Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=1788063

Macro Financial Determinants of the Great Financial Crisis:

Implications for Financial Regulation

Gerard Caprio Jr., Vincenzo D‟Apice, Giovanni Ferri and Giovanni Walter Puopolo1

Abstract

We investigate the macro financial determinants of the Great Financial Crisis of 2007-2009 using

data on 83 countries from the period 1998-2006. Our results show that the probability of suffering

the crisis in 2008 was larger for countries having higher levels of credit deposit ratio whereas it was

lower for countries having higher levels of: i) net interest margin, ii) concentration in the banking

sector, iii) restrictions to bank activities, iv) private monitoring. Our findings contribute to the

ongoing discussion that can help policymakers calibrate new regulation, by achieving a reasonable

trade-off between financial stability and economic growth.

JEL Classification: G15; G18; G21

Keywords: Banking Crisis; Government Intervention, Regulation

Author‟s e-mail address: [email protected]; [email protected]; [email protected];

1 Gerard Caprio, Jr., is a William Brough Professor of Economics and Chair of the Center for Development Economics

at Williams College; Vincenzo D‟Apice is economist at the economic research department of Italian Banking

Association and research coordinator at Istituto Einaudi (IstEin), Giovanni Ferri is Chair of the Department of

Economics at University of Bari; and Giovanni Walter Puopolo is assistant professor at Bocconi University. This

paper‟s findings, interpretations, and conclusions are entirely those of the authors and do not necessarily represent the

views of the World Bank, Italian Banking Association and Bocconi University.

Electronic copy available at: http://ssrn.com/abstract=1788063

2

1. Introduction

As much as it was known that the Great Depression of the 1930s was the acid test for any reputable

macroeconomic theory, the outbreak of the Great Financial crisis of 2007-2009 has shaken not only

financial institutions, but also long-held beliefs and theories on how the regulation of the financial

system should be structured.

In turn, ongoing financial regulatory reforms have sparked a vibrant debate among institutions,

academics and practitioners. On the one hand, the Basel Committee, through its consultative

document (BCBS, 2009), seems more focused on the stability of the financial system, arguing that

the costs of the new regulation will be much lower than the relative benefits (BCBS 2010, MAG

2010). On the other hand, the banking industry argues that the new measures could put economic

growth at risk imposing high costs on the financial intermediaries and, in turn, on economic systems

(IIF, 2010). In the middle, some academics argue that the principles implicitly or explicitly

subscribed by the Basel Committee may be questionable to secure more resilient financial systems

(see, among others, Ferri (2001), Barth, Caprio and Levine (2004), (2006), and Caprio (2010)).

Thus, a definitely crucial issue is to know the impact of the future regulation issued by

policymakers upon this trade-off between costs and benefits. However, the question cannot be

addressed without an analysis of the determinants of the financial crisis of 2007-2009. This is

exactly the purpose of this paper. Specifically, using data on 83 countries from 1998 to 2006 and

running cross-country regressions on the determinants of the probability for a country to be in crisis

in 2008, as reported by Laeven and Valencia (2010), we investigate the macro-financial factors

which contributed to the Great Crisis that broke out in 2007. A novel feature of our analysis is to

measure the financial indicators employed as explanatory variables, using the information relative

to the nine years that preceded the Great Financial crisis and not just to the most recent years before

its outbreak. In fact, we firmly believe that the early signals of what happened in 2007-2009 date

back to several years before it was so manifest. Therefore, the use of “dated variables” is justified

by the fact that they contain information about the health of the financial system and, as a

Electronic copy available at: http://ssrn.com/abstract=1788063

3

consequence, may necessarily be linked with the crisis. Unfortunately, however, we do not have

measures of the enforcement of regulation, even though Barth, Caprio and Levine (2011) cite

numerous breakdowns in enforcement as major causes of the recent crisis.

Our results show that, first, countries with a higher credit/deposit ratio had higher probability to be

in crisis in 2008. Next, a few macro determinants negatively impinged on the probability of crisis.

Namely, such probability was lower for countries with a higher level of net interest margin, and/or a

higher level of concentration in the banking sector, and/or more restrictions on bank activities,

and/or higher level of private monitoring. In particular, net interest margin tends to be more

significant the greater the importance of deposits, and to vary inversely with securitization. Banks

such as those in Canada and Italy that had a large and stable deposit base likely paid less for funds

(and so had a higher net interest margin) than those who had to rely on wholesale markets, which

proved to be more volatile. Net interest margin will also tend to be lower for banking systems more

extensively engaged in securitization, both directly as securitization fees displace interest earnings

(and interest on the securities was accruing to off-balance sheet entities), and indirectly as

securitization boosts the supply of credit from non-bank entities and, other things equal, lending

rates will diminish.

Our empirical evidence can help policymakers calibrate new regulations, by achieving a reasonable

trade-off between financial stability and economic growth. Specifically, new regulations should

consider that, compared to the traditional credit risks, it is more difficult to evaluate the new risks,

such as those emanating from the complex financial contracts so deeply entrenched in the originate

to distribute model and playing a major role in the recent crisis. At the very least this suggests

ending or reversing features that arbitrarily fosters securitization, such as ratings requirements,

which by protecting fund managers who comply with them from lawsuits, encourages the purchase

of securities with the requisite due diligence.

The remainder of the paper is structured as follows. Section II provides a review of the literature on

this topic. Section III describes the data and variables used in the econometric specifications.

4

Section IV looks at the empirical results. Section V offers some robustness checks. Section VI

concludes with some lessons and policy implication.

2. Literature Review

Our paper is complementary to two ongoing strands of empirical literature. The first one is the very

active strand that is analysing the causes of the recent global recession. The results of this strand are

still mixed. For example, Rose and Spiegel (2009) use a cross- country approach and examine a

number of potential causes of the recent crisis. They find few clear reliable indicators in the pre-

crisis data of the incidence of the great recession. In fact, in their analysis, just the natural logarithm

of 2006 real GDP per capita and the percentage change in the stock market between 2003 and 2006

are positively correlated with the severity of the crisis.

The second strand of literature, to which our paper is complementary, is the one that is more

focused on the causes of financial crisis. To this regard, Claessens et al (2010) find that the recent

financial crisis has four major features similar to earlier episodes. First, asset prices rapidly

increased in a number of countries before the crisis. Second, a number of key economies

experienced episodes of credit booms ahead of the crisis. Third, there was a dramatic expansion in a

variety of marginal loans. Fourth, the regulation and supervision of financial institutions failed to

keep up with developments. They also find that the recent crisis was different than the previous

ones in at least four new aspects. First, there was a widespread use of complex and opaque financial

instruments. Second, the interconnectedness among financial markets, nationally and

internationally, with the United States at the core, had increased in a short time period. Third, the

degree of leverage of financial institutions accelerated sharply. Fourth, the household sector played

a central role.

However the question addressed in this paper is both different and more limited. It can be stated as

follows: What are the financial structure factors which contributed to the Great Crisis? Thus, the

closest paper to ours is Barth, Caprio and Levine (2004). Using their database on bank regulation

5

and supervision in 107 countries to assess the relationship between specific regulatory and

supervisory practices and banking-sector development, efficiency, and stability, they show that the

likelihood of suffering a major crisis is greater the more countries: (1) restrict bank activities (or

prevent or discourage diversification of income through non-traditional activities); (2) put limits on

foreign bank entry/ownership; (3) or exacerbate moral hazard via a more generous deposit

insurance scheme fragility. On the other hand, neither capital stringency nor official supervisory

powers – which approximate pillars one and two, respectively of Basel II, is robustly linked with

banking crises when controlling for other supervisory/regulatory policies; similarly, there is no

significant association between private-sector monitoring and the likelihood of a banking crisis and

only a weak positive relationship between government ownership and the likelihood of a crisis.

Our work differs from theirs according to several dimensions. First, we refer to the Great Financial

Crisis of 2007-2009 and use a different classification, based on Laeven and Valencia (2010), to

identify countries as borderline crisis or systemic crisis. Second, we extend the set of macro

financial indicators as possible explanatory variables of the probability to be in crisis in 2008.

Third, we do not restrict the observations to a precise year (for example 1999 as done by the already

cited authors), rather we consider the mean from 1998 to 2006 of these financial factors to take into

account the long-term evolution of the financial sector before the Great Crisis broke out in 2007.2

Others relevant papers, relating to the purpose of our research, are the following.

Before the Great Financial crisis of 2007-2009, Demirguc-Kunt and Detragiache (1998) investigate

the relationship between banking crises and measures aimed at increasing the level of financial

liberalization in 53 countries during the period 1980-1995, though they did so with no data on

regulation and supervision. They find that banking crises are more likely to occur in liberalized

financial systems. Mehrez and Kaufmann (2000) employ a multivariate probit model for 56

countries from 1977 to 1997 to examine how the level of corruption (i.e. transparency) affects the

2 Moreover, in this way we limit endogeneity issues. See next sections.

6

likelihood of a financial crises. They report that, in a country where the government policy is

characterized by lack of transparency, banks have incentives to raise credit above the optimal level,

thus increasing the probability of a banking crisis.

On a cross-country analysis, Beck, Demirguc-Kunt and Levine (2006), using data on 69 countries

from 1980 to 1997, study the impact of bank concentration, bank regulation, and national institution

on the probability that a country can experience a systemic banking crisis. Besides the relationship

between systemic banking crises and concentration, they also examine international differences in

bank capital regulations, rules restricting bank entry, regulatory restrictions on bank activities and

the overall institutional environment. They show that crises are less likely in economies

characterized by: 1) more concentrated banking systems; 2) fewer regulatory restrictions on banks,

(i.e. lower barriers to bank entry and fewer restrictions on bank activities); 3) national institutions

that facilitate competition. Finally, Shehzad and De Hann (2009) analyze the impact of financial

reform on systemic and non systemic banking crises in 85 countries, from 1973 to 2002, finding

that certain types of financial reform reduce the likelihood of crisis.

After the Great Financial crisis of 2007-2009, Giannone et al (2010) use indexes of country risk in

cross-section regressions for over one hundred countries. They find that the set of policies that

favour liberalization in credit markets are negatively correlated with the output growth in 2008 and

2009.

Moving to bank-level data, Beltratti and Stulz (2009) analyzed 98 large banks from 20 countries

and investigated whether bank performance is related to bank-level governance, country-level

governance, bank balance sheet and profitability characteristics before the crisis, and country-level

regulation. Their key results were: 1) banks that the market favoured in 2006 had especially poor

returns during the crisis; 2) banks with more shareholder-friendly boards performed worse during

the crisis; 3) banks in countries with stricter capital requirement regulations and with more

independent supervisors performed better; 4) banks in countries with more powerful supervisors

had worse stock returns; 5) large banks with more Tier 1 capital and more deposit financing at the

7

end of 2006 had significantly higher returns during the crisis. Additional contribution related to

micro-level data is De Jonghe (2009). He investigates why some banks are better able to shelter

themselves from the storm by analyzing the impact of revenue diversity of financial corporations on

banking system stability. He shows that the shift to non-traditional banking activities, which

generate commissions, trading and other non-interest income, increases individual banks risks and

thus reduces the stability of the financial system.

3 Data and Methodology

Our database provides information on 83 countries from the period 1998-2008, including OECD as

well as many non-OECD and developing countries.3

4 Table 1 shows descriptive statistics for the

relevant variables.

In order to identify the macro and financial structure factors contributing to the Great Crisis, we run

cross-country regressions on the determinants of the probability that a country will experience crisis

in 2008. Specifically, for 83 countries, we estimate several probit models, robust to

heteroskedasticity, in which the dependent variable is a dummy variable equal to one if the country

is classified as either borderline crisis or systemic crisis according to the definition introduced by

Laeven and Valencia (2010), and zero otherwise. Moreover, to assess the impact of the financial

globalization indicator on the probability of the crisis, we estimate an instrumental-variables probit

model which takes into account the potential endogeneity problem related to the use of this variable.

For robustness check, we run two different specifications: an ordered probit model (in which the

3 Our original sample included 215 countries. However, we drop some countries based on the following criteria: 1)

countries with missing observations for the relevant variables, and 2) countries falling in the bottom 25% of the sample

according to the Credit/GPD ratio, i.e. countries with a Credit/GDP ratio below 14.4%.

4 We select 1998 as starting year because the source of our regulation variables begin in this year. In fact, we take these

variables from the three surveys conducted by Barth, Caprio and Levine (2004). Specifically, survey I was conducted to

asses the state of regulation in 1998, survey II was conducted to asses the state of regulation in 2002, and survey III was

conducted to asses the state of regulation in 2005.

8

dependent variable is a dummy taking the values of 0 in case of no crisis, 1 in case of borderline

crisis, and 2 in case of systematic crisis), and a tobit model (where the dependent variable is the

ratio of financial support offered by the government to Gross Domestic Product).

Here are the variables used in our specifications. The dependent variable is:

CRISIS = dummy equal to 1 if the country is classified as either borderline crisis or systemic crisis

by Laeven and Valencia (2010) and 0 otherwise. The average of this variable is 0.23 with a

standard deviation of 0.42 (see Table 1).

We also provide robustness checks using alternative definitions of crises in section 5.

We use many independent variables to take into account various characteristics of the national

financial systems. In particular, we use the following banking variables:

NET_INTEREST_MARGIN = mean of the accounting value of the bank's net interest revenue, as a

share of its interest-bearing assets, from 1998 to 2006 (source: Beck, Demirgüç-Kunt and

Levine (2000)). This variable measures the banking system orientation towards traditional

activity. Indeed, if this variable decreases, the incentive for banks to look for other income

sources increases (Beck, Demirgüç-Kunt and Levine (2000)). The average of this variable

is 4.3% with a standard deviation of 2.4% (see Table 1).

ROA = mean of average return on assets (net income/total assets) from 1998 to 2006 (source: Beck,

Demirgüç-Kunt and Levine (2000)). This variable measures the banking system

profitability, but it is not influenced by leverage. The average ROA is 1% with a standard

deviation of 1.1%5.

ROE = mean of average return on equity (net income/total equity) from 1998 to 2006 (source: Beck,

Demirgüç-Kunt and Levine (2000)). This variable measures the banking system

profitability. The average ROE is 10.7% with a standard deviation of 10.1%.

5 The negative numbers for the minimum values of ROA and ROE depend on the inclusion in the sample of some

countries suffering a systemic financial crises during 1998-2006: Argentina, Korea, Rep., Japan , Thailand and

Uruguay.

9

COST_INCOME = mean value of total costs as a share of total income of all commercial banks

from 1998 to 2006 (source: Beck, Demirgüç-Kunt and Levine (2000)). This is a measure of

bank efficiency with higher ratios indicating lower levels of cost efficiency. The average of

this variable is 67.7% with a standard deviation of 14.9% (see Table 1).

Z-SCORE = mean value bank z-score from 1998 to 2006 (source: Beck, Demirgüç-Kunt and Levine

(2000)). The z-score is the ratio of return on assets plus capital-asset-ratio to the standard

deviation of return on assets. As a higher z-score indicates that the bank is more stable, this

index can be seen as the inverse of the probability of insolvency. The average of this

variable is 11.3 with a standard deviation of 6.6 (see Table 1).

CREDIT_DEPOSIT = mean value of the ratio of loans to deposits from 1998 to 2006 (source: Beck,

Demirgüç-Kunt and Levine (2000)). While a high loan-deposit ratio indicates high

intermediation efficiency, a ratio significantly above one also suggests that private sector

lending is funded with non-deposit sources, which could result in funding instability (Beck,

Demirgüç-Kunt and Levine (2000)). However, it also could be true that the other sources

of funding are in the form of retail bonds and so they might be as stable as deposits. This

will likely depend on national specificities (such as in the case of Italy). Although the

database does not allow us to tell apart whether the unstable liabilities hypothesis – linked

to wholesale funding – or the relatively stable retail bond funding apply to any specific

country, we suspect the former cases are more frequent than the latter. The average of

credit deposit ratio is 102.2%, with a standard deviation of 38.6% (see Table 1).

CONCENTRATION = mean of assets of the three largest banks as a share of assets of all

commercial banks, from 1998 to 2006 (source: Beck, Demirgüç-Kunt and Levine (2000)).

The average of this variable is 67.4% with a standard deviation of 18.9%.

We take into account the different degree of financial globalization with the following variable:

INT_DEBT_ISS_GROSS_GDP = mean of the gross flow of international bond issues, relative to

GDP, from 1998 to 2006 (source: Beck, Demirgüç-Kunt and Levine (2000)). This variable

10

measures the degree to which a country‟s financial system is interlinked with international

financial markets. The average of international debt issues is 21.9% with a standard

deviation of 25.8% (see Table 1).

We also use five measure of bank regulation:

RESTRICTION = mean value of the “Overall Restrictions” index reported in the three surveys by

Barth, Caprio and Levine (2004). This index measures the degree to which banks face

regulatory restrictions on their activities in: (a) securities markets, (b) insurance, (c) real-

estate, and (d) owning shares in non-financial firms. For each of these four sub-categories,

the value ranges from a 0 to 4, where a 4 indicates the most restrictive regulations on this

sub-category of bank activity. Thus, the index of overall restrictions can potentially range

from 0 to 16. The average of this index is 7.4 with a standard deviation of 1.7 (see Table

1).

PRIVATE MONITORING = mean value of the “Private Monitoring” index reported in the three

surveys by Barth, Caprio and Levine (2004). This index measures the degree to which

regulations empower, facilitate, and encourage the private sector to monitor banks. It is

composed of information on whether (1) bank directors and officials are legally liable for

the accuracy of information disclosed to the public, (2) whether banks must publish

consolidated accounts, (3) whether banks must be audited by certified international

auditors, (4) whether 100% of the largest 10 banks are rated by international rating

agencies, (5) whether off-balance sheet items are disclosed to the public, (6) whether banks

must disclose their risk management procedures to the public, (7) whether accrued, though

unpaid interest/principal enter the income statement while the loan is still non-performing

(8) whether subordinated debt is allowable as part of capital, and (9) whether there is no

explicit deposit insurance system and no insurance was paid the last time a bank failed.

The private monitoring index has a maximum value of 9 and a minimum value of 0, where

larger numbers indicate greater regulatory empowerment of private monitoring of banks.

11

This index can be seen as a measure of Basel Pillar 3. The average of this index is 8.2 with

a standard deviation of 1.3 (see Table 1).

CAPITAL = mean value of the “Capital Regulation” index reported in the three surveys by Barth,

Caprio and Levine (2004). This index includes information on (1) the extent of regulatory

requirements regarding the amount of capital banks must hold and (2) the stringency of

regulations on the source of funds that count as regulatory capital can include assets other

than cash or government securities, borrowed funds, and whether the

regulatory/supervisory authorities verify the sources of capital. Large values indicate more

stringent capital regulations and it can be considered as a proxy of Basel Pillar I. The

average of this index is 6.2 with a standard deviation of 1.5 (see Table 1).

ENTRY = mean value of the “Entry Requirements” index reported in the three surveys by Barth,

Caprio and Levine (2004). This index essentially counts the number of requirements for a

banking license: (1) draft by-laws; (2) intended organizational chart; (3) financial

projections for first three years; (4) financial information on main potential shareholders;

(5) background/experience of future directors; (6) background/experience of future

managers; (7) sources of funds to be used to capitalize the new bank; and (8) market

differentiation intended for the new bank. Thus, this index is a proxy for the hurdles that

entrants have to overcome to get a license. The average of this index is 7.4 with a standard

deviation of 0.9 (see Table 1).

SUPERVISION = mean value of the “Official Supervisory” index reported in the three surveys by

Barth, Caprio and Levine (2004). This index measures the degree to which the country‟s

commercial bank supervisory agency has the authority to take specific actions. It is

composed of information on many features of official supervision: (1) does the supervisory

agency have the right to meet with external auditors about banks? (2) are auditors required

to communicate directly to the supervisory agency about elicit activities, fraud, or insider

abuse? (3) can supervisors take legal action against external auditors for negligence? (4)

12

can the supervisory authority force a bank to change its internal organizational structure?

(5) are off-balance sheet items disclosed to supervisors? (6) can the supervisory agency

order the bank's directors or management to constitute provisions to cover actual or

potential losses? (7) can the supervisory agency suspend the directors' decision to

distribute: a) dividends? b) bonuses? c) management fees? (8) can the supervisory agency

supersede the rights of bank shareholders-and declare a bank insolvent? (9) can the

supervisory agency suspend some or all ownership rights? (10) can the supervisory agency:

a) supersede shareholder rights? b) remove and replace management? c) remove and

replace directors? The official supervisory index has a maximum value of 14 and a

minimum value of 0, where larger numbers indicate greater power. It can be seen as a

measure of Basel pillar 2. The average of this index is 10.9 with a standard deviation of 2.3

(see Table 1).

Finally, we control for other national characteristics such as GDP and population.

In the next section, we provide evidence on the main macro-financial determinants of the Great

Crisis.

4 Empirical Evidence

4.1 Probit model

We start our investigation of the determinants of the probability that a country will experience crisis

in 2008 by estimating the following probit model:6

CRISISi = α + 1 NET_INTEREST_MARGINi + 2 CREDIT_DEPOSITi + 3 CONCENTRATIONi

+ 4 RESTRICTIONi + 5 PRIVATE MONITORINGi + εi, (1)

6 All the regressions are estimated with heteroschedasticity-robust standard errors.

13

where the dependent variable, CRISISi, is a dummy equal to 1 if the country is classified as crisis

and 0 otherwise.

We think that one of the most important banking cause of the recent crisis is the shift from the

“originate to hold (OtH)” model to “originate to distribute (OtD)” model (see, for example, Berndt

and Gupta (2009), Mian and Sufi (2009), Stiglitz (2010), Eichengreen (2009), FSA (2009), D‟Apice

and Ferri (2010), Mishkin (2008), Trichet (2009)). Thus, we use the NET_INTEREST_MARGIN

variable to verify if higher incentive to perform traditional banking activities could be a deterrent

against the crisis. In fact, if this variable decreases, the incentive for banks to look for other income

sources increases (Beck, Demirgüç-Kunt and Levine (2000)).

One of the most striking feature of the 2007-2009 financial crisis was the impact on the money

markets and global liquidity (Cecchetti (2009), Allen and Carletti (2008), Brunnermeier (2009)).

Thus, we use the CREDIT_DEPOSIT variable to verify the role of maturity mismatching. In fact, a

ratio significantly above one also suggests that private sector lending is funded with non-deposit

sources, which could result in funding instability (Beck, Demirgüç-Kunt and Levine (2000)).

Also the structure of the banking system may be an important aspect of the country‟s resilience to

the crisis (Carletti (2010)). In truth, economic theory provides conflicting predictions about the

relationship between concentration and stability. In particular, there are two different views in the

literature. On the one hand, the charter value hypothesis (e.g. Allen and Gale (2000a), (2000b),

(2004b)) argues that concentration enhances stability. On the other hand, optimal contracting

hypothesis (Boyd and De Nicolo, (2005)) argues the opposite. We consider the matter to be an

empirical one, and accordingly, we use the variable CONCENTRATION to proxy the structure of

the banking system.

Many analysis argue that the flaws in the regulatory framework are very important causes of the

crisis (Demirguc-Kunt and Serven (2009), Coval et al. (2009), Buiter (2007), De Michelis (2009)).

To take accounts of regulatory regime characteristics, we use the regulatory indexes provided by

Barth, Caprio and Levine (2004). In the basic specification we use RESTRICTION, as a proxy of

14

regulatory restrictions on banking activities, PRIVATE MONITORING, as a proxy of Basel Pillar

3.

Specification 1 in Table 2 shows the results. First, the coefficient of NET_INTEREST_MARGIN is

negative and statistically significant. This indicates that countries with a higher level of net interest

margin had a lower probability to be in crisis in 2008; higher net interest income is associated with

less securitization, and also might be picking up the impact of competition (e.g. less competitive

systems such as Australia and Canada survived the crisis quite well, though this result might be

related to other features of their regulatory or institutional settings as well). Indeed, a higher level of

net interest margin represents a strong incentive for banks to undertake traditional activities (e.g.

loans), instead of riskier non-traditional activities (e.g. securities trading). Second, the coefficient of

CREDIT_DEPOSIT is positive and statistically significant. This indicates that countries with a

higher credit/deposit ratio had a higher probability to be in crisis in 2008. As a matter of fact, a ratio

significantly above one suggests that bank lending is funded with non-deposit sources. While some

of the other sources may be as stable as customer deposits – i.e. retail bonds funding – several of

these sources alternative to retail deposits can prove highly volatile, such as in the case of interbank

or money market loans. Thus, considering that the 2007-09 crisis featured a dramatic drop in the

availability of wholesale funding, our evidence suggests that in most of the countries the alternative

funding sources were of the volatile type. Moreover, since non-deposit sources (e.g. wholesale

funding) are typically more expensive, higher credit/deposit ratio is associated with lower net

interest margin and, as a consequence, with a higher probability of crisis. Third, the coefficient of

CONCENTRATION is negative and statistically significant. This indicates that countries with a

higher level of concentration in the banking sector had lower probability to be in crisis in 2008, a

finding consistent with the absence, thus far, of a crisis in Australia or Canada. Our result seems in

line with the empirical evidence provided by Beck, Demirgüç-Kunt and Levine (2006) who find

that crises are less likely in economies with more concentrated banking systems. Fourth, the

coefficient of RESTRICTION is negative and statistically significant. This indicates that countries

15

with more restrictions on bank activities had lower probability to be in crisis in 2008. In other

words, regulatory-induced specialization in the banking sector enhances financial stability7. Fifth,

the coefficient of PRIVATE MONITORING is negative and statistically significant, though

previously evidence of a relationship between private monitoring and stability was hard to find.

This indicates that countries with a higher level of private monitoring had a lower probability to be

in crisis in 2008. This finding is in line with the goal of the third pillar of the Basel II Capital

Accord (Barth, Caprio and Levine, (2004))8.

The results in model 1 show high resilience when we include the other independent variables from

model 2 to model 9. Moreover, measures of banking efficiency (cost-income), stability (z-score),

profitability (ROA and ROE), the log of GDP and the log of population are never significant at the

conventional levels. When controlling for the other variables in the base specification of model 1,

the coefficients of CAPITAL and ENTRY turn out positive and significant9. With regard to

CAPITAL, this suggests that countries with a higher level of capital restriction had a higher

probability to be in crisis in 2008. This finding is clearly at odds with the goal of the first pillar of

the Basel II Capital Accord. However, one lesson of the 2008 crisis is that capital adequacy was

almost irrelevant. For example, Northern Rock got in trouble just few weeks after the bank had

announced plans to return excess capital to shareholders. On the other hand, the importance of

capital in lowering risk taking by banks could work in some specific circumstances. For instance,

Laeven and Levine (2010), combining the Bankscope data with the regulatory database, find that

higher capital does lead to safer banks when there is a strategic owner, but when ownership is

highly diversified, higher capital is associated with more risk taking. Indeed, when there is no

strategic (large) owner, then everyone free rides and wants to go for the higher return. On the

contrary, when a strategic owner has control rights, which is like a high franchise value, that keeps

7 The reader should bear in mind that our results pertain to the extreme financial crisis of 2007-09 and generalizing

them to less extreme crisis cases may be inappropriate. The same consideration applies to the counter-intuitive result,

showed hereinafter, that a higher level of Capital increases the probability of crisis. 8 This specification is robust to a Montecarlo simulation with 100 replications.

9 None of these two variables showed significant if regressed individually against the dependent variable.

16

the banks more conservative, just as some concentrated-ownership banks adopted the practice of

plowing more bonuses into deferred equity to keep managers more risk averse.

With regard to ENTRY, the result means that a country with a higher level of entry restriction had a

higher probability to be in crisis in 2008. This result is in accordance with the mainstream view that

entry restrictions build inefficiency and, hence, instability. It should be also noted that this result is

not in contrast with the role of concentration. Indeed, Beck, Demirgüç-Kunt and Levine (2006) find

that competition reduces fragility when controlling for concentration. Finally, the regulatory

variable SUPERVISION is not significant at the conventional levels.

Going back to the base specification, it is worthwhile assessing also the quantitative importance of

the various determinants. Using a dprobit method, column 1‟ in Table 2b shows that the two most

important regressors – respectively among the continuous independent variables

(NET_INTEREST_MARGIN, CREDIT_DEPOSIT and CONCENTRATION) and among the

discrete independent variables (RESTRICTION and PRIVATE MONITORING) are

NET_INTEREST_MARGIN and RESTRICTION. A marginal change in the former (latter)

associates with a 4.4% (7.9%) lower probability of crisis.

4.2 Probit instrumental variables model

Up to here we have not included the variable INT_DEBT_ISS_GROSS_GDP measuring the degree

to which a country‟s financial system is interlinked with international financial markets. This is, of

course, an important variable to consider especially in view of the fact that international contagion

was one of the chief channel to spread the crisis worldwide. However, the inclusion of this

independent variable raises problems of endogeneity. Indeed, there is an extensive literature

studying the possibility that the extent of financial globalization of a country depends not only on

its level of development and on its policies but is influenced by deeper fundamental factors. Just to

quote a few authors, this is one of the chief points made by Acemoglu and Johnson (2005), Collins

(2005), Faria and Mauro (2005), Kose et al. (2006), Spiegel (2008), Tytell and Wei (2005), Wei

17

(2006). Following this literature, to avoid biases in our empirical analysis it is important that we

control for this endogeneity when we include the financial globalization variable in our regressions.

The most common way used in the literature to solve this type of endogeneity problem among the

dependent and the independent variables is through the method of instrumental variables (IV).

Therefore, in our setting, it is natural to use an instrumental variables probit model to measure the

probability of crisis in 2008. Based on this procedure, we estimate simultaneously the following

two equations:10

INT_DEBT_ISS_GROSS_GDPi = α+ γ1 NET_INTEREST_MARGINi + γ2 CREDIT_DEPOSITi + γ3

CONCENTRATIONi + γ4 RESTRICTIONi + γ5 PRIVATE MONITORINGi + γ6 LEGAL ORIGIN –

BRITISHi + γ7 LEGAL ORIGIN – FRENCHi + γ8 LEGAL ORIGIN – SOCIALISTi + γ9 LEGAL

ORIGIN – GERMANi + γ10 ETHNIC FRACTIONALIZATIONi + γ11 RELIGION

FRACTIONALIZATIONi + γ12 LANGUAGE FRACTIONALIZATIONi + ε2i (2)

CRISISi = α + 1 INT_DEBT_ISS_GROSS_GDP_IVi + 2 NET_INTEREST_MARGINi + 3

CREDIT_DEPOSITi + 4 CONCENTRATIONi + 5 RESTRICTIONi + 6 PRIVATE MONITORINGi

+ ε3i (3)

In equation (2), the procedure estimates INT_DEBT_ISS_GROSS_GDP using as control variables

all the regressors of the base specification, i.e. equation (1), plus the variables: LEGAL ORIGINS

(British, French, Socialist and German) taken from La Porta et al. (1997 and following updates),

and ETHNIC, RELIGIOUS and LANGUAGE FRACTIONALIZATION taken from Alesina et al.

(2003). These instruments are among those most widely used in the literature (Beck, Demirgüç-

Kunt, Levine, (2006); Ponczek V., Mattos E., (2009); Glaeser et al. (2004)). In equation (3), the

10 In STATA, the ivprobit command implements Full Information Maximum Likelihood to estimate the binary and

continuous parts of the model simultaneously which will yield consistent standard-errors.

18

procedure uses the predicted estimate of INT_DEBT_ISS_GROSS_GDP from equation (2) and the

other independent variables to estimate the probability to be in crisis in 2008, while the dependent

variable does not change, being the standard dummy equal to 1 if the country is classified as crisis

and 0 otherwise.

From Table 3, we can see that the results obtained with the probit specification remain almost

unchanged as INT_DEBT_ISS_GROSS_GDP_IV is not significant. The only difference is that

CONCENTRATION is no longer significant in this specification (with a p-value of 13%). As

regards the IV approach, the correlation coefficient between the two equations (rho) equals .86. The

likelihood ratio test for whether this is significantly different from zero is reported in the last line of

the output. In this case the p-value is 0.0028. The significance of this correlation coefficient

confirms that the INT_DEBT_ISS_GROSS_GDP variable is endogenous.

The endogeneity problem is an issue which involves exclusively the variable

INT_DEBT_ISS_GROSS_GDP, but not the other regressors used in the probit models 1 to 9. In

fact, on the one hand, it is worthwhile to underline that most of these explanatory variables are

measured as the average of the annual observations from 1998 to 2006, circumstance which clearly

attenuates the potential correlation between the independent variables and the residual in the

regression specifications. On the other hand, following the procedure described in (2) and (3), we

estimated several instrumental-variable probit models, where, in each model, in turn, a regressor of

the base model (1) was treated as potential source of endogeneity. Using the same set of

instruments, the hypothesis of endogeneity was rejected for all these independent variables.11

5. Robustness Checks

In this section we provide evidence about the robustness of our results relative to different model

specifications and crisis definitions. We start by estimating an ordered probit model.

11 Results are not reported and are available upon request.

19

5.1 Ordered Probit Model

As first robustness check, we estimate the following ordered probit model:

ORDERED_CRISISi = α + 1 NET_INTEREST_MARGINi + 2 CREDIT_DEPOSITi + 3

CONCENTRATIONi + 4RESTRICTIONi + 5 PRIVATE MONITORINGi + ε4i. (4)

The only difference with respect to the probit model being the dependent variable which is now

ORDERED_CRISIS (dummy equal to 1 if the country is classified as borderline crisis, equal to 2 if

the country is classified as systemic crisis and 0 otherwise). The average of this variable is 0.36

with a standard deviation of 0.71 (see Table 1).

From Table 4, we can see that even with the ordered probit specification the results obtained with

the probit model remain unchanged.

5.2 Tobit model

As a second robustness check, we want to verify whether our results stand up to replacing dummy-

type crisis indicators with alternative measures of crisis based on continuous-type variables. In this

respect, the most natural measure one can think of is the extent to which public finances had to be

employed to avoid the meltdown of the national banking system. In practice, we take the sum of the

various forms of support provided by the Government to the national banking system and we scale

down the grand total to GDP12

. This crisis measure has the lower bound of zero for those countries

12 As reported in Leaven and Valencia (2010), there are three types of support: i) liquidity support, ii) gross

restructuring costs, and iii) asset purchases and guarantees. We disregard liquidity support for three reasons. First,

strictly speaking, it is provided by the Central Bank and not by the Government. Second, as such, it is impossible to

break it down by country across the Euro zone. Third, more importantly, liquidity support may be a really transient

measure whose cost could be inherently limited. Thus, we use the conservative measure of Government support given

by the sum of restructuring costs and asset purchases (we also disregard the entity of the guarantees as it is difficult to

quantify what their real ex-post cost would actually be).

20

suffering no crisis and the upper bound of 18.5% for the country suffering the most (United

Kingdom).

From an econometric standpoint, the existence of both a lower bound and an upper bound to the

range of the dependent variable calls for employing a Tobit approach rather than an OLS-type

specification. In practice, the Tobit model we estimate is the following:

CRISIS_COST_GDPi = α + 1 NET_INTEREST_MARGINi + 2 CREDIT_DEPOSITi + 3

CONCENTRATIONi + 4RESTRICTIONi + 5 PRIVATE MONITORINGi + ε5i. (5)

With respect to the base probit model, the dependent variable is now CRISIS_COST_GDP (a

variable that measures the cost of public support to the financial system as a ratio to GDP). The

average of this variable is 1.11 with a standard deviation of 3.20 (see Table 1).

From Table 5, we can see that the results obtained with the probit model remain almost unchanged.

The only difference is that PRIVATE MONITORING is no longer significant at the conventional

level (with a p-value of 11%).

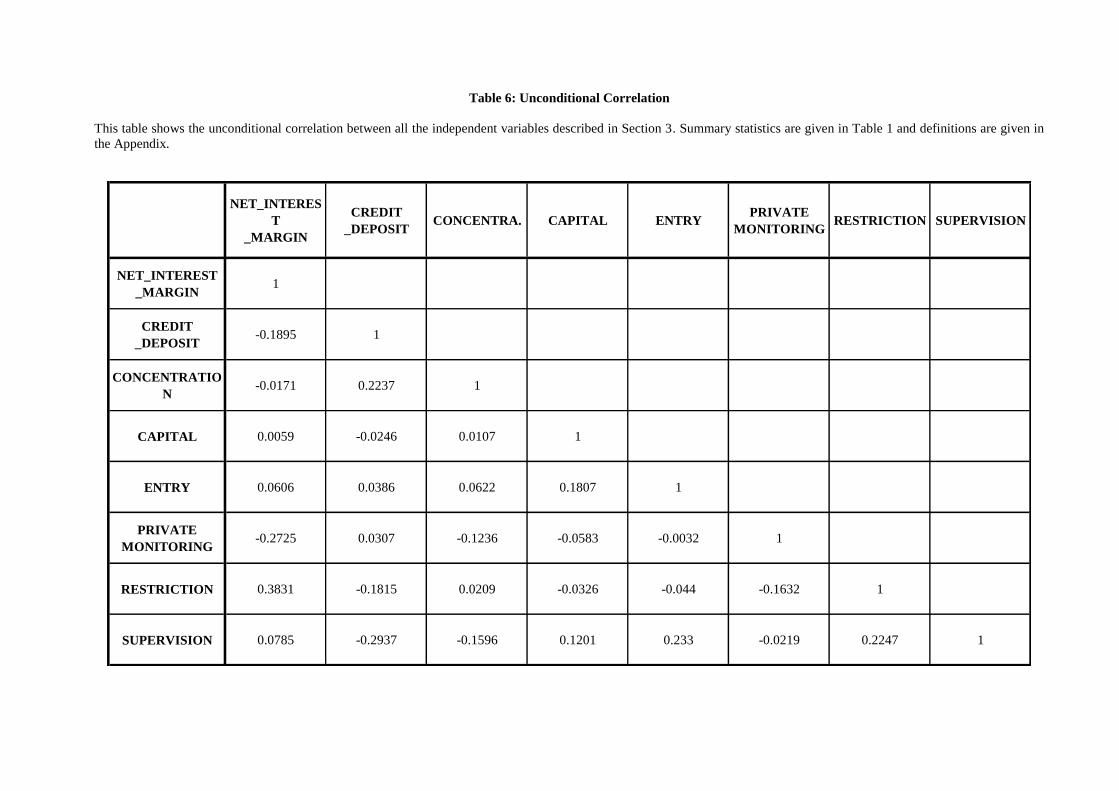

5.3. Multicollinearity

The independent variables used to characterize the basic model (1) belong to a quite heterogeneous

group of financial indicators. However, on the one hand, there are the accounting variables like

NET_INTEREST_MARGIN, COST_INCOME, ROA and ROE which are observed annually and

have to do with the balance sheet of the banks, therefore belonging to the category of financial

performance indicators, whereas, on the contrary, the variables RESTRICTION, PRIVATE

MONITORING, CAPITAL, ENTRY and SUPERVISION refer to the indices reported in the three

surveys by Barth, Caprio and Levine (2004), and somehow reflect the financial background (or

structure) of the countries. Given the different nature of the independent variables used in the

21

regressions, one may suspect that the “structure variables” could have an impact not only on the

probability for a country to be in crisis in 2008, but also on some of the “performance variables”,

giving rise to a clear problem of multicollinearity.

In this section, we consider the issue of potentially-correlated regressors and show that, once

multicollinearity is taken into account, our results still hold.

In order to detect the presence of multicollinearity we compute the unconditional correlation

between the independent variables used in the base model (1). The results of Table 6 show that all

the correlation coefficients are smaller than │0.4│, and 27 out of 28 observations even smaller than

│0.3│. This evidence suggests that, in general, the linear relationship between any pair of these

variables is quite weak, and, most importantly, that the “structure variables” do not have a big

influence on the “performance variables”. However, the presence of a correlation coefficient close

to 0.4 might induce a minimum degree of suspect of multicollinearity between the variables

NET_INTEREST_MARGIN and RESTRICTION, both used as regressors in equation (1).

We take into account these results and estimate a slightly different base specification probit model.

We first regress NET_INTEREST_MARGIN on RESTRICTION (and a constant), that is:

NET_INTEREST_MARGINi = γ0 + γ1 RESTRICTION i +ξi. (6)

Then, we estimate the residual ξ and use it as explanatory variable in the following probit model:

CRISISi = α + 1 RESIDUALi + 2 CREDIT_DEPOSITi + 3 CONCENTRATIONi + 4

RESTRICTIONi + 5 PRIVATE MONITORINGi + εi, (7)

where the variable RESIDUALi is the estimated residual of regression (6).13

13 Both equations (6) and (7) are estimated with heteroskedasticity robust standard errors.

22

The rationale behind this two-step procedure is quite intuitive. In fact, by regressing

NET_INTEREST_MARGIN on RESTRICTION we are isolating the effects of the independent

variable and let the residual capture all the other random factors which may influence

NET_INTEREST_MARGIN.

Table 7 panel A and B shows that, respectively, in equation (6) the coefficient of RESTRICTION is

indeed significant, and, most importantly, in equation (7), the substitution of the variable

NET_INTEREST_MARGIN with the variable RESIDUAL does not alter the validity of our base

specification.14

In fact, the estimated coefficient of RESIDUAL is negative and significant, while all

the other regressors are qualitatively unchanged.

6. Conclusions

Although there is growing consensus that regaining stability - today as much as it did in the 1930s -

requires better regulation of the marketplace (D‟Apice and Ferri, (2010)), there is little consensus as

to what „better‟ would entail. More of the same seems hardly a satisfactory response. In previous

decades, banking systems underwent deep transformation progressively moving away from a type

of banking centred on personal relationships to hinge on more standardised and impersonal

approaches. The change, designed to reach unprecedentedly high returns, theorised by some

consultants and academics, prescribed gearing the banks with financial markets and modifying the

bank business model. This had a notable impact on the transformation of some banking systems –

those that shifted toward a new business model (e.g. originate to distribute, OTD) - , while others

remained firmly fastened to a traditional business model (e.g. originate to hold, OTH). The results

in this paper show that a more traditional banking system had a lower probability to be in crisis in

14 We have also tried different cases of suspect multicollinearity. Specifically, we regressed 1)

NET_INTEREST_MARGIN on RESTRICTION and PRIVATE_MONITORING, and 2) CREDIT_DEPOSIT on

SUPERVISION. Then, we used the estimated residual of 1) and/or 2) in the probit model, and no difference showed up.

23

2008. Thus, a return to an old style banking, like the one prevailing during the Quite Period in the

US after the Great Depression (Gorton (2009)), is being considered in some quarters.

The results we reached in this paper provide fuel to that discussion. In particular we touched upon

five important aspects. First, countries with a higher level of net interest margin had a lower

probability to be in crisis in 2008. Indeed, a higher level of net interest margin represents a strong

incentive for banks to undertake traditional activities (e.g. loans) instead of riskier non-traditional

activities (e.g. securities trading). Second, countries with a higher credit/deposit ratio were more

likely unstable, unless the additional funding was provided via retail sources (such as through retail

bonds like in Italy). As a matter of fact, a ratio significantly high suggests that bank lending is

funded with non-deposit sources, which could result in funding instability. Moreover, since non-

deposit sources (e.g. wholesale funding) are typically more expensive, higher credit/deposit ratio is

associated with lower net interest margin and, as a consequence, with a higher probability of crisis.

Third, countries with a higher level of concentration in the banking sector had a lower probability to

be in crisis in 2008. Indeed, a more concentrated banking system implies that the bank‟s charter

value is higher and, as a consequence, the incentive for bank owners and managers to take excessive

risk is lower. Apparently, the beneficial bank‟s charter value effect on risk taking seems to have

prevailed – in our sample of countries – on the possible additional detrimental effect passing

through the impact of the level of competition on manager compensation schemes. Compensation

policy seemed, in fact, to be a factor in the crisis; countries with a lot of merger activity in banking

tended to have compensation systems that favored growth of banks‟ balance sheets (rewarding

return without much attention if any to risk), and these countries seemed to have the most severe

problems in the crisis (see Barth, Caprio, and Levine (2011)). Fourth, countries with stiffer

restrictions on bank activities were less likely unstable in 2008. This finding might be interpreted as

a sort of regulatory-induced specialization in the banking sector that enhances financial stability.

However, it is important to note that it contrasts with earlier studies (Barth, Caprio, and Levine

(2006)), and might in fact be a proxy for enforcement – countries that cared about imposing activity

24

restrictions might have been enforcing other regulations, and thus it might be enforcement rather

than the restrictions that matter. Unfortunately we do not have good direct measures of enforcement

to test this interpretation. Fifth, countries with a higher level of private monitoring had a lower

probability to be in crisis in 2008 (this in contrast to earlier research – Barth, Caprio, and Levine

(2006) - which found private monitoring important in a variety of areas but with no significance for

stability).

Our empirical evidence can help policymakers calibrate new regulations, by achieving a reasonable

trade-off between financial stability and economic growth. At present governments are moving in

the direction of higher capital requirements in response to the vulnerabilities highlighted in the

paper. This requires some care. Recent years saw both countries with traditional approaches to

banking (Ireland, Spain, Eastern Europe) and those that moved to a more securitized approach (the

U.S) plunge into serious crisis. The fact that capital was mostly not significant should give

regulators pause: like doctors who used leeches (and thought that they were helping patients), or

econometricians who go into a dark room looking for a black cat that is not there and scream „I‟ve

got it,‟ they may be settling for a popular cure in lieu of one that actually works. And as Laeven and

Levine (2010) find, the impact of capital requirements might vary with the ownership structure of

banks. Instead, ending those features of the broader regulatory framework that artificially boosts

securitization, and divulging and verifying more information about risk taking in banking (so that

market monitoring might work) are suggested. Thus, the Authorities should carefully consider the

macro financial determinants of the Great Crisis, especially now that a significant increase in

minimum bank capitalisation is being decided within the framework of Basel 3.

25

References

Acemoglu, D., Johnson, S., (2005), “Unbundling Institutions”, Journal of Political Economy, vol.

113(5), pages 949-995, October.

Alesina A., Devleeschauwer A., Easterly W., Kurlat S., Wacziarg R., (2003), “Fractionalization”,

Journal of Economic Growth, 8, 155-194.

Allen F., Gale D., (2000a), “Comparing Financial System”, MIT Press, Cambridge, MA.

Allen F., Gale D., (2000b), “Financial Contagion”, Journal of Political Economy.

Allen F., Gale D., (2004), “Asset Price Bubbles and Monetary Policy, in Meghnad Desai and Yahia

Said (eds.), Global Governance and Financial Crisis, Routledge, London, 19-42.

Allen F., Carletti E., (2008), “The Role of Liquidity in Financial Crises”, Jackson Hole Conference

Proceedings, Federal Reserve Bank of Kansas City, 379-412.

Barth J., Caprio G. Jr., Levine R., (2004), “Bank Regulation and Supervision: What Works Best?”,

Journal of Financial Intermediation 13, 205–248.

___________________________, (2006). “Rethinking Bank Regulation: Till Angels Govern”,

Cambridge University Press

___________________________, 2011, “The Guardians of Finance: Getting Them to Work for

Us”, MIT Press forthcoming.

Basel Committee on Banking Supervision, (2009), "Strengthening the Resilience of the Banking

Sector", Consultative Document.

___________________________________, (2010), “An Assessment of the Long-Term Economic

Impact of the New Regulatory Framework”.

Beck T., Demirgüç-Kunt A., Levine R., (2000), "A New Database on Financial Development and

Structure", World Bank Economic Review 14, 597-605.

Beck T., Demirgüç-Kunt A., Levine R., (2006), “Bank Concentration, Competition and Crises: First

Results”, Journal of Banking and Finance 30, 1581-1603.

26

Beltratti A., Stulz R.M., (2009), “Why Did Some Banks Perform Better During the Credit Crisis? A

Cross-Country Study of the Impact of Governance and Regulation”, NBER WP 15180.

Berndt A., Gupta A., (2009), “Moral Hazard and Adverse Selection in the Originate-to-Distribute

Model of Bank Credit”, Journal of Monetary Economics 56: 725-743.

Boyd J., De Nicolo G., Jalal A., (2005), “The Theory of Bank Risk Taking and Competition

Revisited”, IMF WP.

Brunnermeier M., (2009), “Deciphering the Liquidity and Credit Crunch 2007-08”, Journal of

Economic Perspectives, 23(1), 77-100.

Buiter, V., (2007), “Lessons from the 2007 Financial Crisis,” Background Paper Submitted to the

UK Treasury Select Committee, December 11, 2007.

Caprio G. Jr., (2010), "Financial Regulation in a Changing World: Lessons from the Recent Crisis",

Paper prepared for the VII Colloquium on “Financial Collapse: How are the Biggest Nations

and Organizations Managing the Crisis?”.

Carletti E., (2010), “Competition, Concentration and Stability in the Banking Sector”, IstEin WP no

8.

Cecchetti, Stephen G., (2009), “Crisis and Responses: The Federal Reserve in the Early Stages of

the Financial Crisis,” Journal of Economic Perspectives, 23(1), Winter, 51-76.

Claessens S., Köse M.A., Terrones M.E., (2010), £The Global Financial Crisis: How Similar? How

Different? How Costly?, Tüsiad-Koç University, Working Paper 1011.

Collins S.M., (2005), “Comments on “Financial Globalization, Growth, and Volatility in

Developing Countries,” by Eswar Prasad, Kenneth Rogoff, Shang-Jin Wei, and M. Ayhan

Kose,” forthcoming in Globalization and Poverty, ed. by Ann Harrison.

Coval J., Jurek J., Stafford E., (2009), “The Economics of Structured Finance”, Journal of

Economic Perspectives, 23(1), Winter, 3-25.

D‟Apice V., Ferri G., (2010), “Financial Instability: Toolkit for Interpreting Boom and Bust Cycle”,

Palgrave Macmillan Studies in Banking and Financial Institutions, London.

27

De Jonghe O., (2009), “Back to the Basics in Banking? A Micro-Analysis of Banking System

Stability”, forthcoming in Journal of Financial Intermediation.

De Michelis A., (2009), “Overcoming the Financial Crisis in the United States,” OECD Economics

Department Working Paper no. 669.

Demirguc-Kunt A., Detragiache E., (1998), “Financial Liberalization and Financial Fragility”,

World Bank Policy Research Working paper No 1917.

Demirguc-Kunt, A., Serven L, (2009), “Are the Sacred Cows Dead?: Implications of the Financial

Crisis for Macro and Financial Policies”, World Bank Policy Research Working Paper no.

4807, January.

Eichengreen B., (2009), “Anatomy of the financial crisis”, in The First Global Financial Crisis

of the 21st Century Part II: June – December, 2008, edited by Andrew Felton and Carmen M.

Reinhart, vox.org publication.

Faria A., Mauro P., (2005), “Institutions and the External Capital Structure of Countries”, IMF

Working Paper 04/236.

Feldstein M., (2009), “The Economic Stimulus and Sustained Economic Growth,” Full Statement

for the House Democratic Steering and Policy Committee, January 7.

Ferri G., (2001), "Capital Adequacy Requirements: Impact and Evolution", Opening Remarks, as

guest editor, of the special issue (no. 3/2001) Economic Notes.

Financial Services Authority (FSA), (2009), “The Turner Review A regulatory response to the

global banking crisis”.

Giannone D., Lenza M., Reichlin L., (2010), “Market Freedom and the Global Recession”, ECGI

Working Paper Series in Finance, 288/2010.

Glaeser E.L., La Porta R., Lopez-De-Silanes F., Shleifer A., (2004), “Do Institutions Cause

Growth?”, Journal of Economic Growth 9, 271-303.

28

Gorton G.B., (2009), “Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007”,

Prepared for the Federal Reserve Bank of Atlanta‟s 2009 Financial Markets Conference:

Financial Innovation and Crisis, May 11-13, 2009.

Institute of International Finance (2010), "Interim Report on the Cumulative Impact on the Global

Economy of Proposed Changes in the Banking Regulatory Framework".

Kose M.A., Prasad E., Rogoff R., Wei S-J., (2006), “Financial Globalization: A Reappraisal”, IMF

WP 06/189.

Laeven, L., Levine R., (2010), “Bank Governance, Regulation and Risk Taking”, Journal of

Financial Economics, forthcoming.

Laeven L., Valencia F., (2010), "Resolution of Banking Crises: The Good, the Bad, and the Ugly",

IMF WP 10/146.

La Porta, R., Lopez-de-Silanes F., Shleifer A., Vishny R.W., (1997), Legal Determinant of External

Finance, The Journal of Finance, 52 (3): 1131-150.

Macroeconomic Assessment Group of the Financial Stability Board and Basel Committee on

Banking Supervision, (2010), Assessing the macroeconomic impact of the transition to

stronger capital and liquidity requirements, Bank for International Settlements.

Mehrez G., Kaufman D., (2000), “Transparency, Liberalization and Banking Crises”, World Bank

Policy Research Working Paper No. 2286.

Mian A., Sufi A., (2009), "The Consequences of Mortgage Credit Expansion: Evidence from the

U.S. Mortgage Default Crisis", Quarterly Journal of Economics 124, no. 4.

Mishkin F, (2008), “Global Financial Turmoil and the World Economy,” Caesarea Forum of the

Israel Democracy Institute, Eilat, Israel, July 2.

Ponczek V., Mattos E., (2009), "Institutions and economic volatility: democracy versus risk of

expropriation", Journal of Economic Studies, Vol. 36 Iss: 2, pp.184 – 194.

Rose A., Spiegel M, (2009), “The Causes and Consequences of the 2008 Crisis:Early Warning,”

Global Journal of Economics, forthcoming.

29

Shehzad C.T., De Hann J., (2009), “Financial Reform and Banking Crises”, CESifo Working Paper

No. 2870.

Spiegel M., (2008), “Financial Globalization and Monetary Policy Discipline: A Survey with New

Evidence from Financial Remoteness”, Federal Reserve Bank of San Francisco Working

Paper 2008-10, July.

Stiglitz J., (2010), “Freefall: America, Free Markets, and the Sinking of the World Economy”, WW

Norton & Company, NY, USA.

Trichet J., (2009), “What Lessons Can be Learned from the Economic and Financial Crisis?,”

speech at the 5e Recontres de l‟Entreprise Européenne, Paris, France, March 17.

Tytell, I., Wei S-J., (2005): “Global Capital Flows and National Policy Choices,” mimeo.

Wei S-J.(2006), “Connecting two views on financial globalization: Can we make further

progress?”, Journal of the Japanese and International Economies 20 459–481.

30

Table 1: Summary Statistics

Independent variable are calculated for each country as average over 1998-2006. Detailed definitions are given in the

Appendix.

Mean Std. Min Max Obs

Dependent Variables:

CRISIS

(probit model)0.23 0.42 0.00 1.00 83

CRISIS ORDERED

(ordered probit model)0.36 0.71 0.00 2.00 83

CRISIS_COST_GDP

(tobit model)1.11 3.20 0.00 18.50 83

Independent Variables:

NET_INTEREST_MARGIN 4.3% 2.4% 0.9% 12.8% 83

CREDIT_DEPOSIT 102.2% 38.6% 35.8% 248.8% 83

CONCENTRATION 67.4% 18.9% 24.8% 100.0% 83

RESTRICTION 7.4 1.7 3.3 12.0 83

PRIVATE MONITORING 8.2 1.3 5.5 11.0 83

COST_INCOME 67.7% 14.9% 29.8% 108.5% 83

Z-SCORE 11.3 6.6 4.2 39.2 81

ROA 1.0% 1.1% -1.8% 4.4% 83

ROE 10.7% 10.1% -26.6% 50.1% 83

CAPITAL 6.2 1.5 3.0 10.0 83

ENTRY 7.4 0.9 3.7 8.0 83

SUPERVISION 10.9 2.3 5.0 14.3 82

INT_DEBT_ISS_GROSS_GDP 21.4% 25.6% 0.0% 146.0% 73

31

Table 2: Probit Specification

Probit estimation with dependent variable = CRISIS (dummy equal to 1 if the country is classified as either borderline

crisis or systemic crisis by Laeven and Valencia and 0 otherwise). *, ** and *** indicate statistical significance of the

parameters at 10, 5 and 1 percent significance level respectively. Robust standard errors appear in parenthesis.

Summary statistics are given in Table 1 and definitions are given in the Appendix.

Variables Probit 1 Probit 2 Probit 3 Probit 4 Probit 5

NET_INTEREST_MARGIN -0.241** -0.232** -0.251** -0.27** -0.24**

(0.112) (0.117) (0.115) (0.116) (0.111)

CREDIT_DEPOSIT 0.017*** 0.017*** 0.017*** 0.018*** 0.017***

(0.005) (0.005) (0.005) (0.005) (0.005)

CONCENTRATION -0.024** -0.023** -0.024** -0.024** -0.023*

(0.012) (0.011) (0.011) (0.012) (0.012)

RESTRICTION -0.43*** -0.434*** -0.461*** -0.413*** -0.435***

(0.125) (0.126) (0.124) (0.125) (0.128)

PRIVATE MONITORING -0.386** -0.377** -0.408** -0.36** -0.389**

(0.173) (0.166) (0.176) (0.165) (0.181)

COST_INCOME -0.004

(0.011)

Z-SCORE -0.019

(0.024)

ROA 0.221

(0.185)

ROE -0.004

(0.02)

CONSTANT 5.971*** 6.132*** 6.712*** 5.536*** 6.05***

(2.093) (2.231) (2.061) (1.979) (2.251)

Number of observations 83 83 81 83 83

Pseudo R-square 0.418 0.418 0.402 0.426 0.418

Wald Chi-square (p-value) 0 0 0 0 0

32

Table 2 (cont): Probit Specification

Probit estimation with dependent variable = CRISIS (dummy equal to 1 if the country is classified as either borderline

crisis or systemic crisis by Laeven and Valencia and 0 otherwise). *, ** and *** indicate statistical significance of the

parameters at 10, 5 and 1 percent significance level respectively. Robust standard errors appear in parenthesis.

Summary statistics are given in Table 1 and definitions are given in the Appendix.

Variables Probit 6 Probit 7 Probit 8 Probit 9 Probit 1'

NET_INTEREST_MARGIN -0.257** -0.248** -0.254** -0.243** -0.044**

(0.12) (0.119) (0.12) (0.106)

CREDIT_DEPOSIT 0.018*** 0.016*** 0.021*** 0.017*** 0.003***

(0.005) (0.005) (0.005) (0.005)

CONCENTRATION -0.025** -0.022* -0.023** -0.022* -0.004**

(0.012) (0.012) (0.012) (0.011)

RESTRICTION -0.466*** -0.458*** -0.498*** -0.448*** -0.079***

(0.121) (0.119) (0.13) (0.134) .

PRIVATE MONITORING -0.39** -0.39** -0.387** -0.419** -0.070**

(0.184) (0.178) (0.171) (0.173)

CAPITAL 0.232*

(0.129)

ENTRY 0.364*

(0.206)

SUPERVISION 0.158

(0.101)

LOG GDP 0.021

(0.108)

LOG POP 0.05

(0.18)

CONSTANT 4.857** 3.537 4.376* 5.318*

(2.398) (2.593) (2.538) (2.983)

Number of observations 83 83 82 82 83

Pseudo R-square 0.454 0.438 0.441 0.418 0.417

Wald Chi-square (p-value) 0 0 0 0 0

33

Table 3: Instrumental Variables Specification

We estimate simultaneously the following two equations: (1) INT_DEBT_ISS_GROSS_GDP = α+ γ1

NET_INTEREST_MARGIN + γ2 CREDIT_DEPOSIT + γ3 RESTRICTION + γ4 PRIVATE MONITORING + γ5 LEGAL

ORIGIN – BRITISH + γ6 LEGAL ORIGIN – FRENCH + γ7 LEGAL ORIGIN – SOCIALIST + γ8 LEGAL ORIGIN –

GERMAN + γ9 ETHNIC FRACTIONALIZATION + γ10 RELIGION FRACTIONALIZATION + γ11 LANGUAGE

FRACTIONALIZATION + ε1 ; (2) CRISIS = α + 1 INT_DEBT_ISS_GROSS_GDP + 2

NET_INTEREST_MARGIN + 3 CREDIT_DEPOSIT + 4 RESTRICTION + 5 PRIVATE MONITORING + ε2. In the

equation (1) we instrument INT_DEBT_ISS_GROSS_GDP with all variables in the equation (2) plus legal origins

(British, French, Socialist, German) and ethnic, religious and language fractionalization. In the equation (2) we use the

coefficient of INT_DEBT_ISS_GROSS_GDP from equation 1 and the other independent variables to estimate the

probability to be in crisis in 2008 (the dependent variable is a dummy equals to 1 if the country is classified as crisis and

0 otherwise). *, ** and *** indicate statistical significance of the parameters at 10, 5 and 1 percent significance level

respectively. Robust standard errors appear in parenthesis. Summary statistics are given in Table 1 and definitions are

given in the Appendix.

Variables IV Probit

INT_DEBT_ISS_GROSS_GDP_IV -0.019

(0.014)

NET_INTEREST_MARGIN -0.176**

(0.081)

CREDIT_DEPOSIT 0.018***

(0.005)

CONCENTRATION -0.017

(0.012)

RESTRICTION -0.366***

(0.122)

PRIVATE MONITORING -0.387***

(0.138)

CONSTANT 5.664**

(2.347)

Number of observations 71

Wald Chi-square (p-value) 0

Wald test of exogeneity (p-value) 0

34

Table 4: Ordered Probit Specification

Ordered probit estimation with dependent variable = ORDERED_CRISIS (dummy equal to 1 if the country is classified

as borderline crisis, equal to 2 if the country is classified as systemic crisis by Laeven and Valencia and 0 otherwise. *,

** and *** indicate statistical significance of the parameters at 10, 5 and 1 percent significance level respectively.

Robust standard errors appear in parenthesis. Summary statistics are given in Table 1 and definitions are given in the

Appendix.

Variables Ordered Probit

NET_INTEREST_MARGIN -0.253**

(0.103)

CREDIT_DEPOSIT 0.018***

(0.005)

CONCENTRATION -0.032***

(0.012)

RESTRICTION -0.472***

(0.124)

PRIVATE MONITORING -0.325**

(0.157)

P-value 0

Pseudo R-square 0.368

Number of observations 83

35

Table 5: Tobit Specification

Tobit estimation with left-censoring limit = 0 and dependent variable = CRISIS_COST_GDP (variable as provided by

Laeven and Valencia that measures the cost of public support to the financial system in term of GDP. *, ** and ***

indicate statistical significance of the parameters at 10, 5 and 1 percent significance level respectively. Robust standard

errors appear in parenthesis. Summary statistics are given in Table 1 and definitions are given in the Appendix.

Variables Tobit

NET_INTEREST_MARGIN -1.494**

(0.702)

CREDIT_DEPOSIT 0.108***

(0.037)

CONCENTRATION -0.196**

(0.096)

RESTRICTION -2.772***

(0.972)

PRIVATE MONITORING -1.565

(0.968)

CONSTANT 32.019***

(10.362)

P-value 0

Pseudo R-square 0.189

Number of observations 83

Table 6: Unconditional Correlation

This table shows the unconditional correlation between all the independent variables described in Section 3. Summary statistics are given in Table 1 and definitions are given in

the Appendix.

NET_INTERES

T

_MARGIN

CREDIT

_DEPOSIT CONCENTRA. CAPITAL ENTRY

PRIVATE

MONITORINGRESTRICTION SUPERVISION

NET_INTEREST

_MARGIN 1

CREDIT

_DEPOSIT -0.1895 1

CONCENTRATIO

N-0.0171 0.2237 1

CAPITAL 0.0059 -0.0246 0.0107 1

ENTRY 0.0606 0.0386 0.0622 0.1807 1

PRIVATE

MONITORING-0.2725 0.0307 -0.1236 -0.0583 -0.0032 1

RESTRICTION 0.3831 -0.1815 0.0209 -0.0326 -0.044 -0.1632 1

SUPERVISION 0.0785 -0.2937 -0.1596 0.1201 0.233 -0.0219 0.2247 1

Table 7: Multicollinearity Check

OLS estimation and dependent variable = NET_INTEREST_MARGIN. *, ** and *** indicate statistical significance of

the parameters at 10, 5 and 1 percent significance level respectively. Robust standard errors appear in parenthesis.

Summary statistics are given in Table 1 and definitions are given in the Appendix.

Panel A

Variables OLS

RESTRICTION 0.524***

(5.46)

CONSTANT 0.42

(0.6)

Observations 83

R-squared 0.15

Panel B

Variables Probit 10

RESIDUAL -0.241*

(-2.16)

CREDIT_DEPOSIT 0.0174***

-3.83

CONCENTRATION -0.0235*

(-2.04)

RESTRICTION -0.556***

(-4.18)

PRIVATE MONITORING -0.386*

(-2.22)

CONSTANT 5.870**

(2.83)

Observations 83

Pseudo R-squared 0.418

38

Appendix: Variable Definitions and Sources

Dependent variable probit model:

CRISIS

Dependent variable ordered probit model:

ORDERED_CRISIS

Dependent variable tobit

model:CRISIS_COST_GDP

Indipendent variables:

NET INTEREST MARGIN

BANK CREDIT / BANK DEPOSITS

CONCENTRATION

RESTRICTION

PRIVATE MONITORING

COST_INCOME

Z-SCORE

ROE

ROA

CAPITAL

ENTRY

SUPERVISION

INT_DEBT_ISS_GROSS_GDP Mean of the gross flow of international bond issues, relative to GDP, from 1998

to 2006 (source: Beck, Demirgüç-Kunt and Levine; 2000).

Mean value of the ratio of loans to deposits from 1998 to 2006 (source: Beck,

Demirgüç-Kunt and Levine; 2000).

Mean value of the “Official Supervisory” index reported in the three surveys

(source: Barth, Caprio and Levine, 2004).

Mean value of the “Private Monitoring” index reported in the three surveys

(source: Barth, Caprio and Levine, 2004).

Mean value bank z-score from 1998 to 2006 (source: Beck, Demirgüç-Kunt and

Levine; 2000).

Mean value of the “Entry Requirements” index reported in the three surveys

(source Barth, Caprio and Levine; 2004).

Mean of the accounting value of bank's net interest revenue, as a share of its

interest-bearing assets, from 1998 to 2006 (source Beck, Demirgüç-Kunt and

Levine; 2000)

Variable as provided by Laeven and Valencia (2010) that measures the cost of

public support to the financial system in term of GDP.

Mean of assets of three largest banks as a share of assets of all commercial

banks, from 1998 to 2006 (source Beck, Demirgüç-Kunt and Levine; 2000).

Dummy equal to 1 if the country is classified as borderline crisis, equal to 2 if

the country is classified as systemic crisis and 0 otherwise (source: Laeven

and Valencia; 2010).

Dummy equal to 1 if the country is classified as either borderline crisis or

systemic crisis by Laeven and Valencia (2010) and 0 otherwise.

Mean value of the “Capital Regulation” index reported in the three surveys

(source Barth, Caprio and Levine; 2004).

Mean of average return on assets (net income/total equity), from 1998 to 2006

(source Beck, Demirgüç-Kunt and Levine; 2000).

Mean of average return on assets (net income/total assets), from 1998 to 2006

(source Beck, Demirgüç-Kunt and Levine; 2000).

Mean of total costs as a share of total income of all commercial banks, from

1998 to 2006 (source Beck, Demirgüç-Kunt and Levine; 2000).

Mean value of the “Overall Restrictions” index reported in the three surveys

(source Barth, Caprio and Levine; 2004).