Embed Size (px)

Citation preview

Transnational Capitalism and Class Formation

JERRY HARRIS

ABSTRACT: Within studies of global capitalism class formation is

analyzed from two different viewpoints: network theory and political

economy. The principal factor determining the emergence of a

transnational capitalist class (TCC) is the relations of production. The

questions of how production and labor are organized, and how and by

whom value is expropriated are primary and point to a hegemonic and

cohesive TCC. Network theory, while helpful in creating a more

complex picture, stresses sociological perceptions of class that

underestimate transnational class formation.

HOW DO WE ANALYZE the formation of a transnational capitalist class

(TCC)? Within studies of global capitalism there are various interpretations

as to the nature and cohesion of the TCC. Research has covered different areas, but

the two main fields have been in political economy and network theory. Those

concerned mainly with exploring transnational corporate investments and

production, capital flows, labor relations and the state tend to see a consolidated

TCC. Others whose primary research examines relationships between firms, their

boards and elite policy groups see a weakly constituted class or regional community.

These are not overly sharp divisions; both overlap and those in the field learn from

each other. But the differences in epistemology are worth exploring because they

2

lead to different conclusions, which impact both theory and practice.

A historical understanding should begin with the formation of the industrial

bourgeoisie. Here a few basic and brief observations are important in understanding

the later emergence of the TCC. Modern capitalism always had a global impulse,

seeking to encompass the entire world in market relations. One of the most

fundamental engines that allowed the bourgeoisie to transform production was a

revolution in the tools of production leading to a reorganization of work and new

relations of production between the owners of capital and the working class. Class

struggle not only occurred between workers and capitalists, but also between

capitalists and the old agrarian ruling class, as new methods in the expropriation of

surplus value were created. These various levels of conflict helped define the

contours of class relationships, and occurred across political, economic, cultural and

social boundaries.

If we begin to trace modern capitalism with the start of the industrial

revolution in the 1760s, we see the consolidation of capitalist state power and class

formation unfolded over an extended period. During this process industrial and

financial families established themselves and expanded their wealth, based on their

ownership of the means of production and capital. The process didn't culminate

until the end of World War I, with the fall of the German Kaiser, the Russian Czar,

the Austrian-Hungarian Empire and the Ottoman Empire. The tremendous

economic energy and power of industrial transformation altered political and state

3

structures. Personal networks thicken through education, intermarriage, common

investments, social ties and political clubs. As political and cultural changes

occurred, they further consolidated the economic transformations, particularly

through the establishment of a regulatory and governance structure mediated by the

state. In turn the state helped promote and protect expansion abroad. This general

line of uneven development over an extended period, led by a revolution in the

means of production and the reorganization of work and wealth, holds true for the

development of the TCC. As capitalism always had global dimensions, a path of

development leading from national to transnational class formation was inherent in

its internal logic.

Although capitalist expansion has led to a transnational economic system, this

doesn’t mean that all national forms and expressions of capital have been swept

away. As with the century-long development of industrial capitalism, transnational

capitalism is undergoing an extended process of consolidation. Each country

assimilates into global production, finance and governance at its own pace,

determined by many historical and cultural factors. Consequently, national rivalries

can still be expressed on the international political stage. The relationships and

reciprocal influences between nation-centric imperialism and transnational

capitalism are complex and ongoing (Harris, 2003; 2005). Such questions deserve

their own study, but this paper will concentrate on class formation.

4

Class Formation, Production and Accumulation

The TCC has emerged through distinct practices embedded in the

transnational economy (Sklair, 2001; Robinson, 2004; Harris, 2008; Liodakis,

2010). Major economic indicators include: foreign direct investment, cross-border

financial flows, cross-border mergers and acquisitions, foreign investment activity

by sovereign wealth funds, the transnational character of stock ownership, foreign

affiliates, tax havens, global assembly lines, intra-firm trade, the vast network of

national sub-contractors tied to transnational corporations (TNCs), the ratio of

foreign-owned assets, employment and sales to similar national figures, and the

percent of foreign revenues and profits. Capitalist accumulation operates through

these globalized circuits, and few remained untouched either in the commodities

they buy or sell.

Organizing and directing these activities determines the TCC’s position in the

relations of production, the creation of value and its expropriation. The

reorganization of manufacturing into transnational value chains, and the

expropriation of value through global financialization are core features that

characterize TCC formation. For the owners and directors of TNCs and financial

institutions, their daily existence is immersed in global strategies of competition and

accumulation. This immersion is seen in organizational forms when corporations

have a decisive portion of their assets, employment, sales and profits linked to world-

spanning circuits of accumulation. At that point daily decisions, as well as long-term

5

strategy, must consider the management of assembly lines, labor relations,

marketing, competitive threats, regulatory structures, tax regimes and other such

factors from an integrative global perspective.

When Jeff Immelt, the CEO of General Electric, was asked what he was most

proud of, he answered:

If I took just one thing to focus on in terms of being proud, it would

probably be the global footprint. We’ve gone from a company a decade

ago that was 70% inside the United States to a company today that’s

65% outside the United States. . . . If you look over the last decade, not

just at GE but at other large companies, the biggest secular change in

the last decade is this opening up of the global market. Companies need

to be confident competitors in every corner of the world. That’s what

we are at GE. (Wharton, 2013.)

For Immelt and other members of the TCC, global accumulation and

production are essential features of modern firms. The production of value and its

expropriation have a global geography. The national market becomes one of many

and a national strategy for growth and survival disappears, replaced by transnational

economic necessities. A dominant corporate culture is created by the most efficient

and profitable TNCs and encoded as best business practices. While some individual

capitalist may have internalized social responsibility and others may internalize a

sense of nationalism, all adhere to strategies and decisions that will produce profits

6

within a global capitalist system of monopoly competition.

The relations between capital and labor also undergo important shifts

conforming to the new geography. The TCC relies on a global labor force that has

integrated millions of workers from China, India, Russia, Brazil and dozens of other

countries. Between 1999 and 2008 TNCs in the United States shed 2.1 million

domeestic jobs while adding 2.2 million abroad (BEA, 2013). As new workers are

brought into new circuits of production and profit, others are dispossessed of their

jobs and means to a livelihood. The deepening of cross-border investments and

manufacturing has extended transnational relationships to labor (Struna, 2009).

Forms of production that depend on global assembly lines organize workers in new

formations subject to hierarchical power centralized on a transnational scale. These

new relations have undercut the necessity for a social contract with the working class

in the west, resulting in greater insecurity, austerity for millions and the growth of

temporary and part-time labor.

Li & Fung, the Hong Kong garment TNC, is a good example of global assembly

line organization. Li & Fung owns no factories, no sewing machines and no fabric

mills, but takes orders from the world’s biggest clothing retailers. What the

corporation does offer is 15,000 suppliers in over 60 countries working for the lowest

wages. In 2012 they had $21.8 billion in revenues. Because of their size, like Wal-

Mart they can set wages and conditions throughout the industry. As chief executive

Bruce Rockowitz stated, “We definitely are part of bringing prices down, there’s no

7

question about that, because we are arbitraging factories and countries all the time”

(Urbina and Bradsher, 2013). Such global arbitrage, and the speed at which it takes

place, is an expression of the new transnationalized relations of production. But not

only is Li & Fung’s unskilled and semi-skilled labor globalized, so too is its

managerial staff. Its 830 senior executives come from over 40 different countries,

half of whom have worked in two or more countries (Li & Fung, 2013).

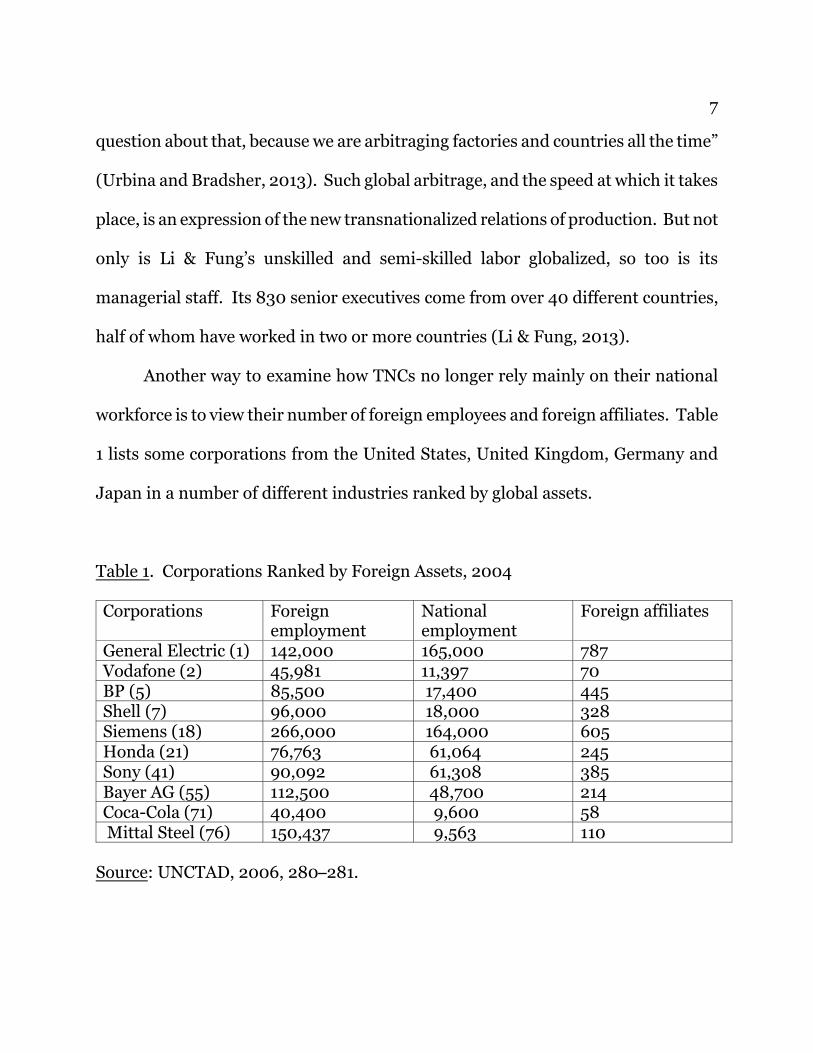

Another way to examine how TNCs no longer rely mainly on their national

workforce is to view their number of foreign employees and foreign affiliates. Table

1 lists some corporations from the United States, United Kingdom, Germany and

Japan in a number of different industries ranked by global assets.

Table 1. Corporations Ranked by Foreign Assets, 2004

Corporations Foreignemployment

Nationalemployment

Foreign affiliates

General Electric (1) 142,000 165,000 787Vodafone (2) 45,981 11,397 70BP (5) 85,500 17,400 445Shell (7) 96,000 18,000 328Siemens (18) 266,000 164,000 605Honda (21) 76,763 61,064 245Sony (41) 90,092 61,308 385Bayer AG (55) 112,500 48,700 214Coca-Cola (71) 40,400 9,600 58 Mittal Steel (76) 150,437 9,563 110

Source: UNCTAD, 2006, 280S281.

8

The most fundamental aspect of transnational class membership is not, as

network theorists argue, corporate board members linked through a network of TNC

firms. Rather, it is the global organization of labor and assets under a centralized

corporate hierarchy in which the primary appropriation of surplus value takes place

through transnationalized financial investments. The core membership of the TCC

are those who organize, finance and lead this process. This is carried out by financial

firms, corporate boards and elite policy bodies in and out of government. But class

formation is never limited to its leadership cadre. And so the linkage between

members of these bodies is of secondary importance to the institutional and

organizational structures built to accommodate, secure and expand global profits,

production and the reorganization of labor. In effect, class formation is situated in

the relations of production. It is these relationships that produce the driving internal

logic that members of the class follow, whether in a subjective or objective manner.

The pooling of capital through common financial investments becomes crucial

to the process of consolidating TCC structure and class cohesion. The integration of

economic interests via FDI, mergers and acquisitions, joint ventures, stock

ownership, cross-border financial flows, loans and debt all weave together a shared

multi-trillion-dollar transnational economy. All this vast economic activity is not

designed to produce more jobs in one’s own nation or pay taxes to expand one’s own

state. There is no national agenda, only a process of transnational accumulation and

monopoly competition based on the global organization of finance and production.

9

A key power is the control over decisions concerning where to invest capital.

With established best practices on how to run a business, strategies are set by

commonly held beliefs on the most efficient use of labor, tax avoidance, global

sourcing, shareholder value, competitive dominance, and so on. Within this set of

theory and practice, investment decisions are made based on who produces the best

returns. When BlackRock invests in the Chinese oil corporation Sinopec they are

investing for thousands of private and institutional owners of capital. BlackRock

does not need to control Sinopec. Transnational investors trust that Sinopec’s

statist/corporate leadership will act within transnational capitalist theory and

practice to return a profit on their investments. Since everyone must attract

investors, the ability to direct financial flows becomes the locus of power.

Class Formation and Network Theory

One important aspect of this process is the integration of operational

leadership as the composition of corporate boards and elite policy centers link key

players, and incorporate TCC individuals of different national origins. These

networks deepen the structure of the TCC by cultivating political and social

integration. Mutual membership on TNC boards, elite political committees and

exclusive clubs also provides sites where TCC members develop leadership cadre,

create common projects, and form shared cultural attitudes and economic

assumptions (Carroll, 2010; Staples, 2012). Adding an American to the board of a

10

Chinese corporation or a German to the board of a Russian bank is not done so these

individuals can be national representatives of their countries’ interests. The aim is

to increase the profits and monopoly position of the TNC, not the nation. In effect,

they work for the class, not the nation.

Elite network theory has a long history, including G. William Domhoff (1967),

C. Wright Mills (1956), and Robert Michels (1915), among others. But my main

concern will focus on a new trend that uses this theoretical framework to analyze the

TCC. This new area of investigation, tracing elite corporate networks as it relates to

TCC theory, has been carried out in a number of detailed studies, the most complete

and richly done by William Carroll. This important and valuable work creates a

picture of the organic development of the TCC on a sociological level. It strengthens

and expands our understanding of class formation. These relationships, however,

are primarily built upon changes in the relations of production and the appropriation

of surplus value organized by the TCC. Although joining a board or policy institute

promotes greater self awareness for a class through networking, it doesn’t create the

class. Rather, it is a reflection of membership in it. Power is a class question, not an

individual one. How many links are held by board members is a secondary question,

because the class relationship between global labor and transnational capital takes

place with or without boardrooms networked through individuals. Therefore, it is

in the relations between capital and labor and the mode of accumulation where class

formation is primarily rooted.

11

When network research becomes too narrowly focused on personal ties rather

than relations of production, this can lead to weak conclusions based on constricted

evidence. For example, Burris and Staples state: “The emergence of a transnational

capitalist class as a truly global phenomenon is a very long way from realization and

probably unlikely for the foreseeable future” (Burris and Staples, 2012, 13). Their

position is closely aligned to the Atlantic ruling class thesis of Kees Van der Pijl,

(1984) as they contend: “The combined evidence is much stronger and relatively

consistent for the emergence of a more circumscribed transnational capitalist class,

centered in the North Atlantic region” (Burris and Staples 2012, 1).

In their study of the Eurozone, Dudouet, Gremont and Vion reach a more

constricted conclusion: “From the whole European elite network structure, we draw

out data showing that the Dutch, German Italian, and French networks are deeply

rooted in national business communities, and have not substituted these for

transnational networks” (Dudouet, Gremont & Vion, 2012, 139). They go on to argue

that “transnational connections within the global network are the work of a very few

key actors” (2012, 142). Accordingly, there is not enough evidence to establish the

existence of the TCC.

To reach such conclusions network theorists analyze class formation from a

narrow sociological viewpoint. Take, for example, this statement: “If one is

interested in transnational class formation and the interpersonal relations that

facilitate transnational class identity and class cohesion, then the preferred approach

12

would surely be to study the structure and evolution of person-to-person (director-

to-director) networks” (Burris and Staples, 2012, 7). Consequently, their analysis is

reduced to the personal relationships of directors linked through TNCs and policy

bodies. In some studies this leads to wonderfully detailed illustrations of

interconnecting relationships. But if over-emphasized, it turns the investigation of

class formation into something akin to mapping Facebook friends. With all its

emphasis on who knows whom on what board, one relationship that seems to

disappear is that between capital and labor. For network theorists, if firms lack links

between board members the TCC has no substantial formation; even when surplus

value is expropriated through transnational circuits, production coordinated into

global assembly lines, and investments pour in from around the world.

TNC board positions are also given a place of privilege far beyond the

hundreds of other personal class ties that exist. A short list might include: schools,

fraternities and sororities, exclusive communities for homes, favorite restaurants,

hotels and vacation spots, family and friendship ties that link to further connections

at dinners, weddings and parties, golf outings, polo clubs, political fund-raisers,

philanthropic work, boards of cultural organizations, business relationships outside

board membership, bargaining at the WTO and IMF, networking at Davos, retreats

at the Bohemian Club, and so on. So to conclude that there is little evidence for the

existence of a global TCC based primarily on ties among corporate directors is a

limited argument, even in sociological terms.

13

Interconnecting board relationships are also a narrow method by which to

examine power, leadership and class formations within TNCs. Speaking to his

leadership core at GE, Immelt explains:

If you want to manage a company as big as GE, you’ve got to know the

top 200 to 300 people really well. The only way I can run GE well is if

I handpick the top couple of hundred people. They have to be a

manifestation of the company, its values and my values. You need to

have this unique ownership of the senior leadership of the company.

(Wharton, 2012.)

This “unique ownership” and system of values is another way by which TCC

consciousness and practice develops. These 300 people are outside the board, but

as the leadership core they wield a good deal of power and have direct contact with

leaders at other global corporations and financial institutions.

Where does this leadership come from? Immelt explains further:

I think leadership has a very short shelf life, and so every few years, we

look outside the company to see what others are doing: What’s Google

doing? What’s the U. S. Military Academy doing? What are they

teaching at the Communist Party School in Beijing? What is McKinsey

teaching its people? I’m paranoid about keeping up-to-date with

attracting and retaining great leaders from Bangalore to Boston and

everywhere around the world. (Wharton, 2012.)

14

Consequently, TCC cadre, their recruitment, training and the rich rewards in stocks

and income that come with elite positions, is a global talent search for the best and

brightest.

Carroll’s work generally avoids a reductionist analysis. With reference to

personal networking among corporate interlocks he states: “Our findings underline

a certain disjuncture between class formation as a sociocultural process and the

economic process of capital accumulation” (Carroll, 2010, 225). Importantly, Carroll

recognizes the advanced state of the transnational economy and its uneven

sociocultural development, so there is a distinction between objective and subjective

class formation. But Carroll seems to be searching for comprehensive relationships

based on historic nation-centric patterns of class formation. Commenting on his

research into board interlocks of TNCs, he writes:

With very few exceptions, transnational interlocks are not vehicles of

strategic control SS they occur independently of transnational

intercorporate ownership. In this sense, there is no evidence of the

formation of transnational enterprise groups SS sets of giant firms

whose boards interlock and whose shares are owned in blocs that

enable coordinated strategic control over major corporations based in

multiple countries. Rather, intercorporate ownership relations,

typically emanating from financial institutions and consisting of

holdings of considerable less than 5 percent of share capital, express the

cross-penetration of investment and the developing solidarities of a

transnational corporate community. (2012, 69S70.)

15

Carroll’s approach to TCC formation is situated in finding individuals within

transnational corporate blocs with coordinated strategic control. Anything less is a

“community” but not a class. But global class formation does not necessarily have

to follow historic forms from the nationSstate era. Control of national markets

through enterprise blocs was an essential step in the formation of the monopoly

capitalist class. This by necessity took place among nationally based capitalists,

often organized around families and banks. Strategic control of industries could be

achieved through blocs grouped around banking families such as Morgan or

Rockefeller.

Italy is a country that long maintained, quoting Carroll, “sets of giant firms

whose boards interlock and whose shares are owned in blocs that enable coordinated

strategic control.” Enrico Cuccia, founder of Mediobanca, was key in building over-

lapping investments for Italy’s most powerful families. These included the Agnellis,

the Benettons, the Ligrestis, the Pesentis, the Pirellis, and later Silvio Berlusconi.

Cross-shareholdings included airports, auto, banking, construction, hotels,

insurance, leisure, media and telecoms. Such arrangements held off foreign

investments, but when the economic crisis hit losses spread like a contagion through

the interlinked corporations, causing historic losses. Now, in what was described as

brutal bloodletting, the old partnerships have been ripped apart. Foreign

acquisitions have taken over many of Italy’s best-known companies, while the Italian

corporations themselves have globalized their holdings and investments. The old

16

national system of enterprise blocs became a barrier to transnational expansion, as

well as an obstruction to capital investments into Italy (Sanderson, 2013).

Class Formation and Financialization

If the national system of class formation situated in enterprise blocs has

broken down, what structures and methods have taken its place? Carroll correctly

notes that “intercorporate ownership relations, typically [emanate] from financial

institutions.” Here is a key element, but Carroll overlooks its importance. Financial

institutions have become central to the organization of capital and TCC formation,

but not in the sense of creating clusters of industrial blocs under their control.

Financialization has changed the trajectory of power, resulting in trillions of dollars

of investments in tens of thousands of global spanning corporations. In fact,

corporations themselves have become something to own, dismantle and sell as a

commodity. The hedge fund industry is based in such activity. For such investors,

strategic control of enterprise blocs are not the main expression of power. The power

to engage in a flexible regime of transnational investments, and to direct the vast

rapid flows of global capital, are at the core of their expropriation of value and class

formation.

As Paul Sweezy pointed out:

The locus of economic power has shifted along with the ascendancy of

17

financial capital. It has long been taken for granted, especially among

radicals, that the seat of power in capitalist society was in the

boardrooms of a few hundred giant multinational corporations . . . [but]

real power is not so much in corporate boardrooms as in the financial

markets. (Sweezy, 1994.)

Consequently, it is not necessary to have transnational enterprise blocs with linked

representatives to constitute a united self-conscious class. With globalization TCC

subjective cohesion is created by common ideology, shared practice, mutual

investments and a broad range of social interactions.

Boards and CEOs do have a large amount of power over where to locate

factories, determination of wages, with whom to sub-contract, with whom to merge,

whom to acquire, and so forth. Such decision-making power certainly has significant

impact on the lives of workers and is a critical factor in defining the relations of

production. But such decision are made within the theory and practice of neoliberal

ideology common to the entire TCC. Executives come and go; the average tenure of

a Fortune 500 CEO is just 3.5 years. Rather than emphasizing a handful of linked

board members, what needs to be emphasized is the structural character of TNCs

and transnational financial investments.

Central to our understanding of the TCC is an investment company such as

BlackRock, the world’s largest with $3.65 trillion of held assets. If we look at just one

of their funds, BlackRock Variable Series Funds, Inc., there is $6.3 billion invested

in 475 common stocks in 34 countries, $729 million in 95 corporate bonds covering

18

24 countries, plus investment vehicles in 16 different currencies (2012, 7S12). And

that is just the first few pages of a longer report. BlackRock does not control any of

these 570 companies. But BlackRock does invest for transnational capitalists

throughout the world. Do all these investors sit on boards or have control over the

strategic decisions of these corporations? Of course not. But they are part of the

financialization of capitalism, through which they appropriate surplus value from

laboring men and women the world over.

Such activity is central to the development of the TCC, and constitutes a locus

of power outside the boardroom. In effect, financial firms have become the

organizing centers for transnational capital. Their activity is to direct global

investments for the TCC and act as a major channel for the expropriation of value.

They do this not as representatives of national capital, but for capitalists from any

country. Goldman Sachs, Barclays and Deutschbank are not national champions,

but transnational financial monopolies competing for world investors, investing the

world over, and often cross-investing with each other. Ties among individual

directors help in business transactions, but they are not the main element in class

formation. Rather, the trillions of dollars flowing through these firms, how these

investments are organized and for whom SS these factors are central to TCC

formation.

Although board links are emphasized by network theorists, BlackRock tends

to frown on directors who sit on too many boards. BlackRock calls this

19

“overboarding,” and in 2012 voted against three Coca-Cola directors because each

served on more than four boards. This strongly suggests that as a financial

institution BlackRock is not interested in linked enterprise blocs, but in directors

who can focus on maximum returns without divided attention. As the largest

shareholding institution in the world they wield tremendous power, voting at 14,872

shareholder meetings. Of these 3,800 were in the United States, where BlackRock

is the largest shareholder in 20% of U. S. corporations. Even so BlackRock has never

put forward a single shareholder proposal (Craig, 2013). For BlackRock, their

holdings do not constitute an enterprise bloc in the historic sense, where strategic

control was brought to bear in an array of boardrooms. Instead, BlackRock’s

financial strategy is determined by the rate of return on each of its capital

investments.

An important study, by the Swiss Federal Institute of Technology in Zurich,

mapped ownership among TNCs, providing significant insight into the process of

financialization. Going through a database of 37 million companies and investors,

they focused on 43,060 TNCs. Examining shareholding networks, the study found

a core group of 147 predominantly financial institutions that constituted a “super-

entity,” controlling about 40% of the entire network (Coghlan and Mackenzie, 2011).

In examining investors grouped mainly in these super-entities, the study found

47,819 major individual and institutional shareholders from 190 countries involved

in the world’s dominant 15,491 TNCs (Vitali, Glattfelder and Battiston, 2011).

20

Furthermore, investors represented by these financial companies may act for

additional institutional and individual investors. So in the BlackRock Variable Series

Funds, from the example above, we might find Vanguard or State Street investing for

their clients into BlackRock. Thus the 47,819 major investors actually accounts for

a greater number, since institutional investors represent multiple individual

interests.

The integrated global character of securities and stocks, seen in data from the

U. S. Bureau of Economic Analysis, provides further evidence. In 2010, U. S.Sheld

foreign securities and stocks were $5.471 trillion, while private foreign-held

securities and stocks inside the United States were $6.113 trillion and foreign official-

held securities in the United States were $4.373 trillion (BEA, 2013). Here we have

over $15 trillion in cross-border stocks and securities representing extensive TCC

investments that merge financial and corporate interests regardless of borders and

board members. The much larger figure of externally held assets and liabilities of

banks and non-banks sat at $64.7 trillion in March, 2012 (BIS, 2012). Such sizeable

cross-border flows represent large clusters of transnational investors. The pivotal

role of financial institutions in directing these trillions of dollars reveals their role as

economic organizing centers for the TCC.

Carroll recognizes the power of finance. He writes of

an extensive network of intercorporate ownership [with] a few key

21

financial institutions playing key integrative roles. Within this new

finance capitalism, investments are rarely matched by the directorial

ties. . . . Rather, power resides in the exit option SS the capacity of

institutions to invest and divest in any of a wide range of companies.

(Carroll, 2012, 70.)

Carroll’s observations are right on target, but his emphasis here is not on the power

of finance. Instead his main focus is on “weak capital and directorial relations that

are transnational in scope SS the latter furnishing the basis for an emerging

transnational capitalist class” (Carroll, 2012, 72). The problem doesn’t lie in his

research; in fact, Carroll well understands political economy. Rather it is in the

assumption that a necessary prerequisite of personal relationships must exist, based

on linked TNCs and policy boards, for class formation to fully emerge. “Weak

directorial relations” result in deficient class cohesion. Therefore, because financial

investments are “rarely matched by directorial ties,” he overlooks their importance.

What is missing for Carroll is a completed organic sociological condition within the

TCC, which he elevates over the more firmly established class relationship between

global finance capital and labor and the manner in which surplus value is

expropriated.

Cliff Staples comes to a position affirming the TCC through his study of the

Business Roundtable. Staples hunts down 49 “inner circle” members of the

Roundtable from a group of 661 inner circle CEOs from the Fortune 500. He then

goes on to examine how the Roundtable “joined a super-group of CEOs” in a lobby

22

organization called World Business Leaders for Growth, concluding that this group

brings “representatives of the transnational capitalist class together under one

umbrella, and arguably is the best example of transnational capitalist class

consciousness, solidarity and political action to date” (Staples, 2012, 116). Like

Carroll, Staples is focused on individuals and their numbers. Class formation is to

be found in rooms where powerful individuals sit down together and make decisions.

That is an interesting topic and occupies an important place in TCC theory. But

class formation is not reducible to small numbers of individuals and groups. Credit

Suisse reports some 84,700 people with investable assets above $50 million, 29,000

with over $100 million. As Credit Suisse points out, “the wealth portfolios of (these)

individuals are also likely to be similar, dominated by financial assets and, in

particular, equity holdings in public companies traded in international markets”

(Freeland, 2012, 5 ). Additional indicators of TCC depth are private client assets held

by high-net-worth individuals. These funds have hit $1.75 trillion in Switzerland,

$1.69 trillion in the United Kingdom and $1.63 trillion in Singapore (Grant, 2013).

Such numbers provide a broader understanding of the TCC, and the key role played

by financial institutions. Without such references, network theory is reduced to

something akin to David Rothkopf’s “superclass,” which puts the global elite at about

6,000 individuals in key business, military and political positions (Rothkopf, 2008).

David Peetz and Georgina Murray sum up the broader relationship between

finance capital and corporations in their detailed study on links between TNCs and

23

capital ownership. They write:

Finance capital not only lends the money to corporations enabling them

to expand, and dictates their movements in share markets that signal

the success or failure of corporate management, it also owns the

corporation. . . . in the end industrial capital is finance capital. . . .

Today corporations that follow the logic of finance capital SS the logic

of money SS dominate the world. Their logic is not the logic of

individuals but the logic of a class. (Peetz and Murray, 2012, 50.)

Consequently, unlike Carroll who sees transnational elite networks, Peetz and

Murray conclude that “now we can also speak of a true transnational class” (ibid.).

Class Formation Technology and Labor

Financialization has expanded through the use of new information

technologies, allowing capitalists to become immensely wealthy with the use of a

minimum amount of labor. Bain Capital issued a report on the tremendous over-

accumulation of capital that uncovers the intensity of this contradiction.

the relationship between the financial economy and the underlying real

economy has reached a decisive turning point. . . . By 2010 global

capital had swollen to some $600 trillion, tripling over the past two

decades. Today, total financial assets are nearly 10 times the value of

the global output of all goods and services (creating) a world that is

24

structurally awash in capital. (Bain Report, 2012).

Bain’s “decisive turning point” denotes the rupture between socially necessary labor

and the creation of surplus value. It has meant a flood of money into speculative

activities that feeds financialization. It also allows investment CEOs to claim billions

of dollars in annual salaries and the obscene rise in wealth of the top one-tenth of

one percent. On one hand, technology has reduced the need for labor, while

globalization has opened access to a mass of super-exploited workers. The result in

the United States and the European Union is that millions are expelled from the

labor force, and face a broken social contract that the TCC no longer sees any reason

to maintain.

The contradiction between the socialized nature of work and the private

ownership of the means of production is accentuated by the technological tools of

financial production. The labor involved in trillions of dollars in speculative finance

is carried out by a very small section of the global work force. Moreover, about half

of all daily trades are done by computer algorithms written by a handful of experts

and run without daily human input. The former chief technical officer at Goldman

Sachs reported that trading strategies were done by “50,000 servers just doing

simulations,” and he noted many more have since been added (Hardy, 2013). So

important is the speed of the technology that a number of trading firms have moved

from New York to Newark to be within blocks of SWIFT, the company that runs the

25

super-computer through which world trades are processed. Fiberoptic cables

transmit data at about one foot every billionth of a second, so physical closeness

gives a microsecond advantage in the speed of information and the ability to profit

from it. These huge data centers have no workers, but are filled with racks of servers

in vast rooms lit only by the blinking lights of computers.

The money markets are one way to examine this phenomenon. This is simply

money trading money, making currencies a commodity rather than a form of

exchange. These trades are done by algorithms looking for arbitrage, or the very

small differences in the price of a currency that exists at the same time in different

places. When the algorithms read the mathematical formulas and figures they are

programmed to look for, transnational trades are conducted in less than a second.

Billions flash back and forth over borders to totals that hit $1.7 trillion a day. It is

hard to understand what one trillion means. But to get an idea, one trillion seconds

equals 36,000 years, while one million seconds is only twelve-and-a-half days.

The wealth of Henry Ford depended on the day-to-day expropriation of value

created by tens of thousands of auto workers. And this expropriation could only

occur when workers took their place on the assembly line. But Goldman Sachs gains

vast riches from the operation of their computers working without the input of daily

human labor. This rupture between socially necessary labor time and wealth is one

element that gives the TCC growing freedom from any nationally based working

class. It inflates the space between the real economy and finance capital.

26

The speed with which finance capital can invest and withdraw capital is a key

aspect of its power. The daily control of enterprise blocs is now overshadowed by the

power and velocity of money. It is the power of financial institutions to invest or

withdraw funds that drives stock prices and enforces neoliberal efficiencies.

Consequently, the holders of stocks, bonds, equities, securities and derivatives can

drive the decision-making process of corporate boards that affect the daily lives of

workers, no matter where the border line is drawn. Owners of capital, whose use of

labor is minimum, now drive the real economy where the vast majority of labor

works. It is no wonder this mode of accumulation has produced a TCC wedded to the

ideology of austerity. Keynesianism has little place in a world in which the distance

between the capitalist class and labor has never been greater.

The transnationalization of finance not only affects TNCs; its logic now defines

the morality, identity and personal financial strategies of the TCC. Their world

outlook is one reason why tax evasion has become such a widespread phenomenon.

Both corporations and individuals have abandoned any sense of national duty with

the multi-trillion cross-border movement of capital. The manner in which TNCs and

investors accumulate wealth has naturally become the manner by which

transnational capitalists deposit and protect their personal wealth. Records leaked

from just three off-shore tax havens in the British Virgin Islands, the Cook Islands

and Singapore revealed information on more than 120,000 companies and nearly

130,000 individuals from more than 170 countries. Other offshore havens, such as

27

the Cayman Islands, hold even larger accounts and greater numbers. The McKinsey

Consulting Group estimates that between $21 to $32 trillion of hidden wealth is piled

into tax havens, with global banks such as UBS and Deutsche Bank deeply involved

in helping their clients hide their money (Gladstone, 2013). Further evidence is seen

in reports from U. S. transnationals that state 43% of their overseas profits are

generated from tax havens, although only seven percent of their foreign investments

and just four percent of their foreign workers are in those countries (Huang, 2013).

Off-shore havens have also become a common vehicle by which FDI is carried out in

order to avoid tax rates. The common practice of hiding profits and wealth, and

sharing information on how to pursue and structure tax havens, is another way the

TCC forms. It creates shared assumptions about the control over personal and

corporate wealth, while discarding concerns over social responsibilities.

Anthony van Fossen did a detailed study of tax havens in which he accounted

for 70 different sites and reported that 19% of the personal wealth of high-net-worth

individuals were in offshore financial centers as of 2009. The recent exposure of

offshore records will probably reveal even more. van Fossen concludes: “The

transnationalization of capitalist wealth has been far more extensive and globally

encompassing than the transnationalization of boards of the world’s large

corporations and elite corporate policy groups” (van Fossen, 2012, 82). His

observation goes to the heart of TCC formation. The linking of boards and policy

groups is important and will continue. But this process is propelled forward by the

28

transnationalization of finance and wealth.

Conclusion

To understand the extent and nature of the attacks on the world’s working

class, it is important to understand the cohesion and hegemonic position of the TCC.

Austerity in the North and structural adjustment programs in the South result from

a break with industrial era nation-centric capitalism.

The bourgeois democratic revolutions in the United States and France were

based on a revolutionary alliance between the capitalist class, craftsmen, workers,

farmers and peasants. This created a historic dialectic that encompassed a

contradictory and tension-filled relationship that nevertheless allowed for the

incorporation of demands from the working masses into capitalist society. As a

result, the working-class opposition has always existed inside the capitalist dialectic

to produce democratic outcomes. Gramsci best explained this in his theory on

hegemony, revealing the twin aspects of consensus and coercion. While force and

violence were always present, consensus was the main tool of more developed

capitalist societies (Gramsci, 1971). This contradiction, built into the very origins of

the industrial relations of production, produced the political flexibility that has

allowed capitalism to adopt and continue to exist.

The socialist movement sought to transcend this dialectic, to take a qualitative

leap beyond into a new dialectic based on working-class state power. This was the

29

only way to resolve the permanent contradiction inherent in capitalism: the fact that

bourgeois rule would never allow the full development of mass democracy because

it would undermine capitalist class power. Yet socialist and working-class demands

were sooner or later folded into an ever-evolving capitalism SS never in the way

envisioned by and called for by revolutionary activists, but in a way that allowed for

both the economic and political social contract to expand. This was particularly so

after the Great Depression and war against fascism, both of which pushed the

capitalist class into further concessions.

The left has often viewed the working-class opposition, its strikes and social

rebellions, as belonging to the socialist side of history, rather than as an essential

feature held within nation-centric capitalism. Yet the very definition of the modern

nationSstate revolves around citizenship, and the political and economic rights that

became part of modern society. The social contract was an essential expression of

one’s identity in belonging to the nation. That identity, of the working class as

stakeholders in capitalist society, was present from the first days of the barricades

in Paris or guerrilla fighters in the woods of North America. The working masses

have always been the contradictory opposite that creates the dialectic. From the

moment the Parisian masses read the Declaration of the Rights of Man they took

liberty, equality and fraternity as their own, not as rights exclusively reserved for

property owners. When Thomas Jefferson declared that “all men are created equal”

and endowed with “unalienable Rights,” farmers and workers possessed those ideas

30

as their own. The long and never-ending struggle over citizenship and democracy

arose from these revolutionary beginnings.

But just as socialists have sought to resolve this contradictory historic

relationship, the capitalist class has also wished to escape it. This is where

globalization comes to bear, because it allows capitalism to advance that goal. World

financialization and production have meant that the capitalist class can at long last

jettison the burdensome relationship with their own national working class. This is

why understanding the TCC as a coherent and hegemonic class is important.

Nation-centric capitalism was historically, and by economic and political necessity,

based on a tension-filled alliance with its own working class. This relationship has

been ruptured by the reorganization of capitalism on a transnational level. The

consensus side of Gramsci’s hegemonic relationship, as the key feature of nation-

centric capitalism, is being replaced by a new technocratic authoritarianism (Harris,

and Davidson, 2013; DuRand and Martinot, 2012). Democratic will is pushed aside

by transnational bodies that enforce austerity over popular opposition. Coercion, the

threat of unemployment, poverty, repression, spying and jail have become the

weapons of choice. The Associated Press reported that over their working life 80%

of adults in the United States will live in near poverty, be jobless or on welfare (Yen,

3013). The litany of attacks on public institutions, jobs, and the environment doesn’t

have to be repeated here. Just read your daily newspaper, no matter the country in

which you live.

31

The global shift in power is not the strategy of any single nation or hegemonic

state. Nor is it the result of a weakly organized and incomplete transnational

capitalist class. It is the strategic objective of a capitalist class transformed by

globalization. The manner in which production is organized and value expropriated

allows the capitalist class to break out of its historic nation-centric dialectic. It was

trapped within a formal relationship of equal citizenship, and burdened with

concessions conceded to its nationally organized laboring classes. But capitalism

has succeeded in creating a new dialectic. Not by one state nor for one state, but for

the class as a whole on a global scale. The struggle is far from over, and crisis-prone

globalization is far from consolidated. But to prepare for the challenges ahead we

must have a clear understanding of what and who we face, and why differences in

epistemology have their implications and consequences.

DeVry University

1250 N. Wood St.

Chicago, IL 60618

REFERENCES

Bain Reports. 2012. “A World Awash in Capital.” Insights (November 14).

BIS. Bank of International Settlements. 2012. “Detailed Tables on Preliminary

32

Locational and Consolidated Banking Stats at End of June 2012.” Monetary

and Economic Department. http://www.bis .org/statist ics/

rppb1210_detailed.pc

BlackRock. 2012. Annual Report (December 31). BlackRock Variable Series Funds,

Inc.

BEA. Bureau of Economic Analysis. 2010. “U. S. Net International Investment

P os i t i on at th e Yearen d 2009. ” h t t p s : / / w w w . b e a . org /

mnewsreleases/international/intinv/intinvnewsrelease.htm

SSSSSS. 2013. PBS.org/wgh/pages/frontline/the-state-of-the-American-middle-

class-in-eight-chapters

Burris, Val, and Clifford Staples. 2012. “In Search of a Transnational Capitalist

Class: Alternative Methods for Comparing Director Interlocks Within and

Between Nations and Regions.” International Journal of Comparative

Sociology, 53, 323.

Business Week. 2013. http://investing.businessweek/research/stocks/private/

person.asp?personId=9176800

Carroll, William K. 2010. The Making of a Transnational Capitalist Class: Corporate

Power in the 21st Century. London/New York: Zed Books.

SSSSSS. 2012. “Capital Relations and Directorate Interlocking: The Global Network

in 2007.” Pp. 54S75 in Financial Elites and Transnational Business: Who

Rules the World? Cheltenham, UK: Edward Elgar Publishing.

33

CDH. 2013. http://www.cdhfund.com/en/index.html

Coghlan, Andy, and Debora MacKenzie. 2011. “Revealed SS The Capitalist Network

that Runs the World.” www.newscientist.com/science-in-society

Craig, Susanne. 2013. “The Giant of Shareholders, Quietly Stirring.” New York

Times (May 18).

Domhoff, G. William. 1967. Who Rules America? Englewood, New Jersey:

Prentice-Hall.

Dudouet, Frabcius-Xavier, Eric Gremont, and Antoine Vion. 2012. “Transnational

Business Networks in the Eurozone: A Focus on Four Major Stock Exchange

Indices.” Pp. 124S145 in Financial Elites and Transnational Business: Who

Rules the World? Cheltenham UK: Edward Elgar Publishing.

DuRand, Cliff, and Steve Martinot, eds. 2012. Recreating Democracy in a

Globalized State. Xxxxxxxxx: Clarity Press.

Freeland, Chrystia. 2012. Plutocrats: The Rise of the New Global Super-Rich and

the Fall of Everyone Else. New York: Penguin.

Gladstone, Rick. 2013. “Vast Hidden Wealth Revealed in Leaked Records.” New

York Times (April 4).

Gramsci, Antonio. 1971. Selections from the Prison Notebooks of Antonio Gramsci.

New York: International Publishers.

Grant, Jeremy. 2013. “Singapore Funds Benefit from Asian Wealth.” Financial

Times (July 23).

34

Hardy, Quinten. 2013. “A Strange Computer Promises Great Speed.” New York

Times (March 21).

Harris, Jerry. 2003. “Power in Transnational Class Theory.” Science & Society,

67:3, 329S338.

SSSSSS. 2005. “To Be or Not to Be: The Nation-Centric World Order Under

Globalization.” Science & Society, 69:3, 329S340.

SSSSSS. 2008. The Dialectics of Globalization; Economic and Political Conflict in

a Transnational World. Newcastle upon Tyne, UK: Cambridge Scholars

Publishing.

Harris, Jerry, and Carl Davidson. 2013. “Globalization and the Crisis of

Democracy.” Perspectives on Global Development and Technology,

12:1S2,181S193.

Huang, Chye-Ching. 2013. “An Unneeded Gift to Corporations.” New York Times

(April 11).

Li & Fung. 2013. http://www.funggroup.com/eng/about/managers

Liodakis, George. 2010. Totalitarian Capitalism and Beyond. Surrey, UK: Ashgate

Publishing.

Michels, Robert. 1915. A Sociological Study of the Oligarchical Tendencies of

Modern Democracy. London: Jarrold & Sons.

Mills, C. Wright. 1956. The Power Elite. Oxford/New York: Oxford University

Press.

35

Peetz, David, and Georgina Murray. 2012. “The Financialization of Global

Corporate Ownership.” Pp. 26S53 in Financial Elites and Transnational

Business: Who Rules the World? Cheltenham, UK: Edward Elgar Publishing.

Robinson, William I. 2004. A Theory of Global Capitalism: Production, Class, and

State in a Transnational World. Baltimore, Maryland/London: The Johns

Hopkins University Press.

Rothkopf, David. 2008. Superclass: The Global Power Elite and the World They Are

Making. New York: Farrar, Straus and Giroux.

Sanderson, Rachel. 2013. “Italian Business: No Way Back.” Financial Times

(August 20).

Sklair, Leslie. 2001. The Transnational Capitalist Class. Oxford: Blackwell.

Staples, Clifford L. 2012. “The Business Roundtable and the Transnational

Capitalist Class.” Pp. 100S123 in Financial Elites and Transnational Business:

Who Rules the World? Cheltenham, UK: Edward Elgar Publishing.

Struna, Jason. 2009. “Towards a Theory of Global Proletarian Fractions.”

Perspectives on Global Development and Technology, 8:2S3, 230S262.

Sweezy, Paul M. 1994. “The Triumph of Financial Capital.” Monthly Review, 46:2

(June), 9S10.

UNCTAD. United Nations Conference on Trade and Development. 2006. World

Investment Report 2006. New York/Geneva: United Nations.

Urbina, Ian, and Keith Bradsher. 2013. “Linking Factories to the Malls, Middleman

36

Pushes Low Costs.” New York Times (August 7).

van der Pijl, Kees. 1984. The Making of an Atlantic Ruling Class. London: Verso.

van Fossen, Anthony. 2012. “The Transnational Capitalist Class and Tax Havens.”

Pp. 76S99 in Financial Elites and Transnational Business: Who Rules the

World? Cheltenham, UK: Edward Elgar Publishing.

Vitali, Stefania, James B. Glattfelder, and Stefano Battiston. 2011. “The Network of

Global Corporate Control.” Systems Design (July 28).

Wharton School of Business. 2013. “GE’s Jeff Immelt on Leadership, Global Risk

and Growth.” http://knowledge.wharton.upenn.edu/article.cfm?

articleid=3241

Yen, Hope. 2013. “Exclusive: Signs of Declining Economic Security.”

http://bigstory.ap.org/article/exclusive-4-5-us-face-near-poverty-no-work-0