Embed Size (px)

Citation preview

MGT 4301 Business Policy & Corporate Strategy FALL 2015

In partial fulfillment of the Business Policy & Corporate

Strategy course

Supervised by Dr. Abderrahman Hassi

1

STRATEGIC MANAGEMENT TEAM

2

ACKNOWLEDGMENT

“On behalf of our capstone project team, about the company Accor-

Risma, we would like to thank all the people who helped us and without whom

the full realization of this report would not have been possible.

First, we would like to address our sincerest thanks to our professor Dr.

Abderrahman Hassi, for his guidance and advice throughout this semester.

Similarly, we would like to thank Dr. Nicolas Hamelin, Dr. Imad Jabbouri, Mr.

Driss El Moudni deputy manager of Nozidées, Mr. Ahmed Debbagh owner of

the Domotiqua franchise in Morocco, Mr. Hassan Smili and Gumbo Kibelloh,

affiliate managers at ad4Game, and Dr. Abdelhamid Bennani Bouchiba for their

assistance and support during our research and analyses.

We would also like to express our deep thanks to Mr. Hassan Lahlou,

regional sales manager at Accor, for giving us precious insights about the

company.

Finally, we would like to thank our families for their support and care

during our whole years at Al Akhawayn University, and especially for their

encouragements during this final period.”

3

EXECUTIVE SUMMARY

AccorHotels is a French adventure that began in 1967 and reached Morocco in 1993

through a consortium of eight founder organizations. With more than 37 hotels throughout the

kingdom, Accor Maroc or Accor-Risma is one of the major players of the country’s tourism

sector even with the current political instability in the MENA region.

Throughout this report, a thorough analysis of the company’s situation was realized.

With a definition of the current objectives, strategies and issues, internal and external

assessment tools were utilized in order to evaluate and clearly determine Accor-Risma’s

position in Morocco. Therefore, leading us to a clear establishment of the matters that needed

to be addressed through our strategy formulation phase.

Through our study and analysis, we noticed that Accor-Risma is facing management

problems as well as irregularities in its accounting operations without forgetting about the

crisis faced by the tourism industry this past years, therefore, our main goal was to

successfully implement three alternative strategies that could realistically be taken into

consideration in the professional setting of Accor-Risma. The application of the theoretical

knowledge of the “Business Policy & Corporate Strategy” course material helped us in the

realization of the necessary matrices indicating the right strategic management decisions to

undertake. In addition to the BCG, SPACE, Grand and I/E matrices, as well as clear and

concise financial evaluations, we used the QSPM matrix to narrow down the best direction

and the best means that had to be chosen for Accor-Risma sustainable performance.

Finally, we implemented the three strategies we think are most appropriate to Accor-

Risma’s current situation in Morocco based on our analyses of the micro and macro

environment of the organization. According to our team, the appropriate solutions would be to

implement a market penetration through a the opening of a new brand of Accor’s economic

range near the location of the new ESSEC business school in order to get more customer

engagement, a product development with the introduction of the artificial intelligence

Domotiqua Fibaro system in the luxurious range products of the brand, and finally a market

penetration through the opening of a new Ibis entity, nearby the upcoming international

airport of Rabat-Salé.

4

TABLE OF CONTENTS

STRATEGIC MANAGEMENT TEAM .................................................................................. 1

ACKNOWLEDGMENT ........................................................................................................ 2

EXECUTIVE SUMMARY ...................................................................................................... 3

TABLE OF CONTENTS ....................................................................................................... 4

TABLE OF FIGURES ........................................................................................................... 7

LIST OF ACRONYMS: ....................................................................................................... 11

I. COMPANY INTRODUCTION ..................................................................................... 12

1.1 HISTORY OF ACCORHOTELS: ............................................................................................................ 12

1.2 ACCOR-RISMA IN MOROCCO: ............................................................................................................ 13

Key Dates ......................................................................................................................... 14

1.3 ACCOR-RISMA’S BRANDS IN MOROCCO: .......................................................................................... 15

1.4 ACCOR-RISMA’S SHAREHOLDERS: ..................................................................................................... 17

1.5 ACCOR-RISMA’S SUBSIDIARIES: ......................................................................................................... 17

II. OBJECTIVES, STRATEGIES & ISSUES OF ACCOR-RISMA .................................... 18

2.1 CURRENT OBJECTIVES: ............................................................................................................................. 18

2.2 CURRENT STRATEGIES: ............................................................................................................................. 18

2.3 CURRENT ISSUES: ...................................................................................................................................... 19

III. MISSION & VISION ................................................................................................. 20

3.1 VISION STATEMENT: .................................................................................................................................. 20

3.2 MISSION STATEMENT: ............................................................................................................................... 20

3.3 RECOMMENDED VISION STATEMENT: ...................................................................................................... 20

3.4 RECOMMENDED MISSION STATEMENT: ................................................................................................... 21

IV. EXTERNAL AUDIT .................................................................................................. 22

4.1 INDUSTRY ANALYSIS: ................................................................................................................................ 22

Industry SWOT analysis ................................................................................................ 22

Forecasted International Tourism Arrivals ................................................................. 24

Forecasted Travel and Receipts ..................................................................................... 25

4.2 PEST ANALYSIS: ....................................................................................................................................... 27

Political Factors: ............................................................................................................. 27

Economic Factors: .......................................................................................................... 27

Social Factors: ................................................................................................................. 30

Technological forces: ...................................................................................................... 32

3.3 THE PORTER’S FIVE FORCES MODEL: ..................................................................................................... 32

Upscale and Luxury Range ............................................................................................. 33

Rivalry among existing firms: ........................................................................................ 33

5

Potential entry of new competitors: .............................................................................. 33

Bargaining power of suppliers: ...................................................................................... 34

Bargaining power of customers: .................................................................................... 34

Threat of substitute products: ....................................................................................... 34

Midscale and Economic Range ....................................................................................... 35

Rivalry among existing firms: ........................................................................................ 35

Potential entry of new competitors: .............................................................................. 35

Bargaining power of suppliers: ...................................................................................... 35

Bargaining power of customers: .................................................................................... 36

Threat of substitute products: ....................................................................................... 36

4.4 EXTERNAL FACTOR EVALUATION MATRIX ...................................................................................... 36

Opportunities: ................................................................................................................. 37

Threats: ............................................................................................................................ 38

4.5 COMPETITIVE PROFILE MATRIX .............................................................................................................. 39

V. INTERNAL AUDIT ...................................................................................................... 40

5.1 COMPANY IMAGE AUDIT ........................................................................................................................... 40

5.2 FINANCIAL ANALYSIS: ............................................................................................................................... 42

Growth Ratios: ................................................................................................................ 42

Profitability Ratios: ........................................................................................................ 43

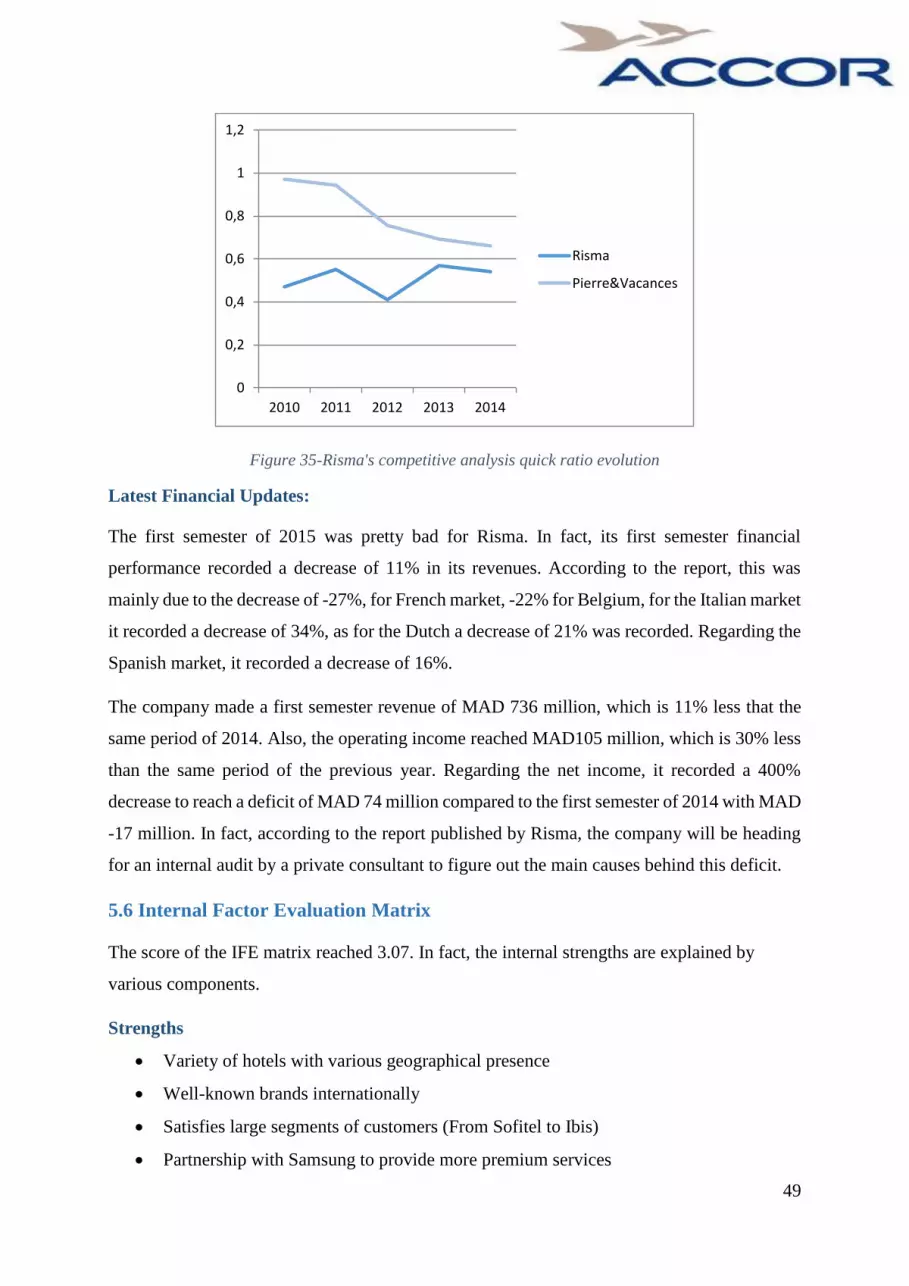

Competitive Analysis: Accor vs Pierre&Vacances ...................................................... 44

Leverage Ratios: .............................................................................................................. 45

Liquidity Ratios: ............................................................................................................. 47

Latest Financial Updates: ............................................................................................... 49

5.6 INTERNAL FACTOR EVALUATION MATRIX............................................................................................... 49

Strengths .......................................................................................................................... 49

Weaknesses ...................................................................................................................... 50

VI. MAIN ISSUE ............................................................................................................ 52

VII. OBJECTIVES OF THIS REPORT ............................................................................ 52

7.1 SHORT TERM OBJECTIVES ......................................................................................................................... 52

7.2 LONG TERM OBJECTIVES ........................................................................................................................... 52

VIII. STRATEGY ANALYSIS & CHOICE ........................................................................ 53

8.1 THE MATCHING STAGE ............................................................................................................................. 53

Matching SWOT ............................................................................................................... 54

SPACE Matrix .................................................................................................................. 56

BCG Matrix ...................................................................................................................... 57

I/E Matrix .......................................................................................................................... 58

6

Grand Strategy Matrix ...................................................................................................... 59

8.2 DECISION STAGE ........................................................................................................................................ 60

QSPM ................................................................................................................................ 60

IX. STRATEGY IMPLEMENTATION ............................................................................ 62

9.1 STRATEGY I: PRODUCT DEVELOPMENT – FIBARO DOMOTIQUA ...................................................... 62

Product Description: ......................................................................................................... 63

Where to implement? ........................................................................................................ 65

Financial Evaluation ......................................................................................................... 66

9.2 STRATEGY II: MARKET PENETRATION – ADAGIO ACCESS .............................................................. 76

What is Adagio? ................................................................................................................ 76

Financial Evaluation ......................................................................................................... 81

Revenue’s Estimation: Scenario Analysis ........................................................................ 84

9.3 STRATEGY III: MARKET PENETRATION – IBIS HOTEL RABAT-SALÉ AIRPORT .............................. 89

When & where & why to implement this strategy ........................................................... 89

Financial Evaluation ......................................................................................................... 94

Revenue Estimation: Scenario Analysis ........................................................................... 97

X. RECOMMENDATIONS............................................................................................. 102

XI. CONCLUSION ....................................................................................................... 106

XII. REFERENCES ...................................................................................................... 107

XIII. APPENDICES ....................................................................................................... 113

APPENDIX A: CURRENT ORGANIZATIONAL CHART OF ACCOR-RISMA ...................................................... 113

APPENDIX B: SPACE MATRIX COMPONENTS ............................................................................................... 114

7

TABLE OF FIGURES

Figure 1. Accor In Morocco ..................................................................................................... 13

Figure 2- Accor's brands logos ................................................................................................. 16

Figure 3- Pie chart of Accor-Risma's main shareholders ......................................................... 17

Figure 4- Evolution of Total Arrivals to Morocco, 2002-2019 (BMI, 2015) .......................... 24

Figure 5- Top Markets by Arrivals in Morocco (BMI, 2015) .................................................. 24

Figure 6-Chart of the top markets in Morocco (BMI, 2015) ................................................... 25

Figure 7-Moroccan International Tourism and Receipt 2011-2018f (BMI, 2015) .................. 26

Figure 8-International Tourism Industry Receipt Evolution 2011-2018 f ............................... 26

Figure 9- Occupancy rate in registered accommodation establishments in August (OTM,

2015) ......................................................................................................................................... 28

Figure 10- Occupancy rates in registered accommodation establishments from January to

August (OTM, 2015) ................................................................................................................ 28

Figure 11- Moroccan Population Growth rate ( ....................................................................... 30

Figure 12- Porter’s Five Forces Model applied to luxury brands ............................................ 33

Figure 13-Porter’s Five Forces model applied to midscale & economic brands ..................... 35

Figure 14- External Factor Evaluation Matrix ......................................................................... 39

Figure 15- Accor-Risma's competitive profile matrix.............................................................. 40

Figure 16- Accor's indictors in social mention ......................................................................... 41

Figure 17- Number of Google searches of Accor in the UK and France (GoogleAdwords,

2015) ......................................................................................................................................... 41

Figure 18-Finacial Key Performance Indicators for Risma ..................................................... 42

Figure 19-Risma's revenue evolutions in MAD million from 2010 to 2014 ........................... 42

Figure 20- Risma's Net income evolution (2010-2014) ........................................................... 43

Figure 21- Risma's Profitability Ratios 2010-2014 .................................................................. 43

Figure 22-ROA - Risma's competitive Analyis ........................................................................ 44

8

Figure 23- Risma's competitive analysis: ROA Evolution (2010-2014) .................................. 44

Figure 24- Risma's competitive Analysis: ROE ....................................................................... 45

Figure 25- Risma's Competitive Analysis: ROE evolution (2010-2014) ................................. 45

Figure 26- Degree of Financial Leverage ................................................................................ 45

Figure 27- Degree of Financial Leverage Evolution (2010-2014) ........................................... 46

Figure 28- Debt to Equity Ratio ............................................................................................... 46

Figure 29- Debt To Asset Ratio Evolution ............................................................................... 46

Figure 30-Debt to Total Assets ................................................................................................ 47

Figure 31- Debt to total Asset Evolution ................................................................................. 47

Figure 32- Risma's current Ratio .............................................................................................. 48

Figure 33- Risma's quick Ratio evolution ................................................................................ 48

Figure 34- Risma's competitive analysis quick ratio ................................................................ 48

Figure 35-Risma's competitive analysis quick ratio evolution................................................. 49

Figure 36- Risma's IFE ............................................................................................................. 51

Figure 37- SWOT Matrix ......................................................................................................... 53

Figure 38- Matching Swot matrix ............................................................................................ 56

Figure 39- Accor-Risma's SPACE matrix ................................................................................ 57

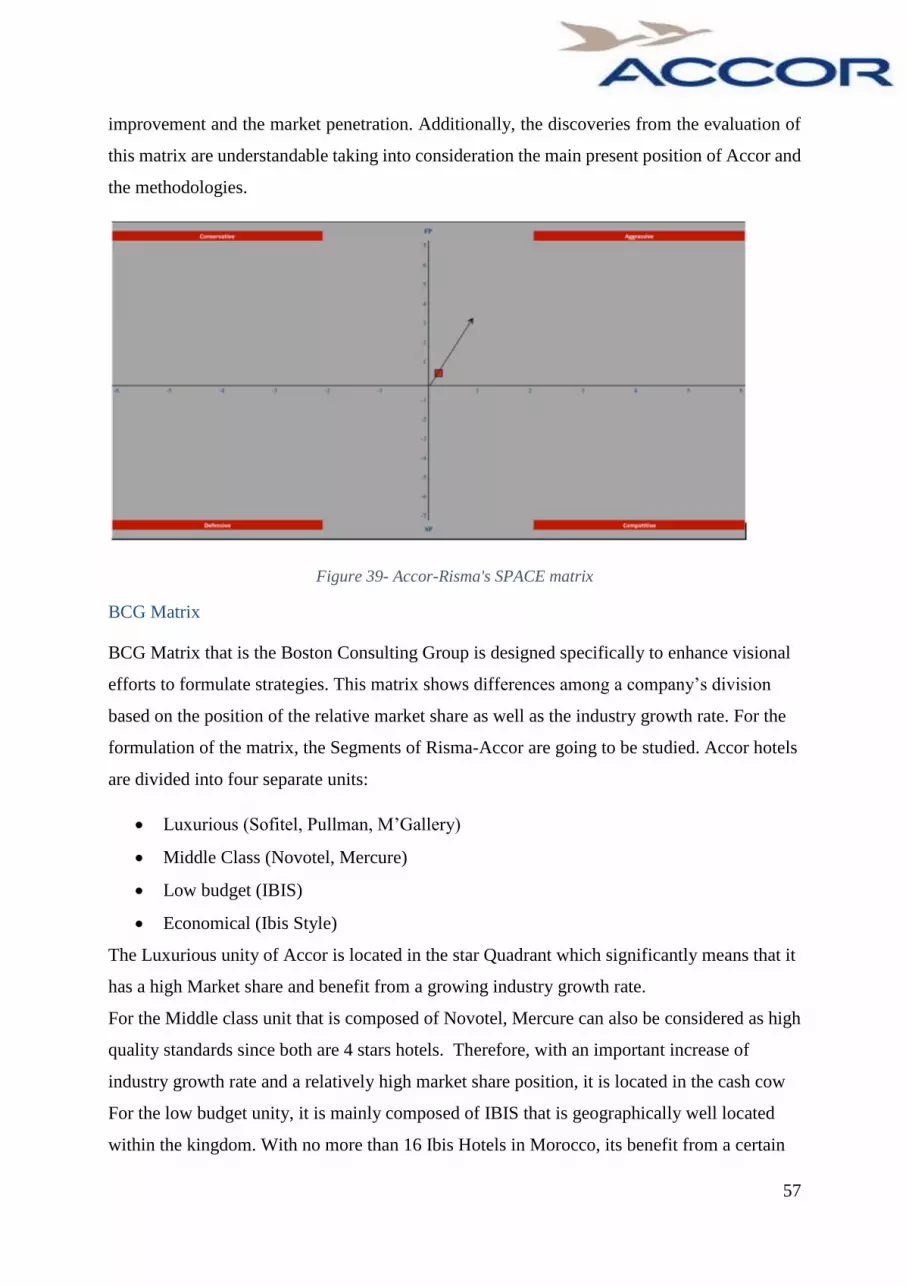

Figure 40-Accor-Risma's BCG Matrix .................................................................................... 58

Figure 41-Accor-Risma's I/E Matrix ........................................................................................ 59

Figure 42- Accor-Risma's Grand Strategy Matrix ................................................................... 59

Figure 43-Accor-Risma's QSPM Matrix .................................................................................. 61

Figure 44- Risma's WACC for Strategy I ................................................................................ 67

Figure 45-Full Pack Cost per Unit ........................................................................................... 67

Figure 46-Sofitel Morocco and Rooms Available ................................................................... 68

Figure 47-Fibaro Domotiqua Initial Investment ...................................................................... 69

Figure 48-Full Pack Depreciation Expense Fibaro Domotiqua .............................................. 69

9

Figure 49-Sofitel RevAr 2014 ................................................................................................. 70

Figure 50-ARR Increase Scenario Strategy I ........................................................................... 71

Figure 51- Forecasted Revenue First Scenario ........................................................................ 71

Figure 52- Forecasted Operating Before Tax Revenue ............................................................ 72

Figure 53-: ARR Increase Second Scenario ............................................................................. 72

Figure 54- Forecasted Revenue Second Scenario Strategy I ................................................... 73

Figure 55- Forecasted Operating Before Tax Revenue ............................................................ 73

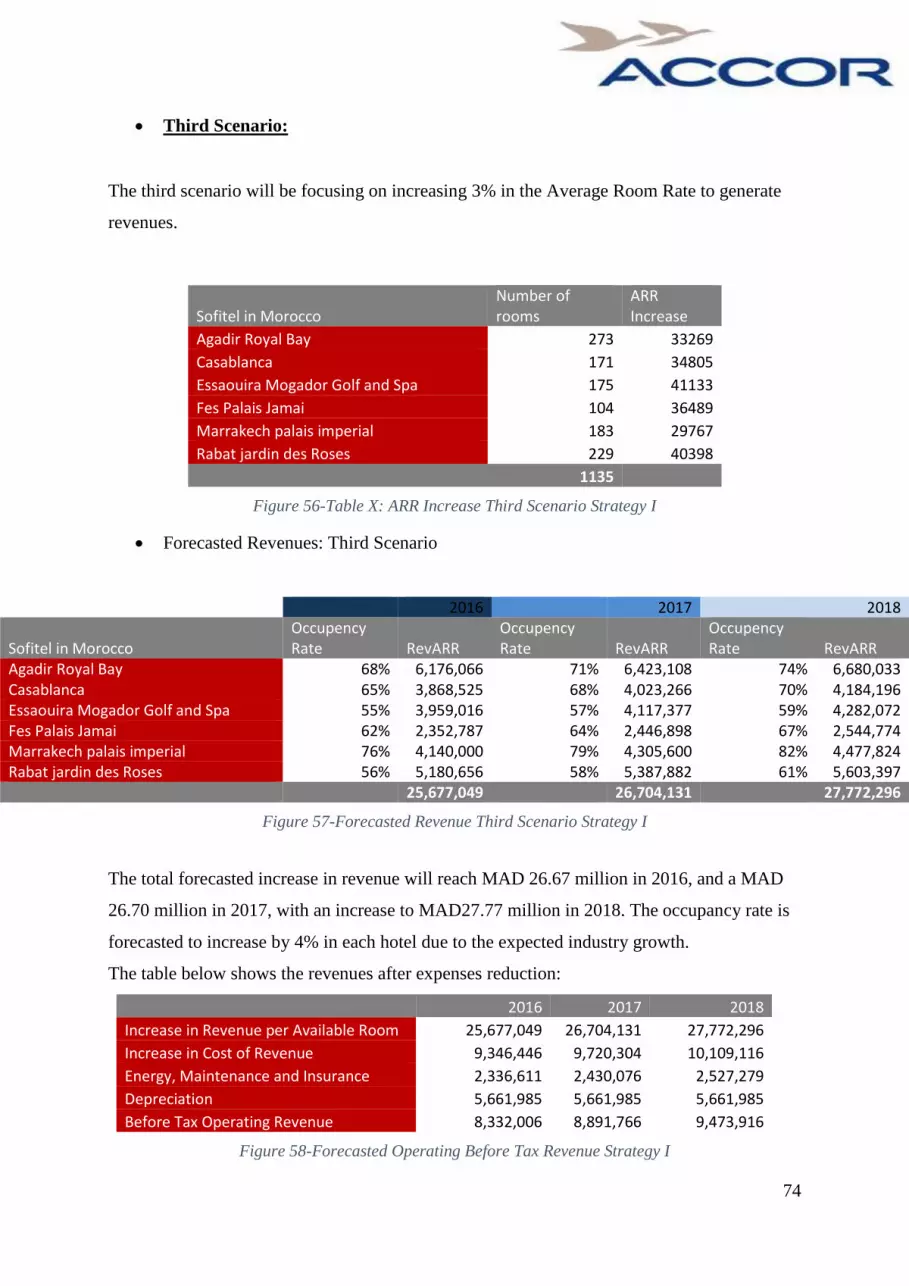

Figure 56-Table X: ARR Increase Third Scenario Strategy I .................................................. 74

Figure 57-Forecasted Revenue Third Scenario Strategy I ....................................................... 74

Figure 58-Forecasted Operating Before Tax Revenue Strategy I ............................................ 74

Figure 59-NPV and Scenario Analysis Strategy I .................................................................... 75

Figure 60-Discount Adagio Packages (adagio-city.com, 2015) .............................................. 80

Figure 61-Initial Investment and Budget Allocation Strategy II .............................................. 82

Figure 62-First Year Forecasted Revenue Strategy II .............................................................. 82

Figure 63-Forecasted Revenues: Optimistic Scenario Strategy II ........................................... 84

Figure 64- Payback Schedule Optimistic ScenarioStrategy II ................................................. 85

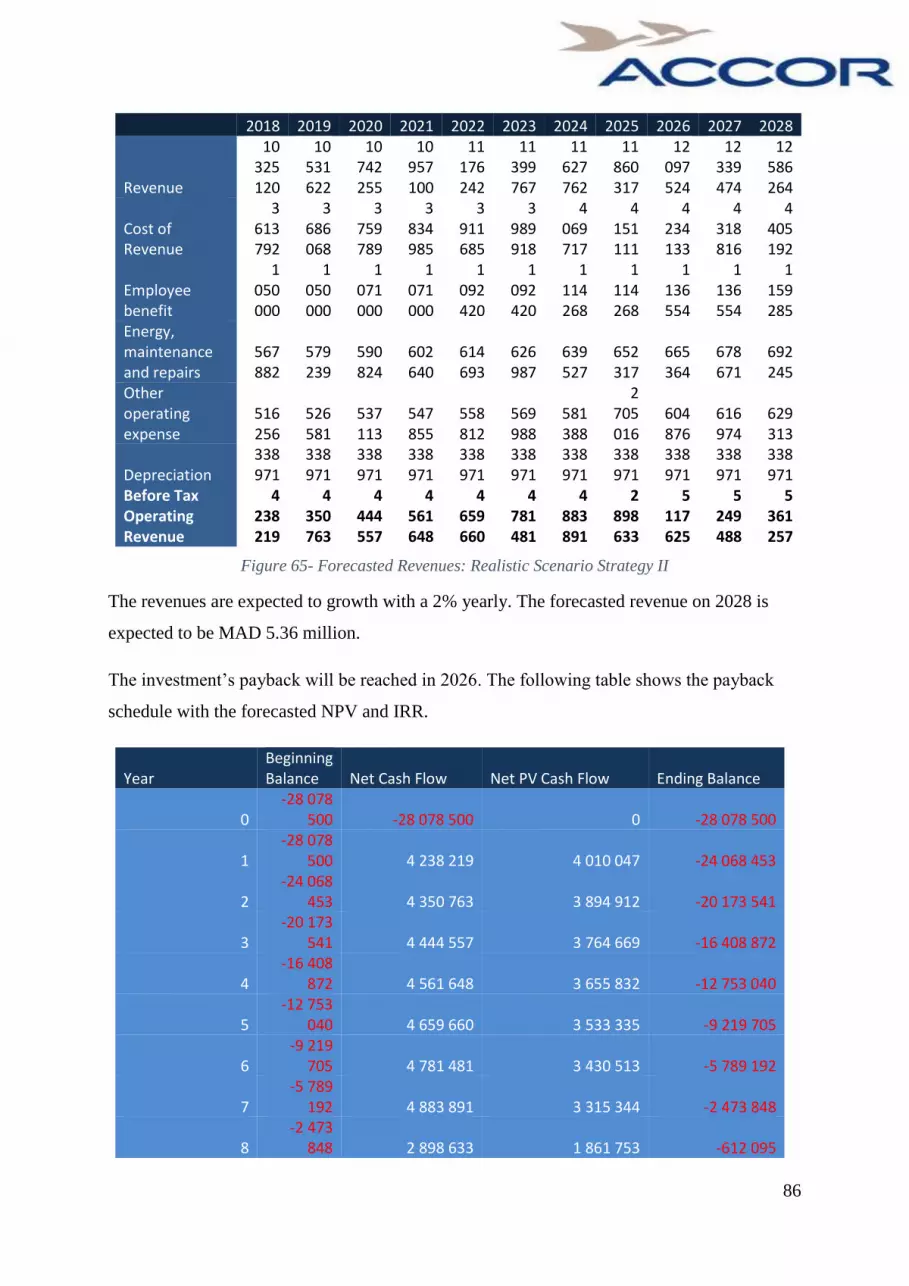

Figure 65- Forecasted Revenues: Realistic Scenario Strategy II ............................................. 86

Figure 66- Payback Schedule: Realistic Scenario Strategy II .................................................. 87

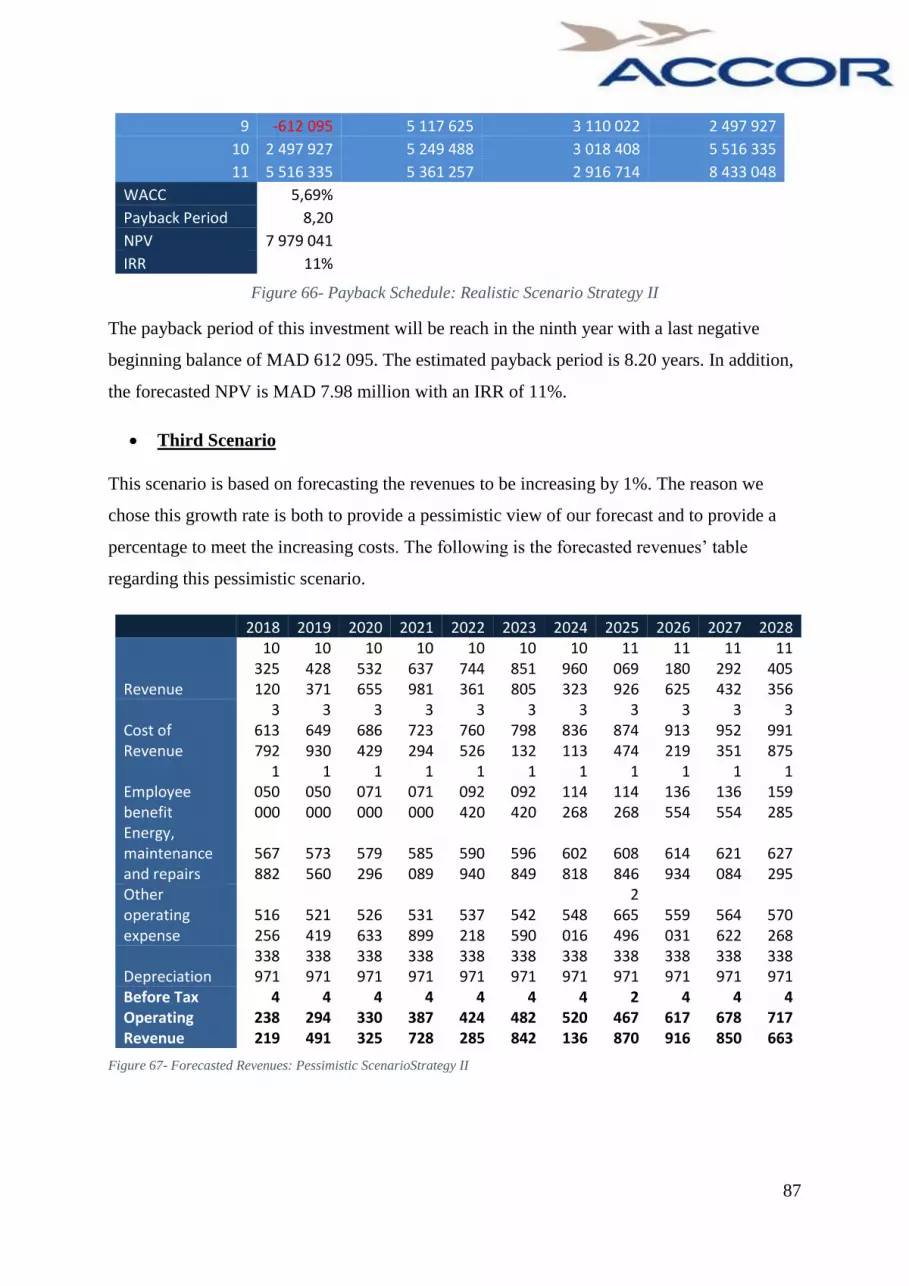

Figure 67- Forecasted Revenues: Pessimistic ScenarioStrategy II .......................................... 87

Figure 68- Payback Schedule: Pessimistic Scenario ................................................................ 88

Figure 69-Flow rate of passengers (Rabat-Salé, 2014) ............................................................ 93

Figure 70-Table X: Ibis Rabat-Salé Budget Allocation ........................................................... 94

Figure 71-Ibis Rabat-Salé Initial Investment ........................................................................... 95

Figure 72- Ibis Rabat-Salé Airport Forecasted RevAR (2018) ................................................ 96

Figure 73-Table X: Depreciation Table Ibis Rabat-Salé Airport ............................................. 97

Figure 74- Ibis Rabat-Salé Airport Revenue Optimistic Scenario ........................................... 98

10

Figure 75-Payback Period Schedule: Optimistic Scenario....................................................... 98

Figure 76-Ibis Rabat-Salé Airport Revenue Realistic Scenario ............................................... 99

Figure 77-Payback Period Schedule: Realistic Scenario ....................................................... 100

Figure 78-Ibis Rabat-Salé Airport Revenue Pessimistic Scenario ......................................... 101

Figure 79-Payback Period Schedule: Pessimistic Scenario ................................................... 101

Figure 80- (Statistica, 2015) ................................................................................................... 102

Figure 81-(Google Adwords, 2015) ....................................................................................... 102

Figure 82-Evolution of searches for Hotels in Morocco from the UK & France .................. 103

Figure 83-(World Bank Data, 2015) ...................................................................................... 104

Figure 84- World Bank Data, 2015 ........................................................................................ 105

Figure 85-Total Available Market in top 6 European countries ............................................ 105

11

List of Acronyms:

RISMA: Société d’Investissement & Propriétaire Hôtelier

ANIT: Association Nationale des Investisseurs touristiques

BCG: Boston Consulting Group

BMI: Business Monitor International

CPM: Competitive Profile Matrix

CRM: Customer Relationship Management

CIMR: Caisse Interprofessionnelle Marocaine de Retraite

EFE: External Factor Evaluation

FNIH: Fédération Nationale de l’Industrie Hôtelière

IFE: Internal Factor Evaluation

MAMDA: Mutuelle Agricole Marocaine d’Assurance

MCMA: Mutuelle Centrale Marocaine d’Assurance

ONA: Omnium Nord-Africain, now SNI: Société Nationale d’investissement

ONCF: Office Nationale des Chemins de Fer

OTM: Observatoire du Tourisme Marocain

QSPM: Quantitative Strategic Planning Matrix

SWOT: Strengths-Weaknesses-Opportunities-Threats

SPACE: Strategic Position and Action Evaluation

TOM: Top of Mind

12

I. Company introduction

With over than 3,700 hotels and 480,000 rooms in 92 countries in the five continents,

AccorHotels is considered as a world leader in the hotel industry. The French group with its

seventeen brands all over the world, ranging from luxury to small budget hotels, employing

more than 180,000 people, has made €5454 million in revenue last year.

1.1 History of AccorHotels:

It all began in 1967 with the opening of the first Novotel in Lille (France) by Gérard

Pélisson and Paul Dubrule who will create SIEH (Société d’Investissement et d’Exploitation

Hôteliers). The first hotel of the Ibis brand is launched in 1974 in Bordeaux. After what, SIEH

acquires the Courtepaille, Mercure and Sofitel brands. In 1983, Accor is born after the merger

of SIEH and Jacques Borel International. In 1985, Accor creates the Formula 1 brand, a new

concept in budget hotels and it continues its diversification and international expansion by the

takeover in 1990 of Motel 6 in the United States, the acquisition of the “Compagnie

Internationale des Wagons-Lits et du Tourisme” in 1991 and the creation of Accor Casinos in

1997 (Luc, 1997). 2010 constitutes a turning point in the group’s history: it decides to focus on

its hotel operations and separates from its Accor Services branch activities that will become

“Edenred” and separately publicly traded in the Paris stock exchange market (Blachez e.t. all,

2011). In 2011, the groups signs off its “LeNôtre” division for €75 Million. During the same

year, it also launched a unique study in the hotel industry; Accor launched a study measuring

its environmental impact, in order to have complete and reliable information to enhance its

strategy in this area. In 2013, AccorJobs.com gets 1st place for best business online recruitment

sites in Europe. Accor consolidates its leadership in Africa by signing the construction of 50

hotels in Angola in July 2015 (Accorhotels-group.com, 2015). Over the past 40 years, Accor

has gained expertise and stronger brands which basically position them as essential for all

market segments worldwide. They have been strengthening their performances in the fields of

operations effectiveness and hotels’ distribution. Their fidelity program, the “AccorHotels

Club” has over than 13 million members, including over two million in Asia. Sebastien Bazin,

named CEO of the group in 2013, gave a boost to the multinational company and redirected its

objectives towards a long-term vision. With a greater focus on the new threats challenging the

hotel industry and the means to utilize them to their advantage, AccorHotels is said to “open a

new hotel every two days” (Leymarie, 2015). AccorHotels is set to build the hotel business of

13

tomorrow based on a bold and innovative vision of their professions (AccorHotels-group,

2015).

1.2 Accor-Risma in Morocco:

Today, as an official member of the ANIT and FNIH associations, Accor-Risma

represents one of the major key players in the Moroccan hotel and services industry.

Risma was created by the French group Accor in 1993 as a private company, to first establish

their first two “holiday villages” under the name of Coralia in Agadir and Marrakech. In 1996,

Accor strengthens its position in Morocco by signing an agreement with the Moroccan

government with an objective to reach a capacity of 7000 rooms and becomes an incorporated

company. Three years later, Accor partners with a group of Moroccan institutions such as

Asma Invest, BMCE Bank, Nexity, RMA-Watanya, CFG Déceloppement and the MAMDA-

MCMA group, with the goal of creating a new tourism operator of reference in the kingdom.

Since 1999, Risma follows a constant and uninterrupted development of new units which

allowed them to establish a total of 27 hotels following the international standards and norms

in strategic locations of the kingdom. In 2006, Risma is the first Moroccan touristic company

to make its initial public offering at the Casablanca Stock Exchange (Risma.com, 2014). This

IPO allowed the group to acquire funds and finance the construction of its hotels. It was then

complemented by the creation of Accor Gestion Maroc that would become in charge of the

operations. In late December 2014, RMA-Watanya buying more shares reached a total of 30%

right behind Accor S.A (33%), and showing potential to supplant the French initial

shareholder. However, Accor remains the first shareholder and will continue to be linked to

Risma by a management contract through its subsidiary Accor Gestion Maroc (Ndiaye, 2014).

Amine Echcherki is the current chairman of the management board

succeeding to Azeddine Guessous and before him Marc Thépot, a key

figure of the fast growing development of the company over the past

decade. The latter undoubtedly marked the hotel industry in Morocco, by

leading the development of the Accor group since 200, he directly

participated in Risma’s IPO in 2006 (Challenge.ma, 2015). Please refer to

Appendix A.1 for the organizational structure of Accor- Risma. It even

achieved an occupancy rate of 60% of the overall Moroccan hotel industry

in 2011, despite the difficult regional context of political crises at that

time (Taleb, 2012). Headquartered in Casablanca, Accor-Risma seems to Figure 1. Accor In Morocco

14

have become the ultimate hub in Africa (A.J, 2014) and considered as a true success, the

Moroccan model of Accor is expected to be replicated elsewhere in Africa by investing in

hotels in Morocco and choosing to operate hotels it owns, Accor-Risma is set to be implanted

permanently on the Moroccan soil serving a diverse customer base, mainly European and

Moroccan and equally using their services while both on business trips and holidays

benefiting from the strong territorial coverage and smart locations in the cities (Marot, 2012).

Key Dates

1993: Accor creates Risma and opens Coralia Palmariva in Marrakech and Coralia La

Kasbah in Agadir.

1996: Risma becomes an incorporated company through the signature of the framework

agreement with the Moroccan government.

1997: ONA and ONCF acquire 66.66% of the Moussafir chain that will develop

subsequently under the brand Ibis Moussafir.

1998: Signature of the management rental agreement for a renewable period of twenty

years of the Palais Jamai as well as the the Almohades chain, but for a period of five

years, that would be managed under the Mercure brand in Agadir, Tangier and

Casablanca.

1999: Acquisition of the Scheherazade hotel in Rabat operating under the Mercure brand

as well. Risma opens capital for Moroccan investors.

2000: Opening of the Sofitel Mogador in Essaouira.

2001: Opening of two Ibis hotels in Meknes and Tangier.

2002: Acquisition of the remaining 60% of the Fastotel Company, owner of the Sofitel

Diwan. Opening of the Sofitel Marrakech and Ibis Moussafir in Fnideq.

2007: Acquisition of the Emirotel Company, owner of Rabat’s Hilton and its management

under the Sofitel name starting 2009.

2009: Opening of the first Suite Novotel in Morroco. Rebranding the Sofitel Diwan under

the M’Gallery signature.

2010: Change in governance with the setting up in March of a new board structure

composed of three members against five before then.

15

1.3 Accor-Risma’s Brands in Morocco:

Established in 13 cities, Accor-Risma offers an approximate number of 5179 rooms with

more than 35 hotels all over the kingdom’s territory. With a new Sofitel in Tetouan this year

and the potential opening of a second one in Casablanca (Barrahou, 2014), Accor-Risma is

benefiting from good brand awareness for most of its products and is planning to grow

accordingly.

1 Suite Novotel: Located in the Hivernage neighborhood of Marrakech, the Suite Novotel

offers travelers on medium stay a cozy atmosphere, modular suites of 30m², and

innovative services like free massages or the loan of a vehicle as well as a gourmet

boutique. Everything is designed to enable a client here for business or leisure to live a

stay in complete autonomy and freedom (AccorHotels -group, 2015).

16 Ibis: Present in Agadir, Marrakech, Ouarzazate, Casablanca, Rabat, El Jadida, Fes,

Meknes, Tangier, Fnideq, and Oujda, Ibis guarantees ultimate comfort with welcoming

and fully equipped rooms, modern reception arias and its new food offer Ibis Kitchen.

Attentive and efficient, Ibis offers the highest level of service within its class: reception

being open round the clock, breakfast being served from 4 am to midday, and a snacks’

bar, Ibis’ constant exigence has been rewarded by the ISO 9001 certification (AccorHotels

-group, 2015).

3 Mercure This midrange category of Accor’s is in harmony with every location it settles

in. Mercure hotels share the same uncompromising commitment to quality and are a real

alternative to standard or independent hotels would it be in Rabat, Nador or Al-Hoceima

(AccorHotels -group, 2015).

1 Novotel: The Novotel Casablanca city center offers its services in the heart of one of the

major cosmopolitan cities, near to business districts and touristic areas. Through a

consistent offer, Novotel contributes to the well-being of business and leisure travelers; a

welcoming and technophile atmosphere, spacious and adaptable rooms, balanced meals

around the clock, meeting and fitness rooms as well as spaces dedicated for children

(AccorHotels-group, 2015).

2 Pullman: Pullman reconciles business and leisure by offering its hyper-connected,

nomadic and cosmopolitan customers a fusion of efficiency and pleasure in their travels,

whether for business or personal reasons. Pullman embodies the “Work hard, play hard”

spirit and offers a new perception of the upscale hotel. With a warm and expert’s

16

welcome, and customized offers and services, the Pullman Mazagan Royal Golf & Spa as

well as the Pullman Marrakech Palmeraie Resort and Spa invite their clients to an

innovative and powerful experience (AccorHotels -group, 2015).

6 Sofitel: Sofitel offers contemporary hotels and resorts adapted to luxury hotels’ guests

of today in search of aesthetics, comfort and excellence. Located in the heart of a major

city or located in a more intimate and sumptuous place, every Sofitel offers a genuine

experience of the art of the French way of life with the best of local refinement. Sofitel

celebrates the design, gastronomy and culture in Agadir, Essaouira, Casablanca,

Marrakech, Rabat, Fez and more recently Tetouan (AccorHotels-group, 2015).

2 M’Gallery: M’Gallery is a unique collection of upscale hotels selected for their

authentic personalities and own characteristics. Its Heritage range brings together hotels

full of history. The Signature one reflects an aesthetic universe and the style a personality

that contributed to its creation or decoration. Finally, the Serenity range promises a safe

haven by the sea, in the countryside, or in the mountains. Rabat’s Diwan hotel and Al

Medina Essaouira Thalassa Sea & Spa invite travelers to experience memorable moments

(AccorHotels -group, 2015).

4 Ibis Budget: The reference brand of the low-cost segment is smart and casual. It

combines simplicity with the essential around a convivial atmosphere in Agadir, Fez, El

Jadida and Tangier for low prices. Ibis Budget is the ideal option for customers in search

of autonomy. It offers rooms for one to three people, free Wi-Fi and gourmet breakfast

(AccorHotels -group, 2015).

Figure 2- Accor's brands logos

17

1.4 Accor-Risma’s shareholders:

The main shareholders of Accor-Risma are: Accor S.A with 33.34% shares of the

company , followed by RMA WATANIYA with 29.59 % and BMCE Bank, Maghreb Siyaha

fund a subsidiary of FinanceCom, SIET, Accor’s direct subsidiary, T CAPITAL Group, the

CIMR and finally the MCMA-MAMDA group as shown in the figure bellow:

Figure 3- Pie chart of Accor-Risma's main shareholders

1.5 Accor-Risma’s subsidiaries:

Risma’s hotel perimeter is legally spread over several limited companies owned directly or

indirectly by Risma:

Moussafir hotels SA

Moussaf SA.

HCH SA. (Horizons Compétences Hôtellières)

Chayla SA.

Marrakech Plaza SA.

Fastotel SA.

Emirotel SA.

AGM, Accor Gestion Maroc has the mission of hotel management but also a mandate to

develop the interests of Risma. For efficiency and performance matters, AGM and Risma

have been taking their distances in terms of relationships between hotel manager and

owner, as an approach to accelerate growth and focus on the valuation of its brands and

hospitality expertise (Baazi, Fanion & Thiam, 2011).

18

II. Objectives, Strategies & Issues of Accor-Risma

2.1 Current Objectives:

Despite its pole position in the hotel industry worldwide, since the appointment of

Sébastien Bazin as CEO, the whole group has shifted directions. Accor-Risma’s new

objective is to become Morocco’s benchmark hotel operator based on the following new

principles:

A new name, a new identity, a new promise: AccorHotels, Feel Welcome.

Sustainably reinforce its strong position by acquiring more market shares and

empowering its loyalty program “AccorHotels Club”.

Enhance its corporate social responsibility through the Planer 21 program for

sustainable development.

The brands of the group were split into three distinct categories: Luxury & upscale, midscale

and economic; in order to enable the group to consolidate its expertise accordingly and secure

its leadership in each segment. Accor-Risma is looking forward to maximizing royalties,

improve its CRM and therefore loyalty by the implementation of strategies specific to each

brand of the different ranges present on the market.

2.2 Current Strategies:

Among Accor-Risma’s current strategies is to sustain the development of the economic

offer existing around the Ibis brand. Accor-Risma is also financially set to:

Reduce its short-term debt and consequently improve its solvency or solvability?

Financing a part of the investments for the necessary renovations needed to maintain

the competitiveness of certain strategic assets.

Maintaining its current assets.

Accor-Risma will continue to focus on its strategic assets and to work on an asset

management policy aiming for the optimization of its current assets. In other words Accor-

Risma is planning to invest if and only if good opportunities arise and do not unbalance its

financial structure (Dassouli, 2014).

19

2.3 Current Issues:

During the past decade, the success of Accor-Risma has been clearly noticed in

Morocco since the different hotels among the different ranges of the brand benefit from a

great brand awareness and has 8% market share of the country hotel industry (ALM, 2015).

However it has been facing financial and managerial issues as well as the impacts of the Arab

Spring and the recent tragic events in the neighboring region. The main issues Risma is facing

are:

The association of Morocco as a potentially dangerous country. The fact that

Morocco is categorized by 75% of the British population, as a country to avoid

among the other Muslim countries facing political instability (Bayo, 2015).

The concrete decrease of the foreign tourists coming to Morocco. At 2015’s first

trimester, travel revenues recorded in late April were 5.3% lower than last year’s

first trimester with a 16.3 billion MAD against 17.2 billion MAD previously

(Korso, 2015).

The French demand for hotels in Morocco has been decreasing by 9% in late April

2015 in comparison with the French amount of reservations in Morocco during the

same period during the last years (Berrada, 2015).

Accor-Risma focuses on debts to finance its investments (FinancialAfrik, 2015).

Accor-Risma is still behind in the digitalization phase of its commercialization

operations, since its website contains only few information about the hotels present

in the Kingdom’s territory.

Accor-Risma does not focus yet on its media, marketing coverage in Morocco.

Accor-Risma has not yet launched its own system of online reservation

(Khennach, 2015).

The managerial and financial roles are not well defined between AccorHotels-

group and Risma are not clearly defined which creates uncertainties within the

company’s workforce and its organizational structure seen as too blurred (Agence

Ecofin, 2015).

The distance Risma-Accor took from its core competencies by building and

opening a residence counting 34 villas named “Jardin des Roses”, which makes us

believe in a will of diversification instead of focusing on its principal objective that

is to be the leader of the hotel industry in Morocco (ALM, 2015).

20

III. Mission & Vision

The vision and the mission are statements that are exceptionally vital and necessary to the

setup of focused purposes and planning good methodologies in the elaboration of a firm’s

objectives and strategies.

3.1 Vision Statement:

Risma is a “hotel investor serving the Moroccan Tourism sector” (risma, 2015).

3.2 Mission Statement:

The mission statement is a key feature in the determination of the culture, objectives and

attitude of a company. Risma’s current mission statement is the following:

“Risma is the first tour operator in Morocco. Resolutely involved in the dynamic of a

continuous evolution, Risma aims to consolidate its role as leader in the tourism industry and

to support the national strategy of the touristic development “Vision 2020” in order to make of

Morocco one of the top 20 destinations in the world”

3.3 Recommended Vision Statement:

To become the kingdom’s leader in the tourism industry as Morocco’s exclusive

representative of AccorHotels-group.

We analyzed Accor’s old vision statement and we figured out that there was a lack of

transparency about their operations. Moreover, this innovative vision statement comprises their

desire to be the pioneers as franchisors and key player in the Moroccan tourism industry.

After analyzing Accor-Risma’s mission statement we figured out that it did not include the

consumers, nor the market, not the products or its services in detail which are essential to

21

illustrate the identity of the company to the public. Moreover, the company did not mention nor

refer to the technology, which is an essential point when it comes to the hotel industry nowadays

in the high and fast internet penetration witnessed worldwide. In addition to that, the company

did not mention no desire to grow nor it did contain the philosophy and values of the internal

organization, nor did it state the concern for employees. Furthermore, Accor-Risma did not

include their willingness to improve its corporate social responsibility.

Evaluation of Accor’s Mission Statement

3.4 Recommended Mission Statement:

To become Morocco’s first hotel company that aims to be a model of corporate citizenship

through its exclusive franchising of AccorHotels’ brands. With Sofitel, Pullman, M’Gallery,

Novotel, Ibis & Adagio, we aim to provide a shelter that will make all kind of travelers

comfortable and feel like home. Risma is keen to be in a constant improvement of its work

quality, perseverance and reactivity to enrich the experience of both our staff and clients. We

also aim to digitalize our processes for more precision and productivity while keeping in touch

with its Moroccan roots by involving the local talent pool.

Evaluation of the new mission statement:

Components Accor’s Mission Evaluation

1. Customers All kind of travelers

2. Products or services Luxury brands, Midscale, economic

3. Markets Low, middle and high income Moroccans and internationals

4. Technology Digitalize our processes

5. Concern for growth Constant improvement

6. Philosophy Aim to provide a shelter for all

7. Self-Concept Main world’s driving inn administrator

8. Concern for public image be a model of corporate citizenship

9. Concern for employees Involving the local talent pool

22

IV. External Audit

4.1 Industry Analysis:

The tourism industry is one of the most important contributors to the Moroccan

economy’s development. In fact, the total services contribute by 53% to the overall Moroccan

GDP with a 9% contribution from the tourism industry. The sector is expected to growth in

the four upcoming years. According to the World Travel & Tourism Council, the tourism

industry is a major focus of many international investments. It is important to mention that the

industry receipts totaled MAD 180 billion in 2014. The industry secures 871 000 jobs, which

represents 7.6% from the total employment.

Industry SWOT analysis

According to Business Monitor International’s report of 2015, the Moroccan tourism industry

includes has several strengths, weaknesses, opportunities, and threats:

Strengths

Morocco is a genuinely safe destination, which was not as seriously influenced as

different nations in the region by the Arab Spring and related challenges.

Morocco offers a wide range of sorts of tourism, from shoreline occasions to social

tourism in areas, for example, Marrakech.

The nation pulls in vacationers from distinctive parts of the world, with higher quantities

of Arab sightseers now supplementing effectively high quantities of guests from

Europe.

Gradually enhancing business environment empowering foreign investments.

Weaknesses

The Moroccan tourism market is still affected by the slow economic growth after the

world economic crisis

Transport facilities and infrastructure need more improvement, to pull in hoteliers and

luxury seeking tourists, especially in country regions.

More utilities infrastructure required with both water and power associations needing

improvement.

23

Opportunities

Large development potential in landings and enhancing inhabitance rates supporting

development.

Rise in travelers requires more hotels, crosswise over spending plan and top of the line

ranges. Smaller destinations outside principle urban areas, for example, the Atlas

Mountains, pulling in more tourists.

Increasing travel associations including low cost airline destinations.

Threats

Infrastructure and facilities like water could be put under weight by a quick increment

in tourism numbers and potential congestion in hotspots as Marrakech, particularly once

the full impacts of ease flights from Europe kick in.

Danger of terrorist attacks could hinder potential guests.

Disputable detainment of a British tourist in 2014 could impact entries from this key

market going ahead.

According to the same source, the report forecasted the Moroccan Tourism sector to be a

growing one after the low increase in 2011 and 2012:

“Morocco has recovered from disappointing growth in arrivals in 2011 and

2012 to an extent, when the tourism industry was affected by the economic

crisis in the Eurozone, which impacted upon arrivals from several major

source markets, such as France and Spain. Arrivals were also affected by the

after-effects of the April 2011 suicide bomb attack on a popular tourist café

in Marrakech, which killed 16 people, as well as uncertainty ahead of the

parliamentary election of November 2011 - a period marked by several

demonstrations across the country. The elections passed peaceably and, in

general, Morocco appears to have escaped the unrest that affected many of

its neighbors. Arrivals largely recovered in 2013 and 2014, and we are

expecting to see solid growth in the inbound tourism market moving forward;

by 2018, we expect arrivals to Morocco to reach 12.7mn, up from 11.1mn in

2015” (BMI, 2015).

24

The above graph shows a forecasted increase in Total arrivals in Morocco reaching 13

million tourists in 2019. In addition, the forecasted tourism receipt will reach $12.6

billion, which is around MAD126.6 billion. This proves that the Moroccan tourism

industry is a growing market, as it is expected to generate income. Mainly the income

from the international tourism in Morocco is generated using foreign country, which

increases the country reserve from foreign currencies mainly US Dollar and Euro.

Forecasted International Tourism Arrivals

The main markets contributing in the Morocco tourism industry are the European ones.

The following table shows the top 6 markets by arrivals in Morocco, with a forecasted

of arrivals up to 2018.

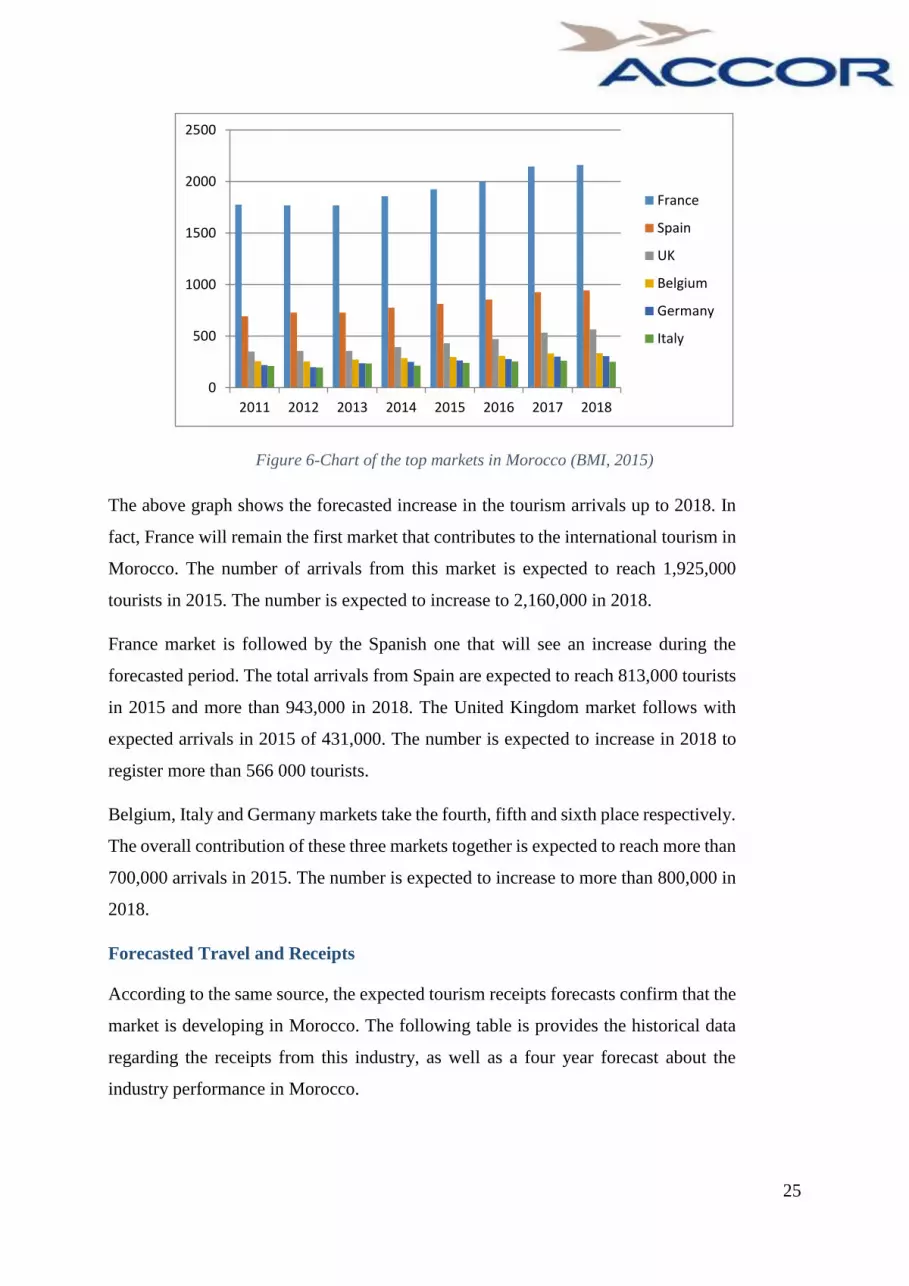

Figure 5- Top Markets by Arrivals in Morocco (BMI, 2015)

Figure 4- Evolution of Total Arrivals to Morocco, 2002-2019 (BMI, 2015)

25

Figure 6-Chart of the top markets in Morocco (BMI, 2015)

The above graph shows the forecasted increase in the tourism arrivals up to 2018. In

fact, France will remain the first market that contributes to the international tourism in

Morocco. The number of arrivals from this market is expected to reach 1,925,000

tourists in 2015. The number is expected to increase to 2,160,000 in 2018.

France market is followed by the Spanish one that will see an increase during the

forecasted period. The total arrivals from Spain are expected to reach 813,000 tourists

in 2015 and more than 943,000 in 2018. The United Kingdom market follows with

expected arrivals in 2015 of 431,000. The number is expected to increase in 2018 to

register more than 566 000 tourists.

Belgium, Italy and Germany markets take the fourth, fifth and sixth place respectively.

The overall contribution of these three markets together is expected to reach more than

700,000 arrivals in 2015. The number is expected to increase to more than 800,000 in

2018.

Forecasted Travel and Receipts

According to the same source, the expected tourism receipts forecasts confirm that the

market is developing in Morocco. The following table is provides the historical data

regarding the receipts from this industry, as well as a four year forecast about the

industry performance in Morocco.

0

500

1000

1500

2000

2500

2011 2012 2013 2014 2015 2016 2017 2018

France

Spain

UK

Belgium

Germany

Italy

26

2011 2012 2013 2014

2015

f

2016

f

2017

f

2018

f

Tourism receipts, MADbn 91 84.9 88.9 95.9 101.8 107.3 116.7 123.1

Tourism receipts, MADbn, % y-o-y 11.3 -6.7 4.7 7.9 6.2 5.4 8.7 5.5

Tourism receipts, transport services, MADbn 14.41 15.5 13.2 14.31 15.45 16.46 18.04 19.12

Tourism receipts, transport services, MADbn, % y-o-y 16 7.5 -14.8 8.4 8 6.6 9.6 6

Tourism receipts, travel items, MADbn 59.27 57.84 61.42 65.87 70.56 74.7 81.07 85.43

Tourism receipts, travel items, MADbn, % y-o-y 4.97 -2.4 6.18 7.25 7.11 5.87 8.53 5.37

Figure 7-Moroccan International Tourism and Receipt 2011-2018f (BMI, 2015)

The above table shows a great contribution of the transport services to the Moroccan

tourism industry. In fact, the transport services are expected to contribute by

MAD15.45 billion to the industry. In addition, the sector historically registered an

increase for all the period apart from 2012, where the receipts decreased by 6.7%. This

decrease was mainly due to the decrease of traveling by 2.4%.

The above graph shows the evolution of the tourism industry receipts between 2011

and 2014 with a four years forecast. In fact, the international tourism is a growing

market, and is expected to continue growing with fluctuating rates. Indeed, the total

tourism receipts are expected to reach MAD101.8 billion in 2015. This forecasted

receipt will be composed of MAD15.45 billion from transport services and MAD

70.56 billion from travel items.

0

20

40

60

80

100

120

140

2011 2012 2013 2014 2015 f 2016 f 2017 f 2018 f

Tourism receipts, MADbn

Tourism receipts, transportservices, MADbn

Tourism receipts, travelitems, MADbn

Figure 8-International Tourism Industry Receipt Evolution 2011-2018 f

27

4.2 PEST ANALYSIS:

Political Factors:

Morocco is one of the oldest monarchies in the world. King Mohamed IV started his

reign in 1999. The Moroccan kingdom has been flexible with the changes needed by the

people, such as the new constitution implemented by the government in 2011 that aims to

give more transparency in the electoral sessions as well as more power to the people that were

seeking for dynamism within our society. In addition, Morocco has being investing in the

health care and educational system in order to improve those sectors as well as improve its

human development index. The Moroccan government has being putting a lot of efforts for

the sake of development of the country and the improvement of important sectors. In addition

the Moroccan kingdom is the most stable region in North Africa with a strategic position

giving access to both the Atlantic Ocean and the Mediterranean Sea. The Moroccan

government started to be more flexible to the people’s demands in order to avoid strikes and

misbehaviors. As we can notice, the Arab spring did not have a big impact on Morocco

compared to neighboring countries, thanks to the efforts made by the government in order to

make elections transparent for the public and in giving more power to the head of the

government that is chosen by the public.

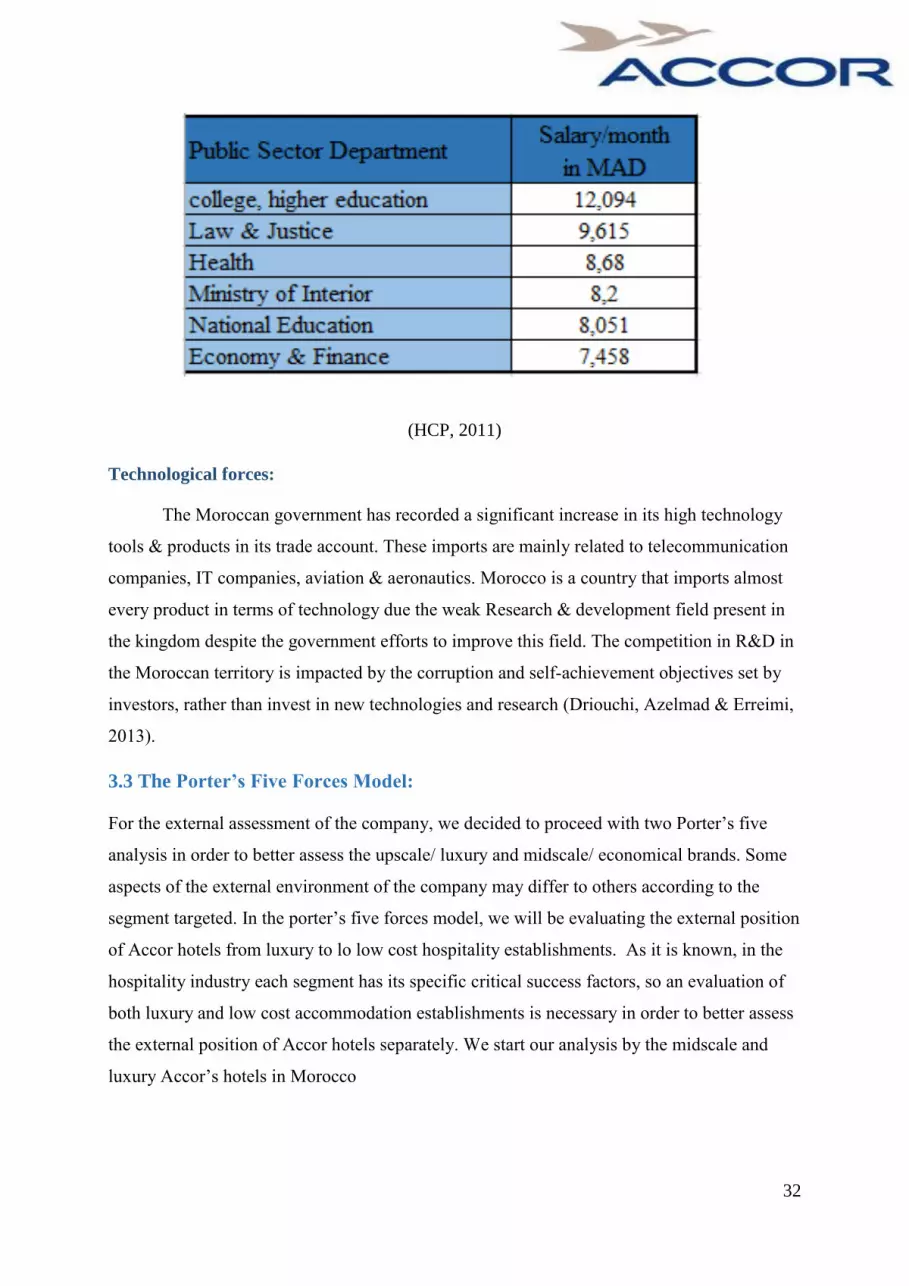

Economic Factors:

The Moroccan economy has been experiencing a stable growth for the last decade. In

order to attract new investors and grow, the Moroccan government is offering subsidies and

financial help for some projects to boost the tourism sector (OTM, 2015). The number of

tourists coming to Morocco has been increasing for the last five years, recording an increase

of 7% compared to the previous year, nearly a million additional tourists in 2015. Also, we

can see in the table below the occupancy rate of accommodation establishment variation. The

table details the occupancy rate of hotels, specifying the region, the period of the stay and the

average duration of the stay in the Moroccan kingdom. The table is specific to the period from

January to August (Figure 9).

The second table of occupancy rate for accommodation establishment is specific to the period

of august. During this period of the year, Morocco has the largest inflow of tourists, which is

making the occupancy rate of the establishments higher (Figure 10).

28

Considering the negative variation of the occupancy rate, the Moroccan hospitality market

still has an estimated average of 43% occupancy rate.

The increase of inflow of tourists and the decrease in the occupancy rate can be explained by

the new threat for the Hospitality establishments that is Airbnb. Airbnb is website made to

list, find and rent apartments, villas, etc. The website’s network is already spread worldwide

reaching 190 countries, 34000 cities, and a total number of listings exceeding 1.5 million

announcements available on the website. The website allows different transactions for its

member, from renting to exchanging houses between members which is starting to be a threat

Figure 10- Occupancy rates in registered accommodation establishments from January to August (OTM, 2015)

Figure 9- Occupancy rate in registered accommodation establishments in August (OTM, 2015)

29

for the industry. In order to minimize the impact of this threat, Accor has launched its Ibis

Budget Hotels to stay competitive in the price and give a quality/price ratio convenient for

potential customers. In addition, Ibis hotels always beneficiate from strategic positioning in

big cities; a factor that impacts heavily the choice of potential customers.

Considering the decrease of the occupancy rate of accommodation establishment compared to

last year’s, Hotels present in the territory are making efforts to keep their customers by

sending promotional offers during holidays period. These promotional offers may give more

incentive to potential customers rather than switching to substitute services (Motels,

apartments, camping, etc.)

According to the “statistiques sur le tourisme au Maroc” report, the number of tourists arrived

in the territory has increased of 7% compared to five years ago, and investments in the

tourism sector has increased thanks to the government efforts to boost the tourism industry

through its vision “Morocco 2030”.

The main sectors of the Moroccan GDP are:

Agriculture 14.6%

Industry 27,3%

Services 58,1%

The Moroccan agricultural sector generated 11.56 billion USD in 2013 and expecting

to reach 17 billion USD within 2020. In order to achieve its objectives, the Moroccan

government is attracting investors by implementing a new strategy for the sector. A

completely new approach for investors, the Moroccan government is planning to lease

600,000 hectares to local & foreign investors.

The Moroccan industry sector is expected to grow based on the forecasts of the

different markets in the industry; textile, automotive and food processing industries. The

industry sector in Moroccan GDP is contributing from 25 to 35%, the variation of the Industry

sector contribution to the GDP can be explained by the performance of the agricultural sector

of the period. Since the agricultural sector is depending on the weather, its contribution to the

GDP is not fixed but highly variable. The Moroccan government is investing and putting a lot

of efforts in the industry sector, in order to attract new investors and grow its economy. The

contribution of the industry sector has grown from year to year, even to exceed the

agricultural sector’s contribution in the year 2010. (Agriculture: 14.7%/ Industry: 38.9%)

30

The Moroccan services sector contributes up to 58.1% in the GDP and employs more

than 35% of the local workforce. The sector is mainly composed of tourism,

telecommunication, transportation and IT industries. The tourism is considered as the main

source of inflow of foreign currencies, thanks to the increase of the number of tourists

arriving in the Moroccan frontiers. In order to grow and develop the Moroccan tourism, the

government has implemented a new project Morocco 2030. For its vision to 2030, Morocco

plans to create new hospitality establishment in order to form and train its workforce for the

tourism industry, also encourage accommodation establishment to get accreditations and

develop new qualifications during trainings. Those reforms are meant to attract new investors

by offering good infrastructures and a qualified local workforce.

Social Factors:

The Moroccan government has been very active in improving its current economy sectors.

However, in doing so the country must improve its educational as well as health care system

in order to offer a good primary education and take care of its population. As stated in the

objectives of the Morocco vision 2030, Morocco is planning the opening of numerous

formation establishments for the hospitality institutions as well as the improvement of

educational systems that will aim to form a qualified workforce.

The Moroccan population recorded an increase in its population from 19.8 million in 1980 to

33.01 million in 2014 with an expected population of 42.9 million in 2050 (ESCWA, 2012).

Period Population Growth Rate (%)

1980-1985 2.36

1985-1990 2.04

1990-1995 1.68

1995-2000 1.35

2000-2005 0.96

2005-2010 0.98

2010-2015* 1.41

Figure 11- Moroccan Population Growth rate (

31

For the Moroccan population age composition, the Moroccan population for the under 15

years old has been decreasing from 1980 and is expected to continue this movement in 2050.

However, the working age population (15-64) has been increasing from 1980 to 2010

recording an increase from 52.9% to 66.9%, with an expected forecast to be reaching 66.8%

in 2035. For the proportion of elderly population (+65), it has witnessed an increase from

1985 to 2005, recording a variation from 3% to 5% with forecasted growth until 2050 to be

reaching 15.2% (ESCWA, 2012).

For the population by gender, the HCP released a study in 2013 showing the gender

proportion in the Moroccan population with 50.34% for women and 49.64% for men.

In addition, a significant drop in the unemployment rate from 13.8% to 9% that is showing the

growth of the Moroccan’s economy, also the human development index that has been

improving thanks to the reforms implemented by the government concerning the health care

and educational system. Also, a study conducted by the HCP in 2011 indicates that 68% of

youngsters watch TV and listen to radio regularly while the remaining third claim to use

internet as a primary source of research, entertainment & information (HCP, 2011).

32

(HCP, 2011)

Technological forces:

The Moroccan government has recorded a significant increase in its high technology

tools & products in its trade account. These imports are mainly related to telecommunication

companies, IT companies, aviation & aeronautics. Morocco is a country that imports almost

every product in terms of technology due the weak Research & development field present in

the kingdom despite the government efforts to improve this field. The competition in R&D in

the Moroccan territory is impacted by the corruption and self-achievement objectives set by

investors, rather than invest in new technologies and research (Driouchi, Azelmad & Erreimi,

2013).

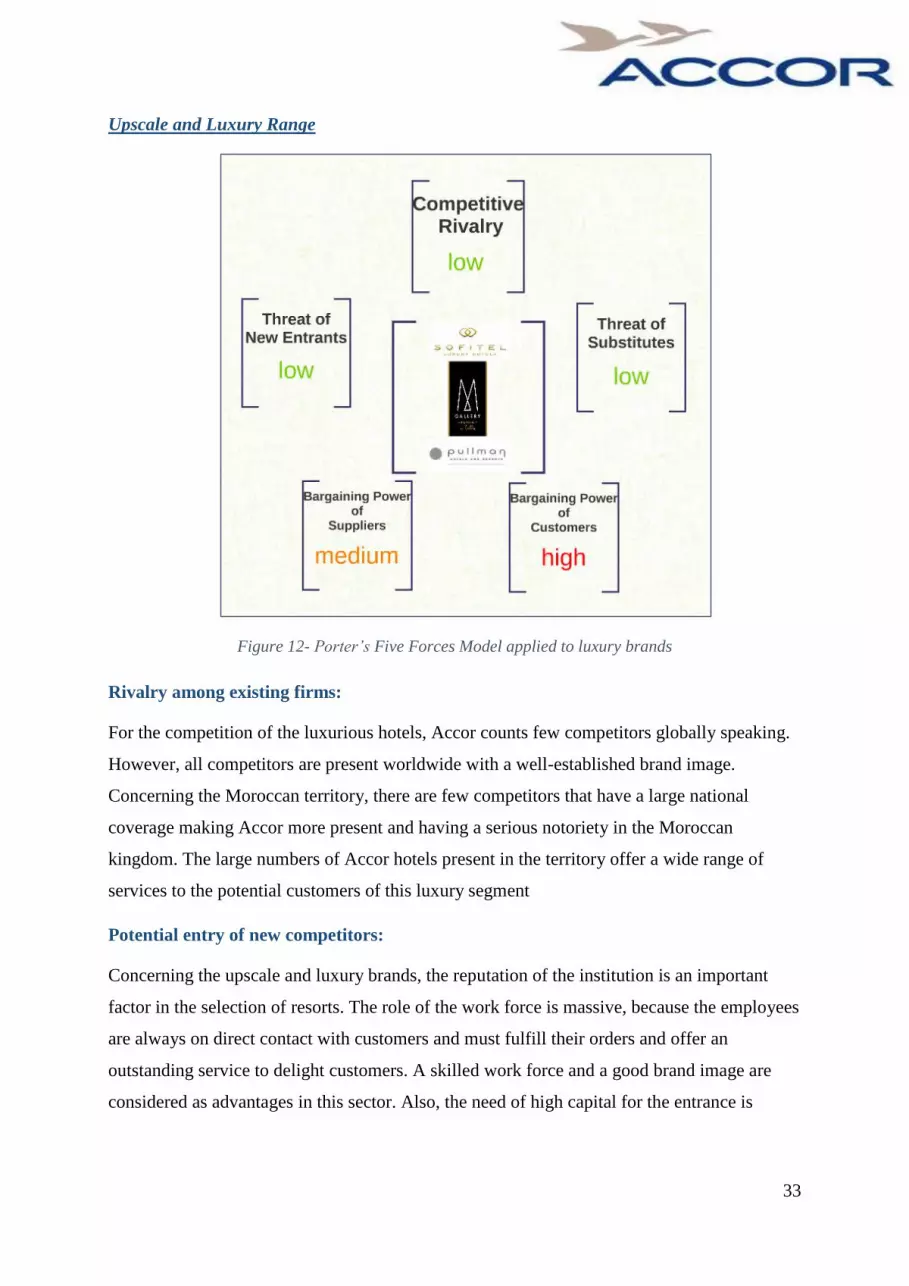

3.3 The Porter’s Five Forces Model:

For the external assessment of the company, we decided to proceed with two Porter’s five

analysis in order to better assess the upscale/ luxury and midscale/ economical brands. Some

aspects of the external environment of the company may differ to others according to the

segment targeted. In the porter’s five forces model, we will be evaluating the external position

of Accor hotels from luxury to lo low cost hospitality establishments. As it is known, in the

hospitality industry each segment has its specific critical success factors, so an evaluation of

both luxury and low cost accommodation establishments is necessary in order to better assess

the external position of Accor hotels separately. We start our analysis by the midscale and

luxury Accor’s hotels in Morocco

33

Upscale and Luxury Range

Figure 12- Porter’s Five Forces Model applied to luxury brands

Rivalry among existing firms:

For the competition of the luxurious hotels, Accor counts few competitors globally speaking.

However, all competitors are present worldwide with a well-established brand image.

Concerning the Moroccan territory, there are few competitors that have a large national

coverage making Accor more present and having a serious notoriety in the Moroccan

kingdom. The large numbers of Accor hotels present in the territory offer a wide range of

services to the potential customers of this luxury segment

Potential entry of new competitors:

Concerning the upscale and luxury brands, the reputation of the institution is an important

factor in the selection of resorts. The role of the work force is massive, because the employees

are always on direct contact with customers and must fulfill their orders and offer an

outstanding service to delight customers. A skilled work force and a good brand image are

considered as advantages in this sector. Also, the need of high capital for the entrance is

34

imperative in order to offer a high quality stay with the best furniture and entertainments for

customers.

Bargaining power of suppliers:

Hotel chains have many types of suppliers from services to goods. For the services, the hotels

outsource its maintenance of materials to external companies. For the goods, hotels have

contracts with furniture manufacturers (beds, tables, etc.) and get supplied on a daily basis of

food for the restoration services of the hotel chain. Given the notoriety of Accor and its wide

coverage globally, Accor has a certain power over customers because the company represents

big orders from suppliers making them one of their major customers.

Bargaining power of customers:

In the luxury sector, the customer is king. Customers have much higher expectations than the

budget brand’s customers. The customers expect a high quality service from the hotel as well

as devoted employees to ensure the satisfaction of customers. The high price of the stay must

be associated with an outstanding quality service that will make the customers come back to

the hotel. Also, customer loyalty is one of the key success factors in the luxury segment,

Hotels must keep track of their customers as well as send promotional offers to give them

more incentives to come back.

Threat of substitute products:

As mentioned earlier, the key success factors of the luxurious hotel industry are the

outstanding customer service, hygiene and strong brand name/ notoriety. The threat of

substitute product is low in this segment due differentiation strategies used by each resort and

high efforts to keep their customers loyal.

35

Midscale and Economic Range

Rivalry among existing firms:

The competition in the low budget hospitality market is high due to high potential alternatives

and high number of potential customers available in the Market. However, Accor

differentiates itself from competitors by offering a good customers service as well as high

hygiene standard of its institutions. In addition, the Accor chain is one of the few in the

hospitality industry to offer a free breakfast for all the types of formulas available in their

hotels, even for the low budget staying.

Potential entry of new competitors:

For future perspectives, the Moroccan government is working on the plan Maroc 2030 in

order to improve its tourism sector. In order to attract new investors in the Moroccan soil, the

government is giving financial help through the FDMT (Fond Marocain pour le development

touristique). The financial aid varies depending on each project, its location and the risk

associated to the project. According to invest In Morocco, a budget of 24 billion Moroccan

dirhams MAD has been allocated by banks for the Project Morocco 2030.

Bargaining power of suppliers:

As mentioned earlier, Accor’s suppliers are from different operating fields from service to

goods. From food supplies for restoration services to services for maintenance and furniture

for the hotels, Accor is dealing with a large number of suppliers. For the Moroccan soil,

Figure 13-Porter’s Five Forces model applied to midscale &

economic brands

36

Accor is largest hospitality chain with thirty-four hotels spread around the territory giving

them a high bargaining power over suppliers. In addition, the services provided to Accor are

available in the market, which give them more alternatives in their supplier selection.

Bargaining power of customers:

For the low-budget/economical hotels, Customers have less bargaining power compared to

upscale segment due to the price paid for the service offered. However, Accor is offering

extra free services for its customers that competitors fail to offer. The access to the Wi-Fi is

free for all the customers even in the rooms; the breakfast is offered for any formula chosen,

and clean and impeccable rooms for customers no matter the standing of the hotel chosen.

Threat of substitute products:

In opposition to the upscale/ luxurious segment, the low budget hospitality industry faces a

high threat regarding the substitute products present in the market. In the low budget industry,

the customers tend to think about the convenience of their choice, a price/quality ratio, rather

than staying loyal to one brand. For the substitute products, we can list low rated hotels, non-

rated hotels, apartments for rent and camping, etc. These substitutes may offer more space for

customers at an affordable price, the case of apartment rentals during holiday periods.

4.4 External Factor Evaluation Matrix

Accor scored 2.69 in the external factors evaluation assessing the strong external position

of the company, and its competitiveness in the hospitality market.

Opportunities:

Demand for more lodging supply

Morocco’s strategic geographic location

Growing urbanization

Increase of tourists arrivals

Demand for more lodging supply in France

Decrease of illiteracy rate

Threats:

Foreign currency exchange rate fluctuation

Rise of Airbnb

Political instability in the south region of Morocco

37

Rough competition in Morocco

Opportunities:

As stated earlier, the number of tourists’ arrival has recorded a 7% increase compared

to 2014; nearly an additional million tourists. Referring to the table of occupancy rate

of the different regions in Morocco, we can see that the regions of the kingdom with

most visits are Marrakech, Agadir & Casablanca respectively. Moreover, the majority

of the hotels belonging to Accor chain are located in those regions and are well spread

over the regions with different formulas offered to customers from different

purchasing buying power.

In 2016, France will be hosting the euro cup, which is considered as an opportunity

for Accor to exploit. In addition to that, the current strategies of Accor consist of

spread their hospitality establishment in Europe and flood the Moroccan market with

low cost/ economical accommodation establishment, such as ibis, ibis budget & ibis

style. We chose to give a rating of 3 to the opportunity because of the compatibility of

the opportunity with the current strategies of Accor, as well as the number of potential

customers targeted thanks to the European cup organized in France.

According to the HCP study, the urbanization rate has been increasing since 2010, to

record a 4% positive growth. The growing urbanization implies that more workforce

available in the market place, as well as a decreasing rate of unemployment. We

choose to put a rating of 2 because we believe that the growing urbanization has not a

big impact of the external position of Accor.

For the strategic positioning Opportunity, Morocco is enjoying a perfect geographic

position with an access to both the Atlantic Ocean & the Mediterranean Sea. In

addition to that, Accor is the largest hotels chains present in the Moroccan kingdom,

with 34-accommodation establishment spread over the territory with well-established

brand image & a variety of formulas to attract all potential customers. Thus, we

allocated a rating 3 to the strategic positioning of the Accor chain in the Moroccan

kingdom.

For the Morocco vision 2030, the Moroccan government is boosting its tourism sector

by opening new accommodation establishment forming institutions in order to create a

qualified local workforce for foreign investors, the subsidies offered by the

government for the hospitality industry are effective in attracting new foreign

investors and training programs for the workforce offered by the government. We

38

choose a rating of 4 for the first opportunity thanks to the help & assistance provided

by the government to investors (Maroc vision 2030, 2014).

For the decrease of the illiteracy rate, it is associated with the government effort made

to improving both the health care and educational system. By doing so, the public has

access to these resources and the social middle class is most likely expected to grow

which will create more potential customers to the Accor group and the hospitality

industry. We chose to allocate a rating of 2 to the opportunity because the opportunity

may exploitable on the long run and its impact also is for coming years, not on the

short run.

Threats:

The foreign currency exchange rate fluctuation is a factor to be considered by

investors in the selection of the country to invest in. The Moroccan MAD does not

have a significant variation, since the currency variation has reached a maximum of +-

0.06%. In addition, the Moroccan MAD is an attractive currency to foreign investors,

and the availability of opportunities in the hospitality sector since the industry is

growing.(Bank al Maghrib, 2010)

Airbnb is a website that aims to find and list lodging items. The website constitute a

real threat to the hospitality industry, since it can be considered as a substitute product

for potential customers. The website offers new services such as the exchange of