Embed Size (px)

Citation preview

http://iaeme.com/Home/journal/IJM 482 [email protected]

International Journal of Management (IJM) Volume 11, Issue 8, August 2020, pp. 482-491, Article ID: IJM_11_08_046 Available online at http://iaeme.com/Home/issue/IJM?Volume=11&Issue=8 ISSN Print: 0976-6502 and ISSN Online: 0976-6510 DOI 10.34218/IJM.11.8.2020.046 :

© IAEME Publication Indexed Scopus

REQUIREMENTS AND OBSTACLES OF ACTIVITY-BASED BUDGETING (ABB)

IMPLEMENTATION IN JORDANIAN PUBLIC-SHARING PHARMACEUTICAL COMPANIES

Dr. Ziad Odeh Al-Aamaedeh Associate Professor, Accounting Department, College of Business Administration,

Mutah University, Jordan

ABSTRACT This study aimed to identify the availability of the necessary technical

requirements to implement Activity-Based Budgeting (ABB) in Jordanian public- sharing pharmaceutical companies' availability of qualified human resources

necessary to it there. As well as to identify availability of the existence of obstacles that limit the implementation of Activity-Based Budgeting in Jordanian public-sharing pharmaceutical companies. The population and the sample of the study consisted of all Jordanian public-sharing pharmaceutical companies during the study counted 8

companies. A questionnaire for data collection was developed and distributed to financial and costs department managers. In order to analyze data collected and to test study hypotheses, arithmetic mean, standard deviation and one-sample T test were

used. The analysis concluded the necessary technical requirement to implement Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical

companies as well as the qualified human resources to do this, nevertheless there are obstacles limiting the implementation Activity-Based Budgeting (ABB) in Jordanian

public-sharing pharmaceutical companies. The study recommended that it is necessary to implement Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies and to perform further studies in other sectors.

Key words: Activity-Based Budgeting Cite this Article: Dr. Ziad Odeh Al-Aamaedeh, Requirements and Obstacles of

Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies, 11(8), 2020, International Journal of Management,

pp. 482-491. http://iaeme.com/Home/issue/IJM?Volume=11&Issue=8

1. INTRODUCTION The development in the economic environment has led to the development of various

managerial accounting methods and Activity-Based Budgeting (ABB) is one of these

Requirements and Obstacles of Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies

http://iaeme.com/Home/journal/IJM 483 [email protected]

methods. Because Activity-Based Budgeting (ABB) is of great importance controlling, planning and evaluating performance in industrial and service companies, this study emerged

to identify the requirements and constraints of implementing Activity-Based Budgeting (ABB) in Jordanian public-0sharing pharmaceutical companies.

The Problem of the Study: The study problem can be presented by asking the following questions:

Are the technical Requirements for implementing Activity-Based Budgeting (ABB) available in Jordanian public-sharing pharmaceutical companies?

Are the necessary human resources available to Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies?

Are there obstacles that limit the implementation of Activity-Based Budgeting (ABB) in Jordanian public pharmaceutical companies?

1.1. The Importance of the Study The importance of the study stems from the importance of the pharmaceutical industry, as it is considered one of the most important industrial sectors in Jordan. Moreover, Activity-Based

Budgeting (ABB) is considered one of the most important modern managerial accounting methods in controlling, and planning and evaluating performance, nevertheless, the studies that tackled this topic are very scarce. Therefore, this study came to identify the requirements and obstacles of implementing Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies.

1.2. Objectives of the Study This study seeks to achieve the following objectives:

To identify the availability of the technical requirements for implementing Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies?

To identify the availability of the necessary human resources available to Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies?

To identify the availability of obstacles that limit the implementation of Activity-Based Budgeting (ABB) in Jordanian public pharmaceutical companies?

1.3. Study Hypotheses Based on the study problem and its objectives, the study will test the following hypotheses: Ho1: The technical Requirements for implementing Activity-Based Budgeting (ABB) are not available in Jordanian public-sharing pharmaceutical companies?

Ho2: The necessary human resources are not available to implement Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies? Ho3: There are no obstacles limiting the implementation of Activity-Based Budgeting (ABB) in Jordanian public pharmaceutical companies?

2. PREVIOUS STUDIES (Al-Hashimi & Mohammed, 2018) study entitled “Activity Based Costing applications in the

preparation of operating budget in the public health sector - Applied research in the Department of Health in Thi- The aim of this study is to motivate the health Qar governorate.” sector to use Activity Based Costing (ABC) to enable th sector to provide more accurate isinformation on the cost of its services as well as to strict the cost control through operating

Dr. Ziad Odeh Al-Aamaedeh

http://iaeme.com/Home/journal/IJM 484 [email protected]

budgets prepared based on activities, so as to improve its services and reduce its costs. The researchers sought to achieve this goal by designing an ABC to Haboubi Teaching Hospital based on information collected from official documents, reports and records of the hospital as well as field visits and interviews with a number of hospital administration officials. The main

conclusions of the study were that the preparation of the operating budget in service organizations in general and health organizations in particular is different from industrial

business due to the different characteristics of health services from the characteristics of products, as the health service is produced and delivered at the same time, therefore, the

determination and control of its costs requires the identification of the various activities on which the providing of the health service is based and then assigning its costs and preparing the budget for each activity.

(Nader & Haidar, 2015) ing systems applied in entitled “Evaluation of budget

government hospitals and the possibility of applying Activity-Based Budgeting: A field al Study of Lattakia.” This study aimed to evaluate the budget system applied in the

governmental hospitals in Lattakia, and to search and to investigate the possibility of the application of (Activity-Based Budgeting). To achieve the objectives of the study a

questionnaire was designed including questions related to various aspects of the existing budget, and the availability of administrative, financial, technical and environmental

potentials. The questionnaire was distributed to the financial and administrative department officials in the Directorate of Health in addition to the staff of government hospitals in the province. The most important results of the study are: the budget system applied in hospitals

do not meet the requirements, and that there are many obstacles and problems facing the possibility of applying (Activity-Based Budgeting) in hospitals under study. Based on the

findings the researchers recommended the need for appropriate infrastructure apply to (Activity-Based Budgeting) by activating the use of modern technology, and to

provide sufficient resources as well as to create the necessary political, economic and legal conditions for the application of (Activity-Based Budgeting) to utilize their advantages in cost management and exploitation of resources.

(Farhat & Yassin, 2017) study entitle -Based d “The Possibility of Applying Activity

Budgeting in Banks: Field Study on Private Banks Listed on The Damascus Stock Exchange.” The purpose of this study is to demonstrate the extent to which private banks listed on the Damascus Stock Exchange can apply modern cost management tools to plan and to prepare

budgets by using ABB. The research focused on the concepts of cost management and Activity-Based Budgeting (ABB) and the components of its application, as well as the

availability of these components in private banks. The study was based on descriptive approach, through design of a questionnaire, and distributing it to some employees in private banks listed on Damascus Stock Exchange. The data were analyzed using Statistic Packagal e

foe Social Sciences (SPSS) version 20.0. The research found that the fundamentals of applying activity-based budgeting system are not available in private banks listed on

Damascus Stock Exchange, and that private banks do not take into account the application of effective cost management. A number of recommendations were made.

(Capusneanu, Boca, Barbu, Rof, & Topor, 2013) entitled “Implementation of Activity-Based Budgeting method in the economic

entities from mining industry of Romania”. This study aim to emphasize the importance ed of the Activity-Based Budgeting (ABB) implementation within the entities in the mining

industry of Romania. The study concluded that the application of Activity-Based Budgeting (ABB) leads to reduce costs and to improve performance as well as will affect the employees’

behavior through the use of financial and non-financial performance indicators. Moreover,

Requirements and Obstacles of Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies

http://iaeme.com/Home/journal/IJM 485 [email protected]

applying Activity-Based Budgeting (ABB) leads to improve the accuracy of costs’ estimation of the level of each activity and to limit the unused energy at operations and activities level.

(Foroghi, Haghighi Parapari, & Rasaiian, 2012) study entitled “Feasibility of the Implementation of Activity- Based Costing (ABC) in Operational Budgeting of Government Agencies: A Case Study of Government Agencies of Isfahan Province. This study aimed to ”

investigate the factors affecting the implementation of Activity Based Costing (ABC) in operational budgeting of governmental agencies in Isfahan province-Iran. The study adopted the descriptive approach and utilized the questionnaire as a tool for data collection. Copies of

the questionnaire were distributed to 50 governmental agencies in Isfahan province. The conclusion drawn from the current study is that governmental agencies of Isfahan province do not possess the necessary factors for implementation of Activity Based Costing in operational

budgeting such as: employees’ qualifications, technical abilities, legal, procedural and organizational authority and political, administrative and organizational acceptance. As well as the study found it is very difficult to perform reforms in the field of operational budget preparation in governmental agencies in Isfahan province.

(Szatmary, 2011) Activity-study entitled “ Based Budgeting in Higher Education.” The

study aimed to identify the benefits of applying Activity-based budgeting in higher education institutions. The study was performed as an applied study at University of Washington in the

United States of America since this university has applied Activity-based budgeting in 2010/2011. The study concluded that Activity-based budgeting helped the university to make decisions related to salaries and marketing. As well as ABC HELPED the university to make

decision related to exclude non-profitable educational programs and to evaluate the fiscal performance of the programs, scientific research and rationalizing the distribution of

university resources.

3. THEORETICAL FRAMEWORK 3.1. Definition of Activity Based Budgeting (Kaplan & Anderson, 2007) defined Activity Based Budgeting (ABB) as a tactic pursue to maximize the revenues and to reduce the costs by forecasting the resources required for the project based on expected changes in activities and operations within the organization. But, (Atkinson, Kaplan, Matsumura, & Young, 2012) defined it as that approach in formulating

budget concentrating on identifying expected costs of activities and the mechanism connecting these activities together and determining the required resources based on expected activities. So, it is a system extended from the main system in determining the costs of each activity that is Activity based costing (ABC). While (Schalkwyk, 2012) believes that Activity based Budgeting is a budgeting system works to estimate the required resources only to meet

the needs of organization’s activities to achieve the goals pursued by the organization in a

more precise way. Accordingly, it is an approach based on future planning and estimation of the organization’s requirements of resources and activities to help in making decisions and

determining the future fiscal requirements to cover these planned activities and resources. Whereas, (Balick, 2010) defined it as the correct utilization of resources to support the main activities according to the volumes of these activities.

3.2. Stages of Preparing Activi -Based Budgets ty(Capusneanu, Boca, Barbu, Rof, & Topor, 2013) summarized the stages of Activity-Based Budgeting by the followings:

Estimate the volume of materials needed to produce the goods or services by estimating the expected volume and value of sales.

Dr. Ziad Odeh Al-Aamaedeh

http://iaeme.com/Home/journal/IJM 486 [email protected]

Estimate the necessary operational activities for each level in unit production based on the structure of activities according to the ABC system.

Determine the required resources to carry out these activities (i.e. determine the type of the required resource and the amount required from these resources).

Aggregate the total estimated costs of activities and total estimated resources. Determine the expected production capacity based on the total activities and sources, re

thus determine the untapped production capacity, which is necessary for the purpose of periodic adjustment in the form of the budget according to the circumstances and fluctuations surrounding the organization.

3.3. Obstacles of Implementing Activity-Based Budgeting (ABB) There are many obstacles facing the implementation of Activity-based budgeting (ABB) that could be summarized as follows (Moustafa, 2005):

Resisting changes by employees: When introducing a modern system in preparing budgets and changing the traditional system, here one finds resistance to change by employees.

Lack of support from senior management: Lack of support by the higher management board of the facility for the modern system in preparing Activity-based budgeting

(ABB), for fear of increasing costs. Lack of trained accountants: The modern entrance to Activity-based budgeting (ABB)

requires a number of trained accountants with high experience, and in the absence of trained accountants, it is difficult to apply the modern entrance to the budgets and may lead to incorrectly setting future goals, thus increasing costs.

Lack of experience and ability to use electronic devices: The lack of staff with experience in using electronic devices prevents the proper and feasible implementation of the Activity Based Budgeting System (ABB).

The difficulty of implementing Activity Based Budgeting System (ABB) in estimating costs: The inability to define and estimate costs prevents the implementation of the

modern entrance to budgets, therefore it is necessary to implement Activity Based costing system (ABC) through which the organization can determine costs in an accurate way.

The difficulty of analyzing and determining value-added activities accurately: due to interference and diversity of products and services consequently the costs interference of products and services making it too difficult for the management of the organization to analyze and to determine value-added activities accurately.

3.4. The Fundamentals of Implementing the Budget S tem Based on Activities ysHigher management's awareness of the importance of implementing the activities budget: One of the most important elements for effective implementation of this system is the support and awareness of senior management of the importance of implementing the budget system based on activities.

Availability of a sound organizational structure: There must be a sound organizational structure that clearly identifies authorities and responsibilities. The structure should be

flexible to facilitate the necessary adjustments when implementing the budget, and to involve different managerial levels in preparing the budget, making them more aware of the costs of their activities.

Requirements and Obstacles of Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies

http://iaeme.com/Home/journal/IJM 487 [email protected]

Availability of computerized accounting systems: Computerized accounting systems help provide the necessary information for planning and budgeting. It also better determines the cost of the products and services provided, and the cost of the activities carried out. It shows the cost of unexploited energy at the level of each activity.

Availability of qualified human resources: Qualified human resources are required to facilitate the implementation of Activity Based Budgeting (ABB), and to make workers

accept change continuously. Increased competition: The increasing intensity of competition among organizations and

the emergence of international agreements that facilitated the movement and the exchange of goods and services, made the world a small village. This forced organizations to review their

used cost systems, to update them on an ongoing basis, and to implement modern management accounting methods, including the Activity Based Budgeting (ABB).

4. STUDY METHODOLOGY This study is divided into two sections:

Theoretical study: the researcher referred to secondary sources related to the subject of the study (books, periodicals, scientific journals and Arabic and foreign articles related to the field of the study).

Field study: the required data were collected with the aid of a questionnaire distributed to the sample of the study, data were analyzed using SPSS to test the hypothesis of the study to reach conclusions and to make recommendations.

The study population and its sample: the study population and its sample consisted of all Jordanian public-sharing pharmaceutical industries companies enlisted in Amman Stock

Exchange (ASE) during the time of the study counted 8 companies. Copies of the questionnaire were distributed to financial managers and heads of costs department in these companies.

Methods of data collection: the researcher referred to the secondary sources related to the subject of the study, which are books, periodicals, scientific journals and Arab and foreign articles about the subject of the study.

A special questionnaire has also been developed for this study, based on the theoretical framework, and it has been distributed to financial managers and heads of companies' cost departments and was received by hand. The questionnaire questions have been formulated in a way that helps easy measurement. Five-point Likert scale was adopted (strongly disagree,

disagree, neutral, agree and strongly agree). To test the validity of the results of the questionnaire, it was presented to a group of experts, specialists and university professors. Reliability Analysis was used to calculate Cronbach’s alpha correlation coefficient. Data analysis methods: For the purposes of achieving the objectives of the study and testing its hypotheses, an analytical descriptive approach was used to demonstrate the availability of

the technical requirements necessary to implement Activity Based Budgeting (ABB) Jordanian public-sharing pharmaceutical companies. In addition to clarify the availability of

qualified human resources necessary to implement Activity Based Budgeting (ABB) Jordanian public-sharing pharmaceutical companies. As well as, to investigate he existence of obstacles that limit the implementation of Activity Based Budgeting (ABB) Jordanian public-sharing pharmaceutical companies.

Dr. Ziad Odeh Al-Aamaedeh

http://iaeme.com/Home/journal/IJM 488 [email protected]

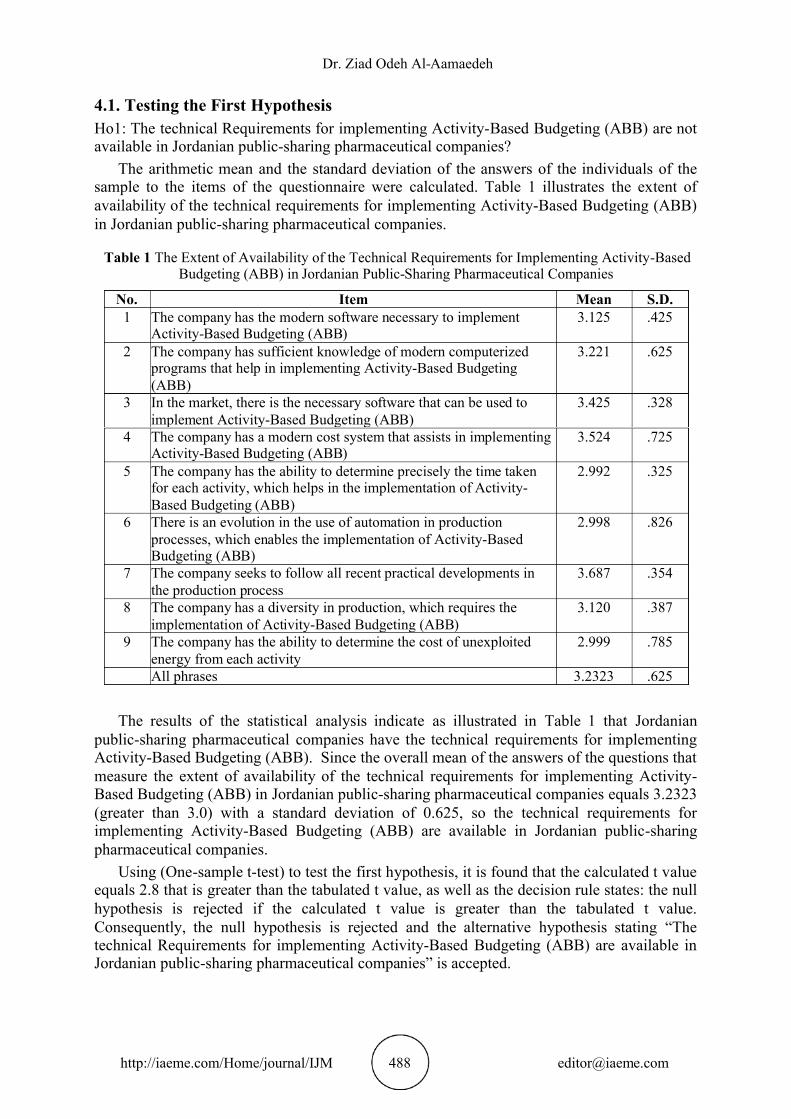

4.1. Testing the First Hypothesis Ho1: The technical Requirements for implementing Activity-Based Budgeting (ABB) are not available in Jordanian public-sharing pharmaceutical companies?

The arithmetic mean and the standard deviation of the answers of the individuals of the sample to the items of the questionnaire were calculated. Table 1 illustrates the extent of

availability of the technical requirements for implementing Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies.

Table 1 The Extent of Availability of the Technical Requirements for Implementing Activity-Based Budgeting (ABB) in Jordanian Public-Sharing Pharmaceutical Companies

No. Item Mean S.D. 1 The company has the modern software necessary to implement

Activity-Based Budgeting (ABB) 3.125 .425

2 The company has sufficient knowledge of modern computerized programs that help in implementing Activity-Based Budgeting (ABB)

3.221 .625

3 In the market, there is the necessary software that can be used to implement Activity-Based Budgeting (ABB)

3.425 .328

4 The company has a modern cost system that assists in implementing Activity-Based Budgeting (ABB)

3.524 .725

5 The company has the ability to determine precisely the time taken for each activity, which helps in the implementation of Activity-Based Budgeting (ABB)

2.992 .325

6 There is an evolution in the use of automation in production processes, which enables the implementation of Activity-Based Budgeting (ABB)

2.998 .826

7 The company seeks to follow all recent practical developments in the production process

3.687 .354

8 The company has a diversity in production, which requires the implementation of Activity-Based Budgeting (ABB)

3.120 .387

9 The company has the ability to determine the cost of unexploited energy from each activity

2.999 .785

All phrases 3.2323 .625

The results of the statistical analysis indicate as illustrated in Table 1 that Jordanian public-sharing pharmaceutical companies have the technical requirements for implementing Activity-Based Budgeting (ABB). Since the overall mean of the answers of the questions that measure the extent of availability of the technical requirements for implementing Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies equals 3.2323

(greater than 3.0) with a standard deviation of 0.625, so the technical requirements for implementing Activity-Based Budgeting (ABB) are available in Jordanian public-sharing pharmaceutical companies.

Using (One-sample t-test) to test the first hypothesis, it is found that the calculated t value equals 2.8 that is greater than the tabulated t value, as well as the decision rule states: the null

hypothesis is rejected if the calculated t value is greater than the tabulated t value. Consequently, the null hypothesis is rejected and the alternative hypothesis stating “The

technical Requirements for implementing Activity-Based Budgeting (ABB) are available in Jordanian public-sharing pharmaceutical companies” is accepted.

Requirements and Obstacles of Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies

http://iaeme.com/Home/journal/IJM 489 [email protected]

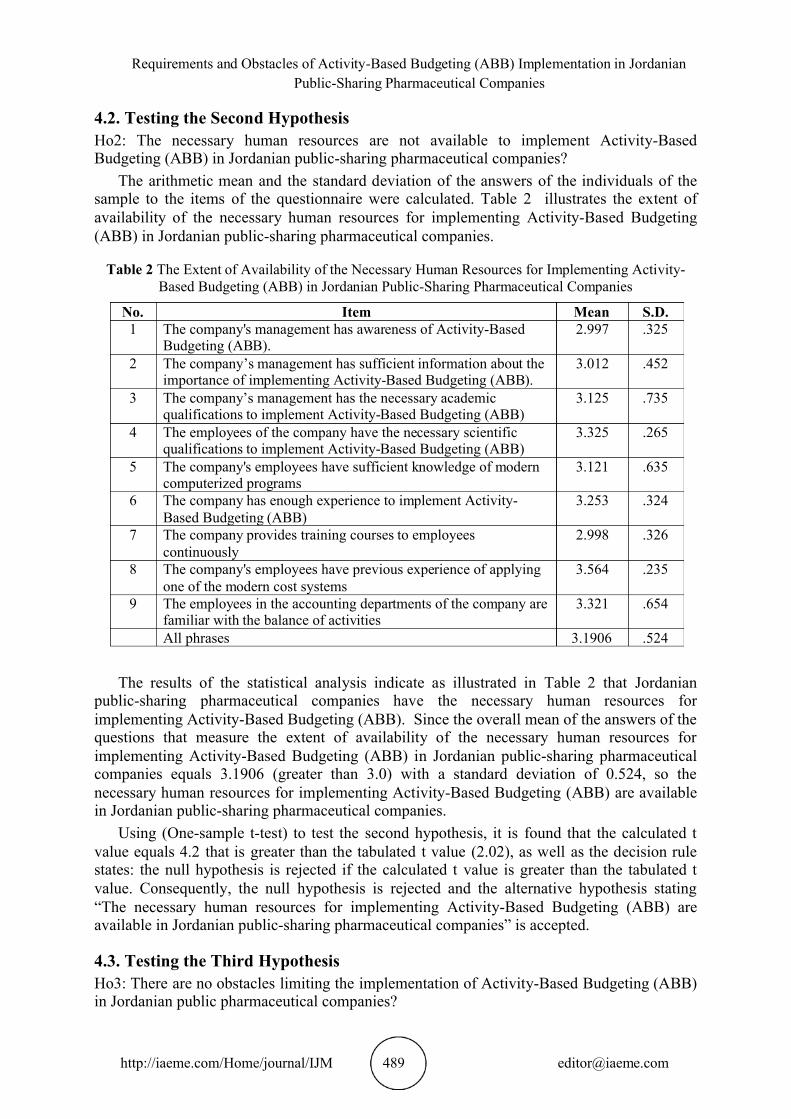

4.2. Testing the Second Hypothesis Ho2: The necessary human resources are not available to implement Activity-Based

Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies? The arithmetic mean and the standard deviation of the answers of the individuals of the

sample to the items of the questionnaire were calculated. Table 2 illustrates the extent of availability of the necessary human resources for implementing Activity-Based Budgeting

(ABB) in Jordanian public-sharing pharmaceutical companies.

Table 2 The Extent of Availability of the Necessary Human Resources for Implementing Activity-Based Budgeting ( ) in Jordanian Public-Sharing Pharmaceutical Companies ABB

No. Item Mean S.D. 1 The company's management has awareness of Activity-Based

Budgeting (ABB). 2.997 .325

2 The company’s management has sufficient information about the importance of implementing Activity-Based Budgeting (ABB).

3.012 .452

3 The company’s management has the necessary academic qualifications to implement Activity-Based Budgeting (ABB)

3.125 .735

4 The employees of the company have the necessary scientific qualifications to implement Activity-Based Budgeting (ABB)

3.325 .265

5 The company's employees have sufficient knowledge of modern computerized programs

3.121 .635

6 The company has enough experience to implement Activity-Based Budgeting (ABB)

3.253 .324

7 The company provides training courses to employees continuously

2.998 .326

8 The company's employees have previous experience applying ofone of the modern cost systems

3.564 .235

9 The employees in the accounting departments of the company are familiar with the balance of activities

3.321 .654

All phrases 3.1906 .524

The results of the statistical analysis indicate as illustrated in Table 2 that Jordanian public-sharing pharmaceutical companies have the necessary human resources for

implementing Activity-Based Budgeting (ABB). Since the overall mean of the answers of the questions that measure the extent of availability of the necessary human resources for

implementing Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies equals 3.1906 (greater than 3.0) with a standard deviation of 0.524, so the

necessary human resources for implementing Activity-Based Budgeting (ABB) are available in Jordanian public-sharing pharmaceutical companies.

Using (One-sample t-test) to test the second hypothesis, it is found that the calculated t value equals 4.2 that is greater than the tabulated t value (2.02), as well as the decision rule states: the null hypothesis is rejected if the calculated t value is greater than the tabulated t

value. Consequently, the null hypothesis is rejected and the alternative hypothesis stating “The necessary human resources for implementing Activity-Based Budgeting (ABB) are available in Jordanian public- sharing pharmaceutical companies” is accepted.

4.3. Testing the Third Hypothesis Ho3: There are no obstacles limiting the implementation of Activity-Based Budgeting (ABB) in Jordanian public pharmaceutical companies?

Dr. Ziad Odeh Al-Aamaedeh

http://iaeme.com/Home/journal/IJM 490 [email protected]

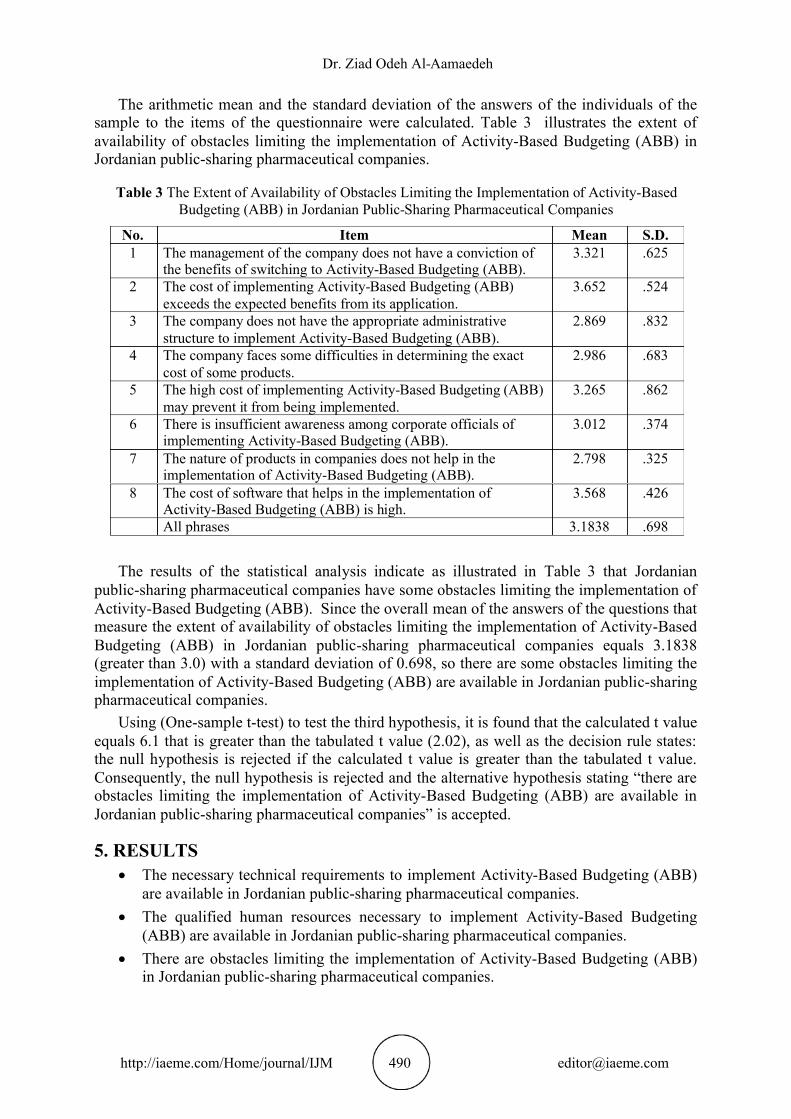

The arithmetic mean and the standard deviation of the answers of the individuals of the sample to the items of the questionnaire were calculated. Table 3 illustrates the extent of

availability of obstacles limiting the implementation of Activity-Based Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies.

Table 3 The Extent of Availability of Obstacles Limiting the Implementation of Activity-Based Budgeting (ABB) in Jordanian Public-Sharing Pharmaceutical Companies

No. Item Mean S.D. 1 The management of the company does not have a conviction of

the benefits of switching to Activity-Based Budgeting (ABB). 3.321 .625

2 The cost of implementing Activity-Based Budgeting (ABB) exceeds the expected benefits from its application.

3.652 .524

3 The company does not have the appropriate administrative structure to implement Activity-Based Budgeting (ABB).

2.869 .832

4 The company faces some difficulties in determining the exact cost of some products.

2.986 .683

5 The high cost of implementing Activity-Based Budgeting (ABB) may prevent it from being implemented.

3.265 .862

6 There is insufficient awareness among corporate officials ofimplementing Activity-Based Budgeting (ABB).

3.012 .374

7 The nature of products in companies does not help in the implementation of Activity-Based Budgeting (ABB).

2.798 .325

8 The cost of software that helps in the implementation of Activity-Based Budgeting (ABB) is high.

3.568 .426

All phrases 3.1838 .698

The results of the statistical analysis indicate as illustrated in Table 3 that Jordanian public-sharing pharmaceutical companies have some obstacles limiting the implementation of Activity-Based Budgeting (ABB). Since the overall mean of the answers of the questions that measure the extent of availability of obstacles limiting the implementation of Activity-Based

Budgeting (ABB) in Jordanian public-sharing pharmaceutical companies equals 3.1838 (greater than 3.0) with a standard deviation of 0.698, so there are some obstacles limiting the implementation of Activity-Based Budgeting (ABB) are available in Jordanian public-sharing pharmaceutical companies.

Using (One-sample t-test) to test the third hypothesis, it is found that the calculated t value equals 6.1 that is greater than the tabulated t value (2.02), as well as the decision rule states: the null hypothesis is rejected if the calculated t value is greater than the tabulated t value. Consequently, the null hypothesis is rejected and the alternative hypothesis stating “there are

obstacles limiting the implementation of Activity-Based Budgeting (ABB) are available in Jordanian public-sharing pharmaceutical companies” is accepted.

5. RESULTS The necessary technical requirements to implement Activity-Based Budgeting (ABB)

are available in Jordanian public-sharing pharmaceutical companies. The qualified human resources necessary to implement Activity-Based Budgeting

(ABB) are available in Jordanian public-sharing pharmaceutical companies. There are obstacles limiting the implementation of Activity-Based Budgeting (ABB)

in Jordanian public-sharing pharmaceutical companies.

Requirements and Obstacles of Activity-Based Budgeting (ABB) Implementation in Jordanian Public-Sharing Pharmaceutical Companies

http://iaeme.com/Home/journal/IJM 491 [email protected]

RECOMMENDATIONS Companies must overcome the obstacles that the implementation of Activity-Based

Budgeting (ABB). The necessity of implementing the implementation of Activity-Based Budgeting

(ABB) in Jordanian public pharmaceutical companies, because of its importance in planning, control and performance evaluation.

The need for companies to pay attention to modern managerial accounting methods. Conducting more studies on the implementation of Activity-Based Budgeting (ABB)

in other sectors.

REFERENCES [1] -Hashimi, A., & Mohammed, S. (2018). Activity Based Costing applications in the Al

preparation of operating budget in the public health sector - Applied research in the Department of Health in Thi-Qar governorate. Univesity of Thi-Qar Journal, 13 (1), 10-37.

[2] Atkinson, A., Kaplan, R., Matsumura, E., & Young, S. (2012). Management Accounting: Information for Decision Making and Strategy Execution (Sixth Edition ed.). Boston, MA: Pearson Education.

[3] Balick, B. (2010, March 10). Activity-Based-Budgeting: Preview of Academic Impacts for UW fACULTY. Washington: Chair of the Faculty Senate.

[4] Capusneanu, S., Boca, I., Barbu, C.-M., Rof, L.-M., & Topor, D. (2013). Implementation of Activity-Based Budgeting Method in the Economic Entities from Mining Industry of

Romania. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(1), 26 34. –

[5] Farhat, M., & Yassin, A. (2017). The Possibility Of Applying Activity-Based Budgeting In Banks: Field Study On Private Banks Listed on The Damascus Stock Exchange. Tishreen

University Journal for Research and Scientific Studies -Economic and Legal Sciences Series, 39(4), 91-110.

[6] Foroghi, D., Haghighi Parapari, M., & Rasaiian, A. (2012). Feasibility of the Implementation of Activity-Based Costing. (ABC) in Operational Budgeting of Government Agencies: A Case Study of Government Agencies of Isfahan Province. Quarterly Journal of Health Accounting, 1(1), 47-62.

[7] Kaplan, S., & Anderson, S. (2007). What-If Analysis and Activity-Based Budgeting: Forecasting Resource Demands. In S. Kaplan, & S. Anderson, Time-Driven Activity-Based

Costing: A Simpler and More Powerful Path to Higher Profits (pp. 85-106). Boston, Massachusetts: Harvard Business Press.

[8] Moustafa, E. (2005, June). An Application of Activity‐Based‐Budgeting in Shared Service Departments and Its Perceived Benefits and Barriers under Low‐IT Environment Conditions.

Journal of Economic and Administrative Sciences, 21(1), 42-72. [9] Nader, N., & Haidar, W. (2015). Evaluation of budgeting systems applied in governmental

hospitals and the possibility of applying Activity-Based Budgeting: A field Study of Lattakia. Tishreen University Journal for Research and Scientific Studies -Economic and Legal

Sciences Serie, 37(5), 83-99. [10] Schalkwyk, A. (2012). Setting Water Service Tariffs Sustainable Technologies. Official

Journal of the Institute of Municipal Finance Officers, IMFO, 12. [11] Szatmary, D. P. (2011). Activity-Based Budgeting in Higher Education. Continuing Higher

Education Review, 75, 69-85.