Embed Size (px)

Citation preview

This article was downloaded by: [Instituto de Pesquisas e Estudos Florest]On: 21 September 2012, At: 11:06Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH,UK

European Accounting ReviewPublication details, including instructions for authorsand subscription information:http://www.tandfonline.com/loi/rear20

Investment Decisions onLong-term Assets: IntegratingStrategic and FinancialPerspectivesFábio Frezatti a , Diógenes de Souza Bido b , Ana PaulaCapuano da Cruz c , Marcelo Francini Girão Barroso a &Maria José de Camargo Machado aa Department of Accounting and Actuarial Sciences,School of Economics, Business and Accounting,University of São Paulo, São Paulo, Brazilb Center for Social and Applied Sciences, MackenziePresbyterian University, São Paulo, Brazilc Institute of Economic, Business and AccountingSciences, Federal University of Rio Grande, RioGrande, Brazil

Version of record first published: 21 Sep 2012.

To cite this article: Fábio Frezatti , Diógenes de Souza Bido, Ana Paula Capuanoda Cruz, Marcelo Francini Girão Barroso & Maria José de Camargo Machado (2012):Investment Decisions on Long-term Assets: Integrating Strategic and FinancialPerspectives, European Accounting Review, DOI:10.1080/09638180.2012.718672

To link to this article: http://dx.doi.org/10.1080/09638180.2012.718672

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes.Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expresslyforbidden.

The publisher does not give any warranty express or implied or make anyrepresentation that the contents will be complete or accurate or up todate. The accuracy of any instructions, formulae, and drug doses should beindependently verified with primary sources. The publisher shall not be liablefor any loss, actions, claims, proceedings, demand, or costs or damageswhatsoever or howsoever caused arising directly or indirectly in connectionwith or arising out of the use of this material.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

Investment Decisions on Long-termAssets: Integrating Strategic andFinancial Perspectives

FABIO FREZATTI∗, DIOGENES DE SOUZA BIDO∗∗, ANA PAULACAPUANO DA CRUZ†, MARCELO FRANCINI GIRAO BARROSO∗

and MARIA JOSE DE CAMARGO MACHADO∗

∗Department of Accounting and Actuarial Sciences, School of Economics, Business and

Accounting, University of Sao Paulo, Sao Paulo, Brazil, ∗ ∗Center for Social and Applied Sciences,

Mackenzie Presbyterian University, Sao Paulo, Brazil, †Institute of Economic, Business and

Accounting Sciences, Federal University of Rio Grande, Rio Grande, Brazil

(Received: September 2010; accepted: July 2011)

ABSTRACT This paper aimed to verify how companies formalise the decisions andcontrol on long-term investments. In particular, an analysis of the published literaturereveals a relevant gap between the strategic and financial perspectives in addressing thisissue, and Agency Theory was proposed as a linking construct to bridge this gap. Asurvey was conducted among 82 companies, and the data were treated using thestructural equation modelling technique. The results of this survey indicate that firmswith intensive external funding use sophisticated capital budgeting methods morefrequently when evaluating the profitability of their long-term investment proposals. Asthese methods require detailed information, these firms use additional appraisalmechanisms to conduct their investment analysis more frequently. Additionalmechanisms are also used if the long-term investment is funded by external sources andperceived as a riskier investment. These deeply analysed long-term investmentproposals often appear and are decided as a part of the strategic planning processinstead of being strongly associated with the budgeting process. Finally, these long-terminvestments, which are funded externally, analysed using sophisticated methods andmechanisms and decided as a part of the strategic planning cycle, are more tightlycontrolled than other investments. These findings help to reduce the heuristics withinthe related literature.

European Accounting Review

iFirst Article, 1–40, 2012

Correspondence Address: Fabio Frezatti, Department of Accounting and Actuarial Sciences, School

of Economics, Business and Accounting, University of Sao Paulo, Av. Prof. Luciano Gualberto, 908,

FEA 3, Sala 226, Sao Paulo, SP 05508-900, Brazil. Email: [email protected]

Paper accepted by Markus Granlund.

European Accounting Review

iFirst Article, 1–40, 2012

0963-8180 Print/1468-4497 Online/12/000001–40 # 2012 European Accounting Associationhttp://dx.doi.org/10.1080/09638180.2012.718672Published by Routledge Journals, Taylor & Francis Ltd on behalf of the EAA.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

1. Introduction

Long-term investment decisions are fundamental to the maintenance of organis-

ations, affecting their managerial structuring process over diverse time horizons.

Such decisions demand analyses of (i) the risk they might pose; (ii) the need for

long-term funding; (iii) the demand for an integrated decision process regarding

the overall long-term view of the organisation; (iv) the involvement of distinct

hierarchical levels; and (v) the useful life span of the assets involved.

Considering the range of consequences that long-term investments can entail

and the contingent nature of the expected future benefits for a given economic

scenario (Papadakis, 1995), long-term investment decisions should be made

through structured projects and should be controlled through formal and specific

initiatives (Pirttila and Sandstrom, 1995).

Times of economic growth generally encourage the search for new business

opportunities. This often means new investments, but it also promotes changes

in working capital elements and raises opportunities for long-term assets.

However, changes in the economic environment may render unfeasible the nego-

tiated (and expected) return on investments. For instance, if long-term funding

resources become scarce and investment plans are postponed during times of gen-

eralised financial crises, decision-makers change their development premises,

and predetermined long-term investments may be abandoned. The ordinary struc-

tured management of long-term investments may not prevent unexpected crises,

but it might provide an understanding of the motivation for the investment,

expectations for the investment, the occurrences that should be anticipated and

the corrective measures that should be taken before, during, and after the

investment.

In addition to the financial perspective, the longer term sustainability of the

organisation should be considered. Long-term investment decisions should be

prioritised in structured decision processes, consistent with the organisation’s

sustainability demands. From a managerial perspective, such a management

control system (involving structured decision processes) must support the align-

ment of investment managers’ behaviours with strategic organisational goals

(Slagmulder, 1997; Alkaraan and Northcott, 2007). Despite the relevance of

long-term investment decisions, Kensinger and Martin (1988) found a lack of

academic dialogue on this topic between the proponents of the strategy literature

or the finance literature. Hence, the need to establish a link between finance

theory and the diverse strategic ramifications of long-term investments motivates

the development of the research presented in this article.

The gap addressed in this paper refers to this dialogue between the approach

focused on strategic planning and the approach designed to maximise long-

term financial decisions. We seek to refine the theories of both perspectives.

Keating (1995) indicated three theoretical development stages for research

scope possibilities: theory discovery, theory refinement, and theory refutation.

Theory refinement represents a loosely defined and less-clear contribution to

2 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

the field and requires the interaction of theoretical propositions and supporting

data.

Parallel to the lack of connection between the financial and strategic

approaches, this study is motivated by specific considerations. There is little evi-

dence regarding the use of formal analytical investment instruments in Brazilian

companies. Moreover, the Brazilian economy has witnessed long inflation

periods and conjuncture issues, which have jeopardised the credibility of man-

agement control in Brazilian organisations (Frezatti et al., 2012). Hence, the Bra-

zilian entrepreneurial context is appropriate for an exploration of long-term

investment decisions.

In sum, from a perspective of structured, long-term investment analysis, we

expect to contribute to the identification and understanding of the factors that

guide decision-making and control. There is currently little empirical knowledge

about these factors (Alkaraan and Northcott, 2007). Integrating these factors

demands managerial maturity within an organisation (i.e. a specific combination

that articulates both strategic and financial analyses). Thus, we posit the follow-

ing research question: how do companies handle long-term investments, and, in

particular, how do they integrate the strategic and financial issues related to such

investments?

We developed an empirical investigation to verify the use of capital budgeting

methods and mechanisms within structured long-term investment decision pro-

cesses as well as the use of methods to control these decisions. The aim was to

identify the strategic and financial elements that inform decision processes. A

sample of Brazilian companies was used in this investigation.

2. Literature Review

In this section, we draw on the theoretical elements that will be discussed

throughout the remainder of this study.

2.1 Agency Theory (AT)

Strategy and finance represent separate strands of thought supporting long-term

investment decisions. Each line of thought has its own rationale for organis-

ational improvement and considers different elements and perspectives. They

are derived from different epistemological perspectives and require an integrative

approach to ‘sew’ them into a cohesive whole. The ‘sewing’ we propose may

accomplish this task and allow the two perspectives to be operational when

combined.

To ‘sew’ these two approaches together, we propose a framework within AT

that can be applied to diverse elements, such as investment decisions, risk analy-

sis, and capital structure as well as capital planning processes, methods, and

mechanisms. This framework privileges the principal’s perspective but also con-

siders the perspectives of ownership vs. control and corporate responsibility

Investment Decisions on Long-term Assets 3

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

(Jensen and Meckling, 1976). Although it recognises other stakeholders, it

assumes that their roles are modulated by the principal’s interests in strategic

decisions. This framework is criticised for not incorporating sufficient tools for

the operationalisation of empirical analyses and for using only relevant elements

to drive the analysis (Tiessen and Waterhouse, 1983; Lambert, 2006). Neverthe-

less, in the context of the present research, we draw on AT to clarify how organ-

isations incorporate elements of corporate governance into their managerial

structures.

AT addresses the relationship between a principal and one (or more) agent(s) in

economic exchanges (Jensen and Meckling, 1976). Agency is configured as a

social engagement process that is limited in time and provides present and

future orientations based on previous information (Emirbayer and Mische,

1998). Furthermore, AT addresses the

‘separation of ownership and control’, the ‘social responsibility’ of

business, the definition of a ‘corporate objective function’, the determi-

nation of an optimal capital structure, the specification of the content of

credit agreements, the theory of organisations, and the supply side of the

completeness of markets problems. (Jensen and Meckling, 1976, p. 1)

These implications stem from the consequences of this principal–agent

relationship, stressing the need to consider management activities.

Long-term investment decisions affect and are affected by agency conflicts due

to the agent’s and the principal’s distinct perceptions of risk, the agent’s relation-

ship with the principal (particularly regarding the agent’s performance assess-

ment by the principal), and the appraisal methods and mechanisms that support

each party’s decision processes. Although the two parties must have similar

beliefs to make the relationship possible (Tiessen and Waterhouse, 1983), and

even if the agents are encouraged to adopt a cooperative attitude, they generally

manifest perceptions that inform their decision processes differently from the

respective principals (Eisenhardt, 1989).

In this sense, various authors (Van Horne, 1995; Rappaport, 1998; Brealey

and Myers, 2005/2002) have noted that a rationality component is needed in

the relationship between principals and agents. This component demands

analytical mechanisms that support the decision processes regarding these

investments and hence (potentially) minimise associated agency conflicts.

These mechanisms are typically materialised through performance information

that is generated for planning and controlling activities. Thus, the demand for

objective instruments that may support investment analyses and assessments

is part of the onus resulting from the agency relationship. Finally, even if AT

is rooted in information economics, we must conjugate it with the elements

addressed by management control and other theoretical branches (Lambert,

2006).

4 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

2.2 Long-term Assets and Strategic Investments

Despite the existence of diverse long-term capital budgeting analysis and assess-

ment techniques, other factors can affect managers’ decisions regarding long-

term assets. For example, pressure from external entities wishing to gain

control of a firm may negatively impact that firm’s performance because this

pressure can induce managers to sacrifice long-term results to improve present

results (Shleifer and Vishny, 1986; Stein, 1988). Conversely, Israel and Ma

(1999) concluded that this type of pressure actually encourages investments in

long-term projects. The authors argued that ‘investment inefficiency under

pressure of acquisition is more probable in the form of over-investment in

long-term projects than in the form of over-investment in short-term projects’

(Israel and Ma, 1999, p. 3).

Investments in long-term assets can be divided into strategic and non-strategic

investments (Slagmulder, 1997; Asrilhant et al., 2004). Although this classifi-

cation is relevant, it is difficult to characterise strategic investments. Slagmulder

(1997) and Haka (2007) criticised the focus that directs this topic towards its con-

nection with an organisation’s formal plans more than its actual strategies. This

focus does not support the perspective defended by Simons (1995), which high-

lighted the need to account for the planning process in diagnostic control and in

interactive control.

Although various definitions of strategic investments are available in the litera-

ture, in this study, they are considered to have a significant effect on the organ-

isation as a whole and on long-term performance (Marsh et al., 1988; Butler

et al., 1991; Ghemawat, 1991; Carr and Tomkins, 1996; Slagmulder, 1997; Asril-

hant et al., 2004). One premise is that there would be greater concern with using

capital budgeting methods and mechanisms to support the analysis if investment

projects were strategic. Thus, the relevance of these investments becomes contex-

tual and is derived from the specific relationship between an investment and its

impact on the business, with different possible interpretations as a result of

each organisation’s interest, and they take the form of investment projects.

2.3 Formal Planning Instruments: Strategic Planning and Budget

Long-term assets demand analyses based on long-term investment appraisal

methods and mechanisms (Papadakis, 1995; Horngren et al., 1996), such as the

organisation’s strategic planning. Additionally, these appraisal methods make

the long term compatible with the short term, and the mechanisms for both

time horizons should be made feasible (Ward and Grundy, 1996). In this case,

the mechanism for the long term is strategic planning, and the mechanism for

the short term is budgeting. Thus, after a decision has been made, its practice

and control become possible. A formal capital budgeting analysis represents

not only a decision instrument but also a communication instrument among the

agents (Van Cauwenbergh et al., 1996).

Investment Decisions on Long-term Assets 5

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

The existing literature is highly fragmented and divergent in its treatment of the

association between the strategic and financial aspects of discussion and planning.

Thus, the authors and theories that permit a dialogue between these knowledge

areas need to be identified (Carr and Tomkins, 1996). The epistemological roots

of the different academic fields can partially explain this divergence. For

example, certain finance researchers believe that investments should only be

made if they increase stockholder value (Lee, 1985; Shapiro, 1998). In this case,

financial assessment logic underlies the analysis-and-decision process, and the

theoretical foundations of the analysis are based on return and capital cost concepts,

among others. By contrast, Mintzberg (1994) argues that creativity and intuition are

the critical elements for identifying and choosing a strategy and thus for selecting an

investment project. Conversely, Shapiro (1998) argues that the approval of an invest-

ment project should derive from the analysis of its positive net present value (NPV).

Mintzberg et al. (1998) argue that investment projects do not constitute strategies;

rather, these projects can impede the formation of strategies.

AT contributes to the alignment of these diverse considerations because it

requires a contacting structure that formalises the goals negotiated between the

principal and agent for both the long- and short-term horizons (Jensen and Meck-

ling, 1976). This perspective identifies the structured planning process, which

covers the strategic planning and the budget and is developed as desired by the

entity. Aspects of structure are also necessary for assessing and analysing risks

during the capital budgeting process.

In conclusion, finance and strategy are complementary areas based on different

epistemological premises that need to be ‘sewn’ together to permit broader appli-

cability. AT produces the perception that a planning instrument is necessary for

determining future directions and that such an instrument provides the conditions

that enable the eventual results to be financially controlled.

2.4 Investment Funding

One of the relevant decisions foreseen in AT is related to the funding of business

operations (Lambert, 2006). Jensen and Meckling (1976) address the relevance of

investment funding as a variable in terms of resources, funding costs, and risk. As

a result of the long horizon of return, investments in these assets require long-

term funding. In many cases, this funding will only be available in the form of

loans. Loans generate considerable costs for companies, and according to the

logical foundation of finance, an investment is only feasible if it exceeds the

cost of the capital invested in it. Therefore, the capital source chosen for an

investment not only produces alterations in a company’s capital structure but is

also intrinsically connected to the investment decision itself.

Recent studies discuss other theories that explain the choice of a given capital

structure (Graham and Harvey, 2002): trade-off theory (Brigham and Ehrhardt,

2006), in which the limit of indebtedness is the moment when the costs generated

by that debt exceed the benefits generated by the fiscal tax economy; and pecking

6 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

order theory (Myers, 1984), which is based on AT and in which information

asymmetry demands that companies rank their choices of funding sources.

Given that an organisation’s strategic planning is one of the tools used to

monitor agency problems and that the choice to invest in long-term assets is

made when this planning is structured, firms are expected to define their

funding sources when they make long-term investment decisions. As the

chosen funding form is a relevant variable in the investment decision, companies

that need capital from third parties typically seek to intensify their use of analyti-

cal instruments to support their decisions.

2.5 Risk Analysis

AT does not specify what types of risks should be accounted for and what forms

of risk should be perceived and either mitigated or eliminated. The one risk expli-

citly mentioned in AT is financial risk (Jensen and Meckling, 1976). Lambert

(2006) finds a relevant theme related to the differing levels of risk perception

between a principal and an agent. If a given risk exists, then the agent’s remunera-

tion becomes a relevant element that affects his or her behaviour. In addition, an

investment project funded by third-party resources should be considered to be

more risky than an identical project funded by the organisation’s own resources

because those outside interests should be remunerated regardless of whether the

project itself generates positive results. When addressing risk in investment pro-

jects (because in most cases, risks are complicated and convoluted, rendering the

discussion complex), we do not specify each type of risk considered by the

manager. Rather, the most relevant issue is the manager’s attitude towards

the principal’s expectations. This approach finds support in the literature, as

the manager is expected to adopt a non-passive attitude, whereas the belief that

an active manager is merely acting for his or her own benefit has generally

declined (Subramaniam, 2006).

2.6 Capital Budgeting Analysis: Methods and Additional Mechanisms

The distinction between capital budgeting methods (tools used to analyse the ade-

quacy of a project) and additional mechanisms (tools that help improve the analy-

sis of a project from a financial perspective) is relevant, as the latter represent an

improvement over the former. Furthermore, additional mechanisms cannot be

used if capital budgeting methods were not used previously.

According to Alkaraan and Northcott (2006), traditional capital budgeting

methods use metrics such as the following: (i) the NPV of cash flow; (ii) the

internal return rate (IRR); (iii) the simple payback and adjusted payback; (iv)

the profitability rate; and (v) the adjusted IRR. These metrics are frequently men-

tioned in the literature (Lee, 1985; Pike, 1996; Carr and Tomkins, 1998; Rappa-

port, 1998; Arnold and Hatzopoulos, 2000; Graham and Harvey, 2001; Alkaraan

and Northcott, 2006; Verbeeten, 2006; Haka, 2007). Stewart (1991) recommends

Investment Decisions on Long-term Assets 7

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

the residual income approach, which he calls economic value added (EVA), as a

comprehensive appraisal method for evaluating investment projects. It differs

from other methods in that it is based not on cash flows but on economic

results. Thus, EVA permits investment analysis, decision, and control.

Capital budgeting methods can be combined with certain additional appraisal

mechanisms, such as simulations, real options, beta analysis, benchmarking, and

value chain analysis (Carr and Tomkins, 1998; Alkaraan and Northcott, 2006).

These alternatives are derived from different approaches to address a project’s

level of risk and ‘hidden’ opportunities. Despite the previously mentioned pos-

sibilities, it should be observed that intuition and decision-making processes that

do not employ formal assessment methods can also be used. In fact, given suffi-

cient supporting information for financial analyses, these approaches can

enhance the decision process, as certain factors cannot be expressed in figures

(Welsch et al., 1988; Van Cauwenbergh et al., 1996). However, what is

questioned in this investigation is the lack of a formalised structure for

making long-term investment decisions and the means by which this deficiency

can generate a gap in managerial accountability within the company’s planning

process.

3. Theoretical Model and Hypotheses

This paper attempts to refine a set of existing constructs related to finance and

strategy and ‘sew’ together the loose threads of these constructs. This ‘sewing’

can be performed through the following methodological scheme: (i) localisation

of theoretical field, with broad links to both perspectives; (ii) identification of

constructs related to strategy and finance and to the main theoretical field; (iii)

organisation of constructs into a model form; (iv) operationalisation of variables

for data gathering and empirical analysis; and (v) discussion regarding the set of

related constructs.

The potential and applicability of AT were developed through this study,

which used the theory to ‘sew’ strategy and long-term finance together. Hirsch

et al. (1987) postulated that this theory demands the use of complementary the-

ories that are grounded in compatible epistemological perspectives and that

permit the confluence of premises. Moreover, under AT, the possibility of co-

opting the hired agent (who has the power in the organisation to decide on

matters of various durations) allows the various strategic and finance constructs

to be related and made operational.

Thus, the theoretical model developed for supporting the empirical research

considers the following elements related to capital budgeting methods and invest-

ment decisions: (i) the parallel funding decision; (ii) the assessment of the per-

ceived risk; (iii) the strategic planning aspect of the decision process itself; (iv)

the budgeting aspect of the decision process; (v) the use of appraisal methods

and additional mechanisms for supporting the decision process; and (vi)

project control.

8 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

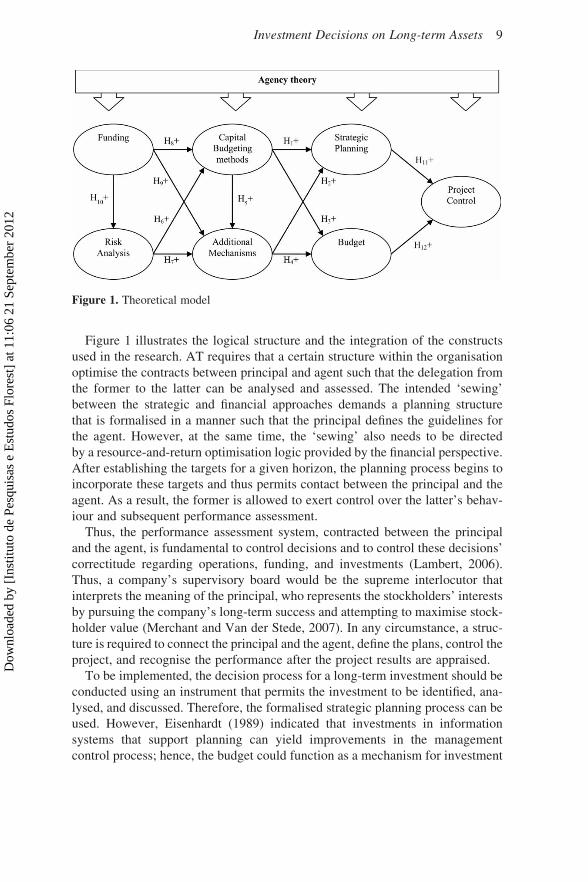

Figure 1 illustrates the logical structure and the integration of the constructs

used in the research. AT requires that a certain structure within the organisation

optimise the contracts between principal and agent such that the delegation from

the former to the latter can be analysed and assessed. The intended ‘sewing’

between the strategic and financial approaches demands a planning structure

that is formalised in a manner such that the principal defines the guidelines for

the agent. However, at the same time, the ‘sewing’ also needs to be directed

by a resource-and-return optimisation logic provided by the financial perspective.

After establishing the targets for a given horizon, the planning process begins to

incorporate these targets and thus permits contact between the principal and the

agent. As a result, the former is allowed to exert control over the latter’s behav-

iour and subsequent performance assessment.

Thus, the performance assessment system, contracted between the principal

and the agent, is fundamental to control decisions and to control these decisions’

correctitude regarding operations, funding, and investments (Lambert, 2006).

Thus, a company’s supervisory board would be the supreme interlocutor that

interprets the meaning of the principal, who represents the stockholders’ interests

by pursuing the company’s long-term success and attempting to maximise stock-

holder value (Merchant and Van der Stede, 2007). In any circumstance, a struc-

ture is required to connect the principal and the agent, define the plans, control the

project, and recognise the performance after the project results are appraised.

To be implemented, the decision process for a long-term investment should be

conducted using an instrument that permits the investment to be identified, ana-

lysed, and discussed. Therefore, the formalised strategic planning process can be

used. However, Eisenhardt (1989) indicated that investments in information

systems that support planning can yield improvements in the management

control process; hence, the budget could function as a mechanism for investment

Figure 1. Theoretical model

Investment Decisions on Long-term Assets 9

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

identification, analysis, and discussion, which should occur if the project were

unknown when the overall strategic plan was approved. Projects of this type

can derive from emerging opportunities identified by managers.

Regardless of whether a project is derived from the formalised planning

process or from an emerging opportunity, it must be adequately funded. Thus,

funding for long-term investments should be analysed and approved together

with their analysis, as the fundraising process affects an organisation’s risk and

its control over the project’s return. The project’s opportunity cost is related to

the weights of its funding sources. Capital budgeting methods are instruments

that allow managers to understand, prioritise and decide on new spending

while considering the monetary limitations and a project’s return profile.

Additional appraisal mechanisms include tools that enhance further analyses, pri-

marily by revealing, mitigating and avoiding project risks.

In accordance with Simons’s (1995) approach, interactive control systems

should follow the evolution of events, measure them, and correct deviations as

necessary. This approach also applies to an organisation’s investment projects.

In general, after an organisation’s strategy is formulated and clarified, it can be

effectively controlled. This adaptability should be foreseen in planning-and-

control processes, where the organisation monitors its planning, follows the

development of its decisions and adjusts them when necessary (Merchant and

Van der Stede, 2007). Merchant and Van der Stede argued that this control

extends to investment projects in not only fixed assets but also other resources,

such as those related to working capital. Thus, interactive control systems can

not only verify the comparison between what was accomplished and foreseen

but also alter plans as a result of conjuncture alterations. The findings of Van

Horne (1995) are consistent with this hypothesis.

Based on the presented constructs, hypotheses are proposed and classified into

two groups according to when they occur relative to the investment decision: (i)

formalisation of the decision, which is related to the planning instruments; and

(ii) control, which is related to the procedures for controlling projects after

they are put into practice.

3.1 Formalisation of the Decision Regarding Long-term Investments

From the financial perspective, the analysis of new investment projects seeks to

identify projects that increase company value (Lee, 1985; Welsch et al., 1988;

Ward and Grundy, 1996; Rappaport, 1998). New investment projects should

derive from stockholders’ expectations and aspirations, be planned through

instruments with long- and short-term views, and capture the organisation’s

characteristics and demands in terms of the structure, funding capacity, and

sophistication of the analysis process (Ward and Grundy, 1996).

Strategic planning, capital budgeting and budget formation are identified as a

sequence of planning cycles (Merchant and Van der Stede, 2007). The first is the

formal instrument that guides the other planning cycles and includes a large

10 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

number of processes that consider the organisation’s mission, objectives, and

strategies. Capital budgeting should be part of the strategic planning cycle,

which identifies the programmes or projects to be put into practice in future

years and the resources those projects are expected to consume (Merchant and

Van der Stede, 2007). Thus, the capital budgeting cycle provides the conditions

under which the foreseen strategies are implemented. The budget, in turn, is the

annual plan and is aimed at the practical execution of the decisions made in the

strategic planning and/or capital budgeting cycles.

Scenarios change, resulting in new emerging opportunities and revealing signs

of new investment projects identified through the organisation’s interactive con-

trols (Simons, 1995). These potential projects should not simply be ignored if

they have not been foreseen in the formal strategic planning cycle. Instead, the

pursued strategic elements can be analysed, and the project can be approved

and put into practice based on the annual budget. In these conditions, the relevant

aspect of the process is that the organisation’s strategic view lies behind the

decision process.

The discussed planning and budgeting cycles are useful for deliberations

regarding investments, as they assist in characterising and assessing projects

through the methods indicated earlier (i.e. the value added to the company, the

short- and long-term perspectives of projects, and the capturing of organisational

characteristics and demands). Capital budgeting decisions demand funding with

specific costs that should be paid and remunerated. To support the decision

process, an analysis should be conducted prior to the investment decision to

assess whether the investment return covers the funding cost. Through the appli-

cation of capital budgeting methods and additional appraisal mechanisms, firms

can make decisions regarding investments by identifying, quantifying, and/or

mitigating risks (Kim and Farragher, 1981; Verbeeten, 2006) and by directing

the project management towards achieving the desired performance. However,

resource allocation is rarely analysed mechanically and is often exclusively

based on financial analysis (Merchant and Van der Stede, 2007).

When investigating the use of capital budget methods relative to the invest-

ment type (strategic vs. non-strategic), Alkaraan and Northcott (2006) verified

that companies are increasingly using methods based on discounted cash flow

techniques (NPV and IRR) for strategic investments. From the corporate view-

point, this trend makes sense, as identifying the value added by an investment,

which can be performed by using the NPV technique, is fundamental to the

decision-making process (Ward and Grundy, 1996).

In the comparative study, Carr and Tomkins (1998) found that even for a more

generally accepted method, such as discounted cash flow, strategic projects put

greater emphasis on the use of assessment techniques, which suggests that the

trend noted above is relevant. According to Alkaraan and Northcott (2007),

most managers believe that financial assessments are one of the primary means

for strategically evaluating investment proposals, as such proposals should

demonstrate sufficient profitability before being implemented. A financial

Investment Decisions on Long-term Assets 11

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

assessment plays two main roles in the process – the role of communication

among agents and the decision role – but it should not be regarded as the only

pathway to decisions (Van Cauwenbergh et al., 1996).

Thus, long-term investments decided upon during the strategic planning

process drive the use and intensity of both traditional assessment methods and

additional appraisal mechanisms. It should be noted that a more efficient use

of resources is demanded by those additional mechanisms than the traditional

methods. Thus, the first two hypotheses are established:

H1: Greater adherence to the use of capital budgeting methods for analysing

investments is positively associated with making decisions on the project

during the strategic planning process.

H2: Greater adherence to the use of additional mechanisms for analysing

investments is positively associated with making decisions on the project

during the strategic planning process.

Mintzberg et al. (1998) criticised the capital budgeting approach for detaching

the organisation’s future from the strategic view. They believed that investment

plans are connected to previously defined strategies and do not stimulate new

strategic initiatives. In particular, their criticism includes two relevant com-

ponents: (i) new projects do not contribute to the creation of strategies, and (ii)

the updated set of strategies and investment projects are detached from each

other. The first criticism is circumstantial, and the second is derived from the

existing inertia in structured planning processes, among other reasons.

Given an organisation’s planning cycle, both criticisms can be applicable at

times, as planned investment projects need to adhere to the accepted organis-

ational strategies to a certain degree. In this sense, new opportunities that

emerge after the strategic review cycle will demand an organisational decision:

should they be accepted and implemented, or should those opportunities await

the next planning cycle? In a situation in which competitiveness is fundamental,

new opportunities that demand investment projects can be discussed and

approved when the next year’s budget is discussed. Although the project is con-

sidered over a shorter time window, this practice permits the organisation to

discern the potential impacts of the funding, asset amortisation, and other

factors of the project within a particular time horizon. Another possibility is

that the project will not be discussed and its effects on the company’s activities

will not be formally perceived, which can increase the organisation’s risk by

causing the firm to ignore knowledge regarding the project’s relevant impacts

and initiatives.

As project decisions are made within the framework of a tactical planning

instrument (i.e. the budget), would the decision to put a new project into practice

be tabled until the next strategic planning cycle? Certainly, relevant arguments

may need to be analysed in further depth. Moreover, a deeper financial analysis

of recent project proposals may be needed to decrease risk. By contrast, managers

12 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

have less time to consider a project than planners or organisational leaders. Thus,

a fast analysis of a potential project will employ methods and mechanisms to

assess the elements that are considered most critical and thereby produce a

more simplified perspective of that project than would have been created if the

project had been delayed until the subsequent strategic planning cycle. In

addition, less relevant projects can be found (Arnold and Hatzopoulos, 2000).

These projects are discussed in the budgeting cycle to allow a greater portion

of the strategic planning cycle to be devoted to the analysis of more relevant stra-

tegic projects.

Thus, a financial analysis can refer to the frequency and intensity of using the

aforementioned methods and mechanisms. Arnold and Hatzopoulos (2000) ques-

tioned particular companies and explored whether they always used these

methods. The results indicated that, although NPV and IRR were cited as the

most used methods, half of the respondent companies did not use these tech-

niques in any of their analyses. Therefore, the analytical process utilised in this

investigation considers factors that are inherent within each project under the

assumption that lower amounts of operational investments might be approved

without the same analytical rigor as would be utilised for higher amounts. In

that sense, depending on the related variables, the literature permits variations

in the logic for the establishment of criteria and priorities. Accordingly, we for-

mulate the next three hypotheses:

H3: Greater adherence to the use of capital budgeting methods for analysing

investments is positively associated with making decisions on the project

through the budgeting process.

H4: Greater adherence to the use of additional mechanisms for analysing

investments is positively associated with making decisions on the project

through the budgeting process.

H5: Greater adherence to the use of capital budgeting methods for analysing

investments is positively associated with the use of additional mechanisms.

The diverse risks associated with alternative strategies are considered to be a

relevant theme from the strategic perspective (Ward and Grundy, 1996), particu-

larly for managers, who are assumed to be more risk-averse than their principals

(Subramaniam, 2006). Thus, risk analysis in investment decisions can indicate

different perceptions of risk. To develop risk analysis, managers can utilise

different approaches that can be segmented into two basic categories: (i) a quali-

tative approach, which lacks numerical measurements; and (ii) a quantitative

approach, which numerically assesses a project’s impact on the company’s

value. The first approach does not directly allow a ‘bridge’ to the perspective

of the finance literature to be identified. The second provides a method to indicate

the impact of risk on expected results. Therefore, in addition to verifying value

creation, additional mechanisms can treat risk. The following mechanisms are

mentioned in the literature: (i) sensitivity analysis; (ii) risk adjustment in the

Investment Decisions on Long-term Assets 13

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

discount rate or in the shortening of the payback period; and (iii) probability

analysis, simulation, and beta analysis (Pratt, 1998). Pike (1996) and Alkaraan

and Nortchcott (2006) indicate that the use of these additional mechanisms has

been increasing and that companies have made more use of sensitivity analysis,

which is the simplest of those mechanisms listed above. None of these authors

have found evidence of differences in risk treatment when the investments are

considered to be strategic.

Van Horne (1995) notes that once an investment project is accepted, the firm’s

future cash flows will be influenced. Consequently, he shows that managers

should be prepared to adjust their cash flow expectations after a project is

accepted and states that cash flow considerations should be part of a project’s

analysis, including both methods and mechanisms, such as simulation and real

options evaluations.

The use of simpler mechanisms to measure risk was also emphasised in the

study sample of Arnold and Hatzopoulos (2000). The respondents indicated

that if a manager is excessively concerned with measuring probabilities to the

point of using more sophisticated models, he or she may feel less motivated to

make an effort to accomplish the project. As uncertainties increase, however,

managers tend to intensify the analysis, even if they do so through simple

methods, such as scenario analysis (Van Cauwenbergh et al., 1996).

Verbeeten (2006) verified this trend for risk consideration in Dutch companies

that used more sophisticated mechanisms, such as real options. The results of that

study indicate that as financial uncertainties increase, companies become more

likely to adopt more sophisticated investment appraisal mechanisms. However,

production inputs and social and market uncertainties do not influence the adop-

tion of analysis mechanisms. Generally, companies simultaneously use various

analysis mechanisms that consider risk. Another important point is that the con-

sideration of risk in investment analysis is a pre-analysis action; that is, a man-

ager’s perception of the project’s risk level is incorporated by raising the

project’s discount rate or through other mechanisms that will be used within an

upcoming analysis (Alkaraan and Northcott, 2007).

In accordance with Gaver and Gaver (1993), Ho and Pike (1998) demonstrate

that in companies with more risky and aggressive strategies, management remu-

neration systems focused on the long term, and systems that support investment

project information tend to use more sophisticated risk treatment mechanisms

during project analysis. According to Lee (1985), investment analysis should

include judgements regarding non-financial elements, and the use of methods

and mechanisms helps managers to understand and explain the project’s risk

dimension. This approach suggests the following:

H6: Greater adherence to the use of capital budgeting methods for analysing

investments is positively associated with concerns regarding the analysis of

perceived risk.

H7: Greater adherence to the use of additional mechanisms for analysing

14 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

investments is positively associated with concerns regarding the analysis

of risk.

Irrespective of the conceptual financial approach chosen to analyse capital

structure and cost, investment funding sources guide the analysis of putative

project investments (Arnold and Hatzopoulos, 2000). If a company has a cash

surplus and self-funding capacity, a formal analysis still exists; nonetheless,

the approval standards are relaxed (Van Cauwenbergh et al., 1996), which may

indicate that project analysis tends to be deeper for investment situations using

third-party resources. This conclusion contains implications for the risk

perceptions of the agents and their consequent reactions. Moreover, this result

is consistent with AT, which specifies a situation in which agents develop con-

tractual relationships to maximise the owners’ welfare (Jensen and Meckling,

1976). From a pragmatic perspective, financing the investment with loans

impacts the owner’s risk perspective and demands a more careful investment

analysis.

For example, Van Horne (1995) argues that the funding source for new

investments may have a limiting potential over the strategic decision. In

other words, managers’ concerns regarding the strategic feasibility of a

project include the capacity to acquire funding for the resources needed for

that project. External funding capacity, in turn, is affected by income distri-

bution decisions, an approach that is exclusively assessed from an organis-

ation’s financial perspective. Thus, this approach is affected by external

factors. Given these conditions, a capital structure that incorporates a relatively

high cost of capital will affect the strategic discussion regarding the acceptance

of the project.

Jensen and Meckling (1976) evaluated the capital funding issue, which was

also addressed subsequently by Lambert (2006). Lee (1985), in turn, discussed

capital rationing as a result of two factors: (i) limits to acquiring capital and

(ii) the possibility of obtaining funding at an adequate cost to develop the

project (i.e. the opportunity cost that makes the project feasible). These elements

have a relevant influence on the investment decisions in that they help support

project identification and choose projects for implementation. Thus, the type of

funding required for a project impacts not only its risk and opportunity costs

but also the formality and depth of the analysis. Given this consideration, the fol-

lowing hypotheses are presented:

H8: A greater need to define the use of loans and more relevant opportunity

costs are positively associated with the use of capital budgeting methods.

H9: A greater need to define the use of loans and more relevant opportunity

costs are positively associated with the use of additional mechanisms.

H10: A greater need to define the use of loans is positively associated with

greater levels of risk analysis.

Investment Decisions on Long-term Assets 15

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

3.2 Control of Long-term Investments: The Dependent Variable

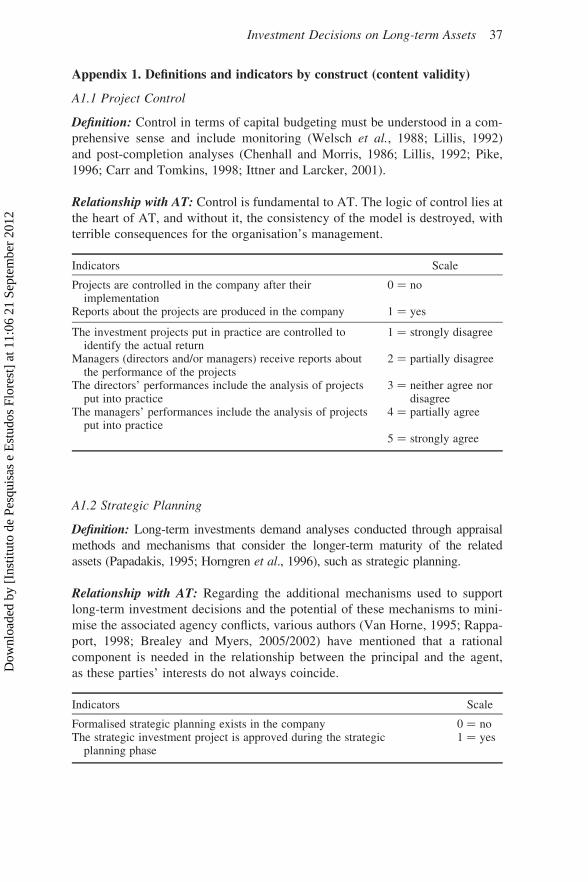

Control is fundamental for AT. If the formalised plans for a specific project are

developed, they must be followed and reported upon from a particular moment

onwards to ensure the accountability of the investments. The logic of control

lies at the heart of AT, and without this control, the consistency of the model

would be destroyed, with terrible consequences for the organisation’s

management.

To a certain extent, this research considers the existence of a formal structured

planning process. The investment plan stems from this process, along with other

managerial instruments that contain the resource allocation decisions for long-

term assets that may be put into practice at a future time. The control of projects

occurs from the moment when they are materialised and should continue until the

promised return is achieved. Thus, the strategic plan and capital budget should be

analysed separately because the investment decision can be made and should be

reflected in either instrument, although the literature indicates that the strategic

plan should contain these decisions (Steiner, 1979; Mintzberg et al., 1998).

Ward and Grundy (1996) suggested that the manner and complexity of using

capital budgeting methods are related to the organisations’ lifecycle stages and

that mature companies have the capital structure and financial sophistication

needed to handle projects in a more complex and comprehensive way. Moreover,

strategic planning, capital budgeting, and budget controlling are realities in the

organisation’s management processes (Frezatti et al., 2010). As planning

exists, control becomes possible.

Control with regard to long-term investments must be understood in a compre-

hensive sense and includes the monitoring of projects during their implemen-

tation (Welsch et al., 1988; Lillis, 1992) and during the post-completion

performance analyses (Chenhall and Morris, 1986; Lillis, 1992; Pike, 1996;

Carr and Tomkins, 1998; Ittner and Larcker, 2001). In other words, when

capital is being expended on a project, especially key projects, it is important

to compare and explain how the actual expenditures of the project differ from

the estimated spending of the ‘economically justifiable’ amount that was author-

ised (Welsch et al., 1988). This procedure is expected to be reported to ade-

quately senior levels of management. After the project expenditures have been

finished, a post-completion audit might be provided for major projects, as ‘it is

intended to provide information about how realistic (in terms of investment

worth) the planning phase was and why any deficiencies occurred’ (Welsch

et al., 1988, p. 421).

When considering capital budgeting as a planning-and-control process invol-

ving strategic and tactical spending on long-term investments (Welsch et al.,

1988), one must elaborate a comprehensive view of the investment, funding

and return portfolio during the establishment of the planning instrument. In

accordance with this line of reasoning, Steiner (1979) indicates that projects

should be approved based on a strategic investment appraisal instrument and

16 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

that the budget should support the exercise and monitoring of project approval

decisions. In this context, the managerial logic dictates that those controlling

these investment decisions consider both the long-term benefit expectations

and the short-term pressures. This consideration generates a demand for more

sophisticated financial instruments (Ward and Grundy, 1996). Thus, if a

project is approved during the strategic planning process, it is likely to be rel-

evant, strategic for the organisation and controllable in terms of its investment

timeframe and expected performance. By contrast, if the project is decided

upon during the budgeting process, it will require stronger control because the

project in question was not a part of the entire deliberation cycle.

Thus, based on the perception that certain projects may not be approved during

the strategic planning process but rather gain approval during the budgeting

process, we wonder whether and to what extent the latter projects will be con-

trolled. Hence, the following hypotheses are established:

H11: Projects approved during the strategic planning process are later con-

trolled.

H12: Projects approved through the budgeting process are later controlled.

3.3 Control Variables: Economic Sector and Size

Certain business sectors adhere strongly to the conceptual model because of their

higher tradition of long-term investments and characteristic risk profiles. Accord-

ing to the literature (Verbeeten, 2006, p. 114), a correlation exists between an

organisation’s economic sector and the use of more sophisticated capital budget-

ing methods and mechanisms: the financial, construction, and utilities (e.g. gas,

energy, and telecommunications) sectors use these methods and mechanisms reg-

ularly when making investment decisions (Asrilhant et al., 2004). Despite this

evidence, Alkaraan and Northcott (2006) did not find evidence that the industry

sector influences the use of risk analysis in capital budgeting processes, but their

sample was limited to manufacturing companies. Therefore, our study includes

the economic sector as a control variable.

Company size is another variable that influences the adoption of capital bud-

geting methods and mechanisms, as the larger the company is, the more analyti-

cal resources are available for supporting the financial analysis of potential

investments (Merchant, 1981; Chenhall, 2003; Verbeeten, 2006).

4. Method

4.1 Main Elements of Method are: Sample Selection, Research Instrument,

and Respondents

The sample chosen for this study was derived from the companies listed in

Melhores & Maiores 2009, which is based on data from 2008. The yearbook

Investment Decisions on Long-term Assets 17

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

Melhores & Maiores – ‘the best and the largest’ – is a Brazilian publication

developed by the University of Sao Paulo’s team and Abril Publishing. Since

1974, it has ranked the best (evaluated based on a self-developed index) and

the largest (as judged by adjusted annual sales) companies in Brazil. For approxi-

mately 900 of the 1825 companies in Melhores & Maiores 2009, we verified that

company investments in long-term assets increased from 2004 to 2008. From this

set of 900 organisations (the target population), a convenience sample of 82 was

obtained. All of the companies in the study sample were large organisations,

according to the size classification criterion established by the Banco Nacional

de Desenvolvimento Economico e Social (BNDES – Brazilian Development

Bank; BNDES, 2010), a financial institution of the federal government that con-

stitutes the primary source of long-term funding for investments in all Brazilian

economic segments.

A closed-ended questionnaire divided into blocks attempted to map infor-

mation regarding the following issues: (i) the perceived relevance of long-term

investments in the companies under analysis; (ii) investment characteristics (stra-

tegic and non-strategic); (iii) capital budgeting methods and mechanisms; (iv) the

management instruments available in the organisation; and (v) the decision-

making hierarchy.

The content validity was checked using indicators developed from the refer-

ences in the measurement model; the reflective approach was utilised for the con-

sidered variables to measure the constructs (Jarvis et al., 2003). The indicators for

this approach were derived from the theoretical constructs, and the hypotheses

were developed in Section 3 and are presented in Tables 1–9. Binary, three-

point and five-point Likert scales were used.

Data were collected via electronic mail from January to March 2010, with tech-

nical support from the Formsite electronic survey system.

Information regarding the respondents’ academic education, time since gradu-

ation and professional functions in their organisations indicate adequate levels of

professional maturity, seniority, and education for the research conducted in this

study. In particular, 92% of the respondents had graduated in Accountancy,

Business Administration, or Economics; 18% of the respondents were directors;

39% were managers/coordinators; and 16% were analysts. The other respondents

held positions as superintendents, supervisors, and accountants, among other

occupations, and 58% of the 82 respondents had graduated more than 10 years

ago.

4.2 Model Estimation

The structural equation modelling (SEM) technique was used to estimate the pre-

viously proposed theoretical model. SEM appeared to be appropriate for evaluat-

ing the data, as it permits the following approaches: (i) estimate models with a

dependent variable that becomes independent in subsequent relations of depen-

dence (path analysis); and (ii) include latent variables that are measured

18 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

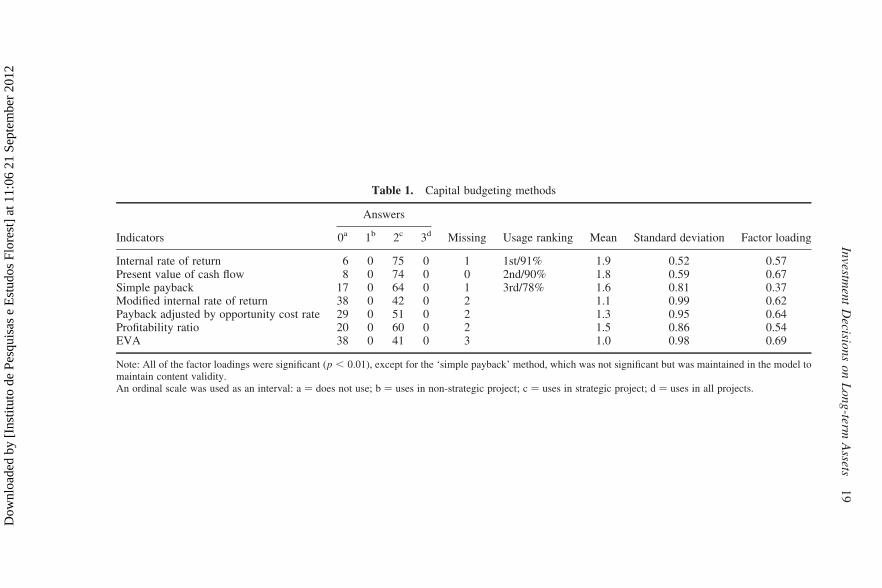

Table 1. Capital budgeting methods

Indicators

Answers

Missing Usage ranking Mean Standard deviation Factor loading0a 1b 2c 3d

Internal rate of return 6 0 75 0 1 1st/91% 1.9 0.52 0.57Present value of cash flow 8 0 74 0 0 2nd/90% 1.8 0.59 0.67Simple payback 17 0 64 0 1 3rd/78% 1.6 0.81 0.37Modified internal rate of return 38 0 42 0 2 1.1 0.99 0.62Payback adjusted by opportunity cost rate 29 0 51 0 2 1.3 0.95 0.64Profitability ratio 20 0 60 0 2 1.5 0.86 0.54EVA 38 0 41 0 3 1.0 0.98 0.69

Note: All of the factor loadings were significant (p , 0.01), except for the ‘simple payback’ method, which was not significant but was maintained in the model tomaintain content validity.An ordinal scale was used as an interval: a ¼ does not use; b ¼ uses in non-strategic project; c ¼ uses in strategic project; d ¼ uses in all projects.

Investm

ent

Decisio

ns

on

Lo

ng

-termA

ssets1

9

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

indirectly (Hair et al., 2010). The data were processed using the SmartPLS

2.0.M3 software (Ringle et al., 2005).

5. Discussion

5.1 Descriptive Aspects of the Field Research

To distinguish the characteristics of the respondents’ companies, we accounted

for the following elements: (i) the company’s economic sector, (ii) whether the

company’s ownership is publicly traded, (iii) the company’s share of long-term

assets relative to total assets, (iv) the company’s total annual billing, and (v)

the company’s indebtedness ratio. The company sectors were defined by the

Melhores & Maiores publication, and a concentration of firms was found in

certain areas, such as food/drink, tobacco, iron, steel, and energy.

Most of the companies in the sample were not publicly traded (79.27%).

Non-current assets comprised a relevant part of the total assets for the

sampled companies (more than 50% in most sectors). The gross billing for

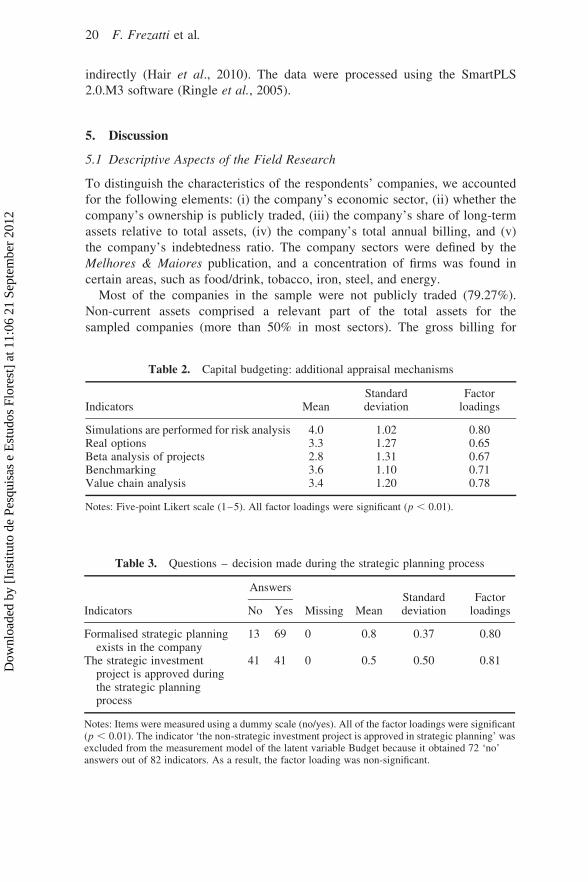

Table 2. Capital budgeting: additional appraisal mechanisms

Indicators MeanStandarddeviation

Factorloadings

Simulations are performed for risk analysis 4.0 1.02 0.80Real options 3.3 1.27 0.65Beta analysis of projects 2.8 1.31 0.67Benchmarking 3.6 1.10 0.71Value chain analysis 3.4 1.20 0.78

Notes: Five-point Likert scale (1–5). All factor loadings were significant (p , 0.01).

Table 3. Questions – decision made during the strategic planning process

Indicators

Answers

Missing MeanStandarddeviation

FactorloadingsNo Yes

Formalised strategic planningexists in the company

13 69 0 0.8 0.37 0.80

The strategic investmentproject is approved duringthe strategic planningprocess

41 41 0 0.5 0.50 0.81

Notes: Items were measured using a dummy scale (no/yes). All of the factor loadings were significant(p , 0.01). The indicator ‘the non-strategic investment project is approved in strategic planning’ wasexcluded from the measurement model of the latent variable Budget because it obtained 72 ‘no’answers out of 82 indicators. As a result, the factor loading was non-significant.

20 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

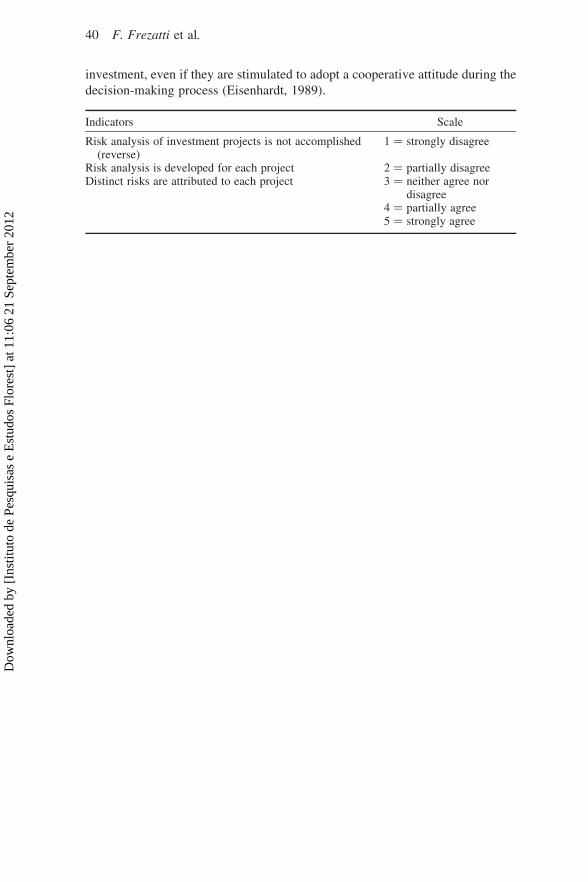

Table 5. Questions – risk analysis

Indicators MeanStandarddeviation

Factorloadings

Risk analysis of investment projects is notaccomplished (reverse)

4.1 1.34 0.49

Risk analysis is developed for each project 4.2 0.81 0.88Distinguished risks are attributed to each project 3.5 1.18 0.89

Notes: Five-point Likert scale (1–5). All of the factor loadings were significant (p , 0.01).

Table 6. Questions – funding

Indicators

Answers

Missing MeanStandarddeviation

Factorloadings0a 1b 2c

Locus of decisions forstrategic investmentprojects

11 35 35 1 1.3 0.69 0.81

Locus of decisions for non-strategic investmentprojects

11 53 17 1 1.1 0.58 0.82

Previously definedopportunity cost rate

9 34 36 3 1.3 0.66 0.79

Note: All of the factor loadings were significant (p , 0.01).Three-point scale was used: a ¼ decision can occur at both times or outside of a formal planninginstrument; b ¼ decision in the budget; and c ¼ decision in strategic planning.

Table 4. Questions – decision occurs during the budgeting process

Indicators

Answers

Missing MeanStandarddeviation

FactorloadingsNo Yes

The strategic investmentproject is approved duringthe budgeting process

48 34 0 0.4 0.50 0.99

The non-strategic investmentproject is approved duringthe budgeting process

15 67 0 0.8 0.39 0.40

Notes: Items were measured using a dummy scale (no/yes). The first factor loading was significant (p, 0.01), but the second was not; it was maintained in the model to maintain the content validity. Theindicator ‘A formalised budget exists in the company’ was excluded from the measurement model ofthe latent variable Budget because 80 ‘yes’ answers were obtained out of 82 indicators. As a result, thefactor loading was non-significant.

Investment Decisions on Long-term Assets 21

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

2008 indicates that all of the companies are large, according to the BNDES

(2010) criteria. However, the range of the data for this element is very wide

(i.e. from millions to billions of dollars). The companies under analysis were

highly capitalised, which is a common characteristic in Brazil. Consequently,

we expected the following to be true: (i) the large share of companies with

similar approaches towards investment projects would represent a bias factor

in our analysis of long-term investment decisions; (ii) there would be a relative

decision-pattern homogeneity among the researched organisations given that all

are of sufficient size to ensure widespread resource availability for investments;

and (iii) the commonly observed differences between publicly traded and non-

publicly traded companies would be found within the research results.

5.2 Univariate Analyses

The descriptive statistics for the indicators used to measure the latent variables

are initially presented here (the factor loadings were obtained from the esti-

mations of the complete model). Thus, we explored how the respondents perceive

investment projects.

Table 1 indicates that the three most used capital budgeting methods were NPV

of the cash flow, internal rate of return, and simple payback. This result is con-

sistent with previous findings (Arnold and Hatzopoulos, 2000; Graham and

Harvey, 2001; Alkaraan and Northcott, 2006), which indicated that NPV and

IRR are the most relevant methods in their rankings. However, the distance

between the valuation of payback and the two other methods can be a source

of concern because in certain cases, the analyses did not consider the return

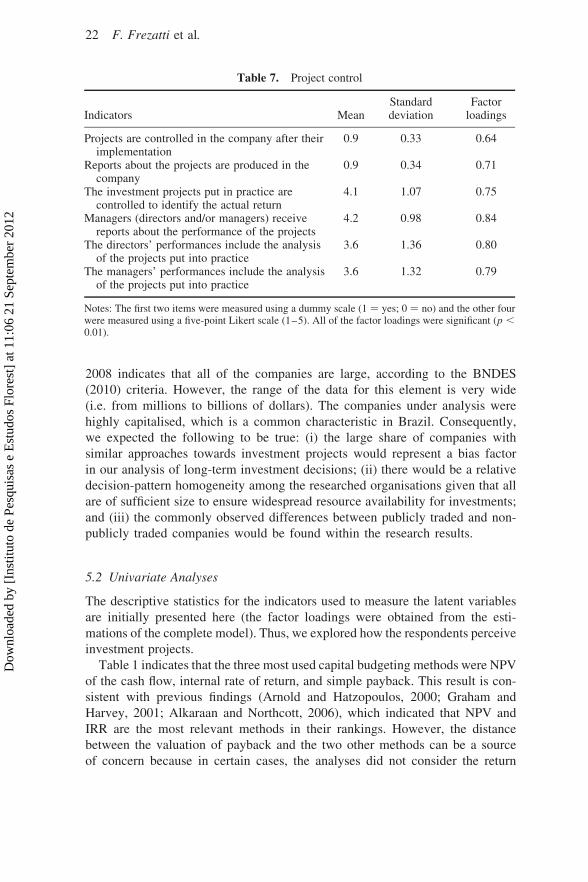

Table 7. Project control

Indicators MeanStandarddeviation

Factorloadings

Projects are controlled in the company after theirimplementation

0.9 0.33 0.64

Reports about the projects are produced in thecompany

0.9 0.34 0.71

The investment projects put in practice arecontrolled to identify the actual return

4.1 1.07 0.75

Managers (directors and/or managers) receivereports about the performance of the projects

4.2 0.98 0.84

The directors’ performances include the analysisof the projects put into practice

3.6 1.36 0.80

The managers’ performances include the analysisof the projects put into practice

3.6 1.32 0.79

Notes: The first two items were measured using a dummy scale (1 ¼ yes; 0 ¼ no) and the other fourwere measured using a five-point Likert scale (1–5). All of the factor loadings were significant (p ,0.01).

22 F. Frezatti et al.

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

horizon, which constitutes a relevant variable in the risk analysis of a project. As

for EVA, this strategy is selective and was only used by a smaller group of

entities.

In addition, Table 2 provides information regarding additional investment

appraisal mechanisms. From this table, it is clear that simulations are frequently

employed auxiliary mechanisms. In their simplest form, these simulations can be

found in the form of a sensitivity test or even a set of elements that includes other

mechanisms.

The time and method by which an investment project was approved and con-

sidered part of the formal planning process were fundamental aspects of the man-

agement model (Table 3). In particular, strategic planning was predominant in the

project approval process, which is in line with the theoretical expectations.

Strategic projects were also approved in the budgeting process. In a few cases,

certain projects were not approved through any formal instrument, which

implies a deviation from theory and increases the risk involved in managing

the project returns. Non-strategic projects, in turn, were approved in the budget-

ing process. Based on the data, we can determine that the term ‘strategic’ does not

distinguish the project type or lead to distinctions in its funding or decision

process.

The profiles of the researched companies provoked a bias towards long-term

projects that is reflected in Table 4. This bias indicates that there is a trend

towards relatively longer projects that consequently possess a well-defined risk

scenario. Thus, we expect the studied companies to use appraisal instruments

to analyse and support their decision processes and to control the development

of investments within these organisations’ tactical horizons.

The risk perspective was captured through three items (Table 5): the develop-

ment of risk analysis in general (captured reversely), individualised analysis, and

risk attribution per project. The answers show that each project was analysed.

However, the companies attributed individualised risk levels to each project

less frequently, which impoverishes the analysis from the decision process

perspective.

Table 6 indicates that funding for long-term investments was not defined in the

strategic planning instrument for all of the strategic investments, whereas funding

for certain non-strategic projects was defined in the same instrument. This finding

is consistent with the above result, as the term ‘strategic’ does not necessarily

refer to a project decided upon within the strategic planning instrument. Oppor-

tunity cost can be characterised in the same way (i.e. as lacking any association

with whether it is defined in the strategic planning phase). A relevant portion of

strategic projects ends up being approved during the budgeting process, and the

opportunity cost is also typically defined when the budget is structured. The con-

sequences of dislocating the project decision to the moment when the budget is

structured can either confirm a strategic action or change the characteristics of

the strategic action to resemble the characteristics of tactical actions. The

research did not manage to capture and dimensionally analyse this possibility,

Investment Decisions on Long-term Assets 23

Dow

nloa

ded

by [

Inst

ituto

de

Pesq

uisa

s e

Est

udos

Flo

rest

] at

11:

06 2

1 Se

ptem

ber

2012

but this result provides an opportunity to discuss the risk that an organisation

assumes if it decides to undertake a long-term investment without considering

its corresponding long-term funding.

Control of a project is vital to the management of an organisation (Table 7). In

this sense, the finding that a project is controlled after its implementation is rel-

evant for both performance management and organisational management. The

fact that directors and managers are charged for the results of the projects is con-

sistent with the literature and relevant to the maintenance of these results (Sub-

ramaniam, 2006). Although this last element is not as predominant as the

others, it scores relatively high, reinforcing its relevance.

5.3 Multivariate Analyses

The model presented in Figure 1 was estimated through partial least square–path

modelling (PLS–PM) instead of linear structural relations (LISREL) or other

estimation methods. This estimation method was chosen because it offers the fol-

lowing advantages: (i) it permits the use of latent variables, which would not be

possible with the alternatives; (ii) PLS–PM simultaneously estimates both the

measurement model (relation between the indicators and latent variables) and

the structural model (relations among the latent variables); (iii) LISREL supposes

data normality, whereas PLS–PM makes no suppositions regarding the data dis-

tribution (Henseler et al., 2009); and (iv) LISREL requires samples of more than

200 cases, whereas PLS–PM demanded a sample of 82 cases for the present

study (a quantity supported by Henseler et al., 2009) to reach an 80% statistical

power, which is the minimum level recommended by Hair et al. (2010) for detect-

ing a significant medium-sized effect (Cohen, 1977).

5.3.1 Measurement model assessment

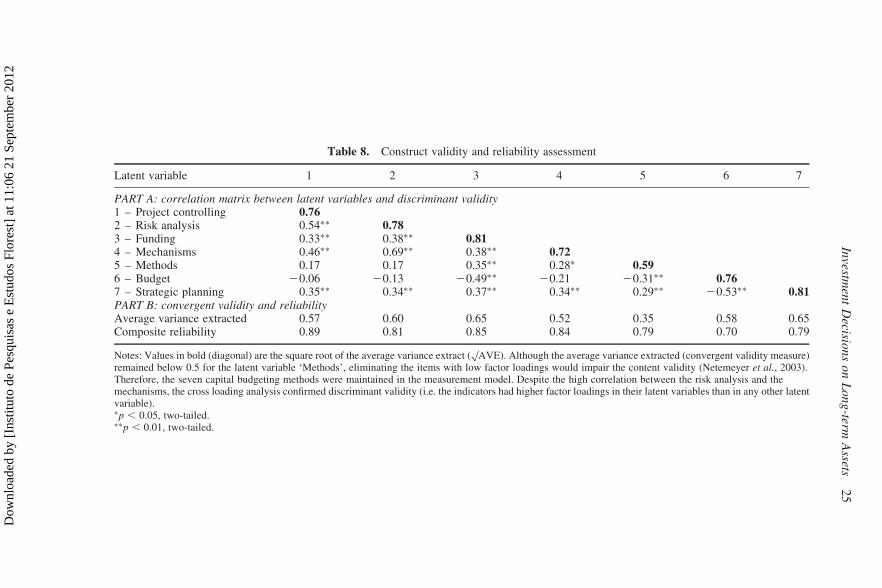

Convergent validity was assessed through factor loadings with significant values

for all but one; an average extracted variance (AVE) higher than 0.5 was also

used for this assessment (Fornell and Larcker, 1981), except for the latent vari-