Embed Size (px)

Citation preview

Sales Desk

Milan Office +39 02 8829 211

New York Office +1 212 991 4745

London Office +44 (0) 207 8625 530

Biancamano

13 April 2011 Industrials Initiating Coverage

Price: € 1.55 Target price: € 2.50 Outperform

Simonetta Chiriotti

Equity Analyst

+39 02 8829 933

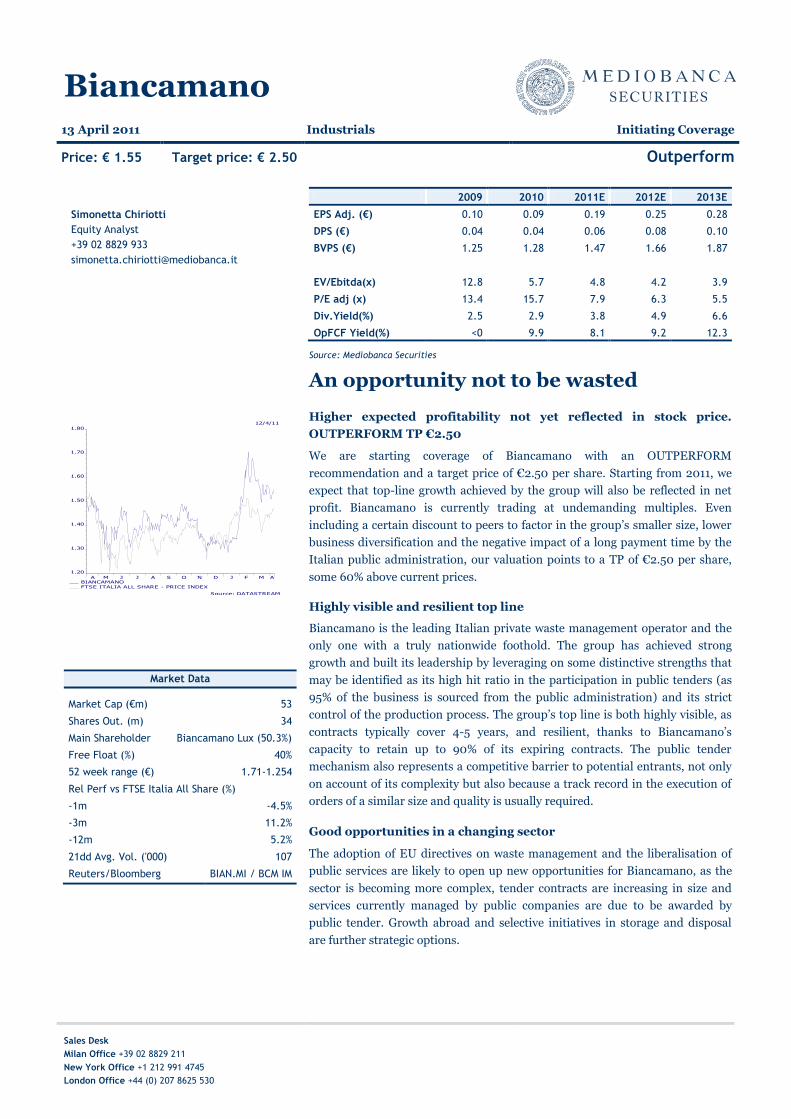

2009 2010 2011E 2012E 2013E

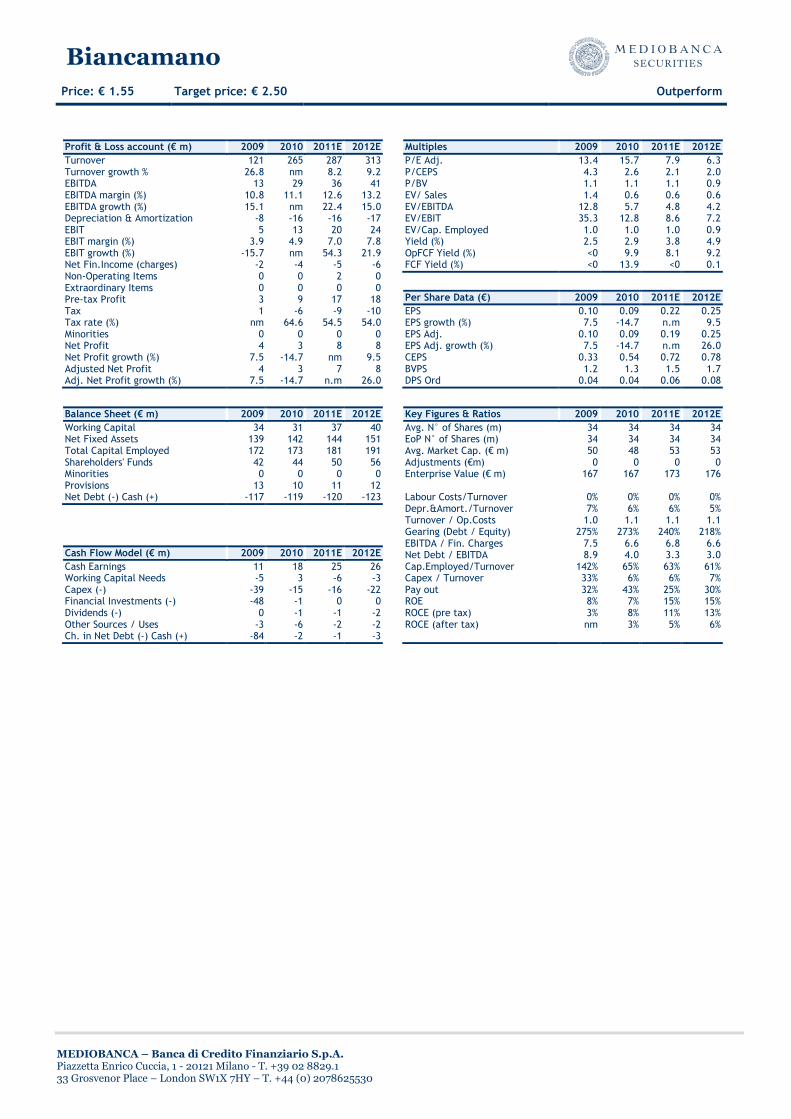

EPS Adj. (€) 0.10 0.09 0.19 0.25 0.28

DPS (€) 0.04 0.04 0.06 0.08 0.10

BVPS (€) 1.25 1.28 1.47 1.66 1.87

EV/Ebitda(x) 12.8 5.7 4.8 4.2 3.9

P/E adj (x) 13.4 15.7 7.9 6.3 5.5

Div.Yield(%) 2.5 2.9 3.8 4.9 6.6

OpFCF Yield(%) <0 9.9 8.1 9.2 12.3

Source: Mediobanca Securities

An opportunity not to be wasted

Higher expected profitability not yet reflected in stock price.

OUTPERFORM TP €2.50

We are starting coverage of Biancamano with an OUTPERFORM

recommendation and a target price of €2.50 per share. Starting from 2011, we

expect that top-line growth achieved by the group will also be reflected in net

profit. Biancamano is currently trading at undemanding multiples. Even

including a certain discount to peers to factor in the group‟s smaller size, lower

business diversification and the negative impact of a long payment time by the

Italian public administration, our valuation points to a TP of €2.50 per share,

some 60% above current prices.

Highly visible and resilient top line

Biancamano is the leading Italian private waste management operator and the

only one with a truly nationwide foothold. The group has achieved strong

growth and built its leadership by leveraging on some distinctive strengths that

may be identified as its high hit ratio in the participation in public tenders (as

95% of the business is sourced from the public administration) and its strict

control of the production process. The group‟s top line is both highly visible, as

contracts typically cover 4-5 years, and resilient, thanks to Biancamano‟s

capacity to retain up to 90% of its expiring contracts. The public tender

mechanism also represents a competitive barrier to potential entrants, not only

on account of its complexity but also because a track record in the execution of

orders of a similar size and quality is usually required.

Good opportunities in a changing sector

The adoption of EU directives on waste management and the liberalisation of

public services are likely to open up new opportunities for Biancamano, as the

sector is becoming more complex, tender contracts are increasing in size and

services currently managed by public companies are due to be awarded by

public tender. Growth abroad and selective initiatives in storage and disposal

are further strategic options.

12/4/11

A M J J A S O N D J F M A

1.20

1.30

1.40

1.50

1.60

1.70

1.80

BIANCAMANOFTSE ITALIA ALL SHARE - PRICE INDEX

Source: DATASTREAM

Market Data

Market Cap (€m) 53

Shares Out. (m) 34

Main Shareholder Biancamano Lux (50.3%)

Free Float (%) 40%

52 week range (€) 1.71-1.254

Rel Perf vs FTSE Italia All Share (%)

-1m -4.5%

-3m 11.2%

-12m 5.2%

21dd Avg. Vol. ('000) 107

Reuters/Bloomberg BIAN.MI / BCM IM

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 2

Contents

Executive summary 3

Valuation 5

Company profile 10

Snapshot 10

Waste management 12

Disposal and storage 19

Competitive environment and strategy 21

Moving towards European best practice 21

Growth in the core business in Italy and abroad 25

Financials 27

2006-2010: building the leadership in waste management 27

2011–2013 forecasts: further growth and a focus on profitability 32

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 3

Executive summary Biancamano is the leader among Italian private waste management operators and the only company

with a truly nationwide foothold. Waste management accounts for the largest part of the business

while operations in treatment and disposal declined following the shutdown of Ponticelli.

The group‟s distinctive strengths are its strong success in winning public tenders (as 95% of the

business is sourced from the public administration) and the strict control of the production process.

Strong track record in public tenders

Public tenders in Italy are complex and strictly regulated. Since the public administration accounts for

95% of total revenues, Biancamano sources most of its business from participating in public tenders.

The group focuses almost exclusively on tenders based on the best economic offer i.e. tenders in which

the awarding rule is not the lower price but the best economic offer in terms of quality of the service,

project and, to a lesser extent, price.

Sourcing its business from public tenders and formalising the relationship with its customers in long-

term contracts has a positive impact on the group in terms of:

Visibility - long-term contracts mean that the group may count on a large backlog covering

the following four to five years.

Resilience – the group‟s turnover is highly resilient due to the ability of Biancamano to retain

up to 90% of expiring business when a tender is renewed, resulting in a positive impact on

profitability.

Competitive strength - the public tender mechanism represents a barrier to entry for new

competitors not only because of their complex bureaucracy but also because they set specific

requirements to allow bidders to participate. In particular, a track record in the execution of

similar order by size, technical characteristics and type of territory are usually required.

In 2010 the group examined 2,185 tenders and made an offer for 59. It won 30 contracts out of the 59

bids, a high 51% success ratio.

Strict control of the production process

Local operations are linked to the centre via a computerised system that allows the strict monitoring of

people and vehicles, to increase operational efficiency and control costs. The system is very extensive

since it has to connect some 3,000 vehicles and 3,700 employees serving customers in 16 regions, and

has to be easily scalable because each new tender means additional vehicles and employees. Waste

management is both capital (investment in vehicles) and labour intensive. As far as the employees are

concerned, it should be underlined that specific regulation is applied in the case of contracts with the

public administration. When a contract with a public entity is lost the related employees are taken over

by the winner thus making the management of the labour force more flexible and the whole business

less risky. Conversely, not being able to choose the labour force from scratch makes it even more

important to be able to organise, co-ordinate and control people. The group-wide IT-based planning

and control system is an essential tool in achieving this goal.

High capex and net working capital (NWC) requirements

Financially the business requires strong capex paid upfront and a relatively large investment in

working capital due to the slow payments by the public administration. When Biancamano wins a new

contract with the public administration, the company has to buy the vehicles to provide the service

immediately, with an investment that amounts to some 10% of the cumulative revenues. Conversely,

the fees from the public administration are billed monthly but actually settled with a delay of several

months thus determining the necessity to finance growing NWC.

Leasing and an “opportunistic” use of factoring are used by Biancamano to control and give flexibility

to its financial position.

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 4

Operations in the storage and disposal segment have had a setback

While waste management operations (the collection and transportation of urban waste) grew steadily,

the group‟s treatment and disposal activities suffered a setback. Through its subsidiary Ponticelli,

Biancamano owns and manages a landfill in Imperia that in 2010 was temporarily shutdown. Even if

re-opened, prospects here are limited as the plant has almost reached its full capacity.

Biancamano is developing some new niches in this area, a new Waste Electric and Electronic

Equipment (WEEE) plant is due to open in Mondovì; however, we do not expect strong growth from

these developments in the near future.

Strong growth opportunities for Biancamano in a changing sector

While being still behind the standards that characterise most advanced European countries, the Italian

waste management sector is gradually moving towards best practices. Due to the adoption of EU

directives on waste management and the liberalisation of public services, the sector is becoming more

complex, contracts tendered are increasing in size and services currently managed by public

companies are due to be assigned in public tenders opened to private players. This challenging and

dynamic scenario will offer strong growth opportunities for Biancamano, the private sector leader. The

company is well placed to obtain a growing share in the domestic market due to its strong track record

in public tenders and its solid organisation. Growth abroad and selective initiatives in storage and

disposal are further strategic options.

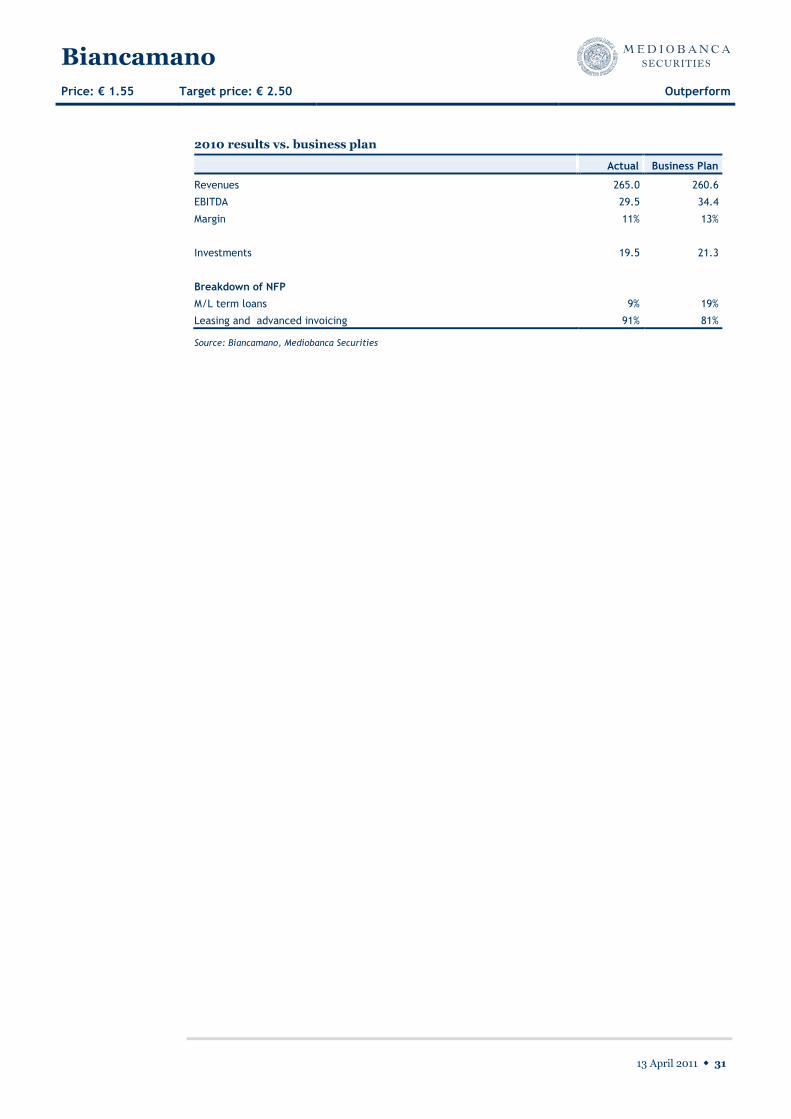

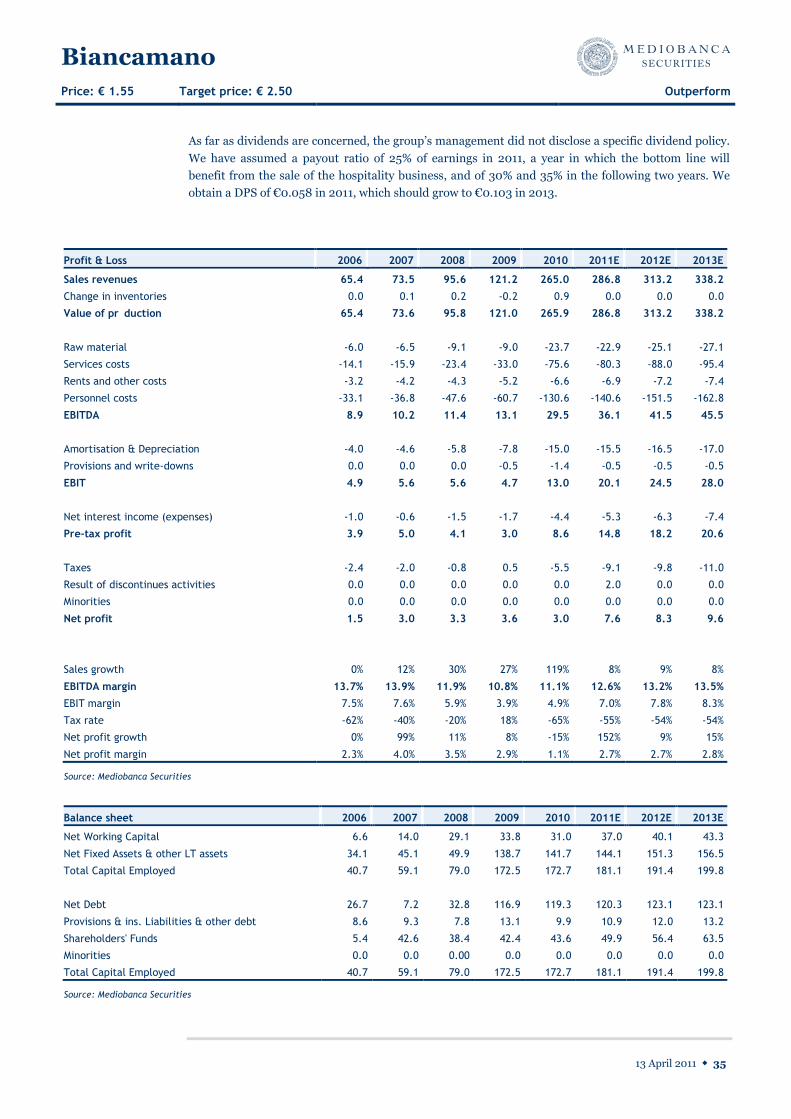

Sales growth to be reflected at the bottom line starting from 2011

2006-2010 has been characterised by a strong growth, both organic and through the acquisition of

MSA, driving Biancamano‟s top line from €65m to €265m. Waste management margins improved

strongly in 2010 benefiting from economies of scale and higher profitability of new contracts.

However, recovery at the consolidated level was partially offset by the closure of the Ponticelli landfill,

while at the bottom line progress was impacted by higher taxes.

Going forward, we expect that the improvement in the top line and EBITDA will be reflected in the

group‟s bottom line. In 2011-2013 we expect high single-digit annual revenues growth and a 235 bps

margin recovery. While debt will continue to be controlled (due to an “opportunistic” use of factoring),

we expect the bottom line to finally start reflecting the group‟s increased size.

Starting coverage with OUTPERFORM recommendation; TP €2.50

We have based our valuation of Biancamano on peer multiples and DCF. While peer multiples point to

a very significant upside for Biancamano, we believe that a certain discount should be applied to the

stock to reflect its lower size and business diversification and the negative impact of slow payment by

the Italian public administration. Our target price of €2.5 per share is based on our conservative DCF

valuation and the bottom end of the range of peer multiples and points to an upside some 60% above

the current price.

Main risks: low liquidity and regulation

We have identified two specific risks for Biancamano:

1. Low liquidity due to the stock‟s modest free float – excluding Biancamano Lux, the treasury

shares and some other stable shareholders, the group‟s free float amounts to around 40% of

the total or about €20m at current prices.

2. Regulation and exposure to the public administration – while sector regulation today offers

more opportunities than threats, it cannot be denied that the group operates in a highly

regulated business environment and exposure to the public administration could become

more challenging going forward.

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 5

Valuation We have based our valuation of Biancamano on peer multiples and DCF. While peer

multiples point to very significant upside for Biancamano, we believe that a certain

discount should be applied to the stock to reflect its small size, lower business

diversification and the negative impact of slow payment by the Italian public

administration. Our target price of €2.50 per share weights equally our conservative

DCF valuation and a valuation that reflects the bottom end of the peer group multiples

and points an upside above 80% to the current price.

Biancamano is the only operator in the waste management sector listed in Italy, while in Europe

Groupe Pizzorno, Seche Environnement SA and Shanks Group PLC are the main players. In the US,

Republic Services Inc and Waste Connections Inc have leading positions. Similar to Biancamano,

these companies are active in waste management (collection and transportation) but have larger

operations in the area of waste treatment and disposal.

Group Pizzorno – Group Pizzorno (€190m turnover in 2010) is a French-based company

which provides both pure waste management services (waste collection, transport, selection,

street cleaning) accounting for some 76% of revenues, and waste treatment, 24% of turnover

(storage and processing facilities for household garbage, industrial wastes, slurries and slag).

France accounts for 80% of net sales while the remaining 20% comes from its subsidiaries in

Morocco, Tunisia and Mauritania.

Seche Environnement SA – the group (€402.1m revenues in 2010) is the third-largest

operator in France for waste treatment, recycling and storage. The group also offers site

decontamination services (waste sorting and transportation, site rehabilitation, and soil

decontamination). Net sales by activity are split as follows: 59% hazardous waste and 41%

non-hazardous waste.

Shanks Group PLC – Shanks Group PLC (£685m sales in 2010) is a UK-based waste

management company operating in the UK, the Netherland, Belgium and Canada. The

company offers a full range of waste collection, transport, recycling, treatment, and disposal

services, including landfill and incinerator operations, and hazardous waste collection and

disposal systems.

Republic Services Inc – this is an US group (US$8.1bn sales in 2010) involved in the

collection, transfer and disposal of non-hazardous solid waste for commercial, industrial and

residential customers. Republic Services Inc serves millions of residential customers under

contracts with more than 2,800 municipalities.

Waste Connections Inc - Waste Connections (US$1.32bn sales in 2010) is an integrated

solid waste services company that provides waste collection, transfer, disposal and recycling

services in mostly secondary markets in the Western and Southern US. The company serves

more than two million residential, commercial and industrial customers across 27 states.

Our second group of peers include companies that are active in both waste management/treatment

and in other services. These companies are either public utilities or service providers. For all these

companies waste management is a leading contributor to their revenues and operating profits while

we have excluded from the sample the Italian utility Iren for which waste management accounts only

7% of EBITDA.

Hera – this is the Italian utility with the greatest focus on waste management, a sector that

accounted for 18% of 2010 revenues (2010 revenues €3,669m) and is the largest contributor

to the group‟s EBITDA, accounting for 32.1% of the total. Gas is the second-largest

contributor to EBITDA (31.9%), followed by water (23%) and electricity (9.8%).

Our peer sample

includes pure waste

management

companies...

...and diversified

players with a strong

presence in waste

management

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 6

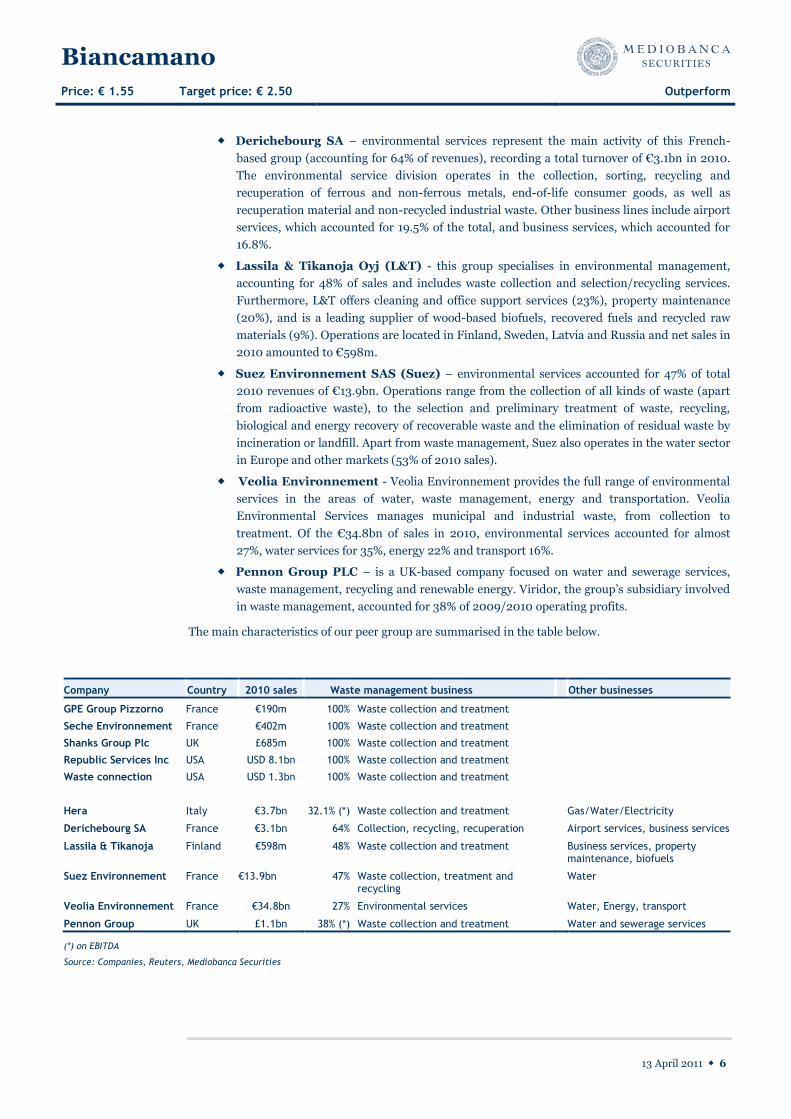

Derichebourg SA – environmental services represent the main activity of this French-

based group (accounting for 64% of revenues), recording a total turnover of €3.1bn in 2010.

The environmental service division operates in the collection, sorting, recycling and

recuperation of ferrous and non-ferrous metals, end-of-life consumer goods, as well as

recuperation material and non-recycled industrial waste. Other business lines include airport

services, which accounted for 19.5% of the total, and business services, which accounted for

16.8%.

Lassila & Tikanoja Oyj (L&T) - this group specialises in environmental management,

accounting for 48% of sales and includes waste collection and selection/recycling services.

Furthermore, L&T offers cleaning and office support services (23%), property maintenance

(20%), and is a leading supplier of wood-based biofuels, recovered fuels and recycled raw

materials (9%). Operations are located in Finland, Sweden, Latvia and Russia and net sales in

2010 amounted to €598m.

Suez Environnement SAS (Suez) – environmental services accounted for 47% of total

2010 revenues of €13.9bn. Operations range from the collection of all kinds of waste (apart

from radioactive waste), to the selection and preliminary treatment of waste, recycling,

biological and energy recovery of recoverable waste and the elimination of residual waste by

incineration or landfill. Apart from waste management, Suez also operates in the water sector

in Europe and other markets (53% of 2010 sales).

Veolia Environnement - Veolia Environnement provides the full range of environmental

services in the areas of water, waste management, energy and transportation. Veolia

Environmental Services manages municipal and industrial waste, from collection to

treatment. Of the €34.8bn of sales in 2010, environmental services accounted for almost

27%, water services for 35%, energy 22% and transport 16%.

Pennon Group PLC – is a UK-based company focused on water and sewerage services,

waste management, recycling and renewable energy. Viridor, the group‟s subsidiary involved

in waste management, accounted for 38% of 2009/2010 operating profits.

The main characteristics of our peer group are summarised in the table below.

Company Country 2010 sales Waste management business Other businesses

GPE Group Pizzorno France €190m 100% Waste collection and treatment

Seche Environnement France €402m 100% Waste collection and treatment

Shanks Group Plc UK £685m 100% Waste collection and treatment

Republic Services Inc USA USD 8.1bn 100% Waste collection and treatment

Waste connection USA USD 1.3bn 100% Waste collection and treatment

Hera Italy €3.7bn 32.1% (*) Waste collection and treatment Gas/Water/Electricity

Derichebourg SA France €3.1bn 64% Collection, recycling, recuperation Airport services, business services

Lassila & Tikanoja Finland €598m 48% Waste collection and treatment

Business services, property maintenance, biofuels

Suez Environnement France €13.9bn 47% Waste collection, treatment and recycling

Water

Veolia Environnement France €34.8bn 27% Environmental services Water, Energy, transport

Pennon Group UK £1.1bn 38% (*) Waste collection and treatment Water and sewerage services

(*) on EBITDA

Source: Companies, Reuters, Mediobanca Securities

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 7

At current prices, Biancamano‟s multiples are undemanding. The group‟s 2011 PE ratio is 8x even after

adjusting earnings for the capital gain expected from the sale of the hospitality business. Additionally,

the stock looks cheap in terms of EV/EBITDA, EV/EBIT and cash flow.

Biancamano price multiples (2011e/12e/13e at current market price)

€ 2007 2008 2009 2010 2011e 2012e 2013e

EV/Sales 1.4 1.0 1.4 0.6 0.6 0.6 0.5

EV/EBITDA 10.0 8.2 12.8 5.6 4.8 4.2 3.9

EV/EBIT 18.3 16.7 35.3 12.7 8.6 7.2 6.3

P/E 32.1 18.5 14.2 14.9 8.0 6.3 5.5

P/CF 14.1 6.6 4.5 2.5 2.1 2.0 1.9

Yield 1.6% 0.0% 2.4% 3.0% 3.8% 4.9% 6.6%

Source: Mediobanca Securities

Biancamano peers‟ multiples are summarised in the table below. The differences among the two

segments, pure waste management companies vs. diversified groups, do not appear to be significant

and, in general, multiples are similar on the various metrics.

Country Company Currency Price Mkt Cap PER Gross Yield EV/EBIT P/CFPS

Local € m 11E 12E 13E 10 11E 11E 12E 13E 11E 12E 13E 11E 12E 13E

Waste management 11,551 15.7 13.5 12.8 2.0% 2.1% 7.4 6.8 6.5 11.2 10.1 9.3 7.1 7.0 4.9

France GPE GROUPE PIZZORNO E 18.6 74 8.8 7.8 n.a. 1.9% 2.3% n.a. n.a. n.a. 7.2 6.5 n.a. n.a. n.a. n.a.

France SECHE ENVIRONNEMENT E 63.4 547 13.7 12.5 10.0 2.1% 2.4% 6.7 6.2 5.6 10.1 9.5 8.5 6.3 6.4 4.6

UK SHANKS GROUP PLC. £ 117.2 527 18.9 15.0 12.2 2.6% 2.6% 6.5 6.0 5.4 13.5 12.1 10.4 5.3 6.3 5.1

USA REPUBLIC SVS.INCO. U$ 29.9 7,993 15.8 13.8 12.3 2.7% 2.7% 6.8 6.4 5.9 10.4 9.8 9.0 7.3 6.8 n.a.

USA WST.CONNECTIONS INCO. U$ 30.2 2,410 21.1 18.2 16.8 1.0% 0.5% 9.6 8.6 8.9 14.7 12.8 n.a. 9.6 8.7 n.a.

Waste management & other services 24,216 15.1 13.3 12.0 3.6% 4.4% 6.9 6.4 6.0 12.0 10.9 10.1 5.4 4.9 4.6

Italy HERA SPA E 1.7 1,884 15.4 14.1 13.0 4.7% 5.9% 5.9 5.7 5.6 10.7 10.2 10.0 4.4 4.2 4.6

France DERICHEBOURG E 6.0 1,029 9.9 8.2 7.7 0.0% 1.5% 5.7 4.8 4.5 8.9 7.3 6.6 5.3 4.4 4.3

Finland LASSILA & TIKANOJA PLC E 12.8 497 14.9 13.1 11.9 3.4% 4.5% 6.6 6.0 5.5 12.3 10.6 9.4 6.3 6.0 5.6

France SUEZ ENVIRONNEMENT CO. E 14.7 7,189 16.5 14.7 12.9 4.4% 4.7% 5.9 5.6 5.3 12.3 11.5 10.6 4.1 3.9 3.6

France VEOLIA ENVIRONNEMENT E 22.2 11,076 16.7 14.9 13.0 5.5% 5.6% 6.7 6.4 6.1 11.8 11.1 10.4 3.7 3.4 3.3

UK PENNON GROUP PLC. £ 626.5 2,542 17.0 14.9 13.3 3.7% 3.9% 10.5 9.8 9.2 16.1 14.8 13.7 8.6 7.5 6.2

Total 35,768 15.3 13.4 12.3 2.9% 3.3% 7.1 6.6 6.2 11.6 10.6 9.9 6.1 5.8 4.7

Average 15.3x 13.4x 12.3x 2.9% 3.3% 7.1x 6.6x 6.2x 11.6x 10.6x 9.9x 5.3x 5.0x 4.5x

Median 15.8x 14.1x 12.6x 2.7% 2.7% 6.7x 6.1x 5.6x 11.8x 10.6x 10.0x 5.3x 4.4x 4.6x

EV/EBITDA

Source: Datastream, Mediobanca Securities

We have focused our valuation on 2011 multiples. On the basis of the pure waste management

companies we obtain a valuation range of €3.0-€5.0 per share, with the bottom obtained using an

EBIT multiple (11x) and the top with a cash flow multiple. The diversified companies produce a range

in valuation for Biancamano of €2.9-€4.0 per share.

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

PER

EV/EBITDA

EV/EBIT

P/CF

Source: Mediobanca Securities

Biancamano is

currently trading at

undemanding multiples

2011 multiples point to

a valuation above €3.0

per share

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 8

The valuation based on peer multiples points to very significant upside. However, at the moment we

would apply a certain discount to peer-based valuation to reflect some characteristics of Biancamano:

1) Lower size – with a market cap of around €50m, Biancamano is much smaller and less liquid

than the peers included in the sample.

2) Lower exposure to treatment and disposal operations - while Biancamano is focused almost

exclusively on waste collection, its competitors have strong operations in treatment, recycling

and disposal, activities with high operating profitability and growth prospects. Going forward

Biancamano hopes to increase slightly these operations; however, due to the specific

characteristics of the sector in Italy, we do not expect strong growth in this area.

3) Impact of slow payments by the Italian public administration – the abnormally slow

payments of the Italian public administration are not reflected at the EBIT or EBITDA level,

but have a cost for Biancamano that should be included in the valuation.

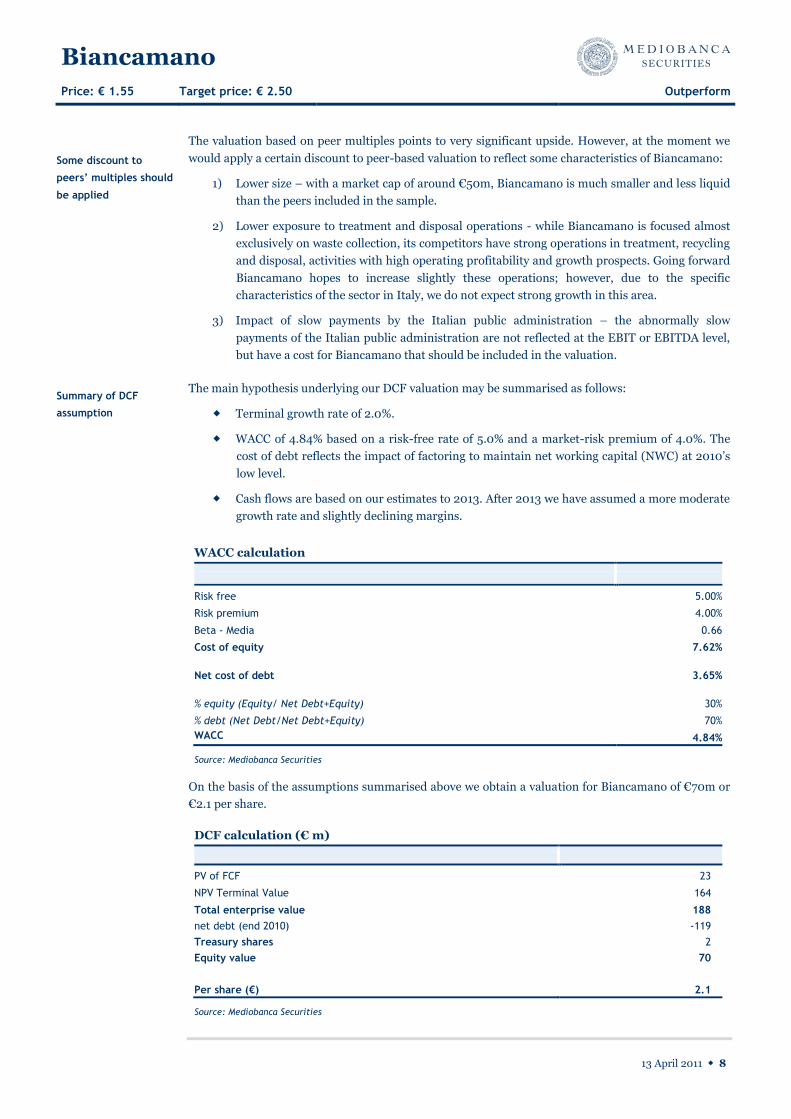

The main hypothesis underlying our DCF valuation may be summarised as follows:

Terminal growth rate of 2.0%.

WACC of 4.84% based on a risk-free rate of 5.0% and a market-risk premium of 4.0%. The

cost of debt reflects the impact of factoring to maintain net working capital (NWC) at 2010‟s

low level.

Cash flows are based on our estimates to 2013. After 2013 we have assumed a more moderate

growth rate and slightly declining margins.

WACC calculation

Risk free 5.00%

Risk premium 4.00%

Beta - Media 0.66

Cost of equity 7.62%

Net cost of debt 3.65%

% equity (Equity/ Net Debt+Equity) 30%

% debt (Net Debt/Net Debt+Equity) 70%

WACC 4.84%

Source: Mediobanca Securities

On the basis of the assumptions summarised above we obtain a valuation for Biancamano of €70m or

€2.1 per share.

DCF calculation (€ m)

PV of FCF 23

NPV Terminal Value 164

Total enterprise value 188

net debt (end 2010) -119

Treasury shares 2

Equity value 70

Per share (€) 2.1

Source: Mediobanca Securities

Some discount to

peers’ multiples should

be applied

Summary of DCF

assumption

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 9

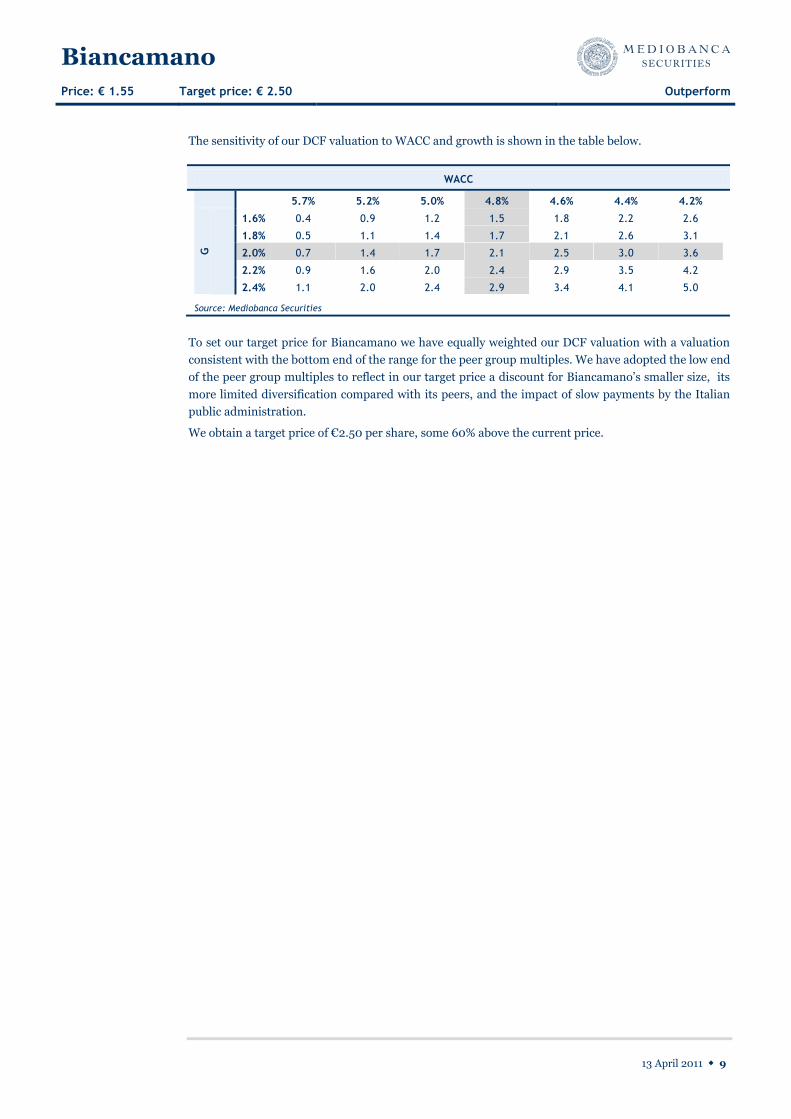

The sensitivity of our DCF valuation to WACC and growth is shown in the table below.

WACC

5.7% 5.2% 5.0% 4.8% 4.6% 4.4% 4.2% G

1.6% 0.4 0.9 1.2 1.5 1.8 2.2 2.6

1.8% 0.5 1.1 1.4 1.7 2.1 2.6 3.1

2.0% 0.7 1.4 1.7 2.1 2.5 3.0 3.6

2.2% 0.9 1.6 2.0 2.4 2.9 3.5 4.2

2.4% 1.1 2.0 2.4 2.9 3.4 4.1 5.0

Source: Mediobanca Securities

To set our target price for Biancamano we have equally weighted our DCF valuation with a valuation

consistent with the bottom end of the range for the peer group multiples. We have adopted the low end

of the peer group multiples to reflect in our target price a discount for Biancamano‟s smaller size, its

more limited diversification compared with its peers, and the impact of slow payments by the Italian

public administration.

We obtain a target price of €2.50 per share, some 60% above the current price.

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 10

Company profile Biancamano is the leader among Italian private waste management operators and the

only company with a truly nationwide foothold. Waste management accounts for the

largest part of the business while operations in storage and treatment declined

following the shutdown of Ponticelli.

The group’s distinctive strengths are its success in winning public tenders (as 95% of the

business is sourced from the public administration) and in the strict control of the

production process. While the public tender mechanism represents a barrier to entry

for potential competitors, public contracts give strong visibility and resilience to the

group’s top line. Local operations are linked to the centre via a computerised system

that allows a strict monitoring of people and vehicles, to increase operational efficiency

and control costs. Financially the business requires strong capex paid upfront and a

relatively large investment in working capital due to the slow payments by the public

administration. Leasing and an “opportunistic” use of factoring are used by

Biancamano to control and give flexibility to its financial position.

Snapshot

Biancamano is the Italian leader in the waste management sector. The group is active in the area of

urban cleaning services and has a smaller operation in the disposal and storage of urban waste and

waste from differentiated collection. Biancamano SpA operates as a holding company, co-ordinating

the activity of two specialised subsidiaries: Aimeri Ambiente in waste management and Ponticelli in

waste storage and treatment.

Group’s structure

99.98%

PONTICELLI

95%

AIMERI

AMBIENTE

5%

Waste management Storage & treatment

50.3%

PIERPAOLO PIZZIMBONE

MASSIMODEL BECCHI

70% 3.3%26.7%

BIANCAMANO

49.7%

BIANCAMANO LUXEMBOURG

GIOVANNI BATTISTA PIZZIMBONE

OTHER SHAREHOLDERS

0.9%

Source: Biancamano, Mediobanca Securities

In 2004 Giovanni Battista Pizzimbone, a manager of Ponticelli SRL, created Biancamano SpA and

through this company acquired Ponticelli, which at that time was active both in waste disposal/storage

and in waste management. In the same year, Biancamano acquired Aimeri Ambiente from the Green

Holding group and transferred Ponticelli‟s operations in waste management to Aimeri.

The main Italian

private operator in the

waste management

sector

A group created by

experienced managers

aggregating leading

companies in

environmental services

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 11

Both Ponticelli and Aimeri, at the time of the acquisition by Biancamano, had long-term experience in

environmental services. Founded in 1973, Aimeri was a leading company in waste management in

Northern Italy while Ponticelli had operated in waste storage and disposal since 1977 and in waste

management since the end of the 1980s.

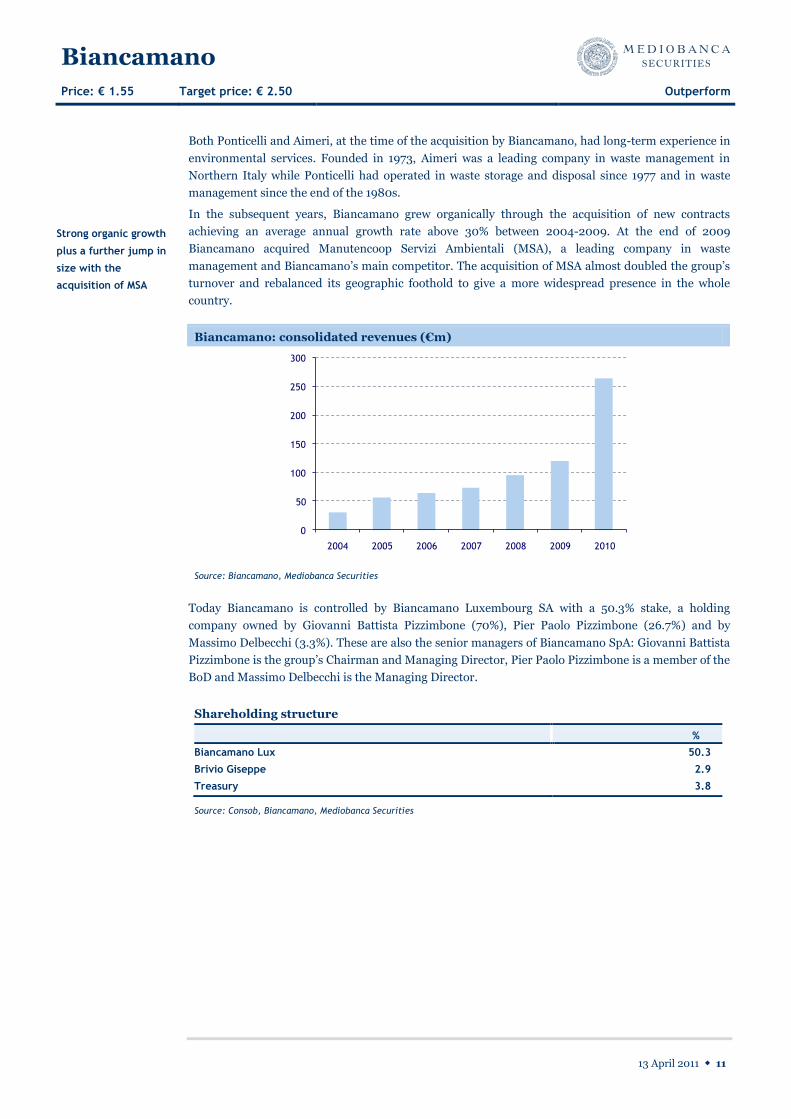

In the subsequent years, Biancamano grew organically through the acquisition of new contracts

achieving an average annual growth rate above 30% between 2004-2009. At the end of 2009

Biancamano acquired Manutencoop Servizi Ambientali (MSA), a leading company in waste

management and Biancamano‟s main competitor. The acquisition of MSA almost doubled the group‟s

turnover and rebalanced its geographic foothold to give a more widespread presence in the whole

country.

Biancamano: consolidated revenues (€m)

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010

Source: Biancamano, Mediobanca Securities

Today Biancamano is controlled by Biancamano Luxembourg SA with a 50.3% stake, a holding

company owned by Giovanni Battista Pizzimbone (70%), Pier Paolo Pizzimbone (26.7%) and by

Massimo Delbecchi (3.3%). These are also the senior managers of Biancamano SpA: Giovanni Battista

Pizzimbone is the group‟s Chairman and Managing Director, Pier Paolo Pizzimbone is a member of the

BoD and Massimo Delbecchi is the Managing Director.

Shareholding structure

%

Biancamano Lux 50.3

Brivio Giseppe 2.9

Treasury 3.8

Source: Consob, Biancamano, Mediobanca Securities

Strong organic growth

plus a further jump in

size with the

acquisition of MSA

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 12

Waste management

Waste management, run through the subsidiary Aimeri Ambiente, represents the bulk of the group‟s

operations accounting for 93% of revenues in 2009 and 99% in 2010.

Waste management includes a number of different activities:

Collection and transportation of urban waste to disposal and storage centres – waste may be

collected either door-to-door or from large containers located in public areas (road

collection) and may be both undifferentiated or differentiated (glass, paper, plastic, etc.) or

hazardous waste (out of date medications, flat batteries, toxic or inflammable containers,

etc.). Biancamano always operates in urban waste and not in industrial/specialist waste.

Street cleaning services – general street cleaning involves the cleaning of the entire road

network either manually of using machinery. These services may also include the emptying of

rubbish bins, the weeding and cleaning of areas following commercial activities, fairs or

parades, and snow clearing.

Other related services – to customise its services to the customers‟ needs, Aimeri may offer

services such as the management and maintenance of containers used for the collection of

waste, computerised management of services (giving the customer the opportunity to closely

monitor the services provided by Aimeri), information awareness campaigns, and the

management of call centres.

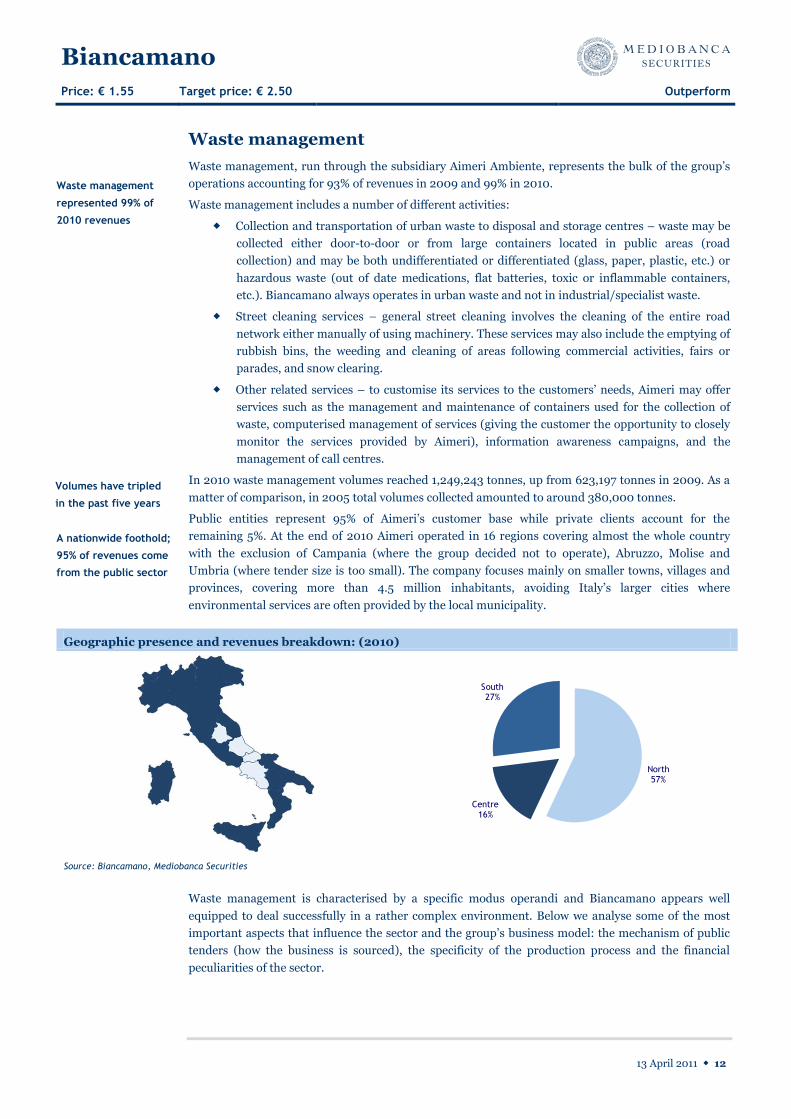

In 2010 waste management volumes reached 1,249,243 tonnes, up from 623,197 tonnes in 2009. As a

matter of comparison, in 2005 total volumes collected amounted to around 380,000 tonnes.

Public entities represent 95% of Aimeri‟s customer base while private clients account for the

remaining 5%. At the end of 2010 Aimeri operated in 16 regions covering almost the whole country

with the exclusion of Campania (where the group decided not to operate), Abruzzo, Molise and

Umbria (where tender size is too small). The company focuses mainly on smaller towns, villages and

provinces, covering more than 4.5 million inhabitants, avoiding Italy‟s larger cities where

environmental services are often provided by the local municipality.

Geographic presence and revenues breakdown: (2010)

North57%

Centre16%

South27%

Source: Biancamano, Mediobanca Securities

Waste management is characterised by a specific modus operandi and Biancamano appears well

equipped to deal successfully in a rather complex environment. Below we analyse some of the most

important aspects that influence the sector and the group‟s business model: the mechanism of public

tenders (how the business is sourced), the specificity of the production process and the financial

peculiarities of the sector.

Waste management

represented 99% of

2010 revenues

Volumes have tripled

in the past five years

A nationwide foothold;

95% of revenues come

from the public sector

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 13

Strong track record in public tenders

Business from public entities can be only be acquired by winning public tenders. The sector is

regulated by the “Public Procurement Code” (Dl 163/06) that identifies two possible awarding rules:

Lower price – in this case the contract is awarded to the bidder that offers the lowest price.

Best economic offer – the contract is awarded to the bidder that makes the best economic

offer in terms of: quality of the service, characteristics of the machinery and equipment used

to provide the service, environmental impact and price.

Aimeri Ambiente rarely participates in tenders that include the lower price as an awarding rule

because in these tenders no value is given to the provider‟s planning and management capabilities.

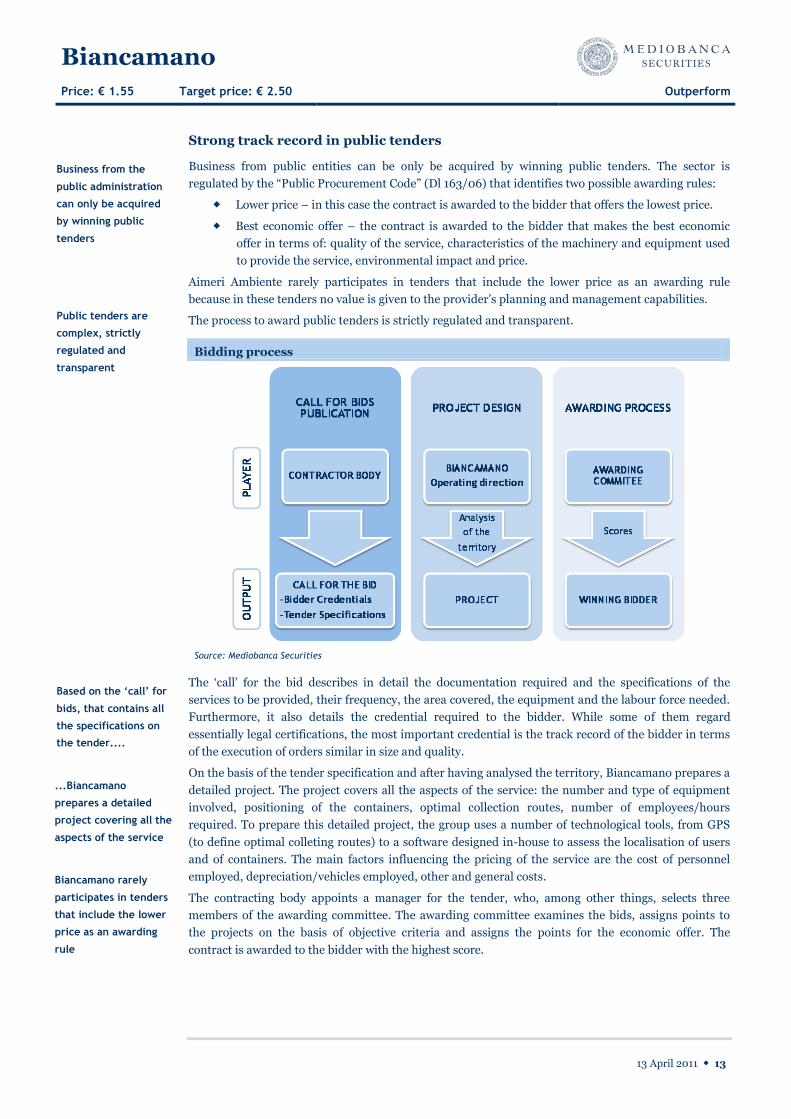

The process to award public tenders is strictly regulated and transparent.

Bidding process

Source: Mediobanca Securities

The „call‟ for the bid describes in detail the documentation required and the specifications of the

services to be provided, their frequency, the area covered, the equipment and the labour force needed.

Furthermore, it also details the credential required to the bidder. While some of them regard

essentially legal certifications, the most important credential is the track record of the bidder in terms

of the execution of orders similar in size and quality.

On the basis of the tender specification and after having analysed the territory, Biancamano prepares a

detailed project. The project covers all the aspects of the service: the number and type of equipment

involved, positioning of the containers, optimal collection routes, number of employees/hours

required. To prepare this detailed project, the group uses a number of technological tools, from GPS

(to define optimal colleting routes) to a software designed in-house to assess the localisation of users

and of containers. The main factors influencing the pricing of the service are the cost of personnel

employed, depreciation/vehicles employed, other and general costs.

The contracting body appoints a manager for the tender, who, among other things, selects three

members of the awarding committee. The awarding committee examines the bids, assigns points to

the projects on the basis of objective criteria and assigns the points for the economic offer. The

contract is awarded to the bidder with the highest score.

Business from the

public administration

can only be acquired

by winning public

tenders

Public tenders are

complex, strictly

regulated and

transparent

Based on the ‘call’ for

bids, that contains all

the specifications on

the tender....

...Biancamano

prepares a detailed

project covering all the

aspects of the service

Biancamano rarely

participates in tenders

that include the lower

price as an awarding

rule

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 14

Contracts typically offer the winner a fixed fee for a defined number of years; the variable components

are usually negligible. For example, the last contract won in 2010 to provide waste management

services in Rapallo (Liguria) is due to earn Biancamano €3.8m per year for four years for a total

amount of €15m. On average, contracts are worth €1m-€3m per year and have a duration between five

and eight years. The fixed annual fee is subject to annual revisions on the basis of inflation, of fuel

prices and changes in the cost of labour, and additional amounts may be added if the parties have

agreed to include some supplementary services.

Local authorities today tend to extend the duration of the contracts and to enlarge the area served to

optimise bidding costs. To do so, the contracting body is often an ATO, Ambito Territoriale Ottimale,

i.e. an entity covering an area typically as large as a province, or a consortium of municipalities. In

these cases bidders set up JVs/consortia (so called ATI or Associazione Temporanea d‟Impresa), in

which Biancamano is usually the leader with a 70%/80% stake, and after winning the bid they split the

territory in areas in which each partner operates independently.

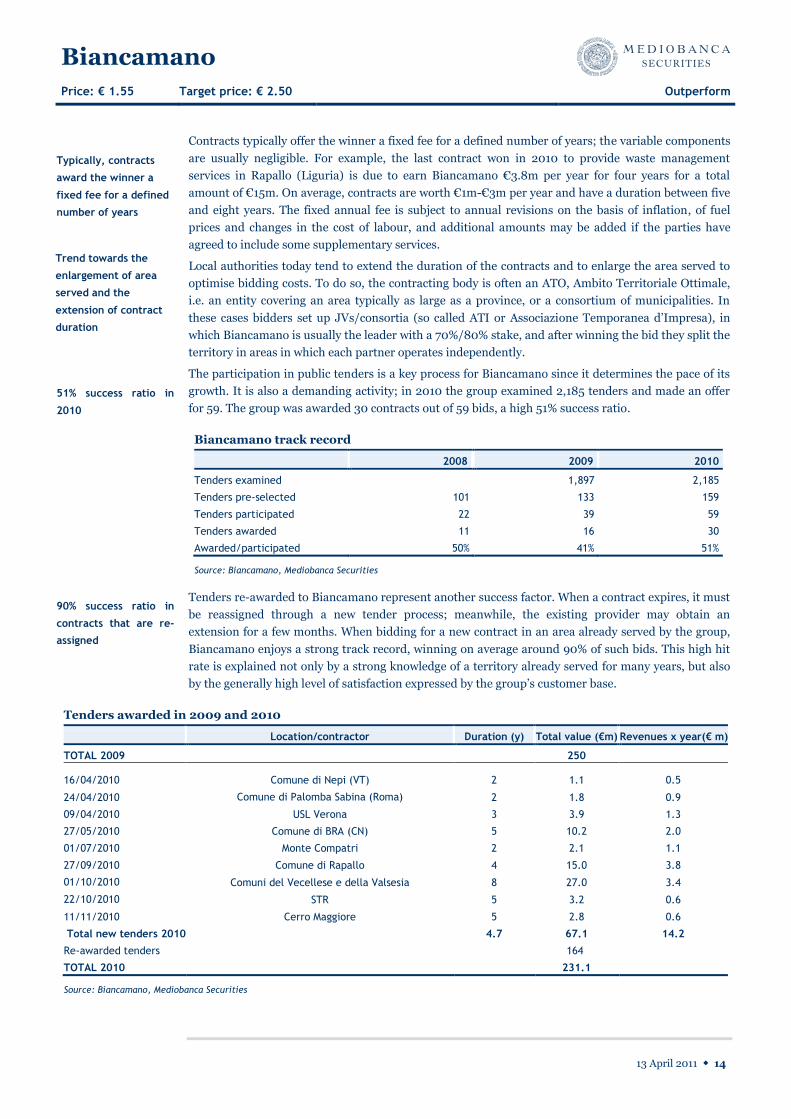

The participation in public tenders is a key process for Biancamano since it determines the pace of its

growth. It is also a demanding activity; in 2010 the group examined 2,185 tenders and made an offer

for 59. The group was awarded 30 contracts out of 59 bids, a high 51% success ratio.

Biancamano track record

2008 2009 2010

Tenders examined 1,897 2,185

Tenders pre-selected 101 133 159

Tenders participated 22 39 59

Tenders awarded 11 16 30

Awarded/participated 50% 41% 51%

Source: Biancamano, Mediobanca Securities

Tenders re-awarded to Biancamano represent another success factor. When a contract expires, it must

be reassigned through a new tender process; meanwhile, the existing provider may obtain an

extension for a few months. When bidding for a new contract in an area already served by the group,

Biancamano enjoys a strong track record, winning on average around 90% of such bids. This high hit

rate is explained not only by a strong knowledge of a territory already served for many years, but also

by the generally high level of satisfaction expressed by the group‟s customer base.

Tenders awarded in 2009 and 2010

Location/contractor Duration (y) Total value (€m) Revenues x year(€ m)

TOTAL 2009 250

16/04/2010 Comune di Nepi (VT) 2 1.1 0.5

24/04/2010 Comune di Palomba Sabina (Roma) 2 1.8 0.9

09/04/2010 USL Verona 3 3.9 1.3

27/05/2010 Comune di BRA (CN) 5 10.2 2.0

01/07/2010 Monte Compatri 2 2.1 1.1

27/09/2010 Comune di Rapallo 4 15.0 3.8

01/10/2010 Comuni del Vecellese e della Valsesia 8 27.0 3.4

22/10/2010 STR 5 3.2 0.6

11/11/2010 Cerro Maggiore 5 2.8 0.6

Total new tenders 2010 4.7 67.1 14.2

Re-awarded tenders 164

TOTAL 2010 231.1

Source: Biancamano, Mediobanca Securities

Typically, contracts

award the winner a

fixed fee for a defined

number of years

Trend towards the

enlargement of area

served and the

extension of contract

duration

51% success ratio in

2010

90% success ratio in

contracts that are re-

assigned

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 15

As reported in the table above, the acquisition of new business in the past number of years has been

strong. In particular, in 2009, new business was boosted by Terra dei Fenici, a contract to provide

waste management services in Sicily and specifically in the area of Marsala, Alcamo, Favignana and

Pantelleria for a total of some 220,000 users. The contract is worth €160m over seven years pointing

to a contribution of almost €23m per year.

Sourcing its growth from public tenders and formalising the relationship with its customers in long-

term contracts has a positive impact on the group in terms of:

Visibility - long-term contracts mean that the group may report a large backlog covering the

following four to five years. The group does not regularly update this figure. However, at the

end of 2009 Biancamano disclosed a backlog of around €200m per year in 2010-2012, a

figure that we expect to be still valid in 2011-2012. In March 2011, the group declared that it

had full visibility on 80% of its FY 2011 turnover target, implying that the backlog on the

current year amounted to around €230m. Furthermore, even if no official figure is disclosed,

the group has already secured a good part of the business expected for the following years.

Resilience – the group‟s turnover is highly resilient due to the ability of Biancamano to retain

up to 90% of expiring business when a tender is renewed. This is also a key point in terms of

profitability as bids for areas already served often generate a higher profitability because the

group has already made some investments for that contract and assets can be partially re-

used if the contract is won again or sold.

Competitive strength - from a competitive point of view, the public tender mechanism

represents a barrier to entry for new competitors not only because of their complex

bureaucracy but also because they set specific requirements to allow bidders to participate. In

particular, call for tenders usually require a track record in the execution of similar orders by

size, technical characteristics and type of territory, thus making the size and past history of

the company an import competitive strength.

The public tender

mechanism represents

a barrier to enter

while public contracts

give strong visibility

and resilience to the

group's top line

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 16

Strict control of the production process

Biancamano directly provides services through its employees and utilising vehicles owned by the

group. The use of subcontractors is not frequent and is usually limited to some seasonal activities like

weeding or snow clearing.

The group has a centralised structure. Locally, Biancamano has only a small premise in each territory

served, just a road yard where the vehicles are parked and a small administrative operation. However,

local operations are linked to the centre and monitored through a computerised system that allows

strict control on the vehicles and people involved in local activities and the production in real time of a

P&L for these operations. The group‟s system is based on GPS receivers positioned on most vehicles

and on transponders placed on the waste containers that are connected to the central IT system. The

system enables the company to:

track in real time the position of the vehicles and control, even after some time, the route

covered and the time employed to empty the containers;

plan in advance the optimal route for the various vehicles on the basis of the positioning of

the containers;

check the number of times each container is emptied to bill this item specifically to the

customer if this is included in the contract;

analyse the productivity of each vehicle in terms of speed, stops, length covered to optimise

operating costs.

The system described above is very extensive, since it connects some 3,000 vehicles and 3,700

employees serving customers in 16 regions, and has to be easily scalable because each new tender

means additional vehicles and employees.

Operating data

2006 2007 2008 2009 2010

Number of employees (avg) 1,058 1,154 1,434 1,720 3,698

Number of operating centres 32 38 39 74 84

Number of regions 7 9 11 17 16

Number of municipalities 200 210 248 461 n.a

Number of inhabitants (m) 1 1.3 1.5 4.4 n.a

Number of vehicles 912 1,121 1,182 2,739 3,035

Source: Biancamano, Mediobanca Securities

As reported in the table above, waste management is both capital (investment in vehicles) and labour

intensive. As far as the employees are concerned, it should be underlined that specific regulation is

applied in the case of contracts with the public administration. The most important aspect is that

when a contract with a public entity is lost, the related employees are taken over by the winner thus

making the management of the labour force more flexible and the whole business less risky.

Conversely, not being able to choose the labour force from scratch makes it even more important to be

able to organise, co-ordinate and control people. The group-wide IT-based planning and control

system is an essential tool in achieving this goal.

Labour force details

Average number 2006 2007 2008 2009 2010

Management - 2 2 2 4

Staff 80 76 83 99 203

Workers 968 1,064 1,326 1,592 3,296

Consultants on an ongoing basis 10 13 23 27 24

Total 1,058 1,154 1,434 1,720 3,527

Source: Biancamano, Mediobanca Securities

The group directly

provides urban

cleaning services;

limited use of

subcontractors

Local operations are

linked to the centre

with a computerised

system that allows a

strict monitoring of

people and vehicles

An extensive and

scalable system

A highly labour

intensive sector

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 17

Financing capex and NWC

Biancamano has to finance its growth both in terms of capex and working capital; for each new

contract it has to sustain relatively large investments in vehicles upfront while dealing with the public

administration in Italy means extremely slow payments.

When Biancamano wins a new contract with the public administration, the company has immediately

to buy the vehicles to provide the service; conversely, the fees from the public administration are billed

monthly but are typically settled with a delay of several months.

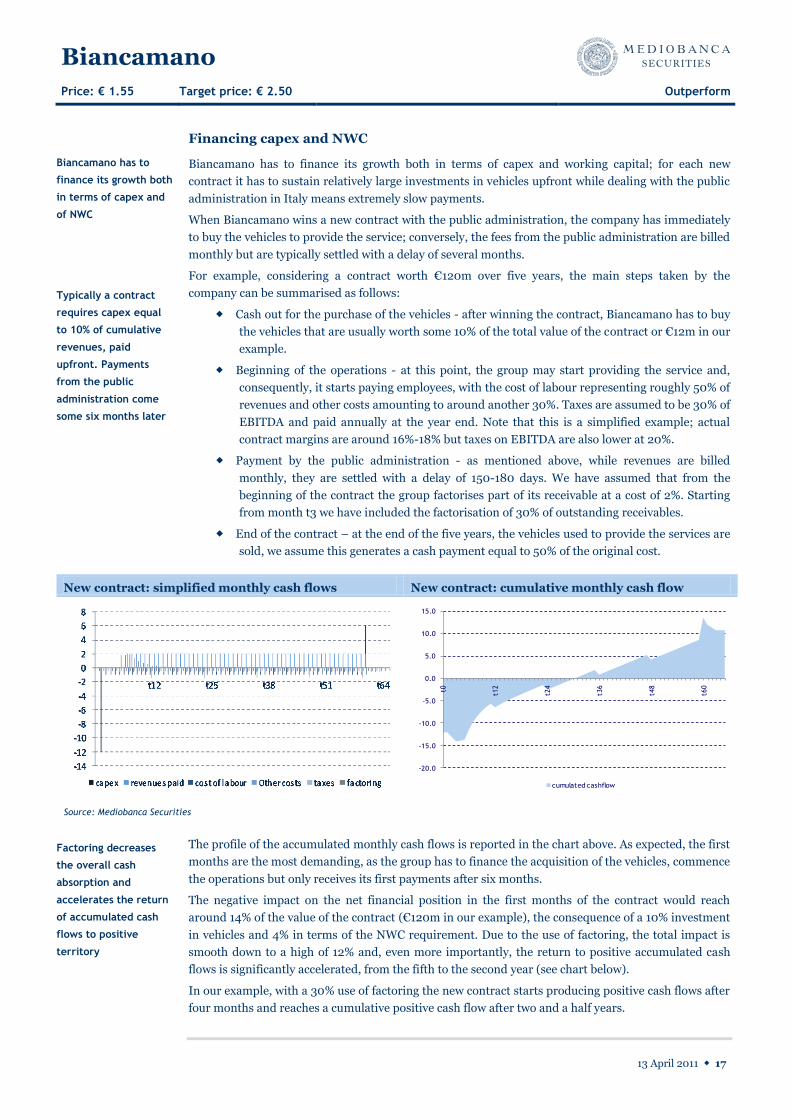

For example, considering a contract worth €120m over five years, the main steps taken by the

company can be summarised as follows:

Cash out for the purchase of the vehicles - after winning the contract, Biancamano has to buy

the vehicles that are usually worth some 10% of the total value of the contract or €12m in our

example.

Beginning of the operations - at this point, the group may start providing the service and,

consequently, it starts paying employees, with the cost of labour representing roughly 50% of

revenues and other costs amounting to around another 30%. Taxes are assumed to be 30% of

EBITDA and paid annually at the year end. Note that this is a simplified example; actual

contract margins are around 16%-18% but taxes on EBITDA are also lower at 20%.

Payment by the public administration - as mentioned above, while revenues are billed

monthly, they are settled with a delay of 150-180 days. We have assumed that from the

beginning of the contract the group factorises part of its receivable at a cost of 2%. Starting

from month t3 we have included the factorisation of 30% of outstanding receivables.

End of the contract – at the end of the five years, the vehicles used to provide the services are

sold, we assume this generates a cash payment equal to 50% of the original cost.

New contract: simplified monthly cash flows New contract: cumulative monthly cash flow

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

t0

t12

t24

t36

t48

t60

cumulated cashflow

Source: Mediobanca Securities

The profile of the accumulated monthly cash flows is reported in the chart above. As expected, the first

months are the most demanding, as the group has to finance the acquisition of the vehicles, commence

the operations but only receives its first payments after six months.

The negative impact on the net financial position in the first months of the contract would reach

around 14% of the value of the contract (€120m in our example), the consequence of a 10% investment

in vehicles and 4% in terms of the NWC requirement. Due to the use of factoring, the total impact is

smooth down to a high of 12% and, even more importantly, the return to positive accumulated cash

flows is significantly accelerated, from the fifth to the second year (see chart below).

In our example, with a 30% use of factoring the new contract starts producing positive cash flows after

four months and reaches a cumulative positive cash flow after two and a half years.

Biancamano has to

finance its growth both

in terms of capex and

of NWC

Typically a contract

requires capex equal

to 10% of cumulative

revenues, paid

upfront. Payments

from the public

administration come

some six months later

Factoring decreases

the overall cash

absorption and

accelerates the return

of accumulated cash

flows to positive

territory

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 18

New contract – impact of factoring Renewal: cumulated monthly cash flow

-20%

-15%

-10%

-5%

0%

5%

10%

15%

t0 t12 t24 t36 t48 t60

30% factoring 0% factoring

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

t0

t12

t24

t36

t48

t60

cumulated cashflow

Source: Mediobanca Securities

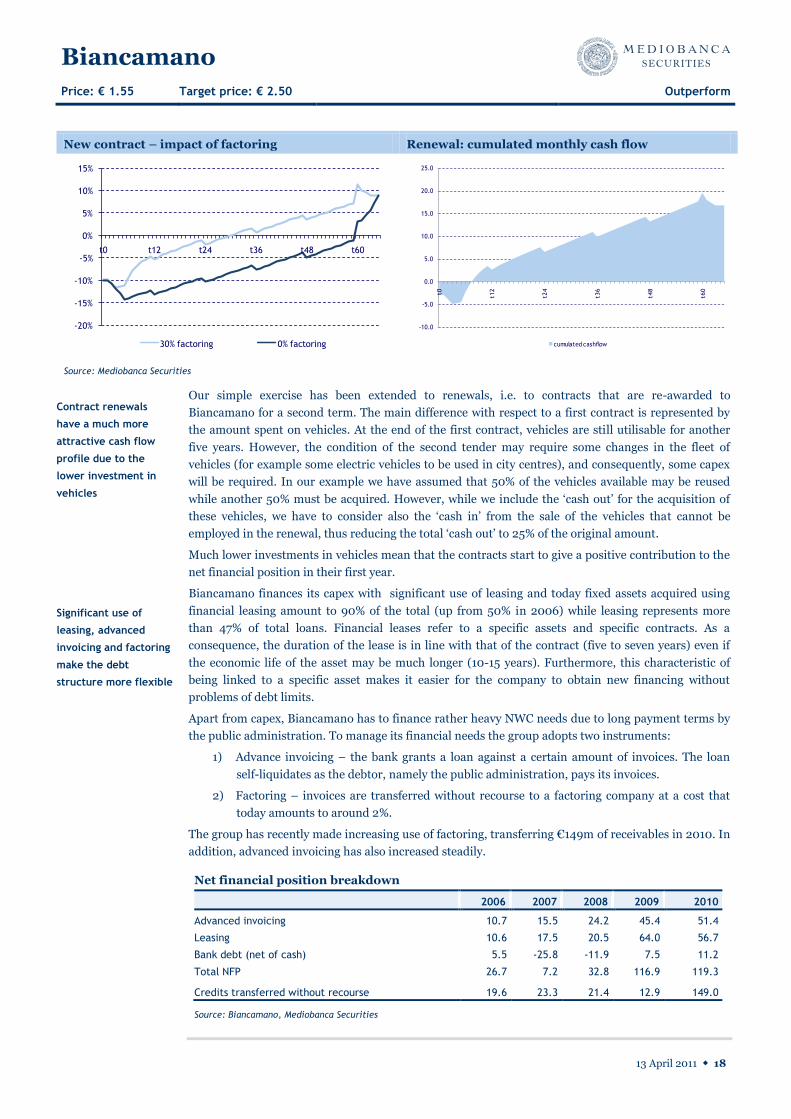

Our simple exercise has been extended to renewals, i.e. to contracts that are re-awarded to

Biancamano for a second term. The main difference with respect to a first contract is represented by

the amount spent on vehicles. At the end of the first contract, vehicles are still utilisable for another

five years. However, the condition of the second tender may require some changes in the fleet of

vehicles (for example some electric vehicles to be used in city centres), and consequently, some capex

will be required. In our example we have assumed that 50% of the vehicles available may be reused

while another 50% must be acquired. However, while we include the „cash out‟ for the acquisition of

these vehicles, we have to consider also the „cash in‟ from the sale of the vehicles that cannot be

employed in the renewal, thus reducing the total „cash out‟ to 25% of the original amount.

Much lower investments in vehicles mean that the contracts start to give a positive contribution to the

net financial position in their first year.

Biancamano finances its capex with significant use of leasing and today fixed assets acquired using

financial leasing amount to 90% of the total (up from 50% in 2006) while leasing represents more

than 47% of total loans. Financial leases refer to a specific assets and specific contracts. As a

consequence, the duration of the lease is in line with that of the contract (five to seven years) even if

the economic life of the asset may be much longer (10-15 years). Furthermore, this characteristic of

being linked to a specific asset makes it easier for the company to obtain new financing without

problems of debt limits.

Apart from capex, Biancamano has to finance rather heavy NWC needs due to long payment terms by

the public administration. To manage its financial needs the group adopts two instruments:

1) Advance invoicing – the bank grants a loan against a certain amount of invoices. The loan

self-liquidates as the debtor, namely the public administration, pays its invoices.

2) Factoring – invoices are transferred without recourse to a factoring company at a cost that

today amounts to around 2%.

The group has recently made increasing use of factoring, transferring €149m of receivables in 2010. In

addition, advanced invoicing has also increased steadily.

Net financial position breakdown

2006 2007 2008 2009 2010

Advanced invoicing 10.7 15.5 24.2 45.4 51.4

Leasing 10.6 17.5 20.5 64.0 56.7

Bank debt (net of cash) 5.5 -25.8 -11.9 7.5 11.2

Total NFP 26.7 7.2 32.8 116.9 119.3 Credits transferred without recourse 19.6 23.3 21.4 12.9 149.0

Source: Biancamano, Mediobanca Securities

Contract renewals

have a much more

attractive cash flow

profile due to the

lower investment in

vehicles

Significant use of

leasing, advanced

invoicing and factoring

make the debt

structure more flexible

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 19

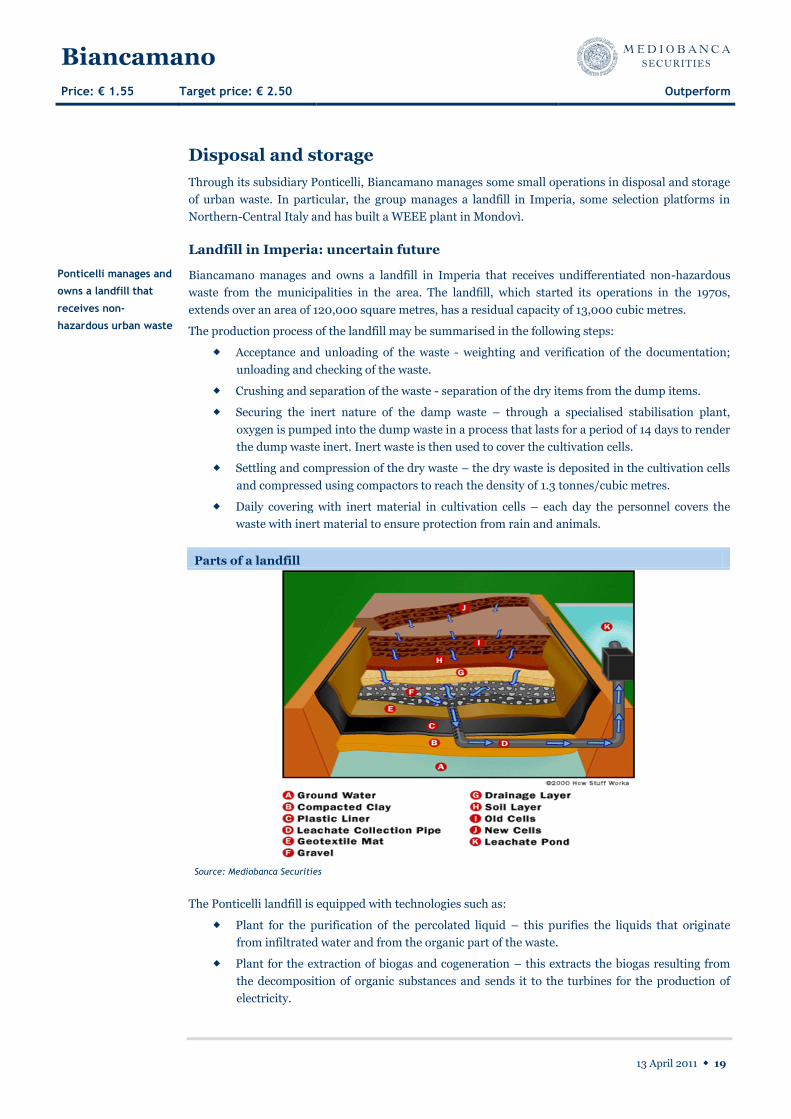

Disposal and storage

Through its subsidiary Ponticelli, Biancamano manages some small operations in disposal and storage

of urban waste. In particular, the group manages a landfill in Imperia, some selection platforms in

Northern-Central Italy and has built a WEEE plant in Mondovì.

Landfill in Imperia: uncertain future

Biancamano manages and owns a landfill in Imperia that receives undifferentiated non-hazardous

waste from the municipalities in the area. The landfill, which started its operations in the 1970s,

extends over an area of 120,000 square metres, has a residual capacity of 13,000 cubic metres.

The production process of the landfill may be summarised in the following steps:

Acceptance and unloading of the waste - weighting and verification of the documentation;

unloading and checking of the waste.

Crushing and separation of the waste - separation of the dry items from the dump items.

Securing the inert nature of the damp waste – through a specialised stabilisation plant,

oxygen is pumped into the dump waste in a process that lasts for a period of 14 days to render

the dump waste inert. Inert waste is then used to cover the cultivation cells.

Settling and compression of the dry waste – the dry waste is deposited in the cultivation cells

and compressed using compactors to reach the density of 1.3 tonnes/cubic metres.

Daily covering with inert material in cultivation cells – each day the personnel covers the

waste with inert material to ensure protection from rain and animals.

Parts of a landfill

Source: Mediobanca Securities

The Ponticelli landfill is equipped with technologies such as:

Plant for the purification of the percolated liquid – this purifies the liquids that originate

from infiltrated water and from the organic part of the waste.

Plant for the extraction of biogas and cogeneration – this extracts the biogas resulting from

the decomposition of organic substances and sends it to the turbines for the production of

electricity.

Ponticelli manages and

owns a landfill that

receives non-

hazardous urban waste

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 20

The landfill gave a contribution to revenues of around €6m-€8m per annum until 2009 with a high

EBITDA ratio of around 30%. In April 2010 the activity at the site, which was expected to reach full

capacity at the end of 2010, was suspended and the plant temporarily closed. The reasons for the

temporary shutdown were a request by the Province of Imperia for the landfill‟s technical stability to

be checked and a request by the Court for checks to be made on the original authorisation for the

landfill to be opened. While the situation is still uncertain, these checks are not expected to have a

negative outcome for Biancamano as the group has already obtained a positive opinion in terms of

technical stability while, as far as the authorisation is concerned, no complaints have been made about

Biancamano as the dispute relates to the process undertaken by the Province of Imperia. However,

even if the original landfill starts its operations again, it is due to reach its full capacity in a few

months.

Selection platforms and WEEE plant

Biancamano manages three selection platforms and one landfill located in Northern/Central Italy.

These activities are sometimes part of a larger contract of urban cleaning while at other times they

have been tendered separately. Altogether, the group‟s selection platforms produce roughly €1m of

revenues with EBITDA margins of around 10%-15%.

More interesting is the WEEE plant due to open in April 2011 in Mondovì (Cuneo). This is a higher

growth segment able to deliver high margins (EBITDA above 50%) due to the fact that the activity

produces both fees from the treatment operations and revenues from the sale of the metals recovered

in the process.

The Mondovì plant, in which the group has invested around €4.8m, will treat some 10,000 tonnes of

WEEE per year with a potential turnover of around €2.0m.

The landfill had almost

reached its full

capacity even before

the temporary

shutdown in April 2010

WEEE plants appear as

a new interesting niche

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 21

Competitive environment and strategy While being still behind the standards that characterise most advanced European

countries, the Italian waste management sector is gradually moving towards best

practice. Due to the adoption of EU directives and the liberalisation of public services,

the sector is becoming more complex, contracts tendered are increasing in size and

services currently managed by public companies are due to be assigned in public

tenders. This challenging and dynamic scenario will offer strong growth opportunities

for Biancamano, the private sector leader. The company is well placed to obtain a

growing share in the domestic market due to its strong track record in public tenders

and its solid organisation. Growth abroad and selective initiatives in storage and

disposal are further strategic options.

Moving towards European best practice

After a long period of moderate but constant growth, in the past few years, total production of urban

waste in Italy has exhibited a flat trend, remaining stable at around 32.5m tonnes while production per

inhabitant fell slightly, from a peak of 550kg/person in 2006 to 541kg/person in 2008. The recent

trend is explained not only by weak GDP growth and household expense growth in the period, but also

by the measures implemented in many areas to minimise the production of urban waste through the

introduction of tariffs levied on households on the basis of the amount of waste produced, the

diffusion of composting and other changes.

Italy: Total urban waste production (m tons) Per capita production (kg/person)

0

5

10

15

20

25

30

35

North Centre South

420

440

460

480

500

520

540

560

Source: ISPRA, Mediobanca Securities

The per capita production of urban waste in Italy is comparable with that of other major European

countries such as France, Germany and the UK. Eastern European countries show a much lower level

of production while higher levels are usually visible in Northern Europe.

Lower consumption

rates are reflected in a

slight decrease in per

capita waste

production

Per capita production

in Italy is comparable

with that of other

major EU countries

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 22

Per capita urban waste production (kg/person)

294

550

801

0 100 200 300 400 500 600 700 800

CZ

PL

RO

EL

HU

PT

BE

SE

UE 25

FR

IT

UE 15

DE

UK

ES

AT

NL

DK

Source: ISPRA, Mediobanca Securities

The chart below shows the portion of recycling in total volumes. At a national level, recycling rates

reached 30.6% in 2008, up from 22.7% in 2004. However, differences among the various areas of the

country are still significant and while in Northern Italy recycling rates reached 45.5% in 2008 (in line

with the targets set by law in 2006), in the South of the country recycling is still limited to just 14.4%.

The trend is positive, however, and since 2004 the portion of waste recycled increased by 35% at the

national level due to a 25%/28% increase in North/Central Italy and 80% growth in the South.

Recycling rates (% over total volumes)

35.5

18.3

8.1

22.7

45.5

22.9

14.7

30.6

0

5

10

15

20

25

30

35

40

45

50

North Centre South Tot. Italy

2004 2005 2006 2007 2008

Target 2008

Target 2007

Source: ISPRA, Mediobanca Securities

Major differences are also visible among European countries. As shown in the chart below, on the

basis of 2006 figures, we can identify some countries such as Belgium and Germany that were already

approaching recycling rates of 60% while most other countries stood at around 40%. Southern

Europe, including Italy, ranged between 10% and 20%.

Recycling rates show

major differences in

the various areas of

the country

Lower recycling rates

in Southern Europe

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 23

Recycling rates: international comparison

Source: IEEP, Mediobanca Securities

In terms of urban waste treatment, the trends that characterised Italy in the past few years are

summarised in the chart below. In 2008 waste sent to landfill still amounted to almost 48% of the

total but has exhibited a continuous decrease since 2003 in favour of incineration (11.3% of the total)

and more markedly of recycling (including composting) that reached 41% of the total.

Waste treatment: Italy 2006-2008 Waste treatment: international comparison (2006)

55.847.9

9.0

11.3

35.140.8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008

Landfill Incineration Recycling & composting

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

DE NL FR IT UK ES PO RO BG EU27

Landfill Incineration Recycling (incl. Composting)

Source: Ispra, Mediobanca Securities

With respect to other major European countries, Italy shows a greater use of landfill; for countries

such as France, the Netherland, Sweden, Belgium or Denmark landfill usage is below 10%. A reduction

of waste sent to landfill is a common trend in Europe and between 1995 and 2007 waste sent to landfill

declined by around 30%, from 274kg to 209kg per capita. In Italy total and per capita values showed a

reduction of around 30%. Among countries with a large landfill usage it is worth mentioning the UK

where a similar reduction (-29%) has been obtained from the 2001 peak.

Conversely waste incinerated is growing and since 1995 per capita amounts incinerated has increased

from 69kg to 110kg at the European level. In Italy, despite the strong growth recorded in the past few

years (per capita amounts have almost tripled since 1995), waste incinerated represents only some

10% of the total vs. 30%-35% for countries such as Germany, France or the Netherlands.

48% of waste still sent

to landfill in Italy

despite the fall

recorded in the past

few years

Europe: trend towards

reduction of waste

sent to landfill in

favour of incineration

In Italy, waste

incinerated remains

well below the

European average

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 24

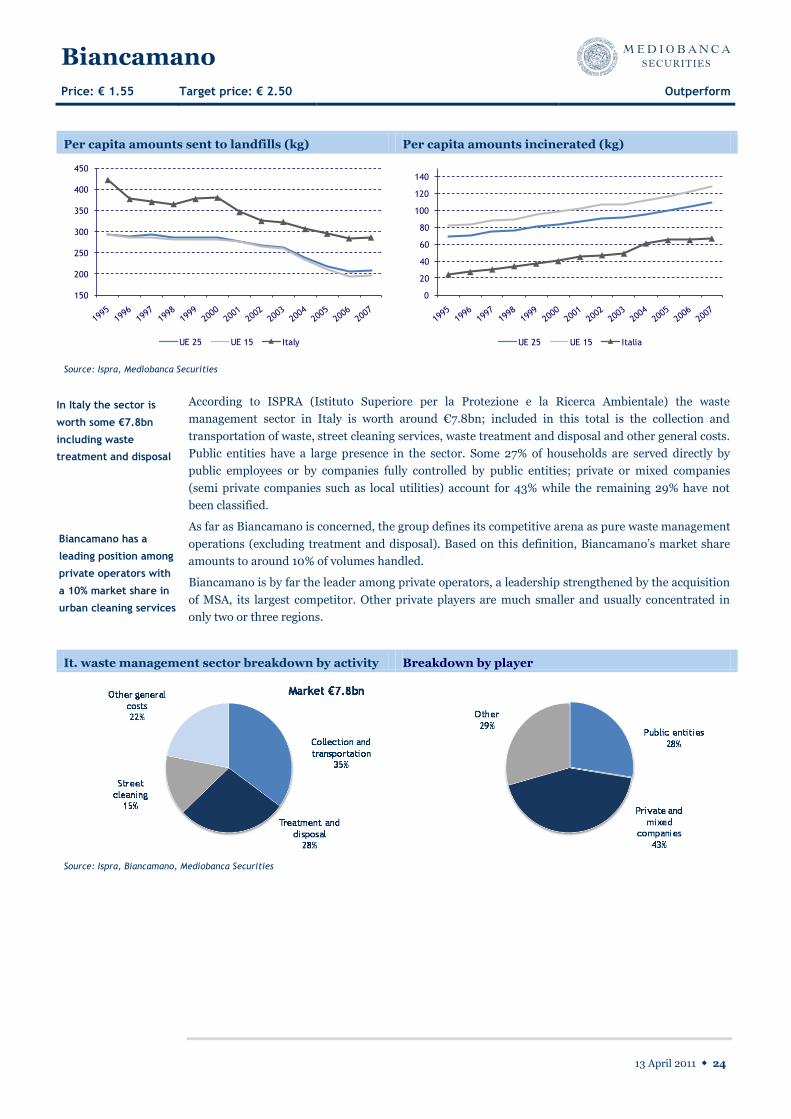

Per capita amounts sent to landfills (kg) Per capita amounts incinerated (kg)

150

200

250

300

350

400

450

UE 25 UE 15 Italy

0

20

40

60

80

100

120

140

UE 25 UE 15 Italia

Source: Ispra, Mediobanca Securities

According to ISPRA (Istituto Superiore per la Protezione e la Ricerca Ambientale) the waste

management sector in Italy is worth around €7.8bn; included in this total is the collection and

transportation of waste, street cleaning services, waste treatment and disposal and other general costs.

Public entities have a large presence in the sector. Some 27% of households are served directly by

public employees or by companies fully controlled by public entities; private or mixed companies

(semi private companies such as local utilities) account for 43% while the remaining 29% have not

been classified.

As far as Biancamano is concerned, the group defines its competitive arena as pure waste management

operations (excluding treatment and disposal). Based on this definition, Biancamano‟s market share

amounts to around 10% of volumes handled.

Biancamano is by far the leader among private operators, a leadership strengthened by the acquisition

of MSA, its largest competitor. Other private players are much smaller and usually concentrated in

only two or three regions.

It. waste management sector breakdown by activity Breakdown by player

Source: Ispra, Biancamano, Mediobanca Securities

In Italy the sector is

worth some €7.8bn

including waste

treatment and disposal

Biancamano has a

leading position among

private operators with

a 10% market share in

urban cleaning services

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 25

Growth in the core business in Italy and abroad

The evolution of the waste management sector in Italy is expected to accelerate over the next few years

and Biancamano can leverage its already strong position to reinforce its leadership.

Two main trends are shaping the Italian market:

1. gradual adoption of the EU directives;

2. liberalisation of the market for public services.

The Waste Framework Directive (2008/08 EC) is the benchmark for the sector. The directive

established a legal framework directed at controlling the whole waste management cycle, from

production to disposal, focusing in particular on prevention, recycling and re-use. The main effects of

this legislation are an increasing attention to recycling rates in general and the specific focus on some

materials. WEEE is one of the main topics as the directive sets specific targets in terms of EEE

collected while other specific issues targeted are packaging and hazardous waste.

A second directive that is due to affect Biancamano is the directive on late payments recently approved

by the EU (2011/7). Following the implementation of this directive, which is due to come in to force in

March 2013, public administration will have to settle its payments within 60 days. Should the directive

be implemented effectively, Biancamano would receive material relief in its financial management that

currently is burdened by the slowness of payments by the public administration (on average around

180-200 days).

The new EU directive will certainly focus the attention on the problem of abnormal late payments by

the Italian public administration. However, some observers underline that legislation against late

payments already exists in Italy and but it has not prevented the current situation. As a consequence,

only the contextual adoption of a new system of sanctions for the public administration is likely to

change the current detrimental modus operandi.

The progressive liberalisation of public services in Italy represents another source of change and an

opportunity for Biancamano. By the end of 2011 all local public services must be assigned through

public tenders (D.L. 135 25/08/2009). As far as waste management services are concerned, currently

some 28% of users are served directly by companies fully owned by the local authorities. Following the

implementation of this decree, all these services will have to be re-assigned with public tenders

allowing the participation of private or mixed companies.

The adoption of EU directives and the liberalisation of public services are due to gradually re-shape

the waste management sector in Italy along the following lines:

Market concentration – waste management services are increasingly tendered by ATO,

Ambito Territoriale Ottimale, i.e. entities covering an area typically as large as a province or

including several municipalities. Serving larger areas requires that service providers achieve a

larger size because a track record on contracts similar in size and technical characteristics is

required. In this type of contest, large players are clearly favoured while smaller operators

tend to exit the market.

Increasing duration of contracts - the market is seeing a trend towards the extension of the

duration of contract to optimise the costs (and time) of the tender process with the effect of

increasing revenue visibility and stability for the players in the sector.

Higher complexity – the reduction in waste production and the increase in recycling rates are

the main goals of EU waste legislation. Both these goals strongly affect the collection process

as they require that those who produce the waste are made responsible for the quantity and

the quality (in terms of differentiation) of the waste produced. The final effect of this process

is to increase door-to-door collection with respect to the road collection from large containers

and, going forward, to implement some form of tracking of the quantity and quality produced

by the individual users. While the cost of collection for the municipality increases, the cost of

Waste Framework

Directive: increasing

focus of prevention,

recycling and re-use

The gradual adoption

of EU directives and

the liberalisation of

public services are

reshaping the waste

management sector

Directive on late

payments: 60 days

maximum delay in

payments by the public

administration by 2013

Liberalisation of public

services: by end-2011

services provided by

public companies must

be assigned through

public tenders

Changes in legislation

are favouring market

concentration, longer

contracts and market

complexity

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 26

treatment and disposal is lower. For Biancamano the trend is favourable as it moves the

market toward higher margin services while at the same time making smaller players less

competitive.

In this scenario, Biancamano‟s strategy is to focus on growth in the core business of waste collection in

Italy and to start looking for opportunities abroad. In addition, the group intends to avail of the

opportunities that could arise in the area of treatment and disposal, carefully selecting activities that

offer growth and low risk.

Growth in waste management collection in Italy - the liberalisations and modernisation of the

waste management sector in Italy represents a strong growth opportunity for Biancamano. The group

will tender for new contracts in its traditional segment of small/medium towns and rural areas but will

also participate in tenders for services currently managed by public and semi public companies. The

group‟s track record, its planning capacity, its experience in managing complex contracts should allow

Biancamano to reap a growing share of the new business especially in a sector in which more skilled

operators are required due to its growing comlexity.

Growth in waste management abroad – Biancamano is monitoring the tenders launched in

other European and in some CEE countries to acquire more information with a view to an expansion

in those markets. Furthermore, the group is making a survey of small and medium sized players in

these markets as it is also considering the possibility of acquiring small/medium sized companies with

a strong local presence.

Growth in selected areas of waste treatment and disposal – with its large presence in the

business of waste collection, Biancamano is in a privileged position to assess the potential that could

arise in waste disposal and treatment operations in some specific segments and areas. The group is not

interested in entering the waste disposal and treatment sector with large investments as would be

required to buy another landfill or to build an incinerator because in this sector large capex is

associated with high risks. Biancamano is monitoring some segments of the waste disposal business,

such as the treatment of WEEE, where some new investments could follow after the opening of the

Mondovì (CN) plant.

At the moment it is not possible to anticipate the location or type of investment that will be made in

the area of waste disposal. What is important to underline is that the activity of waste collection gives

the group a clear view of the amounts and type of waste produced in the various areas and (bearing in

mind that transportation costs should be reduced) of the type of plant that could be successful in that

specific contest.

Biancamano: growth in

Italy leveraging on the

group’s superior skills

and stronger

organisation

The group is

monitoring tenders and

competitors abroad

Knowledge of local

specifics will help the

group in entering

specific niches of

treatment and disposal

Biancamano

Price: € 1.55 Target price: € 2.50 Outperform

13 April 2011 ◆ 27

Financials 2006-2010 has been characterised by strong growth, both organic and through the

acquisition of MSA, driving Biancamano’s top line from €65m to €265m. Waste

management margins improved strongly in 2010 benefiting from economies of scale

and higher profitability of new contracts. However, recovery at the consolidated level

was partially offset by the closure of the Ponticelli landfill, while at the bottom line

progress was impacted by higher taxes. Going forward, we expect that the improvement

in the top line and EBITDA will be reflected in the group’s bottom line. In 2011-2013 we

expect high single-digit annual revenue growth and a 235 bps margin recovery. While

debt will continue to be controlled (due to an “opportunistic” use of factoring) we

expect the bottom line to finally start reflecting the group’s increased size.

2006-2010: building the leadership in waste management

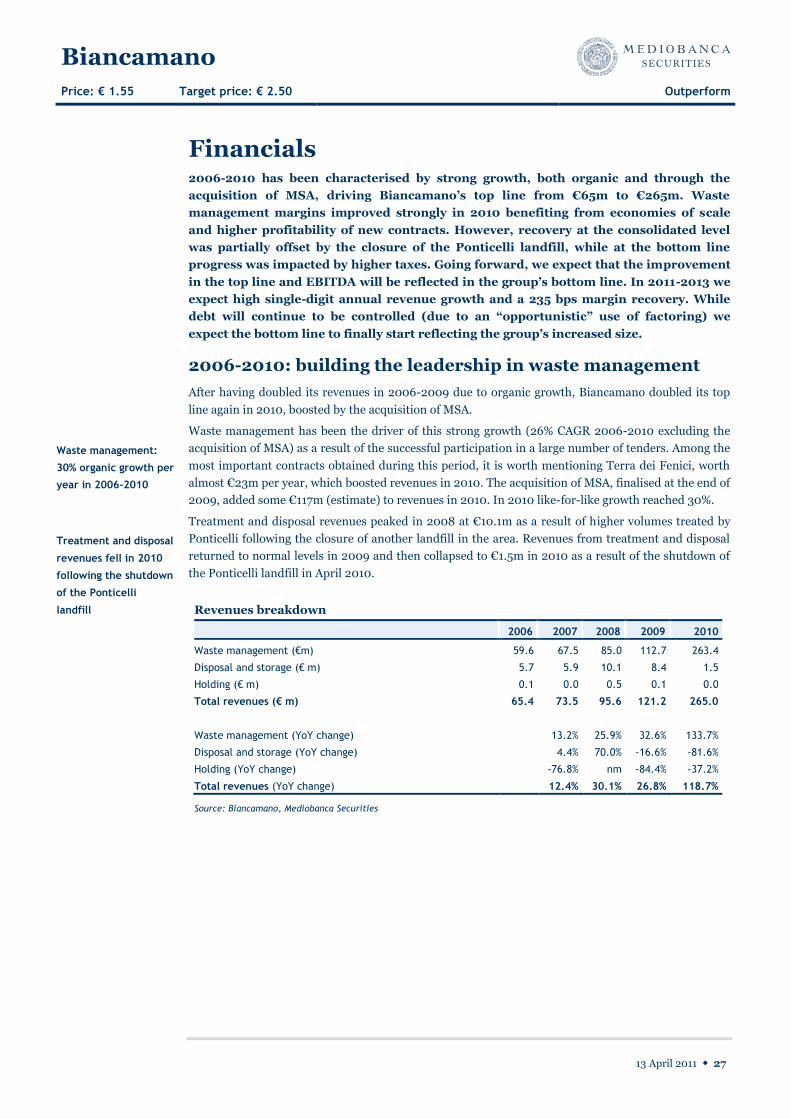

After having doubled its revenues in 2006-2009 due to organic growth, Biancamano doubled its top

line again in 2010, boosted by the acquisition of MSA.

Waste management has been the driver of this strong growth (26% CAGR 2006-2010 excluding the

acquisition of MSA) as a result of the successful participation in a large number of tenders. Among the

most important contracts obtained during this period, it is worth mentioning Terra dei Fenici, worth

almost €23m per year, which boosted revenues in 2010. The acquisition of MSA, finalised at the end of

2009, added some €117m (estimate) to revenues in 2010. In 2010 like-for-like growth reached 30%.

Treatment and disposal revenues peaked in 2008 at €10.1m as a result of higher volumes treated by

Ponticelli following the closure of another landfill in the area. Revenues from treatment and disposal

returned to normal levels in 2009 and then collapsed to €1.5m in 2010 as a result of the shutdown of

the Ponticelli landfill in April 2010.

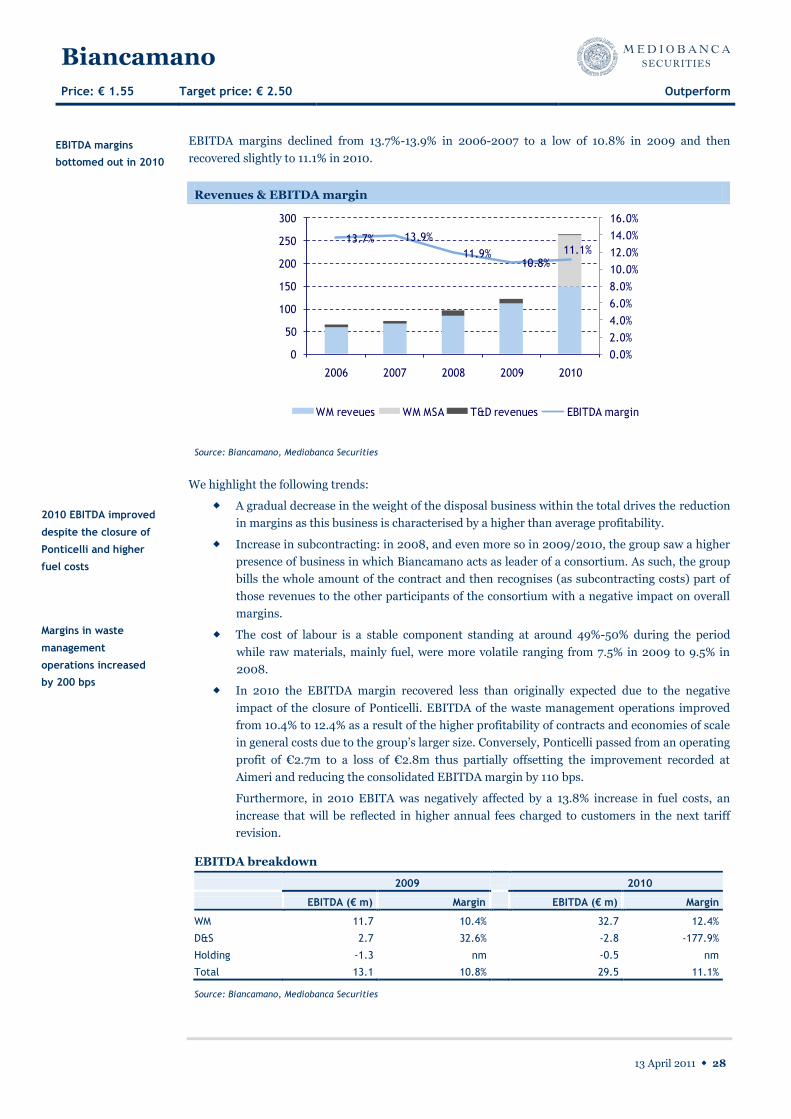

Revenues breakdown