Embed Size (px)

Citation preview

Product management and the marketing of financialservices

Jeffrey StrieterAssistant Professor, Department of Business Administration, SUNY Brockport,New York, USAAshok K. GuptaProfessor of Marketing, College of Business Administration, Ohio University,Athens, Ohio, USAS.P. RajDistinguished Professor of Marketing, School of Management, SyracuseUniversity, Syracuse, New York, USADavid WilemonProfessor of Marketing and Director of the Innovation Management Program,School of Management, Syracuse University, Syracuse, New York, USA

Background

The commercial banking industry has

undergone significant change in the past 15

years. From the origin of commercial bank-

ing, the cost of its key ingredient ± money ±

was controlled. The business activities in

which banks could and could not compete

were largely determined by legislation (Sul-

livan, 1986). Today, large commercial banks

operate in a far more dynamic marketplace.

The cost of funds fluctuates rapidly and there

is increased competition from both inside

and outside the traditional banking industry

(Yang, 1990). Federal and state legislation

continues to exert influence on the industry,

products and customers are increasingly

sophisticated and the rate of change in the

industry continues unabated (LeGrand,

1992). Such rapidly changing circumstances

have prompted a number of significant

changes in traditional bank management.

Challenges confronting bank managers

include developing: a capacity to meet and

exceed the performance levels of sophisti-

cated competitors; a customer-focussed mar-

keting approach; an ability to manage

numerous and often very diverse products

and services; a capability to measure both

market performance and product profitabil-

ity; and initiative and entrepreneurial

thinking within their organizations (Cooper

et al., 1994; Cosse and Swan, 1983; Franozoni,

1991; Wichman, 1989, 1986).

In response to the need for more responsive

management approaches, banks began

implementing product management. First

used in 1927, by Procter & Gamble, product

management is a logical choice when pro-

ducts are quite different from one another or

if the number of products offered is too large

to be managed by a functional department

(Kotler, 1984). Major benefits of the product

management system include: improved cus-

tomer focus, product specialization and co-

ordination, maximum use of resources,

product accountability and the generation of

new ideas. Placing a single person or even a

department in charge of a product or a group

of products is more likely to assure that no

product is overlooked in the marketplace

(Eckles and Novotny, 1984).

Banks have used the product management

system for over a decade. While some banks

continue to find new applications for product

management, other banks are scaling back

their reliance on product management in

favor of more traditional management

approaches (Berggren and Dewar, 1992).

Although there is much anecdotal evidence

of the uses and applications of product

management in banking, little systematic

research has been conducted to examine the

organizational and individual issues

encountered in applying product manage-

ment to large full-service commercial banks.

In fact, our literature review revealed few

previously published studies focussing on the

major conceptual issues of product manage-

ment in banking.

Unfortunately, many banking organiza-

tions adopt the product management system

without completely understanding it and

without providing the necessary support

(Cummings et al., 1989). Despite the many

benefits product management offers both

commercial banks and package goods mar-

keters, there are several management and

organizational issues which must be dealt

with for product management to be success-

ful. One stream of research specifically

explores the challenges product managers

The current issue and full text archive of this journal is available at

http://www.emerald-library.com

[ 342 ]

International Journal of BankMarketing17/7 [1999] 342±354

# MCB University Press[ISSN 0265-2323]

KeywordsBanking, Financial services,

Marketing, Product management,

USA

AbstractOne of the most important devel-

opments in banking is the

increased emphasis on marketing

a wide array of financial services.

This emphasis has led to the

adoption of the product manage-

ment system in one form or an-

other by many large, full-service

commercial banks. The transition

to a product management system

has required banks to change how

they organize and manage their

operations. Examines several of

the major challenges and issues

faced by product managers in the

banking environment, namely, the

identification of the product man-

ager's task responsibilities; the

role of organizational support in

facilitating product management;

the influence of organizational

culture; and the impact of power

and conflict on product managers

and the product management sys-

tem. Also examines how product

managers assess their job perfor-

mance, work satisfaction, and the

performance of the overall product

management system in their bank.

The authors thank TedRuddick for his assistanceduring the early phases ofthis research. They alsoappreciate the efforts of theproduct managers whoshared their knowledge,expertise, andorganizational wisdom withthem during this study.

encounter in the package goods industry

(Lysonski, 1985; Reid, 1988). A second

research stream explicates the issues con-

cerning the application of product manage-

ment to the management of services

(Lysonski et al., 1988; Southerst, 1994). Other

research into the application of product

management has focussed on decision-

making authority and interpersonal rela-

tionships (Churchill and Pecotich, 1982;

Cummings et al., 1984; Hise and Kelly, 1978;

Kelly and Hise, 1979), the role of strategic

planning and product management (Crosse

and Swan, 1983) and product managers' job

satisfaction and job performance and their

relationship to select organizational beha-

vioral variables (Cummings et al., 1989).

However, we know far less about the organi-

zational and individual issues and how they,

in turn, influence the performance of product

management systems in commercial

banking.

Focus

This exploratory study is designed to identify

and examine the major issues and challenges

of product management systems in large

commercial banks. We began our study with

a thorough review of the germane literature

on product management as used in the

packaged goods industries, services and

banking. This literature review revealed

several insights which provided the concep-

tual focus for this study. For example, we

found that, despite the increasingly wide-

spread application of product management in

banking, researchers have seldom probed the

roles of the organization and the individual

product managers in carrying out this

dynamic activity. Based on our literature

review (Cooper et al., 1994; Cummings et al.,

1984, 1989; LeGrand, 1992; Lysonski, 1985;

Reid, 1988; Reidenbach and Moak, 1986), we

hypothesized that there are four major fac-

tors which have a significant influence on

product managers in banking:

1 task responsibilities;

2 organizational support;

3 organizational culture; and

4 power/conflict issues.

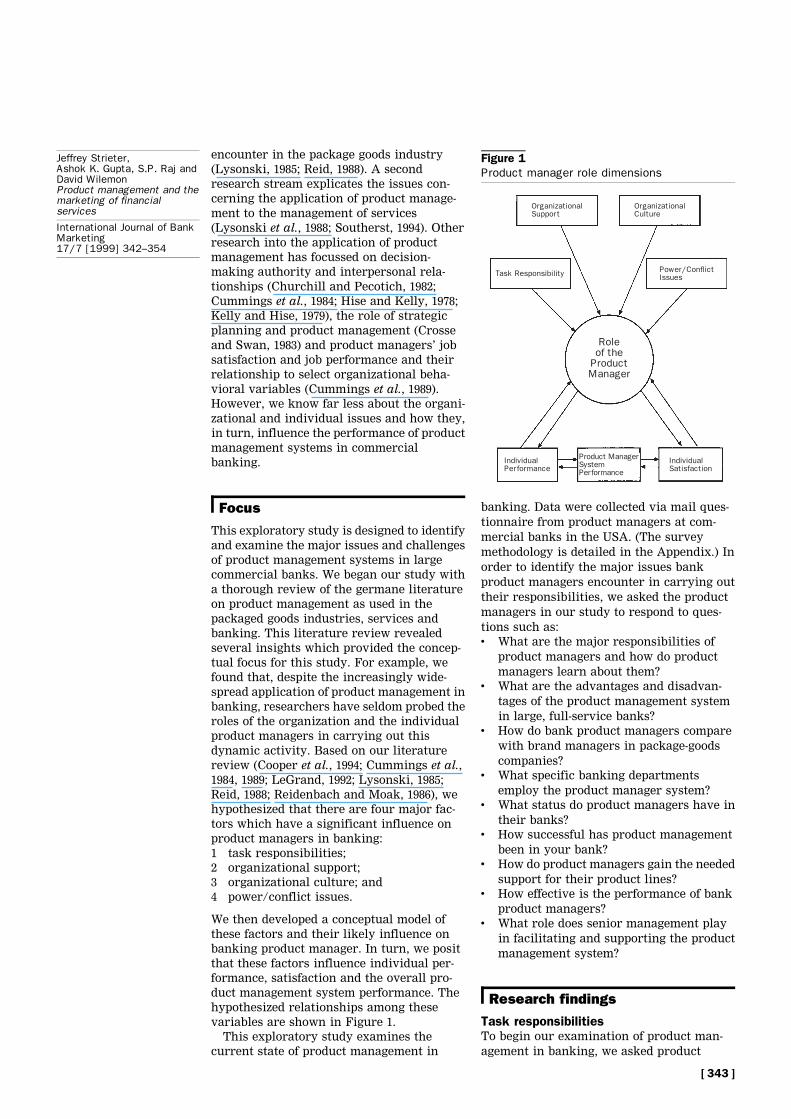

We then developed a conceptual model of

these factors and their likely influence on

banking product manager. In turn, we posit

that these factors influence individual per-

formance, satisfaction and the overall pro-

duct management system performance. The

hypothesized relationships among these

variables are shown in Figure 1.

This exploratory study examines the

current state of product management in

banking. Data were collected via mail ques-

tionnaire from product managers at com-

mercial banks in the USA. (The survey

methodology is detailed in the Appendix.) In

order to identify the major issues bank

product managers encounter in carrying out

their responsibilities, we asked the product

managers in our study to respond to ques-

tions such as:. What are the major responsibilities of

product managers and how do product

managers learn about them?. What are the advantages and disadvan-

tages of the product management system

in large, full-service banks?. How do bank product managers compare

with brand managers in package-goods

companies?. What specific banking departments

employ the product manager system?. What status do product managers have in

their banks?. How successful has product management

been in your bank?. How do product managers gain the needed

support for their product lines?. How effective is the performance of bank

product managers?. What role does senior management play

in facilitating and supporting the product

management system?

Research findings

Task responsibilitiesTo begin our examination of product man-

agement in banking, we asked product

Figure 1Product manager role dimensions

[ 343 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

managers in large commercial banks to share

with us details about their specific job

responsibilities.

Understanding job expectationsAlmost one-half of the product managers

indicated that they learned what was

expected of them from their on-the-job ex-

periences. Approximately one-third (32 per-

cent) indicated that they received significant

direction from their superiors, while 18

percent stated that their roles were generally

well defined owing to the existence of a

product management system in their banks.

A total of 54 percent felt they had consider-

able freedom in shaping their own jobs,

including both defining their areas of re-

sponsibility and making significant changes

in these activities. Many of the product

managers noted that they had to `̀ make their

own way'' in their organizations. We did not

determine whether this freedom reflects

management's confidence in the product

manager concept or is simply due to an

incomplete understanding by management of

the role of product management and its

relationship to other management functions.

As one manager stated:The commodity nature of most products in

banks creates a position of influence for the

product manager, but offers no specific

direction or leadership.

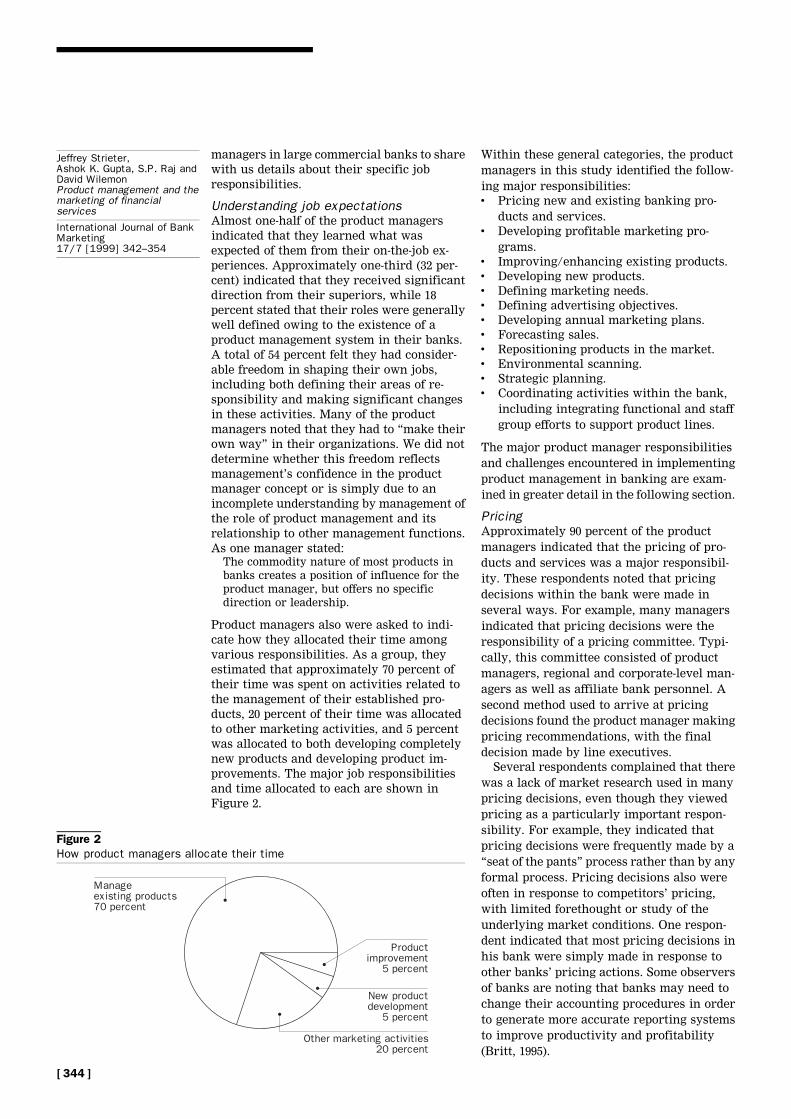

Product managers also were asked to indi-

cate how they allocated their time among

various responsibilities. As a group, they

estimated that approximately 70 percent of

their time was spent on activities related to

the management of their established pro-

ducts, 20 percent of their time was allocated

to other marketing activities, and 5 percent

was allocated to both developing completely

new products and developing product im-

provements. The major job responsibilities

and time allocated to each are shown in

Figure 2.

Within these general categories, the product

managers in this study identified the follow-

ing major responsibilities:. Pricing new and existing banking pro-

ducts and services.. Developing profitable marketing pro-

grams.. Improving/enhancing existing products.. Developing new products.. Defining marketing needs.. Defining advertising objectives.. Developing annual marketing plans.. Forecasting sales.. Repositioning products in the market.. Environmental scanning.. Strategic planning.. Coordinating activities within the bank,

including integrating functional and staff

group efforts to support product lines.

The major product manager responsibilities

and challenges encountered in implementing

product management in banking are exam-

ined in greater detail in the following section.

PricingApproximately 90 percent of the product

managers indicated that the pricing of pro-

ducts and services was a major responsibil-

ity. These respondents noted that pricing

decisions within the bank were made in

several ways. For example, many managers

indicated that pricing decisions were the

responsibility of a pricing committee. Typi-

cally, this committee consisted of product

managers, regional and corporate-level man-

agers as well as affiliate bank personnel. A

second method used to arrive at pricing

decisions found the product manager making

pricing recommendations, with the final

decision made by line executives.

Several respondents complained that there

was a lack of market research used in many

pricing decisions, even though they viewed

pricing as a particularly important respon-

sibility. For example, they indicated that

pricing decisions were frequently made by a

`̀ seat of the pants'' process rather than by any

formal process. Pricing decisions also were

often in response to competitors' pricing,

with limited forethought or study of the

underlying market conditions. One respon-

dent indicated that most pricing decisions in

his bank were simply made in response to

other banks' pricing actions. Some observers

of banks are noting that banks may need to

change their accounting procedures in order

to generate more accurate reporting systems

to improve productivity and profitability

(Britt, 1995).

Figure 2How product managers allocate their time

[ 344 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

Product development/productimprovementOf the product managers, 91 percent indi-

cated that another major responsibility in-

cluded improving/enhancing existing bank

products or services. Despite the reported

importance of improving/enhancing existing

bank products, product managers indicated

they devoted only 10 percent of their time to

such activities. Developing new products was

a major responsibility for 80 percent of the

bank product managers, and approximately

three-quarters indicated defining marketing

needs (76 percent) and scanning the envir-

onment for new opportunities (74 percent) as

additional major responsibilities. Yet, only 34

percent indicated that market-testing new

products was a major responsibility. Ap-

proximately one-quarter (24 percent) indi-

cated marketing research was a major

responsibility. Once again, several respon-

dents indicated there was little market re-

search or competitive analysis conducted

before the introduction of new products.

Several product managers also expressed

concern about coordination problems during

both the introduction of new products and

when existing products were changed or

modified. Since commercial banks conduct

their business in many different branch

locations and affiliate offices, e.g. state-wide,

nationally and even globally, a successful

introduction requires that the market objec-

tives for new products be communicated to

many, diverse facilities. When the branch

offices or affiliates do not understand the

product itself, the reason for the introduc-

tion, or the overall marketing strategy, the

introduction is not likely to be successful.

The areas identified as problematic included

the lack of training and educating line

officers, the continually changing banking

environment, servicing national and global

customers and communications with a

diverse, international salesforce. Several of

the PMs noted that they had the general

responsibility for new product introductions

and existing product modifications without

the necessary authority to implement such

programs effectively.

Planning and forecastingApproximately one-half of the product man-

agers surveyed (50 percent) were required to

prepare a three- or five-year plan for their

products or services. Strategic planning was

a major responsibility for approximately two-

thirds (66 percent) of the product managers.

These plans frequently required the approval

of different bank managers. Frequently, the

review and approval authority included

other product line managers, the director of

product management, sales director, and

other functional area managers (such as the

trust and commercial banking departments).

In many instances, the approval of senior

management was also required. One man-

ager remarked:Generic products developed in a centralizedenvironment may not fit specific local mar-

kets. Product objectives may differ from local

unit plans and direction.

Cross-functional coordinationIn addition to the coordination problems

associated with new or existing products,

many managers expressed problems coordi-

nating their efforts with other departments

within the bank. One manager expressed this

concern:There is a corporate-level product manage-

ment group which facilitates product offer-ings to all affiliate banks. The affiliate banks,

in turn, coordinate the product offerings

between functional areas within each bank.

My overall rating of the effectiveness of

coordination with the bank as a whole is, atbest, average.

Another coordination challenge noted is the

problem of `̀ shared responsibility'' within a

bank. Functional bank managers responsible

for products sold within their respective

groups (retail banking, trust services, com-

mercial lending) can feel threatened by pro-

duct management in general, or by a specific

manager of a particular product. Sensing a

loss of responsibility and control over their

own `̀ turf'', some banking line managers may

not support the efforts of product managers.

One cause of this problem is that the role of

product managers in banking is generally not

as well-defined as the role of PMs in consumer

goods. We posit that one consequence is

increased stress, conflict, and role ambiguity

for bank product managers.

Organizational supportIn one study of bank marketers, it was found

that the biggest hindrance to the develop-

ment of new bank services was the lack of

commitment and support to manage new

service development (Bowers and Wallace,

1986). In our study, we examined several

indicators of organizational support, includ-

ing the availability of support services and

information, status in the organization, and

compensation. Slightly more than half of the

product managers' departments had their

own marketing services support group.

These groups conducted marketing research,

advertising, and other functions to support

the product managers' efforts. Many other

product managers, however, stated that they

did not have sufficient organizational sup-

port to fulfill their job responsibilities

[ 345 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

adequately. Surprisingly, only 18 percent of

the product managers exercised any direct

authority over other bank marketing per-

sonnel. The marketing personnel who did

report to the product managers typically

included personnel with sales and marketing

research responsibilities. Several of the pro-

duct managers expressed concern about the

lack of direct authority over those supporting

organizational functions they considered

important to their success.

Resource availability/managementattentionApproximately 45 percent of the product

managers felt they usually had sufficient

information to perform their jobs effectively.

When asked to indicate how often they found

themselves concerned with obtaining the

necessary financial resources, 21 percent

indicated that their level of concern was mid-

way between `̀ rarely'' and `̀ always'' on a five-

point scale and 17 percent indicated that they

sometimes could obtain adequate assistance.

Many of the product managers in our study

also expressed concern about obtaining suffi-

cient senior management attention. A total of

12 percent stated that they rarely received the

required attention. Less than 4 percent

indicated that they always received sufficient

senior management support. One-half of the

group (51 percent) ranked senior management

attention between `̀ rarely sufficient'' and

`̀ sometimes sufficient'' on a five-point scale.

Departments which utilize the productmanager systemProduct managers were asked to indicate

which departments within their banks

employed the product management system

and how long each had utilized the system.

Several of the banks introduced product

management in the mid-1970s, but most of the

respondents indicated that this system has

been used within their banks since the early

to mid-1980s. Some banks implemented pro-

duct management in one department as an

`̀ experiment''. Other banks adopted product

management concurrently across several

different banking departments. We found

that product management was used in most

major bank departments, including interna-

tional, retail, financial analysis, trust ser-

vices, cash management, and corporate.

Status of product managers in banksIn order to assess the general acceptance of

product managers in banking, we asked

product managers to indicate their percep-

tion of their status in the bank relative to

other managers. Of the product managers, 41

percent felt they possessed at least an aver-

age amount of status compared with other

managers of similar responsibility within the

bank, and one-third (32 percent) rated their

status more than average. A total of 14

percent stated that they enjoyed a great deal

of status compared with other managers

within the bank, while 12 percent indicated

they had less than an average amount of

status.

Factors that enhance productmanagement performance in banksTo examine more closely the perceived

requirements for effective product manage-

ment in banks, we asked product managers to

list the `̀ conditions'' they would recommend

that a colleague investigate before accepting

a position as a product manager with another

bank. Several of the responses indicated that

potential applicants should investigate the

availability of the necessary resources to

accomplish their responsibilities. It was

suggested that an ideal situation was one in

which the product management group had its

own marketing research and marketing

communications staff. Many also suggested

the resources necessary to develop and

market banking products and services suc-

cessfully should be available within a pro-

duct management group.

Our respondents also noted the importance

of both clearly-defined product performance

objectives from senior management and a

regular process for reviewing and revising

goals with senior management. Many noted

that, if senior management does not explicitly

state what a product manager is to accom-

plish, product managers should make certain

that they have the flexibility and autonomy

needed to define their own roles. Some

individuals will find such a situation unac-

ceptable and one to avoid since they must

cope with an unstructured job environment

with little formal authority. This can lead to

stress, uncertainty and dissatisfaction. For

example, one study of product managers

found job satisfaction was inversely related to

role ambiguity (Cummings et al., 1989).

Management's commitment to a product

management system is indicated by a will-

ingness actively to specify the roles, respon-

sibilities, and accountabilities of product

managers. PMs should have clearly-defined

performance objectives from senior manage-

ment, and a regular process for reviewing

and revising new and existing goals with

their managers. Several product managers

also expressed a need for a compensation

system which rewards high performance.

One product manager expressed concern

about the potential negative impact of inac-

curate cost allocation on performance mea-

sures in his bank.

[ 346 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

Organizational culture

Sathe (1985) defines culture as `̀ the set of

important assumptions (often unstated) that

members of a community share in common''.

Organizations accomplish those goals and

objectives which the organizational culture

sanctions. Organizations often find they can

devise new strategies that make sense from a

financial or marketing point of view, yet they

cannot implement their strategies because

they require assumptions, values, and ways

of working that are too far out of line with the

organization's prior assumptions (Franwick

et al., 1994; Schein, 1985). In order better to

understand the cultural environment in

which bank product managers function, we

asked managers to express the degree of

competition that exists among product man-

agers within their departments. Only 2

percent indicated that the competition was

`̀ very intense'', while 44 percent stated that

competition between product managers did

not exist within their departments.

Several product managers expressed a

concern that the very close personal rela-

tionships which banks develop with some of

their key customers can act as a barrier to

the successful implementation of a bank-wide

product manager system. For example, one

customer may get certain service charges

waived without requesting this be done,

while other customers may not enjoy the

same privilege in spite of their requests for

such waivers. In a similar vein, a line officer

might not offer a product that is being

promoted by a product manager because the

line officer fears the offered product may

damage the ongoing relationship with a

customer. Such behavior can create man-

agement and profit/loss problems for product

managers because it can directly affect the

relationship with a customer. In many

instances, the bank-customer relationship

involves multiple products. When this is the

case, specific product profitability (and cost-

ing) becomes increasingly difficult to mea-

sure.

Power/conflict issuesProduct management can offer commercial

banks many opportunities for product

growth and development. Although many

banks have made progress in implementing

product management in recent years, others

have not been able to realize the potential

product management offers. Wichman (1989)

states that, in order to be effective, product

managers must be able to cross organiza-

tional lines informally and operate in areas

beyond their immediate responsibilities.

This can result in task-related conflicts

between different functional groups and sub-

cultures within an organization (Sathe, 1985).

To examine these issues, we asked product

managers to tell us about the power and

conflict issues they encountered when they

performed their responsibilities. Based on

their responses, we were able to identify a

number of different conflicts which develop

between the product management groups and

other departments or staff groups within the

bank who support the PMs' product lines

(Brown, 1983). Frequently, the conflicts

involved issues of responsibility and author-

ity as well as various interdepartmental

conflicts. Disagreements also arise over task

priorities and resource allocations. Schedul-

ing and quality control conflicts develop

when there is no clear agreement within the

bank's department concerning these issues.

One product manager expressed the problem

this way:We have all of the usual responsibilities ofproduct managers, but have little or noresponsibility over operations, marketing,account officers, or other staff groups. Whatmight be a high priority to the productmanager, based on market need, may be oflittle consequence to others. Thus the productmanager is forced to spend an inordinateamount of time convincing others of themerits of the product. The smallest projectfrequently takes an inordinate amount oftime to complete.

Obtaining sufficient resources and organiza-

tional commitment is another source of

conflict identified in this study. We found

that some banks attempted to operate with

their current level of resources rather than

provide the additional resources needed by

their PMs. In such cases, PMs find it

necessary to obtain the needed resources,

such as a management information system,

by `̀ fighting'' and/or reallocating resources

from existing product lines. Inadequate pro-

duct information and incomplete analysis

can lead to other problems, including poor

pricing decisions, establishing inaccurate

sales targets, poor scheduling, and other

operating problems. Several of our respon-

dents suggested that product managers

should have cross-divisional responsibility

for the products and services they support.

This, in turn, can reduce the conflict and

power struggles encountered by PMs.

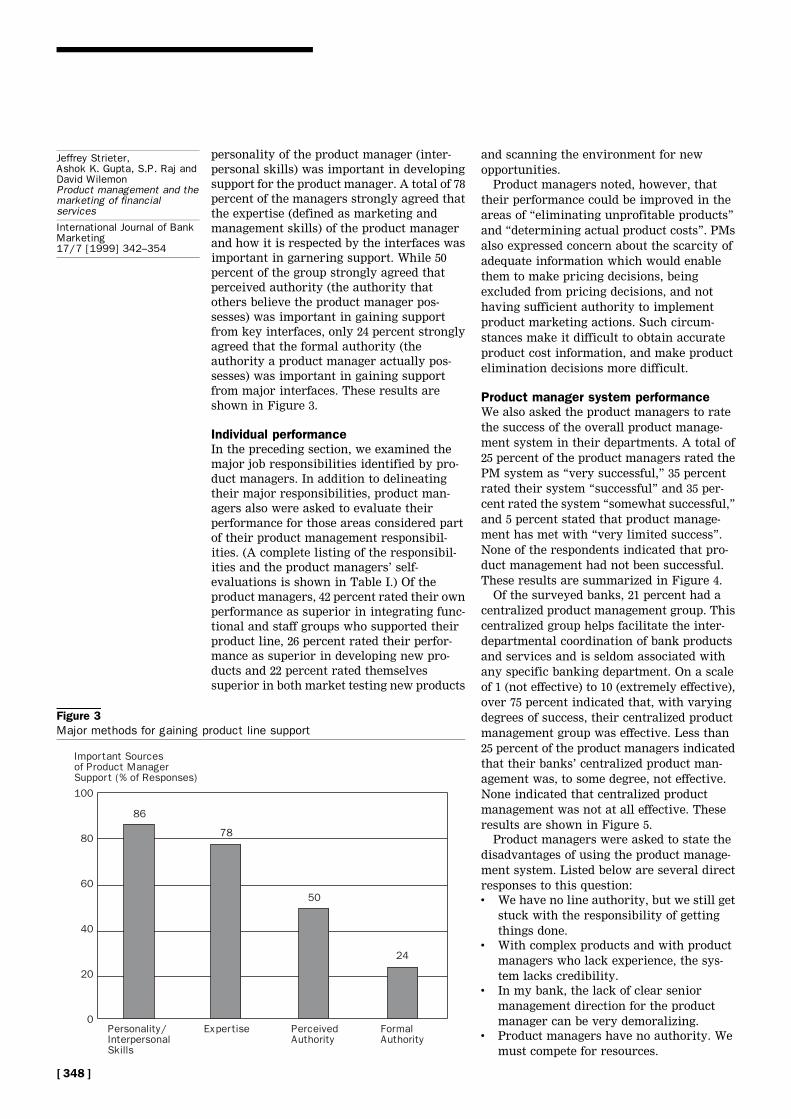

Product managers were asked about the

methods they perceived as most important in

obtaining assistance from other areas within

the bank that supported their product lines

(see Figure 3). Generally, these supporting

areas included key interfaces (functional

areas) not under the direct control of the

product management group. Of the man-

agers, 86 percent strongly expressed that the

[ 347 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

personality of the product manager (inter-

personal skills) was important in developing

support for the product manager. A total of 78

percent of the managers strongly agreed that

the expertise (defined as marketing and

management skills) of the product manager

and how it is respected by the interfaces was

important in garnering support. While 50

percent of the group strongly agreed that

perceived authority (the authority that

others believe the product manager pos-

sesses) was important in gaining support

from key interfaces, only 24 percent strongly

agreed that the formal authority (the

authority a product manager actually pos-

sesses) was important in gaining support

from major interfaces. These results are

shown in Figure 3.

Individual performanceIn the preceding section, we examined the

major job responsibilities identified by pro-

duct managers. In addition to delineating

their major responsibilities, product man-

agers also were asked to evaluate their

performance for those areas considered part

of their product management responsibil-

ities. (A complete listing of the responsibil-

ities and the product managers' self-

evaluations is shown in Table I.) Of the

product managers, 42 percent rated their own

performance as superior in integrating func-

tional and staff groups who supported their

product line, 26 percent rated their perfor-

mance as superior in developing new pro-

ducts and 22 percent rated themselves

superior in both market testing new products

and scanning the environment for new

opportunities.

Product managers noted, however, that

their performance could be improved in the

areas of `̀ eliminating unprofitable products''

and `̀ determining actual product costs''. PMs

also expressed concern about the scarcity of

adequate information which would enable

them to make pricing decisions, being

excluded from pricing decisions, and not

having sufficient authority to implement

product marketing actions. Such circum-

stances make it difficult to obtain accurate

product cost information, and make product

elimination decisions more difficult.

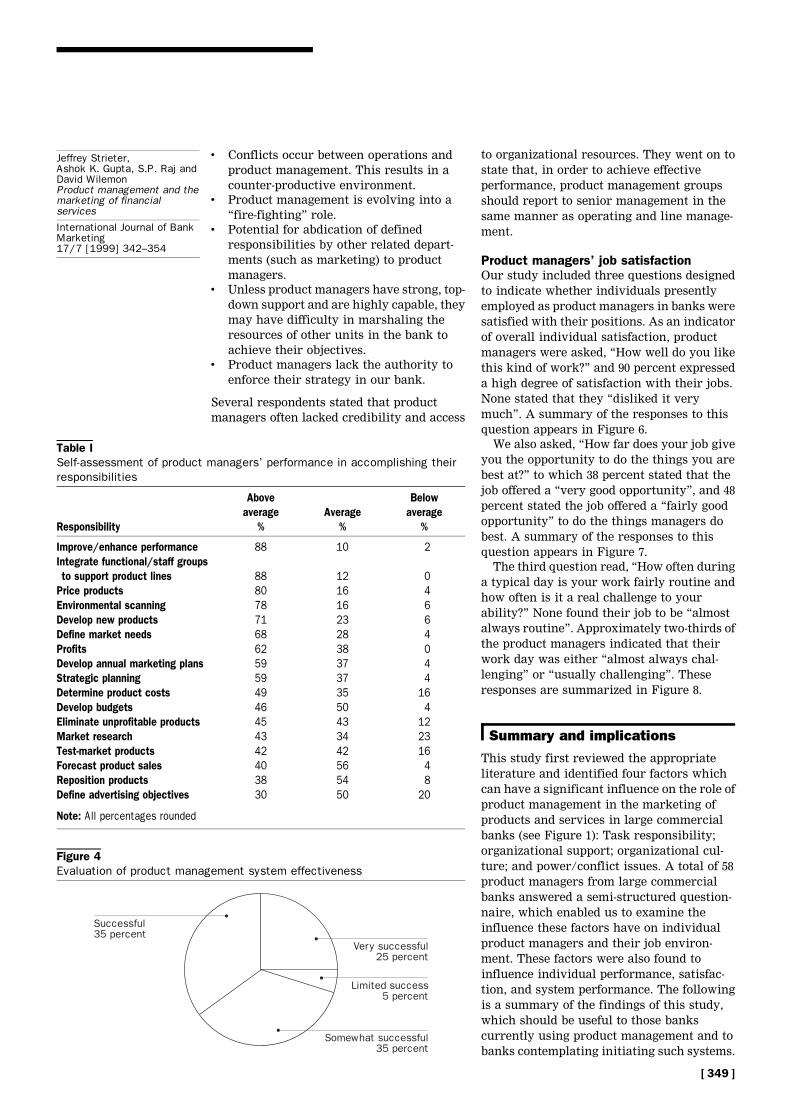

Product manager system performanceWe also asked the product managers to rate

the success of the overall product manage-

ment system in their departments. A total of

25 percent of the product managers rated the

PM system as `̀ very successful,'' 35 percent

rated their system `̀ successful'' and 35 per-

cent rated the system `̀ somewhat successful,''

and 5 percent stated that product manage-

ment has met with `̀ very limited success''.

None of the respondents indicated that pro-

duct management had not been successful.

These results are summarized in Figure 4.

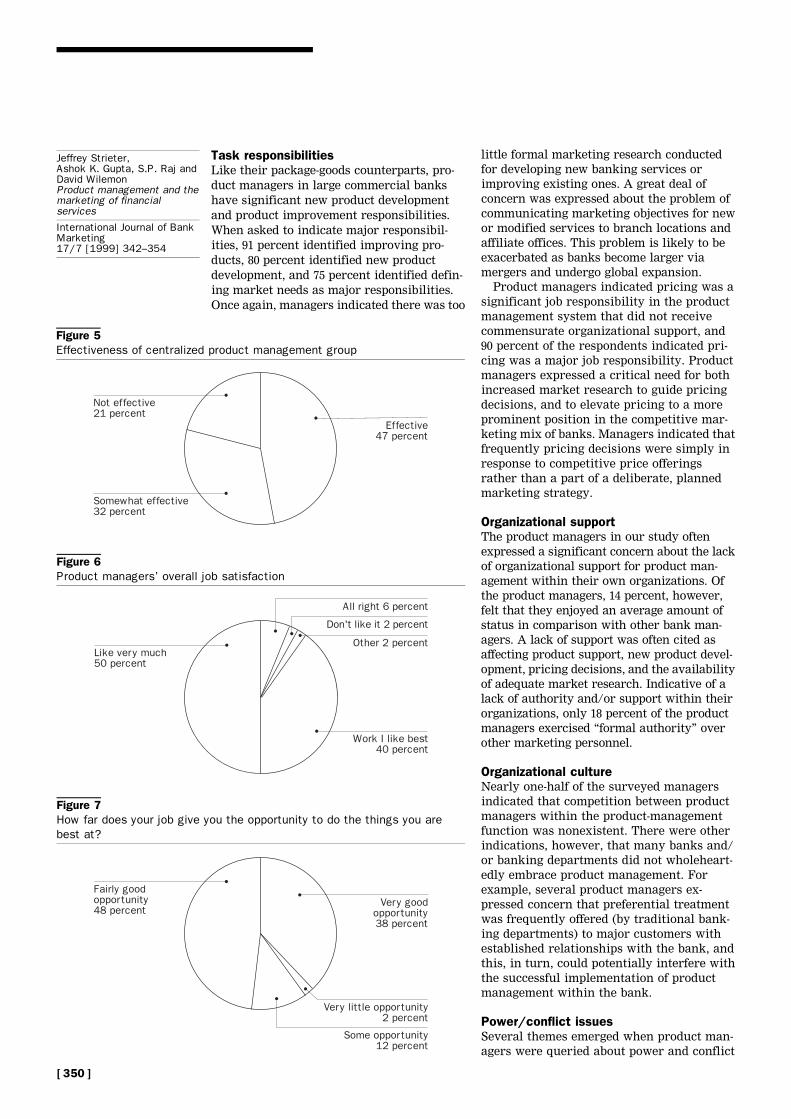

Of the surveyed banks, 21 percent had a

centralized product management group. This

centralized group helps facilitate the inter-

departmental coordination of bank products

and services and is seldom associated with

any specific banking department. On a scale

of 1 (not effective) to 10 (extremely effective),

over 75 percent indicated that, with varying

degrees of success, their centralized product

management group was effective. Less than

25 percent of the product managers indicated

that their banks' centralized product man-

agement was, to some degree, not effective.

None indicated that centralized product

management was not at all effective. These

results are shown in Figure 5.

Product managers were asked to state the

disadvantages of using the product manage-

ment system. Listed below are several direct

responses to this question:. We have no line authority, but we still get

stuck with the responsibility of getting

things done.. With complex products and with product

managers who lack experience, the sys-

tem lacks credibility.. In my bank, the lack of clear senior

management direction for the product

manager can be very demoralizing.. Product managers have no authority. We

must compete for resources.

Figure 3Major methods for gaining product line support

[ 348 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

. Conflicts occur between operations and

product management. This results in a

counter-productive environment.. Product management is evolving into a

`̀ fire-fighting'' role.. Potential for abdication of defined

responsibilities by other related depart-

ments (such as marketing) to product

managers.. Unless product managers have strong, top-

down support and are highly capable, they

may have difficulty in marshaling the

resources of other units in the bank to

achieve their objectives.. Product managers lack the authority to

enforce their strategy in our bank.

Several respondents stated that product

managers often lacked credibility and access

to organizational resources. They went on to

state that, in order to achieve effective

performance, product management groups

should report to senior management in the

same manner as operating and line manage-

ment.

Product managers' job satisfactionOur study included three questions designed

to indicate whether individuals presently

employed as product managers in banks were

satisfied with their positions. As an indicator

of overall individual satisfaction, product

managers were asked, `̀ How well do you like

this kind of work?'' and 90 percent expressed

a high degree of satisfaction with their jobs.

None stated that they `̀ disliked it very

much''. A summary of the responses to this

question appears in Figure 6.

We also asked, `̀ How far does your job give

you the opportunity to do the things you are

best at?'' to which 38 percent stated that the

job offered a `̀ very good opportunity'', and 48

percent stated the job offered a `̀ fairly good

opportunity'' to do the things managers do

best. A summary of the responses to this

question appears in Figure 7.

The third question read, `̀ How often during

a typical day is your work fairly routine and

how often is it a real challenge to your

ability?'' None found their job to be `̀ almost

always routine''. Approximately two-thirds of

the product managers indicated that their

work day was either `̀ almost always chal-

lenging'' or `̀ usually challenging''. These

responses are summarized in Figure 8.

Summary and implications

This study first reviewed the appropriate

literature and identified four factors which

can have a significant influence on the role of

product management in the marketing of

products and services in large commercial

banks (see Figure 1): Task responsibility;

organizational support; organizational cul-

ture; and power/conflict issues. A total of 58

product managers from large commercial

banks answered a semi-structured question-

naire, which enabled us to examine the

influence these factors have on individual

product managers and their job environ-

ment. These factors were also found to

influence individual performance, satisfac-

tion, and system performance. The following

is a summary of the findings of this study,

which should be useful to those banks

currently using product management and to

banks contemplating initiating such systems.

Table ISelf-assessment of product managers' performance in accomplishing theirresponsibilities

Responsibility

Aboveaverage

%Average

%

Belowaverage

%

Improve/enhance performance 88 10 2Integrate functional/staff groupsto support product lines 88 12 0

Price products 80 16 4Environmental scanning 78 16 6Develop new products 71 23 6Define market needs 68 28 4Profits 62 38 0Develop annual marketing plans 59 37 4Strategic planning 59 37 4Determine product costs 49 35 16Develop budgets 46 50 4Eliminate unprofitable products 45 43 12Market research 43 34 23Test-market products 42 42 16Forecast product sales 40 56 4Reposition products 38 54 8Define advertising objectives 30 50 20

Note: All percentages rounded

Figure 4Evaluation of product management system effectiveness

[ 349 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

Task responsibilitiesLike their package-goods counterparts, pro-

duct managers in large commercial banks

have significant new product development

and product improvement responsibilities.

When asked to indicate major responsibil-

ities, 91 percent identified improving pro-

ducts, 80 percent identified new product

development, and 75 percent identified defin-

ing market needs as major responsibilities.

Once again, managers indicated there was too

little formal marketing research conducted

for developing new banking services or

improving existing ones. A great deal of

concern was expressed about the problem of

communicating marketing objectives for new

or modified services to branch locations and

affiliate offices. This problem is likely to be

exacerbated as banks become larger via

mergers and undergo global expansion.

Product managers indicated pricing was a

significant job responsibility in the product

management system that did not receive

commensurate organizational support, and

90 percent of the respondents indicated pri-

cing was a major job responsibility. Product

managers expressed a critical need for both

increased market research to guide pricing

decisions, and to elevate pricing to a more

prominent position in the competitive mar-

keting mix of banks. Managers indicated that

frequently pricing decisions were simply in

response to competitive price offerings

rather than a part of a deliberate, planned

marketing strategy.

Organizational supportThe product managers in our study often

expressed a significant concern about the lack

of organizational support for product man-

agement within their own organizations. Of

the product managers, 14 percent, however,

felt that they enjoyed an average amount of

status in comparison with other bank man-

agers. A lack of support was often cited as

affecting product support, new product devel-

opment, pricing decisions, and the availability

of adequate market research. Indicative of a

lack of authority and/or support within their

organizations, only 18 percent of the product

managers exercised `̀ formal authority'' over

other marketing personnel.

Organizational cultureNearly one-half of the surveyed managers

indicated that competition between product

managers within the product-management

function was nonexistent. There were other

indications, however, that many banks and/

or banking departments did not wholeheart-

edly embrace product management. For

example, several product managers ex-

pressed concern that preferential treatment

was frequently offered (by traditional bank-

ing departments) to major customers with

established relationships with the bank, and

this, in turn, could potentially interfere with

the successful implementation of product

management within the bank.

Power/conflict issuesSeveral themes emerged when product man-

agers were queried about power and conflict

Figure 5Effectiveness of centralized product management group

Figure 6Product managers' overall job satisfaction

Figure 7How far does your job give you the opportunity to do the things you arebest at?

[ 350 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

issues in their organizations. Product man-

agers stated that difficulties frequently arose

between product management groups and

other bank departments over goals, organi-

zational priorities, resource allocations,

various `̀ turf'' issues, scheduling and inade-

quate product market information. Many

times, these conflicts resulted in pitting

individual product managers or a product

management group against others in the

organization. Approximately 86 percent

strongly agreed that the interpersonal skills

of the product manager was important in

soliciting support and maintaining effective

working relations with other groups. Over

three-quarters (78 percent) stated that the

expertise of the product manager was im-

portant in resolving conflicts, establishing

goals and objectives, and in carrying out a

wide range of product manager responsibil-

ities. One half (50 percent) stated that

perceived authority was important as a

means of gaining support when product

managers interacted with other members of

his/her own organization, and 24 percent

stated formal authority was important under

these circumstances.

Individual performanceProduct managers were asked to identify

specific changes needed in their organization

to improve their individual performance.

PMs often responded that they needed more

information and increased authority to

implement specific product management ob-

jectives. Product managers further indicated

that improvements in the areas of product

cost determination and product elimination

decisions offered the potential significantly

to impact individual product manager per-

formance and enhance the overall effective-

ness of the product management system in

banks.

Product management system performanceOverall, product managers stated the effec-

tiveness of the product management system

was positive, with a range of 25 percent

rating it `̀ very successful'' to 5 percent rating

it a `̀ limited success''. While product man-

agers may enjoy organizational support and

individual success, overall the product man-

agement system in many large commercial

banks needs further refinement and

improvement. When asked to compare the

centralized product management group with

the individual application of product man-

agement systems within the bank, managers

indicated the centralized product manage-

ment function was rated less effective.

Individual satisfaction and performanceThe overall reactions to questions concern-

ing job satisfaction, job challenges and

opportunities were positive, ranging from 50

percent liking their job `̀ very much'' to 2

percent `̀ not liking'' their job. Most product

managers found their jobs both challenging

and rewarding.

Product managers emphatically stated that

their performance could be improved by

eliminating wasteful, time-consuming activ-

ities and by having more accurate account-

ing systems in place to aid in determining

actual product/service costs. Product man-

agers also expressed the need for market

research and communications support at the

product management group level. A strong

need was expressed for clearly defined per-

formance objectives and a regular process for

reviewing and revising performance goals

and objectives.

Managerial implications andrecommendations

The study of product management in banking

reveals several important considerations.

Major findings include:

1 Banks and other financial services orga-

nizations considering product manage-

ment need to study carefully the

implications for senior managers, bank

functional managers, and the product

managers before implementing such sys-

tems. Our study suggests that many banks

first adopt product management and then

attempt to work out the details as the

system is implemented. This approach can

result in many serious problems and may

affect the ultimate success of product

management. For most banks, the adop-

tion of product management requires

changing the way banks `̀ do business''.

Considerable thought and preparation

Figure 8How often is your work fairly routine and how often is it a real challenge toyour ability?

[ 351 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

need to be given to what specific respon-

sibilities product managers will have, how

the inevitable conflicts that arise can best

be managed, and how product managers

and functional managers will be recog-

nized and rewarded for their collaborative

efforts. Thus, a considerable amount of

`̀ up front'' work needs to be done to

implement a product management system

successfully. Not to attend to these issues

is likely to result in poor performance,

frustration and even failure.

2 Training issues also need to be addressed

in order to implement product manage-

ment effectively. Much of the general

knowledge about product management is

based on package goods. Frequently,

banking product managers are hired from

package goods companies. Other product

managers may be selected from within the

bank for their knowledge of the product

and bank operations and not for their

marketing expertise or experience with

product management. Product managers

from other environments must be made

aware of the banking environment and

the marketing of financial services. We

found few banks which undertake con-

centrated educational programs for their

product managers. Similarly, those man-

agers and staff specialists who interact

with product managers need instruction

on how best to interact with and support

product managers. Again, if such training

is not offered, serious conflicts and power

struggles may evolve resulting in poor

performance. Team building, marketing

and communication courses can be parti-

cularly useful. Training courses also can

be designed to give senior managers an

understanding of their responsibilities in

support of a product management system.

3 Product managers are frequently held

directly responsible for the success of the

products which they manage. We identi-

fied two issues which need to be dealt with

in order to maximize the effectiveness of

product management:

First, implicit with success is profitabil-

ity. In many instances, product managers

indicated that they lacked the information

required efficiently to measure profitabil-

ity. Product managers also indicated a lack

of control over other cost-related factors

which directly affected profitability.

Second, for a particular product to be

successful, a product manager may need

to assume more responsibility for the

product. To give product managers `̀ com-

plete control and authority'' over each of

their products could be chaotic and lead to

excessive duplication of efforts, and could

ultimately result in self-sustaining auton-

omous units. On the other hand, it is

difficult for a product manager (who

depends on the work of others not under

his/her direct control) to be solely

responsible for the success of a product.

As noted, the organizational environ-

ment must be carefully managed in order

to maximize the effectiveness of product

management. Product managers must be

provided with both the information

needed to maximize the success of their

products and the ability to monitor and

coordinate those aspects of the business

which are not directly under their control

but which affect the overall success of

their products.

In some cases, banks may not be using

`̀ real'' product management even though

they use the term `̀ product manager''.

Because product management is new and

many managers lack significant experi-

ence with the system, these managers may

erroneously assume that a particular

product manager has the necessary sup-

port and resources within the organiza-

tion to accomplish the desired objectives.

In order to realize the full benefit of

product management, senior bank man-

agement must create an organizational

system which supports the application of

product management. The following are

desirable characteristics of the product

manager in banks (Wixon, 1986):. They give full-time attention to their

product-market activities.. They are marketing specialists whose

most valuable qualification is their

marketing experience and insight.. They consider and plan for all of the

activities within the organization

which will affect their products.. They coordinate the many different

functional activities throughout the

banking organization by acting as a

resource to the department heads who

actually implement the plans of the

product management group.

4 For those banks which are not presently

using product management but do wish to

implement such a system, we recommend

beginning with one banking department

and using these experiences as key learn-

ings for implementing the system else-

where. For example, a bank may start

product management in its retail group

then migrate the concept to trust services

or to their corporate banking department.

5 In addition to profitability, product man-

agers indicated a need for other measures

of the performance of the product

[ 352 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

management system. Examples of mea-

sures which should be considered include:. Profits.. Market share/sales.. Product/service line profits.. New customers gained.. Number of new financial services of-

fered.. Customer satisfaction.. Service management efficiency.

Finally, as experience with the product

management system grows, it will become

easier to establish performance benchmarks

as well as specially designed training pro-

grams to enhance product management per-

formance. While banks have learned much

about the product management system, many

questions remain unanswered.

Future research opportunities

This study is by design exploratory. We

believe there are several questions which

warrant additional research. We propose the

following for future study:

1 Why are some banking product manager

systems implemented more quickly than

others? What factors facilitate and hinder

successful implementation?

2 Do large amounts of boundary-spanning

activities produce more stress for product

managers in banks?

3 What type of marketing support is most

needed by bank product managers? How

can it best be obtained?

4 What developments are occurring in how

product management systems are orga-

nized? Are there trends toward centra-

lized, decentralized, or other forms of

product management organizations?

5 How does experience in banking product

management affect a manager's career?

6 Is there an identifiable lifecycle of bank-

ing product management implementa-

tion? If so, are there specific stages within

the implementation cycle?

7 What structural changes, if any, do banks

need to make to accommodate product

management systems?

8 What challenges are faced by product

managers as their banks have moved into

global markets?

9 What has been the influence of total

quality management (TQM) initiatives on

the role of product managers and product

management in banking?

10 What mechanisms facilitate learning and

the cross-fertilization of ideas among

banking departments that employ product

managers?

Conclusions

When carefully implemented and managed,

the product management system can improve

the development and management of a wide

variety of financial services. There remains

much to learn about the system and how it

can be used most effectively. We hope that

more rigorous research and analysis will

follow this exploratory study.

ReferencesBerggren, E. and Dewar, R. (1991-1992), `̀ Is product

management obsolete?'', Journal of Retail

Banking, Vol. 13 No. 4, Winter, pp. 27-32.

Bowers, M.R. and Wallace, E.S. Jr (1986), `̀ New

directions in product development'', Bank

Marketing, April, pp. 22-4.

Britt, P. (1995), `̀ Activity-based accounting can

boost profits'', America's Community Banker,

Vol. 4 No. 5, May, p. 46.

Brown, L. (1983), Managing Conflict at Organiza-

tional Interfaces, Addison-Wesley, Reading,

MA.

Churchill, G.A. and Pecotich, A. (1982), `̀ A

structural equation investigation of the pay-

satisfaction-valence relationship among

salespeople,'' Journal of Marketing, Vol. 47,

Fall, pp. 114-24.

Cooper, R.G., Easingwood, C.J. and Edgett, S.

(1994), `̀ What distinguishes the top perform-

ing new products in financial services'',

Journal of Product Innovation Management,

Vol. 11 No. 4, September, pp. 281-99.

Cosse, T.J. and Swan, J.E. (1983), `̀ Strategic

market planning by product managers ± room

for improvement'', Journal of Marketing, Vol.

47 No. 3, Summer, pp. 92-102.

Cummings, W.T., Jackson, D.W. Jr and Ostrom,

L.L. (1984), `̀ Differences between industrial

and consumer product managers'', Industrial

Marketing Management, Vol. 13 No. 3, August,

pp. 171-80.

Cummings, W.T., Jackson, D.W. Jr and Ostrom,

L.L. (1989), `̀ Examining product managers'

job satisfaction and performance using

selected organizational behavior variables'',

Journal of the Academy of Marketing Science,

Vol. 17 No. 2, Spring, pp. 147-56.

Eckles, R.W. and Novotny, T.J. (1984), `̀ Industrial

product managers: authority and responsi-

bility'', Industrial Marketing Management,

Vol. 13, May, pp. 71-5.

Franwick, G.L., Ward, J.C., Hutt, M.D. and

Reingen, P.H. (1994), `̀ Evolving patterns of

organizational beliefs in the formation of

strategy'', Journal of Marketing, Vol. 58 No. 2,

April, pp. 96-110.

Franzoni, L. (1991), `̀ Playing the numbers game'',

Bank Marketing, Vol. 23 No. 10, October,

pp. 20-3.

Hise, R.T. and Kelly, J.P. (1978), `̀ Product man-

agement on trial'', Journal of Marketing, Vol.

42 No. 4, October, pp. 28-33.

[ 353 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354

Kelly, J.P. and Hise, R.T. (1979), `̀ Industrial and

consumer goods product managers are dif-

ferent'', Industrial Marketing Management,

Vol. 8 No. 4, November, pp. 325-32.

Kotler, P. (1984), `̀ Marketing organization and

implementation'', Chapter 23 in Marketing

Management Analysis, Planning, and Control,

Prentice-Hall, Inc. Englewood Cliffs, NJ.

LeGrand, J.E. (1992), `̀ A product in need of

management'', Bankers Magazine, Vol. 175

No. 6, November-December, pp. 73-6.

Lysonski, S. (1985), `̀ A boundary theory investi-

gation of the product manager's role'', Jour-

nal of Marketing, Vol. 49, Winter, pp. 26-40.

Lysonski, S., Singer, A. and Wilemon, D. (1988),

`̀ Coping with environmental uncertainty and

boundary spanning in the product manager's

role'', Journal of Services Marketing, Vol. 2

No. 4, Fall, pp. 16-26.

Reid, D.M. (1988), `̀ Towards effective product

management'', European Journal of Market-

ing, Vol. 22 No. 5, pp. 32-43.

Reidenbach, R.E. and Moak, D. L. (1986),

`̀ Exploring retail bank performance and new

product development: a profile of industry

practices'', Journal of Product Innovation

Management, Vol. 3, pp. 187-94.

Sathe, V. (1985), Culture and Related Corporate

Realities, Richard D. Irwin, Inc., Homewood, IL.

Schein, E.H. (1985), Organizational Culture and

Leadership, Jossey-Bass, San Francisco, CA.

Southerst, J. (1994), `̀ Suddenly, it all makes

sense'', Canadian Business, Vol. 67 No. 3,

March, pp. 39-42.

Sullivan, B.F. (1986), `̀ Meeting the challenge of

controlling banking costs and developing

pricing strategies'', Journal of Bank Research,

Autumn, pp. 178-81.

Wichman, W.J. (1986), `̀ Marketing commentary:

the case for product management'', United

States Banker, August, pp. 36-8, 42.

Wichman, W.J. (1989), `̀ Product management: still

a way to go'', Bank Marketing, March, pp. 44-6.

Wixon, D. (1986), `̀ Making product management

work for your bank'', Bank Marketing, May,

pp. 36-41.

Yang, G. (1990), `̀ A new approach to measuring

productivity profitability'', Bankers Magazine,

Vol. 173 No. 5, September/October, pp. 33-9.

Appendix. MethodologyThis investigation focussed on large commer-

cial banks in the USA. Size of the banks was

determined by the total dollars on deposit in

the bank. A letter was sent to senior market-

ing officials in each of the 50 largest banks to

determine whether a product manager system

existed within their department or bank, and

if they would nominate product managers

who might participate in the study. In those

instances where it was not possible to obtain

the names of the senior marketing officers, a

letter was sent to the president of the bank,

asking him to suggest a knowledgeable official

in the bank who could assist us in the

identification of those managers with product

management responsibility. Approximately 25

percent of the banks contacted stated that they

did not have a product management system.

Another 25 percent indicated that they were in

the initial stages of implementing such a

system and did not have enough experience to

participate. Approximately 50 percent of the

banks contacted noted that they did have an

active product management system. From

those banks which utilized product manage-

ment, we obtained the names of 115 product

managers from 25 different banks. Question-

naires were sent to these product managers

along with a letter outlining the purpose of the

study, and 58 questionnaires were completed

and returned. The overall response rate was

approximately 50 percent.

We used a combination of approaches in

designing our research questionnaire. First,

we examined the writings and research on

product management in banking. Although

this is not a robust body of literature, we were

able to glean a number of important insights

into the problems and challenges product

managers often encounter in fulfilling their

tasks and responsibilities. Second, the litera-

ture on product management as practiced in

consumer and industrial product companies

was helpful in identifying potential similari-

ties and differences between product man-

agement in banking and its applications in

other industries. Third, we surveyed the

general management literature for factors

which shape and influence managerial roles,

particularly those roles which require con-

siderable integration and support of various

functional groups beyond the immediate

authority of the product manager. The general

management literature also helped identify

how the environment of managers, e.g. cul-

ture, values, and norms, can influence man-

agerial performance. Finally, one of the

authors had extensive experience in helping

implement a complex product management

system in one of the largest US full-service

commercial banks.

A semi-structured questionnaire was used

to collect the data. The instrument was

designed from data obtained from 15 pilot

interviews with managers responsible for

product management systems and product

managers in two large commercial banks. The

questionnaire contained 36 questions. The

questions included open-ended, yes-no, and

agree-disagree responses. Each product man-

ager who cooperated in the study was assured

complete anonymity. The sample included

product managers from various banking

departments such as retail, corporate, inter-

national, and trust services.

[ 354 ]

Jeffrey Strieter,Ashok K. Gupta, S.P. Raj andDavid WilemonProduct management and themarketing of financialservices

International Journal of BankMarketing17/7 [1999] 342±354