Embed Size (px)

Citation preview

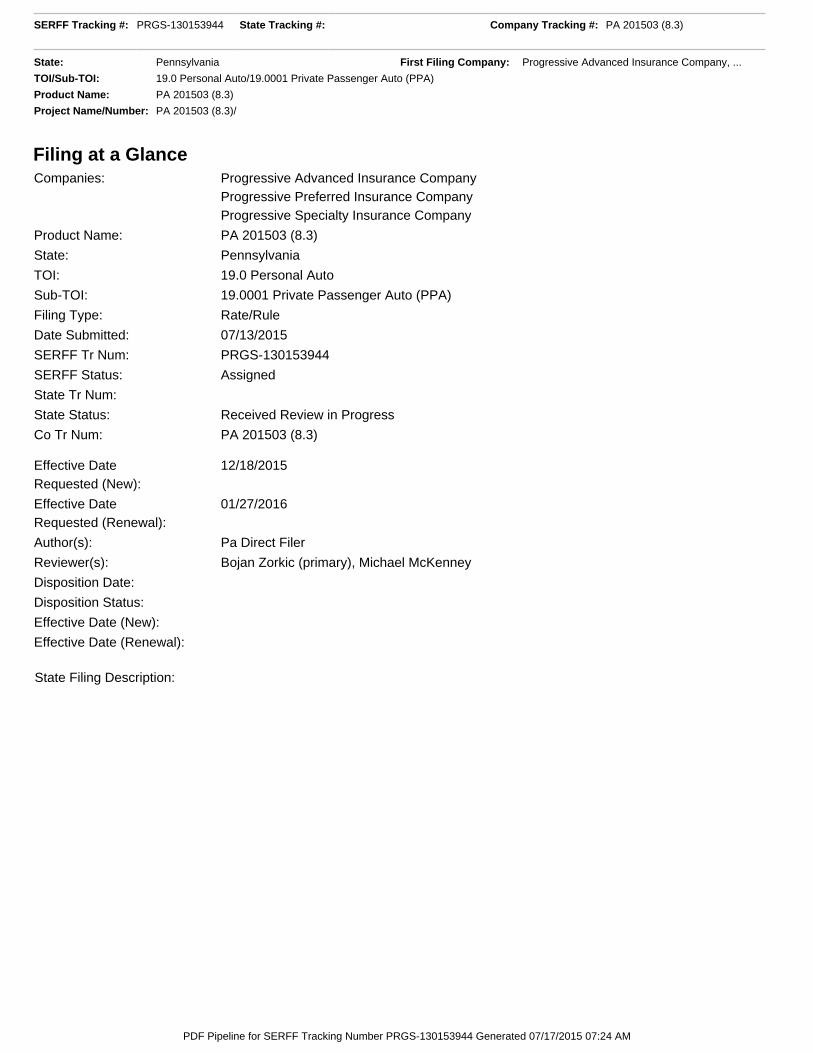

Filing at a Glance

Companies: Progressive Advanced Insurance CompanyProgressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Product Name: PA 201503 (8.3)

State: Pennsylvania

TOI: 19.0 Personal Auto

Sub-TOI: 19.0001 Private Passenger Auto (PPA)

Filing Type: Rate/Rule

Date Submitted: 07/13/2015

SERFF Tr Num: PRGS-130153944

SERFF Status: Assigned

State Tr Num:

State Status: Received Review in Progress

Co Tr Num: PA 201503 (8.3)

Effective DateRequested (New):

12/18/2015

Effective DateRequested (Renewal):

01/27/2016

Author(s): Pa Direct Filer

Reviewer(s): Bojan Zorkic (primary), Michael McKenney

Disposition Date:

Disposition Status:

Effective Date (New):

Effective Date (Renewal):

State Filing Description:

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

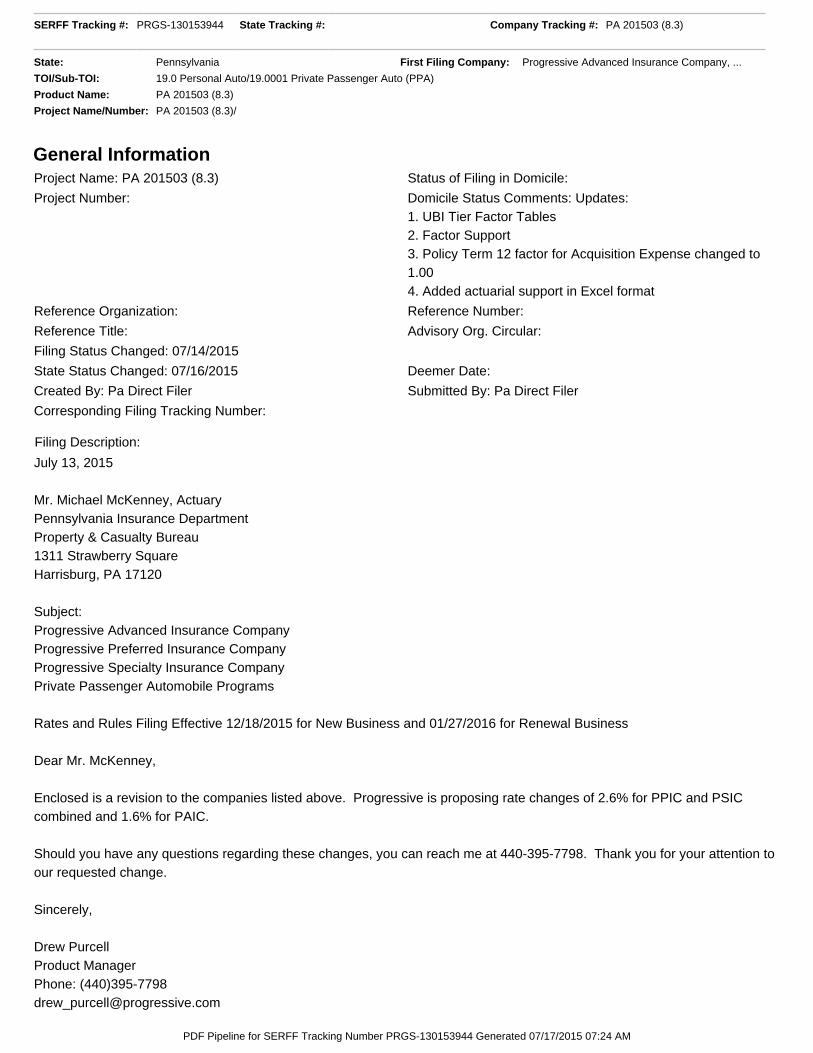

General Information

Project Name: PA 201503 (8.3) Status of Filing in Domicile:

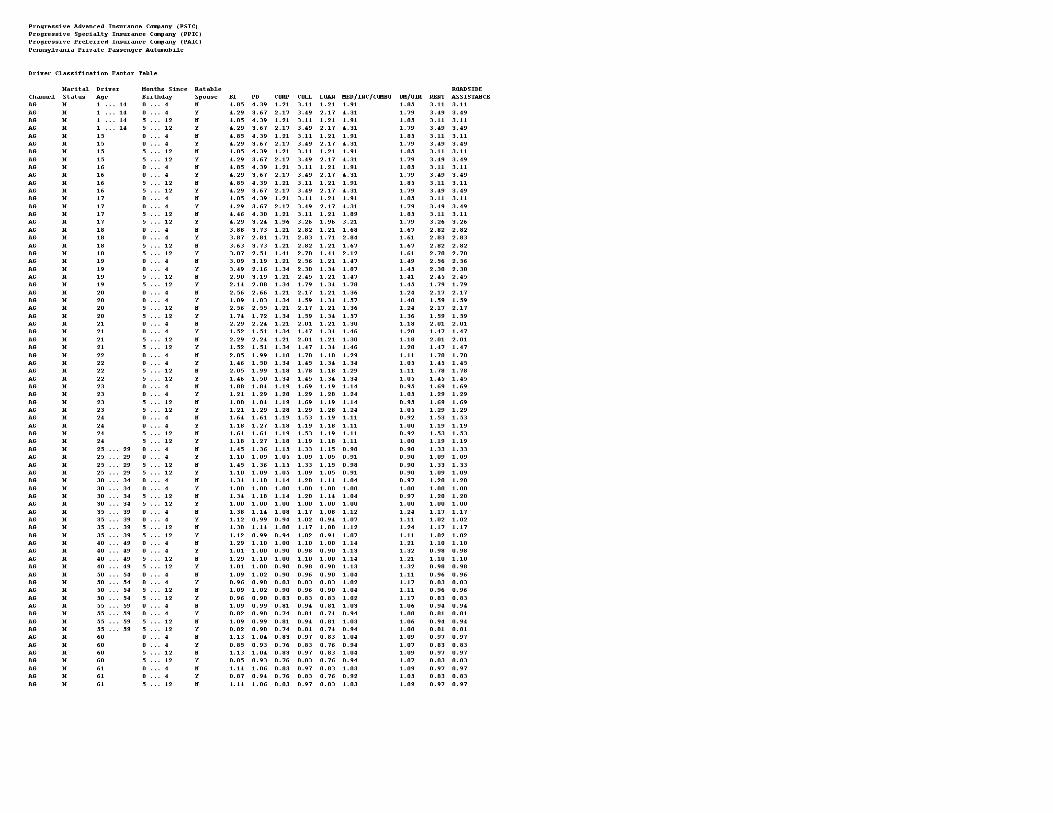

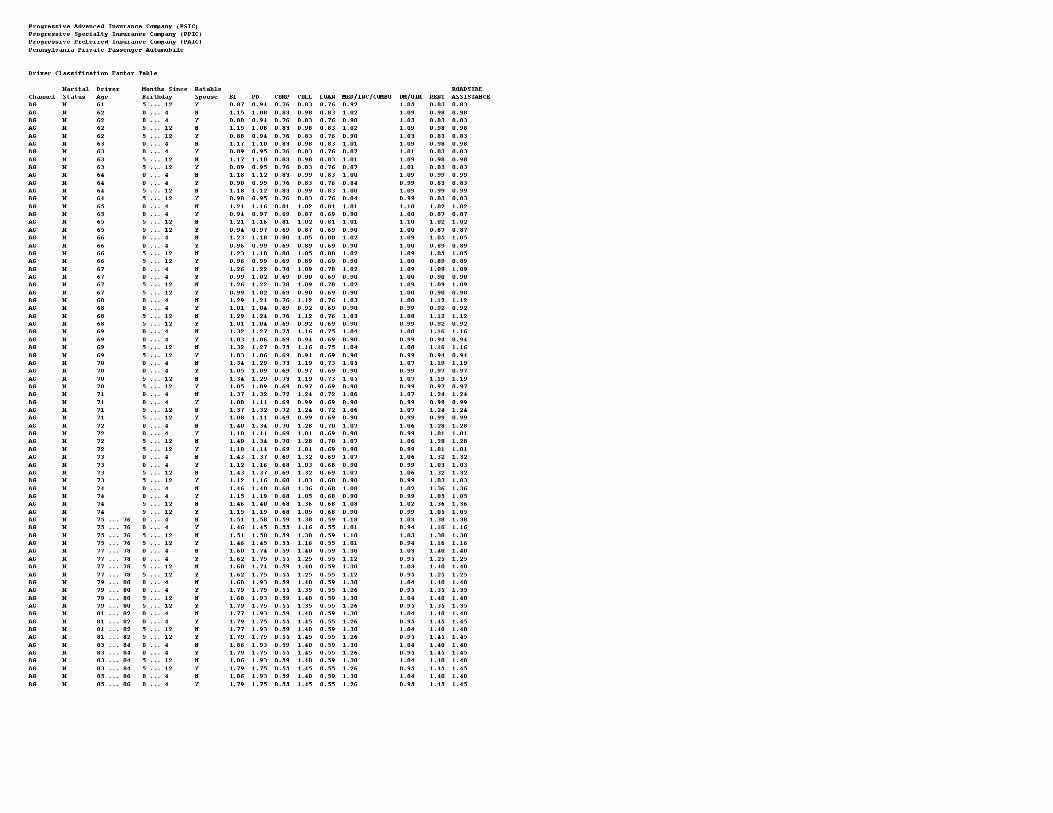

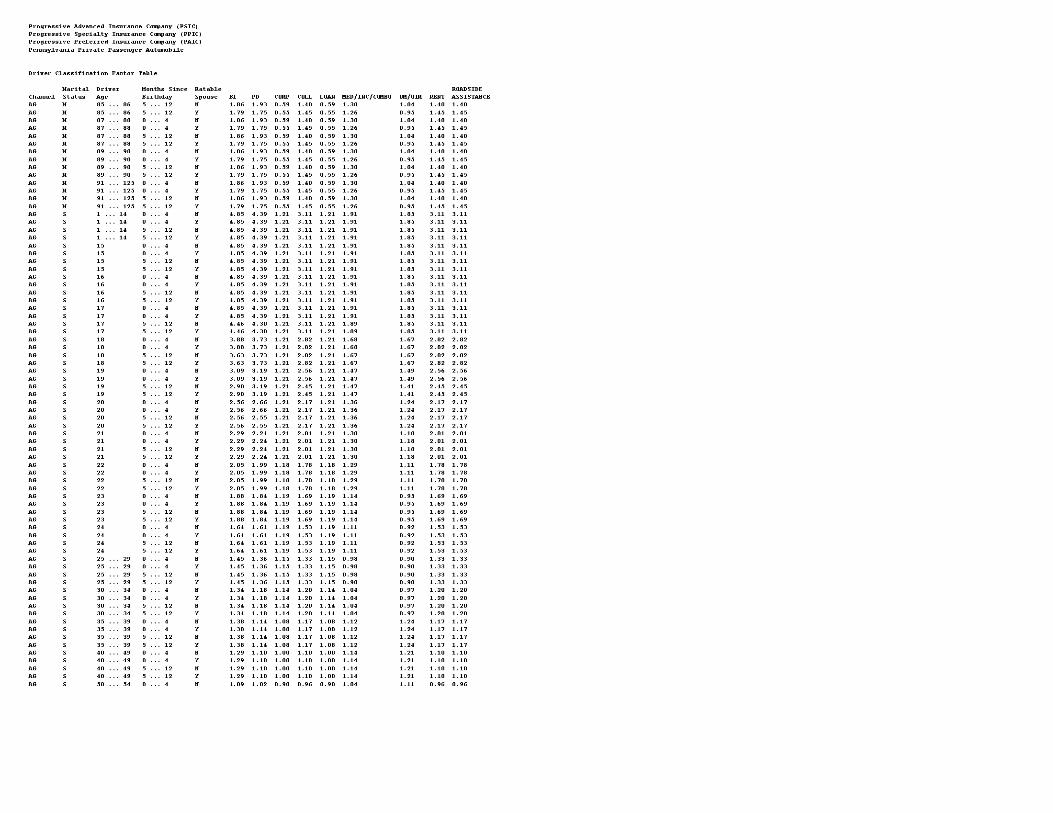

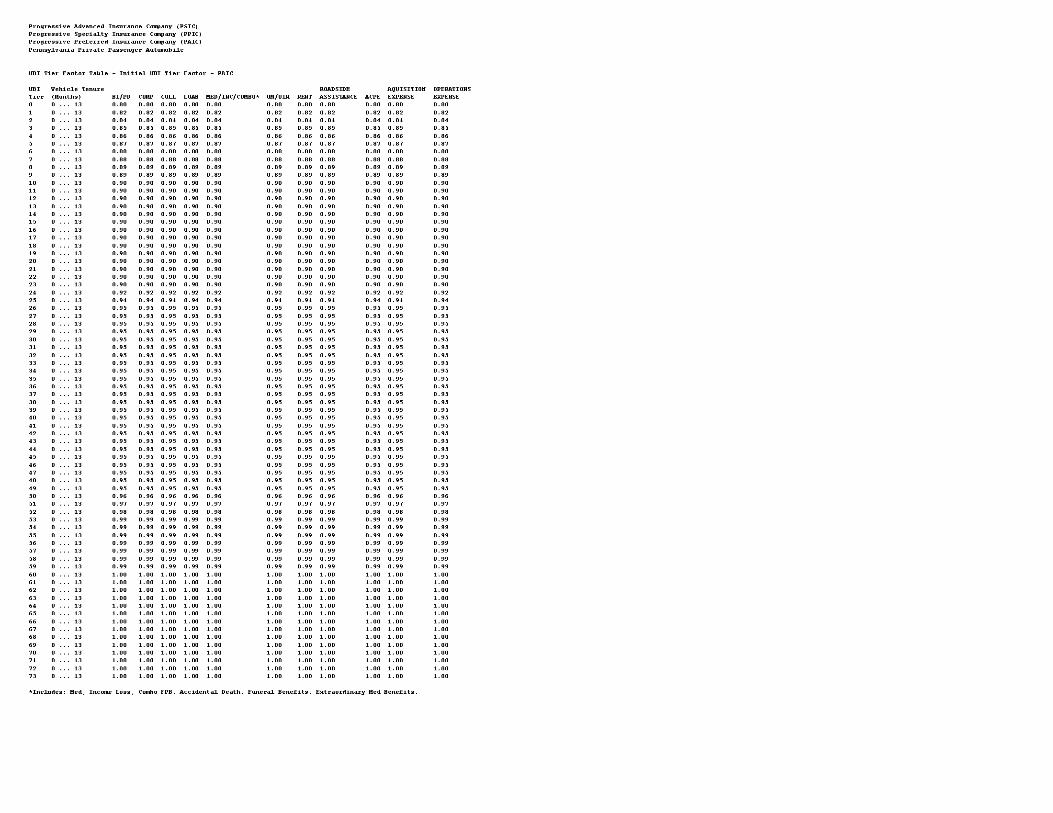

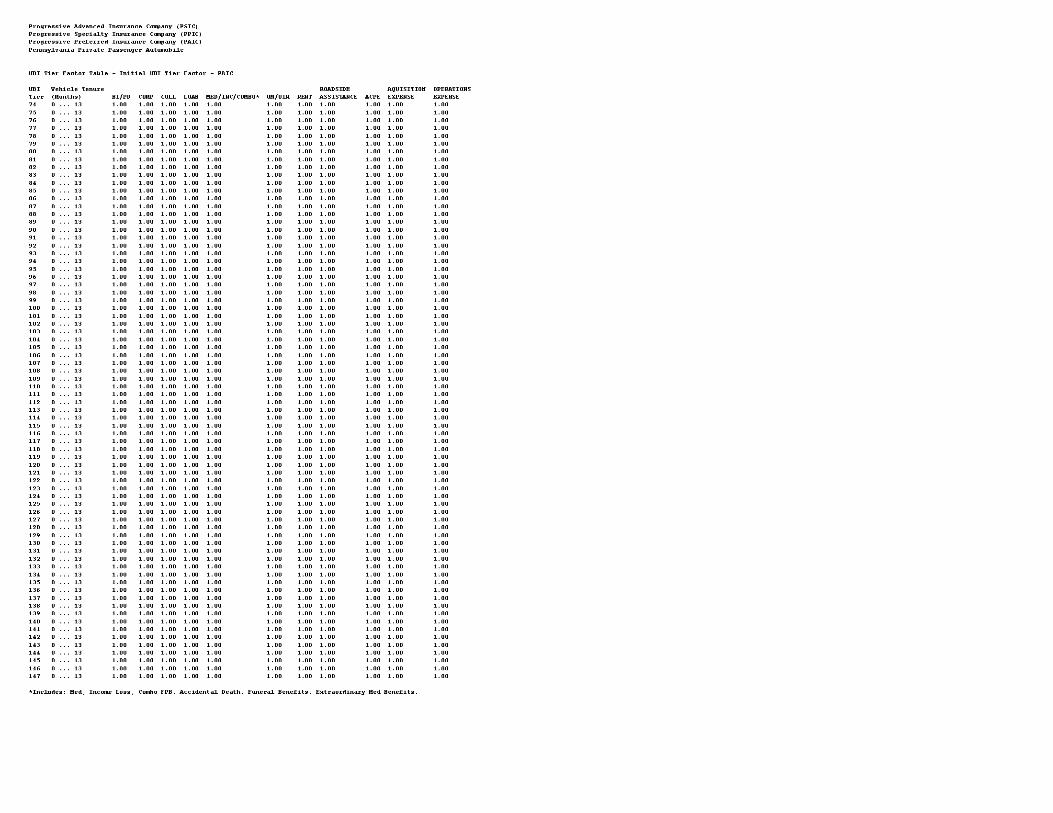

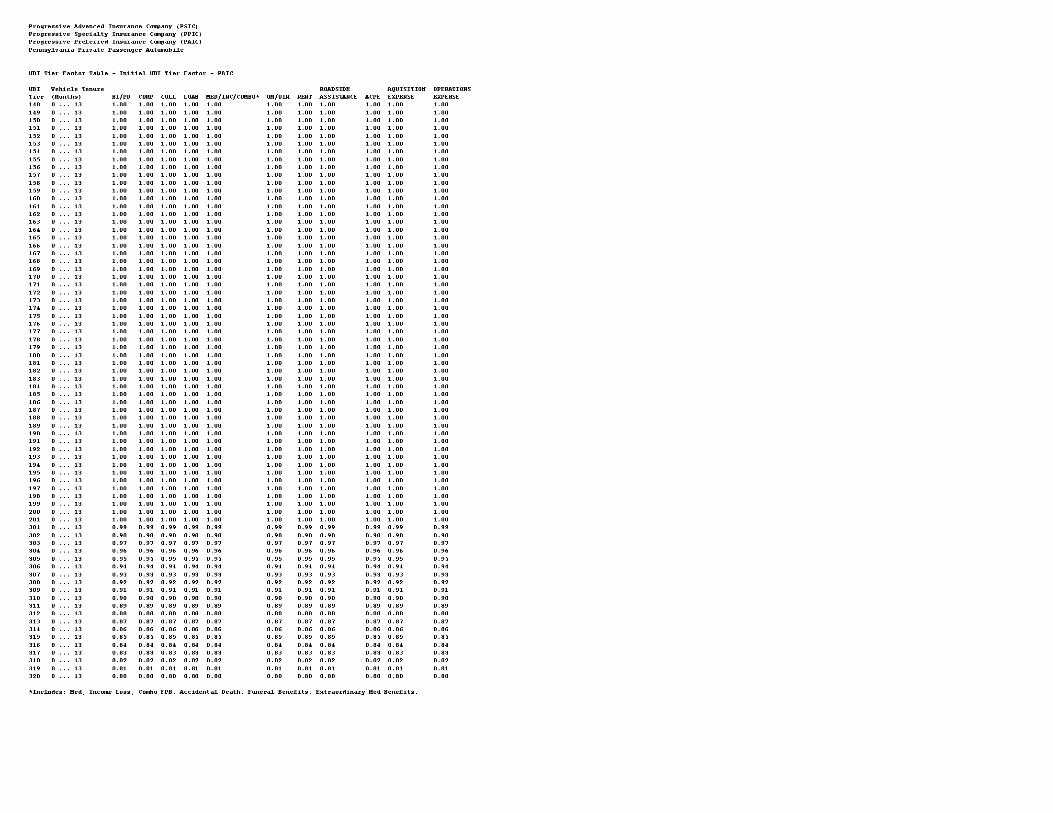

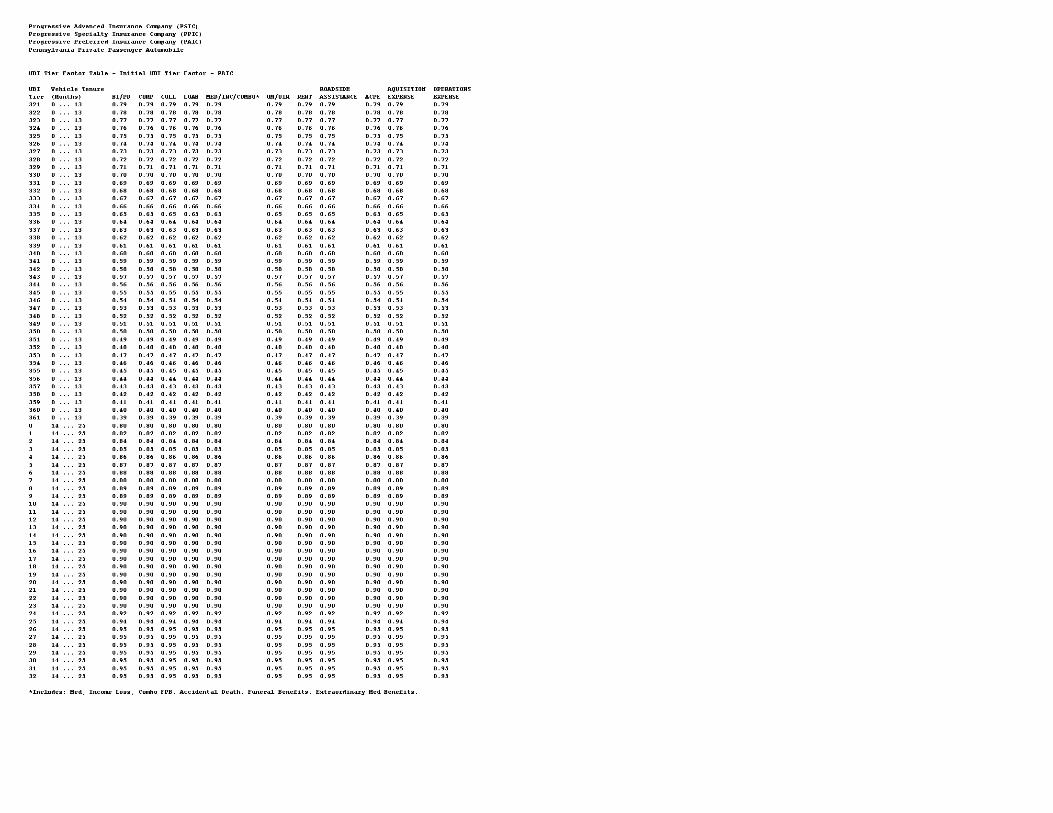

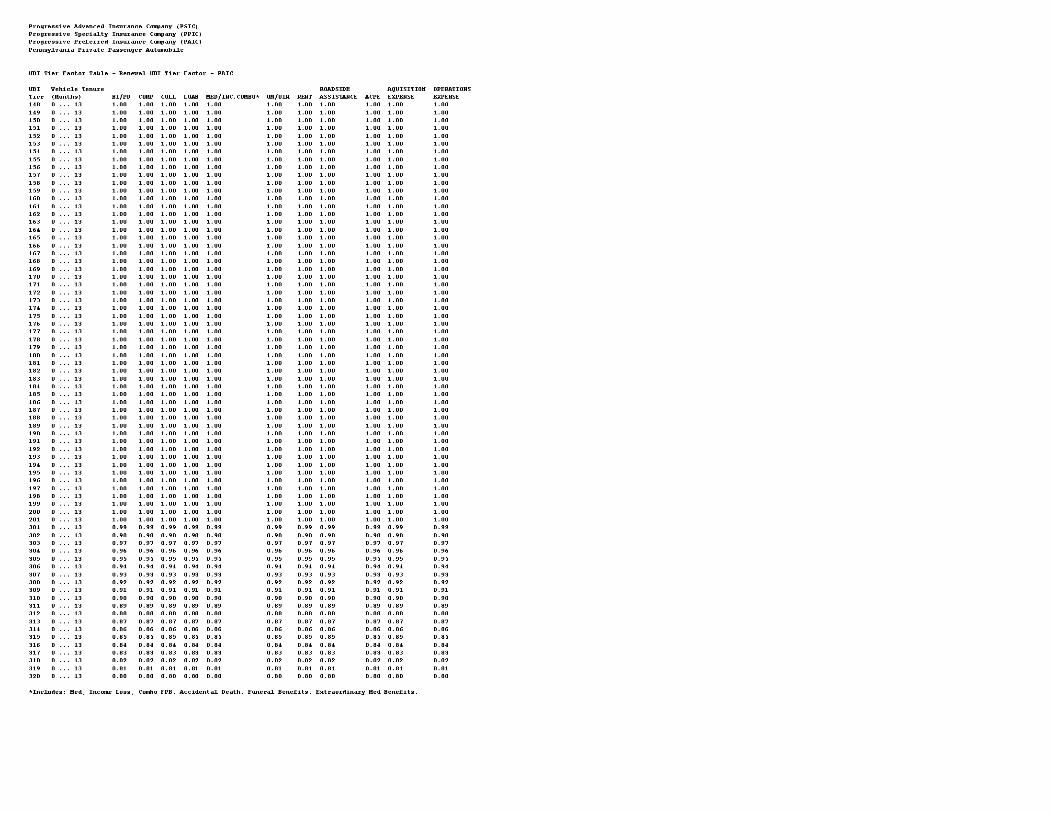

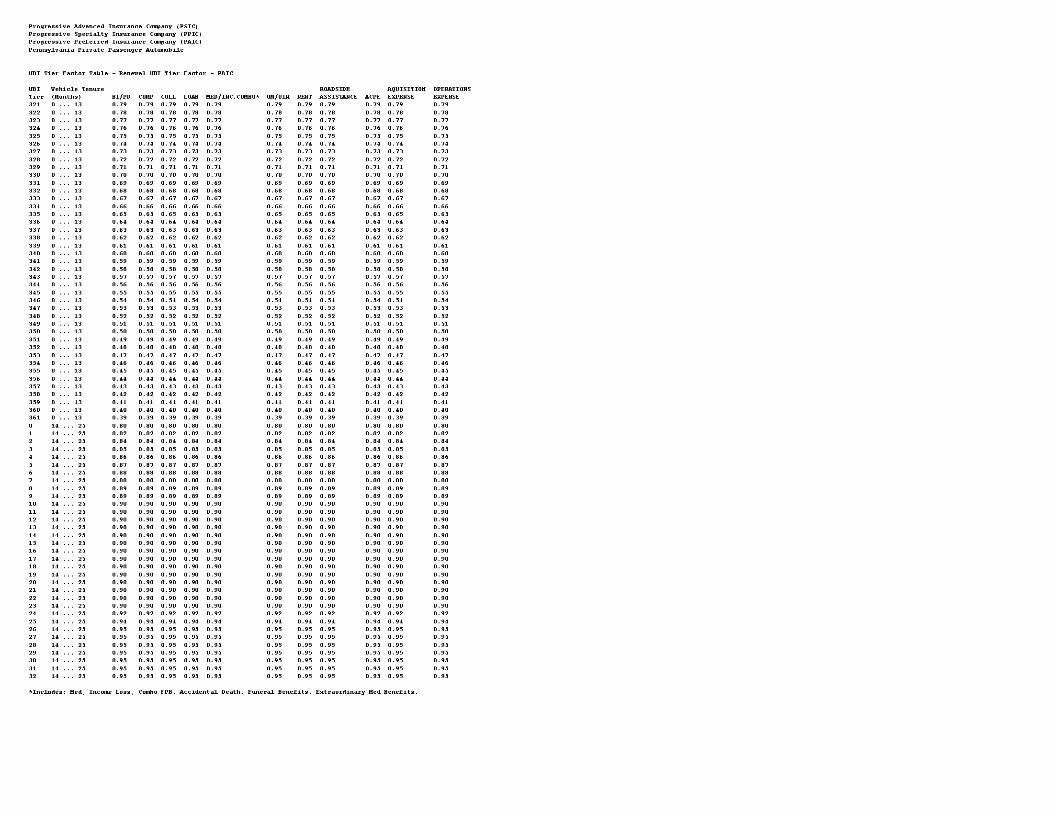

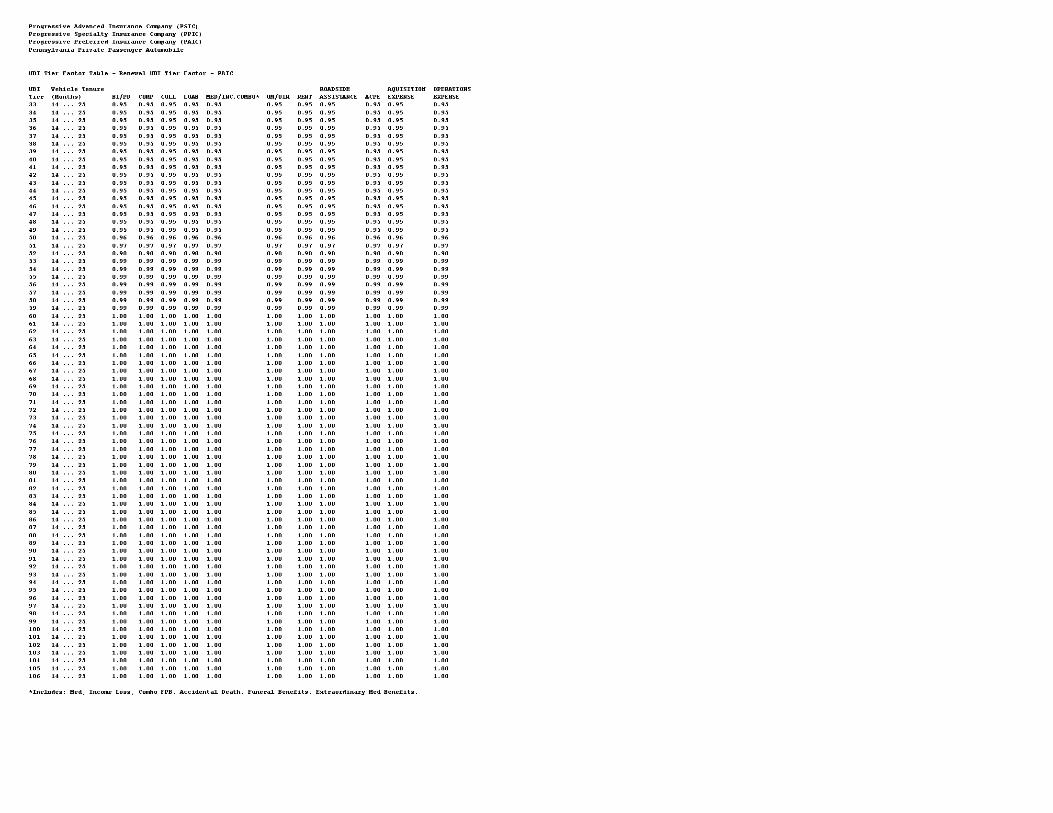

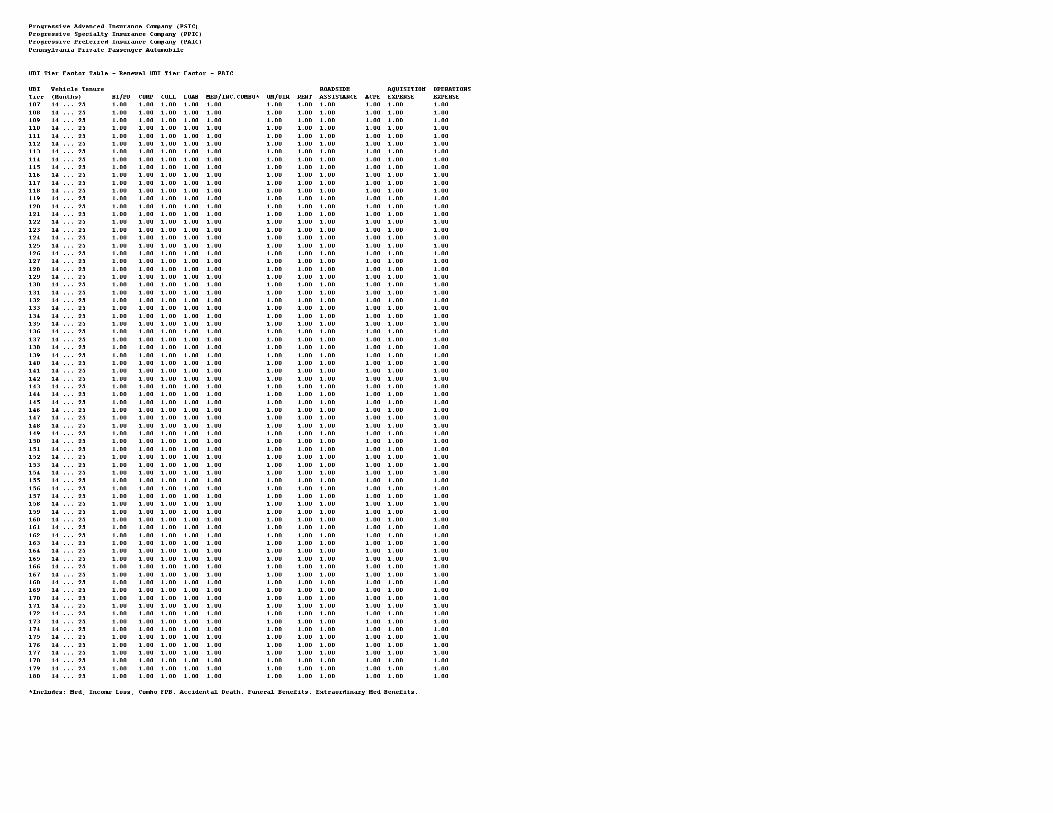

Project Number: Domicile Status Comments: Updates:1. UBI Tier Factor Tables2. Factor Support3. Policy Term 12 factor for Acquisition Expense changed to1.004. Added actuarial support in Excel format

Reference Organization: Reference Number:

Reference Title: Advisory Org. Circular:

Filing Status Changed: 07/14/2015

State Status Changed: 07/16/2015 Deemer Date:

Created By: Pa Direct Filer Submitted By: Pa Direct Filer

Corresponding Filing Tracking Number:

Filing Description:

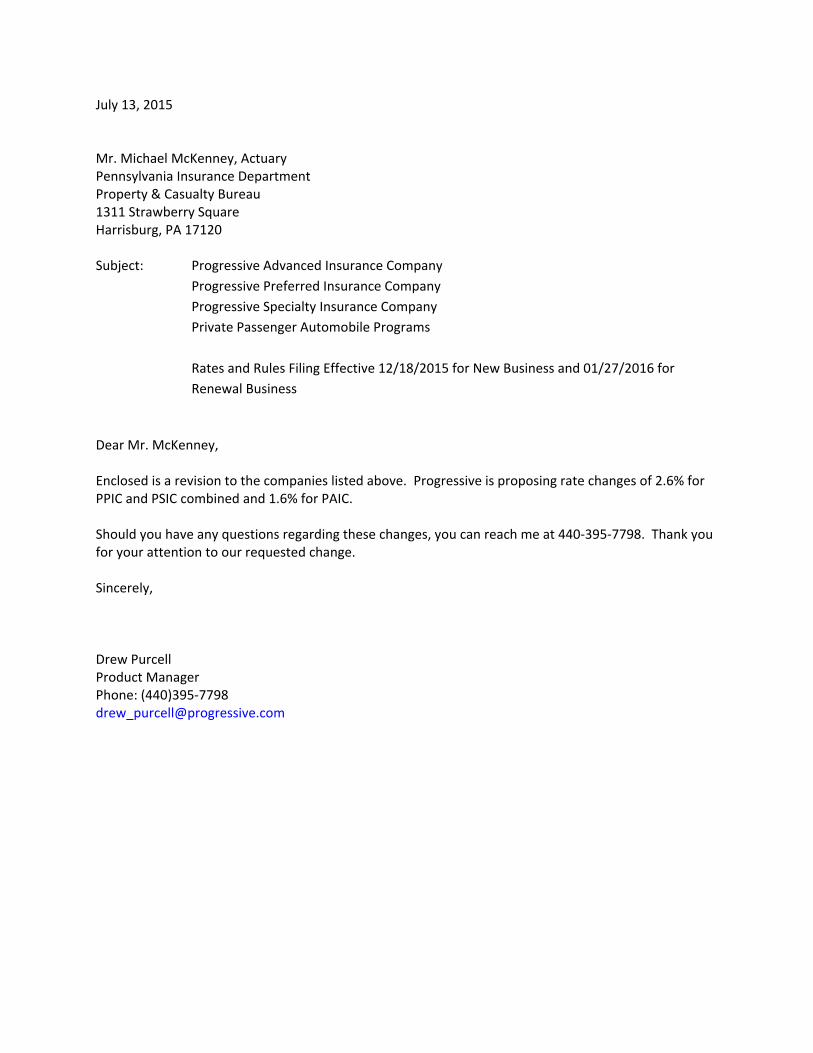

July 13, 2015

Mr. Michael McKenney, ActuaryPennsylvania Insurance DepartmentProperty & Casualty Bureau1311 Strawberry SquareHarrisburg, PA 17120

Subject:Progressive Advanced Insurance CompanyProgressive Preferred Insurance CompanyProgressive Specialty Insurance CompanyPrivate Passenger Automobile Programs

Rates and Rules Filing Effective 12/18/2015 for New Business and 01/27/2016 for Renewal Business

Dear Mr. McKenney,

Enclosed is a revision to the companies listed above. Progressive is proposing rate changes of 2.6% for PPIC and PSICcombined and 1.6% for PAIC.

Should you have any questions regarding these changes, you can reach me at 440-395-7798. Thank you for your attention toour requested change.

Sincerely,

Drew PurcellProduct ManagerPhone: (440)[email protected]

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

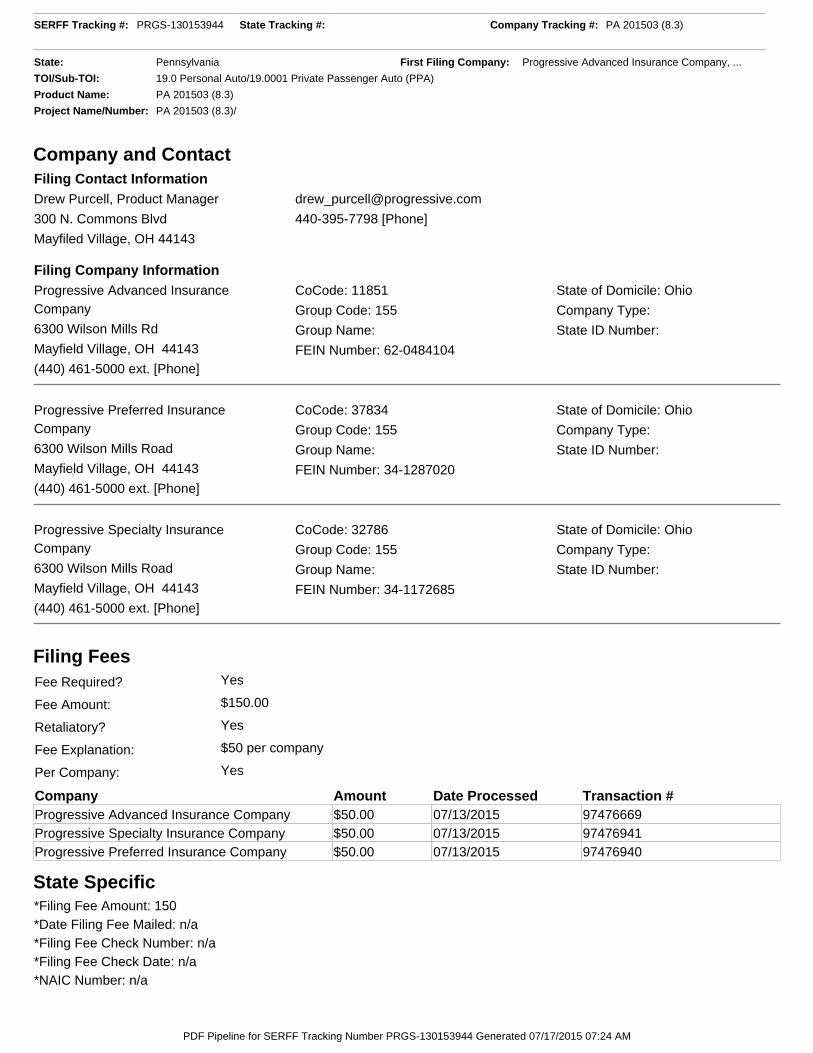

Company and Contact

Filing Fees

State Specific

Filing Contact InformationDrew Purcell, Product Manager [email protected]

300 N. Commons Blvd

Mayfiled Village, OH 44143

440-395-7798 [Phone]

Filing Company InformationProgressive Advanced InsuranceCompany

6300 Wilson Mills Rd

Mayfield Village, OH 44143

(440) 461-5000 ext. [Phone]

CoCode: 11851

Group Code: 155

Group Name:

FEIN Number: 62-0484104

State of Domicile: Ohio

Company Type:

State ID Number:

Progressive Preferred InsuranceCompany

6300 Wilson Mills Road

Mayfield Village, OH 44143

(440) 461-5000 ext. [Phone]

CoCode: 37834

Group Code: 155

Group Name:

FEIN Number: 34-1287020

State of Domicile: Ohio

Company Type:

State ID Number:

Progressive Specialty InsuranceCompany

6300 Wilson Mills Road

Mayfield Village, OH 44143

(440) 461-5000 ext. [Phone]

CoCode: 32786

Group Code: 155

Group Name:

FEIN Number: 34-1172685

State of Domicile: Ohio

Company Type:

State ID Number:

Fee Required? Yes

Fee Amount: $150.00

Retaliatory? Yes

Fee Explanation: $50 per company

Per Company: Yes

Company Amount Date Processed Transaction #Progressive Advanced Insurance Company $50.00 07/13/2015 97476669Progressive Specialty Insurance Company $50.00 07/13/2015 97476941Progressive Preferred Insurance Company $50.00 07/13/2015 97476940

*Filing Fee Amount: 150*Date Filing Fee Mailed: n/a*Filing Fee Check Number: n/a*Filing Fee Check Date: n/a*NAIC Number: n/a

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

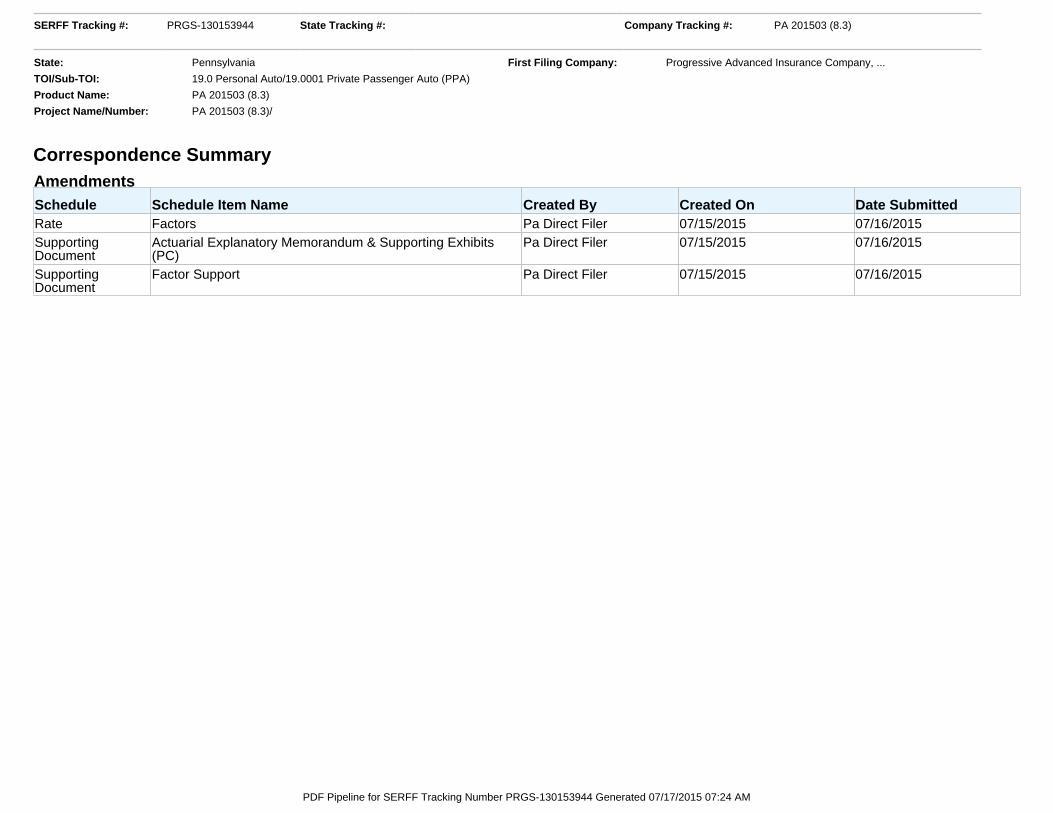

Correspondence Summary AmendmentsSchedule Schedule Item Name Created By Created On Date SubmittedRate Factors Pa Direct Filer 07/15/2015 07/16/2015SupportingDocument

Actuarial Explanatory Memorandum & Supporting Exhibits(PC)

Pa Direct Filer 07/15/2015 07/16/2015

SupportingDocument

Factor Support Pa Direct Filer 07/15/2015 07/16/2015

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

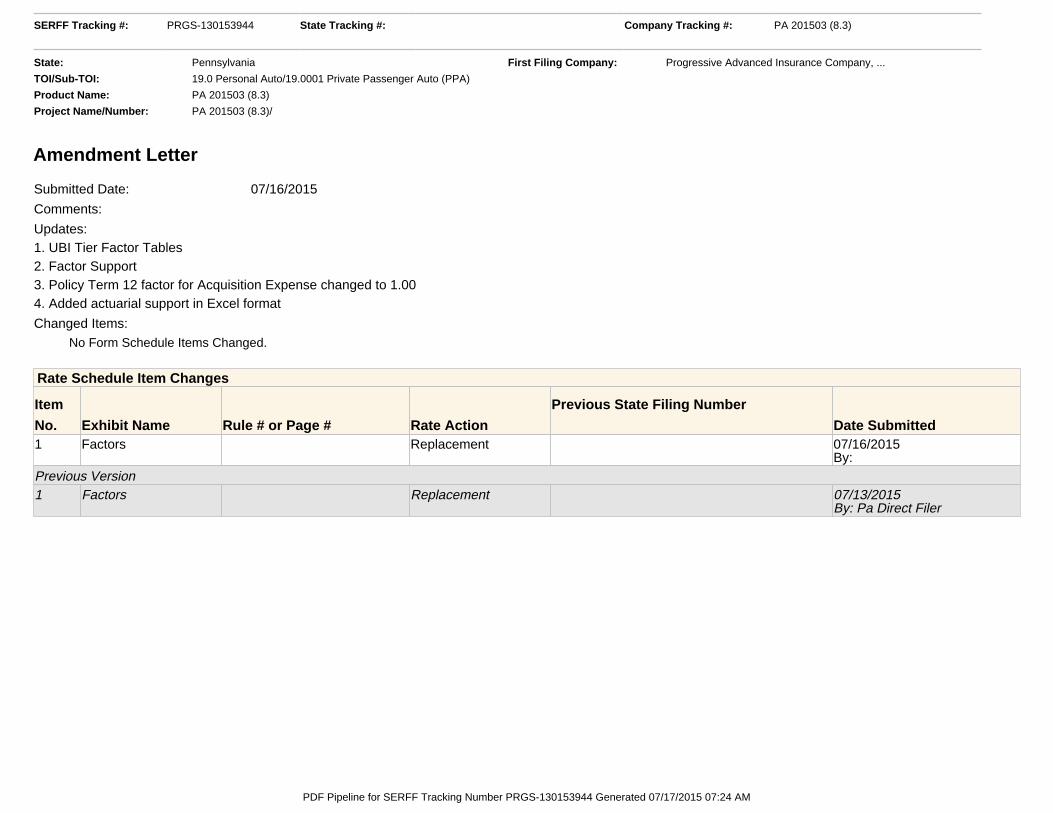

Amendment Letter

Submitted Date: 07/16/2015

Comments:

Updates:1. UBI Tier Factor Tables2. Factor Support3. Policy Term 12 factor for Acquisition Expense changed to 1.004. Added actuarial support in Excel format

Changed Items: No Form Schedule Items Changed.

Rate Schedule Item Changes

Item

No. Exhibit Name Rule # or Page # Rate Action

Previous State Filing Number

Date Submitted1 Factors Replacement 07/16/2015

By:Previous Version1 Factors Replacement 07/13/2015

By: Pa Direct Filer

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

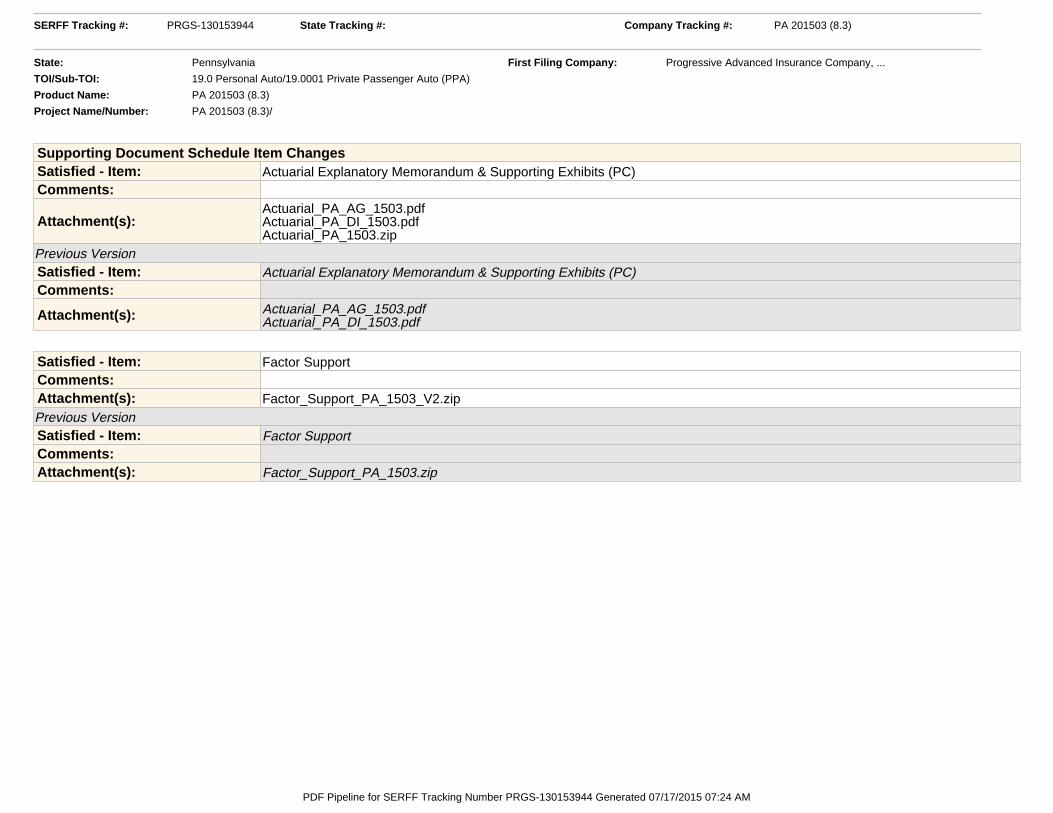

Supporting Document Schedule Item ChangesSatisfied - Item: Actuarial Explanatory Memorandum & Supporting Exhibits (PC)Comments:

Attachment(s):Actuarial_PA_AG_1503.pdfActuarial_PA_DI_1503.pdfActuarial_PA_1503.zip

Previous VersionSatisfied - Item: Actuarial Explanatory Memorandum & Supporting Exhibits (PC)Comments:

Attachment(s): Actuarial_PA_AG_1503.pdfActuarial_PA_DI_1503.pdf

Satisfied - Item: Factor SupportComments:Attachment(s): Factor_Support_PA_1503_V2.zipPrevious VersionSatisfied - Item: Factor SupportComments:Attachment(s): Factor_Support_PA_1503.zip

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

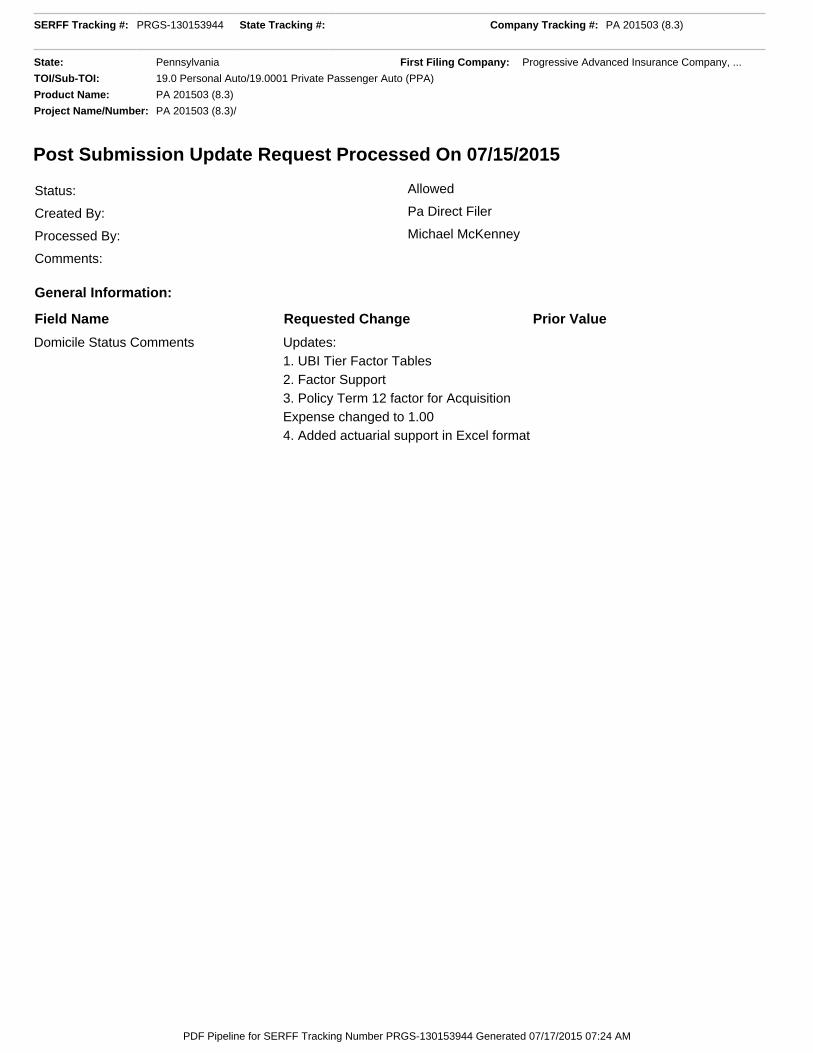

Post Submission Update Request Processed On 07/15/2015

Status: Allowed

Created By: Pa Direct Filer

Processed By: Michael McKenney

Comments:

General Information:

Field Name Requested Change Prior Value

Domicile Status Comments Updates:1. UBI Tier Factor Tables2. Factor Support3. Policy Term 12 factor for AcquisitionExpense changed to 1.004. Added actuarial support in Excel format

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

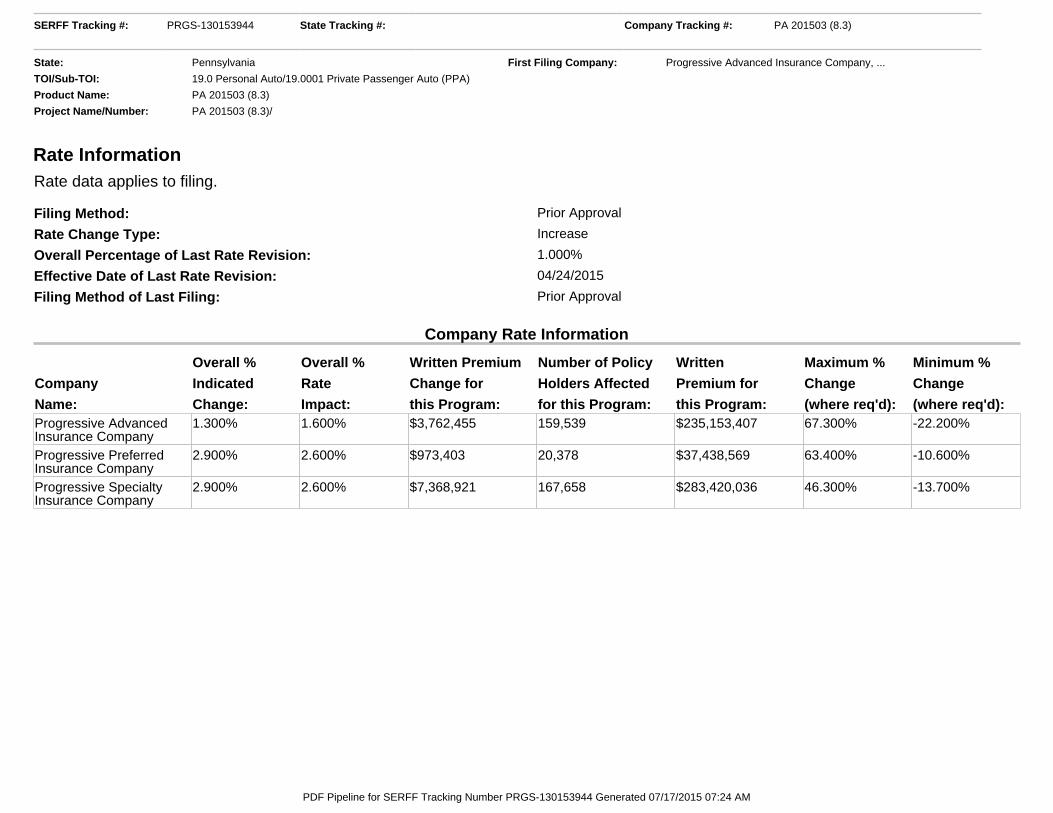

Rate Information Rate data applies to filing.

Filing Method: Prior Approval

Rate Change Type: Increase

Overall Percentage of Last Rate Revision: 1.000%

Effective Date of Last Rate Revision: 04/24/2015

Filing Method of Last Filing: Prior Approval

Company Rate Information

Company

Name:

Overall %

Indicated

Change:

Overall %

Rate

Impact:

Written Premium

Change for

this Program:

Number of Policy

Holders Affected

for this Program:

Written

Premium for

this Program:

Maximum %

Change

(where req'd):

Minimum %

Change

(where req'd):Progressive AdvancedInsurance Company

1.300% 1.600% $3,762,455 159,539 $235,153,407 67.300% -22.200%

Progressive PreferredInsurance Company

2.900% 2.600% $973,403 20,378 $37,438,569 63.400% -10.600%

Progressive SpecialtyInsurance Company

2.900% 2.600% $7,368,921 167,658 $283,420,036 46.300% -13.700%

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

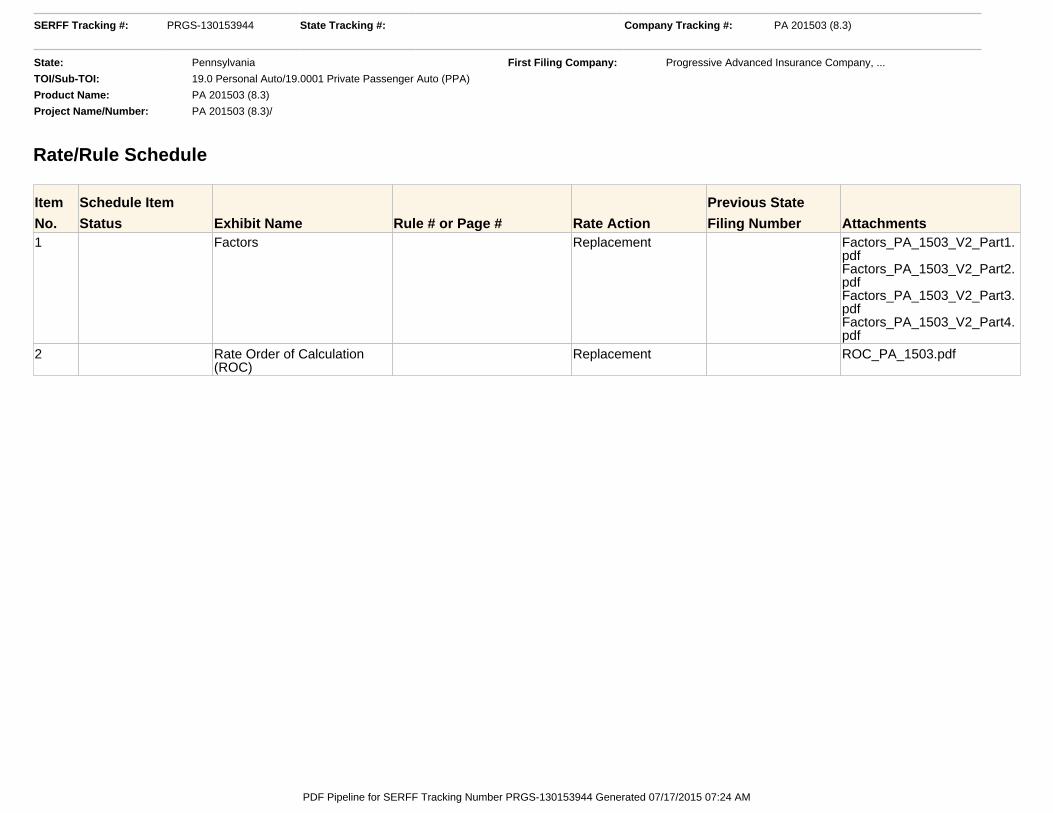

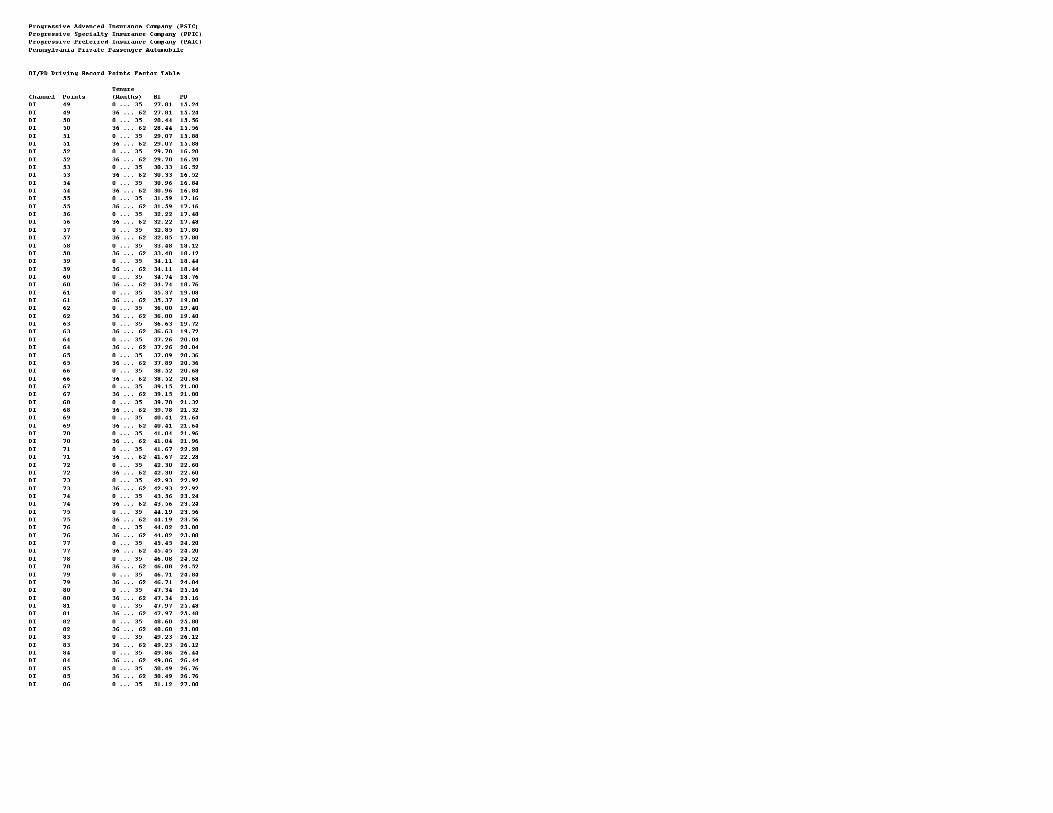

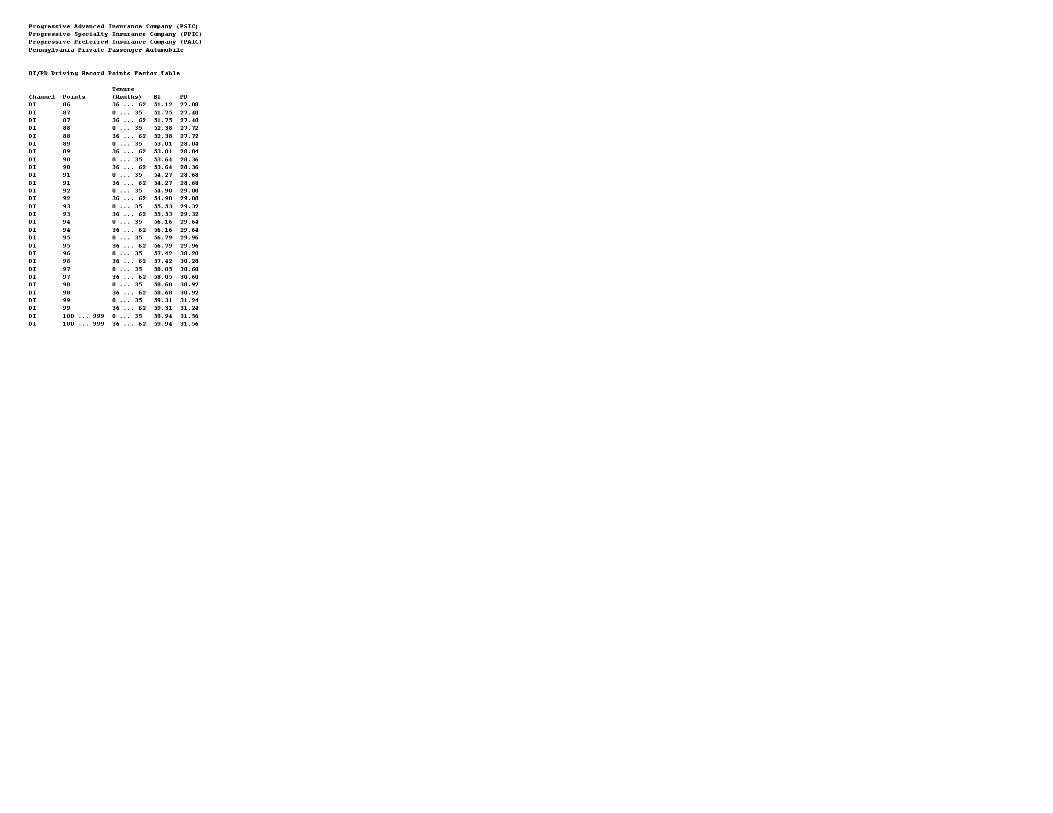

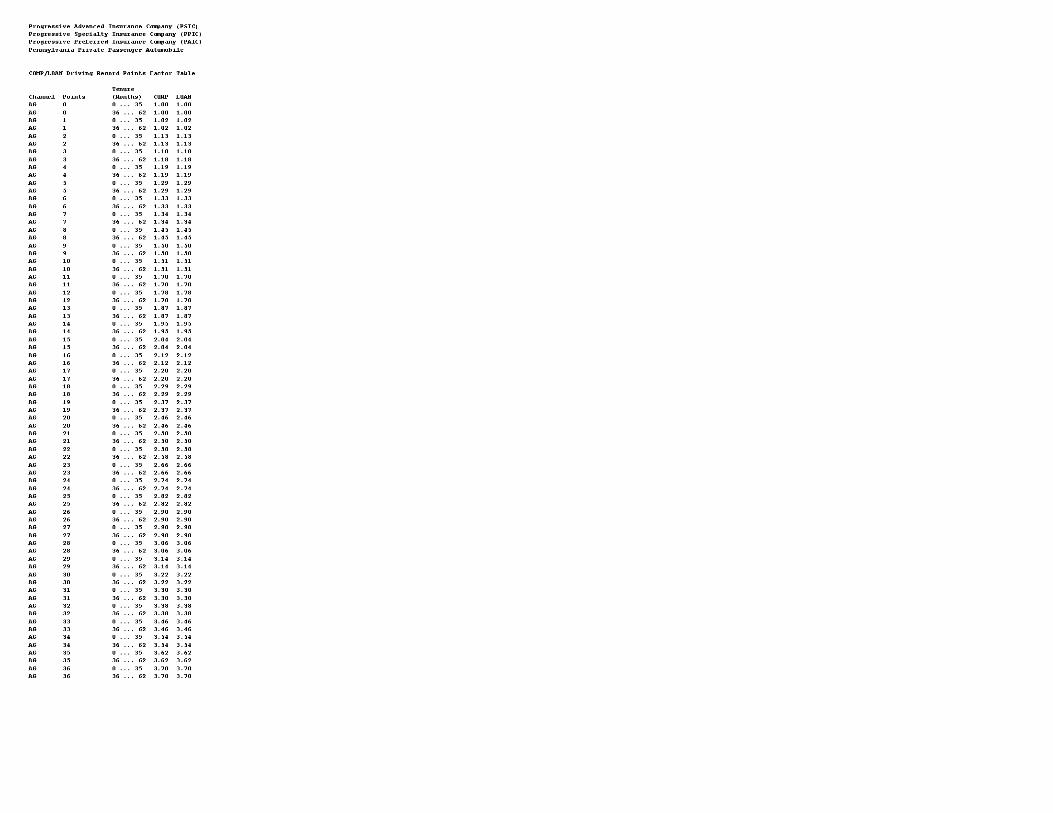

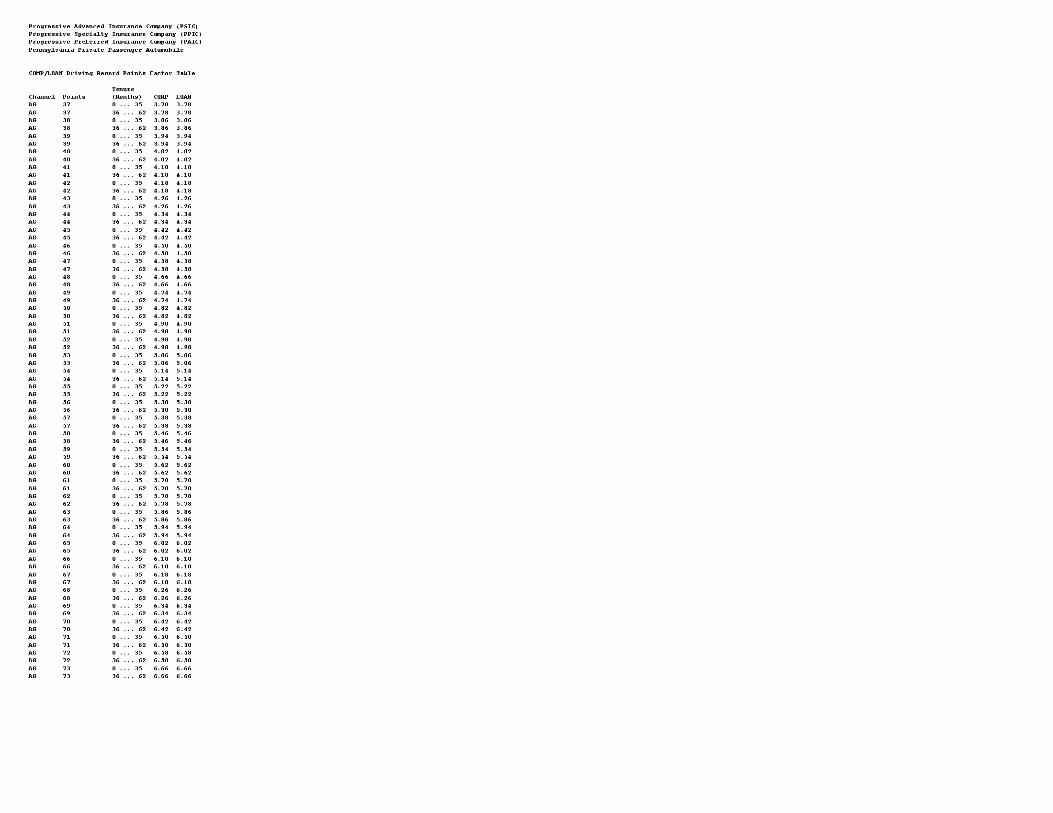

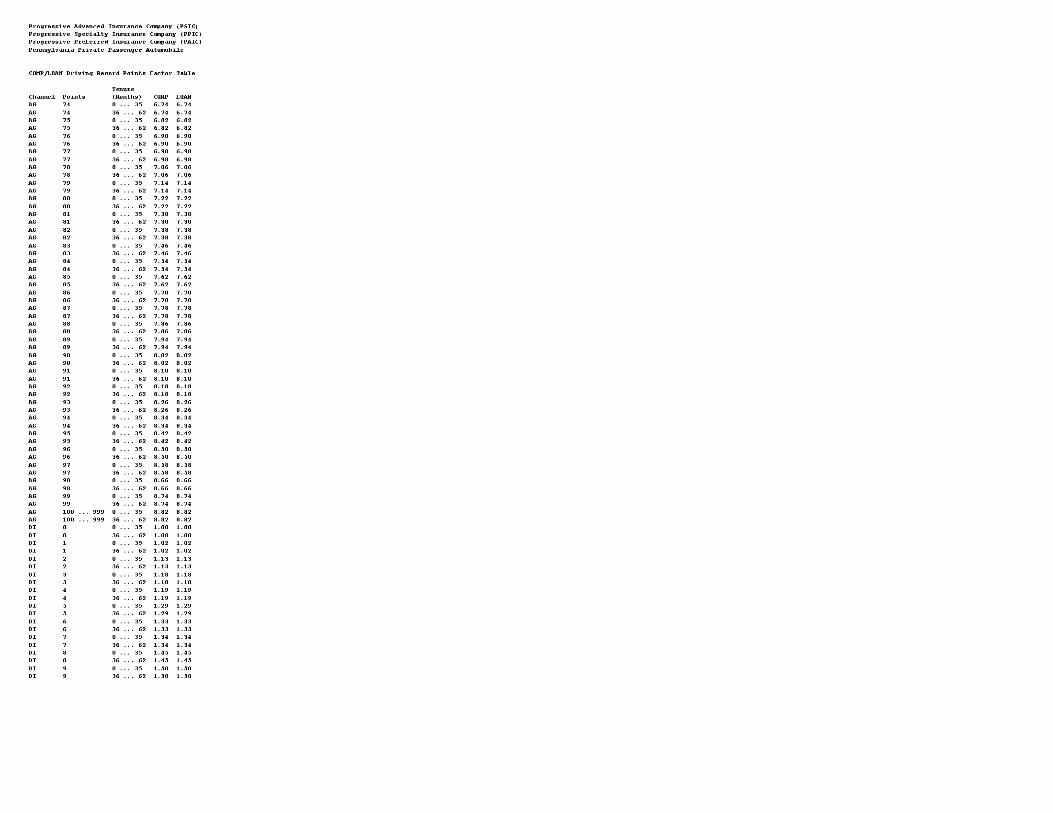

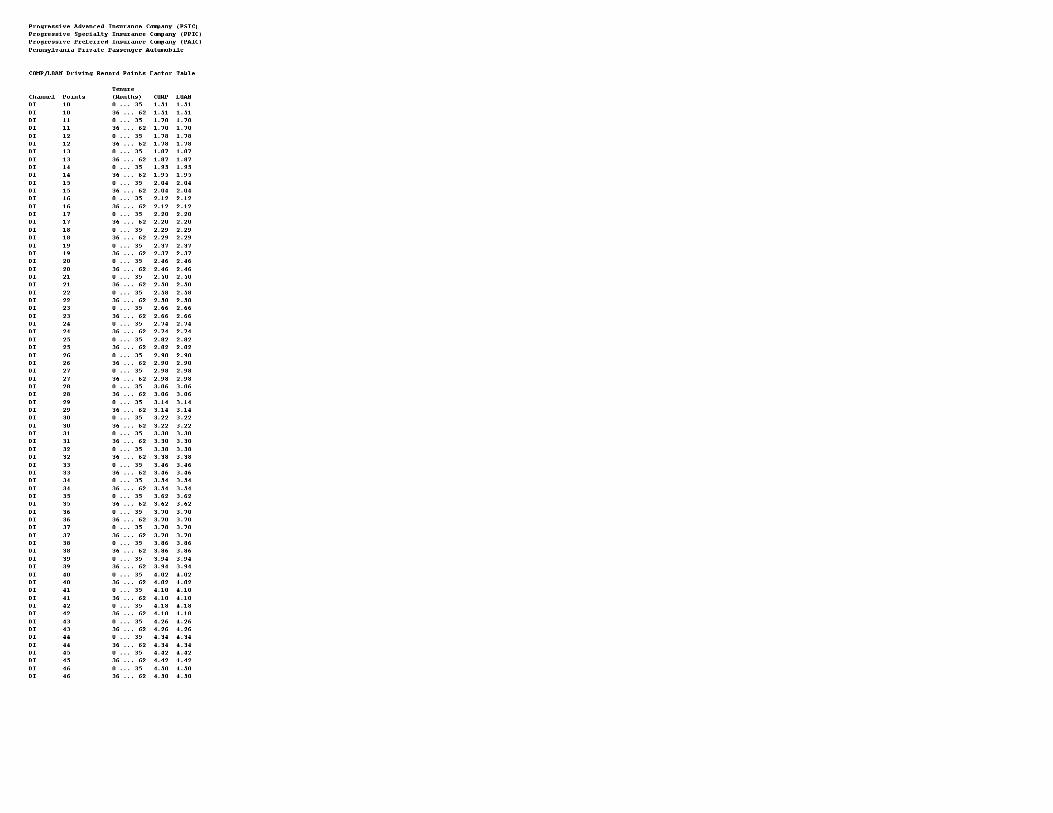

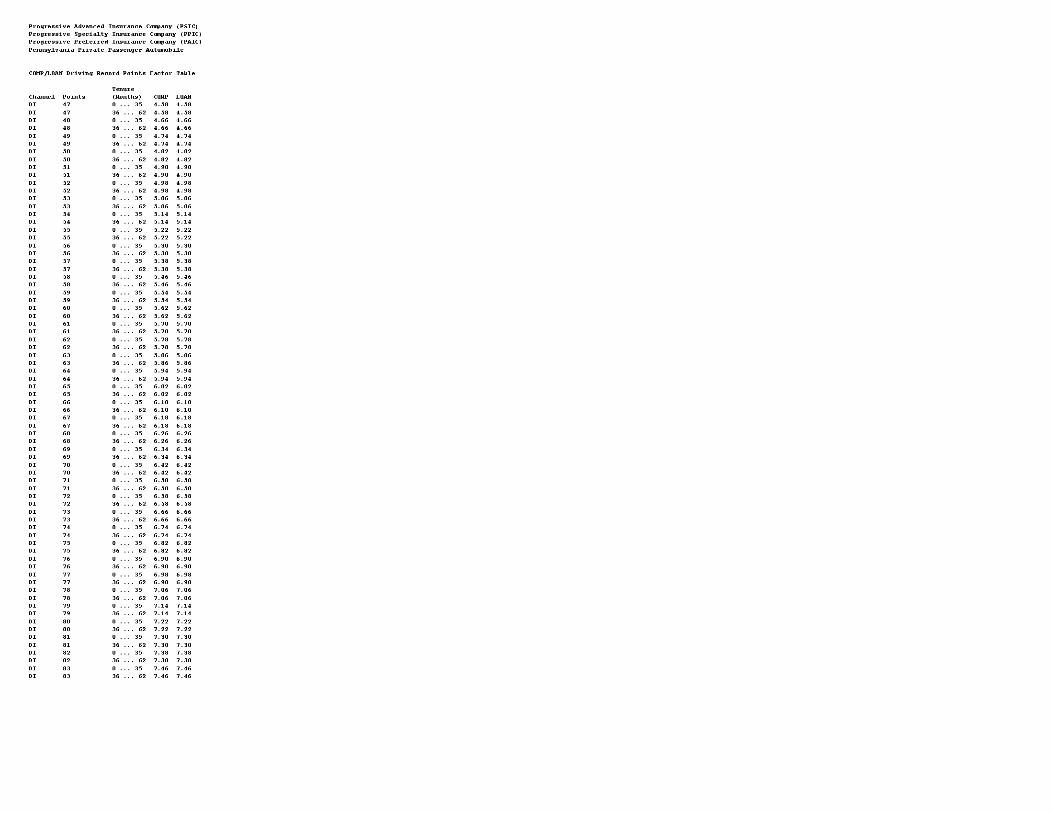

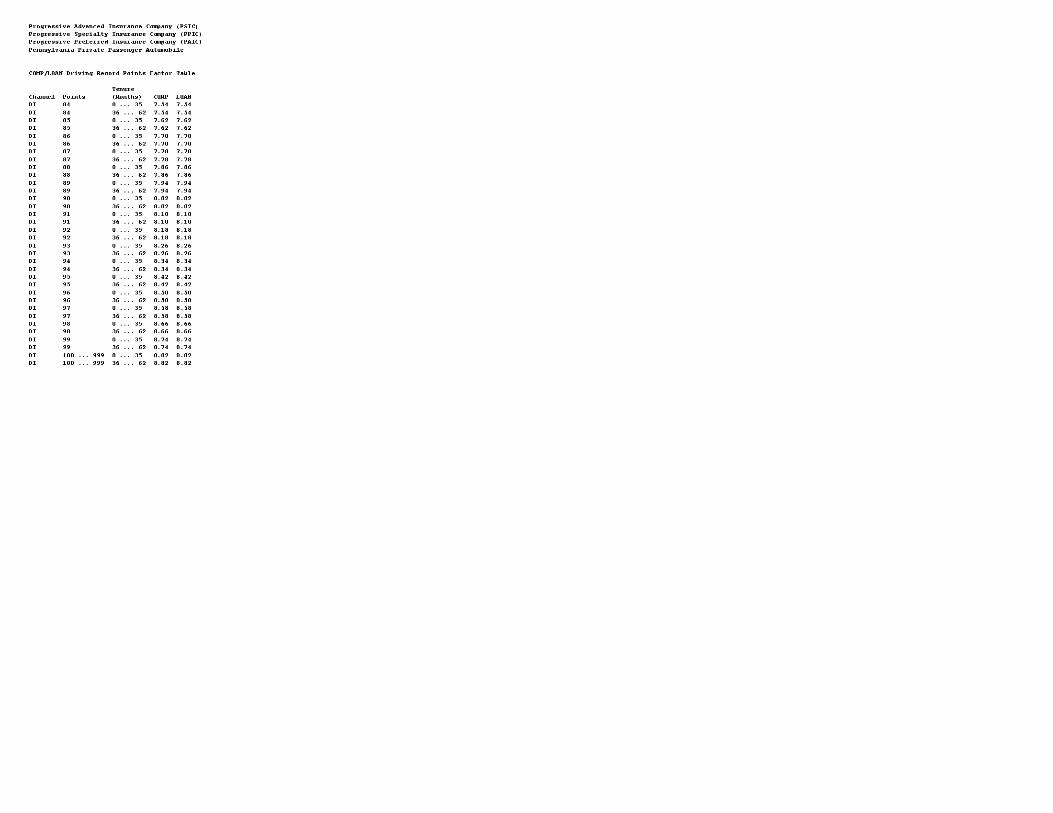

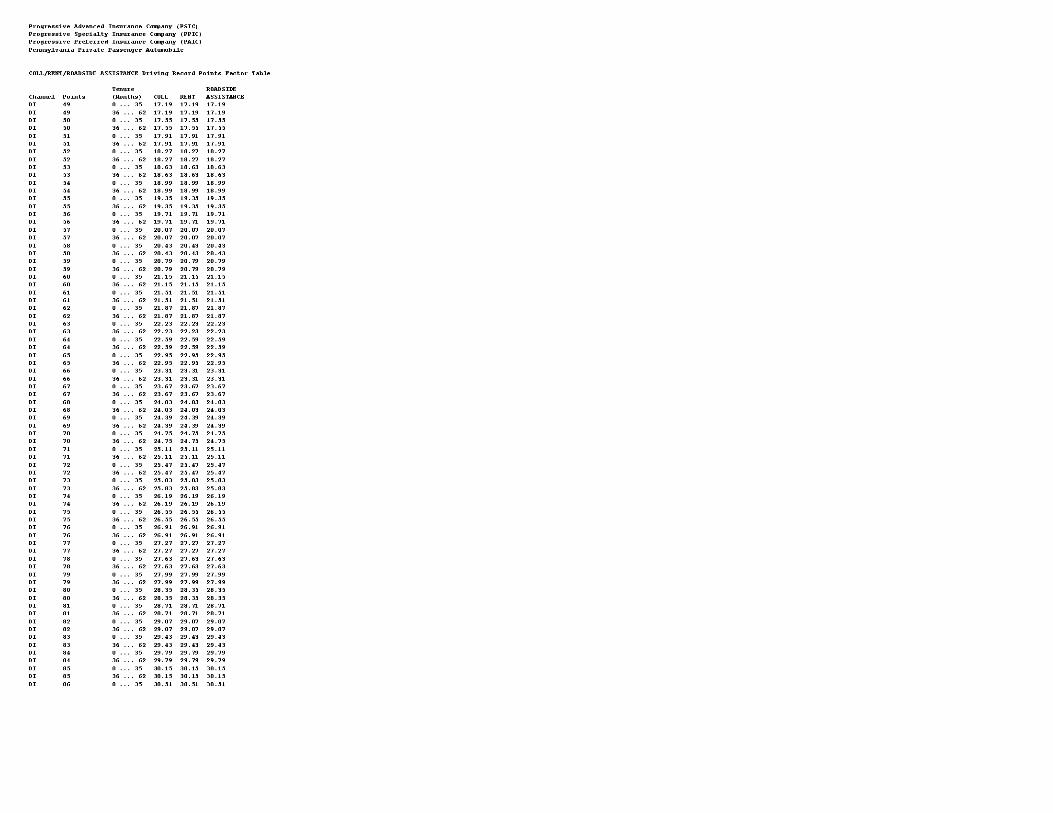

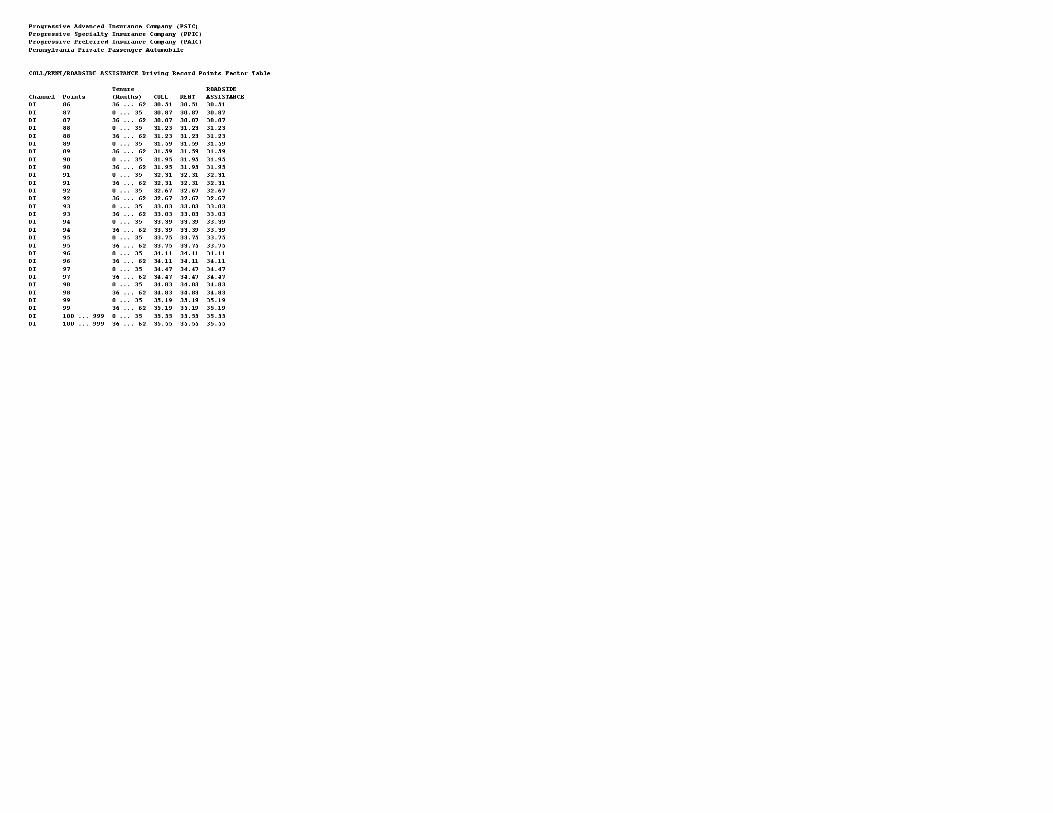

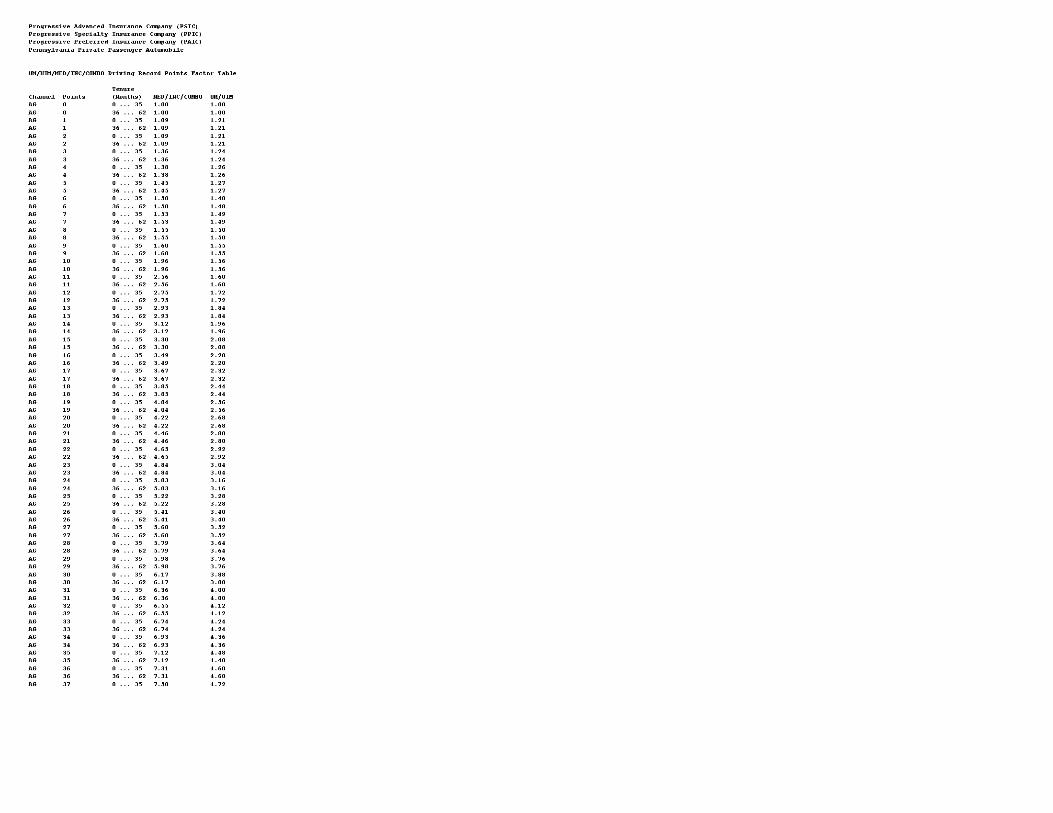

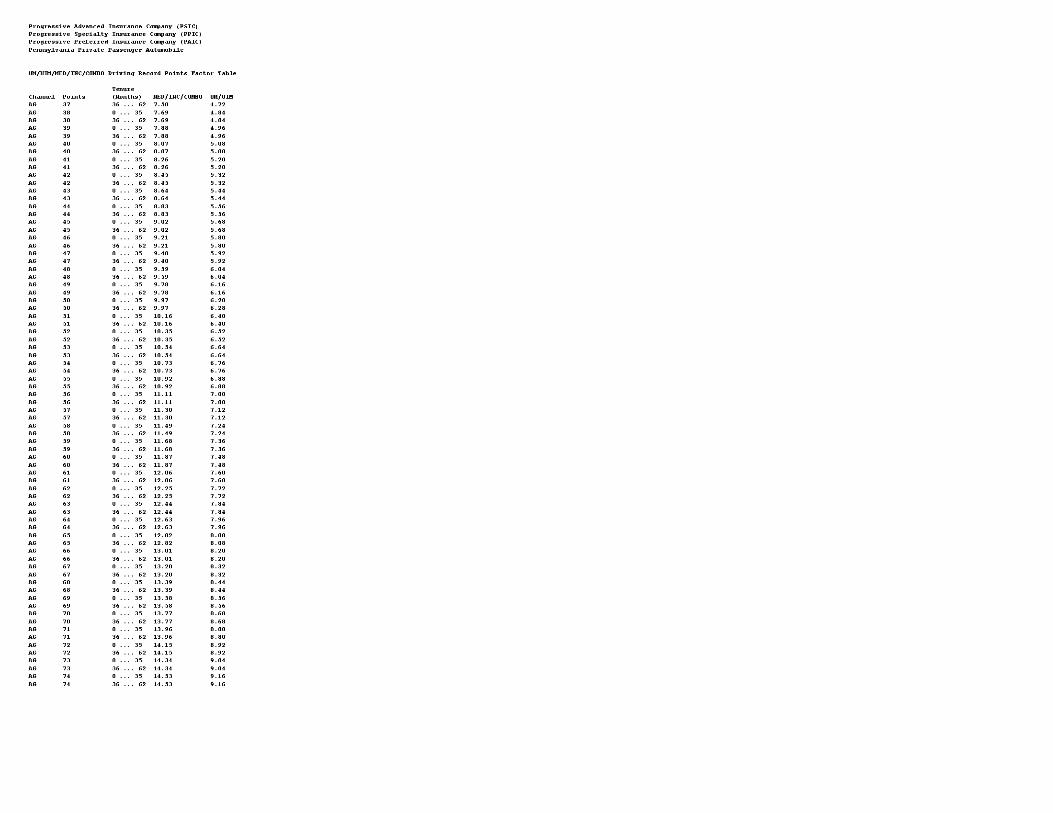

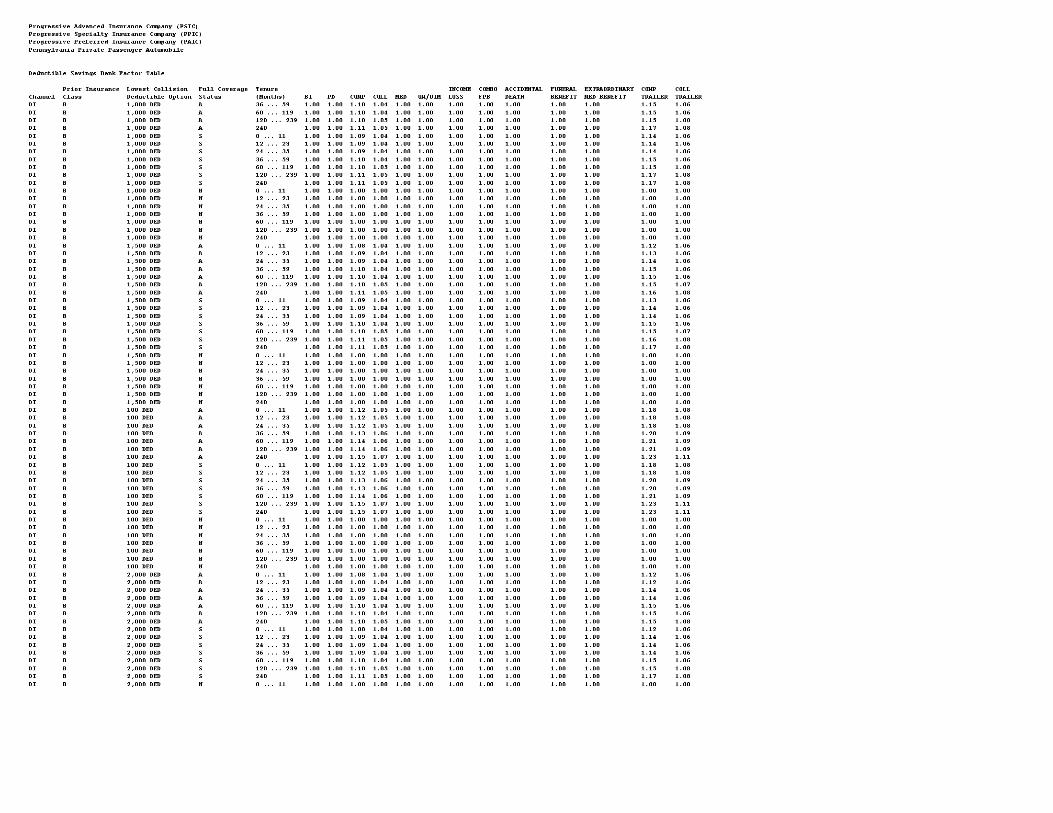

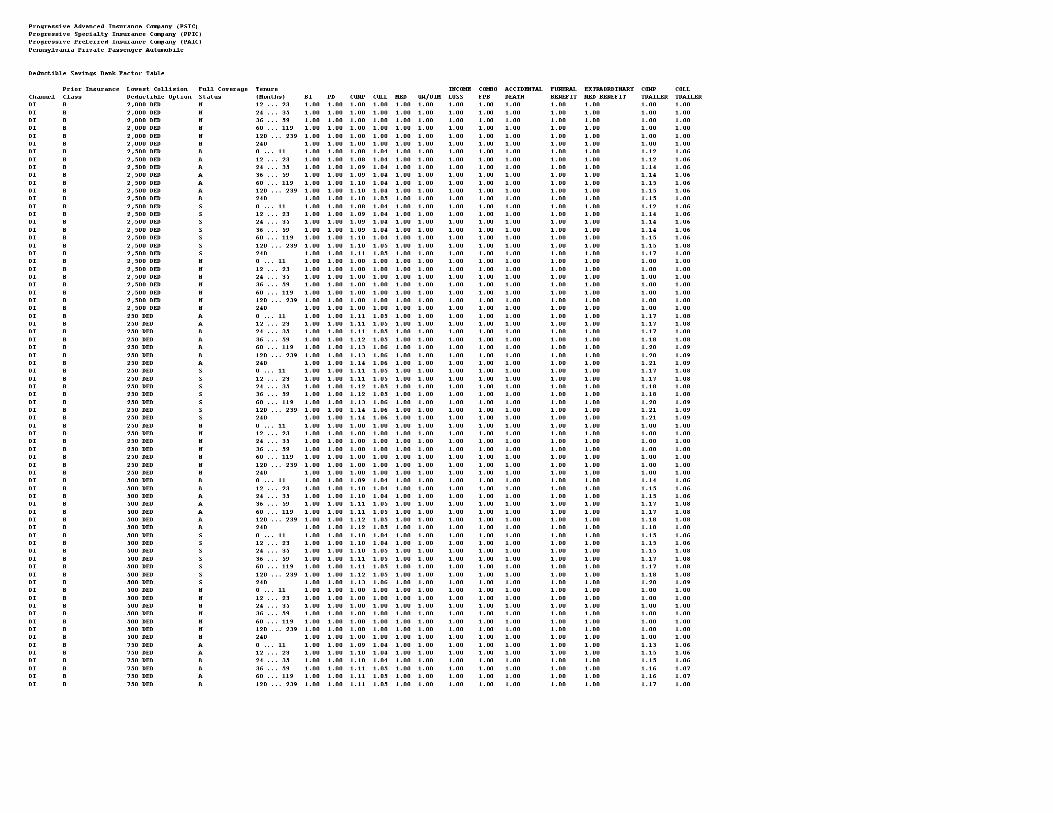

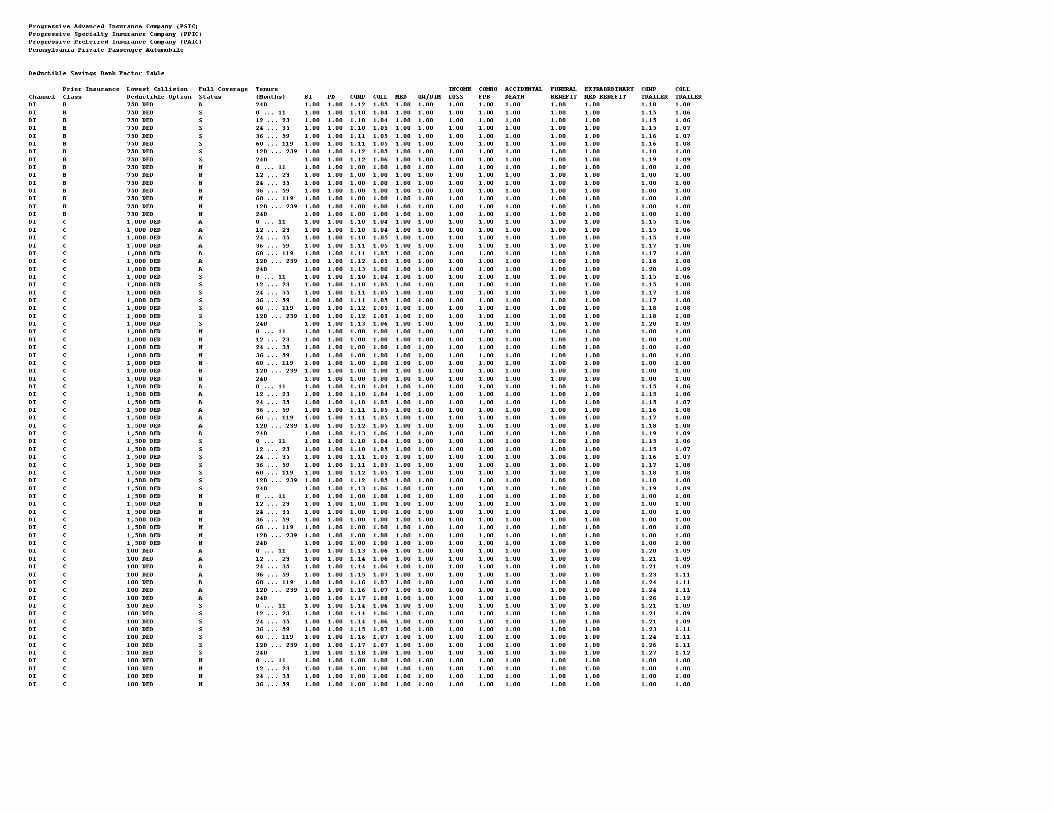

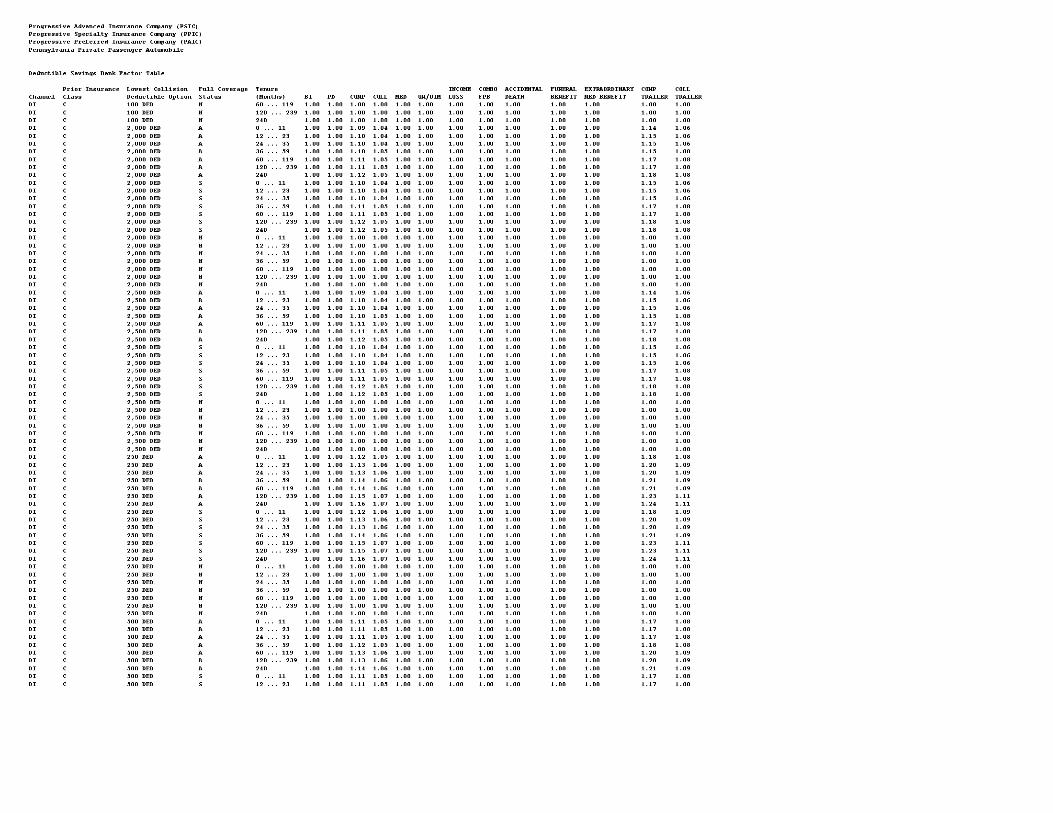

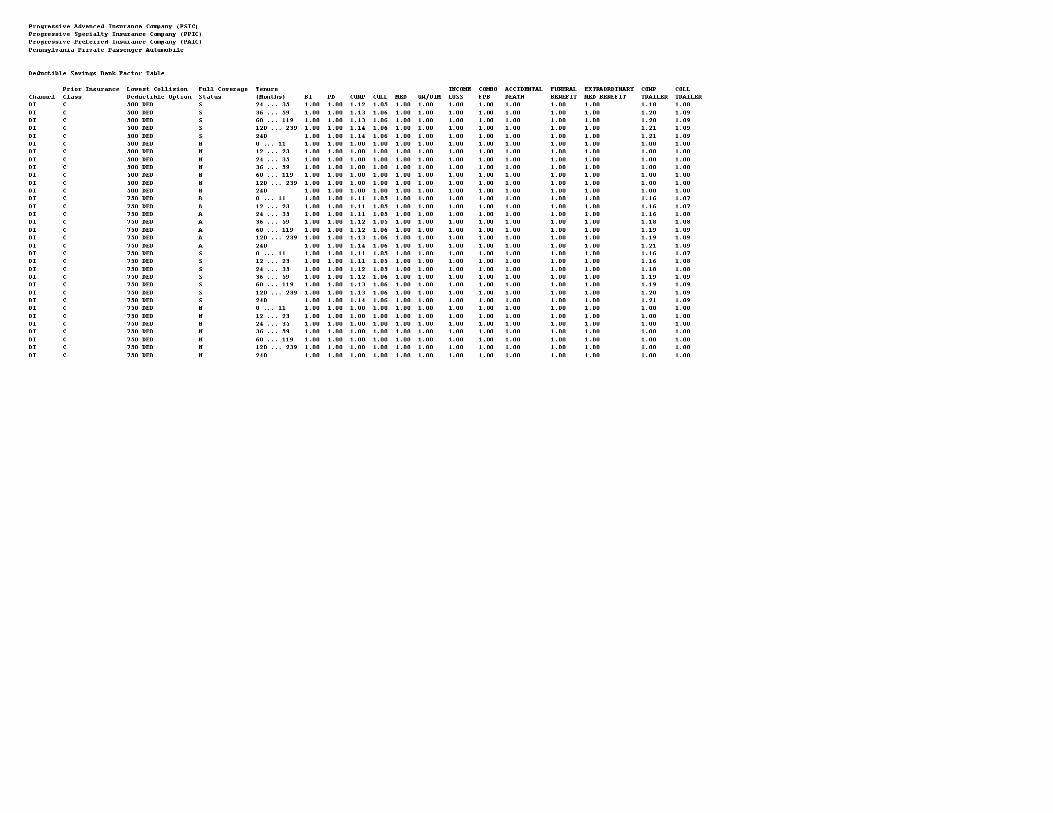

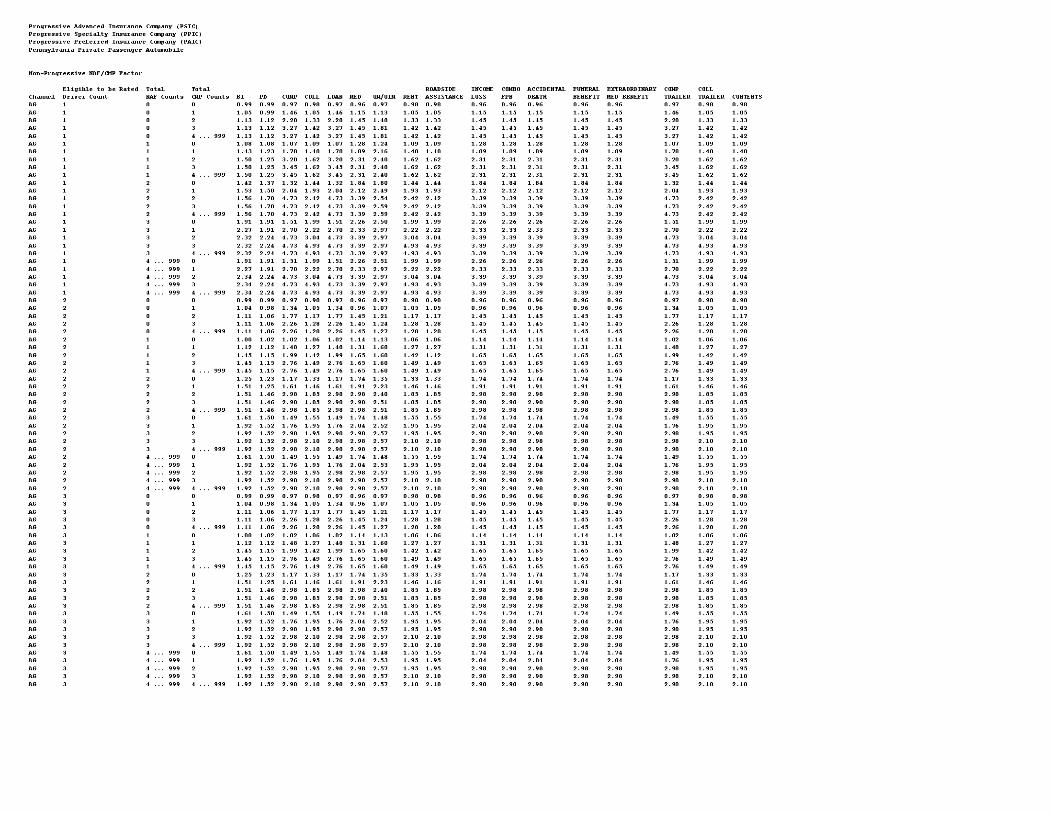

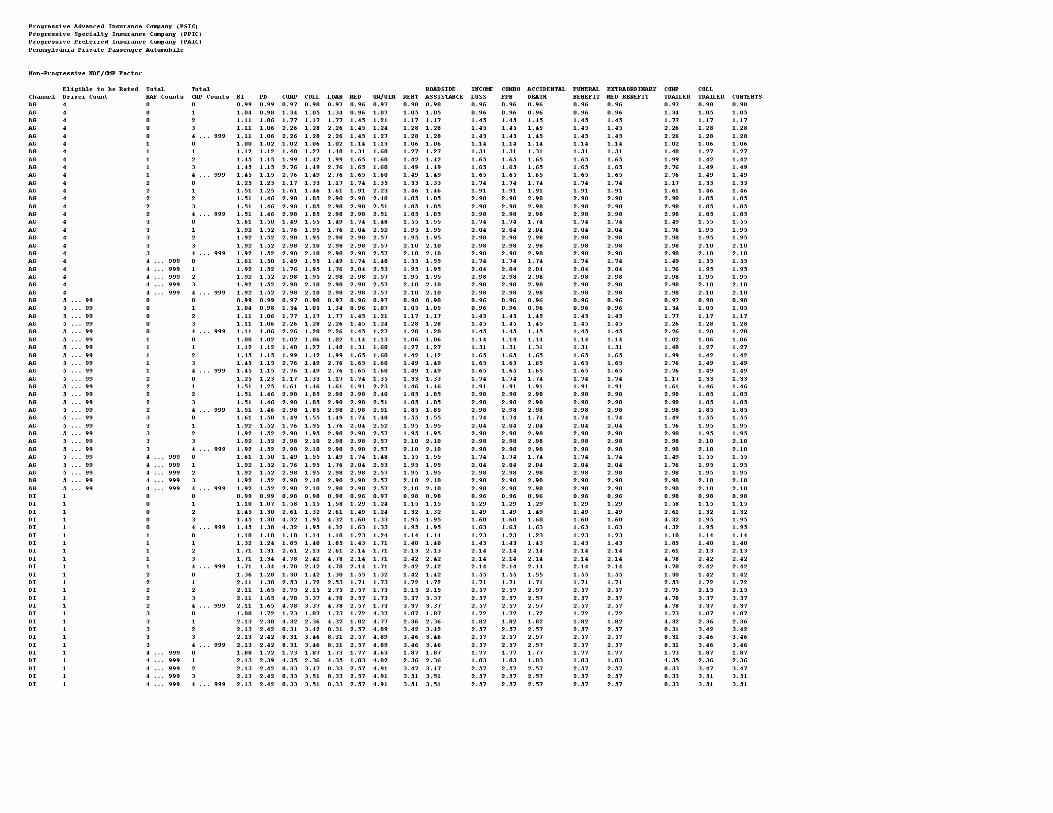

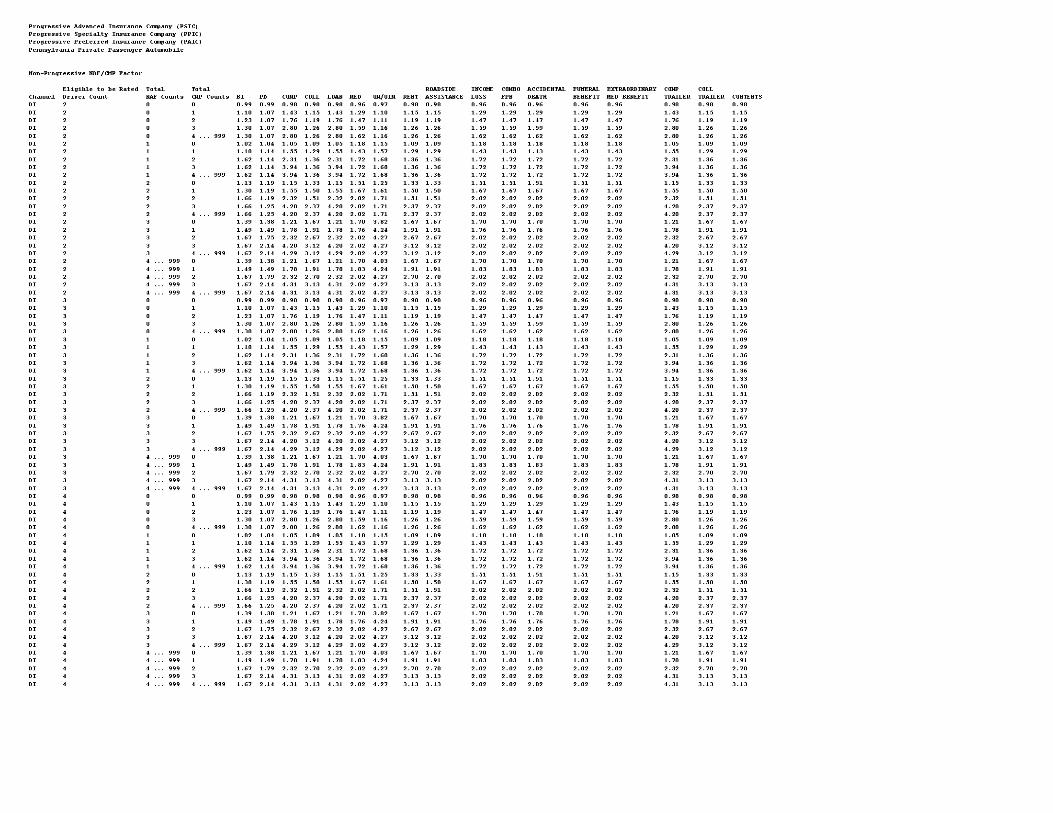

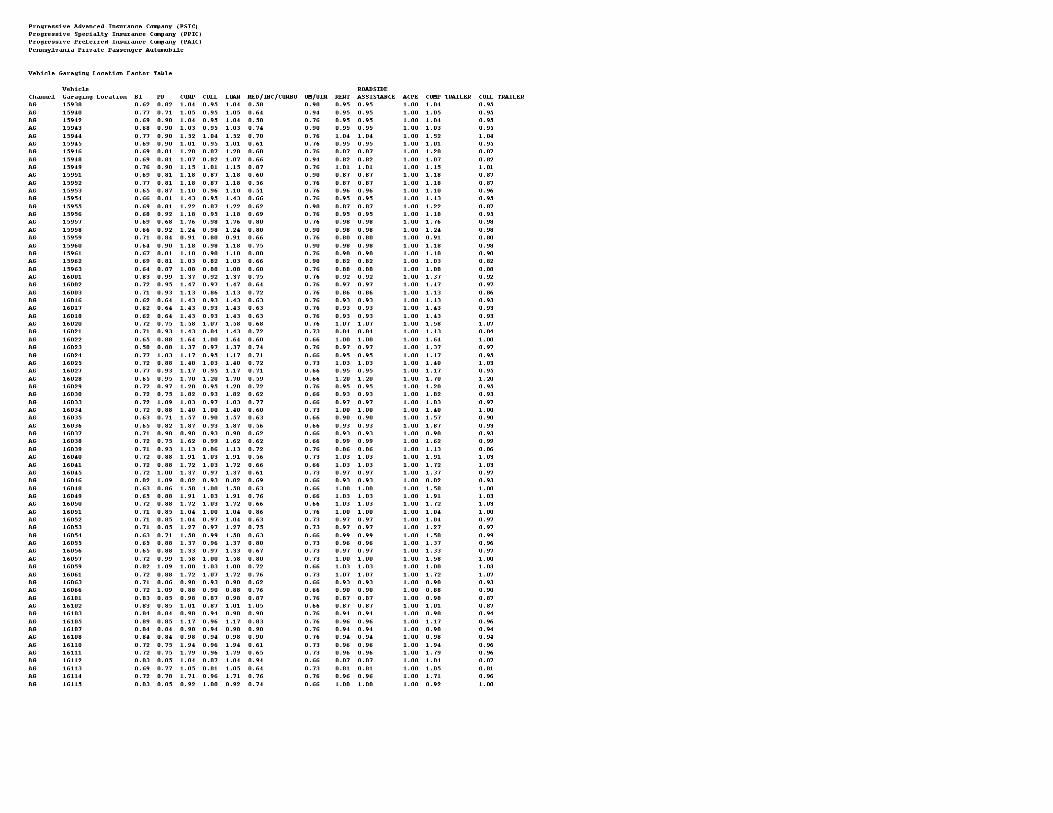

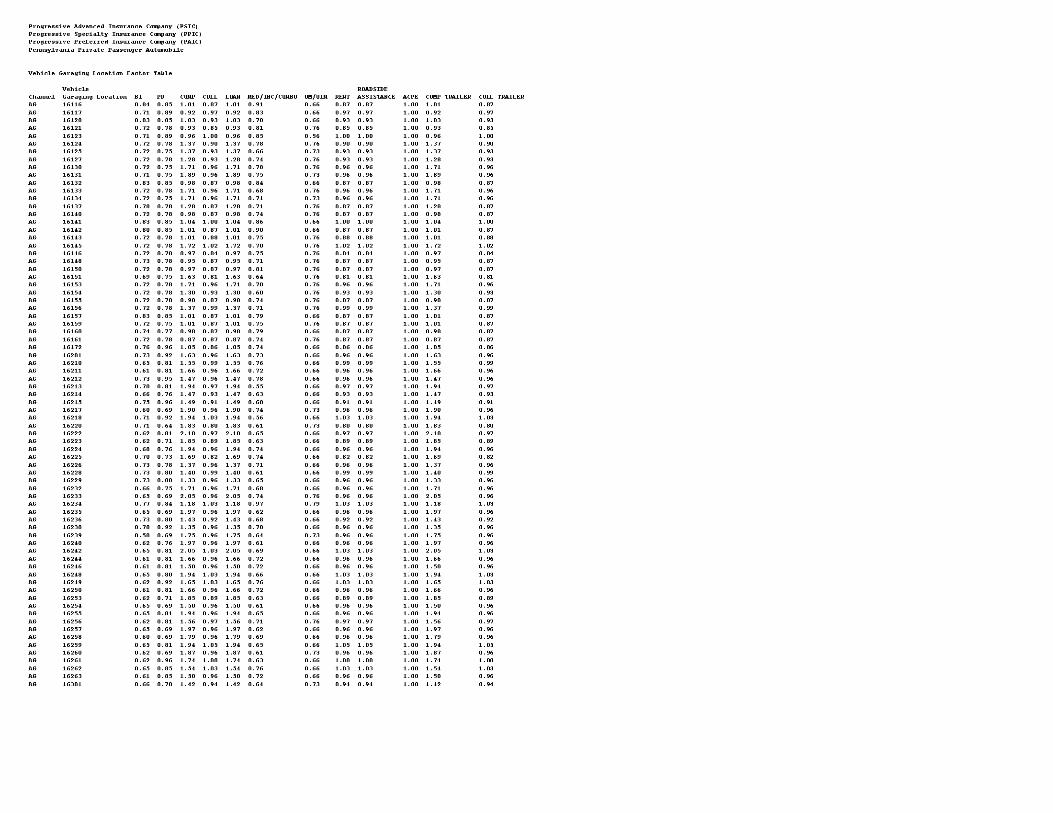

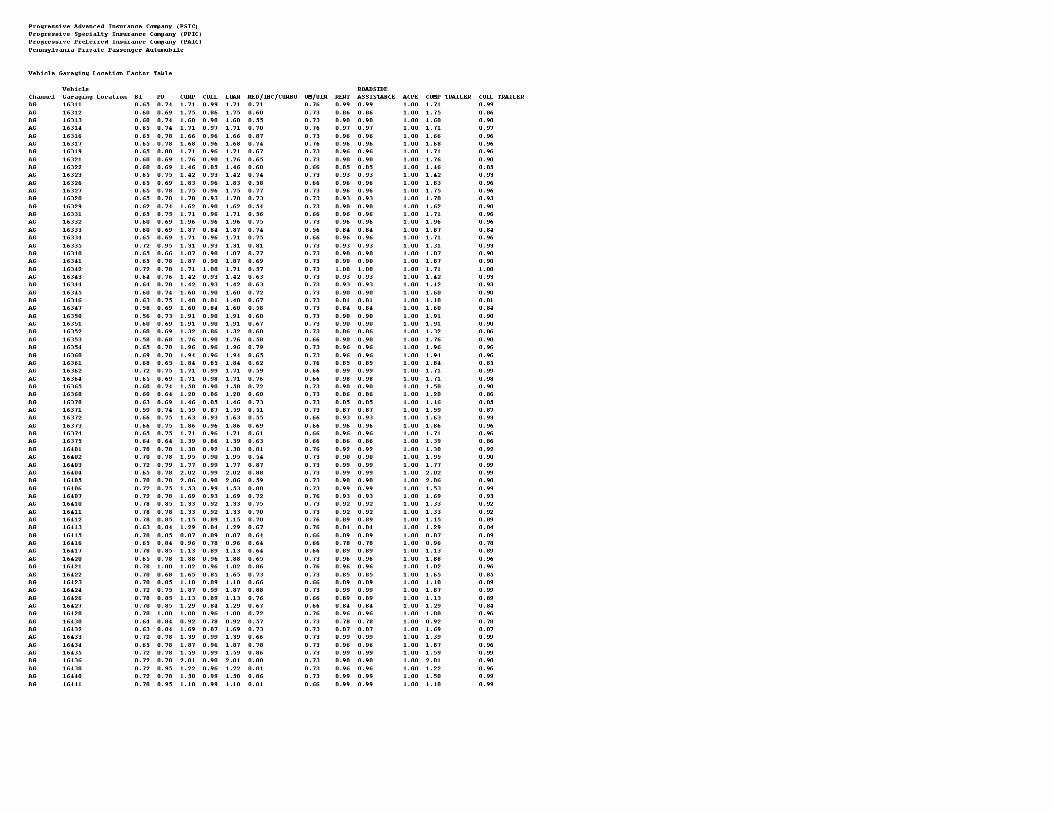

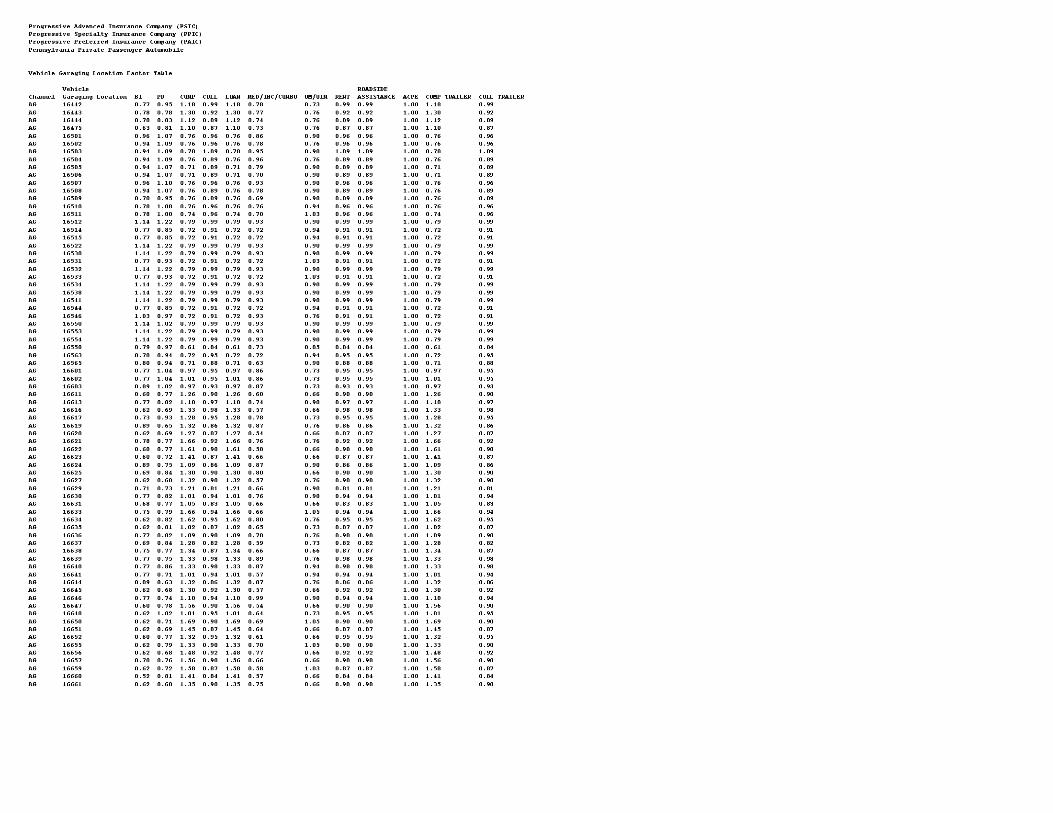

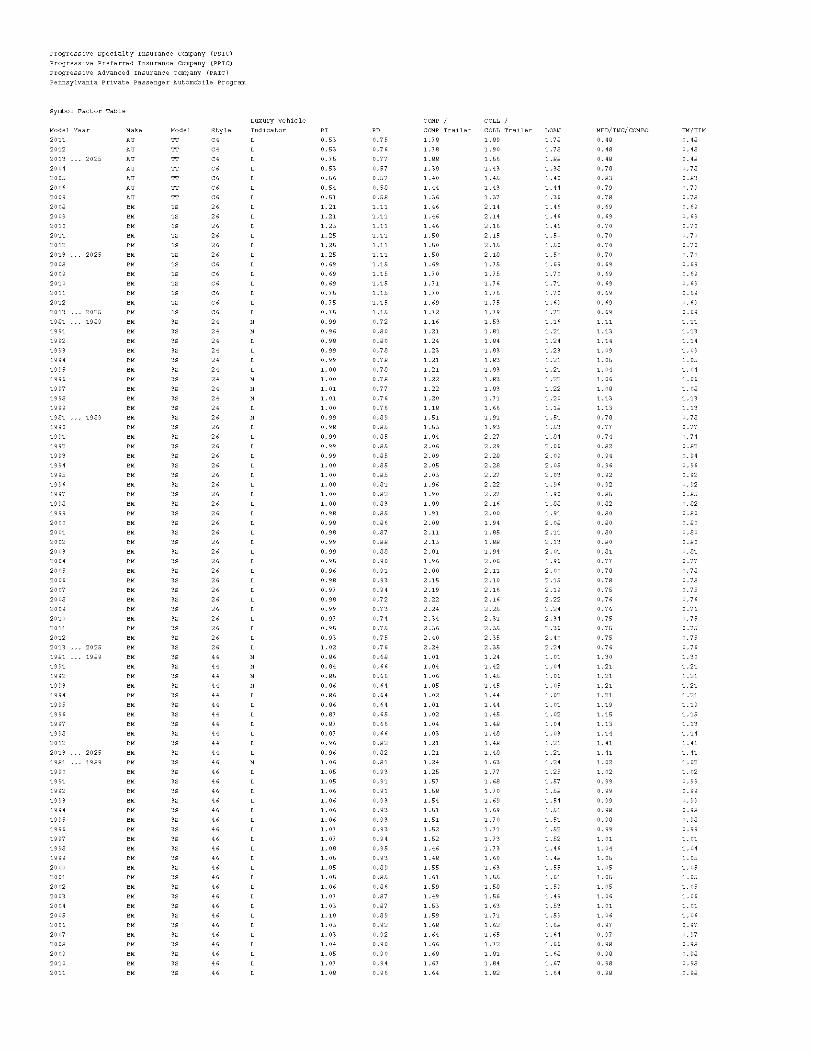

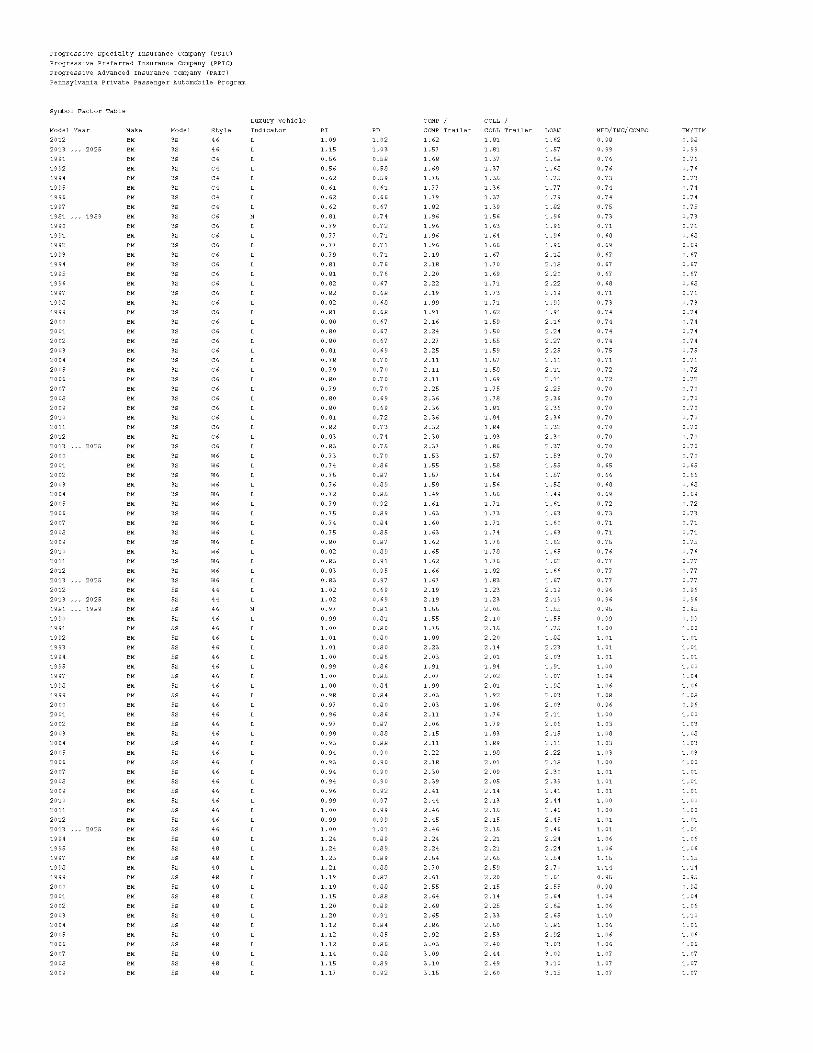

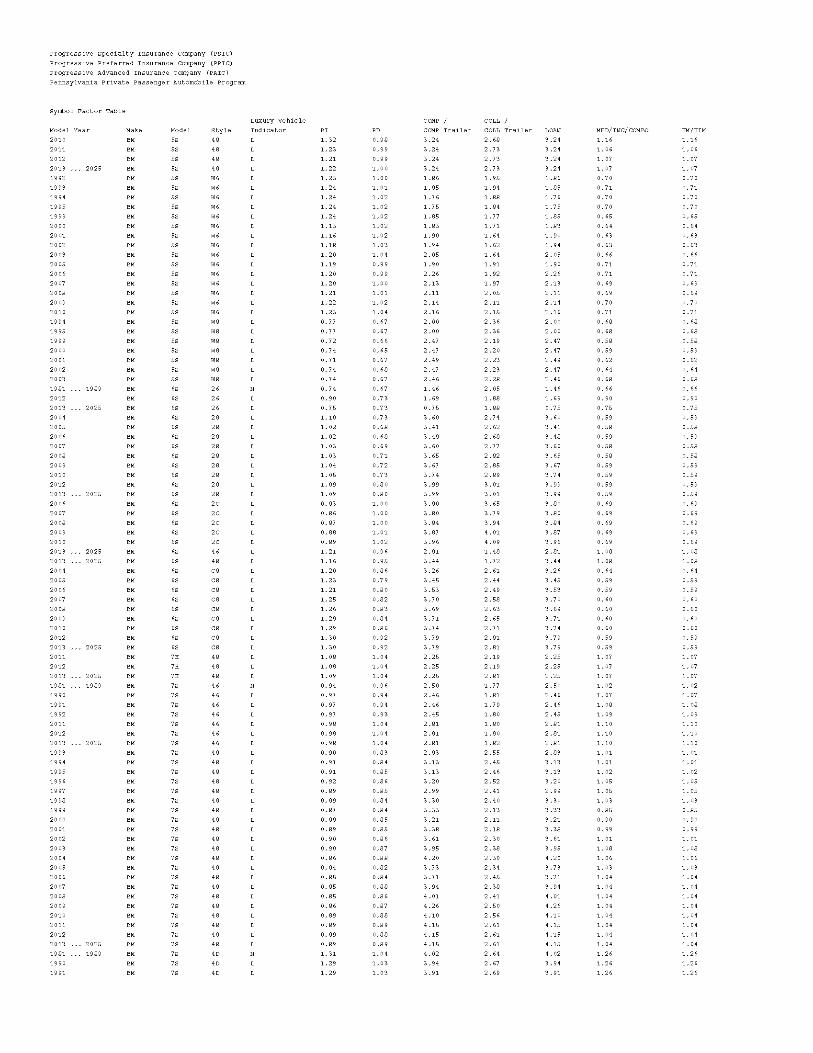

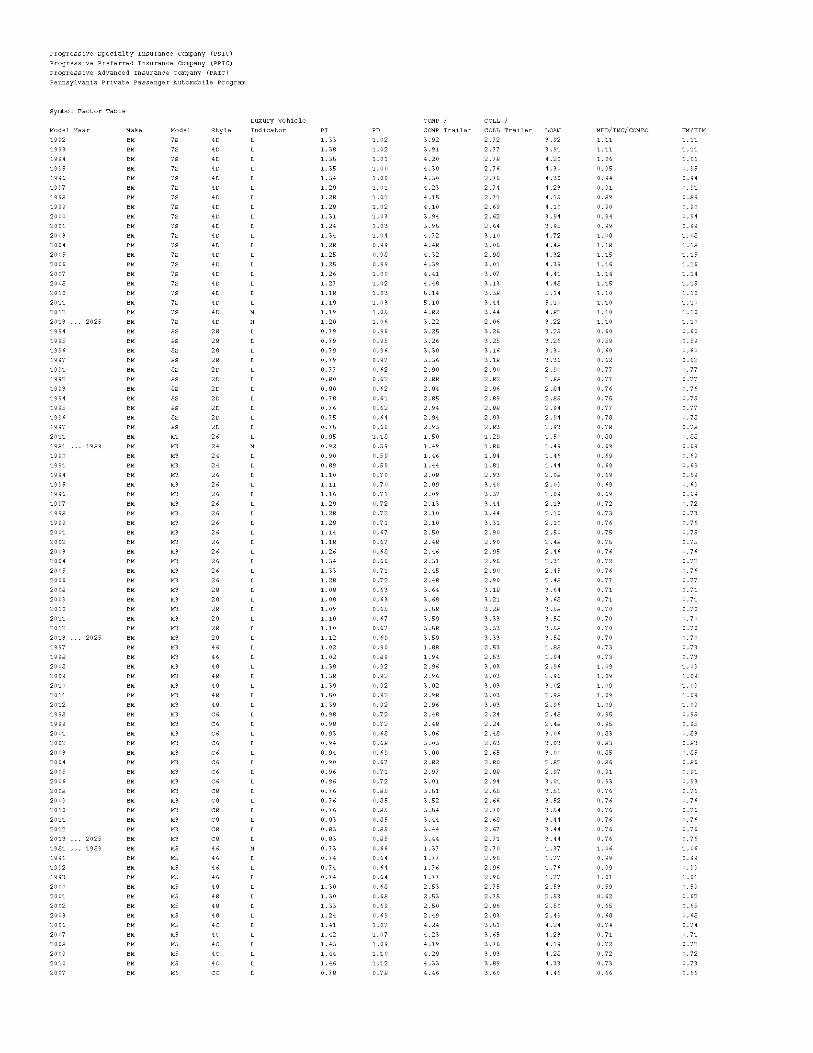

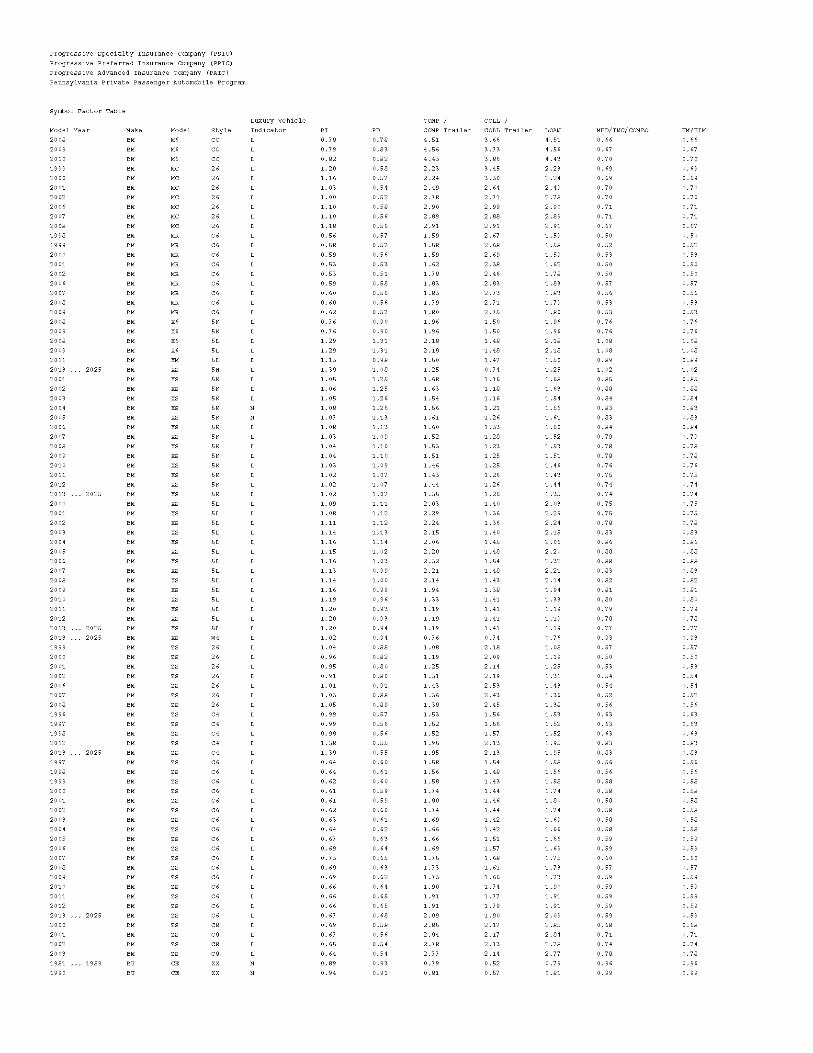

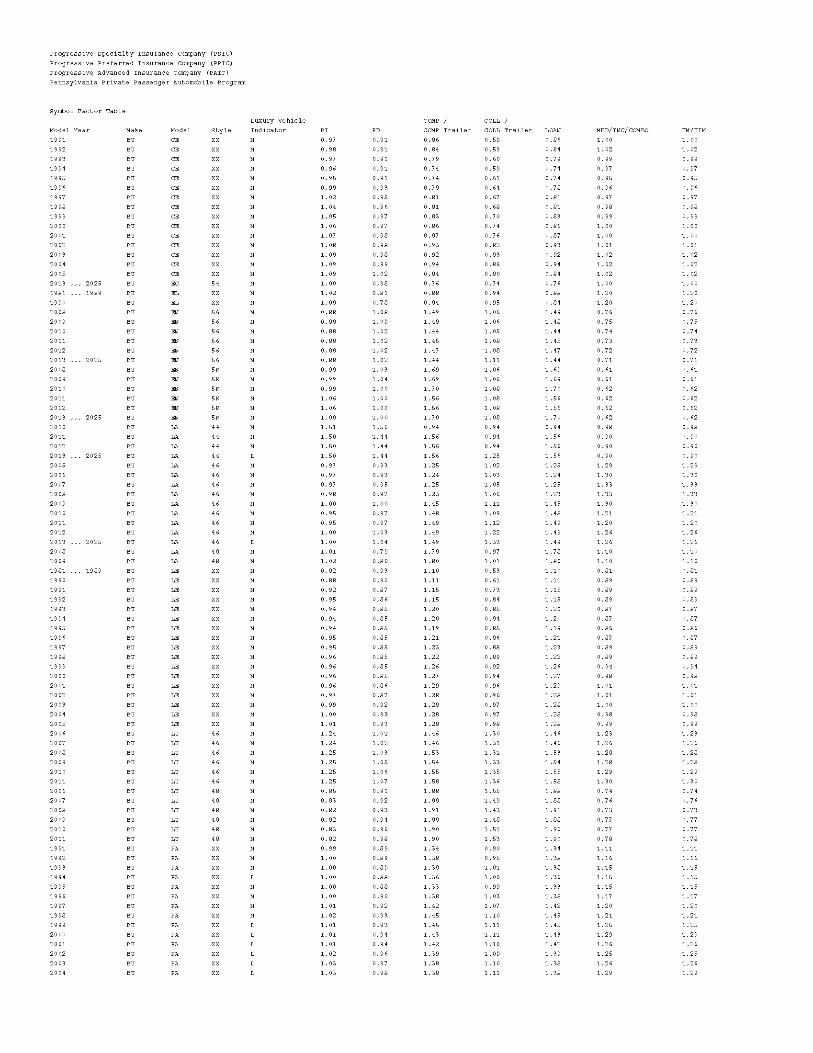

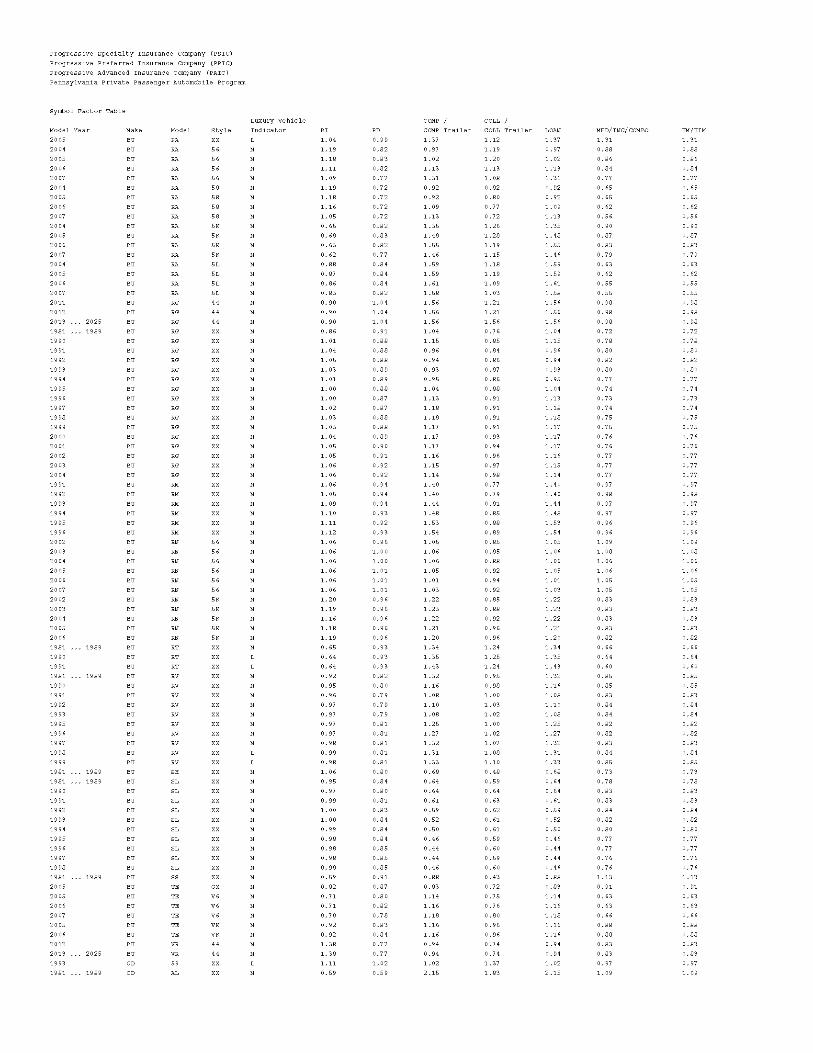

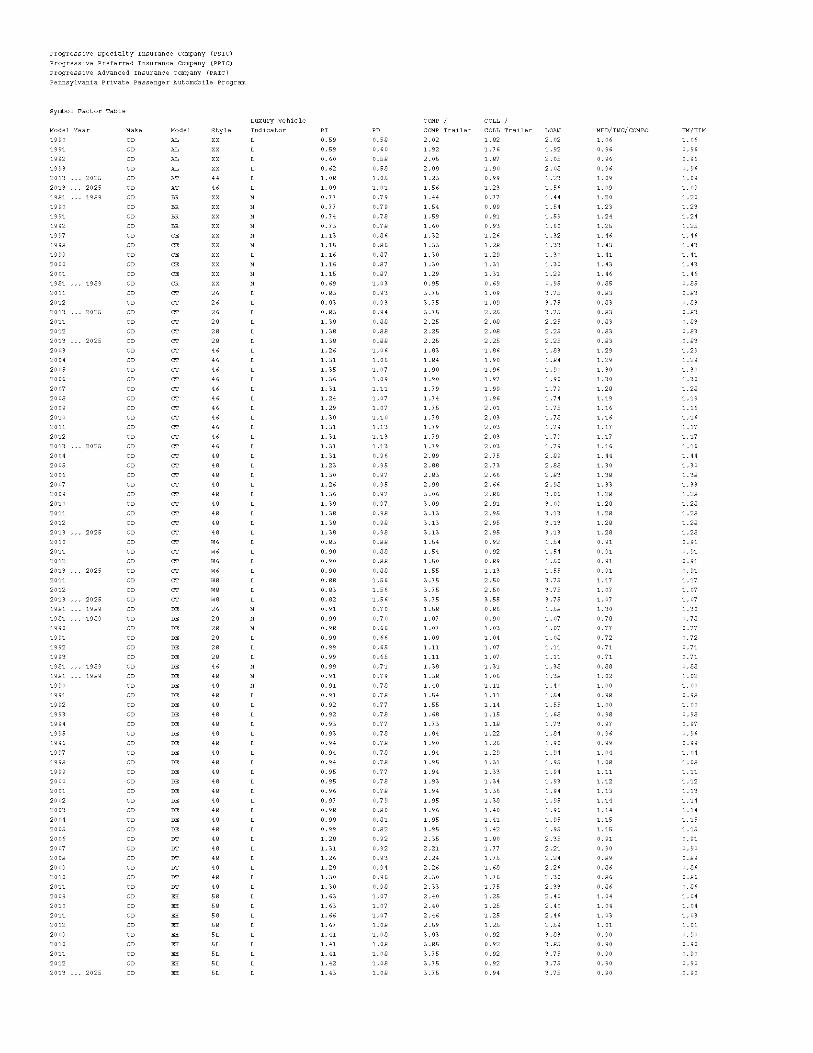

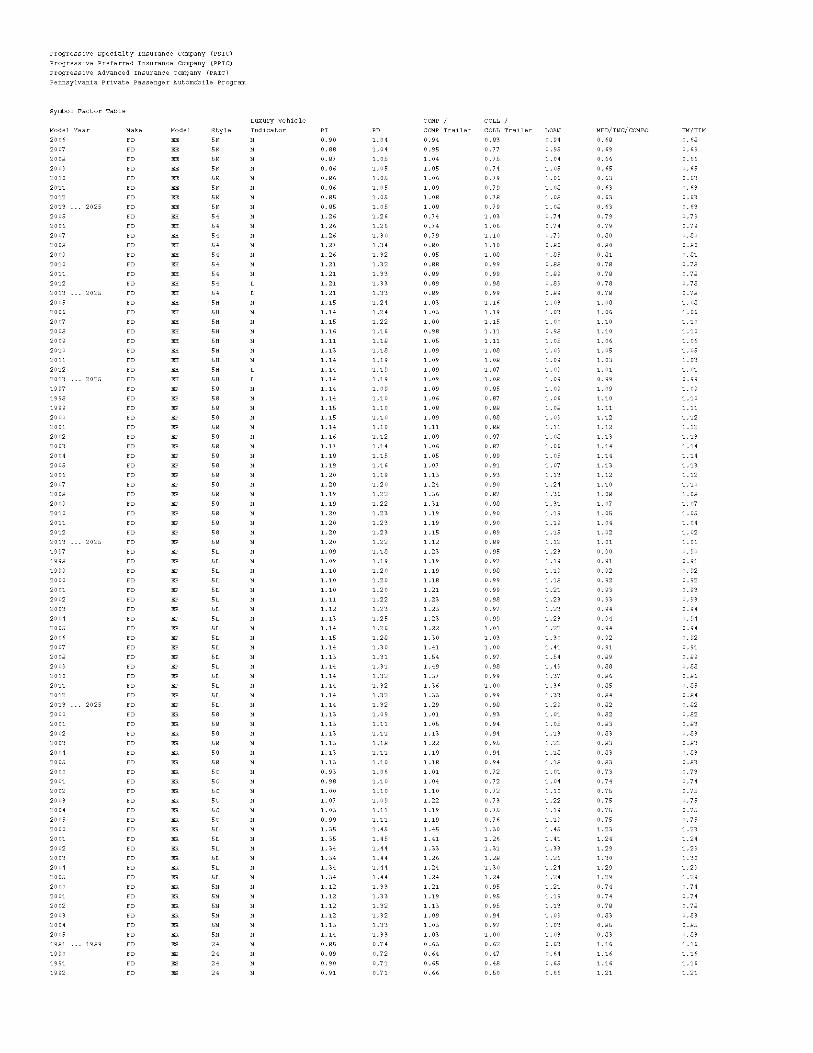

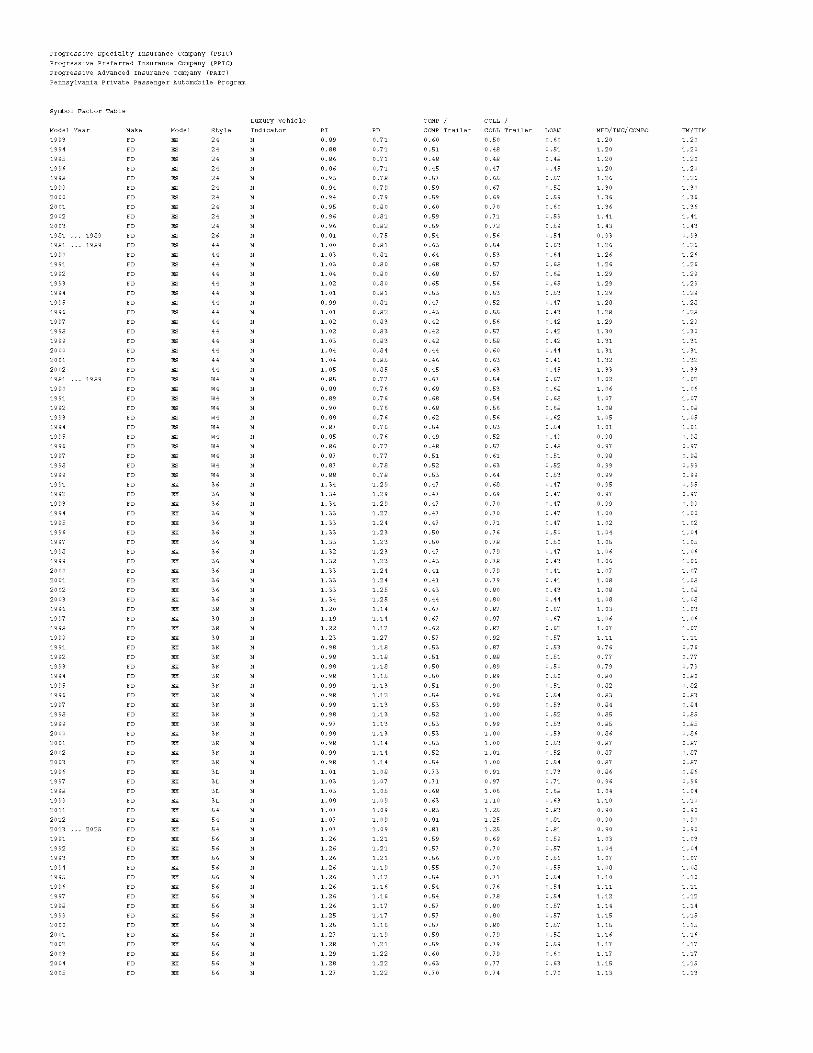

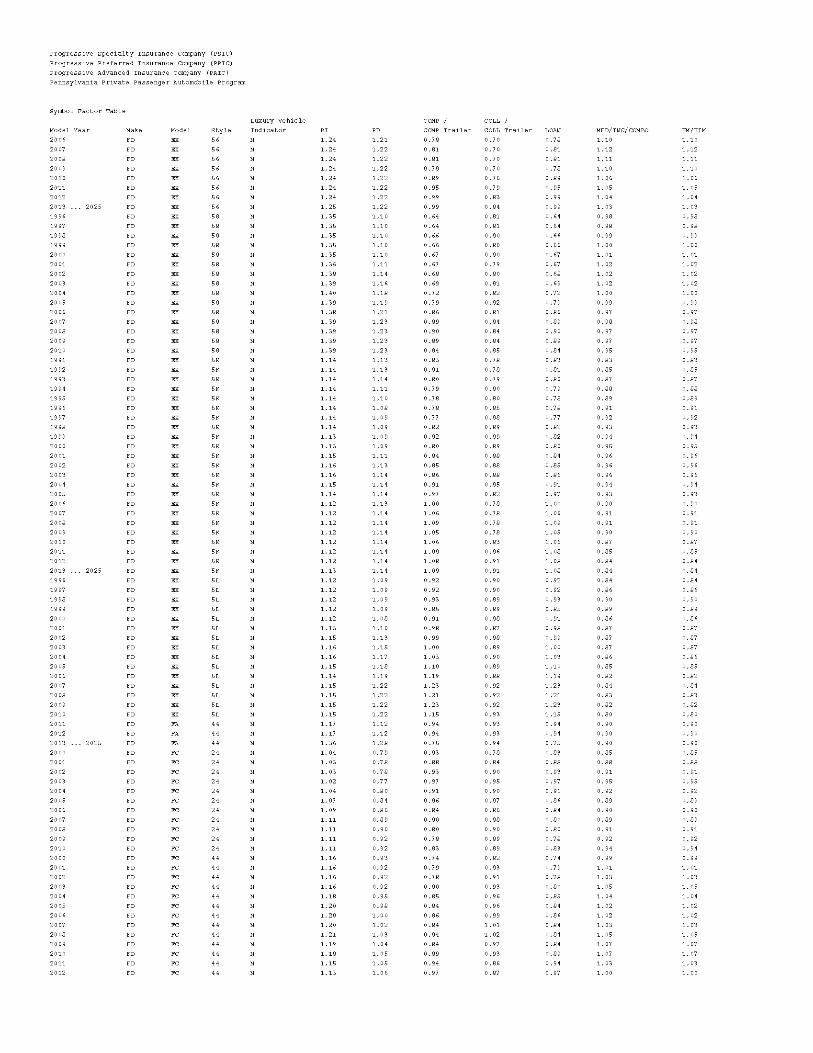

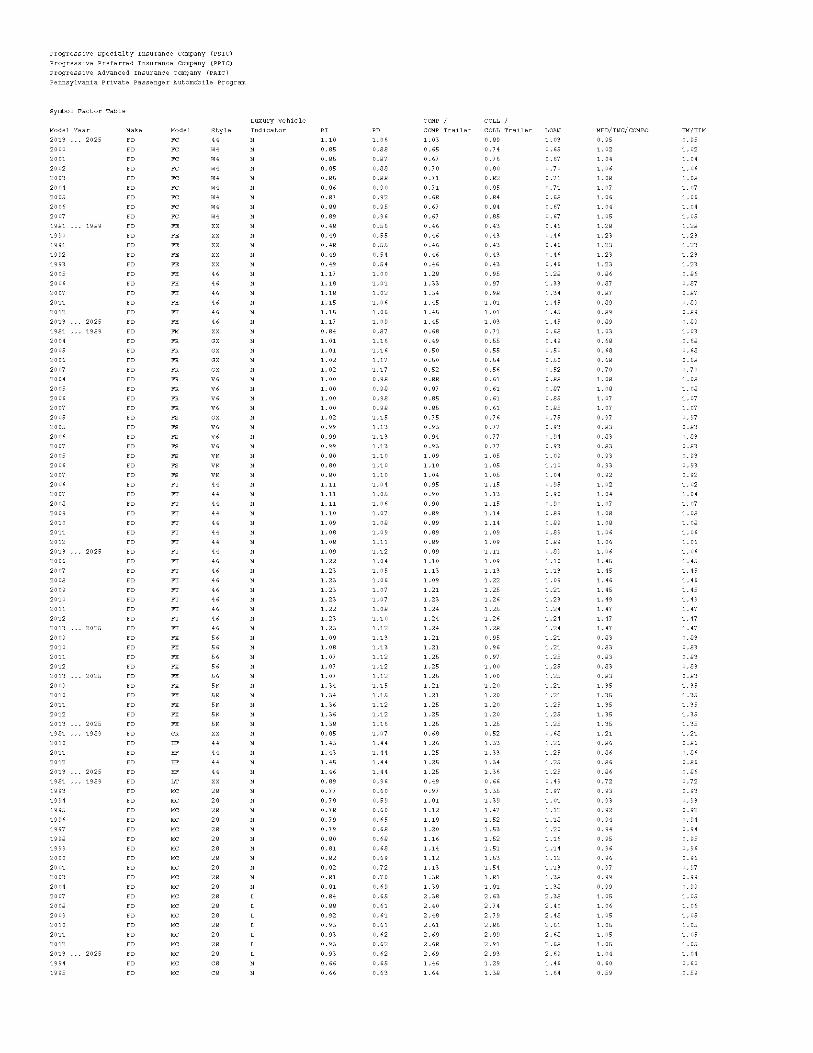

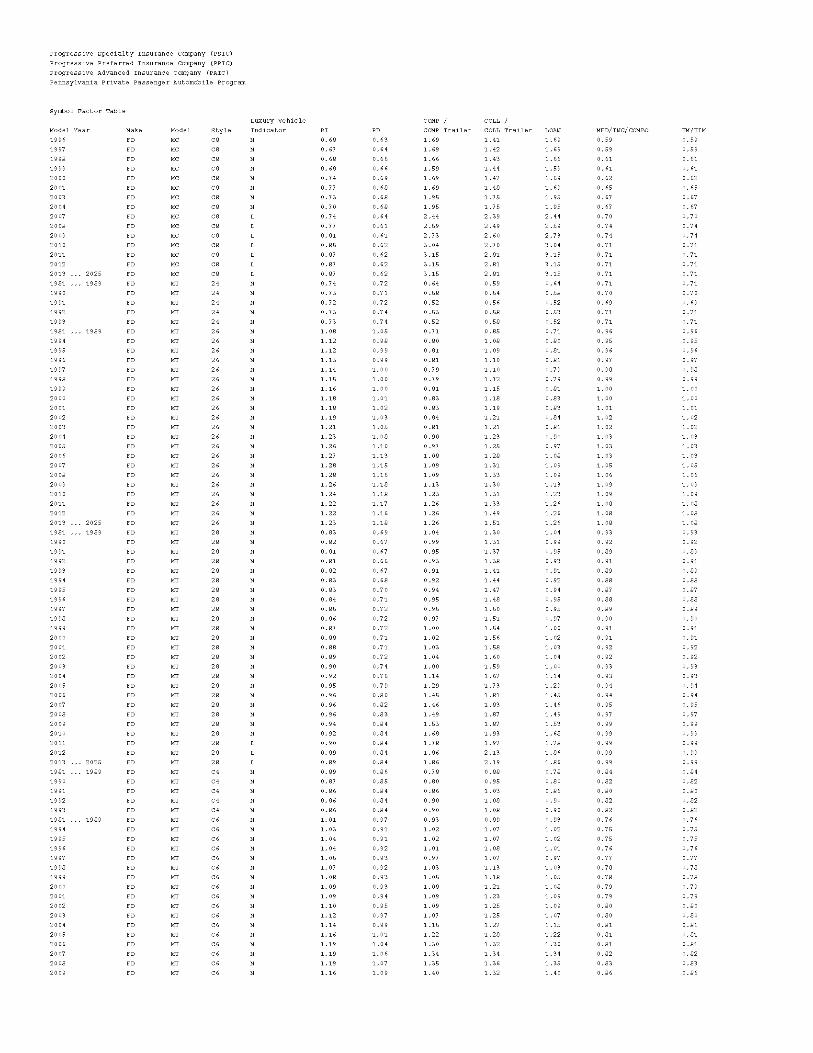

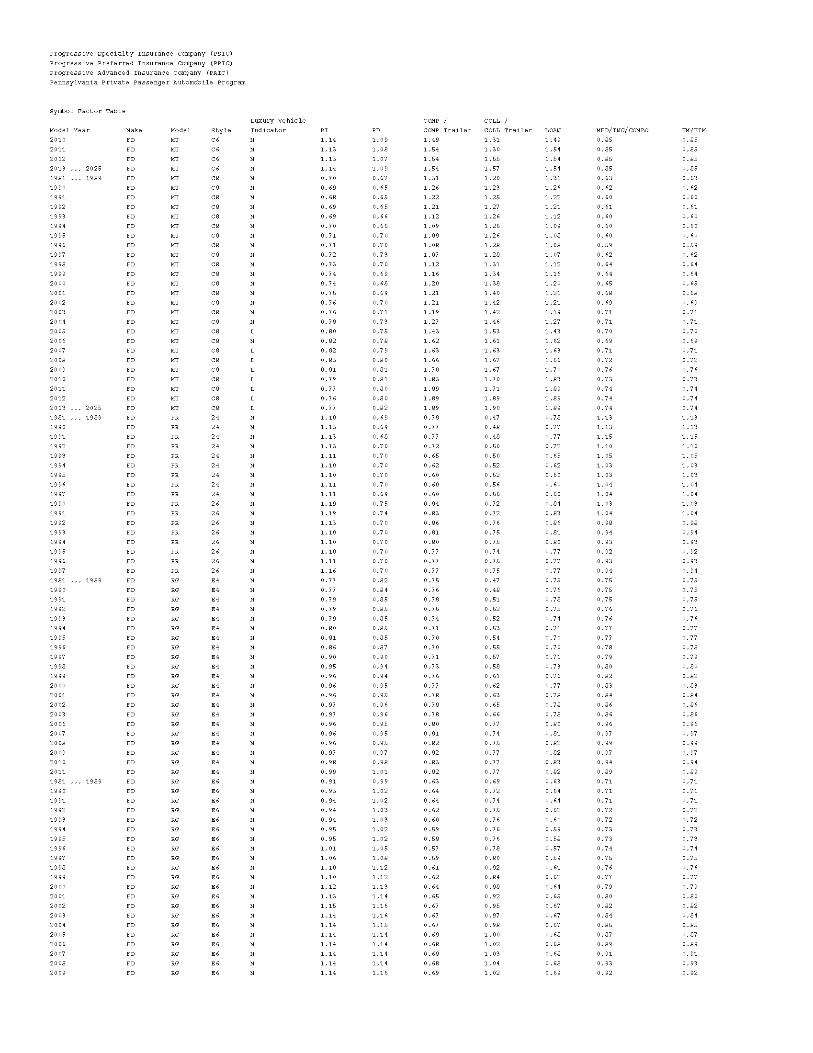

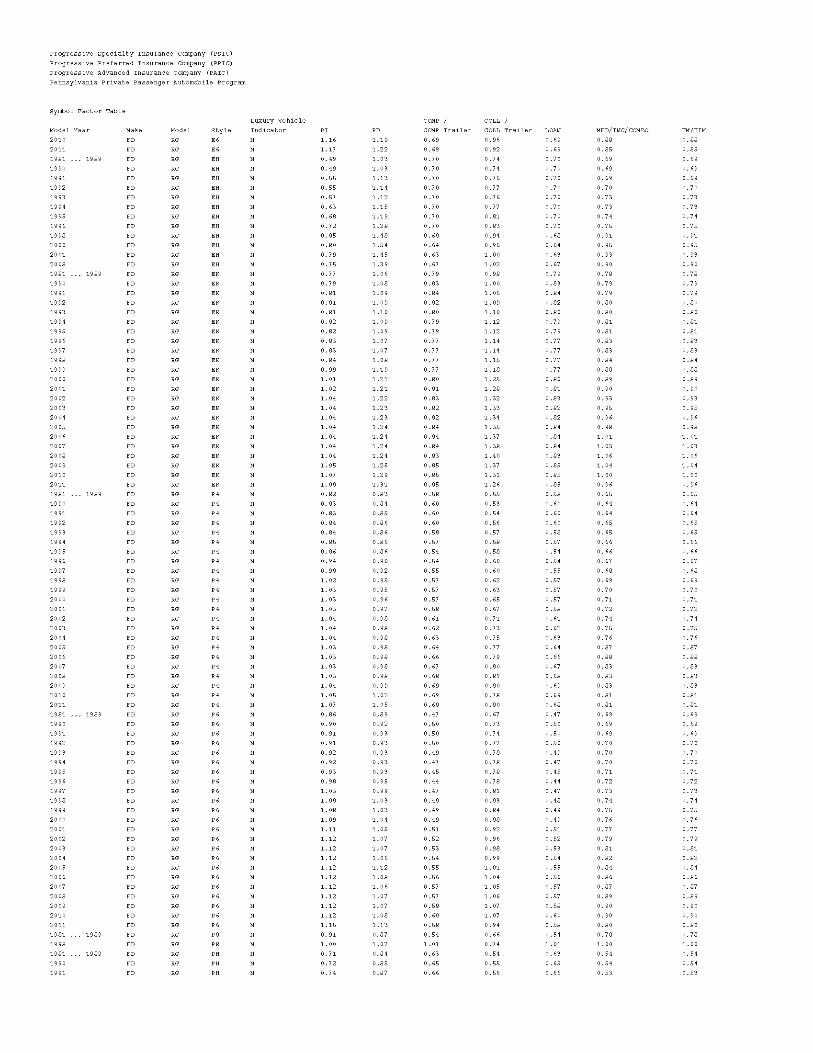

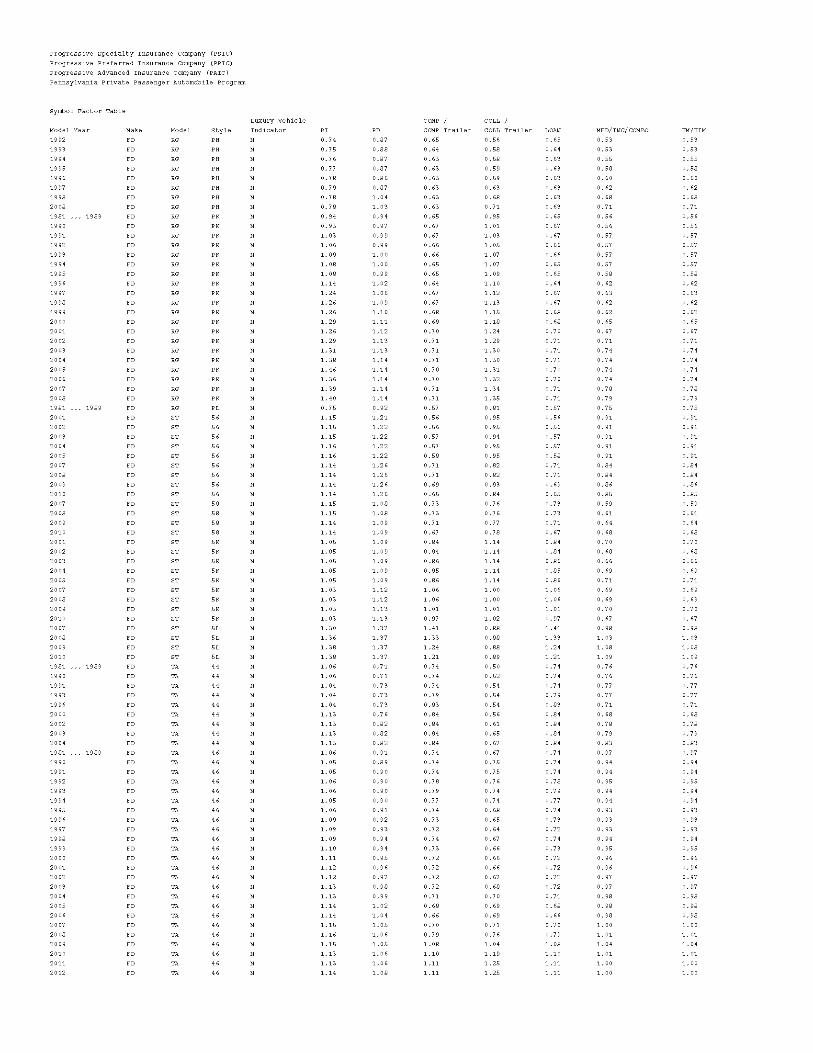

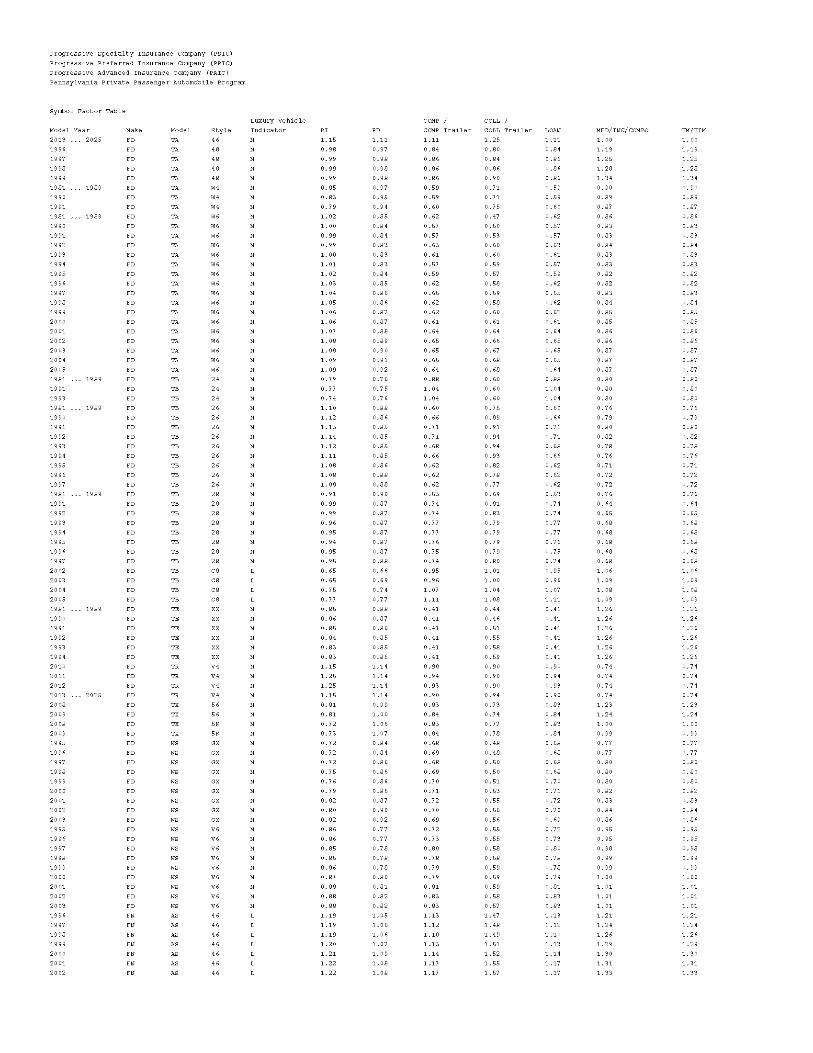

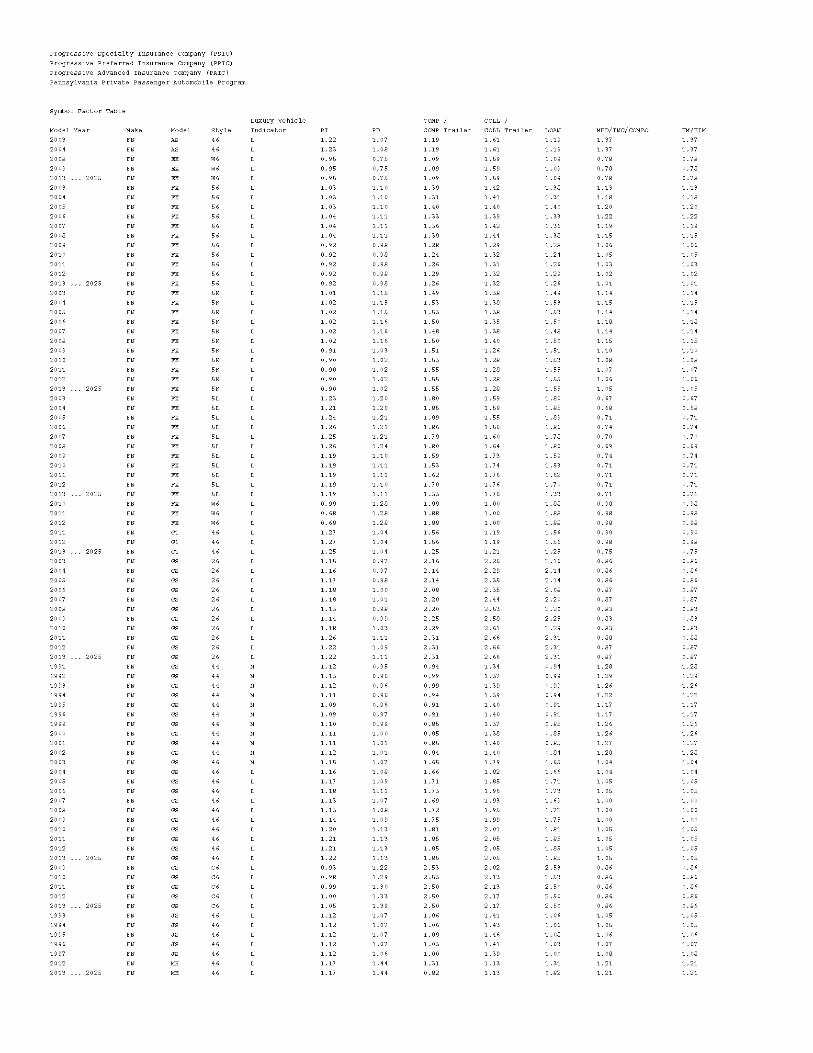

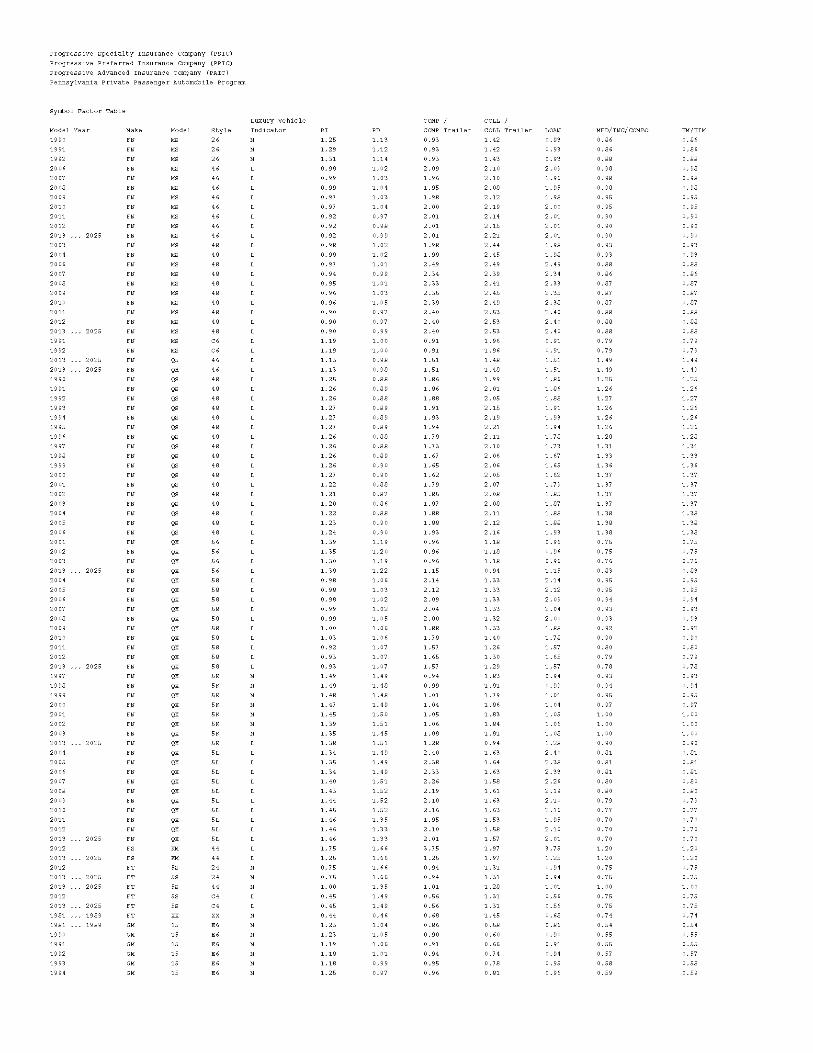

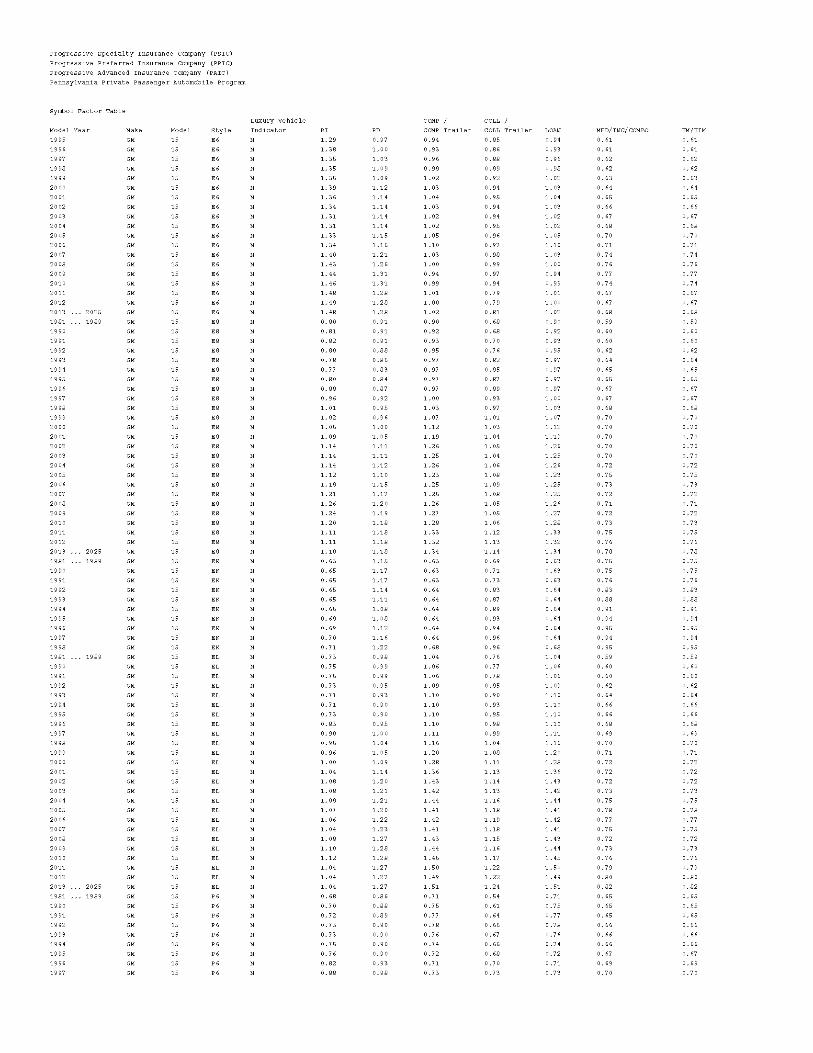

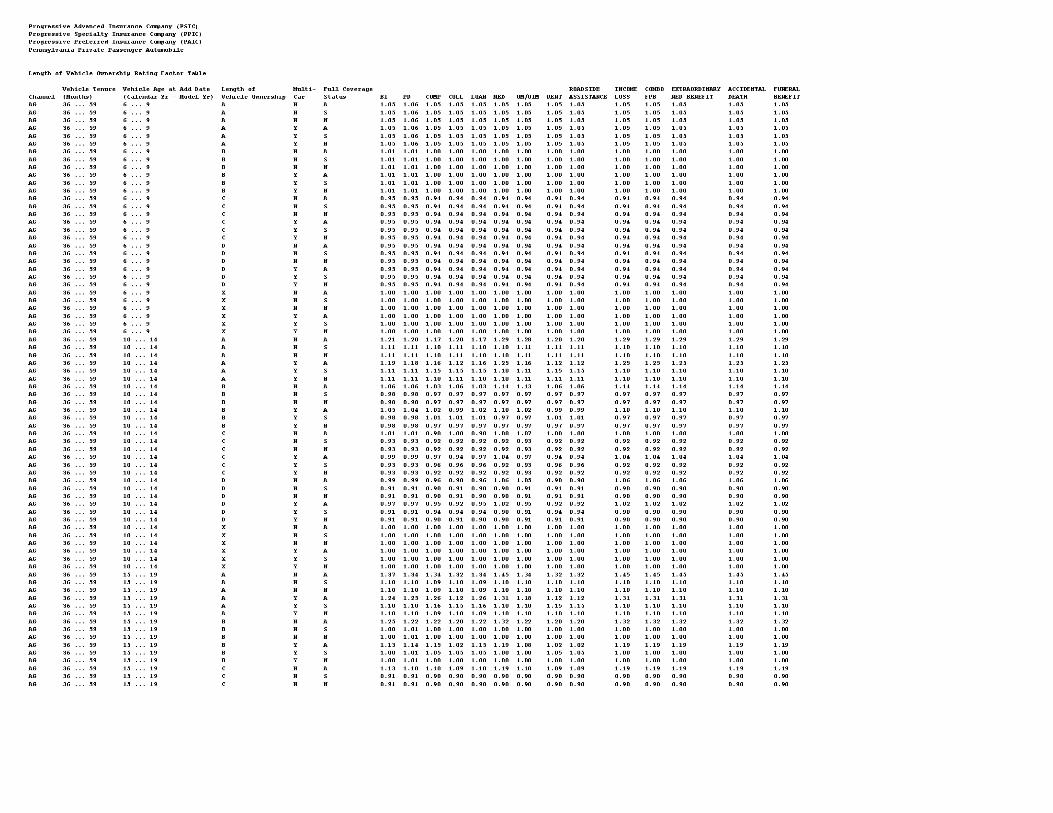

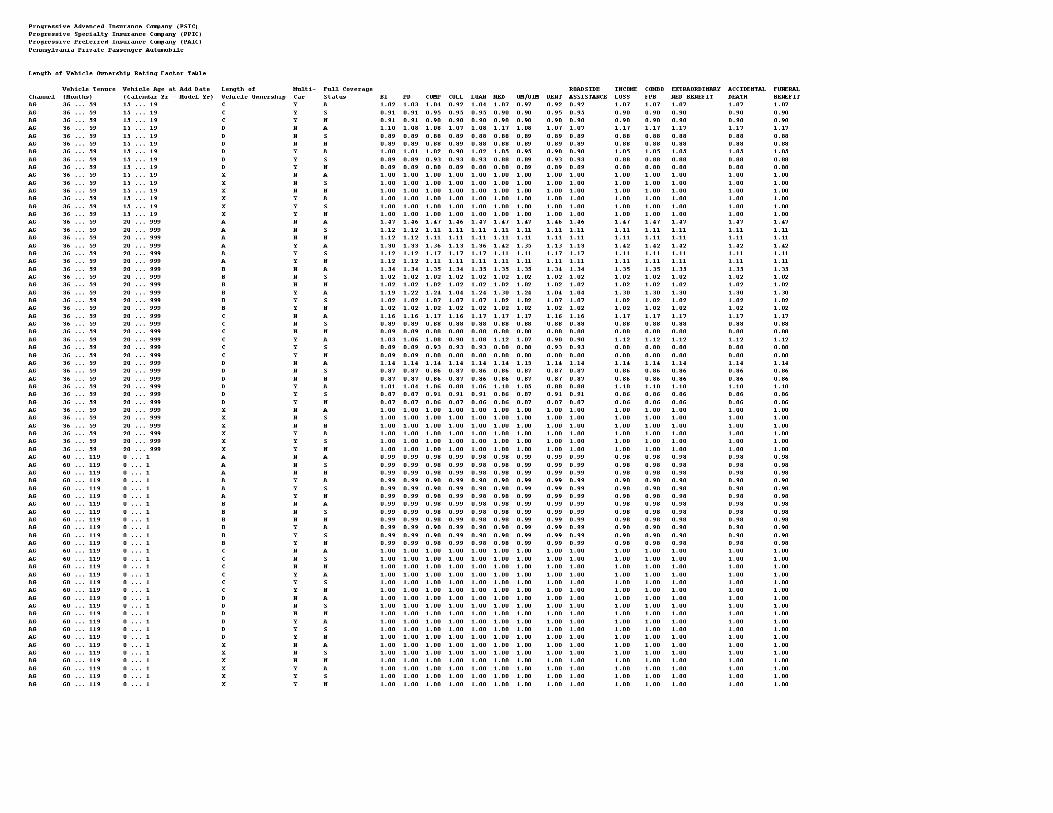

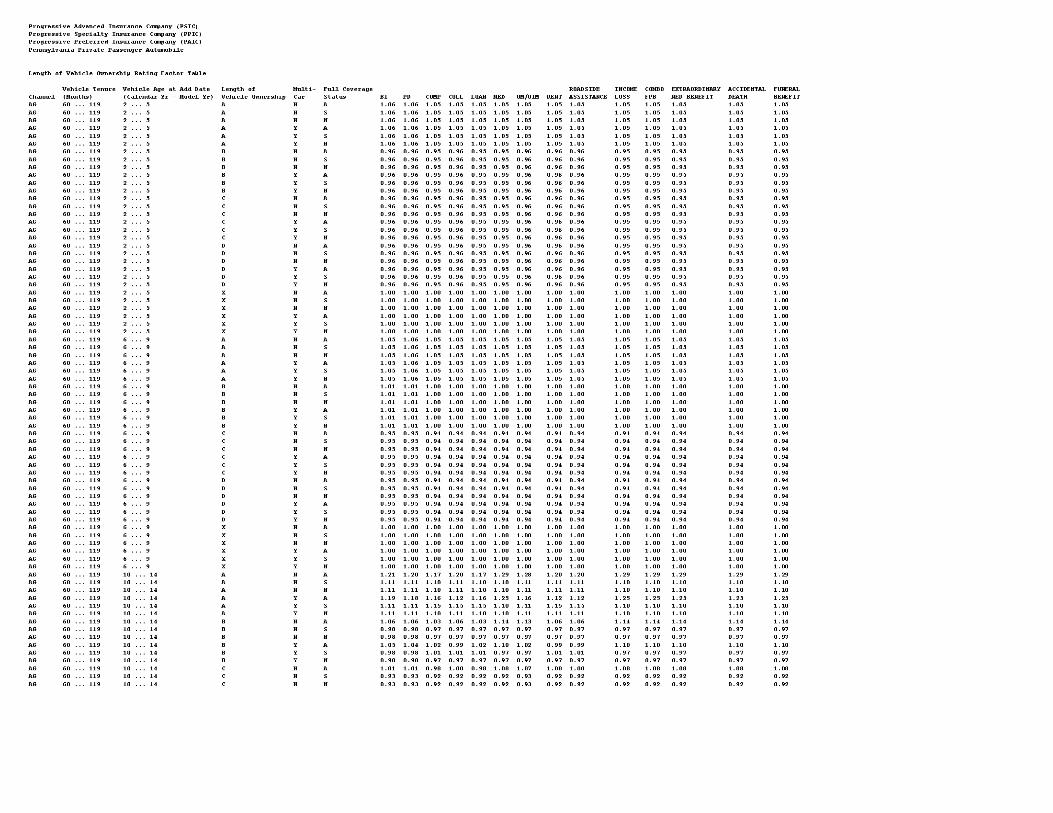

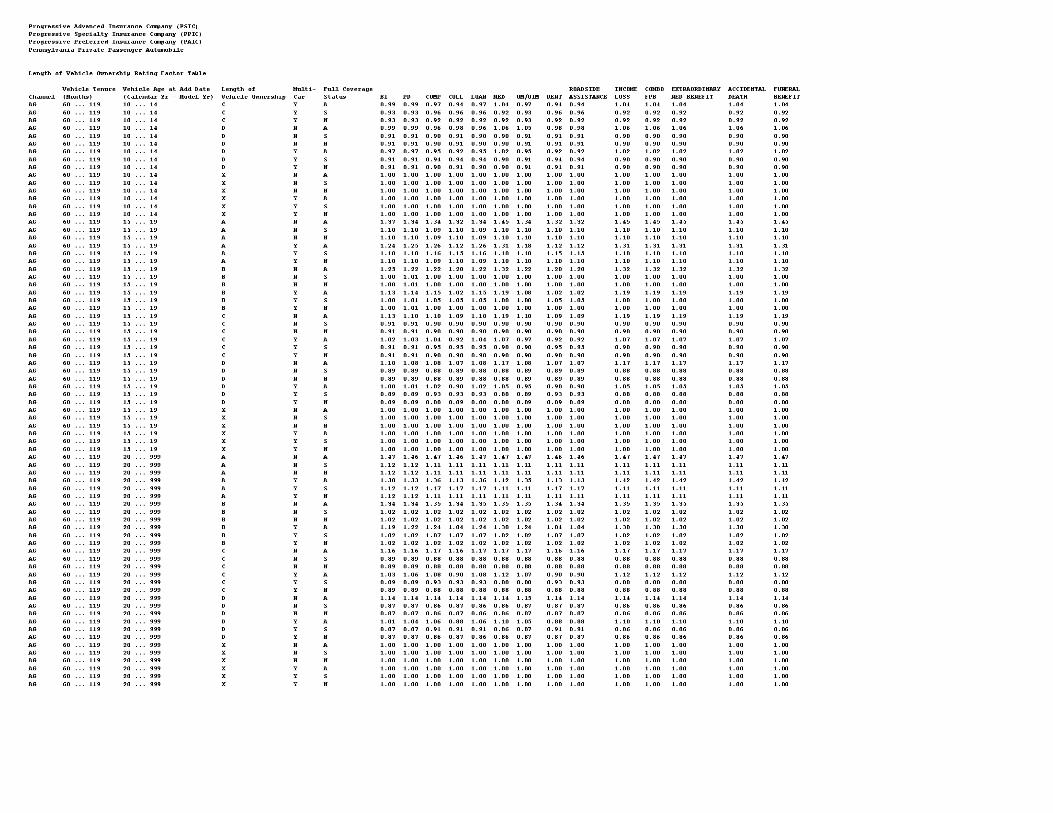

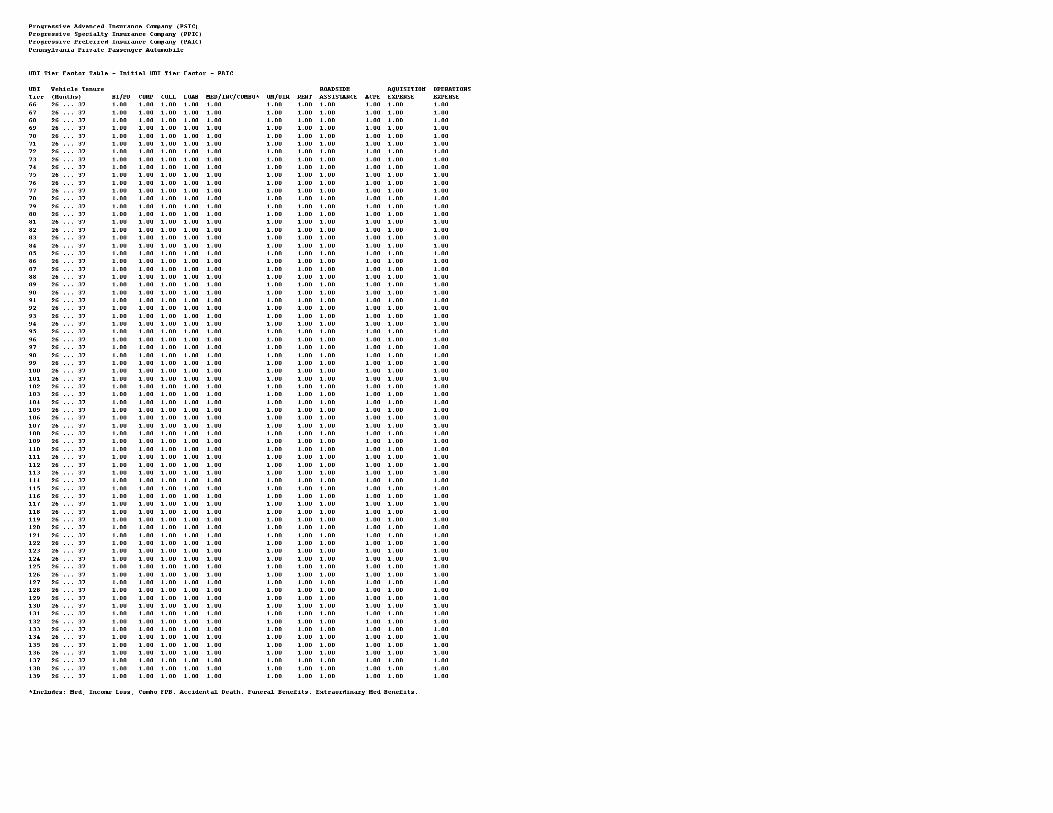

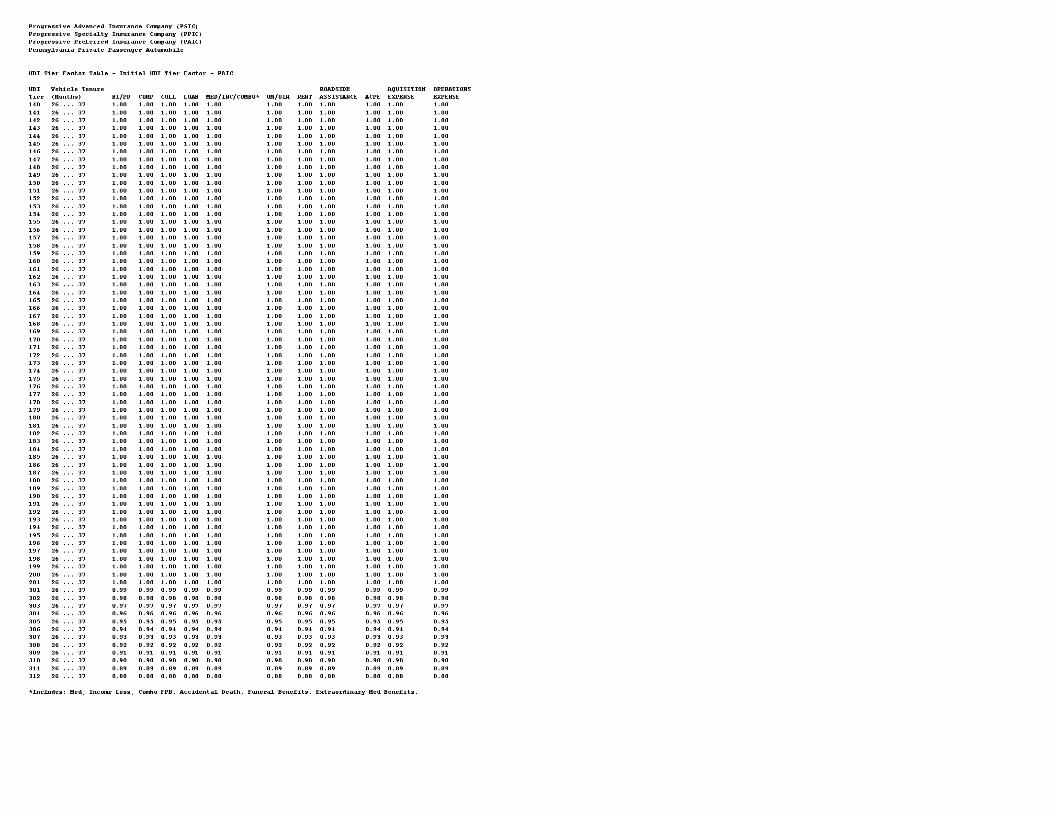

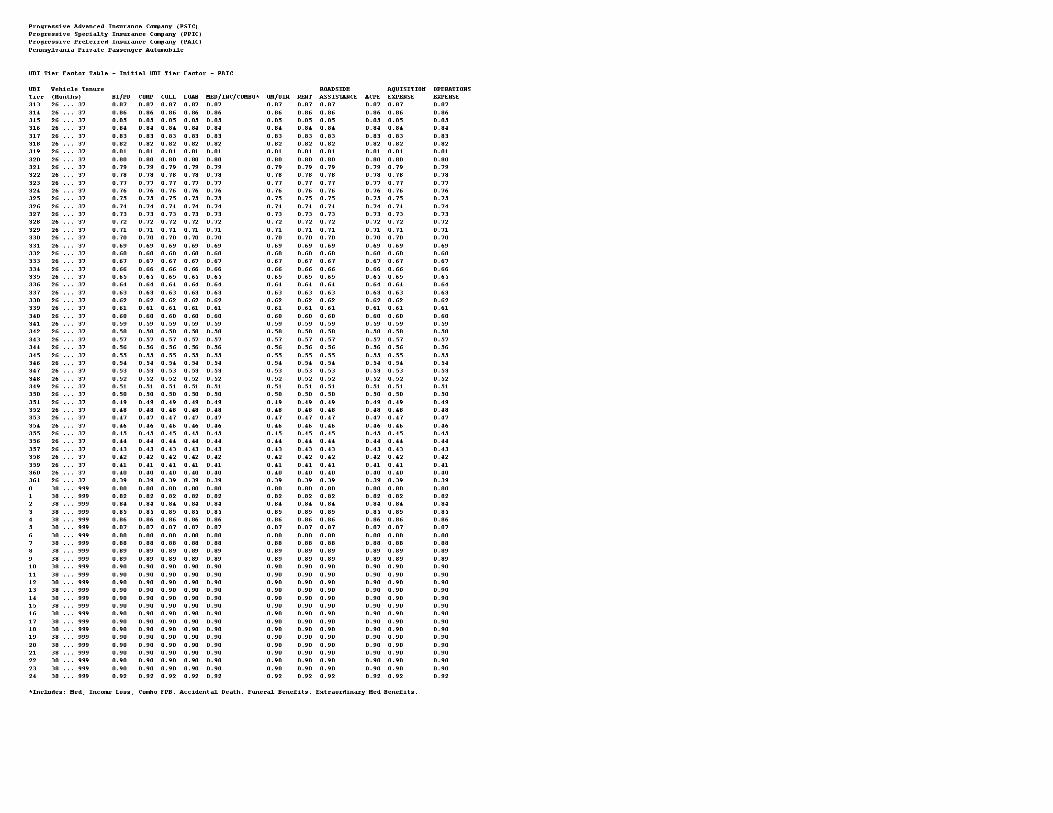

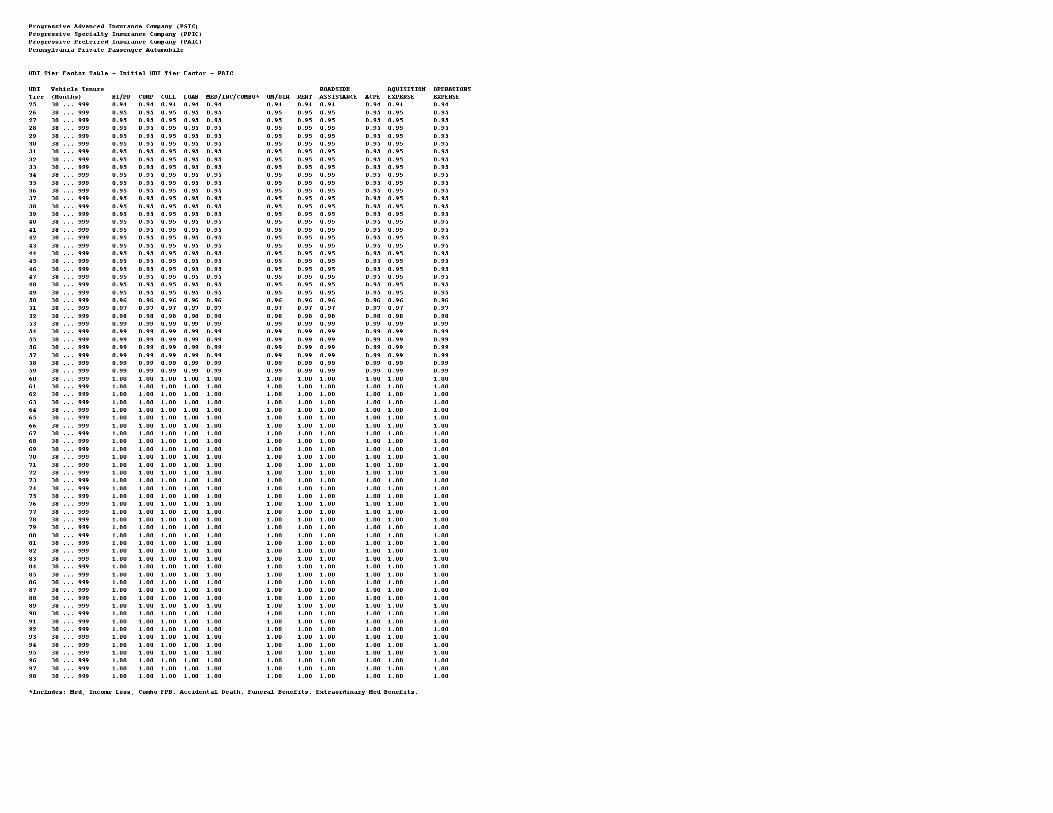

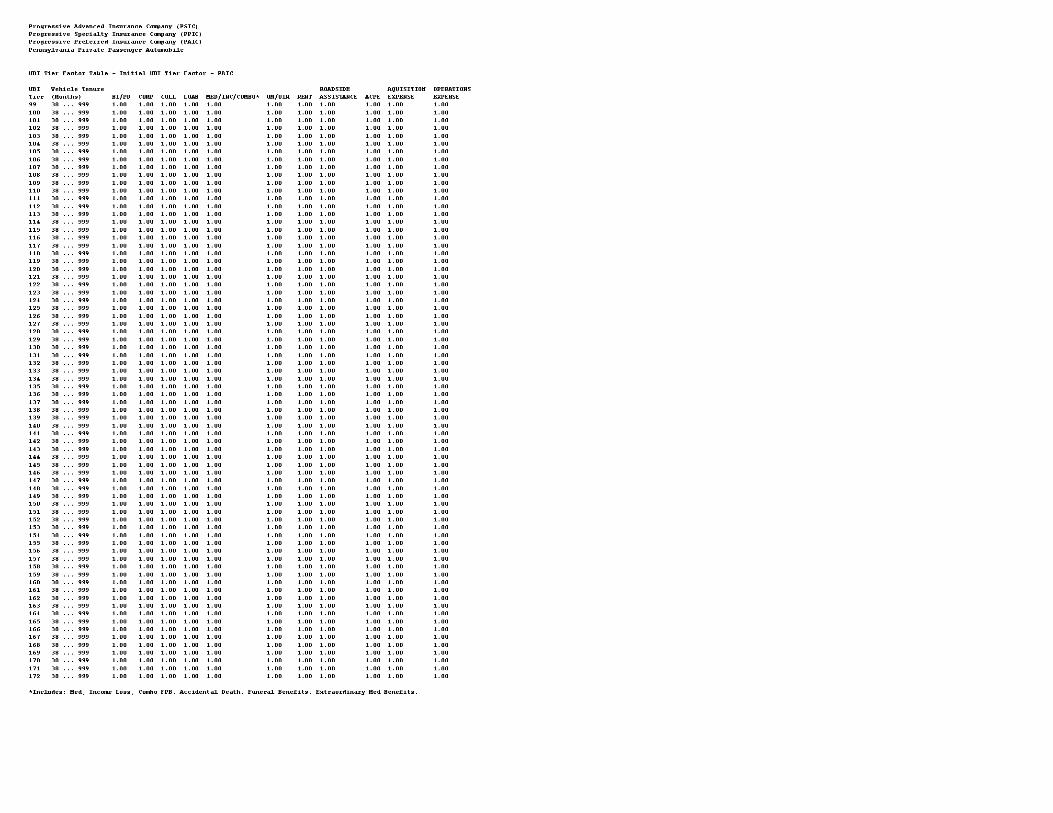

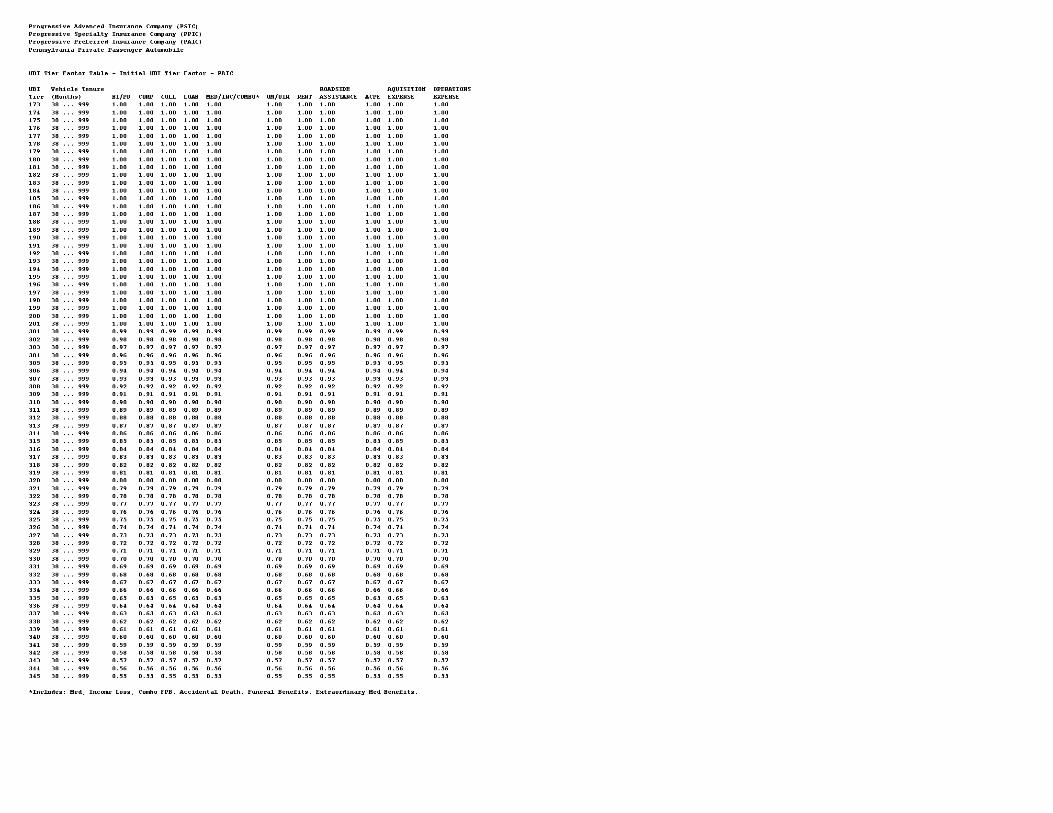

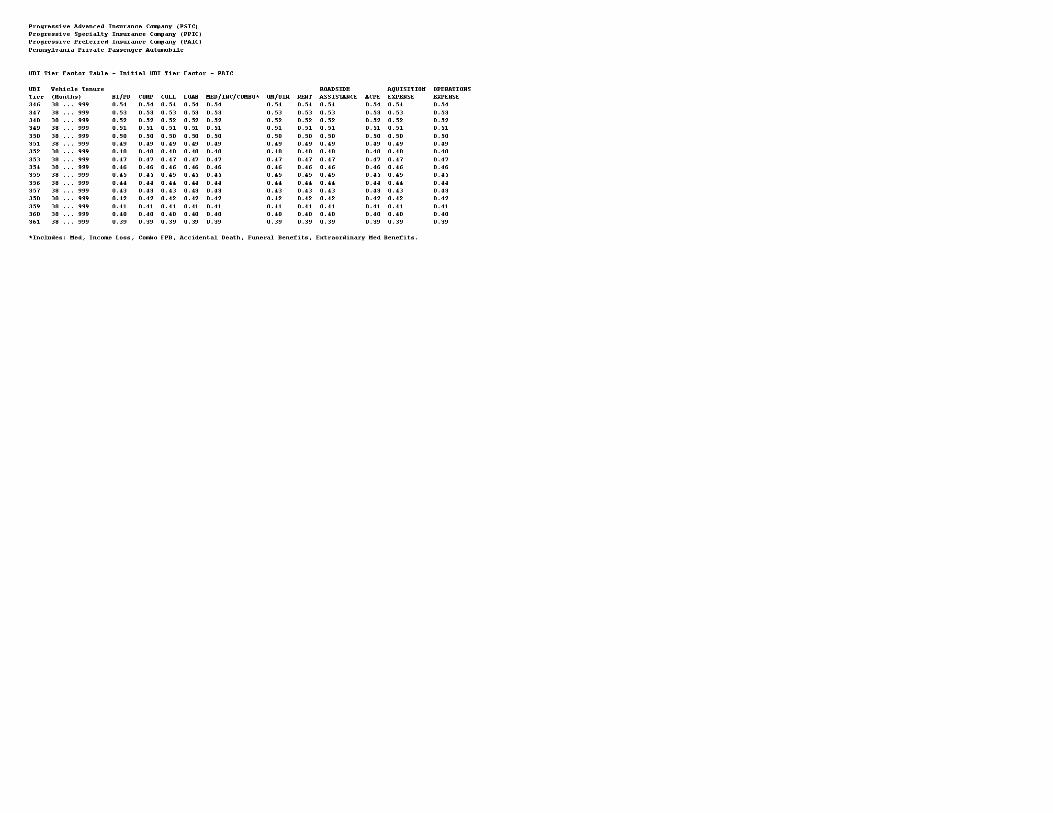

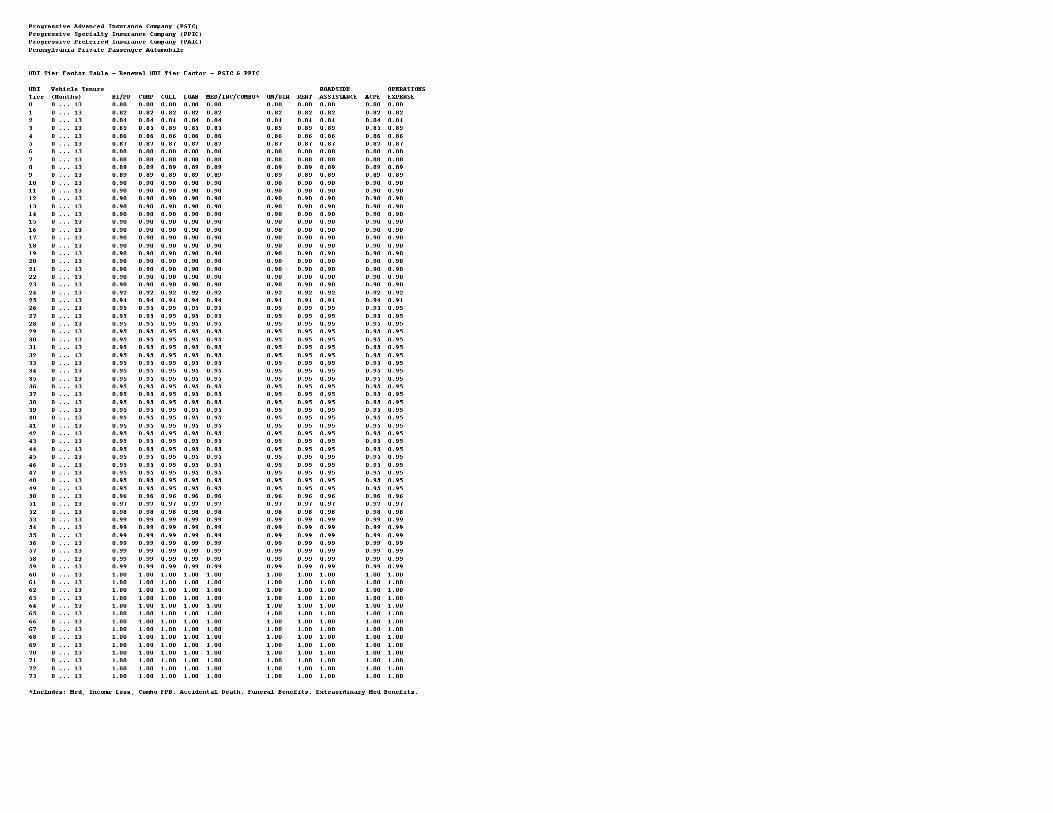

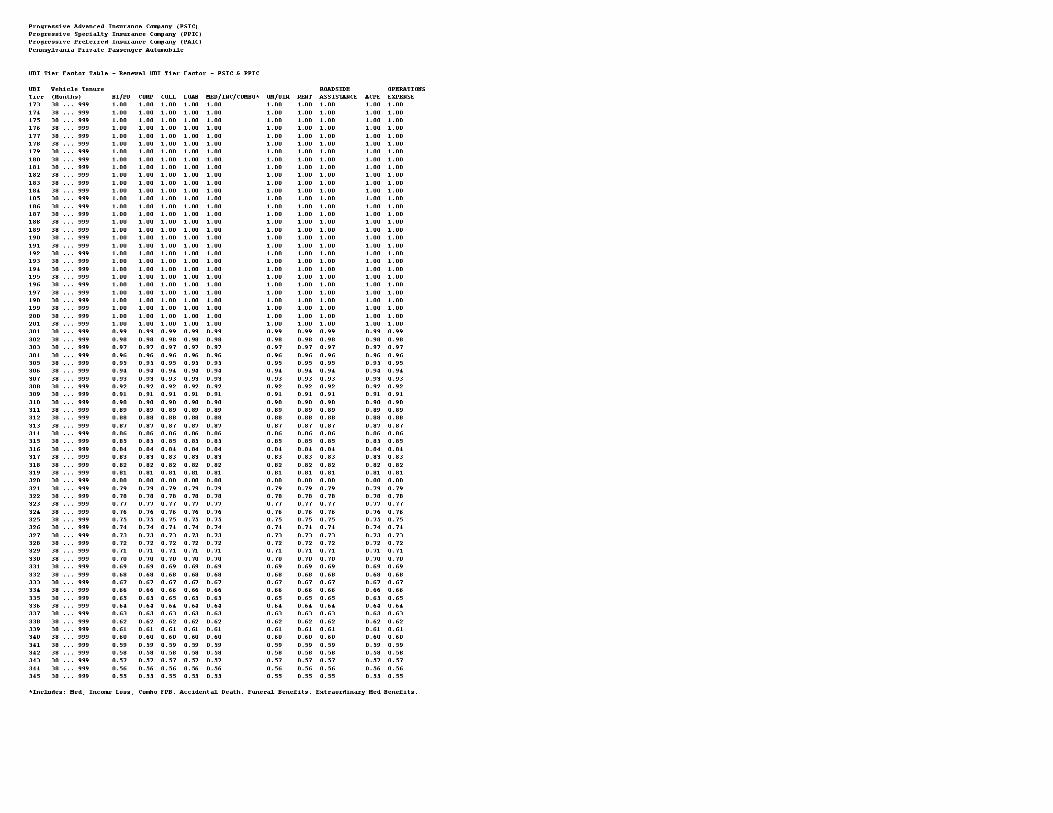

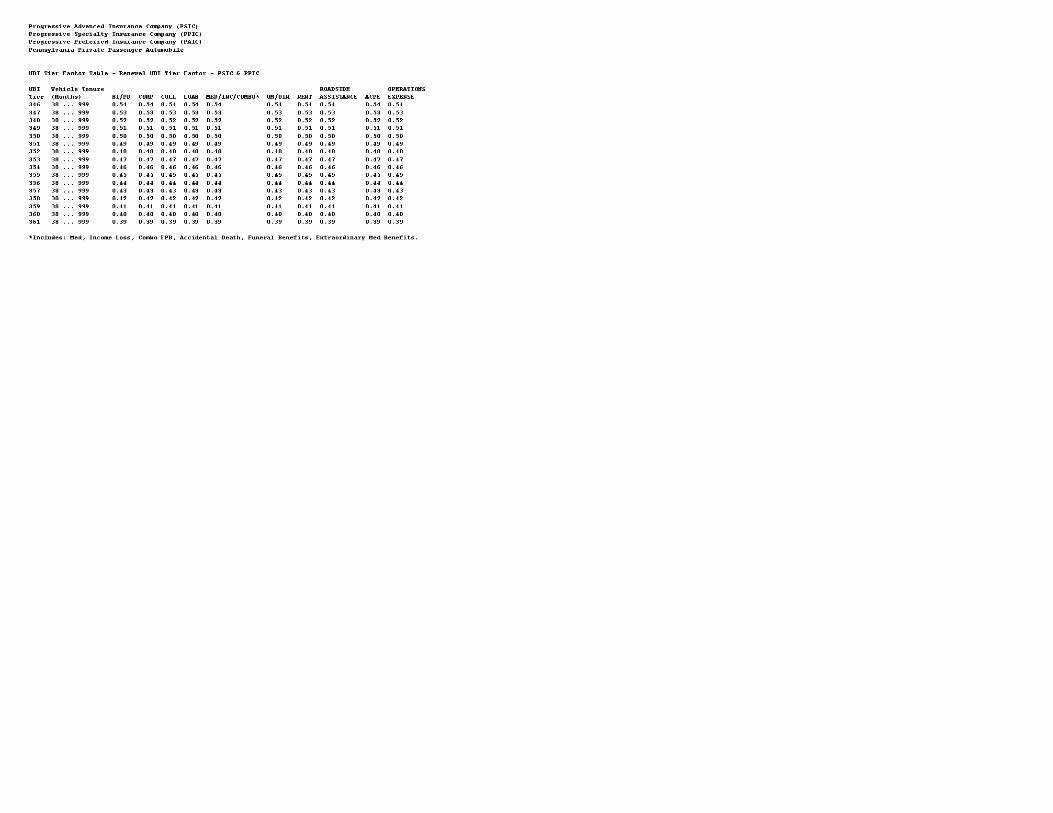

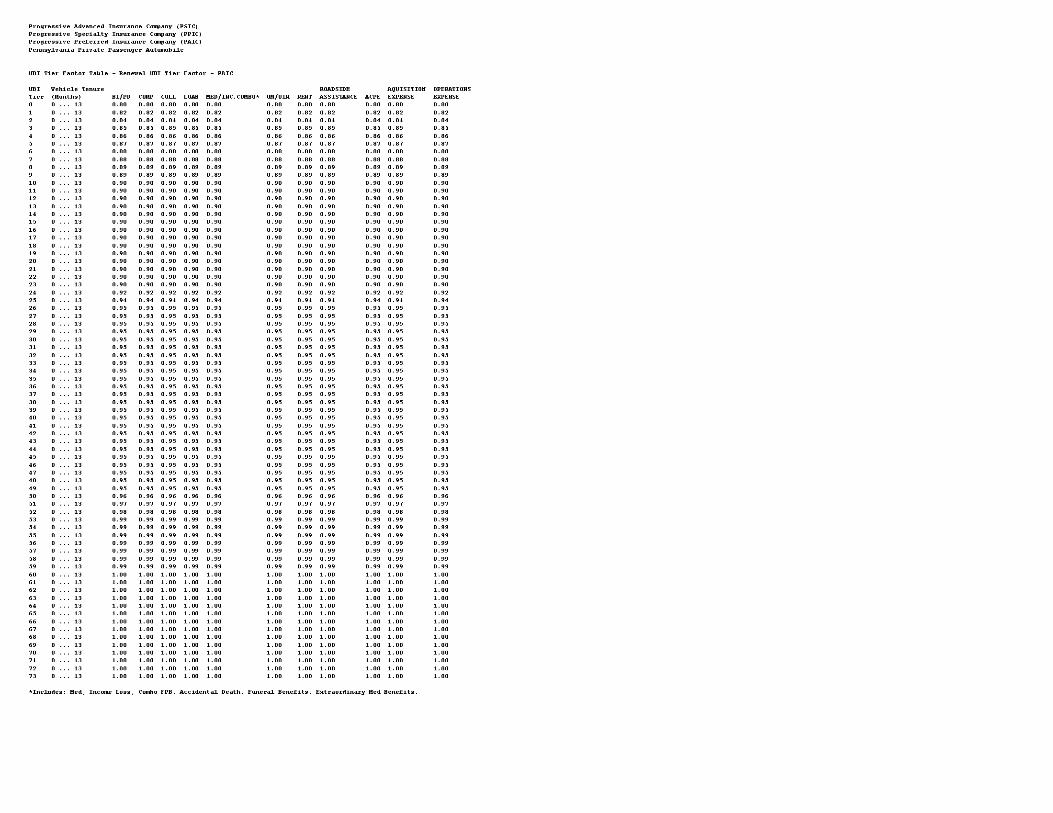

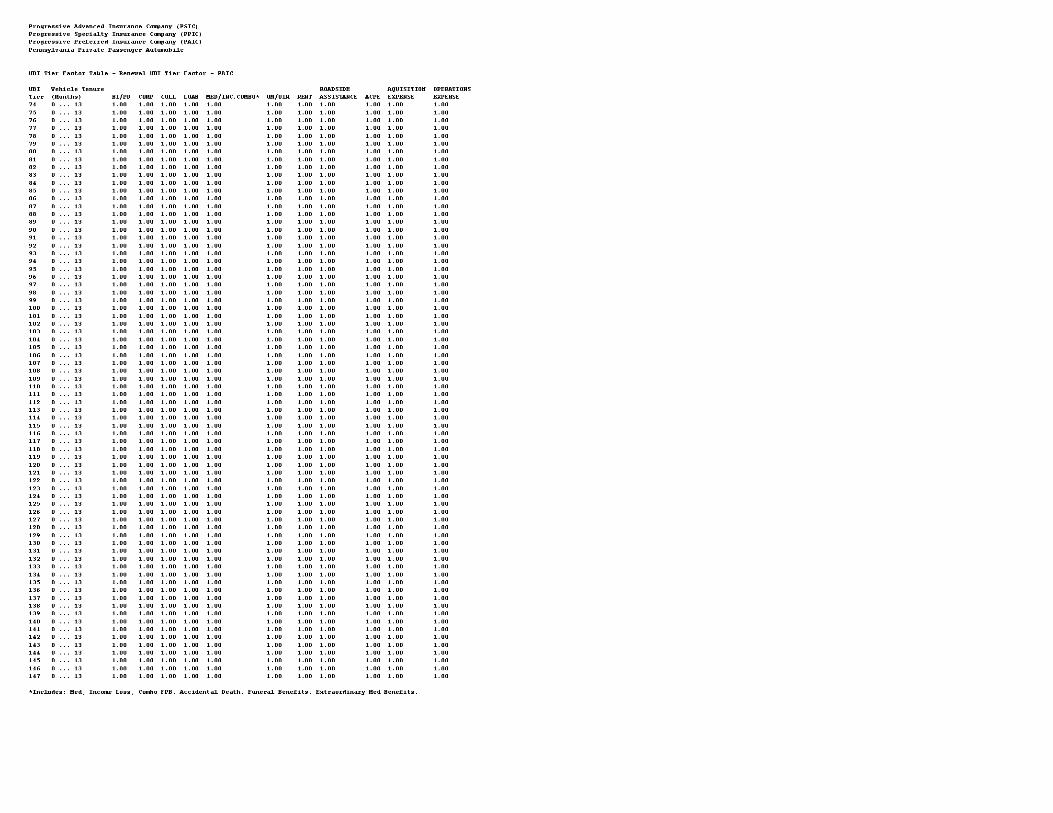

Rate/Rule Schedule

Item

No.

Schedule Item

Status Exhibit Name Rule # or Page # Rate Action

Previous State

Filing Number Attachments1 Factors Replacement Factors_PA_1503_V2_Part1.

pdfFactors_PA_1503_V2_Part2.pdfFactors_PA_1503_V2_Part3.pdfFactors_PA_1503_V2_Part4.pdf

2 Rate Order of Calculation(ROC)

Replacement ROC_PA_1503.pdf

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

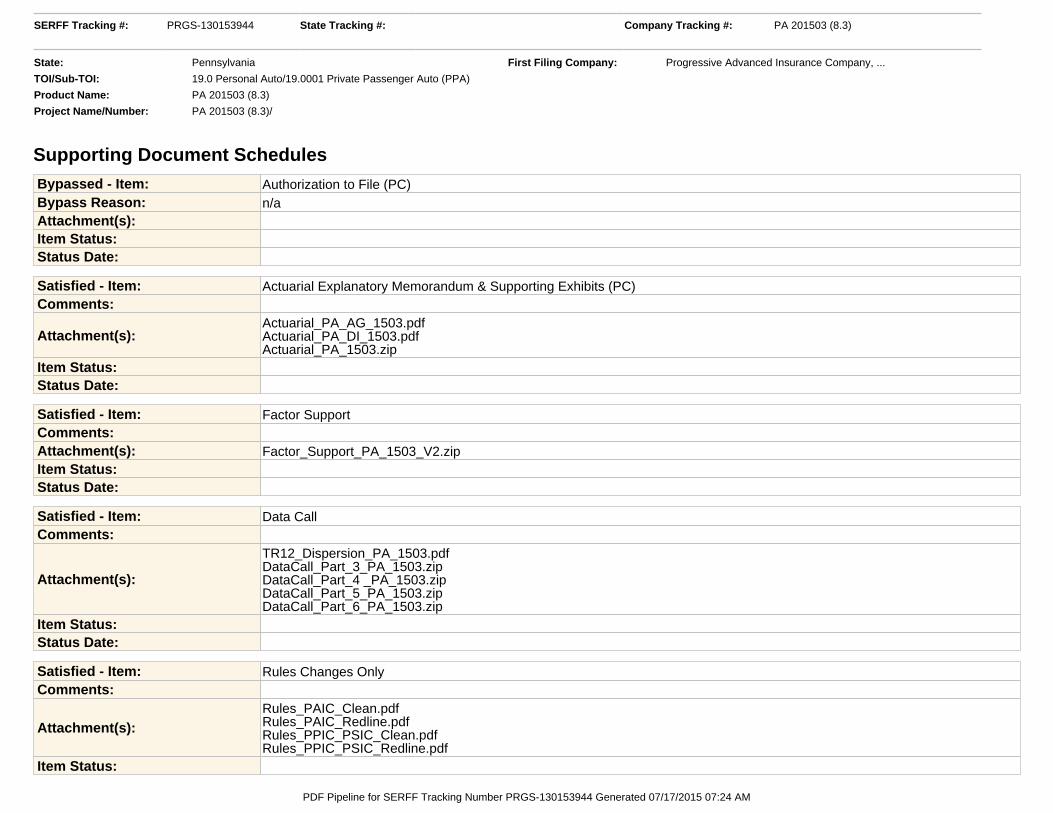

Supporting Document Schedules Bypassed - Item: Authorization to File (PC)Bypass Reason: n/aAttachment(s):Item Status:Status Date:

Satisfied - Item: Actuarial Explanatory Memorandum & Supporting Exhibits (PC)Comments:

Attachment(s):Actuarial_PA_AG_1503.pdfActuarial_PA_DI_1503.pdfActuarial_PA_1503.zip

Item Status:Status Date:

Satisfied - Item: Factor SupportComments:Attachment(s): Factor_Support_PA_1503_V2.zipItem Status:Status Date:

Satisfied - Item: Data CallComments:

Attachment(s):

TR12_Dispersion_PA_1503.pdfDataCall_Part_3_PA_1503.zipDataCall_Part_4 _PA_1503.zipDataCall_Part_5_PA_1503.zipDataCall_Part_6_PA_1503.zip

Item Status:Status Date:

Satisfied - Item: Rules Changes OnlyComments:

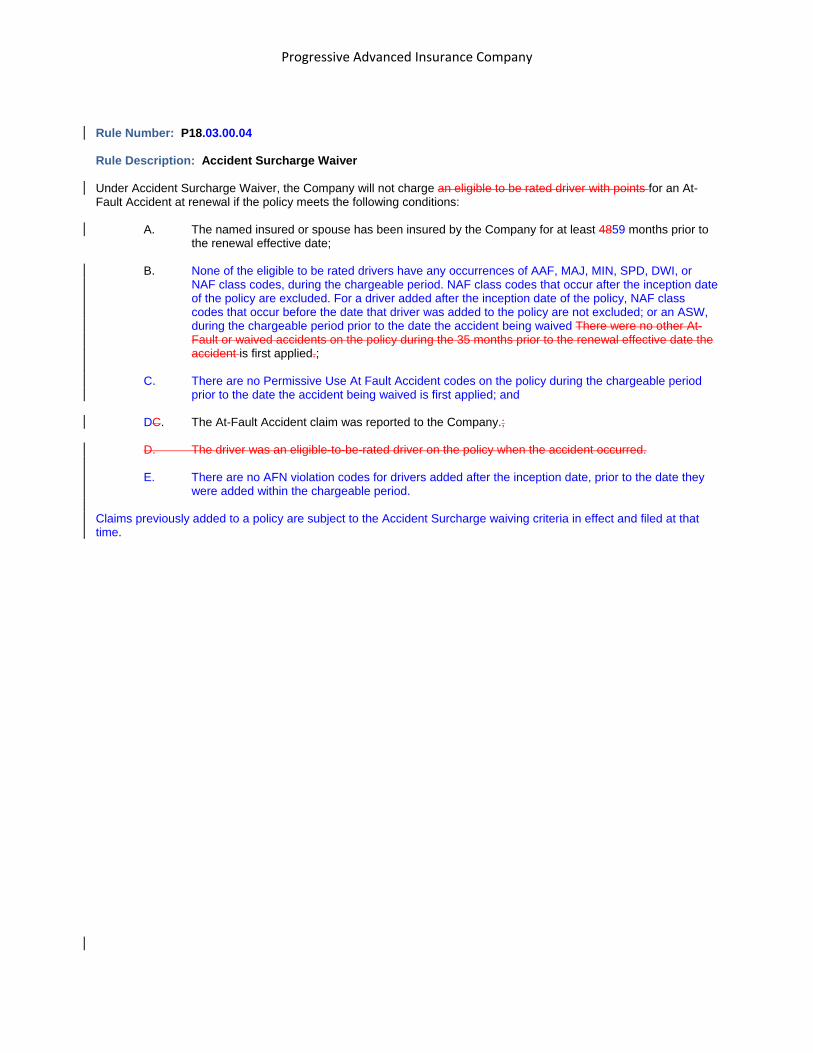

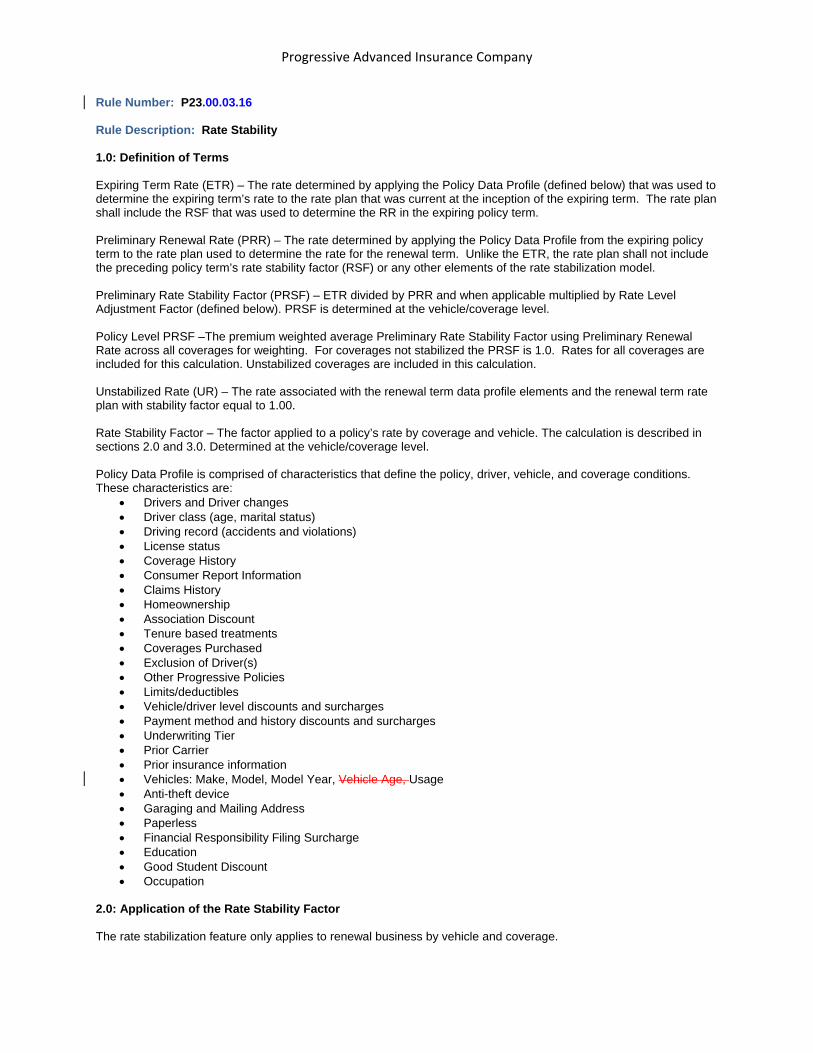

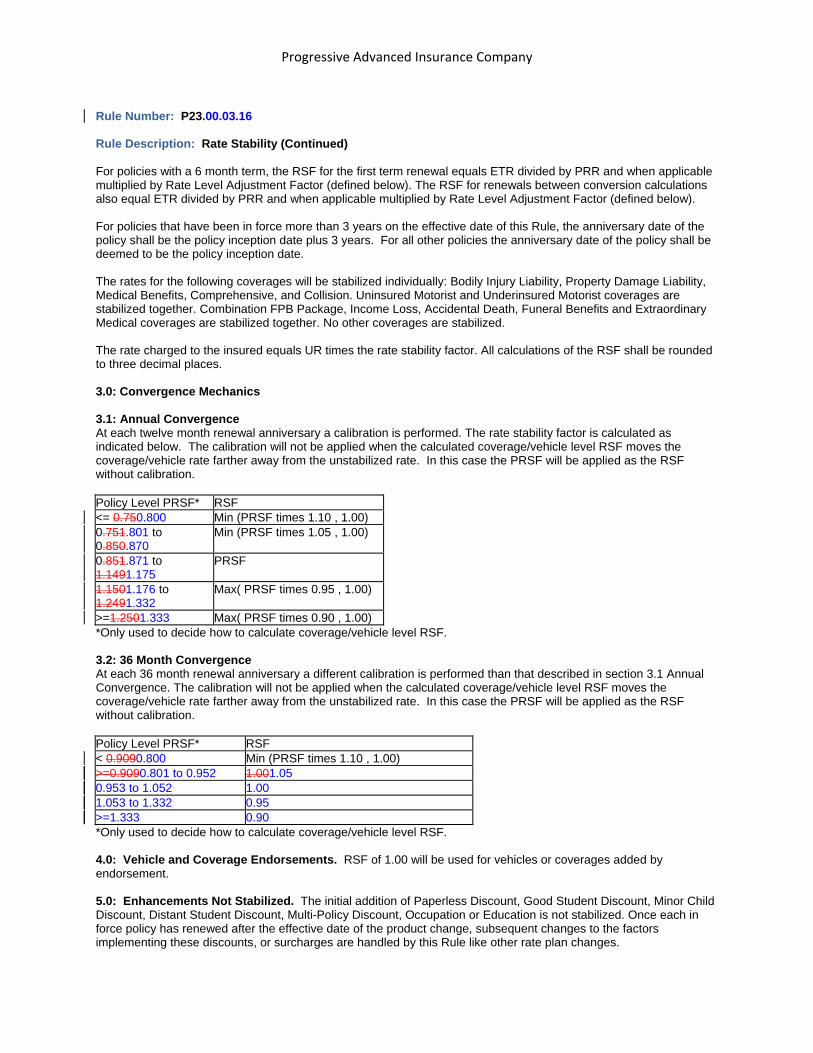

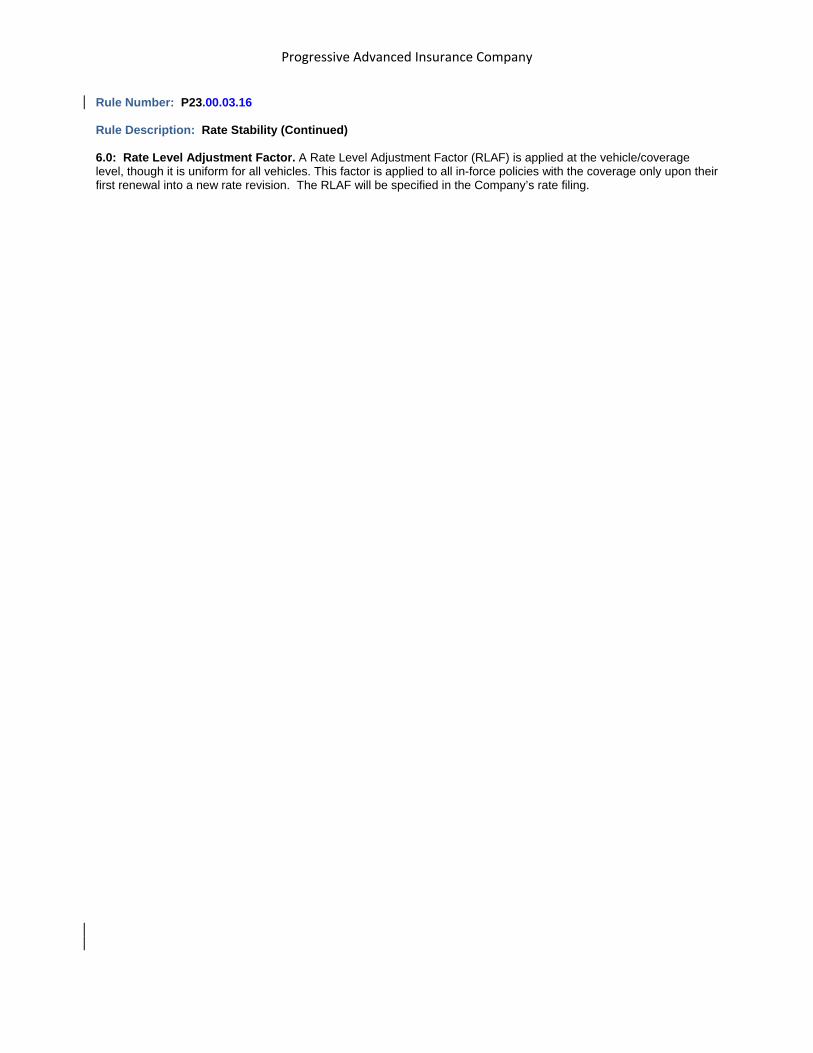

Attachment(s):Rules_PAIC_Clean.pdfRules_PAIC_Redline.pdfRules_PPIC_PSIC_Clean.pdfRules_PPIC_PSIC_Redline.pdf

Item Status:

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

Status Date:

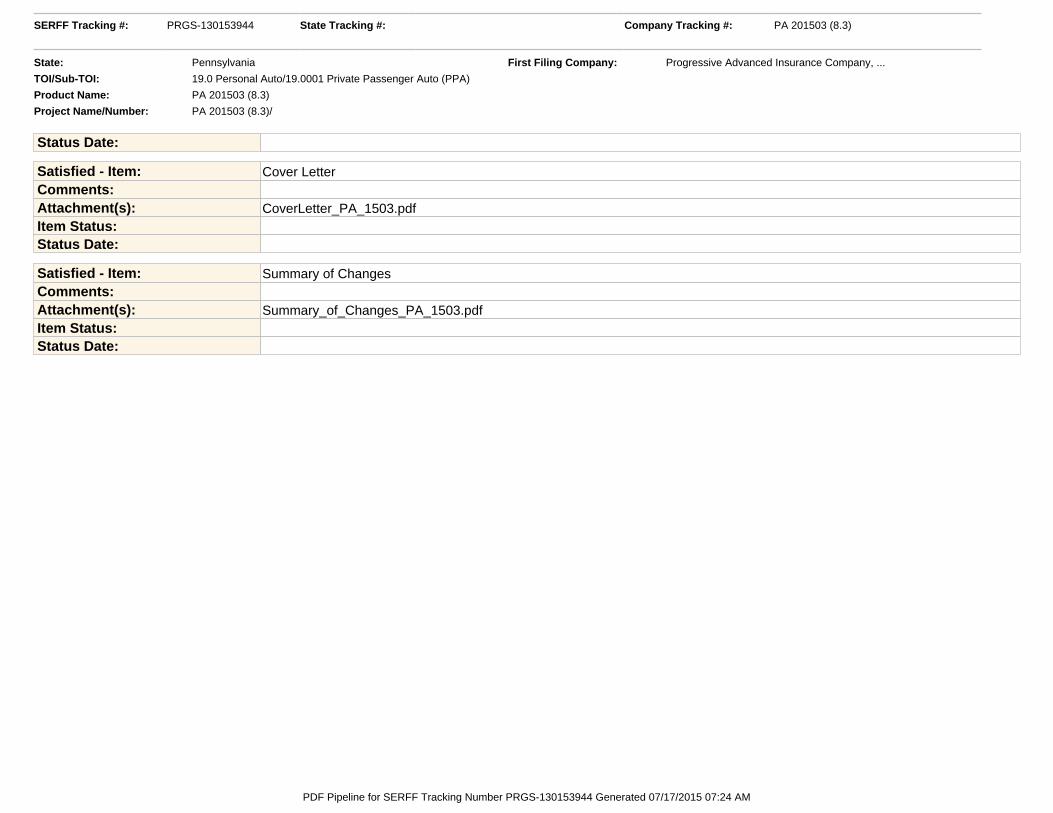

Satisfied - Item: Cover LetterComments:Attachment(s): CoverLetter_PA_1503.pdfItem Status:Status Date:

Satisfied - Item: Summary of ChangesComments:Attachment(s): Summary_of_Changes_PA_1503.pdfItem Status:Status Date:

SERFF Tracking #: PRGS-130153944 State Tracking #: Company Tracking #: PA 201503 (8.3)

State: Pennsylvania First Filing Company: Progressive Advanced Insurance Company, ...

TOI/Sub-TOI: 19.0 Personal Auto/19.0001 Private Passenger Auto (PPA)

Product Name: PA 201503 (8.3)

Project Name/Number: PA 201503 (8.3)/

PDF Pipeline for SERFF Tracking Number PRGS-130153944 Generated 07/17/2015 07:24 AM

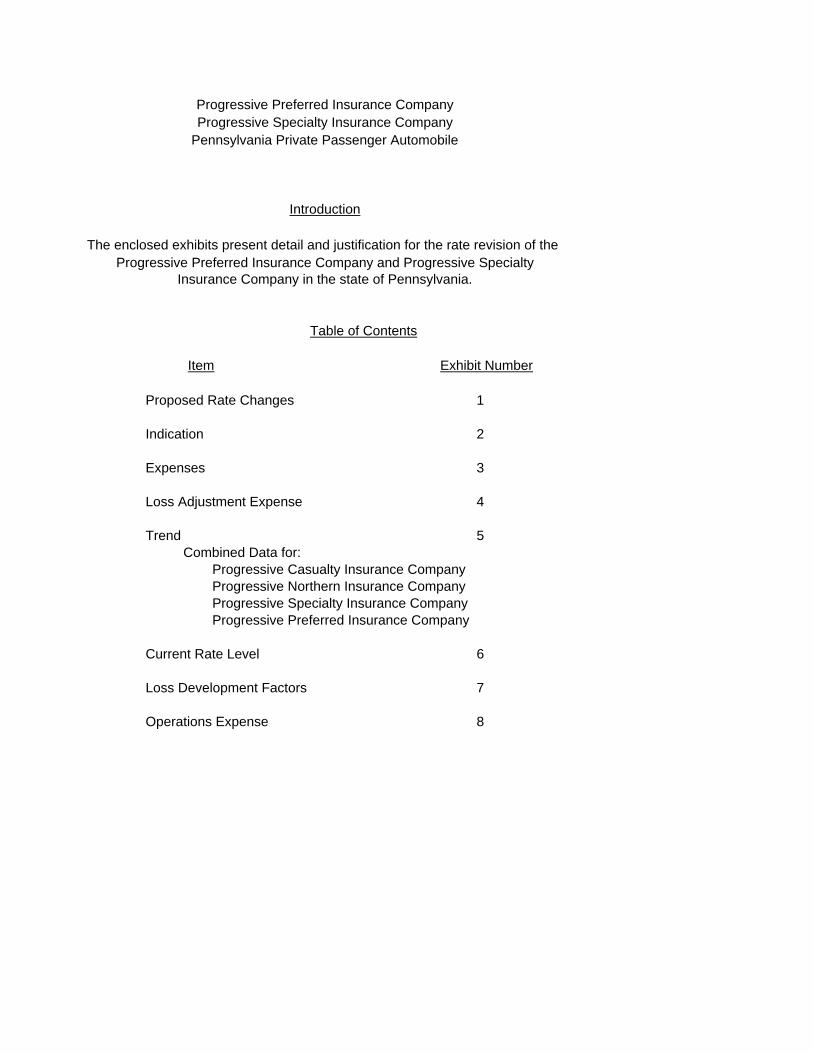

Introduction

The enclosed exhibits present detail and justification for the rate revision of the

Insurance Company in the state of Pennsylvania.

Table of Contents

Item Exhibit Number

Proposed Rate Changes 1

Indication 2

Expenses 3

Loss Adjustment Expense 4

Trend 5 Combined Data for:

Progressive Casualty Insurance CompanyProgressive Northern Insurance CompanyProgressive Specialty Insurance CompanyProgressive Preferred Insurance Company

Current Rate Level 6

Loss Development Factors 7

Operations Expense 8

Pennsylvania Private Passenger Automobile

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Progressive Preferred Insurance Company and Progressive Specialty

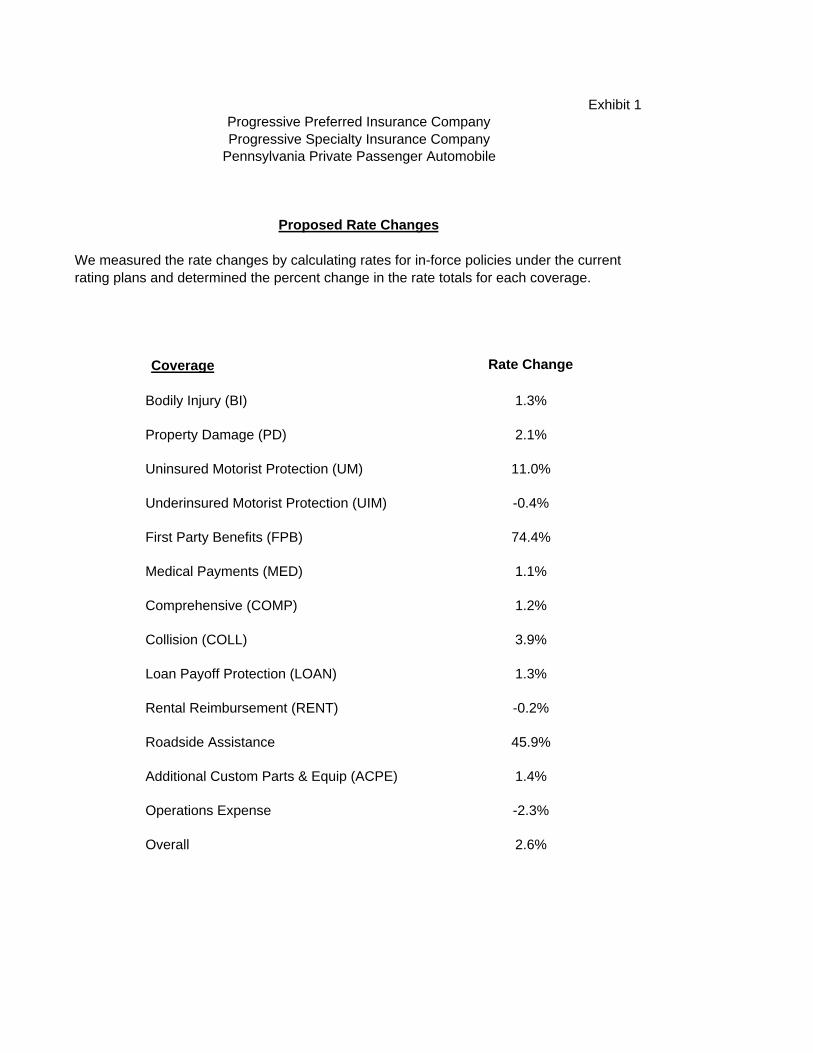

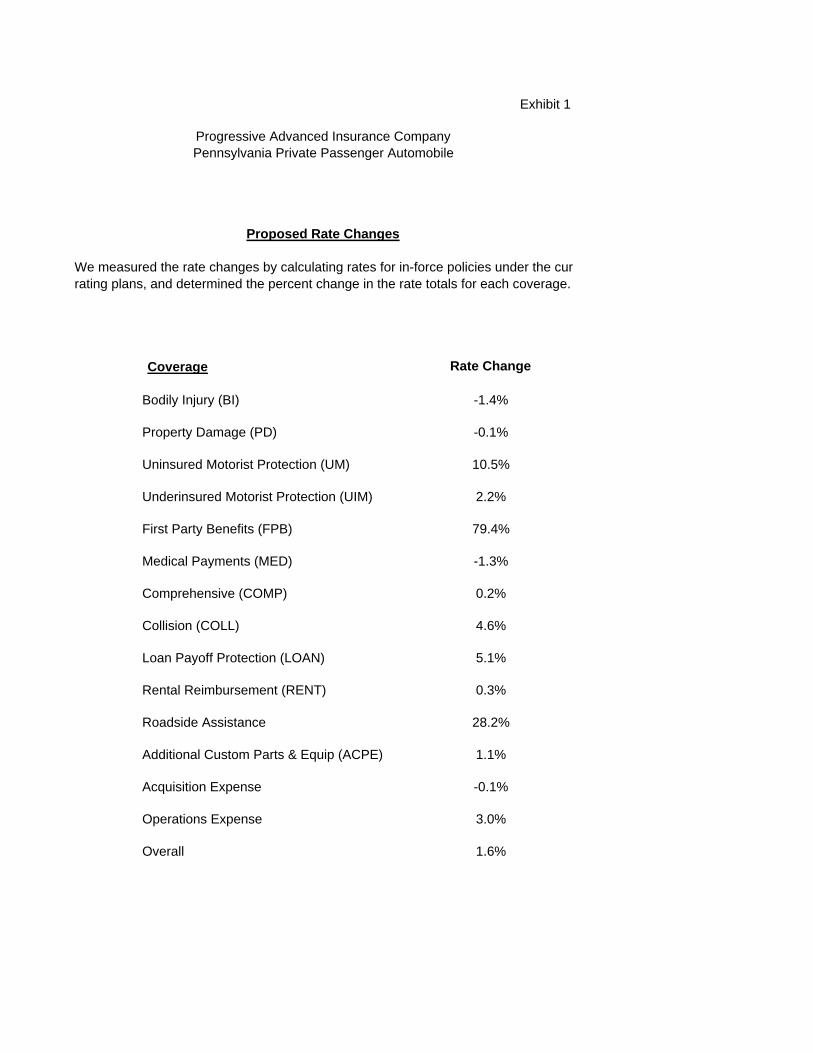

Exhibit 1

We measured the rate changes by calculating rates for in-force policies under the current rating plans and determined the percent change in the rate totals for each coverage.

Coverage Rate Change

Bodily Injury (BI) 1.3%

Property Damage (PD) 2.1%

Uninsured Motorist Protection (UM) 11.0%

Underinsured Motorist Protection (UIM) -0.4%

First Party Benefits (FPB) 74.4%

Medical Payments (MED) 1.1%

Comprehensive (COMP) 1.2%

Collision (COLL) 3.9%

Loan Payoff Protection (LOAN) 1.3%

Rental Reimbursement (RENT) -0.2%

Roadside Assistance 45.9%

Additional Custom Parts & Equip (ACPE) 1.4%

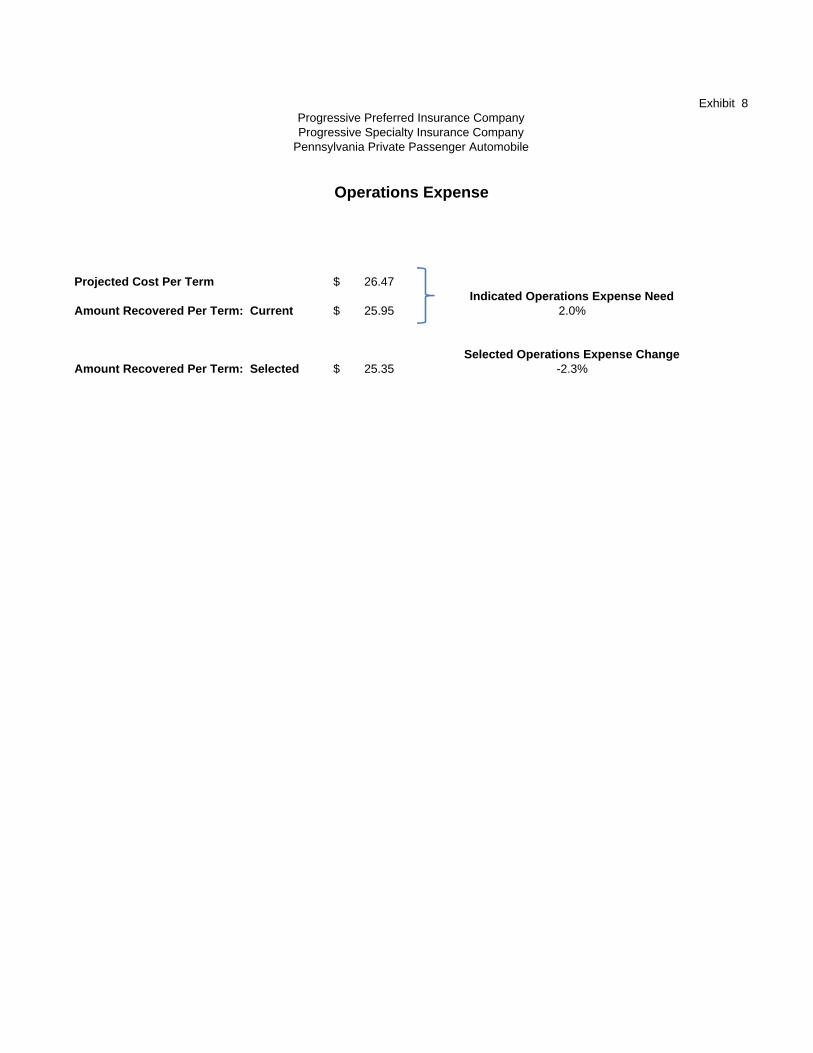

Operations Expense -2.3%

Overall 2.6%

Proposed Rate Changes

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

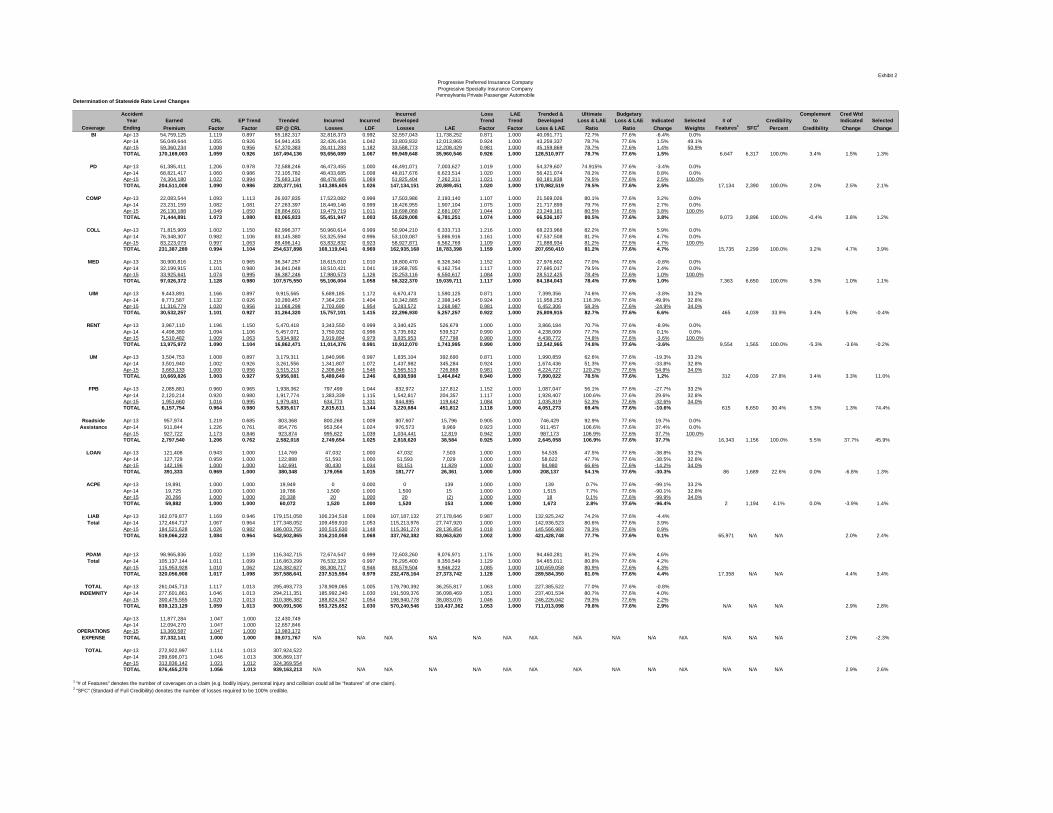

Exhibit 2Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger AutomobileDetermination of Statewide Rate Level Changes

Accident Incurred Loss LAE Trended & Ultimate Budgetary Complement Cred WtdYear Earned CRL EP Trend Trended Incurred Incurred Developed Trend Trend Developed Loss & LAE Loss & LAE Indicated Selected # of Credibility to Indicated Selected

Coverage Ending Premium Factor Factor EP @ CRL Losses LDF Losses LAE Factor Factor Loss & LAE Ratio Ratio Change Weights Features1 SFC2Percent Credibility Change Change

BI Apr-13 54,759,125 1.119 0.897 55,182,317 32,818,373 0.992 32,557,043 11,738,252 0.871 1.000 40,091,771 72.7% 77.6% -6.4% 0.0%Apr-14 56,049,644 1.055 0.926 54,941,435 32,426,434 1.042 33,803,832 12,013,865 0.924 1.000 43,259,337 78.7% 77.6% 1.5% 49.1%Apr-15 59,360,234 1.008 0.956 57,370,383 28,411,283 1.182 33,588,773 12,208,429 0.981 1.000 45,159,869 78.7% 77.6% 1.4% 50.9%TOTAL 170,169,003 1.059 0.926 167,494,136 93,656,089 1.067 99,949,648 35,960,546 0.926 1.000 128,510,977 78.7% 77.6% 1.5% 6,647 6,317 100.0% 3.4% 1.5% 1.3%

PD Apr-13 61,385,411 1.206 0.978 72,588,246 46,473,455 1.000 46,491,071 7,003,627 1.019 1.000 54,379,607 74.915% 77.6% -3.4% 0.0%Apr-14 68,821,417 1.060 0.986 72,105,782 48,433,685 1.008 48,817,676 6,623,514 1.020 1.000 56,421,074 78.2% 77.6% 0.8% 0.0%Apr-15 74,304,180 1.022 0.994 75,683,134 48,478,465 1.069 51,825,404 7,262,311 1.021 1.000 60,181,838 79.5% 77.6% 2.5% 100.0%TOTAL 204,511,008 1.090 0.986 220,377,161 143,385,605 1.026 147,134,151 20,889,451 1.020 1.000 170,982,519 79.5% 77.6% 2.5% 17,134 2,390 100.0% 2.0% 2.5% 2.1%

COMP Apr-13 22,083,544 1.093 1.113 26,937,835 17,523,082 0.999 17,503,986 2,193,140 1.107 1.000 21,569,026 80.1% 77.6% 3.2% 0.0%Apr-14 23,231,159 1.082 1.081 27,263,397 18,449,146 0.999 18,426,955 1,907,104 1.075 1.000 21,717,899 79.7% 77.6% 2.7% 0.0%Apr-15 26,130,188 1.049 1.050 28,864,601 19,479,719 1.011 19,698,068 2,681,007 1.044 1.000 23,249,181 80.5% 77.6% 3.8% 100.0%TOTAL 71,444,891 1.073 1.080 83,065,833 55,451,947 1.003 55,629,008 6,781,251 1.074 1.000 66,536,107 80.5% 77.6% 3.8% 9,073 3,896 100.0% -0.4% 3.8% 1.2%

COLL Apr-13 71,815,909 1.002 1.150 82,996,377 50,960,614 0.999 50,904,210 6,333,713 1.216 1.000 68,223,968 82.2% 77.6% 5.9% 0.0%Apr-14 76,348,307 0.982 1.106 83,145,380 53,325,594 0.996 53,103,087 5,886,916 1.161 1.000 67,537,508 81.2% 77.6% 4.7% 0.0%Apr-15 83,223,073 0.997 1.063 88,496,141 63,832,832 0.923 58,927,871 6,562,769 1.109 1.000 71,888,934 81.2% 77.6% 4.7% 100.0%TOTAL 231,387,289 0.994 1.104 254,637,898 168,119,041 0.969 162,935,168 18,783,398 1.159 1.000 207,650,410 81.2% 77.6% 4.7% 15,735 2,299 100.0% 3.2% 4.7% 3.9%

MED Apr-13 30,900,816 1.215 0.965 36,347,257 18,615,010 1.010 18,800,470 6,326,340 1.152 1.000 27,976,602 77.0% 77.6% -0.8% 0.0%Apr-14 32,199,915 1.101 0.980 34,841,048 18,510,421 1.041 19,268,785 6,162,754 1.117 1.000 27,695,017 79.5% 77.6% 2.4% 0.0%Apr-15 33,925,641 1.074 0.995 36,387,246 17,980,573 1.126 20,253,116 6,550,617 1.084 1.000 28,512,425 78.4% 77.6% 1.0% 100.0%TOTAL 97,026,372 1.128 0.980 107,575,550 55,106,004 1.058 58,322,370 19,039,711 1.117 1.000 84,184,043 78.4% 77.6% 1.0% 7,363 6,650 100.0% 5.3% 1.0% 1.1%

UIM Apr-13 9,443,891 1.166 0.897 9,915,565 5,689,185 1.172 6,670,473 1,590,125 0.871 1.000 7,399,356 74.6% 77.6% -3.8% 33.2%Apr-14 9,771,587 1.132 0.926 10,280,457 7,364,226 1.404 10,342,885 2,398,145 0.924 1.000 11,958,253 116.3% 77.6% 49.9% 32.8%Apr-15 11,316,779 1.020 0.956 11,068,298 2,703,690 1.954 5,283,572 1,268,987 0.981 1.000 6,452,306 58.3% 77.6% -24.9% 34.0%TOTAL 30,532,257 1.101 0.927 31,264,320 15,757,101 1.415 22,296,930 5,257,257 0.922 1.000 25,809,915 82.7% 77.6% 6.6% 465 4,039 33.9% 3.4% 5.0% -0.4%

RENT Apr-13 3,967,110 1.196 1.150 5,470,418 3,343,550 0.999 3,340,425 526,679 1.000 1.000 3,866,184 70.7% 77.6% -8.9% 0.0%Apr-14 4,498,380 1.094 1.106 5,457,071 3,750,932 0.996 3,735,692 539,517 0.990 1.000 4,238,009 77.7% 77.6% 0.1% 0.0%Apr-15 5,510,482 1.009 1.063 5,934,982 3,919,894 0.979 3,835,953 677,798 0.980 1.000 4,438,772 74.8% 77.6% -3.6% 100.0%TOTAL 13,975,972 1.090 1.104 16,862,471 11,014,376 0.991 10,912,070 1,743,995 0.990 1.000 12,542,965 74.8% 77.6% -3.6% 9,554 1,565 100.0% -5.3% -3.6% -0.2%

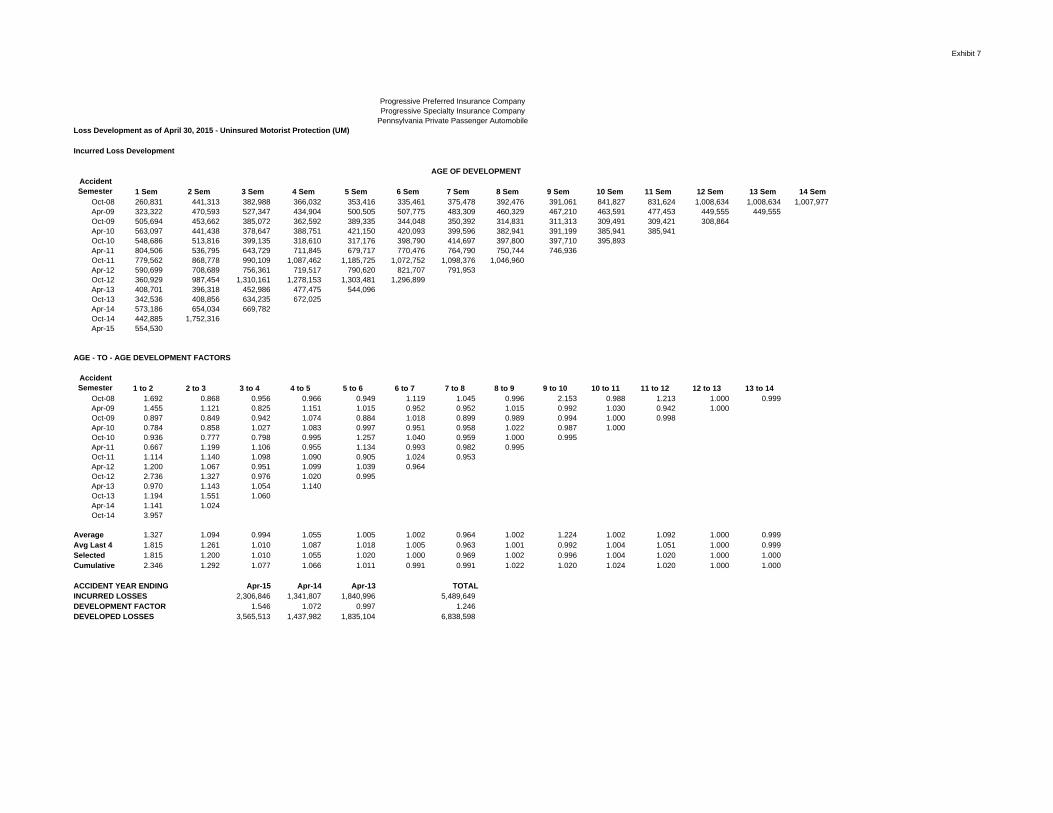

UM Apr-13 3,504,753 1.008 0.897 3,179,311 1,840,996 0.997 1,835,104 392,690 0.871 1.000 1,990,859 62.6% 77.6% -19.3% 33.2%Apr-14 3,501,940 1.002 0.926 3,261,556 1,341,807 1.072 1,437,982 345,284 0.924 1.000 1,674,436 51.3% 77.6% -33.8% 32.8%Apr-15 3,663,133 1.000 0.956 3,515,213 2,306,846 1.546 3,565,513 726,868 0.981 1.000 4,224,727 120.2% 77.6% 54.9% 34.0%TOTAL 10,669,826 1.003 0.927 9,956,081 5,489,649 1.246 6,838,598 1,464,842 0.940 1.000 7,890,022 78.5% 77.6% 1.2% 312 4,039 27.8% 3.4% 3.3% 11.0%

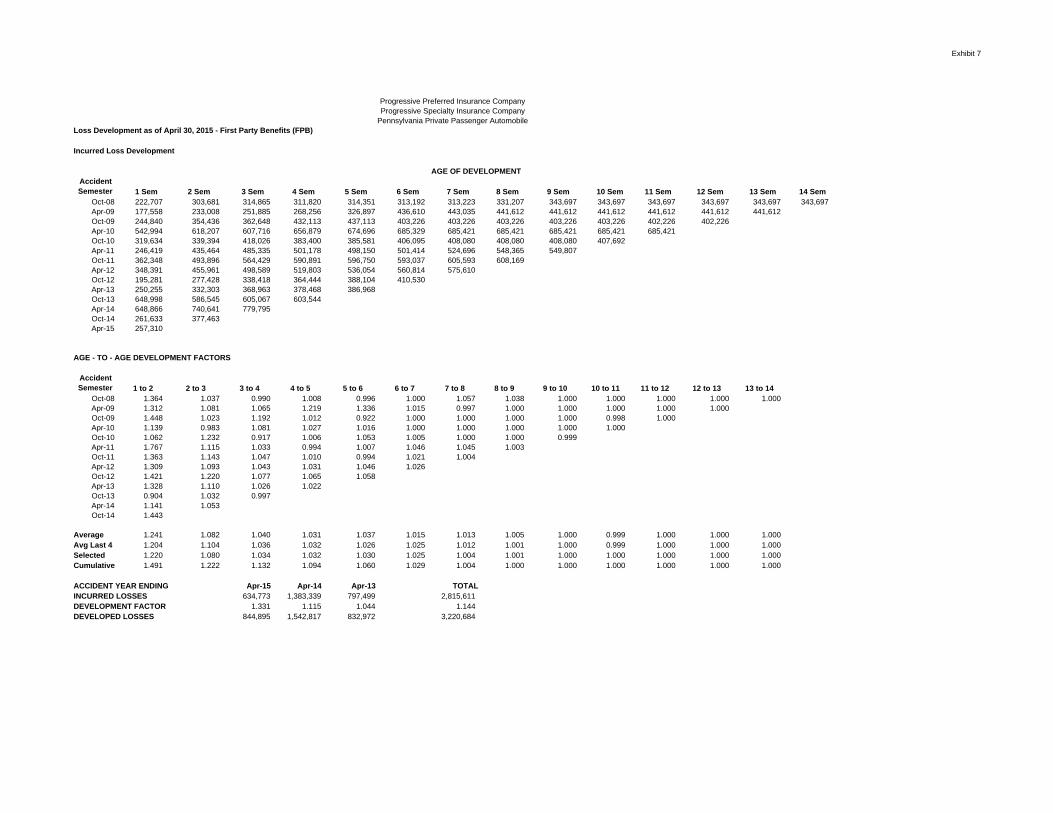

FPB Apr-13 2,085,881 0.960 0.965 1,938,362 797,499 1.044 832,972 127,812 1.152 1.000 1,087,047 56.1% 77.6% -27.7% 33.2%Apr-14 2,120,214 0.920 0.980 1,917,774 1,383,339 1.115 1,542,817 204,357 1.117 1.000 1,928,407 100.6% 77.6% 29.6% 32.8%Apr-15 1,951,660 1.016 0.995 1,979,481 634,773 1.331 844,895 119,642 1.084 1.000 1,035,819 52.3% 77.6% -32.6% 34.0%TOTAL 6,157,754 0.964 0.980 5,835,617 2,815,611 1.144 3,220,684 451,812 1.118 1.000 4,051,273 69.4% 77.6% -10.6% 615 6,650 30.4% 5.3% 1.3% 74.4%

Roadside Apr-13 957,974 1.219 0.685 803,368 800,268 1.009 807,607 15,796 0.905 1.000 746,429 92.9% 77.6% 19.7% 0.0%Assistance Apr-14 911,844 1.226 0.761 854,776 953,564 1.024 976,573 9,969 0.923 1.000 911,457 106.6% 77.6% 37.4% 0.0%

Apr-15 927,722 1.173 0.846 923,874 995,822 1.039 1,034,441 12,819 0.942 1.000 987,173 106.9% 77.6% 37.7% 100.0%TOTAL 2,797,540 1.206 0.762 2,582,018 2,749,654 1.025 2,818,620 38,584 0.925 1.000 2,645,058 106.9% 77.6% 37.7% 16,343 1,156 100.0% 5.5% 37.7% 45.9%

LOAN Apr-13 121,408 0.943 1.000 114,769 47,032 1.000 47,032 7,503 1.000 1.000 54,535 47.5% 77.6% -38.8% 33.2%Apr-14 127,729 0.959 1.000 122,888 51,593 1.000 51,593 7,029 1.000 1.000 58,622 47.7% 77.6% -38.5% 32.8%Apr-15 142,196 1.000 1.000 142,691 80,430 1.034 83,151 11,829 1.000 1.000 94,980 66.6% 77.6% -14.2% 34.0%TOTAL 391,333 0.969 1.000 380,348 179,056 1.015 181,777 26,361 1.000 1.000 208,137 54.1% 77.6% -30.3% 86 1,689 22.6% 0.0% -6.8% 1.3%

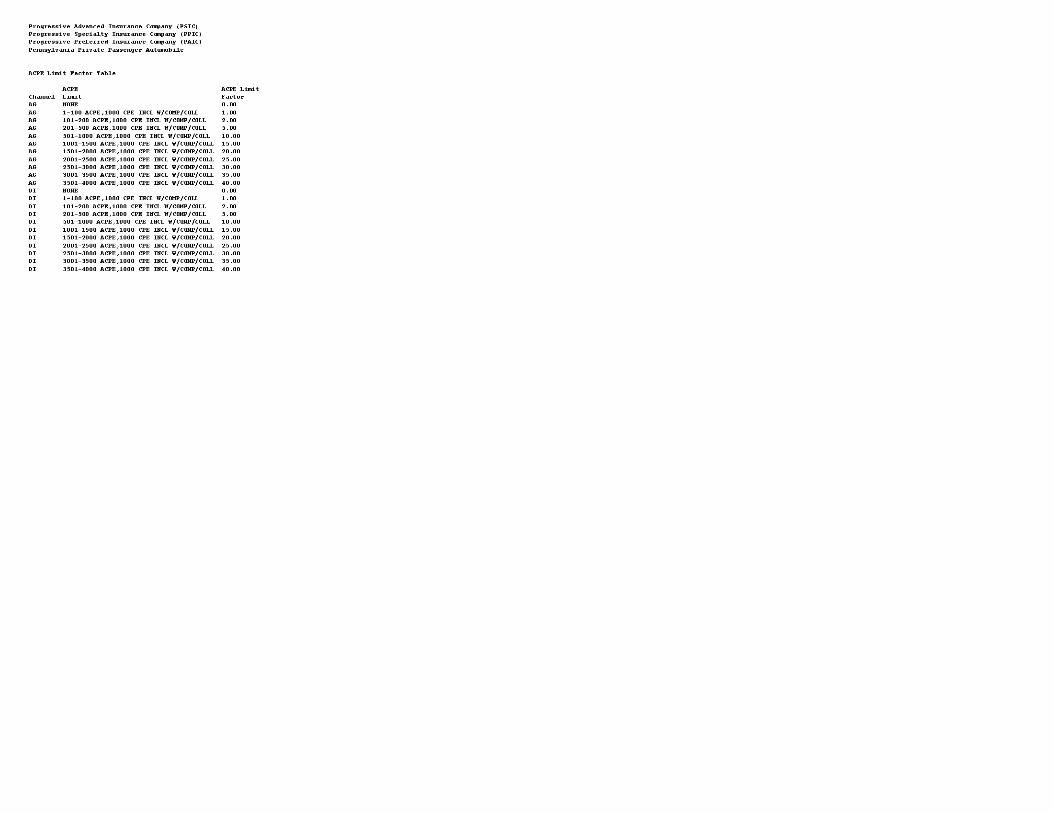

ACPE Apr-13 19,891 1.000 1.000 19,949 0 0.000 0 139 1.000 1.000 139 0.7% 77.6% -99.1% 33.2%Apr-14 19,725 1.000 1.000 19,786 1,500 1.000 1,500 15 1.000 1.000 1,515 7.7% 77.6% -90.1% 32.8%Apr-15 20,266 1.000 1.000 20,338 20 1.000 20 (2) 1.000 1.000 18 0.1% 77.6% -99.9% 34.0%TOTAL 59,882 1.000 1.000 60,072 1,520 1.000 1,520 153 1.000 1.000 1,673 2.8% 77.6% -96.4% 2 1,194 4.1% 0.0% -3.9% 1.4%

LIAB Apr-13 162,079,877 1.169 0.946 179,151,058 106,234,518 1.009 107,187,132 27,178,846 0.987 1.000 132,925,242 74.2% 77.6% -4.4%Total Apr-14 172,464,717 1.067 0.964 177,348,052 109,459,910 1.053 115,213,976 27,747,920 1.000 1.000 142,936,523 80.6% 77.6% 3.9%

Apr-15 184,521,628 1.026 0.982 186,003,755 100,515,630 1.148 115,361,274 28,136,854 1.018 1.000 145,566,983 78.3% 77.6% 0.9%TOTAL 519,066,222 1.084 0.964 542,502,865 316,210,058 1.068 337,762,382 83,063,620 1.002 1.000 421,428,748 77.7% 77.6% 0.1% 65,971 N/A N/A 2.0% 2.4%

PDAM Apr-13 98,965,836 1.032 1.139 116,342,715 72,674,547 0.999 72,603,260 9,076,971 1.176 1.000 94,460,281 81.2% 77.6% 4.6%Total Apr-14 105,137,144 1.011 1.099 116,863,299 76,532,329 0.997 76,295,400 8,350,549 1.129 1.000 94,465,011 80.8% 77.6% 4.2%

Apr-15 115,953,928 1.010 1.062 124,382,627 88,308,717 0.946 83,579,504 9,946,222 1.085 1.000 100,659,058 80.9% 77.6% 4.3%TOTAL 320,056,908 1.017 1.098 357,588,641 237,515,594 0.979 232,478,164 27,373,742 1.128 1.000 289,584,350 81.0% 77.6% 4.4% 17,358 N/A N/A 4.4% 3.4%

TOTAL Apr-13 261,045,713 1.117 1.013 295,493,773 178,909,065 1.005 179,790,392 36,255,817 1.063 1.000 227,385,522 77.0% 77.6% -0.8%INDEMNITY Apr-14 277,601,861 1.046 1.013 294,211,351 185,992,240 1.030 191,509,376 36,098,469 1.051 1.000 237,401,534 80.7% 77.6% 4.0%

Apr-15 300,475,555 1.020 1.013 310,386,382 188,824,347 1.054 198,940,778 38,083,076 1.046 1.000 246,226,042 79.3% 77.6% 2.2%TOTAL 839,123,129 1.059 1.013 900,091,506 553,725,652 1.030 570,240,546 110,437,362 1.053 1.000 711,013,098 79.8% 77.6% 2.9% N/A N/A N/A 2.9% 2.8%

Apr-13 11,877,284 1.047 1.000 12,430,749Apr-14 12,094,270 1.047 1.000 12,657,846

OPERATIONS Apr-15 13,360,587 1.047 1.000 13,983,172EXPENSE TOTAL 37,332,141 1.000 1.000 39,071,767 N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 2.0% -2.3%

TOTAL Apr-13 272,922,997 1.114 1.013 307,924,522Apr-14 289,696,071 1.046 1.013 306,869,137Apr-15 313,836,142 1.021 1.012 324,369,554TOTAL 876,455,270 1.056 1.013 939,163,213 N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 2.9% 2.6%

1 "# of Features" denotes the number of coverages on a claim (e.g. bodily injury, personal injury and collision could all be “features” of one claim).2 "SFC" (Standard of Full Credibility) denotes the number of losses required to be 100% credible.

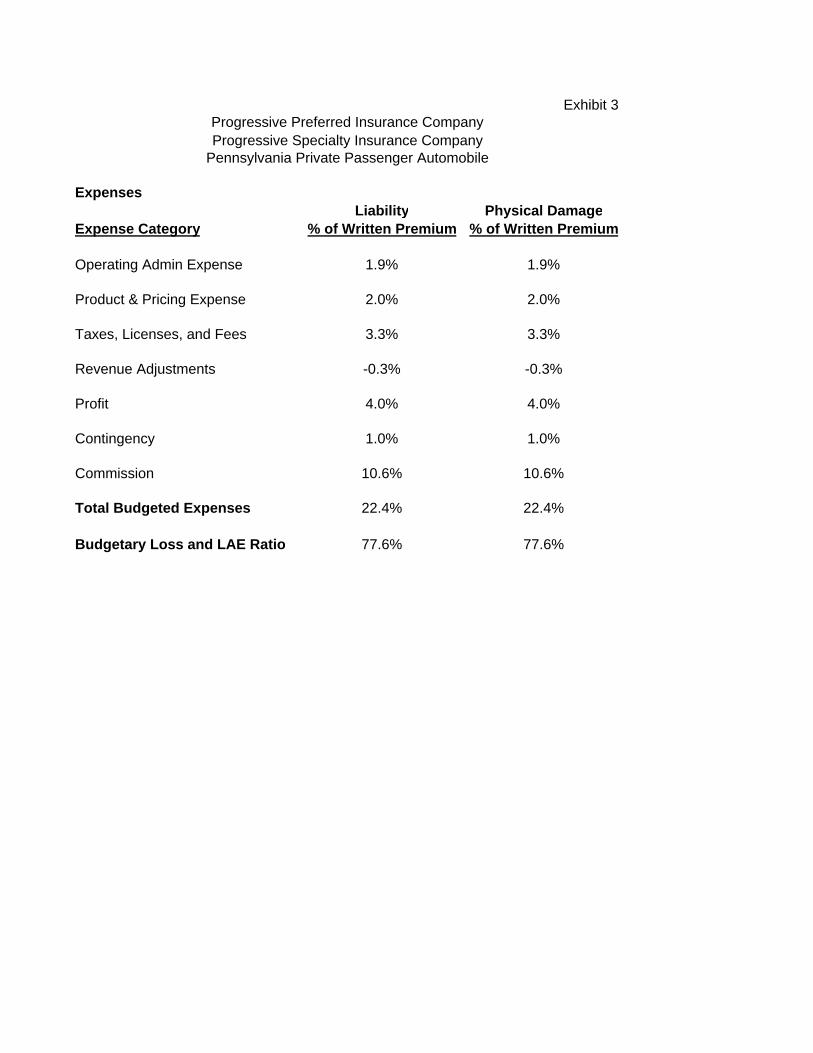

Exhibit 3Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

ExpensesLiability Physical Damage

Expense Category % of Written Premium % of Written Premium

Operating Admin Expense 1.9% 1.9%

Product & Pricing Expense 2.0% 2.0%

Taxes, Licenses, and Fees 3.3% 3.3%

Revenue Adjustments -0.3% -0.3%

Profit 4.0% 4.0%

Contingency 1.0% 1.0%

Commission 10.6% 10.6%

Total Budgeted Expenses 22.4% 22.4%

Budgetary Loss and LAE Ratio 77.6% 77.6%

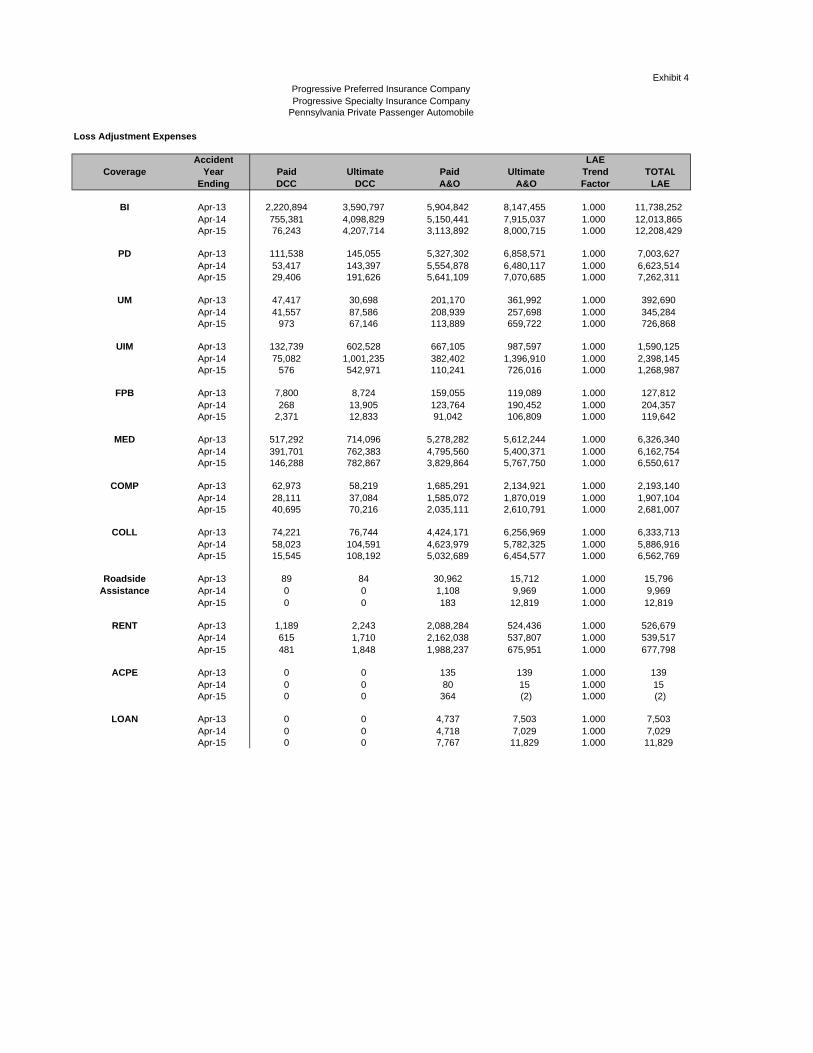

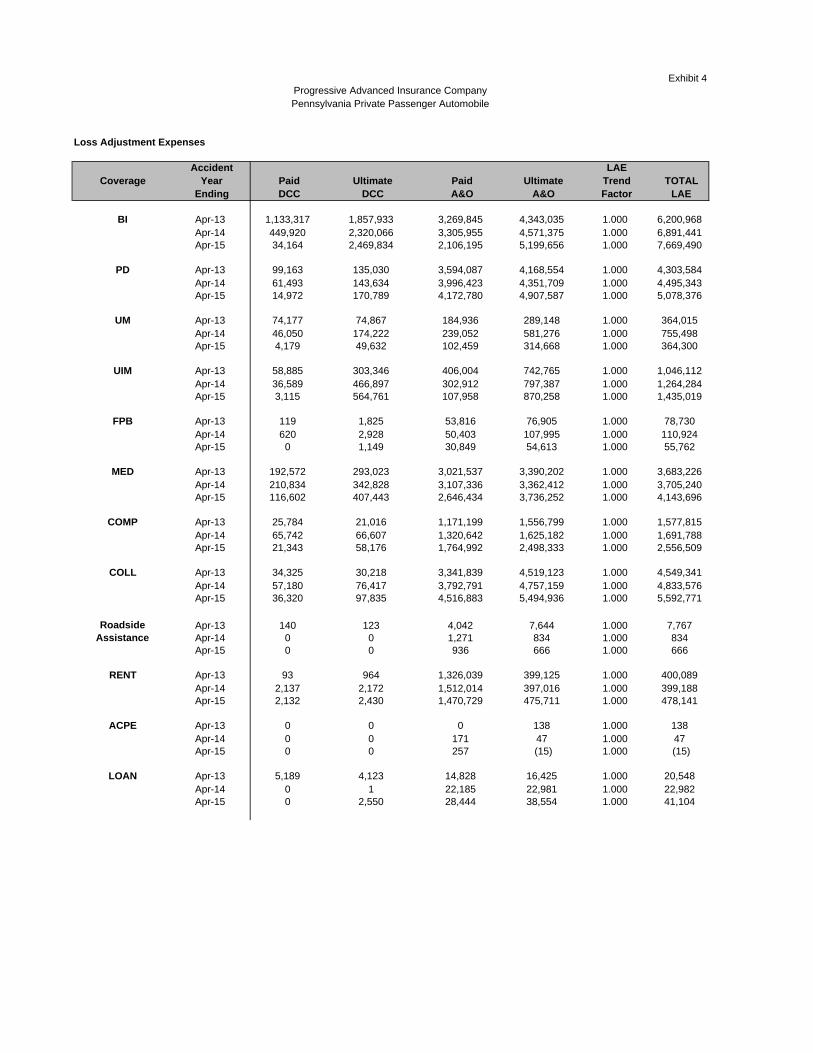

Exhibit 4Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

Loss Adjustment Expenses

Accident LAECoverage Year Paid Ultimate Paid Ultimate Trend TOTAL

Ending DCC DCC A&O A&O Factor LAE

BI Apr-13 2,220,894 3,590,797 5,904,842 8,147,455 1.000 11,738,252Apr-14 755,381 4,098,829 5,150,441 7,915,037 1.000 12,013,865Apr-15 76,243 4,207,714 3,113,892 8,000,715 1.000 12,208,429

PD Apr-13 111,538 145,055 5,327,302 6,858,571 1.000 7,003,627Apr-14 53,417 143,397 5,554,878 6,480,117 1.000 6,623,514Apr-15 29,406 191,626 5,641,109 7,070,685 1.000 7,262,311

UM Apr-13 47,417 30,698 201,170 361,992 1.000 392,690Apr-14 41,557 87,586 208,939 257,698 1.000 345,284Apr-15 973 67,146 113,889 659,722 1.000 726,868

UIM Apr-13 132,739 602,528 667,105 987,597 1.000 1,590,125Apr-14 75,082 1,001,235 382,402 1,396,910 1.000 2,398,145Apr-15 576 542,971 110,241 726,016 1.000 1,268,987

FPB Apr-13 7,800 8,724 159,055 119,089 1.000 127,812Apr-14 268 13,905 123,764 190,452 1.000 204,357Apr-15 2,371 12,833 91,042 106,809 1.000 119,642

MED Apr-13 517,292 714,096 5,278,282 5,612,244 1.000 6,326,340Apr-14 391,701 762,383 4,795,560 5,400,371 1.000 6,162,754Apr-15 146,288 782,867 3,829,864 5,767,750 1.000 6,550,617

COMP Apr-13 62,973 58,219 1,685,291 2,134,921 1.000 2,193,140Apr-14 28,111 37,084 1,585,072 1,870,019 1.000 1,907,104Apr-15 40,695 70,216 2,035,111 2,610,791 1.000 2,681,007

COLL Apr-13 74,221 76,744 4,424,171 6,256,969 1.000 6,333,713Apr-14 58,023 104,591 4,623,979 5,782,325 1.000 5,886,916Apr-15 15,545 108,192 5,032,689 6,454,577 1.000 6,562,769

Roadside Apr-13 89 84 30,962 15,712 1.000 15,796Assistance Apr-14 0 0 1,108 9,969 1.000 9,969

Apr-15 0 0 183 12,819 1.000 12,819

RENT Apr-13 1,189 2,243 2,088,284 524,436 1.000 526,679Apr-14 615 1,710 2,162,038 537,807 1.000 539,517Apr-15 481 1,848 1,988,237 675,951 1.000 677,798

ACPE Apr-13 0 0 135 139 1.000 139Apr-14 0 0 80 15 1.000 15Apr-15 0 0 364 (2) 1.000 (2)

LOAN Apr-13 0 0 4,737 7,503 1.000 7,503Apr-14 0 0 4,718 7,029 1.000 7,029Apr-15 0 0 7,767 11,829 1.000 11,829

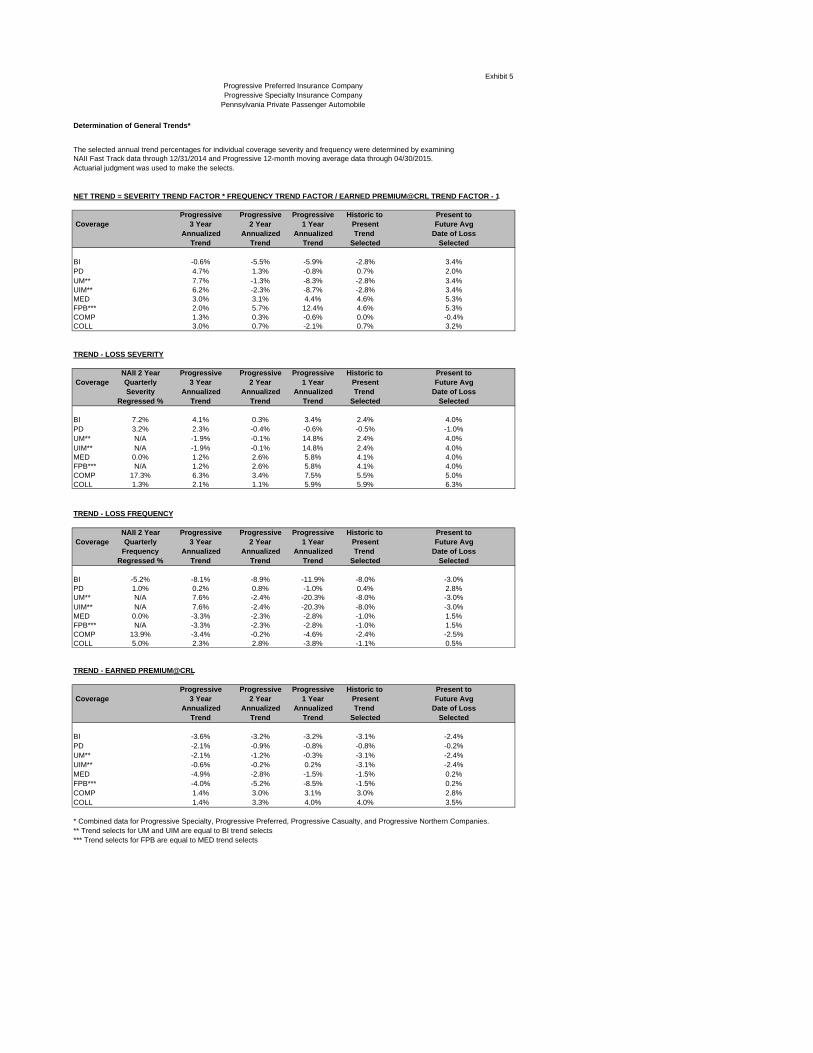

Exhibit 5Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

Determination of General Trends*

The selected annual trend percentages for individual coverage severity and frequency were determined by examiningNAII Fast Track data through 12/31/2014 and Progressive 12-month moving average data through 04/30/2015.Actuarial judgment was used to make the selects.

NET TREND = SEVERITY TREND FACTOR * FREQUENCY TREND FACTOR / EARNED PREMIUM@CRL TREND FACTOR - 1

Progressive Progressive Progressive Historic to Present toCoverage 3 Year 2 Year 1 Year Present Future Avg

Annualized Annualized Annualized Trend Date of LossTrend Trend Trend Selected Selected

BI -0.6% -5.5% -5.9% -2.8% 3.4%PD 4.7% 1.3% -0.8% 0.7% 2.0%UM** 7.7% -1.3% -8.3% -2.8% 3.4%UIM** 6.2% -2.3% -8.7% -2.8% 3.4%MED 3.0% 3.1% 4.4% 4.6% 5.3%FPB*** 2.0% 5.7% 12.4% 4.6% 5.3%COMP 1.3% 0.3% -0.6% 0.0% -0.4%COLL 3.0% 0.7% -2.1% 0.7% 3.2%

TREND - LOSS SEVERITY

NAII 2 Year Progressive Progressive Progressive Historic to Present toCoverage Quarterly 3 Year 2 Year 1 Year Present Future Avg

Severity Annualized Annualized Annualized Trend Date of LossRegressed % Trend Trend Trend Selected Selected

BI 7.2% 4.1% 0.3% 3.4% 2.4% 4.0%PD 3.2% 2.3% -0.4% -0.6% -0.5% -1.0%UM** N/A -1.9% -0.1% 14.8% 2.4% 4.0%UIM** N/A -1.9% -0.1% 14.8% 2.4% 4.0%MED 0.0% 1.2% 2.6% 5.8% 4.1% 4.0%FPB*** N/A 1.2% 2.6% 5.8% 4.1% 4.0%COMP 17.3% 6.3% 3.4% 7.5% 5.5% 5.0%COLL 1.3% 2.1% 1.1% 5.9% 5.9% 6.3%

TREND - LOSS FREQUENCY

NAII 2 Year Progressive Progressive Progressive Historic to Present toCoverage Quarterly 3 Year 2 Year 1 Year Present Future Avg

Frequency Annualized Annualized Annualized Trend Date of LossRegressed % Trend Trend Trend Selected Selected

BI -5.2% -8.1% -8.9% -11.9% -8.0% -3.0%PD 1.0% 0.2% 0.8% -1.0% 0.4% 2.8%UM** N/A 7.6% -2.4% -20.3% -8.0% -3.0%UIM** N/A 7.6% -2.4% -20.3% -8.0% -3.0%MED 0.0% -3.3% -2.3% -2.8% -1.0% 1.5%FPB*** N/A -3.3% -2.3% -2.8% -1.0% 1.5%COMP 13.9% -3.4% -0.2% -4.6% -2.4% -2.5%COLL 5.0% 2.3% 2.8% -3.8% -1.1% 0.5%

TREND - EARNED PREMIUM@CRL

Progressive Progressive Progressive Historic to Present toCoverage 3 Year 2 Year 1 Year Present Future Avg

Annualized Annualized Annualized Trend Date of LossTrend Trend Trend Selected Selected

BI -3.6% -3.2% -3.2% -3.1% -2.4%PD -2.1% -0.9% -0.8% -0.8% -0.2%UM** -2.1% -1.2% -0.3% -3.1% -2.4%UIM** -0.6% -0.2% 0.2% -3.1% -2.4%MED -4.9% -2.8% -1.5% -1.5% 0.2%FPB*** -4.0% -5.2% -8.5% -1.5% 0.2%COMP 1.4% 3.0% 3.1% 3.0% 2.8%COLL 1.4% 3.3% 4.0% 4.0% 3.5%

* Combined data for Progressive Specialty, Progressive Preferred, Progressive Casualty, and Progressive Northern Companies.** Trend selects for UM and UIM are equal to BI trend selects*** Trend selects for FPB are equal to MED trend selects

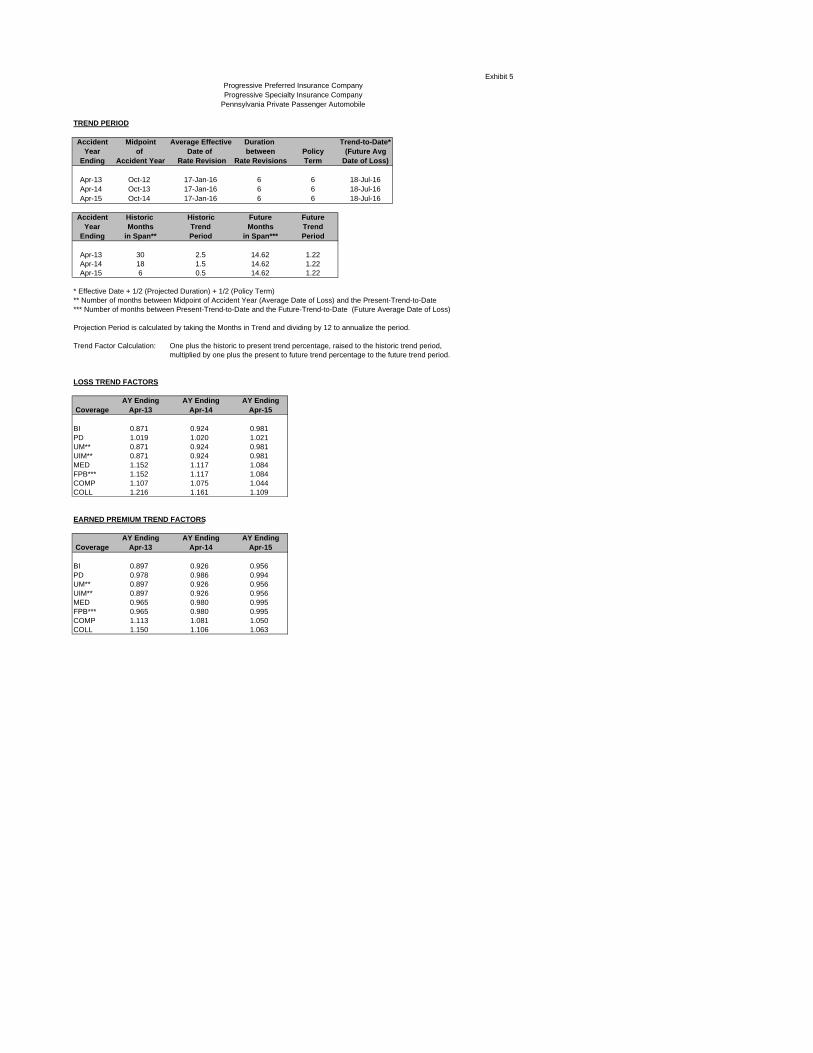

Exhibit 5Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

TREND PERIOD

Accident Midpoint Average Effective Duration Trend-to-Date*Year of Date of between Policy (Future Avg

Ending Accident Year Rate Revision Rate Revisions Term Date of Loss)

Apr-13 Oct-12 17-Jan-16 6 6 18-Jul-16Apr-14 Oct-13 17-Jan-16 6 6 18-Jul-16Apr-15 Oct-14 17-Jan-16 6 6 18-Jul-16

Accident Historic Historic Future FutureYear Months Trend Months Trend

Ending in Span** Period in Span*** Period

Apr-13 30 2.5 14.62 1.22Apr-14 18 1.5 14.62 1.22Apr-15 6 0.5 14.62 1.22

* Effective Date + 1/2 (Projected Duration) + 1/2 (Policy Term)** Number of months between Midpoint of Accident Year (Average Date of Loss) and the Present-Trend-to-Date *** Number of months between Present-Trend-to-Date and the Future-Trend-to-Date (Future Average Date of Loss)

Projection Period is calculated by taking the Months in Trend and dividing by 12 to annualize the period.

Trend Factor Calculation: One plus the historic to present trend percentage, raised to the historic trend period,multiplied by one plus the present to future trend percentage to the future trend period.

LOSS TREND FACTORS

AY Ending AY Ending AY EndingCoverage Apr-13 Apr-14 Apr-15

BI 0.871 0.924 0.981PD 1.019 1.020 1.021UM** 0.871 0.924 0.981UIM** 0.871 0.924 0.981MED 1.152 1.117 1.084FPB*** 1.152 1.117 1.084COMP 1.107 1.075 1.044COLL 1.216 1.161 1.109

EARNED PREMIUM TREND FACTORS

AY Ending AY Ending AY EndingCoverage Apr-13 Apr-14 Apr-15

BI 0.897 0.926 0.956PD 0.978 0.986 0.994UM** 0.897 0.926 0.956UIM** 0.897 0.926 0.956MED 0.965 0.980 0.995FPB*** 0.965 0.980 0.995COMP 1.113 1.081 1.050COLL 1.150 1.106 1.063

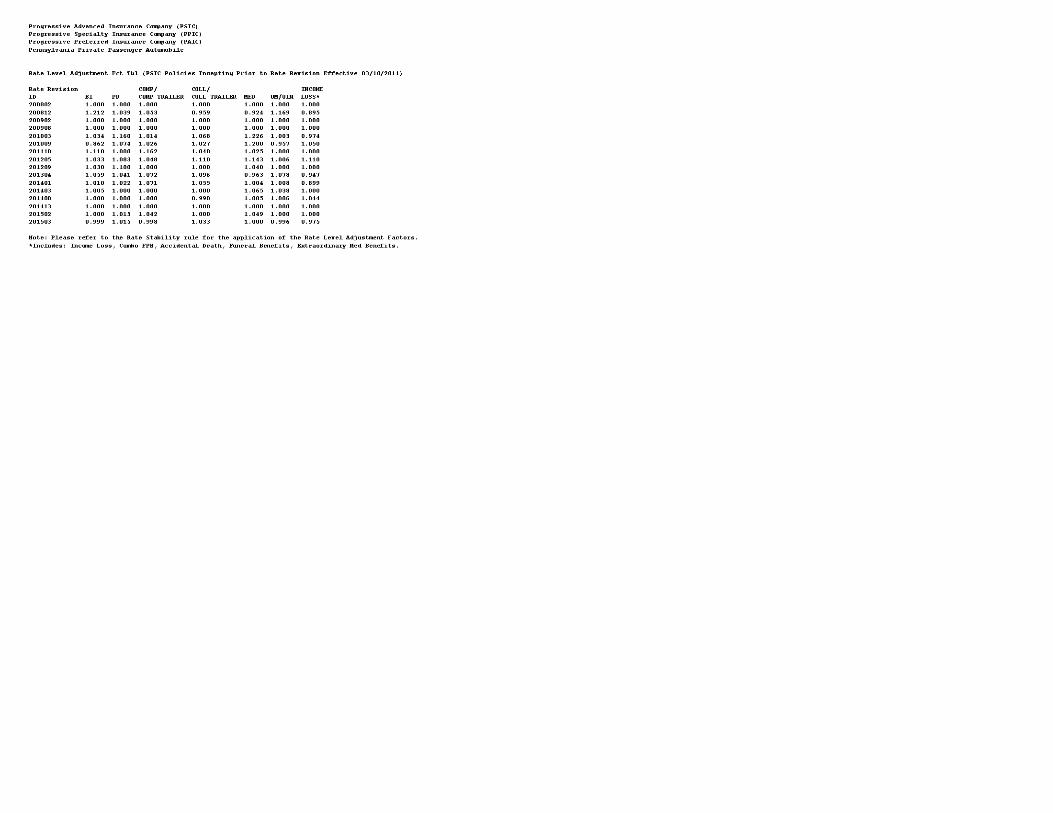

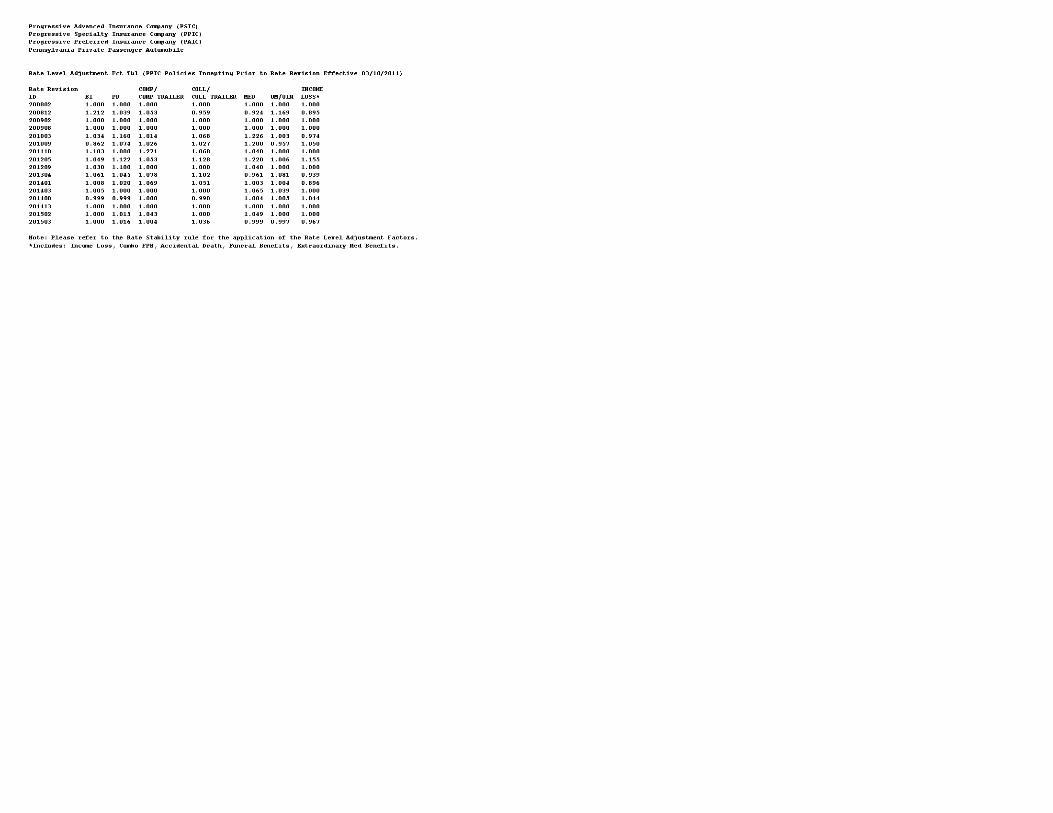

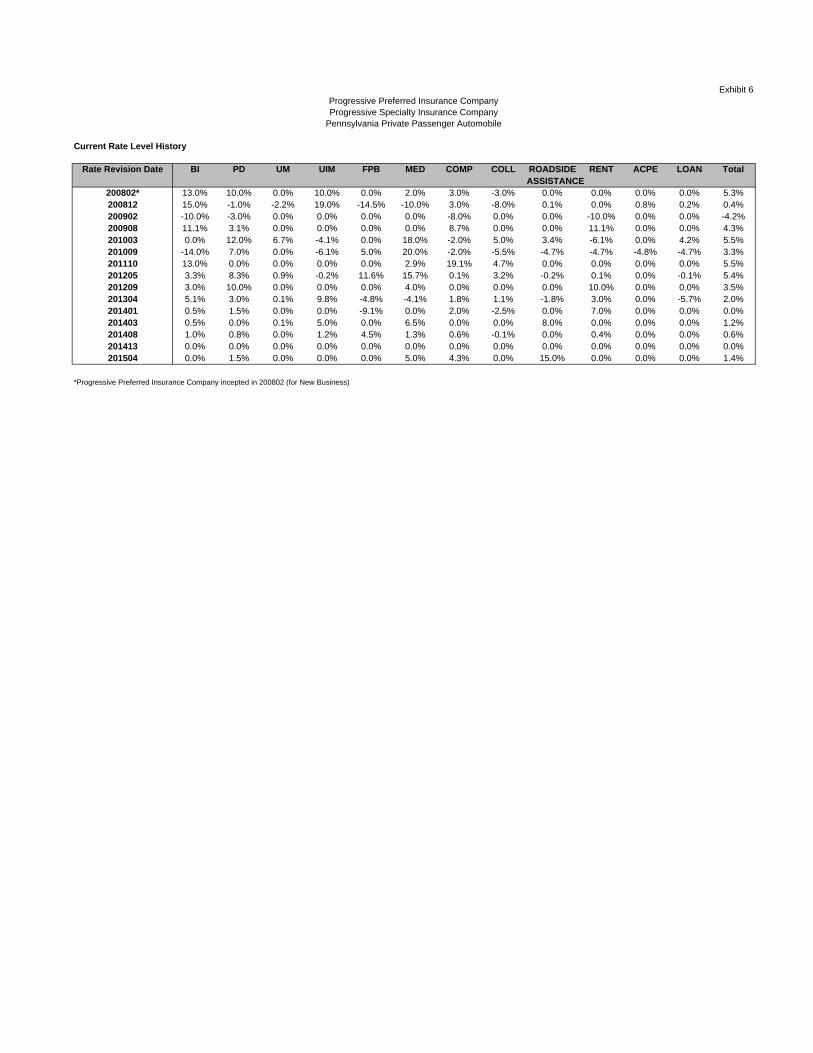

Exhibit 6

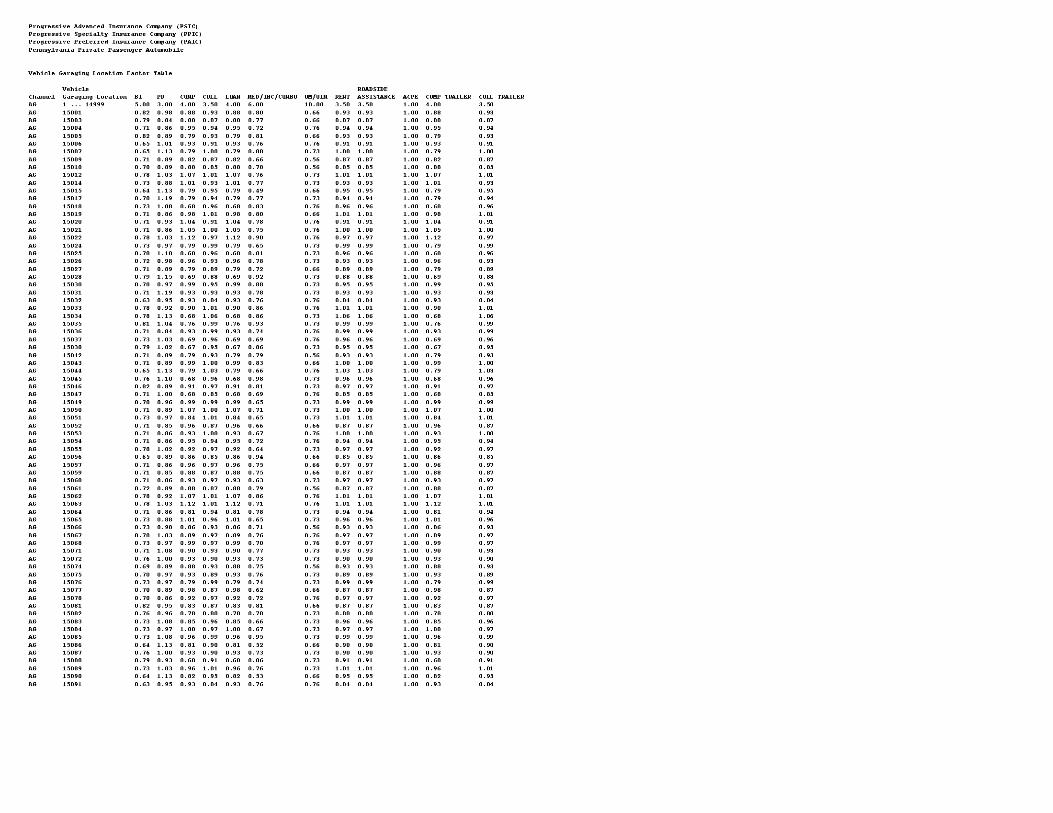

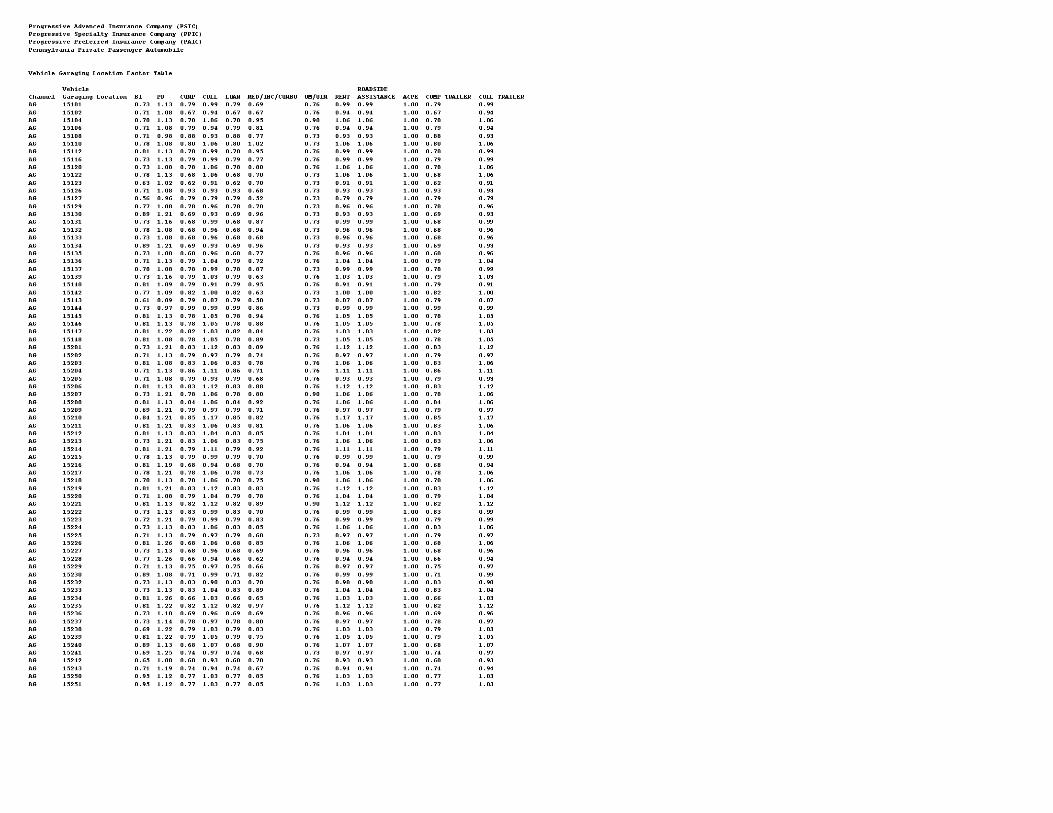

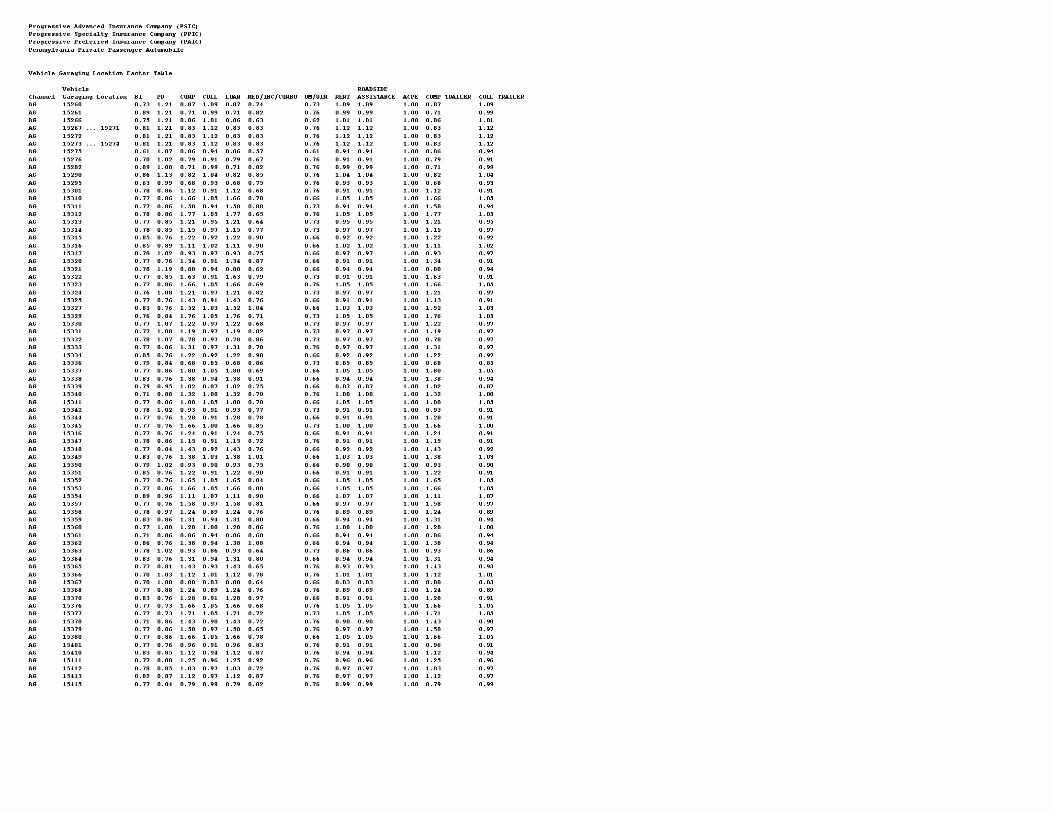

Rate Revision Date BI PD UM UIM FPB MED COMP COLL ROADSIDE RENT ACPE LOAN TotalASSISTANCE

200802* 13.0% 10.0% 0.0% 10.0% 0.0% 2.0% 3.0% -3.0% 0.0% 0.0% 0.0% 0.0% 5.3%200812 15.0% -1.0% -2.2% 19.0% -14.5% -10.0% 3.0% -8.0% 0.1% 0.0% 0.8% 0.2% 0.4%200902 -10.0% -3.0% 0.0% 0.0% 0.0% 0.0% -8.0% 0.0% 0.0% -10.0% 0.0% 0.0% -4.2%200908 11.1% 3.1% 0.0% 0.0% 0.0% 0.0% 8.7% 0.0% 0.0% 11.1% 0.0% 0.0% 4.3%201003 0.0% 12.0% 6.7% -4.1% 0.0% 18.0% -2.0% 5.0% 3.4% -6.1% 0.0% 4.2% 5.5%201009 -14.0% 7.0% 0.0% -6.1% 5.0% 20.0% -2.0% -5.5% -4.7% -4.7% -4.8% -4.7% 3.3%201110 13.0% 0.0% 0.0% 0.0% 0.0% 2.9% 19.1% 4.7% 0.0% 0.0% 0.0% 0.0% 5.5%201205 3.3% 8.3% 0.9% -0.2% 11.6% 15.7% 0.1% 3.2% -0.2% 0.1% 0.0% -0.1% 5.4%201209 3.0% 10.0% 0.0% 0.0% 0.0% 4.0% 0.0% 0.0% 0.0% 10.0% 0.0% 0.0% 3.5%201304 5.1% 3.0% 0.1% 9.8% -4.8% -4.1% 1.8% 1.1% -1.8% 3.0% 0.0% -5.7% 2.0%201401 0.5% 1.5% 0.0% 0.0% -9.1% 0.0% 2.0% -2.5% 0.0% 7.0% 0.0% 0.0% 0.0%201403 0.5% 0.0% 0.1% 5.0% 0.0% 6.5% 0.0% 0.0% 8.0% 0.0% 0.0% 0.0% 1.2%201408 1.0% 0.8% 0.0% 1.2% 4.5% 1.3% 0.6% -0.1% 0.0% 0.4% 0.0% 0.0% 0.6%201413 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%201504 0.0% 1.5% 0.0% 0.0% 0.0% 5.0% 4.3% 0.0% 15.0% 0.0% 0.0% 0.0% 1.4%

*Progressive Preferred Insurance Company incepted in 200802 (for New Business)

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

Current Rate Level History

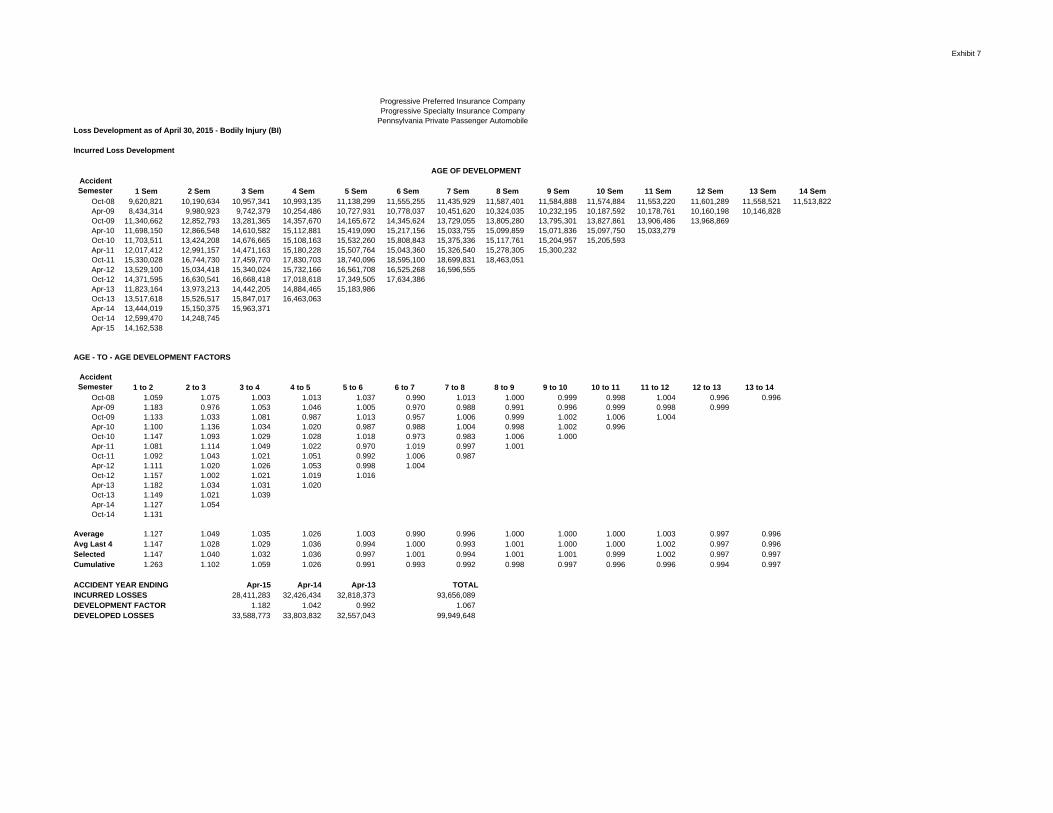

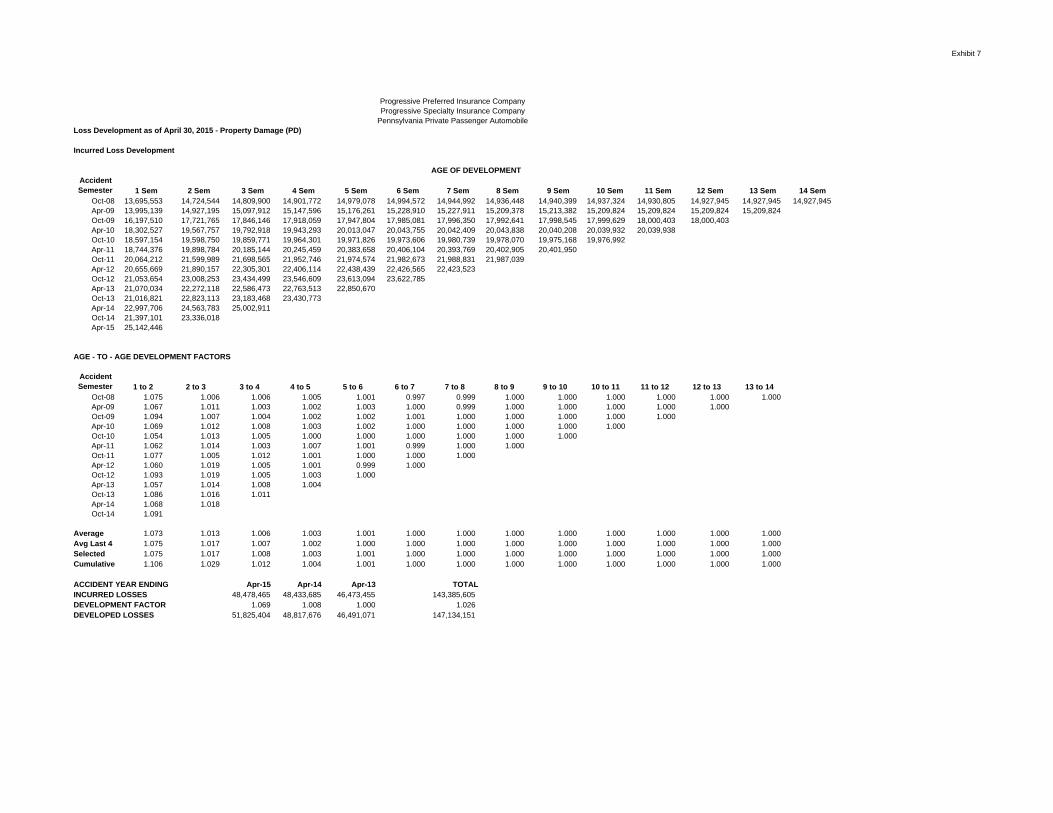

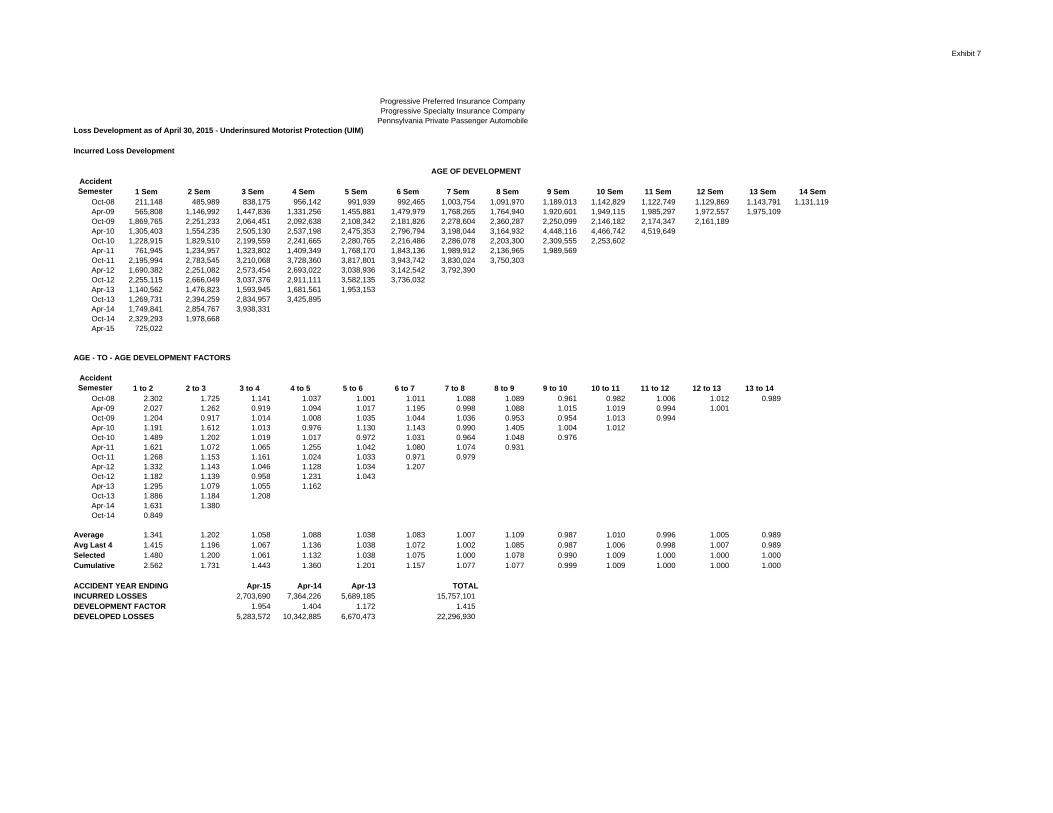

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Bodily Injury (BI)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 9,620,821 10,190,634 10,957,341 10,993,135 11,138,299 11,555,255 11,435,929 11,587,401 11,584,888 11,574,884 11,553,220 11,601,289 11,558,521 11,513,822Apr-09 8,434,314 9,980,923 9,742,379 10,254,486 10,727,931 10,778,037 10,451,620 10,324,035 10,232,195 10,187,592 10,178,761 10,160,198 10,146,828Oct-09 11,340,662 12,852,793 13,281,365 14,357,670 14,165,672 14,345,624 13,729,055 13,805,280 13,795,301 13,827,861 13,906,486 13,968,869Apr-10 11,698,150 12,866,548 14,610,582 15,112,881 15,419,090 15,217,156 15,033,755 15,099,859 15,071,836 15,097,750 15,033,279Oct-10 11,703,511 13,424,208 14,676,665 15,108,163 15,532,260 15,808,843 15,375,336 15,117,761 15,204,957 15,205,593Apr-11 12,017,412 12,991,157 14,471,163 15,180,228 15,507,764 15,043,360 15,326,540 15,278,305 15,300,232Oct-11 15,330,028 16,744,730 17,459,770 17,830,703 18,740,096 18,595,100 18,699,831 18,463,051Apr-12 13,529,100 15,034,418 15,340,024 15,732,166 16,561,708 16,525,268 16,596,555Oct-12 14,371,595 16,630,541 16,668,418 17,018,618 17,349,505 17,634,386Apr-13 11,823,164 13,973,213 14,442,205 14,884,465 15,183,986Oct-13 13,517,618 15,526,517 15,847,017 16,463,063Apr-14 13,444,019 15,150,375 15,963,371Oct-14 12,599,470 14,248,745Apr-15 14,162,538

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.059 1.075 1.003 1.013 1.037 0.990 1.013 1.000 0.999 0.998 1.004 0.996 0.996Apr-09 1.183 0.976 1.053 1.046 1.005 0.970 0.988 0.991 0.996 0.999 0.998 0.999Oct-09 1.133 1.033 1.081 0.987 1.013 0.957 1.006 0.999 1.002 1.006 1.004Apr-10 1.100 1.136 1.034 1.020 0.987 0.988 1.004 0.998 1.002 0.996Oct-10 1.147 1.093 1.029 1.028 1.018 0.973 0.983 1.006 1.000Apr-11 1.081 1.114 1.049 1.022 0.970 1.019 0.997 1.001Oct-11 1.092 1.043 1.021 1.051 0.992 1.006 0.987Apr-12 1.111 1.020 1.026 1.053 0.998 1.004Oct-12 1.157 1.002 1.021 1.019 1.016Apr-13 1.182 1.034 1.031 1.020Oct-13 1.149 1.021 1.039Apr-14 1.127 1.054Oct-14 1.131

Average 1.127 1.049 1.035 1.026 1.003 0.990 0.996 1.000 1.000 1.000 1.003 0.997 0.996Avg Last 4 1.147 1.028 1.029 1.036 0.994 1.000 0.993 1.001 1.000 1.000 1.002 0.997 0.996Selected 1.147 1.040 1.032 1.036 0.997 1.001 0.994 1.001 1.001 0.999 1.002 0.997 0.997Cumulative 1.263 1.102 1.059 1.026 0.991 0.993 0.992 0.998 0.997 0.996 0.996 0.994 0.997

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 28,411,283 32,426,434 32,818,373 93,656,089DEVELOPMENT FACTOR 1.182 1.042 0.992 1.067DEVELOPED LOSSES 33,588,773 33,803,832 32,557,043 99,949,648

AGE OF DEVELOPMENT

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Property Damage (PD)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 13,695,553 14,724,544 14,809,900 14,901,772 14,979,078 14,994,572 14,944,992 14,936,448 14,940,399 14,937,324 14,930,805 14,927,945 14,927,945 14,927,945Apr-09 13,995,139 14,927,195 15,097,912 15,147,596 15,176,261 15,228,910 15,227,911 15,209,378 15,213,382 15,209,824 15,209,824 15,209,824 15,209,824Oct-09 16,197,510 17,721,765 17,846,146 17,918,059 17,947,804 17,985,081 17,996,350 17,992,641 17,998,545 17,999,629 18,000,403 18,000,403Apr-10 18,302,527 19,567,757 19,792,918 19,943,293 20,013,047 20,043,755 20,042,409 20,043,838 20,040,208 20,039,932 20,039,938Oct-10 18,597,154 19,598,750 19,859,771 19,964,301 19,971,826 19,973,606 19,980,739 19,978,070 19,975,168 19,976,992Apr-11 18,744,376 19,898,784 20,185,144 20,245,459 20,383,658 20,406,104 20,393,769 20,402,905 20,401,950Oct-11 20,064,212 21,599,989 21,698,565 21,952,746 21,974,574 21,982,673 21,988,831 21,987,039Apr-12 20,655,669 21,890,157 22,305,301 22,406,114 22,438,439 22,426,565 22,423,523Oct-12 21,053,654 23,008,253 23,434,499 23,546,609 23,613,094 23,622,785Apr-13 21,070,034 22,272,118 22,586,473 22,763,513 22,850,670Oct-13 21,016,821 22,823,113 23,183,468 23,430,773Apr-14 22,997,706 24,563,783 25,002,911Oct-14 21,397,101 23,336,018Apr-15 25,142,446

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.075 1.006 1.006 1.005 1.001 0.997 0.999 1.000 1.000 1.000 1.000 1.000 1.000Apr-09 1.067 1.011 1.003 1.002 1.003 1.000 0.999 1.000 1.000 1.000 1.000 1.000Oct-09 1.094 1.007 1.004 1.002 1.002 1.001 1.000 1.000 1.000 1.000 1.000Apr-10 1.069 1.012 1.008 1.003 1.002 1.000 1.000 1.000 1.000 1.000Oct-10 1.054 1.013 1.005 1.000 1.000 1.000 1.000 1.000 1.000Apr-11 1.062 1.014 1.003 1.007 1.001 0.999 1.000 1.000Oct-11 1.077 1.005 1.012 1.001 1.000 1.000 1.000Apr-12 1.060 1.019 1.005 1.001 0.999 1.000Oct-12 1.093 1.019 1.005 1.003 1.000Apr-13 1.057 1.014 1.008 1.004Oct-13 1.086 1.016 1.011Apr-14 1.068 1.018Oct-14 1.091

Average 1.073 1.013 1.006 1.003 1.001 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Avg Last 4 1.075 1.017 1.007 1.002 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Selected 1.075 1.017 1.008 1.003 1.001 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Cumulative 1.106 1.029 1.012 1.004 1.001 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 48,478,465 48,433,685 46,473,455 143,385,605DEVELOPMENT FACTOR 1.069 1.008 1.000 1.026DEVELOPED LOSSES 51,825,404 48,817,676 46,491,071 147,134,151

AGE OF DEVELOPMENT

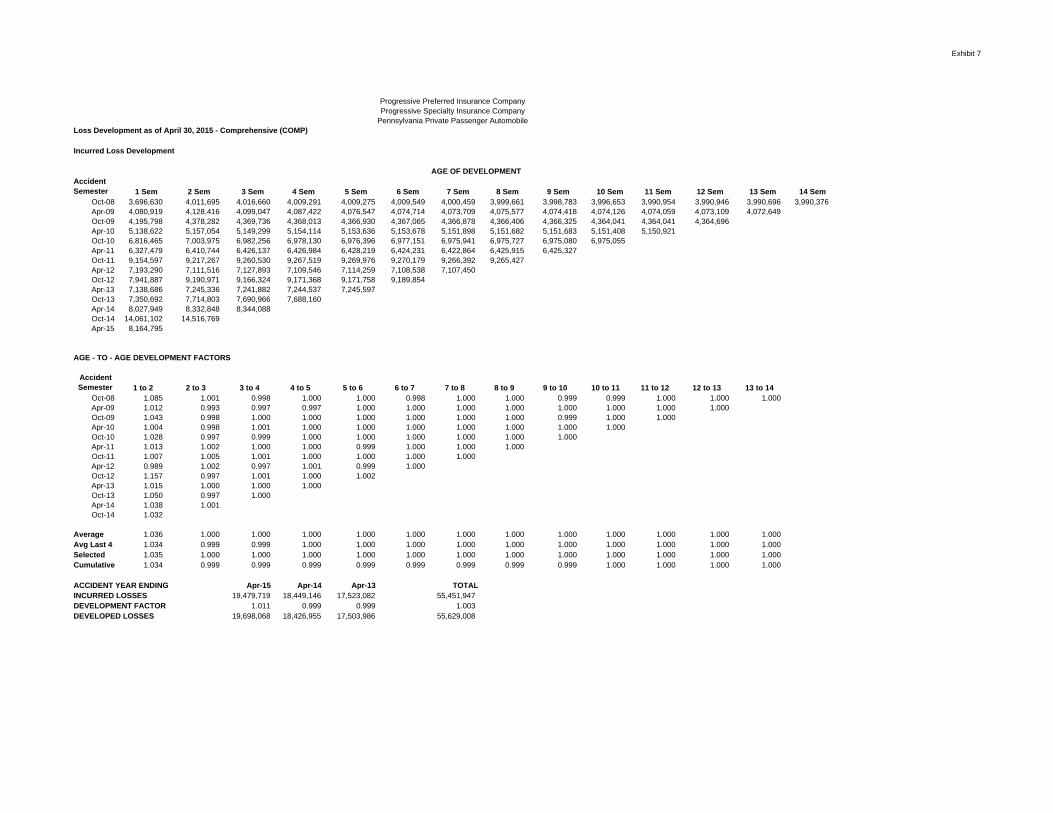

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Comprehensive (COMP)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 3,696,630 4,011,695 4,016,660 4,009,291 4,009,275 4,009,549 4,000,459 3,999,661 3,998,783 3,996,653 3,990,954 3,990,946 3,990,696 3,990,376Apr-09 4,080,919 4,128,416 4,099,047 4,087,422 4,076,547 4,074,714 4,073,709 4,075,577 4,074,418 4,074,126 4,074,059 4,073,109 4,072,649Oct-09 4,195,798 4,378,282 4,369,736 4,368,013 4,366,930 4,367,065 4,366,878 4,366,406 4,366,325 4,364,041 4,364,041 4,364,696Apr-10 5,138,622 5,157,054 5,149,299 5,154,114 5,153,636 5,153,678 5,151,898 5,151,682 5,151,683 5,151,408 5,150,921Oct-10 6,816,465 7,003,975 6,982,256 6,978,130 6,976,396 6,977,151 6,975,941 6,975,727 6,975,080 6,975,055Apr-11 6,327,479 6,410,744 6,426,137 6,426,984 6,428,219 6,424,231 6,422,864 6,425,915 6,425,327Oct-11 9,154,597 9,217,267 9,260,530 9,267,519 9,269,976 9,270,179 9,266,392 9,265,427Apr-12 7,193,290 7,111,516 7,127,893 7,109,546 7,114,259 7,108,538 7,107,450Oct-12 7,941,887 9,190,971 9,166,324 9,171,368 9,171,758 9,189,854Apr-13 7,138,686 7,245,336 7,241,882 7,244,537 7,245,597Oct-13 7,350,692 7,714,803 7,690,966 7,688,160Apr-14 8,027,949 8,332,848 8,344,088Oct-14 14,061,102 14,516,769Apr-15 8,164,795

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.085 1.001 0.998 1.000 1.000 0.998 1.000 1.000 0.999 0.999 1.000 1.000 1.000Apr-09 1.012 0.993 0.997 0.997 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Oct-09 1.043 0.998 1.000 1.000 1.000 1.000 1.000 1.000 0.999 1.000 1.000Apr-10 1.004 0.998 1.001 1.000 1.000 1.000 1.000 1.000 1.000 1.000Oct-10 1.028 0.997 0.999 1.000 1.000 1.000 1.000 1.000 1.000Apr-11 1.013 1.002 1.000 1.000 0.999 1.000 1.000 1.000Oct-11 1.007 1.005 1.001 1.000 1.000 1.000 1.000Apr-12 0.989 1.002 0.997 1.001 0.999 1.000Oct-12 1.157 0.997 1.001 1.000 1.002Apr-13 1.015 1.000 1.000 1.000Oct-13 1.050 0.997 1.000Apr-14 1.038 1.001Oct-14 1.032

Average 1.036 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Avg Last 4 1.034 0.999 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Selected 1.035 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Cumulative 1.034 0.999 0.999 0.999 0.999 0.999 0.999 0.999 0.999 1.000 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 19,479,719 18,449,146 17,523,082 55,451,947DEVELOPMENT FACTOR 1.011 0.999 0.999 1.003DEVELOPED LOSSES 19,698,068 18,426,955 17,503,986 55,629,008

AGE OF DEVELOPMENT

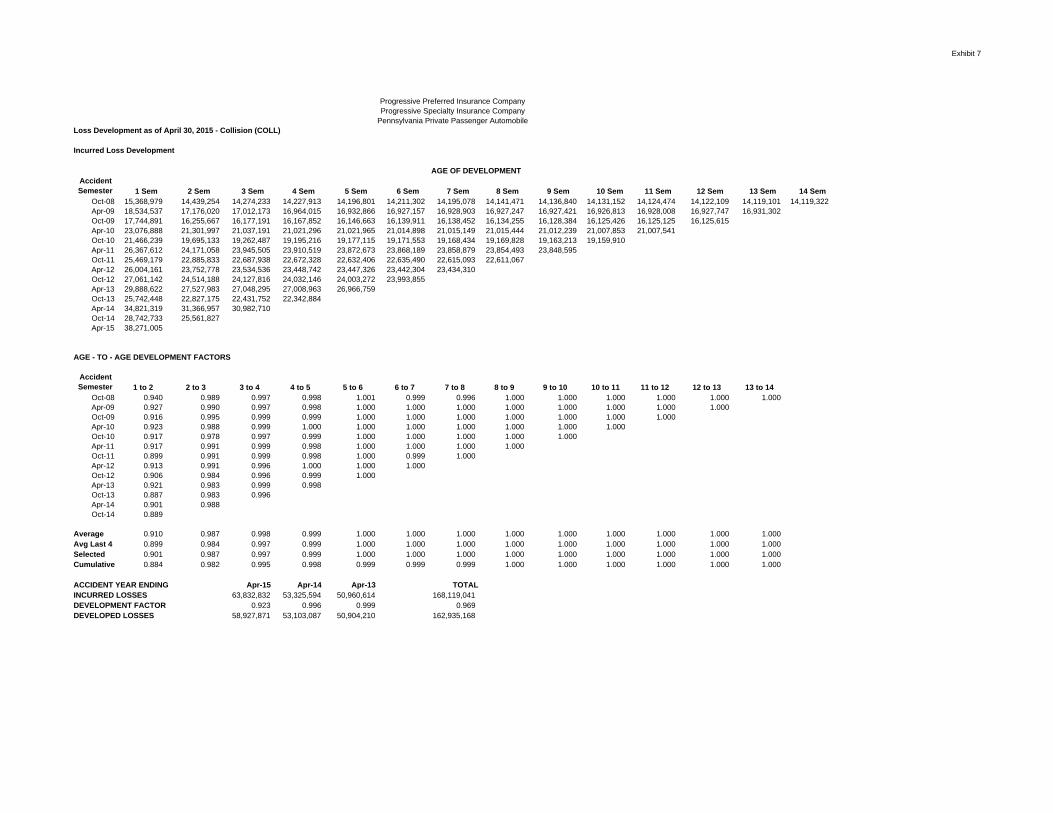

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Collision (COLL)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 15,368,979 14,439,254 14,274,233 14,227,913 14,196,801 14,211,302 14,195,078 14,141,471 14,136,840 14,131,152 14,124,474 14,122,109 14,119,101 14,119,322Apr-09 18,534,537 17,176,020 17,012,173 16,964,015 16,932,866 16,927,157 16,928,903 16,927,247 16,927,421 16,926,813 16,928,008 16,927,747 16,931,302Oct-09 17,744,891 16,255,667 16,177,191 16,167,852 16,146,663 16,139,911 16,138,452 16,134,255 16,128,384 16,125,426 16,125,125 16,125,615Apr-10 23,076,888 21,301,997 21,037,191 21,021,296 21,021,965 21,014,898 21,015,149 21,015,444 21,012,239 21,007,853 21,007,541Oct-10 21,466,239 19,695,133 19,262,487 19,195,216 19,177,115 19,171,553 19,168,434 19,169,828 19,163,213 19,159,910Apr-11 26,367,612 24,171,058 23,945,505 23,910,519 23,872,673 23,868,189 23,858,879 23,854,493 23,848,595Oct-11 25,469,179 22,885,833 22,687,938 22,672,328 22,632,406 22,635,490 22,615,093 22,611,067Apr-12 26,004,161 23,752,778 23,534,536 23,448,742 23,447,326 23,442,304 23,434,310Oct-12 27,061,142 24,514,188 24,127,816 24,032,146 24,003,272 23,993,855Apr-13 29,888,622 27,527,983 27,048,295 27,008,963 26,966,759Oct-13 25,742,448 22,827,175 22,431,752 22,342,884Apr-14 34,821,319 31,366,957 30,982,710Oct-14 28,742,733 25,561,827Apr-15 38,271,005

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 0.940 0.989 0.997 0.998 1.001 0.999 0.996 1.000 1.000 1.000 1.000 1.000 1.000Apr-09 0.927 0.990 0.997 0.998 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Oct-09 0.916 0.995 0.999 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000Apr-10 0.923 0.988 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000Oct-10 0.917 0.978 0.997 0.999 1.000 1.000 1.000 1.000 1.000Apr-11 0.917 0.991 0.999 0.998 1.000 1.000 1.000 1.000Oct-11 0.899 0.991 0.999 0.998 1.000 0.999 1.000Apr-12 0.913 0.991 0.996 1.000 1.000 1.000Oct-12 0.906 0.984 0.996 0.999 1.000Apr-13 0.921 0.983 0.999 0.998Oct-13 0.887 0.983 0.996Apr-14 0.901 0.988Oct-14 0.889

Average 0.910 0.987 0.998 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Avg Last 4 0.899 0.984 0.997 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Selected 0.901 0.987 0.997 0.999 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000Cumulative 0.884 0.982 0.995 0.998 0.999 0.999 0.999 1.000 1.000 1.000 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 63,832,832 53,325,594 50,960,614 168,119,041DEVELOPMENT FACTOR 0.923 0.996 0.999 0.969DEVELOPED LOSSES 58,927,871 53,103,087 50,904,210 162,935,168

AGE OF DEVELOPMENT

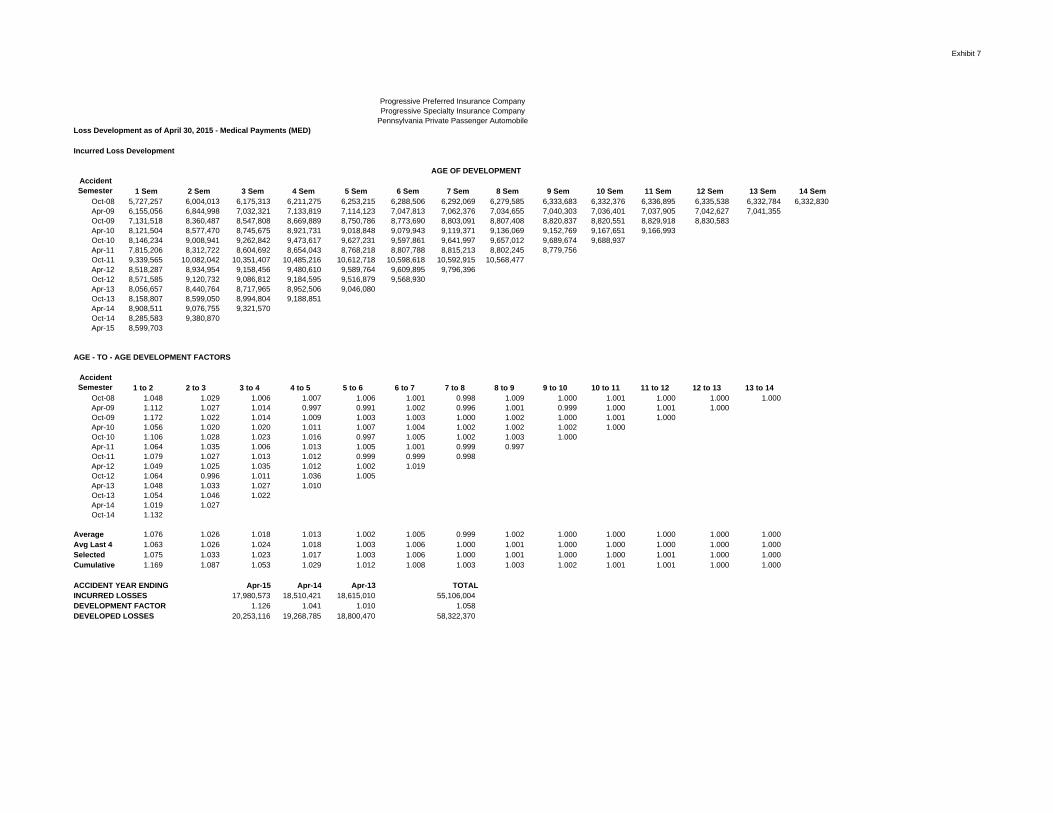

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

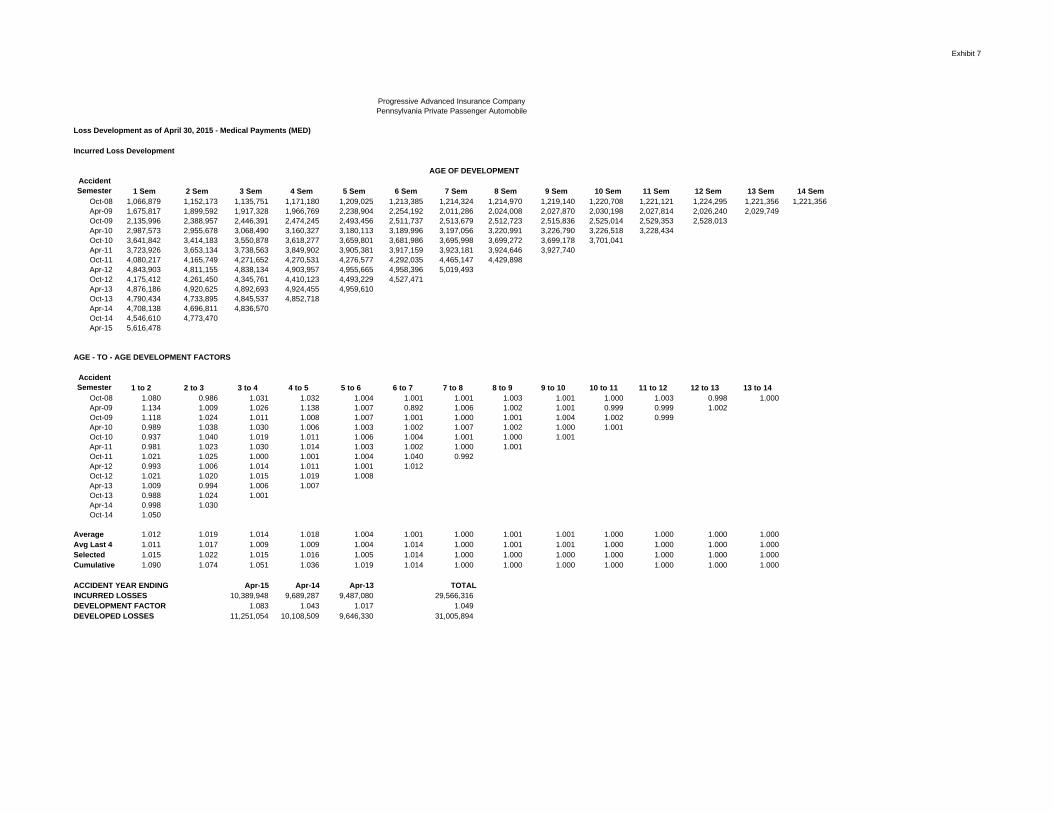

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Medical Payments (MED)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 5,727,257 6,004,013 6,175,313 6,211,275 6,253,215 6,288,506 6,292,069 6,279,585 6,333,683 6,332,376 6,336,895 6,335,538 6,332,784 6,332,830Apr-09 6,155,056 6,844,998 7,032,321 7,133,819 7,114,123 7,047,813 7,062,376 7,034,655 7,040,303 7,036,401 7,037,905 7,042,627 7,041,355Oct-09 7,131,518 8,360,487 8,547,808 8,669,889 8,750,786 8,773,690 8,803,091 8,807,408 8,820,837 8,820,551 8,829,918 8,830,583Apr-10 8,121,504 8,577,470 8,745,675 8,921,731 9,018,848 9,079,943 9,119,371 9,136,069 9,152,769 9,167,651 9,166,993Oct-10 8,146,234 9,008,941 9,262,842 9,473,617 9,627,231 9,597,861 9,641,997 9,657,012 9,689,674 9,688,937Apr-11 7,815,206 8,312,722 8,604,692 8,654,043 8,768,218 8,807,788 8,815,213 8,802,245 8,779,756Oct-11 9,339,565 10,082,042 10,351,407 10,485,216 10,612,718 10,598,618 10,592,915 10,568,477Apr-12 8,518,287 8,934,954 9,158,456 9,480,610 9,589,764 9,609,895 9,796,396Oct-12 8,571,585 9,120,732 9,086,812 9,184,595 9,516,879 9,568,930Apr-13 8,056,657 8,440,764 8,717,965 8,952,506 9,046,080Oct-13 8,158,807 8,599,050 8,994,804 9,188,851Apr-14 8,908,511 9,076,755 9,321,570Oct-14 8,285,583 9,380,870Apr-15 8,599,703

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.048 1.029 1.006 1.007 1.006 1.001 0.998 1.009 1.000 1.001 1.000 1.000 1.000Apr-09 1.112 1.027 1.014 0.997 0.991 1.002 0.996 1.001 0.999 1.000 1.001 1.000Oct-09 1.172 1.022 1.014 1.009 1.003 1.003 1.000 1.002 1.000 1.001 1.000Apr-10 1.056 1.020 1.020 1.011 1.007 1.004 1.002 1.002 1.002 1.000Oct-10 1.106 1.028 1.023 1.016 0.997 1.005 1.002 1.003 1.000Apr-11 1.064 1.035 1.006 1.013 1.005 1.001 0.999 0.997Oct-11 1.079 1.027 1.013 1.012 0.999 0.999 0.998Apr-12 1.049 1.025 1.035 1.012 1.002 1.019Oct-12 1.064 0.996 1.011 1.036 1.005Apr-13 1.048 1.033 1.027 1.010Oct-13 1.054 1.046 1.022Apr-14 1.019 1.027Oct-14 1.132

Average 1.076 1.026 1.018 1.013 1.002 1.005 0.999 1.002 1.000 1.000 1.000 1.000 1.000Avg Last 4 1.063 1.026 1.024 1.018 1.003 1.006 1.000 1.001 1.000 1.000 1.000 1.000 1.000Selected 1.075 1.033 1.023 1.017 1.003 1.006 1.000 1.001 1.000 1.000 1.001 1.000 1.000Cumulative 1.169 1.087 1.053 1.029 1.012 1.008 1.003 1.003 1.002 1.001 1.001 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 17,980,573 18,510,421 18,615,010 55,106,004DEVELOPMENT FACTOR 1.126 1.041 1.010 1.058DEVELOPED LOSSES 20,253,116 19,268,785 18,800,470 58,322,370

AGE OF DEVELOPMENT

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

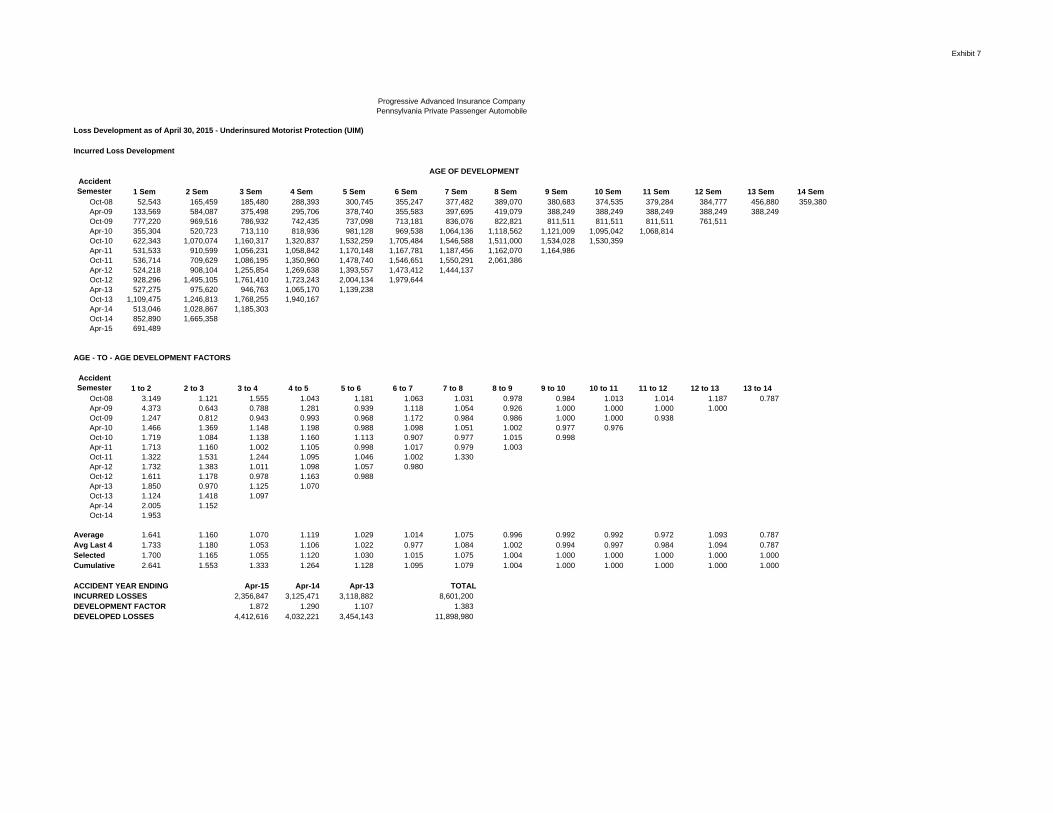

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Underinsured Motorist Protection (UIM)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 211,148 485,989 838,175 956,142 991,939 992,465 1,003,754 1,091,970 1,189,013 1,142,829 1,122,749 1,129,869 1,143,791 1,131,119Apr-09 565,808 1,146,992 1,447,836 1,331,256 1,455,881 1,479,979 1,768,265 1,764,940 1,920,601 1,949,115 1,985,297 1,972,557 1,975,109Oct-09 1,869,765 2,251,233 2,064,451 2,092,638 2,108,342 2,181,826 2,278,604 2,360,287 2,250,099 2,146,182 2,174,347 2,161,189Apr-10 1,305,403 1,554,235 2,505,130 2,537,198 2,475,353 2,796,794 3,198,044 3,164,932 4,448,116 4,466,742 4,519,649Oct-10 1,228,915 1,829,510 2,199,559 2,241,665 2,280,765 2,216,486 2,286,078 2,203,300 2,309,555 2,253,602Apr-11 761,945 1,234,957 1,323,802 1,409,349 1,768,170 1,843,136 1,989,912 2,136,965 1,989,569Oct-11 2,195,994 2,783,545 3,210,068 3,728,360 3,817,801 3,943,742 3,830,024 3,750,303Apr-12 1,690,382 2,251,082 2,573,454 2,693,022 3,038,936 3,142,542 3,792,390Oct-12 2,255,115 2,666,049 3,037,376 2,911,111 3,582,135 3,736,032Apr-13 1,140,562 1,476,823 1,593,945 1,681,561 1,953,153Oct-13 1,269,731 2,394,259 2,834,957 3,425,895Apr-14 1,749,841 2,854,767 3,938,331Oct-14 2,329,293 1,978,668Apr-15 725,022

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 2.302 1.725 1.141 1.037 1.001 1.011 1.088 1.089 0.961 0.982 1.006 1.012 0.989Apr-09 2.027 1.262 0.919 1.094 1.017 1.195 0.998 1.088 1.015 1.019 0.994 1.001Oct-09 1.204 0.917 1.014 1.008 1.035 1.044 1.036 0.953 0.954 1.013 0.994Apr-10 1.191 1.612 1.013 0.976 1.130 1.143 0.990 1.405 1.004 1.012Oct-10 1.489 1.202 1.019 1.017 0.972 1.031 0.964 1.048 0.976Apr-11 1.621 1.072 1.065 1.255 1.042 1.080 1.074 0.931Oct-11 1.268 1.153 1.161 1.024 1.033 0.971 0.979Apr-12 1.332 1.143 1.046 1.128 1.034 1.207Oct-12 1.182 1.139 0.958 1.231 1.043Apr-13 1.295 1.079 1.055 1.162Oct-13 1.886 1.184 1.208Apr-14 1.631 1.380Oct-14 0.849

Average 1.341 1.202 1.058 1.088 1.038 1.083 1.007 1.109 0.987 1.010 0.996 1.005 0.989Avg Last 4 1.415 1.196 1.067 1.136 1.038 1.072 1.002 1.085 0.987 1.006 0.998 1.007 0.989Selected 1.480 1.200 1.061 1.132 1.038 1.075 1.000 1.078 0.990 1.009 1.000 1.000 1.000Cumulative 2.562 1.731 1.443 1.360 1.201 1.157 1.077 1.077 0.999 1.009 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 2,703,690 7,364,226 5,689,185 15,757,101DEVELOPMENT FACTOR 1.954 1.404 1.172 1.415DEVELOPED LOSSES 5,283,572 10,342,885 6,670,473 22,296,930

AGE OF DEVELOPMENT

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

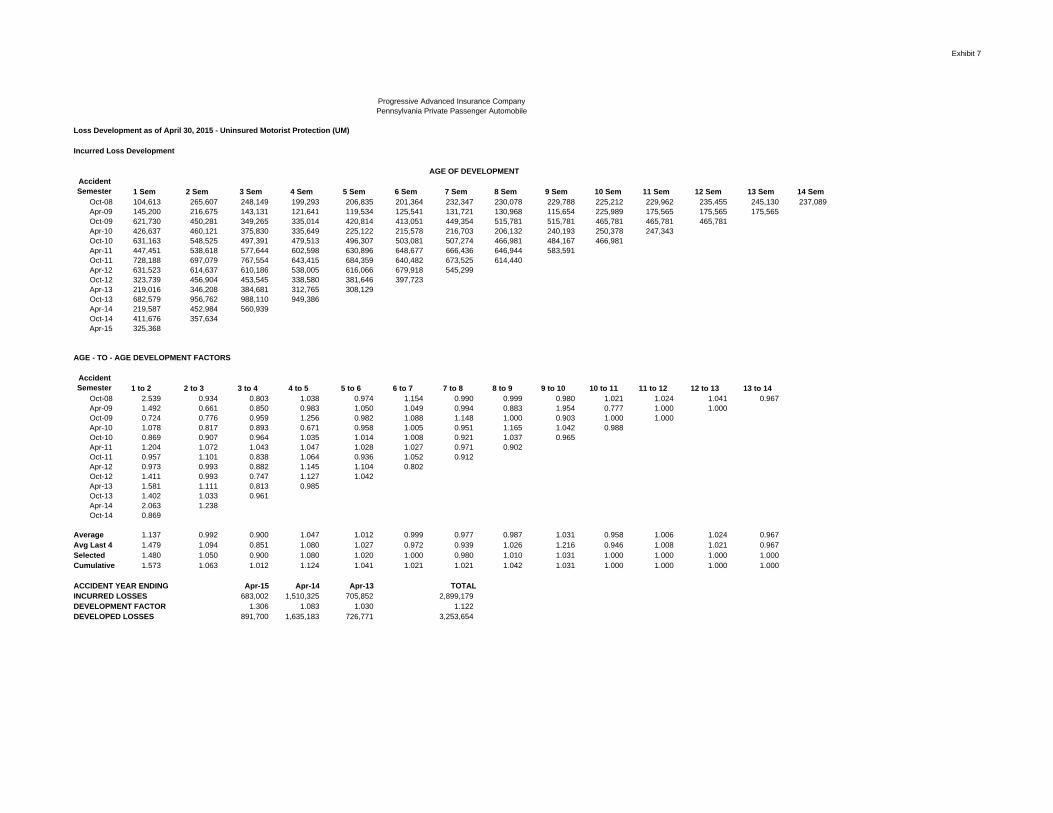

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - Uninsured Motorist Protection (UM)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 260,831 441,313 382,988 366,032 353,416 335,461 375,478 392,476 391,061 841,827 831,624 1,008,634 1,008,634 1,007,977Apr-09 323,322 470,593 527,347 434,904 500,505 507,775 483,309 460,329 467,210 463,591 477,453 449,555 449,555Oct-09 505,694 453,662 385,072 362,592 389,335 344,048 350,392 314,831 311,313 309,491 309,421 308,864Apr-10 563,097 441,438 378,647 388,751 421,150 420,093 399,596 382,941 391,199 385,941 385,941Oct-10 548,686 513,816 399,135 318,610 317,176 398,790 414,697 397,800 397,710 395,893Apr-11 804,506 536,795 643,729 711,845 679,717 770,476 764,790 750,744 746,936Oct-11 779,562 868,778 990,109 1,087,462 1,185,725 1,072,752 1,098,376 1,046,960Apr-12 590,699 708,689 756,361 719,517 790,620 821,707 791,953Oct-12 360,929 987,454 1,310,161 1,278,153 1,303,481 1,296,899Apr-13 408,701 396,318 452,986 477,475 544,096Oct-13 342,536 408,856 634,235 672,025Apr-14 573,186 654,034 669,782Oct-14 442,885 1,752,316Apr-15 554,530

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.692 0.868 0.956 0.966 0.949 1.119 1.045 0.996 2.153 0.988 1.213 1.000 0.999Apr-09 1.455 1.121 0.825 1.151 1.015 0.952 0.952 1.015 0.992 1.030 0.942 1.000Oct-09 0.897 0.849 0.942 1.074 0.884 1.018 0.899 0.989 0.994 1.000 0.998Apr-10 0.784 0.858 1.027 1.083 0.997 0.951 0.958 1.022 0.987 1.000Oct-10 0.936 0.777 0.798 0.995 1.257 1.040 0.959 1.000 0.995Apr-11 0.667 1.199 1.106 0.955 1.134 0.993 0.982 0.995Oct-11 1.114 1.140 1.098 1.090 0.905 1.024 0.953Apr-12 1.200 1.067 0.951 1.099 1.039 0.964Oct-12 2.736 1.327 0.976 1.020 0.995Apr-13 0.970 1.143 1.054 1.140Oct-13 1.194 1.551 1.060Apr-14 1.141 1.024Oct-14 3.957

Average 1.327 1.094 0.994 1.055 1.005 1.002 0.964 1.002 1.224 1.002 1.092 1.000 0.999Avg Last 4 1.815 1.261 1.010 1.087 1.018 1.005 0.963 1.001 0.992 1.004 1.051 1.000 0.999Selected 1.815 1.200 1.010 1.055 1.020 1.000 0.969 1.002 0.996 1.004 1.020 1.000 1.000Cumulative 2.346 1.292 1.077 1.066 1.011 0.991 0.991 1.022 1.020 1.024 1.020 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 2,306,846 1,341,807 1,840,996 5,489,649DEVELOPMENT FACTOR 1.546 1.072 0.997 1.246DEVELOPED LOSSES 3,565,513 1,437,982 1,835,104 6,838,598

AGE OF DEVELOPMENT

Exhibit 7

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

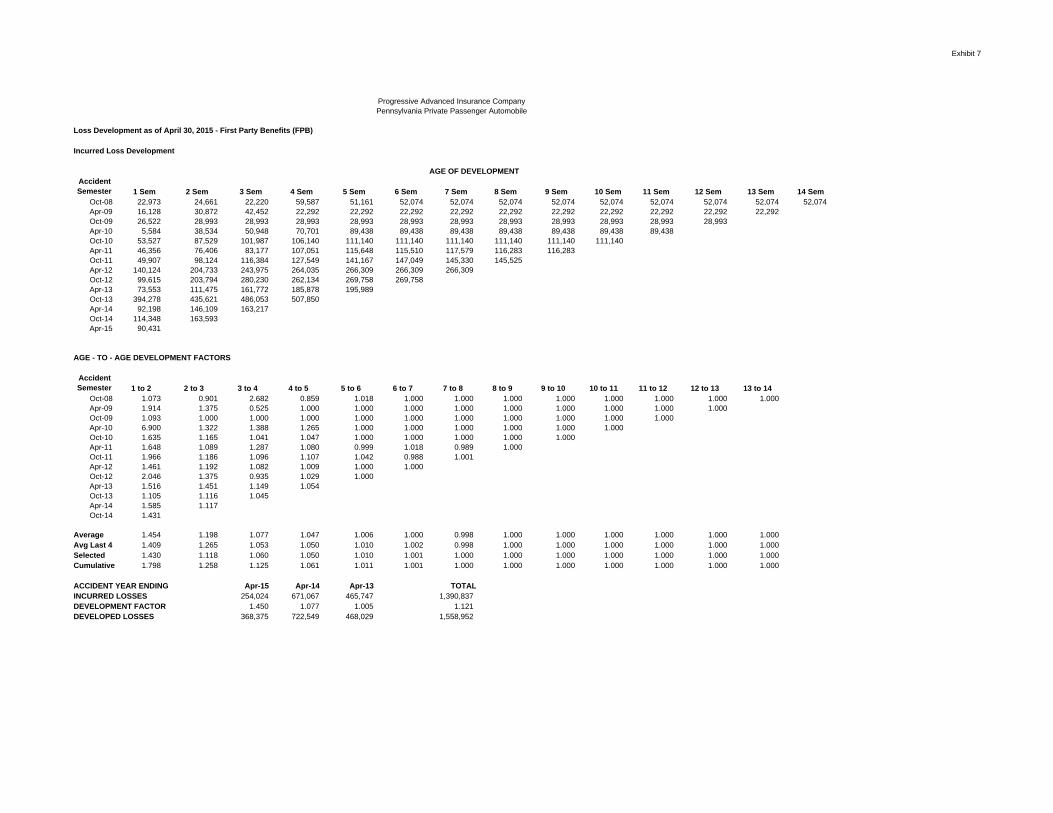

Pennsylvania Private Passenger AutomobileLoss Development as of April 30, 2015 - First Party Benefits (FPB)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 222,707 303,681 314,865 311,820 314,351 313,192 313,223 331,207 343,697 343,697 343,697 343,697 343,697 343,697Apr-09 177,558 233,008 251,885 268,256 326,897 436,610 443,035 441,612 441,612 441,612 441,612 441,612 441,612Oct-09 244,840 354,436 362,648 432,113 437,113 403,226 403,226 403,226 403,226 403,226 402,226 402,226Apr-10 542,994 618,207 607,716 656,879 674,696 685,329 685,421 685,421 685,421 685,421 685,421Oct-10 319,634 339,394 418,026 383,400 385,581 406,095 408,080 408,080 408,080 407,692Apr-11 246,419 435,464 485,335 501,178 498,150 501,414 524,696 548,365 549,807Oct-11 362,348 493,896 564,429 590,891 596,750 593,037 605,593 608,169Apr-12 348,391 455,961 498,589 519,803 536,054 560,814 575,610Oct-12 195,281 277,428 338,418 364,444 388,104 410,530Apr-13 250,255 332,303 368,963 378,468 386,968Oct-13 648,998 586,545 605,067 603,544Apr-14 648,866 740,641 779,795Oct-14 261,633 377,463Apr-15 257,310

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.364 1.037 0.990 1.008 0.996 1.000 1.057 1.038 1.000 1.000 1.000 1.000 1.000Apr-09 1.312 1.081 1.065 1.219 1.336 1.015 0.997 1.000 1.000 1.000 1.000 1.000Oct-09 1.448 1.023 1.192 1.012 0.922 1.000 1.000 1.000 1.000 0.998 1.000Apr-10 1.139 0.983 1.081 1.027 1.016 1.000 1.000 1.000 1.000 1.000Oct-10 1.062 1.232 0.917 1.006 1.053 1.005 1.000 1.000 0.999Apr-11 1.767 1.115 1.033 0.994 1.007 1.046 1.045 1.003Oct-11 1.363 1.143 1.047 1.010 0.994 1.021 1.004Apr-12 1.309 1.093 1.043 1.031 1.046 1.026Oct-12 1.421 1.220 1.077 1.065 1.058Apr-13 1.328 1.110 1.026 1.022Oct-13 0.904 1.032 0.997Apr-14 1.141 1.053Oct-14 1.443

Average 1.241 1.082 1.040 1.031 1.037 1.015 1.013 1.005 1.000 0.999 1.000 1.000 1.000Avg Last 4 1.204 1.104 1.036 1.032 1.026 1.025 1.012 1.001 1.000 0.999 1.000 1.000 1.000Selected 1.220 1.080 1.034 1.032 1.030 1.025 1.004 1.001 1.000 1.000 1.000 1.000 1.000Cumulative 1.491 1.222 1.132 1.094 1.060 1.029 1.004 1.000 1.000 1.000 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 634,773 1,383,339 797,499 2,815,611DEVELOPMENT FACTOR 1.331 1.115 1.044 1.144DEVELOPED LOSSES 844,895 1,542,817 832,972 3,220,684

AGE OF DEVELOPMENT

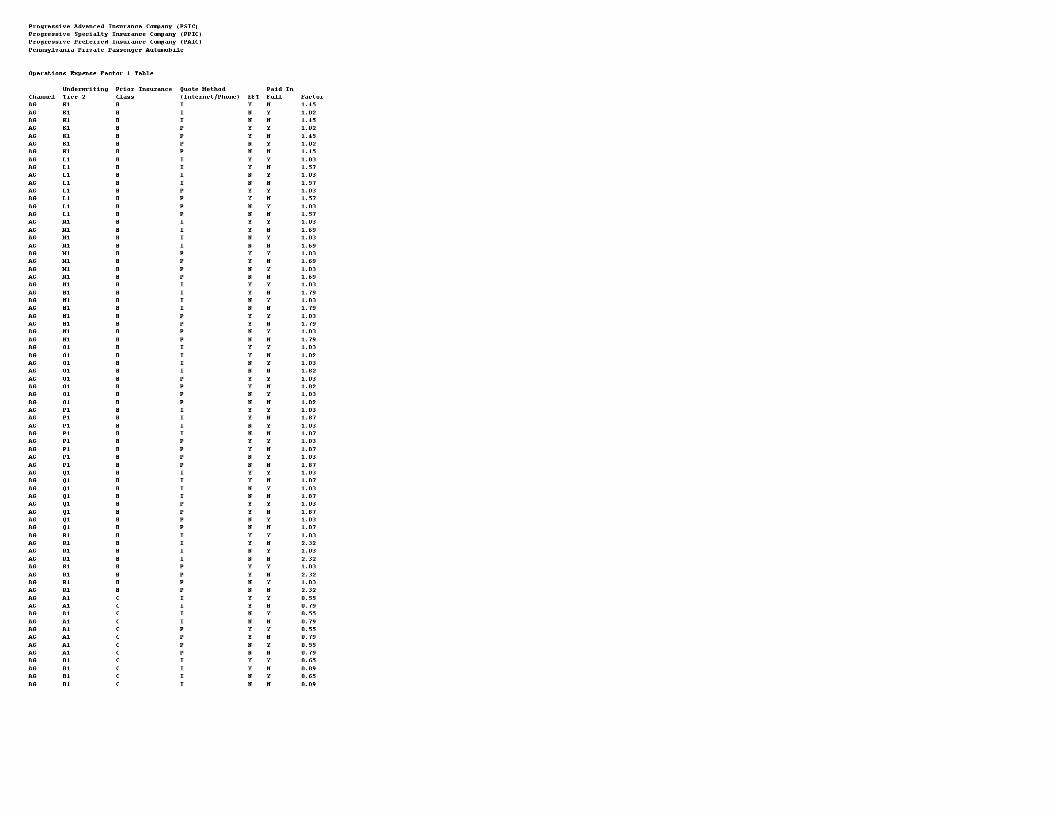

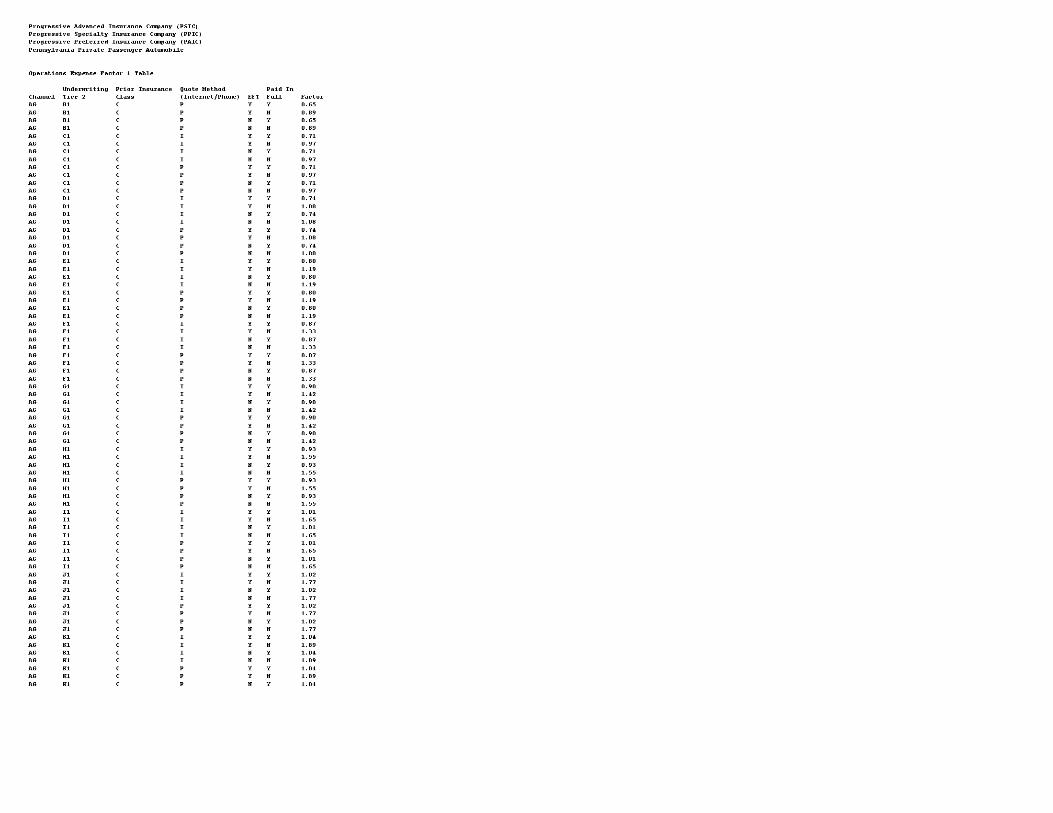

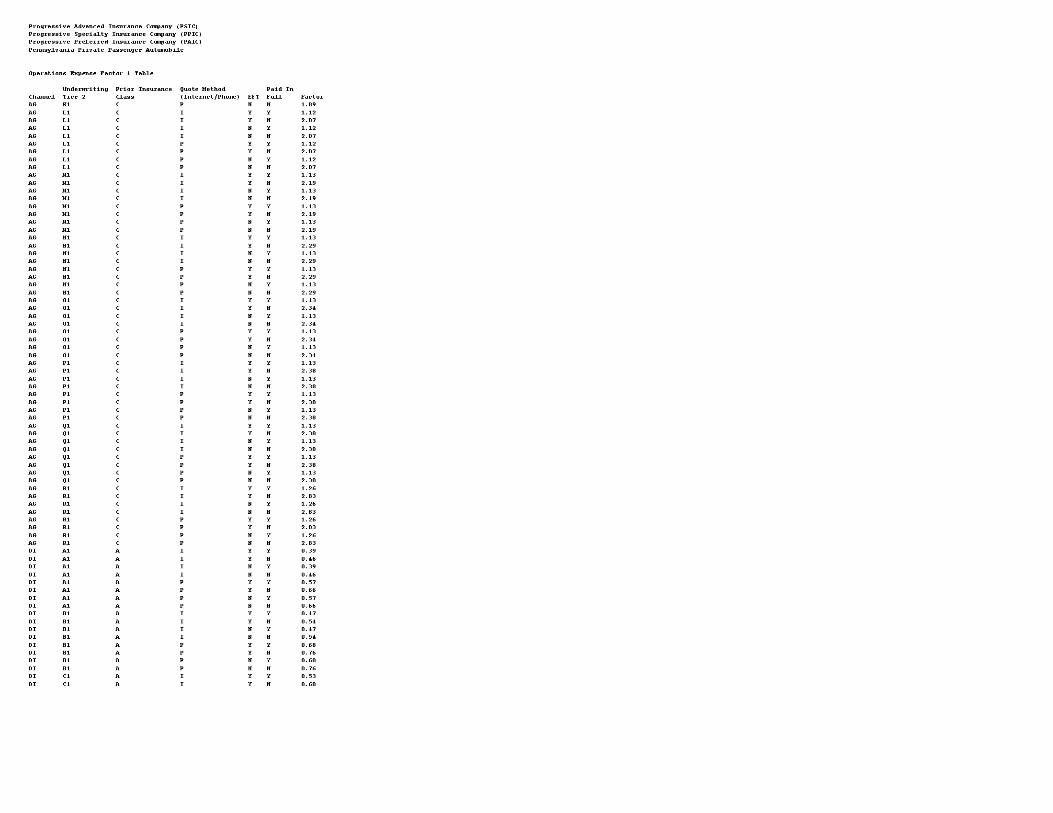

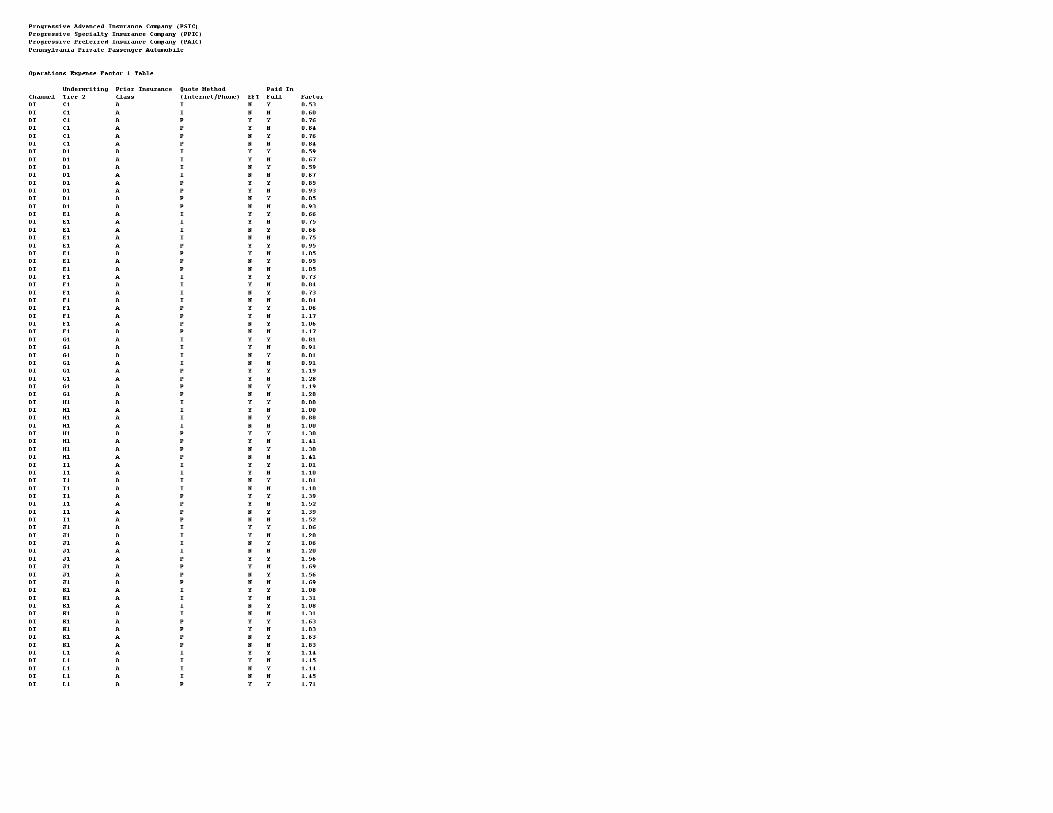

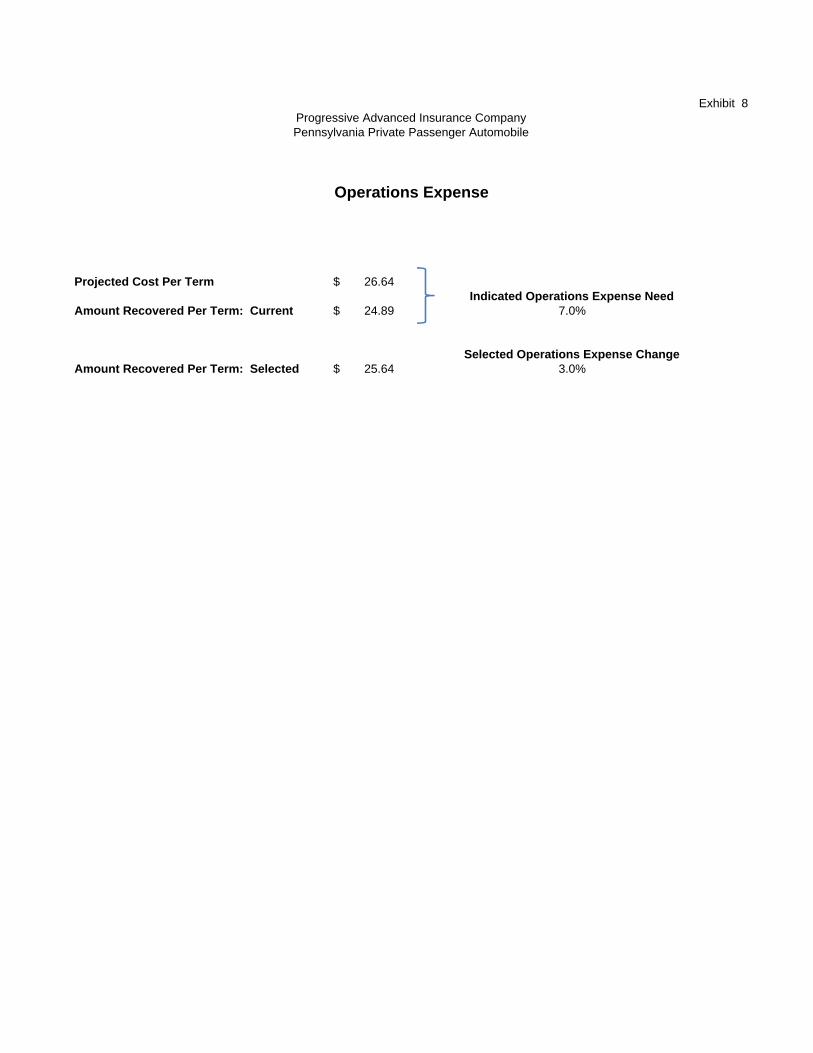

Exhibit 8

Projected Cost Per Term 26.47$

Amount Recovered Per Term: Current 25.95$

Amount Recovered Per Term: Selected 25.35$ -2.3%

Progressive Preferred Insurance CompanyProgressive Specialty Insurance Company

Pennsylvania Private Passenger Automobile

Operations Expense

Selected Operations Expense Change

Indicated Operations Expense Need2.0%

Introduction

The enclosed exhibits present detail and justification for the rate revision of the Progressive Advanced Insurance Company in the state of Pennsylvania.

Table of Contents

Item Exhibit Number

Proposed Rate Changes 1

Indication 2

Expenses 3

Loss Adjustment Expense 4

Trend 5 Combined Data for:

Progressive Advanced Insurance CompanyProgressive Direct Insurance Company

Current Rate Level 6

Loss Development Factors 7

Operations Expense 8

Pennsylvania Private Passenger AutomobileProgressive Advanced Insurance Company

Exhibit 1

We measured the rate changes by calculating rates for in-force policies under the currating plans, and determined the percent change in the rate totals for each coverage.

Coverage Rate Change

Bodily Injury (BI) -1.4%

Property Damage (PD) -0.1%

Uninsured Motorist Protection (UM) 10.5%

Underinsured Motorist Protection (UIM) 2.2%

First Party Benefits (FPB) 79.4%

Medical Payments (MED) -1.3%

Comprehensive (COMP) 0.2%

Collision (COLL) 4.6%

Loan Payoff Protection (LOAN) 5.1%

Rental Reimbursement (RENT) 0.3%

Roadside Assistance 28.2%

Additional Custom Parts & Equip (ACPE) 1.1%

Acquisition Expense -0.1%

Operations Expense 3.0%

Overall 1.6%

Proposed Rate Changes

Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Exhibit 2Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Determination of Statewide Rate Level Changes

Accident Incurred Loss LAE Trended & Ultimate Budgetary Complement Cred WtdYear Earned CRL EP Trend Trended Incurred Incurred Developed Trend Trend Developed Loss & LAE Loss & LAE Indicated Selected # of Credibility to Indicated Selected

Coverage Ending Premium Factor Factor EP @ CRL Losses LDF Losses LAE Factor Factor Loss & LAE Ratio Ratio Change Weights Features1 SFC2 Percent Credibility Change ChangeBI Apr-13 28,852,054 0.998 0.899 25,888,816 16,227,001 0.991 16,074,970 6,200,968 0.825 1.000 19,467,405 75.2% 88.6% -15.2% 0.0%

Apr-14 30,838,323 0.983 0.928 28,138,139 17,228,678 1.055 18,179,390 6,891,441 0.902 1.000 23,288,598 82.8% 88.6% -6.6% 47.7%Apr-15 33,236,060 0.992 0.957 31,576,073 17,530,480 1.182 20,719,102 7,669,490 0.986 1.000 28,093,701 89.0% 88.6% 0.4% 52.3%TOTAL 92,926,438 0.991 0.929 85,603,028 50,986,159 1.078 54,973,461 20,761,899 0.911 1.000 70,849,705 86.0% 88.6% -3.0% 4,470 6,317 84.1% 4.9% -1.5% -1.4%

PD Apr-13 34,293,685 1.155 0.950 37,629,374 27,394,367 1.001 27,422,276 4,303,584 0.904 1.000 29,104,735 77.3% 88.6% -12.7% 0.0%Apr-14 37,359,105 1.137 0.965 40,971,873 31,790,708 1.006 31,976,477 4,495,343 0.938 1.000 34,484,194 84.2% 88.6% -5.0% 0.0%Apr-15 44,948,007 1.042 0.979 45,876,685 33,856,056 1.068 36,172,728 5,078,376 0.973 1.000 40,256,393 87.7% 88.6% -1.0% 100.0%TOTAL 116,600,797 1.106 0.965 124,477,931 93,041,131 1.027 95,571,481 13,877,304 0.941 1.000 103,845,321 87.7% 88.6% -1.0% 12,343 2,390 100.0% 0.3% -1.0% -0.1%

COMP Apr-13 13,147,232 1.052 1.130 15,622,078 9,422,331 1.000 9,418,309 1,577,815 1.088 1.000 11,822,716 75.7% 88.6% -14.6% 0.0%Apr-14 14,051,247 1.110 1.090 17,009,645 12,194,167 1.001 12,200,956 1,691,788 1.067 1.000 14,710,539 86.5% 88.6% -2.4% 0.0%Apr-15 16,891,618 1.096 1.053 19,486,821 13,782,421 1.017 14,014,183 2,556,509 1.047 1.000 17,224,945 88.4% 88.6% -0.3% 100.0%TOTAL 44,090,098 1.087 1.087 52,118,544 35,398,919 1.007 35,633,448 5,826,112 1.065 1.000 43,758,200 88.4% 88.6% -0.3% 7,088 3,896 100.0% 0.2% -0.3% 0.2%

COLL Apr-13 46,496,455 0.966 1.130 50,741,733 34,855,919 0.999 34,832,799 4,549,341 1.286 1.000 49,351,839 97.3% 88.6% 9.7% 0.0%Apr-14 51,529,481 0.988 1.090 55,493,202 41,138,130 0.998 41,070,595 4,833,576 1.200 1.000 54,108,761 97.5% 88.6% 10.0% 0.0%Apr-15 60,146,531 1.010 1.053 63,976,136 53,054,060 0.927 49,197,388 5,592,771 1.119 1.000 60,651,061 94.8% 88.6% 7.0% 100.0%TOTAL 158,172,466 0.990 1.087 170,211,070 129,048,109 0.969 125,100,782 14,975,688 1.192 1.000 164,111,661 94.8% 88.6% 7.0% 13,256 2,299 100.0% 3.7% 7.0% 4.6%

MED Apr-13 14,627,610 1.106 0.962 15,571,010 9,487,080 1.017 9,646,330 3,683,226 0.972 1.000 13,059,951 83.9% 88.6% -5.4% 0.0%Apr-14 15,786,880 1.085 0.974 16,679,107 9,689,287 1.043 10,108,509 3,705,240 0.988 1.000 13,691,479 82.1% 88.6% -7.4% 0.0%Apr-15 18,599,528 1.009 0.986 18,501,892 10,389,948 1.083 11,251,054 4,143,696 1.004 1.000 15,439,934 83.5% 88.6% -5.8% 100.0%TOTAL 49,014,019 1.063 0.974 50,752,008 29,566,316 1.049 31,005,894 11,532,161 0.989 1.000 42,191,364 83.5% 88.6% -5.8% 5,126 6,650 87.8% 1.7% -4.9% -1.3%

UIM Apr-13 5,520,232 1.034 0.901 5,147,956 3,118,882 1.107 3,454,143 1,046,112 0.825 1.000 3,896,766 75.7% 88.6% -14.6% 31.1%Apr-14 5,810,423 1.026 0.929 5,538,486 3,125,471 1.290 4,032,221 1,264,284 0.902 1.000 4,901,203 88.5% 88.6% -0.2% 32.9%Apr-15 6,649,130 1.002 0.958 6,383,338 2,356,847 1.872 4,412,616 1,435,019 0.986 1.000 5,784,831 90.6% 88.6% 2.3% 36.0%TOTAL 17,979,785 1.020 0.931 17,069,781 8,601,200 1.383 11,898,980 3,745,414 0.911 1.000 14,582,799 85.3% 88.6% -3.8% 369 4,039 30.2% 4.9% 3.0% 2.2%

UM Apr-13 3,207,068 0.940 0.901 2,718,636 705,852 1.030 726,771 364,015 0.825 1.000 963,809 35.5% 88.6% -60.0% 31.1%Apr-14 3,383,592 0.945 0.929 2,971,183 1,510,325 1.083 1,635,183 755,498 0.902 1.000 2,230,374 75.1% 88.6% -15.3% 32.9%Apr-15 3,712,170 0.977 0.958 3,473,511 683,002 1.306 891,700 364,300 0.986 1.000 1,243,309 35.8% 88.6% -59.6% 36.0%TOTAL 10,302,830 0.955 0.931 9,163,330 2,899,179 1.122 3,253,654 1,483,813 0.908 1.000 4,437,492 48.6% 88.6% -45.2% 275 4,039 26.1% 4.9% -7.4% 10.5%

RENT Apr-13 2,604,621 1.046 1.105 3,011,064 2,077,068 1.000 2,076,573 400,089 0.997 1.000 2,469,730 82.0% 88.6% -7.5% 0.0%Apr-14 2,848,015 1.048 1.073 3,204,105 2,652,479 0.999 2,649,096 399,188 0.998 1.000 3,041,815 94.9% 88.6% 7.1% 0.0%Apr-15 3,419,063 1.017 1.042 3,623,798 2,821,942 0.987 2,784,033 478,141 0.998 1.000 3,257,872 89.9% 88.6% 1.4% 100.0%TOTAL 8,871,699 1.035 1.071 9,838,968 7,551,489 0.994 7,509,701 1,277,418 0.998 1.000 8,769,418 89.9% 88.6% 1.4% 7,299 1,565 100.0% -2.2% 1.4% 0.3%

Roadside Apr-13 735,736 1.473 0.555 601,224 801,731 1.004 804,827 7,767 0.938 1.000 762,949 126.9% 88.6% 43.2% 0.0%Assistance Apr-14 722,393 1.350 0.652 636,313 962,613 1.011 973,377 834 0.958 1.000 933,055 146.6% 88.6% 65.5% 0.0%

Apr-15 747,894 1.193 0.767 684,844 1,015,168 1.032 1,047,323 666 0.978 1.000 1,024,447 149.6% 88.6% 68.8% 100.0%TOTAL 2,206,023 1.338 0.651 1,922,380 2,779,512 1.017 2,825,528 9,268 0.960 1.000 2,720,451 149.6% 88.6% 68.8% 16,872 1,156 100.0% 15.1% 68.8% 28.2%

FPB Apr-13 611,404 1.033 0.962 607,591 465,747 1.005 468,029 78,730 0.972 1.000 533,678 87.8% 88.6% -0.9% 31.1%Apr-14 604,198 1.067 0.974 627,968 671,067 1.077 722,549 110,924 0.988 1.000 824,733 131.3% 88.6% 48.2% 32.9%Apr-15 668,138 1.024 0.986 674,620 254,024 1.450 368,375 55,762 1.004 1.000 425,616 63.1% 88.6% -28.8% 36.0%TOTAL 1,883,740 1.041 0.974 1,910,179 1,390,837 1.121 1,558,952 245,416 0.987 1.000 1,784,027 93.2% 88.6% 5.2% 243 6,650 19.1% 1.7% 2.7% 79.4%

LOAN Apr-13 331,564 0.889 1.000 294,806 131,737 1.000 131,737 20,548 1.000 1.000 152,285 51.7% 88.6% -41.7% 31.1%Apr-14 339,103 0.965 1.000 327,092 226,493 1.024 231,822 22,982 1.000 1.000 254,804 77.9% 88.6% -12.1% 32.9%Apr-15 370,115 1.006 1.000 372,257 351,315 1.108 389,093 41,104 1.000 1.000 430,197 115.6% 88.6% 30.4% 36.0%TOTAL 1,040,783 0.955 1.000 994,155 709,544 1.061 752,652 84,634 1.000 1.000 837,285 83.3% 88.6% -6.0% 353 1,689 45.7% 0.0% -2.7% 5.1%

ACPE Apr-13 12,514 1.000 1.000 12,515 0 0.000 0 138 1.000 1.000 138 1.1% 88.6% -98.8% 31.1%Apr-14 15,005 1.000 1.000 15,006 6,513 1.000 6,513 47 1.000 1.000 6,560 43.7% 88.6% -50.7% 32.9%Apr-15 18,924 1.000 1.000 18,925 350 1.000 350 (15) 1.000 1.000 335 1.8% 88.6% -98.0% 36.0%TOTAL 46,443 1.000 1.000 46,446 6,863 1.000 6,863 169 1.000 1.000 7,033 15.4% 88.6% -82.7% 3 1,194 5.0% 0.0% -4.1% 1.1%

LIAB Apr-13 87,112,054 1.078 0.932 87,563,383 57,398,930 1.007 57,792,519 15,676,635 0.889 1.000 67,026,344 76.5% 88.6% -13.6%Total Apr-14 93,782,522 1.063 0.952 94,926,756 64,015,536 1.041 66,654,328 17,222,730 0.933 1.000 79,420,581 83.7% 88.6% -5.6%

Apr-15 107,813,034 1.016 0.972 106,486,119 65,070,356 1.134 73,815,574 18,746,643 0.982 1.000 91,243,784 85.7% 88.6% -3.3%TOTAL 288,707,611 1.050 0.953 288,976,258 186,484,822 1.063 198,262,422 51,646,008 0.938 1.000 237,690,708 82.3% 88.6% -7.2% 42,927 N/A N/A -1.8% 0.3%

PDAM Apr-13 63,328,122 0.993 1.118 70,283,420 47,288,785 0.999 47,264,244 6,555,699 1.227 1.000 64,559,658 91.9% 88.6% 3.6%Total Apr-14 69,505,245 1.018 1.083 76,685,362 57,180,395 0.999 57,132,360 6,948,415 1.157 1.000 73,055,533 95.3% 88.6% 7.5%

Apr-15 81,594,145 1.030 1.049 88,162,781 71,025,257 0.949 67,432,369 8,669,176 1.096 1.000 82,588,856 93.7% 88.6% 5.7%TOTAL 214,427,512 1.015 1.080 235,131,563 175,494,437 0.979 171,828,974 22,173,289 1.152 1.000 220,204,047 93.7% 88.6% 5.7% 24,770 N/A N/A 5.8% 3.7%

TOTAL Apr-13 150,440,176 1.042 1.007 157,846,803 104,687,715 1.004 105,056,763 22,232,334 1.041 1.000 131,586,002 83.4% 88.6% -5.9%INDEMNITY Apr-14 163,287,767 1.044 1.006 171,612,118 121,195,931 1.021 123,786,688 24,171,145 1.037 1.000 152,476,114 88.8% 88.6% 0.3%

Apr-15 189,407,180 1.022 1.005 194,648,900 136,095,613 1.038 141,247,944 27,415,819 1.037 1.000 173,832,640 89.3% 88.6% 0.8%TOTAL 503,135,123 1.035 1.006 524,107,821 361,979,259 1.022 370,091,396 73,819,297 1.038 1.000 457,894,756 88.9% 88.6% 0.3% N/A N/A N/A 1.5% 1.8%

Apr-13 20,054,353 1.000 1.000 20,054,353Apr-14 22,605,363 1.000 1.000 22,605,363

ACQUISITION Apr-15 26,689,893 1.000 1.000 26,688,010EXPENSE TOTAL 26,689,893 1.000 1.000 26,688,010 N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A -2.6% -0.1%

Apr-13 7,988,306 1.039 1.000 8,296,757Apr-14 8,807,180 1.039 1.000 9,147,249

OPERATIONS Apr-15 10,103,675 1.039 1.000 10,493,806EXPENSE TOTAL 26,899,161 1.000 1.000 27,937,811 N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 7.0% 3.0%

TOTAL Apr-13 178,482,835 1.037 1.006 186,197,913Apr-14 194,700,309 1.039 1.005 203,364,730Apr-15 226,200,748 1.020 1.004 231,830,716TOTAL 556,724,177 1.032 1.006 621,393,358 N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 1.3% 1.6%

1 "# of Features" denotes the number of coverages on a claim (e.g. bodily injury, personal injury and collision could all be “features” of one claim).2 "SFC" (Standard of Full Credibility) denotes the number of losses required to be 100% credible.

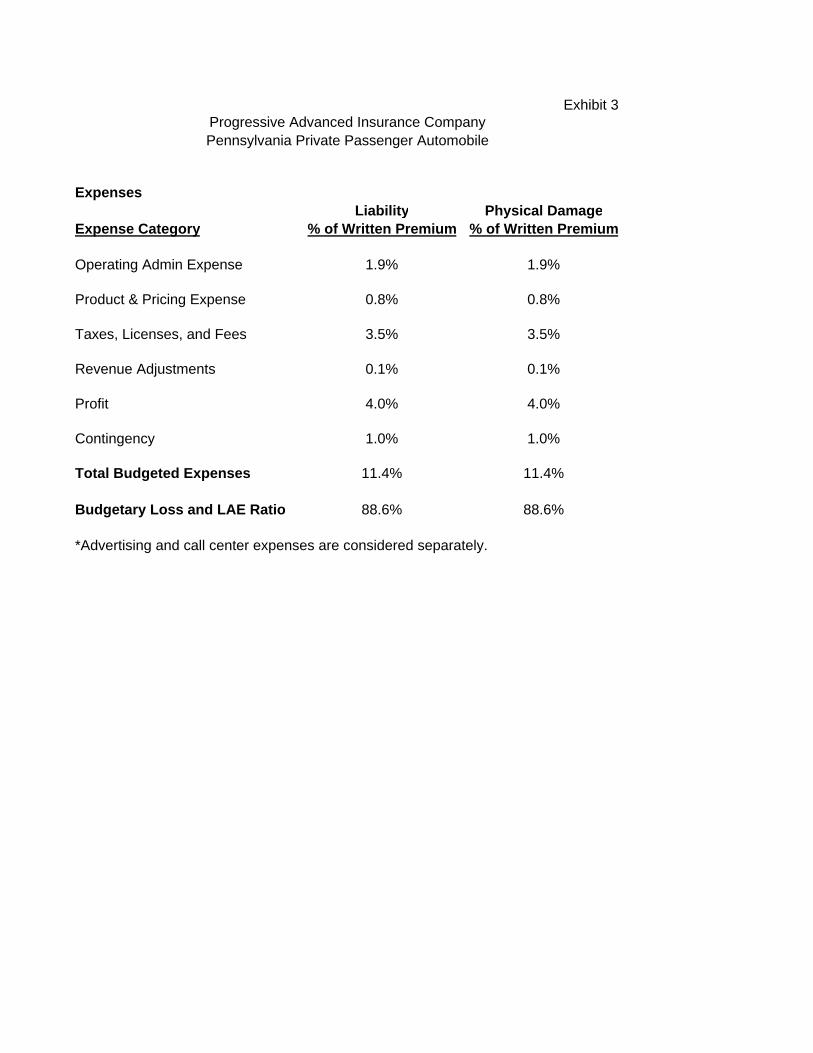

Exhibit 3Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

ExpensesLiability Physical Damage

Expense Category % of Written Premium % of Written Premium

Operating Admin Expense 1.9% 1.9%

Product & Pricing Expense 0.8% 0.8%

Taxes, Licenses, and Fees 3.5% 3.5%

Revenue Adjustments 0.1% 0.1%

Profit 4.0% 4.0%

Contingency 1.0% 1.0%

Total Budgeted Expenses 11.4% 11.4%

Budgetary Loss and LAE Ratio 88.6% 88.6%

*Advertising and call center expenses are considered separately.

Exhibit 4Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Loss Adjustment Expenses

Accident LAECoverage Year Paid Ultimate Paid Ultimate Trend TOTAL

Ending DCC DCC A&O A&O Factor LAE

BI Apr-13 1,133,317 1,857,933 3,269,845 4,343,035 1.000 6,200,968Apr-14 449,920 2,320,066 3,305,955 4,571,375 1.000 6,891,441Apr-15 34,164 2,469,834 2,106,195 5,199,656 1.000 7,669,490

PD Apr-13 99,163 135,030 3,594,087 4,168,554 1.000 4,303,584Apr-14 61,493 143,634 3,996,423 4,351,709 1.000 4,495,343Apr-15 14,972 170,789 4,172,780 4,907,587 1.000 5,078,376

UM Apr-13 74,177 74,867 184,936 289,148 1.000 364,015Apr-14 46,050 174,222 239,052 581,276 1.000 755,498Apr-15 4,179 49,632 102,459 314,668 1.000 364,300

UIM Apr-13 58,885 303,346 406,004 742,765 1.000 1,046,112Apr-14 36,589 466,897 302,912 797,387 1.000 1,264,284Apr-15 3,115 564,761 107,958 870,258 1.000 1,435,019

FPB Apr-13 119 1,825 53,816 76,905 1.000 78,730Apr-14 620 2,928 50,403 107,995 1.000 110,924Apr-15 0 1,149 30,849 54,613 1.000 55,762

MED Apr-13 192,572 293,023 3,021,537 3,390,202 1.000 3,683,226Apr-14 210,834 342,828 3,107,336 3,362,412 1.000 3,705,240Apr-15 116,602 407,443 2,646,434 3,736,252 1.000 4,143,696

COMP Apr-13 25,784 21,016 1,171,199 1,556,799 1.000 1,577,815Apr-14 65,742 66,607 1,320,642 1,625,182 1.000 1,691,788Apr-15 21,343 58,176 1,764,992 2,498,333 1.000 2,556,509

COLL Apr-13 34,325 30,218 3,341,839 4,519,123 1.000 4,549,341Apr-14 57,180 76,417 3,792,791 4,757,159 1.000 4,833,576Apr-15 36,320 97,835 4,516,883 5,494,936 1.000 5,592,771

Apr-13 140 123 4,042 7,644 1.000 7,767Apr-14 0 0 1,271 834 1.000 834Apr-15 0 0 936 666 1.000 666

RENT Apr-13 93 964 1,326,039 399,125 1.000 400,089Apr-14 2,137 2,172 1,512,014 397,016 1.000 399,188Apr-15 2,132 2,430 1,470,729 475,711 1.000 478,141

ACPE Apr-13 0 0 0 138 1.000 138Apr-14 0 0 171 47 1.000 47Apr-15 0 0 257 (15) 1.000 (15)

LOAN Apr-13 5,189 4,123 14,828 16,425 1.000 20,548Apr-14 0 1 22,185 22,981 1.000 22,982Apr-15 0 2,550 28,444 38,554 1.000 41,104

Roadside Assistance

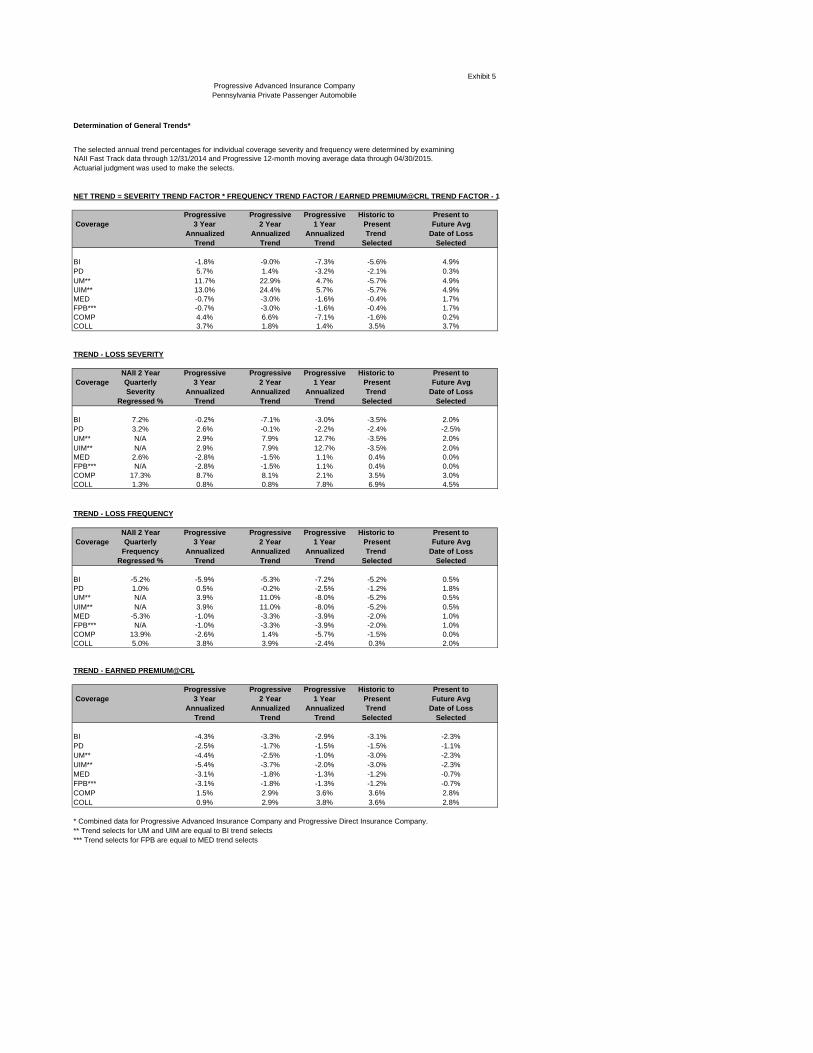

Exhibit 5Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Determination of General Trends*

The selected annual trend percentages for individual coverage severity and frequency were determined by examiningNAII Fast Track data through 12/31/2014 and Progressive 12-month moving average data through 04/30/2015.Actuarial judgment was used to make the selects.

NET TREND = SEVERITY TREND FACTOR * FREQUENCY TREND FACTOR / EARNED PREMIUM@CRL TREND FACTOR - 1

Progressive Progressive Progressive Historic to Present toCoverage 3 Year 2 Year 1 Year Present Future Avg

Annualized Annualized Annualized Trend Date of LossTrend Trend Trend Selected Selected

BI -1.8% -9.0% -7.3% -5.6% 4.9%PD 5.7% 1.4% -3.2% -2.1% 0.3%UM** 11.7% 22.9% 4.7% -5.7% 4.9%UIM** 13.0% 24.4% 5.7% -5.7% 4.9%MED -0.7% -3.0% -1.6% -0.4% 1.7%FPB*** -0.7% -3.0% -1.6% -0.4% 1.7%COMP 4.4% 6.6% -7.1% -1.6% 0.2%COLL 3.7% 1.8% 1.4% 3.5% 3.7%

TREND - LOSS SEVERITY

NAII 2 Year Progressive Progressive Progressive Historic to Present toCoverage Quarterly 3 Year 2 Year 1 Year Present Future Avg

Severity Annualized Annualized Annualized Trend Date of LossRegressed % Trend Trend Trend Selected Selected

BI 7.2% -0.2% -7.1% -3.0% -3.5% 2.0%PD 3.2% 2.6% -0.1% -2.2% -2.4% -2.5%UM** N/A 2.9% 7.9% 12.7% -3.5% 2.0%UIM** N/A 2.9% 7.9% 12.7% -3.5% 2.0%MED 2.6% -2.8% -1.5% 1.1% 0.4% 0.0%FPB*** N/A -2.8% -1.5% 1.1% 0.4% 0.0%COMP 17.3% 8.7% 8.1% 2.1% 3.5% 3.0%COLL 1.3% 0.8% 0.8% 7.8% 6.9% 4.5%

TREND - LOSS FREQUENCY

NAII 2 Year Progressive Progressive Progressive Historic to Present toCoverage Quarterly 3 Year 2 Year 1 Year Present Future Avg

Frequency Annualized Annualized Annualized Trend Date of LossRegressed % Trend Trend Trend Selected Selected

BI -5.2% -5.9% -5.3% -7.2% -5.2% 0.5%PD 1.0% 0.5% -0.2% -2.5% -1.2% 1.8%UM** N/A 3.9% 11.0% -8.0% -5.2% 0.5%UIM** N/A 3.9% 11.0% -8.0% -5.2% 0.5%MED -5.3% -1.0% -3.3% -3.9% -2.0% 1.0%FPB*** N/A -1.0% -3.3% -3.9% -2.0% 1.0%COMP 13.9% -2.6% 1.4% -5.7% -1.5% 0.0%COLL 5.0% 3.8% 3.9% -2.4% 0.3% 2.0%

TREND - EARNED PREMIUM@CRL

Progressive Progressive Progressive Historic to Present toCoverage 3 Year 2 Year 1 Year Present Future Avg

Annualized Annualized Annualized Trend Date of LossTrend Trend Trend Selected Selected

BI -4.3% -3.3% -2.9% -3.1% -2.3%PD -2.5% -1.7% -1.5% -1.5% -1.1%UM** -4.4% -2.5% -1.0% -3.0% -2.3%UIM** -5.4% -3.7% -2.0% -3.0% -2.3%MED -3.1% -1.8% -1.3% -1.2% -0.7%FPB*** -3.1% -1.8% -1.3% -1.2% -0.7%COMP 1.5% 2.9% 3.6% 3.6% 2.8%COLL 0.9% 2.9% 3.8% 3.6% 2.8%

* Combined data for Progressive Advanced Insurance Company and Progressive Direct Insurance Company.** Trend selects for UM and UIM are equal to BI trend selects*** Trend selects for FPB are equal to MED trend selects

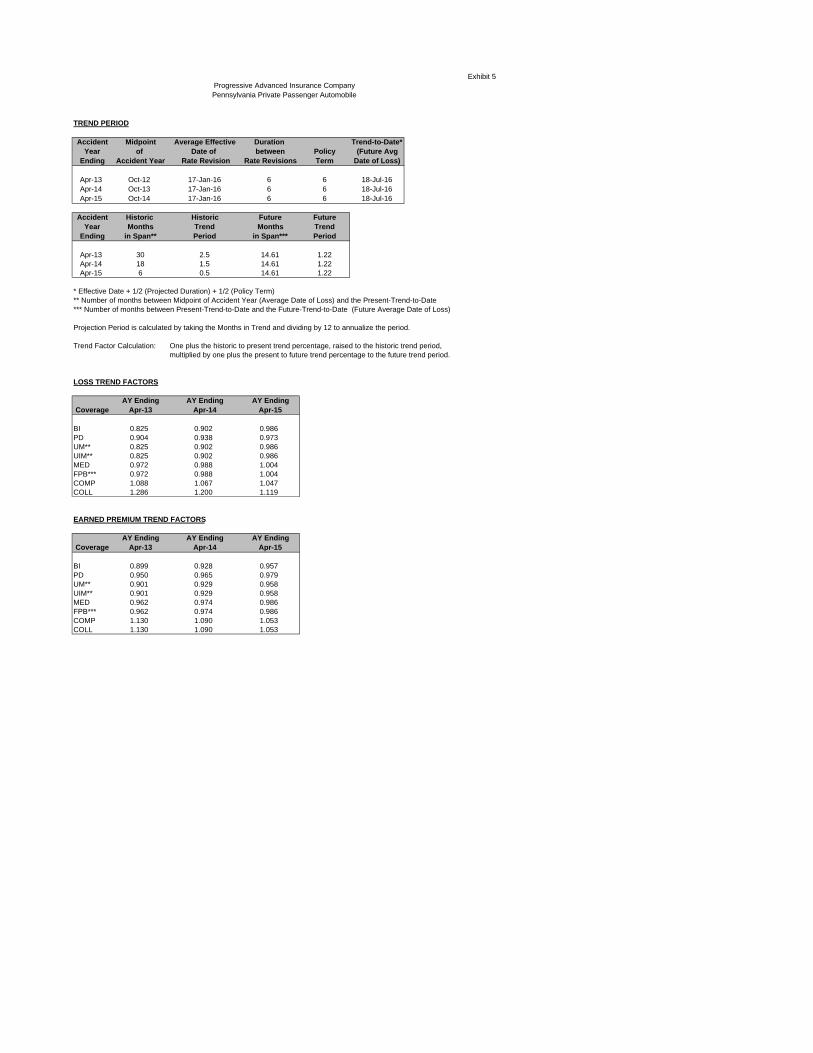

Exhibit 5Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

TREND PERIOD

Accident Midpoint Average Effective Duration Trend-to-Date*Year of Date of between Policy (Future Avg

Ending Accident Year Rate Revision Rate Revisions Term Date of Loss)

Apr-13 Oct-12 17-Jan-16 6 6 18-Jul-16Apr-14 Oct-13 17-Jan-16 6 6 18-Jul-16Apr-15 Oct-14 17-Jan-16 6 6 18-Jul-16

Accident Historic Historic Future FutureYear Months Trend Months Trend

Ending in Span** Period in Span*** Period

Apr-13 30 2.5 14.61 1.22Apr-14 18 1.5 14.61 1.22Apr-15 6 0.5 14.61 1.22

* Effective Date + 1/2 (Projected Duration) + 1/2 (Policy Term)** Number of months between Midpoint of Accident Year (Average Date of Loss) and the Present-Trend-to-Date *** Number of months between Present-Trend-to-Date and the Future-Trend-to-Date (Future Average Date of Loss)

Projection Period is calculated by taking the Months in Trend and dividing by 12 to annualize the period.

Trend Factor Calculation: One plus the historic to present trend percentage, raised to the historic trend period,multiplied by one plus the present to future trend percentage to the future trend period.

LOSS TREND FACTORS

AY Ending AY Ending AY EndingCoverage Apr-13 Apr-14 Apr-15

BI 0.825 0.902 0.986PD 0.904 0.938 0.973UM** 0.825 0.902 0.986UIM** 0.825 0.902 0.986MED 0.972 0.988 1.004FPB*** 0.972 0.988 1.004COMP 1.088 1.067 1.047COLL 1.286 1.200 1.119

EARNED PREMIUM TREND FACTORS

AY Ending AY Ending AY EndingCoverage Apr-13 Apr-14 Apr-15

BI 0.899 0.928 0.957PD 0.950 0.965 0.979UM** 0.901 0.929 0.958UIM** 0.901 0.929 0.958MED 0.962 0.974 0.986FPB*** 0.962 0.974 0.986COMP 1.130 1.090 1.053COLL 1.130 1.090 1.053

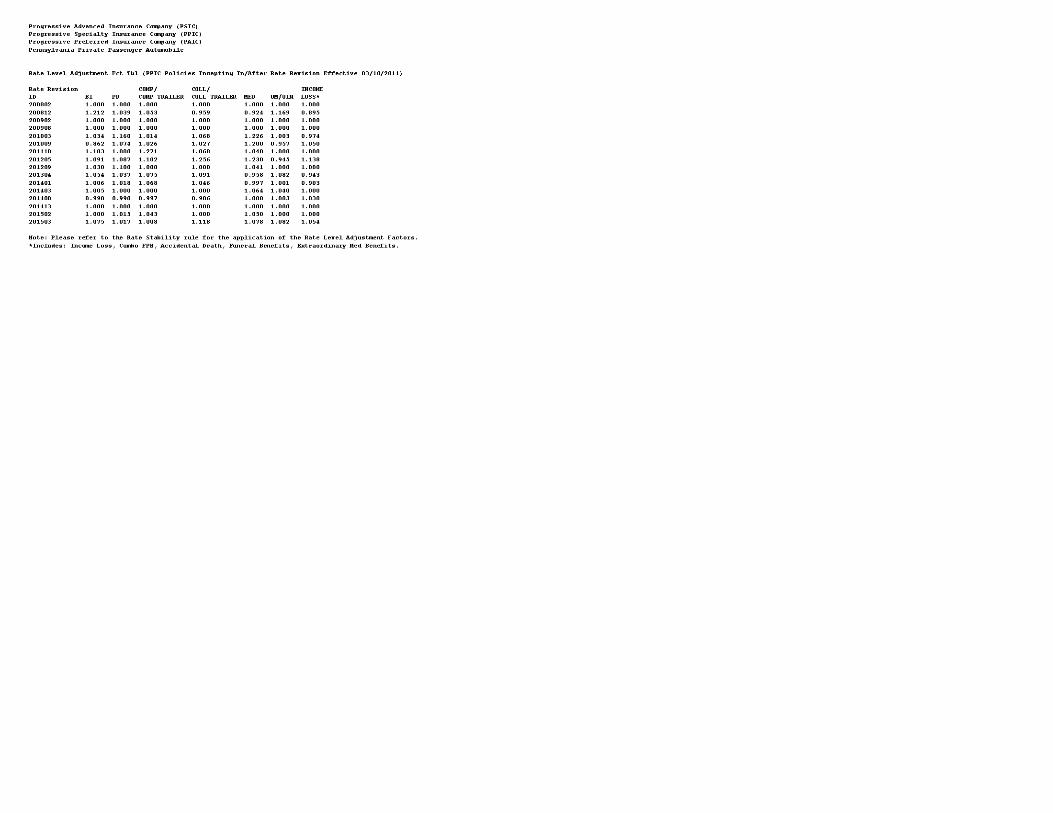

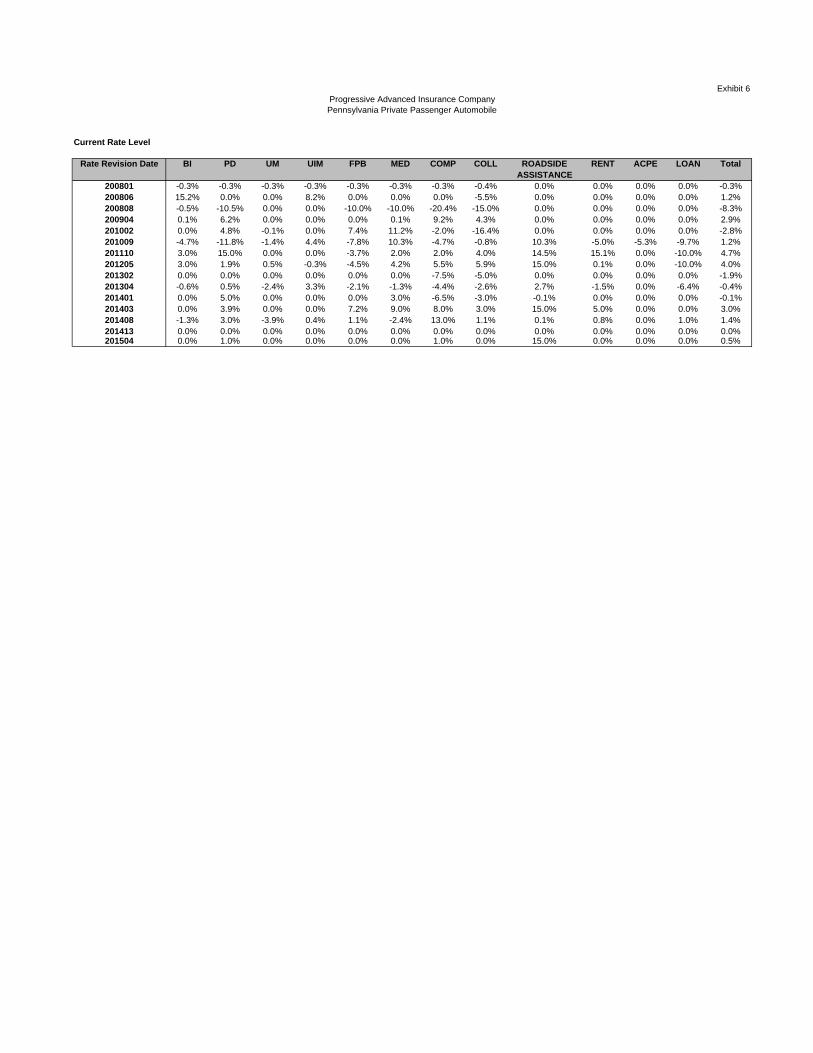

Exhibit 6

Rate Revision Date BI PD UM UIM FPB MED COMP COLL ROADSIDE RENT ACPE LOAN TotalASSISTANCE

200801 -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.4% 0.0% 0.0% 0.0% 0.0% -0.3%200806 15.2% 0.0% 0.0% 8.2% 0.0% 0.0% 0.0% -5.5% 0.0% 0.0% 0.0% 0.0% 1.2%200808 -0.5% -10.5% 0.0% 0.0% -10.0% -10.0% -20.4% -15.0% 0.0% 0.0% 0.0% 0.0% -8.3%200904 0.1% 6.2% 0.0% 0.0% 0.0% 0.1% 9.2% 4.3% 0.0% 0.0% 0.0% 0.0% 2.9%201002 0.0% 4.8% -0.1% 0.0% 7.4% 11.2% -2.0% -16.4% 0.0% 0.0% 0.0% 0.0% -2.8%201009 -4.7% -11.8% -1.4% 4.4% -7.8% 10.3% -4.7% -0.8% 10.3% -5.0% -5.3% -9.7% 1.2%201110 3.0% 15.0% 0.0% 0.0% -3.7% 2.0% 2.0% 4.0% 14.5% 15.1% 0.0% -10.0% 4.7%201205 3.0% 1.9% 0.5% -0.3% -4.5% 4.2% 5.5% 5.9% 15.0% 0.1% 0.0% -10.0% 4.0%201302 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% -7.5% -5.0% 0.0% 0.0% 0.0% 0.0% -1.9%201304 -0.6% 0.5% -2.4% 3.3% -2.1% -1.3% -4.4% -2.6% 2.7% -1.5% 0.0% -6.4% -0.4%201401 0.0% 5.0% 0.0% 0.0% 0.0% 3.0% -6.5% -3.0% -0.1% 0.0% 0.0% 0.0% -0.1%201403 0.0% 3.9% 0.0% 0.0% 7.2% 9.0% 8.0% 3.0% 15.0% 5.0% 0.0% 0.0% 3.0%201408 -1.3% 3.0% -3.9% 0.4% 1.1% -2.4% 13.0% 1.1% 0.1% 0.8% 0.0% 1.0% 1.4%201413 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%201504 0.0% 1.0% 0.0% 0.0% 0.0% 0.0% 1.0% 0.0% 15.0% 0.0% 0.0% 0.0% 0.5%

Current Rate Level

Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Exhibit 7

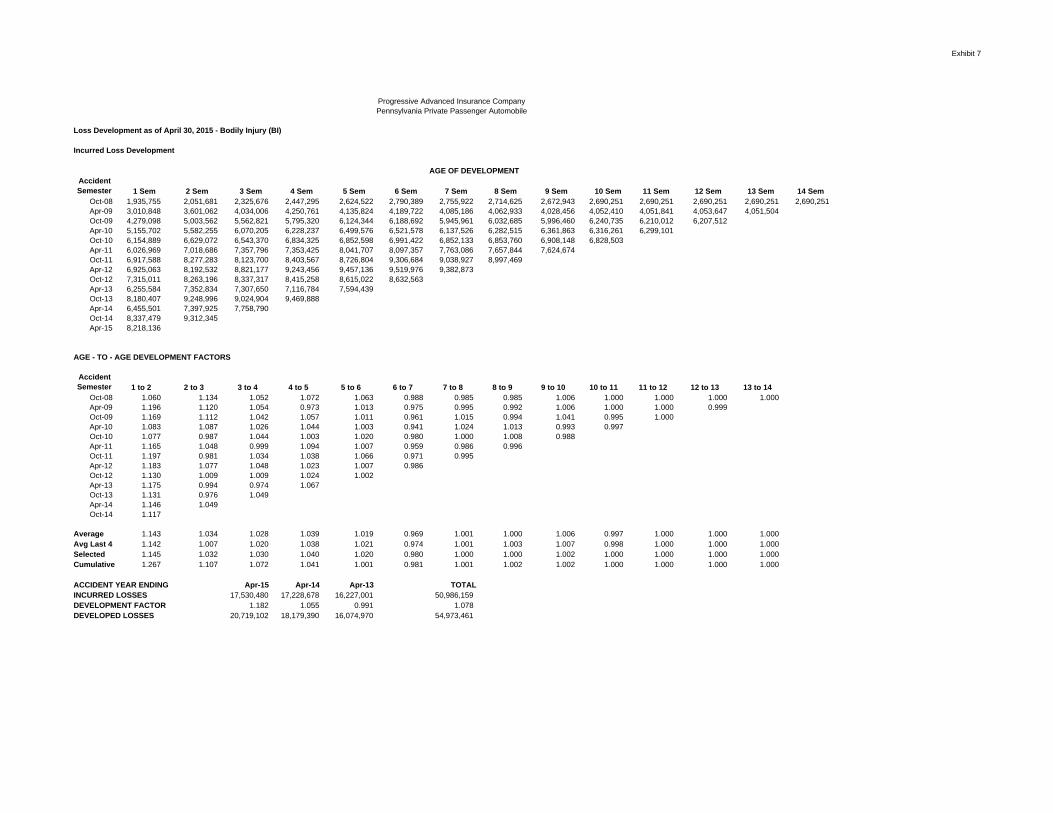

Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Loss Development as of April 30, 2015 - Bodily Injury (BI)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem

Oct-08 1,935,755 2,051,681 2,325,676 2,447,295 2,624,522 2,790,389 2,755,922 2,714,625 2,672,943 2,690,251 2,690,251 2,690,251 2,690,251 2,690,251Apr-09 3,010,848 3,601,062 4,034,006 4,250,761 4,135,824 4,189,722 4,085,186 4,062,933 4,028,456 4,052,410 4,051,841 4,053,647 4,051,504Oct-09 4,279,098 5,003,562 5,562,821 5,795,320 6,124,344 6,188,692 5,945,961 6,032,685 5,996,460 6,240,735 6,210,012 6,207,512Apr-10 5,155,702 5,582,255 6,070,205 6,228,237 6,499,576 6,521,578 6,137,526 6,282,515 6,361,863 6,316,261 6,299,101Oct-10 6,154,889 6,629,072 6,543,370 6,834,325 6,852,598 6,991,422 6,852,133 6,853,760 6,908,148 6,828,503Apr-11 6,026,969 7,018,686 7,357,796 7,353,425 8,041,707 8,097,357 7,763,086 7,657,844 7,624,674Oct-11 6,917,588 8,277,283 8,123,700 8,403,567 8,726,804 9,306,684 9,038,927 8,997,469Apr-12 6,925,063 8,192,532 8,821,177 9,243,456 9,457,136 9,519,976 9,382,873Oct-12 7,315,011 8,263,196 8,337,317 8,415,258 8,615,022 8,632,563Apr-13 6,255,584 7,352,834 7,307,650 7,116,784 7,594,439Oct-13 8,180,407 9,248,996 9,024,904 9,469,888Apr-14 6,455,501 7,397,925 7,758,790Oct-14 8,337,479 9,312,345Apr-15 8,218,136

AGE - TO - AGE DEVELOPMENT FACTORS

Accident Semester 1 to 2 2 to 3 3 to 4 4 to 5 5 to 6 6 to 7 7 to 8 8 to 9 9 to 10 10 to 11 11 to 12 12 to 13 13 to 14

Oct-08 1.060 1.134 1.052 1.072 1.063 0.988 0.985 0.985 1.006 1.000 1.000 1.000 1.000Apr-09 1.196 1.120 1.054 0.973 1.013 0.975 0.995 0.992 1.006 1.000 1.000 0.999Oct-09 1.169 1.112 1.042 1.057 1.011 0.961 1.015 0.994 1.041 0.995 1.000Apr-10 1.083 1.087 1.026 1.044 1.003 0.941 1.024 1.013 0.993 0.997Oct-10 1.077 0.987 1.044 1.003 1.020 0.980 1.000 1.008 0.988Apr-11 1.165 1.048 0.999 1.094 1.007 0.959 0.986 0.996Oct-11 1.197 0.981 1.034 1.038 1.066 0.971 0.995Apr-12 1.183 1.077 1.048 1.023 1.007 0.986Oct-12 1.130 1.009 1.009 1.024 1.002Apr-13 1.175 0.994 0.974 1.067Oct-13 1.131 0.976 1.049Apr-14 1.146 1.049Oct-14 1.117

Average 1.143 1.034 1.028 1.039 1.019 0.969 1.001 1.000 1.006 0.997 1.000 1.000 1.000Avg Last 4 1.142 1.007 1.020 1.038 1.021 0.974 1.001 1.003 1.007 0.998 1.000 1.000 1.000Selected 1.145 1.032 1.030 1.040 1.020 0.980 1.000 1.000 1.002 1.000 1.000 1.000 1.000Cumulative 1.267 1.107 1.072 1.041 1.001 0.981 1.001 1.002 1.002 1.000 1.000 1.000 1.000

ACCIDENT YEAR ENDING Apr-15 Apr-14 Apr-13 TOTALINCURRED LOSSES 17,530,480 17,228,678 16,227,001 50,986,159DEVELOPMENT FACTOR 1.182 1.055 0.991 1.078DEVELOPED LOSSES 20,719,102 18,179,390 16,074,970 54,973,461

AGE OF DEVELOPMENT

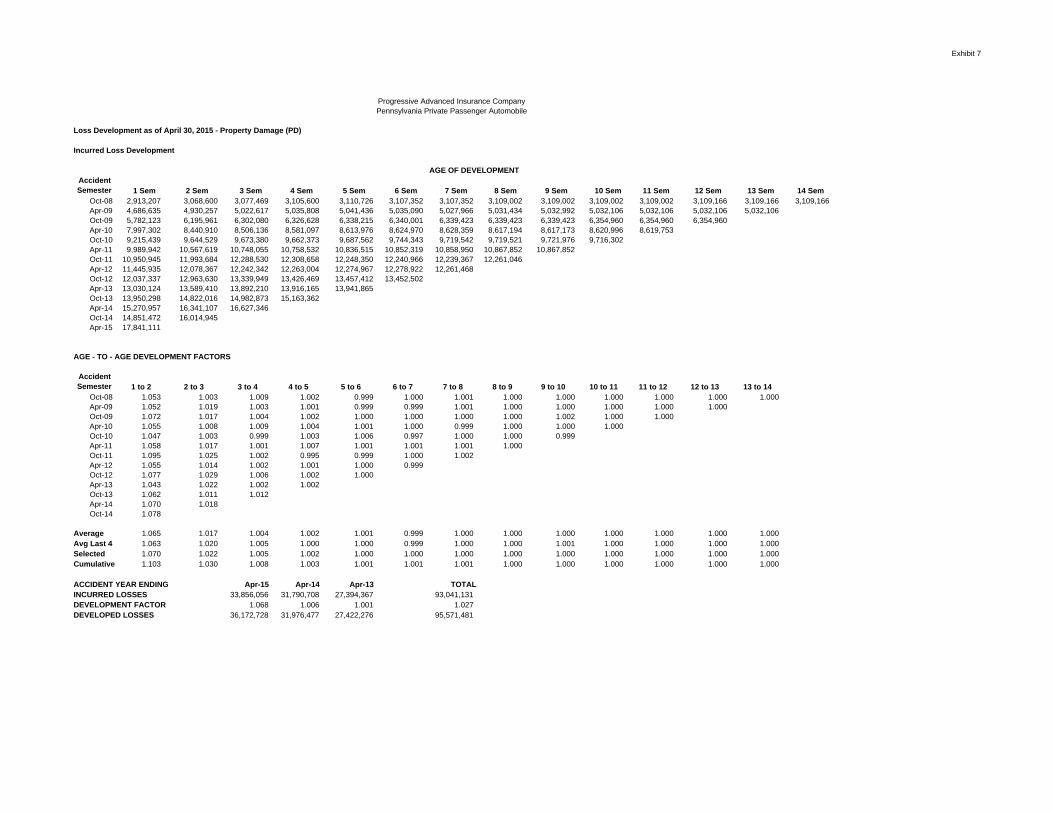

Exhibit 7

Progressive Advanced Insurance CompanyPennsylvania Private Passenger Automobile

Loss Development as of April 30, 2015 - Property Damage (PD)

Incurred Loss Development

Accident Semester 1 Sem 2 Sem 3 Sem 4 Sem 5 Sem 6 Sem 7 Sem 8 Sem 9 Sem 10 Sem 11 Sem 12 Sem 13 Sem 14 Sem