Embed Size (px)

Citation preview

* *

* *

* C H A P T E R N O . 7 . *

* AN ANALYTICAL STUDY OF THE * * *

* ACCOUNTS (STUDY YEAR 1 9 9 0 ) . * •X *

121

C H A P T E R - 7.

An Analytical Study of The Accounts

(Study Year 1990)

The year 1990 is taken for analytical study of

the accounts of the Public Distribution System accounts of

the Akola district. In this chapter the cost of the

essential commodities supplied through the public

districtuion system is taken. The variation from January

to December is comparitively studied and an average cost

is derived from it. The total supply of the all the

commodities and its cost is also tharoughty analysed in

relation to the turnover of the commodities in every month

of the every year. The total cost payment of all the

commodities is studied comparatively with every item. In

the content of other items payment of each item is in the

form of cash payment by cheque, partical payment is

studied thoroughly and its accounting is taken for study.

The accounts system is then examined analytically and

critically to asses the soundness of the system.

The audit reports of the essential commodities

by the public distribution system authority is taken for

analytical study and on the basis of its analysis the

variation of the public distribution system is tested.

Finally the turnover in money, goods, labour is

comparitively and individually in detail. This chapter

will enlighten the economic process and its accounting,

auditing and it willprove the viability of the public

distribution system.

122

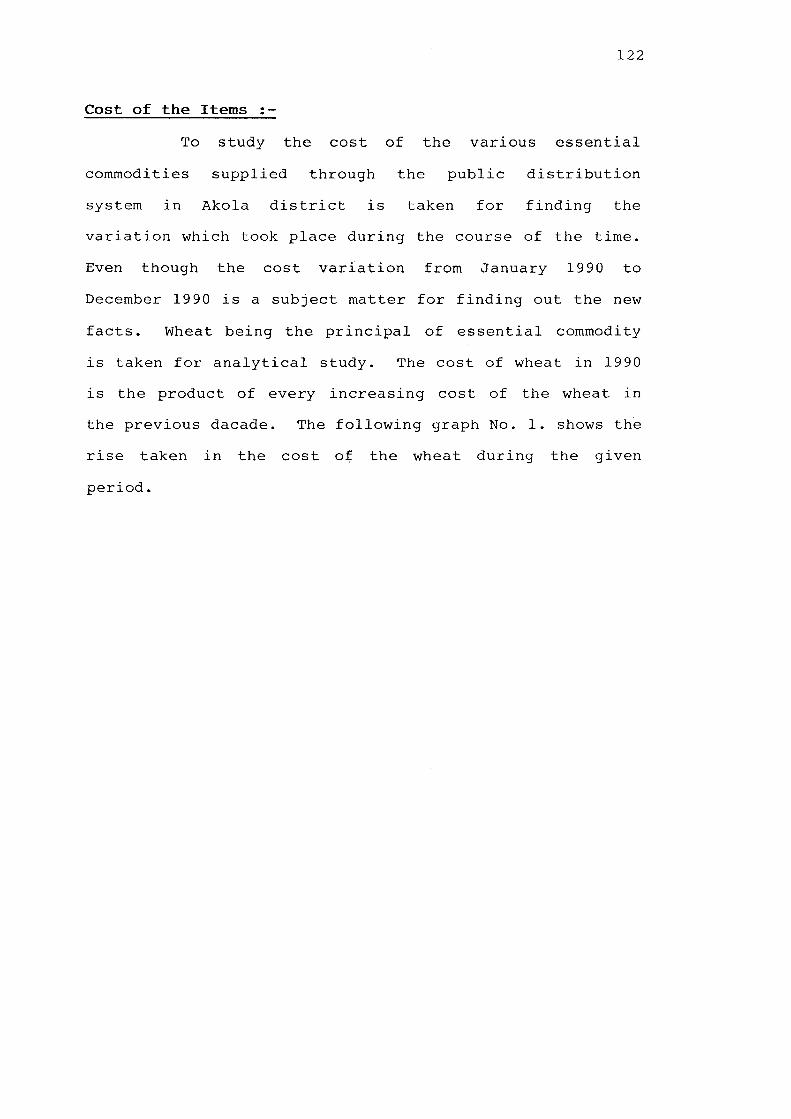

Cost of the Items :-

To study the cost of the various essential

commodities supplied through the public distribution

system in Akola district is taken for finding the

variation which took place during the course of the time.

Even though the cost variation from January 1990 to

December 1990 is a subject matter for finding out the new

facts. Wheat being the principal of essential commodity

is taken for analytical study. The cost of wheat in 1990

is the product of every increasing cost of the wheat in

the previous dacade. The following graph No. 1. shows the

rise taken in the cost of the wheat during the given

period.

\2^^ R

Graph Ho. 1.

310

300

290

280

270

260

250

240

230

220

210

200

190

180

170

160

150

140

RISE IN COST OF WHEAT IN RS DURING THE YEAR 1981 TO 1990 UScalfi 1 Cw. 20 R3.)

/

/

^

/ J'

, /

/ /

V \

t

A /

1

^ - f

r"

i 1 F

ir"

^ " ^ • f 1

1

CO

Tj-

>

^ ^ \> rA

CO CO

9 2̂ 9

M

\ "^

9 \ f N

;>

PERIOD

a COST

9' 9

123

During 1990 the total cost of wheat supplied in

the Akola district was 8,23,750 lakhs. This amount was

send to the Divisional Headquarter.

District authorities of the Akola district

supplied the rice costing Rs. 19,33,750 to the fair price

shops of the Akola district.

The consumers of the Akold district purchased

Jowar from the Fair Price Shops of the Akola district

costing Rs. 53,64,000/- only.

The sugar supplied by the District Public

Distribution on System to the ration card holders of the

district amounts to Rs. 82,37,250/- only.

The cost of the edible oil supplied through the

Public Distribution System was worth of 2,49,78,480/- Rs.

only.

The total cost of the supplied wheat by the

District Public Distribution System authority in 1990 was

Eighty two billion four hundred sixty three million three

hundred thirteen thousand four hundred eighty only in

number that is 82,46,33,13,480/- Rs. only.

In 1981 the cost of the wheat stabilised at the

cost of rupees 156.70 per quintal. In the year 1982 the

rise in the cost of wheat was Rs. 164 per quintal. Again

the cost was increased by Rs. 24.20 per quintal in 1983 to

1984. The cost of wheat per quintal decreased by 19.30.

In 1986 again the cost of wheat stabiised at Rs. 187.70 per

quintal.

124

On 1st. May 1987 the cost of wheat crosed

Rs. 200/- mark and it continously increased thereafter that

is 202 to 221 and then in 1990 it stabilised at Rs. 254.80

per quintal. Table No. 27. gives the cost of the wheat

since 1979 to 1992.

Table No. 27.

The cost of the Wheat in Rupees.

Sr.No. Date & Year

1) 25 October 1979

2) 1 April 1981

3) 16 November 1981

4) 1 July 1982

5) 1 August 1982

6) 22 April 1983

7) 16 October 1984

8) 1 February 1986

9) 1 May 1987

10) 16 February 1988

11) 1 April 1988

12) 16 December 1988

13) 2 May 1990

14) 4 January 1992

15) 1 July 1992

In -godown issue rate in Quintal

141.10

156.70

156.70

157.10

173.50

197.70

178.40

197.70

202.40

212.10

221.70

221.80

254.80

306.60

300.40

Retail rate per kilo

1.45

1.61

1.62

1.63

1.80

2.05

1.85

2.05

2.10

2.20

2.30

2.35

2.70

3.25

3.25

125

From the above table it became very clear that

on 1st. April 1981 to 2nd. May 1990 the cost of the wheat

increased from Rs. 156 to 264 per quintal the difference in

the cost of wheat per quintalwas Rs. 98. Which is 60% of

the cost of the wheat in 1981.

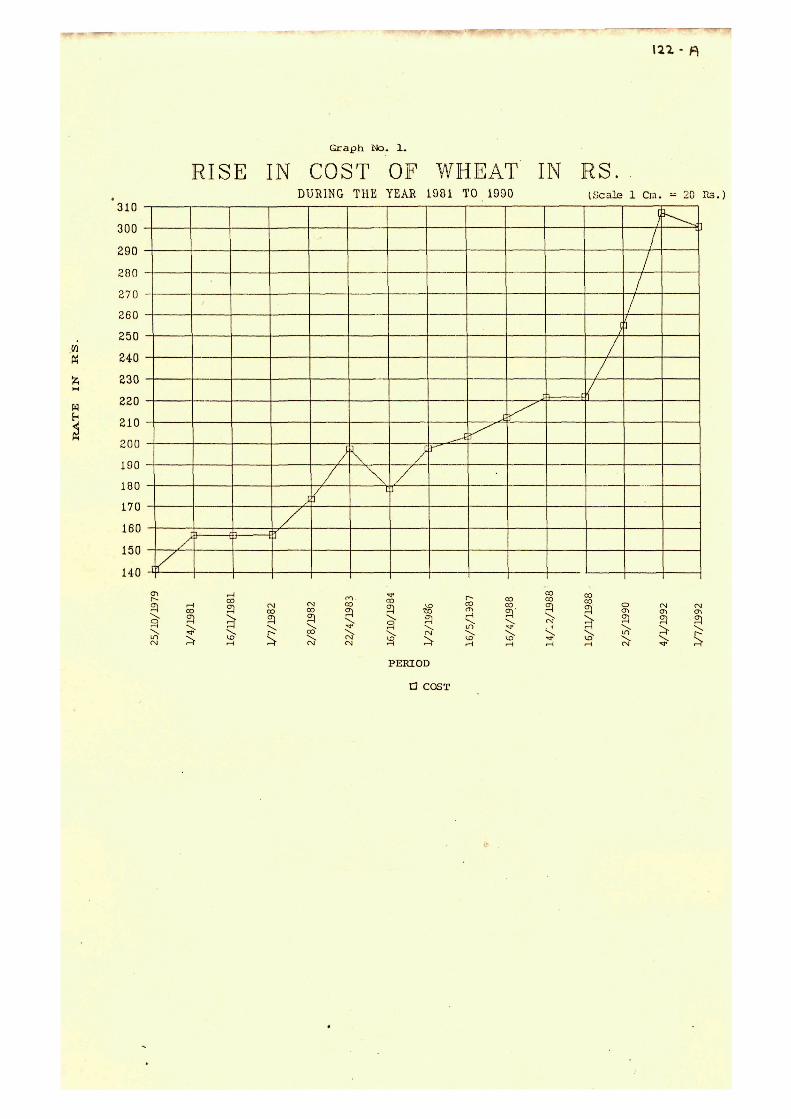

The rate of opened market for the essential

commodities are given in the table No. 28 and than

presented in the graph No. 2. And the cost of the

essential commodities in the Fair Price Shops as on 3rd

August 1990 is given in the graph No. 3.

las-B

G r a p h No. 2 .

OPEN MARKET RATES OF

w N N h P

« N

A.

M

100 -

\

ESSENTIAL COMMODITIES A3

[ ^ _ , •( \

\ >

- -

ON 0 3 / 0 0 / 9 0

r--^'\

(Sca le 1 Cm.=

\1 \

1 k .

50 Rs.)

A

If

•XJ (0 E n) ta

c c x: u

•̂ 3 J

•ij

w

c (0

>

„H

c rd > i

r~\

(0 ^ J > a1

a! K

COMMODITIES

<D •r) la n o

I ;,! o 1 ^

a KATli

c ni Vl

O m o

• ' ; 1 o

I I S - C

Graph No. 3 .

RATES OF ESSENTIAL COMMODITIES IN

w

» ft, P

a «

w

550

500

450

400

350

300

250

200

a

FAIR PRICE SHOP AS ON 0 3 / 0 8 / 9 0 (Sacalfi 1 Cm.= 50 Rs.)

e 3

QJ

s

3 CO

.̂ ?i s

rH D «

IS

y ? • S tn 0 i-i

en 3 (Q

•g 1 *H "o H

126

Table No. 28.

Open Market rate of the essential commodity on 3-8-90.

Sr.-No.

Item Wholesale rate per Quintal

Retail rate Kilogram.

1) Rice

a) Basmati

b) Chinner

c) Luchi

2) Wheat

a) Sarbeti

b) Lokwan

c) Kalyan

3) Jowar

a) Hybreed

b) Govran

4 ) Bajari.

a)

5) Ghana - Dal

6) Tur - Dal

7) Udidh - Dal

8) Sugar

9) Gur

a) Gaoran

b) Ankapalli

10) Groundnut oil

11) Musterd oil

12) Refined oil

830-850 9.00

600 7.00

425-430 5.00

330-340 3.50

310-320 3.30

290-315 3.25

140-155

170-200

175-185

965

1110-1250

750-800

775-785

1.55 - 1.65

1.90 - 2.15

2.00

10.50

12.50 - 13.50

9.00 - 9.50

8.00

450-500

625

314

275

268

5.00 -

6.50 -

34.00

28.00

27.00

- 5.50

- 7.00

n^-j>

Graph No. 4.

COMPARATIVE STUDY OOF THE COST OF GOODS

m

P

n H

900

800

700

600

500

400

IS s :c o

& CO

a,

•U fd

IN OPEN MARKET & FAIR PRICE SHOPS

o s i Id

a,

(1)

* -a 0 "' 1^ bi

COMMODITIES

ORATES

J en P

(Scale 1 Cm. = 50 Rs.)

a, en

(1)

« pi.

o

.51

s tn o

127

2. 3.

13) Karadi oil

14) Vanaspati (15 Kg.)

15) Tea

16) Salt

17) Onion

18) Potatoes

19) Dry chilly

20) Washing Soap

200

560

900

72-

180

190

1150

38

•75

28.00

37.00

58.00 -

1.00

2.50 -

3.00

12.00

3.50

- 60.00

- 3.00

The consumer of the Fair Price Shop had to pay

lesser amount for essential commodities than the consumer

of openmarket, but the quality of goods differs. The

Fair Price Shops consumer received inferior quality of

goods.

The comparision between the cost given in Graph

No. 2. and Graph No. 3 is given for easy understanding.

In Graph No. 4 to distinguish them qualitabively

quantatively.

128

Total Supply and Cost :-

The supply of essential commodities through

Public Distribution System is not constant. To study the

variation in the supply of the essential commodities, the

supply of wheat, rice, sugar and edible oil are taken and

studied. Since 1986 to 1990. The supply of wheat and

rice in 1986 to 1990 is given in the Graph No. 5 likev/ise

the supply of sugar, edible oil is given in the following

Graph No. 6 and Graph No. 7 to study the fluctuation month

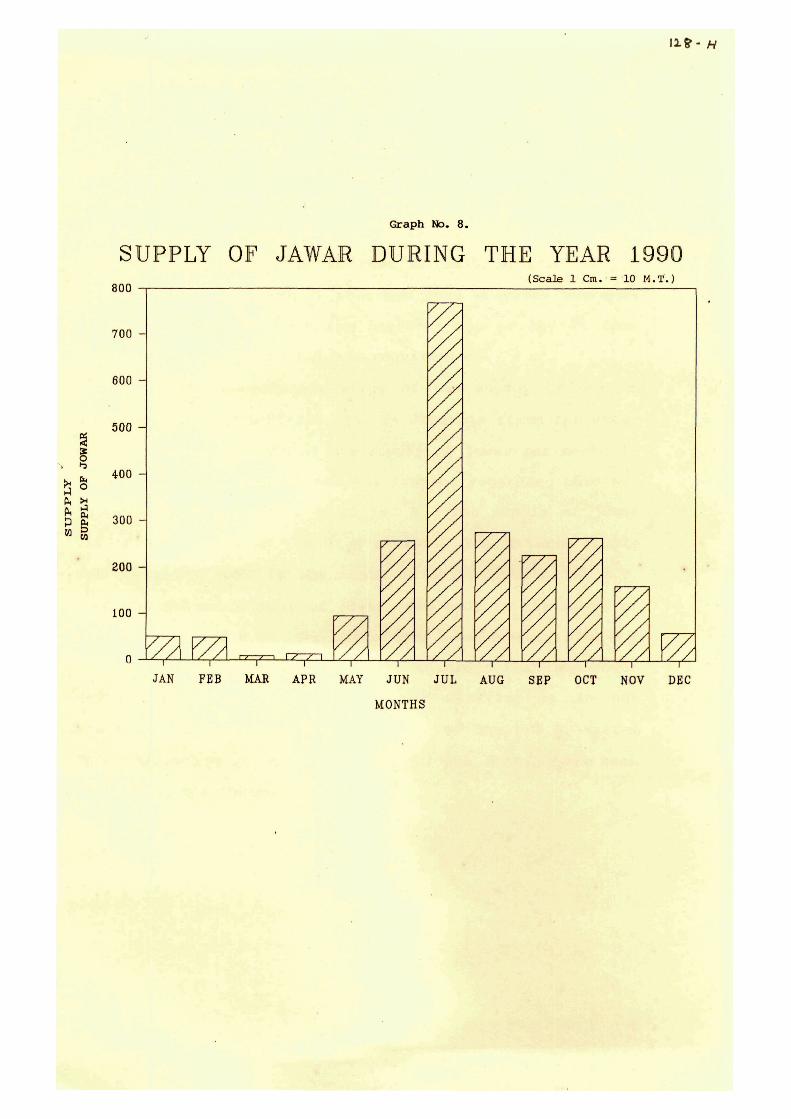

wise, the supply of Jowar in the months of 1990 is taken

and presented in the Graph No. 8.

128- £

2„

m

1-1 0 A, A A* H

w

Graph No. 5 .

SUPPLY OF WHEAT AND RICE

4-5

40 -

3b -

30 -

25 -

20 -

15 -

10 -

5 -

n 1

^

-X^ 1

/ /

V

DURING

y//

/ / /

1

r 1986 TO 1990

1 1

/ .

(Scale 1 Cm. = 1000 M.T.)

V^ 1 1

/ / /

1

^

y/^ 1

1986 1986

1̂ i

1987 1987

s

1988 1988 1989

1̂'

1989

1̂

1990 1990

s

COMMODITIES

»28-F

>̂ 0

D ^

to

Graph No. 6.

SUPPLY OF SUGAR DURING 1986 TO 1990 (Scale 1 Cm. = 1000 M.T.)

120 -

HO -1

100 -

90 -

80 -

70 -

60 -

50 -

40 -

30 -

20 -

10 -

0 -

gg%

s /vy/z^ /vy/v /y^yx" 'V////

/M

^

/ / /

• / /

VA

4̂

VA / / /

< ^

y///A

/ / / / / /

V///A

S / y y ^ /v//^ /vyyy 'VV///

W/. 1986. 1987. 1988

YEARS

1989. 1990.

i2«-Q

Graph No. 7 .

SUPPLY OF EDIBLE OIL

H

i i h O

0< B< D CO

O K O.D

3 -

2.5 -

2 -

1.5 -

1 -

0.5 -

n u

/ ^

^

/ y / /

/ / /

vyy w,

/ /

DURING 1986 TO 1990

' / / / / /

/ / "^ / /

y ^ V////

1

/ / /

(Sca l e 1 Citi

/ / / /

w / / / /

1

^

= 1000 M

//A

\

.T.)

/ /

V/ 1986 1987 1988 1990

YEARS

I1&- H

G r a p h No. 8 .

SUPPLY OF JAWAR DURING THE YEAR 1990

g

800

700 -

600

500 -

400

300

200 -

100 -

(Sca l e 1 Cm. = 10 M.T. )

I ^ y I \ y / \ j ^ 1 I p I I I p . — J . . — . — . - ^ — p — • • • |- •—-^-t—•—"—r

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

MONTHS

129 The comparative study of the edible oil supplied

from 1986 to 1990 is given in graph No. 9 from the study

of graph No. 9 maximum metric tones of oil was supplied in

1986 and minimum quantity was supllied by in 1990. The

difference between them is that of 1821 M.T. of edible

oil. This figure reveals thetruth that whenever there is

a short supply of wheat the customer has to buy it from

the open market to fulfil his requirement.

The comparative study of the supply of one of

the essential commodities that is Jowar is taken for study

to find out varitions in the supply of jowar per month in

the year 1990. The statistical figures regarding this are

given in the following graph No. 9. The supply of jowar

is totally based on the crop season. The maximum supply

of jowar was made in the month of July that is 768 M.T.

and the minimum supply of jowar was made in the month of

March that is 8 M.T. The difference between two 13760 M.T

This fluctuations makes it clear that the jowar

even though the main crop of the district it is not

comsumed evenly throughout the year and the P.D.S. system

also doesn't give any importance to the continueous even

supply to the customer.

130

By analysing graph No. 10 the researcher finds

out the following facts that is the supply of rise varies

from year to year. It was maximum in 1989 and minimum in

1990, the difference between them was of 6450 M.T. This

shows that the supply of rise is not made as per the

requirement of the cardholder but it is based on the

availability of the rice with the Food Corporation of

India.

Wheat is the most essential commodity to be

supplied to the customers of Fair Price Shop. But even in

this commidity the variation in its supply astonishes the

researcher.

In the year 1987 the supply was 40500 M.T. to

the supply of 21475 M.T. in 1986. The difference in these

two is 19,025 M.T. the difference in the supply of wheat

shows that the customer of Fair Price Shop can not depend

on them for the supply of wheat as such he will have by it

whenever it is not available in the Fair Price shop from

the open market.

The supply of sugar is made from the levy and

the sugar acquired from the open market. The variation in

the supply of sugar from year to year. The maximum suply

was made in 1986 that is 1,13,878 M.T. and the minumum

supply was made in 1990 that is 1,07,500 M.T. The

difference between them is that of 6,378 M.T. The

comparision can be easily understood by stating graph No.10

9'

/ 3 6 - 1

M 0

Graph No. 9.

TOTAL COST OF SUPPLIED WHEAT,JAWAR, SUGAR,EDIBLE OIL & RICE IN 1990 (Scale 1 Cm.= 10,00,000 Rs.)

yu

80 -

70 -

60 -

50 -

40 -

30 -

20 -

10 -

0 - / / / / / / \ V7

/ / /

' ̂

VA

v/ A

///

V/

• / /

^ VA

4^ JAWAR SUGAR RICE

COMMODITIES

EDIBLE OIL WHEAT

131

System of Payment :-

Once the cost of the item is decided by the

government, the purchaser has to pay the cost of the total

commodity in the prescribed proformas or in the given mode

of payment. The supply of commodities and its payments is

as per the chart given below:-

Chart No. 17.

Supply of Commodities and it' s Payments.

Purchases from Food Corporation

of India

CENTRAL GOVERNMENT

STATE GOVERNMENT

cultivators &

from open

Market.

M CD •H +j •H

o

o o

o

a a, CO

DIVISION

DISTRICT

TREASURY

Bo

n tr (D a ^T* en

e°

n H QJ H i r t cn

riff h 0 C

i£3

rr n or

I—' OJ 3 cn

*x) OJ

<̂ 3 ro 3 r t

!_,. 3

n OJ 0) 3-

TEHSIL

CARD HOLDER Jc • Jr • o •

CUSTOMER

132

The above chart indicates that the supply of

goods is from top to bottom and its payment is always from

bottom to top.

The payments of the item are payed differently

at the different levels as shows in the chart No.-17.

the Fair Price Shops card-holder is a customer

and hepays in cash what so ever he buys form the related

Fair Price Shops as per the cost fixed by the Government

from time to time.

The authorised Fair Price Shop owners purchased

their commodity at a given rate through chalan from the

Food Corporation of India. The cost given in the chalan

is to be paid in cash in the treasury, Akola. There after

it is official transaction of payment up to the top.

Sometimes the payment is made through drafts or cheques.

The daily transactions of the payments of the commodityat

treasury level is maintained. The treasury submits the

cash and accounts to the divisional headquarters of the

Amravati division on fortnightly. The division submits

the accounts and payment officially to the state

Government on the monthly bases. The state Government

makes money from other transactions related to it on

fiscal bases. At the Government level that is Central

Government and state Government makes the payment to the

food corporation of India in cash. Likewise the payment

from bottom to top is carried out regularly.

133

Accounting system ;-

The accounting in Public Distribution System

scheme is done as per Food Manual of the Government of

Maharashtra. For this purpose there is an accounts branch

in the District supply office headed by a senior

accountant who belongs to Maharashtrsa. Finance & Accounts

service of Government of Maharashtra.

Accounting under Public Distribution System is

commerical nature and double entry book keeping. There

are prescribed register as per Food Manual such as in

Daybook, cashbook, FLA II, PLA 'g' classified abstract

registers etc. The entries in these registers are based

on the monthly prescribed returns received from the

Government on the monthly prescribed returns received from

the Government godowns through Tahasildar of the district

and also the figures which are shown in the monthly

returns in monthly returns by the Tehsildar dully rec

onciled with the order and treasury Personal Led(-.er

Accounts passbook etnd initial transaction maintained by

the accounts branch of District Supply Office.

All the transaction under Public Distribution

System should have the double effect so that ary mistake

of mioclassif ication or omni&:(;ri is noticed j rnmodiately,

under double entry book keeping accountinc^ is divicec: ; r:

four parts such as Persons] Account, Ecal Account,

Mominator Fictitious Account, Goods Account, Credit Account

Asset Account, Liability Account, Capital-Account.

134

(a) There is a personal ledger account in the name

of collector which is controlled by the treasury of

Accountant General.

(b) There are two type of payment, one is direct payment

to party and another is drawn self by District Supply

Office and then paid to party in another district.

(c) Drawl from Personal Ledger Accounts,'Government Capital

Account' is only by issuing Personal Ledger Accounts

cheques to treasury for payment.

(d) If a cheque drawn by District Supply Office for

payment of telephone, electricity, water bills to

Tehsildar or transport and labour contract or of

supplier of the district Akola and the cheque is

issued and the receipt is acquired, the amount is

entered in the cash book of District supply Officer.

The purpose of issuing cheque is mentioned. The

account of cost of the foodgrains required to be paid

to the Food Corporation of India or other

district suppliers is specified. Then District

Supply Office has to draw the cheque on self account

the Demand draft is issued to the cerncerned party.

Then all the entries regarding the payment is filled

in the accounts book. Straight and horizental

totalling art is carried out for the cross checking

and then entries in the cashbook and ledger are

totalled again for verification. This is called

cross checking.

135

The District Supply Office has to submit

monthly and yearly account to the financial advisor and

deputy secretary, Food and civil supplies department of

government of Maharashtra. In the form of dully

undersigned by District Supply Office, Akola.

1) Store and stock account.

2) Cash Account.

3) Caomplied Account.

4) Suspense Account.

5) Profit and Loss Account.

Once the District Supply Office, Akola submits

all the accounts to the higher authorities and receive

its receipt. Accounting procedure at district level is

complete.

Auditing :-

Mere scruting of bills at the time of payment

is not an audit. Therefore the audit of District Supply

Office transaction is done by the Audit party of Finance

Advisor & District Supply Officer, Bombay. Audit party

from Finance Advisor and Deputy Secretary and Accounts

General has performed the yearly audit of District

Supply Officer's account periodically on percentage

basis as possed audit by selecting one month's

transaction.

The audit party has to see and judge whether

the claimants are genuine or not whether the District

Supply Office is competant for sanctioning claims which

deal with the withdrawl of the amount whether the

136

withdrawl is propered that is or ruled and prescribed is

fully observed or not whether the payment has been paid

properly, whether accounting has been done as per the

rules and whether receipt acknowledgement are proper or

not. Then further recounting of all the accounts is

verified. The audit party then certifies it with the

auditing certificate signed by the Chief Auditor. And

thus the auditing procedure is complete.

If certain drawbacks are found while auditing,

then the auditor follows the following procedure :-

As per audit objection and observation, the

mistakes shall be complied by taking suitable action as

per rule and order. For example :-

If some of the money transactions made are

more than that of financial power of the District Supply

Office or Collector, that transaction is required,

retrospective sanction from higher and compitent

authority. Over payment will be recovered from the

receiptents.

The audit party prepare the audit report far

the concerned period. Then the audit report is issued

by the District Supply Office under the signature of

Accounts Officer of Finance Advisor and Deputy

Secretary, Bombay for compliance within one month from

the date of receipt.

137

Total Turnover :-

As explained earlier that the accounting

system in Public Distribution System is in double entry

book-keeping, there is no profit making tendency of the

Government. These are number of commodities which are

covered under the Act of essential commodity Act of

India. The turnover of money labour etc. by Public

Distribution System in Akola District is given below.

A) Money:-

The State Government has placed the certain

errors of Rupees at the disposal of the collector by

spending the personal ledger account in the name of the

collector. The Government has authorised the collector

to delegate his drawing disbursing power under the

Public Distribution System to the District Supply

Officer due to his busy schedule.

The Tehsildar under the control of the

collector, collected the money from the local Fair Price

Shop dealser and credites it in the treasury under Major

head Personal Ledger Account, 4408 - Capital out lay on

Food? the District Supply Office who is under delegated

power of the collector. Studies the credit draws the

ammount from treasury by issuing the Personal Ledger

Account cheque. The yearly receipt and payment under

the Personal Ledger Accounts for the year 1989-90 was

14,07,15,631, 14,71,43,779 respectively. It's break up

into the monthly tornover is shown in the Annexture

No. 1.

138

Annexture No. 1•

Monthly receipt of Payment from Personal Ledger Account

For 1989 - 90.

Month Receipt Payment

April 1989 1,56,49,418.30 99,79,250

May 1989 88,20,390.00 94,97,140

June 1989 95,93,278.00 1,32,49,822

July 1989 85,96,909.00 1,61,75,992

August 1989 70,44,179.00 91,62,938

September 1989 70,11,570.00 1,16,07,709

October 1989 1,55,32,811.00 1,09,29,114

November 1989 1,12,40,139.00 1,17,52,095

December 1989 1,49,80,497.00 1,14,23,954

January 1990 1,54,10,594.00 2,57,86,381

February 1990 1,36,26,986.00 1,05,20,449

March 1990 1,32,68,860.00 70,58,929

Total 14,07,15,631.00 14,71,43,779

B) Goods :-

The tornover of Goods under Public Distribution

System is mainly based on the Wheat, Rice Supplied by the

Food Corporation Of India, oil from Government of

Maharashtra through Food and Civil Supply Department and

sugar from the sugar factory. Recently the Government of

139

Maharashtra has introduced other essential commodities in

Public Distribution System such as. Soap, Machis, Dal,

Rova, Ata & Maidha etc.

Details of Turnover of the goods under Public

Distribution System are as follows:-

1) Wheat and Rice :-

Monthly quota of wheat and rice has been fixed

by the state Government of the District on the basis of

units of ration cards of the district. An information

regarding wheat and rice quota is given by the state

Government. The District Supply Office draws the ammount

from the treasury for the purchases of the wheat and rice.

The District Supply Office draws Demand Draft in favour of

Food Corporation of India and sends it along with the

order to local depot of Food Corporation of India. As per

order, the whear and the rice are issued by the Depot and

onward sold to the Fair Price Shop on payment made into

treasury by them through challans.

2) Oil and Dal ;-

These items have been supplied from the Food and

Civil Supply Department of the District and gets the

payment by telegraphic transfer from the Personal Ledger

Account of Collector.

3) Sugar :-

There are authorised nominees for the sale

purchase of sugar from the sugar factory on the

authorisation of the Government on the basis of monthly

quota. First the nominee have to credit the Ammount at

140

the ex-factory rate into the challan officer, which he get

the sugar quota from the sugar factory on the basis of the

permit issued by the District Supply Office.

Subsidies rates are fixed by the Government

under the Public Distribution System. The difference

between Exfactory rate and selling rate is term as rebate

to the nominees.

Turnover for the year 1989 to 1990 on account

of sugar was 4,65,900-17-650 Qnt. Rs. Rs. 13,20,10,529.

Details of monthly break up of sugar. Turnover is shown

in Annexture No. 2.

Annexture No. 2•

Monthly Turnover of the Goods.

Year Items Receipt Quantity Value Issue - Value Quantity

1989 Wheat 321114-21-650 Q. 65507300 315461-00-000 66126948

Rice 128955-42-000 Q. 42120712 76268-00-000 37075849

Oil 15830-54-000 Q. 24392517 15558-35-000 25549971

465900-17-650 132010529

141

C) Labour :-

Every year under the Public Distribution System

the turnover of Labour is studied at the level of

Government godowns situated in the Tehsil, Collector

appoints a labour contractor for each godowns. The coolie

charges are fixed by the Government. In special situation

the Government has authorised the Public Distribution

System staff to fix the rate of physical labourers as per

the local situation.

The labour contractor has to work as per

instructions of the Godown keeper for loading, unloading,

checking, stacking etc. As per the works up the labour

contractor has to submit the monthly coolie bills through

the godown keeper and Tehsildar. On certification of the

labour work bill by the Tehsildar, the District Supply

Office makes the payment to the labour contractor, after

verification of the labour bill with the extract of labour

Register yearly payment 1980-90 per bags comes to

Rs. 4,06,864/- the monthly brack up is shown in Annexture

No. 3.

Annexture No. 3.

Yearly turnover (Handling) of foodqrain bags with Coolie

charges for the year 1989-90.

Year Handling of num.ber Hamali charges lems. of bags.. Govt. Labour contrac-Godowns tor

1989-90 47,086 bags. 4,06,844 Wheat

Rice

Jowar

142

D) Transportation :-

The Government has to make available the

foodgrain in Taluka godown for distribution through Fair

Price Shops under the Public Distribution System. For

this purpose transport of foodgrain within the District

and ouL of the District are necessary. For this work, the

collector is authorised by the Government to appoint a

transport contractor by inviting open tenders on

transportation rates.

Transportation bills submitted to the District

Supply Office by the transoprt contractor is checked on

the transport passes in which loading and receiving

weights. The loss of grain in transit is derieved and the

charges of transoprt action are paid to the transport

contractor. In 1990 the turnover of foodgrains amount

23,18,167 bags and its transportation charges are Rs.

2,31,816/-. The monthly transportation of foodgrain from

the main godown, Akola to the Tehsils is given in

Annexture No. 4.

Annexture No. 4 .

Number of foodgrain bags transported within District from

Akola Headquarter to the various Government Godowns in the

District during 1989-90.

Year No.of bags Tranport Cost of transportation

1989-90 15,18,167 23,18,167

143

E) Other :-

There are various kinds of receipt and

expenditure takes place in the transaction under Public

Distribution System which are to be shown as a part of

trading account such as

a) 1) Sale of Old grains.

2) Security deprecation .

3) Labour charges received from Transport

Contractor.

4) Road shortage received from Transport contractor,

5) Cost of Ration cards sold etc.

b) 1) Payment of Godown rent.

2) Payment of advertisement.

3) Payment towards cost of stationary-

4) Payment telephone, electricity, Water charges of

godown.

5) Payment towards tarpolin, Fumigation, Pestisides

etc.

c) 1) Payment to Food Corporation of India A/c. of

foodgrains received.

2) Payment of Finance Advisor and Deputy Secretary

In Government of Bombay.

3) Receipt from other District and states on amount

of grain exported.

4) Recovery payment from advances from Parties and

godown etc.

144

The analytical study presented in this chapter

will give a clearcut understanding for the comparative

study with Amravati, Buldhana and yeotmal districts and

will be benificial for giving the interpretation of the

new facts discovered during the detail and in depth study.