Embed Size (px)

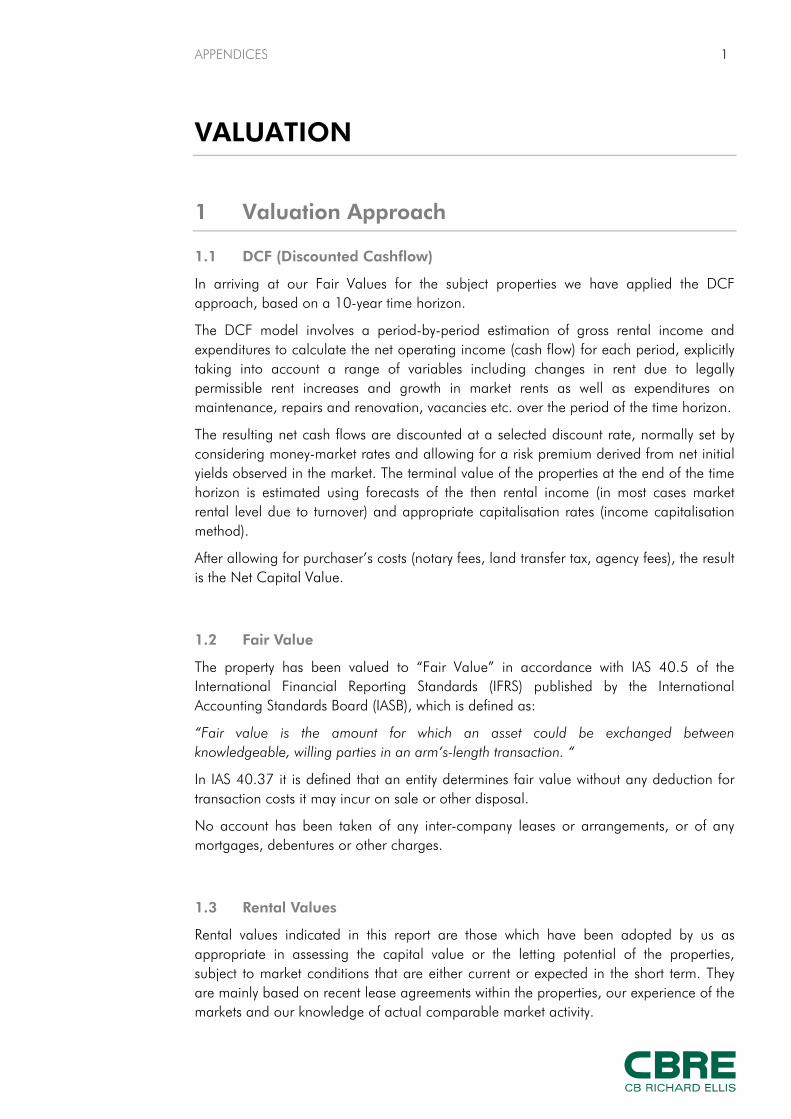

Citation preview

STRICTLY CONFIDENTIAL – FOR ADDRESSEE ONLY

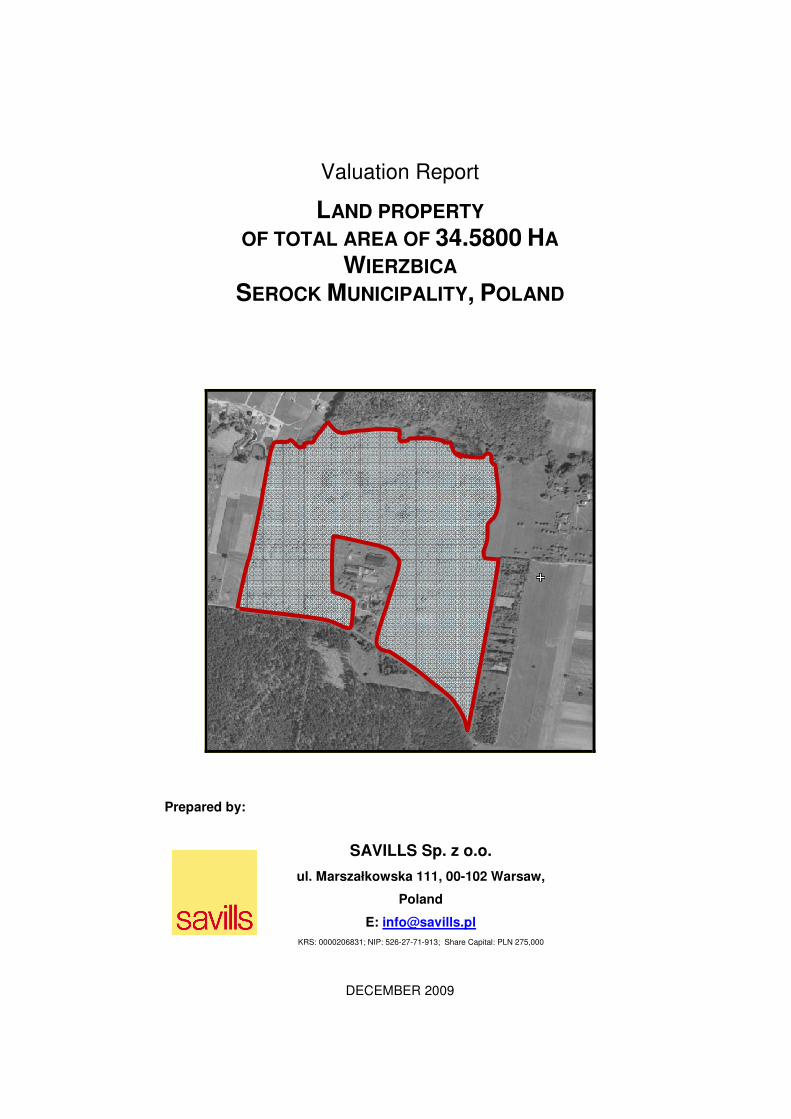

Valuation Report

PANGAEA REAL ESTATE LTD

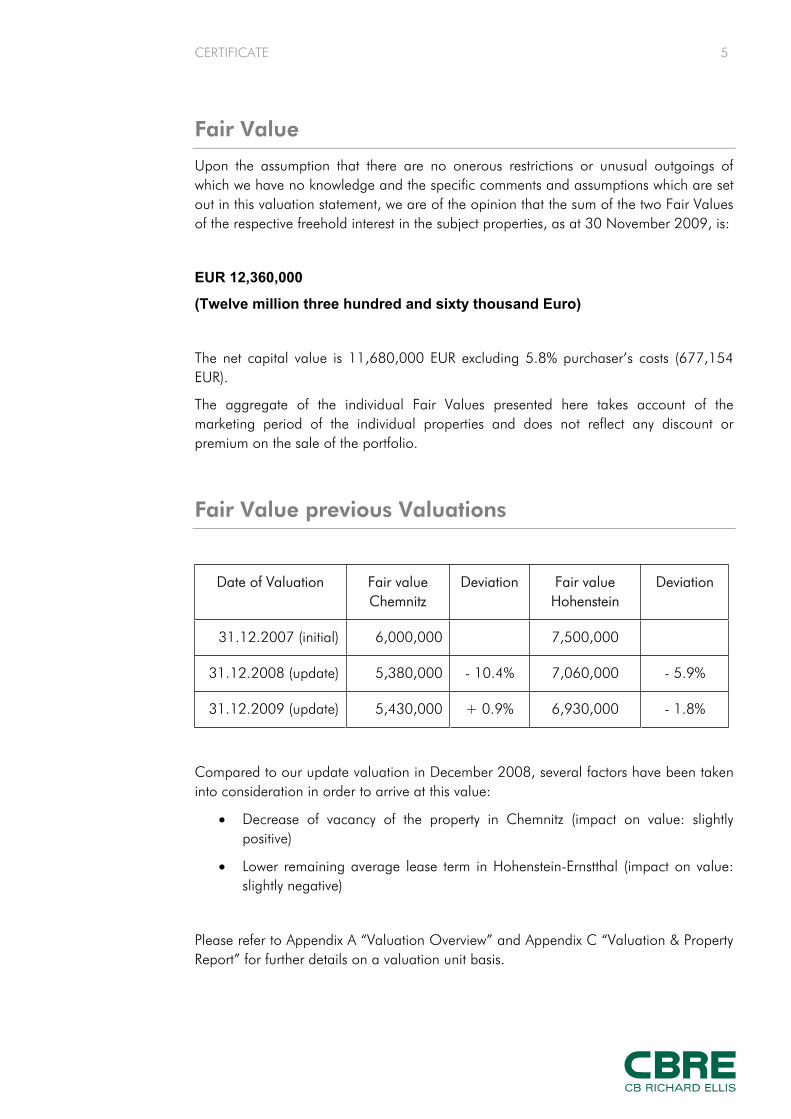

Of the following Property LAND PLOTS OF 2,397,107 SQUARE METERS LOCATED ON

THE INTERSECTION OF

PULKOVSKOE AND VOLKHONSKOE HIGHWAYS IN SAINT PETERSBURG, RUSSIA Valuation Date: 30TH OF NOVEMBER 2009 Report Issue Date: 24TH OF DECEMBER 2009

Prepared by Cushman & Wakefield Stiles & Riabokobylko 125047, Moscow, 6 Gasheka St., Ducat Place III Tel: +7 (495) 797-9600 Fax: +7 (495) 797-9601

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 2 -

Table of Contents

A INTRODUCTION ....................................................................................................................- 5 -

1 INSTRUCTIONS............................................................................................................................................................ - 6 - 2 BASIS OF VALUATION............................................................................................................................................... - 7 - 3 ASSUMPTIONS, DEPARTURES AND RESERVATIONS .................................................................................... - 8 - 4 INSPECTION.................................................................................................................................................................. - 8 - 5 SOURCES OF INFORMATION ................................................................................................................................ - 9 - 6 TOWN PLANNING..................................................................................................................................................... - 9 - 7 STRUCTURE................................................................................................................................................................... - 9 - 8 SITE AND CONTAMINATION................................................................................................................................ - 9 - 9 GENERAL COMMENT .............................................................................................................................................. - 10 - 10 MARKET UNCERTAINTY........................................................................................................................................ - 11 - 11 VALUATION ................................................................................................................................................................ - 12 - 12 CONFIDENTIALITY................................................................................................................................................... - 12 - 13 PREVIOUS VALUATIONS MADE BY THE VALUER ........................................................................................ - 12 - 14 DISCLOSURE AND PUBLICATION...................................................................................................................... - 14 -

B PROPERTY SCHEDULE........................................................................................................- 15 -

1 LOCATION .................................................................................................................................................................. - 16 -

2 DESCRIPTION ............................................................................................................................................................. - 20 - 3 ENVIRONMENTAL CONSIDERATIONS ............................................................................................................ - 24 - 4 TENURE ......................................................................................................................................................................... - 24 - 5 MARKET COMMENTARY........................................................................................................................................ - 26 - 6 VALUATION METHODOLOGY AND COMMENTARY ............................................................................... - 37 - 7 VALUATION SUMMARY.......................................................................................................................................... - 49 -

C APPENDIXES .........................................................................................................................- 50 -

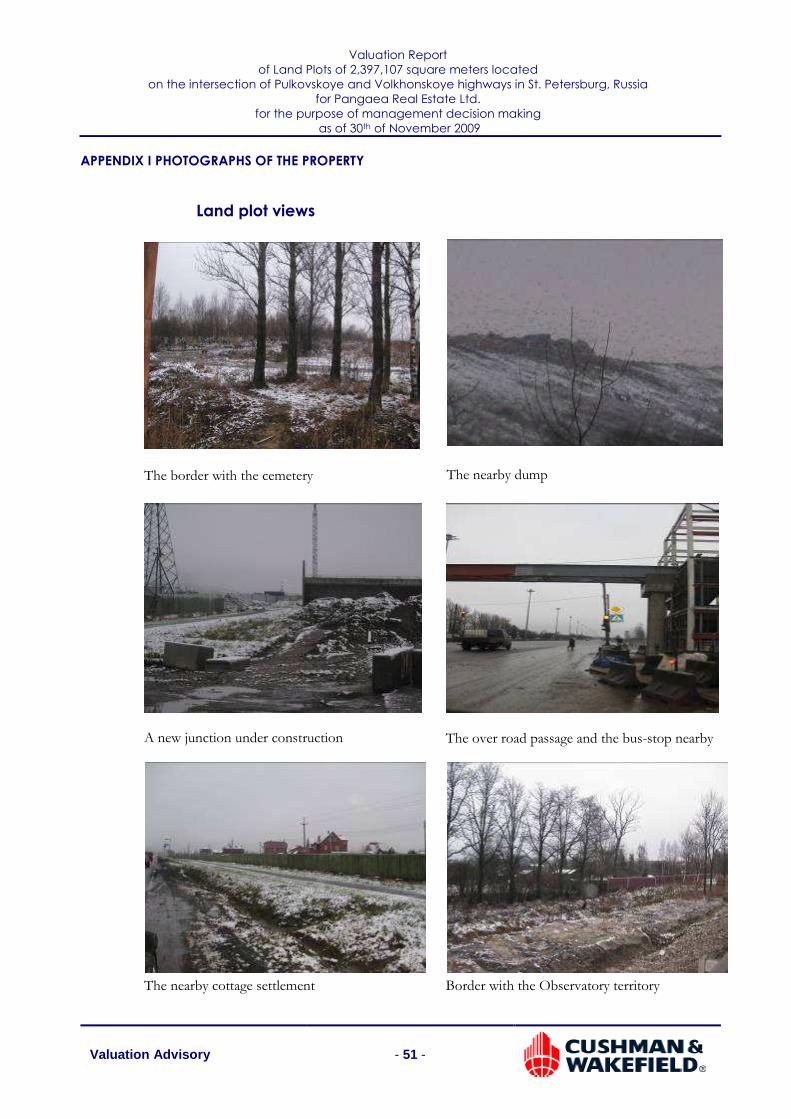

APPENDIX I PHOTOGRAPHS OF THE PROPERTY.................................................................................................... - 51 -

APPENDIX II INFORMATION SUPPLIED ........................................................................................................................ - 52 -

APPENDIX III VALUATION LICENSES............................................................................................................................. - 53 -

APPENDIX IV PRINCIPAL TERMS AND CONDITIONS OF APPOINTMENT AS VALUERS.......................... - 56 -

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 3 -

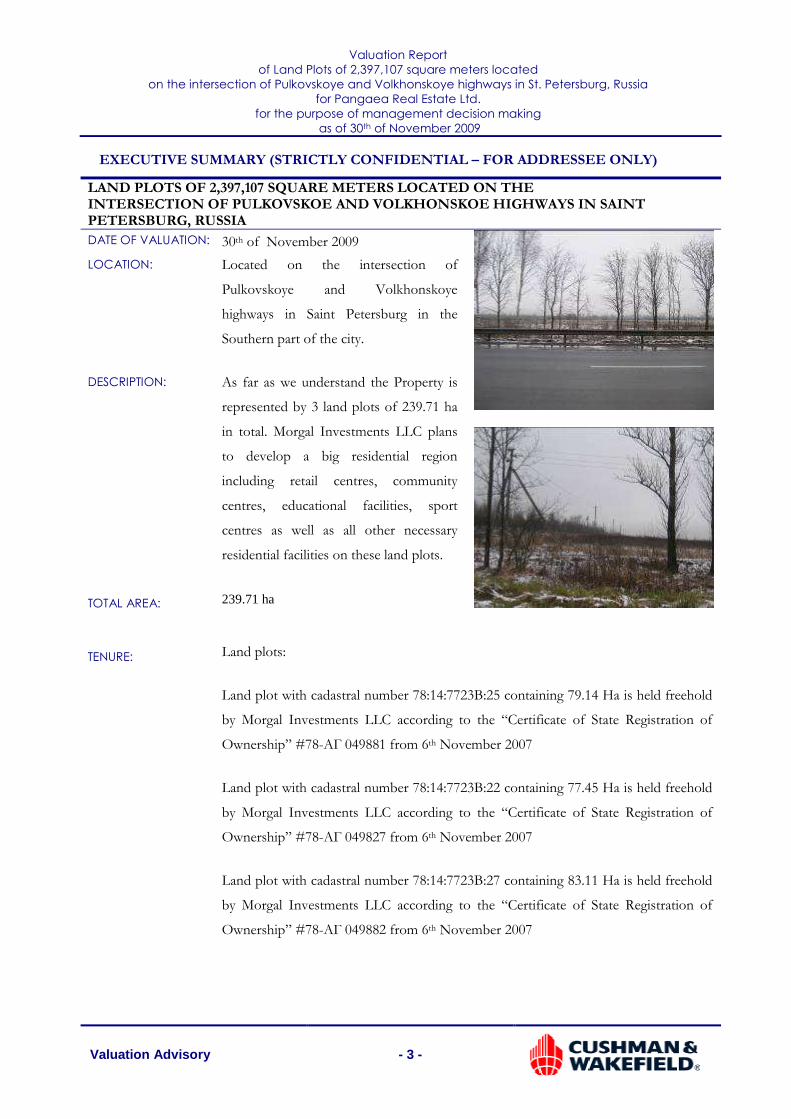

EXECUTIVE SUMMARY (STRICTLY CONFIDENTIAL – FOR ADDRESSEE ONLY)

LAND PLOTS OF 2,397,107 SQUARE METERS LOCATED ON THE INTERSECTION OF PULKOVSKOE AND VOLKHONSKOE HIGHWAYS IN SAINT PETERSBURG, RUSSIA

DATE OF VALUATION: 30th of November 2009

LOCATION: Located on the intersection of

Pulkovskoye and Volkhonskoye

highways in Saint Petersburg in the

Southern part of the city.

DESCRIPTION: As far as we understand the Property is

represented by 3 land plots of 239.71 ha

in total. Morgal Investments LLC plans

to develop a big residential region

including retail centres, community

centres, educational facilities, sport

centres as well as all other necessary

residential facilities on these land plots.

TOTAL AREA: 239.71 ha

TENURE: Land plots:

Land plot with cadastral number 78:14:7723B:25 containing 79.14 Ha is held freehold

by Morgal Investments LLC according to the “Certificate of State Registration of

Ownership” #78-АГ 049881 from 6th November 2007

Land plot with cadastral number 78:14:7723B:22 containing 77.45 Ha is held freehold

by Morgal Investments LLC according to the “Certificate of State Registration of

Ownership” #78-АГ 049827 from 6th November 2007

Land plot with cadastral number 78:14:7723B:27 containing 83.11 Ha is held freehold

by Morgal Investments LLC according to the “Certificate of State Registration of

Ownership” #78-АГ 049882 from 6th November 2007

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 4 -

LAND PLOTS OF 2,397,107 SQUARE METERS LOCATED ON THE INTERSECTION OF PULKOVSKOE AND VOLKHONSKOE HIGHWAYS IN SAINT PETERSBURG, RUSSIA

Buildings:

There are three dilapidated non-residential pieces of property located on the subject

land plots.

The Property cadastral number 78:7723B:7:34 containing 52.1 square meters is

freehold by Morgal Investments LLC starting from 17 September 2007 as stated in

Ownership Registration Certificate #78-АГ 049883 from 6 November 2007.

The Property cadastral number 78:7723B:7:35 containing 219.5 square meters is

freehold by Morgal Investments LLC starting from 17 September 2007 as stated in

Ownership Registration Certificate #78-АГ 049884 from 6 November 2007.

The Property cadastral number 78:7723B:7:36 containing 52.1 square meters is

freehold by Morgal Investments LLC starting from 17 September 2007 as stated in

Ownership Registration Certificate #78-АГ 049885 from 6 November 2007.

Notices from the Federal Registration Service regarding the change of the allowed

usage of the land plots from “for agricultural use” into the “for allocation of

residential buildings” made in the National Land Title Register:

� Notice #78-78-01/0073/2009-018 from 24.02.2009 (for the land plot with the cadastral number 78:14:7723B:22)

� Notice #78-78-01/0073/2009-033 from 24.02.2009 (for the land plot with the cadastral number 78:14:7723B:27)

� Notice #78-78-01/0073/2009-050 from 24.02.2009 (for the land plot with the cadastral number 78:14:7723B:25)

TENURE: The Land Plot belongs to the category “land of settlement” with an allowed usage

“for allocation of residential buildings”

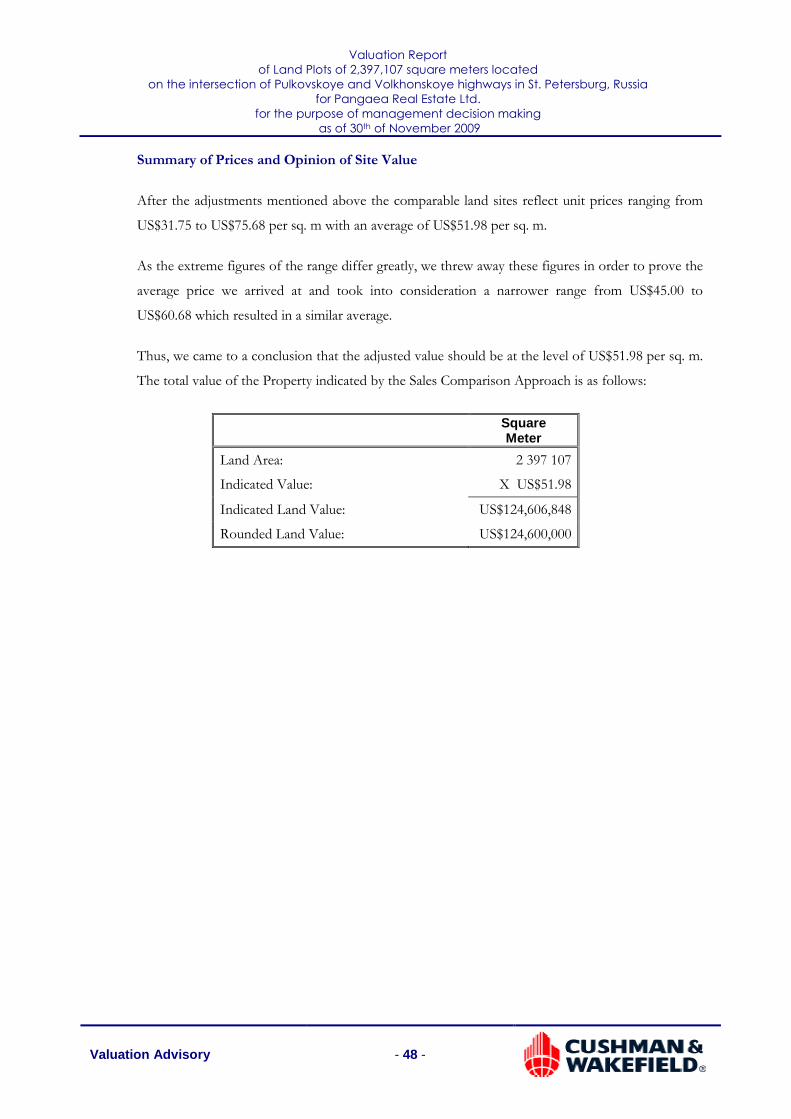

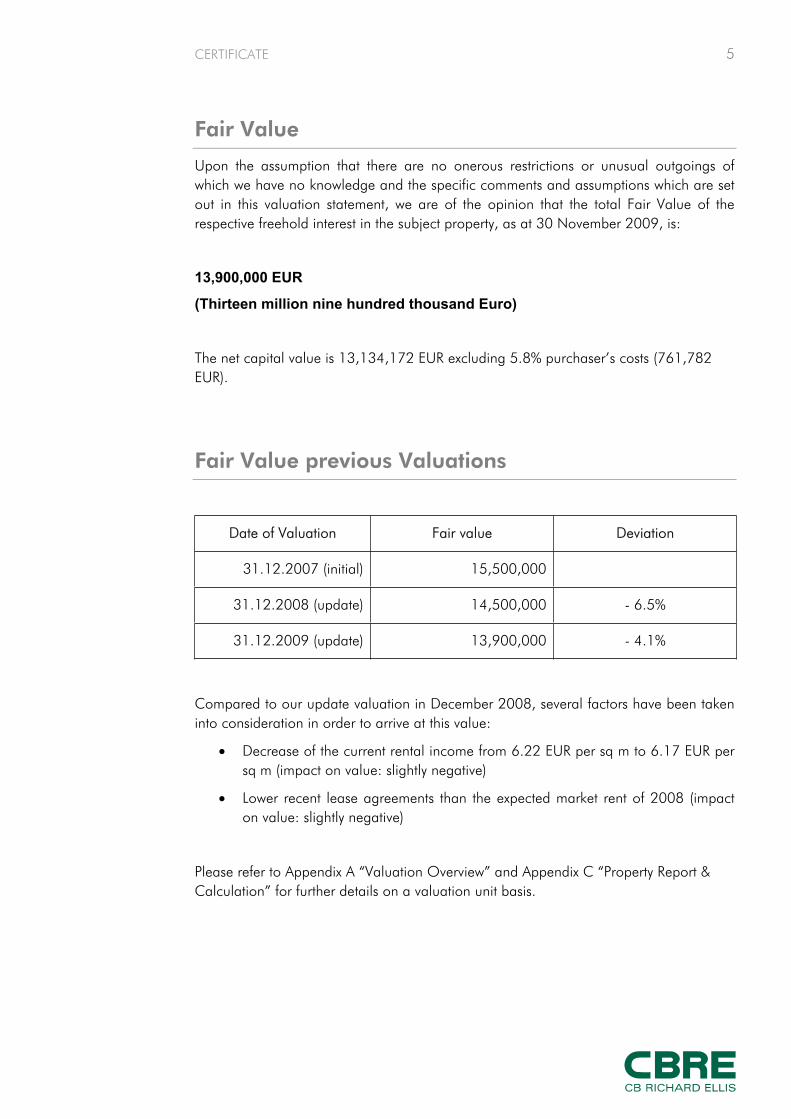

MARKET VALUE: Market Value of the freehold interest in the subject land plots as of the date of

valuation is: US$124 600 000

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 5 -

A INTRODUCTION

Real Estate Consultants

Ducat Place III, Gasheka ul. 6

Moscow 125047

Phone+7 495 797 9600

Fax+7 495 797 9601

www.cushwake.com

Valuation Advisory - 6 -

Strictly Confidential - For Addressee Only Pangaea Real Estate LTD 14 Shenkar Street, Herzelia, Israel For the attention of Mr. Barak Rosen and Mr. Asaf Touchmeir Our Ref: # 08-019254 from 30th November 2009 24th of December 2009 Dear Sirs

Valuation of Land Plots of 239.71 ha in Total located on the intersection of

Pulkovskoe and Volkhonskoe highways in Saint Petersburg, Russia ("the

Property") for Pangaea Real Estate LTD (“the Client”).

1 INSTRUCTIONS

1.1 Confirmation of Instructions

In accordance with your request we have inspected the above land plots (herein referred to as the

“Property”) and made all necessary enquiries to provide you with our Opinion as to the Market

Value of the freehold interest in the Property.

We understand from the instructions received by the Client that the valuation will be used for the

Client’s management decision making.

The Client shall use and publish the Report as a basis for determining the relative value of Pangaea

Israel (T.R.) Ltd. and Pangaea Real Estate Ltd. in the merger process.

The Client or any of Pangaea Real Estate Ltd. subsidiaries shall be entitled to publish the Report in

any immediate report published according to the Israeli Securities Regulations or within their

published financial statements and/or prospectus.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 7 -

1.2 Conflicts of Interest

We confirm that there are no conflicts of interest in our advising you on the value of the Property

under the assumed conditions as instructed.

1.3 Inspections

The Property was inspected externally on 4th of December 2009. No measurement survey has been

carried out by Cushman & Wakefield Stiles & Riabokobylko (“C&W S&R”). We have relied entirely

on the site areas provided to us by the Client. We have assumed that these are correct.

1.4 Background to the Valuation

In accordance with the information on the land areas provided to us by the Client, the Property

currently represents three land plots of 239.71 ha in total located on the intersection of Pulkovskoye

and Volkhonskoye highways in Saint Petersburg, Russia.

As far as we understand the Property is represented by three land plots of 239.71 ha in total, which

are zoned as “land of settlement for allocation of residential buildings”. The Client presented plans

for developing a big residential district including retail centres, community centres, educational

facilities, sport centres as well as all other necessary residential facilities on these land plots.

2 BASIS OF VALUATION

The valuation has been prepared in accordance with the Practice Statements contained in the RICS

Appraisal and Valuation Standards ("the Red Book") published by The Royal Institution of

Chartered Surveyors and updated in January 2008 (6th edition). The valuation has been prepared by

a valuer who conforms to the requirements as set out in the Red Book, acting in the capacity of an

independent valuer.

We have prepared our valuation according to Israeli "Security Law Regulations (periodic and

immediate statements) - 1970" (8B) and in accordance with the requirements of the Red Book.

Our valuation was carried out on the following basis:

2.1 Background to the Valuation

PS 3.2 of the Red Book defines Market Value as:

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 8 -

“The estimated amount for which a property should exchange on the date of valuation between a

willing buyer and a willing seller in an arm’s length transaction after proper marketing wherein the

parties had each acted knowledgeably, prudently and without compulsion.”

We set out in paragraph 9.3 of our Principal Terms and Conditions of Appointment as Valuers

(attached in Appendix IV of this Valuation Report – herein referred to as the “Report”), the

relevant basis of valuation.

3 ASSUMPTIONS, DEPARTURES AND RESERVATIONS

As assumptions is stated in the Glossary to the Red Book to be a “supposition taken to be true”

(“assumption”). Assumptions are facts, condition or situations affecting the subject of, or approach

to, a valuation that, by agreement, need to be verified by a Valuer as part of the valuation process.

In undertaken our valuations, we have made a number of assumptions and have relied on certain

source on information. We believe that the assumptions we have are reasonable, taking into

account our knowledge of the properties, and the contents of report made available to us.

However, in the event that any of these assumptions prove to incorrect then our valuations should

be reviewed. The assumptions we have made for the purposes of our valuations are referred to

below.

We have based our valuations on our inspection of the Land Plots and information supplied to us

by the Company and the results of our other enquiries.

We have made an assumption that the information the Company and its professional advisers have

supplied to us in respect of the Properties is both full and correct.

It follows that we have made an assumptions that details of all matters likely to affect value within

their collective knowledge such prospective lettings, outstanding requirements under legislation and

planning decisions have been made available to us and that information is up to date.

In terms of the Assumptions which we have made and which are summarized within this Valuation

Report, the Company has confirmed that our Assumptions are correct as far as they are aware. In

the event that any of our Assumptions prove to be incorrect, the valuation contained in this

valuation report should be reviewed and modified as necessary.

4 INSPECTION

We inspected the subjected land plots on the 4th of December 2009.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 9 -

5 SOURCES OF INFORMATION

We have based our Valuation on our inspection of the Property and information supplied to us by

the Client and the results of our other enquiries.

6 TOWN PLANNING

We have not made formal searches, but have generally relied on verbal enquiries and any informal

information received from the Local Planning Authority or from the Company.

Each valuation is on the basis that the property has been erected either prior to planning control or

in accordance with a valid planning permission and is being occupied and used without any breach

of planning or building regulations. Except where stated otherwise, each valuation is on the basis

that each property is not affected by proposals for road widening, Compulsory Purchase, planning

inquiry, or archaeological investigation.

Each valuation reflects our opinion of an appropriate development that could reasonably be

expected to form the basis of a bid for a property by a third party. Therefore our valuations do not

necessarily reflect the Company’s intended investment /development program.

7 STRUCTURE

We have neither carried out a structural survey of each property, nor tested any services or other

plant or machinery. We are therefore unable to give any opinion on the condition of the structure

or services at any property. Each valuation takes into account any information supplied to us and

any defects noted during our inspection, but otherwise are on the basis that there are no latent

defects, wants of repair or other matters which would materially affect each valuation.

We have not inspected those parts of each property which are covered, unexposed or inaccessible

and each valuation is on the basis that they are in good repair and condition.

We have not investigated the presence or absence of High Alumina Cement, Calcium Chloride,

Asbestos and other deleterious materials. In the absence of information to the contrary, each

valuation is on the basis that no hazardous or suspect materials or techniques have been used in the

construction of any property. You may wish to arrange for investigations to be carried out to verify.

8 SITE AND CONTAMINATION

We have not investigated ground conditions/stability and each valuation is on the basis that any

buildings have been constructed, having appropriate regard to existing ground conditions. Where

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 10 -

the property has development potential, our valuation is on the basis that there are no adverse

ground conditions which would affect building costs. However, where you have supplied us with a

building cost estimate, we have relied on it being based on full information regarding existing

ground conditions. We have considered the Company’s construction estimates in the light of typical

market norms.

We have not carried out any investigations or tests, nor been supplied with any information from

you or from any relevant expert that determines the presence or otherwise of contamination

(including any ground water). Accordingly, our valuation has been prepared on the basis that there

are no such matters that would materially affect our valuation. Should this basis be unacceptable to

you or should you wish to verify that this basis is correct, you should have appropriate

investigations made and refer the results to us so that we can review our valuation.

9 GENERAL COMMENT

Our Report is derived from the analysis of recent market transactions, together with our market

knowledge derived from the Firm’s agency coverage.

A valuation is a prediction of price, not a guarantee and different Valuers can properly arrive at

different opinions of potential future worth.

We have made subjective judgements during our approach in arriving at our Valuation and whilst

we consider these to be both logical and appropriate they are not necessarily the same as would be

made by a purchaser. The purpose of the valuation does not alter the approach to the valuation.

Property values can change substantially, even over short periods of time, and so our opinion of

value could differ significantly if the date of valuation was to change. If you wish to rely on our

valuation as being valid on any other date you should consult us first.

Should you contemplate a sale, we strongly recommend that the property is given proper exposure

to the market. In a rapidly rising market, or in the case of a property with development potential,

the inclusion of a 'clawback' provision in the sale contract should also be considered, so that further

sums become payable if the property is quickly re-sold at a profit.

You should not rely on this report unless any reference to tenure, tenancies and legal title has been

verified as correct by your legal advisers.

Our Valuation is exclusive of any Value Added Tax.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 11 -

10 MARKET UNCERTAINTY

Where uncertainty could have a material effect on an opinion of value, the Red Book requires a

valuer to draw attention to this, indicating the cause of the uncertainty and the degree to which this

is reflected in the valuation reported.

The global banking crisis and consequent reduction in the availability of debt, coupled with the

economic downturn, have caused property values to experience sharp falls in value and liquidity,

with very few transactions being completed.

Although recent transactions could be considered distressed, it is inappropriate to conclude that all

recent market activity represents forced transactions. An imbalance between supply and demand

(for example, fewer buyers than sellers) is not always a determinant of a forced transaction. A seller

might be under financial pressure to sell, but it is still able to sell at a market price if there is more

than one potential buyer in the market and a reasonable amount of time is available for marketing.

Similarly, transactions initiated during bankruptcy should not automatically be assumed to be

forced.

It has been held that valuers may properly conclude within a range of values. This range is likely to

be greater in an illiquid market where inherent uncertainty exists and a greater degree of judgement

must therefore be applied.

Some parts of the market, particularly for secondary or vacant properties, have experienced

particularly nil transaction volumes. As a consequence, there’s hardly any market evidence upon

which to base our valuation and so we have had to exercise a greater degree of judgement than

usual. We have considered both current and historic market evidence available and endeavoured to

reflect current market sentiment, although the signals are mixed.

We strongly recommend that you keep the valuation of the subject property under review. You

should also anticipate a longer marketing period than would previously have been expected in the

event that the property is offered for sale.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 12 -

11 VALUATION

11.1 Market Value

Subject to the contents of this Report and based on current values, we estimated the Market Value

of the freehold interest in the Property.

We are of the opinion that the Market Value of the freehold interest in the Property as of 30th of

November 2009 is:

US$124 600 000

(ONE HUNDRED TWENTY FOUR MILLION SIX HUNDRED THOUSAND US

DOLLARS)

The findings contained in our Report are based on calculations, conclusions and other information

obtained as a result of market research, on our expertise in the course of which we received certain

information.

12 CONFIDENTIALITY

The contents of this Report are intended to be confidential to the addressees and for the specific

purpose stated. Consequently, and in accordance with current practice, no responsibility is accepted

to any other party in respect of the whole or any part of its contents. Before the Report or any part

of its contents are reproduced or referred to in any document, circular or statement or disclosed

orally to a third party, our written approval as to the form and context of such publication or

disclosure must first be obtained. For avoidance of doubt, such approval is required whether or not

this firm is referred to by name and whether or not our Report is combined with others.

The Report should only be reproduced, in accordance with any of the above requirements, in full

and including all of the assumptions and conditions pertaining thereto. No part of the Report shall

be reproduced in isolation.

13 PREVIOUS VALUATIONS MADE BY THE VALUER

According to Clause 5 of the Israeli "Security Law Regulations (periodic and immediate statements)

- 1970" (8B) we are instructed to list the details of previous valuations made by Cushman &

Wakefield Stiles & Riabokobylko.

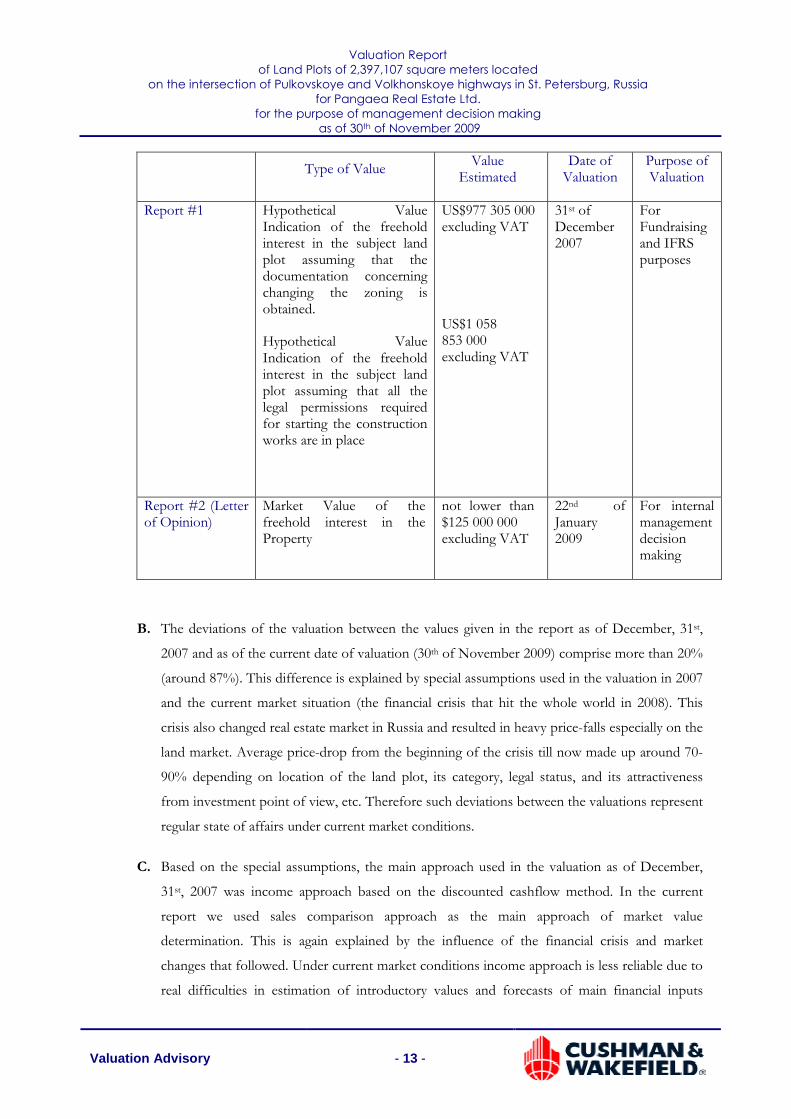

A. During the three years preceding the Effective Date of the Valuation we made 2 valuation

reports. Short summary of these reports in presented in the table below.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 13 -

Type of Value

Value Estimated

Date of Valuation

Purpose of Valuation

Report #1 Hypothetical Value Indication of the freehold interest in the subject land plot assuming that the documentation concerning changing the zoning is obtained.

Hypothetical Value Indication of the freehold interest in the subject land plot assuming that all the legal permissions required for starting the construction works are in place

US$977 305 000 excluding VAT

US$1 058 853 000 excluding VAT

31st of December 2007

For Fundraising and IFRS purposes

Report #2 (Letter of Opinion)

Market Value of the freehold interest in the Property

not lower than $125 000 000 excluding VAT

22nd of January 2009

For internal management decision making

B. The deviations of the valuation between the values given in the report as of December, 31st,

2007 and as of the current date of valuation (30th of November 2009) comprise more than 20%

(around 87%). This difference is explained by special assumptions used in the valuation in 2007

and the current market situation (the financial crisis that hit the whole world in 2008). This

crisis also changed real estate market in Russia and resulted in heavy price-falls especially on the

land market. Average price-drop from the beginning of the crisis till now made up around 70-

90% depending on location of the land plot, its category, legal status, and its attractiveness

from investment point of view, etc. Therefore such deviations between the valuations represent

regular state of affairs under current market conditions.

C. Based on the special assumptions, the main approach used in the valuation as of December,

31st, 2007 was income approach based on the discounted cashflow method. In the current

report we used sales comparison approach as the main approach of market value

determination. This is again explained by the influence of the financial crisis and market

changes that followed. Under current market conditions income approach is less reliable due to

real difficulties in estimation of introductory values and forecasts of main financial inputs

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 14 -

(rental rates, discount rates, construction terms, sales schedule, etc.). Even small alterations of

initial data make great differences in the results because of high level of sensitivity of the

model. Therefore Sales Comparison Approach is more reasonable and advisable for application

at present.

14 DISCLOSURE AND PUBLICATION

We are aware and agree to the publication of our valuation report and the filing thereof in any

required filling under any security laws applicable in Israel.

Yours faithfully,

For and on behalf of Cushman & Wakefield

TIMOTHY MILLARD MRICS

Partner

KONSTANTIN LEBEDEV MRICS

Deputy Head of Valuation Advisory Department

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 15 -

B PROPERTY SCHEDULE

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 16 -

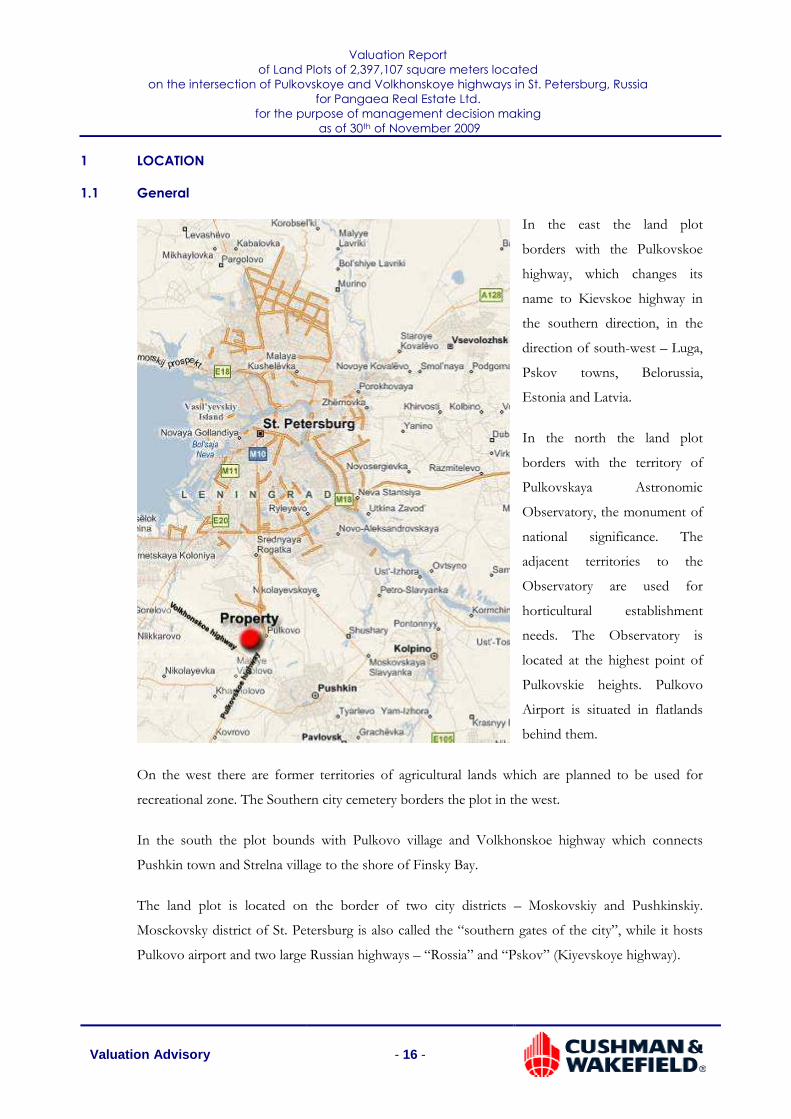

1 LOCATION

1.1 General

In the east the land plot

borders with the Pulkovskoe

highway, which changes its

name to Kievskoe highway in

the southern direction, in the

direction of south-west – Luga,

Pskov towns, Belorussia,

Estonia and Latvia.

In the north the land plot

borders with the territory of

Pulkovskaya Astronomic

Observatory, the monument of

national significance. The

adjacent territories to the

Observatory are used for

horticultural establishment

needs. The Observatory is

located at the highest point of

Pulkovskie heights. Pulkovo

Airport is situated in flatlands

behind them.

On the west there are former territories of agricultural lands which are planned to be used for

recreational zone. The Southern city cemetery borders the plot in the west.

In the south the plot bounds with Pulkovo village and Volkhonskoe highway which connects

Pushkin town and Strelna village to the shore of Finsky Bay.

The land plot is located on the border of two city districts – Moskovskiy and Pushkinskiy.

Mosckovsky district of St. Petersburg is also called the “southern gates of the city”, while it hosts

Pulkovo airport and two large Russian highways – “Rossia” and “Pskov” (Kiyevskoye highway).

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 17 -

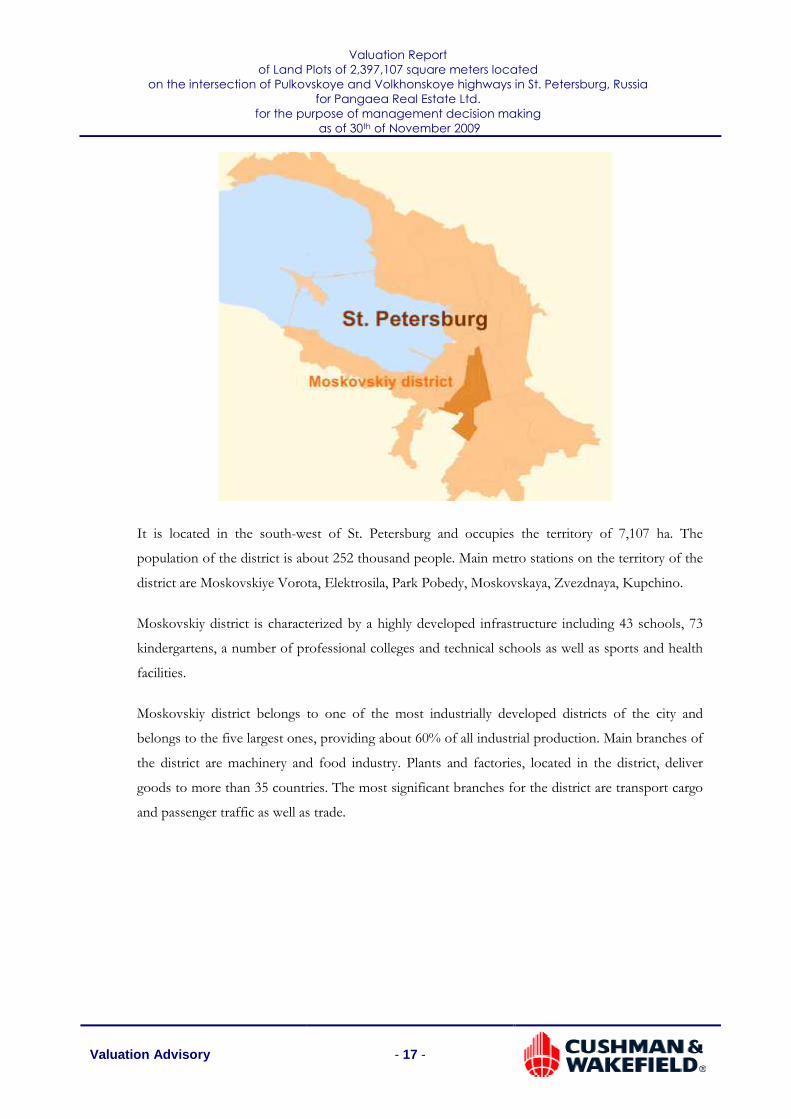

It is located in the south-west of St. Petersburg and occupies the territory of 7,107 ha. The

population of the district is about 252 thousand people. Main metro stations on the territory of the

district are Moskovskiye Vorota, Elektrosila, Park Pobedy, Moskovskaya, Zvezdnaya, Kupchino.

Moskovskiy district is characterized by a highly developed infrastructure including 43 schools, 73

kindergartens, a number of professional colleges and technical schools as well as sports and health

facilities.

Moskovskiy district belongs to one of the most industrially developed districts of the city and

belongs to the five largest ones, providing about 60% of all industrial production. Main branches of

the district are machinery and food industry. Plants and factories, located in the district, deliver

goods to more than 35 countries. The most significant branches for the district are transport cargo

and passenger traffic as well as trade.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 18 -

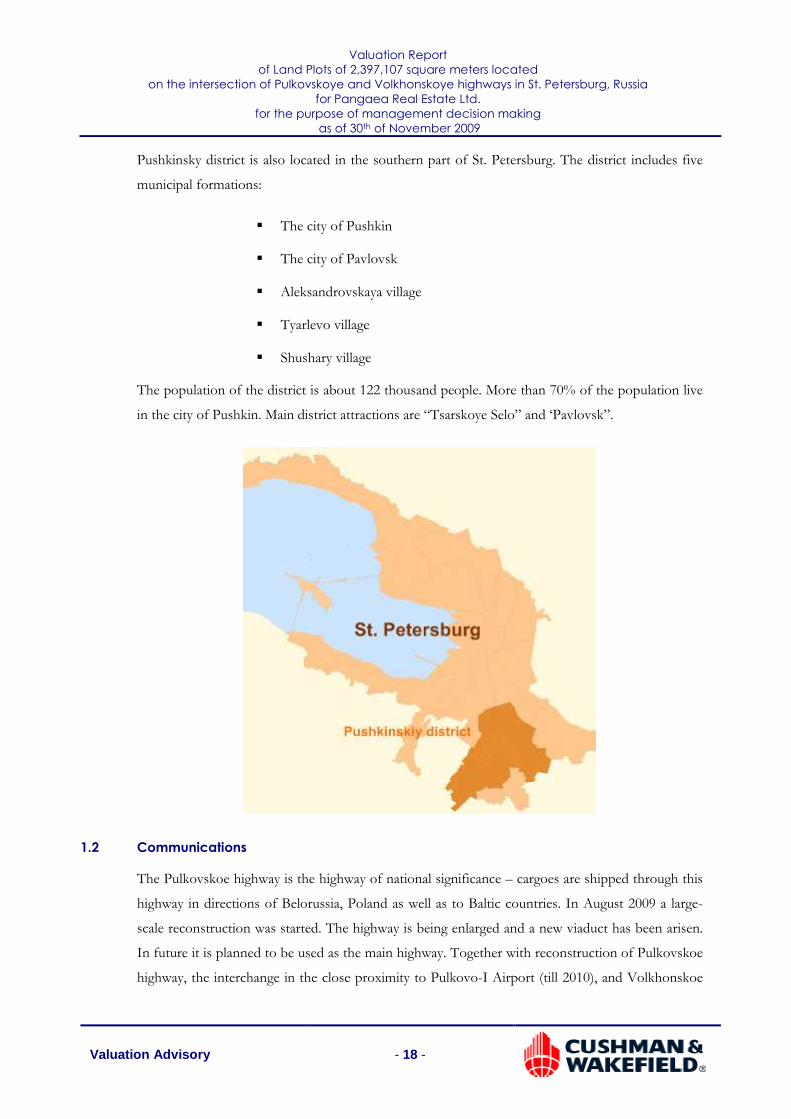

Pushkinsky district is also located in the southern part of St. Petersburg. The district includes five

municipal formations:

� The city of Pushkin

� The city of Pavlovsk

� Aleksandrovskaya village

� Tyarlevo village

� Shushary village

The population of the district is about 122 thousand people. More than 70% of the population live

in the city of Pushkin. Main district attractions are “Tsarskoye Selo” and ‘Pavlovsk”.

1.2 Communications

The Pulkovskoe highway is the highway of national significance – cargoes are shipped through this

highway in directions of Belorussia, Poland as well as to Baltic countries. In August 2009 a large-

scale reconstruction was started. The highway is being enlarged and a new viaduct has been arisen.

In future it is planned to be used as the main highway. Together with reconstruction of Pulkovskoe

highway, the interchange in the close proximity to Pulkovo-I Airport (till 2010), and Volkhonskoe

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 19 -

highway towards Pushkin town, it is also planned to construct a new road interchanges – between

Pulkovskoe and Volkhonskoe highways in particular; construct a new road crossing Krasnoselskoe

highway (till 2015) and a road to Pushkin town. Recently the works to connect Encircling highway

to the Pulkovskoe highway were accomplished.

Currently there are no long-term plans of city committees to build any main roads or streets

crossing the subject land plot.

We estimate that the time to drive from the subject land plot to the centre of Saint Petersburg is

about 30-40 minutes depending on traffic conditions. The time to drive to Pushkin town is about

10-15 minutes.

There is a big interchange as well as terminal of public transportation heading to several directions

close to the border between the subject land plot and Pulkovskoe highway. There is a large public

transportation to Pushkin town, to Krasnoe Selo village (through Volkhonskoe highway) as well as

to Gatchina town. There is a quite convenient connection to the southern part of the city as well.

About three kilometres away from the subject land plot there is a railway towards south-west

direction from the Baltiysky railway station of the city. It is facing the direction of Gatchina, Luga

and Pskov towns. The nearest railway station Alexandrovskaya is situated 3.5 kilometres away from

the subject land plot.

Pulkovo Airport is located in a close proximity to the subject land plot. Pulkovo-I Airport is 7.5

kilometres away and Pulkovo-II – 7 kilometres.

Pulkovo Airport has two main terminals:

1. Pulkovo-1 is intended for internal flights

services and flights across CIS.

2. Pulkovo-2 is intended for international

flights.

Pulkovo Airport takes the forth place among all

Russian airports according to the number of passengers carried.

To summarise, the site accessibility can currently be described as being satisfactory.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 20 -

2 DESCRIPTION

2.1 General

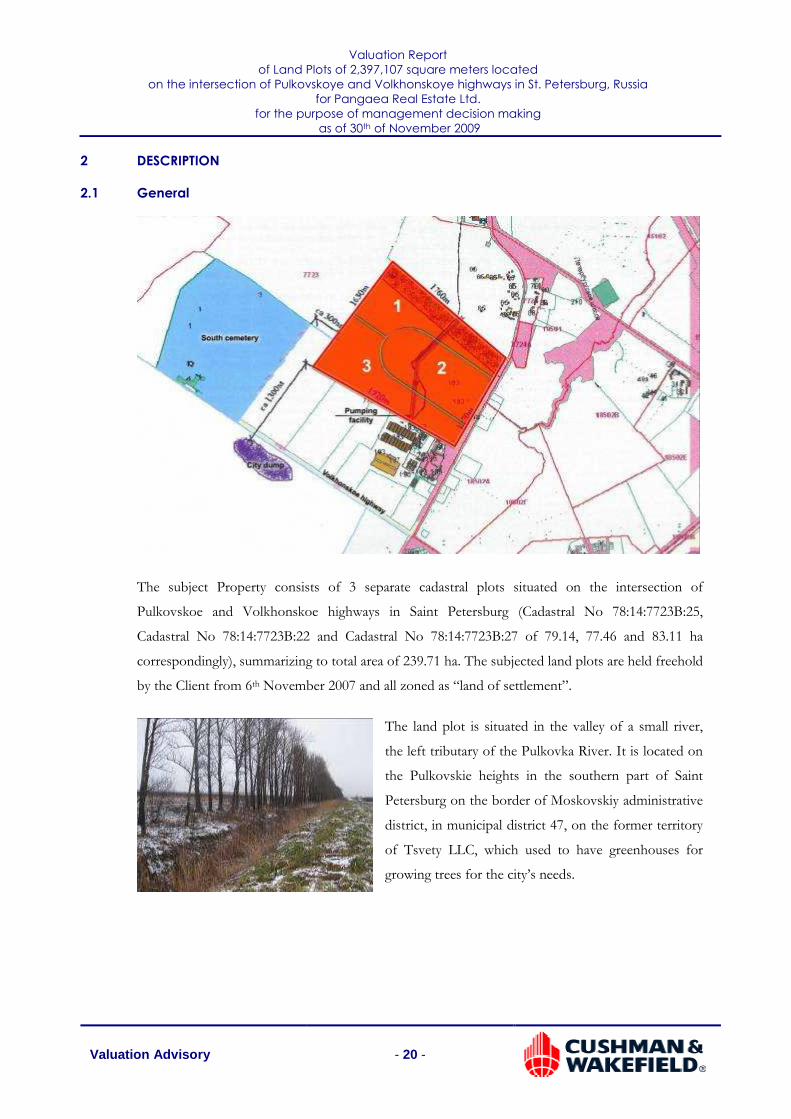

The subject Property consists of 3 separate cadastral plots situated on the intersection of

Pulkovskoe and Volkhonskoe highways in Saint Petersburg (Cadastral No 78:14:7723B:25,

Cadastral No 78:14:7723B:22 and Cadastral No 78:14:7723B:27 of 79.14, 77.46 and 83.11 ha

correspondingly), summarizing to total area of 239.71 ha. The subjected land plots are held freehold

by the Client from 6th November 2007 and all zoned as “land of settlement”.

The land plot is situated in the valley of a small river,

the left tributary of the Pulkovka River. It is located on

the Pulkovskie heights in the southern part of Saint

Petersburg on the border of Moskovskiy administrative

district, in municipal district 47, on the former territory

of Tsvety LLC, which used to have greenhouses for

growing trees for the city’s needs.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 21 -

Most part of the territory is cultivated with forest

plantations including fine woods such as oaks and ash-

trees aging from 5 up to around 25 years old. Some

horticultural establishments are located on the territory

of the land plot as well. The rest part of the territory is

empty. There are three dilapidated non-residential

pieces of property on the land plots as well. Those are

held freehold by the Client. The properties are

registered in the real estate cadastre (Cadastral No

78:7723B:7:34, Cadastral No 78:7723B:7:35, Cadastral

No 78:7723B:7:36), have an address (Pulkovskoe

highway 103 letter “O”, “P” and “П” correspondingly)

and have a total area of 52.1, 219.5 and 52.1 square

metres correspondingly). According to the available

copies of “Certificate of State Registration of

Ownership” all the tree buildings are non-residential.

The building located at the address Pulkovskoe highway 103 letter “P” is a building of former

pumping station which previously was used to supply water for melioration of the greenhouses’

territory. It is located in the north-west part of the land plot, on the bank of a pond. Currently the

building is totally empty.

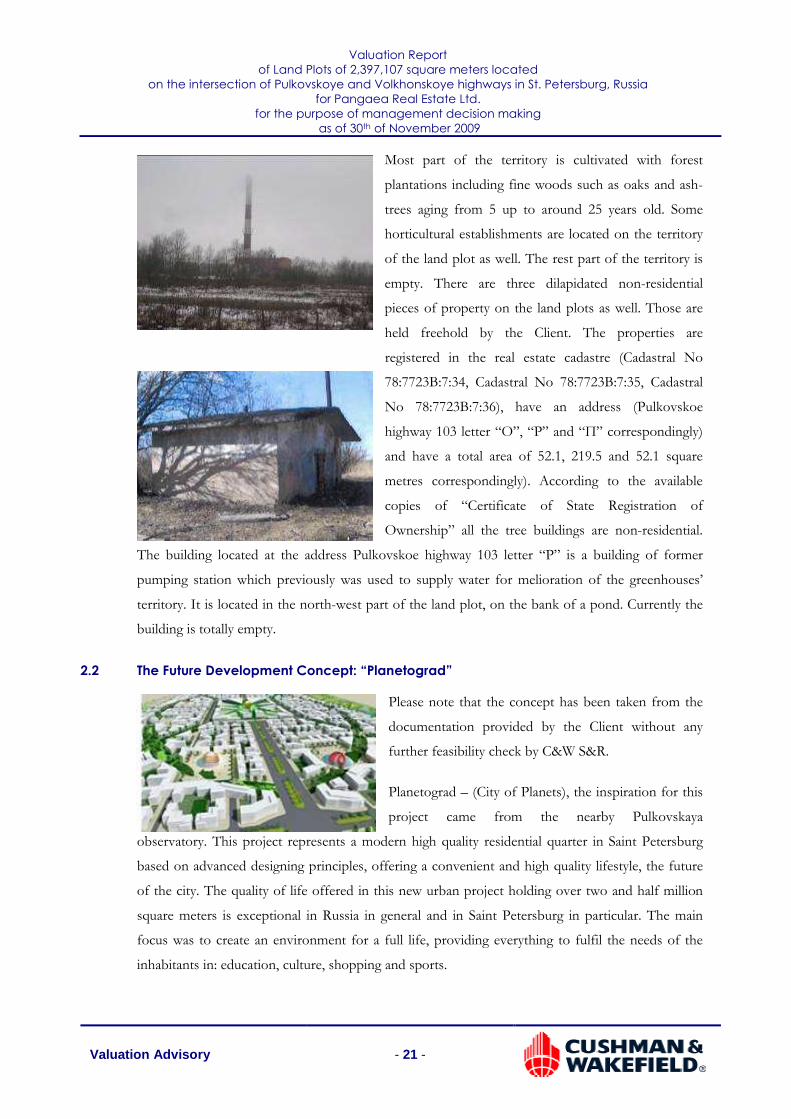

2.2 The Future Development Concept: “Planetograd”

Please note that the concept has been taken from the

documentation provided by the Client without any

further feasibility check by C&W S&R.

Planetograd – (City of Planets), the inspiration for this

project came from the nearby Pulkovskaya

observatory. This project represents a modern high quality residential quarter in Saint Petersburg

based on advanced designing principles, offering a convenient and high quality lifestyle, the future

of the city. The quality of life offered in this new urban project holding over two and half million

square meters is exceptional in Russia in general and in Saint Petersburg in particular. The main

focus was to create an environment for a full life, providing everything to fulfil the needs of the

inhabitants in: education, culture, shopping and sports.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 22 -

Pulkovskaya observatory was established in 1833. It is now the central and main institute of cosmos

study in Russia also known in the professional world of cosmos study worldwide.

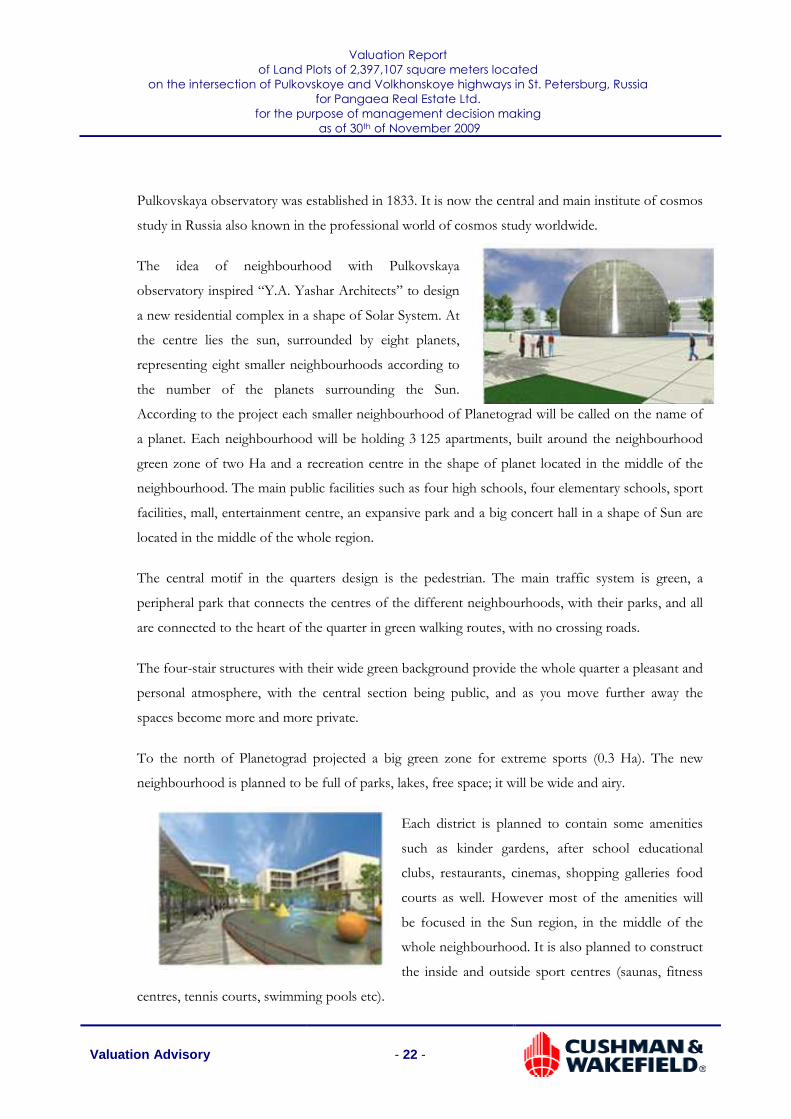

The idea of neighbourhood with Pulkovskaya

observatory inspired “Y.A. Yashar Architects” to design

a new residential complex in a shape of Solar System. At

the centre lies the sun, surrounded by eight planets,

representing eight smaller neighbourhoods according to

the number of the planets surrounding the Sun.

According to the project each smaller neighbourhood of Planetograd will be called on the name of

a planet. Each neighbourhood will be holding 3 125 apartments, built around the neighbourhood

green zone of two Ha and a recreation centre in the shape of planet located in the middle of the

neighbourhood. The main public facilities such as four high schools, four elementary schools, sport

facilities, mall, entertainment centre, an expansive park and a big concert hall in a shape of Sun are

located in the middle of the whole region.

The central motif in the quarters design is the pedestrian. The main traffic system is green, a

peripheral park that connects the centres of the different neighbourhoods, with their parks, and all

are connected to the heart of the quarter in green walking routes, with no crossing roads.

The four-stair structures with their wide green background provide the whole quarter a pleasant and

personal atmosphere, with the central section being public, and as you move further away the

spaces become more and more private.

To the north of Planetograd projected a big green zone for extreme sports (0.3 Ha). The new

neighbourhood is planned to be full of parks, lakes, free space; it will be wide and airy.

Each district is planned to contain some amenities

such as kinder gardens, after school educational

clubs, restaurants, cinemas, shopping galleries food

courts as well. However most of the amenities will

be focused in the Sun region, in the middle of the

whole neighbourhood. It is also planned to construct

the inside and outside sport centres (saunas, fitness

centres, tennis courts, swimming pools etc).

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 23 -

The streets in Planetograd are planned very wide and straight, which allows an easy and fast access

to all districts avoiding traffic jams. Moreover, as it was mentioned before, there is a pedestrian

access from each district to the centre with no crossroads which allows children to reach their

schools without crossing any road, which will decrease the possibility of accidents in the region.

As was said above the complex will consist of eight quite independent residential districts according

to the amount of the planets in the Solar System. This idea allows the developer to divide the

project to eight smaller and independent ones, which will allow merging risks and investments. In

total it is planned to build 25 000 apartments. 31 250 parking lots will allow convenient access to

the whole complex, providing that there will never be any problems with parking space all over the

region.

As was mentioned above the subject land plot is located on the Pulkovskoye and Volkhonskoye

highways in Saint Petersburg. There is a good public transport connection between the land plot

and southern part of Saint Petersburg, Pushkin town and other towns in the region.

The development of the land plot is to be started in 12-18 months and end in 2016.

2.2.1 Limitation conditions for the future construction

The request for limitations of the construction was received from Pulkovskaya observatory.

In order to decrease unfavourable factors disturbing the activity of the observatory there are several

requests that must be fulfilled:

• the buildings in the complex should not be higher than 21.75 meters1;

• there must not be new sources of concentrated emission of heat such as boiler pipe;

• new premises must contain a reliable heat insulation to decrease the amount of warm air

coming from the buildings;

• there must neither be vertical or horizontal strong sources of lights towards the direction of the

observatory, nor any illumination of the sky;

• the total observatory main building dome illuminance would not get over 0.05 luxmeter;

• there must be some green plantations in order to screen the light coming out of the windows

facing the observatory.

1 According to the current planning the height of the buildings is 12 meters, which fulfils the limitation

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 24 -

2.3 Site Area

According to documentation available to us the Property is represented by three land plots

extending to 239.71 ha in total.

3 ENVIRONMENTAL CONSIDERATIONS

We have not carried out any investigations or tests, nor have been supplied with any information

from the owner or from any relevant expert that determines the presence or otherwise of pollution

or contaminative substances or any other land (including any ground water).

However, we would like to mention that there are several environmental issues that must be taken

into consideration:

• The plot is located about 1.3 kilometres from the city garbage dump, which rises high above a

hill and can be seen well from the southern and western sides of the plot. This can affect the

air purity, especially while the dump is burning. However, this is only possible when the south-

eastern wind is blowing which happens in average 30 days annually. Moreover, at 1.3

kilometres the smell disperses. Moreover, according to the new development planning this

dump is planned to be removed from the place.

• The western side of the plot borders the Southern city cemetery.

Considering all said above we would not expect there to be any outstanding environmental or

archaeological issues.

4 TENURE

As it was said above the Client has the freehold in all the mentioned land plots:

• cadastral number 78:14:7723B:25 containing 79.14 ha is held freehold according to the

“Certificate of State Registration of Ownership” #78-АГ 049881 from 6th November 2007,

• cadastral number 78:14:7723B:22 containing 77.45 ha is held freehold according to the

“Certificate of State Registration of Ownership” #78-АГ 049827 from 6th November 2007,

• cadastral number 78:14:7723B:27 containing 83.11 ha is held freehold according to the

“Certificate of State Registration of Ownership” #78-АГ 049882 from 6th November 2007)

As well as the following non-residential pieces of property located on the subject land plots:

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 25 -

• The Property cadastral number 78:7723B:7:34 containing 52.1 square meters is freehold by

Morgal Investments LLC starting from 17 September 2007 as stated in Ownership

Registration Certificate #78-АГ 049883 from 6 November 2007.

• The Property cadastral number 78:7723B:7:35 containing 219.5 square meters is freehold by

Morgal Investments LLC starting from 17 September 2007 as stated in Ownership

Registration Certificate #78-АГ 049884 from 6 November 2007.

• The Property cadastral number 78:7723B:7:36 containing 52.1 square meters is freehold by

Morgal Investments LLC starting from 17 September 2007 as stated in Ownership

Registration Certificate #78-АГ 049885 from 6 November 2007.

In January 2009 allowed usage of the mentioned land plots has been changed which was changed

from “for agricultural use” into the “for allocation of residential buildings”. This was stated in the

Federal Registration Service and made in the National Land Title Register:

• Notice #78-78-01/0073/2009-018 from 24.02.2009 (for the land plot with the cadastral

number 78:14:7723B:22)

• Notice #78-78-01/0073/2009-033 from 24.02.2009 (for the land plot with the cadastral

number 78:14:7723B:27)

• Notice #78-78-01/0073/2009-050 from 24.02.2009 (for the land plot with the cadastral

number 78:14:7723B:25)

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 26 -

5 MARKET COMMENTARY

5.1 Brief Economy Overview

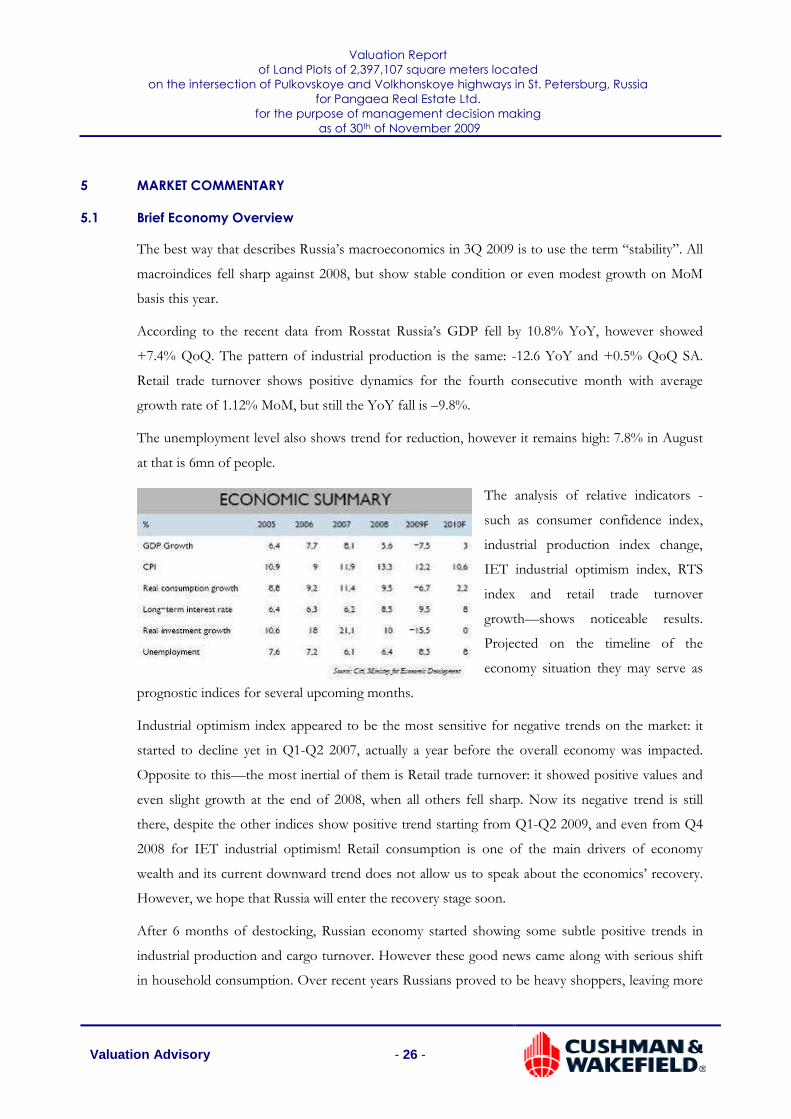

The best way that describes Russia’s macroeconomics in 3Q 2009 is to use the term “stability”. All

macroindices fell sharp against 2008, but show stable condition or even modest growth on MoM

basis this year.

According to the recent data from Rosstat Russia’s GDP fell by 10.8% YoY, however showed

+7.4% QoQ. The pattern of industrial production is the same: -12.6 YoY and +0.5% QoQ SA.

Retail trade turnover shows positive dynamics for the fourth consecutive month with average

growth rate of 1.12% MoM, but still the YoY fall is –9.8%.

The unemployment level also shows trend for reduction, however it remains high: 7.8% in August

at that is 6mn of people.

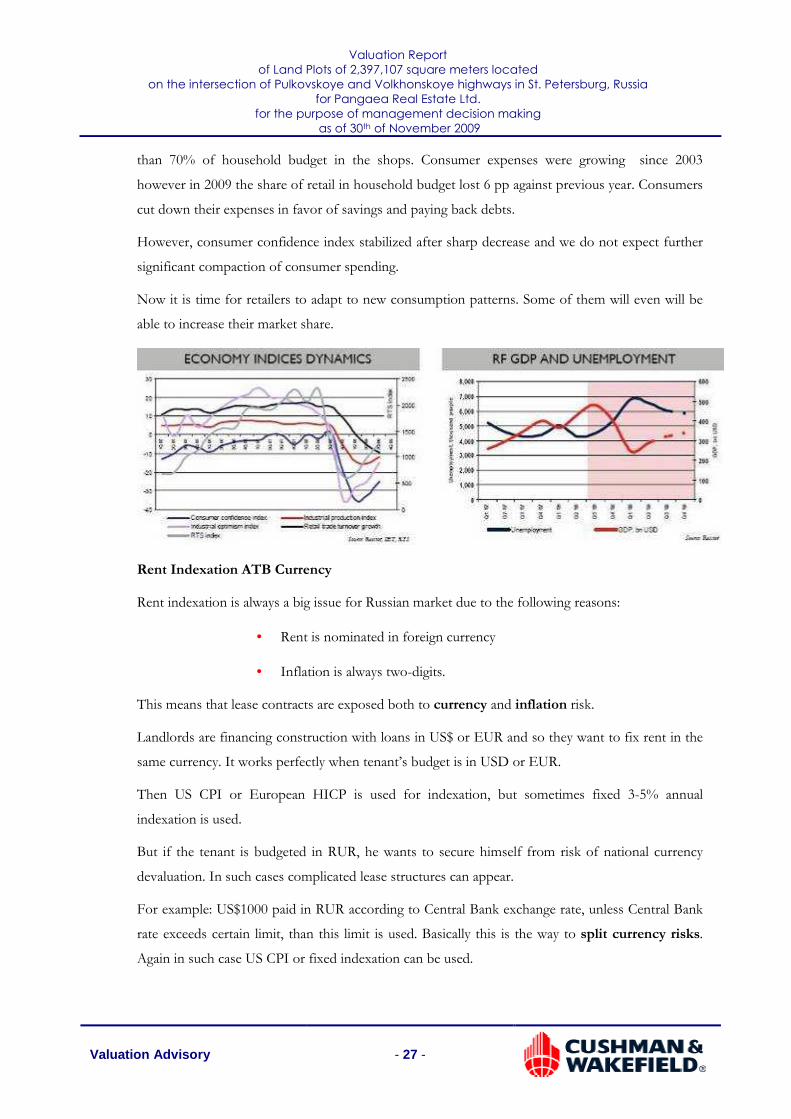

The analysis of relative indicators -

such as consumer confidence index,

industrial production index change,

IET industrial optimism index, RTS

index and retail trade turnover

growth—shows noticeable results.

Projected on the timeline of the

economy situation they may serve as

prognostic indices for several upcoming months.

Industrial optimism index appeared to be the most sensitive for negative trends on the market: it

started to decline yet in Q1-Q2 2007, actually a year before the overall economy was impacted.

Opposite to this—the most inertial of them is Retail trade turnover: it showed positive values and

even slight growth at the end of 2008, when all others fell sharp. Now its negative trend is still

there, despite the other indices show positive trend starting from Q1-Q2 2009, and even from Q4

2008 for IET industrial optimism! Retail consumption is one of the main drivers of economy

wealth and its current downward trend does not allow us to speak about the economics’ recovery.

However, we hope that Russia will enter the recovery stage soon.

After 6 months of destocking, Russian economy started showing some subtle positive trends in

industrial production and cargo turnover. However these good news came along with serious shift

in household consumption. Over recent years Russians proved to be heavy shoppers, leaving more

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 27 -

than 70% of household budget in the shops. Consumer expenses were growing since 2003

however in 2009 the share of retail in household budget lost 6 pp against previous year. Consumers

cut down their expenses in favor of savings and paying back debts.

However, consumer confidence index stabilized after sharp decrease and we do not expect further

significant compaction of consumer spending.

Now it is time for retailers to adapt to new consumption patterns. Some of them will even will be

able to increase their market share.

Rent Indexation ATB Currency

Rent indexation is always a big issue for Russian market due to the following reasons:

• Rent is nominated in foreign currency

• Inflation is always two-digits.

This means that lease contracts are exposed both to currency and inflation risk.

Landlords are financing construction with loans in US$ or EUR and so they want to fix rent in the

same currency. It works perfectly when tenant’s budget is in USD or EUR.

Then US CPI or European HICP is used for indexation, but sometimes fixed 3-5% annual

indexation is used.

But if the tenant is budgeted in RUR, he wants to secure himself from risk of national currency

devaluation. In such cases complicated lease structures can appear.

For example: US$1000 paid in RUR according to Central Bank exchange rate, unless Central Bank

rate exceeds certain limit, than this limit is used. Basically this is the way to split currency risks.

Again in such case US CPI or fixed indexation can be used.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 28 -

Sometimes one can find in the contract statements like: “US$1000 paid in RUR at rate of 25 RUR

per US$” This indeed means Ruble nominated rent but allow parties to pretend that this is dollar

rent. In such case Russian CPI can be applied.

In today’s “low” market, landlords wish to factor in the rent not only devaluation and inflation but

also an expected future growth of market rents. This is a matter of hard negotiations between

parties. Sometimes fixed rents are offered like US$500 in first year, US$700 in second, US$800 in

the following years.

5.2 Investment Market

Q3 2009 brought activity to the investment market, as the summer vacation season came to end a

couple of noticeable events took place: International investment forum in Sochi, Investment forum

of VTB in Moscow, cancellation of Sberbank limitations for individual credits and two consequent

reductions of refinancing rate by Central bank: by 0.25 and 0.5 pp accordingly.

All these events may be characterized as an appeal to potential investors. Here are some factors that

make Russian functionaries troubled and force them to make serious steps to increase capital

inflow.

1. In 2008 capital outflow resulted US$130 bn, Q1 2009 showed US$27.6 bn and additional US$ 39

bn flew out of Russian economy in Q3. Thus, the officially forecasted level of 42 bn USD has been

already exceeded and, that is more important, now it is Russian capital as well.

2. For now Russia’s gold and FX reserves account to about US$550 bn, the Reserve fund gives

US$140 bn more and National Welfare fund adds more US$32 bn to this basket. In the spot of

economy stabilization in two upcoming years both will be completely drawn out.

3. Recently published IMF research named India and China as the main drivers of world economy

growth for the near future.

Now emerging markets are generating about 30% of the world GDP, according to IMF data.

However, according to EPFR Global, the investments into emerging markets are still 1/8 of the

ones for the developed countries. Thus the investment market of the emerging countries is

underestimated and, if the forecasts are correct, we will see the increasing capital inflow into these

countries. But at the same time this report says that the downfall of Russia’s economy appeared to

be worse than expected thus Russia may find itself out of BRIC.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 29 -

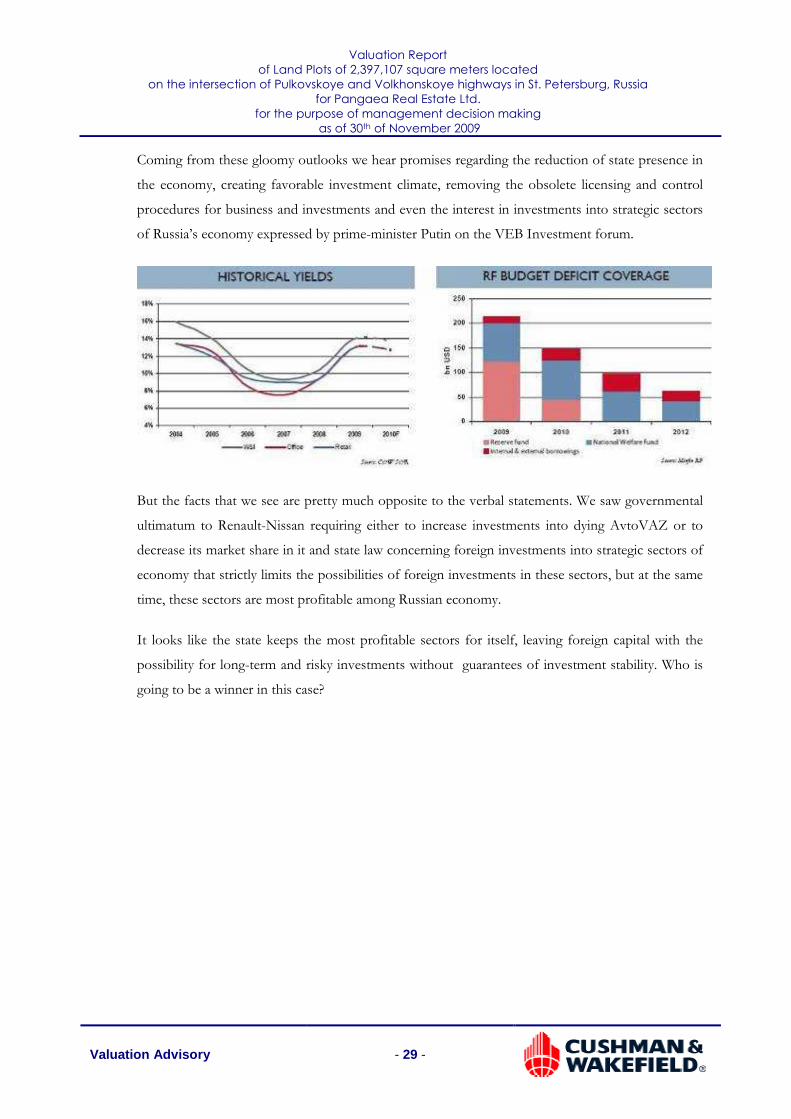

Coming from these gloomy outlooks we hear promises regarding the reduction of state presence in

the economy, creating favorable investment climate, removing the obsolete licensing and control

procedures for business and investments and even the interest in investments into strategic sectors

of Russia’s economy expressed by prime-minister Putin on the VEB Investment forum.

But the facts that we see are pretty much opposite to the verbal statements. We saw governmental

ultimatum to Renault-Nissan requiring either to increase investments into dying AvtoVAZ or to

decrease its market share in it and state law concerning foreign investments into strategic sectors of

economy that strictly limits the possibilities of foreign investments in these sectors, but at the same

time, these sectors are most profitable among Russian economy.

It looks like the state keeps the most profitable sectors for itself, leaving foreign capital with the

possibility for long-term and risky investments without guarantees of investment stability. Who is

going to be a winner in this case?

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 30 -

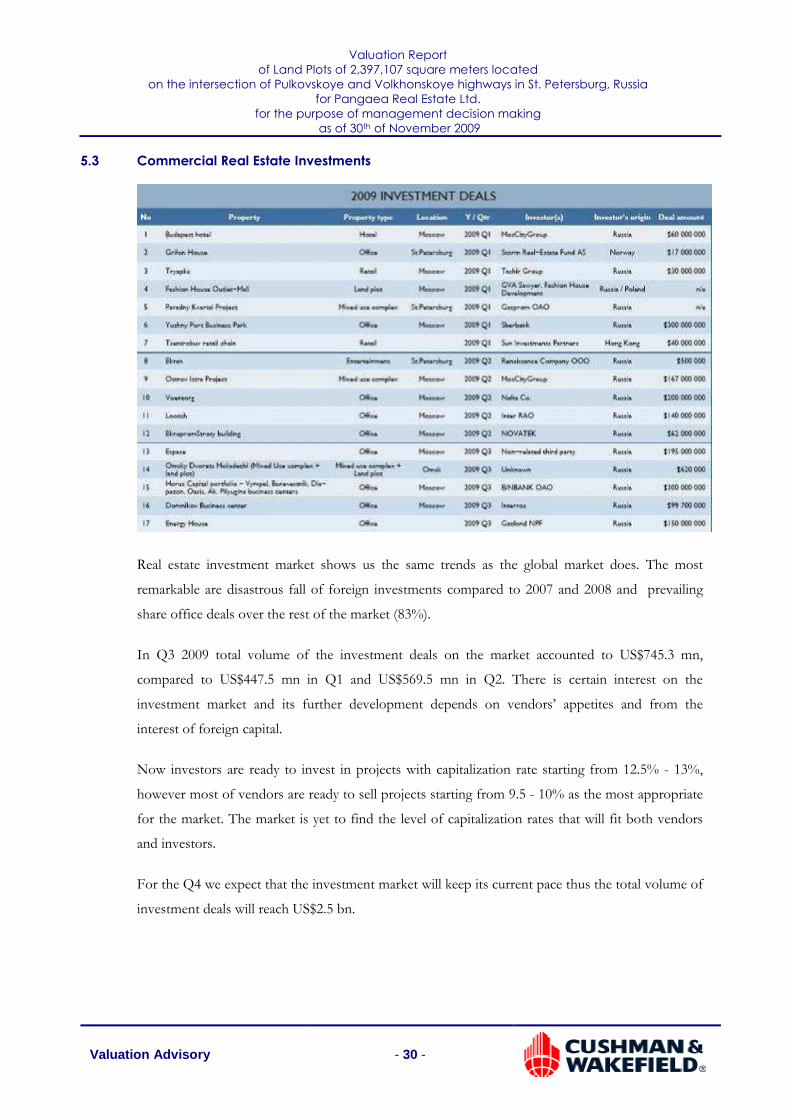

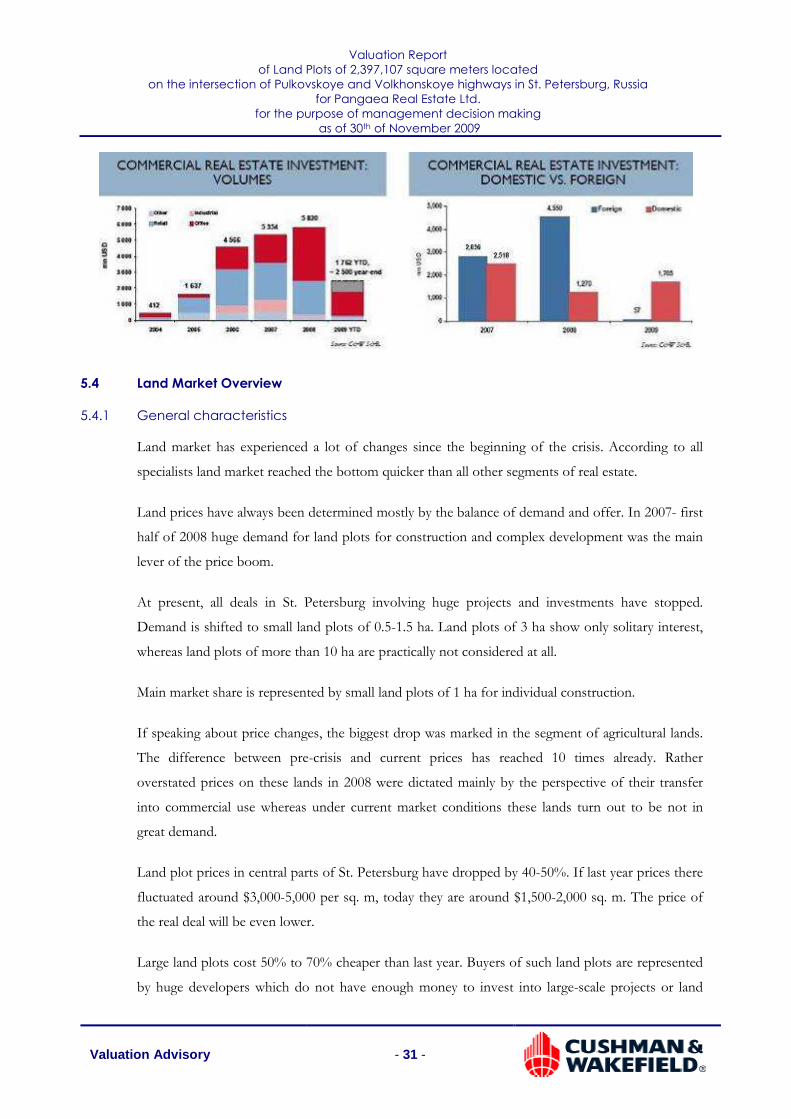

5.3 Commercial Real Estate Investments

Real estate investment market shows us the same trends as the global market does. The most

remarkable are disastrous fall of foreign investments compared to 2007 and 2008 and prevailing

share office deals over the rest of the market (83%).

In Q3 2009 total volume of the investment deals on the market accounted to US$745.3 mn,

compared to US$447.5 mn in Q1 and US$569.5 mn in Q2. There is certain interest on the

investment market and its further development depends on vendors’ appetites and from the

interest of foreign capital.

Now investors are ready to invest in projects with capitalization rate starting from 12.5% - 13%,

however most of vendors are ready to sell projects starting from 9.5 - 10% as the most appropriate

for the market. The market is yet to find the level of capitalization rates that will fit both vendors

and investors.

For the Q4 we expect that the investment market will keep its current pace thus the total volume of

investment deals will reach US$2.5 bn.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 31 -

5.4 Land Market Overview

5.4.1 General characteristics

Land market has experienced a lot of changes since the beginning of the crisis. According to all

specialists land market reached the bottom quicker than all other segments of real estate.

Land prices have always been determined mostly by the balance of demand and offer. In 2007- first

half of 2008 huge demand for land plots for construction and complex development was the main

lever of the price boom.

At present, all deals in St. Petersburg involving huge projects and investments have stopped.

Demand is shifted to small land plots of 0.5-1.5 ha. Land plots of 3 ha show only solitary interest,

whereas land plots of more than 10 ha are practically not considered at all.

Main market share is represented by small land plots of 1 ha for individual construction.

If speaking about price changes, the biggest drop was marked in the segment of agricultural lands.

The difference between pre-crisis and current prices has reached 10 times already. Rather

overstated prices on these lands in 2008 were dictated mainly by the perspective of their transfer

into commercial use whereas under current market conditions these lands turn out to be not in

great demand.

Land plot prices in central parts of St. Petersburg have dropped by 40-50%. If last year prices there

fluctuated around $3,000-5,000 per sq. m, today they are around $1,500-2,000 sq. m. The price of

the real deal will be even lower.

Large land plots cost 50% to 70% cheaper than last year. Buyers of such land plots are represented

by huge developers which do not have enough money to invest into large-scale projects or land

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 32 -

banking. Middle-size land plots (1-3 ha) suffered the least as they are mostly interesting for small

groups of investors who do not dare to enter a project alone – these land plots have become 20-

40% cheaper.

In general offer is much higher than demand now. When crisis struck, the market was going

through a mass cottage development boom. But around 75-80% of all developers left their projects,

putting their land assets on sale.

Though the number of land plots for sale has doubled, the largest in-flow of offers represents lands

without any engineering pre-works, agricultural land and other low-liquid land (with legal problems

or encumbrances), whereas demand today is oriented on fully prepared land plots. At present

investors only sell land assets, and buyers are represented by end-customers (industrial companies,

retail and service companies, etc.)

It is practically impossible speak about any kind of regular price formation under current market

situation, where every land plot owner determines the discount relying on his own economic

realities.

At present prices are at the level of US$100 per sq. m of projected improvements against US$400-

500 before crisis. If land is included into the price of 1 sq. m then development of 1 sq. m will cost

around US$2,000 against US$2,500 before crisis. It is quite obvious that developers who saved

some free cash are in a very good position now as it is very profitable to buy land and build at

present.

Land plot prices depend greatly on the market conditions. Even small change of price of the end-

product (apartments or retail spots) leads to the change in the land price. Land component in the

general price of the end-product takes no more than 10%. Therefore land has become several times

cheaper notwithstanding the fact that the end-product price (apartments or rental rates) has

dropped only by 20%. Nevertheless if the end-product becomes more expensive, land prices will

immediately go up.

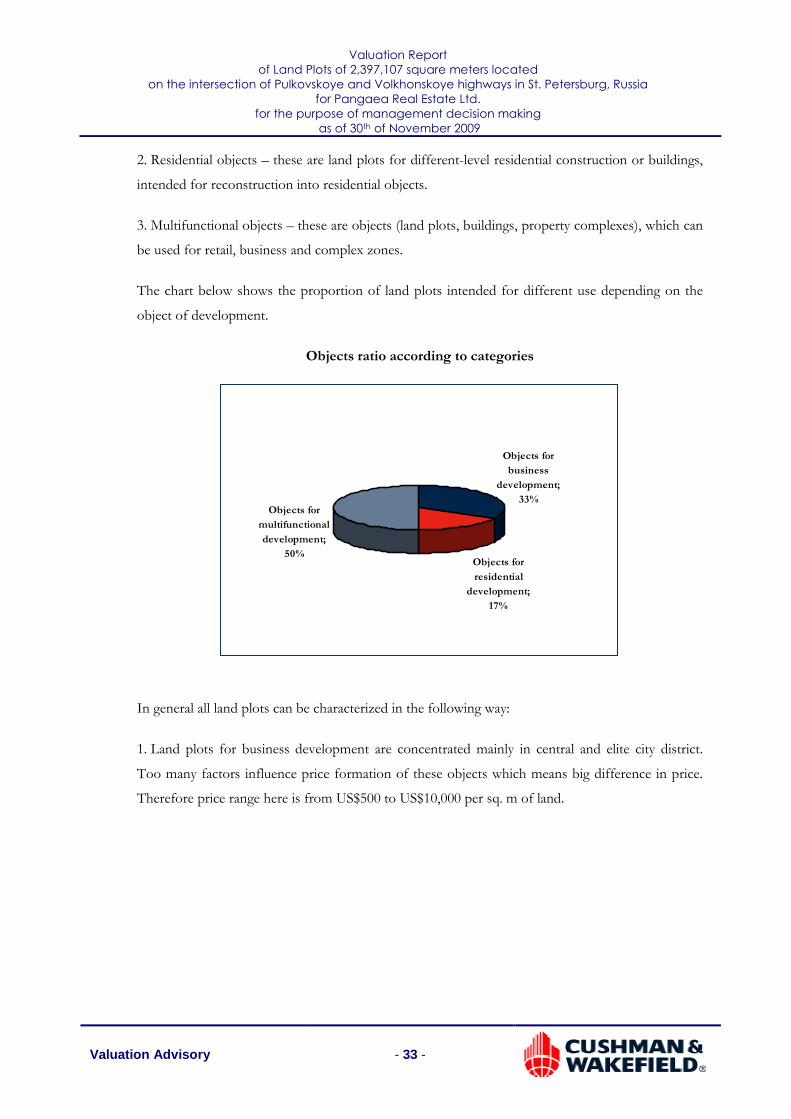

5.4.2 Land Plot Offer in St. Petersburg as of Q3 2009

All represented land plots are divided into three categories:

1. Business objects – these are objects (buildings, building complexes), intended for reconstruction

for allocation of business-centers, hotels, banks, etc.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 33 -

2. Residential objects – these are land plots for different-level residential construction or buildings,

intended for reconstruction into residential objects.

3. Multifunctional objects – these are objects (land plots, buildings, property complexes), which can

be used for retail, business and complex zones.

The chart below shows the proportion of land plots intended for different use depending on the

object of development.

Objects ratio according to categories

Objects for

business

development;

33%

Objects for

residential

development;

17%

Objects for

multifunctional

development;

50%

In general all land plots can be characterized in the following way:

1. Land plots for business development are concentrated mainly in central and elite city district.

Too many factors influence price formation of these objects which means big difference in price.

Therefore price range here is from US$500 to US$10,000 per sq. m of land.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 34 -

2. Land plots for residential construction are represented on the map below:

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 35 -

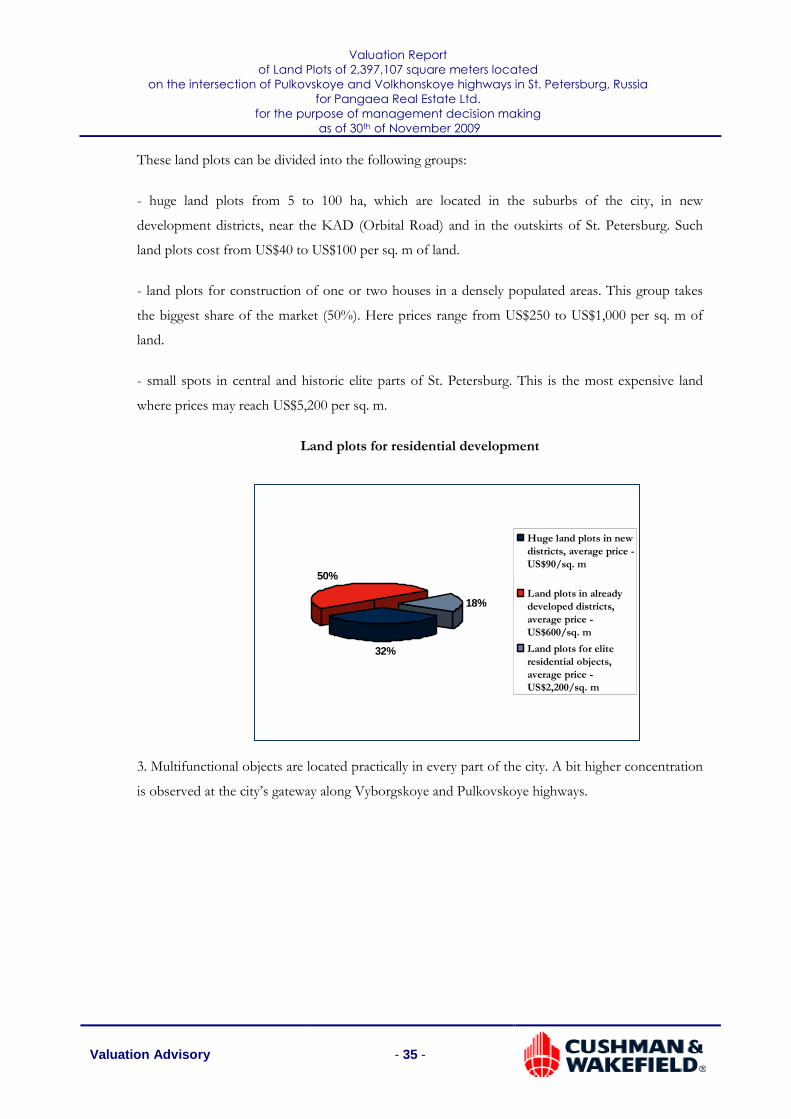

These land plots can be divided into the following groups:

- huge land plots from 5 to 100 ha, which are located in the suburbs of the city, in new

development districts, near the KAD (Orbital Road) and in the outskirts of St. Petersburg. Such

land plots cost from US$40 to US$100 per sq. m of land.

- land plots for construction of one or two houses in a densely populated areas. This group takes

the biggest share of the market (50%). Here prices range from US$250 to US$1,000 per sq. m of

land.

- small spots in central and historic elite parts of St. Petersburg. This is the most expensive land

where prices may reach US$5,200 per sq. m.

Land plots for residential development

32%

50%

18%

Huge land plots in new

districts, average price -

US$90/sq. m

Land plots in already

developed districts,

average price -

US$600/sq. m

Land plots for elite

residential objects,

average price -

US$2,200/sq. m

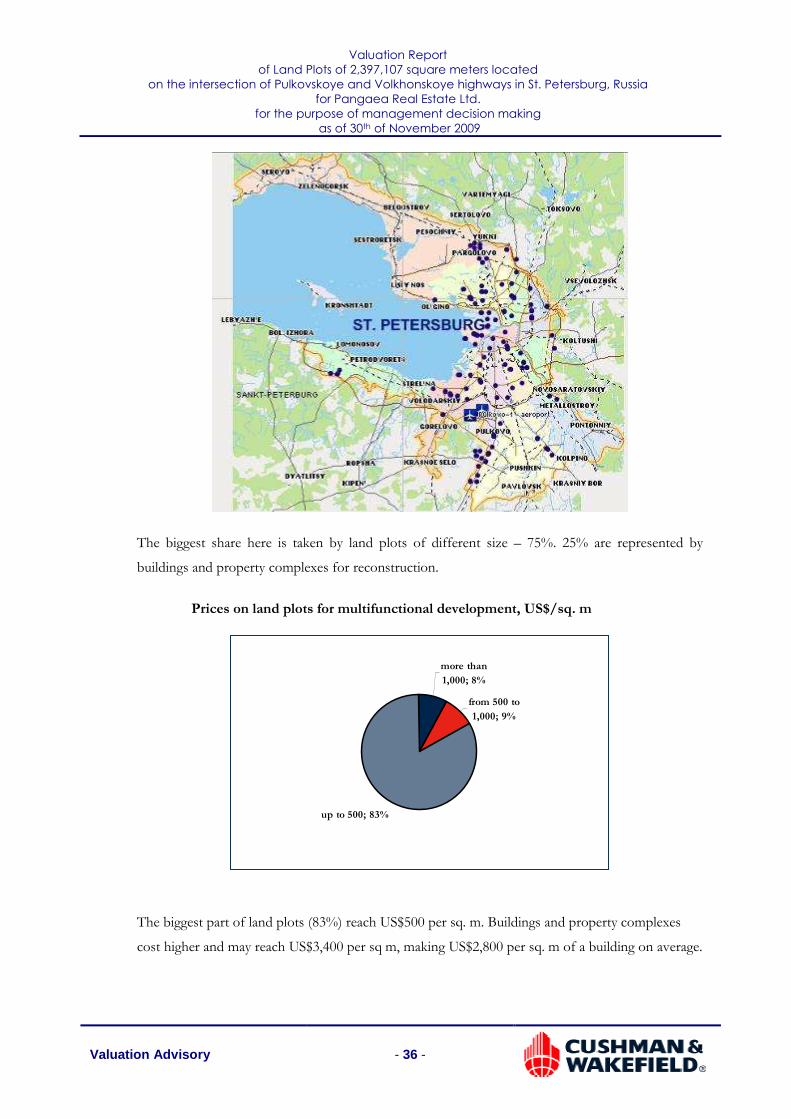

3. Multifunctional objects are located practically in every part of the city. A bit higher concentration

is observed at the city’s gateway along Vyborgskoye and Pulkovskoye highways.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 36 -

The biggest share here is taken by land plots of different size – 75%. 25% are represented by

buildings and property complexes for reconstruction.

Prices on land plots for multifunctional development, US$/sq. m

more than

1,000; 8%

from 500 to

1,000; 9%

up to 500; 83%

The biggest part of land plots (83%) reach US$500 per sq. m. Buildings and property complexes

cost higher and may reach US$3,400 per sq m, making US$2,800 per sq. m of a building on average.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 37 -

6 VALUATION METHODOLOGY AND COMMENTARY

There are three generally adopted approaches used to value property: The Sales Comparison

Approach; The Income Approach; and The Cost Approach. We have valued the Property using the

Income Approach, taking into account sales comparables. The cost approach has not been used as

this produces a “Non-Market Value” suitable for financial statements relating only to “specialised

properties”. A description of mentioned above approaches and how these relate to the Russian

Market, follows.

In preparing our valuation we have relied upon our knowledge of the investment market and the

available evidence which is summarised in our market commentary:

The Cost Approach

Under IVS this approach is relevant to specialised properties (i.e. properties that are rarely if ever

sold on the open market … due to their uniqueness which arises from their specialised nature and

design of the buildings, their configuration, size, location or otherwise) and Limited Market

Property (i.e. properties that because of market conditions, unique features, or other factors attract

relatively few buyers).

The Income Approach

In the Income approach, an estimate is made of prospective economic benefits of ownership.

These amounts are discounted and/or capitalised at appropriate rates of return in order to provide

an indication of value.

The most commonly used technique for assessing market value within the Income Approach is

Discounted Cashflow. This is a financial modelling technique based on explicit assumptions

regarding the prospective cashflow to a property or business and the costs associated with being

able to generate the income. To this assessed cashflow is applied a market-derived discount rate to

establish a present value of the income stream. This Net Present Value (“NPV”) is an indication of

Market Value.

For the purposes of this valuation we consider the Income Approach to be unreliable. Due to the

global financial crisis that has resulted in a crisis of real estate market all over the world, any analysis

and estimates of the value of the property by means of the Income Approach are hindered by a lot

of uncertainties in the real estate sphere as a whole. For instance, it is hard to predict and forecast

any trends and dynamics of rental rates (and, as a result, future cash flows of owners of properties

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 38 -

on the market). Also the lack of transactions on the market poses certain difficulties in assessing

discount and capitalization rates used in Income Approach analysis. Thus, in current situation this

method based solely on our own assumptions can be misleading and that is why it should not be

used for the purposes of this valuation.

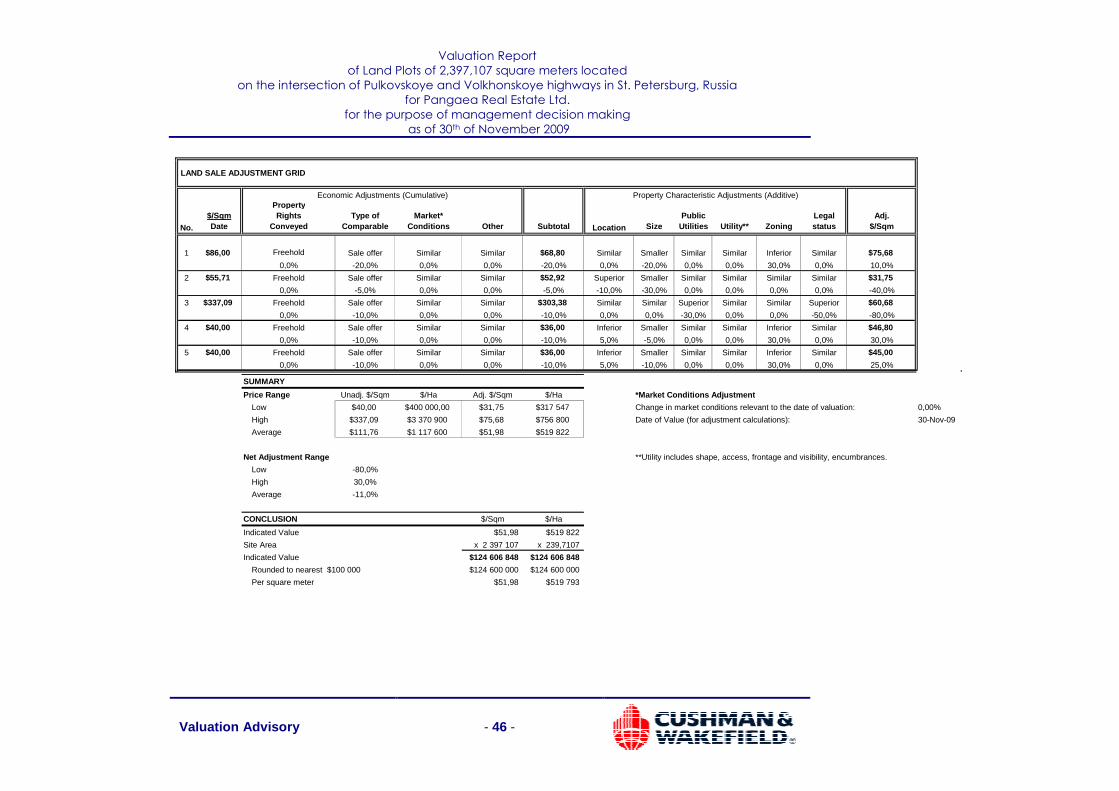

The Sales Comparison Approach

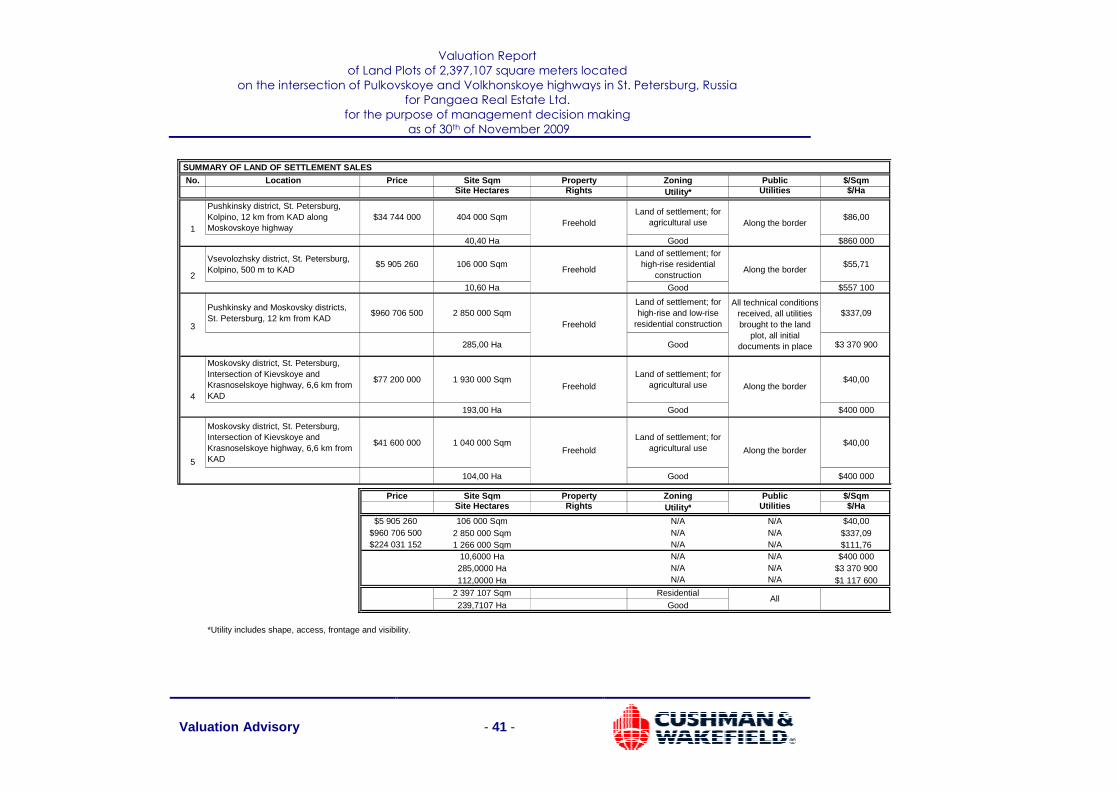

We used the Sales Comparison Approach to develop an opinion of land value. In this method, we

analyzed prices for which sellers currently offer similar sites in this area. While making comparisons,

we adjusted the prices for differences between the Property and the comparable sites. On the

following pages we give a summary of pertinent details of sites currently available for sale that we

compared to the site appraised.

This method involves analysing all available information on sales of comparable properties that

have taken place and making adjustments in the prices achieved to reflect the differences in the

properties sold and the Property to be valued. This approach hinges on the availability of reliable

market evidence of comparable sales. Distinction must be drawn between information that is

known to be accurate and reported information that is second hand or at best hearsay. Only

information that is known to be accurate can be relied upon with any degree of comfort to provide

an accurate valuation

Real estate developers make qualitative and quantitative judgments while planning acquisition of a

site with development potential such as the Property. Subjectively, a developer considers the nature

of surrounding land uses and proximity to complimentary services to a potential project.

Objectively, the physical and functional attributes of the site and the cost of preparing it for

construction must be calculated. Many aesthetic and economic factors lying between these two

considerations tend to influence the final result.

Special Assumption - Using prices from inactive markets2

A quoted market price in an active market for an identical asset or liability is most representative of

fair value and is required to be used (generally without adjustment). Transaction prices in inactive

markets might be inputs when measuring fair value, but may not be determinative.

2 Using judgment to measure the fair value of financial instruments when markets are no longer active. An IASB Staff Summary. October 2008.

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 39 -

Characteristics of an inactive market include a significant decline in the volume and level of trading

activity, the available prices vary significantly over time or among market participants or the prices

are not current. However, these factors alone do not necessarily mean that a market is no longer

active and determining that a market is not active requires judgement. An active market is one in

which transactions are taking place regularly on an arm’s length basis. What is ‘regularly’ is a matter

of judgement and depends upon the facts and circumstances of the market for the instrument being

measured at fair value.

Regardless of the level of activity, transaction prices that do not represent distressed transactions

cannot be ignored when measuring fair value using a valuation technique, although they might

require significant adjustment based on unobservable data. When a market becomes inactive, it is

not appropriate to conclude that all market activity represents forced liquidations or distress sales.

However, it is also not appropriate to conclude automatically that any transaction price is

determinative of fair value. Determining fair value in a market that has become inactive depends on

the facts and circumstances and may require the use of significant judgement. Regardless of the

valuation technique used, an entity must include appropriate risk adjustments that market

participants would make, such as for credit and liquidity.

Global Assumptions

We used the Sales Comparison Approach to develop an opinion of land value. In this method, we

analyzed prices offered by owners for similar sites in the market. In making comparisons, we

adjusted the sale prices for differences between this site and the comparable sites. If the comparable

was superior to the subject, a downward adjustment was made to the comparable sale. If inferior,

an upward adjustment was made. We present on the following pages a summary of pertinent details

of sites recently sold that we compared to the subject site.

In the valuation of the freehold interest in the property, the Sales Comparison Approach has been

used to establish prices being paid for comparably zoned land. The most widely used and market

oriented unit of comparison for properties with characteristics similar to those of the subject is the

sale price per square meter of land area. All transactions utilized in this analysis are analyzed on this

basis.

The major elements of comparison utilized to value the subject site include the property rights

conveyed, economic terms, accompanying the sale, conditions or motivations surrounding the sale,

Valuation Report

of Land Plots of 2,397,107 square meters located

on the intersection of Pulkovskoye and Volkhonskoye highways in St. Petersburg, Russia

for Pangaea Real Estate Ltd.

for the purpose of management decision making

as of 30th of November 2009

Valuation Advisory - 40 -

changes in market conditions since the sale, the location of the real estate, its utility and the physical

characteristics of the property.