Embed Size (px)

Citation preview

SPM Savings BankCondensed Consolidated Interim

Financial Statements1 January - 30 June 2007

SPM Savings BankDigranesgata 2310 Borgarnes

Reg. no. 610269-5409

Page PageEndorsement and Signatures of the Board of Directors and the Managing Director .......................... 3 Consolidated Interim Statement of Cash Flow ......... 8

Independent Auditor's Review Report ........................... 4 Notes to the Consolidated Interim Financial Statements:

Consolidated Interim Income Statement ........................ 5 General information ............................................... 9

Consolidated Interim Balance Sheet .............................. 6 Notes ...................................................................... 23

Consolidated Interim Statement of Changes in Capital ...................................................... 7

Contents

Consolidated Interim Financial Statementsof SPM Savings Bank 30 June 2007________________________________________ 2 ________________________________________

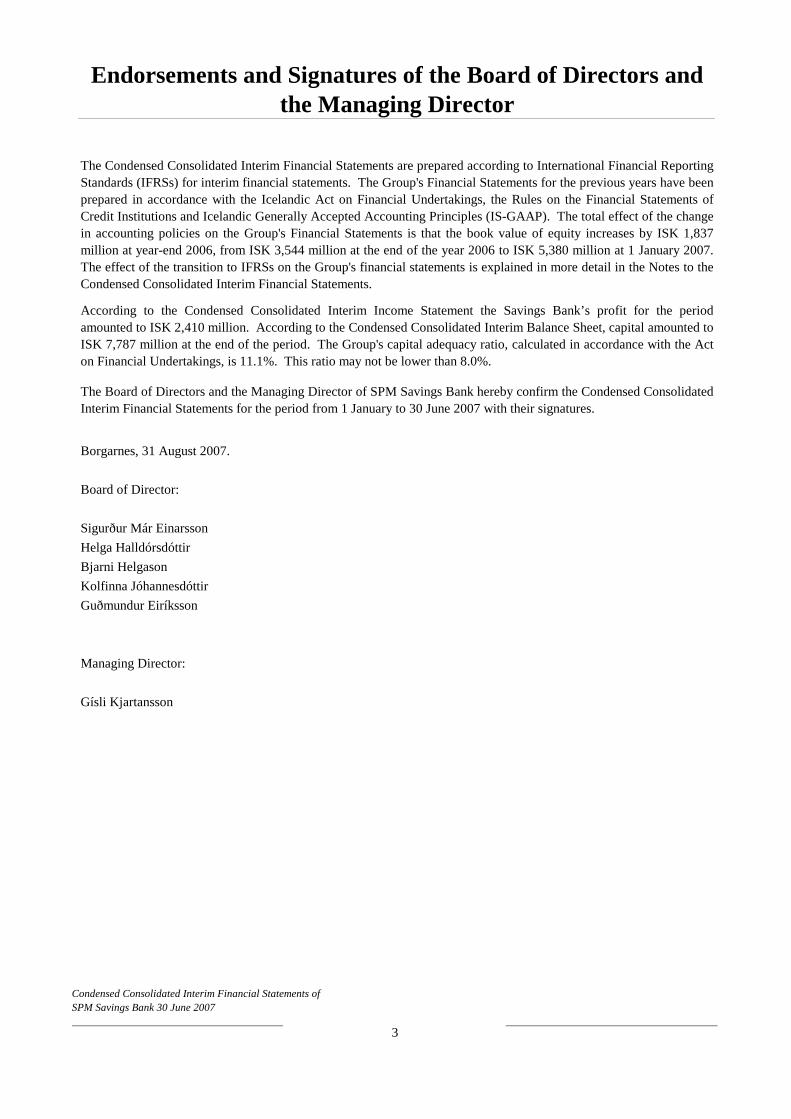

Borgarnes, 31 August 2007.

Board of Director:

Sigurður Már Einarsson

Helga Halldórsdóttir

Bjarni Helgason

Kolfinna Jóhannesdóttir

Guðmundur Eiríksson

Managing Director:

Gísli Kjartansson

Endorsements and Signatures of the Board of Directors and the Managing Director

The Condensed Consolidated Interim Financial Statements are prepared according to International Financial ReportingStandards (IFRSs) for interim financial statements. The Group's Financial Statements for the previous years have beenprepared in accordance with the Icelandic Act on Financial Undertakings, the Rules on the Financial StatementsofCredit Institutions and Icelandic Generally Accepted Accounting Principles (IS-GAAP). The total effect of the changein accounting policies on the Group's Financial Statementsis that the book value of equity increases by ISK 1,837million at year-end 2006, from ISK 3,544 million at the end ofthe year 2006 to ISK 5,380 million at 1 January 2007.The effect of the transition to IFRSs on the Group's financial statements is explained in more detail in the Notes to theCondensed Consolidated Interim Financial Statements.

According to the Condensed Consolidated Interim Income Statement the Savings Bank’s profit for the periodamounted to ISK 2,410 million. According to the Condensed Consolidated Interim Balance Sheet, capital amounted toISK 7,787 million at the end of the period. The Group's capital adequacy ratio, calculated in accordance with the Acton Financial Undertakings, is 11.1%. This ratio may not be lower than 8.0%.

The Board of Directors and the Managing Director of SPM Savings Bank hereby confirm the Condensed ConsolidatedInterim Financial Statements for the period from 1 January to 30 June 2007 with their signatures.

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007_______________________________________

3_______________________________________

To the Board of Directors of SPM Savings Bank.

Introduction

Scope of Review

Conclusion

Reykjavík, 31 August 2007.

KPMG hf.

Hlynur Sigurðsson

Independent Auditors' Review Report

We have reviewed the accompanying Condensed Consolidated Interim Balance Sheet of SPM Savings Bank as of June30, 2007 and the related statements of income, changes in equity and cash flows for the six-month period then ended,and a summary of significant accounting policies and other explanatory notes. Management is responsible for thepreparation and fair presentation of this interim financial information in accordance with International FinancialReporting Standard IAS 34,Interim Financial Reporting. Our responsibility is to express a conclusion on this interimfinancial information based on our review.

We conducted our review in accordance with International Standard on Review Engagements 2410,“Review ofInterim Financial Information Performed by the Independent Auditor of the Entity.” A review of interim financialinformation consists of making inquiries, primarily of persons responsible for financial and accounting matters, andapplying analytical and other review procedures. A review is substantially less in scope than an audit conducted inaccordance with International Standards on Auditing and consequently does not enable us to obtain assurance that wewould become aware of all significant matters that might be identified in an audit. Accordingly, we do not express anaudit opinion.

Based on our review, nothing has come to our attention that causes us to believe that the accompanying interimfinancial information does not give a true and fair view of the financial position of the entity as at June 30, 2007, andof its financial performance and its cash flows for the six month period then ended in accordance with IAS 34,Interim Financial Reporting.

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007_______________________________________

4_______________________________________

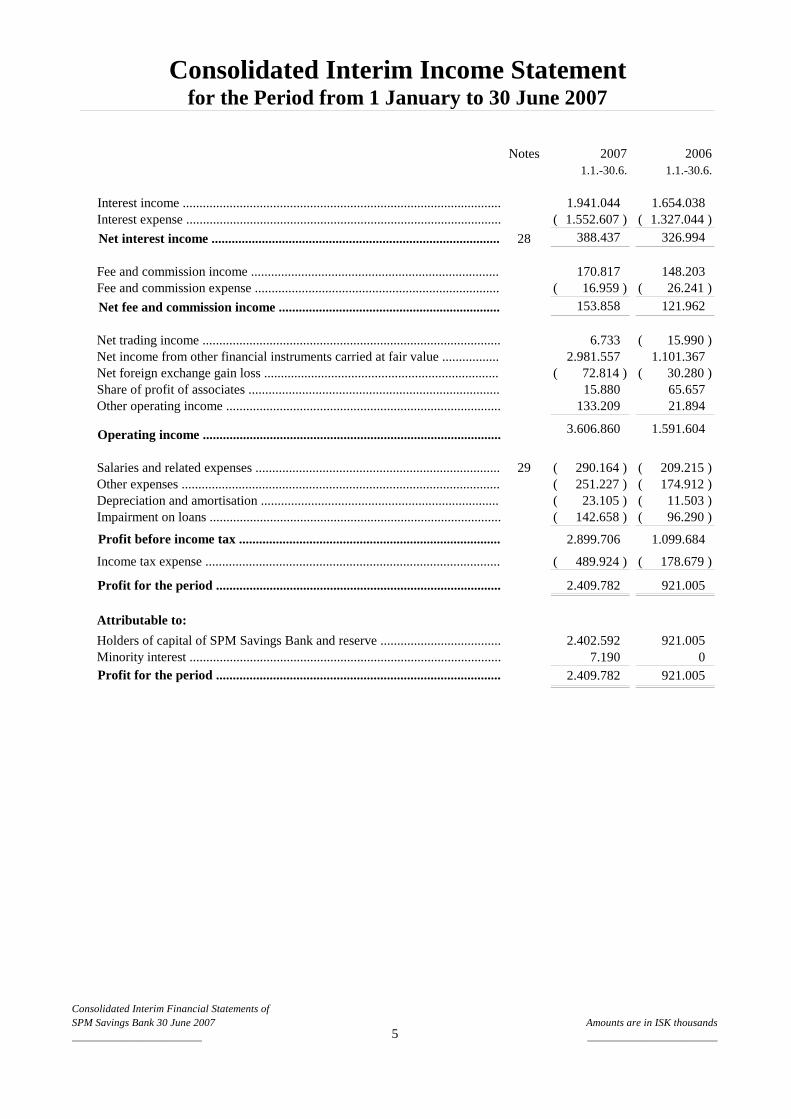

Notes 2007 20061.1.-30.6. 1.1.-30.6.

1.941.044 1.654.038 1.552.607 )( 1.327.044 )(

28 388.437 326.994

170.817 148.203 16.959 )( 26.241 )(

153.858 121.962

6.733 15.990 )( 2.981.557 1.101.367

72.814 )( 30.280 )( 15.880 65.657

133.209 21.894

3.606.860 1.591.604

29 290.164 )( 209.215 )( 251.227 )( 174.912 )( 23.105 )( 11.503 )(

142.658 )( 96.290 )(

2.899.706 1.099.684

489.924 )( 178.679 )(

2.409.782 921.005

2.402.592 921.005 7.190 0

2.409.782 921.005

Attributable to:

Holders of capital of SPM Savings Bank and reserve ....................................Minority interest .............................................................................................Profit for the period .....................................................................................

Profit before income tax ..............................................................................

Profit for the period .....................................................................................

Income tax expense ........................................................................................

Salaries and related expenses .........................................................................

Depreciation and amortisation .......................................................................Impairment on loans .......................................................................................

Consolidated Interim Income Statement

Net trading income .........................................................................................Net income from other financial instruments carried at fair value .................

Fee and commission expense .........................................................................Fee and commission income ..........................................................................

Interest income ...............................................................................................Interest expense ..............................................................................................

for the Period from 1 January to 30 June 2007

Net interest income ......................................................................................

Net fee and commission income ..................................................................

Other operating income ..................................................................................Share of profit of associates ...........................................................................Net foreign exchange gain loss ......................................................................

Other expenses ...............................................................................................

Operating income .........................................................................................

Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007________________________ 5

Amounts are in ISK thousands________________________

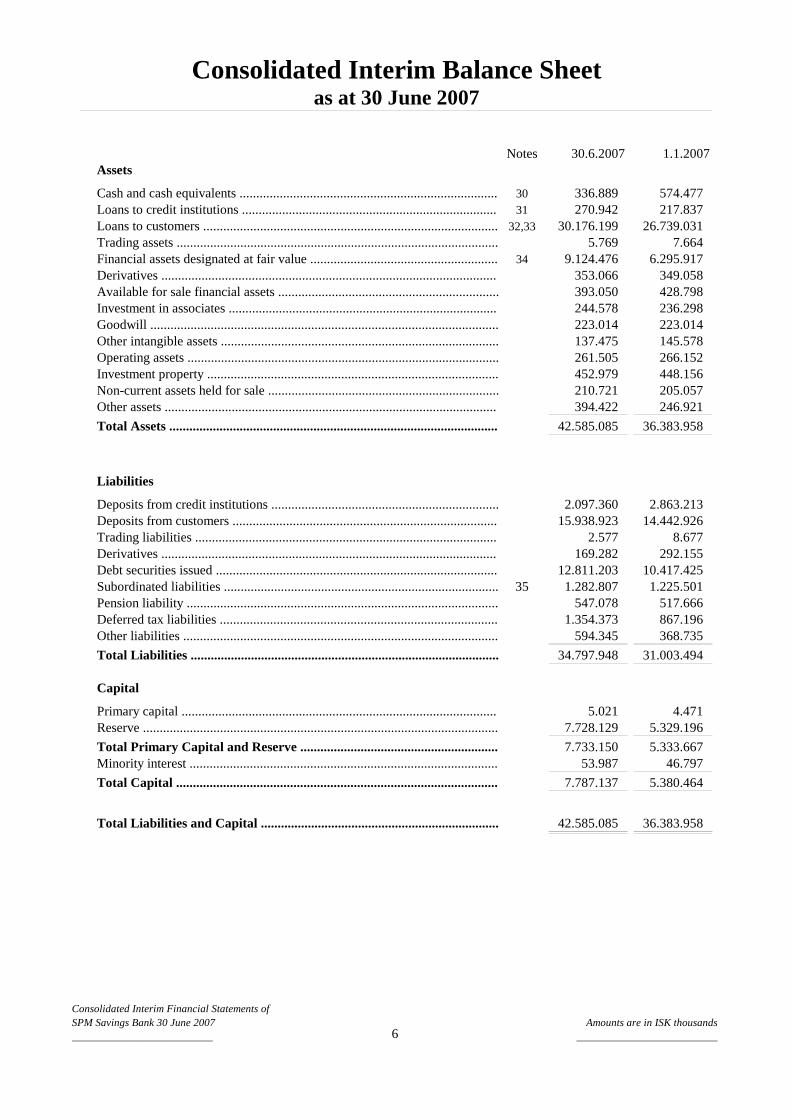

Notes 30.6.2007 1.1.2007Assets

30 336.889 574.477 31 270.942 217.837

32,33 30.176.199 26.739.031 5.769 7.664

34 9.124.476 6.295.917 353.066 349.058 393.050 428.798 244.578 236.298 223.014 223.014 137.475 145.578 261.505 266.152 452.979 448.156 210.721 205.057 394.422 246.921

42.585.085 36.383.958

Liabilities

2.097.360 2.863.213 15.938.923 14.442.926

2.577 8.677 169.282 292.155

12.811.203 10.417.425 35 1.282.807 1.225.501

547.078 517.666 1.354.373 867.196

594.345 368.735

34.797.948 31.003.494

Capital

5.021 4.471 7.728.129 5.329.196

7.733.150 5.333.667 53.987 46.797

7.787.137 5.380.464

42.585.085 36.383.958

Pension liability .............................................................................................

Debt securities issued ....................................................................................

Available for sale financial assets ..................................................................

Other intangible assets ...................................................................................

Investment property .......................................................................................

Derivatives ....................................................................................................

Total Assets ..................................................................................................

Non-current assets held for sale .....................................................................

Goodwill ........................................................................................................

Cash and cash equivalents .............................................................................

as at 30 June 2007

Loans to credit institutions ............................................................................

Derivatives ....................................................................................................Financial assets designated at fair value ........................................................Trading assets ................................................................................................

Total Liabilities and Capital .......................................................................

Other assets ...................................................................................................

Deposits from credit institutions ....................................................................

Other liabilities ..............................................................................................

Minority interest ............................................................................................

Total Liabilities ............................................................................................

Total Primary Capital and Reserve ...........................................................

Total Capital ................................................................................................

Deferred tax liabilities ...................................................................................

Consolidated Interim Balance Sheet

Primary capital ..............................................................................................Reserve ..........................................................................................................

Subordinated liabilities ..................................................................................

Deposits from customers ...............................................................................Trading liabilities ..........................................................................................

Loans to customers ........................................................................................

Investment in associates ................................................................................

Operating assets .............................................................................................

Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 6

Amounts are in ISK thousands__________________________

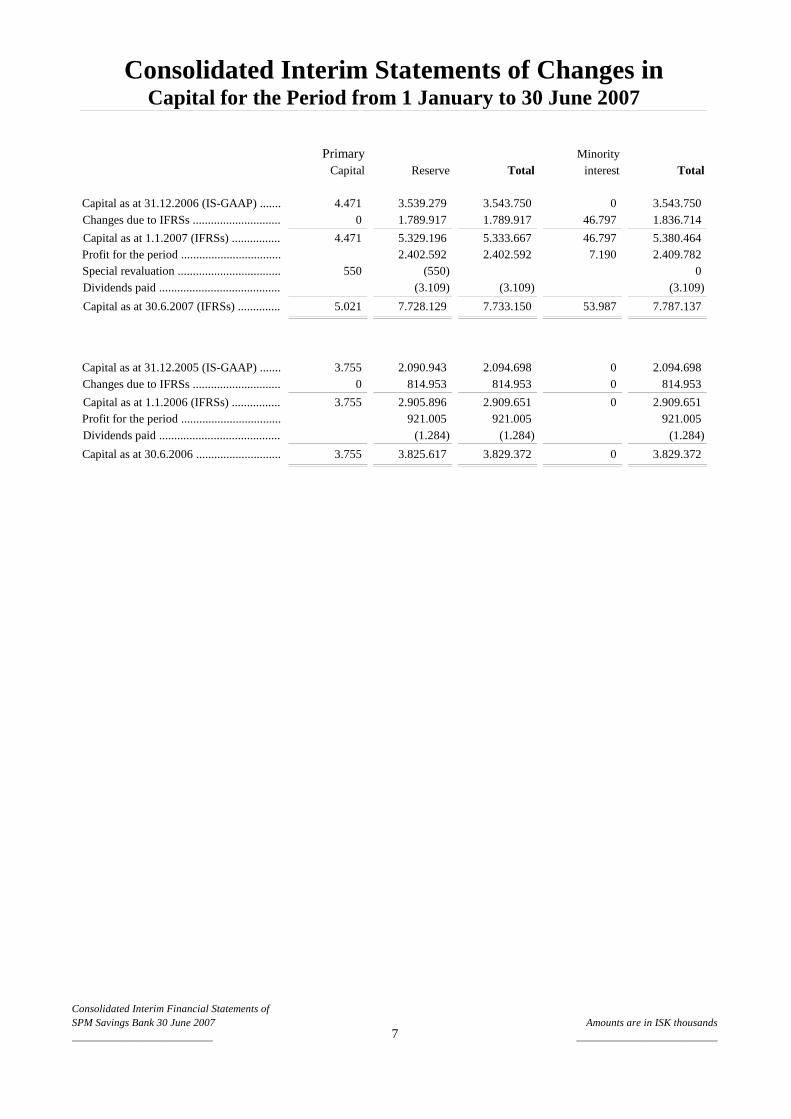

Primary MinorityCapital Reserve Total interest Total

Capital as at 31.12.2006 (IS-GAAP) ....... 4.471 3.539.279 3.543.750 0 3.543.750 Changes due to IFRSs ............................. 0 1.789.917 1.789.917 46.797 1.836.714

Capital as at 1.1.2007 (IFRSs) ................ 4.471 5.329.196 5.333.667 46.797 5.380.464 Profit for the period ................................. 2.402.592 2.402.592 7.190 2.409.782 Special revaluation .................................. 550 (550) 0 Dividends paid ........................................ (3.109) (3.109) (3.109)

Capital as at 30.6.2007 (IFRSs) .............. 5.021 7.728.129 7.733.150 53.987 7.787.137

Capital as at 31.12.2005 (IS-GAAP) ....... 3.755 2.090.943 2.094.698 0 2.094.698 Changes due to IFRSs ............................. 0 814.953 814.953 0 814.953

Capital as at 1.1.2006 (IFRSs) ................ 3.755 2.905.896 2.909.651 0 2.909.651 Profit for the period ................................. 921.005 921.005 921.005 Dividends paid ........................................ (1.284) (1.284) (1.284)

Capital as at 30.6.2006 ............................ 3.755 3.825.617 3.829.372 0 3.829.372

Consolidated Interim Statements of Changes inCapital for the Period from 1 January to 30 June 2007

Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 7

Amounts are in ISK thousands__________________________

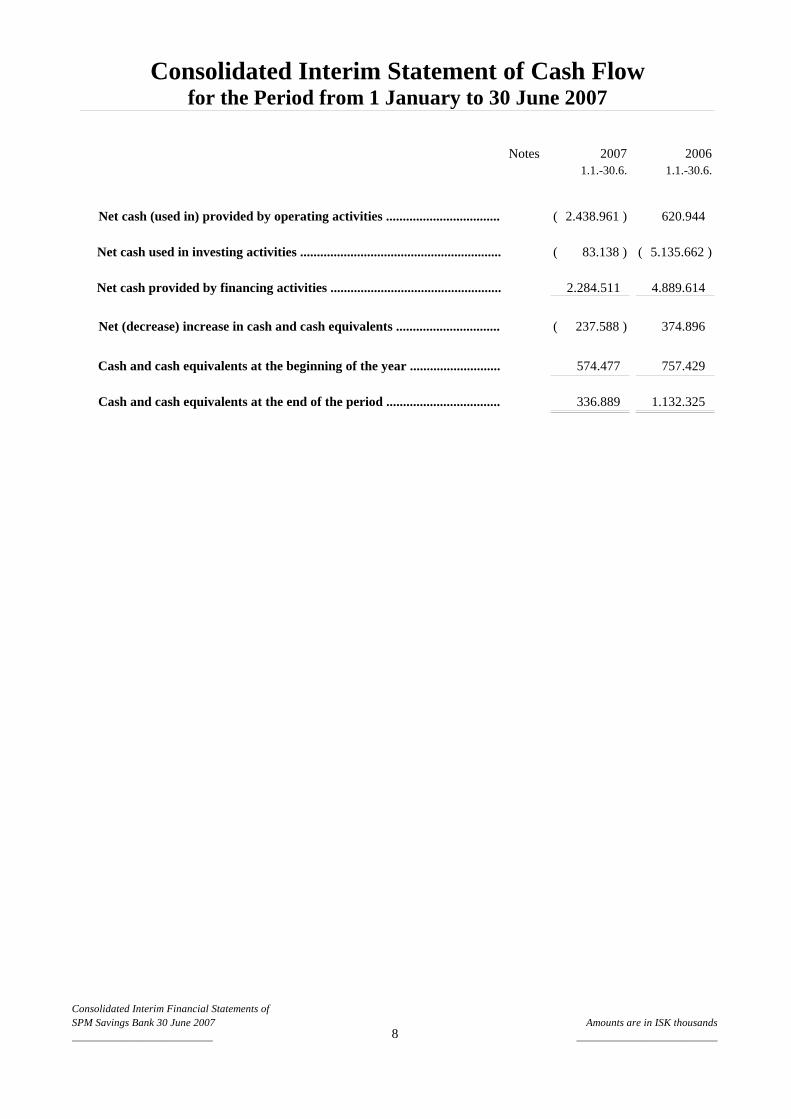

Notes 2007 20061.1.-30.6. 1.1.-30.6.

2.438.961 )( 620.944

83.138 )( 5.135.662 )(

2.284.511 4.889.614

237.588 )( 374.896

574.477 757.429

336.889 1.132.325

Net cash (used in) provided by operating activities ..................................

Cash and cash equivalents at the end of the period ..................................

Net (decrease) increase in cash and cash equivalents ...............................

Consolidated Interim Statement of Cash Flowfor the Period from 1 January to 30 June 2007

Net cash provided by financing activities ...................................................

Net cash used in investing activities ............................................................

Cash and cash equivalents at the beginning of the year ...........................

Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 8

Amounts are in ISK thousands__________________________

General information

1. Reporting entity

2. Basis of preparation

a) Statement of compliance

b) Basis of measurement

c) Functional and presentation currency

d) Use of estimates and judgements

The preparation of the Condensed Consolidated Interim Financial Statements in conformity with IFRS requiresmanagement to make judgements, estimates and assumptions,which affect the application of accounting policiesand the reported amounts of assets and liabilities as well asincome and expenses. The estimates and underlyingassumptions are based on historical experience and variousother factors that are believed to be reasonable underthe circumstances, the results of which form the basis of making the judgements about carrying amounts of assetsand liabilities that are not readily apparent from other sources. Actual results may differ from these estimates.

These Condensed Consolidated Interim Financial Statements are prepared and presented in Icelandic króna (ISK),which is the Group's functional currency. Except as indicated, financial information presented has been roundedto the nearest ISK thousand.

These interim accounts have been prepared in accordance with International Reporting Standars (IFRSs) forinterim accounts. These are the Group's first IFRS condensed interim accounts for part of the period covered bythe first IFRS annual accounts and IFRS 1,First-time Adoption of International Financial ReportingStandardshas been applied. The condensed interim accounts do not include all of the information required for full annualaccounts.

The Condensed Consolidated Financial Statements were approved by the Board of Directors on 31 August 2007.

The Condensed Consolidated Interim Financial Statements are prepared on the historical cost basis except thattrading assets and liabilities and financial instruments designated at fair value through profit and loss are measuredat fair value.

Non-current assets and disposal groups held for sale are measured at the lower of carrying amount and fair valueless costs to sell, unless IFRS 5 requires that another measurement basis shall be used.

Notes to the Consolidated Interim

SPM Savings Bank is a company incorporated and domiciled in Iceland. The Condensed Consolidated InterimFinancial Statements for the period 1 January 1 to 30 June 2007 comprise SPM Savings Bank (the parent) and itssubsidiaries (together referred to as "the Group") and the Group's. The address of the Savings Bank isDigranesgata 2 in Borgarnes.

The Condensed Consolidated Interim Financial Statements have been prepared in accordance with InternationalFinancial Reporting Standards (IFRS) for interim financial statements.

SPM Savings Bank main purpose is to offer banking services toindividuals and corporates. SPM Savings Bankoffers services in areas of commercial banking, brokerage.

Financial Statements

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 9

Amounts are ISK thousands__________________________

2. Basis of preparation, contd.:

Summary of significant accounting policies

3. Basis of consolidation

a) Subsidiaries

b) Transactions eliminated on consolidation

The estimates and underlying assumptions are reviewed on anongoing basis. Revisions to accounting estimatesare recognised in the period in which the estimate is revisedif the revision affects only that period or in the periodof the revision and future periods if the revision affects both current and future periods.

Information about areas of estimation uncertainty and judgements made by management in applying accountingpolicies that have the most significant effect on the amounts recognised in the Condensed Consolidated InterimFinancial Statements is provided in note 26.

The accounting policies set out below have been applied consistently to all periods presented in these CondensedConsolidated Interim Financial Statements. They have alsobeen used for the preparation of the opening IFRSbalance sheet at 1 January 2006 for the purpose of adopting IFRS.

Subsidiaries are entities controlled by the Group. Controlexists when the Group has the power to govern thefinancial and operating policies of an entity so as to obtainbenefits from its activities. Control usually exists whenthe Group holds more than 50% of the voting power of the subsidiary. In assessing control, potential voting rightsthat are currently exercisable or convertible, if any, are taken into account. The Condensed ConsolidatedFinancial Statements of subsidiaries are included in the Consolidated Financial Statements from the date thatcontrol commences until the date that control ceases.

The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The costof an acquisition is measured as the fair value, at the date ofexchange, of the assets given, liabilities incurred orassumed and equity instruments issued, plus cost directly attributable to the acquisition. Identifiable assetsacquired and liabilities and contingent liabilities assumed in a business are measured initially at their fair values atthe acquisition date, irrespective of the extent of any minority interest. The excess of the cost of acquisition overthe fair value of the Group's share of the identifiable net assets acquired is recorded as goodwill. If the costofacquisition is less than the fair value of the net assets of the subsidiary acquired, the difference is recogniseddirectly in the income statement.

Intragroup balances, unrealised gains and losses or incomeand expenses arising from intragroup transactions, areeliminated in the Condensed Consolidated Interim Financial Statements. Unrealised gains arising fromtransactions with associates and jointly controlled entities are eliminated to the extent of the Group's interest in theentity. Unrealised losses are eliminated in the same way as unrealised gains, but only to the extent that there is noevidence of impairment.

Notes to the Consolidated Interim Financial Statements, contd.:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 10

Amounts are ISK thousands__________________________

4. Foreign currency

5. Associates

6. Interest income and expense

Transactions in foreign currencies are translated at the foreign exchange rate ruling at the date of the transaction.Monetary assets and liabilities denominated in foreign currencies are translated to Icelandic króna at the foreignexchange rate ruling at the reporting date. Non-monetary assets and liabilities that are measured in termsofhistorical cost in a foreign currency are translated using the exchange rate at the date of the transaction. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are translated toIcelandic krónas at foreign exchange rates ruling at the dates the fair value was determined. Foreign exchangedifferences resulting from translation to Icelandic króna is recognised in the income statement.

Notes to the Consolidated Interim Financial Statements, contd.:

Once a financial asset or a group of similar financial assetshas been written down as a result of impairment loss,interest income is recognised at the rate of interest used for the purpose of calculating the impairment loss.Interest income on financial assets which have been writtendown as a result of impairment is calculated based ontheir net carrying amount.

Associates are those entities in which the Group has significant influence over the financial and operating policydecisions but not control over those policies. Significantinfluence generally exists when the Group holds between20% and 50% of the voting power, including potential voting rights, if any. Investments in associates are initiallyrecognised at cost.

The Condensed Consolidated Interim Financial Statements include the Group's share of the total recognised gainsand losses of associates on an equity accounted basis, from the date the significant influence commences until thedate it ceases. When the Group's share of loss exceeds its interest in an associate, the Group's carrying amount isreduced to zero and recognition of further losses is discontinued except to the extent that the Group has incurredlegal or constructive obligations or made payments on behalf of the associate. If the associate subsequentlyreports profits, the investor resumes recognising its share of those profits only after its share of the profits equalsthe share of losses not recognised.

Interest income and expense are recognised in the income statement on an accrual basis using the effective interestmethod. Interest income and expense includes the amortisation of any discount or premium or other differencesbetween the initial carrying amount of a financial instrument and its maturity amount, calculated using theeffective interest method.

The effective interest rate is the rate that exactly discounts estimated future cash flows through the expected lifeofthe financial instrument or, when appropriate, a shorter period, to the net carrying amount of the financial asset orfinancial liability. When calculating the effective interest rate, the Group estimates the cash flows considering allcontractual terms of the financial instrument, but it does not consider future credit losses.

Interest income and expense presented in the income statement include:

- interest on financial assets and liabilities at amortised cost on an effective interest rate basis

Interest income and expense on all trading assets and liabilities are considered to be incidental to the Group’strading operations and are presented together with all other changes in the fair value of trading assets andliabilities in net trading income.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 11

Amounts are ISK thousands__________________________

6. Interest income and expense, contd.:

7. Impairment

a) Impairment on loans

Individually assessed loans

The carrying amount of the Group's assets, other than trading assets and financial assets designated at fair value, isreviewed at each balance sheet date to determine whether there is any indication of impairment. If any suchindication exists, the asset's recoverable amount is estimated. An impairment is recognised in the incomestatement whenever the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount.

Impairment loss is calculated by comparing the carrying amount of individual loans with the present value of theirexpected future cash flows, discounted at their original effective interest rate. In the case of loans at variableinterest rates, the discount rate used is their current effective interest rate. The carrying amount of impaired loansis reduced through the use of an allowance account.

- the complexity of determining the aggregate amount and ranking of all creditor claims and the extent to which legal and insurance uncertainties are evident; - the realisable value of security (or other credit mitigants) and likelihood of successful repossession; and - the likely deduction of any costs involved in recovery of amounts outstanding.

Impairment losses on individually assessed loans are determined by an evaluation of the exposures on a case-by-case basis. The Group assesses at each balance sheet date whether there is any objective evidence that individualloans are impaired. This procedure is applied to all loans that are considered individually significant. In makingthe assessment, the following factors are considered:

- the Group's aggregate exposure to the customer; - the amount and timing of expected receipts and recoveries;

Two methods are used to calculate impairment losses, one based on an assessment of individual loans and theother based on a collective assessment. Losses expected as aresult of future events, no matter how likely, are notrecognised.

- the likely dividend available on liquidation or bankruptcy;

Fair value chanes of derivatives are split into interest income and net income from other financial instrumentscarried at fair value and presented in the corresponding line items in the income statement.

- general national or local economic conditions connected with the assets in the group.

(i) significant financial difficulty of the borrower;(ii) a breach of contract, such as a default on installments or on interest or principal payments;(iii) the Group granting to the borrower, for economic or legal reasons relating to the borrower's financial difficulty, a refinancing concession, that the lender would not otherwise consider;

(iv) it becomes probable that the borrower will enter bankruptcy or undergo other financial reorganisation; (v) the disappearance of an active market for that financial asset because of financial difficulties; or (vi) observable data indicating that there is a measurable decrease in the estimated future cash flows from a group of loans, even if the decrease cannot yet be identified with the individual financial assets in the group, including:

- adverse changes in the payment status of borrowers in the group; or

Notes to the Consolidated Interim Financial Statements, contd.:

Objective evidence of impairment includes information about the following events and conditions:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 12

Amounts are ISK thousands__________________________

7. Impairment, contd.:

Collectively assessed loans

Loan write-offs

Reversal of impairment

Assets acquired in exchange for loans

b) Calculation of recoverable amount

The collective impairment loss is determined after taking into account:

Loans are written off, partially or in full, when there is no realistic prospect of recovery.

Notes to the Consolidated Interim Financial Statements, contd.:

Where loans have been individually assessed and no evidenceof loss has been identified, these loans are groupedtogether on the basis of similar credit risk characteristics for the purpose of calculating a collective impairmentloss. This loss covers loans that are impaired at the balancesheet date but which will not be individually identifiedas such until some time in the future.

Non-financial assets acquired in exchange for loans in order to achieve an orderly realisation are recorded asassets held for sale and reported in the balance sheet. The asset acquired is recorded at the lower of its fair valueless costs to sell and the carrying amount of the loan, net of impairment allowance amounts, at the dateofexchange. No depreciation is provided in respect of assets held for sale. Any subsequent write-down of theacquired asset to fair value less costs to sell is recorded asan impairment loss and included in the incomestatement. Any subsequent increase in the fair value less costs to sell, to the extent this does not exceed thecumulative impairment loss, is recognised in the income statement.

Estimates of changes in future cash flows for groups of assets are consistent with changes in observable data fromperiod to period, for example changes in property prices, payment status, or other factors indicative of changes inthe probability of losses on the group and their magnitude. The methodology and assumptions used for estimatingfuture cash flows are reviewed regularly by the Group to minimise any differences between loss estimates andactual losses.

- future cash flows in a group of loans evaluated for impairment are estimated on the basis of the contractual cash flows of the assets;

- historical loss experience in portfolios of similar risk characteristics (for example, by industry sector, loan grade or product); - the estimated period between a loss occurring and that loss being identified and evidenced by the establishment of an allowance against the loss on an individual loan;

- management's experienced judgement as to whether the current economic and credit conditions are such that the actual level of inherent losses is likely to be greater or less than that suggested by historical experience.

If, in a subsequent period, the amount of an impairment loss decreases and the decrease can be related objectivelyto an event occurring after the impairment was recognised, the previously recognised impairment loss isrecognised as revenue in the income statement.

The recoverable amount of the Group's investments in financial assets carried at amortised cost is calculated as thepresent value of estimated future cash flows, discounted at the original effective interest rate.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 13

Amounts are ISK thousands__________________________

7. Impairment, contd.:

c) Impairment of goodwill

8. Income tax expense

9. Cash and cash equivalents

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be availableagainst which the asset can be utilised. Deferred tax assetsare reviewed at each reporting date and reduced to theextent that it is no longer probable that the related tax benefit will be realised.

Cash and cash equivalents in the Statement of Cash Flows consist of cash, demand deposits with the Central Bankand demand deposits with other credit institutions.

The recoverable amount of other assets is the greater of their net selling price and value in use. In assessing valuein use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate thatreflects current market assessments of the time value of money and the risks specific to the asset. For an asset thatdoes not generate largely independent cash inflows, the recoverable amount is determined for the cash-generatingunit to which the asset belongs.

An impairment loss in respect of goodwill is not reversed.

Income tax expense comprises current tax and deferred tax. Income tax expense is recognised in the incomestatement, except to the extent that it relates to items recognised directly in equity in which case it is recognised inequity.

The recoverable amount of other assets is the greater of their fair value less costs to sell and value in use. Inassessing value in use, the estimated future cash flows are discounted to their present value using a pre-taxdiscount rate that reflects current market assessments of the time value of money and the risks specific to the asset.For an asset that does not generate largely independent cashinflows, the recoverable amount is determined for thecash-generating unit to which the asset belongs.

The Group assesses whether there is any indication of impairment of goodwill on annual basis, with expertanalysis being commissioned if necessary. Goodwill is written down for impairment. Gains or losses realised onthe disposal of subsidiaries include any unamortised balance of goodwill relating to the subsidiary disposed of.

An impairment loss is recognised if the carrying amount of anasset or its cash-generating unit exceeds itsrecoverable amount. A cash-generating unit is the smallestidentifiable asset group that generates cash flows thatlargely are independent from other assets and groups. Impairment losses are recognised in profit or loss.Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amountof the other assets in the unit (group of units) on a pro rata basis.

The deferred income tax liability has been calculated and recognised in the balance sheet. The calculation isbased on the difference between balance sheet items as presented in the tax return on one hand, and in theCondensed Consolidated Interim Financial Statements on the other, taking into consideration tax losses carriedforward. This difference is due to the fact that the tax assessment is based on premises that differ from thosegoverning the Condensed Consolidated Interim Financial Statements, mostly due to temporary differences arisingfrom the recognition of revenues and expenses in the tax returns and in the Condensed Consolidated InterimFinancial Statements.

Notes to the Consolidated Interim Financial Statements, contd.:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 14

Amounts are ISK thousands__________________________

10. Trading assets and liabilities

11.

b) Derivatives held for risk management purposes

b) Embedded derivatives

12. Loans

Derivatives

Derivative assets and liabilities are initially recognised and subsequently measured at fair value in the balancesheet. Fair value changes of derivatives are spilt into interest income and net income from other financialinstruments carried at fair value and presented in the corresponding line items in the income statement.

Derivatives held for risk management purposes include all derivative assets and liabilities that are not classified astrading assets or liabilities. Derivatives held for risk management purposes are measured at fair value in thebalance sheet. The treatment of changes in their fair value depends on their classification into the followingcategories:

Loans are initially recognised at fair value, which is the cash advanced, plus any transaction costs. Subsequently,they are measured at amortised cost using the effective interest method. Accrued interest is included in thecarrying amount of the loans.

Trading assets and liabilities are initially recognised and subsequently measured at fair value in the balance sheetwith transaction costs taken directly to profit or loss. Allchanges in fair value are recognised as part of netfinancial income in profit or loss. Interest and dividend income on these assets are included in interest income and net financial income line items in the income statement.

Derivatives may be embedded in another contractual arrangement (a “host contract”). The Group accounts forembedded derivatives separately from the host contract when the host contract is not itself carried at fair valuethrough profit or loss, and the characteristics of the embedded derivative are not clearly and closely related to thehost contract. Separated embedded derivatives are accounted for depending on their classification, and arepresented in the balance sheet together with the host contract.

Trading assets and liabilities are those assets and liabilities that the Group acquires or incurs principally for thepurpose of selling or repurchasing in the near term, or holdsas part of a portfolio that is managed together forshort-term profit or position taking. Trading assets consist of bonds, shares and derivatives with positive fairvalue. Trading liabilities consist of derivatives with negative fair values.

Notes to the Consolidated Interim Financial Statements, contd.:

Loans are non-derivative financial instruments with fixedor determinable payments that are not quoted in anactive market, other than those that the Group designates upon initial recognition as at fair value. Loans includeloans provided by the Group to its customers, participationin loans from other lenders and purchased loans thatare not quoted in an active market and which the Group has no intention of selling immediately or in the nearfuture.

When the Group purchases a financial asset and simultaneously enters into an agreement to resell the asset (or asubstantially similar asset) at a fixed price on a future date (“reverse repo or stock borrowing”), the arrangement isaccounted for as a loan or advance, and the underlying asset is not recognised in the Group’s financial statements.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 15

Amounts are ISK thousands__________________________

13. Financial assets designated at fair value

14. Available-for-sale

15. Determination of fair value

16. Financial assets and liabilities

a) Recognition

b) Derecognition

The Group designates certain financial assets upon their initial recognition as financial assets at fair value whendoing so results in more relevant information, including information provided internally to key managementpersonnel. Fair value changes are recognised in the income statement.

Interest income is recognised in profit or loss using the effective interest method. Dividend income is recognisedin profit or loss when the Group becomes entitled to the dividend.

The Group initially recognises loans, deposits, debt securities issued and subordinated liabilities on the date thatthey are originated. All other financial assets and liabilities (including assets and liabilities designated at fairvalue through profit or loss) are initially recognised on the trade date at which the Group becomes a party to thecontractual provisions of the instrument.

Available-for-sale investments are non-derivative investments that are not designated as another categoryoffinancial assets. All other available-for-sale investments are carried at fair value.

Notes to the Consolidated Interim Financial Statements, contd.:

Other fair value changes are recognised directly in equity until the investment is sold or impaired and the balancein equity is recognised in profit or loss.

The determination of fair value of financial assets and financial liabilities that are quoted in an active market isbased on quoted prices. For all other financial instrumentsfair value is determined by using valuation techniques.A market is considered active if quoted prices are readily and regularly available and those prices represent actualand regularly occurring market transactions on an arm's length basis.

Valuation techniques include recent arm's length transactions between knowledgeable, willing parties, if available,reference to the current fair value of other instruments that are substantially the same, the discounted cash flowanalysis and option pricing models. Valuation techniques incorporate all factors that market participants wouldconsider in setting a price and are consistent with acceptedmethodologies for pricing financial instruments.Periodically, the Group calibrates the valuation technique and tests it for validity using prices from any observablecurrent market transactions in the same instrument, without modification or repackaging, or based on anyavailable observable market data.

The Group derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or ittransfers the rights to receive the contractual cash flows on the financial asset in a transacion in whichsubstantially all the risks and rewards of ownership of the financial asset are transferred. Any interest intransferred fiancial assets that is created or retained by the Group is recognised as a separate asset or liability.

Financial liabilities are recognised when the Group becomes a party to the contractual provisions of the liabilityinstrument. Financial liabilities are derecognised when the obligation of the Group is discharged or cancelled orexpires.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 16

Amounts are ISK thousands__________________________

16. Financial assets and liabilities, contd.:

c) Offsetting

d) Amortised cost measurement

17. Operating assets

50 years5-7 years

18. Intangible assets

a) Goodwill

b) Other intangible assets

Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legallyenforceable right to offset the recognised amounts and there is an intention to settle on a net basis.

Notes to the Consolidated Interim Financial Statements, contd.:

Income and expenses are presented on a net basis only when permitted by the accounting standards, or for gainsand losses arising from a group of similar transactions such as in the Group’s trading activity.

The amortised cost of a financial asset or liability is the amount at which the financial asset or liability is measuredat initial recognition, minus principal repayments, plus or minus the cumulative amortisation using the effectiveinterest method of any difference between the initial amount recognised and the maturity amount, minus anyreduction for impairment.

The Group recognises in the carrying amount of operating assets the cost of replacing part of such an item whenthat cost is incurred if it is probable that the future economic benefits embodied with the item will flow to theGroup and the cost of the item can be measured reliably. All other costs are expensed in the income statementwhen incurred.

Depreciation is recognised in the income statement on a straight-line basis over the estimated useful lives of eachcomponent of an item of operating assets. The estimated useful lives are as follows:

Office equipment fixtures and cars ...............................................................................................Real estate .....................................................................................................................................

All business combinations after 1 January 2004 are accounted for by applying the purchase method. Goodwill hasbeen recognised on the acquisition of subsidiaries and associates. In respect of business acquisitions that haveoccurred since 1 January 2004, goodwill represents the difference between the cost of the acquisition and the fairvalue of the net identifiable assets acquired.

Items of operating assets are measured at cost less accumulated depreciation and impairment losses.

Goodwill is measured at cost less any accumulated impairment losses. Goodwill is allocated to cash-generatingunits and is no longer amortised but is tested annually for impairment. In respect of associates, the carryingamount of goodwill is included in the carrying amount of the investment in the associate.

Intangible assets other than goodwill that are acquired by the Group are stated at cost less accumulatedamortisation and impairment losses.

As long as the residual value is not immaterial, it is reassessd annually.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 17

Amounts are ISK thousands__________________________

18. Intangible assets, contd.:

c) Amortisation

10 years5 years

19. Leased assets

20. Deposits

21. Debt securities issues

22. Subordinated liabilities

Subordinated liabilities are initially recognised at fairvalue less attributable transaction costs. Subsequently,theyare measured at amortised cost using the effective interestmethod. Accrued interest is included in their carryingamount.

Subordinated liabilities are bonds issued by the Group withsubordinated terms. Subordinated liabilities have thecharacteristics of equity in being subordinated to other liabilities of the Group. In the calculation of equity ratio,these bonds are included in equity, as shown in note 36. On onehand, there are bonds with no maturity date thatthe Savings Bank may not retire until 2015 and then only with the approval of the Financial SupervisoryAuthority. These bonds qualify as Tier I capital. On the other hand there are bonds with maturity dates over thenext 10 years. The loans are entered as liabilities with accrued interest and indexation at year-end.

Amortisation is charged to the Income Statement on a straight-line basis over the estimated useful livesofintangible assets. Goodwill with an indefinite useful lifeis systematically tested for impairment at each BalanceSheet date. Other intangible assets are amortised from the date they are available for use. The estimated usefullives are as follows:

Business restrictive provision .......................................................................................................Customers relationships ................................................................................................................

Notes to the Consolidated Interim Financial Statements, contd.:

The Group's borrowings consist of issued bonds and loans from credit institutions. Borrowings are initiallyrecognised at fair value less attributable transaction costs. Subsequently, they are measured at amortised costusing the effective interest method. Accrued interest is included in their carrying amount.

Deposits are measured initially at fair value and subsequently at amortised cost.

Leases in terms of which the Group assumes substantially allthe risks and rewards of ownership are classified asfinance leases. Upon initial recognition the leased asset is measured at an amount equal to the lower of its fairvalue and the present value of the minimum lease payments. Subsequent to initial recognistion, the asset isaccounted for in accordance with the accounting policy applicable to that asset.

Other leases are operating leases and, except for investment property, the leased assets are not recognised on theGroup's balance sheet. Investment property held under an operating lease is recognised on the Group's balancesheet at its fair value.

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 18

Amounts are ISK thousands__________________________

23. Pension liabilities

24. Other assets and other liabilities

25. Capital

a) Primary capital

b) Reserve

c) Dividends on primary capital

26. Critical accounting estimates and judgements in applying accounting policies

a) Impairment losses on loans and advances

b) Fair value of financial instruments

Profit for the year is recognised in reserve. Dividends paid and revaluation of primary capital decreases reserve.

The liability recognised in the balance sheet in respect of defined benefit pension obligation is the present valueofthe obligation at the balance sheet date. The defined benefit obligation is calculated annually by independentactuaries using the projected unit credit method. The present value of the defined benefit obligation is determinedby discounting the estimated future cash outflows using interest rates of government bonds that are denominatedin the currency in which the benefits will be paid, and that have terms to maturity approximating to the termsofthe related pension liability. The discount rate used for the pension liability is 2.0%.

Other assets and other liabilities are measured at cost.

The fair value of financial instruments that are not quoted in active markets are determined by using valuationtechniques which are reviewed regularly by qualified independent personnel. All models that are used must beapproved and calibrated to ensure that outputs reflect actual data.

Dividends on primary capital are recognised in equity in theperiod in which they are approved by the Group'sprimary capital holders.

The Group reviews its loan portfolios to assess impairment at least on a three months basis. In determiningwhether an impairment loss should be recorded in the income statement, the Group makes judgements as towhether there is any observable data indicating that there is a measurable decrease in the estimated future cashflows from a portfolio of loans before the decrease can be identified with an individual loan in that portfolio. Thisevidence may include observable data indicating that therehave been changes in the payment status of borrowersin a group or economic conditions. Management uses estimates based on historical loss experience for assets withsimilar credit risk characteristics and objective evidence of impairment similar to those in the portfolio whenscheduling its future cash flows. The methodology and assumptions used for estimating both the amount andtiming of future cash flows are reviewed regularly to reduceany differences between loss estimates and actual lossexperience.

When primary capital is repurchased, the amount of the consideration paid, including directly attributable costs, isrecognised as a change in capital. Revaluation of primary capital increases primary capital.

Notes to the Consolidated Interim Financial Statements, contd.:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 19

Amounts are ISK thousands__________________________

Risk management

27.

27.

a) Credit risk

b) Liquidity risk

Financial risk management

The Savings Bank has exposure to the following risks from its use of financial instruments:- Credit risk- Liquidity risk- Market risk- Operational risk

The Savings Bank's Board of Directors has established a framework for risk management. In that framework arespecified rules for the Savings Bank in which the risk policyis defined and limits established for all the majorcategories of risk.

The board has established a risk committee, who is responsible for developing and monitoring group riskmanagement. The risk committee consists of the four directors of the Savings Bank and the Managing Director.The directors are responsible for the activities of their respective divisions.

Financial risk management, contd.:

The role of risk management is to identify significant riskswithin the Savings Bank's operations and ensure thatthe total risk exposure is within the limit framework established by the board of directors.

Credit risk is the risk of financial loss to the Savings Bank if a customer or counterparty to a financial instrumentfails to meet its contractual obligations, and arises principally from the Savings Banks loans to customers and toother banks and investment securities.

The Savings Bank is bound by the regulatory maximum limit on single exposures of 25% of regulatory capital.The Board of Directors has limited the Managing Director general lending authority to 10% of the Savings Bank'sregulatory capital. The Managing Director has the authority to exceed the 10% limit in the case of loans tofinancial institutions and municipalities. The Managing Director has delegated defined credit lines and limits for aspecified list of counterparties to directors and certain staff members.

The risk policy states that exposure to a certain industry must not exceed 30% of total assets. The provisioning atthe Savings Bank is based on IFRS guidelines. Additions to the provisions for credit losses are made throughimpairment on loans. All impaired claims are reviewed and analysed at least every three months. Impairment isreversed only when the credit quality has improved to the extent where there is reasonable assurance of timelycollection of principal and interest in accordance with the original contractual terms.

Liquidity risk is the risk that the group will encounter difficulty in meeting obligations from its financial liabilities.

The Savings Banks approach to managing liquidity is to ensure, as far as possible, that it will always havesufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurringunacceptable losses or risking damage to the Savings Bank'sreputation. The Savings Banks liquidity is managedby the Treasury so as to ensure that the Savings Bank can meet both foreseeable and unexpected payments asdescribed above.

Notes to the Consolidated Interim Financial Statements, contd.:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 20

Amounts are ISK thousands__________________________

27.

c) Market risk

i) Interest risk

ii) Equity risk

iii) Currency risk

d) Operational risk

Market risk is the risk that changes in market prices, such asinterest rate, equity prices, foreign exchange ratesand credit spreads (not relating to changes in the obligor’s/issuer’s credit standing) will affect the Savings Bank'sincome or the value of its holdings of financial instruments. The objective of market risk management is tomanage and control market risk exposures within acceptable parameters, while optimising the return on risk.

Interest rate risk is the risk to earnings and capital arising from adverse movements in interest rates. It arises froma mismatch in the maturity of assets and liabilities or the type of interest rates (fixed, floating, indexed, non-indexed). Interest rate risk is measured on a regular basis by assessing the impact of a 100 basis point shift in theyield curve. The risk measured may not exceed 10% of the Savings Bank's adjusted equity. Furthermore, thecomposition of assets and liabilities carrying fixed or floating interest rates and indexed and non-indexed interestrates are measured regularly.

The Savings Bank owns listed and, to a limited extent, unlisted equity shares. The Savings Bank is thereforeexposed to price fluctuations of these assets. Shares are held mainly on a strategic basis but also for tradingpurposes.

Currency risk is the risk of loss due to changes in foreign currency prices. Fluctuations in currency prices affectthe Savnings Bank's assets and liabilities denominated in foreign currencies.

The Savings Bank's currency balance is managed by the Treasury and monitored by risk management. TheSavings Bank's general policy is to keep a neutral position but speculative short-term positions may be takenwithin the currency exposure limits set by the risk framework and the currency exposure limits set by the CentralBank of Iceland.

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with theGroup’s processes, personnel, technology, and infrastructure, and from external factors other than credit, marketand liquidity risks such as those arising from legal and regulatory requirements and generally accepted standardsof corporate behaviour. Operational risks arise from all ofthe Savings Bank's operations and are faced by allbusiness entities.

The Savings Bank has established a set of internal rules, which are either set by the Board of Directors or, on theauthority of the Board, by the Managing Director. These internal rules govern all the most important aspects of the Banks operations and are intended to ensure that the SavingsBank observes all rules and regulations set by theauthorities as well as those laid down in the Articles of association of the Savings Bank and established by itsBoard of Directors.

The Savings Bank has outsourced all its major information and communications technology services to Teris (TheComputer Centre for Icelandic Savings Banks) which is ownedby SPM and other Savings Banks in Iceland. Terisfocuses on serving financial institutions with total ICT-solutions by providing all operations and servicesassociated with the processing and safekeeping of financial information with emphasis on confidentiality, integrityand availability. The company is certified according to ISO/IEC 27001, thereby complying with the requirementsof the financial Supervisory Authority in Iceland regarding ICT-operations within financial institutions.

Notes to the Consolidated Interim Financial Statements, contd.:

Financial risk management, contd.:

Consolidated Interim Financial Statement ofSPM Savings Bank 30 June 2007__________________________ 21

Amounts are ISK thousands__________________________

Notes to the Income Statement

Net interest income

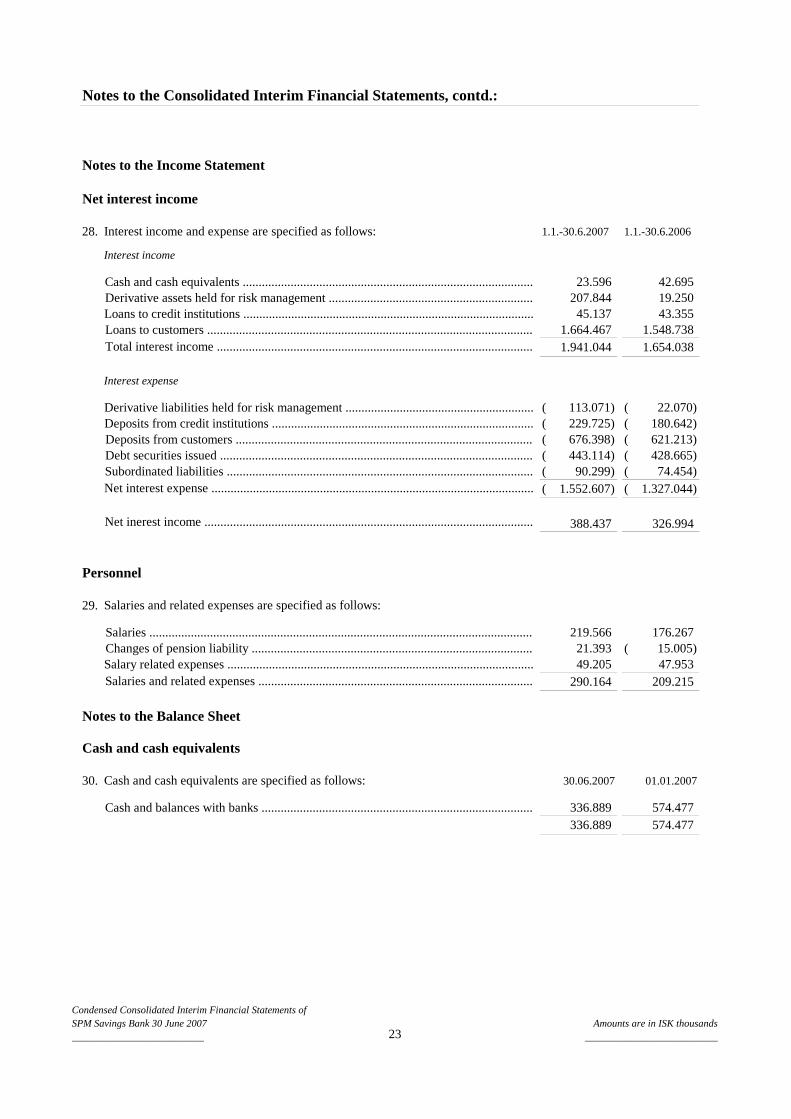

28. Interest income and expense are specified as follows: 1.1.-30.6.2007 1.1.-30.6.2006

Interest income

23.596 42.695 207.844 19.250 45.137 43.355

1.664.467 1.548.738 1.941.044 1.654.038

Interest expense

113.071)( 22.070)( 229.725)( 180.642)( 676.398)( 621.213)( 443.114)( 428.665)( 90.299)( 74.454)(

1.552.607)( 1.327.044)(

388.437 326.994

Personnel

29. Salaries and related expenses are specified as follows:

219.566 176.267 21.393 15.005)( 49.205 47.953

290.164 209.215

Notes to the Balance Sheet

Cash and cash equivalents

30. Cash and cash equivalents are specified as follows: 30.06.2007 01.01.2007

336.889 574.477 336.889 574.477

Cash and cash equivalents ...........................................................................................Derivative assets held for risk management ................................................................Loans to credit institutions ...........................................................................................Loans to customers ......................................................................................................

Notes to the Consolidated Interim Financial Statements, contd.:

Debt securities issued ..................................................................................................

Salaries ........................................................................................................................

Derivative liabilities held for risk management ...........................................................Deposits from credit institutions ..................................................................................

Subordinated liabilities ................................................................................................Net interest expense .....................................................................................................

Net inerest income .......................................................................................................

Deposits from customers .............................................................................................

Total interest income ...................................................................................................

Salaries and related expenses ......................................................................................

Cash and balances with banks .....................................................................................

Changes of pension liability ........................................................................................Salary related expenses ................................................................................................

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 23

Amounts are in ISK thousands__________________________

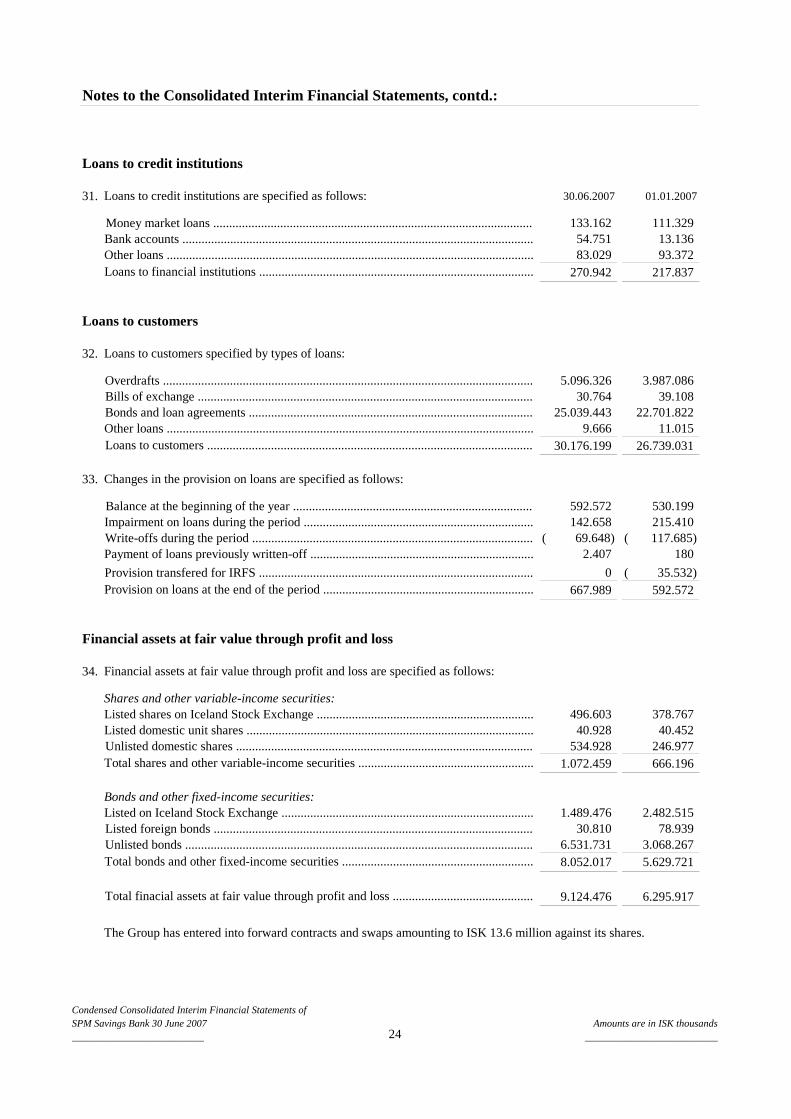

Loans to credit institutions

31. Loans to credit institutions are specified as follows: 30.06.2007 01.01.2007

133.162 111.329 54.751 13.136 83.029 93.372

270.942 217.837

Loans to customers

32. Loans to customers specified by types of loans:

5.096.326 3.987.086 30.764 39.108

25.039.443 22.701.822 9.666 11.015

30.176.199 26.739.031

33. Changes in the provision on loans are specified as follows:

592.572 530.199 142.658 215.410 69.648)( 117.685)(

2.407 180

0 35.532)( 667.989 592.572

Financial assets at fair value through profit and loss

34. Financial assets at fair value through profit and loss are specified as follows:

Shares and other variable-income securities:496.603 378.767 40.928 40.452

534.928 246.977 1.072.459 666.196

Bonds and other fixed-income securities:1.489.476 2.482.515

30.810 78.939 6.531.731 3.068.267 8.052.017 5.629.721

9.124.476 6.295.917

Balance at the beginning of the year ...........................................................................

Payment of loans previously written-off ......................................................................

Provision transfered for IRFS ......................................................................................

Impairment on loans during the period ........................................................................Write-offs during the period ........................................................................................

The Group has entered into forward contracts and swaps amounting to ISK 13.6 million against its shares.

Bills of exchange .........................................................................................................

Loans to customers ......................................................................................................

Bonds and loan agreements .........................................................................................

Unlisted domestic shares .............................................................................................

Other loans ...................................................................................................................

Loans to financial institutions ......................................................................................

Overdrafts ....................................................................................................................

Notes to the Consolidated Interim Financial Statements, contd.:

Total finacial assets at fair value through profit and loss ............................................

Total bonds and other fixed-income securities ............................................................

Provision on loans at the end of the period ..................................................................

Money market loans ....................................................................................................

Other loans ...................................................................................................................Bank accounts ..............................................................................................................

Listed shares on Iceland Stock Exchange ....................................................................Listed domestic unit shares ..........................................................................................

Listed on Iceland Stock Exchange ...............................................................................Listed foreign bonds ....................................................................................................Unlisted bonds .............................................................................................................

Total shares and other variable-income securities .......................................................

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 24

Amounts are in ISK thousands__________________________

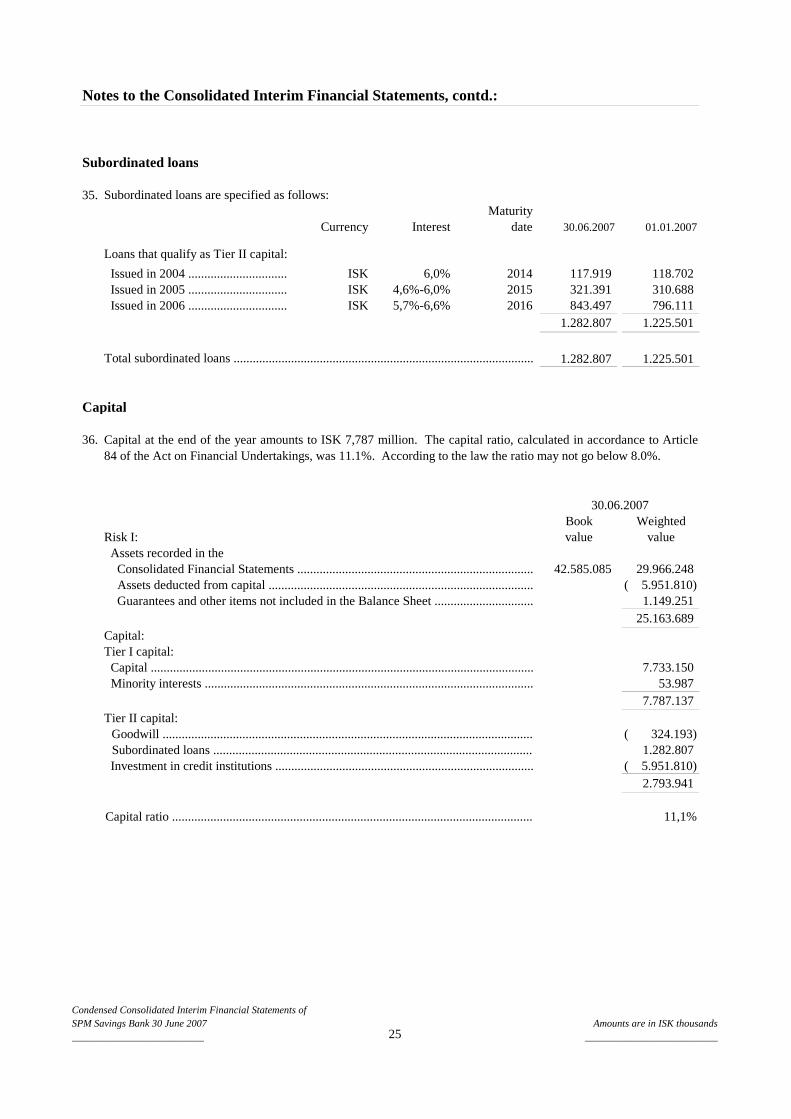

Subordinated loans

35. Subordinated loans are specified as follows:Maturity

Currency Interest date 30.06.2007 01.01.2007

Loans that qualify as Tier II capital:

ISK 6,0% 2014 117.919 118.702 ISK 4,6%-6,0% 2015 321.391 310.688 ISK 5,7%-6,6% 2016 843.497 796.111

1.282.807 1.225.501

1.282.807 1.225.501

Capital

36.

Book WeightedRisk I: value value

42.585.085 29.966.248 5.951.810)( 1.149.251

25.163.689 Capital:Tier I capital:

7.733.150 53.987

7.787.137 Tier II capital:

324.193)( 1.282.807 5.951.810)( 2.793.941

11,1%

Minority interests .......................................................................................................

Subordinated loans .................................................................................................... Goodwill ....................................................................................................................

Capital at the end of the year amounts to ISK 7,787 million. The capital ratio, calculated in accordance to Article84 of the Act on Financial Undertakings, was 11.1%. According to the law the ratio may not go below 8.0%.

30.06.2007

Assets recorded in the

Investment in credit institutions .................................................................................

Capital ratio .................................................................................................................

Issued in 2004 ...............................

Issued in 2006 ............................... Issued in 2005 ...............................

Notes to the Consolidated Interim Financial Statements, contd.:

Consolidated Financial Statements .......................................................................... Assets deducted from capital ................................................................................... Guarantees and other items not included in the Balance Sheet ...............................

Capital ........................................................................................................................

Total subordinated loans ..............................................................................................

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 25

Amounts are in ISK thousands__________________________

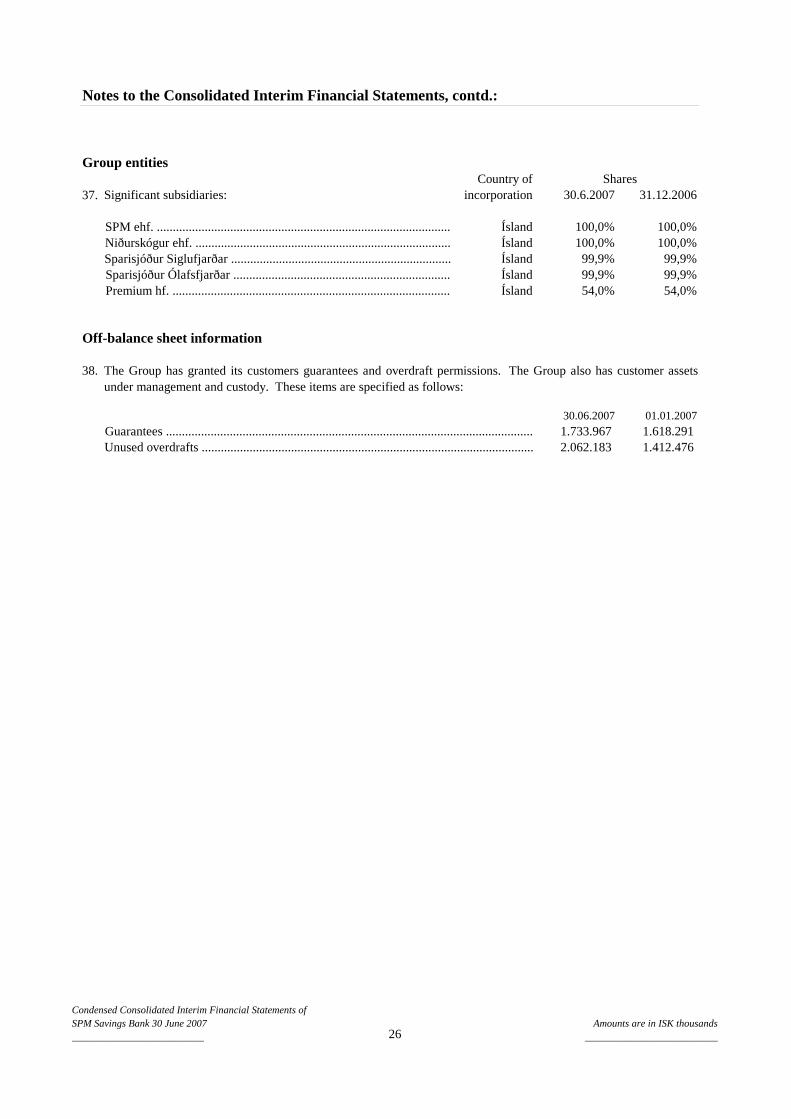

Group entitiesCountry of Shares

37. Significant subsidiaries: incorporation 30.6.2007 31.12.2006

Ísland 100,0% 100,0%Ísland 100,0% 100,0%Ísland 99,9% 99,9%Ísland 99,9% 99,9%Ísland 54,0% 54,0%

Off-balance sheet information

38.

30.06.2007 01.01.20071.733.967 1.618.291 2.062.183 1.412.476

Notes to the Consolidated Interim Financial Statements, contd.:

The Group has granted its customers guarantees and overdraft permissions. The Group also has customer assetsunder management and custody. These items are specified as follows:

Sparisjóður Siglufjarðar .....................................................................

Unused overdrafts ........................................................................................................Guarantees ...................................................................................................................

Niðurskógur ehf. ................................................................................SPM ehf. ............................................................................................

Sparisjóður Ólafsfjarðar ....................................................................Premium hf. .......................................................................................

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 26

Amounts are in ISK thousands__________________________

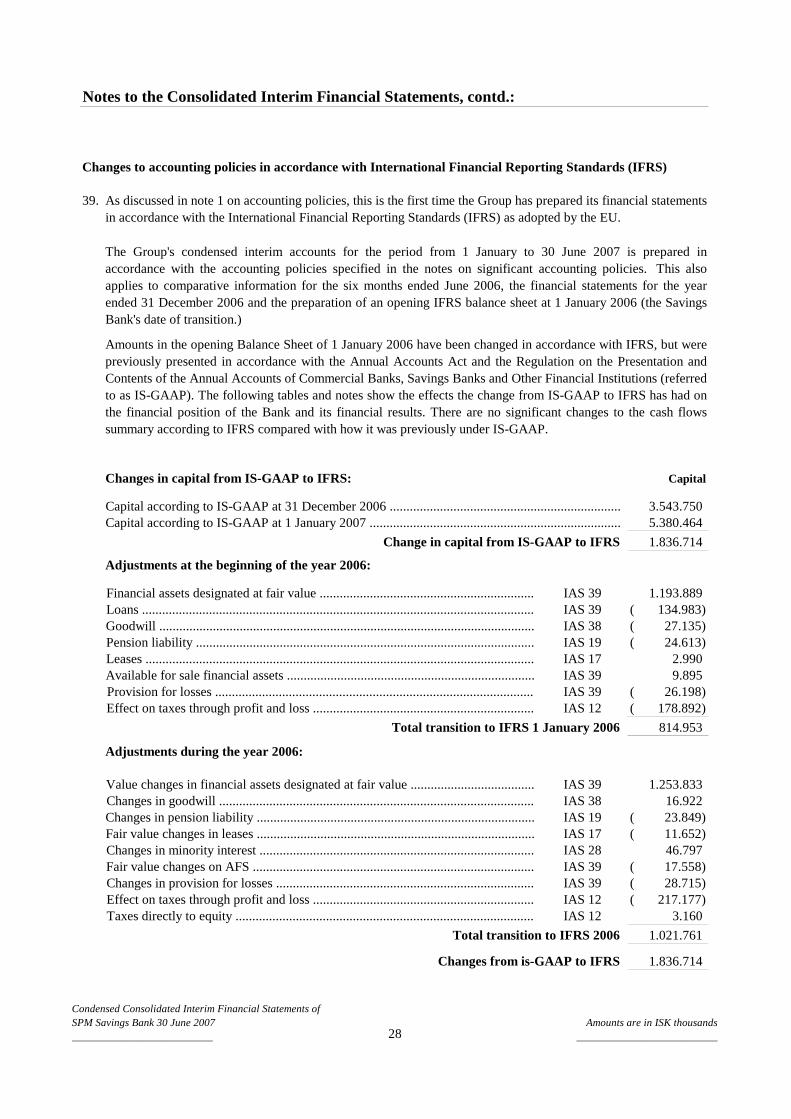

Changes to accounting policies in accordance with International Financial Reporting Standards (IFRS)

39.

Changes in capital from IS-GAAP to IFRS: Capital

3.543.750 5.380.464

1.836.714

Adjustments at the beginning of the year 2006:

IAS 39 1.193.889 IAS 39 134.983)( IAS 38 27.135)( IAS 19 24.613)( IAS 17 2.990 IAS 39 9.895 IAS 39 26.198)( IAS 12 178.892)(

814.953

Adjustments during the year 2006:

IAS 39 1.253.833 IAS 38 16.922 IAS 19 23.849)( IAS 17 11.652)( IAS 28 46.797 IAS 39 17.558)( IAS 39 28.715)( IAS 12 217.177)( IAS 12 3.160

1.021.761

1.836.714

Total transition to IFRS 2006

Changes from is-GAAP to IFRS

Financial assets designated at fair value ................................................................Loans .....................................................................................................................

Provision for losses ...............................................................................................Effect on taxes through profit and loss ..................................................................

Goodwill ................................................................................................................Pension liability .....................................................................................................Leases ....................................................................................................................Available for sale financial assets ..........................................................................

Changes in goodwill ..............................................................................................Changes in pension liability ...................................................................................Fair value changes in leases ...................................................................................

Notes to the Consolidated Interim Financial Statements, contd.:

Changes in minority interest ..................................................................................

Value changes in financial assets designated at fair value .....................................

Change in capital from IS-GAAP to IFRS

As discussed in note 1 on accounting policies, this is the first time the Group has prepared its financial statementsin accordance with the International Financial Reporting Standards (IFRS) as adopted by the EU.

The Group's condensed interim accounts for the period from 1January to 30 June 2007 is prepared inaccordance with the accounting policies specified in the notes on significant accounting policies. This alsoapplies to comparative information for the six months endedJune 2006, the financial statements for the yearended 31 December 2006 and the preparation of an opening IFRSbalance sheet at 1 January 2006 (the SavingsBank's date of transition.)

Amounts in the opening Balance Sheet of 1 January 2006 have been changed in accordance with IFRS, but werepreviously presented in accordance with the Annual Accounts Act and the Regulation on the Presentation andContents of the Annual Accounts of Commercial Banks, Savings Banks and Other Financial Institutions (referredto as IS-GAAP). The following tables and notes show the effects the change from IS-GAAP to IFRS has had onthe financial position of the Bank and its financial results. There are no significant changes to the cash flowssummary according to IFRS compared with how it was previously under IS-GAAP.

Capital according to IS-GAAP at 1 January 2007 ...........................................................................Capital according to IS-GAAP at 31 December 2006 .....................................................................

Total transition to IFRS 1 January 2006

Fair value changes on AFS ....................................................................................Changes in provision for losses .............................................................................Effect on taxes through profit and loss ..................................................................Taxes directly to equity .........................................................................................

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 28

Amounts are in ISK thousands__________________________

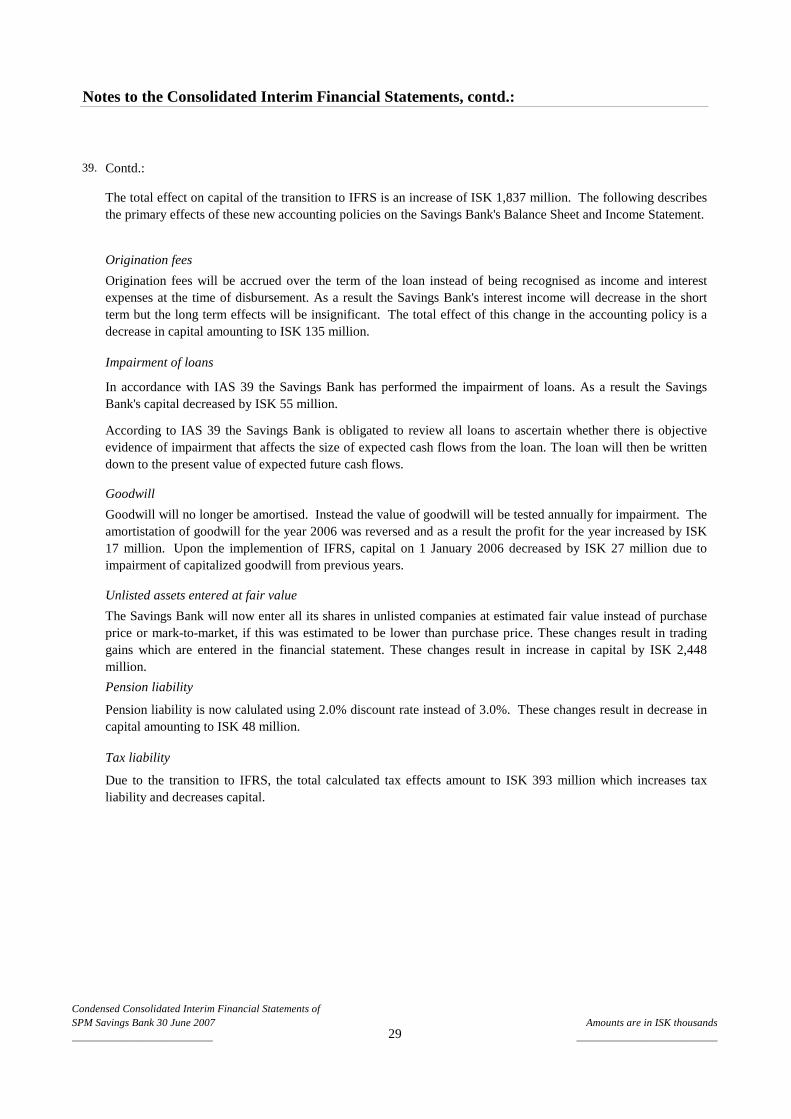

39. Contd.:

Origination fees

Impairment of loans

Goodwill

Unlisted assets entered at fair value

Pension liability

Tax liability

Due to the transition to IFRS, the total calculated tax effects amount to ISK 393 million which increases taxliability and decreases capital.

Origination fees will be accrued over the term of the loan instead of being recognised as income and interestexpenses at the time of disbursement. As a result the SavingsBank's interest income will decrease in the shortterm but the long term effects will be insignificant. The total effect of this change in the accounting policy is adecrease in capital amounting to ISK 135 million.

In accordance with IAS 39 the Savings Bank has performed the impairment of loans. As a result the SavingsBank's capital decreased by ISK 55 million.

Pension liability is now calulated using 2.0% discount rateinstead of 3.0%. These changes result in decrease incapital amounting to ISK 48 million.

Goodwill will no longer be amortised. Instead the value of goodwill will be tested annually for impairment. Theamortistation of goodwill for the year 2006 was reversed andas a result the profit for the year increased by ISK17 million. Upon the implemention of IFRS, capital on 1 January 2006 decreased by ISK 27 million due toimpairment of capitalized goodwill from previous years.

The Savings Bank will now enter all its shares in unlisted companies at estimated fair value instead of purchaseprice or mark-to-market, if this was estimated to be lower than purchase price. These changes result in tradinggains which are entered in the financial statement. These changes result in increase in capital by ISK 2,448million.

The total effect on capital of the transition to IFRS is an increase of ISK 1,837 million. The following describesthe primary effects of these new accounting policies on the Savings Bank's Balance Sheet and Income Statement.

According to IAS 39 the Savings Bank is obligated to review all loans to ascertain whether there is objectiveevidence of impairment that affects the size of expected cash flows from the loan. The loan will then be writtendown to the present value of expected future cash flows.

Notes to the Consolidated Interim Financial Statements, contd.:

Condensed Consolidated Interim Financial Statements ofSPM Savings Bank 30 June 2007__________________________ 29

Amounts are in ISK thousands__________________________

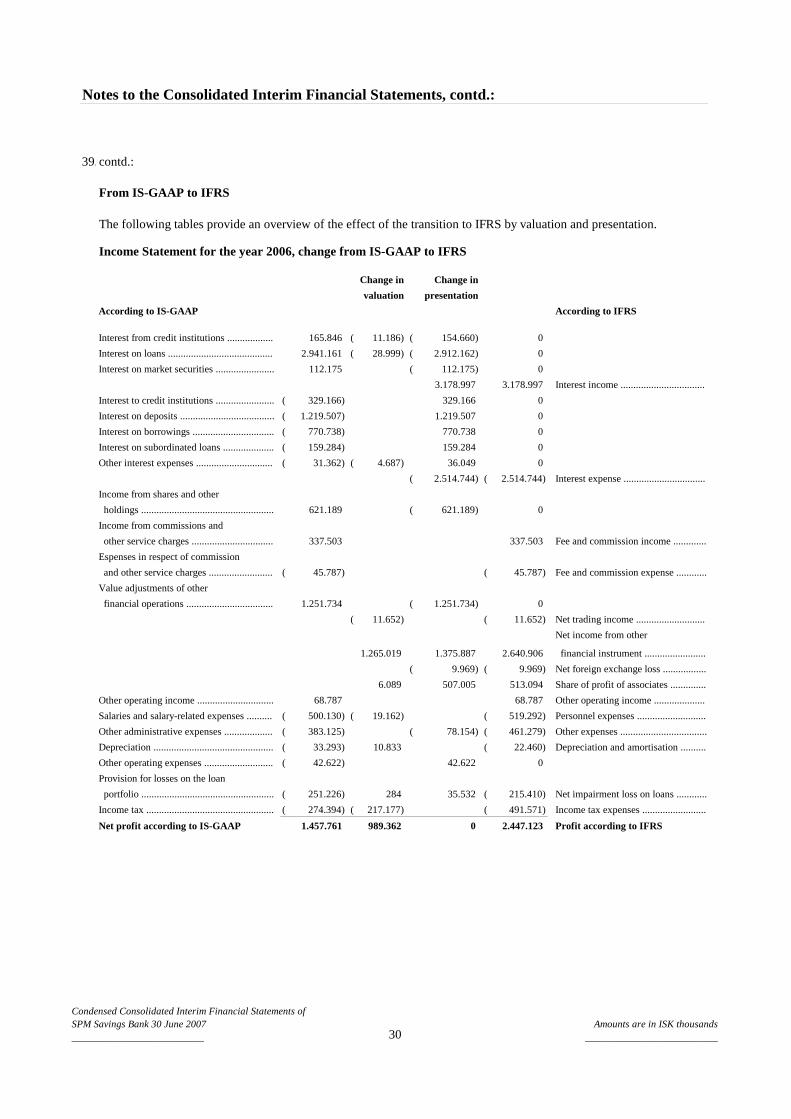

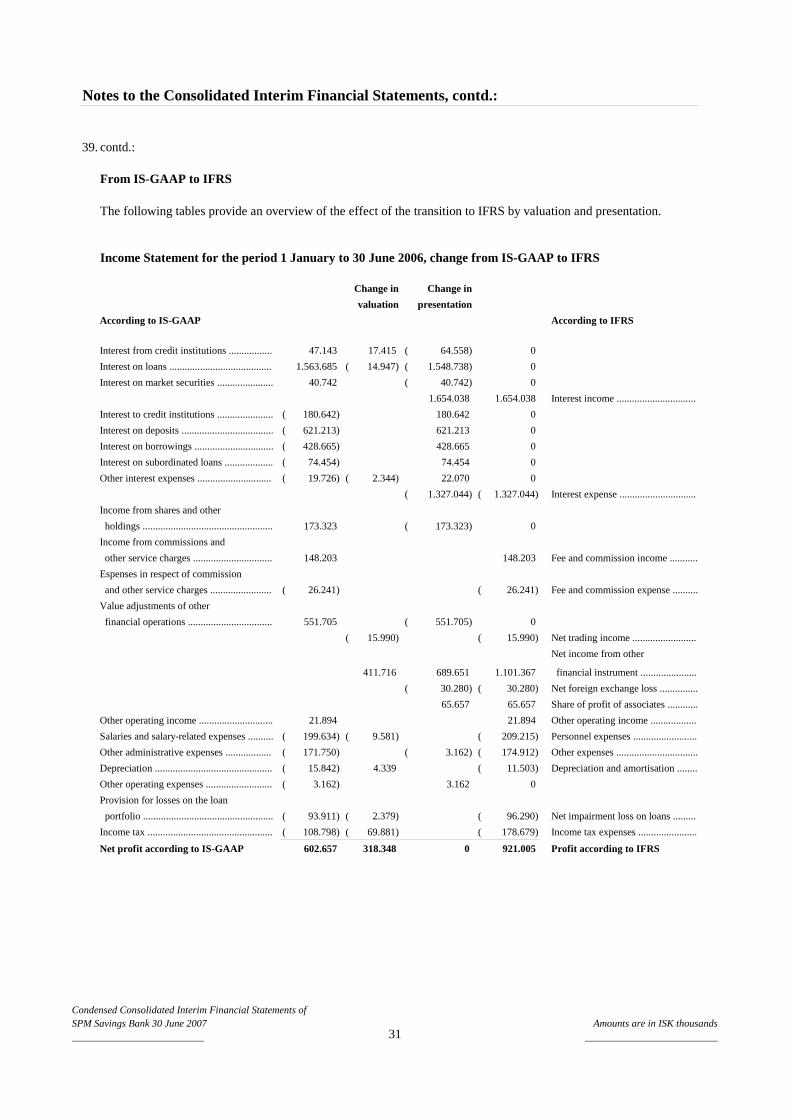

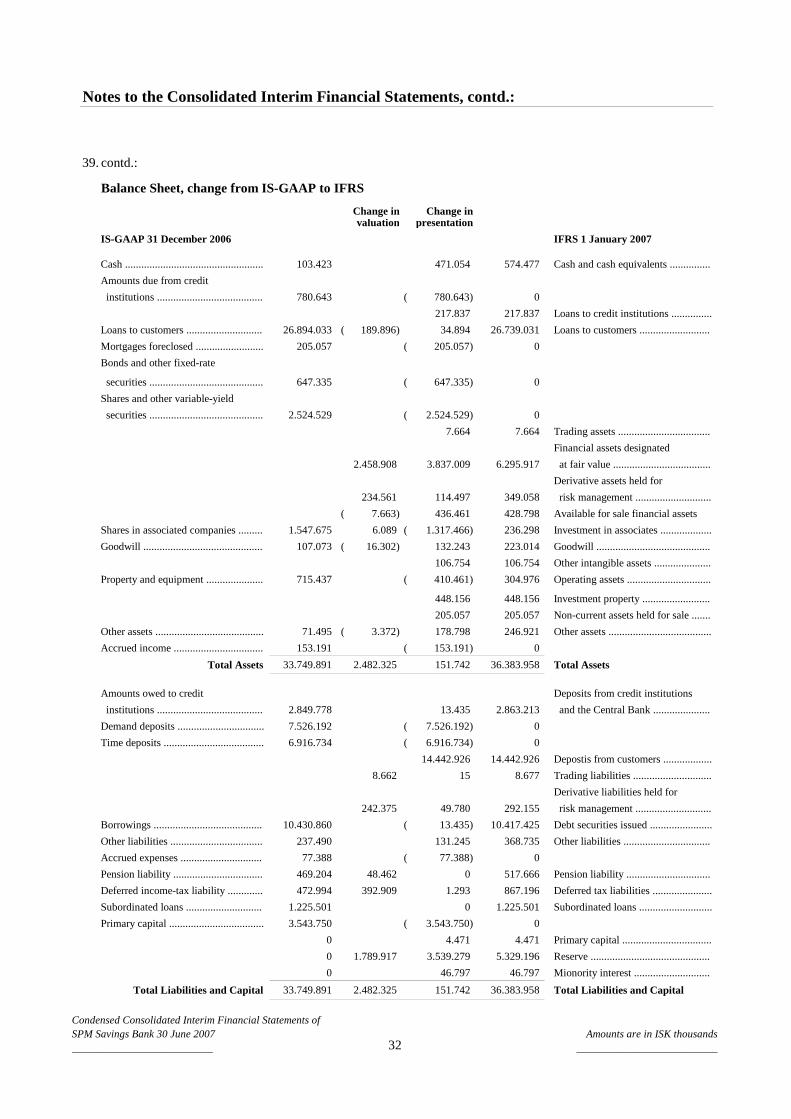

39.

From IS-GAAP to IFRS

Income Statement for the year 2006, change from IS-GAAP to IFRS

Change in Change in

valuation presentation

According to IS-GAAP According to IFRS

Interest from credit institutions .................. 165.846 11.186)( 154.660)( 0

Interest on loans ......................................... 2.941.161 28.999)( 2.912.162)( 0

Interest on market securities ....................... 112.175 112.175)( 0

3.178.997 3.178.997 Interest income .................................

Interest to credit institutions ....................... 329.166)( 329.166 0

Interest on deposits ..................................... 1.219.507)( 1.219.507 0

Interest on borrowings ................................ 770.738)( 770.738 0

Interest on subordinated loans .................... 159.284)( 159.284 0

Other interest expenses .............................. 31.362)( 4.687)( 36.049 0

2.514.744)( 2.514.744)( Interest expense ................................

Income from shares and other

holdings .................................................... 621.189 621.189)( 0

Income from commissions and

other service charges ................................ 337.503 337.503 Fee and commission income .............

Espenses in respect of commission

and other service charges ......................... 45.787)( 45.787)( Fee and commission expense ............

Value adjustments of other

financial operations .................................. 1.251.734 1.251.734)( 0

11.652)( 11.652)( Net trading income ...........................

Net income from other

1.265.019 1.375.887 2.640.906 financial instrument ........................

9.969)( 9.969)( Net foreign exchange loss .................

6.089 507.005 513.094 Share of profit of associates ..............