Embed Size (px)

Citation preview

THE BUSINESS VALUE OF TECHNOLOGY

Jive’s social business plan 10 | The Internet, gone horribly wrong 13 Feds try Office cloud 18 | In search of cloud ROI 39 | War on business, part II 48

JUNE 21, 2010

[Plus]RIGHT TECH, WRONG TACKWhy unified communications is veering off course p.35

Your mother was right—you need to share ... your company’s data, that is. It may be the most important contribution IT can make to the business. p.26

By Michael Healey

SHARE!

A UBM TechWeb Publication® CAN $5.95, US $4.95

informationweek.com

THE BUSINESS VALUE OF TECHNOLOGY

Copyright 2010 United Business Media LLC. Important Note: This PDF is provided solely as a reader service. It is not intended for reproduction or public distribution. For article reprints, e-prints and permissions please contact: PARS International Corp., 102 West 38th Street, Sixth Floor, New York, NY 10018; (212) 221-9595www.magreprints.com/quickquote.asp

2 June 21, 2010 informationweek.com

June 21, 2010 Issue 1,271

CONTENTSTHE BUSINESS VALUE OF TECHNOLOGY

COVER STORY

Share!Data sharing improvesrelationships withcustomers and suppliersand can improveefficiency, butcompanies aren’t doing enough

26

18 QuickTakesOffice In The CloudDefense agency pilots Excel,Word, and more as services

New Federal Control MeasuresWhite House tries to get abetter grip on IT spending

19 Go Online And Feel Better WellPoint plans to pay fortreatment via video, chat, phone

IBM Acquires CoremetricsIt’s IBM’s latest move to offermore analytics

20 A Better BlackBerry RIM has plans to get more appson its phones

Security In The CloudMicrosoft gives Azure developersbest practices for securing apps

22 South Africa Scores CRM GoalTourism board adds CRM to meet World Cup demand

Oracle’s BPM Plan It’s unifying its suite to take onIBM, SAP, and pure-play vendors

22

INFORMATIONWEEK (ISSN 8750-6874) is published 24 times a year (once in January,July,August,and December;twice in February,March,April,and November;and three times in May,June,September,and October) by United Business Media LLC,600 Com-

munity Drive, Manhasset, NY 11030. INFORMATIONWEEK is free to qualified management and professional personnel involved in the management of information systems.One-year subscription rate for U.S. is $199.00; for Canada is $219.00.Registered

for GST as United Business Media LLC. GST No. R13288078, Customer No. 2116057, Agreement No. 40011901. Return undeliverable Canadian addresses to Bleuchip International, P.O. Box 25542, London, ON, N6C 6B2. Overseas air mail rates are: Africa,

Central/South America,Europe,and Mexico,$459.00 for one year.Asia,Australia,and the Pacific,$489.00 for one year.Mail subscriptions with check or money order in U.S.dollars payable to INFORMATIONWEEK.For subscription renewals or change of ad-

dress,please include the mailing label and direct to Circulation Dept., INFORMATIONWEEK,P.O.Box 1093,Skokie, IL 60076-8093.Periodicals postage paid at Manhasset,NY,and additional mailing offices.POSTMASTER:Send address changes to INFORMA-

TIONWEEK,United Business Media LLC,P.O.Box 1093,Skokie, IL 60076-8093.Address all inquiries,editorial copy,and advertising to INFORMATIONWEEK,600 Community Drive,Manhasset,NY 11030.PRINTED IN THE USA

35 Big Promise,Modest Gains Unified communications iscritical, but plans are veeringoff course

39 Cloud ROI: AGrounded View Make sure you’re getting aclear fiscal perspective

4 LinksResearch And ConnectReports from InformationWeekAnalytics, events, and more

8 CIO ProfilesSmooth SailingCUNA Mutual CIO Rick Royhas his mind on the high seas

10 Global CIOBy Bob EvansJive focuses on social businesssoftware and deals withTwitter, Google, and CSC

13 Internet EvolutionBy Stephen SaundersEverything you think youknow about the future of theInternet is wrong

48 Down To BusinessBy Rob PrestonReaders weigh in on columnabout the war on business

6 Editorial Contacts 6 Advertiser Index

4 June 21, 2010 informationweek.com

iPad In The EnterpriseWe take Apple’s new platform through its paces, in theoffice and on the road.

informationweek.com/alert/ipad

Master Your Windows 7 RolloutMigrating to Win 7? Make sure you have a planby checking our list of concrete actions allcompanies should undertake as they add thenew OS to their IT road maps.

windows7.informationweek.com

Server Technology Hits A CrossroadsThe server market is changing rapidly, forced into a tech-nological transition by several broad and simultaneouslyemerging trends. Don’t make the wrong turn.

informationweek.com/analytics/servers2010

Data Deduplication’s Expanding ProfileDeduplication can help you get a handle on storageissues and save money. Find out if the technology is agood fit for your company.

dedupe.informationweek.com

After Disaster StrikesNow that server virtualization is widespread, can weleverage it to make true business continuity a reality—or at least make recovering from disaster faster?

informationweek.com/analytics/virtualbcdr

InformationWeek AnalyticsTake a deep dive with these reports

[ ]

David Berlind sits

down to talk with

Aneesh Chopra,

federal CTO, about

the progress that’s

been made in open

government.informationweek.com/video/fedcto

WatchIt Now

Government Progress:Feds work toward moretransparency [

Private Clouds And YouAttend a virtual event June 23 on creating and leveragingprivate clouds and learn how this strategy could affectyour business’ critical systems and information.techweb.com/private-cloud

Black Hat Conference The Black Hat USA conference will help you stayahead of security trends as they emerge. Thisyear’s event will be hosted at Caesars Palace in LasVegas, July 24-29.blackhat.com

Business Intelligence For The Midsize BusinessJoin Intelligent Enterprise’s Doug Henschen for a Webcaston the latest trends in BI and research on priorities withinmidsize companies. It happens June 22.informationweek.com/1271/midsize

Get PublishedUpload your white paper to the TechWeb Digital Library. informationweek.com/whitepaper

Resources to Research, Connect, CommentLinks

Facebook, iGoogle, And MoreAccess our portfolio of social networking tools, includingFacebook applications and fan page, iGoogle widget,FriendFeed content, Twitter headlines, and RSS feeds.informationweek.com/take.jhtml

Take InformationWeek With You[ ]

Subscribe to our more than 700 reports atanalytics.informationweek.com

Never MissA Report

>> Accelerating Wall Street—Next Stop: Nanosecondsinformationweek.com/analytics/nanosecond

>> 2010 Strategic Securityinformationweek.com/analytics/security2010

>> Beyond Adding Boxes: Smart Strategies For Growthinformationweek.com/analytics/servertco

>> Next Stop,VDI: Going All In On Virtualizationinformationweek.com/analytics/vdimodels

>> Research: Global CIOComing June 28

>> Is The U.S. A Broadband Backwater?Coming July 12

informationweek.com6 June 21, 2010

Print, Online, Newsletters, Events, Research

John Siefert Senior VP and Publisher, InformationWeek Business TechnologyNetwork, [email protected] 949-223-3642

Bob Evans Senior VP and Global CIO Dir., [email protected] 412-661-3091

Rob Preston VP and Editor In Chief, [email protected] 516-562-5692

John Foley Editor, [email protected] 516-562-7189

Chris Murphy Editor, [email protected] 414-906-5331

Art Wittmann VP and Director, Analytics, [email protected] 408-416-3227

Alexander Wolfe Editor In Chief, InformationWeek.com,[email protected] 516-562-7821

Stacey Peterson Executive Editor, Quality, [email protected] 516-562-5933

Lorna Garey Executive Editor, Analytics, [email protected] 978-694-1681

Stephanie Stahl Executive Editor, [email protected] 703-266-6030

Fritz Nelson VP,Editorial Director, [email protected] 949-223-3608

David Berlind Chief Content Officer,TechWeb, [email protected] 978-462-5315

REPORTERSCharles BabcockEditor At LargeOpen source, infrastructure, [email protected] 415-947-6133

Thomas ClaburnEditor At LargeSecurity, search,Web [email protected] 415-947-6820

Paul McDougall Editor At LargeSoftware, IT services, [email protected]

Marianne Kolbasuk McGee Senior Writer IT management and [email protected] 508-697-0083

J. Nicholas Hoover Senior EditorDesktop software, Enterprise 2.0,[email protected] 516-562-5032

Andrew Conry-Murray New Products and Business Editor Information and content [email protected] 724-266-1310

W. David Gardner News Writer Networking, telecom [email protected]

Antone Gonsalves News WriterProcessors, PCs, [email protected]

Eric Zeman Mobile, wireless [email protected]

CONTRIBUTORSMichael Biddick [email protected]

Michael A. Davis [email protected]

Jonathan Feldman [email protected]

Randy George [email protected]

Michael Healey [email protected]

EDITORSMike FrattoManaging Editor/Labs Networking and security [email protected] 315-299-3558

Jim Donahue Chief Copy Editor [email protected]

ART/DESIGNMary Ellen Forte Senior Art Director [email protected]

Sek Leung Senior Designer

INFORMATIONWEEK ANALYTICSanalytics.informationweek.com

Art Wittmann VP and Director [email protected] 408-416-3227

Lorna GareyExecutive Editor, Analytics [email protected] 978-694-1681 Heather Vallis Managing Editor, Research [email protected] 508-416-1101

INFORMATIONWEEK.COMCora Nucci Managing Editor, Features and Reviews [email protected] 508-416-1130

Roma Nowak Senior Director,Online Operations andProduction [email protected] 516-562-5274

Tom LaSusa Managing Editor, Newsletters [email protected]

Jeanette Hafke Web Production Manager [email protected]

Joy Culbertson Web Producer [email protected]

Nevin BergerSenior Director, User Experience [email protected]

Steve GilliardSenior Director,Web Development [email protected]

INFORMATIONWEEK VIDEOinformationweek.com/tv

Fritz Nelson Executive Producer [email protected]

INFORMATIONWEEK BUSINESSTECHNOLOGY NETWORK

DarkReading.comSecurityTim Wilson, Site [email protected]

IntelligentEnterprise.comApp ArchitectureDoug Henschen, Editor In Chief [email protected]

NetworkComputing.comNetworking, Communications,and StorageMike Fratto, Site [email protected]

PlugIntoTheCloud.comCloud ComputingJohn Foley, Site [email protected]

InformationWeek SMBTechnology for Small and Midsize BusinessBenjamin Tomkins, Site [email protected]

Dr. Dobb’s The World of Software DevelopmentJonathan Erickson, Editor In [email protected]

READER SERVICESInformationWeek.com The destination forbreaking IT news, and instant analysis

Electronic Newsletters Subscribe to InformationWeek Daily and other newsletters atinformationweek.com/newsletters/subscribe.jhtml

Events Get the latest on our live events and Netevents at informationweek.com/events

Analytics Go to analytics.informationweek.com for original research and strategic advice

How To Contact Usinformationweek.com/contactus.jhtml

Editorial Calendar informationweek.com/edcal

Back IssuesE-mail: [email protected]:888-664-3332 (U.S.);847-763-9588 (outside U.S.)

Reprints Wright’s Reprints, 1-877-652-5295Web: wrightsreprints.com/reprints/?magid=2196E-mail: [email protected]

List Rentals Merit Direct LLCPhone: (914) 368-1083 E-mail: [email protected]

Media Kits And Advertising Contactscreateyournextcustomer.com/contact-us

Letters To The Editor E-mail [email protected]. Include name, title,company, city, and daytime phone number.

SubscriptionsWeb: informationweek.com/magazine E-mail:[email protected] Phone:888-664-3332 (U.S.) 847-763-9588 (outside U.S.)

ADVISORY BOARD

Dave Bent Senior VP and CIO,United Stationers

Robert Carter Executive VP andCIO, FedEx

Michael Cuddy VP and CIO,Toromont Industries

Laurie Douglas Senior CIO, Publix Super Markets

Dan Drawbaugh CIO, University ofPittsburgh Medical Center

Kent Kushar VP and CIO,E.&J. Gallo Winery

Carolyn Lawson Director, E-Services,California Office of the CIO

Jason Maynard Senior Analyst,Berkowitz Capital

Randall Mott Sr. Executive VP andCIO, Hewlett-Packard

Jeffrey Neville CIO, Eastern Mountain Sports

Denis O’Leary Former Executive VP,Chase.com

C.K. Prahalad Professor of BusinessAdministration,University of Michigan

Mykolas Rambus Head of Technol-ogy and Special Projects,Forbes Media

M.R. Rangaswami Founder,Sand Hill Group

Manjit Singh VP and CIO,Chiquita Brands International

David Smoley CIO, Flextronics

Ralph J. Szygenda Former GroupVP and CIO, General Motors

Peter Whatnell CIO, Sunoco

Please direct all inquires to reporters in the relevantbeat area.

IInnddeexxFor Advertising and Sales Contactsgo to createyournextcustomer.com/contact-us or call Martha Schwartz (212) 600-3015

[ ]American Express www.americanexpress.com ..C4

Autonomy www.autonomy.com .........................11

CDW Corp. www.cdw.com .....................................3

CenturyLink www.centurylink.com ....................34

Citrix www.citrix.com ...........................................33

DTsearch Corp. www.dtsearch.com ....................42

EMC www.emc.com .......................................24,25

Eset www.eset.com ................................................7

Hewlett-Packard www.hp.com .............................5

IBM www.ibm.com ...................................16,17,23

ICC www.icc.com ............................................38,43

iDashboards www.idashboards.com ..................44

InterSystems www.intersystems.com ................C3

ITWatchDogs www.itwatchdogs.com ................42

Kace www.kace.com ............................................31

Marriott www.residenceinn.com ........................29

Microsoft www.microsoft.com ..............C2,1,9,41

Motorola www.motorola.com .............................15

PhoneFactor www.phonefactor.com .................45

SMS Memory Module Assembly ............................

www.smsassembly.com ........................................42

Verdasys www.verdasys.com ..............................12

Verizon Wireless www.verizonwireless.com ......21

Copyright 2010 United Business

Media LLC All rights reserved.

8 June 21, 2010 informationweek.com

Career TrackHow long at current company:I’ve been with CUNA MutualGroup, a financial services provider,for 6-1/2 years.

Career accomplishment I’m mostproud of: Developing and imple-menting a stronger customer per-spective within the CIO role afterleading customer operations forCUNA Mutual for three years.

Most important career influencer:One of my important career influ-encers early on was Dennis Kuester,who is now the chairman of theboard for Marshall and Ilsley. Over aspan of 12 years, I worked for himdirectly and indirectly in many dif-ferent and diverse roles. Consis-tently, he provided sound guidanceon leadership, managing organiza-tions, and creating and executingbusiness strategy. He was a pivotalmentor for me who catapulted mycareer to the next level.

Decision I wish I could do over:We attempted a project replacementwithout adequate business processengineering. I have new check-points in place now to ensure wehave the right information andprocesses for the future.

On The JobIT budget: $100 million

Size of IT team: 670 employeesand contractors

How I measure IT effectiveness:We measure IT effectiveness throughthe business value is delivered, howthe project is aligned with businessstrategy, and thought leadership inthe technology. We use a projectscorecard as our gauge for tracking

RICK ROYSenior VP and CIO, CUNAMutual Group

Colleges/degrees: Marquette Univer-sity, MBA in information technologyand finance; University of Wisconsin-Milwaukee, BBA in management infor-mation systems

Leisure activities: Competitive sail-boat racing and cruising, and some iceboating when the conditions are right!

Biggest business-related pet peeve:Leaders behaving like victims of theircircumstances instead of using theircircumstances to drive positive change

If I weren’t a CIO, I’d be ... a sailingcharter boat captain in the Caribbean

the business results and value. Be-fore a project is approved, it mustalso have a clear plan to generatebusiness results within six months.If it doesn’t, we need to questionwhy we’re doing this project.

Top initiatives:

>> Business intelligence

>> Virtualization

>> Sales force automation

VisionAdvice for future CIOs: Your job isall about people: customers, em-ployees, partners, and peers.

The next big thing for my busi-ness will be ... how we can driverevenue growth. For example, howwe can leverage new proven tech-nology to deliver revenue that abusiness unit may not be aware of,like we did with our voice signaturetechnology, which delivered signifi-cant improvement in sales.

Best way to cope with the eco-nomic downturn: These unprece-dented times reinforce the impor-tance that CIOs, and all leaders,must demonstrate to their CEOsand CFOs what cost containmentstrategies are in place that alsodrive value and align with businessstrategies.

The federal government’s toptechnology priority should be ...data integration.

Kids and technology careers: Ihaven’t steered my children towarda tech career, but I wouldn’t dis-courage them either. It has beengood to me.

CIOprofiles Read other CIO Profiles at informationweek.com/topexecs

10 June 21, 2010 informationweek.com

G

L O B A L C I OG

L O B A L C I OPromising a social media experience

tuned for the enterprise, Jive Softwareis launching the social business soft-

ware category with a new platform that in-corporates the Twittersphere, mobile socialtools from CSC, and a presence on theGoogle Apps Marketplace.

In some ways, privately held Jive is an un-likely candidate for such an ambitious under-taking. While well known among its cus-tomers and the social media community, it’sstill an outsider in the enterprise world andamong many CIOs.

That standing is changing—and quickly.Jive’s annual run rate is approaching$100 million, and it has 15 millionusers among its 3,000 customers,including some very large com-panies deploying its communica-tion, collaboration, and socialmedia tools to engage with cus-tomers, employees, and partners.

New CEO Tony Zingale, who ran Mer-cury before it was acquired by Hewlett-Packard for $4.5 billion four years ago, prom-ised CIOs a profoundly new approach tomanaging the information explosion. “The in-novation of social in the consumer space hashad a ripple effect in the enterprise, forcingmass adoption of social business practices,”he said in a statement. “Today’s announce-ment positions Jive even more firmly as theleader in this multibillion-dollar market.”

Jive aims to succeed by making social busi-ness software its core focus rather than afringe product to be bolted on the edge, andby leveraging three key partnerships:

Twitter: Jive customers will “now be ableto quickly address any conversations hap-pening on Twitter in a user-friendly Jive inter-face.” The release adds that “spotty access toconversations that happen on the social Web”can lead to “brand interruption.”

Google Apps Marketplace: Noting thatJive’s presence on the Google marketplacewill accelerate the possibility of “social busi-ness in the cloud,” Jive said it expects to findtraction among business executives who“have realized that the traditional way of pur-chasing, deploying, and managing softwarehas to change.”

CSC: In Jive’s wide-ranging partnershipwith this IT services heavyweight, CSC willlaunch a social business practice, develop mo-bile social business apps for Jive’s customers,and market Jive’s new social business productsto CSC customers worldwide. In addition,

CSC’s becoming a leading reference ac-count, as Jive’s products are used by

almost 50,000 CSC employees. Chris Lochhead, who’s been

named to Jive’s board and is serv-ing as a strategic adviser, offered

this perspective on why CIOsflooded with apps and add-ons and

portals and social experiments will bewilling to give Jive a shot.

“If you look across the major drivers thatbusinesses are trying to cope with today, it’semployees via collaboration, it’s customersvia loyalty, and it’s the social Web and all theintelligence it can offer,” Lochhead said in aphone conversation. “Some of our competi-tors can play in one or two of those areas, butnot in all three. Jive’s products have beenbuilt from the beginning to support all threeof those initiatives, and that’s why we feel wecan turn social business in the enterprisefrom a bunch of disconnected experimentsinto a real enterprise-level strategic tool.”

Bob Evans is senior VP and director ofInformationWeek’s Global CIO unit. Formore Global CIO perspectives, check outinformationweek.com/blog/globalcio, or writeto Bob at [email protected].

Can Jive Drive Social Business?

Jive aims to succeed

by focusing only

on social business

software and by

leveraging deals

with Twitter, Google,

and CSC

globalCIOB O B E VA N S

Dear InformationWeek Reader:I regret to inform you that everything you

think you know about the future of the Inter-net is wrong. Sorry.

Further, there are only two opinions aboutthe future: mine, which is right, and “every-body else’s,” which is not right.

The conventional wisdom is positive—giddy, really—about what the Internet holdsfor the planet’s expanding connected popula-tion. It envisions an Internet where usersworldwide enjoy speedy, inexpensive Inter-net connections. As this new society devel-ops, national identities are subsumed byknowledge into a global community whoseusers are enabled, even emancipated, by theInternet and the information it carries.

But suppose for a moment this is not thefuture. What if the “wisdom of crowds” turnsout to be the ignorance of the masses? In fact,what if the Internet is a “really bad thing” forthe world and its population?

Decline And Fall (Mainly Fall)The Internet of the late 20th century was

chaotic—an unregulated, borderless virtualentity that grew organically based on U.S.technological innovation and its ability to al-low users to anonymously access vastamounts of information for free.

The media have been silent on the possi-bility that a network so vast could be any-thing other than a great enabling force formankind. But the journey to the Internet’sdarker side has already begun with a game-changing addition to the Web’s most popu-lar application: search.

Search engines like Google and Bing, so-cial networks like Facebook, computer soft-ware developers like Microsoft, and e-com-merce sites like Amazon and eBay nowmonitor and store information about users’search activity and use this data to create pro-

files about who the searchers are (identity),where they are (location), what they want(preferences), how much money they have(financial status), and what they are likely todo or buy next (predictive analysis).

These profiles are already valuable to com-panies looking to target consumers in the vir-tual world with advertising for their real-world goods. But as the Internet replacestraditional supply chains, these profiles areset to become an asset of almost inestimableworth—the equivalent of the commoditiesthat powered the Industrial Revolution.

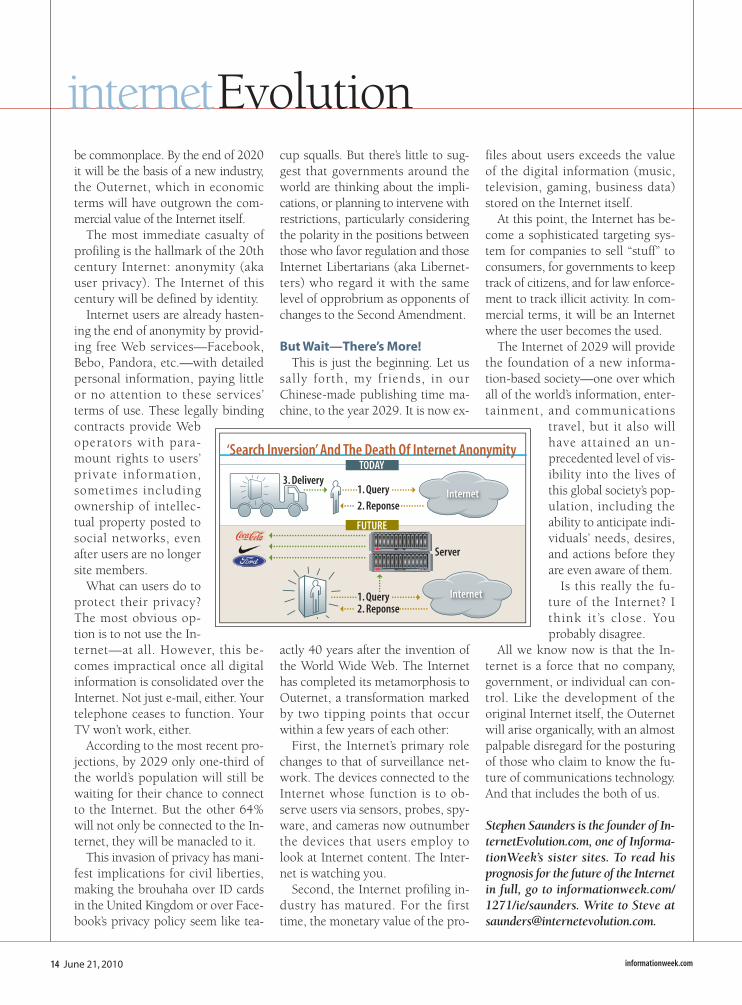

At this point, a phenomenon called “searchinversion” takes place. Today’s Internet searchfunction morphs from being a useful tool forusers to search for products to an essentialtool for companies to search for customers.

User profiles become assets owned by thecompanies that developed them or, eventu-ally, commodities to be bought and sold on“profile markets” or “identity exchanges”—the digital DNA equivalents of the financialand commodities exchanges on whichstocks, oil, and gold are traded.

Companies like Google and Facebook arepioneers in the areas of profiling and searchinversion, but the Internet’s nature (distrib-uted, standards-based, open to all) makes iteasy for others to follow their lead. Any Webcompany that owns servers storing user infor-mation can participate in profiling, as can anynetwork service provider providing the pipes.

Profiling will take off fast for another rea-son: It’s legal. It doesn’t have to be an invasiveactivity. It’s not necessary, for example, toread e-mails or listen in on Skype calls in or-der to create prescient profiles. “Pattern-ing”—or knowing which sites users visit,with whom they communicate, and how of-ten—provides companies with more thanenough data to create a valuable user profile.

By the middle of this decade, profiling will

Superhighway To Hell

The conventional

wisdom is positive—

giddy, really—about

the future of the

Internet. It’s time

to trash the

conventional wisdom.

S T E P H E N S AU N D E R S

informationweek.com

Evolutioninternet

June 21, 2010 13

be commonplace. By the end of 2020it will be the basis of a new industry,the Outernet, which in economicterms will have outgrown the com-mercial value of the Internet itself.

The most immediate casualty ofprofiling is the hallmark of the 20thcentury Internet: anonymity (akauser privacy). The Internet of thiscentury will be defined by identity.

Internet users are already hasten-ing the end of anonymity by provid-ing free Web services—Facebook,Bebo, Pandora, etc.—with detailedpersonal information, paying littleor no attention to these services’terms of use. These legally bindingcontracts provide Weboperators with para-mount rights to users’private information,sometimes includingownership of intellec-tual property posted tosocial networks, evenafter users are no longersite members.

What can users do toprotect their privacy?The most obvious op-tion is to not use the In-ternet—at all. However, this be-comes impractical once all digitalinformation is consolidated over theInternet. Not just e-mail, either. Yourtelephone ceases to function. YourTV won’t work, either.

According to the most recent pro-jections, by 2029 only one-third ofthe world’s population will still bewaiting for their chance to connectto the Internet. But the other 64%will not only be connected to the In-ternet, they will be manacled to it.

This invasion of privacy has mani-fest implications for civil liberties,making the brouhaha over ID cardsin the United Kingdom or over Face-book’s privacy policy seem like tea-

cup squalls. But there’s little to sug-gest that governments around theworld are thinking about the impli-cations, or planning to intervene withrestrictions, particularly consideringthe polarity in the positions betweenthose who favor regulation and thoseInternet Libertarians (aka Libernet-ters) who regard it with the samelevel of opprobrium as opponents ofchanges to the Second Amendment.

But Wait—There’s More!This is just the beginning. Let us

sally forth, my friends, in ourChinese-made publishing time ma-chine, to the year 2029. It is now ex-

actly 40 years after the invention ofthe World Wide Web. The Internethas completed its metamorphosis toOuternet, a transformation markedby two tipping points that occurwithin a few years of each other:

First, the Internet’s primary rolechanges to that of surveillance net-work. The devices connected to theInternet whose function is to ob-serve users via sensors, probes, spy-ware, and cameras now outnumberthe devices that users employ tolook at Internet content. The Inter-net is watching you.

Second, the Internet profiling in-dustry has matured. For the firsttime, the monetary value of the pro-

files about users exceeds the valueof the digital information (music,television, gaming, business data)stored on the Internet itself.

At this point, the Internet has be-come a sophisticated targeting sys-tem for companies to sell “stuff” toconsumers, for governments to keeptrack of citizens, and for law enforce-ment to track illicit activity. In com-mercial terms, it will be an Internetwhere the user becomes the used.

The Internet of 2029 will providethe foundation of a new informa-tion-based society—one over whichall of the world’s information, enter-tainment, and communications

travel, but it also willhave attained an un-precedented level of vis-ibility into the lives ofthis global society’s pop-ulation, including theability to anticipate indi-viduals’ needs, desires,and actions before theyare even aware of them.

Is this really the fu-ture of the Internet? Ithink it ’s close. Youprobably disagree.

All we know now is that the In-ternet is a force that no company,government, or individual can con-trol. Like the development of theoriginal Internet itself, the Outernetwill arise organically, with an almostpalpable disregard for the posturingof those who claim to know the fu-ture of communications technology.And that includes the both of us.

Stephen Saunders is the founder of In-ternetEvolution.com, one of Informa-tionWeek’s sister sites. To read hisprognosis for the future of the Internetin full, go to informationweek.com/1271/ie/saunders. Write to Steve [email protected].

14 June 21, 2010 informationweek.com

Evolutioninternet

‘Search Inversion’ And The Death Of Internet Anonymity

1. Query3. Delivery

2. Reponse

Server

1. Query2. Reponse

Internet

Internet

TODAY

FUTURE

18 June 21, 2010 informationweek.com

The Defense InformationSystems Agency, an arm

of the Department of De-fense that provides com-puter systems and servicesto the military, plans to testthe feasibility of offering Mi-crosoft’s Office 2010 pro-ductivity apps and personalstorage as hosted services.

The pilot program, due toget under way in the thirdquarter, will involve deliver-ing Excel, OneNote, Power-Point, Word, and a personaldocument store as services.The services, dubbed VOf-fice and VDrive, respec-tively, would be hosted inDISA’s data centers andmade available to users onthe military’s unclassifiednetwork.

DISA CIO Henry Sien-kiewicz, speaking last weekat InformationWeek’s Gov-ernment IT Leadership Fo-rum in Washington, D.C.,emphasized that the Office-as-a-service pilot testshouldn’t be interpreted asa move away from the con-ventional desktop configu-ration in which the Officesuite runs on a PC or lap-top. “I want to be clear thatthis is not as if we are transi-tioning anyone to a Web-based application,” Sien-kiewicz said. “We just wantto see how this works. It’sone way of saying, How dowe use the cloud effectively?”

The pilot program will letDISA assess the security is-sues associated with deliv-ering productivity applica-tions and storage servicesover a network, albeit fromwithin the relative safety ofDISA’s firewall.

Early AdopterThe tests are being planned

in coordination with the De-fense Department’s office ofthe assistant secretary of de-fense for networks and infor-mation integration. DISAhad planned to announce itsplans in May at the agency’scustomer partnership con-ference in Nashville, Tenn.,but that event was floodedout following torrential rainsin the area.

DISA has been an earlyadopter of the cloud model,offering on-demand IT re-sources to Defense Depart-ment branches from itsRapid Access Computing En-vironment (RACE), hostedSharePoint services, platformas a service via its Forge.milsite, and other hosted appli-cations and cloud services.

In one example of howDISA’s cloud services areused, the Army is usingRACE and Forge.mil in sup-port of its Apps for theArmy software developmentcompetition.

—J. Nicholas Hoover([email protected])

The White House is tryingto get a better grip on al-

most $80 billion in federalIT spending, putting newemphasis on data centerconsolidation and IT projectmanagement.

“We’ve got to make surethat we don’t continue tothrow good money afterbad,” federal CIO Vivek Kun-dra said last week at Informa-tionWeek’s Government ITLeadership Forum. For fiscal2011, $79.4 billion is bud-geted for federal IT, a 1.6%decrease over what was en-acted in fiscal 2010—and thefirst such decline in 20 years.

President Obama releaseda memo this month in-structing federal agencies to“immediately adopt a policyagainst expanding data cen-ters beyond current levels,”and Kundra says a “zerogrowth” policy will be re-flected in the fiscal 2012budget. Currently, fed agen-cies operate more than1,100 data centers.

In addition, the Office ofManagement and Budget,where Kundra works, isbringing increased oversightto IT spending via metrics-based project and perform-ance management. Kundrasaid OMB will redouble ef-forts around its “TechStat”meetings, where Kundraworks with fed agency CIOsto fix underperforming ITprojects.

Kundra hinted at broadermoves that will likely addressthe modernization of finan-cial systems used by the feds.Financial system upgradestoo often end up overbudgetand short of requirements,according to a draft OMBmemo obtained by Informa-tionWeek. The White Houseapparently plans to mandateshorter development timeframes and increased OMBoversight, and a temporarypostponement of any finan-cial system upgrades.

—J. Nicholas Hoover([email protected])

[QUICKTAKES]EXPANDING PORTFOLIO

Defense Agency To TestOffice As Cloud Service

‘ZERO GROWTH’ POLICY

Federal CIO OutlinesNew Control Measures

Kundra: Stop throwinggood money after bad[

Deb

bie

Wel

l/Fl

ickr

[QUICKTAKES]

June 21, 2010 19

IBM execs weren’t kiddingwhen they said analytics

would be a key part of thevendor’s acquisition strategy.

Its agreement to acquireCoremetrics, a privatelyheld developer of businessanalytics software, marksIBM’s latest move to offermore software and expertiseto help customers extractmeaningful informationfrom raw data.

Coremetrics softwarehelps marketing depart-ments optimize online cam-paigns by providing in-sights into sales, customerinteractions, Web site traf-f ic, and other metrics.

Specific products managesearch engine bids, target e-mail campaigns, and makecross-selling recommenda-tions. The product is deliv-ered as a service.

Coremetrics customersinclude Bank of America,Victoria’s Secret, Virgin At-lantic, and Office Depot.

IBM says it plans to add thevendor’s 230 employees toits own operations.

In May, IBM CEO SamPalmisano laid out a five-year road map, which in-cluded about $20 billion foracquisitions through 2015,with an emphasis on busi-ness analytics and optimiza-tion. In analytics and opti-mization, it has spent $11billion on 18 companiessince 2005, with almost halfof that for business intelli-gence software providerCognos and $1.2 billion forpredictive analytics vendorSPSS. —Paul McDougall

MARKETING INSIGHT

IBM Acquiring Analytics Specialist

WellPoint, one of thiscountry’s largest health

insurers—33 million mem-bers are on its plans—willstart letting patients gettreated over video, chat, andtelephone later this year, asign of the industry’s growingacceptance of online care.

Using an online platformfrom American Well, physi-cians can review members’clinical information, speakwith and see a patient, pre-scribe medications, and sug-gest follow-up care. Well-Point plans to start theprogram in select markets inthe fourth quarter.

It’s significant to have sucha major industry player sup-port online visits becausedoctors won’t embrace tele-medicine until insurance

companies are willing to payfor such visits.

WellPoint says it’s tryingto make healthcare more ac-cessible and convenient, es-pecially in rural areas.WellPoint also wants to seecare offered in the least-ex-pensive setting, “making thepatient’s home an attractiveoption,” says IDC analystIrene Berlinsky.

For online care to suc-ceed, a key factor will beidentifying the types of visitsand ailments best-suited forsuch diagnoses, Berlinskysays. Doctors will also needto ease patient fears aboutsubquality care, and doctorswill need to be convincedthere’s no increased mal-practice liability. People willalso need adequate broad-

band and Web cameras.Telemedicine is slowly

gaining support from pay-ers, who are seeking waysto reduce costs and im-prove outcomes associatedwith chronic illnesses, suchas diabetes and heart dis-ease, that may benefit frommore regular in-home as-sessments. They also seeexpansion opportunities inrural areas.

That was a driver in an-other recent American Welldeal, with the Hawaii Med-ical Service Association andBlue Cross Blue Shield ofHawaii, to link Hawaiian pa-tients online with specialistssuch as dermatologists andcardiologists. —Nicole Lewis

and Marianne Kolbasuk McGee ([email protected])

EARLY MOMENTUM

Insurers Back Online Healthcare TWITTER’S JITTERSIs Twitter key to your market-ing strategy? Don’t count onit always being up thismonth.The company blamesrecord traffic and the com-plexity of its systems for morethan five hours of downtimein June and warns users toexpect a “rocky few weeks.”People posted 64 milliontweets a day in May, and theWorld Cup brought biggerspikes than it could handle.

X86 ALTERNATIVE?Silicon Valley startup Sea-Micro’s new 10U rack-mountserver uses 512 low-powerIntel Atom processors in itsbid to beat out x86 machinesto run Web applications. Sea-Micro claims it uses 75% lesspower and space than simi-larly powered x86 servers. At$139,000 apiece, it bettersave on power.

MORE SECURE MOBILITYJuniper Networks’ new JunoPulse is a downloadable SSLVPN client that verifies a de-vice’s compliance with end-point security policies andcreates secure connectionsto a company’s network. Itworks for PCs but may bemost appealing for compa-nies dealing with a growingnumber of employee smart-phones. It works with theiPhone as well as Windowsand Nokia Symbian devices.

SHANGHAI E-TEXTBOOKS Shanghai thinks it could be-come China’s first city toscrap paper textbooks in fa-vor of e-books—a wildlyambitious plan it hopes toinstitute within five years.The city’s education com-mission is now planning itsfirst trials. But Huang Shan-ming, a city adviser, says itshould save money. Throughhigh school, Shanghai stu-dents use 213 textbooksthat cost $256. The EastChina Normal UniversityPress estimates that, if massproduced, the total e-bookcost could be around $146.

IBM Analytics DealsSPSS July 2009, predictiveanalytics

Exeros May 2009, data discovery

Cognos January 2008,business intelligence

20 June 21, 2010 informationweek.com

Microsoft is providingdevelopers with best

practices for securing appli-cations that reside in itsWindows Azure cloud com-puting environment.

Its new paper, “SecurityBest Practices For WindowsAzure Applications,” coversservice layer and applicationsecurity, Azure’s built-in pro-tections, the network infra-structure, and hardeninguser privilege services. It ex-plains threats that Azureapps could be susceptibleto, such as port scanningand denial of service, andways to prevent them.

Azure has several securityservices that address the

sticky identity managementproblem surrounding thecloud, including WindowsIdentity Foundation, ActiveDirectory Federation Ser-vices 2.0, and WindowsAzure AppFabric AccessControl Service.

People building softwareor hosting services in thecloud need to “understandthat they must also buildsoftware with security inmind from the start,” bloggedMichael Howard, principalsecurity program manager onMicrosoft’s Security Develop-ment Lifecycle team.

At the service layer of thecloud framework, develop-ers should map their regular,

noncloud security require-ments for apps to WindowsAzure services. Any remain-ing threats must be handledby the application or ser-vice, the paper says. Amongthe tips Microsoft offers:

>> Use a custom domainrather than *servicename*.cloudapp.net in order toseparate the cloud from theenterprise space since the

cloudapp.net namespace isused by all Azure customers.

>> Isolate Web roles andseparate duties in order tolimit users’ access to whatthey need to do their jobs.

>>Use multiple storagekeys so there’s no single pointof failure if one is breached.

—Kelly Jackson Higgins,DarkReading.com

CLOUD SECURITY

Microsoft Offers Advice For Securing Azure Apps

Research In Motion, in aneffort to attract more de-

velopers and make its Black-Berry smartphones more ap-plication centric, will offer ahost of new user experienceand performance enhance-ments, and expand the wayusers can pay for apps.

Probably the most signifi-cant change is letting usersuse credit cards or carrierbilling to pay for apps. Untilnow, PayPal was the onlyway to pay for them.

RIM, which is making thechanges later this summer inits App World 2.0 app plat-form, also introduced Black-Berry ID, which aspires tobecome a standard part of al-most everything users do on-line, providing a single user

account regardless of deviceor network. BlackBerry cus-tomers will be able to use theID at RIM’s Web store. Black-Berry ID, combined with thenew payment options, givesusers a simpler way to moveapplications between devicesand manage applicationportfolios.

Developers at BlackBerry’sDevCon and Wireless Enter-prise Symposium were mostexcited about the new pay-ment methods, according toa RIM source, since it willgive users more flexibility,which should, in turn, drivemore app purchases. RIM’scatalog has more than 6,500apps and gets 1 milliondownloads a day among its20 million active users. It’s

no slouch, but it certainlydoesn’t have the applicationfootprint (nor mindshare) ofApple or Google.

For companies, carrierbilling raises concerns thatemployees will rack up hugebills on the corporate ac-count. Fundraising drives,like the Haiti earthquake re-lief effort, have brought thisissue into more urgent view.So RIM lets administratorsset policies to block thesetypes of transactions or toblock carrier billing on cor-porate-controlled devices.

Other enhancements areaimed at helping users man-age their applications. AppWorld 2.0 search will usebetter weighting and rele-vance metrics to provide bet-

ter search results. The MyWorld part of App World(where your application ac-tivity is stored and managed)shows the status of all appli-cations—what’s installed,what’s pending, what’s onyour memory card, andwhat you’ve deleted.

Another cool feature letsdevelopers put QR bar codesin apps. Today, you can scanQR bar codes with yourBlackBerry—say withinBlackBerry Messenger, to getcontacts from another user.Now a developer could puta bar code on a marketingcampaign for their app, andif users scan it, they’ll betaken right to that app in thestore. —Fritz Nelson,

BLACKBERRY APP WORLD 2.0

RIM Adds Single User ID, New Billing Options

[QUICKTAKES]

Data: InformationWeek Analytics 2010 Cloud GRC Survey,January 2010

Top Cloud Computing Concerns

54%

51%

49%

Security defects in the technology itself

Unauthorized access to or leak of proprietary information

Unauthorized access to or leak of customers’ information

22 June 21, 2010 informationweek.com

The 2010 FIFA WorldCup is bringing as many

as 300,000 soccer fans toSouth Africa. To cope withan anticipated tenfold in-crease in visitor calls andonline contacts, SouthAfrican Tourism turned toSalesforce.com. It’s an exam-ple of how the speed andscalability of software as aservice can change IT strat-egy—both before and after amajor event.

The typical South Africatourist comes to visit itswildlife parks and reserves.Visitors for the World Cupare different, and not just be-cause there are a lot more ofthem. Many spectators are

first-time visitors to thecountry, and with 64matches in nine cities, peo-ple will travel within thecountry more than usual.Typically, South AfricanTourism handles previsitcalls from would-be tourists,not real-time help withtravel logistics.

“We had to turn our callcenter inside out to handlecalls from within SouthAfrica,” says William Price,global manager of e-mar-keting at South AfricanTourism. To replace an ag-ing custom-built CRM sys-tem, it looked at seven on-premises CRM systems andthree SaaS options. Once it

picked Salesforce, the SaaSapplication was running inabout three weeks.

The agency’s also usingSalesforce tools for trackingand responding to com-ments on Twitter and Face-book, and it launched afeedback portal throughSalesforce Ideas, an elec-tronic survey capabilitythrough which the agencycan gather crowdsourcedtips on transportation logis-tics and favorite side trips.

Perhaps just as interestingas the ramp-up capability is

the agency’s ability to shedthose costs once the WorldCup’s over. Price plans tophase out the old CRM sys-tem, which is still handlingcalls from outside of SouthAfrica, and replace it mostlywith Salesforce, though withmany fewer seats.

“We may cut the numberof licenses we’ll need byhalf,” Price says, “but it’s apowerful CRM tool that wecan also use for knowledgemanagement.”

—Doug Henschen([email protected])

CLOUD SCALE

How To Ramp CRMUp—And Back Down

The success or failure ofOracle’s new business

process management suitewill have as much to dowith how well Oracle sellsits middleware and upcom-ing Fusion applications asthe power of the suite itself.

Oracle’s Business ProcessManagement Suite 11g ismeant to integrate a collec-tion of BPM technologiesgained through acquisitions.A component of Oracle Fu-sion Middleware 11g, thesuite is an important enablerof business control overend-to-end processes, bethey focused on system-to-system integration, auto-mated content workflows,

case management, or worksuch as exception handlingthat requires a person’sinvolvement.

BPM suites are designedto give managers, businessanalysts, and non-technicalusers a way to monitor andcontrol processes withouthelp from IT. The categorywas pioneered by pure-playvendors, but megavendorsincluding Oracle, IBM, andSAP have acquired or devel-oped most of the requiredcomponents. Oracle’s BPMSuite 11g consolidates tech-nologies from acquisitionsof Collaxa, BEA Systems,and pure-play Fuego.

Oracle executives are ea-

ger to compare their newsuite with the less-integratedportfolio now offered byIBM, which includes sys-tems-integration-centricWebSphere technologies,content-centric BPM ac-quired from FileNet, and therecently acquired Lombardisuite, which is aimed moreat human-centric processes.

Other vendors combin-ing SOA infrastructure, in-tegration middleware, andBPM include Tibco, whichacquired Staffware wayback in 2004. Software AGacquired WebMethods in2007 and process modelingpioneer IDS Scheer in2009. Progress Software ac-

quired Savvion in 2009.Competition will be a fac-

tor, but Oracle BPM Suite11g will likely ride the coat-tails of Oracle Fusion Mid-dleware and yet-to-be-re-leased Fusion Applications,which will upgrade legacyOracle, PeopleSoft, Siebel,and JD Edwards software.The same dependency existsbetween SAP NetWeaverBPM, introduced in 2009,and SAP applications. Foreach of them, they don’thave to be the best BPMsuite, just the best option forextending processes aroundOracle or SAP apps.

—Doug Henschen ([email protected])

BATTLE OF THE SUITES

Oracle Unifies Its Process Management Platform

[QUICKTAKES]

What, no vuvuzela?[

Ach

imSc

hei

dem

ann

/EPA

/Lan

do

v

Your mother was right: Sharing is good! Here’s how sharing data improves relationships with suppliers and customers and can vastly improve corporate efficiency. By Michael Healey

As IT organizationschange their focus from cost cutting to

growth, one of the single best things they

can do for their businesses is enable effec-

tive data sharing. Sounds like a no-

brainer, right? The right data sharing can

open new markets, win new customers,

improve relationships with existing cus-

tomers, and expedite jobs from materials

delivery to inventory management to pay-

ment reconciliation.

Yet data sharing, particularly auto-

mated systems that give your external

SHARE!

[COVER STORY]

June 21, 2010 27informationweek.com

business partners access to your datawhen they want it, are not ubiquitousor easy, and the level of data sharingof any kind is surprisingly low atpoints before and after the sale, ourexclusive research finds. Your col-leagues resist data sharing, but they’renot the only problem. IT is way tooslow at creating such integrations—taking months, not days, to build newlinks, in many cases.

FedEx and UPS make package track-ing so simple, it’s easy to take that capa-bility for granted. Yet only half of com-panies even share order status withcustomers. Meanwhile, in the most so-phisticated supply chains, companiesshare data as deep as inventory levelswith key customers, such as manufac-turers looking to coordinate just-in-timedeliveries. With vendors, electronic in-voicing is the simplest level of sharing.On the other end of the spectrum arecompanies that share point-of-sale datawith vendors, something fewer than onein six companies in our survey do.

It’s such an important trend thatIBM in late May said it would pay $1.4billion for Sterling Commerce, an inte-gration software and services companyowned by AT&T. While the deal didn’tattract a lot of attention, it was IBM’slargest acquisition in three years. Theappeal to IBM is straightforward: Datasharing and integration projects al-ways require some custom integrationand ongoing maintenance of the links.Therein is the opportunity for IBM’sconsulting and services army, and thechallenge for most IT organizations.But the problems go well beyond cre-ating and maintaining data integrationlinks. Our survey of 281 IT profes-sionals finds that while technology ispart of the problem, organizational re-sistance is a bigger obstacle.

Almost every company we sur-veyed shares data with someone.Most (74%) share data with cus-tomers, while 62% share data withsuppliers. Almost half of respondentsare required to share data with other

third parties, mostly governmentagencies. Yet there’s wide disparity indata sharing strategies: A fourth con-sider it a top IT priority, about a thirdbuild connections on request, while22% admit they resist data sharing tosome extent.

When it comes to what frustratesdata sharing efforts, the classic cul-prit, budget limitations, tops the listof survey respondents, followed bycomplaints about the multiple sets of

tools and the care and feeding re-quired by legacy connections. How-ever, we suspect that it goes deeperthan any technology.

Sales, manufacturing, or merchan-dising tend to drive the decision tobuild new data sharing relationshipswith suppliers and customers.“They’re usually the starting pointand are a major factor in getting aprogram expanded,” says Jim Frome,chief strategy officer at EDI software-as-a-service provider SPS Commerce.That trio historically doesn’t have thegreatest relationship with IT in manyorganizations, Frome says. Yet IT re-ally needs to have an active role ineducating the different teams aboutcapabilities and options availableboth internally and externally.

Unfortunately, IT doesn’t typicallyget to play that role, or even tries toavoid it. “The company doesn’t reallycare about sharing data,” says onesenior developer summing up histeam’s sentiment. “There’s usually aninitial scream to get the integrationproject done as quickly as possible tomeet a short-term target, then it’snever looked at again. No attempt togrow it, no ongoing review, no deeperanalysis, and no feedback unlesssomething breaks.”

IT needs to break out of this reactivemode. IT’s expected to create an inte-gration point, but is it also trying topromote its use? IT can shine here witha bit of evangelizing.

One Northeast distributor was try-ing to figure out a way to cut costs. Ithad a few clients who had been doingelectronic transactions for years andwere relatively happy, but most of itscustomers relied on good old paper. ITcame forward with an idea to build asales campaign to push all forms ofstreamlined invoicing, including inte-grated data and electronic invoicing.

After some initial pushback by thesales team, which was overriddenthanks to huge support from finance,the campaign was approved. The result

Data: InformationWeek Analytics DataSharing and Integration Survey of 209business technology professionals atcompanies exchanging data withcustomers, April 2010

Initial orders

Shipment status, tracking, and invoicing

Order status

Quotes

Web traffic analytics

Traditional point-of-sale reports

Marketing and lead tracking

Product development and testing information

Detailed POS reports (sales by end user)

Warranty and service details

Internal stocking levels

Data Exchanges In PlaceOr Planned With Customers

In productionPiloting/testingPlanning/budgeting

53%

50%

49%

46%

32%

30%

30%

28%

28%

26%

25% 12% 12%

7% 13%

8% 11%

9% 12%

12% 12%

8% 11%

10% 11%

11% 7%

8% 11%

6% 9%

10% 7%

DATA SHARING

28 June 21, 2010 informationweek.com

[COVER STORY] DATA SHARING

was a 20% increase in customersswitching from paper, saving a fewthousand dollars a month and two fullhead counts in terms of man-hours.

Why We Don’t ShareIT has an opportunity to evangelize

because companies’ data sharingdoesn’t go very deep, which is evidentwhen we look at actual sharing levelsin our research. For companies thatshare data with customers, initial orderfeeds are either in production or beingpiloted or planned by 70% of respon-dents. However, the level of informa-tion sharing varies widely as you movethrough the phases of the sales process.

The least amount of sharing occursprior to the sale of a product; most or-ganizations don’t share any productdevelopment, Web traffic, or mar-keting data, and most don’t evenquote information electronically withcustomers.

Once a sale is made, there’s a spikein sharing, with 53% sharing the initialorder details electronically. Then thedrop-off resumes as fewer and fewer or-ganizations bother sharing order status,tracking information, invoicing, salesreports, or warranty details.

While not everyone in the company

may be receptive to new data sharingefforts, you can usually find an ally inthe CFO’s office. We spoke with multi-ple integration vendors for this survey,and they all point to one of the hottesttrends in data sharing: electronic rec-onciliation of payments. A step be-yond invoicing, it ties payment trans-actions directly back into the coresystems, reducing reconciliation andpayment cycles. A CFO’s dream.

Here’s how it works: A U.S. sportsequipment manufacturer thought itwas missing a lot of opportunities totake cash discounts from suppliers. Ithad the cash to make payments, butthe processing took too long. Hiringmore staff wasn’t feasible. The manu-facturer opted to push for electronicpayment processing of invoices, evenadding incentives for suppliers to billelectronically. It was able to offset thecost of the incentives and add to thebottom line by paying earlier and tak-ing 90% of the potential early-paymentdiscounts—up from 30%.

Perhaps the only thing worse thanan IT organization not taking the leadon data sharing is when IT is left outof the process. One example: A largeU.S. manufacturer of educational prod-ucts was deep into a review of its pric-ing strategy. It had a mishmash of in-formation about current prices,supplier-recommended costs, andcompetitors.

The primary teams involved—mer-chandising, purchasing, and f i-nance—set up a plan that includedcost and pricing feeds from sup-pliers and different divisions, andsome from old-fashioned Web scrap-

Get This And All Our Reports

Become an InformationWeek Analyticssubscriber: $99 per person per month,multiseat discounts available.

Subscribe and get our full report,“Data Sharing:Time To Play Nice,”atinformationweek.com/analytics/edi

This report includes 30 pages of action-oriented analysis, packed with 19 charts.

What you’ll find:

> Survey responses from 281 IT professionals

> Best practices on internal processes and selling projects to management

> ROI spreadsheets on e-invoicing, stock-level sharing, marketing data,and product service data

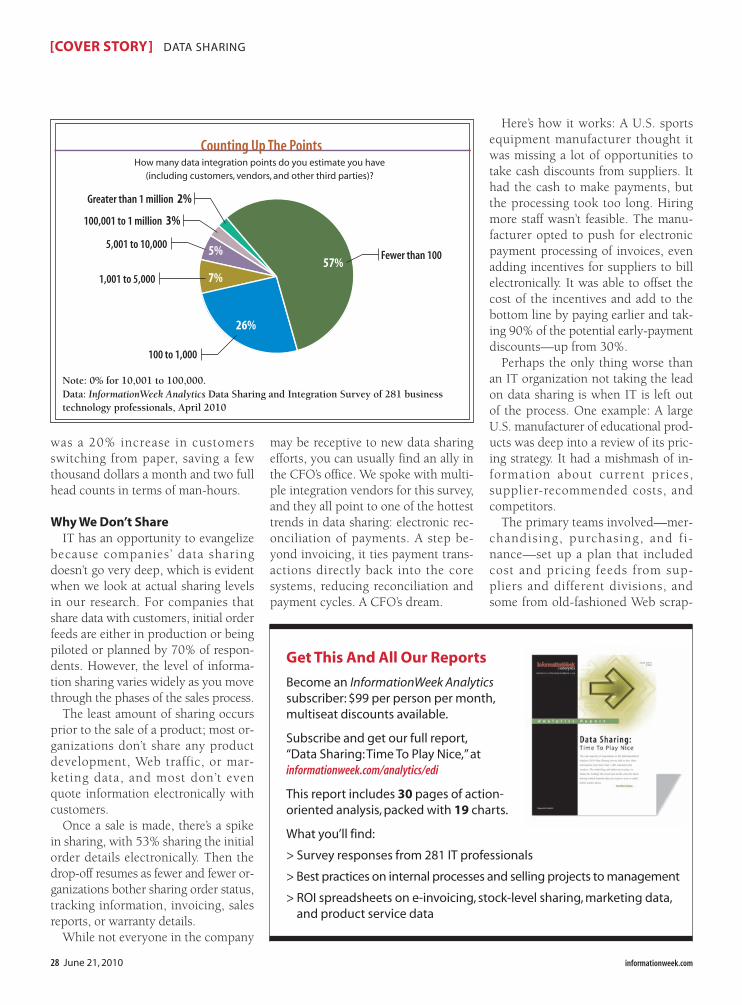

Data: InformationWeek Analytics Data Sharing and Integration Survey of 281 businesstechnology professionals, April 2010

Note: 0% for 10,001 to 100,000.

How many data integration points do you estimate you have(including customers, vendors, and other third parties)?

Fewer than 100

100,001 to 1 million 3%

57%

Greater than 1 million 2%

5,001 to 10,000

1,001 to 5,000

100 to 1,000

5%

26%

7%

Counting Up The Points

30 June 21, 2010 informationweek.com

[COVER STORY] DATA SHARING

ing. The project created a ton of ex-citement, particularly when datastarted coming in.

However, the project was doomed toExcel hell; the manufacturer had thedata, but not the systems to do any-thing with it. IT has a choice: It couldsee such efforts as just another rogueproject foisted upon them, or as agolden opportunity to help the com-pany succeed in an area getting ham-mered with spending cutbacks. Whatwould your team’s reaction be? Excite-ment, disdain, fear, anger?

The Insurmountable QueueYou know the right answer, but we

suspect most would react negativelygiven the potential to crush budgetsand supersede existing projects. That’sa manageable problem, a matter of set-ting the right priorities. A bigger prob-lem is if IT simply doesn’t have theability to respond quickly to new re-quests. Too many companies can’tmove fast enough.

When we asked how long it wouldtake their teams to establish a newdata link with a customer or supplierwhen both have compatible connec-tivity options, only 23% could do itin less than a week. Another 41%could get it done in a month and therest would “add it to a list.” And that’sfor compatible systems.

The response when a new integra-tion point is needed is even moretroubling. Only 29% could get itdone in a month or less. Eleven per-cent said it would take more than sixmonths and 10% were willing to ad-mit they can’t (or won’t) do it—atleast not themselves.

Regardless of how long it takes tobuild the links, we’re not very good atgetting a lot of customers and vendorsto take advantage of the options. Awhopping 83% of respondents havefewer than 1,000 different connectionsin total—customers, suppliers, andthird parties combined.

Here’s how we see it: A midsize,

$200 million company that has an av-erage order size of $1,000 wouldlikely have more than 20,000 clientsand 2,000 to 5,000 suppliers. A largerenterprise is likely to have more than100,000 possible connections. Whereshould you be?

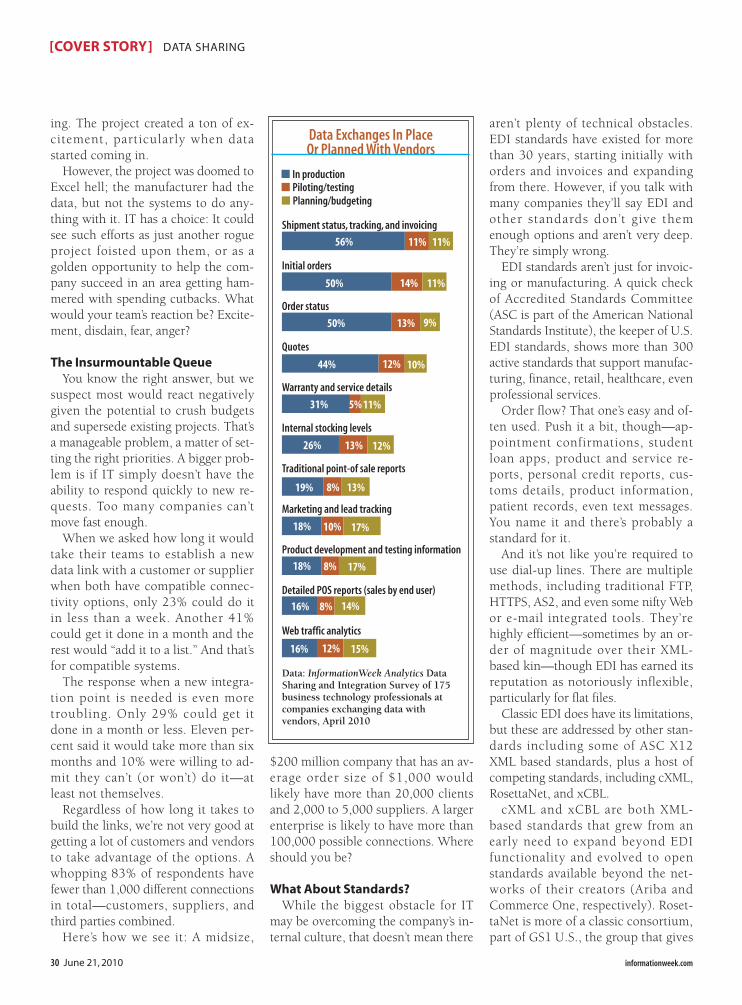

What About Standards?While the biggest obstacle for IT

may be overcoming the company’s in-ternal culture, that doesn’t mean there

aren’t plenty of technical obstacles.EDI standards have existed for morethan 30 years, starting initially withorders and invoices and expandingfrom there. However, if you talk withmany companies they’ll say EDI andother standards don’t give themenough options and aren’t very deep.They’re simply wrong.

EDI standards aren’t just for invoic-ing or manufacturing. A quick checkof Accredited Standards Committee(ASC is part of the American NationalStandards Institute), the keeper of U.S.EDI standards, shows more than 300active standards that support manufac-turing, finance, retail, healthcare, evenprofessional services.

Order flow? That one’s easy and of-ten used. Push it a bit, though—ap-pointment confirmations, studentloan apps, product and service re-ports, personal credit reports, cus-toms details, product information,patient records, even text messages.You name it and there’s probably astandard for it.

And it’s not like you’re required touse dial-up lines. There are multiplemethods, including traditional FTP,HTTPS, AS2, and even some nifty Webor e-mail integrated tools. They’rehighly efficient—sometimes by an or-der of magnitude over their XML-based kin—though EDI has earned itsreputation as notoriously inflexible,particularly for flat files.

Classic EDI does have its limitations,but these are addressed by other stan-dards including some of ASC X12XML based standards, plus a host ofcompeting standards, including cXML,RosettaNet, and xCBL.

cXML and xCBL are both XML-based standards that grew from anearly need to expand beyond EDIfunctionality and evolved to openstandards available beyond the net-works of their creators (Ariba andCommerce One, respectively). Roset-taNet is more of a classic consortium,part of GS1 U.S., the group that gives

Shipment status, tracking, and invoicing

Initial orders

Order status

Quotes

Warranty and service details

Internal stocking levels

Traditional point-of sale reports

Marketing and lead tracking

Product development and testing information

Detailed POS reports (sales by end user)

Web traffic analytics

56%

50%

50%

11% 11%

14%

13%

11%

9%

44%

31%

12%

5%

10%

11%

26%

19%

13%

8%

12%

13%

18%

18%

10%

8%

17%

17%

16%

16%

8%

12%

14%

15%

Data: InformationWeek Analytics DataSharing and Integration Survey of 175business technology professionals atcompanies exchanging data withvendors, April 2010

Data Exchanges In PlaceOr Planned With Vendors

In productionPiloting/testingPlanning/budgeting

32 June 21, 2010 informationweek.com

us the 10-digit UCC bar codes weknow and love. None of them is auniversal standard, but they addsome critical frameworks for Web-centric or interactive sessions. All arefree standards, open to anyone whowants to use them.

Here’s the rub: While standards ex-ist, they are often ignored by large ven-dors creating data exchanges. If a stan-dard doesn’t serve the interests of aparticular provider, that provider sim-ply doesn’t follow the standard and in-stead makes up its own. If a vendor isbig enough or you want its business,IT just adapts. It doesn’t matter ifthere’s one standards group or five,many companies, especially Web-cen-

tric ones, opt to roll their own—eithercreating a new format or modifyingone to suit their needs. One case inpoint is online pricing information.

The Web Catalog NightmareGetting your product and pricing in-

formation on the Web is now a criticalpart of almost every company’s go-to-market strategy. It doesn’t matter if yousell consumer, business, or industrialgoods; users go online to check yourpricing. If you don’t provide such data,your customers are likely to find somerogue price posted by a partner orcompetitor, or even an old customercontract that’s floating around. Worsecase, they’ll find nothing useful and

simply go to a competitor who doesprovide pricing. The tendency of indi-viduals to Google it is the new norm.

[COVER STORY] DATA SHARING

In order to electronically transfer form-based data be-tween entities, the systems doing the transfer mustagree on a number of parameters. Electronic data inter-change (EDI) exists at the application layer to make that

conversation among systems possible.Some of those parameters can be negotiated during the

transfer session; others must be agreed to beforehand. Suchparameters as the transport medium, transport protocol, au-thentication, encryption, and format of the data itself must beagreed upon at some point.

In well-architected systems, a change in one parameterdoesn’t necessarily imply a change in another. For instance,moving from serial lines to a private or public network ideallyshouldn’t require new authentication and encryption choices.In practice,de facto standards crop up for electronic transfer—so transmitting data to a particular vendor may require usingFTP via the public Internet and GS1-formatted documents, be-cause “that’s how they do it.” Wal-mart, for instance, requiresthe AS2 protocol, which uses HTTPS and SMIME for transport,encryption, and session control.

Originally, EDI documents were designed to be as small aspossible to facilitate transfer over slow serial lines. Because oftheir terse nature, they were often open to interpretation. Ifan order came in for 12 boxes of screws, it might not be clear ifthe sender intended to get 12 boxes containing 100 screwseach, or 12 larger cases containing say 50 boxes of 100 screwseach.The only way to fully resolve these issue was to test each

connection to ensure both sender and receiver agreed on theformat, and then test again if a new class of product came up.

The interpretation issue isn’t limited to EDI, and computerscience’s answer to the problem is the Extensible Markup Lan-guage. XML allows for more extensive grammar definition andtherefore the ability to produce nonambiguous (or at leastless ambiguous) business documents.

The two largest sanctioned bodies for EDI standards areAmerican National Standards Institute’s ASC X12 committee,which creates standards for North America,and Edifact,which issanctioned by the United Nations and creates standards largelyused outside of the United States.While these standards are of-ten codeveloped by the two bodies and are widely used, theyare also widely ignored or extended in proprietary ways.

One challenge with XML based systems is that XML is ex-tensible, and standards often form only the base of a com-pany’s or public entity’s usage. Unique extensions are oftendeveloped for good reason, but they require unique support.

Other entities, such as GS1 (formerly UCC—the folks whodictate the universal bar codes), have grown their own sets ofstandards that partially overlap with those of X12 and Edifact.GS1 is a U.S. entity whose standards are largely aimed at sup-ply chain management. It has subsidiaries including Roset-taNet, which works in the business-to-business space and islargely used by the electronics industry. Other groups exist toserve the chemical, pharmaceutical, and energy industries.

—Art Wittmann ([email protected])

The Fundamentals Of EDISTANDARDS, BUT ...

IBM-STERLING DEAL

$1.4 BillionValue of the deal announced on May 24

18,000Total Sterling Commerce customers

2,500Number of Sterling Commerceemployees worldwide joining IBM WebSphere

There is a sharp group of companies in our survey thathave identified this challenge and are publishing priceand product information beyond their main Web page.They’re publishing to government sites, Amazon, andGoogle, as well as to business-to-business integration ven-dors like Ariba.

Good news, right? Not for IT. Amazon, Google, and mostgovernment online systems don’t follow anyone’s stan-dard—not the EDI 832 standard, not cXML, not Roset-taNet, or anyone else’s standard for product information.Your team has to create and maintain a feed for those ven-dors separately, dealing with the different field require-ments and rules on a case-by-case basis.

IT needs to let this reality sink in. The existing levels ofstandards and interoperability aren’t going to improve anytime soon. Don’t wait for it. The Web has transformedbusiness and social relationships on multiple levels. How-ever, the most successful Web-centric vendors don’t wanttrue interoperability.

Take your supply chain team out for a beer and you’llhear the story. Ariba for one set of clients (or vendors),EDIOne for another, GXS for the largest clients, SPS for theretail channel, EduMart for the education market, and soon. Most offer one or more of the standards, but each hasits own rules and none of them share.

Google, Microsoft, and Amazon aren’t any better. Eachhas critical sets of data you either want or need to be a partof, but don’t expect these guys to have a standard you canuse interchangeably among them. Google made waves byadding product feeds to its basic search service. Loading aproduct feed is free, but you have to follow its rules: sepa-rate field definitions and upload processes with no “free”way to simply point to an existing data feed.

There’s no way Google’s going to make it easier for acompany to publish prices on Google by pulling from acompetitor’s search site. It’s the No. 1 destination, andGoogle wants to keep it that way.

This resistance to sharing even extends to the growingSaaS sector. Some vendors, such as Salesforce.com, arepushing their own data clouds as a place to connect. Butonce you integrate with Salesforce, it’s hard to get out. It’llsend you a nice spreadsheet. That’s it. Here’s your data.Good luck. Also, would it be possible to integrate compet-ing data systems? Possible, if you’re flowing data into ERPor other enterprise apps. But another division using Sugar-CRM or Oracle CRM?

You already know the answer. Not gonna happen for along time. Don’t gripe about it; plan around it.

Michael Healey is president of Yeoman Technology Group,an engineering and research firm. You can write to us [email protected].

June 21, 2010 35informationweek.com

The buzz around enterpriseunified communications isloud, and getting more so asIT spending loosens. The

problem is, in our experience and con-firmed by our InformationWeek Analyt-ics 2010 Unified CommunicationsSurvey of 406 business technologyprofessionals, enterprise-wide UC pro-grams that have a truly transformativeimpact on business processes are alltoo rare.

For example, videoconferencing haslately hogged the spotlight. But too of-ten we see IT groups set up expensivevideo systems and walk away, withnary an hour of training or any plan totrack whether employees even use thetool. From the CFO’s perspective, con-sumer-class applications, such asSkype and Yahoo Messenger, seem toprovide much the same benefit as en-terprise-class systems, without all thehassle and expense. No wonder we’refaced with frustration, misunderstand-ings, and elusive ROI.

Trust us: Your users know what’s outthere, and they know when their ITdepartments are hunkering down orworse, dismissing their needs. Onewary survey respondent says of UC:“While this would cut down on waste-ful e-mails, I suspect it would ramp upthe number of distractions an em-ployee has in any given day, and that itwould consume a lot of the employee’stime with little return.”

When you start confusing collabora-tion with wasting time, you’re seriouslymissing the point.

There’s still time to turn this ship

around. The market forecasters think itwill happen, with Infonetics Researchpredicting the enterprise UC segmentwill grow from $256 million in 2010 to$398 million by 2014 in North Amer-ica, according to a May study.

But it will take a few key commit-ments on IT’s part, some easier to ac-complish than others. First, buildtraining into the budget—and we don’tmean allowing for a help desk stafferto spend an hour lecturing employees.Then, leverage business intelligenceprinciples to help drive UC adoptionand speed ROI. Make very sure yournetwork is ready for the load, and planahead for interoperability by keepingan eye on standards.

And finally, cede control to the busi-ness units. That one might be thetoughest, but it’s also the most impor-tant. As we discuss in depth in our In-

formationWeek Analytics UC report,available to subscribers at informationweek.com/analytics/uctoday, technicalglitches are generally seen as the majorcause of disappointing UC implemen-tations. In reality, IT often brings prob-lems on itself by ignoring the end-userexperience and failing to have businessleaders set the strategic direction forthe project.

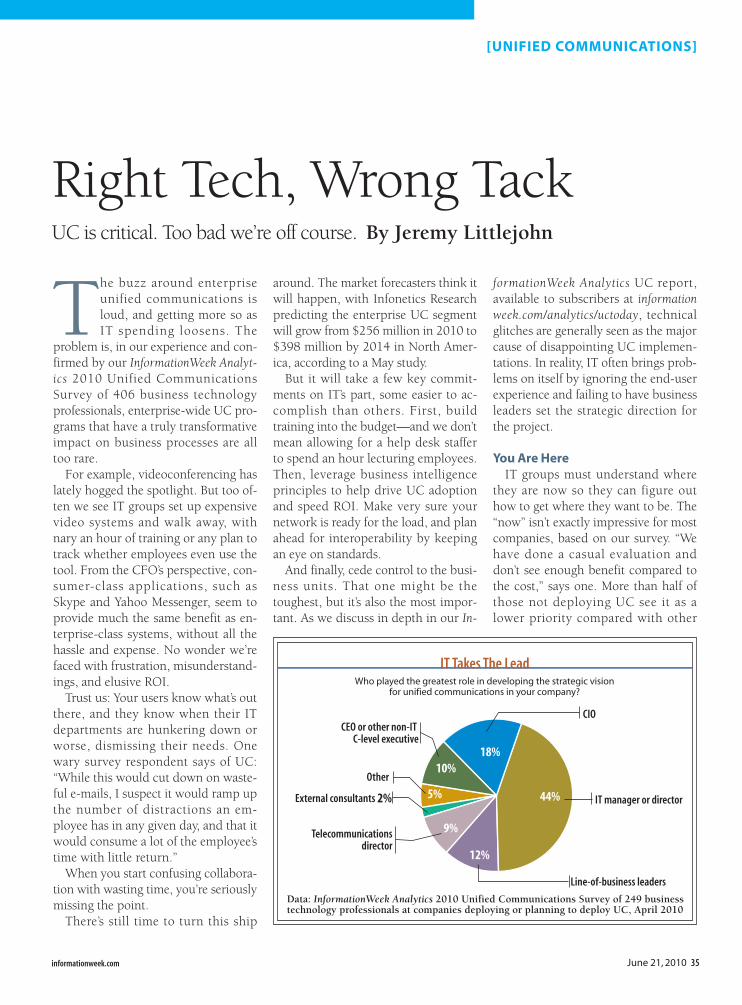

You Are HereIT groups must understand where

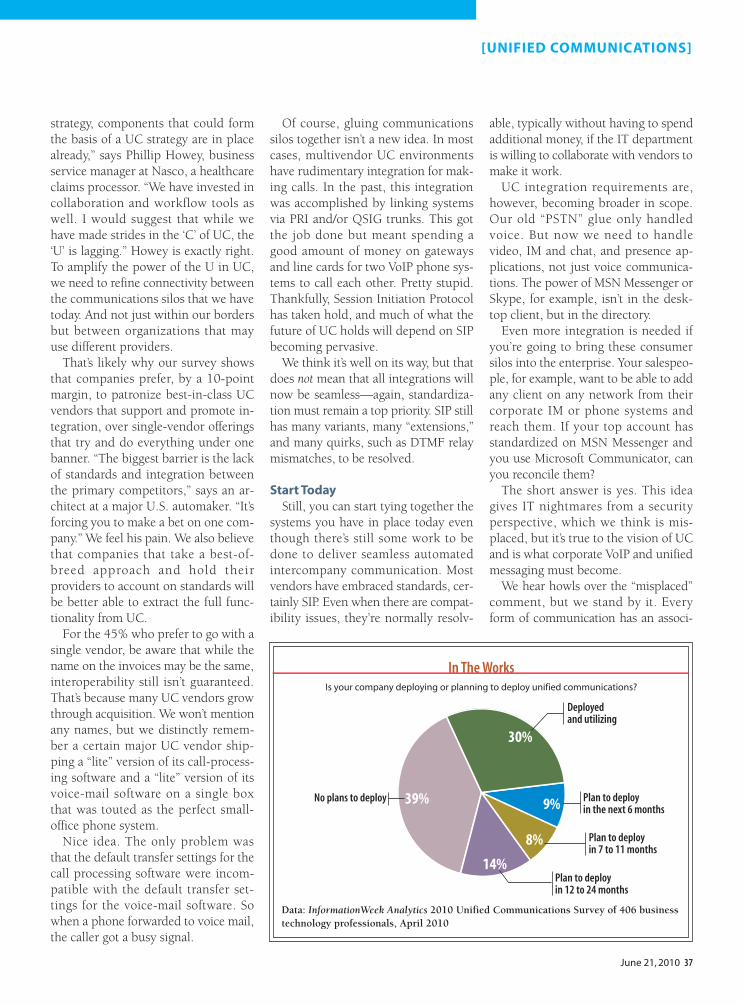

they are now so they can figure outhow to get where they want to be. The“now” isn’t exactly impressive for mostcompanies, based on our survey. “Wehave done a casual evaluation anddon’t see enough benefit compared tothe cost,” says one. More than half ofthose not deploying UC see it as alower priority compared with other

UC is critical. Too bad we’re off course. By Jeremy Littlejohn

Right Tech, Wrong Tack

[UNIFIED COMMUNICATIONS]

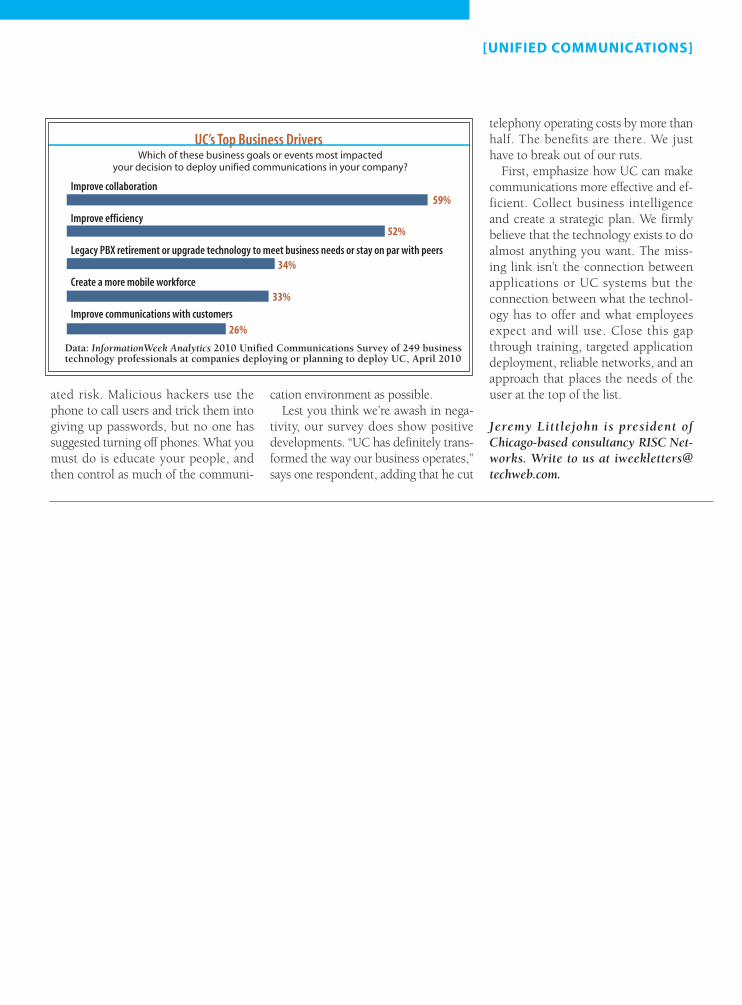

Data: InformationWeek Analytics 2010 Unified Communications Survey of 249 businesstechnology professionals at companies deploying or planning to deploy UC, April 2010

Who played the greatest role in developing the strategic visionfor unified communications in your company?

CIO

External consultants

18%

CEO or other non-ITC-level executive

Other

Telecommunicationsdirector

Line-of-business leaders

2% 5%

10%

9%

12%

44% IT manager or director

IT Takes The Lead

36 June 21, 2010 informationweek.com

projects, and 34% say they see no de-finitive business value. Ouch. Just 10%of those with UC plans have a non-ITC-level executive playing a key role indeveloping a strategic vision. Only14% rate integrating UC with enter-prise applications as a very importantpriority. The No. 1 and No. 2 keys tosuccess? Voice over IP and unifiedmessaging.

What is this, 1997? And why thedispirited outlook? Are IT teams facinginsurmountable technical or interoper-ability hurdles, or perhaps nonexistentbudgets?

Not in most cases. Of course, theconcept of “virtual” everything has cap-tured the minds and pocketbooks of IT,and to be fair it’s much easier to showthe cost savings of going from sevenservers to one than it is to show howmuch you saved or earned becauseyour client got to the right employeefaster or a videoconference saveddozens of phone calls. The biggest chal-lenge, however, is poor user adoption,our survey finds. Technology can helphere; the aforementioned high-defini-tion and desktop videoconferencingapplications are impressive and can en-tice employees into at least trying thesystem. But there is no killer applica-tion that can singlehandedly pull a UCproject out of the bog.

Speeds And FeedsWhile getting employees to actually

use UC applications is the singlelargest factor in a successful rollout andin achieving ROI, it’s not all about softskills and selling your services. Ensur-ing your infrastructure is sized to han-dle the traffic is also very important. Inour experience, IT gets only one shotto hook users on a new application. Ifit fails out of the gate or provides sub-optimal performance because of net-work problems, you’re sunk.

We asked respondents about theirtop concerns regarding their networks’ability to provide appropriate qualityof service to UC applications. Aging in-

frastructures with limited WAN band-width top the list. These concerns arevalid, especially if you need to providePower over Ethernet.

Video, the current UC darling, doesrequire a significant effort to trans-port. Thus the relative dismissal ofcarrier WAN service-level agreementswas very surprising; only 4% of re-spondents say this is a concern. To theother 96%, we’d tell you about aclient we worked with several yearsago that used AT&T to connect itsbank branches. IT was assured that itwould get bandwidth that could

“burst” to a full T1, which seemedsufficient for UC. When VoIP was de-ployed, the company experiencedvery poor performance. It turns outthat the carrier was offering a “burst”of traffic by dropping packets into avirtually bottomless queue some-where in its cloud. Traffic got throughall right—after a short 800- or 900-millisecond delay. AT&T assured usthat it was within its SLA for band-width because it did in fact deliver thepackets, instead of dropping them, sobuyer beware.

And remember: Trust but verify. Youcan see drops and delays on your gear,but you can’t see them on your WANprovider’s equipment, especially ifyou’re buying services like MPLS. It’scritical to the success of UC that younegotiate, understand, and test yourcarriers’ SLAs. You may wind up fight-ing battles that span weeks and evenmonths to get UC applications likevideo to work properly. This wastedtime and erosion of user goodwill killsyour adoption and erases any oppor-tunity for ROI.

Furthermore, IT must not considerUC purely a network initiative. “As weroll out UC, we are struggling withwhere support should fall,” says an ITarchitect for a large manufacturingfirm. “This is a new paradigm.” Ourfirm will provide about 200 voice andvideo readiness analytics engagementsthis year, and about half the time, the“Windows” or “server” teams won’twant to participate. They don’t feel thatUC will impact them, or that they’reresponsible for its success. They’redead wrong. If you’re still engaging inturf wars between IT and telecom, weguarantee you’re depriving your com-pany of collaborative opportunities.

The Power Of UC Is In The “U”Even with an end-user-focused ap-

proach, a unified IT team and a net-work that’s ready to perform, there arestill formidable integration hurdles.

“While UC hasn’t been an overt

Get This AndAll Our Reports

Become an InformationWeek Analytics subscriber for $99 perperson per month, with multiseatdiscounts available, and get ourfull report on unified communi-cations. Go to informationweek.com/analytics/uctoday

This report includes 43 pages ofaction-oriented analysis, packedwith 26 charts.

What you’ll find:

> Nine barriers to UC adoptionand advice on beating the odds.

> Respondents’ top vendor picksin three vital UC technologies.

> Our guide to achieving ROI.Hint: The cost of a system rarelyaligns with its popularity.

June 21, 2010 37

strategy, components that could formthe basis of a UC strategy are in placealready,” says Phillip Howey, businessservice manager at Nasco, a healthcareclaims processor. “We have invested incollaboration and workflow tools aswell. I would suggest that while wehave made strides in the ‘C’ of UC, the‘U’ is lagging.” Howey is exactly right.To amplify the power of the U in UC,we need to refine connectivity betweenthe communications silos that we havetoday. And not just within our bordersbut between organizations that mayuse different providers.