Embed Size (px)

Citation preview

Contents

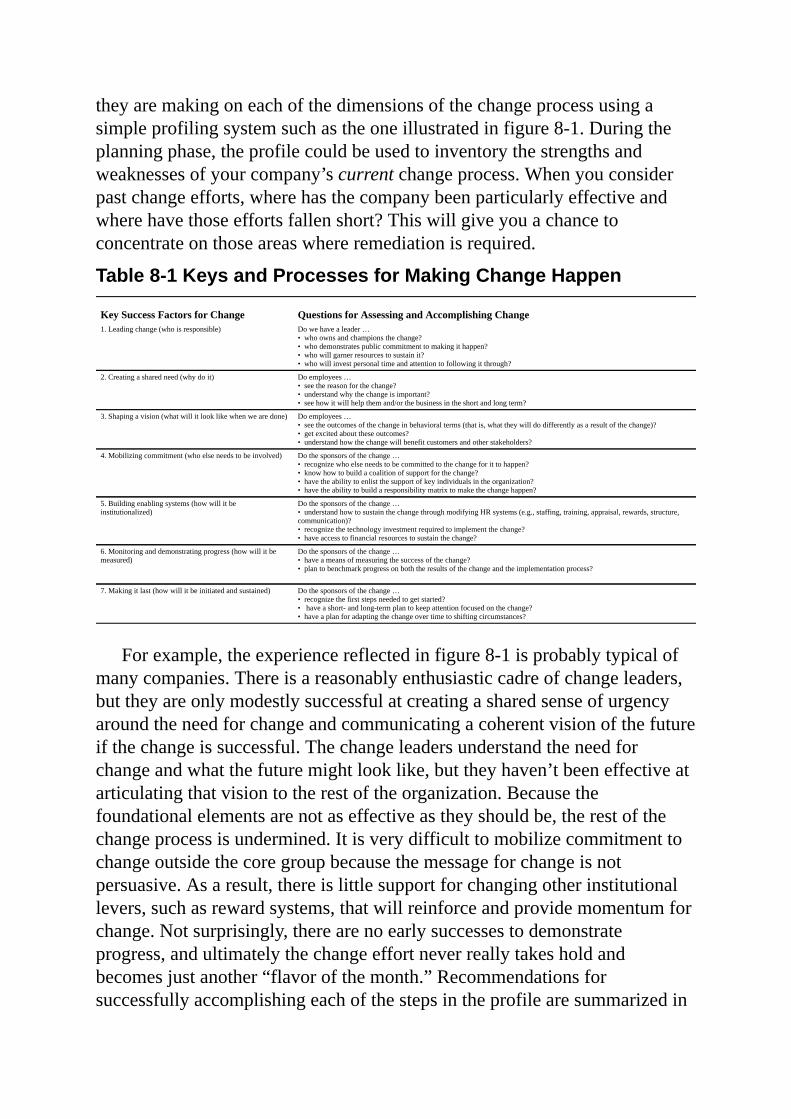

1HRasaStrategicPartner:TheMeasurementChallenge

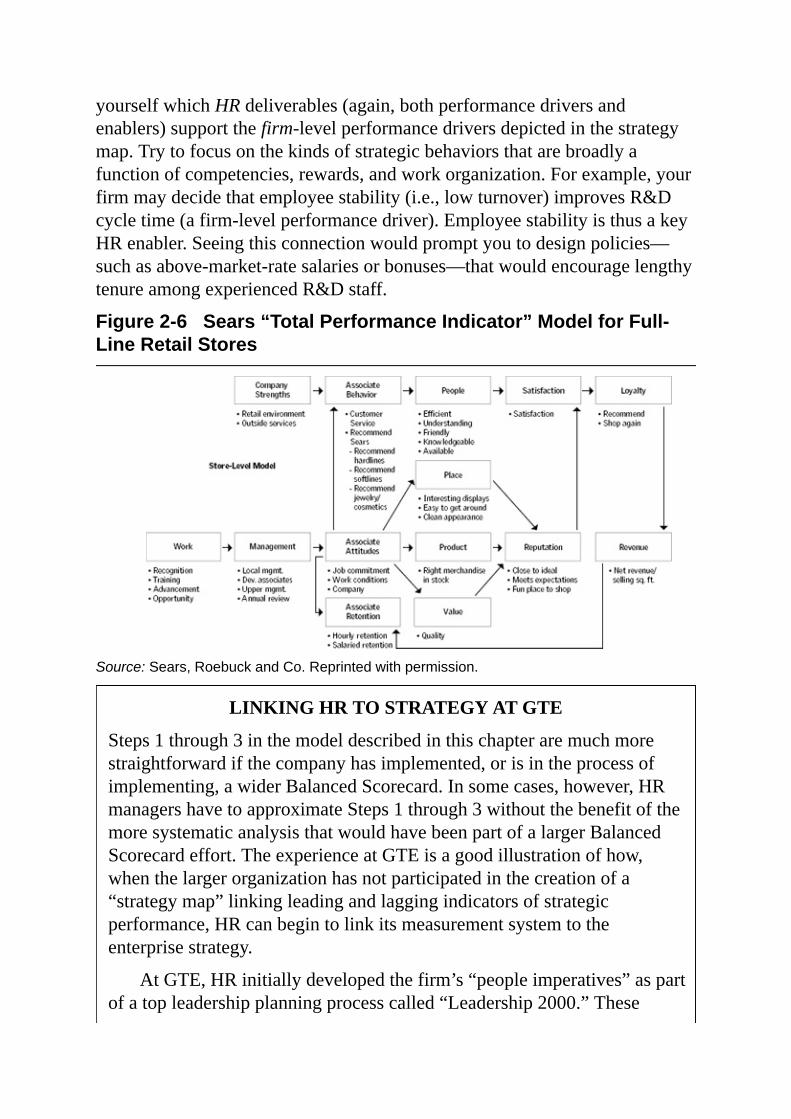

2ClarifyingandMeasuringHR’sStrategicInfluence:IntroductiontoaSeven-StepProcess

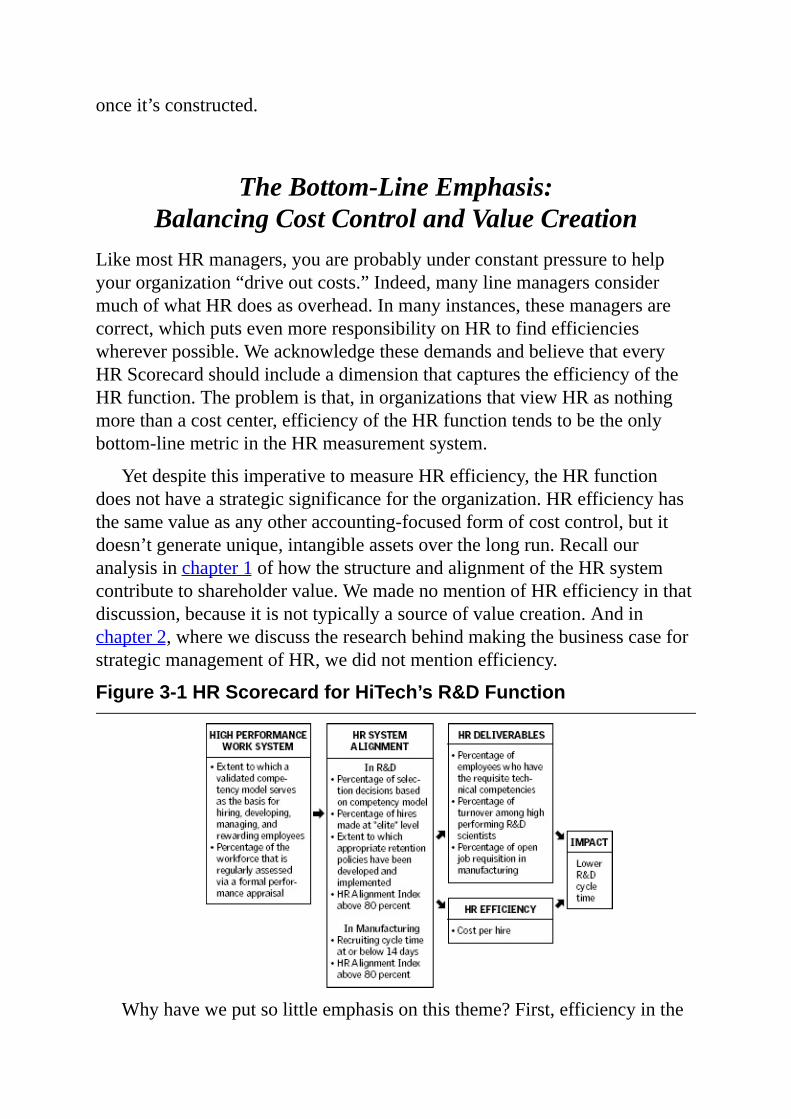

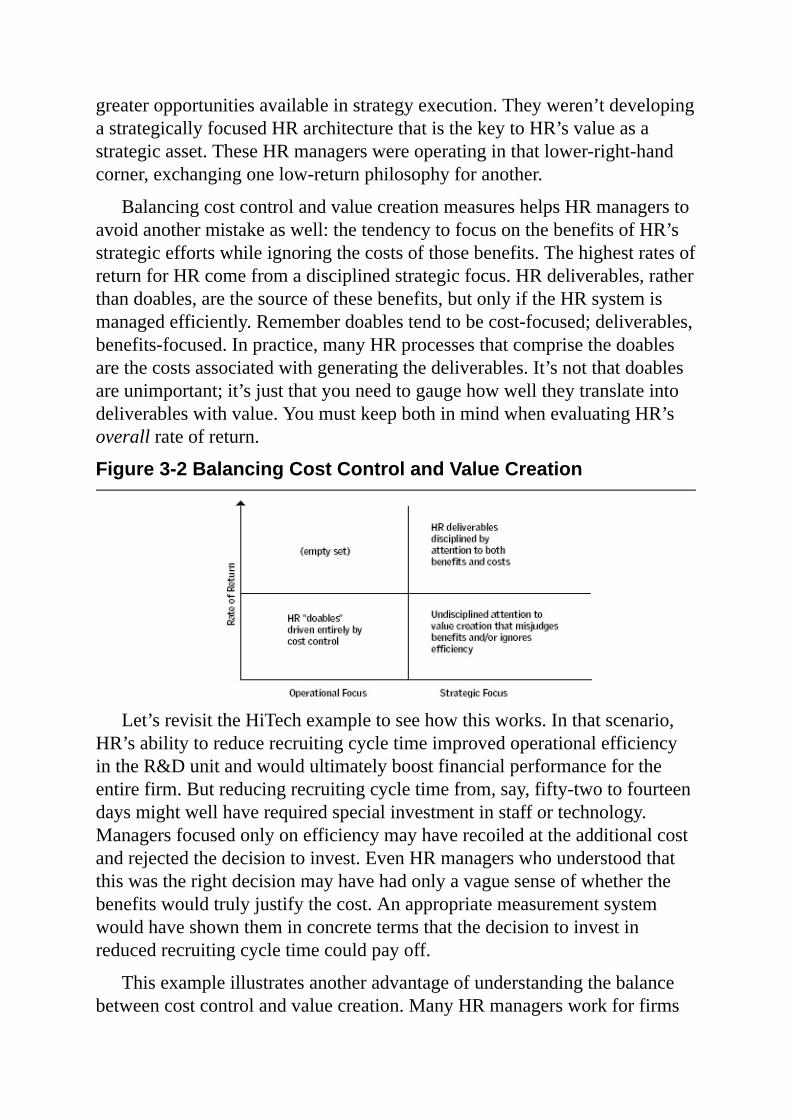

3CreatinganHRScorecard

4Cost-BenefitAnalysesforHRInterventions

5ThePrinciplesofGoodMeasurement

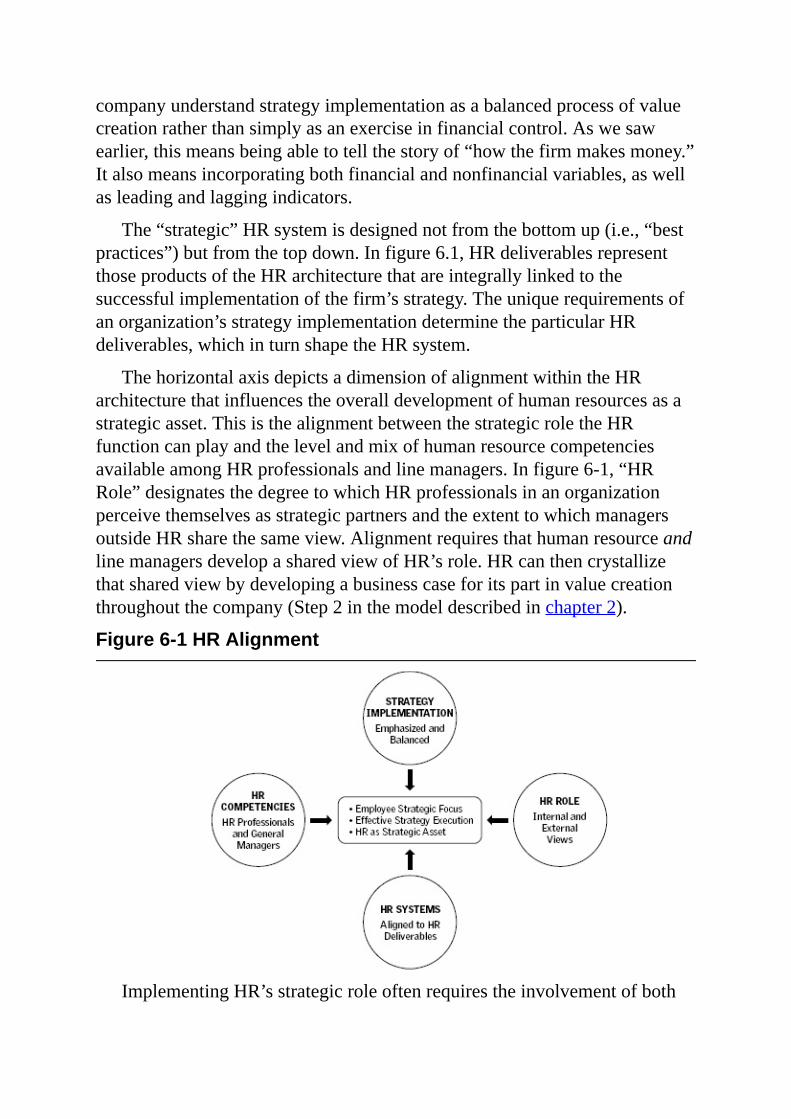

6MeasuringHRAlignment

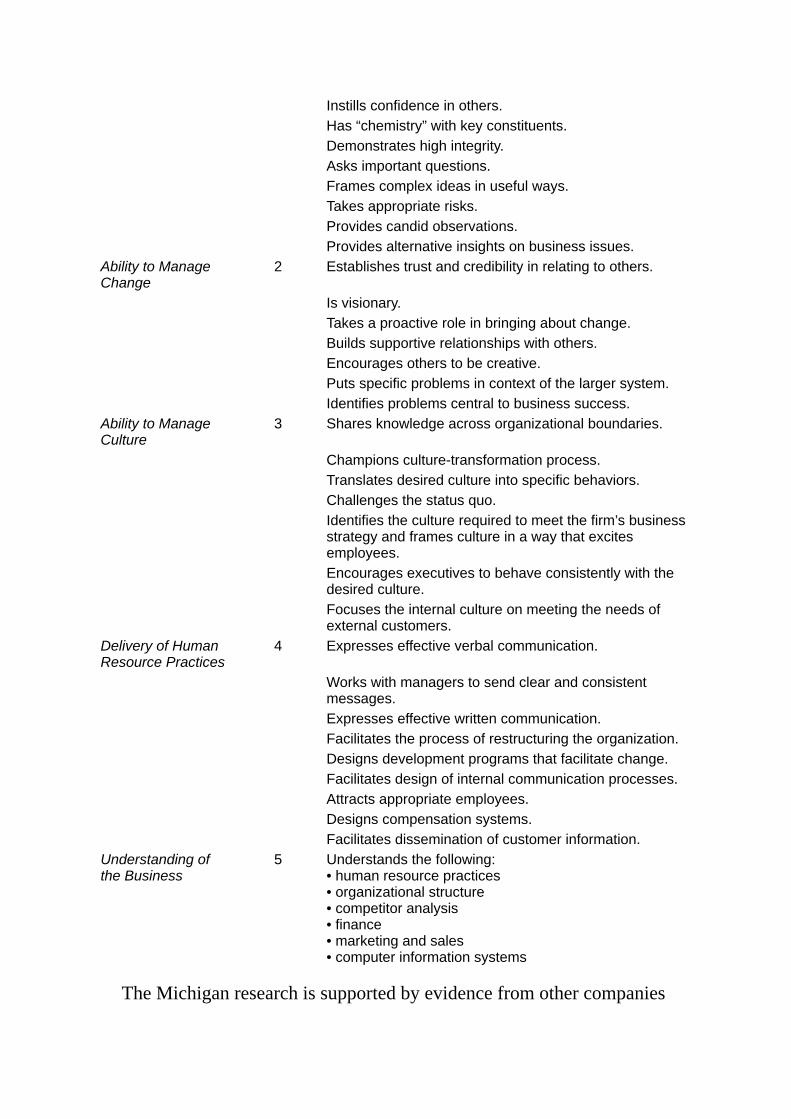

7CompetenciesforHRProfessionals

8GuidelinesforImplementinganHRScorecard

Appendix:ResearchandResults

Notes

AbouttheAuthors

Foreword

BOBKAPLANANDIFIRSTINTRODUCEDtheideaofaBalancedScorecardina1992HarvardBusinessReviewarticle.1Sincethattimewe,andourconsultingorganization,havehadtheopportunitytodesignBalancedScorecardsinmorethan200companies.Thesedesignsalwaysstartwiththesamesimplequestion,Whatisyourstrategy?Thisexperiencehasgivenusfarreachinginsightsintothewaysthatexecutiveteamsthinkaboutstrategyandtheirorganizations.Thetypicalexecutiveteamhasahighdegreeofawarenessandconsensusaroundthefinancialstrategy,aswellastheprioritiesforoperationalprocessimprovement.Theytypicallyhavelimitedconsensusaroundcustomerstrategies(i.e.,whoarethetargetsegments,whatisthevalueproposition),althoughthishasimprovedinrecentyears.Buttheworstgradesarereservedfortheirunderstandingofstrategiesfordevelopinghumancapital.Thereislittleconsensus,littlecreativity,andnorealframeworkforthinkingaboutthesubject.Worseyet,wehaveseenlittleimprovementinthisoverthepasteightyears.

Thegreatestconcernhereisthat,intheNewEconomy,humancapitalisthefoundationofvaluecreation.(Variousstudiesshowthatupto85percentofacorporation’svalueisbasedonintangibleassets.)Thispresentsaninterestingdilemma:Theassetthatismostimportantistheleastunderstood,leastpronetomeasurement,and,hence,leastsusceptibletomanagement.Clearly,weareatawatershed.Asaneweconomicmodelripplesthroughtheeconomy,anewscienceofmanagementisneeded.Inaneconomywherevaluecreationisdominatedbyhumancapitalandotherintangibleassets,therecanbenobetterstartingpointforthisnewsciencethanwiththemeasurementofhumanresourcestrategies.TheHRScorecarddoesjustthatandprovidesanimportantstepforwardinourabilitytomanagestrategy.

Severalfacetsofthebookwillmakelastingcontributions.First,the

developmentofcausalmodels,whichshowtherelationshipofHRvaluedriverswithbusinessoutcomes,takestheBalancedScorecardtothenextlevelofsophistication.Second,theresearchintothedriversofhigh-performanceHRorganizationsgivesexecutivesaframeworkwithwhichtobuildstrategiesforhumancapitalgrowth.Andfinally,theirinsightsintothecompetenciesrequiredbyHRprofessionalslaythegroundworkforanorganizationthatcandeliveronthepromiseofitsmeasurementsystems.

Wecan’tmanagesomethingthatwecan’tdescribe.Measurementisthelanguageusedtodescribeorganizationsandstrategy.Throughtheframeworks,research,andcasesencompassedinthiswork,theauthorshavegivenusanewgenerationoftoolstomeasureandmanagethecreationofhumancapital.TheHRScorecardshouldbeessentialreadingfortheNewEconomymanager.

DAVIDNORTON

BOSTON,MASSACHUSETTS

PrefaceandAcknowledgments

PROFESSIONALSINHUMANRESOURCESareincreasinglychallengedtotakeamorestrategicperspectiveregardingtheirroleintheorganization.WefindthatasHRprofessionalsrespondtothischallenge,measuringHR’sperformanceanditscontributiontothefirm’sperformanceconsistentlyemergesasakeytheme.Thisshouldcomeasnosurprise.Thelastdecadehasbeenhighlightedbyanever-increasingappreciationforthevalueofintangibleassetsandtheassociatedtrendtowardstrategicperformancemeasurementsystemssuchasRobertKaplanandDavidNorton’sBalancedScorecard.NewopportunitiesforHRprofessionals,newdemandsforHR’saccountability,andnewperspectivesonmeasuringorganizationalperformancehaveallconverged.ThisbookisintendedtoguideHRmanagersthroughthechallengeoftheseconvergingtrends.ItisbasedonmorethanadecadeofacademicresearchontheHR-firmperformancerelationshipandgroundedbyourconsultingworkinawiderangeofcompanies.Theresultisanewapproachtomanagingafirm’s“HRarchitecture”(thesumoftheHRfunction,thebroaderHRsystem,andresultingemployeebehaviors)asastrategicasset,aswellasmeasuringitscontributiontothefirm’sperformance.

Ourwork(somewouldcallitanobsession)inmeasuringHRbeganwithoureffortstotrytounderstandwhether,andifsobyhowmuch,thisbroaderHRarchitecturecontributestofirmsuccess.OverthelastdecadewehavecollecteddataonHRmanagementqualityfromnearly3,000firmsandhavematchedthesedatawithemployeeturnover,productivity,stockmarket,andaccountingperformancemeasures.We’vevisitedthesecompanies,followedtheirperformanceovertime,writtencasesaboutthem,andsubjectedthemtodetailedstatisticalanalyses.Alloftheseactivitieshaveledustothesamebroadconclusion:FirmswithmoreeffectiveHRmanagementsystems

consistentlyoutperformtheirpeers.

Yet,inourteachingandconsultingworkwithexecutivesweconsistentlyconfronted(andwereconfrontedby)thesameparadox:EvidencethatHRcancontributetofirmsuccessdoesn’tmeanthatitisnoweffectivelycontributingtosuccessinanygivenbusiness.Managers(HRandline)haverepeatedlychallengeduswiththequestion,Basedonyourresearch,howcanImakeHRastrategicassetinmyfirm?

WehavecometobelievethatthecapacitytodesignandimplementastrategicHRmeasurementsystem—whatwecallinthisbookanHRScorecard—representsanimportantleverthatfirmscanusetodesignanddeployamoreeffectiveHRstrategy.However,implementingeffectivemeasurementsystemsisnoteasy;ifitwere,wewouldseealotmoreofthem.Inaddition,beingheldaccountableforresultsthroughmeasurementcanbethreatening.Manymanagerswillavoiditiftheycan.Butbasedonourexperience,firmsfrequentlyunderinvestintheirpeople—and,justasimportant,investinthewrongways.Moreover,manyfirmsseemtobeunawareoftheconsequencesoftheirinvestmentdecisionsinvolvingpeople.Themosteffectivewayweknowtochangethecalculusistodevelopameasurementsystemdesignedtolinkpeople,strategy,andperformance.Thisiswhatthisbookisintendedtodo.

ACKNOWLEDGMENTS

Thisprojectdrawsinspirationandwisdomfromtheeffortsandsupportofmanyindividuals.WeareespeciallyindebtedtoGarrettWalker,directorofHRPlanning,MeasurementandAnalysisatGTE(nowVerizon),andSteveKirn,VPforInnovationandOrganizationalDevelopmentatSears.GarrettandStevewereverygenerouswithboththeirtimeandtheirpatience,providingawindowintothebestcurrentworkonHRmeasurementsystems.ThereaderwillalsoquicklyrecognizetheintellectualdebtweowetoBobKaplanandDaveNorton.Wehavebenefitednotonlyfromtheirworkon“balanced”strategicperformancemeasurement,butalsofromthepassionandgenerositywithwhichtheysharethoseideas.BrianBeckerandMarkHuselidwouldalsoliketothankReedKellerandBobLindgrenofPriceWaterhouseCoopers,LLCfortheirvisionandenthusiasmaboutmeasuringHR’simpactonfirmperformance.Theydisplayedaconfidenceintheseideas,andinus,atatimewhentheseideasweren’tverywellaccepted.

Ourworkhasalsobenefitedimmenselyfromtheinfluenceofawidevarietyofcolleagues.WewouldparticularlyliketothankJaneBarnes,DickBeatty,WayneBrockbank,SusanJackson,SteveKerr,JeffreyPfeffer,andRandallSchulerfortheirabilitytoframetheissuesaboutmeasurementandtheirwillingnesstodebatetheseideasandsharetheirinsights.CarolTutzauer’sfamiliaritywiththeGalileoprogramwasanessentialcontributiontochapter6.WayneCasciohasalsohadanimportantinfluenceonourthinking,especiallyevidentinchapter4.

ThisprojectwouldnothavebeenpossiblewithoutthefinancialsupportoftheSchoolofManagementandLaborRelationsatRutgersUniversity,theHumanResourcePlanningSociety,andtheSHRMFoundation.Inadditiontofundingmuchofthisresearch,RutgersalsoprovidedMarkwithasabbaticaltoworkonthisproject.MarkwouldalsoliketothankhisgraduatestudentsinHRStrategy,HRMeasurement,andFinancialAnalysisforHRManagers,whocontinuallychallengehimandhelphimtorefinehisthinking.

WealsooweaspecialdebtofgratitudetotheeditorsattheHarvardBusinessSchoolPress.Thereaderwillbenefitfromthegentle,butfirm,effortsofNicolaSabinandLaurieJohnsontomoveusawayfromournaturaltendenciestowritelikeacademics.

Finally,wearemostgratefultoourfamilies,whoprovideloveandsupporttoovaluabletomeasure.

BRIANE.BECKER

MARKA.HUSELID

DAVEULRICH

1

HRASASTRATEGICPARTNERTheMeasurementChallenge

HowcanweensurethatHRisatthetable—andnotonthetable?

ASYOUBEGINTOREADTHISBOOK,takeamomenttoreflectonyourfirm’shumanresources“architecture”—thesumoftheHRfunction,thebroaderHRsystem,andtheresultingemployeebehaviors.Whyarethesethreefeaturesimportant?HowdoestheHRarchitecturehelpyourcompanytoexcelinthemarketplace?

Ifyourorganizationislikemost,you’reprobablyfindingitdifficulttoanswerthesequestions.Inourexperience,manyHRmanagementteamshaveawell-developedvisionoftheirdepartment’sstrategicvalue(atleastfromtheperspectiveofHR),buttheCEOandseniorlinemanagersareatbestskepticalofHR’sroleinthefirm’ssuccess.Worse,inmanyfirms,executiveswanttobelievethat“peopleareourmostimportantasset,”buttheyjustcan’tunderstandhowtheHRfunctionmakesthatvisionareality.

Whatexplainsthissituation?Webelievethattheseproblemshavethesamerootcause:HR’sinfluenceonfirmperformanceisdifficulttomeasure.Considertheelementsandoutcomesofyourfirm’shumanresourcesarchitecturethataretrackedonaregularbasis.Youmighthaveincludedtotalcompensation,employeeturnover,costperhire,thepercentageofemployeeswhohadaperformanceappraisalinthelasttwelvemonths,andemployeeattitudessuchasjobsatisfaction.NowconsiderthoseHRattributesthatyoubelievearecrucialtotheimplementationofyourfirm’scompetitivestrategy.Hereyoumightmentionacapableandcommittedworkforce,developmentofessentialemployeecompetencies,oratrainingsystemthathelpsyouremployeeslearnfasterthanyourcompetitors.

HowwelldoyourexistingHRmeasurescapturethe“strategicHR

drivers”thatyouidentifiedinyoursecondlist?Formostfirmstherewon’tbeaveryclosematch.Moreimportant,eveninfirmswhereHRprofessionalsthinkthereisaclosematch,frequentlytheseniorexecutivesdonotagreethatthissecondlistactuallydescribeshowHRcreatesvalue.Ineithercase,thereisadisconnectbetweenwhatismeasuredandwhatisimportant.

Thesequestionsarefundamental,becauseneweconomicrealitiesareputtingpressureonHRtowidenitsfocusfromtheadministrativeroleithastraditionallyplayedtoabroader,strategicrole.Astheprimarysourceofproductioninoureconomyhasshiftedfromphysicaltointellectualcapital,seniorHRmanagershavecomeunderfiretodemonstrateexactlyhowtheycreatevaluefortheirorganizations.Moreimportant,theyhavebeenchallengedtoserveincreasinglyasstrategicpartnersinrunningthebusiness.

Butwhatdoesitmeantobeastrategicasset?Theliteraturedefinesthetermas“thesetofdifficulttotradeandimitate,scarce,appropriable,andspecializedresourcesandcapabilitiesthatbestowthefirm’scompetitiveadvantage.”1Thinkaboutthedifferencebetweentheabilitytoaligneveryemployee’seffortswiththecompany’soverallvision,andaninnovativepolicysuchas360-degreeperformanceappraisals.Thefirstisastrategiccapabilitywhosecauseislargelyinvisibletocompetitors;thesecondisapolicythat,althoughinitiallyinnovative,isvisibletocompetitors—andthusquicklycopied.Simplyput,strategicassetskeepafirm’scompetitiveedgesharpforthelonghaul—butbydefinitiontheyaredifficulttocopy.

ThusHR’sproblem—thatitsimpactonfirmstrategyisdifficulttosee—istheveryqualitythatalsomakesitaprimesourceofsustainablecompetitivepotential.Buttorealizethispotential,humanresourcemanagersmustunderstandthefirm’sstrategy;thatis,itsplanfordevelopingandsustaininganadvantageinthemarketplace.Then,theymustgrasptheimplicationsofthatstrategyforHR.Inshort,theymustmovefroma“bottom-up”perspective(emphasizingcomplianceandtraditionalHR)toa“top-down”perspective(emphasizingtheimplementationofstrategy).Finally,theyneedinnovativeassessmentsystemsthatwillletthemdemonstratetheirinfluenceonmeasuresthatmattertoCEOs,namely,firmprofitabilityandshareholdervalue.

THEEVOLVINGPICTUREOFHR:FROMPROFESSIONALTOSTRATEGIC

PARTNER

RecentdecadeshavewitnesseddramaticshiftsintheroleofHR.Traditionally,managerssawthehumanresourcefunctionasprimarilyadministrativeandprofessional.HRstafffocusedonadministeringbenefitsandotherpayrollandoperationalfunctionsanddidn’tthinkofthemselvesasplayingapartinthefirm’soverallstrategy.

EffortstomeasureHR’sinfluenceonthefirm’sperformancereflectedthismind-set.Specifically,theoristsexaminedmethodologiesandpracticesthatarefocusedattheleveloftheindividualemployee,theindividualjob,andtheindividualpractice(suchasemployeeselection,incentivecompensation,andsoforth).Theideawasthatimprovementsinindividualemployeeperformancewouldautomaticallyenhancetheorganization’sperformance.

AlthoughsuchresearchattemptedtoextendtherangeofHR’sinfluence,itdidlittletoadvanceHRasanewsourceofcompetitiveadvantage.ItprovidedscantinsightintothecomplexitiesofastrategicHRarchitecture.Andsimplyput,itdidn’tencourageHRmanagerstothinkdifferentlyabouttheirrole.

Inthe1990s,anewemphasisonstrategyandtheimportanceofHRsystemsemerged.Researchersandpractitionersalikebegantorecognizetheimpactofaligningthosesystemswiththecompany’slargerstrategyimplementationeffort—andassessingthequalityofthatfit.Indeed,althoughmanykindsofHRmodelsareinusetoday,wecanthinkofthemasrepresentingthefollowingevolutionofhumanresourcesasastrategicasset:

Thepersonnelperspective:Thefirmhiresandpayspeoplebutdoesn’tfocusonhiringtheverybestordevelopingexceptionalemployees.

Thecompensationperspective:Thefirmusesbonuses,incentivepay,andmeaningfuldistinctionsinpaytorewardhighandlowperformers.Thisisafirststeptowardrelyingonpeopleasasourceofcompetitiveadvantage,butitdoesn’tfullyexploitthebenefitsofHRasastrategicasset.

Thealignmentperspective:Seniormanagersseeemployeesasstrategicassets,buttheydon’tinvestinoverhaulingHR’scapabilities.Therefore,theHRsystemcan’tleveragemanagement’sperspective.

Thehigh-performanceperspective:HRandotherexecutivesviewHRasasystemembeddedwithinthelargersystemofthefirm’sstrategyimplementation.Thefirmmanagesandmeasurestherelationship

betweenthesetwosystemsandfirmperformance.

We’relivinginatimewhenaneweconomicparadigm—characterizedbyspeed,innovation,shortcycletimes,quality,andcustomersatisfaction—ishighlightingtheimportanceofintangibleassets,suchasbrandrecognition,knowledge,innovation,andparticularlyhumancapital.ThisnewparadigmcanmarkthebeginningofagoldenageforHR.Yetevenwhenhumanresourceprofessionalsandseniorlinemanagersgraspthispotential,manyofthemdon’tknowhowtotakethefirststepstowardrealizingit.

Inourview,themostpotentactionHRmanagerscantaketoensuretheirstrategiccontributionistodevelopameasurementsystemthatconvincinglyshowcasesHR’simpactonbusinessperformance.Todesignsuchameasurementsystem,HRmanagersmustadoptadramaticallydifferentperspective,onethatfocusesonhowhumanresourcescanplayacentralroleinimplementingthefirm’sstrategy.WithaproperlydevelopedstrategicHRarchitecture,managersthroughoutthefirmcanunderstandexactlyhowpeoplecreatevalueandhowtomeasurethevalue-creationprocess.

Learningtoserveasstrategicpartnersisn’tjustawayforHRpractitionerstojustifytheirexistenceordefendtheirturf.Ithasimplicationsfortheirverysurvivalandforthesurvivalofthefirmasawhole.IftheHRfunctioncan’tshowthatitaddsvalue,itrisksbeingoutsourced.Initself,thisisn’tnecessarilyabadthing;outsourcinginefficientfunctionscanactuallyenhanceafirm’soverallbottomline.However,itcanwastemuch-neededpotential.Withtherightmind-setandmeasurementtools,theHRarchitecturecanmeanthedifferencebetweenacompanythat’sjustkeepingpacewiththecompetitionandonethatissurgingahead.

Arecentexperienceofoursgraphicallyillustratesthisprinciple.Inacompanywevisited,weaskedthepresidentwhatmostworriedhim.Hequicklyrespondedthatthefinancialmarketwasvaluinghisfirm’searningsathalfthatofhiscompetitors’.Insimpleterms,hisfirm’s$100ofcashflowhadamarketvalueof$2,000,whilehislargestcompetitor’s$100ofcashflowhadamarketvalueof$4,000.Heworriedthatunlesshecouldchangethemarket’sperceptionofthelong-termvalueofhisorganization’searnings,hisfirmwouldremainundervaluedandpossiblybecomeatakeovertarget.Healsohadalargeportionofhispersonalnetworthinthefirm,andheworriedthatitwasnotvaluedashighlyasitcouldbe.

WhenweaskedhimhowhewasinvolvinghisHRexecutiveingrapplingwiththisproblem,hedismissedthequestionwithawaveofhishandandsaid,“MyheadofHRisverytalented.Butthisisbusiness,notHR.”He

acknowledgedthathisHRdepartmenthadlaunchedinnovativerecruitingtechniques,performance-basedpaysystems,andextensiveemployeecommunications.Nevertheless,hedidn’tseethosefunctions’relevancetohisproblemofhowtochangeinvestors’perceptionsofhisfirm’smarketvalue.

Sixmonthsafterourmeeting,acompetitoracquiredthefirm.

ThesadtruthisthattheHRexecutiveinthisstorymissedavaluableopportunity.IfhehadunderstoodandknownhowtomeasuretheconnectionbetweeninvestmentsinHRarchitectureandshareholdervalue,thingsmighthaveturnedoutdifferently.Armedwithanawarenessofhowinvestorsvalueintangibles,hemighthavehelpedhispresidentbuildtheeconomiccaseforincreasedshareholdervalue.

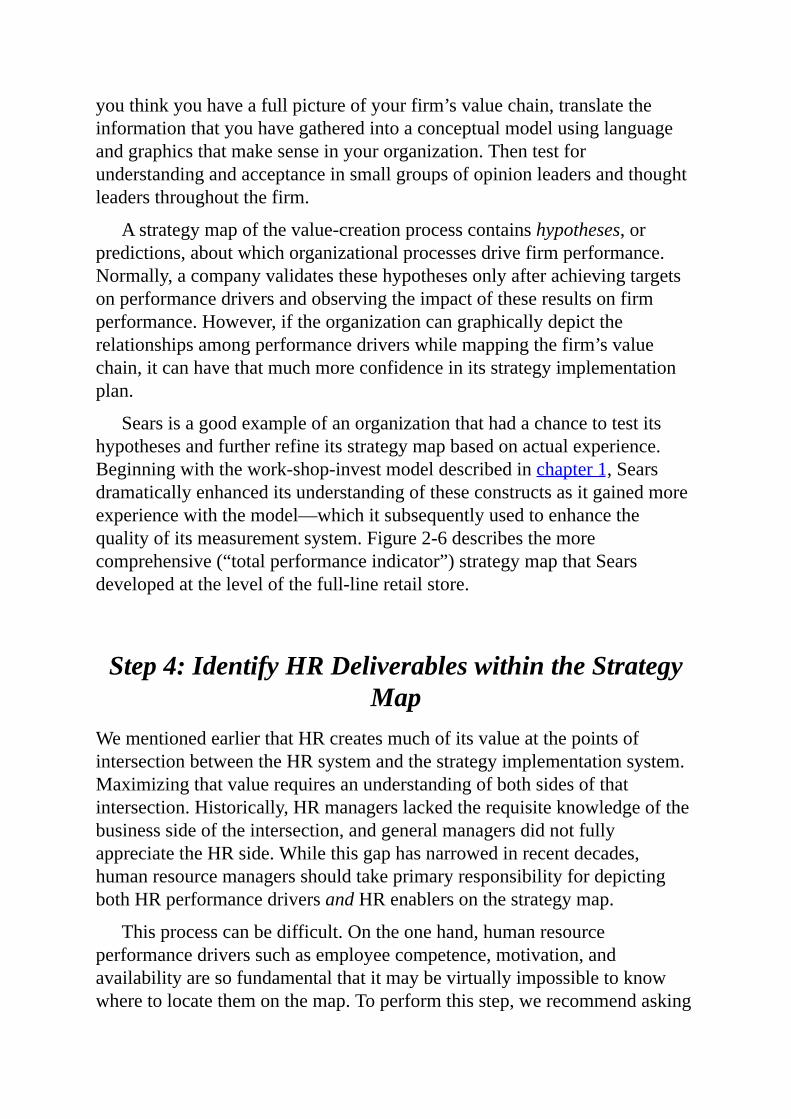

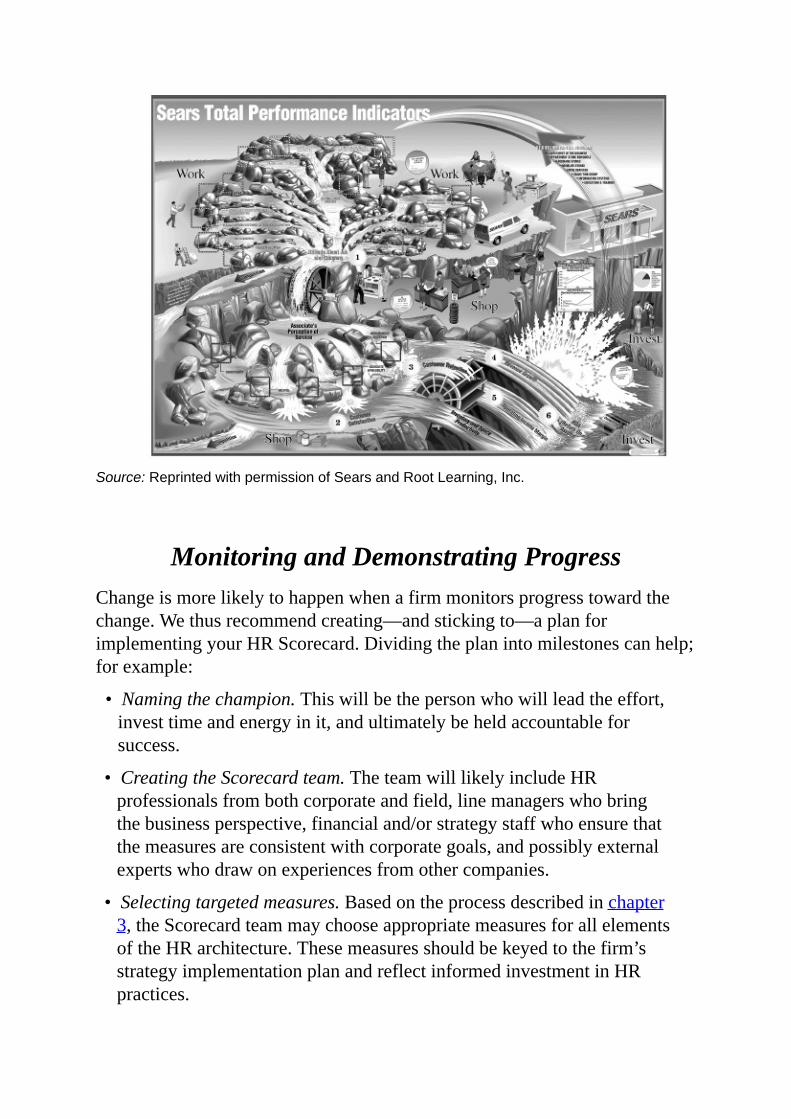

ThestoryofSears,RoebuckandCo.’srecenttransformationstandsinstarkcontrasttothisanecdoteandshowswhatcompaniescanachievewhentheydoalignHRwiththelargerorganization’sstrategy.2Afterstrugglingwithlackoffocusandlossesinthebillionsintheearly1990s,Searscompletelyoverhauleditsstrategyimplementationprocess.LedbyArthurMartinez,aseniormanagementteamincorporatedthefullrangeofperformancedriversintotheprocess,fromtheemployeethroughfinancialperformance.Then,theyarticulatedanew,inspiringvision:ForSearstobeacompellingplaceforinvestors,theysaid,thecompanymustfirstbecomeacompellingplacetoshop.Forittobeacompellingplacetoshop,itmustbecomeacompellingplacetowork.

ButSearsdidn’tjustleavethisstrategicvisionintheexecutivesuiteortypeituponlittlecardsforemployeestoputintheirwallets.Itactuallyvalidatedthevisionwithharddata.Searsthendesignedawaytomanagethisstrategywithameasurementsystemthatreflectedthisvisioninallitsrichness.Specifically,theteamdevelopedobjectivemeasuresforeachofthethree“compellings.”Forexample,“supportforideasandinnovation”helpedestablishSearsasa“compellingplacetowork.”Similarly,byfocusingonbeinga“funplacetoshop,”Searsbecameamore“compellingplacetoshop.”3Theteamextendedthisapproachfurtherbydevelopinganassociatedseriesofrequiredemployeecompetenciesandidentifyingbehavioralobjectivesforeachofthe“3-Cs”atseverallevelsthroughtheorganization.Thesecompetenciesthenbecamethefoundationonwhichthefirmbuiltitsjobdesign,recruiting,selection,performancemanagement,compensation,andpromotionactivities.SearsevencreatedSearsUniversityinordertotrainemployeestoachievethenewlydefinedcompetencies.Theresultwasasignificantfinancialturnaroundthatreflectednotonlya“strategic”influence

forHRbutonethatcouldbemeasureddirectly.

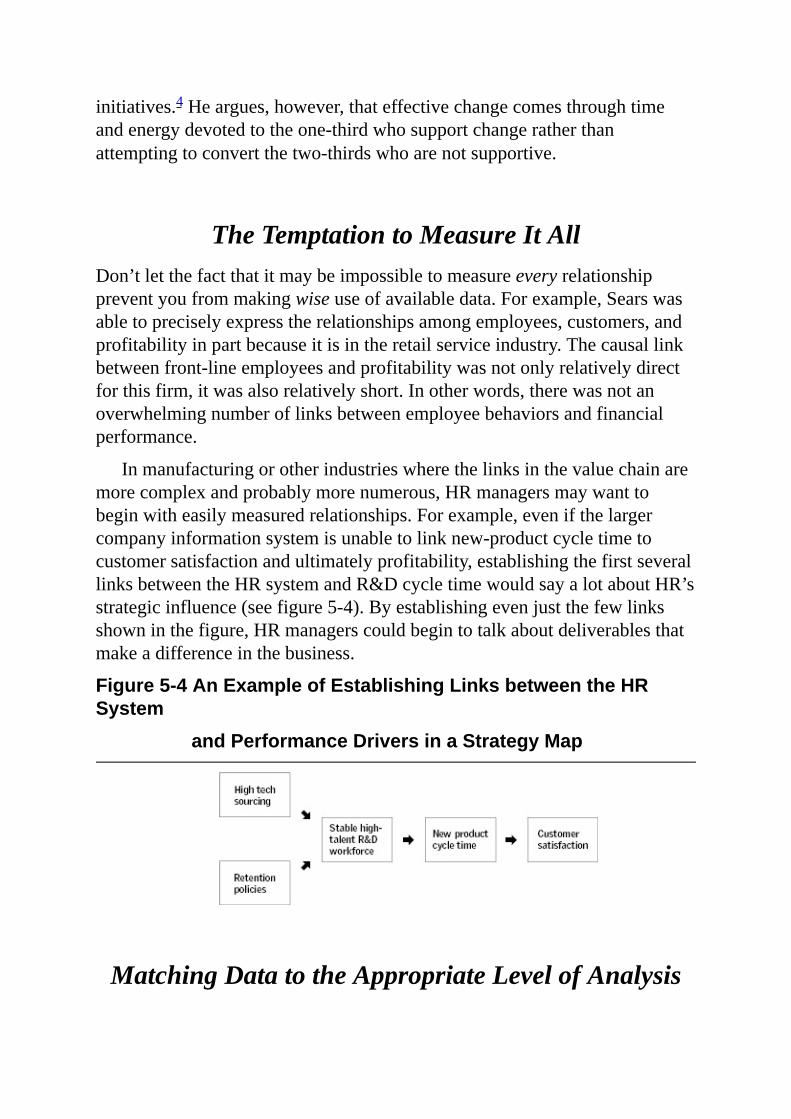

FewfirmshavetakensuchacomprehensiveapproachtothemeasurementofstrategyimplementationasSearshas.Granted,retailserviceindustriesarecharacterizedbyaclear“lineofsight”betweenemployeesandcustomers.Thustheirvalue-creationstoryiseasiertoarticulate.Butthatdoesn’tmeanthatotherindustriescan’taccomplishthisfeat.Thechallengesmaybegreater—butsoaretherewards.

WHYHR?WHYNOW?

Considerthefollowing:

Inmostindustries,itisnowpossibletobuyontheinternationalmarketplacemachineryandequipmentthatiscomparabletothatinplacebytheleadingglobalfirms.Accesstomachineryandequipmentisnotthedifferentiatingfactor.Abilitytouseiteffectivelyis.Acompanythatlostallofitsequipmentbutkepttheskillsandknowhowofitsworkforcecouldbebackinbusinessrelativelyquickly.Acompanythatlostitsworkforce,whilekeepingitsequipment,wouldneverrecover.4

Thisexcerptcapturesthedifferencebetweenphysicalandintellectualcapital—andrevealstheuniqueadvantagesofthelatter.TheCoca-ColaCompany’sexperiencetestifiestothisreality.Accordingtothen-CFOJamesChestnut,aftertransferringthebulkofitstangibleassetstoitsbottlers,Coke’s$150billionmarketvaluederivedlargelyfromitsbrandandmanagementsystems.5

Theevidenceisunmistakable:HR’semergingstrategicpotentialhingesontheincreasinglycentralroleofintangibleassetsandintellectualcapitalintoday’seconomy.Sustained,superiorbusinessperformancerequiresafirmtocontinuallyhoneitscompetitiveedge.Traditionally,thisefforttooktheformofindustry-levelbarrierstoentry,patentprotections,andgovernmentalregulations.Buttechnologicalchange,rapidinnovation,andderegulationhavelargelyeliminatedthosebarriers.Becauseenduring,superiorperformancenowrequiresflexibility,innovation,andspeedtomarket,competitiveadvantagetodaystemsprimarilyfromtheinternalresourcesandcapabilitiesofindividualorganizations—includingafirm’sabilitytodevelopandretainacapableandcommittedworkforce.Asthekeyenablerofhuman

capital,HRisinaprimepositiontoleveragemanyotherintangiblesaswell,suchasgoodwill,researchanddevelopment,andadvertising.

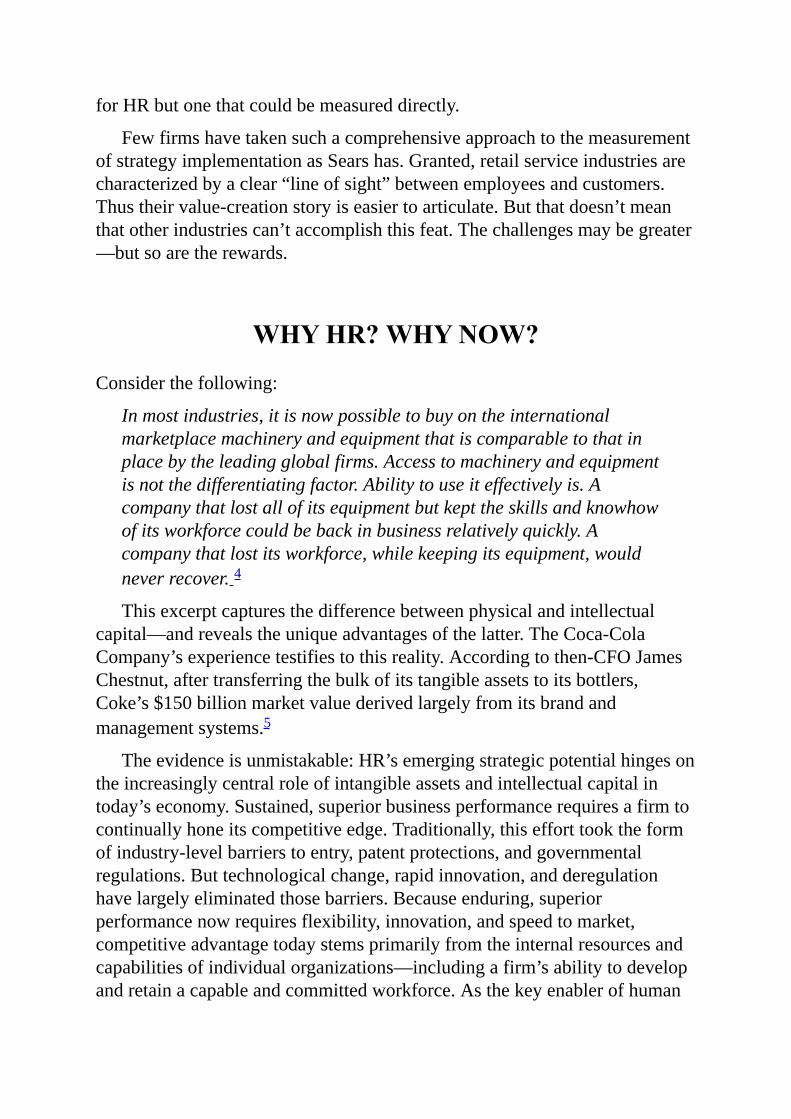

Table1-1takesacloserlookatthemajordifferencesbetweentangibleandintangibleassets.ItalsosuggeststhatmanagingHRrequiresvastlydifferentskillsfromthoseneededtomanagetangibleassets.Inparticular,thebenefitsofHRasanassetarenotalwaysvisible—theycometolightonlywhentheHRroleisskillfullyalignedwithanotherintangibleasset:theorganization’sstrategyimplementationsystem.

Table1-1TangibleversusIntangibleAssets

TangibleAssets IntangibleAssetsReadilyvisible InvisibleRigorouslyquantified DifficulttoquantifyPartofthebalancesheet NottrackedthroughaccountingInvestmentproducesknownreturns AssessmentbasedonassumptionsCanbeeasilyduplicated CannotbeboughtorimitatedDepreciateswithuse AppreciateswithpurposefuluseHasfiniteapplications HasmultipleapplicationswithoutvaluereductionBestmanagedwith“scarcity”mentality Bestmanagedwith“abundance”mentalityBestleveragedthroughcontrol BestleveragedthroughalignmentCanbeaccumulatedandstored Dynamic,shortshelflifewhennotinuse

Source:HubertSaint-Onge,ConferenceBoardpresentation,Boston,MA,October17,1996.Reprintedwithpermission.

INTANGIBLEASSETSGENERATETANGIBLEBENEFITS

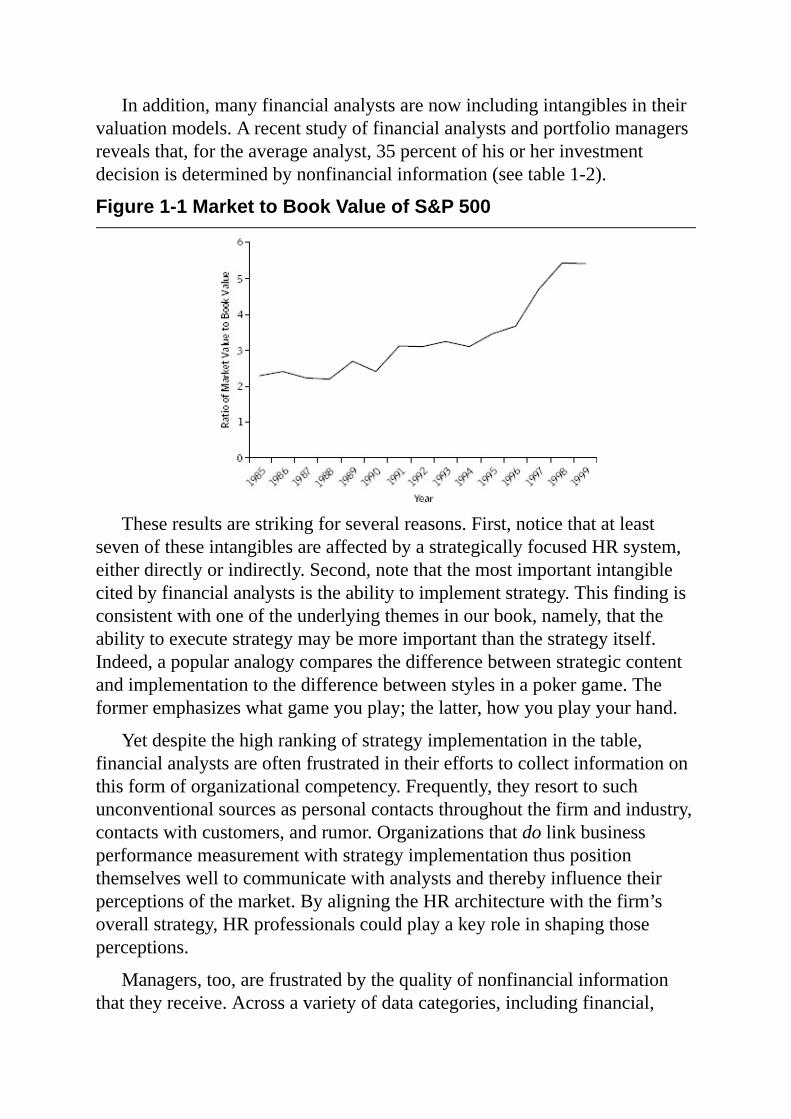

Theincreasingimportanceoforganizationalcapabilitiesandintangibleassetsismuchmorethanacademicspeculation.TrendsinU.S.equitymarketsalsoreflectthisshift.Specifically,thesemarketshaveshownaconsistentwideningintheratioofthemarketvalueofafirm(i.e.,theshareholders’assessmentofthefirm’svalue)toitsbookvalue(theshareholders’initialinvestment).Thisratiohasmorethandoubledinthelasttenyearsalone(seefigure1-1).Thisphenomenoniswidespread,butit’sparticularlynoteworthyincompaniesthatrelyheavilyonintellectualcapitalastheirsourceofcompetitiveadvantage.Someofthesefirmshaveinventedentirelynewbusinessmodelsbasedlargelyonintangibleassets.Forexample,DellandAmazon.com,whichessentiallydealincommodities,havereapedextraordinarygainsinshareholdervaluethroughtheirmanagementsystems.

Inaddition,manyfinancialanalystsarenowincludingintangiblesintheirvaluationmodels.Arecentstudyoffinancialanalystsandportfoliomanagersrevealsthat,fortheaverageanalyst,35percentofhisorherinvestmentdecisionisdeterminedbynonfinancialinformation(seetable1-2).

Figure1-1MarkettoBookValueofS&P500

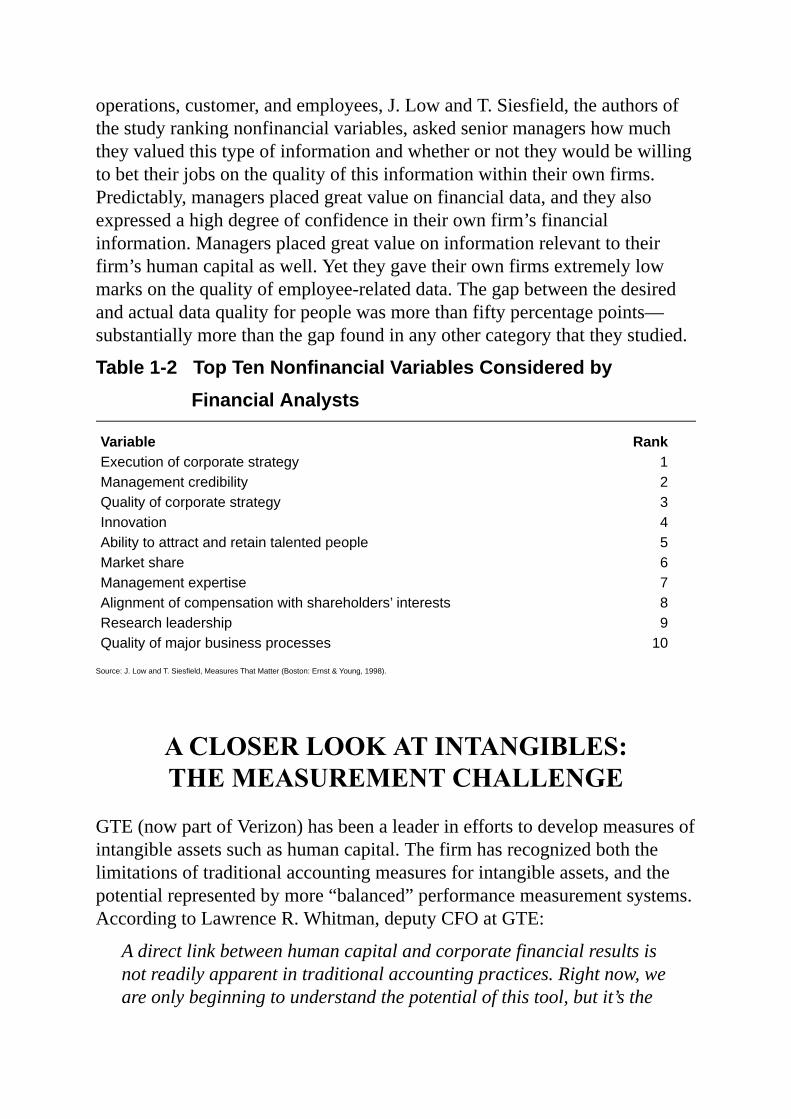

Theseresultsarestrikingforseveralreasons.First,noticethatatleastsevenoftheseintangiblesareaffectedbyastrategicallyfocusedHRsystem,eitherdirectlyorindirectly.Second,notethatthemostimportantintangiblecitedbyfinancialanalystsistheabilitytoimplementstrategy.Thisfindingisconsistentwithoneoftheunderlyingthemesinourbook,namely,thattheabilitytoexecutestrategymaybemoreimportantthanthestrategyitself.Indeed,apopularanalogycomparesthedifferencebetweenstrategiccontentandimplementationtothedifferencebetweenstylesinapokergame.Theformeremphasizeswhatgameyouplay;thelatter,howyouplayyourhand.

Yetdespitethehighrankingofstrategyimplementationinthetable,financialanalystsareoftenfrustratedintheireffortstocollectinformationonthisformoforganizationalcompetency.Frequently,theyresorttosuchunconventionalsourcesaspersonalcontactsthroughoutthefirmandindustry,contactswithcustomers,andrumor.Organizationsthatdolinkbusinessperformancemeasurementwithstrategyimplementationthuspositionthemselveswelltocommunicatewithanalystsandtherebyinfluencetheirperceptionsofthemarket.ByaligningtheHRarchitecturewiththefirm’soverallstrategy,HRprofessionalscouldplayakeyroleinshapingthoseperceptions.

Managers,too,arefrustratedbythequalityofnonfinancialinformationthattheyreceive.Acrossavarietyofdatacategories,includingfinancial,

operations,customer,andemployees,J.LowandT.Siesfield,theauthorsofthestudyrankingnonfinancialvariables,askedseniormanagershowmuchtheyvaluedthistypeofinformationandwhetherornottheywouldbewillingtobettheirjobsonthequalityofthisinformationwithintheirownfirms.Predictably,managersplacedgreatvalueonfinancialdata,andtheyalsoexpressedahighdegreeofconfidenceintheirownfirm’sfinancialinformation.Managersplacedgreatvalueoninformationrelevanttotheirfirm’shumancapitalaswell.Yettheygavetheirownfirmsextremelylowmarksonthequalityofemployee-relateddata.Thegapbetweenthedesiredandactualdataqualityforpeoplewasmorethanfiftypercentagepoints—substantiallymorethanthegapfoundinanyothercategorythattheystudied.

Table1-2TopTenNonfinancialVariablesConsideredbyFinancialAnalysts

Variable RankExecutionofcorporatestrategy 1Managementcredibility 2Qualityofcorporatestrategy 3Innovation 4Abilitytoattractandretaintalentedpeople 5Marketshare 6Managementexpertise 7Alignmentofcompensationwithshareholders’interests 8Researchleadership 9Qualityofmajorbusinessprocesses 10

Source:J.LowandT.Siesfield,MeasuresThatMatter(Boston:Ernst&Young,1998).

ACLOSERLOOKATINTANGIBLES:THEMEASUREMENTCHALLENGE

GTE(nowpartofVerizon)hasbeenaleaderineffortstodevelopmeasuresofintangibleassetssuchashumancapital.Thefirmhasrecognizedboththelimitationsoftraditionalaccountingmeasuresforintangibleassets,andthepotentialrepresentedbymore“balanced”performancemeasurementsystems.AccordingtoLawrenceR.Whitman,deputyCFOatGTE:

Adirectlinkbetweenhumancapitalandcorporatefinancialresultsisnotreadilyapparentintraditionalaccountingpractices.Rightnow,weareonlybeginningtounderstandthepotentialofthistool,butit’sthe

measurementprocessthat’simportant.…Onceweareabletomeasureintangibleassetsmoreaccurately,Ithinkinvestorsandfinanceprofessionalswillbegintolookathumancapitalmetricsasanotherindicatorofacompany’svalue.6

Clearly,businesspeopleeverywhererecognizetheimportanceofintangiblesintoday’smarketplace.Yetmanagingtheseintangiblesischallenging,foranumberofreasons.Foronething,theaccountingsystemsinusetodayevolvedduringatimewhentangiblecapital,bothfinancialandphysical,constitutedtheprincipalsourceofprofits.Duringthistime,thoseorganizationsthathadthemostaccesstomoneyandequipmentenjoyedahugecompetitiveadvantage.Withtheemphasisonknowledgeandintangibleassetsintoday’seconomy,conventionalaccountingsystemsactuallycreatedangerousinformationaldistortions.Asjustoneexample,thesesystemsencourageshort-termthinkingwithrespecttothemanagementofintangibles.Why?Becauseexpendituresintheseareasaretreatedasexpensesratherthaninvestmentsinassets.Bycontrast,investmentsinbuildingsandmachineryarecapitalizedanddepreciatedovertheirusefullives.Considertheseniormanagerfacedwiththedecisiontoinvest$10millioninhardassetsor$10millioninpeople.Inpracticalterms,whenafirminvests$10milliondollarsinabuildingorotherphysicalasset,thisinvestmentisdepreciatedovertime,andearningsarereducedgraduallyoveratwenty-orthirty-yearperiod.Incontrast,a$10milliondollarinvestmentinpeopleisexpensedinitsentirety(andthereforeearningsarereducedby$10milliondollars)duringthecurrentyear.Formanagerswhosepayistiedtothisyear’searnings(asmanyare),thechoiceofinvestmentisobvious.

Asaresult,companiesunderfinancialpressuretendtoinvestinphysicalcapitalattheexpenseofhumancapital—eventhoughthelattermaywellgeneratemorevalue.Thiskindofpressurecanleadtopoordecisions:forinstance,toinitiatearoundoflayoffssolelytogarnershort-term“costsavings.”Researchhasrepeatedlyshownthatafteralayoff,themarketmayinitiallyrespondwithajumpinsharevalue.However,investorsofteneventuallyloseallofthesegains,andsometimesmore.7Thispatternisn’tsurprising,giventhatpeopleareacrucialsourceofcompetitiveadvantageratherthananexpensiveluxurythatshouldbeminimized.

Thebottomlineisthis:Ifcurrentaccountingmethodscan’tgiveHRprofessionalsthemeasurementtoolstheyneed,thentheywillhavetodeveloptheirownwaysofdemonstratingtheircontributiontofirmperformance.ThefirststepistodiscardtheaccountingmentalitythatsaysthatHRisprimarilyacostcenterinwhichcostminimizationistheprincipalobjectiveand

measureofsuccess.Atthesametime,HRmanagersmustgrasptherareopportunityaffordedthembythistransitionalperiod.Investorshavemadeitclearthattheyvalueintangibleassets.It’suptoHRtodevelopanewmeasurementsystemthatcreatesrealvalueforthefirmandsecureshumanresources’legitimateplaceasastrategicpartner.

THEHRARCHITECTUREASASTRATEGICASSET

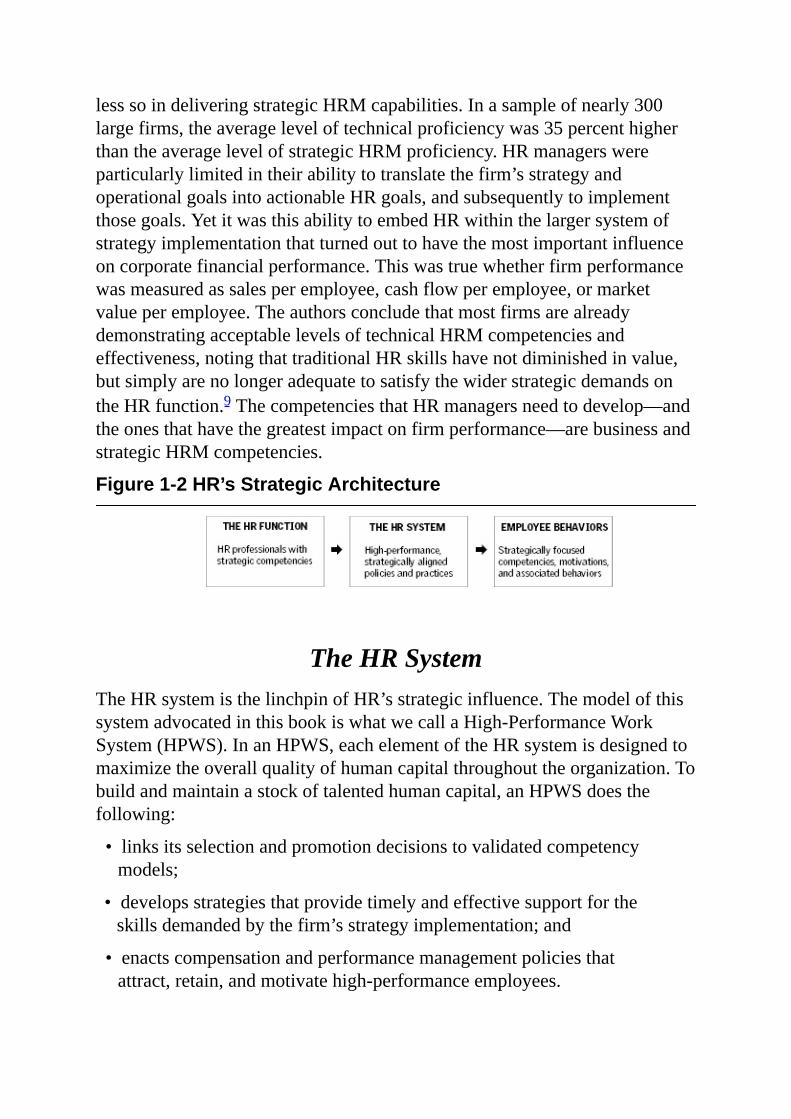

Ifthefocusofcorporatestrategyistocreatesustainedcompetitiveadvantage,thefocusofHRstrategyisequallystraightforward.ItistomaximizethecontributionofHRtowardthatsamegoal,therebycreatingvalueforshareholders.ThefoundationofastrategicHRroleisthethreedimensionsofthe“valuechain”representedbythefirm’sHRarchitecture:thefunction,thesystem,andemployeebehaviors.ThinkingaboutHR’sinfluenceonfirmperformancerequiresafocusonmultiplelevelsofanalysis.Weusetheterm“HRarchitecture”tobroadlydescribethecontinuumfromtheHRprofessionalswithintheHRfunction,tothesystemofHR-relatedpoliciesandpractices,throughthecompetencies,motivations,andassociatedbehaviorsofthefirm’semployees.8(Seefigure1-2.)

TheHRFunctionThefoundationofavalue-creatingHRstrategyisamanagementinfrastructurethatunderstandsandcanimplementthefirm’sstrategy.NormallytheprofessionalsintheHRfunctionwouldbeexpectedtoleadthiseffort.ThisimpliesadeparturefromthetraditionalfunctionalorientationofmanyHRmanagersandawiderunderstandingofthestrategicrolethatHRmightplayinthefirm.Forexample,MarkHuselid,SusanJackson,andRandallSchulerpointoutthathumanresourcesmanagement(HRM)effectivenesshastwoessentialdimensions.Thefirst,technicalHRM,includesthedeliveryofHRbasicssuchasrecruiting,compensation,andbenefits.Thesecond,strategicHRM,involvesdeliveringthoseservicesinawaythatdirectlysupportstheimplementationofthefirm’sstrategy.

HuselidandhiscolleaguesfoundthatmostHRmanagerswereveryproficientinthedeliveryoftraditionalortechnicalHRMactivities,butmuch

lesssoindeliveringstrategicHRMcapabilities.Inasampleofnearly300largefirms,theaverageleveloftechnicalproficiencywas35percenthigherthantheaveragelevelofstrategicHRMproficiency.HRmanagerswereparticularlylimitedintheirabilitytotranslatethefirm’sstrategyandoperationalgoalsintoactionableHRgoals,andsubsequentlytoimplementthosegoals.YetitwasthisabilitytoembedHRwithinthelargersystemofstrategyimplementationthatturnedouttohavethemostimportantinfluenceoncorporatefinancialperformance.Thiswastruewhetherfirmperformancewasmeasuredassalesperemployee,cashflowperemployee,ormarketvalueperemployee.TheauthorsconcludethatmostfirmsarealreadydemonstratingacceptablelevelsoftechnicalHRMcompetenciesandeffectiveness,notingthattraditionalHRskillshavenotdiminishedinvalue,butsimplyarenolongeradequatetosatisfythewiderstrategicdemandsontheHRfunction.9ThecompetenciesthatHRmanagersneedtodevelop—andtheonesthathavethegreatestimpactonfirmperformance—arebusinessandstrategicHRMcompetencies.

Figure1-2HR’sStrategicArchitecture

TheHRSystemTheHRsystemisthelinchpinofHR’sstrategicinfluence.ThemodelofthissystemadvocatedinthisbookiswhatwecallaHigh-PerformanceWorkSystem(HPWS).InanHPWS,eachelementoftheHRsystemisdesignedtomaximizetheoverallqualityofhumancapitalthroughouttheorganization.Tobuildandmaintainastockoftalentedhumancapital,anHPWSdoesthefollowing:

•linksitsselectionandpromotiondecisionstovalidatedcompetencymodels;

•developsstrategiesthatprovidetimelyandeffectivesupportfortheskillsdemandedbythefirm’sstrategyimplementation;and

•enactscompensationandperformancemanagementpoliciesthatattract,retain,andmotivatehigh-performanceemployees.

Theitemsonthislistmayseemobvious.However,theyarevitalstepsinimprovingthequalityofemployeedecision-makingthroughouttheorganization—somethingthatmakesgoodbusinesssenseastraditionalcommand-and-controlmanagementmodelsincreasinglygooutoffashion.Inshort,forHRtocreatevalue,afirmneedstostructureeachelementofitsHRsysteminawaythatrelentlesslyemphasizes,supports,andreinforcesahigh-performanceworkforce.

Butadoptingahigh-performancefocusforindividualHRpoliciesandpracticesisnotnearlyenough.Weusethetermsystemintentionallyhere.ThinkingsystemicallyemphasizestheinterrelationshipsoftheHRsystem’scomponentsandthelinkbetweenHRandthelargerstrategyimplementationsystem.Itistheselinkagesbetweenasystem’scomponents—notanyindividualcomponentitself—thatmakeasystemmorethanjustthesumofitsparts(see“TheLawsofSystemsThinking”).

THELAWSOFSYSTEMSTHINKING

Thinkingsystematicallyisafoundationalcompetencyforseveralstepsinourmodel,becausecertainstepsrequireunderstandingwhathappenswhenmultiplesystemsintersect.Whileacomprehensivetreatmentofsystemsthinkingiswellbeyondthescopeofthisbook,wewouldliketorevisitseveralpertinent“lawsofsystemsthinking”describedbymanagementtheoristPeterM.Senge.*

Today’sProblemsComefromYesterday’s“Solutions.”HRmanagersoperatewithinalargerorganizationalsystem,aswellaswithintheHRsystem.Problems“solved”inonepartofthebusinessoftencropupasnewproblemsinanother.Forexample,topmanagersfacemountingpressurefrominvestorstoboostprofits.Theycutcostsbylayingoffstaff,particularlymiddlemanagers.ThissatisfiesWallStreet,butinthreeorfouryears,thecompanyfindsitselffacedwithaleadershipcrisis.Moreover,HRisstuckwithbothadevelopmentandrecruitingproblem.Systems-savvyHRmanagerscanpointoutthelinksbetweentheseproblemsandsuggestwaystocutstaffthatprotectthefirm’scadreoffutureleaders.

TheEasyWayOutUsuallyLeadsBackIn.Oneimportantbenefitofsystemsthinkingisthatithelpsustoadoptnewperspectivesonproblems.Toooften,werelyoncomfortableandfamiliarsolutionsthathaveworkedinthepast.Totrulyserveasstrategicpartners,humanresourceprofessionalsmustviewHR’svalue-creationrole—

particularlyHRenablers—inawholenewlightandresistthetemptationtouse“tried-and-true”butoutdatedideas.

CauseandEffectAreNotCloselyRelatedinTimeandSpace.Thislawspeakstothedifferencebetweenleadingandlaggingindicators.HR’sinfluenceonfirmperformanceislikelytobemuchlessdirectthanthatofotherstrategicdrivers.ThislagbetweencauseandeffectforHRperformancedriversdoesn’tdiminishtheirultimateinfluence,butitdoesmakeitdifficulttoidentifyandmeasurethatinfluence.Manyseniormanagersrelyprimarilyonconventional,financialperformancemeasures—whicharelaggingindicators.Theyoftentrytosolvefinancialproblemsbyimmediatelycuttingcostsratherthanidentifyingthefundamentalsourcesoftheproblem.Pressuredbytheshort-termdemandsofcapitalmarkets,theyseekthequickfix—onlytodiscoverthatsuchsolutionseitherdon’tlastoractuallyworsentheoriginalproblem.

TheHighestLeveragePointsAreOftentheLeastObvious.Seasonedsystemsthinkersconstantlylookforthelessobvioussolutiontoaproblem.Notsurprisingly,formostCEOs,theobvioussolutionstoimprovedperformancehaverarelyincludedHR.

Thisisthechallengefacinghumanresourceprofessionals.Problemsinfinancialperformancegeteveryone’sattention,butnoonethinksabouthowHRcanhelp.Nevertheless,becauseHRdriversaresofoundational,smallchangesinhowthey’remanagedgathermomentumastheyworktheirwaythroughthestrategyimplementationprocess.Forexample,atSears,amere4-percentincreaseinemployeesatisfactionreverberatedthroughtheprofitchain,eventuallyliftingmarketcapitalizationbynearly$250million.†

CuttinganElephantinHalfDoesn’tGetYouTwoSmallerElephants;ItGetsYouaMess.Inotherwords,ifyoutrytodissectasystem,expectingtobeabletoexamineitspartsinisolation,youmayendupdestroyingit.Organizationsarecomplexsystemsthatinvolveinteractionswithinandbetweenmanydifferentsubsystems.Thus,theyarebestunderstoodfromasystemwideperspective.Yetmostmanagersthinkoftheirfirm’ssubsystemsasfunctionsandlimittheirattentiontotheirown“turf.”Functionalleadersmight“seethefirm’sproblemsclearly,butnoneseehowthepoliciesoftheirdepartmentinteractwith[thoseof]others.”‡AsSengeargues,it’stheinteractions

betweensystemsandamongasystem’spartsthatgeneratebothproblemsandpotentialleveragepointsforchange.Dependingonthesituation,differentsysteminteractionswillbemoreorlessimportantatvarioustimes.Skilledmanagers—includingthoseHRprofessionalswhowanttobemorethanjustadministrators—knowwhichinteractionsmostrequiretheirattention,andwhen.

*PeterSenge,TheFifthDiscipline(Doubleday:NewYork,1990),57–67.†AnthonyJ.Rucci,StevenP.Kirn,andRichardT.Quinn,“TheEmployee-Customer-ProfitChainatSears,”HarvardBusinessReview76,no.1(1998):87.‡Senge,TheFifthDiscipline,66.

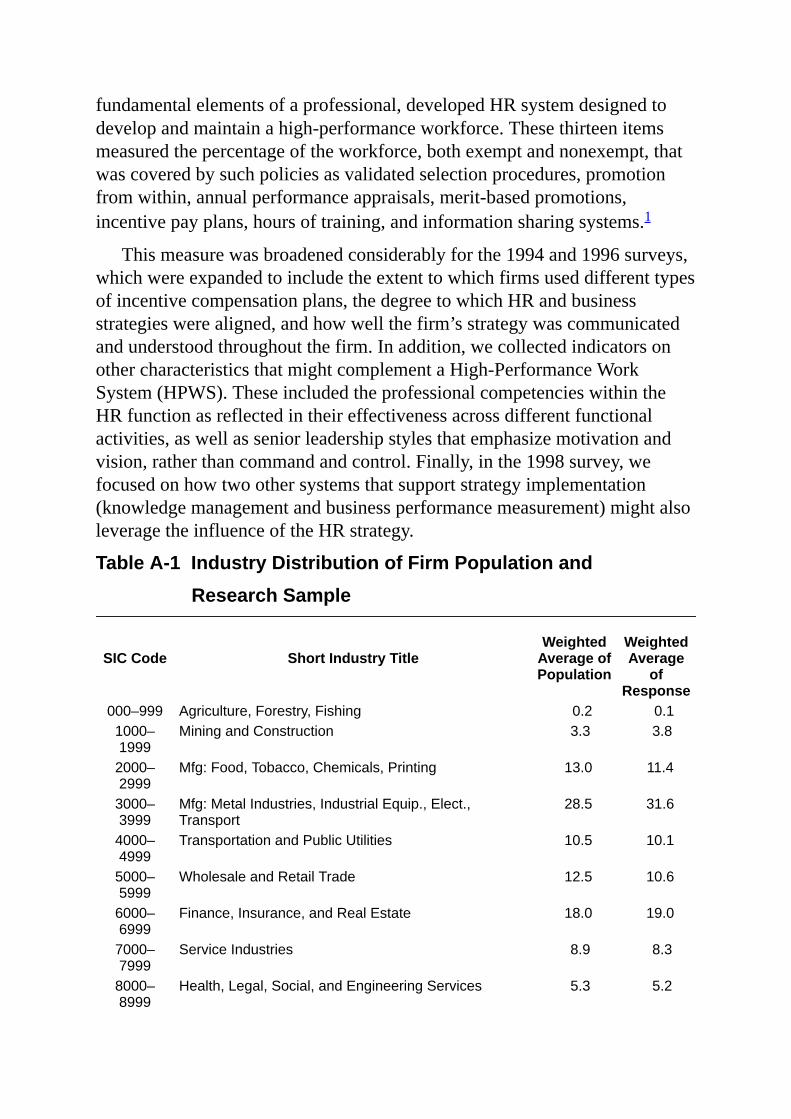

OurdescriptionoftheHPWSraisestheobviousquestion:What,exactly,arethespecificpoliciesandpracticesthatleadtohighperformance?Since1990,twoofushaveconductedabiannualsurveyoftheHRmanagementsystemsinU.S.publiclyheldcompanies.ThefoundationofthisresearchefforthasbeenabiannualsurveyofHRsystemsthattargetsabroadcross-sectionofpubliclytradedfirms:firmswithsalesgreaterthan$5millionandmorethan100employees.ThesedataonHRsystemsarethenmatchedwithpubliclyavailabledataonfinancialperformance.Thisresearchprogramisongoingandnowincludesmorethan2,800corporations.10

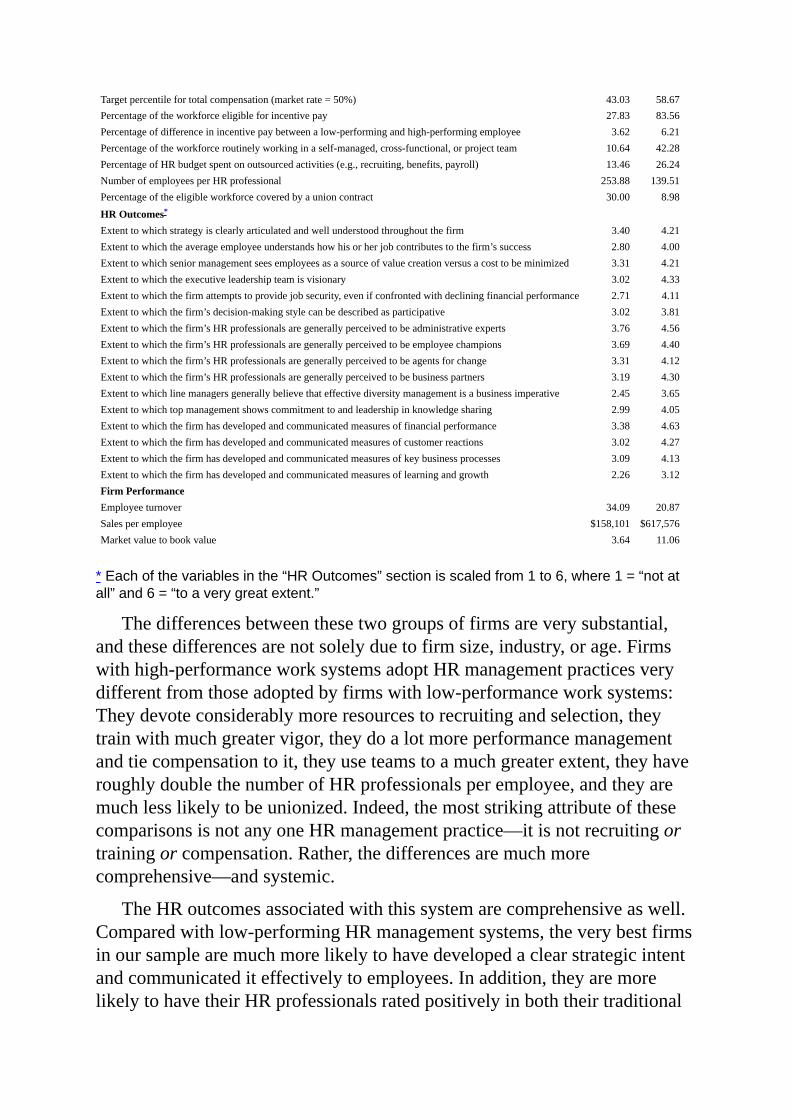

EachsurveyenabledustoconstructanHPWSindexthatmeasurestheextenttowhichafirm’sHRsystemisconsistentwiththeprinciplesofahigh-performanceHRstrategy.Table1-3comparesfirmsinour1998sampleatthetwoendsofthehigh-performanceHRcontinuum.BasedonourHPWSindex,wecalculatedeachfirm’spercentilerankinginoursampleandthencomparedfirmsrankedinthetopdecileontheHPWSindexwiththoseinthebottomdecileonseveralcharacteristics.Theresultsintable1-3arebasedonthe429firmsinour1998sample.However,theresultsareveryrobustandhighlysimilarforour1992,1994,and1996samples.11

Table1-3ComparisonofHighandLowHRManagementQuality

Bottom10%HRIndex(42firms)

Top10%HRIndex(43firms)

HRPractices Numberofqualifiedapplicantsperposition 8.24 36.55Percentagehiredbasedonavalidatedselectiontest 4.26 29.67Percentageofjobsfilledfromwithin 34.90 61.46PercentageinaformalHRplanincludingrecruitment,development,andsuccession 4.79 46.72Numberofhoursoftrainingfornewemployees(lessthan1year) 35.02 116.87Numberofhoursoftrainingforexperiencedemployees 13.40 72.00Percentageofemployeesreceivingaregularperformanceappraisal 41.31 95.17Percentageofworkforcewhosemeritincreaseorincentivepayistiedtoperformance 23.36 87.27Percentageofworkforcewhoreceivedperformancefeedbackfrommultiplesources(360) 3.90 51.67

Targetpercentilefortotalcompensation(marketrate=50%) 43.03 58.67Percentageoftheworkforceeligibleforincentivepay 27.83 83.56Percentageofdifferenceinincentivepaybetweenalow-performingandhigh-performingemployee 3.62 6.21Percentageoftheworkforceroutinelyworkinginaself-managed,cross-functional,orprojectteam 10.64 42.28PercentageofHRbudgetspentonoutsourcedactivities(e.g.,recruiting,benefits,payroll) 13.46 26.24NumberofemployeesperHRprofessional 253.88 139.51Percentageoftheeligibleworkforcecoveredbyaunioncontract 30.00 8.98

HROutcomes*

Extenttowhichstrategyisclearlyarticulatedandwellunderstoodthroughoutthefirm 3.40 4.21Extenttowhichtheaverageemployeeunderstandshowhisorherjobcontributestothefirm’ssuccess 2.80 4.00Extenttowhichseniormanagementseesemployeesasasourceofvaluecreationversusacosttobeminimized 3.31 4.21Extenttowhichtheexecutiveleadershipteamisvisionary 3.02 4.33Extenttowhichthefirmattemptstoprovidejobsecurity,evenifconfrontedwithdecliningfinancialperformance 2.71 4.11Extenttowhichthefirm’sdecision-makingstylecanbedescribedasparticipative 3.02 3.81Extenttowhichthefirm’sHRprofessionalsaregenerallyperceivedtobeadministrativeexperts 3.76 4.56Extenttowhichthefirm’sHRprofessionalsaregenerallyperceivedtobeemployeechampions 3.69 4.40Extenttowhichthefirm’sHRprofessionalsaregenerallyperceivedtobeagentsforchange 3.31 4.12Extenttowhichthefirm’sHRprofessionalsaregenerallyperceivedtobebusinesspartners 3.19 4.30Extenttowhichlinemanagersgenerallybelievethateffectivediversitymanagementisabusinessimperative 2.45 3.65Extenttowhichtopmanagementshowscommitmenttoandleadershipinknowledgesharing 2.99 4.05Extenttowhichthefirmhasdevelopedandcommunicatedmeasuresoffinancialperformance 3.38 4.63Extenttowhichthefirmhasdevelopedandcommunicatedmeasuresofcustomerreactions 3.02 4.27Extenttowhichthefirmhasdevelopedandcommunicatedmeasuresofkeybusinessprocesses 3.09 4.13Extenttowhichthefirmhasdevelopedandcommunicatedmeasuresoflearningandgrowth 2.26 3.12FirmPerformance Employeeturnover 34.09 20.87Salesperemployee $158,101 $617,576Marketvaluetobookvalue 3.64 11.06

*Eachofthevariablesinthe“HROutcomes”sectionisscaledfrom1to6,where1=“notatall”and6=“toaverygreatextent.”

Thedifferencesbetweenthesetwogroupsoffirmsareverysubstantial,andthesedifferencesarenotsolelyduetofirmsize,industry,orage.Firmswithhigh-performanceworksystemsadoptHRmanagementpracticesverydifferentfromthoseadoptedbyfirmswithlow-performanceworksystems:Theydevoteconsiderablymoreresourcestorecruitingandselection,theytrainwithmuchgreatervigor,theydoalotmoreperformancemanagementandtiecompensationtoit,theyuseteamstoamuchgreaterextent,theyhaveroughlydoublethenumberofHRprofessionalsperemployee,andtheyaremuchlesslikelytobeunionized.Indeed,themoststrikingattributeofthesecomparisonsisnotanyoneHRmanagementpractice—itisnotrecruitingortrainingorcompensation.Rather,thedifferencesaremuchmorecomprehensive—andsystemic.

TheHRoutcomesassociatedwiththissystemarecomprehensiveaswell.Comparedwithlow-performingHRmanagementsystems,theverybestfirmsinoursamplearemuchmorelikelytohavedevelopedaclearstrategicintentandcommunicatediteffectivelytoemployees.Inaddition,theyaremorelikelytohavetheirHRprofessionalsratedpositivelyinboththeirtraditional

andstrategicroles.Theyarealsomorelikelytohavedevelopedacomprehensivemeasurementsystemforcommunicatingnonfinancialinformationtoemployees.

Finally,firmswiththemosteffectiveHRmanagementsystemsexhibiteddramaticallyhigherperformance:Employeeturnoverwasclosetohalf,salesperemployeewerefourtimesasgreat,andtheratiooffirmmarketvaluetothebookvalueofassets—akeyindicatorofmanagementquality,asitindicatestheextenttowhichmanagementhasincreasedshareholders’initialinvestment—wasmorethanthreetimesaslargeinhigh-performingcompanies.

AnHPWSisitselfastrategyimplementationsystem,embeddedwithinthefirm’slargerstrategyimplementationsystem.HRintersectswiththatlargersystematmanydifferentpointsandperhapswithmultipleelementsoftheHRsystematthesamepoint.Understandinghowtoidentifythosepointsofintersectioninyourownfirm,andhowtoaligntheHRsystemaccordingly,isthekeytosecuringastrategicroleforHRandknowinghowtomeasureHR’simpactonvaluecreation.Inaddition,firmsmustconstantlysharpentheirawarenessofhowwelltheHRsystem’scomponentsarealigned,thatis,howmuchtheyreinforceorconflictwithoneanother.Asanexampleofreinforcement,afirmmightcombineabove-marketpaypolicieswithcomprehensiveperformancemanagementsystems.Thiscombinationletsthefirmcultivateatalentedapplicantandemployeepool,andrecognizeandrewardthebestemployeesforsuperiorperformance.Bycontrast,whenthesecomponentsareinconflict,anorganizationmightencourageemployeestoworktogetherinteams,butthenprovideraisesbasedonindividualcontributions.

Inshort,anHPWSdirectlygeneratesuniquecustomervalue,oritleveragesotherrelatedsourcesofsuchvalue.Incertainserviceindustries,theemployee-customerrelationshipissovisiblethatitsimpactonvaluecreationisunmistakable.Butformostfirms,valuederivesfromoperationalprocessesorinnovationsthataffectthecustomerinlessobviousways.ItisthesefirmsthatmostneedtoarticulatethestrategyimplementationprocessandthenaligntheHRsystemtosupportthatprocess.Anditisinthesefirms,wheresuchalignmentsandstrategiesarenoteasilyobservedandthusimitatedbycompetitors,thatHRhasthegreatestpotential.

Inourview,thisalignmentprocessmustbeginwithaclearunderstandingofthefirm’svaluechain—asolidcomprehension,throughoutthefirm,ofwhatkindofvaluetheorganizationgeneratesandexactlyhowthatvalueis

created.Forexample,everyfirmshouldbeabletodescribehowitsultimatefinancialgoalsarelinkedtokeysuccessfactorsatthelevelofitscustomers,operations,people,andITsystems.RobertKaplanandDavidNortonhavecoinedtheterm“strategymap”todescribetheserelationships.12Withthissharedunderstandingofthevalue-creationprocess,theorganizationcanthendesignastrategyimplementationmodelthatspecifiesneededcompetenciesandemployeebehaviorsthroughoutthefirm.Thefirm’ssystemformanagingpeoplecanthenbegearedtowardthegenerationofthesecompetenciesandbehaviors.Infact,akeydistinguishingcharacteristicofaHigh-PerformanceWorkSystemisnotjusttheadoptionofappropriateHRpoliciesandpracticessuchasemployeeacquisition,development,compensation,andperformancemanagement,butalsothewayinwhichthesepracticesaredeployed.InanHPWS,thefirm’sHRpoliciesandpracticesshowastrongalignmentwiththefirm’scompetitivestrategyandoperationalgoals.Moreover,eachHPWSwillbedifferent.Nosinglebestexampleexists;eachorganizationmustcustomizeitssystemtomeetitsownuniquestrengthsandneeds.Forexample,table1-3showsthathigh-performingfirmsarecharacterizedbygreateruseofincentivepay.However,thebehaviorsandoutcomesthatarebeingreinforcedwilldiffersubstantiallyacrossfirmsandstrategies.

StrategicEmployeeBehaviorsUltimatelyanydiscussionofthestrategicroleofhumanresourcesorhumancapitalwillimplicitlyfocusontheproductivebehaviorsofthepeopleintheorganization.Inonesensethisisalmosttautologicalsinceitisonlythroughbehaviorsthathumanbeingscaninfluencetheirenvironment.Weareinterested,however,incertaintypesofemployeebehaviorsandnotothers.Inchapter2wedescribeourownresearchlinkingemployeestrategicfocustofirmperformance.Thisworkemphasizestheimportanceofaligningorganizationalprocessesandsupportsystemssothattheyencourageandmotivateanunderstandingof“thebigpicture.”Similarly,wedefinestrategicbehaviorsasthesubsetofproductivebehaviorsthatdirectlyservetoimplementthefirm’sstrategy.Thesestrategicbehaviorswillfallintotwogeneralcategories.Thefirstwouldbethecorebehaviorsthatflowdirectlyfrombehavioralcorecompetenciesdefinedbythefirm.Thesearebehaviorsthatareconsideredfundamentaltothesuccessofthefirm,acrossallbusinessunitsandlevels.Thesecondaresituation-specificbehaviorsthatareessentialatkeypointsinthefirm’sorbusinessunit’svaluechain.Anexampleoftheselatterbehaviorsmightbethecross-sellingskillsrequiredinthebranchofa

retailbank.

IntegratingafocusonbehaviorsintoanoverallefforttoinfluenceandmeasureHR’scontributiontofirmperformanceisachallenge.Whichonesareimportant?Howshouldtheybe“managed”?Weneedtokeepafewpointsinmind.First,theimportanceofthebehaviorswillbedefinedbytheirimportancetotheimplementationofthefirm’sstrategy.Understandinghowpeopleandprocesseswithinthefirmactuallycreatevalueisthefirststep.Thatanalysiswillrevealboththekindsofbehaviorsthataregenerallyrequiredthroughoutthefirmandthosewithspecificvalueatkeypointsinthevaluechain.Second,it’sessentialtorememberthatwedon’taffectstrategicbehaviorsdirectly.TheyaretheendresultofthelargerHRarchitecture.EspeciallyimportantistheinfluenceofanHRsystemthatisalignedwiththefirm’sstrategy.

ALIGNINGPERFORMANCEMEASUREMENTAND

STRATEGYIMPLEMENTATION

Youareundoubtedlyfamiliarwiththeassertionthat“whatgetsmeasuredgetsmanaged—andwhatgetsmanagedgetsaccomplished.”Buthowtrueisthis,really?Canmeasuringorganizationalprocessesprovidecompetitiveadvantage?Webelievethatdevelopingmeasurementcompetencyisimportant,becauseitcanaddvalueatthelevelofthefirm.Butfewmanagers(HRorotherwise)havestrongcompetenciesinthisarea.Inrecentyears,HRmanagershavebeenaskedtolearnaboutfinanceandaccounting.Now,theymusthonetheirmeasurementskillsaswell.

Wearenotthefirsttoemphasizetheimportanceofmeasuringbusinessperformancefromtheperspectiveofstrategyimplementation,ratherthanrelyingsimplyonfinancialresults.RobertKaplanandDavidNorton’sBalancedScorecardapproachpioneeredthisconceptofmovingbeyondmerefinancialmeasurement.13Tousethistool,afirmmustspecifynotonlythefinancialelementsofitsvaluechainbutalsothecustomer,businessprocess,andlearningandgrowthelements.Then,itmustdeveloptangiblewaystoassesseach.

ThepremiseunderlyingtheBalancedScorecardapproachisthatseniormanagershavepaidfartoomuchattentiontothefinancialdimensionsof

performance,andnotenoughattentiontotheforcesthatdrivethoseresults.Afterall,financialmeasuresareinherentlybackward-looking.Because“performancedrivers”arewithinmanagement’scontrolnow,theentireBalancedScorecardmeasurementsystemencouragesmanagerstoactivelyengagewiththestrategyimplementationprocess,ratherthansimplymonitorfinancialresults.Byspecifyingthevitalprocessmeasures,assessingthem,andregularlycommunicatingthefirm’sperformanceonthesecriteriatoemployees,managersensurethattheentireorganizationparticipatesinstrategyimplementation.TheBalancedScorecardapproachthusmakesstrategyeveryone’sbusiness.

THEPURPOSEOFTHISBOOK

Inthisbook,weaddressthecrucialquestionofhowHRpractitionerscanmeasuretheircontributiontotheirfirm’sstrategyimplementation—andthusbeatthetableandnotonthetable.Webelievethateffectivemeasurementsystemsservetwoimportantpurposes:Theyguidedecisionmakingthroughouttheorganization,andtheyserveasabasisforevaluatingperformance.Themeasurementapproachwedescribeaddressesthesetwopurposesinthreeways.First,itencouragesaclear,consistent,andsharedviewofhowthefirmcanimplementitsstrategyateachlevelintheorganization.Itwon’tguaranteethateveryemployeecanarticulatetheentirevalue-creationprocess,butitshouldensurethateachemployeehasaclearunderstandingofhisorherownroleintheprocess.Useofourmodelalsobuildsconsensusaroundhowdifferentelementswithintheorganizationcontributetovaluecreation.

Second,ourapproachforcesmanagerstofocusonthe“vitalfew”measuresthatreallymakeadifference.Anyonecouldeasilygeneratefiftyormoremeasuresoffirmperformance,acrossavarietyofcategories.Yetthisexercisewouldprobablybecounterproductivebecausethatmanymeasureswouldbedifficulttotrack.Wearguethatatrulyeffectivemeasurementsystemcontainsnomorethantwenty-fivemeasures.

Third,thisapproachletspractitionersexpressthesevitalfewmeasuresintermsthatlinemanagersandseniorexecutiveswillunderstand—andvalue.InHR,conventionalmeasuresofcostcontrol,suchashoursoftraining,timetofillanopeningposition,andeventurnoverratesandemployeesatisfaction,willcontinuetolackcredibilityunlesstheyareshowntoinfluencekey

performancedriversinthebusiness.

We’vealsoorganizedthebookaroundtwocentraltenets.Thefirstisthatafirm’sHRarchitecture—particularlytheHRmanagementsystem—canhaveasubstantialimpactonfirmperformance.ThisthesiswillprobablycomeasnosurprisetomostHRprofessionals.Theybelievethatthefieldhasalwaysbeenimportant,evenifmanymanagersoutsidetheHRfunctiondidn’trecognizeitstruevalue.Butforthefirsttime,HRhasthepotentialtoboostthebottomlinebyamethodotherthansimplybyminimizingcosts.ToparaphraseC.K.PrahaladandGaryHamel,HRprofessionalsarenowinapositiontobecomenumeratormanagers(contributingtotop-linegrowth)ratherthanjustdenominatormanagers(cuttingcostsandreducingoverhead).14However,toexertthisinfluenceonfirmperformance,theHRsystemhastobeembeddedintheorganization’sstrategyimplementation,thatlargermanagementsystemthatisthekeytosustainedcompetitiveadvantageandfinancialsuccess.

ThisstrategicrolealsorequiresnewcompetenciesonthepartofHRprofessionals.Tobesure,theHRfieldhasmadehugetechnicalstridesinthelasttwentyyears.Nevertheless,ithasessentiallybeendoingthesamethings,thoughbetterandmoreefficiently.TheneweconomicparadigmrequiresthatHRprofessionalsdodifferentthings,inanentirelydifferentrole.Thismeansmorethanjustunderstandingthefirm’sarticulatedstrategy.BeingastrategicpartnerrequiresthatHRprofessionalscomprehendexactlywhatcapabilitiesdrivesuccessfulstrategyimplementationintheirfirms—andhowHRaffectsthosecapabilities.Thisisachallengingtask,forHR’straditionalrolesasadministrativeexperts,employeechampions,andagentsofchangearenolessimportantinthisnewenvironment.

Thesecondkeytenetofthisbookfollowsdirectlyfromthefirst.ItreflectsthetwomostcommonquestionswehearfromHRpractitioners:

•HowcanwemeasurethevalueofwhatwedoinHRintermsthatlineandgeneralmanagerswillunderstandandrespect?Forexample,howcanwedeterminethereturnoninvestment(ROI)ofanewtraininganddevelopmentprogram?

•HowcanHRmetricsbeincorporatedinmyorganization’smeasuresofbusinessperformance?

Todemonstrateitsstrategiccontributiontoseniorlinemanagers,HRneedsameasurementsystemthatfocusesontwodimensions:

•costcontrol(drivingoutcostsintheHRfunctionandenhancingoperationalefficiencyoutsideofHR),and

•valuecreation(ensuringthattheHRarchitectureintersectswiththestrategyimplementationprocess)

Aswe’veseen,KaplanandNorton’sBalancedScorecardframeworkhasreceivedenormousattention,inpartbecauseitincorporatesmeasuresthatdescribetheactualvalue-creationprocessratherthanfocusingonjustthefinancialresultsthattraditionalaccountingmethodsassess.Itisaframeworkthatwewilldrawonheavilyinthisbook.Inaddition,weseektostrengthenanaspectoftheBalancedScorecardapproachthatNortonandKaplanthemselvesacknowledgetobeitsweakestfeature—thequestionofhowbesttointegrateHR’sroleintoafirm’smeasurementofbusinessperformance.Theynotethefollowing:

[W]henitcomestospecificmeasuresconcerning[HRandpeople-relatedissues]companieshavedevotedvirtuallynoeffortformeasuringeitheroutcomesorthedriversofthesecapabilities.Thisgapisdisappointing,sinceoneofthemostimportantgoalsforadoptingthescorecardmeasurementandmanagementframeworkistopromotethegrowthofindividualandorganizationalcapabilities.…[This]reflectsthelimitedprogressthatmostorganizationshavemadelinkingemployees…andorganizationalalignmentwiththeirstrategicobjectives.15

OurbookisdesignedtoclosethegapthatKaplanandNortonhaveidentified.TheframeworkthatwepresentherewillhelpHRpractitionersdeveloptheconceptualandoperationaltoolstheyneedtostructuretheirroleinawaythataddsunmistakablevalue.Moreover,itwillshowthemhowtodemonstratethosegainsintermsthatseniorHRmanagersandotherleaderswillfindcompelling.

OURFOCUSONHRMANAGERS

ThereaderwillseethatwehaveorganizedourworkaroundtheroleoftheHRprofessionalratherthanthegeneralmanager.Byadoptingsuchafocus,wedonotmeantogivetheimpressionthatlinemanagersplayanunimportantroleinmakingHRastrategicasset.Infact,theappropriatevaluesandbehaviorsofanorganization’sleadershipteamarekeyprerequisitesforHRtorealizethepotentialrolewedescribeinthisbook.Inaddition,therearemanygeneralmanagerswhosetraditionalviewofHR’srolewouldbenefitfromanintroductiontotheseideas.Nevertheless,HRmanagershavethegreatest

professionalstakeinthefutureroleofHRintheirorganizations,andthereforewehavechosentoorientthebooktotheirparticularchallenge.

USINGTHISBOOK

ThenextfivechaptersinthisbookshowyouhowtoactuallycreateameasurementsystemforassessingHR’scontributiontovaluecreationinyourfirm.Chapter2describesaseven-stepprocessthatwilllaythefoundationforHR’sstrategicinfluence.WespecificallyhighlighttheimportanceofastrategicallyfocusedHRarchitectureasaprerequisiteforameasurementsystemthatcanlinkHRwithfirmperformance.

Chapter3thenlaysoutaprocessfordevelopingtheHRScorecardbasedontheconceptsdiscussedinchapter2.Wespecificallydiscusshowtoincorporateconceptssuchasefficiency,valuecreation,andalignmentintheHRmeasurementsystem.

HRmeasurementalsomeansbeingabletoevaluateHRprogramsandinitiativeswiththesamerigorasdecisionselsewhereintheorganization.Inchapter4wedescribeaprocessforcost-benefitanalysisthatwillallowHRprofessionalstodeterminethereturnoninvestmentforthesedecisions.

Chapter5offersaprocessforvalidatingthequalityofthemeasurementsystemyoudevelopandthedataitgenerates.Hereweexplorewaystodeterminewhen“enoughisenough,”defineaccountabilitiesforthemeasurementprocess,andpresentguidelinesfordevelopingmeasurementchampionsinyourorganization.

Chapter6focusesononeofthemostdifficultmeasurementchallengesforafirmattemptingtomanageHRasastrategicasset—theproblemofalignment.Inthischapterwedescribeseveralwaystothinkaboutalignmentandofferseveralalternativemeasurementapproaches.

Chapter7discussestheprevailingcompetencymodelsforHRprofessionalsandhowourviewofwhatconstitutesanappropriatesetofHRcompetenciesisinfluencedbythedemandsofastrategicmeasurementinitiative.

Inchapter8weconcludewithadiscussionofthechallengesinvolvedinimplementingastrategicallyfocusedHRarchitectureandHRScorecard.Wedevelopaseven-stepmodelforplanningandevaluatingthechangemanagementactivitiesassociatedwiththeimplementationefforts.

Forthosereadersinterestedinthefullextentofthetheoreticalunderpinningsofourapproach,wehavealsoprovidedanappendixatthebackofthisbookdescribingourresearchinmoredetail.

AFINALNOTEOFADVICEANDENCOURAGEMENT

Clearly,designinganynewmeasurementsystemforintangibleassetsisn’teasy—ifitwere,mostcompanieswouldhavealreadydoneit.Embracingthischallengetakestimeandalotofcarefulthought.Weencourageyoutoprogressthrougheachchapterinthisbookinsequenceandtoactivelyengagewiththeconceptsasmuchaspossible.ThismeansthinkingabouthowyourownHRarchitectureoperatesandidentifyingwaysinwhichyoucancustomizeourapproachtomeettheuniqueneedsandcharacteristicsofyourfirm.WealsofullyexpectyoutoinvolveyourentireHRstaffinmasteringthetoolsdescribedinthisbook.Afterall,realinnovationcomesonlywhenpeopleworktogetheronthemostpressingchallengesoftheworkplace.

2

CLARIFYINGANDMEASURINGHR’SSTRATEGICINFLUENCE

IntroductiontoaSeven-StepProcessItwasexcitingstuff.WecouldseehowemployeeattitudesdrovenotjustcustomerservicebutalsoturnoverandthelikelihoodthatemployeeswouldrecommendSearsanditsmerchandisetofriends,family,andcustomers.Wediscoveredthatanemployee’sabilitytoseetheconnectionbetweenhisorherworkandthecompany’sstrategicobjectiveswasadriverofpositivebehavior.…Wewerealsoabletoestablishfairlyprecisestatisticalrelationships.Webegantoseeexactlyhowachangeintrainingorbusinessliteracyaffectedrevenues.

ANTHONYJ.RUCCI,STEVENP.KIRN,

ANDRICHARDT.QUINN1

THISQUOTATIONCAPTUREStheenergythatcanbecreatedwhenanorganizationalignsitsHRarchitecturewithitslargerplanforstrategyimplementation—anddevisesawaytomeasurethatalignment.IfwetakeacloserlookatSears’transformationalexperience,wecanseethatthecompany’seffortcenteredontellingthe“story”ofhowvalueiscreatedwithintheorganization.Specifically,Searsexecutivesclarifiedhowtheiremployeesdrivecustomersatisfactionandhowthatsatisfaction,inturn,fuelsoverallfirmperformance.Theythenreinforcedthestorybyinvolvingabroadcross-sectionofseniormanagers,providingdevelopmentalopportunitiesforthosesupervisorswholackedtheleadershipskillsneededtoimplementthenewstrategy,andrealigningtheHRsystemtosupportthestrategy.

Equallyimportant,theydesignedameasurementsystemthatletthemtesttheirhypothesesabouthowemployeebehaviors,customersatisfaction,andfinancialperformancearealllinked.Inotherwords,Searsmovedbeyondthe

hypotheticalanddevisedwaystodemonstrateobjectivelyHR’scontributiontoimplementationofthecompany’snewstrategy.Humanresourcemanagerscouldnowcitehardevidencethat“a5-pointimprovementinemployeeattitudeswilldrivea1.3-pointimprovementincustomersatisfaction,whichinturnwilldrivea.5%improvementinrevenuegrowth.”2

BALANCEDPERFORMANCEMEASUREMENT

ToachievethekindofstrategyalignmentthatSearsaccomplished,acompanymustengageinatwo-stepprocess.First,managershavetounderstandfullythe“story”ofhowvalueiscreatedintheirfirm.Oncetheyachievethisunderstanding,theycanthendesignameasurementsystembasedonthatstory.Wecanthinkofthisprocessintermsoftwogeneralquestions:

First,howshouldstrategybeimplementedinourfirm?Thisisanotherwayofaskinghowthefirmgeneratesvalue.Askingthisquestionfocusestheorganizationontwodimensionsofthestrategyimplementationstory:

Breadth:Thecompanymustattendtomorethanfinancials,whicharejusttheoutcomesofstrategyimplementation.Totrulygraspthevalue-creationstory,theorganizationmustalsofocusonperformancedrivers(suchascustomerloyalty)thatithasidentifiedas“keysuccessfactors.”

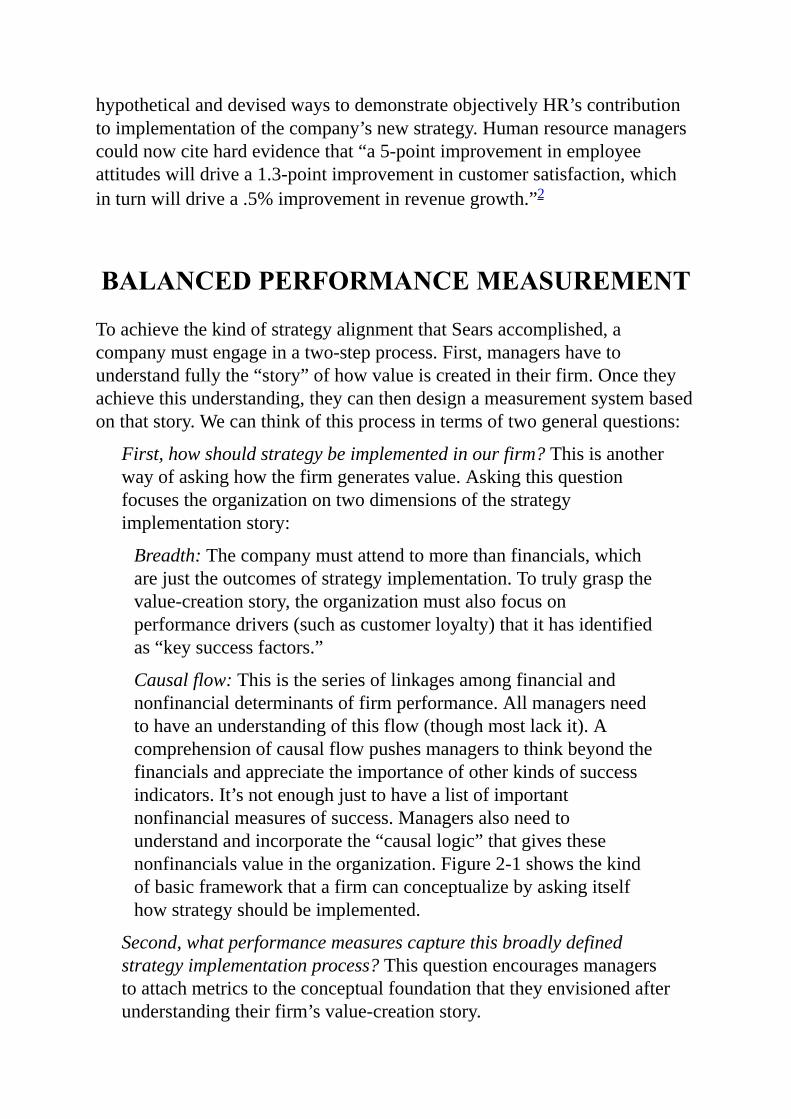

Causalflow:Thisistheseriesoflinkagesamongfinancialandnonfinancialdeterminantsoffirmperformance.Allmanagersneedtohaveanunderstandingofthisflow(thoughmostlackit).Acomprehensionofcausalflowpushesmanagerstothinkbeyondthefinancialsandappreciatetheimportanceofotherkindsofsuccessindicators.It’snotenoughjusttohavealistofimportantnonfinancialmeasuresofsuccess.Managersalsoneedtounderstandandincorporatethe“causallogic”thatgivesthesenonfinancialsvalueintheorganization.Figure2-1showsthekindofbasicframeworkthatafirmcanconceptualizebyaskingitselfhowstrategyshouldbeimplemented.

Second,whatperformancemeasurescapturethisbroadlydefinedstrategyimplementationprocess?Thisquestionencouragesmanagerstoattachmetricstotheconceptualfoundationthattheyenvisionedafterunderstandingtheirfirm’svalue-creationstory.

Oncehigh-levelmanagershaveaddressedthesetwoquestions,theymustthencommunicateittomiddlemanagersandfront-lineemployees.Thatway,everymemberoftheorganizationknowshowtosupportthefirm’ssuccess.Thesequestionsalsohelptheorganizationdecidehowtoallocateresourcessoastobreathelifeintothevalue-creationstory.Finally,andmostimportant,theinsightsgeneratedbythequestionsguidethedecisionsthateveryemployeemakes,everyday.

Figure2-1ASimpleIllustrationofValueCreation

Source:RobertS.KaplanandDavidP.Norton,(Boston,MA:HarvardBusinessSchoolPress,1996),31.

Balancedperformance-measurementmodels,suchastheonewepresentinthisbook,pulltheanswerstothesetwoquestionstogetherinapowerfulassessmenttool.Themodelrecognizestheimportanceofbothintangibleandtangibleassets,andoffinancialandnonfinancialmeasures.Italsoacknowledgesthecomplex,value-generatingconnectionsamongthefirm’scustomers,operations,employees,andtechnology,3andintegratesHR’sroleinanunprecedentedway.Finally,themodelhighlightstheimportantdistinctionbetweenlaggingandleadingindicators.Laggingindicators,suchasfinancialmetrics,typicallyreflectonlywhathashappenedinthepast.Suchmetricsmayaccuratelymeasuretheimpactofpriordecisions,buttheywon’thelpyoutomaketoday’sdecisions,nordotheyguaranteefutureoutcomes.Thepopularanalogycomparesusingthemtoguidedecisionsaboutthefuturetodrivingyourcarbylookingintherearviewmirror!Therefore,youalsoneedasetofmetricscalledleadingindicators.Thiswillbedifferentforeachfirm,butexamplesmightincludeR&Dcycletime,customersatisfaction,oremployeestrategicfocus.Theseindicatorsassessthestatusofthekeysuccessfactorsthatdriveimplementationofthefirm’sstrategy.Andbytheirverynature,theyemphasizethefutureratherthanthepast.

INTEGRATINGHRINTOBUSINESSPERFORMANCE

MEASUREMENT:UNDERSTANDINGHRDELIVERABLES

GraspingtherelationshipsamongkeysuccessfactorsisessentialformeasuringHR’straditionallyelusiveroleindrivingorganizationalperformance.OnceacompanyfirmlyanchorsHRinitsstrategyimplementationsystem,itcanthenseetheconnectionsbetweenHRandthecompany’ssuccessdrivers.BymeasuringHR’seffectonthesedrivers,thefirmcanquantifyHR’soverallstrategicimpact.

TointegrateHRintoabusiness-performancemeasurementsystem,managersmustidentifythepointsofintersectionbetweenHRandtheorganization’sstrategyimplementationplan.WecanthinkofthesepointsasstrategicHRdeliverables,namely,thoseoutcomesoftheHRarchitecturethatservetoexecutethefirm’sstrategy.ThisisincontrasttoHR“doables”thatfocusonHRefficiencyandactivitycounts.Thesedeliverablescomeintwocategories:performancedriversandenablers.HRperformancedriversarecorepeople-relatedcapabilitiesorassets,suchasemployeeproductivityoremployeesatisfaction.Eventhoughthesemayseemsoimportantastobegeneric,thereisactuallynosinglecorrectsetofperformancedrivers.Eachfirmcustom-identifiesitsownsetbasedonitsuniquecharacteristicsandtherequirementsofitsstrategyimplementationprocess.

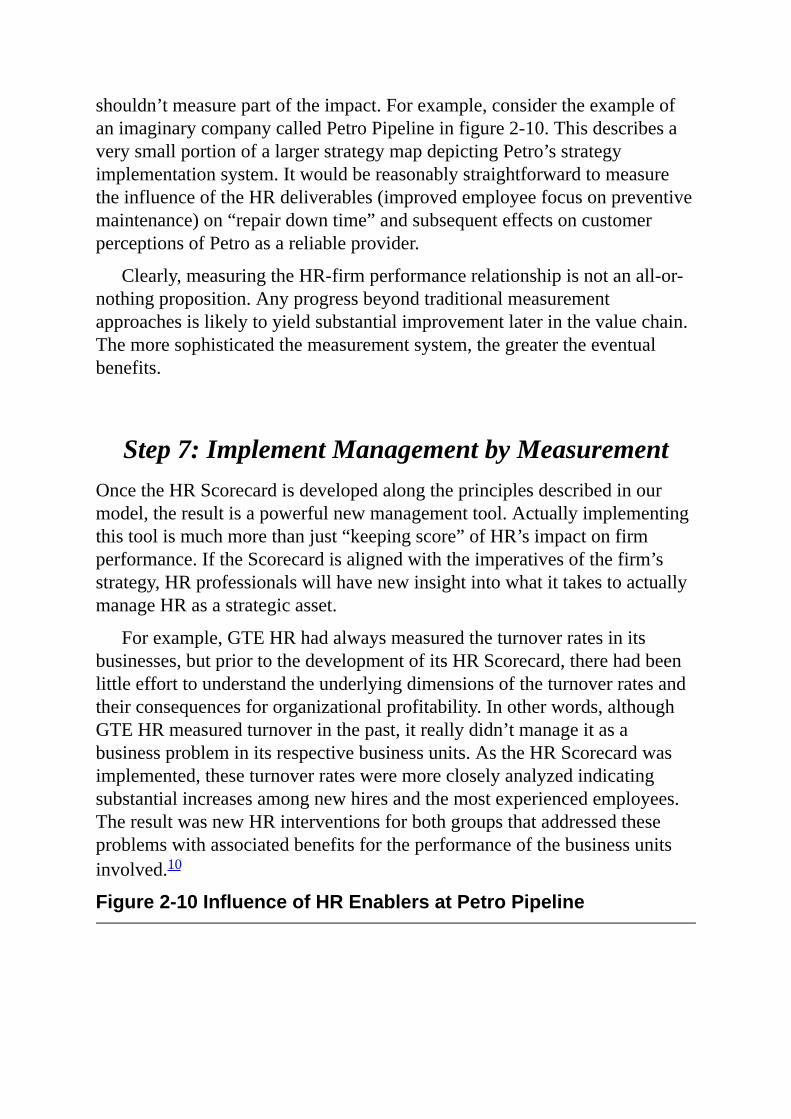

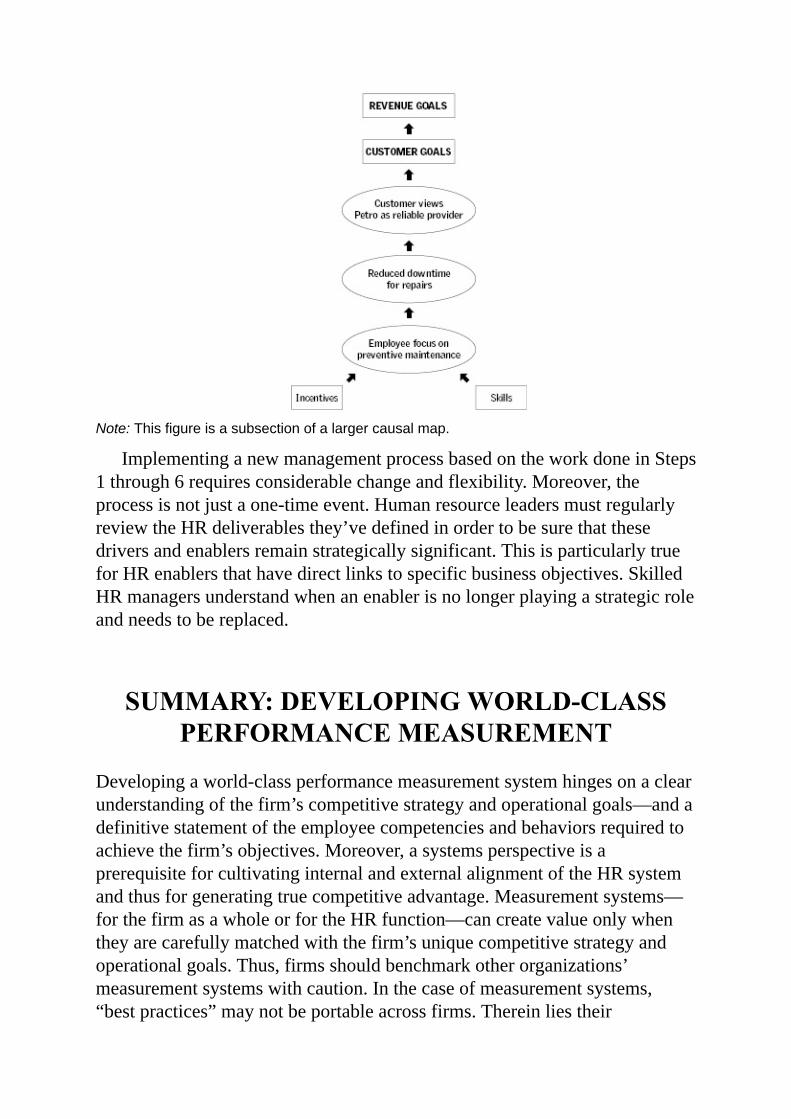

Enablersreinforceperformancedrivers.Forexample,aparticularchangeinacompany’srewardstructuremightencouragepreventivemaintenanceratherthanreactivemaintenance.Anemphasisonpreventivemaintenancemightinturn“enable”aperformancedrivercalled“on-timedelivery.”Anyperformancedrivermayhaveseveralenablers.Theenablersthemselves,inisolation,mayseemmundane,but—aswe’llsee—theircumulativeeffectcanhavestrategicimportance.

Let’slookatthesetwocategoriesofHRdeliverablesingreaterdetail.

HRPerformanceDriversPerhapsnotsurprisingly,humanresourcemanagerstendtofocusonHRperformancedriversinattemptingtodemonstratetheirstrategicinfluence.

Butalltoooften,theymerelyasserttheimportanceofaparticulardriver,suchasemployeesatisfaction,withoutbeingabletomakethebusinesscaseforitsprimacy.ThispredicamentstemsfromthedifficultiesinherentindiscerningHR’sactualcontributiontooverallmissionandstrategy.Becauseofthisdifficulty,companiesoftenexperienceadisconnectbetweenthemetricstheyuseandtheHRpoliciestheyinstitute.Forexample,onefirmweknowofincorporatesvarioussophisticatedmeasuresintoitsbonuscompensationsystem,butHR’smeasuresconsistofsimplehurdlesthatanymanagercanachieve(forinstance,“100percentofdirectreportshavefiledacareerdevelopmentplan”).SuchsimplisticmeasuresundermineHR’scredibilityinthewiderorganization.

ThecredibilityofHRmeasuresisparticularlyimportantwhenfinancialandnonfinancialperformancemeasuresconflict.Inevitably,therecomesatimewhenpeoplemeasuresareup,butfinancialsaredown.Naturally,theCFOobjectstopayingbonuseswhen“performance”doesn’twarrantit.However,suchreactionsmissanessentialpoint:Balancedperformancemeasurementmeanspayingattentiontobothlaggingandleadingindicators.And,it’stheleadingindicators—suchasHRmeasures—thatreallydrivevaluecreationintheorganization.ThehesitationtorewardmanagerswhenpeoplemeasuresareupandfinancialmeasuresaredownreflectsalackofagreementamongexecutivesthatHRmeasuresinfactdrivetheentirecompany’sperformance.Inthisexample,therewardsystemhasbeen“balanced”toaddresssomevagueconcernabout“peopleissues,”butnoonecanarticulatehowthesemeasuresreflectvaluecreationinthefirm.

Moreover,managersoftendon’tunderstandthedelaysinherentinleadingindicators.HighHRscoresinthefaceoflowfinancialsactuallysignalimprovedfinancialsinthefuture,assumingthatotherleadingindicatorsarealsopositive.Thereverseisequallytrue,ofcourse.StrongfinancialsinthefaceofweakHRdriversandotherleadingindicatorsshouldraiseconcernsaboutfuturefinancialperformance.Thelesson?Becausetrulybalancedperformancemeasurementsystemsreflectbothcurrentandfuturefinancialperformance,managersmustinterpretthemdifferentlyfromthewaytheydotraditionalperformancemeasures.

IdentifyingkeyHRperformancedriverscanbechallenging,becausetheyareuniquetoeachfirm.TheexperienceatQuantumCorporationoffersanaptexample.AtQuantum,aleadingmanufacturerofharddisksandcomputerperipherals,executivesemphasizesomethingtheycall“time-to-volume.”InQuantum’sview,beingfirsttomarketdoesnotmeanbeingfirsttoannounceordemonstrateanewproduct.4Rather,itmeansthatcustomersactuallyget

thenewproductstheywant,whentheywantthem,andinthequantitiestheyrequire.Time-to-volumehingesonrapidproductdevelopment—withoutthesacrificeofquality—plustheabilitytorampupproductionfastenoughtomeetcustomers’needs.Quantumidentifiedasetofvaluebehaviors,suchasstayingflexibleandadaptable,takinginitiativeforone’sowndevelopment,andresolvingissuesinanobjectivemanner,asonetime-to-volumedriver.Thereisnothingadhocorsymbolicabouttheimportanceofthesebehaviorstothesuccessofthecompany.Quantumintegratesthemdirectlyintoitsperformancecriteriaandgivesthemequalweightwithmoretraditionalperformancemeasures.Indeed,one-halfofbonusandmeritpayisbasedonfinancialresults,andone-halfonanemployee’sadherencetothevaluebehaviors.Asoneseniorexecutiveobserved,“Youcan’tsimply‘getresults’toooftenwhileleavingapileofdeadbodiesbehindyou.”

HREnablersAswementioned,HRenablersreinforcecoreperformancedrivers.Toprovideanotherexample,ifafirmidentifiesemployeeproductivityasacoreperformancedriver,then“re-skilling”mightbeanenabler.WeencouragehumanresourcemanagerstofocusasmuchonHRenablersastheydoonHRperformancedrivers,buttodramaticallyexpandtheconcept.Forinstance,ratherthanthinkingjustintermsofHR-focusedenablersinyourorganization(thoseenablersthatinfluencethemorecentralHRperformancedrivers),trythinkingabouthowspecificHRenablersalsoreinforceperformancedriversintheoperations,customer,andfinancialsegmentsoftheorganization.

Ourexperiencewithamajormoney-centerbankillustrateswhatcanhappenwhenmanagersdon’tconnectHRenablerswithvariousperformancedriversinthebroaderorganization.Thisparticularbankhaddecidedtoshiftthefocusofitsretailbusinessfromservicetosales.Thebankidentifiedasetofperformancedriversthatincludedincreasedcross-sellingtoexistingcustomers,tellerproductknowledge,andsalesskills.However,itsHRenablersstillemphasizedservice.Forinstance,theorganizationstillhadthefollowing:

•trainingprogramsthatfocusedonserviceratherthansales;

•performanceappraisalandmeritpaythatrewardedserviceratherthansales;

•hiringpracticesbasedonservicecompetenciesratherthansales

competencies;

•turnoverratesthatunderminedrelationshipbuildingbetweentellersandretailcustomers;and

•lowpayandbenefitsfortellers,whowereconsideredoverheadratherthanasourceofrevenuegrowth.

BecauseofthedisconnectbetweenitsnewgoalsandoutdatedHRenablers,thebankfailedtoachieveitssalesandprofitabilitytargets.Withouttheproperlyalignedenablers,itwassimplyunabletoimplementitsnewsalesstrategy.ThelessonhereisthattheentireHRsysteminfluencesemployeebehaviorfrommanypoints.ThusHRhasthatmanymoreopportunitiestoenable—orimpede—thefirm’skeyperformancedrivers.

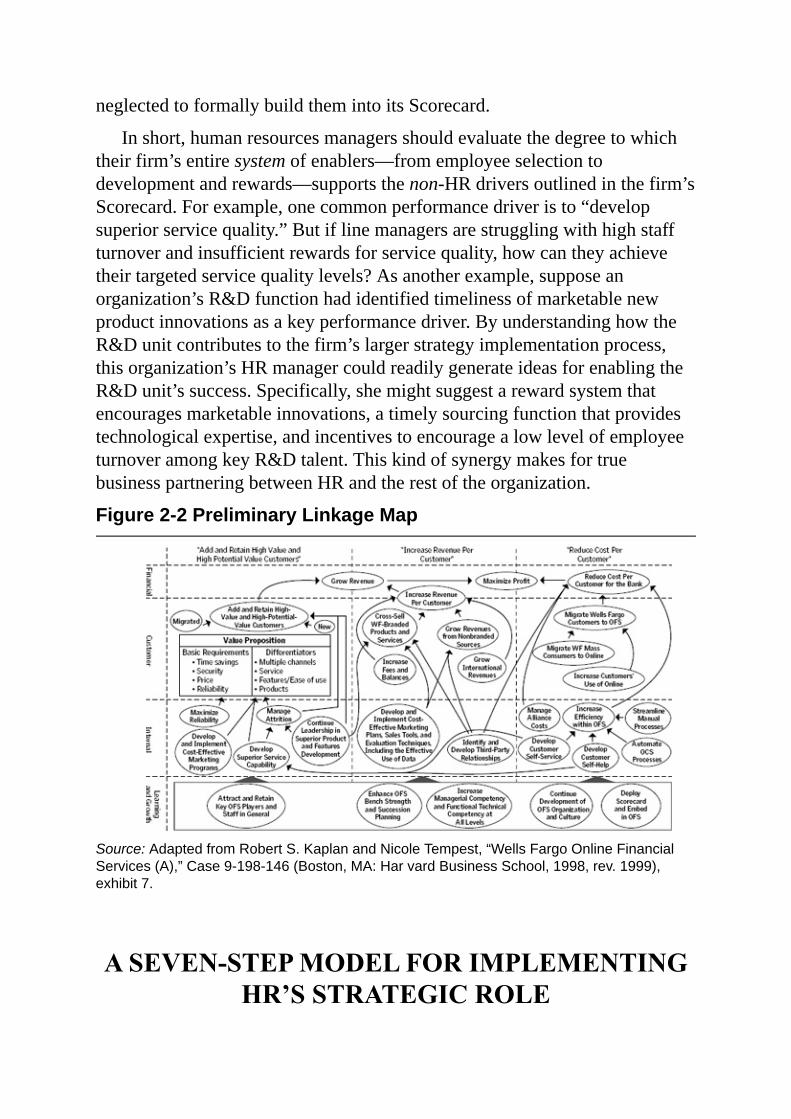

AnotherexamplefromthebankingindustryillustrateshoweasyitistooverlookthepowerofHRenablers.WhentheWellsFargoOnlineFinancialServices(OFS)groupimplementedaBalancedScorecardtomeasurethefirm’soverallprogresstowarditsgoalsofgrowingrevenueandmaximizingprofits,itidentifiedthreekeystrategicdrivers5:

•addandretainhigh-valueandhigh-potential-valuecustomers;

•increaserevenuepercustomer;and

•reducecostpercustomer.

Figure2-2articulatesthe“story”ofhowOFSexpectedtoachievethosegoals.OFSalsoidentifiedseveralHRperformancedriversthatitfeltwouldplayanimportantpartinthesuccessofitsstrategy,shownintheLearningandGrowthsectionofthefigure:

•attractandretainkeyOFSplayersandstaff;

•enhanceOFSbenchstrengthandsuccessionplanning;

•increasemanagerialcompetencyandfunctionalcompetencyatalllevels;

•continuedevelopmentoftheOFSorganizationandculture;and

•deploytheScorecardandembeditinOFS.

AccordingtoMaryD’Agostino,VPofstrategyatOFS,acknowledgingtheseHRdriverssignaledanimportantstepforWellsFargo,inwhichtheculture“embracesfinancialmeasures.”ButOFSmanagersneverachievedconsensusonhowtheseHRdriversdirectlyaffectedthethreestrategicgoals.Asaresult,whilethecompanyagreedtomonitorthesedriversyearly,it

neglectedtoformallybuildthemintoitsScorecard.

Inshort,humanresourcesmanagersshouldevaluatethedegreetowhichtheirfirm’sentiresystemofenablers—fromemployeeselectiontodevelopmentandrewards—supportsthenon-HRdriversoutlinedinthefirm’sScorecard.Forexample,onecommonperformancedriveristo“developsuperiorservicequality.”Butiflinemanagersarestrugglingwithhighstaffturnoverandinsufficientrewardsforservicequality,howcantheyachievetheirtargetedservicequalitylevels?Asanotherexample,supposeanorganization’sR&Dfunctionhadidentifiedtimelinessofmarketablenewproductinnovationsasakeyperformancedriver.ByunderstandinghowtheR&Dunitcontributestothefirm’slargerstrategyimplementationprocess,thisorganization’sHRmanagercouldreadilygenerateideasforenablingtheR&Dunit’ssuccess.Specifically,shemightsuggestarewardsystemthatencouragesmarketableinnovations,atimelysourcingfunctionthatprovidestechnologicalexpertise,andincentivestoencouragealowlevelofemployeeturnoveramongkeyR&Dtalent.ThiskindofsynergymakesfortruebusinesspartneringbetweenHRandtherestoftheorganization.

Figure2-2PreliminaryLinkageMap

Source:AdaptedfromRobertS.KaplanandNicoleTempest,“WellsFargoOnlineFinancialServices(A),”Case9-198-146(Boston,MA:HarvardBusinessSchool,1998,rev.1999),exhibit7.

ASEVEN-STEPMODELFORIMPLEMENTINGHR’SSTRATEGICROLE

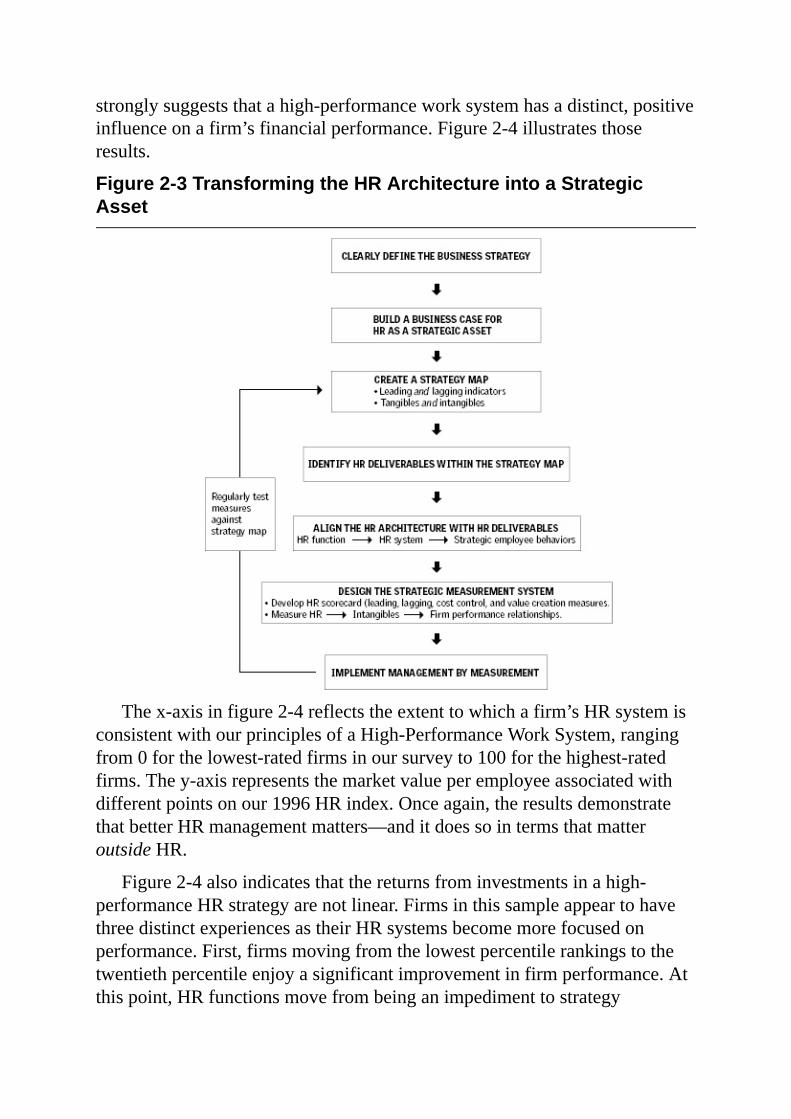

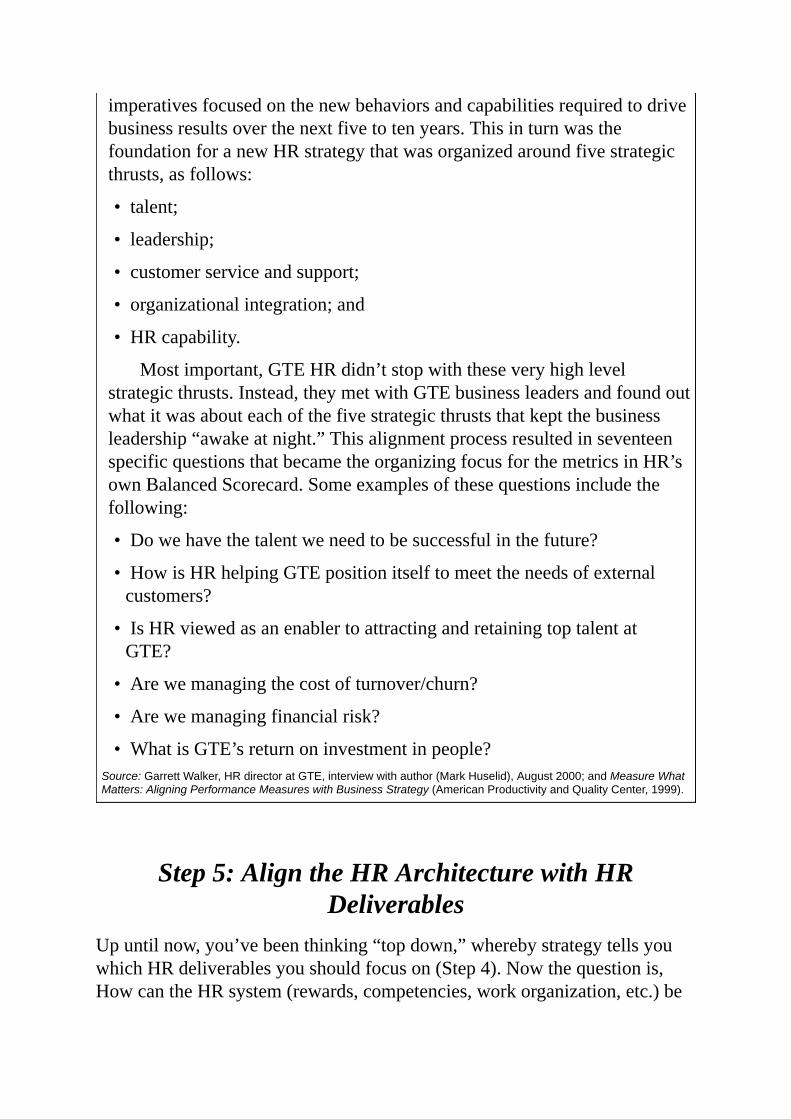

HowcanHRformalizethiskindofstrategicrole?Figure2-3illustrateshowHRcanlinkitsdeliverablestothefirm’sstrategyimplementationprocess.Whileweelaborateonvariouscomponentsofthismodelinsubsequentchapters,wesummarizeitforyouinthefollowingsevensteps:

Step1:ClearlyDefineBusinessStrategyAtthestrategy-development“table,”seniorHRleadersprovideanessentialperspective.Byfocusingonhowtoimplementthestrategyratherthansolelyonwhatthestrategyconsistsof,theycanfacilitateadiscussionabouthowtocommunicatethefirm’sgoalsthroughouttheorganization.Whenstrategicgoalsarenotdevelopedwithaneyetowardhowtheywillbeimplementedandcommunicatedthroughouttheorganization,theytendtobecomeverygeneric—forexample,“maximizeoperatingefficiency,”or“increasepresenceininternationalmarkets,”or“improveproductivity.”Thesegoalsaresovaguethatindividualemployeessimplycan’tknowhowtotakeactiontoachievethem.Worse,employeescan’trecognizethemasuniquetotheirfirm.Toillustrate,weoftenrunasimpleexperimentinourexecutiveeducationclasses.Weaskparticipantstowritedowntheirfirm’smissionorvisionstatement,whichwethenretype(removinganymentionofthefirm’sname)andredistributeamongthegroup.Nextweaskparticipantstopickouttheirownmissionandvisionstatementsfromthiscollection.Thesestatementsaresovague—andsosimilar—thatmostfinditverydifficulttodoso.

Clarifyingyourorganization’sstrategyinprecisetermscantakepractice.Thekeythingistostatethefirm’sgoalsinsuchawaythatemployeesunderstandtheirroleandtheorganizationknowshowtomeasureitssuccessinachievingthem.

Step2:BuildaBusinessCaseforHRasaStrategicAsset

Onceafirmclarifiesitsstrategy,humanresourceprofessionalsneedtobuildaclearbusinesscaseforwhyandhowHRcansupportthatstrategy.Inmakingthisbusinesscase,youhavethebenefitofadecadeofsystematicresearchtosupportyourrecommendations.Whileacomprehensivereviewofthisresearchisbeyondthescopeofthisbook,wecanhighlightthekeyresults.First,evidencegatheredfromfournationalsurveysandmorethan2,800firms

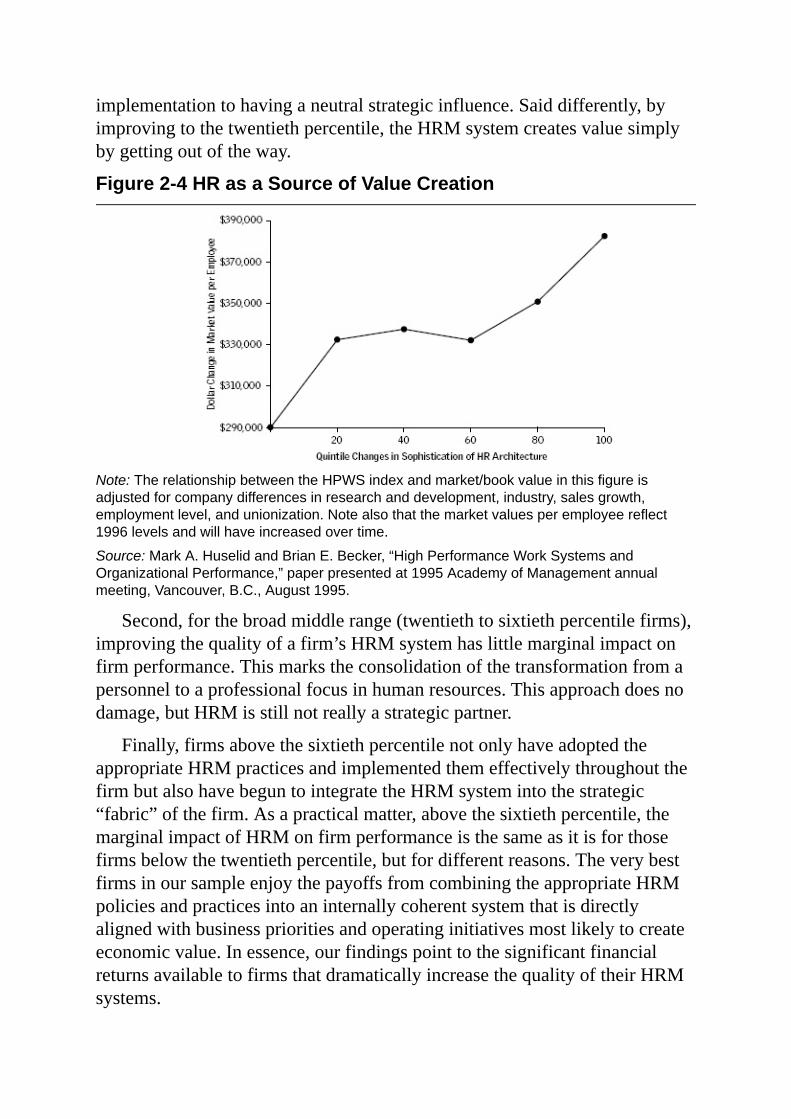

stronglysuggeststhatahigh-performanceworksystemhasadistinct,positiveinfluenceonafirm’sfinancialperformance.Figure2-4illustratesthoseresults.

Figure2-3TransformingtheHRArchitectureintoaStrategicAsset

Thex-axisinfigure2-4reflectstheextenttowhichafirm’sHRsystemisconsistentwithourprinciplesofaHigh-PerformanceWorkSystem,rangingfrom0forthelowest-ratedfirmsinoursurveyto100forthehighest-ratedfirms.They-axisrepresentsthemarketvalueperemployeeassociatedwithdifferentpointsonour1996HRindex.Onceagain,theresultsdemonstratethatbetterHRmanagementmatters—anditdoessointermsthatmatteroutsideHR.

Figure2-4alsoindicatesthatthereturnsfrominvestmentsinahigh-performanceHRstrategyarenotlinear.FirmsinthissampleappeartohavethreedistinctexperiencesastheirHRsystemsbecomemorefocusedonperformance.First,firmsmovingfromthelowestpercentilerankingstothetwentiethpercentileenjoyasignificantimprovementinfirmperformance.Atthispoint,HRfunctionsmovefrombeinganimpedimenttostrategy

implementationtohavinganeutralstrategicinfluence.Saiddifferently,byimprovingtothetwentiethpercentile,theHRMsystemcreatesvaluesimplybygettingoutoftheway.

Figure2-4HRasaSourceofValueCreation

Note:TherelationshipbetweentheHPWSindexandmarket/bookvalueinthisfigureisadjustedforcompanydifferencesinresearchanddevelopment,industry,salesgrowth,employmentlevel,andunionization.Notealsothatthemarketvaluesperemployeereflect1996levelsandwillhaveincreasedovertime.

Source:MarkA.HuselidandBrianE.Becker,“HighPerformanceWorkSystemsandOrganizationalPerformance,”paperpresentedat1995AcademyofManagementannualmeeting,Vancouver,B.C.,August1995.

Second,forthebroadmiddlerange(twentiethtosixtiethpercentilefirms),improvingthequalityofafirm’sHRMsystemhaslittlemarginalimpactonfirmperformance.Thismarkstheconsolidationofthetransformationfromapersonneltoaprofessionalfocusinhumanresources.Thisapproachdoesnodamage,butHRMisstillnotreallyastrategicpartner.

Finally,firmsabovethesixtiethpercentilenotonlyhaveadoptedtheappropriateHRMpracticesandimplementedthemeffectivelythroughoutthefirmbutalsohavebeguntointegratetheHRMsystemintothestrategic“fabric”ofthefirm.Asapracticalmatter,abovethesixtiethpercentile,themarginalimpactofHRMonfirmperformanceisthesameasitisforthosefirmsbelowthetwentiethpercentile,butfordifferentreasons.TheverybestfirmsinoursampleenjoythepayoffsfromcombiningtheappropriateHRMpoliciesandpracticesintoaninternallycoherentsystemthatisdirectlyalignedwithbusinessprioritiesandoperatinginitiativesmostlikelytocreateeconomicvalue.Inessence,ourfindingspointtothesignificantfinancialreturnsavailabletofirmsthatdramaticallyincreasethequalityoftheirHRMsystems.

Whiletheseeffectsarefinanciallysignificant,keepinmindthattheydonotrepresentamagicbullet.Thatis,simplechangesinanHRpracticewillnotimmediatelysendafirm’sstockpricesoaring.RememberthatourHRmeasuredescribesanentirehumanresourcesystem.Changingthissystembythemagnituderequiredtoenjoythesegainstakestime,insight,andconsiderableeffort.It’sfairtosaythatitrequiresatransformationoftheHRfunctionandsystem.Ifitcouldbedoneovernight,humanresourcesystemswouldbeeasilyimitatedandwouldquicklylosemuchoftheirstrategiccharacter.

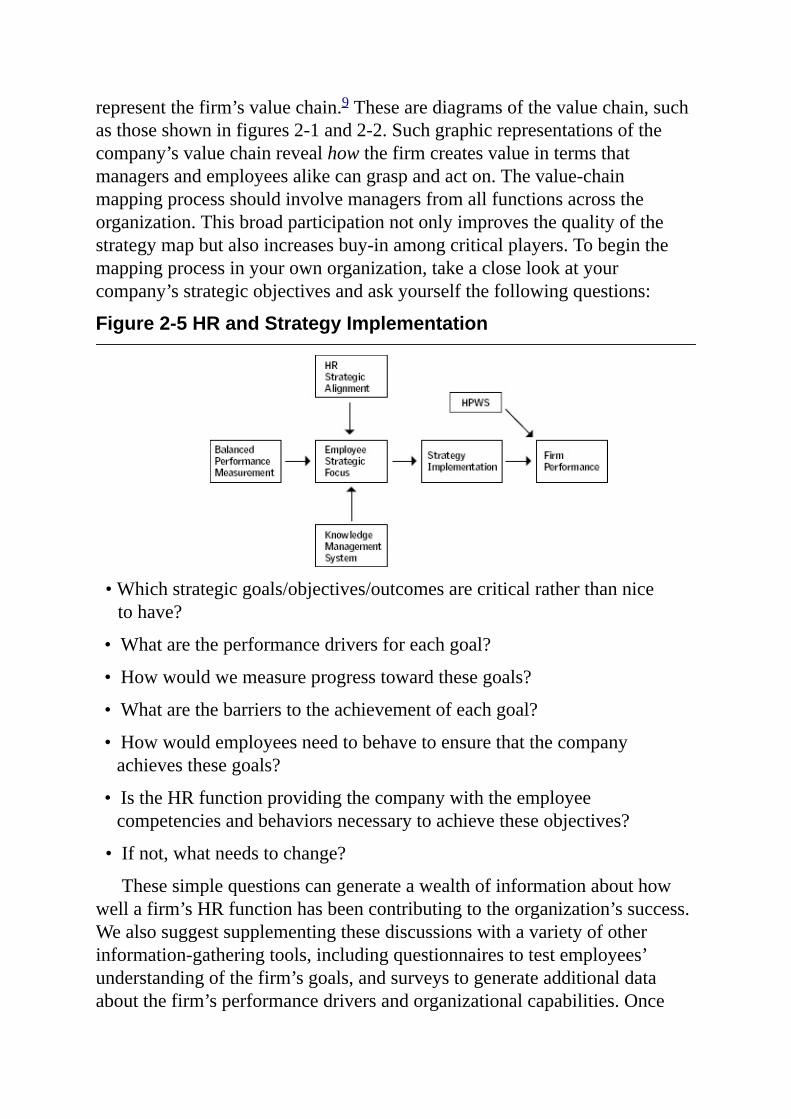

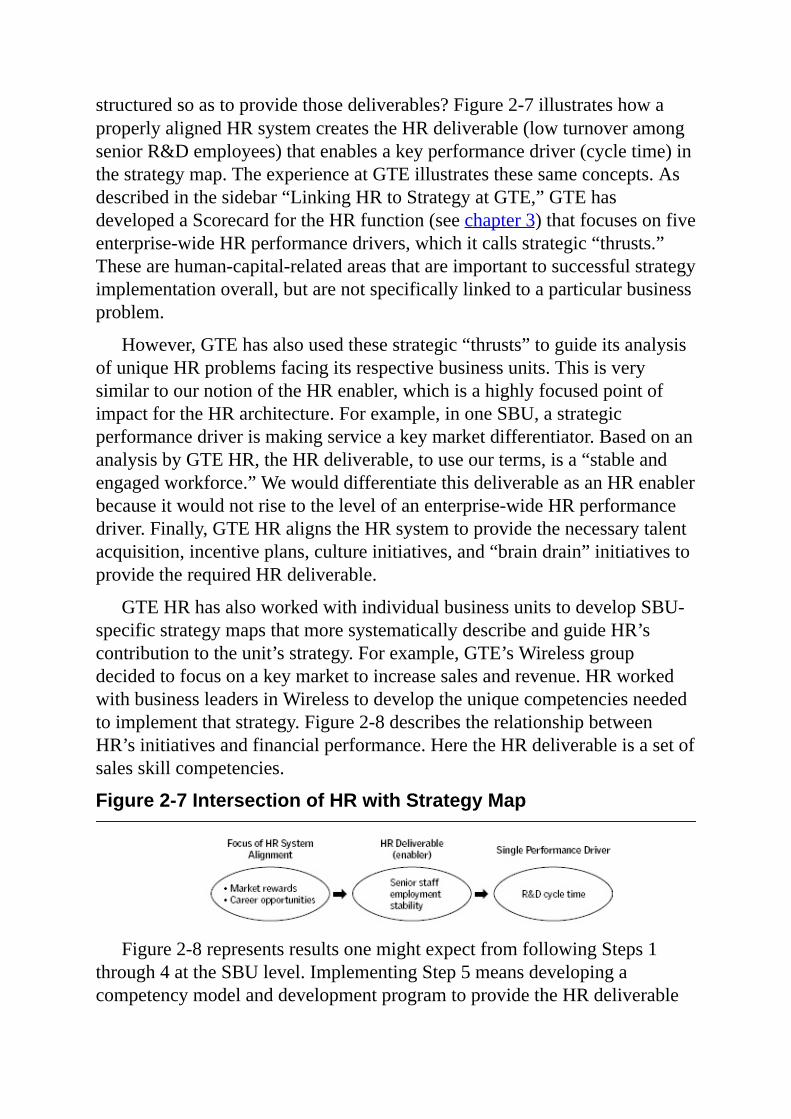

ThebusinesscaseforastrategicHRrolemustalsoincorporateHR’skeyinfluenceonstrategyimplementationandtheroleofstrategicallyfocusedmeasurementsystems.Figure2-5describesthemodelforsuchabusinesscasebasedonourmostrecentsurveyofmorethan400firms.6Theseresultstellasimplebutpowerfulstory.Consistentwiththepremiseofthisbook,ourresearchsuggeststhatstrategyimplementation,ratherthanstrategycontent,differentiatessuccessfulfromunsuccessfulfirms.Itissimplymucheasiertochooseanappropriatestrategythanitistoimplementiteffectively.Moreover,successfulstrategyimplementationisdrivenbyemployeestrategicfocus,HRstrategicalignment,andabalancedperformancemeasurementsystem.Thelinchpinofsuccessfulstrategyimplementationisastrategicallyfocusedworkforce,whichwecouldconsidertheultimateHRperformancedriver.Finally,abalancedperformancemeasurementsystem,intandemwithanalignedHRsystemandeffectiveknowledgemanagement,isthefoundationforastrategicallyfocusedorganization.7

Step3:CreateaStrategyMapClarifyingyourfirm’sstrategysetsthestageforimplementingthatstrategy.Butitisjustthefirststep.Inmostorganizations,thecustomervalueembodiedinthefirm’sproductsandservicesistheresultofacomplex,cumulativeprocess—whatMichaelPorterreferstoasthefirm’svaluechain.8Allfirmshaveavaluechain—eventhosethathaven’tarticulatedit—andthecompany’sperformancemeasurementsystemmustaccountforeverylinkinthatchain.

Todefinethevalue-creationprocessinyourorganization,werecommendthatthetop-andmid-levelmanagerswhowillbeimplementingthefirm’sstrategydevelopwhatBobKaplanandDaveNortoncallastrategymapto

representthefirm’svaluechain.9Thesearediagramsofthevaluechain,suchasthoseshowninfigures2-1and2-2.Suchgraphicrepresentationsofthecompany’svaluechainrevealhowthefirmcreatesvalueintermsthatmanagersandemployeesalikecangraspandacton.Thevalue-chainmappingprocessshouldinvolvemanagersfromallfunctionsacrosstheorganization.Thisbroadparticipationnotonlyimprovesthequalityofthestrategymapbutalsoincreasesbuy-inamongcriticalplayers.Tobeginthemappingprocessinyourownorganization,takeacloselookatyourcompany’sstrategicobjectivesandaskyourselfthefollowingquestions:

Figure2-5HRandStrategyImplementation

•Whichstrategicgoals/objectives/outcomesarecriticalratherthannicetohave?

•Whataretheperformancedriversforeachgoal?

•Howwouldwemeasureprogresstowardthesegoals?

•Whatarethebarrierstotheachievementofeachgoal?

•Howwouldemployeesneedtobehavetoensurethatthecompanyachievesthesegoals?

•IstheHRfunctionprovidingthecompanywiththeemployeecompetenciesandbehaviorsnecessarytoachievetheseobjectives?

•Ifnot,whatneedstochange?

Thesesimplequestionscangenerateawealthofinformationabouthowwellafirm’sHRfunctionhasbeencontributingtotheorganization’ssuccess.Wealsosuggestsupplementingthesediscussionswithavarietyofotherinformation-gatheringtools,includingquestionnairestotestemployees’understandingofthefirm’sgoals,andsurveystogenerateadditionaldataaboutthefirm’sperformancedriversandorganizationalcapabilities.Once

youthinkyouhaveafullpictureofyourfirm’svaluechain,translatetheinformationthatyouhavegatheredintoaconceptualmodelusinglanguageandgraphicsthatmakesenseinyourorganization.Thentestforunderstandingandacceptanceinsmallgroupsofopinionleadersandthoughtleadersthroughoutthefirm.

Astrategymapofthevalue-creationprocesscontainshypotheses,orpredictions,aboutwhichorganizationalprocessesdrivefirmperformance.Normally,acompanyvalidatesthesehypothesesonlyafterachievingtargetsonperformancedriversandobservingtheimpactoftheseresultsonfirmperformance.However,iftheorganizationcangraphicallydepicttherelationshipsamongperformancedriverswhilemappingthefirm’svaluechain,itcanhavethatmuchmoreconfidenceinitsstrategyimplementationplan.