Embed Size (px)

Citation preview

INR 15A monthly Capital Markets & Lifestyle Magazine by the Bombay Stock Exchange Brokers' Forum (BBF)

CLOSING THE CRITICAL GAPS TO PROTECT PERSONAL INFORMATION INVEST IN ETFS TO COMPLIMENT YOUR MUTUAL FUND | |INVESTMENTS TIME TO BLOW THE WHISTLE: CORPORATE VIGILENCE MECHANISM BROKING INDUSTRY REGULATIONS AND

| |POSSIBLE IMPACT ON RETAIL BROKERS BUDGET & SECTOR IMPACT COMPLIANCE TO GOOD GOVERNANCE - SEBI’S |NOTEWORTHY INITIATIVE YOUR SECRET TEACHER TO LIFE & LIVING

|

Volume 9 | Issue 12

IAN RUSSELL

SWARUP MOHANTY

ZERICK DASTUR

TEJAS KHODAY

AYUSH AGGARWAL

DEVDUTTA MODAK

JYOTSNAAHUJA

INVESTMENT INDUSTRYASSOCIATION OF CANADA

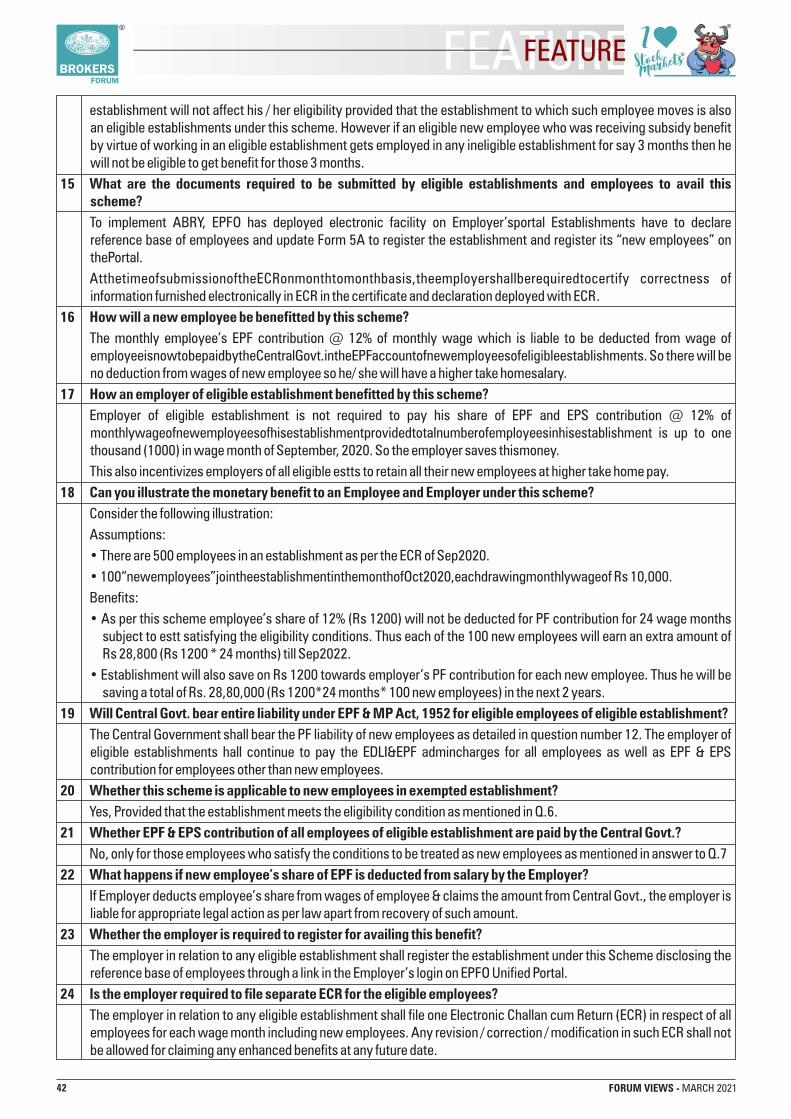

MIRAE ASSET INVESTMENTMANAGERS (INDIA) PVT. LTD.

ADVOCATES &SOLICITORS

FYERS

SMC PRIVATEWEALTH

AXAR DIGITALSERVICES PVT. LTD.

THE WHITESPACE

March 2021

MORE

2

UTTAM BAGRI HEMANT MAJETHIA ANURAG BANSAL RAJIV CHOKSEYChairman | BBF Vice Chairman | BBF Secretary | BBF Jt. Treasurer | BBF

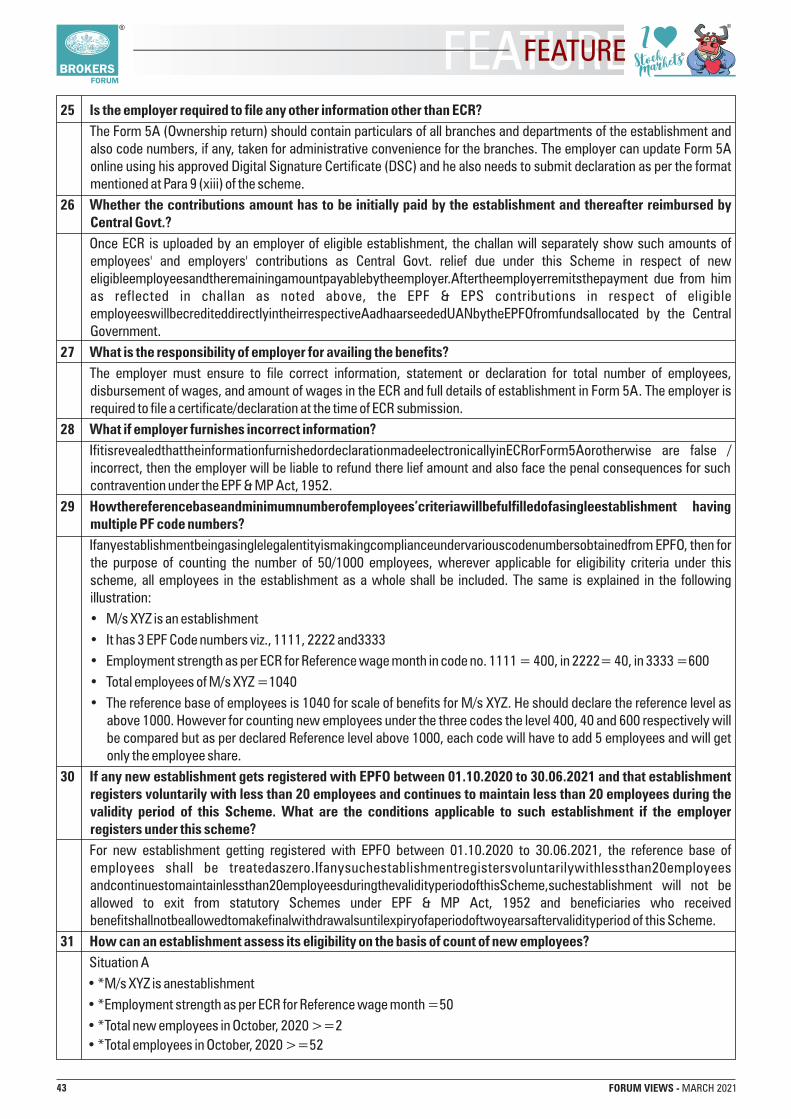

BCB BrokeragePvt. Ltd.

VenturaSecurities Ltd.

SMC GlobalSecurities Ltd.

KR Choksey Shares& Securities Pvt. Ltd.

EXECUTIVE COMMITTEE

GOVERNING BOARD MEMBERS

3 FORUM VIEWS - MARCH 2021

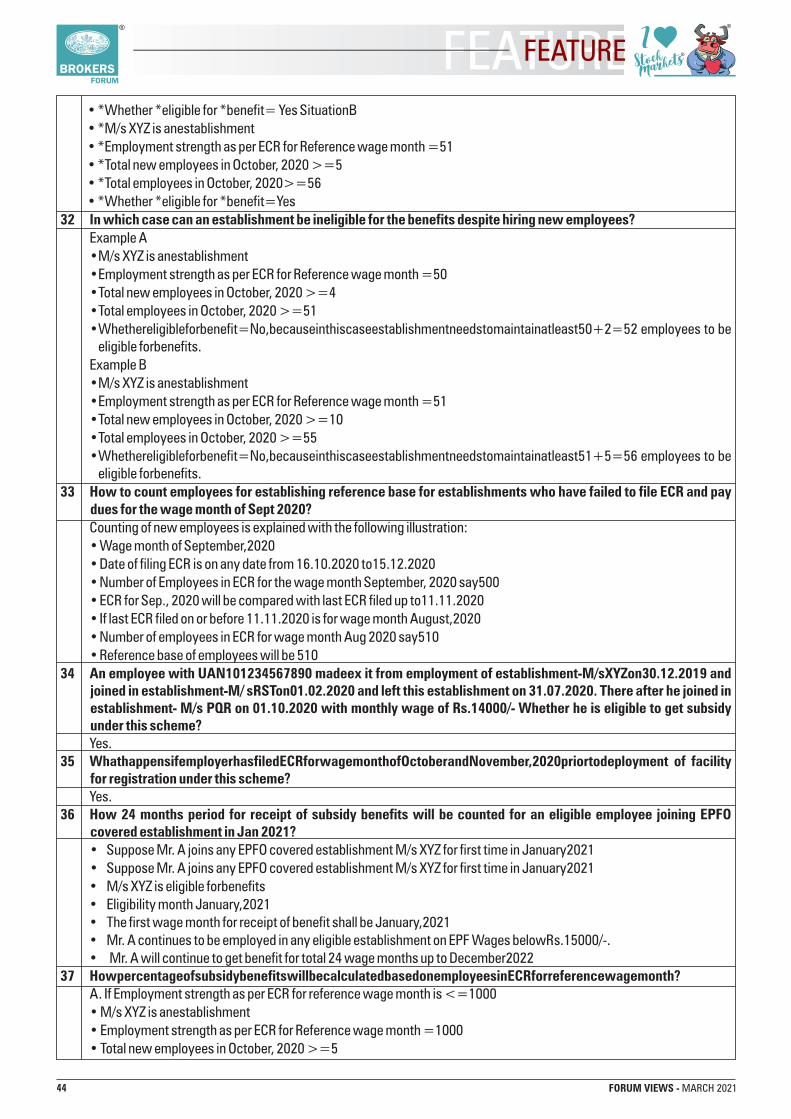

BOMBAY STOCK EXCHANGE BROKERS’ FORUM (BBF)GOVERNING BOARD 2020 - 21

Anup GuptaSykes & Ray

Equities India Ltd.

Cyrus KhambataPaytm

Money Ltd.

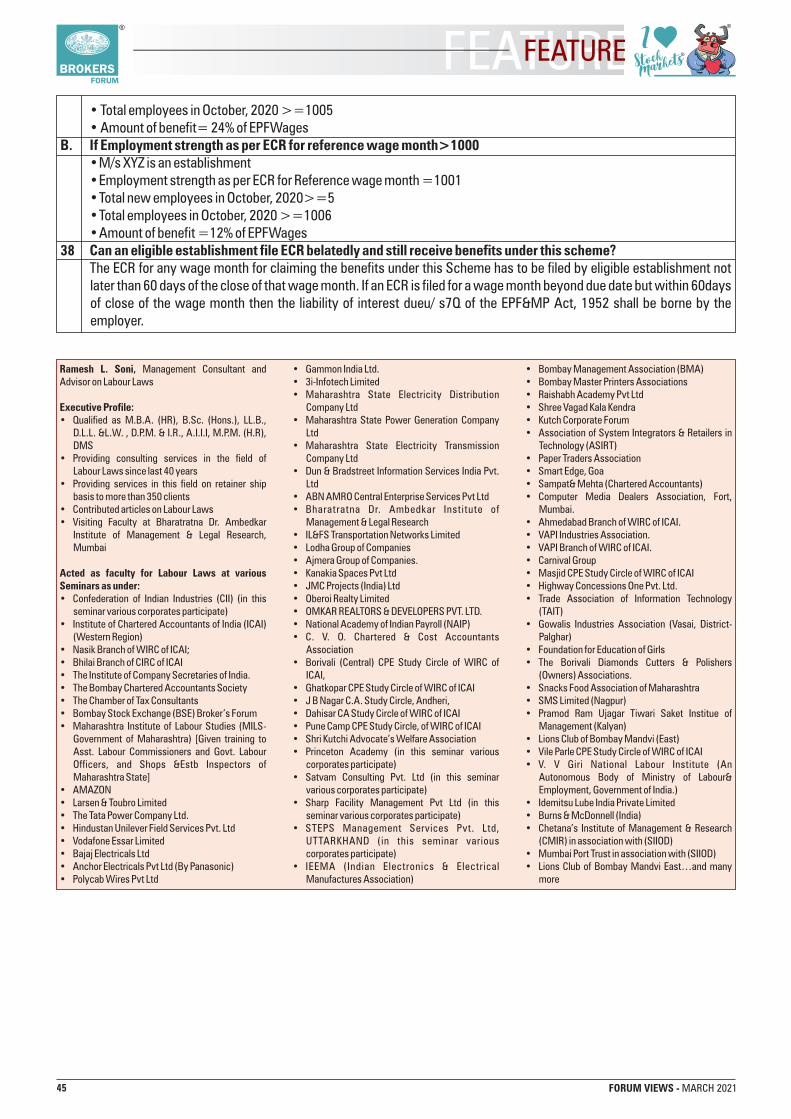

Kamlesh JhaveriJhaveri

Securities Ltd.

Ketan MarwadiMarwadi Shares& Finance Ltd.

Madhavi VoraULJK Securities

Pvt. Ltd.

Naresh RanaVishwas Fincap

Services Pvt. Ltd.

Neeraj ChoksiNJ India

Invest Pvt. Ltd.

Nirav GandhiJM FinancialServices Ltd.

Nithin KamathZerodha

Securities Pvt. Ltd.

Paresh ShahP.C.S.

Securities Ltd.

Parth NyatiSwastika

Investmart Ltd.

Pradeep GuptaAnand Rathi Share

& Stock Brokers Ltd.

S. P. ToshniwalSunlight

Broking LLP

Sandeep NayakCentrum

Broking Ltd.

Santanu SyamAngel

Broking Ltd.

Sunil SardaSystematix Shares& Stocks India Ltd.

Vineet BhatnagarPhillip Capital

(India) Pvt. Ltd.

Vivek GuptaGEPL Capital

Pvt. Ltd.

KUSHAL A. SHAHJt. Secretary | BBF

RatnakarSecurities Pvt. Ltd.

LALIT MUNDRATreasurer | BBF

Suresh RathiSecurities Pvt. Ltd.

Ajit SanghviMSS Securities

Pvt. Ltd

Kishor KansagraPragya Securities

Pvt. Ltd.

Purav Fozdar Axiom Share

Broking Pvt. Ltd.

Disclaimer: This magazine is meant for information purposes only and does not constitute any opinion or guidelines or recommendation on any course of action to be followed by the reader(s). It is not intended to be used as trading or investment advice by anybody and should not in any way be treated as a recommendation. The information contained in this magazine does not constitute or form part of and should not be construed as, any offer for purchase or sale of any product or service. While the information in the magazine has been compiled from sources believed to be reliable and in good faith, readers may note that the contents thereof including text, graphics, links or other items are provided without warranties of any kind. Bombay Stock Exchange Brokers' Forum (BBF) expressly disclaims any warranty as to the accuracy, correctness, reliability, timeliness, merchantability or fitness for any particular purpose, of this magazine. Bombay Stock Exchange Brokers' Forum (BBF) shall also not be liable for any damage or loss of any kind, howsoever caused as a result (direct or indirect) of the use of the information or data contained in this magazine. Any alteration, transmission, photocopied distribution in part or in whole or reproduction of any form of this magazine or any part thereof without prior consent of Bombay Stock Exchange Brokers' Forum (BBF) is prohibited.

Printed, Published and Edited by Dr. VISPI RUSI BHATHENA, PhD (h.c.)

& Dr. V. ADITYA SRINIVAS on behalf of Bombay Stock Exchange Brokers' Forum (BBF),printed at KSHITIJ PRINTERS, 49, Parsi Panchayat Road, Ashok Ind. Estate, 1st, Floor,Andheri (East) Mumbai - 400 069. and published from Bombay Stock Exchange Brokers'Forum (BBF), 808 A,P. J. TOWERS, DALAL STREET, FORT, MUMBAI - 400 001.Editor: Dr. V. ADITYA SRINIVAS | Design by: Harshad Gajera | Photographer: Sanjeev Dubey

Write to us: We would be happy to hearfrom you! Do send in your suggestions,feedback and comments via email [email protected] us: www.brokersforumofindia.com

BBF Steering CommitteeUttam Bagri (Chairman)Hemant Majethia (Vice-Chairman)Anurag Bansal (Secretary)Lalit Mundra (Treasurer)Kushal A. Shah (Jt. Secretary)Rajiv Choksey (Jt. Treasurer)

Follow us on: @bbfindia /bsebrokersforum/brokersforumofindia c/bbfindia/

4 FORUM VIEWS - MARCH 2021

12YourQuestionsAnswered

06GlobalInsights

CLOSING THE CRITICALGAPS TO PROTECTPERSONALINFORMATION

INVEST IN ETFS TOCOMPLIMENT YOURMUTUAL FUNDINVESTMENTS

ASIA-PACIFIC MARKETSMONTHLY HIGHLIGHTSAND INSIGHTS

18 Insights

2021 BUDGET DELIVERSRESET MODE(ALT + CTRL + DELETE)TO REBOOT AND REENGINEERINDIA GROWTH HORIZON

38 Feature

COMPLIANCE CALENDARREGULATORY PULSECIRCULARS

50 RegulatoryAssistance

Nurturing Lifestyle61

DIGITAL DETOX

YOUR SECRET TEACHERTO LIFE & LIVING

IMMUNITY

RIGHT TO PROPERTYUNDER THE CONSTITUTIONOF INDIA, 1950

CYBERSECURITYIN HEALTHCARE

FAQS ON ATMANIRBHARBHARAT ROZGAR YOJANA

EXECUTIVE PRESENCE

TIME TO BLOW THEWHISTLE: CORPORATEVIGILENCE MECHANISM

FRAMEWORK FORENABLING ANCILLARYSERVICES ATINTERNATIONALFINANCIAL SERVICESCENTRES (“IFSC”)

BROKING INDUSTRYREGULATIONS AND POSSIBLEIMPACT ON RETAIL BROKERS

BUDGET & SECTOR IMPACT

COMPLIANCE TO GOODGOVERNANCE - SEBI’SNOTEWORTHY INITIATIVE

SIP YOUR GOALSAT NEW HIGH

INVESTOR’S FIRST FRONTIER:RISK ASSESSMENTAND ASSET ALLOCATION

WHAT DOES THE RECENTBROAD MARKET RALLY INMARKETS TELLS US?

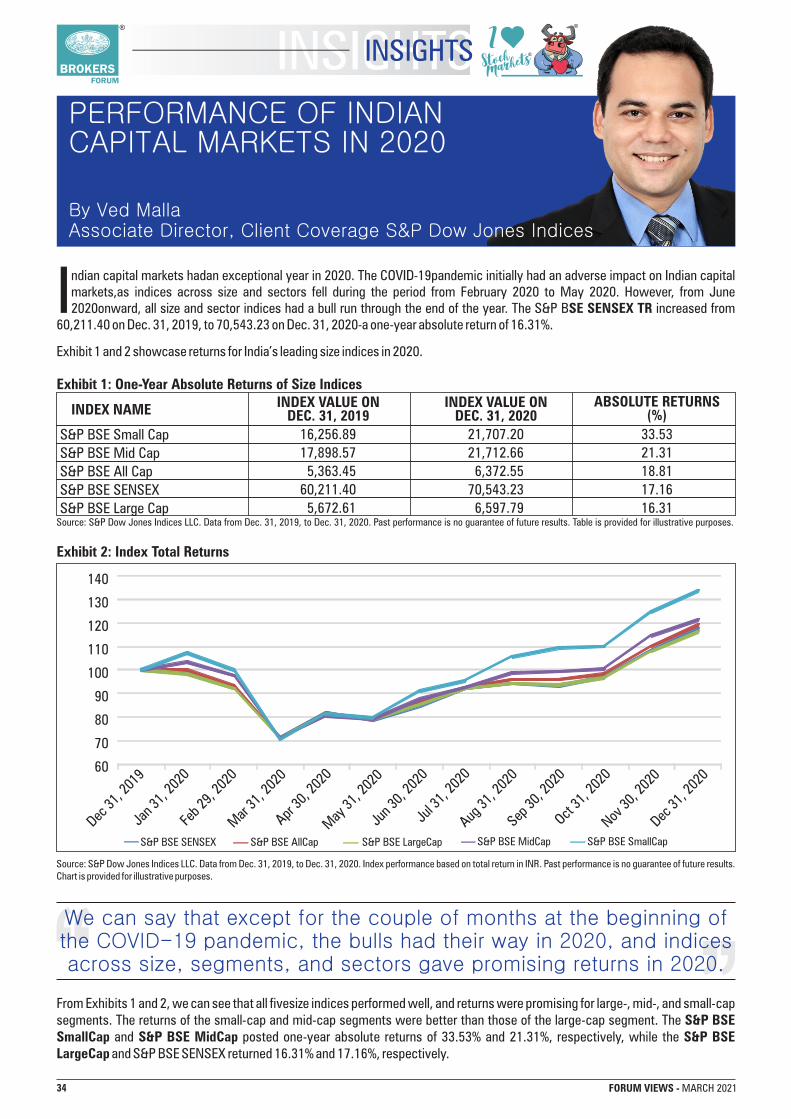

PERFORMANCE OF INDIANCAPITAL MARKETS IN 2020

THE NEXT PHASE OFECONOMIC REFORM BEGINS:AN OVERVIEW

5 FORUM VIEWS - MARCH 2021

ceo & coo message

Dr. Aditya Srinivas

next year. The direct tax was kept unchanged. The agriculture cess of Rs. 2 was added to petrol and Rs. 4 to diesel aimed to generate revenue to make up for the fiscal deficit.

RBI monetary policy also echoed the intent that growth is the priority of the

g o v e r n m e n t a n d p e g g e d t h e G D P growth to be at 10.55% for the next year. The outlook for inflation has also been pegged at 5% which is the normal range. The

WelcomeDr. Vispi RusiBhathena,PhD (h.c.)

to magazine.Forum Views

The RBI maintained its

accommodative stand to

ensure that growth is

the vital aspect and

interest rates will move

up only when economy

is completely out of

woods.

RBI maintained its accommodative stand to ensure that growth is the vital aspect and interest rates will move up only when economy is completely out of woods.

The Foreign Institutional Investors have invested Rs. 29000 crores in January and February 2021 (till Feb 10th) as they have appreciated the boldness in the budget for CAPEX which will set the ball rolling for higher economic growth.

The rollout of vaccination has created positive environment for the overall economic growth and spending spirits will be back soon in the economy.

BUDGET GAVE NEW LIFE TO ECONOMY AND MARKETS

The Indian Economy seems to be all guns blazing with the stock markets touching lifetime high. The Budget spelled out clear intention of the government that Growth cannot be compromised. The very fact that CAPEX target has been kept at Rs. 5.54 lakh crores were one of the biggest welcome moves taken by the stock market. The BSE SENSEX gave clear thumps up by moving up more than 5% on the Budget day. The Government stand to make vital expenditure in the field of health care was also vital factor as the health care is going to be prime importance.

The Budget also made road for the fiscal deficit which is pegged at 9.5% for the current year and target of 6.8% for the

On the BBF front:

BBF Seminars and Events

Topic Date

Sexual Harassment of Womenat Work (POSH)NCDEX - Investor ResolutionMechanismNew Developments at CDSL

Monday,22-FebruaryWednesday,17-FebruaryFriday,5-February

6 FORUM VIEWS - MARCH 2021

IAN RUSSELLPresident and CEO

Investment Industry Association of Canada (IIAC)

The European Union law on data protection and privacy, the GDPR (General Data Protection Regulation), has become the path-breaking template for protecting personal information in many foreign jurisdictions.

7 FORUM VIEWS - MARCH 2021

The BBF is a key member of ICSA, the global organization of nineteen securities industry associations. Founded in 1988, ICSA provides a forum for member associations to understand developments, exchange views, and collaborate to work for better global capital markets. (www.icsa.global).

ICSA members have been invited to submit contributions to Forum Views. The following is from the Investment Industry Association of Canada.

CLOSING THE CRITICAL GAPS TO PROTECTPERSONAL INFORMATION

control”. As previewed earlier, new legislation grants individuals rights, including the right to access and amend their information, the right to dispose with their information, the right to transfer personal information among organizations, and the right to be informed of how predictions, recommendations or decisions are made by an automated decision-making system.

The core obligation of the investment dealer firms under the proposed legislation is to implement a “privacy management program” that includes policies, practices and procedures respecting the protection of personal information; how inquiries and complaints are received and dealt with; the training and information provided to staff; and the development of materials to explain firms’ policies and procedures to fulfil their obligations. We anticipate the eventual regulations will be principles-based to enable broad applicability across the corporate sector.

Firms will be required to develop policies and procedures consistent with the sensitivity and volume of personal information under their control. Further, these policies and procedures will be subject to review and approval by the Office of the Privacy Commissioner and will be monitored against the approved compliance standard. The new legislation imposes substantial penalties for non-compliance under broader “order-making power” of the Privacy Commissioner, with the Commissioner and new Personal Information and Data Protection Tribunal to impose fines and penalties.

For the most cost-efficient regulatory outcome, investment dealers in the financial sector could request to operate under an approved certification program that includes “a code of practice that provides for substantially the same or greater protection of personal information as some or all of the protection provided under the Act”. The dealers would elect the recognized self-regulatory organization, the Investment Industry Regulatory Organization of Canada (IIROC), with its resources as the regulator of the business activities of the dealer, as the integral part of the certification program. IIROC, in conjunction with member firms, would develop the codes of practice and provide the compliance oversight of the privacy management program and other practices, given its regulatory infrastructure.

The proposed legislation promises an effective protection for personal information, an important guidepost for harmonized rules in the provincial/territorial statutes, and the features for a flexible and efficient regulatory structure. We are hopeful that, as coming discussions unfold, potential will be realized.

Ian Russell has been President and CEO of the Investment Industry Association of Canada since its inauguration in April 2006. Previously, Ian was Senior Vice-President, Industry Relations and Representation, at the Investment Dealers Association of Canada (IDA).

In his more than 20-year tenure with the IDA and the IIAC, Ian has participated actively in many committees and working groups involved in regulatory and tax issues related to the securities industry and capital markets in Canada.

Ian is a past Chairman of ICSA.

espite the intensive public policy focus during the long-standing COVID-19 pandemic, the federal government of DCanada has persevered to release proposed legislation to

update and modernize Canada’s privacy laws and increase Canadians’ control over their data and personal information.

The proposed legislation builds on earlier legislative proposals and will replace the outdated long-serving Personal Information Protection and Electronic Documents Act (PIPEDA). Rapid advances of digitalization, automated or algorithmic decision-making, and recent testimony before the U.S. Congress on the misuse of personal information on the internet suggest much higher standards of regulation of personal information are long overdue.

The European Union law on data protection and privacy, the GDPR (General Data Protection Regulation), has become the path-breaking template for protecting personal information in many foreign jurisdictions. The Canada-EU Comprehensive Economic Trade Agreement (CETA) necessitates GDPR compliance (adequacy) for many Canadian businesses that offer goods or services to individuals in the EU.

The Investment Industry Association of Canada (IIAC), representing 115 Canadian investment dealers in the country, has been a strong advocate for renewal of the laws protecting privacy and personal information. Firms in our industry collectively administer 14 million client accounts with extensive personal data and information and, therefore, support comprehensive privacy legislation imposing uniform, transparent and high standards of protection for personal financial information across the country.

Close federal-provincial/territorial coordination is important to ensure the framework is streamlined and simplified to reduce the regulatory burden, minimize confusion and uncertainty, and ensure effective enforcement of standards.

The draft privacy legislation requires valid consent from individuals to collect, use and disclose their personal information, with narrow exemptions, but the validity of the consent is now based upon information being provided in “plain language”, and consent has to be expressly obtained. It removes the burden of having to obtain consent when that consent does not provide any meaningful privacy protection. An organization is accountable for personal information that is “under its

Key findings:

ASIA-PACIFIC MARKETSMONTHLY HIGHLIGHTS

AND INSIGHTS

• M&A Activity By Country, Sector

• Initial Public Offerings

• Private Equity Investments And Buyouts

• Venture Capital Investments

• Market Attributes: Index Dashboard

Contact Information: If you have any questions relating to the content featured in the publication, please contact [email protected]

Disclaimer: Copyright © 2021 by S&P Global Market Intelligence, a division of S&P Global Inc. All rights reserved.

These materials have been prepared solely for information purposes based upon information generally available to the public and from sources believed to be reliable. No content (including index data, ratings, credit-related analyses and data, research, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P Global Market Intelligence or its affiliates (collectively, S&P Global). The Content shall not be used for any unlawful or unauthorized purposes. S&P Global and any third-party providers, (collectively S&P Global Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Global Parties are not responsible for any errors or omissions, regardless of the cause, for the results obtained from the use of the Content. THE CONTENT IS PROVIDED ON “AS IS” BASIS. S&P GLOBAL PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Global Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

S&P Global Market Intelligence’s opinions, quotes and credit-related and other analyses are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P Global Market Intelligence assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P Global Market Intelligence does not act as a fiduciary or an investment advisor except where registered as such. S&P Global keeps certain activities of its divisions separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain divisions of S&P Global may have information that is not available to other S&P Global divisions. S&P Global has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

S&P Global Ratings does not contribute to or participate in the creation of credit scores generated by S&P Global Market Intelligence. Lowercase nomenclature is used to differentiate S&P Global Market Intelligence PD credit model scores from the credit ratings issued by S&P Global Ratings.

S&P Global may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P Global reserves the right to disseminate its opinions and analyses. S&P Global's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P Global publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

8 FORUM VIEWS - MARCH 2021

GLOBAL INSIGHTSGLOBAL INSIGHTS

9 FORUM VIEWS - MARCH 2021

GLOBAL INSIGHTSGLOBAL INSIGHTS

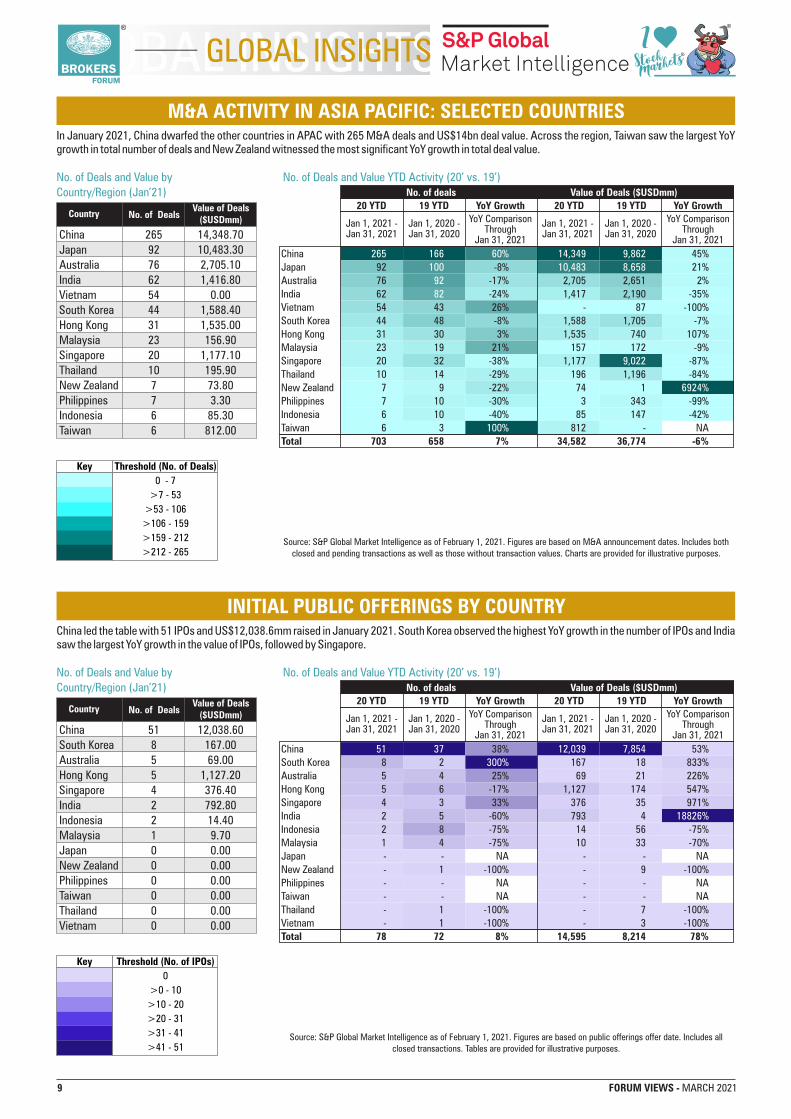

M&A ACTIVITY IN ASIA PACIFIC: SELECTED COUNTRIESIn January 2021, China dwarfed the other countries in APAC with 265 M&A deals and US$14bn deal value. Across the region, Taiwan saw the largest YoY growth in total number of deals and New Zealand witnessed the most significant YoY growth in total deal value.

Source: S&P Global Market Intelligence as of February 1, 2021. Figures are based on M&A announcement dates. Includes both closed and pending transactions as well as those without transaction values. Charts are provided for illustrative purposes.

Key Threshold (No. of Deals)

0 - 7

>7 - 53

>53 - 106

>106 - 159

>159 - 212

>212 - 265

No. of Deals and Value by

Country/Region (Jan’21)

No. of Deals and Value YTD Activity (20’ vs. 19’)

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

No. of deals Value of Deals ($USDmm)

China 45%

Japan 92 -8% 21%

Australia 76 -17% 2,705 2,651 2%

India 62 -24% 1,417 2,190 -35%

Vietnam 54 43 26% - 87 -100%

South Korea 44 48 -8% 1,588 1,705 -7%

Hong Kong 31 30 3% 1,535 740 107%

Malaysia 23 19 21% 157 172 -9%

Singapore 20 32 -38% 1,177 -87%

Thailand 10 14 -29% 196 1,196 -84%

New Zealand 7 9 -22% 74 1

Philippines 7 10 -30% 3 343 -99%

Indonesia 6 10 -40% 85 147 -42%

Taiwan 6 3 812 - NA

Total 703 658 7% 34,582 36,774 -6%

265 166 60% 14,349 9,862

100 10,483 8,658

92

82

9,022

6924%

100%

Country No. of DealsValue of Deals

($USDmm)

China 265 14,348.70

Japan 92 10,483.30

Australia 76 2,705.10

India 62 1,416.80

Vietnam 54 0.00

South Korea 44 1,588.40

Hong Kong 31 1,535.00

Malaysia 23 156.90

Singapore 20 1,177.10

Thailand 10 195.90

New Zealand 7 73.80

Philippines 7 3.30

Indonesia 6 85.30

Taiwan 6 812.00

INITIAL PUBLIC OFFERINGS BY COUNTRYChina led the table with 51 IPOs and US$12,038.6mm raised in January 2021. South Korea observed the highest YoY growth in the number of IPOs and India saw the largest YoY growth in the value of IPOs, followed by Singapore.

Source: S&P Global Market Intelligence as of February 1, 2021. Figures are based on public offerings offer date. Includes all closed transactions. Tables are provided for illustrative purposes.

No. of Deals and Value YTD Activity (20’ vs. 19’)

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

No. of deals Value of Deals ($USDmm)

China 38% 53%

South Korea 8 2 167 18 833%

Australia 5 4 25% 69 21 226%

Hong Kong 5 6 -17% 1,127 174 547%

Singapore 4 3 33% 376 35 971%

India 2 5 -60% 793 4

Indonesia 2 8 -75% 14 56 -75%

Malaysia 1 4 -75% 10 33 -70%

Japan - - NA - - NA

New Zealand - 1 -100% - 9 -100%

Philippines - - NA - - NA

Taiwan - - NA - - NA

Thailand - 1 -100% - 7 -100%

Vietnam - 1 -100% - 3 -100%

Total 78 72 8% 14,595 8,214 78%

51 37 12,039 7,854

300%

18826%

No. of Deals and Value by

Country/Region (Jan’21)

Country No. of DealsValue of Deals

($USDmm)

China 51 12,038.60

South Korea 8 167.00

Australia 5 69.00

Hong Kong 5 1,127.20

Singapore 4 376.40

India 2 792.80

Indonesia 2 14.40

Malaysia 1 9.70

Japan 0 0.00

New Zealand 0 0.00

Philippines 0 0.00

Taiwan 0 0.00

Thailand 0 0.00

Vietnam 0 0.00

Key Threshold (No. of IPOs)

0

>0 - 10

>10 - 20

>20 - 31

>31 - 41

>41 - 51

10 FORUM VIEWS - MARCH 2021

GLOBAL INSIGHTSGLOBAL INSIGHTS

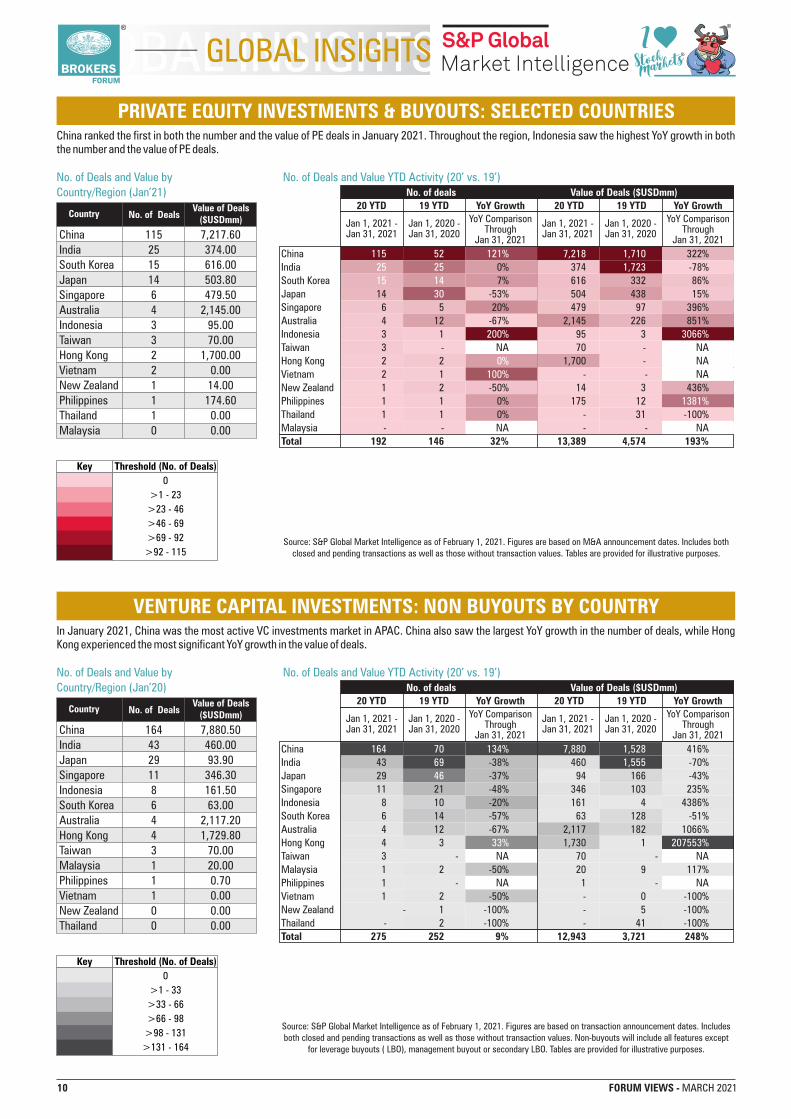

VENTURE CAPITAL INVESTMENTS: NON BUYOUTS BY COUNTRYIn January 2021, China was the most active VC investments market in APAC. China also saw the largest YoY growth in the number of deals, while Hong Kong experienced the most significant YoY growth in the value of deals.

Source: S&P Global Market Intelligence as of February 1, 2021. Figures are based on transaction announcement dates. Includes both closed and pending transactions as well as those without transaction values. Non-buyouts will include all features except

for leverage buyouts ( LBO), management buyout or secondary LBO. Tables are provided for illustrative purposes.

No. of Deals and Value by

Country/Region (Jan’20)

No. of Deals and Value YTD Activity (20’ vs. 19’)

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

No. of deals Value of Deals ($USDmm)

China 416%

India 43 -38% 460 -70%

Japan 29 -37% 94 166 -43%

Singapore 11 21 -48% 346 103 235%

Indonesia 8 10 -20% 161 4 4386%

South Korea 6 14 -57% 63 128 -51%

Australia 4 12 -67% 2,117 182 1066%

Hong Kong 4 3 1,730 1

Taiwan 3 - NA 70 - NA

Malaysia 1 2 -50% 20 9 117%

Philippines 1 - NA 1 - NA

Vietnam 1 2 -50% - 0 -100%

New Zealand - 1 -100% - 5 -100%

Thailand - 2 -100% - 41 -100%

Total 275 252 9% 12,943 3,721 248%

164 70 134% 7,880 1,528

69 1,555

46

33% 207553%

Country No. of DealsValue of Deals

($USDmm)

China 164 7,880.50

India 43 460.00

Japan 29 93.90

Singapore 11 346.30

Indonesia 8 161.50

South Korea 6 63.00

Australia 4 2,117.20

Hong Kong 4 1,729.80

Taiwan 3 70.00

Malaysia 1 20.00

Philippines 1 0.70

Vietnam 1 0.00

New Zealand 0 0.00

Thailand 0 0.00

Key Threshold (No. of Deals)

0

>1 - 33

>33 - 66

>66 - 98

>98 - 131

>131 - 164

PRIVATE EQUITY INVESTMENTS & BUYOUTS: SELECTED COUNTRIESChina ranked the first in both the number and the value of PE deals in January 2021. Throughout the region, Indonesia saw the highest YoY growth in both the number and the value of PE deals.

Key Threshold (No. of Deals)

0

>1 - 23

>23 - 46

>46 - 69

>69 - 92

>92 - 115Source: S&P Global Market Intelligence as of February 1, 2021. Figures are based on M&A announcement dates. Includes both

closed and pending transactions as well as those without transaction values. Tables are provided for illustrative purposes.

No. of Deals and Value YTD Activity (20’ vs. 19’)

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

Jan 1, 2021 -Jan 31, 2021

Jan 1, 2020 -Jan 31, 2020

YoY ComparisonThrough

Jan 31, 2021

No. of deals Value of Deals ($USDmm)

No. of Deals and Value by

Country/Region (Jan’21)

Country No. of DealsValue of Deals

($USDmm)

China 115 7,217.60

India 25 374.00

South Korea 15 616.00

Japan 14 503.80

Singapore 6 479.50

Australia 4 2,145.00

Indonesia 3 95.00

Taiwan 3 70.00

Hong Kong 2 1,700.00

Vietnam 2 0.00

New Zealand 1 14.00

Philippines 1 174.60

Thailand 1 0.00

Malaysia 0 0.00

China 322%

India 0% 374 -78%

South Korea 7% 616 332 86%

Japan 14 -53% 504 438 15%

Singapore 6 5 20% 479 97 396%

Australia 4 12 -67% 2,145 226 851%

Indonesia 3 1 95 3

Taiwan 3 - NA 70 - NA

Hong Kong 2 2 1,700 - NA

Vietnam 2 1 - - NA

New Zealand 1 2 -50% 14 3 436%

Philippines 1 1 0% 175 12

Thailand 1 1 0% - 31 -100%

Malaysia - - NA - - NA

Total 192 146 32% 13,389 4,574 193%

115 52 121% 7,218 1,710

25 25 1,723

15 14

30

200% 3066%

0%

100%

1381%

11 FORUM VIEWS - MARCH 2021

GLOBAL INSIGHTSGLOBAL INSIGHTS

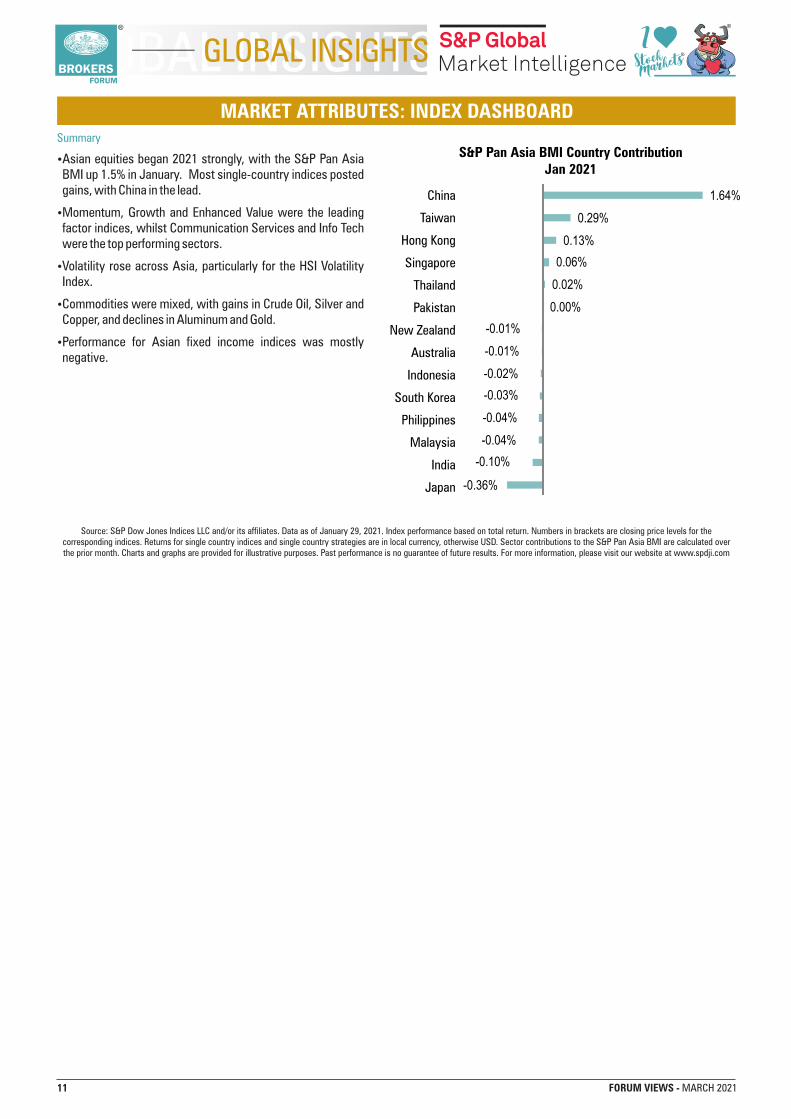

MARKET ATTRIBUTES: INDEX DASHBOARD

ŸAsian equities began 2021 strongly, with the S&P Pan Asia BMI up 1.5% in January. Most single-country indices posted gains, with China in the lead.

ŸMomentum, Growth and Enhanced Value were the leading factor indices, whilst Communication Services and Info Tech were the top performing sectors.

ŸVolatility rose across Asia, particularly for the HSI Volatility Index.

ŸCommodities were mixed, with gains in Crude Oil, Silver and Copper, and declines in Aluminum and Gold.

ŸPerformance for Asian fixed income indices was mostly negative.

Summary

Source: S&P Dow Jones Indices LLC and/or its affiliates. Data as of January 29, 2021. Index performance based on total return. Numbers in brackets are closing price levels for the corresponding indices. Returns for single country indices and single country strategies are in local currency, otherwise USD. Sector contributions to the S&P Pan Asia BMI are calculated over the prior month. Charts and graphs are provided for illustrative purposes. Past performance is no guarantee of future results. For more information, please visit our website at www.spdji.com

-0.36%

-0.10%

-0.04%

-0.04%

-0.03%

-0.02%

-0.01%

-0.01%

0.00%

0.02%

0.06%

0.13%

0.29%

1.64%China

Taiwan

Hong Kong

Singapore

Thailand

Pakistan

New Zealand

Australia

Indonesia

South Korea

Philippines

Malaysia

India

Japan

S&P Pan Asia BMI Country ContributionJan 2021

12 FORUM VIEWS - MARCH 2021

SWARUP MOHANTYCEO and Associate DirectorMirae Asset Investment Managers(India) Pvt. Ltd.

INVEST IN ETFS TO COMPLIMENT YOURMUTUAL FUND INVESTMENTS

Going ahead in the domestic market if alpha

continuous to shrink specially in the large-cap segment, we may witness quick adoption of ETFs among the investors.

Further, the pandemic has accelerated the need to diversify one’s portfolio

beyond the home bias. In such cases ETFs become an excellent tool to take exposure in the foreign

market.

What are Exchange Traded Funds (ETF)?Exchange traded funds are passive schemes, which aim to track a particular market index like Sensex, Nifty, Nifty Bank etc. ETFs invest in a basket of stocks which replicate the index. These funds do not aim to beat the index like actively managed mutual fund schemes; they aim to minimize the tracking error. Tracking error is difference in returns of the ETF and that of the index. When investing in ETF you should expect to get the index returns, if any, nothing more and nothing less.

Advantages of ETFs

Growth of ETF Industry in India

• Cost: The biggest advantage of ETFs is cost. The expense ratio of ETFs can be upto 1.5 to 2.25% lower than actively managed funds. Actively managed funds need to beat their benchmark by that margin to match returns of comparable ETFs. Over long investment tenors the cost advantage of ETFs can be of significant advantage to investors.

• Simplicity: Investing in ETF is much simpler than investing in actively managed funds. You do not have to analyze past performance, understand the fund manager’s investment style e.g. Growth, Value or study fund’s performance in up and down markets etc. Simply you may select an index and invest in a low cost ETF, which tracks that index.

The year 2020 witnessed launch of new ETFs across the industry tracking various indices such as IT, themes such as ESG and general broad-based market indices. Industry wide AUM of all the ETFs at the end of Jan 2021 stood at Rs.278,376 Cr. showing rise of 53% from Jan 2020.(Source: AMFI). Though ETFs have been in existence in India for 20 years, the growth in ETF actually can be witnessed in last 5-6 years. Some of the reasons which have contributed to rise in ETF AUM in India are:

• Government’s use of ETFs as a preferred route for disinvestment has increased the participation of retail investors.

• ETFs are being used by EPFO and private Provident Fund bodies to take exposure to the equity market.

• Shrinking alpha in active fund space has made even an average investor aware about the benefit of plain vanilla ETFs like NIFTY, Sensex etc.

13 FORUM VIEWS - MARCH 2021

• Regulators measures such as categorization of funds along with benchmarking them against Total Return Index variants has improved the performance evaluation significantly.

Further, what is exciting is to see rise in participation of retail investors in ETFs. For instance, no. of retail folio in ETFs other than gold stood at 2,50,034 in Dec 2015. This has increased at an annual rate of 57% per annum to 15,03,033 in Dec 2019. In last one year this has more than doubled to 33,81,776 folio in Dec 2020.(Source: AMFI) . It highlights that investor has adapted ETFs at much faster pace than most of us would have anticipated.

pandemic has accelerated the need to diversify one’s portfolio beyond the home bias. In such cases ETFs become an excellent tool to take exposure in the foreign market. However, with the rise and usage of ETFs it becomes critical for asset managers to facilitate smooth functioning of the ETFs with continuous market making via Authorized Participants on the exchange.

We think ETFs are going to play very crucial role in coming times for an investor’s portfolio. An active investor can form his portfolio with 75% using actively managed fund and the rest 25% he can allocate to ETF as satellite portfolio (the exact allocation will depend on clients risk profile, time horizon etc..). What this 25% will do is that it will reduce his risk of underperforming the benchmark significantly. The investor desires to generate significant excess return but also acknowledges the risk associate with it and to minimize the impact he is using ETF.

On the other hand, an investor can form his core portfolio using large cap ETFs like NIFTY 50 and take exposure in other asset classes using mutual funds.

Apart from forming the portfolio, investors can use ETFs for • Buying and selling on exchange at intraday levels with

an aim to generate additional returns• Taking beta exposure when he or she is unsure in which

fund to invest• Take focussed yet low cost exposure in various

segments of the market

Overall we believe both Active and Passive products need to co-exist for an investors and an ETF is multi-functional product that can supplement existing portfolio of mutual fund investor.

Active v/s Passive Investing: Debate

Swarup is the Chief Executive Officer (CEO) and Associate Director of Mirae Asset Investment Managers (India) Pvt. Ltd. He has over 27 years of experience in the field of financial services including 20 years plus experience in Asset Management Sales. He is overall responsible for the India AMC. He has been associated with the AMC as Head - Sales from July 2011. Prior to this assignment, Swarup was National Sales Head - Retail, India with Religare Asset Management Co. Ltd. He has also been associated with organizations like Aditya Birla Sun Life AMC Ltd., Franklin Templeton Asset Management (India) Pvt. Ltd. & Kotak Mahindra Asset Management Company Ltd. in sales responsibilities. He holds a degree in PGDBM and B.COM (HONS.).

He is also a director on the following companies:• Mirae Asset Global Investments (India) Private Limited• Mirae Asset Venture Investments (India) Private Limited• Mirae Asset Financial Services (India) Private Limited

Overall we believe both Active and Passive

products need to co-exist for an investors and an ETF is multi-functional product

that can supplement existing portfolio of mutual

fund investor.

This shift where investors want to add ETFs in his/her portfolio along with active funds is largely because of consistent underperformance of large-cap funds. While some of the active fund houses have done well, but overall at an aggregate industry level, performance is lagging, which has made investor cautious about the cost that is being levied. The simplicity of the product is what makes ETFs more appealing. Apart from simplicity, the low cost, tradability feature, transparent portfolio, focused exposure and accessibility in terms of an investor sitting in any foreign country taking exposure to Indian markets and vice-versa has contributed to the rise and popularity of ETF. Globally today ETFs are preferred route of investment vehicle if somebody wants to capture and get benefitted from particular theme such as ESG, cloud computing, robotic and artificial intelligence etc. More and more ETFs are being adopted to take smart-beta exposures.

Going ahead in the domestic market if alpha continuous to shrink specially in the large-cap segment, we may witness quick adoption of ETFs among the investors. Further, the

14 FORUM VIEWS - MARCH 2021

ZERICK DASTUR

Advocates & Solicitors

TIME TO BLOW THE WHISTLE:CORPORATE VIGILENCE MECHANISM

Thomas Jefferson, the 3rd President of the United States

of America is said to have once remarked, “Let the eye of

vigilance never be closed.”

This prescient statement continues to be applicable

even today and applies universally across spheres.

1. Introduction into the whistle-blower mechanism: What is the regulatory mechanism governing whistler blowing in the corporate sector?Thomas Jefferson, the 3rd President of the United States of America is said to have once remarked, “Let the eye of vigilance never be closed.”

This prescient statement continues to be applicable even today and applies universally across spheres.

The term ‘whistle-blowing’ is a relatively recent entry into the vocabulary of public and corporate affairs, although the phenomenon itself is not new. It refers to the process by which insiders go public with their claims of malpractices by, or within, organisations - usually after failing to remedy the matters from the inside, and often at great personal risk to themselves.

India has recently seen a number of corporate scams and frauds particularly in listed companies. Some of the largest frauds the market has seen have been detected by whistleblower complaints and tip-offs. Hence having an appropriate internal vigilance mechanism which encourages timely reporting of a wrong doing and at the same time provides adequate protection for those who come forward with vital information was felt necessary. Section 177(9) of the Companies Act, 2013 requires every listed company and such other class of company as provided under the corresponding rules, to set-up a vigil mechanism for directors and employees to report bonafide concerns and issues in a specified manner.

Listed companies are also specifically governed by the Securities and Exchange Board of India (“SEBI”) (Listing Obligations and Disclosure Requirements) Regulations, 2015 (the “Regulations”), where Regulation 22 provides for the formulation of a vigil mechanism for directors and

2. Who is a whistle blower? Discuss the requirements of company policy in relation to this vigil mechanism.Broadly, a whistle blower is one who reports or discloses to the concerned authorities, any fraudulent or unethical activity or any other activity which he has reason to believe or knows to have a malafide intent. Such information is usually made in writing and shared with the persons as provided by the company on their website.

The Listing Regulations requires that every listed company provide on its website, the policy in relation to this vigil mechanism. The extent of coverage of such whistle-blower policy includes all employees, director and any individual

employees to report genuine concerns. The Regulations further require that the vigil mechanism shall provide for adequate safeguards against victimization of director(s) or employee(s) or any other person who avail the mechanism and also provide for direct access to the chairperson of the audit committee in appropriate or exceptional cases.

15 FORUM VIEWS - MARCH 2021

associated in any manner with the company including consultants or shareholders. A typical whistle-blower policy covers the following aspects: defines a whistle blower, provides the various types of information that may be reported, the manner of reporting, the kind of information required while making a disclosure, the persons to whom various types of information may be reported to along with contact details including an e-mail address, a phone number or a fax number or a form to directly provide the necessary details along with the steps / process flow to be undertaken once the report is submitted and the type of protection post reporting.

Additionally, with effect from December 2019, SEBI has also introduced an incentive / reward scheme to incentivize persons to report concerns relating to insider trading.

Even Section 46 of the Competition Act, 2002, provides for a leniency regime for any vital disclosure of information. It provides that the Competition Commission may, if it is satisfied that any producer, seller, distributor, trader or service provider included in any cartel, which is alleged to have violated section 3 of the Act dealing with anti-competitive agreements, has made a full and true disclosure in respect of the alleged violations and such disclosure is vital, impose upon such producer, seller, distributor, trader or service provider a lesser penalty as it may deem fit, than leviable under this Act or the rules or the regulations. The CCI has also notified the Competition Commission of India (Lesser Penalty) Regulations, 2009 (the “Lesser Penalty Regulations”) which inter alia provide the procedure, conditions to be met and the corresponding quantum of leniency.

Zerick Dastur is Proprietor of the Law Firm, practicing in the field of Court litigation, Dispute Resolution, Arbitration and Competition Law. He is a triple Gold Medalist from Mumbai University. His practice covers diverse areas of Corporate Commercial and Regulatory disputes, Competition Law and Securities Law. He is representing a number of clients in the Port Sector, Infrastructure and Mining Sectors. He has represented clients in domestic and international, commercial arbitration matters and has acted for clients on mergers, acquisitions and other transactional matters. His practice involves representing clients before various Courts, Statutory Tribunals and Regulators including the Securities Appellate Tribunal, Competition Commission of India, the Securities and Exchange Board of India and the Tariff Authority for Major Ports. He was a former Partner at the Law Firm, J. Sagar Associates.

He has litigation experience before the Hon’ble Supreme Court, various State High Courts as well as a number of Tribunals and Regulatory Bodies. He has been involved in a number of matters involving issues of Constitution Law. He has been involved in matters involving defense of Auditors and Corporate clients before various Civil/Criminal Courts/Tribunals and Regulators in connection with Corporate frauds and scams. He has also advised various clients in matters involving shareholder disputes and minority actions before the NCLT and CLB.

He has advised clients in connection with Competition Law issues in everyday business operations including issues relating to anti-competitive agreements and abuse of dominance by enterprises. He also practices Securities Law and appears before the Securities Appellate Tribunal and the SEBI.

He has also written a number of Articles for various national publications on various Corporate, Commercial and Competition Law issues.

He writes for various national newspapers and publications on Corporate, Commercial and Competition Law. He is a regular speaker at events organised by VC Circle, Indian Merchant Chambers, Economic Times, Corporate Knowledge Foundation and the World Zoroastrian Chamber of Commerce.

He is a Member of the Law Committee of Indian Merchant Chambers.

(Advocate Zerick Dastur and Advocate Harini Subramani)

Views expressed are personal and do not constitute legal advice

The Listing Regulations requires that every listed company provide on its website, the policy in relation to this vigil mechanism. The extent of

coverage of such whistle-blower policy includes all employees,

director and any individual associated in any manner with

the company including consultants or shareholders.

Many a time company policies also provide for allowing a report to be issued anonymously if required subject to providing all necessary documents and any other conditions

The reporting mechanism is also encouraged by SEBI in connection with detection and prevention of insider trading. An ‘Informant’ has been defined under the SEBI (Prohibition of Insider Trading) Regulations, 2015 in the following manner:

an individual(s), who voluntarily submits to the Board a Voluntary Information Disclosure Form relating to an alleged violation of insider trading laws that has occurred, is occurring or has a reasonable belief that it is about to occur, in a manner provided under these regulations, regardless of whether such individual(s) satisfies the requirements, procedures and conditions to qualify for a reward.

3. Which are the other laws and regulations where reporting and vigilance is encouraged?

16 FORUM VIEWS - MARCH 2021

ROSHAN KUMAR BAJAJDirectorJPNR Corporate Consultants Pvt. Ltd.

FRAMEWORK FOR ENABLING ANCILLARY SERVICESAT INTERNATIONAL FINANCIAL SERVICES CENTRES (“IFSC”)

This framework shall be applicable to all ancillary

service providers (hereinafter referred to as “service

provider(s)”) engaged in one or more permissible ancillary

services within the IFSC.

This is our thirty-fourth release in the series of awareness articles on IFSC

1.0 Synopsis of the previous release

2.0 Coverage in the current release

3.0 Applicability

4.1 Ancillary services

In our last releases, we had discussed about International Financial Services Centres Authority (Bullion Exchange) Regulations, 2020 in International Financial Services Centre (“IFSC”).

The International Financial Services Centres Authority (IFSCA) hereby consider the importance of professional and other service providers for the development of financial products, financial services and financial institutions in IFSC, hence IFSCA has provided the framework for enabling ancillary services at International Financial Services Centres vide circular no. F.No. 206/IFSCA/Anc.Aux/2020-21 dated February 10, 2021.

This framework shall be applicable to all ancillary service providers (hereinafter referred to as “service provider(s)”) engaged in one or more permissible ancillary services within the IFSC.

• Ancillary services:Ancillary services shall mean those services which directly or indirectly aid, help, assist or strengthen or are attendant upon or connected with the services, as detailed under sub-clauses (i) to (xi) of clause (e) of sub-section (1) of section 3 of the IFSCA Act, 2019 i.e.

(I) buying, selling, or subscribing to a financial product or agreeing to do so;

(ii) acceptance of deposits;

(iii) safeguarding and administering assets consisting of financial products, belonging to another person, or agreeing to do so;

(iv) effecting contracts of insurance;

(v) offering, managing or agreeing to manage assets consisting of financial products belonging to another person;

(vi) exercising any right associated with a financial product or financial service;

(vii) establishing or operating an investment scheme;

(viii) maintaining or transferring records of ownership of a financial product;

(ix) underwriting the issuance or subscription of a financial product;

(x) providing information about a person's financialstanding or creditworthiness;

(xi) selling, providing, or issuing stored value or payment instruments or providing payment services.

17 FORUM VIEWS - MARCH 2021

• Permissible ancillary services:The service providers may engage in any one or more of the following activities:

(i) Legal, Compliance and Secretarial;

(ii) Auditing, Accounting, Bookkeeping and Taxation Services;

(iii) Professional & Management Consulting Services;

(iv) Administration, Assets Management Support Services and Trusteeship Services;

(v) Any other services as approved by IFSCA from time to time.

The following entities are eligible to act as a service provider so as to provide permissible ancillary services pertaining to activities in relation to financial products, financial services and financial institutions in the IFSC:

(i) Any existing or newly incorporated entity set up in the IFSC or

(ii) Any Indian or foreign incorporated entity by establishing a branch or a subsidiary.

Service providers can provide permissible services to any one or more of the following:

(I) Entity(ies) set up in the IFSC;

(ii) Financial services entities from foreign jurisdictions for various activities in the IFSCs in India or other related activities overseas;

(iii) Indian entities who propose to open, set up or carry out operations in IFSCs or foreign jurisdiction, provided consideration is received in freely convertible foreign currency.

• Currency for conduct of business:

Service providers shall transact in freely convertible foreign currency only. However, the service providers may defray their administrative expenses in INR by maintaining an INR account.

• Fees for Ancillary Service Provider

Following fee is applicable for the Ancillary Service Provider:

5.1 Eligibility Cariteri for acting as a Service Provider

6.1 Service Recipients

7.1 Operational Compliances to be complied with

For more information & queries, please contactJPNR Corporate Consultants Private Limited (www.jpnrgroup.com)

Roshan Kumar Bajaj [FCA, CIFRS]

He is a Director in JPNR Corporate Consultants Private Limited which is a business advisory and consultancy company, incorporated under Companies Act, 2013. The company is engaged in providing services related to Goods and

The article isco-authored by

CS Jhalak Jain

Services Tax, advisory services to International Financial Service Centre [Gujarat International Finance Tec-City (GIFT)]. During his association with Deloitte earlier, he has gained rich experience in providing Audit and Assurance services to various large Corporate including Telecom, FMCG, Cement, Consumer Appliances, Port, Healthcare, Hospitality sectors, Steel, Mining etc. He has expertise in providing services relating to IFRS and Ind-AS also and has handled domestic and international projects for the same. He also contributes to various articles relating to his domain.

Particular FeeApplication FeeRegistration Fee

USD 500USD 2,000 (for 5 years)

• Maintenance of Books of Accounts, Records and DocumentsEvery service provider shall maintain its books of accounts, records, and documents in such foreign currency, as may be declared at the time of making an application.

• Submissions of Report / Information(i) Every service provider shall furnish the following

information to the IFSCA:

a. Annual financial statements for the entity registered.

b. Confirmation of compliance with the regulations, circulars, guidelines and/or directions as issued by the International Financial Services Centres Authority from time to time.

c. Details of material regulatory action, if any.

(ii) Every service provider authorized by the IFSCA shall submit the financial information to the IFSCA in US Dollar, unless otherwise specified by the IFSCA.

(iii) The IFSCA from time to time may call for any information, documents, or records as it may deem necessary from the service provider.

International Financial Services Centres Authority has widened the scope for the professionals and other service providers for the development of financial products, financial services and financial institutions at IFSC which directly or indirectly aid, help, assist or strengthen or are dependent upon or connected with the primary services.

8.0 Conclusion

18 FORUM VIEWS - MARCH 2021

he Indian Finance Minister decided to navigate valiantly through global Tpandemic crisis in conjunction with

numerous measures announced since last year of Covid-19 in the form of stimulus package, to confidently present the 2021 Budget after a year long economy slowdown. The Budget was not only aimed for speedy recovery but was designed towards growth trajectory of the Indian economy since the plunge in economic activities in 2020 echoed by various credit agencies, focused to achieve the ambitious target of USD 5 trillion economy since the introduction of medical cure.

The promotion of 2021 Budget by the Indian Finance Minister to deliver a landmark event given the constraints of pandemic since a century, is directionally appreciated considering the incessant efforts made by the Government to overcome challenges by setting high bench mark in adopting counter cyclical expansionary steps as a medieval concept. The measures are expected to boost GDP growth both directly, and indirectly building a cascading effect on private consumption, expenditure and investment thus causing a positive outlook on the Indian economy.

The prominent areas of focus by 2021 Budget addressed by the Government to offer impetus in the Indian economy are:• Adding resources without raising tax• Encouraging spending and savings• Managing fiscal deficit with alternate

resource mobilisation• Creating an investment climate to

become a global manufacturing hub

The economic revitalising package released in phases during lockdown was bespoke to provide cushion to the vulnerable sections of the society and the small businesses hence, with steady unwinding of lockdown restrictions, the

The promotion of 2021 Budget by the Indian Finance Minister to deliver a landmark

event given the constraints of

pandemic since a century, is directionally

appreciated considering the

incessant efforts made by the Government to overcome challenges by setting high bench

mark in adopting counter cyclical

expansionary steps as a medieval concept.

INSIGHTSINSIGHTS

demand is likely to boost consumption. The economic recovery inched back on track since normalisation aided by stimulus measures initiated to boost investment climate by introducing Production Linked Incentives, enhancing capital expenditure and other steps also contributing towards Make in India initiative. The change in strategy reflects that the fiscal policy offered flexibility to adjust with an ever evolving situation for a resilient recovery.

2021 BUDGET DELIVERS RESET MODE(ALT + CTRL + DELETE) TO REBOOT ANDREENGINEER INDIA GROWTH HORIZON

By CA Shailendra SharmaAssociate Director, Products (Advisory)Asset Services, Edelweiss Financial Services Ltd.

the Indian Budget, also a barometer of the fiscal and policy reforms to provide an outcome of the steps introduced by the Indian Government over the year. The progressive measure implemented last year, fostered India to retain its 63rd rank in the World Bank's Ease of Doing Business Index supported by strong prediction of economic recovery post March 31 with expectation of revival in real GDP growth in double digit territory by the end of next financial year.

The capital market has always been a substantial contributor to the Indian economy which experienced record high net inflows of ~ INR 2.1 trillion from the foreign portfolio investors (FPIs) in the capital market since last year up to December compared to investments in the same period in 2019-20. The indigenous institutions were not left behind with their contribution of ~ INR 2.76 trillion by the domestic fund industry. The enhanced FPI and domestic participation triggered Indian capital markets to touch new highs resulting in S&P BSE Sensex benchmark index to rise by 68.9 percent and Nifty 50 index of National Stock Exchange (NSE) gained by 70.3 percent in January 20, 2021 and reaching its peak as on date.

The performance and potential of the insurance sector is assessed using two indicators-Insurance penetration and Insurance Density. In 2019-20 the year of health care, mobilised gross direct premium of Non-Life insurers at ~ INR 1.89 trillion, as against ~INR 1.69 trillion last year, recording a growth of 11.45 percent. Conversely, Life insurance recorded a premium of ~ INR 5.73 trillion in 2019-20against INR ~ 5.08 trillion last year, registering a growth of 12.75 percent where, the renewal premium accounted for 54.75 percent of the total premium received by the life insurers.

The column aims to elaborate on the capital markets and financial services sector that briefly articulates and provides an insight on the 2021 Budget proposal introduced specifically in the financial service segment that plays a vital role to propel the Indian economy.

The Economic Survey was a precursor to

Brief snapshot of the 2021 Economic Survey

19 FORUM VIEWS - MARCH 2021

INSIGHTSINSIGHTS

Interestingly, the Government’s aim to protect the society through social security echoed an overall growth in the Assets Under Management (AUM) of National Pension Scheme to INR ~ 4.94 trillion as compared to INR ~ 3.71 trillion last year, thereby recording a substantial growth of 33.3 percent with maximum growth reg is tered by a l l - C i t i zen mode l CorporateSector and State Government Sector.

The total debt issuance in the primary market rose by 29.7 percent to ~ INR 5.99 trillion during 2020-21 compared to ~ INR 4.63 trillion in the corresponding period of the previous year. Since April- December 2020, the amount raised through private placement of debt increased by 32.2 percent to ~ INR 5.95 trillion where the amount raised through public debt issues declined by 67 percent.

In the lending space, Private Sector Banks exhibited greater transmission of fresh loans however, Public Sector Banks (PSB) reflected greater transmission of outstanding loans for easing the cycle. The NBFC sector witnessed marginal credit growth of 3 percent rising to ~ INR 23.8 trillion in March 2020 compared to 17.7 percent growth in the previous year. Non-Banking Financial Company (NBFCs) also witnessed slowdown in their growth due to isolated credit events in few large NBFCs and challenges in accessing capital. The banks continued to support NBFCs with their offtake expanding by9.2 percent YoY till October 2020, well above the overall bankcredit growth. The sector also benefitted from the liquidity infusing measures announced by the Reserve Bank of India (RBI) during the pandemic.

Besides the focus on financial services segment, the Economic Survey also published the following policy updates on the economy as under:• India’s GDP projection to contract by

7.7 percent in the ongoing financial year due to pandemic, but a strong V-shaped growth recovery of ~ 11 percent is expected in the financial year 2021-22 being in line with IMF’s prediction..

• India remains a preferred investment destination in FY 2020-21 with FDI soring amidst global asset, in equities having strong prospects of quicker recovery in emerging economies reflected by FPI

inflows at record high of USD 9.8 billion in November 2020, as investors’ risk appetite returned. Despite the disruptions being witnessed globally, FDI inflows into India’s services sector grew robustly by 34 percent YoY during April-September 2020 to reach US$ 23.6 billion.• Forex reserves rose to record levels of

USD 586.1 billion as on January 08, 2021 to cover 18 months’ worth of import in December 2020.

• Monthly Goods and Service Tax (GST) collection crossed the INR 1 trillion mark consecutively since last 3 months, reaching its highest levels in December 2020 since the introduction of GST

• India also entered the top-50 innovating countries for the first time in 2020 since the inception of Global Innovation Index in 2007, ranking first in Central and South Asia, and third amongst lower-middle-income group economies.

The preparation of this year Budget has been unique, motivated against all odds under challenging circumstances, owing to global slowdown since last year Budget. Government with an objective to counter effect of pandemic intermittently released 'Aatmanirbhar' (self-reliant) Package and other reforms for sustained recovery through 3-4 mini Budgets since May 2020. The concept of Atmanirbhar Bharat (Make in India) is part of PMs’ vision reflected in 2021 Budgetbased on 6 pillar approach aimed to strengthen the objective of indigenous produce to resolve fiscal deficit expected at 6.8 percent. The contours of Budget proposals and capital outlay arethemed under the following structure:• AtmaNirbhar Bharat programmes• Performance-linked incentives• Boost for domestic manufacturing• Improved credit access for enterprises• Moratorium on interest payments• Thrust on affordable housing

The Budget also contemplated policy for an on-goingemphasis of the Government on administrative ease, transparency, and simplification of legal provisions through policy reforms by introducing liberal expenditure measures like:

Budget conceptualised to Reset,Reengineer and Reboot Indian economythrough counter cyclical steps

• Establish a Development Finance Institution (DFI) to be capitalised with INR 200 billion to launch National Asset Monetisation Pipeline to fund and mobilise new infra projects. The new DFI aims to build a lending portfolio of INR 5 trillion in 3 years

• INR 3 trillion outlay for power sector including power transmission assets of INR 70 billion is to be transferred to Power Grid InvIT

• Eliminate overregulation currently creating impedimentan towards ease of doing business where schemes like PLI Scheme will make India an integral part of global supply chain and Infrastructure development a key role in the overall economic growth

• Allocate INR 15 billion to boost digital transactions and facilitate setting-up a world class Fintech hub in GIFT City IFSC

• Set-up an Asset Reconstruction C o m p a n y ( A R C ) a n d A s s e t Management Company (AMC)to help banks tackle bad loans permitting sale of distressed assets to Alternate Investment Funds (AIFs)

• Separate administration structure to promote ease of doing business including multi-state co-operative for ease of doing business

• Permit One Person Companyto grow without any restrictions on paid up capital and turnover by encouraging start-ups for a structured legal entity recognition to help attract accredited investors

• Rationalise security market regulations under capital one market code being a significant step towards ease of doing business to go a long way in attracting foreign investments in India

• Design investors’ charter to assimilate rights of all financial investors across all financial products

• Increase FDI limits in the insurance sector from 49 to 74 percent and permitting foreign ownership and controls with conditions

In summary, the 2021 Budget is focused to provide clarity regarding the long-standing issues to promote certainty and boost foreign investor confidence. The Budget intends to overhaul the tax

2021 Budget proposals to Reengineer, Refine and Revitalise the financial services sector

20 FORUM VIEWS - MARCH 2021

INSIGHTSINSIGHTS

administrative system to encourage a trust based system for ease of compliance. A high level analysis and brief insight on the Budget proposals are briefly explained.

• The induction of IFSC since 2015 created an enhanced interest for the investors considering multiple activities and amendments to the IFSC Regulations in the form of FPI, AIF, Portfolio Manager, Investment advisers, etc. The implementation of FPI Regulations had an underlying objective to re-domicile Indian administered offshore funds back in India by offering incentives for relocation.

Budget proposes to incentives offshore fund managers on relocation to IFSC, with capital gains tax exemption to such offshore Fund and its investors / shareholders relocating only as an AIF Category I, II or III located in IFSC (Resultant Fund) on or before 31 March 2023 pursuant to such relocation. Other consequential amendments to relocation like carried cost and period of holding of offshore Fund is available to the Resultant Fund without any impact on carry forward losses of Indian company due to change in beneficial voting power pursuant to relocation can prevail.• Relocation of eligible offshore fund

managers qualify for exemption from applicability of business connection in India subject to satisfaction of conditions prescribed under safe harbour rules. It is proposed that safe harbour rules will not apply (or apply with modification) to an eligible investment fund or its eligible fund manager, if the fund manager is located in an IFSC and has commenced operations on or before the 31st day of March, 2024.

• Income of an investment division situated in Offshore Banking Units (OBU) in IFSC shall qualify to claim exemption where such investment division is AIF Category III registered commencing its operations on or before 31 March 2024.

• In line with the Aircraft leasing regulations introduced in the IFSC, it is proposed that aircraft leasing activitiesin the form of royalty earned by non-resident from lease of Aircraft to a unit in an IFSC or income from transfer of Aircraft / Aircraft engine given on lease is eligible for 100 percent tax holiday on

1. International Financial Services Centre (IFSC)

satisfaction of the prescribed conditions.• Income from transfer of non-deliverable

forward contract of non-resident from OBU in IFSC would qualify for tax e x e m p t i o n w h e r e s u c h O B U commenced operations in IFSC on or before 31 March 2024.

Key impact assessment: The Government’s attempt and concerted efforts to onshore the off shored fund activities in India has potentially improved liquidity and is able to draw investors’ attention to attract investments in the Country. 2021 Budget with introduction of tax neutrality on re-domiciliation and other incentives for IFSC entities on Aircraft leasing will renew investor interest to explore India as a comparative destination amongst other global Financial Service Centres for their investment activities. Perhaps an extension of similar benefits to FPIs migrating to IFSC would promote volume and liquidity and go a long way to encourage investment activities from IFSC.

Investments made by SWFs and PFs qualifies for exemption from interest, dividend and capital gains arising from investment in specified infrastructure in India by specified persons, including SWFs and PFs on satisfaction of several conditions. In order to encourage additional participation of SWFs and PFs to invest in infrastructure of India, the Budget proposes to relax conditions like: • Permit investment in Category I or II AIFs

with lower threshold from 100 percent investment in a company or enterprise carrying on specified infrastructure activities to 50 percent investment.

• Allow eligible investments through a holding company being a domestic company, set up and registered on or after 1 April 2021 having minimum 75 percent of investment in infrastructure company(s).

• Permit investment in registered NBFC as an Infrastructure Finance Company notified as Infrastructure Debt Fund-Non-Banking Financial Companies under Reserve Bank Directions, with at least 90 percent lending to one or more infrastructure companies or enterprises.

• All the above situation where the criteria of 50 percent / 75 percent / 90 percent are not satisfied the exemption shall be calculated / computed proportionately.

2. Sovereign wealth fund (SWF) and pension funds (PF)

• Permit Category I or II AIF in which SWFs / PFs have invested, to make investment in InvITs.

• SWFs / PFs can explore specified loans or borrowings directly or indirectly withend use restrictions for the purpose of making investment in India however, assets can be distributed to lenders of eligible loans only in case of dissolution of SWF / PF.

• SWFs / PFs restricted participation in the operational activities of the investee entities, but permitted appointment of directors for monitoring the investment and remove restriction to undertake commercial activity.

• Eligibility for PFs as liable to tax in their home countries clarified to have specific exemption on their incomes is eligible to apply for exemption.

Key impact assessment: The provision of incentivising global SWF / PF introduced in last year Budget for investment in capital intensive sector like infrastructure receiveda dreary response. The budget recognising such impediment to build attractiveness in this category, proposed to liberalise various conditions associated with such investments by SWF / PF, shall potentially appeal investors to explore investment in the infrastructure sector to maximise their returns from India. The recent amendment by the government to bring UAE at par with other eligible country to qualify for privileged FPI license is a step in the right direction to offer SWF / PF diversified investment opportunity in infrastructure projects in India.

• In the last year Budget, dividend income has been taxable in the hands of the investors effective 1 April 2020. The tax provisions on payments to FPI provides for withholding tax on income from securities excluding capital gains and interest at the rate of 20 percent. Unfortunately, the provision prescribes specified tax rates absent application of the tax treaty benefit at the time of tax withholding.

In order to align the withholding tax provision for payments to FPI, the Budget proposed to settle the anomaly by providing withholding tax at a lower taxrate of 20 percent or at the prescribed tax treaty rate where:

3. Dividend tax benefit to investment vehicles and FPIs

21 FORUM VIEWS - MARCH 2021

INSIGHTSINSIGHTS

• Tax treaty exists between India and the respective jurisdiction of the FPI; and

• FPI has furnished a TRC to the payer• The withholding tax on REIT/InvITis

inapplicable where dividend income is credited or paid to eligible investors like insurance companies / insurers. The Budget aimed at counter cyclical approach, proposed to extend relief of non-withholding of tax on payment of dividend to business trusts where dividend income is credited or paid to REIT/InvIT by specified SPV or payment of dividend income to any other person.

Key impact assessment: The proposed amendments for lower or minimal withholding tax on income distribution to the investors either for FPIs or REIT/InvIT shall repose investor confidence by optimising their returns and minimising tax leakage by addressing cash trap considerations of the investors supported by offering certainty for compliance.

• Amount received under Unit Linked Investment Plan (ULIP), a life insurance product including the sum allocated as bonus on such policy is exempt where the annual premium payable during the term of the policy does not exceed 10 percent of the actual capital sum assured. Aimed to provide benefit to small and genuine taxpayers of life insurance, Budget amends to withdraw exemption on proceeds received from such ULIP issued on or after 1 February 2021, where the premium amount payable in any year during the policy tenure exceeds INR0.25 million in respect of one or more than one ULIP.

• ‘Zero Coupon Bonds’ (ZCB) under the given tax guidelines are bonds issued by infrastructure Capital Company, infrastructure capital fund or Public Sector Company or scheduled banks. In order to broaden the scope of capital funds availability in the infrastructure sector, Budget proposed to permit Infrastructure Debt Funds (IDF) to issue ZCB where the income earned by IDFs from such bonds is exempt from tax.

• RBI permitted voluntary migration of primary co-operative bank into a

4. Other amendments

banking company through transfer of Assets and Liabilities. Accordingly, to expand the scope of business reorganisation, transfer of a capital asset by the co-operative bank to the B a n k i n g C o m p a n y t o w a r d s conversion, and allotment of shares of converted banking company to the shareholders of the existing co-operative bank shall be treated business reorganisation and regarded as exempt transfer for capital gain tax purpose.

• Ideally, Goodwill cannot be regarded as a depreciable asset and based on the nature of business, Goodwill would normally appreciate without any depreciation to its value akin to immovable property. Accordingly, it is proposed that Goodwill of a business or profession cannot be regarded as an asset hence, does not qualify for depreciation.

Key impact assessment: The amendment to ULIP can be a dampener in the structured equity product of the insurance company largely targeted for high networth investors but, small refinement to launch ULIP for low income category investors could widen the base and scope of the product given the renewed interest and valuation of the indices. The extended clarifications on other provisions like goodwill, tax neutrality for conversion and ZCB will provide tax certainty and depth in the investment activities in India.

Globally countries have lauded India’s pragmatic approach best suited for a resilient recovery of its economy since the adverse impact of pandemic, converse to the simplist ic st imulus package implemented by many offshore countries. The Indian Budget since health crisis receded has set a benchmark to focus on the growth trajectory considering a year long slow impact on the economy, proposing an array of fiscal inclusion measure of Aspirational, Economic Development and Caring India, targeted to achieve USD 5 trillion economy by recalibrating the financial architecture to help the sectors move from pillar to post.

The Government announced setting-up an institution to address the stressed assets in the banking space through an ARC

Key takeaways

model, areassuringstand for banking sector since the industry was on the cusp of bad loan spurt due to pandemic. Besides, the proposal seems to also support job creation, promoting infrastructure spending and creating equilibrium between demand and supply for improving liquidity and directional utilisation towards development. In the present economic situation, proactive approach of the Government to reset the economy and provide rationalisation of the tax provisions is an encouraging step for recovery and revival.

The proposal to minimise deficit target and improve allocation in identified infrastructure spending should promote impulsive growth in the economy but, may require balancing anyform of decline in global trade, high commodity prices and snugger external financing conditions causing any adverse implications on the cu r ren t account ba lances . The Government has set an ambitious target of developing infrastructure in the country with funding of large scale infrastructure p ro j ec ts backed by s t ruc tu red investments from SWF / PF to minimise the challenge of financial constraints and stress on borrowings.

Apropos, the Budget proposals delibera-ted on providing clarity on some open issues and streamlining legislaturesfor certainty and to boost foreigninvestor confidence. The proposal are concentrated to overhaul the tax administrative framework by introducing faceless tax assessments, developing robust dispute resolution mechanism, and revoking aged provisions to encourage a trust based system for ease of compliances. Although, some questions may still remain unaddressed it will be interesting to explore how, the Budget proposal will support the agile financial service sector poised to interest new investment avenues in India from the investors and acclaim India a preferred investment destination.

Shailendra Sharma is an Indian CPA associated with multinational financial services firm in India. The views expressed in the column are personal in nature based on the professional experience, research and capabilities that does not in any manner represent or resemble or express the views or opinion or facts of the organisation, group, firm or other bodies affiliated with.

22 FORUM VIEWS - MARCH 2021

BROKING INDUSTRY REGULATIONS ANDPOSSIBLE IMPACT ON RETAIL BROKERS

By Tejas KhodayCEO & Co-Founder, FYERS

rom the debilitating effects of Covid19, to the crazy market Fvolatility during the ensuing

lockdowns, to a slew of sweeping reforms undertaken by the market regulator SEBI and the V shaped recover that led to historic market rally, the year 2020 & 2021 so far have been phenomenal for the broking industry, and will be remembered for times to come.

The retail participation in stock markets, especially by millennials, has increased exponentially since the lockdown of March 2020. Even though new investors’ count increased by the millions during the year, only a few well-established brokerages were able to capture a decent share of the expanding market. Being associated with capital markets for many years, experienced hands find it as one of the fastest-evolving regulatory phases of this generation. Perhaps, an equivalent of the early 1990s when SEBI replaced the Controller of Capital Issues (CCI) to modernize India's markets

For years, unfair & non-compliant practices of several brokerage firms destroyed immeasurable amounts of investors wealthas well as faith in the equity ecosystem. A crisis of public confidence arose as few brokers went off-track and defrauded investors, or went bust due to misplaced risk management priorities. For instance, the recent IL&FS and Allied Financial fiasco, news of a massive scandal at Karvy Stock Broking sent everyone into a tailspin and it didn't stop there! In 2020, around 18 brokers defaulted on NSE & BSE. Witnessing things go from bad to worse from side-lines wasn't making it any better for other brokers. It was time for SEBI to proactively take matters into their own hands and change the approach and regulations, in order to protect retail investors interest.

A quick summary of the regulatory changes and their possible impact on retail brokers.

excessive leverage was detrimental to retail investors. Though many debates and discussions ensued among market participants, SEBI was firm in its decision and restricted intraday leverage bya maximum of 5X for equities and mandatory SPAN margins for derivatives. This totally nullifies any competitive advantage that traditional players enjoyed so far. The phased implementation of this new rule offers sufficient time to all brokerages in adjusting to the evolving landscape.