Embed Size (px)

Citation preview

21 November 2017 Strategy Research

Securitization Market Watch

UniCredit Research page 1 See last pages for disclaimer.

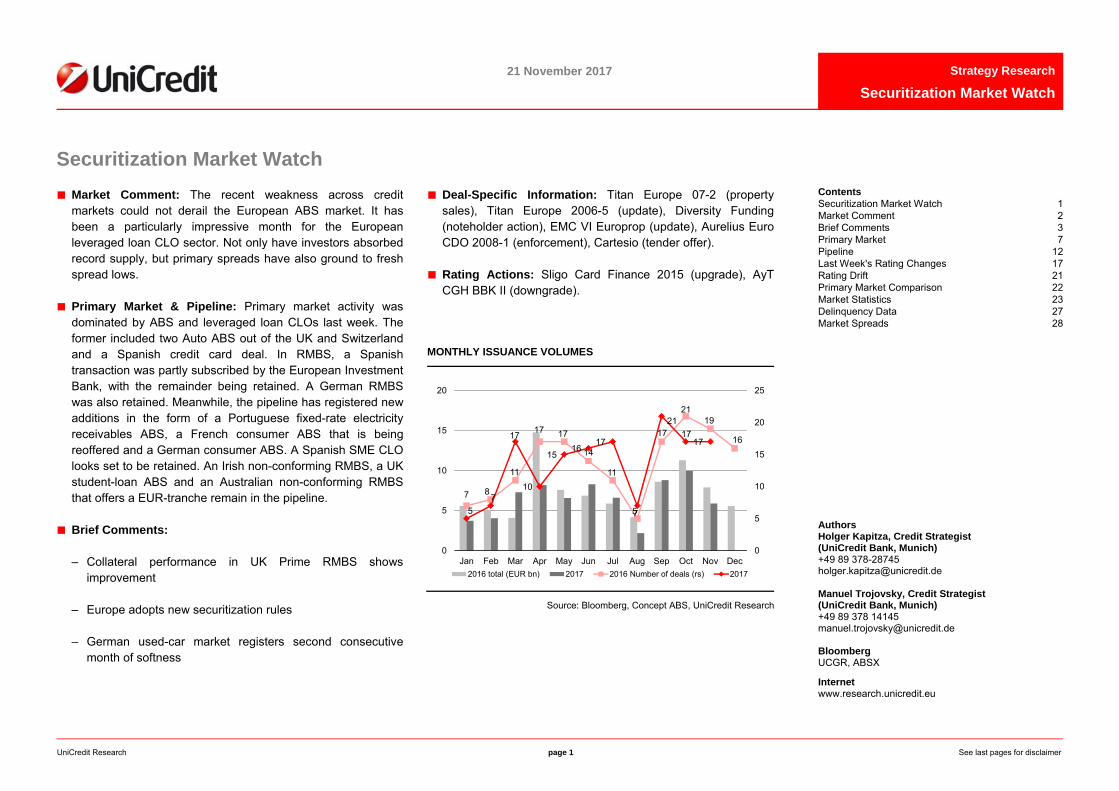

Securitization Market Watch ■ Market Comment: The recent weakness across credit

markets could not derail the European ABS market. It has been a particularly impressive month for the European leveraged loan CLO sector. Not only have investors absorbed record supply, but primary spreads have also ground to fresh spread lows.

■ Primary Market & Pipeline: Primary market activity was dominated by ABS and leveraged loan CLOs last week. The former included two Auto ABS out of the UK and Switzerland and a Spanish credit card deal. In RMBS, a Spanish transaction was partly subscribed by the European Investment Bank, with the remainder being retained. A German RMBS was also retained. Meanwhile, the pipeline has registered new additions in the form of a Portuguese fixed-rate electricity receivables ABS, a French consumer ABS that is being reoffered and a German consumer ABS. A Spanish SME CLO looks set to be retained. An Irish non-conforming RMBS, a UK student-loan ABS and an Australian non-conforming RMBS that offers a EUR-tranche remain in the pipeline.

■ Brief Comments:

– Collateral performance in UK Prime RMBS shows improvement

– Europe adopts new securitization rules

– German used-car market registers second consecutive month of softness

■ Deal-Specific Information: Titan Europe 07-2 (property sales), Titan Europe 2006-5 (update), Diversity Funding (noteholder action), EMC VI Europrop (update), Aurelius Euro CDO 2008-1 (enforcement), Cartesio (tender offer).

■ Rating Actions: Sligo Card Finance 2015 (upgrade), AyT CGH BBK II (downgrade).

MONTHLY ISSUANCE VOLUMES

Source: Bloomberg, Concept ABS, UniCredit Research

Contents Securitization Market Watch 1Market Comment 2Brief Comments 3Primary Market 7Pipeline 12Last Week's Rating Changes 17Rating Drift 21Primary Market Comparison 22Market Statistics 23Delinquency Data 27Market Spreads 28

Authors Holger Kapitza, Credit Strategist (UniCredit Bank, Munich) +49 89 378-28745 [email protected] Manuel Trojovsky, Credit Strategist (UniCredit Bank, Munich) +49 89 378 14145 [email protected] Bloomberg UCGR, ABSX

Internet www.research.unicredit.eu

7 8

11

17 17

14

11

5

17

2119

16

57

17

10

1516

17

7

2117

17

0

5

10

15

20

25

0

5

10

15

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 total (EUR bn) 2017 2016 Number of deals (rs) 2017

21 November 2017 Strategy Research

Securitization Market Watch

UniCredit Research page 2 See last pages for disclaimer.

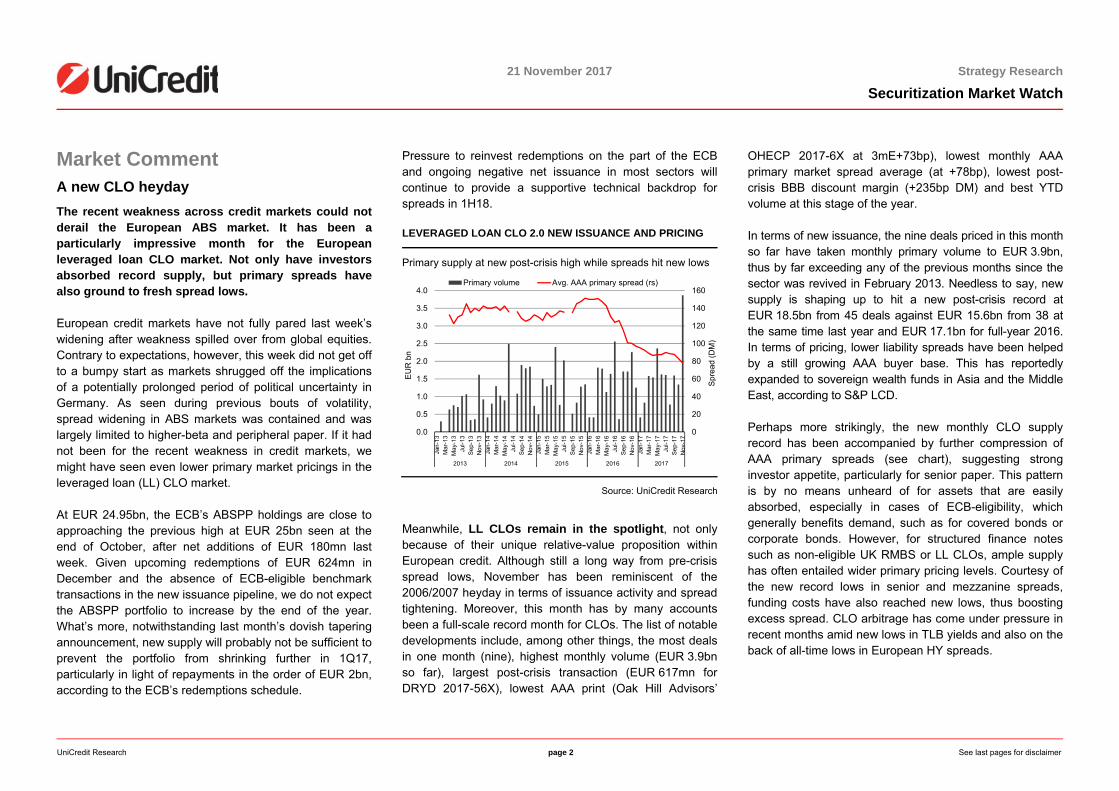

Market Comment A new CLO heyday The recent weakness across credit markets could not derail the European ABS market. It has been a particularly impressive month for the European leveraged loan CLO market. Not only have investors absorbed record supply, but primary spreads have also ground to fresh spread lows.

European credit markets have not fully pared last week’s widening after weakness spilled over from global equities. Contrary to expectations, however, this week did not get off to a bumpy start as markets shrugged off the implications of a potentially prolonged period of political uncertainty in Germany. As seen during previous bouts of volatility, spread widening in ABS markets was contained and was largely limited to higher-beta and peripheral paper. If it had not been for the recent weakness in credit markets, we might have seen even lower primary market pricings in the leveraged loan (LL) CLO market.

At EUR 24.95bn, the ECB’s ABSPP holdings are close to approaching the previous high at EUR 25bn seen at the end of October, after net additions of EUR 180mn last week. Given upcoming redemptions of EUR 624mn in December and the absence of ECB-eligible benchmark transactions in the new issuance pipeline, we do not expect the ABSPP portfolio to increase by the end of the year. What’s more, notwithstanding last month’s dovish tapering announcement, new supply will probably not be sufficient to prevent the portfolio from shrinking further in 1Q17, particularly in light of repayments in the order of EUR 2bn, according to the ECB’s redemptions schedule.

Pressure to reinvest redemptions on the part of the ECB and ongoing negative net issuance in most sectors will continue to provide a supportive technical backdrop for spreads in 1H18.

LEVERAGED LOAN CLO 2.0 NEW ISSUANCE AND PRICING

Primary supply at new post-crisis high while spreads hit new lows

Source: UniCredit Research

Meanwhile, LL CLOs remain in the spotlight, not only because of their unique relative-value proposition within European credit. Although still a long way from pre-crisis spread lows, November has been reminiscent of the 2006/2007 heyday in terms of issuance activity and spread tightening. Moreover, this month has by many accounts been a full-scale record month for CLOs. The list of notable developments include, among other things, the most deals in one month (nine), highest monthly volume (EUR 3.9bn so far), largest post-crisis transaction (EUR 617mn for DRYD 2017-56X), lowest AAA print (Oak Hill Advisors’

OHECP 2017-6X at 3mE+73bp), lowest monthly AAA primary market spread average (at +78bp), lowest post-crisis BBB discount margin (+235bp DM) and best YTD volume at this stage of the year.

In terms of new issuance, the nine deals priced in this month so far have taken monthly primary volume to EUR 3.9bn, thus by far exceeding any of the previous months since the sector was revived in February 2013. Needless to say, new supply is shaping up to hit a new post-crisis record at EUR 18.5bn from 45 deals against EUR 15.6bn from 38 at the same time last year and EUR 17.1bn for full-year 2016. In terms of pricing, lower liability spreads have been helped by a still growing AAA buyer base. This has reportedly expanded to sovereign wealth funds in Asia and the Middle East, according to S&P LCD.

Perhaps more strikingly, the new monthly CLO supply record has been accompanied by further compression of AAA primary spreads (see chart), suggesting strong investor appetite, particularly for senior paper. This pattern is by no means unheard of for assets that are easily absorbed, especially in cases of ECB-eligibility, which generally benefits demand, such as for covered bonds or corporate bonds. However, for structured finance notes such as non-eligible UK RMBS or LL CLOs, ample supply has often entailed wider primary pricing levels. Courtesy of the new record lows in senior and mezzanine spreads, funding costs have also reached new lows, thus boosting excess spread. CLO arbitrage has come under pressure in recent months amid new lows in TLB yields and also on the back of all-time lows in European HY spreads.

0

20

40

60

80

100

120

140

160

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep-

13N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4Se

p-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Sep-

15N

ov-1

5Ja

n-16

Mar

-16

May

-16

Jul-1

6Se

p-16

Nov

-16

Jan-

17M

ar-1

7M

ay-1

7Ju

l-17

Sep-

17N

ov-1

7

2013 2014 2015 2016 2017

Spr

ead

(DM

)

EU

R b

n

Primary volume Avg. AAA primary spread (rs)

21 November 2017 Strategy Research

Securitization Market Watch

UniCredit Research page 3 See last pages for disclaimer.

This compression took a breather last week, which offered some buying opportunities for CLO managers amid the temporary weakness in secondary leveraged loans on the back of softness in HY and equity markets. That said, the re-pricing was brief and contained and thus of little help to managers ramping up transactions. Moreover, sourcing new loans remains challenging amid the drop in preferred M&A-related financings in the primary and a wave of less-preferred repricings and refinancings. Overall, S&P LCD reports that at 3.19%, the average all-in YTM for BB rated institutional loans in 3Q17 is the lowest it has been in the past twelve months. Single-B new-issue YTM are also hitting record lows, with an average of 3.82% for the three months to the end of October.

Aside from LL CLOs, primary market activity was dominated by ABS last week. In Auto ABS, Close Brothers priced its GBP 309.5mn Orbita Funding 2017-1 plc (ORBTA 2017-1), with the Class A spread being set at 1mL+55bp, in line with guidance. On the same day, Emil Frey Group launched its second leasing deal from its SWMOBI platform, First Swiss Mobility 2017-2 AG. The structure’s CHF-denominated fixed-rate tranches come in 3Y WAL bullet format and printed at coupons of 0% (Class A), 1% (B) and 2% (C). Also in ABS, WiZink Master (WZNK 2017-3), Santander’s Spanish credit card ABS, was also launched. The EUR 200.8mn Class A (AA+/AA high, 3Y WAL) was priced at 1mE+45, at the tight end of guidance. In retained transactions, Deutsche Bank launched its EUR 2.5bn Wendelstein 2017-1 UG Prime RMBS transaction and BBVA closed its EUR 1.8bn BBVA RMBS 18 FT. In SME CLOs, CaixaBank will retain the EUR 1.85bn PYMES 9 FT.

On the supply front, the ABS pipeline has seen three notable additions in the past seven days. First, Crédit Agricole is reoffering the Class A of its previously retained Consumer ABS GNKGO 2017-SF1. Second, Energias de Portugal is offering Class A of its Volta V Electricity Receivables Securitisation in fixed-rate format. Third, Santander Consumer will bring another deal from its SC Germany platform to market (SCGC 2017-1), although the transaction will not be publicly marketed. A look at the 2016 predecessor transaction, which had a similar structure, suggests that the floating-rate lower mezzanine and junior classes might be preplaced while the senior and upper mezzanine classes might be retained. Elsewhere, Taurus 2017-2 UK DAC, the UK single-loan CMBS by BAML, is expected to price tomorrow. The transaction enjoys solid coverage across the capital structure (Classes A to E). Guidance for the AAA class (4.95Y WAL) has been released in the 3mL+85-90 (will price in range) area.

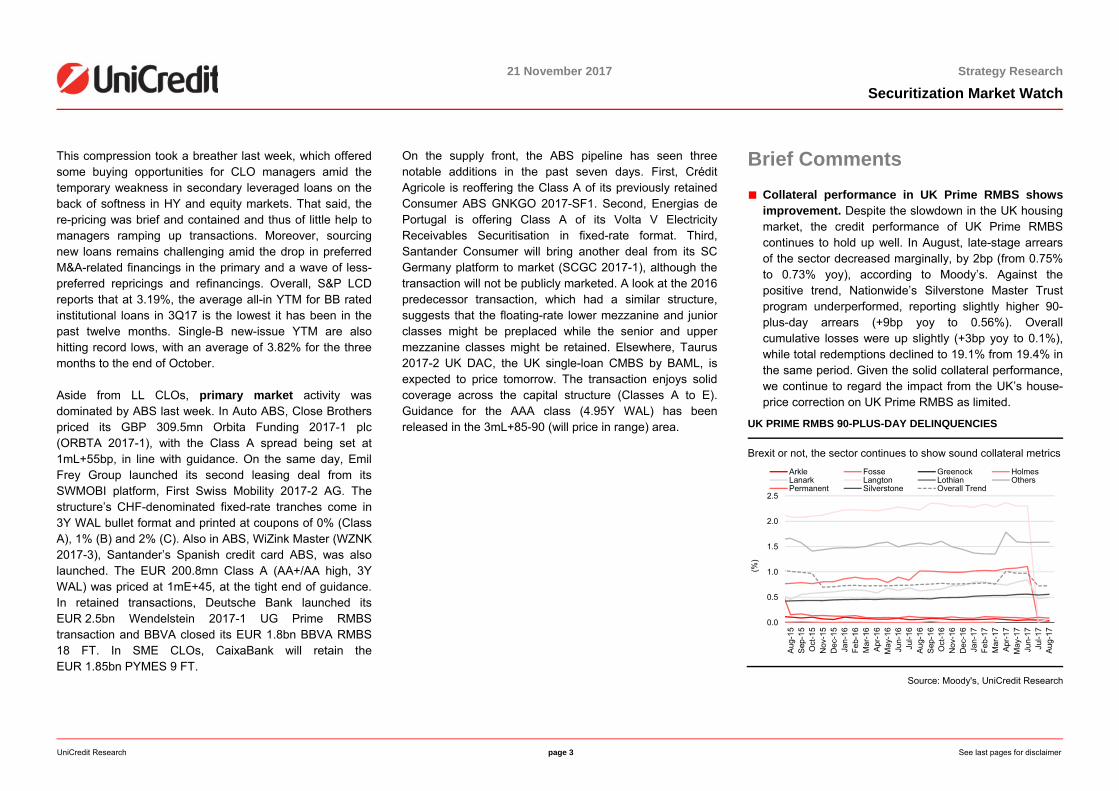

Brief Comments ■ Collateral performance in UK Prime RMBS shows

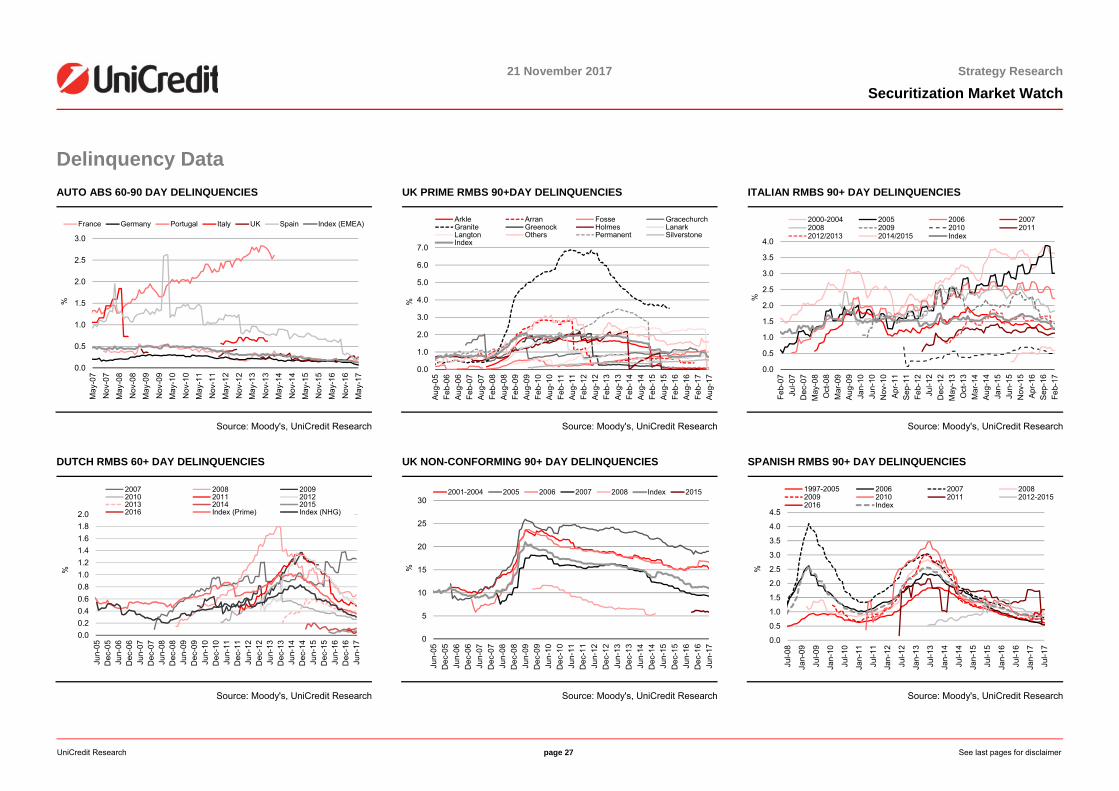

improvement. Despite the slowdown in the UK housing market, the credit performance of UK Prime RMBS continues to hold up well. In August, late-stage arrears of the sector decreased marginally, by 2bp (from 0.75% to 0.73% yoy), according to Moody’s. Against the positive trend, Nationwide’s Silverstone Master Trust program underperformed, reporting slightly higher 90-plus-day arrears (+9bp yoy to 0.56%). Overall cumulative losses were up slightly (+3bp yoy to 0.1%), while total redemptions declined to 19.1% from 19.4% in the same period. Given the solid collateral performance, we continue to regard the impact from the UK’s house-price correction on UK Prime RMBS as limited.

UK PRIME RMBS 90-PLUS-DAY DELINQUENCIES

Brexit or not, the sector continues to show sound collateral metrics

Source: Moody's, UniCredit Research

0.0

0.5

1.0

1.5

2.0

2.5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16Fe

b-16

Mar

-16

Apr

-16

May

-16

Jun-

16Ju

l-16

Aug

-16

Sep

-16

Oct

-16

Nov

-16

Dec

-16

Jan-

17Fe

b-17

Mar

-17

Apr

-17

May

-17

Jun-

17Ju

l-17

Aug

-17

(%)

Arkle Fosse Greenock HolmesLanark Langton Lothian OthersPermanent Silverstone Overall Trend

21 November 2017 Strategy Research

Securitization Market Watch

UniCredit Research page 4 See last pages for disclaimer.

■ Europe adopts new securitization rules. The new European securitization framework was approved by the European Council on 20 November. This follows the approval by the European Parliament on 26 October and the agreements reached between the European Presidency, the Council and the Parliament earlier in May. With that and following intense discussions over the last few years, the path is now more or less clear for a new EU securitization framework, which will be applied to new deals, to be issued from 1 January 2019. The new rules, which will bring the EU broadly in line with the Basel IV securitization framework, lay down a new framework for simple, transparent and standardized (STS) securitization transactions (link); the regulation also sets out new methods for calculating capital requirements for securitization positions (link). While we expect the new framework to result in higher capital charges compared to the old rules, which is not justified given the collateral performance of European securitization deals, we positively note that there will be a grandfathering of outstanding securitizations until 31 December 2019. In this context, the EBA continued with its consultation process on the discussion of the significant risk transfer in securitization. As part of this process, the EBA is requested to review the implementation of the EBA guidelines on significant risk transfer (SRT) from July 2014 and to provide binding technical standards to the European Commission. In a public hearing, which took place on 17 November, the EBA laid out its proposals on the SRT assessment, structural features, quantitative tests and the regulatory treatment of NPL securitization deals (link). However, results of the discussion have not yet been published.

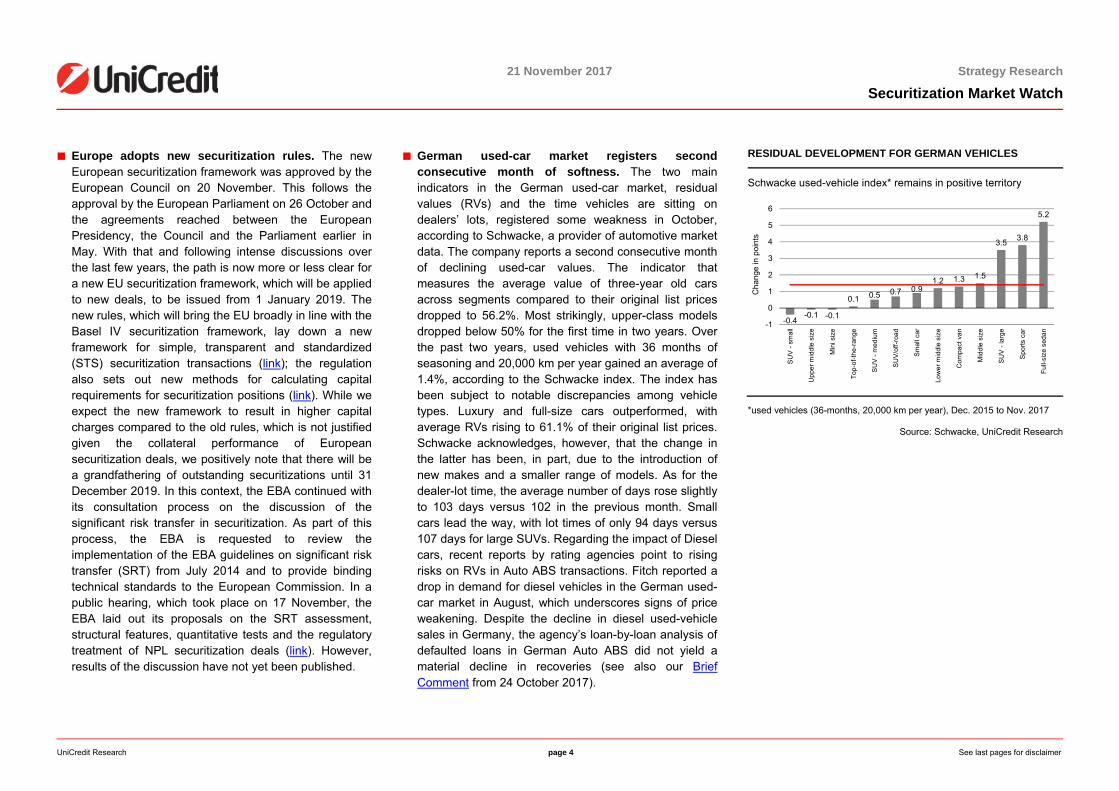

■ German used-car market registers second consecutive month of softness. The two main indicators in the German used-car market, residual values (RVs) and the time vehicles are sitting on dealers’ lots, registered some weakness in October, according to Schwacke, a provider of automotive market data. The company reports a second consecutive month of declining used-car values. The indicator that measures the average value of three-year old cars across segments compared to their original list prices dropped to 56.2%. Most strikingly, upper-class models dropped below 50% for the first time in two years. Over the past two years, used vehicles with 36 months of seasoning and 20,000 km per year gained an average of 1.4%, according to the Schwacke index. The index has been subject to notable discrepancies among vehicle types. Luxury and full-size cars outperformed, with average RVs rising to 61.1% of their original list prices. Schwacke acknowledges, however, that the change in the latter has been, in part, due to the introduction of new makes and a smaller range of models. As for the dealer-lot time, the average number of days rose slightly to 103 days versus 102 in the previous month. Small cars lead the way, with lot times of only 94 days versus 107 days for large SUVs. Regarding the impact of Diesel cars, recent reports by rating agencies point to rising risks on RVs in Auto ABS transactions. Fitch reported a drop in demand for diesel vehicles in the German used-car market in August, which underscores signs of price weakening. Despite the decline in diesel used-vehicle sales in Germany, the agency’s loan-by-loan analysis of defaulted loans in German Auto ABS did not yield a material decline in recoveries (see also our Brief Comment from 24 October 2017).

RESIDUAL DEVELOPMENT FOR GERMAN VEHICLES

Schwacke used-vehicle index* remains in positive territory

*used vehicles (36-months, 20,000 km per year), Dec. 2015 to Nov. 2017 Source: Schwacke, UniCredit Research

-0.4-0.1 -0.1

0.1 0.5 0.7 0.91.2 1.3 1.5

3.5 3.8

5.2

-1

0

1

2

3

4

5

6

SU

V - s

mal

l

Upp

er m

iddl

e si

ze

Min

i siz

e

Top-

of-th

e-ra

nge

SU

V - m

ediu

m

SU

V/of

f-roa

d

Sm

all c

ar

Low

er m

iddl

e si

ze

Com

pact

van

Mid

dle

size

SU

V -

larg

e

Spo

rts c

ar

Full-

size

sed

an

Cha

nge

in p

oint

s

UniCredit Research page 5 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

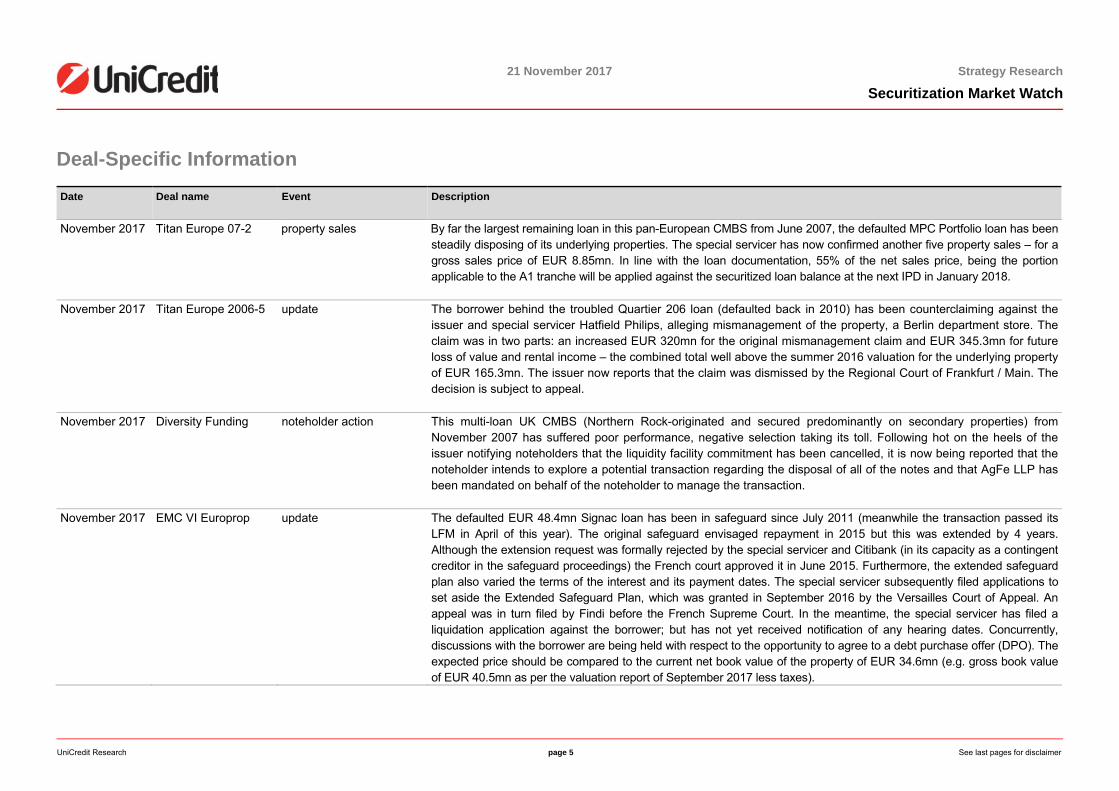

Deal-Specific Information Date Deal name Event Description

November 2017 Titan Europe 07-2 property sales By far the largest remaining loan in this pan-European CMBS from June 2007, the defaulted MPC Portfolio loan has been steadily disposing of its underlying properties. The special servicer has now confirmed another five property sales – for a gross sales price of EUR 8.85mn. In line with the loan documentation, 55% of the net sales price, being the portion applicable to the A1 tranche will be applied against the securitized loan balance at the next IPD in January 2018.

November 2017 Titan Europe 2006-5 update The borrower behind the troubled Quartier 206 loan (defaulted back in 2010) has been counterclaiming against the issuer and special servicer Hatfield Philips, alleging mismanagement of the property, a Berlin department store. The claim was in two parts: an increased EUR 320mn for the original mismanagement claim and EUR 345.3mn for future loss of value and rental income – the combined total well above the summer 2016 valuation for the underlying property of EUR 165.3mn. The issuer now reports that the claim was dismissed by the Regional Court of Frankfurt / Main. The decision is subject to appeal.

November 2017 Diversity Funding noteholder action This multi-loan UK CMBS (Northern Rock-originated and secured predominantly on secondary properties) from November 2007 has suffered poor performance, negative selection taking its toll. Following hot on the heels of the issuer notifying noteholders that the liquidity facility commitment has been cancelled, it is now being reported that the noteholder intends to explore a potential transaction regarding the disposal of all of the notes and that AgFe LLP has been mandated on behalf of the noteholder to manage the transaction.

November 2017 EMC VI Europrop update The defaulted EUR 48.4mn Signac loan has been in safeguard since July 2011 (meanwhile the transaction passed its LFM in April of this year). The original safeguard envisaged repayment in 2015 but this was extended by 4 years. Although the extension request was formally rejected by the special servicer and Citibank (in its capacity as a contingent creditor in the safeguard proceedings) the French court approved it in June 2015. Furthermore, the extended safeguard plan also varied the terms of the interest and its payment dates. The special servicer subsequently filed applications to set aside the Extended Safeguard Plan, which was granted in September 2016 by the Versailles Court of Appeal. An appeal was in turn filed by Findi before the French Supreme Court. In the meantime, the special servicer has filed a liquidation application against the borrower; but has not yet received notification of any hearing dates. Concurrently, discussions with the borrower are being held with respect to the opportunity to agree to a debt purchase offer (DPO). The expected price should be compared to the current net book value of the property of EUR 34.6mn (e.g. gross book value of EUR 40.5mn as per the valuation report of September 2017 less taxes).

UniCredit Research page 6 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Date Deal name Event Description

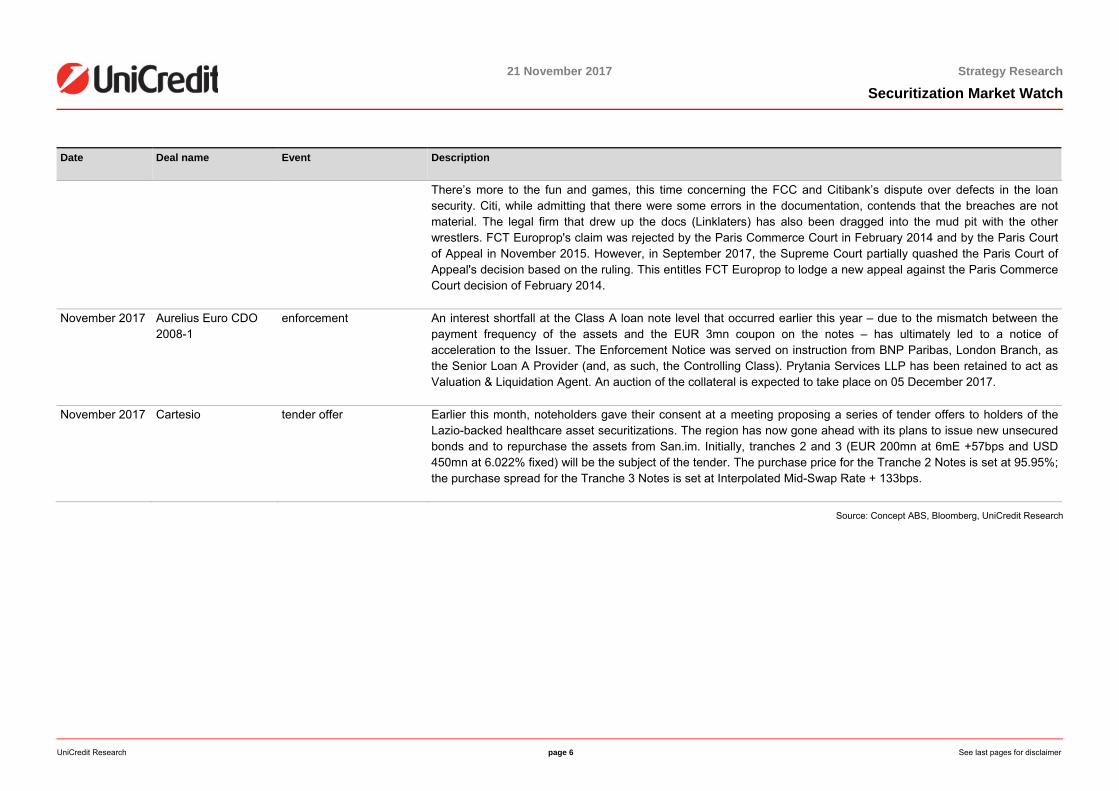

There’s more to the fun and games, this time concerning the FCC and Citibank’s dispute over defects in the loan security. Citi, while admitting that there were some errors in the documentation, contends that the breaches are not material. The legal firm that drew up the docs (Linklaters) has also been dragged into the mud pit with the other wrestlers. FCT Europrop's claim was rejected by the Paris Commerce Court in February 2014 and by the Paris Court of Appeal in November 2015. However, in September 2017, the Supreme Court partially quashed the Paris Court of Appeal's decision based on the ruling. This entitles FCT Europrop to lodge a new appeal against the Paris Commerce Court decision of February 2014.

November 2017 Aurelius Euro CDO 2008-1

enforcement An interest shortfall at the Class A loan note level that occurred earlier this year – due to the mismatch between the payment frequency of the assets and the EUR 3mn coupon on the notes – has ultimately led to a notice of acceleration to the Issuer. The Enforcement Notice was served on instruction from BNP Paribas, London Branch, as the Senior Loan A Provider (and, as such, the Controlling Class). Prytania Services LLP has been retained to act as Valuation & Liquidation Agent. An auction of the collateral is expected to take place on 05 December 2017.

November 2017 Cartesio tender offer Earlier this month, noteholders gave their consent at a meeting proposing a series of tender offers to holders of the Lazio-backed healthcare asset securitizations. The region has now gone ahead with its plans to issue new unsecured bonds and to repurchase the assets from San.im. Initially, tranches 2 and 3 (EUR 200mn at 6mE +57bps and USD 450mn at 6.022% fixed) will be the subject of the tender. The purchase price for the Tranche 2 Notes is set at 95.95%; the purchase spread for the Tranche 3 Notes is set at Interpolated Mid-Swap Rate + 133bps.

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 7 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

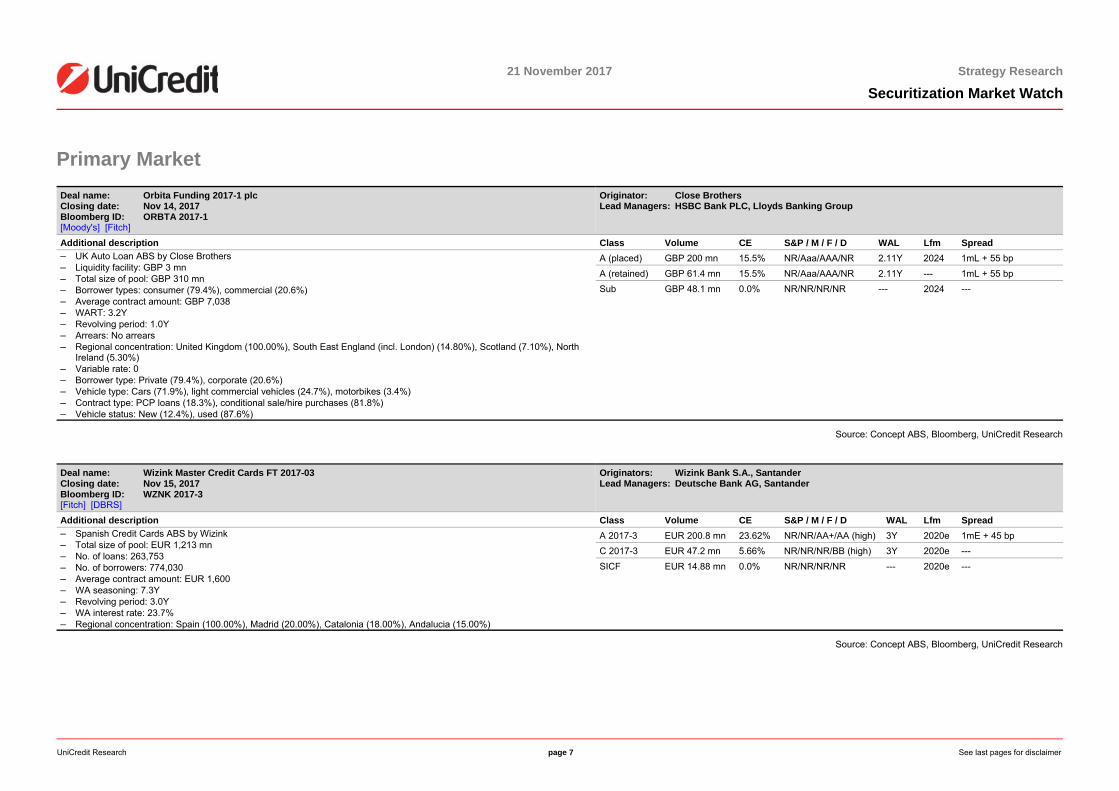

Primary Market Deal name: Orbita Funding 2017-1 plc Closing date: Nov 14, 2017 Bloomberg ID: ORBTA 2017-1 [Moody's] [Fitch]

Originator: Close Brothers Lead Managers: HSBC Bank PLC, Lloyds Banking Group

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – UK Auto Loan ABS by Close Brothers – Liquidity facility: GBP 3 mn – Total size of pool: GBP 310 mn – Borrower types: consumer (79.4%), commercial (20.6%) – Average contract amount: GBP 7,038 – WART: 3.2Y – Revolving period: 1.0Y – Arrears: No arrears – Regional concentration: United Kingdom (100.00%), South East England (incl. London) (14.80%), Scotland (7.10%), North

Ireland (5.30%) – Variable rate: 0 – Borrower type: Private (79.4%), corporate (20.6%) – Vehicle type: Cars (71.9%), light commercial vehicles (24.7%), motorbikes (3.4%) – Contract type: PCP loans (18.3%), conditional sale/hire purchases (81.8%) – Vehicle status: New (12.4%), used (87.6%)

A (placed) GBP 200 mn 15.5% NR/Aaa/AAA/NR 2.11Y 2024 1mL + 55 bp A (retained) GBP 61.4 mn 15.5% NR/Aaa/AAA/NR 2.11Y --- 1mL + 55 bp Sub GBP 48.1 mn 0.0% NR/NR/NR/NR --- 2024 ---

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Wizink Master Credit Cards FT 2017-03 Closing date: Nov 15, 2017 Bloomberg ID: WZNK 2017-3 [Fitch] [DBRS]

Originators: Wizink Bank S.A., Santander Lead Managers: Deutsche Bank AG, Santander

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Spanish Credit Cards ABS by Wizink – Total size of pool: EUR 1,213 mn – No. of loans: 263,753 – No. of borrowers: 774,030 – Average contract amount: EUR 1,600 – WA seasoning: 7.3Y – Revolving period: 3.0Y – WA interest rate: 23.7% – Regional concentration: Spain (100.00%), Madrid (20.00%), Catalonia (18.00%), Andalucia (15.00%)

A 2017-3 EUR 200.8 mn 23.62% NR/NR/AA+/AA (high) 3Y 2020e 1mE + 45 bp C 2017-3 EUR 47.2 mn 5.66% NR/NR/NR/BB (high) 3Y 2020e --- SICF EUR 14.88 mn 0.0% NR/NR/NR/NR --- 2020e ---

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 8 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

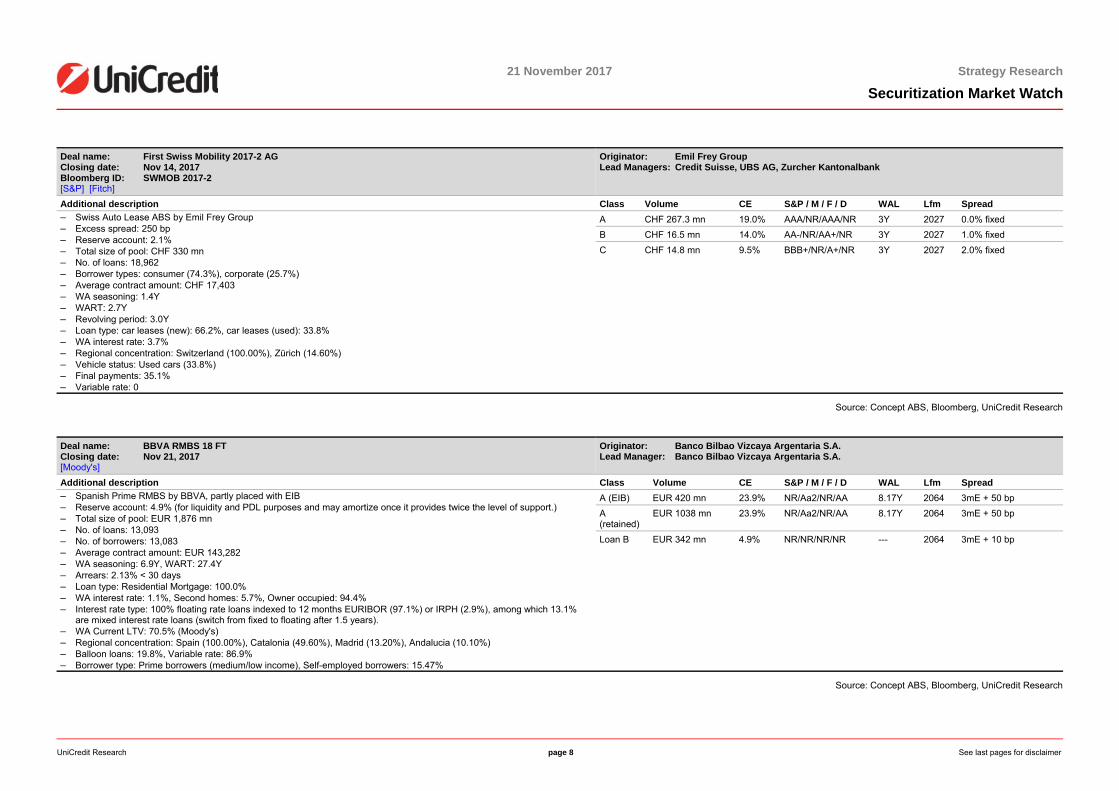

Deal name: First Swiss Mobility 2017-2 AG Closing date: Nov 14, 2017 Bloomberg ID: SWMOB 2017-2 [S&P] [Fitch]

Originator: Emil Frey Group Lead Managers: Credit Suisse, UBS AG, Zurcher Kantonalbank

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Swiss Auto Lease ABS by Emil Frey Group – Excess spread: 250 bp – Reserve account: 2.1% – Total size of pool: CHF 330 mn – No. of loans: 18,962 – Borrower types: consumer (74.3%), corporate (25.7%) – Average contract amount: CHF 17,403 – WA seasoning: 1.4Y – WART: 2.7Y – Revolving period: 3.0Y – Loan type: car leases (new): 66.2%, car leases (used): 33.8% – WA interest rate: 3.7% – Regional concentration: Switzerland (100.00%), Zürich (14.60%) – Vehicle status: Used cars (33.8%) – Final payments: 35.1% – Variable rate: 0

A CHF 267.3 mn 19.0% AAA/NR/AAA/NR 3Y 2027 0.0% fixed B CHF 16.5 mn 14.0% AA-/NR/AA+/NR 3Y 2027 1.0% fixed C CHF 14.8 mn 9.5% BBB+/NR/A+/NR 3Y 2027 2.0% fixed

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: BBVA RMBS 18 FT Closing date: Nov 21, 2017 [Moody's]

Originator: Banco Bilbao Vizcaya Argentaria S.A. Lead Manager: Banco Bilbao Vizcaya Argentaria S.A.

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Spanish Prime RMBS by BBVA, partly placed with EIB – Reserve account: 4.9% (for liquidity and PDL purposes and may amortize once it provides twice the level of support.) – Total size of pool: EUR 1,876 mn – No. of loans: 13,093 – No. of borrowers: 13,083 – Average contract amount: EUR 143,282 – WA seasoning: 6.9Y, WART: 27.4Y – Arrears: 2.13% < 30 days – Loan type: Residential Mortgage: 100.0% – WA interest rate: 1.1%, Second homes: 5.7%, Owner occupied: 94.4% – Interest rate type: 100% floating rate loans indexed to 12 months EURIBOR (97.1%) or IRPH (2.9%), among which 13.1%

are mixed interest rate loans (switch from fixed to floating after 1.5 years). – WA Current LTV: 70.5% (Moody's) – Regional concentration: Spain (100.00%), Catalonia (49.60%), Madrid (13.20%), Andalucia (10.10%) – Balloon loans: 19.8%, Variable rate: 86.9% – Borrower type: Prime borrowers (medium/low income), Self-employed borrowers: 15.47%

A (EIB) EUR 420 mn 23.9% NR/Aa2/NR/AA 8.17Y 2064 3mE + 50 bp A (retained)

EUR 1038 mn 23.9% NR/Aa2/NR/AA 8.17Y 2064 3mE + 50 bp

Loan B EUR 342 mn 4.9% NR/NR/NR/NR --- 2064 3mE + 10 bp

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 9 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

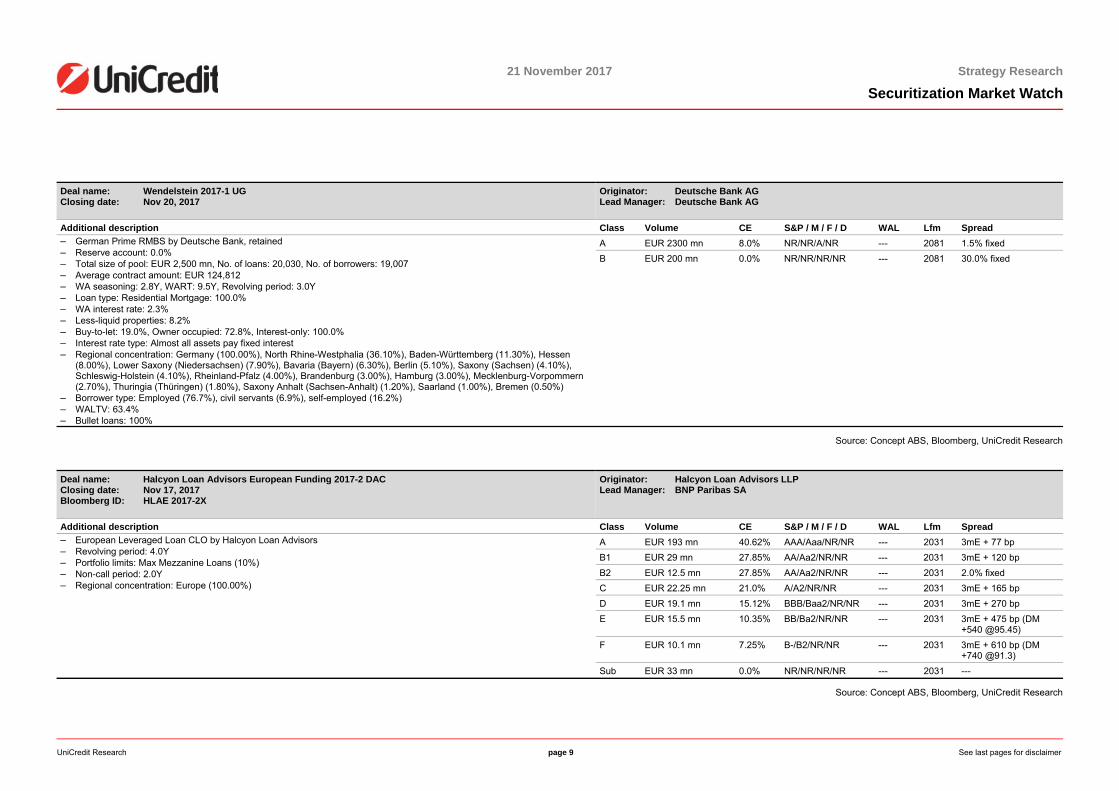

Deal name: Wendelstein 2017-1 UG Closing date: Nov 20, 2017

Originator: Deutsche Bank AG Lead Manager: Deutsche Bank AG

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – German Prime RMBS by Deutsche Bank, retained – Reserve account: 0.0% – Total size of pool: EUR 2,500 mn, No. of loans: 20,030, No. of borrowers: 19,007 – Average contract amount: EUR 124,812 – WA seasoning: 2.8Y, WART: 9.5Y, Revolving period: 3.0Y – Loan type: Residential Mortgage: 100.0% – WA interest rate: 2.3% – Less-liquid properties: 8.2% – Buy-to-let: 19.0%, Owner occupied: 72.8%, Interest-only: 100.0% – Interest rate type: Almost all assets pay fixed interest – Regional concentration: Germany (100.00%), North Rhine-Westphalia (36.10%), Baden-Württemberg (11.30%), Hessen

(8.00%), Lower Saxony (Niedersachsen) (7.90%), Bavaria (Bayern) (6.30%), Berlin (5.10%), Saxony (Sachsen) (4.10%), Schleswig-Holstein (4.10%), Rheinland-Pfalz (4.00%), Brandenburg (3.00%), Hamburg (3.00%), Mecklenburg-Vorpommern (2.70%), Thuringia (Thüringen) (1.80%), Saxony Anhalt (Sachsen-Anhalt) (1.20%), Saarland (1.00%), Bremen (0.50%)

– Borrower type: Employed (76.7%), civil servants (6.9%), self-employed (16.2%) – WALTV: 63.4% – Bullet loans: 100%

A EUR 2300 mn 8.0% NR/NR/A/NR --- 2081 1.5% fixed B EUR 200 mn 0.0% NR/NR/NR/NR --- 2081 30.0% fixed

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Halcyon Loan Advisors European Funding 2017-2 DAC Closing date: Nov 17, 2017 Bloomberg ID: HLAE 2017-2X

Originator: Halcyon Loan Advisors LLP Lead Manager: BNP Paribas SA

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Halcyon Loan Advisors – Revolving period: 4.0Y – Portfolio limits: Max Mezzanine Loans (10%) – Non-call period: 2.0Y – Regional concentration: Europe (100.00%)

A EUR 193 mn 40.62% AAA/Aaa/NR/NR --- 2031 3mE + 77 bp B1 EUR 29 mn 27.85% AA/Aa2/NR/NR --- 2031 3mE + 120 bp B2 EUR 12.5 mn 27.85% AA/Aa2/NR/NR --- 2031 2.0% fixed C EUR 22.25 mn 21.0% A/A2/NR/NR --- 2031 3mE + 165 bp D EUR 19.1 mn 15.12% BBB/Baa2/NR/NR --- 2031 3mE + 270 bp E EUR 15.5 mn 10.35% BB/Ba2/NR/NR --- 2031 3mE + 475 bp (DM

+540 @95.45) F EUR 10.1 mn 7.25% B-/B2/NR/NR --- 2031 3mE + 610 bp (DM

+740 @91.3) Sub EUR 33 mn 0.0% NR/NR/NR/NR --- 2031 ---

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 10 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

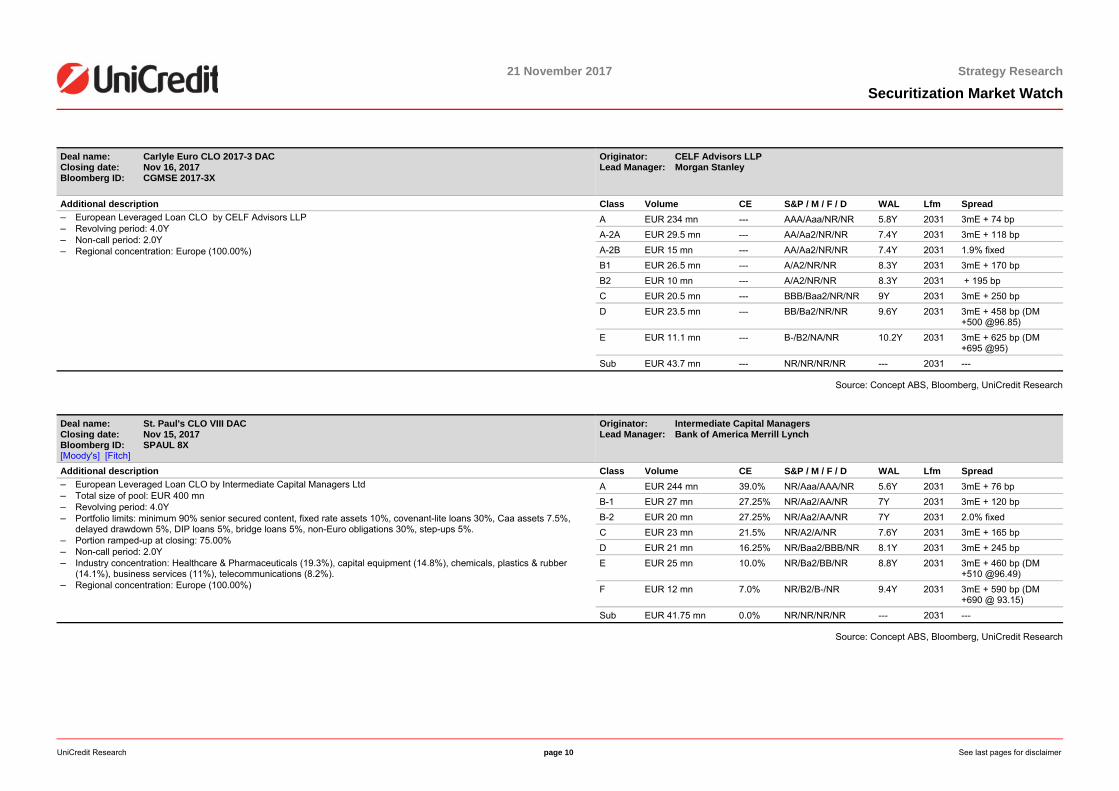

Deal name: Carlyle Euro CLO 2017-3 DAC Closing date: Nov 16, 2017 Bloomberg ID: CGMSE 2017-3X

Originator: CELF Advisors LLP Lead Manager: Morgan Stanley

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by CELF Advisors LLP – Revolving period: 4.0Y – Non-call period: 2.0Y – Regional concentration: Europe (100.00%)

A EUR 234 mn --- AAA/Aaa/NR/NR 5.8Y 2031 3mE + 74 bp A-2A EUR 29.5 mn --- AA/Aa2/NR/NR 7.4Y 2031 3mE + 118 bp A-2B EUR 15 mn --- AA/Aa2/NR/NR 7.4Y 2031 1.9% fixed B1 EUR 26.5 mn --- A/A2/NR/NR 8.3Y 2031 3mE + 170 bp B2 EUR 10 mn --- A/A2/NR/NR 8.3Y 2031 + 195 bp C EUR 20.5 mn --- BBB/Baa2/NR/NR 9Y 2031 3mE + 250 bp D EUR 23.5 mn --- BB/Ba2/NR/NR 9.6Y 2031 3mE + 458 bp (DM

+500 @96.85) E EUR 11.1 mn --- B-/B2/NA/NR 10.2Y 2031 3mE + 625 bp (DM

+695 @95) Sub EUR 43.7 mn --- NR/NR/NR/NR --- 2031 ---

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: St. Paul's CLO VIII DAC Closing date: Nov 15, 2017 Bloomberg ID: SPAUL 8X [Moody's] [Fitch]

Originator: Intermediate Capital Managers Lead Manager: Bank of America Merrill Lynch

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Intermediate Capital Managers Ltd – Total size of pool: EUR 400 mn – Revolving period: 4.0Y – Portfolio limits: minimum 90% senior secured content, fixed rate assets 10%, covenant-lite loans 30%, Caa assets 7.5%,

delayed drawdown 5%, DIP loans 5%, bridge loans 5%, non-Euro obligations 30%, step-ups 5%. – Portion ramped-up at closing: 75.00% – Non-call period: 2.0Y – Industry concentration: Healthcare & Pharmaceuticals (19.3%), capital equipment (14.8%), chemicals, plastics & rubber

(14.1%), business services (11%), telecommunications (8.2%). – Regional concentration: Europe (100.00%)

A EUR 244 mn 39.0% NR/Aaa/AAA/NR 5.6Y 2031 3mE + 76 bp B-1 EUR 27 mn 27.25% NR/Aa2/AA/NR 7Y 2031 3mE + 120 bp B-2 EUR 20 mn 27.25% NR/Aa2/AA/NR 7Y 2031 2.0% fixed C EUR 23 mn 21.5% NR/A2/A/NR 7.6Y 2031 3mE + 165 bp D EUR 21 mn 16.25% NR/Baa2/BBB/NR 8.1Y 2031 3mE + 245 bp E EUR 25 mn 10.0% NR/Ba2/BB/NR 8.8Y 2031 3mE + 460 bp (DM

+510 @96.49) F EUR 12 mn 7.0% NR/B2/B-/NR 9.4Y 2031 3mE + 590 bp (DM

+690 @ 93.15) Sub EUR 41.75 mn 0.0% NR/NR/NR/NR --- 2031 ---

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 11 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

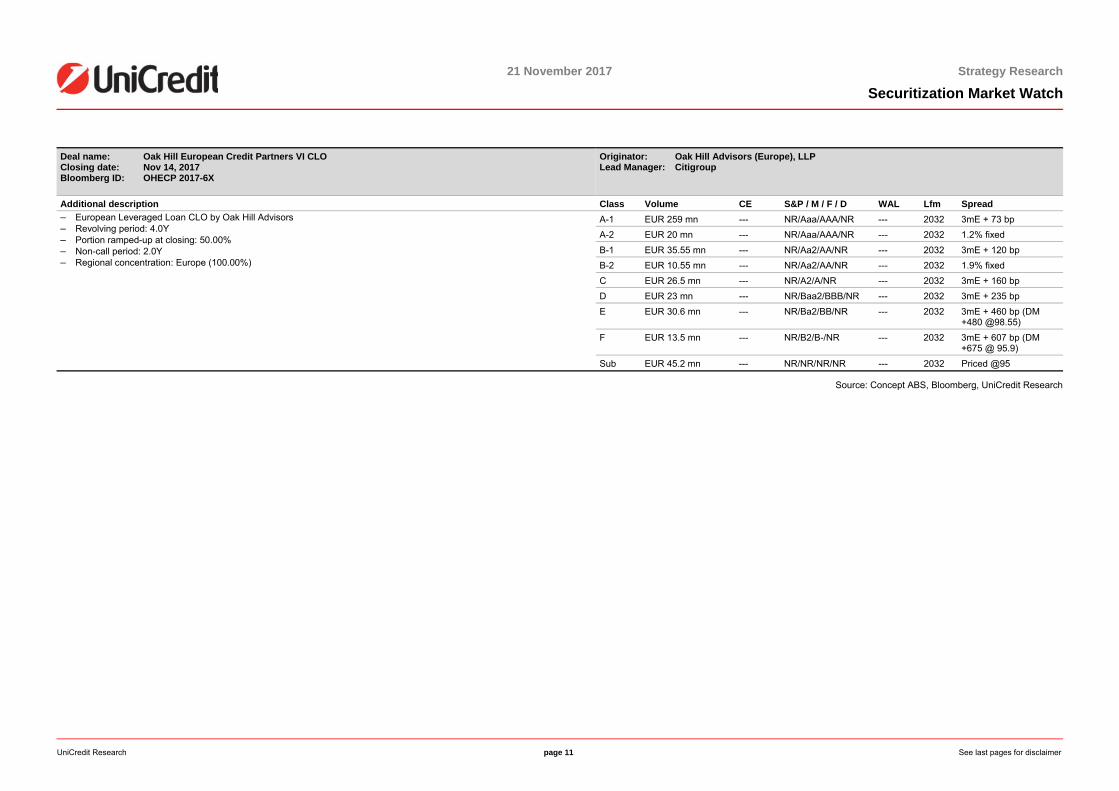

Deal name: Oak Hill European Credit Partners VI CLO Closing date: Nov 14, 2017 Bloomberg ID: OHECP 2017-6X

Originator: Oak Hill Advisors (Europe), LLP Lead Manager: Citigroup

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Oak Hill Advisors – Revolving period: 4.0Y – Portion ramped-up at closing: 50.00% – Non-call period: 2.0Y – Regional concentration: Europe (100.00%)

A-1 EUR 259 mn --- NR/Aaa/AAA/NR --- 2032 3mE + 73 bp A-2 EUR 20 mn --- NR/Aaa/AAA/NR --- 2032 1.2% fixed B-1 EUR 35.55 mn --- NR/Aa2/AA/NR --- 2032 3mE + 120 bp B-2 EUR 10.55 mn --- NR/Aa2/AA/NR --- 2032 1.9% fixed C EUR 26.5 mn --- NR/A2/A/NR --- 2032 3mE + 160 bp D EUR 23 mn --- NR/Baa2/BBB/NR --- 2032 3mE + 235 bp E EUR 30.6 mn --- NR/Ba2/BB/NR --- 2032 3mE + 460 bp (DM

+480 @98.55) F EUR 13.5 mn --- NR/B2/B-/NR --- 2032 3mE + 607 bp (DM

+675 @ 95.9) Sub EUR 45.2 mn --- NR/NR/NR/NR --- 2032 Priced @95

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 12 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Pipeline

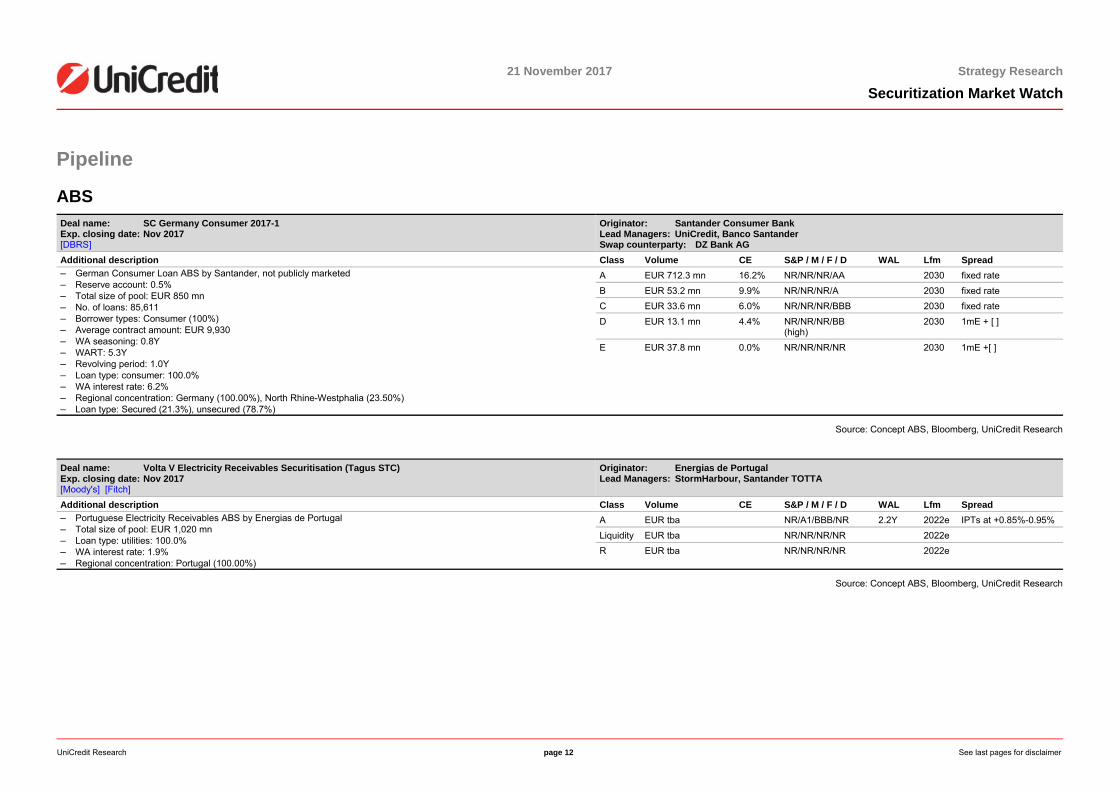

ABS Deal name: SC Germany Consumer 2017-1 Exp. closing date: Nov 2017 [DBRS]

Originator: Santander Consumer Bank Lead Managers: UniCredit, Banco Santander Swap counterparty: DZ Bank AG

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – German Consumer Loan ABS by Santander, not publicly marketed – Reserve account: 0.5% – Total size of pool: EUR 850 mn – No. of loans: 85,611 – Borrower types: Consumer (100%) – Average contract amount: EUR 9,930 – WA seasoning: 0.8Y – WART: 5.3Y – Revolving period: 1.0Y – Loan type: consumer: 100.0% – WA interest rate: 6.2% – Regional concentration: Germany (100.00%), North Rhine-Westphalia (23.50%) – Loan type: Secured (21.3%), unsecured (78.7%)

A EUR 712.3 mn 16.2% NR/NR/NR/AA 2030 fixed rate B EUR 53.2 mn 9.9% NR/NR/NR/A 2030 fixed rate C EUR 33.6 mn 6.0% NR/NR/NR/BBB 2030 fixed rate D EUR 13.1 mn 4.4% NR/NR/NR/BB

(high) 2030 1mE + [ ]

E EUR 37.8 mn 0.0% NR/NR/NR/NR 2030 1mE +[ ]

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Volta V Electricity Receivables Securitisation (Tagus STC) Exp. closing date: Nov 2017 [Moody's] [Fitch]

Originator: Energias de Portugal Lead Managers: StormHarbour, Santander TOTTA

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Portuguese Electricity Receivables ABS by Energias de Portugal – Total size of pool: EUR 1,020 mn – Loan type: utilities: 100.0% – WA interest rate: 1.9% – Regional concentration: Portugal (100.00%)

A EUR tba NR/A1/BBB/NR 2.2Y 2022e IPTs at +0.85%-0.95% Liquidity EUR tba NR/NR/NR/NR 2022e R EUR tba NR/NR/NR/NR 2022e

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 13 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

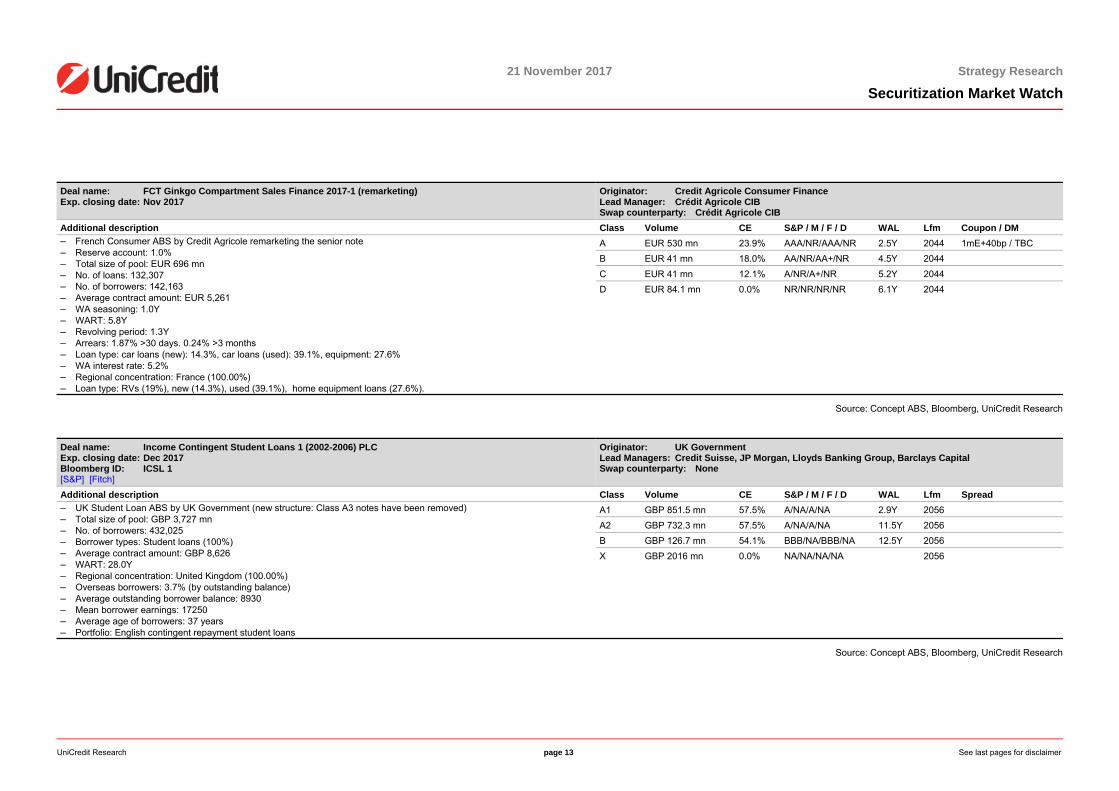

Deal name: FCT Ginkgo Compartment Sales Finance 2017-1 (remarketing) Exp. closing date: Nov 2017

Originator: Credit Agricole Consumer Finance Lead Manager: Crédit Agricole CIB Swap counterparty: Crédit Agricole CIB

Additional description Class Volume CE S&P / M / F / D WAL Lfm Coupon / DM – French Consumer ABS by Credit Agricole remarketing the senior note – Reserve account: 1.0% – Total size of pool: EUR 696 mn – No. of loans: 132,307 – No. of borrowers: 142,163 – Average contract amount: EUR 5,261 – WA seasoning: 1.0Y – WART: 5.8Y – Revolving period: 1.3Y – Arrears: 1.87% >30 days. 0.24% >3 months – Loan type: car loans (new): 14.3%, car loans (used): 39.1%, equipment: 27.6% – WA interest rate: 5.2% – Regional concentration: France (100.00%) – Loan type: RVs (19%), new (14.3%), used (39.1%), home equipment loans (27.6%).

A EUR 530 mn 23.9% AAA/NR/AAA/NR 2.5Y 2044 1mE+40bp / TBC B EUR 41 mn 18.0% AA/NR/AA+/NR 4.5Y 2044 C EUR 41 mn 12.1% A/NR/A+/NR 5.2Y 2044 D EUR 84.1 mn 0.0% NR/NR/NR/NR 6.1Y 2044

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Income Contingent Student Loans 1 (2002-2006) PLC Exp. closing date: Dec 2017 Bloomberg ID: ICSL 1 [S&P] [Fitch]

Originator: UK Government Lead Managers: Credit Suisse, JP Morgan, Lloyds Banking Group, Barclays Capital Swap counterparty: None

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – UK Student Loan ABS by UK Government (new structure: Class A3 notes have been removed) – Total size of pool: GBP 3,727 mn – No. of borrowers: 432,025 – Borrower types: Student loans (100%) – Average contract amount: GBP 8,626 – WART: 28.0Y – Regional concentration: United Kingdom (100.00%) – Overseas borrowers: 3.7% (by outstanding balance) – Average outstanding borrower balance: 8930 – Mean borrower earnings: 17250 – Average age of borrowers: 37 years – Portfolio: English contingent repayment student loans

A1 GBP 851.5 mn 57.5% A/NA/A/NA 2.9Y 2056 A2 GBP 732.3 mn 57.5% A/NA/A/NA 11.5Y 2056 B GBP 126.7 mn 54.1% BBB/NA/BBB/NA 12.5Y 2056 X GBP 2016 mn 0.0% NA/NA/NA/NA 2056

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 14 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

RMBS Deal name: Grand Canal Securities 2 DAC Exp. closing date: Nov 2017 Bloomberg ID: GCS 2 [Moody's]

Originators: Irish Nationwide, Springboard Mortgages Lead Manager: Morgan Stanley

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Irish non-standard RMBS by Mars securitizing non-performing and performing loans – Total size of pool: EUR 542 mn – No. of loans: 3,191 – No. of borrowers: 2,464 – Average contract amount: EUR 220,100 – WA seasoning: 10.6Y – WA interest rate: 4.0% – Buy-to-let: 17.0% – Self-certified: 49.9% – Interest-only: 22.7% – Regional concentration: Ireland (100.00%), Dublin (20.00%), Cork (9.00%), Kildare (6.00%), Meath (6.00%), Galway (5.00%),

Louth (5.00%), Wexford (5.00%), Wicklow (5.00%) – Borrower type: Performing, non-performing – WALTV: 113.91% – Loan type: Secured assets performing (16%), secured assets non-performing (84%) – Self-employed borrowers: 43.6% – Fixed interest: 0

A EUR 241.91 mn 55.4% NR/A2/NR/A 2.76Y 2058 IPTs at +mid 100s bp B EUR 9.763 mn 53.6% NR/Baa3/NR/BBB

(low) 3.88Y 2058 IPTs at +high 200s-300

bp area C EUR 10.577 mn 51.65% NR/Ba1/NR/BB (low) 3.88Y 2058 IPTs at +mid 500s bp D EUR 12.475 mn 49.35% NR/Ba3/NR/B (low) 3.88Y 2058 IPTs at +mid 700s bp E1 EUR 12.738 mn 47.0% NR/NR/NR/NR 3.83Y 2058 IPTs at +mid 900s bp E2 EUR 12.738 mn 44.65% NR/NR/NR/NR 2058 E3 EUR 12.738 mn 42.3% NR/NR/NR/NR 2058 F EUR 216.96 mn 0.0% NR/NR/NR/NR 2058 P EUR 12.5 mn 40.0% NR/NR/NR/NR 2058

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Liberty Series 2017-4 Trust Exp. closing date: Nov 2017 [Moody's] [Fitch]

Originator: Liberty Financial Lead Managers: Commonwealth Bank of Australia, Deutsche Bank AG, NAB, Westpac Swap counterparties: Commonwealth Bank of Australia, National Australia Bank Ltd

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – Australian non-conforming RMBS by Liberty Financial, including EUR tranche – Total size of pool: AUD 700 mn – No. of loans: 1,771 – No. of borrowers: 1,596 – Average contract amount: AUD 395,257 – WA seasoning: 0.7Y, WART: 29.0Y – Arrears: 0.97%<1 month – WA interest rate: 5.2%, Buy-to-let: 42.6%, Owner occupied: 57.4% – County court judgment: 2.2%, Bankruptcy order/IVA: 0.1%, Self-certified: 2.9%, Interest-only: 39.1% – Interest rate type: Fixed rate loans (3.6%), variable rate loans (96.4%) – Regional concentration: Australia (100.00%), New South Wales (36.80%), Victoria (35.30%), Queensland (15.90%) – Borrower type: Credit-impaired (2.3%), non-conforming (12.1%), investment mortgages (42.63%) – CLTV: 73.2% – Self-employed borrowers: 11.4% – Variable rate: 96.4% – Property type: House and semi (84.1%), unit (15.7%), land (0.2%)

A1a AUD 70 mn 35.0% NR/Aaa/AAA/NR A1b AUD 385 mn 35.0% NR/Aaa/AAA/NR A1c EUR tba 35.0% NR/Aaa/AAA/NR A2 AUD 166.6 mn 11.2% NR/Aaa/AAA/NR B AUD 33.6 mn 6.4% NR/Aa2/NR/NR C AUD 12.6 mn 4.6% NR/A2/NR/NR D AUD 9.1 mn 3.3% NR/Baa2/NR/NR E AUD 4.9 mn 2.6% NR/Ba2/NR/NR F AUD 6.3 mn 1.7% NR/B2/NR/NR G AUD 11.9 mn 0.0% NR/NR/NR/NR

Source: Concept ABS, Bloomberg, UniCredit Research

UniCredit Research page 15 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

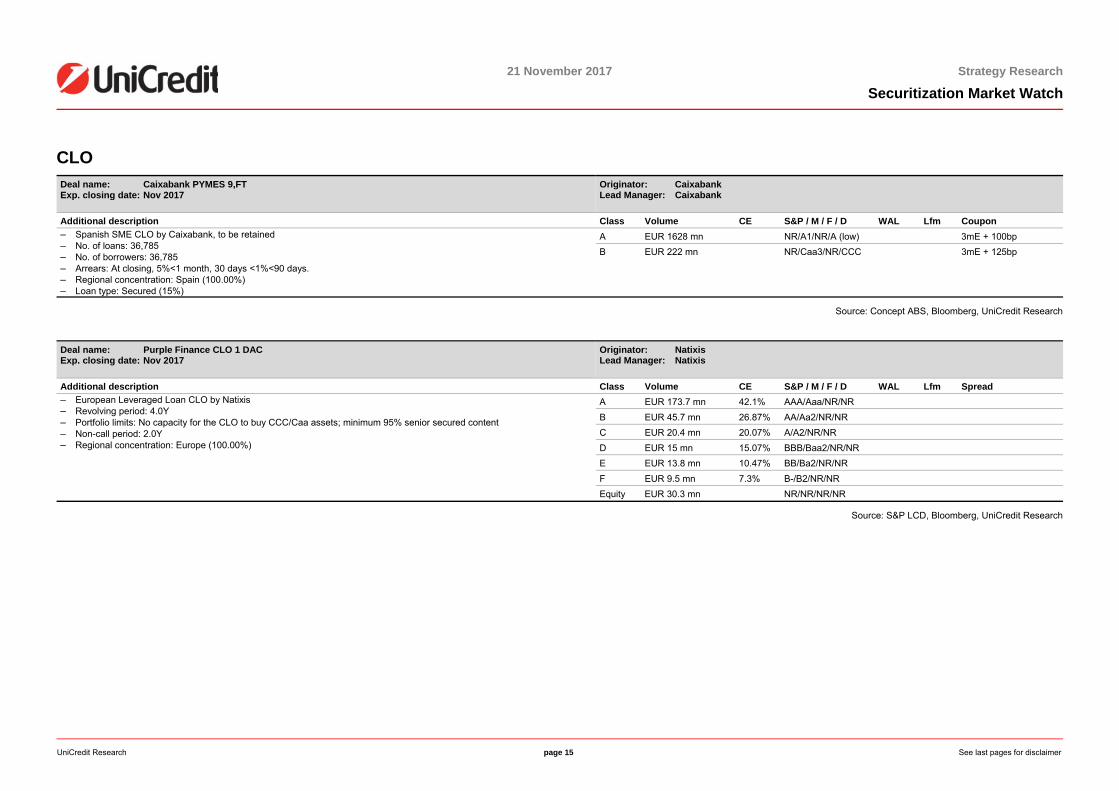

CLO Deal name: Caixabank PYMES 9,FT Exp. closing date: Nov 2017

Originator: Caixabank Lead Manager: Caixabank

Additional description Class Volume CE S&P / M / F / D WAL Lfm Coupon – Spanish SME CLO by Caixabank, to be retained – No. of loans: 36,785 – No. of borrowers: 36,785 – Arrears: At closing, 5%<1 month, 30 days <1%<90 days. – Regional concentration: Spain (100.00%) – Loan type: Secured (15%)

A EUR 1628 mn NR/A1/NR/A (low) 3mE + 100bp B EUR 222 mn NR/Caa3/NR/CCC 3mE + 125bp

Source: Concept ABS, Bloomberg, UniCredit Research

Deal name: Purple Finance CLO 1 DAC Exp. closing date: Nov 2017

Originator: Natixis Lead Manager: Natixis

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Natixis – Revolving period: 4.0Y – Portfolio limits: No capacity for the CLO to buy CCC/Caa assets; minimum 95% senior secured content – Non-call period: 2.0Y – Regional concentration: Europe (100.00%)

A EUR 173.7 mn 42.1% AAA/Aaa/NR/NR B EUR 45.7 mn 26.87% AA/Aa2/NR/NR C EUR 20.4 mn 20.07% A/A2/NR/NR D EUR 15 mn 15.07% BBB/Baa2/NR/NR E EUR 13.8 mn 10.47% BB/Ba2/NR/NR F EUR 9.5 mn 7.3% B-/B2/NR/NR Equity EUR 30.3 mn NR/NR/NR/NR

Source: S&P LCD, Bloomberg, UniCredit Research

UniCredit Research page 16 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

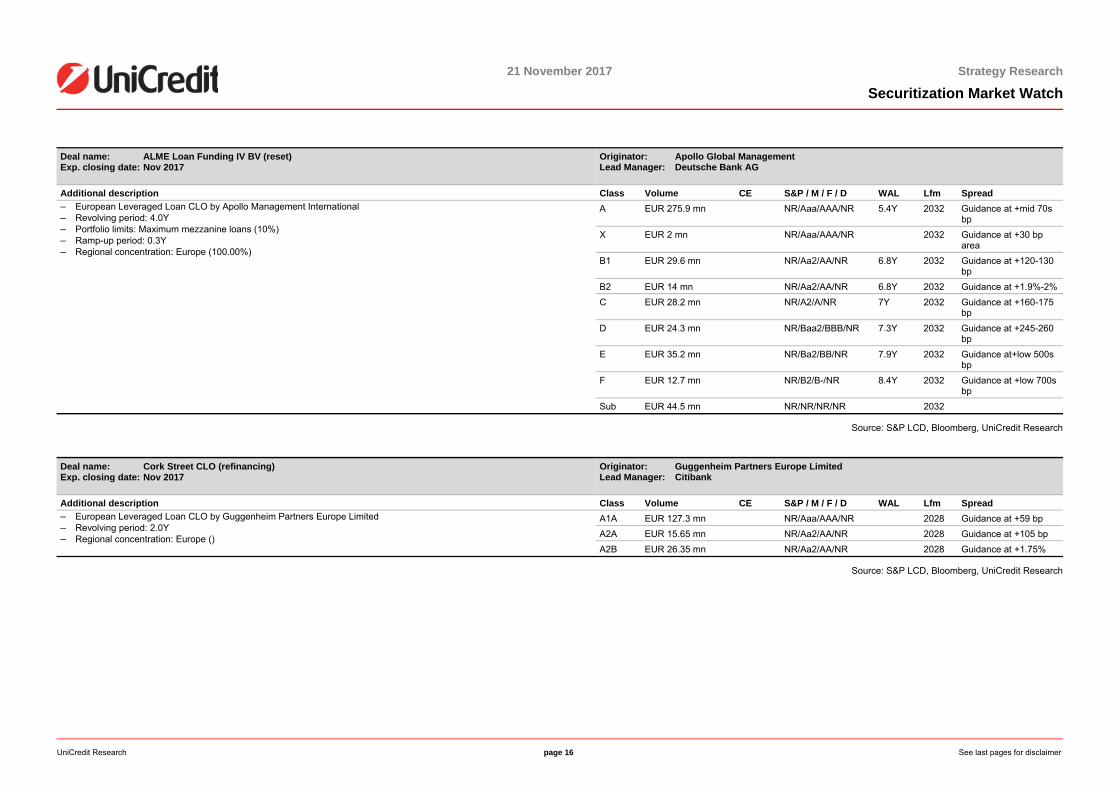

Deal name: ALME Loan Funding IV BV (reset) Exp. closing date: Nov 2017

Originator: Apollo Global Management Lead Manager: Deutsche Bank AG

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Apollo Management International – Revolving period: 4.0Y – Portfolio limits: Maximum mezzanine loans (10%) – Ramp-up period: 0.3Y – Regional concentration: Europe (100.00%)

A EUR 275.9 mn NR/Aaa/AAA/NR 5.4Y 2032 Guidance at +mid 70s bp

X EUR 2 mn NR/Aaa/AAA/NR 2032 Guidance at +30 bp area

B1 EUR 29.6 mn NR/Aa2/AA/NR 6.8Y 2032 Guidance at +120-130 bp

B2 EUR 14 mn NR/Aa2/AA/NR 6.8Y 2032 Guidance at +1.9%-2% C EUR 28.2 mn NR/A2/A/NR 7Y 2032 Guidance at +160-175

bp D EUR 24.3 mn NR/Baa2/BBB/NR 7.3Y 2032 Guidance at +245-260

bp E EUR 35.2 mn NR/Ba2/BB/NR 7.9Y 2032 Guidance at+low 500s

bp F EUR 12.7 mn NR/B2/B-/NR 8.4Y 2032 Guidance at +low 700s

bp Sub EUR 44.5 mn NR/NR/NR/NR 2032

Source: S&P LCD, Bloomberg, UniCredit Research

Deal name: Cork Street CLO (refinancing) Exp. closing date: Nov 2017

Originator: Guggenheim Partners Europe Limited Lead Manager: Citibank

Additional description Class Volume CE S&P / M / F / D WAL Lfm Spread – European Leveraged Loan CLO by Guggenheim Partners Europe Limited – Revolving period: 2.0Y – Regional concentration: Europe ()

A1A EUR 127.3 mn NR/Aaa/AAA/NR 2028 Guidance at +59 bp A2A EUR 15.65 mn NR/Aa2/AA/NR 2028 Guidance at +105 bp A2B EUR 26.35 mn NR/Aa2/AA/NR 2028 Guidance at +1.75%

Source: S&P LCD, Bloomberg, UniCredit Research

UniCredit Research page 17 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

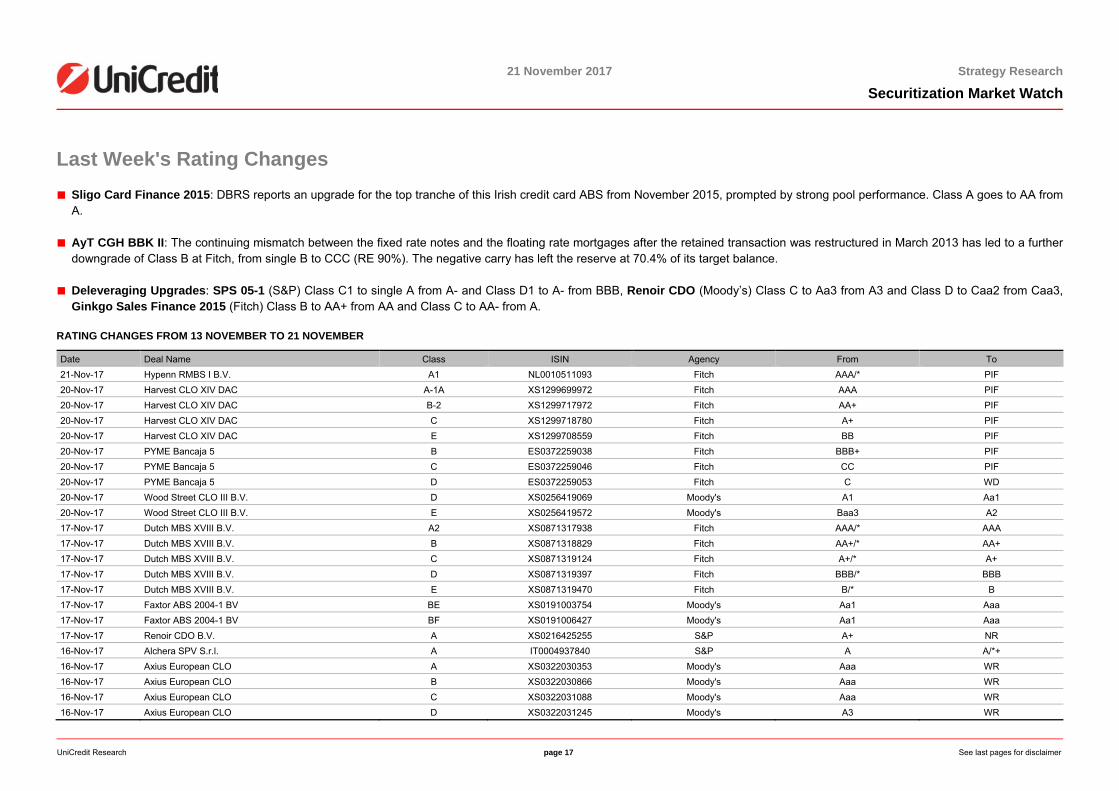

Last Week's Rating Changes ■ Sligo Card Finance 2015: DBRS reports an upgrade for the top tranche of this Irish credit card ABS from November 2015, prompted by strong pool performance. Class A goes to AA from

A.

■ AyT CGH BBK II: The continuing mismatch between the fixed rate notes and the floating rate mortgages after the retained transaction was restructured in March 2013 has led to a further downgrade of Class B at Fitch, from single B to CCC (RE 90%). The negative carry has left the reserve at 70.4% of its target balance.

■ Deleveraging Upgrades: SPS 05-1 (S&P) Class C1 to single A from A- and Class D1 to A- from BBB, Renoir CDO (Moody’s) Class C to Aa3 from A3 and Class D to Caa2 from Caa3, Ginkgo Sales Finance 2015 (Fitch) Class B to AA+ from AA and Class C to AA- from A.

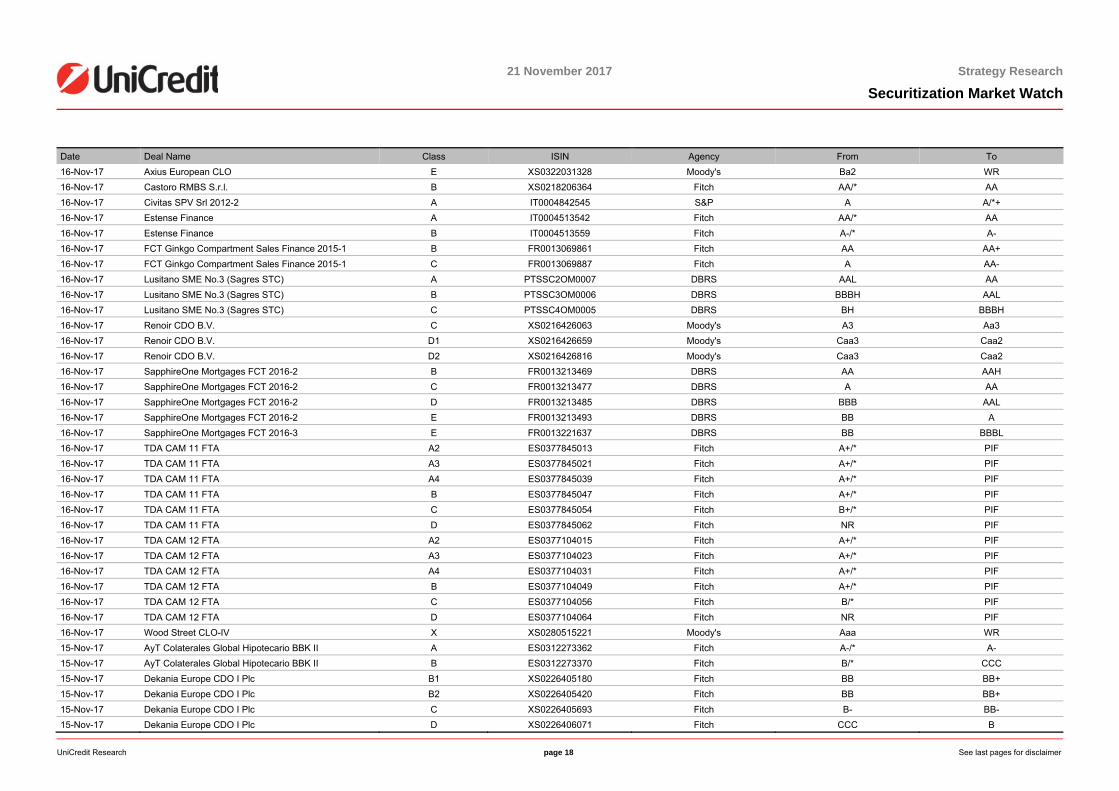

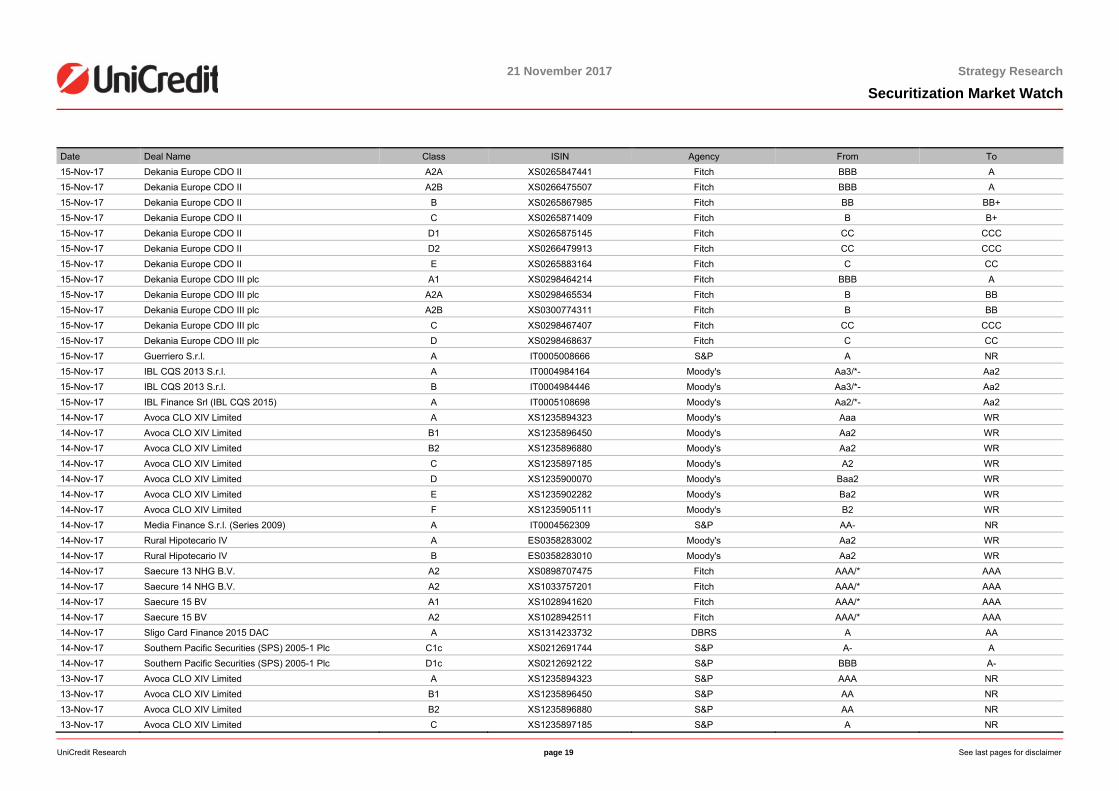

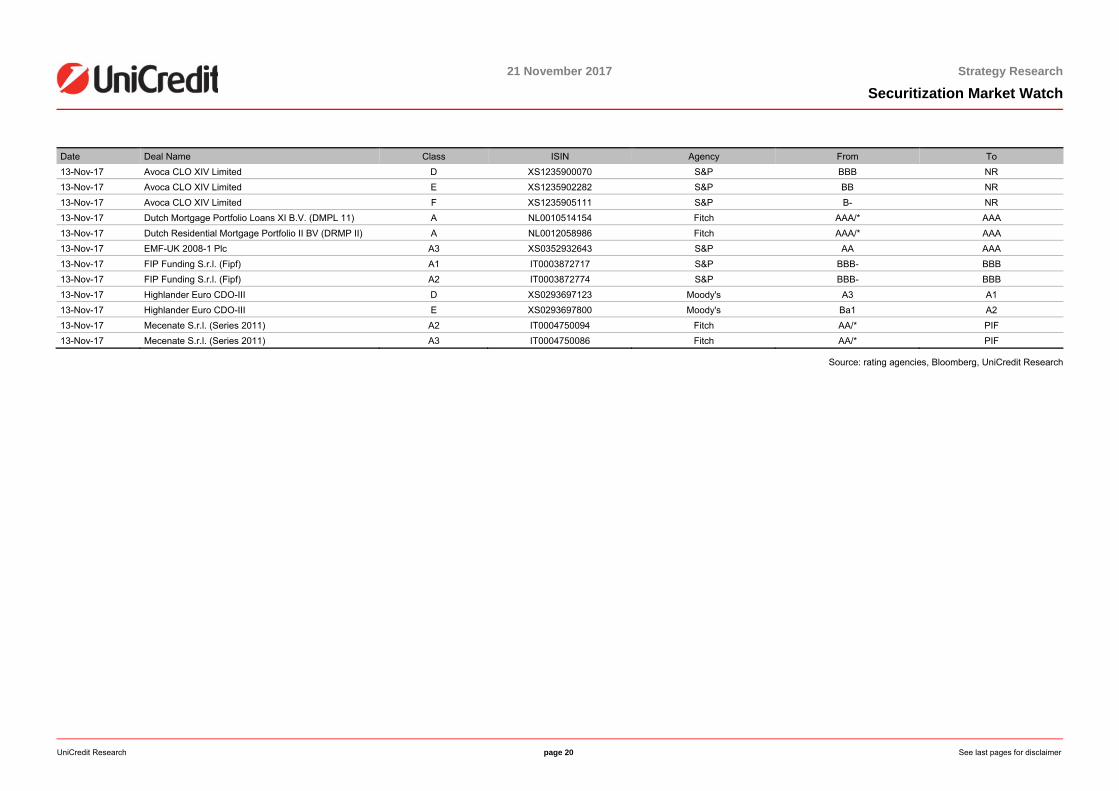

RATING CHANGES FROM 13 NOVEMBER TO 21 NOVEMBER

Date Deal Name Class ISIN Agency From To 21-Nov-17 Hypenn RMBS I B.V. A1 NL0010511093 Fitch AAA/* PIF 20-Nov-17 Harvest CLO XIV DAC A-1A XS1299699972 Fitch AAA PIF 20-Nov-17 Harvest CLO XIV DAC B-2 XS1299717972 Fitch AA+ PIF 20-Nov-17 Harvest CLO XIV DAC C XS1299718780 Fitch A+ PIF 20-Nov-17 Harvest CLO XIV DAC E XS1299708559 Fitch BB PIF 20-Nov-17 PYME Bancaja 5 B ES0372259038 Fitch BBB+ PIF 20-Nov-17 PYME Bancaja 5 C ES0372259046 Fitch CC PIF 20-Nov-17 PYME Bancaja 5 D ES0372259053 Fitch C WD 20-Nov-17 Wood Street CLO III B.V. D XS0256419069 Moody's A1 Aa1 20-Nov-17 Wood Street CLO III B.V. E XS0256419572 Moody's Baa3 A2 17-Nov-17 Dutch MBS XVIII B.V. A2 XS0871317938 Fitch AAA/* AAA 17-Nov-17 Dutch MBS XVIII B.V. B XS0871318829 Fitch AA+/* AA+ 17-Nov-17 Dutch MBS XVIII B.V. C XS0871319124 Fitch A+/* A+ 17-Nov-17 Dutch MBS XVIII B.V. D XS0871319397 Fitch BBB/* BBB 17-Nov-17 Dutch MBS XVIII B.V. E XS0871319470 Fitch B/* B 17-Nov-17 Faxtor ABS 2004-1 BV BE XS0191003754 Moody's Aa1 Aaa 17-Nov-17 Faxtor ABS 2004-1 BV BF XS0191006427 Moody's Aa1 Aaa 17-Nov-17 Renoir CDO B.V. A XS0216425255 S&P A+ NR 16-Nov-17 Alchera SPV S.r.l. A IT0004937840 S&P A A/*+ 16-Nov-17 Axius European CLO A XS0322030353 Moody's Aaa WR 16-Nov-17 Axius European CLO B XS0322030866 Moody's Aaa WR 16-Nov-17 Axius European CLO C XS0322031088 Moody's Aaa WR 16-Nov-17 Axius European CLO D XS0322031245 Moody's A3 WR

UniCredit Research page 18 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Date Deal Name Class ISIN Agency From To 16-Nov-17 Axius European CLO E XS0322031328 Moody's Ba2 WR 16-Nov-17 Castoro RMBS S.r.l. B XS0218206364 Fitch AA/* AA 16-Nov-17 Civitas SPV Srl 2012-2 A IT0004842545 S&P A A/*+ 16-Nov-17 Estense Finance A IT0004513542 Fitch AA/* AA 16-Nov-17 Estense Finance B IT0004513559 Fitch A-/* A- 16-Nov-17 FCT Ginkgo Compartment Sales Finance 2015-1 B FR0013069861 Fitch AA AA+ 16-Nov-17 FCT Ginkgo Compartment Sales Finance 2015-1 C FR0013069887 Fitch A AA- 16-Nov-17 Lusitano SME No.3 (Sagres STC) A PTSSC2OM0007 DBRS AAL AA 16-Nov-17 Lusitano SME No.3 (Sagres STC) B PTSSC3OM0006 DBRS BBBH AAL 16-Nov-17 Lusitano SME No.3 (Sagres STC) C PTSSC4OM0005 DBRS BH BBBH 16-Nov-17 Renoir CDO B.V. C XS0216426063 Moody's A3 Aa3 16-Nov-17 Renoir CDO B.V. D1 XS0216426659 Moody's Caa3 Caa2 16-Nov-17 Renoir CDO B.V. D2 XS0216426816 Moody's Caa3 Caa2 16-Nov-17 SapphireOne Mortgages FCT 2016-2 B FR0013213469 DBRS AA AAH 16-Nov-17 SapphireOne Mortgages FCT 2016-2 C FR0013213477 DBRS A AA 16-Nov-17 SapphireOne Mortgages FCT 2016-2 D FR0013213485 DBRS BBB AAL 16-Nov-17 SapphireOne Mortgages FCT 2016-2 E FR0013213493 DBRS BB A 16-Nov-17 SapphireOne Mortgages FCT 2016-3 E FR0013221637 DBRS BB BBBL 16-Nov-17 TDA CAM 11 FTA A2 ES0377845013 Fitch A+/* PIF 16-Nov-17 TDA CAM 11 FTA A3 ES0377845021 Fitch A+/* PIF 16-Nov-17 TDA CAM 11 FTA A4 ES0377845039 Fitch A+/* PIF 16-Nov-17 TDA CAM 11 FTA B ES0377845047 Fitch A+/* PIF 16-Nov-17 TDA CAM 11 FTA C ES0377845054 Fitch B+/* PIF 16-Nov-17 TDA CAM 11 FTA D ES0377845062 Fitch NR PIF 16-Nov-17 TDA CAM 12 FTA A2 ES0377104015 Fitch A+/* PIF 16-Nov-17 TDA CAM 12 FTA A3 ES0377104023 Fitch A+/* PIF 16-Nov-17 TDA CAM 12 FTA A4 ES0377104031 Fitch A+/* PIF 16-Nov-17 TDA CAM 12 FTA B ES0377104049 Fitch A+/* PIF 16-Nov-17 TDA CAM 12 FTA C ES0377104056 Fitch B/* PIF 16-Nov-17 TDA CAM 12 FTA D ES0377104064 Fitch NR PIF 16-Nov-17 Wood Street CLO-IV X XS0280515221 Moody's Aaa WR 15-Nov-17 AyT Colaterales Global Hipotecario BBK II A ES0312273362 Fitch A-/* A- 15-Nov-17 AyT Colaterales Global Hipotecario BBK II B ES0312273370 Fitch B/* CCC 15-Nov-17 Dekania Europe CDO I Plc B1 XS0226405180 Fitch BB BB+ 15-Nov-17 Dekania Europe CDO I Plc B2 XS0226405420 Fitch BB BB+ 15-Nov-17 Dekania Europe CDO I Plc C XS0226405693 Fitch B- BB- 15-Nov-17 Dekania Europe CDO I Plc D XS0226406071 Fitch CCC B

UniCredit Research page 19 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Date Deal Name Class ISIN Agency From To 15-Nov-17 Dekania Europe CDO II A2A XS0265847441 Fitch BBB A 15-Nov-17 Dekania Europe CDO II A2B XS0266475507 Fitch BBB A 15-Nov-17 Dekania Europe CDO II B XS0265867985 Fitch BB BB+ 15-Nov-17 Dekania Europe CDO II C XS0265871409 Fitch B B+ 15-Nov-17 Dekania Europe CDO II D1 XS0265875145 Fitch CC CCC 15-Nov-17 Dekania Europe CDO II D2 XS0266479913 Fitch CC CCC 15-Nov-17 Dekania Europe CDO II E XS0265883164 Fitch C CC 15-Nov-17 Dekania Europe CDO III plc A1 XS0298464214 Fitch BBB A 15-Nov-17 Dekania Europe CDO III plc A2A XS0298465534 Fitch B BB 15-Nov-17 Dekania Europe CDO III plc A2B XS0300774311 Fitch B BB 15-Nov-17 Dekania Europe CDO III plc C XS0298467407 Fitch CC CCC 15-Nov-17 Dekania Europe CDO III plc D XS0298468637 Fitch C CC 15-Nov-17 Guerriero S.r.l. A IT0005008666 S&P A NR 15-Nov-17 IBL CQS 2013 S.r.l. A IT0004984164 Moody's Aa3/*- Aa2 15-Nov-17 IBL CQS 2013 S.r.l. B IT0004984446 Moody's Aa3/*- Aa2 15-Nov-17 IBL Finance Srl (IBL CQS 2015) A IT0005108698 Moody's Aa2/*- Aa2 14-Nov-17 Avoca CLO XIV Limited A XS1235894323 Moody's Aaa WR 14-Nov-17 Avoca CLO XIV Limited B1 XS1235896450 Moody's Aa2 WR 14-Nov-17 Avoca CLO XIV Limited B2 XS1235896880 Moody's Aa2 WR 14-Nov-17 Avoca CLO XIV Limited C XS1235897185 Moody's A2 WR 14-Nov-17 Avoca CLO XIV Limited D XS1235900070 Moody's Baa2 WR 14-Nov-17 Avoca CLO XIV Limited E XS1235902282 Moody's Ba2 WR 14-Nov-17 Avoca CLO XIV Limited F XS1235905111 Moody's B2 WR 14-Nov-17 Media Finance S.r.l. (Series 2009) A IT0004562309 S&P AA- NR 14-Nov-17 Rural Hipotecario IV A ES0358283002 Moody's Aa2 WR 14-Nov-17 Rural Hipotecario IV B ES0358283010 Moody's Aa2 WR 14-Nov-17 Saecure 13 NHG B.V. A2 XS0898707475 Fitch AAA/* AAA 14-Nov-17 Saecure 14 NHG B.V. A2 XS1033757201 Fitch AAA/* AAA 14-Nov-17 Saecure 15 BV A1 XS1028941620 Fitch AAA/* AAA 14-Nov-17 Saecure 15 BV A2 XS1028942511 Fitch AAA/* AAA 14-Nov-17 Sligo Card Finance 2015 DAC A XS1314233732 DBRS A AA 14-Nov-17 Southern Pacific Securities (SPS) 2005-1 Plc C1c XS0212691744 S&P A- A 14-Nov-17 Southern Pacific Securities (SPS) 2005-1 Plc D1c XS0212692122 S&P BBB A- 13-Nov-17 Avoca CLO XIV Limited A XS1235894323 S&P AAA NR 13-Nov-17 Avoca CLO XIV Limited B1 XS1235896450 S&P AA NR 13-Nov-17 Avoca CLO XIV Limited B2 XS1235896880 S&P AA NR 13-Nov-17 Avoca CLO XIV Limited C XS1235897185 S&P A NR

UniCredit Research page 20 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Date Deal Name Class ISIN Agency From To 13-Nov-17 Avoca CLO XIV Limited D XS1235900070 S&P BBB NR 13-Nov-17 Avoca CLO XIV Limited E XS1235902282 S&P BB NR 13-Nov-17 Avoca CLO XIV Limited F XS1235905111 S&P B- NR 13-Nov-17 Dutch Mortgage Portfolio Loans XI B.V. (DMPL 11) A NL0010514154 Fitch AAA/* AAA 13-Nov-17 Dutch Residential Mortgage Portfolio II BV (DRMP II) A NL0012058986 Fitch AAA/* AAA 13-Nov-17 EMF-UK 2008-1 Plc A3 XS0352932643 S&P AA AAA 13-Nov-17 FIP Funding S.r.l. (Fipf) A1 IT0003872717 S&P BBB- BBB 13-Nov-17 FIP Funding S.r.l. (Fipf) A2 IT0003872774 S&P BBB- BBB 13-Nov-17 Highlander Euro CDO-III D XS0293697123 Moody's A3 A1 13-Nov-17 Highlander Euro CDO-III E XS0293697800 Moody's Ba1 A2 13-Nov-17 Mecenate S.r.l. (Series 2011) A2 IT0004750094 Fitch AA/* PIF 13-Nov-17 Mecenate S.r.l. (Series 2011) A3 IT0004750086 Fitch AA/* PIF

Source: rating agencies, Bloomberg, UniCredit Research

UniCredit Research page 21 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

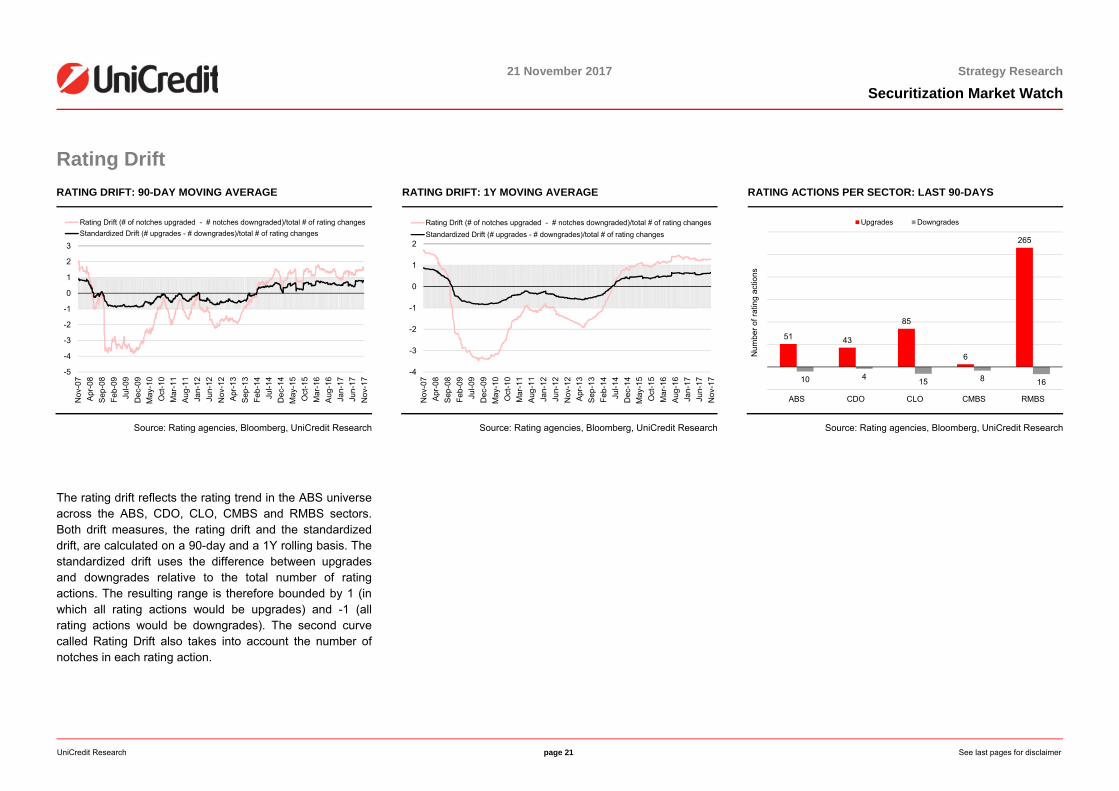

Rating Drift RATING DRIFT: 90-DAY MOVING AVERAGE

Source: Rating agencies, Bloomberg, UniCredit Research

The rating drift reflects the rating trend in the ABS universe across the ABS, CDO, CLO, CMBS and RMBS sectors. Both drift measures, the rating drift and the standardized drift, are calculated on a 90-day and a 1Y rolling basis. The standardized drift uses the difference between upgrades and downgrades relative to the total number of rating actions. The resulting range is therefore bounded by 1 (in which all rating actions would be upgrades) and -1 (all rating actions would be downgrades). The second curve called Rating Drift also takes into account the number of notches in each rating action.

RATING DRIFT: 1Y MOVING AVERAGE

Source: Rating agencies, Bloomberg, UniCredit Research

RATING ACTIONS PER SECTOR: LAST 90-DAYS

Source: Rating agencies, Bloomberg, UniCredit Research

-5

-4

-3

-2

-1

0

1

2

3

Nov

-07

Apr

-08

Sep

-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan-

12Ju

n-12

Nov

-12

Apr

-13

Sep

-13

Feb-

14Ju

l-14

Dec

-14

May

-15

Oct

-15

Mar

-16

Aug

-16

Jan-

17Ju

n-17

Nov

-17

Rating Drift (# of notches upgraded - # notches downgraded)/total # of rating changesStandardized Drift (# upgrades - # downgrades)/total # of rating changes

-4

-3

-2

-1

0

1

2

Nov

-07

Apr

-08

Sep

-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan-

12Ju

n-12

Nov

-12

Apr

-13

Sep

-13

Feb-

14Ju

l-14

Dec

-14

May

-15

Oct

-15

Mar

-16

Aug

-16

Jan-

17Ju

n-17

Nov

-17

Rating Drift (# of notches upgraded - # notches downgraded)/total # of rating changesStandardized Drift (# upgrades - # downgrades)/total # of rating changes

51 43

85

6

265

10 4 15 8 16

ABS CDO CLO CMBS RMBS

Num

ber o

f rat

ing

actio

ns

Upgrades Downgrades

UniCredit Research page 22 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

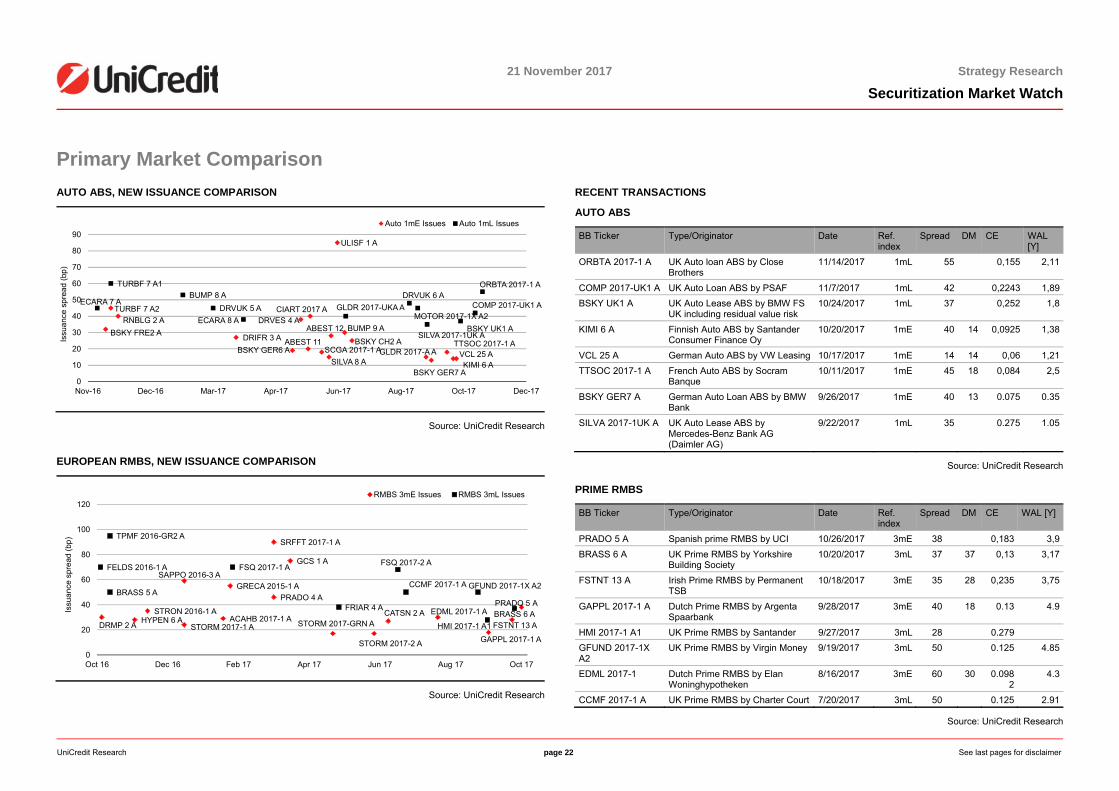

Primary Market Comparison AUTO ABS, NEW ISSUANCE COMPARISON

Source: UniCredit Research

EUROPEAN RMBS, NEW ISSUANCE COMPARISON

Source: UniCredit Research

RECENT TRANSACTIONS

AUTO ABS

BB Ticker Type/Originator Date Ref. index

Spread DM CE WAL [Y]

ORBTA 2017-1 A UK Auto loan ABS by Close Brothers

11/14/2017 1mL 55 0,155 2,11

COMP 2017-UK1 A UK Auto Loan ABS by PSAF 11/7/2017 1mL 42 0,2243 1,89 BSKY UK1 A UK Auto Lease ABS by BMW FS

UK including residual value risk 10/24/2017 1mL 37 0,252 1,8

KIMI 6 A Finnish Auto ABS by Santander Consumer Finance Oy

10/20/2017 1mE 40 14 0,0925 1,38

VCL 25 A German Auto ABS by VW Leasing 10/17/2017 1mE 14 14 0,06 1,21 TTSOC 2017-1 A French Auto ABS by Socram

Banque 10/11/2017 1mE 45 18 0,084 2,5

BSKY GER7 A German Auto Loan ABS by BMW Bank

9/26/2017 1mE 40 13 0.075 0.35

SILVA 2017-1UK A UK Auto Lease ABS by Mercedes-Benz Bank AG (Daimler AG)

9/22/2017 1mL 35 0.275 1.05

Source: UniCredit Research PRIME RMBS

BB Ticker Type/Originator Date Ref. index

Spread DM CE WAL [Y]

PRADO 5 A Spanish prime RMBS by UCI 10/26/2017 3mE 38 0,183 3,9 BRASS 6 A UK Prime RMBS by Yorkshire

Building Society 10/20/2017 3mL 37 37 0,13 3,17

FSTNT 13 A Irish Prime RMBS by Permanent TSB

10/18/2017 3mE 35 28 0,235 3,75

GAPPL 2017-1 A Dutch Prime RMBS by Argenta Spaarbank

9/28/2017 3mE 40 18 0.13 4.9

HMI 2017-1 A1 UK Prime RMBS by Santander 9/27/2017 3mL 28 0.279 GFUND 2017-1X A2

UK Prime RMBS by Virgin Money 9/19/2017 3mL 50 0.125 4.85

EDML 2017-1 Dutch Prime RMBS by Elan Woninghypotheken

8/16/2017 3mE 60 30 0.0982

4.3

CCMF 2017-1 A UK Prime RMBS by Charter Court 7/20/2017 3mL 50 0.125 2.91

Source: UniCredit Research

BSKY FRE2 A

TURBF 7 A2RNBLG 2 A

DRIFR 3 ABSKY GER6 A

DRVES 4 ACIART 2017 A

ABEST 11SCGA 2017-1 A

ABEST 12

SILVA 8 A

ULISF 1 A

BUMP 9 ABSKY CH2 A

GLDR 2017-A A

BSKY GER7 A

TTSOC 2017-1 AVCL 25 AKIMI 6 A

ECARA 7 A

TURBF 7 A1BUMP 8 A

DRVUK 5 AECARA 8 A

GLDR 2017-UKA ADRVUK 6 A

MOTOR 2017-1X A2

SILVA 2017-1UK ABSKY UK1 A

COMP 2017-UK1 A

ORBTA 2017-1 A

0

10

20

30

40

50

60

70

80

90

Nov-16 Dec-16 Mar-17 Apr-17 Jun-17 Aug-17 Oct-17 Dec-17

Issu

ance

spr

ead

(bp)

Auto 1mE Issues Auto 1mL Issues

DRMP 2 A HYPEN 6 ASTRON 2016-1 A

SAPPO 2016-3 A

STORM 2017-1 AACAHB 2017-1 A

GRECA 2015-1 A

SRFFT 2017-1 A

PRADO 4 A

GCS 1 A

STORM 2017-GRN A

STORM 2017-2 A

CATSN 2 A EDML 2017-1 A

GAPPL 2017-1 A

FSTNT 13 A

FELDS 2016-1 A

TPMF 2016-GR2 A

BRASS 5 A

FSQ 2017-1 A

FRIAR 4 A

FSQ 2017-2 A

CCMF 2017-1 A GFUND 2017-1X A2

HMI 2017-1 A1BRASS 6 A

0

20

40

60

80

100

120

Oct 16 Dec 16 Feb 17 Apr 17 Jun 17 Aug 17 Oct 17

Issu

ance

spr

ead

(bp)

RMBS 3mE Issues RMBS 3mL Issues

PRADO 5 A

UniCredit Research page 23 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

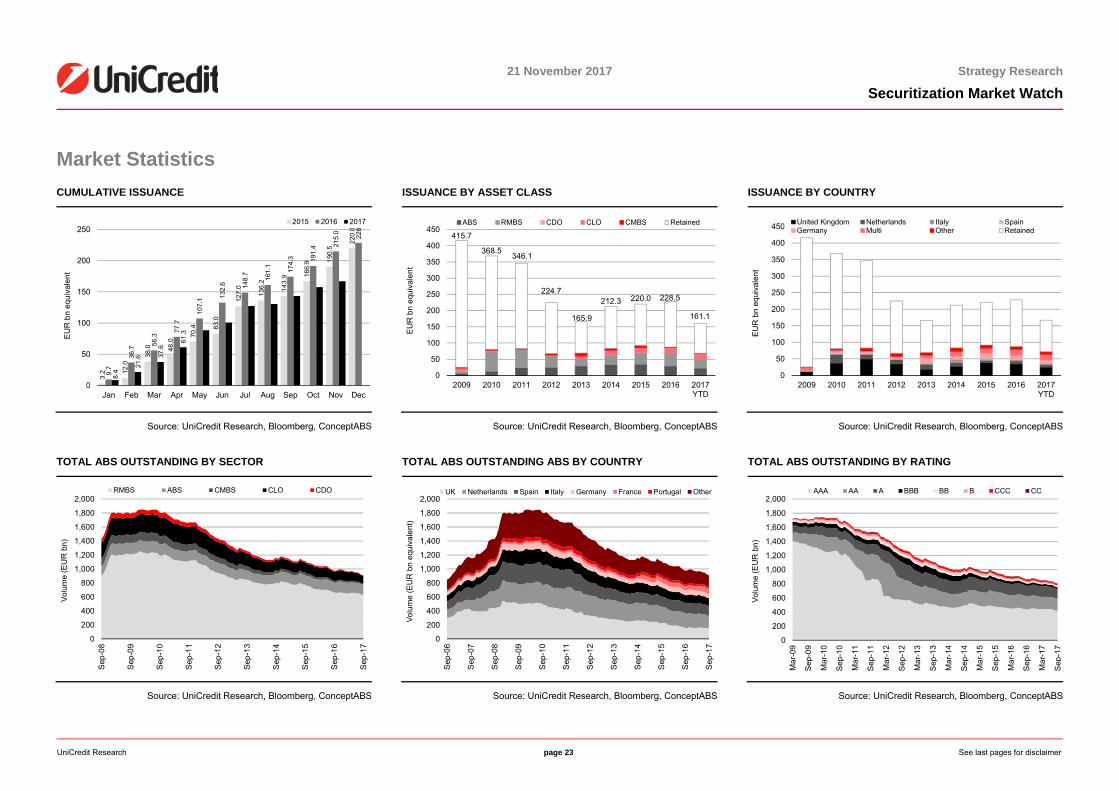

Market Statistics CUMULATIVE ISSUANCE

Source: UniCredit Research, Bloomberg, ConceptABS

TOTAL ABS OUTSTANDING BY SECTOR

Source: UniCredit Research, Bloomberg, ConceptABS

ISSUANCE BY ASSET CLASS

Source: UniCredit Research, Bloomberg, ConceptABS

TOTAL ABS OUTSTANDING ABS BY COUNTRY

Source: UniCredit Research, Bloomberg, ConceptABS

ISSUANCE BY COUNTRY

Source: UniCredit Research, Bloomberg, ConceptABS

TOTAL ABS OUTSTANDING BY RATING

Source: UniCredit Research, Bloomberg, ConceptABS

3.2 12

.0

38.0 48

.0

70.4 83

.0

127.

0

136.

2

143.

9 166.

9 190.

5

220.

0

9.7

36.7

56.3

77.7

107.

1 132.

6 148.

7

161.

1

174.

3 191.

4 215.

0

228.

5

8.4

21.6 37

.6

61.3

0

50

100

150

200

250

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

EU

R b

n eq

uiva

lent

2015 2016 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Sep

-08

Sep

-09

Sep

-10

Sep

-11

Sep

-12

Sep

-13

Sep

-14

Sep

-15

Sep

-16

Sep

-17

Volu

me

(EU

R b

n)

RMBS ABS CMBS CLO CDO

415.7

368.5 346.1

224.7

165.9

212.3 220.0 228.5

161.1

0

50

100

150

200

250

300

350

400

450

2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

EU

R b

n eq

uiva

lent

ABS RMBS CDO CLO CMBS Retained

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

Sep

-11

Sep

-12

Sep

-13

Sep

-14

Sep

-15

Sep

-16

Sep

-17

Volu

me

(EU

R b

n eq

uiva

lent

)

UK Netherlands Spain Italy Germany France Portugal Other

0

50

100

150

200

250

300

350

400

450

2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

EU

R b

n eq

uiva

lent

United Kingdom Netherlands Italy SpainGermany Multi Other Retained

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

Sep

-16

Mar

-17

Se p

-17

Volu

me

(EU

R b

n)

AAA AA A BBB BB B CCC CC

UniCredit Research page 24 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

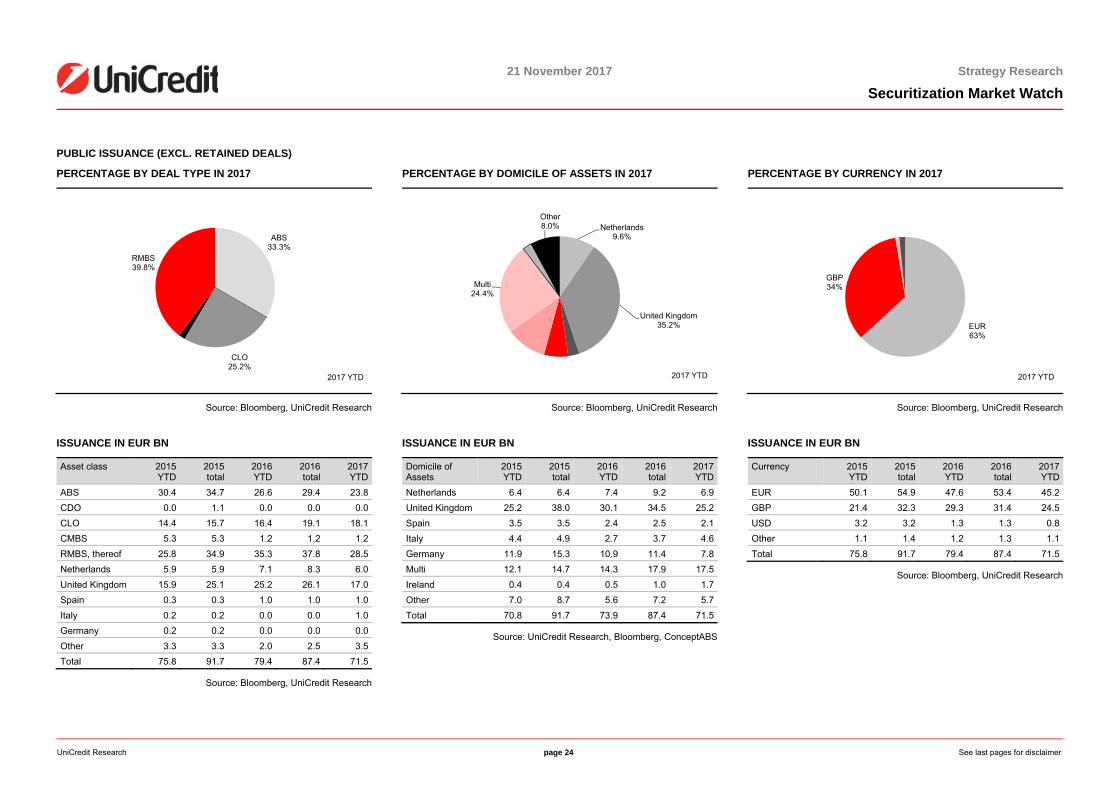

PUBLIC ISSUANCE (EXCL. RETAINED DEALS)

PERCENTAGE BY DEAL TYPE IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Asset class 2015 YTD

2015 total

2016 YTD

2016 total

2017 YTD

ABS 30.4 34.7 26.6 29.4 23.8CDO 0.0 1.1 0.0 0.0 0.0CLO 14.4 15.7 16.4 19.1 18.1CMBS 5.3 5.3 1.2 1.2 1.2RMBS, thereof 25.8 34.9 35.3 37.8 28.5Netherlands 5.9 5.9 7.1 8.3 6.0United Kingdom 15.9 25.1 25.2 26.1 17.0Spain 0.3 0.3 1.0 1.0 1.0Italy 0.2 0.2 0.0 0.0 1.0Germany 0.2 0.2 0.0 0.0 0.0Other 3.3 3.3 2.0 2.5 3.5Total 75.8 91.7 79.4 87.4 71.5

Source: Bloomberg, UniCredit Research

PERCENTAGE BY DOMICILE OF ASSETS IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Domicile of Assets

2015 YTD

2015 total

2016 YTD

2016 total

2017 YTD

Netherlands 6.4 6.4 7.4 9.2 6.9United Kingdom 25.2 38.0 30.1 34.5 25.2Spain 3.5 3.5 2.4 2.5 2.1Italy 4.4 4.9 2.7 3.7 4.6Germany 11.9 15.3 10.9 11.4 7.8Multi 12.1 14.7 14.3 17.9 17.5Ireland 0.4 0.4 0.5 1.0 1.7Other 7.0 8.7 5.6 7.2 5.7Total 70.8 91.7 73.9 87.4 71.5

Source: UniCredit Research, Bloomberg, ConceptABS

PERCENTAGE BY CURRENCY IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Currency 2015 YTD

2015 total

2016 YTD

2016 total

2017 YTD

EUR 50.1 54.9 47.6 53.4 45.2 GBP 21.4 32.3 29.3 31.4 24.5 USD 3.2 3.2 1.3 1.3 0.8 Other 1.1 1.4 1.2 1.3 1.1 Total 75.8 91.7 79.4 87.4 71.5

Source: Bloomberg, UniCredit Research

ABS33.3%

CLO25.2%

RMBS39.8%

2017 YTD

Netherlands9.6%

United Kingdom35.2%

Multi24.4%

Other8.0%

2017 YTD

EUR63%

GBP34%

2017 YTD

UniCredit Research page 25 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

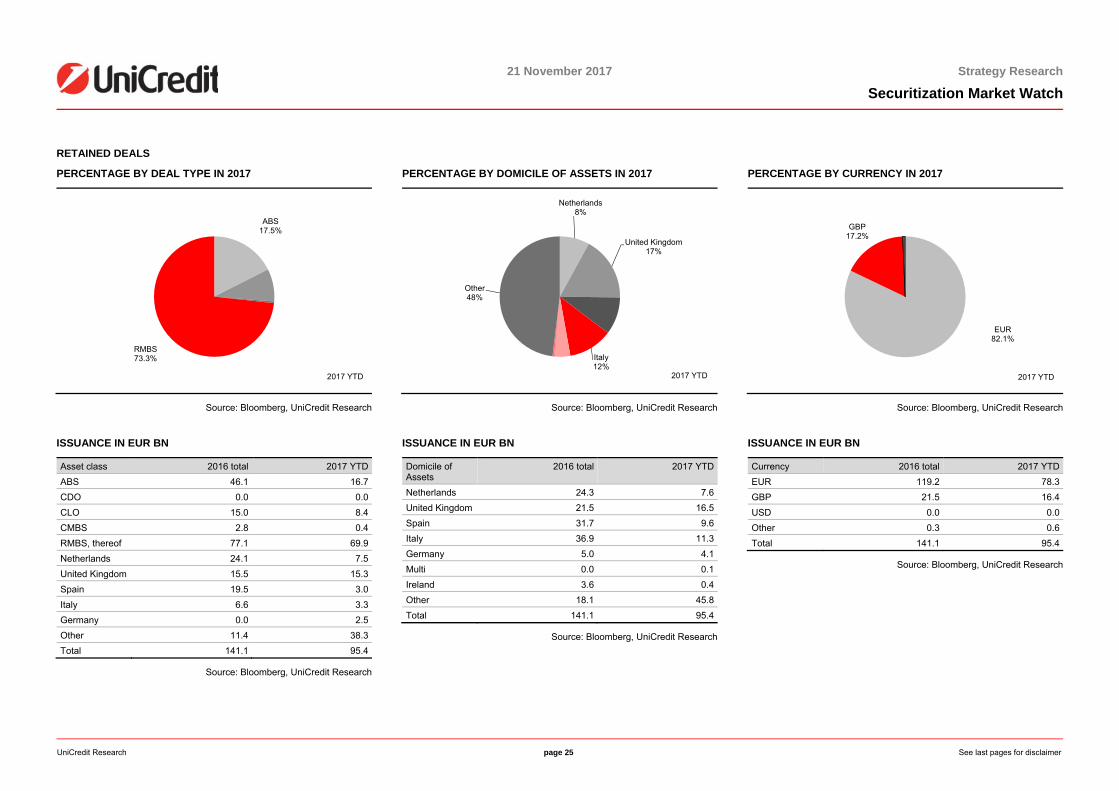

RETAINED DEALS

PERCENTAGE BY DEAL TYPE IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Asset class 2016 total 2017 YTDABS 46.1 16.7CDO 0.0 0.0CLO 15.0 8.4CMBS 2.8 0.4RMBS, thereof 77.1 69.9Netherlands 24.1 7.5United Kingdom 15.5 15.3Spain 19.5 3.0Italy 6.6 3.3Germany 0.0 2.5Other 11.4 38.3Total 141.1 95.4

Source: Bloomberg, UniCredit Research

PERCENTAGE BY DOMICILE OF ASSETS IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Domicile of Assets

2016 total 2017 YTD

Netherlands 24.3 7.6United Kingdom 21.5 16.5Spain 31.7 9.6Italy 36.9 11.3Germany 5.0 4.1Multi 0.0 0.1Ireland 3.6 0.4Other 18.1 45.8Total 141.1 95.4

Source: Bloomberg, UniCredit Research

PERCENTAGE BY CURRENCY IN 2017

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

Currency 2016 total 2017 YTD EUR 119.2 78.3 GBP 21.5 16.4 USD 0.0 0.0 Other 0.3 0.6 Total 141.1 95.4

Source: Bloomberg, UniCredit Research

ABS17.5%

RMBS73.3%

2017 YTD

Netherlands8%

United Kingdom17%

Italy12%

Other48%

2017 YTD

EUR82.1%

GBP17.2%

2017 YTD

UniCredit Research page 26 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

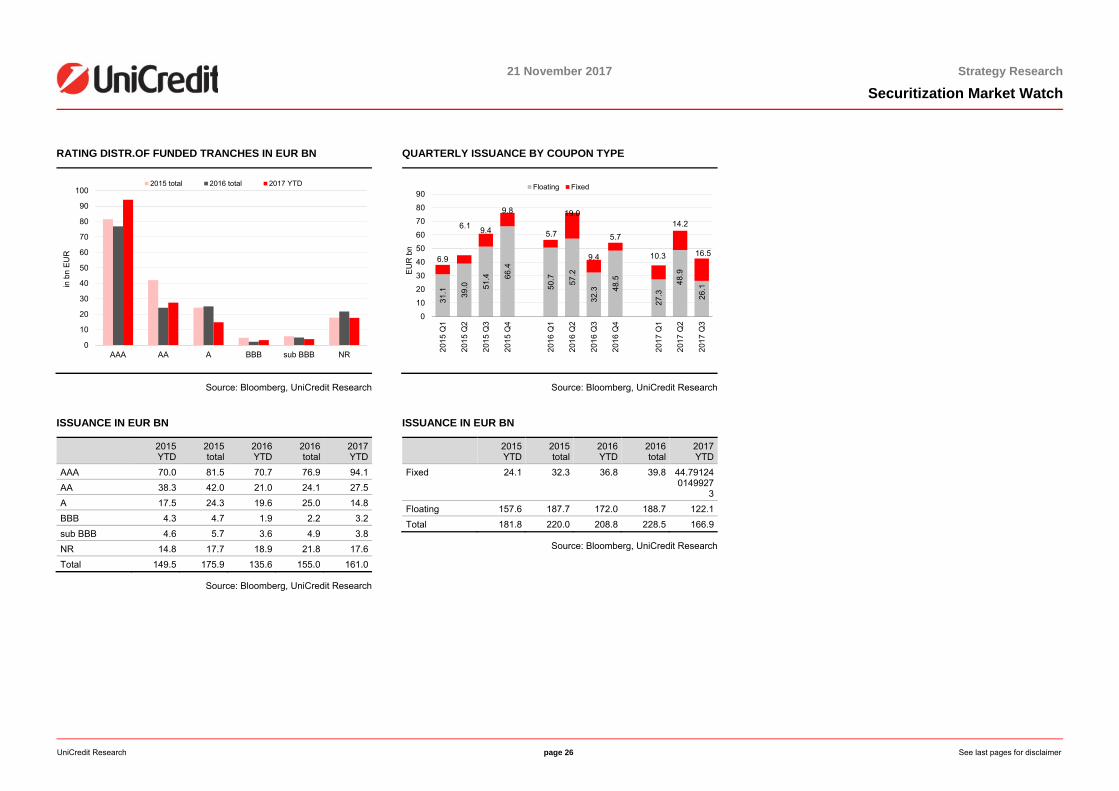

RATING DISTR.OF FUNDED TRANCHES IN EUR BN

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

2015 YTD

2015 total

2016 YTD

2016 total

2017 YTD

AAA 70.0 81.5 70.7 76.9 94.1AA 38.3 42.0 21.0 24.1 27.5A 17.5 24.3 19.6 25.0 14.8BBB 4.3 4.7 1.9 2.2 3.2sub BBB 4.6 5.7 3.6 4.9 3.8NR 14.8 17.7 18.9 21.8 17.6Total 149.5 175.9 135.6 155.0 161.0

Source: Bloomberg, UniCredit Research

QUARTERLY ISSUANCE BY COUPON TYPE

Source: Bloomberg, UniCredit Research

ISSUANCE IN EUR BN

2015 YTD

2015 total

2016 YTD

2016 total

2017 YTD

Fixed 24.1 32.3 36.8 39.8 44.791240149927

3Floating 157.6 187.7 172.0 188.7 122.1Total 181.8 220.0 208.8 228.5 166.9

Source: Bloomberg, UniCredit Research

0

10

20

30

40

50

60

70

80

90

100

AAA AA A BBB sub BBB NR

in b

n EU

R

2015 total 2016 total 2017 YTD

31.1 39

.0 51.4 66

.4

50.7 57.2

32.3 48

.5

27.3

48.9

26.1

6.9

6.1 9.4

9.8

5.7

19.0

9.4

5.7

10.3

14.2

16.5

0

10

20

30

40

50

60

70

80

90

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

EU

R b

n

Floating Fixed

UniCredit Research page 27 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

Delinquency Data AUTO ABS 60-90 DAY DELINQUENCIES

Source: Moody's, UniCredit Research

DUTCH RMBS 60+ DAY DELINQUENCIES

Source: Moody's, UniCredit Research

UK PRIME RMBS 90+DAY DELINQUENCIES

Source: Moody's, UniCredit Research

UK NON-CONFORMING 90+ DAY DELINQUENCIES

Source: Moody's, UniCredit Research

ITALIAN RMBS 90+ DAY DELINQUENCIES

Source: Moody's, UniCredit Research

SPANISH RMBS 90+ DAY DELINQUENCIES

Source: Moody's, UniCredit Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

May

-07

Nov

-07

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Nov

-14

May

-15

Nov

-15

May

-16

Nov

-16

May

-17

%

France Germany Portugal Italy UK Spain Index (EMEA)

0.00.20.40.60.81.01.21.41.61.82.0

Jun-

05D

ec-0

5Ju

n-06

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Ju

n-14

Dec

-14

Jun-

15D

ec-1

5Ju

n-16

Dec

-16

Jun-

17

%

2007 2008 20092010 2011 20122013 2014 20152016 Index (Prime) Index (NHG)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Aug-

05Fe

b-06

Aug-

06Fe

b-07

Aug-

07Fe

b-08

Aug-

08Fe

b-09

Aug-

09Fe

b-10

Aug-

10Fe

b-11

Aug-

11Fe

b-12

Aug-

12Fe

b-13

Aug-

13Fe

b-14

Aug-

14Fe

b-15

Aug-

15Fe

b-16

Aug-

16Fe

b-17

Aug-

17

%

Arkle Arran Fosse GracechurchGranite Greenock Holmes LanarkLangton Others Permanent SilverstoneIndex

0

5

10

15

20

25

30

Jun-

05D

ec-0

5Ju

n-06

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Ju

n-14

Dec

-14

Jun-

15D

ec-1

5Ju

n-16

Dec

-16

Jun-

17

%

2001-2004 2005 2006 2007 2008 Index 2015

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Feb-

07Ju

l-07

Dec

-07

May

-08

Oct

-08

Mar

-09

Aug

-09

Jan-

10Ju

n-10

Nov

-10

Apr-1

1S

ep-1

1Fe

b-12

Jul-1

2D

ec-1

2M

ay-1

3O

ct-1

3M

ar-1

4A

ug-1

4Ja

n-15

Jun-

15N

ov-1

5Ap

r-16

Sep

-16

Feb-

17

%

2000-2004 2005 2006 20072008 2009 2010 20112012/2013 2014/2015 Index

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

%

1997-2005 2006 2007 20082009 2010 2011 2012-20152016 Index

UniCredit Research page 28 See last pages for disclaimer.

21 November 2017 Strategy Research

Securitization Market Watch

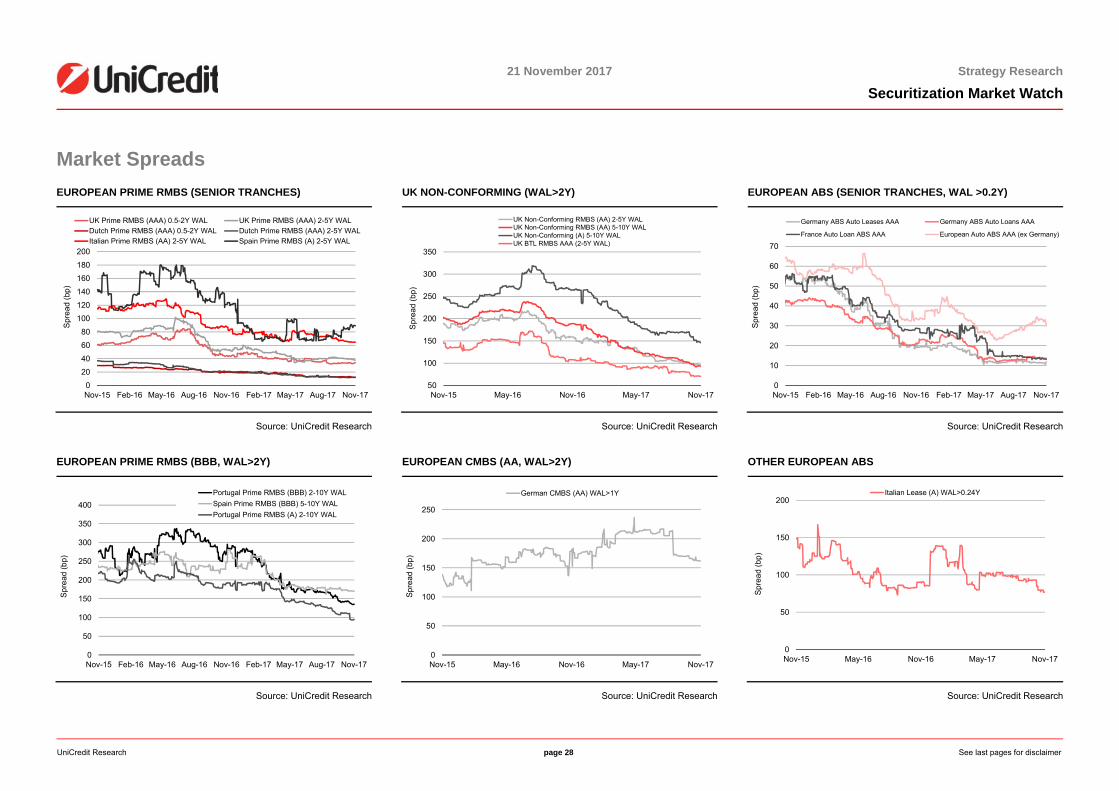

Market Spreads EUROPEAN PRIME RMBS (SENIOR TRANCHES)

Source: UniCredit Research

EUROPEAN PRIME RMBS (BBB, WAL>2Y)

Source: UniCredit Research

UK NON-CONFORMING (WAL>2Y)

Source: UniCredit Research

EUROPEAN CMBS (AA, WAL>2Y)

Source: UniCredit Research

EUROPEAN ABS (SENIOR TRANCHES, WAL >0.2Y)

Source: UniCredit Research

OTHER EUROPEAN ABS

Source: UniCredit Research

0

2040

60

80

100120

140

160180

200

Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17 Nov-17

Spr

ead

(bp)

UK Prime RMBS (AAA) 0.5-2Y WAL UK Prime RMBS (AAA) 2-5Y WALDutch Prime RMBS (AAA) 0.5-2Y WAL Dutch Prime RMBS (AAA) 2-5Y WALItalian Prime RMBS (AA) 2-5Y WAL Spain Prime RMBS (A) 2-5Y WAL

0

50

100

150

200

250

300

350

400

Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17 Nov-17

Spre

ad (b

p)

Portugal Prime RMBS (BBB) 2-10Y WALSpain Prime RMBS (BBB) 5-10Y WALPortugal Prime RMBS (A) 2-10Y WAL

50

100

150

200

250

300

350

Nov-15 May-16 Nov-16 May-17 Nov-17

Spr

ead

(bp)

UK Non-Conforming RMBS (AA) 2-5Y WALUK Non-Conforming RMBS (AA) 5-10Y WALUK Non-Conforming (A) 5-10Y WALUK BTL RMBS AAA (2-5Y WAL)

0

50

100

150

200

250

Nov-15 May-16 Nov-16 May-17 Nov-17

Spr

ead

(bp)

German CMBS (AA) WAL>1YGerman CMBS (AA) WAL>1Y

0

10

20

30

40

50

60

70

Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17 Nov-17

Spr

ead

(bp)

Germany ABS Auto Leases AAA Germany ABS Auto Loans AAA

France Auto Loan ABS AAA European Auto ABS AAA (ex Germany)

0

50

100

150

200

Nov-15 May-16 Nov-16 May-17 Nov-17

Spre

ad (b

p)

Italian Lease (A) WAL>0.24Y

21 November 2017 Strategy Research

Securitization Market Watch

UniCredit Research page 29

Disclaimer Our recommendations are based on information obtained from, or are based upon public information sources that we consider to be reliable but for the completeness and accuracy of which we assume no liability. All estimates and opinions and projections and forecasts included in the report represent the independent judgment of the analysts as of the date of the issue unless stated otherwise. This report may contain links to websites of third parties, the content of which is not controlled by UniCredit Bank. No liability is assumed for the content of these third-party websites. We reserve the right to modify the views expressed herein at any time without notice. Moreover, we reserve the right not to update this information or to discontinue it altogether without notice. This analysis is for information purposes only and (i) does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any financial, money market or investment instrument or any security, (ii) is neither intended as such an offer for sale or subscription of or solicitation of an offer to buy or subscribe for any financial, money market or investment instrument or any security nor (iii) as an advertisement thereof. The investment possibilities discussed in this report may not be suitable for certain investors depending on their specific investment objectives and time horizon or in the context of their overall financial situation. The investments discussed may fluctuate in price or value. Investors may get back less than they invested. Changes in rates of exchange may have an adverse effect on the value of investments. Furthermore, past performance is not necessarily indicative of future results. In particular, the risks associated with an investment in the financial, money market or investment instrument or security under discussion are not explained in their entirety. This information is given without any warranty on an "as is" basis and should not be regarded as a substitute for obtaining individual advice. Investors must make their own determination of the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy and their legal, fiscal and financial position. As this document does not qualify as an investment recommendation or as a direct investment recommendation, neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Investors are urged to contact their bank's investment advisor for individual explanations and advice. Neither UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch nor any of their respective directors, officers or employees nor any other person accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. This analysis is being distributed by electronic and ordinary mail to professional investors, who are expected to make their own investment decisions without undue reliance on this publication, and may not be redistributed, reproduced or published in whole or in part for any purpose. Responsibility for the content of this publication lies with: UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank a) UniCredit Bank AG (UniCredit Bank, Munich or Frankfurt), Arabellastraße 12, 81925 Munich, Germany, (also responsible for the distribution pursuant to §34b WpHG). The company belongs to UniCredit Group. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28 , 60439 Frankfurt, Germany. b) UniCredit Bank AG London Branch (UniCredit Bank, London), Moor House, 120 London Wall, London EC2Y 5ET, United Kingdom. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany and subject to limited regulation by the Financial Conduct Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS, United Kingdom and Prudential Regulation Authority 20 Moorgate, London, EC2R 6DA, United Kingdom. Further details regarding our regulatory status are available on request.