Embed Size (px)

Citation preview

Management Studies (2020) Vol. 10, No. 2, 39 – 49

What do we know about the financial consequences of the

WorldCom accounting scandal?

Katharina Ganschow Leuphana University Lüneburg,

Universitätsallee 1, 21335 Lüneburg, Germany; [email protected]

Leon Kulemann Leuphana University Lüneburg,

Universitätsallee 1, 21335 Lüneburg, Germany; [email protected]

Finn Ripp Leuphana University Lüneburg,

Universitätsallee 1, 21335 Lüneburg, Germany; [email protected]

Lisa Zastrow Leuphana University Lüneburg,

Universitätsallee 1, 21335 Lüneburg, Germany; [email protected]

MANAGEMENT

STUDIES

journal homepage: www.managementstudies.org

Abstract

At which point does a fraud become a scandal and where can one draw the line? Which extent and effects can a

fraud have? Using the example of the WorldCom scandal in 2002, these questions will be addressed and further

investigated. This paper deals with the economic and social consequences of such a fraud case and approaches

the effects to the present day. Using economic theories and practical examples, the extent will be explained in

detail. The fraud is rooted in the organizational misbehavior which was caused, on the one hand, by the wrong

decisions based on the personal interest of the top managers and, on the other hand, revenue-seeking Wall Street

analysts giving intentionally wrong information. During the 1990s, MCI WorldCom bought-up many competitive

companies, which led to a significant increase in its reported revenues. To carry on this fast-paced development,

the company distorted its balance sheet by capitalizing on line costs and releasing accruals while booking them

as expenses, not as expenditures. Finally, as the fraud was disclosed by the internal audit in 2002, the stock price

fell immediately from almost $65 to below $1 a share.

1 Introduction

The WorldCom accounting scandal of 2002 is seen as one of the biggest scandals in the United States corporate

scandal history. The impacts of this particular corporate scandal had severe effects on shareholders, as well as

stakeholders and the whole market at its time, as the following elaboration will show on different levels.

The scandal is of legislative, ethical, and practical relevance - the consequences of which can still be seen in our

current corporate structures. Besides the ethical and practical relevance, which will become apparent when diving

into the specific facts of the scandal, the legislative relevance is depicted in the Sarbanes-Oxley Act. The Sarbanes-

Oxley Act comprises what changes were implemented in the legislation restricting possibilities for accounting

fraud (Norris, 2005). The whole scandal around WorldCom can be seen as a prime example of organizational

misbehavior and the possible outcomes leading to grave consequences, especially when having a look at its course

40 Ganschow et al.

Management Studies 10 (2020) 39 - 49

and impacts. Through analyzing the timeline of the scandal, the need for stakeholders and shareholders to maintain

a skeptical view of their respective company’s performance, as well as the individual behavior of executives,

becomes apparent, particularly concerning accounting related statements. Bearing this in mind; “WorldCom’s

demise set a record for the largest bankruptcy in the world, shoving Enron aside for that honor” (Markham, 2015)

- this provides a glimpse of the majority of the scandal. In consideration of those aspects, this report covers a

detailed overview focusing on the consequences of the scandal and researching the question “To what extent can

the WorldCom accounting scandal be seen as a paradigm for organizational misbehavior and what are the resulting

consequences?”.

2 Theoretical Foundation

The assumptions that will be made in the following report are based on the broad lines of the agency theory and

stakeholder-agency theory. The approach of the agency theory describes a diverge principal-agent relationship

and argues about their parallels (Hill and Jones, 1992). This theory assumes that the agents are self-interested,

boundedly rational, and different in their goals and risk-taking (Payne and Petrenko, 2019). Through the

implementation of the theory, one takes into consideration the best interest of each individual and thus can be used

to describe the relationship between managers and shareholders (Hill and Jones, 1992). The relationship usually

comes along with information asymmetry and disagreement between the parties and is therefore to be handled

carefully (Payne and Petrenko, 2019). This theory can be used to understand and explain corporate governance

from different points of view and helps to analyze external relationships with a critical approach (Payne and

Petrenko, 2019). The stakeholder-agency theory includes an extension of the assumptions made in the agency

theory, furthermore adding a stakeholder perspective. This extension can be used to illustrate the organizational

behavior or misbehavior within a company, it highlights the external impacts and consequences (Hill and Jones,

1992). In addition to the financial aspect, the agency theory, the stakeholder-agency theory also considers market

processes whereas the individual inefficient behavior plays a major role (Hill and Jones, 1992). Through

incorporating these theoretical approaches, it becomes evident that the characteristics of the WorldCom

accounting scandal apply to a significant degree. The case is considered a prime example of these assumptions

made in the agency, as well as the stakeholder-agency theory. These already mentioned assumptions can be

exemplified based on official statements describing the scandal as “[…] a result of knowing misconduct directed

by a few senior executives […]. The fraud was the consequence of the way WorldCom’s Chief Executive Officer,

Bernard J. Ebbers, ran the Company.” (Report of Investigation, 2003, p.1). Keeping the theoretical foundation in

mind, the WorldCom scandal is highly relevant in a scientific way and shows different levels of organizational

misbehavior and its financial implications to a great extent.

3 Methodology

To provide comprehensive information around the WorldCom accounting scandal, the report will focus on the

main characteristics of the case. This means it will take a deeper look into the aspects of organizational

misbehavior, continuous growth, balance sheet distortion, and the financial implications and consequences. All

containing information results from a structured and detailed literature review elaborated in the following and

compiled in a critical view. Until now, research concerning this particular case has mainly focused on the

circumstances and impacts illustrating the characteristics of the WorldCom scandal mostly separately. This report

will provide information surrounding the main facts of the scandal. Through highlighting these facts, the report

will focus on the consequences and thus enable an overall view and understand the correlations between all of the

important factors.

The research question “To what extent can the WorldCom accounting scandal be seen as a paradigm for

organizational misbehavior and what are the resulting consequences?” will help to find a common thread and

creating a connection leading to a reasonable conclusion. In this context, the practical- as well as the research-

relevance becomes apparent and illuminates a new approach to understanding the WorldCom accounting scandal.

Ganschow et al. 41

Management Studies 10 (2010) 39 - 49

4 Literature Review

4.1. Background and Synopsis

The company WorldCom was established in 1983 in the United States and started as a small carrier in Mississippi

(Capital-Redaktion, 2020). As WorldCom started a series of acquisitions of other telecommunication firms in

1990, including “MCI“ in 1989, and becoming “MCI WorldCom“ the company pursued the corporate objective

of becoming one of the leading long-distance carriers in the United States. This helped them become the second-

largest provider and leading operator of internet infrastructure until their downfall (Lyke and Jickling, 2002;

Capital-Redaktion, 2020). The early success of the company built the foundation of the events that followed

throughout the years (Report of Investigation, 2003). After the end of the “dot com“ boom in 2001 - which was

mainly influenced by overly optimistic projections of the internet growth and resulted in a recession of the

economy - MCI WorldCom started struggling (Lyke and Jickling, 2002). Financial trouble started to hit the

company which was caused by the pressure of maintaining their widely known reputation of success (Report of

Investigation, 2003). At this time shareholders, as well as stakeholders, were highly affected by the company’s

performance (Lyke and Jickling, 2002). The detailed information about the financial situation and impacts will be

examined in the following parts of the Literature Review. In 2002 MCI WorldCom announced incorrect

accounting by more than $3.8 billion in 2001 and the first quarter of 2002 (Lyke and Jickling, 2002). This

confession did not only affect the company, its financial situation, and its reputation but also the financial markets

(Chuvakin and Gertmenian, 2003). Although the fraud occurred to be the result of the misbehavior of a few key

executives like Bernard J. Ebbers, the whole company - meaning approximately 80.000 employees and every

stakeholder involved - suffered major losses (Report of Investigation, 2003; Chuvakin and Gertmenian, 2003).

US Securities and Exchange Commission charged the company with fraud on June 26th, 2002 leading to the

company filing for bankruptcy on July 21st, 2002 (Lyke and Jickling, 2002). The fraud affected the whole economy

leaving major consequences to deal with and resulting in a reconsideration of corporate structures (Norris, 2005;

Chuvakin and Gertmenian, 2003).

4.2. Organizational Misbehavior

MCI WorldCom sets the priority for achieving business success on the strategy of growth through acquisitions

(Report of Investigation, 2003). Accordingly, the stock price was the currency for takeovers of other companies.

For that, keeping the company’s stock price high and increasing it continuously was of great importance (Report

of Investigation, 2003; Wilmarth, 2007). But due to the rising competition on national and international levels as

well as overinvestment, MCI WorldCom’s revenues declined after the fourth quarter of the year 1999 and the

previously used acquisition policy could not be implemented anymore (Wilmarth, 2007). However, to continue

their business and to satisfy Wall Street’s expectations, they created an “illusion of stability” (Harmantzis, 2004,

p.3) by falsifying financial statements which finally lead to the corporate scandal and following the largest

bankruptcy in American history (Cernusca, 2007). Organizational misbehavior includes various factors

influencing the resulting misleading. According to Grant, the two main factors driving these events are the

immoral behavior of individuals as well as “inadequate oversight by boards, auditors, investment analysts,

regulators and the media” (Grant, 2006, p. 362). The resulted facts that emerged during the investigation of the

MCI WorldCom case can refer to this statement.

4.2.1. Corporate Culture

Although MCI WorldCom consists of different departments and thousands of employees, the fraud can be

attributed to three top managers of the company. The Chief Executive Officer Bernie Ebbers helped the company

to grow and achieve success. Together with his close associates Scott Sullivan, the Chief Financial Officer, and

David Myers, the Controller, he had full control over the company (Pandey and Verma, 2004). The strong and

focused leadership of the top managers establishes an autocratic structure (Zekany et al., 2004). The atmosphere

dominated by the leaders and managers left hardly the opportunity to question or doubting decisions that were

initiated by higher positioned managers (Pandey and Verma, 2004; Soltani, 2014; Zekany et al., 2004). Moreover,

the headquarters of each department were geographically separated and placed at different states which limited

the internal communication and thus facilitated the concealment of the financial truth. While the headquarter for

network operations was based in Texas, the department for Human Resources was located in Florida, and the legal

department in Washington, D.C., MCI WorldCom’s general accounting group was located in Clinton, Mississippi

(Kaplan and Kiron, 2004; Report of Investigation, 2003). From there, Ebbers, Sullivan, and Myers had a good

position to conceal the actual financial condition of the company (Markham, 2015). It is known that the financial

fraud was suspected and recognized by the General Accounting Group which was responsible for the

42 Ganschow et al.

Management Studies 10 (2020) 39 - 49

implementation of the entries but also employees working in other financial and accounting sections. But because

of the dominant policy of the executives, none of them reported the falsification (Report of Investigation, 2003).

4.2.2. Unethical Behavior of Individuals

The CEO, Bernie Ebbers, had a personal interest in the continuing sham of stability. Besides his work for MCI

WorldCom, he had several private businesses, inter alia, hotels, real estate ventures, timberlands, a luxury yacht

building company, an operating marina, a country club, a trucking company, and a minor league hockey club

(Pandey and Verma, 2004, p. 118). They were mainly financed by commercial bank loans which he secured by

his personal MCI WorldCom stock (Pandey and Verma, 2004). The number of loans was high and to protect his

property, he was willing to take illegal accounting actions. Also, MCI WorldCom had a high reputation in the

financial world and for a long time a frontrunner for investors and Wall Street analysts. (Harmantzis, 2004;

Soltani, 2014). After the MCI WorldCom stock reached its stock peak of $64.51 in June 1999, the institutional

investors and Wall Street analysts were confident about the continuing success and increasing revenue. This

attitude was fostered by the MCI WorldCom investment bankers, especially the leading telecommunications

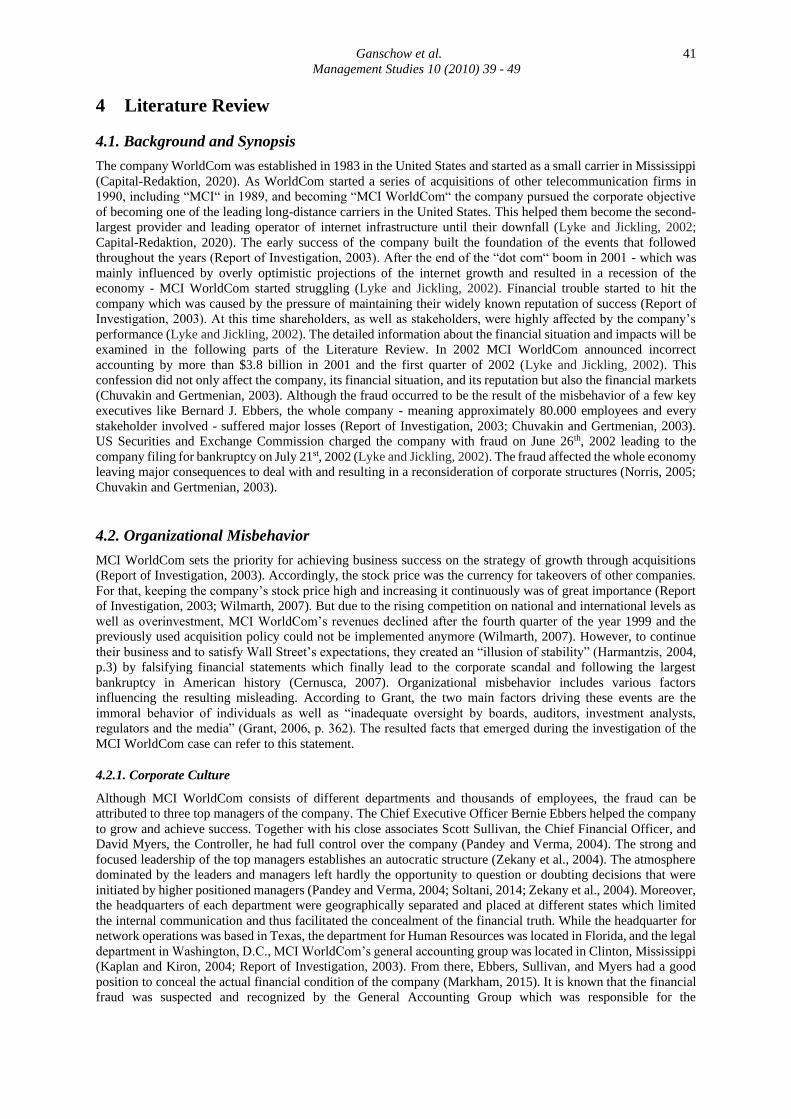

equity analyst at Salomon Smith Barney, Jack Grubman (Sidak, 2003). He built up a close relationship with MCI

WorldCom’s CEO and became a close advisor (Wilmarth, 2007). According to Green, the telecommunication

company providing the analyst with exclusive information to get beneficial public dissemination (Green, 2004,

p.45). Grubman promoted misleading equity research of MCI WorldCom to investors and recommended

participation in initial public offerings of other companies (Sidak, 2003). He gave these statements in exchange

for lucrative investment banking business, even though he was aware of the fact that the company was overvalued

(Port, & Doss, 2011; Sidak, 2003). As Grubman’s opinion had a high reputation among investors, they trust his

“independent and objective research” (Green, 2004, p.45).

Figure 1: Possible WorldCom Conspiracies in Restraint of Trade (Sidak, 2003, p. 247)

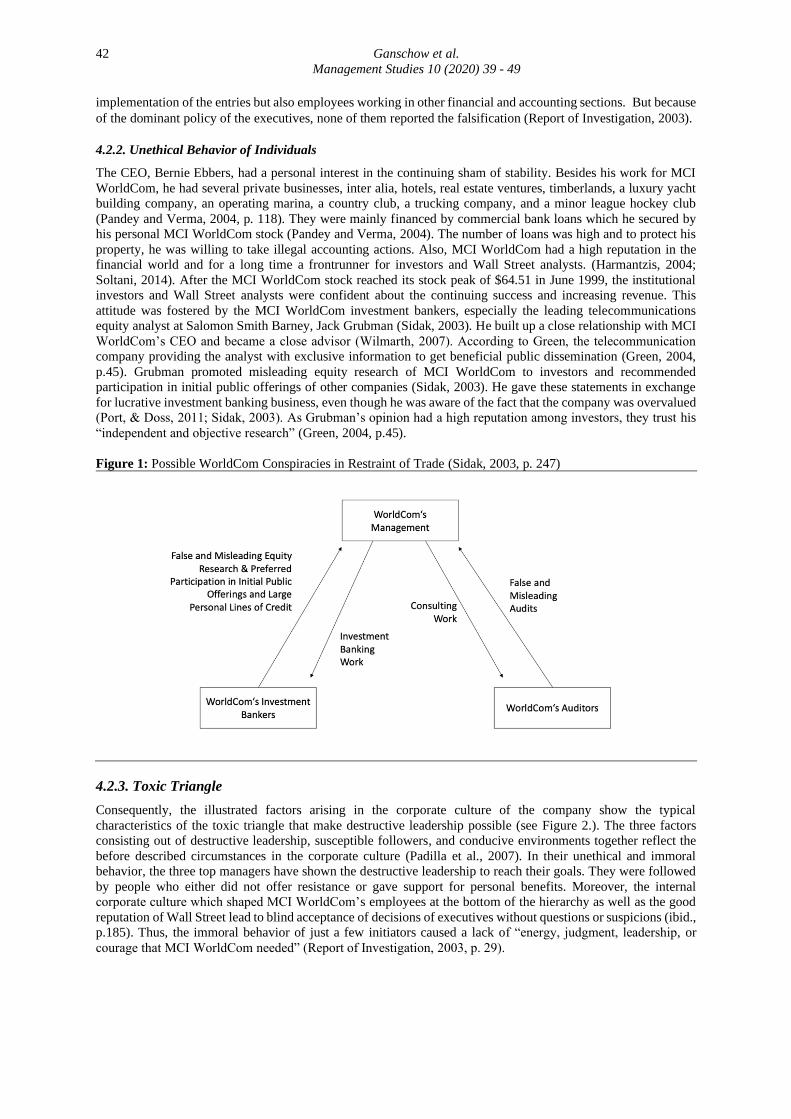

4.2.3. Toxic Triangle

Consequently, the illustrated factors arising in the corporate culture of the company show the typical

characteristics of the toxic triangle that make destructive leadership possible (see Figure 2.). The three factors

consisting out of destructive leadership, susceptible followers, and conducive environments together reflect the

before described circumstances in the corporate culture (Padilla et al., 2007). In their unethical and immoral

behavior, the three top managers have shown the destructive leadership to reach their goals. They were followed

by people who either did not offer resistance or gave support for personal benefits. Moreover, the internal

corporate culture which shaped MCI WorldCom’s employees at the bottom of the hierarchy as well as the good

reputation of Wall Street lead to blind acceptance of decisions of executives without questions or suspicions (ibid.,

p.185). Thus, the immoral behavior of just a few initiators caused a lack of “energy, judgment, leadership, or

courage that MCI WorldCom needed” (Report of Investigation, 2003, p. 29).

Ganschow et al. 43

Management Studies 10 (2010) 39 - 49

Figure 2: The toxic triangle: elements in three domains related to destructive leadership (Padilla et al., 2007,

p.180)

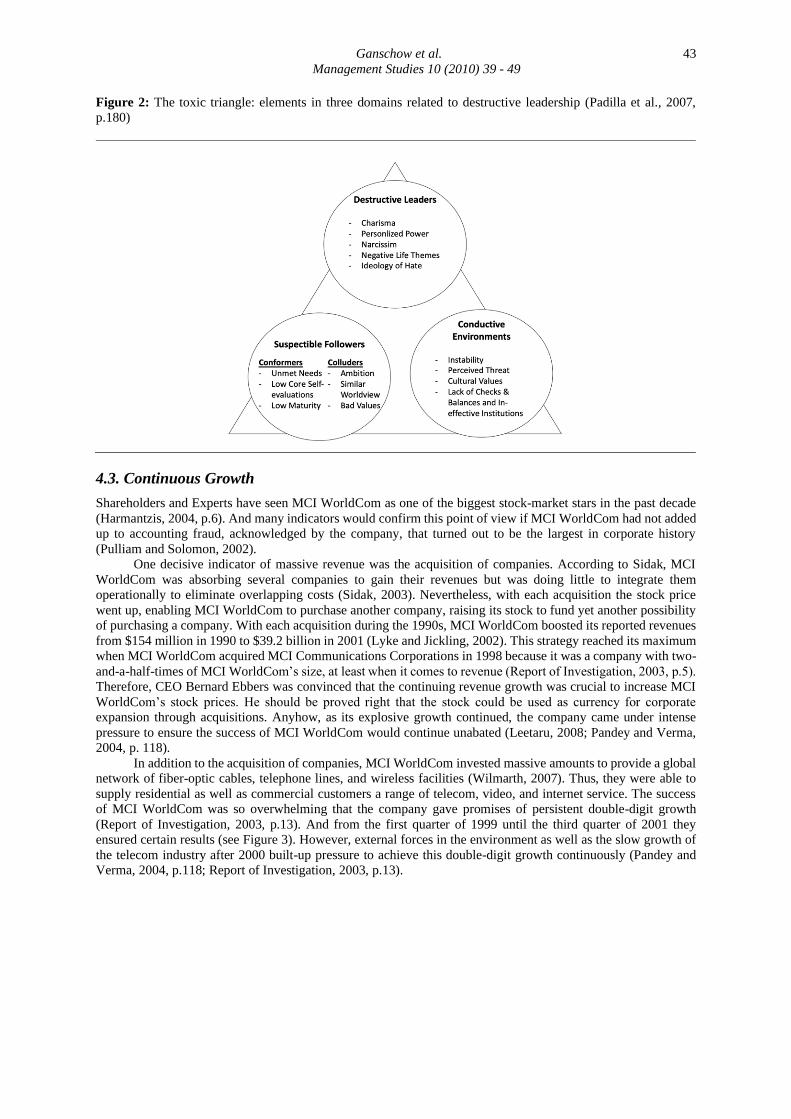

4.3. Continuous Growth

Shareholders and Experts have seen MCI WorldCom as one of the biggest stock-market stars in the past decade

(Harmantzis, 2004, p.6). And many indicators would confirm this point of view if MCI WorldCom had not added

up to accounting fraud, acknowledged by the company, that turned out to be the largest in corporate history

(Pulliam and Solomon, 2002).

One decisive indicator of massive revenue was the acquisition of companies. According to Sidak, MCI

WorldCom was absorbing several companies to gain their revenues but was doing little to integrate them

operationally to eliminate overlapping costs (Sidak, 2003). Nevertheless, with each acquisition the stock price

went up, enabling MCI WorldCom to purchase another company, raising its stock to fund yet another possibility

of purchasing a company. With each acquisition during the 1990s, MCI WorldCom boosted its reported revenues

from $154 million in 1990 to $39.2 billion in 2001 (Lyke and Jickling, 2002). This strategy reached its maximum

when MCI WorldCom acquired MCI Communications Corporations in 1998 because it was a company with two-

and-a-half-times of MCI WorldCom’s size, at least when it comes to revenue (Report of Investigation, 2003, p.5).

Therefore, CEO Bernard Ebbers was convinced that the continuing revenue growth was crucial to increase MCI

WorldCom’s stock prices. He should be proved right that the stock could be used as currency for corporate

expansion through acquisitions. Anyhow, as its explosive growth continued, the company came under intense

pressure to ensure the success of MCI WorldCom would continue unabated (Leetaru, 2008; Pandey and Verma,

2004, p. 118).

In addition to the acquisition of companies, MCI WorldCom invested massive amounts to provide a global

network of fiber-optic cables, telephone lines, and wireless facilities (Wilmarth, 2007). Thus, they were able to

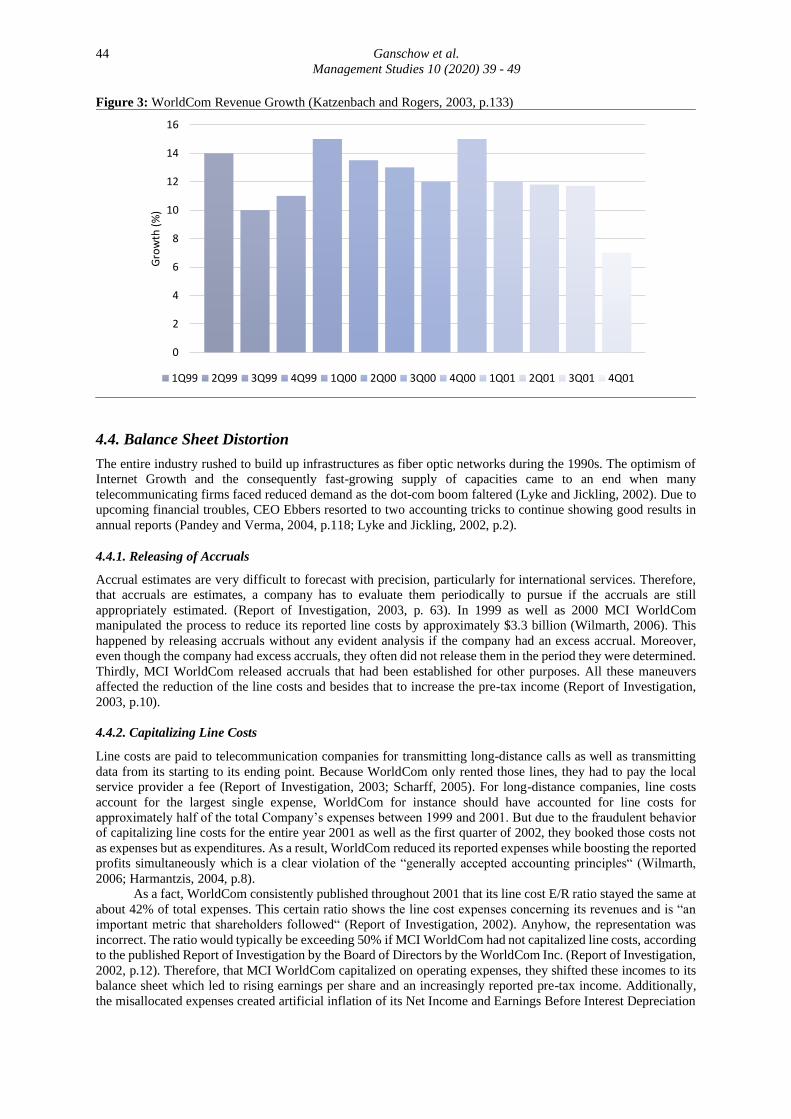

supply residential as well as commercial customers a range of telecom, video, and internet service. The success

of MCI WorldCom was so overwhelming that the company gave promises of persistent double-digit growth

(Report of Investigation, 2003, p.13). And from the first quarter of 1999 until the third quarter of 2001 they

ensured certain results (see Figure 3). However, external forces in the environment as well as the slow growth of

the telecom industry after 2000 built-up pressure to achieve this double-digit growth continuously (Pandey and

Verma, 2004, p.118; Report of Investigation, 2003, p.13).

44 Ganschow et al.

Management Studies 10 (2020) 39 - 49

Figure 3: WorldCom Revenue Growth (Katzenbach and Rogers, 2003, p.133)

4.4. Balance Sheet Distortion

The entire industry rushed to build up infrastructures as fiber optic networks during the 1990s. The optimism of

Internet Growth and the consequently fast-growing supply of capacities came to an end when many

telecommunicating firms faced reduced demand as the dot-com boom faltered (Lyke and Jickling, 2002). Due to

upcoming financial troubles, CEO Ebbers resorted to two accounting tricks to continue showing good results in

annual reports (Pandey and Verma, 2004, p.118; Lyke and Jickling, 2002, p.2).

4.4.1. Releasing of Accruals

Accrual estimates are very difficult to forecast with precision, particularly for international services. Therefore,

that accruals are estimates, a company has to evaluate them periodically to pursue if the accruals are still

appropriately estimated. (Report of Investigation, 2003, p. 63). In 1999 as well as 2000 MCI WorldCom

manipulated the process to reduce its reported line costs by approximately $3.3 billion (Wilmarth, 2006). This

happened by releasing accruals without any evident analysis if the company had an excess accrual. Moreover,

even though the company had excess accruals, they often did not release them in the period they were determined.

Thirdly, MCI WorldCom released accruals that had been established for other purposes. All these maneuvers

affected the reduction of the line costs and besides that to increase the pre-tax income (Report of Investigation,

2003, p.10).

4.4.2. Capitalizing Line Costs

Line costs are paid to telecommunication companies for transmitting long-distance calls as well as transmitting

data from its starting to its ending point. Because WorldCom only rented those lines, they had to pay the local

service provider a fee (Report of Investigation, 2003; Scharff, 2005). For long-distance companies, line costs

account for the largest single expense, WorldCom for instance should have accounted for line costs for

approximately half of the total Company’s expenses between 1999 and 2001. But due to the fraudulent behavior

of capitalizing line costs for the entire year 2001 as well as the first quarter of 2002, they booked those costs not

as expenses but as expenditures. As a result, WorldCom reduced its reported expenses while boosting the reported

profits simultaneously which is a clear violation of the “generally accepted accounting principles“ (Wilmarth,

2006; Harmantzis, 2004, p.8).

As a fact, WorldCom consistently published throughout 2001 that its line cost E/R ratio stayed the same at

about 42% of total expenses. This certain ratio shows the line cost expenses concerning its revenues and is “an

important metric that shareholders followed“ (Report of Investigation, 2002). Anyhow, the representation was

incorrect. The ratio would typically be exceeding 50% if MCI WorldCom had not capitalized line costs, according

to the published Report of Investigation by the Board of Directors by the WorldCom Inc. (Report of Investigation,

2002, p.12). Therefore, that MCI WorldCom capitalized on operating expenses, they shifted these incomes to its

balance sheet which led to rising earnings per share and an increasingly reported pre-tax income. Additionally,

the misallocated expenses created artificial inflation of its Net Income and Earnings Before Interest Depreciation

0

2

4

6

8

10

12

14

16

Gro

wth

(%

)

1Q99 2Q99 3Q99 4Q99 1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01

Ganschow et al. 45

Management Studies 10 (2010) 39 - 49

and Amortization (EBITDA). All in all, with this “financial gimmickry“ (Report of Investigation, p.5) MCI

WorldCom capitalized $3.06 billion in 2001 and $797 billion in the first three months of 2002. (Langlois 2002;

Harmantzis 2004, p.8). Without the distortion, the company would have faced a pre-tax loss in three of the five

quarters where the improper entries occurred (Report of Investigation, 2003, p. 11). As an example, in the second

quarter of 2001, the company published a pre-tax income of nearly $160 million but without the improper

capitalization of $560 million for that quarter MCI WorldCom would have reported a loss of approximately $400

million (see Table 1).

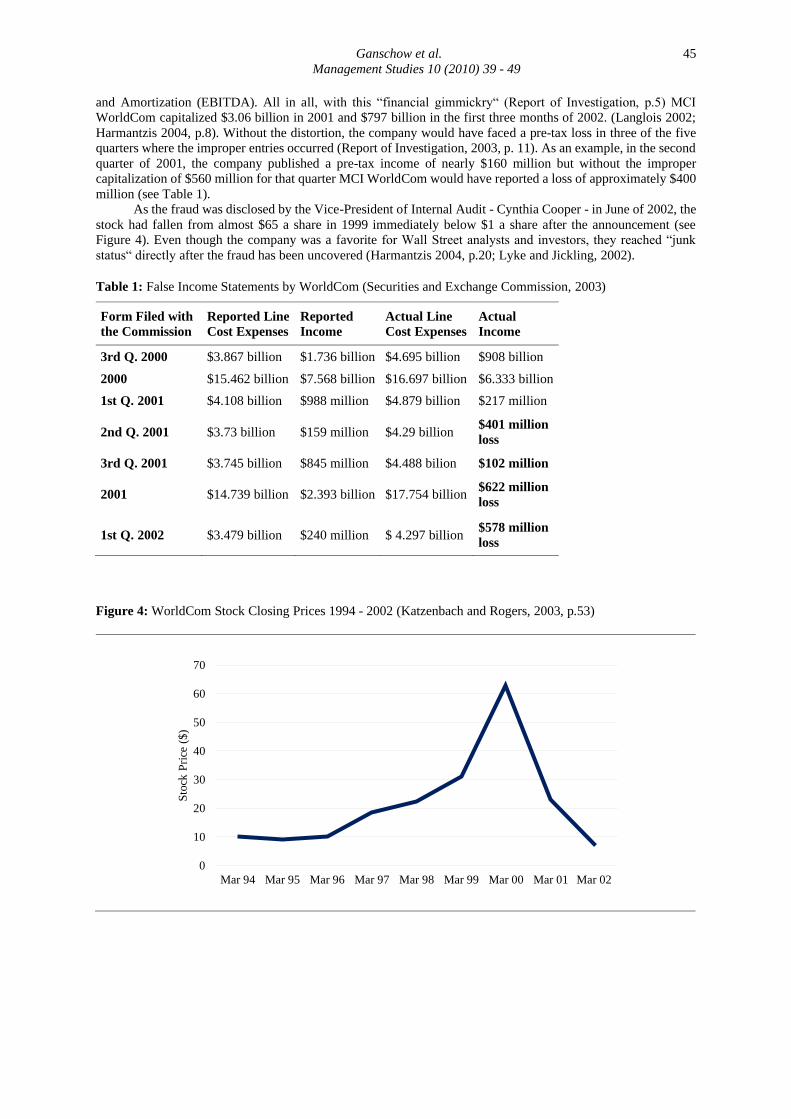

As the fraud was disclosed by the Vice-President of Internal Audit - Cynthia Cooper - in June of 2002, the

stock had fallen from almost $65 a share in 1999 immediately below $1 a share after the announcement (see

Figure 4). Even though the company was a favorite for Wall Street analysts and investors, they reached “junk

status“ directly after the fraud has been uncovered (Harmantzis 2004, p.20; Lyke and Jickling, 2002).

Table 1: False Income Statements by WorldCom (Securities and Exchange Commission, 2003)

Form Filed with

the Commission

Reported Line

Cost Expenses

Reported

Income

Actual Line

Cost Expenses

Actual

Income

3rd Q. 2000 $3.867 billion $1.736 billion $4.695 billion $908 billion

2000 $15.462 billion $7.568 billion $16.697 billion $6.333 billion

1st Q. 2001 $4.108 billion $988 million $4.879 billion $217 million

2nd Q. 2001 $3.73 billion $159 million $4.29 billion $401 million

loss

3rd Q. 2001 $3.745 billion $845 million $4.488 bilion $102 million

2001 $14.739 billion $2.393 billion $17.754 billion $622 million

loss

1st Q. 2002 $3.479 billion $240 million $ 4.297 billion $578 million

loss

Figure 4: WorldCom Stock Closing Prices 1994 - 2002 (Katzenbach and Rogers, 2003, p.53)

Mar 94 Mar 95 Mar 96 Mar 97 Mar 98 Mar 99 Mar 00 Mar 01 Mar 02

0

10

20

30

40

50

60

70

Sto

ck P

rice

($

)

46 Ganschow et al.

Management Studies 10 (2020) 39 - 49

4.5. Financial Implications and Consequences

4.5.1. Consequences of the fraud

The WorldCom scandal had multifaceted consequences on its internal and external environment. On July 21st of

2002, MCI WorldCom filed for reorganization in bankruptcy under Chapter eleven of the Bankruptcy Code which

presupposes the continued existence of the company with protection from their debtors. The investigations

commenced as external third parties such as the SEC, The Justice Department and the state of Mississippi

discovered the fraud. In addition to the governmental regulations, MCI WorldCom was sued by private creditors.

On May 19th of 2003, a final judgment of the SEC terminated the investigations. As to monetary relief, it included

a civil penalty in the amount of $ 2.25 billion, a payment of $ 500.000 in cash, and a transfer of ten million shares

of common stock in the reorganized company (SEC, 2006). The company’s debt of $ 41 billion was diminished

in April 2003 due to a deal with bondholders struck by Michael Capellas to reduce the debt to $ 5 billion for equity

(Business Week, 2003). Richard C. Breeden, a former SEC chairman, who was appointed by the US District Court

as Corporate Monitor of WorldCom, drew up a report stating 78 ways to restore trust in the company, a lot of

which was translated into action in the following years.

4.5.2. Internal Consequences

4.5.2.1. Removing of top management

The most immediate consequence of the fraud was removing the responsible executives from their positions. CEO

Bernard J. Ebbers resigned on the 29th of April 2002. It was discovered that he had taken a high amount of loans

from the company which was later on forgiven for him to give up his assets in MCI WorldCom (Ashraf, 2011).

Ebbers was sentenced to 25 years in prison and died just shortly after his release in 2020. CFO Scott Sullivan was

fired in 2002 and was sentenced to five years in prison. Controller David Myers resigned when the fraud was

discovered and got a prison sentence of one year and one day (Bayot and Farzad, 2005).

4.5.2.2 Restructuring the company

Top management had to be replaced almost immediately to maintain the companies’ existence. With Michael

Capellas, who brought a reputation for integrity and forthrightness in his leadership skills, a new CEO was chosen

(Pandey, 2006). The CFO position was filled with Viktoria Harker, who was replaced a year later by Robert

Blakely, an experienced manager with complicated financial reconstructions (Manager Magazin, 2003). Breeden

called these changes a “good progress“ and especially outlined the fact that all of them were from outside the

company and separated from the scandal (Breeden, 2003). In addition to the top management, more than 400 new

finance and accounting employees were hired, while WorldCom let go of 17.000 of its 85.000 existing employees

(Ashraf, 2011). Furthermore, a Code of Ethics was established and a Corporate Ethics Office was created to build

an ethical work culture. Additionally, the new CEO Capellas established a Zero Tolerance Policy (Pandey, 2006).

To ensure transparency within the company, the new board of directors provided a mixture of corporate skills

such as finance, accounting, regulatory experience or technology, and a Public Company Accounting Oversight

Board, as a part of the Sarbanes-Oxley Act, was established to oversee the audit of WorldCom and protect the

interests of shareholders and stakeholders (Breeden, 2003; pcaobus.org). The board decided to separate the roles

of chairman and chief executive officer in March 2004 so the interests and duties of the CEO will no longer

determine the company’s behavior (Pandey, 2006 P. 147). In April 2003 MCI WorldCom transformed MCI and

relocated its headquarter from Clinton in Mississippi to Ashburn in Virginia. In this process, the finance and

accounting department in Clinton, Mississippi, was shut down (Breeden, 2003).

4.5.3. External Consequences

4.5.3.1. Consequences on Investors

The external consequences of the fraud had an impact on the people who invested in MCI WorldCom.

Consequently, the investors suffered under great losses as the price was at 83 cents per share when the stock

market closed on the 30th of April 2002. Three years before, it peaked at about $64.50. In pre-market trading on

that day, it sunk to 9 cents (Langlois, 2002). This led to an investor’s loss of $175 Billion which is nearly three

times the loss in the Enron Scandal. Another victim of the fraud was the New York State Common Retirement

Fund including Assets of New York State, Police, and Fire Department. The loss here was over $300 Million of

its investments in MCI WorldCom which was ruining the retirement savings of thousands of people (Kadlec,

2002).

Ganschow et al. 47

Management Studies 10 (2010) 39 - 49

4.5.3.2. Consequences on other Companies

Furthermore, the MCI WorldCom fraud influenced other companies in different ways such as the market.

According to Gil Sadka, accounting frauds like MCI WorldCom „can have a serious adverse effect on the market“

(Sadka, 2006, p. 27). These effects can result after a certain amount of past time but can be also noticeable during

other companies committed. It is obvious that the MCI WorldCom fraud distorted the economic gains of acquiring

new customers, and caused other companies a high financial loss. An example is C. Michael Armstrong, former

CEO of AT&T, claiming his company made wrong investment decisions, such as cutting 20.000 jobs (Ashraf,

2011). But not just the companies in the telecommunications sector were affected by the biggest accounting fraud

in US history. The change in regulations also made it a lot harder for international companies to enter the market

of the US.

4.5.3.3. Consequences on regulations

MCI WorldCom was a crime “so large it changed the law” (New York Times, 2005). One reaction was the

Sarbanes Oxley act, a US federal law that was passed by the congress on the 30th of July 2002. This law was

developed as a consequence of the accounting scandals of MCI WorldCom and Enron and improved the reliability

of accounting in the capital market of the US by different new regulations.

“Especially section 404 that requires companies to assess the strength of internal controls and to report any

material weakness, and it requires to opine whether the controls are adequate“ (New York Times, 2005).

Moreover, it forbids loans to members of the top management. The situation might have been different if Ebbers

loans of an estimated 400 million were denied.

4.5.4. General Consequences

Moreover, the accounting scandal led to a general distrust in financial information given by companies. „Not only

did the economy suffer from devalued businesses and widespread layoffs, but several companies-most notably,

MCI WorldCom - appear to have resorted to financial deception to mask poor performance. This fraud

compounded the downturn by shaking investors' confidence in the truthfulness of financial statements (Abernathy,

2003, p. 3).

This led to higher capital costs and fewer investments in the telecommunications industry (Sidak, 2003 P.

240). Also, many contributions for public programs like the Universal Service Fund or Telecommunications Relay

Service were calculated based on the wrong numbers. This had a bad impact on MCI WorldCom because they

had to pay more than they had capacity but good for the public which was benefiting from the higher payments

(Ashraf, 2011).

5 Limitations

Based on the research question “To what extent can the WorldCom accounting scandal be seen as a paradigm for

organizational misbehavior and what are the resulting consequences?” an overall view of the scandal and the

consequences was examined. The purpose of this report was, on the one hand, to highlight the internal hierarchy

of the company and the resulting lack of transparency, and on the other hand, to identify the financial

consequences for all stakeholders. However, the findings evince limits and results with impulses and

recommendations for future research on the specific case. The development potential for further investigations is

at the ethical perspectives on the case. Most of the literature focuses on the external consequences and drives,

supported by financial implications. Contrastly, descriptions of internal circumstances of the company were

lacking in its accuracy and precision. Consequently, the investigation of ethical drives requires depth to guarantee

a valid assessment of the case. Also, the described results mainly highlight the consequences with respect to the

company and its investors. It was a scandal of such enormous proportions, it was impacting not just the company

but diverse shareholders. Therefore, another recommendation for future searches is a concentration on the impact

on the economy as a whole, the bond market as well as customers.

6 Summary and Outlook

Over the last decades, the importance of transparency between companies and shareholders gained increasing

attention. Reinforced through the financial crisis in 2008, shareholders seem to be more doubtful in terms of

making investments prematurely. In particular, violating accounting principles as it has happened at the

WorldCom scandal is inevitably leading to the irreparable credibility of a company in relation to its stakeholders.

Therefore, the issue that is addressed by this report was to expose what the main abuses of the disclosed fraud

were but much more important screening out the lessons of the organizational misbehavior. One decisive aspect

48 Ganschow et al.

Management Studies 10 (2020) 39 - 49

in terms of misbehavior was trying to maintain high growth even though the dot-com boom faltered. The entire

industry faced reducing demand but instead of realigning the companies structure to find a legal solution, MCI

WorldCom harmed its Shareholders with fraudulently accounting tricks as capitalizing line costs.

Consequently, the fraud could only happen in order to the corporate culture within the company shaped by

top managers creating a dominant atmosphere leaving no room for doubts. Here, the top managers as well as other

highly respected individuals run on their agendas and their operational purposes which made the long concealment

possible. The fraud had implications for many participants on the market. It undermined the trust in financial

statements given by companies in general which can be seen by the fraud's effect on regulations and law. These

were supposed to prevent fraud like the one that happened with WorldCom in the future.

However, the latest accounting scandal of Wirecard shows that the prevention of fraud in this dimension

seems to be difficult to avoid. Even though there have been various examples of incomprehensible hierarchies

leading to violations of accounting principles, managers are ignoring potential implications when it comes to

precarious decisions. As a consequence, a comprehensive change has to be transmitted: Besides a more transparent

communication between the management and shareholders, particularly audit firms need to take action when it

comes to doubtful positions on the balance sheet of companies.

References

Abernathy, K. (2003). Written Statement on the State of Competition in the Telecommunications Industry.

Ashraf, J. (2011). The accounting fraud @ worldcom: the causes, the characteristics, the consequences, and the

lessons learned, Florida.

Bayot, J. & Farzad, R. (2005). Ex-WorldCom Officer Sentenced to 5 Years in Accounting Fraud. Retrieved

from https://www.nytimes.com/2005/08/https://www.nytimes.com/2005/08/12/business/exworldcom-

officer-sentenced-to-5-years-in-accounting-fraud.html (last access: 14.7.2020).

Blackburn, R.B. (2003). Civ No. 02-CV-4963 (JSR). (Securities and Exchange Commission).

Breeden, R. (2003). Restoring trust, Report to the United States District Court on Corporate Governance For

The Future of MCI, Inc.

Capital-Redaktion (2020). Western von Gestern. Der Untergang von Worldcom-Chef Bernie Ebbers. Retrieved

from https://www.capital.de/wirtschaft-politik/der-untergang-von-worldcom-chef-bernie-ebbers (last

access: 28.06.2020).

Cernusca, L. (2007). Ethics in Accounting: The Worldcom Inc. Scandal. Lex ET Scientia International Journal,

14, 239-248.

Chuvakin, N. V. & Gertmenian, L. W. (2003). Predicting Bankruptcy in the WorldCom Age. How to determine

when it is safe to grant credit.

Grant, R. (2006). The Strategic Background to Corporate Accounting Scandals. The Long Range Planning

Journal, 39, 361-383.

Green, S. (2004). A Look at the Causes, Impact and Future of the Sarbanes-Oxley Act. J. Int'l Bus. & L., 3, 33-

45.

Harmantzis, F. (2004). Inside the Telecom Crash: Bankruptcies, Fallacies and Scandals-a Closer Look at the

Worldcom Case. Fallacies and Scandals-a Closer Look at the Worldcom Case (March 30, 2004), 3-6.

Hill, C. W., & Jones, T. M. (1992). Stakeholder‐agency theory. Journal of management studies, 29(2), 131-154.

Kadlec, D. (2002). Worldcon. Content Time.

Kaplan, R. S., & Kiron, D. (2004). Accounting fraud at WorldCom (pp. 9-104). Boston, MA: Harvard Business

School.

Langlois, S. (2002). WorldCom's $3.8 billion scandal. Retrieved from https://www.marketwatch.com/story/

worldcom-future-in-doubt-amid-38billion-scandal (last access: 27.06.2020).

Leetaru, K. (2008). An open source study of international media coverage of the WorldCom scandal. Journal of

International Communication, 14(2), 66-86.

Lyke, B & Jickling, M. (2002). WorldCom: The accounting scandal. Congressional Research Service Report for

Congress, 29, 1-6.

Manager Magazin. (2003): Der die Kastanien aus dem Feuer holt. Retrieved from https://www.manager-

magazin.de/unternehmen/karriere/a-244743.html (last accessed 10.7.2020).

Markham, J. W. (2015). A financial history of modern US corporate scandals: From Enron to reform.

Routledge.

Norris, F. (2005): Market place; A Crime So Large It changed The Law, Section C, Page 1 of the National

edition, New York Times. Retrieved from https://www.nytimes.com/2005/07/14/business/a-crime-so-

large-it-changed-the-law.html (last access: 28.06.2020).

Padilla, A., Hogan, R., & Kaiser, R. B. (2007). The toxic triangle: Destructive leaders, susceptible followers,

and conducive environments. The Leadership Quarterly, 18(3), 176-194.

Ganschow et al. 49

Management Studies 10 (2010) 39 - 49

Pandey, S. C., & Verma, P. (2004). WorldCom Inc. Vikalpa, 29(4), 113–126.

Pandey, S. C. & Verma, P (2006): From Worldcom to MCI.

Payne, G. T., & Petrenko, O. V. (2019). Agency Theory in Business and Management Research. Retrieved

from https://oxfordre.com/business/view/10.1093/acrefore/9780190224851.001.0001/acrefore-

9780190224851-e-5 (last access: 28.06.2020).

Port, R. C., & Doss (2011). J. R. Holmes v. Grubman.

Pulliam, S & Deborah, S. (2002) How three unlikely sleuths exposed fraud at WorldCom. The Wall Street

Journal.

Sadka, G. (2006). The Economic Consequences of Accounting Fraud in Product Markets: Theory and a Case

from the US Telecommunications Industry (WorldCom), 17-18.

Scharff, M. M. (2005). Understanding WorldCom's accounting fraud: Did groupthink play a role?. Journal of

Leadership & Organizational Studies, 11(3), 109-118.

Securities and Exchange Commission. (2006): Additional Information for Investors Regarding the Potential

Distribution of the SEC's Civil Penalty Judgment Against WorldCom, Inc. in the SEC v. WorldCom

Case.

Sidak, J. (2003). The failure of good intentions: The worldcom fraud and the collapse of american

telecommunications after deregulation. Yale Journal on Regulation, 20(2), 207-268.

Soltani, B. (2014). The anatomy of corporate fraud: A comparative analysis of high profile American and

European corporate scandals. Journal of business ethics, 120(2), 251-274.

Wilmarth Jr, A. E. (2007). Conflicts of interest and corporate governance failures at universal banks during the

stock market boom of the 1990s: the cases of Enron and WorldCom. Corporate Governance in

Banking: A Global Perspective, 28- 37.

WorldCom (Firm). Board of Directors. Special Investigative Committee, Beresford, D. R., Katzenbach, N. D.,

& Rogers, C. B. (2003). Report of investigation. Findlaw.

Zekany, K. E., Braun, L. W., & Warder, Z. T. (2004). Behind closed doors at WorldCom: 2001. Issues in

Accounting Education, 19(1), 101-117.