Embed Size (px)

Citation preview

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

33

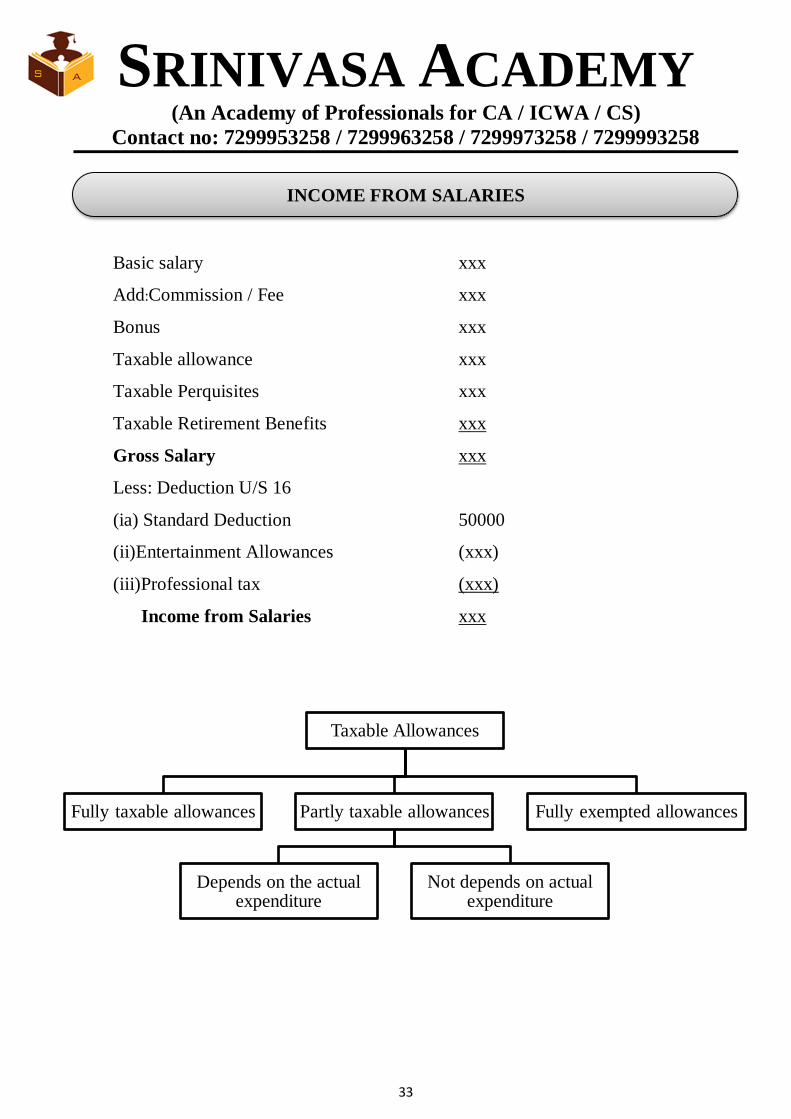

Basic salary xxx

Add:Commission / Fee xxx

Bonus xxx

Taxable allowance xxx

Taxable Perquisites xxx

Taxable Retirement Benefits xxx

Gross Salary xxx

Less: Deduction U/S 16

(ia) Standard Deduction 50000

(ii)Entertainment Allowances (xxx)

(iii)Professional tax (xxx)

Income from Salaries xxx

INCOME FROM SALARIES

Taxable Allowances

Fully taxable allowances Partly taxable allowances

Depends on the actual expenditure

Not depends on actual expenditure

Fully exempted allowances

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

34

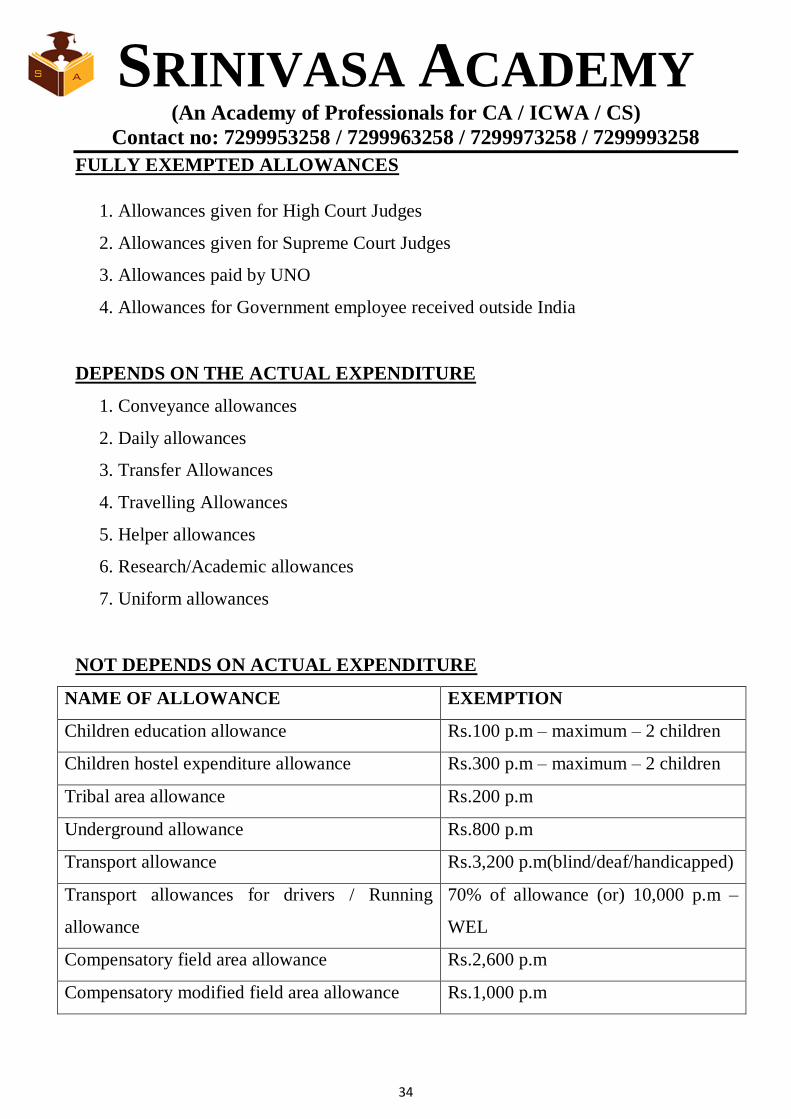

FULLY EXEMPTED ALLOWANCES

1. Allowances given for High Court Judges

2. Allowances given for Supreme Court Judges

3. Allowances paid by UNO

4. Allowances for Government employee received outside India

DEPENDS ON THE ACTUAL EXPENDITURE

1. Conveyance allowances

2. Daily allowances

3. Transfer Allowances

4. Travelling Allowances

5. Helper allowances

6. Research/Academic allowances

7. Uniform allowances

NOT DEPENDS ON ACTUAL EXPENDITURE

NAME OF ALLOWANCE EXEMPTION

Children education allowance Rs.100 p.m – maximum – 2 children

Children hostel expenditure allowance Rs.300 p.m – maximum – 2 children

Tribal area allowance Rs.200 p.m

Underground allowance Rs.800 p.m

Transport allowance Rs.3,200 p.m(blind/deaf/handicapped)

Transport allowances for drivers / Running

allowance

70% of allowance (or) 10,000 p.m –

WEL

Compensatory field area allowance Rs.2,600 p.m

Compensatory modified field area allowance Rs.1,000 p.m

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

35

High altitude allowance(armed forces)

9,000 ft – 15,000 ft

Above 15,000 ft

Rs.1,060 p.m

Rs.1,600 p.m

Special compensatory highly active field area

allowance(armed forces)

Rs.4,200 p.m

Counter insurgency allowance(armed forces

operating away from permanent locations)

Rs.3,900 p.m

Island duty allowance(armed forces operating in

Andaman & Nicobar & Lakshadweep)

Rs.3,250 p.m

Special compensatory hilly area allowance Rs.800 (or) Rs.300 p.m depending on

the location

Rs.7,000 p.m in Siachen

House Rent Allowances

House Rent Allowances xxx

LESS: Exemption xxx

Taxable HRA xxx

Least of the following

1. HRA received

2. Rent paid -10% of salary

3. 40% of salary (other Cities) / 50% of salary (Metropolitan cities )

NOTE: Salary = Basic + DA (Forming Part) + % on Turnover

Metropolitan cities

Chennai

Mumbai

Calcutta

Delhi

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

36

FULLY TAXABLE ALLOWANCES

1. City Compensatory Allowances

2. Dearness Allowances

3. Tiffin / Lunch / Dinner Allowances

4. Servant Allowances

5. Interim Allowances

6. Warden Allowances / Proper Allowances

7. Non-practicing Allowances

8. Over time Allowances

9. Any other cash Allowances

10. Medical Allowances

11. Entertainment Allowances

RETIREMENT BENEFITS

Voluntary Retirement Scheme

Provident Fund

Pension

Gratuity

Leave Encashment

Retrenchment Compensation

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

37

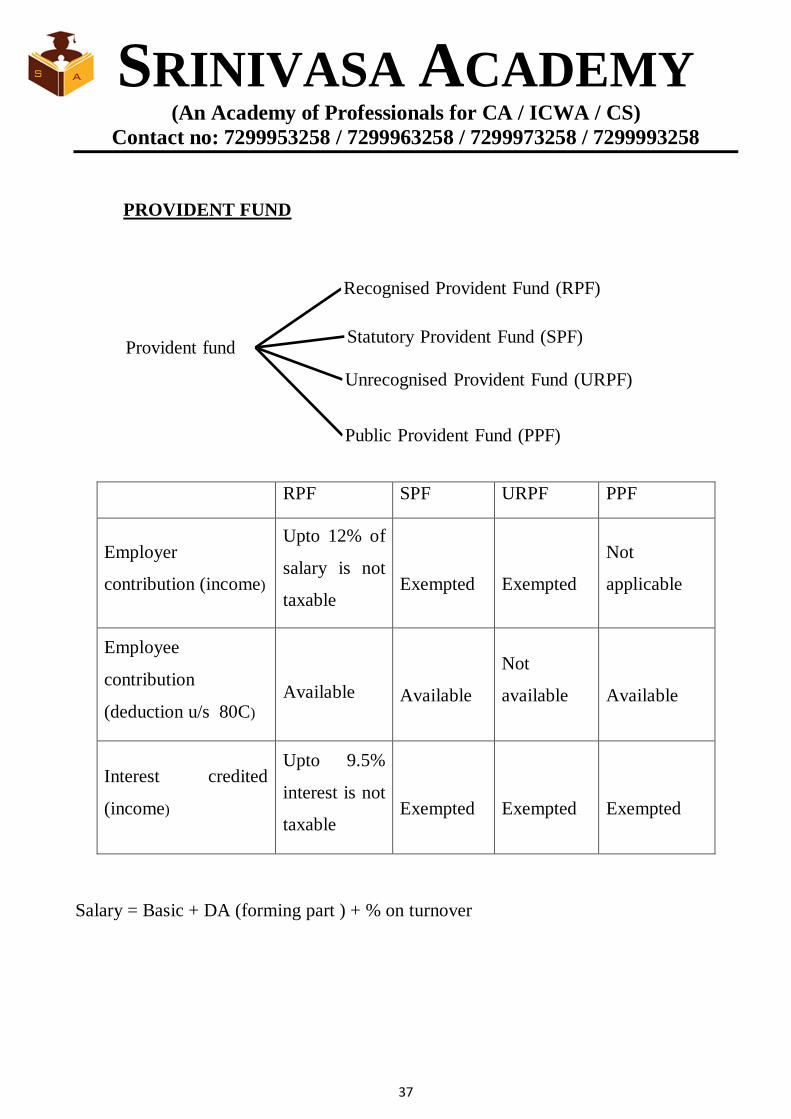

PROVIDENT FUND

RPF SPF URPF PPF

Employer

contribution (income)

Upto 12% of

salary is not

taxable

Exempted

Exempted

Not

applicable

Employee

contribution

(deduction u/s 80C)

Available

Available

Not

available

Available

Interest credited

(income)

Upto 9.5%

interest is not

taxable

Exempted

Exempted

Exempted

Salary = Basic + DA (forming part ) + % on turnover

Provident fundStatutory Provident Fund (SPF)

Recognised Provident Fund (RPF)

Unrecognised Provident Fund (URPF)

Public Provident Fund (PPF)

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

38

Least of the following

1. Actually received.

2. Rs.3,00,000 – exempted earlier.

3. Average monthly salary X 10

4. Average monthly salary X unearned leave

Average Salary = Basic + DA (forming part ) + % on turnover. Preceding the 10

months retirement

PENSION

Commuted pension

Govt employee

Exempted

Non-govt employee

When gratuity received

1/3 X Full value of pension

When gratuity not received

1/2 X Full value of pension

Uncommuted pension

Fully taxable

LEAVE SALARY / LEAVE ENCASHMENT

During the service

Fully taxable

After the service

Govt employee

Exempted

Non-govt employee

Leave salary XXX

Less: Exemption XXX

XXX

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

39

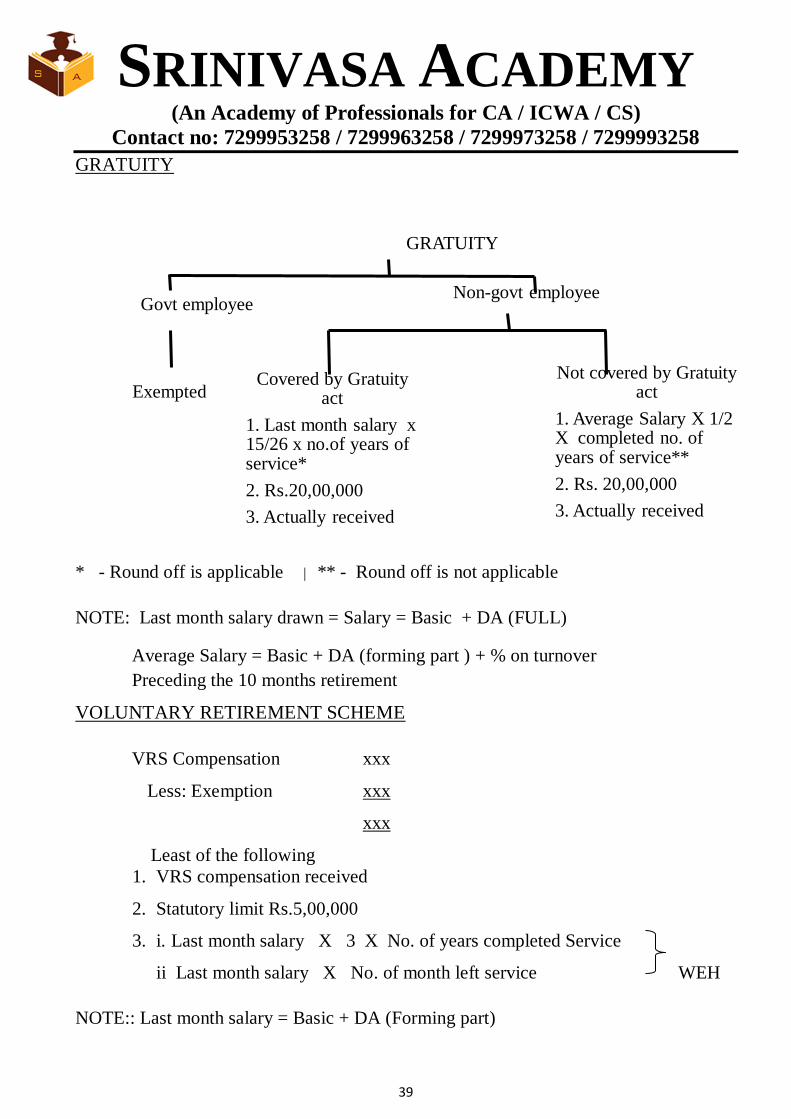

GRATUITY

* - Round off is applicable | ** - Round off is not applicable

NOTE: Last month salary drawn = Salary = Basic + DA (FULL)

Average Salary = Basic + DA (forming part ) + % on turnover

Preceding the 10 months retirement

VOLUNTARY RETIREMENT SCHEME

VRS Compensation xxx

Less: Exemption xxx

xxx

Least of the following

1. VRS compensation received

2. Statutory limit Rs.5,00,000

3. i. Last month salary X 3 X No. of years completed Service

ii Last month salary X No. of month left service WEH

NOTE:: Last month salary = Basic + DA (Forming part)

GRATUITY

Non-govt employee

Covered by Gratuity act

1. Last month salary x 15/26 x no.of years of service*

2. Rs.20,00,000

3. Actually received

Govt employee

Not covered by Gratuity act

1. Average Salary X 1/2 X completed no. of years of service**

2. Rs. 20,00,000

3. Actually received

Exempted

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

40

RETRENCHMENT COMPENSATION

Actually received xxx

Less: Exemption xxx

xxx

Least of the following:

1. Actually received

2. Rs.5,00,000

3. Average monthly salary X 15/26 X No. of years service

Note

Average monthly salary = preceding 3 month salary from the date of

Retirement

Salary includes all except PF and Bonus

DEDUCTIONS:

16(ia) Standard deduction

16 (ii) Entertainment Allowances

16 (iii) Professional Tax

Standard deduction

Rs.50,000 (or) the amount of salary

WEL

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

41

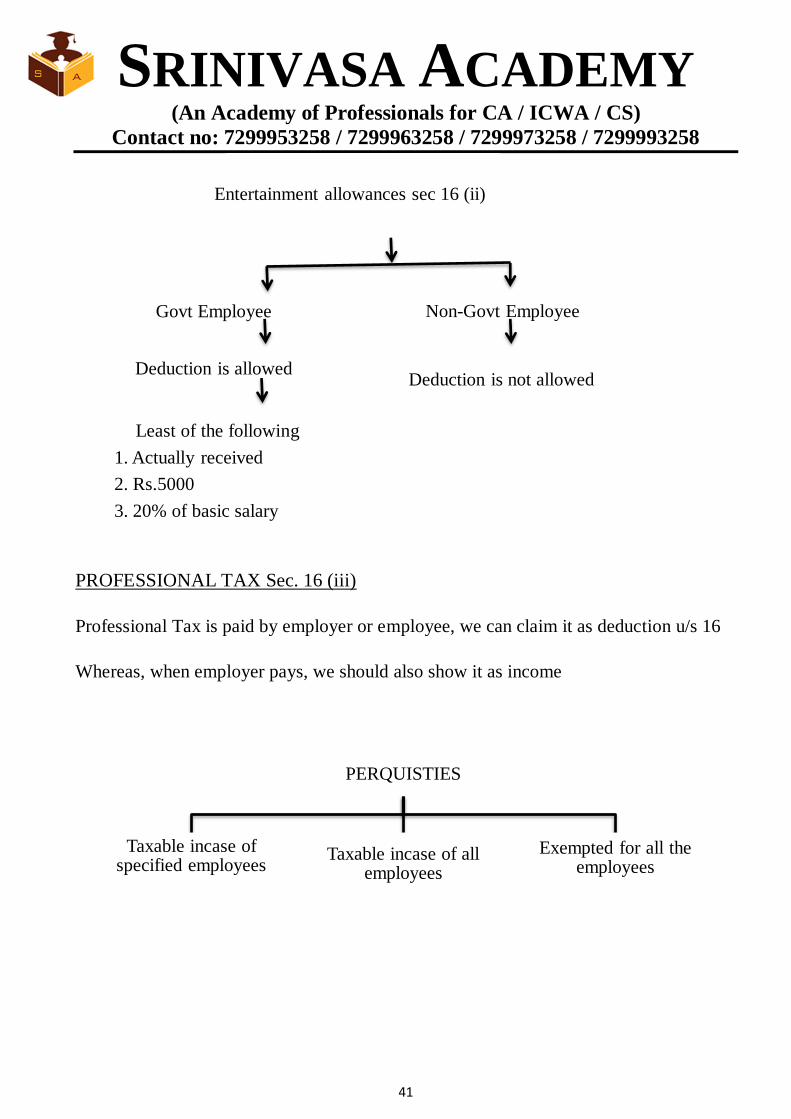

PROFESSIONAL TAX Sec. 16 (iii)

Professional Tax is paid by employer or employee, we can claim it as deduction u/s 16

Whereas, when employer pays, we should also show it as income

Entertainment AllowanceEntertainment allowances sec 16 (ii)

Govt Employee

Deduction is allowed

Least of the following

1. Actually received

2. Rs.5000

3. 20% of basic salary

Non-Govt Employee

Deduction is not allowed

PERQUISTIES

Taxable incase of specified employees

Taxable incase of all employees

Exempted for all the employees

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

42

TAXABLE FOR SPECIFIED EMPLOYEES:

SPECIFIED EMPLOYEE:

i. Director

ii. Substantial interest / 20% of voting power / shares above (i) $ (ii) clause

are not satisfied

iii. Salary should exceed Rs.50,000 p.a

Note: Salaries includes all, including entertainment allowances, and profession at taxes

1. Services of gardener, Sweeper, Watchman, Personal Attender

2. Usage of gas / Water / Electricity

3. Educational facilities in the concessional rate

4. Valuation of motor car

5. Free / concessional – Transport facility

1. Services of Sweeper / Gardener / Watchman / PA

Total Salary paid xxx

Less: Amount paid by employee xxx

Taxable perks xxx

2. Usage : Gas / Water / Electricity

Actual cost xxx

Less: Amount paid by employee xxx

Taxable Perks xxx

3. Free / Concessional Educational Facilities

Cost incurred by the employer xxx

Less: exemption Rs.1000 per month xxx

xxx

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

43

Less: Amount paid by the employee xxx

Taxable Perks xxx

4. Transport Facilities

Actual Cost xxx

Less: Amount paid by the employee xxx

Taxable Perks xxx

TAXABLE INCASE OF ALL EMPLOYEES

1. Rent Free Accommodation

2. Concessional Rent

3. Obligation from employer to employee

4. Approved super annulation Fund (exceeds Rs.1,50,000)

5. Specified shares or sweat equity shares

6. Fringe benefits

Salary = Basic + DA (R/B) + Bonus + Commission + Fee + Taxable Allowances

Rent Free Accommodation

Govt employee

License fee

Non-Govt employee

Owned by the Employer

2.Population exceeds 10 L to 25 L (10% of salary)

1.Population UPTO 10 lakhs (7.5% of Salary)

3. Above 25 L (15% of salary)

Not owned by the Employer

15% of salary

(or) WEL

Rent paid

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

44

Unfurnished RFA xxx

Add: 10 % of cost / Actual Cost* xxx

Furnished RFA xxx

Less: Amount paid by employee xxx

(concessional rent) xxx

*Actual Cost = Rent paid for the furnished house

7. Fringe Benefit:

Meal - Rs.50 per meal

Credit card / Club expenditure xxx

Less: Amount paid by employee xxx

xxx

Use of movable assets (other than computer and laptop)

10 % of cost xxx

Less: Paid by employee xxx

xxx

Interest free / concessional Loan

i. Exceeds Rs.20,000 Taxable

ii. Medical treatment, except for cancer, AIDS, TB

Gift in Kind

Exceeds Rs.5000 is taxable

Transfer of property

Computer / Electronics - 50% of WDV

Motor Car - 20% of WDV

Other assets - 10% of SLM

Valuation of Motor car

Owned by the Employer Owned by the Employee

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

45

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

46

Owned by the employer

Official use

Nil

Personal use

Actual Cost xxx

Add : 10% cost xxx

xxx

Less: Amount paid

by employee (xxx)

xxx

Partly Official / Partly personal

Running / maintenance by employer

Upto 1.6 cc

Rs.1800 p.m.

Add : Driver Salary Rs.900 p.m.

Exceed 1.6cc

Rs.2400 p.m.

Add: Driver salary Rs.900 p.m.

Running / maintenance by employee

Upto 1.6 cc

Rs.600 p.m.

Add: Driver salary Rs.900 p.m.

Exceed 1.6 cc

Rs.900 p.m.

Add: Driver salary Rs.900

p.m.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

47

Owned by the employee

Official use

Nil

Personal use

Actual Cost xxx

Less: Amount paid

by employee (xxx)

xxx

Partly Official / Partly personal

Running / maintenance by employer

Actual cost xxx

Less: upto 1.6cc-Rs.1800 p.m

Exceeds1.6cc-Rs.2400 p.m ( xxx)

Less:Driver salary-900 p.m ( xxx)

Taxable perks xxx

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

48

EXEMPTED PERQUISITES:

PERQUISITES NATURE

Telephone Provided by employer to employee at his

residence

Transport facility Provided by employer engaged in the

business of carrying passengers (or) goods

to employees

Privilege passes and tickets Provided by Indian Railways to employees

Perquisites allowed outside India by

Government

Provided by Government of India to

citizens residing outside India.

Contribution to Staff Group Insurance

scheme.

Provided by Employer to Employee

Annual premium on personal accident

policy

Provided by employer to employee

Refreshment Provided by employer to employee during

working hours.

Subsidised lunch Provided by employer to employee upto

Rs.50

Recreational facilities Provided by employer to employee

Training expenses Provided by employer to employee

Amount paid to RPF or approved

superannuation fund

Provided by employer to employee

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

49

The following perquisites provided to judges of High court / Supreme court /

Ministers of Parliament:

Medical facilities (upto certain limits)

Rent – free official residence

Rent – free furnished residence

Conveyance facility

LEAVE TRAVEL CONCESSION (LTC):

Limit of exemption: Exemption will be available in respect of two journeys

performed in a block of four calendar years(Amount actually spent).

Leave travel concession

Journey performed by

Air

Amount not exceeding air

economy fair of the National Carrier by the shortest route

Rail

Amount not exceeding air-

conditioned first class rail fare by the

shortest route

Recognised public transport system

Amount not exceeding first class or deluxe class fare by the shortest route

No recognised public transport system

Amount equivalent to air-conditioned first

class rail fare

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

50

EMPLOYEE’S STOCK OPTION PLAN (ESOP): DETERMINATION OF

FMV

LEAVE TRAVEL CONCESSION[SEC.10(5)]

MODE OF TRAVEL CLASS OF TRAVEL AMOUNT EXEMPT

AIRWAYS ECONOMY CLASS TRAVEL CHARGES ON SHORTEST ROUTE

TRAIN 1ST CLASS AC TRAVEL CHARGES ON SHORTEST ROUTE

RECOGNISED TRANSPORT DELUXE CLASS TRAVEL CHARGES ON SHORTEST ROUTE

OTHER TRANSPORT - 1ST CLASS AC FARE AS PER RAILWAYS

VALUE OF PERQUISITE:

FMV of securities or sweat equity shares xxx

Less: Amount recovered from the employee xxx

Value Of Perquisite xxx

FMV

Unlisted company

As determined by merchant banker

Listed company

Trading on the date of vesting of option

Listed in one rse

Avg of opening & closing price

Listed in more than one rse

Avg of opening and closing price in stock exchange that records the highest volume of

trading

No trading on the date of vesting of

option

Listed in one rse

Closing price of share

Listed in more than one rse

Closing price in stock exchange that records the highest volume

of trading

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

51

MEDICAL FACILITIES:

The following medical facilities are exempted:

Note:

i)Such expenditure should be approved by RBI.

ii)The expenses in respect of traveling of the patient & attendant will be exempt if

the employee’s gross total income computed before including the said expenditure

does not exceed Rs.2,00,000/-

Medical Facilities

Hospital maintained by

employer

Hospital maintained by Government

(or) approved by Principal

Chief Commissioner

Premium paid on health

insurance policy of employee approved by Government

Reimbursement of premium paid on health

insurance policy approved by Government

Expenditure incurred abroad(Refer note)

For medical treatment

travel and stay abroad of patient & attendant

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

52

QUICK REFERENCE FOR MEANING OF SALARY:

GRATUITY (covered under

Payment of Gratuity Act)

(Basic salary + D.A.) last drawn

GRATUITY (not covered

under Payment of Gratuity

Act)

(Basic salary + D.A.[forming part of Retirement

Benefits] + Commission as a percentage on

turnover) Average of last 10 months preceding the

year of retirement

LEAVE ENCASHMENT (Basic salary + D.A.[forming part of Retirement

Benefits] + Commission as a percentage on

turnover) Average of last 10 months immediately

from the retirement

VOLUNTARY

RETIREMENT

(Basic salary + D.A.[forming part of Retirement

Benefits] + Commission as a percentage on

turnover) last drawn

RENT FREE

ACCOMODATION

(Basic + D.A. [forming part of Retirement

Benefits] + Commission as a percentage on

turnover + Bonus + Fees + Any other taxable

allowance + Any other monetary benefits

excluding perquisite)

SPECIFIED EMPLOYEE (Basic + DA + Commission + Bonus + Fees +

Any other taxable allowance + Any other

monetary benefits – Deduction u/s 16)

ENTERTAINMENT

ALLOWANCE

(DEDUCTION U/S 16(ii))

Only basic salary

ALL OTHER CASES Basic salary + D.A.(forming part of retirement

benefits) + Commission as a percentage on

turnover

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

53

Allowances

1. Mr.Giri who resides, in Chennai, get Rs.6,00,000 p.a. as basic salary. He

receives Rs.1,00,000 p.a. as house rent allowance. Rent paid by him is

Rs.80,000 p.a. find out the amount of taxable house rent allowance for the AY

2020-21.

2. Mr. Gurvindar who is posted in Delhi but resides in Noida, gets Rs.90,000 per

annum as basic pay. He gets Rs.13,500 per annum as house rent allowance,

though he pays Rs.18,000 per annum as rent. During the previous year 2019-

20, he receives Rs.7,500 as advance salary of April 2019. Can he claim the

entire amount of house rent allowance as exempt from tax for the assessment

year 2020-2021.

3. Compute taxable salary of Mr.M for the assessment year 2020-21

Nature of allowance Amount of

allowance Rs.

Amount

actually

spent Rs.

Amount

chargeable for

tax* Rs.

1. conveyance allowance for official

purpose 25000 23000

2.Travelling allowance for official

purpose 15000 18000

Practice Problems

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

54

3.transfer allowance given at the time of

transfer of Arvind from Goa to Varanasi 20000 18000

4.Helper allowance for engaging helper

for official purposes 60000 45000

5.research allowance 50000 45000

6.uniform allowance for official

purposes 10000 12000

*Amount chargeable to tax shall be lower of amount of allowance or

amount actually spent for the purpose whichever is lower.

4. Mr. x is employed at Hyderabad at the Basic Salary of Rs.25,000 p.m. and he is

also getting following allowances:

Rs. P.m.

1 Dearness allowance 2000

2 Lunch allowance 1000

3 Servant allowance (He is paying Rs.1,200 p.m. to a

servant)

1000

4 Transport allowance 1000

5 Education allowance @ 200 p.m. per child for three

children

6 Hostel allowance to one child 500

7 Conveyance allowance 800

8 Overtime allowance 2000

9 Officiating allowance 2000

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

55

10 Cash allowance 1200

11 Entertainment allowance 2000

12 Medical allowance 800

13 City compensatory allowance 600

14 House rent allowance 5000

He is having family house at the place of his posting but he is living in a

rented house and is paying a rent of Rs.7,000 p.m. find out his gross

salary.

5. Mr. Chonga is an area manager of M/s Bokaro, Steels Co.Ltd. During the

financial year 2019-20, he gets the following emoluments from his employer:

Basic salary

Up to 31.8.2019 Rs. 20,000 p.m.

From 01.9.2019 Rs. 25,000 p.m.

Transport allowance Rs. 2800 p.m.

Contribution to recognized provident fund 15% of basic salary

Children education allowance Rs.500 p.m. for two children

City compensatory allowance Rs. 300 p.m.

Hostel expenses allowance Rs.380 p.m. for two children

Tiffin allowance (Actual expenses Rs.3700) Rs. 5,000 p.a.

Tax paid on employment Rs.2500

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

56

Leave salary

6. Mr. H was employed by Elite Ltd, up to March 15, 2000. At the time of leaving

Elite Ltd, he was paid Rs.3,50,000 as leave salary out of which Rs.72,000 was

exempt from tax under section 10(10AA)(ii). Thereafter he joined XYZ (P) Ltd.

and received Rs.5,00,250 as leave salary at the time of his retirement on

December 31, 2019. Determine the amount of taxable leave salary from the

following information.

Salary at the time of retirement (per month)

Average salary received during 10 months ending on

Dec,31,2019

. from March 1, 2019 to July 31, 2019 (per month)

. from August 1, 2019 to December 31, 2019 (per month)

Duration service(a)

Leave entitlement for every year of service (b)

Leave availed while in service ©

Rs.28,000

Rs.27,000

Rs.27,500

14 year & 8 month

44 days

80 days

17.866 Months

Gratuity

7. Mr.L an employee of Lovely Co. Ltd., receives Rs.1,20,000 as gratuity. He is

covered by the payment of Gratuity Act, 1972. He retires on December 1,2019 after

rendering service of 29 years and 8 months. At the time of retirement his monthly

basic salary and dearness allowance (40% forming part of retirement benefit) was

Rs. 4,000 and Rs.1,500 respectively. Is the entire amount of gratuity exempt from

tax?

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

57

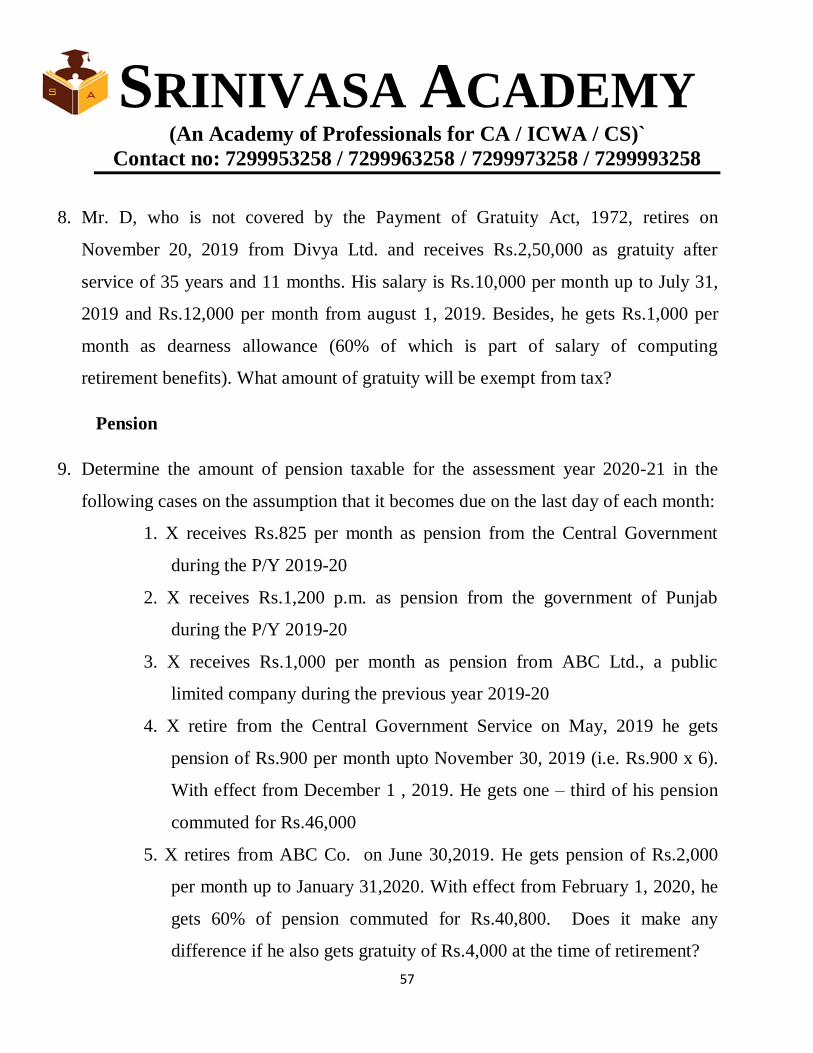

8. Mr. D, who is not covered by the Payment of Gratuity Act, 1972, retires on

November 20, 2019 from Divya Ltd. and receives Rs.2,50,000 as gratuity after

service of 35 years and 11 months. His salary is Rs.10,000 per month up to July 31,

2019 and Rs.12,000 per month from august 1, 2019. Besides, he gets Rs.1,000 per

month as dearness allowance (60% of which is part of salary of computing

retirement benefits). What amount of gratuity will be exempt from tax?

Pension

9. Determine the amount of pension taxable for the assessment year 2020-21 in the

following cases on the assumption that it becomes due on the last day of each month:

1. X receives Rs.825 per month as pension from the Central Government

during the P/Y 2019-20

2. X receives Rs.1,200 p.m. as pension from the government of Punjab

during the P/Y 2019-20

3. X receives Rs.1,000 per month as pension from ABC Ltd., a public

limited company during the previous year 2019-20

4. X retire from the Central Government Service on May, 2019 he gets

pension of Rs.900 per month upto November 30, 2019 (i.e. Rs.900 x 6).

With effect from December 1 , 2019. He gets one – third of his pension

commuted for Rs.46,000

5. X retires from ABC Co. on June 30,2019. He gets pension of Rs.2,000

per month up to January 31,2020. With effect from February 1, 2020, he

gets 60% of pension commuted for Rs.40,800. Does it make any

difference if he also gets gratuity of Rs.4,000 at the time of retirement?

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

58

Comprehensive (Allowances, Pension, Leave Salary & Gratuity)

10. Mr. Ashok, who retired from the services of Hotel Taj Ltd, on 31.1.2020

after putting on service for 5 years, received the following amounts from the

employer for the year ending on 31.3.2020:

Salary @ Rs.16,000 p.m. comprising of basic salary of Rs.10,000.

Dearness allowance of Rs.3,000, City compensatory allowance of

Rs.2,000 and Night duty allowance of Rs.1,000

Pension @ 30% of basic salary from 1.2.2020

Leave salary of Rs.75,000 for 225 days of leave accumulated during 5

years @ 24 days leave in each year. He has not availed any earned

leave during his tenure of 5 years and utilized only his casual leave

Gratuity of Rs.50,000

Compute the total income of Mr.Ashok for the assessment year 2020-21

Provident Fund

11. For the previous year 2019-20, Udai submits the following information –

Basic salary: Rs.1,80,000; dearness allowance : Rs.60,000 (46% of which is

part of salary for retirement benefits) commission: Rs.6,000 (i.e. 1% of

Rs.6,00,000 being turnover achieved by Udai) and children education

allowance for his 2 children : Rs.7200. the employer contributes Rs.20,000

towards provident fund to which a matching contribution is made by Udai.

Interest credited in the provident fund account on March 15, 2020 @ 11%

comes to Rs.93500. Income of Udai from other sources is Rs.1,00,000. Find

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

59

out the net income of Udai for the assessment year 2020-21 if the provident

fund is

(a) Statutory provident fund

(b) Recognized provident fund

(c) Unrecognized provident fund.

Comprehensive

(Allowances, Pension, Leave Salary, Gratuity & Provident fund)

12. On the basis of the following information compute the taxable income of

Om Prakash under the hear “Salaries” for the assessment year 2020-21

Particulars Rs.

(i) Basic pay

(ii) Dearness allowance

(iii) Entertainment allowance

(iv) Tribal area allowance

(v) His own contribution towards statutory provident

fund

(vi) Employer’s contribution

(vii) Interest credited to SPF @ 10% p.a.

(viii) House rent allowance

8400 p.m.

1200 p.m.

750 p.m.

350 p.m.

1000 p.m.

1000 p.m.

13000

1600 p.m.

Om Prakash is an employee of the Government of UP. He is paying Rs.2400 p.m.

as house rent.

13. Mrs. Lakshmi aged about 66 years is a Finance Manager of M/s Lakshmi & Co.

Pvt Ltd., based at Calcutta, She is in continuous service since 1967 and receives

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

60

the following salary and perks from the company during the year ending

31.03.2020

i) Basic Salary (50000 x 12) = Rs.600000

ii) D.A. (20000x12)-Rs.240000 (forms part of pay for retirement benefits)

iii) Bonus – 2 months basic pay

iv) Commission – 0.1% of the turnover of the company. The turnover for the

F.Y. 2019-20 was Rs.15.00 crores

v) Contribution of the employer and employee to the PF Account Rs.300000

each

vi) Interest credited to P.F. Account at 8.5% - Rs.60000

vii) Entertainment Allowance Rs.30000

viii) Hostel allowance for three children Rs.5000 each

Compute the total income for the Assessment Year 2020-21

Voluntary Retirement Scheme: (VRS)

14. From the following information given by Mr.Shiva Shankaran, find the amount

of

Employer - A limited company

Date of retirement - 31st October 2019

Years of Service - 28 years

Amount received from employer - Rs.2,49,000

Salary at the time of retirement - Rs.9,500 p.m.

Actual date of retirement - 31st, march 2021

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

61

Deduction U/S 16 (ia), (ii) & (iii) from Salary

15. Mr.Bharat who joined the ABC (P) Ltd in 1955, he receives Rs.9000 as basic

salary and Rs.400 per month as entertainment allowance during the previous year

2019-20. Determine the amount of income chargeable under the hear “Salaries”.

16. Mr.Raja an employee of the central government, gets Rs.6000 p.m. as basic salary

and is entitled to Rs.1,500 p.m. as entertainment allowance. Compute the

deduction U/S 16 (ii) from gross salary

17. Mr. V.J., an employee of the central government, gets Rs.10,000 p.m. as basic

salary and is entitled to Rs.2,500 p.m. as entertainment allowance. Compute the

taxable entertainment allowance U/S . 16(ii)

18. Compute the net salary in the following cases for the assessment year 2020-21

a. Basic salary Rs.10,000 p.m. DA Rs.500 p.m., CCA Rs.200 p.m. Commission

Rs.500 p.m. Bonus700 p.m.. Professional tax paid by employer Rs.1,200.

Employer’s contribution to SPF R.3,000 p.m. Interest credited to SPF during

2019-2020 Rs.30,000 at 15% A is Govt. employee.

He is receipt of Entertainment allowance @ Rs.1,000 per month

b. Basic salary Rs.3,000 p.m. DA Rs.200 p.m. Bonus Rs.5,000. Professional tax

paid by Assessee Rs.1,500. Entertainment allowance received from his

employer @ 500 per month. His employer is a Ltd. Company

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

62

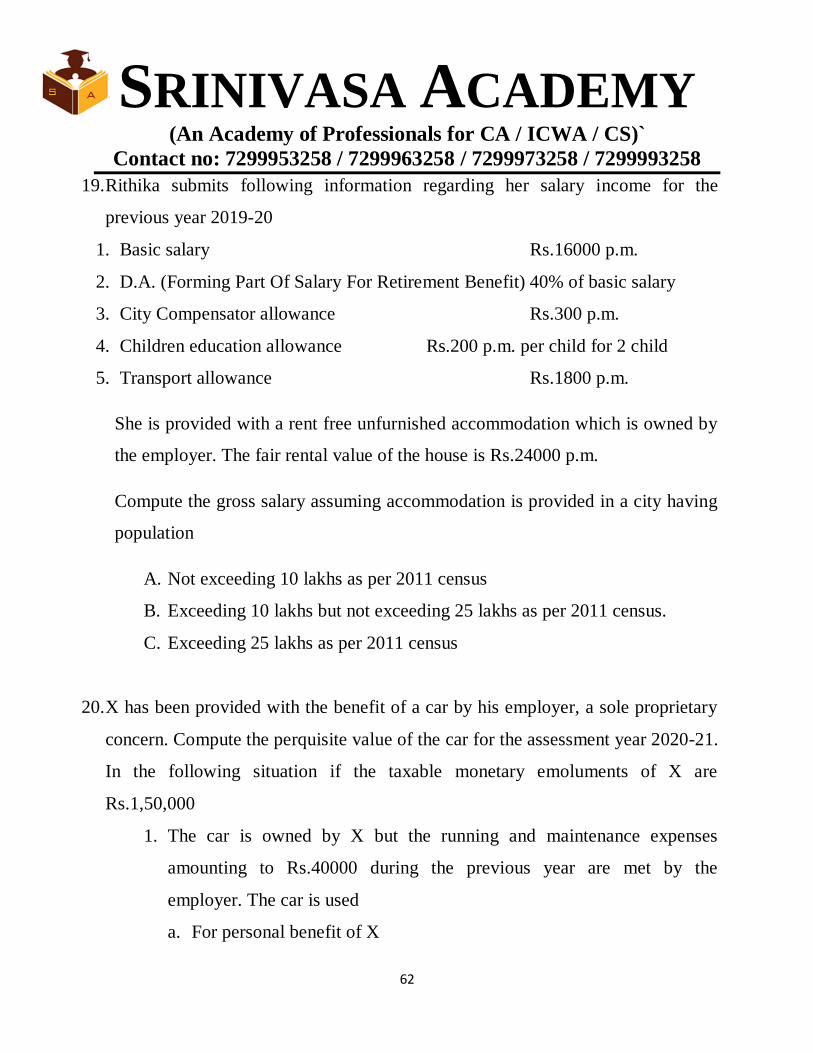

19. Rithika submits following information regarding her salary income for the

previous year 2019-20

1. Basic salary Rs.16000 p.m.

2. D.A. (Forming Part Of Salary For Retirement Benefit) 40% of basic salary

3. City Compensator allowance Rs.300 p.m.

4. Children education allowance Rs.200 p.m. per child for 2 child

5. Transport allowance Rs.1800 p.m.

She is provided with a rent free unfurnished accommodation which is owned by

the employer. The fair rental value of the house is Rs.24000 p.m.

Compute the gross salary assuming accommodation is provided in a city having

population

A. Not exceeding 10 lakhs as per 2011 census

B. Exceeding 10 lakhs but not exceeding 25 lakhs as per 2011 census.

C. Exceeding 25 lakhs as per 2011 census

20. X has been provided with the benefit of a car by his employer, a sole proprietary

concern. Compute the perquisite value of the car for the assessment year 2020-21.

In the following situation if the taxable monetary emoluments of X are

Rs.1,50,000

1. The car is owned by X but the running and maintenance expenses

amounting to Rs.40000 during the previous year are met by the

employer. The car is used

a. For personal benefit of X

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

63

b. Only for official duties

c. 30% for personal benefit and 70% for official use

2. The employer provides a car of 1.5 ltr. Engine cubic capacity costing

Rs.500000 exclusively for the personal benefit of X. The expenses

incurred on the car are Rs.52000

3. The employer provides a car (below 1.6 lt.) along with a driver to X party

for official and partly for personal purpose. The expenses incurred by the

company are:

a. Running and maintenance expenses Rs.32000

b. Driver’s salary Rs.36000

4. In case(3) the employer maintains a log book and it is established than

30% of the total coverage of the car is for personal use of X and 70% for

official duties

5. The employer provides a car (above 1.6 It) to X which is used for official

work and is also used by X for commuting from his residence to office

and back

6. X is provided with 2 cars to be used for official and personal work and

the following information is available from the company’s records:

Car 1 Exceeding Car 2 Below

1.6 It. Rs. 1.6 It. Rs.

Cost of the car 600000 400000

Running and maintenance 60800 48000

Salary of driver 44000 44000

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

64

21. Mr. K Sonu is Asst. Manager of a Textile company of Jaipur, since 1987. He has

submitted the following particulars of his income for the financial year 2019-20

I. Basic salary Rs.46,000

II. Dearness allowance Rs.5,000 per month (Rs.200 p.m. enters into

retirement benefits)

III. Education allowance for two children at Rs.150 p.m. per child

IV. Commission on sales 1% of turnover of Rs.10,00,000

V. Entertainment allowance Rs.700 p.m.

VI. Travelling allowance for his official tours Rs.30,000. The entire amount

is spent on the official tour.

VII. He was given cloth worth Rs.1,000 by his employer free cost

VIII. He resides in the flat of the company. Its market rent is Rs.2,000 p.m. A

watchman and a cook have been provides by the company at the flat who

are paid Rs.4,00 per month each

IX. He has been provided with a motor car of 1.8 ltr. Engine capacity for his

official as well as personal use. The running and maintenance costs are

borne by the Company.

X. Rent of house recovered from Sonu Rs.4,600

Compute income from salaries for the assessment year 2020-21. Assume the

population of Jaipur is 26 lakhs as per 2011 census.

22.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

65

23. Sri Bhagawan Das is a Purchase Officer in a company in Jaipur. He furnished the

following particulars regarding his income for previous year 2019-20

i. Basic salary Rs.84000

ii. Bonus Rs.5000

iii. Dearness allowance Rs.3000 p.m.

iv. Travelling allowance Rs.45000. He spends Rs.30000 for official purpose;

v. Reimbursement of medical bills Rs.25000 (treatment was done in a

Government hospital India)

vi. He lived a bungalow belonging to the company. Its fair rent is Rs.2500per

month. The company has provided on his bungalow, the facility of a

watchmen and a cook each of whom is being paid a salary of Rs.250 per

month. The company paid in respect of this bungalow Rs.5000 for electric

bills and Rs.3000 for water bills

vii. He has been provided with 1.5 ltr. Engine capacity car for official and

personal use. The company maintenance and running expenses of the car

(including diver ) are borne by the company.

viii. The following amount were deposited in his provided fund account;

a. Own contribution Rs.8400

b. Company’s contribution Rs.12000 and

c. Interest @ 12% p.a. Rs.12600

ix. Rent of house recovered from Sri Bhagawan Das Rs.3600

Compute his taxable income from salary for the assessment year 2018-10.

Assume the population of Jaipur is 26 lakhs as per 2011 census.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

66

24. Mr. Vignesh, Finance manager of KLM Ltd, Mumbai, furnished the following

particulars for the financial year 2019-20

I. Salary Rs.46000 per month

II. Value of medical facility in hospital maintained by the company Rs.7000

III. Rent free accommopdation owned by the company

IV. Houseing loan of Rs.600000 at the interest rate of 6% p.a. (No repayment

made during the year. SBI Rate 10% p.a.)

V. Gifts in kind made by the coomapny on the occasion of wedding

anniversary of Mr.Vignesh Rs.4,750

VI. A wodden table and 4 chair wer provided to Mr.Vignesh at his residence

(dining table) This was purchased on 1.5.14 for Rs.60000 and sold to

Mr.Vignesh on 1.8.2017 Rs.30,000. This was given for use from the date

of purchase by employer to Mr.Vignesh

VII. Personal purchase through credit card provided by the company

amounting to Rs.10,000 was paid by the company. No part of the amount

was recovered from Mr.Vignesh

VIII. An ambassador car which was purchased by the company on 16.7.14 for

Rs.250000 was sold to the assessee on 14.7.17 for Rs.80,000

Other income received by the assessee during the previous year 2017-18

a. Interest on Fixed Deposits with a company Rs.5000

b. Income from specified mutual fund Rs.3000

c. Interest on bank deposits of a minor married daughter Rs.3000

Compute the Gross Total Income of Mr.Vignesh and the tax thereon for the

Assessment year 2020-21

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

67

1. Compute his income under the head salary of PKJ the assessment year 2020-21 from the

following information submitted to you:

Sl. No. Particulars Rs.

1. Basic Salary 20,000 p.m.

2. D.A. (60% of which is part of retirement benefits) 10,000 p.m.

3. Children education allowance (for two children) 200 p.m. per

child

4. Free lunch for 300 days in the office during office hours 80 per meal

5. Reimbursement of expenses incurred on credit card provided by

the employer

10,000

6. Gift of Titan watch 12,000

7. Rent free unfurnished accommodation at Delhi, the fair rent value of which is

Rs. 84,000

p.a.

8. Motor car of 1.8 litre with driver both for official and private purposes

9. Watchman facility by the employer. Wages of watchman paid by employer

1,000 p.m.

10. Telephone facility at his residence. The employer has incurred expenses of Rs.

15,000 for the same.

COMPREHENSIVE PRACTICE PROBLEMS

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

68

2. Mrs. Z has the following income during the previous year 2019-20:

Sl. No. Particulars Rs.

1 Salary 3,10,000

2 Dearness Allowance (forming part of salary for retirement benefits) 72,000

3 Medical Allowance (Actual expenditure Rs. 28,000) 30,000

4 Education Allowance (for three children) 5,200

5 Rent free house in Delhi for which Z Ltd., the employer, paid Rs. 5,000 per

month as rent. The house is equipped with rented furniture. The rent of the

furniture is Rs. 3,000 per month.

6 The employer had provided her a domestic servant, a sweeper and a watchman.

The

employer paid Rs. 500 per month to each.

7 The employer spent Rs. 2,500 on her refresher course.

8 The employer paid her telephone bills of 22,200

9 Profession tax paid by Mrs. Z 1,200

Compute her taxable income for the assessment year 2020-21 assuming that she has

no other income.

3. Mr. K. Sikri is Asstt. Manager of a Textile Company of Jaipur, since 1991. He has

submitted the following particulars of his income for the financial year 2019-20:

(i) Basic salary Rs.2,40,000.

(ii) Dearness Allowance Rs. 5,000 per month (Rs. 200 p.m. enters into

retirement benefits).

(iii) Education allowance for two children at Rs. 150 p.m. per child.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

69

(iv) Commission on sales 1% of turnover of Rs.10,00,000.

(v) Entertainment allowance Rs. 700p.m.

(vi) Travelling Allowance for his official tours Rs. 30,000. The entire amount is

spent on the official tour.

(vii) He was given cloth worth Rs. 1,000 by his employer free of cost.

(viii) He resides in the flat of the company. Its market rent is Rs. 12,000 p.m.

A watchman and a cook have been provided by the company at the bungalow

who are paid Rs. 400 per month each.

(ix) He has been provided with a motor car of 1.8 ltr. engine capacity for his

official as well as personal use. The running and maintenance costs are borne

by the Company.

(x) Employer's contribution to R.P.F. is Rs. 40,000 and the interest credited to this

fund at 13% rate amounted to Rs.16,250.

(xi) Contribution by Sikri to recognised provident fund Rs.40,000.

(xii) Rent of house recovered from Sikri Rs. 1,500p.m.

Compute income from salaries for the assessment year 2020-21. Assume the

population of Jaipur is 26 lakhs as per 2001 census.

4. P, a Director of XYZ Pvt. Ltd. Pune is offered an employment with the following two

alternative packages:

Particulars I (Rs.) II (Rs.)

Basic Pay per annum 1,38,000 1,38,000

Conveyance allowance for private use 9,000 —

Motor car facility for private use of P and his family members — 9,000

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

70

(valued)

Entertainment Allowance 18,000 —

Club facility (Valued) — 18,000

Children Education Allowance (for 2 children) 9,700 —

Free Education Facility in an institution run by the employer for

Children

(Valued)

9,700

Rent Free unfurnished house with fair rental value 30,000 30,000

Which of the two packages should P opt for on the assumption that both employer and

employeewillcontribute20%ofthebasicpaytowardsanunrecognisedprovidentfund?Assume

the population of Pune is more than 25 lakhs as per 2001census.

5. Mr. J is Manager of a HUF of Jaipur (population exceeds 25 lakhs). He has submitted

the following particulars of his income for the AY 2020-2021 i.e. PY 2019-2020

I. Net Salary Rs. 80,000 after TDS of Rs. 6,000, contribution to RPF Rs. 9,000 and

rent of bungalow @5% of salary.

II. Dearness Allowance Rs. 1,000 per month (Rs.200 pm enters into retirement

benefits).

III. Education Allowance for two children at Rs.150 pm per child.

IV. Commission on sales Rs.10,000.

V. Entertainment Allowance Rs.1,000 per month.

VI. Travelling Allowance for his official tours Rs.30,000, Actual expenditure on tours

Rs. 22,000.

VII. He was given shirts worth Rs.4,800 by employer free of cost (employer is

manufacturer of shirts).

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

71

VIII. He resides in the bungalow belonging to HUF. Its fair rent is Rs.1,500 pm A

gardener, watchman and a cook have been provided by the employer at the

bungalow who are paid Rs.1,300 per month each.

IX. He has been provided with a motorcar of 1.8 liter (1800 cc) for his official as well

as personal use. The running and maintenance costs are borne by the HUF.

X. Employer’s contribution of RPF is Rs. 7,000 and interest credited to fund @13% pa

was Rs.16,250.

His employer paid in December 2019 for his medical treatment in London

Rs.80,000, Rs.7,5000 for travelling in this connection and Rs. 25,000 for stay there.

6. Mr. Goyal receives the following emoluments during the previous year ending

31.03.2020.

Basic pay Rs. 40,000

Dearness Allowance Rs. 15,000

Commission Rs. 10,000

Entertainment allowance Rs. 4,000

Medical expenses reimbursed Rs. 25,000

Professional tax paid Rs. 2,000 (Rs. 1,000 was paid by his

employer)

Mr. Goyal contributes Rs. 5,000 towards recognized provident fund. He has no

other income. Determine the income from salary for A.Y. 2020-21, if Mr. Goyal is

a State Government employee.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

72

7. Mr. Balaji, employed as Production Manager in Beta Ltd., furnishes you the

following information for the year ended31.03.2020:

I Basic salary upto

31.10.2019

Rs. 50,000 p.m.

Basic salary from

01.11.2019

Rs. 60,000 p.m.

Note: Salary is due and paid on the last day of every month.

ii. Dearness allowance @ 40% of basic salary.

iii. Bonus equal to one month salary. Paid in October 2019 on basic salary

plus dearness allowance applicable for that month.

iv. Contribution of employer to recognized provident fund account of the

employee@16% of basic salary.

v. Professional tax paid Rs. 2,500 of which Rs. 2,000 was paid by the

employer.

vi. Facility of laptop and computer was provided to Balaji for both official

and personal use. Cost of laptop Rs. 45,000 and computer Rs. 35,000

were acquired by the company on01.12.2019.

vii. Motor car owned by the employer (cubic capacity of engine

exceeds1.60 litres) provided to the employee from 01.11.2019 meant for

both official and personal use. Repair and running expenses of Rs.

45,000 from 01.11.2019 to 31.03.2020, were fully met by the employer.

The motor car was self-driven by the employee.

viii. Leave travel concession given to employee, his wife and three children

(one daughter aged 7 and twin sons aged 3). Cost of air tickets

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

73

(economy class) reimbursed by the employer Rs. 30,000 for adults and

Rs. 45,000 for three children. Balaji is eligible for availing exemption

this year to the extent it is permissible in law.

Compute the salary income chargeable to tax in the hands of Mr. Balaji for the

assessment year 2020-21.

8. Ms. Suhaani, a resident individual, aged 33 years, is an assistant manager of

Daily Needs Ltd. She is getting a salary of Rs. 48,000 per month. During the

previous year 2019-20, she received the following amounts from her

employer.

(i) Dearness allowance (10% of basic pay which forms part of salary

for retirement benefits).

(ii) Bonus for the previous year 2018-19 amounting to Rs. 52,000 was

received on 30thNovember,2019.

(iii) Fixed Medical allowance of Rs. 48,000 for meeting medical

expenditure.

(iv) She was also reimbursed the medical bill of her father dependent on

her amounting to Rs.4,900.

(v) Ms. Suhaani was provided;

a laptop both for official and personal use. Laptop was acquired

by the company on 1stJune, 2017 at Rs.35,000.

a domestic servant at a monthly salary of Rs. 5,000 which was

reimbursed by her employer.

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

74

(vi) Daily Needs Ltd. allotted 700 equity shares in the month of October

2019 @ Rs. 170 per share against the fair market value of Rs. 280

per share on the date of exercise of option by Ms. Suhaani. The fair

market value was computed in accordance with the method

prescribed under the Act.

(vii) Professional tax Rs. 2,200 (out of which Rs. 1,400 was paid by the

employer).

Compute the Income under the head “Salaries” of Ms. Suhaani for the assessment

year 20-21.

9. Ms. Poorvisha is the HR Manager in Poorni Textiles Ltd. She gives you the

following particulars for the yearended31-03-2020:

- Basic Salary Rs. 1,00,000 p.m.

- Dearness Allowance Rs. 24,000 p.m. (30% of which forms part of

retirement benefits).

- Bonus Rs.21,000 p.m.

- Heremployer-

companyhasprovidedherwithanaccommodationon1stApril,2019 at a

concessional rent. The house was taken on lease by the company for

Rs.12,000 p.m. Ms.Poorvisha occupied the house from1st November

2019,Rs.4,800 p.m is recovered from the salary of Ms. Poorvisha.

- The employer gave her a gift voucher of Rs. 10,000 on her birthday.

- She contributes 18% of her salary (Basic Pay plus DA) towards

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

75

recognised provident fund and the company contributes the same

amount.

- Uniform allowance Rs.24,000.

- The company pays medical insurance premium to effect insurance on the

health of Ms. Poorvisha Rs. 20,000.

- Motor car owned by the employer (Cubic capacity of engine exceeds 1.6

liters) provided to Ms. Poorvisha from 1st November, 2019 which is used

for both official and personal purposes. Repair and running expenses of Rs.

70,000 were fully met by the company. The motor car was self-driven by

the employee.

Compute the income chargeable to tax under the head “Salaries” in the hands of Ms.

Poorvisha. Brief note on treatment of each item is required.

10. Mr. Subramani is Senior Manager (Finance) of VKS Steel Ltd. The particulars of

h-is emoluments for the year ended 31.03.2020 are given below:

Basic Salary Rs. 60,000 per month

Dearness Allowance Rs. 40,000 per month (30% is for

retirement benefit) Annual performance Incentive Rs.1,80,000

House Rent Allowance Rs. 10,000 per month

Mr. Subramani pays rent of Rs.20,000 per month for a flat occupied from

1stNovember, 2019 at Erode, Tamil Nadu.

He received gift voucher of Rs.6,000 from the employer on the occasion of

his marriage anniversary.

The employer provided him a motor car (cubic capacity of the engine

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

76

exceeds 1.6 liters) without chauffeur with effect from 1st December,

2019. Running and maintenance expenses of Rs. 30,000 were fully borne

by the employer. The car is used by Mr. Subramani both for official and

private purposes.

The employer paid the following premiums for Mr. Subramani:

(i) Medical insurance premiumRs.12,000

(ii) Life insurance premium Rs.15,000

(iii) Accident insurance premiumRs.10,000

Tax on employment paid to Erode Municipal Corporation by Mr. Subramani Rs.

5,000. Compute the income chargeable to tax under the head "Salaries" in the hands of

Mr. Subramani for AssessmentYear2020-21.

11. Mr. Kamal employed in Rajini Mfg. Co. Ltd., Mumbai as General Manager

furnishes the following information for the year ended 31.03.2020:

Particulars Amount (Rs.)

Basic salary (per month) 50,000

Dearness Allowance (eligible for retirement benefits) 80% of basic

salary

House Rent Allowance (per month) 10,000

Rent paid by him Rs. 15,000 per month for 6 months and Rs.

20,000

per month for balance 6 months (at Mumbai)

City Compensatory Allowance (per month) 2,500

Medical reimbursements (annual) 13,000

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

77

Gymkhana club annual membership fee reimbursed by employer 20,000

Mobile phone bill reimbursed by the employer (Used for both

official and personal use)

37,500

Motor car (cubic capacity of engine 2.2 litres) owned by the

employee but the maintenance expenses fully met by the

employer (Motor car was used both for personal and official use)

85,800

Cash gift paid by the employer in appreciation of performance on

01.012020

30,000

Contribution to recognized provident fund :

Employee 1,20,000

Employer 90,000

Contribution to National Pension Trust:

Employee 60,000

Employer 55,000

Medical insurance premium paid by means of uncrossed cheque 18,000

You are requested compute the total income of Mr. Kamal for the assessment year

2020-21.

12. Mr. Raghu is employed with Yes Power Co Ltd. as General Manager

(Finance) at Kolkata. He furnishes you the following information for

theyearended31.03.2020.

Basic salary (per month) 40,000

Dearness allowance (per month) eligible for retirement benefits 30,000

SRINIVASA ACADEMY (An Academy of Professionals for CA / ICWA / CS)`

Contact no: 7299953258 / 7299963258 / 7299973258 / 7299993258

78

Rent-free accommodation is provided.

A car was provided to him from 01.06.2019 (engine cubic capacity more

than 1.6 litres). It is used both for official and personal purposes. Running

expenses are fully met by employer. Mr. Raghu drives the car himself.

Provident fund contribution of both employer and employee 12% of basic

pay and dearness allowance.

Fixed tiffin allowance (per annum) 20,000

Fixed medical allowance (per annum) 30,000

Credit card annual fee paid by employer (used for personal purposes) 7,000

Only son of Mr. Raghu is given free education in the school run by the

employer. Cost of education is 1,500 per month.

Loan taken by Mr. Raghu from provident fund during the year 50,000

Compute the total income of Mr.Raghu for the assessment year 2020-21.