Embed Size (px)

Citation preview

© 2012 Rockwell Publishing

Financing Residential Real Estate

Lesson 5:

Finance Instruments

© 2012 Rockwell Publishing

Introduction

This lesson will cover:types of finance instrumentshow instruments workcommon provisions

© 2012 Rockwell Publishing

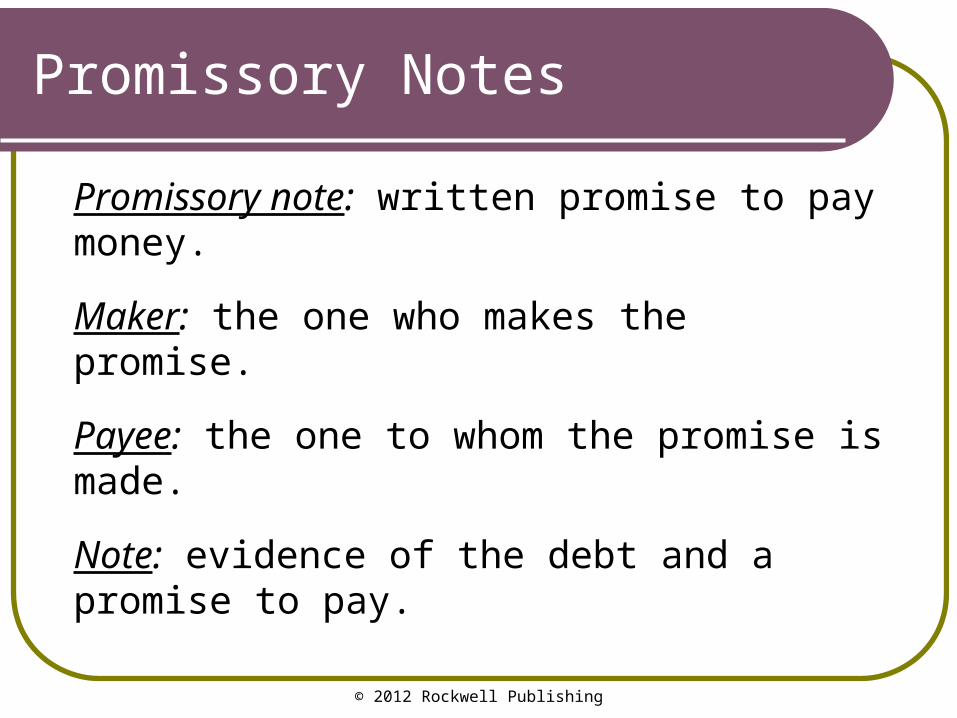

Promissory Notes

Promissory note: written promise to pay money.

Maker: the one who makes the promise.

Payee: the one to whom the promise is made.

Note: evidence of the debt and a promise to pay.

© 2012 Rockwell Publishing

Promissory Notes

Can be brief, simple document. Usually contains:

names of partiesamount of debtinterest ratehow/when money is to be repaid

Basic provisions

© 2012 Rockwell Publishing

Promissory Notes

Must be signed by maker.

If certain requirements are met, it’s a negotiable instrument: right to receive payment can be transferred by endorsement.

Basic provisions

© 2012 Rockwell Publishing

Promissory Notes

Negotiable instrument requirements: written, unconditional promiseto pay a certain sum of moneyon demand or on a certain datepayable to order or to bearersigned by maker

Negotiability

© 2012 Rockwell Publishing

Promissory Notes

“Without recourse” endorsement: issue of future payment strictly between maker and third party the instrument is endorsed to.

Original payee not liable if maker fails to pay.

Without recourse

© 2012 Rockwell Publishing

Promissory Notes

Holder in due course: someone who buys negotiable instrument:

for valuein good faithwithout notice of defenses

Even if maker has defense against original payee, maker still required to pay holder in due course.

Holder in due course

© 2012 Rockwell Publishing

Promissory Notes

Promissory notes classified as to how principal and interest are paid off.

Straight note: periodic payments are interest only, with principal due on maturity date.

Installment note: periodic payments include both principal and interest.

Types of notes

© 2012 Rockwell Publishing

SummaryPromissory Notes

• Maker

• Payee

• Negotiable instrument

• Without recourse

• Holder in due course

• Straight note

• Installment note

© 2012 Rockwell Publishing

Security Instruments

In real estate transactions, promissory note is accompanied by security instrument:

mortgagedeed of trust

Gives lender right to foreclose on property if borrower defaults.

Purpose

© 2012 Rockwell Publishing

Security Instruments

If no collateral, lender can still enforce promissory note.

Lender sues borrower, obtains judgment.But borrower may be “judgment-proof.”

Secured lender much more likely to collect payment.

Purpose

© 2012 Rockwell Publishing

Security Instruments

Personal property used as collateral for early forms of secured lending.

Borrower gave lender possession of collateral property until loan repaid.

Lender kept property if loan wasn’t repaid.

Historical background

© 2012 Rockwell Publishing

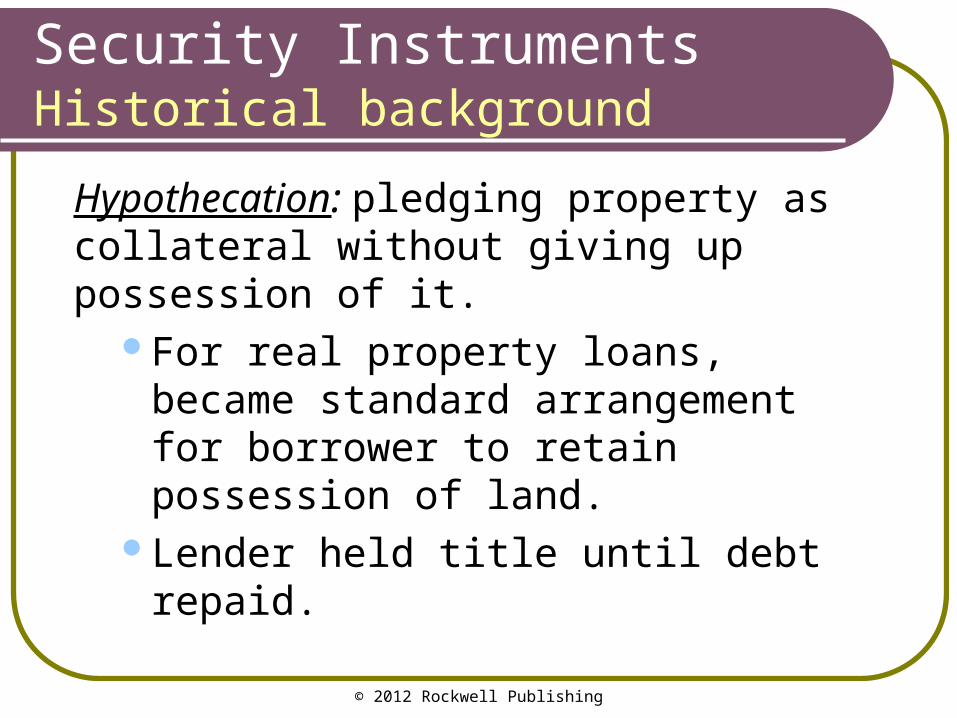

Security Instruments

Hypothecation: pledging property as collateral without giving up possession of it.

For real property loans, became standard arrangement for borrower to retain possession of land.

Lender held title until debt repaid.

Historical background

© 2012 Rockwell Publishing

Security Instruments

Legal title: title transferred only as collateral, without possessory rights.

Equitable title: property rights retained by borrower, without legal title.

Historical background

© 2012 Rockwell Publishing

Security Instruments

Eventually, transfer of legal title wasn’t necessary. More common to place lien against borrower’s property.

Lien: financial encumbrance on owner’s title, allowing lienholder to foreclose on property to collect debt.

Historical background

© 2012 Rockwell Publishing

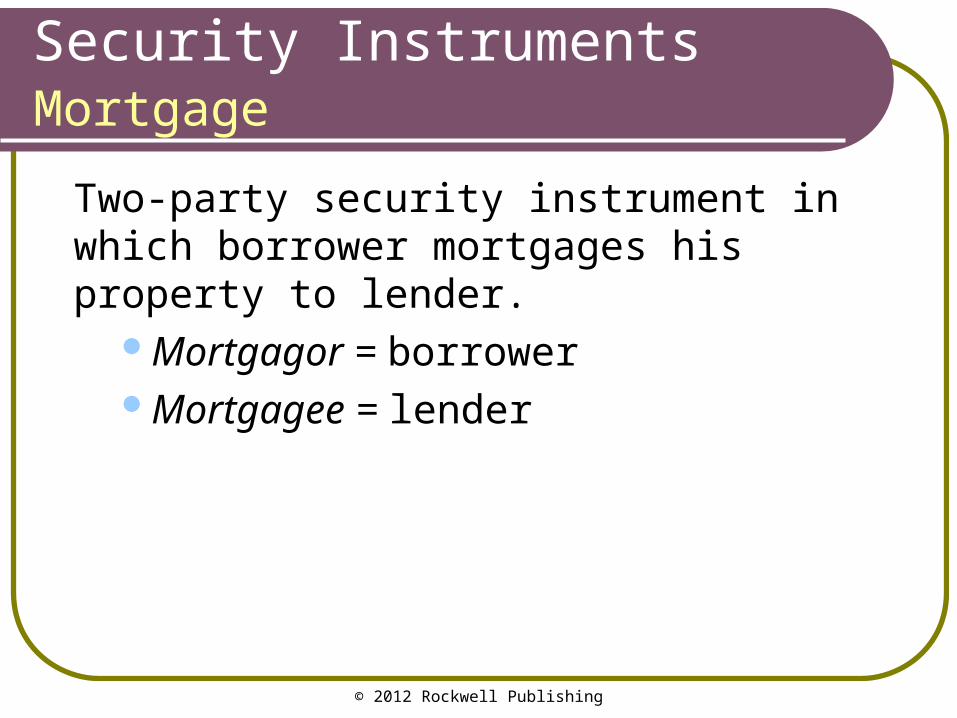

Security Instruments

Two-party security instrument in which borrower mortgages his property to lender.

Mortgagor = borrowerMortgagee = lender

Mortgage

© 2012 Rockwell Publishing

Mortgages

Mortgage must include:names of partiesaccurate legal description of property

Also must identify promissory note it secures.

Basic provisions

© 2012 Rockwell Publishing

Mortgages

Mortgagor promises to:pay property taxes keep property insured against

fire and other hazardsmaintain structures in good repair

Mortgagee has right to inspect property.

Covenants

© 2012 Rockwell Publishing

Mortgages

Satisfaction of mortgage: document given to mortgagor by mortgagee after mortgage is paid off, releasing property from lien.

Mortgagor records document.

Satisfaction

© 2012 Rockwell Publishing

Security Instruments

Similar to mortgage, but involves three parties, rather than two.

Grantor/trustor = borrowerBeneficiary = lenderTrustee = neutral third party

Trustee arranges for release of property or foreclosure, as necessary.

Deed of trust

© 2012 Rockwell Publishing

Deeds of Trust

Deed of trust usually includes same basic provisions found in mortgage:

names of partiesproperty description identification of promissory note grantor’s promises to pay taxes and insure

propertybeneficiary’s right to inspect

property

Basic provisions

© 2012 Rockwell Publishing

Deeds of Trust

Deed of reconveyance: document releasing property from lien, executed by trustee when loan is paid off.

Recorded by grantor.

Reconveyance

© 2012 Rockwell Publishing

SummarySecurity Instruments

• Hypothecation

• Legal title

• Equitable title

• Lien

• Mortgage

• Satisfaction of mortgage

• Deed of trust

• Deed of reconveyance

© 2012 Rockwell Publishing

Security Instruments

Key difference between deeds of trust and mortgages: procedures used for foreclosure.

Foreclosure

© 2012 Rockwell Publishing

Foreclosure

At one time, judicial foreclosure was only option.

Lender filed lawsuit against borrower.Sheriff’s sale ordered by court if borrower

found to be in default.

Alternative to judicial foreclosure was eventually developed.

Methods

© 2012 Rockwell Publishing

Methods of Foreclosure

Nonjudicial foreclosure is generally associated with deeds of trust.

Lender doesn’t have to file lawsuit.Trustee arranges for property to be

sold at trustee’s sale.Property sold to highest bidder.

Judicial vs. nonjudicial

© 2012 Rockwell Publishing

Methods of Foreclosure

Nonjudicial foreclosure requires power of sale clause in security instrument.

Power of sale clause: authorizes trustee to sell property in event of default.

All deeds of trust contain one.May be included in mortgage, but usually

not.

Power of sale

© 2012 Rockwell Publishing

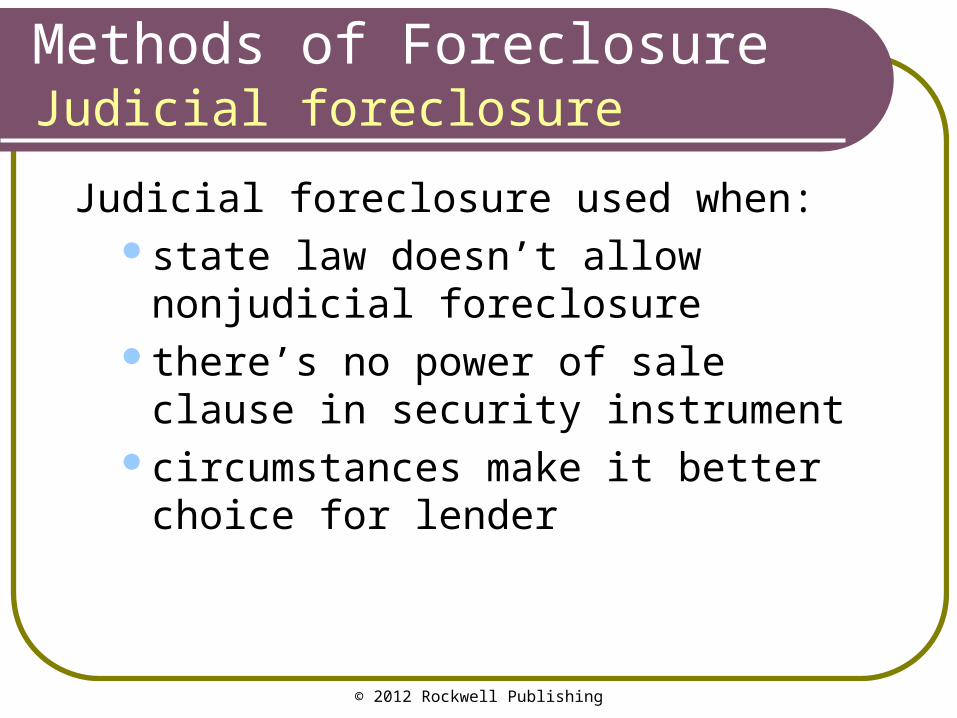

Methods of Foreclosure

Judicial foreclosure used when:state law doesn’t allow nonjudicial

foreclosurethere’s no power of sale clause in

security instrumentcircumstances make it better choice for

lender

Judicial foreclosure

© 2012 Rockwell Publishing

Judicial Foreclosure

1. Acceleration of debt

2. Foreclosure lawsuit

3. Equitable redemption or cure and reinstatement

4. Writ of execution

5. Sheriff’s sale

6. Statutory redemption

7. Sheriff’s deed

Steps in judicial foreclosure

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

1. Acceleration of debt: if mortgagor defaults, mortgagee notifies mortgagor that entire outstanding loan balance is due.

2. Foreclosure lawsuit: unless mortgagor pays off accelerated debt, mortgagee files foreclosure action.

Acceleration & Lawsuit

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

3. Equitable redemption or cure & reinstatement: while lawsuit is pending, mortgagor has right to stop proceedings by paying mortgagee.

Depending on state law, may be:equitable right of redemption, orright to cure and reinstate.

Stopping a pending foreclosure

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

Equitable right of redemption: mortgagor’s right to stop proceedings by paying entire amount owed, plus costs.

Loan is paid off and property is redeemed.

Stopping a pending foreclosure

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

Cure and reinstatement: mortgagor may “cure” default by paying just delinquent amount plus costs.

Foreclosure proceedings terminate, loan is reinstated.

Stopping a pending foreclosure

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

4. Writ of execution: if loan not cured or redeemed, judge schedules hearing to determine if default exists.

If so, judge issues writ of execution.Directs sheriff to seize and sell

property.

Court order

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

5. Sheriff’s sale: public auction where property is sold to highest bidder.

Purchaser given certificate of sale. Proceeds of sale pay costs and debt.

Sale of property

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

If proceeds aren’t enough to pay off foreclosed mortgage, court may award deficiency judgment against debtor for amount of deficiency.

Sale of property

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

6. Statutory right of redemption: additional period after sheriff’s sale to redeem property.

Must pay purchaser amount paid at auction, plus interest.

Depending on state law, period can be 6 months to 2 years.

After sheriff’s sale

© 2012 Rockwell Publishing

Judicial Foreclosure Steps

7. Sheriff’s deed given to purchaser at end of redemption period.

State law may allow purchaser to:take possession of property

immediately, orcollect rent from debtor during

redemption period.

Rights of sheriff’s sale purchaser

© 2012 Rockwell Publishing

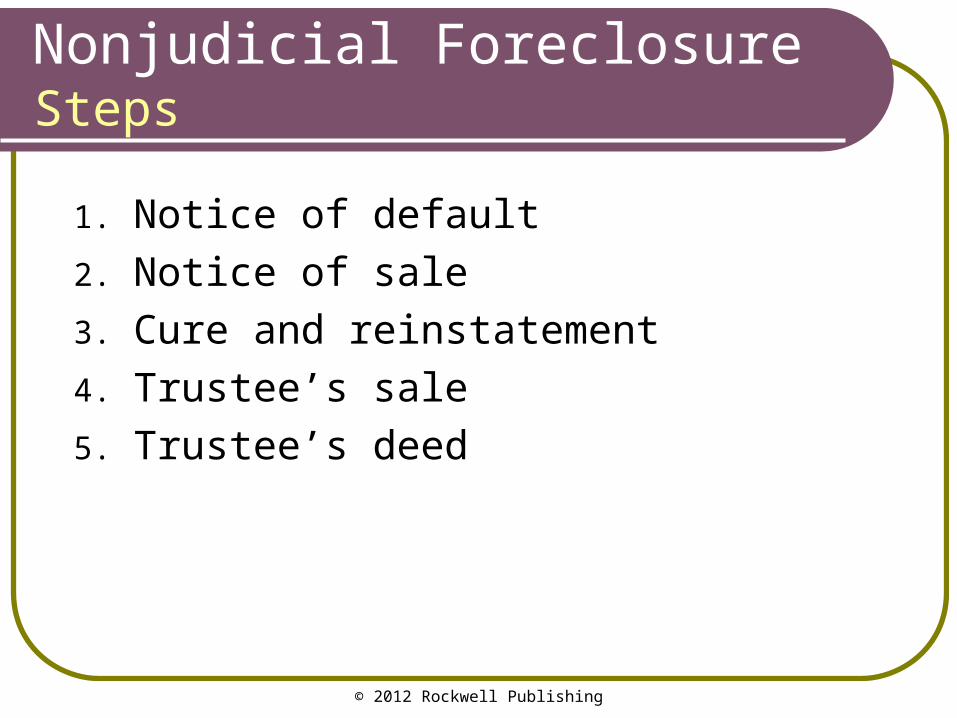

Nonjudicial Foreclosure

1. Notice of default

2. Notice of sale

3. Cure and reinstatement

4. Trustee’s sale

5. Trustee’s deed

Steps

© 2012 Rockwell Publishing

Nonjudicial Foreclosure Steps

1. Notice of default: to begin, trustee must give notice of default to grantor.

2. Notice of sale: trustee must wait certain time after notice of default before issuing notice of sale. Usually 3 to 6 months.

Notice to borrower

© 2012 Rockwell Publishing

Nonjudicial Foreclosure Steps

3. Cure and reinstatement: grantor allowed to cure default and reinstate loan by paying delinquent amounts plus costs.

Right ends shortly before trustee’s sale.No right of redemption after trustee’s

sale.

Stopping the foreclosure

© 2012 Rockwell Publishing

Nonjudicial Foreclosure Steps

4. Trustee’s sale: like sheriff’s sale, trustee’s sale is public auction.

Proceeds first applied to costs, then to debt, then junior liens.

Sale of property

© 2012 Rockwell Publishing

Nonjudicial Foreclosure Steps

5. Trustee’s deed: highest bidder receives trustee’s deed immediately after sale.

Debtor’s title terminates immediately.Must vacate property within short period

(such as 30 days).

No redemption period

© 2012 Rockwell Publishing

Nonjudicial Foreclosure

State law may place restrictions on nonjudicial foreclosures, such as:

requiring post-sale redemption period for agricultural property

prohibiting beneficiary from obtaining deficiency judgment after sale

Restrictions

© 2012 Rockwell Publishing

Judicial vs. Nonjudicial

Judicial foreclosure advantages:borrower can’t reinstate loanright to deficiency judgment

Nonjudicial foreclosure advantages:quick and inexpensive

Lender’s point of view

© 2012 Rockwell Publishing

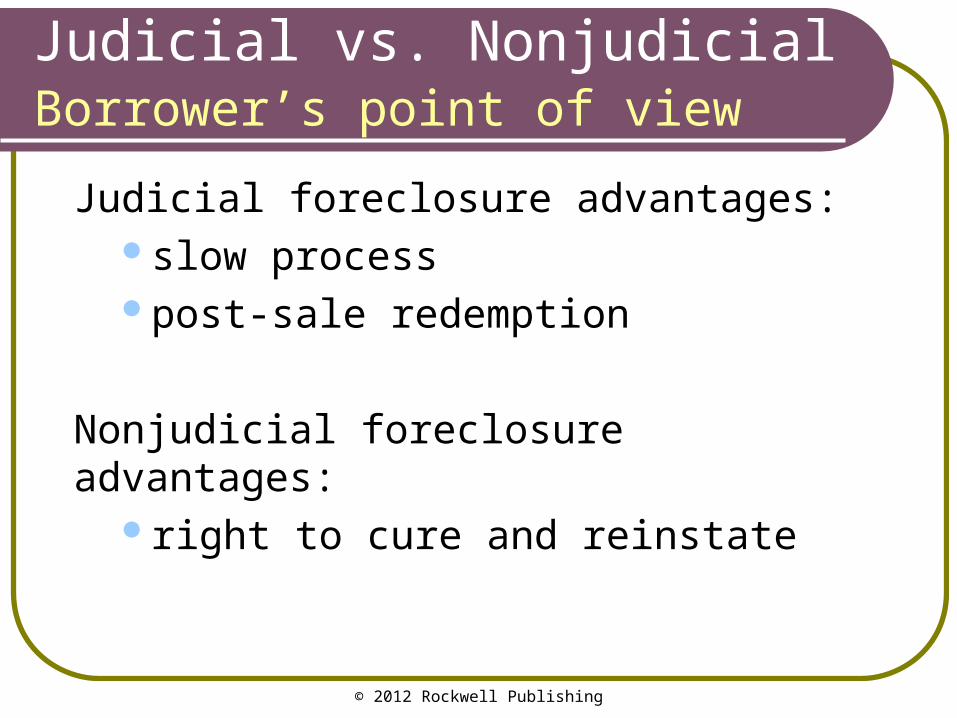

Judicial vs. Nonjudicial

Judicial foreclosure advantages:slow processpost-sale redemption

Nonjudicial foreclosure advantages:right to cure and reinstate

Borrower’s point of view

© 2012 Rockwell Publishing

SummaryForeclosure

• Judicial foreclosure• Equitable right of redemption• Sheriff’s sale• Deficiency judgment• Statutory right of redemption• Nonjudicial foreclosure• Power of sale• Cure and reinstatement• Trustee’s sale

© 2012 Rockwell Publishing

Alternatives to Foreclosure

Three alternatives allow borrowers who can no longer make payments to avoid foreclosure:

loan workoutdeed in lieushort sale

© 2012 Rockwell Publishing

Alternatives to Foreclosure

All three alternatives require lender’s consent.

Lender’s incentives to cooperate:avoiding foreclosure costsending money-losing situation

more quickly

Lender’s consent needed

© 2012 Rockwell Publishing

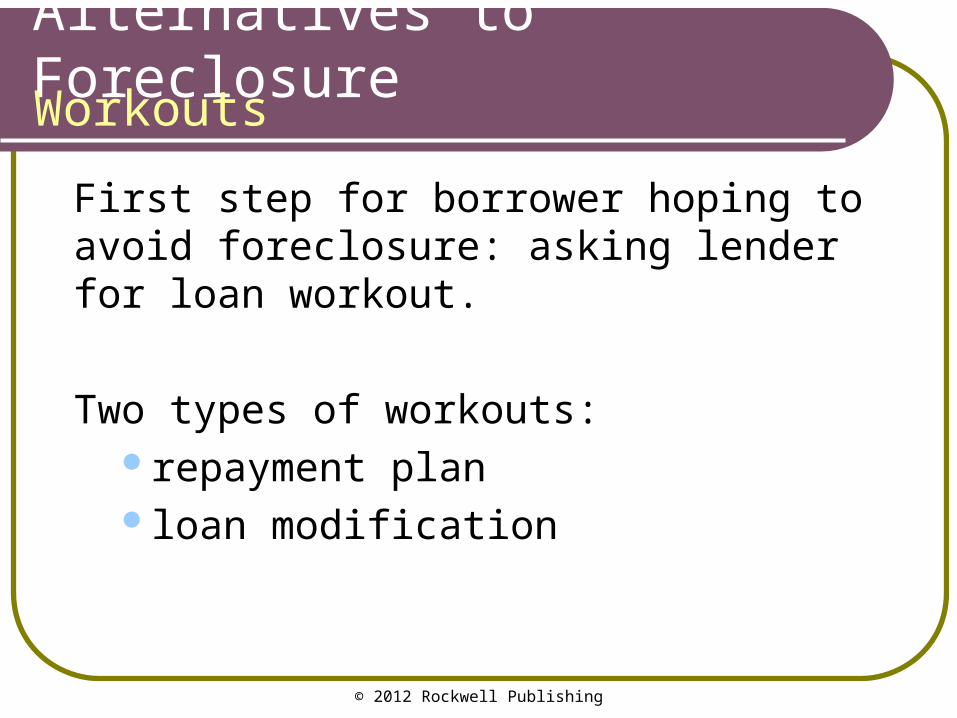

Alternatives to Foreclosure

First step for borrower hoping to avoid foreclosure: asking lender for loan workout.

Two types of workouts:repayment planloan modification

Workouts

© 2012 Rockwell Publishing

Workouts

With repayment plan, lender allows borrower to change timing of limited number of payments.

Borrower in more dire situation may need loan modification: permanent change in terms of repayment (like reduced principal or interest rate).

Repayment plans / loan modifications

© 2012 Rockwell Publishing

Alternatives to Foreclosure

If borrower can’t negotiate workout and will lose property anyway, can offer lender deed in lieu.

If lender accepts deed in lieu:borrower deeds property to lenderdebt satisfied

Deed in lieu of foreclosure

© 2012 Rockwell Publishing

Deed in Lieu of Foreclosure

Lender agrees to release borrower even though property is usually worth less than amount owed.

Lender could require borrower to sign promissory note for shortfall, but that isn’t typical.

Settlement of debt

© 2012 Rockwell Publishing

Deed in Lieu of Foreclosure

Compared to foreclosure, deed in lieu is:simplerless public

Borrower’s credit rating suffers almost as much as from foreclosure.

Impact on borrower

© 2012 Rockwell Publishing

Deed in Lieu of Foreclosure

Lender takes title subject to other liens.Not like foreclosure, which extinguishes

junior liens.

Junior liens

© 2012 Rockwell Publishing

Alternatives to Foreclosure

Short sale: when borrower sells property to third party for less than amount owed.

Borrower facing foreclosure may ask lender to approve short sale.

If lender approves buyer, lender receives sale proceeds and releases lien.

Short sales

© 2012 Rockwell Publishing

Short Sales

Like ordinary sale, short sale doesn’t extinguish junior liens.

If there are junior liens, short sale must be approved by all lienholders.

Junior lienholders unlikely to consent.

Junior liens

© 2012 Rockwell Publishing

Alternatives to Foreclosure

To arrange workout, deed in lieu, or short sale, borrower contacts loan servicer.

May need approval from more than onedepartment or entity.

Obtaining lender’s consent

© 2012 Rockwell Publishing

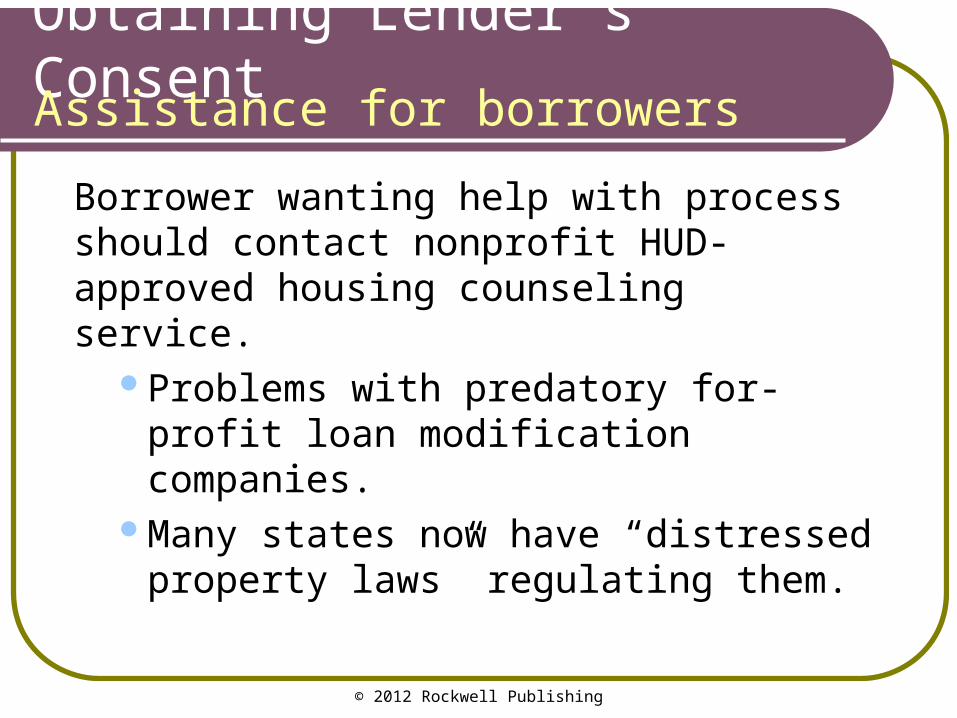

Obtaining Lender’s Consent

Borrower wanting help with process should contact nonprofit HUD-approved housing counseling service.

Problems with predatory for-profit loan modification companies.

Many states now have “distressed property laws” regulating them.

Assistance for borrowers

© 2012 Rockwell Publishing

Obtaining Lender’s Consent

If loan has been securitized, it’s difficult to obtain consent.

Under some MBS contracts, any purchaser (investor) can object and prevent loan modification or settlement.

Impractical to obtain consent of all investors.

Securitized loans

© 2012 Rockwell Publishing

Alternatives to Foreclosure

Generally, IRS views debt relief (reduction in amount owed) as income.

Borrower who enters arrangement reducing amount owed may have to pay income tax on debt relief.

Income tax implications

© 2012 Rockwell Publishing

Alternatives to Foreclosure

Exceptions: debt relief not taxed if:debt was secured by principal residence

and forgiven between 2007-2012debtor was insolvent when debt forgiven

Income tax implications

© 2012 Rockwell Publishing

SummaryAlternatives to Foreclosure

• Loan workout

• Repayment plan

• Loan modification

• Deed in lieu

• Short sale

• Housing counseling service

• Distressed property laws

• Debt relief

© 2012 Rockwell Publishing

Finance Instrument Provisions

Rights and responsibilities of borrower and lender may be affected by:

subordination clauselate charge provisionprepayment provisionpartial release clauseacceleration clausealienation clause

© 2012 Rockwell Publishing

Finance Instrument Provisions

Subordination clause: gives a mortgage lower priority than another mortgage that will be recorded later on.

Common in construction financing.

Subordination clauses

© 2012 Rockwell Publishing

Finance Instrument Provisions

Promissory notes usually provide for late charges if borrower doesn’t make payments on time.

State laws may override late charge provision, to protect borrowers from excessive charges.

Late charge provisions

© 2012 Rockwell Publishing

Finance Instrument Provisions

Prepayment provision: imposes penalty on borrower who repays some or all of principal before due.

Prepayment deprives lender of some of interest it expected to receive over loan term.

Prepayment provisions

© 2012 Rockwell Publishing

Finance Instrument Provisions

Not standard in residential loan agreements.Fannie Mae/Freddie Mac promissory

note gives borrower right to prepay.Prepayment penalties prohibited with

FHA and VA loans.Dodd-Frank Act places new restrictions

on prepayment penalties.

Prepayment provisions

© 2012 Rockwell Publishing

Finance Instrument Provisions

Partial release clause: obligates lender to release part of property from lien when part of debt is paid.

Typically found in deed of trust or mortgage that covers subdivision, allowing release of individual lot from lien when lot is sold.

Partial release clauses

© 2012 Rockwell Publishing

Finance Instrument Provisions

Acceleration clause: allows lender to declare outstanding loan balance due immediately in event of default.

Most lenders wait 90 days before accelerating.

Some states now have laws requiring specific waiting period.

Acceleration clauses

© 2012 Rockwell Publishing

Finance Instrument Provisions

Alienation clause: prevents borrower from selling security property without lender’s permission unless loan paid off at closing.

If title transferred without permission, lender can accelerate loan.

Also called due-on-sale clause.

Alienation clauses

© 2012 Rockwell Publishing

Alienation Clauses

Most alienation clauses triggered by transfer of any significant interest in property.

Includes long-term leases, or leases with options to purchase.

Lender can’t forbid transfer, but can demand payment of loan.

Triggered by transfer of any interest

© 2012 Rockwell Publishing

Alienation Clauses

To understand purpose of alienation clause, consider what happens when borrower sells property without paying off loan.

Transfer of title without loan payoff

© 2012 Rockwell Publishing

Alienation Clauses

Three possibilities:

1. New owner takes title subject to loan but

does not assume it.

2. New owner assumes loan but original borrower is not released.

3. New owner assumes loan and lender agrees to release original borrower.

Transfer of title without loan payoff

© 2012 Rockwell Publishing

SummaryFinance Instrument Provisions

• Subordination clause

• Late charge provision

• Prepayment provision

• Partial release clause

• Acceleration clause

• Alienation clause

• Assumption

© 2012 Rockwell Publishing

Types of Real Estate Loans

Junior mortgage: mortgage with lower lien priority than another against same property.

Senior mortgage: mortgage with higher lien priority than another on same property.

At foreclosure, junior mortgage paid only after senior has been paid in full.

Junior or senior mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Lien having most senior (first) position is called first mortgage.

Junior mortgages may be referred to as second mortgage, third mortgage, etc.

First mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Purchase money mortgage: any mortgage loan used to finance purchase of property that is collateral for loan.

A mortgage that buyer gives to seller in seller-financed transaction.

Purchase money mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Home equity loan: loan secured by mortgage against borrower’s equity in home she already owns. (Interest rates higher than on purchase loans.)

Equity: difference between property’s market value and total liens against it.

Home equity loan

© 2012 Rockwell Publishing

Types of Real Estate Loans

Home equity line of credit (HELOC): line of credit with limit and minimum monthly payments; homeowner can draw upon as needed.

Automatically secured by borrower’s home.

Home equity loan

© 2012 Rockwell Publishing

Types of Real Estate Loans

Refinancing: new loan used to pay off existing mortgage against same property.

Often used:to take advantage of market interest rate

decreasewhen balloon payment due on existing

loan

Refinance mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Bridge loan: provides cash for purchase of new home pending sale of old home.

Secured by equity in old home.Usually has interest-only payments.Also called swing loan or gap loan.

Bridge loan

© 2012 Rockwell Publishing

Types of Real Estate Loans

Budget mortgage: loan with monthly payments that include property taxes and hazard insurance.

Lender holds tax and insurance portions of borrower’s payments in impound account until payments due.

Budget mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Package mortgage: loan secured by personal property as well as real property.

Alternatively, personal property may be financed separately, using separate security agreement.

Lender must file financing statement with Secretary of State.

Package mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Blanket mortgage: loan secured by more than one parcel of land; contains partial release clause.

Partial release clause: requires lender to release some of security property from lien when portion of debt is paid off.

Blanket mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Construction loan: short-term loan used to finance construction on land already owned by borrower.

Once construction completed, construction loan replaced by take-out loan.

Borrower repays amount over specified term.

Construction loan

© 2012 Rockwell Publishing

Types of Real Estate Loans

Nonrecourse mortgage: loan that gives lender no recourse against borrower.

Lender’s only remedy in event of default is foreclosure on collateral property.

Borrower not personally liable for loan repayment.

Nonrecourse mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Participation mortgage: allows lender to participate in earnings generated by mortgaged property, in addition to collecting interest payments.

Shared appreciation mortgage: entitles lender to share of increase in property’s value.

Participation / shared appreciation

© 2012 Rockwell Publishing

Types of Real Estate Loans

Wraparound mortgage: new mortgage that includes existing first mortgage on property.

Used almost exclusively in seller-financed transactions.

Wraparound mortgage

© 2012 Rockwell Publishing

Types of Real Estate Loans

Reverse mortgage: provides elderly homeowners source of income, without requiring sale of home.

Homeowner borrows against equity.Monthly check from lender.Borrower required to be over certain age.Home sold after death to repay loan.

Reverse mortgage

© 2012 Rockwell Publishing

SummaryTypes of Real Estate Loans

• Purchase money mortgage• Home equity loan or HELOC• Refinancing• Bridge loan• Budget mortgage• Package mortgage• Blanket mortgage• Construction loan• Nonrecourse mortgage• Wraparound mortgage• Reverse mortgage