Embed Size (px)

Citation preview

Polen Capital Investment Funds plc

(an open-ended umbrella investment company with variable capital and segregated liability between

Funds incorporated with limited liability in Ireland under the Companies Act 2014 as amended with

registration number 522617 and established as Undertakings for Collective Investment in Transferable Securities pursuant to

the European Communities (Undertakings for Collective Investment in

Transferable Securities) Regulations, 2011 (S.I. No. 352 of 2011), as amended and Central Bank (Supervision and

Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities)

Regulations, 2019

CONDENSED INTERIM REPORT AND

UNAUDITED FINANCIAL STATEMENTS

For the financial period ended

30 June 2022

Polen Capital Investment Funds plc

1

2022 Condensed Interim Report &

Unaudited Financial Statements

Information Only for German Investors

No notification pursuant to Sec. 310 of the German Capital Investment Code (Kapitalanlagegesetzbuch) has been filed for the

following sub-funds and the shares in these sub-funds may not be marketed to investors in the Federal Republic of Germany:

Polen Capital International Growth Fund

Polen Capital Global Emerging Markets Growth Fund

Polen Capital Global SMID Company Growth Fund

Information Only For Swiss Investors

The state of the origin of the fund is Ireland. The representative is ACOLIN Fund Services AG, Leutschenbachstrasse 50, CH-8050

Zurich. The paying agent is NPB Neue Privat Bank AG, Limmatquai 1 / am Bellevue, CH-8024 Zurich. The prospectus, the Key

Investor Information Documents, the articles of association, the list of purchases and sales as well as the annual and semi-annual

reports may be obtained free of charge from the representative. In respect of the units distributed in and from Switzerland, the place of

performance and jurisdiction is at the registered office of the representative.

The total expense ratio (TER) was calculated based on the version currently applicable of the “Guidelines on the calculation and

disclosure of the Total Expense Ratio (TER) of collective investment schemes” of the Swiss Funds & Asset Management Association

(SFAMA).

For the period from 01 July 2021 to 30 June 2022:

Sub-fund(s) Share class(es) TER (%)

Polen Capital Focus U.S.

Growth Fund

CHF Class (Institutional) 0.80

CHF Class (Retail) 1.55

EUR Class (Institutional) 0.80

EUR Class (Institutional Unhedged) 0.80

EUR Class (Retail) 1.55

EUR Class (Retail Unhedged) 1.55

EUR D Class (Institutional Unhedged Distributing) 0.70

GBP Class (Institutional) 0.79

GBP Class (Institutional Unhedged) 0.80

GBP Class (Institutional Unhedged Distributing) 0.80

GBP Class (Retail) 1.55

GBP D Class (Institutional Unhedged Distributing) 0.70

U.S. Dollar A Class (Retail) 1.55

U.S. Dollar C Class (Retail) 1.80

U.S. Dollar Class (Institutional) 0.80

U.S. Dollar Class (Retail) 1.55

U.S. Dollar D Class (Institutional Unhedged) 0.69

U.S. Dollar E Class (Retail) 1.55

U.S. Dollar N Class (Retail) 1.95

Sub-fund(s) Share class(es) TER (%)

Polen Capital U.S. Small

Company Growth Fund

U.S. Dollar Class (Institutional) 1.25

U.S. Dollar A Class (Retail) 2.01

U.S. Dollar C Class (Retail) 2.26

Polen Capital Investment Funds plc

2

2022 Condensed Interim Report &

Unaudited Financial Statements

Contents

Page

Information Only For German Investors 1

Information Only For Swiss Investors 1

Organisation 3

Background to Company 4 - 6

Investment Manager’s Report 7 - 21

Statement of Financial Position 22 - 24

Statement of Comprehensive Income 25 - 27

Statement of Changes in Net Assets Attributable to Holders of Redeemable Participating Shares 28 - 30

Statement of Cash Flows 31 - 36

Notes to the Condensed Financial Statements 37 - 62

Schedule of Investments

Polen Capital Focus U.S. Growth Fund 63 - 65

Polen Capital U.S. Small Company Growth Fund 66 - 67

Polen Capital International Growth Fund 68 - 70

Polen Capital Global Emerging Markets Growth Fund 71 - 74

Polen Capital Global SMID Company Growth Fund 75 - 77

Schedule of Significant Portfolio Changes

Polen Capital Focus U.S. Growth Fund 78 - 79

Polen Capital U.S. Small Company Growth Fund 80 - 81

Polen Capital International Growth Fund 82 - 83

Polen Capital Global Emerging Markets Growth Fund 84 - 85

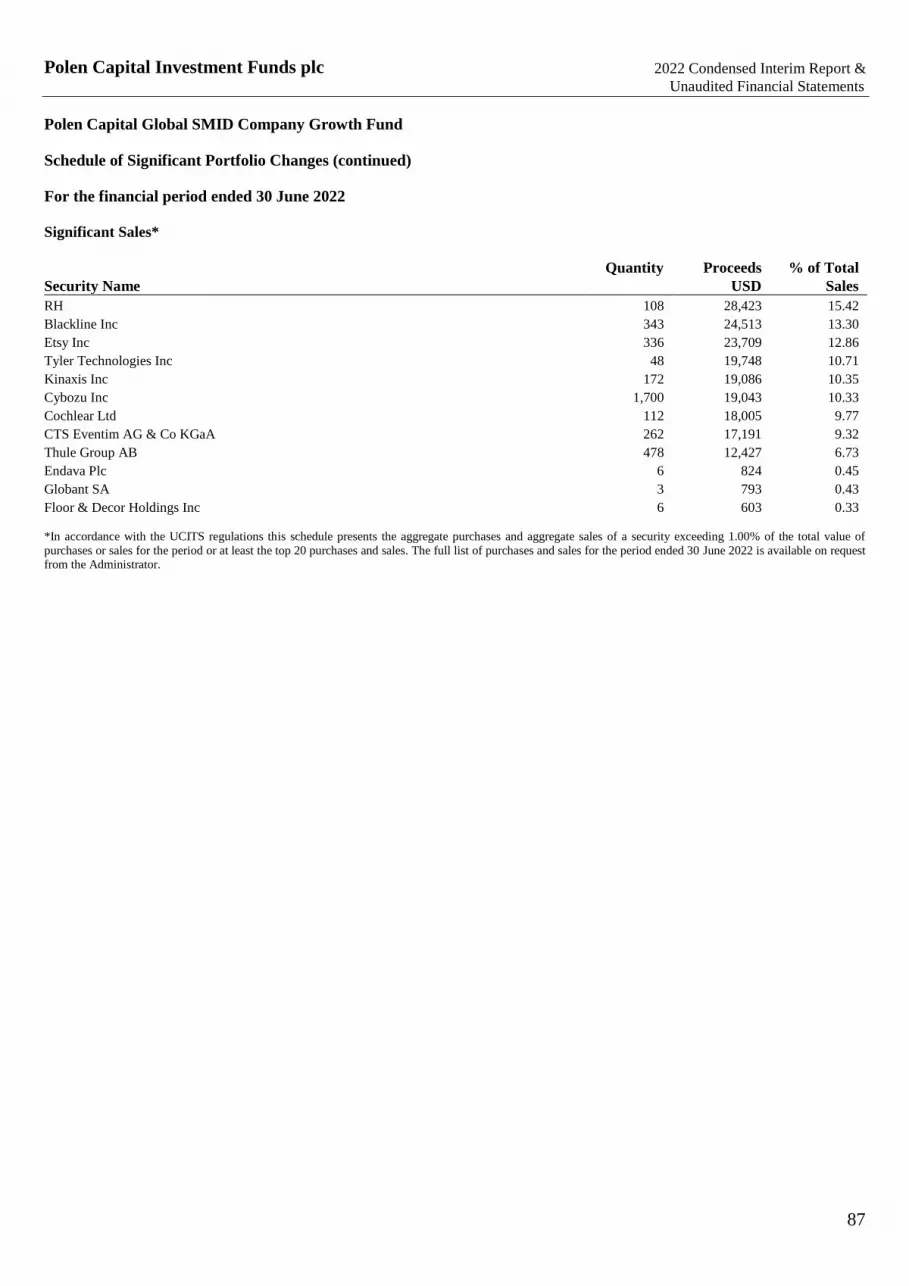

Polen Capital Global SMID Company Growth Fund 86 - 87

Appendix

Securities Financing Transactions Regulation 88

Polen Capital Investment Funds plc

3

2022 Condensed Interim Report &

Unaudited Financial Statements

Organisation

Directors

Bronwyn Wright (Irish)3

Brian Goldberg (U.S.)1

Kevin O'Neill (Irish)2

Mike Guarasci (U.S.)1

Jason Mullins (Irish)1

Registered Office of the Company

Polen Capital Investment Funds plc

4th Floor,

One George's Quay Plaza,

George's Quay, Dublin 2

Ireland

Investment Manager and Distributor

Polen Capital Management, LLC

1825 NW Corporate Blvd

Suite 300

Boca Raton

FL 33431

USA

Manager

Amundi Ireland Limited

1 George's Quay Plaza

George's Quay

Dublin 2

Ireland

Sub-Investment Manager

For Polen Capital Global Emerging Markets Growth Fund

Polen Capital UK LLP

1st Floor

15-18 Austin Friars

London

EC2N 2HE

United Kingdom

Depositary

RBC Investor Services Bank S.A., Dublin Branch

4th Floor,

One George's Quay Plaza,

George's Quay, Dublin 2

Ireland

Company Secretary

Tudor Trust Limited

33 Sir John Rogerson’s Quay

Dublin 2

Ireland

Administrator

RBC Investor Services Ireland Limited 4th Floor,

One George's Quay Plaza,

George's Quay, Dublin 2

Ireland

Independent Auditor

PricewaterhouseCoopers

Chartered Accountants and Statutory Audit Firm

One Spencer Dock

North Wall Quay

Dublin 1

Ireland

Legal Advisers

Dillon Eustace

33 Sir John Rogerson’s Quay

Dublin 2

Ireland

Sponsoring Broker

Dillon Eustace

33 Sir John Rogerson’s Quay

Dublin 2

Ireland

1 Non-Executive Director. 2 Independent Non-Executive Director. 3 Independent Non-Executive Director and Chairman.

Polen Capital Investment Funds plc

4

2022 Condensed Interim Report &

Unaudited Financial Statements

Background to Company

Polen Capital Investment Funds plc (the “Company”) is an open-ended umbrella investment company with variable capital and with

limited liability. The Company is structured as an umbrella fund and may comprise several portfolios of assets. The share capital of

the Company may be divided into different sub-funds (the “Funds”) each representing a separate portfolio of assets and further sub-

divided, to denote differing characteristics attributable to particular Shares, into “Classes”. The functional currency of the Funds is

U.S. Dollar.

At the financial period end there were five Funds which had been launched in the umbrella.

Launch Date Polen Capital Focus U.S. Growth Fund 8 March 2013

Polen Capital International Growth Fund 31 December 2018

Polen Capital U.S. Small Company Growth Fund 31 December 2018

Polen Capital Global Emerging Markets Growth Fund 16 October 2020

Polen Capital Global SMID Company Growth Fund 31 January 2022

Investment Objective and Policy

Polen Capital Focus U.S. Growth Fund

The investment objective of the Fund is to seek long-term growth of capital. The Fund seeks to achieve its investment objective by

investing typically in a focused portfolio of high quality common stocks of large capitalization companies (market capitalisations

greater than $10 billion at time of purchase) which are listed or traded on Recognised Exchanges in the United States of America

and which, in the view of the Investment Manager, have a sustainable competitive advantage. The Fund may from time to time also

purchase the common stock of companies whose shares are listed or traded on Recognised Markets in the United States of America

which have a market capitalisation of less than $10 billion at the time of purchase if the Investment Manager is of the opinion that

the stock represents a particularly attractive investment opportunity.

The Fund will measure its performance against the Russell 1000 Growth Index and the S&P 500 Index (the “Benchmarks”). The

Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes

those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Growth

Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. The index is completely

reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect

growth characteristics. The S&P 500 Index measures the performance of the top 500 large-cap companies listed on stock exchanges

in the U.S. The Fund is considered to be actively managed in reference to the Benchmarks by virtue of the fact that it uses the

Benchmarks for performance comparison purposes. Certain of the Fund’s securities may be components of and may have similar

weightings to the Benchmarks. However, the Benchmarks are not used to define the portfolio composition of the Fund or as a

performance target and the Fund may be wholly invested in securities which are not constituents of the Benchmarks. Any change to

the indices against which the performance of the Fund is measured will be disclosed in the annual or half-yearly report of the

Company issued subsequent to such change being effected.

For this Fund of the Company, underlying investments do not take into account the EU criteria for environmentally sustainable

economic activities.

Polen Capital International Growth Fund

The investment objective of the Fund is to seek long-term growth of capital. The Fund seeks to achieve its investment objective by

investing typically in a focused portfolio of high quality common stocks of large capitalization companies (market capitalisations

greater than $5 billion at time of purchase) which are listed or traded on Recognised Exchanges globally (including those domiciled

in emerging markets) and which, in the view of the Investment Manager, have a sustainable competitive advantage. Investment in

emerging market securities will comprise no more than the greater of 35% of the Fund’s Net Asset Value or 150% of the

Benchmark’s emerging market weighting as of the latest calendar quarter-end. The Fund may from time to time also purchase the

common stock of companies whose shares are listed or traded on Recognised Markets globally which have a market capitalisation

of less than $5 billion at the time of purchase if the Investment Manager is of the opinion that the stock represents a particularly

attractive investment opportunity. The Fund may also invest in Global Depositary Receipts, American Depositary Receipts,

European Depositary Receipts, and International Depositary Receipts where deemed appropriate by the Investment Manager in

order to achieve the investment objective of the Fund.

Polen Capital Investment Funds plc

5

2022 Condensed Interim Report &

Unaudited Financial Statements

Background to Company (continued)

Investment Objective and Policy (continued)

Polen Capital International Growth Fund (continued)

The Fund will measure its performance against the MSCI All Country World Index (“ACWI”) (ex-USA) (the “Benchmark”). The

MSCI ACWI (ex-USA) captures large and mid-cap companies across 22 of 23 Developed Markets countries (excluding the U.S.)

and 24 Emerging Markets countries. The index covers approximately 85% of the global investable equity opportunity set outside

the U.S. The Fund is considered to be actively managed in reference to the Benchmark by virtue of the fact that it uses the

Benchmark to define the maximum emerging market exposure of the Fund but the Benchmark is not used to define the portfolio

composition of the Fund. Certain of the Fund’s securities may be components of and may have similar weightings to the

Benchmark. However, the Fund may be wholly invested in securities which are not constituents of the Benchmark. The Fund may

also use the Benchmark for performance comparison purposes, however it is not used as a performance target. Any change to the

index against which the performance of the Fund is measured will be disclosed in the annual or half-yearly report of the Company

issued subsequent to such change being effected.

For this Fund of the Company, underlying investments do not take into account the EU criteria for environmentally sustainable

economic activities.

Polen Capital U.S. Small Company Growth Fund

The investment objective of the Fund is to seek long-term growth of capital. The Fund seeks to achieve its investment objective by

investing typically in a focused portfolio of high quality common stocks of small companies (market capitalisations within the

range of the market capitalizations of companies in the Russell 2000 Index and the S&P Small Cap 600 Index on a rolling three

year basis at time of purchase) which are listed or traded on Recognised Exchanges in the United States of America and which, in

the view of the Investment Manager, have a sustainable competitive advantage. The Fund may from time to time also purchase the

common stock of companies whose shares are listed or traded on Recognised Markets in the United States of America which have a

market capitalisation outside of the small company definition described in the preceding paragraph at the time of purchase if the

Investment Manager is of the opinion that the stock represents a particularly attractive investment opportunity. The Fund may also

invest in American Depositary Receipts where deemed appropriate by the Investment Manager in order to achieve the investment

objective of the Fund.

The Fund will measure its performance against the Russell 2000 Growth Index. The Russell 2000 Growth Index measures the

performance of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Fund is

considered to be actively managed in reference to the Russell 2000 Growth Index and the S&P Small Cap 600 Index (the

“Benchmarks”) by virtue of the fact that it uses each of the Benchmarks to define the characteristics of the securities held by the

Fund. Certain of the Fund’s securities may be components of and may have similar weightings to the Benchmarks. However, the

Fund may be wholly invested in securities which are not constituents of the Benchmarks. The Fund may also use the Russell 2000

Growth Index for performance comparison purposes, however it is not used as a performance target. Any change to the index

against which the performance of the Fund is measured will be disclosed in the annual or half-yearly report of the Company issued

subsequent to such change being effected.

For this Fund of the Company, underlying investments do not take into account the EU criteria for environmentally sustainable

economic activities.

Polen Capital Global Emerging Markets Growth Fund

The investment objective of the Fund is to seek long-term growth of capital. The Fund seeks to achieve the investment objective

through investment in a well-diversified portfolio of equity securities of issuers in the Emerging Markets or of issuers established

outside of the Emerging Markets, which have a predominant proportion of their assets or business operations in the Emerging

Markets and which are listed, traded or dealt in or on Recognised Exchanges worldwide. It is not proposed to concentrate

investments in any one industry or sector. The Fund may from time to time also purchase the common stock of companies whose

shares are listed or traded on Recognised Exchanges globally which have substantial business in, or revenues from Emerging

Markets if the Investment Manager is of the opinion that the stock represents a particularly attractive investment opportunity in

accordance with its Investment strategy. The Fund may invest up to 20% of net assets in securities which are listed or traded on the

Moscow Exchange. The Fund may also invest in Global Depositary Receipts, American Depositary Receipts, European Depositary

Receipts, and International Depositary Receipts where deemed appropriate by the Investment Manager in order to gain exposure to

international stocks rather than purchasing the stock directly from the underlying company in order to achieve the investment

objective of the Fund. Investment by the Fund in these instruments will limit the need for the Fund to transact in foreign currencies

to achieve the investment objective of the Fund.

Polen Capital Investment Funds plc

6

2022 Condensed Interim Report &

Unaudited Financial Statements

Background to Company (continued)

Investment Objective and Policy (continued)

Polen Capital Global Emerging Markets Growth Fund (continued)

The Fund is considered to be actively managed in reference to MSCI Emerging Markets Index (the “Benchmark”) by virtue of the

fact that it uses the Benchmark for performance comparison purposes. The Benchmark is a free float-adjusted market capitalization

weighted index that is designed to measure the equity market performance of emerging markets. Certain of the Fund’s securities

may be components of and may have similar weightings to the Benchmark. However, the Benchmark is not used to define the

portfolio composition of the Fund or as a performance target and the Fund may be wholly invested in securities which are not

constituents of the Benchmark.

For this Fund of the Company, underlying investments do not take into account the EU criteria for environmentally sustainable

economic activities.

Polen Capital Global SMID Company Growth Fund

The investment objective of the Fund is to seek long-term growth of capital. The Fund seeks to achieve its investment objective

through investment in a well-diversified portfolio of global equity securities of small and mid cap companies (market capitalisations

within the range of the market capitalisations of companies in the MSCI ACWI SMID Cap Index (the “Benchmark”) at the time of

purchase) which are listed, traded or dealt in or on Recognised Exchanges worldwide. While the Investment Manager will monitor

position size, country and sector weightings, it is not proposed to concentrate investments in any one country, industry or sector.

The Fund is considered to be actively managed in reference to the Benchmark by virtue of the fact that it uses the Benchmark to

define the characteristics of the securities held by the Fund. Certain of the Fund’s securities may be components of and may have

similar weightings to the Benchmark. However, the Fund may be wholly invested in securities which are not constituents of the

Benchmark. The Fund may also use the Benchmark for performance comparison purposes, however it is not used as a performance

target.

For this Fund of the Company, underlying investments do not take into account the EU criteria for environmentally sustainable

economic activities.

Polen Capital Investment Funds plc

7

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report

For the financial period ended 30 June 2022

Polen Capital Focus U.S. Growth Fund

The sell-off that began in 4Q'21 and continued into 1Q'22 accelerated this past quarter. Using the S&P 500 as a proxy for the U.S.

market, the current magnitude of the downdraft has been 3x faster than the bursting of the tech bubble in 2000-02. Concerns about

inflation—recently running above 8%—and rising interest rates continued, especially as the Federal Reserve began raising rates by

25, 50, and 75 basis points in March, May, and June, respectively. The Federal Reserve is clearly trying to clamp down on inflation

by raising the cost of borrowing, and the central bank expects to continue with aggressive rate hikes through the rest of this year.

As we exited the first half of the year, the bigger concern seemed to be about the possibility and severity of a looming recession,

which would not be surprising after a period of high inflation and higher interest rates. Indeed, the yield on the 10-year Treasury

note hit a high of nearly 3.5% in mid-June (up from about 1.5% only a few months ago) but has since retreated below 3% at the

time of this writing. It appears, at least when looking at the bond market, that inflation and higher rates may cause less demand for

products and services. If this does occur, inflation itself would likely begin to ease, and interest rates might stay relatively low.

We previously discussed the negative impact on the share prices of "long-duration equities" from the quick rise in interest rates.

Companies with more of their market value derived from future free cash flows are most susceptible to valuation impacts from an

abrupt change in interest rates. Many of these companies, particularly those that are digitally focused, such as digital advertising

businesses like Alphabet and Meta and e-commerce businesses like Amazon, have been robust stock market outperformers for

years. During the pandemic, they saw their revenue growth accelerate, and as the world reopened, their revenue growth slowed

considerably. The rate-induced selling that we have seen in these types of businesses seems to have been magnified by the shorter-

term revenue growth slowdown these companies are experiencing in 2022.

In hindsight, it seems clear that many digitally focused businesses that were driving secular growth trends pre-COVID had a bigger

pull forward in demand in 2020 and the first half of 2021 than we had expected. Though many of them, including Alphabet, Meta,

and Align Technology, are growing slower than we would have expected this year, which has affected share prices in the short-

term, we do not see a substantial change in the longer-term growth rates, market opportunity or earnings power for most of them

We still anticipate nearly 20% annualized earnings per share growth from the Polen Capital Focus U.S. Growth Fund (the “Fund”)

over the coming five years.

It is possible that the U.S. has already entered a recession. Recessions are normal. Economies don't grow all the time. The U.S.

economy has strong underlying foundational properties that have allowed it to grow at an incredible rate for almost two and a half

centuries. Still, there have been and will continue to be periods of negative GDP growth from time to time. Many companies must

retreat and cut investments in talent, product development, marketing, and other areas during periods of economic weakness. Most

companies either have little product/service differentiation versus competitors, in our view, or offer products and services that their

customers do not deem as essential. As a result, demand for their products and services tends to be tied closely to the health of the

overall economy. These types of businesses need to conserve cash when times are tough because their revenue and margins contract

when the economy contracts.

In our experience though, there is a much smaller group of companies—the companies we look for and seek to invest in—that are

typically far more resilient. We believe they can continue to grow revenue and earnings even when economic growth pauses or

temporarily contracts. These are companies that, according to our research, have strong competitive advantages, differentiated

products and services, secular growth prospects, and cash-rich balance sheets. These characteristics generally allow our Fund’s

companies to continue to invest during these tougher times, further widening their competitive advantages while most others are

conserving and contracting.

Most of the market sell-off we have witnessed over the last nine months has more to do with a re-setting of valuations based on

interest rate expectations, in our view.

Going forward, particularly if we remain in a more difficult economic environment, we expect to see the resilience of revenue and

earnings growth rise in importance in a more growth-challenged world.

All businesses will be affected by recessions to some degree. Still, based on our past experience and the high hurdles we hold our

companies to, we expect that the growth in our Fund portfolio companies' earnings, vis-à-vis the market, will compare quite

favourably as they have in other recessions.

Polen Capital Investment Funds plc

8

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital Focus U.S. Growth Fund (continued)

Fund Activity

Most of our holdings had double-digit stock price declines during the most recent quarter, but we've seen very little change in the

long-term competitive positions or growth prospects of these companies. As such, we have begun to shift weightings a bit within

the Fund. We have sold our position in MSCI outright in the second quarter. We have redeployed the cash from these sales into

existing holdings where we see more compelling values.

Many of these are in our fastest growing and most competitively advantaged businesses, like Adobe. We are currently witnessing

what we see as large dislocations in valuations, especially in companies commonly classified as faster-growing technology and

internet businesses. We are already taking advantage of these dislocations.

As an example of a valuation dislocation, we've recently taken advantage of, we added to our position in Adobe in the second

quarter. It is now one of our top three holdings at just under 7% of the Fund. According to our research, Adobe has a near monopoly

on digital content creation software globally and is a highly advantaged digital marketing and analytics business. The business

continues to grow revenues and profits robustly, even in the face of large currency headwinds and macroeconomic weakness in

parts of Europe.

We expect the company to continue to grow earnings at a high-teens or better rate for the foreseeable future on the back of robust

secular growth tailwinds in digital content creation and consumption. Adobe's tools are the de facto standards for various

applications such as graphics and video editing. In addition, Adobe stands to be a leader in providing tools for creators to develop

aspects of the immersive internet (metaverse) as that develops as well.

Adobe's share price has sold off considerably despite its healthy ongoing growth, similar to certain other companies commonly

classified as technology businesses. It is now valued at less than 23x consensus 2023 earnings estimates. This is a discount to

companies like Coca-Cola, Colgate, Clorox, McDonald's, and Proctor & Gamble. Each of these consumer staples companies could

be considered a good business by any unbiased observer. Yet, our research tells us that each one is also likely to only grow earnings

at a single-digit pace because they face more competition and sell into more mature markets than Adobe. The last time we saw

dominant, faster-growing businesses like Adobe trading at discounts to more challenged, slower-growing consumer staples

businesses like Coca-Cola was in late 2008/early 2009 during the Financial Crisis. We are not making a market call, but we are

starting to see valuation discrepancies that we can take advantage of for our Fund.

Fund Performance

Airbnb was one of our largest detractors from performance in the second quarter. Airbnb is the clear market leader in private rental

bookings globally, according to market research firm Euromonitor. The business is currently firing on all cylinders, with revenue

and earnings growth well above our expectations and long-term estimates. It would be easy to say that it is because as the world

reopens, people are traveling for the first time in two years, providing a short-term benefit to the company. But, Airbnb also grew

quickly in 2021 when people were still hesitant to travel and preferred staying close to home. The company's growth in 2022 is not

an easy comparison like it is for online travel agencies (which are more hotel-oriented), airlines, and hotels. In fact, Airbnb's

business has outpaced the hotel industry growth by more than 1,250 basis points per year since 2019, showing far more resilience

than hotels and online travel agencies.

Airbnb didn't invent the private rental market, but it developed a better offering and helped it scale with robust network effects and

a system of trust protecting travellers and hosts alike. It has diligently removed friction from the marketplace to catalyze demand.

The business model has very high incremental profit margins. When the company went public only a year and a half ago, it had

pretax profit margins on a non-GAAP3basis of approximately 5% by our calculations. This year, those margins should approach

30%. In addition, the company has generated approximately $3 billion in free cash flow over the last 12 months. The runway for

growth in private rental is very long, especially considering that hybrid work will likely remain for the long-term, allowing for more

business/leisure trips that work better in Airbnbs than hotels, in our view.

At the same time, Airbnb's network effect of more property listings drives more travellers to make more bookings, which again

drives more listings. This virtuous cycle helps to create the potential for huge barriers to entry for its competitors. As we see it, the

decline in the stock price year-to-date seems to have little to do with the long-term fundamentals of the business. Instead, it has

more to do with the general sell-off in faster-growing technology and internet businesses and short-term concerns around how travel

might fare in 2023 following a solid 2022.

Polen Capital Investment Funds plc

9

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital Focus U.S. Growth Fund (continued)

We agree that Airbnb will have a very tough growth comparison in 2023, especially if a recession is in store. But, we see many

years of double-digit growth ahead driven by durable competitive advantages and management's persistent investment to make

booking on Airbnb the first place travellers go for unique and differentiated stays. Indiscriminate selling due to macroeconomic

fears and how they might impact Airbnb's business over the next year rather than focusing on the next 5-10 years is the definition of

missing the forest for the trees, in our view.

Revisiting Netflix –We See Light in the Darkness, but Still Much Wood to Chop

We believed that the slowdown in Netflix's subscriber growth was most likely due to the reopening of the economy post-COVID-19

and not a competitive or maturation issue. We came to this conclusion because churn remained quite low (which was unlikely if

there was a competitive problem), and the slowdown was broad-based by geography. To us, this likely meant that maturation was

unlikely as even countries with low streaming penetration were seeing the same slowness in new users as those that were more

mature.

Earlier this quarter, Netflix again warned that net new subscriber additions would be negative (fewer new subscribers than those

churning off). They also disclosed for the first time that there are over 100 million households globally (including 30 million in the

U.S. and Canada) that use Netflix but don't pay for it by sharing someone else's password. This is a much larger number than we

expected and indicates that maturation is a real issue, especially in the U.S. and Western Europe.

In the intermediate term, we believe that the addressable market for Netflix is the roughly 450 million homes with smart TVs, often

the preferred method for watching long-form video. In the longer term, the market could be closer to the one billion households

with broadband internet access (excluding China). Watching on laptops and mobile devices can also be a good experience for many,

and over a long enough period, we would expect these households without smart TVs today will eventually own at least one. With

the new disclosure though, Netflix is already reaching roughly 320 million of the 450 million smart TV households (220 million

paying households plus 100 million non-paying password borrowers), which is the better metric for the medium-term addressable

market.

While we are not enthusiastic about the company being much further along in its subscriber adoption journey than we previously

thought due to excessive password-sharing, the potential for monetizing these users remains intriguing. An obvious positive is that

these 100 million households already use and seem to enjoy Netflix. But the big question is, how can you extract value out of them

if they have been unwilling to pay for a subscription? Certainly, there are many reasons why people borrow subscription passwords.

Netflix, in response to the slowdown in growth, has said it will embark on two new strategies. First, it intends to stop allowing

account holders to share their passwords without some payment. Second, the company plans to introduce a lower-cost subscription

that also presents users with advertisements to extract value for the company while offering a more cost-effective plan for

consumers. It remains unclear just how effective these two strategies will be as the details of both have not yet been articulated. But,

interpreting the thoughts management has provided thus far, we expect a few different options are on the table and that this will

involve a good amount of trial and error.

Netflix doesn't want to cut off people that are borrowing someone's password. They want to be able to keep them viewing and allow

for passwords to be shared for a fee (likely well below a full subscription fee). The ad-supported model could be free with ads or a

low-cost subscription with ads. And, it may be different by geography as some markets are far more price sensitive than others. It

will be very important that Netflix thread the needle properly to not alienate users and not incentivize too many of them to trade

down to cheaper subscriptions.

In our view, we'd like to see the company use advertising not only to bring new subscribers to the service but also to monetize

shared passwords. Forcing new fees on subscribers to pay for password sharing is likely to introduce friction and negative brand

equity at a time when consumers' wallets are already stretched. But, introducing ads to those who are borrowing passwords and not

paying does not financially burden the subscription owner and still allows the borrower to watch Netflix without an out-of-pocket

expense. This could be a win-win that should also provide significant incremental revenue to Netflix.

While advertisements can feel inconvenient for some, we think most people accept the trade-off between lower out-of-pocket costs

and seeing ads, particularly as ads become more relevant and engaging over time. The vast majority of linear T.V. and almost all

streaming companies now offer ad-supported models that most consumers accept. If someone does not like seeing ads, the full

subscription price option without ads will remain. The advertising model can be lucrative. Hulu alone generated over $2 billion in

advertising revenue in 2021 with a much smaller and less engaged user base than Netflix.

Polen Capital Investment Funds plc

10

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital Focus U.S. Growth Fund (continued)

We believe that as we exit 2022, Netflix will likely be growing its user base again on the back of a new, rich content slate and easy

comparisons with the tough 2022 period. They will also be launching new monetization schemes, especially advertising plans that

could open incremental revenue opportunities. That said, there is still much work to be done, and it's not as if competition is getting

any less intense. We still need more information from the company to better understand their new monetization strategies, but we

feel that the market has already priced in a dire situation when there is potentially light at the end of the tunnel.

There is much wood to chop for Netflix management, but we are being patient as we see opportunity. Most importantly, we

continue to see a service enjoyed by over 300 million people worldwide that is difficult for competitors to match on a global scale.

This is especially true for the large and important original programming category, an area where Netflix still has a clear lead in

viewership time versus all competitors, including in the U.S., where competition is the fiercest. We have seen plenty of examples of

weak products and services failing to monetize, but we have not seen many examples of unique products and services that are

globally scaled with hundreds of millions of engaged users failing to receive fair value from those who consume, even if it takes

longer than expected to get there.

Outlook

We have seen unusual volatility and surprising downside performance in share prices of many of our holdings despite what we

believe are businesses with strong competitive advantages and growth prospects. The confluence of macroeconomic issues

(inflation, interest rates, recession risks, etc.) and the post-COVID-19 reverberations across industries (difficult comparisons and

capacity utilization after large investments) have made for a challenging year so far. That said, our team has been methodically

examining each of our holdings, assessing the durability of competitive advantages and growth prospects.

We are disciplined in adhering to our investment philosophy but also dispassionate when it comes to stock price movements.

Our research indicates that the vast majority of our holdings are executing well on their strategic paths and growth initiatives, and

we feel confident in the ability to generate mid-teens or better earnings per share growth over the coming five years. We are also

evaluating new potential investments as valuation dislocations are occurring across our investible universe.

Thank you for your interest in Polen Capital and the Polen Capital Focus U.S. Growth Fund. Please feel free to contact us with any

questions or comments.

Sincerely,

Dan Davidowitz and Brandon Ladoff

11 August 2022

Polen Capital Investment Funds plc

11

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital International Growth Fund

International equities broadly declined in the first half of 2022. The Russia-Ukraine conflict, stubbornly high inflation, aggressive

central bank measures, and supply chain challenges all contributed to asset valuation reductions. A clear tightening bias from

central banks dampened some speculative fire that characterized markets in recent years. Liquidity conditions added to the multiple

compression that hit growth stocks. Overall, the markets on June 30 paid significantly less for a dollar's worth of earnings than they

did on January 1.

Many of our steady and stable holdings, including those we believe provide ballast for the Polen Capital International Growth Fund

(the “Fund”), were down in step with the broader market.

Despite share price movements, most of these companies reported robust results, with long-term growth initiatives continuing

briskly and management teams expressing confidence about their business trajectories.

Fund Performance & Attribution

The Fund's exposure to companies within the consumer discretionary, health care, and information technology sectors detracted

from performance in the most recent quarter. Risk-off sentiment has punished these sectors while favouring those in safe havens

like consumer staples. Materials, an area to which we typically carry little exposure, also benefitted the Index in the quarter. The

Fund style was challenged by growth and quality underperforming the benchmark.

Our most significant contributors to performance on an absolute basis over the second quarter were Unilever, Walmart de México,

and Tencent Holdings Ltd.

Multinational consumer goods company Unilever showed robust price increases overall, with minimal impact on volume, resulting

in faster-than-expected sales growth during the quarter. Indeed, higher inflation can be a positive change for companies with

favourable brands like Unilever as these conditions make it easier for the biggest brands to raise prices, continue spending on

advertising, and take share. We believe the appointment of an activist investor to Unilever's board in June will help spur additional

growth.

Walmart de México, Central America's leading retailer, sustained momentum in e-commerce, marketplace, connectivity solutions,

financial services, and advertising, which helped support its ongoing growth.

Our most significant absolute detractors from performance over the quarter were adidas AG, Siemens Healthineers, and

MercadoLibre. With no changes to their underlying businesses during the quarter, we strongly believe these companies were swept

up in indiscriminate selling unrelated to business fundamentals. Our view on the long-term prospects of all three remains positive.

Fund Activity

We increased our position in Globant S.A. during the quarter and exited Walmart de México. We reduced our position in Experian

and Dassault Systèmes SE.

Globant is a leading technology consulting company based in Argentina. As many businesses seek help with digital transformation,

Globant is seeing strong demand for its services that we expect will persist for years to come and drive earnings growth above 25%.

Since our initial purchase in January at a 1% weight, Globant's valuation has become more attractive, providing an opportunity to

add to our position incrementally.

While Walmart de México's business continues to perform as we expected, its stock valuation has crept higher. Over the more than

five years that we have owned the company, it delivered persistent net income growth and dividends. A surprisingly strengthening

peso further aided our compounded total returns. We believe the business is less likely to deliver on our future return expectations

based on valuations, so we decided to take profits and redeploy the proceeds to more favourable opportunities.

Multinational consumer credit reporting company Experian continues to execute well, and shares reflect a positive outlook for its

core Credit Bureau services and success in the consumer services segment. Given Experian's full but fair valuation and the rising

interest rate environment, we felt it prudent to trim our weighting in the company.

France-based Dassault Systèmes is a leading provider of enterprise software solutions in the computer-aided design industry.

Dassault has shown remarkable resilience in its growth and earnings in recent quarters; however, we again trimmed our position to

use the proceeds to add to a faster-growing business trading for the same valuation multiple (Globant).

Polen Capital Investment Funds plc

12

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital International Growth Fund (continued)

Outlook

We continue to run the Fund with a focus on robust and profitable businesses poised to grow their earnings at above- market rates

over the next five years.

Our optimism also stems from competitively advantaged companies on our watch list that we currently do not own but could

become more compelling options as valuations come in.

While uncertain and volatile markets can signal slower near-term economic growth, the divergence between business fundamentals

and stock prices has created attractive entry points for investment in companies with outsized long-term return potential.

As ever, we are confident in the time-tested philosophy driving our growth investing approach. Thank you for your interest in Polen

Capital and the Polen Capital International Growth Fund. Please contact us with any questions.

Sincerely,

Todd Morris and Daniel Fields

11 August 2022

Polen Capital Investment Funds plc

13

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital U.S. Small Company Growth Fund

The Polen Capital U.S. Small Company Growth Fund (the “Fund”) performance was disappointing in the second quarter and full

first half of the year, on both an absolute and relative basis. Amidst higher inflation, slowing economic growth, tightening monetary

policy, and widespread uncertainty, the Russell Growth 2000 Index delivered its worst first-half performance in its more than 40-

year history. There was nowhere to hide with most of the Index constituents delivering negative returns. Growth stocks faced the

greatest pressure. While we own a range of businesses on a growth-to-safety spectrum within an overall growth-oriented

framework, our longer duration, higher multiple investments along with our consumer discretionary holdings were particularly hard

hit. We generally avoid cyclical and commodity businesses like energy for several reasons including our core Flywheel investment

criteria, ESG (Environmental, Social, and Governance) considerations, and our need for strong balance sheets. It is important to

acknowledge that this under-exposure hurt us while still being clear that we do not intend to change our core discipline.

The underlying health of our businesses remains robust, even amidst a worsening economic outlook. As a reminder, in good times

and in bad, one of the key tenants of our Flywheel is investing in businesses with strong balance sheets that can self- fund growth.

We believe this allows them to invest, grow, and emerge stronger in and following challenging economic or funding environments.

However, this does not mean we sit idle. We have been working hard all year to leverage our distinctive collaborative team

approach to look at our investments from all angles and perspectives. As we promise, we are unafraid to update our views. We’ve

made some adjustments to manage the evolving risk landscape as detailed later in this note. We are still pleased with the balance

and ballast in our Fund as it stands today.

While we believe our clients are aligned with our long-term investment horizon, we never like to underperform for any period as

has been the case so far this year. We recognize that sometimes macroeconomic factors weigh more heavily on stock prices than

fundamental company results, and, there are some steps we could have taken to buffer the impact such as reducing some exposure

to consumer discretionary. However, our North Star is to remain focused on long-term intrinsic value creation, and we believe our

ability to see through the noise and act with the conviction of our disciplined research process will ultimately drive significant long-

term returns.

There remains a lot of uncertainty around how long high inflation will last, whether it will trigger a recession, how bad it will be,

and how high rates will need to go. While it’s tempting to make predictions, it’s far more prudent to recognize that the answers are

unknowable.

Instead, we stay focused on what we can understand: the quality of a business, the robustness, and repeatability of the business

model, the quality of a management team, and the team’s experience navigating difficult environments, and the investments a

company can make to solidify and expand its competitive advantages. Changing macroeconomic and pandemic conditions have the

biggest impact on stock prices over the short term.

However, over the long term, the value of a business is a function of the compounding of earnings, free cash flow, and high returns

on capital. By these metrics, we believe opportunities in our investment universe are better than they’ve been in several years and

offer attractive prospects for long-term investors. We are using the factor driven stock market volatility to our advantage, adding

new opportunities in companies in our library that previously did not meet our expected IRR hurdles. We are selling or trimming

companies that have held up well but may be more vulnerable to the changing market conditions. With respect to risk management,

we have been selling companies with less financial flexibility and focusing on adding more sector breadth where applicable.

We are mindful that in more challenging environments, it can be tempting to sell investments that aren’t working and assume

continued weakness.

Sometimes this is the best time to own these investments or buy more from a fundamental perspective.

With any changes that we make, our goal is to enhance quality and expected risk-adjusted returns.

It is often good to buy small-cap growth stocks during challenging times like these. Our focus continues to be on finding what we

believe to be high-quality companies that benefit from long-term secular trends; are well-positioned in their respective markets;

have robust, cash-generative business models; and are run by talented management teams. We believe these qualities provide

businesses with the ability to grow in any market environment and are important drivers of long-term performance. We have not

changed our view that the stocks in our Fund have the potential to at least double in value over a five-year period, with some

offering far more upside especially after the recent drawdown. We believe that maintaining our focus high-quality growth

companies with the best risk-reward tradeoff that are well positioned to drive cash flow and earnings growth over the next 5 years

will generate long-term performance for the Portfolio, regardless of volatility in the underlying economy and shorter-term rotations

in the market.

Polen Capital Investment Funds plc

14

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital U.S. Small Company Growth Fund (continued)

Fund Performance & Attribution Challenging stock selection in consumer discretionary and financials, where we believe there is a disconnect between the

performance of the underlying businesses and their stock prices, drove Fund underperformance. Cyclical sectors (energy, materials)

on one end of the spectrum and defensives (consumer staples, utilities) on the other were the only sectors that materially

outperformed the benchmark.

Except for consumer staples, our focus on high-quality, sustainable growth makes it easier to steer away from most of these sectors.

Our above-benchmark exposure to growth also detracted from performance over the quarter, as did our below- benchmark

exposures to the value and dividend yield factors.

The top absolute contributors to the Fund’s performance over the most recent quarter included AMN Healthcare, Bumble, and

Azenta.

AMN Healthcare is a provider of temporary health care staffing in the U.S. A tightened labour market and higher-than-average

turnover in the health care industry precipitated by the pandemic are helping to drive pricing and volume growth for the company.

We do not believe the company’s current results are sustainable, especially the well above average pricing the company is currently

benefitting from. Given its relative performance and the wide range of outcomes over the next few years as health care starts to

normalize, we trimmed our position in the company.

Online dating company Bumble has been successfully executing its core strategic priorities focused on driving scale and

engagement, monetization, and profitability. We are excited about the market potential for online dating and believe Bumble can

take share and leverage its brand in adjacent categories. This is a category we believe should be resilient no matter what happens

with the economy.

Azenta is a health care company that focuses on biological sample management. The company, previously known as Brooks

Automation, re-branded as Azenta after selling its semiconductor business earlier this year. The company is the only end-to-end

provider of reliable cold-chain sample management solutions and genomic services and benefits from the trend towards sample

outsourcing by pharmaceutical and diagnostic companies.

The most significant absolute detractors from the Fund’s performance over the most recent quarter included Warby Parker,

Revolve, and Progyny.

Warby Parker is an omnichannel retailer of prescription glasses, contacts, and sunglasses. The market’s rapid shift toward favouring

profitable companies posed challenges for the company in the quarter as did weaker results which were pandemic-related. Warby

Parker is less profitable at this stage of its lifecycle as it invests in building out its retail footprint. We expect the company to be

cash-flow positive within a year as it continues to benefit from scale and as retail foot traffic and productivity of the company’s

retail stores return to normal as pandemic conditions ease. We may have had the opportunity to add this holding at a more ideal

price. However, we remain excited about the long-term growth potential of the business, and the expected IRR.

Revolve is an e-commerce fashion company we believe is executing well. The stock weakness during the period was more

sentiment-driven as the market grew increasingly concerned about consumer spending in a recession. We acknowledge that there

could be some softness in the company’s near-term results as consumers tighten their purse strings, but we believe there remains

tremendous long-term potential for this business. We have also observed that Revolve’s management team is exceptional when it

comes to navigating unprecedented challenges, as they did during the pandemic and have a long history of doing so since being

founded in 2003 and bootstrapped by their founders. Management preparedness is an important marker we are looking for during

this challenging time and Revolve’s management team is unquestionably in this area. We added to our position on this weakness.

Progyny is a fertility benefits manager for self-insured companies and their employees. Like Revolve, the underlying fundamentals

of the business remain robust, and we believe the outsized weakness during the quarter was sentiment-driven based on investors’

recessionary fears. In our view, this is a short-sighted concern that overlooks Progyny’s nascent opportunity to penetrate a large and

rapidly growing market with an advantaged, “patient-first” business model. Progyny’s comprehensive fertility solutions are top of

mind for employers looking to drive better diversity, equity and inclusion efforts and it’s also a way for companies to stay

competitive in attracting and retaining talent. As a medical benefits provider, they should be relatively insulated should economic

conditions worsen, especially compared to more "nice to have" employee benefits.

Polen Capital Investment Funds plc

15

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital U.S. Small Company Growth Fund (continued)

Fund Activity

We had more trading activity than usual in recent months.

We are using the stock market volatility to enhance the Fund’s quality and expected risk- adjusted returns while remaining well

positioned for the long term.

We took advantage of drawdowns in existing holdings’ stock prices over the second quarter to add to our positions in cloud-based,

e- commerce restaurant brand platform Olo, e-commerce fashion company Revolve, and insurance brokerage company Goosehead

Insurance. We also added to our position in investment management services firm Hamilton Lane after initiating a smaller position

in the company earlier this year.

We have taken advantage of new opportunities in companies in our library that previously didn’t meet our expected IRR hurdles,

initiating new positions in Five Below Inc., Azenta Life Sciences Inc., Doximity, Inc., and SiteOne Landscape Supply, Inc.

Five Below is a leading, high-growth, value retailer in the U.S. with a differentiated and durable customer value proposition. This is

a company we had previously owned in the Fund but sold it during the pandemic as we were concerned about the company's ability

to thrive during the pandemic with a business model reliant on physical storefronts and foot-traffic.

With more comfort that the economy is reopening and considering the stock's big pullback over the past several months, Five

Below is a compelling investment once again. The things that have us most excited are the company's potential to grow its store

base, its compelling store economics, the investments the company is making to remodel its stores, and its value orientation in a

potentially difficult economy. We are excited about the company's plans to triple its store base by 2030 and double its top and

bottom line by 2025. Based on expectations of 15% square footage growth annually, modest store comps, and limited margin

improvement over the next eight years as the company grows its store base as planned, we believe there is significant upside from

current levels.

Azenta is the only end-to-end global provider of reliable cold-chain life science sample management solutions and genomic

services. The company is competitively advantaged in a very attractive industry that is growing 10 - 12% as more and more drugs

are developed in an increasingly complex environment. Due to the nature of its business, its customer relationships are often

enduring. The average sample is stored for three years, with some stored for over a decade. Long term, we believe the company will

deliver attractive growth, margin expansion, continued mergers and acquisition opportunities, and the potential for share buybacks

over time. From a portfolio management perspective, Azenta gives us exposure to the robust research and development trends in

biotechnology and pharma without concentrated FDA risk or earnings losses.

Doximity is a productivity and professional network app for doctors that derives its revenues primarily from advertising dollars

spent by biopharma companies on its platform. Its unique value proposition lies in its targeted physician list desired by drug

companies. Doximity is an attractive alternative or supplement to an industry that has historically focused its ad spend on sales reps.

Doximity is uniquely high growth and already a very profitable business with a 33% operating margin. It has attractive software-

like economics without having to spend much to acquire users or customers. While the company clearly had some benefit from the

pandemic, it is still early in tapping into a growing, $8B market with multiple avenues for growth. The sell-off in recent IPOs has

created an attractive risk-reward opportunity to start a position.

SiteOne is the largest and only nation-wide wholesale distributor of landscape products in the U.S. Given its scale, SiteOne offers

an accessible network for suppliers with limited distribution resources. The company’s landscaping focus, which is more recurring

in nature than other consumer markets, gives it a resilient earnings profile even in the event of an economic downturn. SiteOne has

also demonstrated success through highly accretive acquisitions of small local players. Given its industry’s fragmentation, we

believe the company has a long runway for growth. Going forward, we expect earnings per share to compound at a low double-digit

rate for the next five years, driven again by +5% organic same store sales growth, +5% growth from acquisitions, flat to expanding

margins, and potential returns of capital in the form of share repurchases or dividends. We recognize that some recent margin gains

may revert in the near- term, but believe this is a rock-solid, high-quality company that can compound earnings for many years and

that the current valuation sufficiently discounts near-term uncertainty.

In the most recent quarter, we reduced our positions in a few existing holdings. This included Endava, AMN Healthcare, and

AppFolio.

Our reduced position in IT consulting company Endava reflects the above-average risk related to the Russia-Ukraine conflict and

the possibility that it extends to Moldova, which represents 9% of Endava’s revenues and where 12% of the company's employees

are based.

Polen Capital Investment Funds plc

16

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital U.S. Small Company Growth Fund (continued)

We trimmed our position in property management software company AppFolio to redeploy the capital into what we believe to be

superior alternatives. The stock held up relatively well this year, and it was a source of funds for adding to new and existing

positions.

As referenced above, AMN Healthcare, performed well during the period. We reduced our position size on the margin due to risk

management given a widening range of outcomes over the next few years as the healthcare system returns to a new normal. AMN

remains a top holding.

We’ve completely sold companies that we believe may be more vulnerable to the changing market conditions and those with less

financial flexibility including Malibu Boats LLC., Trupanion, and BigCommerce Holding Inc.

On Malibu Boats LLC we are concerned about the considerable demand pull-forward during the pandemic combined with the rise

in interest rates and inflationary pressures the consumer is currently facing. The business continues to perform well but we know

from past downturns that this is an industry that is more vulnerable to these types of pressures, and that the environment can change

quickly. The company's stock has held up better than most companies in our Fund in the YTD period, making it a good source of

funds to redeploy into companies with less vulnerability to the changing economic conditions and more compelling risk reward

profiles.

We sold Trupanion because we are concerned about the deteriorating unit economics of the business. Changes in how vets operated

during COVID disrupted Trupanion’s strategic advantage for onboarding new pets at vet offices.

This forced Trupanion to compete in undifferentiated DTC (direct-To-consumer) sales channels with other pet insurers and increase

experimentation for pet acquisition. This significantly increasing per pet acquisition cost and moving away from the discipline we

had seen from management historically.

This is a key variable in the unit economics and free cash flow (FCF) generation that Trupanion would be able to earn from each of

its covered pets. While the veterinary community has largely overcome the challenges of COVID-19, we lack confidence that

management can curb pet acquisition spend in the intermediate term while also investing in future growth channels. This can both

hamper growth and is a major obstacle to generating free cash flow FCF. This is a clear and likely persistent Flywheel violation.

Management may be making correct and rational decisions to ensure the multi-decade success of the business, but the declining unit

economics of the business and lack of FCF makes it less compelling in the current environment and over our investment horizon.

Finally, we sold BigCommerce due to clear Flywheel violations. We are concerned about the company's deteriorating profitability

and reliance on external sources of capital. BigCommerce is facing numerous challenges including developer resources in Ukraine

and the potential for staffing challenges in a still challenging labour market for engineers.

Outlook The macroeconomic environment is complex and unpredictable. This unpredictability stems from interplay between

macroeconomic data points, external shocks or their reversal, the Fed’s actions, and how consumers and businesses react. This

creates a series of junctures in which multiple scenarios are possible. What we are observing in many companies we follow is a

natural reaction to uncertainty, which is a slowdown in the front edge of consumer discretionary, a lengthening of sales cycles, and

more caution around building inventory. There may be tougher times ahead, and we are prepared for it. We are expecting growth to

slow in the face of difficult comparisons and the weakening outlook. This compounds uncertainty around near-term predictions and

valuation multiples. Companies that benefited from the pandemic may look particularly volatile with a short-term view.

This is exactly why we stay focused on the long-term. While it may be hard to believe with short-term lens influenced by fear and

uncertainty, the long-term picture is far clearer than the market would suggest, and by and large, our long-term view and conviction

in our portfolio companies is unchanged. This allows us to confidently sift through the noise and take advantage of price

dislocation. This also highlights the benefit of owning Flywheel companies as we define them. These are long-term secular winners,

still in the early innings of their growth, with durable businesses models and balance sheets that are built to keep them robust when

others are weak. Time and patience are required for the fundamentals to play out. We cannot predict the short-term even though we

believe significant bad news is priced in.

Despite all the challenges, the opportunity set in small-cap is attractive. High-quality, small-cap companies have greater latent

potential for growth relative to more mature businesses. The best small cap growth companies can quickly reduce spending and

inflect profitability if needed given their high starting levels of investment. We believe the best-of-the-best small-cap companies

will take advantage of adjacencies and have a better potential opportunity set for value-added acquisitions.

Polen Capital Investment Funds plc

17

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital U.S. Small Company Growth Fund (continued)

Of course, many companies do not meet this high hurdle, which is why we hold a concentrated portfolio of companies that do not

just offer growth and high returns, but also durability, robust financial models, the ability to self-fund growth, and what we believe

to be superior management teams.

We believe great investing requires a clear and proven philosophy, a disciplined process and conviction. It also requires great

humility and a willingness to change your view when the evidence requires it. We look forward to keeping you updated on our

views in future commentary.

Thank you for your interest in Polen Capital and the Polen Capital U.S. Small Company Growth Fund. Please contact us with any

questions.

Sincerely,

Rayna Lesser Hannaway

11 August 2022

Polen Capital Investment Funds plc

18

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital Global Emerging Markets Growth Fund

Share prices globally—including those in emerging markets— remained under pressure in the second quarter of 2022, adding to an

already challenging start to the year. In our view, some of the reasons for the declines this year have been very rational. With

inflation moving higher globally and interest rates following suit, markets are naturally baking in higher discount rates, and some of

the frothy valuations of the past years have come home to roost.

We have been concerned for a while about the number of companies in the market with unprofitable business models raising capital

on the promise of significant returns tomorrow.

There was no way of knowing when this would unwind; however, history has shown that no matter how painful it can be – and

sometimes for a long time – fundamentals tend to win out in the end.

In such unwinding environments, it is not uncommon for markets to throw the proverbial "baby out with the bathwater." We believe

this is playing out now. Companies we regard as high quality are selling off as much if not more than those with significantly less

solid fundamental underpinnings simply because of the industry they operate in.

Going forward, we have no idea how much further markets can or will fall. However, it looks likely that global interest rates and

funding sources will get tighter from here on. This is probably not good news for companies with weak fundamental underpinnings

or cash flows to support valuations. Nevertheless, in our opinion, it is a good time to be an active investor. We feel very confident

in the companies we own in the Polen Capital Global Emerging Markets Growth Fund (the “Fund”), their robust business models,

and the valuations many of them are now trading on.

Emerging markets were not exempt from global pressures in the second quarter. Yet, the drawdown was less severe than across

their developed counterparts. This was partly because China, the largest emerging market, had already been heavily punished

during the previous twelve months. It was also probably a reflection of the emerging market asset class as a whole having missed

out on some of the exuberance that found its way into global markets in recent years.

Chinese equities closed the period higher after the world's second-largest economy relaxed some of its COVID-19-related

lockdowns and showed early signs of easing tensions on the regulatory front, particularly within the technology sector.

While easing lockdowns are a favourable tailwind in the short term, we would be cautious in cheering too early as the Chinese

government remains committed, albeit in an increasingly isolated way, to a zero COVID-19 policy. Despite the government's

efforts, achieving this goal is something that, at least as we stand today, looks unlikely to succeed over the long term.

Fund Performance & Attribution From an absolute perspective, our most significant contributors to performance over the most recent quarter were Autohome, Phu

Nhuan Jewelry, and Prosus.

Autohome is China's leading online car classified company and one company that, in our view, was unfairly punished in reaction to

China's regulatory crackdown last year. Autohome saw a steep decline in its share price in 2021 as most tech-related companies

sold off, irrespective of the actual direct impact of regulatory changes or how cash-generative their businesses were.

While earnings of Autohome did soften during the year as the global chip shortage weighed on new car sales, we expect the

company to return to the earnings growth levels it has historically delivered. The company's 70% share price decline in 2021 left it

trading on levels we considered very attractive, and we took the opportunity to increase our position earlier in the year. Despite the

bounce during the quarter, we still view the company as materially undervalued.

Headquartered in Vietnam, Phu Nhuan Jewelry produces, sells, and trades jewellery and related products. PNJ is the leading

formalized jewellery retailer in a growing industry (and country) still primarily dominated by "Mom and Pop" stores. Year to date,

profits are up about 50% year-over-year, which in our view, represents solid growth for a company trading at less than 20x forward

earnings. As PNJ rolls out new stores and customers continue to be attracted to purchasing from a brand they trust, we expect PNJ

will continue compounding at high rates of return.

Prosus is a Netherlands-headquartered holding company with a 30% stake in Tencent Holdings Ltd. We have historically viewed

Prosus as an attractive vehicle for investing in Tencent, given that Prosus's market cap—including several other promising

businesses—is significantly lower than its direct stake in Tencent.

After trying multiple times to close the discount without much success, the firm's management announced that it would begin to

gradually sell down some of its Tencent holdings and use the proceeds to buy back shares, leading to a jump in Prosus's share price.

Polen Capital Investment Funds plc

19

2022 Condensed Interim Report &

Unaudited Financial Statements

Investment Manager’s Report (continued)

For the financial period ended 30 June 2022

Polen Capital Global Emerging Markets Growth Fund (continued)

The most significant absolute detractors from performance over the quarter were MercadoLibre, Karoooo, and Titan.

As written in our Q4 2021 commentary, some significant differences exist between the underlying profitability of e- commerce

companies in emerging markets. However, MercadoLibre was punished during the quarter in part because of the sector it happens

to operate in. Given its robust cash flow generation, we believe MercadoLibre is well-poised to continue delivering solid cash flows

that will enable it to support its operations fully. Going forward, we expect the business to continue growing and providing value-

added services to its customers across the continent. In turn, we capitalized on the weakness during the quarter to opportunistically

increase our position in MercadoLibre.

Karoooo is a leading South African and Southeast Asian provider of highly precise vehicle tracking services that help its customers

improve their logistics operations' efficiency, safety, and security. Despite the price weakness during the quarter and year-to-date,

the company continues to deliver solid operating results, with subscribers and revenues for the full year ending February 2021

increasing by 17% and 20%, respectively. During the quarter, we spoke with Zak Calisto, CEO of Karoooo, about the business and

its plans for the future. Following our discussion, we remain very impressed with the company's strategy, quality of management,

and ability to continue compounding cash flows for many years.

Titan is the leading jewellery retailer in India. While it has made a solid recovery operationally since the early days of the

pandemic, so has its share price. With valuations under the limelight, it is not surprising to see some profit-taking action. Though

our team remains confident in the company's long-term structural growth story, we reduced our holding late last year to reflect more

demanding near-term valuations.

Fund Activity

During the most recent quarter, we increased our positions in Momo.com, Wizz Air, MercadoLibre, Tencent Music Entertainment

Group, and Alibaba Group Holding and exited President Chain Store. We also reduced our positions in Raia Drogasil SA, United

Spirits Limited, and Colgate-Palmolive (India) Ltd.

We used share-price weakness over the quarter to increase our positions in Taiwan-based e-commerce company Momo.com, low-

cost airline Wizz Air and online marketplace MercadoLibre. We have discussed these three businesses in recent quarterly

commentaries, and we believe in each case that the share price movements we have seen this year are not reflective of their