Embed Size (px)

Citation preview

Market Trends: Multienterprise/B2B Infrastructure Market, Worldwide, 2009-2014

Dataquest Note G00200571, Fabrizio Biscotti, Paolo Malinverno, Benoit J. Lheureux, Thomas Skybakmoen, 14 July 2010, R3569 7142011

During the next five years, the multienterprise/business-to-business (B2B) infrastructure market will continue to grow at a steady pace. This period will offer good opportunities for existing providers and market consolidators and strong potential for new entrants — particularly if they are already players in the application integration and middleware space — although substantial investment in sales, marketing and product functionalities will be required to displace well-established incumbents and to gain market share. In addition, the B2B market is already crowded in some regions (such as the U.S. and parts of Western Europe).

Key Findings

• Thefastest-growingsegmentsaremanagedfiletransferasaservice(MFTaaS)forB2B,cloudservicesintegrationasaserviceandB2Bintegrationoutsourcing(BIO),whicharebenefitingfromincreasingendusers’attentiononcloudandmanagedservices.

• Between2010and2014,weexpectGlobal2000companiestoatleastdoubletheirmultienterprisetraffic(transactions,documentsandprocessexecutionevents),andthiswillhaveasignificantimpactontheamountofspendingthatgoestowardmultienterprise/B2Binfrastructure.

• Onekeydriverfortherevenuegrowthofmultienterprise/B2Binfrastructuretechnologieswillbethatmidsizetolargebusinesseswillneedtoimplementseveraldifferentstylesofmultienterprisecollaborationtomeetdiverseexternalbusinesspartnerrequirements.Thisissettobeadriverforsoftwaresegmentssuchasmultienterprise/B2BgatewaysandforservicesegmentssuchasB2BIntegrationoutsourcing.

• E-invoicingprojectswillbeincreasinglycommon,duetonewregulationsandpressureonreducingcosts,especiallyinsomecountriesofWesternEurope(suchasSpainandGermany)andofSouthAmerica(suchasMexicoandBrazil).

2Recommendations

• Endusersshouldplacegreatcareinassessingvendorviability.BecausetheoutsourcingB2Bintegrationfunctionality(integrationasaservice,IaaS)andB2Bprojects(BIO)makesavendorapartnerintheB2Bintegrationproject,vendorviabilitymusthaveasubstantialweightinevaluationsforintegrationserviceprovidersintermsofvendorsizeandsupportqualityinyourlocalgeography

• Vendorsshouldfocusonmodularofferingsinwhichcustomerscanstartsmallandincrementallybuildwithtime.Thisisbecause,giventhestillchallengingeconomicconditions,endusersaremorewaryaboutlargeprojectsandtherelativecostsandprefertostartsmallandgrowincrementallyovertime.

• Vendorsshouldbepreparedwithcustomerreferencesandafocusedgo-to-marketstrategythatwillputthemasapointofcontactforanycompanylookingattherationalizationoftheirB2Binfrastructures.

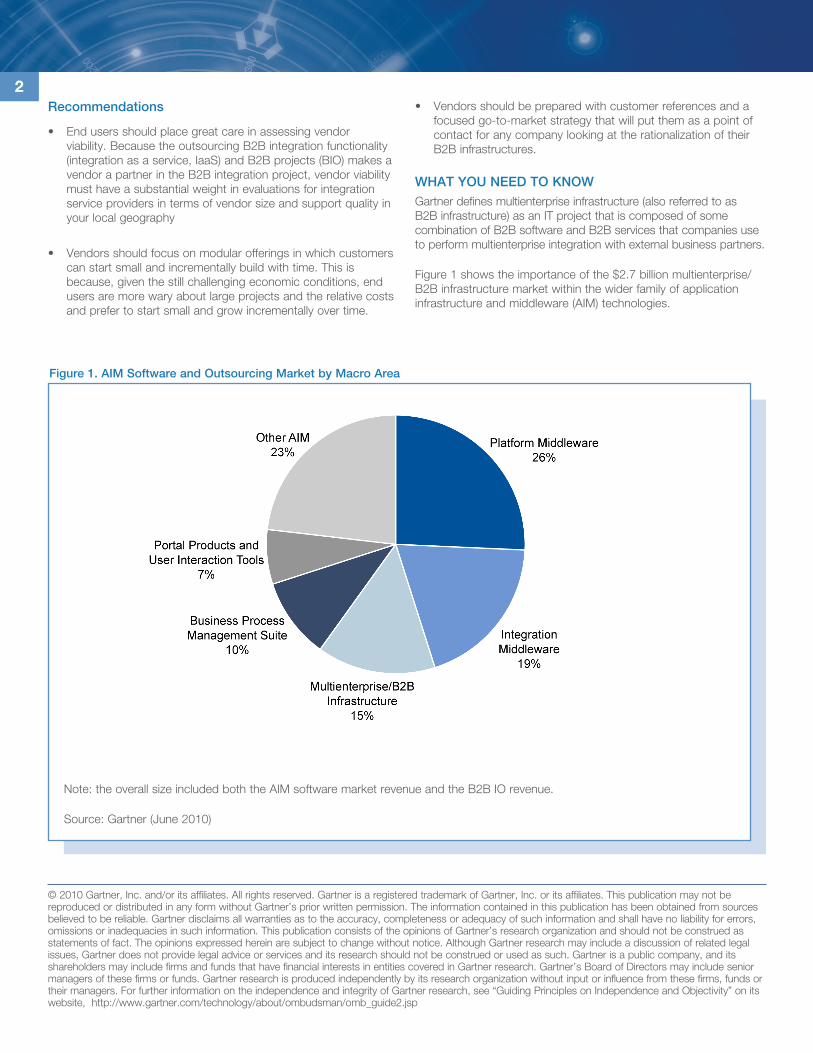

WHAT YOU NEED TO KNOWGartnerdefinesmultienterpriseinfrastructure(alsoreferredtoasB2Binfrastructure)asanITprojectthatiscomposedofsomecombinationofB2BsoftwareandB2Bservicesthatcompaniesusetoperformmultienterpriseintegrationwithexternalbusinesspartners.

Figure1showstheimportanceofthe$2.7billionmultienterprise/B2Binfrastructuremarketwithinthewiderfamilyofapplicationinfrastructureandmiddleware(AIM)technologies.

©2010Gartner,Inc.and/oritsaffiliates.Allrightsreserved.GartnerisaregisteredtrademarkofGartner,Inc.oritsaffiliates.ThispublicationmaynotbereproducedordistributedinanyformwithoutGartner’spriorwrittenpermission.Theinformationcontainedinthispublicationhasbeenobtainedfromsourcesbelievedtobereliable.Gartnerdisclaimsallwarrantiesastotheaccuracy,completenessoradequacyofsuchinformationandshallhavenoliabilityforerrors,omissionsorinadequaciesinsuchinformation.ThispublicationconsistsoftheopinionsofGartner’sresearchorganizationandshouldnotbeconstruedasstatementsoffact.Theopinionsexpressedhereinaresubjecttochangewithoutnotice.AlthoughGartnerresearchmayincludeadiscussionofrelatedlegalissues,Gartnerdoesnotprovidelegaladviceorservicesanditsresearchshouldnotbeconstruedorusedassuch.Gartnerisapubliccompany,anditsshareholdersmayincludefirmsandfundsthathavefinancialinterestsinentitiescoveredinGartnerresearch.Gartner’sBoardofDirectorsmayincludeseniormanagersofthesefirmsorfunds.Gartnerresearchisproducedindependentlybyitsresearchorganizationwithoutinputorinfluencefromthesefirms,fundsortheirmanagers.ForfurtherinformationontheindependenceandintegrityofGartnerresearch,see“GuidingPrinciplesonIndependenceandObjectivity”onitswebsite,http://www.gartner.com/technology/about/ombudsman/omb_guide2.jsp

Figure 1. AIM Software and Outsourcing Market by Macro Area

Note:theoverallsizeincludedboththeAIMsoftwaremarketrevenueandtheB2BIOrevenue.

Source:Gartner(June2010)

3Theobjectiveofmultienterpriseinfrastructureistoexchangebusinessdata(forexample,customerorsupplygoodsdata)ortolinkandautomatebusinessprocesses(forexample,order-to-cashorprocure-topay)betweentwoormorecompaniesinawaythatiseasiertomanage,faster,more-affordableandmore-accuratethanmanualapproachesorcustomcoding.Toaccomplishtheseobjectives,companiesusearangeofapproaches,suchasbuildingoroutsourcingtheB2Binfrastructure,orusingtraditionalbatchelectronicdatainterchange(EDI)atoneextreme,emergingcloudservicesattheotherextreme,Webservices-basedSOAoracombinationofanyoftheseapproachestoB2B.Forthisreason,therearecurrentlyseveralmultienterprise/B2Binfrastructureofferingsavailableinthemarketwithsimilarlydifferenttractionandprospectsforgrowth.

ThewaveofmergersandacquisitionsthatischaracterizingtheoverallAIMmarketandthespecificB2Bintegrationmarketisamajordisrupterthatwillcontinuetoshapethevendorlandscapeduringtheforecastperiod.Changesinthevendorlandscape(suchas,IBMacquiringSterlingCommercemighttriggeroraccelerateacquisitioningmovesbyitsmaincompetitors)willoffernewopportunities,butalsomorereasonsforcautionbyuserorganizations.OrganizationshavingtoaddressB2Brequirementsmustassesscarefullythebalancebetweenextraspecializedpure-playB2Bvendors(typicallysmallerandnimbler)andvendorsthatofferB2Binconjunctionwithotherintegrationproductsandservices.Dealswillhavetofocusontheabilityofvendorstohavesufficientresourcesanddomainexpertisetomeetdiverse,geographic-andvertical-specificB2Bproject-scoperequirementsthatarelikelytoexpandinthefuture.

AsfarasdiversewaysofdeliveringB2Bcapabilities,wehaveidentifiedninesegments,includingpurelysoftwareofferingsandserviceofferings,composingtheB2Binfrastructureportfolio;eachofthesesegmentsaddressesdifferentB2Bprojectrequirementsandhasspecificprosandcons;somearelegacytechnology,andsomeareemergingofferings,buttheyallplayaroleinthecurrentorganization’squestforB2Bintegrationportfolioconsolidation.Thesegmentscomposingthemultienterprise/B2BInfrastructureportfolioareasfollows:

• BIO

• Traditionale-commerceIaaS

• CloudservicesIaaS

• Managedfiletransfer(MFT)forB2B

• MFTaaSforB2B

• Service-orientedarchitecture(SOA)governancesoftwareforB2B

• Stand-alonemultienterprise/B2Bgateways

• Embeddedmultienterprise/B2Bgateways

• Electronicdatainterchange(EDI)translators(stand-alone)

Stand-aloneEDItranslatorsoftwareistypicallylicensedfromanEDIsoftwareproviderortraditionalvalue-addednetwork(VAN)thatisfocusedprimarilyonthetranslationofEDIdataintointernaldataformats.TherearealsoembeddedEDItranslatorsthatareofferedasfunctionalitywithinmultienterprise/B2Bgateways.However,thisembeddedcomponentisfairlycommoditized,anditsrevenuecontributionisrecognizedintherevenuesizeofmultienterprise/B2Bgateways.

B2Bgatewaysoftwareismiddlewareusedtoconsolidateandcentralizeacompany’smultienterprisedata,application,processintegrationandinteroperabilityrequirementswiththoseofexternalbusinesspartners.

MFTsoftwareenablescompaniestoautomate,compress,restart,secure,log,analyzeandauditthetransferofdatafromoneendpointtoanother,often(notalways)includingexternalbusinesspartners.

SOAgovernancesoftwareforB2BprojectsisdrivenbytheemergenceofSOAoverall,whichhelpscoordinatethegovernanceoftheservicesinvolved.BecauseSOAismakingasignificantinroadintotheB2Bspace,thereisagrowingmarketopportunityforofferingsaddressingthespecificneedsofSOAgovernancewithinB2Bprojects.

IaaSismultienterpriseintegrationcapabilities(suchasthatofB2Bgatewaysoftware)hostedinamultitenantenvironmentanddeliveredasaserviceratherthanassoftware.TraditionallyknownasEDIVANs,vendorsofferingIaaSarecalled“integrationserviceproviders.”Thissegmentiscomposedbytraditionale-commerceIaaS,cloudservicesIaaSandMFTaaSforB2B.

B2BIntegrationoutsourcingisaspecificcategoryofITprojectoutsourcingthatcombinesoutsourcingyourtechnicalB2Binfrastructure(IaaS)andyourB2Bproject(thatis,thepeopleandprocesses).Mostofe-invoicingprojectswillbeinthissegment.

OntheB2Bsoftwareside,akeytrendisthatthemarketforstand-aloneEDItranslators,SOAgovernancetechnologies,andMFTisquicklybeingabsorbedintoB2Bgatewaysoftware.Sofar,mostSOAgovernancesoftwareforB2Bprojectsaresoldasastand-alone,butovertimethisfunctionalitywillincreasinglybecomeavailableasanembeddedfeatureofB2BgatewaysoftwareandcloudserviceIaaS.Ontheserviceside,B2BIntegrationoutsourcingincreasinglyisdeployedusinganIaaSofferingasthetechnologybackbone,whichlowersoverallprojectcostsbecauseitleveragessharedB2Binfrastructure.

KEY TRENDSIntegrationisnolongeraprojectbetweentwoapplications.Itisacross-companyandbetween-companydisciplinethatincreasinglyinvolvesallofanorganization’sapplications,externalbusinesspartnersandcloudservices.The“dumb”networkthatusedtoonlytransferbulkfilesbetweenapplicationsandtradingpartnersisturningintoa“smart”networkthatincorporatesdiverseintegrationfunctionality,includingcommunications,translationandworkflow,increasinglyimplementedbyapplicationvendorsandusersusinganSOA.TheB2Bdisciplinealsonowmustincludecloudservicesintegration—forexample,howtolinkservicesfromsolutionssuchassalesforce.comtoon-premisesapplications.SuccessfulorganizationswillcombinetraditionalintegrationandemergingSOA

4andWeb-nativeapproachessuchasWeb-orientedarchitecture(WOA)andcloudAP’stosolvediverseapplicationintegrationandinteroperabilityrequirements.Thescopeoftheseeffortswillinvolveinternalandexternalapplications,thelatterincludinge-commercetradingpartnersandexternalserviceproviders(ESPs),suchasserviceintegratorsandsoftwareasaservice(SaaS)providers.

AtypicalITinfrastructureincludesadapters;datatransformationenginesandextraction,transformationandloading(ETL)tools;integrationbrokers,managedfiletransferandbusinessprocessmanagerstoorchestratemessageflows,Webserviceschoreographyandbusinessprocessexecution;eventmanagement;andalertingfacilitiesforbusinessactivitymonitoring(BAM).OrganizationswillthenneedB2BinfrastructuretoextendtheirITinfrastructuretoexternalbusinesspartners,includingprovisioningtoolstosimplifytheprocess.

The B2B Vendor Landscape — More Consolidation Ahead Whenpure-playapplicationintegrationvendorscametomarketinthemid-1990s,productsintroducedhadabasesetoffeaturesthatincludeddatatransformation,intelligentrouting,message-orientedmiddleware,amessagewarehouseandadministration/management.Whenlargesuitevendors(suchasOracle)enteredthemarket(inthelate1990s),theyalsoofferedsimilartypesofbasefeatures.However,thenumberoffeaturesinproductsfrompure-playvendorshasbeenextendedtoincludeworkflow,internalintegrationfeatures(suchasadaptersforpackagedapplications),processvisibilityandotherformsofBAM.Theneteffectofthisovertimeisthatthedistinctionbetweenpure-playB2Bproductsandpure-playinternalintegrationproductsisblurring,andincreasingB2Bcapabilitieswillsimplybeafeatureofanyintegrationmiddleware.Furthermore,webelievethatthepure-playB2Bmarketwillultimatelyceasetoexist,althoughstand-aloneB2Bproductsandserviceswillcontinuetobeavailableforatleastthenextdecade.

WeexpecttheB2BmarkettoconsolidatearoundfewerB2Bspecialists,whilewealsoexpecttraditionalAIMvendors(particularlysuitevendors)toconsiderexpandingintothemultienterprise/B2Binfrastructurespace.Asaconsequence,theB2BsuitevendorsandtheAIMvendorswillincreasinglybattlehead-to-head;theformerwillpromotetheirabilitytodeliverspecificexpertiseandexcellenceintheB2Bspace,includingmuch-neededverticalknowledge,whilethelatterwillcapitalizeontheirabilitytoreachouttoasizableexistingcustomerbaseandtothoseorganizationslookingfora“goodenough”B2Bsolution.

ThemainchallengeforB2Bspecialistswillbetoreachouttothesamevariety(intermsofverticalmarketsandgeography)ofexistingcustomersthatatypicalAIMvendormightbeabletoreach.ThiswillbeincreasinglydifficultwhenfacingamegavendorthatisstartingtoplayinB2B.Furthermore,byexploitingexistingrelationshipsandcross-sellingandupsellingB2Bfunctionalitytotheirexistingcustomers,AIMvendorsobtainthepotentialcompetitiveadvantageofshorteningsalescycletimesandbeingabletooffer(veryoften,goodenough)B2Bfunctionalityatadiscountedrateontopofothermiddlewareofferings.Also,forthecustomers,it’smucheasiertoconnectanyB2BextensionintosomethingthatisalreadypluggedintoandintegratedwiththeirITsystems.

Multienterprise/B2BgatewaysoftwarewouldgenerallybetheentrypointtotheB2BmarketfortraditionalAIMplayersthatcanpotentiallyofferB2Bgatewayfunctionalitieswithinwiderintegrationsuiteofferings.Thisisbecausethemultienterprise/B2Bgatewaymarketiscomposedofmiddlewaretechnologyfrommultipledisciplines,includingintegrationsuites,enterpriseservicebuses,applicationserversandapplicationplatformsuites,EDItranslators,MFTandtheB2B-enabledintegrationmiddlewarethatisincreasinglyavailablewithpackagedapplications.Ingeneral,vendorsofferinganyofthesemiddlewaretechnologieswouldfinditeasiertoalsotrytoaddresstheB2Bgatewayneedsoftheircustomers.

Ontheintegrationservicesside,wehaveseensubstantialmarketconsolidation,whichwillcontinueinthenextyears.RecentexamplesincludeIBM’sacquisitionsofCastIronandSterlingCommerceandtheGXSmergerwithInovis.Overall,theexpansionofpure-playintegrationvendors(mostofwhichalreadyoffersomekindofB2Bfunctionality)willcauseincreasedpressureonsmallerB2Bplayers,someofwhichwillultimatelylosemarketshareand/orbecomeappealingacquisitiontargets.WebelievethattherecentSPSCommerceIPO—wasexecutedatleastinpartbecauseofpressurefromlargerprovidersandaneedtoraisecapitaltobettercompete.

Multienterprise/B2B Infrastructure Market OutlookInsizingthemultienterprise/B2Binfrastructuremarket,weconsideredsomecomponentsthataresoldasaspecificstand-aloneB2Bproductorasafunctionalitypartofasuite.

Multienterprise/B2B Gateway Software ForecastMultienterprise/B2BgatewaysolutionsaresoldbyB2Bspecialistsasastand-aloneproduct(suchasthosesoldbySterlingCommerce(nowpartofIBM),Axway,GXS,SeeburgerAG,SoftwareAGandGenerix)orasafunctionalitywithinabroaderintegrationsuite(suchasthosesoldbyTibco,SoftwareAG,OracleandMicrosoft).

AsshowninTable1,theoverallmultienterprise/B2Bgatewaymarketisexpectedtogrowatasingle-digitratethrough2014,outpacingtheoverallApplicationInfrastructureandMiddlewaresoftwaremarket.

Multienterprise/B2Bgatewayscontinuetobeinhighdemandfromorganizationsofeverysize,regardlessofindustryexpertise.Vendorshaveexpandedthefunctionalityofthemultienterprise/B2Bgatewayfromprimarilyprovidingameansofconsolidatingandcentralizingacompany’sB2Bcommunications(regardlessofthesizeandtypeofdata),toprovidingsomeinternalintegration(resultingintheeventualexternalizationoftheintegrateddata),andprovidinganinfrastructureincludinginnovativecommunitymanagementcapabilitiesforautomatingandmonitoring(frombothatechnologyandbusinessprocesspointofview)interactionswithexternalbusinesspartners.Thisevolvedfunctionalitygivescompaniestheflexibilitynecessarytosupportthemyriadofcurrentandemergingtransportandcommunicationsprotocols,aswellassecuritystandardsandmechanisms.

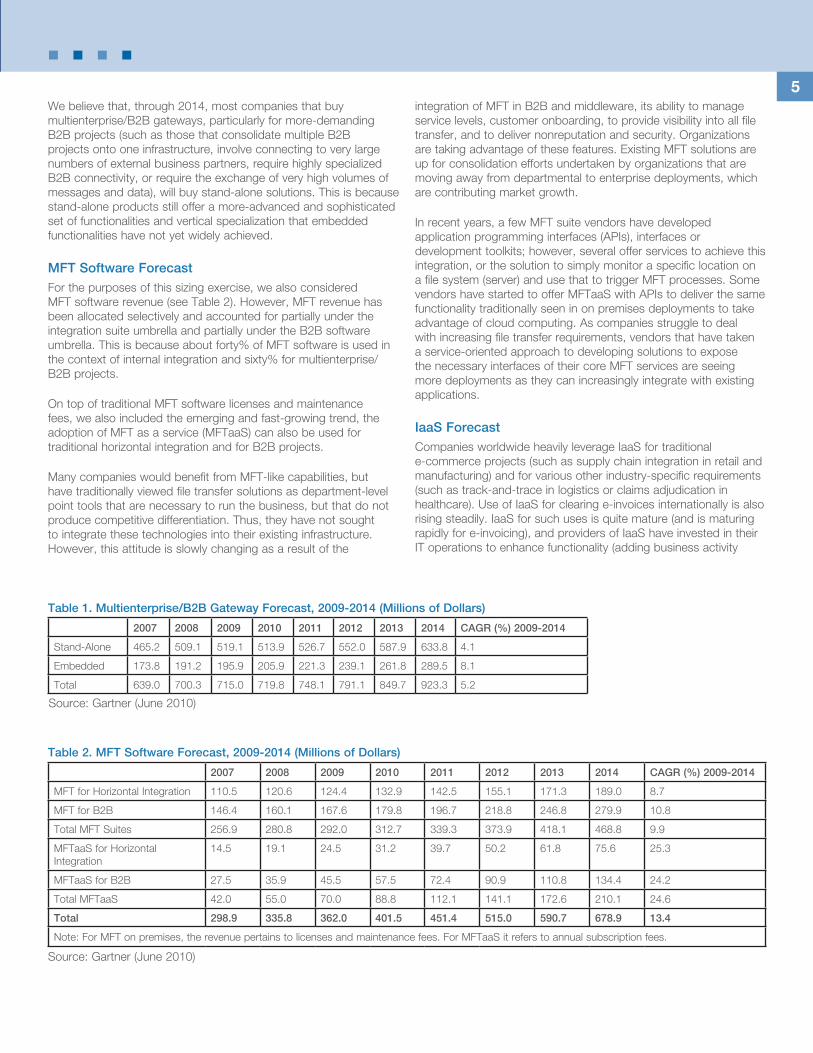

5Webelievethat,through2014,mostcompaniesthatbuymultienterprise/B2Bgateways,particularlyformore-demandingB2Bprojects(suchasthosethatconsolidatemultipleB2Bprojectsontooneinfrastructure,involveconnectingtoverylargenumbersofexternalbusinesspartners,requirehighlyspecializedB2Bconnectivity,orrequiretheexchangeofveryhighvolumesofmessagesanddata),willbuystand-alonesolutions.Thisisbecausestand-aloneproductsstillofferamore-advancedandsophisticatedsetoffunctionalitiesandverticalspecializationthatembeddedfunctionalitieshavenotyetwidelyachieved.

MFT Software Forecast Forthepurposesofthissizingexercise,wealsoconsideredMFTsoftwarerevenue(seeTable2).However,MFTrevenuehasbeenallocatedselectivelyandaccountedforpartiallyundertheintegrationsuiteumbrellaandpartiallyundertheB2Bsoftwareumbrella.Thisisbecauseaboutforty%ofMFTsoftwareisusedinthecontextofinternalintegrationandsixty%formultienterprise/B2Bprojects.

OntopoftraditionalMFTsoftwarelicensesandmaintenancefees,wealsoincludedtheemergingandfast-growingtrend,theadoptionofMFTasaservice(MFTaaS)canalsobeusedfortraditionalhorizontalintegrationandforB2Bprojects.

ManycompanieswouldbenefitfromMFT-likecapabilities,buthavetraditionallyviewedfiletransfersolutionsasdepartment-levelpointtoolsthatarenecessarytorunthebusiness,butthatdonotproducecompetitivedifferentiation.Thus,theyhavenotsoughttointegratethesetechnologiesintotheirexistinginfrastructure.However,thisattitudeisslowlychangingasaresultofthe

integrationofMFTinB2Bandmiddleware,itsabilitytomanageservicelevels,customeronboarding,toprovidevisibilityintoallfiletransfer,andtodelivernonreputationandsecurity.Organizationsaretakingadvantageofthesefeatures.ExistingMFTsolutionsareupforconsolidationeffortsundertakenbyorganizationsthataremovingawayfromdepartmentaltoenterprisedeployments,whicharecontributingmarketgrowth.

Inrecentyears,afewMFTsuitevendorshavedevelopedapplicationprogramminginterfaces(APIs),interfacesordevelopmenttoolkits;however,severalofferservicestoachievethisintegration,orthesolutiontosimplymonitoraspecificlocationonafilesystem(server)andusethattotriggerMFTprocesses.SomevendorshavestartedtoofferMFTaaSwithAPIstodeliverthesamefunctionalitytraditionallyseeninonpremisesdeploymentstotakeadvantageofcloudcomputing.Ascompaniesstruggletodealwithincreasingfiletransferrequirements,vendorsthathavetakenaservice-orientedapproachtodevelopingsolutionstoexposethenecessaryinterfacesoftheircoreMFTservicesareseeingmoredeploymentsastheycanincreasinglyintegratewithexistingapplications.

IaaS ForecastCompaniesworldwideheavilyleverageIaaSfortraditionale-commerceprojects(suchassupplychainintegrationinretailandmanufacturing)andforvariousotherindustry-specificrequirements(suchastrack-and-traceinlogisticsorclaimsadjudicationinhealthcare).UseofIaaSforclearinge-invoicesinternationallyisalsorisingsteadily.IaaSforsuchusesisquitemature(andismaturingrapidlyfore-invoicing),andprovidersofIaaShaveinvestedintheirIToperationstoenhancefunctionality(addingbusinessactivity

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

Stand-Alone 465.2 509.1 519.1 513.9 526.7 552.0 587.9 633.8 4.1

Embedded 173.8 191.2 195.9 205.9 221.3 239.1 261.8 289.5 8.1

Total 639.0 700.3 715.0 719.8 748.1 791.1 849.7 923.3 5.2

Table 1. Multienterprise/B2B Gateway Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

MFTforHorizontalIntegration 110.5 120.6 124.4 132.9 142.5 155.1 171.3 189.0 8.7

MFTforB2B 146.4 160.1 167.6 179.8 196.7 218.8 246.8 279.9 10.8

Total MFT Suites 256.9 280.8 292.0 312.7 339.3 373.9 418.1 468.8 9.9

MFTaaSforHorizontalIntegration

14.5 19.1 24.5 31.2 39.7 50.2 61.8 75.6 25.3

MFTaaSforB2B 27.5 35.9 45.5 57.5 72.4 90.9 110.8 134.4 24.2

Total MFTaaS 42.0 55.0 70.0 88.8 112.1 141.1 172.6 210.1 24.6

Total 298.9 335.8 362.0 401.5 451.4 515.0 590.7 678.9 13.4

Note:ForMFTonpremises,therevenuepertainstolicensesandmaintenancefees.ForMFTaaSitreferstoannualsubscriptionfees.

Table 2. MFT Software Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

6monitoringandimprovedcommunitymanagement),andtodriveincreasingscaleandefficiencies(switchingtomore-modern,scalableIaaSarchitectures).ThoseITmodernizations,combinedwithincreasingadoptionandtheprevailingperceptionthatIaaSisincreasinglyacommodity,havebeendrivingdownIaaSpricesfornearlyadecade.Nevertheless,IaaSfortraditionale-commerceisstillavaluableITserviceforcompaniesdoingB2Bintegration;therefore,adoptioncontinuestoincrease,asindicatedbytheincreasingnumbersofcompaniesandtransactionshandledbytheprovidersofIaaSeachyear(generallyrangingfroma10%to100%increaseinthenumberofcompaniesservedandtransactionsexchangedperyear,dependingonthesizeoftheprovider).Thistrendhasbeenconsistentworldwideyeartoyear—evenduringthecurrentworldwiderecession—asmorecompaniesseekoutsourcing(subscription)alternativestothesignificant(capital)costofexpandingB2BinfrastructureandstaffingwhenitisnecessarytoscaleuptheirB2Bprojects.AsIaaSincreases,SaaSapplicationsusingIaaSwillincreasesteadilytoo.Table3showsthesizeandgrowthrateofthedifferentcomponentsoftheIaaSsegment.

CloudserviceintegrationisarelativelynewB2Bintegrationprojectscenario,yetthebuyersofIaaSforcloudserviceintegrationrangefromline-of-businessITbuyers—primarilyonlyfocusedonthecloudservicetoon-premisesintegrationproblem—tomore-traditionalITbuyers—focusedoncloudserviceintegrationandontraditionale-commerceintegration.ProvidersofIaaSforcloudserviceintegrationoftenselldirectlytoITend-users;theyalsosellasubstantialproportionoftheirIaaSservices(weestimate50%)throughITchannelpartners.

ThisisbecausemanyITservicesproviders—particularlySaaSproviders—mustaddresscloudserviceintegration,yetwouldprefertoinvesttheirlimitedR&Dcapabilitiesondifferentiatedfunctionalitythatbuildsabarriertoentryintheirtargetmarkets,ratherthanmakingsubstantialinvestmentstosolveatechnicallycomplicatedintegrationproblem.FouryearsagotherewasbasicallynomarketforIaaSforcloudserviceintegration.Today,

weestimatethatcompaniesspend$50milliononIaaSforcloudserviceintegration,andthatthisITmarketsegmentwillgrowat23.5%CAGRforthenextfiveyears.

Overall Multienterprise/B2B Infrastructure Market ForecastThemultienterprise/B2Binfrastructuremarketispoisedforgoodgrowthduringthenextfiveyears.Itwillbedrivenbytheincreasingmaturityandadoptionofvariousrelatedstandards—suchasXML,SOA,Webservices,cloudcomputing,globaldatasynchronization(GDS),andforecasting—combinedwiththeincreasingmaturityandflexibilityoftheintegrationofSaaS.

Furthermore,thereisalreadyagoodsetofreferenceorganizationssuccessful(generallyintermsofprocessimprovementsandcostsavings)inmultienterprisecollaboration,reportingbottom-lineandtop-linerevenueincreasesattributedtoincreasedautomation,lowercostsandimprovedprocessexecution,whichimprovesbusinesspartnerrelationshipsandattractsnewbusiness.Theprospectsforgrowthremainpositivebecausetheneedforinterenterprisecollaborationdoesnotshowanysignsofdiminishing.

Tosizethemarket,weconsideredtotalsoftwarerevenue(fromnewlicenses,maintenanceandtechnicalsupport)generatedbysalesofstand-aloneandembeddedmultienterprise/B2Bgateways,MFTforB2B,EDItranslators(stand-alone),andSOAgovernancesoftwareforB2Bproducts.ForIaaS,weconsideredsubscriptionrevenue(inourdefinition,partofmaintenance),andforB2BIntegrationoutsourcing,weestimatedrevenuegeneratedexcludingprofessionalservicesfees.

In2009,weestimatetheoverallmultienterprise/B2Binfrastructuremarketgeneratedalmost$2.8billion(seeFigure2).Themarketwillgrowata9.0%CAGR,whichisabout2percentagepointshigherthanthegrowthweexpectfortheoverallapplicationinfrastructureandmiddlewaremarket.

7

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

TraditionalE-CommerceIaaS

946.3 969.2 849.2 775.5 714.0 662.0 617.9 573.5 -7.5

CloudServicesIaaS 35.3 41.7 50.4 61.5 75.8 94.3 116.9 145.0 23.5

MFTaaSforB2B 27.5 35.9 45.5 57.5 72.4 90.9 110.8 134.4 24.2

Total 1,009.0 1,046.7 945.1 894.5 862.1 847.2 845.6 853.0 -2.0

Table 3. IaaS Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

Figure 2. Multienterprise/B2B Infrastructure Market Forecast, 2009-2014

Source:Gartner(June2010)

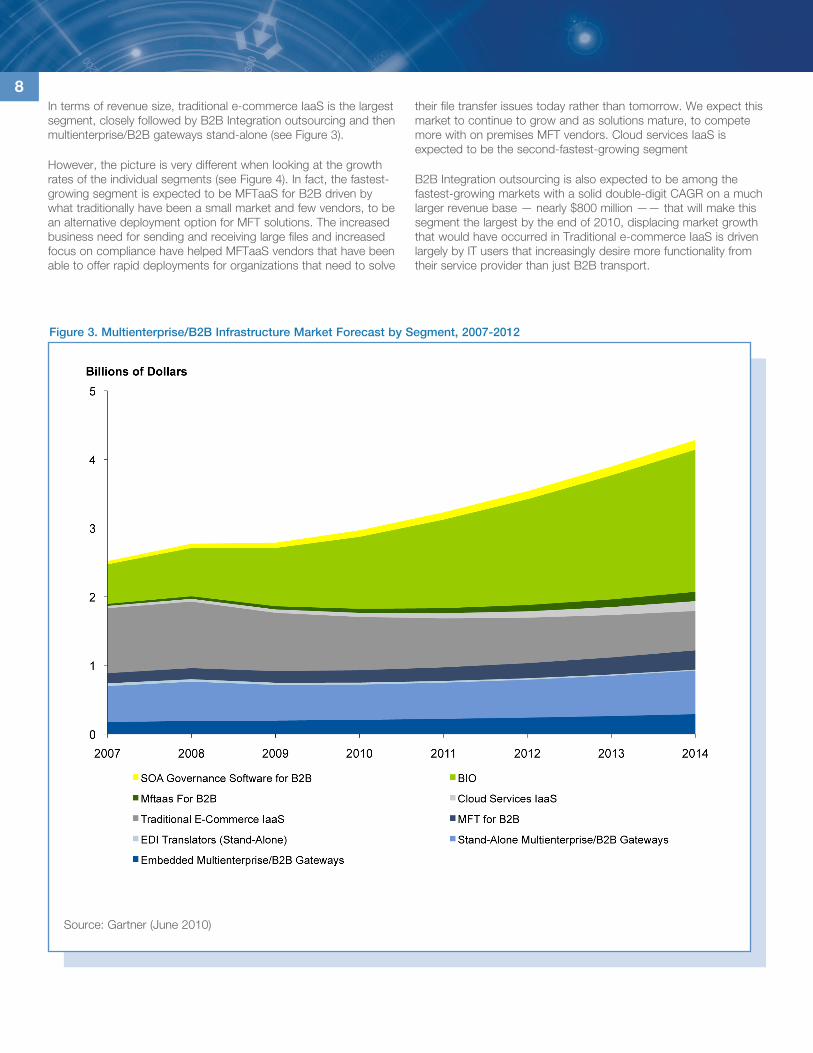

8Intermsofrevenuesize,traditionale-commerceIaaSisthelargestsegment,closelyfollowedbyB2BIntegrationoutsourcingandthenmultienterprise/B2Bgatewaysstand-alone(seeFigure3).

However,thepictureisverydifferentwhenlookingatthegrowthratesoftheindividualsegments(seeFigure4).Infact,thefastest-growingsegmentisexpectedtobeMFTaaSforB2Bdrivenbywhattraditionallyhavebeenasmallmarketandfewvendors,tobeanalternativedeploymentoptionforMFTsolutions.TheincreasedbusinessneedforsendingandreceivinglargefilesandincreasedfocusoncompliancehavehelpedMFTaaSvendorsthathavebeenabletoofferrapiddeploymentsfororganizationsthatneedtosolve

Figure 3. Multienterprise/B2B Infrastructure Market Forecast by Segment, 2007-2012

Source:Gartner(June2010)

theirfiletransferissuestodayratherthantomorrow.Weexpectthismarkettocontinuetogrowandassolutionsmature,tocompetemorewithonpremisesMFTvendors.CloudservicesIaaSisexpectedtobethesecond-fastest-growingsegment

B2BIntegrationoutsourcingisalsoexpectedtobeamongthefastest-growingmarketswithasoliddouble-digitCAGRonamuchlargerrevenuebase—nearly$800million——thatwillmakethissegmentthelargestbytheendof2010,displacingmarketgrowththatwouldhaveoccurredinTraditionale-commerceIaaSisdrivenlargelybyITusersthatincreasinglydesiremorefunctionalityfromtheirserviceproviderthanjustB2Btransport.

9

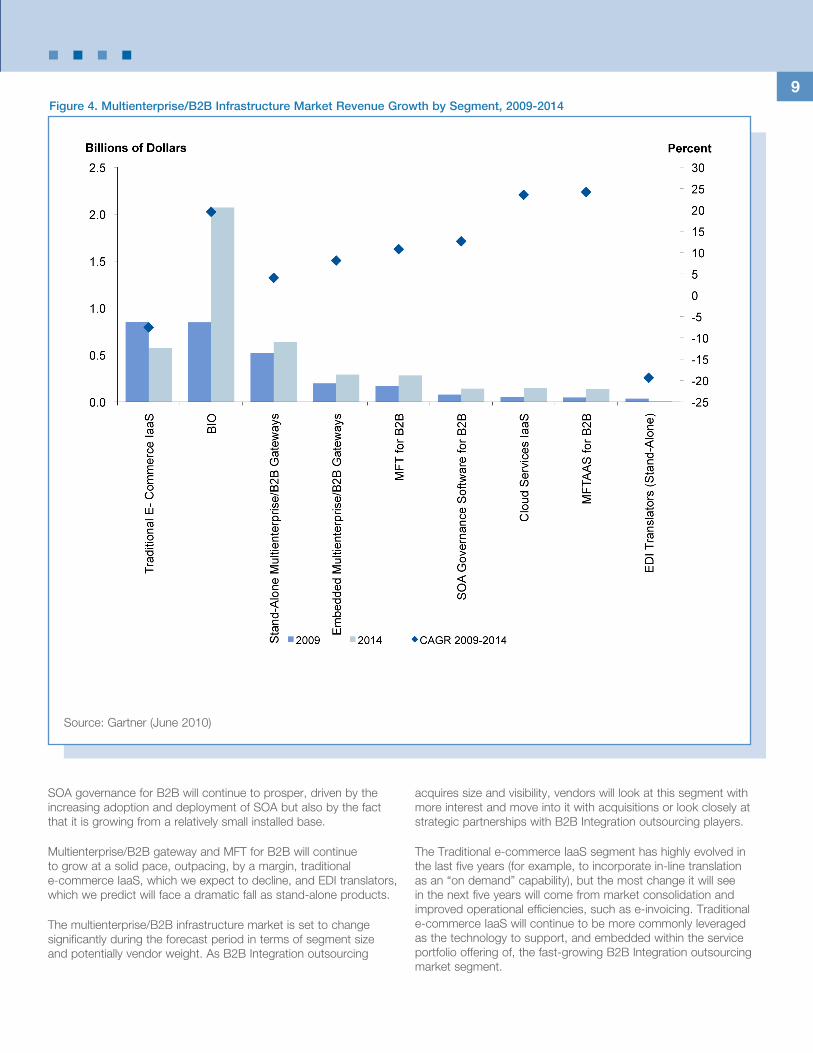

SOAgovernanceforB2Bwillcontinuetoprosper,drivenbytheincreasingadoptionanddeploymentofSOAbutalsobythefactthatitisgrowingfromarelativelysmallinstalledbase.

Multienterprise/B2BgatewayandMFTforB2Bwillcontinuetogrowatasolidpace,outpacing,byamargin,traditionale-commerceIaaS,whichweexpecttodecline,andEDItranslators,whichwepredictwillfaceadramaticfallasstand-aloneproducts.

Themultienterprise/B2Binfrastructuremarketissettochangesignificantlyduringtheforecastperiodintermsofsegmentsizeandpotentiallyvendorweight.AsB2BIntegrationoutsourcing

acquiressizeandvisibility,vendorswilllookatthissegmentwithmoreinterestandmoveintoitwithacquisitionsorlookcloselyatstrategicpartnershipswithB2BIntegrationoutsourcingplayers.

TheTraditionale-commerceIaaSsegmenthashighlyevolvedinthelastfiveyears(forexample,toincorporatein-linetranslationasan“ondemand”capability),butthemostchangeitwillseeinthenextfiveyearswillcomefrommarketconsolidationandimprovedoperationalefficiencies,suchase-invoicing.Traditionale-commerceIaaSwillcontinuetobemorecommonlyleveragedasthetechnologytosupport,andembeddedwithintheserviceportfolioofferingof,thefast-growingB2BIntegrationoutsourcingmarketsegment.

Figure 4. Multienterprise/B2B Infrastructure Market Revenue Growth by Segment, 2009-2014

Source:Gartner(June2010)

10CONTRIBUTING FACTORS TO TRENDSMultienterprise/B2Binfrastructureproductswillcontinuetoseetractioninthemarketbecausemultienterprisecollaborationofallformswillcontinuetoproliferate.Thereareseveraldriversandinhibitorsofthismarket,bothonthetechnologysideandthebusinessside.

Market DriversTechnologydriversincludethefollowing:

• Morecompaniesareadoptingalong-termplantoconsolidatediversemultienterpriseprojectsontoasharedinfrastructure.Thiswilllikelytakeyears,andinsomecases,fullconsolidationisnotevenpossible,butthegeneralapproachisconsistentwithouradviceforconsolidatinginternalintegrationprojectsontoasharedinfrastructure,withsimilarbenefitsandchallenges.BenefitsincludelowerB2Bprojectcosts(fromeconomiesofscale),amore-consistentapproachtodoingintegration,betterprovisioningtools,consistentapplicationofsecuritypolicies,andimprovedandmore-consistentprocessvisibilityandgovernance.

• Themarketisbeinghelpedbytheincreasingmaturityandadoptionofvariousrelatedstandards,suchasXML,SOA,Webservices,portals,GDS,CPFR,RosettanetandeXML.

• Thewholemarketisgettinganincreaseinspendingandaninjectionofinnovationbecauseoftherapidproliferationofcloudservices,andtheneedtointegratethosewitheachother(cloudtocloud)andwithon-premisesapplications.

• SaaScustomersincreasinglyneedtointegratetheirinternalapplicationsdirectlywiththesoftwarefunctionalityavailablefromSaaSproviders.Manycompaniesarebeginningtoshopforasingle-sourcesolutionofB2Binfrastructuredeliveredassoftwareandservices.

Businessdriversincludethefollowing:

• MultienterpriseB2Binquiriesaredrivenbyincreasedcompliancerequirements,suchasthatmandatedbytheU.S.Sarbanes-OxleyAct,theHealthInsurancePortabilityandAccountabilityAct,BaselII,e-invoicingregulationsinEuropeandSouthAmerica,andconcernsaboutconsistentsecurityandauditing.Toprotectthemselvesfromfuturesecurityviolationsandcompliancerisk,companiesareincreasinglyconsideringlimitingtheproliferationofuncoordinatedB2Bprojects.Theynowlookatdeployingacompanywidemultienterpriseintegrationstrategy,perhapsusingaphasedapproachtocontrolcostsandminimizedisruptiontocurrentprojects.

• Themarketisbeinghelpedbymore-visiblebusinessimpact,withcompaniesthataresuccessfulinmultienterprisecollaborationreportingbottom-lineandtop-linerevenueincreasesandcostsavingsattributedtoincreasedautomation,lowercostsandimprovedprocessexecution(visibilityand

control).Thisimprovesbusinesspartnerrelationshipsandattractsnewbusiness,particularlywhenmultienterpriseprojectsincludeprocessmonitoringandintelligence(suchasdatavalidation,compliancemanagement,andsupplierandvendorrelationshipmanagement).

• Multienterprise/B2Binfrastructuredeploymentshaveextensivelyprovedtoincreasetop-linerevenuevianewservicesandcustomers,andincreasedcompetitivedifferentiation.Thereisalreadyasizablenumberofreferenceaccountsofmultienterprisesuccessesacrossregionsandverticalmarketsthathelpdecisionmakersleantowardmultienterprise/B2Binfrastructureadoption.

• Theever-increasinginternationalizationofeconomiesandincreasedinterdependenceoforganizationsoperatingacrossregionsalsohelpsthismarket.

• Therapidadoptionofe-invoicing(especiallyinareaswhereregulationsmandateit)andlogisticsvisibilityisexpandingexistingB2Bprojectsandcreatingnewones.

• OutsourcingofnoncorecompetencieswillincreasinglysustainIaaSuseandgrowB2Bintegrationoutsourcing.SMBscanbenefitfromB2BoutsourcingbecauseB2Bprojectsaregenerallyaresource-intensive,complexITtaskthatcanbecost-effectivelyoutsourcedtoESPs.LargecompaniescanalsobenefitfromB2Boutsourcing,particularlywhenthereisadesiretoapplylimitedinternalITresourcestohigher-priorityinternalITprojects,suchasERPupgradesorCRMprojects,orwhenconsolidatingexisting(frequentlynationallybased)B2Binfrastructures.

Market InhibitorsDespiterecentgains,therearestillinhibitorstoadoptingvariousformsofenterprisecollaboration,whichpressurethemarketnottogrowatthedouble-digitratesseeninthepast.

Technologyinhibitorsincludethefollowing:

• Securityinteroperability(forexample,therearenoubiquitousformsofauthentication)anddifficultiesinintegration(mostinternalapplicationsarestillnot“multienterpriseready”)remainissues.Furthermore,intherushtomarket,manycompanieslookingtointegratevariousinfrastructureandapplicationsalsooverlookthesecurityvulnerabilitiescausedbyboltingtogetherinternalandexternalsystems.

• Technicalcompatibilityisstillanunresolvedissuebecausemostapplicationsarenotinherentlydesignedforcollaboration.

• B2Bstandardsaretoonumerousandstillincomplete,andcustomizationisstillneeded(WebservicesandSOAarenotwidelyusedinB2Bprojects).

11• Masterdatamanagementispoorlyunderstoodinhighly

distributedsystems.

• Therearefearsrelatedtolegalissuesandintellectualproperty(IP)protectioninherentinanyformofcollaboration.Oneaspectofthisistheexposureofsensitiveorproprietarybusinessprocesslogicordatatoexternalbusinesspartners.AnotheraspectofthisisestablishingclearIPownershipforIPimplementedbetweencompanies(suchaswithinanIaaSorB2BIntegrationoutsourcingsolution).

Businessinhibitorsincludethefollowing:

• Theeconomyin2008and2009hitthemanufacturingsectorparticularlyhard;thissectorisastrongconsumerofB2Btechnologies.Although2010issettobetheyearofrecovery,itisanticipatedtobeafairlyslowyearformosteconomicallymatureregionsintheworldinwhichthebulkofmultienterprise/B2Binfrastructurespendingisconcentrated.Atthisstage,theimpactofspendingfromemergingregionsinthismarketisminimalandnotsettoovercomeanycontinuedsluggishperformanceofEuropeortheU.S.Theeconomyremainsacrucialfactorinthefortunesofthismarketovertheforecastperiod.

• Resistancetochangehashurtthemarket,ashastheaversiontowardtheculturaladaptationneededwhenimplementingamultienterprisestrategicdeployment.Departmentalstaffgenerallyresistschange,andinsomecases,keydecision-makingindividualsmighthaveahiddenagendathatwouldbeunderminedbyanyformofopennessandcollaboration.Forexample,thefearofworkforcereductionorlossofcontrolwhenoutsourcingaB2BprojectcouldmakeinternalITmanagersreluctanttooutsourceB2Bprojects(versusimplementingthemin-house).

• Mostcompaniesarestillattheearlystagesofimplementingmultienterprise/B2Binfrastructure,developingbestpracticesfortrustandIPandestablishingmutuallybeneficialincentives,investments,risksandrewards.Thispartneruneasinessshowsitselfalsointheunwillingnesstoinvesttimeandresourcesincollaboration.

• ComparedwiththeirunderstandingofthebusinessvalueofinternalITprojects,ITstaffmembersonB2Bprojectshavelessexperienceofmeasuringandmakingthebusinessvalueofmultienterprise/B2Binfrastructureunderstoodatthemanagementlevel.Realmeasurementsofvalueareofparamountimportance.

• Differentnationalregulationswillstillmakethedeploymentofinternationale-invoicingprojectschallenging:thesolutionofthosechallenges,especiallyfromaBIOperspective,willstillremainoneoftheirmajorsellingpointsintheshortterm(twotothreeyears),whilethedifferencewillsmoothupininternationalmarket.

ANALYSISThemultienterprise/B2Bgatewaysoftwaremarketispoisedtogrowatasteadypaceduringthenextfiveyears.Thismarketofferstheopportunityforvendorsto“gettheirfootinthedoor”ofasegmentoftheAIMmarketthatisamongthefastest-growingandthathassomeofthemostpotential.

Infact,allthemajorintegrationandplatformvendorshaveanarticulatedconsistentandfocusedstrategyofexploitingmultienterprise/B2Bgateways,usedforthemanagementofexchangeddataandprocesses,tocreaterecurringsalesopportunitiesforvendors.Thepresenceoftheirmultienterprise/B2Bgatewaysinacompany’sinfrastructurecouldpresumablycreatevendorpresenceandvendoropportunitytoselllarger,more-expensivetechnologies,especiallynowthatthemegavendorshavestartedtoplayinB2B.ThisiswhywebelievethattheembeddedB2Bgatewayfunctionalitieswithinsuiteswillcontinuetothrive.

Ontheotherhand,stand-alonesolutionswillcontinuetooffergood(andinmanycasesbetter)verticalfunctionalityandexpertise.Unlikeseveralmiddlewaretechnologiesthatarehorizontalinnature(suchasapplicationservers),integrationplatformsareexpectedtocomewithsomevertical“flavor”fromaproductperspectiveandfromago-to-marketapproach.Here,verticalmarketscansignificantlyinfluencethedevelopmentoftheproduct,andsomeindustrieswilldemandthatspecificprotocols(suchasRosettaNetforhigh-techmanufacturing,Odettefortheautomotiveindustry,theChemicalIndustryDataExchange,thePetroleumIndustryDataExchange,theSocietyforWorldwideInterbankFinancialTelecommunication,ACORDforinsuranceandHealthLevel7forhealthcare)beincorporatedinmultienterprise/B2Btransactions.

Multienterprise/B2Binfrastructuretoolscontinuetobeinhighdemandfromorganizationsofeverysize,butparticularlyfrommidsizeandlargecompanies,regardlessofindustrysector,ascompaniescontinuetolookfortheflexibilitynecessarytosupportthemyriadofcurrentandemergingtransportandcommunicationsprotocols,securitystandards,auditingandprocesstracking,andexternalbusinesspartnerprovisioningmechanisms.

Vendor Recommendations

• By2014,weexpectatleastone-thirdoforganizationswithuncoordinatedB2Binfrastructurestore-implementthemascentralizedB2Bgateways(andtwothirdsasBIO).RationalizationoftechnologyandproductswillbeadrivingforceacrossITdepartmentslookingatB2Bprojects.Bepreparedwithcustomerreferencesandacleargo-to-marketstrategythatputsyouasapointofcontactforanycompanylookingattherationalizationoftheirB2Binfrastructures.

• Focusyourvaluepropositiononthebusinessissuesyousolve,suchasimprovingbusinessprocessdiscovery,design,integrationandmanagement,orimprovingoperatingcosts(suchasforsupplychainintegrationprojects)orsolvingmandatorycompliancetospecificregulationsratherthanonthemerefeatureandfunctionalitiesofyourproduct.

12• Newcustomersarestillhardtocomeby,eveninthisgrowing

market,sogiveyourcurrentcustomerbasemoreattentionforbothretentionandupsellingopportunities.Insomeregions,notablyEurope,butalsoSouthAmerica,thismeansnotonlyprovidingbetterlocalizedsoftwarebutalsospecializedsolutionsfortheregionalmarket,intermsofsupportinggeospecificpackages,protocols,standards,regulationsandbusinesspractices.

• Traditionally,multienterprise/B2Bgatewaydealshavebeenreasonablylow-priced,andtheaveragedealsizeisincreasing,althoughmoderately.Focusonmodularofferingsinwhichcustomerscanstartsmallandincrementallybuildwithtime.

• Multienterprise/B2Binfrastructuretechnologyisnowbeingadoptedbymainstreamorganizations,whicharenotasinterestedintechnologyforthetechnology’ssakebutwishtofindsolutionstobusinessproblemsinstead.Vendorsmusthaveasolution-oriented/verticallyfocusedvalueproposition:ThisismostlikelytoincludesomeformofIaaSandBIO.

• Pickaviableandcommittedintegratorforeachlocationandsizeofcompanythatyoutarget.NorthAmericancompaniesprefertousepackagedbusinessapplications,whichtheydonotcustomize.Europeancompaniesprefertouselegacyapplications.WhenEuropeancompaniesbuypackagedapplications,theytendtocustomizethemmore.Asaresult,theinfluenceofserviceproviders,especiallysystemintegrators,ismuchstrongerinEuropethanintheU.S.Regionalspecificandcountry-specificsystemintegratorsarekeychannelstomarketforB2Bsoftware,especiallywhenitcomestotacklingthemidmarket.

• Thecombinationofproliferatingmultienterpriseprojects,differentimplementationapproachestomultienterpriseinteroperabilityandsourcingoptionsiscreatingagrowingmarketsegmentofuserswhowanttoprocuremultienterprise/B2Binfrastructure,includingB2BsoftwareandB2Bservices,fromoneprovider.Despitethistrend,mostcompaniestodaycontinuetoseparatelyprocureB2BsoftwareandB2Bservicesfortheirmultienterpriseprojects(indifferentgeographies).Thus,vendorscontinuetocompeteaggressivelyintheseparateB2Bsoftwareandservicemarkets.Inresponse,savvyB2BvendorsshouldincreasinglyofferahybridB2Binfrastructureportfolio,includingsoftwareandservices,orpartnerwithvendorsofferingacomplementarysoftwareandservicesolutionthattheyaremissingintheirownportfolio.

• Vendorsshouldunderstandthekeytrendsthataredrivingend-userpreferencesfortheirmultienterprise/B2Binfrastructureandbalancetheirproductportfolio,marketingmessageandstrategicalliancesaccordingly.Somekeyissuesinthemindsofendusersinclude:

• TheneedtosynchronizetheirB2Bstrategywiththeirinternalintegrationstrategy,businessprocessmanagementstrategyandapplicationsourcingstrategy.

• Thechallengeofimplementinga“portfolioapproach”toB2Bprojectsbyleveragingmatureandinnovativeapproaches,suchasEDIandSOA.

• ThedecisiontomakeorbuyB2Binfrastructuresolutions.

• TheneedtoconsolidatetheirB2BprojectsontoonesharedB2Binfrastructure—Consolidatebuy-sideandsell-sideprojectsontothesameinfrastructureandconsolidatemultipleVANcontractstoonevendor(andlowertheirrates).Thisdriver,inparticular,ismakingmoreITusersseekaB2BsolutionthatcansupportallformsofB2Binteraction,includingEDIandXML,batchanddiscretetransactions,andsoforth.

• TheneedtoleverageprocessvisibilityandBAMintheirB2Bprojects.

User Recommendations

• Theexpectedmoderateeconomicgrowththrough2014willputpressureonITbudgets.Buyersneedtomastertheirabilitytousetheirmore-containedITbudgets,whichinvariablywillleavelittleroomtomaneuverforexperimentationandforenterprisewidedeployments,aswellasformore-targetedandoftendepartmentalpurchases.

• Vendorsareunderpressurefromincreasedcompetitioninthemultienterprise/B2Bgatewaysoftwarespacecomingfrommegavendors,suiteprovidersandbusinessapplicationvendorsexpandingtheirfunctionalitiesintothisfieldandfromITservicescompaniesofferingalternativewaysofdeliveringB2Bintegration(suchasIaaS).Vendorswillbeeagertoconcludeasaleatatimeinwhichdealsarebecomingfiercelycompetitive;therefore,thepossibilitiesforaskingfordiscountsandfavorablecontracttermshaveincreased.

• Recognizingtheinevitablebusinesspressureposedbycross-companyandbetween-companycollaborationandmatchingittoonesetoftechnologies,insteadofaseriesofprojects,isthefirststepfororganizationstowardaneffectiveandfunctionalB2Bproject.Organizationsshouldestablishwell-setexpectationsfor“justgoodenough”ITandsharedincentivesandriskwiththeirexternalbusinesspartnerswithintheircollaborationnetwork.

• Beawarethatmultienterprise/B2Binfrastructureprojectswillincreasinglyinvolveavarietyoftechnologiesasthe“dumb”networkevolvestobecomea“smart”networkthatincorporatesdiverseintegrationandcollaborationfunctionality,includingcommunications,translation,BPMandcollaborativetools,increasinglyimplementedusinganSOA.Successfulcompanieswillleveragetraditionalandprocessintegration,aswellasSOA,tosolvediverseapplicationintegrationandinteroperabilityrequirements.InternalITinfrastructurewillincludeadapters;datatransformationenginesandETLtools;integrationbrokersandbusinessprocessmanagerstoorchestratemessageflow,Webserviceschoreographyandbusinessprocessexecution;andeventmanagementandalertingfacilitiesforBAM.

13• Recognizethatthefirststepindevelopingaviable

multienterprisestrategyisacknowledgingthatmultiple,autonomousmultienterprise/B2Binfrastructureprojectsanda“onesizefitsall”approachtomultienterprisecollaborationarelong-terminhibitorstodevelopingaholistic,flexibleapproachtodiversebusinessrequirements.Abigchallengeforcompaniesispreventingpreconceivedassumptions—suchas“EDIisdead,”“Webservicesarecool,”or“wecanuseonestandardforallmultienterprise/B2Bcollaboration”—fromunintentionallyhinderingtheimplementationofaflexibleandbalancedapproachtoamultienterprisecollaborationstrategy.

• Organizationsplanningtoembarkintoamultienterprise/B2Binfrastructureprojectshouldemphasizetheskillsandbusinessabilitiesnecessarytohandlesuccessfullyavarietyoftechnologies.

• Bewarethatabigchallengewillbeorganizationalandculturalchange—slowlyelevatingseparatemultienterprise/B2Binfrastructureprojectsfrombeing“whollyowned”bydiscreteITgroupstobeingpartofaholistic,companywide,multienterprisestrategy,andideally,asharedmultienterpriseITinfrastructure,whichcomeswithafreshsetofgovernanceissues.Solutions—intheformofmodernmultienterprise/B2BgatewaysoftwareorasIaaSfrommodernintegrationserviceproviders—canhelpcompaniesconsolidatetheirB2BITinfrastructuresandbettermeettherequirementsestablishedinamultienterprisestrategy.Business-levelmetricsandtheircrediblemeasurementswillhelpbusinessexecutivesestablishalinkbetweenthequalityofexecutionoftheirmultienterprise/B2Binfrastructureprojectsandcompanyprofitability.

• Companieswithinternationalmultienterpriseintegrationrequirementsshouldusetechnologyandservicevendorswithsufficientfunctionality,resourcesanddomainexpertisetomeetdiverse,country-specificmultienterprise/B2Binfrastructureproject-scoperequirements.Thisisparticularlytruefore-invoicing.Usersofsmallermultienterprise/B2Binfrastructuretechnologyprovidersshouldanticipatetheimpactofmergersandfurtherconsolidation.Multienterprisesoftwareandserviceprovidersshouldcontinuetoinvestinexpandingcross-countrymultienterprise/B2Binfrastructureprojectopportunities.

• Nomatterwhatverticalorfinancialshapeyourcompanyisin,lookfore-invoicingprojectsavingsopportunities.Don’twaitforregulationsandinteroperabilitytogetbetter;youcanreapgoodbenefitsfrome-invoicingtoday.

Acronym Key and Glossary Terms

AIM applicationinfrastructureandmiddleware

APS applicationplatformsuite

B2B business-to-business

BAM businessactivitymonitoring

BIO B2Bintegrationoutsourcing

BPM businessprocessmanagement

CPFR collaborativeplanning,forecastingandreplenishment

EDI electronicdatainterchange

ESP externalserviceprovider

ETL extraction,transformationandloading

GDS globaldatasynchronization

IaaS integrationasaservice

IP intellectualproperty

MFT managedfiletransfer

MFTaaS filetransferasaservice

SaaS softwareasaservice

SOA service-orientedarchitecture

VAN value-addednetwork