Embed Size (px)

Citation preview

MIDLANDS STATE UNIVESITY

FACULTY OF COMMERCE

DEPARTMENT OF BUSINESS MANAGEMENT

PROJECT TOPICRISK AND RISK MANAGEMENT DISCLOSURES AS A CORPORATE GOVERNANCE

MEASURE

A CASE OF THE ZSE LISTED BANKING AND FINANCIAL INSTITUTIONS

DISSERTATION SUBMITTED BY

R101551P

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS OF THE

HONOURS DEGREE IN BUSINESS MANAGEMENT

GWERU, ZIMBABWE

NOVEMBER 2013

b

APPROVAL FORM

The undersigned certify that they have supervised the student

dissertation entitled Risk and risk management disclosures as a

corporate governance measure: A case of the ZSE listed Banking

and Financial Institutions submitted in partial fulfillment of

the requirements of the Bachelor of Commerce in Business

Management Honours Degree at Midlands State University.

…………………………………….

………………………………

SUPERVISOR

DATE

……………………………………..

……………………………..

CHAIRPERSON

DATE

i

…………………………………….

………………………………

EXTERNAL EXAMINER

DATE

RELEASE FORM

NAME OF AUTHOR R101551P

DISSERTATION TITLE INVESTGATION ON RISK AND RISK

MANAGEMENT DISCLOSURE AS A CORPORATE

GOVERNANCE MEASURE: A CASE OF THE ZSE

LISTED BANKING AND FINANCIAL

INSTITUTIONS

DEGREE TITLE BACHELOR OF COMMERCE HONOURS IN

BUSINESS MANAGEMENT

ii

YEAR GRANTED 2013

Permission is granted to the Midlands State University to produce

single copies of this dissertation and to lend or sell such

copies for private, scholarly or scientific research purpose

only. The author does reserve other publication rights and

neither the project nor extensive extracts from it may be printed

or otherwise be reproduced without the author’s written

permission.

SIGNED ………………………………………

PERMANENT ADDRESS 92 HARARE DRIVE GREYSTON PARK

HARARE, ZIMBABWE

DATE ……………………………………….

DEDICATION

I dedicate this research project to my family and friends for

their support and inspiration throughout my studies

iii

ACKNOWLEDGEMENTS

All glory and honor to the almighty God for guidance and

protection throughout my studies.

iv

I wish to acknowledge the guidance and support I received from my

supervisor who made it possible for this research study to be

complete. I am indebted to thank all my family and friends who

supported me through financially and spiritual during the course

of my study. Not forgetting to express my gratitude my friend

Bonelite Mavurawa for being a pillar of strength and support in

my studies and made this piece of work possible.

v

ABSTRACT

This study aims at examine the risk and risk management

disclosures as corporate governance measures by listed Banking

and Financial institutions in Zimbabwe. The collapse of many

banking institutions that span form 1999 to 2005 in Zimbabwe has

triggered the need to conduct a research in this sector. In

response to the crisis the central bank introduced The Code1 on

corporate governance in 2004 and Minimum disclosures requirements

in 2007 so as to curb systematic collapse of the financial sector

and restore the banking public confidence. The objective of this

study was to investigate the level of compliance of listed

financial institutions with the Reserve Bank of Zimbabwe Minimum

risk management disclosures requirements of 2007, extent of Basel

2 implementation and measures in place to warrant compliance.

Previous research indicated greater disclosures are in favor of

financial risk than non-financial risk. Also the corporate

governance frameworks which mandate the disclosures of risk

management have been implemented to foster compliance in the USA,

Canada, Brazil, Germany, France, Portugal, Netherlands, Malaysia,

United Arab Emirates and South Africa respectively. Descriptive

and case study approach were employed in the study. Content

vi

analysis was conducted to measure the extent and level of risk

management disclosure in the annual reports of listed banking

financial institutions .A content analysis was performed to

examine the informative of the risk disclosures. Population of

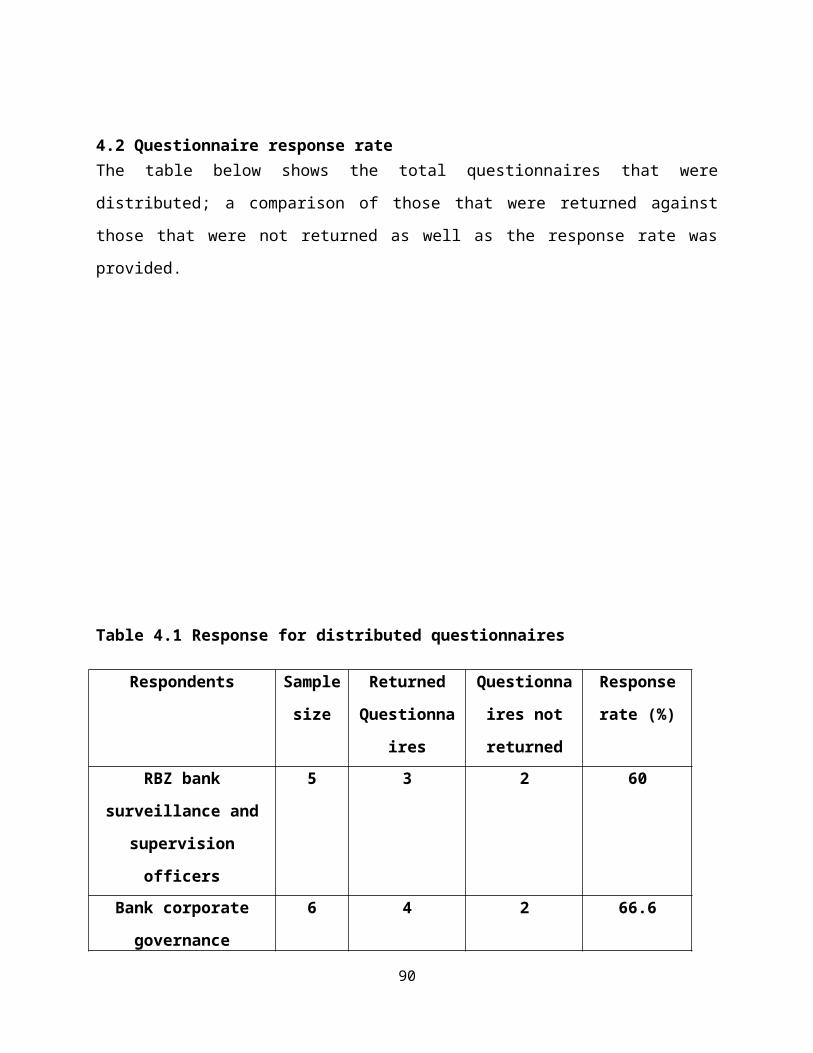

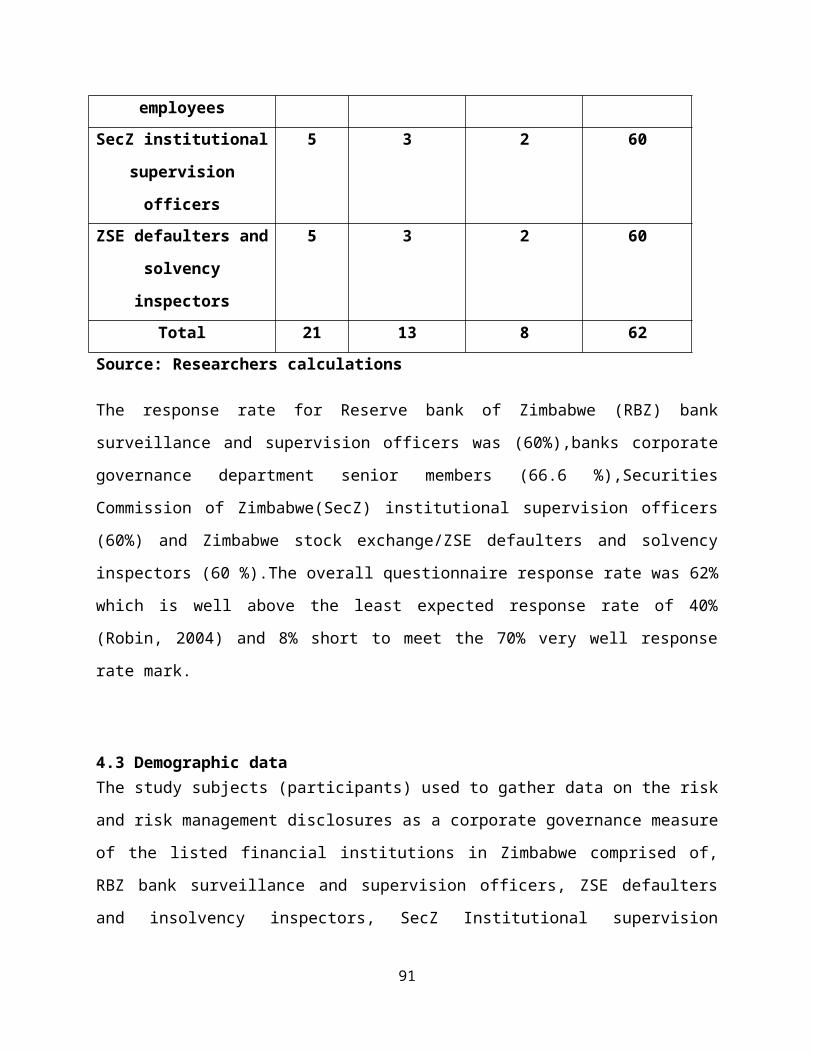

the study comprised of regulatory officials from ZSE, SecZ, RBZ

and listed financial institutions. Research findings shows that

financial risks are being disclosed in greater detail as compared

to non-financial risks, however risk management disclosures are

not detailed enough to enable stakeholders in making an informed

decision. The study also found deficiency in monitoring and

enforcing of corporate governance practices from relevant

regulatory authorities. Therefore the study concluded that there

was limited compliance with the Reserve Bank of Zimbabwe minimum

risk disclosures requirements. The Basel 2 implementation is

lagging behind and there is no cooperation of regulatory

institutions in monitoring and enforcement of market discipline

frame works as well as a lack of good governance in listed

financial institutions. The study recommend the adoption of a

legislative approach in the implementation of governance codes,

Multi-lateral approach in ensuring market discipline and

introduction of penalties on institutions and managers in case of

non-compliance.

Table of Contents

APPROVAL FORM..................................................i

vii

RELEASE FORM..................................................iiDEDICATION...................................................iiiACKNOWLEDGEMENTS..............................................ivABSTRACT.......................................................vLIST OF TABLES................................................xiLIST OF APPENDICES...........................................xiiLIST OF ACRONYMS............................................xiiiDEFINITION OF KEY TERMS......................................xivCHAPTER 1......................................................1GENERAL INTRODUCTION...........................................11.0 Introduction..............................................11.1 Background of the study...................................11.2 Problem statement.........................................61.3 Research objectives.......................................61.4 Research questions........................................61.5 Significance of the study.................................71.6 Assumptions of the study..................................91.7 Scope of the study........................................91.8 Limitations of the study.................................101.9 Chapter summary..........................................10

CHAPTER 2.....................................................11LITERATURE REVIEW.............................................112.0 Introduction.............................................112.1 The concepts of risk.....................................112.1.1 Risk management........................................122.1.2 Risk management disclosure...........................12

viii

2.2 Previous research findings on risk and risk management disclosures..................................................122.3 Corporate Governance in Zimbabwe and risk management disclosure in comparison with other countries................142.3.1 Companies Act........................................142.3.2 Zimbabwe Stock Exchange Act Chapter 24:18............162.2.3 Securities Act Chapter 24:25.........................17

2.3 Corporate governance in banking and financial institutions of Zimbabwe..................................................192.3.1 The Banking Act 24:20................................202.3.2 The RBZ Code 1.......................................20

2.4 Development and implementation of corporate governance and challenges adopting codes....................................212.4.1 “Comply or explain” principle........................222.4.2 Legislation of corporate governance codes............242.4.3 The “Comply or else” approach........................262.4.4 “Box ticking” approach...............................26

2.5 Risk management disclosure and Corporate Governance......272.5.1 Transparency and accountability......................272.5.2 Openness.............................................292.5.3 Good board practices.................................292.5.4 Fairness.............................................302.5.5 Turnbull Guidance (Internal control: Revised Internal Control Guidance for Directors on the Combined Code 2005). .302.5.6 King 3 report (South Africa, 2009)...................302.5.7 Malaysia Code on Corporate Governance (2012).........31

2.6 Risk Management Disclosure Requirements, Regulations, Accounting standards and Conventions.........................31

ix

2.6.1 Basel 2 Convention...................................322.6.2 Portuguese Companies Code (Codigo das Sociedades Comercias).................................................332.6.3 Securities and Exchange Commission (USA).............332.6.4 Sarbanes Oxley act (USA).............................332.6.5 International Financial Reporting Standards (IFRS). . .33

2.7 Theories of risk management disclosure...................352.7.1 Agency theory........................................352.7.2 Signalling theory....................................362.7.3 Political cost theory................................362.7.4 Legitimacy theory....................................37

2.8 Merits of risk management disclosure.....................372.8.1 Encourage better risk management in banks............372.8.2 Focusing on future events (forward looking)..........382.8.3 Reduced cost of capital..............................382.8.4 Improves Accountability..............................39

2.9 Demerits of risk management disclosures..................392.9.1 Commercial sensitive information.....................392.9.2 Unreliability of forward-looking information.........40

2.10 Chapter summary.........................................41CHAPTER 3.....................................................42METHODOLOGY...................................................423.0 Introduction.............................................423.1 Research Design..........................................423.1.2 Qualitative and quantitative approaches..............433.1.3 Descriptive..........................................433.1.4 Case study...........................................44

x

3.2 Population...............................................453.2.1 Target Population....................................453.2.3 Sampling.............................................453.2.4 Sampling technique...................................463.2.5 Non-probability sampling.............................463.2.7 Sample size..........................................473.3.1 Secondary data.......................................483.3.2 Primary data.........................................493.3.2.3 Self-administered questionnaire....................503.3.2.4 Questioner design..................................503.3.2.5 Close questionnaires...............................50

3.4 Research Validity........................................513.4.1 Validity.............................................513.4.2 Reliability..........................................52

3.5 Data analysis and Data Presentation......................523.5.1 Qualitative data analysis............................523.5.2 Content Analysis.....................................523.5.3 Data presentation....................................53

3.6 Ethical considerations in research.......................533.7 Chapter summary..........................................54

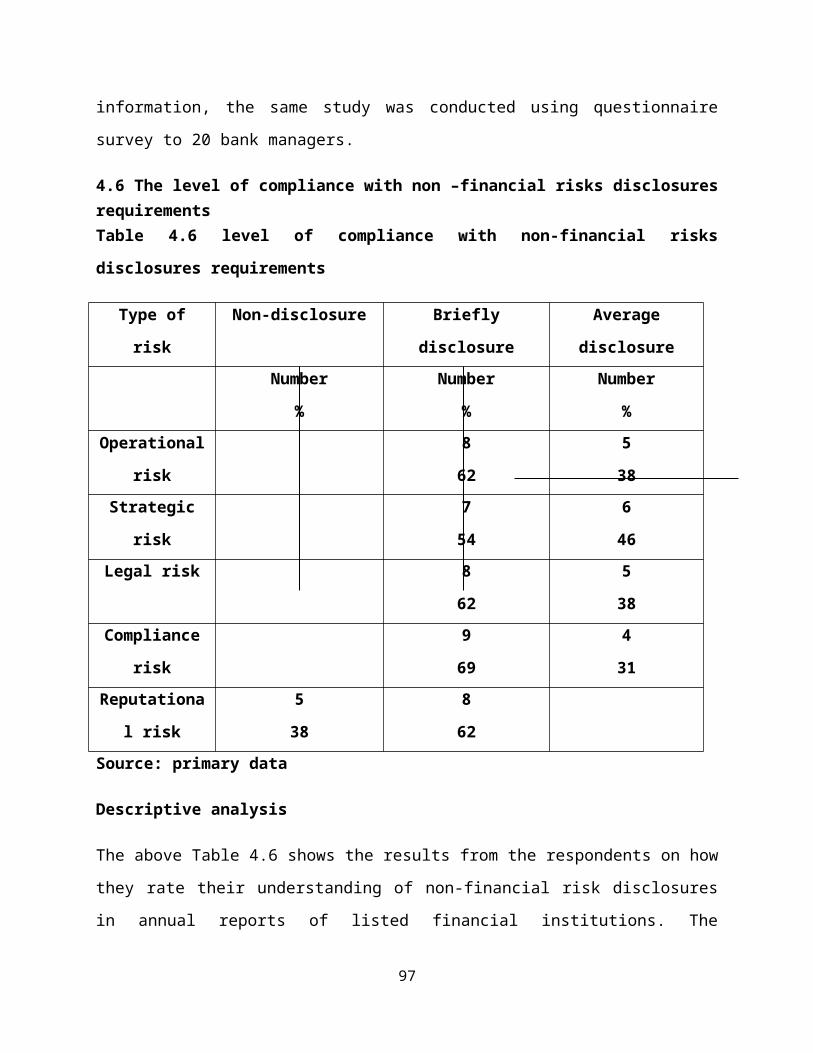

Chapter 4.....................................................55Data presentation, interpretation and analysis................554.1 Introduction.............................................554.2 Questionnaire response rate..............................554.3 Demographic data.........................................564.4 The extent of financial and non-financial risks disclosures.............................................................57

xi

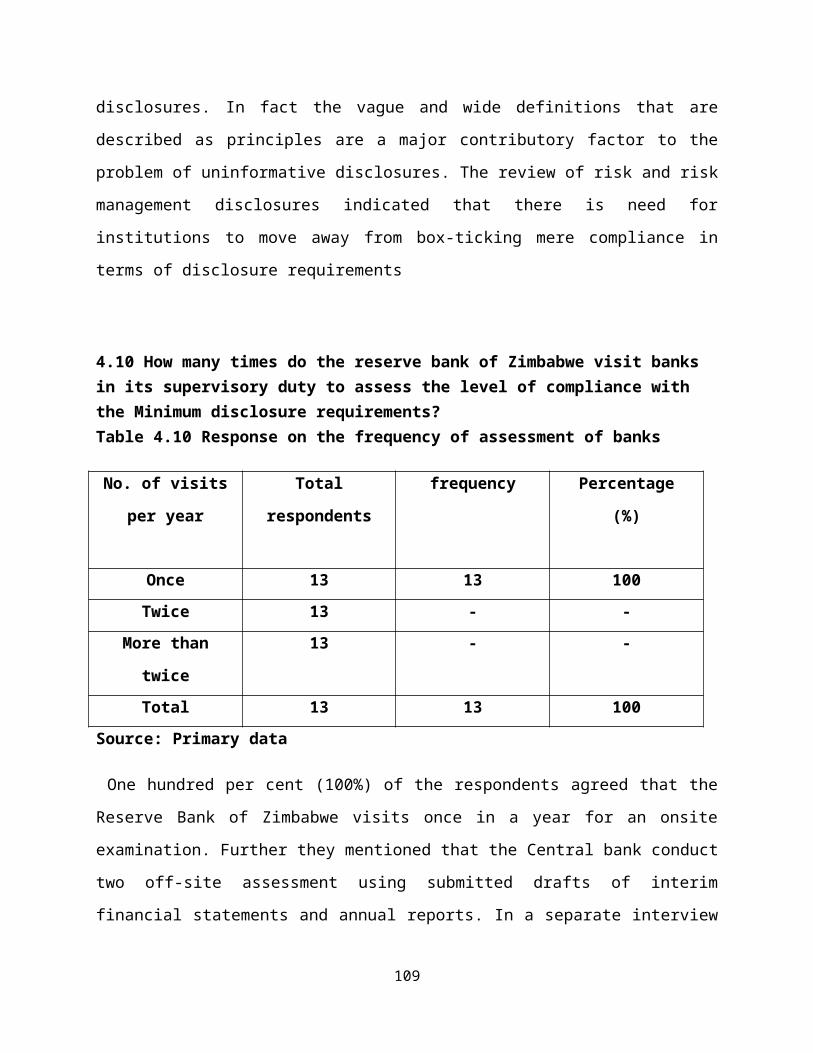

4.5 level of compliance with financial risks disclosure requirements.................................................594.6 The level of compliance with non –financial risks disclosures requirements.....................................604.7 The extent of implementation and compliance with the RBZ minimum disclosures requirements and Basel 2 recommendations. 624.9 Analysis and discussion of the risk and risk management disclosure and the extent of compliance with RBZ minimum disclosure requirements and Basel 2..........................654.10 How many times do the reserve bank of Zimbabwe visit banksin its supervisory duty to assess the level of compliance with the Minimum disclosure requirements?.........................674.11 How does the Zimbabwe Stock exchange determine whether listed banking institutions are complying with other regulations which are not in the Zimbabwe stock exchange Act such as the RBZ Minimum disclosure requirements..............684.12 What are the measures being implemented by Securities Commission of Zimbabwe to ensure compliance with the RBZ minimum disclosure requirements and Basel 2 recommendation.. .694.13 Chapter summary.........................................70

CHAPTER 5.....................................................71Summary of findings, conclusions, recommendations and areas of further study.................................................715.0 Introduction.............................................715.1.1 Summary findings.....................................725.1.2 The extent of disclosures on financial and non-financial risks............................................725.1.3 Level of compliance with RBZ minimum risk disclosures requirement................................................72

xii

5.1.4 The extent of compliance with RBZ minimum disclosure requirements and Basel 2...................................725.1.5 Frequency of on-site examination by RBZ in its supervisory role...........................................735.1.6 Zimbabwe stocks exchange assessment on whether listed institutions are in compliance with regulations which are noton the Zimbabwe stock exchange Act such as the RBZ minimum disclosures requirements...................................73

5.2 Conclusions..............................................735.3 Recommendations..........................................755.4 Areas of further study...................................75

References:...................................................77APPENDICES....................................................86

xiii

LIST OF TABLES

Table

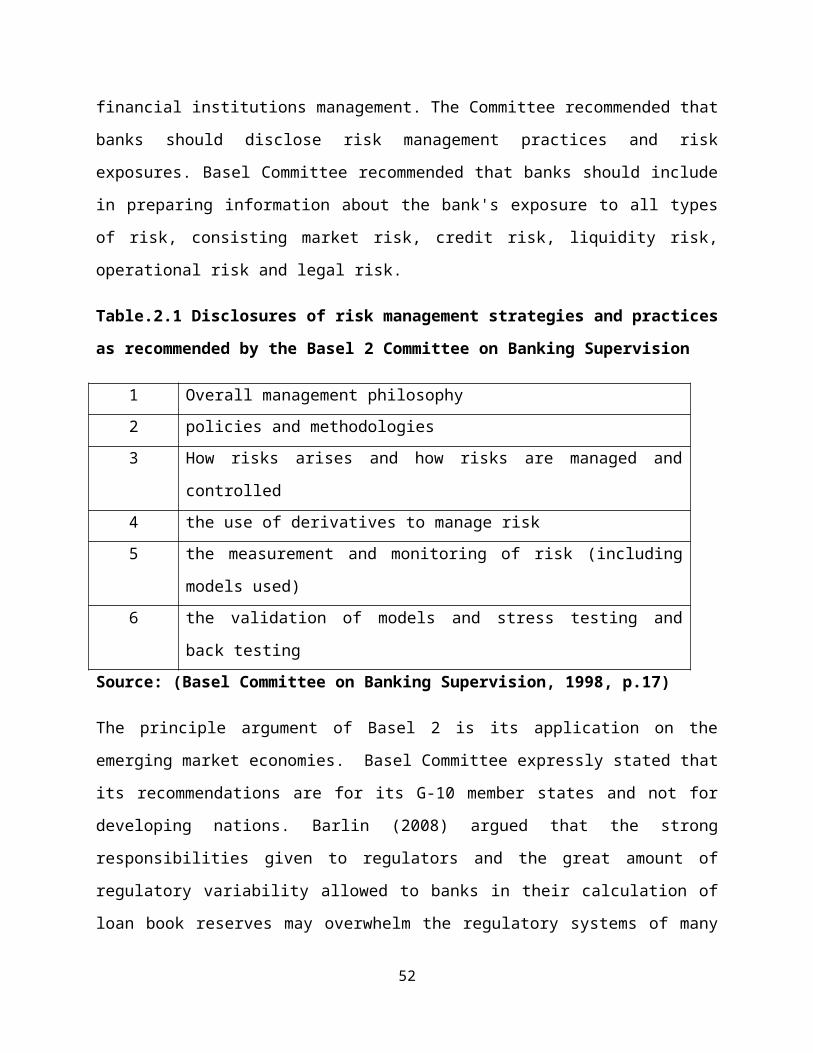

2.1 Basel 2 risk management disclosures

requirements

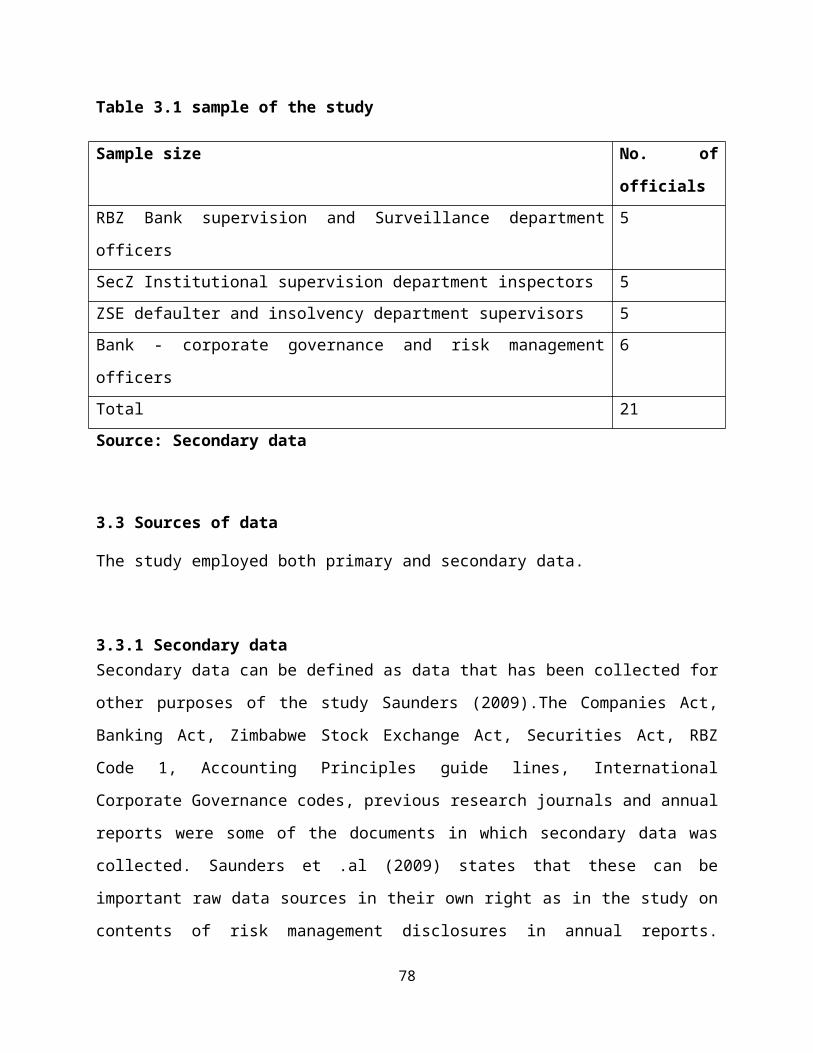

3.1 Sample of the study

4.1 Response for distributed

questionnaires

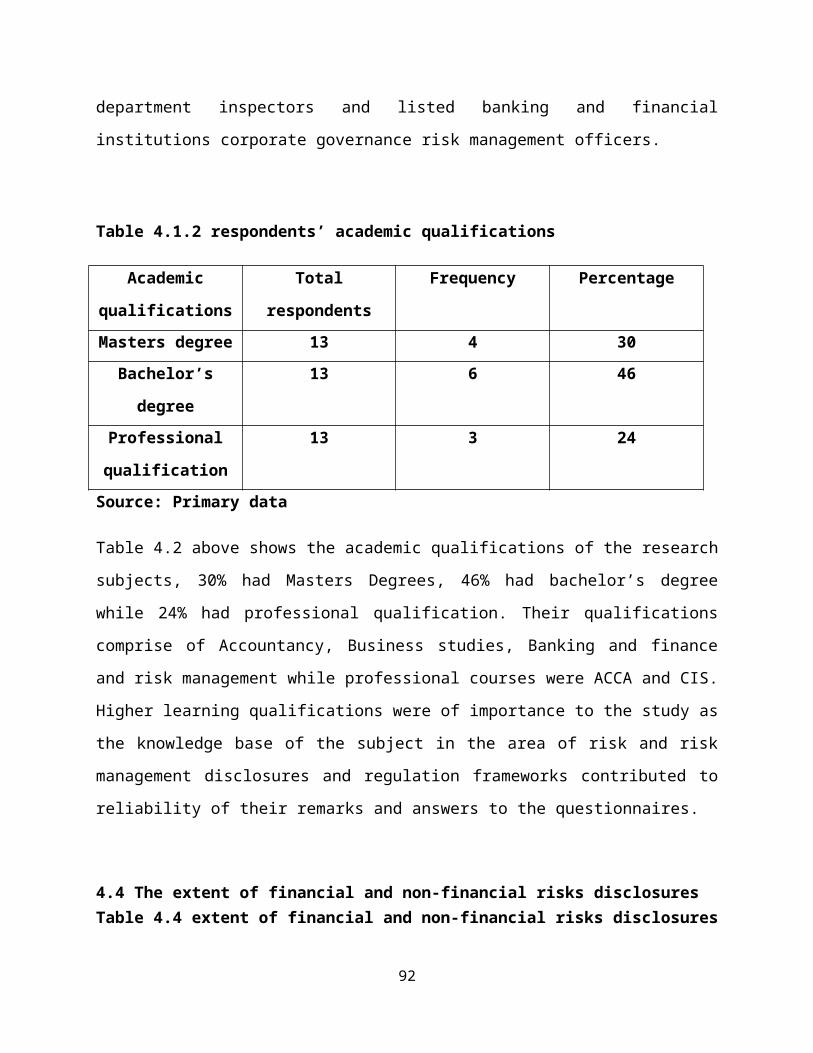

4.1.2 Respondents academic qualifications

4.4 Extent of disclosures of financial

and non-financial risks

4.5 Level of compliance with financial risks disclosures requirements

4.6 Level of compliance with non-

financial risks disclosures requirements

4.7 Implementation and compliance with

the RBZ minimum disclosures

requirements and Basel 2

recommendations

4.8 Risk management disclosure in annual

of financial institutions

xiv

4.10 Response on the frequency of

assessment of banks

LIST OF APPENDICES

Appendix 1 Cover letter

Appendix 2 Questionnaire

xv

LIST OF ACRONYMS

ACCA Association of Chartered Certified

Accountants

BSSL Bank Supervision, Surveillance and

Licensing

BIS Bank of International Settlement

xvi

CACG Commonwealth Association of Corporate

Governance

CIS Chartered Institute of Secretaries

COSO Commission of Sponsoring Organizations

ICAZ Institute of Chartered Accountancy of

Zimbabwe

ICAEW Institute of Chartered Accountancy of

England and Wales

IFRS7 International Financial Reporting

Standards 7

MPS Monetary Policy Statement

RBZ Reserve Bank of Zimbabwe

SEC Securities Exchange Commission

SOX Sarbanes-Oxley Act

UAE United Arab Emirates

UK United Kingdom

USA United States of America

SECZ Securities Commission of Zimbabwe

ZSE Zimbabwe Stock Exchange

xvii

xviii

DEFINITION OF KEY TERMS

Corporate governance- is the framework of rules, relationships,

systems and processes within and by which authority is exercised and

controlled in corporation. It encompasses the mechanisms by which

companies, and those in control are held to account, It influences how

the objectives of the company are set and achieved, how risk is

monitored and assessed, and how performance is optimized (Australian

Corporate Governance code 2006)

Risk- is defined as anything that can create hindrances in the

way of achievement of certain objectives

Financial risks – defined financial risks as risks that have an

immediate effect on assets and liabilities in monetary term

Non-financial risks- are risks that can affect an organizations

that arises from the operating environment or in the organization

Risk management- these are measures that a put in place to

mitigate, hedge or reduce the possible impact of unfavorable

events

xix

Risk management disclosure- this is the dissemination of

information on risk management systems that are in place in an

organization through the annual reports

xx

CHAPTER 1

GENERAL INTRODUCTION

1.0 Introduction The last few years has witnessed an exponential growth in demand

for corporate disclosures. The worldwide financial crisis is a

key driver for increased disclosure demands, particularly in risk

matters (Woods, Dowd and Humphrey, 2008). In order to satisfy the

raising demands for information and warrant corporate

transparency and accountability, there seems to be general

agreement that new reporting approaches are needed (Beatti,

McInnes and Fearnely,2004).Although there are several significant

developments in the area revolving around the reporting topic,

there exist a considerable information gap. Specifically

reporting on risk in general (Beretta and Bozzolan, 2004) and the

risks inherent in intangible resources appear to be

underdeveloped (Buhk, Neilsen, Gormsen and Mouritsen, 2004). Many

developing economies such as Africa and Zimbabwe in particular

recognises that a competitive banking sector is necessary for

sustainable economic growth and that corporate governance in the

form of corporate risk transparency fosters a stable and vibrant

banking sector(Carletti and Hertman, 2003). Richer information is

not necessarily linked to positive returns’ but economic theory

presents contradictory expectations regarding the advantages of

1

greater banking stability through enhanced disclosures. More

information is rather associated with both beneficial and

negative externalities .Hence richer corporate risk management

disclosures and transparency, can influence sensible bank risk-

taking through market discipline (Barth et. al. 2004).

1.1 Background of the study Banks are risk- taking enterprises operating in an increasingly

unpredictable and unstable business environment that are required

to provide a multitude of information about their activities. The

Asian financial crisis of 1997-1998(Jayaraman and Kothari, 2012)

and the recent credit crunch of 2007-2009 have led to increased

calls arguing for even more risk and its management disclosure

(Durst et.al, 2008). Information on risk is essential to

determine the risk profile of a company, the accuracy of

securities price forecast, the estimation of market value and the

probability of corporate failure (Lang and Lundholm 1996; Beretta

and Bozzolan, 2004).Despite the critical role attributed to

banks, it is surprising this sector is apparently under

researched with respect to (risk) disclosure (Woods, Dowd and

Humphrey, 2009)

Zimbabwe’s financial sector crisis can be traced back in the

late 90’s up to the new millennium era, under different economic

conditions, financial sector regulations, political and

government set up as well as different central bank governors.

The deregulation of the financial sector of early 1990s exposed2

the banking sector to structural vulnerability and risk

management cum corporate governance challenges (Muranda,

2006) .Since 1995 depositors and financial sector investors have

lost their funds either deposited or invested in the bank without

prior warning or publication of challenges being or likely to be

faced by the banks either through press release or annual

reports.

The need for depositor and investors’ interest protection and

notification through risk and risk management disclosure was

underscored by bank failures in the 1995-2001, mainly Universal

Merchant Bank, United Merchant Bank, Zimbabwe building society

and First National Building Society (The Herald 31 May 2013).

Three banks were liquidated and nine others were put under

curatorship (Monetary Policy Statement 2006). It was reported in

the 2013 Monetary Policy Statement under the heading troubled

banks that banks failure of 2004 was due to weak governance, poor

risk taking and deficiency risk management.

The following is a list of some of and a brief explanation events

of those troubled banks: Trust Bank was put under the custody of

a curator in 2004 and then liquidated the same year after it was

discovered that that the bank was facing serious liquidity

problems, emanating from non- performing loans, poor risk

management systems while this information was kept out of public

eye through risk and risk management non-disclosure. Intermarket

Bank in March 2004 was placed under curatorship by the Central

3

bank after facing serious liquidity challenges, high level of

non-performing loans amounting Z$174 billion which was unearthed

by the curator. Barbican Bank started to face liquidity problems

in 2003 but had since late 90’s engaged in over expansion

activities against low capital to support its expansion projects

including across – boarder investments in South Africa. In 2003

the bank was placed under the curator citing poor risk management

systems and weak corporate governance structures. Later on in

2004 it was decided to liquidate Barbican bank by the Central

Bank. Royal bank was put under curatorship in 2004 due to a

number of deficiencies including high level of non-performing

loans and chronic liquidity challenges. Time Bank, CFX Bank

Limited CFX Merchant Bank, Intermarket Building Society and

Intermarket discount House were all faced operational challenges.

Risk management deficiencies were frequently associated with

every bank that failed.

It is in light of these bank failures that the Government

through the Reserve Bank Of Zimbabwe drafted the statutory

legislature Minimum Disclosure Requirements in 2004 and was

published three years later in 2007 (BLSS 2007).In this

regulation it is stipulated that banking institutions must

disclose the following risk and mitigation systems in place

credit risk, foreign exchange risk, interest rate risk, liquidity

risk, strategic risk, reputational risk, operational risk,

institution and market risk, legal and compliance risk .The RBZ

Minimum Disclosure Requirements also mandated listed financial

4

institutions to disclose their compliance with the BLSS 2007 in

their annual reports. After the 2003-2004 financial crises the

nation lost investors and depositors’ confidence and the events

that follow was the effort by the Reserve Bank of Zimbabwe in

trying to address risk management systems and their disclosure so

as to win back public confidence. The Central bank move on to

redraft the Minimum Disclosure Requirement of 2004, through the

use of the Basel 2 Conversion publication of 2004 also known as

the Basel Committee on Banking Supervision which contained the

infamous Pillar 3 or Market Discipline .The Basel 2 Accord

clearly stated that a bank should publicly disclose quantitative

and qualitative information about its risk exposure, including

its strategies for managing risk (BIS 2003) .This action was

taken as measure to promote corporate risk transparency and

effective market discipline to ensure that both depositors and

investors will be aware of the level of risk that is faced by

their banks and the risk management system being

implemented(jayaraman, 2012).After the Minimum Disclosure

Regulation was gazetted and became operational in 2004, the same

year witnessed the biggest financial sector crisis .

In year 2007 the Central bank fully adopted the principles set up

in Basel 2 Accord which were based on the fact that market

discipline imposes strong incentives on banks to maintain a

strong capital base to cushion potential future losses arising

from its risk exposures. BLSS 2007 was published with the revised

Minimum Disclosures Requirements ,in this revised edition more

5

risk management and disclosures were provided by stipulating that

all banking institution were expected to provide sufficient,

timely and detailed information that allows stakeholders to make

meaningful assessment of the bank’s financial condition and

performance, business conditions, risk profile, risk management

practices, corporate governance and compliance practices(BLSS 9

Jan, 2007).The following were major addition; capital adequacy

compliance or minimum capital requirement for banks as a pre-

condition to be licensed and to the continuance of license ,

credit risk mitigation methods such Standardised Approach,

Foundation Internal Ratings –Based Approach (IRB) and Internal

Ratings Based approach; description of stress testing method

applied, disclosure of the organisational structure of the risk

management function, procedures, policies on limits including

types of limits and how they were established

However despite the previously mentioned developments trouble

continued to rock the Zimbabwean financial sector. On June 3,

2011 the RBZ Governor announced it had put ReNaissance Merchant

bank under curatorship after filing for bankruptcy as a result of

poor corporate governance practices and failure to meet the

minimum capital threshold (Financial Gazzette 9 June 2011). In

June 2012 Interfin Bank Limited was put under curatorship citing

liquidity crisis. Depositors failed to access their funds at the

announcement of its failure without prior publications of operating

problems and possible risk of collapse. When the news was published

all Interfin bank branches had no cash at their disposal. Genesis

6

Merchant bank voluntarily surrendered its banking license to the

Central bank and was closed on 11 June 2012 this was as result

of failure to satisfy the minimum capital threshold requirement.

Genesis bank was shut down without prior publication of its

challenges and possible failure in its previous financial

statements.27 July 2012 barely a month after the collapse of

Genesis bank and Interfin bank, Royal Bank surrendered its

banking license citing failure to meet the requisite of minimum

capital threshold in stipulated time frame, conduct of banking

business without sound administrative and risk management

procedures , poor accounting practices and, liquidity constraints

with a negative gap amounting US$3.03 million in the critical 0-7

day time band resulting in the bank imposing a minimum withdrawal

limit of US$50 per day. High non-performing loans that spans to

15 months up to July 30 2012 since the commencement of Royal bank

operations were unearthed. The defaulted loans was as much as

99.92% of the total loan book of US$ 1.52 million to 31 May

2012.In the same press statement it was mentioned that the bank

was fully aware of the level of the non-performing loans, but it

was misrepresenting information and data presented to the RBZ

(Royal bank press statement July 2012).

In more recent developments in Zimbabwe’s financial sector

AFRASIA Kingdom Bank in particular, has continued to raise public

concern about the compliance of the banking sector with the

corporate governance practices in risk and risk management

disclosure and their risk management systems in place. On 10 May

7

2013 it was reported that AFRASIA Kingdom bank was in a serious

trouble arising from a huge US$ 21 million non-performing loan

which had weakened its financial position(News Day 10 May

2013).This also raises quires over the compliance of banking

institutions with the RBZ Minimum Capital Threshold and its

disclosure as the total capitalisation of Kingdom bank was

reported to be US$ 28.79 million (Monetary Policy statement Jan

2013) yet its non-performing loan was said to be a massive US$ 21

million leaving the bank with US$ 7,79 million as actual capital

in position, while such capital discrepancy only came to public

knowledge after a newspaper report instead of a financial

report or press statement. On the 30th of June 2013 came another

shocking news of the listed Pan-African bank BancABC Financial

holdings when it was reported that the bank had its property

worth US$10 million attached by the Harare Messenger of Court

over a US$ 11million “debt’’ owed to a Belgian diamond company

‘Mackie Diamonds’.It was later uncovered that this occurred after

a diamond deal that went sour between BancABC and one of its

client ,Mr Jamal Joseph Hamed who was said to have been given US$

20 million in 2010 to purchase rough diamonds from Marange.

However Mr Hamed failed to repay the amount leading to the bank

withholding some of the funds amounting US$ 11 million belonging

to Mr Hamed and Mackie Diamonds, who are said to have been part

of the deal. This resulted in the Belgian firm pursuing the

matter through the courts and won the case against Banc ABC.

However further investigations revealed that the US$ 20 Million

8

under-performing loan was never recorded in BancABC books and

also never disclosed in its annual reports since 2010 (Bulawayo

24 NEWS 13 June 2013).

Over the past 10 years there have been recurrent instances of

Zimbabwean Banks collapsing or, being weakened so that the

Reserve Bank of Zimbabwe has had to intervene, pursuit in its

supervisory role on financial institutions. Its interventions

have ranged from forced closure of some banks, placement under

curatorship of other banks to introduction of various regulation

including risk management and its disclosure. However, despite

such controls and measures, the stability of various banks and

security of both investors and depositors funds in those banks

has continued to be uncertain without the disclosure of the risk

managements systems in place.

1.2 Problem statementDespite a progressively intensified monitoring and control of

banking sector by RBZ, are banking and financial institutions

trading on the Zimbabwe stock exchange complying with the Reserve

Bank of Zimbabwe minimum risk and risk management disclosure

requirements.

1.3 Research objectivesThis research aims at providing empirical evidence to the risk

management disclosure as a corporate governance measure of listed

9

banking and finance institutions of Zimbabwe. Specifically, the

objectives of this research are to:

assess whether there is conformity between corporate risk

management disclosure practices in listed banking and

financial institutions and the RBZ Minimum Disclosure

Requirements in risk management disclosures.

Investigate the level of risk management disclosure of

financial instruments information among listed banking and

financial institution in Zimbabwe from 2009 to 2012.

examine whether listed banking institutions of Zimbabwe are

providing more information than statutorily required in

their annual financial reports

assess the extent of implementation of Basel 2 in Zimbabwe

listed banking institutions

are there consequences associated with failure to meet the

RBZ Minimum Disclosure Requirements faced by listed banking

institutions in Zimbabwe.

1.4 Research questions1. What is the extent of compliance of listed banking

institutions in Zimbabwe with the required disclosures of

the Reserve Bank of Zimbabwe minimum risk and risk

management disclosures?

10

2. Is there conformity between corporate risk management

disclosure by Zimbabwe’s listed banking institutions and

stipulated Minimum Disclosure Requirements

3. Do listed banking institutions in Zimbabwe disclose

discretionary risk management information than required?

4. What is the extent of Zimbabwean listed banking institutions

in implementing the Basel 2

5. What are the consequences of non-compliance with Reserve

Bank of Zimbabwe Minimum Risk Management Disclosure

requirements?

1.5 Significance of the studyCompulsory and voluntary disclosure of financial information in

corporate annual reports and their determinants have attracted

considerable research attention in the developed countries than

developing ones (Akhtaruddin, 2005 ).Alan Edkins (2009) studied

risk disclosure and re-establishing legitimacy in the event of a

crisis, this research was focused on a case of Northern rock

building society United Kingdom. Dennis Taylor (2011) carried out

a research on corporate risk disclosure and the influence of

institutional shareholders and audit committees. Allen. N.

Berger, Thomas Kick and Klans Schaeck studied the effect of

executive board composition (gender, educational qualifications,

age and their areas of specialisation with risk disclosures. Dirk

Horing and Helmut (2011) carried out an investigation on risk

disclosure practices in the European Insurance Industries. Dr11

Yainis Anagonostopolus and Rosemary Skordoluis (2009) researched

on the risk disclosure policies in Greek Banking industries

including both listed and non-listed banks. The research findings

in the developed countries especially in the European Union (EU)

have aided the government of these nations to revamp their risk

and risk management compliance mechanisms. They have also

assisted the government in issuing out directives that facilitate

the harmonization process and invariably bring all community

companies up to a reasonable level of disclosure. However these

studies and their findings may not be applicable in African

Countries and Zimbabwe in particular as they were carried out in

different economies, political set up, cultural, educational and

literature development. Only a handful of studies have been

carried out in developing countries (Africa) relating to issues

of disclosure practices in risk and corporate governance issues.

Jackie Young studied (2011) Corporate Governance and risk

management a South African perspective. The disclosure of

operational risk in Tunisian companies was conducted by Weal

Hemrit and Mournira Ben Arab (2011).

In Zimbabwe only a single study was conducted by Jacob Mavingi

who researched on Merchant banks and conformity to International

best practices in risk management. The research was conducted

through a survey method by administering questioners and

conducting interviews to targeted individuals working in those

merchant banks. In all these researches they have concerned with

corporate attributes and their effect to risk disclosures and

12

without any agreed concrete conclusion or result in those studies

as different researchers argued the results of others. Corporate

risk management disclosure has remained under researched

especially on listed financial institutions in Africa and

Zimbabwe. Therefore, the following have been identified as the

gaps that currently exist in knowledge.

There exist no comprehensive study on the compliance of

the listed Zimbabwe’s banking and financial

institutions with risk and risk management disclosures

in relations to corporate governance practices.

The analysis of previous researchers was mainly focused

on corporate attribute and risk taking and disclosure

while risk management has been left out in these

researches.

The rapid changes in risk and risk management

disclosure regulations, growing awareness on corporate

governance and stakeholder relations calls for a

constant update.

This study aims to fill the current gap observed by considering

the following:

Current annual reports for the year ended December 2012

Regulatory requirements in risks disclosures operational at

the time of the research both local and international

Risk and risk management disclosures in relationship to

corporate governance in banking and financial institutions

13

The role being played by regulatory institutions in ensuring

that firms are in compliance with risk disclosures

requirements and consequence for non-compliance

Opinions and views of regulatory officials and users

financial reports on the risk and risk management disclosure

practices of listed financial institutions in Zimbabwe

As Zimbabwe is a developing country and its risk management and

disclosure practices are still at an emerging stage. Academic

literature in risk reporting field is limited or currently

unavailable, therefore this research is expected to be one of the

fundamental study on current risk reporting and management

practices in the banking and financial sector of Zimbabwe.

Research on risk management disclosure in banking sector of

Zimbabwe will enable students and professionals already in the

industry to have a thorough understanding of the nature of

corporate risk management disclosure in developing countries and

enhance the quality of literature in the subject in matter.

The study will pave way for other researchers to further

investigate other topics related to risk management disclosures

and factors that influence the practices.

This research is also of significant to the government,

investors, business management, regulatory bodies, educators,

researchers, accountants, auditors and scholars particularly in

the field of banking, finance, accounting and risk management as

it will cast more light and add understanding on corporate risk

14

management disclosure in relation to corporate governance

practices.

1.6 Assumptions of the studyThe research on disclosure of risk management as a corporate

governance practices was conducted under the following

assumptions

If companies were to convey risk management information to

shareholders, the annual report would be only logical and

practicable choice of media.

This research effectively assumes that if any of the listed

financial institutions under review fails to report any

assessed risk or risk management disclosure requirement it

is simply non-compliant with the particular required

disclosure.

1.7 Scope of the study The concept of disclosures in this research will be limited to

risk and risk management disclosures

The study will be focused on listed financial institutions as

they are regulated by the Zimbabwe Stocks Exchange Act,

Securities Act, Banking Act and are the one which are mandated to

publish annual reports these banks ABC Holdings, CBZ Holdings, ZB

Holdings, FBC Holdings, Barclays Bank Zimbabwe and NMB bank

15

The study will focus on the information that have been published

in annual reports of the trading period from 2009 to 2012 as this

time was characterised by low inflation rates, stable political

environment and a multi-party government as well as the multi-

currency system

Secondly the research on the annual report will be confined to

the risk management disclosures section of the annual report of

firms chosen in the sample. Banking institutions not listed on

the Zimbabwe Stock exchange are not taken into consideration as

they are not of paramount interest to the investors and are

outside the scope of this work.

1.8 Limitations of the studySample size was small as the banks that were involved in the

study were the one that were listed on the Zimbabwe stock

exchange on the closing day of 30 June 2012.As a result the study

findings may not be generalised to other banks not listed on the

stock market.

Another limitation of the study arise from the use of content

analysis which tend to be inevitably subjective and results may

not be generalised (Linsley and shrives, 2006) there for the

study resort to triangulation using both primary and secondary

data to ensure validity

16

1.9 Chapter summaryThis chapter was an insight into the topic of the research in

terms of background of the study, in an attempt to pinpoint the

need to investigate the risk management disclosure. In this

chapter main elements that will guide the study were outlined

which are statement of the problem, research objectives,

significance of the study, research questions, the scope of the

study, assumptions as well as limitations of the study. The

following chapter (two) will review the literature that the

researcher used to gain knowledge in risk and risk management

disclosures as well as corporate governance in particular.

CHAPTER 2

LITERATURE REVIEW

2.0 IntroductionThis chapter aims to put the study into context by discussing a

wide range of literature the researcher devoured before and

during the research process. In the chapter an overview of the

following will be provided so as to enhance the readers

appreciation of the subject under study ;the legal frame work17

that govern companies in Zimbabwe in comparison with other

foreign mechanisms, those that govern listed firms and banking

institutions. These comprise the Companies Act, Banking Act,

Securities Act, RBZ regulations and requirement, IFRS, Basel 2

convention, with particular emphasis on the risk and risk

management disclosure regulatory framework. The chapter also

discusses risk management disclosure theories corporate

governance implementation practices and the motives behind

compliance and non-compliance with risk management disclosures.

2.1 The concepts of riskRisk in this study is conceptualised as a hazard, threat, harm or

expected loss that might affect the business or its operations

(Lupton, 1999).Risk is a potential that events expected or

unanticipated, may have an adverse effect on the banking

institution’s net worth (capital), earnings, set goals and

objectives (RBZ –Risk-Based supervision Policy 2006).Risks that

are faced by banks can be categorised as financial and non-

financial risks. Jorion (1997) defined financial risks as risks

that have an immediate effect on assets and liabilities in

monetary term. Types of financial risks comprise of credit risk,

market risk, foreign exchange risk, interest rate risk, liquidity

risk, and non-financial risks are strategic, reputational,

operational risk, legal compliance risk and operational risk

(BSBC 2001).

18

2.1.1 Risk managementRisk management is the mitigation or measures that are put in

place by the directors or senior management to identify, measure,

monitor and control risk so as to reduce the negative impact of

or eliminate possible risks Identified (Bessis 1988; Fischer and

Veilmeyer, 2004). According to COSO (2004) "risk management is a

process, affected by an entity's board of directors, management

and other personnel, applied in strategy setting and across the

enterprise, designed to identify potential events that may affect

the entity, and manage risk to be within its risk appetite, to

provide reasonable assurance regarding the achievement of entity

objectives(COSO,2004). Mertens and Blij (2008) defined risk

management as all activities and measures which are aimed at

controlling risks. In this regard the focus of risk management is

on prevention of the adverse effects of threat in the event they

occur.

2.1.2 Risk management disclosureBaretta and Bozzolan (2004) defined risk disclosure as the

communication of information concerning firms' strategies,

characteristics, operations and other external factors that have

the potential to affect expected results. Risk and risk

management disclosure is therefore the dissemination of or

publication of risks that might negatively affect a particular

bank and risk management systems that are being implemented

19

through annual financial report. In particular, more information

regarding banks’ risk profile is highly demanded, as this would

help stakeholders to better evaluate the risk exposure of a

certain bank and measures implemented to tackle it (Linsley and

Shrives 2005; Tricker, 2009).

2.2 Previous research findings on risk and risk managementdisclosuresIn a study conducted by Angela Ma et al (2012), using a sample

all 300 listed companies on the Australian Stocks Exchange

identified the following (a) 90 per cent simply documented

phrases in their annual reports regarding regulatory changes to

express the management’s willingness to comply with all

regulatory and statutory requirements. In view of this extract it

highlights that only 10 per cent of listed firms in Australia

provided detailed information pertaining to legal and compliance

risk management with Australian Stocks Exchange Corporate

Governance Practices requirements.

In Italy, a research in the annual reports of 85 listed companies

on the Italian stock exchange by Beretta and Bozzolan (2004)

discovered that Italian institutions willingly disclosed their

future risk management strategies (35.9 %),however, expected

effectiveness of implementing those strategies were rarely

disclosed thus only (15.5%) communicated such information. In the

same study it was found that Italian annual reports lacked

information about decisions and actions taken to manage risks as

20

evidenced by only 16.2% of all firms to be disclosing such

information.

A study by Kongprajya (2010) in Thailand of 30 listed companies,

conclude that Thai companies financial risk disclosures were the

most popular among all types of risk disclosures. This was

further explained by the fact that "financial risk is complex to

understand as they are usually related to technical terms and

sometimes sophisticated calculations (Kongprajya, 2010).

Therefore financial risks are assumed to require more

clarification as compared to other types of risks which are also

referred to as non- financial risks.

Research findings by Carlon et al (2000) of an examination of

annual reports of 54 Australian companies in the mining industry

discovered variations in the level and detail of voluntary risks

disclosure. In another study which recorded similar results

reported by Lajili and Zaghal (2003) that examined annual reports

of 300 listed Canadian companies and discovered voluntary risks

disclosures in annual reports are presented in qualitative nature

lacking specificity and detail or depth. A study by Woods and

Reber (2003) who conducted an investigation on the risk

disclosures of six German institutions and six British companies

for the year 2000 and 2001 respectively conclude that there was

an increase in risk disclosures by German companies after GAS 5.

In another separate study by Mousa and Elmar using content

analysis of 48 companies listed on the Bahraini Capital Market

21

reported that interest rate disclosures were dominant in in both

financial risk sections while operational risk was common in non-

financial risk section.

These previous study triggered the need to enhance knowledge in

this area of study at a local level, by investigating the

disclosure practices in risk and risk management in Zimbabwe’s

banking and financial institutions listed on the stock market.

2.3 Corporate Governance in Zimbabwe and risk management disclosure in comparison with other countriesCorporate operations in Zimbabwe are governed by the Common Law

which has some elements of the Roman-Dutch Law (Tsumba, 2002).

Corporate Law is engraved in the Companies Act of 1951 of which

every organisation that operate in Zimbabwe is expected to

conduct its business in line the Companies Act chapter 23:04

regardless of their size, nature of industry or whether private

or public corporation. For companies that wish to or trade on the

Financial market they are further mandated to comply with the

listings requirements embedded in the Zimbabwe Stock Exchange Act

Chapter 24:18 and the Securities Act Chapter 24:25 of 2010 which

was issued by the Securities Commission of Zimbabwe .Apart from

the three mentioned Acts of law Financial institutions whether

incorporated in Zimbabwe or in another countries are subject to

the Banking act Chapter 24:20.

22

2.3.1 Companies Act The Companies act Chapter 23:04 is the one which vested fiduciary

duties of the directors’ to conduct their work in utmost most

good faith on behalf of shareholders. Company directors are held

accountable for any event arising in their exercise of duties

during their tenure of office. Thus the interest of the

shareholders comes first in their day to day execution of duties.

Zimbabwe's Companies Act requires company accounts to be prepared

in accordance with the adopted IFRS 7, there for even the annual

financial statements should also be prepared in line with the

same principles.

Zimbwa (2005) argued that the Companies Act stipulates only the

basic minimum requirements thus disclosure rules are supplemented

by pronouncements of the professional accountancy body the

Institute of Charted Accountancy of Zimbabwe (ICAZ). Implicitly,

the Companies Act requires published financial statements to be

factually correct and presented in all material respects in

accordance with the generally acceptable accounting practice

Stephen (Owusu-Ansah, 2000).In the same study of Owusu-Ansah

(2000) argued that the Companies Act of Zimbabwe does not

mandate the disclosure of risk management.

The lack of a clear section of law that deal with requirements

of risk management disclosures pose problematic in information

reporting, thus polarise the practices of risk reporting in

general and good governance in particular. Risk management

disclosures recommended in Accounting standard do not stipulate

23

their strict compliance and the dissemination of such information

are left at the discretion of managers. While this is a critical

governance issue absence of an act of law means good governance

will not flourish in the country. In comparison to South

Africa’s Companies Act which adopted the King 3 report and made

it mandatory that institutions must apply the codes in their

financial statements.

The success of the King report in more recent time is a result of

a significant decision which was made to incorporate the King

Report into the South African Companies Act. Under this regime

disclosures became mandatory and breach of which attracts penalty

for the contravention of a statutory regulation. In light of the

resurgence of financial institutions failures of 2001, 2004 and

recent scandals in financial sector of 2013 which are associated

with poor risk management. A stringent arm of Law can help in the

restoration of sanity in the Zimbabwean finance sector.

In Germany as a response to infamous corporate crisis and

failures, the German government passed the legislative law on

Corporate control and Transparency “KonTrag-Gestez zur Kontrolle und

Transparenz im Unternehmensbereichamendedss” (Durst, 2005).Germany

banks are required to disclose their risk exposure that are

regulated by the articles 289(1) and 315(1) in the HGB and the

German Accounting Standards GAS 5-10:representing a legislative

standard that is unique in the world so far (Homolle, 2009).GAS 5

require institutions to report information about their risk

24

management system, qualitative and quantitative data on relevant

risks. The German Accounting standards also requires disclosures

about risk forecast and relevant accompanied information which

are compulsory, referring to GAS 5.9-10,5.18,15.83-91

(Dobler,2008). This shows a sharp distinction from other

accounting standards which only recommend these disclosure and

not require them. Under GAS the reporting of risks facing an

institution must include non -financial risks and non-market

risk. Further it also requires the explanation of corporate risk

management and risk forecast.

It is such firm stance toward good governance that need to be

factored in the Companies Act of Zimbabwe that can help to

enforce the disclosures of risk management while spearheading

good governance in the business environment.

2.3.2 Zimbabwe Stock Exchange Act Chapter 24:18For companies wishing to trade their securities on the stock

market in Zimbabwe are further obliged to abide with listings

requirements of the Zimbabwe stock exchange Act. Listings rules

require that annual published accounts report certain information

in addition to that demanded by the Companies Act. For instance

institutions annual reports must disclose the aggregate of the

direct and indirect interests of directors in the share capital

of listed company, distinguishing between beneficial and non-

beneficial interest (s.8.52 (d)). Companies trading on the stock

25

market are mandated to disclose relevant material information

necessary to help present and potential investors to evaluate

their financial position and performance. Zimbwa (2005) argued

that corporate governance disclosures are largely voluntary on

the stock market; citing that there are no provisions in the

Zimbabwe stock Exchange Act regarding the disclosure of or

discussion of risk management in annual reports, though strongly

encouraged by the accounting profession.

In comparison the Emirates Securities and Commodity Market

Authority (ES&CMA) listing conditions encourage organisations to

disclose risk-related information with an appropriate level of

transparency "UAE Federal Act NO.4 OF 2000"(Hassan, 2012).The

ES&CMA also passed the UAE Code of Corporate Governance that

encourages as part of best practice, to have regular procedures

allowing for the determination, measurement and disclosure of

their risks (Khaleej Times, 2006) and (ES&CMA decision R/23,

2007).The participation of securities market in corporate

governance is required in Zimbabwe to encourage corporates in

adoption of good governance practices. The effort that arises

from stock market regulatory authorities is likely to yield quick

and successful results in restoration and maintenance of

corporate governance practices as well as market transparency.

Another mechanism of risk management disclosures regulation that

is lacking from the Zimbabwe’s stock market is that of Novo

Mercado of Brazil which is an independent body from Bovespa Stock

26

Exchange. This requires companies to comply with more rigorous

corporate governance standards relating to shareholders rights

and transparency. Under the Novo Mercado’s rules shareholders may

submit any disputes relating to the listing rules to binding

arbitration in Brazil. These provisions give shareholders of Novo

Mercado’s companies a forum entirely separate from the Brazil

judicial system to seek redress for violations of their rights as

shareholders” (Milstein et al, 2005). The Novo Mercado regulation

system exhibit how the stock exchange can be a strong tool to

enforce corporate governance codes or practices in emerging

markets like Zimbabwe, even when the judicial and legal systems

are inefficient. The calibration and reformation of stock

exchange rules is relatively simple than for Companies Acts.

Rather more essentially, the threat of delisting enable the stock

exchange with distinct ability to enforce compliance with the

regulations set by other institutions that seek to install and

maintain market discipline.

The stocks exchange is endowed with a unique self -enforcement

capabilities to impose sanctions. This ability of stock exchanges

to act as enforcers in their own right is demonstrated by the

London Stock Exchange adoption of Cadbury Report as part of the

listing rules which mandate institutions to comply with corporate

governance codes recommendations or publicly explain the reasons

behind their non-compliance (Millstein, et al, 2005). One of the

Listings Agreements of the India Stocks Exchange is that

Independent directors shall periodically review legal compliance

27

and as well as the boards disclosures on risk management.

Millstein, et al (2005) put forward that Stock exchange listings

requirements can adopt voluntary standards so as to ensure that

corporates do adhere to them as stocks exchange enjoys monopoly

therefore they have more enforcement powers.

Absence of risk management disclosures in the rules and listings

requirements on the Zimbabwe stock market plays down the effort

to attain good governance. Thus there is need to adopt from other

countries mechanisms that are being implemented to ensure fluent

implementation and success of the good governance.

2.2.3 Securities Act Chapter 24:25The securities Act Chapter 24:25 of 2010 took a great stride

trying to foster corporate governance practices in Zimbabwe in

which risk management disclosures are recommended. The Securities

Act corporate governance guide lines for listed companies was

composed in line with the Cadbury and the Combined Codes of

United Kingdom, King 1, 2 and 3 of South Africa and Commonwealth

Association for Corporate Governance (CACG).The objectives of

this Act is to reinforce corporate governance practices by listed

institutions and foster the standards of self-regulation so as

their governance to be in line with the international standards.

In section 3:4 of the Securities Act on accountability and audit

stated that “the board should ensure that the financial

statements are presented in line with the international financial

28

reporting standards (IFRS) adopted in Zimbabwe”. Thus there

should be no divergence of reporting in annual financial

statements of listed institutions. Under section 3.4.1 the board

is required to maintain a sound system of internal controls to

safeguard the shareholders investments and assets. However the

Securities Act like other companies regulatory frameworks in

Zimbabwe remains silent on risk management disclosures in annual

reports.

In comparison with Canada the provincial securities commissions

have set out requirements for disclosure and discussion of risks

in annual reports. According to the guidelines, Canada's Ontario

securities Commission 2008 requested the disclosure of

information on the enterprises main risks as well as the

consequences of these for corporate activities and performance

and also the strategies implemented to manage them (Dia and

Zeghal, 2012).These measure are in recognition of the fact that

governance issues need to be enforced through the use of a

securities market mechanism that have direct contact with

institutions through listings requirements and listings

continuation.

Section 1.7 of the Securities Act stated that “every registered

institution must disclose in its annual reports and statements of

directors as to whether the corporate body is complying with

these guidelines on corporate governance, while section 1.8

stated that “where a registered institution is not in full

29

compliance with these guide lines the directors must indicate the

steps the company will take to adhere to full compliance”.

Governance issues are not mandatory as shown by the “Comply or

explain” approach which lack penal sanction. While in Malaysia,

the listing requirements of 2001 delineate the requirements for

financial reporting disclosures matters relating to corporate

governance and continuing listing obligations. Companies are

subject to fines and sanctions by Bursa Malaysia. Malaysian

Securities of Commission (SC) issued statutory legislations such

as The Bursa Malaysia Listing Requirements (Abdullah and Chen,

2010). Furthermore the Bursa Malaysia Listing Requirements

mandate all listed companies to disclose their compliance with

The Code on Corporate Governance of Malaysia in their annual

reports. Such an initiative is profoundly significant to

reinforce the effectiveness of internal governance in line with

corporate governance code (Abdullah and Chen, 2010).Thus the

recognition of the importance of compliance with governance

recommendations by Bursa Malaysia (Malaysia Stock Exchange)

strengthened compliance, improve market discipline and promote

transparency at institutional level.

In U.S.A companies are required by the Securities Exchange

Commission to disclose key information about their risk

management practices Item 305 of SEC Regulations S-K Quantitative

and Qualitative Disclosures about Market Risk (Lijili and Zeghal,

2005). This is another development from established markets were

30

the securities commission plays a pivotal role in warranting

success of good governance on the market.

Implementation of good governance codes can be successful in

Zimbabwe when there exist multi-lateral and mandatory regulations

which constantly monitor progress and educating senior management

to raise their awareness and knowledge on the need to disclose

risk management and how they can be disseminated in a clear way.

The discussion aimed to shed light on the regulations that govern

corporate activities as well as highlighting their weakness in

the good governance and risk management in particular. Other

foreign regulations that have been implemented in a bid to

enhance good governance and their possible effect they may render

if adopted in Zimbabwe were also reviewed.

2.3 Corporate governance in banking and financial institutions ofZimbabweIn Zimbabwe banks has gone through two different phases. Since

independence in 1980-1990 banks operated under quasi-command

economy in which the government had control of the financial

sector (Tsumba, 2002). Corporate governance though still

important was not given much attention it deserved. Monetary

policy and bank supervision were conducted in a passive manner as

the controls in place at that time ensured that risks were kept

at minimum levels. Such controls however limited the activities

of banking sector. While the Reserve bank undertook limited

31

supervision of banks during the 80s era, it is not surprising

that the country never experienced banks failure at all. Banks

profitability and viability were warranted as there was no

competition in the financial sector. Thus corporate governance

was not a cause to concern for banks as their customers were

guaranteed a return under the cost plus pricing that was in

place. In light of this there was no incentive to insist on sound

corporate governance principles on banks (Tsumba, 2002).

The financial sector reforms of 1991 lead to the removal of the

command system of economy and pave way for the entrance of many

institutions in the financial sector. Deregulation of the

financial sector heralded the advent of new players such as

commercial banks, discount houses and later by asset management

companies. During the period from 1991 to 2000 there exist few

regulatory frame works meant to govern financial sector in

particular. Onsite examination was introduced in 1996 by the

central bank with the primary focus on the commercial and

merchant banks (Tsumba, 2000). In 2000 the government of Zimbabwe

enacted the Banking Act Chapter 24:20 to regulate the financial

sector.

2.3.1 The Banking Act 24:20In section 45 (1) Banking Act provided the Reserve Bank of

Zimbabwe with strong, legal basis for supervising financial

institutions to ensure that they comply with the Act. Section 45

32

(2) empowered the Central bank with functions of monitoring and

supervising banking institutions through analysis of documents

and information supplied to it and obtaining of information at

the premises of the banking institution concerned.

2.3.2 The RBZ Code 1After a series of financial sector crisis in Zimbabwe, the

Central bank using its mandate from the Banking Act issued

Guideline/Code 1-2004 of corporate governance. The major

highlight of the code1 principles were (1.51) Risk management,

(1.5.3) High quality financial disclosures, (2.1) authority and

duties of shareholders, leadership of the banking institution,

role and functions of the board and duties and responsibilities

of the board. Zimbwa (2005) argued that code1 was marred by

presence of vague statements which were not worth abiding with as

they were not likely to change corporate governance in practice.

Further the author pointed out that lack of enforcement of the

code to succeed as well as being published, while leaving its

adoption to the discretion of those institutions which had come

across with the code.

An analysis in other Codes originating from Central banks of

other countries in monitoring corporate governance frameworks in

Malaysia for example; the Code on Corporate Governance was

approved by the Ministry of Finance (Norman et al, 2005) and it

was released by the Securities Commission and enforce by The

Stock Exchange Requirement (Abdullah and Chen, 2010). Such a

combined force of regulatory institutions in support of Corporate

33

Governance code is essential in any country that is eager to

implement a Code that will face a relatively weak resistance and

eventual success. However absence of such a will power from

Zimbabwean Government and the Market Regulatory body can be a

stumbling block toward attainment of market transparency goal and

efficient banking sector. Tsumba (2002) argued that the

Zimbabwe stock exchange does not support institutions that seek

to promote market discipline citing the Johannesburg stock

exchange adoption and support of the King report in 1994 which

was initiated as a private business initiative by Institute of

directors of South Africa and it was made part of listings and

listing continuation requirements .While implementation of Good

Corporate Governance is voluntary in Zimbabwe

Also in comparison with United Arab Emirate (UAE) regulatory

framework which impose mandatory requirements that exert pressure

on listed institutions to publish risk information in their

annual reports. The UAE securities market listing conditions

require the disclosure of risk-related information (Hassan,

2012).The UAE Central Bank regulations compel UAE financial

institutions to incorporate risk information in their annual

reports (Central Bank of UAE,2006 and Al-Taminmi ,2008).However,

the scope or extent of that disclosure is at the management

discretion (Obay,2009) In the UAE, the Emirates Security and

Commodity Market Authority(ES&CMA) and UAE Central Bank issues

regulations or guidelines that affect risk disclosures.

Furthermore the UAE Institute of internal Audit (IIA-UAE chapter)

34

share information to enhance knowledge about risk reporting among

different institutions. Thus the partnership between different

regulatory institutions in advocating for risk management

disclosure is essential to promote the desire to adopt practices

which are considered as worth of implementing.

2.4 Development and implementation of corporate governance and challenges adopting codesTo date Zimbabwe has not yet produced its own code of corporate

governance; codes that are currently in use were adopted from

other states. Though the business leaders in Zimbabwe has

undertaken effort to come up with locally produced codes, the

document under construction is more of a blue print of the King 2

and Cadbury report in particular. The Zimbabwean situation calls

for the exercise of caution against code "transplanting" from

established to developing economies or from one state to another

ignoring factors such as ownership, control structures and the

economic environment that influence institutions and behaviour.

Wong (2008) mentioned that many codes sit on the shelves of their

drafters because no local institutions have assumed any

leadership role in promoting their implementation. Lack of

support from the government and regulatory authorities has

contributed in hampering the successful development,

implementation and enforcement of corporate governance in

Zimbabwe.

35

Clearly demarcated lines between legislation and provisions must

be drawn to facilitate prohibition of pernicious behaviour by

management and board members by law. The problem associated with

lack of compliance with the corporate governance principles lead

to development of measure in various countries in a bid to ensure

compliance. A number of approaches to ensure success of corporate

governance were designed and implemented which consist of the

“comply and explain” approach of the UK and legislation of the

Sarbanes Oxley Act of the USA.

2.4.1 “Comply or explain” principleThe “comply or explain” also known as “if not why not” was

pronounced in United Kingdom in 1992 upon introduction of the

Cadbury report as to how it will work. The essence behind the

principle is that compliance with the code is not mandatory, but

that disclosure relating to compliance is (Macneil and Li, 2006).

Securities Commission of Zimbabwe adopted the same principle as

to apply to Securities Act Chapter 24:25 of 2010.In the act it

was stated that every listed institution has to disclose in

annual reports if they did not comply with the codes. Thus in its

nature the code’s principles are not mandatory to abide with but

only disclosure of non-compliance is mandatory.

The "comply or explain" code allows for companies not to comply

with the recommendation if they can prove that good governance

can still be attained. Thus success of the whole document is then

36

left in the hands of directors as to whether they wish to

implement the codes or they will choose to ignore then explain as

to why they did not comply with the principle. “Governance codes

have proved popular because they are seen as flexible instruments

that rely on market mechanism for their development,

implementation, enforcement and subsequent evolution; in contrast

to the more rigid and prescriptive nature of mandatory

legislation and regulation, corporate governance codes not only

accommodate-but in fact expect-some degree of non-compliance with

their provision” (Wong, 2008). Companies are not expected to

follow all provisions on a one size fit all basis, rather where

individual rules are not appropriate for a particular

organisational settings, companies are expected even actively

encourage to, deviate (D.seidl et al, 2012).The Combined Codes

for instance explicitly stated that: “Whilst shareholders have

every right to challenge companies' explanations if they are not

convincing ,they should not be automatically be treated as

breaches (Financial Reporting Council, 2006)

This further weakens the position of adopting a “comply or

explain” approach when dealing with corporate governance as it is

non-legislative. If the principles laid down in the codes are to

succeed as a result of public sympathy there is no point for them

to be accepted and implemented as they are a mere recommendation

instead of a mandate. Another point is the “box ticking”

reporting manifest under “comply or explain” regime.

37

Successful development and implementation of corporate governance

in UK through a “comply or explain” approach on addressing

governance issues in place of regulations was attributed to many

factors that characterised the UK market. These factors consist

of the long history of self-regulatory of the United Kingdom’s

institutions such that the Cadbury report was accepted by many

institutions, “ with a tradition of self-regulation stretching

back hundreds of years the UK provides a highly conducive

environment for voluntary codes” (Wong, 2008).Differences in

culture and tradition in various countries means the success of

corporate governance codes based on culture of voluntary self-

regulatory cannot be guaranteed outside United Kingdom

specifically in Zimbabwe where the topic of corporate governance

is still at infancy stage. Secondly Wong (2008) stated that the

UK media plays a pivotal role in information dissemination on

matters to do with compliance, soon after information on code

compliance is published through annual financial statements, the

British media plays an important role in analysing it and

informing investors of significant codes breaches (Wong,

2008) .Fear of such media onslaught means institutions in the

United Kingdom are compelled to comply with corporate governance

codes to avoid media attention. Such kind of mechanism does not

prevail in all countries as each nation got particular topic that

get more attention. Therefore if the role of media is essential

for success of a code it will remain effective in UK until such a

time when all countries experience the same development in media

38

fraternity. Furthermore Wong (2008) added that the high number of

institutional-medium to long term investors plays a pivotal role

in ensuring that listed institutions are in compliance with code.

Institutional and long term investors are the one who are more

concerned with how corporate governance is adhered to as they

invest large amounts of funds and for long period so they want to

be satisfied that proper governance is in place to guarantee a

return on their investment and the safety of their funds. Based

on such mentioned factors “comply or explain” principle cannot

guarantee a successful development and implementation of

corporate governance in other countries such as Zimbabwe in

particular, given absence of conducive environment which enable

the success of self-regulatory regulations.

2.4.2 Legislation of corporate governance codes “Governance codes have proved popular because they are seen as

flexible instruments that rely on market mechanism for their

development, implementation, enforcement and subsequent

evolution; in contrast to the more rigid and prescriptive nature

of mandatory legislation and regulation, corporate governance

codes not only accommodate-but in fact expect-some degree of non-