Embed Size (px)

Citation preview

Eco-Branding The Case of Änglamark

02/2006-5314

This case was written by Renato J. Orsato, Senior Research Fellow at the INSEAD Business in Society (IBiS) Centre, at INSEAD, and Andrea Öström, Project Manager at Ekologiskt Marknadscentrum, Malmö, Sweden, as a basis for class discussion rather than to illustrate either effective or ineffective handling of an administrative situation.

Copyright © 2006 INSEAD

N.B. PLEASE NOTE THAT DETAILS OF ORDERING INSEAD CASES ARE FOUND ON THE BACK COVER. COPIES MAY NOT BE MADE WITHOUT PERMISSION.

Copyright © 2006 INSEAD 02/2006-5314 1

“When you go shopping, move your hand and pick organic meat, milk or eggs, so that we can boost the organic production. By doing so, there will be more animals living a more free and natural life.”

“Remember that, each time you pick an Änglamark organic egg, you let a hen out to see the light of the sun and feel the green grass under her claws. The more people that buy organic eggs, the more hens will have the chance to live under such conditions. In other words, normal conditions, with the possibility to behave naturally and eat organic food. Exactly like you.”

http://www.coop.se

Introduction

Food retailing in Sweden is a competitive business. Although there are only a few players, the market is ruled by fierce price rivalry. And even when higher returns resulting from differentiation strategies are possible, they tend to be very risky.

Retailers that have used environmental and social arguments to differentiate their products learned how difficult is to deploy and maintain such strategies. The tradeoff between price and environmental attributes of products is a constant challenge for consumer retention.

It is in this context that a special type of differentiation strategy − eco-branding − has been developed; it carries the promise of generating competitive advantage.

Food Retailing in Sweden

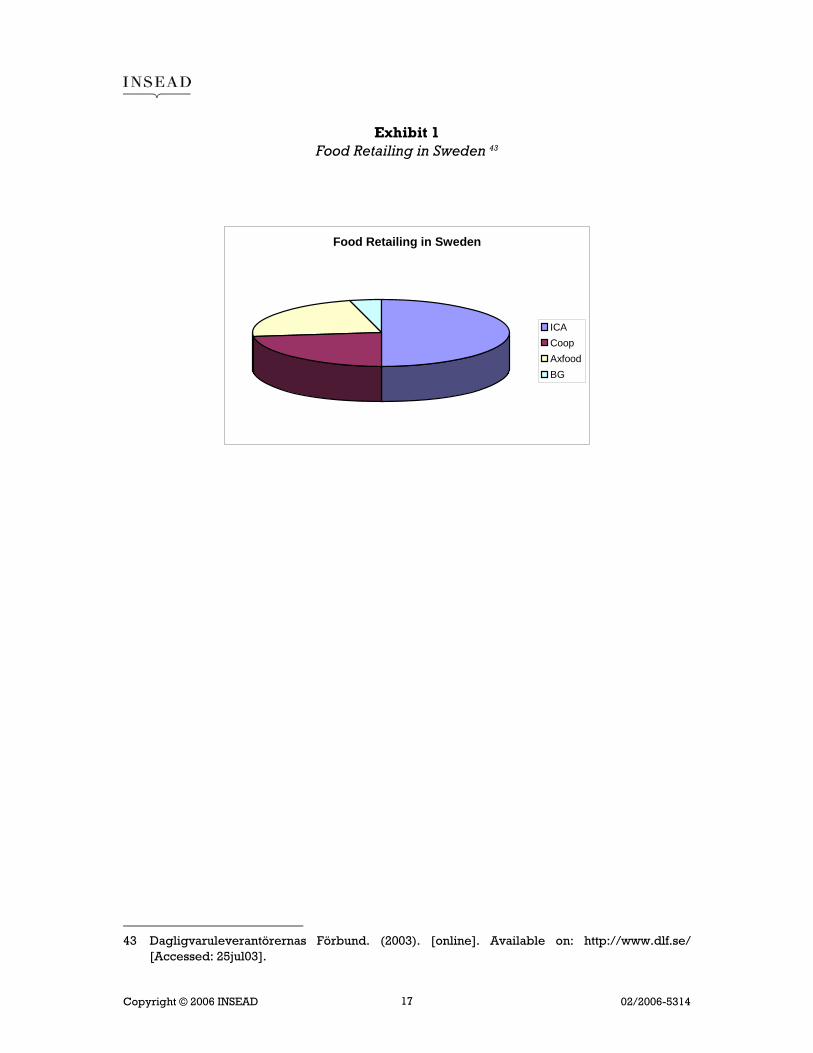

Food retailing1 in Sweden is concentrated in three large firms: ICA, Coop and Axfood. Together, these companies control more than 95% of the market. Industry rivalry is very strong, and there is increasing pressure from Swedish low-price chains as well as the new competitors, such as the German retailer, Lidl.

As Exhibit 1 shows, ICA is the dominant player with almost 50% of the market. Coop Sverige and Axfood share the remaining part of the market with approximately 23% each, and Bergendahls Gruppen, with 4%.2

1 In fact, ‘food retailing’ also covers ‘non-food products’, such as cleaning materials and

kitchenware. Possibly, the term ‘supermarket’ depicts the industry more accurately, since most lay citizens have a quite clear understanding what a supermarket is. Nonetheless, since the term ‘food retailing’ is well established among practitioners and academics, we also adopt it in this case.

2 Dagligvaruleverantörernas Förbund. (2003). Available on: http://www.dlf.se/.[Accessed 25 July 03].

Copyright © 2006 INSEAD 02/2006-5314 2

The Market Leader: ICA AB

ICA AB is owned by the Swedish ICA Förbundet Invest, the Norwegian Canica and the Dutch Royal Ahold, and manages food retailing in Sweden, Norway and the Baltic countries, with 3,000 stores and 40,000 employees.3

The vision of ICA is to “facilitate everyday life and become the leading retail trade company in Northern Europe”. In order to get there, ICA aims to be in the lead in every market the company operates – a position it certainly achieved in Sweden. An aggressive strategy has led to the control of 50% of the market. Today, around 4,000 persons work in the 1,764 stores throughout the country, generating a net turnover of around 7.90 billion Euros (€)4 in 2003, (71.98 billion SEK) – which represents an increase of 1.5%, compared to the previous year.5

ICA manages two business models: ICA and Netto. The ICA stores are a full service concept, where consumers can find the standard assortment, with various product brands such as the corporate brand, ICA, which aims to be on par with the market leader, but at a lower price; a low-price brand, Euroshopper, and the ecological brands, ICA ekologiskt and Skona. Besides its own brands, ICA also offers a range of brands from other suppliers.6

Netto is a Danish concept owned by Dansk Supermarked, operating in Sweden under a joint-venture with ICA. Netto is the low-price chain of ICA that offers ‘hard discount’. The first Netto stores opened in 2002, and by 2005 there were 73 of them. Rapid market response is a key element of the strategic approach guiding Netto. The marketing strategy builds on ICA − indeed, a very strong retailer brand – offering standard quality at a lower price.7

ICA is a member cooperative, so the store managers are also owners of the organization. Indeed, some industry experts believe that this is a key contributor to the success of ICA: membership is an additional motivation for store managers to achieve economic results.

The Owner of Änglamark: Coop Sverige

Coop Sverige was originally the food retailer of KF, then under the name KF Svenska Detaljhandeln. KF is a relatively old organization – it was founded in 1899. Today, KF is formed by 63 consumer associations with a combined membership of

3 ICA. (2003). Om ICA. [online]. Available on: www.ica.se [Accessed: 7 November 03]. 4 All values presented in this case have been converted from Swedish Kronor (SEK) to Euro (€),

based on the average currency rate for the period January-March 2004, according to: www.x-rates.com (2004, March 22). The values do not include inflation during the period. Since the numbers are intended to give an idea of magnitude, precision is not a key element. Therefore, they represent an approximate value of the original currency.

5 ICA. (2003). [online]. ICA presenterar resultatet för 2003. Available on: www.ica.se. [Accessed: 22 March 04].

6 ICA. (2003). Våra varumärken. [online]. Available on: www.ica.se. [Accessed: 4 August 03]. 7 ICA. (2003). Netto. [online]. Available on: www.ica.se. [Accessed: 27 September 05].

Copyright © 2006 INSEAD 02/2006-5314 3

2.9 million.8 The cooperative values are central in defining the organization. Originally, the mission of KF was to ‘defend’ consumer rights to have reasonably priced ‘original’ food (mainly organic), provided with transparent information (or ‘value for money’).

After 2001, Coop Sverige (henceforth, Coop, for short) became a fully owned subsidiary of Coop Norden. Coop manages the food retail industry in the Swedish market under two business models: Coop Konsum and Coop Forum. Coop Konsum is the ‘city supermarket’, with 373 stores around the country, and has a clear orientation toward ecology and food excellence. Coop Forum is formed by 43 ‘hypermarkets’ located outside the city center, providing ‘everything under one roof’. In 2004, the turnover of Coop was €2.97 billion (27,000 million SEK),9

Coop operates with its own brands (or ‘private brands’) as well as with brands of its suppliers. The private brand portfolio consists of three concepts: (i) low-price, (ii) standard and (iii) ecological. The low-price brand, Blå Vitt, was launched in 1979 and was recently substituted with x-tra, the common low-price brand of Coop Norden. Signum (standard brand) was launched in 1995 and stands for quality but at lower price than the market leaders. Signum has been converted into Coop as a common standard brand for Coop Norden. The third brand concept is the ecological one − Änglamark − the main focus of this case study.10

Low-Price Leadership: Axfood AB

Axfood AB runs food retail businesses in Sweden and Finland, employing more than 33,000 people. In Sweden, Axfood operates with several different business models, and has a total of 500 stores; around half of them are fully owned by Axfood and the rest are franchised. Hemköp, Willy and Willy’s hemma are Axfood’s own concepts. Hemköp is a full service concept. Willy and Willy’s hemma, launched in 2002, are low-price concepts, as well as Spar, which is one of the franchise chains, with 130 stores. Other franchises are Tempo and Vivo.

Axfood leads the low-price segment with approximately 260 stores. Indeed, the low-price strategy seems to have paid off. The turnover of Axfood increased from €3.2 billion (29 billion SEK) in 1999 to €3.7 billion (33.32 billion SEK) in 2003. In the same period, the results after tax rose from €16 million (141 million SEK) to €75 million (684 million SEK). The business idea of Axfood is to create, operate and develop successful food retail chains, fully owned or franchised (...) and be a

8 KF. (2004). Vad innebär medlemskapet? [online]. Available on:

www.kf.se/templates/Page____263.aspx [Accessed: 15 November 2005]. 9 Coop Sverige. (2004). Företagsinformation. [online]. Available on: www.coop.se [Accessed: 15

November 2005]. 10 Coop. (2004). Coop koncepten. [online]. Available on:

http://www.coop.se/se/articles/article_group.jhtml?menuLocation=1&utilLocation=116&articleIndex=1&pageIndex=1&categoryIndex=120. [Accessed: 22 March 04].

Copyright © 2006 INSEAD 02/2006-5314 4

challenge in the Scandinavian market through clear and unique offers to consumers”.11

In the early 1990s, Axfood was a leader in proactive environmental strategies. The group saw a market opportunity in portraying a proactive image, promoting values of quality, environmental protection and health within the chain, Hemköp.12 Such an image, however, eroded over time. Axfood distanced itself from such values, and today, price seems to be its main competitive focus.

A Small Family-Owned Competitor: Bergendahls Gruppen

Bergendahls Gruppen is a family-owned business that has a strong presence in southern Sweden, where it holds a 10% market share. One of the members of the group, AGs, specializes on the Scanian market (the southern Swedish region) and local producers, with stores such as Favör and Skånsk Matglädje. With 2,000 employees, in 2002, the group generated a turnover of €454 million (4.1 billion SEK) and results after tax of €9 million (81 million SEK).13

A New Entrant: The German Lidl

Lidl is a German retailer that entered the Scandinavian market in late 2003. An aggressive strategy led to Lidl opening stores in 11 Swedish cities, with 65 stores planned to open in Norway.

Lidl is very competitive in the low-price segment, benefiting from economies of scale to supply its stores with products shipped from a central warehouse in Germany. According to a representative of a market analysis firm, this will soon generate a ‘price war’ in Sweden. Rivalry in certain product categories such as milk, coffee, mineral water, flour, sugar, salt, frozen meals, detergents, fish, and meat will be extremely high.14

Gröna Konsum and the Creation of Änglamark

On the 100th anniversary in 1999, the mission of KF was extended to the sustainability concept:

Through cooperation, Coop shall facilitate and brighten up the daily life of all the people who want to live in a better world, by creating

11 Axfood Annual Report 2003. [online]. Available on: www.axfood.se. [Accessed: 22 March 04]. 12 Strannegård, L. (1995). Kundorienterad miljöstrategi – fallet Hemköp. In: Miljöstrategier – Ett

företagsekonomiskt perspektiv. Nerenius & Santérus Förlag, Stockholm. 13 Bergendahls Gruppen (2003). Fakta. [online]. Available on:

http://www.bergendahls.se/fakta/fakta.htm [Accessed: 7 November 03]. 14 Horntvedt, A. (2003). [online]. Lidl kom till Sverige igår. Nationen. 26 September 2003.

Available on: http://www.nationen.no/naeringsliv/article756957.ece [Accessed: 14 November 03].

Copyright © 2006 INSEAD 02/2006-5314 5

sustainable solutions that contribute to economic, ecological and social values.15

Such a step is a continuation of the policy initiated in late 1980s, when the company went through an image crisis. An ‘attitude survey’ revealed that consumers hardly associated KF with the foundational values of the organization − consumer rights to have reasonably priced ‘original’ and non-manipulated food provided with transparent information. Apart from being perceived as more proactive toward environmental protection, consumers did not differentiate KF from competitors in any other respect.

At that time, the Consumer Association of Stockholm (KFS) was concerned with the environmental impact of some products. The presence of pesticides and allergens in food, as well as animal welfare, were among the main preoccupation of KFS. Such concerns motivated the association to start selling ‘alternative food’ through Konsum stores in Stockholm, and create the first ecological brand, Lanthandeln, in 1986.

This development led to the renaming of the stores: from Konsum to Gröna Konsum (Green Konsum). At the same time, an internal assessment identified that, of all activities performed by the retailer, products had the highest environmental impact. For this reason, the environmental policy adopted in 1990 focused on reducing the impact of products, rather than on the organizational processes (activities) performed in the stores. As part of this policy, Coop Konsum would offer consumers at least one ecologically friendly alternative in each product category.16

Consumers, Eco-products and Eco-brands

The task of finding the best possible way to reach the eco-product goal was assigned to a working team of three staff members. Two members of the team had previous environment-related knowledge, and one had experience in marketing and branding.

After analyzing the results of consumer surveys on organic food, the team identified three reasons why ecological products had not yet succeeded in the market. One reason was price. Ecologically-oriented products (or ‘eco-products’, for short) tended to be too expensive. The second reason was quality; on average, eco-products performed and tasted worse than conventional ones. Finally, such products were simply too difficult to find in the store.

Based on these findings, the team elaborated the values and the functions that ecological products should have in order to succeed. They should ‘function’ similarly to conventional products, i.e., they should taste good and perform well. 15 Coop. (2003). [online]. Coops löfte. [online]. Available on www.coop.se [Accessed: 27-06-03]. 16 Terrvik, E. (2001). Att kanalisera hållbarhet – hur dagligvaruföretag översätter miljökrav till

handling. En studie om egna varumärken i handeln. Bokförlaget BAS, Handelshögskolan, Göteborg.

Copyright © 2006 INSEAD 02/2006-5314 6

Ecological products should not be more expensive than conventional ones, the message should be clear, and the products easy to find.

The working team concluded that the creation of a private brand would be the best approach to market eco-products. The eco-brand would communicate the ecological orientation of a wide range of products in a coherent and consistent way, making it easier for consumers to find the products in the stores. Besides, a private eco-brand would ‘force’ the top management to prioritize the development of ecological products.

Developing Änglamark

Tests with focus groups showed that the name Änglamark invoked positive values, associating the name with the Swedish soul, identity, and with nature. The name for the eco-brand was selected based on this association. Indeed, the meaning associated with the name, the intrinsic characteristics of the products as well as the strategy for product mix and pricing determined the initial success of Änglamark.

The product mix included both food and non-food products. Since the volume of food was higher than that of non-food products, while the turnover was lower, extending the brand to both categories would increases its exposure to consumers, as well as generating economies of scale in advertising. Hence, in principle, food and non-food categories should be complementary.

Änglamark Criteria

The development of Änglamark was based on previous experience of Coop in building two other ‘private brands’ − Signum and Blå Vitt. In simple terms, Änglamark would be quite similar to the other brands, with added environmental, health and ethical values. Änglamark products build on six standpoints, or criteria, which should be seen in a holistic perspective and evaluated in relation to the market leader.17

• Eco-labeling: Änglamark products should, as a minimum, fulfill the requirements of eco-labeling schemes such as (See Exhibit 2):

− KRAV for food products

− The Scandinavian Swan, Good Environmental Choice (Bra Miljöval), or the EU Flower for non-food products

• Carbon dioxide emissions: Änglamark products should not impact the level of carbon dioxide emissions.

• Packaging: Änglamark products should have the right type and amount of packaging.

17 Coop Sverige. (2002, May 22). Pocket platform Änglamark? Internal document.

Copyright © 2006 INSEAD 02/2006-5314 7

• Renewable material: Änglamark products should use renewable materials in packaging and raw materials.

• Health: Änglamark products should contribute to higher levels of perceived well-being.

• Ethics: Änglamark products should have a high ethical level.

• Quality: Änglamark products should have the same quality in taste and function as the product leader in each product category.

Even if the aim is to fulfill the criteria of the above-mentioned eco-labeling schemes, around 10% of the Änglamark food products do not carry the KRAV label. The reason for this is that, in some cases, KRAV criteria are much stricter than the EU criteria. In some cases, Änglamark products use eco-labeling criteria of other accredited European labeling organizations.

The carbon dioxide criterion has not been very well developed since it has not been a prime focus so far. The health and ethical criteria are also less developed than the environmental criteria. But for some products, third party labels are used. In the case of detergents, for example, the asthma and allergy association (Astma- och Allergiförbundet) recommends Änglamark products. Products such as coffee and bananas carry the Fair Trade label (Rättvisemärkt), which means that they have been produced in accordance with human rights conventions.18

Änglamark Price Policy

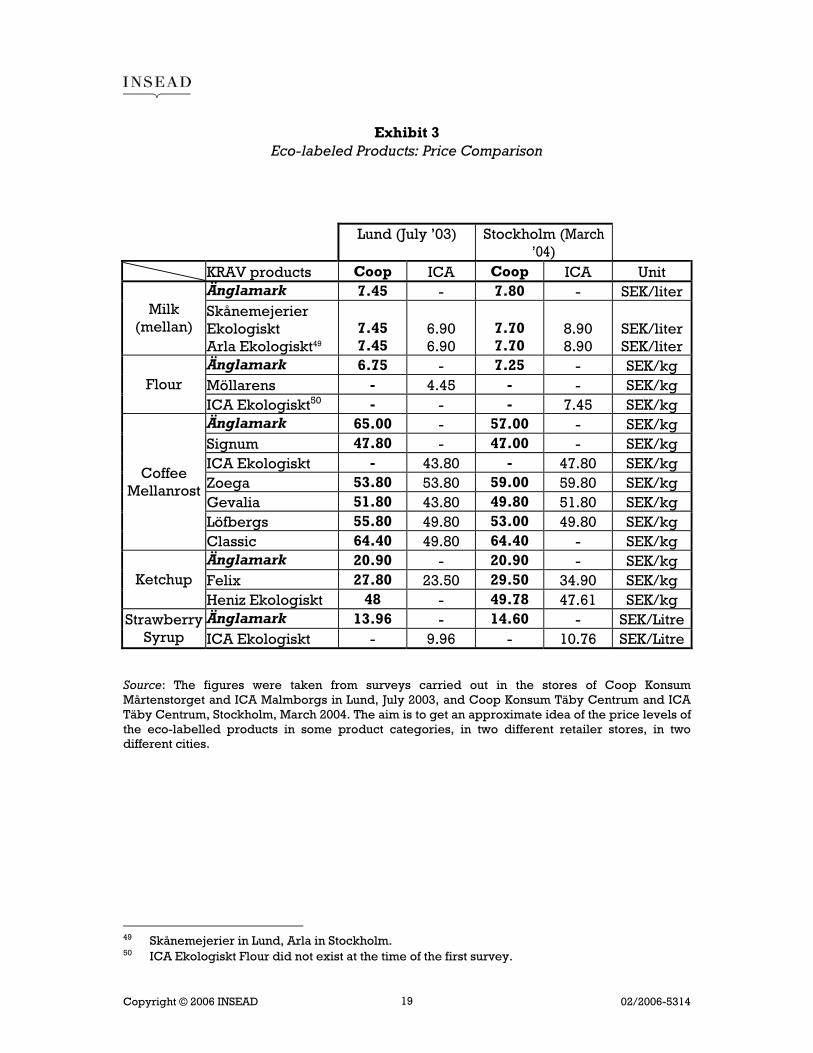

In principle, Coop strategists decided that Änglamark products should be able to compete with product leaders of Konsum stores, as well as the eco-products of rival retailers. Änglamark food products should not be more expensive than the organic alternatives of ‘product leaders’ in the store (i.e., the best selling products in each product category) and, whenever possible, should not be more expensive than the organic assortment of other retailers.

For this reason, Coop adopted a price strategy that considers the margins of the products in absolute terms (Swedish crowns), instead of profit margins in percentage. Änglamark should have the same profit margins (in crowns) as the product leaders.19 For instance, if the cost of the product leader is €10, and a margin of 10% is applied (€1), the final price to consumers is €11. The margin of Änglamark in that product category should then be €1 (rather than 10%). So, if the cost of an Änglamark product is €12, the price will be €13 (€12 + €1).

Nonetheless, as shown in Exhibit 3, in some categories, such as coffee and strawberry syrup, Änglamark products are actually more expensive than rival 18 Coop Konsum. (2003). Märkliga märken. [Online].

http://www.konsum.se/konsum/jsp/Crosslink.jsp?d=292&a=3889. [Accessed: 25 November 03].

19 Terrvik, E. (2001). Att kanalisera hållbarhet – hur dagligvaruföretag översätter miljökrav till handling. En studie om egna varumärken i handeln. Bokförlaget BAS, Handelshögskolan, Göteborg.

Copyright © 2006 INSEAD 02/2006-5314 8

products. Because some competitors comply with the minimum environmental requirements only, they are able to offer products at lower prices. In order to beat competitors’ prices in some product categories, the environmental requirements and quality of Änglamark products would eventually have to be lowered − even if the brand managers at Coop would rather avoid such measure.

Änglamark in Perspective

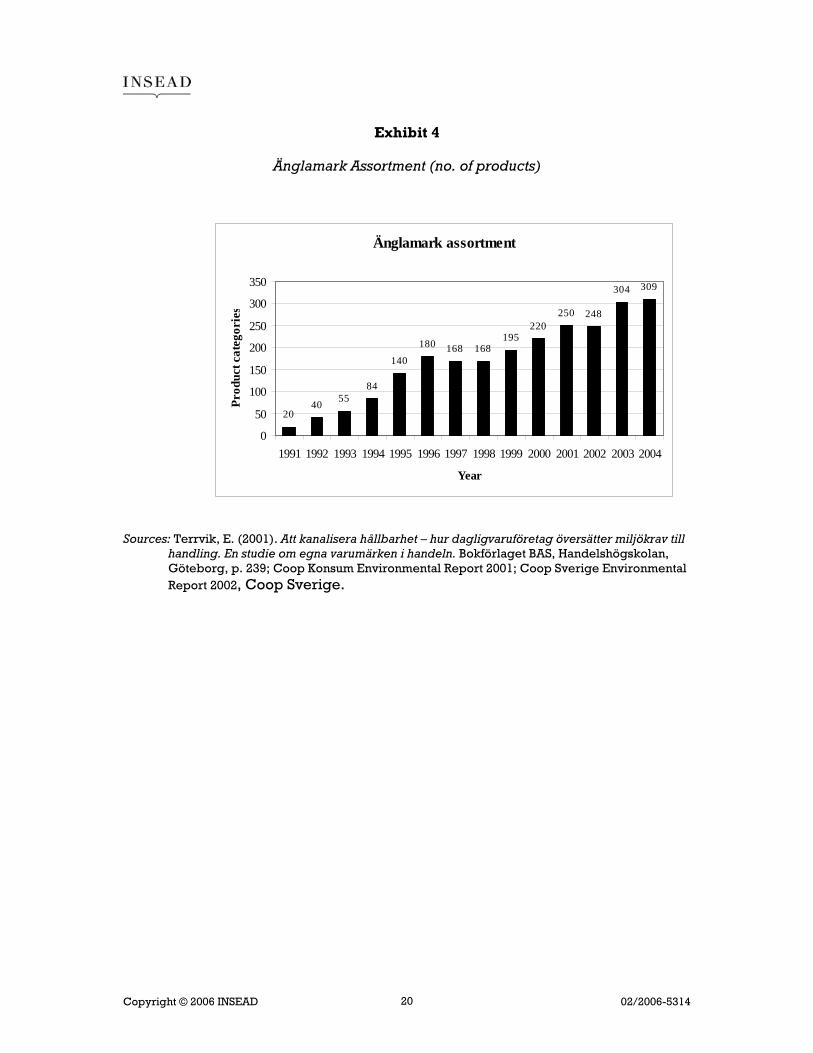

Änglamark was launched in September 1991. Exhibit 4 presents the development of the assortment and sales of the brand. The increase was strongest at the beginning of the 1990s: the assortment increased from 20 products in 1991 to 180 products in 1996.

In September 2000, the brand platform of Änglamark was modified with its re-launch. An attitude survey had previously identified a group of consumers concerned with environmental, health and ethical issues, formed mainly by women in the 19-35 age group, and some up to 49. Many of these women, who represent around 25% of the market, are holders of a discount card (MedMera), which means that they are members of KF/Coop. The re-launch aimed at reaching this group of consumers, which is much broader than the ‘traditional green’ segment of around 10-15%. With the re-launch of the brand, the assortment was upgraded and in 2002, there are around 250 Änglamark products in 90 categories.

After the creation of Coop Norden, efforts and resources have been (re)directed to the development of Coop - the common brand of Coop Norden. This meant some cost cuttings and refocusing of Änglamark. From 309 product categories the Änglamark brand in 2004, Änglamark assortment decreased to 275 product categories in 2005.

Even though Änglamark will remain the leading eco-brand of Coop, its assortment has been reduced. In some cases, Änglamark has been withdrawn from a product category because other leading brands have developed organic alternatives and taken over the segment because they can meet consumer demands more effectively than Änglamark. In these cases, one could say that Änglamark has reached its goal, since its main mission is to push and drive the development of organic products. For example, Änglamark was a pioneer in ecological milk, which forced Arla (the largest Dairy company of Sweden) to produce and sell ecological milk. Today, Arla has a large range of ecological dairy products; Änglamark is not needed any longer in that category.

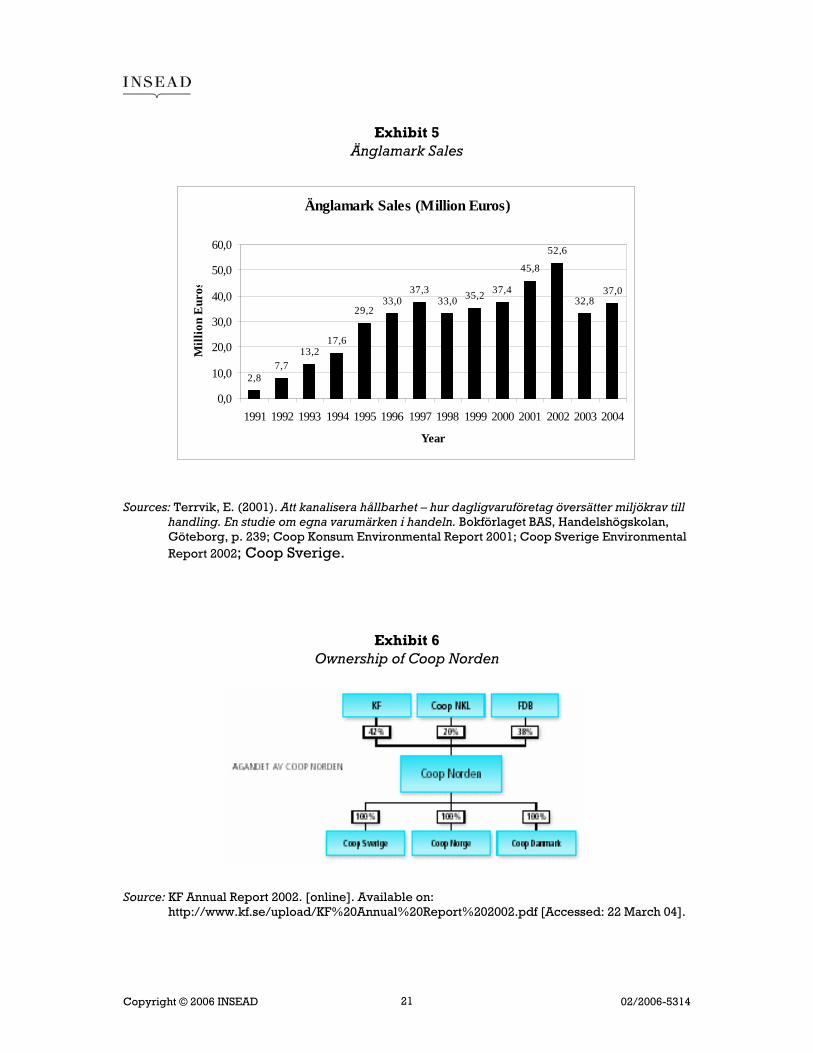

As shown in Exhibit 5, the turnover of Änglamark increased from €2.8 million (25 million SEK) in 1991 to €52.6 million (478 million SEK) in 2002. During 1998 and 1999, there was a slump in sales, but with the re-launch of the brand in September 2000, they quickly recovered. The aim of the re-launch was to increase the volume of sales 3 to 4 times in three years. Although sales did increase 22% in 2001 and 15% in

Copyright © 2006 INSEAD 02/2006-5314 9

2002, the original − and indeed ambitious − goal was not fulfilled. By 2004 the sales have decreased to €37.0 million (336 million SEK)20.

Strategic Products and First Mover Advantage

For Coop managers, ‘strategic product categories’ are those that, at certain moments, become ‘an issue’ for the media and customers. Detergents were such a category at the beginning of the 1990s, requiring manufacturers to develop and market biodegradable and eco-labeled products. More recently, the development of the fast food trend has increased the demand for ready-made meals and processed food.

Being first in strategic product categories has been of crucial importance for the development of Änglamark. The company was able to respond rapidly to the emerging ‘food issues’ with an organic product alternative, under the brand Änglamark. In its first five years (1991-1996), Änglamark was the first organic alternative in all food, and often in non-food, categories, covering more than 80% of products. Such a move gave Coop a ‘first mover advantage’.

In order to sell high volumes of eco-products, Coop used Änglamark to compete directly with market leaders in each product category. Since Änglamark offered products that performed as well as the conventional ones, it gradually gained consumers from market leaders. Competitors eventually reacted to Änglamark and developed their own ecological brands. Today, almost all market leaders have an organic product alternative. Nonetheless, in some product categories, Änglamark may have caused more than an eventual ‘dent’ in the market share; its presence may be a lasting one.

Vertical Integration and Collaboration

Coop’s first mover advantage was facilitated by its organizational structure. The group was vertically integrated in several food product categories: organic bread, charcuterie and some processed food, such as pea soup, rice porridge and baked beans, were supplied in bulk by production units of corporations owned by Coop, such as Juvelbagarna and the Goman group.

Collaborative schemes also played an important role in the development of Änglamark. Saltå Kvarn, a producer of organic grain products, developed the first organic fruit muesli for Coop.

Coop Norden and the Future of Änglamark

Coop Norden was formed in 2001 as a result of the merger of the Danish, Norwegian and Swedish cooperatives. With more than 2,000 stores, around 28,000 employees and a turnover of €8.5 billion (77.36 Billion SEK)21 in 2002, Coop 20 Coop Sverige. 21 Coop Norden Annual Report 2002. [online]. Available on www.coop.se. [Accessed: 22-03-04].

Copyright © 2006 INSEAD 02/2006-5314 10

Norden is one of the largest food retailers in Scandinavia. As Exhibit 6 shows, the Swedish consumer cooperative, KF, owns 42% of Coop Norden, the Danish cooperative, FDB, owns 38%, and the Norwegian NKL owns 20%.

The creation of Coop Norden aimed at improving the purchasing power of the member organizations (Coop Sverige, FDB and NKL), so they could respond more effectively to the increasing competition based on price from Netto (ICA) and Axfood, as well as the recently established German retailer Lidl. Nonetheless, the creation of the group generated extra costs – at least in the short term. In 2002, Coop Norden had an after-tax deficit of €23 million (205 million SEK).22 Since then the organization is under pressure to make extensive overhead cost reductions while dealing with the price competition. Many at Coop Konsum are concerned. As Thomas Evertsson, Manager of Coop Konsum stated:

“Price is a restriction; we do not want our customers to leave our stores (…) so our prices need to be modified; they are a little bit too high compared to those of our competitors”.

Fierce competition and poor results after the creation of Coop Norden led Coop Sverige to reorganization. In order to meet consumer needs more effectively, new business models were created and introduced in 2003: Coop Nära as the small ‘shop on the corner’, Coop Extra as full service stores with lower prices, while Coop Konsum remained the ‘green stores’ and Coop Forum remains a hypermarket with ‘everything under one roof’.

Sales of Eco-products at Coop Sverige: A Good Performance?

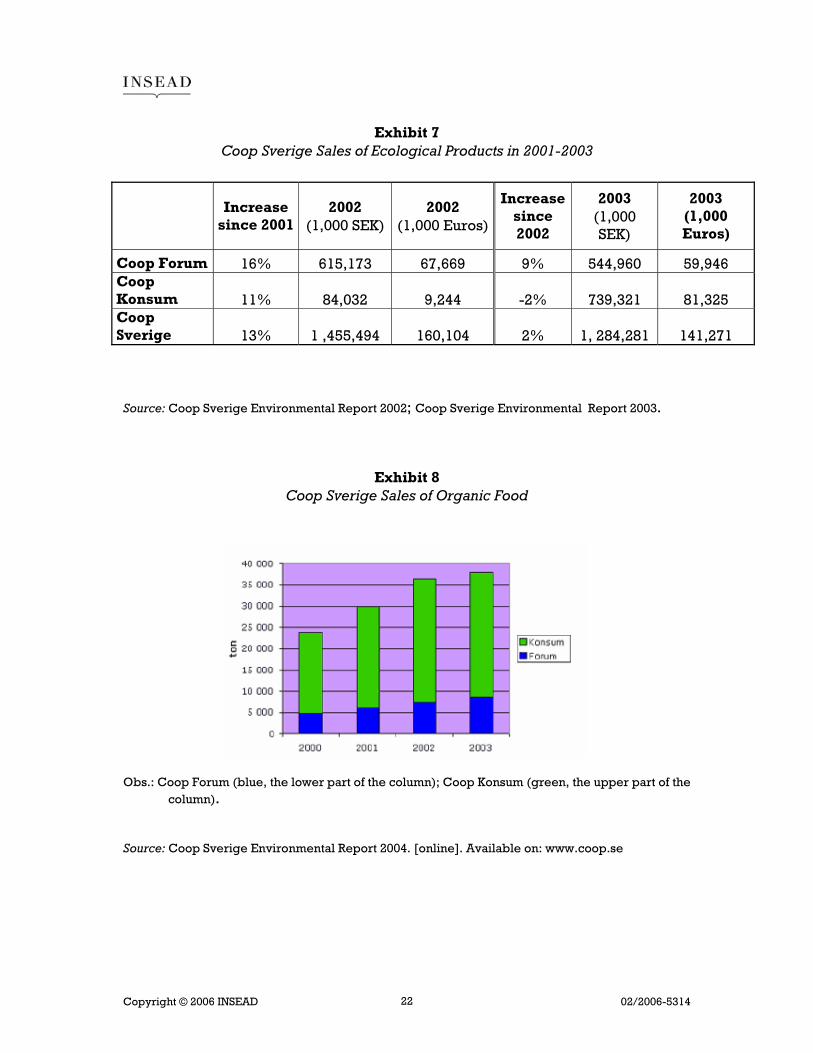

In 2002, Coop Sverige had more than 2,000 ecological products in its assortment (i.e., all eco-labeled products, including Änglamark). Exhibit 7 shows that this assortment generated a turnover of approximately €160 million (1.45 billion SEK), a 13 percent increase from 2001 to 2002. Overall, sales of (food and non-food) ecological products represented 0.5 percent of the total sales of Coop.23

Exhibit 8 also shows that in the recent past there has been a strong increase in sales of organic food products at Coop. In total, organic food represented 3% of total sales of food in 2002.24 Lately, sales of organic food have increased more than the non-food category. A possible explanation for this may be that ecological non-food products were developed earlier (in the 1990s) than food products. Hence, the growth in organic food is higher in past years.

Finally, even though Coop still has the largest assortment of ecological products in its industry (1,200 product categories25), in 2004 the total sales of ecological products (in tons) decreased 13.7 percent, compared to previous year26.

22 Coop Norden Annual Report 2002. [online]. Available on www.coop.se. [Accessed: 22-03-04]. 23 Coop Norden Annual Report 2002. [online]. Available on www.coop.se. [Accessed: 22-03-04]. 24 Coop Norden Annual Report 2002. [online]. Available on www.coop.se. [Accessed: 22-03-04]. 25 Coop Sverige. (Online). Coops miljöarbete. Available on www.coop.se . [Accessed: 27

October 2005]

Copyright © 2006 INSEAD 02/2006-5314 11

Supply Chain Management: Small or Large Suppliers?

Finding, developing and managing suppliers is time consuming and costly. Since Coop has invested heavily in the development of its suppliers, maintaining long-term relationships is the main policy now. But such a policy is not without problems.

At the beginning of the 1990s, there were few suppliers of organic food products. Most of them were small, ‘specialized pioneers’, who helped Coop Sverige to develop the competences and the assortment of eco-products. This situation has changed a lot in the past few years. Today, there is not only a much larger number of suppliers of organic food, but these suppliers are larger, and offer lower prices and better guarantees of compliance with food safety standards than smaller ones.

Since Änglamark products need to be safe as well as price competitive, such a situation creates a ‘moral dilemma’ for Coop. Ecological production is more costly for the smaller suppliers, and some are, to a large extent, dependent on Coop as a client. For this reason, forcing prices down for small suppliers could lead to ‘cheating’. Finding the optimum price level for small suppliers is a current pressuring issue for Coop.

Finally, even if large suppliers can offer lower prices and better product safety, there are some advantages with the smaller suppliers. They are, in general, more flexible, motivated and attentive. A large supplier may be more interested in developing own ecological brands rather than Änglamark, and lack of commitment has been a problem in some cases.

Supplier Certification: Extra Cost or Advantage?

With the introduction in 2002 of new EU legislation on food safety,27 an increasing number of requirements have to be met, and the Swedish Food Agency has established the minimum requirements of risk management following the principles of HACCP (Hazardous Critical Control Points).28 In order to satisfy such demands, Coop requires suppliers to have a risk management plan according to the HACCP principles, and undergo periodic revision of facilities.

Furthermore, the EU law decrees that organic food products be certified according to EU standards on organic food.29 Swedish producers often deal with certification themselves, but purchase managers at Coop need to be more

26 Coop Norden Annual Report 2004. (Online). Etik och ekologi i korthet. Available on:

http://www.coopnorden.com/2004/sv/index.html. [Accessed: 27 October 2005]. 27 Regulation (EC) 178/2002 of the European Parliament and Council of 28 January 2002. Laying

down the general principles and requirements of food law, establishing the European Food Safety Authority and laying down procedures in matters of food safety.

28 Swedish Food Agency (Sveriges Livsmedelsverk). (2002). Egentillsyn med HACCP. [online]. Available on: www.slv.se [Accessed: 22 March 04]

29 Council regulation (EEC) 2092/91 of 24 June 1991 on organic production of agricultural products and indications referring thereto on agricultural products and foodstuffs.

Copyright © 2006 INSEAD 02/2006-5314 12

involved in the process of guiding foreign suppliers toward KRAV certification. Since the whole chain has to be certified − all the way back to the producer of raw materials − ecological certification of suppliers is complex and time consuming.

Since Coop demanded this kind of control much earlier than it became a requirement, the HACCP legislation may actually generate some advantages. Eco-innovation for the development of Änglamark products required close collaboration with suppliers, with insights into suppliers’ ways of controlling processes and product safety. Now, this closeness could be used for the purposes of HACCP certification. Since small suppliers are more dependent on Coop, they are also more interested in fulfilling their requirements.

Nonetheless, the benefits of working with small suppliers may not compensate the inconveniences. Small suppliers cannot guarantee the same product safety as larger suppliers can; nor can they match the prices of larger suppliers.

Too Late for Another ‘First Mover Advantage’?

Today, first mover advantage is more difficult to achieve in the new ‘strategic product categories’: ready-made meals. Although Coop was one of the first retailers to offer ‘processed organic food’ in items such as bread and pea soup, these were relatively easy to produce organically because of vertical integration.

Today, organic alternatives of most categories of processed food would require more resources from Coop. The reason is simple. Coop will have to develop these products with its pool of suppliers and: (i) suppliers of organic food are often small and may not have the capacity to develop new products at the same pace or at the same low prices as competitors of Änglamark; (ii) eco-labeling criteria still need to be developed for these product categories. Coop may need to invest more resources in helping KRAV to develop such criteria. Even so, Coop is launching products in the field of half ready-made meals, such as organic fresh pasta, fresh salmon products.

What Consumers Want, Really?

In 1999, a survey30 of 2,400 randomly chosen people, representative of the Swedish population, found that 41% buy organic food at least once a month (frequent buyers), while 50% buy organic food at least four times a year (less frequent buyers). According to the survey, the most cited reasons for buying organic food are environmental concerns, quality, health and nutrition. The study concluded that the demand could be expected to increase since the majority of the organic food buyers think that they will buy KRAV labelled food more often in the future (75% of the frequent buyers and 50% of the less frequent).

30 LUI Marknadsinformation AB. (1999). Rapport: Konsumentundersökning om ekologiska

produkter. 30-7866. Hans E. Holmberg. Stockholm.

Copyright © 2006 INSEAD 02/2006-5314 13

Overall, lower prices would increase the purchasing frequency for both frequent and less frequent buyers. A broader assortment would make the frequent buyers buy more often, while for the less frequent buyers, information was more important. Convenience and accessibility was not decisive for increasing the purchasing frequency; probably because KRAV products are bought in the store where the rest of the food shopping is done. Better visibility would increase the demand of frequent buyers, but greater credibility of the information was not a decisive factor.

Consumer surveys carried out in 1998-200131 found that health was a stronger argument for the purchasing of organic food than the environment. A representative of the Consumer Association of Stockholm (KFS) believes that young people are more concerned with health issues than with environmental ones. In her opinion, people today feel a constant ‘lack of something’, be it vitamins, minerals, time or whatever, and this may be a reason for the increasing health concern. There is also more awareness in society about the link between dietary habits and common welfare diseases, such as diabetes, obesity, high cholesterol and bone fragility.32

The diet of the Swedish population has changed in the last decade, as national surveys on dietary habits have revealed.33 In one way, it has improved; the consumption of root vegetables, juice, rice, and pasta has increased. In other ways, however, it has worsened, since the consumption of snacks, sweets, soft drinks and alcohol has also increased. The changes are related to gender, age and education. Low levels of education and smoking are generally related to bad eating habits, especially among men, and women tend to have better dietary habits than men.

Convenience, in the sense of close location and accessibility of the store, is an important factor in the choice of food outlet. In simple terms, consumers tend to buy from the closest supermarket. In this respect, the profile of the retailer may influence only marginally the purchasing behavior of consumers. Indeed, convenience seems to be such a crucial variable in food retailing that differentiation strategies may not pay off.

31 Mat 21. (2002). Vem gillar ekologiska livsmedel – och varför?.Institutionen för folkhälso – och

vårdvetenskap, 3 October 2002, Uppsala Universitet, Sweden. (Who likes ecological food – and why? Documentation from seminar about consumer attitudes and behavior in relation to ecological food.) Mat 21 is a Swedish research project on food and sustainability, 1997-2005

32 Swedish Food Agency (Svenska Livsmedelsverket). (2003). Säker mat. (Safe food). [online] Available on: http://www.slv.se/templates/SLV_Page____7715.aspx. [Accessed: 28 September 2005].

33 Becker W, Pearson M. (2002). Riksmaten 1997-98. Befolkningens kostvanor och näringsintag. Metod – och resultatanalys. Livsmedelsverket, Uppsala. National surveys on the dietary habits of the Swedish population carried out by the Swedish Food Agency in 1989 and 1997-98.

Copyright © 2006 INSEAD 02/2006-5314 14

What should the Marketing Campaign Focus on?

The aim of Coop is to influence consumers to ‘move the hand’ and, when faced with the choice of an ecological or a conventional alternative, pick the ecological one − given that the prices are comparable. Coop combines in-store marketing, such as shelf indications and a wide assortment, with aggressive marketing campaigns on TV, aimed to raise positive public opinion about eco-products.

Although many consumers may have been sensitized to the advantages of eco-products, an Änglamark TV campaign in 2001 put in evidence the interests of an important player in the food business. The Swedish Grain Growers (Sveriges Spannmålsodlare) sued Coop in the Market Court claiming that the advertisement called The Toxic Film was comparative marketing. The advertisement showed a waiter spraying pesticides on the food of two people in a restaurant, presuming that it was something ‘normal’.

Coop lost the case against the Swedish Grain Growers and the film was banned from TV. The following TV commercials of Coop followed the same line of argument of The Toxic Film, and the Swedish Grain Growers sued Coop once again – this time at the Stockholm District Court, claiming that this was comparative marketing. The Association was then claiming indemnification of €500,000 (5 million SEK).

While the parties were disputing the case in Court, environmental organizations, such as KRAV, TCO Development, SIS Miljömärkning och Världsnaturfonden WWF (World Wildlife Fund), expressed their deep concern about the potential negative outcome of the trial. In case Coop Sverige was found guilty, it would have serious consequences for future communication of environmental benefits of organic food.34

The trial generated a lot of publicity, and until the case was solved in December 2003, the marketing campaign had to be put on hold, resulting in direct and indirect losses for Coop. Throughout the process, Coop argued that the message portrayed in the ads was of informative and of the opinion-forming kind, and that it should therefore be protected under the ‘freedom of speech’ law, rather than being subject to the marketing laws. With this argument, Coop won the case; it was declared not guilty on all counts, and the Swedish Grain Growers had to pay court expenses of €110,000 (1 million SEK) to Coop.35

The lesson was apparently learned. By 2005, the marketing campaign was much less aggressive. A campaign with the theme “You’ve only got one body” has been

34 Jansson, K. (2003-09-22). Spannmålsodlarna stämmer KF på 5 miljoner kronor. [online].

Available on: http://www.resume.se/pub/nyhet.asp?art_id=15805. [Accessed: 12 November 03].

35 Söderberg, L. (2003). Glädjande dom i Stockholms tingsrätt. KRAV mailet nr. 11, 2003. [online]. Available on: http://www.krav.se/krav.asp?ID=89&tab=press&option=senaste&type=presskontakt [Accessed: 16 December 03].

Copyright © 2006 INSEAD 02/2006-5314 15

launched, with pictures of fruits and vegetables forming images of body parts, in combination with special prices on fruits and vegetables. According to Thomas Johansson, Manager of Market and Business Development at Coop Sverige36:

“For both us and our customers, health and ecology is closely related. Health is about what you eat. Ecology is about how it is produced”

Considering that Coop is the leader in ecological food, it is just wise to link the current societal preoccupation with health to ecological issues.

Are Competitors Threatening Änglamark?

Even if competitors have been less proactive than Coop in developing eco-oriented brands, they have not been alien to such marketing strategy. ICA created the eco-brand, Skona, in 1991 for chemical technical products, and Sunda in 1993 for organic food. ICA Ekologiskt has substituted Sunda, but Skona remains with 32 products.37 In 2002, ICA Ekologiskt expanded from 370 to 440 products.38 This represents a 20% increase in the eco-oriented food assortment, which resulted also in 20% growth in sales of organic products.39

In 2004, even though ICA reduced the number of ecological product categories, there was an increase of 15.5 percent in sales of ecological products40. ICA Ekologiskt and dairy products were responsible for most of this increase. According to Kerstin Lindwall, Environmental Manager of ICA AB, the increase in both volume and sales means a larger share of the market. According to Ms Lindwall, ICA is aiming at taking over the leading role in ecology, which has always belonged to Coop41.

How can Änglamark’s Success be Measured?

Success of Änglamark could be measured by the extent to which the brand conveys Coop’s commitment toward sustainable development. Coop has taken on the mission to promote change toward ecological sustainability via the mass commercialization of ecological products. In this respect, a way of evaluating the brand success is via the growth in the number of Änglamark products, such as those presented in Exhibit 4.

36 Coop Sverige. (Online). Pressmeddelande 2005-09-30. Coop Konsum ökar satsningen på hälsa.

Available on: http://se.yhp.waymaker.net/coop/popup/coop_sverige.asp [Accessed: 27 October 2005]

37 ICA. (2003). Våra varumärken. [online]. Available on: http://www.ica.se/ [Accessed: 4 August 03].

38 ICA Environmental Report 2002. [online]. Available on: www.ica.se [Accessed: 4 August 03]. 39 KRAV. (2003). Ekologiskt ökar hos ICA. KRAV mailet nr. 9, 2003. 40 ICA AB. (Online). Rapport om etik och samhällsansvar 2004. Available on: www.ica.se

[Accessed: 27 October 2005] 41 Ekoweb Sverige. (Online). Ekowebs Nyhetsbrev, vecka 38, 2005. ICA nu största aktören på

ekologiska livsmedel. Available on: www.ekoweb.nu [Accessed: 27 October 2005]

Copyright © 2006 INSEAD 02/2006-5314 16

As a ‘value-based brand’ − i.e., built around the values of environment, health and ethics − Änglamark’s success could also relate to the link consumers establish between Änglamark products and sustainable development. Indeed, besides health attributes of Änglamark products and their ‘value for money’, the company tracks consumer behavior to assess such a link. Results in 2003 show that 90% of Swedish consumers are acquainted with the brand, 50% of them associate it with sustainable development, and 15% occasionally buy Änglamark products. According to a consumer survey conducted in 2005, Änglamark is the brand with the strongest association to ecology and ethics42.

A more ‘objective’ way of evaluating the brand’s success is via sales of Änglamark products. Exhibit 3 shows that a substantial number of consumers buy Änglamark. Although this is certainly a good indicator, the question is: how satisfied are these customers?

In other words, a third way of measuring brand success relates to customer satisfaction. Indeed, Coop has often used ‘attitude surveys’ to measure Änglamark’s success. But because consumer attitude tends to differ from their real purchasing habits, some managers believe that the day’s cash is a more reliable way of measuring success. Purchases made by the 400,000 consumers who shop at Coop’s stores every day constitute objective indicators of purchasing choice of all products in the stores. The day’s cash ‘method’, however, provides very little information about the consumer profile. The database of the members’ discount card, MedMera, could disclose such information. Since 80% of the consumers of Coop are also members of KF (and thereby members of Coop), the MedMera database could provide vital information about them. Nonetheless, Swedish regulations about personal confidentiality and the lack of organizational resources limit this possibility.

Overall, it seems that information on consumer preferences is still weak to further developing the brand. This is not rare, since Swedish companies have surprisingly little information about consumers’ actual green purchasing behavior.

42 LUI, Livsmedel Undersökningar Insikt.

Copyright © 2006 INSEAD 02/2006-5314 17

Exhibit 1 Food Retailing in Sweden 43

Food Retailing in Sweden

ICA CoopAxfoodBG

43 Dagligvaruleverantörernas Förbund. (2003). [online]. Available on: http://www.dlf.se/

[Accessed: 25jul03].

Copyright © 2006 INSEAD 02/2006-5314 18

Exhibit 2 Eco-Labelling Organizations

KRAV is the Swedish control organization for organic food production, labeling and marketing; an association representing the whole food chain. KRAV controls and certifies organic food production, restaurants and food stores. The aim of ecological production is an improved circulation of nutrients, and therefore the KRAV regulation does not allow artificial fertilizers, pesticides and GMOs (Genetically Modified Organisms).44

Svenska Demeterförbundet, a non-profit consumer association, is the Swedish control organization for biodynamic production. Svenska Demeterförbundet controls food production (plant cultivation, animal raising, processed food), restaurants and food stores.45

Bra Miljöval (Good Environmental Choice) is the eco-label of the Swedish Society for Nature Conservation (SNF), a non-profit organization. Bra Miljöval has criteria for non-food products, focusing on the raw material and chemicals used in production, as well as energy use and recycling.46

The Swan (Svanen) is an eco-label established by the Nordic Council of Ministers, managed by SIS Miljömärkning AB, on commission by the Swedish Government. There are Swan criteria for 60 non-food product groups, from hotel services, furniture to detergents and paper. The criteria aim to minimize the negative environmental impacts in the product life cycle, from raw material extraction, to production and end-of-life.47

The EU-Flower is an eco-label established by the EU (European Union). The Swedish Government commissioned SIS Miljömärkning AB to manage the EU Flower in the country. At the moment, EU-flower has criteria for 21 non-food product groups, in the area of perishable goods and services. The criteria aim to achieve the least negative environmental impacts along the product life cycle, from raw material extraction, to production and end-of-life.48

44 KRAV (2004, February 19). [online]. Available on:

http://www.krav.se/krav.asp?Id=2&tab=fakta_krav_marke&option=omkravsregler&type=omregler.

45 Demeterförbundet. (2004, February 19). [online]. Available on: http://www.demeter.nu/index.htm.

46 SNF. (2004, February 19) [online]. Available on: http://www.snf.se/bmv/kriterier-index.cfm 47 Svanen. (2004, February 19). [online]. Available on:

http://www.svanen.nu/omsvan/basfakta.asp. 48 EU blomman. (2004, February 19). Available on:

http://www.blomman.nu/default.asp?nav=arbete.

Copyright © 2006 INSEAD 02/2006-5314 19

Exhibit 3 Eco-labeled Products: Price Comparison

Lund (July ’03) Stockholm (March

’04) KRAV products Coop ICA Coop ICA Unit

Änglamark 7.45 - 7.80 - SEK/liter Milk

(mellan) Skånemejerier Ekologiskt Arla Ekologiskt49

7.45 7.45

6.90 6.90

7.70 7.70

8.90 8.90

SEK/liter SEK/liter

Änglamark 6.75 - 7.25 - SEK/kg Möllarens - 4.45 - - SEK/kg Flour ICA Ekologiskt50 - - - 7.45 SEK/kg Änglamark 65.00 - 57.00 - SEK/kg Signum 47.80 - 47.00 - SEK/kg ICA Ekologiskt - 43.80 - 47.80 SEK/kg Zoega 53.80 53.80 59.00 59.80 SEK/kg Gevalia 51.80 43.80 49.80 51.80 SEK/kg Löfbergs 55.80 49.80 53.00 49.80 SEK/kg

Coffee Mellanrost

Classic 64.40 49.80 64.40 - SEK/kg Änglamark 20.90 - 20.90 - SEK/kg Felix 27.80 23.50 29.50 34.90 SEK/kg Ketchup Heniz Ekologiskt 48 - 49.78 47.61 SEK/kg Änglamark 13.96 - 14.60 - SEK/Litre Strawberry

Syrup ICA Ekologiskt - 9.96 - 10.76 SEK/Litre

Source: The figures were taken from surveys carried out in the stores of Coop Konsum Mårtenstorget and ICA Malmborgs in Lund, July 2003, and Coop Konsum Täby Centrum and ICA Täby Centrum, Stockholm, March 2004. The aim is to get an approximate idea of the price levels of the eco-labelled products in some product categories, in two different retailer stores, in two different cities.

49 Skånemejerier in Lund, Arla in Stockholm. 50 ICA Ekologiskt Flour did not exist at the time of the first survey.

Copyright © 2006 INSEAD 02/2006-5314 20

Exhibit 4

Änglamark Assortment (no. of products)

Änglamark assortment

2040 55

84

140180 168 168

195220

250 248

304 309

0

50

100

150

200

250

300

350

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Year

Prod

uct c

ateg

orie

s

Sources: Terrvik, E. (2001). Att kanalisera hållbarhet – hur dagligvaruföretag översätter miljökrav till handling. En studie om egna varumärken i handeln. Bokförlaget BAS, Handelshögskolan, Göteborg, p. 239; Coop Konsum Environmental Report 2001; Coop Sverige Environmental Report 2002, Coop Sverige.

Copyright © 2006 INSEAD 02/2006-5314 21

Exhibit 5 Änglamark Sales

Änglamark Sales (Million Euros)

2,87,7

13,217,6

29,233,0

37,333,0 35,2 37,4

45,8

52,6

32,837,0

0,0

10,0

20,0

30,0

40,0

50,0

60,0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Year

Mill

ion

Eur

os

Sources: Terrvik, E. (2001). Att kanalisera hållbarhet – hur dagligvaruföretag översätter miljökrav till handling. En studie om egna varumärken i handeln. Bokförlaget BAS, Handelshögskolan, Göteborg, p. 239; Coop Konsum Environmental Report 2001; Coop Sverige Environmental Report 2002; Coop Sverige.

Exhibit 6 Ownership of Coop Norden

Source: KF Annual Report 2002. [online]. Available on: http://www.kf.se/upload/KF%20Annual%20Report%202002.pdf [Accessed: 22 March 04].

Copyright © 2006 INSEAD 02/2006-5314 22

Exhibit 7 Coop Sverige Sales of Ecological Products in 2001-2003

Increase

since 2001 2002

(1,000 SEK) 2002

(1,000 Euros)

Increase since 2002

2003 (1,000 SEK)

2003 (1,000 Euros)

Coop Forum 16% 615,173 67,669 9% 544,960 59,946 Coop Konsum 11% 84,032 9,244 -2% 739,321 81,325 Coop Sverige 13% 1 ,455,494 160,104 2% 1, 284,281 141,271

Source: Coop Sverige Environmental Report 2002; Coop Sverige Environmental Report 2003.

Exhibit 8 Coop Sverige Sales of Organic Food

Obs.: Coop Forum (blue, the lower part of the column); Coop Konsum (green, the upper part of the column).

Source: Coop Sverige Environmental Report 2004. [online]. Available on: www.coop.se