Embed Size (px)

Citation preview

© 2015 First Data Corporation. All Rights Reserved.

DIGITAL PAYMENTS – USERS AND INFLUENCERS

DIGITAL PAYMENTS SUMMIT SEPTEMBER 30TH 2015

Espen TranoyManager Director First Data HellasRegional Manager CEE and SEE

© 2015 First Data Corporation. All Rights Reserved.

The Millennials – the “Unbanked” Generation

80MAMERICANS BORN

2020MILLENNIALS PEAK

46%OF ALL U.S INCOME

1,5MGREEKS BORN

?OF ALL GREEK INCOME

1

© 2015 First Data Corporation. All Rights Reserved.

User Characteristics

2

in

© 2015 First Data Corporation. All Rights Reserved.

Millennials Want to hold their Bank at Arm’s Length

71% 33% 71% 33%Would rather go to

the dentist than listen to what banks

say.

Believe they won'tneed a bank in five

years.

Consider their banking relationship to be transactional

rather than relationship-driven.

Are open to switching

banks within the next

90 days.

Millennials are increasingly using online payment methods in place of cash and checks:

47% 43%Of consumers have already transferred money to someone electronically.

List online banking as the first or second most valuable aspect of their day-to-day

banking experience; 23% list mobile banking.

3

© 2015 First Data Corporation. All Rights Reserved.

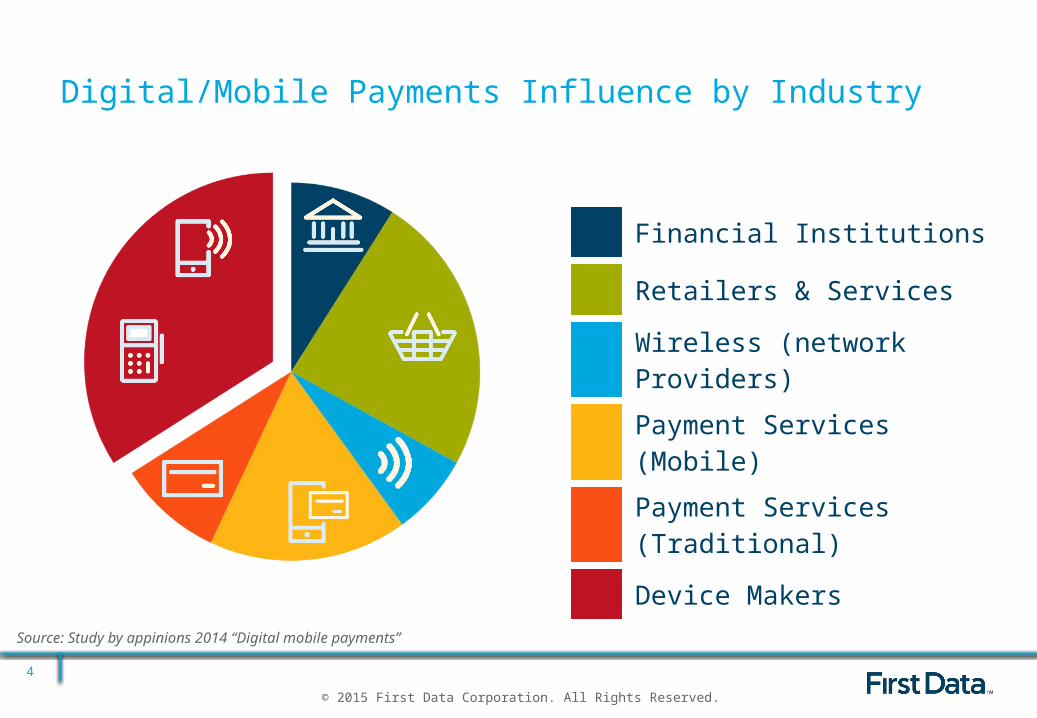

Digital/Mobile Payments Influence by Industry

4

Financial Institutions

Retailers & Services

Wireless (network Providers)

Payment Services (Mobile)

Payment Services (Traditional)

Device Makers

Source: Study by appinions 2014 “Digital mobile payments”

© 2015 First Data Corporation. All Rights Reserved.

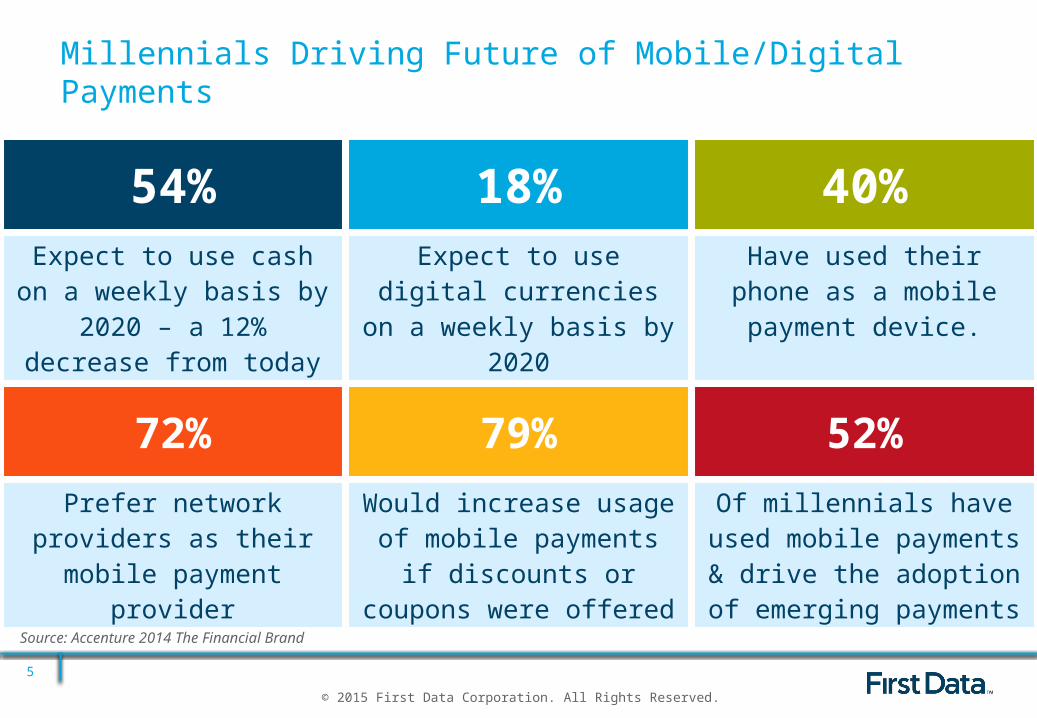

Millennials Driving Future of Mobile/Digital Payments

5

54% 18% 40%Expect to use cash on a weekly basis by 2020 – a 12% decrease from today

Expect to use digital currencies on a weekly

basis by 2020

Have used their phone as a mobile payment device.

72% 79% 52%

Prefer network providers as their mobile payment

provider

Would increase usage of mobile payments if

discounts or coupons were offered

Of millennials have used mobile payments & drive the adoption of emerging

payments

Source: Accenture 2014 The Financial Brand

© 2015 First Data Corporation. All Rights Reserved.

What do the Millennials want from their Bank?

6

27%Would consider a

branchless digital bank

51% Want their bank to

proactively recommend products/services for their

financial needs

71%Consider their banking

relationship to be transactional rather than

relationship driven

48% Are interested in real-time

and forward looking spending analysis

Source: Accenture 2014 The digital disruption n Banking

© 2015 First Data Corporation. All Rights Reserved.

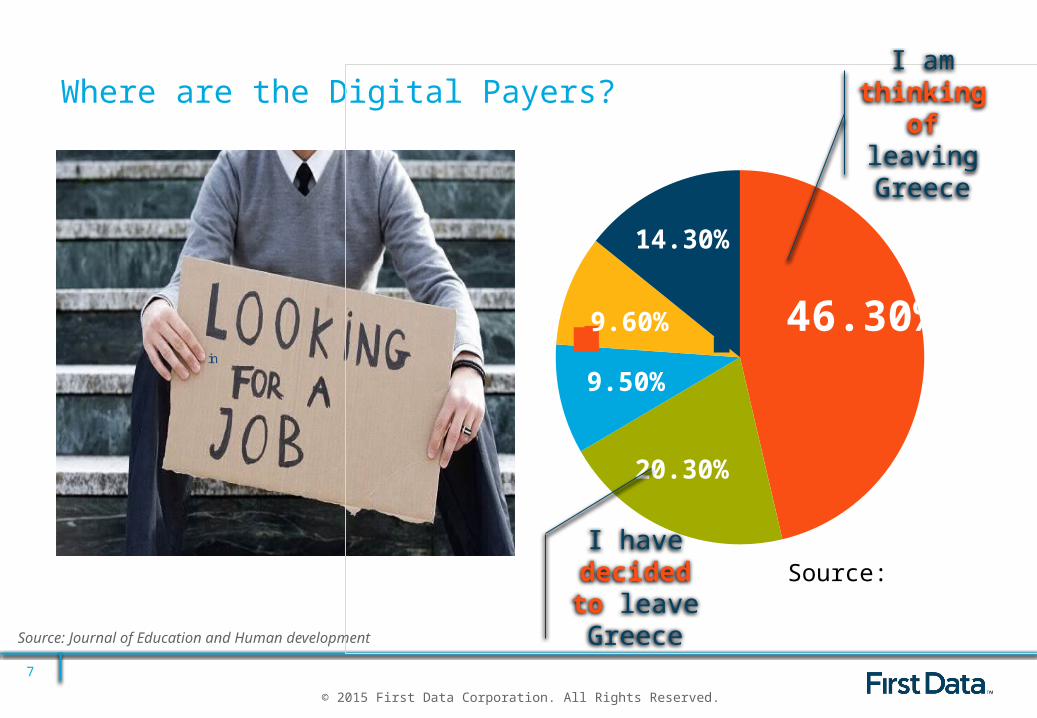

Where are the Digital Payers?

7

in

46.30%

20.30%

9.50%

9.60%

14.30%

Chart TitleI am

thinking of leaving

Greece

I have decided to

leave Greece

Source:

Source: Journal of Education and Human development

© 2015 First Data Corporation. All Rights Reserved.

What will Evolve in Greece?

8

© 2015 First Data Corporation. All Rights Reserved.

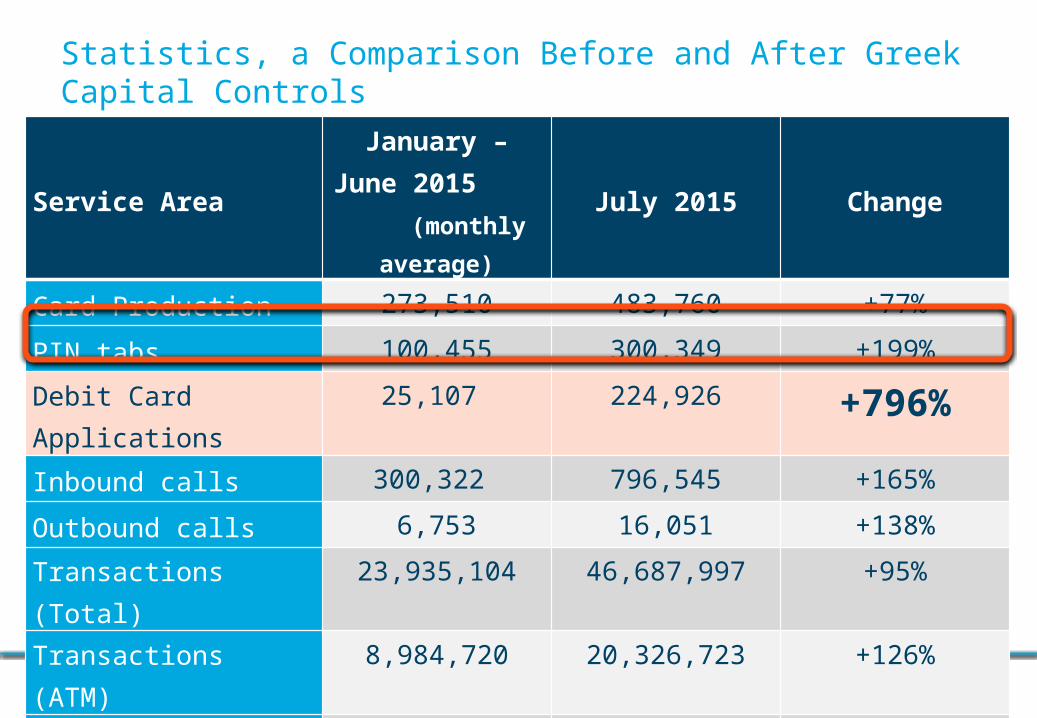

Statistics, a Comparison Before and After Greek Capital Controls

9

Service AreaJanuary – June

2015 (monthly average)

July 2015 Change

Card Production 273,510 483,760 +77%

PIN tabs 100,455 300,349 +199%

Debit Card Applications 25,107 224,926 +796%Inbound calls 300,322 796,545 +165%

Outbound calls 6,753 16,051 +138%

Transactions (Total) 23,935,104 46,687,997 +95%

Transactions (ATM) 8,984,720 20,326,723 +126%

Transactions (POS) 10,057,410 19,120,184 +90%

Transactions (Issuing) 4,892,974 7,241,090 +48%

MIPS 191,509 281,035 +47%