Embed Size (px)

Citation preview

www.bursamids.com

MIDF RESEARCH is a unit of MIDF AMANAH INVESTMENT BANK

Kindly refer to the last page of this publication for important disclosures

02 June 2017 | Initiation

Spritzer Berhad Buy

A Thirst for Growth Target Price (TP): RM2.83

INVESTMENT HIGHLIGHTS

• Market leader with over 40% market share in Malaysia

• Increase production by 20% in next three years

• Undisrupted profit growth for the past 5 years

• Initiate with Buy and TP of RM2.83

Business Overview:

Spritzer is a market leader in bottled drinking and mineral water with an

annual production capacity of 650 million litres from 15 production lines

in three of its plants in Taiping, Shah Alam and Yong Peng. Brands sold

by the company include Spritzer, Cactus, Summer, Tinge and Pop.

Investment Theses:

1. Strong brand with over 40% market share in Malaysia.

Spritzer is a household name in Malaysia with a market share of

over 40% for bottled water and over 50% for mineral water. The

mineral water to drinking water ratio it produces is 70:30. The

company has won 69 awards in the past 27 years.

2. Increase production by 15-20% in next three years. The

company could further increase its production capacity by another

15% in the next two to three years through enhancements on its

water production lines. Moreover, management plans to build a

new fully automated warehouse in its Taiping plant to meet the

increase in sales and production.

3. Undisrupted profit growth for the past 5 years. Thanks to its

dominant market position, Spritzer has been charting undisrupted

growth in the last five years. Its 2012 to 2016 net profit CAGR was

30%. We expect the company to continue its upward climb in FY18

as it solidifies its existing market share while it expands into new

markets.

Valuation:

Initiate with BUY recommendation and target price of RM2.83

based on 17x FY18F EPS of 16.6 sen. The PER of 17x is a 35% discount

to the average PER of other beverage companies listed on Bursa such

as Fraser and Neaves, Dutch Lady and Nestle. The discount ascribed is

due to Spritzer’s smaller market cap. We like Spritzer for its i) resilient

earnings due to its defensive business model, ii) strong position as

market leader in Malaysia’s bottled water industry and iii) strong

balance sheet with net cash position as of end-FY16.

RETURN STATS

Price (1 June 2017) RM2.44

Fair Value RM2.83

Expected Share Price

Return +16.0%

Expected Dividend Yield +2.3%

Expected Total

Return +18.3%

STOCK INFO

KLCI 1,763.11

Bursa / Bloomberg 7103 SPZ MK

Board / Sector Main / Consumer

Syariah Compliant Yes

Issued shares (m) 182.58

Market cap. (RM’m) 445.50

Price over NA 1.52

52-wk price Range RM2.19-RM2.60

Beta (against KLCI) 0.63

3-mth Avg Daily Vol 0.21m

3-mth Avg Daily Value RM0.49m

Major Shareholders (%)

Yee Lee Corporation 31.96

Yee Lee Holdings S/B 12.49

Dato’ Lim Kok Boon 6.81

Price Performance (%) Absolute Relative

1 month 2.1 3.0

3 months 6.1 3.7

12 months -4.3 -11.5

MIDF RESEARCH Friday, 02 June 2017

2

INVESTMENT STATISTICS

FYE Dec FY14* FY15* FY16** FY17F FY18F

Revenue (RM’m) 238.75 253.67 185.94 308.02 335.30

Pretax Profit (RM’m) 28.31 31.96 18.27 29.82 40.01

Net Profit (RM’m) 21.57 22.81 12.51 22.66 30.41

EPS (sen) 11.81 12.49 6.85 12.41 16.65

EPS growth (%) 12.13 5.75 N/A N/A 34.18

PER (x) 19.53 15.66 N/A 19.66 14.65

Net Dividend (sen) 4.0 5.0 3.5 4.7 5.5

Dividend yield (%) 1.64 2.05 1.43 1.93 2.25

Gearing (x) 0.34 0.18 0.07 0.09 0.09

ROE (%) 11.48 10.58 4.34 7.50 9.42

ROA (%) 7.01 7.32 3.40 6.00 7.58

NTA per share (RM) 1.03 1.18 1.58 1.66 1.77

Price to NTA (x) 2.36 2.06 1.54 1.47 1.38

Source: Company, MIDF Research *FYE May **May to Dec 2016, seven months only due to change in financial year end

Source: Bloomberg

DAILY PRICE CHART

Ng Bei Shan

[email protected] 03-2173 8461

MIDF RESEARCH Friday, 02 June 2017

3

A. KEY INVESTMENT THESES

One of the local pioneers in the bottled water industry. Spitzer’s drinking water production business was set up in

1989, held under the private company owned by the Lim family. The family eventually listed the mineral water and

packaging business as Spritzer Bhd in 2000. Spritzer owns two mineral water plants in Taiping, Perak and Yong Peng,

Johor and one distilled water plant at Shah Alam, Selangor. The three plants are strategically located as the Taiping

plant can serve both the northern, west coast and central regions. The drinking water plant in Shah Alam can serve the

central region, which is the most populous zone, while the Yong Peng plant serves the southern and Singapore markets.

These locations are crucial to the distribution of Spritzer’s products as logistics costs are significant for bottled water as

they are bulky and heavy. The Taiping plant, which sits on a 330-acre parcel, is home to its flagship brand Spritzer. It

has nine production lines in Taiping, three in Shah Alam and three in Yong Peng, Johor. The utilisation rate for all 15

production lines ranges from 70% to 75% with a capacity of 650 million litres per year. The three plants help to mitigate

operational risks compared to companies operating from a single plant.

Exhibit 1: Spritzer’s flagship mineral water brand contributes over one-third to its sales

Source: Company

Market leader with over 40% market share in Malaysia. Spritzer is a household name in Malaysia with a market

share of over 40% for bottled water and over 50% for mineral water. Brands under its wing includes Spritzer, Cactus,

Summer, Tinge and Pop. It has been a dominant player since establishment as it enters the bottled water market almost

three decades ago. In the past two to three years, its market share expanded to 40%. The mineral water to drinking

water ratio it produces is 70:30. The company has won 69 awards in the past 27 years, inferring that its products are

well received and recognised. Management aims to increase its market share through more advertising and promotional

campaigns. There are two variants of bottled water: mineral water, which is water sourced from underground and

drinking water, which is from treated water provided by Syabas.

Strong brand equity in Spritzer. Its flagship brand which is packaged in the recognisable light green, has been the

number one mineral water in Malaysia, according to market studies by AC Nielsen. The Spritzer range of products

contributes over a-third to the group’s overall sales. Spritzer commands a higher margin compared to its other brands as

it is marketed as a more premium product as it is generally priced 8% to 30% higher than its branded competitors. It is

also able to garner volume because it is much more affordable than imported premium brands like Volvic and Evian

because retail prices for Spritzer are about 40% to 60% cheaper. The brand is built through tireless marketing activities

that enhance its brand equity over time. Among some of the strategies adopted include the buying of shelve in

prominent locations. It is also a sponsor for the upcoming SEA Games, which could improve its branding and increase its

exposure to the regional audience.

MIDF RESEARCH Friday, 02 June 2017

4

Market share expansion to drive growth. Spritzer commands over 40% of the bottled water market share locally.

Growth opportunities will come from market share expansion as well as increasing its exports. In Malaysia, it targets to

penetrate mamaks and coffee shops through distributors specialising in the segment. Overseas sales account for about

7% of its overall revenue. It exports to Singapore, Hong Kong, Taiwan, Papua New Guinea, Brunei and China. Singapore

is a market where it can tighten its grip while it continues its advertising and promotional efforts in China.

Increase production by 15% to 20% by 2020. The company could further increase its production capacity by

another 20% in the next two to three years through enhancements on its water production lines. There is room for the

company to add two or more production lines in the next three years once its utilisation rate exceeds 75%. Moreover,

management plans to build a new fully automated warehouse in its Taiping plant to meet the increase in sales and

production. We believe that the new warehouse could help to boost its production efficiency due to the easing of the

current bottleneck at its current warehouse in Taiping. We estimate that the new automated warehouse may cost up to

RM50m depending on the layout and machinery specifications. The construction of the new facility will take up to three

years and the investment will be expensed over the period with construction cost funded through internally-generated

funds and some debt. We do not expect the construction of the warehouse to affect its financial position as it is in a net

cash position as of end-2016 while operating cash flow is expected to be robust at RM25m in FY17.

Integrated facilities offer cost advantage. Spritzer is able to maintain reasonable profit margins because of its

integrated facilities that include its in-house manufacturing of packaging products. We understand that packaging makes

up about 70% of its costs of goods sold. Its Taiping plant houses three preform production lines which allow it to

manage it packaging cost better.

Exhibit 2: A bird’s eye view on Spritzer’s plant in Taiping

Source: Company

Backed by an established distributor. As a 32.5%-owned associate of Bursa-listed Yee Lee Corp Bhd, Spritzer is

able to tap into its parents’ wide network of distribution for growth. The symbiotic relationship reduces the risks of

potential contractual disagreements compared to that with other third party distributors. Yee Lee was established in

1968 and has a sales network of 18 branches and distribution facilities throughout Malaysia. Yee Lee has a turnover of

RM1.06b in FY16 and a market cap of RM474m.

MIDF RESEARCH Friday, 02 June 2017

5

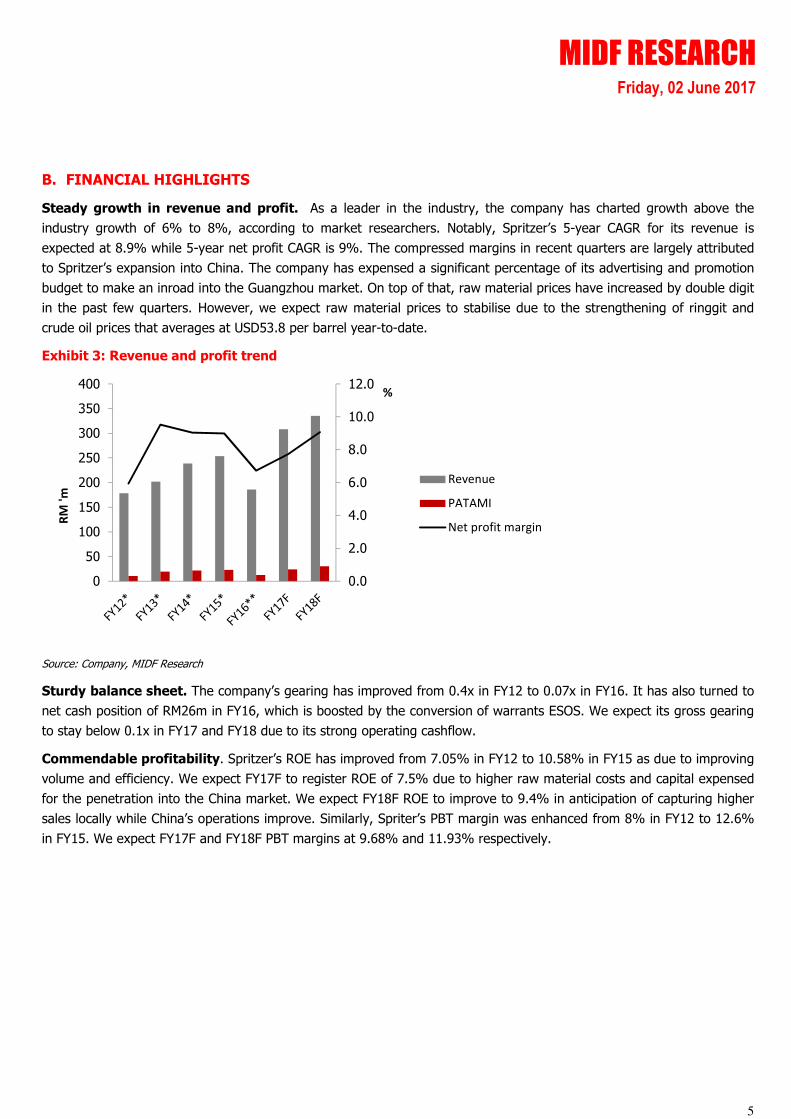

B. FINANCIAL HIGHLIGHTS

Steady growth in revenue and profit. As a leader in the industry, the company has charted growth above the

industry growth of 6% to 8%, according to market researchers. Notably, Spritzer’s 5-year CAGR for its revenue is

expected at 8.9% while 5-year net profit CAGR is 9%. The compressed margins in recent quarters are largely attributed

to Spritzer’s expansion into China. The company has expensed a significant percentage of its advertising and promotion

budget to make an inroad into the Guangzhou market. On top of that, raw material prices have increased by double digit

in the past few quarters. However, we expect raw material prices to stabilise due to the strengthening of ringgit and

crude oil prices that averages at USD53.8 per barrel year-to-date.

Exhibit 3: Revenue and profit trend

Source:

Source: Company, MIDF Research

Sturdy balance sheet. The company’s gearing has improved from 0.4x in FY12 to 0.07x in FY16. It has also turned to

net cash position of RM26m in FY16, which is boosted by the conversion of warrants ESOS. We expect its gross gearing

to stay below 0.1x in FY17 and FY18 due to its strong operating cashflow.

Commendable profitability. Spritzer’s ROE has improved from 7.05% in FY12 to 10.58% in FY15 as due to improving

volume and efficiency. We expect FY17F to register ROE of 7.5% due to higher raw material costs and capital expensed

for the penetration into the China market. We expect FY18F ROE to improve to 9.4% in anticipation of capturing higher

sales locally while China’s operations improve. Similarly, Spriter’s PBT margin was enhanced from 8% in FY12 to 12.6%

in FY15. We expect FY17F and FY18F PBT margins at 9.68% and 11.93% respectively.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0

50

100

150

200

250

300

350

400%

RM

'm

Revenue

PATAMI

Net profit margin

MIDF RESEARCH Friday, 02 June 2017

6

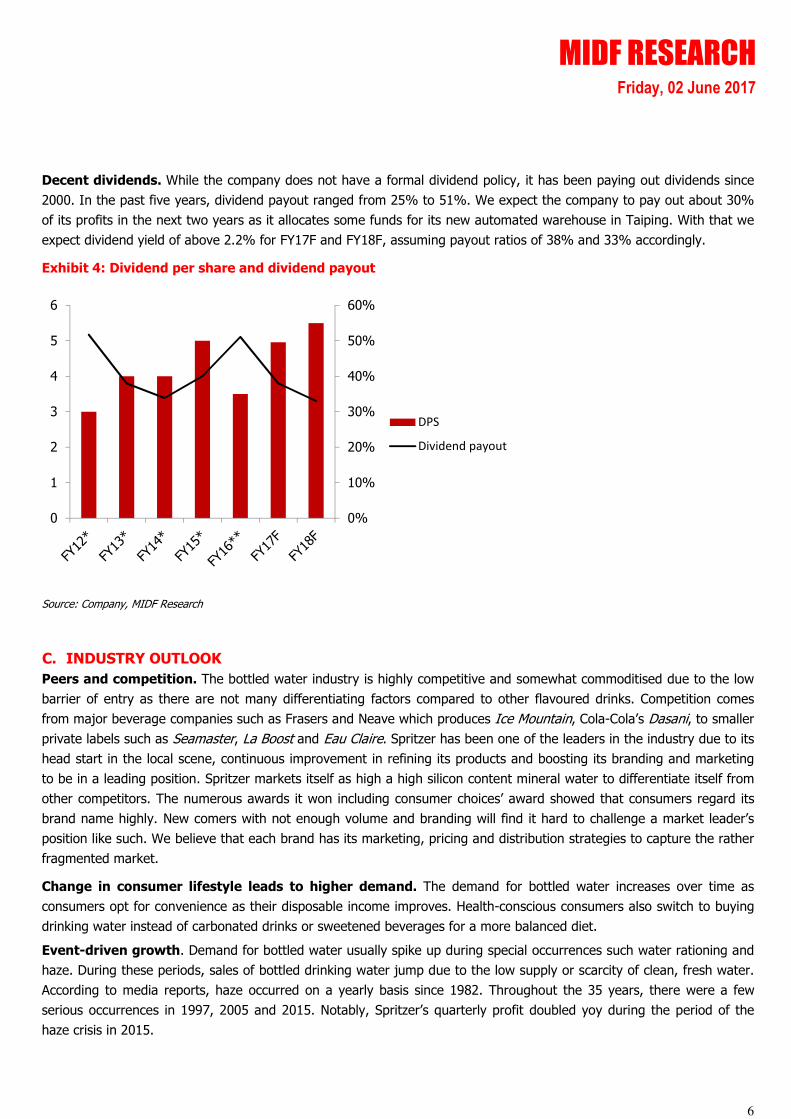

Decent dividends. While the company does not have a formal dividend policy, it has been paying out dividends since

2000. In the past five years, dividend payout ranged from 25% to 51%. We expect the company to pay out about 30%

of its profits in the next two years as it allocates some funds for its new automated warehouse in Taiping. With that we

expect dividend yield of above 2.2% for FY17F and FY18F, assuming payout ratios of 38% and 33% accordingly.

Exhibit 4: Dividend per share and dividend payout

Source: Company, MIDF Research

C. INDUSTRY OUTLOOK

Peers and competition. The bottled water industry is highly competitive and somewhat commoditised due to the low

barrier of entry as there are not many differentiating factors compared to other flavoured drinks. Competition comes

from major beverage companies such as Frasers and Neave which produces Ice Mountain, Cola-Cola’s Dasani, to smaller

private labels such as Seamaster, La Boost and Eau Claire. Spritzer has been one of the leaders in the industry due to its

head start in the local scene, continuous improvement in refining its products and boosting its branding and marketing

to be in a leading position. Spritzer markets itself as high a high silicon content mineral water to differentiate itself from

other competitors. The numerous awards it won including consumer choices’ award showed that consumers regard its

brand name highly. New comers with not enough volume and branding will find it hard to challenge a market leader’s

position like such. We believe that each brand has its marketing, pricing and distribution strategies to capture the rather

fragmented market.

Change in consumer lifestyle leads to higher demand. The demand for bottled water increases over time as

consumers opt for convenience as their disposable income improves. Health-conscious consumers also switch to buying

drinking water instead of carbonated drinks or sweetened beverages for a more balanced diet.

Event-driven growth. Demand for bottled water usually spike up during special occurrences such water rationing and

haze. During these periods, sales of bottled drinking water jump due to the low supply or scarcity of clean, fresh water.

According to media reports, haze occurred on a yearly basis since 1982. Throughout the 35 years, there were a few

serious occurrences in 1997, 2005 and 2015. Notably, Spritzer’s quarterly profit doubled yoy during the period of the

haze crisis in 2015.

0%

10%

20%

30%

40%

50%

60%

0

1

2

3

4

5

6

DPS

Dividend payout

MIDF RESEARCH Friday, 02 June 2017

7

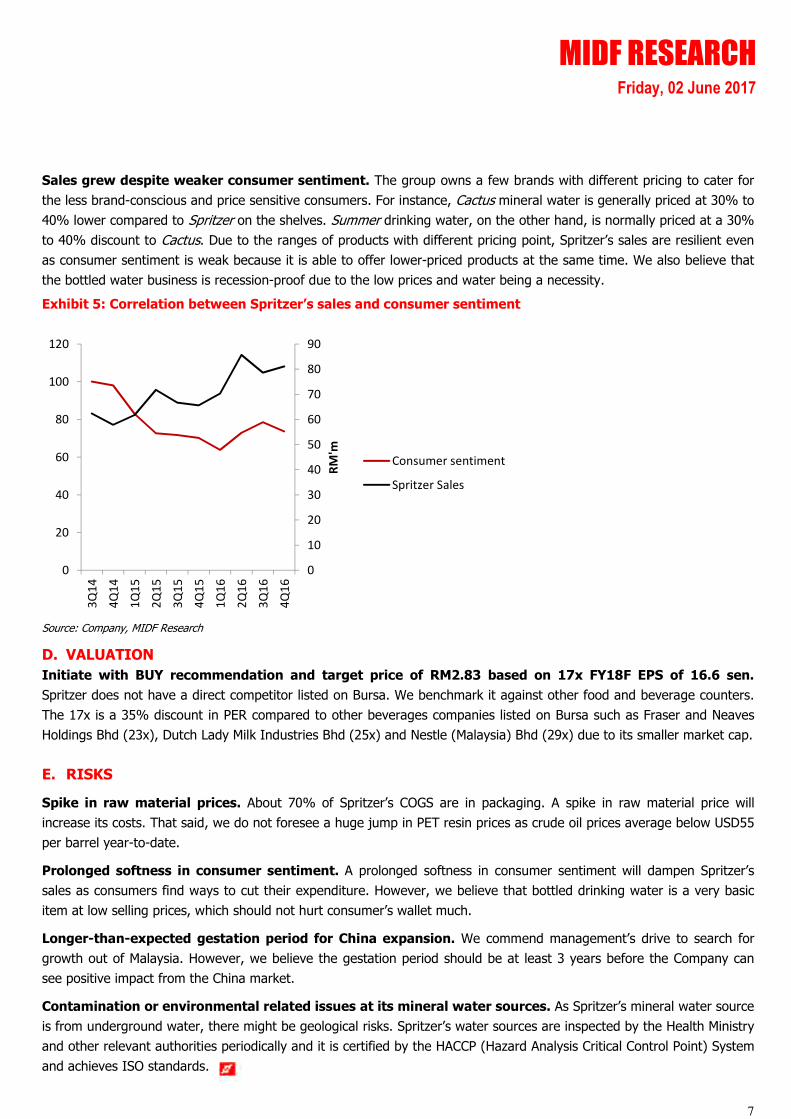

Sales grew despite weaker consumer sentiment. The group owns a few brands with different pricing to cater for

the less brand-conscious and price sensitive consumers. For instance, Cactus mineral water is generally priced at 30% to

40% lower compared to Spritzer on the shelves. Summer drinking water, on the other hand, is normally priced at a 30%

to 40% discount to Cactus. Due to the ranges of products with different pricing point, Spritzer’s sales are resilient even

as consumer sentiment is weak because it is able to offer lower-priced products at the same time. We also believe that

the bottled water business is recession-proof due to the low prices and water being a necessity.

Exhibit 5: Correlation between Spritzer’s sales and consumer sentiment

Source: Company, MIDF Research

D. VALUATION

Initiate with BUY recommendation and target price of RM2.83 based on 17x FY18F EPS of 16.6 sen.

Spritzer does not have a direct competitor listed on Bursa. We benchmark it against other food and beverage counters.

The 17x is a 35% discount in PER compared to other beverages companies listed on Bursa such as Fraser and Neaves

Holdings Bhd (23x), Dutch Lady Milk Industries Bhd (25x) and Nestle (Malaysia) Bhd (29x) due to its smaller market cap.

E. RISKS

Spike in raw material prices. About 70% of Spritzer’s COGS are in packaging. A spike in raw material price will

increase its costs. That said, we do not foresee a huge jump in PET resin prices as crude oil prices average below USD55

per barrel year-to-date.

Prolonged softness in consumer sentiment. A prolonged softness in consumer sentiment will dampen Spritzer’s

sales as consumers find ways to cut their expenditure. However, we believe that bottled drinking water is a very basic

item at low selling prices, which should not hurt consumer’s wallet much.

Longer-than-expected gestation period for China expansion. We commend management’s drive to search for

growth out of Malaysia. However, we believe the gestation period should be at least 3 years before the Company can

see positive impact from the China market.

Contamination or environmental related issues at its mineral water sources. As Spritzer’s mineral water source

is from underground water, there might be geological risks. Spritzer’s water sources are inspected by the Health Ministry

and other relevant authorities periodically and it is certified by the HACCP (Hazard Analysis Critical Control Point) System

and achieves ISO standards.

0

10

20

30

40

50

60

70

80

90

0

20

40

60

80

100

120

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

RM

'm

Consumer sentiment

Spritzer Sales

MIDF RESEARCH Friday, 02 June 2017

8

Source: Company, MIDF Research

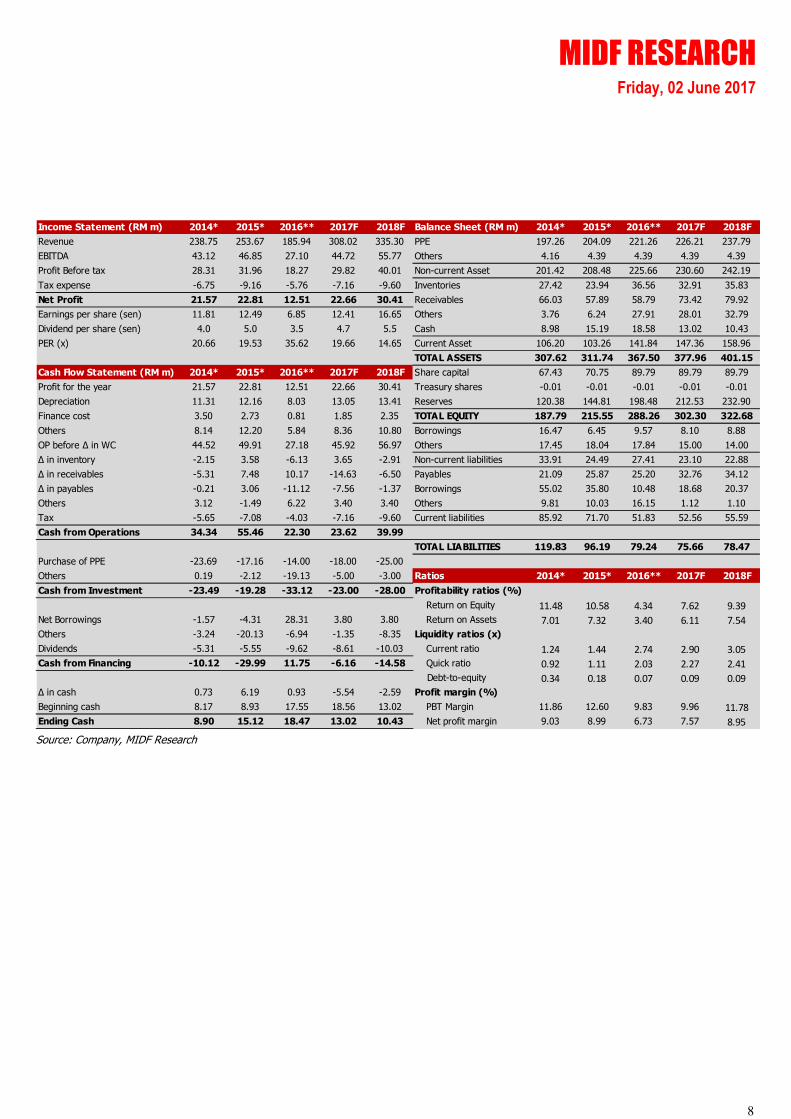

Income Statement (RM m) 2014* 2015* 2016** 2017F 2018F Balance Sheet (RM m) 2014* 2015* 2016** 2017F 2018F

Revenue 238.75 253.67 185.94 308.02 335.30 PPE 197.26 204.09 221.26 226.21 237.79

EBITDA 43.12 46.85 27.10 44.72 55.77 Others 4.16 4.39 4.39 4.39 4.39

Profit Before tax 28.31 31.96 18.27 29.82 40.01 Non-current Asset 201.42 208.48 225.66 230.60 242.19

Tax expense -6.75 -9.16 -5.76 -7.16 -9.60 Inventories 27.42 23.94 36.56 32.91 35.83

Net Profit 21.57 22.81 12.51 22.66 30.41 Receivables 66.03 57.89 58.79 73.42 79.92

Earnings per share (sen) 11.81 12.49 6.85 12.41 16.65 Others 3.76 6.24 27.91 28.01 32.79

Dividend per share (sen) 4.0 5.0 3.5 4.7 5.5 Cash 8.98 15.19 18.58 13.02 10.43

PER (x) 20.66 19.53 35.62 19.66 14.65 Current Asset 106.20 103.26 141.84 147.36 158.96

TOTAL ASSETS 307.62 311.74 367.50 377.96 401.15

Cash Flow Statement (RM m) 2014* 2015* 2016** 2017F 2018F Share capital 67.43 70.75 89.79 89.79 89.79

Profit for the year 21.57 22.81 12.51 22.66 30.41 Treasury shares -0.01 -0.01 -0.01 -0.01 -0.01

Depreciation 11.31 12.16 8.03 13.05 13.41 Reserves 120.38 144.81 198.48 212.53 232.90

Finance cost 3.50 2.73 0.81 1.85 2.35 TOTAL EQUITY 187.79 215.55 288.26 302.30 322.68

Others 8.14 12.20 5.84 8.36 10.80 Borrowings 16.47 6.45 9.57 8.10 8.88

OP before ∆ in WC 44.52 49.91 27.18 45.92 56.97 Others 17.45 18.04 17.84 15.00 14.00

∆ in inventory -2.15 3.58 -6.13 3.65 -2.91 Non-current liabilities 33.91 24.49 27.41 23.10 22.88

∆ in receivables -5.31 7.48 10.17 -14.63 -6.50 Payables 21.09 25.87 25.20 32.76 34.12

∆ in payables -0.21 3.06 -11.12 -7.56 -1.37 Borrowings 55.02 35.80 10.48 18.68 20.37

Others 3.12 -1.49 6.22 3.40 3.40 Others 9.81 10.03 16.15 1.12 1.10

Tax -5.65 -7.08 -4.03 -7.16 -9.60 Current liabilities 85.92 71.70 51.83 52.56 55.59

Cash from Operations 34.34 55.46 22.30 23.62 39.99

TOTAL LIABILITIES 119.83 96.19 79.24 75.66 78.47

Purchase of PPE -23.69 -17.16 -14.00 -18.00 -25.00

Others 0.19 -2.12 -19.13 -5.00 -3.00 Ratios 2014* 2015* 2016** 2017F 2018F

Cash from Investment -23.49 -19.28 -33.12 -23.00 -28.00 Profitability ratios (%)

Return on Equity 11.48 10.58 4.34 7.62 9.39

Net Borrowings -1.57 -4.31 28.31 3.80 3.80 Return on Assets 7.01 7.32 3.40 6.11 7.54

Others -3.24 -20.13 -6.94 -1.35 -8.35 Liquidity ratios (x)

Dividends -5.31 -5.55 -9.62 -8.61 -10.03 Current ratio 1.24 1.44 2.74 2.90 3.05

Cash from Financing -10.12 -29.99 11.75 -6.16 -14.58 Quick ratio 0.92 1.11 2.03 2.27 2.41

Debt-to-equity 0.34 0.18 0.07 0.09 0.09

∆ in cash 0.73 6.19 0.93 -5.54 -2.59 Profit margin (%)

Beginning cash 8.17 8.93 17.55 18.56 13.02 PBT Margin 11.86 12.60 9.83 9.96 11.78

Ending Cash 8.90 15.12 18.47 13.02 10.43 Net profit margin 9.03 8.99 6.73 7.57 8.95

MIDF RESEARCH Friday, 02 June 2017

9

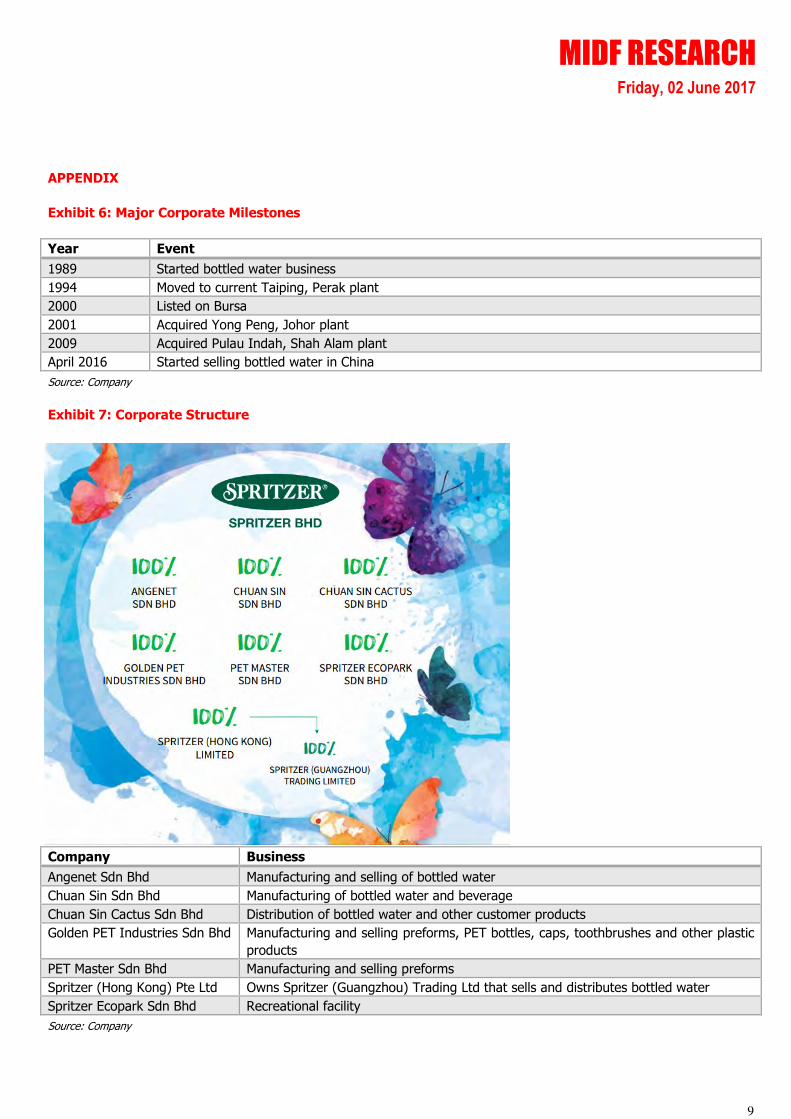

APPENDIX

Exhibit 6: Major Corporate Milestones

Year Event

1989 Started bottled water business

1994 Moved to current Taiping, Perak plant

2000 Listed on Bursa

2001 Acquired Yong Peng, Johor plant

2009 Acquired Pulau Indah, Shah Alam plant

April 2016 Started selling bottled water in China

Source: Company

Exhibit 7: Corporate Structure

Source: Company

Company Business

Angenet Sdn Bhd Manufacturing and selling of bottled water

Chuan Sin Sdn Bhd Manufacturing of bottled water and beverage

Chuan Sin Cactus Sdn Bhd Distribution of bottled water and other customer products

Golden PET Industries Sdn Bhd Manufacturing and selling preforms, PET bottles, caps, toothbrushes and other plastic

products

PET Master Sdn Bhd Manufacturing and selling preforms

Spritzer (Hong Kong) Pte Ltd Owns Spritzer (Guangzhou) Trading Ltd that sells and distributes bottled water

Spritzer Ecopark Sdn Bhd Recreational facility

MIDF RESEARCH Friday, 02 June 2017

10

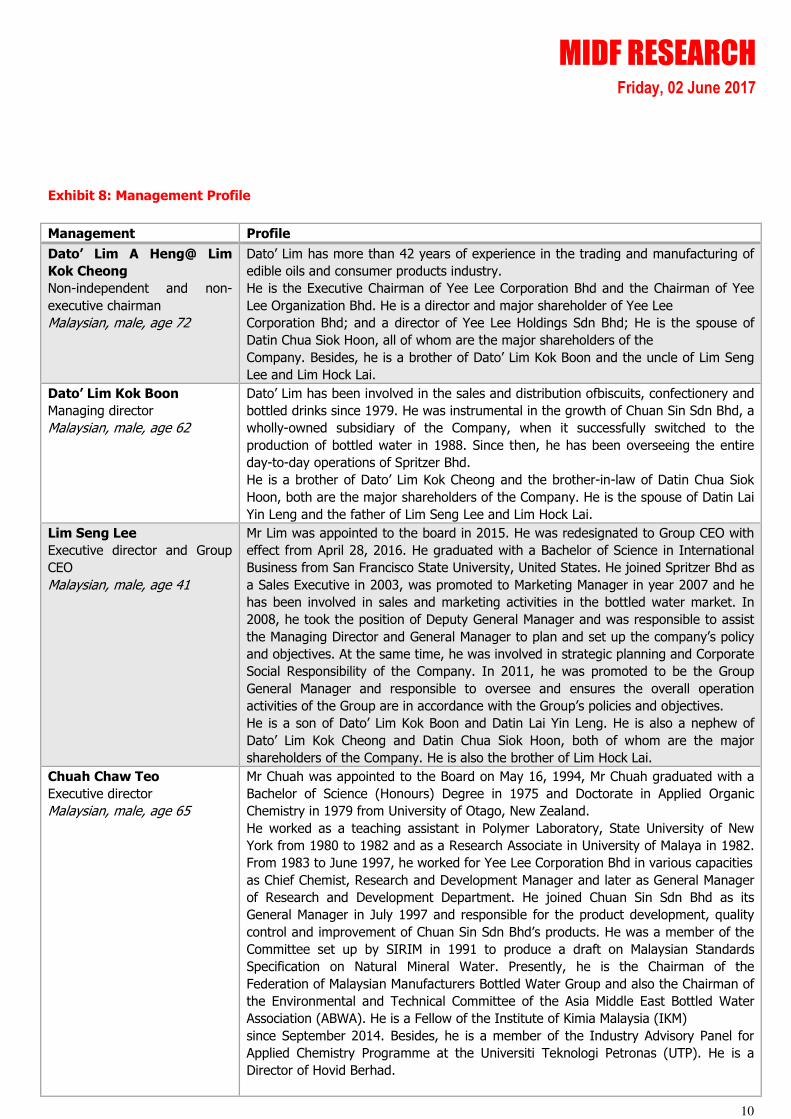

Exhibit 8: Management Profile

Management Profile

Dato’ Lim A Heng@ Lim

Kok Cheong

Non-independent and non-

executive chairman

Malaysian, male, age 72

Dato’ Lim has more than 42 years of experience in the trading and manufacturing of

edible oils and consumer products industry.

He is the Executive Chairman of Yee Lee Corporation Bhd and the Chairman of Yee

Lee Organization Bhd. He is a director and major shareholder of Yee Lee

Corporation Bhd; and a director of Yee Lee Holdings Sdn Bhd; He is the spouse of

Datin Chua Siok Hoon, all of whom are the major shareholders of the

Company. Besides, he is a brother of Dato’ Lim Kok Boon and the uncle of Lim Seng

Lee and Lim Hock Lai.

Dato’ Lim Kok Boon

Managing director

Malaysian, male, age 62

Dato’ Lim has been involved in the sales and distribution ofbiscuits, confectionery and

bottled drinks since 1979. He was instrumental in the growth of Chuan Sin Sdn Bhd, a

wholly-owned subsidiary of the Company, when it successfully switched to the

production of bottled water in 1988. Since then, he has been overseeing the entire

day-to-day operations of Spritzer Bhd.

He is a brother of Dato’ Lim Kok Cheong and the brother-in-law of Datin Chua Siok

Hoon, both are the major shareholders of the Company. He is the spouse of Datin Lai

Yin Leng and the father of Lim Seng Lee and Lim Hock Lai.

Lim Seng Lee

Executive director and Group

CEO

Malaysian, male, age 41

Mr Lim was appointed to the board in 2015. He was redesignated to Group CEO with

effect from April 28, 2016. He graduated with a Bachelor of Science in International

Business from San Francisco State University, United States. He joined Spritzer Bhd as

a Sales Executive in 2003, was promoted to Marketing Manager in year 2007 and he

has been involved in sales and marketing activities in the bottled water market. In

2008, he took the position of Deputy General Manager and was responsible to assist

the Managing Director and General Manager to plan and set up the company’s policy

and objectives. At the same time, he was involved in strategic planning and Corporate

Social Responsibility of the Company. In 2011, he was promoted to be the Group

General Manager and responsible to oversee and ensures the overall operation

activities of the Group are in accordance with the Group’s policies and objectives.

He is a son of Dato’ Lim Kok Boon and Datin Lai Yin Leng. He is also a nephew of

Dato’ Lim Kok Cheong and Datin Chua Siok Hoon, both of whom are the major

shareholders of the Company. He is also the brother of Lim Hock Lai.

Chuah Chaw Teo

Executive director

Malaysian, male, age 65

Mr Chuah was appointed to the Board on May 16, 1994, Mr Chuah graduated with a

Bachelor of Science (Honours) Degree in 1975 and Doctorate in Applied Organic

Chemistry in 1979 from University of Otago, New Zealand.

He worked as a teaching assistant in Polymer Laboratory, State University of New

York from 1980 to 1982 and as a Research Associate in University of Malaya in 1982.

From 1983 to June 1997, he worked for Yee Lee Corporation Bhd in various capacities

as Chief Chemist, Research and Development Manager and later as General Manager

of Research and Development Department. He joined Chuan Sin Sdn Bhd as its

General Manager in July 1997 and responsible for the product development, quality

control and improvement of Chuan Sin Sdn Bhd’s products. He was a member of the

Committee set up by SIRIM in 1991 to produce a draft on Malaysian Standards

Specification on Natural Mineral Water. Presently, he is the Chairman of the

Federation of Malaysian Manufacturers Bottled Water Group and also the Chairman of

the Environmental and Technical Committee of the Asia Middle East Bottled Water

Association (ABWA). He is a Fellow of the Institute of Kimia Malaysia (IKM)

since September 2014. Besides, he is a member of the Industry Advisory Panel for

Applied Chemistry Programme at the Universiti Teknologi Petronas (UTP). He is a

Director of Hovid Berhad.

MIDF RESEARCH Friday, 02 June 2017

11

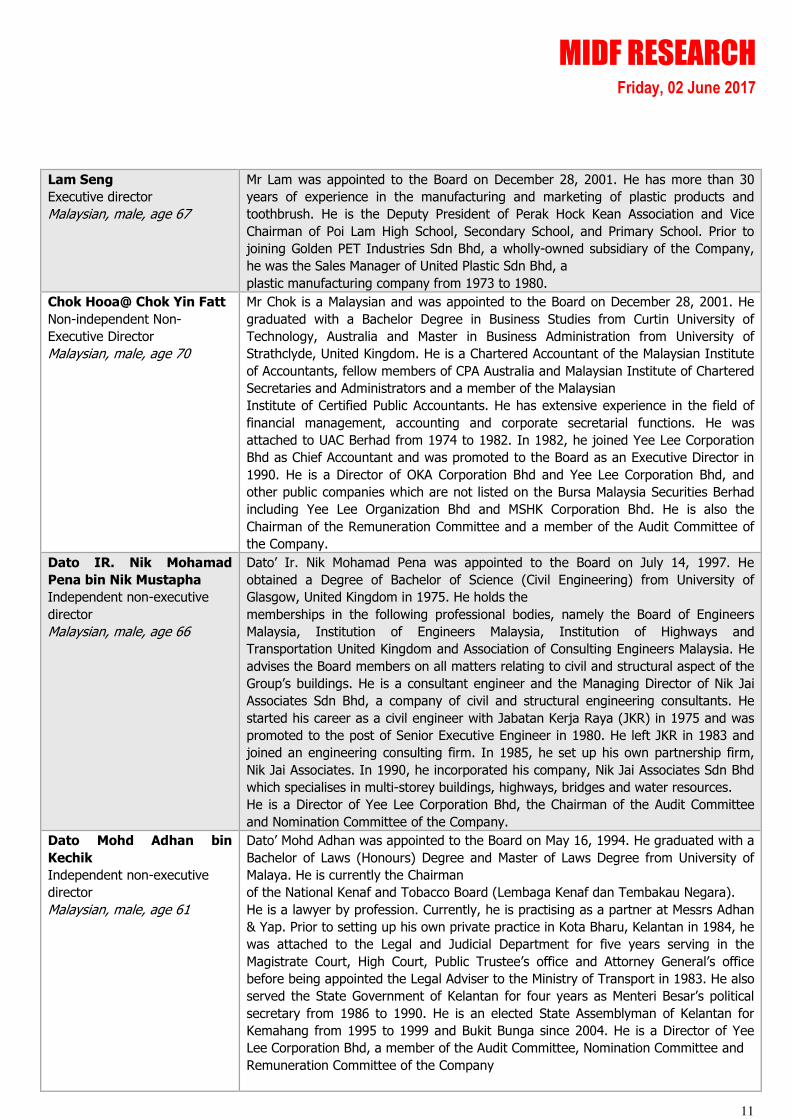

Lam Seng

Executive director

Malaysian, male, age 67

Mr Lam was appointed to the Board on December 28, 2001. He has more than 30

years of experience in the manufacturing and marketing of plastic products and

toothbrush. He is the Deputy President of Perak Hock Kean Association and Vice

Chairman of Poi Lam High School, Secondary School, and Primary School. Prior to

joining Golden PET Industries Sdn Bhd, a wholly-owned subsidiary of the Company,

he was the Sales Manager of United Plastic Sdn Bhd, a

plastic manufacturing company from 1973 to 1980.

Chok Hooa@ Chok Yin Fatt

Non-independent Non-

Executive Director

Malaysian, male, age 70

Mr Chok is a Malaysian and was appointed to the Board on December 28, 2001. He

graduated with a Bachelor Degree in Business Studies from Curtin University of

Technology, Australia and Master in Business Administration from University of

Strathclyde, United Kingdom. He is a Chartered Accountant of the Malaysian Institute

of Accountants, fellow members of CPA Australia and Malaysian Institute of Chartered

Secretaries and Administrators and a member of the Malaysian

Institute of Certified Public Accountants. He has extensive experience in the field of

financial management, accounting and corporate secretarial functions. He was

attached to UAC Berhad from 1974 to 1982. In 1982, he joined Yee Lee Corporation

Bhd as Chief Accountant and was promoted to the Board as an Executive Director in

1990. He is a Director of OKA Corporation Bhd and Yee Lee Corporation Bhd, and

other public companies which are not listed on the Bursa Malaysia Securities Berhad

including Yee Lee Organization Bhd and MSHK Corporation Bhd. He is also the

Chairman of the Remuneration Committee and a member of the Audit Committee of

the Company.

Dato IR. Nik Mohamad

Pena bin Nik Mustapha

Independent non-executive

director

Malaysian, male, age 66

Dato’ Ir. Nik Mohamad Pena was appointed to the Board on July 14, 1997. He

obtained a Degree of Bachelor of Science (Civil Engineering) from University of

Glasgow, United Kingdom in 1975. He holds the

memberships in the following professional bodies, namely the Board of Engineers

Malaysia, Institution of Engineers Malaysia, Institution of Highways and

Transportation United Kingdom and Association of Consulting Engineers Malaysia. He

advises the Board members on all matters relating to civil and structural aspect of the

Group’s buildings. He is a consultant engineer and the Managing Director of Nik Jai

Associates Sdn Bhd, a company of civil and structural engineering consultants. He

started his career as a civil engineer with Jabatan Kerja Raya (JKR) in 1975 and was

promoted to the post of Senior Executive Engineer in 1980. He left JKR in 1983 and

joined an engineering consulting firm. In 1985, he set up his own partnership firm,

Nik Jai Associates. In 1990, he incorporated his company, Nik Jai Associates Sdn Bhd

which specialises in multi-storey buildings, highways, bridges and water resources.

He is a Director of Yee Lee Corporation Bhd, the Chairman of the Audit Committee

and Nomination Committee of the Company.

Dato Mohd Adhan bin

Kechik

Independent non-executive

director

Malaysian, male, age 61

Dato’ Mohd Adhan was appointed to the Board on May 16, 1994. He graduated with a

Bachelor of Laws (Honours) Degree and Master of Laws Degree from University of

Malaya. He is currently the Chairman

of the National Kenaf and Tobacco Board (Lembaga Kenaf dan Tembakau Negara).

He is a lawyer by profession. Currently, he is practising as a partner at Messrs Adhan

& Yap. Prior to setting up his own private practice in Kota Bharu, Kelantan in 1984, he

was attached to the Legal and Judicial Department for five years serving in the

Magistrate Court, High Court, Public Trustee’s office and Attorney General’s office

before being appointed the Legal Adviser to the Ministry of Transport in 1983. He also

served the State Government of Kelantan for four years as Menteri Besar’s political

secretary from 1986 to 1990. He is an elected State Assemblyman of Kelantan for

Kemahang from 1995 to 1999 and Bukit Bunga since 2004. He is a Director of Yee

Lee Corporation Bhd, a member of the Audit Committee, Nomination Committee and

Remuneration Committee of the Company

MIDF RESEARCH Friday, 02 June 2017

12

Source: Company

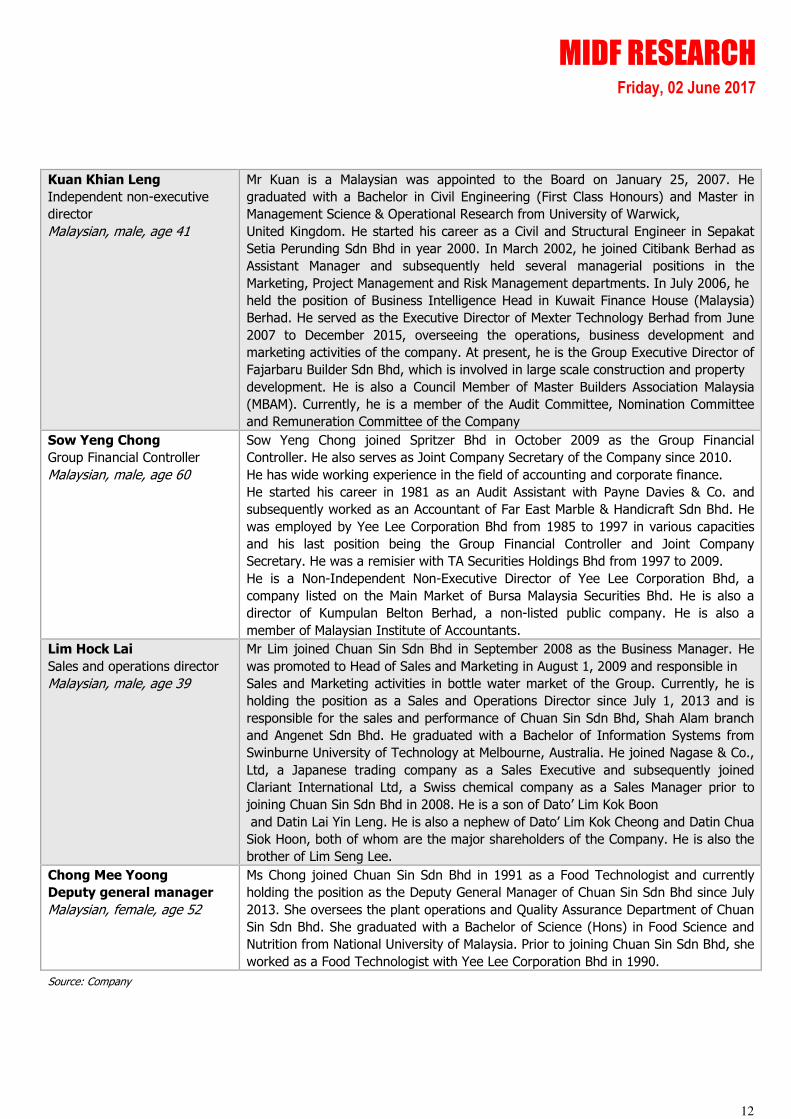

Kuan Khian Leng

Independent non-executive

director

Malaysian, male, age 41

Mr Kuan is a Malaysian was appointed to the Board on January 25, 2007. He

graduated with a Bachelor in Civil Engineering (First Class Honours) and Master in

Management Science & Operational Research from University of Warwick,

United Kingdom. He started his career as a Civil and Structural Engineer in Sepakat

Setia Perunding Sdn Bhd in year 2000. In March 2002, he joined Citibank Berhad as

Assistant Manager and subsequently held several managerial positions in the

Marketing, Project Management and Risk Management departments. In July 2006, he

held the position of Business Intelligence Head in Kuwait Finance House (Malaysia)

Berhad. He served as the Executive Director of Mexter Technology Berhad from June

2007 to December 2015, overseeing the operations, business development and

marketing activities of the company. At present, he is the Group Executive Director of

Fajarbaru Builder Sdn Bhd, which is involved in large scale construction and property

development. He is also a Council Member of Master Builders Association Malaysia

(MBAM). Currently, he is a member of the Audit Committee, Nomination Committee

and Remuneration Committee of the Company

Sow Yeng Chong

Group Financial Controller

Malaysian, male, age 60

Sow Yeng Chong joined Spritzer Bhd in October 2009 as the Group Financial

Controller. He also serves as Joint Company Secretary of the Company since 2010.

He has wide working experience in the field of accounting and corporate finance.

He started his career in 1981 as an Audit Assistant with Payne Davies & Co. and

subsequently worked as an Accountant of Far East Marble & Handicraft Sdn Bhd. He

was employed by Yee Lee Corporation Bhd from 1985 to 1997 in various capacities

and his last position being the Group Financial Controller and Joint Company

Secretary. He was a remisier with TA Securities Holdings Bhd from 1997 to 2009.

He is a Non-Independent Non-Executive Director of Yee Lee Corporation Bhd, a

company listed on the Main Market of Bursa Malaysia Securities Bhd. He is also a

director of Kumpulan Belton Berhad, a non-listed public company. He is also a

member of Malaysian Institute of Accountants.

Lim Hock Lai

Sales and operations director

Malaysian, male, age 39

Mr Lim joined Chuan Sin Sdn Bhd in September 2008 as the Business Manager. He

was promoted to Head of Sales and Marketing in August 1, 2009 and responsible in

Sales and Marketing activities in bottle water market of the Group. Currently, he is

holding the position as a Sales and Operations Director since July 1, 2013 and is

responsible for the sales and performance of Chuan Sin Sdn Bhd, Shah Alam branch

and Angenet Sdn Bhd. He graduated with a Bachelor of Information Systems from

Swinburne University of Technology at Melbourne, Australia. He joined Nagase & Co.,

Ltd, a Japanese trading company as a Sales Executive and subsequently joined

Clariant International Ltd, a Swiss chemical company as a Sales Manager prior to

joining Chuan Sin Sdn Bhd in 2008. He is a son of Dato’ Lim Kok Boon

and Datin Lai Yin Leng. He is also a nephew of Dato’ Lim Kok Cheong and Datin Chua

Siok Hoon, both of whom are the major shareholders of the Company. He is also the

brother of Lim Seng Lee.

Chong Mee Yoong

Deputy general manager

Malaysian, female, age 52

Ms Chong joined Chuan Sin Sdn Bhd in 1991 as a Food Technologist and currently

holding the position as the Deputy General Manager of Chuan Sin Sdn Bhd since July

2013. She oversees the plant operations and Quality Assurance Department of Chuan

Sin Sdn Bhd. She graduated with a Bachelor of Science (Hons) in Food Science and

Nutrition from National University of Malaysia. Prior to joining Chuan Sin Sdn Bhd, she

worked as a Food Technologist with Yee Lee Corporation Bhd in 1990.

MIDF RESEARCH Friday, 02 June 2017

13

MIDF RESEARCH is part of MIDF Amanah Investment Bank Berhad (23878 - X).

(Bank Pelaburan)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

DISCLOSURES AND DISCLAIMER

This report has been prepared by MIDF AMANAH INVESTMENT BANK BERHAD (23878-X) pursuant to

the Mid and Small Cap Research Scheme (“MidS”) administered by Bursa Malaysia Berhad. This report

has been produced independent of any influence from Bursa Malaysia Berhad or the subject company.

Bursa Malaysia Berhad and its group of companies disclaim any and all liability, howsoever arising, out

of or in relation to the administration of MidS and/or this report. It is for distribution only under such

circumstances as may be permitted by applicable law.

Readers should be fully aware that this report is for information purposes only. The opinions contained

in this report are based on information obtained or derived from sources that we believe are reliable.

MIDF AMANAH INVESTMENT BANK BERHAD makes no representation or warranty, expressed or

implied, as to the accuracy, completeness or reliability of the information contained therein and it

should not be relied upon as such.

This report is not, and should not be construed as, an offer to buy or sell any securities or other

financial instruments. The analysis contained herein is based on numerous assumptions. Different

assumptions could result in materially different results. All opinions and estimates are subject to

change without notice. The research analysts will initiate, update and cease coverage solely at the

discretion of MIDF AMANAH INVESTMENT BANK BERHAD.

The directors, employees and representatives of MIDF AMANAH INVESTMENT BANK BERHAD may

have interest in any of the securities mentioned and may benefit from the information herein.

Members of the MIDF Group and their affiliates may provide services to any company and affiliates of

such companies whose securities are mentioned herein This document may not be reproduced,

distributed or published in any form or for any purpose.

MIDF AMANAH INVESTMENT BANK : GUIDE TO RECOMMENDATIONS

STOCK RECOMMENDATIONS

BUY Total return is expected to be >15% over the next 12 months.

TRADING BUY Stock price is expected to rise by >15% within 3-months after a Trading Buy rating has been

assigned due to positive newsflow.

NEUTRAL Total return is expected to be between -15% and +15% over the next 12 months.

SELL Total return is expected to be <-15% over the next 12 months.

TRADING SELL Stock price is expected to fall by >15% within 3-months after a Trading Sell rating has been

assigned due to negative newsflow.

SECTOR RECOMMENDATIONS

POSITIVE The sector is expected to outperform the overall market over the next 12 months.

NEUTRAL The sector is to perform in line with the overall market over the next 12 months.

NEGATIVE The sector is expected to underperform the overall market over the next 12 months.