Embed Size (px)

Citation preview

Development Policy Review, 2008, 26 (5): 529-553

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute.

Published by Blackwell Publishing, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

The Economic Partnership Agreements: Rationale, Misperceptions and Non-trade Aspects

Louise Curran, Lars Nilsson and Douglas Brew∗ The European Union and the African, Caribbean and Pacific (ACP) countries entered a new era in 2008. The Cotonou trade regime and the WTO waiver legitimising it have expired, and the long anticipated, and much debated, move to Economic Partnership Agreements (EPAs) has begun. This article explains the background and analyses the ‘alternatives’ to EPAs, in order to tackle common misperceptions. Moving on from what has been the focus of debates, namely, the reciprocal liberalisation required under WTO rules, it sheds some light on the non-goods trade aspects of EPAs which, while integral to economic policy, are inherently hard to quantify and often skimmed over in existing studies or addressed in ideological terms. Key words: Economic Partnership Agreements, rationale, misperceptions, WTO, non-trade aspects

1 Introduction The European Union has a long history of partnership with the countries of the Africa, Caribbean and Pacific (ACP) grouping, including trade relations stimulated by highly preferential market access to the EU under the Cotonou Agreement or the Everything but Arms (EBA) initiative. Over 95% of ACP exports entered the EU duty-free in 2006. However, despite this preferential treatment, ACP trade with the EU has not diversified and has steadily declined over the last 30 years. Clearly, preferential market access alone has not been adequate to stimulate export-led growth in the ACP.

At the same time, non-ACP developing countries have not been granted similar treatment. This is incompatible with the principle of most favoured nation (MFN) treatment set out in Article I of the GATT and with the ‘Enabling Clause’ covering special treatment of developing countries. The EU was therefore forced to seek a series of waivers from other World Trade Organisation members to enable its special trade regime for the ACP to continue. The latest of these waivers was only agreed in Doha in

∗Louise Curran is at the Toulouse Business School; Lars Nilsson and Douglas Brew are in the DG Trade, European Commission, Rue de la Loi, Wetstraat 200, B-1049 Brussels ([email protected]). They would like to thank Yves Bourdet for comments on an earlier draft of this article and to acknowledge the support on statistical extractions provided by Claudio Gasparini and Michael Pajot. The article represents the views of the authors and not the position of the European Commission.

530 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

2001 with the express condition that new WTO-compatible trade arrangements must be agreed by the end of 2007, after which the waiver expired.

The negotiations on this last waiver were difficult and there was no realistic chance of a further extension from WTO members,1 who expected the ACP and EU to abide by their promises to bring their trade regime into conformity with WTO rules. Those doubting the willingness of developing countries to question such special treatment need look no further than the long and bitter ‘banana wars’ during which non-ACP countries have challenged a series of frameworks established by the EU to provide market access for ACP bananas since 1996.2

In the ACP-EU Partnership Agreement, signed in Cotonou on 23 June 2000 (hereafter referred to as the Cotonou Agreement), the parties agreed to conclude new WTO-compatible trading arrangements, so-called ‘economic partnership agreements’ (EPAs), which aim at progressively removing barriers and enhancing co-operation in all areas relevant to trade.3 The purpose of the EPAs is to help the ACP to integrate into the world economy and to promote their sustainable development as well as poverty reduction. In order to be WTO-compatible, EU-ACP trade relations have to move from a context framed by a GATT Article I waiver to one framed by the rules on free trade agreements (FTAs) and/or customs unions, i.e. Article XXIV of the GATT. The precise interpretation of the requirements of Article XXIV has subsequently spurred perhaps the most contentious debates in relation to the EPAs.

Despite the breadth of the EPA coverage, the debate around them usually focuses on goods trade and the potential negative effects of a change to a situation compatible with WTO rules, while concentrating on the elements of the agreements related to trade and market access. Critics see the EPAs as an attempt by the EU to force open developing country markets, with mercantilist interests in mind; they fear that this will lead to the closure of ACP factories, the undermining of regional trade and major losses in government revenues.4 However, they too often forget that the status quo is no longer an option for EU-ACP relations. Not only is it a situation of declining value of preferences and falling ACP trade shares, but other developing countries simply will not accept a solution that does not conform with the international legal framework, as explained above.

Moreover, although WTO compatibility is essential for EPAs, they are not straightforward FTAs. While a legally secure trade regime is crucial for investor confidence, this aspect is only one part of the EPA agenda. This is why EPA

1. Several concessions were required to other developing countries to secure the waiver, notably extra access

for tuna from several Asian countries and for bananas from Latin America. 2. Consultations are ongoing with Colombia on this issue and a final WTO panel report was due to confirm

in March 2008 an interim ruling of December 2007 finding in favour of Ecuador. 3. Formal negotiations at the level of all ACP countries started in September 2002. In October 2003, regional

negotiations got under way with West Africa and Central Africa, in February 2004 with Eastern and Southern Africa and in April 2004 with the Caribbean. The non-reciprocal preferences under the Cotonou Agreement, for which a waiver in the WTO until 2007 was granted, continued to apply in the meantime.

4. For example, an informal coalition of NGOs including 11.11.11, ActionAid, Bread for the World, Church Development Service, Oxfam International, and Enda on 14 February 2007 called on the European Commission to stop pressuring Africa to agree new trade relationships by the end of the year, warning that the current proposals would have very damaging implications for development, see www.oxfam.org.uk/applications/blogs/pressoffice/2007/02/ngos_denounce_eu_pressure_over.html.

EPAs: Rationale, Misperceptions and Non-trade Aspects 531

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

negotiations remain very much ongoing despite the fact that ACP-EU goods trade relations are now compatible with the relevant WTO provisions. EU-ACP trade relations have always rested on strong co-operation well beyond their trade-related aspects, and this will continue with the EPAs. The combination of transparent rules, increased co-operation, legal security, support for regional integration and links to development finance makes EPAs unique. Nevertheless, the European Commission recognises that it is essential to reduce any risks of negative impacts by careful design of the EPAs and accompanying development support measures.

This article seeks to elucidate the debate by explaining what the EPAs will be and, perhaps more importantly, what they will not be. It clarifies the rationale for the EPA approach, points to some common misperceptions in the existing assessment of their economic impact, and sheds some light on non-trade aspects rarely touched upon in existing studies. An important aim of the article is also to explain the reasons why the EU and the ACP see the EPAs as the only feasible means to secure ACP development in a way which will be acceptable to the non-ACP developing countries.

Section 2 briefly takes stock of EU-ACP trade relations over the past decades. Section 3 sets out the legal context and demonstrates why the Cotonou trade regime has to change to be WTO-compliant. Section 4 presents the EU’s offer in terms of market access in goods under the EPAs, and discusses the existing literature on the economic impact of the EPAs, arguing that in many cases the underlying assumptions are flawed. Section 5 discusses so-called ‘alternatives’ to EPAs, while Section 6 reviews the services and non-trade components of the EPAs and their likely economic impact. Section 7 presents the outcome of the negotiations thus far and the interim agreements concluded, and discusses the next steps in EPA negotiations. Finally, Section 8 provides some conclusions.

2 EU-ACP trade relations: a short overview

If market access had been the key to development, the ACP countries would be amongst the richest in the developing world. Since 1975 they have been offered increasing access to the EU market and the vast majority of their products now enter EU markets duty-free. Under the Cotonou Agreement of 2000, all industrial products (a definition which includes fisheries) originating in ACP countries were exempted from EU customs duties, while preferences for agricultural products were differentiated.5 However, even for those products not fully covered, since 2001 the ACP least developed countries (LDCs) could choose to use the provisions of the EBA (Everything but Arms) scheme, which is part of the EU’s Generalised System of Preferences (GSPs), to gain duty-free access to EU markets. Moreover, for certain products (bananas, beef and veal, and sugar), the EU provides special market access for non-LDCs via the so-called commodity protocols.

5. Tropical products which do not compete with European products enter the EU market duty-free.

Temperate products enjoy an exemption or reduction of customs duties, while fruits and vegetables are subject to seasonal restrictions. Other agricultural products face quantitative restrictions or are excluded from preferential treatment.

532 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

Yet, the ACP countries have become increasingly marginalised on the EU market. Their mediocre trade performance compared with the group of ‘all developing countries’ became evident in the late 1980s and early 1990s and was further exacerbated in the beginning of the 2000s. This development can be attributed in part to the fact that economic growth in low-income countries (as defined by the World Bank) has surpassed that in the ACP in all but three of the last 30 years,6 the respective average growth rates being 4.6% and 2.8%. Today, the ACP share of EU trade stands at less than 3%, although the EU is an important market for the ACP, especially for their agricultural goods, taking 23% of their exports.

The EU-ACP trading relationship is to a large extent based on complementarity, with ACP exports still overwhelmingly made up of raw materials. Over 60% of ACP exports to the EU by value now consist of just four basic commodities – oil and gas (41%), diamonds (13%), cocoa (6%) and aluminium (about 3%) – while EU exports are concentrated in manufactured goods (machinery (30%) and vehicles (10%)). EU exports to and imports from the ACP have mirrored each other quite closely. In the period 1975-2006, in all but five years, the EU has had a trade deficit with the grouping. Recent trends of increased ACP exports and a shift in the trade balance are almost exclusively due to high oil prices.

There are also regional differences in the EU’s trade with the ACP. West Africa is by far the EU’s largest trading partner among the ACP regions, followed by the Caribbean and the SADC group. The ACP regions of Central Africa, Pacific and the SADC group show, by and large, a surplus in their trade with the EU over the 2002-6 period, while the opposite holds true for the Caribbean and Eastern and Southern Africa. EU trade with West Africa shows a deficit in three of the last five years, including the two latest years for which figures are available. 3 The EPAs and the legal context While only part of the overall package, an essential element of the EPAs is that they will ensure that trade relations between the EU and the ACP are WTO-compatible. There are two key legal frameworks of relevance to the EU’s relations with the ACP: first, the so-called ‘enabling clause’, which allows signatories to accord differential and more favourable treatment to developing countries,7 and, second, the legal basis governing preferential trade agreements between countries – Article XXIV of the GATT. Both these frameworks will be briefly considered in order to clarify exactly the requirements to which future EU-ACP relations need to conform. 3.1 The ‘enabling clause’ The ‘enabling clause’, agreed in 1979, allows contracting parties to grant preferential tariff treatment to products originating in developing countries in accordance with the

6. In 1976, 1979 and in 1991. It should be noted that the figures are limited by availability, as growth figures

for all ACP countries are not available in all years. 7. GATT decision of 28 November 1979 (L/4903), Differential and more favourable treatment reciprocity

and fuller participation of developing countries.

EPAs: Rationale, Misperceptions and Non-trade Aspects 533

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

GSP, namely, non-reciprocal and non-discriminatory preferences beneficial to the developing countries. It also allows special treatment of the group of countries classified as LDCs by the UN. The implication of the enabling clause is that all non-LDCs should be treated equally by the party providing market access.

The problem, in this context, is that the ACP group does not correspond to the LDC grouping. Although most ACPs are poor, only half of them are LDCs. For the ACP’s treatment under the Cotonou Agreement to be WTO-compatible, the EU would have to provide the same preferential treatment to all of the 178 developing countries which are eligible for the EU GSP. As we shall see later, this would be problematic not only for the EU, where sensitivities on market access for large developing countries are a political reality, but also for the ACP. They would see their preferential access eroded and would find it difficult to compete with non-ACP developing countries, many of which are very competitive in key ACP exports. Thus, a solution which seeks to achieve legal compatibility through the enabling clause does not seem to be a feasible option.

3.2 GATT Article XXIV The other option available to ensure the continuance and strengthening of ACP access to EU markets is therefore through agreements under GATT Article XXIV. This article enables WTO member states to provide preferential market access in the context of a customs union or a free trade area, provided that substantially all trade (SAT) between the parties is liberalised, that trade barriers on the whole are not increased as a result of the agreement and that the formation is concluded within a reasonable length of time.

However, the two key principles here – ‘substantially all trade’ (SAT) and ‘a reasonable length of time’ – are not defined in the GATT, thus leaving them open to interpretation. Critics of the EPAs insist that the EU is interpreting these principles too stringently in order to force open ACP markets. However, the fact is that agreements which do not clearly meet such criteria are likely to be challenged in the WTO.

Concerning the first principle, SAT, there is no baseline figure agreed in the WTO, although precedent indicates that a figure of around 90% (including both the volume of trade and the number of tariff lines) is acceptable to members. The EU for its part aims for at least a 90% threshold when negotiating its FTAs. The coverage in its Trade, Development and Co-operation Agreement (TDCA) with South Africa, a country that is at a higher level of development compared with most ACPs, is 91%.

In the situation of legal uncertainty, some NGOs and ACP negotiators have argued that lower figures would be needed to avoid negative impacts of the EPAs. For instance, TWN Africa and Oxfam (2007) argue that, to avoid any negative impact from an EPA, Kenya would need to exclude more than half its trade from liberalisation with the EU. If Kenya liberalises 50% of its imports from the EU and the EU liberalises 100% that would indicate that, overall, approximately 75% of trade between the two would be liberalised (depending on the trade balance). Perez and Karingi (2006) argue that if African countries reciprocate with tariff elimination on 60% of their European imports, the EPA would be neutral in terms of output. This, in turn, points to an overall degree of trade liberalisation of approximately 80%.

For the EPAs to be seen as WTO-compatible, if the EU fully liberalises its imports from the ACP, the ACP will have to liberalise less than 90% of trade. Depending on the

534 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

balance of trade between the parties this could lead to liberalisation of 80% or less.8 In the South African case, the EU liberalised 95% of its import trade and South Africa 86%.

On the question of the ‘reasonable length of time’ for implementation, WTO members agreed in 1994 that it should exceed 10 years only in ‘exceptional cases’.9 In the EU’s TDCA with South Africa, the transitional period was set at 12 years. Unless the rules governing Article XXIV are changed,10 the substantially longer lead times of 20 or 25 years suggested by some ACP negotiators and NGOs would need to be justified on the grounds of being exceptional, a concept which is difficult, although not impossible, to establish. A 2006 UNECA report has pointed out that there are international precedents for periods longer than 10 years, for example the Canada-Chile FTA, which has a 19.5 year implementation period (Lang, 2006). What the UNECA report fails to do, however, is to distinguish between timeframes in the sense of Article XXIV and the overall timeframe for the implementation of the full agreement. If an FTA is to meet the requirements of Article XXIV, it must liberalise substantially all trade in a reasonable time period. The parties to an agreement can then agree on any timeframe they want to liberalise the remaining sectors which are included in the accord, but this does not need to be liberalised in order for the accord to be WTO-compatible. In the case of the Canada-Chile FTA, for example, according to Canadian and Chilean submissions to the WTO, the agreement eliminates tariffs on 99.8% of trade, covering 99% of tariff lines (WTO, 1998).

4 Assessing the impact of the EPAs 4.1 The EU’s market access offer under the EPAs The EU has agreed to remove all remaining quota and tariff limitations on access to the EU market for ACP goods. This covers all products, including agricultural goods like beef, dairy products, cereals and all fruit and vegetables, and applies immediately following the initialling of the agreements (by those countries which have done so) – with a phase-in period for rice and sugar.11 This means that goods entering the EU and originating in an ACP country that is party to an EPA are subject to the same tariff-free treatment as LDCs already have under the EBA, with the exception of rice and sugar, the phase-in period for which lasts until 2015.

However, market access is about more than tariffs, and the Rules of Origin (RoO) under the EPAs will offer improvements over those for the GSP and EBA. They will be based on the Cotonou rules, with improvements, where requested by the ACP, in the

8. It is important to remember that the liberalisation commitments of each party, as far as the volume of trade

is concerned, depend on the balance of trade between the two partners. Each ACP region is in a different position as far as trade balances are concerned, so an asymmetric EPA has different implications across regions.

9. Uruguay Round Agreement: Understanding on the Interpretation of Article XXIV of the General Agreement on Tariffs and Trade 1994, http://www.wto.org/english/docs_e/legal_e/10-24_e.htm

10. See Desta (2006) on discussion of the legal context and its potential evolution. 11. The only exception is South Africa which has not been offered exactly the same concession, and a number

of globally competitive products will continue to pay import duties.

EPAs: Rationale, Misperceptions and Non-trade Aspects 535

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

areas of main export interest to them (fisheries, textiles and agriculture).12 As far as fisheries is concerned, the RoO are relaxed in key areas for all ACP countries, with a special far-reaching relaxation for the Pacific, in view of its special situation. In agriculture, each region has determined and negotiated special derogations or relaxations considered important.

In textiles and clothing, the key change (which has been included in all initialled agreements) is a move from the so-called ‘double transformation rule’ to the ‘single transformation rule’. Global sourcing is allowed and tolerance rules no longer apply. In practice, this means that the ACP can import fabric from any country to produce clothes which can then be exported duty- and quota-free to the EU. It should be noted that these rules are more liberal than the US has been offering to certain African countries under its AGOA scheme. In the EU’s case, there are no limits on the volume of clothes that may be exported to the EU, the agreement is permanent, the rules are not subject to discretionary political selection criteria and they are offered under WTO-compatible agreements.

It is important to understand one key element of the political economy of these negotiations. Unlike other current or likely EU FTAs, in the case of the EPAs the European Commission has not been subject to any significant lobbying by EU industry for either tariff protection or market access in the ACP region. The unfortunate fact is that most ACP industries are too uncompetitive and markets too small and underdeveloped to be of concern or interest to EU business. In this sense these negotiations have differed significantly from traditional FTA negotiations in that there has been no long ‘defensive list’ of products which the EU wished to protect, or ‘offensive list’ of products which it wished to see liberalised. Within the boundaries of the need to conform to the SAT requirement, which calls for a certain opening of the ACP market, but also provides certain flexibility, the EU has been open to discuss whichever exclusions the ACP countries consider to be in their best development interests, while providing full market access on their side. We shall return to this issue in Section 7.

4.2 Common misperceptions Over the period of these negotiations there have been numerous attempts to assess the likely impact of the EPAs on ACP economies (but clearly, given the timeframe, none so far on the actual outcome of the market-access negotiations for goods). For several reasons, most of these efforts have been inadequate. Unless important pitfalls (such as access to data and quality of data) are recognised and proper methodologies and underlying assumptions used, unsound policy conclusions are drawn on the basis of flawed analyses.

First, to get a proper view of the impact of trade policy change, we need to look at not only the static effects of tariff changes but also the dynamic effects of these impacts within the rest of the economy. If resources are being used to produce goods in which

12. Interim Rules of Origin attached to the EPA Market Access Regulation, Council Regulation (EC)

1528/2007 apply pending the signature of the EPA and Interim Agreements to which the final regionally specific RoO are attached. The interim RoO bring forward key improvements in the regional RoO.

536 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

the country is not competitive and trade liberalisation means that uncompetitive firms abandon the market, economic theory indicates that these resources (capital and labour) will move into other activities which are more productive (static effect). Trade liberalisation can also affect the steady-state levels of production factors such as human and physical capital and thus have dynamic effects on output and welfare.

The best way to model such interactive processes is to use a computable general equilibrium (CGE) framework. Unfortunately, the most widely used database to carry out such assessments, the Global Trade Analysis Project (GTAP) database, does not include any of the ACP regions, as the detailed data required are not yet available. Individual countries, especially those in southern Africa, are modelled, but the ‘rest of sub-Saharan Africa’ group is large, about 35 countries, making it very difficult to pinpoint impacts. Overall, trying to establish the real impact of the EPAs through a CGE modelling exercise, as some have tried to do (Perez and Karingi, 2006; Tekle et al., 2006), is therefore unsatisfactory as the database stands. The European Commission is currently sponsoring a project, together with the World Bank, to disaggregate the GTAP database according to the EPA regions. The dataset is now being finalised and tested and its completion will facilitate region-specific analyses.

Up to now, however, efforts to quantify the impacts of EPAs have tended to fall back on more static models which look at the existing situation, in terms of trade and tariffs, and model the static impact of change. Although this ‘partial equilibrium’ approach is useful for identifying products vulnerable to import surges or losses in tariff revenue, it is not one which gives an indication of overall impact. Almost by definition, it leads to negative impacts, as it emphasises increased ACP imports, with no counter-weighing increase in exports or production due to the activity fuelled in other parts of the economy. This is the approach taken in many EPA studies, including many of those by UNECA (for example, Ben Hammouda et al., 2006, 2005; Milner et al., 2005).

Secondly, there are serious data problems with even this basic approach. Analysis of the trade data encompassed in the World Bank’s Integrated Trade Solution (WITS) database, on which many of these studies are based, indicates that there are major discrepancies in the data for intra-ACP trade, especially in Africa. For example, intra-sub-Saharan Africa exports are on average 25% higher than imports in the early 2000s.13 This figure is far too high to be explained in the usual way, by a potential difference in cif and fob charges. Even trade flows to and from the EU in the database do not always correspond to the figures from Eurostat. This is probably because of use of different statistical regimes, an additional issue which researchers do not seem to have taken seriously. As a result, the extent to which we can have confidence in the projected outcomes is limited.

Thirdly, the way in which ‘sensitive products’ (those likely to remain protected) are defined in the negotiations is key. One basic approach to simulation could simply be to analyse the production structure in the ACP countries and compare this with the structure of imports from the EU, so as to identify sectors or products in which competition may increase following the implementation of the EPAs. However, such data are generally not available at a useful level of disaggregation. Another way would be to choose products for exclusion so as to minimise the impact on tariff revenue in the

13. Based on an extraction made in October 2006.

EPAs: Rationale, Misperceptions and Non-trade Aspects 537

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

ACP, or to simply liberalise those tariff lines where the highest tariffs are found (the approach taken by Stevens and Kennan, 2006), which requires updated tariff data to take account of ongoing tariff liberalisation in many of the ACP countries, partly due to their own regional integration efforts.

Fourthly, studies often make unrealistic assumptions on negotiating outcomes. There is a substantial difference between trade being liberalised over a 10- or 15-year period and the frequent assumption in studies that trade would be fully liberalised from day one of the agreement entering into force (an eventuality that is not envisaged by any party). There will be substantial asymmetry in the agreements, with the ACP countries required to liberalise not only substantially less than the EU but also at a slower pace. Certain duties, for example on luxury products not produced in most ACP regions, such as wines or luxury cars, can easily be replaced by excise duties collected at the border (similarly to Value Added Tax payable on imports) further offsetting losses.

Fifthly, a comprehensive approach to revenue impacts would need to estimate the efficiency of tariff revenue collection in the ACP, rather than simply assuming full collection, as many studies do. Problems with customs efficiency, plus a welter of special exemptions, which tend to apply in particular to the kind of luxury products and industrial inputs that the EU exports, mean that actual collection rates are often well below theoretical levels. Thus losses in tariff revenue are likely to be far below predictions. Busse et al. (2004) estimate average duty collection efficiencies in West Africa at 67%, falling as low as 30% for some key markets such as Ghana (Busse et al., 2004: Table 13). The IMF estimates effective duty collection rates in the Eastern Caribbean to be 60% (IMF, 2005).

Somewhat related to this point, there is also a need to examine the link between tariff levels and the prevalence of corruption/smuggling, in order to analyse whether reducing/eliminating tariffs could help to tackle these problems and therefore increase collection rates – thus counteracting shortfalls in tariff revenue. Moreover, one would have to take account of the fact that tariff revenue may actually increase, at least initially, during the implementation period of the agreements if imports and/or tariff collection rates increase as tariffs are lowered.

Finally, studies model those aspects which are readily quantifiable – trade and tariffs. However, these are only one element of the agreements, which will also cover many other elements which are more difficult to quantify, but which have the potential to bring substantial benefits to the ACP. These elements will be considered in Section 5.

4.3 Overview of existing quantitative studies The Overseas Development Institute has analysed the key studies on the EPAs which use general and partial equilibrium models (ODI, 2006). On this basis, its general conclusion is that the trade-creation effects are greater than trade-diversion and that the welfare effects are positive and in most cases significant, for almost all countries.14 The

14. However, the ODI also emphasises that the results should be carefully interpreted in the light of caveats

such as lack of detail in the estimations and the assumption that tariff cuts will be translated into proportionate reduction of prices and passed on to consumers. On the other hand, the modelling

538 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

ODI further notes that these welfare gains have to be weighted against the tariff revenue losses following EPAs. The studies reviewed by the ODI focus on specific ACP or EPA regions or on sub-Saharan Africa (SSA) as a whole. A great many region-specific studies have been carried out recently, while there are far fewer studies assessing the impact of the EPAs for the ACP as a whole or for all the ACP regions. This is partly due to data reasons, as elaborated above.

Due to the use of different methodologies, with associated weaknesses and assumptions on transitional periods and scope of the EPAs, etc., it is difficult to usefully compare the outcome of different studies. We shall not attempt here to cover all of the studies on individual regions or countries which have been undertaken in recent years, some of which are referred to above. We shall focus here on a few recent, comprehensive studies which cover most ACP countries and regions in a consistent manner. Table 1 presents the key results of these studies. They differ quite significantly in some aspects. For instance, the estimated export effects of the EPAs in Bouët et al. (2007) are significantly higher than Perez’s (2006) estimates. Similarly, the small negative impact on the ACP’s GDP in Perez’s study is contradicted in the study by Bouët et al., which forecasts a positive impact on GDP in all individual regions except the ‘Rest of West, Central and Eastern Africa’, where the estimated negative impact is small. In particular, the estimated positive impact of 5.1% in real income for the Southern African Development Community (SADC) is noteworthy, as is the positive impact forecast on its tariff revenue.15

The third study in the table is a CEPII study financed by the European Commission, the objective of which was to evaluate the trade effects of the EPAs and the impact on tariff revenue in the ACP. The study improves on previous research on the effects of the EPAs in a number of aspects. It is exceptional in its detailed approach and in that it covers all ACP regions and countries. It evaluates the effects of the EPAs compared with the only WTO-compatible option, the GSP. Furthermore, it analyses the effects of excluding certain products from liberalisation under two different scenarios at a detailed product level (HS6), taking into account that some products are covered by special protocols and that the balance of trade between the EU and the ACP affects the scope of products that may be excluded from ACP liberalisation, as explained above. The study also separates the effects on tariff revenue into a direct effect arising from trade liberalisation vis-à-vis the EU and an indirect effect in terms of trade diversion applying an estimate of average tariff collection rates in the ACP. The results of the study indicate that the benefits from trade creation (€5 billion) will be approximately twice as large as the losses from trade diversion for the ACP as a whole, indicating (but not confirming) positive welfare impacts of the EPAs. The volume of ACP exports

frameworks are static and thus do not capture the potential positive productivity effects arising from, for example, competition and scale.

15. This positive impact is due to the fact that, firstly, SADC has a small share of imports originating from the EU and will lose less than other regions from tariff reduction. Secondly, SADC countries (except South Africa) trade a lot with other SADC countries (including South Africa), so trade diversion will mainly take place on previously untaxed trade flows and will thus not be associated with tariff revenue losses. Thirdly, as the simulations indicate, SADC manages to increase its exports significantly as a result of the end of EU protection in meat and sugar. Assuming that the current account balance is kept constant, imports from all countries will therefore also increase and bring new tariff revenues.

EPAs: Rationale, Misperceptions and Non-trade Aspects 539

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

Tab

le 1

: S

umm

ary

of s

elec

ted

res

ults

of

rece

nt

incl

usiv

e EP

A s

tud

ies

(€ m

. an

d %

)

Stud

y A

CP

liber

alis

atio

n/ye

ar

Reg

ion

Welfare (€ m.)

Real GDP (€ m.)

Real GDP (%)

Loss in tariff revenue (%)

Fiscal loss (% of GDP)

Trade creation (%)

Trade diversion (%)

ACP exports (€ m.)

ACP imports (€ m.)

80%

in 2

008

All

AC

P -8

51

-183

0.

7

P

erez

(20

06),

C

GE

CA

RIC

OM

-8

1

0.2

162a

2238

a

Pa

cifi

c -1

34

1.

6

13

6a 12

54a

SAD

C (

rest

of)

-2

4

0.4

118a

677a

SSA

-6

12

1.

0

95

4a 64

17a

80%

in 2

035

All

AC

P

≈9

000

Bou

ët e

t al.

(200

7), C

GE

Car

ibbe

an a

nd P

acif

ic

0.5b

13.5

6000

ESA

2.

3 17

.1

30

00

R

est o

f A

fric

a

-100

Res

t of

Wes

t, C

entr

al a

nd

Eas

tern

Afr

ica

-0.1

39

.3

48

00

SAD

C

5.1b

-1.8

7100

All

AC

P

25.4

0.

7 17

.7

3.6

10.7

a 17

.7a

Font

agne

et a

l. (2

008)

, PE

80

% in

202

2, e

xclu

ding

m

ainl

y ag

ricu

ltur

al p

rodu

cts

Car

ibbe

an

15

.5

0.8

27.1

3.

1 25

.2a

27.1

a

C

EM

AC

41.2

0.

8 17

.2

7.2

7.3a

17.2

a

C

OM

ES

A

20

.5

0.7

20.7

3.

4 25

.5a

20.7

a

Pa

cifi

c

8.5

0.2

-0.2

-0

.2

37.1

a -0

.2a

SAD

C

22

.0

0.4

10.6

2.

5 6.

6a 10

.6a

EC

OW

AS

37

.8

0.7

15.1

4.

6 4.

0a 15

.1a

N

otes

: a)

to a

nd f

rom

the

EU

; b)

real

inco

me,

% C

GE

com

puta

ble

gene

ral e

quili

briu

m m

odel

and

PE

par

tial e

quil

ibri

um m

odel

.

540 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute.

Development Policy Review 26 (5)

to the EU in 2022 is forecast to increase by close to 11% compared with the situation under the GSP.16 ACP imports from the EU are forecast to increase by about 18% on average. The maximum loss for the ACP as a whole in terms of total tariff revenue is estimated to be about 25%, corresponding to 0.6% of GDP. The most affected regions in this context are Central Africa and West Africa.

5 ‘Alternatives’ to EPAs? Article 37:6 of the Cotonou Agreement contains provisions under which the European Commission agrees to consider alternative trade arrangements for any non-LDCs which decide that they are not in a position to conclude an EPA. This article had a deadline of 2004 that was subsequently extended to 2006. However, at the May 2007 ACP-EU Joint Council of Ministers, all the ACP regions issued declarations of their commitment to conclude EPAs by the end of the year. Nevertheless, it is interesting to review briefly those studies that either assume or propose non-EPA solutions or so-called ‘alternative’ EPA solutions.

Most studies compare a hypothetical EPA with the status quo, which is not a realistic baseline.17 The reason why the Cotonou Agreement proposed such radical change in EU-ACP relations was that the status quo was generally agreed to be legally untenable. As outlined above, waivers in the WTO for continued preferential access for the ACP are not likely to be forthcoming indefinitely. Thus, in the absence of EPAs the EU-ACP relationship would need to move towards the other alternative legal framework – the Enabling Clause.

The most likely means to achieve this is through the provision of access under the GSP. The EU general GSP scheme covers about 7,200 products. Non-sensitive products (slightly less than half of the products covered) enjoy duty-free access, while sensitive products (mainly agricultural products, but also textiles, clothing, footwear and fish) benefit from a tariff reduction of 3.5 percentage points of ad valorem duties compared with the MFN tariff and a 30% reduction of specific duties (with a few exceptions).18 For textiles and clothing, the reduction is 20% of the ad valorem MFN duty rate.19

Thus any impacts of EPAs need to be compared with the lesser levels of market access, compared with the Cotonou Agreement, which would be available in the absence of an agreement. The analysis by Perez (2006) would indicate that a reversion to the GSP would make little difference to most ACP countries, with the fall in exports of $0.9 bn mainly balanced by increased exports in other markets. Looking at the situation in more detail, however, there is good reason to believe that a reversion to the GSP would have significant impacts on trade flows for several countries. The key potential difficulty with the GSP for ACP countries, apart from the fact that it is less generous than the Cotonou Agreement, is that it is ‘generalised’ – in other words it covers all developing countries, including very competitive ones such as China and

16. Compared with the Cotonou Agreement, the increase would be about 5.5%. 17. One of the few exceptions is the presentation by Fontagne et al. (2006). 18. Tariffs are suspended if preferential treatment results in (ad valorem) duties of 1% or less, or in specific

duties of €2 or less. 19. This concerns mainly products in chapters 50-63 of the Harmonised System (HS).

EPAs: Rationale, Misperceptions and Non-trade Aspects 541

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

India. This fact is not taken adequately into account by many commentators, with an exception of Stevens and Kennan (2007).

If the ACP countries were to fall back to a GSP level of market access, this would seriously reduce their absolute preferences and preferential margin vis-à-vis other developing countries on the EU market and probably have a strong impact on their exports. For example, Persson and Wilhelmsson (2007) estimate that moving from Cotonou/Lomé preferences would reduce the export-creating effects of preferences from around 30% to 3-4% (or nil, as the latter figure is statistically insignificant in their regression).20 Falling back on the GSP also has disadvantages in terms of the lack of security in market access (the GSP is revised every 10 years, with minor interim revisions). This undermines the capacity for market access to stimulate investment.

Several commentators have suggested that if the standard GSP is not an option, then the EU’s special incentive arrangement for sustainable development under its GSP+ scheme would be a good alternative to EPAs (Bilal, 2007; Perez, 2006; Draper, 2007; TWN Africa and Oxfam, 2007). The GSP+ is more generous than the standard GSP scheme; it allows for duty-free access to the EU market of all the goods covered by the general GSP scheme.21 However, the European Commission estimates that under a GSP+ regime non-LDC ACP exporters would have been liable for theoretical duties of €750 million on 2005 exports to the EU, as compared with zero under an EPA regime.22

In addition, GSP+ has a specific objective of stimulating sustainable development. To be eligible to apply,23 beneficiaries must have ratified and effectively implemented 16 core human and labour rights conventions and 11 conventions related to the environment and governance principles, as well as demonstrating that their countries are ‘vulnerable’. A vulnerable country is one that (i) has not been classified by the World Bank as a high-income country during three consecutive years, (ii) whose five largest sections of its GSP-covered imports to the EU represent more than 75% in value of its total GSP-covered imports and (iii) whose GSP-covered imports to the EU represent less than 1% in value of the EU’s total GSP-covered imports.

It seems unlikely that any ACP country would have difficulty in conforming to these ‘vulnerability’ criteria in principle; however, the level of ratification and implementation of the relevant conventions is very variable. A brief look at the situation at the end of 2007 indicates that, of all ACP countries, only the Seychelles has implemented the relevant conventions. Thus significant efforts would be required before most ACP countries could qualify for GSP+. Allowing ACP countries access to GSP+ benefits without ratifying the relevant conventions is not an option, as this would undermine the whole ‘sustainable development’ objective of the scheme, as well as its WTO compatibility.

Even if all ACP countries did qualify through such ratifications, the scheme would not provide such generous market access as EPAs, or even maintain the status quo. This

20. Lower impacts are expected in LDCs. 21. However, for products for which Common Customs Tariff duties also include ad valorem duties, the

specific duties are not eliminated. 22. Calculations based on trade data from COMEXT. These observations do not hold, of course, for LDCs,

which already have quota- and tariff-free access to the EU market under the EBA. 23. There is a rigorous application and vetting process that permits applications every 3 years. Those for 2009-

12 will be considered in October 2008.

542 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

is largely because the GSP+ does not include two key ACP exports – sugar and bananas. Although they made up only 4% of ACP exports to the EU in 2005, certain regions, such as the Caribbean, are significantly more dependent on these two products. In addition, in the case of West Africa, shipping lines carrying bananas also support the export of other tropical fruits. Studies consistently show that many ACP countries are internationally uncompetitive in the production of both these products (for example, Gillson et al., 2005). This is especially the case for the Caribbean, which is heavily dependent on both. In the case of sugar, even the EU’s agreed internal reforms, which will cut prices by 36%, will render several ACP suppliers uncompetitive, perhaps with the exception of Belize and Guyana (Gillson et al., 2005).

Some have suggested simply expanding the GSP+ scheme to include these few key exports (Perez, 2006). However, by definition this access would have to be extended to all suppliers qualified for the scheme. As this includes several Latin American countries with potential supply capacity in one or both of these key exports, the likely outcome would be severe erosion of ACP exports, as explained in Curran (2007).

Thus the most feasible alternative to EPAs for non-LDC ACP countries – GSP or GSP+ for those who qualify – cannot provide similar levels of market access to the current system or an EPA. If EPAs are not concluded, market access for ACP countries to the EU market will inevitably deteriorate, with subsequent loss of exports, jobs and foreign exchange. The EU has worked consistently to avoid such an outcome, concentrating its efforts on achieving a satisfactory outcome to the EPA negotiations. Nevertheless, those countries which have not initialled an agreement now find themselves in a situation where their market access ‘reverts’ to the GSP.

6 The non-trade aspects: key elements which are too

often sidelined There are many elements of the EPAs which do not relate to the simple opening of goods markets through tariff reductions. Some are related to trade and others are not. These ‘non-trade’ aspects have become increasingly important with the gradual lowering of tariff barriers in recent decades. Most are difficult to quantify and therefore tend to be sidelined from any existing impact studies of EPAs. It is important to note that the objective of the EU in these areas is not to enforce EU-type rules in the ACP regions, but rather to foster agreement, especially within regional groupings, on minimum standards. 6.1 Trade facilitation The reduction in the physical and institutional barriers to trade has enormous potential to increase both trade volumes and the benefits which economies gain from them, particularly in developing countries. A number of studies indicate that trade facilitation is the major source of gains from the Doha Development Agenda (DDA), in particular for developing countries. The estimates are rough, but there is a broad consensus that

EPAs: Rationale, Misperceptions and Non-trade Aspects 543

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

trade facilitation could double the gains from goods liberalisation (Hertel and Keeney, 2006; Wilson et al., 2004).

The potential savings from trade facilitation are unsurprising when the complexities of trading in developing countries are considered. UNECA has estimated the extent of certain barriers to trade in Africa, and finds that the average delay at sub-Saharan African customs is 12 days, compared with 5.5 days in East Asia (UNECA, 2004). Analysis by ECOWAS found that there were between 7 and 2 checkpoints per 100km along intra-ECOWAS highways (quoted in Alaba, 2006). Delays in trading have serious implications for a country’s exports. Persson has estimated that a reduction of exporting delays by one day in ACP countries would stimulate exports on average by 1% (Persson, 2007). In a cross country study, Nordas found that a reduction of 10% in the export time increases exports by between 8% and 27%, depending on the sector and country of destination (Nordas, 2006).

The quality of the infrastructure is a key factor in stimulating trade. Coulibaly and Fontagne (2005) find that if all inter-state roads in the West African Economic and Monetary Union (WAEMU)24 were paved, countries would trade three times more than at present. This effect is particularly important for land-locked countries, for whom shipping goods through a transit country accounts for 4% of trade costs. A recent study by Morrissey et al. (2007) of the non-trade aspects of EPAs found that trade facilitation measures could make an important contribution to economic growth and efficiency through increased revenue collection, reductions in trade costs and promotion of greater regional co-operation.

6.2 Rules, standards and regional integration Clear and predictable rules are a key factor in business efficiency, as industry needs a predictable environment to flourish. Studies have consistently shown that a favourable regulatory environment is a key stimulant for foreign direct investment (Görg et al., 2007). In addition, the positive impacts of FDI on economic growth appear to be magnified in a sound regulatory context (Busse and Groizard, 2006). Morrissey et al. (2007) reviewed the regulatory elements of EPAs and found that the types of regulatory reforms proposed should improve the business environment and make investment more attractive.

Investment decisions and sourcing of supplies and inputs are affected by the extent to which countries can meet formal and informal standards related to quality, sanitary protection and marketing. The security of intellectual property affects choices over outsourcing of production and transfer of technology. The EPAs seek also to enhance co-operation, build regional ACP institutions and capacity and harmonise legal and institutional frameworks within the ACP regions themselves in all of these areas, in order to help diversify production away from price-driven basic commodity exports towards quality-driven value added and integrated production systems.

Regional integration and the development of regional institutions – building credible regional markets with common rules for business – could make a huge difference to the attractiveness of the ACP for business. The small size of ACP markets

24. UEMOA in French.

544 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

is one of the key reasons why they have had difficulty attracting FDI beyond the narrow extractive industry sector (Morrissey et al., 2007; UNCTAD, 2007). Building regional markets will help domestic industry to become more efficient as well as making these markets more attractive for FDI.

6.3 Investment, competition and procurement In terms of the key areas of investment and competition, Morrissey et al. (2007) reviewed the evidence and found that there is support in the literature for the provision of predictable frameworks in both these areas. In the case of investment, the inclusion of investment provisions in regional integration agreements has been shown to stimulate investment (Levy et al., 2002; Dee and Gali, 2003). Whether it is the investment provisions themselves, or the predictability and ‘locking-in’ of reforms that the regional agreements provide, is subject to debate; however, the positive impact on the investment climate seems clear (see also Evenett et al., 2006). Indeed, an UNCTAD report noted the positive effect of recent ‘business-friendly’ African reforms in attracting increased FDI (UNCTAD, 2007). Minimum provisions on national treatment and non-discrimination within the EPA context would help to magnify this effect and provide further security.

Anti-competitive practices are certainly widespread in ACP countries (Evenett et al., 2006); thus there is potential for important impacts from the establishment of a more transparent and predictable competition framework. As a priority, hard-core cartels need to be addressed. Effectively dealing with such cartels on a regional level should not only improve the competitive environment, but also demonstrate the benefits of active competition policy, stimulating further efforts in the future. Although host governments may wish to protect certain industries for a variety of reasons, it is clear that a more competitive environment reduces prices and benefits consumers and there is some evidence that this is conducive to growth. The OECD has estimated that improving competitiveness policy in developing countries to the level prevalent in the OECD would increase per capita GDP by almost 8% on average (OECD, 2006). In the same way, opening up government procurement has been shown to reduce prices significantly – by around 30% in the EU (European Commission, 2004).

6.4 Good governance Research has consistently found that good governance is a key factor in stimulating foreign direct investment. Asiedu (2006) found that corruption and political instability discourage FDI in Africa, while an efficient legal system and a good investment framework have the opposite effect. Obwona (2001) finds that macroeconomic and political stability has been more important than incentive schemes in stimulating FDI in Uganda, where he finds a positive relationship between FDI and GDP growth. Mlambo (2005) surveys the existing situation in southern Africa and concludes that countries in the region need to reduce regulation, enforce property rights, improve the bureaucracy and reduce corruption if they are to increase FDI flows.

Busse et al. (2005) emphasise the importance of institutional quality in supporting growth in the ACP and note the potential of the Cotonou Agreement to contribute to

EPAs: Rationale, Misperceptions and Non-trade Aspects 545

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

improving the quality of institutions. Busse and Gröning (2007) find evidence that trade liberalisation can help to improve governance in developing countries. They note that if the EPAs do lead to closer economic (and political) links between the EU and ACP countries, governance in the latter group could improve significantly. They conclude that the EU approach towards deeper regional integration finds support in their research.

6.5 Services Although not a ‘non-trade’ aspect, the question of the effects of the liberalisation of services trade has been omitted from most analyses of the impact of the EPAs, usually for the same reason as for non-trade aspects – lack of reliable data. Analysis of services on an ACP basis is limited but UNCTAD (2006) data provide a reasonable proxy, showing that the sector is the largest contributor to GDP in the poorest countries (42% and growing, compared with 33% and falling for agriculture). Given the important role of services as intermediate inputs for most industries, an inefficient services sector is costly for the economy as a whole. For example, in many ACP industries a reduction of goods tariffs alone without a parallel liberalisation of services could mean that the potential positive effect of goods liberalisation would not fully materialise.

Services are key to economic growth and, unlike many other FTAs, EPAs seek to be comprehensive trade agreements that include agreements on trade in services. Any agreement must be compatible with GATS Article V, which is based on similar principles to GATT Article XXIV; the EU will similarly ensure symmetry in commitments with the ACP.

6.6 Development support While not directly part of the economic rationale, EPAs provide the opportunity to co-ordinate economic reform with development finance. Related support will include capacity-building for sectors of the economy that face adjustment problems, customs reform, regional integration, support for fiscal adjustment and monitoring and funds to help offset any observed fiscal losses. Support to EPAs and regional integration lies behind the decision to increase regional allocations to the ACP from the European Development Fund (EDF) over the period 2008-13 by 50% to €1.8 billion out of an overall co-operation package of €22 bn.

EPA-related development support provided by the EDF will be complemented by financial assistance from EU Member States, but specific financial commitments will not form part of the EPA agreements. This is to avoid any implied conditionality or link between the depth of ACP reform commitments and the disbursement of development finance, to respect the competences of EU and ACP institutions and to ensure that trade reform is based on incentives linked to economic rationale rather than external financing.

Nevertheless, in order to ensure that EPAs contain no unaffordable commitments, the negotiating process has established specific co-ordination bodies to identify the associated capacity-building needs and earmark support within national and regional development finance planning processes. Institutions linked to EPA implementation

546 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

will subsequently provide a platform to co-ordinate and monitor the delivery and effectiveness of that support.

All interim agreements, apart from the Pacific and the East African Community, contain extensive provisions on development co-operation. They follow a largely similar approach which includes (i) a general provision referring to Cotonou rules and procedures, EDF financing and efforts from Member States and other donors and (ii) more detailed provisions identifying areas of support, mainly trade-related rules and, in certain cases, productive sectors, fiscal adjustment costs and regional funds. Two agreements, with the EAC and the Eastern and Southern African countries, contain a detailed chapter on fisheries, while the agreements with ESA and Central Africa also refer to accompanying documents which establish agreed broad priorities for support.

7 State of play by region When it became clear that full EPAs would not be agreed in all ACP regions by the end of 2007, EU Member States gave their backing to the Commission to negotiate interim agreements where needed to ensure that a new, legally secure, goods trade regime was in place for as many of the 36 ACP non-LDCs as possible by 1 January 2008.25 As the Commission had set out in its October 2007 Communication on EPAs, these agreements also had to avoid obstructing ACP regional integration and continue to steer a course towards full EPAs. The resulting trade regimes applying to ACP countries from 1 January 2008 are as follows. There is a comprehensive EPA agreed with the Caribbean region and a series of interim agreements based on new WTO-compatible goods trade arrangements for the other ACP regions. All the interim agreements are explicitly drafted to provide the basis for subsequent comprehensive regional EPA agreements. Nevertheless, like the full EPAs, the interim agreements are compatible with the requirements of Article XXIV of GATT, while using the existing flexibility of WTO rules to protect sensitive and growing ACP industries. As the agreements all include immediate liberalisation on the EU side,26 any decision to liberalise more than 80% of trade volume over 15 years was made by the ACP themselves.

In the Caribbean a full regional EPA with all 15 CARIFORUM countries covering all subjects, including services, rules, trade in goods and development support has been initialled. In Southern Africa there are interim agreements with Botswana, Lesotho, Namibia, Swaziland and Mozambique. In addition, there is an agenda and timetable for progressing towards a full EPA in 2008. Angola is expected to join the agreement. South Africa, which already has a WTO-compatible free trade agreement with the EU and is unaffected by the expiry of the Cotonou trade regime, has not joined the interim EPA but is expected to remain engaged in negotiations with a view to initialling the interim EPA and possibly a full EPA.

In East Africa, there is an interim agreement with the East African Community and interim agreements with five Eastern and Southern African countries. The final

25. Council Conclusions on Economic Partnership Agreements at the 2831st External Relations Council

meeting, Brussels, 19-20 November 2007. 26. With short transition periods for rice (until 2010) and sugar (until 2015). In 2005 these products accounted

for less than 2.5% of ACP exports to the EU.

EPAs: Rationale, Misperceptions and Non-trade Aspects 547

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

structure of a full regional EPA is still under discussion. The objective is to ensure that it builds on the existing EAC Customs Union without undermining the longer-term regional vision for COMESA, the Common Market of Eastern and Southern Africa.

In the Pacific, an interim agreement has been concluded with the two countries that account for almost all of the region’s trade with the EU – Papua New Guinea and Fiji. Other non-LDCs in the region have negligible goods trade with the EU and did not seek to sign WTO-compatible goods trade agreements at this stage, being more interested in a services-based EPA. The objective, however, remains the agreement of a full regional EPA covering the whole region by the end of 2008.

In West Africa, there are interim agreements with two of the three non-LDCs, Côte d’Ivoire and Ghana. Nigeria, the only other non-LDC in the region, has made clear its lack of interest in negotiating an EPA at this stage. In Central Africa, Cameroon has initialled an agreement and Gabon has indicated its wish to conclude an interim agreement using the same text but with a goods market-access schedule specific to Gabon appended. Congo (Brazzaville) declined to negotiate an interim agreement. As an oil exporter, like Nigeria, it views its interests differently from most other ACP countries. According to Machin (2006), 95-96% of both countries’ exports to the EU in 2001 were in products where MFN duty rates are zero and preferences therefore offer no incentive.

The Caribbean EPA contains the full range of institutions necessary for the implementation and monitoring of the agreement. The provisions of the interim agreements vary according to the content of the agreements and the nature and scope of various ‘rendezvous clauses’. These clauses were negotiated together with a series of accompanying political declarations to define how further negotiations towards a comprehensive regional EPA will be handled. This process varies by region. The SADC agreement foresees that further negotiations will expand the agreed interim text into a full regional EPA and therefore establishes the full range of EPA institutions. On the other hand, the West Africa agreements foresee that they will be entirely replaced by a regional EPA and they therefore establish only the minimum institutions necessary for the functioning of the goods-based interim agreement.

The concrete objectives for the forthcoming negotiations are: (i) to turn sub-regional and multi-country interim agreements into genuine regional EPAs bringing in all countries, non-LDCs and LDCs alike; (ii) to build on the emerging EPAs to form comprehensive agreements with the greatest possible coverage on issues like services and rules. This will build on existing ACP regional integration agendas and, in a number of cases, is already foreseen as an ongoing process, with commitments taken after a period of capacity-building; (iii) to follow up on EU commitments on Aid for Trade by concluding the 10th EDF regional programmes and delivering on EU commitments in this area as set out in the EU Aid for Trade strategy; and (iv) to present initialled texts to the Council for signature, to the Parliament and to notify the WTO of existing agreements.

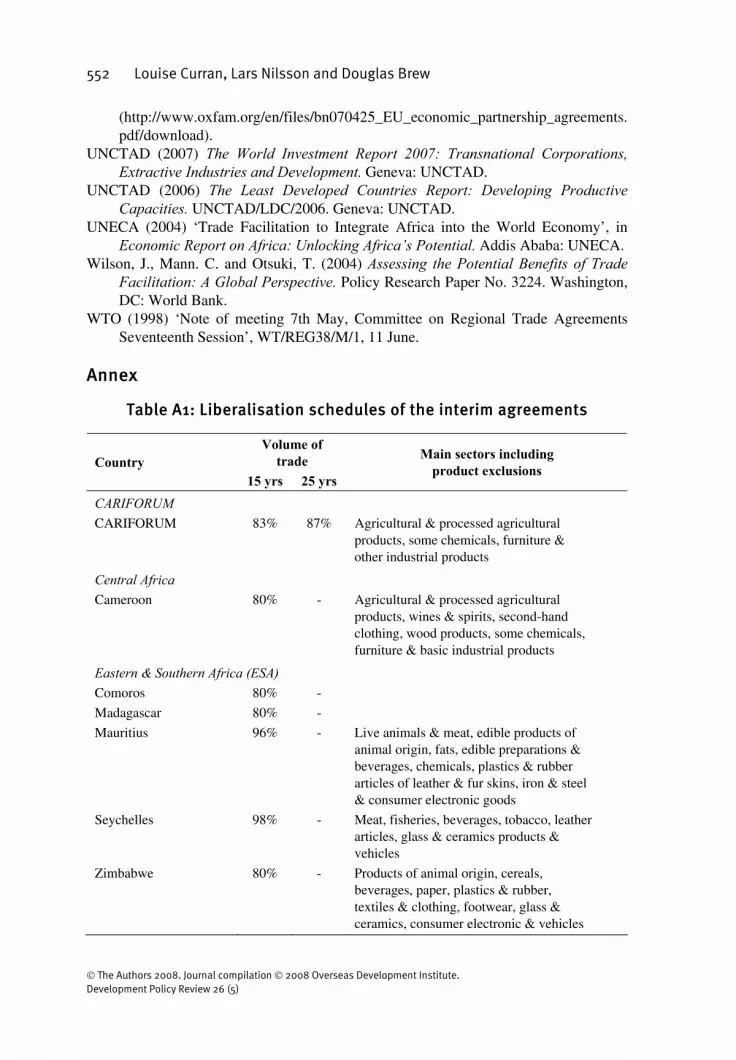

An initial analysis of the liberalisation coverage of the different agreements on the ACP side is summarised in Annex 1. It is worth noting that some ACP countries have chosen to liberalise their imports by more than the 80% which might have been expected. The schedules also focus on lowering duties on the essential goods and inputs the ACP need in the early stages of industrialisation, while continuing to protect

548 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

sensitive and growing industries. The figures do not show the additional market opening over and above the situation under Cotonou or the change in tariff protection; some tariff rates included in the liberalisation analysis are either low or zero or concern tariff lines where there is no EU production or export trade.

There has been some controversy over the potential of interim agreements to disrupt ACP regional integration. However, in reality this fear is unfounded, as they form the basis for harmonised ACP regional trade regimes and avoid the political and economic disruption that would otherwise have resulted from the end of the Cotonou trade regime. There is now a duty-free trade regime covering the vast majority of ACP countries, which is certainly an improvement on the situation in 2007 when ACP regions were split between non-LDCs which paid Cotonou duties on agricultural products and LDCs which had the full duty-free trade regime of the EBA. Moreover, these agreements are called ‘interim’ for a reason. They were negotiated under time pressure to prevent trade disruption, but with the full intention that they will be replaced as part of a move to full EPAs; thus the original objective of supporting ACP regional integration remains unchanged. Importantly, they have created real policy space for the ACP regions which, free from divisive deadlines and the threat of legal challenges to non-LDC market access, can now approach EPA negotiations on their own terms.

8 Summary and conclusion The objective of the EPA process is to promote sustainable development in the ACP, including by supporting the ACP’s own regional integration processes. The greater trade and economic integration between the EU and the ACP promoted by EPAs will act as a stepping stone to bring about the gradual integration of the ACP countries into the world economy. The agreements will be consistent with WTO rules but, where they promote ACP development, will also go beyond agreements reached in the WTO.

EU liberalisation of trade will be more far-reaching and rapid than that of the ACP, to allow the gradual phasing in of change and the protection of sensitive industry on the ACP side. However, one of the main motivations for EPAs is the recognition that goods market access alone is not sufficient to promote growth. The inclusion of services trade and the creation of transparent, predictable and regional rules on ‘non-trade’ issues such as investment, public procurement and competition policy are essential for effective economic governance and will be key to attracting more local and foreign investment in the ACP and thus ensuring that growth and development follow trade policy reform.

The EU-ACP joint conclusion that the EPAs are the most appropriate way to break the current negative trends in EU-ACP trade and to move forward is also motivated by the understanding that the EPAs are not simply trade agreements, but co-ordinated packages of measures supported by extensive development assistance. This approach enables the EU-ACP relationship to go further than simply protecting EU-ACP goods trade from legal challenge. It provides a structured framework for co-ordinating reform with EU development assistance and supporting the emerging regional economic communities of the ACP. The latter are seen as a key economic and political objective by many politicians on both the EU and ACP sides.

These multiple advantages were the reason why EU and ACP leaders agreed in the Cotonou Agreement to negotiate EPAs as the best option for framing future EU-ACP

EPAs: Rationale, Misperceptions and Non-trade Aspects 549

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

trade relations. However, much criticism has failed to centre on this broad approach and has focused on assumptions that the status quo is acceptable in development terms, or that the impact of EPAs will come from changes in the tariff regime measured against a baseline of continued unilateral ACP preferences in EU markets – often with the further assumption that the value of these preferences will be unaffected by preference erosion or direct competition with other developing regions.

The EU and the ACP have taken significant steps in recent months towards a successful conclusion to EPA negotiations that tackle these assumptions and are rather based on a comprehensive analysis of the problems in ACP-EU trade relations. The Caribbean region in particular has shown that it is possible to establish a comprehensive, ambitious agreement between an ACP region and the EU. More needs now to be done to secure coherent approaches in the other ACP regions and to consolidate the results achieved so far. For this to happen, other ACP regions will need to define, collectively, where their key interests and ambitions lie and to work with the EU to match these to their regional capacity and integration strategies. This will not be straightforward, but the EU continues to believe that such ambitious agreements are not only feasible but essential to foster long-term growth and development and to finally break ACP dependence on primary commodity exports and EU preferences.

first submitted March 2008 final revision accepted April 2008

References Alaba, O. (2006) ‘EU-ECOWAS EPA: Regional Integration, Trade Facilitation and

Development in West Africa’. Paper presented at the GTAP conference, Addis Ababa, June.

Asiedu, E. (2006) ‘Foreign Direct Investment in Africa: The Role of Natural Resources, Market Size, Government Policy, Institutions and Political Stability’, World Economy 29 (1): 63-77.

Ben Hammouda, H.; Karingi, S.; Idrissa Ouedraogo, B.; Oulmane, N. and Sadni-Jallab, M. (2006) Assessing the Consequences of the Economic Partnership Agreement on the Ethiopian Economy. African Trade Policy Centre, Work in Progress, No 43. Addis Ababa: UNECA.

Ben Hammouda, H., Rémi, L. and Sadni-Jallab, M. (2005) Evaluation de l’accord de partenariat économique entre l’union européenne et le Mali. African Trade Policy Centre, Work in Progress, No 24. Addis Ababa: UNECA.

Bilal, S. (2007) Concluding EPA Negotiations: Legal and Institutional Issues. Policy Management Report 12. Maastricht: ECDPM.

Bouët, A., Laborde, D. and Mevel, S. (2007) Searching for an Alternative to Economic Partnership Agreements. IFPRI Research Brief No. 10. Washington, DC: IFPRI.

Busse, M. and Gröning, S. (2007) Does Trade Liberalisation Lead to Better Governance? An Analysis of the Proposed ACP/EU Economic Partnership Agreements. Hamburg: Hamburg Institute of International Economics (HWWI).

Busse, M., and Groizard, J. L. (2006) Foreign Direct Investment, Regulations and Growth. Policy Research Working Paper No. 3882. Washington, DC: World Bank.

550 Louise Curran, Lars Nilsson and Douglas Brew

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

Busse, M., Borrmann, A. and Neuhaus, S. (2005) Trade, Institutions and Growth: An Empirical Analysis of the Proposed ACP/EU Economic Partnership Agreements for ECOWAS Countries. Working Paper. Hamburg: Hamburg Institute of International Economics.

Busse, M., Borrmann, A. and Grossman, H. (2004) The Impact of ACP/EU Economic Partnership Agreements on ECOWAS Countries: An Empirical Analysis of Trade and Budget Effects. Hamburg: Hamburg Institute of International Economics.

Coulibaly, S. and Fontagne, L. (2005) ‘South-South Trade: Geography Matters’, Journal of African Economies 15 (2): 313-41.

Curran, L. (2007) ‘Response to the Article “Are the Economic Partnership Agreements a First-bet Optimum for the ACP Countries?”, Perez, R. (2006) 40 (6)’, Journal of World Trade 41: 243-4.

Dee, P. and Gali, J. (2003) The Trade and Investment Effects of Preferential Trading Arrangements. NBER Working Paper No. 10160. Cambridge, MA: NBER.

Desta, M. G. (2006) ‘EC-ACP Economic Partnership Agreements and WTO Compatibility: An Experiment in North-South Inter-Regional Agreements’, Common Market Law Review 43: 1343-79.

Draper, P. (2007) ‘EU-Africa Trade Relations: The Political Economy of Economic Partnership Agreements’, Jan Tumlir Policy Essay No. 02 (http://www.ecipe.org/ publications/jan-tumlir-policy-essays/).

European Commission (2004) ‘Measuring the Impact of Public Procurement Policy, First Indicators, Single Market News’, March (available at http://ec.europa.eu/ internal_market/smn/smn20/s20mn18.htm#fn1).

Evenett, S., Jenny, F. and Meier, M. (2006) ‘A Database of Allegations of Private Anti-Competitive Practices in Sub-Saharan Africa’ (available at www.evenett.com/ ssafrica.htm).

Fontagne, L., Laborde, D. and Mitaritonna, C. (2008) An Impact Study of the EU-ACP Economic Partnership Agreements (EPAs)in the Six ACP Regions. CEPII Working Paper No. 4, April (http://www.cepii.fr/anglaisgraph/workpap/pdf/2008/wp2008-04.pdf).

Fontagne, L., Laborde, D. and Mitaritonna, C. (2006) ‘Analyse d’impact en équilibre partiel de l’application des APE concernant les aspects commerciaux et tarifaires’, Communication from the Farm Foundation (http://www.farm-foundation.org/ IMG/pdf/COLLAPE_presentation_cepii__.pdf).

Gillson, I., Hewitt, A. and Page, S. (2005) Forthcoming Changes in the EU Banana/Sugar Markets: A Menu of Options for an Effective EU Transitional Package. International Economic Development Group Report. London: ODI.

Görg, H., Morrissey, O. and Manop, U. (2007) Investment and Sources of Investment Finance in Developing Countries. GEP Research Paper No. 2007/16 (http://ssrn.com/abstract=975915).

Hertel, T. and Keeney, R. (2006) ‘What’s at Stake: The Relative Importance of Import Barriers, Export Subsidies and Domestic Support’, in K. Anderson and W. Martin (eds), Agricultural Trade Reform and the DDA. Washington, DC: World Bank.

IMF (2005) ‘IMF Country Report Eastern Caribbean Currency Union: Selected Issues’. Chapter V, IMF Country Report 05/305. Washington, DC: IMF.

EPAs: Rationale, Misperceptions and Non-trade Aspects 551

© The Authors 2008. Journal compilation © 2008 Overseas Development Institute. Development Policy Review 26 (5)

Lang, R. (2006) Renegotiating GATT Article XXIV: A Priority for African Countries Engaged in North-South Trade Agreements. African Trade Policy Centre, Work in Progress No. 33. Addis Ababa: UNECA.

Levy, E., Stein, E. and Daude, C. (2002) Regional Integration and the Location of FDI. Working Paper No. 492. Washington, DC: Inter-American Development Bank.

Machin, M. (2006) ‘Preference Utilisation and Tariff Reduction in EU Imports from ACP Countries’, The World Economy.

Milner, C. et al. (2005) ‘Some Simple Analytics of the Trade and Welfare Effects of Economic Partnership Agreements’, Journal of African Economies 14 (3): 327-58.

Mlambo, K. (2005) ‘Reviving Foreign Direct Investments in Southern Africa: Constraints and Policies’, African Development Review 17 (3).

Morrissey, O.; Milner, C.; Falvey, R.; Zgovu, E. and Chimia, L. A. (2007) ‘The Link between EU-ACP Economic Partnership Agreements and Institutional Reforms’. Report prepared for DG Trade of the European Commission.

Nordas, H. (2006) Time as a Trade Barrier: Implications for Low-income Countries. OECD Economic Studies No. 42, 2006/1. Paris: OECD.