Embed Size (px)

Citation preview

WWEEEEKK 22

1

1

Lecture Notes

Week Two, Day One(Session I: 08:30 – 10:30)

Program on the Appraisal of Infrastructure Projects with Private

Participation

2

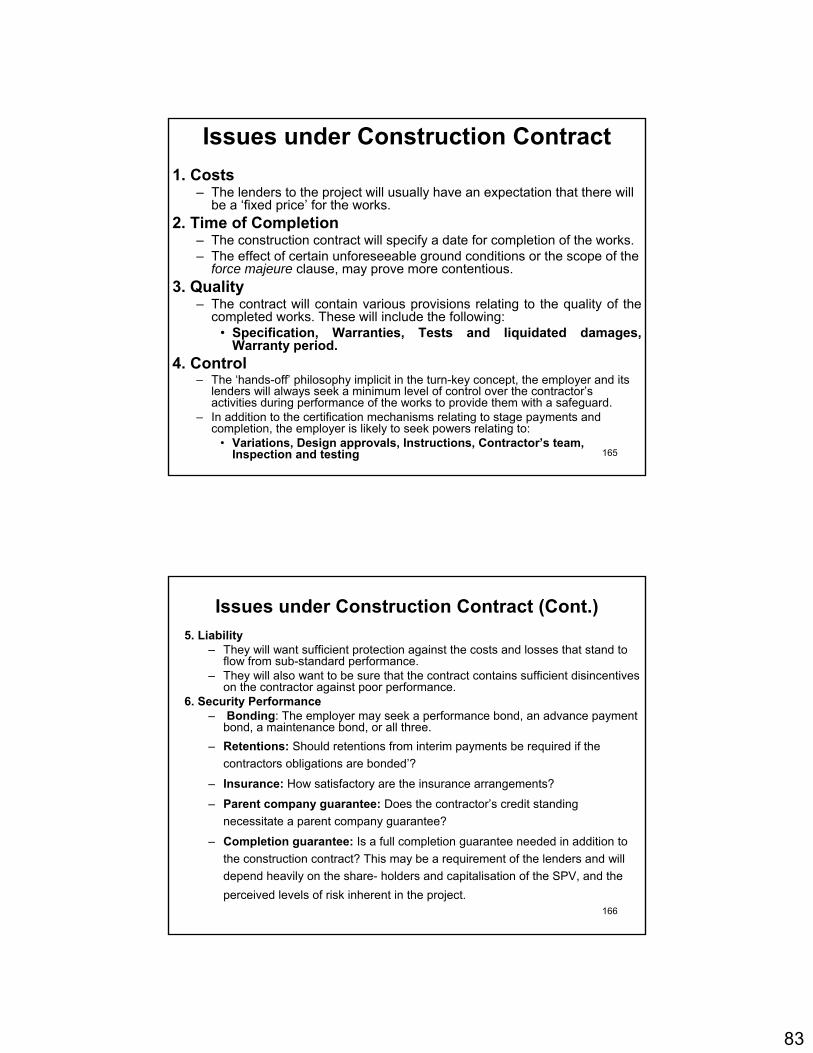

COSTS AND BENEFITS OF

ELECTRICITY INVESTMENTS

2

3

Economic Valuation of Additional Electricity Supply

• Willingness to pay for new connections• Willingness to pay for more reliable

service• Resource cost savings from replacement

of more expensive generation plants• Marginal cost pricing

4

ECONOMIC VALUE OF ELECTRICITYFOR NEW CONNECTIONS OR FOR REDUCTION OF

WITH ROTATING POWER SHORTAGES

Assuming willingness to pay (WTP) of all customers are also evenly distributed from highest 0P’ to lowest P0

m:

Economic Value of Additional Power Supply = ((PMAX+ P0m)/2) * (Q’-Q0)

Shaded area = economic value of shortage power

(Q’-Q0) = Power shortage, evenly rotated to all customers

Q00

P0m

PMAX=P’ D

FC

D0

S0

B

Quantity

$

Q’

3

5

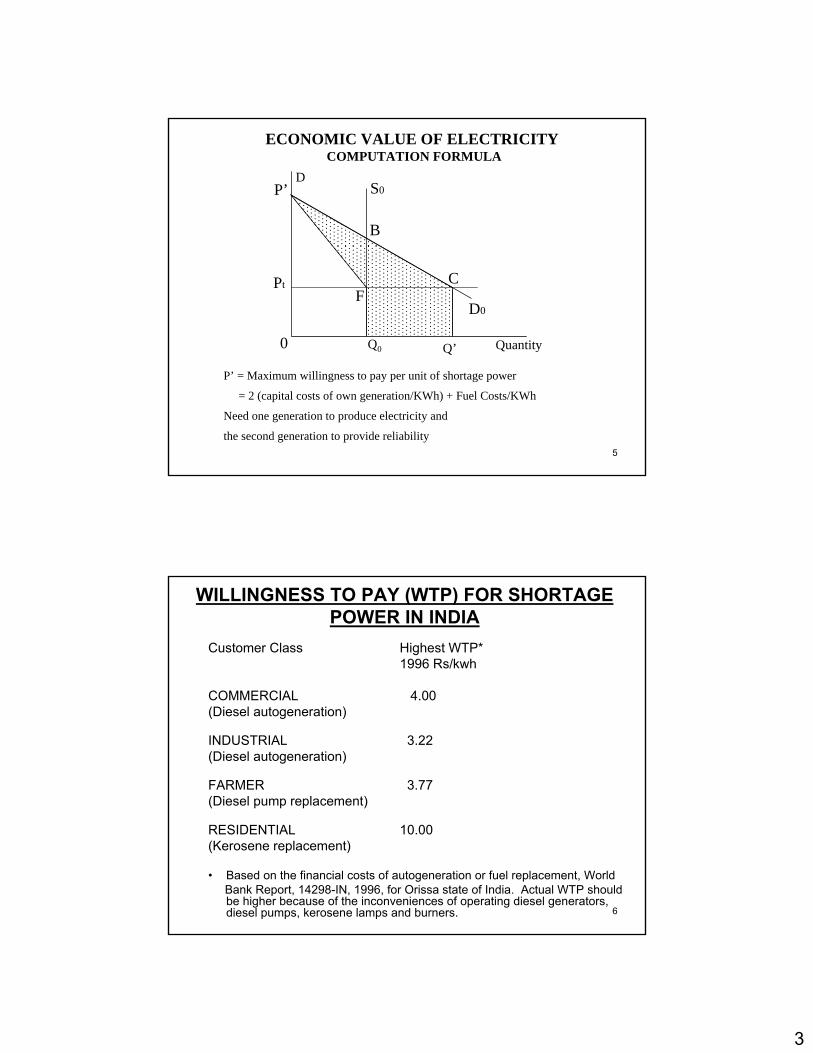

ECONOMIC VALUE OF ELECTRICITY COMPUTATION FORMULA

P’ = Maximum willingness to pay per unit of shortage power

= 2 (capital costs of own generation/KWh) + Fuel Costs/KWh

Need one generation to produce electricity and

the second generation to provide reliability

0

Pt

P’D

F

Q0

C

D0

S0

B

QuantityQ’

6

WILLINGNESS TO PAY (WTP) FOR SHORTAGE POWER IN INDIA

Customer Class Highest WTP*1996 Rs/kwh

COMMERCIAL 4.00(Diesel autogeneration)

INDUSTRIAL 3.22(Diesel autogeneration)

FARMER 3.77(Diesel pump replacement)

RESIDENTIAL 10.00(Kerosene replacement)

• Based on the financial costs of autogeneration or fuel replacement, WorldBank Report, 14298-IN, 1996, for Orissa state of India. Actual WTP should be higher because of the inconveniences of operating diesel generators, diesel pumps, kerosene lamps and burners.

4

7

Total Own-generation Cost ($/kWh) 0.169

Average Power Price (Gross of Tax, $/kWh) 0.037

Maximum Willingness To Pay ($/kWh) 0.212

Average Willingness To Pay ($/kWh) 0.125

OWN-GENERATION COST AND WILLINGNESS TO PAY IN MEXICO

8

1. Based on willingness to pay• Based on customers survey

2. Based on actual costs to users

3. Based on linear relationship between GDP and electricity consumption of industrial/commercial users

Estimated Cost of Power Failure

5

9

Estimated Cost of Power Failure*1. Based on Willingness to Pay

• Based on customers survey (Contingent valuation)Ontario Hydro Estimates of Outage Costs (1981 US$/kwh)

Duration Large Small Commercial ResidentialManufacturers Manufacturers

1 min 58.76 83.25 1.96 0.1720 min 8.81 13.56 1.66 0.151 hr 4.35 7.16 1.68 0.052 hr 3.75 7.35 2.52 0.034 hr 1.87 8.13 2.10 0.038 hr 1.80 6.42 1.89 0.0216 hr 1.45 4.96 1.75 0.02Average** 2.15 6.38 1.98 0.12All groups average***: 1.96 Average power price: 0.025

Average willingness for power during outage = 78.4 times average power price.

English Estimate (1996): 4 $/kwh* C.W. Gellings and J.H. Chamberlin, Demand-Side Management: Concepts and Methods,

Liburn, Georgia, The Fairmont Press, Inc., 1988. ** Based on system simulation model *** Based on shares: 13.5/13.5/39/34 %.

10

Estimated Cost of Power Failure (continued)

2. Based on actual costs to users (Loss in contribution to profits)

* Source: Table 7-10, Roop Jyoti, Investment Appraisal of Management Strategies for Addressing Uncertainties in Power Supply in the Context of Nepalese Manufacturing Enterprises, PhD Thesis, The Kennedy School of Government, Harvard University,December, 1998.

Year 1 2 3 4 5

Firm 1 5.56 2.73 5.01 1.50 3.43 Firm 2 3.31 2.86 1.71 3.24 3.76 Firm 3 15.25 11.77 14.37 12.16 5.26 Average each year 8.04 5.79 7.03 5.63 4.15 Average all years 6.13

COST OF POWER FAILURE IN NEPAL*(Multiples of electric tariff)

6

11

Estimated Cost of Power Failure (continued)San Diego (sudden outage of a few hours)*

(1981 US $/kwh)

Industrial CommercialDirect User 2.79 2.40Employees of Direct User 0.21 0.09Indirect User 0.12 0.13Total 3.12 2.62Multiples of Av Tariff** 62.4 52.4

Key West, Florida (rotating blackout for 26 days)*% of Cost MultiplesTime of Price

Nonresidential Users 4.8 $2.30/kwh 46.0

* Electric Power Research Institute study EPRI EA-1215, 1981, Vol. 2. ** Average price in 1981 is 0.05 $/kwh.

12

Estimated Cost of Power Failure (continued)

3. Based on linear relationship between GDP and electricity consumption of industrial/commercial users*

Outage cost = 1.35 (1981$/kwh) Or:

= 27 (multiples of the average power price)

* M. L. Telson, “The Economics of Alternative Levels of Reliability for Electric Power Generation Systems,” Bell Journal of Economics, Autumn, 1975.

7

13

Summary:Average power outage cost ranges from 6 to 80 times of the average power price.

14

Investment in New Generation to obtain Cost

Savings

8

15

8760 hrs

CapacityMW

Load Duration Curve hours for Year

8760 hrs

CapacityMW

Load Curve hours for Year

Peak hours Off-Peak hours

16

Calculation of Marginal Cost of Electricity Supply

• During the off-peak hours when the capacity is not fully utilized, the marginal cost in any given hour is the marginal running cost (fuel and operating cost per Kwh) of the most expensive plant operating during that hour.

• During the peak hours, when generation capacity is fully utilized, the marginal cost of electricity per Kwh is equal to the marginal running cost of the most expensive plant running at the time plus the capital costs of adding more generation capacity, expressed as a cost per Kwh of peak energy supplied.

9

17

2

3

4 MC1=0.03/KWH

Optimal Stacking of Thermal

MC2=0.04/KWH

MC3=0.05/KWH

MC4=0.08+ 400(0.15)/1000=0.14/KWH

H2 H3 H4

1000 1500 4500

CapacityKwH

0.08 $4001

0.05 $6002

0.04 $7003

0.03 $10004

Fuel Cost

Capital Cost

Plant

H4 solve for the minimum number of hours to run a plant 4 or the maximum number to run plant 3.

v = r+ d =0.15v(K4)+f4(H4)=v(K3)+f3(H4)

0.15(1000)+0.03(H4)=0.15(700)+0.04(H4)(150-105)=0.4(H4)-0.03(H4)

45=0.01H4

H4=4500

1

18

Contribution to Generation Investments

Hours Price MC Amount $/yr.Plant 1: 1000 * (0.14 – 0.08) = 60

Plant 2: 1000 * (0.14 – 0.05) = 90

Plant 3: 1000 * (0.14 – 0.04) = 100

Plant 4: 1000 * (0.14 – 0.03) = 110

Plant 3: 500 * (0.05 – 0.04) = 5

Plant 4: 500 * (0.05 – 0.03) = 10

Plant 4: 3000 * (0.04 – 0.03) = 30

Total contribution per year = $405

Annualized Cost of Generation Investments

Capital Annual Cost v Cost

Plant 1: 400 * 0.15 = 60

Plant 2: 600 * 0.15 = 90

Plant 3: 700 * 0.15 = 105

Plant 4: 1000 * 0.15 = 150

Total capital cost of system $405 per year.

90

100

110

1000 1500 4500

60

5

10 30

60

90

105

150Plant 4

Plant 3

Plant 2

Plant 1

Total: $ 405

10

19

Stacking Problem: when do we replace a thermal plant?

Output of plant #5 that substitutes for plant #1 = Q1

H2

KW

1 (2)

2 (3)

3 (4)

4 (5)

Hydro storage

H1

H3

H4

Output of plant #5 that substitutes for plant #2 = Q2

Output of plant #5 that substitutes for plant #3 = Q3

Output of plant #5 that substitutes for plant #4 = Q4

Load curve for plants 2,3,4 after 5 is introduced

0.025

0.034

0.043

0.052

0.081

Marginal Running Cost per Kwh

Plant No.

• Assume plant #5 has equal capacity to each of the other plants we would then have to shift all of the plants up one stage in production, thus there is no need to use plant number one now.

Benefits to Plant #5: It is going to be producing most of the time. Part of the time 5 is effectively substituting for 4, part for 3, part for 2, and part for 1.

The question is whether or not we should build plant #5. We use the most efficient plant first and then use the next most efficient and so on until the least efficient we need to meet demand.

20

Two approaches to calculating benefits

A. The new plant is used to substitute for part of the other plants that now do not produce as much as previously:Benefits Q4 x (0.03 – 0.02)

Q3 x (0.04 – 0.02)Q2 x (0.05 – 0.02)Q1 x (0.08 – 0.02)Total A

B. Alternative approach• Let H1, H2, H3, H4, be amount of electricity previously produced by plants 1

to 4.

Original Total Cost New Total CostH4 x 0.03 H4 x 0.02H3 x 0.04 H3 x 0.03H2 x 0.05 H2 x 0.04H1 x 0.08 H1 x 0.05Total B Total C

Total A = Total B -Total C. • We now compare total A with the annual capital cost of plant 5.

11

21

The Situation where variations in the efficiency of thermal plants are taken into account

The optimum price to charge at any hour is the marginal running cost of the oldest (least efficient) thermal plant that is in operation during that hour.

In this case, the benefits attributable to an investment in new capacityturn out to be the savings in system costs that the investment makespossible; and the present value of expected benefits is

[ ]∑ ∑∞

+=

−−

=

+−1

1

1)1()()(),(

jt

tjj

krjCkCtkH

C(k) - the marginal running cost of a plant built in year kH(k,t) - the number of kilowatt-hours in the production of which a new

plant would substitute for plants built in year kC(j) – running cost of plant j

22

When the plant is new, it is generating benefits all the time, but as it ages, and is supplanted at the base of the system by more

efficient plants, it generates benefits only part of the time.

Given this, the key investment criterion can be represented quite simply if we assume that the function

[ ]∑ −=−

=

1j

1k)j(C)k(C)t,k(H)t,j(B

Declines exponentially through time at annual rate of y.

.....,)r1(

)y1(B)r1(

)y1(Br1

)y1(B3

31J

2

21J1J +

+−

++−

++− +++

12

23

Marginal Cost Pricing of Electricity

• Efficient pricing of electricity.The basic assumption that we make is that the demand for electricity is increasing over time, 5-10% each year. Therefore with existing capacity economic rents will increase over time.

24

Growth of Economic Rent Over Time

A B

Dt0

Dt1

Dt2

Q

Price of electricity • If choice is to either stay at

A capacity forever, or to stay at B forever, then we add up the consumer surpluses between A and B to see if B plant is worthwhile to install.

A B

Dt0

Dt1

Dt2

Q

Price of electricity

C

0

0

• If we expand capacity from A to B to C in subsequent time period.

Benefits of ABenefits of B

Benefits of C

13

25

Load Curve for Hours of Day

• We start with the assumption that all we have are homogeneous thermal plants.

Qt0

Qt1

Hours of day

Capacity in K.W.

0

K0

• If demand increases to Qt1 we either ration the available electricity or we build more capacity.

26

Load Curve for Hours of Day• by varying the price of electricity through time we can spread out

demand so that it does not exceed capacity.

Qt00

Hours of day

Capacity in K.W.

0

K0

• It is possible to keep quantity demanded constant by varying theprice with the use of a surcharge.

• Let Ki be the length of time each surcharge is operative. Si is the difference between MC and the price charged, then:

12

3

4

Surcharge cents

Si = Surcharge

∑=m

iiiKS rent economic Total

• It is the economic rent accruing to the existing capacity.

14

27

Example• A kilowatt is the measure of capacity.

• 1 K.W. of capacity can produce 8760 Kilowatt hour (KWH) per year.

• Assume it costs $400 /kw of capital cost, and the social opportunity cost of capital plus depreciation = 12%. Therefore we need $48 of rent per year before we install another additional k.w. of capacity.

• As demand increases through time we require a higher surcharge in order to contain capacity. Price used to ration capacity.

• This will generate more economic rent, and if this rent is big enough it would warrant an expansion of capacity.

• The objective of pricing in this way is to have it reflect social opportunity cost or supply price.

• In practical cases the price does not vary continuously with time but we have surcharges that go on and off at certain time periods.

28

Example (Cont’d)

• The “Load Factor” = KWH generated/8760 kwh

• Capital costs of per KW of capacity = 400/KW

• 10% interest + 2% depr = $48/yr

• Marginal running costs = 3 cents per KWH

• Peak hours are 2400 out of the year

• Off peak optimal charge is 3 cents per KWH

• On peak optimal charge is 5 cents per KWH

• Implicit rent of any new capacity = 2400 x 2 cents = $48/year

15

29

Choice of different types of Electricity Generation Technologies to make

Electricity Generation System

• Thermal Generation:– Nuclear– Large fossil fuel plants– Combined cycle plants– Gas turbines

• Hydro Power– Run of the Stream– Daily Reservoir– Pump Storage

30

Thermal vs. Hydro Generation

• The thermal capacity is relatively homogeneous if capacity costs are higher generally fuel costs are lower. e.g. Coal plant versus combined cycle plant.

• With hydro storage or use of the stream every particular site is different.

• Costs may range over a 5 fold difference.

16

31

Run of the Stream• No choice of when the water will come.• Water comes at a zero marginal cost, therefore should use

it when it comes.• Suppose river runs for 8760 hrs. at full generation capacity. • We will assume that the highest potential output during the

year of the run of the stream is always less than total demand. Some thermal is being used.

• Peak hours = 2400• Off peak hours = 6360• Savings as compared to thermal plant (from previous example)• 2400 x 5¢ 120.00 Peak rationed price = 5 ¢• 6360 x 3¢ 190.80 off peak MRC of thermal = 3 ¢

310.80 per yearQuestion: Is US$ 310.80 per year enough to pay for run of

stream capital plus running costs?

32

Daily Reservoir• Constructed to meet the peak day hours.• To store water during the off peak for use during the

peak hours.• We don't generate any more electricity but we use the

same amount of water and use it to produce peak priced electricity i.e. (5¢) instead of off peak (3¢) electricity.

• Instead of 2400 x 5 ¢ = $120.006360 x 3 ¢ = $190.80

= $310.80• We get 8760 x 5 ¢ = $438.00. Net benefits = $127.20• The costs are that of building the reservoir and the

additional hydro generating capacity so as to generate more electricity in the peak hours.

17

33

Daily Reservoir (Cont’d)• If previous run of stream generated 100 KW for 24

hours, now we will generate 300 KW for 8 hours.

• The gain from this switch in water is what we compare with the extra cost.

• If we now produce off peak electricity with thermal instead of run-of-the stream then this opportunity cost is calculated when calculating the opportunity costs of the daily reservoir.

• The additional marginal running costs of the thermal plants needed to meet the off peak demand are deducted from the benefits of switching off-peak run-of-stream water to peak time water.

34

Pump Storage• We use off peak electricity to pump water up to a high area so that it can

be released to produce electricity during peak demand periods.

Example:

• It takes 1.4 KWH off peak to produce 1KWH on peak

• Off peak value = 3 ¢ KWH Peak = 5 ¢ KWH

• There is a profit here of [(5¢ - 3¢*1.4) = (5¢ - 4.2 ¢)] = 0.8 ¢/KWH of peak hour generated

• Pump storage is becoming feasible because of the existence of nuclear and very large fossil fuel plants.

• These plants are very costly to shut off and on.

• Therefore, their surplus in off peak hours is very cheap electricity.

• With large storage at top and bottom of till, a very small stream is all that is needed to produce a very large power station and use nuclear power to pump water back up on off peak hours.

18

35

Multipurpose Dams• Multipurpose dams are used for irrigation, power and flood control. • However, with multipurpose dams it is possible to have conflicting

objectives.• For example, it may be the case that irrigation water is needed in

summer, but electrical power is at its lowest demand in summer. • We may have to adjust prices of electricity to shift some of the

demand to times when irrigation water is required.• The different objectives have to be weighted.• A useful solution is to provide the water during the peak time hours

for electricity and then build a small regulatory dam to provide water for irrigation.

• The conflicting objectives may cause us to not have any optimal strategy over the year, but we still may be able to maximize during the day.

• In this case we still will have to have a larger thermal capacity than in the case of no irrigation objective.

36

How do we price for the peak if the alternative is thermal generation?

• Assume quantity of water available is fixed.

• With an increase in peak demand we have to increase the thermal capacity and it is based on this cost that we have to calculate the peak time surcharge.

Hydro

8760 hrs

Capacity

Thermal 2

Hydro

Thermal 1

Suppose system peak = 2,400 hours Thermal peak = 4,000 hours• It is over the 4,000 hours that we spread the capital costs of new thermal

plants. If $48/kw needed per year to cover the capital costs then we only require a surcharge of 1.2 ¢/Kwh (4800¢/4000hrs. = 1.2¢/Kwh)

• To find the price that should be charged for electricity during the peak hours, we add the capacity charge of 1.2 ¢ to the costs marginal running cost of the least efficient thermal plant operating during these hours.

• As long as we peak with hydro storage then the benefit of increasing hydro is the thermal peak cost.

2400 4000

19

37

Lecture Notes

Week Two, Day One(Session II: 10:15 – 12:00)

Program on the Appraisal of Infrastructure Projects with Private

Participation

APPRAISAL OF

EL-KUREIMAT

COMBINED

CYCLE POWER PLANT

20

39

PROPOSED EL KUREIMAT (MODULE II) PLANT

• Proposed El Kureimat Combined Cycle Power Project is about 90 km south of Cairo

• Inside the existing El Kureimat Power Station

• Module II will not share any facilities with the existing plant

• Construction of 750 MW (2x250 MW gas turbine and 1x250 MW steam turbine) combine cycle power plant• Construction period: start in 2005, two gas turbines

operational in 2008 and steam turbine in 2009• Total cost € 264.1 million with foreign component of

72.9% • A loan application to AfDB for € 173.6 million (65.7%),

government guarantee is offered

40

PLANT OPERATION• Project operational life is 40 years from 2008• Replacement investment for the gas turbines after 25 years • Plant net generation capacity is 691 MW after deducting ISO factor

(5%) and auxiliary consumption (3%)• Annual plant utilization rate is 80%, reduced by 0.50% p.a.• Fuel Cost: natural gas consumption rate of 0.16 m3/kWh, supplied

by state gas utility to project at 0.141 EGP/m3 (US$ 2.35 cent/m3)• Operations and Maintenance (O&M) Costs: Fixed generation O&M is

estimated at US$ 15.8 million p.a. and variable O&M at 1.57 US$/MWh

• Periodic maintenance of gas turbines every 5 years at a cost of US$ 10 million

• Terms for AfDB loan: interest rate of 4.5% p.a.; repayment period of 20 years, including a 5-year grace period and a commitment charge of 0.25%

21

41

ELECTRICITY SECTOR IN EGYPT • Unlike a number of other countries, Government of Egypt places

a high priority on having a well-managed electricity system that supports every sector of economy

• Growth in electricity demand, that mirrors the economic development, averaged 6.2% p.a. over period of 1999-2004

• No power shortages have been experienced in Egypt during the last decade

• Egyptian Electricity Holding Company (EEHC) is integrated utility that is responsible for generation, transmission and distribution of electric power

• EEHC consists of 15 companies, organized by function and geographical area: 5 generation, 1 transmission and 9 distribution companies

• On generation side, total installed capacity at the end of 2004 was 14,091 MW: 2,100 MW of hydro, 11,914 MW of thermal and 77 MW of wind

• Thermal units type: 8.9% gas turbines, 73.8% steam turbines, and 17.4% combine cycle units

42

PURPOSE OF PROJECT APPRAISAL

• Government of Egypt is the guarantor for loan, and EEHC is the borrower and executing agency with excellent past record

• What do we need to worry about?

• Six specific questions:1) Does the project ensure the least-cost way of meeting power

demand by EEHC?2) What is the magnitude of financial benefits realized by the

electric utility?3) What are the cashflow implications for the utility in terms of

servicing the debt obligations of the proposed project? 4) To what extent does this project contribute to Egyptian

economy?5) Who are stakeholders and by how much do they benefit, or

lose, as a consequence of this project?6) What are the risk factors that affect the project and how can

the uncertainty and risk exposure be mitigated?

22

43

“WITH” AND “WITHOUT” PROJECT• Egyptian authorities realized decades ago that it is worthwhile to

maintain a modern power system in order to have an affordable and reliable energy supply

• Country has the second largest power system on African continent, and 99% of potential consumers have been connected to grid, one of highest rates among all developing countries

• Under the “without” project scenario EEHC will supply sufficient electricity to meet the demand it faces, regardless where additional power might come from: own generation or purchases from private BOOT plants

• The “without” scenario would also include other elements of the proposed system expansion plan, which will enhance the reliability and generation capacity of the utility until 2014/15

• Specific feature of the “with” scenario of this project is that with implementation of this new efficient combine cycle plant, projected demand will be met at a lower generation cost to EEHC

44

• The incremental change introduced by the plant is change in the mix of plants that EEHC would operate

• Currently, during the off-peak the company uses a number of steam plants in base load together with a few existing combine cycle plants and its limited hydro potential; while at the peak time, additional capacity is provided by gas turbines

• Since both steam and gas units operate with a substantially higher fuel and O&M costs, proposed plant will enable EEHC to reduce the use of its most inefficient units

• Therefore, financial benefits from proposed plant are savings ofrunning costs of steam plants during the off-peak regime, and savings on operation and capital cost of gas plants at the system peak

• No additional energy sales should be credited as financial benefits

23

45

Impact of Project on System Dispatch (MWh/year)

8,760 hours/year

Hydro and Wind

Combined Cycle

Steam Units

Gas Units

Capacity (MW)

Replacement of gas units during peak times (MWh/year)

Replacement of steam units during off- peak times (MWh/year)

700 hours/year

46

FINANCIAL BENEFITS• Off-Peak Savings: cash saved by the electric utility on operation of

steam plants. Average fuel consumption on steam plants is 0.202 m3/kWh of natural gas while consumption by proposed combine cycle plant is only 0.161 m3/kWh. Average O&M costs of existing steam plants are EGP 4.0 Piaster/kWh, while proposed plant has EGP 3.4 Piaster/kWh. The off-peak load is supplied by hydro, wind, existing combine cycle and steam units during 8060 hours/year.

• Peak Savings: summation of the peak fuel savings, peak O&M savings and capital costs associated with the installation of gas turbines for reserve capacity. Average system fuel consumption on gas plants is 0.375 m3/kWh of natural gas. Average O&M costs on gas units are EGP 4.0 Piaster/kWh. Capital savings are basicallythe avoided cost of gas turbine capacity, and it is estimated as EGP 31.4 Piaster/kWh (US$ 5.22 cent/kWh).

• Capital savings on installation of gas turbine capacity: cost of gas turbine installed is US$ 400 per kW, expected to serve 25 years, generating a weighted average cost of capital (WACC) for project of 5.0% p.a., then the annual depreciation charge is US$ 16 p.a., and the required return on capital is US$ 20.5 p.a.

• Total capital charge per annum will be US$ 36.51 per kW of installed capacity. This charge must be amortized over amount ofenergy generated during a year. Since gas turbines are operated 700 hours/year then the corresponding capital charge on energy amounts to US$ 5.22 cent/kWh = 36.51 US$/kW / 700 hours.

24

47

Cash Flow Statement for Project: Total Investment Perspective, 2005 prices (million EGP)

INFLOWS 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2020 2025 2030 2033 2035 2040 2045 2048System off-peak cost savings 0 0 0 111 275 324 323 322 322 321 316 306 297 285 188 275 265 256 0System peak cost savings 0 0 0 53 134 159 158 157 159 158 157 152 146 141 92 136 131 126 0Other revenues 0 0 0 22 55 65 66 66 64 65 64 62 61 59 37 56 54 52 290

Total Inflows 0 0 0 186 463 548 547 545 545 544 536 520 504 485 317 467 450 434 290OUTFLOWS

Investment Costs 160 673 836 333 88 0 0 0 0 0 0 0 0 0 644 0 0 0 0Operating Costs

Fuel costs 0 0 0 60 152 181 182 182 178 179 178 173 168 164 103 155 150 145 0O&M 0 0 0 47 101 109 109 108 169 108 108 106 105 103 48 102 100 99 0Labor 0 0 0 19 33 33 33 33 33 34 34 34 35 36 36 37 38 38 0Change in working capital 0 0 0 24 -2 0 1 1 1 1 1 1 1 1 2 1 1 1 5

Total Outflows 160 673 836 482 372 323 324 324 381 321 320 314 309 304 834 294 288 283 5NET CASH FLOW BEFORE FINANCING -160 -673 -836 -297 92 225 223 221 165 222 216 206 195 182 -517 172 162 151 285

Add: loan disbursement 114 468 571 163 58 0 0 0 0 0 0 0 0 0 0 0 0 0 0Less: Loan repayment + fees + charges 3 7 26 50 57 58 141 135 128 122 116 89 67 0 0 0 0 0 0NET CASH FLOW AFTER FINANCING -49 -211 -290 -184 93 167 82 86 36 100 100 117 129 182 -517 172 162 151 285

FNPV, real (million EGP) @ ROE: 6% 740.1FIRR: 12.3%

Levelized energy cost, real (US cent/kWh) 1.71

ADSCR = Net system savings over project debt repayments 1.58 1.64 1.28 1.82 1.86 2.30 2.93DSCR = PV of net system savings over PV of project debt repayments 1.91 1.95 2.00 2.10 2.14 2.46 2.93

48

ELECTRIC UTILITY AND DEBT SERVICE

• EEHC is an integrated utility responsible for generation, transmission and distribution of electric power in Egypt. To meet projected energy demand, EEHC has developed an expansion plan that aims at expanding the generation and transmission capacity between 2005 and 2012.

• Tariffs: The average system tariff is EGP 14.22 piaster/kWh (US$ 2.37 cent/kWh). Government has allowed EEHC to raise tariffs by not more than 5.0% a year over the period 2005-10 in nominal terms. There is no automatic mechanism linking tariffs to inflation.

• Billing Cycle and Accounts Receivable: All customers are metered and billing cycle of EEHC is about 150 days at the end of 2004. The bulk of A/R is owed by government and public sector. Government has approved a number of measures in an effort to settle its accounts with the EEHC over next years.

25

49

EEHC Cash Flow Projection and Debt Service, Current Prices (billion

EGP)REVENUES 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Sales of Energy 12.3 13.9 15.7 17.7 20.0 22.6 25.1 27.9 30.3 31.4 32.5 33.6 34.8 36.0 37.3 38.6 40.0 41.4 42.8 44.4 45.9 47.5Change in Accounts Receivable 0.2 0.3 0.6 0.1 0.0 0.0 -0.5 -0.6 -0.5 -0.2 -0.2 -0.2 -0.2 -0.2 -0.3 -0.3 -0.3 -0.3 -0.3 -0.3 -0.3 -0.3Other revenues 0.8 0.9 1.0 1.1 1.2 1.4 1.5 1.7 1.8 1.9 1.9 2.0 2.1 2.2 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.8

Total Revenues 13.4 15.1 17.3 18.9 21.2 24.0 26.1 29.0 31.7 33.1 34.2 35.4 36.7 38.0 39.3 40.7 42.1 43.6 45.1 46.7 48.4 50.1EXPENDITURES

Investment Costs 5.8 6.0 7.5 8.0 9.1 8.8 8.7 8.6 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Operating Costs

Fuel costs 3.4 3.9 4.4 4.8 5.3 5.9 6.7 7.5 8.6 8.9 9.1 9.5 9.9 10.3 10.7 10.9 11.4 11.8 12.3 12.8 13.1 13.7Purchases for sale 1.7 1.8 1.9 1.9 2.0 2.1 2.1 2.2 2.3 2.4 2.4 2.5 2.6 2.7 2.8 2.9 3.0 3.1 3.2 3.3 3.4 3.6Salaries and wages 3.2 3.6 4.1 4.7 5.2 5.9 6.7 7.6 8.4 8.4 8.9 9.3 9.7 10.2 10.4 10.9 11.4 11.9 12.5 12.7 13.4 14.0Materials & services input 1.9 2.2 2.4 2.8 3.2 3.6 4.0 4.5 5.0 5.2 5.2 5.5 5.7 6.0 6.2 6.2 6.5 6.8 7.2 7.4 7.4 7.8Net interest expenses 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0Change in working capital 1.0 0.6 0.6 0.6 0.6 0.8 1.0 1.1 1.1 0.3 0.3 0.5 0.5 0.6 0.4 0.4 0.6 0.6 0.7 0.5 0.5 0.8

Total Expenditures 19.1 20.1 22.9 24.8 27.5 29.0 31.2 33.5 27.4 27.3 28.0 29.3 30.4 31.8 32.4 33.4 35.0 36.3 37.9 38.7 40.0 41.8NET CASH FLOW BEFORE FINANCIN -5.7 -4.9 -5.5 -5.9 -6.3 -5.1 -5.1 -4.5 4.2 5.8 6.2 6.1 6.3 6.2 6.9 7.3 7.1 7.3 7.2 8.0 8.4 8.2

Add: Loan Disbursements 4.8 4.7 6.1 6.3 7.3 7.0 7.0 6.8 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Less: Additional Interest Expense 0.1 0.4 0.6 0.9 1.2 1.6 2.1 2.5 6.2 6.1 6.0 5.8 5.7 5.6 5.4 5.3 5.1 5.0 4.8 4.7 4.5 4.2NET CASH FLOW AFTER FINANCING -1.0 -0.5 0.0 -0.5 -0.2 0.4 -0.2 -0.2 -2.0 -0.3 0.3 0.3 0.6 0.6 1.5 2.0 2.0 2.3 2.4 3.3 3.9 4.0

Annual Debt Service Coverage Ratio (ADSCR) 1.70 1.66 0.68 0.96 1.04 1.04 1.10 1.11 1.27 1.37 1.39 1.47 1.49 1.71 1.86Debt Service Capacity Ratio (DSCR) 1.21 1.15 1.09 1.15 1.17 1.19 1.22 1.24 1.26 1.26 1.23 1.19 1.12 1.00 1.86

50

TARIFF ADJUSTMENT• No Additional Tariff Increases after 2010: In a situation where

only 5% nominal adjustment is undertaken until 2010 and tariff is inflation-adjusted on annual basis thereafter, EEHC may have some liquidity gaps and will not be able to pay off all its debtobligations without an external injection of funds in 2013-14.

• One-Time Real Increase of Tariffs by 6.0% in 2011: ADSCR is equal 1.0 in worst period of loan repayment, year 2013. This adjustment is in addition to the already committed 5% p.a. nominal tariff increases over the period 2005-10 under the assumption of a 3.5% annual rate of inflation. On top of that, EEHC would have to adjust the tariffs for inflation in followingyears.

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

ADSCR 2.40 2.36 1.00 1.23 1.39 1.41 1.49 1.52 1.70 1.84 1.88 1.99 2.05 2.31 2.50

DSCR 1.65 1.56 1.48 1.54 1.59 1.62 1.65 1.67 1.70 1.70 1.67 1.62 1.52 1.35 2.50

26

51

• Nominal Increase of Tariffs by 5.75% p.a. over 2011-15: Government continues the nominal tariff increase over the period 2011-15 but now with a rate of 5.75% per year.

• The two options, whether to raise tariffs once-for-all by 6.0% in real terms in 2011 or to phase out this increase over 2011-15 through nominal increases of 5.75%, are roughly equivalent, provided that the domestic inflation rate remains within the 3.5% p.a. range.

• Any unexpected increase in the inflation will erode the revenues of the electric utility.

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

ADSCR 1.92 2.13 1.00 1.42 1.67 1.73 1.83 1.88 2.08 2.24 2.31 2.45 2.54 2.83 3.06

DSCR 1.90 1.84 1.77 1.88 1.94 1.98 2.02 2.06 2.09 2.09 2.06 1.99 1.87 1.65 3.06

52

ECONOMIC APPRAISAL• Economic Value of Natural Gas. Egypt is endowed with substantial reserves of natural

gas which are mainly underdeveloped. Domestic prices are regulated by Government and kept low, substantially less than international prices. Industrial users pay 0.220 EGP/m3. EEHC has a preferential agreement with state-controlled natural gas utility EGEAS. Subsidized cost of natural gas for EEHC is 0.141 EGP/m3.

• Netback Value of Natural Gas Exports: Natural gas production sufficiently covers all domestic needs, and the excess is exported as liquefied natural gas (LNG). Shipment of LNG by the EGEAS is facilitated through contracts but contractual prices are not known. A specific formula of LNG price was developed by gas exporters to be used during contract negotiations:

LNG Price (US$/GJ) = 0.1567 * Crude Oil Price (US$/bbl) + 0.79• For crude price of 30 US$/barrel, corresponding price of LNG will be 5.49 US$/GJ.

There are processing and shipping costs for natural gas, comprising about 3.50 US$/GJ, which implies that border value of natural gas is 1.99 US$/GJ. This figure translates into US$ 2.29 per cubic feet. There is an existing gas pipeline to the Module I of El Kureimat plant, no new pipeline will be needed for Module II. The average domestic cost of gas delivery from the EGEAS to the plant is 0.29 US$/cuf.

• Netback value of natural gas is 2.00 US$/cuf (0.057 US$/m3). With exchange rate of 6.0 EGP/US$, netback value is 0.34 EGP/m3.

27

53

Economic Resource Flow Statement, 2005 prices (million EGP)

BENEFITS 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2025 2030 2033 2035 2040 2045 2048System off-peak cost savings 0 0 0 183 451 528 528 527 530 528 517 518 515 515 512 502 488 467 310 450 435 420 0System peak cost savings 0 0 0 83 209 248 248 246 252 250 247 246 245 243 242 239 231 222 145 214 206 199 0Other benefits 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 316

Total Benefits 0 0 0 266 660 776 776 773 781 779 764 764 760 758 755 741 719 689 455 664 641 619 316COSTS

Investment Costs 156 654 812 315 86 0 0 0 0 0 0 0 0 0 0 0 0 0 644 0 0 0 0Operating Costs

Fuel costs 0 0 0 100 255 304 305 305 298 301 299 300 300 289 292 290 283 275 173 261 251 243 0O&M 0 0 0 39 83 89 89 89 146 88 88 88 88 145 87 87 86 85 39 84 83 81 0Labor 0 0 0 18 32 32 32 32 32 33 33 33 33 33 33 33 34 35 35 36 36 37 0Change in working capital 0 0 0 37 -4 -1 0 0 0 0 0 0 0 0 0 0 0 0 2 0 0 0 -21

Total Costs 156 654 812 509 453 425 426 426 477 422 420 421 421 467 412 411 403 395 894 380 370 362 -21NET RESOURCE FLOW -156 -654 -812 -243 207 352 350 347 305 357 343 343 339 291 342 331 316 295 -439 284 271 257 337

NPV, real (million EGP) @ EOCK: 10% 654.7EIRR: 13.8%

Levelized Energy Cost, real (US cent/kWh) 2.42

• Economic Value of Capital Assets and O&M. Investment costs are mainly tradable items, except civil works, economic valuation removes all import duties and other indirect taxes imposed on the items. In addition, values of foreign exchange premium and shadow price ofnon-tradable outlays are incorporated. O&M expenditures are also tradable items.

• For non-tradable civil works, analysis also looks at distortions in inputs markets (i.e., taxes and subsidies on goods and services used in civil works).

54

STAKEHOLDER IMPACTSAllocation of Externalities, 2005 prices (million EGP)

GOVERNMENT Taxes, subsidies, FEP

PETROLEUM EXPORTER Savings

PUBLIC SECTOR Net Impact

BENEFITS System off-peak cost savings 123.1 1,367.3 1,490.4 System peak cost savings 54.0 599.6 653.6 Other revenues -468.8 0.0 -468.8

Total Benefits -291.7 1,966.9 1,675.2 COSTS

Investment Costs -54.4 0.0 -54.4 Operating Costs

Fuel costs 72.9 809.8 882.7 O&M -149.2 0.0 -149.2 Labor -8.0 0.0 -8.0 Change in working capital 3.6 0.0 3.6

Total Costs -135.1 809.8 674.7 NET EXTERNALITY FLOW -156.6 1,157.1 1,000.5

28

55

SENSITIVITY ANALYSIS: CRITICAL FACTORS

Direct effect on the EEHC revenues and profitability. The management controls the efficiency to a large extent.

Invoicing efficiency

Direct effect on the EEHC revenues and profitability. The management controls the efficiency to a large extent.

Collection efficiency

Tremendous impact on the EEHC revenues and profitability. As of now the management can not change the tariffs without approval by the Cabinet of Ministers.

Electricity Tariffs

Large effect on the EEHC generation decisions and, as a consequence, on the project. Beyond management control; based on economic factors and policies.

Electricity Demand Growth

Little impact on the financial results, but it is the main factor of economic viability of the project and allocation of stakeholder impacts. Beyond Egypt’s control.

World price of crude oil

Critical impact on performance of project and electric utility. Beyond management control. The Government directly controls the prices for oil and natural gas in Egypt.

Cost of natural gas to the EEHC

Mainly affects the investment costs and loan repayment. Beyond Egypt’s control; based on EU policies and economy.

EU inflation

Large effects on operating costs, working capital and interest rate on loan. Beyond management control; based on economic factors and policies.

Domestic inflation

Reduction of benefits. Management can control it.Plant utilization

Direct increase of investment costs. Management can control it to a large extent.Investment cost overruns

Impact and risk significanceFactors

56

RISK ANALYSIS• Expected value of financial NPV (EGP 546.9 million) is different from

deterministic outcome of the financial analysis of EGP 740.1 million. • Result also shows that no possibility of having a financial loss exists. • At extreme lower end of possible range, minimum gain (EGP 222.4

million) is about 8.1% of investment value of project, while in best case scenario maximum gain (EGP 869.8 million) is 31.6% of initial value of investment.

Frequency Chart

Certai nty i s 0.21% from -Infini ty to 222.4 milli on EGP

Mean = 546.9.000

.006

.013

.019

.025

0

63

126

189

252

222.4 384.3 546.1 708.0 869.8

10,000 Trials 9,970 Displayed

Forecast: FNPV@ROE

29

57

• Debt service ratios are also tested through risk analysis, using base case of the utility cashflows without additional tariff adjustment beyond 2010 but with assumption of annual inflation adjustment after 2010.

• Expected values of all debt ratios are lower than in deterministic analysis, implying that ability of the EEHC to service debt in a timely manner is not as optimistic as in deterministic analysis.

• In 2011 and 2012, probability of substandard ratios is at a very low level, below one percent. However, in 2013 and 2014 when first debt repayments of loans on EL Kureimat plant and other projects undertaken within the expansion program are due, likelihood of having an insufficient cashflows is 100% certain.

ADSCR DSCR 2011 2012 2013 2014 2015 2011 2012 2013 2014 Deterministic Value: 1.70 1.67 0.68 0.96 1.05 1.21 1.15 1.09 1.15 Risk Statistics:

Mean 1.53 1.51 0.61 0.74 0.83 1.08 1.02 0.96 1.01 St. Dev. 0.24 0.24 0.10 0.11 0.13 0.06 0.05 0.05 0.05 Minimum 0.96 0.92 0.40 0.46 0.51 0.92 0.86 0.80 0.84 Maximum 2.26 2.15 0.87 1.00 1.21 1.28 1.21 1.15 1.18 Prob. Sub-standard 0.1% 0.4% 100% 100% 90.2% 5.7% 35.6% 75.9% 41.6%

58

• In regard to the economic results, economic NPV has recorded an expected value of EGP 473.8 million, and probability of having a return below economic cost of capital of 10.0% real is 2.6%.

• It should be noted that the economic internal rate of return never becomes zero or negative.

• In worst case scenario maximum loss (EGP -169.3 million) is about 7.0% of investment value of project, while in best case scenariomaximum gain (EGP 1,150.2 million) is 47.6%.

Frequency Chart

Certai nty i s 2.58% from -Infini ty to 0.0 mil lion EGP

Mean = 473.8.000

.006

.011

.017

.022

0

55.5

111

166.5

222

-169.3 160.6 490.4 820.3 1,150.2

10,000 Trials 9,909 Displayed

Forecast: ENPV@EOCK

30

59

CONCLUSION

• Nature of proposed combine cycle generation plant is a provision of additional capacity to a large electricity utility. Role of this plant is to substitute existing steam plants during off-peak time and to avoid installation of additional gas turbine capacity during the peak load.

• New efficient combine cycle plant is able to supply power at a lower cost than existing generating units, and within that environment project has a very little chance of weak financial or economic performance.

• On project basis, the service of loan by AfDB is well covered bycash savings that the project will generate for EEHC.

• The repayment of loan is however in hands of EEHC financial operation and unless an additional tariff increases are undertaken in 2010-15, the company is likely to have difficulty with repayment.

60

Lecture Notes

Week Two, Day Two(Session I: 08:30 – 10:00)

Program on the Appraisal of Infrastructure Projects with Private

Participation

31

61

PUBLIC PRIVATE PARTNERSHIPS: The Public

Sector Comparator

62

Private Public Partnerships in Infrastructure

• A major new user of project financing techniques• Infrastructure traditionally financed and managed by

governments• Demand for infrastructure has been growing faster than

government funding available, particularly in emerging economies.

• Recent trend has been to involve the private sector in the supply and provision of these services

• For example: Roads, Bridges and Tunnels, Light Rail Networks, Airports and Airport control Systems, Water and Sanitation, Electricity Generation, Hospitals, Schools, Prisons

32

63

Private Public Partnerships in Infrastructure

• For a PPP to be successful, there has to be a clear benefit for both the public and the private partners

• In the spectrum of public sector verses private sector service delivery, PPPs lie somewhere between simply the government contracting –out of a set of service delivery to the private sector and a complete private market to plan, design, build and operate a facility that provides the service

64

Private Participation in Infrastructure (PPIs)

• Private sector involvement requires commercial rates of return

• Projects have to lend themselves to generating these returns.

• The public partner typically gains in the sense that a desired project is implemented without any financial strain on the budget

33

65

Private Participation in Infrastructure (PPIs)

• In many instances, the governments receive tax payments from the project, and in certain cases, a share of the profits.

• The structure of the partnership can vary along a spectrum from a leading private sector role to a marginal one.

66

Different PPP Models

Degree of Private Sector Involvement

Degr

ee o

f Priv

ate

Sect

or R

isk

Design-Build

Government

Operation / Maintenance Service /License

Design-Build-Operate

Lease-Develop-Operate

Build-Lease-Operate-Transfer

Build-Own-Operate-Transfer

Build-Own-Operate

Buy-Build-Operate

Privatisation

34

67

Public-Private Partnership Models

• Design-Build (DB): Under this model, the government contracts with a private partner to design and build a facility in accordance with the requirements set by the government. After completing the facility, the government assumes responsibility for operating and maintaining the facility. This method of procurement is also referred to as Build-Transfer (BT).

• Design-Build-Maintain (DBM): This model is similar to Design-Build except that the private sector also maintains the facility. The public sector retains responsibility for operations.

68

Public-Private Partnership Models (Cont.)

• Design-Build-Operate (DBO): Under this model, the private sector designs and builds a facility. Once the facility is completed, the title for the new facility is transferred to the public sector, while the private sector operates the facility for a specified period. This procurement model is also referred to as Build-Transfer-Operate (BTO).

• Design-Build-Operate-Maintain (DBOM): This model combines the responsibilities of design-build procurements with the operations and maintenance of a facility for a specified period by a private sector partner. At the end of that period, the operation of the facility is transferred back to the public sector. This method of procurement is also referred to as Build- Operate-Transfer (BOT).

35

69

Public-Private Partnership Models (Cont.)

• Build-Own-Operate-Transfer (BOOT): The government grants a franchise to a private partner to finance, design, build and operate a facility for a specific period of time. Ownership of the facility is transferred back to the public sector at the end of that period.

• Build-Own-Operate (BOO): The government grants the right to finance, design, build, operate and maintain a project to a private entity, which retains ownership of the project. The private entity is not required to transfer the facility back to the government.

70

Public-Private Partnership Models (Cont.)• Design-Build-Finance-Operate/Maintain (DBFO, DBFM or

DBFO/M): Under this model, the private sector designs, builds, finances, operates and/or maintains a new facility under a long-term lease. At the end of the lease term, the facility is transferred to the public sector. In some countries, DBFO/M covers both BOO and BOOT. PPPs can also be used for existing services and facilities in addition to new ones. Some of these models are described below.

• Concession: The government grants a private entity exclusive right to provide operate and maintain an asset over a long period of time in accordance with performance requirements set forth by the government. The public sector retains ownership of the original asset, while the private operator retains ownership over any improvements made during the concession period.

36

71

Public-Private Partnership Models (Cont.)

• Service Contract: The government contracts with a private entity to provide services the government previously performed.

• Management Contract: A management contract differs from a service contract in that the private entity is responsible for all aspects of operations and maintenance of the facility under contract.

72

Public-Private Partnership Models (Cont.)

• Lease: The government grants a private entity a leasehold interest in an asset. The private partner operates and maintains the asset in accordance with the terms of the lease.

• Divestiture: The government transfers an asset, either in part or in full, to the private sector. Generally the government will include certain conditions with the sale of the asset to ensure that improvements are made and citizens continue to be served.

37

73

Public Private Partnerships (PPPs)

Main characteristics of PPPs are:1. Private sector is given responsibilities for one or

more of the following tasks:i. Defining and designing the project ii. Financing the capital costs of the projectiii. Building the capital physical assets (road, bridge)iv. Operating and maintaining the assets in order to deliver the

product/servicev. Significant risks is transferred from the government to private

sector2. Bundling of responsibilities or the

allocation of two or more tasks to a unique partner(s)

3. Allocation of the financing task, private financing.

74

Public Private Partnerships (PPPs)Why PPPs have become an alternative to traditional methods for the provision

of public services?1. Ex ante Competition (Private sector firms compete to do project)

Marshaling the pro-efficiency forces of competition lowers costs.

Competition at the bidding stage, ex ante.Less likely that tax payers will get value for their money if

such ex-ante competition does not exist2. Scarce Skills

Private sector has skills not available in the public sectorAllocate certain tasks to a private partner who has the skills and also the incentive to reform at a high level

3. Poor Labor RelationsPrivate sector through the forces of competition may offer

a skilled, efficient and flexible labor force. The public sector labor management may be inflexible due to tradition, civil service laws, and political protection of certain groups of workers

38

75

Public Private Partnerships (PPPs)4. Innovation

Some parts of the project may need new approaches andinnovative thinkingThe extend of PPPs will depend on the complementarities

between the tasks5. Risk

Major risk can be managed better by private sector (ex.construction-delay risk, being contractor and operator giveincentive to minimize such risk)Political risk is better managed by public sector

6. Economies of scale Private sector is taking advantage of economies of scale fromthe operation of similar project in other jurisdictions, the PPP option becomes more attractive

76

Public Private Partnerships (PPPs)

7. Observability and measurability of qualityConcerns about the quality of servicesThe partnership agreement should specify the requiredquality, provide the measurement of verification of quality andprovide for enforcement of the contracts’ requirement.

8. Constrains on public sector borrowingBeing in depth and further borrowing risk on deteriorating of government, credit rating cost of borrowing increasesAllocating the financial tasks to the private sector

PPPs should be embraced only when they allow government to provide services of an acceptable quality at lower cost to taxpayers (consumers)

39

77

Risk Analysis

• PPPs involve a range of risks:– Construction risks: relate to deign problems, building

cost overrun and project delays– Financial risks: variability in interest rates, exchange

rate and other factors affecting financing costs– Availability risks: relate to continuity and quality of

service provided and in turn depend on “availability”of an asset

– Demand risks: relate to ongoing need for the service– Residual value risk: relate to future market price of

assets

78

Risk Analysis• It is necessary to achieve significant risk transfer in order

to derive the full benefits from the capital inflows from the private sector and the management change

• Financing costs of risk transfer and pricing of risk are important in efficient allocation of risks

• Risk Transfer and Financing Costs– With complete market in risk bearing, project risk is not affected

by the particular source of financing (finance theory)– Incomplete markets in risk bearing affect project risk as sources

of financing defines the risk of project– Various sources of financing will determine how this risk will be

allocated– Private sector transfers risk to financial markets– Governments transfer it to taxpayers in general

40

79

Risk Analysis• Pricing of Risk

– To use PPPs, government must compare cost of public investment and provision of service with using PPPs to provide the service

– PPPs sometimes are an efficient way for government to relieve its risks

– Government has to pay for the risks that it transfers to the private sector

– Project-specific risk (e.g. interruption of supply of building materials, labor problems, unfavorable weather, etc) can be diversified across a number of government or private sector projects and need not be priced by the government

80

Risk Analysis

– Market risk reflects the economic developments that affect all projects and cannot be diversified and should be priced properly

– private sector demands a discount rate that includes a risk premium on the risk free discount rate that typically government uses

41

81

Competition and Regulation in PPPs• Private sector efficiency is main reason for PPPs• Competition is the important source of efficiency

in both the private and public sector• Competition in award of construction and service

contracts necessary to foster competition, managerial improvement and spur innovation

• In the case where private sector sells to public sector, there is little scope for competition after the contract is awarded and government usually regulate prices

• Price regulation and incentive based regulations are used to increase output, hold down prices, limit monopoly profits

82

Prerequisites for PPPs Success

• Political commitment• Good governance• Government expertise• Effective Project Appraisal and Selection

42

83

Risk Transfer• Need for Risk Transfer to the Private Sector

– Determines whether PPPs is a better option than to have public investment and government provision of service

– Influences the appropriateness of accounting and reporting treatment of PPPs

• Risk Transfer and Ownership– PPPs are legally owned by private and are legally

mandated to bear the risks of the project– If government bears ownership related risks, it is in effect

the owner of the asset, and in that case the PPPs will be indistinguishable from traditional methods of financing

– Different risks are associated with owning and operating an asset and risk transfer can be assessed by reference to these rights and obligations

84

Risk Transfer• In the case where ownership related risks are not specified

by PPP contracts, risk transfer can be assessed by reference to the overall risk characteristics of the PPPs

• In the Non-separable contracts (ownership and service elements cannot be distinguished) the balance between demand risks and residual value risk borne by government is used in the UK

• Demand risk is borne by government if service payments to a private operator are independent of future need for the service

• Residual value risk is borne by the government if the asset is transferred to the government at more or less than its residual value

• Other factors such as government guarantees, extent of government influence over asset design and operation can be used to assess the degree of risk that has been transferred away from the government

43

85

Lecture Notes

Week Two, Day Two(Session II: 10:15 – 12:00)

Program on the Appraisal of Infrastructure Projects with Private

Participation

86

ELEMENTS OF

PROJECT FINANCE

44

87

What is Project Finance?

• No universally accepted definition of the term “Project Financing” -- different people use it in different senses.

• Project financing refers to a financing in which lenders to a project look primarily to the cash flow and assets of that project as the source of payment of their loans.

PROJECT FINANCE

88

• Full Recourse - lenders look initially to the cash flow and assets of the project for debt repayment but ultimately can look to a creditworthy sponsor for any shortfalls.

• Non-Recourse - lenders look solely to the cash flow and assets of the project for debt repayment. There is no guarantee that they will be paid.

• Limited Recourse - all financing between full and non-recourse. Lenders look partially to project cash flow and assets for debt repayment. In defined circumstances they look to project sponsors for debt repayment. Two categories:– Fall away, initially full-recourse then non-recourse (e.g. post-

completion)– True limited recourse - residual risks to sponsors (e.g. market)

Three Categories of Project Financing

45

89

Origins and Development of Project Finance

• Project financing had its origins in the energy industry in industrialized countries (oil & gas production loans).

• Later extended to transportation (mainly gas and oil pipelines), mining, utilities and large industrial projects.

• Scope further expanded to include all kinds of infrastructure projects.

• Today even medium-scale projects (US $5 million) can use project finance

90

Main Characteristics of Suitable Investments for Projects Financing

• The ideal candidates for project financing are capital investment projects that

• are capable of functioning as independent economic units,

• can be completed without undue uncertainty, and

• When completed, will be worth demonstrably more than they cost to complete.

46

91

Why Project Financing? (cont’d)

• Project Owners’ Perspective– Achievement of Economics of scale– Risk minimization– Preservation of borrowing capacity and

credit rating– Release of free cash flow– Reduce Legal or Regulatory costs– Country specific accounting and/or tax

benefits

92

Size and Cost of Financing for Projects

• Project financing should be pursued when it will achieve a lower after-tax cost of capital than conventional financing.

• In an extreme case, the sponsors’ credit may be so weak that it is unable to obtain sufficient funds to finance a project at a reasonable cost on its own.

• Project financing may then offer the only practical means available for financing the project.

47

93

Achieving Economies of Scale

• Two or more producers can benefit from joining

together to build a single facility when there are

economies of scale in production.

• For example, two aluminum producers might decide

to build a single aluminum processing plant near a

location where each has a large supply of bauxite.

94

Risk Minimization• A joint venture permits the sponsors to share a

project’s risks.

• If a project’s capital cost is large in relation to the sponsor’s capitalization, a decision to undertake the project alone might jeopardize the sponsor’s future.

• Similarly, a project may be too large for the host country to finance prudently from its treasury.

• To reduce its own risk exposure, the sponsor or host country can enlist one or more joint-venture partners.

48

95

Expanded Debt Capacity• Project financing enables a project sponsor to finance the project

on someone else’s credit.• Often, that someone else is the purchaser(s) of the project’s

output.• If the output purchaser’s credit standing is higher than that of the

project sponsors, the project will be able to borrow funds more cheaply than the project sponsors could on their own.

• A project can rise funds on the basis of contractual commitmentswhen (1) the purchasers enter into long-term contracts to buy the project output and (2) the contract provisions are tight enough to ensure adequate cash flow to the project, enabling it to serviceits debt fully under all reasonably foreseeable circumstances.

• If there are contingencies in which cash flow might be inadequate, supplemental credit support arrangements will be required to cover these contingencies.

96

Release of Free Cash Flow

• The project entity typically has a finite life.

• Its “dividend policy” is usually specified contractually at the time any outside equity financing is arranged.

• Cash flow not needed to cover operating expenses, pay debt service, or make capital improvements-so called free cash flow – must normally be distributed to the project’s equity investors.

• Thus, under a project financing arrangement, it is the equity investors, rather than professional managers (as is normally thecase with companies) who get to decide how the project’s free cash flow will be reinvested.

49

97

Reduced Legal or Regulatory Costs• Certain types of projects, such as cogeneration

projects, involve legal or regulatory costs that an experienced project operator can bear more cheaply than an inexperienced sponsor can.

• For example, a chemical company or an oil company that undertakes a cogeneration project on its own would face significant costs because of an unfamiliar technology and legal and regulatory requirements.

Tax and Accountability Issues– Organizing a project on a project financing basis

with a specific type of organization may lower total tax burden on project

98

Why Project Financing?

• Lenders’ Perspective–Competitive pressures: other

banks are doing the business–Seeking higher returns–Easier to assess risks in project

finance situation

50

99

• Reduced Cost of Resolving Financial Distress Problems

• The structure of a project’s liabilities will normally be less complex than the structure of each sponsor’s liabilities.

• A project entity’s capital structure typically has just one class of debt, and the number of other potential claimants is likely to be small.

Easier to Understand the Nature of the Project’s Business

100

Disadvantages of Project Financing• Project financing will not necessarily lead to a lower cost of capital in

all circumstances.• Project financings are costly to arrange, and these costs may

outweigh the advantages enumerated above.• Complexity of Project Financings: Project financing is structured

around a set of contracts that must be negotiated by all the parties to a project.

• Indirect Credit Support: For any given degree of leverage in the capital structure, the cost of debt is typically higher in a project financing than in a comparable conventional financing because ofthe indirect nature of the credit support. The credit support for a project financing is provided through contractual commitments rather than through a direct promise to pay.

• Higher Transaction Cost: Because of their greater complexity, project financings involve higher transaction costs than comparable conventional financings.

51

101

Main Characteristics of Project Finance (Summary)

– Project is a distinct legal entity.– Project assets, project-related contracts, and

project cash flows are separated to a large degree from the sponsors.

– Sponsors provide limited or no recourse to cash flow from other assets.

– Lenders may have recourse to their funds through other stakeholders through various types of security arrangements.

– Two-phase financing is common.

102

The Basic Elements of a Project Financing

Contractor

Operator

Investors

Input Supply Contract

Construction Contract

Input Supplier

Lenders

Equity Project Finance Debt

Project Company

Support Agreement

Concession Agreement or License

Government or other Public Sector

authorities

Offtake Contract

Offtaker

Operator & Maintenance Contract

Finance

OR

52

103

Legal Ownership Structures for Project Financing

Special Purpose Vehicles(SPV)

104

Legal Ownership Structures for Project Financing

(Special Purpose Vehicle (SPV))• Choice influenced by tax, accounting,

regulatory, risk allocation considerations as well as access to, and cost of, capital.

• Examples of legal ownership forms are:– Undivided Joint Interest– Corporation– Partnership– Limited Liability Company

53

105

Undivided Joint Interest• Liability is several and unlimited• Each sponsor is responsible for providing its pro

rata share of cost. Advantageous if sponsors have different credit strengths.

• Tax consequences flow through directly to sponsors.

• Project is not legal entity for accounting purposes –proportional consolidation of assets and liabilities.

106

Partnership• Can have general partners and limited liability partners

• Must have at least one general partner

• Liability of general partners may be joint or several but liability is unlimited

• Partnership owns assets and raises equity and debt

• Tax consequences flow through directly to sponsors

• Reflection of project’s assets and liabilities on partner’s balance sheets depends on ownership share.

• In USA, full consolidation if over 50%, none if less.

54

107

Corporation• No liability to project owners• Corporation owns assets and raises equity

and debt• Tax consequences do not flow through

directly to sponsors unless there is full consolidation

• Taxation of income at the corporation and shareholder level, with perhaps of tax levels.

• Reflection of project’s assets and liabilities on partner’s balance sheets depends on ownership share.

• In USA, full consolidation if over 50%, none if less.

108

Limited Liability Company• No liability to project owners• Company owns assets and raises equity and

debt• Tax consequences flow through directly to

sponsors (deductions may not include investment tax credits).

• Reflection of project’s assets and liabilities on partner’s balance sheets depends on ownership share.

• In USA, full consolidation if over 50%, none if less.

55

109

Prerequisites for Project Financing

• Financial Analysis

• Economic Analysis

• Risk Analysis

110

Prerequisites for Project Financing(cont’d)

• Financial Analysis is concerned with:

– project’s overall financial viability and sustainability--NPV, financial ratios, etc.

– Project’s ability to service its debt--coverage ratios; and generate sufficient returns--ROA, ROE.

56

111

Prerequisites for Project Financing(cont’d)

• Economic Analysis is concerned with:

– Economic fundamentals of project

– Economic viability of project

112

Prerequisites for Project Financing(cont’d)

• Risk Analysis is concerned with

– identifying the different areas of project risk

– identifying the impact of changes in risky variables on project’s economic and financial viability

57

113

Lecture Notes

Week Two, Day Three(Session I: 08:30 – 10:00)

Program on the Appraisal of Infrastructure Projects with Private

Participation

114

Project Financing and

Managing Project Risks

58

115

Definition of Project Completion• Principle Categories of Risk: Pre-Completion and

Post-Completion• Physical Completion

– Project is physically complete according to technical design criteria.

• Mechanical Completion– Project can sustain production at a specified

capacity for a certain period of time.• Financial Completion (financial sustainability)

– Project can produce under a certain unit cost for a certain period of time & meets certain financial ratios (current ratio, Debt/Equity, Debt Service Capacity ratios)

116

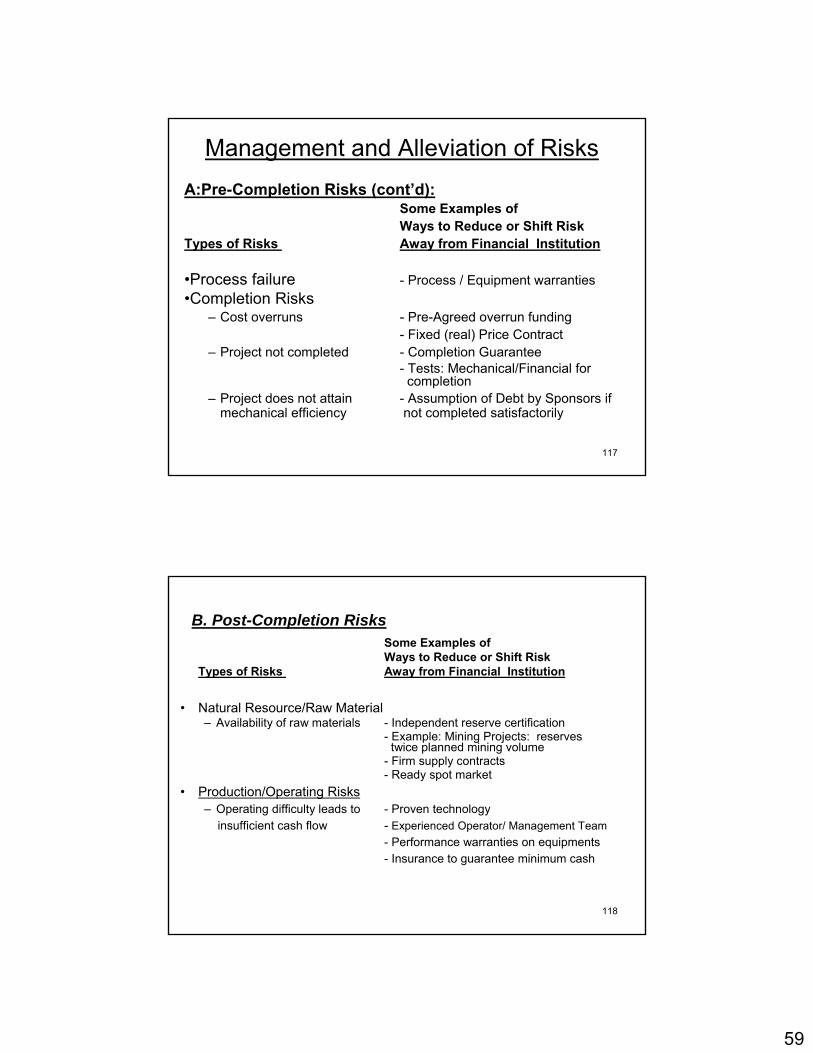

Management and Alleviation of RisksPrinciple Categories of Risk: Pre-Completion and Post-

Completion

A:Pre-Completion Risks:Some Examples ofWays to Reduce or Shift Risk

Types of Risks Away from Financial Institution•Participant Risks

-Sponsor commitment to project - Reduce Magnitude of investment?

-Require Lower Debt/Equity ratio-Finance investment through equity then by debt

– Financially weak sponsor - Attain Third party credit support for weak sponsor (e.g.,Letter of Credit)- Cross default to other sponsors

•Construction/Design defects - Experienced Contractor- Turn key construction contract

59

117

Management and Alleviation of RisksA:Pre-Completion Risks (cont’d):

Some Examples ofWays to Reduce or Shift Risk

Types of Risks Away from Financial Institution

•Process failure - Process / Equipment warranties•Completion Risks

– Cost overruns - Pre-Agreed overrun funding- Fixed (real) Price Contract

– Project not completed - Completion Guarantee- Tests: Mechanical/Financial for completion

– Project does not attain - Assumption of Debt by Sponsors if mechanical efficiency not completed satisfactorily

118

B. Post-Completion RisksSome Examples ofWays to Reduce or Shift Risk

Types of Risks Away from Financial Institution

• Natural Resource/Raw Material– Availability of raw materials - Independent reserve certification

- Example: Mining Projects: reserves twice planned mining volume

- Firm supply contracts- Ready spot market

• Production/Operating Risks– Operating difficulty leads to - Proven technology

insufficient cash flow - Experienced Operator/ Management Team- Performance warranties on equipments- Insurance to guarantee minimum cash

60

119

Some Examples ofWays to Reduce or Shift Risk

Types of Risks Away from Financial Institution

• Market Risk–Volume -cannot sell entire output - Long term contract with

creditworthy buyers: take-or-pay; take-if-delivered; take-and-pay

–Price - cannot sell output at profit - Minimum volume/floor price provisions - Price escalation provisions

• Abandonment Risk–Sponsors walk away from project - Abandonment test in agreement

for banks to run project closure based on historical andprojected costs and revenues

B. Post-Completion Risks

120

FORCE MAJEURE RISK• This category concerns the risk that some discrete event might

impair, or prevent altogether, the operation of the project for a pro-longed period of time after the project has been completed and placed in operation.

• Lenders normally insist on being protected from loss caused by force majeure.

• Certain events of force majeure, such as fires or earthquakes, can be insured against.

• Lenders will require assurances from financially capable partiesthat the project's debt service requirements will be met in the event force majeure occurs.

• If force majeure results in abandonment of the project, lenders typically require repayment of project debt on an accelerated basis – debt service reserve fund.

• In the case of events covered by insurance, lenders will requirethe project sponsors to pledge the right to receive insurance payments as part of the security for project loans.

61

121

ENVIRONMENTAL RISK• Environmental risk is present when the environmental effects

of a project might cause a delay in the project's development or necessitate a costly redesign.

• For example, in connection with a mining project, disposal of tailings is often a very sensitive environmental issue that can add significantly to the cost of operations.

• Interestingly, the frequent changes in environmental regulations in the United States (at both the state and federal levels), and, the legal challenges mounted by environmental groups, have given rise to significant environmental risks for environmentally sensitive projects in the United States.

122

POLITICAL RISK

• Covers range of issues from political risk assurances nationalization/ expropriation changes in tax and other laws, currency inconvertibility, etc.

• Political risk can be ameliorated by borrowing funds for the project from local banks (which would suffer financially if the project is unable to repay project debt because its assets were expropriated).

62

123

• It can also be mitigated by borrowing funds for the project from the World Bank, the Inter-American Development Bank, or some other multilateral financing agency, if the host countryis relying on such agencies to fund public expenditures (expropriation would jeopardize such funding).

• In addition, project sponsors can often arrange political risk insurance to cover a wide range of political risks.– Assumption of debt– Official insurance: OPIC, COFACE, EXIM– Private insurance: AIG, LLOYDS– Offshore Escrow Accounts

POLITICAL RISK MANAGEMENT

124

Some Examples ofWays to Reduce or Shift Risk

Types of Risks Away from Financial Institution

• Other Risks: Not really project risks but may include:–Syndication risk - Secure strong lead financial institution–Currency risk - Currency swaps / hedges –Interest rate exposure - Interest rate swaps –Rigid debt service - Built-in flexibility in debt service

obligations–Hair trigger defaults

63

125

Security Arrangements

126

Security Arrangements

– Ensure project completion (physical, mechanical and financial).

– Upon completion, ensure that project generates sufficient cash to cover operating expenses and meet debt service requirements.

– Ensure that the project can service debt in the event of disruption in operations (including force majeure situations).

Objectives

64

127

Elements of a Security Package

a) Mortgage on project assetsb) Turnkey contractsc) Sale & purchase contractual agreementsd) Sponsors’ commitment/support/pledgese) Financial covenantsf) Guaranteesg) Insuranceh) Escrow funds

128

A) Mortgage on Project Assets

• If financial institution has mortgage on assets of project it can take over assets if loans are not repaid.

• First Mortgage lien on project’s fixed assets (land, buildings and machinery) means that the financial institution has first claim on fixed assets.

• Works well for industrial projects and power projects but not so for other infrastructure projects (such as highway projects).

• Not possible in case of concessions or BOTs—Sponsor guarantees will be necessary

65

129

Mortgage on Project Assets (cont’d)

• Weak Mortgage Legal Framework is often a problem. For example,– No mortgage law in project country– No mortgage of land allowed to foreigners– If fixed assets are mortgaged, no other

assurance can be used by lender.

130

B) Off Take and Supply Contracts• Off take contracts obligate buyers of the of the project’s

output to provide credit support to the project and to share in its risks.

• Raw material supply agreements obligate providers of the project’s inputs to provide credit support to the project and to share in its risks. For example, suppliers of telephone switching and transmission equipment for all phone project.

• Contracts specify certain remedies when deliveries are not received or made.

• Off take and supply agreements are often requested by lenders to provide credit support for a project.

• Often supplemented by sponsors’ assurances and commitments.

66

131

B) Off Take Contracts• Take and Pay (Take-if-Offered)

ContractA contract obligating the buyer of the project’s

output to take delivery and pay for the output only if the project is able to deliver them. No payment is required unless the project is able to make deliveries.

• Take or Pay ContractA contract obligating the buyer of the project’s output to pay for the output, regardless of whether the purchaser takes delivery. Cash payments are usually credited against charges for future delivers.

132

B) Off Take Contracts (cont’d)

• Hell-or-High-Water ContractSimilar to take-or-pay except there are no “outs”. Buyer has to pay in all events even if output is not produced and even in cases of force majeure.

• Throughput AgreementAn agreement according to which the shipper agrees to ship a specified amount of product through the pipeline within a certain time period. Throughput generates sufficient cash to cover operating costs and service debt.

67

133

B) Off Take Contracts (cont’d)

• Cost of Service ContractThis contract requires each sponsor to pay his proportionate share of project costs and receive its share of project output.

• Tolling AgreementThe agreement requires each sponsor to pay its share of tolling charges for processing a raw material. Typically raw material is owned by project sponsors.

134

C) Raw Material Supply Agreements

• Supply or Pay ContractContract obligates the raw material supplier to furnish the required amounts of the raw material specified in the contract or else make payments to the project entity that are sufficient to cover the project’s debt service.

68

135

• An obligation by other buyers to increase their respective shares of purchases in case one of the buyers goes into default; or by a other suppliers of raw material to increase their respective shares of supply if one supplier goes into default, hence enhancing the strength of the agreements.

• Each of the buyers/suppliers coinsures the obligations of the other buyers/suppliers.

• A step-up provision is often included in the purchase and supply contracts if there are multiple buyers of the project’s output/suppliers of raw material.

D) Step-Up Provisions

136

E) Sponsors’ Commitment/ Support/ Pledges

• Project Funds AgreementAgreement by sponsors to provide additional funds as needed--typically until project completion.

69

137

E) Sponsors’ Support (cont’d)

• Share Retention AgreementAn agreement by the shareholders not to sell their shares, or alternatively to hold a specified amount of shares.

138

E) Sponsors’ Support (cont’d)

• Capital Subscription AgreementAn obligation by creditworthy parties to buy the

securities of the project entity for cash to the

extent required to cover any cash short-falls by

the project.

Typically, common stock or subordinated debt

(junior securities)

70

139

E) Sponsors’ Support (cont’d)• Clawback Agreement• An agreement by project sponsors to contribute cash to