Embed Size (px)

Citation preview

DECLARATION

We hereby declare that this thesis is our original research whosefindings have not been presented for another degree in thisuniversity or elsewhere and that all citations in the work havebeen duly acknowledged.

STUDENT’S NAME ID NUMBER SIGNATURE

ANNING AGNES IBS/

0794/10

ANNOR PHILIPA IBS/

0795/10

ANSAH OWUSU IBS/

0796/10

AMOAH STEPHEN IMS/

0133/10

AMOAKO CHARLES KWESI IMS/

0134/10

Supervisors’ Declaration

I hereby declare that we supervised the preparation andpresentation of this thesis in accordance with the rules andregulations of the University for Development Studies (UDS).

[I]

Supervisor’s Name

MR. MUSAH ALHASSAN

Supervisor’sSignature............................

Date.....................................

DEDICATION

We dedicate this work to our parents; love one’s and the

generationunborn.

[II]

ACKNOWLEDGEMENT

We first of all give thanks to the almighty God for giving

us the strength and the courage to undertake this programme

successfully to this far. Our next thanks go to our

outstanding supervisor, Mr. Musah Alhassan who in diverse

ways gave us the best of guidance and directions to come out

with this work. We express to him our deepest appreciation

[III]

to his hard work and love for students and may God richly

bless and guide him for the good of the University in

particular and to Ghana as a whole. More importantly also,

we express our particular indebtedness to the University for

Development Studies for giving us the chance to undertake

this programme. Particularly, our appreciation goes to the

Faculty members of the Department of Management

Administration and to the staff of the School of Business,

not forgetting Rev. Emmanuel Atami, the Head of Department

of School of Business, Mr. Joseph Kofi Nkoah, and Mr. John

Paul and all other staff members for their care and support

for making this program come to fruition. We again,

expressed our thanks to the Mr. Ezekiel Boakye the Manager

of National Investment Bank, Wa branch and Mr. Benjamin

Amenya, staff member. Our last thanks go to the customersof

the bankwhosupported us with technically explanation of our

data.

[IV]

ABSTRACT

It is vital for service providers to obtain feedback from their

customers. This is especially important when a customer has

perceived an unfavourable service experience. One way to receive

feedback from these customers is to encourage and facilitate the

complaint process.Knowledge about complaint behaviour gives the

service provider valuable insight into service problems and how

to improve service offerings, service processes and interactions

to increase customer satisfaction, loyalty and profit. Customers

who have an unfavourable service experience should be encouraged

to complain because if they do not, the provider risk losing the

customer and thus future revenue.This research set forth to know

how the banking sector manages customer’s complaints. The paper

considers a case study of one bank as a means of understanding

the real issues that makes customer complaints.In carrying out

this research; we adopt the descriptive research module which

involves both the quantitative and qualitative research methods.

[V]

A set of questions were administered to the banking staff of

National Investment Bank Ltd and their customers as well to help

know how customer complaints are managed in the banking industry.

Data generated were analyzed using SPSS and Microsoft Excel

software with the aid of tables, figures, columns and charts. The

results of the study generally indicate that, customer complaint

is vital in the banking sector which enables banks to identify

and improve on service failures. Dissatisfaction being met by the

bank with positive responses and action improve is crucial for

the bank to become successful. The findings of the study reveal

that management of N.I.B has mechanism set in place to implement

complaints customers bring in. the service portal routes

complaints to the right personnel to handle it.

[VI]

Table of ContentCHAPTER ONE...........................................1INTRODUCTION........................................................11.0 BACKGROUND OF THE STUDY.......................................1

1.1 THE HISTORY AND BACKGROUND OF THE BANK (N.I.B)..............11.2 PROBLEM STATEMENT...........................................3

1.3 RESEARCH OBJECTIVES.........................................31.4 RESEARCH QUESTION...........................................4

1.5 SIGNIFICANCE................................................41.6 SCOPE OF THE STUDY..........................................4

1.7 LIMITATIONS OF THE STUDY....................................51.8 ORGANIZATION OF THE STUDY...................................5

CHAPTER TWO...........................................6LITERATURE REVIEW...................................................62.0 INTRODUCTION..................................................6

2.1 NATURE OF CUSTOMER COMPLAINTS...............................62.2 CAUSES OF COMPLAINTS........................................8

2.3 TECHNIQUES FOR HANDLING CUSTOMER COMPLAINTS.................82.3.1 Establish a common approach to handling complaints.......8

2.3.2 Analyses and Report Trends...............................92.3.3 Build in customer satisfaction checks....................9

2.4 USEFULNESS OF COMPLAINTS....................................92.5 THE IMPORTANCE OF CUSTOMER COMPLAINT BEHAVIOUR.............11

2.6 SOME FEATURES OF COMPLAINT MANAGEMENT......................132.7 CUSTOMER COMPLAINT BEHAVIOUR IN TODAY’S RESEARCH...........15

2.7.1 Motivation for complaining..............................152.7.2 Antecedents to complaint behaviour......................16

2.7.3 Types of complaint responses............................17

[V]

2.8 LITEERATURE GAP............................................182.9 SUMMARY....................................................18

CHAPTER 3............................................19RESEARCH METHODOLOGY...............................................193.0 INTRODUCTION.................................................19

3.1 AREA OF STUDY..............................................193.2 RESEACH DESIGN.............................................20

3.3 POPULATION.................................................203.4 SAMPLE.....................................................20

3.5 SAMPLING FRAME.............................................213.5.1 Sampling techniques.....................................21

3.5.2 Data analysis...........................................213.6 DATA COLLECTION TECHNIQUES.................................21

3.7 RESARCH INSTRUMENTS OR TOOLS...............................22

CHAPTER FOUR.........................................23PRESENTATION AND ANALYSIS OF DATA COLLECTED........................23

4.0 INTRODUCTION.................................................234.1 CUSTOMER SURVEY............................................23

4.1.1 CUSTOMER BANKING PERIODS WITH N.I.B.....................234.1.2 MOST APPRECIATED SERVICE................................25

4.1.3 DISSATISFACATION IN BANKING SERVICES TO CUSTOMERS.......264.1.4 DO CUSTOMERS COMPLAIN ABOUT DISSATIFIED SERVICES?.......27

4.1.5 DID CUSTOMERS COMPLAIN?.................................284.1.6 EASY/DIFFICULT TO COMPLAIN..............................29

4.1.7 SERVICES TO BE IMPROVED.................................294.1.8 COMPARISON OF N.I.B AND OTHER BANKS ON HOW COMPLIANT S IS MANAGED.......................................................314.1.9 HOW COMPLAINTS SHOULD BE HANDLED........................32

[VI]

4.1.10 RECOMMENDING THE BANK TO OTHER CUSTOMERS...............334.1.12 WHY WOULD YOU RECOMMEND THE BANK TO OTHERS.............34

4.2 INSTITUTIONAL SURVEY.......................................354.2.1 HOW THE MANAGEMENT OF N.I.B MANAGES CUSTOMER COMPLAINTS.35

CHAPTER FIVE.........................................37SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS................375.0 INTRODUCTION.................................................37

5.2 SUMMARY OF FINDINGS........................................375.3 CONCLUSIONS................................................38

5.4 RECOMMENDATIONS............................................38Bibliography................................................40

ACRONYMS....................................................45APPENDIX....................................................46

Questionnaire for management................................46Questionnaire for customers.................................47

List of Figures

Figure 1............................................................24Figure 2............................................................28Figure 3............................................................32

List of Tables

Table 1.............................................................25Table 2.............................................................26Table 3.............................................................27Table 4.............................................................29Table 5.............................................................30Table 6.............................................................31Table 7.............................................................33

[VII]

Table 8.............................................................34

[VIII]

CHAPTER ONE

INTRODUCTION

1.0 BACKGROUND OF THE STUDY.

Within the banking sector, complaints management is becoming an

integral part of business, both from a regulatory perspective and

the customer service stand point. Regulatory bodies are

establishing specific requirement to capture, investigate,

resolve, and report customer complaints. “Customer Expression”

simply states that complaints management is the formal process of

recording and resolving customer complaints (Gerard, 2007).

Houghton (2009) defines “Industry wide trends in the banking

sector as the sales that have decreased industry wide or industry

wide cooperation”. This summarizes common customer experiences in

responds to the changes in banking services. Individual and

aggregate industry trends in complaints behavior are described

including factors that inhabit customer complaints, increasing

the dramatic levels of under-reports. The case is made that

banking industries should affirmatively encourage customer

complaints. This will help the banks identify short comings in

[1]

the product features and service delivery. Thus customer

dissatisfaction will tarnish the bank’s name and image in future.

1.1 THE HISTORY AND BACKGROUND OF THE BANK (N.I.B)

The history of the bank can be traced back to the end of the

Second World War. An association of West African Merchants (AWAM)

was formed when agitations from the indigenes boycotted against

foreign imports by the local population. The colonial

administration decided to establish an entity that will

facilitate the involvement of private indigenous persons in

business. The Gold Coast Industrial Development Corporation

(GCIDC) was therefore established in 1952 with budgetary

appropriations to enable it provide financial support to

indigenes for the establishment of their own businesses.

The Gold Coast Industrial Development Corporation (GCIDC),

encouraged entrepreneurship among the indigenes in the areas of

furniture making and baking. After the independence, the GCIDC

became known as Ghana Industrial Corporation (GIDC) with the

Government of Ghana as the controlling body. The government

transformed the GIDC into the National Investment Bank (NIB) by

[2]

an act of Parliament (Act 163). The NIB was incorporated as an

autonomous joint state private institution on March 22, 1963. It

was established primarily to promote and strengthen rapid

industrialization in all sectors of the Ghanaian economy. The

National Investment Bank Ltd. was therefore the first development

bank in Ghana.

The Act also enabled the National Investment Bank Limited to set

up joint ventures because the Ghanaian manufactures or the

private sector did not have the required funding for start-ups.

NIB on the other hand could lend to enterprises including some of

the defunct regional development corporations. Most of the major

existing industries including Nestle Ghana Limited, Novatel and

many others benefited from NIB’s equity participation or funding

The mission of the National Investment Bank Limited is to offer

the highest-quality, customer-focused banking services to their

clients and to create value for their shareholders.

The National Investment Bank Limited aims at being the most

renowned Ghanaian bank for growth and efficiency.

[3]

The National Investment Bank Limited is said to be one of the

largest financial service institution in Wa Municipality with the

needs of their customers coming first than any other issues.

Their core values are; competence creativity, candor,

collaboration, community, commitment and customer service

excellence.

1.2 PROBLEM STATEMENT

As stated in the background of the company, the company has been

quite successful in serving its customers over the period of

operation .With a number of years in business and experience, NIB

have moved from one stage to another and from growth to growth.

The National Investment Bank still face some problems which are:

In order to offer the highest quality, customer- focused

service banking. National Investment Bank offers support to

local industries and customers in terms of giving loans.

Currently NIB’s responses to customers are not effective.

Customers must queue to be se` rved and ATM machines do

not work either. Loans will be granted when collateral

securities are provided.

[4]

If NIB continues to serve customers in this manner, they

will not only lose customers but also international

investors and customers will move to other banks in the

municipality.

1.3 RESEARCH OBJECTIVES

To find out how effective customer complaints are managed.

To know how customer complaints are responded to in the

bank.

To find out the factors that will make complaint management

effective in the bank.

1.4 RESEARCH QUESTION

How effective are customer complaints managed?

How does management respond to complaints the customer

expresses?

How will the complaint management factors work effectively?

1.5 SIGNIFICANCE

The National Investment Bank focuses on serving its customers

better, collaborate and cooperate with each other to give the

[5]

best service to their cherished customers and shareholders. The

management put in place mechanisms to manage its customer’s

complaints but these mechanisms are not as effective as it must

be. This research when completed will indicate issues that are

worth bringing to the knowledge of management of the bank in

other to serve its cherished customers as the bank seeks to

offer. It also indicates problems or setbacks encountered by the

staff of the Bank in attempt to solve customer problems and

difficulties theywill encounter in their effort to serve

customers effectively. It will help bring out the knowledge and

improvement of understanding in terms of managing customer

complaints.

As a business student, this research gives a mean insight in a

practical situation. It helps give customers the knowledge on how

and when to present a complaint and help improve upon the

reaction of the management and staff of the Bank towards customer

complaints.

1.6 SCOPE OF THE STUDY.

[6]

The studywill cover National Investment Bankin Upper West in the

Northern part of the country. The company is located in WA near

the market circle. The research covers Management and Customers

of the organization.

1.7 LIMITATIONS OF THE STUDY

The difficulties we will encounter in carrying out the project

work are as follows;

The unwillingness of the company to release some information

needed for the work.

We will face some financial difficulties .It will be very

necessary to travel on motor cycles to andfrom one

destination to another for the needed information. Also we

will spend a lot of money on the internet to fish out some

needed information.

The issue of time will be limited in the research work since

the project work has to be done alongside with all academic

works.

1.8 ORGANIZATION OF THE STUDY

[7]

The research reportis organized in five chapters

Chapter one covers the introduction, statement of problem,

research questions, limitations, and the organization of the

study. Chapter two also covers the literature review, brief

introduction on the nature of customer complaints, and its

significant, review of concepts and definitions, related theories

and paradigms, modern perspectives and arguments, literature gap.

In chapter three, detail ofmethodology followed to achieve

results is outlined. It includes the study design, sampling,

sampling techniques and data analysis. Chapter four will comprise

of the presentation and analyzing of data collection. Chapter

five will also include the summary, conclusion, recommendation

and bibliography.

[8]

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

The overall purpose of the study is to look at how customer

complaints can be managed in the banking sector. Customer

complaint is one of those integral parts in the banking .These

complaints that is both formal and regulatory have been the main

aim of this study. Complaint comes from various sectors both

within and outside the organization. This has led to most

problems being encountered in the banking sector (National

Investment Bank). The issue of inappropriate prompt responds to

customer complaints and the lack of special amenities set in

place to address customer complaints are the researcher’s main

focus of this research.

This chapter will look at techniques in handling customer

complaints, importance or usefulness of complaints, the nature of

customer complaints and the benefits to the importance.

2.1 NATURE OF CUSTOMER COMPLAINTS

[9]

Strategies for managing the effects of service incidents on

satisfaction, intention to complain have been studied to restore

exchange balances between a customer, potentially disappointed by

a flawed service, and the “offending” firm. Faulty services and

their management may be seen as an exchange situation in which

players evaluate their profits and losses.

In this context, complaint management may be considered a key,

even an essential, variable within a service-based relationship.

A dissatisfies customer is likely to cut off the relationship or

act in a negative way which may damage the firm. Moreover, it is

admitted that seeking a new customer is generally more costly

than preserving an existing one (Fornell and Wernerfelt, 1987).

Retail banks’ faulty services tend to negatively affect service

quality and consequently customers satisfaction. This state of

affairs tends to intensify the need for an efficient complaints

management system (Sabadie and Prim-AllazI, 2006).

Complaints results from being dissatisfied with services provided

by organizations. Dissatisfaction itself occurs when customers’

expectations are not met by the service provider since

[10]

expectations differ from person to person. It may not be possible

for organizations to satisfy all Customers’. Every organization

that offers to the public is thus likely to receive complaints at

some time. “Not all discontented customers however complain.

Studies of customer satisfaction have revealed that customers are

dissatisfied with their purchase above 25% of the time but that

only about 5% complain”. (Eccles and Durand 1998).

Hinson(2006) further distinguishes between two types of

dissatisfied customers: passives; who do not take action because

they believe complaining is not worth the effort or who instead

of telling a provider tells others and talk to third parties

through negative word of mouth. The second type is “garruls”

(garrulous/talkative people) who insist on their right for

compensation and fair treatment for goods and services.

Most customers feel that complaining to staff of service

organizations in Africa as and when a problem occurs will only

cause additional annoyance and waste of time. If customers have a

problem with service rather than the product, they are even less

likely to say something. Customer will tell their friends and

[11]

family about their problems rather than the service provider. In

general, dissatisfied people will tell between 8 and 10 people

about the bad service they received. Customers whose complaints

are satisfactory resolved often become more loyal than customers

who were never satisfied. “If organizations are to win and retain

customer loyalty they must effectively capture and manage

customer complaint”. This a review- by Eccles and Durand 1998 and

the researcher strongly believes.

2.2 CAUSES OF COMPLAINTS

According to Tumi (2010) leader for “future leaders’

foundations”, the general causes of service complaints include;

failure to perform service when promised; inefficiency, rudeness,

delays and failure to keep customers informed of changes and any

flexibility on the part of the service provider. Some common

causes of complaints also include discourteousness, inept and

incompetent service.

2.3 TECHNIQUES FOR HANDLING CUSTOMER COMPLAINTS

[12]

One cannot talk about the techniques without first looking at the

causes. Kurtus (2007) commented on some techniques for handling

customer complaints. He stated that;

2.3.1Establish a common approach to handling complaints

When the customer pays for a service, it is assumed that the

product will work correctly or that the service received is as

promised. Ideally the customer will no longer have a complain.

Kurtus (2007) explained that “if there is a problem and the

customer complains about it, the company should quickly answer

the complaint and solve the customer’s problem”. This problem

solving is normally done through the company’s customer service

activity. According to Gerald (2007) once complaints are recorded

the nature of the complaint among with the product or service the

complaint is about requires classifications. In the banking

sector, complaint that violates federal laws, or internal bank

policies and procedures, should be classified, separately from

other customer service issues. Once complaints are classified,

the data should be analyzed and reported on a regular basis.

2.3.2 Analyses and Report Trends

[13]

Once complaints are classified the data should be analyzed and

reported on a regular basis. The goal of analysis is to identify

themes or trends that occur with front –line service delivery.

The is done with an eye toward both regulatory matters, and

those that improve customer experiences .Given that many bank

ombudsmen report to their Chief Executive and Board of Directors

on a semi-annual basis ,this ensures complaints management

activities receive senior executive attention and accountability.

2.3.3 Build in customer satisfaction checks

Tumi (2010) explained that after an appropriate interval; say

two weeks get in touch with the customer to confirm that the

company still has a customer. The review mechanism should help in

identifying short comings in product features and delivery.

2.4 USEFULNESS OF COMPLAINTS

The importance or usefulness of complaint to companies or

organizations cannot be overemphasized. The benefits derived from

complaints are enormous.

Zairi (2002) postulates that complaints are useful for the

following reasons:

[14]

They are a way of receiving feedback from customer and therefore

a necessary means for putting into action improvement

plans.Complaints are a necessary tool for preventing complacency

and harnessing internal competencies for optimizing products and

service.

Thereis useful way of measuring performance and allocating

resource to deal with the deficient areas of the service

business.They are a useful “mirror” for gauging internal

performance against competition.Complaints are also useful

exercise tor getting nearer and understanding them

better.Complaining customers are among the most loyal customers.

These views are supported by Eccles and Durand (1998) who have

also noted that;

Research findings have indicated that customers who complain are

also more likely to repurchase, even when their complaint is not

handled satisfactory.Again customers whose problems are recovered

are more likely to say positive thing about the company. This is

explained by reciprocity principle which stipulates that people

like to return favors when something nice has been done for them.

[15]

Complaints are vital to a customer focused service organization.

Complaints provide an opportunity to discover weaknesses in

service provisions; identify areas for improvement and

demonstrate high levels of customer care and resolving issues.

Furthermore effective customer complaints procedures can help

organizations to improve both product and service quality by

offering unhappy customers a method of feeding back information

to the providers of those goods and services. Also complaints are

instrumental in developing a quality culture within organizations

by focusing on customer requirement.

2.5 THE IMPORTANCE OF CUSTOMER COMPLAINT BEHAVIOUR

Perceived service failures experienced by customers are a major

concern for the service personnel’s because of the potential

influence of the service outcome. A complaint allows the service

personnel’s to obtain customer feedback that is useful in making

improvements to increase customer satisfaction, loyalty, long-

term sales and profits (Fornell and Wernefelt 1987). Singh (1991)

argues that providers recognise the extent of customer

dissatisfaction in the marketplace and the handling of service

[16]

recovery as main indicators of customer loyalty, discontent and

welfare. Tax (1998), have further demonstrated that effective

resolution of customer complains can have a positive impact on

customers’ trust and commitment. The complaint handling,

therefore, is a critical "moment of truth" in maintaining and

developing the customer relationships (Berry and Parasuraman

1991).

Successful service companies recognize that while attracting new

customers is important, retaining new customers in a closer

relationship is perhaps more essential for profitability (Johnson

and Selnes 2004). Consequently, dissatisfied customers should be

encouraged to complain (Tax, 1998). A complaint from a customer

and a subsequent lack of service recovery activities has a major

impact on the service company’s financial future. When a service

problem occurs, the service company’s response has the potential

to either emphasize a strong customer relationship or change an

apparently minor distraction into a major incident. Improving a

service company’s customer retention rate by 20 percent has the

same effect on profits as cutting costs by 10 percent (Power and

Driscoll 1992).[17]

Furthermore, it has been estimated that by reducing customer

defections among dissatisfied customers by just 5 percent, a

company can achieve a profit improvement of 25-85 percent

(Reichheld and Sasser Jr. 1990). Complaint handling can be a

significantly superior investment for a service company and can

generate 30- 150 percent return on investment (Brown 2000).

Essentially, the payoff for customer retention is high and a good

complaint response can be used to recover from an unfavourable

service experience and subsequently secure the future of the

company.

In addition to a direct negative effect on the company’s

financial future, the unfavourable service experience may also

have an indirect effect. A customer who has experienced a

negative critical incident or experienced an unfavourable service

may spread negative word-of-mouth communication. By understanding

the complaint process and the customer complaint behaviour, the

service company can learn how to reduce the impact of an

unfavourable service experience or complaint. Dissatisfied

customers often voice their displeasure in the form of negative

word-of-mouth to other current and potential customers (Ah-Keng[18]

and Wan-Yiun Loh 2006). When a negative critical incident occurs,

a company may make the customer into a “terrorist” and engage in

protest activities.

On the other hand, if the complaint is properly handled the

customer may engage in positive wordof- mouth (Blodgett and

Anderson 2000). During recent years, negative word-of-mouth

communication has developed a new dimension due to technological

advancements. There is a large amount of evidence showing that

frustrated and angry customers voice their negative impressions

on the internet. Bailey (2004) has identified four categories for

corporate complaint websites that are used for negative word-of-

mouth communication: (i) Individual sites developed by

disgruntled customers or former employees, (ii) Corporate

complaint sites, (iii) Intermediate sites and (iv).Consumer

protection agency sites.

As mention earlier, customer feedback and complaints are key

drivers for improving different aspects of business and may help

the provider to develop a sustainable company. An effective

complaint management process can be an important quality

[19]

improvement tool. Many studies emphasise that customer feedback

and complaints should be welcomed and encouraged by the service

provider because they generate valuable information (Nyer and

Gopinath 2005). Customer complaints may be useful in many ways:

providing marketing intelligence data (Harrison-Walker 2001),

identifying common service problems (Harari 1992), learning about

organization (Johnston and Mehra 2002), improving service design

and delivery (East 2000), measuring and enhancing the perception

of service quality (Harrison-Walker 2001), and helping strategic

planning (Dröge and Halstead 1991). A customer who does not

complain to the service personnel when having an unfavorable

service experience is of particular concern to any service

company.

It is generally accepted that obtaining feedback from customers’

service experiences is important and if the provider fails to

obtain such valuable feedback, the opportunity to remedy the

problem and retain the customer is lost (Hirschman 1970). The

company’s reputation can also suffer damage from negative word-

of-mouth among dissatisfied customers (Richins 1983b). It is

often asserted that lack of feedback from dissatisfied customers[20]

represents a loss of potential and current customers. Therefore,

it is important to understand the customer’s service evaluation

through increased knowledge about the behavioral process and in

the case of an unfavorable service experience, the complaint

behavior.

2.6 SOME FEATURES OF COMPLAINT MANAGEMENT

As (Fornell and Wernerfelt 1988) suggest, complaint management is

much more general than warranties and guarantees. In their

summary, complaint management typically applies to all customers,

rather than a subset of clients; and it’s closely related to the

reports on quality improvement. Moreover, “effort to facilitate

voicing of complaints" is a crucial part of complaint management.

It also widely recognized that customer complaint mainly is

driven by failing expectation, thus both expectations and quality

realization are essences. These features motivate the basic

ingredients of our model, such as the corrective action as public

good, and the key role of complaining barrier set-up as policy

choice.

[21]

The following stylized facts about complaint behavior are

concerns of our work. First, it’s a famous marketing text- book

even asserts that as much as 95% of dissatisfied customers never

tell the company their problem (Kotler et al 1999). Hence, it

suggests that not complaining is more likely a part of

equilibrium behavior, rather than abnormal action. Second, since

most customer complaints are unsolicited (Richins and Verhage,

1985), economic theory may suggest because of the possible

misreport problem, complaint is not a perfect indicator of

service quality. This is concerned by various researches. For

instance, (Snellman and Vihtkari, 2003) illustrate that the most

frequent complainers are those who actually con- sider themselves

guilty for the outcome.

Doerpinghaus(1991) suggests that disappointed expectations,

rather than poor service quality, may result in complaints. And

it’s recognized that complaint frequency is not significantly

related to the dissatisfaction (Andreasen, 1977). (Halstead et

al, 1996) found that poor performance in one service area may

predispose the complainers to negatively evaluate and complain

other service areas or attributes. Hence consistent with the need[22]

by (TARP, 1991), customer satisfaction may not reach service

quality or customer satisfaction. Finally, despite the claims

made by many firms that complaining is encouraged, substantive

barriers exist. (TARPS, 1991) identify time and effort involved,

ignorance about how to complain, and uncertainty about redress

after complaints as the primary sources of cost.

Moreover, complaining barrier, consequently complain behavior,

varies considerably across countries, industries, even firms.

Many surveys since (Richins and Verhage, 1985) have established

that dissatisfied customers from some specific countries are

significantly less likely to complain, thus culture background

may matter. (TARP, 1992) demonstrates that

complaint/dissatisfaction ratio varies significantly across

industries, in which tourist and luxury products have higher

ratio, and consumer products has the lowest one. (Fornell, 2007)

identifies hospitals, life insurance, airlines and health

insurance as the worst ones in complaints handling, while

supermarkets and automobile work well. Even the firms in the same

industry have quite different complaint handling practices. For

example, Ryanair, the leading low-cost airline in Europe, is[23]

famous for its bad attitude toward complaints and obstruct

procedure to complain10. On the other hand, Southwest Airlines,

the low-cost airline in U.S., maintain the lowest complaint rate

and very high customer’s satisfaction.

2.7 CUSTOMER COMPLAINT BEHAVIOUR IN TODAY’S RESEARCH

Research on customer complaint behaviour has mainly emphasized

three aspects: (i) motivation for complaining, (ii) antecedents

to complaint behaviour and (iii) types of complaint responses.

2.7.1 Motivation for complaining.

Even decades ago, researchers argued that dissatisfaction serves

as the motivation for complaint behavior (Day, 1984). Since then,

several researchers have followed in their footsteps and argued

that dissatisfaction is the main source of complaints. According

to Keaveney (1995), there are several determinants to switching

behaviour, which can be categorized as single or complex types of

determinants. The categories depend on the number of factors

involved in the switching behaviour. These types of determinants

suggest that fully understanding the motivation for complaint

behaviour is complicated. Based on Keaveney’s (1995) research,

[24]

there are three main single sources for complaint behaviour: (i)

core service failure, (ii) service encounter failure and (iii)

responses to failures. Core service failure is the most commonly

reported reason for dissatisfaction (Bitner, 1990). The main

reason for an unsatisfactory outcome in service encounters is the

employee’s response to service delivery system failures (Bitner,

1990).Inadequate response to service failures also increases the

likelihood that dissatisfied customers will complain about the

incident (Bitner, 1994). Oliver (1997) notes that as many as half

of all customer complaining episodes end with even more

dissatisfaction.

2.7.2 Antecedents to complaint behaviorthe idea of linking

consumer’s responses to the intensity of dissatisfaction is not

new. The first model proposing such a relationship was put

forward by (Landon, 1977). More recent research agreed with this

statement (Maute and Forrester 1993). (Richins, 1983), using

severity of the problem as a surrogate for intensity of

dissatisfaction, found a direct relation between intensity and

complaining behaviour. Attitude towards the act of complaining is

conceptualized as an overall effect towards the “goodness or bad”[25]

of complaining to service personnel (Singh and Widing 1991). When

consumers believe that their complaint will be accepted by the

firm and not spread negative word- of- mouth, they become happy

(Anderson and Sullivan, 1993). Bearden el al (2001) argues that

“consumers self-confidence is the extent to which individual feel

capable and assured with respect to his or her market place

decisions and behaviour” and reflects as a consumer in the

marketplace( Adelman 1987).

2.7.3 Types of complaint responses

Several different complaint response models have been suggested

in the past. There are two main types of complaint responses: (i)

complaint models that include intermediate factors in the

complaint process such as justice (Tax, 1998) or emotions (White

and Yi-Ting, 2005) and (ii) complaint response models that are

untainted (Day and Landon Jr. 1977b). The latter complaint models

are most often referenced. Hirschman’s (1970) theory of exit,

voice and loyalty was one of the first to conceptualize customer

complaint responses.

[26]

According to Hirschman (1970), the customer can choose to voice

a complaint to the seller or a third party and then exit the

relationship with the seller through switching or determination.

The model suggests that ‘exit’ or ‘voice’ is dependent on the

degree of customer loyalty. Day and Landon (1977) suggested a

three-level hierarchical classification scheme. The model

distinguished between taking no action and taking some action and

is further subdivided into private and public responses. Private

actions include decisions to stop further purchases and warnings

to friends and/or ceasing to patronize a retail outlet; public

actions include redress-seeking efforts directed toward the

seller, complaints to third-party consumer affairs institutions

and legal action.

Singh (1988) extended and Landon’s (1977) hierarchical model to

a three-dimensional model consisting of private response (e.g.,

negative word-of-mouth), voice response (e.g., seeking redress

from the seller), and third-party response (e.g., taking legal

action or complain to an external third party). Private response

refers to behaviour exhibited within a customer’s own social

sphere. Such behaviour can vary from warning friends and[27]

relatives against using a service provider to deciding not to

purchase from a provider again. Voice response essentially refers

to complaining directly to the offending provider. A customer who

contacts a service provider in person, in writing or by telephone

would be using voice response.

Singh (1988) also included the “no complaint action” in this

category. Third-party response, conversely, refers to complaints

expressed to an external party who are not directly involved with

the offending service provider but who may have some authority or

influence over the provider. Customers who contact customer

protection agencies, lawyers or newspapers as a result of a

dissatisfying experience with a service provider are taking

third-party action (Singh 1988). Exit is when the customer begins

a personal boycott against the service provider to avoid

repeating the original transaction that led to dissatisfaction.

2.8 LITEERATURE GAP

The following research gaps are identified by a reviewing both

national and international literature regarding customer

complaint management .it is consequently found many foreign

[28]

literature failed to acknowledge the effectiveness of initiative

strategies, maintains strategies and services satisfaction to

identified the effectiveness of customer complain management in

any banking industry.

Another important gap which induced the present research is that

the previous researchers did not give any relationship the

service seekers and service providers this present thesis

numerically identified the gap between perception of customers

and bankers.

2.9 SUMMARY

Institutions, organizations and service providers should not take

customer complaints as a dent on their performance but rather as

a sit up call. This will intend yield benefits to the

organization in terms of customer loyalty. Also customer’s

retention in the future will be attained when such complaints are

handled effectively. This is what this chapter has been trying to

do – look at what others have said about how customers’

complaints can be managed: the techniques adopted in managing

[29]

such complaints and the benefits one stands to derive from

managing complaints very well.

CHAPTER 3

RESEARCH METHODOLOGY

3.0 INTRODUCTION

The objective of this chapter is to discuss the method used for

the study. It describes the target population and selected

sample. It also outlines the development and design of the

methods used to administer the questions and designs of the

research plus the study area.

3.1 AREA OF STUDY

The area of study is the Wa municipality of the Upper West

region. It is located in the North West corner of the Upper West

[30]

region of Ghana between latitude of 9°-32W to 10°-20W and

longitude of 1°40N. The town serves as transportation for the

Upper West region of Ghana, with major roads leading Hamile and

North East to Tumu in Upper West region of Ghana. It has annual

rainfall of 879m (34.6in) and the hottest period of year’s day

time temperature; often reach 39o c mean annual temperature.

The municipality covers a landmass area of 1502.336 JKM² and is

divided into five area/town councils to facilitate effective

decentralized administrative, political and development decision-

making and transparent governance. The municipality has a total

population of 107,214 with 52,996 being males and 54,218 females

representing 49.4% to that of males and 50.6% to that of females.

(Wa statistical department)

3.2 RESEACH DESIGN

Mixed approach methodology was use as the research design. This

entails quantitative and qualitative methods. Quantitative

[31]

approach takes into accounts numerical analysis whiles the

quality of the research study too was considered by qualitative

methods.

Effective management of customer complaint helped retain ones

customers, when customers are fully satisfied. It also helped the

organization to identify their weakness in their service

delivery. The study is based on managing customer complaint in

the financial sector. The information gathered was based on how

complaints are received and handled in the banking sectors and

the mechanisms set in place to handle them .To obtain account

data for the study the researcher used both primary and secondary

data. The primary data got through the designing of questionnaire

whilst the secondary data was got from text books to suit the

purpose of the study.

3.3 POPULATION

The population target that the researchers were interested in

studying was the National Investment Bank (NIB) in Wa which

involve the Management, Staff and Customers.

3.4 SAMPLE

[32]

To save time and cost, Forty nine (49) questionnaires were

designed for the Management and Customers of the organization to

be answered, which represent a bigger group or allow the

researcher to obtain data from representative section of the

population from valid conclusion.

3.5 SAMPLING FRAME

Two of the questionnaires were distributed to management and

forty seven to the customers of the National Investment Bank.

3.5.1 Sampling techniques

The researcher used probability and non- probability sampling

techniques in selecting the sample for the study. In order to get

very accurate result for this study, management and customers

were being selected. The researcher used simple random sampling

technique to select the customers and other financial

institutions while the purposive sampling technique was used to

[33]

select the staff. In the purposive sampling, the sample is chosen

to suit the purpose of the study.

3.5.2 Data analysis

In order to make valid assumptions about the information and data

collected, a comprehensive data analysis approach was of

immersive help to bring about logical conclusions and

recommendations. Data wasanalyzed through the use of the

software of Statistical Package for social science (SPSS),

charts, tables and Microsoft excel. Apart from this method,

quantitative and qualitative tools of analysis were also used to

analyze our data where necessary.

3.6 DATA COLLECTION TECHNIQUES

The main sources of data collection for the study were primary

and secondary data. The primary data was obtained using

questionnaires and interviews which would be designed and

administered to the management, staff, customers, and other

customers in different financial institutions by the researchers

in Wa Municipal. The secondary source of data is the already

processed data that we obtain fromorganizations that are

[34]

considered relevant to our study, some of these organizations

include: National Investment Bank (NIB) and others bank in Wa

municipality.

3.7 RESARCH INSTRUMENTS OR TOOLS

Questionnaires were used as our source of obtaining primary

data. The questionnaires were properly designed to aid us

generate appropriate and relevant data for the study. The essence

of the questionnaires is to give the respondents the opportunity

to answer the questions at their leisure time. Both open and

close ended form of questionnaires was used. These forms of

questionnaires, most especially the close ended form is easy to

answer, less expensive and requires less time. The open ended

form is to enable respondents express their opinion on the study

where necessary. The questionnaires were subjected to validation

before administering and this to enable us avoid ambiguity and

other terminologies.

[35]

CHAPTER FOUR

PRESENTATION AND ANALYSIS OF DATA COLLECTED

4.0 INTRODUCTION

This section contains the analysis from the questionnaires

administered in the field of survey. For the purpose of the

analysis and discussion, the study was conducted with two

identified groups which comprise the management and the customers

of bank .A total number of forty-seven (47) customer

questionnaires were selected, two were given to the management of

the bank making a total number of 49 respondents. The

[36]

questionnaires were to find out how N.I.B manages its customer

complains in the Wa municipality and suggest ways to improve upon

the customer care services. The data was analyzed based on the

objectives of the study. The information obtained is presented in

the form of tables and charts in this section. An analysis of the

findings is presented alongside the data obtained.

From the data collected, the following findings were obtained by

the researchers after the analysis of data collected from the

management of the bank. The findings are grouped under the

objectives of the study.

4.1 CUSTOMER SURVEY

4.1.1 CUSTOMER BANKING PERIODS WITH N.I.B.

This is the distribution of respondents and the year each

customer started doing business with the bank. From the response

the researchers had, it can be seen from the fig.1 that none of

the respondents started business with N.I.B between 10 and

11years period. In the fig.1 the analysis shows that, from 7,

9and 12years in doing business with the bank recorded the lowest

customers of one (1) customer each representing 2.1% each. From

[37]

3and 4 years in doing business with the bank recorded the highest

years N.I.B with a total of ten (10) representing 21.3% each of

the total respondents of the study. However, from 5years in doing

business with the bank recorded the second highest, 8 respondents

which represent 17.0%. The next highest of the respondent was

from 6 years which recorded five (5) customer representing 10.6%.

Also from 2 years and 8years recorded four (4) customers each

representing 8.5% each and from 1year recorded the second lowest

customers of three (3) representing 6.4% of the total respondent.

Figure 1

[38]

Source: Field Survey, June 2014

Most of the customers started doing business with N.I.B from the

years 3 and 4. Most customers can be said to be students and few

being workers and laymen as illustrated in fig.1 above. This can

be due to services rendered during those year periods or periods

when the bank had competitive advantage over their competitors.

Management can still attract customer if those mechanisms are put

in place again.

4.1.2 MOST APPRECIATED SERVICE.

[39]

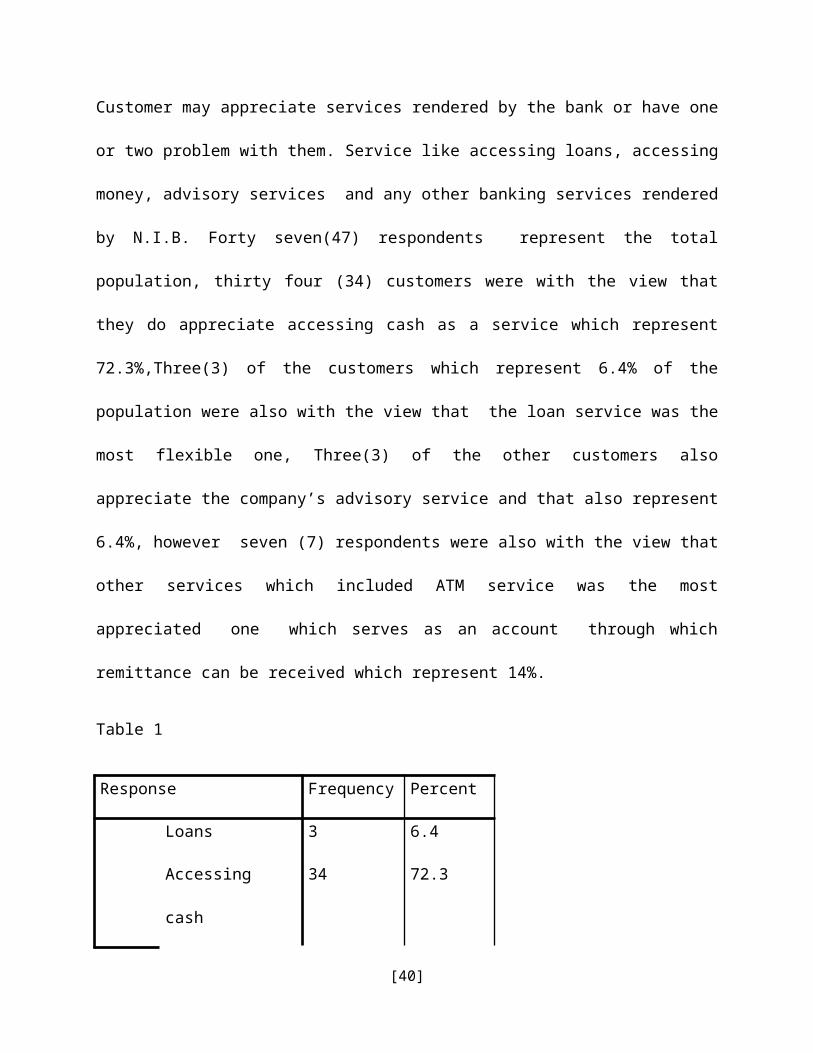

Customer may appreciate services rendered by the bank or have one

or two problem with them. Service like accessing loans, accessing

money, advisory services and any other banking services rendered

by N.I.B. Forty seven(47) respondents represent the total

population, thirty four (34) customers were with the view that

they do appreciate accessing cash as a service which represent

72.3%,Three(3) of the customers which represent 6.4% of the

population were also with the view that the loan service was the

most flexible one, Three(3) of the other customers also

appreciate the company’s advisory service and that also represent

6.4%, however seven (7) respondents were also with the view that

other services which included ATM service was the most

appreciated one which serves as an account through which

remittance can be received which represent 14%.

Table 1

Response Frequency Percent

Loans 3 6.4

Accessing

cash

34 72.3

[40]

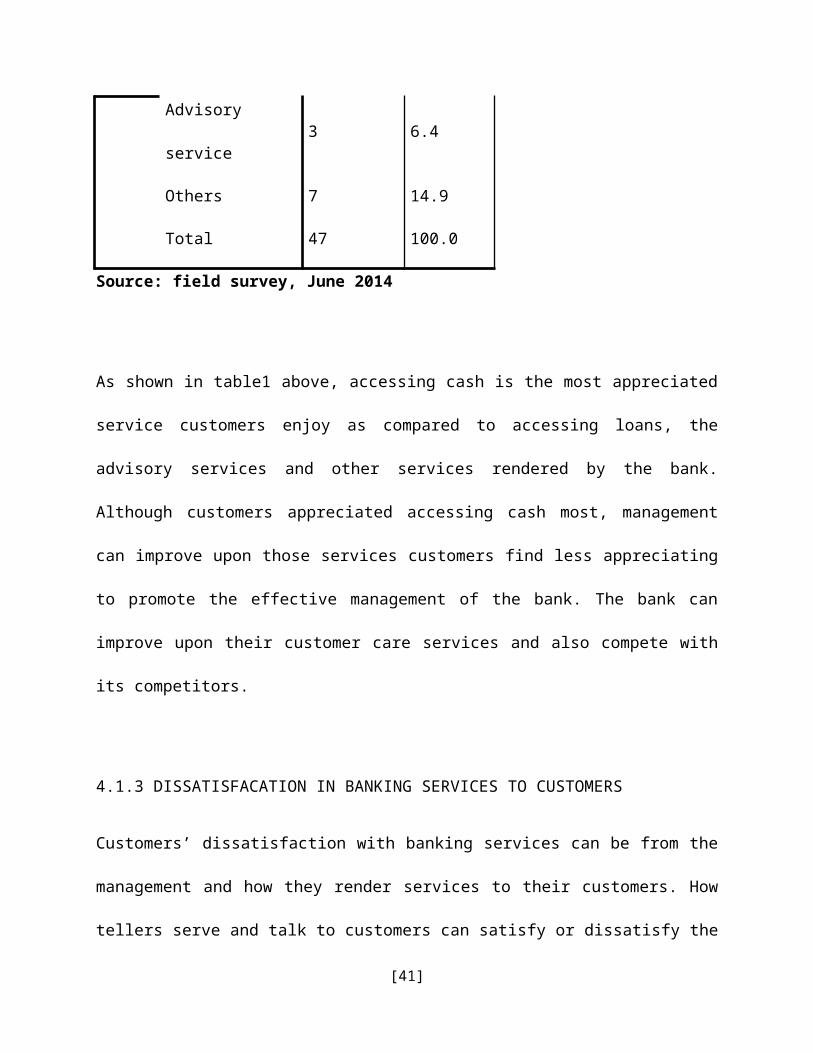

Advisory

service3 6.4

Others 7 14.9

Total 47 100.0

Source: field survey, June 2014

As shown in table1 above, accessing cash is the most appreciated

service customers enjoy as compared to accessing loans, the

advisory services and other services rendered by the bank.

Although customers appreciated accessing cash most, management

can improve upon those services customers find less appreciating

to promote the effective management of the bank. The bank can

improve upon their customer care services and also compete with

its competitors.

4.1.3 DISSATISFACATION IN BANKING SERVICES TO CUSTOMERS

Customers’ dissatisfaction with banking services can be from the

management and how they render services to their customers. How

tellers serve and talk to customers can satisfy or dissatisfy the

[41]

customer. From the questionnaires selected, Twenty seven (27)

customers were with the view that they dissatisfied which is57.4%

and twenty customers (20) respondent who are not dissatisfied in

any services the bank renders which is 42.6%.

Table 2

RESPONSE FREQUENCY PERCENTAGE

Yes 27 57.4

No 20 42.6

Total 47 100.0

Source: field survey, June 2014

From table2 customers who were dissatisfied with the service of

the bank out numbers the customers who are not dissatisfied with

the banking services. Management of N.I.B must improve upon their

customer care in order to satisfy customers and to compete with

its other banking competitors

4.1.4 DO CUSTOMERS COMPLAIN ABOUT DISSATIFIED SERVICES?

Customers complain to management and specified officers on

problem they encounter with services rendered to them. This is

[42]

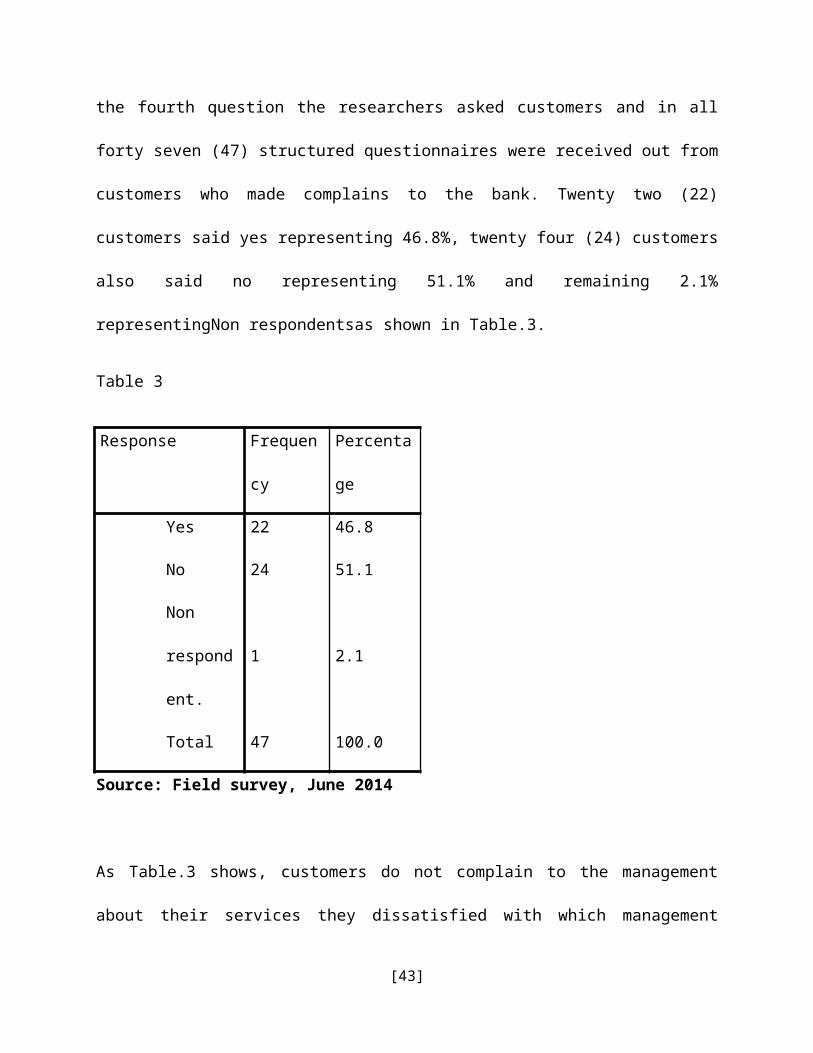

the fourth question the researchers asked customers and in all

forty seven (47) structured questionnaires were received out from

customers who made complains to the bank. Twenty two (22)

customers said yes representing 46.8%, twenty four (24) customers

also said no representing 51.1% and remaining 2.1%

representingNon respondentsas shown in Table.3.

Table 3

Response Frequen

cy

Percenta

ge

Yes 22 46.8

No 24 51.1

Non

respond

ent.

1 2.1

Total 47 100.0

Source: Field survey, June 2014

As Table.3 shows, customers do not complain to the management

about their services they dissatisfied with which management

[43]

should know and they must improve upon. Management must note that

even though customers do not complain they must find ways to know

customers problems and to make it a point to solve those

problems. A competitive advantage can be won by the management

over its competitors.

4.1.5 DID CUSTOMERS COMPLAIN?

In all forty- seven (47) structured questionnaires were received

out of customers who made complains to the bank. Twenty-two (22)

customers said yesrepresenting 46.8%, twenty four (24) customers

also norepresenting 51.1% and remaining 2.1% representing non-

respondent.

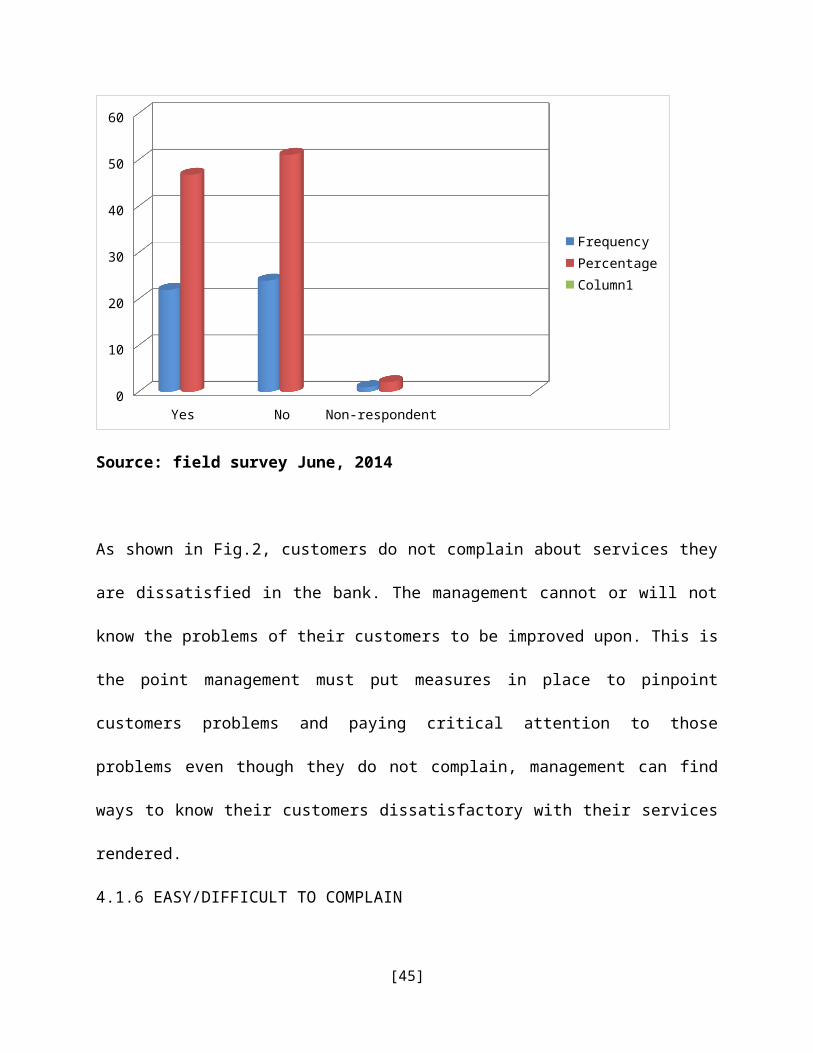

Figure 2

[44]

Yes No Non-respondent0

10

20

30

40

50

60

FrequencyPercentageColumn1

Source: field survey June, 2014

As shown in Fig.2, customers do not complain about services they

are dissatisfied in the bank. The management cannot or will not

know the problems of their customers to be improved upon. This is

the point management must put measures in place to pinpoint

customers problems and paying critical attention to those

problems even though they do not complain, management can find

ways to know their customers dissatisfactory with their services

rendered.

4.1.6 EASY/DIFFICULT TO COMPLAIN

[45]

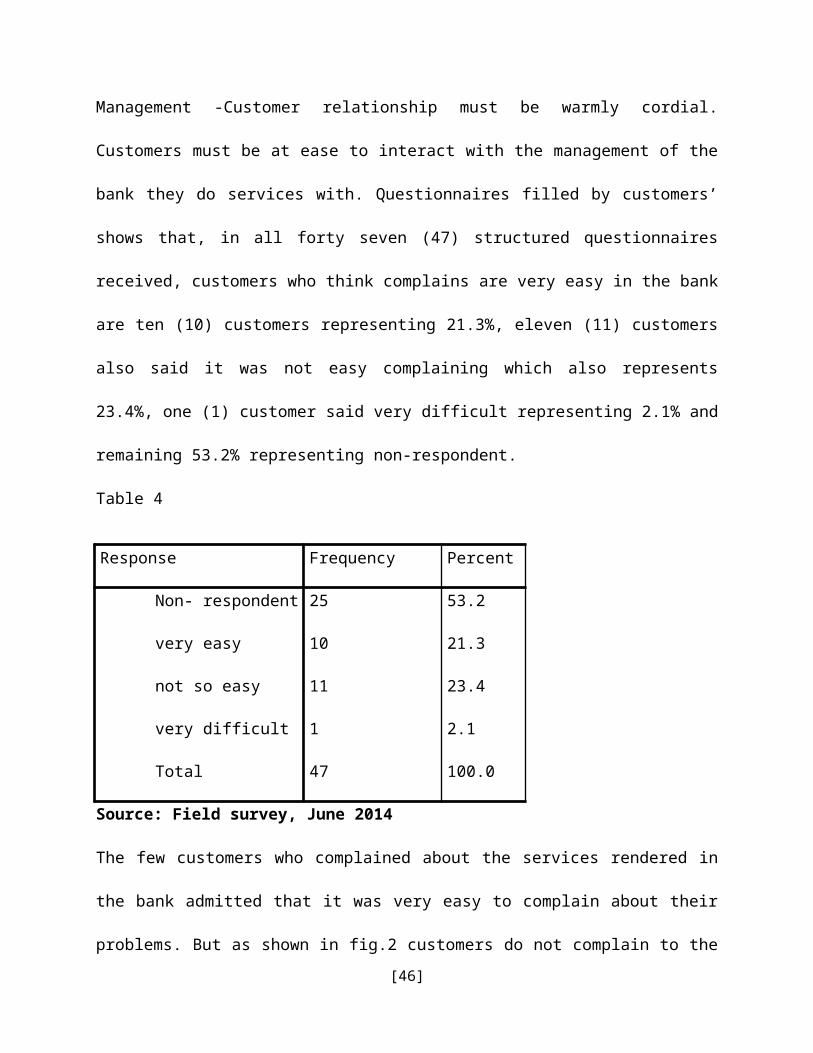

Management -Customer relationship must be warmly cordial.

Customers must be at ease to interact with the management of the

bank they do services with. Questionnaires filled by customers’

shows that, in all forty seven (47) structured questionnaires

received, customers who think complains are very easy in the bank

are ten (10) customers representing 21.3%, eleven (11) customers

also said it was not easy complaining which also represents

23.4%, one (1) customer said very difficult representing 2.1% and

remaining 53.2% representing non-respondent.

Table 4

Response Frequency Percent

Non- respondent 25 53.2

very easy 10 21.3

not so easy 11 23.4

very difficult 1 2.1

Total 47 100.0

Source: Field survey, June 2014

The few customers who complained about the services rendered in

the bank admitted that it was very easy to complain about their

problems. But as shown in fig.2 customers do not complain to the[46]

management of the dissatisfaction in the services they render to

them.

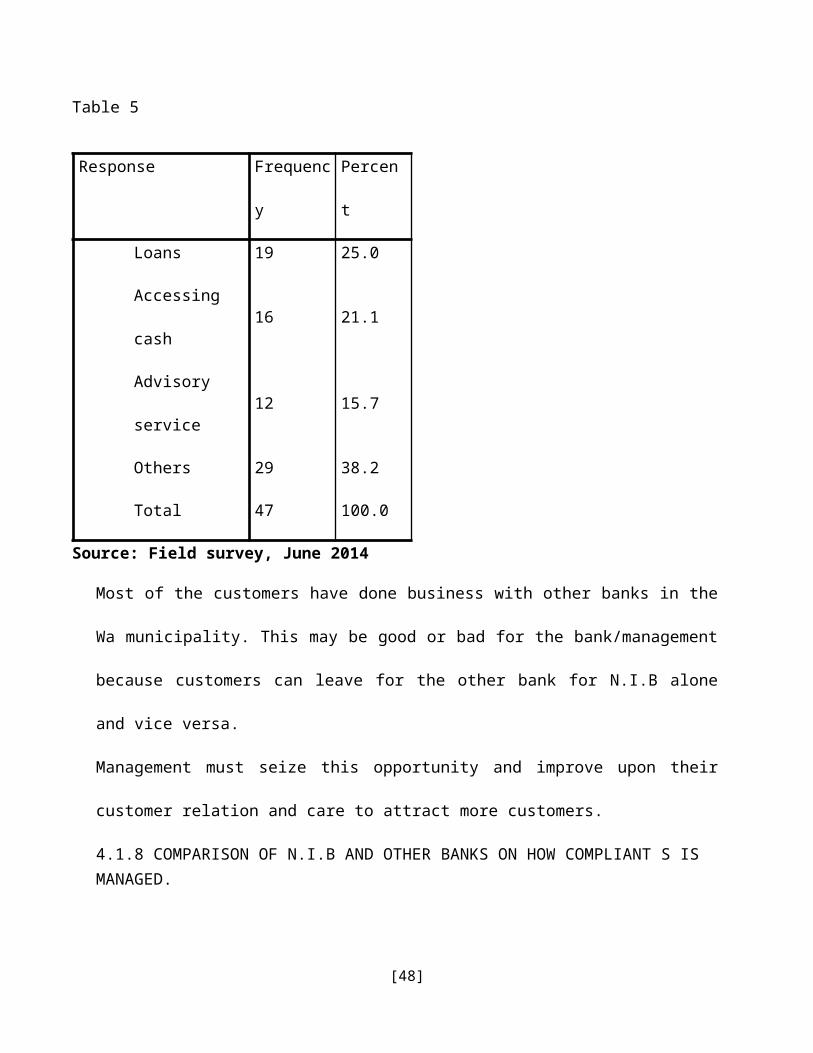

4.1.7 SERVICES TO BE IMPROVED.

Customers of the National Investment Bank think some of the

services must be improved upon. In all forty seven (47)

represents the total population of customers who also think

N.I.B. should improve on their services rendered. Nineteen (19)

customers were with the view that they should improve on their

loan service which is representing 25.0%, sixteen (16) customers

also said they should improve on accessing cash which is

representing 21.1%. However twelve (12) customers also think they

should improve on advisory service which representing 15.7% and

twenty nine customers (29) respondent to other services which is

38.2%.

[47]

Table 5

Response Frequenc

y

Percen

t

Loans 19 25.0

Accessing

cash16 21.1

Advisory

service12 15.7

Others 29 38.2

Total 47 100.0

Source: Field survey, June 2014

Most of the customers have done business with other banks in the

Wa municipality. This may be good or bad for the bank/management

because customers can leave for the other bank for N.I.B alone

and vice versa.

Management must seize this opportunity and improve upon their

customer relation and care to attract more customers.

4.1.8 COMPARISON OF N.I.B AND OTHER BANKS ON HOW COMPLIANT S IS MANAGED.

[48]

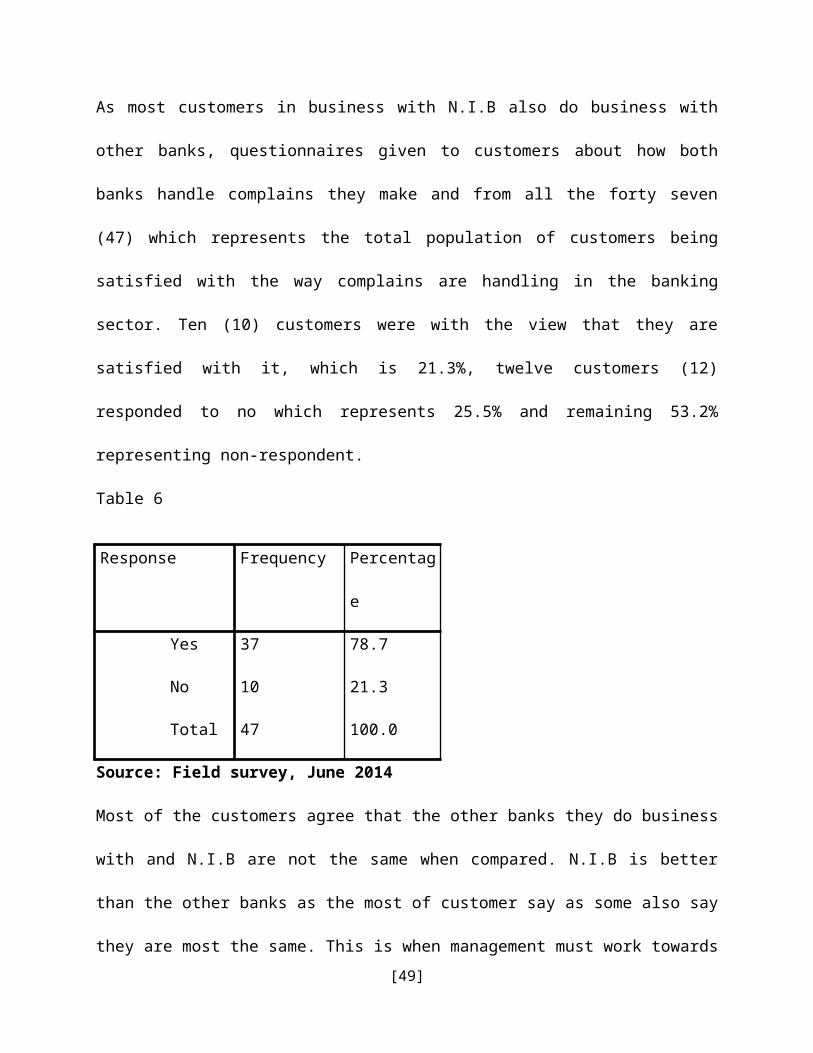

As most customers in business with N.I.B also do business with

other banks, questionnaires given to customers about how both

banks handle complains they make and from all the forty seven

(47) which represents the total population of customers being

satisfied with the way complains are handling in the banking

sector. Ten (10) customers were with the view that they are

satisfied with it, which is 21.3%, twelve customers (12)

responded to no which represents 25.5% and remaining 53.2%

representing non-respondent.

Table 6

Response Frequency Percentag

e

Yes 37 78.7

No 10 21.3

Total 47 100.0

Source: Field survey, June 2014

Most of the customers agree that the other banks they do business

with and N.I.B are not the same when compared. N.I.B is better

than the other banks as the most of customer say as some also say

they are most the same. This is when management must work towards[49]

winning its customers and other customers to help maintain their

competitive advantage and to work effectively to satisfy their

cherished customers.

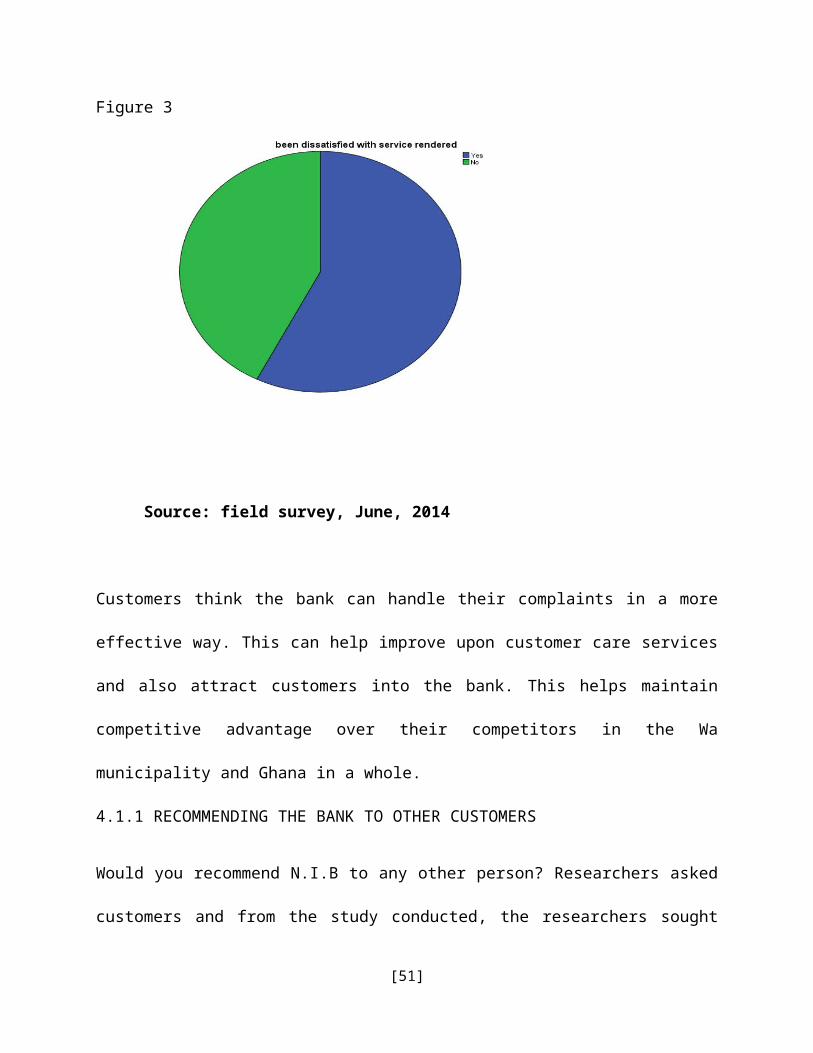

4.1.9 HOW COMPLAINTS SHOULD BE HANDLED

Most people would like to be treated different. Everybody has got

a way in which they prefer to be handled with their issues so as

customers of every institution and banking firms. As everybody

has different views on handling issues, so as customers of N.I.B.

they prefer the management to handle the complaints they make in

a more effective way. Fig.3 is in two sections, the section

marked with blue represents customers who said yes to the

researchers that there’s supposed to be a way management handles

their complaints. And the portion marked with green represents

customers who said no. The customers who said yes recorded 78.7%

and customers with No as their answer recorded 21.3% respectively

as illustrated in fig.3.

[50]

Figure 3

Source: field survey, June, 2014

Customers think the bank can handle their complaints in a more

effective way. This can help improve upon customer care services

and also attract customers into the bank. This helps maintain

competitive advantage over their competitors in the Wa

municipality and Ghana in a whole.

4.1.1 RECOMMENDING THE BANK TO OTHER CUSTOMERS

Would you recommend N.I.B to any other person? Researchers asked

customers and from the study conducted, the researchers sought

[51]

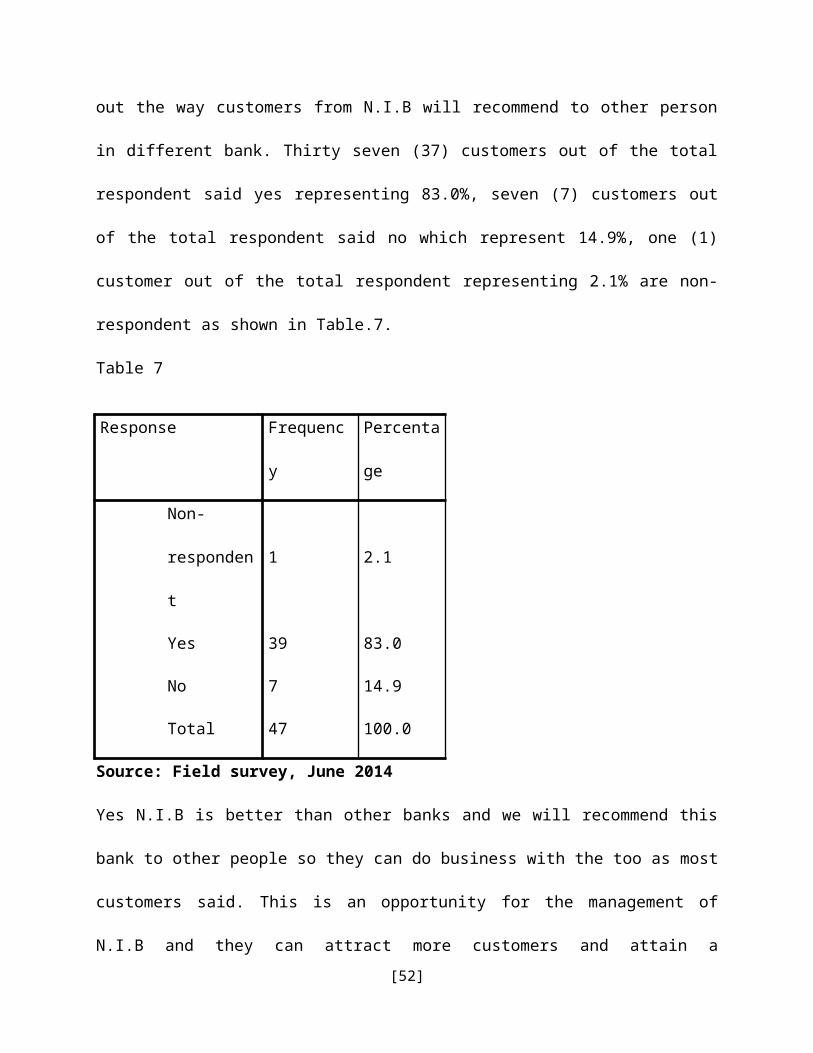

out the way customers from N.I.B will recommend to other person

in different bank. Thirty seven (37) customers out of the total

respondent said yes representing 83.0%, seven (7) customers out

of the total respondent said no which represent 14.9%, one (1)

customer out of the total respondent representing 2.1% are non-

respondent as shown in Table.7.

Table 7

Response Frequenc

y

Percenta

ge

Non-

responden

t

1 2.1

Yes 39 83.0

No 7 14.9

Total 47 100.0

Source: Field survey, June 2014

Yes N.I.B is better than other banks and we will recommend this

bank to other people so they can do business with the too as most

customers said. This is an opportunity for the management of

N.I.B and they can attract more customers and attain a[52]

competitive advantage over their competitors in the Wa

municipality and in Ghana as a whole.

4.1.12 WHY WOULD YOU RECOMMEND THE BANK TO OTHERS

Customers give reasons to why they will recommend N.I.B to other

people as required in the questionnaires researchers provided

out of 47 respondents, 17 respondents representing 36.17% said

they are willing to recommend the bank to others due to the good

nature of the bank services, 13 respondent represent 27.05% will

recommend the bank because of how customer complaint are handled,

8 respondents representing 19.14% will recommend due to their

loan services they offered and 9 respondents representing 19.14%

said they see the bank services as a poor one, since they are

always dissatisfy with the bank services as shown in Table.8.

Table 8

Services Frequency Percentage

Bank services are

good

17 36.17

Customer relation 13 27.05

[53]

Loan services 8 17.02

Poor services 9 19.14

Total 47 100

Source: Field survey, June 2014

As shown in Table.8 above most customers are willing to recommend

the bank to others because their services are of good quality.

Although some still think some of their services are poor,

management can make a difference with this. More customers can

be attracted by the bank if proper measures are put in place.

This can also help the bank compete with its competitors.

4.2 INSTITUTIONAL SURVEY

4.2.1 HOW THE MANAGEMENT OF N.I.B MANAGES CUSTOMER COMPLAINTS

When researchers met the management of the National Investment

Bank, the question “Do you have any customer complaints

mechanism?” was asked. They said yes they do and they made sure

it was effective and met their customers’ requirement. In order

to ensure that, special officials were appointed to take

responsibility of the customer’s complaints they went on to say

[54]

that their complaint management effort as compared to their major

competitors is at Par. With reference to other survey made by the

researchers, due to how management responds to customer

complaints, it can be said to have increased the number of

customers in the bank. The researchers sought to find out the

difference between N.I.B and other banks on how they handle

complaints from customers and in all forty-seven selected from

the total questionnaires, fourteen (14) customers think that they

are the same, seventeen (17) customers were of the view that

N.I.B is better, eight (8) customers also think that they are

better than N.I.B and eight (8) customers of the total population

did not respondent.

The management said they ensure that N.I.B has better complaint

handling mechanisms than any bank in Wa Municipality and they

manage these complaints by assigning special human personnel’s

and they made sure the environment was conducive for the

complainant. The management then assured the complainant that

proper mechanisms will be put in place for the customer

satisfaction.

[55]

Most customers complain about their ATM cards and the machine

itself, their cheque withdrawal books, huge collateral securities

before lending loans and how the place is always busy and jammed

on Mondays. And customers are assured that their problems will be

solved as soon as possible. And customers leave with happy and

smiley faces because we assured them and we make it a point to do

so as soon as possible.

Our major constraints are when the IT networks jams up. Customers

although waits patiently for ours services are disturbed .ATM

machine also become useless when the network jams up.

We still look forward for proper mechanisms to improve upon the

complaint our customers makes. And we make it a point to serve

them better. All these were acquired from the management by the

researchers when two (2) questionnaires were selected from all

three questionnaires given to the management.

Source: Field survey, June 2014

[56]

CHAPTER FIVE

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS

5.0 INTRODUCTION

This chapter gives the overall summary of the research. It will

also discuss the implications of the outcomes and help recommend

proper mechanism for the management to solve the complaints their

customers make. As stated in the problem statement N.I.B has been

[57]

serving their customers successful for sometimes now but still

faces problems with managing its customer complaints. There are

no proper mechanisms put in place to address customer complaints.

Management of the bank does not have appropriate response to

customer complaints. Researchers used both the quantitative and

qualitative approaches in the findings of this research work. In

the researcher’s findings, customers gave ways they expect the

management to handle their complaint and the management are

putting mechanisms in place to satisfy their customers.

5.2 SUMMARY OF FINDINGS.

Management of N.I.B has mechanisms set in place to handle

customer complaints. The service portal was set in place to

implement the complaints customers bring in. The service portal

routes complaints to the right personnel to handle it.

Most customers are satisfied with accessing cash when compared

with other services in bank. They are able to report to the

management of N.I.B of their problems and share their views on

how it can be handled. Also management of the company deemed

complaint to be very useful as it is a tool for measuring

[58]

performance and allocating resource. Complaints are also a way of

receiving feedback from customers and therefore a necessary means

for putting into action improvement plans.

Moreover the company’s complaint handling effort was rated high

above competitors. The major complaints the company receive from

customers are the problems with the ATM machine and cheque book

delays. Loyal customers of N.I.B find it easy to complain to

management about their problems.

Researchers had their findings from the management and customer

of the National Investment Bank. Data was collected and analyzed

based on the researchers’ findings.

5.3 CONCLUSIONS.

From what has been discussed it can be observed that management

sees their customers as very important and handling their

complaints is vital. In view of this management has set in place

complaint handling mechanisms to deal with the customer’s

problem. The researchers however agree with Cosmo Graham that

“the better the complaints are handled the higher the level

customer satisfaction”. This is because the mechanisms set in

[59]

place will help solve customer’s problems and thus increase their

level of satisfaction.

5.4 RECOMMENDATIONS.

The National Investment Bank aims to be the most renewed Ghanaian

bank for growth and efficiency and also to offer the highest-

quality services to its clients and create a value for its

shareholders in their long and short term goals. Although, most

of the questions were answered positively by customers, findings

have indicated that there is more room for improvement. The

researchers recommend that;

The bank should be undergoing training and workshops to

offer more effective customer service for customer

satisfaction.

The management should conduct periodic customer satisfaction

survey since customer complaint level cannot only be used to

measure customer satisfaction in order to improve customer

care services.

Customers should been courage to complain and their

complaints must be given attention and resolved fully. The

[60]

researchers also recommend that customer hot line should be

established to maximize the ease with which customers

complain or make suggestions and inquire about the service

delivered.

Customers of the bank should be asked to rate the company’s

service on key satisfaction factors like speed of service

delivery and friendliness of staff in order for management

to know total performance of the bank.

Banking services such as loans, advisory services and

automatic teller machines (A.T.M) are improved upon and loan

service be made more flexible to attract customers and

improve upon their level of satisfaction. The management can

reduce high collateral securities for easy access to loans.

The above recommendation, if properly adhered will assist N.I.B.

to effectively handle customer complaint and thus satisfy the

customer the right way and retaining them for survival of the

bank.

[61]

Bibliography

Adelman, P. (1987). Occupational Complexity, Control and Income: Relation

Psychological Well-Being in Men and Women. Journal of Applied

Psychology, 72 (November),529-537.

Ah-Keng, K. and Wan-YiunL.E.(2006).The effects of service recovery on

consumer satisfaction: a comparison between complainants and non-

complainants.Journal of Services Marketing,

Bailey, A. A. (2004).Thiscompanysucks.com: the use of the Internet In negative

consumer-to-consumer articulations.Journal of Marketing

Communications.

Bearden, W. O. and Teel J. E. (1983).Selected Determinants of Consumer

Satisfaction and Complaint Reports. Journal of Marketing Research,

20 (1), 21-28.

Berry, L. L. and. ParasuramanA. (1991).Marketing services: competing

through quality. New York: Freepress.

[62]

Bitner, M. J. (1990). Evaluating Service Encounters: The Effects of Physical

Surroundings and Employee Responses. Journal of Marketing, 54 (2),

69-83.

Bitner, M. J., B. H. Booms, and Mohr L. A. (1994).Critical service

encounters: The employee's viewpoint. Journal of Marketing, 58 (4),

95-106.

Blodgett, J. G. and Anderson R. D. (2000).A Bayesian Network Model of

the Consumer Complaint Process. Journal of Service Research, 2

(4), 321

Brown, S. W. (2000). Practicing Best-in-Class Service Recovery. Marketing

Management Journal, 9 (2), 8-9.

Dabholkar, P. (1994). Incorporating Choice into an Attitudinal Framework:

Analyzing Models of Men Comparison Processes. Journal of Consumer

Research, 21(1), 100-119.

Day, R.L. (1984). Modeling choices among alternative responses to

dissatisfaction. Advances in consumer research, 11, pp. 496-499

[63]

Doerpinghaus and Helen I. (1991).An Analysis of Complaint Data in the

Automobile Insurance Industry. Journal of Risk and Insurance, 58,

120-127.

Dröge, C. and HalsteadD. (1991). Post purchase hierarchies of effects: The

antecedents and consequences of satisfaction for complainers versus non

complainers. International Journal of Research in Marketing,

8 (4), 315-28

Dwyer, F. R. andSchurr P. H. (1990).Developing Buyer-Seller Relationships.

Journal of Marketing, 51 (2), 11-27.

East, R. (2000). Complaining as Planned Behavior. Psychology &

Marketing, 17 (12), 1077-98.

Emmanuel Dei Tumi (2007). Customer Service is an Attitude not a

Department.Published by Charted Institutes of Marketing.

Fornell, C (2007). The Satisfied Customer: Winners and Losers in the

Battle for Buyer Preference. New York, NY: Palgrave-

McMillan.

[64]

Fornell, C.andWernefelt B. (1987).Defensive Marketing Strategy by

Customer Complaint Management: A Theoretical Analysis,"

Journal of Marketing Research (24 (November), 337-46.

Gavin E and Durand P. (1998). Complaining Customer Service Recovery and

Continuous improvement.Service quality. Vol. 81 Iss.1,pp. 68-71

Halstead, D, Edward A. M and John O. (1996).Comparing Objective

Service Failures and Subjective Complaints:An Investigation of Domino and Halo

Effects. Journal of Business Research, 36,107-115.

Harari, Marquis, M. and Filiatrault P. (2002), Understanding

Complaining Responses through Consumers' Self-Consciousness

Disposition.Psychology& Marketing, 19 (3), 267-92.

Harrison-Walker, L. J. (2001). E-complaining: a content analysis of an

Internet complaint foru.,Journal of Services Marketing, 15

(4/5), 397-412

Hirschman, A. O. (1990).Exit, voice, and loyalty: responses to decline in firms,

organizations, and states. Cambridge, Mass.: Harvard University

Press

[65]

Incom S.E. (1998).Monetary and Financial work book series. Published by

the Charted Institute of Banker.

Joe Gerard (2007). Sales and marketing.Pitman Publishing

Johnston, R. (1995). The zone of tolerance. International Journal of

Service Industry Management, 6 2), 46-61.

Keaveney, S. M. (1995). Customer switching behavior in service industries: An

exploratory study. Journal of Marketing, 59 (2), 71-82

Kelley, S. W, HoffmanK.D.andDavisM.A. (1993)."A Typology of Retail

Failures and Recoveries, Journal of Retailing, 69 (4), 429-52.

Kotler, P, G, Armstrong, John S. and Veronica W.(1999). Principles

of Marketing. London, UK: Prentice Hall Europe.

Maute, M. and William R. Forrester Jr. (1993).The Structure and

Determinants of Consumer Complaint Intentions and Behavior.Journal of

Economic Psychology, 14 (2), 219-48.

Michael Le Boeuf (1987). How to win customers and keeps them for life.

Pastoral care publishing.

[66]

Nyer, P. U. and Gopinath M. (2005).Effects of complaining versus negative

word of mouth on subsequent changes in satisfaction: The role of public

commitment. Psychology & Marketing

Oliver, R. L. (1997). Satisfaction: A Behavioral Perspective on the Consumer.

New York: McGraw-Hill Companies Inc.

Power, C. and Driscoll L. (1992).Smart Selling: How Companies is winning

over Today's Tougher Customer? Business Week, 8 (3277), 46-48

Reichheld,andSasser W. E. Jr. (1990). Zero defections: Quality comes to

services. Harvard Business Review, 68 (5), 105-11

Richins, M. L. and. Verhage B. J (1985).Cross-cultural differences in

consumer attitudes and their implications for complaint management.

International Journal of Research in Marketing, 2 (3), 197-

206.

Ron Kurtus (revised 6 June 2007). Customer care satisfaction.Australian

standard.

Shields, P. O. (2006).Customer Correspondence: Corporate Responses and

Customer Reactions.Marketing Management Journal, 16 (2), 155-

70

[67]

Singh, J. (1991), Industry Characteristics and Consumer Dissatisfaction. The

Journal of Consumer Affairs, 25 (1), 19-56