Embed Size (px)

Citation preview

179

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

Gadjah Mada International Journal of BusinessMay-August 2005, Vol. 7, No. 2, pp. 179—204

INVESTIGATING THE SIMULTANEITYOF CORPORATE HEDGING AND

DEBT POLICIES:Empirical Evidence from Indonesia*

Iman S. Suriawinata

The primary objective of this paper is to investigate the simulta-neity of corporate hedging and debt policies. Using a pooled sampleof Indonesian non-financial listed firms covering the periods of 1996-2001, the present study finds evidence that corporate hedging and debtpolicies are simultaneously determined. That is, the use of debtsmotivate firms to hedge; but simultaneously, hedging increases debtcapacity and induces firms to borrow more in order to take advantageof the tax benefits arising from additional debt capacity. Anotherimportant finding is that financially distressed firms –as indicated bytheir debt restructuring programs– are less motivated to hedge,because such firms will see that the option values of their equity willincrease as their cash-flow volatilities increase. Therefore, finan-cially distressed firms tend not to hedge; or at least, hedge lessercompared to those of firms that do not experience financial distress.

Keywords: currency derivatives; corporate hedging policy; debt policy

* This paper is a modified version of a part of my doctoral dissertation at the University of Indonesia.I wish to thank my promotors: Prof. Dr. Prijono Tjiptoherijanto and Dr. Ruslan Prijadi for theircontinuous support and valuable assistance, and the chair and members of the examining committee:Prof. Dr. I.G.N. Agung, Dr. T. Sunaryo, and Dr. Indra Widjaja for their useful comments andsuggestions. Nevertheless, I am solely responsible for any remaining errors or omissions.

180

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

Introduction

Anecdotal evidence shows thatmany Indonesian firms use foreign cur-rency debts to finance their operationand investment activities. The interestrate difference between the foreign cur-rency and the Rupiah denominated loansis believed to be a primary reason foremploying foreign currency debts. Nev-ertheless, firms are quite aware thatemploying foreign currency debts toexploit short-term foreign exchangemarket inefficiencies1 will expose themto foreign currency risk which mightthreaten their profitability, or even per-haps their survivability. Therefore, tomitigate the currency risk associatedwith the use of foreign currency de-nominated debts, many Indonesianfirms implement hedging programs withcurrency derivative instruments –suchas currency forwards, futures, swaps,and options.

According to Modigliani-Miller’s(1958, 1963) analysis of capital struc-ture policy, hedging programs do notcreate value for the shareholders be-cause they can omit the firm’s hedgingprogram in their analysis to suit theirindividual risk appetite. If this is so,then why do firms hedge? The answerlies on the fact that the Modigliani-Miller’s (1958, 1963) analysis is basedon the assumptions of perfect capitalmarkets, symmetric information, and

equal access to capital markets. Obvi-ously, all these assumptions are vio-lated in the real world.

Based on capital market imper-fections (e.g. corporate taxes and trans-action costs), financial economists havedeveloped several theories attemptingto explain what motivates firms tohedge. They argue that firms hedge inorder to reduce expected tax liabilitiesand financial distress costs (Smith andStulz 1985), minimize underinvest-ment costs (Froot et al.1993), and alle-viate asset substitution problems aris-ing from agency conflicts betweenshareholders and debt-holders (Culp2001). Therefore, it is claimed that theimplementation of a hedging programby a firm will create value for its share-holders through reductions in tax li-abilities, financial distress costs,underinvestment costs, and agencycosts. Employing a sample of 720 largeUS nonfinancial firms between 1990and 1995, Allayannis and Weston(2001) find a positive relation betweenfirm value –as proxied by Tobin’s Q–and the use of foreign currency deriva-tives. Using data from Indonesian listednon-financial firms between 1996 and2001, Suriawinata (2004) has con-ducted a similar study and has alsofound that corporate hedging programwith currency derivatives enhancesfirm value. However, due to difficul-ties in measuring Tobin’s Q ratios for

1 Using the Indonesian Rupiah/US dollar floating rate data from July 1997 up to July 2002,Suriawinata (2002) has obtained results unsupportive to the UIP (Uncovered Interest-rate Parity)doctrine. Therefore, the results indicate that there are opportunities to exploit interest rate differentialsdue to foreign exchange market inefficiencies – at least in the short term.

181

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

Indonesian firms, Suriawinata (2004)employs the ratio of market-to-bookvalue of equity as a proxy for firmvalue.2

Adding to the literature of corpo-rate hedging theories, Ross (1996) hasproposed an interesting hypothesis re-lating to corporate hedging policy. Heargues that while hedging reduces afirm’s financial distress costs (Smithand Stulz 1985), at the same time hedg-ing also increases the firm’s debt ca-pacity; and therefore, the firm canrealize more tax benefits from the in-creased leverage. Because it is the ex-istence of debts that initially motivatesfirms to hedge, then Ross’s (1996)argument implies a simultaneous rela-

tionship between corporate hedgingand debt policies. Two studies on thedeterminants of hedging policy withinthe context of a simultaneous relation-ship with the debt policy have beenconducted (Geczy et al. 1997; Grahamand Rogers 2002), and the results aremixed. Employing a two-stage Logitregression model, Geczy et al. (1997)do not find a simultaneous relation-ship between hedging decision usingcurrency derivatives and the level ofdebts. On the other hand, employing atwo-stage Tobit regression model,Graham and Rogers (2002) find a posi-tive and significant simultaneous rela-tionship between extent of hedgingusing interest rate and currency de-

2 Varaiya et al. (1987) have shown that Tobin’s Q ratio and the market-to-book value of equity ratioare theoretically equivalent measures of value creation, and their findings confirm that both ratios arealso empirically equivalent measures of value creation.

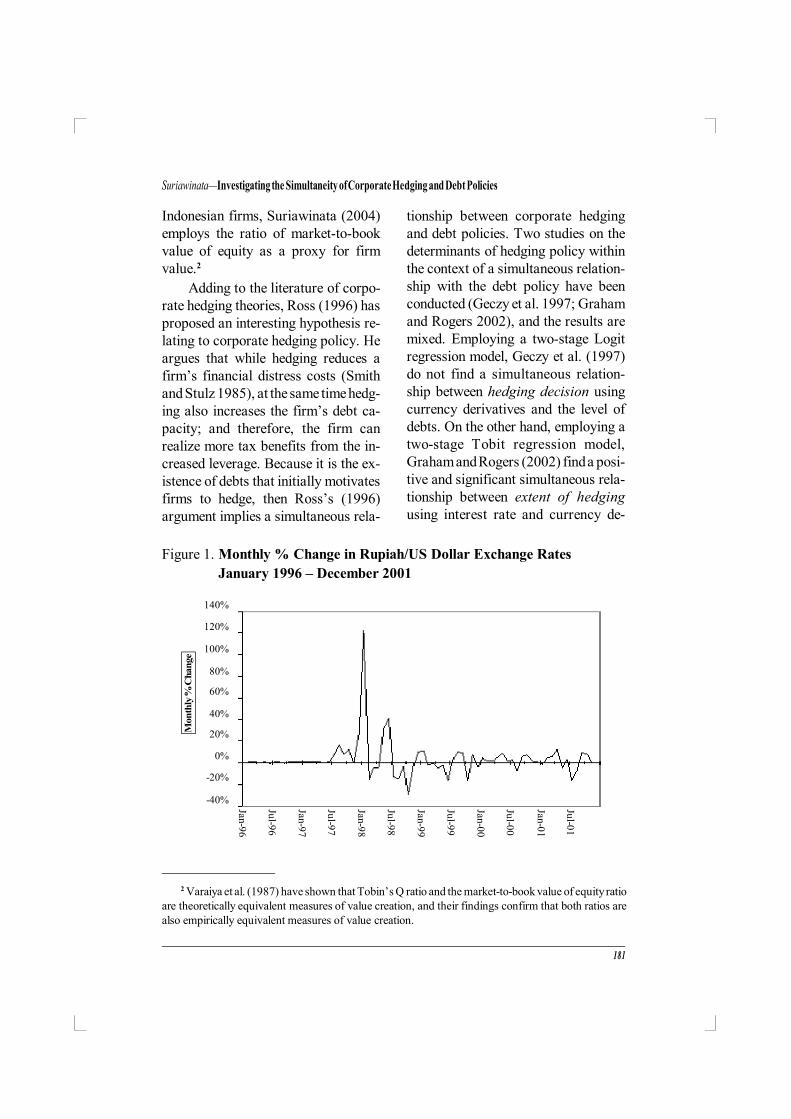

Figure 1. Monthly % Change in Rupiah/US Dollar Exchange Rates

January 1996 – December 2001

140%

120%

100%

80%

60%

40%

20%

0%

-20%

-40%

Mon

thly

% C

han

ge

Jan-98

Jul-9

8

Jan-96

Jul-9

6

Jan-97

Jul-9

7

Jan-99

Jul-9

9

Jan-00

Jul-0

0

Jan-01

Jul-0

1

182

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

rivatives and the level of debts. Hedg-ing decision refers to whether or not afirm hedges its financial exposure,while extent of hedging refers to howmuch notional amount of derivatives afirm holds to hedge.

Using data from Indonesian non-financial listed firms covering the peri-ods of 1996-2001, this paper investi-gates the simultaneity of corporatehedging and debt policies. The presentstudy focuses on the use of foreigncurrency derivatives to hedge againstthe foreign exchange exposure. As canbe seen from Figure 1, the periods ofstudy are mostly dominated by ex-tremely high Rupiah/US Dollar ex-change rate volatilities that have neveroccurred in the history of Indonesianeconomy. Therefore, examining firmshedging policy with currency deriva-tives during the periods of 1996-2001should be interesting.

This study extends previous stud-ies, and employs both Logit and Tobitmodels to investigate the simultaneityof corporate hedging and debt poli-cies. The Logit model is used to exam-ine the relationship between the hedg-ing decision and the debt policy, whilethe Tobit model is used to examine therelationship between the extent of hedg-ing and the debt policy. Since it isobserved that many Indonesian firmsrestructure their debts during the peri-ods of 1996-2001, the present studyalso investigates the effect of debt re-structuring on corporate hedgingpolicy.

Theories of Hedging Motivesand Previous EmpiricalEvidence

The literature on corporate hedg-ing motives can be sub-divided intotwo main streams (Tufano 1996). Thefirst stream focuses on hedging as ameans to maximize shareholder valuethrough reductions in expected tax li-abilities, expected financial distresscosts, underinvestment costs, and as-set substitution costs (e.g. Smith andStulz 1985; Froot et al. 1993; Culp2001). While the second stream fo-cuses on hedging as a means to maxi-mize managerial private utility (e.g.Stulz 1984; Smith and Stulz 1985;DeMarzo and Duffie 1995; Breedenand Viswanathan 1996). However,since the present study investigates thesimultaneity of hedging and debt poli-cies within the context of maximizingshareholder value, the following shalldiscuss only the shareholder valuemaximizing motives of corporate hedg-ing activities.

Shareholder Value MaximizingMotives

Tax Incentive. Smith and Stulz(1985) show that volatility is costlywhen firms have convex effective taxfunctions; and therefore, they arguethat firms hedge in order to reduceexpected future tax liabilities. Con-vexity in corporate income tax arisesfrom: (i) progressivity in income taxrates, (ii) tax preference treatments

183

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

such as tax holiday, and (iii) tax losscarry-forwards. The more convex theeffective tax function of a firm, themore incentive it has to hedge. As anillustration, if a firm has large tax losscarry-forwards and it does not hedge,then continued losses from currencyfluctuations might prevent the firm toutilize the accumulated tax losses tocompensate future income tax liabili-ties.3 Therefore, the tax incentive moti-vation for hedging predicts that hedg-ing is positively related with tax losscarry-forwards.

Empirical evidence regarding taxincentive is unclear. For example,Nance et al. (1993) find moderate evi-dence that hedging firms face moreconvex tax functions. However, Tufano(1996) and Geczy et al. (1997) do notfind supportive evidence that firmshedge in response to tax convexity.Graham and Rogers (2002) even find anegative and significant (at 1%) rela-tionship between corporate hedgingpolicy and tax loss carry-forwards.This later finding contradicts the tax-based motivation for hedging.

Expected Costs of Financial Dis-tress. According to Smith and Stulz(1985), hedging reduces the likelihoodof financial distress or bankruptcy, andtherefore it enhances the value of thefirm. This increase in firm value arisesfrom the reduction in cash flow vola-tility which minimizes the number ofstates that the hedging firm experi-

ences financial difficulty (Nguyen andFaff 2002).

Many studies use debt ratio as anindicator of the likelihood of financialdistress to measure expected distresscosts. Higher debt ratio indicates higherexpected financial distress costs. There-fore, it is predicted that the relationshipbetween debt ratio and corporate hedg-ing policy will be positive.

Previous empirical evidence re-garding financial distress cost hypoth-esis is also mixed. Nance et al. (1993)find a positive but not significant rela-tionship between debt ratio and corpo-rate hedging decision. On the otherhand, Geczy et al. (1997) find a nega-tive but not significant relationship be-tween debt ratio and hedging decision.However, later studies by Graham andRogers (2002) and Nguyen and Faff(2002) find positive and significantrelationships between leverage and cor-porate hedging policy.

Underinvestment Costs. Accord-ing to Froot et al. (1993), costly exter-nal financing is a capital market im-perfection that makes hedging a value-enhancing strategy. Based on peckingorder hypothesis (Myers and Majluf1984) on preference of financingsources, Froot et al. (1993) argue thatunderinvestment costs arise if firmsfind that external financing –either debtor equity– are sufficiently expensivethat firms must reduce their invest-ment spending during times when in-

3 Based on the Indonesian tax laws, a firm can compensate (that is to carry-forward) its current taxlosses against future tax liabilities up until five years.

184

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

ternally generated cash-flows are notsufficient to finance growth opportuni-ties. The underinvestment costs repre-sent the foregone projects’ net presentvalues that would otherwise accrue tothem should the internal funds wereavailable to finance the projects. Withhedging, firms are protected from cash-flow volatilities, and therefore are en-sured that sufficient internally gener-ated cash will be available to takeadvantage of profitable investment op-portunities.

Using different proxies for invest-ment opportunities –e.g. R&D expen-ditures, market-to-book value of eq-uity, and book-to-market value of eq-uity– several studies have empiricallyexamined the underinvestment costhypothesis (Nance et al. 1993; Geczyet al. 1997; Gay and Nam 1998;Haushalter 2000; Graham and Rogers2002; Nguyen and Faff 2002). Most ofthose studies find evidence of a posi-tive and significant relationship be-tween a firm’s hedging activity usingderivatives and its investment opportu-nities.

Asset Substitution Costs. Culp(2001) asserts that asset substitutioncosts arise because of the differentincentives faced by equity and debtholders to take on certain investmentprojects. In the presence of debt fi-

nancing, shareholders are motivatedto select riskier projects than debt-holders are comfortable with.4 How-ever, debt-holders recognize this op-portunistic risk-shifting behavior onthe part of shareholders, and thereforethey impose costly debt covenants formonitoring purposes and they usuallycharge higher lending rates to theprojects. Ostensibly, increased cost ofcapital will reduce the net present valueof the projects. This reduction in theprojects’ NPVs represents the assetsubstitution costs arising from theshareholders’ action of substituting lessrisky projects with those of riskierones. However, asset substitution costscould be substantially reduced for firmsthat hedge their projects’ cash-flows.When cash-flows of debt-fundedprojects are well-hedged, debt-hold-ers would be satisfied with less lend-ing rates compared to those of firmswho do not hedge. With a lower cost ofcapital, the pro-ject’s net present valuewill increase, and so is the sharehold-ers’ wealth.

Lookman (2005) examines therole of hedging in mitigating the assetsubstitution problem arising from theuse of bank debt by oil and gas firms inthe United States. Using a sample ofUS oil and gas producers for the peri-ods of 1999-2000, he finds that firms

4 This follows Jensen and Meckling (1976) who argued that in the presence of debt, shareholdershave a convex claim on a firm’s assets; and therefore, have incentives to increase, rather than decrease,firm risk. In other words, shareholders transfer part of the risk to the debt-holders. That is, if the projectis successful, shareholders will reap most of the benefits; while if it is unsuccessful, debt-holders willbear part of the losses. Additionally, this risk-shifting problem will be more acute in firms with extremely

high leverage.

185

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

with bank debt hedge their exposures tocommodity price risk.

Simultaneity of Corporate Hedg-ing and Debt Policies Stulz (1996),Ross (1996), and Leland (1998) arguethat debt financing motivates firms tohedge, because hedging reduces cash-flow volatility, and therefore decreasesthe probability of bankruptcy and fi-nancial distress. Reductions in the fi-nancial distress costs due to hedgingwill increase the firms’ debt capacity(Ross 1996); and since there are taxbenefits from debt financing, firmswill be induced to borrow more to takeadvantage of the potential additionaltax benefits. However, increased debtwill further increase the likelihood offinancial distress –and thus, firms willhedge more to mitigate the increaseddistress probability. In short, the aboveanalysis suggests that there is a simul-taneous relationship between hedgingand debt policies; that is– hedgingincreases debt capacity, and simulta-neously debt affects hedging policy.

In fact, building on the trade-offtheory of capital structure (Castanias1993), a reduction in the financial dis-tress costs will lead to a greater opti-mal leverage; and hence, more taxbenefits. Ross (1996) has demonstratedthat hedging can result in an enhancedoptimal capital structure, worth an ad-ditional value of approximately 10-15percent for shareholders.

Two studies are known to haveexamined the simultaneous relation-ship between corporate hedging anddebt policies, where both studies adopt

a two-stage estimation technique tocontrol for the simultaneity of the twopolicies. Using a Logit regressionmodel, Geczy et al. (1997) do not findsignificant relationship between thedebt policy and hedging decision.However, by employing a Tobit re-gression model, Graham and Rogers(2002) have found that hedging in-creases debt capacity, and simulta-neously debt also affects hedgingpolicy. Using simultaneous system ofequations, Graham and Rogers (2002)test whether the extent of hedging af-fects the debt ratio, while Geczy et al.(1997) test whether the probability ofhedging affects the debt ratio. Withtheir findings, Graham and Rogers(2002) claim that it is not the yes/nodecision of whether to hedge, but ratherhow much a firm hedges, that affectsthe level of debts.

Methodology

Samples

The initial sample includes all In-donesian non-financial firms listed inthe Jakarta Stock Exchange in any yearwithin the periods of 1996-2001. How-ever, to be included in the final sample,a firm must:

(i) have a complete set of auditedfinancial statements including thenotes to financial statements,

(ii) have a foreign currency exposurearising from imported raw materi-als, export sales, assets or liabili-ties in foreign currencies, or haveforeign subsidiaries,

186

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

(iii) have an adequate disclosure onforeign currency liabilities,

(iv) maintain accounting records inRupiah currency, and

(v) have a positive book value of eq-uity at year end.

Imposing these criteria yields atotal of 1007 firm-year observationsfrom 229 firms.5 Information aboutcorporate hedging with foreign cur-rency derivatives is obtained from notesto financial statements where it is foundthat 245 firm-year observations reportforeign currency derivatives usage -such as currency forwards, futures,swaps, and options. However, only225 firm-year observations report thenotional amount of foreign currencyderivatives held.6 All cross-sectionalunits (N firms) are pooled by year (T

years), and multiple regression analy-ses are then applied to the pooled datato investigate the simultaneity of thecorporate hedging and the capital struc-ture policies. Hence, the present studyemploys a data structure called pooledcross sections over time.7 FollowingWooldridge (2002), this approach as-sumes that every year a new randomsample is taken from the relevant popu-lation.8 However, to control the timeeffects, the present study includes yeardummies in its multiple regression mod-els, where the year 1996 is used as thebasis or benchmark year.9

Hypothesis and Empirical Model

Following Ross (1996), it is hy-pothesized that corporate hedging anddebt policies are simultaneously de-

5 Firms do not have equal number of observations due to new listing, delisting, or failing to meetthe sampling criteria in certain years.

6 Prior to the stipulation of PSAK No. 59 Tahun 1999 which obliges firms to report their derivativesholdings, disclosure of derivatives usage is voluntary. Although many sample firms disclose the notionalamount of their derivatives holdings, yet there are some firms that report the usage of currencyderivatives but not the notional amount. All firms in the sample state that they hold foreign currencyderivatives to hedge against foreign exchange exposure.

7 An alternative approach is to use a panel data set up, where the same sample firms are followedover time, and the data will be structured in blocks of observation, either of T for a given firm i or N fora given year t. However, since firms do not have equal number of observations, then an unbalanced paneldata is obtained. While estimating an unbalanced panel data is possible (Green 2002, 2003), it alsointroduces an attrition bias which is rather complicated to handle (Wooldridge 2002). On the other hand,imposing a balanced panel data would significantly reduce the sample size.

To avoid the loss of many valuable information on firms’ hedging activities, a pooled data approachwith some restrictive assumptions is applied. Therefore, the results of this study should be interpretedby taking into account those restrictive assumptions.

8 If sample firms appear more than one time period, their recurrence are treated as coincidental andignored. In short, if a sample firm does appear in each and every year during the periods of 1996-2001,then the observations will be regarded as 6 different and independent firms. Wooldridge (2002) providesgood discussion that contrasts the pooling of cross section over time approach with that of the panel data.

9 The use of year dummies is basically similar to conducting the Chow test on the pooled data (seeGujarati 2003: 306-310).

187

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

termined. To examine the simultaneityof corporate hedging and debt policies,the present study constructs a systemof structural equations consisting ofhedging policy equation and debt policyequation. The present study followsboth Geczy et al. (1997) and Grahamand Rogers (2002) methodologies ininvestigating the simultaneity of cor-porate hedging and debt policies, andtherefore uses both Logit and Tobitregression models to examine corpo-rate hedging policy. The Logit regres-sion is used to examine the hedgingdecision (yes/no decision), while theTobit regression is used to examine theextent of hedging.10

The debt specification used by thepresent study adopts explanatory vari-ables suggested by Titman and Wessels(1988), Geczy et al. (1997), andHovakimian et al. (2001). FollowingGeczy et al. (1997) and Graham andRogers (2002), the debt equation isestimated by using the OLS method.

Corporate Hedging Policy

The present study develops twohedging policy multiple regressions:the Logit regression to estimate thehedging decision equation, and the Tobitregression to estimate the extent ofhedging equation. As the dependentvariables, the study employs two mea-sures of corporate hedging policy(HEDGING) variables, i.e.: (i) dummyhedging (D_HEDGE) to represent thedecision to hedge in the Logit regres-

sion, and (ii) the total notional amountof foreign currency derivatives con-tract divided by total assets(TOT_HEDGE) to represent the ex-tent of hedging in the Tobit regression.

The followings list the various in-dependent variables used in the Logitand Tobit regressions and describe theirhypothesized relationships with thedependent variables (D_HEDGE andTOT_HEDGE) of each regression.Leverage (DEBT_MVE) is the inde-pendent variable of interest, while otherindependent variables act as controlvariables.

(a) Tax-Loss Carry Forward(TAXLOSS): Firms hedge in orderto reduce expected tax liabilities,and the more convex the tax sched-ule is, the larger the incentive forfirms to hedge. The present studyuses tax-loss carry forwards di-vided by market value of equity toproxy tax incentive, and predicts apositive relationship between tax-loss carry forwards and corporatehedging policy.

(b) Leverage (DEBT_MVE): Firmshedge in order to reduce expectedcosts of financial distress and bank-ruptcy. Higher leverage indicateshigher expected costs of distress,and therefore it is predicted thathigher leverage will lead to moreincentive to hedge. Leverage isproxied by total interest-bearingdebt divided by the market value ofequity.

10 The Tobit model is used because the extent of hedging (represented by the notional amount ofcurrency derivatives holding divided by total assets) is censored at zero.

188

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

(c) Investment Opportunities (BME):Froot et al. (1993) argue that firmsthat have potential investment op-portunities will be motivated tohedge to ensure the availability ofinternal cash-flows to fund futureinvestments. On the other hand,firms with no growth opportunitieswill be less motivated to hedge.Similar to Nance et al. (1993),Geczy et al. (1997) and Grahamand Rogers (2002), this study usesbook-to-market value of equity ra-tio as a proxy for growth opportu-nities. Larger book-to-market valueof equity ratio means lesser growthopportunities. Therefore, this studypredicts a negative relationshipbetween the book-to-market valueof equity ratio with corporate hedg-ing policy.

(d) Business Risk (V_ROA): Thisstudy employs volatility of returnon assets –defined as the volatilityof EBIT to total assets– as a mea-sure of business risk. Higher busi-ness risk implies higher asset sub-stitution costs, and it is predictedthat volatility of return on assets ispositively related with corporatehedging policy.

(e) Liquidity (LIQUID_TL): Firmsmay use substitutes for hedging tomanage risk. For example, firmswith more liquid assets will be lesslikely to face financial distress(Geczy et al. 1997). Therefore, it is

predicted that liquid assets are nega-tively related with corporate hedg-ing policy. The present study usesthe ratio of liquid assets11 to totalliabilities as a proxy for hedgingsubstitute.

(f) Foreign Exchange Exposure(FCL_TA): Obviously, firms holdcurrency derivatives to hedgeagainst foreign exchange exposure.This study uses the ratio of foreigncurrency denominated liabilitiesdivided by total assets to proxyforeign exchange exposure, andpredicts a positive relationship be-tween foreign exchange exposurewith corporate hedging policy.

(g) Firm Size (SIZE_TA): Previousempirical studies provide evidencethat firm size is positively relatedwith corporate hedging policy, in-dicating the existence of economiesof scale in hedging costs (Nance etal. 1993; Mian 1996; Geczy et al.1997; Graham and Rogers 2002).Similar to past research, this studyuses natural logarithm of total as-sets as a proxy of firm size, andpredicts a positive relationship be-tween firm size and corporate hedg-ing policy.

(h) Debt Restructuring (D_RESTRU): The existence of debt re-structuring indicates severe finan-cial distress. It is well known thatthe option value of equity increasesas the probability of financial dis-

11 In this study, liquid assets consisted of: cash and cash equivalents, trade receivables, and notereceivables.

189

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

tress increases. Because the optionvalue of equity of distressed firmswill increase as cash-flows volatil-ity increases, then it would be forthe best interest of such firms ifthey do not hedge.12 The presentstudy uses a dummy variable fordebt restructuring; that is a firmwill be assigned a value of 1 if it isrestructuring its debt, and 0 other-wise. It is predicted that debt re-structuring is negatively relatedwith corporate hedging policy.

(i) Interaction Variables: To accountfor any interaction effects, thepresent study includes two interac-tion variables, i.e. D_RESTRU*DEBT_MVE and D_RESTRU*SIZE_TA in the corporate hedgingpolicy equations. However, thepresent study does not provide anyprediction on the directions of therelationships between the interac-tion variables and corporate hedg-ing policy.

Debt Policy Equation

The dependent variable of the debtpolicy equation is the total interest-bearing debt divided by the marketvalue of equity. The two measures ofcorporate hedging policy (i.e.D_HEDGE and TOT_HEDGE) are

the independent variables of interest,while other independent variables actas control variables. The list of allindependent variables and their hypoth-esized relationships with the dependentvariable are as follows:

(a) Hedging (D_HEDGE orTOT_HEDGE): Ross (1996) as-serts that hedging increases debtcapacity. Therefore, it is predictedthat hedging using foreign currencyderivatives is positively related withdebt.

(b) Selling and General Administra-tion Expenses (SGA): AdoptingTitman and Wessels (1988), SGArepresents firm uniqueness. Sinceuniqueness is negatively relatedwith leverage, the present studypredicts a negative relationshipbetween SGA and debt.

(c) Growth opportunities (BME):According to Titman and Wessels(1988), growth opportunities arecapital assets that add value to afirm but cannot be collateralized.Firms with high growth opportuni-ties are expected to have less debt,and vice versa. Higher book-to-market value of equity (BME)means lower growth opportunities;therefore, the present study pre-dicts a positive relationship be-

12 Hedging reduces volatility, and based on Black and Scholes (1973) option pricing formula, areduction in the volatility of the value of underlying asset decreases the option value. Total asset is theunderlying asset, while debt is the exercise price. Debt restructuring implies that total asset is potentiallyinsufficient to pay debt, therefore it would be better for shareholders of a distressed firm to expose theirfirm’s assets to currency fluctuations to increase the probability that total assets will exceed debt atmaturity. If this is the case, then shareholders would keep the firm; otherwise, shareholders would losenothing as their firm is already at the mercy of debt-holders.

190

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

tween the book-to-market value ofequity and debt.

(d) Profitability (ROA): FollowingMyers and Majluf (1984), firmswith higher profitability will berelying less on debt to finance theirinvestment activities. Therefore, itis predicted that profitability isnegatively related with leverage.The present study uses return onassets –measured by EBIT dividedby total assets– as a proxy forprofitability.

(e) Firm Size (SIZE_TA): Titman andWessel (1988) state that large firmstend to be more diversified and lessprone to bankruptcy. Therefore,larger firms are predicted to behighly leveraged. In this study, firmsize is proxied by natural loga-rithm of total assets.

(f) Asset Tangibility (TANG): Assettangibility affects the amount ofdebt that could be obtained by afirm because creditors generallyrely on tangible assets as debtcollaterals. The present study usesthe ratio of net fixed asset-to-mar-ket value of equity as a proxy forasset tangibility, and predicts apositive relationship between assettangibility and debt levels.

(g) Debt Restructuring (D_RESTRU): The present study arguesthat firms that restructure theirdebts must already have relativelymuch higher debt ratios, otherwisesuch firms would not embark debtrestructuring programs. Therefore,

the present study predicts a posi-tive relationship between the oc-currence of debt restructuring(dummy debt restructuring) anddebt levels.

Previous discussions suggest thathedging can increase debt capacity,and simultaneously debt can affecthedging policy. Therefore, followingGeczy, Minton, and Schrand (1997)and Graham and Rogers (2002), toinvestigate the simultaneity of the hedg-ing decision and the debt policy, thisstudy employs a two-stage estimationtechnique on the structural equationswhich consisted of: corporate hedgingpolicy equation (Logit and Tobit Re-gressions):

HEDGINGit=

1 +

jD_YR

j +

1TAXLOSS

it +

2DEBT_MVF

it +

3BME

it +

4V_ROA

it +

5LIQUID_TL

it +

6FCL_TA

it +

7SIZE_TA

it +

8D_RESTRU

it +

9D_RESTRU

it *

DEBT_MVFit +

10

D_RESTRUit *

SIZE_TAit +

it .........(1)

Debt policy equation (OLS Re-gression):

2001

j=1997

191

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

Table 1. The Hypothesized Relationships between the Dependent Variablesand the Independent Variables of the Corporate Hedging and theDebt Policies

Hedging Debt

Policy Policy

Independent Variables Dependent Variables

D_HEDGE {1,0}

and DEBT_MVE

TOT_HEDGE

Tax Loss Carry-Forwards (TAXLOSS) +

Predicted Value of Debt Ratio (DEBT_MVF) +

Book-to-Market Value of Equity (BME) - +

Volatility of Return on Assets (V_ROA) +

Hedging Substitute (LIQUID_TL) -

Debt Restructurization (D_RESTRU) {1,0} - +

Foreign Currency Liabilities-to-Total Assets (FCL_TA) +

DEBT_MVEit=

1 +

jD_YR

j +

1HEDGINGF

it +

2SGA

it +

3BME

it +

4ROA

it +

5SIZE_TA

it +

7TANG

it +

8D_RESTRU

it +

it ...(2)

The multiple regression in Equa-tion (1) are estimated using two meth-ods, i.e. (i) the Logit method to exam-ine the hedging decision, and (ii) theTobit method to examine the extent ofhedging. For the Logit regression,HEDGING is a binary variable, whereit will be assigned a value of 1 (D_

2001

j=1997

HEDGE= 1) if an examination on thenotes to financial statements revealsthat the firm uses any currency deriva-tives such as forwards, futures, swapsor options for hedging purposes; andwill be assigned a value of 0 (D_HEDGE=0) otherwise. In the Tobitregression, HEDGING is the extent ofhedging (represented by TOT_HEDGE–defined as the notional amount offoreign currency derivatives holdingdivided by total assets) and is censoredat zero.

It must be noted that the aboveequations are the second-stage equa-tions; where DEBT_MVF is the pre-dicted value of the debt ratio obtainedfrom the first-stage estimation of thedebt policy equation, and HEDGINGF

192

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

is the predicted value of D_HEDGEand TOT_HEDGE from the first-stageestimation of the hedging decision equa-tion (Logit regression) and the extent ofhedging equation (Tobit regression)respectively. The present study assumesconstant coefficients over time, but dif-ferent intercept for each year.13 Toaccount for year effects, dummy years(D_YR97 up to D_YR01) are includedin both corporate hedging and debtequations, where the year 1996 is usedas a basis or benchmark year.14 Table 1summarizes the hypothesized relation-ships between the dependent variablesand the independent variables for bothhedging and debt equations.

Results

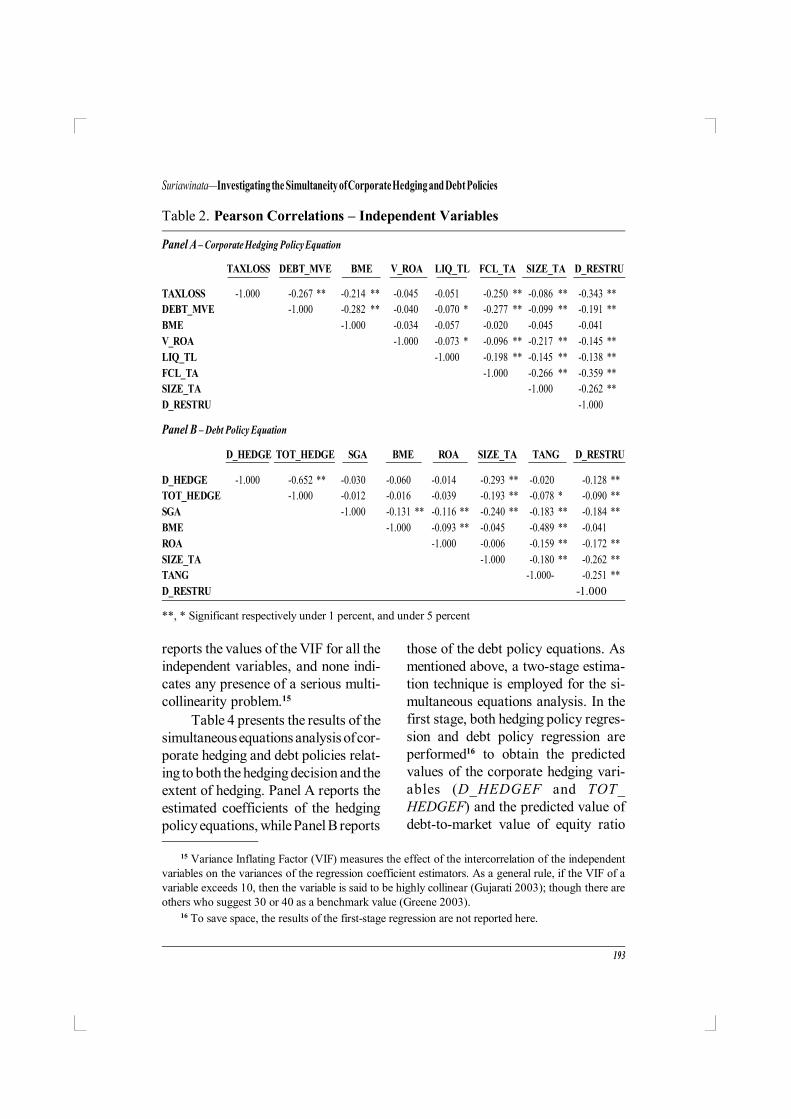

Table 2 reports correlations amongthe independent variables of both hedg-ing and debt equations. Of particularinterest is the positive and significantcorrelation between corporate hedg-ing policy (D_HEDGE and TOT_HEDGE) and firm size (SIZE_TA),indicating the importance of firm sizein corporate hedging policy. Also, it

can be seen that corporate hedgingpolicy is negatively correlated withdebt restructuring (D_RESTRU),which implies that distressed firms areless motivated to hedge because theoption values of their equity will in-crease as volatility increases. There-fore, such firms will be better-off with-out hedging. Another interesting ob-servation is the negative correlationbetween profitability (ROA) and debtrestructuring (D_RESTRU). Thismeans that profitable firms are lesslikely to restructure their debts.

From Table 2, it can also be ob-served that there is no correlation coef-ficient that exceeds 0.8. As a rule ofthumb, for a model involving only twoindependent variables, a correlationcoefficient in excess of 0.8 may sug-gest a serious collinearity problem(Judge et al. 1988; Gujarati 2003).However, the rule will not provide areliable guide if the model involvesmore than two independent variables,as in the case with the present study.Therefore, a more reliable diagnostictool called Variance Inflating Factor(VIF) should be consulted. Table 3

13 Since it has been assumed that each observation represents a different and independent unit (seeNote 8), no additional assumptions are needed about the intercept and coefficient of each cross sectionalunit.

14 To avoid the dummy variable trap, a dummy is assigned only for each year covering 1997 to 2001,whereas the year 1996 is used as the base or benchmark year. Therefore, the intercept a

1 and j

1 represents

the mean value of the benchmark category –that is the year 1996– for equations (1) and (2) respectively.The coefficients (d

j and l

j) associated with each D_YR

j are the differential intercept coefficients, and

they show by how much the value of the intercept for each year j (year 1997 up to 2001) differs fromthe intercept coefficient of the benchmark year (i.e. year 1996).

193

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

reports the values of the VIF for all theindependent variables, and none indi-cates any presence of a serious multi-collinearity problem.15

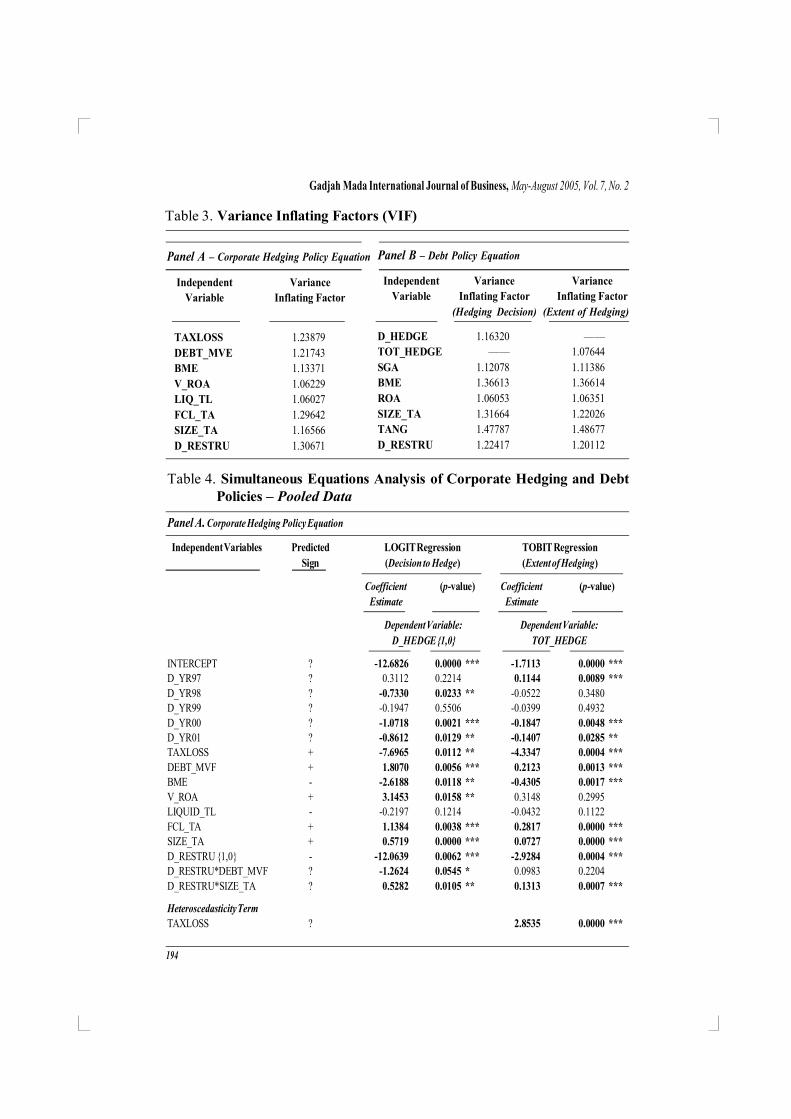

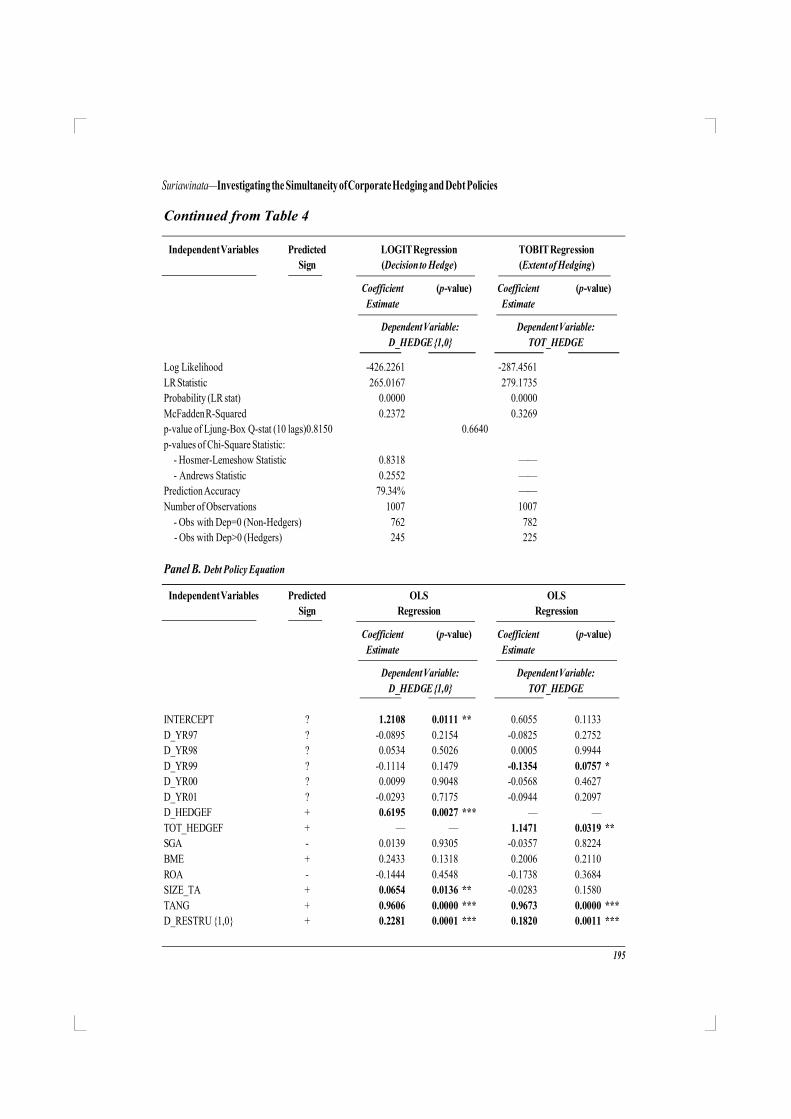

Table 4 presents the results of thesimultaneous equations analysis of cor-porate hedging and debt policies relat-ing to both the hedging decision and theextent of hedging. Panel A reports theestimated coefficients of the hedgingpolicy equations, while Panel B reports

those of the debt policy equations. Asmentioned above, a two-stage estima-tion technique is employed for the si-multaneous equations analysis. In thefirst stage, both hedging policy regres-sion and debt policy regression areperformed16 to obtain the predictedvalues of the corporate hedging vari-ables (D_HEDGEF and TOT_HEDGEF) and the predicted value ofdebt-to-market value of equity ratio

Table 2. Pearson Correlations – Independent Variables

Panel A – Corporate Hedging Policy Equation

TAXLOSS DEBT_MVE BME V_ROA LIQ_TL FCL_TA SIZE_TA D_RESTRU

TAXLOSS -1.000 -0.267 ** -0.214 ** -0.045 -0.051 -0.250 ** -0.086 ** -0.343 **

DEBT_MVE -1.000 -0.282 ** -0.040 -0.070 * -0.277 ** -0.099 ** -0.191 **

BME -1.000 -0.034 -0.057 -0.020 -0.045 -0.041

V_ROA -1.000 -0.073 * -0.096 ** -0.217 ** -0.145 **

LIQ_TL -1.000 -0.198 ** -0.145 ** -0.138 **

FCL_TA -1.000 -0.266 ** -0.359 **

SIZE_TA -1.000 -0.262 **

D_RESTRU -1.000

Panel B – Debt Policy Equation

D_HEDGE TOT_HEDGE SGA BME ROA SIZE_TA TANG D_RESTRU

D_HEDGE -1.000 -0.652 ** -0.030 -0.060 -0.014 -0.293 ** -0.020 -0.128 **

TOT_HEDGE -1.000 -0.012 -0.016 -0.039 -0.193 ** -0.078 * -0.090 **

SGA -1.000 -0.131 ** -0.116 ** -0.240 ** -0.183 ** -0.184 **

BME -1.000 -0.093 ** -0.045 -0.489 ** -0.041

ROA -1.000 -0.006 -0.159 ** -0.172 **

SIZE_TA -1.000 -0.180 ** -0.262 **

TANG -1.000- -0.251 **

D_RESTRU -1.000

**, * Significant respectively under 1 percent, and under 5 percent

15 Variance Inflating Factor (VIF) measures the effect of the intercorrelation of the independentvariables on the variances of the regression coefficient estimators. As a general rule, if the VIF of avariable exceeds 10, then the variable is said to be highly collinear (Gujarati 2003); though there areothers who suggest 30 or 40 as a benchmark value (Greene 2003).

16 To save space, the results of the first-stage regression are not reported here.

194

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

Panel B – Debt Policy Equation

Independent Variance Variance

Variable Inflating Factor Inflating Factor

(Hedging Decision) (Extent of Hedging)

D_HEDGE 1.16320 ——

TOT_HEDGE —— 1.07644

SGA 1.12078 1.11386

BME 1.36613 1.36614

ROA 1.06053 1.06351

SIZE_TA 1.31664 1.22026

TANG 1.47787 1.48677

D_RESTRU 1.22417 1.20112

Table 3. Variance Inflating Factors (VIF)

Panel A – Corporate Hedging Policy Equation

Independent Variance

Variable Inflating Factor

TAXLOSS 1.23879

DEBT_MVE 1.21743

BME 1.13371

V_ROA 1.06229

LIQ_TL 1.06027

FCL_TA 1.29642

SIZE_TA 1.16566

D_RESTRU 1.30671

Table 4. Simultaneous Equations Analysis of Corporate Hedging and DebtPolicies – Pooled Data

Panel A. Corporate Hedging Policy Equation

Independent Variables Predicted LOGIT Regression TOBIT Regression

Sign (Decision to Hedge) (Extent of Hedging)

Coefficient (p-value) Coefficient (p-value)

Estimate Estimate

Dependent Variable: Dependent Variable:

D_HEDGE {1,0} TOT_HEDGE

INTERCEPT ? -12.6826 0.0000 *** -1.7113 0.0000 ***D_YR97 ? 0.3112 0.2214 0.1144 0.0089 ***

D_YR98 ? -0.7330 0.0233 ** -0.0522 0.3480D_YR99 ? -0.1947 0.5506 -0.0399 0.4932

D_YR00 ? -1.0718 0.0021 *** -0.1847 0.0048 ***D_YR01 ? -0.8612 0.0129 ** -0.1407 0.0285 **TAXLOSS + -7.6965 0.0112 ** -4.3347 0.0004 ***

DEBT_MVF + 1.8070 0.0056 *** 0.2123 0.0013 ***BME - -2.6188 0.0118 ** -0.4305 0.0017 ***

V_ROA + 3.1453 0.0158 ** 0.3148 0.2995LIQUID_TL - -0.2197 0.1214 -0.0432 0.1122

FCL_TA + 1.1384 0.0038 *** 0.2817 0.0000 ***SIZE_TA + 0.5719 0.0000 *** 0.0727 0.0000 ***

D_RESTRU {1,0} - -12.0639 0.0062 *** -2.9284 0.0004 ***D_RESTRU*DEBT_MVF ? -1.2624 0.0545 * 0.0983 0.2204

D_RESTRU*SIZE_TA ? 0.5282 0.0105 ** 0.1313 0.0007 ***

Heteroscedasticity Term

TAXLOSS ? 2.8535 0.0000 ***

195

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

Continued from Table 4

Independent Variables Predicted LOGIT Regression TOBIT Regression

Sign (Decision to Hedge) (Extent of Hedging)

Coefficient (p-value) Coefficient (p-value)

Estimate Estimate

Dependent Variable: Dependent Variable:

D_HEDGE {1,0} TOT_HEDGE

Log Likelihood -426.2261 -287.4561

LR Statistic 265.0167 279.1735

Probability (LR stat) 0.0000 0.0000

McFadden R-Squared 0.2372 0.3269

p-value of Ljung-Box Q-stat (10 lags)0.8150 0.6640

p-values of Chi-Square Statistic:

- Hosmer-Lemeshow Statistic 0.8318 ——

- Andrews Statistic 0.2552 ——

Prediction Accuracy 79.34% ——

Number of Observations 1007 1007

- Obs with Dep=0 (Non-Hedgers) 762 782

- Obs with Dep>0 (Hedgers) 245 225

Panel B. Debt Policy Equation

Independent Variables Predicted OLS OLS

Sign Regression Regression

Coefficient (p-value) Coefficient (p-value)

Estimate Estimate

Dependent Variable: Dependent Variable:

D_HEDGE {1,0} TOT_HEDGE

INTERCEPT ? 1.2108 0.0111 ** 0.6055 0.1133

D_YR97 ? -0.0895 0.2154 -0.0825 0.2752

D_YR98 ? 0.0534 0.5026 0.0005 0.9944

D_YR99 ? -0.1114 0.1479 -0.1354 0.0757 *

D_YR00 ? 0.0099 0.9048 -0.0568 0.4627

D_YR01 ? -0.0293 0.7175 -0.0944 0.2097

D_HEDGEF + 0.6195 0.0027 *** — —

TOT_HEDGEF + — — 1.1471 0.0319 **

SGA - 0.0139 0.9305 -0.0357 0.8224

BME + 0.2433 0.1318 0.2006 0.2110

ROA - -0.1444 0.4548 -0.1738 0.3684

SIZE_TA + 0.0654 0.0136 ** -0.0283 0.1580

TANG + 0.9606 0.0000 *** 0.9673 0.0000 ***

D_RESTRU {1,0} + 0.2281 0.0001 *** 0.1820 0.0011 ***

196

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

(DEBT_MVF) respectively. In the sec-ond stage, D_HEDGEF, TOT_HEDGEF, and DEBT_MVF are thenused (instead of their original values)as independent variables in the debtpolicy regression and the hedging policyregression.

The results of the second stageregressions are presented in Table 4.However, before discussing them, itwould be useful to investigate whetherthere are potential econometric prob-lems that may weaken the results. Thepresent study focuses on the potentialproblems of autocorrelation, hetero-scedasticity, and model specificationerrors.

Based on Ljung-Box Q-stats (us-ing 10 lags), no autocorrelation prob-lems are detected for both hedging (Logitand Tobit) and debt (OLS) regression

models. Panel B of Table 4 also reportsthat the Durbin-Watson stats for bothdebt (OLS) equations involving hedg-ing decision and extent of hedging arein the neighborhood of 2, which valueindicates that there is no first-orderautocorrelation in the error terms, ei-ther positive or negative (Gujarati2003).

Even though OLS estimates arestill consistent in the presence ofheteroscedasticity, the conventionalcomputed standard errors are no longervalid, which will cause conclusionsfrom conventionally employed t and Ftests to be misleading. White Hetero-scedasticity Test is a test of the nullhypothesis of no heteroscedasticityagainst heteroscedasticity of some un-known general form. Panel B of Table4 reports high probability values of

Continued from Table 4

Panel B. Debt Policy Equation (Continued)

Independent Variables Predicted OLS OLS

Sign Regression Regression

Coefficient (p-value) Coefficient (p-value)

Estimate Estimate

Dependent Variable: Dependent Variable:

D_HEDGE {1,0} TOT_HEDGE

R-squared 0.3009 0.2978

Adjusted R-squared 0.2924 0.2893

p-value of Ljung-Box Q-stat (10 lags)0.9910 0.9960

Durbin-Watson stat 2.0271 2.0234

Regression F-statistic 35.6504 35.1300

p-value of F-statistic 0.0000 0.0000

p-value of Ramsey RESET F-stat 0.2336 0.1437

p-value of White Het F-stat 0.8352 0.8132

***, **, * Significant for respectively under 1 percent, under 5 percent and under 10%

197

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

White’s F-tests, which mean that thenull hypothesis of no heteroscedasticitycannot be rejected. Therefore, both debtspecifications are homoscedastic.

Employing a Lagrange multipliertest, a multiplicative heteroscedasticity(Greene 2002) caused by TAXLOSSis found in the Tobit regression model.Therefore, the Tobit (extent of hedg-ing) equation is estimated by correctingfor the heteroscedasticity. However,by employing a similar procedure, thepresent study does not find anyheteroscedasticity problem in the Logit(hedging decision) equation.

With regard to model specifica-tion errors, the Logit results indicate nospecification errors as shown by rela-tively high probability values ofHosmer-Lemeshow and Andrews teststatistics. For the Tobit model, the pa-rameter estimates will be inconsistentin the presence heteroscedasticity andnon-normal errors (Greene 2003, Long1997). The problem of hetero-scedasticity has been corrected and dis-cussed in the previous paragraph, butresearch is still ongoing in handling theproblem of non-normal errors (Greene2002).17

17 One solution is to use an alternative error distribution (Greene 2002). Employing an alternativeerror distribution, i.e. extreme value, the author finds that the results are more or less similar with theresults that assume normal errors. However, the results are not reported here.

Figure 2. Testing the Stability of the Coefficients of Debt Policy Equation

40

30

20

10

0

-10

-20

-30

-40

850 875 900 925 950 975 1000

CUSUM ------- 5% Signicicance

198

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

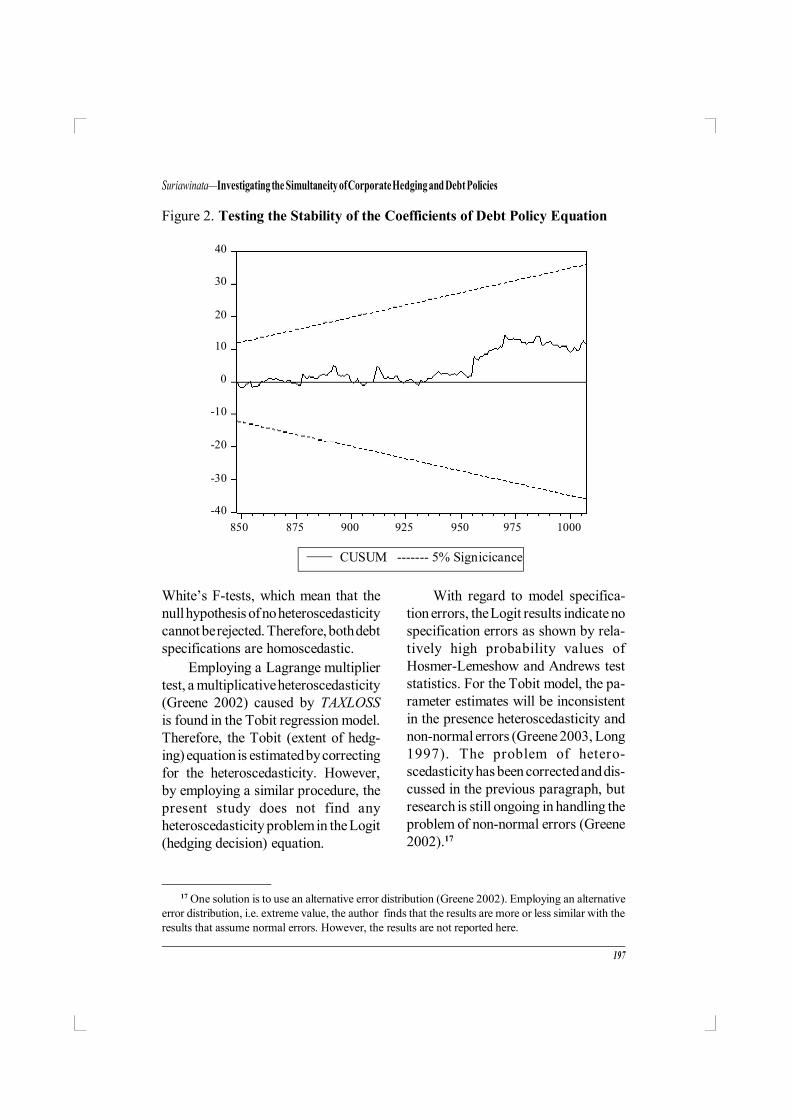

Panel B of Table 4 reports that theprobability values of the Ramsey’sRESET F tests for both OLS regres-sions are above the significance levelof 5 percent, and therefore the resultsindicate that both debt equations arenot mis-specified. Additionally, to testthe stability of the debt policy equa-tion, a CUSUM test is conducted. Ascan be seen from Figure 2, the nullhypothesis of coefficient stability can-not be rejected. Since the results of allthe above diagnostic tests are more orless satisfactory, the followings willthen discuss the results of the esti-mated hedging and debt policies equa-tions.

By examining the sign (whetherpositive or negative) and the statistical

significance of the estimated coeffi-cients of the Logit regression, it can besaid that generally the results supportthe view that firms hedge in order toenhance or increase shareholder value.To be more specific, it can be con-cluded that firms hedge in order toreduce financial distress costs(DEBT_MVF), minimize underinvest-ment costs (BME), and alleviate assetsubstitution problems (V_ROA). How-ever, the results do not provide supportfor the tax incentive (TAXLOSS) hy-pothesis. Graham and Rogers (2002)argue that a significant large amount ofaccumulated tax losses –as in the caseof many Indonesian firms during thecrisis periods– represents financial dis-tress rather than future potential tax

Figure 3. The Effect of Debt Restructuring on the Estimated Probability ofHedging in Relation to the Predicted Debt Ratio

1.0

0.8

0.6

0.4

0.2

0.0

0.0 0.4 0.8 1.2 1.6 2.0 2.4 2.8 3.2

Predicted Debt-to-Market Value of Equity Ratio

Est

imat

ed P

roba

bili

ty o

f H

edg

ing

Without Debt Restructuring

With Debt Restructuring

199

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

saving. Therefore, this later findingactually supports the view that dis-tressed firms are less motivated to hedge.

The results of the Logit regression

also show that corporate hedging deci-sion is: (i) positively related with firm

size (SIZE_TA), (ii) negatively relatedwith liquid assets (LIQUID_TL) -

though not statistically significant, (iii)positively related with foreign ex-

change exposure (FCL_TA), and (iv)negatively related with debt restruc-

turing (D_RESTRU). The estimatedcoefficients of the two interaction

variables (D_RESTRU*DEBT_MVFand D_RESTRU*SIZE_TA) reveal

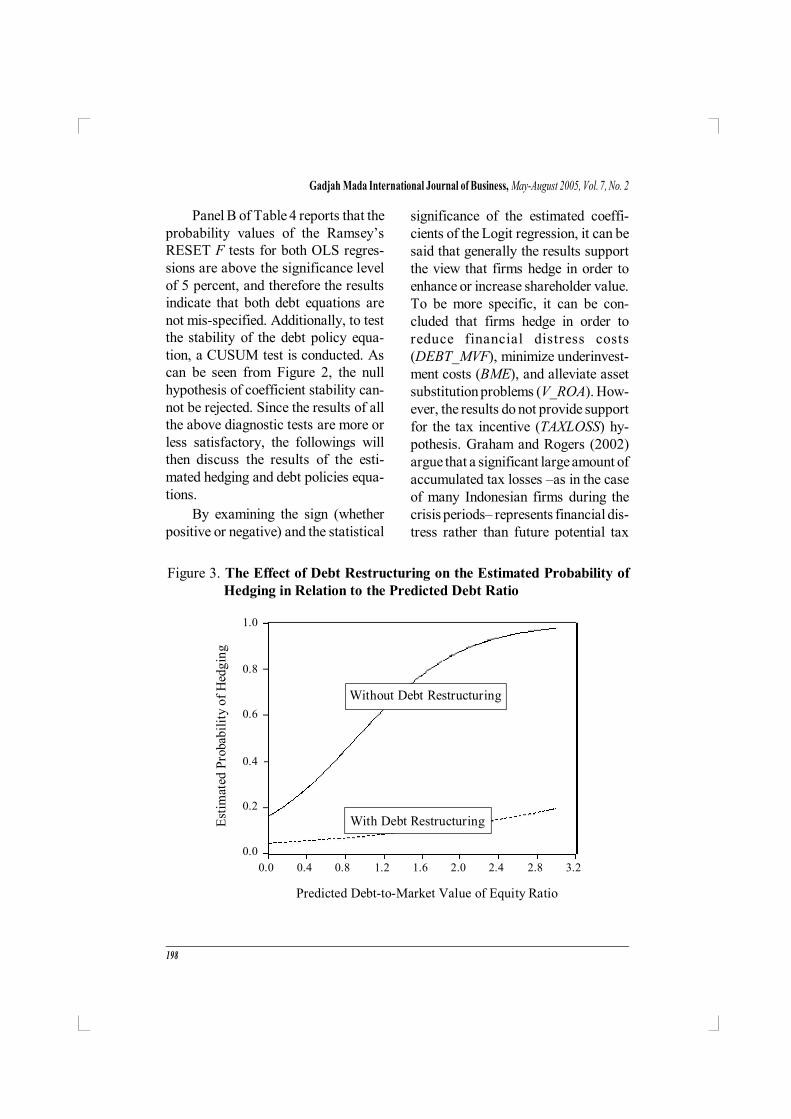

that firms which debts are being re-structured tend not to hedge, but large

firms which debts are being restruc-tured tend to hedge. Figure 3 shows the

relationship between the probability ofcorporate hedging using foreign cur-

rency derivatives with the predictedvalue of debt ratio –with and without

debt restructuring.18

Panel A of Table 4 also reports theresults of the Tobit regression that hasbeen corrected for heteroscedasticitycaused by the ratio of tax-loss carryforwards-to-market value of equity(TAXLOSS). By comparing the re-sults of both Logit and Tobit regres-sions, with the exceptions of two inde-pendent variables (V_ROA andD_RESTRU*DEBT_MVF), it can be

said that generally the independentvariables have similar impacts on thecorporate hedging decision as well ason the extent of hedging. From theLogit and Tobit results, it can be seenthat the volatility of earnings (V_ROA)determines firms’ decision to hedge,but does not determine the notionalamount of foreign currency deriva-tives held by firms for hedging pur-poses. Also, while the interaction vari-able D_RESTRU*DEBT_MVF signi-ficantly and negatively affects firms’decision to hedge, the same variablehas a positive but not significant effecton the extent of corporate hedgingusing foreign currency derivatives.

Panel B of Table 4 reports theresults of OLS regression for the debtpolicy equation. It is interesting tonote that the independent variablesfound to have significant effects on thecorporate debt policy are limited onlyto: (i) corporate hedging policy(D_HEDGEF and TOT_HEDGEF),(ii) firm size (SIZE_TA),19 (iii) assettangibility (TANG), and (iv) debt re-structuring (D_RESTRU). As pre-dicted, debt levels are positively re-lated with asset tangibility. The resultsalso confirm that firms which debts arebeing restructured tend to have higherdebt levels. However, the present find-ing that firm size is negatively relatedwith leverage is in contradiction withprevious findings (e.g. Hovakimian et

18 Using mean values for other independent variables.19 However, firm size (SIZE_TA) is not statistically significant in the debt policy equation relating

to the extent of hedging.

200

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

al. 2001). One plausible explanation isthat during the periods of study –cover-ing the periods of economic crisis– allfirms tend to reduce their debt levels toavoid detrimental effects of rising in-terest rates. However, due to their abil-ity to raise necessary funds to repaydebt, it is argued that only larger firmsthat are capable of successfully reduc-ing their debt levels. Therefore, thepresent study finds that larger firmstend to have lower leverage.

Of significant interest is that theresults of the debt policy equation showthat both the hedging decision(D_HEDGEF) and the extent of hedg-ing using foreign currency derivatives(TOT_HEDGEF) are important fac-tors in the determination of corporatedebt level (significant at 1% and 5%respectively). And since Panel A ofTable 4 has already shown that thepredicted debt level (DEBT_MVF) af-fects both corporate hedging decisionand extent of hedging (significant at1% for both Logit and Tobit regres-sions), the results of the present studyhave provided empirical evidence onthe simultaneity of corporate hedgingand debt policies. In the present study -unlike those of previous results (i.e.Geczy et al. 1997; Graham and Rogers2002), the evidence of simultaneity withthe debt policy is found for both thehedging decision and the extent of hedg-ing.

Summary and Conclusion

It is believed that many Indone-sian firms employ foreign currency

debts in order to exploit interest ratedifferentials arising from the short-term foreign exchange market ineffi-ciencies. However, realizing that suchfunding strategy would expose firmsto foreign exchange rates volatility,many Indonesian firms mitigate theexposure by using foreign currencyderivative instruments, such as cur-rency forwards, futures, swaps, andoptions. The primary focus of thepresent study is to investigate the si-multaneity of corporate hedging anddebt policies. It is argued that firmshedge in order to reduce the probabil-ity of financial distress arising fromdebts; however, reduced probabilityof financial distress will increase firms’debt capacity and will induce them toincrease their debt levels to take ad-vantage of the tax benefits of debts.Therefore, a simultaneous relationshipbetween corporate hedging and debtpolicies is hypothesized.

Using a pooled sample of Indone-sian non-financial listed firms coveringthe periods of 1996-2001, the presentstudy finds evidence that corporatehedging and debt policies are simulta-neously determined. That is, the pres-ence of debts motivates firms to hedge;but hedging also increases firms’ debtcapacity. There are also other impor-tant findings. The results of the presentstudy show that Indonesian firms hedgein order to enhance shareholder valuethrough reductions in financial distressand underinvest-ment costs, and alle-viation of asset substitution problems.The positive relationship between firmsize and corporate hedging activities

201

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

found in this study means that –com-pared to those of smaller ones– largerfirms are more likely to hedge. Whilethis finding might support the conten-tion of the existence of economies ofscale in hedging costs (Nance et al.1993; Mian 1996; Geczy et al. 1997;Graham and Rogers 2002), anotherplausible explanation is that larger firmsmay have more access to currency de-rivative instruments.20 Last but not least,the finding that distressed firms –asindicated by their debt restructuringprograms– are less motivated to hedgeis consistent with the view that leveredequity is an option held by shareholdersagainst the firm’s assets where the valueof debt is the exercise price. Finan-cially distressed firms will see that theoption values of their equity will in-crease as their cash-flow volatilitiesincrease. Therefore, such firms tendnot to hedge; or at least, hedge lessercompared to those of firms that do notexperience financial distress.

Limitations and FutureResearch

The present study imposes twoimportant assumptions. Firstly, it isassumed that observations are drawn

from annual random sampling, and eachobservation drawn is regarded as adifferent and independent firm. Sec-ondly, the regression coefficients esti-mated in the present study are assumedto be constant over time. These twoassumptions may be regarded as toorestrictive. Therefore, the results ofthis study should be interpreted with allthese restrictive assumptions in mind.

Also, data limitation and unknownpotential attrition bias have prevented

the present study to confidently employa panel data approach that could pro-

vide many opportunities to explore bothindividual firm as well as time effects

on the simultaneity of corporate hedg-ing and debt policies. It is hoped that

with more data and better financialstatement disclosures, a balanced panel

data approach for studying corporatehedging policy would be possible in the

near future; and therefore, richer analy-ses and conclusions could be obtained.21

Lastly, other limitation worth men-tioning is that considering the pecu-liarities of the Indonesian macro-eco-nomic conditions during the study pe-riods of 1996 through 2001, the resultsof this study might not be extendableto periods beyond the year 2001.22 The

20 Further examination reveals that large sample firms obtain currency derivative instrumentsthrough OTC markets involving some large reputable global financial institutions such as Credit SuisseFirst Boston, Morgan Stanley, Standard Chartered, Citibank, or Sumitomo Bank. It is doubted thatsmaller firms would have as equal access as their larger counterparts to such financial institutions.

21 Nevertheless, the author has conducted unreported analyses where the results show that neitheran unbalanced panel data approach nor relaxing the assumption of constant coefficient changes thehedging-debt simultaneity conclusion drawn by the present study.

22 Due to lack of adequate financial statement disclosures, conducting a study on Indonesian firms’hedging policy prior to year 1996 would be difficult, if not impossible.

202

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

Rupiah exchange rates during periodssubsequent to year 2001 are seen to beless volatile, and there is also a sort ofwidely held believe within the businesscommunity that the Rupiah currencywould appreciate as the Indonesianeconomic and political climates start toimprove. It is asserted that if firms

believe that the Rupiah exchange ratewould appreciate, they might opt not tohedge their currency exposures; or atleast, they might selectively hedge theircurrency exposures. This asserted se-lective hedging policy should be aninteresting topic for future research.

References

Allayannis, G., and J. P. Weston. 2001. The Use of Foreign Currency Derivatives andFirm Market Value. Review of Financial Studies 14 (1): 243-276.

Bessembinder, H. 1991. Forward Contracts and Firm Value: Investment Incentive andContracting Effects. Journal of Financial and Quantitative Analysis 26 (4): 519-532.

Black, F., and M. Scholes. 1973. The Pricing of Options and Corporate Liabilities.Journal of Political Economy 81: 637-654.

Breeden, D., and S. Viswanathan. 1996. Why Do Firms Hedge? An AsymmetricInformation Model. Working Paper. Duke University.

Castanias, R. 1983. Bankruptcy Risk and Optimal Capital Structure. Journal of Finance38: 1617-1635.

Culp, C. L. 2001. The Risk Management Process: Business Strategy and Tactics. JohnWiley & Sons, Inc.

DeMarzo, P., and D. Duffie. 1995. Corporate Incentives for Hedging and HedgeAccounting. Review of Financial Studies 8: 743-772.

Froot, K. A., D. S. Scharfstein, and J. C. Stein. 1993. Risk Management: CoordinatingCorporate Investment and Financing Policies. Journal of Finance 48: 1629-1657.

Gay, G., and J. Nam. 1998. The Underinvestment Problem and Corporate DerivativesUse. Financial Management 27 (4): 53-69.

Geczy, C., B. A. Minton, and C. Schrand. 1997. Why Firms Use Currency Derivatives.Journal of Finance 52: 1323-1354.

Gujarati, D. N. 2003. Basic Econometrics. 4th Edition. McGraw-Hill Higher Education.

Graham, J. R., and D. A. Rogers. 2002. Do Firms Hedge in Response to Tax Incentives?Journal of Finance 57 (2): 815-839.

Greene, W. H. 2003. LIMDEP - Version 8.0: Econometric Modeling Guide. EconometricSoftware, Inc.

Greene, W. H. 2002. Econometric Analysis. 5th Edition. Prentice Hall.

Haushalter, G.D. 2000. Financing Policy, Basis Risk, and Corporate Hedging: Evidencefrom Oil and Gas Producers. Journal of Finance 55 (1): 107-152.

203

Suriawinata—Investigating the Simultaneity of Corporate Hedging and Debt Policies

Hovakimian, A., T. Opler, and S. Titman. 2001. The Debt/Equity Choice. Journal ofFinancial and Quantitative Analysis 36 (1): 1-24.

Jensen, M.C. 1986. Agency Costs of Free Cash Flow, Corporate Finance and Takeovers.American Economic Review 76: 323-339.

Jensen, M.C., and W. Meckling. 1976. Theory of the Firm: Managerial Behavior,Agency Costs, and the Capital Structure. Journal of Financial Economics 3: 305-360.

Judge, G. G., R. C. Hill, W. E. Griffiths, H. Lutkepohl, and T. C. Lee. 1988. Introductionto the Theory and Practice of Econometrics. 2nd Edition. John Wiley and Sons.

Leland, H. E. 1998. Agency Costs, Risk Management, and Capital Structure. Journal ofFinance 53: 1213-1243.

Leland, H.E. 1994. Corporate Debt Value, Bond Covenants, and Optimal CapitalStructure. Journal of Finance 49 (4): 1213-1252.

Long, J. S. 1997. Regression Models for Categorical and Limited Dependent Variables.Sage Publications.

Lookman, A. 2005. Bank Borrowing and Corporate Risk Management. UnpublishedWorking Paper. Tepper School of Business – Carnegie Melon University.

Mian, S.L. 1996. Evidence on Corporate Hedging Policy. Journal of Financial andQuantitative Analysis 31 (3): 419-439.

Modigliani, F., and M. Miller. 1963. Corporate Income Taxes and The Cost of Capital:A Correction. American Economic Review 53: 433-443.

Modigliani, F., and M. Miller. 1958. The Cost of Capital, Corporation Finance and theTheory of Investment. American Economic Review 48: 261-297.

Myers, S. C. 1977. Determinants of Corporate Borrowing. Journal of Financial Econom-ics 5: 147-175.

Myers, S. C., and N. Majluf. 1984. Corporate Finance and Investment Decisions whenFirms Have Information that Investors do not Have. Journal of Financial Economics13: 187-221.

Nance, D.R., C. W. Smith, and C. W. Smithson. 1993. On the Determinants of CorporateHedging. Journal of Finance 48: 267-284.

Nguyen, H. and Robert Faff. 2002. On the Determinants of Derivative Usage byAustralian Companies. Australian Journal of Management 27 (1): 1-24.

Ross, M. P. 1996. Corporate Hedging: What, Why and How?. Working Paper. Universityof California, Berkeley.

Smith, C. W., and R. Stulz. 1985. The Determinants of Firms’ Hedging Policies. Journalof Financial and Quantitative Analysis 20: 391-405.

Stulz, R. 1996. Rethinking Risk Management. Journal of Applied Corporate Finance. 9:8-24.

Stulz, R. 1990. Managerial Discretion and Optimal Financing Policies. Journal ofFinancial Economics 26: 3-27.

204

Gadjah Mada International Journal of Business, May-August 2005, Vol. 7, No. 2

Stulz, R. 1984. Optimal Hedging Policies. Journal of Financial and Quantitative Analysis19: 127-140.

Suriawinata, I. S. 2004. Apakah Kebijakan Hedging Perusahaan dengan InstrumenDerivatif Valuta Asing Meningkatkan Nilai Pemegang Saham?: Bukti Empiris dariPerusahaan-Perusahaan Non-Finansial yang Terdaftar di Bursa Efek Jakarta.Prasetiya Mulya Management Journal 9 (2): 59-80.

Suriawinata, I. S. 2002. Empirical Testing of International Parity Conditions of theRupiah Exchange Rate against the US Dollar over the Floating Rate Period.Prasetiya Mulya Management Journal 7 (13): 26-45.

Titman, S., and R. Wessels. 1988. The Determinants of Capital Structure Choice. Journalof Finance 43: 1-18.

Tufano, P. 1996. Who Manages Risk? An Empirical Examination of Risk ManagementPractices in the Gold Mining Industry. Journal of Finance 51 (4): 1097-1137.

Varaiya, N., R. A. Kerin, and D. Weeks. 1987. The Relationship between Growth,Profitability, and Firm Value. Strategic Management Journal 8 (5): 487-498.

Wooldridge, J. M. 2002. Econometric Analysis of Cross Section and Panel Data. TheMIT Press.