Embed Size (px)

Citation preview

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

IPTVTechVenture 2006

Kellogg School of ManagementTom Cadwell

Laurence CuaMahesh Jadhav

Ammon MatsudaRob Svetlik

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

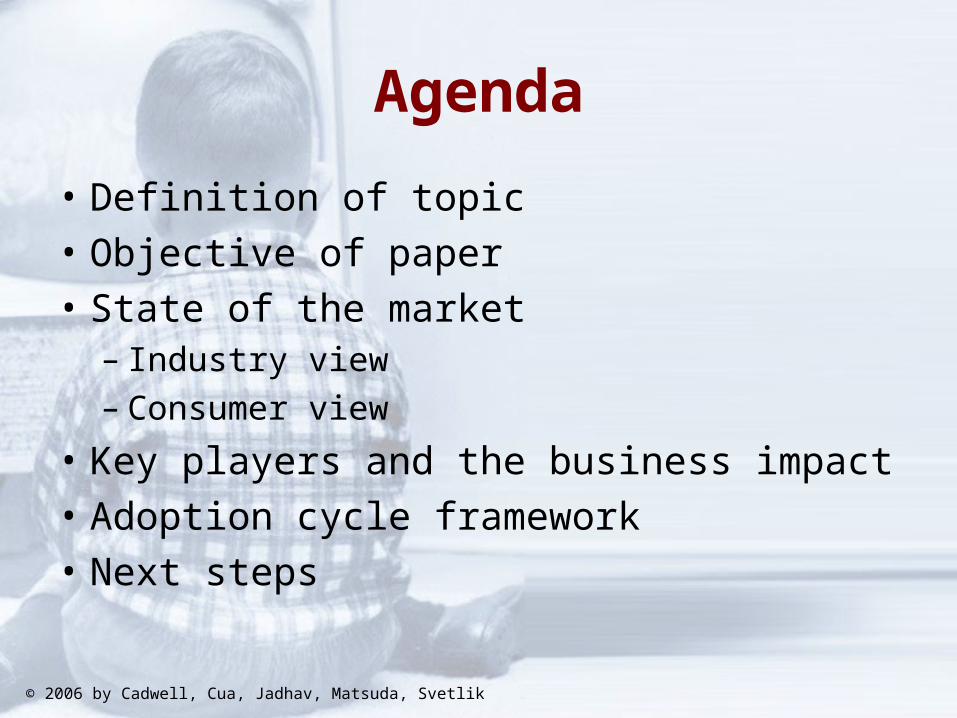

Agenda

• Definition of topic

• Objective of paper

• State of the market– Industry view– Consumer view

• Key players and the business impact

• Adoption cycle framework

• Next steps

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

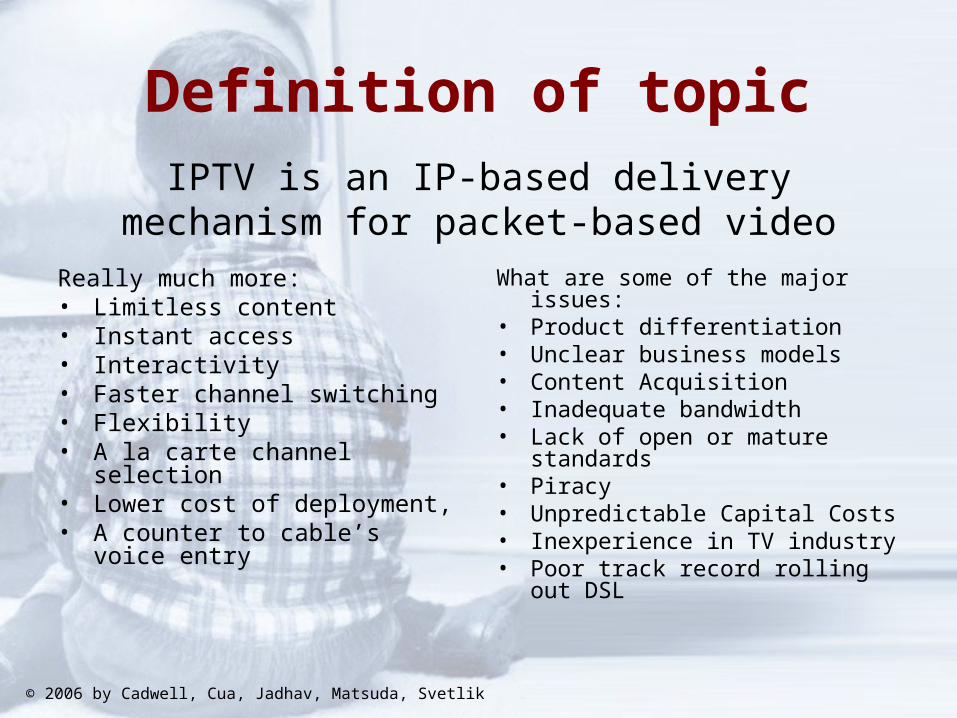

Definition of topic

Really much more:• Limitless content• Instant access• Interactivity• Faster channel switching• Flexibility• A la carte channel selection• Lower cost of deployment,• A counter to cable’s voice entry

What are some of the major issues:• Product differentiation• Unclear business models• Content Acquisition• Inadequate bandwidth• Lack of open or mature standards• Piracy• Unpredictable Capital Costs• Inexperience in TV industry• Poor track record rolling out DSL

IPTV is an IP-based delivery mechanism for packet-based video

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

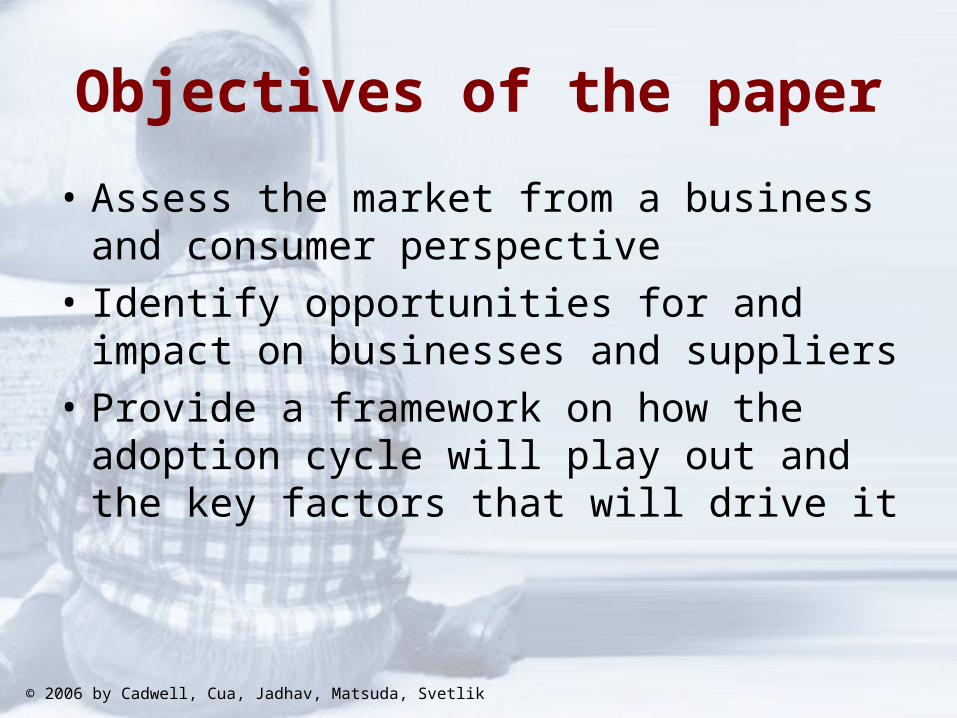

Objectives of the paper

• Assess the market from a business and consumer perspective

• Identify opportunities for and impact on businesses and suppliers

• Provide a framework on how the adoption cycle will play out and the key factors that will drive it

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Global SnapshotAsia• Hong Kong leading• Taiwan, Japan moderate success• Korea stuck in regulation• China, Singapore, India, other in trial

Europe• Italy leading• France, Spain, Nordic areas moderate success• UK, Germany, Ireland in trial

US• SBC/AT&T/Bell South – “Project Lightspeed”• Verizon’s FiOS

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

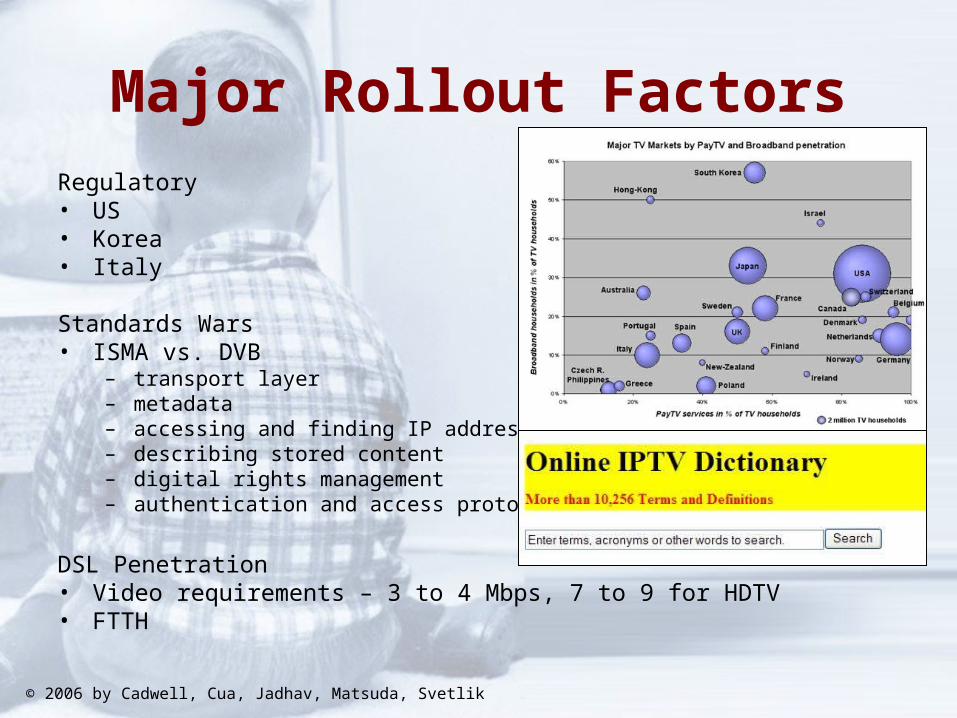

Major Rollout FactorsRegulatory• US• Korea• Italy

Standards Wars• ISMA vs. DVB

– transport layer– metadata– accessing and finding IP addresses– describing stored content– digital rights management– authentication and access protocols

DSL Penetration• Video requirements – 3 to 4 Mbps, 7 to 9 for HDTV• FTTH

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Microsoft Labs demonstration

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

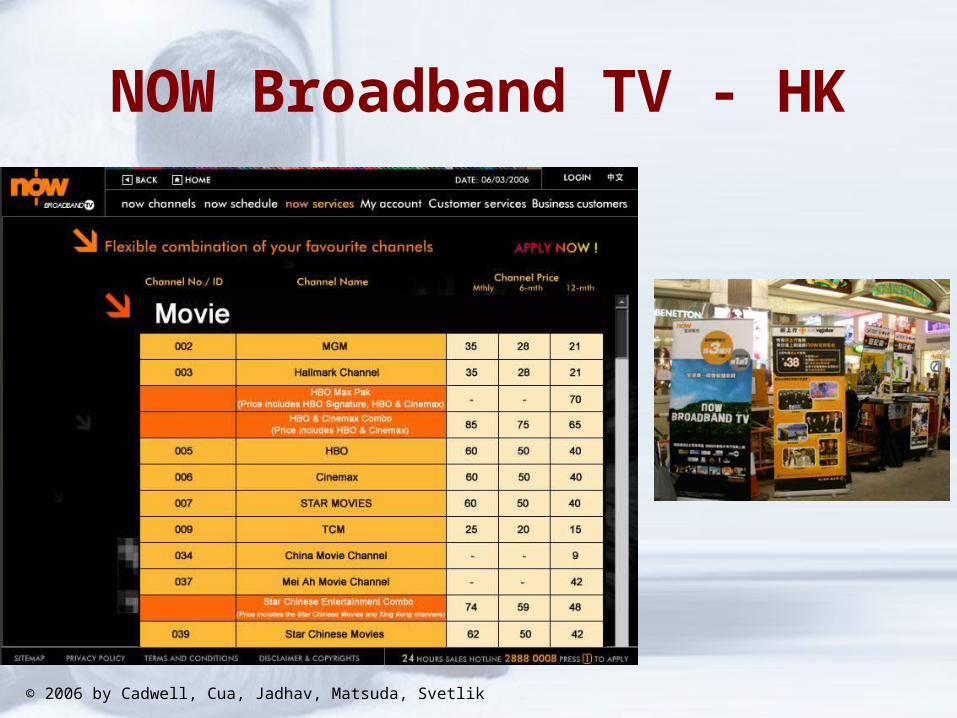

NOW Broadband TV - HK

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Verizon infrastructure buildup

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Consumer habits trends

• Watching content online through the PC is a different consumer experience– “sit up” vs “sit back” experience

• Growing desire for control– DVRs, PVRs, VoD

• Concurrent usage of different media channels– 96% of consumers use two or more media channels

simultaneously for 30% of a day– Watching TV and using the Internet is the number one

combination

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

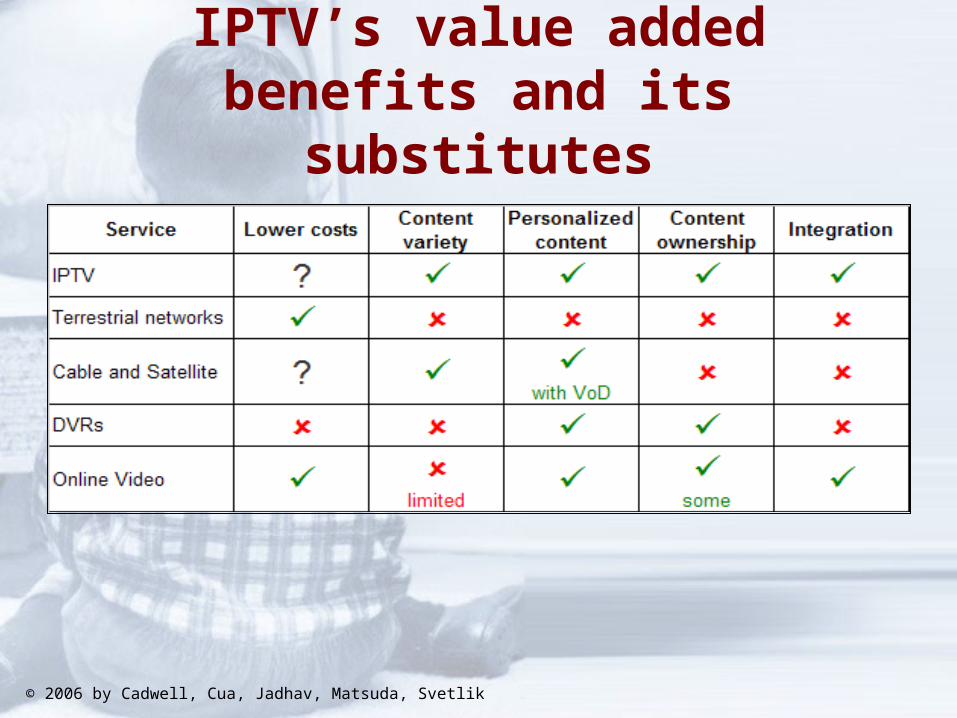

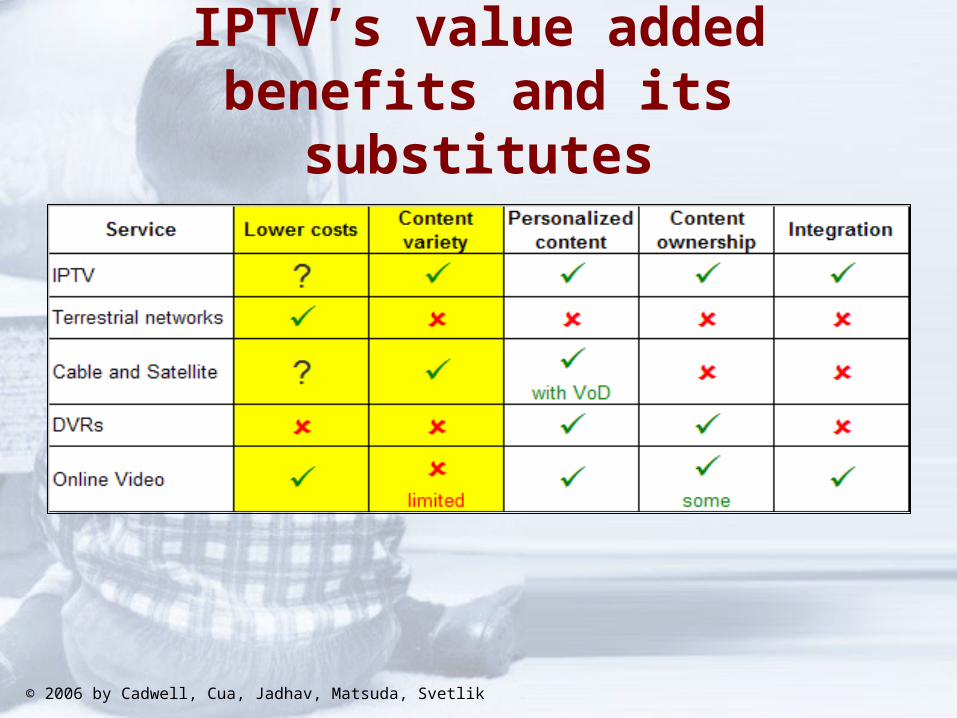

IPTV’s value added benefits and its substitutes

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

IPTV’s value added benefits and its substitutes

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

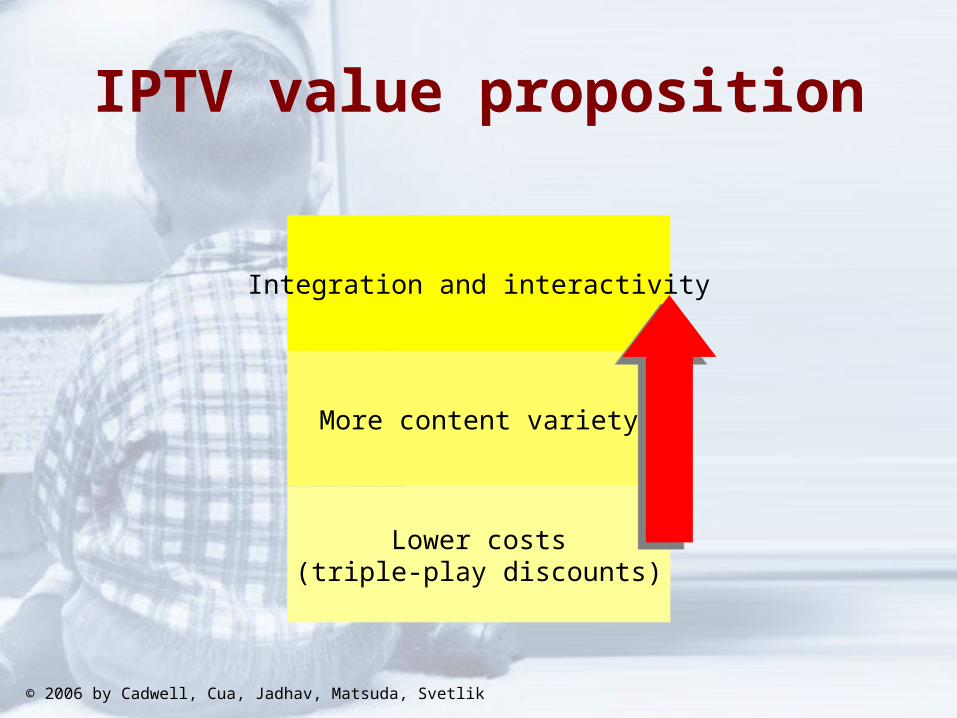

IPTV value proposition

Lower costs(triple-play discounts)

More content variety

Integration and interactivity

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

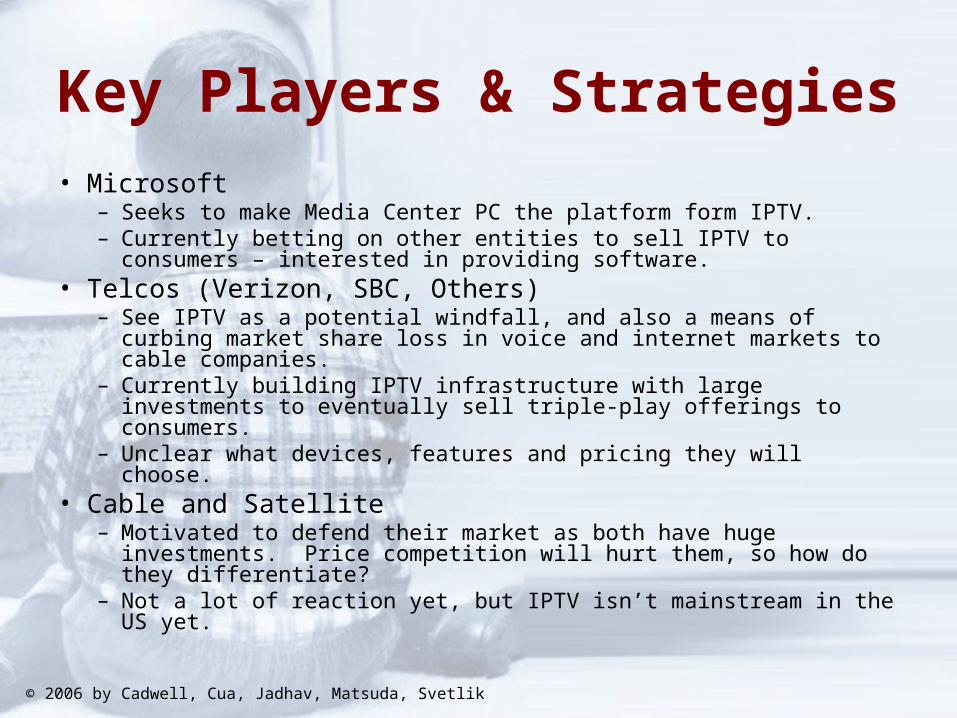

Key Players & Strategies

• Microsoft– Seeks to make Media Center PC the platform form IPTV.– Currently betting on other entities to sell IPTV to consumers –

interested in providing software.• Telcos (Verizon, SBC, Others)

– See IPTV as a potential windfall, and also a means of curbing market share loss in voice and internet markets to cable companies.

– Currently building IPTV infrastructure with large investments to eventually sell triple-play offerings to consumers.

– Unclear what devices, features and pricing they will choose.• Cable and Satellite

– Motivated to defend their market as both have huge investments. Price competition will hurt them, so how do they differentiate?

– Not a lot of reaction yet, but IPTV isn’t mainstream in the US yet.

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

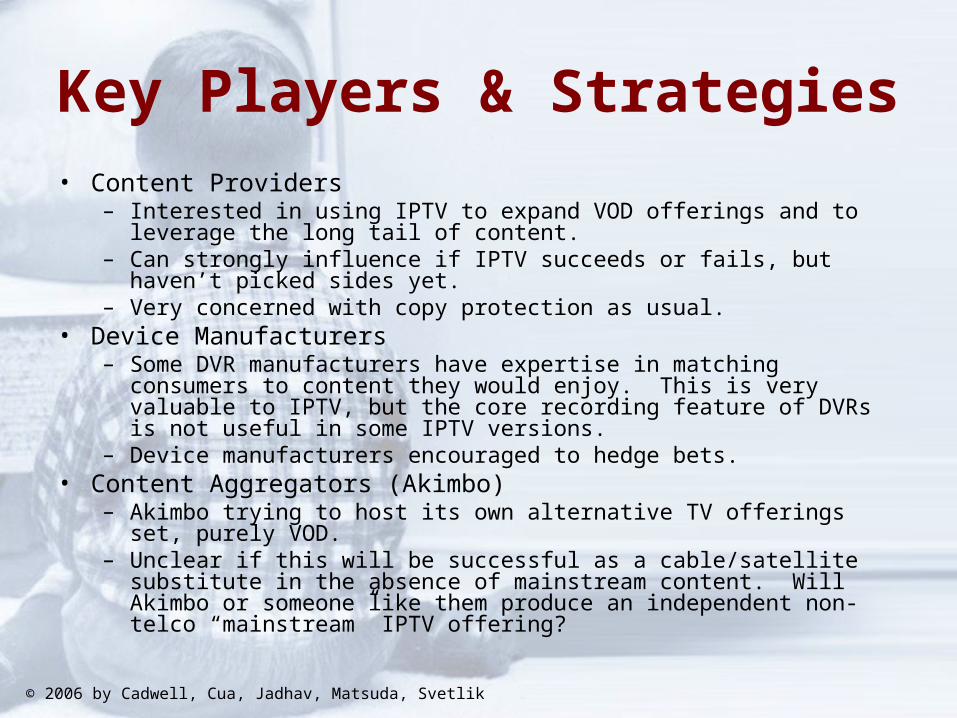

Key Players & Strategies• Content Providers

– Interested in using IPTV to expand VOD offerings and to leverage the long tail of content.

– Can strongly influence if IPTV succeeds or fails, but haven’t picked sides yet.

– Very concerned with copy protection as usual.• Device Manufacturers

– Some DVR manufacturers have expertise in matching consumers to content they would enjoy. This is very valuable to IPTV, but the core recording feature of DVRs is not useful in some IPTV versions.

– Device manufacturers encouraged to hedge bets.• Content Aggregators (Akimbo)

– Akimbo trying to host its own alternative TV offerings set, purely VOD. – Unclear if this will be successful as a cable/satellite substitute in the

absence of mainstream content. Will Akimbo or someone like them produce an independent non-telco “mainstream” IPTV offering?

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Impact on Businesses

• Content Providers– Increase in bargaining power – can influence

who wins.– May benefit from long-tail effects.– May benefit from content innovations.– Will seek direct relationship with consumer,

but unclear if this will occur.– Concerned with copy protection.

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Impact on Businesses

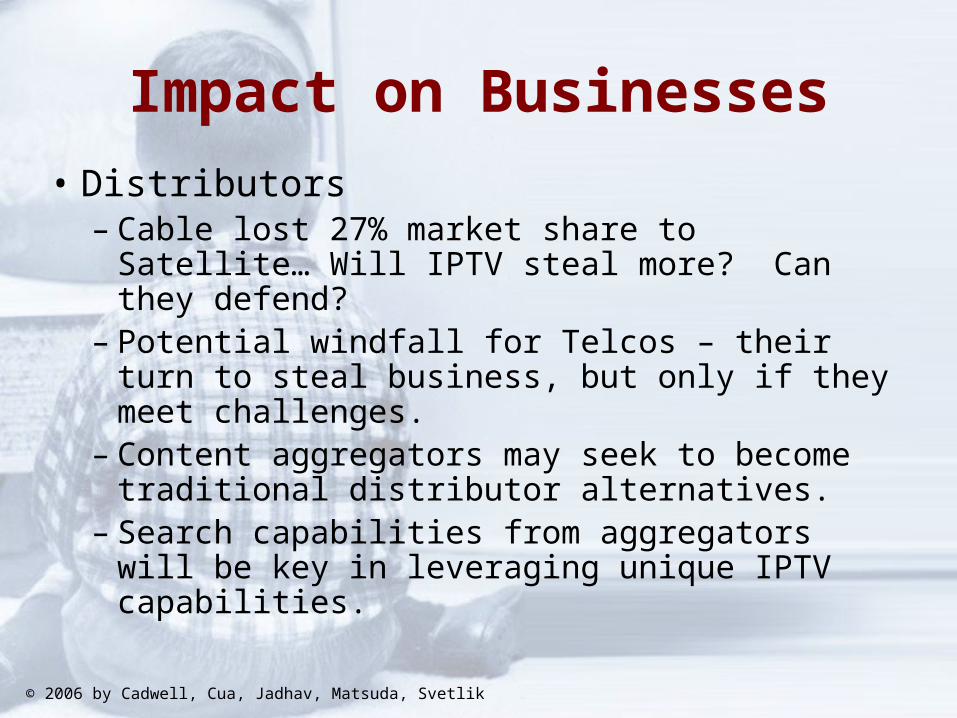

• Distributors– Cable lost 27% market share to Satellite…

Will IPTV steal more? Can they defend?– Potential windfall for Telcos – their turn to

steal business, but only if they meet challenges.

– Content aggregators may seek to become traditional distributor alternatives.

– Search capabilities from aggregators will be key in leveraging unique IPTV capabilities.

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Impact on Businesses

• Device Manufacturers– Probably will not affect TV manufacturers too

much. If Media Center PC takes hold, some opportunities for bundling extenders.

– Set-top box or Media Center PC? Will media center PCs become standard?

– Will DVRs evolve, be replaced, or continue to be used as they are currently?

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Adoption Patterns and value creationPast trends

Migration of intelligence in value network

Co

nsu

mer

ad

op

tio

n

life

cyc

leIn

no

vat

ion

dif

fus

ion

b

y s

up

pli

ers

IPTV Adoption – Analytical Frameworks

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

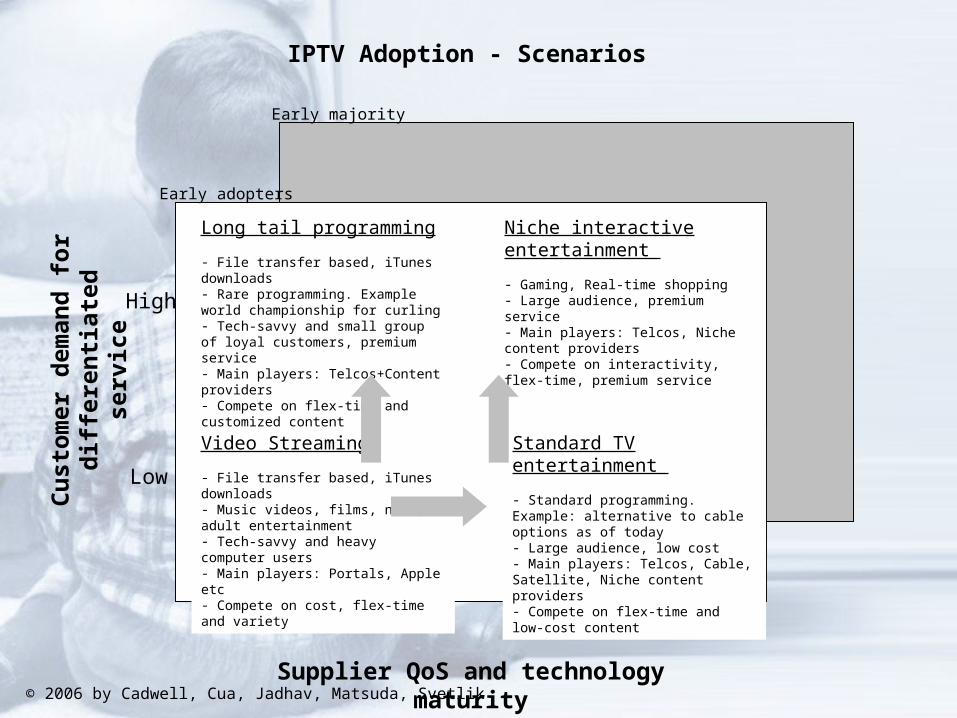

IPTV Adoption - ScenariosC

ust

om

er d

eman

d f

or

dif

fere

nti

ated

ser

vice

Supplier QoS and technology maturity

Low High

High

Low

Video Streaming

- File transfer based, iTunes downloads - Music videos, films, news, adult entertainment- Tech-savvy and heavy computer users- Main players: Portals, Apple etc- Compete on cost, flex-time and variety

Long tail programming

- File transfer based, iTunes downloads - Rare programming. Example world championship for curling- Tech-savvy and small group of loyal customers, premium service- Main players: Telcos+Content providers- Compete on flex-time and customized content

Standard TV entertainment

- Standard programming. Example: alternative to cable options as of today- Large audience, low cost- Main players: Telcos, Cable, Satellite, Niche content providers- Compete on flex-time and low-cost content

Niche interactive entertainment

- Gaming, Real-time shopping - Large audience, premium service- Main players: Telcos, Niche content providers- Compete on interactivity, flex-time, premium service

Early adopters

Early majority

© 2006 by Cadwell, Cua, Jadhav, Matsuda, Svetlik

Next Steps

• Microsoft (Mountain View office)• AT&T/SBC - San Ramon office, focus: IP solutions• Current TV • TiVo – Alviso, CA• Akimbo – San Mateo• ISMA – SF, standards group• Yahoo!• Google• Cisco Systems • Kasenna • OpenTV – SF• Redback Networks – San Jose