Embed Size (px)

Citation preview

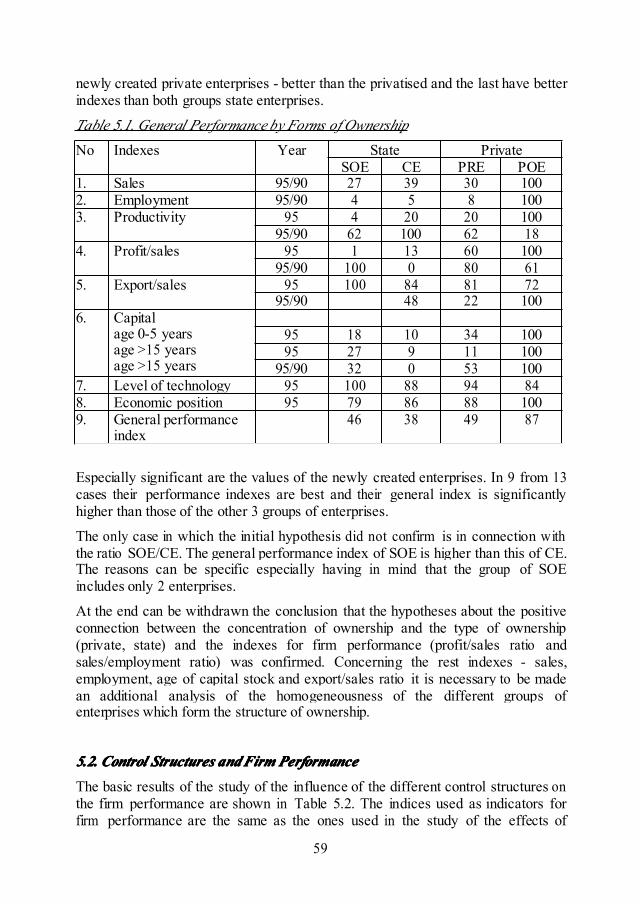

14

PARTPARTPARTPART I.I.I.I. OWNERSHIPOWNERSHIPOWNERSHIPOWNERSHIP CONTROLCONTROLCONTROLCONTROL ANDANDANDAND PERFORMANCE:PERFORMANCE:PERFORMANCE:PERFORMANCE:COUNTRYCOUNTRYCOUNTRYCOUNTRY STUDIESSTUDIESSTUDIESSTUDIES

CHAPTERCHAPTERCHAPTERCHAPTER I.I.I.I. BULGARIA

bybybybyMitkoMitkoMitkoMitko DimitrovDimitrovDimitrovDimitrov andandandand EvgeniEvgeniEvgeniEvgeni PeevPeevPeevPeev

I.I.I.I. OwnershipOwnershipOwnershipOwnershipandandandandControlControlControlControl Structures:Structures:Structures:Structures: AAAAMacro-LevelMacro-LevelMacro-LevelMacro-LevelAnalysisAnalysisAnalysisAnalysis inininin BulgariaBulgariaBulgariaBulgaria

1.1.1.1. OwnershipOwnershipOwnershipOwnership StructureStructureStructureStructure

Changes in the ownership structure are among the most important characteristics ofthe transition to market economy and the conditions in which enterprises operate.In order to study this problem, however, it is not sufficient to just analyse the ratioof state-owned and private enterprises. It should be known whether privateenterprises are privatised former state ones or de novo established, whether stateenterprises are transformed into entities of new legal status, or not. It is thereforenecessary to examine not only the changes in ownership structure and its presentcondition, but also the distribution of enterprises by their legal status.

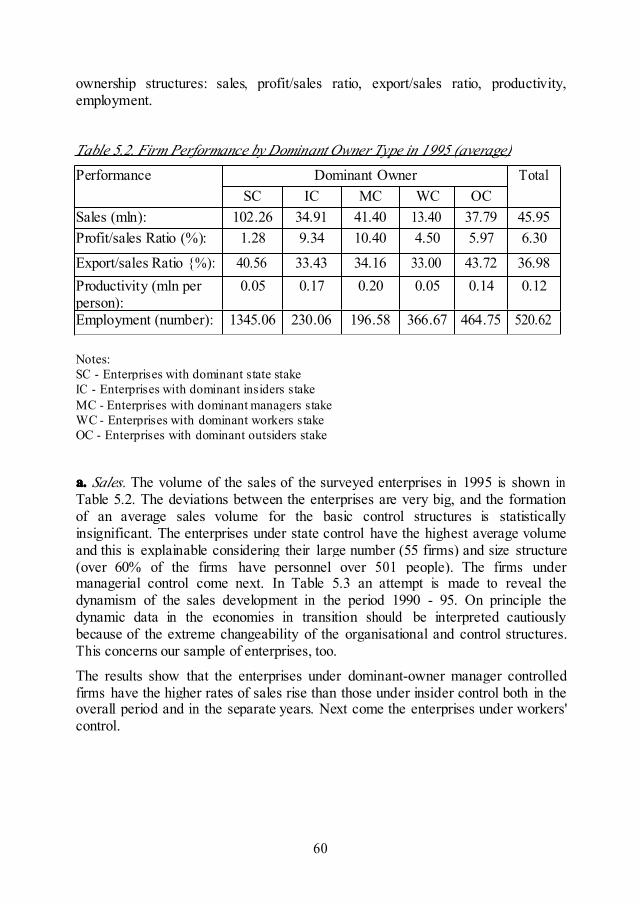

1.1.1.1.1.1.1.1. FormsFormsFormsForms ofofofof EconomicEconomicEconomicEconomicEntitiesEntitiesEntitiesEntities inininin BulgariaBulgariaBulgariaBulgariaThe legal status of economic agents in Bulgaria is regulated by the Law onCommerce1111 which was adopted in June 1991 and which was aiming to harmonisethe Bulgarian legislation with that of developed market economies. It was difficultto obtain a complete identity, since the historical and cultural specifics of differentWest European counties had resulted also in the forms of their economic activity.The goal, therefore, was an approximation rather in the essence and not in theterms, so that the Bulgarian system was made consistent with the western one.

Pursuant to the provisions of the Law on Commerce, a merchant is the commondenotation for any physical or legal person engaged in business activity(purchasing and sale of merchandise, production, services, financial transactions,etc.) in Bulgaria. A merchant can be a commercial company, a cooperative or aperson who has established an enterprise requiring that its activity be conducted asa commercial business. A "merchant" therefore is the most general concept onwhich the Law on Commerce is based.

1 Law on Commerce, State Gazette, 48/18.06.1991.

15

The private merchant is the first form of economic activity envisaged by the Law,which refers to any physical person who is registered at the court and who bearsfull liability for his obligations.

The association of two or more physical or legal persons for the purpose ofperforming business activities is denoted as a commercial company. A commercialcompany shall be any of the following: an unlimited partnership, a limitedpartnership, a private limited company, a public limited company, and a publiclimited partnership.

An unlimited partnership is a company incorporated by two or more personsengaged in business activity (commercial transactions) who bear joint andunlimited liability.

In the case when one or more of the partners bear joint and unlimited liability whilethe liability of the remaining members is limited to the extent of their pledgedcontribution, the commercial company is called a limited partnership. Themanagement and representation of the company is executed by the unlimited liablepartners.

A private limited company (Ltd.) is formed by one or more persons who are heldliable to the extent of their contribution to the company's capital. The managingbodies of the company include the general meeting of the partners and themanaging director. Should the company have more than 50 employees, they shallbe represented at the general meeting with the right to a deliberative vote only.

A public limited company (Pic.) is a company, which has its capital divided intoshares and which is liable to its creditors to the extent of its assets. The managingbodies of Pic. include a general meeting of the members and a board of directors(one-tier system) or a supervisory board and a management board (two-tiersystem). The members of the board of directors, respectively of the managementboard, represent the company jointly, except when provided otherwise by itsarticles of association. The difference comes from the fact that in a two-tier systemthe members of the management board are appointed by the supervisory board andnot directly by the shareholders.

A public limited partnership is similar to the limited partnership except for thataspect that the limited liable partners are issued shares in return for their capital.The company is promoted and managed by the general partners who have a votingright in the general meeting and constitute the board of directors.

Apart from these main forms of merchants, the Law on Commerce provides alsofor the existence of their alliances, or commercial groups, such as consortiums andholdings. The consortium is a contract-based group of merchants, while the holdingis a public limited company established for the purpose of management, withoutengaging in any production or commercial activity of its own.

The Law on Commerce contains also provisions for the legal forms of state- ownedand municipal enterprises, the main of them including the single-person private

16

limited company and the single-person public limited company (corporatised firmswith a hundred percent state participation). The formation of other commercialcompanies or associations thereof is further allowed. It is also provided that, byvirtue of a law, state-owned enterprises can be founded which are not commercialcompanies. The incorporation and transformation of state- owned enterprises insingle-person public (or, private) limited companies is regulated by a special law,while the municipal companies are subject to a resolution by the municipal council.

1.2.1.2.1.2.1.2. EnterprisesEnterprisesEnterprisesEnterprises RestructuringRestructuringRestructuringRestructuring inininin TermsTermsTermsTerms ofofofof OwnershipOwnershipOwnershipOwnership andandandand LegalLegalLegalLegal StatusStatusStatusStatus

The most considerable changes in the industrial organisation of the Bulgarianeconomy are related to its organisation structure. These were accomplished in twomain directions, namely: changes in the organisation forms of state-ownedenterprises and a sharp increase in the number and forms of commercial companiesowned by other economic agents, legal and physical persons mostly.

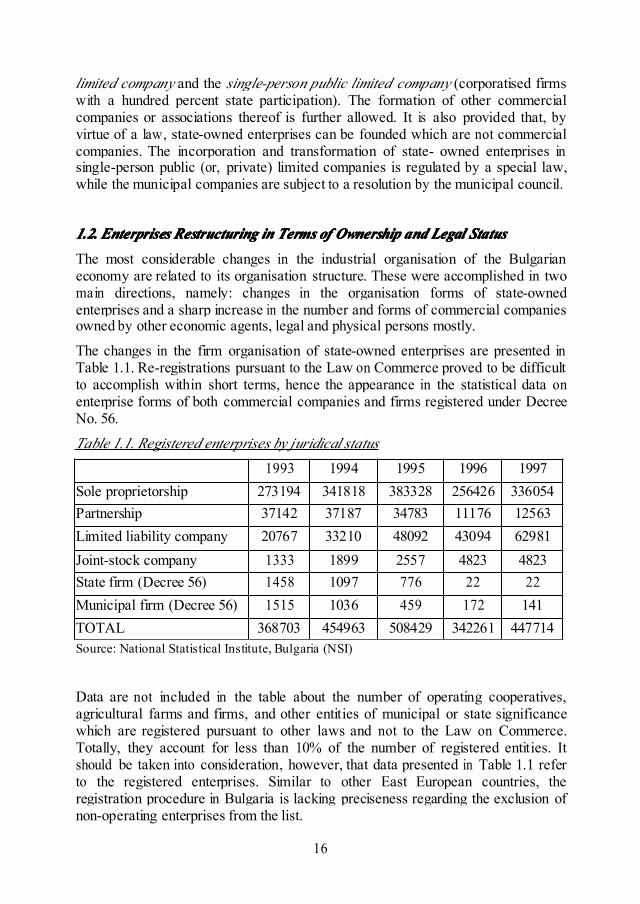

The changes in the firm organisation of state-owned enterprises are presented inTable 1.1. Re-registrations pursuant to the Law on Commerce proved to be difficultto accomplish within short terms, hence the appearance in the statistical data onenterprise forms of both commercial companies and firms registered under DecreeNo. 56.

Table 1.1. Registered enterprises by juridical status

1993 1994 1995 1996 1997Sole proprietorship 273194 341818 383328 256426 336054Partnership 37142 37187 34783 11176 12563Limited liability company 20767 33210 48092 43094 62981Joint-stock company 1333 1899 2557 4823 4823State firm (Decree 56) 1458 1097 776 22 22Municipal firm (Decree 56) 1515 1036 459 172 141TOTAL 368703 454963 508429 342261 447714Source: National Statistical Institute, Bulgaria (NSI)

Data are not included in the table about the number of operating cooperatives,agricultural farms and firms, and other entities of municipal or state significancewhich are registered pursuant to other laws and not to the Law on Commerce.Totally, they account for less than 10% of the number of registered entities. Itshould be taken into consideration, however, that data presented in Table 1.1 referto the registered enterprises. Similar to other East European countries, theregistration procedure in Bulgaria is lacking preciseness regarding the exclusion ofnon-operating enterprises from the list.

17

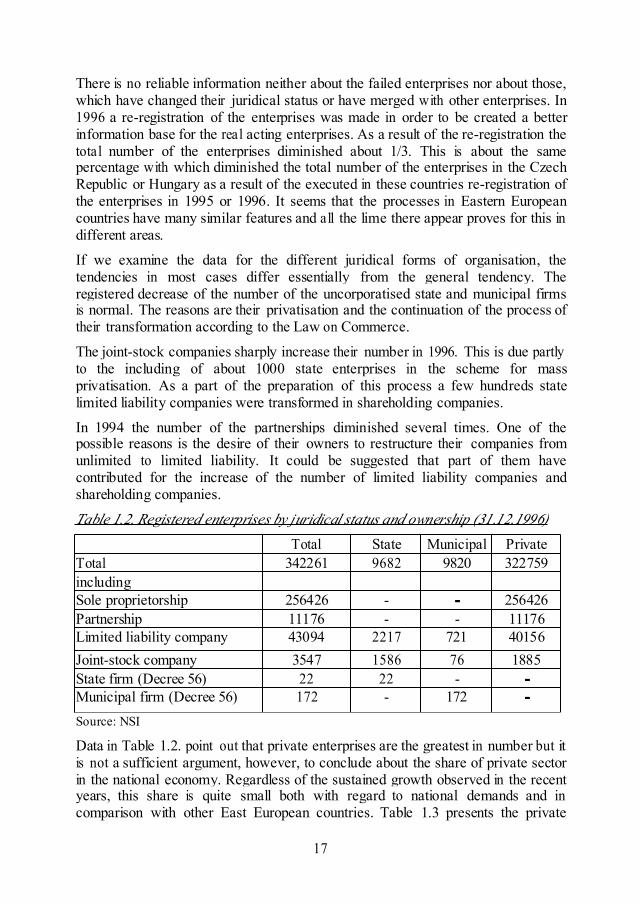

There is no reliable information neither about the failed enterprises nor about those,which have changed their juridical status or have merged with other enterprises. In1996 a re-registration of the enterprises was made in order to be created a betterinformation base for the real acting enterprises. As a result of the re-registration thetotal number of the enterprises diminished about 1/3. This is about the samepercentage with which diminished the total number of the enterprises in the CzechRepublic or Hungary as a result of the executed in these countries re-registration ofthe enterprises in 1995 or 1996. It seems that the processes in Eastern Europeancountries have many similar features and all the lime there appear proves for this indifferent areas.

If we examine the data for the different juridical forms of organisation, thetendencies in most cases differ essentially from the general tendency. Theregistered decrease of the number of the uncorporatised state and municipal firmsis normal. The reasons are their privatisation and the continuation of the process oftheir transformation according to the Law on Commerce.

The joint-stock companies sharply increase their number in 1996. This is due partlyto the including of about 1000 state enterprises in the scheme for massprivatisation. As a part of the preparation of this process a few hundreds statelimited liability companies were transformed in shareholding companies.

In 1994 the number of the partnerships diminished several times. One of thepossible reasons is the desire of their owners to restructure their companies fromunlimited to limited liability. It could be suggested that part of them havecontributed for the increase of the number of limited liability companies andshareholding companies.

Table 1.2. Registered enterprises by juridical status and ownership (31.12.1996)

Total State Municipal PrivateTotal 342261 9682 9820 322759includingSole proprietorship 256426 - ---- 256426Partnership 11176 - - 11176Limited liability company 43094 2217 721 40156Joint-stock company 3547 1586 76 1885State firm (Decree 56) 22 22 - ----Municipal firm (Decree 56) 172 - 172 ----

Source: NSI

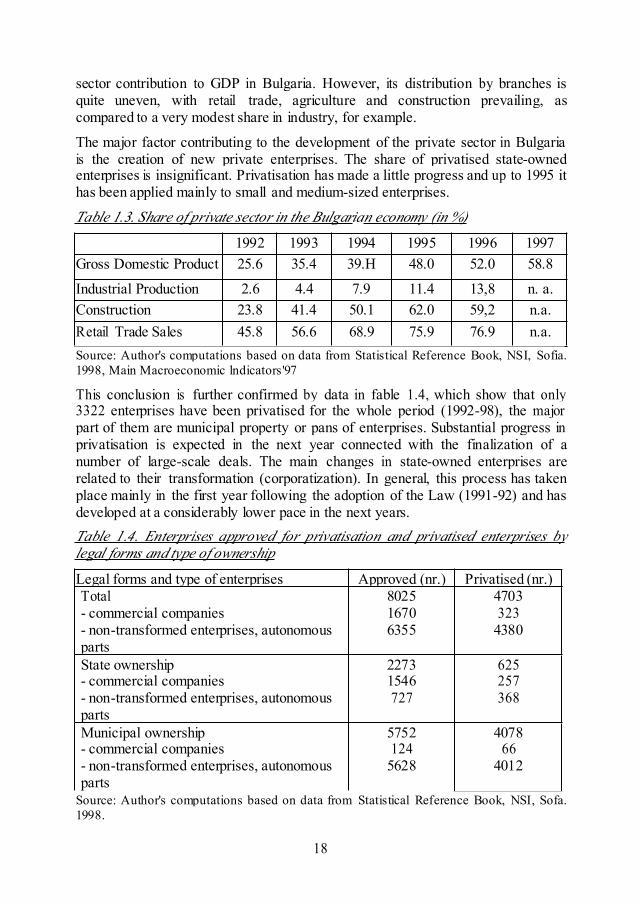

Data in Table 1.2. point out that private enterprises are the greatest in number but itis not a sufficient argument, however, to conclude about the share of private sectorin the national economy. Regardless of the sustained growth observed in the recentyears, this share is quite small both with regard to national demands and incomparison with other East European countries. Table 1.3 presents the private

18

sector contribution to GDP in Bulgaria. However, its distribution by branches isquite uneven, with retail trade, agriculture and construction prevailing, ascompared to a very modest share in industry, for example.

The major factor contributing to the development of the private sector in Bulgariais the creation of new private enterprises. The share of privatised state-ownedenterprises is insignificant. Privatisation has made a little progress and up to 1995 ithas been applied mainly to small and medium-sized enterprises.

Table 1.3. Share of private sector in the Bulgarian economy (in %)

1992 1993 1994 1995 1996 1997Gross Domestic Product 25.6 35.4 39.H 48.0 52.0 58.8

Industrial Production 2.6 4.4 7.9 11.4 13,8 n. a.Construction 23.8 41.4 50.1 62.0 59,2 n.a.Retail Trade Sales 45.8 56.6 68.9 75.9 76.9 n.a.Source: Author's computations based on data from Statistical Reference Book, NSI, Sofia.1998, Main Macroeconomic lndicators'97

This conclusion is further confirmed by data in fable 1.4, which show that only3322 enterprises have been privatised for the whole period (1992-98), the majorpart of them are municipal property or pans of enterprises. Substantial progress inprivatisation is expected in the next year connected with the finalization of anumber of large-scale deals. The main changes in state-owned enterprises arerelated to their transformation (corporatization). In general, this process has takenplace mainly in the first year following the adoption of the Law (1991-92) and hasdeveloped at a considerably lower pace in the next years.Table 1.4. Enterprises approved for privatisation and privatised enterprises bylegal forms and type of ownership

Legal forms and type of enterprises Approved (nr.) Privatised (nr.)Total- commercial companies- non-transformed enterprises, autonomousparts

802516706355

4703323

4380

State ownership- commercial companies- non-transformed enterprises, autonomousparts

22731546727

625257368

Municipal ownership- commercial companies- non-transformed enterprises, autonomousparts

5752124

5628

407866

4012

Source: Author's computations based on data from Statistical Reference Book, NSI, Sofa.1998.

19

After 1993, non-transformed state-owned and municipal firms decreased twice innumber. This was due to two main reasons: first, the continuing process oftransformation, and, second, the privatisation of non-transformed state-ownedenterprises.

Comparing the figures in Table 1.4. on the number of approved for privatisationnon-transformed enterprises it can be concluded about a prevailing policy towardsprivatisation without a preliminary transformation of enterprises.

The general conclusion can be made, therefore, that changes in the ownershipstructure of Bulgarian economy are still at their initial stage. Most probably, thecreation of modern forms of economic organisation will be completed in the nextyears. Certain problems can emerge in the functioning of enterprises, stemmingfrom insufficient changes in ownership patterns.

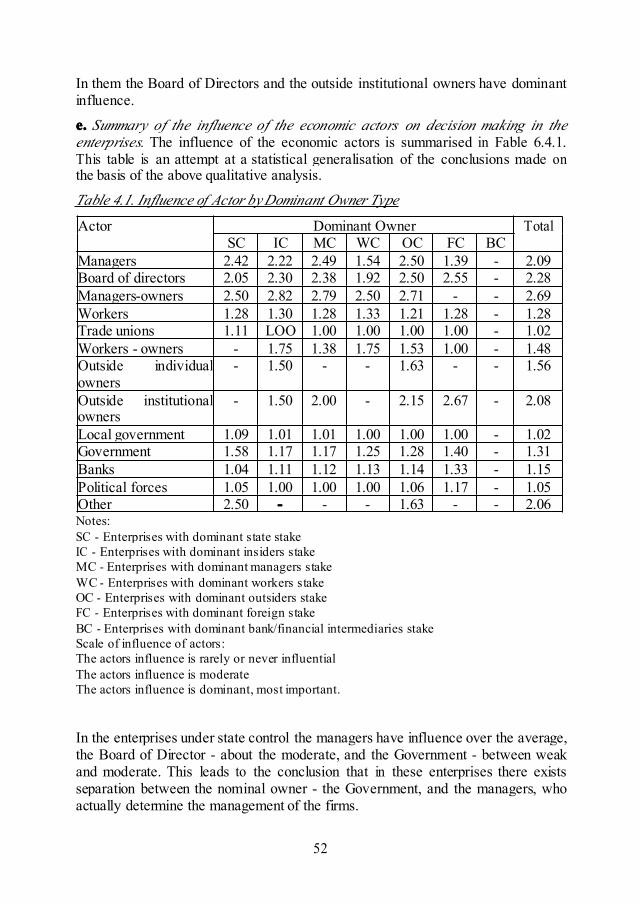

2.2.2.2. ControlControlControlControl StructureStructureStructureStructureEvery randomly selected criterion of types of corporate control in a mixedeconomy fails to reflect faithfully the reality of the Bulgarian transitional economy.The formal quantitative stake in corporate assets does not determine at present whohas real control on particular enterprise and especially on corporatized state-ownedenterprises. A more suitable classification of firms by type of control includes theboth quantitative and qualitative indicators.

According to the classical criterion, corporations may be classified by thefollowing types of control: 1) private control - one party-individual, family,financial group, etc., owns 50-80% of shares; 2) majority control - one party owns50-80% of shares; 3) minority control - one party owns 20-50% of shares; 4)control by legal device; 5) managerial control - if there is no base for externalcontrol.2222

This classification is used by other scholars in order to provide a basis for studyingthe evolution of control structures in a mixed economy. It also serves as a startingpoint for creating a corresponding classification of types of control in a transitioneconomy.

There is no official statistical information about the control types in the Bulgarianeconomy. According to recent publication of the Bulgarian National StatisticalInstitute the ownership distribution in the privatized state enterprises is as follows(percentage of privatized objects): personnel - 32,6, Bulgarian physical persons -33,2, foreign physical persons - 0,4, Bulgarian juridical persons - 30,8 and foreignjuridical persons - 3. (Currant economic conjuncture in Bulgaria, Sofia, 30November, 1997).

2 Berle, A., and Means, G., Modern Corporation and Private Ownership, New York, 1932.

20

Empirical studies show some specific control structures of enterprises in theBulgarian economy in transition.3

2.1.2.1.2.1.2.1. PrivatePrivatePrivatePrivate andandandandMajorityMajorityMajorityMajority ControlControlControlControl

The prevailing types of control of private de novo and privatised companies are theprivate and majority control. One group of the companies under private control arecharacterised with dominant outsider stake of company assets. But these outsideinstitutional shareholders are: 1) firms owned by the company managers and 2)firms with company managerial participation in their ownership. Other group of thefirms under private control have dominant workers stake. But these firms are notprevailing as the former ones.

The companies under majority control are characterised with two groups firms aswell. Some of the enterprises are with dominant outsider stake as this largeshareholder is private firm. Essential feature of these firms are managerialparticipation in the company assets and the board of directors. The other companieshave dominant managerial stake of their assets. One party, usually private firmowned by company managers is the large shareholder in these firms.

The described control structures are characterised with some key features: first, thelarge shareholder has formal effective control on the managerial behaviour throughnominating the members of board of directors, obtaining real companyinformation, hiring and firing of managers. This control type diminishes thetransaction costs for the monitoring over the managers. These costs become lowerthan the ones of companies with dispersed ownership between many smallshareholders; second, the large shareholder brings more risk and has strongermotivation to compel managers for strategies maximising the shareholders wealth.

2.22.22.22.2 ControlControlControlControl BasedBasedBasedBased onononon UnestablishedUnestablishedUnestablishedUnestablishedPropertyPropertyPropertyProperty RightsRightsRightsRights andandandand InterestInterestInterestInterest GroupsGroupsGroupsGroups

Despite 100% state participation in their ownership, the corporatized state-ownedcompanies are mainly under managerial control and interest group control. Thesetypes of control are based on unestablished property rights and informal influenceby groups other than the nominal owner State. This peculiar transition kind ofcontrol is implicit and unstable.

3 See for example, Hare, P., and Peev, E., The Sole-Trader Company and ManagerialBehaviour in a Transitional Economy, Discussion Paper in Economics, No. 94/12, 1994,Heriot-Watt University; Peev, E., and Hare, P., Corporatization and Control in theTransitional Economy, Economic Systems, Vol. 19, No. 4, December 1995, pp. 265-283;Peev. E., and Simmons, C. Property-Rights, Managerial Strategies and EnterpriseAdjustment: Bulgaria in Transition, Journal of Southern Europe and the Balkans, Issue 3,forthcoming, 2000.

21

Unestablished property rights are such property rights structures which fail todetermine clearly who owns company assets, who is a bearer of residual risk, whois a decision-maker, who nominates members of the board of directors. In thisownership structure, however, there are different degrees of managerial discretion.

Another key feature of the control structure of the sole-trader company with ahundred percent state participation is the influence of interest groups other thanState. In the Bulgarian state-owned companies interest groups other than the ownerState are trade unions, political forces, finance groups. In the distinct companiesthey have different degrees of influence on management.

2.3.2.3.2.3.2.3. RetainedRetainedRetainedRetained andandandand ClearClearClearClear GovernmentGovernmentGovernmentGovernment ControlControlControlControl

Among state-owned companies there are also companies with purposefullyretained and clear government control. But their number is small and this controlstructure is not typical of the companies with 100% state participation. The keyfeatures of the control structures observed in the empirical studies are following:first, in the existing so far private sector, private and privatised firms, there isstrong owner type of control that is the base for constraining potential discretionarymanagerial behaviour; second, in the private companies managers participateclosely in company ownership, they have stake of private firms-large owners ofcompany assets, directly own company ownership and seat on the board ofdirectors; third, contrary to the conventional view that 100% state ownership meansstrong government control as well, the state-owned enterprises are characterisedwith of a high potential for managerial discretion.

2.4.2.4.2.4.2.4. ManagerialManagerialManagerialManagerial ControlControlControlControl andandandandMinorityMinorityMinorityMinority ControlControlControlControl

It can be expected that after the mass privatisation many companies, especiallylarge firms, would acquire dispersed ownership structure. Managerial and minoritytypes of control would be emerged. There would be separation of ownership fromcontrol and potential for inefficient managerial behaviour.

3.3.3.3. GovernanceGovernanceGovernanceGovernance structuresstructuresstructuresstructuresExamination of literature shows that in corporations there are agency problemsbetween shareholders and managers that arise as a result of the former and thelatter having different motives different risk-aversion, and different strategies.Because the owners are residual risk-bearers, they are interested in pursuingefficient strategies and there are governance mechanisms for disciplining potentialmanagerial opportunism and shirking. Some governance structures in moderncorporations are: ownership concentration, managerial ownership, the board of

22

directors, managerial compensation, capital and managerial markets, markets foreconomic environment etc.

For the purposes of studying enterprises in transition it is important to know whichof the governance structures surveyed have a basic influence in discipliningmanagers. Empirical studies try to examine some of these governance mechanismsof new established companies in Bulgaria.4

3.1.3.1.3.1.3.1. OwnershipOwnershipOwnershipOwnership ConcentrationConcentrationConcentrationConcentration

The high degree of concentration of company assets at the hands of one party -private firm, firms coalition, etc., is the most important governance mechanism tocompel managers to behave effectively in the newly established private firms andprivatised firms. Because the stockholdings are concentrated the large shareholdersmay receive reliable information about the company's performance. Owners havebroad powers to remove managers. Managers may feel constrained to pursuestrategies, which are in the shareholders' best interests. The struggle for corporatecontrol between top managers, employees, state officers and outsider interestgroups of state-owned companies ends after privatisation. The peculiar separationof ownership from control between these economic agents was transformed inownership concentration and strong control of large shareholders. However, theirbehaviour is not as efficient as predicted the conventional theory because of thespecific transition "crony capitalism'"conditions.

In its policy to shift all the risks of the reforms onto state-owned companies, thestate shows clearly inefficient behaviour. Contrary to the theory, instead of theowner with 100% participation constraining the potential for managerialopportunism in the sole-trader state-owned company, the same opportunism isdemonstrated by the owner himself. The empirical studies provide a number ofexamples about this strange owner motivation. In this unique situation it is notprobably for any one other than the nominal owner to constrain managers andencourage them to pursue strategies for efficient adjustment and restructuring.These efficient agents would be managers or interest groups but the efficiency oftheir behaviour depends on chance and not on the institutional structure given. Inshort, the high state ownership concentration of companies gives rise rathermanagerial discretion than strong government control.

4 Peev. E. Separation of Ownership and Control in the Transition: the Case of Bulgaria,Europe-Asia Studies, vol. 47, No 5, 1995, pp. 859-875 .

23

3.2.3.2.3.2.3.2. ManagerialManagerialManagerialManagerial OwnershipOwnershipOwnershipOwnership

As the governance structure described above this is another important mechanismfor efficient managerial behaviour in the private and privatised firms. Managerstake participation in company property directly or through their ownership stake inthe private firm, the large company shareholder. Both cases have a basic influencein disciplining managers for more efficient behaviour.

In state-owned companies the managers do not take part in ownership because theState has 100% participation. The legal way to change their implicit control overthe company into explicit control based on private established property rights ismanagers to offer privatisation proposals on their own initiative. This futureownership stake is both strong managerial intensive to privatisation and efficientgovernance device constraining managerial opportunism in the transition.

3.33.33.33.3 BoardBoardBoardBoard ofofofof DirectorsDirectorsDirectorsDirectors

In the private and privatised companies established so far the board of directors ischaracterised as institution with real power. The investigations indicate that thisgovernance body has strong influence on strategic decisions. The top-managers siton board of directors in many companies. This shows again that in the newlyestablished private sector managers have explicit control based on their privateownership stake.In the state-owned joint-stock companies the board of directors is a specificgovernance structure. The lack of other shareholders besides the State in thecompanies in question gives grounds to assume that the board of directors isassigned a key role in the control of the enterprises. Empirical investigations,however, reveal that the role of the board of directors in company adjustment isquite passive. Typically, the board of directors of a particular company is appointedby the government and the other interest groups, which take no risk. It is controlledby them and, at the same time, must exhibit a efficient economic behaviour andplease those who determine the membership of the board. But this leads to themembers of the board taking a rather passive role, which depends on their moraland personal human qualities rather than on clear mechanisms for efficientbehaviour.

3.4.3.4.3.4.3.4. CapitalCapitalCapitalCapital andandandandManagerialManagerialManagerialManagerial LabourLabourLabourLabourMarketsMarketsMarketsMarkets

The Bulgarian Stock Exchange - Sofia began to function on 21 October 1997. Thestart of the real transactions based on free supply and demand was on 24 November1997. Till the end of the year only three transactions were concluded. At the sametime OTC markets functioned as well and according to expert estimations the bulkof the transactions were concluded in these markets. Empirical studies indicate thatthe influence of market mechanisms is weak in the prívate and slate-owned firms

24

as well. Top managers have no plans for company participation in capital markets.The market for managerial services is only a fledgling one.

Because the market mechanisms (capital and managerial labour markets and themarket for corporate control) have remained undeveloped, the main incentives forcontrol over managers of private and privatised firms are direct non-market ones.Transaction costs are low because of the high ownership concentration andmanagerial participation of company ownership. This indicates again moreeffective corporate governance of the private companies than the state-owned ones.

However, after the forthcoming "mass" privatisation many companies would obtaindispersed property structure and transaction costs will rise because of need formonitoring of managerial decisions by many small shareholders. Under theseconditions different governance structures requiring lower transaction costs arelikely to be introduced: consolidation of shareholding by proxy battles,concentration of ownership in large blocks and other cheaper mechanisms to giveshareholders more power over management.

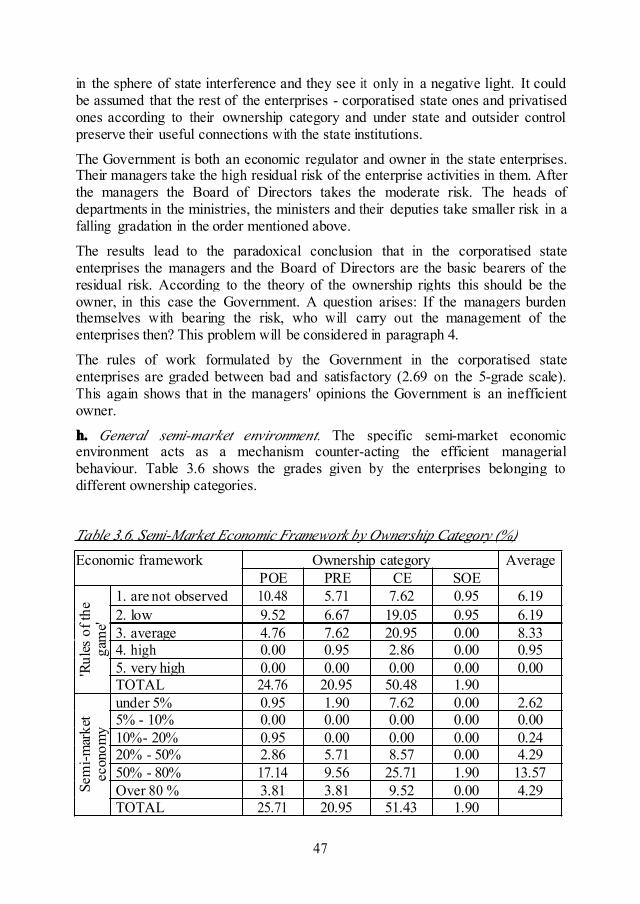

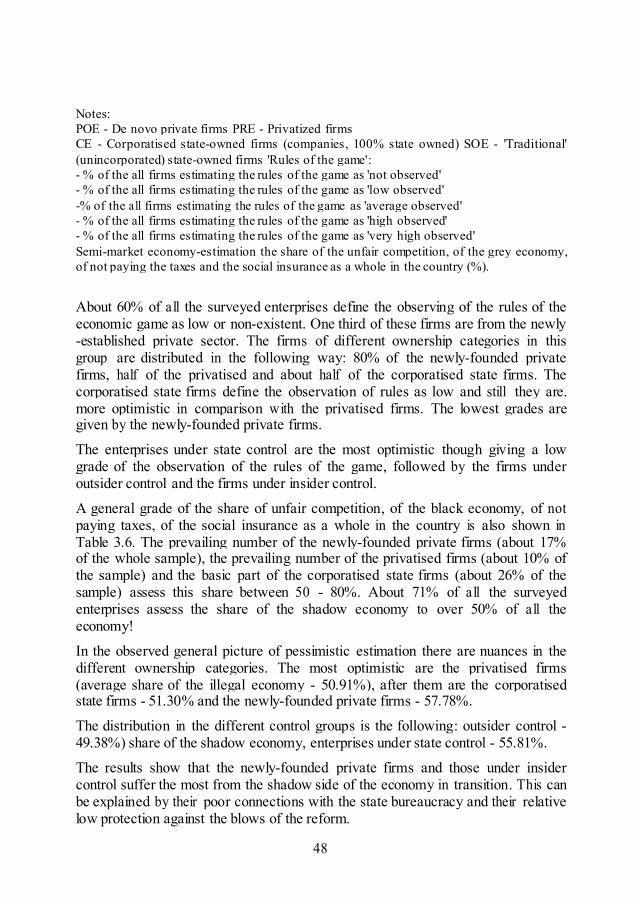

3.5.3.5.3.5.3.5. GeneralGeneralGeneralGeneral Semi-MarketSemi-MarketSemi-MarketSemi-Market EnvironmentEnvironmentEnvironmentEnvironment

The general economic environment in Bulgaria during the period studied ischaracterised as a very unstable and very "noisy". Under these specificcircumstances it is difficult to the owners to decide correctly if bad firmperformance is result of managerial mistakes or good economic position asoutcome of real managerial efforts. The most efficient governance mechanisms ofthe private and privatised firms become ownership concentration and owner-manager participation in decision-making.

In the state-owned companies the formal governance structures described aboveindicate the lack of strict institutional mechanisms for disciplining managers andthe broad scope for managerial discretion. But investigations also show theexistence of specific informal mechanisms for influencing managers. One suchpeculiar mechanism is the struggle between different interest groups for the controlof a given company.

Indicators for this unorthodox "market for corporate control" are the extent ofinvolvement of forces other than the nominally authorised ones in determining theboard of directors and the managers, the extent of involvement of such forces in theday-to-day running of the company, the degree of turnover of the companyexecutives and others. But this quasi-market delays the privatisation and goes onthe existing of the implicit managerial control.

25

4.4.4.4. EnterpriseEnterpriseEnterpriseEnterprise SizeSizeSizeSize StructureStructureStructureStructure

4.1.4.1.4.1.4.1. SourcesSourcesSourcesSources forforforfor ChangeChangeChangeChange ofofofof thethethethe SizeSizeSizeSize StructureStructureStructureStructureThe main reasons for deformed size structure of the enterprises in centrallymanaged economies are, first, the believing that only large-size production andtherefore the large-sized enterprises are effective and second, the wish to manageless at number economic entities which leads to centralisation of the existingenterprises.

At third place we can add the fears that the existing of an autonomous, marketoriented sector of small enterprises will help the economic and political unstabilityof the communist system which led to the continuously liquidation of this groupenterprises in most of the socialist countries.

The overcoming of the deform size structure of the enterprises in the period oftransition to market economy began exactly with the decline of the limitations inthe mentioned fields. First comes the development of the newly-established privateenterprises. Since they are SME as a rule, their vigorous development bought out aconsiderable growth of the relative percentage of these enterprises in the overallstructure. Second, there is the process of decentralisation of the state enterprises.Decentralising brought out growth in the overall number of enterprises anddecrease in the percentage of the large ones. Third, there is the establishing of newstate, municipal etc. non-private enterprises. Fourth, together with these sources ofincrease of the number of the enterprises it is necessary to point out one, whichleads to its decrease - liquidation of the loss-makers.

Another group of factors is connected with the change of the number of theemployees and change of the belonging of an enterprise to a certain size group.First, reducing overmanned on social reasons labour force, which varies from 20%to 40% for the different countries or different branches. Second, one should takeinto account the reduce of the employees because of the reduce of the production.The reasons could be short-term - crisis of the adjustment or middle- term - changeof the specialisation because of opening of the economy.

The mentioned two groups of factors start to act from the beginning of thetransition and it is expected that they would have short-term or middle-terminfluence. Together with them we could expect the influence of long-term factors.First, it can be expected a certain decrease of the number of the enterprises as aresult of the processes of decentralisation and demonopolization of enterprises.Second, further decrease of the number of the employed in an enterprise remainingor even increase the volume of the production as a result of the improvement oflabour productivity which now is a few times lower than it is in the developedcountries.

26

4.2.4.2.4.2.4.2. DecentralisationDecentralisationDecentralisationDecentralisation ofofofof thethethethe StateStateStateState EnterprisesEnterprisesEnterprisesEnterprises

In 1991 in Bulgaria began a process of decentralisation of the big state firms andcomplexes, existing till now, which was connected with establishment of newenterprises from their former production units. The main part of the enterpriseswere decentralised in 1991 although the process continued in the next few years.The number of the state enterprises increased in the industry from 5631 (1989) to3508 (1991) and to 4048 (1994), in the construction from 705 (1989) to 1154(1991) and to 1313 (1993), in the transport from 89 (1989) to 506 (1991) and to651 (1993), etc. After 1994-95 the number of the state enterprises began todecrease because of finishing the process of decentralization and increase in theprocess of privatization.

The analysis of the process of decentralisation of the state enterprises in thecountries from Central and South-Eastern Europe showed the existing of twomodels. The first of them (Bulgaria, Czech Republic), which can be called fulldecentralisation, is characterised with wholly separation of the former combinâtesin their composite enterprises in almost all branches.

As exceptions, subject to specific government decisions are considered usually themilitary production and some vertical combincombincombincombinââââtestestestes of a very important nationalsignificance. This approach is measured with 6-8 times increase in the number ofthe state enterprises.The applying of the second model (Romania), which can be determined as a partlydecentralisation, leads to 2-3 times increase in the number of the enterprises as aresult of the separation of obvious cases of production and economic unconnectedenterprises.

The advantages of the first model are in providing maximum opportunities forinclusion of the enterprises in a new type of division of labour, respectively in anew type of integration at national and international level, in the creation of betterconditions for competitiveness and for abolishing the monopolies.The disadvantages, which were best revealed in the Bulgarian case, are thedifficulties with the management of the many times increased number ofenterprises in conditions when the semi-market environment cannot be used as adisciplining factor. The situation of the Bulgarian enterprises was additionallycomplicated by the delaying of the privatisation.

Probably in order to avoid such weak points, the "full decentralisation" wasexecuted in the Czech Republic in two stages. The first stage was carried out in thebeginning of the reform and the second - as a part of the privatisation process.There were no limits whether to be privatised whole combinâtes, separateenterprises of their specific parts.

The decisions were taken by the state institutions choosing between severalcompeting projects. In this way the possibilities for management remain, the statecould not pass the clear cases of "hidden" privatisation, the executing of "full

27

decentralisation" coincides with the finding of new private owners.

The advantages of the "partly decentralisation" are the easier management and thekeeping of the existing production-technology links. The main disadvantage ishampering the privatisation and putting burdens in front of their restructuring, i.e.conditions for keeping and reproduction of the existing structure of the economyare created.

4.3.4.3.4.3.4.3. CreationCreationCreationCreation ofofofof NewNewNewNewPrivatePrivatePrivatePrivate EnterprisesEnterprisesEnterprisesEnterprises

In Bulgaria the number of the newly created private enterprises increasedextremely fast. Before 1989 they practically have missed, in the end of 1990 theirnumber reached 25 thousand and in the end of 1997 - 380 thousand. The speed ofthe process depends mostly on the conditions in the beginning of the transitionperiod - for example in Hungary the growth is comparatively less because evenbefore 1989 in this country there were conditions for carrying out specific forms ofprivate activity.

The general macroeconomic conditions and the policy concerning the small andmedium business definitely influence the distribution and the stability of the newlycreated private enterprises. The unstable macroeconomic situation in Bulgaria, thehigh interest rates, the high inflation, the crisis in the bank system limited theopportunities for establishment of new private enterprises and led to failure a largepart of also created firms. Besides in Bulgaria there is no policy in favour of thesmall and medium business - there is no a specific law, no financial alleviation, nocreated network for informational and consulting services, for education, etc.

It is necessary the process of establishment of new private enterprises to beencouraged, eased and supported. The reality is different. At least for Bulgaria itcan be said that the new small and medium private enterprises were created in spiteof the lack of a support from the state due to the initiative and the entrepreneurialspirit of the people. The specialised funds for crediting are insufficient and mostlyforeign originated, there is not a law on small and medium business, theentrepreneurship centres are not connected between each other, etc.

4.44.44.44.4 IncreaseIncreaseIncreaseIncreaseofofofof thethethethe TotalTotalTotalTotalNumberNumberNumberNumber ofofofof thethethethe EnterprisesEnterprisesEnterprisesEnterprises

The common tendency which can be seen in all countries from Central and South-Eastern Europe is the very quick increase in the total number of the enterprises(See Table 5.4.1. for Bulgaria). The second common feature is that the main sourceof this increase is the development of small and medium business.

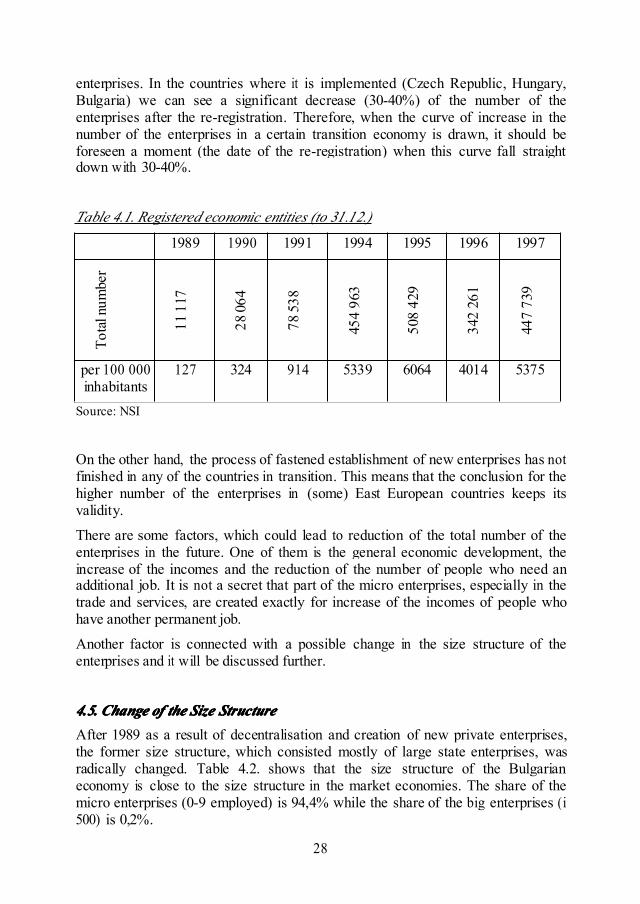

When the significance of the mentioned figures is estimated, it is necessary tomake some specifications. As a rule the total number of the enterprises in EasternEurope includes the number of the registered, not the number of the activeenterprises. One of the used decisions of the problem is re-registration of the

28

enterprises. In the countries where it is implemented (Czech Republic, Hungary,Bulgaria) we can see a significant decrease (30-40%) of the number of theenterprises after the re-registration. Therefore, when the curve of increase in thenumber of the enterprises in a certain transition economy is drawn, it should beforeseen a moment (the date of the re-registration) when this curve fall straightdown with 30-40%.

Table 4.1. Registered economic entities (to 31.12.)

1989 1990 1991 1994 1995 1996 1997

Tota

lnum

ber

1111

7

2806

4

7853

8

454

963

508

429

342

261

447

739

per 100 000inhabitants

127 324 914 5339 6064 4014 5375

Source: NSI

On the other hand, the process of fastened establishment of new enterprises has notfinished in any of the countries in transition. This means that the conclusion for thehigher number of the enterprises in (some) East European countries keeps itsvalidity.

There are some factors, which could lead to reduction of the total number of theenterprises in the future. One of them is the general economic development, theincrease of the incomes and the reduction of the number of people who need anadditional job. It is not a secret that part of the micro enterprises, especially in thetrade and services, are created exactly for increase of the incomes of people whohave another permanent job.

Another factor is connected with a possible change in the size structure of theenterprises and it will be discussed further.

4.5.4.5.4.5.4.5. ChangeChangeChangeChange ofofofof thethethethe SizeSizeSizeSize StructureStructureStructureStructureAfter 1989 as a result of decentralisation and creation of new private enterprises,the former size structure, which consisted mostly of large state enterprises, wasradically changed. Table 4.2. shows that the size structure of the Bulgarianeconomy is close to the size structure in the market economies. The share of themicro enterprises (0-9 employed) is 94,4% while the share of the big enterprises (i500) is 0,2%.

29

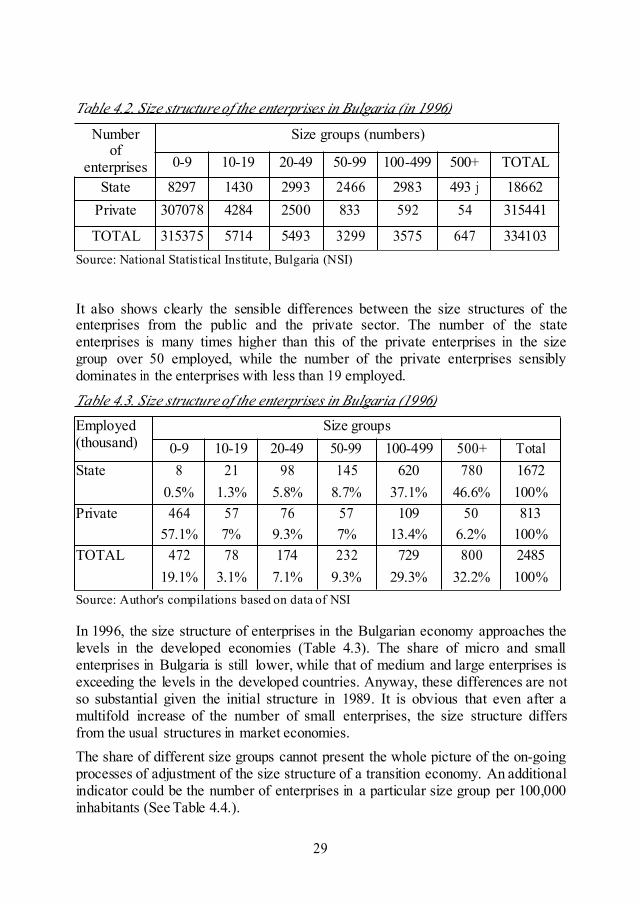

Table 4.2. Size structure of the enterprises in Bulgaria (in 1996)

Numberof

enterprises

Size groups (numbers)

0-9 10-19 20-49 50-99 100-499 500+ TOTAL

State 8297 1430 2993 2466 2983 493 j 18662Private 307078 4284 2500 833 592 54 315441

TOTAL 315375 5714 5493 3299 3575 647 334103Source: National Statistical Institute, Bulgaria (NSI)

It also shows clearly the sensible differences between the size structures of theenterprises from the public and the private sector. The number of the stateenterprises is many times higher than this of the private enterprises in the sizegroup over 50 employed, while the number of the private enterprises sensiblydominates in the enterprises with less than 19 employed.

Table 4.3. Size structure of the enterprises in Bulgaria (1996)

Employed(thousand)

Size groups0-9 10-19 20-49 50-99 100-499 500+ Total

State 8 21 98 145 620 780 16720.5% 1.3% 5.8% 8.7% 37.1% 46.6% 100%

Private 464 57 76 57 109 50 81357.1% 7% 9.3% 7% 13.4% 6.2% 100%

TOTAL 472 78 174 232 729 800 248519.1% 3.1% 7.1% 9.3% 29.3% 32.2% 100%

Source: Author's compilations based on data of NSI

In 1996, the size structure of enterprises in the Bulgarian economy approaches thelevels in the developed economies (Table 4.3). The share of micro and smallenterprises in Bulgaria is still lower, while that of medium and large enterprises isexceeding the levels in the developed countries. Anyway, these differences are notso substantial given the initial structure in 1989. It is obvious that even after amultifold increase of the number of small enterprises, the size structure differsfrom the usual structures in market economies.The share of different size groups cannot present the whole picture of the on-goingprocesses of adjustment of the size structure of a transition economy. An additionalindicator could be the number of enterprises in a particular size group per 100,000inhabitants (See Table 4.4.).

30

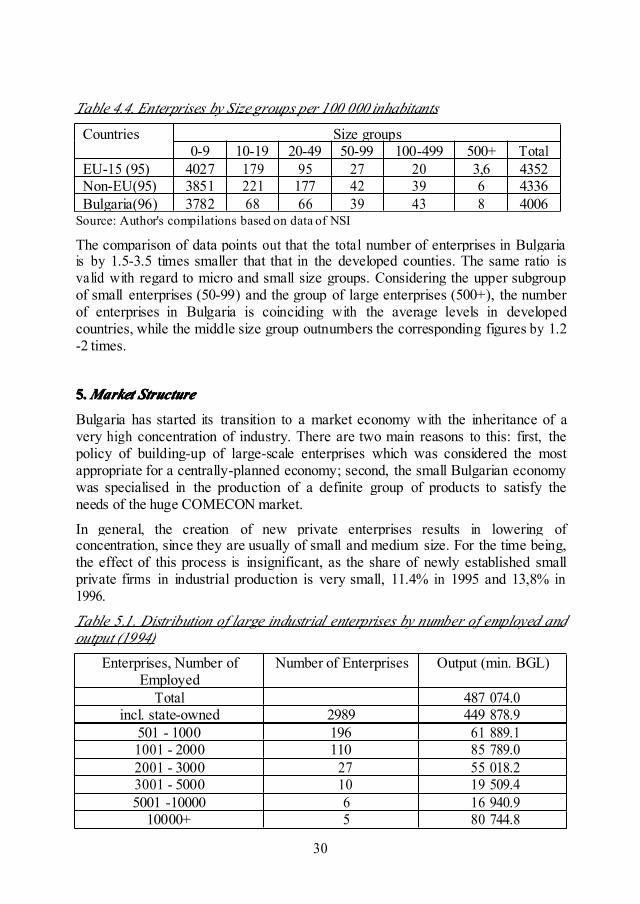

Table 4.4. Enterprises by Size groups per 100 000 inhabitants

Countries Size groups0-9 10-19 20-49 50-99 100-499 500+ Total

EU-15 (95) 4027 179 95 27 20 3,6 4352Non-EU(95) 3851 221 177 42 39 6 4336Bulgaria(96) 3782 68 66 39 43 8 4006

Source: Author's compilations based on data of NSI

The comparison of data points out that the total number of enterprises in Bulgariais by 1.5-3.5 times smaller that that in the developed counties. The same ratio isvalid with regard to micro and small size groups. Considering the upper subgroupof small enterprises (50-99) and the group of large enterprises (500+), the numberof enterprises in Bulgaria is coinciding with the average levels in developedcountries, while the middle size group outnumbers the corresponding figures by 1.2-2 times.

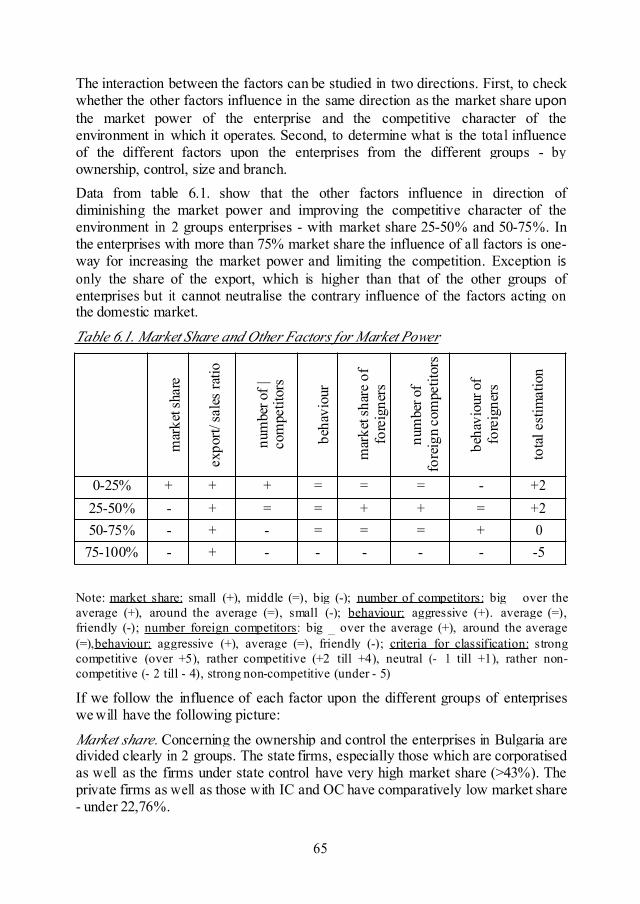

5.5.5.5.MarketMarketMarketMarket StructureStructureStructureStructure

Bulgaria has started its transition to a market economy with the inheritance of avery high concentration of industry. There are two main reasons to this: first, thepolicy of building-up of large-scale enterprises which was considered the mostappropriate for a centrally-planned economy; second, the small Bulgarian economywas specialised in the production of a definite group of products to satisfy theneeds of the huge COMECON market.

In general, the creation of new private enterprises results in lowering ofconcentration, since they are usually of small and medium size. For the time being,the effect of this process is insignificant, as the share of newly established smallprivate firms in industrial production is very small, 11.4% in 1995 and 13,8% in1996.

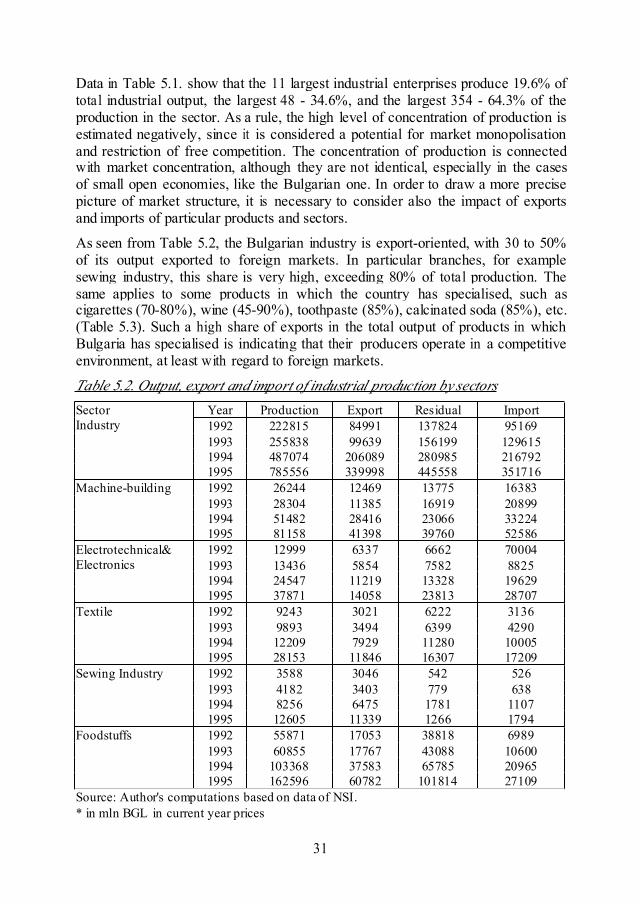

Table 5.1. Distribution of large industrial enterprises by number of employed andoutput (1994)

Enterprises, Number ofEmployed

Number of Enterprises Output (min. BGL)

Total 487 074.0incl. state-owned 2989 449 878.9

501 - 1000 196 61 889.11001 - 2000 110 85 789.02001 - 3000 27 55 018.23001 - 5000 10 19 509.45001 -10000 6 16 940.9

10000+ 5 80 744.8

31

Data in Table 5.1. show that the 11 largest industrial enterprises produce 19.6% oftotal industrial output, the largest 48 - 34.6%, and the largest 354 - 64.3% of theproduction in the sector. As a rule, the high level of concentration of production isestimated negatively, since it is considered a potential for market monopolisationand restriction of free competition. The concentration of production is connectedwith market concentration, although they are not identical, especially in the casesof small open economies, like the Bulgarian one. In order to draw a more precisepicture of market structure, it is necessary to consider also the impact of exportsand imports of particular products and sectors.

As seen from Table 5.2, the Bulgarian industry is export-oriented, with 30 to 50%of its output exported to foreign markets. In particular branches, for examplesewing industry, this share is very high, exceeding 80% of total production. Thesame applies to some products in which the country has specialised, such ascigarettes (70-80%), wine (45-90%), toothpaste (85%), calcinated soda (85%), etc.(Table 5.3). Such a high share of exports in the total output of products in whichBulgaria has specialised is indicating that their producers operate in a competitiveenvironment, at least with regard to foreign markets.

Table 5.2. Output, export and import of industrial production by sectorsSectorIndustry

Year Production Export Residual Import1992 222815 84991 137824 951691993 255838 99639 156199 1296151994 487074 206089 280985 2167921995 785556 339998 445558 351716

Machine-building 1992 26244 12469 13775 163831993 28304 11385 16919 208991994 51482 28416 23066 332241995 81158 41398 39760 52586

Electrotechnical&Electronics

1992 12999 6337 6662 700041993 13436 5854 7582 88251994 24547 11219 13328 196291995 37871 14058 23813 28707

Textile 1992 9243 3021 6222 31361993 9893 3494 6399 42901994 12209 7929 11280 100051995 28153 11846 16307 17209

Sewing Industry 1992 3588 3046 542 5261993 4182 3403 779 6381994 8256 6475 1781 11071995 12605 11339 1266 1794

Foodstuffs 1992 55871 17053 38818 69891993 60855 17767 43088 106001994 103368 37583 65785 209651995 162596 60782 101814 27109

Source: Author's computations based on data of NSI.* in mln BGL in current year prices

32

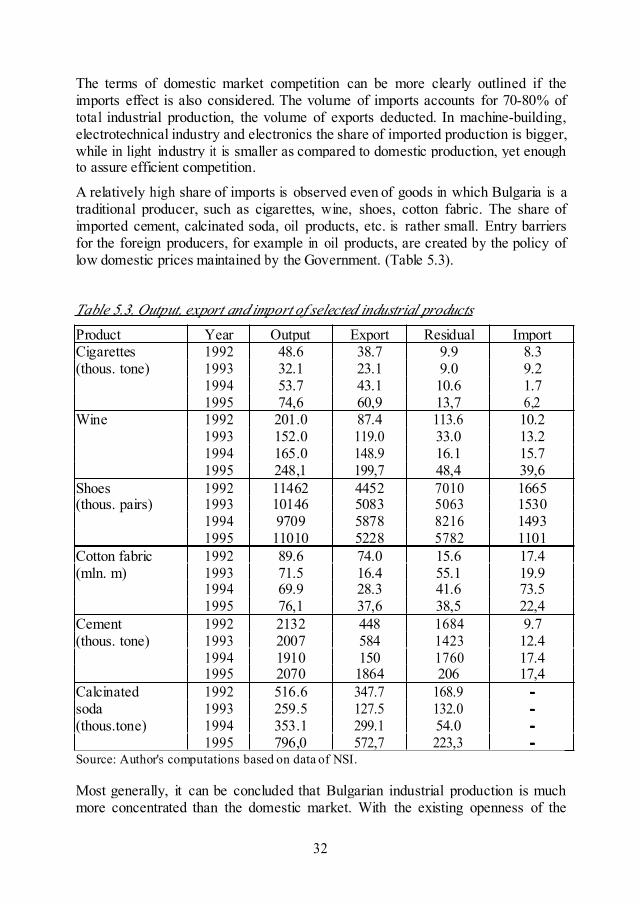

The terms of domestic market competition can be more clearly outlined if theimports effect is also considered. The volume of imports accounts for 70-80% oftotal industrial production, the volume of exports deducted. In machine-building,electrotechnical industry and electronics the share of imported production is bigger,while in light industry it is smaller as compared to domestic production, yet enoughto assure efficient competition.

A relatively high share of imports is observed even of goods in which Bulgaria is atraditional producer, such as cigarettes, wine, shoes, cotton fabric. The share ofimported cement, calcinated soda, oil products, etc. is rather small. Entry barriersfor the foreign producers, for example in oil products, are created by the policy oflow domestic prices maintained by the Government. (Table 5.3).

Table 5.3. Output, export and import of selected industrial products

Product Year Output Export Residual ImportCigarettes(thous. tone)

1992 48.6 38.7 9.9 8.31993 32.1 23.1 9.0 9.21994 53.7 43.1 10.6 1.71995 74,6 60,9 13,7 6,2

Wine 1992 201.0 87.4 113.6 10.21993 152.0 119.0 33.0 13.21994 165.0 148.9 16.1 15.71995 248,1 199,7 48,4 39,6

Shoes(thous. pairs)

1992 11462 4452 7010 16651993 10146 5083 5063 15301994 9709 5878 8216 14931995 11010 5228 5782 1101

Cotton fabric(mln. m)

1992 89.6 74.0 15.6 17.41993 71.5 16.4 55.1 19.91994 69.9 28.3 41.6 73.51995 76,1 37,6 38,5 22,4

Cement(thous. tone)

1992 2132 448 1684 9.71993 2007 584 1423 12.41994 1910 150 1760 17.41995 2070 1864 206 17,4

Calcinatedsoda(thous.tone)

1992 516.6 347.7 168.9 ----1993 259.5 127.5 132.0 ----1994 353.1 299.1 54.0 ----1995 796,0 572,7 223,3 ----

Source: Author's computations based on data of NSI.

Most generally, it can be concluded that Bulgarian industrial production is muchmore concentrated than the domestic market. With the existing openness of the

33

economy, however, all producers should be free to operate in a competitiveenvironment.

6666.... Government-FirmsGovernment-FirmsGovernment-FirmsGovernment-Firms RelationsRelationsRelationsRelationsI Inder the conditions of quasi-market environment and absent market institutions,the state has to fulfil functions similar to that of the market in normal marketeconomies, such as obeying financial discipline, financial restructuring orliquidation of enterprises, etc. In Bulgaria, the main problems in this sphere areconnected with subsidies and budget dotations, liquidation and financialrestructuring of enterprises.

6.1.6.1.6.1.6.1. ProductionProductionProductionProduction SubsidiesSubsidiesSubsidiesSubsidies andandandand BudgetBudgetBudgetBudget DotationsDotationsDotationsDotations

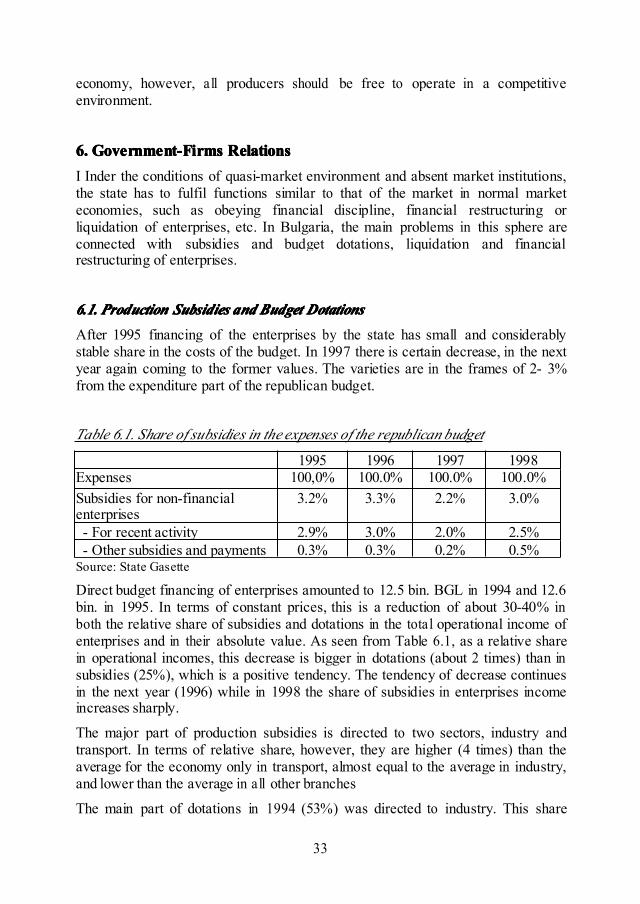

After 1995 financing of the enterprises by the state has small and considerablystable share in the costs of the budget. In 1997 there is certain decrease, in the nextyear again coming to the former values. The varieties are in the frames of 2- 3%from the expenditure part of the republican budget.

Table 6.1. Share of subsidies in the expenses of the republican budget

1995 1996 1997 1998Expenses 100,0% 100.0% 100.0% 100.0%Subsidies for non-financialenterprises

3.2% 3.3% 2.2% 3.0%

- For recent activity 2.9% 3.0% 2.0% 2.5%- Other subsidies and payments 0.3% 0.3% 0.2% 0.5%

Source: State Gasette

Direct budget financing of enterprises amounted to 12.5 bin. BGL in 1994 and 12.6bin. in 1995. In terms of constant prices, this is a reduction of about 30-40% inboth the relative share of subsidies and dotations in the total operational income ofenterprises and in their absolute value. As seen from Table 6.1, as a relative sharein operational incomes, this decrease is bigger in dotations (about 2 times) than insubsidies (25%), which is a positive tendency. The tendency of decrease continuesin the next year (1996) while in 1998 the share of subsidies in enterprises incomeincreases sharply.

The major part of production subsidies is directed to two sectors, industry andtransport. In terms of relative share, however, they are higher (4 times) than theaverage for the economy only in transport, almost equal to the average in industry,and lower than the average in all other branches

The main part of dotations in 1994 (53%) was directed to industry. This share

34

demonstrated a considerable decrease in 1995, down to 21%, yet remained abovethe average for the economy. The highest share of dotations went to construction,while the greatest increase in 1995 was observed in trade, the three sectors thusreceiving about 80% of total volume of dotations.

Production subsidies and dotations are quite unevenly distributed between industrysectors. Nearly a three-quarter of subsidies is directed to coal mining andproduction of electricity. The same branches have also the highest level ofsubsidies per unit of operational income - 2-3 times in electricity and more than 20times in coal mining. The rest of industrial branches are either close to the averagefor the economy (for example, non-ferrous metals) or considerably lower.

In their main part (88%), 1994 dotations were directed to production of electricityand non-ferrous metallurgy. Actually, non-ferrous metallurgy was the only branchdotated in 1995. There was a drastic decrease in dotations for electricity, whiletheir level in the other branches was insignificant.

It can be concluded that the main reason for direct financing of enterprises by thebudget is the maintenance of lower prices of energy carriers. The total increase ofthe share of production subsidies in 1998 is arranged together with theirconcentration. For example their share in carbon industry, non-ferrous metallurgy,wood industry, agriculture and trade decreases sharply, while in electric power andsteam energy, forestry and transport increases. The increased volume of subsidiesis distributed in branches, where the state by social reasons continues to paysubsidies.

6.2.6.2.6.2.6.2. FinancialFinancialFinancialFinancial RestructuringRestructuringRestructuringRestructuring ofofofof EnterprisesEnterprisesEnterprisesEnterprises

The delay of structural reforms in Bulgaria has brought bad financial results in agreat number of enterprises. In April 1996, the Government advanced a programfor restructuring, consisting of two main parts - liquidation, and financialrestructuring of loss-making state-owned enterprises.The program of financial restructuring includes a list of 36 industrial enterprises:15 in machine-building, 5 in electrotechnical industry, 4 in chemistry and oil-processing, 5 in textile, 3 in non-ferrous metallurgy, 2 in ferrous metallurgy, and 2in glass industry.

The total debt of these enterprises amounts to 54.6 bin BGL, which is equal to theircapital (54.5 bin. BGL), or their fixed tangible assets (59 bin. BGL). This is anindicator of a very high degree of decapitalization of enterprises included in theProgram, yet comparing the figures it should be kept into account that a revaluationof assets has not been made in Bulgaria since 1992, therefore the value (resp. price)of these enterprises should several times higher. In terms of current financialresults and indebtedness, enterprises can be classified into 4 main groups, namely:positive results and small debt, positive financial results and very big debt, currentloss and small debt, and current loss combined with very high indebtedness.

35

Obviously, enterprises suffer different problems and the solutions should besearched for each case in particular. Enterprises are given three months to prepareindividual plans for financial restructuring in a one-year term. If they aresuccessful, enterprises would be allowed rescheduling, reduction or cancellation ofold debts; in the opposite case, measures would be undertaken lor their liquidation.Enterprises included in the financial restructuring program ire under thegovernance and supervision of the Ministry of Finance.

6.36.36.36.3.... LiquidationLiquidationLiquidationLiquidation ofofofof EnterprisesEnterprisesEnterprisesEnterprises

Like in some other East European countries, the governments in Bulgaria haveproved to be rather reluctant towards the liquidation of state-owned enterprises. Ihe reason here is neither the absence of adequate legal basis, nor thenon existence of state loss-makers. Actually, there hasn't been adopted aparticular law on bankruptcy, yet the Commercial Law (1991) includes a specialchapter regulating this issue.

It was realised only in spring 1996 that any further delay in the solution of theseproblems would be crucial, and steps were undertaken in two directions: first,working-out a program for liquidation of a part of enterprises in extremely badfinancial condition, and, second, creating the prerequisites for the normalfunctioning and application of already existing legislation regarding the liquidationof loss-making state enterprises.

The program for liquidation has been initiated by the World Bank and theInternational Monetary Fund and is accomplished with the financial and expertassistance of these institutions. There are 64 state-owned companies included in thelist for liquidation, of them 38 in industry. These companies account for 3% of thetotal number of employees, 7% of the fixed assets, and more than 30% of the lossesin the sector. The total debt of enterprises in the list exceeds by 2.6 times theirfixed capital and by 2 times their long-term tangible assets. The goal of theprogram, therefore, is to improve the general performance of the sector, with aminimum negative effect on the employed.

Liquidation procedures have been opened for 27 of enterprises, while theremaining 11 will be privatised. Privatisation deals have been already concludedfor 8 of them, the rest are in process of negotiations with potential buyers.

As a result of the application of the provisions of the Commercial Law regulatingthe liquidation of companies, closing and liquidation procedures have been openedfor another group of 44 loss-making enterprises. These are mainly small- sizedenterprises with a total of 1070 employed.

36

II.II.II.II. Ownership,Ownership,Ownership,Ownership, ControlControlControlControl andandandand EconomicEconomicEconomicEconomic Behaviour:Behaviour:Behaviour:Behaviour: QuestionnaireQuestionnaireQuestionnaireQuestionnaireSurveySurveySurveySurvey inininin BulgariaBulgariaBulgariaBulgaria1.1.1.1. IntroductionIntroductionIntroductionIntroduction105 industrial enterprises were surveyed in Bulgaria. Paragraph 2. describes thesample of the surveyed enterprises. Paragraph 3. reveals the basic characteristics ofthe observed ownership, control and governance structures. Paragraph 4. analysesthe effect of the ownership structures and control on managerial behaviour andParagraph 5. on firm performance. Paragraph 6. analyses the influence of themarket structure, the Government, the industrial sector and size structure on firmperformance.

2.2.2.2. SampleSampleSampleSampleCharacteristicsCharacteristicsCharacteristicsCharacteristicsOwnership structure. The survey comprised four major groups of firms, classifiedaccording to the type of ownership: state-owned (SOE), corporatized state-owned(CE), former state-owned firms which have been privatized (PRE), and privatefirms established de novo (POE). Out of 105 surveyed enterprises 27 were POEs,22 - PREs, 54 - CEs, 2 - SOEs. The insignificant number of the traditional stateenterprises in the sample reflects the insignificant position of this kind ofownership in the Bulgarian industry. Out of all the registered enterprises inBulgaria in 1995, exactly 17,595 are CEs, whereas only 776 are SOEs. Aqualitative analysis can establish that there is not a significant industrial enterprise,which has remained SOEs. All the enterprises important to the country weretransformed in CEs as early as 1990/91.65% of the studied enterprises existed in some other form. 70% of the CEs existedin another form. Most of them were entirely owned by the state. This is typical ofthe transformation of SOEs into corporatised enterprises entirely owned by thestate (CEs). 95.5% of the privatised enterprises existed as state enterprises and4.5% as part of a state enterprise. This is not typical of the privatisation in thecountry where the prevailing number of the privatised enterprises were formed outof parts of state enterprises. But as far as their importance to the economy of thecountry is concerned the privatised firms originating from whole state enterpriseshave priority because as a rule they have bigger assets and a greater number ofpersonnel.Legal form structure. The sole proprietors prevail among the POEs (51.9% of thesample) which is typical of the existing private sector in Bulgaria too. LimitedLiability companies (33.3% of the sample) are the remaining big group of surveyedenterprises. They come third in number in the Bulgarian private sector in 1995.General partnerships were not included in the sample though they come second innumber in the private sector. The lack of precise statistics makes it difficult toestimate the actual share of these enterprises only in the industry. The empiricalwork of the interviewers within the adopted inductive approach did not find even asingle enterprise answering the sample criteria. 68.2% of the surveyed 1'iivatisedfirms are joint-stock companies. The rest are limited liability companies. It is

37

difficult to gather information in order to conclude whether this structure is typicalof the country.

Organisation structure. The average number of plants in the surveyed enterprises isabout 1 in the private sector and 2 in the public one. 6% of the CEs and 9% of thePREs are subsidiaries of other firms. On their part 6% of the CEs, 9% of the PREsand 11% of the POEs have their own subsidiaries. The structure of the samplefollows the tendencies in the development of the organisational structures in theBulgarian industry characterised by decentralisation of the economic units.

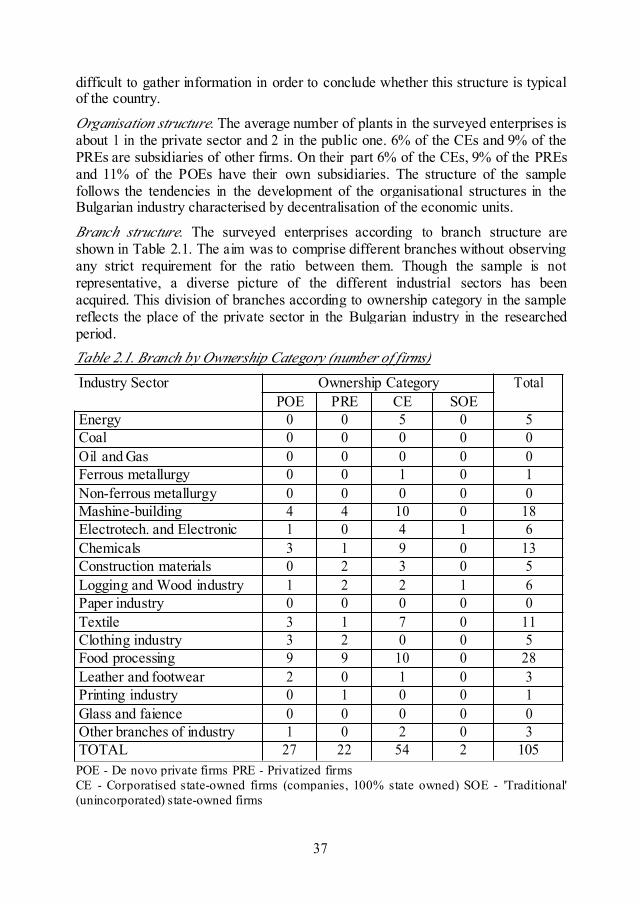

Branch structure. The surveyed enterprises according to branch structure areshown in Table 2.1. The aim was to comprise different branches without observingany strict requirement for the ratio between them. Though the sample is notrepresentative, a diverse picture of the different industrial sectors has beenacquired. This division of branches according to ownership category in the samplereflects the place of the private sector in the Bulgarian industry in the researchedperiod.Table 2.1. Branch by Ownership Category (number of firms)

Industry Sector Ownership Category TotalPOE PRE CE SOE

Energy 0 0 5 0 5Coal 0 0 0 0 0Oil and Gas 0 0 0 0 0Ferrous metallurgy 0 0 1 0 1Non-ferrous metallurgy 0 0 0 0 0Mashine-building 4 4 10 0 18Electrotech. and Electronic 1 0 4 1 6Chemicals 3 1 9 0 13Construction materials 0 2 3 0 5Logging and Wood industry 1 2 2 1 6Paper industry 0 0 0 0 0Textile 3 1 7 0 11Clothing industry 3 2 0 0 5Food processing 9 9 10 0 28Leather and footwear 2 0 1 0 3Printing industry 0 1 0 0 1Glass and faience 0 0 0 0 0Other branches of industry 1 0 2 0 3TOTAL 27 22 54 2 105POE - De novo private firms PRE - Privatized firmsCE - Corporatised state-owned firms (companies, 100% state owned) SOE - 'Traditional'(unincorporated) state-owned firms

38

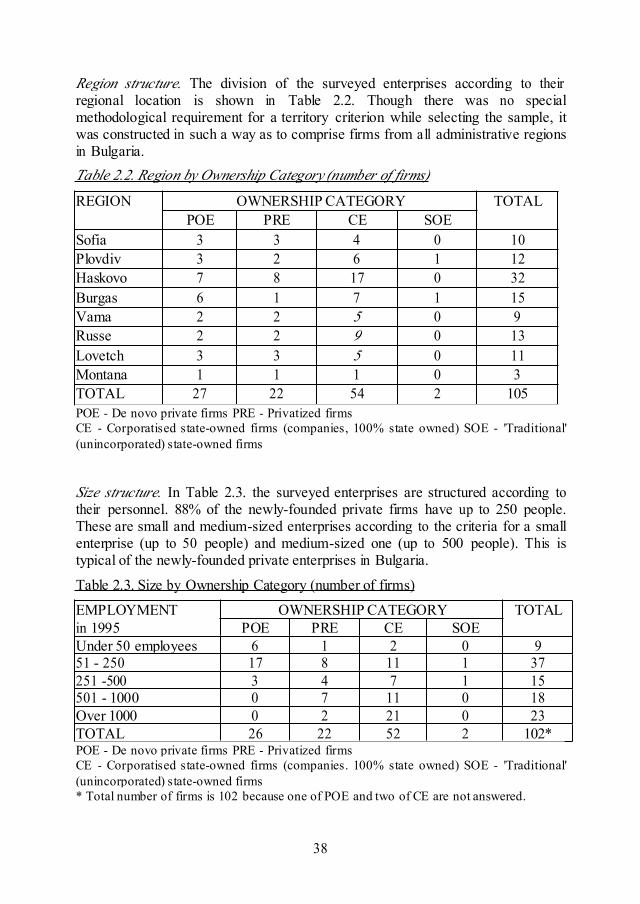

Region structure. The division of the surveyed enterprises according to theirregional location is shown in Table 2.2. Though there was no specialmethodological requirement for a territory criterion while selecting the sample, itwas constructed in such a way as to comprise firms from all administrative regionsin Bulgaria.Table 2.2. Region by Ownership Category (number of firms)

REGION OWNERSHIP CATEGORY TOTALPOE PRE CE SOE

Sofia 3 3 4 0 10Plovdiv 3 2 6 1 12Haskovo 7 8 17 0 32Burgas 6 1 7 1 15Vama 2 2 5 0 9Russe 2 2 9 0 13Lovetch 3 3 5 0 11Montana 1 1 1 0 3TOTAL 27 22 54 2 105POE - De novo private firms PRE - Privatized firmsCE - Corporatised state-owned firms (companies, 100% state owned) SOE - 'Traditional'(unincorporated) state-owned firms

Size structure. In Table 2.3. the surveyed enterprises are structured according totheir personnel. 88% of the newly-founded private firms have up to 250 people.These are small and medium-sized enterprises according to the criteria for a smallenterprise (up to 50 people) and medium-sized one (up to 500 people). This istypical of the newly-founded private enterprises in Bulgaria.

Table 2.3. Size by Ownership Category (number of firms)

EMPLOYMENT OWNERSHIP CATEGORY TOTALin 1995 POE PRE CE SOEUnder 50 employees 6 1 2 0 951 - 250 17 8 11 1 37251 -500 3 4 7 1 15501 - 1000 0 7 11 0 18Over 1000 0 2 21 0 23TOTAL 26 22 52 2 102*POE - De novo private firms PRE - Privatized firmsCE - Corporatised state-owned firms (companies. 100% state owned) SOE - 'Traditional'(unincorporated) state-owned firms* Total number of firms is 102 because one of POE and two of CE are not answered.

39

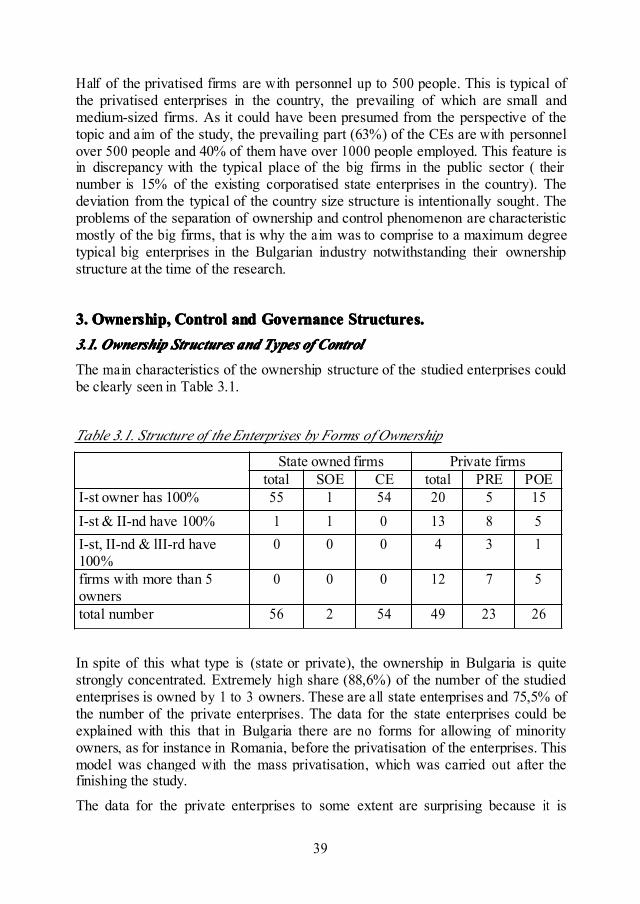

Half of the privatised firms are with personnel up to 500 people. This is typical ofthe privatised enterprises in the country, the prevailing of which are small andmedium-sized firms. As it could have been presumed from the perspective of thetopic and aim of the study, the prevailing part (63%) of the CEs are with personnelover 500 people and 40% of them have over 1000 people employed. This feature isin discrepancy with the typical place of the big firms in the public sector ( theirnumber is 15% of the existing corporatised state enterprises in the country). Thedeviation from the typical of the country size structure is intentionally sought. Theproblems of the separation of ownership and control phenomenon are characteristicmostly of the big firms, that is why the aim was to comprise to a maximum degreetypical big enterprises in the Bulgarian industry notwithstanding their ownershipstructure at the time of the research.

3.3.3.3. Ownership,Ownership,Ownership,Ownership, ControlControlControlControl andandandand GovernanceGovernanceGovernanceGovernance Structures.Structures.Structures.Structures.3.1.3.1.3.1.3.1. OwnershipOwnershipOwnershipOwnership StructuresStructuresStructuresStructures andandandand TypesTypesTypesTypes ofofofof ControlControlControlControl

The main characteristics of the ownership structure of the studied enterprises couldbe clearly seen in Table 3.1.

Table 3.1. Structure of the Enterprises by Forms of Ownership

State owned firms Private firmstotal SOE CE total PRE POE

I-st owner has 100% 55 1 54 20 5 15I-st & II-nd have 100% 1 1 0 13 8 5I-st, II-nd & lII-rd have100%

0 0 0 4 3 1

firms with more than 5owners

0 0 0 12 7 5

total number 56 2 54 49 23 26

In spite of this what type is (state or private), the ownership in Bulgaria is quitestrongly concentrated. Extremely high share (88,6%) of the number of the studiedenterprises is owned by 1 to 3 owners. These are all state enterprises and 75,5% ofthe number of the private enterprises. The data for the state enterprises could beexplained with this that in Bulgaria there are no forms for allowing of minorityowners, as for instance in Romania, before the privatisation of the enterprises. Thismodel was changed with the mass privatisation, which was carried out after thefinishing the study.

The data for the private enterprises to some extent are surprising because it is

40

known that there are fears from dispersion of the ownership in the transitioneconomies in result of the privatisation. In our case there is only weak tendency todispersion which is revealing in the fact that the relative share of the privatisedenterprises, owned by 1+3 owners (69,6%) is lower than of the private enterprisescreated de novo (80,8%).Interesting are 11% of the number of the enterprises which have more than 5owners. The share of the first 5 owners does not exceed 50% as in privatised(29.8%) and in the newly created private enterprises (42,9%).

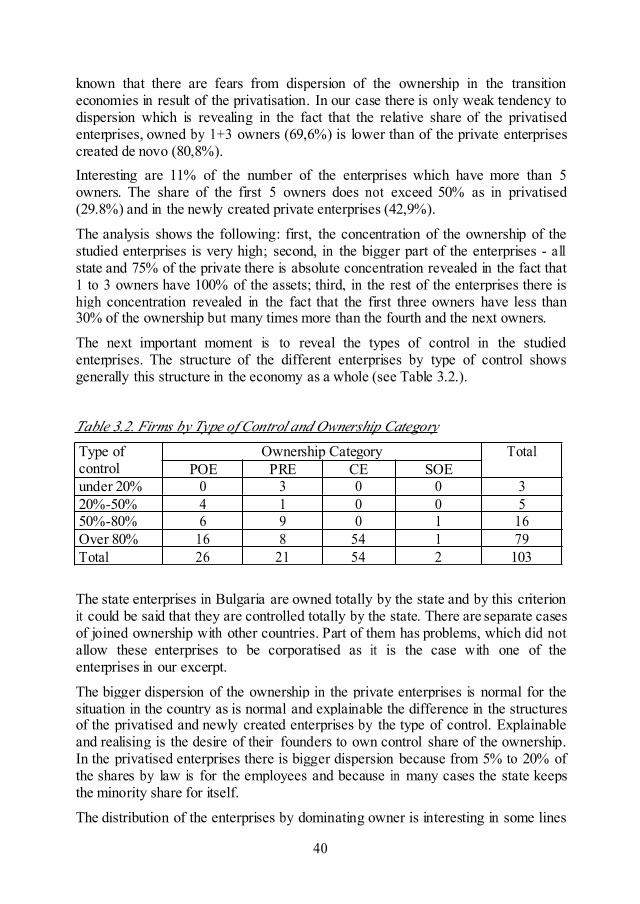

The analysis shows the following: first, the concentration of the ownership of thestudied enterprises is very high; second, in the bigger part of the enterprises - allstate and 75% of the private there is absolute concentration revealed in the fact that1 to 3 owners have 100% of the assets; third, in the rest of the enterprises there ishigh concentration revealed in the fact that the first three owners have less than30% of the ownership but many times more than the fourth and the next owners.

The next important moment is to reveal the types of control in the studiedenterprises. The structure of the different enterprises by type of control showsgenerally this structure in the economy as a whole (see Table 3.2.).

Table 3.2. Firms by Type of Control and Ownership Category

Type ofcontrol

Ownership Category TotalPOE PRE CE SOE

under 20% 0 3 0 0 320%-50% 4 1 0 0 550%-80% 6 9 0 1 16Over 80% 16 8 54 1 79Total 26 21 54 2 103

The state enterprises in Bulgaria are owned totally by the state and by this criterionit could be said that they are controlled totally by the state. There are separate casesof joined ownership with other countries. Part of them has problems, which did notallow these enterprises to be corporatised as it is the case with one of theenterprises in our excerpt.

The bigger dispersion of the ownership in the private enterprises is normal for thesituation in the country as is normal and explainable the difference in the structuresof the privatised and newly created enterprises by the type of control. Explainableand realising is the desire of their founders to own control share of the ownership.In the privatised enterprises there is bigger dispersion because from 5% to 20% ofthe shares by law is for the employees and because in many cases the state keepsthe minority share for itself.

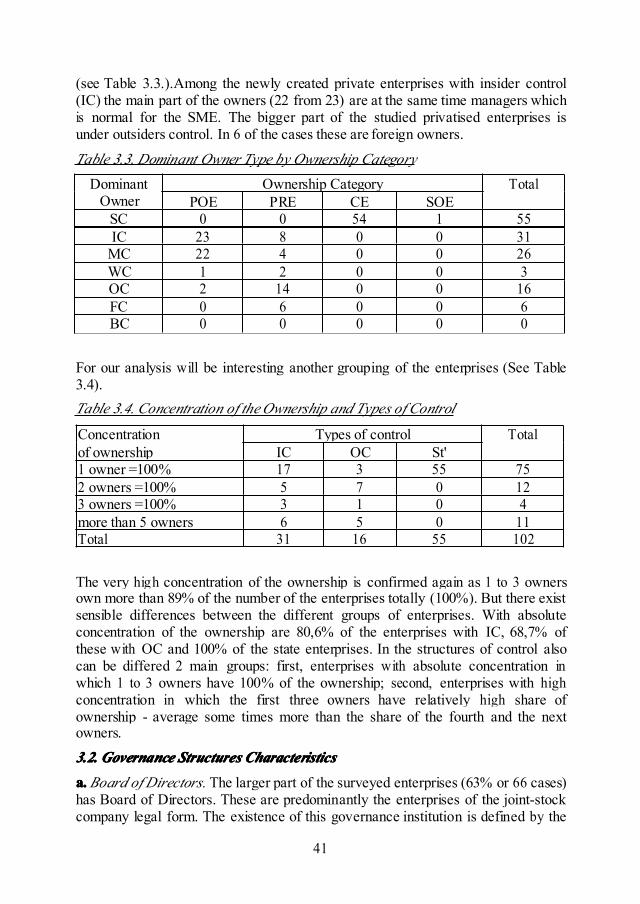

The distribution of the enterprises by dominating owner is interesting in some lines

41

(see Table 3.3.).Among the newly created private enterprises with insider control(IC) the main part of the owners (22 from 23) are at the same time managers whichis normal for the SME. The bigger part of the studied privatised enterprises isunder outsiders control. In 6 of the cases these are foreign owners.

Table 3.3. Dominant Owner Type by Ownership Category

DominantOwner

Ownership Category TotalPOE PRE CE SOE

SC 0 0 54 1 55IC 23 8 0 0 31

MC 22 4 0 0 26WC 1 2 0 0 3OC 2 14 0 0 16FC 0 6 0 0 6BC 0 0 0 0 0

For our analysis will be interesting another grouping of the enterprises (See Table3.4).Table 3.4. Concentration of theOwnership and Types of Control

Concentration Types of control Totalof ownership IC OC St'1 owner =100% 17 3 55 752 owners =100% 5 7 0 123 owners =100% 3 1 0 4more than 5 owners 6 5 0 11Total 31 16 55 102

The very high concentration of the ownership is confirmed again as 1 to 3 ownersown more than 89% of the number of the enterprises totally (100%). But there existsensible differences between the different groups of enterprises. With absoluteconcentration of the ownership are 80,6% of the enterprises with IC, 68,7% ofthese with OC and 100% of the state enterprises. In the structures of control alsocan be differed 2 main groups: first, enterprises with absolute concentration inwhich 1 to 3 owners have 100% of the ownership; second, enterprises with highconcentration in which the first three owners have relatively high share ofownership - average some times more than the share of the fourth and the nextowners.

3.2.3.2.3.2.3.2. GovernanceGovernanceGovernanceGovernance StructuresStructuresStructuresStructures CharacteristicsCharacteristicsCharacteristicsCharacteristics

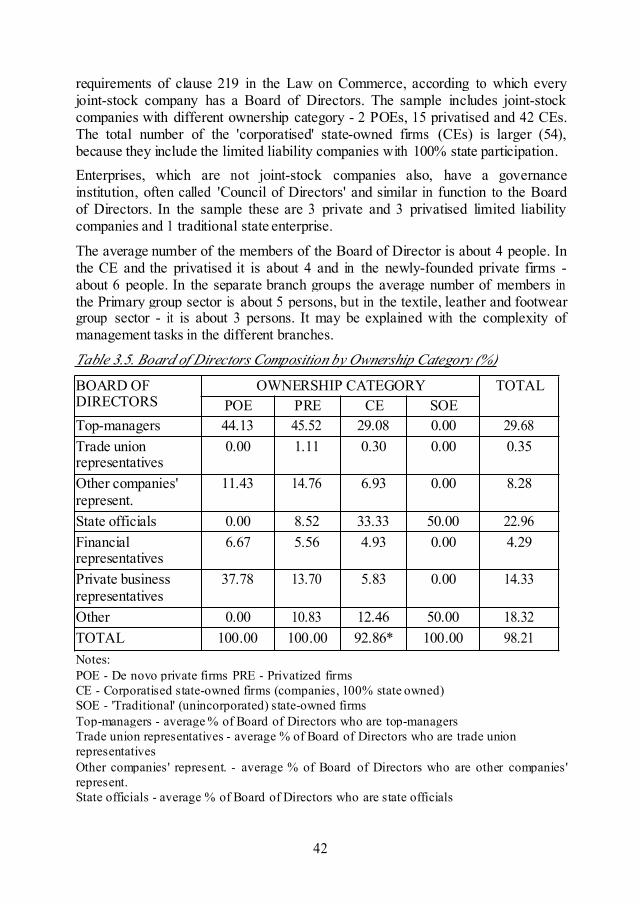

a.a.a.a. Board of Directors. The larger part of the surveyed enterprises (63% or 66 cases)has Board of Directors. These are predominantly the enterprises of the joint-stockcompany legal form. The existence of this governance institution is defined by the

42

requirements of clause 219 in the Law on Commerce, according to which everyjoint-stock company has a Board of Directors. The sample includes joint-stockcompanies with different ownership category - 2 POEs, 15 privatised and 42 CEs.The total number of the 'corporatised' state-owned firms (CEs) is larger (54),because they include the limited liability companies with 100% state participation.Enterprises, which are not joint-stock companies also, have a governanceinstitution, often called 'Council of Directors' and similar in function to the Boardof Directors. In the sample these are 3 private and 3 privatised limited liabilitycompanies and 1 traditional state enterprise.

The average number of the members of the Board of Director is about 4 people. Inthe CE and the privatised it is about 4 and in the newly-founded private firms -about 6 people. In the separate branch groups the average number of members inthe Primary group sector is about 5 persons, but in the textile, leather and footweargroup sector - it is about 3 persons. It may be explained with the complexity ofmanagement tasks in the different branches.

Table 3.5. Board of Directors Composition by Ownership Category (%)

BOARD OFDIRECTORS

OWNERSHIP CATEGORY TOTALPOE PRE CE SOE

Top-managers 44.13 45.52 29.08 0.00 29.68Trade unionrepresentatives

0.00 1.11 0.30 0.00 0.35

Other companies'represent.

11.43 14.76 6.93 0.00 8.28

State officials 0.00 8.52 33.33 50.00 22.96Financialrepresentatives

6.67 5.56 4.93 0.00 4.29

Private businessrepresentatives

37.78 13.70 5.83 0.00 14.33

Other 0.00 10.83 12.46 50.00 18.32TOTAL 100.00 100.00 92.86* 100.00 98.21Notes:POE - De novo private firms PRE - Privatized firmsCE - Corporatised state-owned firms (companies, 100% state owned)SOE - 'Traditional' (unincorporated) state-owned firmsTop-managers - average % of Board of Directors who are top-managersTrade union representatives - average % of Board of Directors who are trade unionrepresentativesOther companies' represent. - average % of Board of Directors who are other companies'represent.State officials - average % of Board of Directors who are state officials

43

Financial representatives - average % of Board of Directors who are financialrepresentativesPrivate business represent. - average % of Board of Directors who are private businessrepresent.Total percentage of CE firms is 92.86 because three of the firms are not answered.

Table 3.5 shows the Board of Directors composition by Ownership Category. Inthe POEs over 80% of the members of the Board of Directors are top-managers andrepresentatives of the private business, and about 10% are people working in therespective enterprise. In the PREs these numbers are respectively about 60% and15%. While the above numbers have been anticipated and explainable, thecomposition of the Council of Directors in the CEs seems strange. In them about18% of the members are representatives of the private business or 'other' economicsubjects difficult to identify.

The Trade Unions have an insignificant presence in the Councils of Directors. Inthe PREs it is a little over 1% and in the POEs and CEs it is 0% or about 0%. Thiscreates a potential for a low level of workers' influence on decision making.

According to expert views of the managers of the surveyed enterprises on the basisof a seven-grade scale, the average influence of the Board of Directors on thestrategic decisions was graded 4.58, bearing in mind that in the CE the grades arelower - 4.21, and in the private sector - higher (POEs - 5.60 and PREs - 5.33). Theassessment of the influence on the operative decisions shows lower levels (3.91 onthe average), but the grading of the firms with different category of ownership isthe same: CEs - 3.62, POEs- 5.60 and PREs- 4.39.

The results above show the more passive role of the Board of Directors at makingboth the strategic and operative decisions in the corporatised state enterprises incomparison with the enterprises in the private sector. On the other hand, in theprivate sector itself the influence of the Board of Directors in the newly-foundedprivate firms is stronger than in the privatised firms.

The high estimation of the influence of the Board of Directors on the operativedecisions in the newly-founded private firms (60% of them define it as very strongand extensive) shows that in these enterprises the Board has taken over untypical ofits nature functions of the operative management. This also reveals the greatercentralisation and the concentration of power of decision making in the samehands. The same tendency has been observed in the privatised enterprises (about50% of them assess the influence of the Board on operative decision making asstrong, very strong and extensive). For comparison, only 32% of the CE givesimilar assessment of the strong role of the Board in operative decision making.b.b.b.b. Supervisory Board. Only 3% of the surveyed enterprises have a SupervisoryBoard in their governance structure. According to the Law on Commerce they havea two-tier system of governance, i.e. Board of Directors and Supervisory Board.For comparison, the enterprises with a one-tire structure are those with a Board of

44

Directors only. The studied enterprises with a Supervisory Board are two privatisedones and one newly-founded private one. However, the case of the newly-foundedprivate enterprise is specific because it has no Board of Directors but only aSupervisory Board, which leads to the conclusion that these are two names for thesame thing and the system has one tier. The average number of the members of theSupervisory Board is 3 people. One of the privatised enterprises is under insidercontrol and the other one is under outsider control. In the first enterprise themembers of the Supervisory Board are representatives of the Trade Unions andother employees of the firm. In the second enterprise the members of theSupervisory Board are top-managers, one of them being an owner of the firm - thebiggest shareholder in the firm. This distribution of the board members aseconomic agents shows that the governance structure of the Supervisory Board isused to acquire more influence of part of the owners on the operations of theenterprises. In Bulgaria, however, this governance mechanism of control over themanagers was not typical in the period of the study.

c.c.c.c. Conflict between managers and Board of Directors (Supervisory Board). In thenewly-founded private enterprises there is full agreement at making the decisions.Such agreement exists in about 70% of the privatised enterprises. These results canbe explained with the merging of interests of the Board of Directors and themanagers in this ownership category.

While the above results are explainable, the high percentage of corporatised stateenterprises (about 87%), saying that there is full agreement between the Board ofDirectors and the managers at decision making cannot be interpreted one-sidedly.On the one hand this could mean curbing the potential managerial opportunism onpart of the institution of the Board as a disciplining mechanism. The highpercentage of private businessmen and other 'non-identifiable' persons in the Boardof Directors in these enterprises casts doubts that the demonstrated unanimity maybe directed against the interests of the enterprise. On the other hand there exists onepurely methodological explanation of the optimistic answers. The managers had toassess the level of their own disagreement with the institution that governed them.This in itself created the potential wish to soften the facts.