Embed Size (px)

Citation preview

TAX INCENTIVES AND REFORMSBY MRS. TITILAYO FOWOKAN (ACA, ACTI)

CITN MPTP, ABEOKUTA, 25 AUGUST 2010

Introduction The topic of this session on Tax Incentives and Reforms came at

the right time when Nigeria is going through reforms in the various sectors of the economy as well as within government establishments. We are all aware of the recent reforms in the Capital Market via the introduction of incentives to attract more investors into the market, Banking and Insurance Industries via recapitalisation and consolidation, Oil & Gas industry via the introduction of Nigerian Content Development Act (NCDA) 2010 and the proposed Petroleum Industry Bill, to mention a few.

Other reforms by government at all levels, worthy of mentioning are in the area of Taxation. Some of these reforms are; the autonomy of the Federal Inland Revenue Service via the enactment of the FIRS Establishment Act 2007 and the recent approval of the National Tax Policy by the Federal Executive Council. At the State level, there is a shift by State governments from relying on Federal allocation to generating revenue internally. Some of the States have increased the tax drive through the enactment of State laws such as Land Use Charge law by Lagos State. The clamour for more revenue by local governments has also resulted into the promulgation of bye-laws to support their demand for various taxes and levies not specifically included in the Taxes and Levies (Approved list of collection) Decree No. 21 of 1998.

2 CITN MPTP, Abeokuta, 25 Aug. 2010

Introduction However, with all the tax reforms embarked upon by the all

levels of government there is no commensurate increase in the level of tax revenue. The reason for this is not far-fetched. This is due to the fact that tax compliance level is still low. Tax payers are skeptical about the sincerity of government and therefore require a level of assurance that government will demonstrate a high level of accountability and responsibility to the populace by ensuring that the revenue generated through taxation are used judiciously for the provision of amenities that will ease the pain of the citizenry.

Our discussions during this session will be centred on the impact of the government reforms in the area of taxation on the investment incentives provided by the same government in the tax legislations.

This paper will therefore be focused on the following: Tax Reforms in Nigeria, Nigeria’s Tax incentives, The effect of the current tax reforms on the existing tax incentives, Effective communication between tax administrators and taxpayers as a form

of tax incentives, and Prudent use of tax funds as an incentive for tax compliance

3 CITN MPTP, Abeokuta, 25 Aug. 2010

Tax Reforms In Nigeria

CITN MPTP, Abeokuta, 25 Aug. 2010

4

Concept of Tax Reform To have a clear understanding of the concept of Tax Reform, we

need to look at the key words, Tax and Reform. Tax is a “compulsory levy imposed on a subject or upon his

property by the government having authority over him”. Tax is the price of social security between the government and the citizenry and it is also an instrument of social engineering which can be used to stimulate general or sectoral economic growth. Reform on the other hand has to do with improvement of a system, an organisation, a law, etc by making changes to it with the aim of getting a better result. The word Reform can be interchanged with the words; improvement, reorganisation, restructuring, modification, alteration, change, development or amendment.

Tax reform is a universal concept. It is the process of changing the way taxes are collected , administered or managed by the government.

Tax reformers have different goals which could be any of the following: to reduce the level of taxation of all people by the government. to make the tax system more/less progressive in its effect. to simplify the tax system. to make the tax system more understandable, or more accountable. to deal with externalities.

5 CITN MPTP, Abeokuta, 25 Aug. 2010

History of Tax Reform in Nigeria

CITN MPTP, Abeokuta, 25 Aug. 2010

6

The history of tax reform in Nigeria could be traced back to the birth of the Federal Board of Inland Revenue (FBIR) in 1939 when the Companies Income Tax Ordinance was enacted. Some of the reforms that had taken place since then include: Introduction of the withholding tax regime. Imposition of 10 percent special levy on bank's excess profits Imposition of 2.5 percent turnover tax on building and construction

companies. Establishment of Federal Inland Revenue Service (FIRS) as the operational

arm of Federal Board of Inland Revenue (FBIR). Setting up of revenue services at other tiers of government (states and

local). Introduction of Value Added Tax (VAT) in 1993.

The recent reform in tax administration is the granting of autonomy to the FIRS via the enactment of the FIRS Establishment Act 2007. The objective of this reform is to reposition the FIRS for greater effectiveness and efficiency in meeting the revenue demands of government. The focus of the reform is on expanding the tax net and increasing the contribution of tax to total revenue in Nigeria.

Government’s Tax Reform Agenda

CITN MPTP, Abeokuta, 25 Aug. 2010

7

The Federal government reform agenda for Nigeria tax system and administration include: Restructuring of the FIRS into an autonomous government agency Amendment to Tax/Regulatory Laws on personal income tax to introduce an

equitable income tax structure and encourage voluntary compliance Amendment of CITA to revise the penalty provisions and increase incentives

for donation to tertiary institutions for research activities. NNPC to act as the hub for FIRS in getting comprehensive information on

arrangements in the upstream sub-sector of the Oil industry Amendment of VATA to remove all inherent ambiguities in the law and

introduce an increase in the rate from 5%.

Another area of tax reform that is potentially an attractive means of financing municipal government in developing countries is the drive for urban property tax, which would be more effective in financing the local governments than the current tenement rate system. As a revenue source, it can provide local governments with access to a broad and expanding tax base as compared to the mix of intergovernmental grants and indirect taxes that now dominate local government revenues. This has been embraced by the Lagos State Government via the enactment of the Land Use Charge Law 2004.

We will focus on the tax reform agenda in relation to FIRS restructuring, being a major leap in the Nigeria’s tax administration.

Reform of Nigerian Tax System

CITN MPTP, Abeokuta, 25 Aug. 2010

8

Even though the Nigerian tax system is fashioned after the UK tax system, it is still far from being comparable to what obtains in some other developing countries.

The reform agenda of government is driven by the recommendations of the Study and Working groups set up between 2003 and 2004 as well as the Stakeholders retreat held in 2005 to review the Nigerian tax system. The reforms identified as expedient and necessary for the system are as follows: Efficient and effective tax administration Stimulation of the non-oil sector of the economy Resolution of contentious issues in tax administration Redistribution of wealth and entrenchment of a more equitable tax system Capacity building for administrators and taxpayers Centralisation of revenue agency and computerisation Reduction in the effective tax rates and simplifying the tax regime Development of a tax policy for Nigeria, etc.

Reasons for FIRS Restructuring

CITN MPTP, Abeokuta, 25 Aug. 2010

9

In a bid to reforms identified by the working groups and stakeholders, the government has taken a bold step to reform the FIRS with the aim of achieving the following objectives: Repositioning the FIRS for greater effectiveness and efficiency in meeting

the revenue demands of government. Administrative efficiency through capacity building at all levels of tax

administration; Improved integrity and ethical standards; Reasonable financial and administrative autonomy; Protection of the taxpayers' rights through professionalism, taxpayer

education. Fair hearing and adjudication of cases and prompt refund mechanism.

Other reasons for the repositioning of the FIRS include: To increase the contribution of tax, being the major source of income for

national development to total revenue especially with regard to non-oil taxes.

To achieve other fiscal objectives and improved services delivery to taxpayer.

Expansion of the tax net. Linkage to other stakeholders such as Corporate Affairs Commission (CAC). Improved policy regime. Scope tax exemptions/waivers. Formulate a national tax policy. Amend tax law (simplify; clarify).

Tax Incentives In Nigeria

CITN MPTP, Abeokuta, 25 Aug. 2010

10

Inflow of Foreign Investments

CITN MPTP, Abeokuta, 25 Aug. 2010

11

We cannot talk about investment incentives in Nigeria without considering the Nigerian Investment Promotion Commission (NIPC). The NIPC Decree 1995 was established on 16th January 1995 to encourage non-Nigerians (both individuals and corporate organisations) to invest and participate in the operations of any Nigerian enterprise with the exception of Petroleum, crude oil and gas enterprises.

To allow participation by non-Nigerians, the shares of the Nigerian enterprises have to be traded on the floor of the Nigerian Stock Exchange (NSE) so that they may be bought in any currency. To further encourage investment by these non-Nigerians, some terms would also be guaranteed subject to the payment of WHT, Income tax and Capital Gains tax. These terms are as follows: There would be an unconditional transferability of funds in and out of the

country The enterprise will not be nationalized or expropriated except in national

interest.

The encouragement of investment by non-Nigerians results in high inflow of foreign currency, and there would be an expected increase in: The rate of return on capital in Nigeria from investors. The number of companies seeking to be listed on the NSE. The number of additional funds available for companies listed on the NSE. PBT and revenue for the federal government, etc.

Effect of Foreign Investment on Taxes

CITN MPTP, Abeokuta, 25 Aug. 2010

12

The availability of foreign funds will make sourcing of funds by companies easier and reduce the cost of these funds with resultant higher PBT and more revenue for the federal government.

CIT and PIT returns will increase as the incomes increase and as turnover increases, the VAT will also increase. Where acquisitions are involved, capital gains tax (CGT) will also increase.

There are usually two sides of a coin. The availability of foreign funds has positive effect on taxes paid to the government while the taxes payable also have effect on the returns made by the foreign investors. With the expectations that taxes collected by government will be higher if more foreign funds are available, the effect of the taxes payable to the government in respect of the investment is worth giving due consideration so as not to have a negative impact on the investors thereby jeopardising the efforts of the government.

To curb the impact of taxes payable on investment, various incentives have been included in the provisions of the tax laws to encourage inflow of foreign funds as well as investment initiatives by Nigerians.

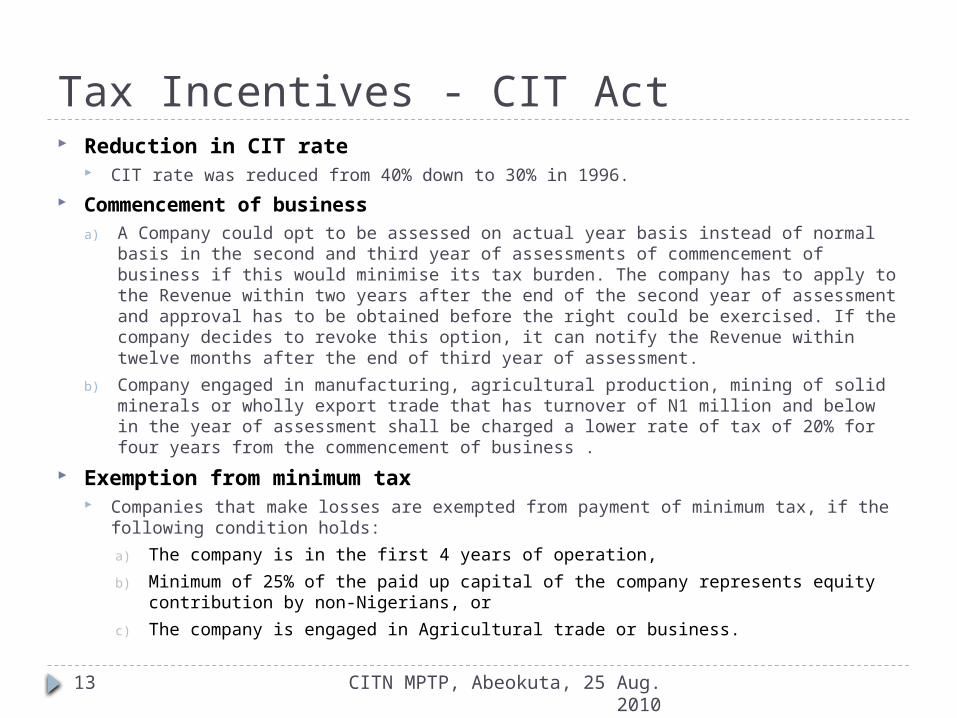

Tax Incentives - CIT Act

CITN MPTP, Abeokuta, 25 Aug. 2010

13

Reduction in CIT rate CIT rate was reduced from 40% down to 30% in 1996.

Commencement of businessa) A Company could opt to be assessed on actual year basis instead of normal

basis in the second and third year of assessments of commencement of business if this would minimise its tax burden. The company has to apply to the Revenue within two years after the end of the second year of assessment and approval has to be obtained before the right could be exercised. If the company decides to revoke this option, it can notify the Revenue within twelve months after the end of third year of assessment.

b) Company engaged in manufacturing, agricultural production, mining of solid minerals or wholly export trade that has turnover of N1 million and below in the year of assessment shall be charged a lower rate of tax of 20% for four years from the commencement of business .

Exemption from minimum tax Companies that make losses are exempted from payment of minimum tax, if the

following condition holds:a) The company is in the first 4 years of operation, b) Minimum of 25% of the paid up capital of the company represents equity

contribution by non-Nigerians, orc) The company is engaged in Agricultural trade or business.

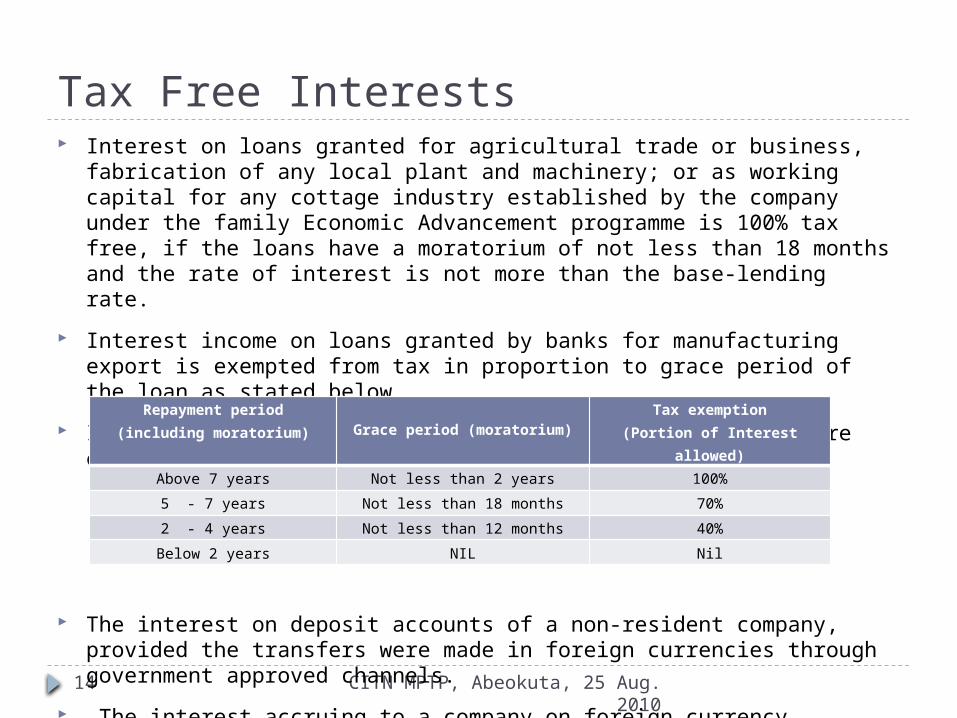

Tax Free Interests

CITN MPTP, Abeokuta, 25 Aug. 2010

14

Interest on loans granted for agricultural trade or business, fabrication of any local plant and machinery; or as working capital for any cottage industry established by the company under the family Economic Advancement programme is 100% tax free, if the loans have a moratorium of not less than 18 months and the rate of interest is not more than the base-lending rate.

Interest income on loans granted by banks for manufacturing export is exempted from tax in proportion to grace period of the loan as stated below.

Interests on foreign loans secured by Nigerian companies are exempted from tax if the following criteria are met:

The interest on deposit accounts of a non-resident company, provided the transfers were made in foreign currencies through government approved channels.

The interest accruing to a company on foreign currency domiciliary accounts in Nigeria.

Repayment period(including moratorium) Grace period (moratorium)

Tax exemption(Portion of Interest

allowed)Above 7 years Not less than 2 years 100%5 - 7 years Not less than 18 months 70%2 - 4 years Not less than 12 months 40%Below 2 years NIL Nil

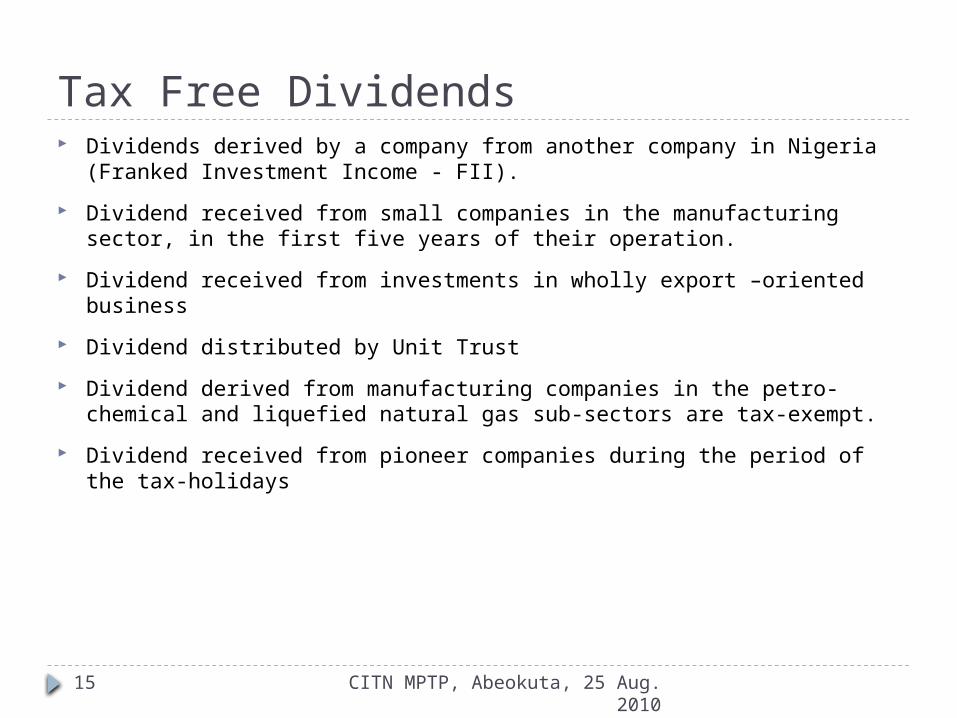

Tax Free Dividends

CITN MPTP, Abeokuta, 25 Aug. 2010

15

Dividends derived by a company from another company in Nigeria (Franked Investment Income - FII).

Dividend received from small companies in the manufacturing sector, in the first five years of their operation.

Dividend received from investments in wholly export –oriented business

Dividend distributed by Unit Trust Dividend derived from manufacturing companies in the petro-

chemical and liquefied natural gas sub-sectors are tax-exempt. Dividend received from pioneer companies during the period of

the tax-holidays

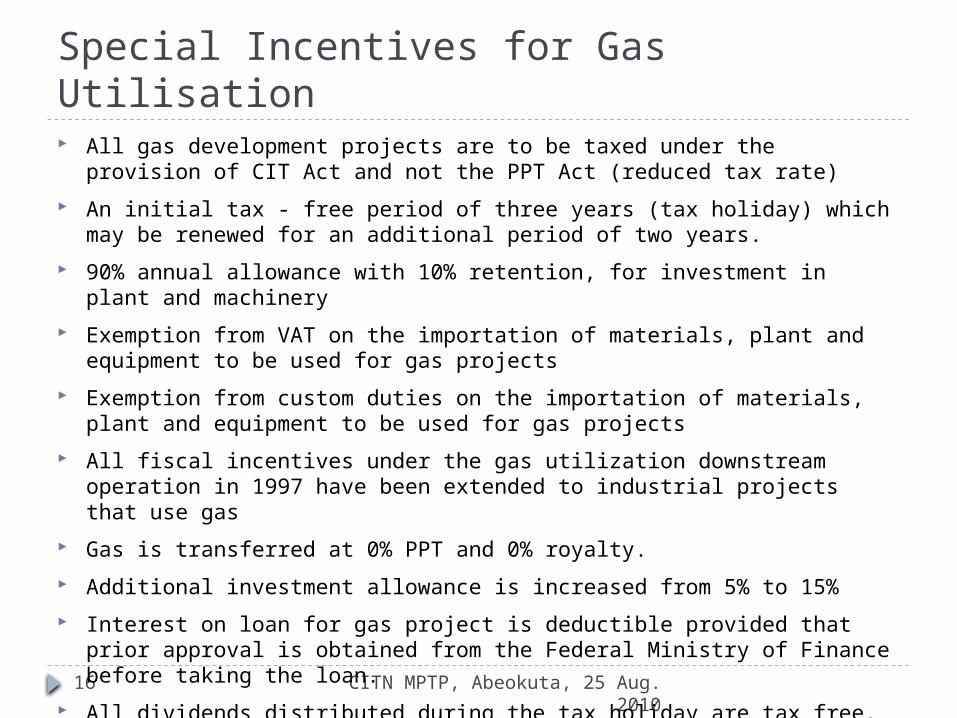

Special Incentives for Gas Utilisation

CITN MPTP, Abeokuta, 25 Aug. 2010

16

All gas development projects are to be taxed under the provision of CIT Act and not the PPT Act (reduced tax rate)

An initial tax - free period of three years (tax holiday) which may be renewed for an additional period of two years.

90% annual allowance with 10% retention, for investment in plant and machinery

Exemption from VAT on the importation of materials, plant and equipment to be used for gas projects

Exemption from custom duties on the importation of materials, plant and equipment to be used for gas projects

All fiscal incentives under the gas utilization downstream operation in 1997 have been extended to industrial projects that use gas

Gas is transferred at 0% PPT and 0% royalty. Additional investment allowance is increased from 5% to 15% Interest on loan for gas project is deductible provided that

prior approval is obtained from the Federal Ministry of Finance before taking the loan.

All dividends distributed during the tax holiday are tax free.

Incentives for Export Business

CITN MPTP, Abeokuta, 25 Aug. 2010

17

The fiscal policy in relation to exports has been to encourage non-oil exports with a view to enhancing foreign exchange receipt from these sectors. The following incentives are available to encourage export business: Profits of any Nigerian company in respect of goods exported from Nigeria

are exempt from tax, provided that the proceeds from such exports are repatriated to Nigeria and are used exclusively for the purchase of raw materials, plant, equipment, and spare parts.

Profits of companies whose supplies are exclusively inputs for the manufacture of products for export are exempt from tax. Such companies are expected to obtain a certificate of purchase of the input from the exporter in order to claim tax exemption.

A company which has incurred expenditure in its qualifying building and plant equipment in an approved manufacturing activity in an Export Processing Zone shall be granted 100% capital allowance in any year of assessment. The company shall not be entitled to investment allowance on the plant and equipment.

All new industrial undertakings, including foreign companies and individuals operating in and outside the Export Free Zone, are to be allowed full tax holidays for the first three consecutive assessment years, provided that: The undertaking is 100% export oriented; the undertaking is not formed by splitting or breaking up or reconstructing a business already

in existence; The total export proceeds of the person or company must not be less than 75% of the total

turnover for the tax holidays to be claimed. Where plant and machinery are transferred to the new company, the tax written-down value of

the asset transferred must not exceed 25% of the total value of plant and machinery in the new company.

The company should also repatriate at least 75% of the export earnings to Nigeria and place it in a Nigerian domiciliary account in order to qualify for the tax holiday

All exports are exempted from VAT.

Incentives for Manufacturing Business

CITN MPTP, Abeokuta, 25 Aug. 2010

18

Expenses on research and development are now deductible for tax purposes.

Low rate of tax for small manufacturing companies for the first five years of commencement of business.

Removal for restriction on capital allowances is now in force. Generous rates of capital allowance abound, thereby further

reducing the tax burden.

Investment Allowance

CITN MPTP, Abeokuta, 25 Aug. 2010

19

This is a tax incentive granted on expenditure on plant, machinery and equipment. It is an outright gift and not deducted from the tax written down value (TWDV). It can only be claimed in the year of purchase otherwise it is forfeited.

The following are the investment allowances that are currently available under the Nigerian tax regime: 10% on plant and equipment 15% investment tax credit can be claimed by a company that

has incurred an expenditure on plant and machinery in replacement for obsolete ones;

25% on the assets of companies engaged in the local fabrication of small tools and machinery; and

15% can also be claimed by a taxpayer who uses the locally fabricated small tools and machine.

Rural investment allowance can be claimed where a company established in a rural area incurs capital expenditure on the provision of facilities such as electricity, water or tarred road for the purpose of a trade or business at least 20 Km away from such facilities provided by Government. The rate of allowance claimable on the Capital expenditure in the first year in addition to initial allowance are as follows : No facilities at all – 100%; No electricity - 50%; No Water – 30%; and No Tarred Road -15%.

Tax incentives for operating in Economic free zones

CITN MPTP, Abeokuta, 25 Aug. 2010

20

There is an Export Free Zone in Onne, which confers tax benefits to companies approved to operate in the Zone. The advantages conferred are as follows: Easy shipping or air freight into Nigeria (no pre-shipment inspection, no Nigerian Maritime Authority (NMA) regulations)

Possibility to transfer cargo under free port status from a terminal operator to the licensee’s designated area.

Limitation of documentation and communication problems between supplier and importer

Direct transfer from Port Harcourt International Airport into the free port Duty free storage of goods with no limitation of time Possibility to release goods with a deferred processing of the Bill of Entry and payment of Customs Duties (scheduling system)

Possibility to re-export without payment of any duties Section 8 of the Decree setting up the zone states clearly that approved enterprises operating within the export free zone shall be exempt from all Federal, State and Local Government taxes, levies and rates related to the portion of its business done within the free trade zone.

100% repatriation of capital and profit 100% foreign ownership No expatriate quota

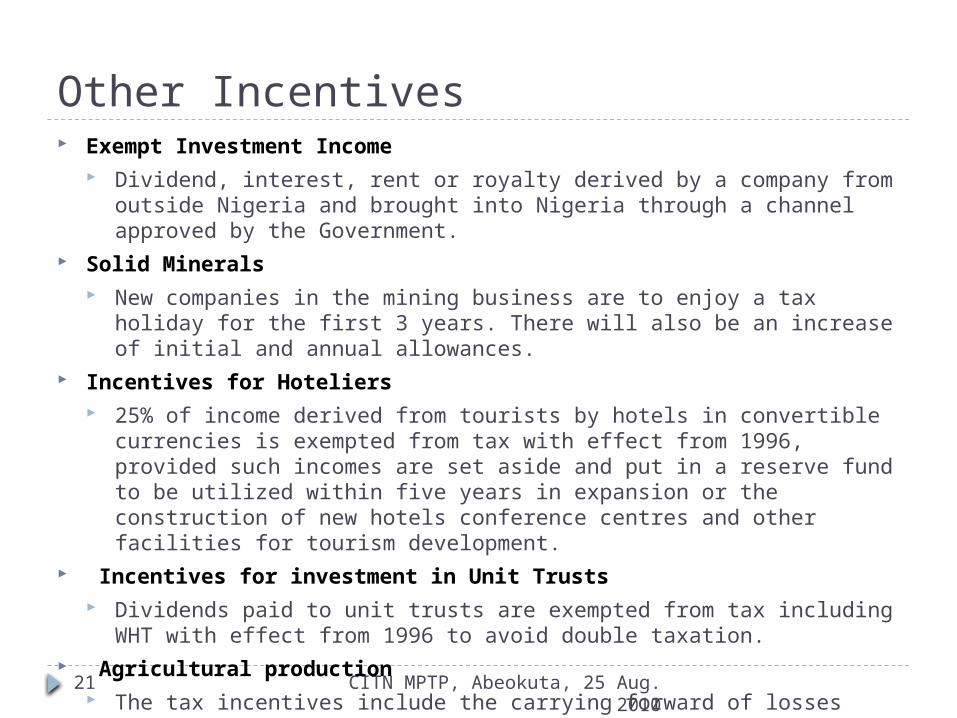

Other Incentives

CITN MPTP, Abeokuta, 25 Aug. 2010

21

Exempt Investment Income Dividend, interest, rent or royalty derived by a company from

outside Nigeria and brought into Nigeria through a channel approved by the Government.

Solid Minerals New companies in the mining business are to enjoy a tax

holiday for the first 3 years. There will also be an increase of initial and annual allowances.

Incentives for Hoteliers 25% of income derived from tourists by hotels in convertible

currencies is exempted from tax with effect from 1996, provided such incomes are set aside and put in a reserve fund to be utilized within five years in expansion or the construction of new hotels conference centres and other facilities for tourism development.

Incentives for investment in Unit Trusts Dividends paid to unit trusts are exempted from tax including

WHT with effect from 1996 to avoid double taxation. Agricultural production

The tax incentives include the carrying forward of losses indefinitely and the non-restriction of capital allowances.

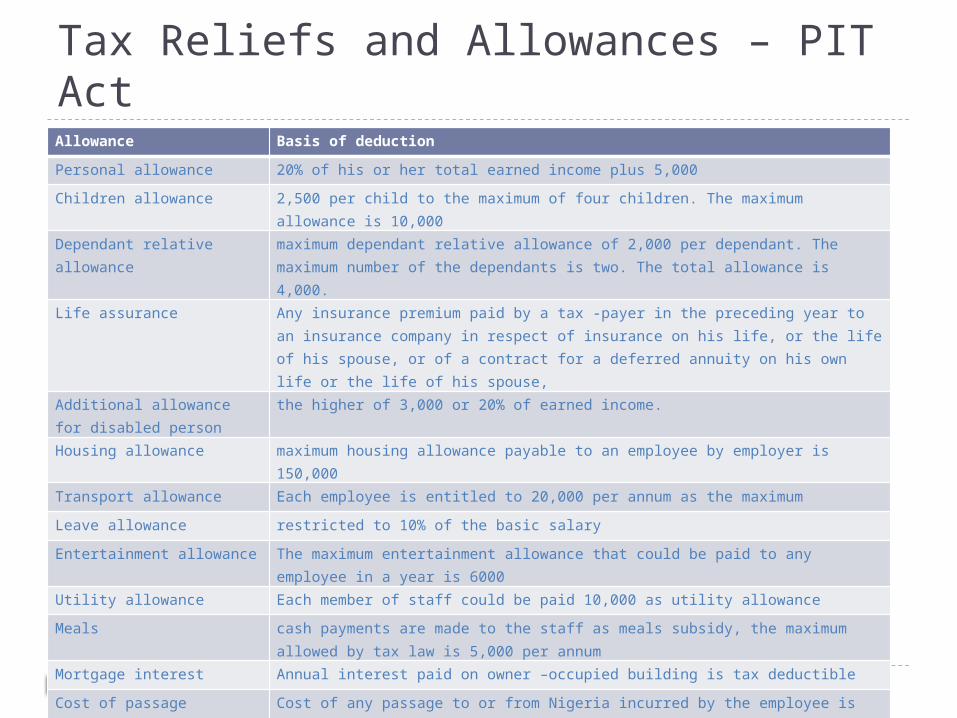

Tax Reliefs and Allowances – PIT Act

CITN MPTP, Abeokuta, 25 Aug. 2010

22

Allowance Basis of deductionPersonal allowance 20% of his or her total earned income plus 5,000Children allowance 2,500 per child to the maximum of four children. The maximum

allowance is 10,000Dependant relative allowance

maximum dependant relative allowance of 2,000 per dependant. The maximum number of the dependants is two. The total allowance is 4,000.

Life assurance Any insurance premium paid by a tax -payer in the preceding year to an insurance company in respect of insurance on his life, or the life of his spouse, or of a contract for a deferred annuity on his own life or the life of his spouse,

Additional allowance for disabled person

the higher of 3,000 or 20% of earned income.

Housing allowance maximum housing allowance payable to an employee by employer is 150,000

Transport allowance Each employee is entitled to 20,000 per annum as the maximumLeave allowance restricted to 10% of the basic salaryEntertainment allowance The maximum entertainment allowance that could be paid to any

employee in a year is 6000Utility allowance Each member of staff could be paid 10,000 as utility allowanceMeals cash payments are made to the staff as meals subsidy, the maximum

allowed by tax law is 5,000 per annumMortgage interest Annual interest paid on owner –occupied building is tax deductibleCost of passage Cost of any passage to or from Nigeria incurred by the employee is

tax exempt. Necessary documents should be submitted as evidence of the cost incurred.

Medical or dental expenses

incurred by the employees are tax-exempt. These are reimbursable expenses and should be supported with necessary documents before they could be tax deductible

Effective Communication between Tax Administrators and Taxpayers

CITN MPTP, Abeokuta, 25 Aug. 2010

23

Effective communication between tax administrators and taxpayers

CITN MPTP, Abeokuta, 25 Aug. 2010

24

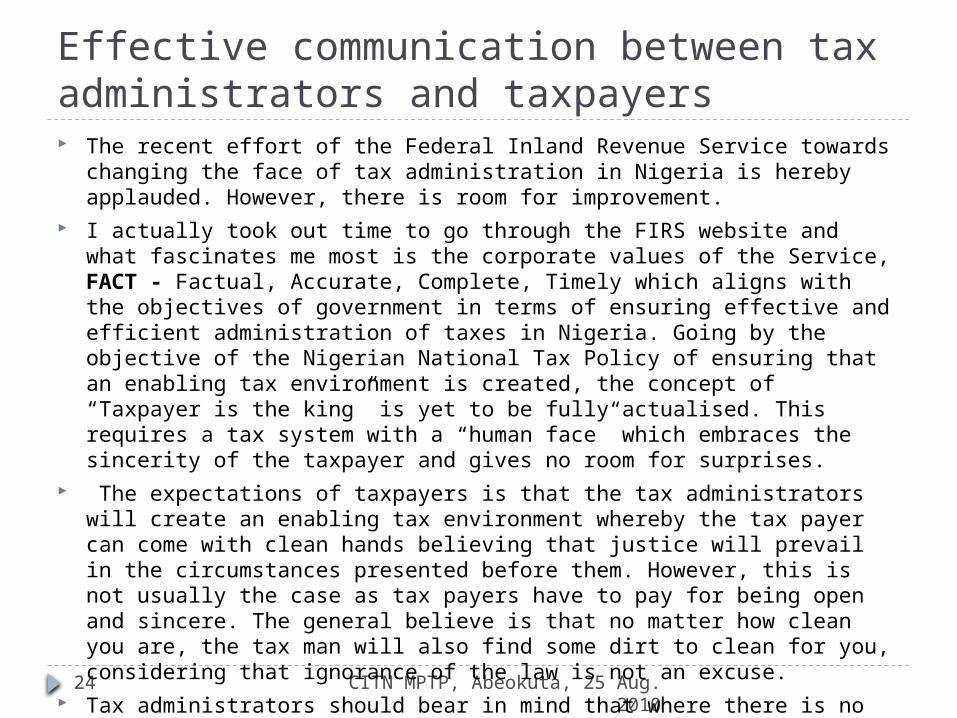

The recent effort of the Federal Inland Revenue Service towards changing the face of tax administration in Nigeria is hereby applauded. However, there is room for improvement.

I actually took out time to go through the FIRS website and what fascinates me most is the corporate values of the Service, FACT - Factual, Accurate, Complete, Timely which aligns with the objectives of government in terms of ensuring effective and efficient administration of taxes in Nigeria. Going by the objective of the Nigerian National Tax Policy of ensuring that an enabling tax environment is created, the concept of “Taxpayer is the king” is yet to be fully actualised. This requires a tax system with a “human face” which embraces the sincerity of the taxpayer and gives no room for surprises.

The expectations of taxpayers is that the tax administrators will create an enabling tax environment whereby the tax payer can come with clean hands believing that justice will prevail in the circumstances presented before them. However, this is not usually the case as tax payers have to pay for being open and sincere. The general believe is that no matter how clean you are, the tax man will also find some dirt to clean for you, considering that ignorance of the law is not an excuse.

Tax administrators should bear in mind that where there is no income or profit we cannot be talking of tax payment. If the actions of the administrators results in the improvement or otherwise of a tax payers business the resultant effect will be felt by both parties.

Communication is a very important tool in building and sustaining relationships. It must be a two way approach and there must be a common understanding of each other for the communication to be effective. Effective communication is achieved when there is positive feedback from both parties.

Effective communication between tax administrators and taxpayers

CITN MPTP, Abeokuta, 25 Aug. 2010

25

Tax payer education and an understanding of tax payers business will go a long way in building confidence in the Nigerian tax system.

The expectations of taxpayers with respect to relationship with tax administrators are as follows: Quality service from the tax administrators with respect to courtesy,

clarity, efficiency and objective assessment of the issues on ground with an open mind.

Sound technical knowledge and skill of the tax administrator with respect to the dynamics of the taxpayer’s industry

Good understanding of the taxpayer’s position and business structures A win-win approach to resolution of the tax issues Professional outlook in approaching issues High level of integrity and the discharge of duties without fear or favour.

We should be moving away from the era of missing taxpayers’ files, begging officers to post withholding tax credits, seeing the tax administrators as a devourer, waiting for long hours before getting the necessary attention; to an era of looking forward to meeting with tax administrators with the assurance that issues will be resolved amicably. Where the tax payer is satisfied with the level of equity in the judgement of the tax administrators, there is usually less resistance.

The recent development in CITN with the signing of the Professional practice Guidelines into law is a step in the right direction which should give the tax administrators some level of comfort that Tax practitioners have been challenged to bridge the gap by joining force with the tax administrators to encourage voluntary compliance.

Encouraging Wilful Tax Compliance

CITN MPTP, Abeokuta, 25 Aug. 2010

26

This is not a difficult task if there are reasonable assurance that the taxpayers money will be seen in action.

Companies have to contend with the need to satisfy their Corporate Social Responsibility goals which can be narrowed down to providing amenities that otherwise should have been provided by Government using tax revenue generated. However, this is not the case. Taxpayers struggle to get the basic necessities of life and at the same time starred in the face with the demand for taxes. Most often than not an average citizen would prefer to pay some premium for his desired comfort level and the willingness to pay is usually driven by the assurance that the resources required to achieve this will be available as and when required.

According to Maslow hierarchy of needs, human needs starts from physiological needs i.e. the basis needs of food, shelter and clothing. This is followed by self esteem needs which will be demanded once the physiological needs are met. At this point, there is a willingness to go an extra mile to get it even if it requires paying a premium.

There are two certainties in life – death and taxes. Under all circumstances, the government is a secured creditor and this implies that whether a Tax payer is willing or not the tax obligations must be fulfilled.

Encouraging Wilful Tax Compliance

CITN MPTP, Abeokuta, 25 Aug. 2010

27

The ridiculous reliefs in the personal income tax law is of great concern to employees considering the rate of increase in income levels. It is rather painful to part with about 18% of ones earnings and still spend money on fuel for generator due to the erratic electricity supply, repair of vehicles due to the bad state of the roads and pay exorbitant school fees due to the fall in the standard of government schools. In the absence of all these basic needs for survival it is difficult to convince a taxpayer that is under the heavy burden of how to take care of these needs to accept a reduction in his disposable income by way of income tax.

An improvement in government’s level of responsibility to the citizenry will receive a reciprocal effect of taxpayers willingness to pay the right tax without being compelled. The level of tax compliance will in no doubt rise even though there may still be room for improvement. The big task ahead of government is the implementation of proposed tax policy and strategies for the country and the restoration of the confidence of Taxpayers in the Nigerian tax system. The provision of social amenities and facilities such as good roads, constant electricity, availability of portable water, well funded and progressive education system, adequate security of life and property are the driving force for achieving a sustainable economy.

A case study of Lagos State Government on the provision of BRT buses and the recent road projects has set the hearts of tax payers within the State on the need to complement the efforts of government through wilful compliance.

Conclusion

CITN MPTP, Abeokuta, 25 Aug. 2010

28

The imposts of the reform have started to manifest as noted in the following: Enhanced uniformity and standards in application of laws and procedures: Co-ordination the various tax types of companies and monitor their activities; Reduction in functional duplications and waste; Information cross-referencing; Faster service delivery to the taxpayers and Higher revenue collection profile.

While the various tax incentives are laudable, it is hoped that policy consistency, stable polity and non-erratic physical infrastructures will also be regarded as complements towards attracting foreign investments.

However, having taken the first step in any tax reform effort which is to undertake a thorough analysis of the existing tax system, government needs to now identify the major constraints and opportunities for improvement. Based on this analysis, an appropriate reform strategy must be designed, focusing on the policy and administrative dimensions as well as the implementation strategy itself.

It is expected that the Tax Administrators will not just be seen by Tax payers as watch dogs but as business partners with the aim of fostering mutually beneficial relationship. With the appropriate education of tax payers by Tax Administrators and the existence of effective communication between the parties, the tax system becomes more effective and the efficiency of the Tax Authorities is also enahanced.

There is no doubt that if government can refocus its attention on meeting the needs of the citizenry in the area of providing a conducive environment that assures the safety of life and property, then every one that has tasted the dividend of democracy by way of good roads, constant electricity, etc will be willing to stand as an advocate of wilful tax compliance.

Thank You

CITN MPTP, Abeokuta, 25 Aug. 2010

29