Embed Size (px)

DESCRIPTION

" Did I really have to declare that to the IRS??? ". How to Come Back into the US Tax System. Town Hall Meeting Dr Guillaume Grisel US Banking and Taxation Part 6 LL.M. (Cambridge), Ph.D., T.E.P. Attorney-at-law, Bonnard Lawson. Swiss-US Estate Planning in a Nutshell. - PowerPoint PPT Presentation

Citation preview

"Did I really have to declare that to the IRS???"

How to Come Back into the US Tax System

Town Hall Meeting Dr Guillaume Grisel

US Banking and Taxation Part 6 LL.M. (Cambridge), Ph.D., T.E.P.Attorney-at-law, Bonnard Lawson

Swiss-US Estate Planning in a Nutshell

Pre- / Post- Nuptial Agreements and Wills

For US Citizens Living in Switzerland

Dr. Guillaume GriselLL.M. (Cambridge), Ph.D., T.E.P.Attorney-at-law, Bonnard Lawson

"Did I really have to declare that to the IRS???"

How to Come Back into the US Tax System

Town Hall Meeting Dr. Guillaume Grisel

US Banking and Taxation Part 6 LL.M. (Cambridge), Ph.D., T.E.P.Attorney-at-law, Bonnard Lawson

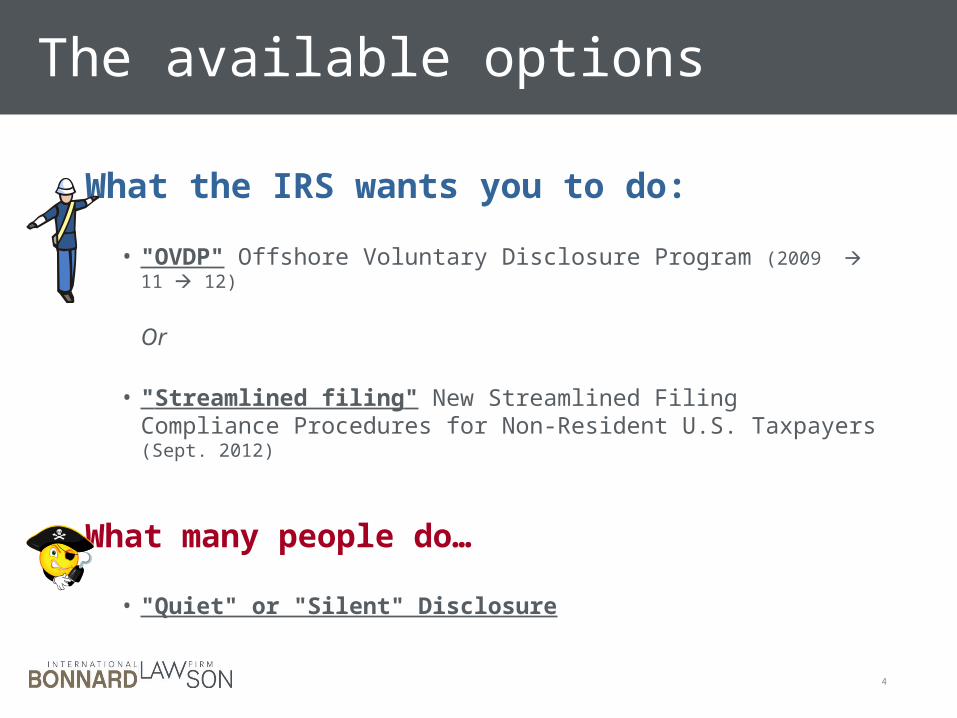

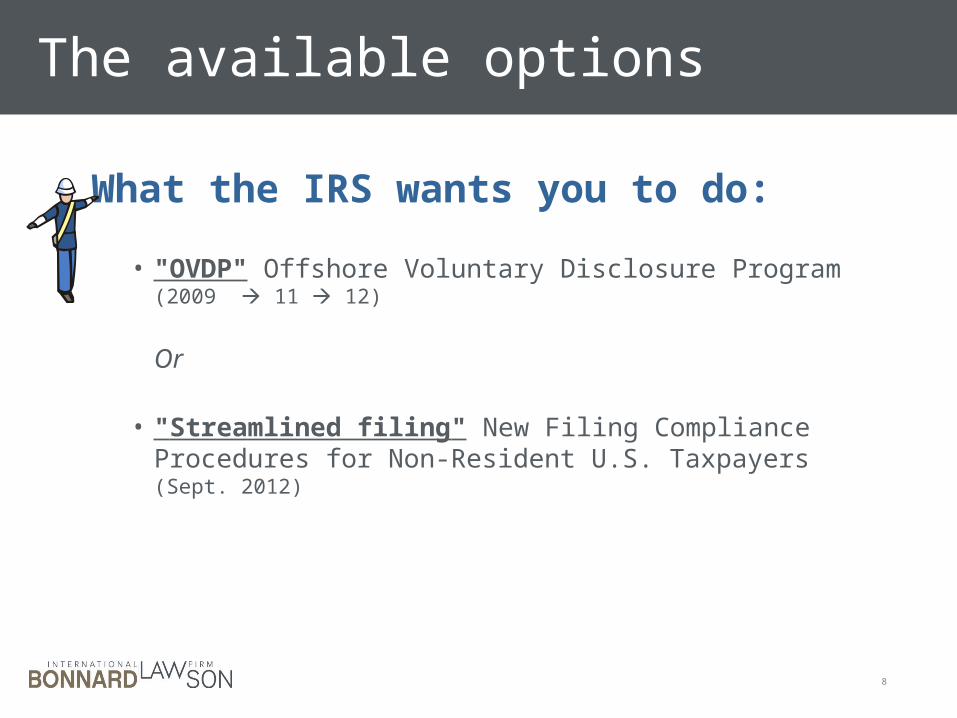

The available options

What the IRS wants you to do:

• "OVDP" Offshore Voluntary Disclosure Program (2009 11 12)

Or

• "Streamlined filing" New Streamlined Filing Compliance Procedures for Non-Resident U.S. Taxpayers (Sept. 2012)

What many people do…

• "Quiet" or "Silent" Disclosure

4

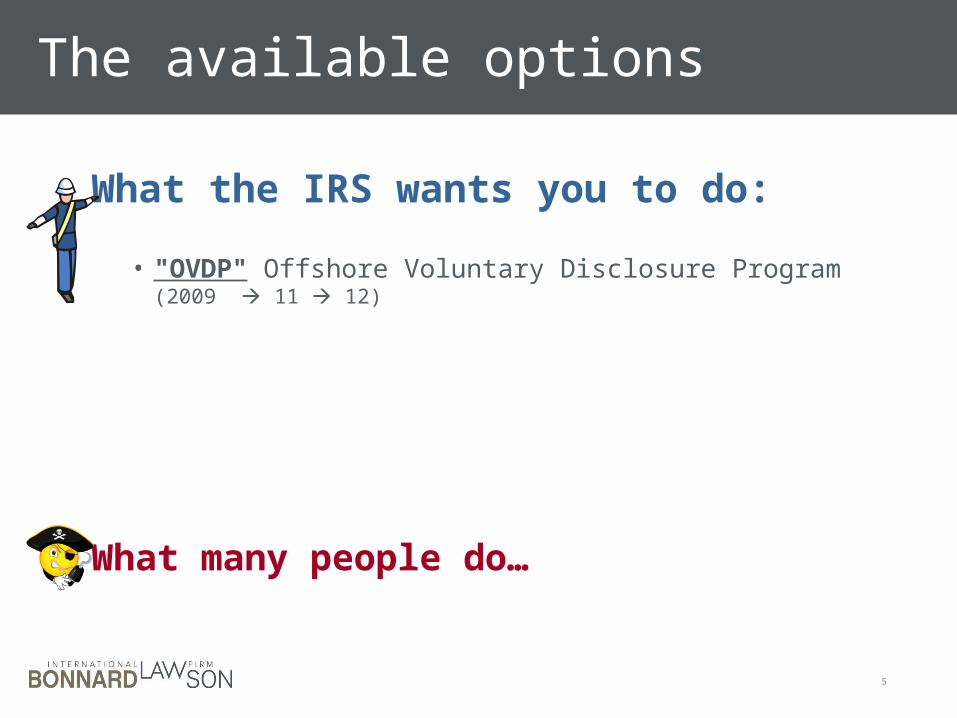

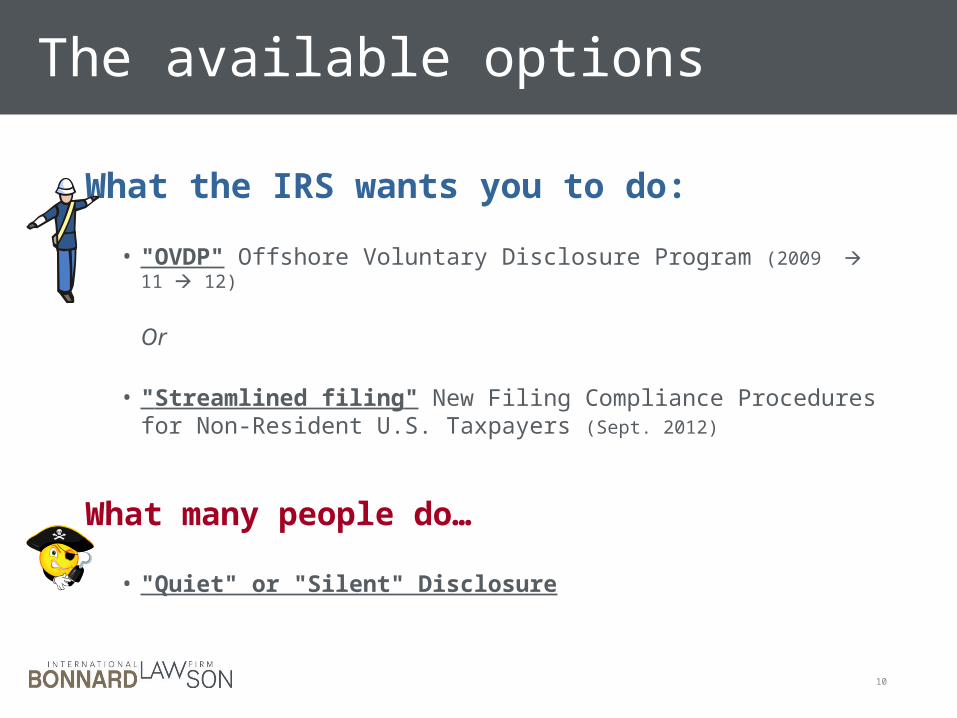

The available options

What the IRS wants you to do:

• "OVDP" Offshore Voluntary Disclosure Program (2009 11 12)

What many people do…

5

OVDP: What you have to pay

• 8 years income tax + interests

• Tax penalties• Accuracy-related penalties (20% of tax due)• Failure to file/pay penalties (up to 25% of tax due each)

• FBAR penalty! • 27.5% of highest value of each offshore account during the 8 last years (!!!)

Can be reduced to 12.5% or even 5% in some (rare) cases

• Your lawyer and your CPA…

OVDP: Up & down sides

Upsides• Quasi-assurance of no criminal prosecution• Predictability of tax and penalties due

Downsides• High penalties (in particular FBAR penalty)• Thorough audit by the IRS• High professional fees (CPA, lawyer)

7

The available options

What the IRS wants you to do:

• "OVDP" Offshore Voluntary Disclosure Program (2009 11 12)

Or

• "Streamlined filing" New Filing Compliance Procedures for Non-Resident U.S. Taxpayers (Sept. 2012)

8

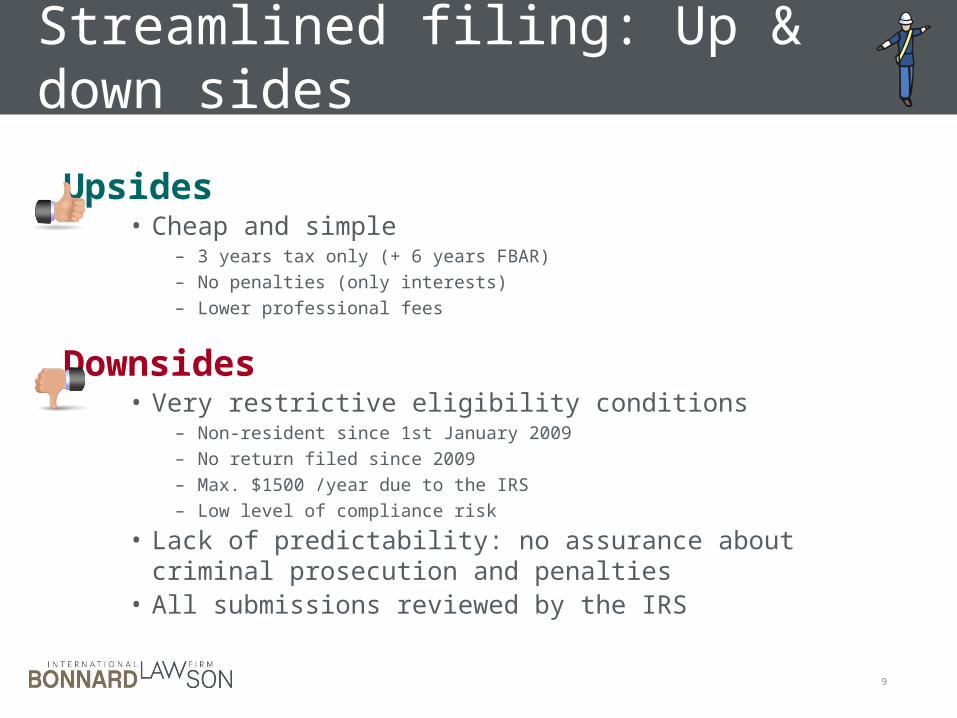

Streamlined filing: Up & down sides

Upsides• Cheap and simple

– 3 years tax only (+ 6 years FBAR)– No penalties (only interests)– Lower professional fees

Downsides• Very restrictive eligibility conditions

– Non-resident since 1st January 2009– No return filed since 2009– Max. $1500 /year due to the IRS– Low level of compliance risk

• Lack of predictability: no assurance about criminal prosecution and penalties

• All submissions reviewed by the IRS

9

The available options

What the IRS wants you to do:

• "OVDP" Offshore Voluntary Disclosure Program (2009 11 12)

Or

• "Streamlined filing" New Filing Compliance Procedures for Non-Resident U.S. Taxpayers (Sept. 2012)

What many people do…

• "Quiet" or "Silent" Disclosure

10

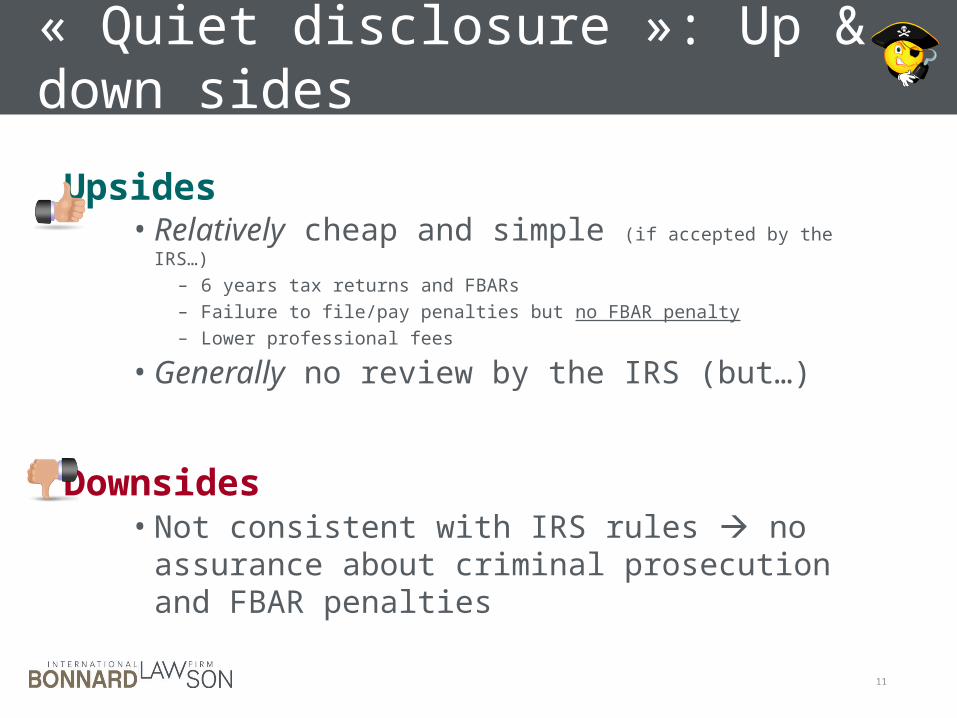

« Quiet disclosure »: Up & down sides

Upsides• Relatively cheap and simple (if accepted by the IRS…)

– 6 years tax returns and FBARs– Failure to file/pay penalties but no FBAR penalty– Lower professional fees

• Generally no review by the IRS (but…)

Downsides• Not consistent with IRS rules no assurance about

criminal prosecution and FBAR penalties

11

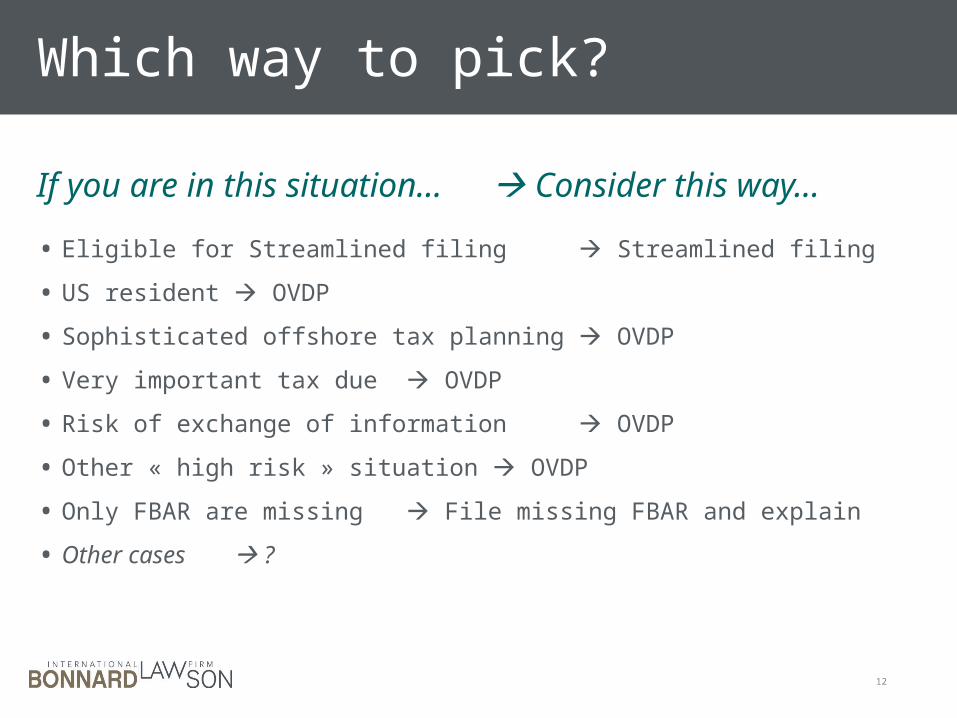

Which way to pick?

If you are in this situation… Consider this way…

• Eligible for Streamlined filing Streamlined filing

• US resident OVDP

• Sophisticated offshore tax planning OVDP

• Very important tax due OVDP

• Risk of exchange of information OVDP

• Other « high risk » situation OVDP

• Only FBAR are missing File missing FBAR and explain

• Other cases ?

12

Swiss-US Estate Planning in a Nutshell

Pre- / Post- Nuptial Agreements and Wills

For US Citizens Living in Switzerland

Dr. Guillaume GriselLL.M. (Cambridge), Ph.D., T.E.P.Attorney-at-law, Bonnard Lawson

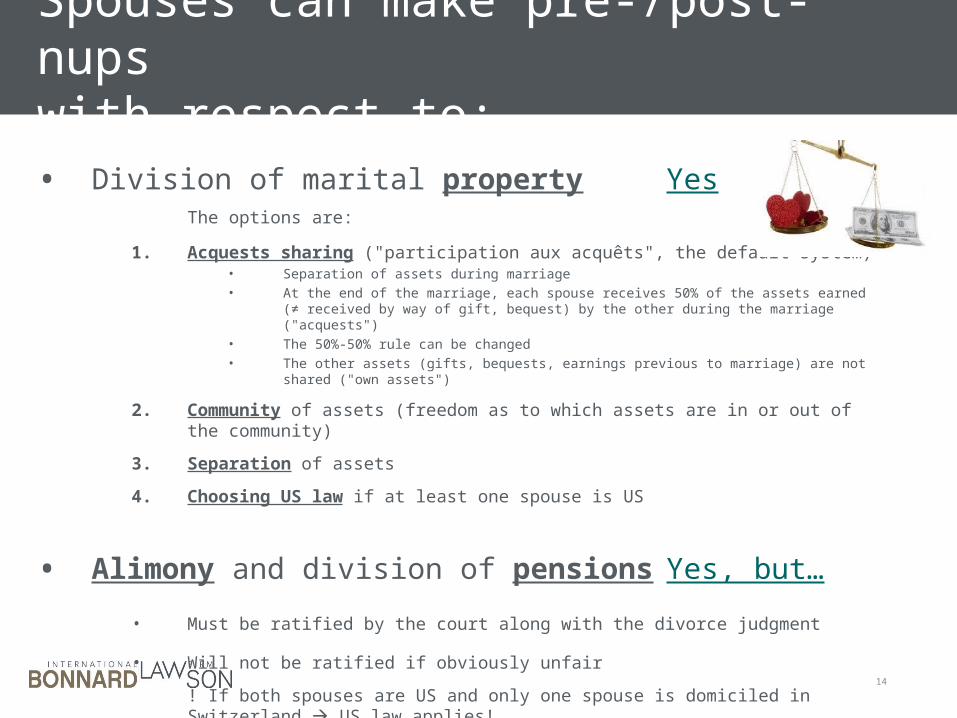

Spouses can make pre-/post-nups with respect to:

14

• Division of marital property Yes The options are:

1. Acquests sharing ("participation aux acquêts", the default system)• Separation of assets during marriage• At the end of the marriage, each spouse receives 50% of the assets earned (≠ received by way of gift, bequest)

by the other during the marriage ("acquests")• The 50%-50% rule can be changed• The other assets (gifts, bequests, earnings previous to marriage) are not shared ("own assets")

2. Community of assets (freedom as to which assets are in or out of the community)

3. Separation of assets

4. Choosing US law if at least one spouse is US

• Alimony and division of pensions Yes, but…

• Must be ratified by the court along with the divorce judgment

• Will not be ratified if obviously unfair

! If both spouses are US and only one spouse is domiciled in Switzerland US law applies!

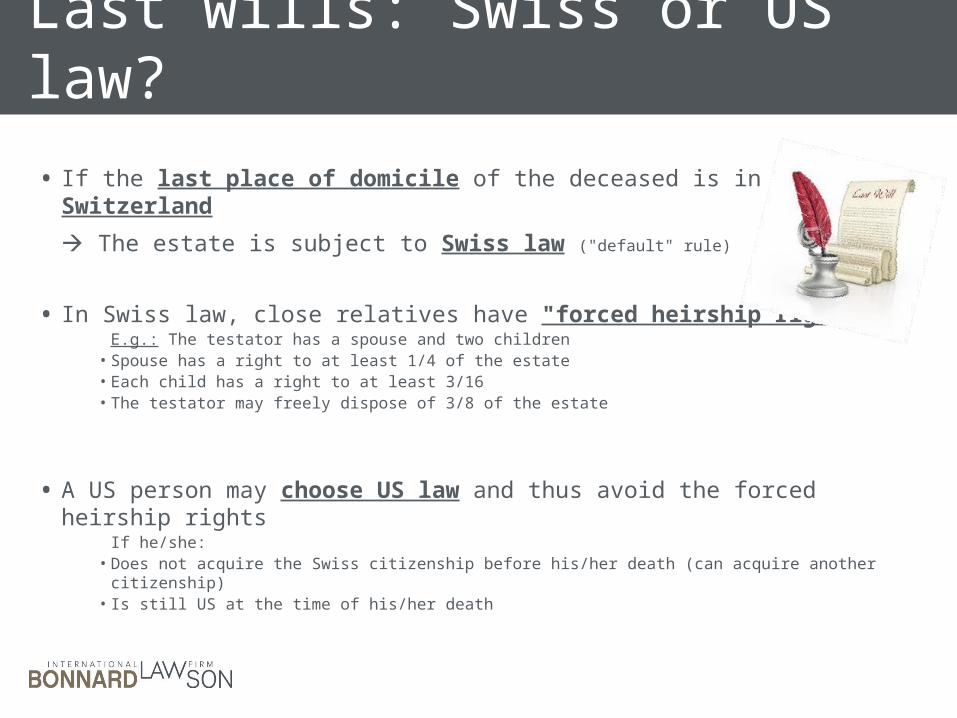

Last wills: Swiss or US law?

• If the last place of domicile of the deceased is in Switzerland

The estate is subject to Swiss law ("default" rule)

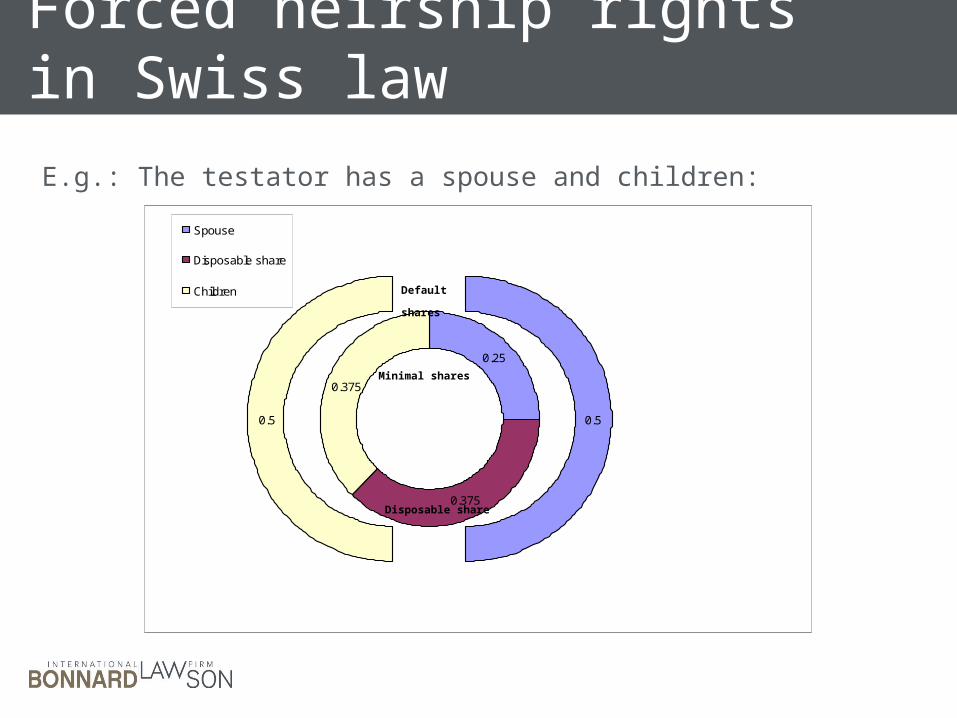

• In Swiss law, close relatives have "forced heirship rights"E.g.: The testator has a spouse and two children• Spouse has a right to at least 1/4 of the estate• Each child has a right to at least 3/16• The testator may freely dispose of 3/8 of the estate

• A US person may choose US law and thus avoid the forced heirship rightsIf he/she:• Does not acquire the Swiss citizenship before his/her death (can acquire another citizenship)• Is still US at the time of his/her death

Forced heirship rights in Swiss law

0.25

0.375

0.375

0.50.5

Spouse

Disposable share

Children Default

shares

Minimal shares

Disposable share

E.g.: The testator has a spouse and children:

Thank you very much for your attention

Should you have any questions…

• Bonnard Lawson – International Law FirmMe Guillaume GRISELRue du Grand-Chêne 8CP 5463CH-1002 Lausanne

• +41(0)21/348’11’88