Embed Size (px)

Citation preview

/~

""-'".'/..-. . - ':"

..•••....•..I ,~; "J:I~"··',.'·I':".".Indian Institute of ManagementXX~ ,AriMCDAH," Ahmedabad IIMA/F &A0484

Sale of ONGC Shares by lacThe Die is CastAfternoon of April 26, 2006. Prof. SK Barua was driving home from the campus of a well-known Institute of Management in Southern India (WlMSl) when he received the call. Mr.SV Narasimhan, Director (Finance), Indian Oil Corporation (laC), was on the line. "Theprice of ONGC (Oil and Natural Gas Corporation) stock has risen again today. Shall we dothe stake sale tomorrow?", he queried. Pulling over, Prof. Barua replied, "Yes, the stockprice has moved up and this may be the right time for stake sale." "Let me talk to Mr.Uplenchwar and then I would ask Mr. Goyal to get in touch with you to make thearrangements for travel and stay", said Mr. Narasimhan. Within ten minutes, Prof. Baruareceived fl call from Mr. Goyal, who had already found out the schedule of flights thatevening from Bangalore to Mumbai. Mr. Goyal informed Prof. Barua that he had alreadycontacted' the merchant bankers and given them the green signal to initiate the process forselling 20% of the ONGC shares held by lac. "Since the market is rising, make sure that thediscount at which we sell the shares is as low as possible. The merchant bankers are likely topush for a higher discount as that would make their task much easier", cautioned Prof.Barua.

, The stake sale had been contemplated and put off few times since the decision was taken bythe Board of roc to sell its holding in ONGC several weeks ago. While the market hadmoved up, the price of ONGC stock had not moved in line with the index. Therefore, theBoard Committee set up for the purpose had been reluctant to effect the sale. The ONGCstock price had finally moved up significantly in the last few days and it appeared anoppqrtune time to sell. Prof. Barua reached home by 15:15 hours. The market had anotherfifte minutes left before closure. He switched on the television to watch the popularbusiness channel, CNBC-TV18, to assess the market mood, while getting ready to catch the

€. \ fo,

flightJ9 ¥ mbai in a few hours. As he watched, to his great surprise, he noticed that a newsflash ~as~streaming at the bottom of the screen informing viewers that it was rumoured thatlac was )t8 sell its stake in ONGC the next day, that is, on April 27. Interrupting the on-going djSy\ission, the anchor for the channel announced that there were as yet unconfirmedreports thllt laC would enter the market to sell a part of its equity stakes in ONGC. Prof.'. ,Barua was upset with this development as it could result is a decline in the closing price ofONC;;Cstock and may negatively impact the price at which the shares could be sold the nextday. He suspected that the potential clients the bankers may have contacted for the stakesale could be the source of this leakage of information to the media. He called up Mr.Narasimhan and queried, "Does this not violate the confidentiality that merchant bankersare required to observe?". Narasimhan mentioned that while the price range indicated inchannels can have some effect on the bids, closing price would not be impacted as the rangefor the same price would be given to the bankers only after the close of the market.

Written by Professor Samir K Barua, Indian Institute of Management Ahmedabad.

Cases of the Indian Institu te of Management, Ahmedabad, are prepared as a basis for classdiscussion. Cases are not designed to present illustrations of either correct or incorrect handling ofadministra tive problems.

© 2010 by Indian Institute of Management, Ahmedabad.

1 •.This document is authorized for use only by K Selvakumar, Xavier Institute of Management and Entrepreneurship.

Copying or posting is an infringement of copyright.

, II

IIMA/F &A'04842 of 11

Acquisition of Stakes in dNGClaC had acquired 9,61 % equlty stake in ONGC in 1999-2000, This was pursuant to thedecision to raise resource for the government by tapping into cash available with the 'rich'public sector undertakings (PSUs) in the petroleum sector, The government's disinvestmentprogramme had been stalled by the political impasse on the issue. Therefore, the idea wasmooted to take away the cash available with the PSUs in the petroleum sector. Thegovernment decided to sell a part of its holdings in each of the three major PSUs in thepetroleum sector (lac, ONGC and GAIL) to the other two, thereby creating cross-holdingamong the companies. The resulting sale of government stakes in these companies led toroc acquiring stakes in ONGC and GAIL and the latter two companies acquiring stakes inlaC The net outcome of the exercise was that the government garnered Rs. 50000 millionfrom the three com panies.

Contemplation of Sale of ONGC SharesThe unprecedented rise in the price of crude by the last quarter of 2005 and the freeze onprices of petroleum products by the government had created a situation whereby the oilrefining and marketing companies had started making cash losses on sale of products.Coupled with high capital expenditure requirement for major ongoing projects, this wasresulting in a huge cash crunch for these companies. The treasury department of laCtherefore prepared a note for consideration of the Board for disinvestment of a portion of theholdings in ONGC and GAIL. A sub-committee of the Board consisting of three directors,Mr. SV Narasimhan, Director (Finance), Mr. AM Uplenchwar, Director (Pipeline) and Prof.SK Barua, Independent Director, was formed to carry out the sale of laC's stake in ONGCand GAIL. The committee was to be assisted by Mr. PK Goyal, Executive Director (Finance)and Mr. SC Jain, General Manager (Finance). The first meeting of the committee took placeon December 29, 2005. After examining the various alternatives available for sale of laC'sstakes in the two companies, the committee decided to opt for sale of shares throughbulk/block trade in the secondary market. This would essentially involve building thedemand book through intermediation of merchant bankers. The first step would thereforebe to identify the merchant bankers who would be entrusted with the task.

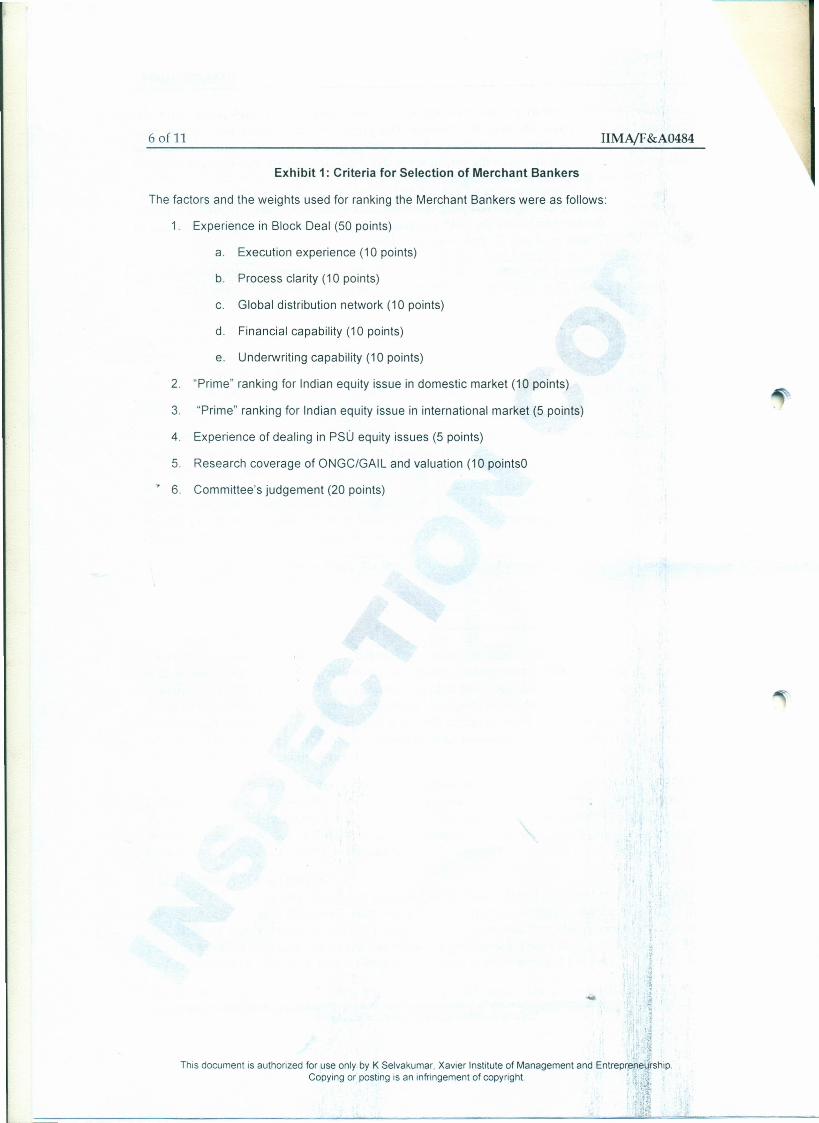

Appointment of Merchant BankersThe top ten merchant bankers based on 'Prime' League Table Ranking for the total amountof equity issues handled in the years 2002-03, 2003-04, 2004-05 and April 'OS to November'OS were invited for presentations to the committee for sale of ONGC and GAIL shares. Eachmerchant banker was given about an hour to present the proposal for sale. The presentationincluded assessment of the way market would move and the timing of sale of laC'sholdings. The criteria for selection of the merchant bankers for sale of ONGC shares arelisted in Exhibit 1. The presentations were scheduled over two days - January 4 & 5,2006.

The third meeting of the committee was held on January 26, 2006. Based on thepresentations, three merchant bankers were short-listed for sale of ONGC shares and invitedto submit their detailed proposals including the financial terms. The bids were evaluatedand JM Morgan Stanley and Citigroup were invited for final round of discussions onFebruary 1, 2006. Pursuant to the discussions, the two merchant bankers agreed to submit ajoint offer.

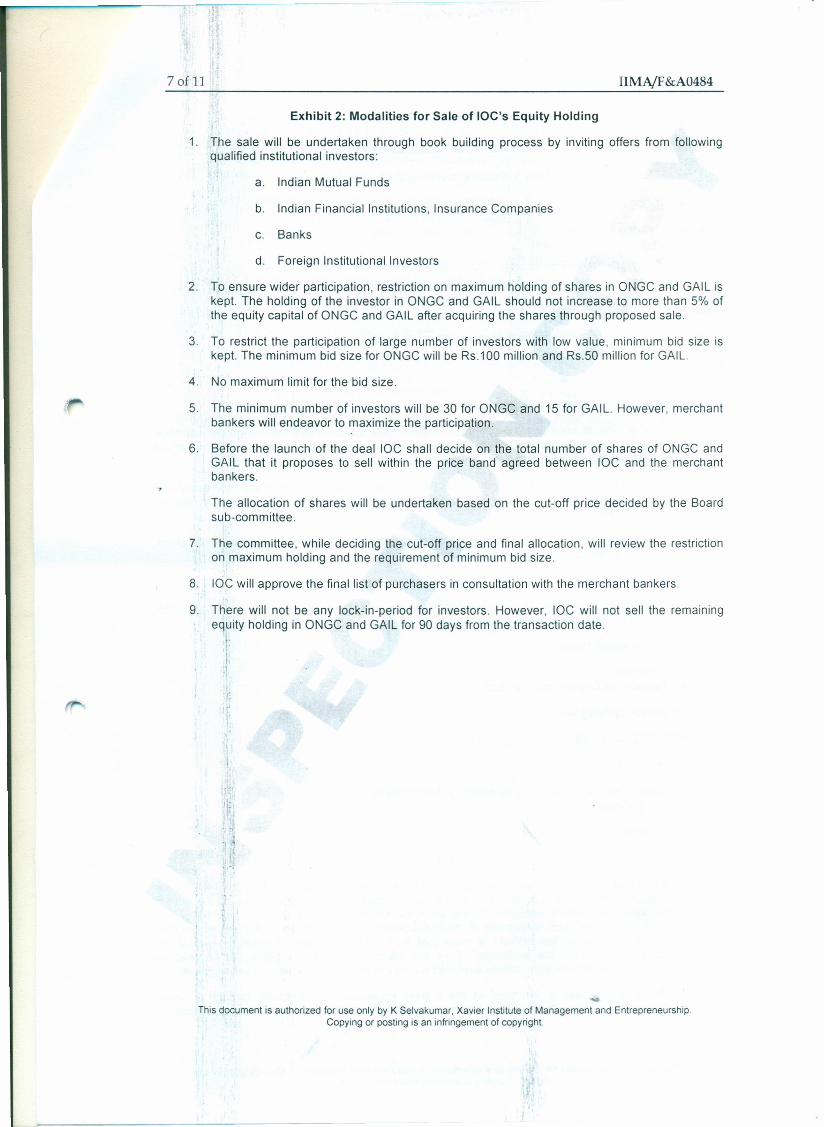

The broad description of the modalities to be followed for sale of laC's stakes in the twocompanies is contained in Exhibit 2. The relevant SEBI regulations governing bulk/blocksale of shares are contained in Exhibit 3.

This document is authorized for use only by K Selvakumar. Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright

3 of 11 IIMAjF&A0484

Terms Offered by Merchant BankersThe salient features of the offer, submitted on February 2, 2006 were as follows:~ Allocation to investors would be made on Dutch basis, that is, at a uniform price.~ The merchant bankers would advise on the price band, based on market feedback.

~ IOC will transfer equal number of shares (SO% of the number of shares to be sold) to JMMorgan Stanley and Citigroup by 16:00 hours on the date prior to the transaction date.

~ The affiliates of the merchant bankers will offer Participatory Notes (P-notes) to itsinvestors and such investors will be eligible for allocations. Merchant Bankers will sharethe names of investors participating through P-notes.

~ The list of investors contacted by the merchant bankers for the transaction and theresponse received from the investors will be provided to IOC on completion of thetransaction.

~ IOC would not sell any further stock of ONGC for a period of 90 days from the date ofsettlement of this transaction.

~ The sale proceeds will be remitted after deduction of Securities Transaction Tax (SIT)through RTGS (Real Time Gross Settlement) system on the third working day followingthe transaction date.

~ The merchant bankers will provide the certificate of payment of SIT and copies of thecontract notes.

~ IOC will execute sale agreement with the merchant bankers.~ The fee quoted by the merchant bankers will be as follows:

Brokerage fee or commission NILStamp duty To be borne by merchant bankers

'L .Exchange transaction charges To be borne by merchant bankers

~ The ~erchant bankers would reimburse actual out of pocket costs incurred by IOC to aI J r i

maximum of Rs. SOO,OOO.(1 1

~ Ir order to secure the performance and in consideration of the contract security as also'. I I

Host contract performance, each merchant banker will pay a non-refundableBierfon-riance fee of Rs. 17.S0 million within three working days from the date ofae:cepta~ce of the proposal as evidenced by mandate letter from IOC. In case thetfunsadion does not get consummated on or before April 30, 2006 then IOC will refundtile enfire non-refundable fee within 7 days thereafter. Further, in case of reduction intlie number of shares sold, IOC would refund a proportionate amount of non-refundable performance fee to each merchant banker within 7 working days from thedate of the transaction.

The Build-up of DemandThe 2,74,13,476 shares of ONGC were transferred from IOC to the merchant bankers'accounts on the afternoon of April 26 for sale of the same the next day. These shares hadalready been dematerialized so that the transfer could occur electronically and thereforequickly. After the transfer was completed, the merchant bankers started contacting theiroffices in other countries to contact institutional investors who had been investing in theIndian. equity market and would therefore be potential buyers of shares on offer. Mutualfunds, insurance companies and banks in India too were contacted by the local office of themerchant bankers to generate demand from within the country. Based on the closing price ofRs. 138S on April 26,2006, the price band using +1 % to -4%, worked out to Rs. 1330 to Rs.

I·,"1\ _

T?is document is authorized for use only by K Selva kumar, Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright.

'\

'I'1'I

11, J1;';1

I'

OJ'

4 of 11 IIMNF &A0484"I· II

"• • 1

1400 per share. The mov.~P1ent of the ,.?~are price of ONGC in the last several lllon ths andthe volumes transacted ar~,\presentedlin Exhibit 4. The average closing prices ,f shares ofONGC at the NSE (National Stock Exchange) for the preceding 7 days, 15 days ~nd 30 dayswere Rs.l341, Rs.1310 and Rs.1272 respectively.

The team from lOC assembled in the' control room' that had been set up in the office of oneof the merchant bankers by 7 a.m. on April 27, 2006. Orders had poured in from a largenumber of global and local investors and the offer for sale had been oversubscribed. Theissue however that was facing the committee was that the price at which the offer had beencompletely subscribed to was below the price expectation, based on the closing price ofApril 26 of ONGC stock. The committee was contemplating even withdrawing the offerentirely, in case the cut-off price was thought to be low, The merchant bankers advised thelOC team that while withdrawal of offer was an option that was technically availa\JI~~to10C, such a move would send a negative signal to the market and selling the shar~J;op alater occasion may become more difficult. r A ~

, J :, 'I"'The scene was chaotic outside thecontrol room as the merchant bankers kept ~ontacti1:llgthebuyers who had already SJll,' srted indicative bids and new potential customers'Ilt1 anattempt to raise the cut-offcprlce at which the entire issue could be sold. By.t8:45 a. '.: 'themerchant bankers were pushing the lOC team to take a view on the allocation so tha,t, thebidders could be informed about the allocation. The team desired that the merchant b~ri' ersshould put in some more effort in raising the cut-off price by negotiating £1'irthh witRthebidders. By 9:10 a.rn. the order book was as follows: ,: ' i :0

.c. 1

Share Price (Rs.)No. of shares No. of investors1399 1,420,563 81350 10,233,026 26

1340 28,271,972 47

1330 29,313,609 511 ;

There were a few bids that were below the minimum size of Rs. 100 million while..beingwithin the price band. The committee decided to accept these bids by relaxing the sizeconstraint to USD 1 million. The committee decided to accept the cut-off price of Rs. 1340 pershare at which the offer was over-subscribed, All applicants who bid at the cut-off or betterprice would receive pro-rata allocation at 96.99% of the number of shares bid for at the cut-off price. The allocation to domestic investors was estimated at about 40%. The rest of theallocation was to foreign investors.

At this price, the sale proceeds after deduction of Securities Transaction tax (Rs.36.70million) would be Rs. 36698.10 million. lOC acquired the shares of ONGC at the price ofRs.162.34 per share in financial year 1999-2000. The capital gain on the sale of ONGC shareswould work out to Rs. 32247.80 million. Pursuant to this sale, lOC's equity holding inONGC would reduce to 7.69% from 9.61%.

The Execution of the OrderThe sale of shares was required to be executed in the NSE, after it opened for trading at 10:00a.m. on April 27. Since the transactions were to be completed while the market was open, theexecution of the transaction required great finesse to ensure that the possible leakage (toother buyers) or shortage (all shares on offer not getting sold) was kept to a minimum. Theorders were to be placed from the Hong Kong offices of the merchant bankers. ' "

~(.

On the morning of April 27, 2006, the market opened weak. The price $.f shareJ~~f ONGCopened above the closing price for the previous day, but became soft quiq<]~1~,l1d kept

"*" ,~? t~~ •

j! ,t,t;1"-, "'~i 'This document is authorized for use only ~~f."$elvakumar, Xavier Institute of Management and Entrepre(le~fsbiP

Copying or poStl~g is an infringement of copyright. \ !~.. "

5 of 11 IIMA/F&A0484

declining steadily thereafter. The transaction had not been put through even after themarkets had been open for over 40 minutes. The price of ONGC share had by the timedeclined by over 2% from the previous day's closing price. The lOC team was gettingconcerned about the tardiness in the execution of the order apparently due to some problemfaced in the foreign office in executing the order.

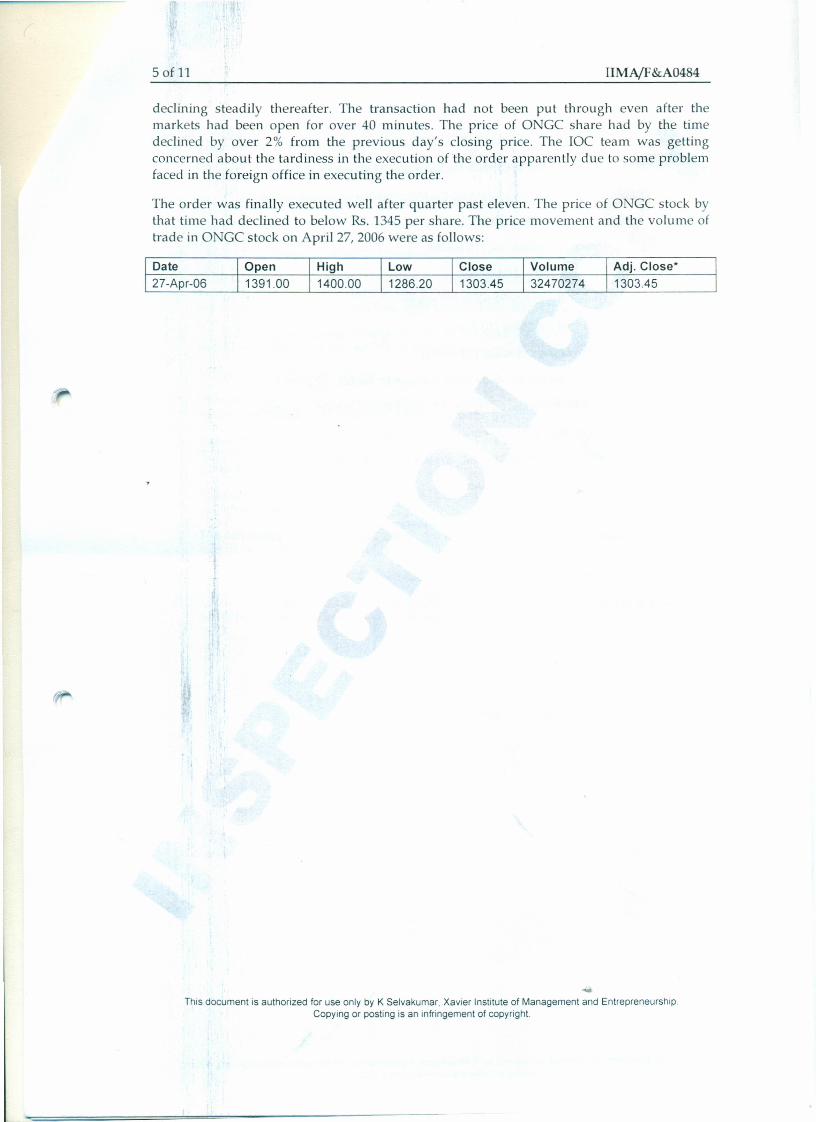

The order was finally executed well after quarter past eleven. The price of ONGC stock bythat time had declined to below Rs. 1345 per share. The price movement and the volume oftrade in 0 GC stock on April 27, 2006 were as follows:

Date Volume Adj. Close*27-Apr-06 32470274 1303.45

-This document is authorized for use only by K Selvakumar, Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright.

6 of 11 IIMA/F &A0484

Exhibit 1: Criteria for Selection of Merchant Bankers

The factors and the weights used for ranking the Merchant Bankers were as follows:

1. Experience in Block Deal (50 points)

a. Execution experience (10 points)

b. Process clarity (10 points)

c. Global distribution network (10 points)

d. Financial capability (10 points)

e. Underwriting capability (10 points)

2. "Prime" ranking for Indian equity issue in domestic market (10 points)

3. "Prime" ranking for Indian equity issue in international market (5 points)

4. Experience of dealing in PSU equity issues (5 points)

5. Research coverage of ONGC/GAIL and valuation (10 pointsO

" 6, Committee's judgement (20 points)

-:f

This document is authorized for use only by K Selvakumar, Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright. '

't'l,i:•• j

~~;.::..

7 of 11 IIMA/F &A0484

Exhibit 2: Modalities for Sale of IOC's Equity Holding

1. The sale will be undertaken through book building process by inviting offers from followingqualified institutional investors:

a. Indian Mutual Funds

b. Indian Financial Institutions, Insurance Companies

c. Banks

d. Foreign Institutional Investors

2. To ensure wider participation, restriction on maximum holding of shares in ONGC and GAIL iskept. The holding of the investor in ONGC and GAIL should not increase to more than 5% ofthe equity capital of ONGC and GAIL after acquiring the shares through proposed sale.

3. To restrict the participation of large number of investors with low value, minimum bid size iskept. The minimum bid size for ONGC will be RS.100 million and RS.50 million for GAIL.

4. No maximum limit for the bid size.

5. The minimum number of investors will be 30 for ONGC and 15 for GAl L. However, merchantbankers will endeavor to maximize the participation.

6. Before the launch of the deal IOC shall decide on the total number of shares of ONGC andGAIL that it proposes to sell within the price band agreed between IOC and the merchantbankers.

The allocation of shares will be undertaken based on the cut-off price decided by the Boardsub-committee.

7. The committee, while deciding the cut-off price and final allocation, will review the restrictionon maximum holding and the requirement of minimum bid size.

8. IOC will approve the final list of purchasers in consultation with the merchant bankers.

9. There will not be any lock-in-period for investors. However, IOC will not sell the remainingequity holding in ONGC and GAIL for 90 days from the transaction date.

rI

.J

This document is authorized for use only by K Selvakumar, Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright.

8 of 11 IIMAjF &A0484

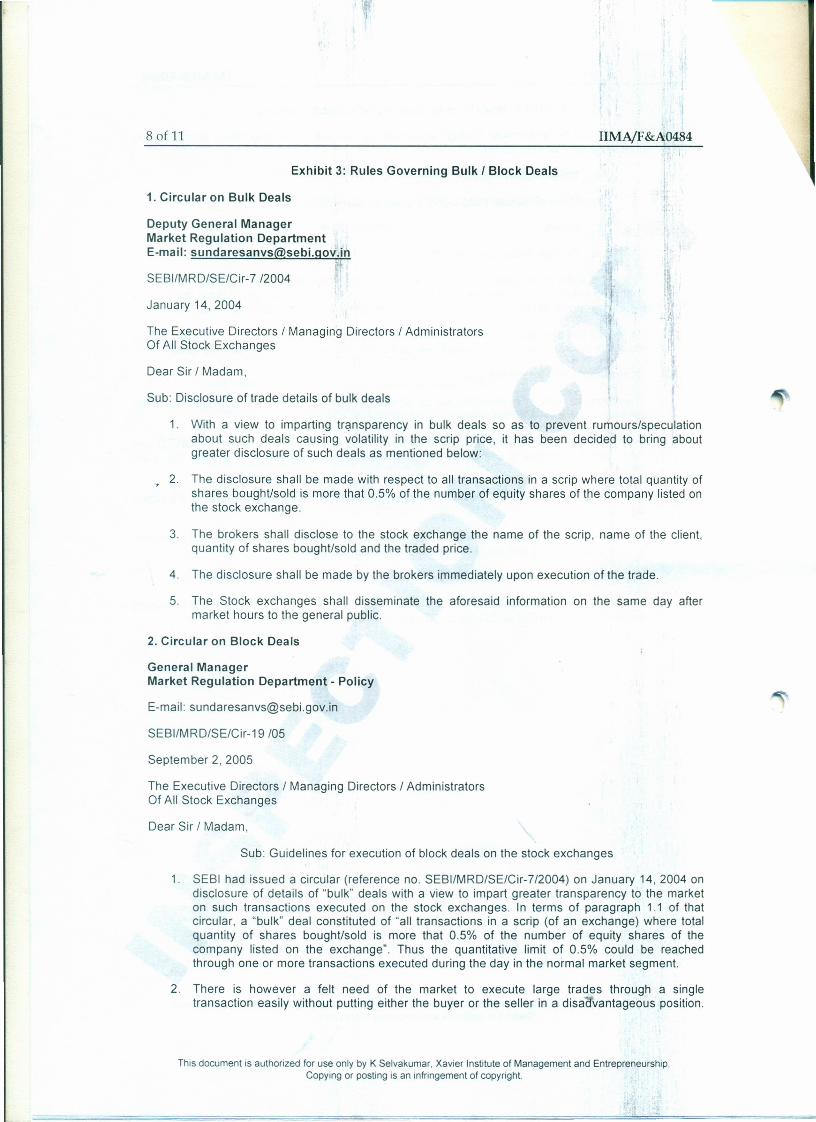

Exhibit 3: Rules Governing Bulk I Block Deals

1. Circular on Bulk Deals

Deputy General ManagerMarket Regulation DepartmentE-mail: [email protected]

SEBI/MRD/SE/Cir-7 /2004

January 14, 2004

The Executive Directors / Managing Directors / AdministratorsOf All Stock Exchanges

Dear Sir / Madam,

Sub: Disclosure of trade details of bulk deals

1. With a view to imparting transparency in bulk deals so as to prevent rumours/speculationabout such deals causing volatility in the scrip price, it has been decided to bring aboutgreater disclosure of such deals as mentioned below:

2. The disclosure shall be made with respect to all transactions in a scrip where total quantity ofshares bought/sold is more that 0.5% of the number of equity shares of the company listed onthe stock exchange.

3. The brokers shall disclose to the stock exchange the name of the scrip, name of the client,quantity of shares bought/sold and the traded price.

4. The disclosure shall be made by the brokers immediately upon execution of the trade.

5. The Stock exchanges shall disseminate the aforesaid information on the same day aftermarket hours to the general public.

2. Circular on Block Deals

General ManagerMarket Regulation Department - Policy

E-mail: [email protected]

SEBI/MRD/SE/Cir-19 /05

September 2, 2005

The Executive Directors / Managing Directors / AdministratorsOf All Stock Exchanges

Dear Sir / Madam,

Sub: Guidelines for execution of block deals on the stock exchanges

1. SEBI had issued a circular (reference no. SEBI/MRD/SE/Cir-7/2004) on January 14, 2004 ondisclosure of details of "bulk" deals with a view to impart greater transparency to the marketon such transactions executed on the stock exchanges. In terms of paragraph 1.1 of thatcircular, a "bulk" deal constituted of "all transactions in a scrip (of an exchange) where totalquantity of shares bought/sold is more that 0.5% of the number of equity shares of thecompany listed on the exchange". Thus the quantitative limit of 0.5% could be reachedthrough one or more transactions executed during the day in the normal market segment.

2. There is however a felt need of the market to execute large trades through a singletransaction easily without putting either the buyer or the seller in a disa vantageous position.

This document is authorized for use only by K Selvakumar, Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright.

9 of 11 IIMA/F &A0484

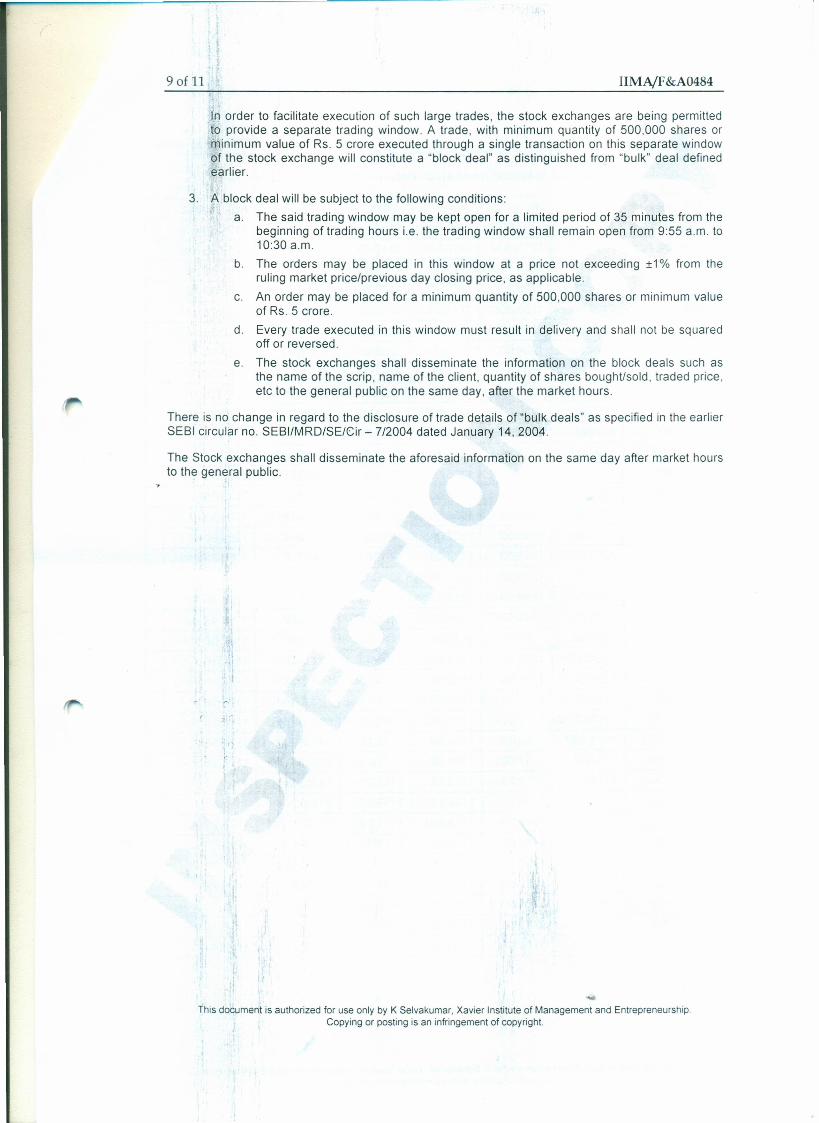

In order to facilitate execution of such large trades, the stock exchanges are being permittedto provide a separate trading window. A trade, with minimum quantity of 500,000 shares orminimum value of Rs. 5 crore executed through a single transaction on this separate windowof the stock exchange will constitute a "block deal" as distinguished from "bulk" deal definedearlier.

3. A block deal will be subject to the following conditions:

a. The said trading window may be kept open for a limited period of 35 minutes from thebeginning of trading hours i.e. the trading window shall remain open from 9:55 a.m. to10:30 a.m.

b. The orders may be placed in this window at a price not exceeding ±1 % from theruling market price/previous day closing price, as applicable.

c. An order may be placed for a minimum quantity of 500,000 shares or minimum valueof Rs. 5 crore.

d. Every trade executed in this window must result in delivery and shall not be squaredoff or reversed.

e. The stock exchanges shall disseminate the information on the block deals such asthe name of the scrip, name of the client, quantity of shares boughUsold, traded price,etc to the general public on the same day, after the market hours.

There is no change in regard to the disclosure of trade details of "bulk deals" as specified in the earlierSEBI circular no. SEBI/MRO/SE/Cir - 7/2004 dated January 14,2004.

The Stock exchanges shall disseminate the aforesaid information on the same day after market hoursto the general public.

, .

-This document is authorized for use only by K Selvakumar. Xavier Institute of Management and Entrepreneurship.Copying or posting is an infringement of copyright.

t '. 1t IIM{\iF&A0484------1

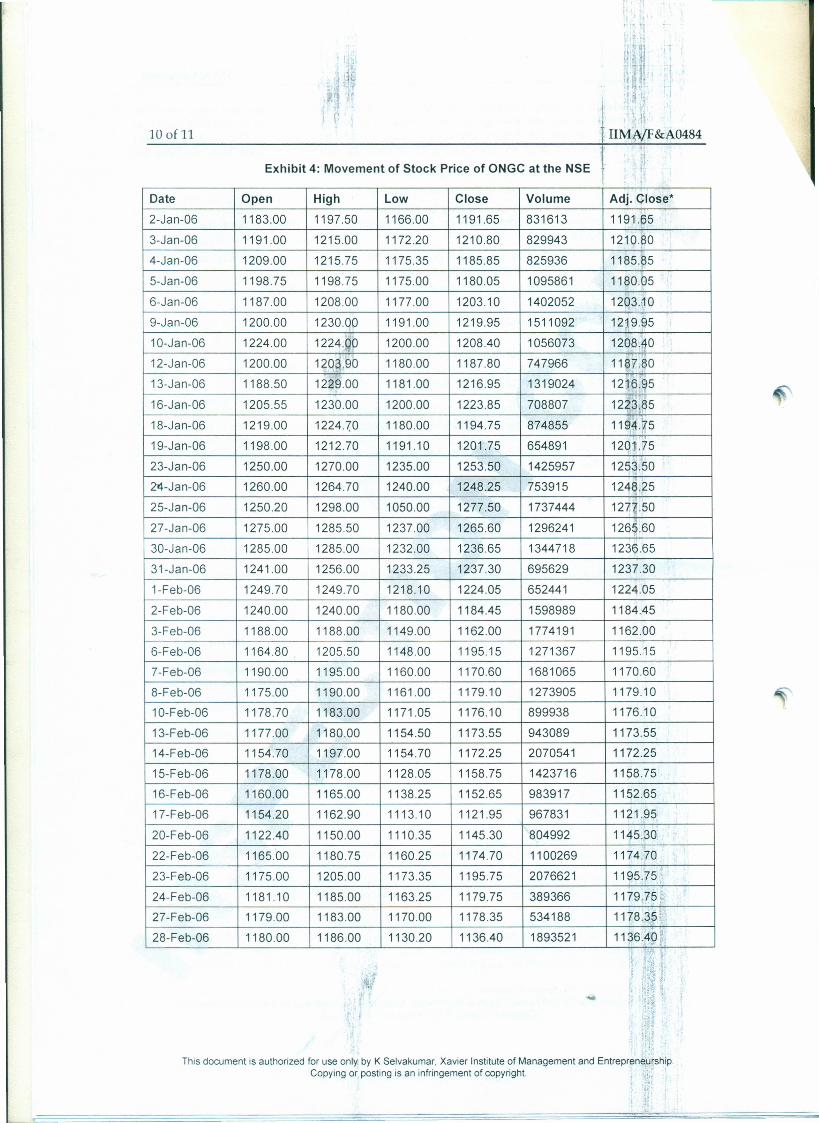

Exhibit 4: Movement of Stock Price of ONGC at the NSE

10 of 11

Date Open High Low Close Volume Adj. Close"2-Jan-06 1183.00 1197.50 1166.00 1191.65 831613 1191.65

3-Jan-06 1191.00 1215.00 1172.20 1210.80 829943 1210.~0

4-Jan-06 1209.00 1215.75 1175.35 1185.85 825936 1185.85

5-Jan-06 1198.75 1198.75 1175.00 1180.05 1095861 1180.05

6-Jan-06 1187.00 1208.00 1177.00 1203.10 1402052 1203.~0

9-Jan-06 1200.00 1230.00 1191.00 1219.95 1511092 12~9.95

10-Jan-06 1224.00 1224.QP 1200.00 1208.40 1056073 1208,~0

12-Jan-06 1200.00 12Q6,90 1180.00 1187.80 747966 1Hl7.80

13-Jan-06 1188.50 1229.00 1181.00 1216.95 1319024 1216.95

16-Jan-06 1205.55 1230.00 1200.00 1223.85 708807 122i3,~5

18-Jan-06 1219.00 1224)0 1180.00 1194.75 874855 119;4.i7,5

19-Jan-06 1198.00 1212.70 1191.10 1201.75 654891 120f75

23-Jan-06 1250.00 1270.00 1235.00 1253.50 1425957 1253.50

24-Jan-06 1260.00 1264.70 1240.00 1248.25 753915 1248.25

25-Jan-06 1250.20 1298.00 1050.00 1277.50 1737444 1271.50

27 -Jan-06 1275.00 1285.50 1237.00 1265.60 1296241 1265,60

30-Jan-06 1285.00 1285.00 1232.00 1236.65 1344718 1236.65

31-Jan-06 1241.00 1256.00 1233.25 1237.30 695629 1237.30

1-Feb-06 1249.70 1249.70 1218.10 1224.05 652441 1224.05

2-Feb-06 1240.00 1240.00 1180.00 1184.45 1598989 1184.45

3-Feb-06 1188.00 1188.00 1149.00 1162.00 1774191 1162.00

6-Feb-06 1164.80 1205.50 1148.00 1195.15 1271367 1195.15

7-Feb-06 1190.00 1195.00 1160.00 1170.60 1681065 1170.60

8-Feb-06 1175.00 1190.00 1161.00 1179.10 1273905 1179.10

10-Feb-06 1178.70 1183.00 1171.05 1176.10 899938 1176.10

13-Feb-06 1177.00 1180.00 1154.50 1173.55 943089 1173.55

14-Feb-06 1154.70 1197.00 1154.70 1172.25 2070541 1172.25

15-Feb-06 1178.00 1178.00 1128.05 1158.75 1423716 1158.75

16-Feb-06 1160.00 1165.00 1138.25 1152.65 983917 1152.65

17-Feb-06 1154.20 1162.90 1113.10 1121.95 967831 1121.95

20-Feb-06 1122.40 1150.00 1110.35 1145.30 804992 1145.30

22-Feb-06 1165.00 1180.75 1160.25 1174.70 1100269 1174.70

23-Feb-06 1175.00 1205.00 1173.35 1195.75 2076621 1195.75

24-Feb-06 1181.10 1185.00 1163.25 1179.75 389366 1179,75,

27-Feb-06 1179.00 1183.00 1170.00 1178.35 534188 1178.35·

28-Feb-06 1180.00 1186.00 1130.20 1136.40 1893521 1136.40 :. '.

-This document is authorized for use only by K Selva kumar, Xavier Institute of Management and Entrepreneurship.

Copying or posting is an infringement of copyright."

11 of 1] IIMA/F &A0484

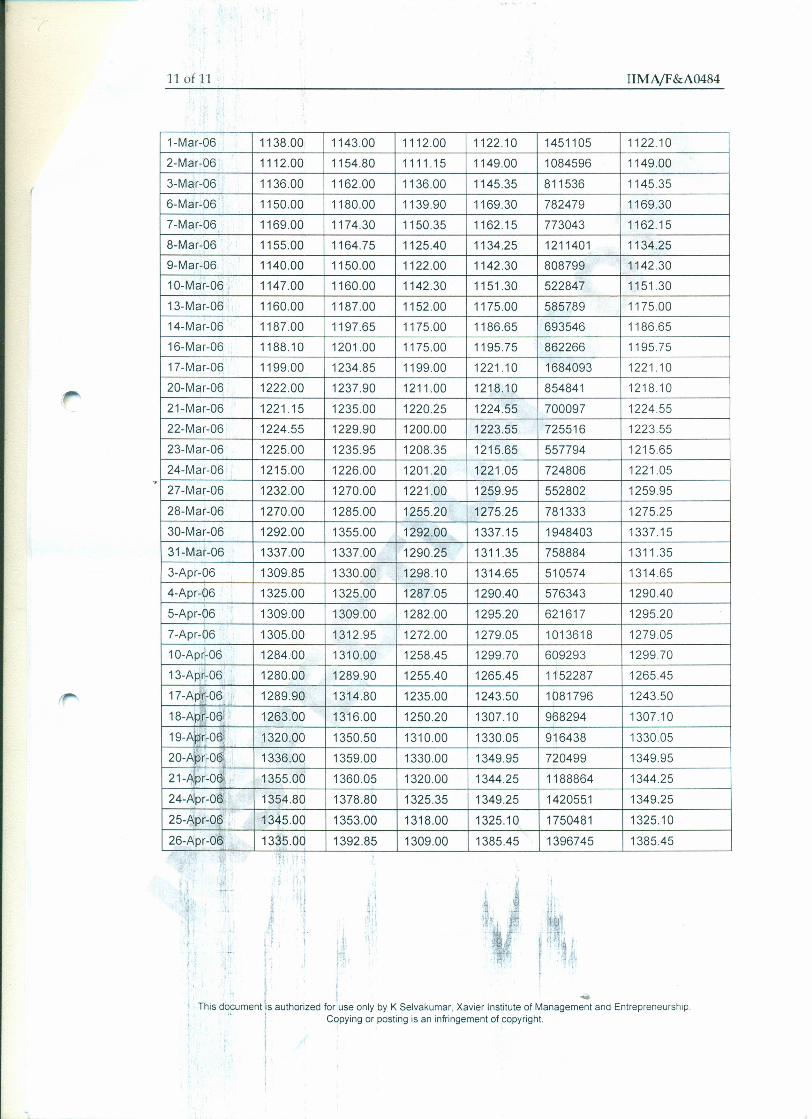

1-Mar-06 1138.00 1143.00 1112.00 1122.10 1451105 1122.10

2-Mar-06 1112.00 1154.80 1111.15 1149.00 1084596 1149.00

3-Mar-06 1136.00 1162.00 1136.00 1145.35 811536 1145.35

6-Mar-06 1150.00 1180.00 1139.90 1169.30 782479 1169.30

7-Mar-06 1169.00 1174.30 1150.35 1162.15 773043 1162.15

8-Mar-06 1155.00 1164.75 1125.40 1134.25 1211401 1134.25

9-Mar-06 1140.00 1150.00 1122.00 1142.30 808799 1142.30

10-Mar-06 1147.00 1160.00 1142.30 1151.30 522847 1151.30

13-Mar-06 1160.00 1187.00 1152.00 1175.00 585789 1175.00

14-Mar-06 1187.00 1197.65 1175.00 1186.65 693546 1186.65

16-Mar-06 1188.10 1201.00 1175.00 1195.75 862266 1195.75

17-Mar-06 1199.00 1234.85 1199.00 1221.10 1684093 1221.10

20-Mar-06 1222.00 1237.90 1211.00 1218.10 854841 1218.10

21-Mar-06 1221.15 1235.00 1220.25 1224.55 700097 1224.55

22-Mar-06 1224.55 1229.90 1200.00 1223.55 725516 1223.55

23-Mar-06 1225.00 1235.95 1208.35 1215.65 557794 1215.65..

24-Mar-06 1215.00 1226.00 1201.20 122105 724806 1221.05

27-Mar-06 1232.00 1270.00 1221.00 1259.95 552802 1259.95

28-Mar-06 1270.00 1285.00 1255.20 1275.25 781333 1275.25

30-Mar-06 1292.00 1355.00 1292.00 1337.15 1948403 1337.15

31-Mar-06 1337.00 1337.00 1290.25 1311.35 758884 1311.35

3-Apr-06 1309.85 1330.00 1298.10 1314.65 510574 1314.65

4-Apr-06 1325.00 1325.00 1287.05 1290.40 576343 1290.40

5-Apr-06 1309.00 1309.00 1282.00 1295.20 621617 1295.20

7-Apr-06 1305.00 1312.95 1272.00 1279.05 1013618 1279.05

1O-Ap~ 06 1284.00 1310.00 1258.45 1299.70 609293 1299.70

13-Ap~06 1280.00 1289.90 1255.40 1265.45 1152287 1265.45

17-Apr-06. 1289.90 1314.80 1235.00 1243.50 1081796 1243.50~18-A\:~r-06U 1263.00 1316.00 1250.20 1307.10 968294 1307.10,19-A ~r.-06 1320.00 1350.50 1310.00 1330.05 916438 133005. '"20-11: ~r-O(( 1336.00 1359.00 1330.00 1349.95 720499 1349.95

21-A,:l!>r-0~ 1355.00 1360.05 1320.00 1344.25 1188864 1344.25

24-Alpr-06' 1354.80 1378.80 1325.35 1349.25 1420551 1349.25

25-A'pr-06' 1345.00 1353.00 1318.00 1325.10 1750481 1325.10

26-Apr-06 1335.00 1392.85 1309.00 1385.45 1396745 1385.45_ ...

,.I~

I;

I

I iI -This document is authorized for use only by K Selvakumar. Xavier Institute of Management and Entrepreneurship.

..• Copying or posting is an infringement of copyright.