Embed Size (px)

Citation preview

Master Thesis

MsC. Business Administration

Marketing Programme 2010-2011

Conceptualizing Customer Value in Property

Development for the Dutch Residential Housing

Market: an Exploratory study

Customer value in property development: an exploratory study Page 2

Conceptualizing Customer Value in Property

Development for the Dutch Residential Housing

Market: an Exploratory study

Name: Maurice van de Vreede

Student number: 0862304

Course: Master Study

Program: Master Marketing

Supervisor Radboud University: Dr. J. Henseler

In favor of internship firm: MAB Development Group B.V.

Supervisor firm: Drs. J.H. Smit

Table of content

Abstract 5

1. Introduction 6

1.1 Introduction 6

1.2 Motivation 6

1.3 Purpose 9

2. Literature study 10

2.1 Value in theoretical perspective 10

2.2 Value in practical perspective 13

2.3 Value in broader perspective 14

3. Qualitative study 15

3.1 Interview design 15

3.2 Results 16

4. Proposed conceptual model 22

4.1 Dominant logic 22 4.2 Delineating basic assumptions 22

5. Quantitative study 25

5.1 Methodology 25

5.2 Survey development 25

5.3 Data collection 26

6. Results 29

6.1 Factor analysis 29

6.2 Structural equation modeling 30

6.3 In-dept analysis 33

Customer value in property development: an exploratory study Page 4

7. Discussion 35

7.1 The role of components to customer value 35

7.2 Attitudes of the consumer 38

8. Conclusions and recommendations 40

8.1 Conclusions 40

8.2 Recommendations 42

9. Contribution, limitations and research directions 44

9.1 Contribution 44

9.2 Limitations 44

9.3 Research directions 45

10. Reflection 46

Reference list 47

Appendix A 52

Appendix B 58

Appendix C 60

Appendix D 63

Appendix E 67

Customer value in property development: an exploratory study Page 5

Abstract

The purpose of this study is to provide insight into which specific components lead to customer

value within the context of property development in the Dutch residential real estate market.

Recent market circumstances have created necessity for property developers to shift focus

towards the needs of the consumer and customer value has become a central issue in

contemporary property development. Literature study provided a formative higher order

construct to model the components (dimensions and drivers/cost-drivers) of customer value.

Subsequently, qualitative research was performed by conducting in-dept interviews with industry

professionals with the goal of gathering input for the quantitative study. The quantitative study

was performed through an online survey in which consumers, registered as active house-

searchers, participated. The formative construct was established from raw data through structural

equation modeling. Results indicate that drivers have far more contribution to differentiate on

customer value than costs. In particular, the driver-dimensions customer attention, conceptuals,

locations, co-creation and branding display considerable effect on customer value. In contrast:

the driver-dimensions installations, casco structure and outdoor space have only weak influence

on customer value. Acquisition-, direct- and operations costs display quite weak effects on

customer value as well. Furthermore, the results imply that service orientation of a developer is

becoming increasingly important with a substantial amount of intangible components focused on

the processes in which a house is created. It is recommended that a developer applies a service

orientation, concentrates on the development process for (mutual) value creation and places the

consumer as a central actor in this process. Moreover, it is recommended to focus strongly on

intangible drivers as customer attention, conceptuals, co-creation and branding. The focus on

locations, as a tangible driver remains important as well. It is recommended that a developer only

focuses on costs as complementary to the focus on drivers.

Customer value in property development: an exploratory study Page 6

1. Introduction 1.1 Introduction

The real estate industry is still governed by a supply regulated market mechanism, in particular in

its development and construction processes (Verveen 2009). This mechanism is based on the

concept that dictates a focus on tangible output and which dominated marketing beliefs in the

early industrial era (Vargo and Lusch 2004). For long, strategic ground positions and political

power fronts protected the industry and brought it financial prosperity (Rengers and van Uffelen

2006). In the Dutch market, a growing population, economic growth and governmental

legislation and incentives boosted the demand for housing. However, recent market conditions

caused high rates of project failure and large losses were incurred by property developers

(Rietdijk 2010). As a consequence, these market conditions urged actors within the industry to

reconsider their business-practices. The needs of the consumer are starting to become the central

focus of developers and the supply-regulated mechanism is becoming obsolete in contemporary

property development. More specifically, a developer has to fulfil those (relevant) needs which

are present in the consumers’ mindset if it wants to attain commitment from the consumer.

Consumer needs are a direct representation of their value-perceptions for a product or service

(Park, Jaworski and MacInnis 1986). Therefore, in the context of this study value for the

consumer (customer value) is the central focus. The choice for this focus stands to reason since

consumers are the ultimate decision makers and their (purchase) decisions have detrimental

consequences for project success. The context of this study is the Dutch residential real estate

market, to provide a wide context of applicability for this study. The research unit is limited to

newly build houses for the retail market (ground-dwelling houses and apartments), because

property developers concentrate on the development of new houses and/or the redevelopment

into new houses. The rental market for houses is not taken into consideration, because this

market is outside of the scope of this study.

1.2 Motivation

Recent developments indicate that the real estate industry is changing. There are causes which

place these developments into perspective. The economic downturn is the first of these causes.

Due to economic uncertainty, demand for houses drastically decreased. This trend was

strengthened by the tightening credit facilities available to consumers (Elsinga, de Jong-Tennekes

Customer value in property development: an exploratory study Page 7

and van der Heijden 2011; Sanders 2009). Strategic (ground) positions of developers dwindled as

well. As consumers, they found it increasingly difficult to attract credit facilities to finance ground

positions and project investments (Knol and Savelkoul 2009). This indicates that consumers who

are in the position to purchase a house are now more critical than ever because of the large

amount of houses available to them. The second cause is socio-economic: the increasing

individualization of the consumer (Gilmore and Pine 2000). For long manifest needs for housing

concealed consumers’ needs to distinguish themselves as individuals. Now that consumers have a

stronger position in the market, they will enforce their needs increasingly upon the developer

towards delivering more individualized solutions for their housing (Verveen 2009). The third

cause is more socio-political in nature. For long, nearly every new residential property project

aimed at increasing value for the developer and the municipality. Municipalities achieved this

through the expropriation of (mostly) agricultural land in urban environments. These lands were

sold to developers, who build large scale uniform housing projects: Vinex areas (Verveen 2009).

However, on national level regulation has been implemented to limit the strategic ground

positions of developers and the agricultural land available for development of these Vinex areas

has drastically been reduced (Knol and Savelkoul 2009). This is socio-political reasoned, since the

government is attempting to recover the unbalance between supply and demand and stabilize the

dislocated market- mechanism (Knol and Savelkoul 2009).

Beyond the scope of economics and politics

The fourth cause is socio-ecological, because environmental considerations affect and reinforce

changes within the industry as well. Collective awareness is growing that, considering the limited

amount of green landscape left in The Netherlands, the focus of property development must

shift from exploiting new land to redeveloping and revitalizing disregarded areas (Traa and

Knoben 2009). Furthermore, the emphasis on new housing projects will increasingly be on

durability. This durability not only translates to eco-friendliness in construction and energy in

housing, but also to the ability of creating comfortable environments for people to live in

(Urbanaviciene and Kaklauskas 2009). Moreover, since many property development projects are

becoming focused on inner-city, high density areas, multiple stakeholder groups will be involved

in the development process. This will increase the complexity of such projects (Michielsen 2010).

The fifth cause is socio-technological. Society is becoming increasingly transparent because

technological advances tighten social interaction among different stakeholder groups. This

enables stakeholder groups to join forces and increase their power towards societal issues

Customer value in property development: an exploratory study Page 8

(Maignan and Ferrell 2004). The days that a power front of a municipality and developer

overarched the interests of other stakeholders are passed behind, in particular because the

increasing importance of social media and communication technology reinforces the power of

stakeholder groups fast. These causes show that the strategic position of a developer has been

affected and necessitate a developer into the position in which it has to acknowledge the needs of

the consumer (and other stakeholder groups) and has to focus on mutual value creation: value for

the firm and value for its stakeholders. As earlier indicated, this study only focuses on value

(creation) for one specific, but important stakeholder group: consumers.

Current state of research

The real estate industry is gradually becoming aware of the shift in power from seller to buyer

and recognizes that is has to focus more on the consumer in property development (de

Lathauwer 2005; Kwee and Hacquebord 2005; Luchjenbroers 2007; Majaama et al. 2008; Tuns et

al. 2010; Verveen 2008). Although industry-specific studies have provided guidelines and models

for structuring processes to achieve and/or increase customer value, none of these studies really

capture the essence of value creation, because a) industry-specific studies are aimed at customer

value but do not conceptualize customer value as such, thereby leaving value as an ultimate but

unknown condition to be satisfied and b) none of these guidelines and models are based on

empirical validation. Mainstream literature (Anderson, Jain, and Chintagunta 1993; Grönroos and

Helle 2010; Heinonen et al. 2010; Lapierre 2000; Ulaga 2003; Ulaga and Eggert 2005; Vargo and

Lusch 2004) really captures the essence of (customer) value by disentangling value into

components and by giving well structured and founded recommendations by which management

can improve their value creation-processes. However, what this research stream lacks is that it

does not capture the essence and complexity of the property development process and does not

account for the industry characteristics that influence such value creation processes. The property

development process is characterized by its longevity, high transaction specific investments and

associated risks (Muller 2005). Each property development project necessitates a unique

approach, not only in the interaction with stakeholder groups but in all relevant technical,

commercial, political, financial and legal aspects of a project (Muller 2005). The unique character

of property development and the special deployment of resources that it brings with it along are

not accounted for in mainstream research. To conclude, mainstream research has provided

valuable insights in customer value, but its generalizability for property development is still too

Customer value in property development: an exploratory study Page 9

limited. As far as known, no earlier attempts have been made to incorporate customer value

empirically in this industry-specific context.

1.3 Purpose

Apparently, when value is reflected, a main generalization between industry-specific and non-

industry-specific research streams can be drawn. A generalization is that both research streams

consider value as some ultimate perception in the mindset of the consumer (Heinonen et al.

2010; Luchjenbroers 2007; Smeets 2010; Verveen 2008; Zeithaml 1988). The mainstream

literature described above indicates that (customer) value is disentangled in components. Without

those components, customer value could not exist. After all, a perception must be a composition

of certain components which cause a condition of customer value. Lapierre (2000) was the first

to confirm the validity of this claim by establishing a construct of components. Therefore, the

main purpose of this study is to provide insight into which specific components lead to customer

value in industry-specific context. The appropriate research question for this study becomes:

Which components of customer value can be identified in the residential property development market?

In the following section, literature study will provide the theoretical foundation(s) for (customer)

value to build further upon. The qualitative study will provide knowledge about the industry-

related components that will be used for modelling customer value. Subsequently, the

quantitative study will concern the modelling of customer value into a construct. The three

subsequent studies are chosen to provide an elaborate as possible methodological approach to

this study. After, results are discussed and conclusions are presented. To conclude,

recommendations and future research directions are provided.

Customer value in property development: an exploratory study Page 10

2. Literature study

2.1 Value in theoretical perspective

Conceptualizations of value

Value has undergone extensive review in academic literature to date. In the academic field, many

conceptualizations of customer value have been proposed. Zeithaml (1988) refers to customer

value as “the consumer’s overall assessment of the utility of a product based on a perception of

what is received and what is given”, while Monroe (1991) refers to customer value as a “ratio of

perceived benefits relative to perceived sacrifice”. Parallel to previous definitions, Flint,

Woodruff and Fisher-Gardial (1997) conceptualize customer value in a business-to-business

context as “the customers’ assessment of the value that has been created for them by a supplier

given the trade-offs between all relevant benefits and sacrifices in a specific-use situation”. Other

studies focus more on the relationship-aspect of value. Ulaga (2003) disentangles the concept of

(relationship) value into four characteristics: a) value is a subjective concept, b) it consists of a

trade-off between benefits and sacrifices, c) benefits and sacrifices can be multi-faceted and d)

value perceptions are relative to competition. Furthermore, Ulaga and Eggert (2005) augment to

the concept of relationship value by stipulating the difference between customer value and

relationship value. Customer value is value that is created from a transactional point of view and

focuses solely on the value and sacrifices that relate to the tangible output of the product or

service. The concept of relationship value, which is derived from relationship marketing, has a

broader perspective because it considers not only the value of the tangible output but also the

value of the relational aspects between customer and supplier. Anderson, Jain, and Chintagunta

(1993) recognize this perspective by implicating that relationship value is “the perceived worth in

monetary units of the set of economic, technical, service and social benefits received by a

customer firm in exchange for the price paid for a product offering, taking into consideration the

available alternative suppliers’ offerings and prices”.

Value identified in constructs

As before indicated, Lapierre (2000) was the first who attempted to establish a construct with 13

value drivers for customer value through quantitative validation. In his study, Eggert (2003)

contributed to the conceptualization of relationship value by introducing a construct for

Customer value in property development: an exploratory study Page 11

relationship value in a business-to-business (B2B) context. Through qualitative research he

distinguished eight relationship value drivers, two of which are costs. In their study, Ulaga and

Eggert (2005), proposed a formative (higher-order) construct of relationship value in B2B

context. In this construct: five relationship benefit dimensions were identified: a) product

benefits, b) service benefits, c) know how benefits, d) time-to-market benefits and e) social

benefits, as well as two relationship sacrifices: a) process costs and, b) price. An asymmetric effect

was confirmed between benefits and sacrifices, because the positive influence of the benefits on

relationship value is stronger than the negative effect of the sacrifices on relationship value. The

distinction between this study and the study of Ulaga (2003) is that this study models a negative

effect of costs to customer value, while Ulaga (2003) models a positive effect of costs to

customer value. Ulaga and Eggert (2005) consider costs as sacrifices, while Ulaga (2003)

considers costs as (alternative) value drivers. In their subsequent study, Ulaga and Eggert (2006)

again used the formative construct to identify which components most strongly influence

relationship value in B2B context. The deviation to the previous study is that the benefit

dimensions were reduced to three and the cost dimensions increased to three. Again, this study

confirmed the validity of the proposed formative construct for (relationship) value.

Dominant logic

Previous indicates that value has been conceptualized and modelled into constructs. Another

distinction among studies resides in the logic under which value is conceptualized. The study of

Vargo and Lusch (2004) indentifies that a shift is taking place: transactions in the market-place

are moving away from the goods-dominant (GD) logic towards the service-dominant (SD) logic.

Value resides decreasingly in tangible output and increasingly in intangible resources as skills,

knowledge, information and collaborative relationships with consumers. Woodruff (1997) reflects

on this by critically examining the concept of customer value. According to his study, ambiguity

exists in the conceptualizations of value because their underlying reasoning is similar but the

indicators from which they are composed and the context in which they operate differ.

Furthermore, Woodruff (1997) identifies a shifting focus in customers’ perceptions from GD-

logic to SD- or CD-logic and recognizes that many conceptualizations based on the GD-logic

seem to come obsolete. As a result of his critique: he introduces a conceptualization in which the

logic-shift in the customers’ perceptions is captured: “Customer value is a customers’ perceived

preference for and evaluation of those product attributes, attribute consequences and experiences

arising from use that facilitate (or block) achieving the customers’ goals and purposes in use

Customer value in property development: an exploratory study Page 12

situations”. Recent research has stretched the boundaries of value even further by placing

emphasis on the experiential value, or value-in-use. In their study, Heinonen et al. (2010) consider

an SD-logic still as a provider-dominant logic and propose value-in-use as the ultimate instrument

to create value. The value-in-use refers to the customer-dominant (CD) logic and reflects the aim

of business to create value by focussing not on which need a product or service satisfies, but on

what desired experience a product can create for the consumer. Soman and Marambi (2009)

stipulate the movement in willingness to pay for economic value (i.e. the value of the tangible

good) to experiential value.

Core assumption of value

It is in particular significant to identify that most mainstream research on value, regardless of

whether customer value or relationship value is addressed, focuses in particular on business

context and/or business-to-business relationships. Only the studies of Gutman (1982), Heinonen

et al. (2010), Vargo and Lusch (2004) and Woodall (2003) focus on business-to-consumer

relationships. However, this does not necessarily imply that value is perceived differently in the

context of consumer and business. Soman and Marambi (2009) support this assumption by

introducing a universally applicable value spectrum: a conceptualization of the value assessment

process in which customer value is shown as the value surplus when consumers (or customers)

compare incremental benefits with incremental costs. Although there is still disagreement about

the exact conceptualization for value, its dominant logic under which it operates and whether it

focuses on the consumer in B2C context (customer value) or the customer in B2B context

(relationship value), there is consensus among research about its core assumption. Value still

reflects the perception of surplus in relation to what consumers (customers in B2B context)

receive and what they have sacrificed, regardless of context and whether this surplus is reflected

as being tangible, intangible or experiential. This argument is also supported by Woodruff (1997),

who implies that there is no dominant logic, but instead they are complementary. Gutman (1982)

proposed such a view years ago by implying that product attributes (tangible), consequences

(intangible) and experiences (experiential) all create value on different levels in the means-end

chain of consumers and therefore function as complementary. Another interesting avenue of

research is provided by Woodall (2003). Woodall (2003) proposes a conceptual framework for

customer value based on extensive case-study. Value is dually based here: on the object (product)

and the subject (consumer). In that sense value is created both for the object based on usage

value and for the consumer based on the experience the object creates. This study therefore

Customer value in property development: an exploratory study Page 13

proposes value under GD/SD-logic and CD-logic simultaneously. Five value dimensions are

provided, two of which based on the object and three based on the subject.

2.2 Value in practical perspective

On the other hand, a diversity of studies has examined which particular activities lead to value.

Flint, Woodruff and Fisher-Gardial (1997) propose a conceptual model that guides customer

perceived-value. However, its purpose is not to provide strategy on how to shape customer value

but on how a supplier can identify events in a customers’ environment that are likely to change

their perceptions of value. From identification of these changing values, offerings that tap into

these (future) values can be created. This study strongly implies the importance of learning

capabilities of a supplier. Sharma and Sheth (1997) propose three ways to create value: a) value

creation through relationships with suppliers, b) value creation through alliance partnering and c)

value creation through relationships with customers. Both Vargo and Lusch (2004) and

Grönroos and Helle (2010) highlight the importance of co-creation initiatives. According to their

studies, it is necessary to create value through intensive collaboration with consumers (customers)

to jointly develop solutions for their needs. Continuing on co-creation, Alam (2006) stipulates

that customer interaction removes the fuzziness in the fuzzy front end of new service

development (NSD) and thereby increasing NSD-success. Hoyer et al. (2010) introduce a

conceptual model in which they identify stimulators and impediments to co-creation. As they

indicate, social media and community building activities are gaining importance as instruments in

the process of co-creation. Industry-specific research is also supportive of co-creation (Tuns et al.

2010), but the study by Verveen (2008) and the publication by Kwee and Hacquebord (2005)

expand the view on co-creation as an extensive collaboration among firm, consumers and

relevant parties in the supply-chain. Heinonen et al. (2010) argue that co-creation alone is not a

sufficient condition for creating (superior) value. This study indicates that co-creation is not an

end itself, but merely a (possible, but not necessary) supportive instrument in value creation.

They argue that instead of focussing on searching how a product fits in the context of the

consumer, a firm should focus on the consumers’ experience(s) to find solutions for problems

the consumer encounters. In industry-specific context Luchjenbroers (2007) indicates that

“consumer experience” in residential projects contributes to customer value, thereby supporting

the assumptions made by Heinonen et al. (2010).

Customer value in property development: an exploratory study Page 14

2.3 Value in broader perspective

Thus far, a diversity of studies has proposed theoretical and practical perspectives on value.

However, there is also a research stream which focuses on value as part of a network, modelling

antecedents and consequences of value in broader perspective. Ulaga and Eggert (2004) explored

what function relationship value has in the broader network of relationship marketing and

whether relationship value can be considered as an important antecedent to relationship quality.

What they found was that in B2B context, relationship value has a direct (positive) influence on

the decision of the customer to continue the relationship with the supplier and indirect (positive)

through the construct of relationship quality (with the dimensions: satisfaction, trust and

commitment). The results show: a) the necessity for business to create (superior) value for the

customer in order to continue its business-activities with the customer, b) to focus on creating

(mutual) trust between customer-supplier, because trust functions as a mediating variable in the

construct of relationship quality and c) that relationship value is an important antecedent to

relationship quality. Grönroos and Helle (2010) elaborate that trust is a necessary ingredient to

create successful relationships for mutual value creation between customer and supplier. The

distinction between both studies is that Ulaga and Eggert (2004) consider trust as part of a

construct that is a consequence of relationship value, while Grönroos and Helle (2010) consider

trust to be an important antecedent for the creation of value. Either way, trust seems to be a

variable that is closely related to value. Furthermore, Chiou and Droge (2006) confirm in B2C-

context that satisfaction leads to an increase by consumers to invest in specific asset investments

(SAI). Satisfaction resembles value to some degree, since both are considered as affective

attitudes in the mind of the consumer that lead to some form of consequence(s) (Chiou and

Droge 2006). SAI are investments done by consumers in the (acquisition of) product(s) or

service(s) of a firm that loose significant value when the consumer switches to competitive

offerings. This closely parallels the study by Ulaga and Eggert (2004) in which there exists a

positive relationship between value and the customers’ choice for continuation with the supplier,

because SAI are considered to be done only when the customer is satisfied with its supplier.

Moreover, Palmatier et al. (2006) have also contributed strongly to value. In their study, they

confirmed that relational mediators similar to those by established by Ulaga and Eggert (2004),

mediate the relationship(s) between value based antecedents and value based outcomes.

Customer value in property development: an exploratory study Page 15

3. Qualitative study

3.1 Interview design

In advance, certain themes to be discussed were set up for the interviews. These were derived

from a variety of (industry-related) sources (studies, publications and news-items) as well as from

the authors’ knowledge. In line with the studies of Lapierre (2000), Ulaga (2003), Ulaga and

Eggert (2005) and Ulaga and Eggert (2006), the themes reflected possible sources of benefits and

sacrifices (costs) for customer value. The interviews contained open questions about the themes.

The questions were formulated as neutral and uniform as possible to reduce response bias

(Robinson, Shaver and Wrightman 1991) Moreover, the open character of the interviews

stimulated participants to provide as rich as possible information about the discussed themes and

their attitudes towards these themes.

Sampling

Interviews were conducted with eight industry professionals from two different property

development firms in The Netherlands. Respondents were contacted either through telephone or

e-mail through the use of references provided by an employee of one of the firms. Respondents

were invited to a face to face interview or an interview conducted through telephone. Ultimately,

six interviews were done face to face and two interviews were conducted by telephone.

Sample

Both firms belong to one of the leading banking-conglomerates in The Netherlands. Although

both firms cooperate on a strategic level, they are autonomously managed. From the eight

interview participants, six of them are employed at firm A and two are employed at firm B. Firm

A specializes in commercial real estate (offices, retail, public functions etc.) and mixed-use

projects (combination of housing with commercial real estate). The development of housing is a

substantial part of the business, but is only initiated as part of mixed use projects. This firm is one

of the leading developers of commercial real estate in The Netherlands. Firm B is the leading

property developer of The Netherlands in the residential market and develops mostly stand-alone

residential projects.

In composing this sample of respondents, one criterion was most important: the multidisciplinary

background of the respondents. By including professionals with different backgrounds and

Customer value in property development: an exploratory study Page 16

different functions within the property development process, similarities and differences were

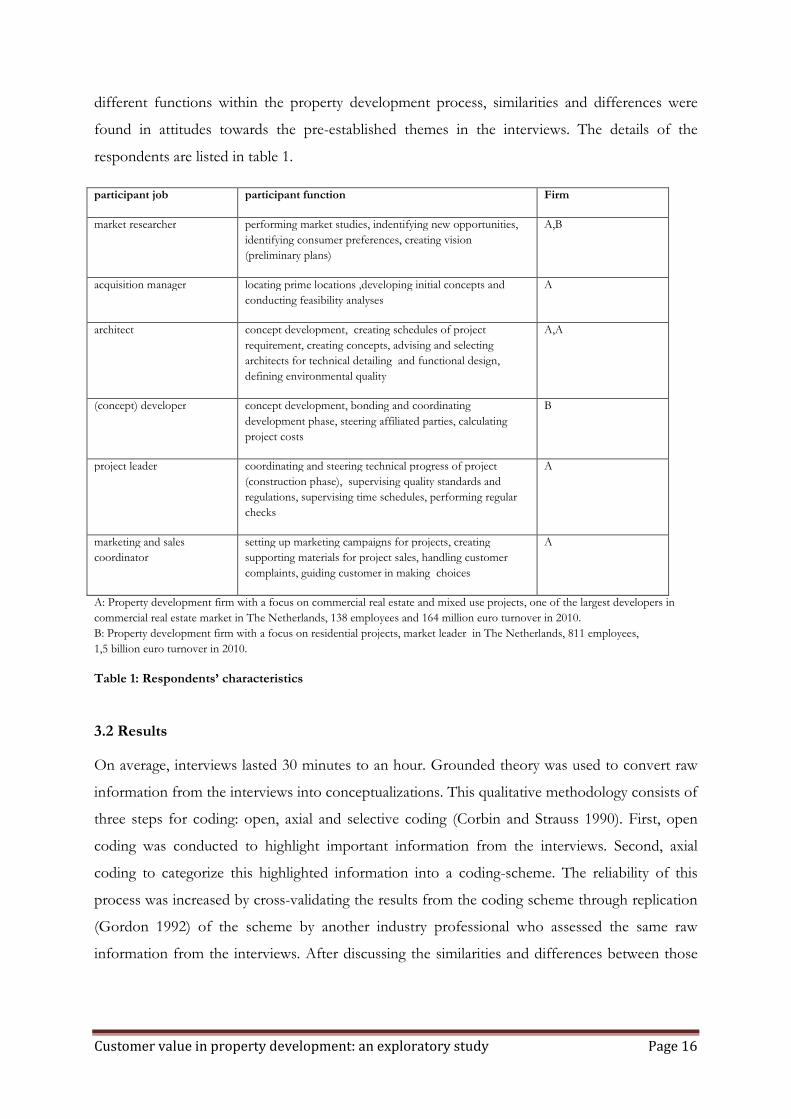

found in attitudes towards the pre-established themes in the interviews. The details of the

respondents are listed in table 1.

participant job participant function Firm

market researcher performing market studies, indentifying new opportunities,

identifying consumer preferences, creating vision

(preliminary plans)

A,B

acquisition manager locating prime locations ,developing initial concepts and

conducting feasibility analyses

A

architect concept development, creating schedules of project

requirement, creating concepts, advising and selecting

architects for technical detailing and functional design,

defining environmental quality

A,A

(concept) developer concept development, bonding and coordinating

development phase, steering affiliated parties, calculating

project costs

B

project leader coordinating and steering technical progress of project

(construction phase), supervising quality standards and

regulations, supervising time schedules, performing regular

checks

A

marketing and sales

coordinator

setting up marketing campaigns for projects, creating

supporting materials for project sales, handling customer

complaints, guiding customer in making choices

A

A: Property development firm with a focus on commercial real estate and mixed use projects, one of the largest developers in

commercial real estate market in The Netherlands, 138 employees and 164 million euro turnover in 2010.

B: Property development firm with a focus on residential projects, market leader in The Netherlands, 811 employees,

1,5 billion euro turnover in 2010.

Table 1: Respondents’ characteristics

3.2 Results

On average, interviews lasted 30 minutes to an hour. Grounded theory was used to convert raw

information from the interviews into conceptualizations. This qualitative methodology consists of

three steps for coding: open, axial and selective coding (Corbin and Strauss 1990). First, open

coding was conducted to highlight important information from the interviews. Second, axial

coding to categorize this highlighted information into a coding-scheme. The reliability of this

process was increased by cross-validating the results from the coding scheme through replication

(Gordon 1992) of the scheme by another industry professional who assessed the same raw

information from the interviews. After discussing the similarities and differences between those

Customer value in property development: an exploratory study Page 17

schemes, a final coherent coding scheme was created. Finally, selective coding was performed in

order to build conceptualizations.

Axial coding

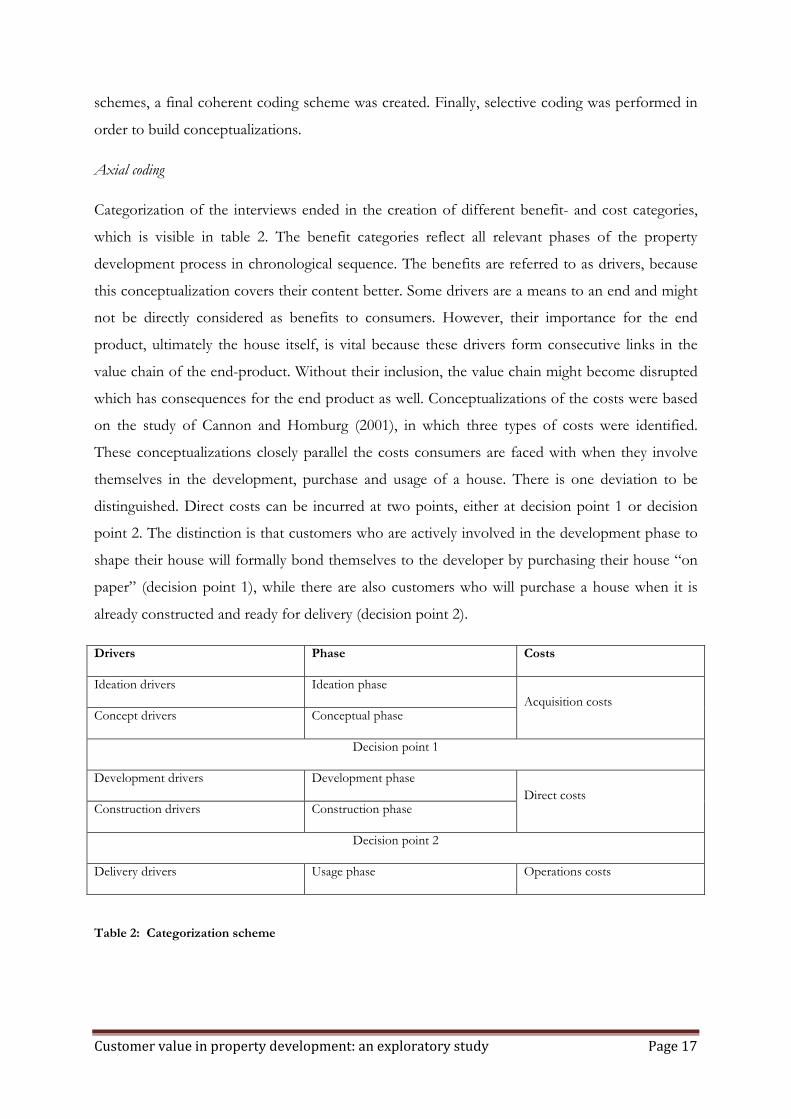

Categorization of the interviews ended in the creation of different benefit- and cost categories,

which is visible in table 2. The benefit categories reflect all relevant phases of the property

development process in chronological sequence. The benefits are referred to as drivers, because

this conceptualization covers their content better. Some drivers are a means to an end and might

not be directly considered as benefits to consumers. However, their importance for the end

product, ultimately the house itself, is vital because these drivers form consecutive links in the

value chain of the end-product. Without their inclusion, the value chain might become disrupted

which has consequences for the end product as well. Conceptualizations of the costs were based

on the study of Cannon and Homburg (2001), in which three types of costs were identified.

These conceptualizations closely parallel the costs consumers are faced with when they involve

themselves in the development, purchase and usage of a house. There is one deviation to be

distinguished. Direct costs can be incurred at two points, either at decision point 1 or decision

point 2. The distinction is that customers who are actively involved in the development phase to

shape their house will formally bond themselves to the developer by purchasing their house “on

paper” (decision point 1), while there are also customers who will purchase a house when it is

already constructed and ready for delivery (decision point 2).

Drivers Phase Costs

Ideation drivers Ideation phase

Acquisition costs Concept drivers Conceptual phase

Decision point 1

Development drivers Development phase

Direct costs Construction drivers Construction phase

Decision point 2

Delivery drivers Usage phase Operations costs

Table 2: Categorization scheme

Customer value in property development: an exploratory study Page 18

Selective coding

The drivers and cost-driver identified from axial coding are conceptualized below:

Ideation drivers

Location: the location of is one of the fundaments of property development and is a well-known

determinant for success. The importance of location is even supported by quantitative research

(Baroussa, Hoesli and Peng 2003). A location can be divided into a) surrounding area

(neighborhood), b) landscape (the surrounding view of the project) and c) surrounding facilities

(schools, shops, sports accommodation, social and cultural functions).

Personal dialogue: a personal dialogue represents a face to face conversation between developer

and consumers in order to discover what their needs are. The developer has a coordinating role

in this phase and its key goal is to provide the necessary tools for consumers to identify their

needs. The secondary goal is to gather this information for further development purposes.

Community building: this is an alternative to the personal dialogue. A developer can establish a

community through a website. Through this website consumers can express their needs. But it is

more of a monologue than it is a dialogue, because there is not a two-way communication.

Furthermore, the developer does not provide tools for the consumer to help express his needs.

Therefore, this alternative generates less in-dept knowledge than the personal dialogue. The

motivation to include this driver is derived from the study of Hoyer et al. (2010).

Concept drivers

Concepts: concepts are a design translation from the needs gathered at the dialogue/community.

The developer incorporates those needs together with technical and legal requirements, as well as

the knowledge and vision of the developer on the project. These elements together compose a

physical design study: concept. Subsequently, these concepts are judged by consumers. Support

to include as important to customer value is provided by the study of van Leent (2009).

Public space: a developer designs and creates public space. Public space is the “shared” space of a

project, functions as a connection between the project and the external environment and

provides a form of identity for the project. Its design consists of a) green structures (i.e. parks

and ponds), b) social structures (i.e. playgrounds and benches) and c) landscape architecture (art

objects and sidewalk design). The study of Verveen (2008) advises to focus on public space, as

having a considerable influence on customer value.

Customer value in property development: an exploratory study Page 19

Development drivers

Co-creation: in co-creation consumers (customers) have attached themselves to the project by

formally committing themselves to a house (decision point 1, table 2). This house is co-created

with the developer within the technical and financial boundaries of the project. The consumer is

involved in a process of decisions about the finish (materials), installations (kitchen, bathroom,

heating etc.) and structure of the house (placing of walls and doors). As elaborated upon in the

literature study, a diversity of studies has indicated the importance of co-creation to customer

value.

Branding: a developer can brand his name and actively promote this brand all its

communications. In such a way, familiarity with projects is increased for consumers. This might

affect their beliefs about the quality of the project and/or developer. It is particularly noteworthy

that there was somewhat disagreement among respondents about the contribution of this driver.

Respondents with more commercial background indicated branding to have an important

contribution to customer value, while the technical oriented respondents did not attribute any

importance to branding for customer value. Although branding is considered as vital for

improving perceived quality and subsequently customer value (Baldauf, Cravens and Binder 2003;

Zeithaml 1988), its contribution in the context of property development has not yet been

determined by research.

Agent: guidance is reflected in the assignment of a fixed agent for consumers (customers). This

agent provides elaborate guidance during the development process, a process in which a

consumer is faced with many choices and uncertainties. Consumers will have the same agent

during the development process to increase the familiarity with the agent and to increase

consumer trust.

Surface: the surface reflects the square meters of living space available in a house. It dictates to a

degree the choices a consumer has to make in decorating the interior. According to one

respondent the dominant value for money trade off is also reflected here, because many

consumers relate the (perceived) value of the end product to the surface (in square meters) that

they get for the price they pay for a house. The presence of a minimum amount of surface is seen

as a basic requirement by Verveen (2008).

Customer value in property development: an exploratory study Page 20

Outdoor space: the outdoor space refers to the outside space of the house that is directly situated

by the house and which is only accessible through the inside of the house. In apartments, this is

often referred to as balcony, loggia or terrace. In ground-dwelling houses, this is referred to as the

garden. The studies of Kwee and Hacquebord (2005) and Meijer (2008) indicate the importance

of outdoor space.

Casco structure: this driver reflects the inside structure of the house. A developer has the ability

to deliver the house casco. This implies that walls, doors and other installations have been

excluded as much as possible. The house is delivered as “bare” as possible on the inside. This

casco structure allows the house to be cheaper, because construction costs of the former

elements are being avoided, as well as it provides the consumer with the opportunity to create

this structure for own cost(s) and risk(s).

Installations: installations are the energy supplying techniques in a house. In particular, there was

a common conviction with the respondents that energy saving installations can be identified as a

relevant driver for customer value. These provisions are often represented as novel techniques

that ensure improved performance in energy-supply while decreasing energy costs and emissions,

but against higher purchasing price. In general, such installations will pay-back the initial

additional investments after several years of use. De Vries (2010) indicates that consumers

attribute value to energy saving installations and are prepared to pay a premium for such

installations if they reduce energy-costs considerably.

Construction drivers

Construction visits: a developer organizes construction visits for consumers (customers). The

consumer has the opportunity to invite relatives to join them to see the progress of the house

and/or the project. The agent will guide the consumer on these occasions on the construction

site.

Personal customer file: in this digital file, progress of the construction is kept. This enables a

much closer relation with the consumer (customer), since the consumer is being involved in the

construction process. The digital file is readily available for the consumer and is updated regularly

by the developer / constructor.

Delivery drivers:

Guidance: at delivery of the house the developer provides an elaborate guidance for the

consumer (customer). This guidance translates to an elaborate explanation of all available

Customer value in property development: an exploratory study Page 21

functions in the house and answering (remaining) questions from the consumer. In property

development, this practice is not common as one might guess.

Flaw minimization: flaws are often present in the house and/or project at delivery. The term

driver might not seem appropriate, because every consumer expects that his house will be

delivered without flaws (Boumeester, Lamain and Mariën 2006). Minimization of flaws at delivery

might therefore be more of a prevention of dissatisfaction (preserver of value), rather than a

value creating driver.

Acquisition costs

Time: acquisition costs refer to all the non-monetary costs that consumers have to make in order

to make the purchase of a house. It refers to all their efforts to bond with the firm as well as their

efforts to participate in the ideation, conceptual and development phase. The largest part of these

costs will be time-related and these costs will increase as the development process progresses. If a

consumer choosing to buy a house in a completed stage (decision point 2, table 2), these

acquisition costs are much lower because a consumer does not have to invest time in co-creation

efforts.

Direct costs

Purchase price: this cost-driver refers to the actual price consumers have to pay for a house.

Construction interest: this cost-driver can be considered as the costs that a consumer (customer)

is obliged to pay to the developer because the developer pre-financed the plot and the

construction of the house. The interest payable by the developer to its financer will be charged to

the consumer above the purchase price.

Operations costs:

Usage costs: the operations costs are reflected as the usage costs. These costs are incurred by the

consumer in daily use of the house and consist of energy – and maintenance costs. There is no

clear subdivision in cost-drivers here, because energy – and maintenance costs are not mutually

exclusive. In general, energy costs are normally higher with low efforts for maintenance and vice

versa.

Customer value in property development: an exploratory study Page 22

4. Proposed conceptual model

4.1 Dominant logic

The literature indicates that the concept of value has transitioned in the past two decades, when a

shift occurred from GD- to SD and from SD- to CD-logic. Although customer value under the

GD-logic is often conceptualized and provides a solid base to build further research on, it must

be recognized that this value is guided through a logic which focuses solely on tangible output of

offerings and neglects the importance of intangible capabilities that contribute to the creation of

value for the consumer (Vargo and Lusch 2004). Property developers are often seen as

manufacturers of tangible products. This is incorrectly assumed because a) the resources to create

the end-product are largely abstract in nature and b) there is a trend visible in which property

developers are only guiding processes for their customers. In these processes, the developer does

not have a financial interest and/or risk in the project, but is merely a service manufacturer for

consumers (Kwee and Hacquebord 2005). Verveen (2008) indicates: “a property developer has

the ability to create value for customers in the development process by applying its intangible

resources, knowledge and skills to guide long-term and complex processes”. This indicates that

the focus of the property development process is gradually shifting towards service-focus (SD-

logic). The CD-logic provides valuable input for further avenues in research on value, but

knowledge in this field is still too preliminary to consider industry-specific application as a real

option for this study. The strongest support is found for modelling customer value under SD-

logic: implying a service orientation for this study towards customer value.

4.2 Delineating basic assumptions

The (proposed) conceptual model will be based on the formative construct proposed by Ulaga

and Eggert (2005) and Ulaga and Eggert (2006). Support is found for this choice, because a) this

model gives a comprehensible interpretation about which components (indicators and

dimensions) constitute the construct of customer value, b) distinctions among the components

based on their effect on customer value are visible, c) the model allows modification to industry-

specific components without losing its core assumptions and d) the model allows the inclusion of

a diversity of components and still retains interpretable. Some distinctions should also be

considered. In contrast to above mentioned studies, customer value instead of relationship value

is the central construct of the conceptual model. While the literature study provides support that

Customer value in property development: an exploratory study Page 23

customer value and relationship value both share the core assumption that value is the offset

when the perceived benefits and costs of a product and/or service are considered, customer

value is more appropriate in the context of this study. This is based on the assumption that

relationship value is confounded and reinforced in an enduring relationship between customer

and supplier in which the relation is based on repetitive purchase of products (Ulaga and Eggert

2005; Ulaga and Eggert 2006). The studies of Arndt (1979), Gadde and Mattsson (1987) and

Wind (1970) provide further support for this assumption. In the context of this study, there is

not an enduring character between a firm and consumer because the purchase of a house is still a

discrete transaction. Vargo and Lusch (2004) and Grönroos and Helle (2010) indicate that the

relationship between consumer and firm is seen as key to achieve customer value, but that these

relationships are not characterized by an enduring character. Customer value is therefore more

appropriate, because it does not necessarily imply the enduring relationship between consumer

and firm (developer).

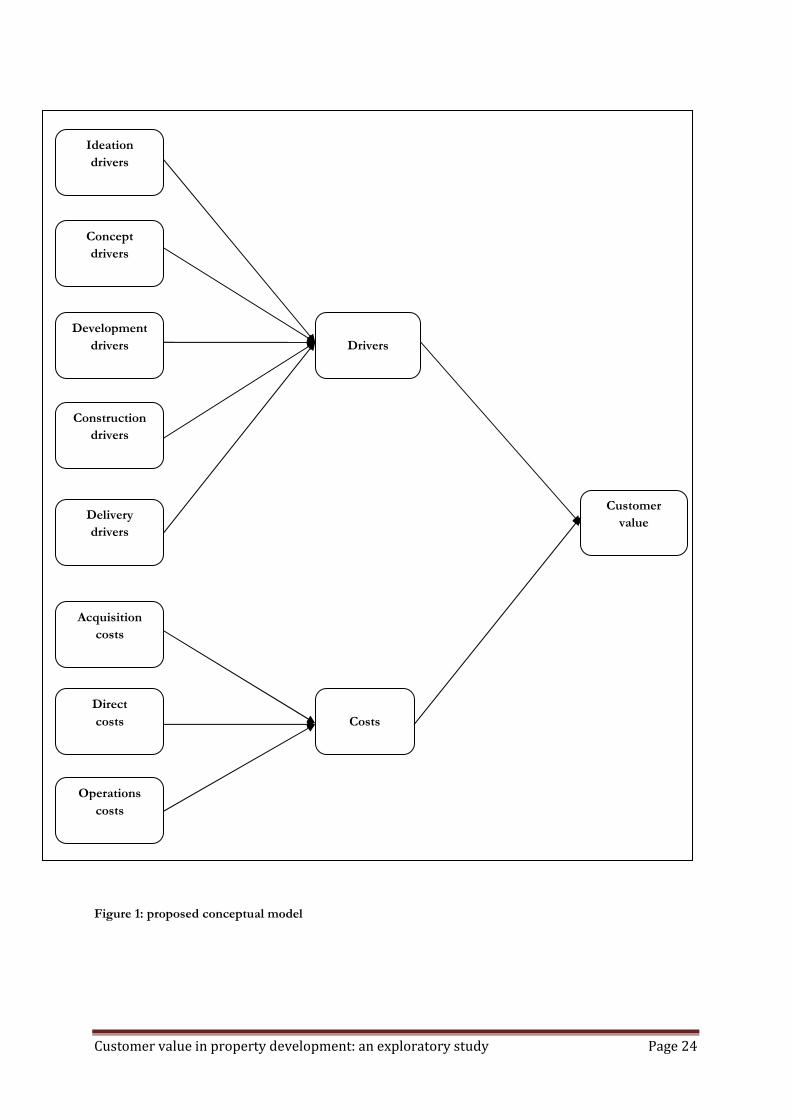

Industry-specific modeling

In the conceptual model, there are three-order dimensions. The identified drivers and costs-

drivers in the qualitative study will form the indicators which are connected to their categories of

drivers and costs. These categories represent the first-order dimensions. The choice to include

the identified categories as first order dimensions is made because every category reflects a

relevant phase of the property development process and every phase has its potential

contribution to customer value. The same applies to costs, since every category of costs reflects a

phase for a consumer in which costs are incurred. The second order dimensions Drivers and

Costs are composite dimensions: they represent all the first order dimensions for drivers and

costs together respectively. To prevent confusion between (cost-) drivers as indicators and

drivers/costs as second dimensions, the second order dimensions are indicated as Drivers and

Costs (capital letter in front). The third order dimension is customer value, representing the focal

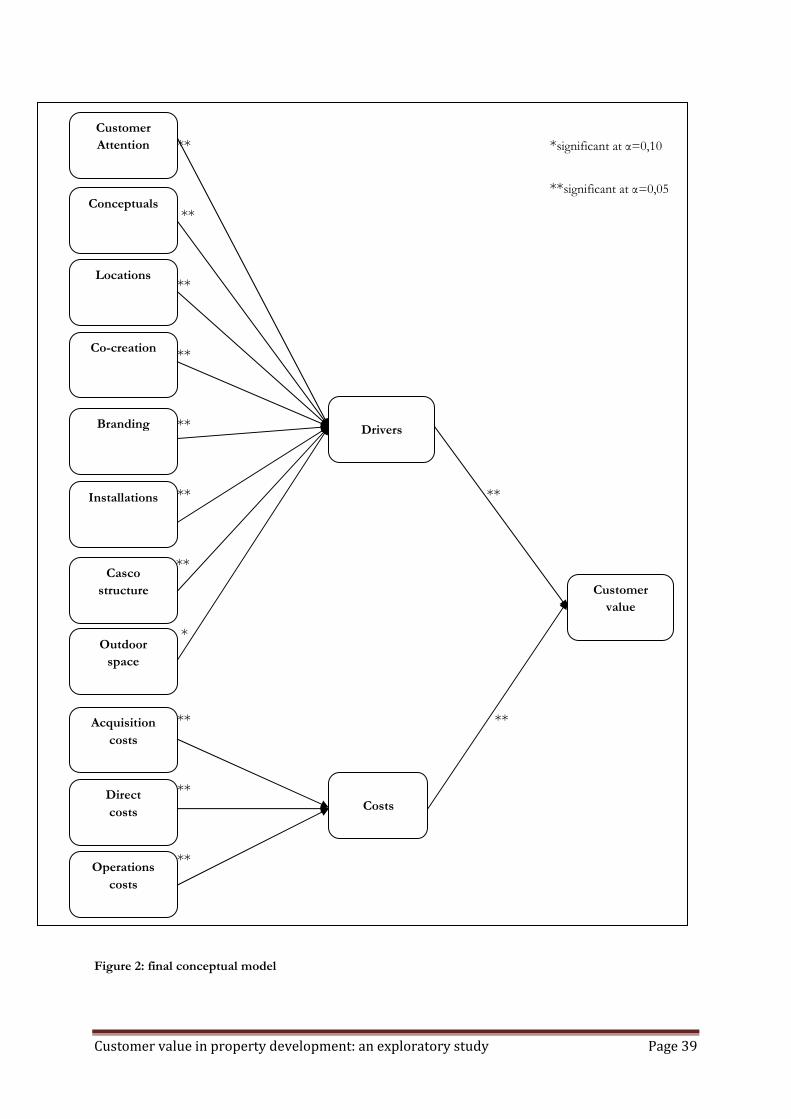

construct of this study. Figure 1 displays the proposed conceptual model.

Customer value in property development: an exploratory study Page 24

Figure 1: proposed conceptual model

Construction

drivers

Delivery

drivers

Drivers

Development

drivers

Concept

drivers

Ideation

drivers

Costs

Customer

value

Operations

costs

Direct

costs

Acquisition

costs

Customer value in property development: an exploratory study Page 25

5. Quantitative study

5.1 Methodology

Structural equation modelling (SEM) was used to establish a construct for customer value. To

assess which indicators from the survey should be included in SEM, exploratory factor analysis

through principal components factoring (PCA) was performed first in SPSS. PCA was not

performed for the first order cost dimensions (and indicators), since previous research already

confirmed the validity of the proposed cost dimensions (Homburg and Cannon 2001). Since the

goal of the factor analysis is data reduction, PCA is considered as a suitable approach (Hair et al.

2006; Costello and Osborne 2005; Suhr 2006). With the data from PCA in place, Partial Least

Squares (PLS) was used for structural equation modelling with the use of SmartPLS 2.0 (2005).

PLS was chosen because its fits the purpose of prediction better than co-variance based structural

equation models and has more (predictive) accuracy when working with samples sizes below 200

(Henseler, Ringle and Sinkovics 2009). Furthermore, in contrast to co-variance based models,

PLS allows the possibility to simultaneously create formative and reflective models and offers

more robustness in formative modelling (Fornell and Bookstein 1982; Henseler, Ringle and

Sinkovics 2009).

5.2 Survey development

Survey design

Survey was chosen as a means to perform the quantitative study. The operationalizations of the

drivers from the qualitative study were translated into Dutch. To increase understanding from the

respondent, (industry-specific) terminology was changed and/or elaborately explained. This

process was conducted together with the industry professional who cross-validated the coding-

process in the qualitative study. All identified drivers and cost-drivers from the qualitative study

were decided to be incorporated in the survey as indicators. The survey was divided into eight

parts. The first five parts reflected the first order dimensions for drivers and the last three parts

reflected the relevant first cost dimensions for costs. Before each dimension was discussed, an

explanation was provided for respondents about its meaning and purpose. Within each

dimension, its underlying indicators were discussed. Before-mentioned operationalizations served

to provide meaning and content to the indicators.

Customer value in property development: an exploratory study Page 26

Measure development

The survey composed a total of 49 stands. Each stand represented an indicator. Respondents

had to indicate to which degree they agreed with a particular stand. A 7-point rating scale

(1=strongly agree and 7=strongly disagree) was used.

In the survey, 38 stands were designed to identify the validity of the proposed conceptual model

and 11 stands were included to acquire more information about the attitudes of the respondents.

More specifically, 8 out of 11 stands were incorporated to indicate to which degree respondents

are willing to pay extra for certain drivers or less when certain drivers are excluded. To envision

the financial consequences of incorporating drivers, consequent amounts were used. A price of €

200.000,- when the driver is included, a price of € 195.000,- when it is not included (premium of

€ 5.000,-). An exception was the premium for branding, this was set at € 2.500,- (€ 200.000,- and

€ 197.500,-) and the discount when choosing for casco structure at € 15.000,- (€180.000,- and €

195.000,-). The comparison-stands were included, because the meaning of value is really shown

when drivers have financial consequences for the consumer and choices have to be made based

on these consequences. Although the amounts are arbitrarily set, they do have the ability to

envision financial consequences to some degree. Also, 3 stands were incorporated to identify the

preference of respondents for certain drivers. In these stands, no financial sacrifices were

included. By including either/or choices for drivers, potential preferences could be revealed that

were not revealed in the stands for validation of the proposed conceptual model. The survey can

be found in Appendix A (in Dutch).

Survey pretest

The survey was pre-tested by two respondents who were non-industry related. From these pre-

tests some minor changes were made in the phrasing and wording of the survey. No major

changes were necessary to make.

5.3 Data collection

Sampling frame

For data collection, a sampling frame with two samples was available. The primary sample

consists of 603 consumers. What characterizes this sample is that it is collected though a CRM

system of a real estate agent. It consists of consumers who have submitted themselves as

“searchers”, meaning that they are (actively or passively) searching for a newly build ground-

dwelling house or apartment. The main advantage of using such a sample is that most of these

Customer value in property development: an exploratory study Page 27

respondents should have a clear view about their housing preferences and they should therefore

be able to indicate quite clearly what value they attribute to housing. This sample has also

limitations in that it only concerns respondents who are searching in a specific region. Nation-

wide preferences and local preferences might diverge.

The secondary sample was provided as a back-up when the response rate of the primary sample

would be insufficient for further analysis. This sample consists of a panel of maximum 500

respondents. A selection criterion was applied. Only respondents who were actively seeking for a

ground-dwelling house or apartment were obliged to take part in the survey. This sample consists

of nationwide consumers and therefore does not have the limitation of the primary sample.

However, the limitation from this sample is that there is no distinction between respondents

based on their preferences for an existing or newly build house. There could be deviation in

preferences based on this search criterion.

Data collection: sampling procedure

Respondents in the primary sample were contacted through email and invited to participate in the

survey, which was administered through an online survey programme. The purpose and relevance

of the survey was explained to the respondents in advance. To increase the willingness to

participate, an incentive was provided to every respondent who completed the survey. The

incentive is a digital book about art and architecture, which reflects the central theme of this

study to some degree.

Data collection: response

From the primary sample of 603 consumers, 110 responses were collected. This amounts to a

response rate of 18,2%. For online surveys, such a response rate is considered as average and

sufficient (Deutskens et al. 2004). However, 21 of those responses were removed because of

excessive missing data. The final sample of responses amounted to 89. Factor analysis requires a

minimum ratio of 5 observations (responses) per indicator (Hair et al. 2006). Since 38 indicators

are used for validation of the proposed conceptual model, the minimum amount of responses

required is 190. Therefore, the secondary sample was used to collect the required responses. 100

panel respondents were invited to participate in the survey. Ultimately all respondents

participated, amounting to a response rate of 100%. None of the responses had to be deleted due

to excessive missing data. From both samples, a total of 189 responses were collected. This is

almost equivalent to the minimum sample size required for factor analysis. It is the expectation

Customer value in property development: an exploratory study Page 28

that during the process some indicators will be deleted and that the required sample size will be

met.

Data collection: respondents’ characteristics

There are some basic respondents’ characteristics. In the final sample, 55% of the respondents

are male, 45% are female. The largest part of the respondents fall within the age-category of 25 to

35 (42%), while the mean age-category is 36 to 45. Furthermore, most of the respondents fall in

the income class of 50.001 to 70.000 euro, while the mean income category is the income

category of 35.001 to 50.000 euro. Moreover, most of the respondents have a higher educational

degree and the mean also lies within this group. Their housing situation also reveals some basic

characteristics about the respondents: 74% of the respondents currently own a house and from

this 74%, a majority of 75% owns a ground-dwelling house, while 25% owns an apartment.

However, the most important characteristic is the searching efforts. 132 of 189 (70%)

respondents indicated that they are still in active search for a newly build house. Of those 132

respondents, 71% are in active search for a ground-dwelling house and 29% are in active search

for an apartment.

Customer value in property development: an exploratory study Page 29

6. Results

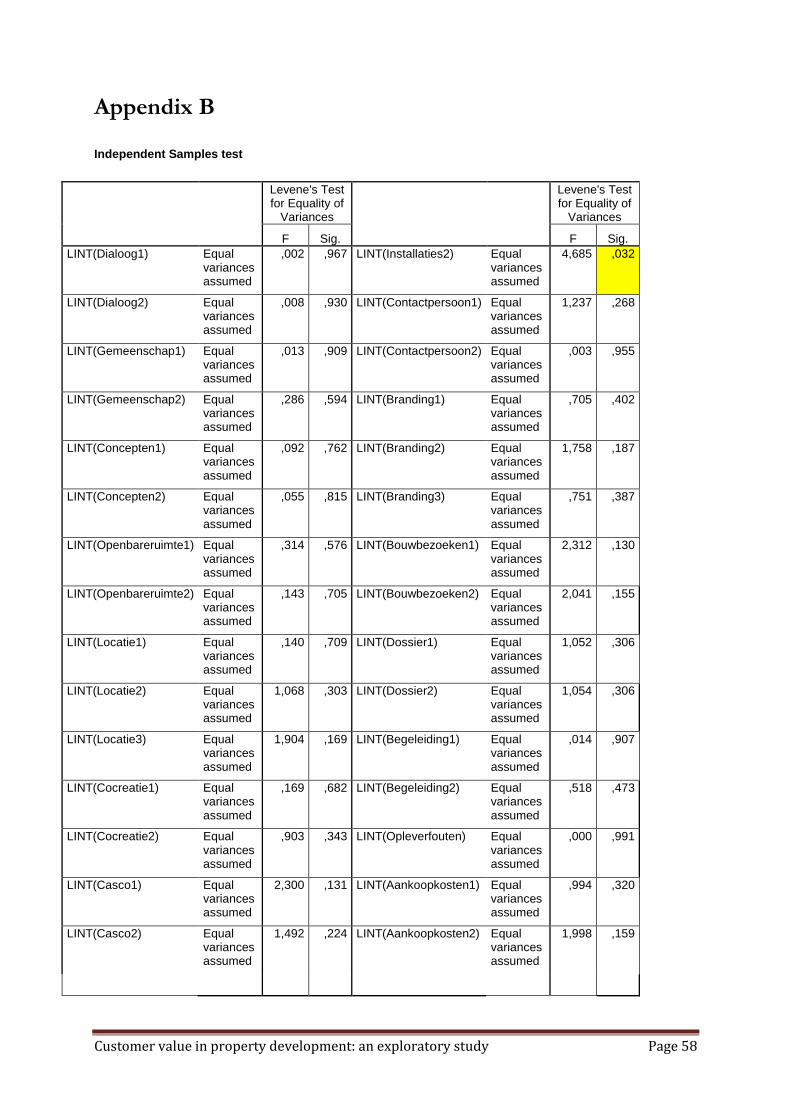

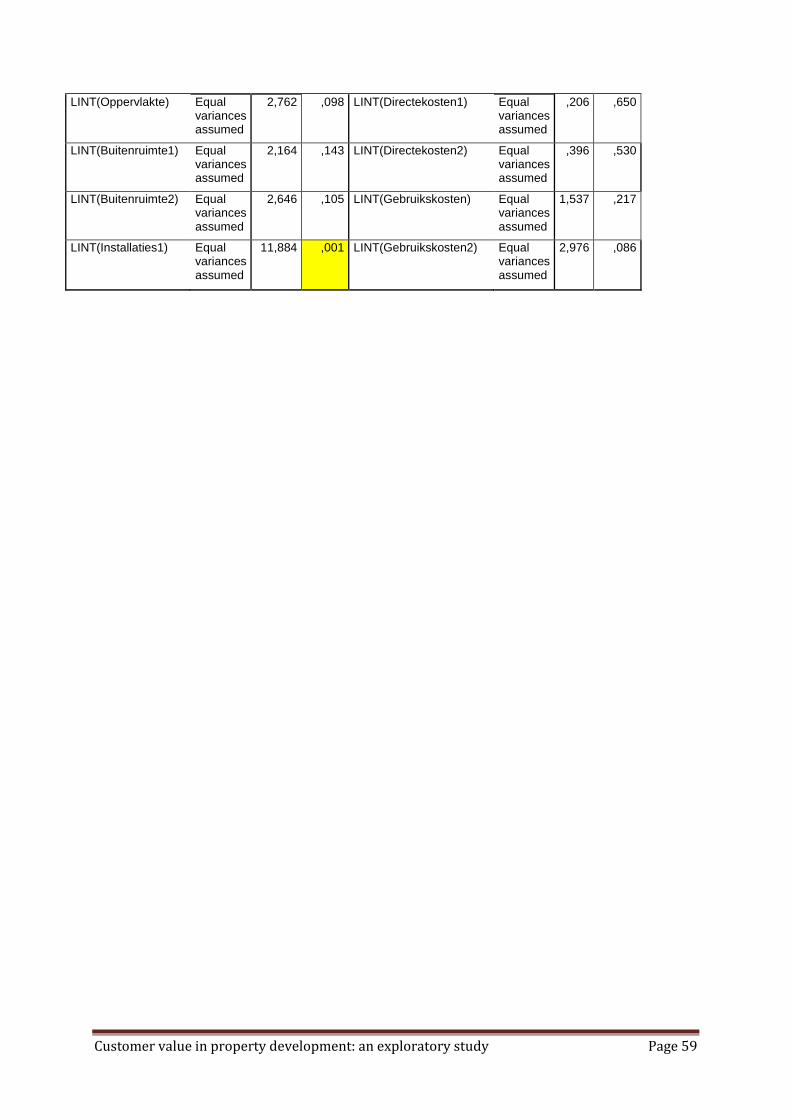

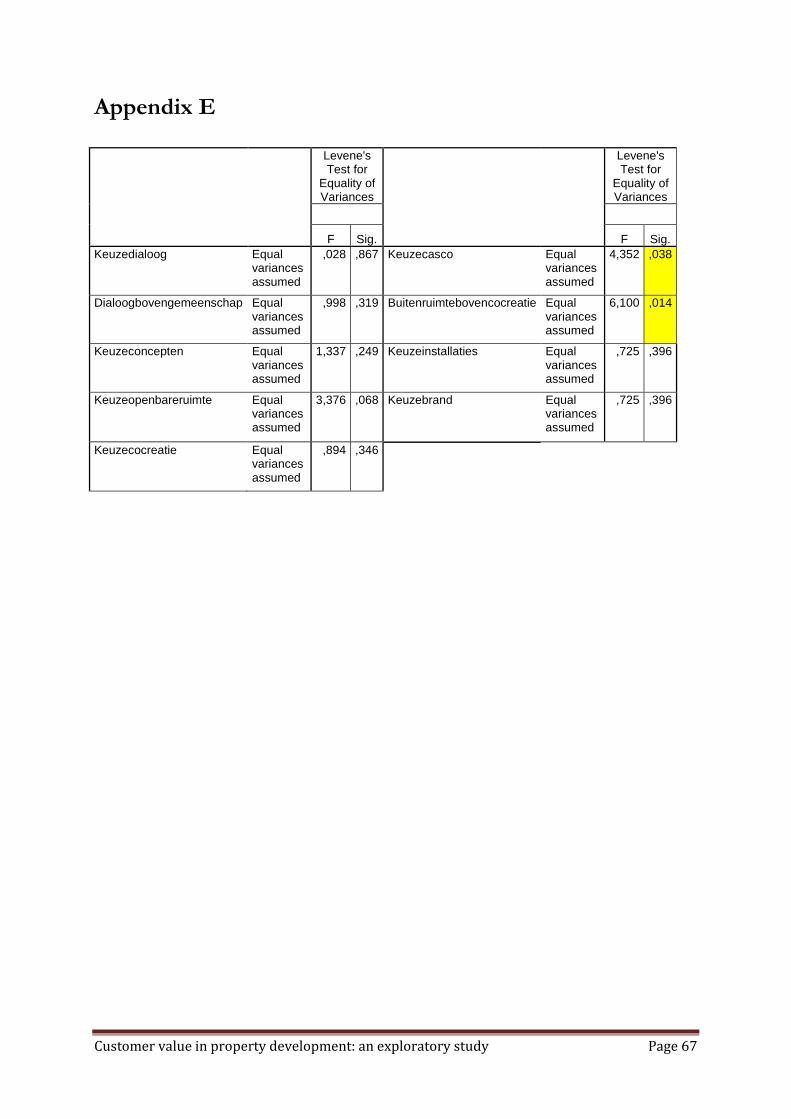

First, response bias was assessed. To check whether significant differences exist between the

primary and the secondary sample, Levene’s test was performed using SPSS at 95% confidence

interval. Accordingly, all indicators except installations 1 and installations 2 are above the 0,05

significance level (Hair et al. 2006). The data displays strong signs of homoscedasticity, because

36 out of 38 indicators do not show a sign of inequality in population variance. It is concluded

that there are no significant differences between the responses from both samples of respondents

(at α = 0,05). Considering the large combined sample size in relation to the large amount of

indicators that show non-significant values, it is not necessary to apply remedies for both

indicators with significant values (Hair et al. 2006). Appendix B displays the output of Levene’s

test.

6.1 Factor analysis

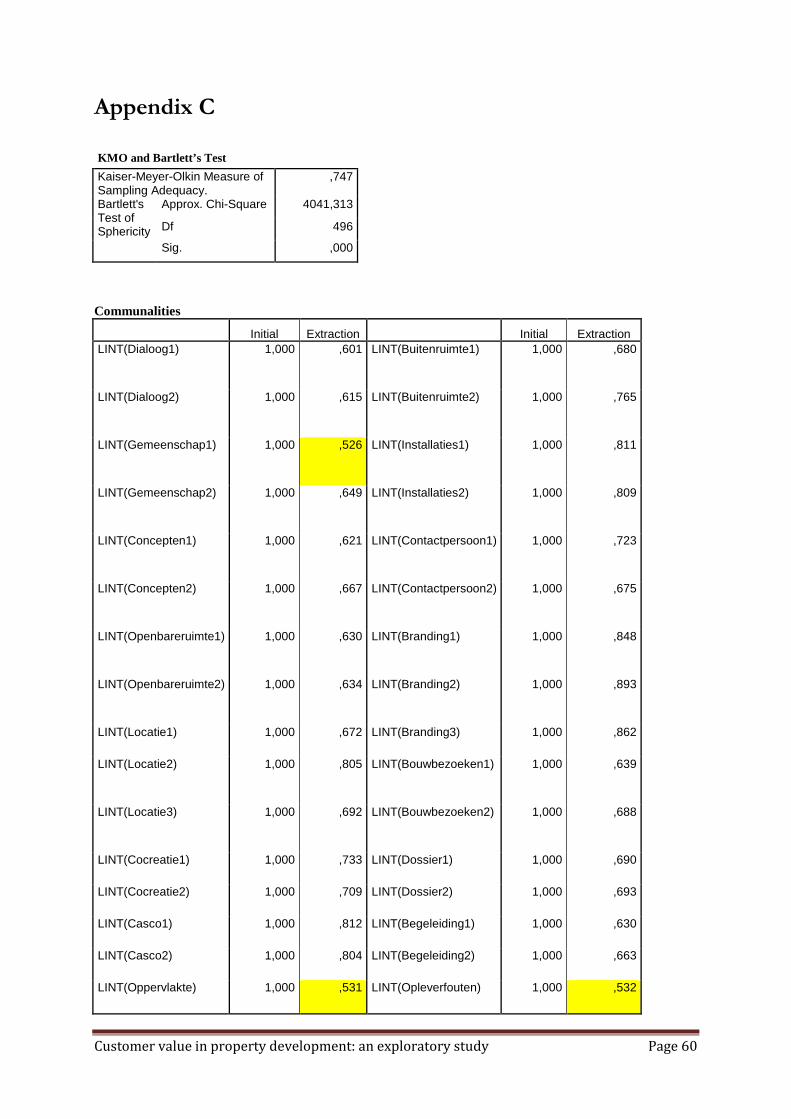

The first step in the process was to check the normality of the data by looking at the skewness

and kurtosis. There do not seem to be extreme values in the data, since all indicators fall within

the statistical norms to assume normality. Excess kurtosis lies within the range of -3/6 and

skewness lies within the range of -3/3 (Fiori 2008; Hair et al. 2006). In the second step

parameters were set for PCA. PCA with varimax rotation was performed on the indicators.

Varimax as a rotational method is appropriate when choosing PCA, because orthogonal rational

methods do not assume correlations between factors. This is in line with the assumptions of PCA

(Hair et al. 2006; Suhr 2006). The third step consisted of judging the output shown by PCA. At

first glance there is a sufficient amount of correlations between indicators above the threshold of

0,4 indicating appropriateness for factor analysis (Hair et al. 2006). The Kaiser-Meyer-Olkin

(KMO) measure of sampling adequacy has a value of 0,747 and Bartlett’s test of sphericity

indicates a value of 0,00. Both values support the assumption of appropriateness for factor

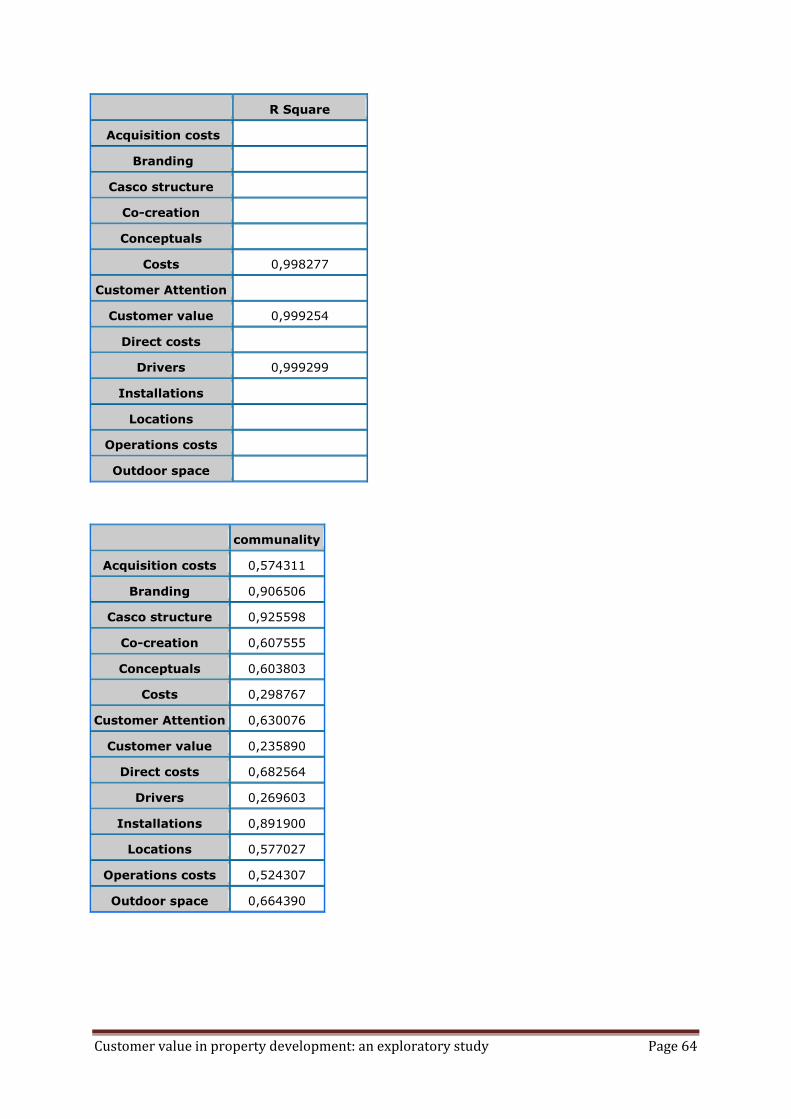

analysis (Hair et al. 2006). The fourth step involves the judgement of the communalities. This

threshold is set at 0,6, following the assumptions made by Yeomans and Golder (1982) that

higher communalities improve the quality of factor analysis. Three indicators (community

building 1, surface and flaw minimization) became candidates for deletion based on their

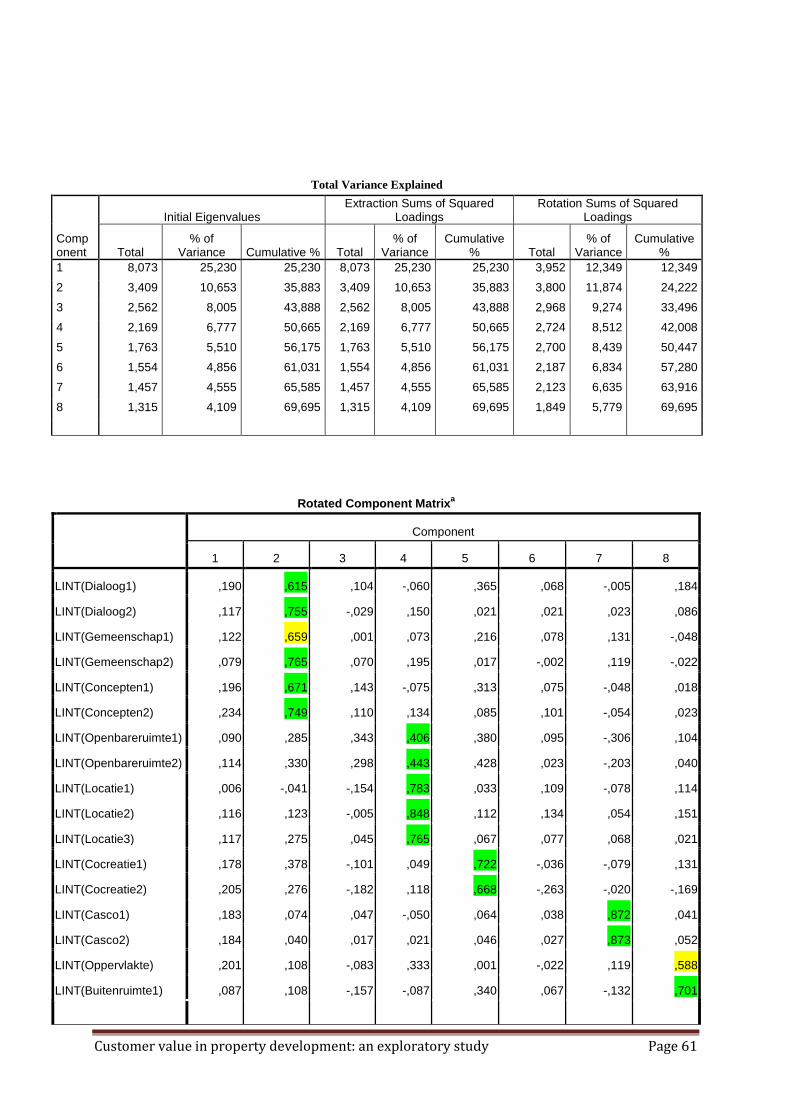

communalities which were lower than 0,6. In the variance matrix, there are 8 factors retained

with an Eigenvalue above 1,0 according to the Kaiser-criterion (Hair et al. 2006). Together these

8 factors explain 69,7% of the variance. The final step involved the rotated component matrix.

All indicators have loadings of 0,5 or higher on their respective factors and no cross-loadings

Customer value in property development: an exploratory study Page 30

have been identified. Based on this criterion (Hair et al. 2006), no indicator should be deleted.

Nonetheless, indicators community building 1, surface and flaw minimization were deleted

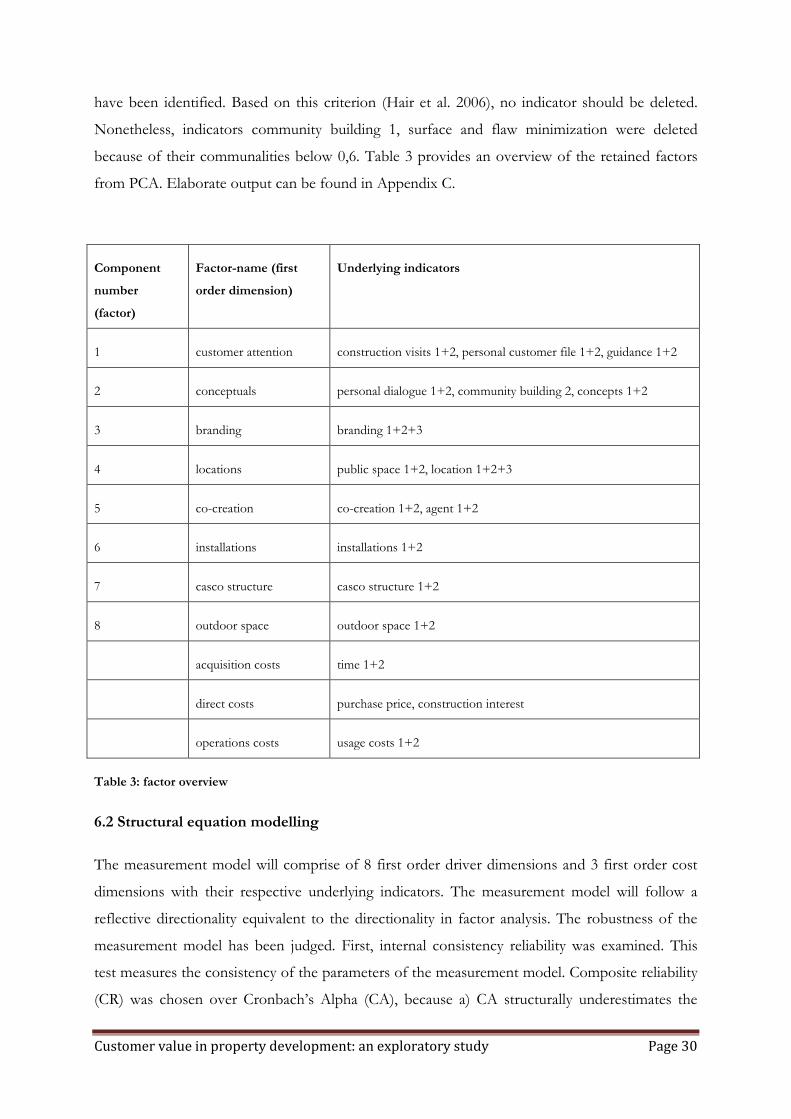

because of their communalities below 0,6. Table 3 provides an overview of the retained factors

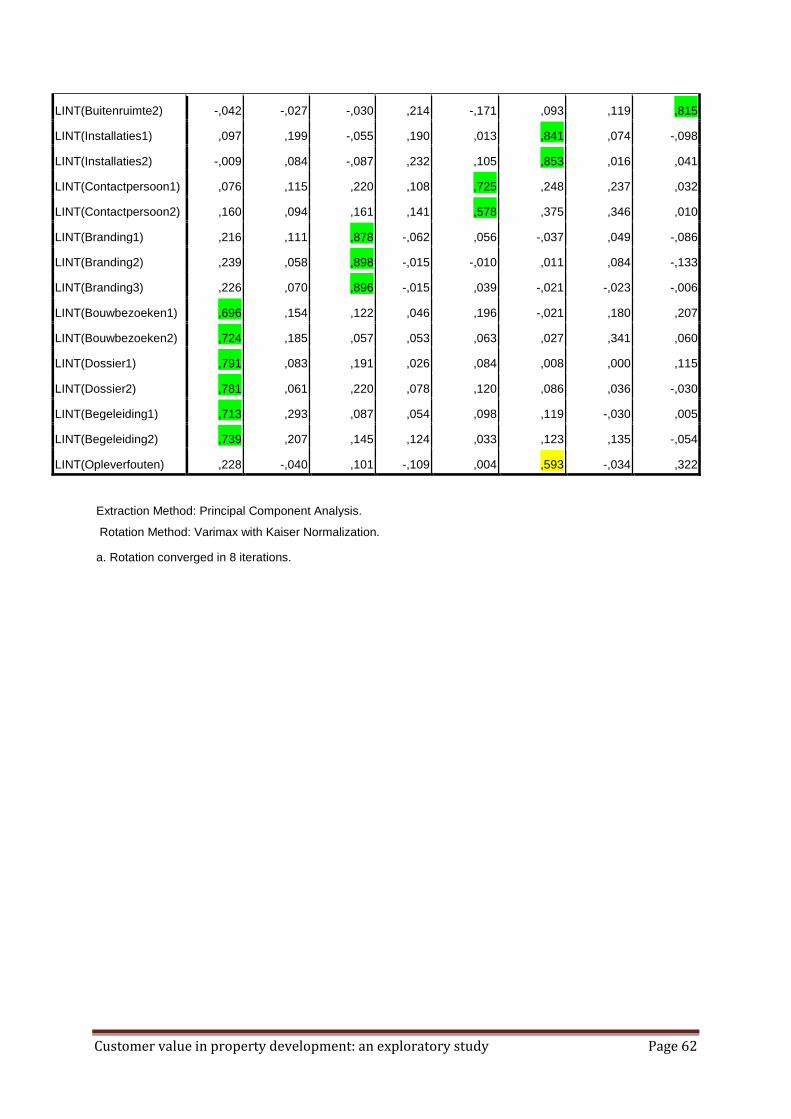

from PCA. Elaborate output can be found in Appendix C.

Component

number

(factor)

Factor-name (first

order dimension)

Underlying indicators

1 customer attention construction visits 1+2, personal customer file 1+2, guidance 1+2

2 conceptuals personal dialogue 1+2, community building 2, concepts 1+2

3 branding branding 1+2+3

4 locations public space 1+2, location 1+2+3

5 co-creation co-creation 1+2, agent 1+2

6 installations installations 1+2

7 casco structure casco structure 1+2

8 outdoor space outdoor space 1+2

acquisition costs time 1+2

direct costs purchase price, construction interest

operations costs usage costs 1+2

Table 3: factor overview

6.2 Structural equation modelling

The measurement model will comprise of 8 first order driver dimensions and 3 first order cost

dimensions with their respective underlying indicators. The measurement model will follow a

reflective directionality equivalent to the directionality in factor analysis. The robustness of the

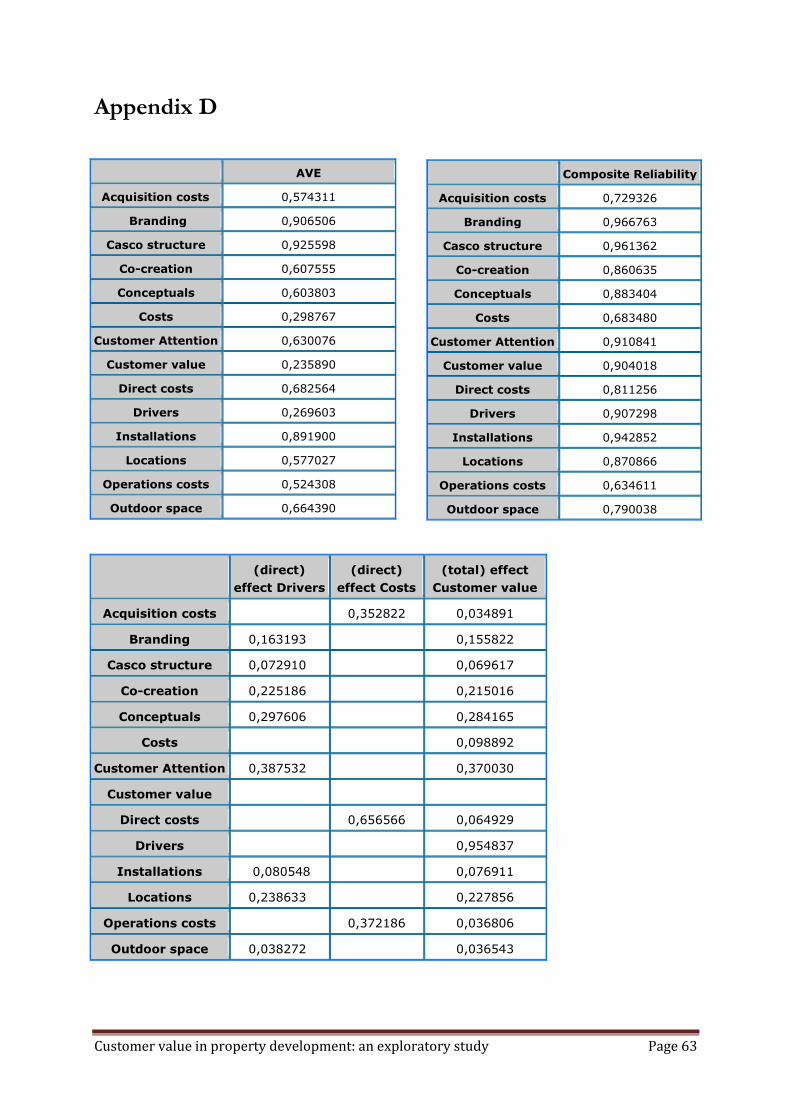

measurement model has been judged. First, internal consistency reliability was examined. This

test measures the consistency of the parameters of the measurement model. Composite reliability

(CR) was chosen over Cronbach’s Alpha (CA), because a) CA structurally underestimates the

Customer value in property development: an exploratory study Page 31

reliability of the first order dimensions (factors) in the measurement model (Raykov 1998) and b)

the CR-coefficient is superior to the CA-coefficient, because CR does not assume that all

indicators in the measurement model are equally weighted (Fornell and Larcker 1981). All

dimensions have values above 0,7, except for the first order dimension operations costs and the

second order dimension Costs which have values of 0,63 and 0,68 respectively. Diamantopoulos

and Siguaw (2000) prescribe a threshold of 0,6 for CR. Since all dimensions denote values above

0,6, none of the constructs will be deleted based on CR. Second, convergent validity was

assessed. Convergent validity indicates the degree to which indicators in a dimension have

similarity in their meaning. There are two methods to assess this: a) through the average variance

each dimension extracts from its indicators (AVE) and b) by looking at the standardized loadings

of the indicators to their respective dimension. AVE has to exceed 0,5 (Fornell and Larcker 1981;

Hair et al. 2006) to show a sufficient amount of convergent validity. All first order dimensions

have AVE values above 0,5. If one looks at the standardized loadings, sufficient convergent

validity is shown when factor loadings exceed 0,5 and a good convergent validity is shown when

loadings exceed 0,7 (Hair et al. 2006). Of the 38 indicators, 34 indicators have loadings that

exceed 0,7, 3 indicators have loadings that exceed 0,5 and only one indicator (usage costs 2) has a

loading below 0,5. This indicator is not directly removed because of its potential contribution to

the model, but is critically monitored. Third, discriminant validity was assessed. Discriminant

validity represents the degree to which indicators actually belong to their respective dimensions.

Discriminant validity will be judged based on the Fornell-Larcker criterion (Fornell and Larcker

1981) which prescribes that the root of the AVE of one dimension has to exceed the correlations

that this dimension has with all other dimensions. This criterion is met. Another way to judge

discriminant validity is by assessing potential cross-loadings (Hair et al. 2006). However, this was

already performed during PCA during which no cross-loadings were indicated. To ensure that no

cross loadings exist in the cost-indicators, these indicators were separately assessed in PLS. Data

confirmed that there were no cross-loadings in the cost-indicators either. Finally, face validity

was reviewed. According to Hair et al. (2006), face validity represents “the extent to which the

content of the items is consistent with the construct definition”. The focus is here on the

coherence between the indicators’ meaning and the definition of their dimension. There are no

numerical criteria available to evaluate this. To ensure some validation, the definition of the

dimensions was discussed with the industry professional who participated earlier in this study. No

changes were required to make in the definition of the dimensions, providing support that there

is coherence between indicators and dimensions. Furthermore, there seems to be a logical

coherence in the grouping of indicators under factors, supporting face validity further. Since the

Customer value in property development: an exploratory study Page 32

purpose of PLS is prediction (as opposed to fit), no fit-indices are available for the measurement

model (Fornell and Cha 1994). All data used to assess the robustness of the measurement model

can be found in Appendix D.

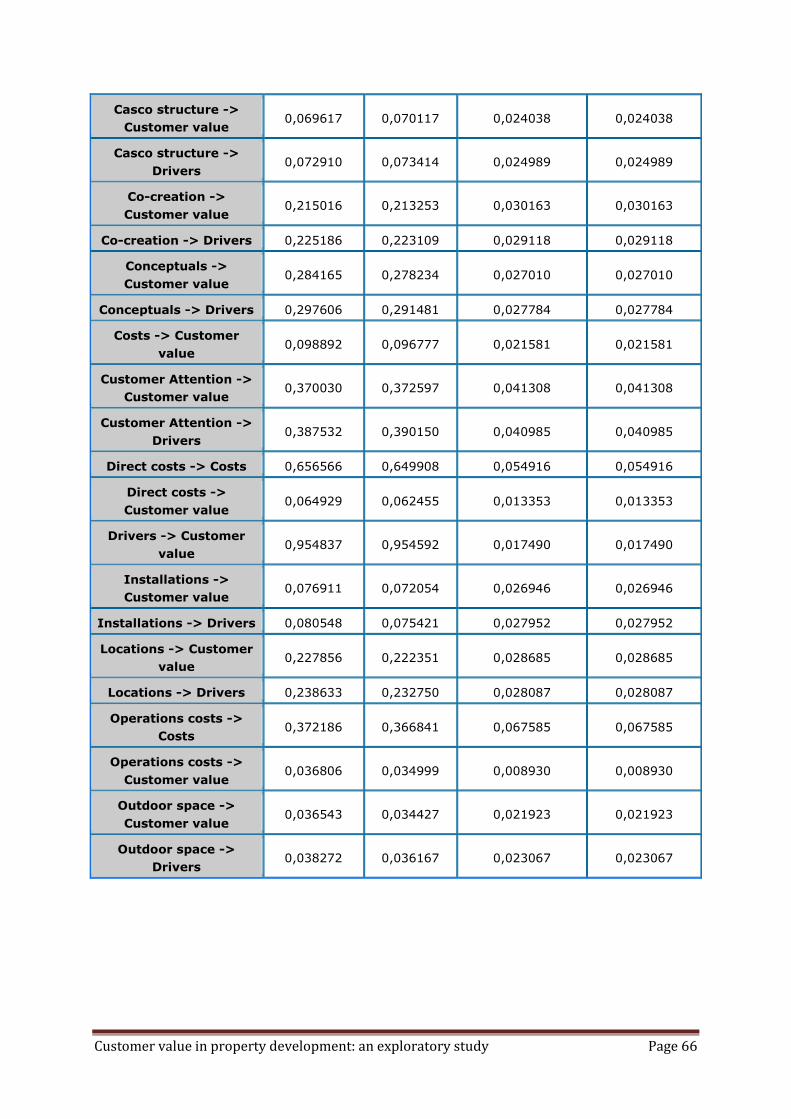

Effects in the structural model

The structural model follows a formative directionality and envisions the relations among the

dimensions. First, the direct effects (regression coefficients) show that customer attention has the

strongest effect on drivers with a regression coefficient of 0,39. This is followed by conceptuals

(0,30), locations (0,24), co-creation (0,23) and branding (0,16). Installations (0,08), casco structure

(0,07) and outdoor space (0,04) have relatively weak effects on drivers. When the costs are

assessed, direct costs have the strongest influence on costs (0,66), followed by operations costs

(0,37) and acquisition costs (0,35). Second, where Drivers has a very strong direct effect on

customer value (0,95), Costs has a relatively weak direct effect on customer value (0,10).

However, the effect of Costs on customer value (its sign) is positive where a negative effect was

anticipated. Third, when the total effects (path coefficients) are taken account, the first order

dimension customer attention still has the strongest effect on customer value (0,37), followed by

conceptuals (0,28), locations (0,23), co-creation (0,22) and branding (0,16). Again, installations

(0,08), casco structure (0,07) and outdoor space (0,04) exhibit a relatively weak effect on

customer value. Because of the strong effect of Drivers on customer value, there is only minor

deviation in direct effects and total effects. When the costs are reviewed another image emerges.

The path coefficients indicate that the total effects of all three cost dimensions on customer value

are relatively weak: direct costs (0,06) provide the strongest effect on customer value, followed by

operations costs (0,04) and acquisition costs (0,03). There is a large deviation between direct and

total effects among the cost-dimensions, which is caused by the relatively weak direct effect of

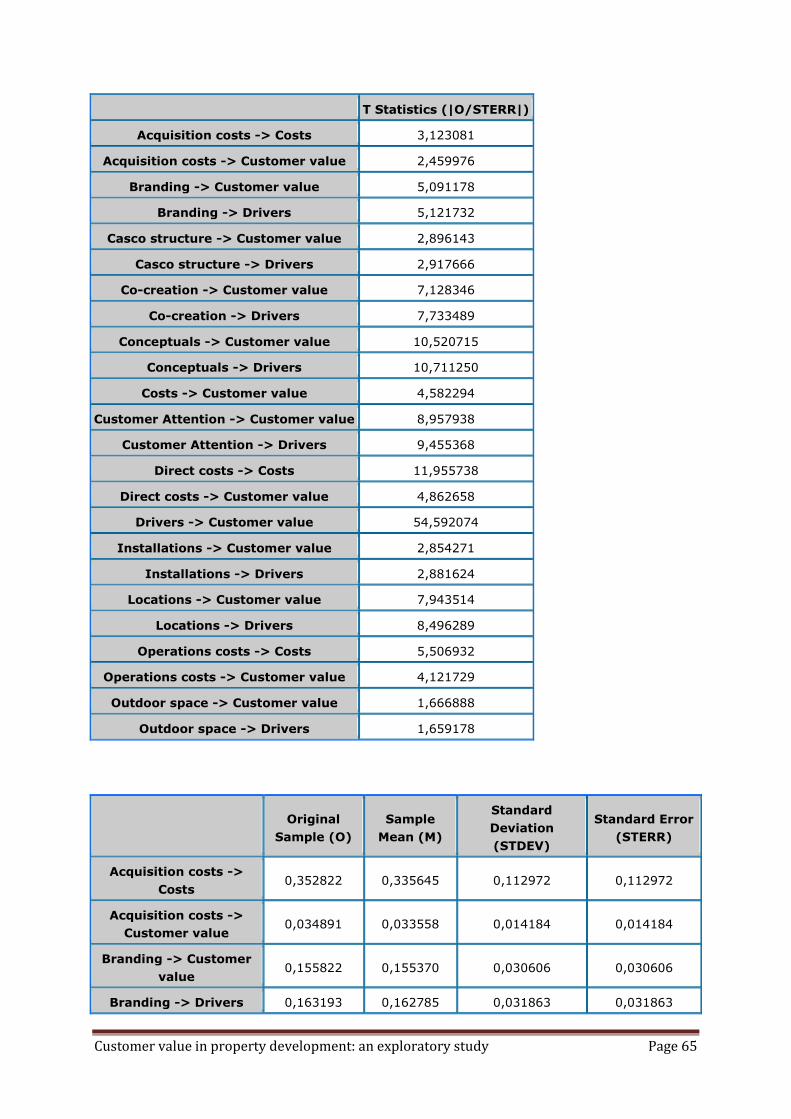

Costs on customer value. A first measure to judge the structural model is the T-statistic.

Bootstrapping was performed to discover relevant T-statistics using the option “no significant

changes” in the SmartPLS 2.0 (2005) bootstrapping menu with a re-sampling number of 400. The

options construct level changes and individual sign changes were not used, because construct

level changes has the potential danger to increase the standard errors of the total effects (path

coefficients) to an unsatisfactory high level when different re-sampling numbers are used

(Tenenhaus et al. 2005), while the individual sign changes is avoided because of a lack of

coherence when the sign from the re-samples is made consistent to the original sample

(Tenenhaus et al. 2005). Support in the data is found that there are no large discrepancies

between the resample mean and original sample mean (only small values for the standard error of

Customer value in property development: an exploratory study Page 33

the mean). This indicates the appropriateness for the option no significant changes. The results

of the bootstrapping procedure indicate that all total effects (path coefficients) are significant at

95% (α = 0,05) confidence interval, except for the total effect of outdoor space on drivers. This

effect is only significant at 90% confidence interval (α = 0,10). The second measure to assess the

structural model is the R-square. The R-square value of Drivers is 0,999 and for Costs it is 0,998.

This results in an R-square for customer value of 0,999. These values seem to indicate that the

robustness of the structural equation model (SEM) is optimal (Chin 1998), since almost all

possible variance in customer value is explained by its underlying dimensions. Because these

values might seem quite extreme, the complete SEM was checked. No errors were found,

indicating support for the validity of these R-square values. A third measure to judge the

structural model is through the effect sizes (f2). The f2 compares the increase in explained

variance by the endogenous dimensions (R-square) with the increase in variance that is

unexplained explained by the endogenous dimensions (Henseler, Ringle and Sinkovics 2009).

This can be tested by excluding one of the second-order dimensions from the model (Wong

2006). When Costs are deleted, the f2 becomes 5 and when Drivers are deleted, the f2 becomes

453. These values are largely above the minimum threshold of 0,02 (Cohen 1988) and can be

considered as very strong. These extreme values are largely due to the fact that the R-square of

customer value has such a high value. Even fractional changes in this R-square result in high

values for f2, because these changes are divided by an even smaller value (1 - R-square included,

or 1 - 0,999). Elaborate output for structural assessment of PLS can be found in appendix D.

6.3 In-dept analysis

The remaining 11 indicators from the survey were also analyzed to provide more meaning to the

data. Two indicators were directly removed from further analysis since they relate to indicators

that were deleted earlier in PCA (surface and flaw minimization). Levene’s test in SPSS indicated

heteroscedasticity in two of the 9 remaining indicators (significant values at 95% confidence

interval, with α = 0,05). These indicators were also deleted for further analysis. Normality of the

remaining indicators was checked and no extreme values were found based on norms for

skewness and kurtosis as applied earlier in this study. Respondents’ level of (dis)agreement with

an indicator was assessed by looking at the mean value on the 7-point rating scale for that

particular indicator. The first indicator revealed respondents’ attitude regarding the indicators

personal dialogue 1 and 2. The consensus is that respondents are willing to pay a premium for a

house when it is created through personal dialogue (mean = 2,39). The second indicator revealed

that respondents prefer personal dialogue over community building (mean = 2,74). This finding

Customer value in property development: an exploratory study Page 34

is supported by the data from SEM, because the indicators personal dialogue 1 and 2 have larger

standardized loadings (0,767 and 0,783) than the indicator community building 2 (0,672) on

conceptuals. The third indicator revealed that respondents are willing to pay a premium for a

house when it is created through concepts (mean = 2,60). The fourth indicator revealed that

respondents are willing to pay a premium for the design of public space (mean = 2,66). The fifth

indicator revealed that respondents have only a very small tendency towards paying a premium

for a house when it is developed through co-creation (mean= 3,57). The sixth indicator pointed

out that respondents have a neutral attitude (neither agree, nor disagree) towards paying a

premium for installations (mean = 3,97). Finally, the seventh indicator revealed that respondents

have a neutral attitude towards paying a premium for a house from a developer which has a

brand(name) (mean = 3,97). Levene’s test for the indicators above is displayed in Appendix E.

Customer value in property development: an exploratory study Page 35

7. Discussion

The results of the three subsequent processes of the quantitative study each provide valuable