Embed Size (px)

Citation preview

( A BRIEF COMPARISON )

BY:- CS RAVI BHUSHAN KUMAREmail:- [email protected]

09990339200www.csinindia.com

• Enacted in the Year 1956 by the First Parliament of the India elected by General Public of India

• First Act of Year1956• Enacted on 18 January

1956• Commenced on 1 April

1956

• Enacted in the Year 2013 by the Fifteenth Parliament of the India.

• 18th Act of Year 2013• Enacted on 29 August

2013• Commenced on 1 April

2014

COMPANIES ACT, 1956 COMPANIES ACT, 2013

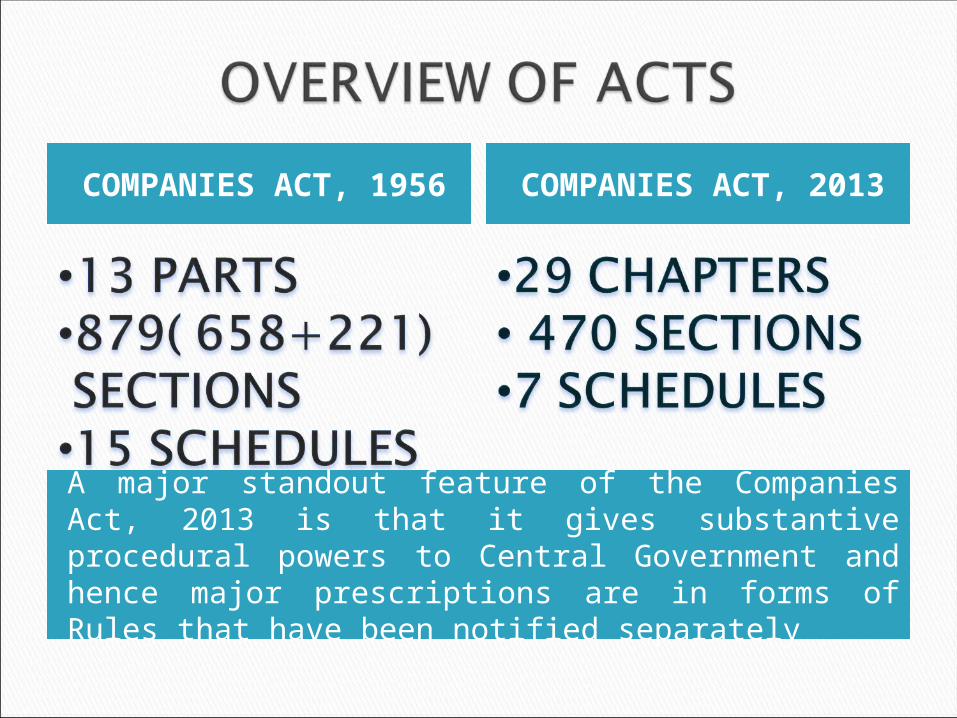

A major standout feature of the Companies Act, 2013 is that it gives substantive procedural powers to Central Government and hence major prescriptions are in forms of Rules that have been notified separately

The Central Government has vested powers to enforce different provisions of the Companies Act, 2013 at different points in time.

No such power existed in the previous Act and the Act was brought to force in entirety

The Central Government was vested with power to amend the applicability of Act based on Geographical Locations.Sec 1(3) – Nagaland620B – Goa, Daman and Diu620C – Jammu and Kashmir

No such provision exists in the Act of 2013 and the Government cannot amend the applicability of the Act based on Geographical Locations

IN• Key managerial

personnel• Resident Director• Auditor Rotation• Dormant company• NFRA• Vigil mechanism• SFIO• Definition of

Subsidiary• Secretarial Audit• Recasting of Account• Private Placement

IN• Key managerial

personnel• Resident Director• Auditor Rotation• Dormant company• NFRA• Vigil mechanism• SFIO• Definition of

Subsidiary• Secretarial Audit• Recasting of Account• Private Placement

OUT• Sole selling agents • Statutory meetings• Convert share into

stock• Qualification shares• Treasury stocks

OUT• Sole selling agents • Statutory meetings• Convert share into

stock• Qualification shares• Treasury stocks

Introduction of New Definitions & Concepts in the Act, which were

not existing in the Companies Act, 1956

One Person Company

Small Company

KMP

Registered Valuer

Associate Company

Dormant Company

Promoters

Class Action Suit

Independent Director

Auditing Standards

Secretarial Audit

By Liability By Type By Listing status

UnlimitedLimited PrivatePublic

By Shares By Guarantee Small

Listed Unlisted

One Person

Q.1. is it compulsory to have a common seal ?Ans: clause 3 of Companies (Amendment) Act 2015

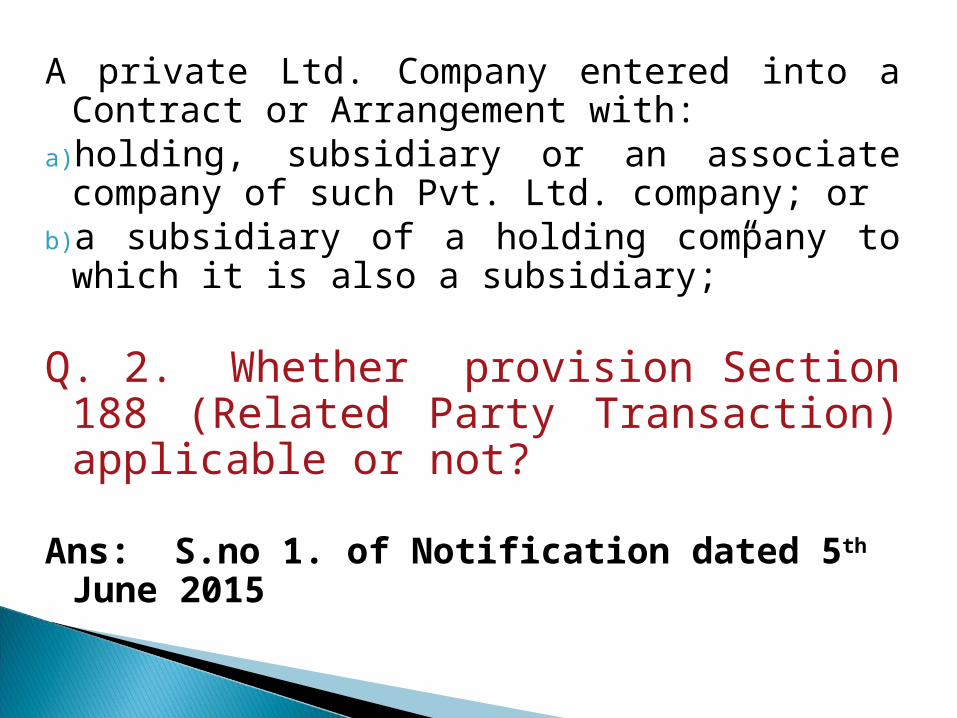

A private Ltd. Company entered into a Contract or Arrangement with:

a)holding, subsidiary or an associate company of such Pvt. Ltd. company; or

b)a subsidiary of a holding company to which it is also a subsidiary;”

Q. 2. Whether provision Section 188 (Related Party Transaction) applicable or not?

Ans: S.no 1. of Notification dated 5th June 2015

Q. 3 How many types of shares can have in a Private ltd Co.?

1. A private companies MAY have only one kind of share capital say preference share capital OR can issue equity shares with differential rights without compliance of following conditions as specified under Rule 4 of the Companies (Share Capital and Debentures) Rules, 2014

2. The private companies can determine voting rights of its equity and preference shareholders in any manner it desires by incorporating suitable provision in its memorandum or articles of association.

RULE 3 OF COMPANIES(SHARE CAPITAL AND DEBENTURE)RULES,2014 MAY BE AMENDED TO DELETE ‘(b)’ i.e. ‘all private companies’.

Ans. S. No. 2 of Notification Dated 5th May 2015

Ans. S. No. of Notification Dated 5th June 2015

Confusing Exemption !!!!!!

Ans. S.No 6 of Notification Dated 5th June 2015

A Private Company may accept from its members deposits up to 100% of aggregate of the paid up share capital and free reserves without fulfilling conditions (a) to (e) u/s 73(2).

But,The Private Company shall file details of deposits so accepted to the Registrar.

MCA may modify Rule 3(3) of the Companies (Acceptance of Deposits) Rules, 2014, which states that maximum amount of deposit that a company may accept from its members shall not exceed 25% of its paid-up share capital and free reserves.

Ans. S. 9 of Notification Dated 5th June 2015

Now While computing the limit of 20 companies, the one person companies, dormant companies, and the private companies with the paid up share capital of less than rupees 100 crores will be excluded.

Section 141(3)(g) limits the number of audits by an auditor to twenty companies.Now the words “other than One person companies, dormant companies, small companies and private companies having paid-up share capital of less than Rs 100 crores” have been inserted after twenty companies.

Ans: S. No 13 of Notification Dated 5th June 2015

Now in a private company an interested director may participate in a board meeting after disclosing his interest.

Although, this provision will certainly lead to ease of decision making by private companies, there seems to be some anomaly. Such an interested director may participate in a Board meeting of a private company after disclosure of his interest but he cannot be counted for the purpose of ascertaining quorum under section 174(3).

Ans. S.No 14. Notification Dated 5th June 2015

Section 185 shall not apply to a private company if the following conditions are fulfilled:

(a)in whose share capital no other body corporate has invested any money;

(b) if the borrowings of such a company from banks or Financial Institutions is less than twice of its paid up share capital or Rs. 50 crores, whichever is lower;and

(c) such a company has no default in repayment of such borrowings subsisting at the time of making transactions u/s 185.

"Public Company" means a company which –a)is not a private company ;b)has a minimum paid-up capital of five lakh rupees or such higher paid-up capital, as may be prescribed ;c)is a private company which is a subsidiary of a company which is not a private company.

o Act of 2013 clearly states that the Private Company subsidiary of the Public Company shall be deemed to be Public Company though it may be Private Company by the virtue of its Articles. Act of 1956 was ambiguous in this regard

“Body Corporate” or “Corporation” includes a company incorporated outside India, but does not include—i.a co-operative society registered under any law relating to co-operative societies; andii.any other body corporate (not being a company as defined in this Act), which the Central Government may, by notification, specify in this behalf;

"Body Corporate" or "Corporation" includes a company incorporated outside India but does not include -a)a corporation sole ;b)a co-operative society registered under any law relating to co-operative societies ; andc)any other body corporate (not being a company as defined in this Act), which the Central Government may, by notification in the Official Gazette, specify in this behalf;

o The Definition is more or less similar just the Corporation Sole which was specifically excluded in Act of 1956 is now included in the Act of 2013

“Associate Company”, in relation to another company, means a company in which that other company has a significant influence, but which is not a subsidiary company of the company having such influence and includes a joint venture company.Explanation.— For the purposes of this clause, “significant influence” means control of at least twenty per cent. of total share capital, or of business decisions under an agreement;

Associate Company is a Related Party [2(76)]

If the Directors are concerned or interested in such associate companies, such director will not be regarded as independent director

Accounts of Associated Company should be consolidated with Accounts of Investing Company [129(3)]

Transaction with Associate Companies included in Transactions under Section 188 [Related Party Transactions]

A Chartered Accountant is not eligible to be appointed as Statutory Auditor of the Company, if he is holding any security, interest, is indebted to or has a business relation with the associate company

The Auditor is barred from providing specified non-audit services to Associate Companies

Annual return of every company shall contain particulars of associate companies

Register of Directors and KMP kept under section 170 shall now include the details of securities held by each of them in Associate Companies as well Act of 2013 prohibits Forward Dealing of Securities of

Associate Companies by the Directors and KMP of the Companies [194]

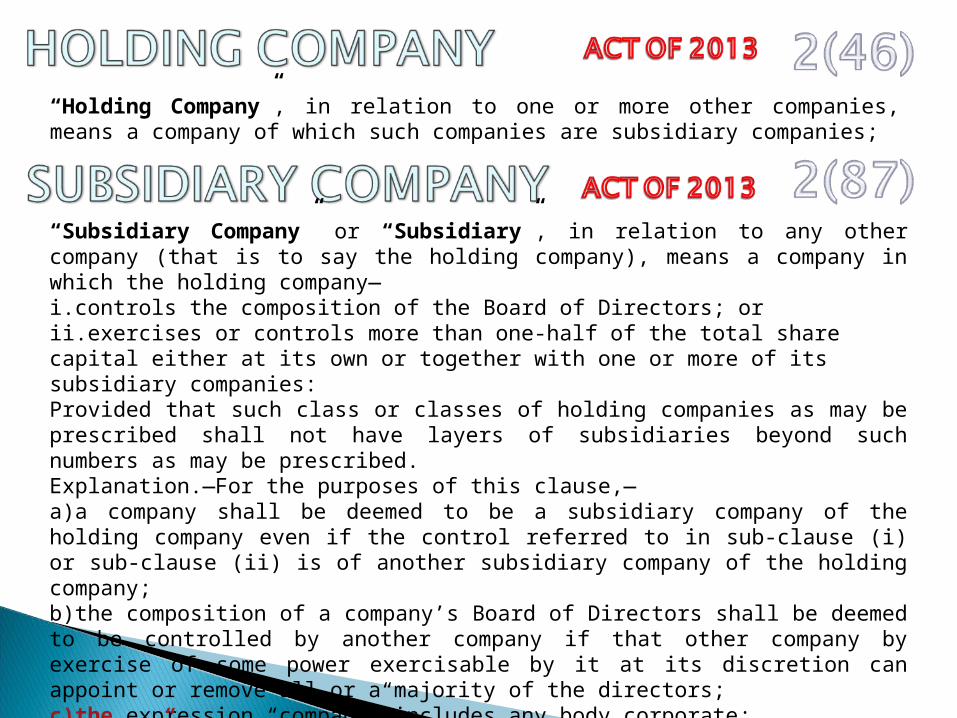

“Holding Company”, in relation to one or more other companies, means a company of which such companies are subsidiary companies;

“Subsidiary Company” or “Subsidiary”, in relation to any other company (that is to say the holding company), means a company in which the holding company—i.controls the composition of the Board of Directors; orii.exercises or controls more than one-half of the total share capital either at its own or together with one or more of its subsidiary companies:Provided that such class or classes of holding companies as may be prescribed shall not have layers of subsidiaries beyond such numbers as may be prescribed.Explanation.—For the purposes of this clause,—a)a company shall be deemed to be a subsidiary company of the holding company even if the control referred to in sub-clause (i) or sub-clause (ii) is of another subsidiary company of the holding company;b)the composition of a company’s Board of Directors shall be deemed to be controlled by another company if that other company by exercise of some power exercisable by it at its discretion can appoint or remove all or a majority of the directors;c)the expression “company” includes any body corporate;d)“layer” in relation to a holding company means its subsidiary or subsidiaries;

For the purposes of this Act, a company shall, subject to the provisions of sub-section (3), be deemed to be a subsidiary of another if, but only if, -a)that other controls the composition of its Board of directors ; orb)that other -

i. where the first-mentioned company is an existing company in respect of which the holders of preference shares issued before the commencement of this Act have the same voting rights in all respects as the holders of equity shares, exercises or controls more than half of the total voting power of such company;

ii. where the first-mentioned company is any other company, holds more than half in nominal value of its equity share capital; or

c) the first-mentioned company is a subsidiary of any company which is that other's subsidiary.

Rule 2(1)(r) of Companies (Specification of definition details) Rules 2014

TOTAL CAPITAL

=PAID UP EQUITY SHARE CAPITAL

+CONVERTIBLE PREFERENCE

SHARE CAPITAL

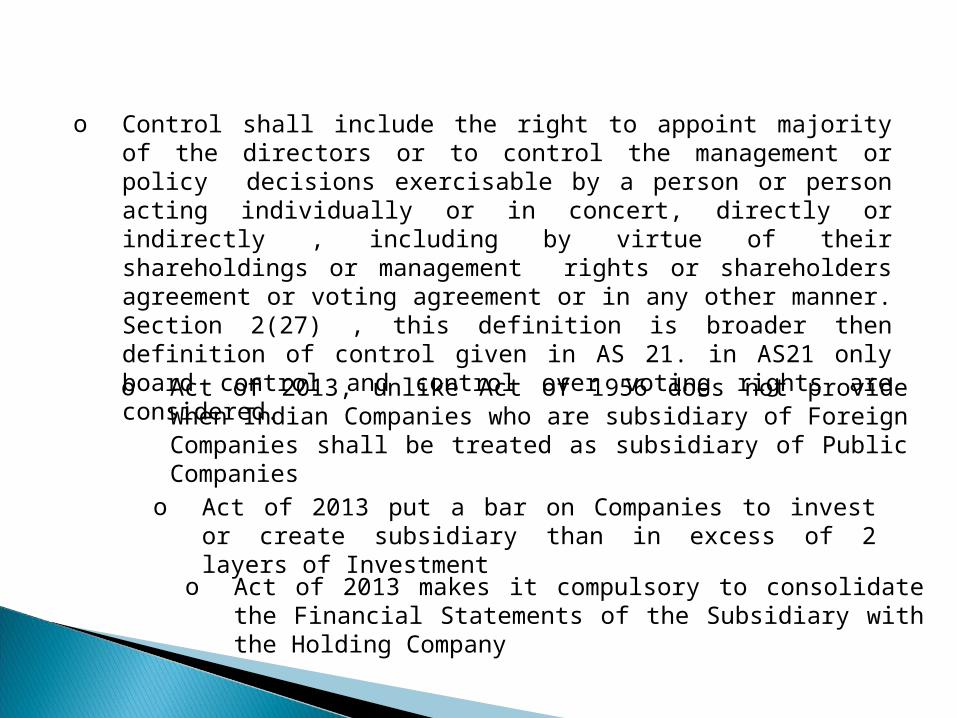

o Control shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or person acting individually or in concert, directly or indirectly , including by virtue of their shareholdings or management rights or shareholders agreement or voting agreement or in any other manner. Section 2(27) , this definition is broader then definition of control given in AS 21. in AS21 only board control and control over voting rights are considered.o Act of 2013, unlike Act of 1956 does not provide When

Indian Companies who are subsidiary of Foreign Companies shall be treated as subsidiary of Public Companies

o Act of 2013 put a bar on Companies to invest or create subsidiary than in excess of 2 layers of Investment

o Act of 2013 makes it compulsory to consolidate the Financial Statements of the Subsidiary with the Holding Company

‘‘Small Company’’ means a company, other than a public company,—

Relatively new concept and provides to classify companies on the basis of Capital and Turnover

Small Companies are exempted to comply or have relaxed application of Laws, e.g. 1. Relaxation to prepare CFS for FY. 2. two board meeting in a calendar year, provided gap between two meeting shall not be more then 90 days. 3. fast track merger without the requirement of court process.

ii. Turnover of which as per its last profit and loss account does not exceed two crores rupees or such higher amount as may be prescribed which shall not be more than twenty crores rupees:

Provided that nothing in this clause shall not apply to—(A) a holding company or a subsidiary company;(B) a company registered under section 8; or(C) a company or body corporate governed by any special Act;

“One Person Company” means a company which has only one person as a member; Now Private Company of Special Character can now have only

one Member and Director Only one Person can now Form a Company

A new provision of Nominee of lone Shareholder of the Company, in case of his/her death or insanity

No such provision existed in Act of 1956, in fact it did not even recognize Foreign OPC as Corporates

The Act provides certain exemptions to OPCs like relaxation in convening Board Meeting, no requirement to convene AGM, relaxation in maintenance of Annual Accounts, etc.

OPC may be of three types :1.A company limited by shares; or2.A company limited by guarantee; or3.An unlimited company

A One Person Company is incorporated as a Private Limited Company

The Member and Nominee should be Natural Persons, Indian Citizens and Resident in India

‘Resident of India’ is a person who has stayed in India for a period of not less than 182 days during immediately preceding Calendar Year One Person cannot incorporate more than one OPC or

become Nominee in more than one OPC

Person who becomes member of another OPC by virtue of being nominee in that OPC shall within 180 days meet the eligibility criterion of being member in one OPC

An existing private company other than a company registered under section 8 of the Act which has paid up share capital of Rs. 50 Lakhs or less or average annual

turnover during the relevant period is Rs. 2 Crore or less may

convert itself into one person company by passing a special resolution in the general meeting.

COMPULSORY CONVERSION:OPC loses its status, if PSC exceeds Rs. 50 Lac or Average Annual Turnover exceeds Rs. 2 Crore in immediate three preceding years

ADULTS ONLY:No minor is eligible to become Nominee or Member of OPC or hold share in Beneficiary Interest

ONLY COMMERCIAL ACTIVITIESOPC cannot be incorporated or converted into a Company under Section 8 of the Act of 2013

NO NBFC OR BANKING CORPORATIONOPC cannot carry out the Banking or Non-Banking Financial Investment activities including Investment in Securities of any Body Corporate

COMPULSORY LOCK-IN PERIODAn OPC cannot voluntarily convert into other forms of Company until two years have elapsed from Incorporation except for operation of Law

The Reserve Bank of India under its Master Circular No. RBI/2013-14/107 RPCD.CO. Plan.BC9/04.09.01/2013-14 dated July 01, 2013 has instructed all Scheduled Commercial Banks (excluding Regional Rural Banks) to increase their involvement in financing of priority sectors, viz., agriculture and small scale industries. The Master Circular provides for the following activities as being eligible for priority sector lending:

PRIORITY SECTOR LENDING

Enterprises

Investment in Plant and Machinery

Manufacturing Sector Service Sector

Micro Do not exceed Rupees 25 Lac

Does not exceed Rupees 10 Lac

SmallMore than Rs. 25 Lac butdoes not exceed Rs. 5 Crore

More than Rs. 10 Lac but doesnot exceed Rs. 2 Crore

One Person Company coming under any of the above categories may fall under priority sector lending. There is enormous scope for One Person Companies to leverage benefits of priority sector lending.

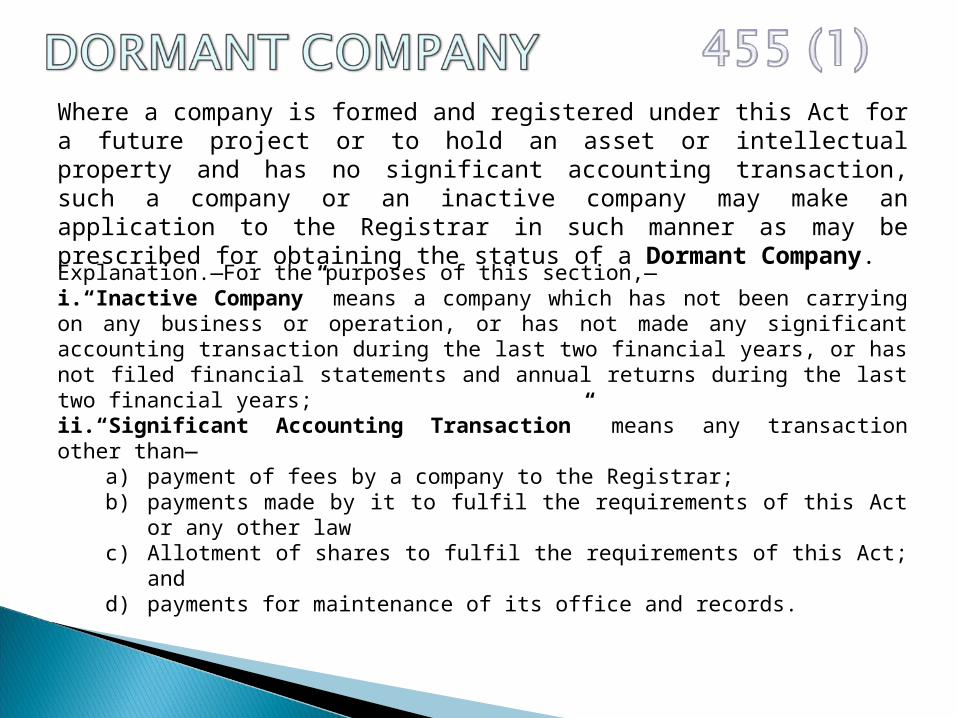

Where a company is formed and registered under this Act for a future project or to hold an asset or intellectual property and has no significant accounting transaction, such a company or an inactive company may make an application to the Registrar in such manner as may be prescribed for obtaining the status of a Dormant Company.

Explanation.—For the purposes of this section,—i.“Inactive Company” means a company which has not been carrying on any business or operation, or has not made any significant accounting transaction during the last two financial years, or has not filed financial statements and annual returns during the last two financial years;ii.“Significant Accounting Transaction” means any transaction other than—

a) payment of fees by a company to the Registrar;b) payments made by it to fulfil the requirements of this Act or any other

lawc) Allotment of shares to fulfil the requirements of this Act; andd) payments for maintenance of its office and records.

No Significant Accounting Transactions in last two Financial Years, or Inactive Company as per Explanation to Section 455(1) of Act of 2013

No inspection, inquiry or investigation has been ordered or taken up or carried out against the Company; and

AND

no prosecution has been initiated and pending against the company under any law; and

the company is neither having any public deposits which are outstanding nor the company is in default in payment thereof or interest thereon; and

the company is not having any outstanding loan, whether secured or unsecured:

Provided that if there is any outstanding unsecured loan, the company may apply after obtaining concurrence of the lender...; and

there is no dispute in the management or ownership of the company and a certificate shall be enclosed with the Application; and

the company does not have any outstanding statutory taxes, dues, duties etc. payable to the Central Government or any State Government or local authorities etc.; and

the company has not defaulted in the payment of workmen’s dues; and the securities of the company are not listed on any stock exchange

Not mandatory to prepare Cash Flow Statement for the Years under Dormancy

Eased norms in convening Board Meeting and only two meetings are required per Financial Year to comply with the relevant provisions

Registrar after issue of notice may tag a Company as Dormant Company, if the Company has not filed the Annual Returns for two consecutive Financial Years

Registrar, may after giving reasonable opportunity of being heard, may strike off a Company which has a Dormant Status for more than 5 consecutive Financial Years

Registrar, may also, tag a Dormant Company as Active if he has reasonable reason to believe that the Company is carrying on Business as an Active Company

Provision of Rotation of Directors are not applicable on Dormant Companies

Prohibition of association or partnership of persons exceeding certain number

The 2013 Act puts a restriction on the number of partners that can be admitted to a partnership at 50. To be specific, the 2013 Act states that no association or partnership consisting of more than the given number of persons as may be prescribed shall be formed for the purpose of carrying on any business that has for its object the acquisition of gain by the association or partnership or by the individual members thereof, unless it is registered as a company under this Act or is formed under any other law for the time being in force: As an exception, the aforesaid restriction would not apply to the following: 1. A Hindu undivided family carrying on any business 2. An association or partnership, if it is formed by professionals who are governed by special acts like the Chartered Accountants Act, etc.[section 464 of 2013 Act]

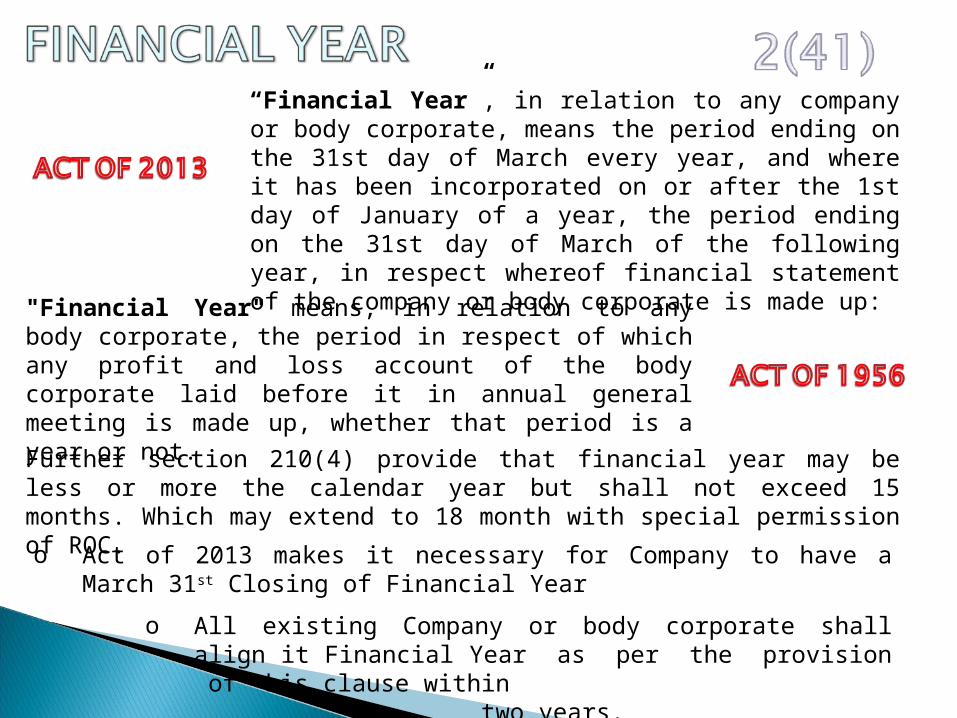

"Financial Year" means, in relation to any body corporate, the period in respect of which any profit and loss account of the body corporate laid before it in annual general meeting is made up, whether that period is a year or not.

o Act of 2013 makes it necessary for Company to have a March 31st Closing of Financial Year

“Financial Year”, in relation to any company or body corporate, means the period ending on the 31st day of March every year, and where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year, in respect whereof financial statement of the company or body corporate is made up:

Further section 210(4) provide that financial year may be less or more the calendar year but shall not exceed 15 months. Which may extend to 18 month with special permission of ROC.

o All existing Company or body corporate shall align it Financial Year as per the provision of his clause within

two years.

o An application can made by a Company or Body Corporate which is Subsidiary of a Company incorporated outside India and is required to follow a different Financial Year for consolidation of its account outside India, the tribunal may, if it is satisfied, allow any period as its financial year, whether or not that period is a year

o A Company with foreign subsidiary will be allowed to adopt different Financial Year only for consolidation of account out side India.

“Auditing Standards” means the standards of auditing or any addendum thereto for companies or class of companies referred to in sub-section (10) of section 143;

In Act of 2013, Auditing Standards are now recognized and have an authoritative value

Auditor has to adhere the norms as prescribed in the AuditingStandards

Auditing Standards issued by Institute of Chartered Accountants of India to apply till the time NFRA come into the existence and Central Government notifies the same.

Auditing Standards would be notified by Central Government on recommendation of NFRA

National Financial Reporting Authority to be constituted under Section 132 of the Act to advise Central Government regarding Accounting Standards

“Financial Statement” in relation to a company, includes—i.a Balance Sheet as at the end of the financial year;ii.a Profit and Loss Account, or in the case of a company carrying on any activity not for profit, an Income and Expenditure Account for the Financial Year;iii.Cash Flow Statement for the Financial Year;iv.a Statement of Changes in Equity, if applicable; andv.any explanatory note annexed to, or forming part of, any document referred to in sub-clause (i) to sub-clause (iv):Provided that the financial statement, with respect to One Person Company, small company and dormant company, may not include the cash flow statement;

Clear Definition of Financial Statements required to be maintained by a Company

Adds Cash Flow Statement to the list of Financial Statement

Gives relief to smaller Companies by exempting to prepared CFS

RELEVANT FACTOR ACCOUNTING STANDARD

COMPANIES ACT 2013

OPCNot a criterion for identification as SMC

Exempted from preparation of Cash Flow Statement

Dormant Not a criterion for identification as SMC

Exempted from preparation of Cash Flow Statement

Small and Medium Sized Companies Vs. Small Company

Turnover ≯Rs. 50 Crore ≯ Rs. 2 Crore

PSC No such requirement≯ 50 Lakh unless higher amount specified

Borrowings ≯Rs. 10 crore Not a criterion

ListingNeither listed nor in the process of Listing

Shall not be Public Company

Special catagoryCompany is not a Bank, FI, carrying insurance business

Company is not be Governed by Special Act nor to be registered under section 8

Holding SubsidiaryCompany is not a holding / subsidiary of non SMC

Company is an independent Company (not a holding subsidiary)

THE CA 2013 REQUIRES MORE COMPANIES TO PREPARE CASH FLOW STATEMENT

“Key Managerial Personnel”, in relation to a company, means-i.the Chief Executive Officer or the managing director or the manager;ii.the company secretary;iii.the whole-time director;iv.the Chief Financial Officer; andv.such other officer as may be prescribed; Section 203 read with Rule 8 of Companies (A&R of MP) Rules

2014 Listed Company and Company with min. paid up Capital of Rs. Ten Crore shall have following full time KMP.

1. MD, CEO, Mgr and in their absence a WTD2. CS; and3. CFOSame person can not be appointed as Chairman and MD/CEO

except AOA provide otherwise or company is in multiple business. In the amendment rules, (Rule 8A) Central Government

made it mandatory for a Company with Min. Capital of Rs. Five Crore to appoint a whole time Company Secretary

“Serious Fraud Investigation Office” means the office referred to in section 211;

Act of 2013 provides Statutory Recognition to SFIO

SFIO can now try the cases in special court who shall take cognizance of the case only on application of SFIO

SEC 211(1) - The Central Government shall, by notification, establish an office to be called the Serious Fraud Investigation Office to investigate frauds relating to a company:Provided that until the Serious Fraud Investigation Office is established under subsection (1), the Serious Fraud Investigation Office set-up by the Central Government in terms of the Government of India Resolution No. 45011/16/2003-Adm-I, dated the 2nd July, 2003 shall be deemed to be the Serious Fraud Investigation Office for the purpose of this section.

SFIO can now initiate investigation into affairs of the Company, prepare and submit the report to special court in the same manner like a Police Officer under CrPC

If any case assigned to SFIO then no other agency of CG/SG shall proceed with investigation in such case in respect of any offence under this Act and in case if any such investigation has already been initiated, it shall not be proceed further with and the concern agency shall transfer the relevant documents and records in respect of such offence under this Act to SFIO [Section 212(2)]

CG may by an order assign the Investigation of a Company to SFIO and its Director in following cases:

On receipt of a Report of the Registrar or Inspector under Section 208 [Investigation Report by ROC / Inspector]

On intimation of a special resolution passed by a company that its affairs are require to be investigate

On intimation of a Special Resolution passed by a company that its affairs are require to be investigate

In Public Interest; or

On request of any Department of State of Central Government

Provided that where the fraud in question involves public interest, the term of imprisonment shall not be less than

three years.

Explanation to Section 447

i. “Fraud” in relation to affairs of a company or any body corporate, includes any act, omission, concealment of any fact or abuse of position committed by any person or any other person with the connivance in any manner, with intent to deceive, to gain undue advantage from, or to injure the interests of, the company or its shareholders or its creditors or any other person, whether or not there is any wrongful gain or wrongful loss;

ii. “Wrongful Gain” means the gain by unlawful means of property to which the person gaining is not legally entitled;

iii. “Wrongful Loss” means the loss by unlawful means of property to which the person losing is legally entitled.

Without prejudice to any liability including repayment of any debt under this Act or any other law for the time being in force, any person who is found to be guilty of fraud, shall be punishable with imprisonment for a term which shall not be less than six months but which may extend to ten years and shall also be liable to fine which shall not be less than the amount involved in the fraud, but which may extend to three times the amount involved in the fraud:

PUNISHMENT

Notwithstanding anything contained in the Code of Criminal Procedure, 1973, the offences covered under following :

Section Particular

7 (5)(6)False information, suppress any information at the time of Incorporation or found false any time in future

8(11) Affair of section 8 company conducted fraudulently

34 Criminal liabilities misstatement in prospectus

36 Fraudulently inducing person to invest money

38(1) For making multiple application by fictitious name for shares

46(5) Issue of duplicate share certificate with intent to defraud

56(7) Transfer of shares by DP or depository with intent to defraud

140(5)If Auditor of company directly or indirectly acted in fraudulently manner

And many more

b. in any affidavit, deposition or solemn affirmation, in or about the winding up of any company under this Act, or otherwise in or about any matter arising under this Act, he shall be punishable with imprisonment for a term which shall not be less than three years but

which may extend to seven years and with fine which may extend to ten lakh rupees.

448. Punishment for false statementSave as otherwise provided in this Act, if in any return, report, certificate, financial statement, prospectus, statement or other document required by, or for, the purposes of any of the provisions of this Act or the rules made there under, any person makes a statement,—a. which is false in any material particulars, knowing it to be false; or

b. which omits any material fact, knowing it to be material, he shall be liable under section 447

449. Punishment for false evidence

Save as otherwise provided in this Act, if any person intentionally gives false evidence—

a. upon any examination on oath or solemn affirmation, authorized under this Act; or

2% of average net profits* made during the 3 immediately preceding financial years Every Financial Year to be calculated in accordance with provisions of section 198

Net Worth ≥ Rs.500 crore

EVERY COMPANY *

To constitute

CSR Committee of the Board

Turnover ≥ Rs.1,000 crore

Net Profit ≥ Rs.5 crore

* during any financial year

Min. 1 Independent Director

The Board Report to disclose the composition of CSR Committee

3 or more

Directors

CSR Committe

e

Recommend the amount of expenditure to be incurred on CSR activities

**activities to be undertaken as specified in Schedule VII of the Companies Act, 2013

Formulate and recommend to the Board, a CSR Policy **

Monitor CSR Policy of the Company

APPLICABILITY Every listed company; and

A company belonging to other class of companies as may be prescribed

Every Public Company having PSC ≥ 50 crore

Every public Company having turnover ≥ 250 Crore

REQUIREMENT OF REGISTERED VALUERS`

Where a valuation is required to be made in respect of –

any property, stocks, shares, debentures, securities, goodwill or any other asset of the Company (“Assets”); or

net-worth of a company; or

its liabilities under the provisions of the Companies Act, 2013

Eligibility: Valuation shall be done by a person having such qualifications and experience and registered as a Valuer in such manner, on such terms and conditions as may be prescribed.

Appointment: Such valuer to be appointed by the Audit Committee or in its absence, by the Board of Directors of the Company

REGISTERED VALUERS (S. 247)

Duties of Valuer

To make an impartial, true and fair valuation of any assets, required to be valued;

To exercise due diligence; To make valuation in accordance with such

rules as may be prescribed; Not to undertake valuation of any asset(s) in

which he has a direct or indirect interest; or becomes so interested at any time during or after the valuation of the assets.

REGISTERED VALUERS (S. 247)

Penal Provisions u/s 247(3)For contravention of provisions of the

section or the rules made thereunder

Fine –Minimum Rs.25,000, but which may extend to Rs.1,00,000; or

In case of intention to defraud the company or its members

Imprisonment up to 1-years; or Fine – Min. Rs.1,00,000. Max.

Rs.5,00,000

REGISTERED VALUERS

National Financial Reporting Authority (NFRA) to be constituted by Central Government to provide for dealing with matters relating to accounting and auditing policies and standards to be followed by companies and their auditors

SRA

A new quasi-judicial body comes up–NFRA

To oversee quality of service of professionals

associated with preparation of financial

statements

To recommending, monitoring and enforcing compliance of accounting and auditing standards

It is a complete new quasi judicial body – complete with Appellate Authority, having powers of a civil court

“Director” means a director appointed to the Board of a company;

"director" includes any person occupying the position of director, by whatever name called

o Act of 2013 excludes the concept of de-facto Director. Only a person who is appointed on the Board of Directors to be called a Director of the Company

o Act of 1956 provided for the Directors who could be called as a Director of the Company without being appointed on the Board

o Act of 2013 lays emphasis on the Director being the member of the Board, while act of 1956 laid the emphasis on the being the director of the Company by the virtue of control and occupation of the post of Director

NEW CONCEPTS RELATING TO DIRECTORS

1. Listed Company 2. Other public Company having PSC ≥100 crore or turnover ≥ 300 crore

WOMAN DIRECTOR [Proviso to S. 149(1)]

RESIDENT DIRECTOR [S. 149(3)]Every company shall have resident director who have stay in India for a total period of not less then 180 days

SMALL SHAREHOLDERS’ DIRECTOR [S. 151] Every listed company may appoint a director of

small share holders small share holders means a share holder who holding shares of nominal value not exceeding Rs. 20000.

• Such director shall be consider as independent director

• Such director shall not non rotational director• Tenure shall not exceed three consecutive year.• Such person can not be director of small

shareholders in more then two company .

SRA

Independent Director

Every Listed Company

Other PUBLIC Company having

Paid-up share capital of Rs.10 cr

or more

Having in aggregate

outstanding loans or Borrowings or

Debentures or Deposits exceeding

Rs. 50 Crores

Turnover of Rs.100 cr or

more

One third of total Number

of Director

Section 139

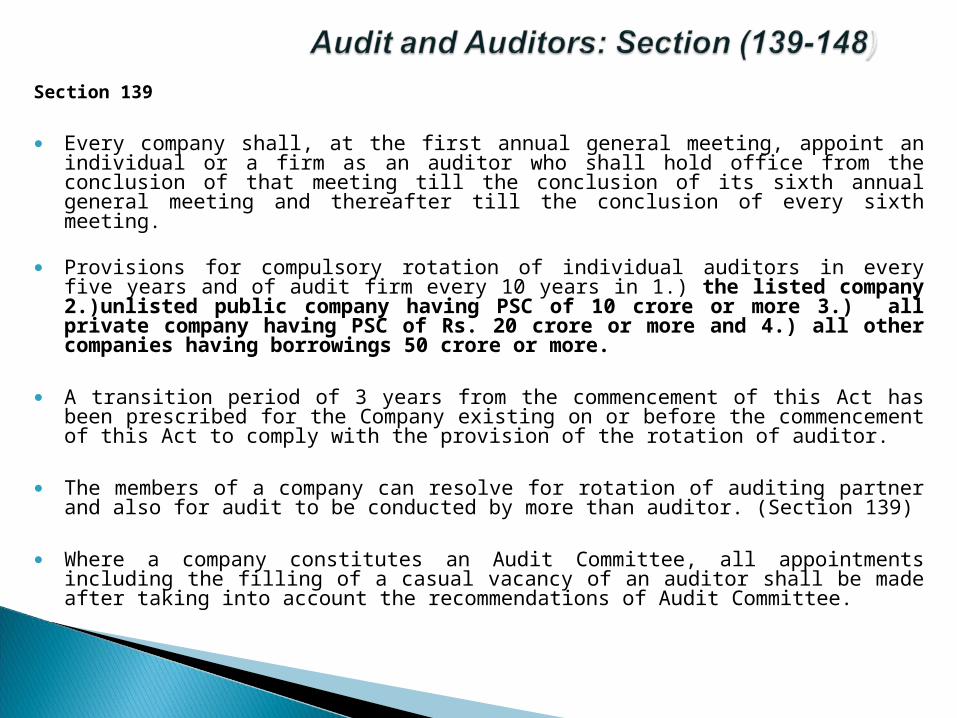

● Every company shall, at the first annual general meeting, appoint an individual or a firm as an auditor who shall hold office from the conclusion of that meeting till the conclusion of its sixth annual general meeting and thereafter till the conclusion of every sixth meeting.

● Provisions for compulsory rotation of individual auditors in every five years and of audit firm every 10 years in 1.) the listed company 2.)unlisted public company having PSC of 10 crore or more 3.) all private company having PSC of Rs. 20 crore or more and 4.) all other companies having borrowings 50 crore or more.

● A transition period of 3 years from the commencement of this Act has been prescribed for the Company existing on or before the commencement of this Act to comply with the provision of the rotation of auditor.

● The members of a company can resolve for rotation of auditing partner and also for audit to be conducted by more than auditor. (Section 139)

● Where a company constitutes an Audit Committee, all appointments including the filling of a casual vacancy of an auditor shall be made after taking into account the recommendations of Audit Committee.

● Appointment is done once for 5 years● Ratification done every year● There is a confusion between the terms “ratification” and “reappointment”.● Mandatory retirement after 5 years in case of individual and 10 years in case of firms● – no auditor/audit firm/ audit firms having common partners, shall take audit for a

consecutive term of 5 years after 5 years have been completed● A person at the time of appointment or reappointment holding appointment as auditor of

more than twenty companies shall not be eligible for appointment. (Section 141 (3) (g))● In case, LLP is appointed as auditor only chartered Accountants is allowed to act and sign

on behalf of the firm. Section 141(2)● Multidisciplinary partnership is allowed. Proviso to Section 141(1)

![basavaraj hiremath [mailto:shrinidhi.pvtltd@gmail.com]environmentclearance.nic.in/writereaddata/... · 1 Ravi Kumar Yadav B.V From: Ravi Kumar Yadav B.V Sent: Friday 24 February 2017](https://img.pdfslide.net/doc/110x75/5f3164a79694af65280317b2/basavaraj-hiremath-mailto-gmailcomenvironmentclearancenicinwritereaddata.jpg)

![[IJCT V3I4P15] Authors: K. Ravi Kumar, P. Karthik](https://img.pdfslide.net/doc/110x75/5888a0911a28ab264b8b5d31/ijct-v3i4p15-authors-k-ravi-kumar-p-karthik.jpg)