Embed Size (px)

Citation preview

Seismic risk perception in the aftermath of Wenchuanearthquakes in southwestern China

Alex Y. Lo

The Kadoorie Institute, University of Hong Kong, Hong Kong

Lewis T.O. Cheung

Department of Social Sciences, The Hong Kong Institute ofEducation, Tai Po, New Territories, Hong Kong

Citation:

Lo, A.Y. and L.T.O. Cheung (in press) Seismic risk perception in the aftermath ofWenchuan earthquakes in southwestern China, Natural Hazards. DOI:http://dx.doi.org/10.1007/s11069-015-1815-6

Publisher version available from authors: [email protected]

2

Abstract

Disruptive earthquakes hit Sichuan Province, China, in 2008. Thisarticle describes the earthquake risk perception of residents inthe most badly damaged area of Sichuan. Specifically, thisresearch explores the extent to which risk perception is relatedto a household’s socioeconomic characteristics and theirfinancial protection from natural hazards. A household survey wasconducted in a special administrative region of Wenchuan County.Residents strongly believe that major earthquakes are unlikely toreturn in the next decade, although potential impacts areexpected to be significant. The perceived likelihood and severityof future earthquake disasters increased with the intensity ofthe damage from past earthquakes, i.e., the most greatly affectedvictims tend to rate the risk higher. Income levels had anegative effect on the perceived earthquake likelihood. Moreover,many local residents did not appear to be financially preparedfor earthquakes. The degree of financial protection fromearthquakes had only modest impacts on risk perception. Theseresults provide mixed evidence for the hypothesis thatindividuals who are better prepared for hazards tend to perceiverelated risks lower than others. We call for further researchinto how rising incomes and the ability to secure disasterfinances affect community resilience to natural hazards.

Keywords: earthquake; risk perception; financial protection; income; community resilience; China

3

1.

2. Introduction

According to the International Disaster Database (2014), the top

ten most devastating earthquakes during 2005-2014 incurred an

economic damage of US$395 billion in total. Japan’s ‘3.11’

earthquake and tsunami in 2011 topped the list by causing

estimated damage of US$210 billion. The second and eighth most

damaging earthquake events, estimated at US$85 billion and US$6.8

billion, respectively, were recorded in China. Casualties and

property damage in these two catastrophic events were

concentrated in Sichuan Province, which is located in

southwestern China; the province had a Gross Domestic Product

(GDP) per capita of ¥29,608 Chinese RMB yuan, or US$4,775, in

2012 (National Bureau of Statistics, 2013).

Earthquakes occur within a very brief period of time.

Effective adaptive and coping efforts crucially rely upon the

extent to which necessary knowledge, resources, and competencies

are organized in advance and are used promptly and effectively

should the need arise (Paton et al., 2010). Arrangements for

post-disaster relief and catastrophe insurance are important for

accelerating economic recovery from major hazardous events

(Botzen, 2013; Lo, 2013). Not all countries or regions, however,

have set up effective mechanisms for providing timely financial

aid to earthquake victims (World Bank, 2010). Members of poor

agricultural communities, such as the remote counties and

4

villages in Sichuan, are particularly vulnerable (Sun et al.,

2010). Local governments and the public sector in these areas

struggle to increase their capital investments in seismic risk

mitigation due to budgetary constraints relative to other

priorities. Because of the shortage of governmental assistance,

households and communities exposed to seismic hazards must take

initiative in risk mitigation and preparation.

Hazard awareness is the most fundamental psychosocial

threshold that must be passed before members of a society can

adjust to impending shocks (Laska, 1990). Early research

suggested that residents of earthquake-prone areas had little

knowledge of the probability or potential damage from a future

disaster (Kunreuther and Slovic, 1978; Palm, 1990), and this

remains largely true in present-day communities (Armas, 2006;

Tian et al., 2014). The public might misperceive or ignore the

risk of earthquakes, which are low-probability events that are

not amenable to direct human control and that are difficult to

predict with high precision (Kung and Chen, 2012). Misperception

and myopic attitudes might result in delays or failures in taking

proper risk-mitigating actions ahead of time to reduce the

potential impacts of the hazard on households and communities.

Understanding how earthquake risks are perceived by the

public is an important first step for assessing a community’s

seismic vulnerability (Armas, 2006, 2008; Palm and Hodgson,

1992). However, few recent international research reports are

5

dedicated to the study of earthquake risk perception (Armas,

2006, 2008; Paton et al., 2010). Such knowledge is very limited

in China, despite the pressing need for public understanding of

seismic hazards to inform organizational practices. Only a

handful of scientific reports have been published in the

aftermath of the 2008 earthquake that devastated Sichuan (Tian et

al., 2014; Zhu et al., 2011). None of these studies were

conducted within the most badly damaged area, i.e., Wenchuan.

Closer investigation is needed to assess the ability of victims

and other residents to cope with future earthquakes and to

identify risk management options for protecting vulnerable groups

from the large-scale destruction of the economy.

This research explores how members of affected villages

perceive the risk of earthquakes in Sichuan’s Wenchuan County.

The general research objective is to determine the extent to

which earthquake risk perception is related to household

characteristics and financial preparedness for coping with

damaging natural catastrophes. We focus on socioeconomic factors

that influence responses, particularly those that may reduce the

perceived risk of hazards. The findings can help hazard managers

target population segments that are least predisposed to adopt

hazard adjustments and can help address perverse incentives for

deferring hazard adjustments.

Evidence was solicited from a household survey conducted in

Wenchuan, where the epicentre of the 2008 massive earthquake

6

measured 7.9 on the Richter scale. This article reports the

findings of this survey. The next section describes the study

area. The survey measures and sampling method are then

introduced. The collected data are analyzed and presented in the

following section. The conclusions section summarizes the

findings and the practical implications of the study.

2. Wenchuan and Recent Earthquakes

Wenchuan County is within the boundary of the Ngawa Tibetan and

Qiang Autonomous Prefecture, which is situated in the

northwestern part of Sichuan Province, People’s Republic of

China. With an area of 4,084 km2, the county was home to 98,780

people in 20111. Our study area is a special administrative

region located within Wenchuan County, i.e., the Wolong National

Nature Reserve. The reserve is 125 km from Chengdu, the

Province’s capital city, and is under the provincial government’s

direct control. The national protected area is best known for its

large giant panda population, conservation and research

facilities. The reserve has a resident population of 5,343, 85%

of whom engage in agriculture-related activities2.

Towns and villages in Wenchuan, including the Wolong

National Nature Reserve, were severely damaged by a catastrophic1 Wenchuan County Population and Family Planning Bureau’s official website. URL: http://www.wcxjsj.gov.cn. Accessed 13 September 2014.2 Wolong National Nature Reserve’s official website. URL: http://wl.forestry.gov.cn/business/htmlfiles/wl/bhqjj/index.html. Accessed 13 September 2014.

7

earthquake on 12 May 2008. Wenchuan County was the epicentre

(31.021°N 103.367°E) of the 7.9-magnitude earthquake. According

to a briefing released by the China Earthquake Administration

(2008), the earthquake occurred along the Longmenshan fault,

which is a thrust structure along the border of the Indo-

Australian Plate and Eurasian Plate; seismic activities were

concentrated near the mid-fracture. The rupture lasted nearly 2

minutes, while the majority of the energy was released within the

first 80 sec. The earthquake started in Wenchuan and propagated

at an average speed of 3.1 kilometres per second at 49° towards

the north-east. The fault was 300 km long. The maximum

displacement was estimated as 9 metres, and the focus was deeper

than 10 km.

According to the International Disaster Database (2014), the

‘5.12’ earthquake was the most destructive natural catastrophe in

China since 1976 and one of the largest earthquakes in human

history in terms of socio-economic losses. The economic damage

costs of this disaster event amounted to US$85 billion

(International Disaster Database, 2014). Swiss Re, a global

reinsurance company, reported a larger number: the total economic

losses were estimated at US$137 billion, whereas insured losses

were only US$0.4 billion (i.e., 0.3% insured) (Swiss Re, 2014).

Therefore, the economic damage created by the Wenchuan earthquake

accounted for 1.9% to 3.1% of China’s GDP in 2008: ¥30,067

billion Chinese yuan (National Bureau of Statistics, 2009) or

US$4,410 billion.

8

Massive casualties were the worst consequence. There were a

total of 87,449 deaths, 375,000 injured, 15 million people made

homeless, 5 million houses destroyed, and 18,500 collapsed

schools (Swiss Re, 2014). For comparison, Japan’s ‘3.11’

earthquake and tsunami in 2011 killed 18,520 individuals and

injured 5,893; 0.4 million people lost their homes. Although the

Japan earthquake was the world’s costliest seismic disaster

within ten years, approximately 16.7% of the total economic

damage was insured (Swiss Re, 2014). The Wenchuan earthquake was

relatively more destructive in terms of the number of casualties

and relative size of insured losses.

Within two years, Sichuan was hit by another major

earthquake (20 April 2013), known as the Lushan or Ya’an

earthquake. The Lushan earthquake was measured at a magnitude of

7.0, and the epicentre was located in Sichuan’s Lushan County,

which is approximately 156 km from Chengdu and only 85 km from

southwestern Wenchuan County. According to Swiss Re (2014), the

2013 earthquake resulted in less damage than the 2008 event: 214

deaths and 13,484 injuries. Nearly US$ 7 billion in economic

losses were recorded, but only 0.4% of these losses were insured.

Both the 2011 and 2013 earthquakes were considered economic

disasters. Enormous unrecoverable losses were incurred, and the

poor agricultural communities in Sichuan were further

impoverished. Sun et al. (2010) reported that the Wenchuan

earthquake more than doubled the poverty rate of 43 counties, and

9

farmers’ per capita net income in these areas decreased from

¥1,873 yuan (approx. US$305) at the end of 2007 to less than

¥1,000 yuan (approx. US$163) in the aftermath of the 2008

catastrophe. Both events suggest that China’s southwestern

population remains economically vulnerable to seismic hazards,

despite the rapid economic growth along the country’s eastern

coast. Enhancing the community’s economic resilience to

unavoidable natural hazards is imperative. More effective coping

strategies for the bulk of rural population are needed. This

endeavour could benefit from an assessment of public responses to

potential threats.

3. Research Hypotheses

This study sought to ascertain how earthquake risk perception is

related to the socio-demographic traits of individuals and to

their financial preparedness for coping with damaging natural

catastrophes. Three working hypotheses were developed to guide

the empirical study. The topics were 1) hazard experience, 2)

financial preparedness for hazards and 3) personal and household

characteristics. The rationale is explained below.

H1: Earthquake risk perception is a function of the personal and household

characteristics of individuals

10

Socio-demographic factors can explain variations in the

perceptions of natural hazards. Gender, for example, is a key

determinant; females generally tend to be more concerned about

environmental hazards, including earthquakes (Lindell and

Whitney, 2000; Kung and Chen, 2012; Armas, 2006). Older and less

educated individuals have greater concern of earthquakes than the

better educated and younger generations (Armas, 2006; Tian et

al., 2014). Personal or household income is negatively associated

with risk perception (Tian et al., 2014). Yet, review studies

show that the explanatory power of these variables changes for

hazard types and locations (Bubeck et al., 2012; Lindell and

Perry, 2000). There is mixed evidence for the ways in which

personal or household characteristics influence risk perception.

Further confirmatory research is needed (Lindell and Perry,

2000).

Apart from these standard socio-demographic variables, we

also explored the implications of several secondary factors for

risk perception. These factors pertain to occupation, source of

income, remittance, home ownership, and insurance, which are all

related to the economic capabilities of individuals and

households. Considering these attributes can help broaden our

understanding of the role of household economic resources in

reducing perceived environmental risks, which have clear

implications for (mal)adaptation to environmental change (Lo,

2014).

11

H2: Earthquake risk perception is positively associated with hazard experience (intensity

of damage)

Previous experience with related hazards is closely linked to

perceived earthquake risk, as supported by recent Chinese

studies, such as Zhu et al. (2011), Kung and Chen (2012) and Tian

et al. (2014). Victims severely impacted by past earthquakes may

strongly believe that the hazard is likely to return in future

and create significant losses. The usual assumption is therefore

a positive relationship between hazard experience and perceived

risk. However, Lindell and Perry (2000) have found mixed evidence

on the role of past experience with earthquakes. While the

frequency of encounters with natural hazards is logically related

to perceived risk, empirical evidence is far from conclusive (Lo,

2013; Tian et al., 2014). Bubeck et al. (2012) argue that an

important determinant of flood risk perception is the extent of

the experience with the negative consequences of flooding rather

than direct experience with flooding per se. Laska (1990) supports

this view. We therefore focused on the intensity of damage to

seek evidence on the effects of hazard experience.

H3: Earthquake risk perception is negatively associated with financial preparedness for

hazards

12

The second objective of this study is to assess the extent to

which Wolong residents are financially prepared for major

earthquakes and how the degree of preparedness varies with

perceived earthquake risk. Few studies are dedicated to exploring

the important linkage between financial preparation and risk

perception. Bubeck et al.’s report (2012) suggests that

households who have made effective financial arrangements for

coping with flooding tend to perceive flood risks as lower. A

person or household acquires flood insurance, for example,

because they believe that it can reduce the risks confronting

them by recovering insured losses of properties and assets.

Consequently, financially better prepared households tend to

perceive risks as lower, particularly in terms of consequences.

This finding may be explained in terms of ‘optimistic bias’,

which refers to the tendency of self-prepared individuals to

perceive the need for additional preparedness as lower than other

people (Helweg-Larsen, 1999; Paton and Johnston, 2001). A cross-

national study also notes that the sense of security and efficacy

has negative impacts on environmental risk perception (Lo, 2014).

We explored such a hypothesis by including a suite of questions

related to financial preparedness in a questionnaire, as

described in the next section.

4. Measures

13

A household survey was conducted in Wolong to address the three

hypotheses. We employed a structured questionnaire to record the

personal and household characteristics of Wolong residents, their

perception and experience with earthquakes, and their ability to

mitigate the resulting economic impacts. How these factors are

related to earthquake risk perception were statistically

analyzed. This section describes the relevant survey items and

questions included in the questionnaire.

The structure of the questionnaire followed a standard

design, beginning with items that are likely to be familiar to

the respondents. The first few questions probed hazard

experience. The questionnaire included a subjective assessment of

the intensity of damage by past earthquakes. The perceived

outcome severity was prompted by the question ‘How damaging was

the last major earthquake to you and your family?’ A five-point

scale, ranging from ‘No damage’ to ‘Extremely damaging’, was

presented to respondents.

This question was followed by two items about earthquake

risk perception, which was enlisted as the dependent variable in

a subsequent statistical analysis. In its simplest form, risk

perception denotes the perceived likelihood of an outcome that

affects what people value and the perceived severity of that

outcome (Renn, 2008). Kunreuther (1996) is convinced that if a

risk is perceived to be sufficiently high, then people would

behave in a way that can mitigate that risk. Advocates of the

14

psychometric paradigm, such as Slovic (1987, 2000), define risk

perception in terms of a range of attributes, including

dreadfulness, controllability, catastrophic potential, newness,

fatality, scientific certainty and distribution of consequences.

Critics argue that the psychometric scale does not fully

apply to perceptions of natural events, such as earthquakes,

because it is more fitting for studies of man-made hazards (Brun,

1992). Seminal work conducted by Lindell and Whitney (2000) also

defines risk perception primarily in terms of perceived

likelihood and impacts. Moreover, the focus of our study is

people’s expectation of the possible return of a disruptive

earthquake and its potential impacts on livelihoods, rather than

the various dimensions of risk perception per se. We therefore

adopted a basic two-dimensional structure for assessing seismic

risk perception, and we do not seek a broad representation of the

risk perception concept.

The questionnaire included two individual statements that

gauged the perceived likelihood and severity of earthquake risk.

The first question was “How likely is Wolong to experience a

magnitude 7 earthquake in the next ten years?” The responses were

recorded on a five-point Likert scale, with options ranging from

‘Very unlikely’ to ‘Very likely’. The second question was “How

much personal damage would another magnitude 7 earthquake cause?”

A different five-point scale was presented to respondents,

ranging from ‘No damage’ to ‘Extremely damaging’.

15

The financial preparedness variables appeared in the middle

of the questionnaire. These questions were generally presented in

terms of access to alternative sources of income or contingency

funds should earthquakes severely affect one’s livelihood. For

example, having multiple sources of income and forms of assets

could reduce the risk of losing the essential basis of livelihood

(Alinovi et al., 2009). Liquid assets require lower transaction

costs to sell; ownership of assets and the ability to liquidate

is particularly important for poor farmers when their income-

generating activities come to a halt during an extended drought

(Keil et al., 2008). Other related attributes include access to

credit (Le Dang et al., 2014), access to insurance (Bubeck et

al., 2012), and availability of remittances from family members

or friends (Adger et al., 2002). These capabilities or

opportunities can maintain the functioning of a household economy

in the aftermath of a disruptive disaster event and can prevent

the significant deterioration of people’s well-being. Finances

can strengthen the sense of security and efficacy but may weaken

the sense of caution towards natural hazards. The knowledge that

effective protection measures have been implemented might produce

perverse effects on the perceived severity of consequences

(Bubeck et al., 2012).

To examine this perspective, a nine-item scale was

constructed to measure the financial preparedness to disruptive

earthquakes. Based on the various studies cited above, notably

Alinovi et al. (2009) and Le Dang et al. (2014), the constructed

16

scale included various attributes, such as income diversity,

asset liquidity, access to loans, and remittance. Full

descriptions are listed in Section 5. Respondents were requested

to assess the statements on a five-point scale.

As a common practice, personal information, such gender,

age, and monthly income, was collected by the last batch of

survey questions to avoid non-response. Survey items for

secondary demographic variables, such as home ownership and

remittance, were distributed in different parts of the

questionnaire, mostly before or after relevant questions about

financial preparedness for hazards.

5. Data collection

The household survey was conducted in the main villages of Wolong

and Gengda in the Wolong National Nature Reserve between March

and May 2014 (Figure 1). These villages are located near (within

40 km) the epicentre of the 2008 Wenchuan earthquakes, and they

experienced significant losses during the event. Each of the

villages has approximately 80 – 100 households. Residents of six

villages within Wolong Town and Gengda Town were invited to

participate in face-to-face interviews based on the structured

questionnaire.

Six local undergraduate students were recruited as research

assistants. These student research assistants were fluent in the

17

local dialect and were trained in the procedure and etiquette of

face-to-face interviews. Each assistant was assigned to one

village and visited every household in that village while

accompanied by a local government officer from the Wolong Nature

Reserve Administration, which granted permission for the

interviews and offered logistical support. One member of each

household age 16 or older was invited to complete the

questionnaire in situ.

The survey was conducted on weekdays and weekends. Each

interview, on average, lasted 15 minutes. All interviewees

received a small gift as a token of appreciation after completing

the survey. A total of 425 local residents were approached and

invited to participate; 380 agreed to be interviewed. Only 371

individuals completed the interviews, yielding an effective

response rate of 89%.

The Wolong National Reserve Administration indicated that

the reserve currently has a population of nearly 5,500, of which

75% are ethnic minorities. We did not have access to accurate

household statistics that could help achieve demographic

representativeness of the sample due to the inherent difficulties

of obtaining socio-demographic census data in China. In contrast

to Western cities, detailed demographic data are not available

for Chinese counties; the data are aggregated to a broad scale,

challenging the generalization of survey findings (Byrne et al.,

forthcoming; Xie et al., 2014).

18

6. Results

The study is based on the 371 complete interviews. Data analysis

was performed by standard statistical software, e.g., SPSS. This

section describes the socio-economic characteristics and risk

perceptions of respondents and presents the results of our

analysis based on multiple regression.

6.1 Socioeconomic characteristics of respondents

As shown in Table 1, the average respondent was 41 years old and

had lived in Wolong for 36 years, suggesting that the majority of

respondents were native. Only 26 (7%) of the respondents did not

report their household income level (one outlier was excluded).

The average and median incomes were ¥1,578 (approx. US$255) and

¥1,000 (approx. US$161) Chinese yuan, respectively, which are

well below the provincial average of ¥2,467 (approx. US$398)

(National Bureau of Statistics, 2013).

More than half of the respondents were female (54.5%). Many

received elementary education only (43.1%), and some attended

middle school (32.5%), whereas less than 10% had a post-secondary

education. This suggests that opportunities for higher education

are limited in Wolong. The sample includes 252 (67.9%) ethnic

Tibetans and only 97 (26.1%) people of Han origin, which is the

19

dominant ethnic group in China. The study area is home to a

relatively large minority community.

Wolong is an agricultural community, and most of the local

residents are associated with the primary agriculture industry.

As many as 70.6% of our survey respondents identified themselves

as farmers, and only 38.8% received all or partial income from

non-agricultural sources. Few respondents (15.5%) received

remittance incomes from other family members. More than half

(60.6%) were homeowners, but only a handful (5.4%) had active

insurance policies on their residential properties.

6.2 Hazard experience and risk perception

A relatively large number of respondents recorded losses in

personal or household properties during major earthquakes in

Sichuan (Figure 2). The majority described the impacts as

extremely damaging (49.5%) and fairly damaging (31.5%). Few

reported no economic loss (3.8%) or minor damage (2.4%), while

the rest experienced mild impacts (12.8%). These results suggest

that most of the local residents interviewed were severely

affected by recent earthquakes, although the amount of the damage

varied.

Despite their personal experience with earthquakes, many

Wolong residents described the possibility of recurring magnitude

7 earthquakes as unlikely (Figure 3). More than half of the

20

respondents felt assured: 50.5% believed that a strong earthquake

was not likely to return, and 14.4% expressed an even stronger

view. Less than 5% acknowledged such a possibility, while 30.4%

admitted uncertainties in the repeat occurrence of a major

seismic disaster. The likelihood of another major earthquake in

the next ten years was generally perceived to be low.

However, if major earthquakes were to occur, most

respondents anticipated substantial impacts on their properties

and assets (Figure 4). The majority believed that it would be

extremely damaging (42.3%) or fairly damaging (36.9%). A small

proportion of respondents were very optimistic (0.8%), while

others anticipated minor damage (8.9%) or moderate damage

(11.1%). Overall, the severity of the next major earthquake was

perceived to be significant.

6.3 Financial preparedness for earthquakes

The self-assessment of the capacity for economically recovering

from disruptive earthquakes generated mixed results (Table 2).

Many Wolong residents (45.2%) were confident that they would be

able to return to work as usual immediately after a strong

earthquake. Notably, there was a modest degree of uncertainty in

their responses (15.6%).

While there was a fair degree of job continuity, diversity

of income and assets was rated low. Less than one-third of

21

respondents had alternative sources of income (29.3%) and assets

other than their current residential properties (25.1%), which

are typically primitive in structure and likely to suffer during

strong earthquakes. Fewer (13.2%) respondents claimed to be able

to easily liquidate their assets should a strong earthquake occur

and financial needs arise.

Commercial means for disaster recovery were limited to a few

respondents. One-third (33.1%) of the residents interviewed

suggested that they had access to insurance that would compensate

for part of their losses due to strong earthquakes. More than

half (54.2%) believed that they could secure finance from banks

or financial institutions for rebuilding their properties, assets

or businesses if these are severely affected by strong

earthquakes. Opportunities for disaster finance were just

emerging in these earthquake-prone communities.

There was greater confidence in the ability to solicit

contingency funds via social channels. More than half (55.8%)

trusted that the local community corporations or their work units

would offer finance for rebuilding properties, assets or

businesses in the aftermath of earthquakes. Most respondents

expected remittance incomes from out-of-town family members

(71.4%) or friends (61%) if their livelihood were to be severely

affected by earthquakes. Thus, local residents are more likely to

depend on socially organized financial assistance than commercial

solutions.

22

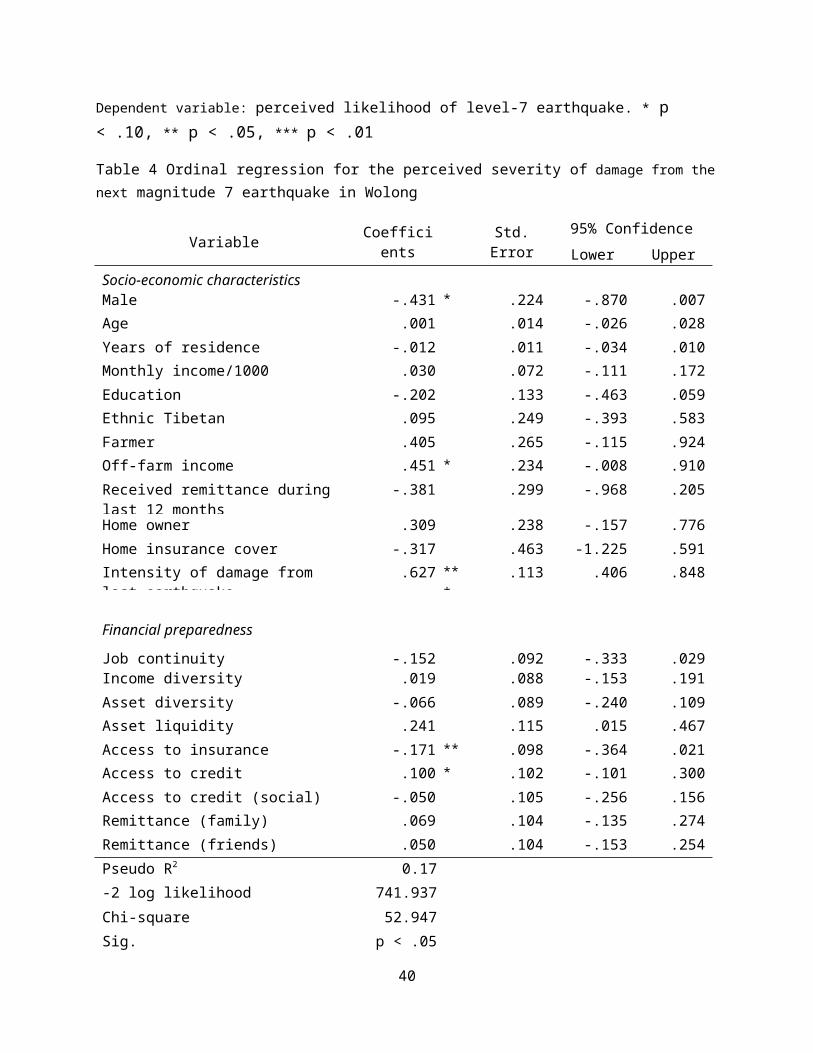

6.4 Regression analysis

To identify the determinants of risk perception, all of the

survey items discussed above were included in regression

modelling. The perceived likelihood and severity of earthquakes

were used as dependent variables. All other items were tested for

their predictive power against these perceptions. Dummy variables

were created for the categorical independent variables listed in

Table 1, namely, gender, education, ethnicity, occupation, off-

farm income, remittance, homeownership, and insurance. Ordinal

regression was performed using SPSS. The regression model

explained 13% of the variation in the perceived likelihood of

earthquakes (Table 3), while the other model accounted for 17% of

the variability in the perceived severity (Table 4). Tests of

parallel lines yielded a satisfactory Chi-square value in both

models (p > .05), suggesting that the proportional odds

assumption was not violated.

The perceived likelihood did not have strong relationship

with the socio-economic characteristics of the respondents (Table

3). Only the household income demonstrated significant negative

impacts, suggesting that wealthier households were less likely to

experience an impending disaster. A weak association was found

between the perceived severity and socio-economic variables

(Table 4). Males and those without off-farm income were less

likely to consider a future magnitude 7 earthquake as very

23

damaging. This result provides limited support for Hypothesis H1

listed in Section 3, i.e., Earthquake risk perception is a function of the

personal and household characteristics of individuals.

There was some supporting evidence for Hypothesis H2, i.e.,

Earthquake risk perception is positively associated with hazard experience (intensity of

damage). The reported intensity of damage from the last earthquake

increased with the perceived likelihood when other variables were

controlled for, although the magnitude of the effects was modest

(Table 3). The intensity of the damage, however, was strongly and

positively related to the perceived severity (Table 4).

Mixed evidence was found for Hypothesis H3, i.e., Earthquake risk

perception is negatively associated with financial preparedness for hazards. Three

financial preparedness variables indicated mixed effects on the

perceived likelihood (Table 3). Job continuity was negatively

associated with the perceived likelihood. Therefore, those

individuals who are able to return to work as usual after

earthquakes tended to perceive the likelihood of repeat major

earthquakes as low. Yet, asset liquidity and access to commercial

credit produced positive impacts. Those individuals who are able

to sell their assets for cash and secure finances were more aware

of a potential disruptive earthquake in the next 10 years. Access

to insurance and commercial credit had significant but opposite

impacts on the perceived disaster severity (Table 4). Holders of

insurance policies were less concerned about the catastrophic

consequences of a future magnitude 7 earthquake than non-policy

24

holders. In contrast, the ability to secure finance increased

with such concern.

7. Discussion

Results of the household survey indicate that most of the Wolong

residents interviewed reported some damage during the major

seismic events in 2008 and 2011. Although there was a strong

belief that magnitude 7 earthquakes were unlikely to return in

the next decade, the potential impacts of such large-scale

seismic hazards were expected to be disruptive. Similar to most

people, the local residents understood major earthquakes as low-

probability high-impact events.

Many Wolong residents did not appear to be financially well-

prepared for earthquakes or other natural hazards. Diversity of

income and assets and asset liquidity were reported to be low.

Some of the respondents might be able to secure disaster finance

from commercial sources, but many have greater access to

contingency funds via social channels. Consistent with the

literature on community resilience to environmental change

(Adger, 2000; Pelling, 2011), these results imply that social

capital is likely to be a main source of financial protection for

rural households, who typically do not have knowledge or

opportunities for arranging disaster finance, in contrast to

urban residents. This finding indicates the importance of

enhancing community resilience to natural hazards by

25

strengthening social ties and directing social dynamics towards

disaster preparation (Lo, 2013; Lo et al., 2012; Xie et al.,

2014).

This inquiry sought to identify factors that influence

earthquake risk perception. We found that the intensity of damage

from past earthquakes consistently predicted the perceived

likelihood and severity of future earthquake disasters, i.e., the

more greatly affected victims tended to rate the risk of

suffering from the same hazard as higher. This finding is logical

and is supported by numerous studies on hazards (Bubeck et al.,

2012; Jackson, 1981; Laska, 1990; Lo, 2013; Miceli et al., 2008;

Zhu et al., 2011). Contrary to Armas’s (2006, 2008) Romania

study, our results show that few socio-demographic variables had

significant impacts on risk perception, and these significant

observations were not consistently predictive across the two

constituent variables.

Nonetheless, the income effects are consistent across

scientific studies. In our research, the monthly income strongly

and negatively impacted the perception of the probability of

future earthquake disasters. Similar results have been reported

by other researchers, such as Lima et al. (2005), Le Dang et al.

(2014), Lo (2014) and Tian et al. (2014). To the extent in which

hazard adjustments are a function of perceived risk, these

results suggest that wealthier households are relatively more

likely to be less cautious of natural hazards because of a

26

(false) sense of security. This finding raises concerns regarding

economic development and adaptation to environmental change,

i.e., would wealth accumulation create perverse incentives for

deferring hazard adjustments? Further research should ascertain

how increasing incomes affect community resilience to natural

hazards.

A related hypothesis is the idea that potential financial

protection can reduce perceived risks (Bubeck et al., 2012; Lo,

2013). This claim has mixed support from our study, as most of

the model variables that represent financial preparedness did not

predict risk perception, and significant predictors did not have

the same signs. More research is needed to replicate such

‘optimistic bias’ in disaster preparation (Helweg-Larsen, 1999;

Paton and Johnston, 2001). We suggest introducing an

effectiveness dimension to construct survey statements. Dang et

al. (2014), for example, made a distinction between the ability

to gain access to credit and perceived usefulness of credit; the

authors showed that the latter had strong impacts on the

perception of adaptation efficacy. A similar approach that

recognizes subjective dimensions could provide more conclusive

evidence on the partially supported hypothesis. This step will be

important for understanding the implications of the increasing

abilities of households to secure disaster finance for community

resilience to natural hazards.

27

8. Conclusions

Major earthquakes hit Sichuan Province, China, in 2008 and 2011

and resulted in massive casualties and economic damage. The

objective of this article was to investigate how rural residents

of Sichuan Wolong perceive earthquake risk and how the perceived

risk is related to the household characteristics and financial

preparedness for coping with damaging natural catastrophes. We

found that many Wolong residents did not anticipate a premature

return of magnitude 7 earthquakes in the following decade but

were aware of the potential disruptive consequences of such

infrequent natural hazards. Personal and household

characteristics, except household income, were not significantly

related to earthquake risk perception. Moreover, hazard

experience influenced the perception of the likelihood and

severity of future earthquake disasters. Wolong residents

indicated a modest level of financial preparation for earthquakes

or other natural hazards. Financial preparedness had mixed

impacts on risk perceptions.

The results of the household survey have practical

implications for policy-making and disaster communication. More

information is needed to inform rural residents of the risks of

natural hazards, including but not limited to earthquakes. Risk

education requires a more complete understanding of how audiences

comprehend various dimensions of hazard risks. A limitation of

our study is the use of a primitive scale for risk perception,

28

which is defined in terms of perceived likelihood and severity.

Although the choice of the scale is supported by our research

objectives, the use of multi-attribute measures, such as the

psychometric approach adopted by Kung and Chen (2012) and Tian et

al. (2014), would have provided a conceptually more complete

analysis and a more solid basis for formulating risk education

strategies.

Additionally, social channels are important for enhancing

community resilience to natural hazards. Coordinating the

activities of rural community corporations or neighbourhood

associations is a way to strengthen social ties between community

members and promote community financing. Governments and aid

organizations should also help local communities set up micro-

finance schemes and inter-community insurance mechanisms (World

Bank, 2010). However, care should be taken when interpreting the

results because the measures of financial preparedness prompt

subjective opinions of respondents, which may not be completely

factual. There may be discrepancies between the actual

availability and respondents’ personal opinions of their access

to credit or their likelihood of receiving remittances. Including

objective measures in the questionnaire, such as estimated values

of liquid assets (Keil et al., 2008) or cash amounts (Alinovi et

al., 2009), may improve the validity of the results.

29

References:

Adger WN (2000) Social and ecological resilience: are they related?Progress in Human Geography 24:347-364.

Adger WN, Kelly PM, Winkels A, Huy LQ, Locke C (2002) Migration,Remittances, Livelihood Trajectories, and Social Resilience. AMBIO:A Journal of the Human Environment 31:358-366.

Alinovi L, Mane E, Romano D (2009) Measuring household resilience tofood insecurity: application to Palestinian households. EC-FAO FoodSecurity Programme: Linking Information and Decision Making toImprove Food.

Armas I (2006) Earthquake Risk Perception in Bucharest, Romania. RiskAnalysis 26:1223-1234.

Armas I (2008) Social vulnerability and seismic risk perception. Casestudy: the historic center of the Bucharest Municipality/Romania.Natural Hazards 47:397-410.

Botzen WJW (2013) Managing extreme climate change risks throughinsurance. Cambridge University Press, Cambridge, England.

Brun W (1992) Cognitive components in risk perception: Natural versusmanmade risks. Journal of Behavioral Decision Making 5:117–132.

Bubeck P, Botzen WJW, Aerts JCJH (2012) A Review of Risk Perceptionsand Other Factors that Influence Flood Mitigation Behavior. RiskAnalysis 32:1481-1495.

Byrne J, Lo AY, Yang J (forthcoming) Residents' understanding of therole of green infrastructure for climate change adaptation inHangzhou, China. Landscape and Urban Planning.

China Earthquake Administration (2008) An analysis of the causes ofthe Wenchuan magnitude 8.0 earthquake. Available fromhttp://www.cea.gov.cn/manage/html/8a8587881632fa5c0116674a018300cf/_content/08_05/30/1212119940937.html. Accessed 13 September 2014.(in Chinese).

Helweg-Larsen M (1999) (The Lack of) Optimistic Biases in Response tothe 1994 Northridge Earthquake: The Role of Personal Experience.Basic and Applied Social Psychology 21:119-129.

International Disaster Database (2014) EM-DAT: The OFDA/CREDInternational Disaster Database - Université Catholique de Louvain -Brussels – Belgium. Available from www.emdat.be/database. Accessed17 February 2015.

Jackson EL (1981) Response to Earthquake Hazard: The West Coast ofNorth America. Environment and Behavior 13:387-416.

Keil A, Zeller M, Wida A, Sanim B, Birner R (2008) What determinesfarmers’ resilience towards ENSO-related drought? An empirical

30

assessment in Central Sulawesi, Indonesia. Climatic Change 86:291-307.

Kung Y-W, Chen S-H (2012) Perception of Earthquake Risk in Taiwan:Effects of Gender and Past Earthquake Experience. Risk Analysis32:1535-1546.

Kunreuther H (1996) Mitigating disaster losses through insurance.Journal of Risk and Uncertainty 12:171-187.

Kunreuther H, Slovic P (1978) Economics, psychology, and protectivebehavior. American Economic Review 68:64-69.

Laska SB (1990) Homeowner Adaptation to Flooding: An Application ofthe General Hazards Coping Theory. Environment and Behavior 22:320-357.

Le Dang H, Li E, Nuberg I, Bruwer J (2014) Farmers’ assessments ofprivate adaptive measures to climate change and influential factors:a study in the Mekong Delta, Vietnam. Natural Hazards 71:385-401.

Lima ML, Barnett J, Vala J (2005) Risk Perception and TechnologicalDevelopment at a Societal Level. Risk Analysis 25:1229-1239.

Lindell MK, Whitney DJ (2000) Correlates of Household Seismic HazardAdjustment Adoption. Risk Analysis 20:13-25.

Lo AY (2013) The Role of Social Norms in Climate Adaptation: MediatingRisk Perception and Flood Insurance Purchase. Global EnvironmentalChange 23:1249–1257.

Lo AY (2014) Negative income effect on perception of long-termenvironmental risk. Ecological Economics 107:51-58.

Lo AY, Chow AT, Cheung SM (2012) Significance of Perceived SocialExpectation and Implications to Conservation Education: TurtleConservation as a Case Study. Environmental Management 50:900-913.

Miceli R, Sotgiu I, Settanni M (2008) Disaster preparedness andperception of flood risk: A study in an alpine valley in Italy.Journal of Environmental Psychology 28:164-173.

National Bureau of Statistics (2009) China Statistics Yearbook.National Bureau of Statistics, Beijing.

National Bureau of Statistics (2013) China Statistics Yearbook.National Bureau of Statistics, Beijing.

Palm R (1990) Natural Hazards: An Integrative Framework for Researchand Planning. Johns Hopkins University Press, Baltimore, MD.

Palm R, Hodgson M (1992) Earthquake Insurance: Mandated Disclosure andHomeowner Response in California. Annals of the Association ofAmerican Geographers 82:207-222.

Paton D, Bajek R, Okada N, McIvor D (2010) Predicting communityearthquake preparedness: a cross-cultural comparison of Japan andNew Zealand. Natural Hazards 54:765-781.

31

Paton D, Johnston D (2001) Disasters and communities: vulnerability,resilience and preparedness. Disaster Prevention and Management: AnInternational Journal 10:270-277.

Pelling M (2011) Adaptation to climate change : from resilience totransformation Routledge, Oxon, U.K.

Renn O (2008) Risk governance: coping with uncertainty in a complexworld. Earthscan, London.

Slovic P (1987) Perception of risk. Science 236:280-285.Slovic P (ed.): (2000) The perception of risk Earthscan, London.Sun M, Chen B, Ren J, Chang T (2010) Natural Disaster's Impact

Evaluation of Rural Households’ Vulnerability: The case of Wenchuanearthquake. Agriculture and Agricultural Science Procedia 1:52-61.

Swiss Re (2014) Sigma Explorer. Available at http://www.sigma-explorer.com/. Accessed 13 September 2014.

Tian L, Yao P, Jiang S-j (2014) Perception of earthquake risk: a studyof the earthquake insurance pilot area in China. Natural Hazards:1-17.

World Bank (2010) Natural Hazards, UnNatural Disasters: The Economicsof Effective Prevention. World Bank, Washington D.C.

Xie XL, Lo AY, Zheng Y, Pan J, Luo J (2014) Generic security concerninfluencing individual response to natural hazards: evidence fromShanghai, China. Area 46:194-202.

Zhu D, Xie X, Gan Y (2011) Information source and valence: Howinformation credibility influences earthquake risk perception.Journal of Environmental Psychology 31:129-136.

32

Table 1 Socioeconomic characteristics of respondents (N = 371)

Socioeconomic variable (continuous)

Measure ValueAge Average 41 yearsYears of residence Average 36 years

Monthly household income (ChineseRMB yuan)

Average ¥1,5781 U.S. dollar / Chinese Yuan = 6.2 (March 2014)

Median ¥1,000

Socioeconomic variable (categorical)

Category Frequency(%)Gender Male 45.5

Female 54.5Education attainment Primary or below 43.1

Junior middleschool

32.5Middle school 15.2Post-secondary

diploma7.3

Universitydegree

1.9

Ethnicity Han 26.1Tibetan 67.9

Other minorities 5.4Primary occupation Farmer 70.6

Otherwise 29.4

Off-farm income Yes 38.8Otherwise 61.2

Received remittance during last 12 months

Yes 15.5Otherwise 84.5

Homeowner Yes 60.6Otherwise 39.4

Home insurance cover Yes 5.4Otherwise 94.6

33

Figure 2 Percentage of respondents by intensity of damage fromthe last earthquake

No damage 3.8%Minor damage 2.4%

Some damage 12.8%

Fairly damaging 31.5%

Extremely damaging 49.5%

How damaging was the last major earthquake to you and

your family?

34

Figure 3 Percentage of respondents by perceived likelihood of magnitude 7 earthquake in Wolong

Very unlikely 14.4%

Not quite possible 50.5%

Maybe 30.4%

Possible 1.9%Very likely 2.7%

How likely is Wolong to experience a magnitude 7 earthquake in the

next ten years?

35

No damage 0.8% Minor damage 8.9%Some damage

11.1%

Fairly damaging 36.9%

Extremely damaging 42.3%

How much personal damage would another magnitude 7 earthquake

cause?

Figure 4 Percentage of respondents by perceived severity of damage from the next magnitude 7 earthquake in Wolong

36

Table 2 Self-assessed household financial preparedness forearthquakes

Variable Survey statement

No /Notmany(1/2)^

Neutral /fair(3)

Yes /

Many(4/5)#

Mean(1-5)

S.D.

(%)Job continuity

Are you able to quickly return to work as usual after a strong earthquake?

38.2 15.6 45.2 3.08 1.26

Income diversity

Do you or your family have alternative sources of income that are unlikely to be affected by strong earthquakes

61.2 8.9 29.3 2.31 1.32

Asset diversity

Do you or your family own any form of asset other than your house?

67.9 6.7 25.1 2.03 1.28

Asset liquidity

Are you able to easily liquidate your assets after a strong earthquake

77.3 8.1 13.2 2.01 1.02

Access toinsurance

Are you able to get commercial insurance that covers part of your potential losses due to strong earthquakes?

55.8 10.8 33.1 2.67 1.22

Access tocredit (commercial)

Are you able to get low-interest loans from banks or financial institutions for rebuilding your properties, assets or businesses ifthese are severely affected by consequences of strong earthquakes?

34.8 10.5 54.2 3.28 1.21

Access tocredit (social)

Would your community corporates or work units offer you loans upon your request, if your livelihood isseverely affected by the consequences of earthquakes?

28.3 15.1 55.8 3.29 1.15

Remittance (family)

Would your family members living outside the town send you money (remittance), if your livelihood isseverely affected by the consequences of earthquakes?

20.0 7.3 71.4 3.86 1.22

Remittanc Would your friends send you 29.1 9.2 61.0 3.48 1.2

37

e (friends)

(remittance), if your livelihood isseverely affected by the consequences of earthquakes?

3

^ negative options include ‘Definitely not / Not at all’ (1) and ‘Probablynot / Not many’ (2). #positive options include ‘Probably / Some’ (4)and ‘Definitely / Many’ (5). Percentages may not add to 100% becauseof missing values. The higher the scores, the greater the financialpreparedness of the households.

38

Table 3 Ordinal regression for the perceived likelihood of having a magnitude 7 earthquake in Wolong in the next ten years

Variable Coefficients

Std.Error

95% ConfidenceIntervalLower Upper

Socio-economic characteristicsMale -.132 .227 -.576 .313Age -.005 .014 -.032 .022Years of residence -.011 .011 -.032 .011Monthly income -.194 *** .074 -.338 -.049Education -.013 .135 -.278 .253Ethnic Tibetan -.298 .251 -.790 .194Farmer .225 .269 -.303 .753Off-farm income -.219 .234 -.679 .240Received remittance during last 12 months

-.361 .305 -.959 .238

Home owner .337 .242 -.137 .811Home insurance cover -.562 .478 -1.499 .374Intensity of damage from last earthquake

.190 * .112 -.030 .410

Financial preparedness

Job continuity -.208 ** .093 -.390 -.025Income diversity .111 .089 -.065 .286Asset diversity -.032 .091 -.209 .146Asset liquidity .268 ** .115 .041 .494Access to insurance -.019 .099 -.213 .175Access to credit (commercial)

.250 ** .105 .045 .456Access to credit (social) -.079 .107 -.288 .131Remittance (family) .079 .107 -.130 .288Remittance (friends) .007 .106 -.200 .215Pseudo R2 0.13-2 log likelihood 701.589Chi-square 39.151Sig. p < .05N 319

39

Dependent variable: perceived likelihood of level-7 earthquake. * p < .10, ** p < .05, *** p < .01

Table 4 Ordinal regression for the perceived severity of damage from thenext magnitude 7 earthquake in Wolong

Variable Coefficients

Std.Error

95% ConfidenceIntervalLower Upper

Socio-economic characteristicsMale -.431 * .224 -.870 .007Age .001 .014 -.026 .028Years of residence -.012 .011 -.034 .010Monthly income/1000 .030 .072 -.111 .172Education -.202 .133 -.463 .059Ethnic Tibetan .095 .249 -.393 .583Farmer .405 .265 -.115 .924Off-farm income .451 * .234 -.008 .910Received remittance during last 12 months

-.381 .299 -.968 .205

Home owner .309 .238 -.157 .776Home insurance cover -.317 .463 -1.225 .591Intensity of damage from last earthquake

.627 ***

.113 .406 .848

Financial preparedness

Job continuity -.152 .092 -.333 .029Income diversity .019 .088 -.153 .191Asset diversity -.066 .089 -.240 .109Asset liquidity .241 .115 .015 .467Access to insurance -.171 ** .098 -.364 .021Access to credit (commercial)

.100 * .102 -.101 .300Access to credit (social) -.050 .105 -.256 .156Remittance (family) .069 .104 -.135 .274Remittance (friends) .050 .104 -.153 .254Pseudo R2 0.17-2 log likelihood 741.937Chi-square 52.947Sig. p < .05

40

N 320Dependent variable: perceived severity of damage from the next level-7 earthquake. * p < .10, ** p < .05, *** p < .01

41