Embed Size (px)

Citation preview

The 2009 Preqin Alternative Investment Advisor ReviewA Guide to the Advisors of Institutional Investors in Alternative Assets

© 2008 Preqin Ltd 1

The 2009 Preqin Alternative Investment Advisor Review - Sample Pages

The 2009 Preqin Alternative Investment Advisor Review

- Sample Pages

© 2008 Preqin Ltd 2

The 2009 Preqin Alternative Investment Advisor Review - Sample Pages

Contents1. Executive Summary 7

2. Data Sources 13

3. Review of Alternative Investment Advisors 17- Breakdown of advisors by location, nature of service, number of staff and

clients, age of fi rm

4. Advisor League Table 27- Overview of the 25 largest advisors by assets under management

5. Advisor Attributes Directory 31- Overview of service coverage, nature of service and location of clients

6. Expert Opinions on the Latest Factors Affecting the Market 37- Watson Wyatt’s Mark Calnan outlines his view of the state of the market

- Courtland Partners’ Rob Negrelli discusses manager fees

- Cambridge Associates on what happens next for large-cap buyout funds

7. Advisors for Most Important 25 Institutional Investors 49- Overview of advisors used by the top 25 institutional investors that employ the

services of advisors

8. Review of Investor Use of Advisors 55- Breakdown of investors by region and fi rm type

9. Investor Survey 63

10. Listings of Investors Showing Advisor Used 73

11. Advisor Profi les 77- Detailed profi les for 100 advisors

12. Index 163- Alphabetical by advisor name

13. Other Publications 167- Other Preqin Products

© 2008 Preqin Ltd 3

Executive Summary - Sample Pages

Advisors are an integral part of the alternative assets

universe, providing investment advice and services

to numerous institutional investors ranging from small

family offi ces all the way up to multi-billion dollar

public pension plans. Whether advisors are acting on

a discretionary or non-discretionary basis, the advice

that they provide to their clients is taken extremely

seriously. As a result it is vital that all fund managers

operating in the alternative asset classes have a

good knowledge of which advisors are advising

which investors, what the advisors are advising them

on, and what they need to do in order to form strong

relationships with these important custodians of

investor capital.

There are over 100 noteworthy advisors of

institutional investors in alternative assets worldwide,

between them responsible for advising over $2

trillion of investments in this area. Why is it that so

many investors are willing to pay considerable fees

to these fi rms to provide investment advice rather

than channelling these funds into setting up in-house

investment teams?

In a survey of 50 institutional investors from around

the world using advisors, Preqin asked respondents

to rate the importance of the different functions

performed by advisors out of fi ve. As the results in

Fig. A show, the most important factor that investors

consider when selecting new advisors is that they

have a proven strong track record in fund selection.

There are over 1,600 different unlisted private

equity, real estate and infrastructure funds currently

on the road seeking capital, along with several

thousand hedge funds seeking to boost their assets

under management. With the variation between

the best and worst performing alternatives funds

being considerable, fund selection is clearly both

an important and challenging prospect for any

investor in alternatives. Investors see their advisor’s

most important role as being able to select the top

performing vehicles, with their resources allowing

Executive SummaryFig. A: Investor Attitudes Towards Advisor Attributes

Very Important

Less Important

Importance Rating

© 2008 Preqin Ltd 4

Executive Summary - Sample Pages

them to undertake detailed due diligence, and their

market knowledge allowing them to review and be

aware of all the opportunities available to them.

Linked to this is the ability of advisors to gain access

to in-demand top tier funds, which was also deemed

highly important by investors. While fundraising for

certain managers remains extremely challenging,

other fund managers with a strong track record, and

excellent past performance may fi nd themselves with

more than enough interested investors to complete

their fundraising. By making commitments via an

advisor, smaller investors stand a much better chance

of gaining access to these funds.

Another factor deemed highly important was

customer service, and good communication between

the advisor and client. An international presence was

deemed important, but less so than the other factors

mentioned, while a competitive price was deemed

the least important factor for investors when seeking

out advisory services. It is clear that investors view

the services that are being provided by advisors as

extremely important and valuable, and are unwilling

to compromise on quality, with the relatively low

importance attached to competitive price showing

that investors are willing to pay a high price in order

to receive what they perceive as the best possible

investment advice.

These responses have some important ramifi cations

for those involved with the management and especially

marketing of alternative investment vehicles. With

the market for alternatives fundraising currently more

competitive than at any other point in the history of the

industry, increasing numbers of institutional investors

are utilising the services of advisors in order to assist

them with fund selection, advice and due diligence. If

a fund manager is able to communicate its strategy

to an advisor in an effective manner, then it can lead

to them potentially gaining a number of commitments

from the advisor’s clients.

With the fundraising market currently in a crowded

state, it is important that fund managers are

maintaining effective communications with advisors

both during a fundraising process, and also during a

fund investment period when new capital is not being

sought. A consistent approach to providing advisors

with information on performance and strategy is vital

in fostering a relationship that can lead to mutually

benefi cial new commitments being made in future

fundraising drives. In order for this to be effective, a

good understanding of the key factors that advisors

are considering, along with a detailed knowledge of

the services they offer and make up of their client

base is of the highest importance.

Contained in the body of the 2009 Preqin Alternative

Investment Advisor Review is the vital information

necessary for managers and fund marketers to

ensure that they are approaching the best advisors

with the most appropriate clients in order to build the

most effective and fruitful relationships possible. The

Review is also an excellent resource for investors

seeking detailed profi les on all advisors active in

this space along with analysis for the latest factors

affecting the market. The Review provides advisors

themselves with comprehensive intelligence on

other fi rms active in this space, and also the latest

trends and breakdown of all areas of the alternative

investment advisor universe.

The alternative assets universe has grown

dramatically in recent years, as many new investors

© 2008 Preqin Ltd 5

Executive Summary - Sample Pages

have made maiden commitments to funds, and

existing investors have been increasing their

allocations. In many ways the name ‘alternatives’ is a

misleading term for what is now a major component

in the portfolios of institutional investors. As the

market has evolved and become more complex, the

importance and stature of advisors in the industry has

also been growing. It is the aim of the 2009 Preqin

Alternative Investment Advisor Review to provide a

comprehensive overview of this signifi cant sector

of the market, and we hope that it proves to be an

effective tool in facilitating and furthering relationships

between investors, advisors and fund managers.

© 2008 Preqin Ltd 6

3. Review of Alternative Investment Advisors - Sample Pages

Location of Advisory Firms

Looking at the geographic location of advisory fi rms

that are active in alternative investments, the majority,

more than two-thirds, are based in North America,

as shown in Fig. 3.4. This is unsurprising, since the

US remains the main hub of alternative investment

activity in the world, with major centres such as New

York for hedge funds and Silicon Valley for venture

capital. Additionally, most of the largest fi rms in terms

of assets advised are headquartered in the US.

Nearly one-quarter of advisory fi rms are based in

Europe, leaving less than 8% based outside of the

two primary regions. Again, this correlates with the

prominence and maturity of alternative investment

activity in the respective regions. The recent growth

in demand for alternative investments in Asia, both

from investors around the world wishing to invest

there and from Asian investors wishing to add

alternative investments to their portfolios, is refl ected

by the fact that many of the larger advisory fi rms that

are headquartered in North America or Europe now

have offi ces in one or several locations in Asia. This

allows them to benefi t from local knowledge when

researching investment opportunities in the region,

as well as providing the opportunity to take on clients

based there. Russell Investment Group and Wilshire

Associates have offi ces in Singapore. Albourne

Partners has offi ces in Japan and Hong Kong, as

well as Singapore.

Age of Advisory Firms

We also took a breakdown of advisory fi rms by the

number of years that they have been operational. As

shown by Fig. 3.5, fi rms that have been operating

for less than 10 years form 27.5% of the population;

23.3% are between 10 and 19 years old; 25.9% have

been running for between 20 and 29 years; 15.8%

for between 30 and 39 years; and 7.5% have been

operational for more than 40 years. These fi gures

show a steady growth in the number of fi rms over

the past 30 years, following the formative period of

the industry prior to that. This would seem to imply

that the demand for general investment advice and

education about, as well as access to, alternative

Fig. 3.4: Advisor Firm Location

© 2008 Preqin Ltd 7

5. Advisors Attributes Directory - Sample Pages

Abbott Capital Management 79 US 1986 4.0 USD 4.0 USD • • • • •Access Capital Advisers 79 Australia 1988 15.0 AUD • • • • • • • • • •Adams Street Partners 80 US 1979 12.0 USD 12.0 USD • • • • •Aksia 81 US 2006 • • • • •Alan Biller and Associates 81 US 1982 50.0 USD • • • • • • • •Albourne Partners 82 UK 1994 200.0 USD 200.0 USD 149 • • • • • •Aldus Equity 82 US 2003 6.0 USD 6.0 USD 25 • • • • •Alpha Associates 83 Switzerland 2004 2.0 USD 2.0 USD 18 • • • • •Alternative Investment Capital 84 Japan 2002 2.0 USD 2.0 USD • • • • • •Altius Associates 85 UK 1998 17.0 USD 17.0 USD 25 • • • • • • •Amanda Advisors 85 Finland 2002 2.4 EUR 2.4 EUR 25 • • • •Arnerich Massena & Associates 86 US 1991 15.0 USD 51 • • • • •Asset Consulting Group 87 US 1989 50.0 USD 47 • • • • • • •Auda International 88 US 1989 5.6 USD 5.6 USD 80 • • • • • • •Babson Capital Management 88 US 1940 100.0 USD 20.8 USD 600 • • • • • • • •Bramdean Asset Management 89 UK 2005 1.3 USD 1.3 USD 13 • • • • • • •Callan Associates 90 US 1973 10.0 USD 175 • • • • • •CAM Private Equity 91 Germany 1998 3.0 EUR 3.0 EUR 42 • • • •Cambridge Associates 91 US 1973 88.2 USD 37.0 USD 885 • • • • • • • • •Canterbury Consulting 92 US 1988 11.0 USD 40 • • • • • •Capital Dynamics 92 Switzerland 1988 20.0 USD 20.0 USD 112 • • • • • • •Central Park Group 93 US 2006 • • • • •Cliffwater 93 US 2004 19.0 USD 19.0 USD 30 • • • • • • • • •Colonial Consulting 94 US 1980 21.0 USD 5.0 USD 41 • • • • • • •Commonfund Capital 94 US 1971 42.0 USD • • • • • • •Consulting Services Group 95 US 1988 36.0 USD 66 • • • • • • •Courtland Partners 96 US 1995 25.0 USD 25.0 USD 27 • • • • •Credit Suisse Customized Fund Investment Group 96 US 2000 14.0 USD 14.0 USD • • • • • •

CTC Consulting 97 US 1981 28.0 USD 11.0 USD 65 • • • • • •DB Advisors 98 US 561.0 USD • • • • • • • • •DeMarche Associates 98 US 1974 53 • • • • • •DTZ Investment Management 99 UK 1970 1.9 GBP 1.9 GBP 29 • • • •Ellwood Associates 99 US 1977 36 • • • • • •

Firm Name Page Location Year Est. Total Assets Advised (bn)

Alt. Assets Advised (bn) No. of Staff

Service Coverage

Nature of Service

Location of Clients

Infra

stru

ctur

e

Gen

eral

Con

sulta

ntPr

ivat

e Eq

uity

Rea

l Est

ate

Dis

cret

iona

ryN

on-D

iscr

etio

nary

Nor

th A

mer

ica

Euro

pe

Res

t of W

orld

Hed

ge F

unds

© 2008 Preqin Ltd 8

9. Investor Survey - Sample Pages

Do you believe your advisor provides good value

for money?

In general LPs agreed that their advisor provided

good value for money, with 29% stating it was excellent

value and 34% believing it was above average. A

minority of 8% thought that the service they received

was below average with regards to value for money

and only 3% commented that it was poor. One small

German insurance company explained their reason

for believing their advisor provided them with good

value for money by stating “we are a small team with

limited experience in alternatives and rely heavily on

our advisor to use their expertise to provide us with

access to top performing funds”.

What are the most important attributes you seek

when reviewing advisors?

For these questions we asked our respondents to rank

a list of attributes by importance. LPs were asked to

rate the criteria out of 5, with 5 being very important

and 1 being the least important. Unsurprisingly, all

the attributes were deemed as fairly important by

investors and this is demonstrated in Fig. 9.11.

Fig. 9.10: Advisors Success At Providing Good Value For Money

Fig. 9.11: Attributes LPs Seek When Reviewing AdvisorsVery Important

Less Important

Importance Rating

© 2008 Preqin Ltd 9

11. Advisor Profiles - Sample Pages

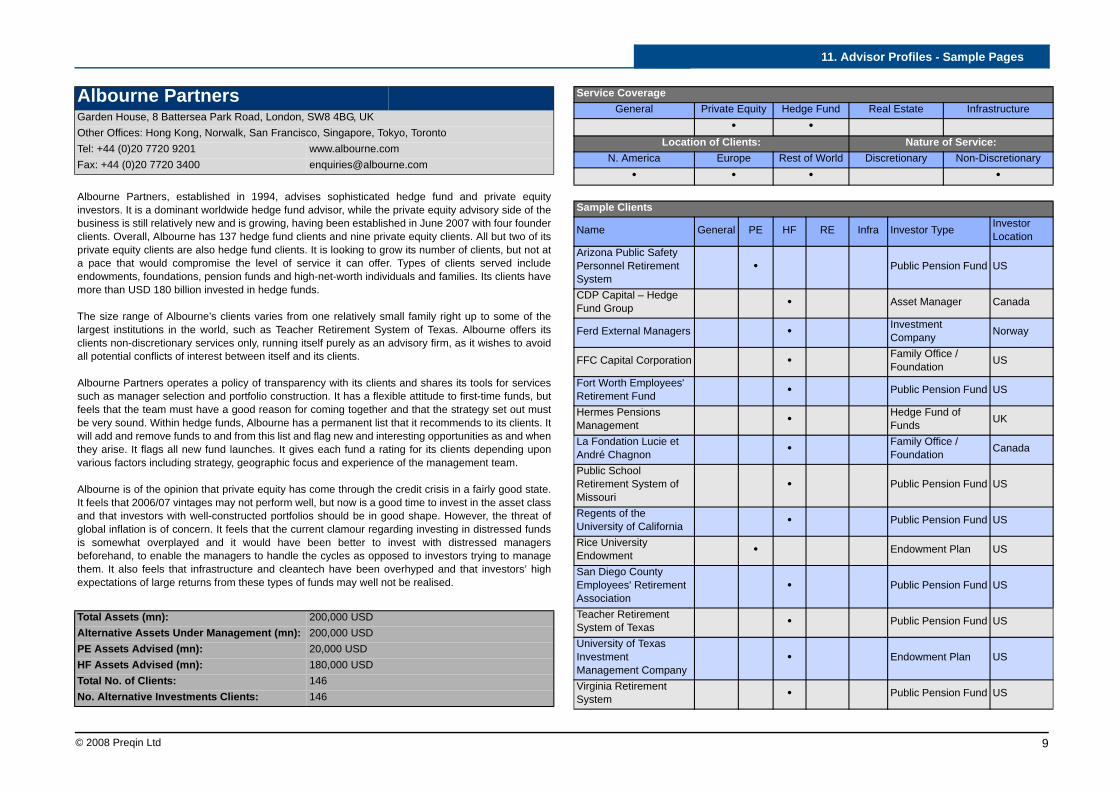

Albourne PartnersGarden House, 8 Battersea Park Road, London, SW8 4BG, UKOther Offices: Hong Kong, Norwalk, San Francisco, Singapore, Tokyo, TorontoTel: +44 (0)20 7720 9201 www.albourne.comFax: +44 (0)20 7720 3400 [email protected]

Albourne Partners, established in 1994, advises sophisticated hedge fund and private equityinvestors. It is a dominant worldwide hedge fund advisor, while the private equity advisory side of thebusiness is still relatively new and is growing, having been established in June 2007 with four founderclients. Overall, Albourne has 137 hedge fund clients and nine private equity clients. All but two of itsprivate equity clients are also hedge fund clients. It is looking to grow its number of clients, but not ata pace that would compromise the level of service it can offer. Types of clients served includeendowments, foundations, pension funds and high-net-worth individuals and families. Its clients havemore than USD 180 billion invested in hedge funds.

The size range of Albourne’s clients varies from one relatively small family right up to some of thelargest institutions in the world, such as Teacher Retirement System of Texas. Albourne offers itsclients non-discretionary services only, running itself purely as an advisory firm, as it wishes to avoidall potential conflicts of interest between itself and its clients.

Albourne Partners operates a policy of transparency with its clients and shares its tools for servicessuch as manager selection and portfolio construction. It has a flexible attitude to first-time funds, butfeels that the team must have a good reason for coming together and that the strategy set out mustbe very sound. Within hedge funds, Albourne has a permanent list that it recommends to its clients. Itwill add and remove funds to and from this list and flag new and interesting opportunities as and whenthey arise. It flags all new fund launches. It gives each fund a rating for its clients depending uponvarious factors including strategy, geographic focus and experience of the management team.

Albourne is of the opinion that private equity has come through the credit crisis in a fairly good state.It feels that 2006/07 vintages may not perform well, but now is a good time to invest in the asset classand that investors with well-constructed portfolios should be in good shape. However, the threat ofglobal inflation is of concern. It feels that the current clamour regarding investing in distressed fundsis somewhat overplayed and it would have been better to invest with distressed managersbeforehand, to enable the managers to handle the cycles as opposed to investors trying to managethem. It also feels that infrastructure and cleantech have been overhyped and that investors’ highexpectations of large returns from these types of funds may well not be realised.

Total Assets (mn): 200,000 USDAlternative Assets Under Management (mn): 200,000 USDPE Assets Advised (mn): 20,000 USDHF Assets Advised (mn): 180,000 USDTotal No. of Clients: 146No. Alternative Investments Clients: 146

Service CoverageGeneral Private Equity Hedge Fund Real Estate Infrastructure

• •Location of Clients: Nature of Service:

N. America Europe Rest of World Discretionary Non-Discretionary• • • •

Sample Clients

Name General PE HF RE Infra Investor Type InvestorLocation

Arizona Public Safety Personnel Retirement System

• Public Pension Fund US

CDP Capital – Hedge Fund Group • Asset Manager Canada

Ferd External Managers • Investment Company Norway

FFC Capital Corporation • Family Office / Foundation US

Fort Worth Employees' Retirement Fund • Public Pension Fund US

Hermes Pensions Management • Hedge Fund of

Funds UK

La Fondation Lucie et André Chagnon • Family Office /

Foundation Canada

Public School Retirement System of Missouri

• Public Pension Fund US

Regents of the University of California • Public Pension Fund US

Rice University Endowment • Endowment Plan US

San Diego County Employees' Retirement Association

• Public Pension Fund US

Teacher Retirement System of Texas • Public Pension Fund US

University of Texas Investment Management Company

• Endowment Plan US

Virginia Retirement System • Public Pension Fund US

© 2008 Preqin Ltd 10

11. Advisor Profiles - Sample Pages

Wellcome Trust • Family Office / Foundation UK

West Virginia Investment Management Board

• Government Agency US

Name Position Tel Email

David Harmston Head of US Client Services

+1 203 852 7116 [email protected]

David Hutchings Head of Private Equity +44 (0)20 7099 0283 [email protected]

Frank Moens Senior HF Advisor +1 416 848 4124 [email protected]

Tom Cawkwell Senior Analyst +1 415 489 7200 [email protected]

Ennis Knupp and Associates Investment Consultant

10 South Riverside Plaza, Suite 1600, Chicago, IL, 60606, USTel: +1 312 715 1700 www.ennisknupp.comFax: +1 312 715 1952

Ennis Knupp and Associates is a Chicago-based investment consulting firm that was established in1981 by Richard Ennis and Jim Knupp. The firm specialises in full consulting and advisory servicesand is owned by 26 key employees, with four principals and 130 employees in total. It has around 160clients, 15-20% of whom have investments in private equity, and advises on aggregate total assets ofUSD 840 billion.

Clients include public pension funds, endowments and foundations, which are the most involved withalternative investments, as well as corporations, universities and hospitals. The size of its clientsvaries from tens of millions up to USD 220 billion, with allocations to alternatives also varyingdependent upon size, goals of the investor and appetite for risk. The majority of Ennis Knupp’s clientsare served on a non-discretionary basis, although more recently the firm has started working withsome clients, including a union pension plan, on a discretionary basis. It offers a full range ofconsulting services, as well as fiduciary audits and operational reviews, education and board/committee governance advice. Its longest advisory relationship stands at more than 20 years.

Ennis Knupp and Associates has grown fairly rapidly, with growth averaging 10% per year over thepast ten years. This growth is controlled to ensure the quality of services provided to existing clientsremains high, and certain teams within the firm have also seen rapid growth. The firm has anapproved list of investment managers for each asset class and conducts approximately 1,400manager meetings each year, adding or removing managers from these lists as necessary.

Whilst Ennis Knupp closely monitors prevailing market conditions, it feels that these do not directlyaffect its advisory positions, as it is not a market timer, maintaining long-term positions andencouraging its clients to diversify their portfolios. The firm and its clients are becoming moreinterested in frontier markets. In terms of first-time fund managers, there is no prerequisite minimumtrack record or level of assets under management. If the manager meets strict requirements after a12-18 month due diligence process then they can be approved, regardless of whether they are first-time managers or not.

Total Assets (mn): 840,000 USDTotal No. of Clients: 160

Service CoverageGeneral Private Equity Hedge Fund Real Estate Infrastructure

• • • • •Location of Clients: Nature Of Service:

N. America Europe Rest of World Discretionary Non-Discretionary• • •

© 2008 Preqin Ltd 11

11. Advisor Profiles - Sample Pages

Sample Clients

Name General PE HF RE Infra Investor Type Investor Location

Arizona State Retirement System • Public Pension Fund US

Arkansas Teachers' Retirement System • Public Pension Fund US

Chicago Park Employees' Annuity & Benefit Fund

• Public Pension Fund US

Chicago Police Pension Fund • Public Pension Fund US

FirstEnergy • Private Sector Pension Fund US

Florida State Board of Administration • Public Pension Fund US

Georgia-Pacific Corporation • Private Sector

Pension Fund US

Harry and Jeanette Weinberg Foundation • Family Office /

Foundation US

Health Care Foundation of Greater Kansas City • Family Office /

Foundation US

Illinois Municipal Retirement Fund • Public Pension Fund US

Kansas Public Employees' Retirement System

• Public Pension Fund US

Lawrence University Endowment • Endowment Plan US

Maine Public Employees Retirement System

• Public Pension Fund US

Maryland State Retirement and Pension System

• Public Pension Fund US

Nebraska Investment Council • Public Pension Fund US

New Hampshire Retirement System • Public Pension Fund US

Pension Benefits Guaranty Corporation • Government Agency US

Policemen's Annuity and Benefit Fund of Chicago

• Public Pension Fund US

San Diego County Employees' Retirement Association

• Public Pension Fund US

Sonoma County Employees' Retirement Association

• Public Pension Fund US

State Universities Retirement System of Illinois

• Public Pension Fund US

United Technologies Pension Fund • Private Sector

Pension Fund US

University of Illinois Endowment • Endowment Plan US

University of Illinois Foundation • Endowment Plan US

Name Position Tel Email

Amy Hauke Senior Investment Analyst

+1 312 715 2937 [email protected]

Brett Nelson Partner in Charge, Private Equity

+1 312 715 1700 [email protected]

David J. Keil Primary Consultant +1 312 715 1700 [email protected]

Doug Patejunas Primary Consultant +1 312 715 1700 [email protected]

Harmony Watling Communications Manager & Associate

+1 312 715 1700 [email protected]

Stephen Cummings CEO and President +1 312 715 1700 [email protected]

Name PrivateEquity

RealEstate Infra. Hedge

Funds Price Order? (Please Tick)

Additional Copies Price

No. Additional

Copies

Charts & Graphs Excel Data Pack **

(Please Tick)2009 Global Hedge Fund Investor Review $795 / £465 / €495 $180 / £110 / €115

2009 Alternative Investment Advisor Review $595 / £350 / €385 $90 / £50 / €60

2008 Real Estate Review $1,345 / £795 / €895 $180 / £110 / €115

2008 Distressed Private Equity Review $795 / £465 / €495 $180 / £110 / €115

2008 PE Performance Monitor $1,345 / £795 / €895 $180 / £110 / €115

2009 PE Fund of Funds Review $1,495 / £885 / €950 $180 / £110 / €115

2009 PE LP Universe $1,345 / £795 / €895 $180 / £110 / €115

2009 Fund Terms Advisor $1,125 / £675 / €715 * $180 / £110 / €115

2008 Infrastructure Review $795 / £465 / €495 $180 / £110 / €115

2008 PERE Fund of Funds Review $795 / £465 / €495 $180 / £110 / €115

2009 Sovereign Wealth Fund Review $595 / £350 / €385 $90 / £50 / €60

2009 Global Private Equity Review $195 / £95 / €140 $150 / £75 / €80

2009 Real Estate Distressed & Debt Review $795 / £465 / €495 $180 / £110 / €115

2009 Private Equity Secondaries Review $1,345 / £795 / €895 $180 / £110 / €115

2009 Preqin PE Cleantech Review $1,345 / £795 / €895 $180 / £110 / €115

Name:

Firm: Address:

Email:

Job Title:

Telephone:

Please Send To:

US Dollars ($) GB Pounds (£) Euros (€)

Please Select Currency for Payment:

Shipping Costs: $40 / £10 / €25 for single publication, $60 / £15 / €37 for multiple publications purchase

Preqin Publications Orderform

More Info:

Please visit www.preqin.com/publications

Completed Order Forms:

Send To:

Scotia House,33 Finsbury Square,London,EC2A 1BBUK

Fax To:

+44 (0)87 0330 5892+1 440 445 9595

Email:

Over the Phone:

+44 (0)20 7065 5100

Charts and Graphs Data Pack Prices: $300 / £180 / €185

Payment Options:

Credit Card Visa AmexMastercard

Cheque enclosed (please make cheque payable to ‘Preqin’)

Please invoice me

Card Number:

Expiration Date:

Name on Card:

Security Code*:

* Price quoted is inclusive of 25% pre-publication discount valid until 12th June 2009.** contains all underlying data for charts and graphs contained in the publication. Only available alongside purchase of the publication.

Visa / Mastercard: the last 3 digits printed on the back of the card.

American Express: the 4 digit code is printed on the front of the card.

*Security Code: