Embed Size (px)

Citation preview

© 2011 Financial Operations Networks LLC

Reducing Financial Risk for Your Organization Regarding Issuing U.S.

Source Income Payments, Payee Documentation, Withholding and

Information ReportingJohn Foertschbeck, CPALynda FoertschbeckIRSCompliance, Inc.

Wednesday, April 13, 2011

www.TheAPNetwork.com Page 2

THE ACCOUNTS PAYABLE

Leadership ConferenceKey Topics• Information reporting and withholding compliance must be a

priority throughout your organization

• Why your company should be concerned

• Potential risks for non-compliance

• Activity that can lead to audits

• Cost of non-compliance

• Third-party providers― Can you outsource your liability?― How reliable is the provider?― Contractual Issues

• Minimizing risk

www.TheAPNetwork.com Page 3

THE ACCOUNTS PAYABLE

Leadership ConferenceWhy is Information Reportinga Potential Risk?• The Federal Government has estimated that the annual tax gap is

$345 billion attributed primarily to non-reporting of income by the payers and/or the payees

• Logical choice — either raise taxes or collect the taxes currently owed

• IRS enforcement is greater than ever — 4,000+ new auditors

• New and modified legislation

• As states search for new revenue sources they are enforcing laws for information reporting, withholding and penalties.— Backup withholding— NRA withholding— Cross-state issues

• Primary targets for the IRS and states are service providers and non-resident aliens

www.TheAPNetwork.com Page 4

THE ACCOUNTS PAYABLE

Leadership Conference

• The responsibility to file information returns rests with the payer

• In the extreme, responsibility for the liability can rest with the “Responsible Person” (executives) IRC 6672― Company officers can be held personally financially responsible

• Third-party administrators― Look at your contract― Ultimate responsibility for reporting and withholding― Who has fiduciary responsibility?

• FINCEN disclosure― Must publically disclose known risks for withholding liabilities, penalties

and interest

Why is Information Reportinga Potential Risk? (Cont’d.)

www.TheAPNetwork.com Page 5

THE ACCOUNTS PAYABLE

Leadership ConferenceCould My Company Be Audited?• Senior IRS officials have instructed all large and mid-size

audit teams to include a review of information reporting and withholding

• All companies are impacted

• Focus on related-party payments

• Full information reporting audits including:― Policies and procedures― Reporting and withholding systems― Payee documentation and practices― Reporting and withholding history

• Once your company has been notified of a planned audit, it is too late to correct failures where possible

• Take action prior to audit to identify and correct failures

www.TheAPNetwork.com Page 6

THE ACCOUNTS PAYABLE

Leadership ConferenceOther Reporting Activity That Could Lead to Audits• Internal IRS programs are used to provide employment tax

audit leads

• Examples:― Failure to implement backup withholding, “B” Notice program, no TIN or

invalid payee TIN and name documentation― Failure to identify non-resident aliens and withhold/deposit proper

NRA withholding― Payers with repeat payees receiving Forms 1099 with missing or

false TINs― Repeat payment of penalties for incorrect, missing or false TINs― Review of Forms 1099-MISC issued to payee where the proceeds are

the payees main source of income― Lack of withholding on payments issued to both U.S. (28%) and NRA

(30%) where the payee TIN not provided or absence of treaty and/or the correct tax rates for treaty withholding rates

www.TheAPNetwork.com Page 7

THE ACCOUNTS PAYABLE

Leadership ConferenceCost of Non-Compliance

• Penalties:―Late filing, missing or false TIN, $100 per document

• Penalty capped at $500K for small corp., $1.5M for large corp.• Example: 7,000 docs with missing TINS, penalty proposal would be

assessed on 5,000 documents for small corp., all 7,000 for large corp. (large corp. cap would be 15,000 documents)

―If intentional disregard penalty is proposed:• $250 per document with no cap

• Liabilities for the amount of withholding NOT deposited

www.TheAPNetwork.com Page 8

THE ACCOUNTS PAYABLE

Leadership Conference

• Failure to implement backup withholding

• Payer is responsible for the amount due to be withheld which then could lead to―Failure to deposit penalties―Failure to pay penalties―Accuracy penalty―Failure to file penalties―Plus interest

• IRC 6672(a) could apply—Can be considered a criminal offense

Cost ofNon-Compliance (Cont’d.)

www.TheAPNetwork.com Page 9

THE ACCOUNTS PAYABLE

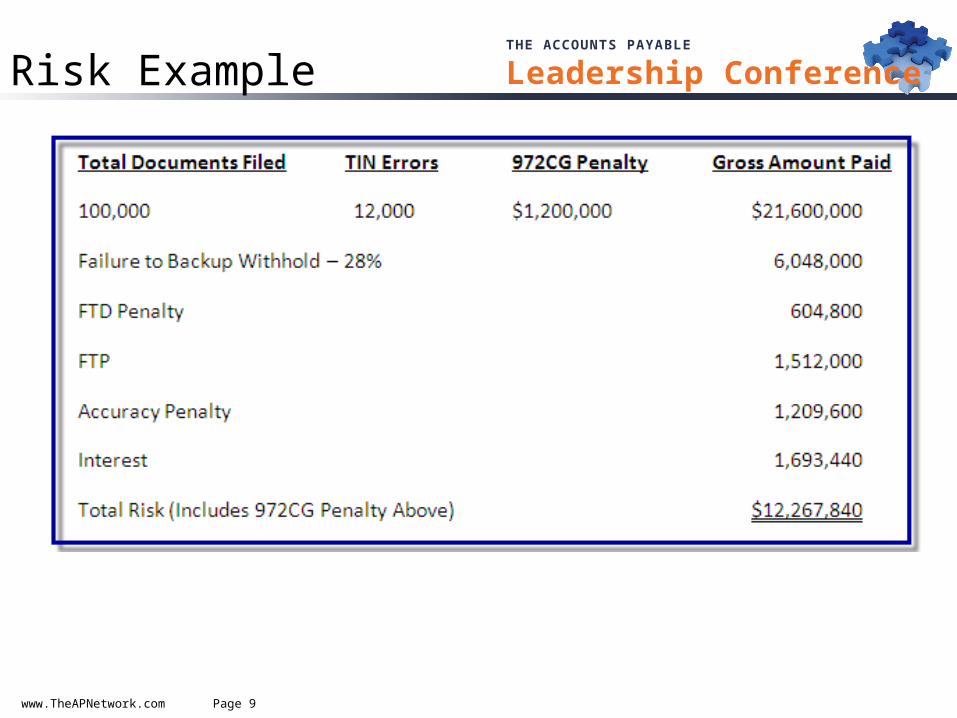

Leadership ConferenceRisk Example

www.TheAPNetwork.com Page 10

THE ACCOUNTS PAYABLE

Leadership ConferenceMinimize Risk

Minimize risk with a compliance review of current process• Review company policy statements on information reporting

―Does it address domestic and NRA payments?―Is there oversight to ensure policy compliance?

• There should be a departmental policy and procedure for any area that could issue payments

• Review training material or programs to train employees on the regulatory requirements

• Review account opening procedures

• Ensure no NRA payments are classified as U.S.

www.TheAPNetwork.com Page 11

THE ACCOUNTS PAYABLE

Leadership Conference

• What steps have you taken to eliminate common errors?

• Are all information returns filed and recipient statements mailed on a timely basis?

• Are corrections filed and corrected recipient statements mailed every 30 days?

• Do you process and report information returns for multiple tax years?

• Do you have the ability to retain the payment activity detail for an account?

Minimize Risk (Cont’d.)

www.TheAPNetwork.com Page 12

THE ACCOUNTS PAYABLE

Leadership Conference

• What steps have you taken to improve your accuracy of TIN and name information?

• Do you require and perform TIN solicitations (Form W-9 or Form W-8 series) for each payee prior to or at time of payment?

• Are TIN solicitations produced and mailed annually as prescribed by the IRS?

• Is backup withholding put into effect when required?• Do you currently interface account status information to payment systems

for the purpose of backup withholding? • Does your current process support “B” Notice matching, notice generation

and status tracking of TIN/name accounts in error?• Does your current process support TIN penalty matching and generate the

appropriate solicitations when necessary?

Minimize Risk (Cont’d.)

www.TheAPNetwork.com Page 13

THE ACCOUNTS PAYABLE

Leadership ConferenceHandling Issues forNon-Resident Aliens

• Do you recertify expiring Form W-8 series as required?

• Do you have a U.S. issued TIN on the Form W-8?

• Are procedures followed to ensure that the proper Form W-8 certification and/or supporting documentation is obtained from the payee when making payments to non-resident aliens?

• Have treaty benefits been allowed? Ensure the review process is correct and well documented.

• Are payments to non-resident aliens reported on Form 1042-S when applicable?

• Does your 1042-S withholding process meet the IRS guidelines for the current treaty rates, types of income and exemptions?

www.TheAPNetwork.com Page 14

THE ACCOUNTS PAYABLE

Leadership ConferenceMiscellaneous Items• Do you have the functionality to report all form

type payments to the IRS, SSA, resident and non-resident states, including U.S. territories?

• Are you capable of processing and reporting information throughout the year to comply with current year state reporting requirements?

• Can you generate all required reporting media and transmittals for original and correction reporting to IRS, SSA, states and U.S. territories?

• Does your process track payment state and resident state to meet state reporting and withholding requirements?

www.TheAPNetwork.com Page 15

THE ACCOUNTS PAYABLE

Leadership Conference

New and Pending Legislation

www.TheAPNetwork.com Page 16

THE ACCOUNTS PAYABLE

Leadership ConferenceImportantLegislative Requirements• Corporate Reporting — passed into law, repealed

April 2011

• Reporting of Purchases of Goods & Materials — passed into law, repealed April 2011

• Increased Penalties — passed

• Section 6050W Merchant Reporting — passed, law

• TIPRA 2005 SEC. 511. withholding on certain payments issued by federal, state or local government entities — passed, law

• FATCA — Foreign Account Tax Compliance Act — passed

www.TheAPNetwork.com Page 17

THE ACCOUNTS PAYABLE

Leadership Conference

Increased PenaltiesEffective January 1, 2011

www.TheAPNetwork.com Page 18

THE ACCOUNTS PAYABLE

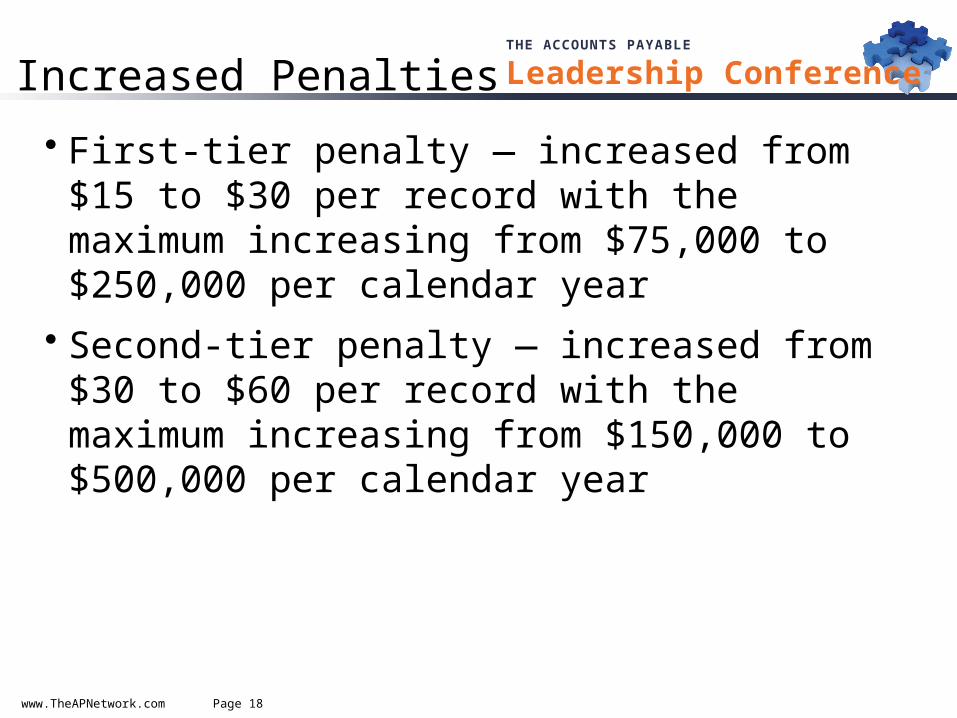

Leadership ConferenceIncreased Penalties

• First-tier penalty — increased from $15 to $30 per record with the maximum increasing from $75,000 to $250,000 per calendar year

• Second-tier penalty — increased from $30 to $60 per record with the maximum increasing from $150,000 to $500,000 per calendar year

www.TheAPNetwork.com Page 19

THE ACCOUNTS PAYABLE

Leadership Conference

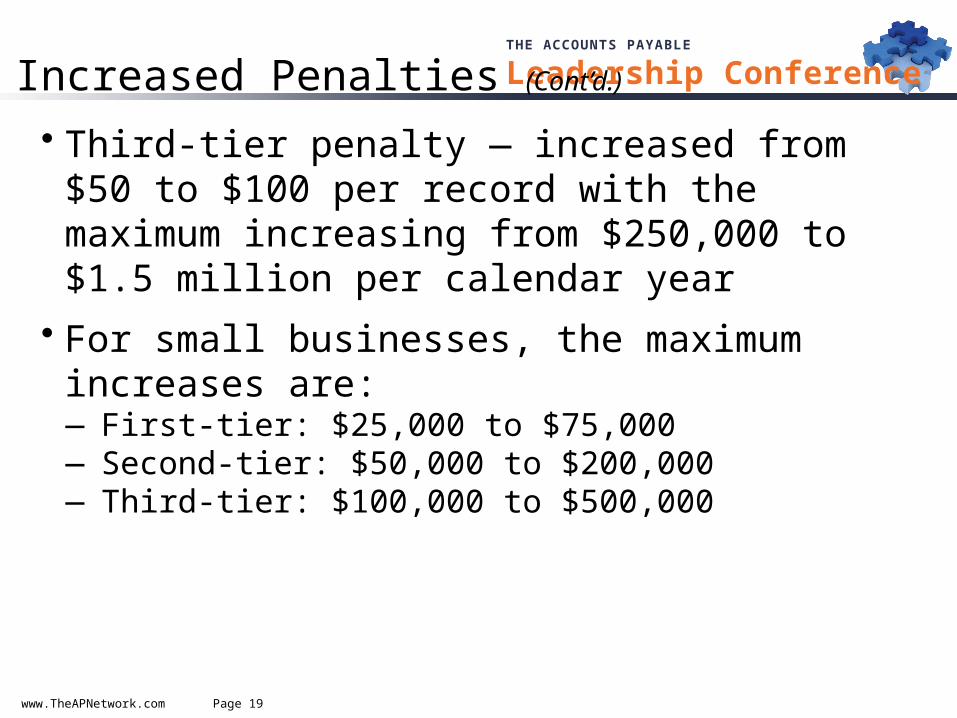

• Third-tier penalty — increased from $50 to $100 per record with the maximum increasing from $250,000 to $1.5 million per calendar year

• For small businesses, the maximum increases are:―First-tier: $25,000 to $75,000―Second-tier: $50,000 to $200,000―Third-tier: $100,000 to $500,000

Increased Penalties (Cont’d.)

www.TheAPNetwork.com Page 20

THE ACCOUNTS PAYABLE

Leadership ConferenceRisk Summary

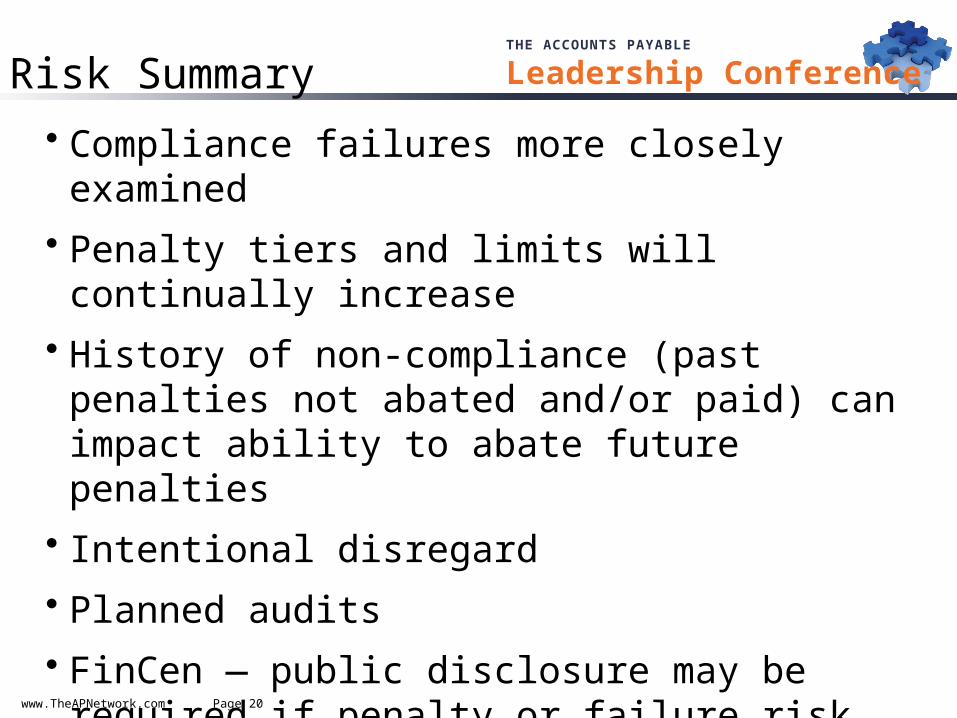

• Compliance failures more closely examined

• Penalty tiers and limits will continually increase

• History of non-compliance (past penalties not abated and/or paid) can impact ability to abate future penalties

• Intentional disregard

• Planned audits

• FinCen — public disclosure may be required if penalty or failure risk becomes known or evident

www.TheAPNetwork.com Page 21

THE ACCOUNTS PAYABLE

Leadership ConferenceThe Legal Stuff

“Any tax advice included in this written or electronic communication was not intended or written to be used, and it cannot be used by the taxpayer for the purpose of avoiding any penalties that may be imposed on the taxpayer by a governmental taxing authority or agency.”

© 2011 Financial Operations Networks LLC

Thank You!If you have further questions:

John Foertschbeck, CPA(410) [email protected]

Lynda Foertschbeck(410) [email protected]

IRSCompliance, Inc.www.irscompliance.org