Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=1504712

DEPARTMENT OF MANAGEMENT RESEARCH PAPERS

STOCK MARKET REACT TO FOREIGN INVESTMENT: THE EFFECTS OF INVESTMENT PURPOSE, STOCK MARKET CHARACTERISTICS,

AND BUSINESS GROUP AFFILIATION

Byoung Youp Lee, Jenifer Piesse and Roger Strange

Research Paper XX

Subject area: International Business

To request a paper please contact: Corresponding Author: Jenifer Piesse Department of Management King’s College London Franklin-Wilkins Building 150 Stamford St London SE1 9NH United Kingdom Tel/Fax: 44 (0)207 848 4164 Email: [email protected]

Electronic copy available at: http://ssrn.com/abstract=1504712

2

STOCK MARKET REACT TO FOREIGN INVESTMENT: THE EFFECTS OF INVESTMENT PURPOSE, STOCK MARKET CHARACTERISTICS,

AND BUSINESS GROUP AFFILIATION

Byoung Youp Lee King’s College London

Department of Management 150 Stamford St, London SE1 9NH

Email: [email protected]

Jenifer Piesse King’s College London

Department of Management 150 Stamford St, London SE1 9NH

Tel: 44 (0)207 848 4164 Email: [email protected]

and University of Stellenbosch, South Africa

Roger Strange School of Business, Management and Economics

University of Sussex Mantell Building, Brighton BN1 9RH

Tel: 44 (0)207 848 4164 Email: [email protected]

Abstract This paper examines how the public announcement of foreign share acquisitions in listed companies affects the share prices of those companies. The dataset contains 422 public announcements of foreign share acquisitions in Korean listed companies over the period from March 2005 to June 2009. The empirical analysis builds upon the findings of previous studies, but also considers the moderating effects of three factors: the motivation of the foreign investor (management participation or pure investment); the characteristics of the stock exchange on which the domestic companies are listed; and the effects of group affiliation. Using event study methods, the abnormal returns are obtained and statistical tests are undertaken between the mean returns for the different sub-groups. A significant 21-day cumulative abnormal return of 1.1% is found for the total sample, and the statistical tests suggest that the factors investigated influence the size of the abnormal gains. JEL classification: G14, G32, G34 Keywords: Corporate governance; foreign investment; blockholders; business groups; event study; emerging markets

3

Stock Market React to Foreign Investment:

The Effects of Investment Purpose, Stock Market Characteristics,

and Business Group Affiliation

1. Introduction

There is a substantial literature investigating how the public announcement of foreign share

acquisitions in listed companies affects the share prices of those companies. These empirical

studies yield mixed results, with some reporting significant positive impacts whilst others find an

inconclusive response. This suggests that the local markets take into account other factors apart

from the simple fact of a foreign share acquisition. In this paper, we consider the possible effects

of investment purpose, stock market characteristics, and business group affiliation on the stock

market response to foreign share acquisitions.

We consider 422 public announcements of foreign share acquisitions in Korean listed

companies over the period from March 2005 to June 2009. The Korean context is particularly

appropriate for this study for a number of reasons. First, Korea is a large economy, has witnessed

substantial inflows of foreign investment since the millennium, and was perhaps the first country

in South East Asia to recover from the 1998 financial crisis. Second, the Korean Government

amended its regulations regarding the disclosure of block acquisitions in 2005 and, since March

2005, has required all investors making a block (5% or more of the total shares) acquisition to

reveal the purpose of their investments. We have thus been able to distinguish in our dataset

between acquisitions that were made with the express intention of the foreign investor

participating in the management of the domestic Korean company, and acquisitions that were

made for (portfolio) investment purposes only. In the former case, we would expect a significant

positive share price response to the announcement but in the latter an an insignificant response.

Third, some of the domestic companies are listed on the long-established Korean Stock Exchange

(KSE), whilst others are listed on the newer Korean Securities Dealers Automated Quotation

(KOSDAQ) exchange. We would expect there to be a much stronger stock market response to

acquisitions of shares in KOSDAQ listed companies than in those listed on the KSE. Fourth,

some of the domestic companies were members of chaebol, whilst others were not. We would

4

expect business group affiliation to have a dampening impact on any stock market reaction, as

participants would expect new investors to exercise little influence over affiliated companies.

The paper is structured as follows. We first review the extant literature on stock market

responses to announcements of foreign share acquisitions, and put forward three testable

hypotheses. We then explain the construction of our dataset, provide some descriptive statistics

for the sample, and explain the main elements of the event study methodology used in this paper.

The empirical results are then presented and discussed, and we conclude by considering briefly

possible avenues for the extension of the analysis in this paper.

2. Literature Review and Hypotheses

There is a considerable literature that examines the effects of the public announcements of

foreign share acquisitions in listed companies on the share prices of those companies. The

strategic importance of foreign investment, particularly in emerging markets, has led to a re-

evaluation of the financial strength of firms when an announcement of international expansion

becomes available to the stock market. This literature includes an enquiry into the motivation for

foreign ownership that is broadly consistent with investors’ internalisation needs (Morck &

Yeung, 1992); an analysis of the potential risk-sharing strategies to ally with multinational

partners in foreign investment (García-Canal & Sánchez, 2006), and a study of the investment

decisions to improve the long-run competitiveness of firms (Woolridge & Snow, 1990). The

appropriate timing of investments to gain future benefits from FDI was found to provide a

positive stock market response by Ding & Sun (1997) and Meschi & Cheng (2002).

Cheng & Fung (1998) examined the stock market response to joint venture

announcements between US and Chinese companies using US stock market data. The results of

this study (using 103 firms during the period 1973–1993) showed a significant 3-day abnormal

return around the event date. Although these results are based on the positive effect from the US

FDI firms, stock market reactions are confined to a few days only around the announcement.

Further regression analysis did not provide any evidence that firm-specific factors contributed to

the size of the abnormal gains. López-Duarte & García-Canal (2007) investigated the stock

market response to FDI announcements made by Spanish companies between 1990 and 2003.

Different categories of ownership and the extent of investors’ involvement were found to explain

5

the positive announcement response. The more engaged investments showed higher abnormal

returns when the announcements were made available to the market. Finally, in a study of the

Singapore stock market, Ding & Sun (1997) investigated whether FDI announcements provided

new information to investors, whether shareholder benefits were a product of their firms’ FDI

decisions, and whether abnormal returns were attainable by trading shares. Their results showed

that an average 2.73% additional return could be observed by investors buying and holding the

stock of an announcing firm 21 days around the announcement date.

This paper considers the stock market reactions to foreign acquisitions of blocks (5% or

more of the outstanding shares) of shares in domestic listed companies. We contend that this

response may well differ according to the intention of the foreign investor, in so far as this is

known to market participants. The foreign investors may well have made their acquisition

because they perceive the target company’s shares are undervalued and/or the company has good

growth prospects. In such cases, the market response is likely to be positive but small, though a

negative price reaction is also possible (Bishop, 1991). In contrast, the foreign investors may

indeed wish to participate in the management of the company. If block investors have the power

to influence the operating performance and corporate strategy of target companies, block

acquisition will trigger the probability of corporate control transfer; change of board members,

management turnover, and so on. Whenever the threat of external blockholders can be regarded

as credible, managers will devote more effort to reach decisions that are shareholder-friendly.

Outside blockholders’ monitoring thus promotes valuable internal control efforts for the

companies (Sudarsanam, 1996). In particular, foreign investors have a tendency to demand better

corporate governance in order to protect their investments. If they are the significant

blockholders, their need to secure their interests will only be amplified. Sometimes block

acquisition with management participation means that subsequent tender offers are imminent.

Mikkelson & Ruback (1985) reported that 26% of the block acquisition announcements were

eventually taken by the block acquirer or a third party within three years. Choi (1991) states that

takeover attempts increase when blockholders already own significant portions of the target

firms. Such foreign block acquisitions will thus have a positive impact on company value as

stock market participants usually expect foreign investors to undertake strong monitoring

activities. Our first hypothesis is thus:

6

H1: The stock market reaction to foreign share acquisitions made with the intention of

management participation will be greater than that to foreign share acquisitions made only for

investment purposes.

There are two competing stock exchanges in Korea: the Korea Stock Exchange (KSE) and

the KOSDAQ (Korean Securities Dealers Automated Quotation) exchange. KSE accounts for the

majority of market capital, as well as listing numerous well-known companies such as Samsung

Electronics and Hyundai Motors. KOSDAQ is mainly comprised of small-sized Korean

Information, Communication and Technology (ICT) and Manufacturing companies. Generally,

investors perceive the KSE market to be more stable than the KOSDAQ market (Shin, 2002), and

there is greater liquidity.

In many countries, foreign investors typically tend to focus on large companies listed on

established stock markets, which demonstrate relatively stable fluctuations in share prices and

trading volumes. Not only are such companies more reliable, but the trading volumes mean that

stocks will be relatively easy to sell if need be. Higher returns may well be possible from

investments in smaller, less liquid companies. Investors intending to acquire substantial blocks of

shares in such companies have the incentive to access information about their targets and to

undertake substantial market analysis. The knowledge that a foreign investor is considering an

acquisition and is carrying out such activities transmits a message about the company’s prospects,

and this information will be reflected in an increase in the company’s share price. Our second

hypothesis is thus:

H2: The stock market reaction to foreign share acquisitions will depend upon the nature of the

stock exchange, and will be greater on smaller, less liquid stock markets.

Business groups are a common feature of the corporate governance system in many

countries, and in Korea they are known as chaebol. Such groups are corporate organisations

which comprise various companies linked through cross-ownership and stock pyramids

(Claessens et al, 2006). Such groups typically make widespread use of internal factor markets,

particularly for finance. Affiliated companies can access the group’s capital and managerial

resources, and may be able to mobilise resources more readily or at a lower cost than in the

external capital market because of reputation benefits and privileged access. Such are the

7

potential benefits of group affiliation, but there are also costs, notably that the operations of the

affiliated companies have to accord with the interests of the group as a whole even if the

company’s objectives are not the same as group objectives. It is thus likely that new investors

will have little opportunity to influence let alone change radically the operations of any company

affiliated to a business group.

H3: The stock market reaction to foreign share acquisitions will be greater in independent

companies than in companies affiliated to business groups.

3. Data and Methodology

The objective of this paper is to consider the possible effects of investment purpose, stock market

characteristics, and business group affiliation on the stock market response to foreign share

acquisitions. In this section, we explain how the data were collected, provide some descriptive

statistics on the composition of the sample, and then outline the event study methodology that we

used to assess the stock market response.

3.1 Data

We constructed our dataset from the publicly accessible website provided by the Korean

Financial Supervisory Service (FSS). The FSS maintains the DART (Data Analysis, Retrieval

and Transfer System; http://dart.fss.or.kr) website for the financial disclosures of listed

companies, including those listed on both KSE and KOSDAQ. Data are available back to 2001.

The financial data and daily stock prices of individual companies were collected from the

database of KisValue. KisValue is maintained and updated by the Korea Information Service

(KIS), a subsidiary of a leading credit rating agency in Korea, which has provided comprehensive

corporate and financial information on all listed KSE and KOSDAQ companies since the early

1980s. Most Korean financial market studies depend on KisValue for its credibility and

expansive data coverage.

As we were interested in assessing the effects of investment purpose, we limited the

dataset to announcements of foreign share acquisitions of more than 5% of the outstanding shares

made between March 29 2005 and June 30 2009. We omitted acquisitions where the foreign

investor already owned more that 5% of the shares in the domestic Korean company and was

8

supplementing its original holding, and this left us with a total of 422 cases. As noted in the

Introduction, investors have to disclose the purpose of their investments: those intending to

participate in the management of the domestic Korean company have to report their

shareholdings using ‘the general form’, whilst those only making a (portfolio) investment fill out

‘the basic form’. We were thus able to distinguish between the 76 acquisitions made for

management purposes (MP) and the 346 acquisitions made for investment only (INV). Table 1

details the breakdown of the two groups over the period 2005-9. As is evident, there was a

marked drop in foreign acquisitions during 2008-09 on account of the global credit crisis.

Table 1

Almost 60% of the sample consisted of companies listed on the KSE (239 cases) with the

remaining 183 companies listed on the KOSDAQ exchange. Interestingly – see Table 2 – there

was a much higher proportion of MP cases amongst the KOSDAQ listed companies (45/183 ≈

25%) than among the KSE listed companies (31/239 ≈ 13%). About one-fifth (86) of the listed

companies were members of chaebol, with the remainder being independent. Very few (8) of the

MP cases were in group-affiliated companies.

Table 2

The mean share acquisition for the whole sample was 7.60%, with a median figure of

5.27% - see Table 3. The average (mean and median) figures for the acquisitions involving

management participation were markedly higher than those for the acquisitions for investment

only, as one might expect. Also, the average (mean and median) figures for the KOSDAQ listed

companies were higher than for the KSE listed companies, and the average figures for the

independent companies were higher than for the chaebol-affiliated companies.

Table 3

3.2 Methodology

The use of event study methodology (Fama et al, 1969) is commonplace in financial

studies assessing the impact of key corporate events such as mergers and acquisitions, the

appointment of new CEOs, major investment or divestments etc. The underlying theory is that an

efficient stock market will react to all publicly-available information. If the market views the

information in a favourable light, then the share price will rise; if the market perceives that the

news is bad for the company then the share price will fall. The stock market response, measured

9

in terms of the average abnormal return (AAR) and the cumulative abnormal return (CAR),

provides an indication of the expected impact of the event on the company.

The ‘event’ in this study is the public announcement of the foreign acquisition of shares

in the domestic Korean company, with the day of the announcement defined as the event day (t =

0). The estimation period is 90 days commencing (t – 120) days before the event day and ending

on (t – 31) days before the announcement. The event period is 61 days, from (t – 30) days before

the announcement to (t + 30) days after the announcement date. Thus, the total number of days

for the empirical study is 151.

t= -120 t= -30 t= 0 t= +30

Event period

Estimation period

Study period

Various approaches have been used in the literature to estimate the abnormal return for a

given stock. We adopt the market model to compute abnormal returns, and use Ordinary Least

Squares (OLS) as the estimation procedure. The market model is defined in Equation (1). The

benchmark index for stocks listed on the KSE is the Korea Composite Stock Price Index

(KOSPI), and the benchmark index for stocks listed on the KOSDAQ exchange is the KOSDAQ

index.

where = yield of an individual stock (i) on day t

= benchmark market index (KOSPI or KOSDAQ) on day t

= regression coefficients of the market model

= the error term for an individual stock (i) on day t

10

The market model computes the rates of return on a security over a particular holding period.

Equation (2) illustrates a basic formula which calculates the abnormal returns of an individual

sample for a day. During the event period [day (t – 30) through day (t + 30)], the daily abnormal

return for each firm, ARit, is calculated. Individual securities are aggregated into portfolios based

on time periods relative to the event date, not calendar time. The average daily abnormal return

(AAR) for a particular time period is calculated as the sum of the abnormal returns at that point

divided by the number of securities in the portfolio. The equation for deriving the AAR of a day

is seen in Equation (3).

are the estimated market model coefficients

The CAR (cumulative abnormal return) from t1 to t2 is the sum of the average abnormal

returns(AAR) for each day for the period and is defined in Equation (4). We estimate mean CARs

for various intervals surrounding the announcement: (t = 0, t = +1), (t = -5, t = +5), (t = -15, t =

+15), (t = -20, t = -1), (t = +1, t = +20) etc. Significance tests were undertaken for both the

average and the cumulative average abnormal returns. The test statistics for AARt and CAR(t1, t2)

are shown in Equation (5) and Equation (6) respectively.

11

4. Results

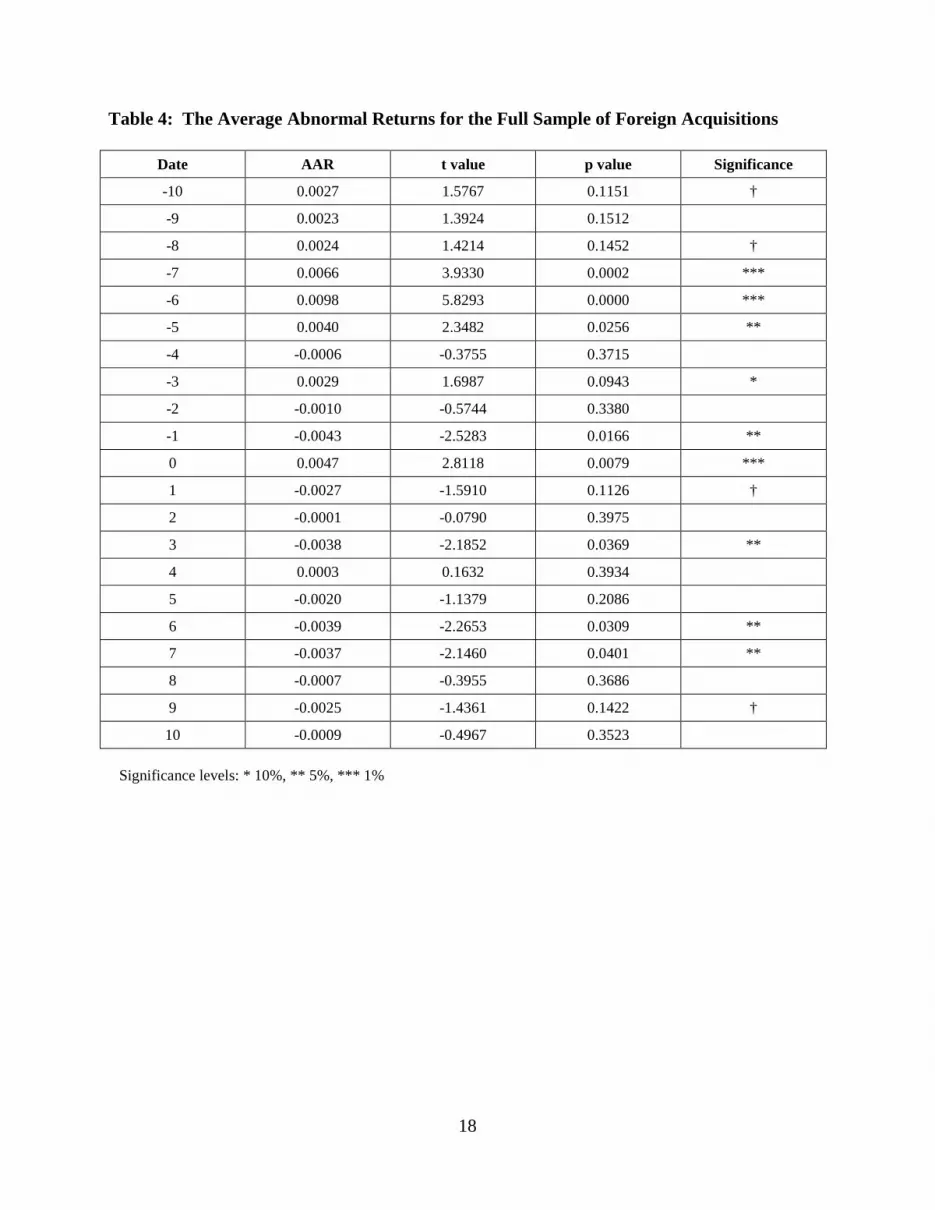

We first explored the stock market reaction using the whole sample of 422 announcements. We

observed a highly significant AAR on the event day (t = 0, AAR = 0.47%, p < 0.01), see Table 4.

Furthermore, the AARs on most days prior to the event are positive and significant, whilst those

on most days after the event are negative. These results suggest that there has been information

leakage regarding foreign block acquisitions. Prior to the disclosure, astute investors may have

had access to information on the block acquisition. They could be at an advantage and buy the

shares of target firms before the public announcement is made. Another explanation of positive

pre-announcement returns results from the natural process of consecutively increasing demand

for shares by foreign block holders. Prior to the disclosure of block acquisitions, foreign investors

buy and hold substantial amounts of shares. Usually, the process of block acquisition takes a

considerable amount of time, a couple of days at least. During the block acquisition, information

of a large investment will be passed to professional investors. Also, foreign investors

subconsciously reveal information about the target firms in the process of gathering information

on investment prospects. However, after the announcement an adverse adjustment of abnormal

price response is observed. Figure 1 shows the AARs and the CARs over the full event period.

The CARs before the event date are positive, but then decline steadily thereafter reflecting the

negative AARs after the event date.

Table 4 and Figure 1

The analysis is then repeated, but separately for acquisitions where management

participation (MP) was intended and where only investment (INV) was intended. The AARs for

both groups are in Table 5, and these show that the AARs for the MP group are generally more

positive than those for the INV group, plus the returns stay positive for longer after the event

12

date. These figures are reflected in the CARs in Figure 2, which show clearly that the average

stock market response to the MP acquisitions is both stronger and longer-lasting than that of the

INV acquisitions. The CARs for the two groups over various intervals were then compared using

t-tests, with interesting results. The CAR (-10, +10) shows a mean difference of +6.9% (p <

0.05), whilst CAR (-5, +5) shows a mean difference of +5.6% (p<0.1) and CAR (-15, +15) shows

a mean difference of +7.1% (p<0.1). The positive differences indicate a higher CAR for the MP

companies than for the INV companies. In conclusion, these results demonstrate that the stock

market takes into account the motivation of the foreign investors, and values investments made

for management participation significantly higher than those made for investment only.

Hypothesis 1 is thus strongly supported.

Table 5 and Figure 2

As noted above, KSE and KOSDAQ have distinct characteristics. KOSDAQ is usually

regarded as more volatile, and KSE has the more stable of the Korean stock markets. The

headlines of the Korean media frequently report news of market manipulations, corporate deceit

and private benefit transfers in KOSDAQ listed companies. The level of self regulation and

market monitoring is relatively low in KOSDAQ, although the standard in the KSE are not

regarded to be particularly high compared with long established stock exchanges such as New

York and London. The AARs for the companies listed on the KSE and on the KOSDAQ

exchange are shown in Table 6. There is a very significant positive AAR of 0.55% (p<0.01) for

the KSE listed companies, but the corresponding figure for the KOSDAQ companies is both

smaller and statistically insignificant. But there is evidence of large positive AARs on the

KOSDAQ exchange from early in the event period (t = -25), and then large negative AARs in the

days after the event date. This is reflected in the CARs in Figure 3, which show the greater

volatility in the KOSDAQ market. The CARs for the companies listed on the two exchanges over

various intervals were then compared using t-tests, with interesting results. The CAR (-15, +15)

shows a mean difference of +4.04% (p < 0.1), whilst CAR (-10, +10) shows a mean difference of

+0.85% (p>0.1) and CAR (-5, +5) shows a mean difference of +2.23% (p<0.1): the positive

figures indicate a higher CAR for the KOSDAQ companies than for the KSE companies. In

conclusion, these results demonstrate the differential responses of investors on the two stock

markets, though this finding is sensitive to the choice of interval. Hypothesis 2 is thus supported,

though with this caveat.

13

Table 6 and Figure 3

Finally, the analysis was again repeated, but separately for those companies that were

affiliated to chaebol and those that were independent. The AARs for both groups are in Table 7,

and these show that the AARs for the independent companies were generally more positive than

those for the affiliated companies, which are often negative though small and statistically

insignificant before the event date. However, the AARs for the independent companies were

often negative after the event date whilst those for the affiliated companies remain small. Neither

group shows a significant AAR on the event date, and very few AARs for the affiliated

companies throughout the event period were statistically significant. These observations are

reflected in the CARs in Figure 4. The plot for the affiliated companies is very flat throughout the

period, suggesting a lack of stock market reaction to the news of foreign share acquisitions. This

is probably because the market judges that foreign investors will have little scope for influencing

the operations of companies that are part of powerful chaebols. In contrast, the CAR plot for the

independent companies rises steeply before the event date, and then fall sharply afterwards. The

CARs for the two groups of companies over various intervals were then compared using t-tests.

The results for the major period CARs show slight differences between the two groups using a t

test although there is a clear difference in the CAR plots. CAR (-10, +10) shows a mean

difference of +2.3% (p > 0.1); CAR (-5, +5) shows a mean difference of +1.2% (p > 0.1); whilst

CAR (-15, +15) has a negative result with a mean difference of -0.45% (p > 0.1). However, the

pre announcement date CARs strongly support hypothesis 3. The CAR (-10, +1) and CAR (-30,

+1) show significant positive mean differences of +2.86% (p < 0.05), +4.64% (p < 0.1)

respectively between the two sample groups. The positive differences indicate a higher CAR for

the independent companies than for the group-affiliated ones. In conclusion, these results

demonstrate that the stock market takes into account the affiliation of the domestic target

companies, and values investment in independent companies significantly higher than that made

in companies affiliated to chaebol. Hypothesis 3 is supported, but careful interpretation would be

needed to extend this result.

Table 7 and Figure 4

14

4. Discussion and Conclusions

Previous studies of stock market reactions to announcement of foreign share acquisitions have

provided inconclusive results. In this paper we have since demonstrated that a possible reason for

this is that there are systematic differences in the market reactions to acquisitions by different

investors and in domestic companies with different organisational structures. In particular, we

have shown that the stock market reaction is greater when investors announce their intention to

participate in management, where markets are more volatile, and in domestic firms that are not

affiliated to business groups.

We have also replicated our analyses using different combinations of these three factors.

Space constraints space precludes reporting these results here in detail, but two results are worthy

of mention. The first is that the differential stock market response to MP and INV acquisitions is

only apparent in companies listed on the KSE and is both significant and long-lasting, whilst

there are no differences in the CARs for MP and INV acquisitions listed on the KOSDAQ

exchange. The higher volatility in the second may mask more subtle effects that result from a

new announcement. The second is that the differential stock market response to MP and INV

acquisitions is only apparent in independent companies, whilst there are no differences in the

CARs for MP and INV acquisitions of group-affiliated companies. This is a sensible result as

affiliated companies are much more difficult to influence.

15

References

Bishop, S. (1991). ‘Pre-bid acquisitions and substantial shareholder notices.’ Australian Journal

of Management, 16(1): 1-34.

Cheng, L & Fung, J (1998). 'An examination of the determinants of stock-price effects of US-

Chinese joint venture announcements.' International Business Review, 7(2): 151-161.

Choi, D. (1991). ‘Toehold acquisitions, shareholder wealth, and the market for corporate control.’

Journal of Financial and Quantitative Analysis, 26(3): 391-407.

Claessens, S., Fan, J. & Lang, L. (2006). ‘The benefits and costs of group affiliation: evidence

from East Asia.’ Emerging Markets Review, 7: 1-26.

Ding, K.D. & Sun, Q. (1997). 'The information content of FDI announcements: evidence from an

emerging market.' International Review of Financial Analysis, 6(1): 63-76.

Fama, E., Fisher, L., Jensen, M.C. & Roll, R. (1969). ‘The adjustment of stock prices to new

information.’ International Economic Review, 9(3): 1-21.

García-Canal, E. & Sánchez, P.L. (2006). ‘The number of partners and the stock market reaction

to domestic and international alliance formation in EU telecom firms.’ International

Business Review, 16(1): 83-108.

Kim, W.S. (2000). ‘Does FDI increase firm value in emerging markets? Harvard University,

Weatherhead Centre for International Affairs, Working Paper 00-03.

López-Duarte, C. & García-Canal, E. (2007). ‘Stock market reaction to foreign direct

investments: interaction between entry modes and FDI attributes.’ Management

International Review, 47(3): 393-422.

Meschi, P.X. & Cheng, L.T.W. (2002). ‘Stock price reactions to Sino-European joint ventures.’

Journal of World Business, 37(2): 119-126.

Mikkelson, W.H. & Ruback, R.S. (1985). ‘An empirical analysis of the interfirm equity

investment process.’ Journal of Financial Economics, 14: 523-553.

Morck, R. & Yeung, B. (1992). ‘Internalization: an event study test.’ Journal of International

Economics, 33(1-2): 41-56.

Sudarsanam, S. (1996). ‘Large shareholders, takeovers and target valuation.’ Journal of Business

Finance & Accounting, 23(2): 295-314.

Ueng, C & Kim, S (1996). ‘Foreign direct investment and shareholders’ wealth: evidence from

the newly industrialized countries (NICS)’ Multinational Business Review, 4(2): 79-85.

16

Woolridge, J.R. and Snow, C.C. (1990). ‘Stock market reaction to strategic investment

decisions.’ Strategic Management Journal, 11(5): 353-363

17

Table 1: Sample statistics - by year and investment purpose

Year Management Participation (MP) Investment Only (INV) Total 2005 10 123 133 (32%) 2006 21 120 141 (33%) 2007 19 83 102 (24%) 2008 20 15 35 (8%) 2009 6 5 11 (3%)

Total 76 346 422

Table 2: Sample statistics - by stock market and group affiliation

Management participation (MP) Investment only (INV) Total

Stock Market KSE 31 208 239

KOSDAQ 45 138 183 Total 76 346 422

Group affiliation Chaebol member 8 78 86

Independent 68 268 336 Total 76 346 422

Table 3: Sample Statistics - average share acquisitions Mean share

acquisition Median share

acquisition Investment purpose

Management participation (n=76) 14.98% 8.66% Investment only (n=346) 5.97% 5.19%

Stock Exchange

KSE (n=239) 6.57% 5.12% KOSDAQ (n=183) 8.93% 5.77%

Group affiliation

Chaebol member (n=86) 6.19% 5.11% Independent (n=336) 7.96% 5.41%

Whole sample (n=422) 7.60% 5.27%

18

Table 4: The Average Abnormal Returns for the Full Sample of Foreign Acquisitions

Date AAR t value p value Significance

-10 0.0027 1.5767 0.1151 †

-9 0.0023 1.3924 0.1512

-8 0.0024 1.4214 0.1452 †

-7 0.0066 3.9330 0.0002 ***

-6 0.0098 5.8293 0.0000 ***

-5 0.0040 2.3482 0.0256 **

-4 -0.0006 -0.3755 0.3715

-3 0.0029 1.6987 0.0943 *

-2 -0.0010 -0.5744 0.3380

-1 -0.0043 -2.5283 0.0166 **

0 0.0047 2.8118 0.0079 ***

1 -0.0027 -1.5910 0.1126 †

2 -0.0001 -0.0790 0.3975

3 -0.0038 -2.1852 0.0369 **

4 0.0003 0.1632 0.3934

5 -0.0020 -1.1379 0.2086

6 -0.0039 -2.2653 0.0309 **

7 -0.0037 -2.1460 0.0401 **

8 -0.0007 -0.3955 0.3686

9 -0.0025 -1.4361 0.1422 †

10 -0.0009 -0.4967 0.3523 Significance levels: * 10%, ** 5%, *** 1%

19

Table 5: The Average Abnormal Returns by Investment Purpose

Date MP (n=76) INV (n=346)

AAR t value AAR t value

-10 0.0051 0.8807 0.0021 1.3002

-9 0.0055 0.9484 0.0016 1.0142

-8 0.0096 1.6516 0.0008 0.4986

-7 0.0075 1.2877 0.0064 3.9574

-6 0.0121** 2.0860 0.0093*** 5.7261

-5 -0.0041 -0.7130 0.0057*** 3.5265

-4 0.0137** 2.3560 -0.0038** -2.3246

-3 0.0088 1.5062 0.0016 0.9631

-2 0.0051 0.8769 -0.0023 -1.4143

-1 -0.0049 -0.8500 -0.0041** -2.5265

0 0.0167*** 2.8750 0.0021 1.2945

1 0.0002 0.0365 -0.0027* -1.6834

2 -0.0010 -0.1739 -0.0001 -0.0679

3 0.0057 0.9859 -0.0056*** -3.4496

4 0.0092 1.5786 -0.0016 -0.9744

5 -0.0045 -0.7763 -0.0005 -0.3125

6 -0.0066 -1.1413 -0.0032* -1.9653

7 -0.0065 -1.1166 -0.0027 -1.6501

8 0.0008 0.1390 -0.0014 -0.8350

9 -0.0051 -0.8806 -0.0022 -1.3422

10 0.0001 0.0226 -0.0009 -0.5548

Significance levels: * 10%, ** 5%, *** 1%

20

Table 6: The Average Abnormal Returns by Stock Exchange

Date KSE (n=239) KOSDAQ (n=183)

AAR t value AAR t value

-10 0.0011 0.5925 0.0046 1.6116

-9 0.0006 0.3039 0.0046 1.6162

-8 0.0013 0.6581 0.0039 1.3438

-7 0.0059*** 3.0279 0.0076** 2.6569

-6 0.0067*** 3.4702 0.0139*** 4.8330

-5 0.0035* 1.7883 0.0046 1.6034

-4 -0.0024 -1.2607 0.0017 0.6011

-3 0.0042** 2.1560 0.0012 0.4014

-2 0.0006 0.2956 -0.0030 -1.0370

-1 -0.0010 -0.4980 -0.0086*** -2.9821

0 0.0055*** 2.8324 0.0038 1.3121

1 -0.0012 -0.6041 -0.0036 -1.2403

2 -0.0001 -0.0359 -0.0005 -0.1874

3 -0.0030 -1.5411 -0.0043 -1.5090

4 0.0010 0.5392(0.3444) -0.0005 -0.1903

5 0.0015 0.7810(0.2935) -0.0048 -1.6744

6 -0.0030 -1.5669(0.1169) -0.0048* -1.6857

7 -0.0022 -1.1303(0.2102) -0.0049* -1.7116

8 0.0012 0.6157(0.3295) -0.0038 -1.3188

9 -0.0040** -2.0770(0.0466) -0.0010 -0.3507

10 -0.0014 -0.7298(0.3051) 0.0002 0.0669

Significance levels: * 10%, ** 5%, *** 1%

21

Table 6: The Average Abnormal Returns by Group Affiliates

Date Group affiliates (n=86) Independent (n=336)

AAR t value AAR t value

-10 -0.0011 -0.3600 0.0036* 1.8810

-9 -0.0032 -1.0823 0.0038** 1.9611

-8 -0.0016 -0.5405 0.0034* 1.7805

-7 0.0053 1.8191 0.0069*** 3.6256

-6 0.0107*** 3.6546 0.0096*** 4.9975

-5 0.0027 0.9315 0.0043** 2.2253

-4 -0.0057* -1.9234 0.0007 0.3406

-3 0.0016 0.5294 0.0032* 1.6665

-2 -0.0049* -1.6763 0.0000 0.0242

-1 -0.0027 -0.9227 -0.0047** -2.4275

0 0.0035 1.1982 0.0050** 2.6322

1 -0.0002 -0.0815 -0.0027 -1.4132

2 -0.0051* -1.7299 0.0010 0.5003

3 -0.0008 -0.2765 -0.0043** -2.2281

4 0.0020 0.6887 -0.0001 -0.0386

5 -0.0012 -0.3963 -0.0012 -0.6498

6 -0.0001 -0.0225 -0.0048** -2.4904

7 0.0007 0.2475 -0.0044** -2.3042

8 -0.0002 -0.0700 -0.0012 -0.6064

9 -0.0050 -1.7087 -0.0021 -1.1056

10 -0.0024 -0.8258 -0.0003 -0.1449 Significance levels: * 10%, ** 5%, *** 1%

22

Figure 1: The Stock Market Response to Foreign Share Acquisitions (whole sample)

Figure 2: The Stock Market Response to Foreign Share Acquisitions: Comparison by Investment Purpose

23

Figure 3: The Stock Market Response to Foreign Share Acquisitions: Comparison by Stock Exchange

Figure 4: The Stock Market Response to Foreign Share Acquisitions: Comparison by Group Affiliation