Embed Size (px)

Citation preview

Th

e P

NC

Fin

ancial S

ervices G

roup, In

c. 2012

An

nu

al R

ep

ort

PNC Financial Services Group2012 Annual Report

Corporate HeadquartersThe PNC Financial Services Group, Inc.

One PNC Plaza, 249 Fifth Avenue

Pittsburgh, PA 15222-2707

412-762-2000

8621_Cvr.indd 18621_Cvr.indd 1 2/27/13 8:59 AM2/27/13 8:59 AM

Stock Listing

The common stock of The PNC Financial

Services Group, Inc. is listed on the New York

Stock Exchange under the symbol PNC.

Stock Transfer Agent and Registrar

Computershare Trust Company, N. A.

250 RoyaII Street

Canton, MA 02021

800-982-7652

Dividend Reinvestment and Stock Purchase Plan

The PNC Financial Services Group, Inc. Dividend

Reinvestment and Stock Purchase Plan enables

holders of common and preferred Series B

stock to conveniently purchase additional shares

of common stock. Obtain a prospectus and

enrollment form at www.computershare.com/pnc

or by contacting Computershare at 800-982-7652.

“PNC is going to win in this environment because

we have the right people, the right culture and the

right business model to deliver for our shareholders,

customers, employees and communities.”

–Jim Rohr, chairman and chief executive offi cer

8621_Cvr.indd 28621_Cvr.indd 2 2/27/13 8:59 AM2/27/13 8:59 AM

From the ChairmanMarch 1, 2013

James E. Rohr

Chairman and Chief Executive Officer

To Our Shareholders,

In nearly every way, today’s banking industry is a world away from the one I joined nearly

41 years ago. New regulations, persistently low interest rates, evolving customer preferences

and stunning enhancements in technology are just some of the differences we see as we

begin 2013. Then as now, one attribute transcends the decades – trust.

Trust is the quality that people seek from a financial institution, and banks that can earn the

confidence of their customers are those that will have enduring success. We believe PNC

is such a bank.

We have strategies for growth, a business model and an approach to risk that drive our

performance. Our products are designed to provide customers with the level of safety and

liquidity they seek and to create opportunities for financial growth. But it is trust that creates

the loyalty necessary to sustain relationships, and that is why we believe customers are the

foundation for revenue potential.

PNC Chairman and Chief Executive Officer Jim Rohr celebrated the 25-year anniversary of PNC trading

on the New York Stock Exchange on October 22, 2012.

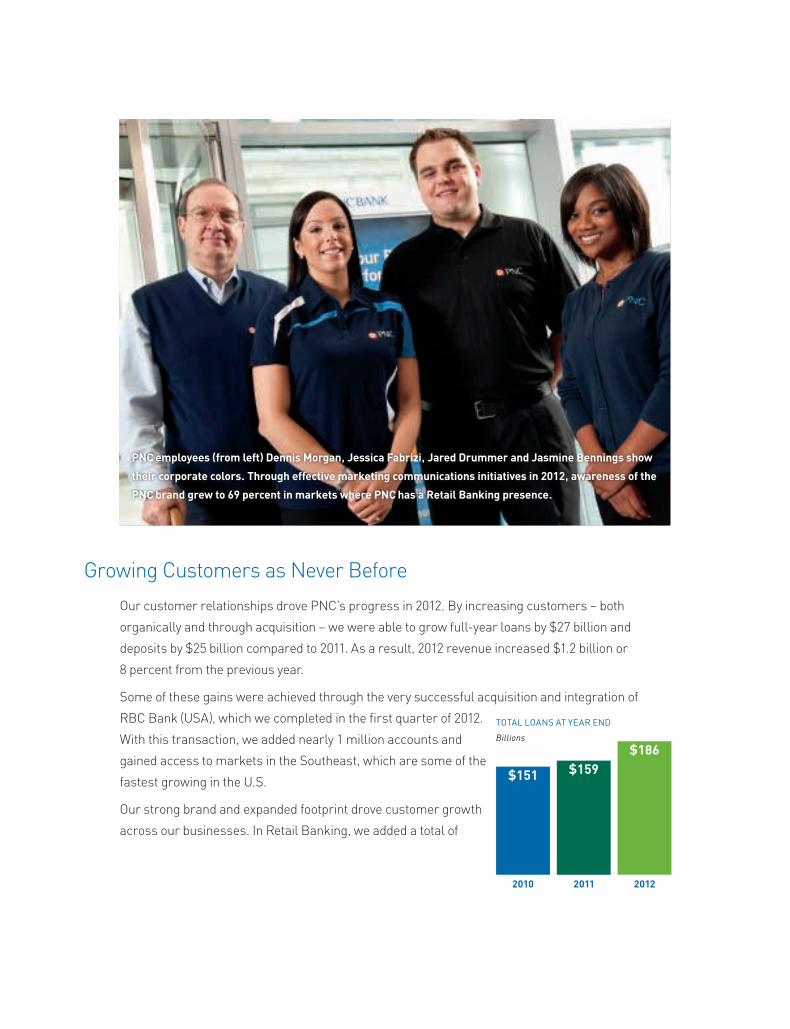

Our customer relationships drove PNC’s progress in 2012. By increasing customers – both

organically and through acquisition – we were able to grow full-year loans by $27 billion and

deposits by $25 billion compared to 2011. As a result, 2012 revenue increased $1.2 billion or

8 percent from the previous year.

Some of these gains were achieved through the very successful acquisition and integration of

RBC Bank (USA), which we completed in the first quarter of 2012.

With this transaction, we added nearly 1 million accounts and

gained access to markets in the Southeast, which are some of the

fastest growing in the U.S.

Our strong brand and expanded footprint drove customer growth

across our businesses. In Retail Banking, we added a total of

Growing Customers as Never Before

ToTal loans aT year end

Billions

$151 $159

2010 2011 2012

$186

PNC employees (from left) Dennis Morgan, Jessica Fabrizi, Jared Drummer and Jasmine Bennings show

their corporate colors. Through effective marketing communications initiatives in 2012, awareness of the

PNC brand grew to 69 percent in markets where PNC has a Retail Banking presence.

There were clearly some pluses and minuses for PNC in 2012.

In addition to our growth in customers and gains in loans,

deposits and revenue, other positives included:

• Our balance sheet liquidity remained strong as

evidenced by our loan-to-deposit ratio of 87 percent

as of December 31, 2012.

• We exceeded our full-year cost reduction target of $550 million.

• Our Tier 1 capital ratio increased following our cash acquisition of RBC Bank (USA)

in March 2012.

There were also a few minuses, some of which reflect the current operating environment.

• Developments in the residential mortgage banking industry required us to set aside

a provision of $761 million primarily for obligations to repurchase loans that were

acquired when we purchased National City. This had a negative impact on revenue.

• On the expense side, residential mortgage foreclosure-related expenses were

$225 million for the year.

• Other expenses included integration costs of RBC Bank (USA) and the noncash charges

related to the redemption of $2.3 billion in high-cost trust preferred securities. Both

provide PNC with benefits in the form of an expanded footprint and lower funding costs,

respectively.

On balance this was a good year for PNC but because of these minuses, our financial results

do not reflect the full potential of the investments we have made and the value we believe

PNC can create for shareholders.

Pluses and Minuses

714,000 net new checking relationships during the year. Of that amount, 254,000 were net

new organic relationships, growth of 4 percent from year-end 2011 or more than double the

population growth rate in our footprint. Over the last three years, from 2010 through 2012, we

acquired about 3,000 new Corporate Banking primary clients. In 2012 compared with 2011,

new primary client acquisitions for our Asset Management Group were 37 percent higher

and Residential Mortgage originations increased by $3.8 billion or 33 percent.

This growth helped to create full year earnings of $3 billion or $5.30 per diluted common

share. Overall, I was pleased – but not entirely satisfied – with our results.

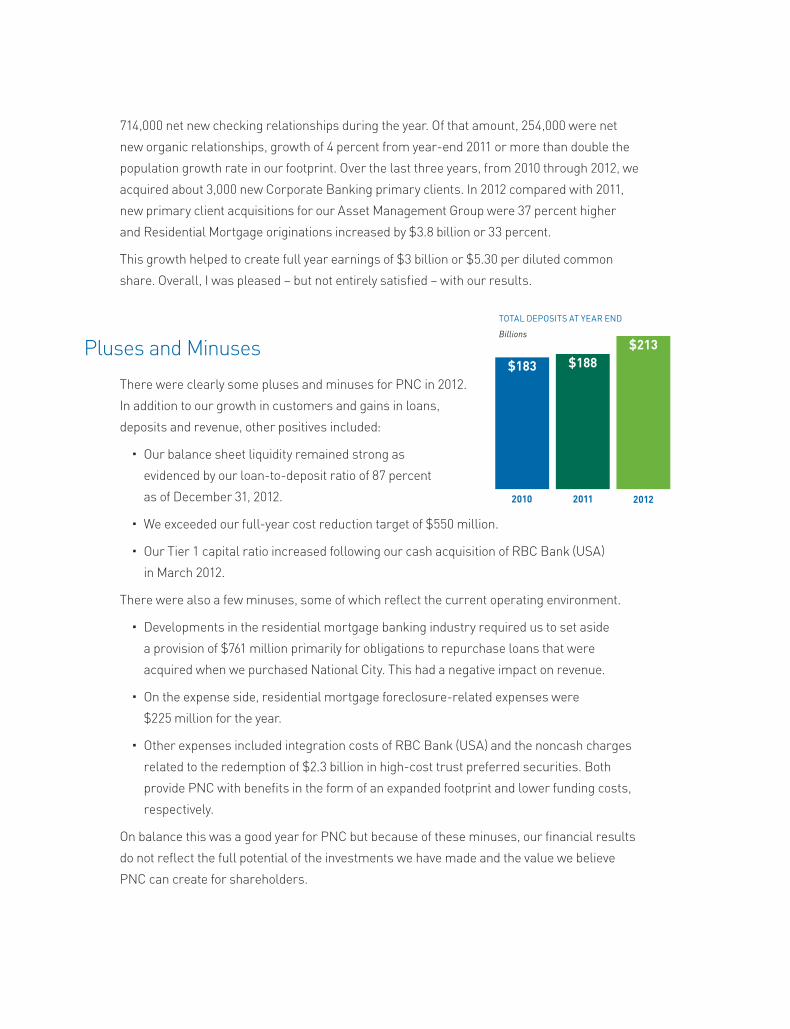

ToTal deposiTs aT year end

Billions

$183 $188

2010 2011 2012

$213

Priorities for 2013

Building on the strong customer growth in our business segments – Retail Banking, Corporate &

Institutional Banking, Asset Management Group and Residential Mortgage – 2013 provides us with

greater opportunities to deepen relationships through cross selling and increase fee-based income,

while we also look to reduce expenses. Additionally, we have established several growth priorities

for 2013.

Across our industry, fewer customers are

regularly using retail branches. In fact 40

percent of PNC’s customers have not visited

a branch in the last three months as more

transactions are being conducted online, at

ATMs and through mobile devices. And the

number of checks deposited by mobile devices

grew from zero to nearly 15,000 per day at PNC

– all in 2012.

Evolving customer preferences along with

low interest rates and a dynamic regulatory

environment have created a new world for

retail banking. We are rethinking nearly

every aspect of this business with a focus on

enhancing customer loyalty by deepening

relationships while lowering costs.

For example, we plan to install nearly

2,500 multi-functional, check-cashing ATMs

this year in addition to the 1,100 we rolled out

in 2012. That would mean that by the end of

2013, approximately half of our ATM network

will allow customers to cash checks, receive

images of their deposits and withdraw cash.

Compared to a branch, these ATMs often

provide greater customer convenience and

have significantly lower transaction costs.

Our innovative Virtual Wallet® product, which

helps customers better manage their money,

now has approximately 1.3 million accounts. In

the fourth quarter of 2012, we became the first

U.S. bank to integrate with Visa’s new digital

wallet service – V.me – which should simplify

e-commerce for Virtual Wallet users.

We are applying this same innovative approach

to a new product that we will be launching

this year for our business banking customers.

It’s called Cash Flow Insight® and provides

business owners with an online tool to help

them better understand their cash flows and

forecast their cash position.

Reflecting customer trends, we also plan to

close more branches in 2013 than we have

in any year in our history. However, PNC will

continue to expand its branch presence in

underpenetrated markets.

As we look ahead, we envision technology-

centered branches that deliver products and

services such as business and commercial

banking, wealth management, investments

and mortgages. This approach should drive

customer loyalty while improving margins. At

the same time, we are looking to increase our

brand equity in the virtual space with the goal

of deeper relationships with our customers.

redefine The reTail banking experience.

CAPTURE MORE OF OUR CUSTOMERS’ INVESTABlE ASSETS.

We estimate that our current customers

have $1.9 trillion in personal investable assets,

but our percentage share of those dollars is

in the single digits, reflecting the fragmented

nature of this industry. With the long-term

goal of doubling the size of our investment and

retirement business, we plan to have annual

conversations with each of our customers.

At a time when many banks are looking to

the mass market, affluent, high net worth

and institutional markets as a source to

increase fee income, we believe PNC’s

highly collaborative culture gives us an

edge as referrals are one of our strengths.

For example, referral sales to our Asset

Management Group last year were up

more than 39 percent compared to 2011,

reflecting strong referral activity from Retail

and Corporate & Institutional Banking. This

helped to produce an increase in total net

inflows, bringing discretionary assets under

management to $112 billion at year-end 2012.

This year, we are looking to expand those

efforts. All of our client-facing employees now

have specific goals in support of our investing

and retirement initiative.

Our open architecture along with our

consultative approach is designed to provide

customers with solutions based on their

individualized needs. It’s our position that this

approach helps to drive our excellent levels of

client retention.

Recognizing that some clients like to manage

aspects of their portfolio on their own, last year

we established the PNC Investment Center and

we introduced brokerage capabilities for our

high net worth customers.

PNC Wealth Insight® was honored by both CIO

and InformationWeek magazines in 2012 as

an innovation that delivers a competitive

advantage. This tool allows wealth management

customers to aggregate their assets – even

those not managed by PNC – and view them

based on how they think about their money.

Given our culture, product and service

capabilities and larger customer base, we feel

this represents another opportunity to diversify

our revenue stream.

Moises Almonte (right), a senior relationship manager in Wealth Management, meets with Mark Nobile

(center), chief operating officer, and Ed Maier, president, of the Susquehanna Brewing Co., a family-owned

craft brewery located in northeastern Pennsylvania.

CONTINUE TO BUIlD OUR PRESENCE IN NEWly ACqUIRED MARkETS.

As this letter goes to press, we have been in

our new Southeastern markets about one year.

In that short space of time, we have established

our brand in highly attractive markets such as

Atlanta, Birmingham, Charlotte and Raleigh,

provided Retail customers with a robust

product set and, from a de novo position,

created an Asset Management and Corporate

& Institutional banking presence.

When we entered the market, we received

thousands of resumes, many from area

competitors. These new hires coupled with

a group of legacy employees who willingly

relocated to warmer climes have allowed

PNC to establish itself as a worthy banking

competitor with strong talent.

Despite a credit market that has become more

competitive for our Corporate & Institutional

Bank, we remain bullish on the opportunities,

and believe that over time, this area will

generate loan and fee income in line with our

more established markets such as Chicago,

Washington, D.C. and Philadelphia.

BUIlD A SUSTAINABlE RESIDENTIAl MORTGAGE BUSINESS.

For most customers, the single most important

financial transaction of their lives is the purchase

of a home. We are committed to investing in this

business to create a strong financial bond with

our customers while delivering bottom-line

returns and burnishing our already strong brand.

Today, we are building a viable, highly integrated

mortgage origination and servicing engine that

is cost efficient and reflects PNC’s business

practices, culture and commitment to customer

service. As refinancing activity eases, this should

drive longer term value for this business. We

are also looking to cross-sell our mortgage

products to existing clients across our footprint.

We are seeing an improving housing market,

something we haven’t experienced since 2008.

Taken together, we see our opportunities with

our residential mortgage business to enhance

customer relationships and help us capture a

greater share of wallet.

PNC’s expansion in the Southeast combined with a commitment to innovation, expense management and energy

efficiency led to the opening of a net-zero energy bank branch in Fort Lauderdale in January 2012.

These priorities along with our commitment to executing give us confidence that we can deliver

shareholder value in 2013.

* PNC believes that tangible book value per common share, a non-GAAP measure, is useful as a tool to help to better evaluate growth of a company’s business apart from the amount, on a per share basis, of intangible assets other than servicing rights included in book value per common share. PNC’s book value per share was $67.05 at year-end 2012, a 41% increase over $47.68 at year-end 2009. Subtracting approximately $9.8 billion ($10.9 billion of goodwill and other intangible assets less $1.1 billion of servicing rights) or $18.54 per share for year-end 2012, and subtracting approximately $10.7 billion ($12.9 billion of goodwill and other intangible assets less $2.2 billion of servicing rights) or $23.09 per share for year-end 2009, results in tangible book value per share of approximately $48.51 for year-end 2012, a 97% increase over approximately $24.59 at year-end 2009.

PNC’s 2012 peer group consists of BB&T Corporation, Bank of America Corporation, Capital One Financial Corporation, Comerica Incorporated, Fifth Third Bancorp, JPMorgan Chase & Co., KeyCorp, M&T Bank Corporation, The PNC Financial Services Group, Inc., Regions Financial Corporation, SunTrust Banks, Inc., U.S. Bancorp, and Wells Fargo & Company.

MANAGE RISk, ExPENSES AND CAPITAl.

Managing credit risk remains a priority for us.

Our nonperforming assets declined from year

end 2011, and our provision for credit losses

and net charge-offs improved in 2012. Overall,

we remain committed to a moderate risk

philosophy.

At PNC, expense management is a part of

our culture, and we have a track record of

executing on our objectives. For 2013 we

increased our continuous improvement

target to $700 million, with the overall goal of

achieving full-year positive operating leverage

on a reported basis and producing stronger

results in 2013.

Our Tier 1 common capital ratio was 9.6

percent as of December 31, 2012, and our

estimated Basel III Tier 1 common capital

ratio on a pro forma basis as of that date was

7.5 percent. Of course that is based on our

current understanding of Basel rules and other

estimates. It remains our goal to be within the

range of 8.0 to 8.5 percent by year-end 2013

without benefit of phase-ins, and we believe

we can get there primarily based on increased

retained earnings in 2013.

Since the financial crisis began in 2008, we

have made strategic decisions to use capital

to grow our franchise for the long term. Over

time, we believe the opportunities associated

with these acquisitions should provide our

shareholders with strong returns.

Our earnings and capital strength supported

our decision to increase the common stock

dividend in the first quarter of 2012 for the

second time in as many years. Our dividend

yield as of December 31, 2012, was 2.76

percent, which we believe makes PNC stock

very attractive in the current low interest rate

environment.

An important

measure of any

stock is its tangible

book value per

share. We almost

doubled our

tangible book value

per share from

the end of 2009 to

year-end 2012, the

highest increase in

our peer group.*

2009 2012

$24.59

$48.51Tangible book Value per share

At Year End

+97%

Our ValuesPerformance

Customer Focus

Respect

Integrity

Diversity

Teamwork

Quality of Life

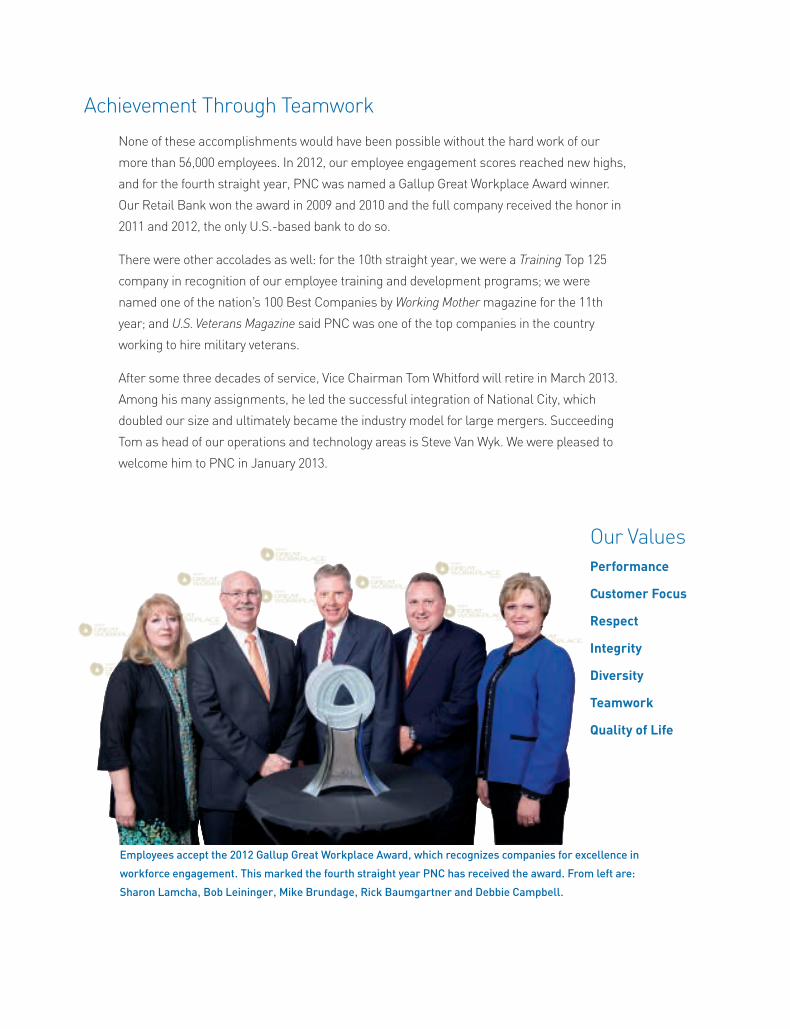

Employees accept the 2012 Gallup Great Workplace Award, which recognizes companies for excellence in

workforce engagement. This marked the fourth straight year PNC has received the award. From left are:

Sharon Lamcha, Bob Leininger, Mike Brundage, Rick Baumgartner and Debbie Campbell.

Achievement Through Teamwork

None of these accomplishments would have been possible without the hard work of our

more than 56,000 employees. In 2012, our employee engagement scores reached new highs,

and for the fourth straight year, PNC was named a Gallup Great Workplace Award winner.

Our Retail Bank won the award in 2009 and 2010 and the full company received the honor in

2011 and 2012, the only U.S.-based bank to do so.

There were other accolades as well: for the 10th straight year, we were a Training Top 125

company in recognition of our employee training and development programs; we were

named one of the nation’s 100 Best Companies by Working Mother magazine for the 11th

year; and U.S. Veterans Magazine said PNC was one of the top companies in the country

working to hire military veterans.

After some three decades of service, Vice Chairman Tom Whitford will retire in March 2013.

Among his many assignments, he led the successful integration of National City, which

doubled our size and ultimately became the industry model for large mergers. Succeeding

Tom as head of our operations and technology areas is Steve Van Wyk. We were pleased to

welcome him to PNC in January 2013.

Giving Back to the Community

At PNC, we have always believed that a company is only as strong as the community it serves. Overall,

we contributed more than $73 million to strengthen communities and enrich lives in the places where

we had a significant presence in 2012.

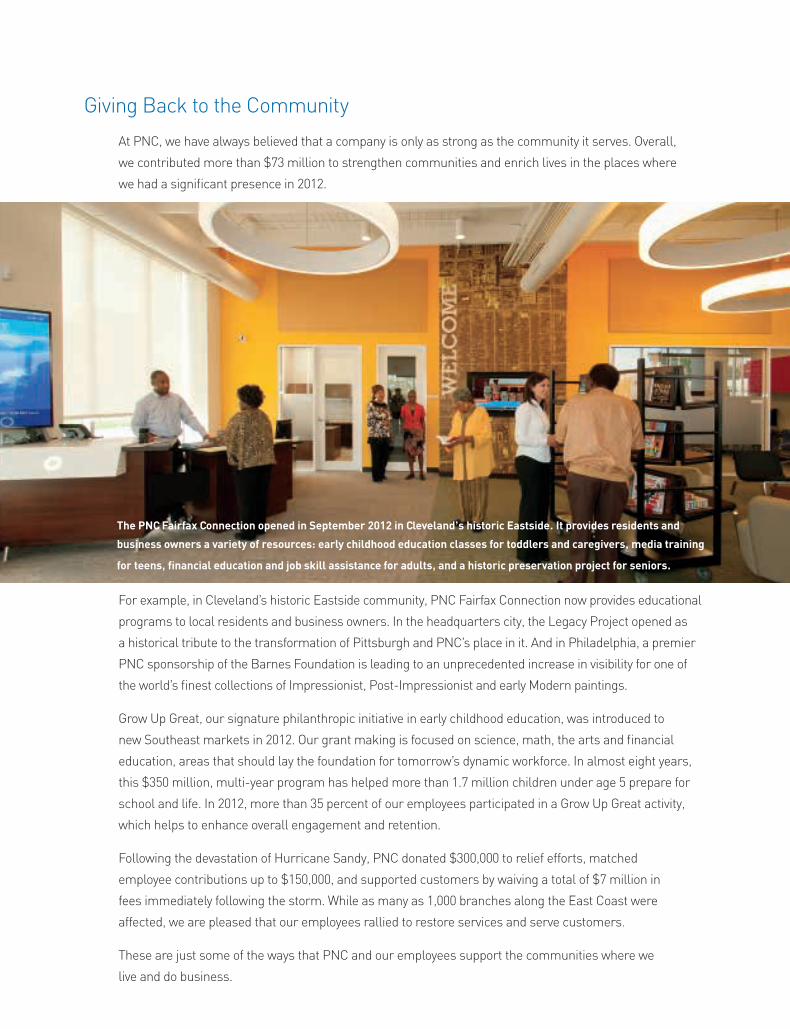

For example, in Cleveland’s historic Eastside community, PNC Fairfax Connection now provides educational

programs to local residents and business owners. In the headquarters city, the legacy Project opened as

a historical tribute to the transformation of Pittsburgh and PNC’s place in it. And in Philadelphia, a premier

PNC sponsorship of the Barnes Foundation is leading to an unprecedented increase in visibility for one of

the world’s finest collections of Impressionist, Post-Impressionist and early Modern paintings.

Grow Up Great, our signature philanthropic initiative in early childhood education, was introduced to

new Southeast markets in 2012. Our grant making is focused on science, math, the arts and financial

education, areas that should lay the foundation for tomorrow’s dynamic workforce. In almost eight years,

this $350 million, multi-year program has helped more than 1.7 million children under age 5 prepare for

school and life. In 2012, more than 35 percent of our employees participated in a Grow Up Great activity,

which helps to enhance overall engagement and retention.

Following the devastation of Hurricane Sandy, PNC donated $300,000 to relief efforts, matched

employee contributions up to $150,000, and supported customers by waiving a total of $7 million in

fees immediately following the storm. While as many as 1,000 branches along the East Coast were

affected, we are pleased that our employees rallied to restore services and serve customers.

These are just some of the ways that PNC and our employees support the communities where we

live and do business.

The PNC Fairfax Connection opened in September 2012 in Cleveland’s historic Eastside. It provides residents and

business owners a variety of resources: early childhood education classes for toddlers and caregivers, media training

for teens, financial education and job skill assistance for adults, and a historic preservation project for seniors.

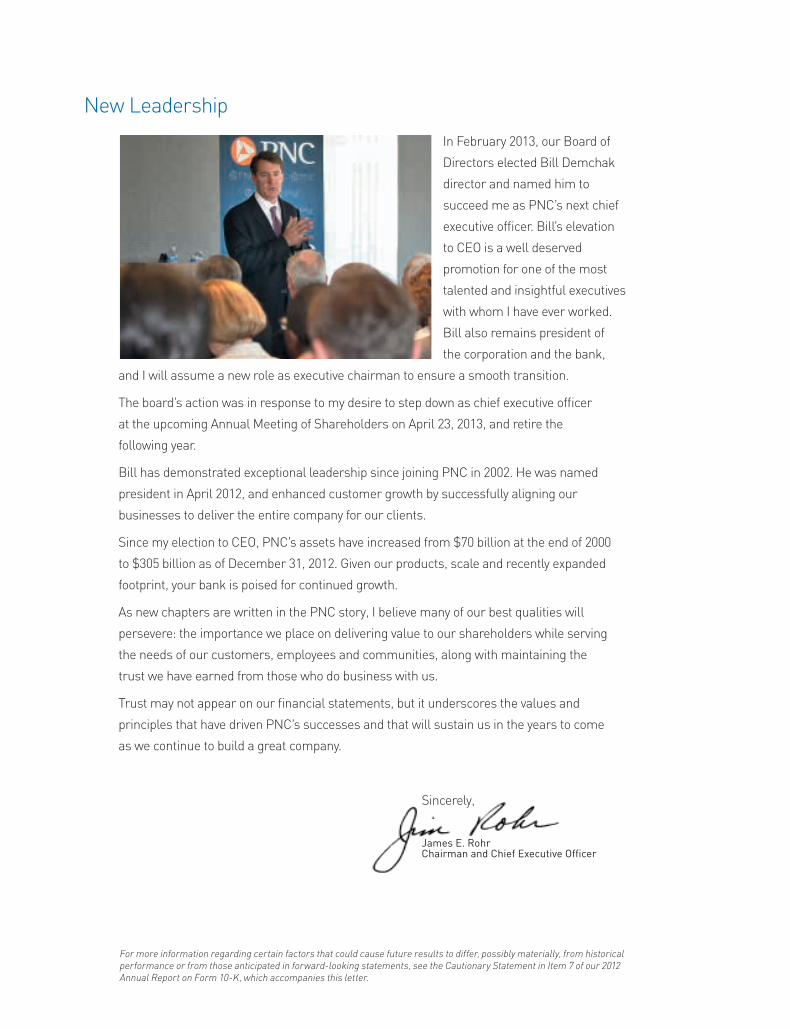

New leadership

In February 2013, our Board of

Directors elected Bill Demchak

director and named him to

succeed me as PNC’s next chief

executive officer. Bill’s elevation

to CEO is a well deserved

promotion for one of the most

talented and insightful executives

with whom I have ever worked.

Bill also remains president of

the corporation and the bank,

and I will assume a new role as executive chairman to ensure a smooth transition.

The board’s action was in response to my desire to step down as chief executive officer

at the upcoming Annual Meeting of Shareholders on April 23, 2013, and retire the

following year.

Bill has demonstrated exceptional leadership since joining PNC in 2002. He was named

president in April 2012, and enhanced customer growth by successfully aligning our

businesses to deliver the entire company for our clients.

Since my election to CEO, PNC’s assets have increased from $70 billion at the end of 2000

to $305 billion as of December 31, 2012. Given our products, scale and recently expanded

footprint, your bank is poised for continued growth.

As new chapters are written in the PNC story, I believe many of our best qualities will

persevere: the importance we place on delivering value to our shareholders while serving

the needs of our customers, employees and communities, along with maintaining the

trust we have earned from those who do business with us.

Trust may not appear on our financial statements, but it underscores the values and

principles that have driven PNC’s successes and that will sustain us in the years to come

as we continue to build a great company.

Sincerely,

James e. rohr chairman and chief executive officer

For more information regarding certain factors that could cause future results to differ, possibly materially, from historical performance or from those anticipated in forward-looking statements, see the Cautionary Statement in Item 7 of our 2012 Annual Report on Form 10-K, which accompanies this letter.

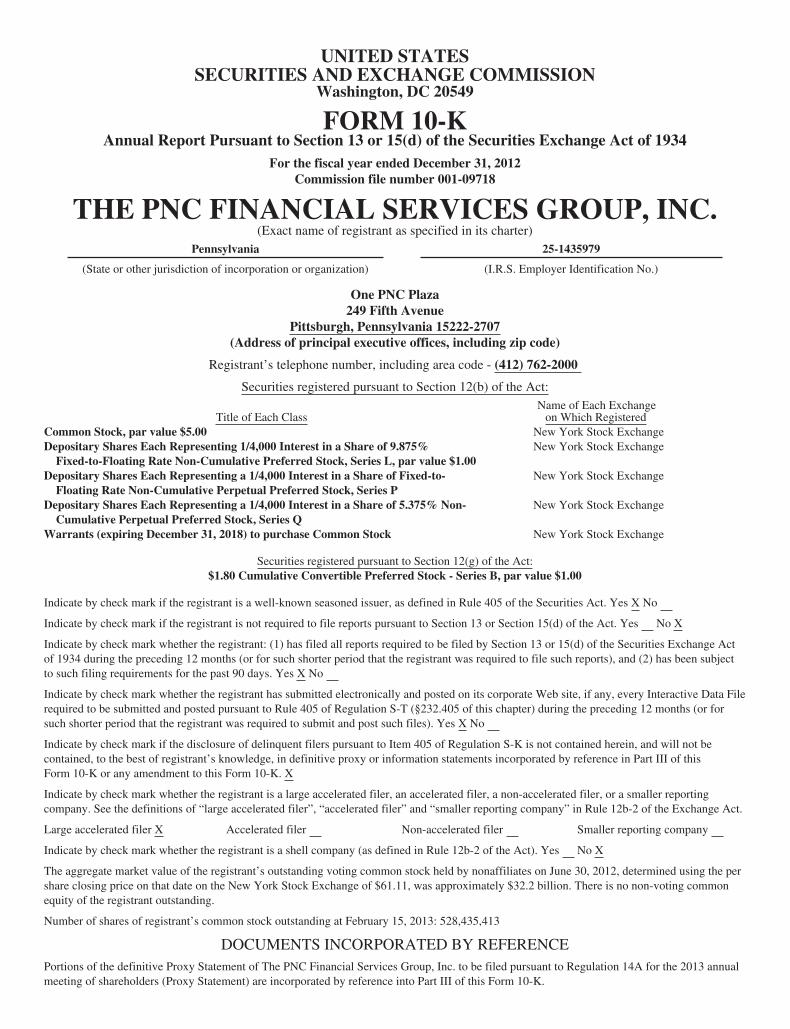

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-KAnnual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2012Commission file number 001-09718

THE PNC FINANCIAL SERVICES GROUP, INC.(Exact name of registrant as specified in its charter)

Pennsylvania 25-1435979

(State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.)

One PNC Plaza249 Fifth Avenue

Pittsburgh, Pennsylvania 15222-2707(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code - (412) 762-2000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each ClassName of Each Exchange

on Which RegisteredCommon Stock, par value $5.00 New York Stock ExchangeDepositary Shares Each Representing 1/4,000 Interest in a Share of 9.875%

Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series L, par value $1.00New York Stock Exchange

Depositary Shares Each Representing a 1/4,000 Interest in a Share of Fixed-to-Floating Rate Non-Cumulative Perpetual Preferred Stock, Series P

New York Stock Exchange

Depositary Shares Each Representing a 1/4,000 Interest in a Share of 5.375% Non-Cumulative Perpetual Preferred Stock, Series Q

New York Stock Exchange

Warrants (expiring December 31, 2018) to purchase Common Stock New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:$1.80 Cumulative Convertible Preferred Stock - Series B, par value $1.00

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes X No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No X

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Actof 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subjectto such filing requirements for the past 90 days. Yes X No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data Filerequired to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or forsuch shorter period that the registrant was required to submit and post such files). Yes X No

Indicate by check mark if the disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not becontained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of thisForm 10-K or any amendment to this Form 10-K. X

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reportingcompany. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer X Accelerated filer Non-accelerated filer Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No X

The aggregate market value of the registrant’s outstanding voting common stock held by nonaffiliates on June 30, 2012, determined using the pershare closing price on that date on the New York Stock Exchange of $61.11, was approximately $32.2 billion. There is no non-voting commonequity of the registrant outstanding.

Number of shares of registrant’s common stock outstanding at February 15, 2013: 528,435,413

DOCUMENTS INCORPORATED BY REFERENCEPortions of the definitive Proxy Statement of The PNC Financial Services Group, Inc. to be filed pursuant to Regulation 14A for the 2013 annualmeeting of shareholders (Proxy Statement) are incorporated by reference into Part III of this Form 10-K.

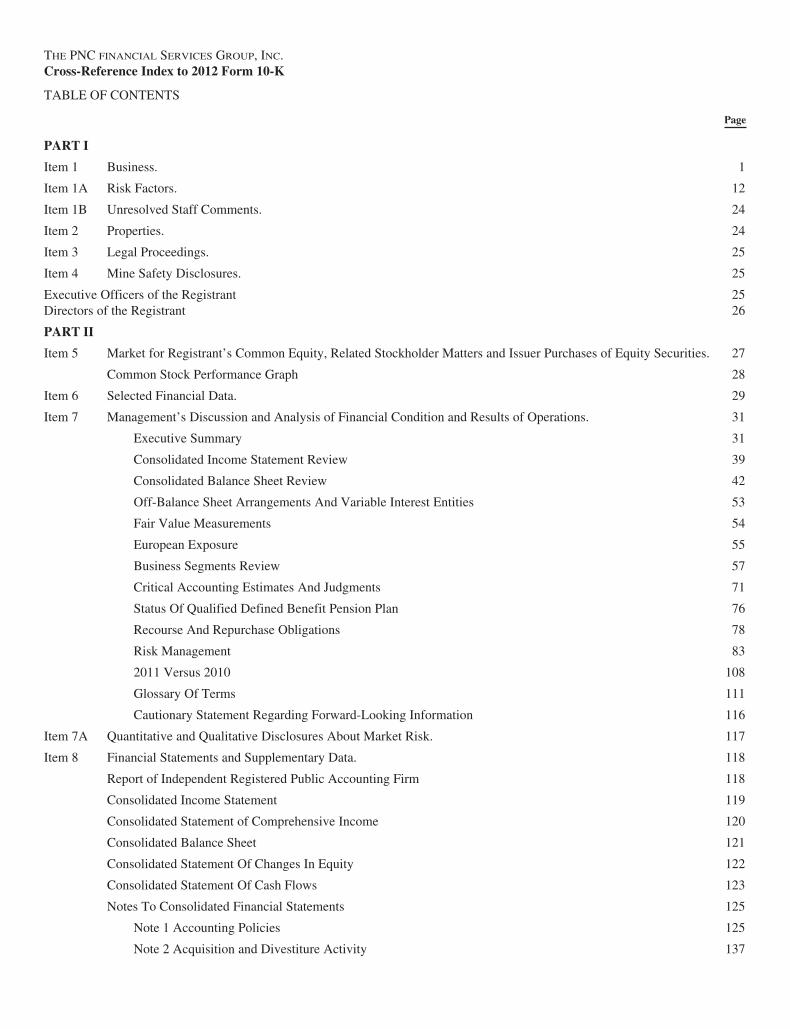

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K

TABLE OF CONTENTS

Page

PART I

Item 1 Business. 1

Item 1A Risk Factors. 12

Item 1B Unresolved Staff Comments. 24

Item 2 Properties. 24

Item 3 Legal Proceedings. 25

Item 4 Mine Safety Disclosures. 25

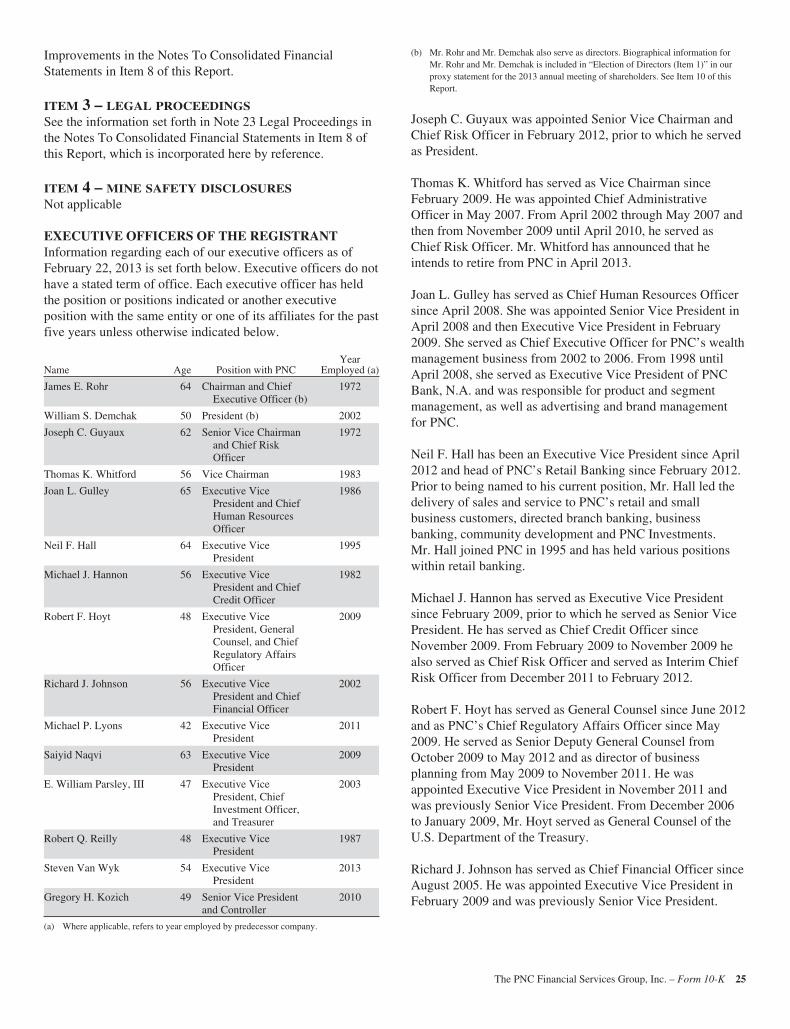

Executive Officers of the Registrant 25Directors of the Registrant 26

PART II

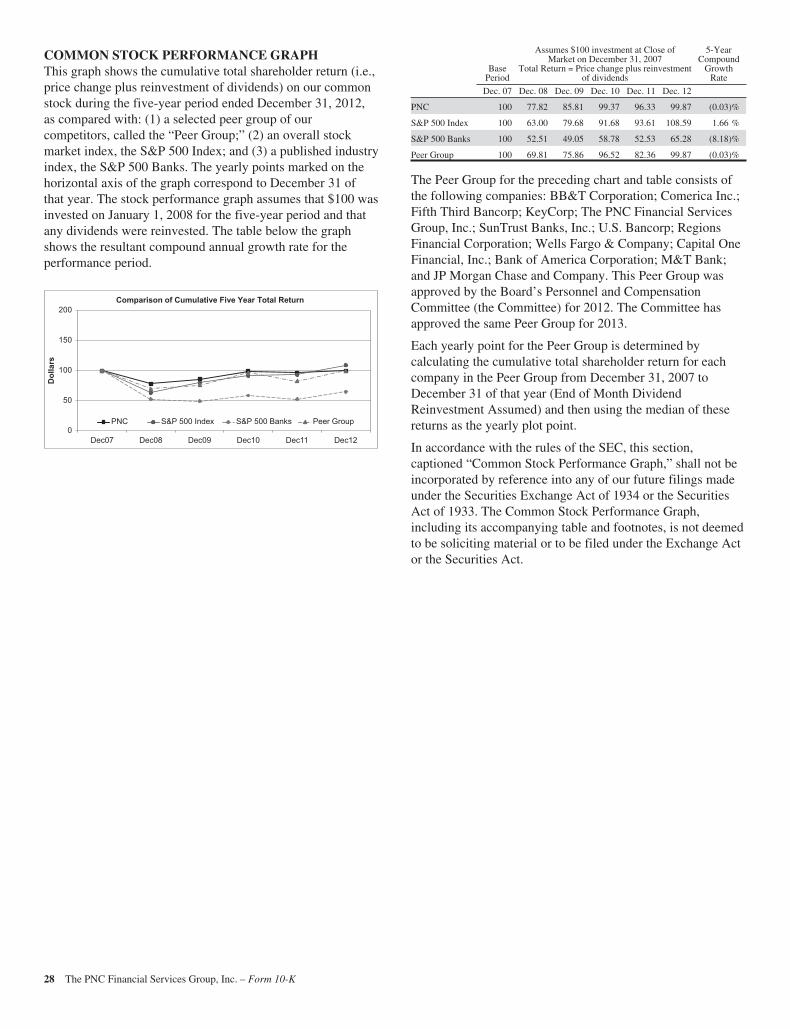

Item 5 Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. 27

Common Stock Performance Graph 28

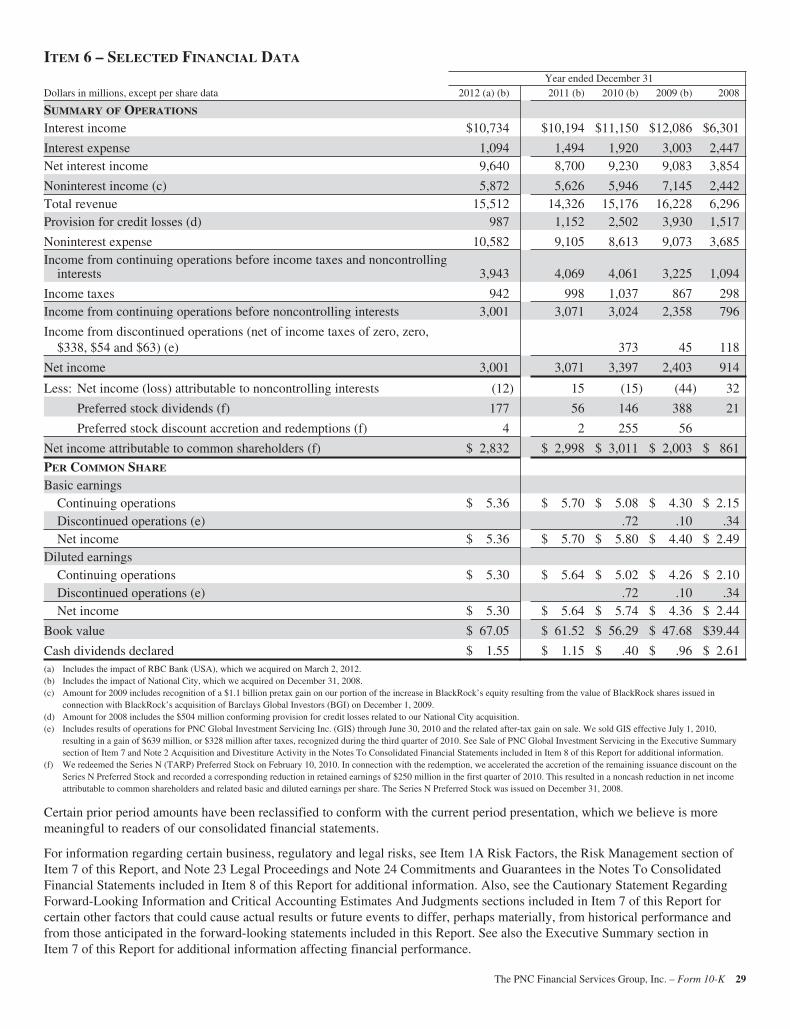

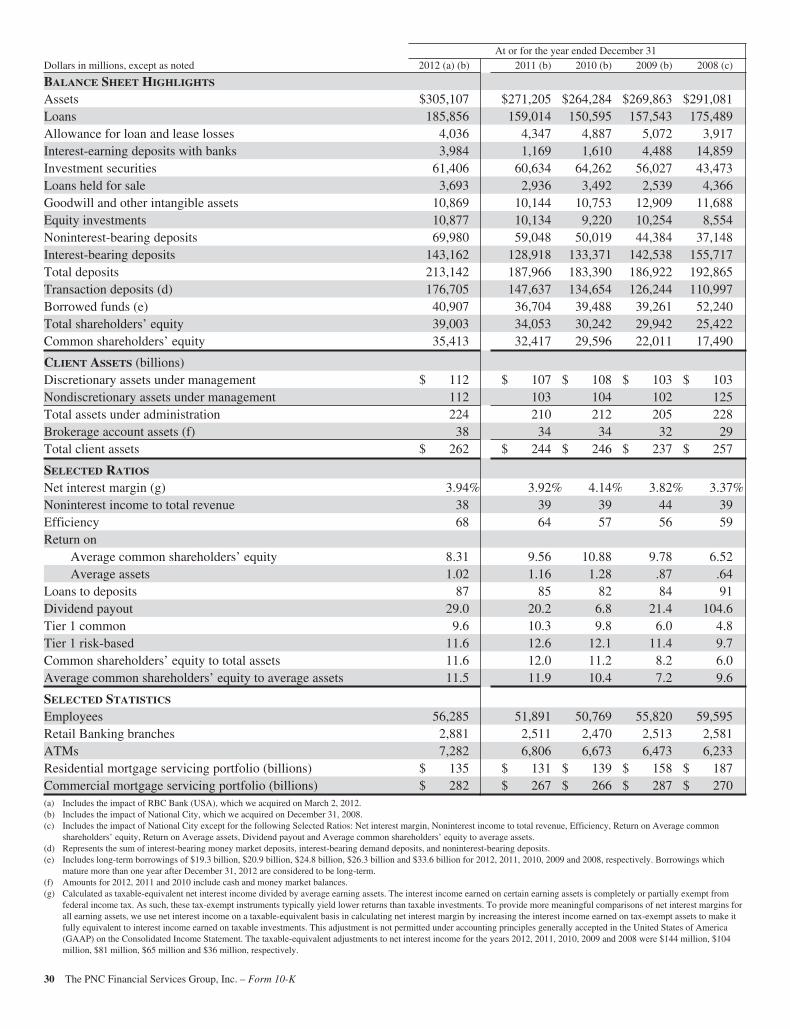

Item 6 Selected Financial Data. 29

Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations. 31

Executive Summary 31

Consolidated Income Statement Review 39

Consolidated Balance Sheet Review 42

Off-Balance Sheet Arrangements And Variable Interest Entities 53

Fair Value Measurements 54

European Exposure 55

Business Segments Review 57

Critical Accounting Estimates And Judgments 71

Status Of Qualified Defined Benefit Pension Plan 76

Recourse And Repurchase Obligations 78

Risk Management 83

2011 Versus 2010 108

Glossary Of Terms 111

Cautionary Statement Regarding Forward-Looking Information 116

Item 7A Quantitative and Qualitative Disclosures About Market Risk. 117

Item 8 Financial Statements and Supplementary Data. 118

Report of Independent Registered Public Accounting Firm 118

Consolidated Income Statement 119

Consolidated Statement of Comprehensive Income 120

Consolidated Balance Sheet 121

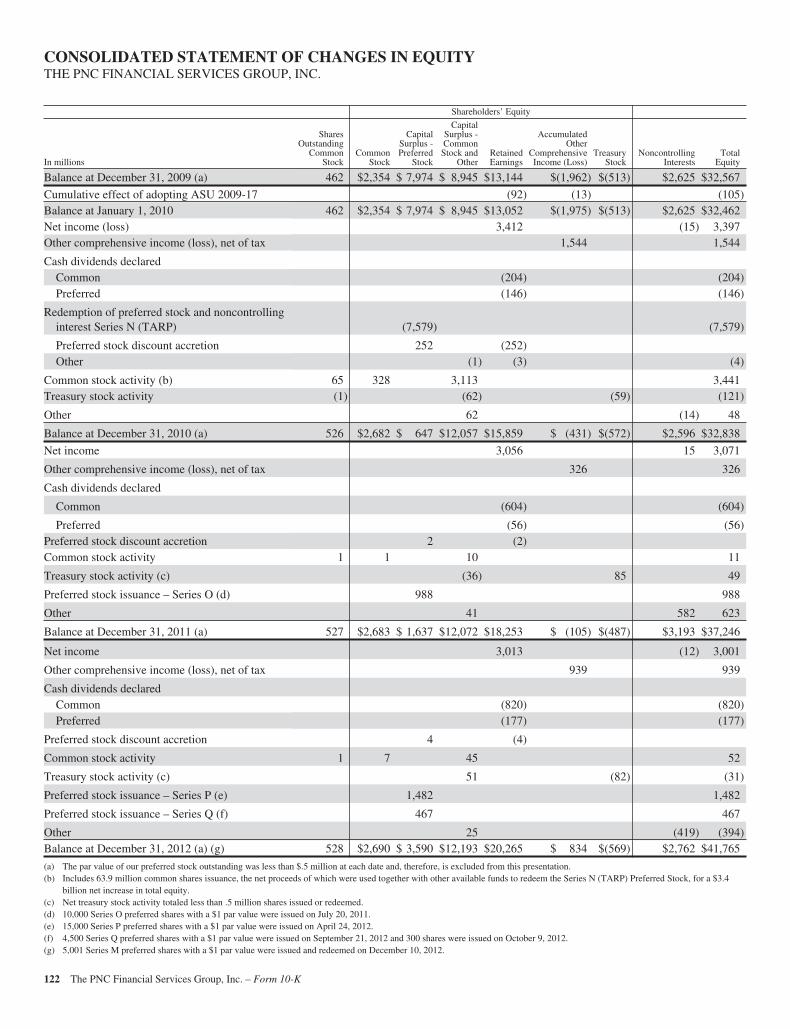

Consolidated Statement Of Changes In Equity 122

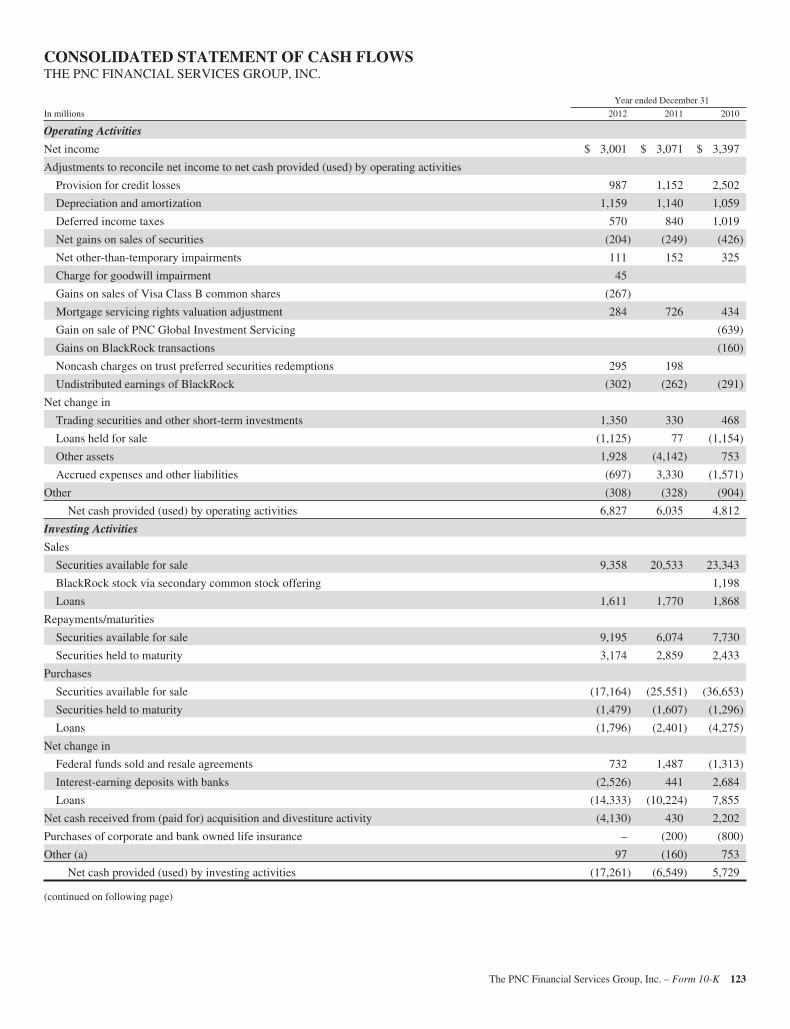

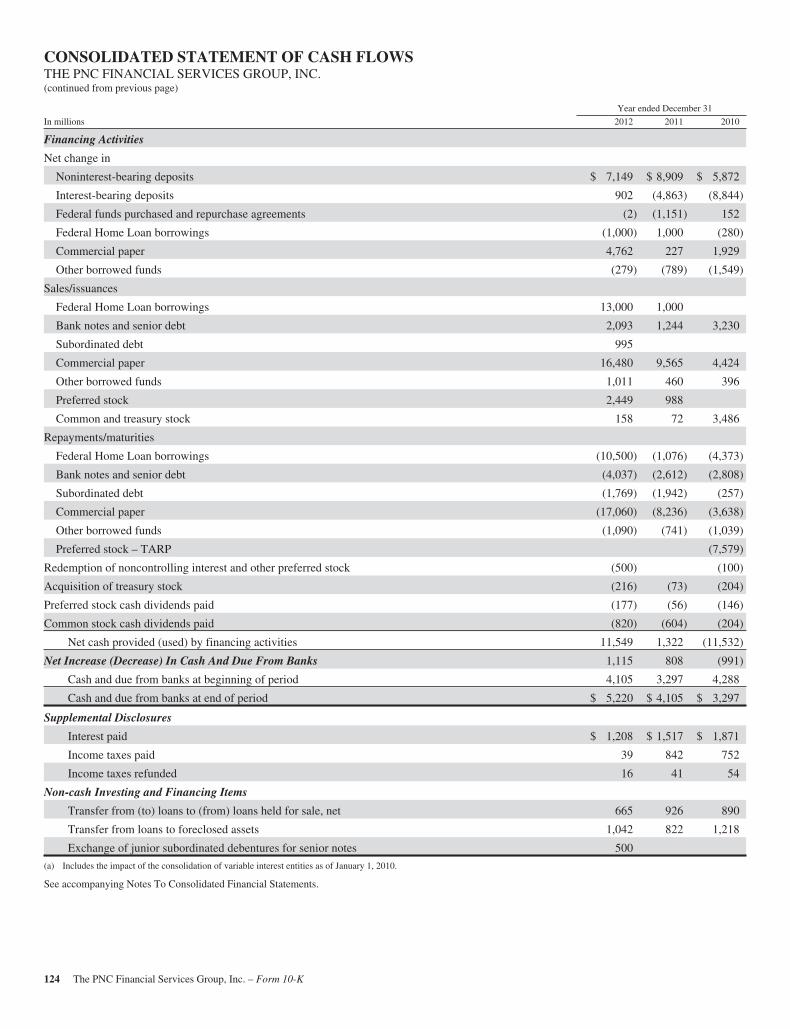

Consolidated Statement Of Cash Flows 123

Notes To Consolidated Financial Statements 125

Note 1 Accounting Policies 125

Note 2 Acquisition and Divestiture Activity 137

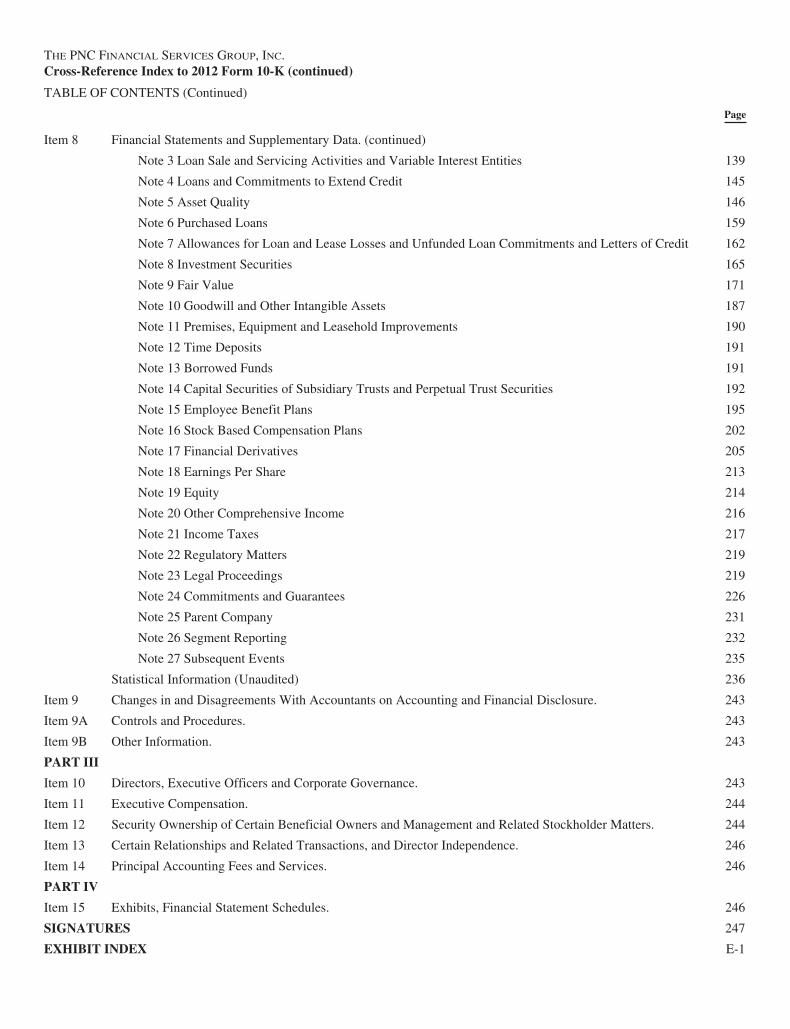

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K (continued)

TABLE OF CONTENTS (Continued)

Page

Item 8 Financial Statements and Supplementary Data. (continued)

Note 3 Loan Sale and Servicing Activities and Variable Interest Entities 139

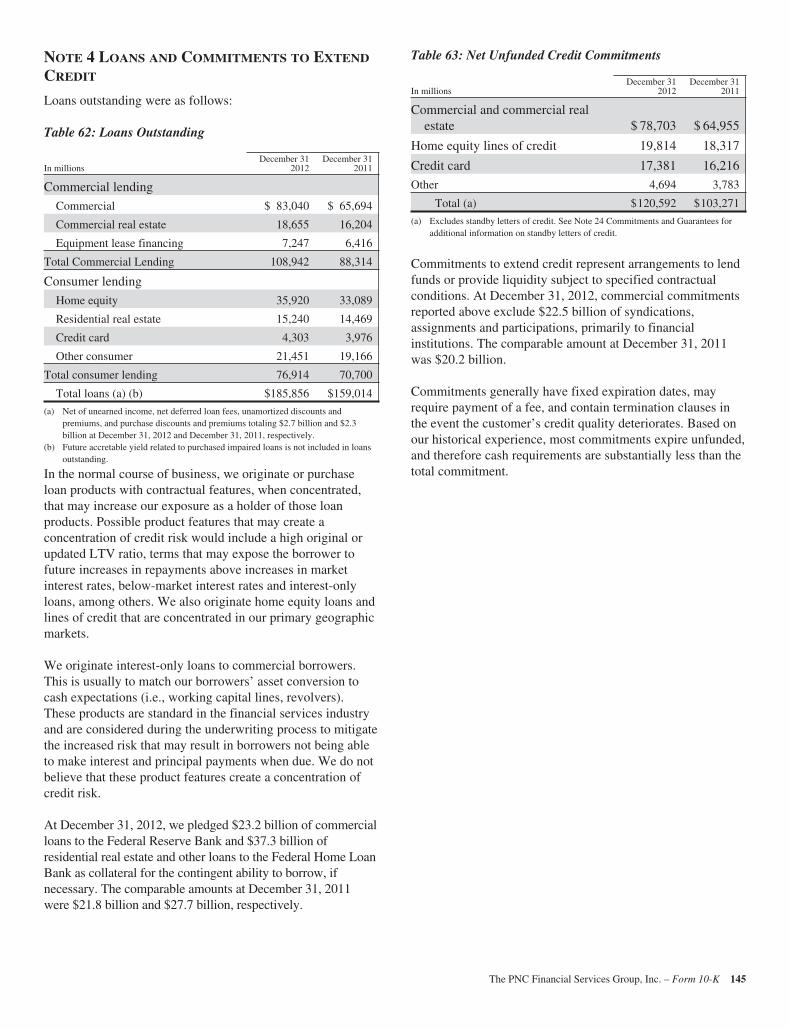

Note 4 Loans and Commitments to Extend Credit 145

Note 5 Asset Quality 146

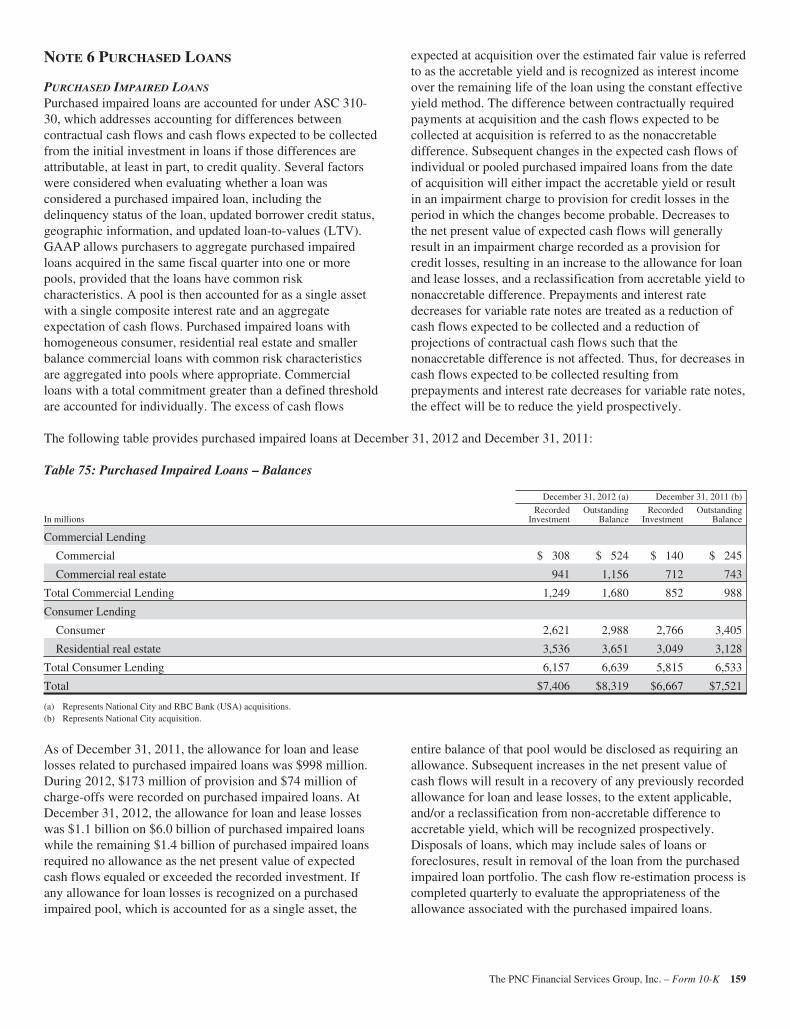

Note 6 Purchased Loans 159

Note 7 Allowances for Loan and Lease Losses and Unfunded Loan Commitments and Letters of Credit 162

Note 8 Investment Securities 165

Note 9 Fair Value 171

Note 10 Goodwill and Other Intangible Assets 187

Note 11 Premises, Equipment and Leasehold Improvements 190

Note 12 Time Deposits 191

Note 13 Borrowed Funds 191

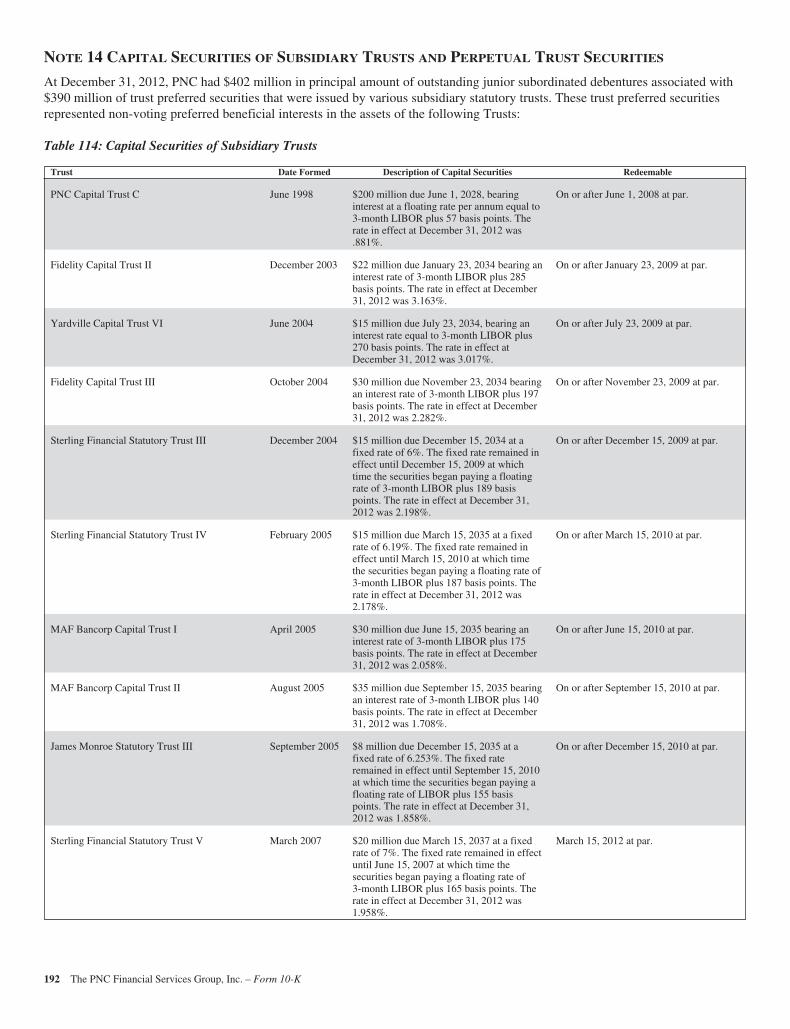

Note 14 Capital Securities of Subsidiary Trusts and Perpetual Trust Securities 192

Note 15 Employee Benefit Plans 195

Note 16 Stock Based Compensation Plans 202

Note 17 Financial Derivatives 205

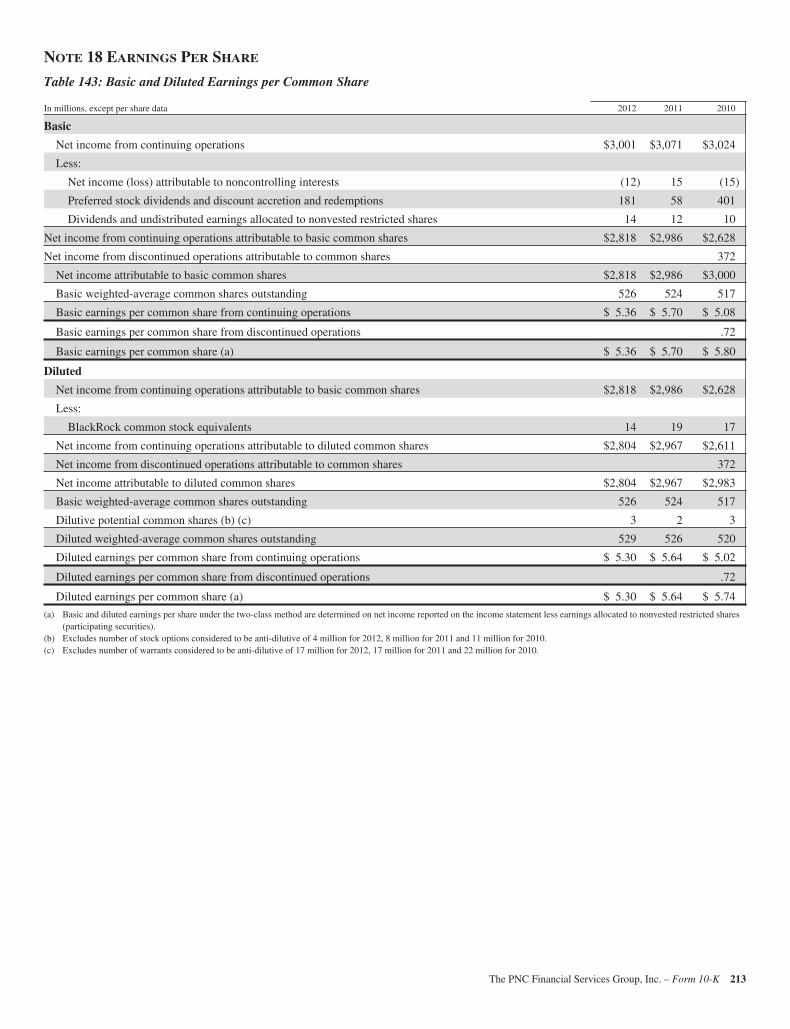

Note 18 Earnings Per Share 213

Note 19 Equity 214

Note 20 Other Comprehensive Income 216

Note 21 Income Taxes 217

Note 22 Regulatory Matters 219

Note 23 Legal Proceedings 219

Note 24 Commitments and Guarantees 226

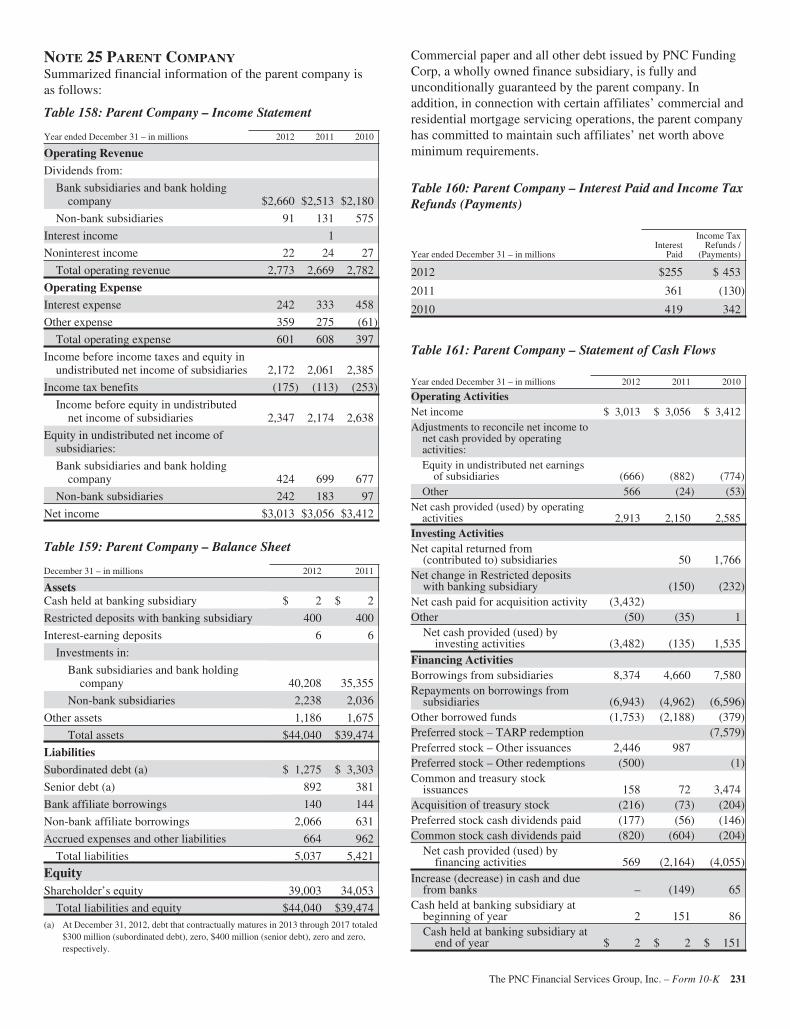

Note 25 Parent Company 231

Note 26 Segment Reporting 232

Note 27 Subsequent Events 235

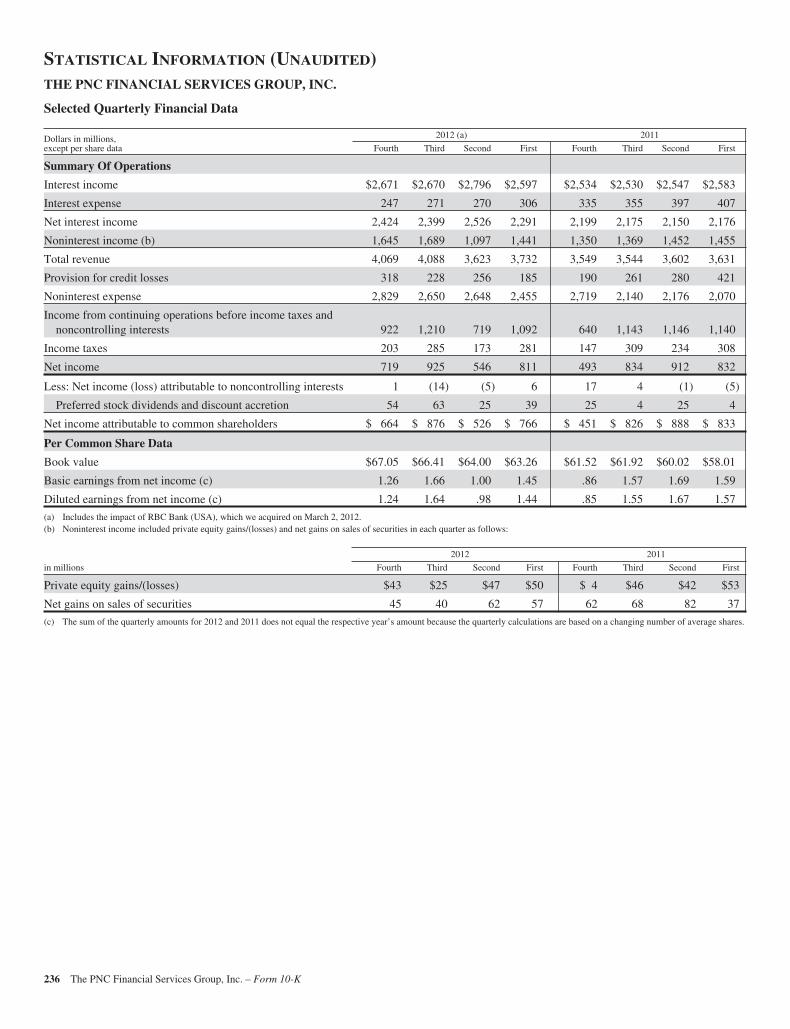

Statistical Information (Unaudited) 236

Item 9 Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. 243

Item 9A Controls and Procedures. 243

Item 9B Other Information. 243

PART III

Item 10 Directors, Executive Officers and Corporate Governance. 243

Item 11 Executive Compensation. 244

Item 12 Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. 244

Item 13 Certain Relationships and Related Transactions, and Director Independence. 246

Item 14 Principal Accounting Fees and Services. 246

PART IV

Item 15 Exhibits, Financial Statement Schedules. 246

SIGNATURES 247

EXHIBIT INDEX E-1

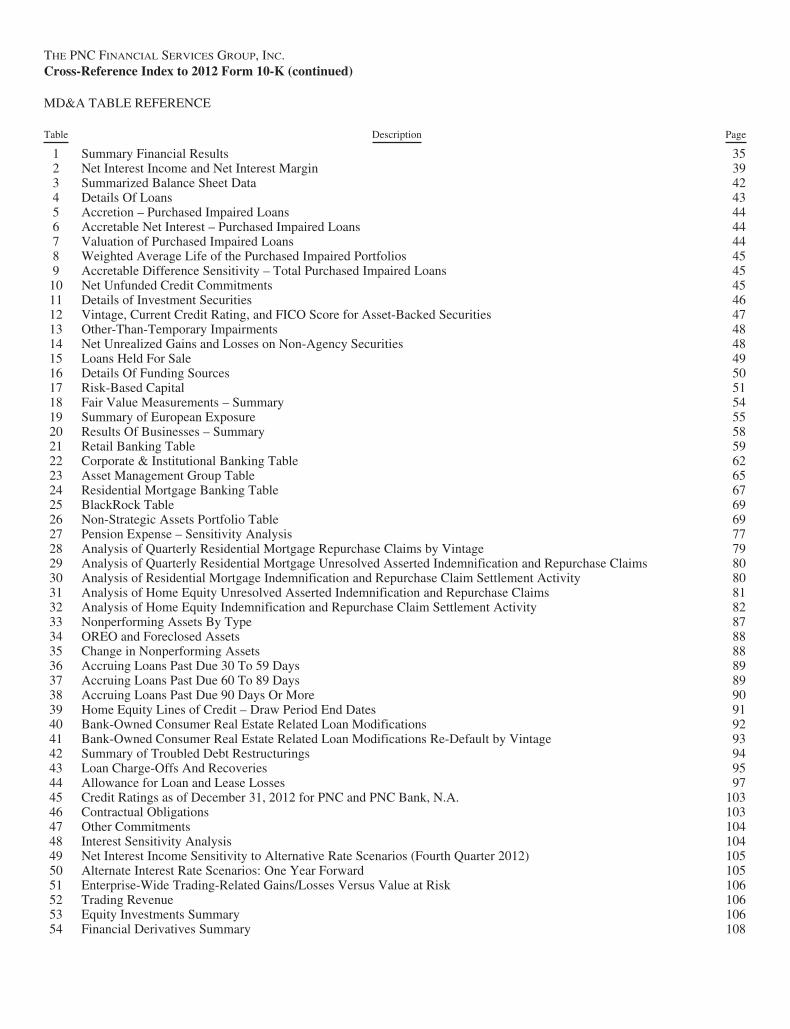

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K (continued)

MD&A TABLE REFERENCE

Table Description Page

1 Summary Financial Results 352 Net Interest Income and Net Interest Margin 393 Summarized Balance Sheet Data 424 Details Of Loans 435 Accretion – Purchased Impaired Loans 446 Accretable Net Interest – Purchased Impaired Loans 447 Valuation of Purchased Impaired Loans 448 Weighted Average Life of the Purchased Impaired Portfolios 459 Accretable Difference Sensitivity – Total Purchased Impaired Loans 4510 Net Unfunded Credit Commitments 4511 Details of Investment Securities 4612 Vintage, Current Credit Rating, and FICO Score for Asset-Backed Securities 4713 Other-Than-Temporary Impairments 4814 Net Unrealized Gains and Losses on Non-Agency Securities 4815 Loans Held For Sale 4916 Details Of Funding Sources 5017 Risk-Based Capital 5118 Fair Value Measurements – Summary 5419 Summary of European Exposure 5520 Results Of Businesses – Summary 5821 Retail Banking Table 5922 Corporate & Institutional Banking Table 6223 Asset Management Group Table 6524 Residential Mortgage Banking Table 6725 BlackRock Table 6926 Non-Strategic Assets Portfolio Table 6927 Pension Expense – Sensitivity Analysis 7728 Analysis of Quarterly Residential Mortgage Repurchase Claims by Vintage 7929 Analysis of Quarterly Residential Mortgage Unresolved Asserted Indemnification and Repurchase Claims 8030 Analysis of Residential Mortgage Indemnification and Repurchase Claim Settlement Activity 8031 Analysis of Home Equity Unresolved Asserted Indemnification and Repurchase Claims 8132 Analysis of Home Equity Indemnification and Repurchase Claim Settlement Activity 8233 Nonperforming Assets By Type 8734 OREO and Foreclosed Assets 8835 Change in Nonperforming Assets 8836 Accruing Loans Past Due 30 To 59 Days 8937 Accruing Loans Past Due 60 To 89 Days 8938 Accruing Loans Past Due 90 Days Or More 9039 Home Equity Lines of Credit – Draw Period End Dates 9140 Bank-Owned Consumer Real Estate Related Loan Modifications 9241 Bank-Owned Consumer Real Estate Related Loan Modifications Re-Default by Vintage 9342 Summary of Troubled Debt Restructurings 9443 Loan Charge-Offs And Recoveries 9544 Allowance for Loan and Lease Losses 9745 Credit Ratings as of December 31, 2012 for PNC and PNC Bank, N.A. 10346 Contractual Obligations 10347 Other Commitments 10448 Interest Sensitivity Analysis 10449 Net Interest Income Sensitivity to Alternative Rate Scenarios (Fourth Quarter 2012) 10550 Alternate Interest Rate Scenarios: One Year Forward 10551 Enterprise-Wide Trading-Related Gains/Losses Versus Value at Risk 10652 Trading Revenue 10653 Equity Investments Summary 10654 Financial Derivatives Summary 108

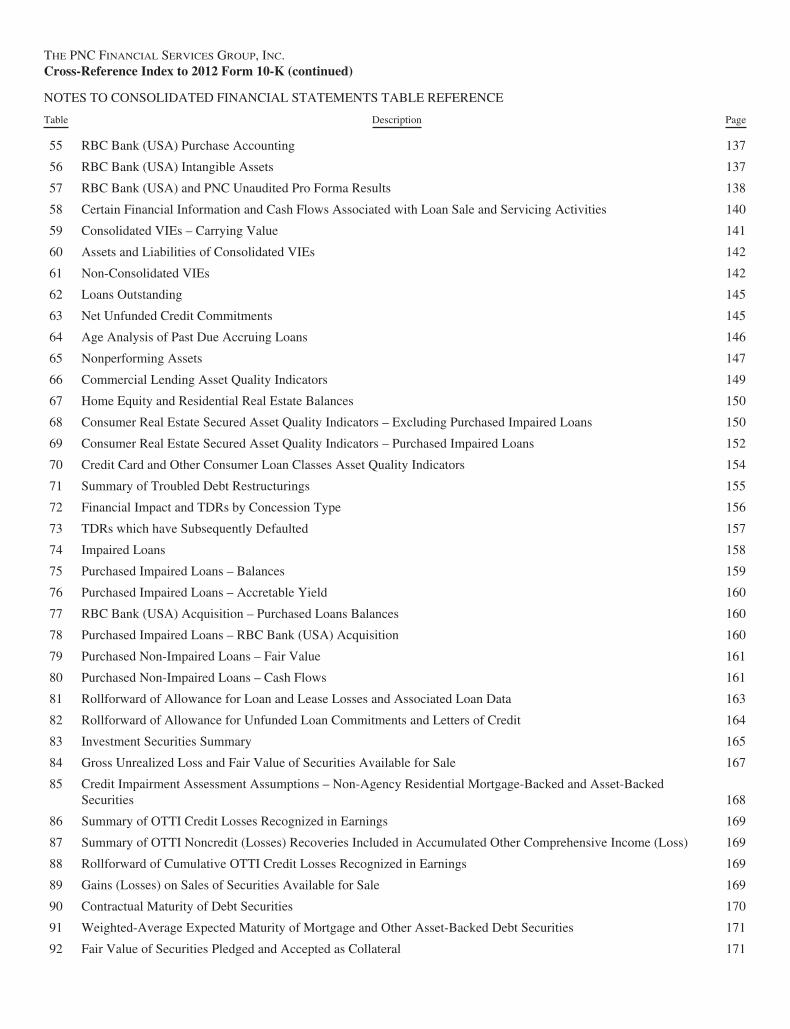

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K (continued)

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS TABLE REFERENCE

Table Description Page

55 RBC Bank (USA) Purchase Accounting 137

56 RBC Bank (USA) Intangible Assets 137

57 RBC Bank (USA) and PNC Unaudited Pro Forma Results 138

58 Certain Financial Information and Cash Flows Associated with Loan Sale and Servicing Activities 140

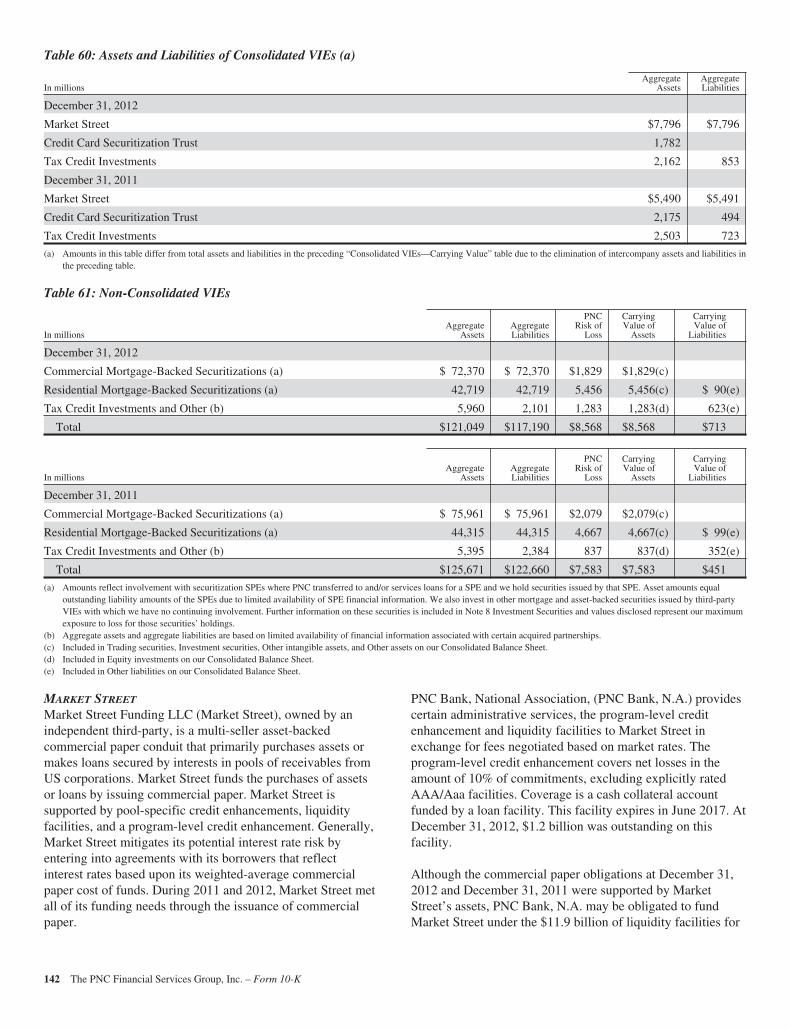

59 Consolidated VIEs – Carrying Value 141

60 Assets and Liabilities of Consolidated VIEs 142

61 Non-Consolidated VIEs 142

62 Loans Outstanding 145

63 Net Unfunded Credit Commitments 145

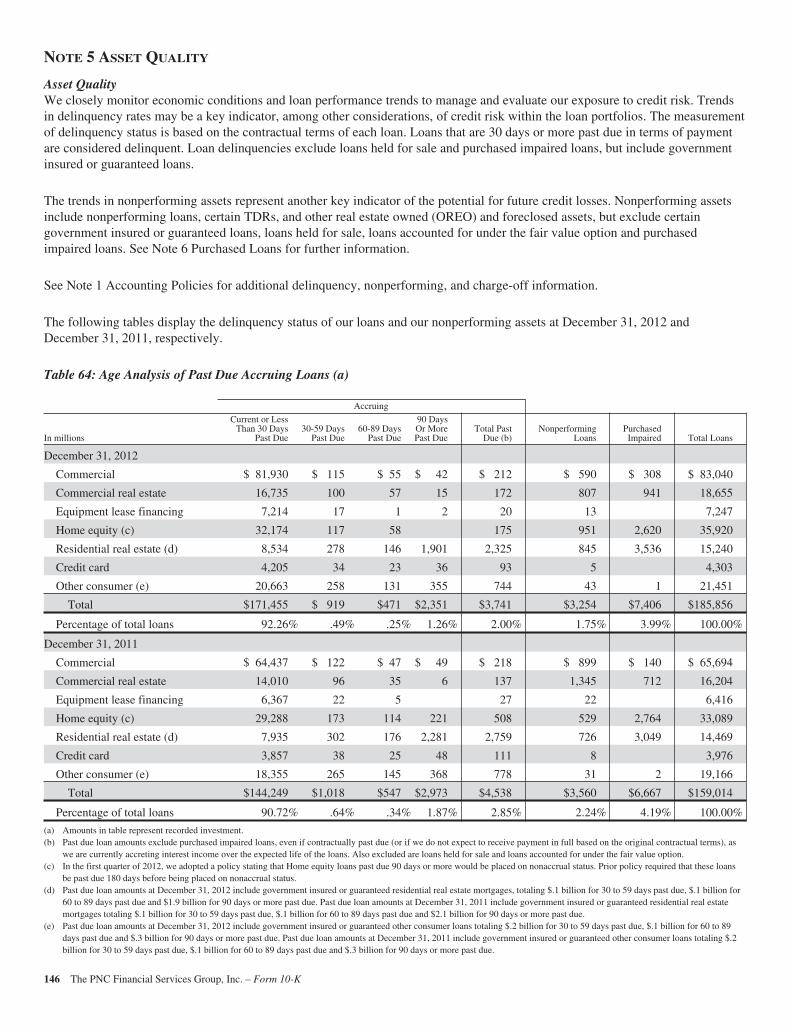

64 Age Analysis of Past Due Accruing Loans 146

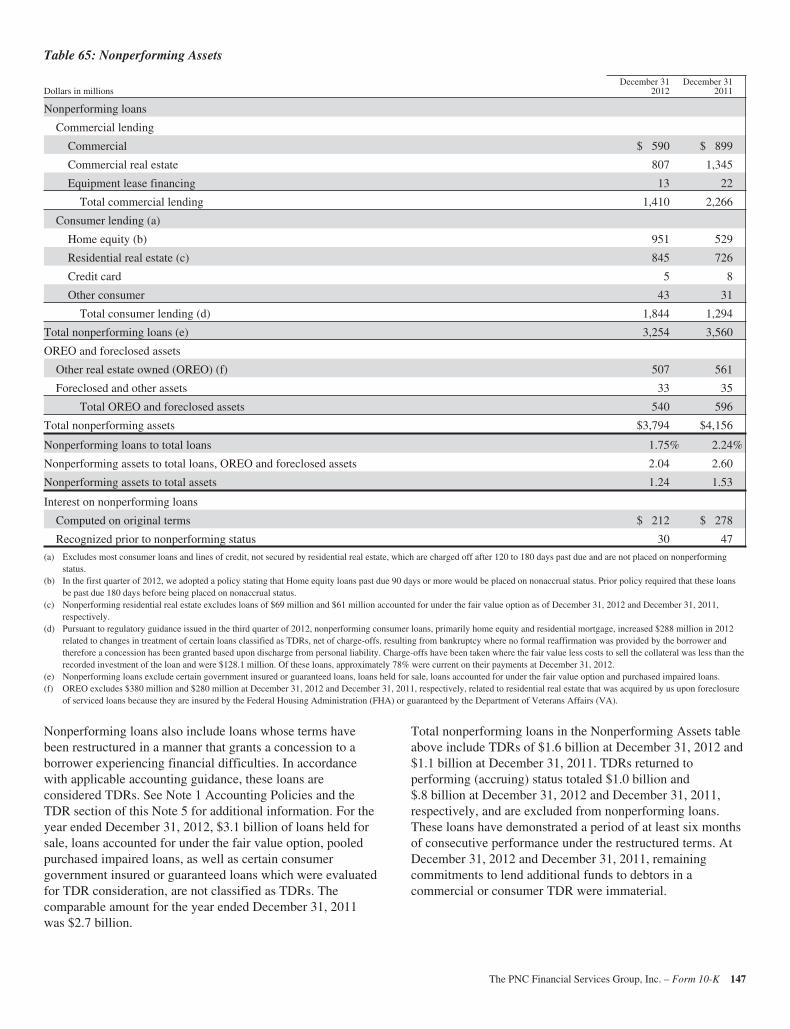

65 Nonperforming Assets 147

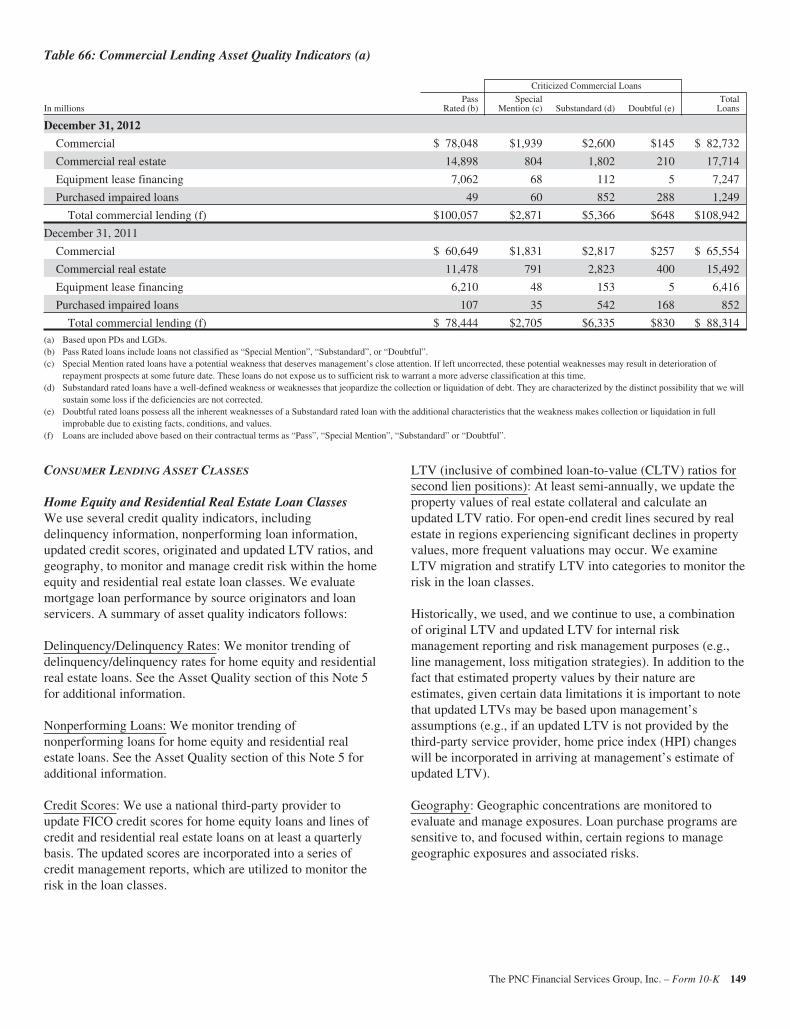

66 Commercial Lending Asset Quality Indicators 149

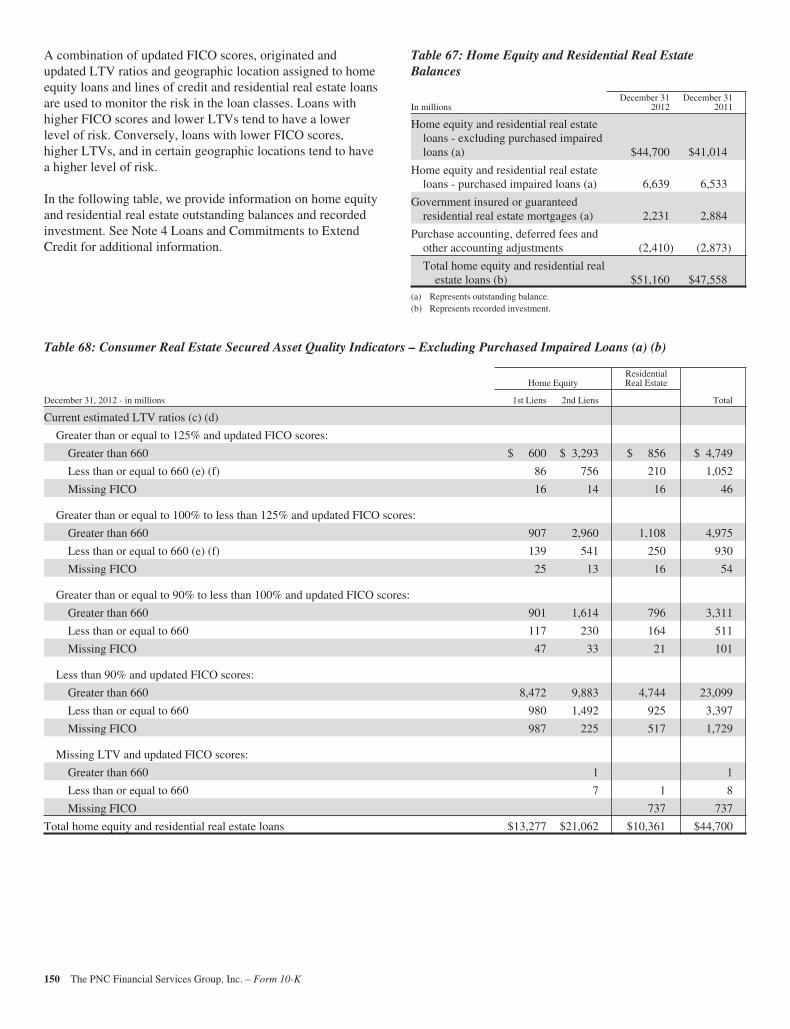

67 Home Equity and Residential Real Estate Balances 150

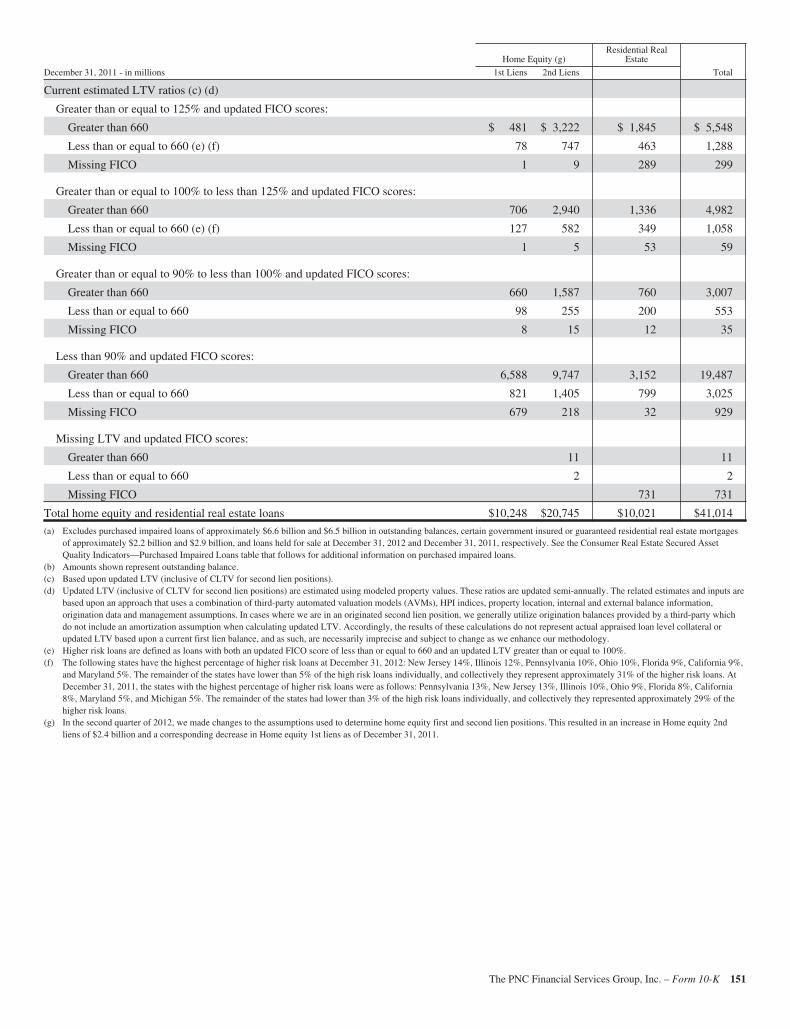

68 Consumer Real Estate Secured Asset Quality Indicators – Excluding Purchased Impaired Loans 150

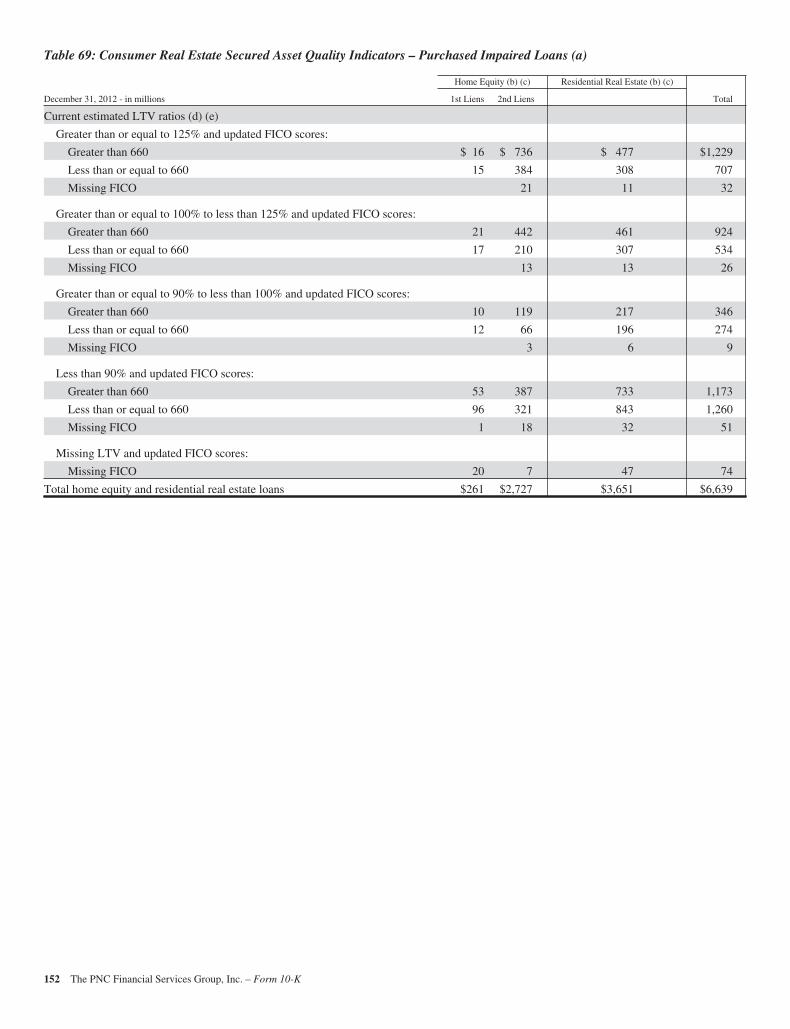

69 Consumer Real Estate Secured Asset Quality Indicators – Purchased Impaired Loans 152

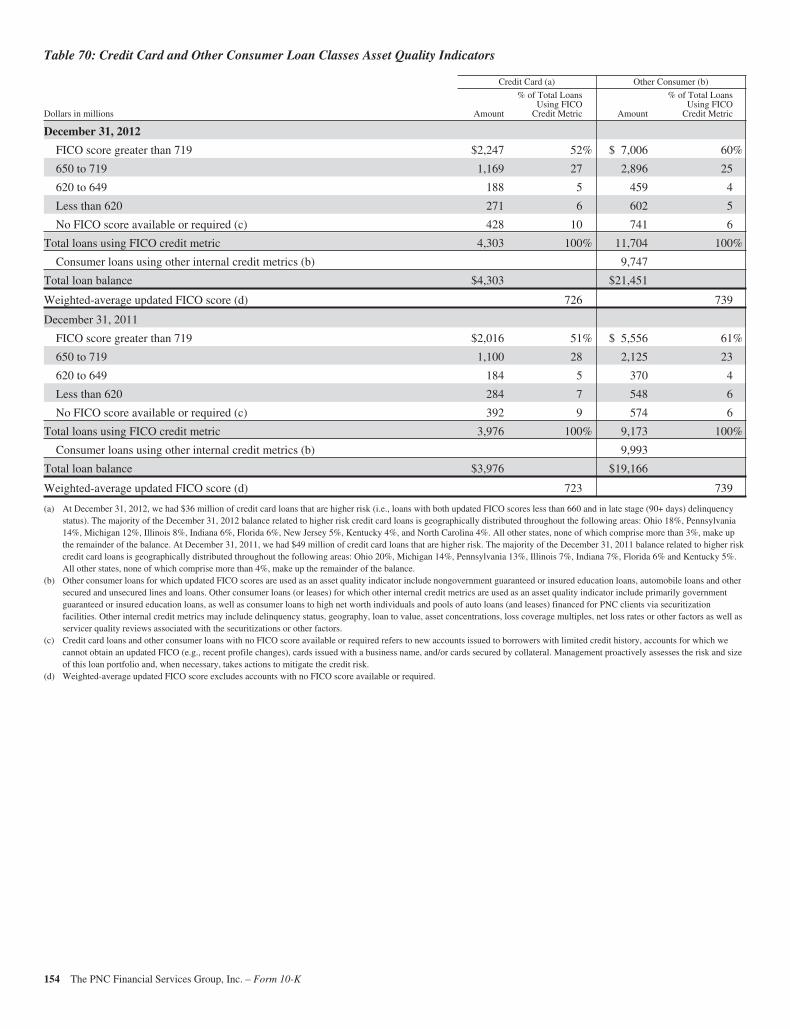

70 Credit Card and Other Consumer Loan Classes Asset Quality Indicators 154

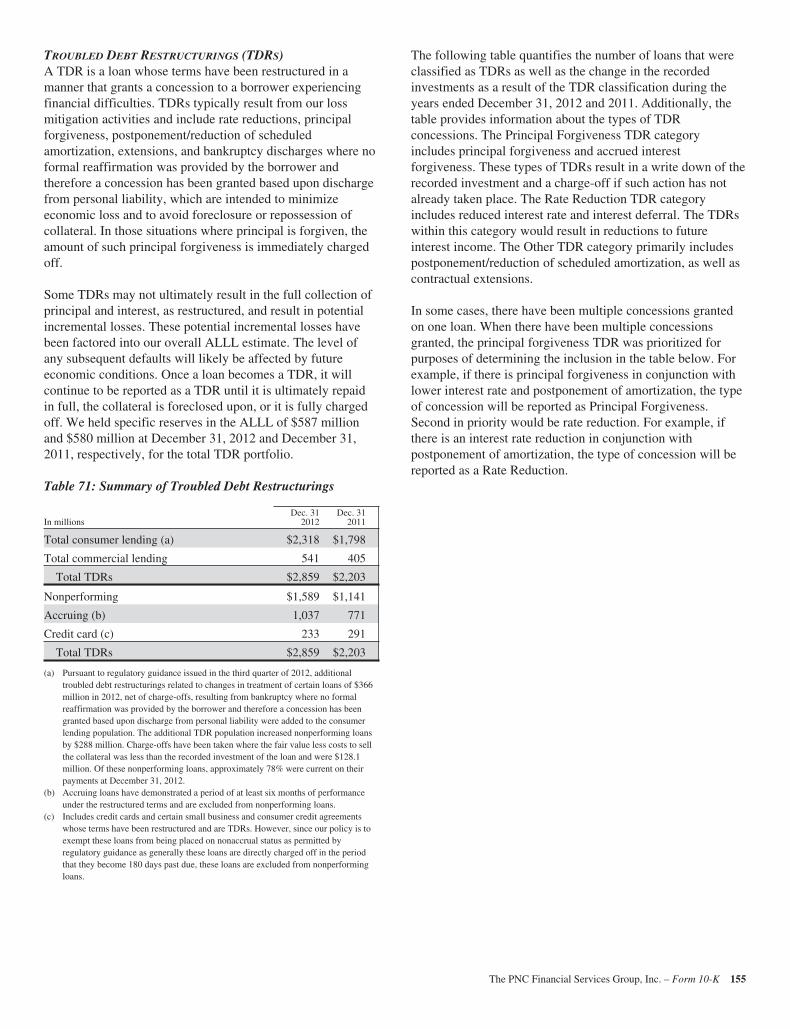

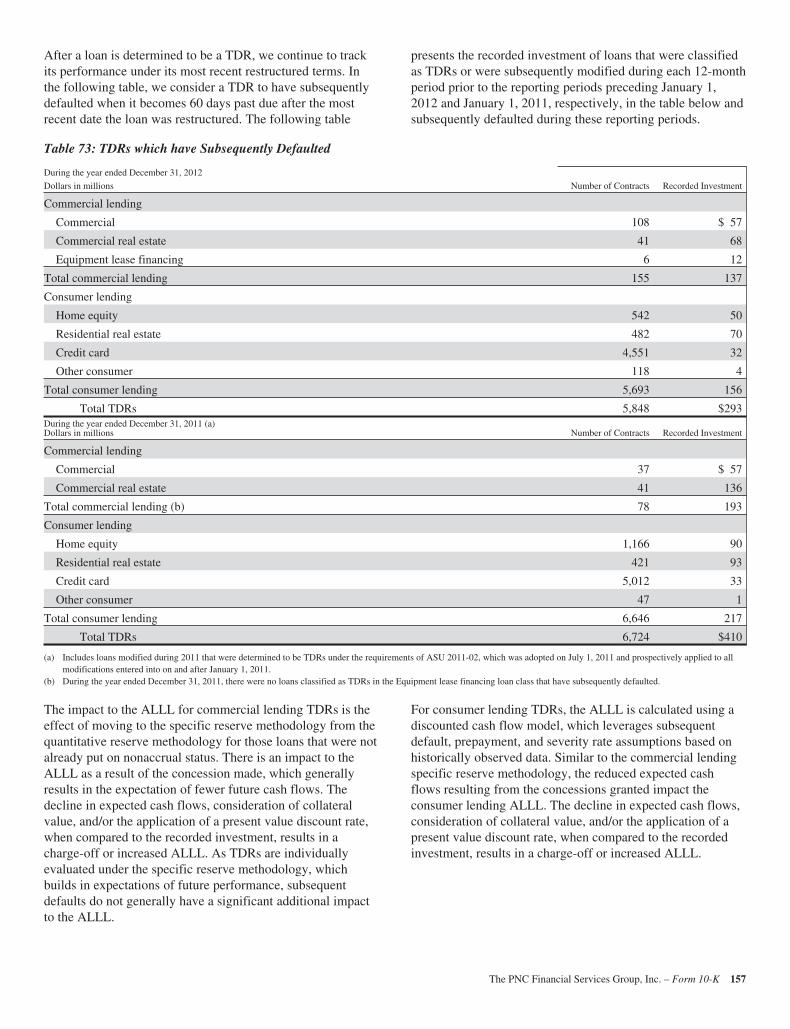

71 Summary of Troubled Debt Restructurings 155

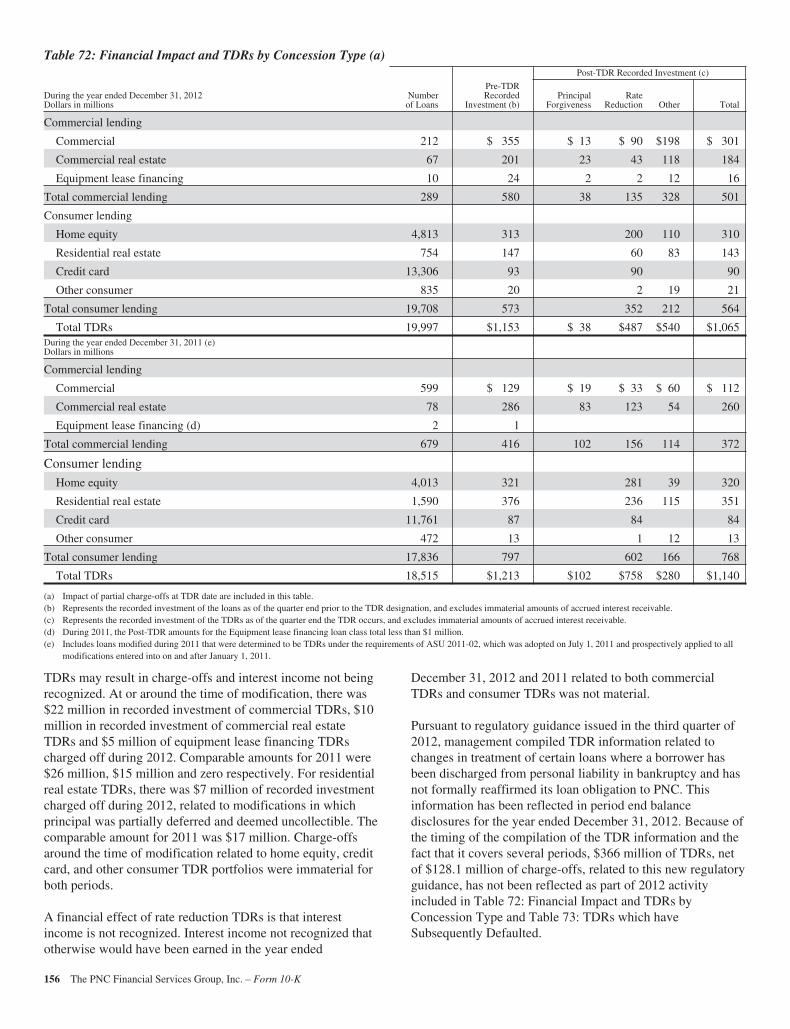

72 Financial Impact and TDRs by Concession Type 156

73 TDRs which have Subsequently Defaulted 157

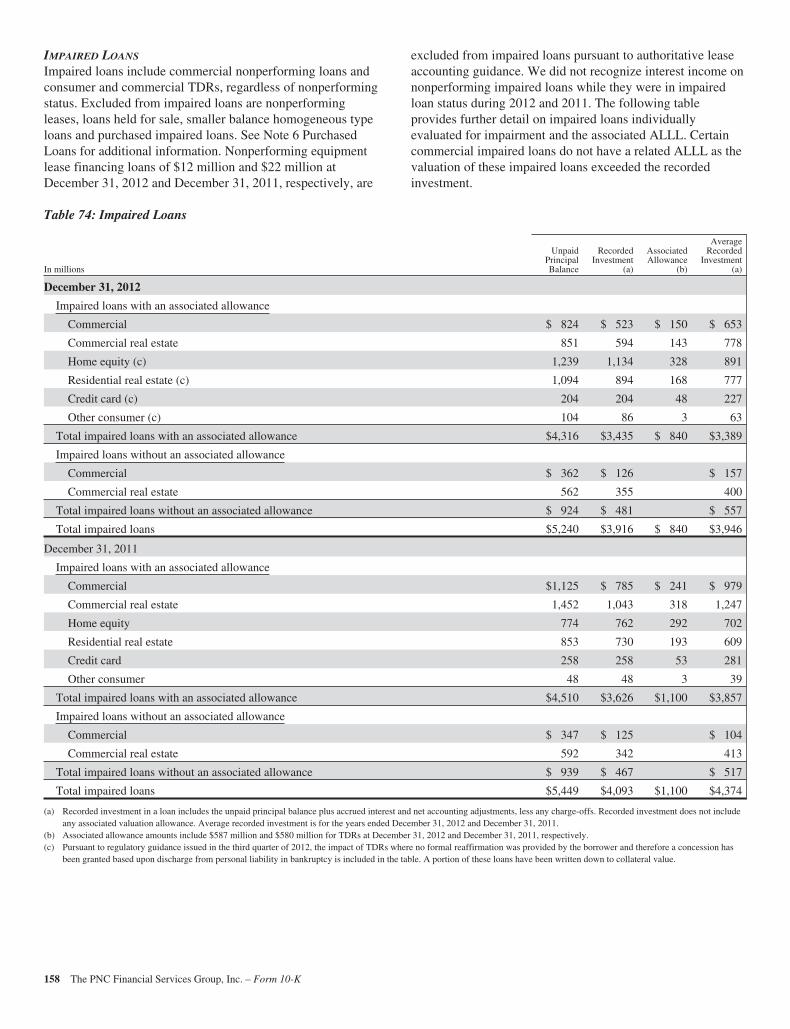

74 Impaired Loans 158

75 Purchased Impaired Loans – Balances 159

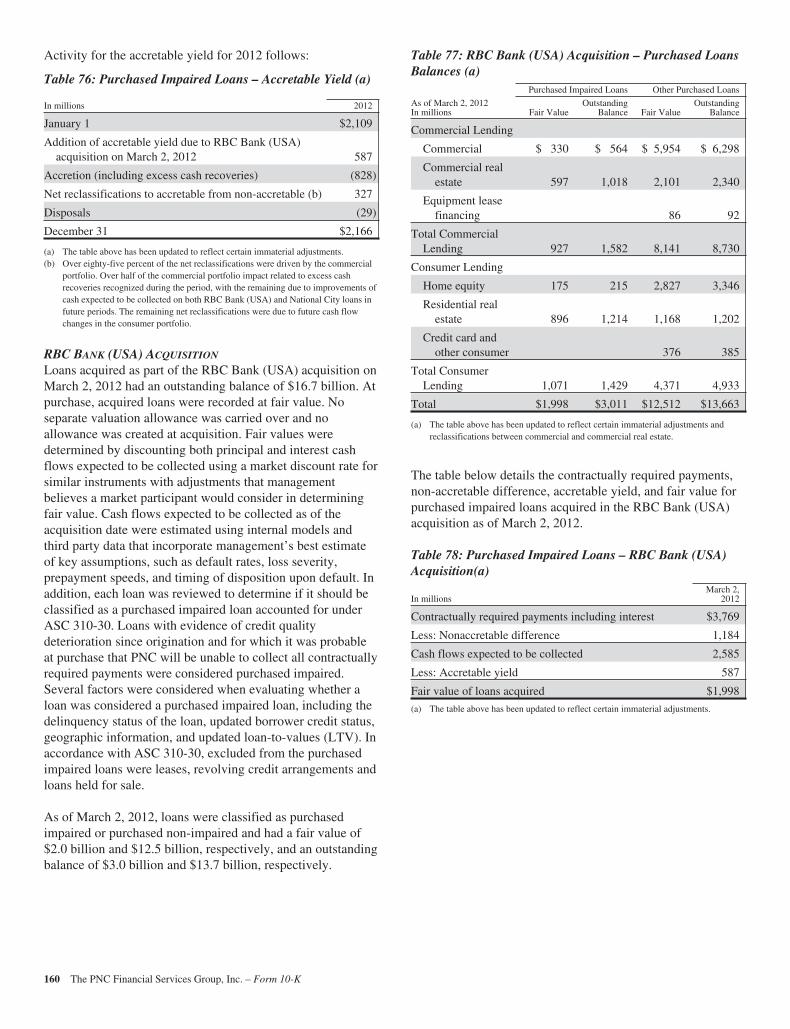

76 Purchased Impaired Loans – Accretable Yield 160

77 RBC Bank (USA) Acquisition – Purchased Loans Balances 160

78 Purchased Impaired Loans – RBC Bank (USA) Acquisition 160

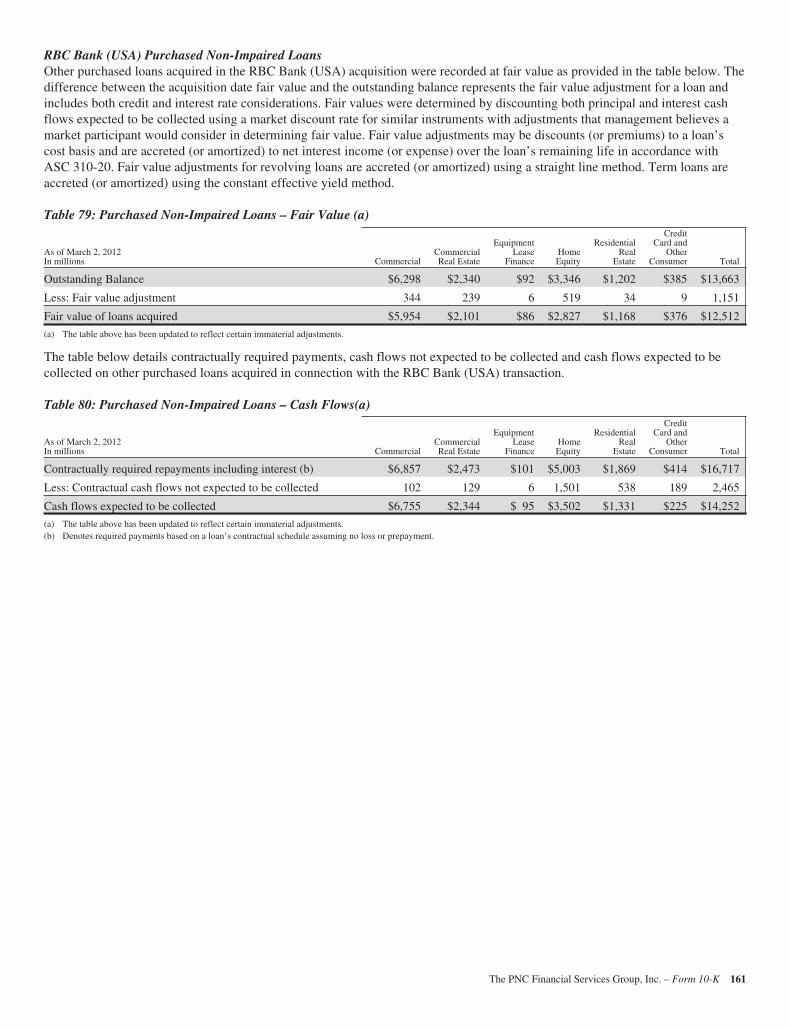

79 Purchased Non-Impaired Loans – Fair Value 161

80 Purchased Non-Impaired Loans – Cash Flows 161

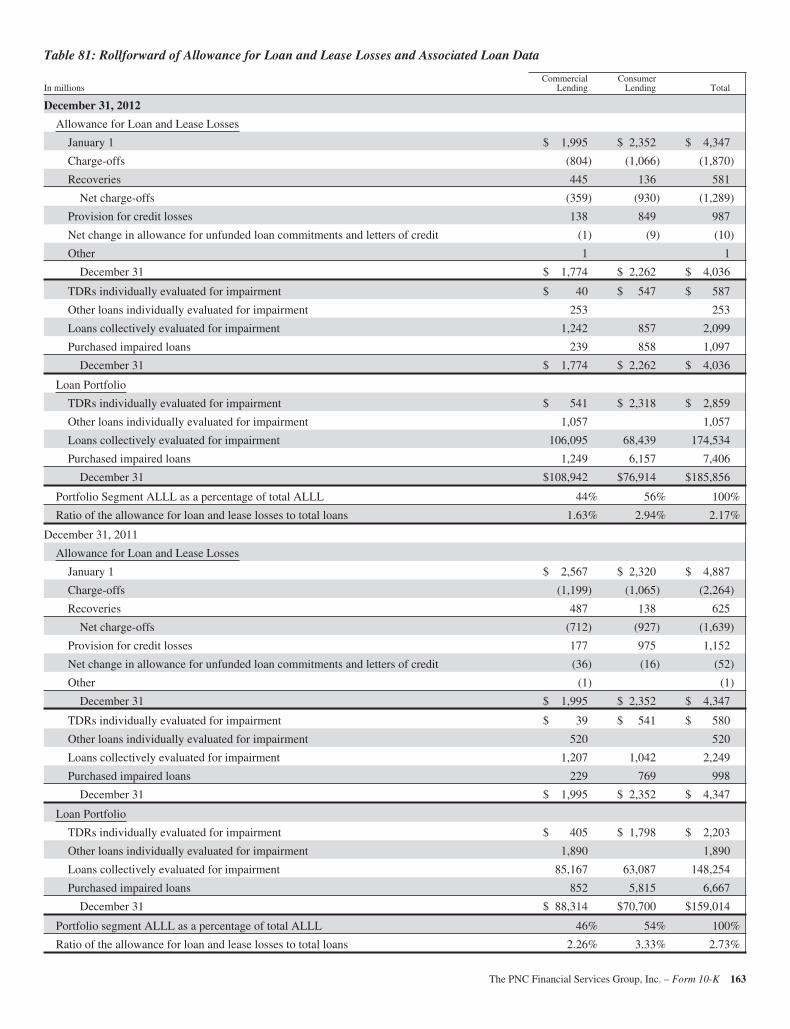

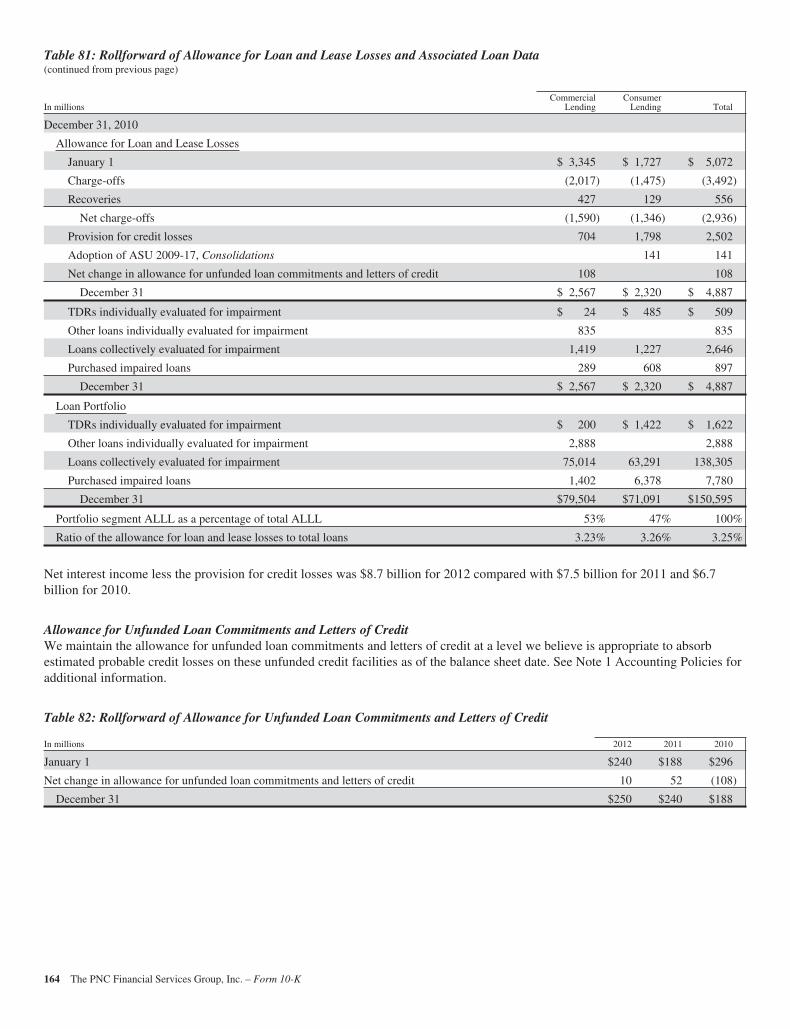

81 Rollforward of Allowance for Loan and Lease Losses and Associated Loan Data 163

82 Rollforward of Allowance for Unfunded Loan Commitments and Letters of Credit 164

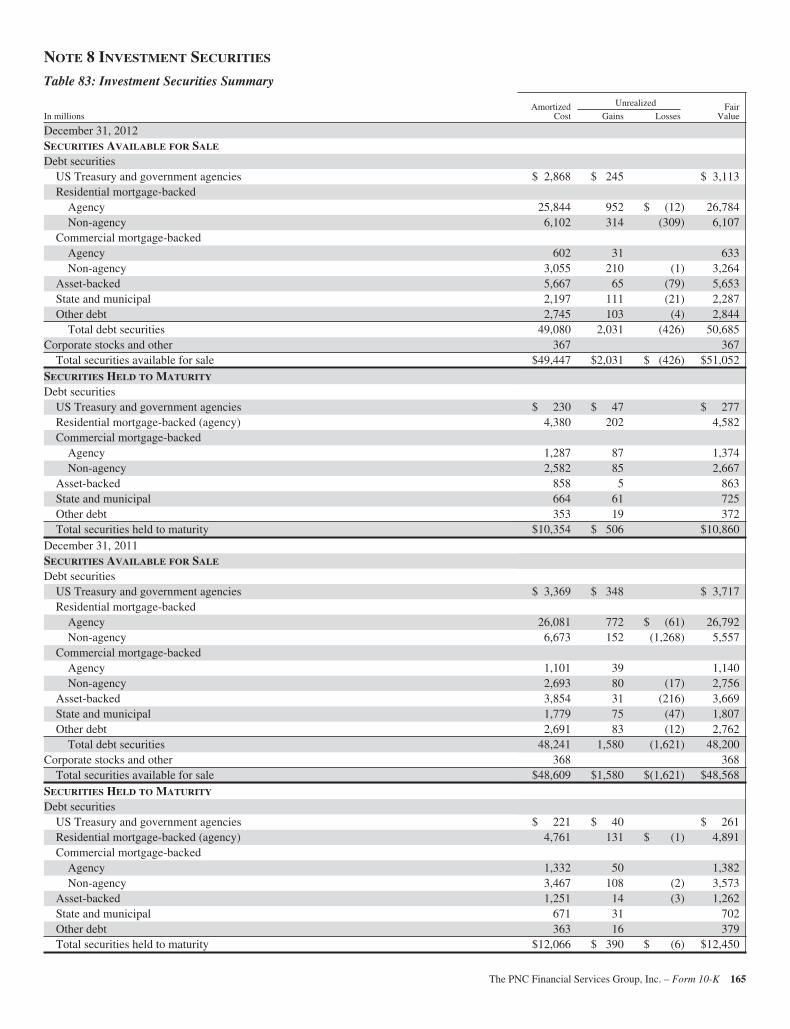

83 Investment Securities Summary 165

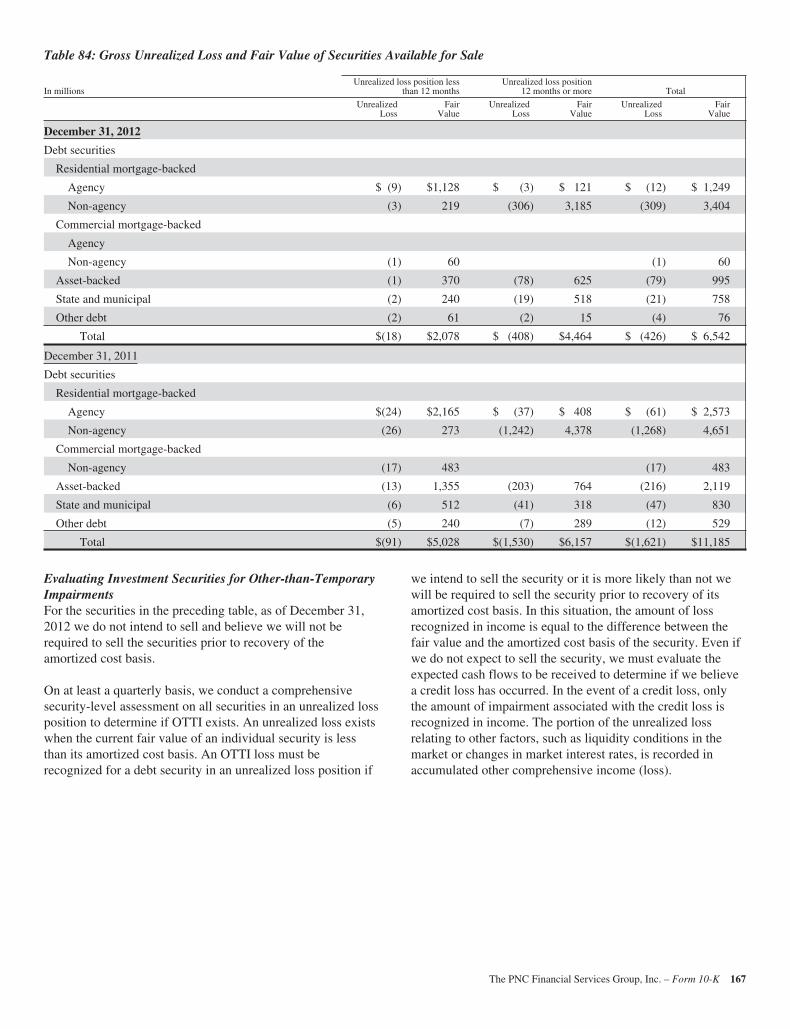

84 Gross Unrealized Loss and Fair Value of Securities Available for Sale 167

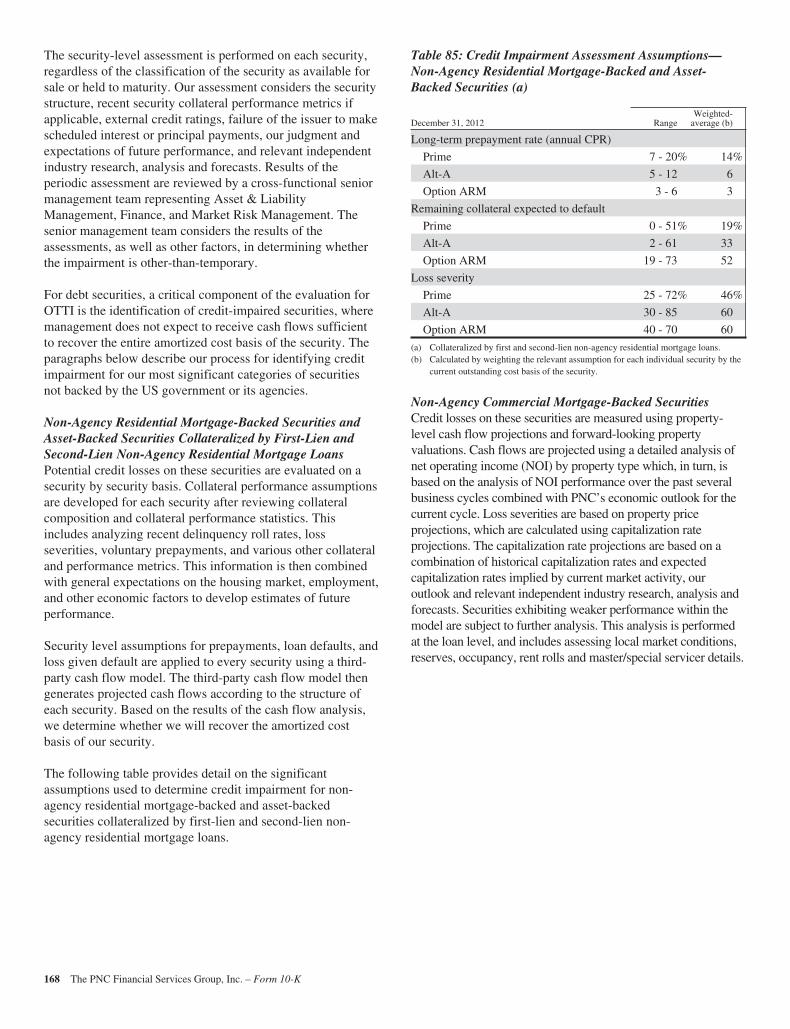

85 Credit Impairment Assessment Assumptions – Non-Agency Residential Mortgage-Backed and Asset-BackedSecurities 168

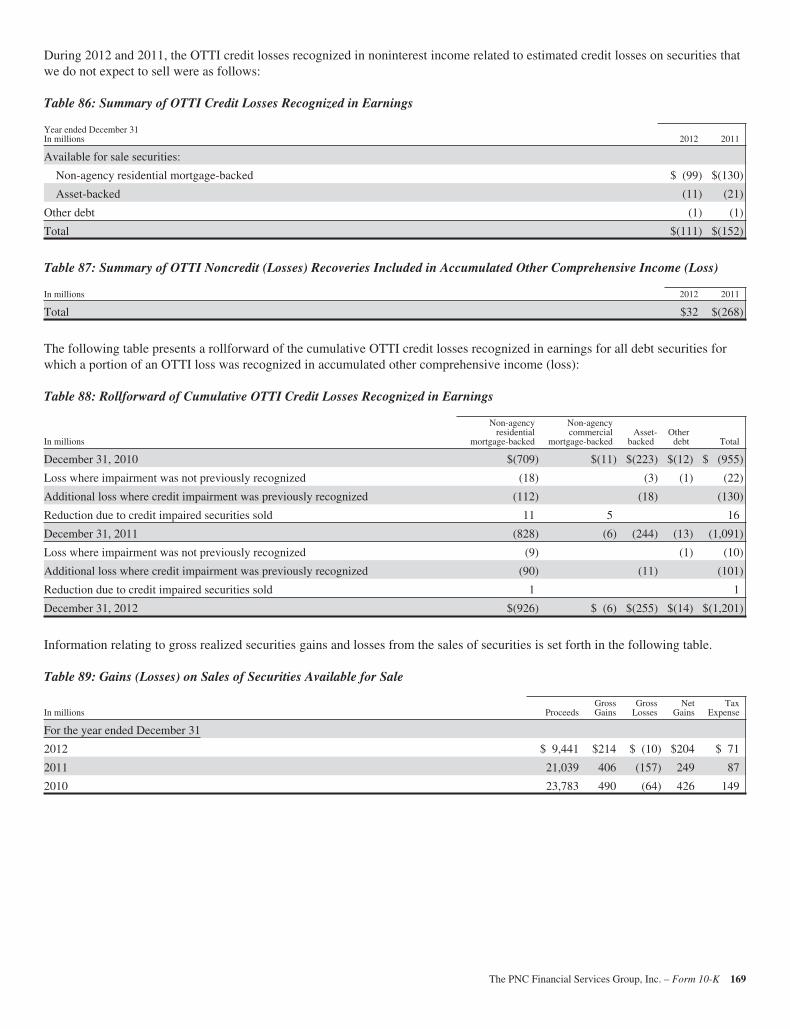

86 Summary of OTTI Credit Losses Recognized in Earnings 169

87 Summary of OTTI Noncredit (Losses) Recoveries Included in Accumulated Other Comprehensive Income (Loss) 169

88 Rollforward of Cumulative OTTI Credit Losses Recognized in Earnings 169

89 Gains (Losses) on Sales of Securities Available for Sale 169

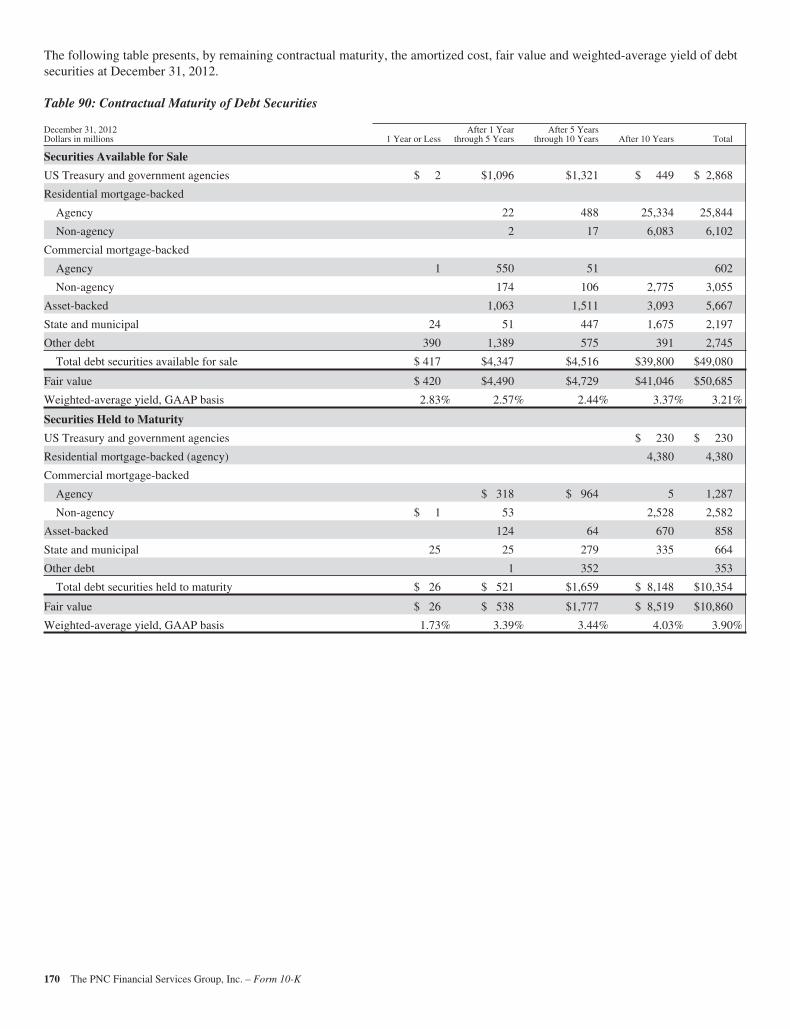

90 Contractual Maturity of Debt Securities 170

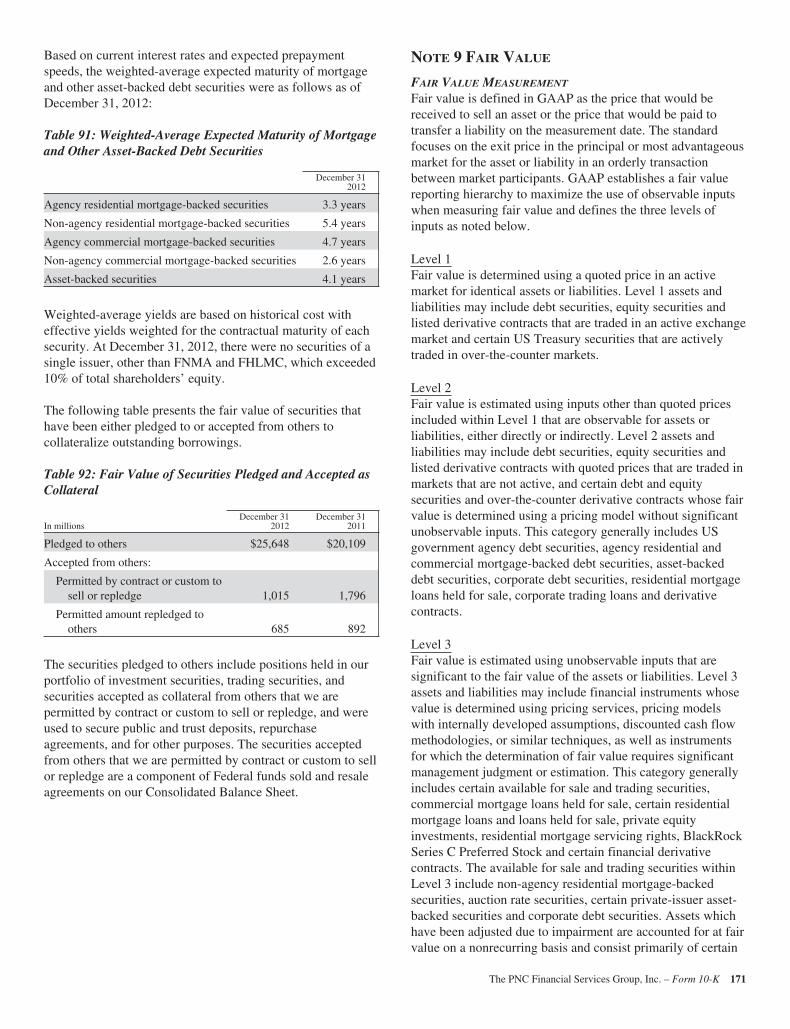

91 Weighted-Average Expected Maturity of Mortgage and Other Asset-Backed Debt Securities 171

92 Fair Value of Securities Pledged and Accepted as Collateral 171

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K (continued)

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS TABLE REFERENCE (Continued)

Table Description Page

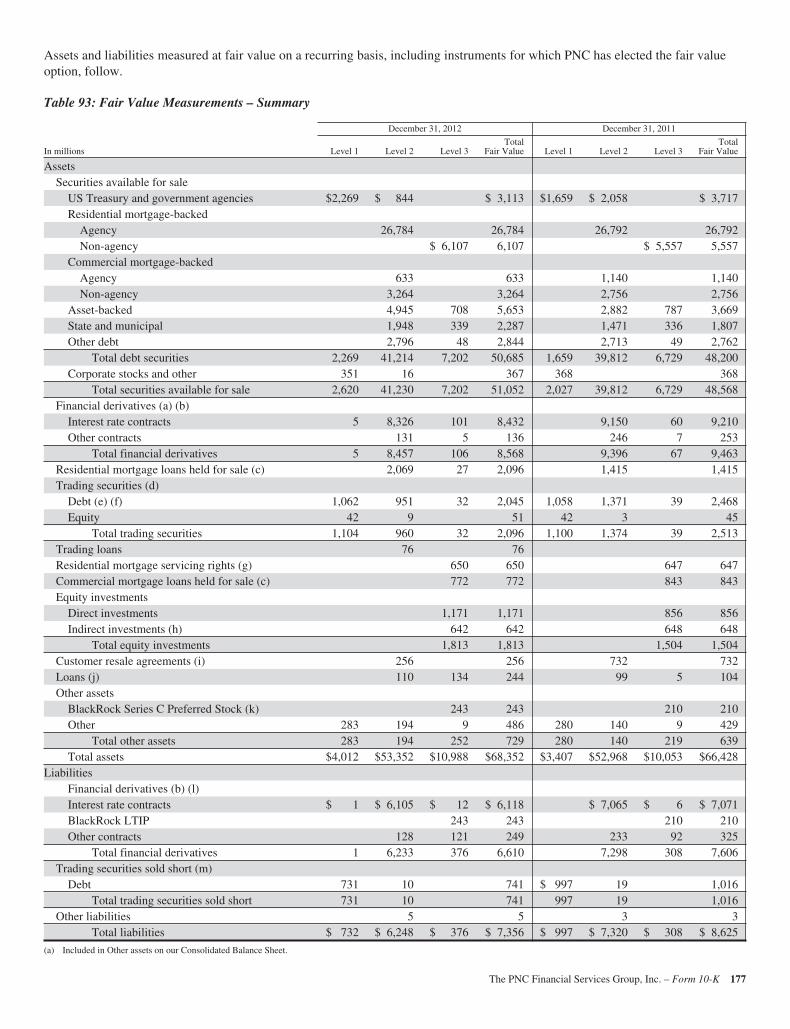

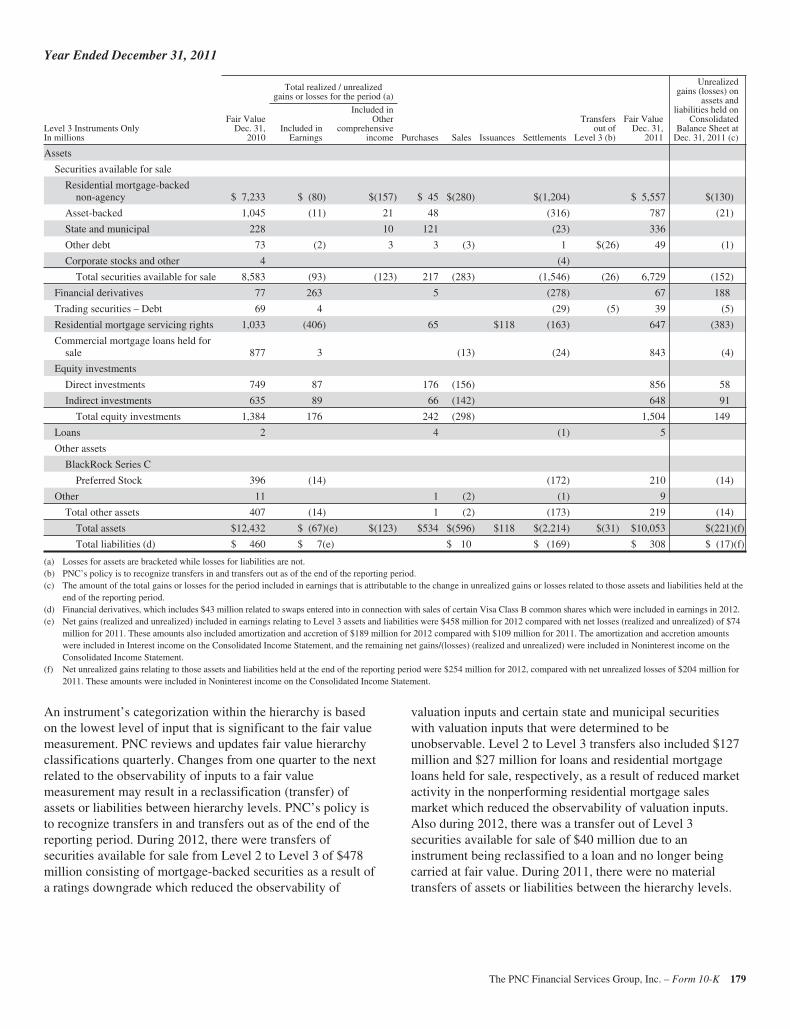

93 Fair Value Measurements – Summary 177

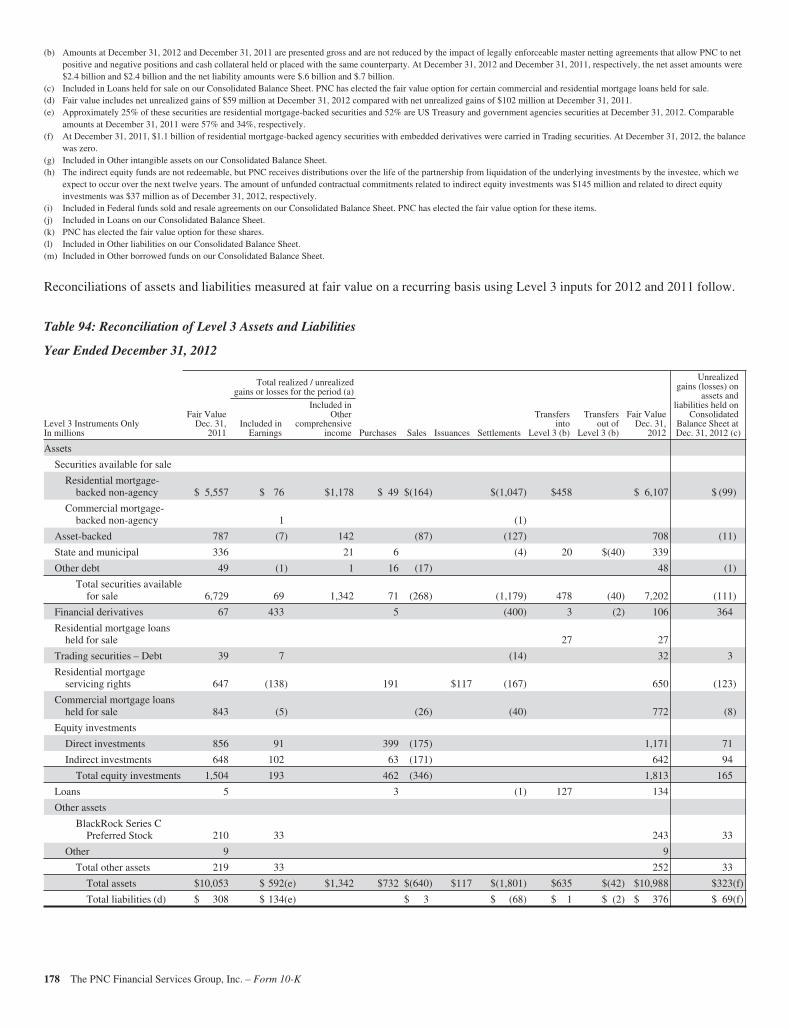

94 Reconciliation of Level 3 Assets and Liabilities 178

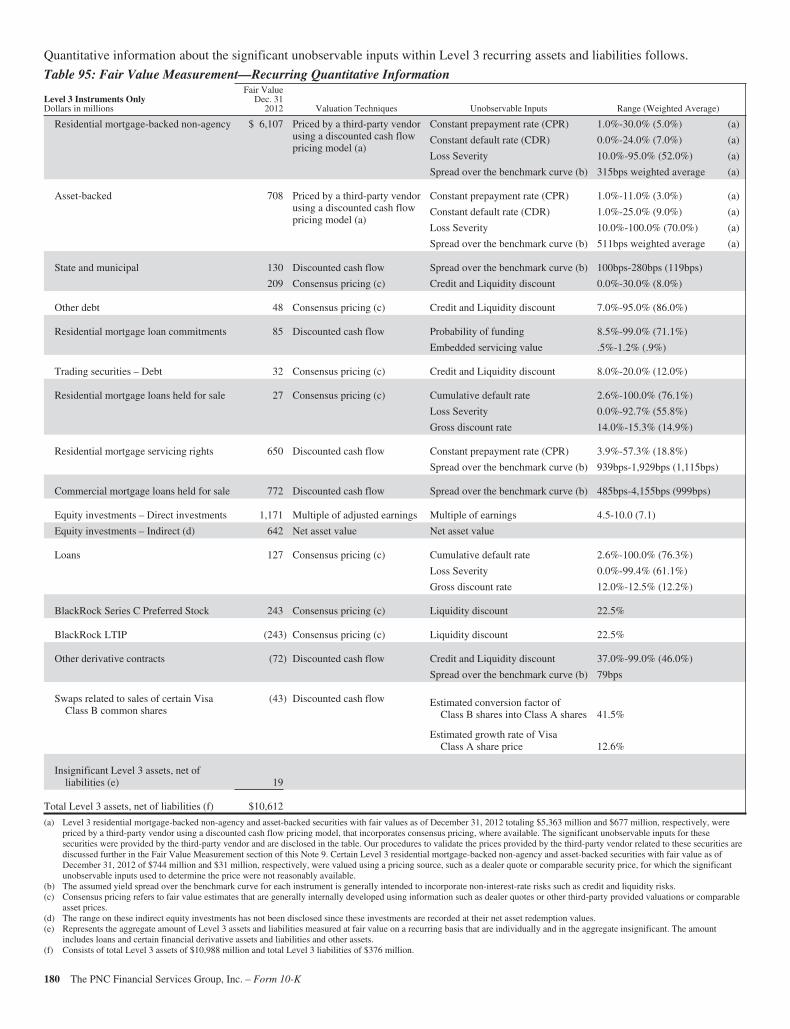

95 Fair Value Measurement – Recurring Quantitative Information 180

96 Fair Value Measurements – Nonrecurring 182

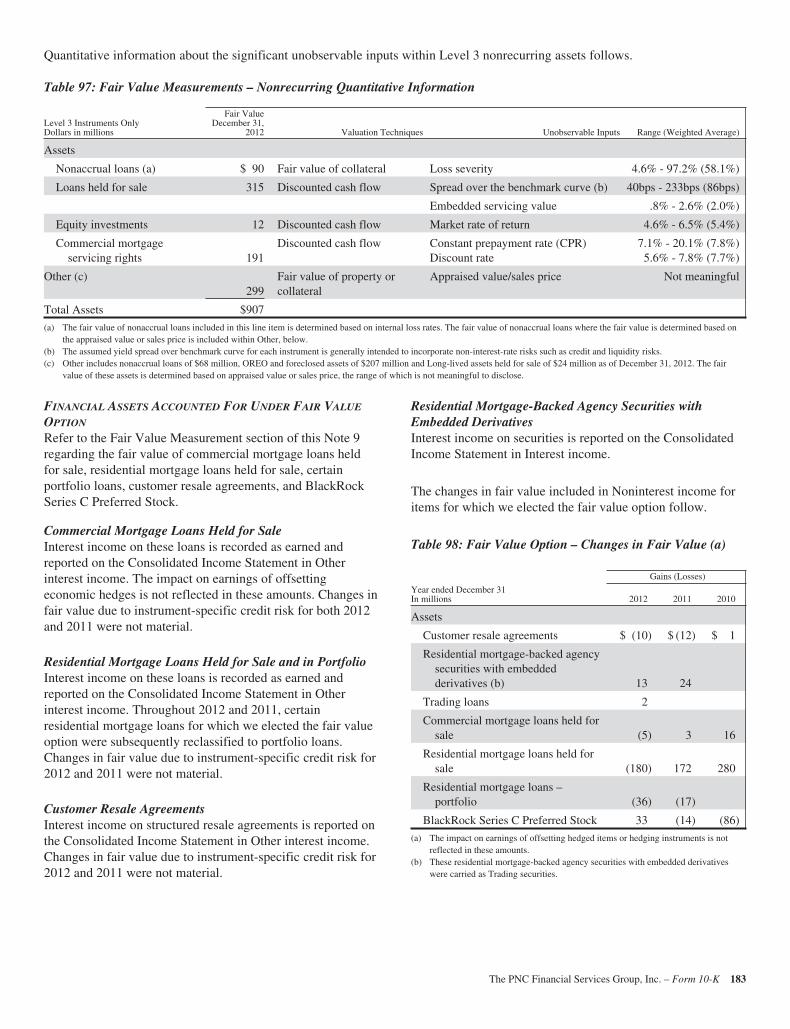

97 Fair Value Measurements – Nonrecurring Quantitative Information 183

98 Fair Value Option – Changes in Fair Value 183

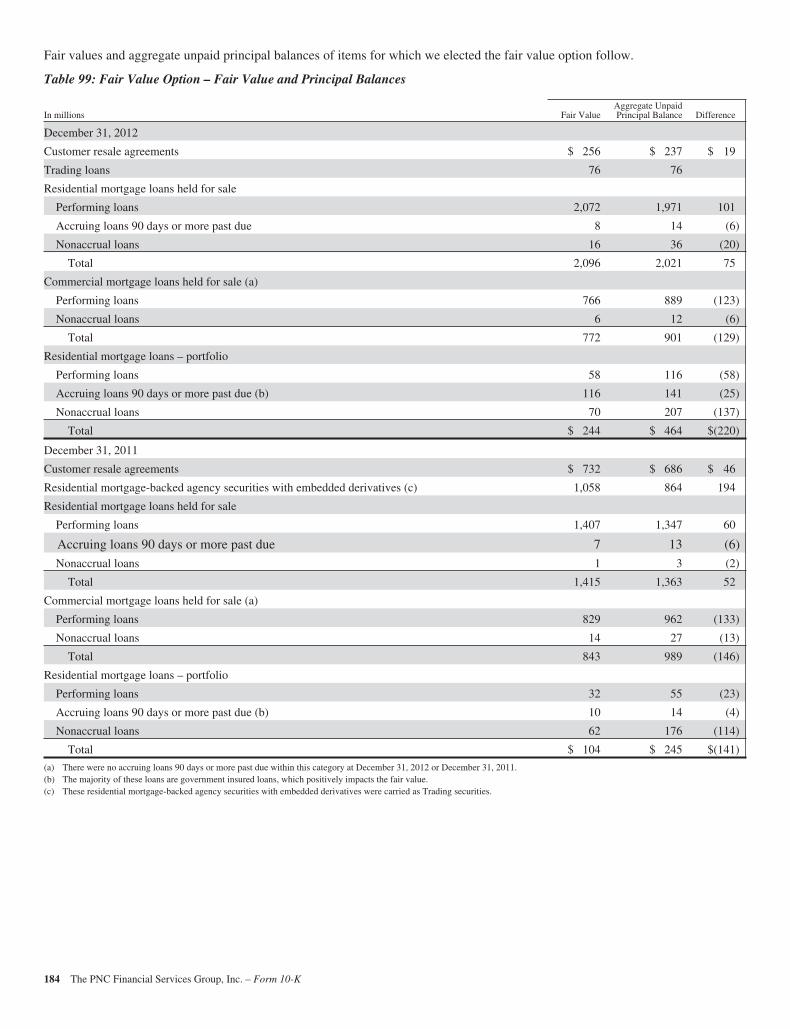

99 Fair Value Option – Fair Value and Principal Balances 184

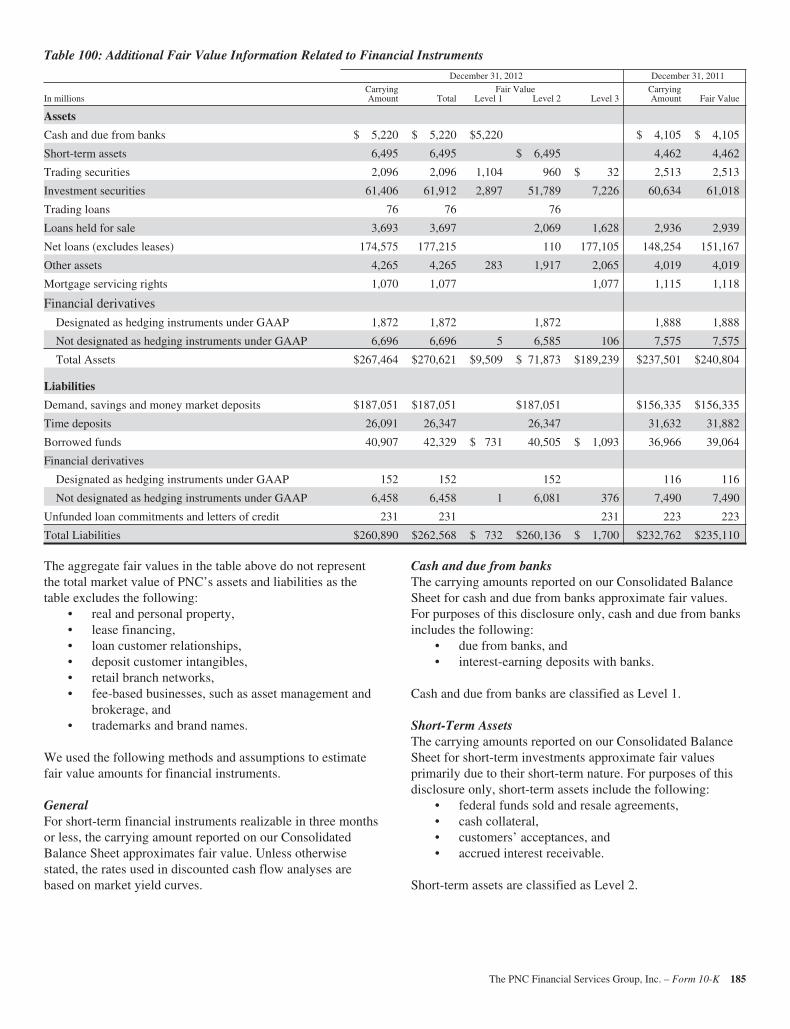

100 Additional Fair Value Information Related to Financial Instruments 185

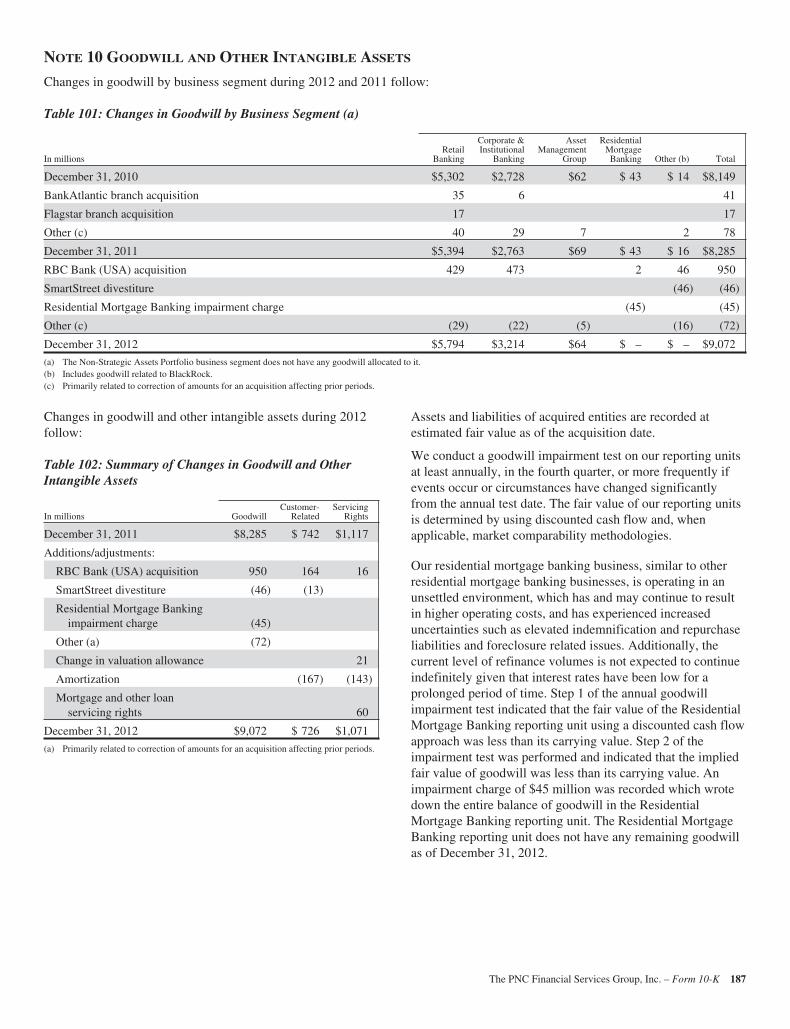

101 Changes in Goodwill by Business Segment 187

102 Summary of Changes in Goodwill and Other Intangible Assets 187

103 Other Intangible Assets 188

104 Amortization Expense on Existing Intangible Assets 188

105 Commercial Mortgage Servicing Rights 188

106 Residential Mortgage Servicing Rights 189

107 Commercial Mortgage Loan Servicing Assets – Key Valuation Assumptions 189

108 Residential Mortgage Loan Servicing Assets – Key Valuation Assumptions 190

109 Fees from Mortgage and Other Loan Servicing 190

110 Premises, Equipment and Leasehold Improvements 190

111 Depreciation and Amortization Expense 190

112 Lease Rental Expense 190

113 Bank Notes, Senior Debt and Subordinated Debt 191

114 Capital Securities of Subsidiary Trusts 192

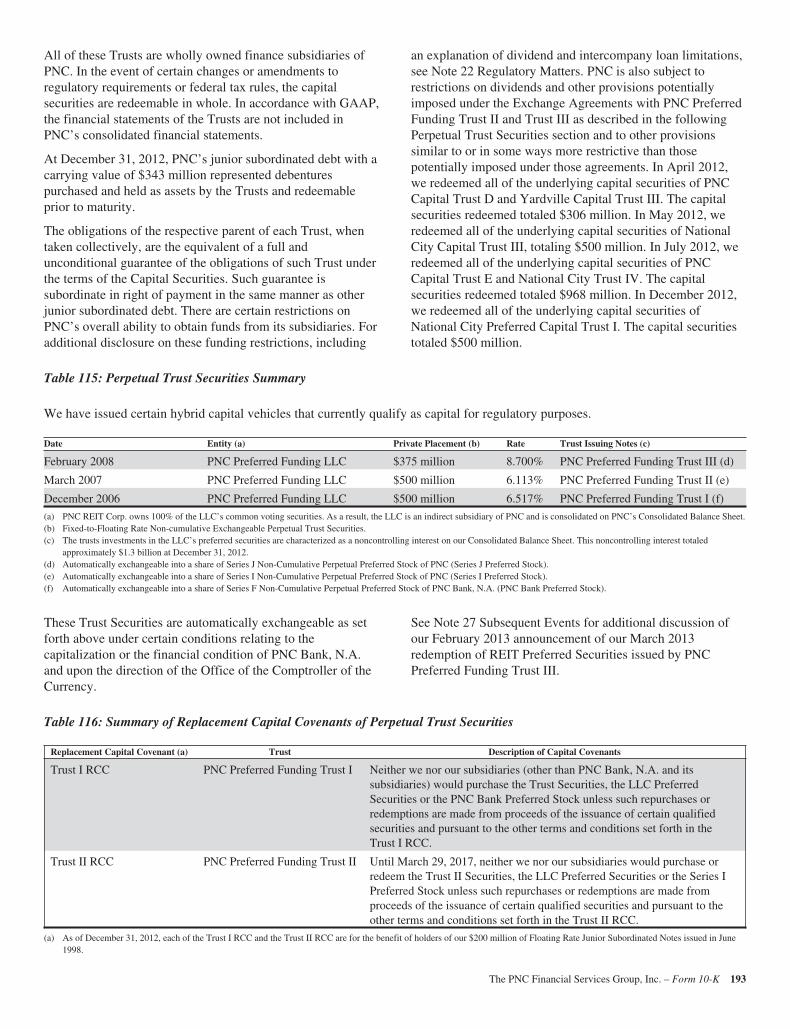

115 Perpetual Trust Securities Summary 193

116 Summary of Replacement Capital Covenants of Perpetual Trust Securities 193

117 Summary of Contractual Commitments of Perpetual Trust Securities 194

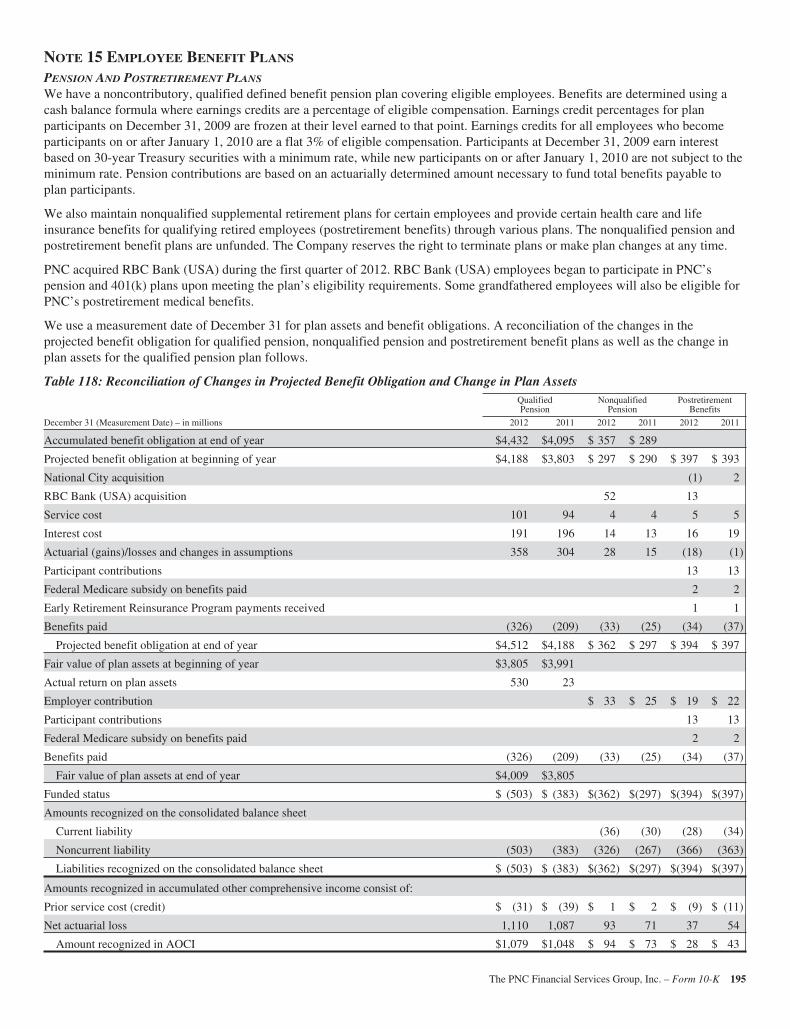

118 Reconciliation of Changes in Projected Benefit Obligation and Change in Plan Assets 195

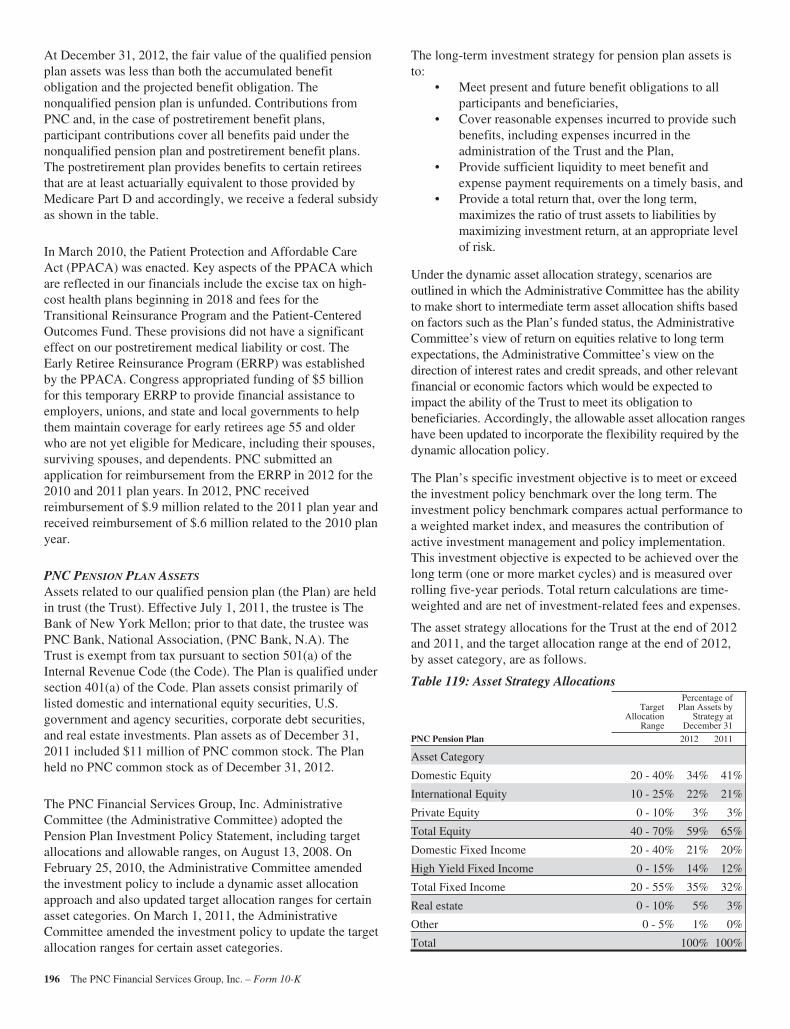

119 Asset Strategy Allocations 196

120 Pension Plan Assets – Fair Value Hierarchy 198

121 Rollforward of Pension Plan Level 3 Assets 199

122 Estimated Cash Flows 199

123 Components of Net Periodic Benefit Cost 200

124 Net Periodic Costs – Assumptions 200

125 Other Pension Assumptions 200

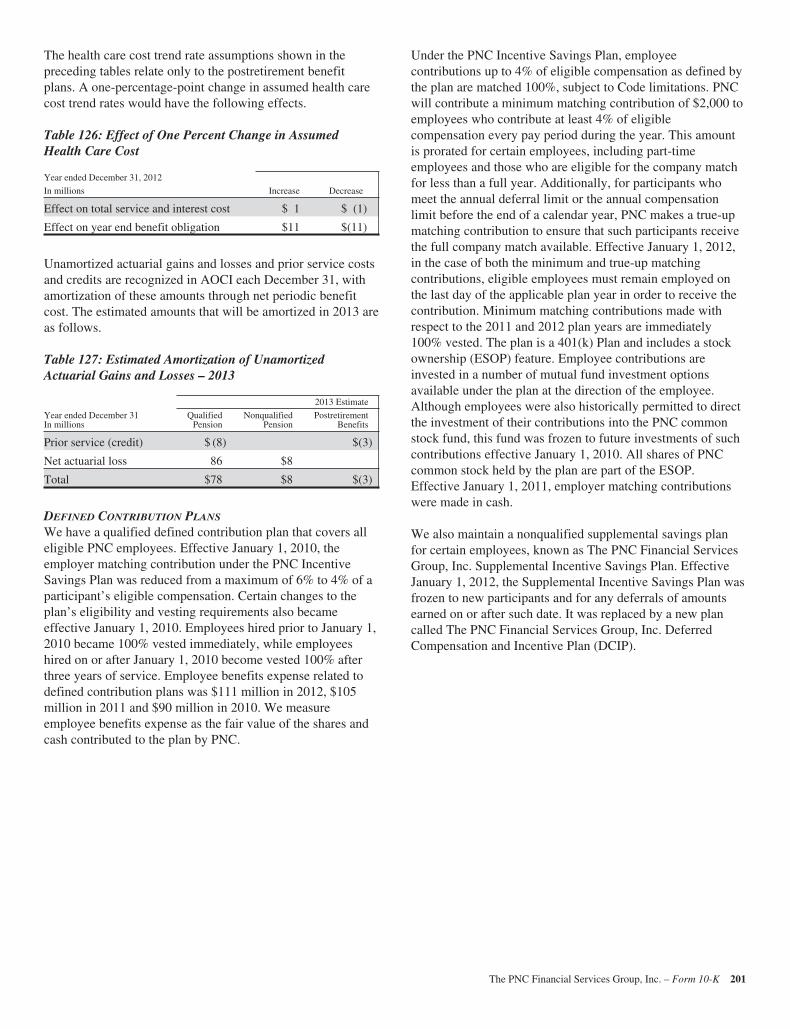

126 Effect of One Percent Change in Assumed Health Care Cost 201

127 Estimated Amortization of Unamortized Actuarial Gains and Losses – 2013 201

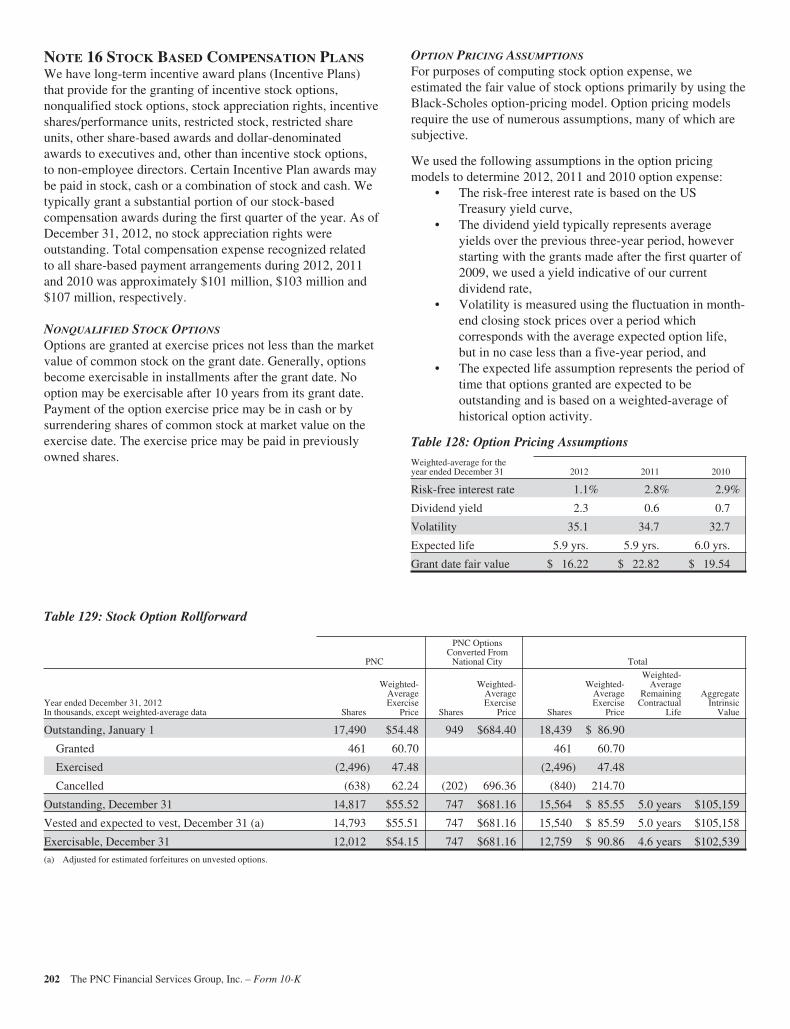

128 Option Pricing Assumptions 202

129 Stock Option Rollforward 202

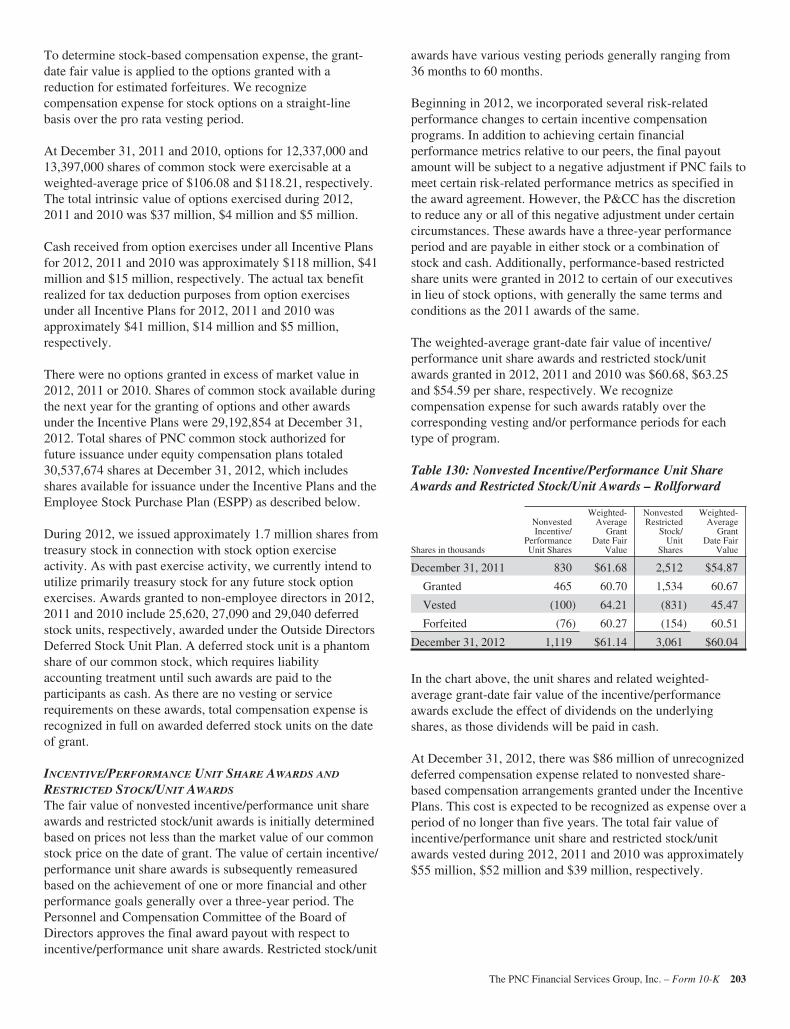

130 Nonvested Incentive/Performance Unit Share Awards and Restricted Stock/Unit Awards – Rollforward 203

131 Nonvested Cash-Payable Restricted Share Unit – Rollforward 204

THE PNC FINANCIAL SERVICES GROUP, INC.Cross-Reference Index to 2012 Form 10-K (continued)

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS TABLE REFERENCE (Continued)

Table Description Page

132 Employee Stock Purchase Plan – Summary 204

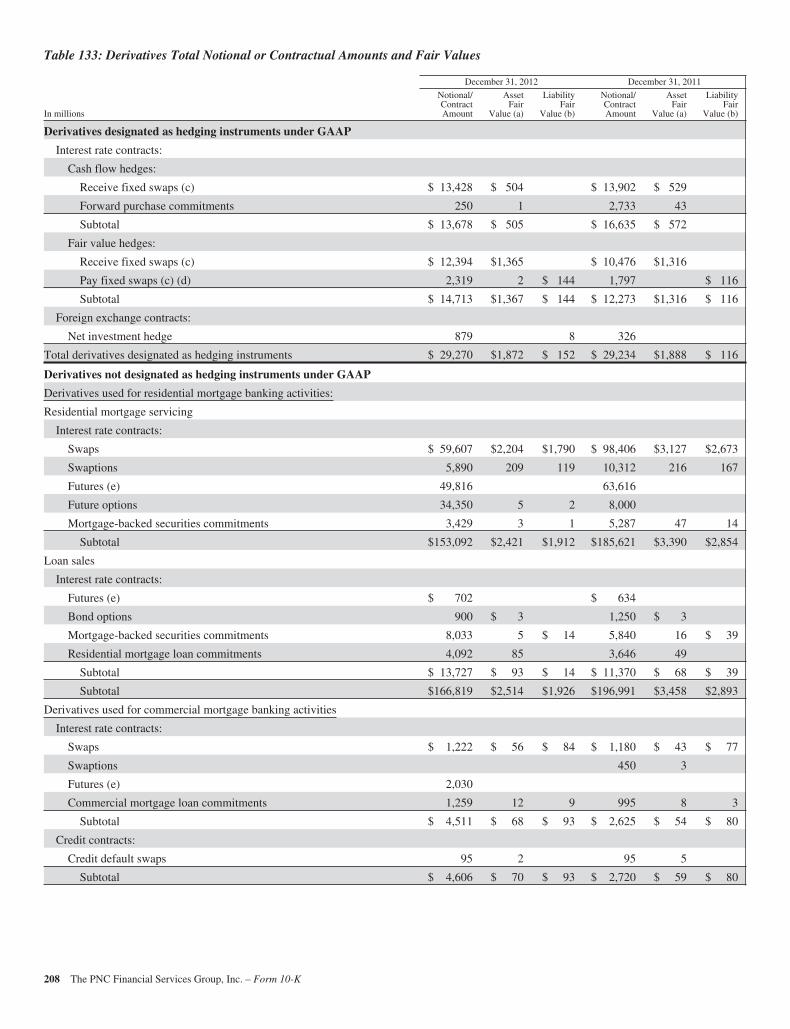

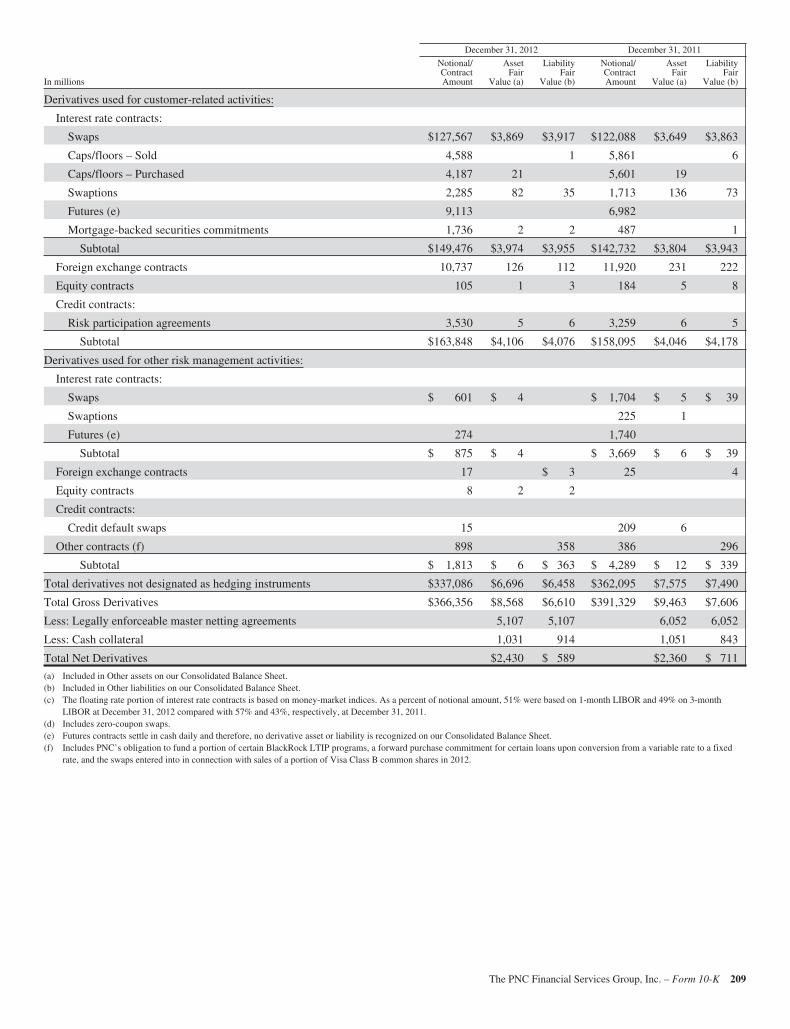

133 Derivatives Total Notional or Contractual Amounts and Fair Values 208

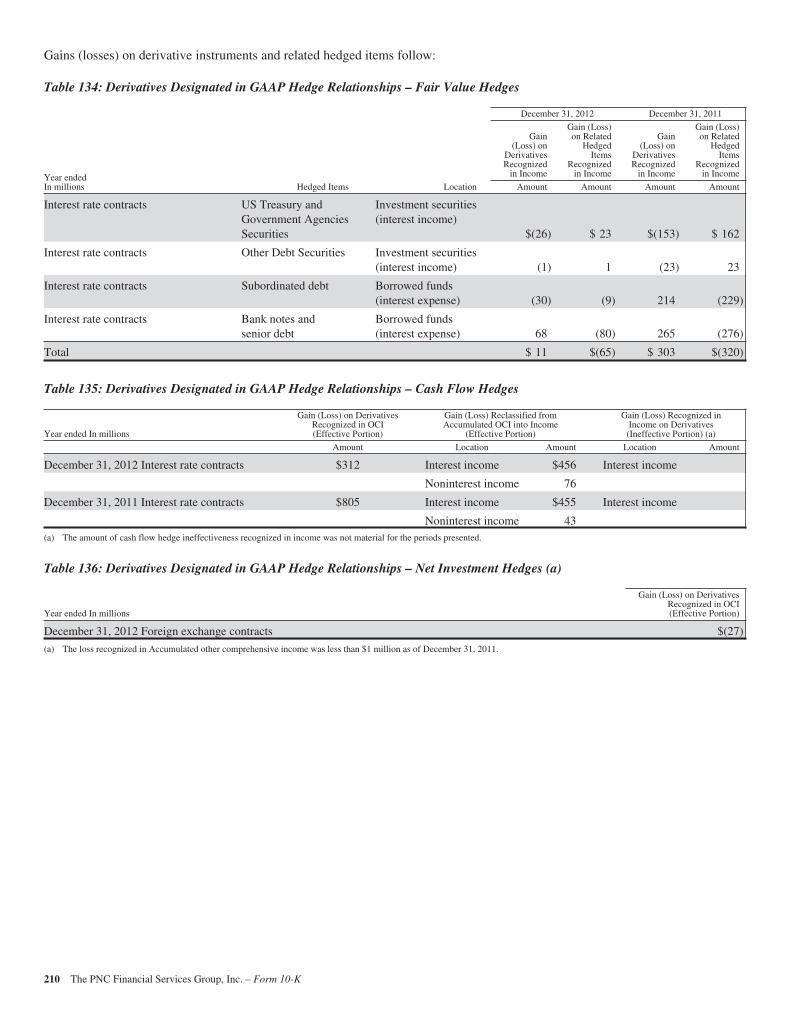

134 Derivatives Designated in GAAP Hedge Relationships – Fair Value Hedges 210

135 Derivatives Designated in GAAP Hedge Relationships – Cash Flow Hedges 210

136 Derivatives Designated in GAAP Hedge Relationships – Net Investment Hedges 210

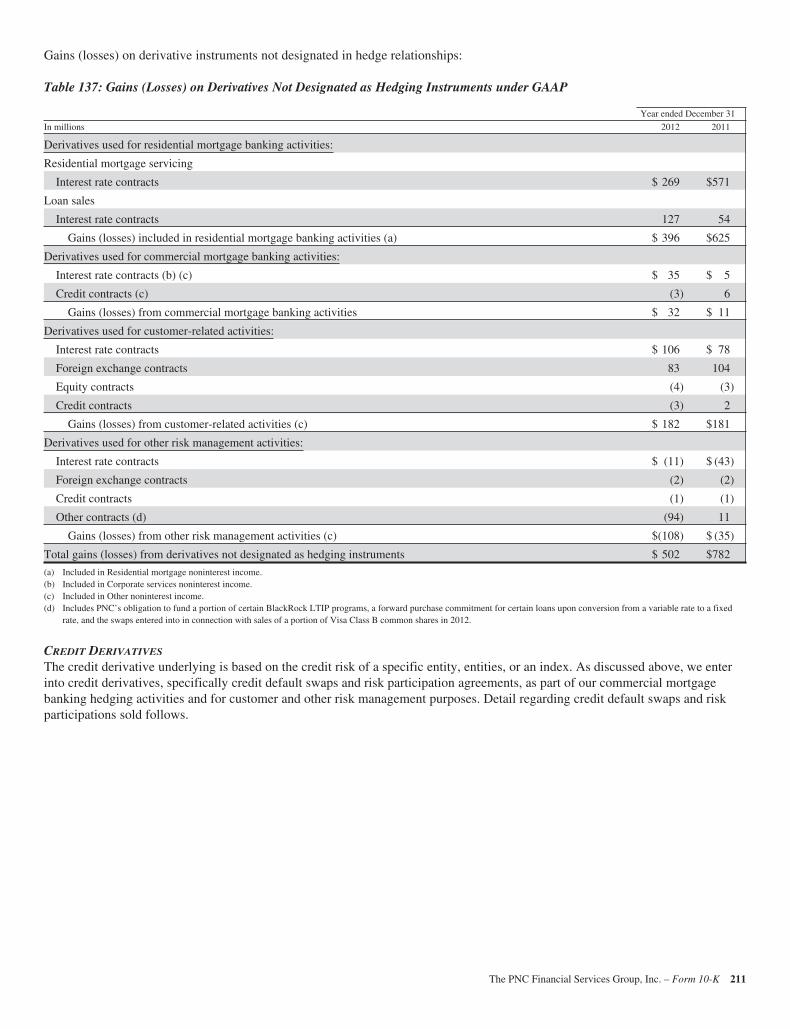

137 Gains (Losses) on Derivatives Not Designated as Hedging Instruments under GAAP 211

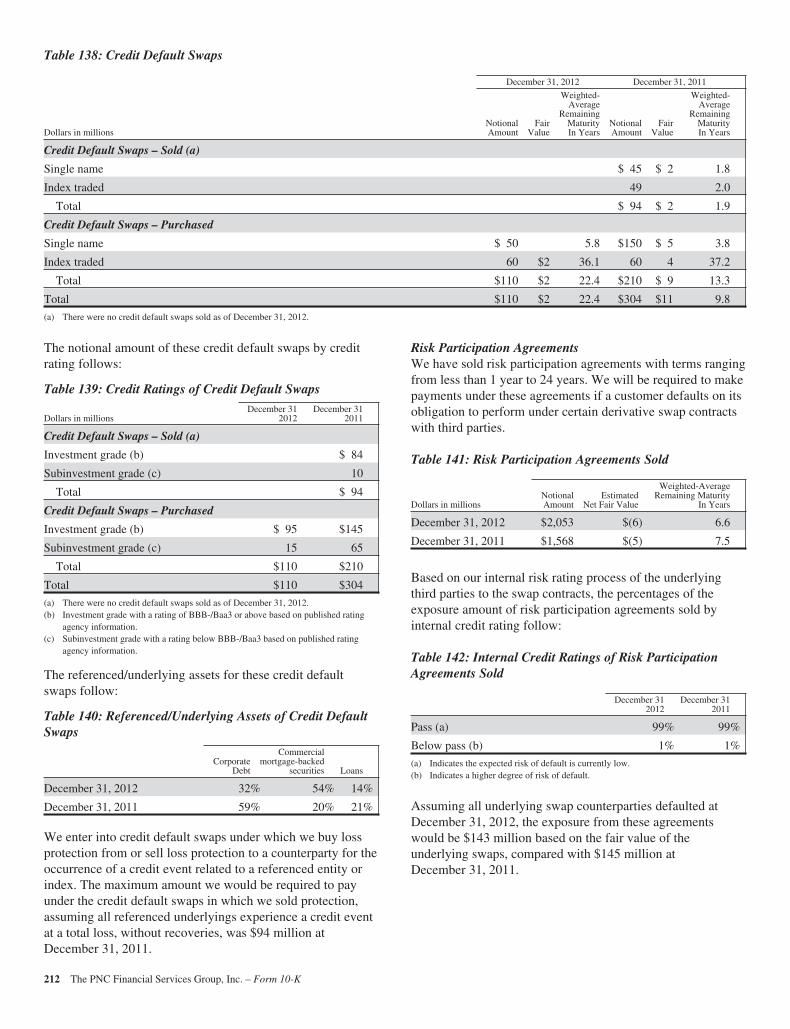

138 Credit Default Swaps 212

139 Credit Ratings of Credit Default Swaps 212

140 Referenced/Underlying Assets of Credit Default Swaps 212

141 Risk Participation Agreements Sold 212

142 Internal Credit Ratings of Risk Participation Agreements Sold 212

143 Basic and Diluted Earnings per Common Share 213

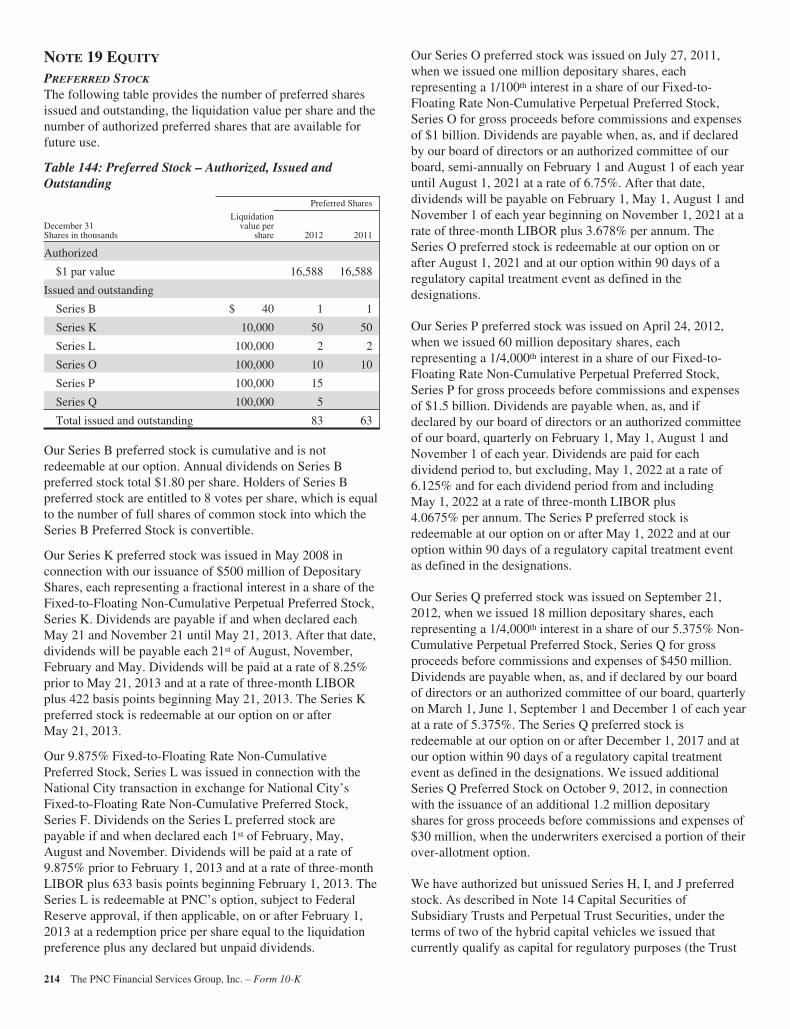

144 Preferred Stock – Authorized, Issued and Outstanding 214

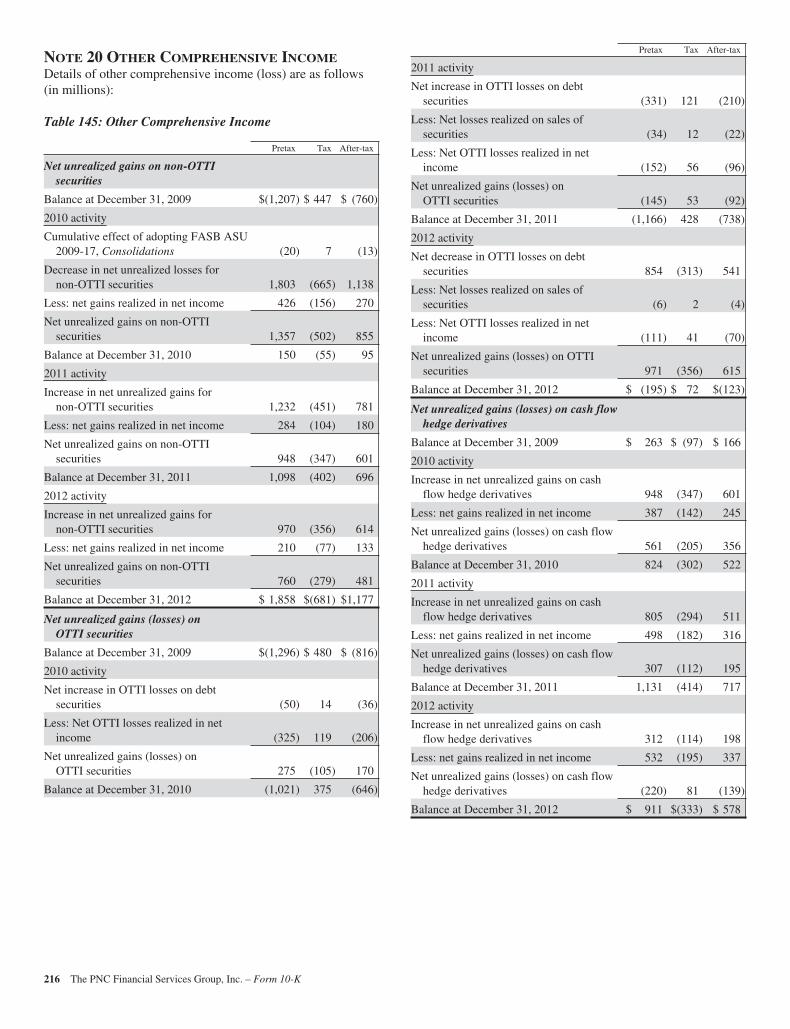

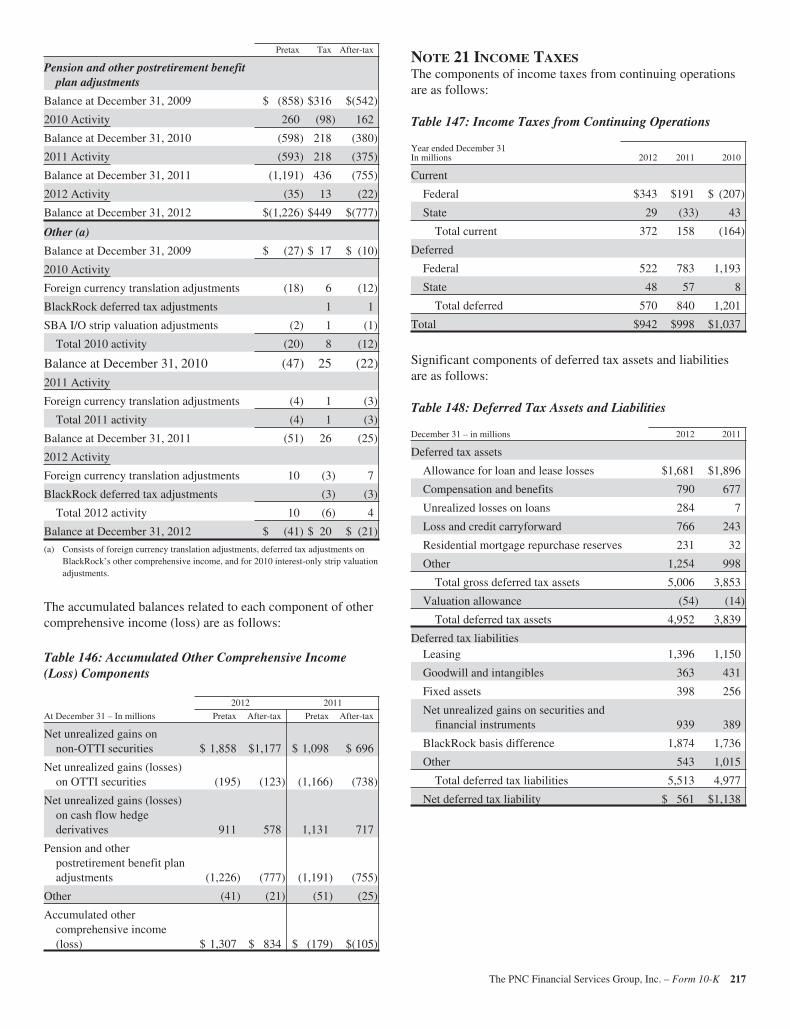

145 Other Comprehensive Income 216

146 Accumulated Other Comprehensive Income (Loss) Components 217

147 Income Taxes from Continuing Operations 217

148 Deferred Tax Assets and Liabilities 217

149 Reconciliation of Statutory and Effective Tax Rates 218

150 Net Operating Loss Carryforwards and Tax Credit Carryforwards 218

151 Changes in Liability for Unrecognized Tax Benefits 218

152 Regulatory Capital 219

153 Net Outstanding Standby Letters of Credit 227

154 Analysis of Commercial Mortgage Recourse Obligations 228

155 Analysis of Indemnification and Repurchase Liability for Asserted Claims and Unasserted Claims 229

156 Reinsurance Agreements Exposure 230

157 Reinsurance Reserves – Rollforward 230

158 Parent Company – Income Statement 231

159 Parent Company – Balance Sheet 231

160 Parent Company – Interest Paid and Income Tax Refunds (Payments) 231

161 Parent Company – Statement of Cash Flows 231

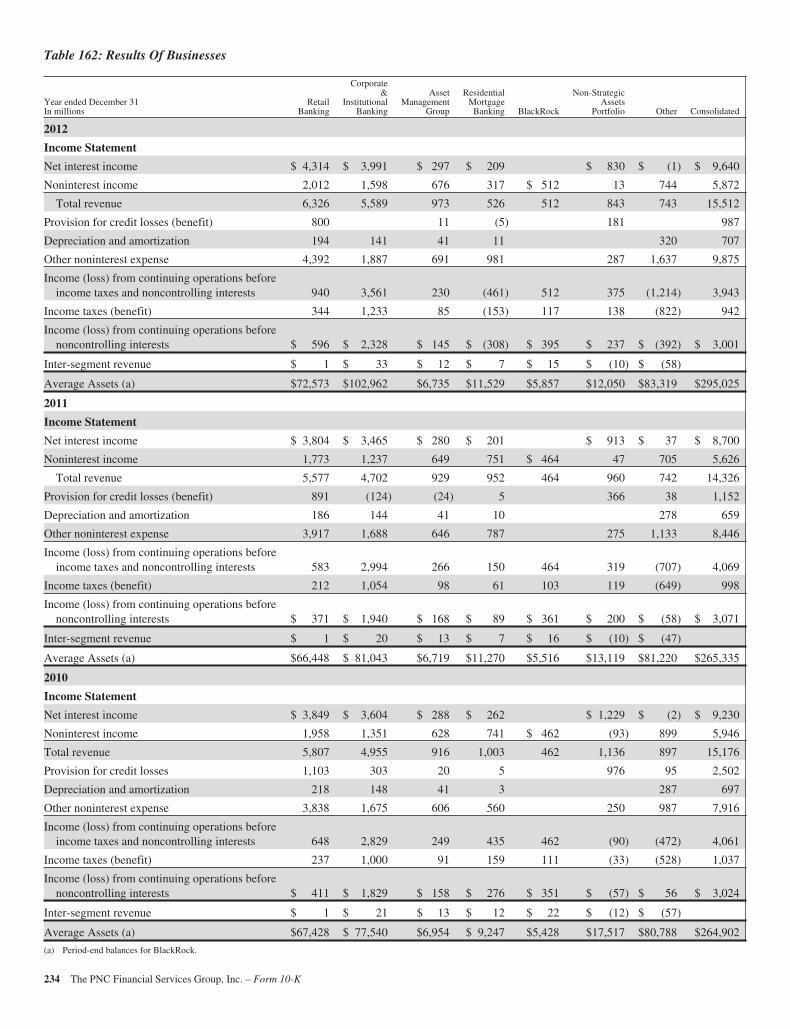

162 Results Of Businesses 234

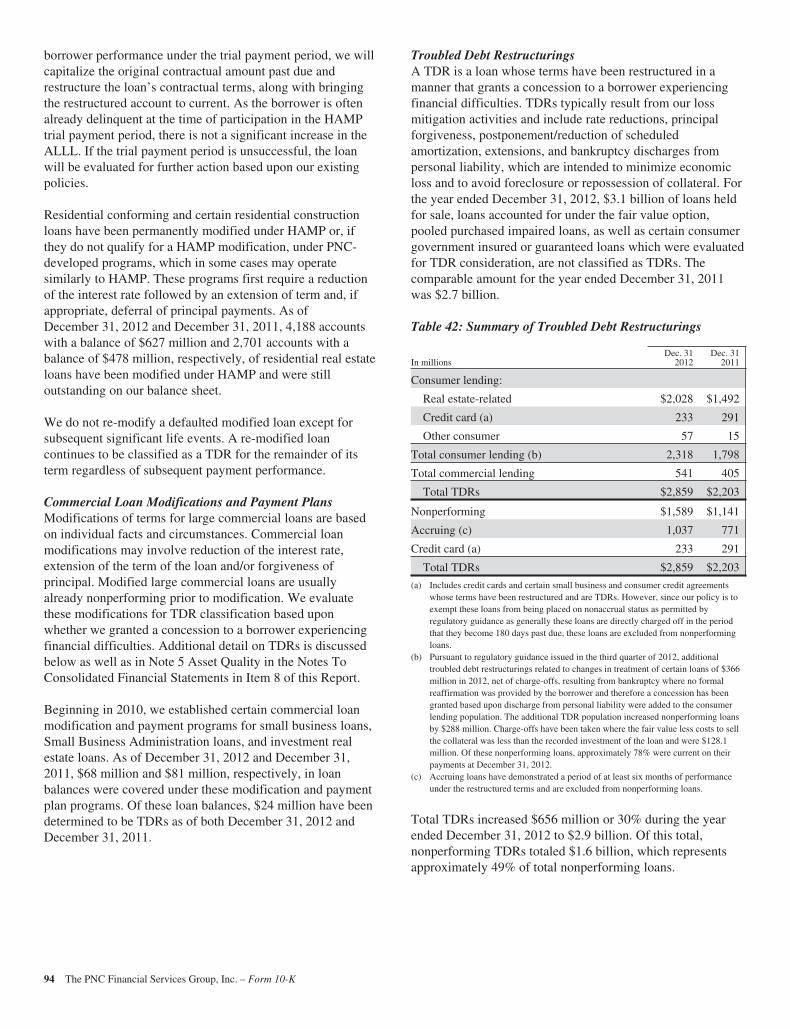

PART IForward-Looking Statements: From time to time, The PNC Financial Services Group, Inc. (PNC or the Corporation) has madeand may continue to make written or oral forward-looking statements regarding our outlook for earnings, revenues, expenses,capital levels and ratios, liquidity levels, asset levels, asset quality, financial position and other matters regarding or affectingPNC and its future business and operations or the impact of legal, regulatory or supervisory matters on our business operations orperformance. This Annual Report on Form 10-K (the Report or Form 10-K) also includes forward-looking statements. With respectto all such forward-looking statements, you should review our Risk Factors discussion in Item 1A, our Risk Management, CriticalAccounting Estimates And Judgments, and Cautionary Statement Regarding Forward-Looking Information sections included inItem 7, and Note 23 Legal Proceedings and Note 24 Commitments and Guarantees in the Notes To Consolidated FinancialStatements included in Item 8 of this Report.

ITEM 1 – BUSINESS

BUSINESS OVERVIEW

Headquartered in Pittsburgh, Pennsylvania, we are one of thelargest diversified financial services companies in the UnitedStates. We have businesses engaged in retail banking,corporate and institutional banking, asset management, andresidential mortgage banking, providing many of our productsand services nationally, as well as products and services in ourprimary geographic markets located in Pennsylvania, Ohio,New Jersey, Michigan, Illinois, Maryland, Indiana, NorthCarolina, Florida, Kentucky, Washington, D.C., Delaware,Alabama, Virginia, Georgia, Missouri, Wisconsin and SouthCarolina. We also provide certain products and servicesinternationally. At December 31, 2012, our consolidated totalassets, total deposits and total shareholders’ equity were$305.1 billion, $213.1 billion and $39.0 billion, respectively.

We were incorporated under the laws of the Commonwealthof Pennsylvania in 1983 with the consolidation of PittsburghNational Corporation and Provident National Corporation.Since 1983, we have diversified our geographical presence,business mix and product capabilities through internal growth,strategic bank and non-bank acquisitions and equityinvestments, and the formation of various non-bankingsubsidiaries.

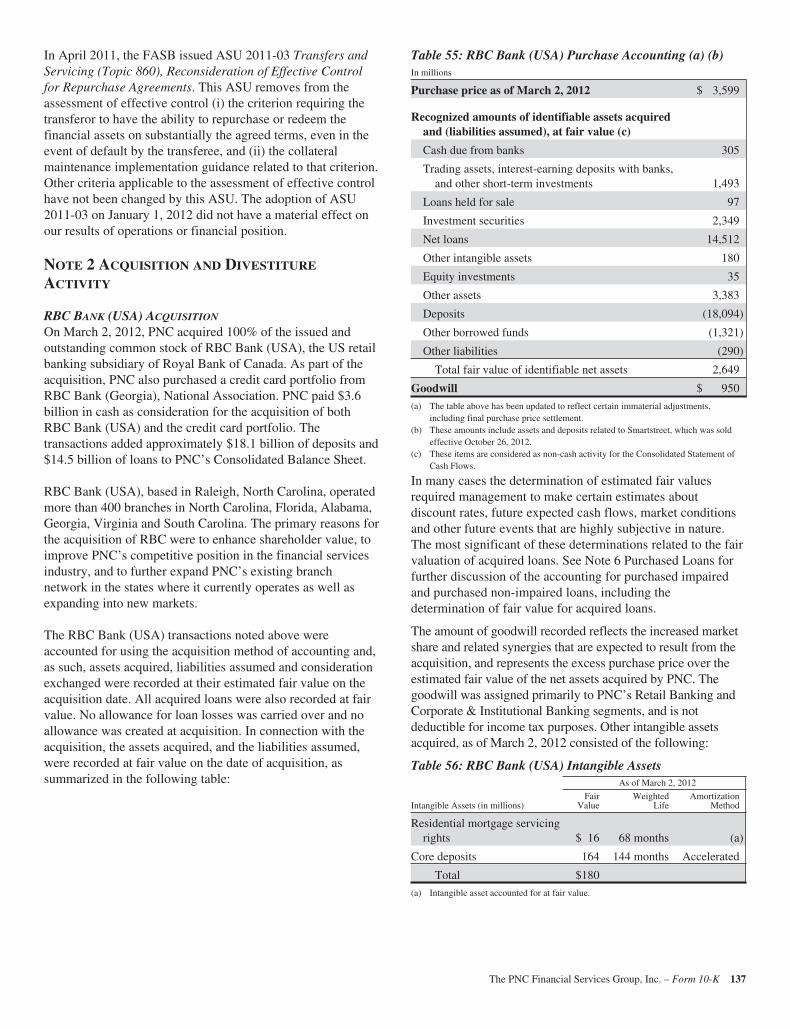

RBC BANK (USA) ACQUISITION

On March 2, 2012, we acquired 100% of the issued andoutstanding common stock of RBC Bank (USA), the U.S.retail banking subsidiary of Royal Bank of Canada. As part ofthe acquisition, PNC also purchased a credit card portfoliofrom RBC Bank (Georgia), National Association. PNC paid$3.6 billion in cash as the consideration for the acquisition ofboth RBC Bank (USA) and the credit card portfolio. Thetransaction added approximately $18.1 billion in deposits,$14.5 billion of loans and $1.1 billion of goodwill andintangible assets to PNC’s Consolidated Balance Sheet. OurConsolidated Income Statement includes the impact ofbusiness activity associated with the RBC Bank (USA)acquisition subsequent to March 2, 2012.

RBC Bank (USA), based in Raleigh, North Carolina, operatedmore than 400 branches in North Carolina, Florida, Alabama,Georgia, Virginia and South Carolina. The primary reasons forthe acquisition of RBC Bank (USA) were to enhance

shareholder value, to improve PNC’s competitive position inthe financial services industry, and to further expand PNC’sexisting branch network in the states where it currentlyoperates as well as expanding into new markets.

SALE OF SMARTSTREET

Effective October 26, 2012, PNC divested certain deposits andassets of the Smartstreet business unit, which was acquired byPNC as part of the RBC Bank (USA) acquisition, to UnionBank, N.A. Smartstreet is a nationwide business focused onhomeowner or community association managers and hadapproximately $1 billion of assets and deposits as ofSeptember 30, 2012. The gain on sale was immaterial and wereduced goodwill and core deposit intangibles of $46 millionand $13 million, respectively.

FLAGSTAR BRANCH ACQUISITION

Effective December 9, 2011, PNC acquired 27 branches in thenorthern metropolitan Atlanta, Georgia area from FlagstarBank, FSB, a subsidiary of Flagstar Bancorp, Inc. Weassumed approximately $210 million of deposits associatedwith these branches. No loans were acquired in thetransaction.

BANKATLANTIC BRANCH ACQUISITION

Effective June 6, 2011, PNC acquired 19 branches in thegreater Tampa, Florida area from BankAtlantic, a subsidiaryof BankAtlantic Bancorp, Inc. We assumed approximately$324 million of deposits associated with these branches. Noloans were acquired in the transaction.

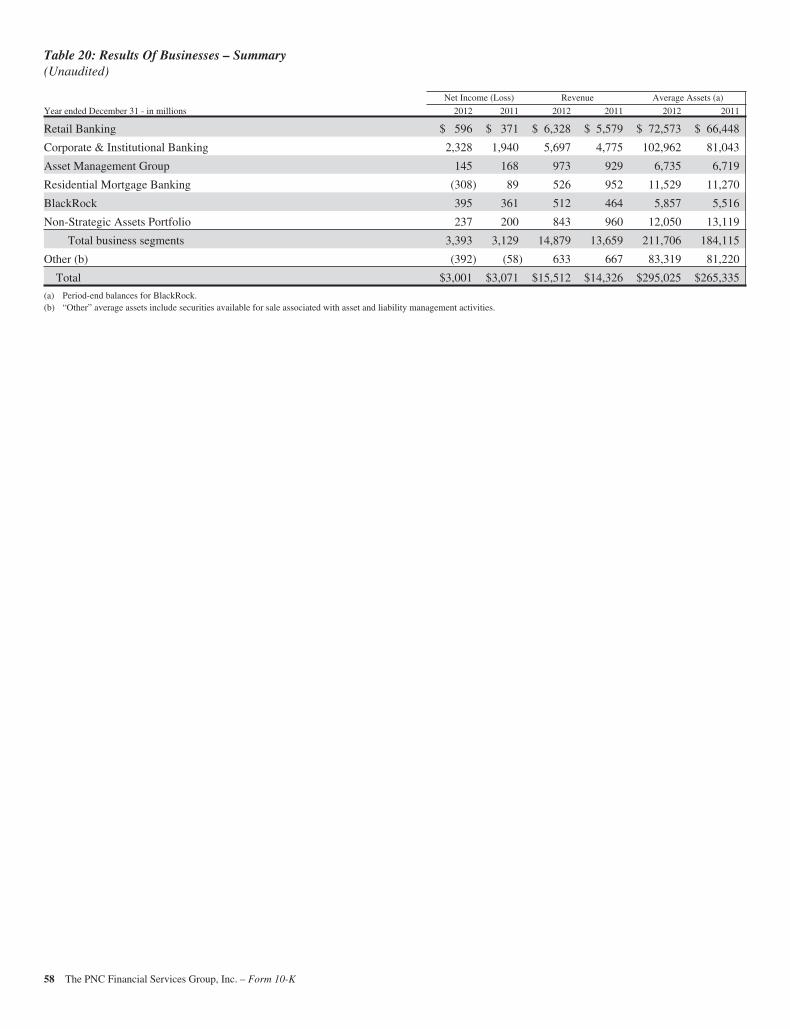

REVIEW OF BUSINESS SEGMENTS

In addition to the following information relating to our lines ofbusiness, we incorporate the information under the captionsBusiness Segment Highlights, Product Revenue, and BusinessSegments Review in Item 7 of this Report here by reference.Also, we include the financial and other information bybusiness in Note 26 Segment Reporting in the Notes ToConsolidated Financial Statements in Item 8 of this Reporthere by reference.

Assets, revenue and earnings attributable to foreign activitieswere not material in the periods presented. Business segmentresults for periods prior to 2012 have been reclassified toreflect current methodologies and current business andmanagement structure and to present those periods on the

The PNC Financial Services Group, Inc. – Form 10-K 1

same basis. Business segment information does not includePNC Global Investment Servicing Inc. (GIS). Results ofoperations of GIS through June 30, 2010 and the related after-tax gain on its sale in the third quarter of 2010 are reflected indiscontinued operations.

Retail Banking provides deposit, lending, brokerage,investment management and cash management services toconsumer and small business customers within our primarygeographic markets. Our customers are serviced through ourbranch network, call centers, online banking and mobilechannels. The branch network is principally located in ourprimary geographical markets.

Our core strategy is to acquire and retain customers whomaintain their primary checking and transaction relationshipswith PNC. We also seek revenue growth by deepening ourshare of our customers’ financial assets, including savings andliquidity deposits, loans and investable assets, includingretirement assets. A key element of our strategy is to expandthe use of lower-cost alternative distribution channels whilecontinuing to optimize the traditional branch network. Inaddition, we have a disciplined process to continually improvethe engagement of both our employees and customers, whichis a strong indicator of customer growth, retention andrelationship expansion.

Corporate & Institutional Banking provides lending, treasurymanagement and capital markets-related products and servicesto mid-sized corporations, government and not-for-profitentities and selectively to large corporations. Lendingproducts include secured and unsecured loans, letters of creditand equipment leases. Treasury management services includecash and investment management, receivables management,disbursement services, funds transfer services, informationreporting and global trade services. Capital markets-relatedproducts and services include foreign exchange, derivatives,loan syndications, mergers and acquisitions advisory andrelated services to middle-market companies, our multi-sellerconduit, securities underwriting and securities sales andtrading. Corporate & Institutional Banking also providescommercial loan servicing, and real estate advisory andtechnology solutions for the commercial real estate financeindustry. Corporate & Institutional Banking provides productsand services generally within our primary geographic markets,with certain products and services offered nationally andinternationally.

Corporate & Institutional Banking is focused on becoming apremier provider of financial services in each of the markets itserves. The value proposition to our customers is driven byproviding a broad range of competitive and high qualityproducts and services by a team fully committed to deliveringthe comprehensive resources of PNC to help each clientsucceed. Corporate & Institutional Banking’s primary goalsare to achieve market share growth and enhanced returns bymeans of expansion and retention of customer relationshipsand prudent risk and expense management.

Asset Management Group includes personal wealthmanagement for high net worth and ultra high net worthclients and institutional asset management. Wealthmanagement products and services include investment andretirement planning, customized investment management,private banking, tailored credit solutions and trustmanagement and administration for individuals and theirfamilies. Institutional asset management provides investmentmanagement, custody and retirement administration services.Institutional clients include corporations, unions,municipalities, non-profits, foundations and endowments,primarily located in our geographic footprint.

Asset Management Group is focused on being one of thepremier bank-held individual and institutional asset managersin each of the markets it serves. The business seeks to deliverhigh quality banking advice and trust and investmentmanagement services to our high net worth, ultra high networth and institutional client sectors through a broad array ofproducts and services. Asset Management Group’s primarygoals are to service our clients, grow the business and deliversolid financial performance with prudent risk and expensemanagement.

Residential Mortgage Banking directly originates primarilyfirst lien residential mortgage loans on a nationwide basis witha significant presence within the retail banking footprint, andalso originates loans through majority owned affiliates.Mortgage loans represent loans collateralized by one-to-four-family residential real estate. These loans are typicallyunderwritten to government agency and/or third-partystandards, and sold, servicing retained, to secondary mortgageconduits of Federal National Mortgage Association (FNMA),Federal Home Loan Mortgage Corporation (FHLMC), FederalHome Loan Banks and third-party investors, or are securitizedand issued under the Government National MortgageAssociation (GNMA) program, as described in more detail inNote 3 Loan Sale and Servicing Activities and VariableInterest Entities in Item 8 of this Report and included here byreference. The mortgage servicing operation performs allfunctions related to servicing mortgage loans, primarily thosein first lien position, for various investors and for loans ownedby PNC. Certain loan applications are brokered by majorityowned affiliates to others.

Residential Mortgage Banking is focused on adding value tothe PNC franchise by building stronger customerrelationships, providing quality investment loans, anddelivering acceptable returns consistent with a moderate riskphilosophy. Our national distribution capability providesvolume that drives economies of scale, risk dispersion, andcost-effective extension of the retail banking footprint forcross-selling opportunities.

BlackRock is a leader in investment management, riskmanagement and advisory services for institutional and retailclients worldwide. BlackRock provides diversified investment

2 The PNC Financial Services Group, Inc. – Form 10-K

management services to institutional clients, intermediary andindividual investors through various investment vehicles.Investment management services primarily consist of themanagement of equity, fixed income, multi-asset class,alternative investment and cash management products.BlackRock offers its investment products in a variety ofvehicles, including open-end and closed-end mutual funds,iShares® exchange-traded funds (ETFs), collective investmenttrusts and separate accounts. In addition, BlackRock providesmarket risk management, financial markets advisory andenterprise investment system services to a broad base ofclients. Financial markets advisory services include valuationservices relating to illiquid securities, dispositions andworkout assignments (including long-term portfolioliquidation assignments), risk management and strategicplanning and execution.

We hold an equity investment in BlackRock, which is a keycomponent of our diversified revenue strategy. BlackRock is apublicly traded company, and additional informationregarding its business is available in its filings with theSecurities and Exchange Commission (SEC).

Non-Strategic Assets Portfolio (formerly, Distressed AssetsPortfolio) includes a consumer portfolio of mainly residentialmortgage and brokered home equity loans and a smallcommercial loan and lease portfolio. We obtained a significantportion of these non-strategic assets through acquisitions ofother companies.

SUBSIDIARIES

Our corporate legal structure at December 31, 2012 consistedof one domestic subsidiary bank, including its subsidiaries,and approximately 141 active non-bank subsidiaries. Our banksubsidiary is PNC Bank, National Association (PNC Bank,N.A.), headquartered in Pittsburgh, Pennsylvania. Foradditional information on our subsidiaries, see Exhibit 21 tothis Report.

STATISTICAL DISCLOSURE BY BANK HOLDING COMPANIES

The following statistical information is included on theindicated pages of this Report and is incorporated herein byreference:

Form 10-K page

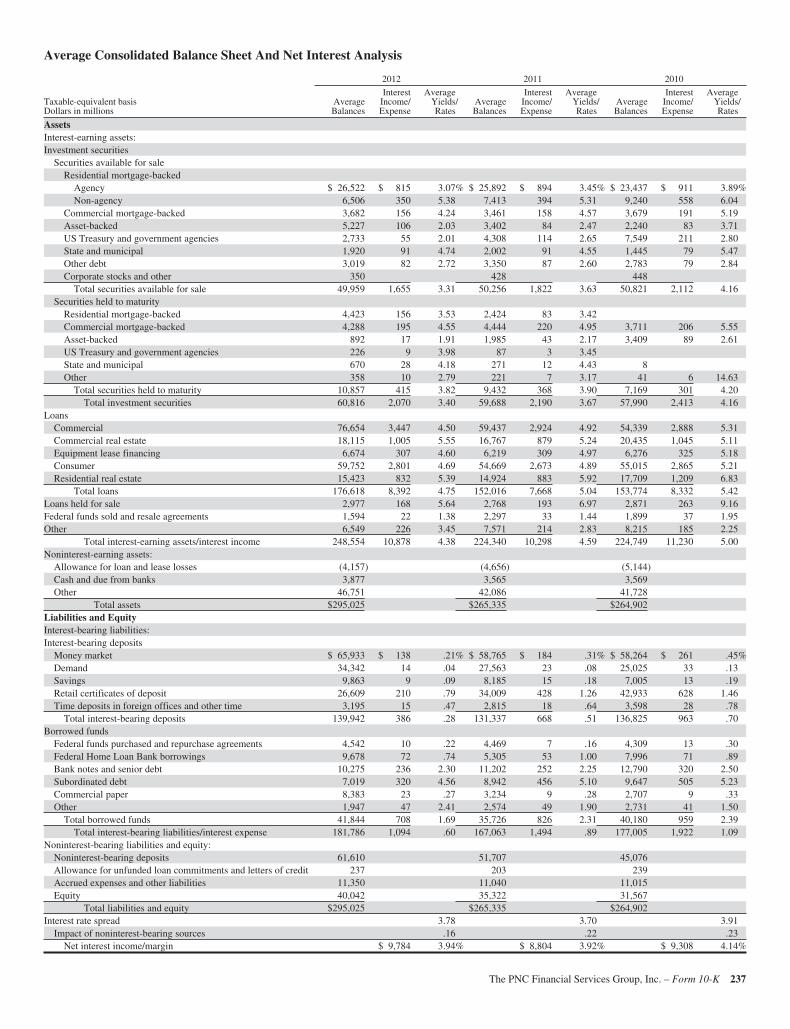

Average Consolidated Balance SheetAnd Net Interest Analysis 237 – 238

Analysis Of Year-To-Year ChangesIn Net Interest Income 239

Book Values Of Securities 46 – 49and 165 – 171

Maturities And Weighted-AverageYield Of Securities 170 – 171

Loan Types 42 – 45, 145 and 240

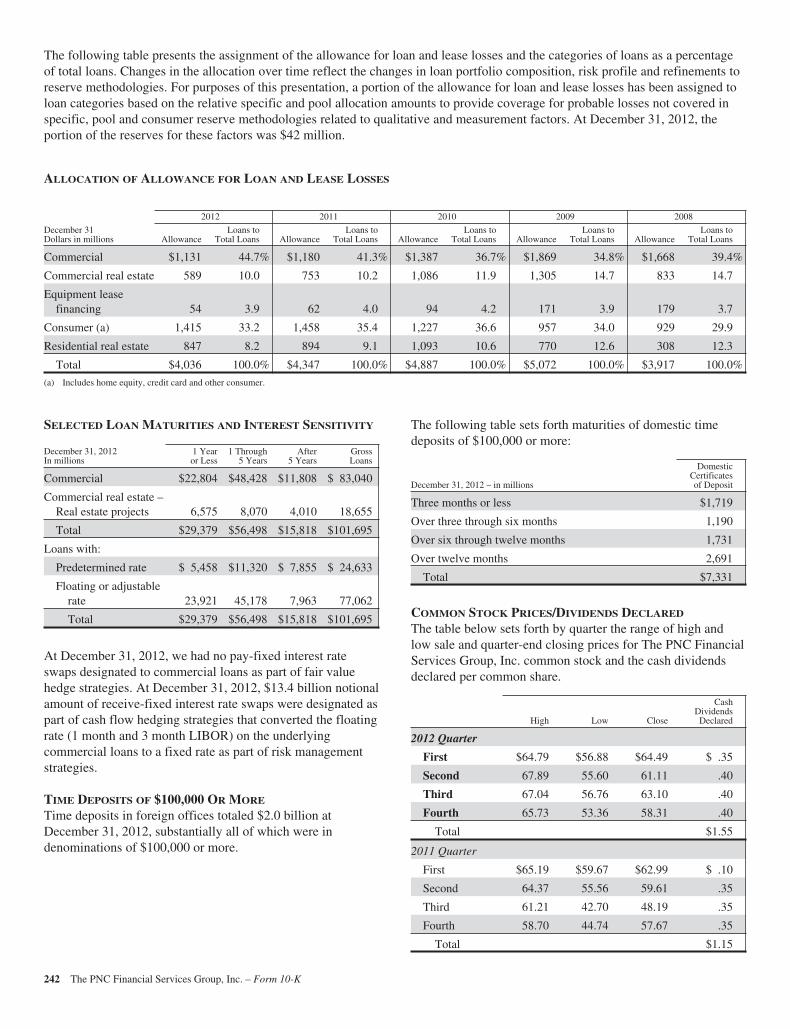

Selected Loan Maturities AndInterest Sensitivity 242

Nonaccrual, Past Due AndRestructured Loans And OtherNonperforming Assets

85 – 95, 130 – 131,146 – 158 and

240 – 241

Potential Problem Loans And LoansHeld For Sale

49 – 50 and86 – 97

Summary Of Loan Loss Experience 95 – 97,146 – 158, 162 – 164

and 241

Assignment Of Allowance For LoanAnd Lease Losses

95 – 97 and242

Average Amount And Average RatePaid On Deposits 237 – 238

Time Deposits Of $100,000 Or More 191 and 242

Selected Consolidated Financial Data 29 – 30

Short-term borrowings – not includedas average balances during 2012,2011, and 2010 were less than 30%of total shareholders’ equity at theend of each period.

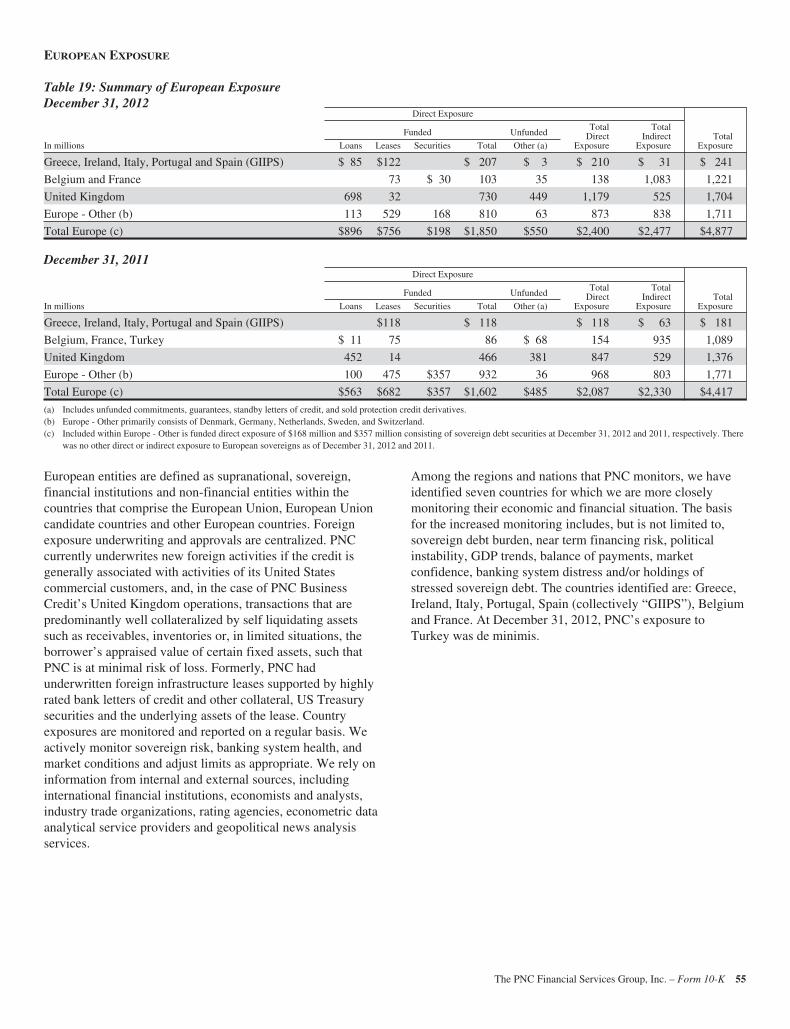

EUROPEAN EXPOSURE

For information regarding our exposure to European entities atDecember 31, 2012 and December 31, 2011, see the EuropeanExposure section included in Item 7 of this Report.

The PNC Financial Services Group, Inc. – Form 10-K 3

SUPERVISION AND REGULATION

OVERVIEW

PNC is a bank holding company registered under the BankHolding Company Act of 1956 as amended (BHC Act) and afinancial holding company under the Gramm-Leach-BlileyAct (GLB Act).

We are subject to numerous governmental regulations, someof which are highlighted below. See Note 22 RegulatoryMatters in the Notes To Consolidated Financial Statements inItem 8 of this Report, for additional information regarding ourregulatory matters. Applicable laws and regulations restrictour permissible activities and investments and requirecompliance with protections for loan, deposit, brokerage,fiduciary, investment management and other customers,among other things. They also restrict our ability torepurchase stock or pay dividends, or to receive dividendsfrom our bank subsidiary, and impose capital adequacyrequirements. The consequences of noncompliance caninclude substantial monetary and nonmonetary sanctions.

In addition, we are subject to comprehensive examination andsupervision by, among other regulatory bodies, the Board ofGovernors of the Federal Reserve System (Federal Reserve)and the Office of the Comptroller of the Currency (OCC),which result in examination reports and ratings (which are notpublicly available) that can impact the conduct and growth ofour businesses. These examinations consider not onlycompliance with applicable laws and regulations, but alsocapital levels, asset quality and risk, management ability andperformance, earnings, liquidity and various other factors. Theresults of examination activity by any of our federal bankregulators potentially can result in the imposition ofsignificant limitations on our activities and growth. Theseregulatory agencies generally have broad discretion to imposerestrictions and limitations on the operations of a regulatedentity where the relevant agency determines, among otherthings, that such operations are conducted in an unsafe orunsound manner, fail to comply with applicable law or areotherwise inconsistent with the regulations or supervisorypolicies of the agency. This supervisory framework couldmaterially impact the conduct, growth and profitability of ouroperations.

The Consumer Financial Protection Bureau (CFPB), a newagency established by the Dodd-Frank Wall Street Reform andConsumer Protection Act (Dodd-Frank), is responsible forexamining PNC Bank, N.A. and its affiliates (including PNC)for compliance with most consumer financial protection lawsand for enforcing such laws with respect to PNC Bank, N.A.and its affiliates. This authority previously was exercised bythe OCC and the Federal Reserve. The CFPB also now hasauthority for prescribing rules governing the provision ofconsumer financial products and services such as credit cards,student and other loans, deposits and residential mortgages.The agency has issued final regulations that impose broad new

requirements relating to our mortgage origination activitiesand the servicing activities we perform for residentialmortgage loans. These regulations include a requirement thatresidential mortgage lenders, like PNC Bank, make a “goodfaith and reasonable determination” at or before the time ofconsummation of a residential mortgage loan that theprospective borrower has a reasonable ability to repay thatloan. The new regulations also include broad newrequirements applicable to servicers of residential mortgageloans, like PNC, which include provisions requiring policiesand procedures relating to how servicers respond to andmanage loans of borrowers who are in default. Most of theseregulations are scheduled to take effect in January of 2014. Inaddition, the CFPB is now considering additional regulationsthat will modify the application and closing disclosures thatmust be provided to borrowers in connection with residentialmortgage loans.

As a result of Dodd-Frank, after July 21, 2011, subsidiaries ofPNC Bank, N.A. are subject to state law and regulation to thesame extent as if they were not subsidiaries of a national bank.Additionally, based on Dodd-Frank, state authorities mayassert that certain state consumer financial laws that providedifferent requirements or limitations than Federal law mayapply to national banks, including PNC Bank, N.A. Such statelaws may be preempted if they meet certain standards set forthin Dodd-Frank or other applicable law. We expect toexperience an increase in regulation of our Retail Banking,Asset Management Group and Residential Mortgage Bankingbusinesses and additional compliance obligations, revenue andcost impacts.

We also are subject to regulation by the SEC by virtue of ourstatus as a public company and by the SEC and theCommodity Futures Trading Commission (CFTC) due to thenature of some of our businesses. Our banking and securitiesbusinesses with operations outside the United States,including those conducted by BlackRock, are also subject toregulation by appropriate authorities in the foreignjurisdictions in which they do business.

As a regulated financial services firm, our relationships andgood standing with regulators are of fundamental importanceto the operation and growth of our businesses. The FederalReserve, OCC, CFPB, SEC, CFTC and other domestic andforeign regulators have broad enforcement powers, and certainof the regulators have the power to approve, deny, or refuse toact upon our applications or notices to conduct new activities,acquire or divest businesses or assets and deposits, orreconfigure existing operations.

We anticipate new legislative and regulatory initiatives overthe next several years, focused specifically on banking andother financial services in which we are engaged. Theseinitiatives would be in addition to the actions already taken byCongress and the regulators, including the Credit CardAccountability, Responsibility, and Disclosure Act of 2009

4 The PNC Financial Services Group, Inc. – Form 10-K

(Credit CARD Act), the Secure and Fair Enforcement forMortgage Licensing Act (the SAFE Act), and Dodd-Frank, aswell as changes to the regulations implementing the RealEstate Settlement Procedures Act, the Federal Truth inLending Act, and the Electronic Fund Transfer Act, includingthe new rules set forth in Regulation E related to overdraftcharges.

Dodd-Frank, which was signed into law on July 21, 2010,comprehensively reforms the regulation of financialinstitutions, products and services. Dodd-Frank requiresvarious federal regulatory agencies to implement numerousnew rules and regulations. Because the federal agencies aregranted broad discretion in drafting these rules andregulations, and many implementing rules either have not yetbeen issued or have only been issued in proposed form, manyof the details and much of the impact of Dodd-Frank may notbe known for many months or years. Among other things,Dodd-Frank provides for new capital standards that eliminatethe treatment of trust preferred securities as Tier 1 regulatorycapital; requires that deposit insurance assessments becalculated based on an insured depository institution’s assetsrather than its insured deposits; raises the minimumDesignated Reserve Ratio (the balance in the DepositInsurance Fund divided by estimated insured deposits) to1.35%; establishes a comprehensive regulatory regime for thederivatives activities of financial institutions; limitsproprietary trading and owning or sponsoring hedge funds andprivate equity funds by banking entities; requires the FederalReserve to establish a variety of enhanced prudentialstandards for bank holding companies with $50 billion ormore in total assets; places limitations on the interchange feescharged for debit card transactions; and establishes newminimum mortgage underwriting standards for residentialmortgages.

Dodd-Frank established the 10-member inter-agency FinancialStability Oversight Council (FSOC), which is charged withidentifying systemic risks and strengthening the regulation offinancial holding companies and certain non-bank companiesdeemed to be “systemically important” and could, inextraordinary cases and in conjunction with the FederalReserve, break up financial firms that are deemed to present agrave threat to the financial stability of the United States.Dodd-Frank also requires the Federal Reserve to establishprudential standards for bank holding companies with totalconsolidated assets equal to or greater than $50 billion that aremore stringent than the standards and requirements applicableto bank holding companies with assets below this threshold,and that increase in stringency for bank holding companiesthat present heightened risk to the financial system. Additionalinformation concerning these enhanced prudential standards isprovided in Item 1A – Risk Factors of this Report. The FSOCmay make recommendations to the Federal Reserveconcerning the establishment and refinement of theseprudential standards and reporting and disclosurerequirements.

Legislative and regulatory developments to date, as well asthose that come in the future, have had and are likely tocontinue to have an impact on the conduct of our business.The more detailed description of the significant regulations towhich we are subject included in this Report is based on thecurrent regulatory environment and is subject to potentiallymaterial change. See also the additional information includedin Item 1A of this Report under the risk factors discussing theimpact of financial regulatory reform initiatives, includingDodd-Frank and regulations promulgated to implement it, onthe regulatory environment for PNC and the financial servicesindustry.

Among other areas that have been receiving a high level ofregulatory focus over the last several years are compliancewith anti-money laundering laws and the protection ofconfidential customer information. In addition, at least in partdriven by the current economic and financial situation, there isan increased focus on fair lending and other issues related tothe mortgage industry. Ongoing mortgage-related regulatoryreforms include measures aimed at reducing mortgageforeclosures.

Additional legislation, changes in rules promulgated by theFederal Reserve, the OCC, the Federal Deposit InsuranceCorporation (FDIC), the CFPB, the SEC, the CFTC, otherfederal and state regulatory authorities and self-regulatoryorganizations, or changes in the interpretation or enforcementof existing laws and rules, may directly affect the method ofoperation and profitability of our businesses. The profitabilityof our businesses could also be affected by rules andregulations that impact the business and financial communitiesin general, including changes to the laws governing taxation,antitrust regulation and electronic commerce.

There are numerous rules governing the regulation of financialservices institutions and their holding companies.Accordingly, the following discussion is general in nature anddoes not purport to be complete or to describe all of the lawsand regulations that apply to us. To a substantial extent, thepurpose of the regulation and supervision of financial servicesinstitutions and their holding companies is not to protect ourshareholders and our non-customer creditors, but rather toprotect our customers (including depositors) and the financialmarkets in general.

The PNC Financial Services Group, Inc. – Form 10-K 5

BANKING REGULATION AND SUPERVISION

Capital Regulations. PNC and PNC Bank, N.A. are subject tothe regulatory capital requirements established by the FederalReserve and the OCC, respectively. In addition, PNC issubject to the Federal Reserve’s capital plan rule and annualcapital stress testing and Comprehensive Capital Analysis andReview (CCAR) process. As part of this annual capitalplanning process, the Federal Reserve undertakes asupervisory assessment of the capital adequacy of bankholding companies (BHCs), including PNC, that have $50billion or more in total consolidated assets. This capitaladequacy assessment is based on a review of a comprehensivecapital plan submitted by each participating BHC to theFederal Reserve that describes the company’s planned capitalactions during the nine quarter review period, as well as theresults of stress tests conducted by both the company and theFederal Reserve under different hypothetical macro-economicscenarios, including a severely stressed scenario provided bythe Federal Reserve (supervisory severely adverse scenario).In evaluating a BHC’s capital plan, the Federal Reserveconsiders a number of factors, including the company’s riskprofile, the strength of the company’s internal capitalassessment process, and whether the company’s projected proforma Basel I Tier 1 common capital ratio under thehypothetical supervisory severely adverse scenario wouldremain above 5 percent throughout the nine quarter planninghorizon even if the company continued with the capitaldistributions proposed under a baseline scenario. In addition,the Federal Reserve evaluates a company’s projected pathtowards compliance with the proposed Basel III regulatorycapital framework. After completing its review, the FederalReserve may object or not object to the firm’s proposedcapital actions, such as plans to pay or increase common stockdividends, reinstate or increase common stock repurchaseprograms, or redeem preferred stock or other regulatorycapital instruments.

In connection with the 2013 CCAR, PNC filed its capital planand stress testing results using financial data as ofSeptember 30, 2012 with the Federal Reserve on January 7,2013. PNC expects to receive the Federal Reserve’s response(either a non-objection or objection) to the capital plansubmitted as part of the 2013 CCAR by March 15, 2013. TheFederal Reserve also has announced that it intends to publishon this date the results of its assessments, including theFederal Reserve’s estimates of the Basel I capital ratios foreach of the largest 19 BHCs participating in the 2013 reviews,including PNC, during the review period under the FederalReserve’s severely adverse macro-economic scenario andapplying the firm’s proposed base case capital distributions.Prior to this release, the Federal Reserve will release onMarch 7, 2013 its estimate of the Basel I capital ratios, as wellas its estimate of certain revenue and loss information, forsuch BHCs under the same supervisory severely adversescenario but applying the common assumptions concerningcapital distributions by firms established by the FederalReserve for the stress tests required by Dodd-Frank (Dodd-

Frank capital action assumptions). PNC also is requiredto publicly disclose, in March 2013, its estimates of certaincapital, revenue and loss information under the samehypothetical supervisory severely adverse macro-economicscenario and applying the Dodd-Frank capital actionassumptions. Federal Reserve regulations also require thatPNC and other large bank holding companies conduct aseparate mid-year stress test using financial data as ofMarch 31st and three company-derived macro-economicscenarios (base, adverse and severely adverse) and publish asummary of the results under the severely adverse scenario inSeptember.

The Federal banking agencies have requested comment onproposed rules to implement the Basel III capital frameworkin the United States. These rules have not yet been finalizedand remain subject to change. For additional information onthese proposed rules, see Recent Market and IndustryDevelopments in Item 7 and Item 1A – Risk Factors in thisReport. PNC’s estimated pro forma Basel III Tier 1 commonratio was 7.5% at December 31, 2012, excluding the benefitsof the transitional phase-in periods provided by Basel III. Thisestimate is based on management’s understanding of theBasel III proposed rules issued by the U.S. banking agenciesin June 2012 and on available data and information as ofDecember 31, 2012. It also reflects our estimates of PNC’srisk-weighted assets under Basel II (with the modificationsproposed in June 2012) and application of the Basel II.5market risk rules that became effective on January 1, 2013.Both our Basel II and Basel III estimates are point in timeestimates and are subject to further regulatory guidance andclarity, as well as the development, refinement, validation andregulatory approval of internal models.

Parent Company Liquidity and Dividends. The principalsource of our liquidity at the parent company level isdividends from PNC Bank, N.A. PNC Bank, N.A. is subject tovarious federal restrictions on its ability to pay dividends toPNC Bancorp, Inc., its direct parent. PNC Bank, N.A. is alsosubject to federal laws limiting extensions of credit to itsparent holding company and non-bank affiliates as discussedin Note 22 Regulatory Matters in the Notes To ConsolidatedFinancial Statements in Item 8 of this Report. Furtherinformation on bank level liquidity and parent companyliquidity and on certain contractual restrictions is alsoavailable in the Liquidity Risk Management portion of theRisk Management section and the Trust Preferred Securitiesportion of the Off-Balance Sheet Arrangements And VariableInterest Entities section of Item 7 of this Report, and in Note14 Capital Securities of Subsidiary Trusts and Perpetual TrustSecurities in the Notes To Consolidated Financial Statementsin Item 8 of this Report.

Federal Reserve rules provide that a bank holding company isexpected to serve as a source of financial strength to itssubsidiary banks and to commit resources to support suchbanks if necessary. Consistent with the “source of strength”

6 The PNC Financial Services Group, Inc. – Form 10-K

policy for subsidiary banks, the Federal Reserve has statedthat, as a matter of prudent banking, a bank holding companygenerally should not maintain a rate of cash dividends unlessits net income available to common shareholders has beensufficient to fully fund the dividends and the prospective rateof earnings retention appears to be consistent with thecorporation’s capital needs, asset quality and overall financialcondition. Further, in providing guidance to the large BHCsparticipating in the 2013 CCAR, discussed above, the FederalReserve stated that it expects capital plans submitted in 2013will reflect conservative dividend payout ratios and net sharerepurchase programs, and that requests that imply commondividend payout ratios above 30% of projected after-tax netincome available to common shareholders will receiveparticularly close scrutiny. The Federal Reserve also hasstated that it expects BHCs that meet the minimum capitalratio requirements under Basel III during the transition periodsprovided by Basel III, but that do not meet the fully-phased inBasel III minimum plus capital conservation buffer ratio of 7percent Tier 1 common (plus any applicable capital surchargefor globally systemically important banks), to maintainprudent earnings retention policies with a view to meeting thisstandard in accordance with the phase-in schedule included inthe agencies’ proposed Basel III rules.

Additional Powers Under the GLB Act. The Gramm–Leach–Bliley Act (GLB Act) permits a qualifying bank holdingcompany to become a “financial holding company” andthereby engage in, or affiliate with financial companiesengaging in, a broader range of activities than wouldotherwise be permitted for a bank holding company. Permittedaffiliates include securities underwriters and dealers, insurancecompanies and companies engaged in other activities that aredetermined by the Federal Reserve, in consultation with theSecretary of the Treasury, to be “financial in nature orincidental thereto” or are determined by the Federal Reserveunilaterally to be “complementary” to financial activities. Webecame a financial holding company as of March 13, 2000. Inorder to be and remain a financial holding company, a bankholding company and its subsidiary depository institutionsmust be “well capitalized” and “well managed.” In addition, afinancial holding company generally may not engage in a newfinancial activity if any of its insured depository institutionsreceived a less than Satisfactory rating at its most recentevaluation under the Community Reinvestment Act (CRA).

The Federal Reserve is the “umbrella” regulator of a financialholding company, with its operating entities, such as itssubsidiary broker-dealers, investment advisers, insurancecompanies and banks, as well as investment companiesadvised by investment adviser subsidiaries of the financialholding company, also being subject to the jurisdiction ofvarious federal and state “functional” regulators with normalregulatory responsibility for companies in their lines ofbusiness.

As subsidiaries of a financial holding company under the GLBAct, our non-bank subsidiaries are generally allowed toconduct new financial activities, and PNC is generallypermitted to acquire non-bank financial companies that haveless than $10 billion in assets, with after-the-fact notice to theFederal Reserve. In addition, our non-bank subsidiaries (andany financial subsidiaries of subsidiary banks) are permitted toengage in certain activities that were not permitted for bankholding companies and banks prior to enactment of the GLBAct, and to engage on less restrictive terms in certain activitiesthat were previously permitted. Among other activities, wecurrently rely on our status as a financial holding company toconduct merchant banking activities and securitiesunderwriting and dealing activities.