Embed Size (px)

Citation preview

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

U.S. DC Power Market Brief

December, 2003

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Meet John Celentano• 30 years in telecom• Involved with telecom power for 25 years • Broad experience in carrier, supplier, and consulting

environments• Research/strategy consulting on public network

infrastructure markets• Supported clients through campaigns worth billions in

sales• Advises equipment manufacturers, service providers,

and investor groups worldwide• Publishes research reports and articles on DC power,

and quoted often in business and trade press

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Discussion Format

• Telecom Market Overview

• DC Power Application Drivers

• Telecom DC Power Market Outlook

• Strategic Considerations

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

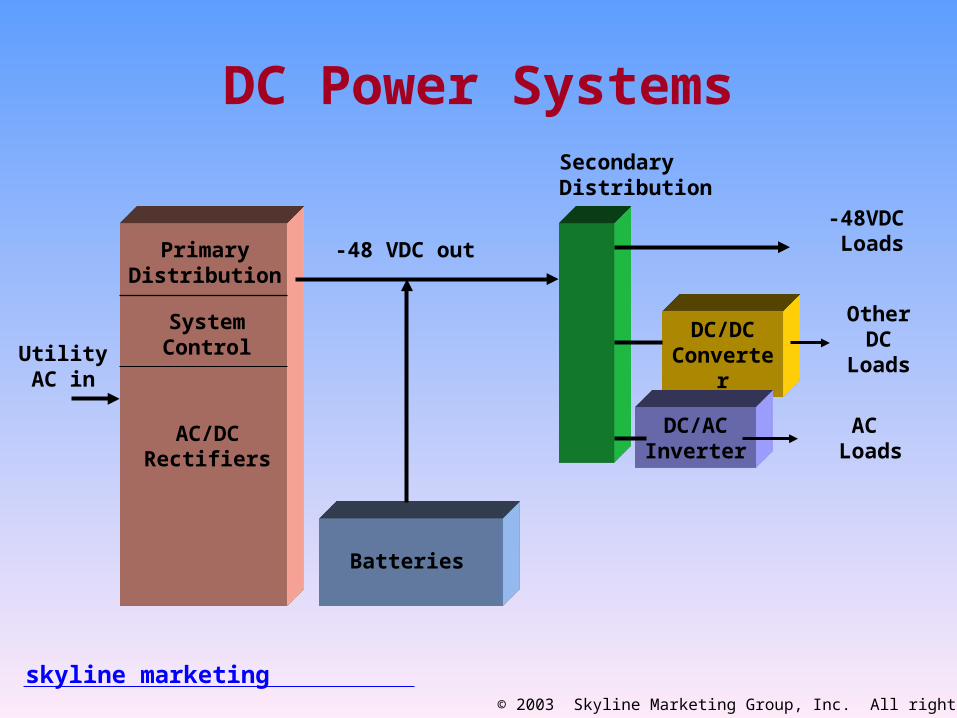

DC Power Systems

PrimaryDistribution

SystemControl

Batteries

UtilityAC in

-48 VDC out

AC/DCRectifiers

-48VDC Loads

DC/DCConverter

DC/ACInverter

AC Loads

OtherDC

Loads

SecondaryDistribution

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

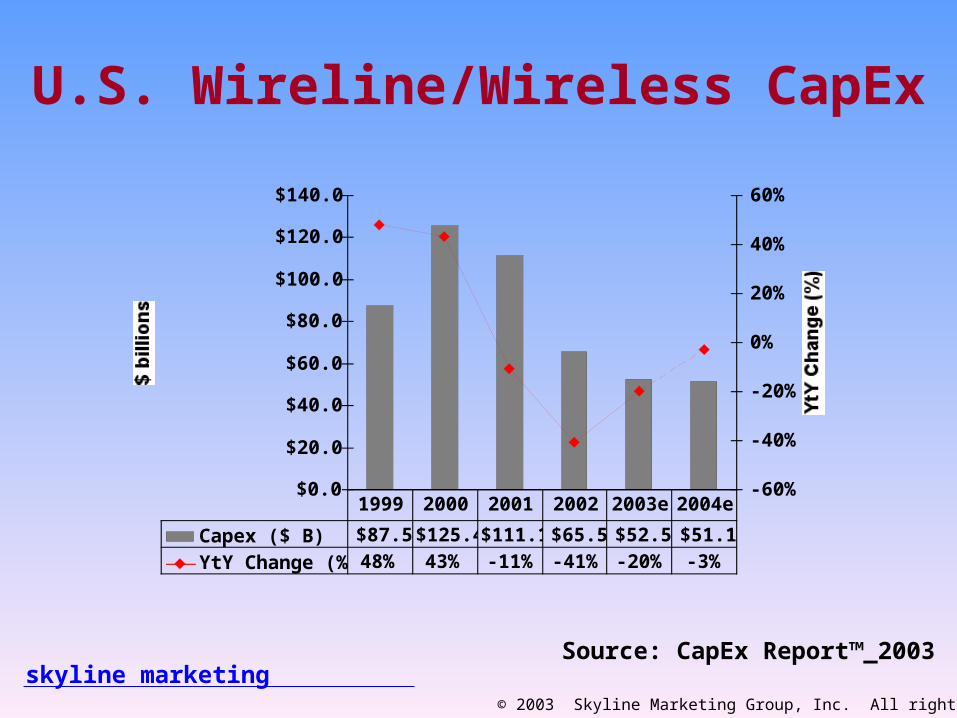

U.S. Wireline/Wireless CapEx

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$ billions

-60%

-40%

-20%

0%

20%

40%

60%

YtY Change (%)

Capex ($ B) $87.5 $125.4 $111.1 $65.5 $52.5 $51.1

YtY Change (%) 48% 43% -11% -41% -20% -3%

1999 2000 2001 2002 2003e 2004e

Source: CapEx Report™_2003

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

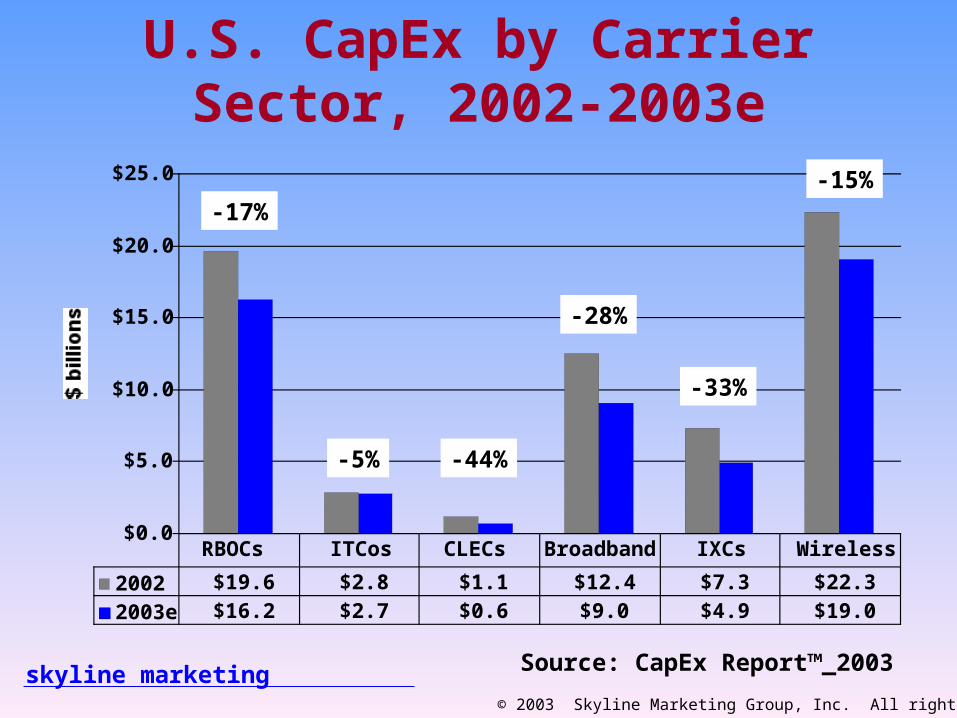

U.S. CapEx by Carrier Sector, 2002-2003e

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$ billions

2002 $19.6 $2.8 $1.1 $12.4 $7.3 $22.3

2003e $16.2 $2.7 $0.6 $9.0 $4.9 $19.0

RBOCs ITCos CLECs Broadband IXCs Wireless

-17%

-5% -44%

-28%

-33%

-15%

Source: CapEx Report™_2003

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

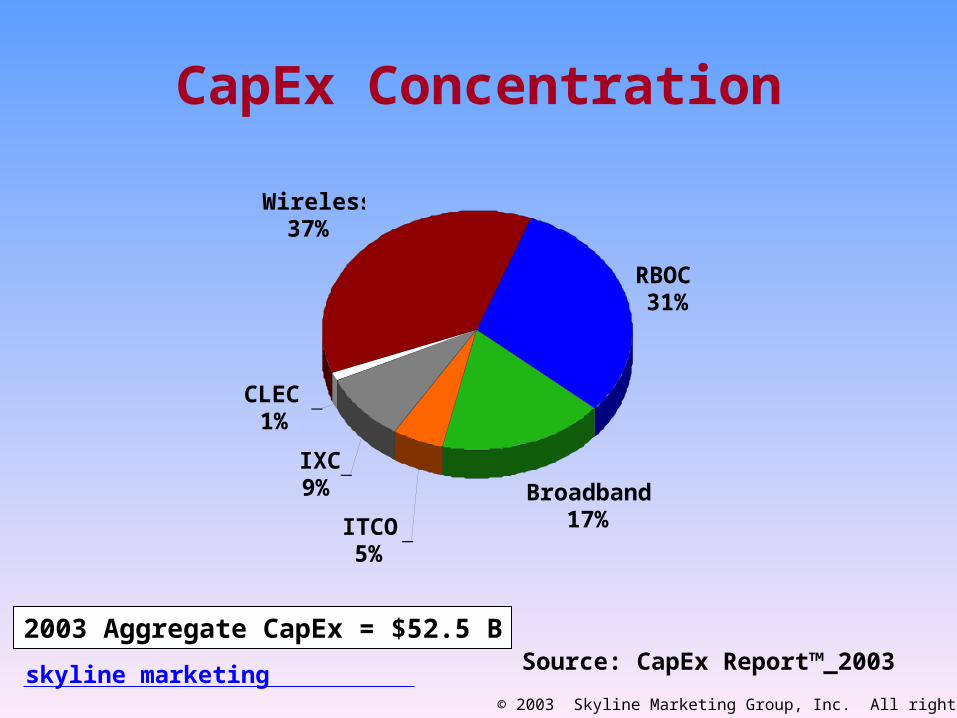

CapEx Concentration

RBOC31%

Broadband17%ITCO

5%

IXC9%

CLEC1%

Wireless37%

2003 Aggregate CapEx = $52.5 BSource: CapEx Report™_2003

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

What We See …

• Flat capex in 2004

• Telco response to cable/wireless threats

• Receding network overcapacity

• Carriers spending for ‘success-based’ demand

• Consolidation happening slowly

• Early stage of long-term technology shifts

• Growth in telecom DC power

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

End Equipment Bright Spots

• Broadband Access

• FTTP

• C2P Migration

• Wireless

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Broadband Access

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

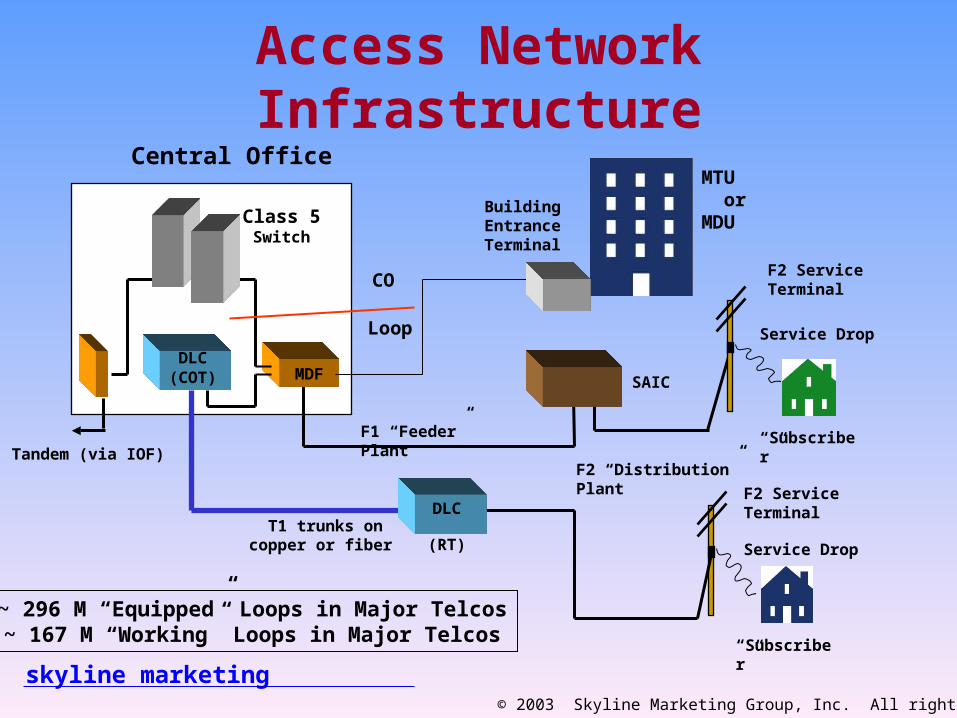

Access Network Infrastructure

“Subscriber”

MDF

F1 “Feeder” Plant

F2 “Distribution” Plant

Service Drop

F2 Service Terminal

Tandem (via IOF)

T1 trunks on copper or fiber

DLC(COT)

Central Office

Service Drop

F2 Service Terminal

BuildingEntranceTerminal

“Subscriber”

MTU orMDUClass 5

Switch

CO

Loop

~ 296 M “Equipped” Loops in Major Telcos~ 167 M “Working” Loops in Major Telcos

DLC (RT)

SAIC

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

DLC Working Lines

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

FoDLC 15.1 17.2 23.9 27.3 28.1 29.1

CuDLC 11.4 12.4 13.6 13.7 12.6 11.4

1997 1998 1999 2000 2001 2002

17%18%

22%24% 24%

% = penetration of Total Working Lines

25%

Source: “An Excess of Access” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

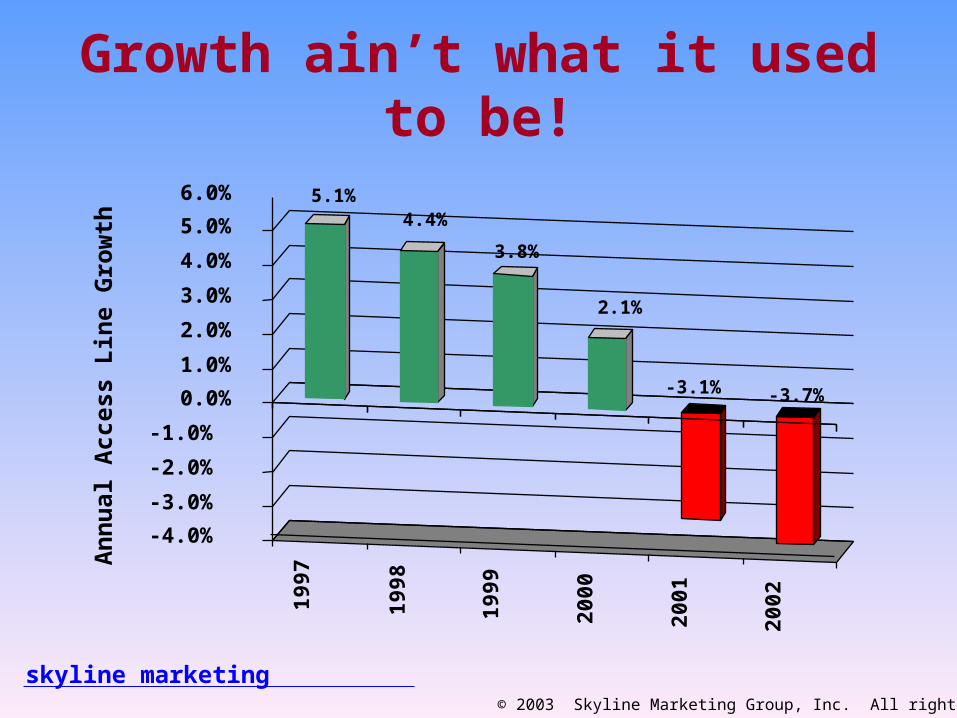

Growth ain’t what it used to be!

19

97

19

98

19

99

20

00

20

01

20

02

5.1%4.4%

3.8%

2.1%

-3.1% -3.7%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

An

nual

Acc

ess

Lin

e G

row

th

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

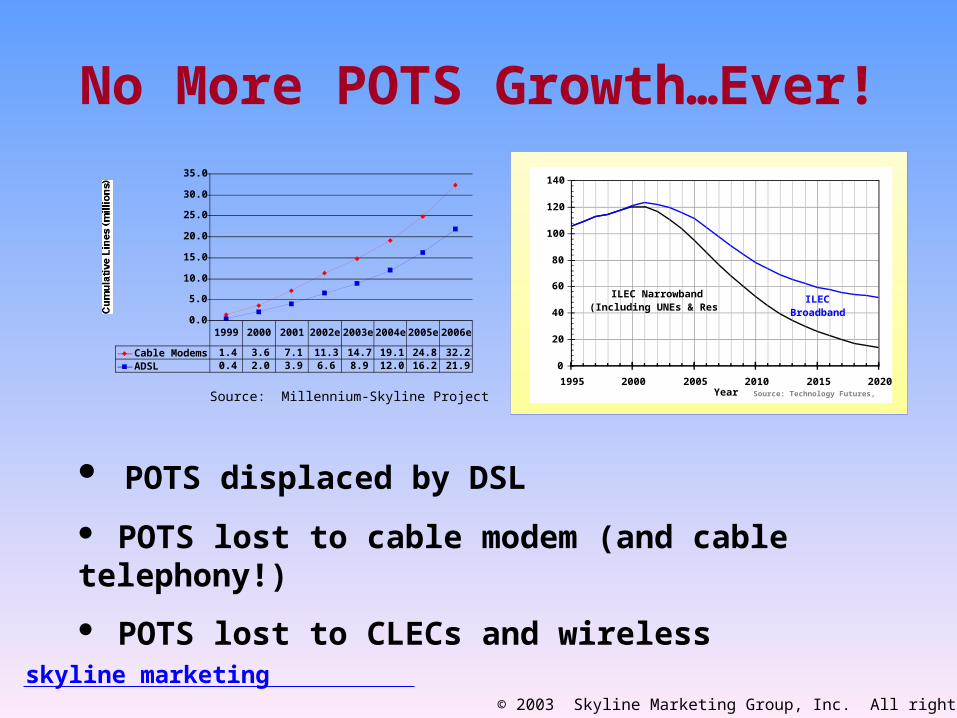

No More POTS Growth…Ever!

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Cable Modems 1.4 3.6 7.1 11.3 14.7 19.1 24.8 32.2ADSL 0.4 2.0 3.9 6.6 8.9 12.0 16.2 21.9

1999 2000 2001 2002e 2003e 2004e 2005e 2006e

0

20

40

60

80

100

120

140

1995 2000 2005 2010 2015 2020Year

Millions of Access Lines

ILEC Narrowband(Including UNEs & Resale)

Source: Technology Futures, Inc.

Competitive Impacts 2002

ILECBroadband

POTS displaced by DSL

POTS lost to cable modem (and cable telephony!)

POTS lost to CLECs and wireless

Source: Millennium-Skyline Project

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

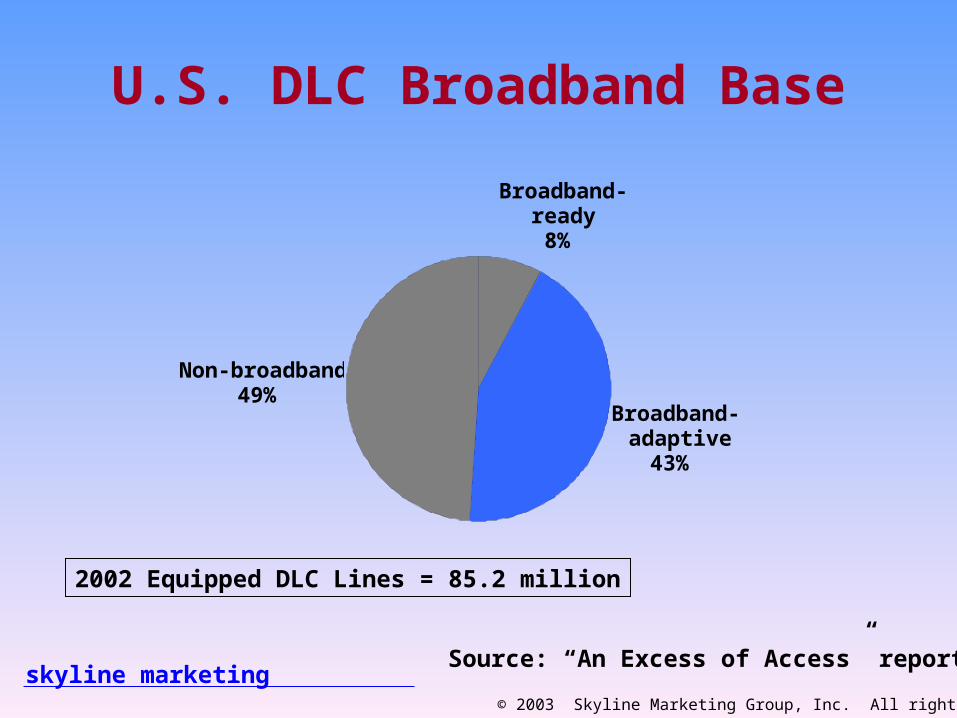

U.S. DLC Broadband Base

Broadband-ready

8%

Broadband-adaptive

43%

Non-broadband49%

2002 Equipped DLC Lines = 85.2 million

Source: “An Excess of Access” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

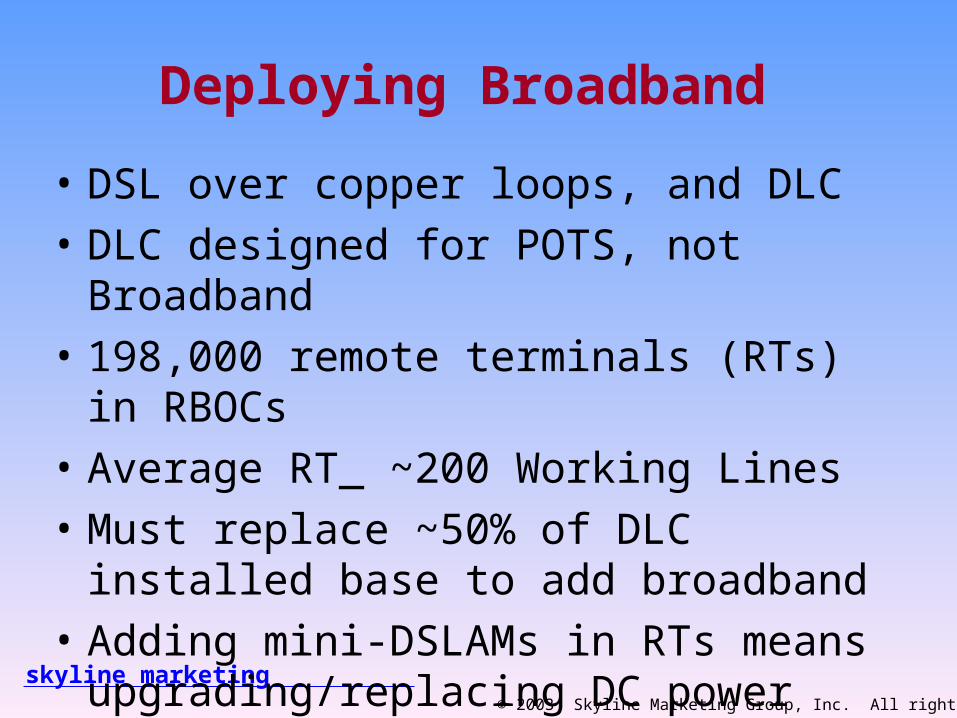

Deploying Broadband

• DSL over copper loops, and DLC

• DLC designed for POTS, not Broadband

• 198,000 remote terminals (RTs) in RBOCs

• Average RT_ ~200 Working Lines

• Must replace ~50% of DLC installed base to add broadband

• Adding mini-DSLAMs in RTs means upgrading/replacing DC power

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

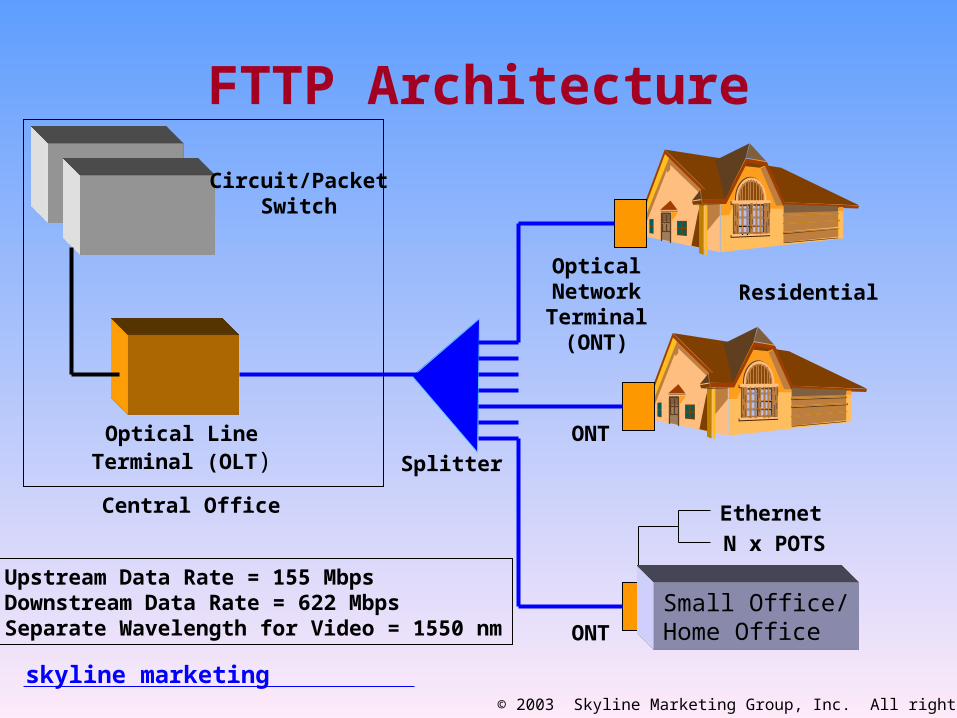

Fiber-to-the-Premise (FTTP)

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

FTTP Architecture

Circuit/PacketSwitch

Optical LineTerminal (OLT) Splitter

Central Office

ResidentialOpticalNetworkTerminal

(ONT)

ONT

ONT

Ethernet

N x POTS

Small Office/Home Office

Upstream Data Rate = 155 MbpsDownstream Data Rate = 622 MbpsSeparate Wavelength for Video = 1550 nm

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Circuit-to-Packet (C2P) Migration

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

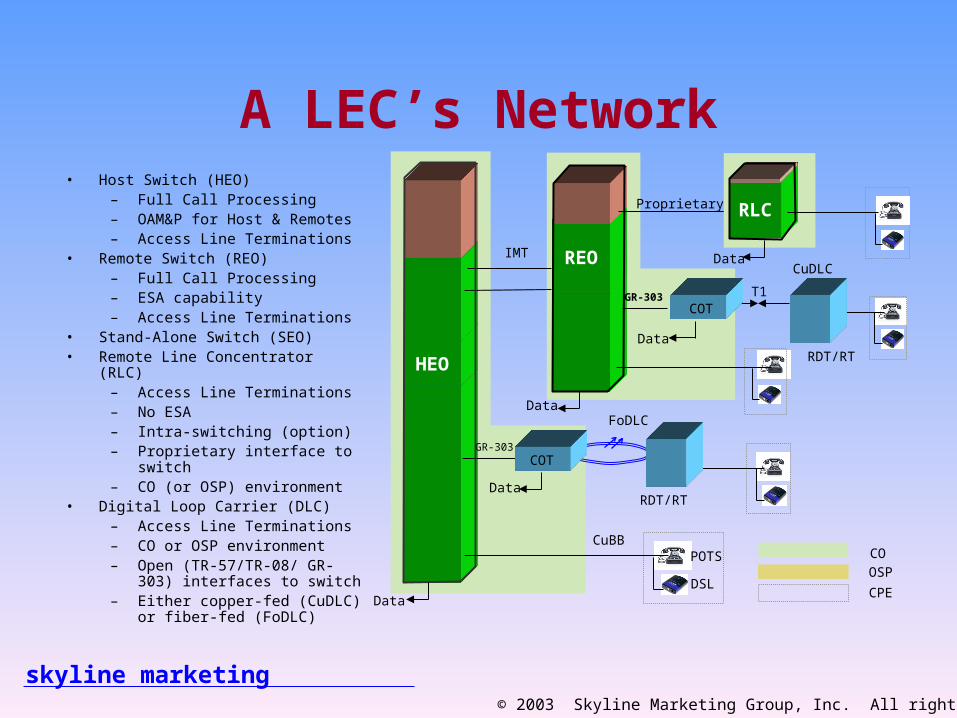

A LEC’s Network• Host Switch (HEO)

– Full Call Processing– OAM&P for Host & Remotes– Access Line Terminations

• Remote Switch (REO) – Full Call Processing– ESA capability– Access Line Terminations

• Stand-Alone Switch (SEO)• Remote Line Concentrator (RLC)

– Access Line Terminations – No ESA– Intra-switching (option)– Proprietary interface to switch– CO (or OSP) environment

• Digital Loop Carrier (DLC)– Access Line Terminations – CO or OSP environment– Open (TR-57/TR-08/ GR-303)

interfaces to switch– Either copper-fed (CuDLC) or

fiber-fed (FoDLC)

HEO

REO

GR-303

Proprietary

IMT

Data

GR-303

Data

Data

Data

RLC

Data

CO

OSP

CPE

POTS

DSL

T1

CuDLC

FoDLC

CuBB

COT

COT

RDT/RT

RDT/RT

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

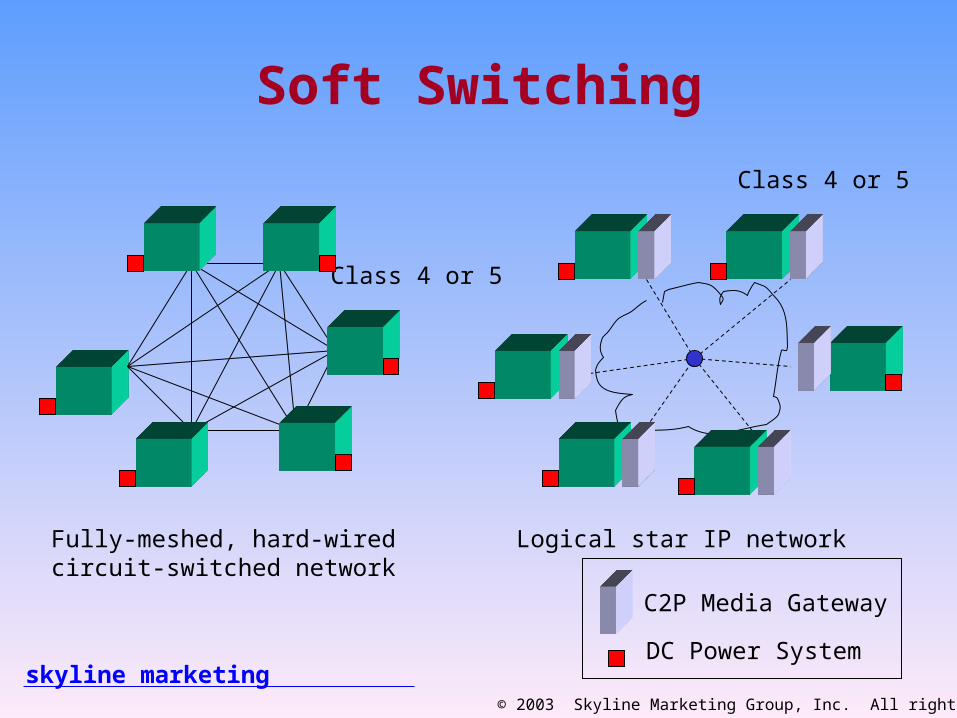

Soft Switching

Fully-meshed, hard-wiredcircuit-switched network

Logical star IP network

Class 4 or 5

Class 4 or 5

C2P Media Gateway

DC Power System

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

C2P Drivers

• IP traffic doubling every year• Better network utilization for multimedia traffic with

“voice-over” technologies, e.g. VoIP, VoATM• Lower operating cost per bit (Moore’s Law)• High-speed transport_SONET, DWDM• Multiple Access technologies_Ethernet, IP, ATM, TDM• Long migration period_10-15 years

– Different migration paths

• DC power adds/upgrades needed at every EO

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

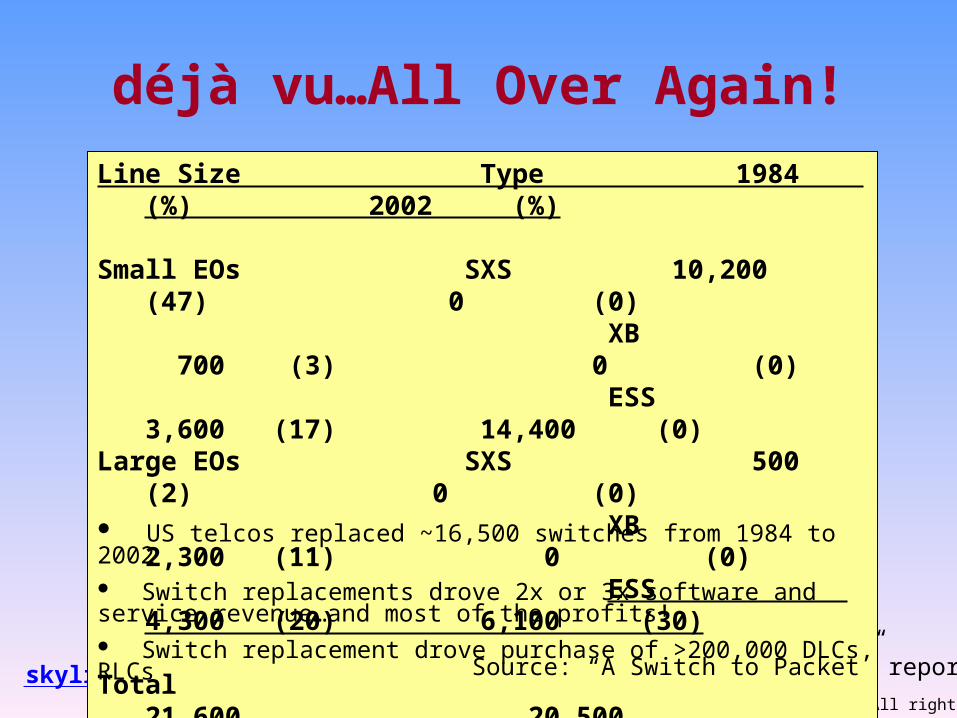

déjà vu…All Over Again!

Line Size Type 1984 (%) 2002 (%)

Small EOs SXS 10,200 (47) 0 (0) XB 700 (3) 0 (0) ESS 3,600 (17) 14,400 (0)Large EOs SXS 500 (2) 0 (0) XB 2,300 (11) 0 (0) ESS 4,300 (20) 6,100 (30)

Total 21,600 20,500

US telcos replaced ~16,500 switches from 1984 to 2002 Switch replacements drove 2x or 3x software and service revenue…and most of the profits! Switch replacement drove purchase of >200,000 DLCs, RLCs

Source: “A Switch to Packet” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

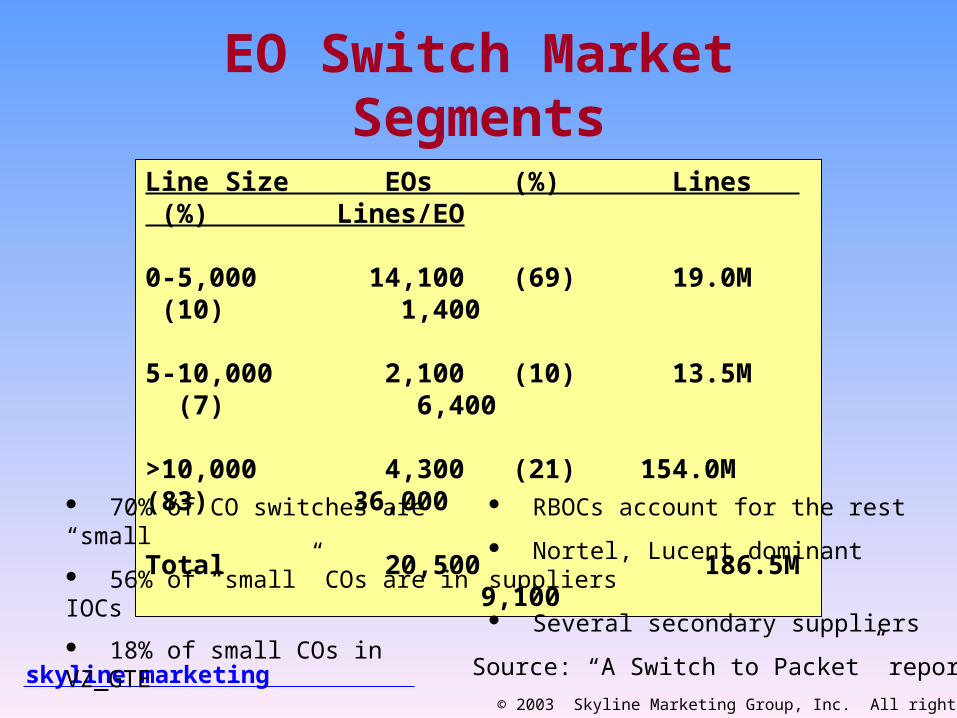

EO Switch Market Segments

Line Size EOs (%) Lines (%) Lines/EO

0-5,000 14,100 (69) 19.0M (10) 1,400

5-10,000 2,100 (10) 13.5M (7) 6,400

>10,000 4,300 (21) 154.0M (83) 36,000

Total 20,500 186.5M 9,100

70% of CO switches are “small”

56% of “small” COs are in IOCs

18% of small COs in VZ_GTE

RBOCs account for the rest

Nortel, Lucent dominant suppliers

Several secondary suppliers

Source: “A Switch to Packet” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

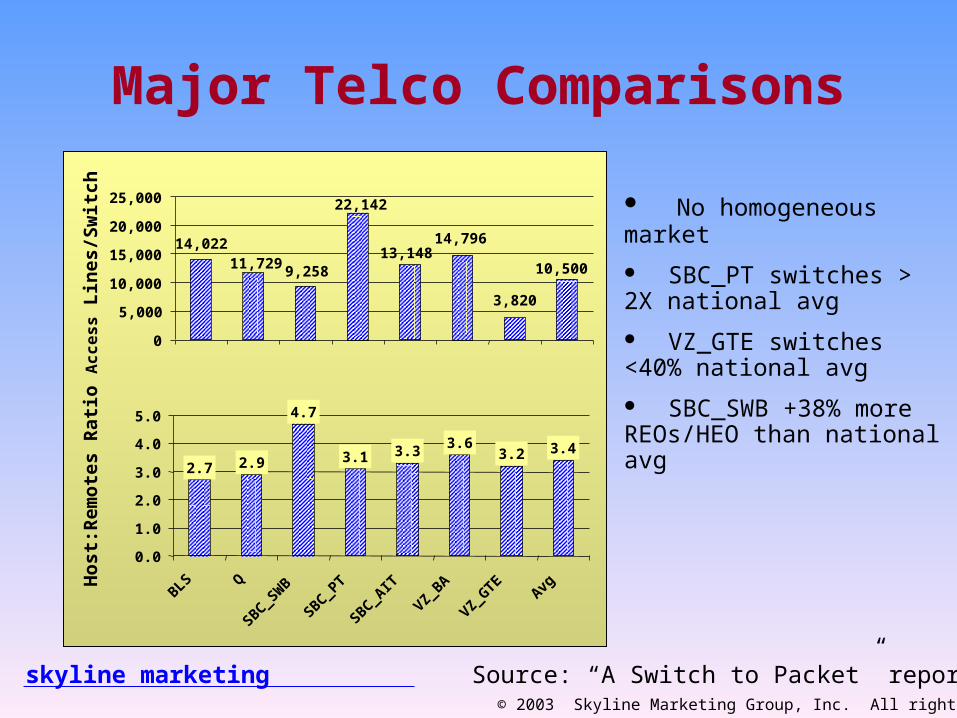

Major Telco Comparisons

10,500

3,820

14,79613,148

22,142

9,25811,72914,022

0

5,000

10,000

15,000

20,000

25,000

Acc

ess

Lin

es/S

wit

ch

3.43.23.63.33.1

4.7

2.92.7

0.0

1.0

2.0

3.0

4.0

5.0

BLS Q

SBC_S

WB

SBC_P

T

SBC_A

IT

VZ_BA

VZ_GTE

Avg

Hos

t:R

emot

es R

atio

No homogeneous market

SBC_PT switches > 2X national avg

VZ_GTE switches <40% national avg

SBC_SWB +38% more REOs/HEO than national avg

Source: “A Switch to Packet” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

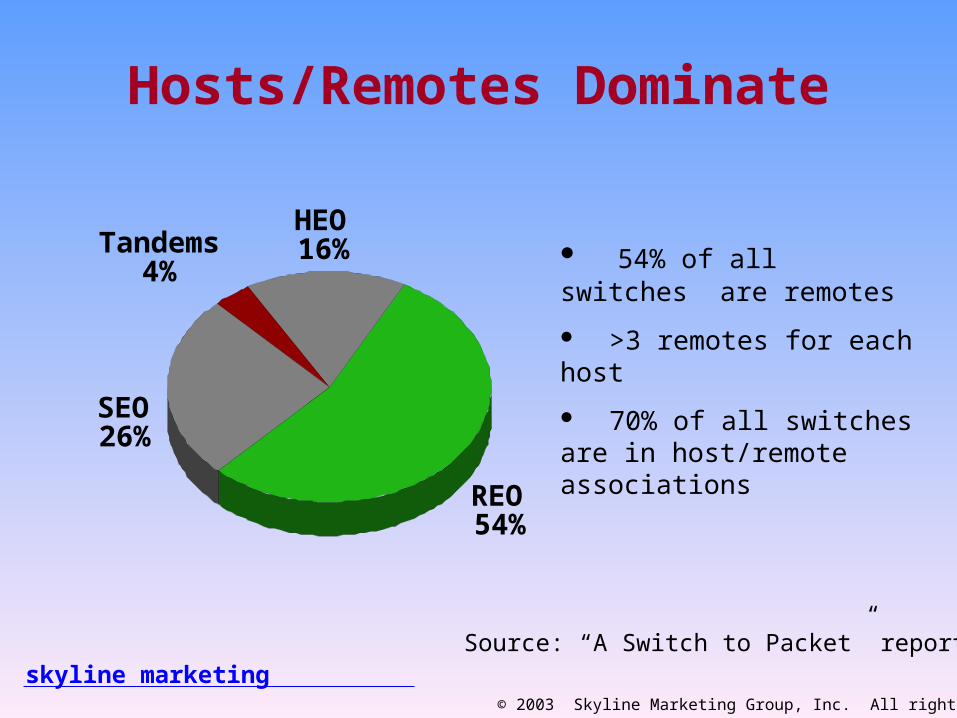

Hosts/Remotes Dominate

HEO16%

REO54%

SEO26%

Tandems4%

54% of all switches are remotes

>3 remotes for each host

70% of all switches are in host/remote associations

Source: “A Switch to Packet” report

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Wireless

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

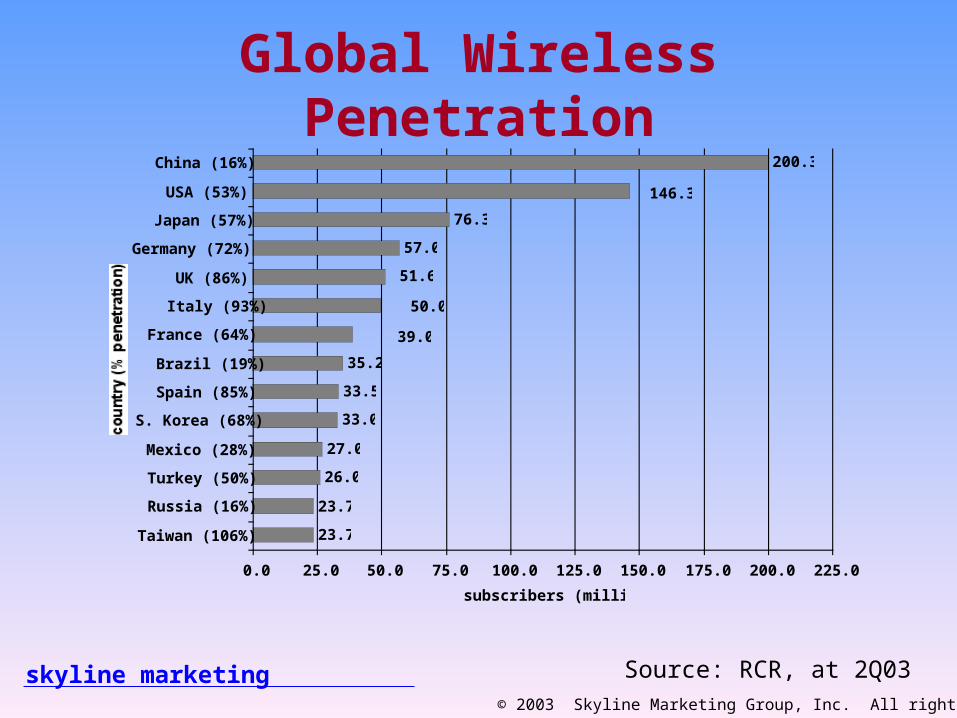

Global Wireless Penetration200.3

76.3

57.0

35.2

33.5

33.0

27.0

26.0

23.7

23.7

51.6

39.0

50.0

146.3

0.0 25.0 50.0 75.0 100.0 125.0 150.0 175.0 200.0 225.0

China (16%)

USA (53%)

Japan (57%)

Germany (72%)

UK (86%)

Italy (93%)

France (64%)

Brazil (19%)

Spain (85%)

S. Korea (68%)

Mexico (28%)

Turkey (50%)

Russia (16%)

Taiwan (106%)

subscribers (millions)

Source: RCR, at 2Q03

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

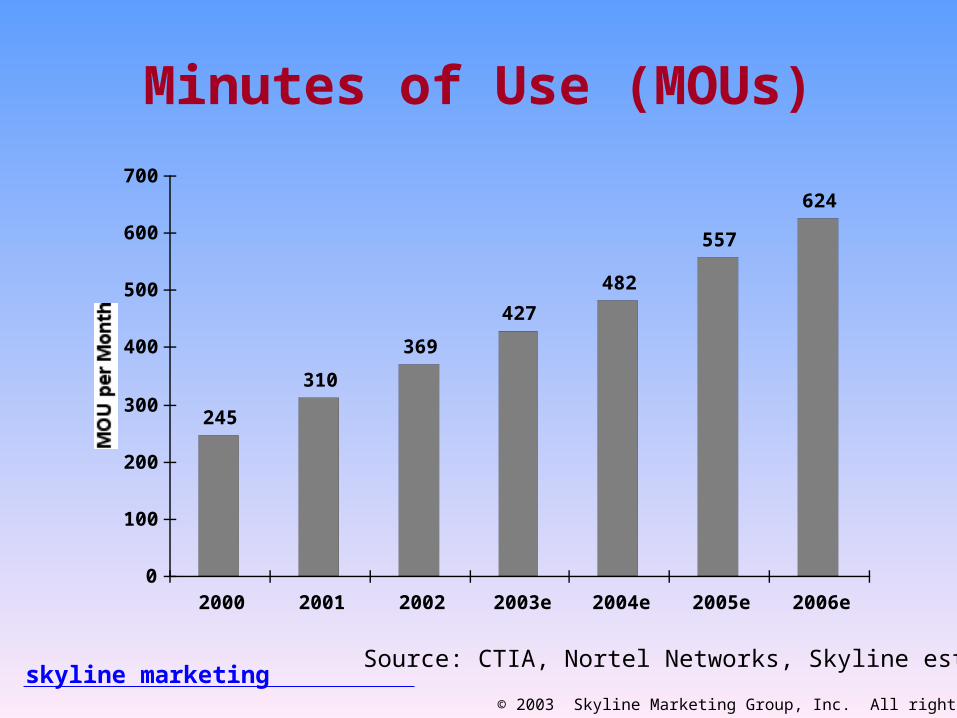

245

310

369

427

482

557

624

0

100

200

300

400

500

600

700

2000 2001 2002 2003e 2004e 2005e 2006e

Source: CTIA, Nortel Networks, Skyline est.

Minutes of Use (MOUs)

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

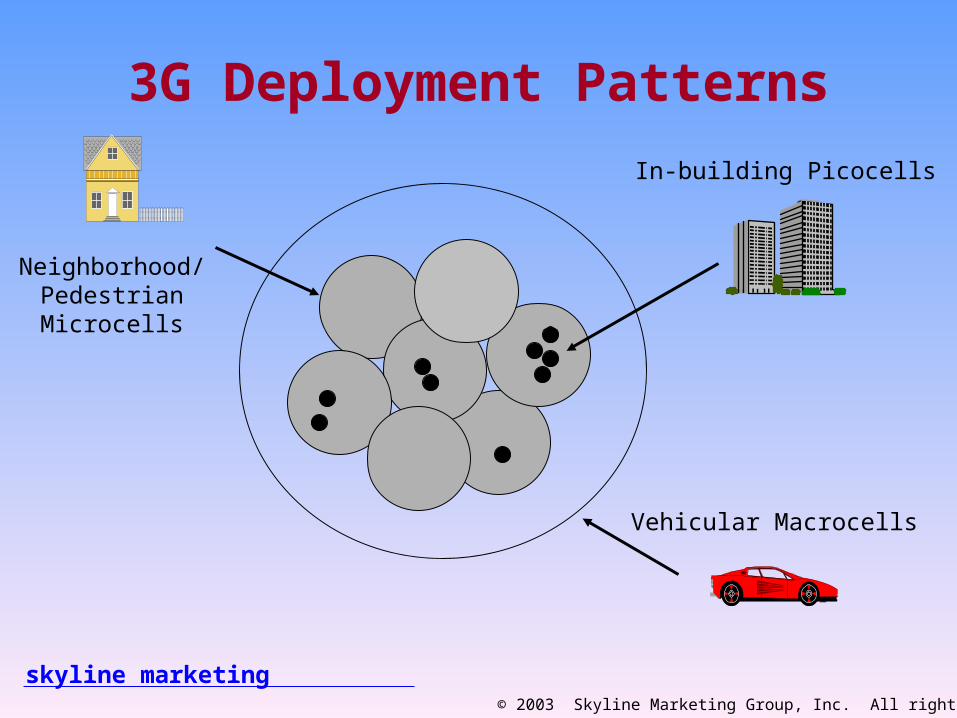

In-building Picocells

Neighborhood/PedestrianMicrocells

Vehicular Macrocells

3G Deployment Patterns

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

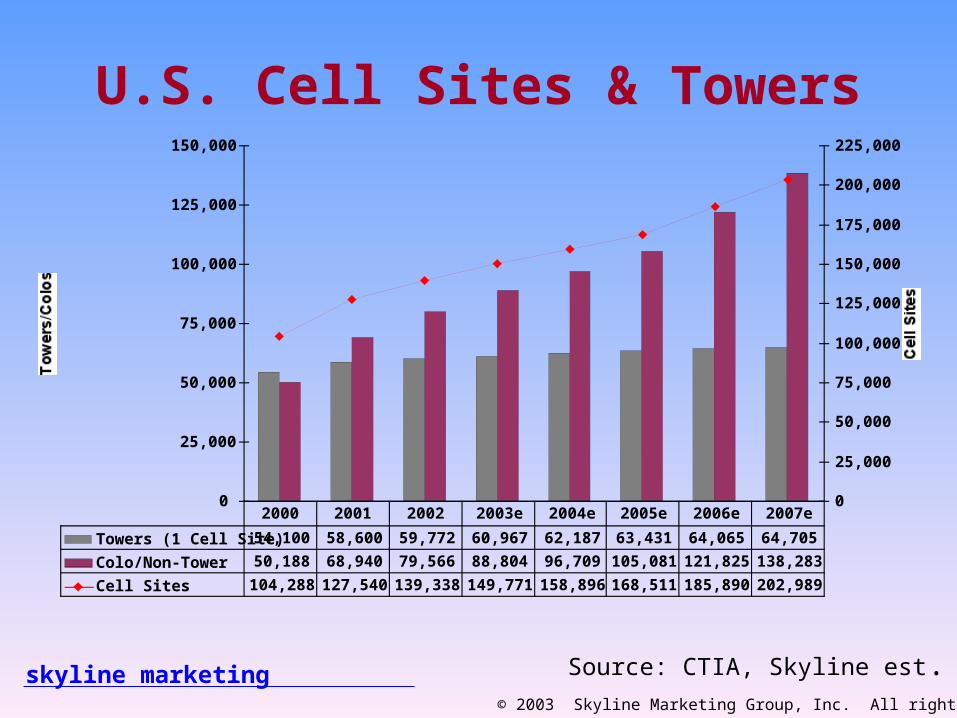

0

25,000

50,000

75,000

100,000

125,000

150,000

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

Towers (1 Cell Site) 54,100 58,600 59,772 60,967 62,187 63,431 64,065 64,705

Colo/Non-Tower 50,188 68,940 79,566 88,804 96,709 105,081 121,825 138,283

Cell Sites 104,288 127,540 139,338 149,771 158,896 168,511 185,890 202,989

2000 2001 2002 2003e 2004e 2005e 2006e 2007e

Source: CTIA, Skyline est.

U.S. Cell Sites & Towers

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

DC Power Market

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

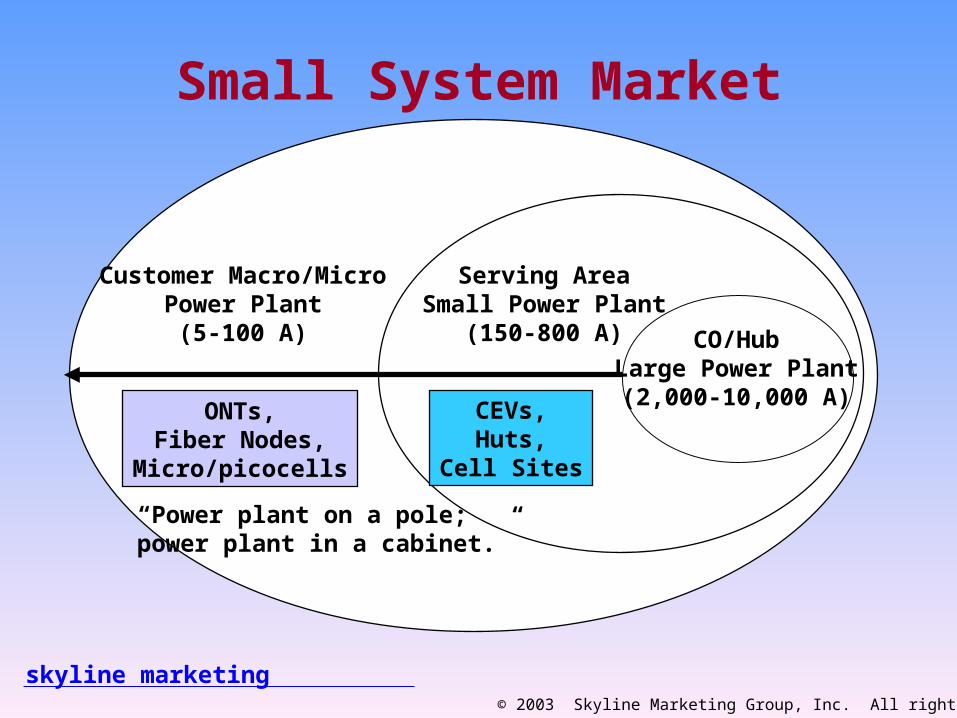

Small System Market

Serving AreaSmall Power Plant

(150-800 A)

Customer Macro/MicroPower Plant

(5-100 A)

CEVs,Huts,

Cell Sites

ONTs,Fiber Nodes,

Micro/picocells

“Power plant on a pole;power plant in a cabinet.”

CO/HubLarge Power Plant

(2,000-10,000 A)

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

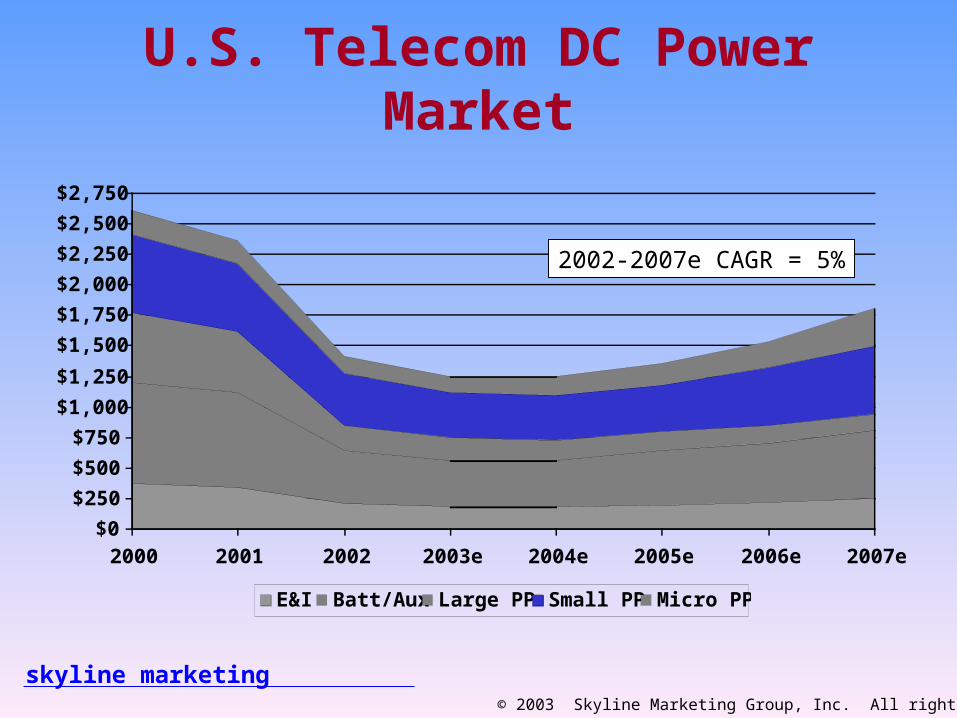

U.S. Telecom DC Power Market

$0

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

2000 2001 2002 2003e 2004e 2005e 2006e 2007e

E&I Batt/Aux Large PP Small PP Micro PP

2002-2007e CAGR = 5%

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Power Product/System Features

• Energy efficiency_90-92+%

• Power density_small size, weight

• Ease of handling_installation, maintenance

• Improved system intelligence

• Short-interval provisioning/maintenance

• Growing interest in alternate energy gear

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Key Decision Factors Criteria

• High availability_“It just has to work”

• Help improve financials_reduce CapEx/OpEx– Competitive first costs– Low maintenance costs– Low operating costs

• Power system management imperative– Remote, hands-off operation

• Supplier knowledge/experience dependency

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Strategic Considerations

• Telecom/IT recovery showing signs of life– Follow the money

• DC power is a replacement business– Focus on small/micro power plant “sweet spot”

• Support moves to “Lights out network”– Offer Total Power Solutions = Equipment + Services

• Sell on a “carrier-by-carrier” basis– Every carrier is different– Help carriers’ achieve their operating goals

skyline marketing© 2003 Skyline Marketing Group, Inc. All rights reserved.

Skyline Marketing Groupwww.skylinemarketing.com

We help you make your numbers!!

![Trade Show Marketing [Skyline Exhibits]](https://img.pdfslide.net/doc/110x75/5552e0bbb4c905014c8b4d96/trade-show-marketing-skyline-exhibits.jpg)