Embed Size (px)

Citation preview

© 2010 AirAdvice, Inc.

Walk a Mile in a Building Owner’s Shoes

© 2010 AirAdvice, Inc.

“Seek first to understand, then to be understood”Stephen Covey

The Seven Habits of Highly Effective People

© 2010 AirAdvice, Inc.

Agenda

• Energy demographics and commercial building markets• Ownership structures and motivations• How to make (or not make) money in commercial real estate

– Property valuation– Economic drivers

• Lease types and the behaviors they drive• Events that create action• Strategies for success

4© 2010 AirAdvice, Inc.

98% 58%

Energy Demographics

0

500

1,000

1,500

2,000

2,500

3,000

Lessthan 5k

5k to10k

10k to25k

25k to50k

50k to100k

100k to200k

200k to500k

Over500k

Building Size (sq. ft.)

No

. o

f B

ldg

s (t

ho

usa

nd

s)

0%

20%

40%

60%

80%

100%

Cu

mu

lati

ve E

ner

gy

Use

(%

of

To

tal)

Cumulative Energy Use No. of Bldgs

Source: Commercial Buildings Energy Consumption Survey (CBECS)

© 2010 AirAdvice, Inc.

Commercial Buildings Markets

0100200300400500600700800900

Office

Servic

e

War

ehou

se

Resta

uran

ts

Retail

Schoo

ls

Religi

ous W

orsh

ip

Public

Mall

s

Hotels

Med

ical O

ffice

Other

Hospi

tals

Nu

mb

er

of

Bu

ild

ing

s (

k)

0

50

100

150

200

250

300

Av

era

ge

Siz

e (

k s

f)

Number of Buildings Average Size

Source: Commercial Buildings Energy Consumption Survey (CBECS)

© 2010 AirAdvice, Inc.

% of Total Floorspace

Warehouse15%

Restaurants4%

Retail6%Schools

14%

Religious Worship

5%

Public7%

Service6%

Office18%

Malls10%

Hotels7%

Other3% Hospitals

3%

Medical Office2%

Source: Commercial Buildings Energy Consumption Survey (CBECS)

© 2010 AirAdvice, Inc.

Ownership Structures

1. Owner occupied• Employees of company owning the building

occupy the space• Examples:

– Corporate campuses, education, public

• Company views property as an asset– May benefit from capital appreciation, but not

primary motivation– Typically longer term view

• Primary motivation– Profitability of business– Reduce costs associated with facilities

© 2010 AirAdvice, Inc.

Ownership Structures

2. Investor Owned• Building owner leases space to other

companies, who occupy the space• Company views property as a “box of

leases”– Return on investment is primary motivation– May have very short term investment horizon

• Examples:– Office buildings, warehouses, retail

© 2010 AirAdvice, Inc.

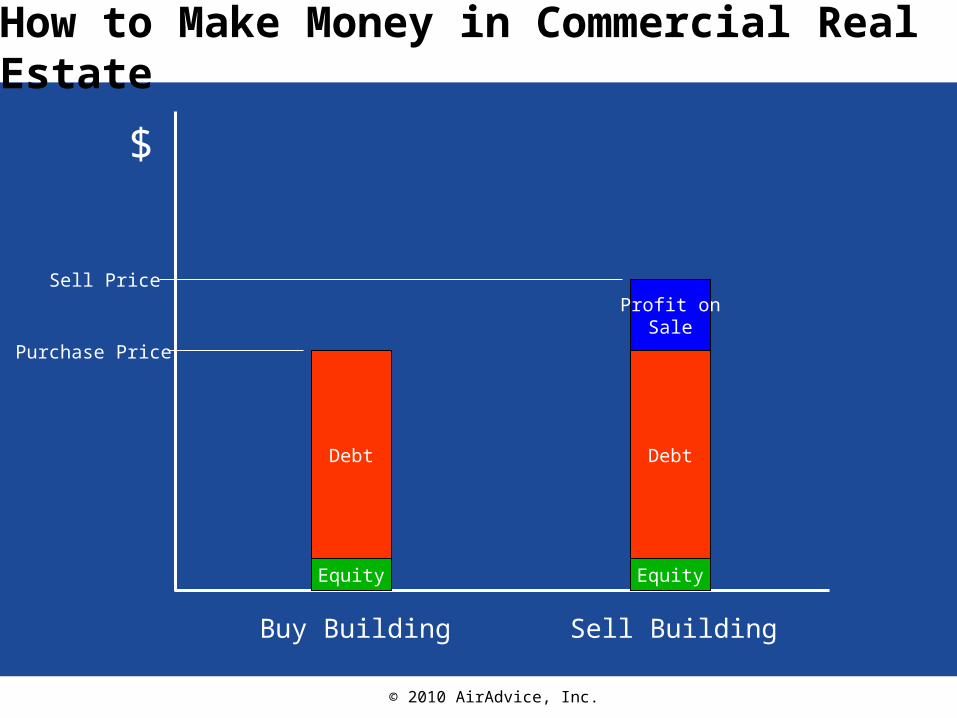

How to Make Money in Commercial Real Estate

Equity

Debt

$

Buy Building

Purchase Price

Sell Building

Equity

Debt

Sell PriceProfit on

Sale

© 2010 AirAdvice, Inc.

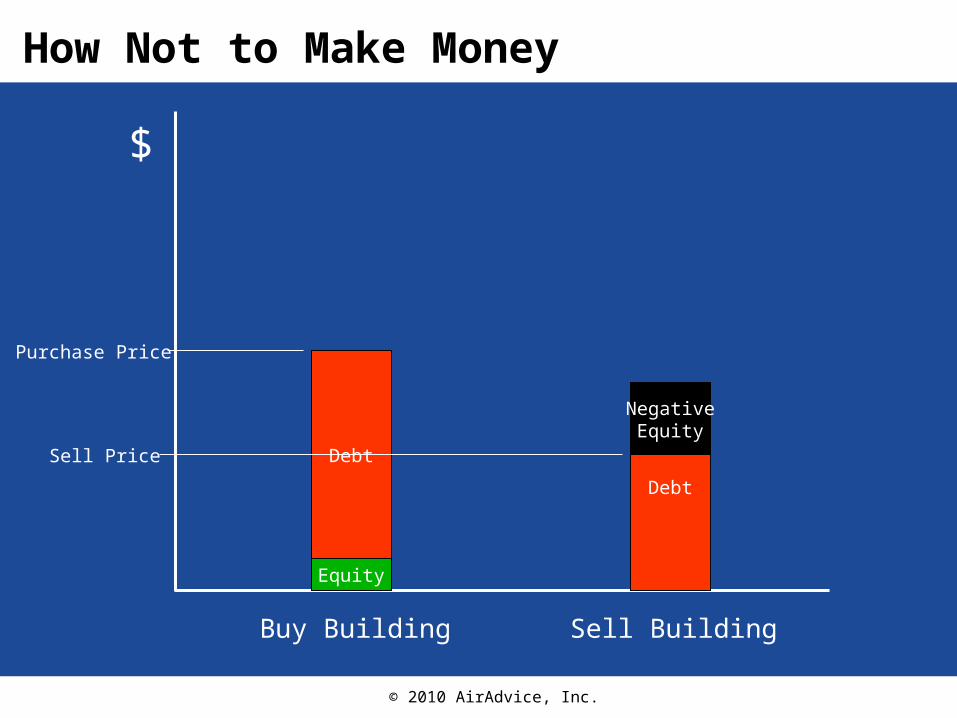

How Not to Make Money

Equity

Debt

$

Buy Building

Purchase Price

Sell Building

Equity

Debt

Sell Price

NegativeEquity

© 2010 AirAdvice, Inc.

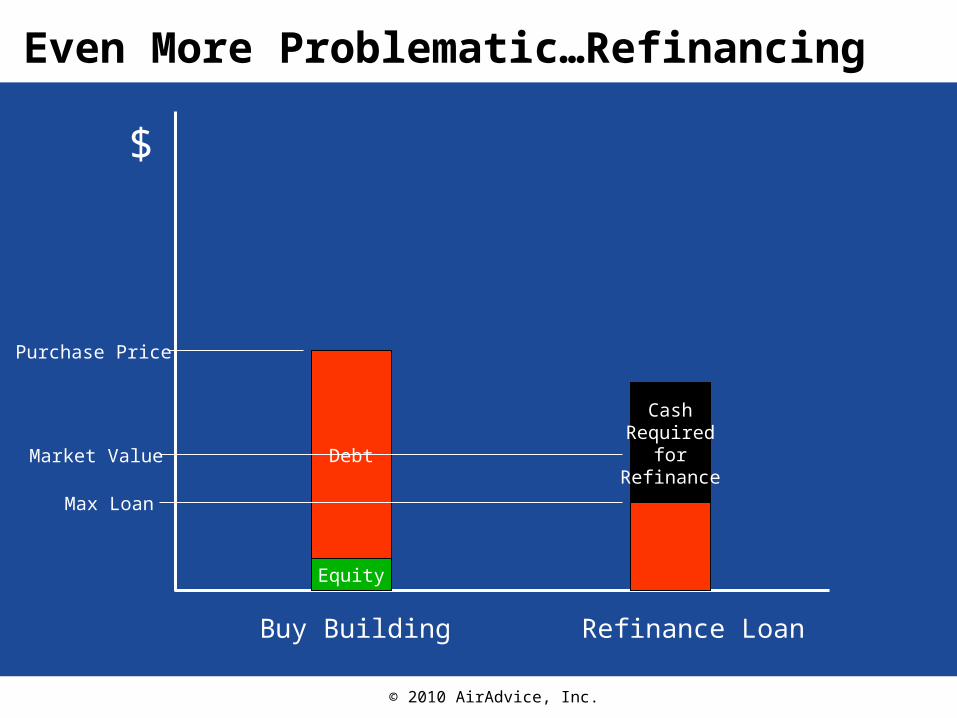

Even More Problematic…Refinancing

$

Equity

Debt

Buy Building

Purchase Price

Refinance Loan

Equity

Debt

Market Value

CashRequired

forRefinance

Max Loan

© 2010 AirAdvice, Inc.

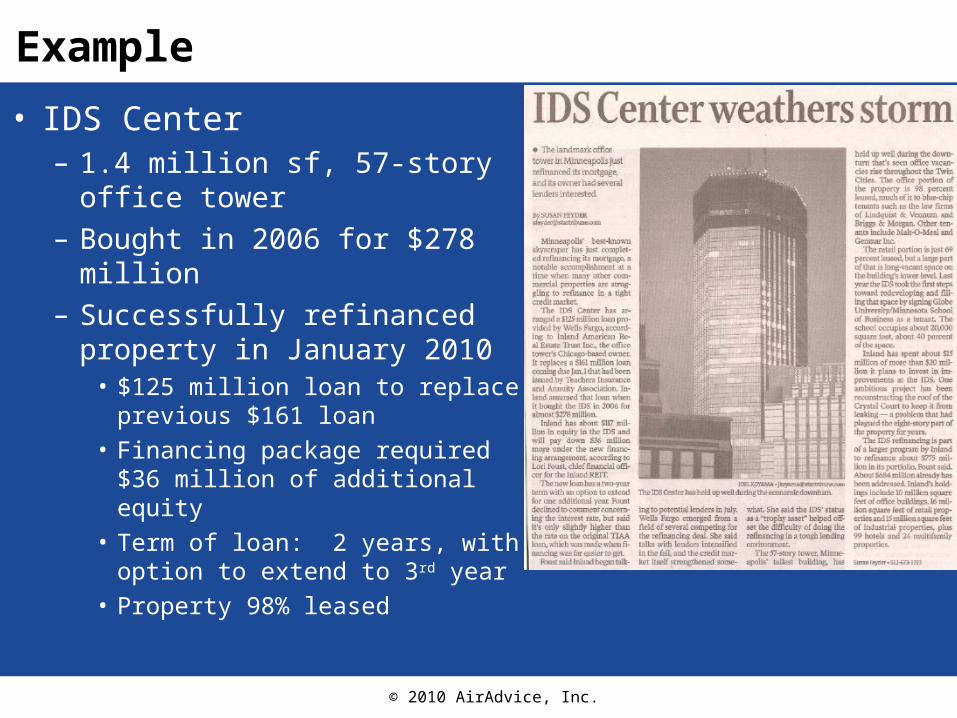

Example

• IDS Center– 1.4 million sf, 57-story office

tower– Bought in 2006 for $278

million– Successfully refinanced

property in January 2010• $125 million loan to replace

previous $161 loan• Financing package required $36

million of additional equity• Term of loan: 2 years, with

option to extend to 3rd year• Property 98% leased

© 2010 AirAdvice, Inc.

Distressed Commercial Properties

• Between 2010 and 2014, $770 billion in commercial loans will be on properties in a negative equity position

Source: Foresight Analytics

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014

% o

f L

oa

ns

Ma

turi

ng

in

N

eg

ati

ve

Eq

uit

y P

os

itio

n

0

0

0

1

1

1

1

© 2010 AirAdvice, Inc.

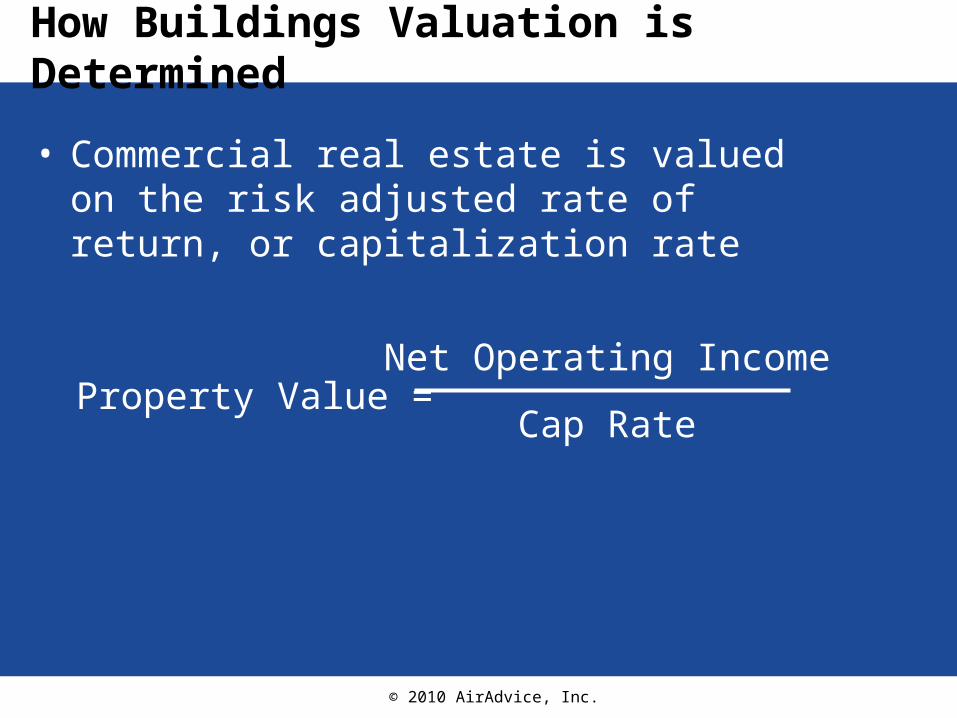

How Buildings Valuation is Determined

• Commercial real estate is valued on the risk adjusted rate of return, or capitalization rate

Property Value = Net Operating Income

Cap Rate

© 2010 AirAdvice, Inc.

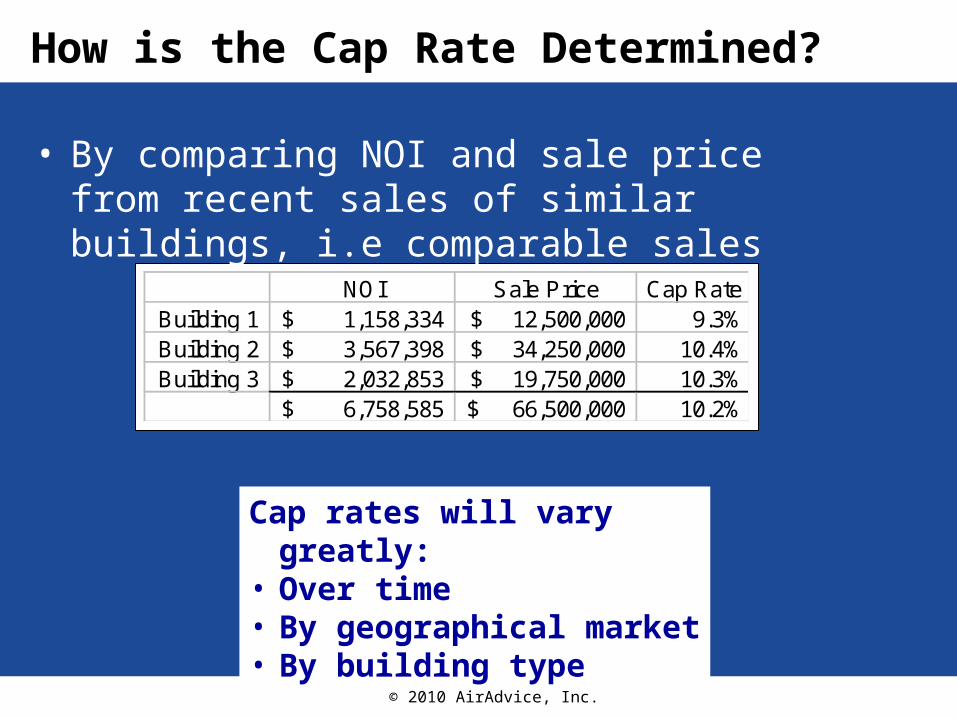

How is the Cap Rate Determined?

• By comparing NOI and sale price from recent sales of similar buildings, i.e comparable sales

NOI Sale Price Cap RateBuilding 1 1,158,334$ 12,500,000$ 9.3%Building 2 3,567,398$ 34,250,000$ 10.4%Building 3 2,032,853$ 19,750,000$ 10.3%

6,758,585$ 66,500,000$ 10.2%

Cap rates will vary greatly:• Over time• By geographical market• By building type

© 2010 AirAdvice, Inc.

Net Operating Income

Net Operating Income = Revenue – Operating Expenses

• Revenue Lease payments Other fees

• Operating Expenses Management / leasing fees Insurance Janitorial Taxes Utilities

© 2010 AirAdvice, Inc.

Where We’re Headed…• “Energy use is the single

largest operating expense in commercial office buildings, representing approximately one-third of typical operating budgets”

© 2010 AirAdvice, Inc.

Energy Savings Drive Higher Asset Value

Building A Building BGross operating income:

Rents 7,038,822$ 7,038,822$ Fees 129,584$ 129,584$

7,168,406$ 7,168,406$ Operating expenses:

Management fees 703,882 703,882$ Insurance 633,494 633,494$ Janitorial 985,435 985,435$

Taxes 1,055,823 1,055,823$ Utilities 1,407,764 1,126,212$

4,786,399 4,504,846

Net Operating Income 2,382,007$ 2,663,560$

Cap Rate 8% 8%

Asset Value 29,775,088$ 33,294,499$

20% lower utilities

$3.4 million higher asset value

© 2010 AirAdvice, Inc.

Turn Price Pressure into Gain

$-

$5,000

$10,000

$15,000

$20,000

Sa

vin

gs

Example:• 100,000 sf

building• $2 per sf in

energy costs• $10,000 cost

of PM agreement

Scenario 210% Reduction Energy Costs

50% Increase in PM Price

Scenario 110% Reduction

in PM Price

© 2010 AirAdvice, Inc.

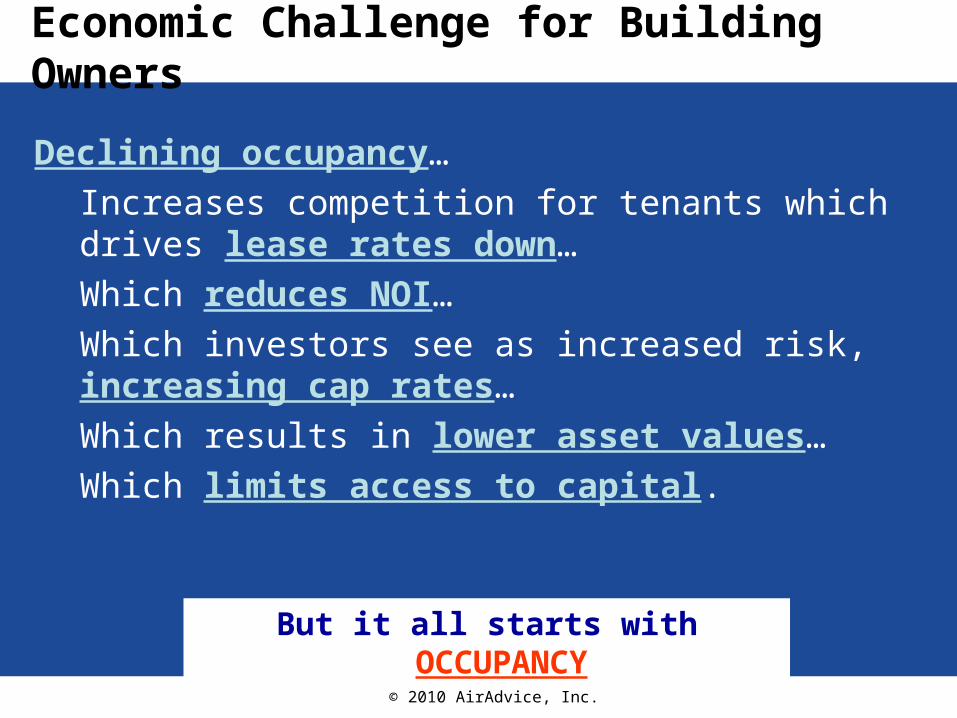

Economic Challenge for Building Owners

Declining occupancy…

Increases competition for tenants which drives lease rates down…

Which reduces NOI…

Which investors see as increased risk, increasing cap rates…

Which results in lower asset values…

Which limits access to capital.

But it all starts with OCCUPANCY

© 2010 AirAdvice, Inc.

Common Lease Types

Lease Type Description Impact of Operating Expenses on NOI

Gross or full service

• Landlord pays all capital and operating expenses

• Lower operating expenses result in higher NOI

Net • Landlord pays capital expenses

• Tenant pays operating expenses

• No direct impact on NOI

Full service w/ base year expenses

• Landlord pays capital expenses and operating expenses up to “base year” amount

• Tenant pays operating expenses above base year amount

• If operating expenses near base year, lower operating expenses can result in higher NOI

© 2010 AirAdvice, Inc.

Behaviors Determined by Lease Type

Gross Lease

Year 1 Year 2

$2.00 persf $1.50 per

sf

$0.50 toLandlord

Net Lease

Year 1 Year 2

$2.00 persf $1.50 per

sf

$0.50 toTenant

Gross Lease w/ Base Year

Year 1 Year 2

$2.00 persf $1.50 per

sf

$1.90Base Year

$0.10 toTenant $0.40 to

Landlord

Landlord generally

motivated to reduce operating

expenses

Landlord may not be motivated

to reduce operating expenses

Motivation depends on

relationship of current

expenses to base year

© 2010 AirAdvice, Inc.

Must Understand Who Pays and Who Benefits

Owner Occupied

Space

Leased Space

Net Lease Gross Lease

Owner Tenant Owner Tenant

Who Pays:

Operating Expenses

Capital Expenses

X

X X

X X

X

Who Directly Benefits: X X X

Benefits Accrue to Owner

Benefits Accrue to Owner

Benefits Accrue to Tenant

© 2010 AirAdvice, Inc.

Pass Throughs

• A common lease clause, even in net leases, allows the building owner to recover capital costs from the tenants for improvements that reduce operating expenses

© 2010 AirAdvice, Inc.

Events that Drive Action

© 2010 AirAdvice, Inc.

Lease Renewal

• Buyer’s market• Building owners are willing to invest for the

benefit of tenant as a retention tool

© 2010 AirAdvice, Inc.

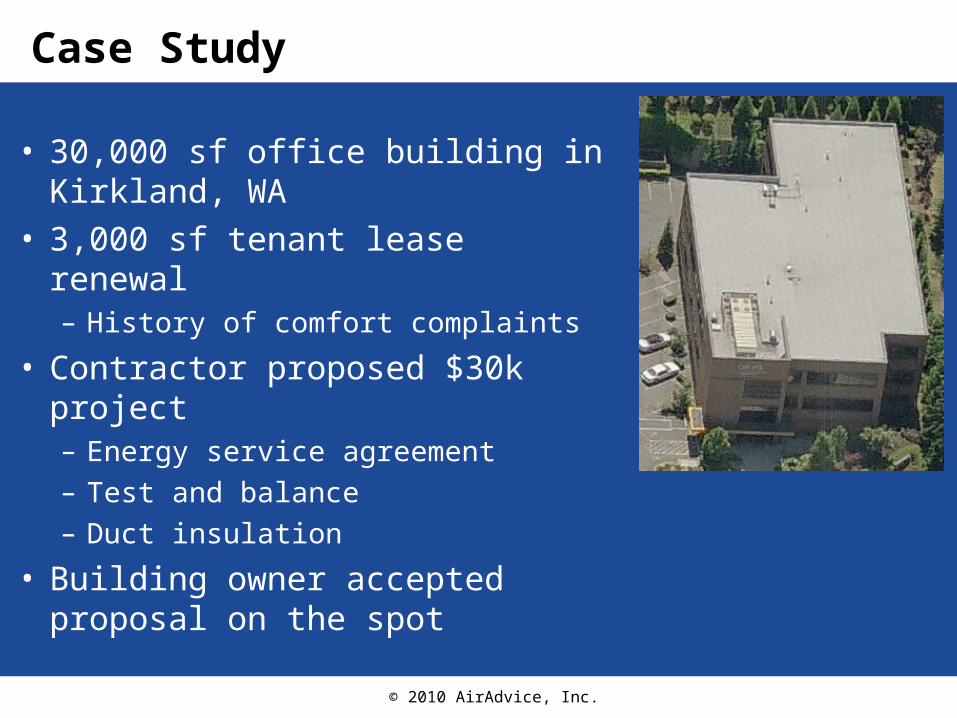

Case Study

• 30,000 sf office building in Kirkland, WA

• 3,000 sf tenant lease renewal– History of comfort complaints

• Contractor proposed $30k project– Energy service agreement– Test and balance– Duct insulation

• Building owner accepted proposal on the spot

© 2010 AirAdvice, Inc.

Case Study

• What’s at risk?– 3,000 sf x $30 per sf = $90,000 per

year in rent– 7 year lease = $630,000 of

guaranteed revenue

• If tenant leaves?– Minimum 6 to 9 months of lost rent =

$45,000 to $67,500

Building owner’s perspective:$30,000 to solve problem doesn’t seem so bad

© 2010 AirAdvice, Inc.

Sale or Refinance of Building

• Building finances will be heavily scrutinized– Revenues– Operating expenses– Cash flow– Condition of systems

• 1-2 years leading up to event is prime time for action

© 2010 AirAdvice, Inc.

Property Condition Assessment (PCA)

• Evaluation of major systems in building– Roof, parking lots, mechanical

• Lenders may require cash escrow for items found deficient– Immediate lump-sum reserve– Ongoing monthly reserves above NOI line

• Replacement of major systems prior to refinancing can be cash flow positive

© 2010 AirAdvice, Inc.

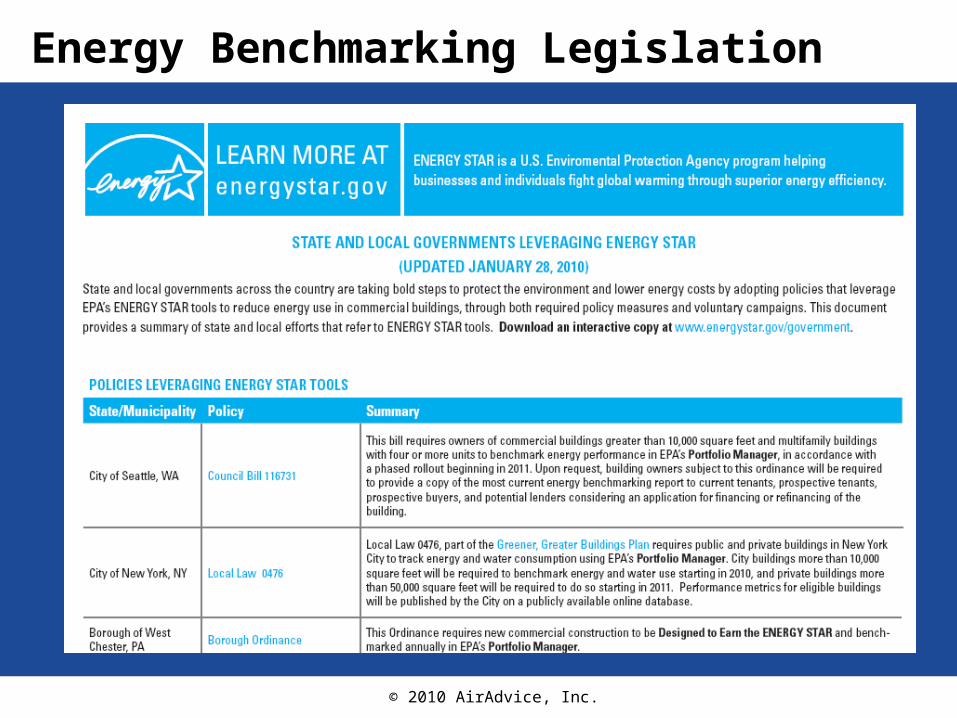

Energy Benchmarking Legislation

• Legislation requires benchmarking:– Sale of building– Refinancing of building– Lease of building to single

tenant

• Most notable legislation passed in:– State of California– State of Washington– New York City– Washington, DC

© 2010 AirAdvice, Inc.

Energy Benchmarking Legislation

© 2010 AirAdvice, Inc.

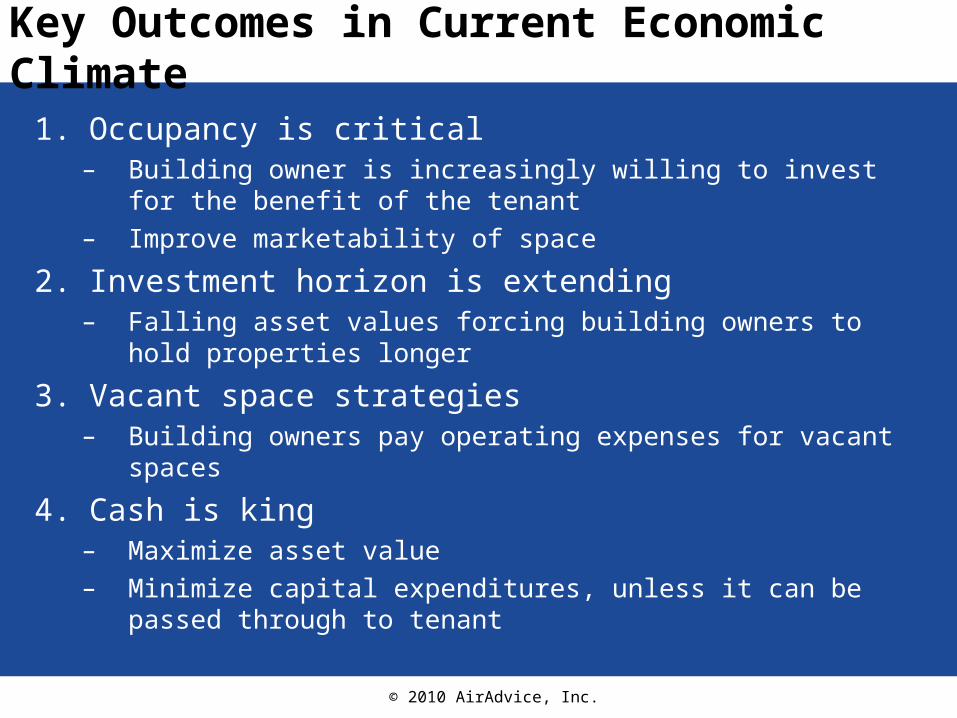

Key Outcomes in Current Economic Climate

1. Occupancy is critical– Building owner is increasingly willing to invest for the benefit of the

tenant– Improve marketability of space

2. Investment horizon is extending– Falling asset values forcing building owners to hold properties

longer

3. Vacant space strategies– Building owners pay operating expenses for vacant spaces

4. Cash is king– Maximize asset value– Minimize capital expenditures, unless it can be passed through to

tenant

© 2010 AirAdvice, Inc.

Strategies for Success

© 2010 AirAdvice, Inc.

Strategies for Success

1. Sell to the right level– Financial decision makers,

not building operator

• When meeting:– Above ground is good– Below ground is bad

Bad Good

© 2010 AirAdvice, Inc.

Tips for Selling to the Right Level

• Ask financially based questions• If your contact doesn’t know the answer, ask

them to who would– Gain a warm introduction to financial decision

maker

© 2010 AirAdvice, Inc.

Target the Correct Decision Making Level

% of Time Goal

Position What Motivates Them Why Talk to Them

10% 20%CFO / COO / Controller

• Overall operating cost and corporate objectives

• Needed to approve decision• Can direct activities

20% 30% VP Finance, VP Operations, VP Facilities

• Reducing operating costs (management pressure)

• Decision maker for service (but not final say on capital expenditures)

60% 45%

Facilities or Plant Manager / Director

or Property Manager

• Happy tenants• Looking good to their

owners

• Can influence decisions• Partner with them to go

upstairs• In the loop w/ current service

provider

10% 5%Building Engineer/Operator

• Minimizing downtime• Reduced complaints

• Close to mechanical equipment

• Need to win them over• May have veto power

© 2010 AirAdvice, Inc.

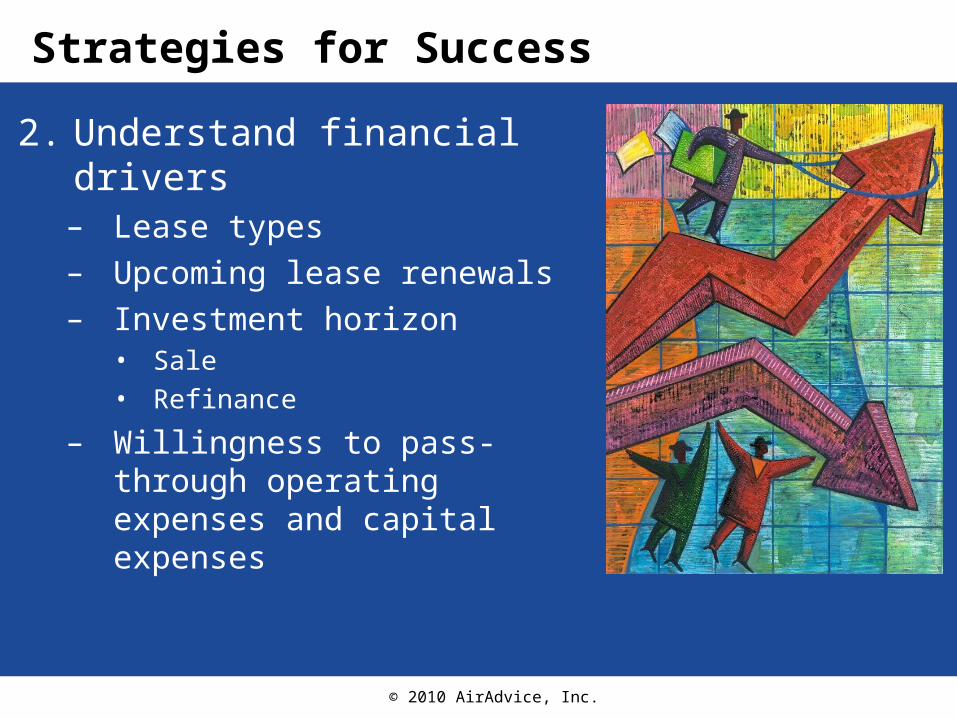

Strategies for Success

2. Understand financial drivers– Lease types– Upcoming lease renewals– Investment horizon

• Sale• Refinance

– Willingness to pass-through operating expenses and capital expenses

© 2010 AirAdvice, Inc.

Strategies for Success

3. Change the buying criteria– Offer something different

© 2010 AirAdvice, Inc.

Change the Buying Criteria

• Current – Price of maintenance agreement or project

• New:– Impact to NOI– Impact to asset value– Impact to broader portfolio financial metrics

© 2010 AirAdvice, Inc.

Strategies for Success

4. Key off action-driving events– Lease renewal– Sale / refinance of building– Energy benchmarking

legislation

© 2010 AirAdvice, Inc.

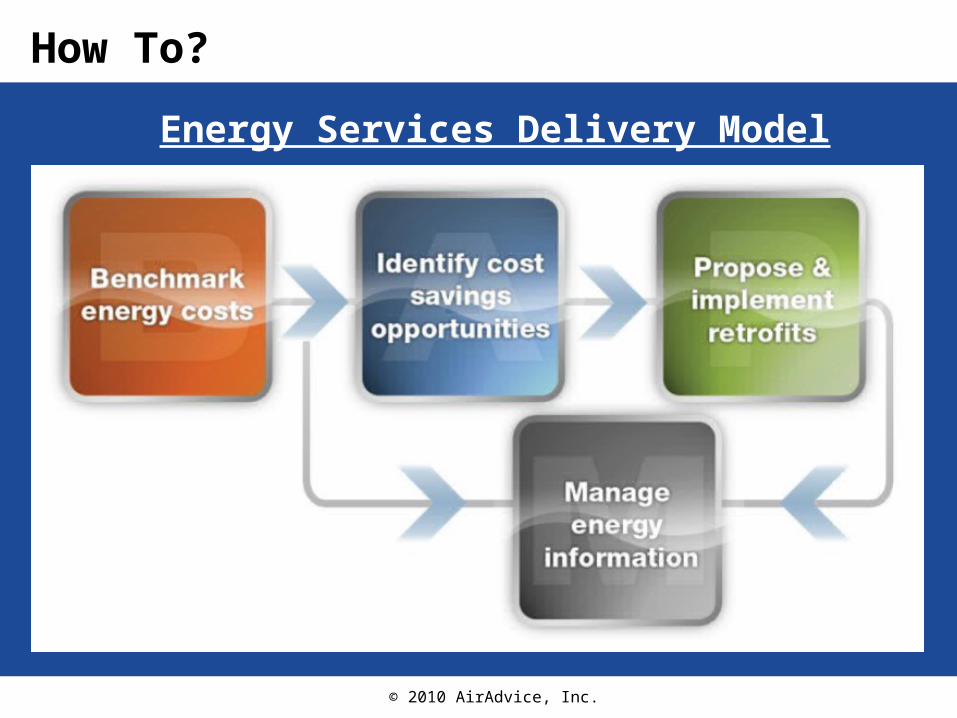

How To?

Energy Services Delivery Model

© 2010 AirAdvice, Inc.

Walk a Mile in a Building Owner’s Shoes• Owner-occupied & investor owned

properties are motivated differently• #1 priority: Occupancy

• Different lease types drive different behaviors– Understand who pays and who

benefits• Events that create action

– Lease renewal– Sale or refinance of building– Energy benchmarking

• Strategies for success1. Target the right level2. Understand financial drivers3. Change the buying criteria4. Key off action-driving events

© 2010 AirAdvice, Inc.

Questions

? ? ?

?

?

?? ?

![Walk a mile in His/Her shoes€¦ · Walk a mile in His/Her shoes [PICK ONE] a collection of short fictional stories Written by: Madyson Smith Senior Communication Honors Major Texas](https://img.pdfslide.net/doc/110x75/5fdc34dd13f54c41bb4d9d99/walk-a-mile-in-hisher-shoes-walk-a-mile-in-hisher-shoes-pick-one-a-collection.jpg)