Embed Size (px)

Citation preview

BASE LISTING DOCUMENT DATED 23 MARCH 2021

If you are in any doubt about any of the contents of this document, you should obtain independent professionaladvice.

Hong Kong Exchanges and Clearing Limited (“HKEX”), The Stock Exchange of Hong Kong Limited (the “StockExchange”) and Hong Kong Securities Clearing Company Limited (“HKSCC”) take no responsibility for thecontents of this document, make no representation as to its accuracy or completeness and expressly disclaim anyliability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contentsof this document.

Non-collateralised Structured ProductsBase Listing Document

relating to Structured Productsto be issued by

UBS AG(incorporated with limited liability in Switzerland)

acting through its London Branch

Sponsor

UBS Securities Asia Limited

This document, for which we accept full responsibility, includes particulars given in compliance with the RulesGoverning the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”) for thepurpose of giving information with regard to us and our standard warrants (“Warrants”), callable bull/bearcontracts (“CBBCs”) and other structured products (together, “Structured Products”) to be listed on the StockExchange from time to time. This document may be updated and/or amended from time to time by way ofaddenda.

We, having made all reasonable enquiries, confirm that to the best of our knowledge and belief the informationcontained in this document is accurate and complete in all material respects and not misleading or deceptive, andthere are no other matters the omission of which would make any statement herein or this document misleading.

The Structured Products involve derivatives. Do not invest in them unless you fully understand and arewilling to assume the risks associated with them.

Investors are warned that the price of the Structured Products may fall in value as rapidly as it may riseand holders may sustain a total loss of their investment. Prospective purchasers should therefore ensurethat they understand the nature of the Structured Products and carefully study the risk factors set out inthis document and, where necessary, seek professional advice, before they invest in the StructuredProducts.

The Structured Products are complex products. You should exercise caution in relation to them. TheStructured Products constitute our general unsecured contractual obligations and of no other person andwill rank equally among themselves and with all our other unsecured obligations (save for those obligationspreferred by law) upon liquidation. If you purchase the Structured Products, you are relying upon ourcreditworthiness, and have no rights under the Structured Products against (a) the company which hasissued the underlying securities; (b) the trustee or the manager of the underlying unit trust; or (c) the indexcompiler of any underlying index. If we become insolvent or default on our obligations under the StructuredProducts, you may not be able to recover all or even part of the amount due under the Structured Products(if any).

CONTENTS

Page

IMPORTANT INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

PLACING AND SALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

OVERVIEW OF WARRANTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

OVERVIEW OF CBBCs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

INFORMATION IN RELATION TO US . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

APPENDIX 1 — TERMS AND CONDITIONS OF WARRANTS . . . . . . . . . . . . . . . . . . . . 43

Part A — Terms and Conditions of Cash Settled Warrants over Single Equities . . . . . . . 44

Part B — Terms and Conditions of Cash Settled Index Warrants . . . . . . . . . . . . . . . . . . 55

Part C — Terms and Conditions of Cash Settled Warrants over Single Unit Trusts . . . . . 63

APPENDIX 2 — TERMS AND CONDITIONS OF CBBCs . . . . . . . . . . . . . . . . . . . . . . . . 74

Part A — Terms and Conditions of Cash Settled Callable Bull/Bear Contracts over

Single Equities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Part B — Terms and Conditions of Cash Settled Callable Bull/Bear Contracts over an

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

Part C — Terms and Conditions of Cash Settled Callable Bull/Bear Contracts over

Single Unit Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

APPENDIX 3 — AUDITOR’S REPORT AND OUR CONSOLIDATED FINANCIALSTATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2020 . . . . . . . 115

APPENDIX 4 — RISK MANAGEMENT AND CONTROL . . . . . . . . . . . . . . . . . . . . . . . . 267

APPENDIX 5 — OPERATING ENVIRONMENT AND STRATEGY . . . . . . . . . . . . . . . . . 319

APPENDIX 6 — A BRIEF GUIDE TO CREDIT RATINGS . . . . . . . . . . . . . . . . . . . . . . . 331

− 2 −

IMPORTANT INFORMATION

What is this document about?

This document is for information purposes only

and does not constitute an offer, an advertisement

or invitation to the public to subscribe for or to

acquire any Structured Products.

What documents should you read beforeinvesting in the Structured Products?

A launch announcement and supplemental listing

document will be issued before the issue date of

each series of Structured Products, which will

include detailed commercial terms of the relevant

series. You must read this document (including

any addendum to this document to be issued from

time to time) together with such launch

announcement and supplemental listing document

(including any addendum to such launch

announcement and supplemental listing document

to be issued from time to time) (together, the

“Listing Documents”) before investing in any

Structured Product. You should carefully study

the risk factors set out in the Listing Documents.

You should also consider your financial position

and investment objectives before deciding to

invest in the Structured Products. We cannot give

you investment advice. You must decide whether

the Structured Products meet your investment

needs before investing in the Structured Products.

Is there any guarantee or collateral for theStructured Products?

No. Our obligations under the Structured

Products are neither guaranteed by any third

party, nor collateralised with any of our assets or

other collaterals. When you purchase our

Structured Products, you are relying on our

creditworthiness only, and of no other person. If

we become insolvent or default on our

obligations under the Structured Products, you

can only claim as our unsecured creditor. In such

event, you may not be able to recover all or even

part of the amount due under the Structured

Products (if any).

What are our credit ratings?

Our long term debt ratings are:

Rating agencyRating as of

22 March 2021

Moody’s Deutschland GmbH(“Moody’s”)

Aa3(stable

outlook)S&P Global Ratings

Europe Limited (“S&P”)A+

(stableoutlook)

Our credit ratings disclosed above are only an

assessment by the rating agencies of our overall

capacity to pay our long term debts.

Aa3 is among the top two major credit rating

categories and is the fourth highest

investment-grade ranking of the ten

investment-grade ratings (including 1, 2 and 3

sub-grades) assigned by Moody’s.

A+ is among the top three major credit rating

categories and is the fifth highest

investment-grade ranking of the ten

investment-grade ratings (including + or -

sub-grades) assigned by S&P.

Please refer to the brief guide in Appendix 6 to

this Base Listing Document for more information

about credit ratings.

Rating agencies usually receive a fee from the

issuers that they rate.

When evaluating our creditworthiness, you

should not solely rely on our credit ratings

because:

• a credit rating is not a recommendation to

buy, sell or hold the Structured Products;

• ratings of companies may involve

difficult-to-quantify factors such as market

competition, the success or failure of new

products and markets and managerial

competence;

− 3 −

• a high credit rating is not necessarilyindicative of low risk. Our credit ratings asof the date immediately preceding the dateof this document are for reference only. Anydowngrading of our credit ratings couldresult in a reduction in the value of theStructured Products;

• a credit rating is not an indication of theliquidity or volatility of the StructuredProducts; and

• a credit rating may be downgraded if ourcredit quality declines.

The Structured Products are not rated.

Our credit ratings are subject to change orwithdrawal at any time within each ratingagency’s sole discretion. You should conductyour own research using publicly availablesources to obtain the latest information withrespect to our credit ratings from time to time.

Are we regulated by the Hong Kong MonetaryAuthority referred to in Rule 15A.13(2) or theSecurities and Futures Commission referred toin Rule 15A.13(3)?

We are a licensed bank regulated by the HongKong Monetary Authority. We are also authorisedand regulated by the Financial MarketSupervisory Authority in Switzerland, andauthorised by the Prudential RegulationAuthority and subject to regulation by theFinancial Conduct Authority and limitedregulation by the Prudential Regulation Authorityin the United Kingdom.

Are we subject to any litigation?

Save as disclosed in this document, we and oursubsidiaries are not aware of any litigation orclaims of material importance pending orthreatened against us or them.

Authorisation for the issue of the StructuredProducts

The issue of the Structured Products wasauthorised by our board of directors on 19September 2001.

Has our financial position changed since lastfinancial year-end?

There has been no material adverse change in ourfinancial or trading position since 31 December2020.

Do you need to pay any trading fees and levies?

The Stock Exchange currently charges a tradingfee of 0.005 per cent. and the Securities andFutures Commission currently charges atransaction levy of 0.0027 per cent. for eachtransaction effected on the Stock Exchangepayable by each of the seller and the buyer andcalculated on the value of the consideration forthe Structured Products. The levy for the investorcompensation fund is currently suspended.

Do you need to pay any tax?

Taxation in Hong Kong

No tax is payable in Hong Kong by way ofwithholding or otherwise in respect of any capitalgains arising on the sale of the StructuredProducts, except that Hong Kong profits tax maybe chargeable on any such gains, which isconsidered as trading gain, in the case of certainpersons carrying on a trade, profession orbusiness in Hong Kong.

You do not need to pay any stamp duty in respectof purely cash settled Structured Products.

Taxation in Switzerland

Under present Swiss law, if you are anon-resident of Switzerland and have not engagedin trade or business through a permanentestablishment within Switzerland during thetaxable year, you will not be subject to any SwissFederal, Cantonal or Municipal income or othertax on gains realised during the year on the saleor redemption of the Structured Products.

There is no tax liability in Switzerland inconnection with the issue of the StructuredProducts. However, Structured Productssubscribed, transferred or redeemed through abank or other dealer resident in Switzerland orLiechtenstein may be subject to Swiss securitiestransfer tax.

− 4 −

Taxation in United States of America

FATCA Withholding Tax

Pursuant to sections 1471 to 1474 of the U.S.Internal Revenue Code of 1986, as amended,commonly known as FATCA, a “foreignfinancial institution” (as defined by FATCA)may be required to withhold on (i) certainpayments of U.S. source income and (ii) “foreignpassthru payments” paid to or in respect ofpersons that fail to meet certain certification,reporting or related requirements. A number ofjurisdictions (including Switzerland) haveentered into, or have agreed in substance to,intergovernmental agreements (“IGAs”) with theUnited States to implement FATCA, whichmodify the way in which FATCA applies in theirjurisdictions.

Under the provisions of the IGAs as currently ineffect, a foreign financial institution in an IGAjurisdiction would generally not be required towithhold under FATCA or an IGA from paymentsthat it makes. Certain aspects of the applicationof the FATCA provisions and IGAs to instrumentssuch as Structured Products, including whetherwithholding would ever be required pursuant toFATCA or an IGA with respect to payments oninstruments such as Structured Products, areuncertain and may be subject to change. Even ifwithholding would be required pursuant toFATCA or an IGA with respect to payments oninstruments such as Structured Products, suchwithholding would not apply to foreign passthrupayments prior to the date that is two years afterthe publication of the final regulations defining“foreign passthru payment” in the U.S. FederalRegister and, provided that Structured Productsare properly treated as debt for U.S. federalincome tax purposes, Structured Products issuedon or prior to the date that is six months after thedate on which final regulations defining foreignpassthru payments are filed with the U.S. FederalRegister generally would be grandfathered forpurposes of FATCA withholding on foreignpassthru payments unless materially modifiedafter such date or classified as equity for U.S.federal income tax purposes. However, ifadditional Structured Products that are notdistinguishable from previously issued StructuredProducts are issued after the expiration of thegrandfathering period and are subject towithholding under FATCA, then withholdingagents may treat all Structured Products,

including the Structured Products offered prior tothe expiration of the grandfathering period, assubject to withholding under FATCA. Holdersshould consult their own tax advisors regardinghow these rules may apply to their investment inthe Structured Products. In the event anywithholding would be required pursuant toFATCA or an IGA with respect to payments on theStructured Products, neither UBS nor any otherperson will be required under the terms of theStructured Products to pay additional amounts asa result of the withholding.

The U.S. federal income tax discussion setforth above is included for general informationonly and may not be applicable dependingupon an investor’s particular situation.Prospective investors should consult their owntax advisers with respect to the taxconsequences to them of the ownership anddisposition of the Structured Products and theunderlying stock, including the taxconsequences under state, local, non-U.S. andother tax laws and the possible effects ofchanges in U.S. federal or other tax laws.

The above information is of a general nature onlyand is not intended to be a comprehensivedescription of all potential relevant taxconsiderations. We do not provide any tax advicefor the Structured Products. Tax treatmentdepends on the individual circumstances of eachclient and clients must therefore seek their owntax advice from a reputable service provider.Prior to entering into a transaction you shouldconsult with your own legal, regulatory, tax,financial and accounting advisors to the extentyou consider it necessary, and make your owninvestment, hedging and trading decisions(including decisions regarding the suitability ofthis transaction) based upon your own judgmentand advice from those advisors you considernecessary.

Placing, sale and grey market dealings

No offers, sales, re-sales, transfers or deliveriesof any Structured Products, or distribution of anyoffering material relating to the StructuredProducts may be made in or from any jurisdictionexcept in circumstances which will result incompliance with any applicable laws orregulations and which will not impose anyobligation on us. See the section “Placing andSale” for further information.

− 5 −

Following the launch of a series of Structured

Products, we may place all or part of that series

with our related party.

The Structured Products may be sold to investors

in the grey market in the period between the

launch date and the listing date. We will report

any dealings in Structured Products by us and/or

any of our subsidiaries or associated companies

in the grey market to the Stock Exchange by the

listing date and such report will be released on

the website of HKEX.

Where can you inspect the relevantdocuments?

The following documents are available for

inspection during usual business hours on any

weekday (Saturdays, Sundays and holidays

excepted) at the offices of UBS Securities Asia

Limited:

(a) the Annual Report 2020 of UBS Group AG

and UBS AG (“Annual Report 2020”);

(b) consent letter of our auditors, Ernst &

Young Ltd (“Auditors”);

(c) this document and any addendum to this

document;

(d) the launch announcement and supplemental

listing document as long as the relevant

series of Structured Products is listed on the

Stock Exchange; and

(e) the instrument executed by us by way of

deed poll on 10 April 2006 which

constitutes the Structured Products.

Requests for photocopies of the above documentswill be subject to a reasonable fee which reflectsthe cost of making such copies.

The Listing Documents are also available on thewebsite of the HKEX at www.hkexnews.hk andour website at http://warrants.ubs.com/en.

各上市文件亦可於香港交易所披露易網站www.hkexnews.hk 以及我們的網站http://warrants.ubs.com/ch 瀏覽。

Have the Auditors consented to the inclusion oftheir report to the Listing Documents?

Our Auditors have given and have not withdrawntheir written consent to the inclusion of theirreport dated 4 March 2021 and/or the referencesto their name in this document, in the form andcontext in which they are included. Their reportwas not prepared for incorporation into thisdocument. The Auditors do not own any of ourshares or shares in our subsidiaries, nor do theyhave the right (whether legally enforceable ornot) to subscribe for or to nominate persons tosubscribe for our securities or securities of any ofour subsidiaries.

Authorised representatives

Bernard Wu and Dougal McAdam, both of 52ndFloor, Two International Finance Centre, 8Finance Street, Central, Hong Kong, are ourauthorised representatives and are authorised toaccept services on our behalf in Hong Kong.

How can you get further information aboutUBS AG or the Structured Products?

You may visit www.ubs.com to obtainfurther information about us andhttp://warrants.ubs.com/en to obtain furtherinformation about the Structured Products.

Governing law of the Structured Products

All contractual documentation for the StructuredProducts will be governed by, and construed inaccordance with, the laws of Hong Kong.

The Listing Documents are not the sole basisfor making an investment decision

The Listing Documents do not take into accountyour investment objectives, financial situation orparticular needs. Nothing in the ListingDocuments should be construed as arecommendation by us or our affiliates to investin the Structured Products or the underlying assetof the Structured Products.

No person has been authorised to give anyinformation or to make any representations otherthan those contained in this document inconnection with the Structured Products, and, ifgiven or made, such information orrepresentations must not be relied upon as havingbeen authorised by us.

− 6 −

HKEX, the Stock Exchange and HKSCC have

made no assessment of, nor taken any

responsibility for, our financial soundness or the

merits of investing in any Structured Products,

nor have they verified the accuracy or the

truthfulness of statements made or opinions

expressed in this document.

This document has not been reviewed by the

Securities and Futures Commission. You are

advised to exercise caution in relation to the offer

of the Structured Products.

Capitalised terms

Unless otherwise specified, capitalised terms

used in this document have the meanings set out

in the terms and conditions of the relevant series

of Structured Products set out in Appendix 1 and

Appendix 2 (together, the “Conditions”).

− 7 −

PLACING AND SALE

General

No action has been or will be taken by us thatwould permit a public offering of any series ofStructured Products or possession or distributionof any offering material in relation to anyStructured Products in any jurisdiction (otherthan Hong Kong) where action for the purpose isrequired.

United States of America

Each series of Structured Products has not been,and will not be, registered under the UnitedStates Securities Act of 1933, as amended (the“Securities Act”) or the securities laws of anystate or other jurisdiction of the United States.The Structured Products do not constitute, andhave not been marketed as, contracts of sale of acommodity for future delivery (or optionsthereon) subject to the U.S. CommodityExchange Act of 1936, as amended (the“Commodity Exchange Act”), and trading in theStructured Products has not been approved by theU.S. Commodity Futures Trading Commission(the “CFTC”) under the Commodity ExchangeAct.

Subject to certain exceptions, StructuredProducts or interests therein, may not at any timebe offered, sold, resold, transferred or delivered,directly or indirectly, in the United States or to,or for the account or benefit of, any U.S. personor to others for offering, sale or resale in theUnited States or to any such U.S. person. Offers,sales and transfers of Structured Products, orinterests therein, in the United States or to U.S.persons would constitute a violation of UnitedStates securities laws unless made in compliancewith the registration requirements of theSecurities Act or pursuant to an exemptiontherefrom. In addition, certain issues ofStructured Products may not at any time beoffered, sold or delivered in the United States orto, or for the account or benefit of, U.S. persons,nor may any U.S. persons at any time trade ormaintain a position in such Structured Products.No person will offer, sell, re-sell, transfer ordeliver any Structured Products or intereststherein within the United States or to U.S.persons, except as permitted by the base placingagreement between us and the Sponsor, acting asmanager. As used herein, “United States” meansthe United States of America (including theStates and the District of Columbia), itsterritories, its possessions and other areas subjectto its jurisdiction; and “U.S. person” means (i)any national or resident of the United States,

including any corporation, partnership or otherentity created or organised in or under the laws ofthe United States or of any political subdivisionthereof, (ii) any estate or trust the income ofwhich is subject to United States income taxationregardless of its source, (iii) “U.S. person as suchterm is defined in (a) Regulation S under theSecurities Act or (b) the Interpretive Guidanceand Policy Statement Regarding Compliance withCertain Swap Regulations promulgated by theCFTC pursuant to the Commodity Exchange Act,or (iv) a person other than a “Non-United StatesPerson” as defined in CFTC Rule 4.7, in eachcase, as such definition is amended, modified orsupplemented from time to time.

In addition, until 40 days after thecommencement of the offering, an offer, sale,re-sale, transfer or delivery of StructuredProducts within the United States by a dealer thatis not participating in the offering may violate theregistration requirements of the Securities Act.

European Economic Area

Each dealer represents and agrees, and eachfurther dealer appointed in respect of theStructured Products will be required to representand agree, that it has not offered, sold orotherwise made available and will not offer, sell,or otherwise make available any StructuredProducts which are the subject of the offering ascontemplated by this Base Listing Document toany retail investor in the European EconomicArea. For the purposes of this provision:

(a) the expression “retail investor” means aperson who is one (or more) of thefollowing:

(i) a retail client as defined in point (11)of Article 4(1) of Directive 2014/65/EU(as amended, “MiFID II”); or

(ii) a customer within the meaning ofDirective 2016/97/EU (as amended,the Insurance Distribution Directive),where that customer would not qualifyas a professional client as defined inpoint (10) of Article 4(1) of MiFID II;or

(iii) not a qualified investor as defined inRegulation (EU) 2017/1129 (asamended and superseded, the“Prospectus Regulation”, theProspectus Directive); and

− 8 −

(b) the expression “offer” includes thecommunication in any form and by anymeans of sufficient information on the termsof the offer and the Structured Products tobe offered so as to enable an investor todecide to purchase or subscribe theStructured Products.

United Kingdom

Each dealer has represented and agreed, and eachfurther dealer appointed in respect of theStructured Products will be required to representand agree, that it has not offered, sold orotherwise made available and will not offer, sellor otherwise make available any StructuredProducts which are the subject of the offeringcontemplated by this Base Listing Document toany retail investor in the United Kingdom. Forthe purposes of this provision:

(a) the expression “retail investor” means aperson who is one (or more) of thefollowing:

(i) a retail client, as defined in point (8)of Article 2 of Regulation (EU) No2017/565 as it forms part of domesticlaw by virtue of the European Union(Withdrawal) Act 2018 (“EUWA”); or

(ii) a customer within the meaning of theprovisions of the Financial Servicesand Markets Act, as amended (the“FSMA”) and any rules or regulationsmade under the FSMA to implementDirective (EU) 2016/97, where thatcustomer would not qualify as aprofessional client, as defined in point(8) of Article 2(1) of Regulation (EU)No 600/2014 as it forms part ofdomestic law by virtue of the EUWA;or

(iii) not a qualified investor as defined inArticle 2 of Regulation (EU)2017/1129 as it forms part of domesticlaw by virtue of the EUWA; and

(b) the expression an “offer” includes thecommunication in any form and by anymeans of sufficient information on the termsof the offer and the Structured Products tobe offered so as to enable an investor todecide to purchase or subscribe for theStructured Products.

Each dealer has represented and agreed, and eachfurther dealer appointed in respect of theStructure Products will be required to representand agree that:

(a) in respect to Structured Products having amaturity of less than one year: (i) it is aperson whose ordinary activities involve itin acquiring, holding, managing ordisposing of investments (as principal oragent) for the purposes of its business; and(ii) it has not offered or sold and will notoffer or sell any Structured Products otherthan to persons whose ordinary activitiesinvolve them in acquiring, holding,managing or disposing of investments (asprincipal or agent) for the purposes of theirbusinesses or who it is reasonable to expectwill acquire, hold, manage or dispose ofinvestments (as principal or agent) for thepurposes of their businesses where the issueof the Structured Products would otherwiseconstitute a contravention of Section 19 ofFSMA by us;

(b) it has only communicated or caused to becommunicated and will only communicateor cause to be communicated an invitationor inducement to engage in investmentactivity (within the meaning of section 21 ofthe FSMA) received by it in connection withthe issue or sale of the Structured Productsin circumstances in which section 21(1) ofthe FSMA does not apply to us; and

(c) it has complied and will comply with allapplicable provisions of the FSMA withrespect to anything done by it in relation toany Structured Products in, from orotherwise involving the United Kingdom.

Switzerland

This document does not constitute an offer anddoes not constitute a prospectus within themeaning of the laws of Switzerland. TheStructured Products may only be offered, sold orotherwise made available to (i) professionalclients as defined in article 4 para. 3 and article5 of the Federal Financial Services Act, “FinSA”)or (ii), if a key information document within themeaning of article 58 FinSA is available, inaccordance with the exemptions as set out inarticle 36 FinSA.

− 9 −

OVERVIEW OF WARRANTS

What is a Warrant?

A Warrant is a type of derivative warrants.

A derivative warrant linked to a share, a unit, anindex or other asset (each an “UnderlyingAsset”) is an instrument which gives the holder aright to “buy” or “sell” the Underlying Asset at,or derives its value by reference to, a pre-setprice or level called the Exercise Price/StrikeLevel on the Expiry Date. It usually costs afraction of the value of the Underlying Asset.

A derivative warrant may provide leveragedreturn to you (but conversely, it could alsomagnify your losses).

How and when can you get back yourinvestment?

Our Warrants are European style warrants. Thatmeans they can only be exercised on the ExpiryDate. A warrant will, upon exercise on the ExpiryDate, entitle the holder to a cash amount calledthe “Cash Settlement Amount” (if positive)according to the Conditions of that warrant.

You will receive the Cash Settlement Amount lessany Exercise Expenses upon settlement at expiry.If the Cash Settlement Amount is equal to or lessthan the Exercise Expenses, no amount is payableto you upon expiry.

How do our warrants work?

Ordinary warrants

The potential payoff of an ordinary warrant iscalculated by us by reference to the differencebetween:

(a) for a warrant linked to a security, theExercise Price and the Average Price; and

(b) for a warrant linked to an index, the StrikeLevel and the Closing Level.

Call warrants

A call warrant is suitable for an investor holdinga bullish view of the price or level of theUnderlying Asset during the term of the warrant.

A call warrant will be exercised if the AveragePrice/Closing Level is greater than the Exercise

Price/Strike Level (as the case may be). The morethe Average Price/Closing Level exceeds theExercise Price/Strike Level (as the case may be),the higher the payoff upon expiry. If the AveragePrice/Closing Level is at or below the ExercisePrice/Strike Level (as the case may be), aninvestor in the call warrant will lose all of hisinvestment.

Put warrants

A put warrant is suitable for an investor holdinga bearish view of the price or level of theUnderlying Asset during the term of the warrant.

A put warrant will be exercised if the AveragePrice/Closing Level is below the ExercisePrice/Strike Level (as the case may be). The morethe Average Price/Closing Level is below theExercise Price/Strike Level (as the case may be),the higher the payoff upon expiry. If the ExercisePrice/Strike Level is at or below the AveragePrice/Closing Level (as the case may be), aninvestor in the put warrant will lose all of hisinvestment.

Other types of warrants

The launch announcement and supplementallisting document applicable to other types ofwarrants will specify the type of such warrantsand whether such warrants are exotic warrants.

The Conditions applicable to each type of ourwarrants are set out in Parts A to C of Appendix1 (as may be supplemented by any addendum orthe relevant launch announcement andsupplemental listing document).

What are the factors determining the price of aderivative warrant?

The price of a derivative warrant generallydepends on the prevailing price or level of theUnderlying Asset. However, throughout the termof a derivative warrant, its price will beinfluenced by a number of factors, including:

(a) the Exercise Price or Strike Level;

(b) the value and volatility of the price or levelof the Underlying Asset (being a measure ofthe fluctuation in the price or level of theUnderlying Asset over time);

− 10 −

(c) the time remaining to expiry: generally, the

longer the remaining life of a derivative

warrant, the greater its value;

(d) the interim interest rates and expected

dividend payments or other distributions on

the Underlying Asset or on any components

comprising the underlying index;

(e) the liquidity of the Underlying Asset;

(f) the supply and demand for the derivative

warrants;

(g) our related transaction costs; and

(h) our creditworthiness.

What is your maximum loss?

Your maximum loss in warrants will be your

entire investment amount plus any transaction

costs.

How can you get information about ourwarrants after issue?

You may visit the website of HKEX

at https://www.hkex.com.hk/products/securities/structured-

products/overview?sc_lang=en or our website at

http://warrants.ubs.com/home/html/warrants_e.html

to obtain information on our warrants or any

notice given by us or the Stock Exchange in

relation to our warrants.

− 11 −

OVERVIEW OF CBBCS

What are CBBCs?

CBBCs are a type of Structured Products thattrack the performance of an Underlying Asset.CBBCs can be issued on different types ofUnderlying Assets as prescribed by the StockExchange from time to time, including:

(a) shares listed on the Stock Exchange;

(b) Hang Seng Index, Hang Seng ChinaEnterprises Index, Hang Seng TECH Indexand Hang Seng China H-Financials Index;

(c) unit trusts listed on the Stock Exchange;and/or

(d) overseas shares, indices, currencies orcommodities (such as oil, gold andplatinum).

A list of eligible Underlying Assets for CBBCs isavailable on the website of HKEX athttps://www.hkex.com.hk/Products/Securities/Structured-Products/Eligible-Underlying-Assets?sc_lang=en

CBBCs are issued either as bull CBBCs or bearCBBCs, allowing you to take either bullish orbearish positions on the Underlying Asset. BullCBBCs are designed for investors who have anoptimistic view on the Underlying Asset. BearCBBCs are designed for investors who have apessimistic view on the Underlying Asset.

Your maximum potential loss in a series ofCBBCs is limited to the purchase price, which isgenerally a fraction of the value of theUnderlying Asset, for the CBBCs plus the costinvolved in your purchase.

CBBCs have a mandatory call feature (the“Mandatory Call Event”) and, subject to thelimited circumstances set out in the relevantConditions in which a Mandatory Call Event maybe reversed, we must terminate our CBBCs uponthe occurrence of a Mandatory Call Event. See“What are the mandatory call features ofCBBCs?” below.

There are 2 categories of CBBCs, namely:

(a) Category R CBBCs; and

(b) Category N CBBCs.

Your entitlement following the occurrence of aMandatory Call Event will depend on thecategory of the CBBCs.

If no Mandatory Call Event occurs, the CBBCswill be exercised automatically on the ExpiryDate by payment of a Cash Settlement Amount (ifany) on the Settlement Date. The Cash SettlementAmount (if any) payable at expiry represents thedifference between the Closing Price/ClosingLevel of the Underlying Asset on the ValuationDate and the Strike Price/Strike Level.

The Conditions applicable to CBBCs are set outin Parts A to C of Appendix 2 (as may besupplemented by any addendum or the relevantlaunch announcement and supplemental listingdocument).

What are the mandatory call features ofCBBCs?

Mandatory Call Event

Subject to the limited circumstances set out in therelevant Conditions in which a Mandatory CallEvent may be reversed, we must terminate theCBBCs if a Mandatory Call Event occurs. AMandatory Call Event occurs if the Spot Price/Spot Level of the Underlying Asset is:

(a) at or below the Call Price/Call Level (in thecase of a bull CBBC); or

(b) at or above the Call Price/Call Level (in thecase of a bear CBBC),

at any time during the Observation Period.

The Observation Period starts from and includingthe Observation Commencement Date of therelevant CBBCs and ends on and including theTrading Day immediately preceding the ExpiryDate.

Subject to the limited circumstances set out in therelevant Conditions in which a Mandatory CallEvent may be reversed and such modification andamendment as may be prescribed by the StockExchange from time to time:

(a) all trades in the CBBCs concluded orrecorded in the Stock Exchange’s systemafter the time of the occurrence of aMandatory Call Event; and

− 12 −

(b) where the Mandatory Call Event occurs

during a pre-opening session or closing

auction session (if applicable), all auction

trades in the CBBCs concluded in such

session,

will be invalid and will be cancelled, and will not

be recognised by us or the Stock Exchange.

The time at which a Mandatory Call Event occurs

will be determined by reference to:

(a) in respect of CBBCs over single equities or

CBBCs over single unit trusts, the Stock

Exchange’s automatic order matching and

execution system time at which the Spot

Price is at or below the Call Price (for a

series of bull CBBCs) or is at or above the

Call Price (for a series of bear CBBCs); or

(b) in respect of CBBCs over index, the time

the relevant Spot Level is published by the

Index Compiler at which the Spot Level is at

or below the Call Level (for a series of bull

CBBCs) or is at or above the Call Level (for

a series of bear CBBCs),

subject to the rules and requirements as

prescribed by the Stock Exchange from time to

time.

Category R CBBCs vs. Category N CBBCs

The launch announcement and supplemental

listing document for the relevant series of CBBCs

will specify whether the CBBCs are Category R

CBBCs or Category N CBBCs.

“Category N CBBCs” refer to CBBCs for which

the Call Price/Call Level is equal to their Strike

Price/Strike Level. In respect of a series of

Category N CBBCs, you will not receive any cash

payment following the occurrence of a Mandatory

Call Event.

“Category R CBBCs” refer to CBBCs for which

the Call Price/Call Level is different from their

Strike Price/Strike Level. In respect of a series of

Category R CBBCs, you may receive a cash

payment called the Residual Value upon the

occurrence of a Mandatory Call Event. Theamount of the Residual Value payable (if any) iscalculated by reference to:

(a) in respect of a bull CBBC, the differencebetween the Minimum Trade Price/Minimum Index Level of the UnderlyingAsset and the Strike Price/Strike Level; and

(b) in respect of a bear CBBC, the differencebetween the Strike Price/Strike Level andthe Maximum Trade Price/Maximum IndexLevel of the Underlying Asset.

You must read the relevant Conditions and therelevant launch announcement and supplementallisting document to obtain further information onthe calculation formula of the Residual Valueapplicable to Category R CBBCs.

You may lose all of your investment in aparticular series of CBBCs if:

(a) in the case of a series of bull CBBCs, theMinimum Trade Price/Minimum IndexLevel of the Underlying Asset is equal to orless than the Strike Price/Strike Level; or

(b) in the case of a series of bear CBBCs, theMaximum Trade Price/Maximum IndexLevel of the Underlying Asset is equal to orgreater than the Strike Price/Strike Level.

How is the funding cost calculated?

The issue price of a CBBC represents thedifference between the initial reference spot priceor level of the Underlying Asset as at the launchdate of the CBBC and the Strike Price/StrikeLevel, plus the applicable funding cost.

The initial funding cost applicable to each seriesof CBBCs will be specified in the relevant launchannouncement and supplemental listing documentfor the relevant series and will fluctuatethroughout the life of the CBBCs as the fundingrate changes from time to time. The funding rateis a rate determined by us based on one or moreof the following factors, including but not limitedto the Strike Price/Strike Level, the prevailinginterest rate, the expected life of the CBBCs,expected notional dividends or distributions inrespect of the Underlying Asset and the marginfinancing provided by us.

− 13 −

Further details about the funding cost applicableto a series of CBBCs will be described in therelevant launch announcement and supplementallisting document.

Do you own the Underlying Asset?

CBBCs convey no interest in the UnderlyingAsset. We may choose not to hold the UnderlyingAsset or any derivatives contracts linked to theUnderlying Asset. There is no restriction throughthe issue of the CBBCs on the ability of us and/orour affiliates to sell, pledge or otherwise conveyall right, title and interest in any UnderlyingAsset or any derivatives products linked to theUnderlying Asset.

What are the factors determining the price of aCBBC?

Although the price of a CBBC tends to followclosely the movement in the value of theUnderlying Asset in dollar value (on theassumption of an entitlement ratio of one CBBCto one Underlying Asset), movement in the priceof the CBBC may not always follow closely themovement in value of the Underlying Asset.

However, throughout the term of a CBBC, itsprice will be influenced by a number of factors,including:

(a) the Strike Price/Strike Level and the CallPrice/Call Level;

(b) the likelihood of the occurrence of aMandatory Call Event;

(c) for Category R CBBCs only, the probablerange of the Residual Value (if any) payableupon the occurrence of a Mandatory CallEvent;

(d) the time remaining to expiry;

(e) the interim interest rates and expecteddividend payments or other distributions onthe Underlying Asset or on any componentscomprising the underlying index;

(f) the liquidity of the Underlying Asset;

(g) the supply and demand for the CBBCs;

(h) the probable range of the Cash SettlementAmounts;

(i) the depth of the market and liquidity of the

Underlying Asset or of the future contracts

relating to the underlying index;

(j) our related transaction costs; and

(k) our creditworthiness.

What is your maximum loss?

Your maximum loss in CBBCs will be your entire

investment amount plus any transaction costs.

How can you get information about our CBBCsafter issue?

You may visit the website of HKEX at

https://www.hkex.com.hk/products/securities/structured-

products/overview?sc_lang=en or our website at

http://warrants.ubs.com/home/html/cbbc_e.html to

obtain information on our CBBCs or any notice given

by us or the Stock Exchange in relation to our CBBCs.

− 14 −

INFORMATION IN RELATION TO US

1. Overview

UBS AG with its subsidiaries (together,“UBS AG consolidated”, or “UBS AGGroup”; together with UBS Group AG,which is the holding company of UBS AG,and its subsidiaries, “UBS Group”,“Group”, “UBS” or “UBS Group AGconsolidated”) provides financial adviceand solutions to private, institutional andcorporate clients worldwide, as well asprivate clients in Switzerland. Theoperational structure of the Group iscomprised of the Group Functions and fourbusiness divisions: Global WealthManagement, Personal & CorporateBanking, Asset Management and theInvestment Bank.

2. Information about the Issuer

2.1. Corporate Information

The legal and commercial name of thecompany is UBS AG.

The company was incorporated under thename SBC AG on 28 February 1978 for anunlimited duration and entered in theCommercial Register of Canton Basel-Cityon that day. On 8 December 1997, thecompany changed its name to UBS AG. Thecompany in its present form was created on29 June 1998 by the merger of Union Bankof Switzerland (founded 1862) and SwissBank Corporation (founded 1872). UBS AGis entered in the Commercial Registers ofCanton Zurich and Canton Basel-City. Theregistration number is CHE-101.329.561.

UBS AG is incorporated and domiciled inSwitzerland and operates under the SwissCode of Obligations as anAktiengesellschaft, a corporation limited byshares. UBS AG’s Legal Entity Identifier(LEI) code is BFM8T61CT2L1QCEMIK50.

According to article 2 of the articles ofassociation of UBS AG dated 26 April 2018,the purpose of UBS AG is the operation of abank. Its scope of operations extends to alltypes of banking, financial, advisory,trading and service activities in Switzerlandand abroad. UBS AG may establish

branches and representative offices as wellas banks, finance companies and otherenterprises of any kind in Switzerland andabroad, hold equity interests in thesecompanies, and conduct their management.UBS AG is authorized to acquire, mortgageand sell real estate and building rights inSwitzerland and abroad. UBS AG mayborrow and invest money on the capitalmarkets. UBS AG is part of the group ofcompanies controlled by the group parentcompany UBS Group AG. It may promotethe interests of the group parent company orother group companies. It may provideloans, guarantees and other kinds offinancing and security for group companies.

The addresses and telephone numbers ofUBS AG’s two registered offices andprincipal places of business are:Bahnhofstrasse 45, CH-8001 Zurich,Switzerland, telephone +41 44 234 1111;and Aeschenvorstadt 1, CH-4051 Basel,Switzerland, telephone +41 61 288 5050.

2.2. UBS’s borrowing and funding structureand financing of UBS’s activities

For information on UBS’s expectedfinancing of its business activities, pleaserefer to “Liquidity and fundingmanagement” in the “Capital, liquidity andfunding, and balance sheet” section of theUBS Group AG and UBS AG Annual Report2020 published on 5 March 2021 (“AnnualReport 2020”).

3. Business Overview

3.1. Organisational Structure of UBS AG

UBS AG is a Swiss bank and the parentcompany of the UBS AG Group. It is 100%owned by UBS Group AG, which is theholding company of the UBS Group. UBSoperates as a group with four businessdivisions and Group Functions.

In 2014, UBS began adapting its legal entitystructure in response to too-big-to-failrequirements and other regulatoryinitiatives. First, UBS Group AG wasestablished as the ultimate parent holdingcompany for the Group.

− 15 −

In 2015, UBS AG transferred its personal &

corporate banking and Swiss-booked wealth

management businesses to the newly

established UBS Switzerland AG, a banking

subsidiary of UBS AG in Switzerland. That

same year, UBS Business Solutions AG, a

wholly owned subsidiary of UBS Group AG,

was established and acts as the Group

service company. In 2016, UBS Americas

Holding LLC became the intermediate

holding company for UBS’s subsidiaries in

the United States (“US”) and UBS’s wealth

management subsidiaries across Europe

were merged into UBS Europe SE, UBS’s

German-headquartered European

subsidiary. In 2019, UBS Limited, UBS’s

United Kingdom (“UK”) headquartered

subsidiary, was merged into UBS Europe

SE.

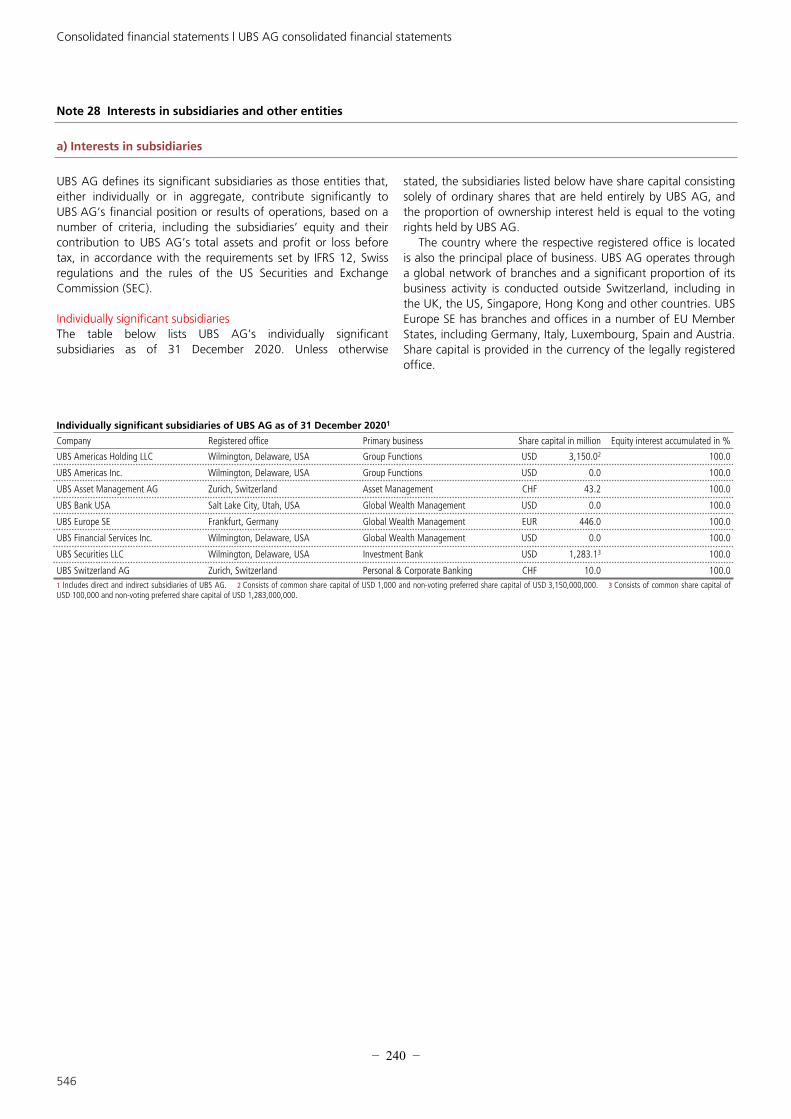

UBS Group AG’s interests in subsidiaries

and other entities as of 31 December 2020,

including interests in significant

subsidiaries, are discussed in “Note 28

Interests in subsidiaries and other entities”

to the UBS Group AG’s consolidated

financial statements included in the Annual

Report 2020.

UBS AG’s interests in subsidiaries and

other entities as of 31 December 2020,

including interests in significant

subsidiaries, are discussed in “Note 28

Interests in subsidiaries and other entities”

to the UBS AG’s consolidated financial

statements included in the Annual Report

2020.

UBS AG is the parent company of, and

conducts a significant portion of its

operations through, its subsidiaries. UBS

AG has contributed a significant portion of

its capital and provides substantial liquidity

to subsidiaries. In addition, UBS Business

Solutions AG provides substantial services

to group companies including UBS AG and

its subsidiaries. To this extent, UBS AG is

dependent on certain of the entities of the

UBS AG Group and of the UBS Group.

3.2. Recent Developments

Accounting, regulatory, legal and otherdevelopments

Swiss COVID-19 loans

In March 2020, the Swiss Federal Counciladopted provisional emergency legislation tosupport small and medium-sized Swisscompanies suffering from substantial reductionsin revenue due to the COVID-19 pandemic. InDecember 2020, the Swiss Parliament approvedthe COVID-19 Joint and Several Guarantee Act,which became effective on 19 December 2020.This Act codified the measures adopted underemergency legislation into ordinary law andprovides for regulation of the loan programs andguarantees over their life cycle. The new Actextends the standard amortization period of loansfrom five to eight years.

IFRS 9 and COVID-19: accounting for expectedcredit losses

In March 2020, the International AccountingStandards Board (the “IASB”) emphasized thatentities should apply appropriate judgment whendetermining the effects of COVID-19 on expectedcredit losses under IFRS 9, given that significantuncertainty exists, particularly related to theassessment of future macroeconomic conditions.

Swiss Financial Market Supervisory Authority(“FINMA”), the European Central Bank (“ECB”)and other banking regulators issued similarstatements emphasizing the need for appropriatejudgment with regard to COVID-19 effects onexpected credit losses. Notwithstanding themeasures taken by regulators and clarifyingstatements, deteriorating economic forecasts havecaused an increase in credit loss expenses andhence greater volatility in the income statement.

Swiss Withholding Tax Act

In April 2020, the Swiss Federal Councillaunched a consultation on various suggestedamendments to the Withholding Tax Act. Basedon the consultation results, the Federal Councilproposed in September 2020 to maintain thewithholding tax on interest carried on bankaccounts by natural persons with tax domicile inSwitzerland and to abolish the tax on all otherinterest payments. As the next step, the FederalCouncil will submit a dispatch to Parliament in

− 16 −

the second quarter of 2021. Furthermore, the

Swiss Federal Council has proposed to extend the

current withholding tax exemption for total

loss-absorbing capacity and additional tier 1

instruments from 2021 until the end of 2026. This

extension will be subject to parliamentary debate

in 2021.

Climate-related risks; environmental, social andgovernance (“ESG”) matters

In January 2021, the Swiss government officiallyexpressed support for the Climate-relatedFinancial Disclosures (“TCFD”). Since thelaunch of the TCFD recommendations in 2017,UBS has continuously improved and expanded itsclimate-related disclosures to demonstrate itsactive engagement for an orderly transition to alow-carbon economy.

In December 2020, the US Federal Reservejoined the Network of Central Banks andSupervisors for Greening the Financial System(the “NGFS”). As a result, all global systemicallyimportant banks (“G-SIBs”) are now supervisedby members of the NGFS. The NGFS advocatesfor a more sustainable financial system andissued a range of prudential supervisory practicesfor climate- and environment-related topics in2020.

Furthermore, the Federal Reserve has indicatedthat it will work closely with other agencies andauthorities, including the Basel Committee onBanking Supervision (“BCBS”) Task Force onClimate-related Financial Risks and the FinancialStability Board (“FSB”), to better understand,measure and mitigate climate-related financialrisks.

In Europe, the ECB has issued a guide onclimate-related and environmental risks andannounced plans for a 2022 climate stress test.Also, the EBA has consulted on the inclusion ofESG matters in supervisory practices, and theEuropean Securities and Markets Authority(“ESMA”) has consulted on DisclosureRegulation technical standards, including adverseimpact requirements. The EU (“EuropeanUnion”) has formally adopted the TaxonomyRegulation with a legislative base for technicalstandards to define a green taxonomy.

NSFR implementation

In September 2020, the Swiss Federal Counciladopted an amendment to the LiquidityOrdinance for the implementation of the netstable funding ratio (“NSFR”). The NSFRregulation was finalized in the fourth quarter of2020 with the release of the revised FINMAliquidity circular, and will become effective on 1July 2021. It applies to UBS Group AG at theconsolidated level and to UBS AG, UBSSwitzerland AG and UBS Swiss FinancialAdvisers AG at the standalone level. UBS is onschedule to operationalize the NSFR regulation;its overall effect on UBS is expected to belimited. In October 2020, the US bankingregulators finalized the NSFR rule for supervisedfirms to ensure a minimum level of stablefunding. The rule becomes effective as of 1 July2021 and will require semi-annual disclosurefrom 1 January 2023. As a Category III firmunder the Federal Reserve’s Tailoring Rule(2019), UBS’s intermediate holding company,UBS Americas Holding LLC, and its subsidiarybank, UBS Bank USA, will be subject to an NSFRrequirement of 85%. In the European Union, theEuropean Commission (the “EC”) adopted theupdated Capital Requirements Regulation in June2019, which will become effective from 28 June2021. The regulation requires UBS Europe SE toprovide a detailed annual NSFR disclosure and asemi-annual NSFR key metrics disclosure.

US CCAR

In June 2020, the Federal Reserve released theresults of its annual Dodd—Frank Act StressTests (“DFAST”) and Comprehensive CapitalAnalysis and Review (“CCAR”).

UBS’s intermediate holding company, UBSAmericas Holding LLC, exceeded minimumcapital requirements under the severely adversescenario and the Federal Reserve did not object toits capital plan. As a result, UBS AmericasHolding LLC will no longer be subject to thequalitative assessment component of CCAR.

Following the completion of the annual DFASTand CCAR, UBS Americas Holding LLC wasassigned a stress capital buffer (an “SCB”) of6.7% under the SCB rule (based on Dodd—FrankAct stress test results and planned futuredividends), which results in the imposition ofrestrictions if the SCB is not maintained abovespecified regulatory minimum capitalrequirements.

− 17 −

The Federal Reserve also conducted sensitivityanalyses to model the economic effects of theCOVID-19 pandemic. As a result of thesesupplementary analyses, the Federal Reservedetermined that firms should resubmit revisedcapital plans based on a new stress scenario. InDecember 2020, the Federal Reserve released theresults of this second CCAR of 2020. UBSAmericas Holding LLC’s projected stress capitalratios exceeded regulatory capital minima underthe updated supervisory scenarios.

Brexit

Following the UK’s withdrawal from the EU on31 January 2020, a regulation grantingequivalence to Switzerland’s stock exchangeswas approved by the UK Parliament and cameinto force on 3 February 2021. In response,Switzerland granted recognition for UK tradingvenues that allows shares issued bySwiss-incorporated companies to be admitted totrading on UK trading venues.

Also, the negotiation on the Trade andCooperation Agreement, which governs therelationship between the EU and the UK on freetrade in certain goods and mutual market access,among other matters, was finalized on 24December 2020.

In September 2020, the EC adopted a temporaryequivalence decision for UK centralcounterparties (“CCPs”) for the purpose offacilitating derivatives clearing. The temporaryequivalence decision, applicable from 1 January2021 until 30 June 2022, does not require UBSEurope SE to migrate its exposures to an EU CCPbefore the end of the transition period.

In March 2019, UBS completed a businesstransfer and cross- border merger of UBS Limitedand UBS Europe SE in order to continue servingEuropean Economic Area (“EEA”) clientsfollowing the end of the transition period. UBScontinues to align its Investment Bank activitiesto respond to ongoing regulatory guidance.

Developments related to the transition away fromLIBOR

The ICE Benchmark Administration (“IBA”), theFCA-regulated and authorized administrator ofLondon Interbank Offered Rate (“LIBOR”), isconsulting on the timing of the cessation of USDLIBOR. IBA expects that one-week and

two-month USD LIBOR settings, and all GBP,JPY, EUR and CHF LIBOR settings, will cease bythe end of 2021, and that the remaining USDLIBOR settings will cease by the end of June2023. The UK Government announced that theFCA will be given additional powers to ensure asmooth wind-down of LIBOR and deal withcertain legacy contracts that cannot easilytransition from LIBOR.

In October 2020, the International Swaps andDerivatives Association (“ISDA”) launched theIBOR Fallbacks Supplement and IBOR FallbacksProtocol, amending the ISDA standard definitionsfor interest-rate derivatives to incorporatefallbacks for derivatives linked to certaininterbank offered rates (“IBORs”). The changescame into effect on 25 January 2021 and, fromthat date, all new cleared and non-clearedderivatives between adhering parties thatreference the definitions now include thesefallbacks. UBS adhered to the protocol sinceNovember 2020, ahead of the effective date inJanuary 2021.

Digitalization

In 2020, the Swiss Parliament passed a revisedSwiss data protection law. The consultation onthe corresponding ordinance is expected to belaunched in the second quarter of 2021 and UBSanticipates both the law and the ordinance tobecome effective as of 1 January 2022. Therevision seeks to improve data protection forindividuals by enhancing the transparency andaccountability rules for companies processingdata, among other measures. This is intended toresult in the equivalence necessary for thecontinued cross-border transmission of data withEU member states.

The Swiss Parliament also adopted the FederalAct on the Adaptation of Federal Law toDevelopments in Distributed Ledger Technology(the “DLT Act”), among other matters, enablingthe introduction of ledger-based securities thatare represented in a blockchain. Part of the DLTAct has become effective as of February 2021,the remainder is expected to enter into force inthe second half of 2021.

The Swiss Parliament also passed the Federal Acton Electronic Identification Services (the “e-IDAct”), thereby introducing a federally recognizedelectronic identity. As a referendum has been

− 18 −

successfully called for, the law will be subject toa public vote in March 2021. In the EU, the EChas outlined its Digital Finance Package, which isfocused on crypto-assets, digital identities,digital operational resilience and retail paymentsstrategy, among other matters. Furthermore, theECB has launched a consultation on a possiblefuture digital euro.

Operational resilience

On the international level, in 2020, the BCBSfinished its consultation on new Principles forOperational Resilience, as well as on therevisions to the existing BCBS Principles for theSound Management of Operational Risk. Finalguidelines are expected to be released in thecourse of 2021. In the UK, the UK PrudentialRegulation Authority (“PRA”) and FCAcompleted their joint consultations on the newUK operational resilience framework, with finalrules expected in March 2021. US bankingregulators have further issued a whitepaper onoperational resilience that broadly aligns with theBCBS and UK proposals but is not applicable toforeign banks, at present. EU institutions are alsoconsidering legislative proposals in relation todigital operational resilience. Addressing theemerging requirements across jurisdictions, UBShas established a global program to enhance itscapabilities on operational resilience and enablealignment with relevant regulatory requirementsand legislation.

3.3. Trend Information

As indicated in the UBS Group AG fourthquarter 2020 report published on 26 January2021, investor sentiment improved in thefourth quarter of 2020, largely on the basisof the strong rebound in economic activityseen through the third quarter, combinedwith greater optimism regarding theavailability and effective distribution ofCOVID-19 vaccines, as well as continuedfiscal and monetary stimulus thatcontributed to generally more positiveviews on the timing and extent of asustainable economic recovery. However,recent developments, including economicand political situations in some largeeconomies and geopolitical tensions, haveagain raised questions around the shape andpace of the recovery. The growingnumbers of COVID-19 infections and

hospitalizations as well as lockdowns andsimilar measures imposed to control thepandemic add to existing concerns about theshape of the overall recovery and theseverity and duration of the effects of thepandemic in certain economic sectors. Inthese uncertain times, UBS’s clientsparticularly value expert guidance and UBSremains focused on supporting them withadvice and solutions. UBS expects itsrevenues in the first quarter of 2021 to bepositively influenced by seasonal factorssuch as higher client activity, comparedwith the fourth quarter of 2020. Higher assetprices should have a positive effect onrecurring fee income in UBS’s assetgathering businesses. However, thecontinued uncertainty in the environmentcould affect both asset prices and clientactivity. While supporting marketsentiment, low and persistently negativeinterest rates and expectations of continuingeasy monetary policy will remain headwindsto net interest income sequentially. With itsbalance sheet for all seasons and itsdiversified business model, UBS remainswell positioned to drive sustainablelong-term value for its clients andshareholders.

Refer to the “Our environment” and “Riskfactors” in the “”Our strategy, businessmodel and environment” section of theAnnual Report 2020 for more information.

4. Board of Directors

The Board of Directors (“BoD”) consists ofat least five and no more than twelvemembers. All the members of the BoD areelected individually by the Annual GeneralMeeting of Shareholders (“AGM”) for aterm of office of one year, which expiresafter the completion of the next AGM.Shareholders also elect the Chairman uponproposal of the BoD.

The BoD meets as often as businessrequires, and at least six times a year.

4.1.1. Members of the Board of Directors

The current members of the BoD are listedbelow. In addition, the UBS announced thatBeatrice Weder di Mauro has decided not to

− 19 −

stand for re-election to the BoD, and that it

intends to appoint Claudia Böckstiegel and

Patrick Firmenich for election to the BoD at

the next AGM.

Member TitleTerm ofoffice

Current principal activities outsideUBS AG

Axel A. Weber Chairman 2021 Chairman of the Board of Directors ofUBS Group AG; board member of theSwiss Bankers Association; TrusteesBoard member of Avenir Suisse; boardmember of the Swiss Finance Council;Chairman of the board of the Instituteof International Finance; member ofthe European Financial ServicesRound Table; member of the EuropeanBanking Group; member of theInternational Advisory Councils of theChina Banking and InsuranceRegulatory Commission and the ChinaSecurities Regulatory Commission;member of the International AdvisoryPanel, Monetary Authority ofSingapore; member of the Group ofThirty, Washington, D.C.; Chairman ofthe Board of Trustees of DIW Berlin;Advisory Board member of theDepartment of Economics, Universityof Zurich; member of the TrilateralCommission.

Jeremy Anderson ViceChairman

2021 Vice-Chairman and SeniorIndependent Director of the Board ofDirectors of UBS Group AG; boardmember of Prudential plc; trustee ofthe UK’s Productivity LeadershipGroup; trustee of Kingham Hill Trust;trustee of St. Helen Bishopsgate.

William C.Dudley

Member 2021 Member of the Board of Directors ofUBS Group AG; senior researchscholar at the Griswold Center forEconomic Policy Studies at PrincetonUniversity; member of the Board ofTreliant LLC; member of the Group ofThirty; member of the Council onForeign Relations; chair of the BrettonWoods Committee’s Advisory Council.

Reto Francioni Member 2021 Member of the Board of Directors ofUBS Group AG; professor at theUniversity of Basel; board member ofCoca-Cola HBC AG (SeniorIndependent Non-Executive Director,chair of the nomination committee);Chairman of the board of SwissInternational Air Lines AG; boardmember of MedTech InnovationPartners AG; executive director andmember of myTAMAR GmBH.

Member TitleTerm ofoffice

Current principal activities outsideUBS AG

Fred Hu Member 2021 Member of the Board of Directors ofUBS Group AG; non-executivechairman of the board of Yum ChinaHoldings (chair of the nomination andgovernance committee); member of theBoard of Ant Group; board member ofIndustrial and Commercial Bank ofChina; board member of Hong KongExchanges and Clearing Ltd.;chairman of Primavera Capital Group;board member of China AssetManagement; board member ofMinsheng Financial Leasing Co.;trustee of the China Medical Board;Governor of the Chinese InternationalSchool in Hong Kong; co-chairman ofthe Nature Conservancy Asia PacificCouncil; director and member of theExecutive Committee of China VentureCapital and Private Equity AssociationLtd.; Global Advisory Board memberof the Council on Foreign Relations.

Mark Hughes Member 2021 Member of the Board of Directors ofUBS Group AG; chair of the Board ofDirectors of the Global Risk Institute;visiting lecturer at the University ofLeeds; senior advisor to McKinsey &Company.

Nathalie Rachou Member 2021 Member of the Board of Directors ofUBS Group AG; member of the Boardof Euronext N.V.; member of theBoard of Veolia Environnement SA.

Julie G.Richardson

Member 2021 Member of the Board of Directors ofUBS Group AG; member of the boardof Yext (chair of the audit committee);member of the board of Vereit, Inc.(chair of the compensationcommittee); member of the board ofDatalog (chair of the audit committee).

Beatrice Wederdi Mauro

Member 2021 Member of the Board of Directors ofUBS Group AG; professor ofinternational economics at theGraduate Institute Geneva (IHEID);president of the Centre for EconomicPolicy Research in London; researchprofessor and distinguished fellow atthe Emerging Markets Institute atINSEAD in Singapore; SupervisoryBoard member of Robert BoschGmbH; member of the FoundationBoard of the International Center forMonetary and Banking Studies(ICMB); member of theFranco-German Council of EconomicExperts; advisor to the Board ofDirectors of Unigestion.

− 20 −

Member TitleTerm ofoffice

Current principal activities outsideUBS AG

Dieter Wemmer Member 2021 Member of the Board of Directors ofUBS Group AG; board member ofØrsted A/S (chair of the audit and riskcommittee); chairman of MarcoCapital Holding, Malta; member of theBerlin Center of CorporateGovernance.

Jeanette Wong Member 2021 Member of the Board of Directors ofUBS Group AG; board member ofEssilorLuxottica; board member ofJurong Town Corporation; boardmember of PSA International; boardmember of FFMC Holdings Pte. Ltd.and of Fullerton Fund ManagementCompany Ltd.; member of theManagement Advisory Board of NUSBusiness School; member of theGlobal Advisory Board, Asia,University of Chicago Booth School ofBusiness; member of the SecuritiesIndustry Council; member of the Boardof Trustees of the National Universityof Singapore.

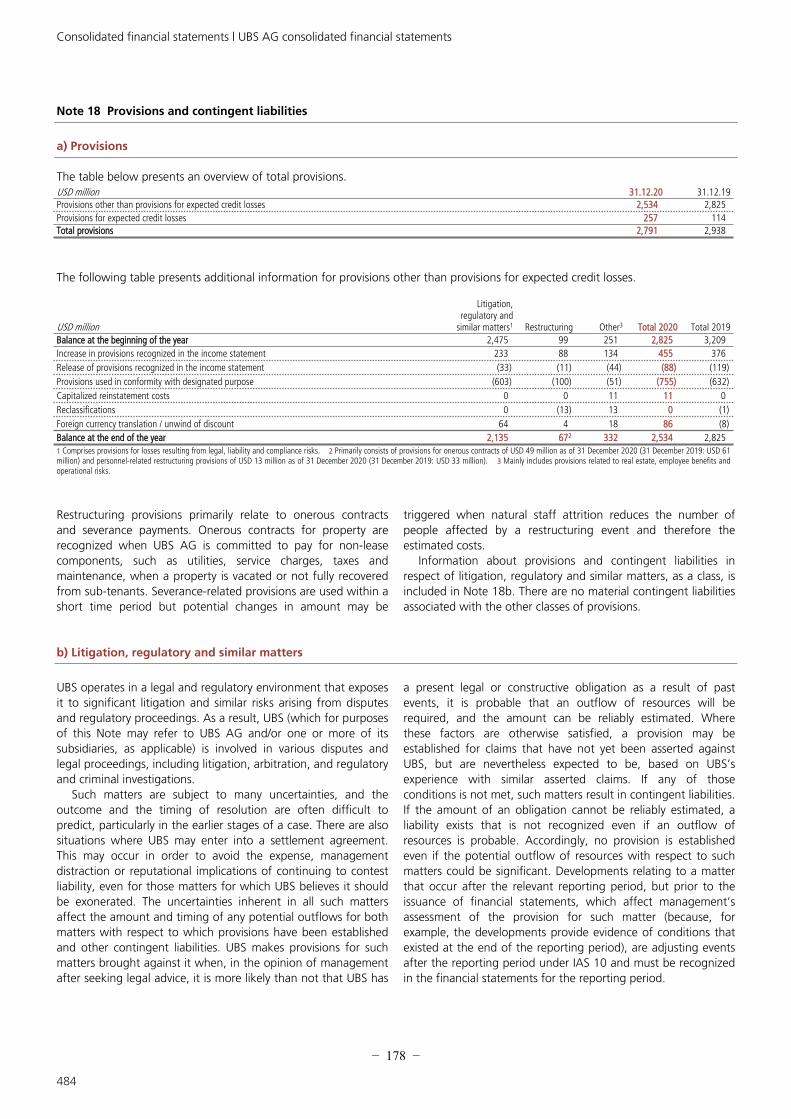

5. Litigation, Regulatory and SimilarMatters

UBS operates in a legal and regulatoryenvironment that exposes it to significantlitigation and similar risks arising fromdisputes and regulatory proceedings. As aresult, UBS (which for purposes of thissection may refer to UBS AG and / or one ormore of its subsidiaries, as applicable) isinvolved in various disputes and legalproceedings, including litigation,arbitration, and regulatory and criminalinvestigations.

Such matters are subject to manyuncertainties, and the outcome and thetiming of resolution are often difficult topredict, particularly in the earlier stages of acase. There are also situations where UBSmay enter into a settlement agreement. Thismay occur in order to avoid the expense,management distraction or reputationalimplications of continuing to contestliability, even for those matters for whichUBS believes it should be exonerated. Theuncertainties inherent in all such mattersaffect the amount and timing of anypotential outflows for both matters withrespect to which provisions have beenestablished and other contingent liabilities.UBS makes provisions for such matters

brought against it when, in the opinion ofmanagement after seeking legal advice, it ismore likely than not that UBS has a presentlegal or constructive obligation as a resultof past events, it is probable that an outflowof resources will be required, and theamount can be reliably estimated. Wherethese factors are otherwise satisfied, aprovision may be established for claims thathave not yet been asserted against UBS, butare nevertheless expected to be, based onUBS’s experience with similar assertedclaims. If any of those conditions is not met,such matters result in contingent liabilities.If the amount of an obligation cannot bereliably estimated, a liability exists that isnot recognized even if an outflow ofresources is probable. Accordingly, noprovision is established even if the potentialoutflow of resources with respect to suchmatters could be significant. Developmentsrelating to a matter that occur after therelevant reporting period, but prior to theissuance of financial statements, whichaffect management’s assessment of theprovision for such matter (because, forexample, the developments provideevidence of conditions that existed at theend of the reporting period), are adjustingevents after the reporting period under IAS10 and must be recognized in the financialstatements for the reporting period.

Specific litigation, regulatory and othermatters are described below, including allsuch matters that management considers tobe material and others that managementbelieves to be of significance due topotential financial, reputational and othereffects. The amount of damages claimed, thesize of a transaction or other information isprovided where available and appropriate inorder to assist users in considering themagnitude of potential exposures.

In the case of certain matters below, UBSstates that it has established a provision, andfor the other matters, it makes no suchstatement. When UBS makes this statementand it expects disclosure of the amount of aprovision to prejudice seriously its positionwith other parties in the matter because itwould reveal what UBS believes to be theprobable and reliably estimable outflow,UBS does not disclose that amount. In some

− 21 −

cases UBS is subject to confidentialityobligations that preclude such disclosure.With respect to the matters for which UBSdoes not state whether it has established aprovision, either: (a) it has not established aprovision, in which case the matter istreated as a contingent liability under theapplicable accounting standard; or (b) it hasestablished a provision but expectsdisclosure of that fact to prejudice seriouslyits position with other parties in the matterbecause it would reveal the fact that UBSbelieves an outflow of resources to beprobable and reliably estimable.

With respect to certain litigation, regulatoryand similar matters for which UBS hasestablished provisions, UBS is able toestimate the expected timing of outflows.However, the aggregate amount of theexpected outflows for those matters forwhich it is able to estimate expected timingis immaterial relative to its current andexpected levels of liquidity over therelevant time periods.

The aggregate amount provisioned forlitigation, regulatory and similar matters asa class is disclosed in “Note 18 Provisionsand contingent liabilities” to the UBS AGaudited consolidated financial statementsincluded in the Annual Report 2020. It is notpracticable to provide an aggregate estimateof liability for UBS’s litigation, regulatoryand similar matters as a class of contingentliabilities. Doing so would require UBS toprovide speculative legal assessments as toclaims and proceedings that involve uniquefact patterns or novel legal theories, thathave not yet been initiated or are at earlystages of adjudication, or as to whichalleged damages have not been quantifiedby the claimants. Although UBS thereforecannot provide a numerical estimate of thefuture losses that could arise from litigation,regulatory and similar matters, UBSbelieves that the aggregate amount ofpossible future losses from this class thatare more than remote substantially exceedsthe level of current provisions. Litigation,regulatory and similar matters may alsoresult in non-monetary penalties andconsequences. For example, thenon-prosecution agreement UBS enteredinto with the US Department of Justice

(“DOJ”), Criminal Division, Fraud Section

in connection with submissions of

benchmark interest rates, including, among

others, the British Bankers’ Association

LIBOR, was terminated by the DOJ based

on its determination that UBS had

committed a US crime in relation to foreign

exchange matters. As a consequence, UBS

AG pleaded guilty to one count of wire

fraud for conduct in the LIBOR matter, paid

a fine and was subject to probation, which

ended in January 2020.

A guilty plea to, or conviction of, a crime

could have material consequences for UBS.

Resolution of regulatory proceedings may

require UBS to obtain waivers of regulatory

disqualifications to maintain certain

operations, may entitle regulatory

authorities to limit, suspend or terminate

licenses and regulatory authorizations and

may permit financial market utilities to

limit, suspend or terminate UBS’s

participation in such utilities. Failure to

obtain such waivers, or any limitation,

suspension or termination of licenses,

authorizations or participations, could have

material consequences for UBS.

The risk of loss associated with litigation,

regulatory and similar matters is a

component of operational risk for purposes

of determining capital requirements.

Information concerning UBS’s capital

requirements and the calculation of

operational risk for this purpose is included

in the “Capital, liquidity and funding, and

balance sheet” section of the Annual Report

2020.

− 22 −

Provisions for litigation, regulatory andsimilar matters by business division and inGroup Functions1

USD million

GlobalWealth

Manage-ment

Personal&

CorporateBanking

AssetManage-

mentInvestment

BankGroup

FunctionsTotal2020

Total2019

Balance at thebeginning of theyear 782 113 0 255 1,325 2,475 2,827

Increase in provisionsrecognized in theincome statement 213 0 0 19 1 233 258

Release of provisionsrecognized in theincome statement (24) (6) 0 (1) (2) (33) (81)

Provisions used inconformity withdesignated purpose (154) (1) 0 (52) (395) (603) (518)

Reclassifications 0 0 0 (3) 3 0 0

Foreign currencytranslation /unwind ofdiscount 44 10 0 10 0 64 (12)

Balance at the end ofthe year 861 115 0 227 932 2,135 2,475

1 Provisions, if any, for matters described in this disclosureare recorded in Global Wealth Management (item C anditem D) and Group Functions (item B). Provisions, if any,for the matters described in items A and F of thisdisclosure are allocated between Global WealthManagement and Personal & Corporate Banking, andprovisions, if any, for the matters described in thisdisclosure in item E are allocated between the InvestmentBank and Group Functions.

A. Inquiries regarding cross-border wealthmanagement businesses

Tax and regulatory authorities in a number ofcountries have made inquiries, served requestsfor information or examined employees located intheir respective jurisdictions relating to thecross-border wealth management servicesprovided by UBS and other financial institutions.It is possible that the implementation ofautomatic tax information exchange and othermeasures relating to cross-border provision offinancial services could give rise to furtherinquiries in the future. UBS has receiveddisclosure orders from the Swiss Federal TaxAdministration (“FTA”) to transfer informationbased on requests for international administrativeassistance in tax matters. The requests concern anumber of UBS account numbers pertaining tocurrent and former clients and are based on datafrom 2006 and 2008. UBS has taken steps toinform affected clients about the administrativeassistance proceedings and their proceduralrights, including the right to appeal. The requestsare based on data received from the German

authorities, who seized certain data related to

UBS clients booked in Switzerland during their

investigations and have apparently shared this

data with other European countries. UBS expects

additional countries to file similar requests.

The Swiss Federal Administrative Court ruled in

2016 that, in the administrative assistance

proceedings related to a French bulk request,

UBS has the right to appeal all final FTA client