Embed Size (px)

Citation preview

Stealth Compensation: Do CEOs Increase Their Pay

by Influencing Dividend Policy?

Kristina Minnick* Department of Finance

Bentley University 781-891-2941

Leonard Rosenthal Department of Finance

Bentley University 781-891-2516

*Corresponding Author Bentley University, 175 Forest St., Waltham, MA 02452 USA

© 2013 by Kristina Minnick and Leonard Rosenthal. All rights reserved.

We would like to thank the participants in the Bentley University Finance Department and the University of Stirling Accounting &Finance Department research seminars, at the 2011 meetings of the Midwest Finance Association and Financial Management Association and the 2012 European Conference of the Financial Management Association for a number of helpful comments. We would especially like to thank Nalinasksha Bhattacharyya, Alan Goodacre, Marcia Millon Cornett, Abe de Jong, Jayant Kale, Katherine Farrell, Melissa Frye, Jeff Netter, Ajay Patel, Kartik Raman, Chip Ryan, Hassan Tehranian, Mathijs van Dijk, Yulia Veld-Merloulova, and an anonymous referee for additional suggestions and insights.

1

Stealth Compensation: Do CEOs Increase Their Pay

by Influencing Dividend Policy?

Companies can increase executive compensation by allowing dividends to be paid on

unvested restricted stocks grants, also known as stealth compensation. Examining all S&P

500 firms over the period 2003-2007, we find that more than half of the dividend paying

firms allow this practice. We look at whether this form of compensation reduces agency

costs or decreases value for shareholders. We find that CEOs’ stealth compensation amounts

to an average $180,000 in additional income, which increases the CEOs’ cash compensation

and total compensation by 9% and 2% respectively. Firms engaging in stealth compensation

have higher dividend payout ratios than those not allowing stealth compensation. For all

firms using stealth compensation, there is a reduction in average ROA and Tobin’s Q over

the long run. However, stealth compensation companies with potential agency issues see a

meaningful improvement in their long run performance. For weakly governed companies,

stealth compensation may act as a bonding mechanism which may serve to reduce agency

costs and therefore increase shareholder value.

JEL classification: M41, M52, J33

Keywords: Executive Compensation; Payout Policy; Firm Performance; Corporate

Governance

2

Stealth Compensation: Do CEOs/Directors Increase Their Pay

by Influencing Dividend Policy?

1. Introduction

With the increased attention on executive compensation, particularly cash compensation,

directors have created alternative ways to enhance a CEO’s compensation (and their own)

without attracting shareholder attention. One such method is allowing management to receive

additional income from dividends on unvested restricted stock grants (RSGs). RiskMetrics

dubbed this type of compensation “stealth compensation” since companies are not required to

clearly report this additional dividend component as part of an executive’s compensation

package.1 It is not surprising that such hidden compensation exists at many firms, given

shareholder pressure to reduce or change how executives are compensated. Chidabaram and

Prabhala (2009) find that firms often engage in behavior to offset restrictions on compensation

by using substitutes that can increase costs to shareholders. In this paper, we examine the degree

to which firms engage in stealth dividend compensation, focusing on CEOs in particular,

whether it is a meaningful contributor to overall compensation packages, and if it creates agency

problems.

Stealth compensation could influence decisions involving dividend policy by creating

incentives for companies to increase their dividend payout, which could either reduce or

exacerbate agency issues. Shareholders of firms with cash flows exceeding their profitable

investment opportunities want excess free cash flow paid out as dividends to prevent wasteful

spending. Directors may use stealth compensation as a tool to motivate CEOs to push for

increased payouts, which ultimately may benefit shareholders. Shareholders would get a higher

current cash return, although at the possible cost of foregoing profitable projects. Additionally,

tax-exempt institutional investors would be attracted to stocks with high dividend payouts since

they are taxed at a lower rate than individual investors (Allen, Bernardo, and Welch, 2000). The

resulting increase in institutional ownership may lead to more active monitoring of the firm,

which could reduce agency issues.

Alternatively, agency issues could be magnified if the CEO, working with the board, uses

stealth compensation to maximize their own as well as the directors’ compensation.

3

Additionally, if the use of stealth compensation motivates managers to pay out cash to

shareholders rather than invest in potentially profitable investments, the overall value of the firm

can be negatively impacted. In particular, companies with risk averse managers or managers

who want to lead “the quiet life” might prefer stealth compensation (Bertrand and Mullainathan,

2003). This too may decrease value for shareholders.

We focus on dividend-paying S&P 500 firms that allow dividends to be paid on unvested

RSGs from 2003 through 2007 and compare them to dividend-paying S&P 500 firms that do not

allow stealth compensation. During this time period, tax preferences between dividends and

capital gains are minimal, which provides a unique opportunity to examine whether stealth

compensation affects dividend policy. We find that CEOs make an extra $180,200 a year on

average from dividends on unvested RSGs. This amounts to 9% of their total cash compensation

and 2% of their total compensation, both significantly greater than for CEOs of firms without

dividend compensation could have received if their firms allowed these payments. In order to

better understand the factors affecting the use and impact of stealth compensation, we

incorporate different measures of governance and institutional ownership into our analysis. We

find that companies that use stealth compensation have greater board independence, higher

institutional ownership, more entrenchment provisions, and lower governance transparency than

companies that do not follow this policy.

Our results are consistent with stealth compensation influencing payout decisions. Stealth

compensation firms have significantly higher dividend payout ratios and spend significantly less

on repurchases than firms that do not engage in this practice. We find that the more RSGs a

company has, the stronger the effect of stealth compensation. Interestingly, we see significantly

higher dividend and lower repurchase payouts in firms that have high institutional ownership and

offer stealth compensation. These results suggest that stealth compensation may act as a bonding

mechanism to ensure that institutional owners get higher dividends, and that entrenched

managers pay out excess free cash. We find a similar result for firms with poor governance and

stealth compensation. We incorporate several methods to deal with endogeneity and find our

overall results are similar.

1Risk Metrics used this term in a 2008 report on dividend compensation and we adopt it in this paper. Under SEC reporting rules, this income is not considered compensation, so firms are not required to include the exact dollar amount executives receives in their proxy statement.

4

Finally, we look at the operating performance of firms engaging in stealth compensation

and those which do not. Firms using stealth compensation experience significantly worse

operating performance, both in terms of ROA and Tobin’s Q, than firms not engaging in this

practice over the subsequent three-year period Interestingly, performance is significantly better

for poorly governed firms that use stealth compensation compared to firms with poor governance

but no stealth compensation. These results provide support for the possibility that stealth

compensation is used by firms with poor governance to reduce agency issues.

Our paper proceeds as follows: section 2 reviews related literature and our motivation,

section 3 describes the data, section 4 discusses our results, and section 5 presents our summary

and conclusions.

2. Literature and motivation

2.1. Literature

There is a vast literature on both dividend policy and executive compensation. Recent

evidence suggests that dividend payout ratios and the number of dividend-paying firms have

declined (Fama and French, 2001), and that share repurchases have become a preferred method

of payout for many firms (Grullon and Michaely, 2002). It has been suggested that one reason

that dividends have become less popular is the increased use of company stock options as a form

of compensation. These options are not protected against the decline in stock price when its goes

ex-dividend. Consequently, their expected value is a decreasing function of dividends payments.

Lambert, Lanen, and Larker (1989), Jolls (1998), Fenn and Liang (2001), and Kahle

(2002) find that the firms offering managers more stock options as compensation tend to pay

dividends to a lesser extent. Chetty and Saez (2005) and Brown, Liang, and Weisbenner (2007)

provide evidence of a negative relationship between executive stock options and the likelihood

of a dividend increase after the 2003 reduction of taxes on dividends. These papers all focus on

the role of options in setting dividend policy. We build on this literature by examining how

another form of compensation, namely stealth compensation, affects dividend policy.

Aboody and Kasznick (2008) assess the underlying rationale for shareholders to design

incentive contracts that induce managers to make payout choices that increase the value of their

stock-based compensation. They find that the 2003 reduction in taxes on dividends resulted in

greater alignment of the desires of individual (tax-paying) shareholders with those of

management by inducing the latter to switch to RSGs from options. Blouin, Raedy, and

5

Shakelford (2011) jointly test the impact of the 2003 tax reduction on individual investors and

management using 2001-2005 data and find that firms with the largest individual ownership

increased dividends relative to share repurchases starting in 2003. Moreover, they argue that

their results are consistent with officers and directors increasing their holdings in order to take

advantage of the reduced taxes on dividends.

Zhang (2013) also looks at the effects of dividend compensation on payout for S&P 500

stocks using the period from 2000 through 2009. She finds that dividend increases are more

likely after 2003 for firms that pay stealth compensation. We also examine stealth compensation

during this period, but focus on the role of governance and the role played by institutional

ownership in determining stealth compensation, as well as the impact of dividend compensation

on future profitability.

Our paper builds on the existing literature in three ways. First, we control for the choice

between stock and option compensation as well as for corporate governance while examining

which firms use dividend compensation, and how dividend compensation may affect a

company’s payout policy. Second. we add to the existing literature by examining whether

allowing executives to receive dividends on unvested RSGs reduces agency issues by providing

a bonding mechanism to motivate entrenched CEOs to pay out dividends. Finally, we examine

whether this form of stealth compensation may ultimately hurt or help shareholders.

2.2. Motivation

Agency issues in firms result from differing objectives between shareholders and the

executive officers of the company. The former want their wealth to be maximized, while the

latter want to maximize their own interests. Jensen (1986) identifies free cash flow as one source

of agency problems. Shareholders want excess cash flow to be used for their benefit through the

payment of dividends, while officers may view this as a reduction in resources they control. The

role of the board is to minimize this conflict through the firm’s compensation plan with

management, including stock based compensation. Thus, the quality of board governance plays

an important role in executive compensation. Since dividends on unvested restricted stock are a

form of compensation, its use can mitigate or exacerbate the agency problem created by free cash

flow.

In the compensation literature there are two views as to how compensation agreements

are reached: optimal contracting or managerial rent extraction. Under optimal contracting theory,

6

directors use executive compensation to help reduce the agency issues between executives and

shareholders, thereby maximizing shareholder wealth. Well-functioning markets for executive

labor should produce a set of contracts that optimally minimizes the expected cost of managers’

self-interest, given available information (Fama and Jensen (1983a, 1983b)). In accordance with

the incentive alignment view, Core and Guay (1999) show that firms award equity grants in a

manner that is consistent with agency and contracting theories.

Optimal contracting theory suggests that stealth compensation may reduce agency issues

by motivating managers to distribute excess cash flow to shareholders. By inducing a larger

payout, stealth compensation may be a mechanism to incentivize managers to attract institutional

investors, which may not be otherwise desired by managers who prefer not to be monitored.

Allen, Bernardo, and Welch (2000) show that firms that pay higher dividends attract more

institutional ownership, which should result in improved monitoring of the firm.

If managers engage in rent extraction, stock based compensation may have the opposite

effect. Goergen and Rennenboog (2011) review research on optimal contracts versus managerial

rent extraction and find more empirical support for the latter. For example, Denis, Hanouna, and

Sarin (2006) show that incentive compensation has a dark side that results in increased risk

taking, resulting in CEOs maximizing their own wealth, sometimes to the detriment of

shareholders. Bebchuk and Fried (2004) suggest that certain executive compensation contracts

can result in rent extraction from shareholders. Stealth compensation may be one form of rent

extraction by motivating managers to obtain additional benefits for themselves by increasing

dividend payouts instead of engaging in more value enhancing activities. Larger dividends

payouts will be detrimental to shareholders if these payments are not sustainable, and if

potentially positive, albeit risky, NPV projects are turned down instead of being funded. Finally,

paying dividends on restricted stock would be preferable to managers if they are entrenched (due

to weak governance), or risk averse because they are desirous of “the quiet life” (see Bertrand

and Mallainaithan (2003). It is worth noting that equity compensation (by itself) was developed

to minimize this kind of behavior. Based on this, we identify three specific research questions

below to try to determine whether stealth compensation alleviates or exacerbates agency issues

2.2.1 Individual Research Questions

The board of directors serves as the primary internal monitoring mechanism to protect the

interests of shareholders by aligning management interests with those of the shareholders. The

7

effectiveness of the board’s efforts can have a considerable effect on shareholder value,

depending on the quality of governance. As a result, studies have looked at factors affecting

governance quality. Among these are board size, share ownership structure, entrenchment

mechanisms and corporate social responsibility/transparency. All of these can bear on the use of

stealth compensation as an alignment mechanism.

With respect to board size, there are conflicting views as to how board composition

affects monitoring and thus performance. Earlier governance papers show that board

composition (the size of the board and percentage of insiders on the board) is related to the

degree of agency problems (Core, Holthausen, and Larcker (1999), Hermalin and Weisbach,

(1991), Yermack (1996)). The traditional literature implies that firms with small boards and a

higher percentage of outsiders will be more concerned about shareholder welfare and firm

performance. However, there is emerging literature which suggests that large boards may not

always be bad. Cheng (2008) finds that it takes more compromises for a larger board to reach

consensus, so decisions of larger boards are less extreme, leading to less variable corporate

performance. Larger boards also bring greater opportunity for more links to the external

environment, especially in unstable economic periods, and hence access to resources that may

improve corporate performance and reduce uncertainty (Korac-Kakabadse, Kakabadse, and

Kouzmin (2001), Platt and Platt (2012) find that larger boards are best positioned to help a firm

remain out of bankruptcy. Companies with more effective board monitoring based on board size

may offer stealth compensation to better align managers and shareholders. Conversely, weak

boards may allow the payment of this extra compensation which increases managers own private

benefits.

Research has shown that ownership structure, both institutional and insider, also plays a

role in the monitoring and governance of a firm. Institutional investors have a much stronger

incentive to monitor companies that they own than individual investors because of their larger

stakes in those companies. Hawley and Williams (2000) provide evidence that the institutional

investors’ fiduciary duty facilitates their attraction to companies with good governance

mechanisms. Bushee and Noe (2000) suggest that institutional investors prefer firms with better

disclosure rankings to reduce monitoring costs. Chung and Zhang (2011) find that institutional

investors will invest more in companies with fewer agency issues. Institutional investors have

problems with firms where economic and voting rights of insiders are not aligned. For example,

8

Giannetti and Simonov (2006) suggest that institutions are reluctant to hold shares of companies

where insiders have a high ratio of control to cash flow rights. Li, Ortiz-Molina, and Zhao (2008)

show that institutions avoid investing in companies with dual-class shares. This literature

suggests that when a discrepancy between the principal shareholder’s cash flow and control

rights exists, the outsiders may view their interests as not being aligned with those of insiders. By

encouraging management to increase dividend payouts, stealth compensation may be a tool used

by the board to try to align insiders’ and outsiders’ incentives.

A number of recent papers confirm the governance role of entrenchment and its effect on

firm performance/shareholder value. For example, Gompers, Ishii, and Metrick (2003) and

Bebchuk, Cohen, and Ferrell (2009) show that firms with relatively more anti-takeover

provisions or weaker shareholder rights have lower valuations. Firms with fewer entrenchment

mechanisms may view stealth compensation as a way to reduce the agency costs of excess free

cash. Conversely, firms with more anti-takeover measures may not care about shareholder

concerns from using the cash flow to pay stealth dividends.

In addition, there is evidence that corporate social responsibility (CSR) is connected to

the quality of corporate governance. Jo and Harjoto (2011) suggest that CSR is an extension of

firms’ efforts to foster effective corporate governance by promoting accountability and

transparency. This results in a positive link between CSR, firm governance and firm

performance. Firms that are more socially responsibly are likely to view stealth compensation as

reducing transparency and the quality of governance. On the other hand, the use of stealth

compensation would be consistent with firms with a lower commitment to CSR and

transparency. The various factors associated with governance quality discussed above lead to our

first research hypothesis:

Q1: Is the use of stealth compensation related to the quality of governance?

As noted earlier, under Jensen’s free cash flow argument (1986), increasing the dividend

or repurchase payout ratios should help reduce agency issues by making it less likely that excess

cash flow will be used on value-destroying projects. If stealth compensation exacerbates agency

issues, we would expect that the use of stealth compensation would be associated with an

increase in dividend payouts and a decrease in repurchase payouts. The former immediately

benefits managers through increased compensation, while the latter may not provide immediate

benefits. On the other hand, for firms with value reducing agency issues, stealth compensation

9

may push managers to favor larger dividend payouts that they otherwise would not want. From

the shareholders’ perspective, increasing dividends (which are difficult to rescind) compared to

repurchase programs, can be a better way to align their interests with those of management.

More formally stated:

Q2: Is the use of stealth compensation positively related to the dividend payout decision

and negatively related to the repurchase decision?

From an agency theory perspective, incorporating incentives such as restricted stock as

well as options into managerial compensation should have the desired effect of motivating

managers to maximize shareholder wealth (Murphy (1993)). Following this line of reasoning,

incentive compensation is driven by economic determinants that are aligned with shareholder

interests and not by poor governance that allows rent-seeking managerial behavior. If this is the

case, paying dividends on RSGs as a form of compensation should lead to a dividend payout

decision that maximizes shareholder wealth.

Q3: Does stealth compensation enhance shareholder wealth? 3. Data

In the annual proxy statement, compensation for the five highest-paid executives is

broken out by categories: cash, bonus/short-term incentive compensation, and long-term

incentive compensation. The latter includes stock awards, stock options, and other compensation.

Both stock awards and options are used to incentivize management to maximize long-term

shareholder value (at least in theory). From 1994 to 2003, boards of directors tended to use stock

options as the principal incentive for management. However, following excessive risk taking

during the late 1990s and the enactment of the Sarbanes-Oxley Act (SOX) in July 2002,

restricted stock grants have increased considerably. Restricted stock comes in two types:

outright grants and performance-related grants. Outright grants vest after a number of years,

while the performance-related grants require certain financial metrics to be met in order to vest.

Restricted stock is not transferable (i.e., saleable) until it vests.

Based on the SEC disclosure rules, public companies can hide information about the

payment of dividends on restricted stock in the fine print of the proxy statement. Instruction 4 to

Item 402(b)(2)(iii)(C) of Regulation S-K (1992) provides that when executives receive dividends

on restricted stock, the firm’s Summary Compensation Table will include a footnote to the

10

Restricted Stock Award column describing when the dividends are paid on restricted shares.2

Moreover, if they determine that this information is not material, they do not have to include it in

the narrative discussion accompanying the compensation tables. In a September 30, 2008 report,

RiskMetrics found that 32% of S&P 500 firms paid dividends on unvested restricted stock. They

noted that some companies interpret the disclosure rules as permitting them to avoid disclosing

the amount of dividends paid on restricted stock as part of executive compensation. As a result,

many firms do not report this compensation outright, although in footnotes they report the

number of RSGs, and how dividends (if any) are treated on those shares. The treatment of

dividends varies, even across dividend-paying firms. Some firms allow dividends to be paid as

soon as they are awarded, while others allow dividends to accumulate (in either cash or

additional restricted shares) and be paid when vesting occurs. Allowing dividends on restricted

stock becomes another form of compensation.

We identify a sample of S&P 500 companies over 2003 to 2007 that pay dividends on

unvested restricted stock. We use this time period for three reasons. First, there is no investor

tax preference between dividends and capital gains from stock repurchases. The enactment of the

Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA) cut the personal tax rate on

dividend income from 38.6% to 15%, and reduced the top rate on long-term capital gains from

20% to 15%. The reduction of dividend income was retroactive to January 2003, while the

reduction in the capital gains tax applies to transactions after May 5, 2003. 3 Second, we end our

analysis in 2007 as a structural change in the economy occurs after that year. The intensification

of the financial crisis led some firms to cut dividends in response, so we don’t want the impact of

the crisis to affect our results. For those S&P 500 companies that pay dividends on unvested,

nonperformance-restricted stock, we determine the proportion of cash and bonus compensation,

and total compensation that these dividend payments represent. Since there is no threshold of

firm performance that has to be met, dividends on these RSGs are automatic. Given the weak

2See Securities and Exchange Commission, “Executive Computation Disclosure,” 57 FR 48126, October 21, 1992, and Securities and Exchange Commission, “Executive Compensation and Related Person Disclosure,”71 FR 53158, September 8, 2006. 3Under U.S. Tax Code, Section 83(b), the person granted restricted stock can elect to pay the tax on the grant up front (within 30 days of the grant). The advantage in doing this is that dividends are treated as dividend income (versus ordinary income without 83(b)) and any gain on the stock is taxed as a long-term capital gain (assuming the stock is held for more than a year and is sold after vesting). Since most firms do not outright report whether 83(b) is chosen, we assume that all the CEOs in our sample take the 83(b) election, which provides an outside estimate of the impact of stealth compensation.

11

reporting requirements, these dividends represent one form of stealth compensation. We also

examine this dividend compensation in relation to the quality of governance measures, the

degree of institutional ownership, and operating and stock market performance.

Using proxy statements, we hand collect information about restricted stock grants in

order to determine the following:

a. Are dividends paid on unvested RSGs for CEOs? (If a company has more than one CEO

in a particular year, we use the CEO who was in office for the greatest portion of the

year.)

b. Are there voting rights on unvested RSGs for CEOs?

c. Do the dividends accumulate on RSGs, and are they paid out when the RSG vests?

d. If the dividends accumulate, is interest paid on this amount? Does the company issue

more RSGs in lieu of cash?

e. Is the treatment of dividends for directors’ RSGs the same as for CEOs’?

f. Is the treatment of dividends for other named executives officers’ (NEOs’) RSGs the

same as for CEOs’?

g. How many years does it take for RSGs to vest?

We are able to collect this information for 482 S&P 500 companies. The number of

dividend-paying companies varies by year. In the few cases where there is ambiguity about

whether dividends are paid on unvested RSGs, we eliminate those observations from the sample.

If a firm does not pay dividends in any particular year, it is dropped from the sample for that

year.4 We refer to firms in our sample that pay stealth compensation to the CEO as stealth firms,

and to those firms that do not as non-stealth firms. Overall, our final sample has 1,834 firm

years for which we have full data.5

4. Results

4.1 Univariate estimations

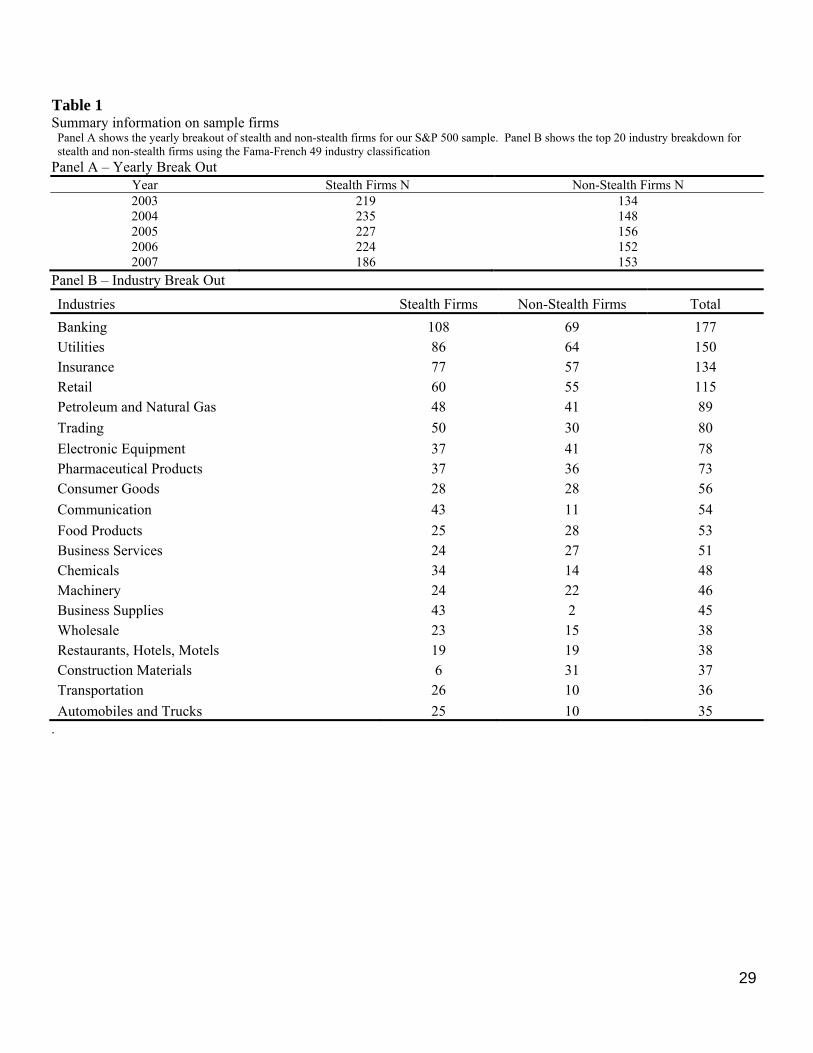

Table 1, Panel A shows the breakout of stealth and non-stealth firms by year. In 2003,

62% of the sample firms paid dividends on unvested RSGs, falling to 55% by 2007. Table 1,

Panel B shows the top 20 industry classifications for our sample using the Fama-French 49

4Our results remain qualitatively the same if we include all firms, including those that do not pay dividends. 5651 of the firm year observations do not have any CEO RSG holdings. Of the 651 observations, 444 are non- stealth firms.

12

industry classification. Our industry breakdown is similar to the general composition of the S&P

500 - the top industries in our sample are banking, utilities, insurance, energy, retail,

manufacturing and technology. Our results remain qualitatively unchanged if we exclude

financial service and utilities. Table 2 provides a summary of data that was hand collected from

proxy statements. Out of 1,091 firm years, 91% of the firms grant voting rights on RSGs, while

for the 743 non-stealth firms, 81% grant voting rights. Additionally, 12% of the stealth

companies allow dividends to be accumulated, which are then paid after vesting and 10% get

interest on the accumulated dividends. Note that 21% of the stealth firm CEOs receive more

RSGs instead of a cash dividend. We find that 80% of directors and 98% of other NEOs receive

the same treatment as the stealth firm CEOs with respect to dividends on RSGs. Finally, the

average time for restricted stock grants to vest is 4.76 years for stealth firms compared to 4.02

years for non-stealth firms; the typical vesting period is three years.6

Next, we examine payout variables, including DPS (dividends per share), PAYOUT (the

total amount of dividends paid divided by net income), DIV/MV and DIV/ASSETS (total

dividends paid divided by market value of equity and by book value of total assets, respectively),

and REPAMT (dollars spent on repurchases minus any decrease in the par value of preferred

stock, divided by the market value of equity). All measures are taken from COMPUSTAT.

Other firm-specific factors that may affect payout policy include G (the moving average

of earnings growth over 20 quarters, following Ferreira and Santa-Clara (2011)), CASHFLOW

(net income plus depreciation and amortization), DEBTRATIO (long-term debt as a percentage of

market value of equity), ASSETS (book value of total assets), SIZE (the logarithm of market

value of equity), WC (working capital scaled by market value of equity), CAPEX (capital

expenditures divided by market value of equity), ROA (net income scaled by total assets), and

BKMK (the ratio of book value of equity to market value of equity). Market value of equity is at

year end. Many of these variables are also employed by Aboody and Kasznik (2008). Table 3

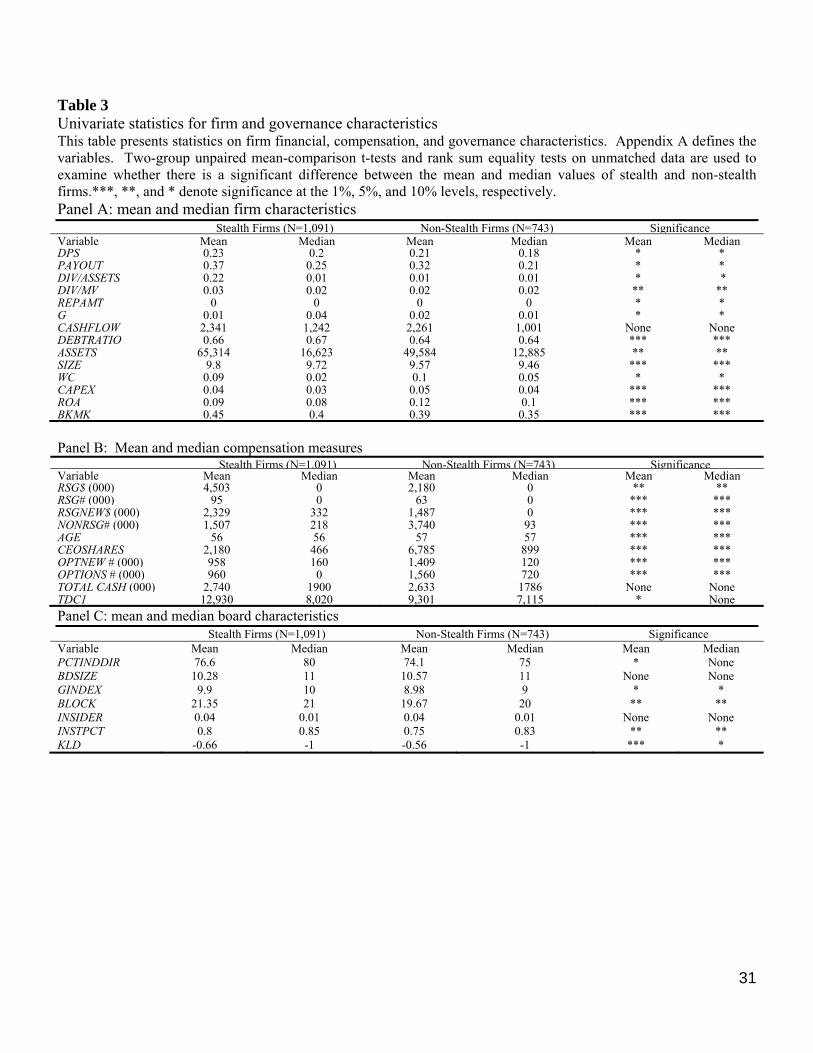

summarizes firm characteristics for all firms over all time periods for our sample.

In Panel A, we show firm payout, operating and market-based characteristics. The first

group of columns represents stealth firms, while the second group is for non-stealth firms. We

find that for all of the dividend measures, the means are modestly significantly higher for stealth

6 http://www.mystockoptions.com/faq/index.cfm/catID/AE9F69E6-3097-43BD-B15BE00AA8F1761C/objectID/D943A157-30A9-11D4-B9080008C79F9E62

13

firms than for non-stealth firms (except for DIV/MV), where the mean is significantly higher at

the 5% level). For the repurchase measure, stealth firms spend modestly, significantly more than

non-stealth firms. Stealth firms have significantly lower mean earnings growth (1%) than non-

stealth firms (2.4%). We find stealth firms and non-stealth firms have similar cashflow, but

stealth firms have a higher debt ratio. Stealth firms are also significantly larger in terms of assets

and market value. Stealth firms have significantly lower working capital and capital

expenditures. Additionally, stealth firms are less profitable based on return on assets, and have

higher ratios of book to market value, indicating lower growth opportunities (both significant at

the 1% level). Overall, the results are consistent with what one would expect for firms with high

dividends.

Panel B summarizes CEO compensation characteristics for the sample of stealth firms

and non-stealth firms, including RSG$ (dollar amount of RSG holdings), RSGNEW$ (dollar

amount of newly granted RSGs), RSG# (the number of RSG shares held by the CEO),

NONRSG# (number of unrestricted share grants), OPTNEW# (the number of new options

granted), and OPTIONS# (the number of options). The results indicate that CEOs of stealth

firms have a significantly greater dollar amount of new grants, and more RSG holdings in both

dollar amount and number of shares. Since stealth firms have lower growth rates and fewer

growth opportunities, these firms may have an incentive to use restricted stock versus options to

reward management. Moreover, lower growth should result in lower stock price appreciation, so

boards can additionally augment their CEOs’ income by allowing stealth compensation. The

results also show that in lieu of RSGs, CEOs of non-stealth firms receive more unrestricted stock

grants and options (significant at the 1% level). Total cash compensation and total compensation

from all sources are similar for both types of firms.

In Panel C, data on governance characteristics is presented for stealth and non-stealth

firms, including PCTINDDIR (the percent of independent directors on the board), and BDSIZE

(the number of directors on the board). We also use two different measures of firm level

governance, the GINDEX and the KLD index. The GINDEX is computed from the Gompers,

Ishii, and Metrick (2003) index of 24 anti-takeover governance provisions (derived from

publications of the Investor Responsibility Research Center) which appear to be beneficial to

management and harmful to shareholders. The KLD index, provided by Kinder, Lydenberg,

Domini, & Co., has been shown by Hong and Kostovesky (2012) to be a good proxy for a

14

company’s corporate social responsibility (CSR). The KLD index also provides transparency

about past and likely future corporate governance performance in that there is a positive link

between CSR, firm governance and firm performance. In the index, corporate governance

concerns are subtracted from corporate governance strengths. Strengths include: Limited

Compensation, Ownership Strength, Transparency Strength, Political Accountability Strength

and Other Strengths. Concerns include High Compensation, Accounting Concern, Transparency

Concern, Political Accountability Concern, and Other Concerns. For each area of strength and

concern, a company gets a one if it is applicable and zero otherwise.

Finally, we look directly at several dimensions of ownership, including institutional

ownership, and insider ownership. We measure institutional ownership as the percent of shares

held by institutions scaled by the total shares outstanding from Thompson Financial 13D filings

(INSTPCT). Using the definition of blockholders in Buchanan, Netter, Poulsen, and Yang

(2012), we count the number of institutional owners in the firm who hold more than 1% of the

equity, and call this BLOCK (similar results are obtained using a 5% threshold). We measure

insider ownership, INSIDERPCT, as executive and director share ownership divided by total

shares outstanding.

The mean percentage of independent directors for stealth firms is 76.6% vs. 74.1% for

non-stealth firms (significant at the 10% level). Board size does not significantly differ between

the groups. However, when comparing various governance and entrenchment measures, we find

that stealth firms have significantly worse governance. On average, stealth firms have

significantly higher anti-takeover provisions compared to non-stealth firms. The KLD index is

also significantly worse for stealth and non-stealth firms (-0.66 versus -0.56). However, stealth

firms tend to have significantly higher institutional ownership and more block holders than non-

stealth firms. In answer to our first research question, these results suggest that the quality of

governance, as well as the make-up of shareholders plays a significant role in the use of stealth

compensation.

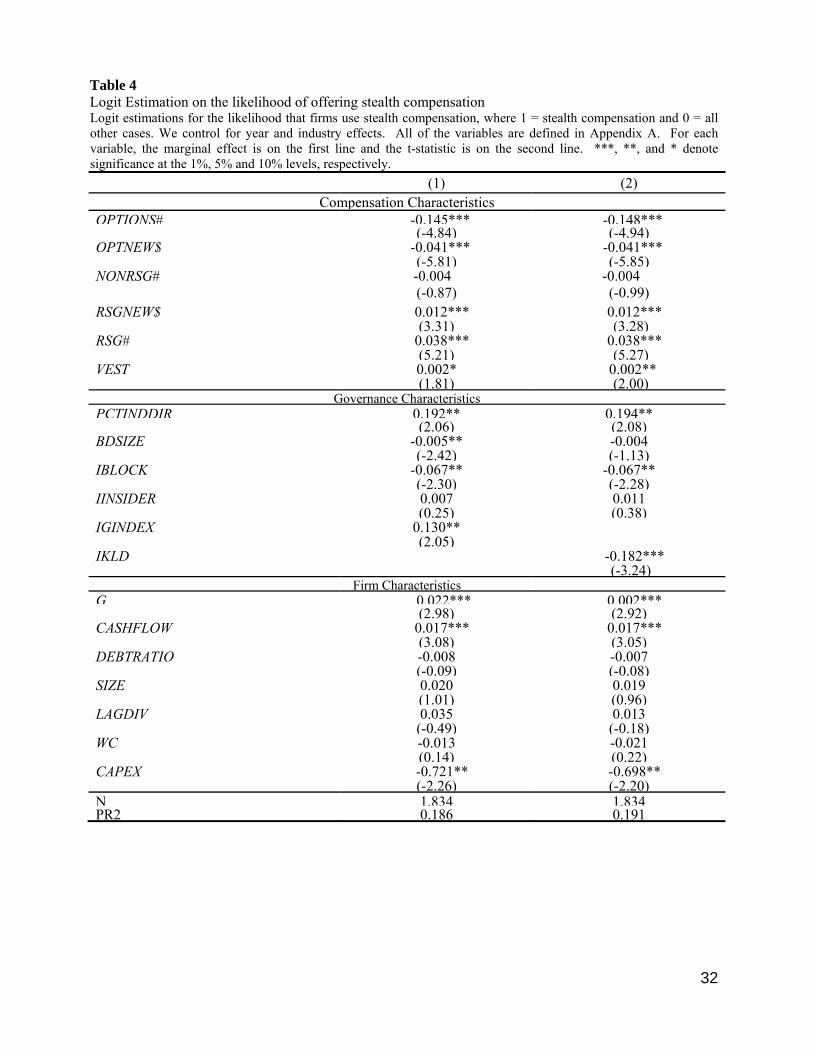

4.2 Logit estimations

We next run multivariate tests, so we first examine the correlations between our

independent variables. None of the governance variables are highly correlated, which suggests

that multicollinearity will not be a problem in our multivariate estimations (correlation tables are

available upon request). We are interested in seeing the particular firm, compensation, and

15

governance characteristics that increase the likelihood that a company will offer its executives

stealth compensation. We run the following logit estimation and report the marginal effects:

STEALTH = b0 + b1-8COMPVARS + b9-13GOVVARS + b14G + b15CASHFLOW +

b16DEBTRATIO + b17SIZE + B18LAGDIV + b19WC + b20CAPEX + ε (1)

where STEALTH is an indicator variable that is equal to one if the firm uses stealth compensation

and zero otherwise. Our firm-specific variables are detailed in Appendix A. COMPVARS are

RSGNEW$, RSG#, NONRSG#, OPTNEW#, OPTIONS#, and VEST (the number of years until

RSGs vest, on average). GOVVARS include the controls PCTINDDIR and BDSIZE. We also

create governance indicator variables, IBLOCK, IINSIDERPCT, IGINDEX and IKLD, that are

equal to one if the variable of interest is in the upper tercile based on the values in a particular

year, and zero otherwise. Additionally, we control for year and industry effects.

The results in Table 4 suggest that executive compensation plays a meaningful role in the

likelihood that stealth compensation is used. Firms which grant new options and which have

options outstanding are significantly less likely to offer stealth compensation to its executives.

The opposite is true for firms with restricted stock, in terms of new grants and restricted shares

held. In addition, the longer the vesting period of the RSGs, the greater the likelihood of stealth

compensation.

There appears to be a connection between stealth compensation and various governance

mechanisms. For example, companies with greater independent director representation have an

increased likelihood of using stealth compensation. Conversely, larger boards are less likely to

use this form of compensation, although only significant in estimation (1). Institutional

ownership also plays an important role in the use of stealth compensation. Companies with a

greater number of blockholders are less likely to engage in stealth compensation. Looking at the

first governance indicator variable, shown in Column 1, the predicted probability of using stealth

compensation is 0.13 greater for firms with high anti-takeover provisions (IGINDEX equal to one)

compared to those with low anti-takeover provisions. For the second indicator variable, shown in

column 2, firms with good governance (IKLD equal to one), the predicted probability of using

stealth compensation decreases by 0.182. (One has to keep in mind that there is a positive

relationship between KLD rating and good governance.)

16

Thus, we have mixed results regarding whether stealth compensation is associated with

agency issues. On one hand, companies with a board composition associated with good

governance are more likely to allow stealth compensation, suggesting that its use is associated

with reducing agency issues. On the other hand, companies with less outside monitoring, more

anti-takeover provisions, and worse social governance rankings are more likely to use stealth

compensation. These results suggest a positive association between agency issues and stealth

compensation. It may be that firms with good as well as with poor governance both use stealth

compensation for differing motivations. Smaller, more independent boards may use stealth

compensation as a way to motivate managers to disgorge excess cash. However, managers at

companies where there is low oversight by outside investors, whose hand may be tied by more

anti-takeover provisions or shareholder apathy, could use the stealth compensation as a way to

increase their own compensation.

Finally, there are some firm characteristics that are significantly associated with the use

of stealth compensation. Firms with high growth and high capital expenditures are less likely to

do so, while firms with high cash flow are more like to engage in stealth compensation.

4.3 Compensation Received from Stealth Compensation

From the univariate results, stealth firms appear to be different than non-stealth firms.

However, the choice to pay dividends on unvested RSGs is not important if the amount of money

that CEOs receive is not economically significant. In Table 5, we measure on a yearly basis how

much additional compensation CEOs of stealth firms receive from dividends versus how much

CEOs of non-stealth firms would have received if they were paid dividends on unvested RSGs

(calculated by multiplying the number of grants by the DPS). CEOs of stealth firms receive

$180,200 per year (on average) in additional income, whereas the CEOs of non-stealth firms

would have only received an additional $96,000. The maximum additional amount in dividends

is $4,340,000, which is not reported in the table. Over the period of this study, the average

amount of stealth compensation represents 9% of all cash compensation and 2% of total

compensation. Both of these percentages are significantly greater than what would have been

received by CEOs of non-stealth firms. The amount of dividends paid increases considerably

over the sample period. In 2003, stealth firms CEOs received almost $129,000 versus only

$52,000 for non-stealth firms. This increased to $263,000 for stealth firms and $238,000 for

non-stealth firms by 2007. It is particularly interesting to note the increased use and size of

17

stealth compensation over time. In 2003, dividend compensation was only 5% of cash

compensation, but rose to 20% by 2007 for stealth firms.

Dividends on unvested RSGs appear to be economically meaningful. In order to better

understand the economic significance and effect of agency issues that may arise from stealth

compensation, we run the following regression:

DIVCOMP =b0 + b1STEALTH + b2-7COMPVARS + b8-12GOVVARS + b13G +

b14CASHFLOW + b14CASHFLOW + b15DEBTRATIO + b16SIZE +

b15LAGDIV + b16WC + b17CAPEX + ε (2)

where DIVCOMP is either dividend compensation scaled by total cash compensation or TDC1.

COMPVARS are RSGNEW$, RSG#, NONRSG#, OPTNEW#, OPTIONS#, and VEST. GOVVARS

include PCTINDDIR, BDSIZE, IBLOCK, IINSIDER, IGINDEX, and IKLD.

The results in Table 5 show that controlling for firm characteristics, CEOs of stealth

firms receive more dividend compensation. For firms offering stealth compensation, there is a

9.6% and 2.1% increase in dividend compensation adjusted by total cash and total compensation,

respectively. We also find that an increase in option compensation (both existing and new

grants) decreases dividend compensation, while new restricted stock grants, and current RS

holdings increase dividend compensation. Examining governance characteristics, we find that

only block ownership and the governance quality indexes affect the amount of dividend

compensation. It is worth noting that although block ownership reduces the likelihood of

offering stealth compensation, there is a positive relation between block ownership and dividend

compensation. A higher GINDEX (where a high value can be interpreted as poor governance) is

also positively related to higher dividend compensation, while there is a negative relationship

between KLD (where a high value can be interpreted as good governance) and dividend

compensation. Based on these results, it is possible that companies with more institutional

ownership use increased dividend income (higher dividends) to reduce agency issues related to

free cash flow. However, CEOs along with the boards of companies with higher managerial

entrenchment and worse governance may also use stealth compensation to increase their own

compensation.

The results from Table 5 suggest that dividend compensation could influence decisions

with respect to dividend policy. As noted earlier, companies that use stealth compensation have

18

higher dividend payouts than companies that do not. Next, we use multivariate analysis to test

whether this result still holds when controlling for other firm characteristics.

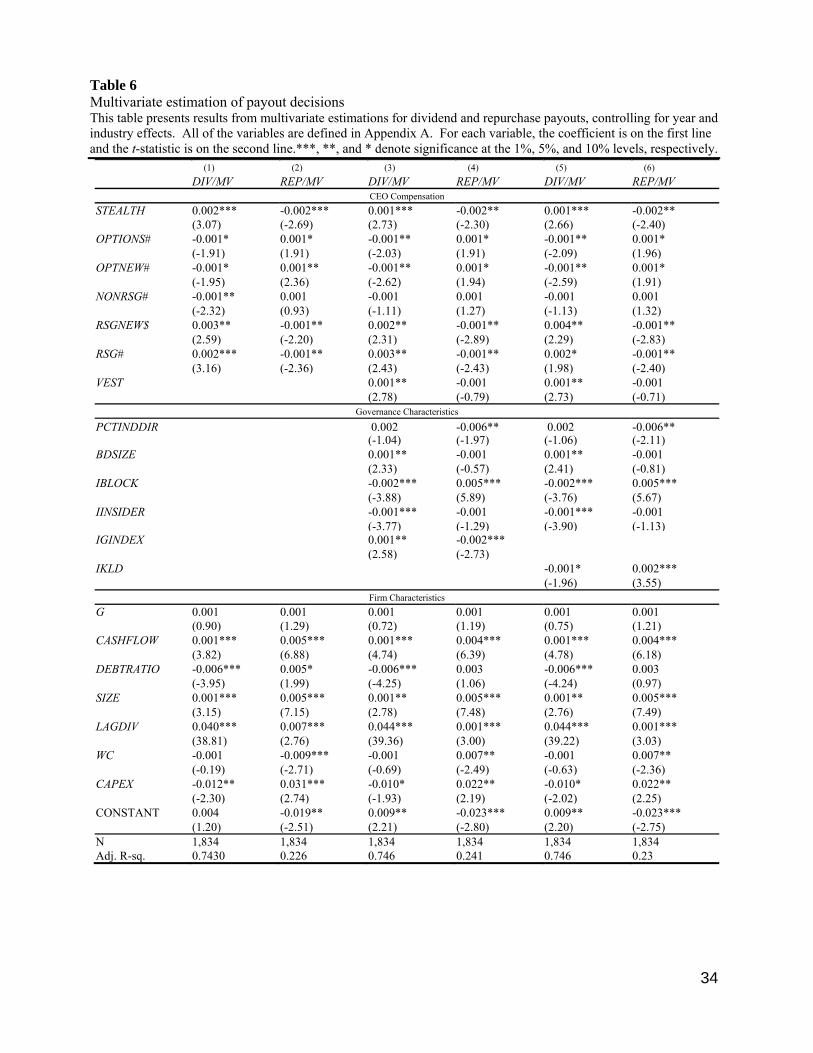

4.4 Payout Estimations We use a model similar to Aboody and Kasznik, and regress two payout measures, on

variables related to stealth compensation, governance, and control variables:

PAYOUT = b0 + b1STEALTH + b2-7COMPVARS + b8-12GOVVARS + b13G +

b14CASHFLOW + b15DEBTRATIO + b16SIZE + b15LAGDIV +

b16WC + b17CAPEX + ε, (3)

where PAYOUT is either: total dividends scaled by market value of equity (DIV/MV) or the

dollar amount spent on repurchases minus any decrease in the par value of preferred stock,

divided by the market value of equity (REP/MV). All other variables are defined in Appendix A.

The results are shown in Table 6.7

The stealth variable is highly positively related to all of the dividend measures and highly

negatively related to repurchases (significant in all cases at the 1% level). Stealth firms pay 0.2%

more dividends and make 0.2% fewer repurchases. Considering the average dividend payout is

2.3%, and repurchase payout is 0.4% over our sample period, this result is economically

significant. Thus, in answer to our second research question, stealth firms pay higher dividends

and repurchase fewer shares.

New option grants as well as option holdings are positively and significantly related to

repurchases, but negatively related to dividend payouts. As Fenn and Liang (2001) suggest,

increases in repurchases may offset option-induced reductions in dividends so that total payouts

remain relatively constant. Firms where CEOs have larger non restricted grants pay significantly

lower dividends. Our results on RSGs are consistent with Aboody and Kasznik (2008). The

dollar amount of new RSGs is positively related to dividends measure and negatively related to

repurchases. The same relationship holds for the number of RSGs held by the CEO. Finally,

vesting is positively and significantly related to the dividend measures, but not related to

repurchases.

In examining board structure, we find that larger boards have a significant positive

relationship with dividends, while the percent of independent directors is significantly,

7 We use a Tobit model instead of a robust OLS model with qualitatively similar results. Additionally, we use dividend per share, payout ratio, and total dividends/assets as a dependent variable with qualitatively similar results.

19

negatively related to repurchases. A one standard deviation change in board size would increase

the dividend payout ratio by 0.065%, while a one standard deviation change in director

independence would reduce repurchases by 0.08%. An increase in institutional block holders

has a highly significant effect on payout, decreasing dividends by 0.2% while increasing

repurchases by 0.5%. These results are consistent with Grinstein and Michaely (2005) who find

that institutions do not prefer firms that pay high dividends but like firms that repurchase shares

more regularly. We also find that greater insider ownership reduces dividends by 0.1%, which is

consistent with Rozeff (1982), who finds that dividend payouts are negatively related to insider

stock holdings. He argues that insider stock ownership provides direct incentive alignment

between managers and shareholders, while dividends serve as a bonding mechanism to reduce

management's scope for making unprofitable investments using internal funds. Thus, insider

stock ownership and dividend policy can be viewed as substitute means of addressing potential

agency problems. Finally, the results from our governance indexes (both IGINDEX and IKLD)

show that poorer governance is associated with a 0.1% increase in dividend payouts and a 0.2%

decrease in repurchase payouts. This is consistent with Knyazeva (2007), who finds that weakly

governed managers make fewer dividend cuts and engage in more dividend smoothing.

The variables measuring firm-specific characteristics show the expected signs. Not

surprisingly, higher cash flow is positively and significantly related to both dividends and

repurchases. Jensen (1986) also contends that higher debt reduces the free cash flow problem,

suggesting that highly levered firms have less cash to pay out to shareholders, which we also

find. Firm debt ratio is positively related to repurchases, but only significant in one case. Firms

may be constrained by loan/bond covenants from raising dividends, but are known to borrow so

that they can repurchase shares, which would result in the signs of the coefficients we observe.

Similar to Fama and French (2001), firm size is positively and highly significantly related to all

dependent variables. Lagged dividends are significantly and positively related to current

dividend measures, but not related to the repurchase measure (except in one case). We find that

working capital is not related to dividend payout but is generally positively related to

repurchases. CAPEX is negatively related to dividends, but is positively related to repurchases. It

is possible that companies that want to conserve their cash flow for working capital investment

and capital expenditures may prefer to use repurchases over dividends.

20

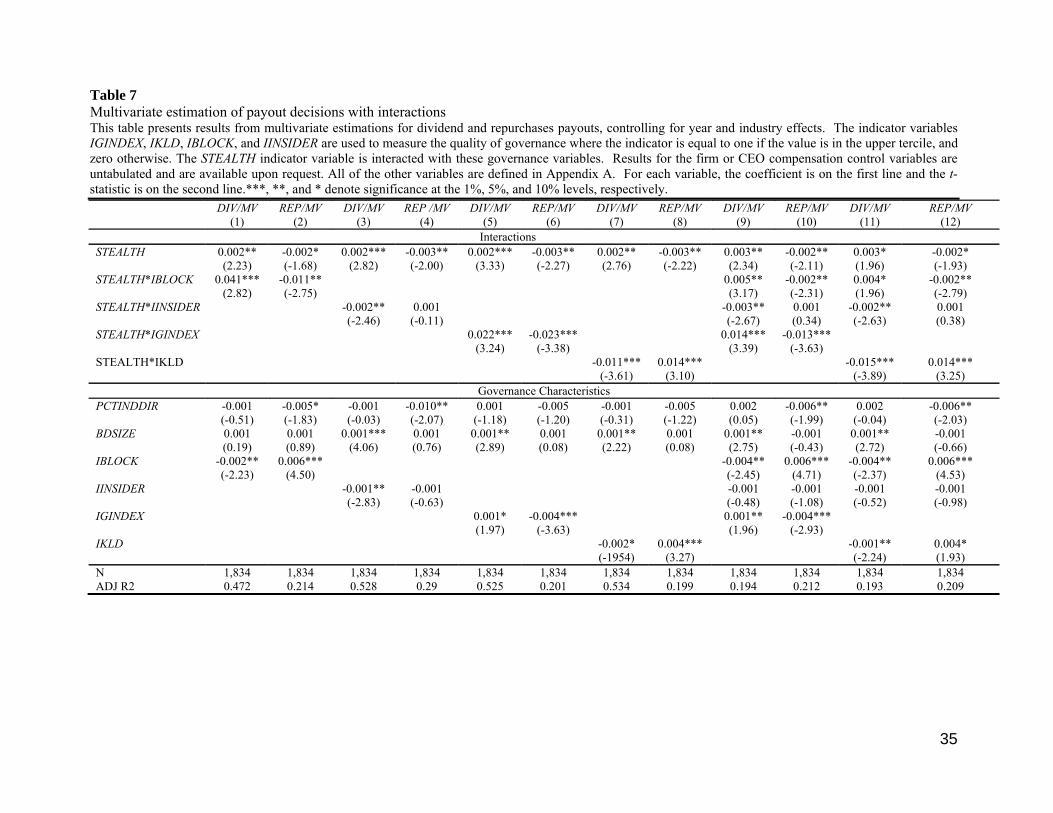

Next, we examine the interactions of governance, ownership, and stealth compensation in

Table 7. From previous tests, we know that greater block ownership reduces the likelihood of

paying stealth compensation as well as the likelihood of dividend payouts. However, the

coefficient on the interaction between block ownership and stealth is positive. A company with

high block ownership, but no stealth compensation experiences a 0.2% decrease in dividend

payout and a 0.6% increase in repurchase payout (columns 1-2). On the other hand, if a firm has

high block ownership and stealth compensation, there is a 4.1% increase in dividend payout and

a 0.7% decrease in repurchases (based on adding the coefficients on STEALTH, IBLOCK, and

the interaction term). The higher payout for stealth firms which have block ownership may

possibly be the result of the block holders preferring dividends to counteract the agency issues

associated with high free cash flow. Since Rozeff (1982) suggests that insider ownership better

aligns managers and shareholders, we next examine whether this relationship holds in the

presence of stealth compensation. As before, we find that companies with stealth compensation

have significantly lower dividend payouts when there is high insider ownership (columns 3).

Finally, to determine whether stealth compensation potentially reduces or increases agency

issues by creating an incentive to increase payouts, we look at the interactions with GINDEX and

KLD (quality of governance indicators). From columns 5-8, we find that poorly governed

companies without stealth compensation increase their dividends by 0.1% to 0.2% (GINDEX and

KLD, respectively), while repurchases increase by 0.4%. However, poorly governed companies

that also have stealth compensation significantly increase their dividend payouts by as much as

2.5% (GINDEX) and 1.1% (KLD), respectively) and decrease their repurchase payouts by as

much as 3.0% (GINDEX) and 1.5% (KLD), respectively.

To better understand how all of these interactions relate to each other, in columns 9-12,

we look at joint estimations involving blockholding, inside ownership and quality of governance.

We find that the governance interactions, with both GINDEX and KLD when coupled with

stealth compensation, show the largest effect on dividend payout (in absolute terms) of all the

joint estimations, We run a Wald test to examine whether there is a significant difference

between the coefficients on STEALTH*IGINDEX (IKLD) and the other interaction terms, and

find that they are significantly different at the 1% level. Overall, the results, suggests that stealth

compensation may act as an important bonding mechanism to increase dividend payouts when

there may be greater agency issues within the firm.

21

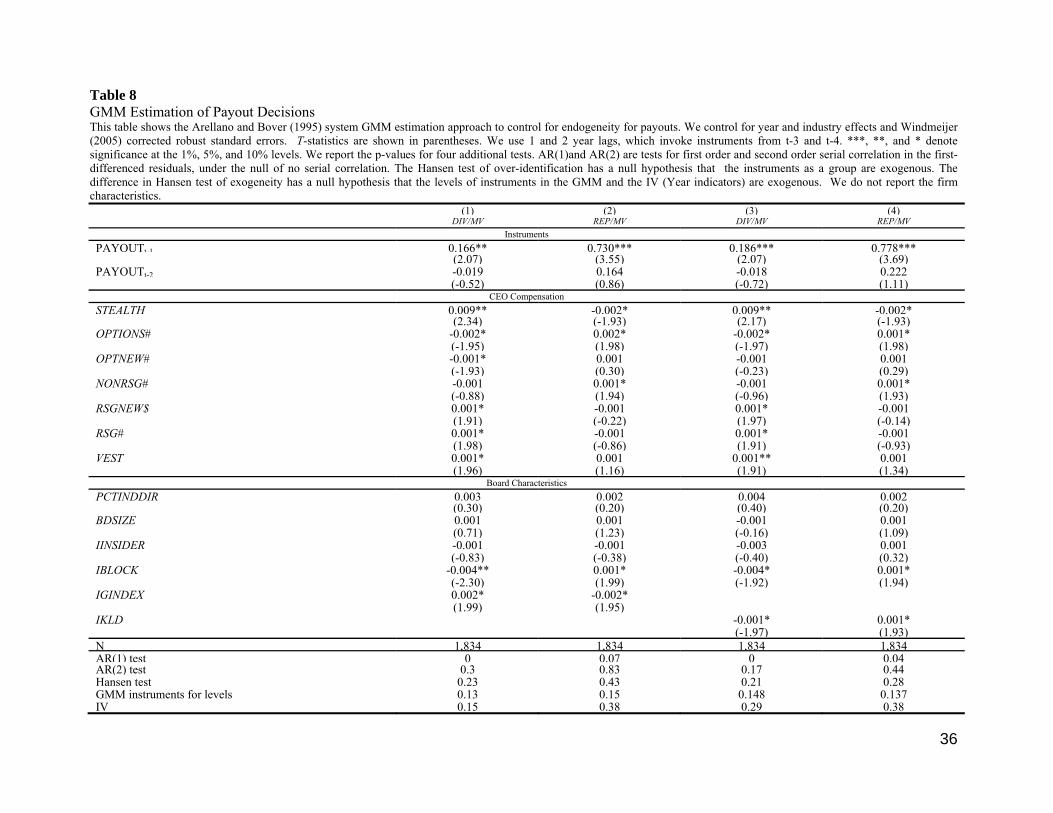

4.5 Robustness Tests

The issue of causality may exist in that stealth compensation may affect dividend policy

or that dividend policy may drive the use of stealth compensation. We employ several different

robustness tests to try to deal with the potential endogeneity concerns. It is very difficult to

determine exogenous factors to control for the relationships being studied. Linck, Netter, and

Wintoki (2012) argue that governance studies often do not control for the dynamic endogeneity

of the data which is not strictly exogenous, and changes over time due to shocks to the firm at

various points in time. Since a firm’s historical decisions can proxy for important governance

attributes such as agency issues or managerial entrenchment, it is important to control for past

decisions, which may be a major determinant of future decisions and future governance

structures. Linck et al. (2012) suggest that the most appropriate method to control for this

endogeneity is a system GMM estimator controlling for historical factors in the form of lags in

the main variable of interest. Their results suggest that fixed effects models are biased because

these models ignore past performance and past governance choices. We test our hypotheses

using a system GMM estimator controlling for year and industry as well as the Windmeijer

(2005) correction. Since our regressor is predetermined, but may not be strictly exogenous, we

use lags of one and two years, which invokes instruments from t-3 and t-4, respectively

(Roodman (2006)). The results are shown in Table 8. We still find that companies with stealth

compensation increase their dividend payout and decrease their repurchase payout - by 0.9%

(significant at the 5% level) and by 0.2% (significant at the 10% level), respectively. The

coefficients on the compensation and governance variables are similar to what we find in Table

6, although we do lose some significance. This is consistent with Linck et al. (2012), who find

that after controlling for endogeneity, governance variables may lose their explanatory power.

We also report the results from tests of the exogeneity of our model. Our assumption is

that a firm’s historical payout policy is exogenous to changes in their current payout decisions.

We use several tests of exogeneity suggested by Arellano and Bond (1991) and Roodman (2006)

to see if our assumption of the exogeneity of payout policy is valid. First, we test for

autocorrelation, as the validity of the instrumental matrix in the Arellano-Bond (AB) estimator

depends on having no autocorrelation. The initial step in the AB estimator takes the first

difference between PAYOUTt-1 - PAYOUTt−2. We use AR (1) and AR (2) tests for first-order

and second-order serial correlation in the first-differenced residuals. Due to first-differencing in

22

the AB estimator, there can be mechanical first-order autocorrelation in the errors (thus, it is not

unusual if the AR (1) test has low p-values). The relevant test involves checking for second-order

autocorrelation in AR (2), where higher p-values are desired, as this shows there is no serial

correlation (Linck et al., 2012). The p-values reported in Table 8 for the AR tests suggest the

underlying conditional errors are not autocorrelated (the AR (1) test yields p-values between 0.00

and 0.07, and the AR (2) test yields p-values between 0.17 and 0.83).

The second step is to further check the exogeneity of the instruments by performing a

Hansen test of over-identifying restrictions. Since the dynamic panel GMM estimator uses

multiple lags as instruments, it is possible that our system is over-identified. The Hansen test has

a null hypothesis that the instruments as a group are exogenous. High p-values for the Hansen

test indicate that the null hypothesis cannot be rejected. Finally, we run two additional tests of

exogeneity of a subset of our instruments. By using a system GMM approach, we are able to

include the level equations in our GMM estimates and use lagged differences as instruments for

these levels. We test this assumption by using a difference in Hansen test of endogeneity. The

high p-values suggest we cannot reject the null hypothesis that these instruments are exogenous.

We also run a difference in Hansen test for the year IVs, and find similar p-values. The lack of

serial correlation suggests that endogeneity is not a significant concern in our approach.

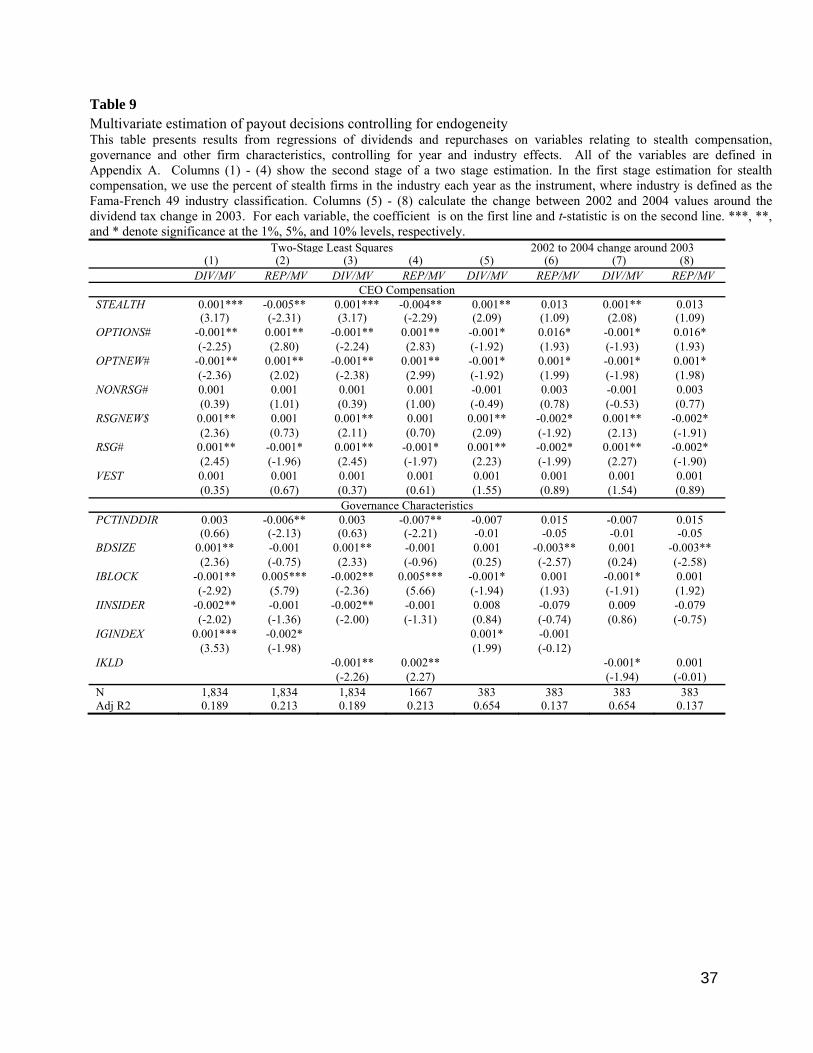

Table 9 shows additional robustness checks. In columns (1-4), we show the results from

a two-stage least squares estimation; in the first stage we regress the percent of stealth firms in

the industry each year as the instrument. We follow the method employed by John and

Knyazeva (2006), where the logic is that industry structure is unique to each industry and

therefore is expected to be exogenous. This is based on the intuition that the percent of stealth

firms in the industry is positively associated with an individual firm’s decision to offer stealth

compensation, and not likely to have a direct impact on individual payout policy. Consistent

with this argument, the percent of firms using stealth in an industry is highly significant in a first

stage regression (untabulated) predicting stealth compensation (the coefficient is 3.36 with a p-

value of 0.00). Thus, identification does not reject the null hypothesis that the instruments are

valid.8 As the table shows, we continue to find a positive relation between dividend payout and

8 First stage F statistics are above 10. The Cragg-Donald test rejects the null hypothesis of weak instruments.

23

(predicted) stealth compensation, and a negative relation between repurchase payout and

(predicted) stealth compensation.

As a final robustness check, we look at the change in dividends around the 2003

dividend tax cut in Table 9, columns (5-8). Using a change-in-change approach, we measure the

change in the payout variables, as well as firm, compensation, and governance characteristics

from 2002 to 2004. We find that companies with stealth compensation the year before the tax

cut are more likely to increase the firm’s dividends the year after the tax cut, which supports the

idea that stealth compensation influences dividend payouts but not repurchases.

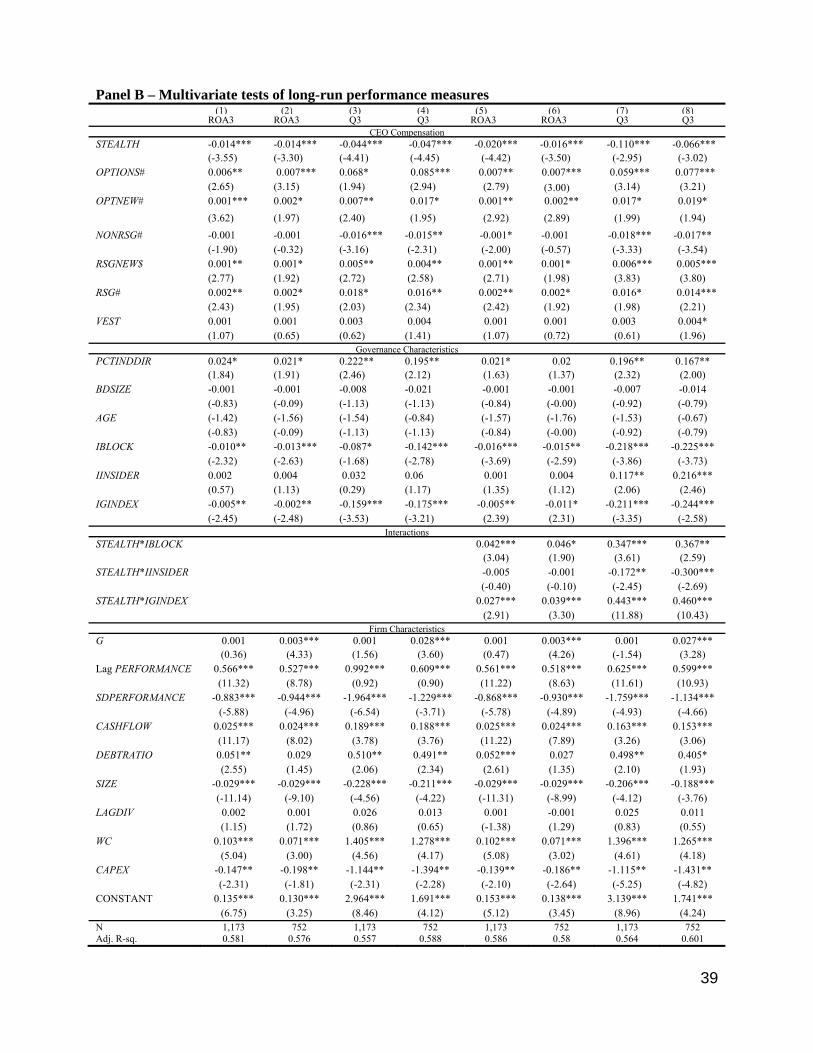

4.6 Performance and Stealth Compensation

Since the goal of management is to maximize long-term shareholder value, it would be

worthwhile to look at the impact of stealth compensation on long-term profitability. We do this

by first comparing the one- and three-year average of return on assets, and Tobin’s Q for both

groups of firms (we also use ROE but do not report it as results are qualitatively similar). Next,

to better understand whether stealth compensation improves or worsens agency issues, we

estimate the relationship between stealth compensation and subsequent firm financial

performance. Agency problems are usually associated with poorer financial performance, if not

in the short run, then in the longer run. Assuming that the use of stealth compensation reflects a

breakdown in the agency relationship, we expect to observe a negative relationship between its

use and subsequent performance. Following Core et al. (1999), we regress the one-and three-

year average of return on assets, return on equity, and Tobin’s Q on firm and governance

characteristics:

PERFORMANCE = b0 + b0 + b1STEALTH + b2-7COMPVARS + b8-13GOVVARS + b14G

+ b15CASHFLOW + b16DEBTRATIO + b17SIZE + b18LAGDIV + b19WC +

b20CAPEX + b21SDPERFORMANCE + ε (4)

where SDPERFORMANCE is the standard deviation of the performance measure (ROA or Q)

for the five years prior to when stealth compensation is paid (similar to Core et al. (1999)). In

addition to the governance variables from the other equations, we also include AGE (the age of

the CEO). All the other variables are defined following equation (3), and we control for year and

industry effects.

Table 10, Panel A, shows the univariate mean and median values of the performance

measures. It is evident that stealth firms have worse performance over the short term (one-year)

24

period as well as the longer term (three-year) period subsequent to paying stealth compensation.

Table 10, Panel B shows the results of Equation (4). We use two measures of growth. The first

measure (G) is EPS growth over the past five years. While the literature shows this to be a good

proxy for growth opportunities (see Ferreira and Santa-Clara (2011)), as a robustness check, we

also use a forward-looking measure (FUTURE G). In columns (2), (4), (6), and (8) we use the

Institutional Brokers’ Estimate System (IBES) long-term growth forecast as our second growth

variable. Note that growth is significantly positively related to performance whether historical or

forecasted growth is used. Stealth compensation is associated with a statistically significant

decline in ROA of 1.4% to 2% and a decline in Q of between 4.4% and 11% over a three-year

period. Since the average ROA for stealth firms is approximately 10%, the regression results

imply a loss of approximately 10% of the sample average ROA. We also find a negative

relationship between IGINDEX and performance, consistent with weak governance leading to

declining performance.

We include the interactions between stealth compensation and ownership, and stealth

compensation and governance. Interestingly, when a company has high block ownership but

does not have stealth compensation, the ROA declines by 1.6% (column 5). However when a

company with high block ownership offers stealth compensation, ROA increases by 0.6% and Q

increases by 1.9% (based on the net effect of STEALTH, IBLOCK and the interaction term). We

see similar results with the IGINDEX. Companies with poor governance and no stealth

compensation experience a 0.5% decline in ROA and a 21.1% decline in Q. On the other hand,

for poorly governed companies with stealth compensation, ROA and Q increase significantly by

0.2% and 12.2%, respectively (the net effect of STEALTH, IGINDEX and the interaction term).

The results suggest that the improvement in performance is markedly greater for poor

governance firms with stealth compensation than for poor governance firms without stealth

compensation. Stealth compensation may actually help alleviate some agency issues, resulting in

better long term performance.

5. Conclusion

We examine the degree to which firms pay dividends on unvested restricted stock grants

of CEOs (stealth compensation), whether it is a meaningful contributor to overall compensation

packages, if it create agency issues for shareholders and affects performance. Our sample

consists of S&P 500 firms over the period 2003-2007 that issue restricted stock and allow

25

dividends to be paid on unvested shares. This period provides a unique opportunity to examine

dividend policy since the tax treatments of dividends and share repurchases are very similar. As

a result, our results are not confounded by tax preferences of CEOs and/or directors.

Stealth firms seem to be different from non-stealth firms. The former have higher cash

flow and lower growth opportunities than the latter. Executives of firms paying dividends on

unvested restricted stock grants make an extra $180,200 a year on average from stealth

compensation, or almost 9% of cash compensation and 2% of total compensation. Stealth firms

pay significantly larger dividends than the non-stealth firms, but repurchase less. For companies

that have stealth compensation, more restricted stock grants result in higher dividend payouts,

which can result in the misalignment of management interests with those of the shareholders.

Several robustness checks on the effect of endogeneity provide overall similar results. In

analyzing the long-run effects of stealth compensation on firm performance, we find that the use

of stealth compensation is associated with a decline in performance. However, for firms with

potential agency problems, firms with stealth compensation have a meaningful improvement in

long-term performance. For firms with weak governance, stealth compensation may act as a

bonding mechanism by promoting increased dividend payouts. The results in this paper may

have policy implications for corporate decision makers. They suggest a possible means by which

weak corporate governance and agency issues arising from free cash flow can be improved by

using stealth compensation.

26

References

Aboody, D., Kasznik, R., 2008. Executive stock-based compensation and firms' cash payout: the role of shareholders' tax-related payout preferences. Rev. Account. Stud. 13, 216-251.

Allen, F., Bernardo, A., Welch, I., 2000. A theory of dividends based on tax clienteles. J. Finance 55, 2499-2536. Arellano, M., Bond, S. 1991. Some tests of specification for panel data: Monte Carlo evidence

and an application to employment equations. Rev. Econ. Stud. 58, 277-297. Bebchuk, L., Fried, J., 2004. Pay without performance: The unfulfilled promise of executive

compensation. Harvard University Press, Cambridge, MA. Bebchuk, L., Cohen A., 2005. The costs of entrenched boards. J. Financ. Econ.78, 409-433. Bebchuk, L., Cohen, A., Ferrell, A., 2009. What matters in corporate governance? Rev. Financ.

Stud. 22,783-827. Bertrand, M., Mullainathan, S., 2003. Enjoying the quiet life? Corporate governance and

managerial preferences. J. Pol. Econ. 111, 1043-1075. Bhagat, S., Black, B., 1999. The uncertain relationship between board composition and firm

performance. Bus. Lawyer 55,921-963. Blouin, J., Raedy, J., Shakelford, D., 2011. Dividends, share repurchases, and tax clienteles:

evidence from the 2003 reduction in shareholder taxes. Account. Rev. 86, 887-914. Brown, J., Liang, N., Weisbenner, N., 2007. Executive financial incentives and payout policy,

firm responses to the 2003 dividend tax cut. J. Finance62, 1935-1965. Buchanan, B., Netter, J., Poulsen, A., Yang, T, 2012. Shareholder proposal rules and practice:

Evidence from a comparison of the US and the UK. Am. Bus. Law. J. 49, 739-803. Bushee, B, 2001. Do institutional investors prefer near-term earnings over long-run value? Cont.

Account. R. 18,207–46. Bushee, B., Noe, C., 2000. Corporate disclosure practices, institutional investors, and stock return volatility. J. Account. R., 171-202. Cheng, S., 2008. Board size and the variability of corporate performance. J. Financ. Econ.87,

157–176. Chetty, R., Saez, E., 2005. Dividends, taxes and corporate behavior: evidence from the 2003

dividend tax cut. Q. J. Econ.120, 791-833. Chidambaran, N., Prabhala, N., 2009. Offsetting behavior and compensation reform. University

of Maryland working paper. Chung, K., Zhang, H., 2011. Corporate governance and institutional ownership. J. Financ. Anal. 46, 247-273. Coles, J., Daniel, N., Naveen, L., 2008. Boards: does one size fit all? J. Financ. Econ. 87, 329-

356. Core, J., Guay, W.,1999. The use of equity grants to manage optimal equity incentive levels. J.

Account. Econ. 28,151-184. Core, J., Holthausen, R., Larcker, D., 1999.Corporate governance, chief executive officer

compensation, and firm performance. J. Financ. Econ. 51, 371-406. Denis, D., Hanouna, P., Sarin, A., 2006. Is there a dark side to incentive compensation? J. Corp.

Finance 12, 467-488. Fama, E., French, K., 2001. Disappearing dividends: changing firm characteristics or lower

propensity to pay? J. Financ. Econ. 60, 3-44. Fama, E., Jensen, M.,1983a. Separation of ownership and control. J. Law Econ 26, 301-325. Fama, E., Jensen, M., 1983b. Agency problems and residual claims. J. Law Econ. 26, 326-350.

27

Fenn, G., Liang, N., 2001. Corporate payout policy and managerial stock incentives. J. Financ. Econ. 60, 45-72.

Ferreira, M., Santa-Clara, P., 2011. Forecasting stock market returns: the sum of the parts is more than the whole. J. Financ. Econ. 100, 514-537.

Giannetti, M., Simonov, A., 2006. Which investors fear expropriation? Evidence from investors’ portfolio choices. J. Financ. 61, 1507-1547.

Goergen, M., Renneboog, L., 2011. Managerial compensation. J. Corp. Finance. 17, 1068-1077. Gompers P., Ishii, J., Metrick, A., 2003. Corporate governance and equity prices. Q. J. Econ.

118, 107-155. Grinstein, Y., Michaely, R., 2005. Institutional holdings and payout policy. J. Financ.60, 1389–

426. Grullon, G., Michaely, R., 2002. Dividends, share repurchases, and the substitution hypothesis.

J. Financ. Econ. 57, 1649-1684. Hawley, J., Williams, A., 2000. The rise of fiduciary capitalism: How institutional investors can

make corporate America more democratic. Philadelphia, PA: University of Pennsylvania Press.

Heckman, J., 1979. Sample selection bias as a specification error. Econometrica 47, 153-161. Hermalin. B.,Weisbach, M., 1991. The effects of board composition and direct incentives on

firm performance. Financ. Manag. 20,101-112. Jagannathan, M., Stephens, C.P., Weisbach, M., 2000. Financial flexibility and choice between

dividends and stock repurchases. J. Financ. Econ 57,355-384. Jensen, M., 1983. Organization theory and methodology. Account. Rev. 58, 319-339. Jensen, M., 1986. Agency costs of free cashflow, corporate finance and takeovers. Am. Econ.

Rev.76, 323-339. Jensen, M., 1993.The modern industrial revolution, exit, and the failure of internal control

systems. J. Finance 48, 831-880. Jensen, M., Meckling, W.K., 1976. Theory of the firm: managerial behavior, agency costs and ownership structure. J. Financ. Econ. 3, 305-360. Jo, H., Harjoto, M., 2011. Corporate governance and firm value: The impact of corporate social

responsibility. J. Bus. Ethics. 103, 351-383. Jolls, C., 1998. Stock repurchases and incentive compensation. NBER Working Paper No. 6467. John, K., Knyazeva , A., 2006. Payout policy, agency conflicts and corporate governance. SSRN

Working Paper. Kahle, K., 2002. When a buyback isn’t a buyback: open market repurchases and employee

options. J. Financ. Econ. 63, 235-261. Knyazeva , A., 2007. Delivering on the dividend promise: corporate governance, managerial

incentives, and dynamic dividend behavior. Unpublished working paper. Korac-Kakabadse, N., Kakabadse A.K., and Kouzmin A., 2001. Board governance and company performance: any correlations? Corp. Gov. 1, 24-30. Lambert, R., Lanen, W., Larker, D., 1989. Executive stock option plans and corporate dividend

policy. J. Financ. Quant. Anal. 24, 409-425. Lamont, O.,1998. Earnings and expected returns. J. Finance. 531563-1587. Li, K., Ortiz-Molina, H., Zhao, X., 2008. Do voting rights affect institutional investment

decisions? Evidence from dual-class firms. Financ. Manage., 37, 713-745. Linck, J., Wintoki, M., Netter, J., 2012. Endogeneity and the dynamics of internal corporate

governance. J. Financ. Econ. 105,581-606.

28

Murphy, K., 1993. Executive compensation. In: Ashenfelter, O. and Card, D. (Eds.), Handbook of Labor Economics3. North-Holland. Amsterdam.

Platt, H. Platt, M., 2012. Corporate board attributes and bankruptcy, J. Bus. R. 65, 1139-1143. RiskMetrics Group. September 30, 2008. Stealth compensation continues in executive

compensation. Roodman, D. 2006. How to Do xtabond2: An introduction to difference and system GMM in

Stata, Center for Global Development, Washington. Rozeff, M., 1982. Growth, beta, and agency costs as determinants of dividend payout ratios. J.

Financ. R. 5, 249-259. Yermack, D., 1996. Higher market valuation of companies with a small board of directors. J.

Financ. Econ. 40, 185-202. Weisbach, M., 1988. Outside directors and CEO turnover. J. Financ. Econ. 20, 431-460. Windmeijer, F., 2005. A finite sample correction for the variance of linear efficient two-step

GMM estimators. J. of Economet. 126, 25-51. Zhang, Dan., 2013. Managerial dividend-paying incentives. Oslo University Working Paper.

29

Table 1 Summary information on sample firms Panel A shows the yearly breakout of stealth and non-stealth firms for our S&P 500 sample. Panel B shows the top 20 industry breakdown for stealth and non-stealth firms using the Fama-French 49 industry classification

Panel A – Yearly Break Out Year Stealth Firms N Non-Stealth Firms N 2003 219 134 2004 235 148 2005 227 156 2006 224 152 2007 186 153

Panel B – Industry Break Out

Industries Stealth Firms Non-Stealth Firms Total

Banking 108 69 177Utilities 86 64 150Insurance 77 57 134Retail 60 55 115Petroleum and Natural Gas 48 41 89

Trading 50 30 80

Electronic Equipment 37 41 78Pharmaceutical Products 37 36 73Consumer Goods 28 28 56

Communication 43 11 54

Food Products 25 28 53Business Services 24 27 51Chemicals 34 14 48Machinery 24 22 46Business Supplies 43 2 45Wholesale 23 15 38Restaurants, Hotels, Motels 19 19 38Construction Materials 6 31 37Transportation 26 10 36

Automobiles and Trucks 25 10 35.

30

Table 2 Summary data for sample firms This table presents summary data on the sample firms segmented by whether the firm uses stealth compensation. For variables that are specific to the use of stealth compensation, the details for non-stealth firms are not available. Appendix A describes the variables.

Stealth Firms Non-Stealth FirmsVoting Rights (VOTE) 0.91 0.81Dividends Paid on RSGs 1 0Accumulate Dividends, Pay on Vesting 0.12 N.A.Vesting Years (VEST) 4.76 4.02Directors Paid Dividends Same as CEO 0.8 N.A.Other Execs Paid Dividends Same as CEO 0.98 N.A.Pays Interest on Accumulated Dividends 0.1 N.A.Receives More RSGs Instead of Cash 0.21 N.A.N 1,091 743

31

Table 3 Univariate statistics for firm and governance characteristics This table presents statistics on firm financial, compensation, and governance characteristics. Appendix A defines the variables. Two-group unpaired mean-comparison t-tests and rank sum equality tests on unmatched data are used to examine whether there is a significant difference between the mean and median values of stealth and non-stealth firms.***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively. Panel A: mean and median firm characteristics Stealth Firms (N=1,091) Non-Stealth Firms (N=743) SignificanceVariable Mean Median Mean Median Mean MedianDPS 0.23 0.2 0.21 0.18 * *PAYOUT 0.37 0.25 0.32 0.21 * *DIV/ASSETS 0.22 0.01 0.01 0.01 * *DIV/MV 0.03 0.02 0.02 0.02 ** **REPAMT 0 0 0 0 * *G 0.01 0.04 0.02 0.01 * *CASHFLOW 2,341 1,242 2,261 1,001 None NoneDEBTRATIO 0.66 0.67 0.64 0.64 *** ***ASSETS 65,314 16,623 49,584 12,885 ** **SIZE 9.8 9.72 9.57 9.46 *** ***WC 0.09 0.02 0.1 0.05 * *CAPEX 0.04 0.03 0.05 0.04 *** ***ROA 0.09 0.08 0.12 0.1 *** ***BKMK 0.45 0.4 0.39 0.35 *** ***

Panel B: Mean and median compensation measures