Embed Size (px)

Citation preview

1

REG Document Review SimulationFederal Taxation › Property Transactions › Section 1231 Assets—Cost Recovery

efficientlearning.com/cpa

Property Transaction 2-3

Question 1 4-7

Question 2 8-11

Question 3 12-15

Question 4 16-19

Question 5 20-23

Exhibit: HEC Tax Depreciation Worksheet 24

Exhibit: Invoice 19 25

Exhibit: Invoice 25 26

Exhibit: Invoice 28 27

Exhibit: Great Buy Invoice 28

Additional Resources: HUD-1 29-31

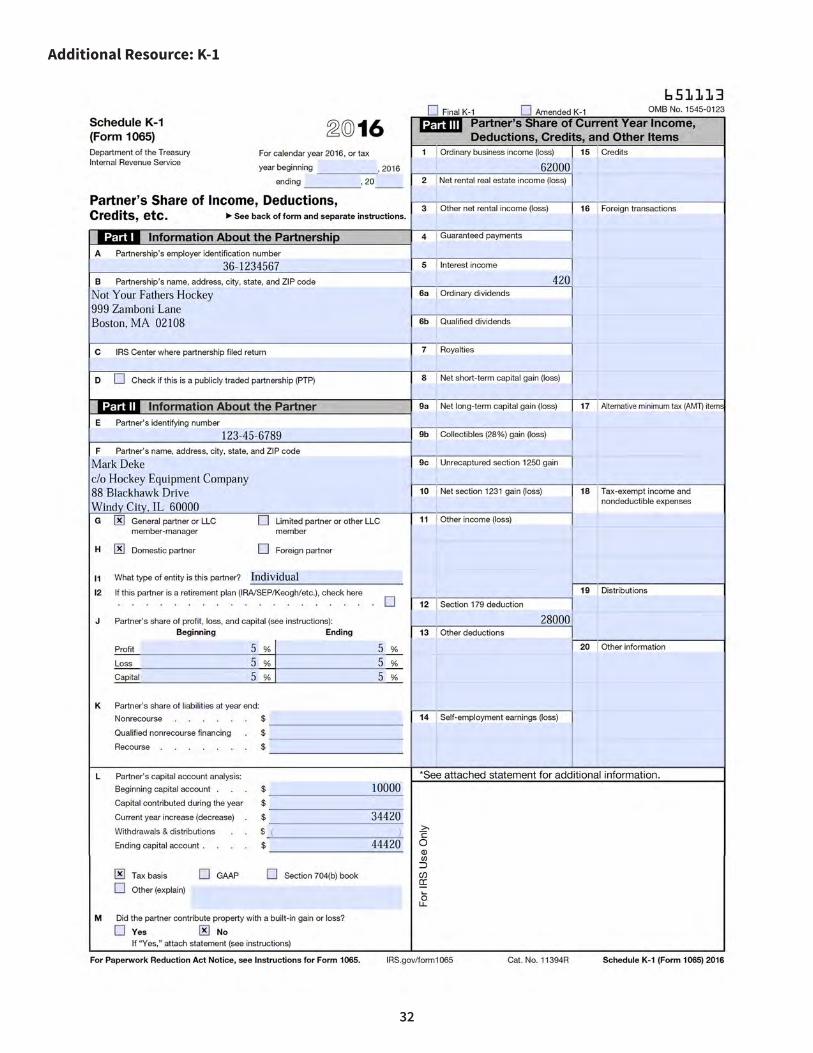

Additional Resources: K-1 32

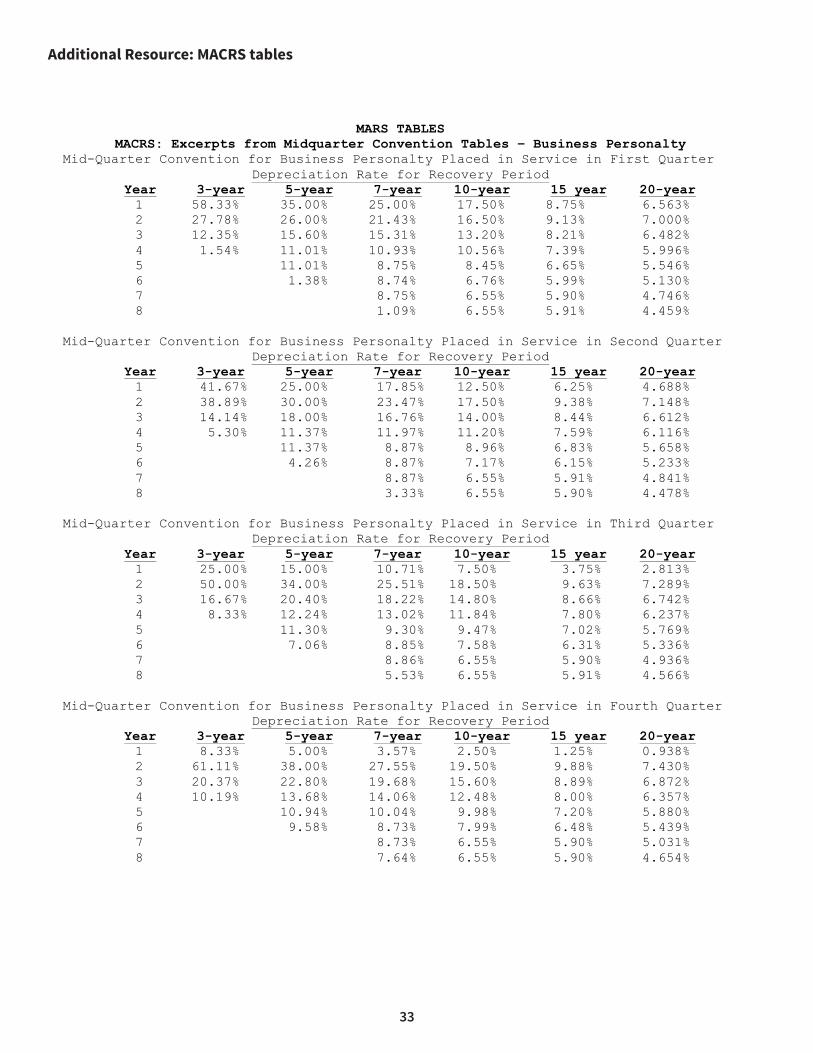

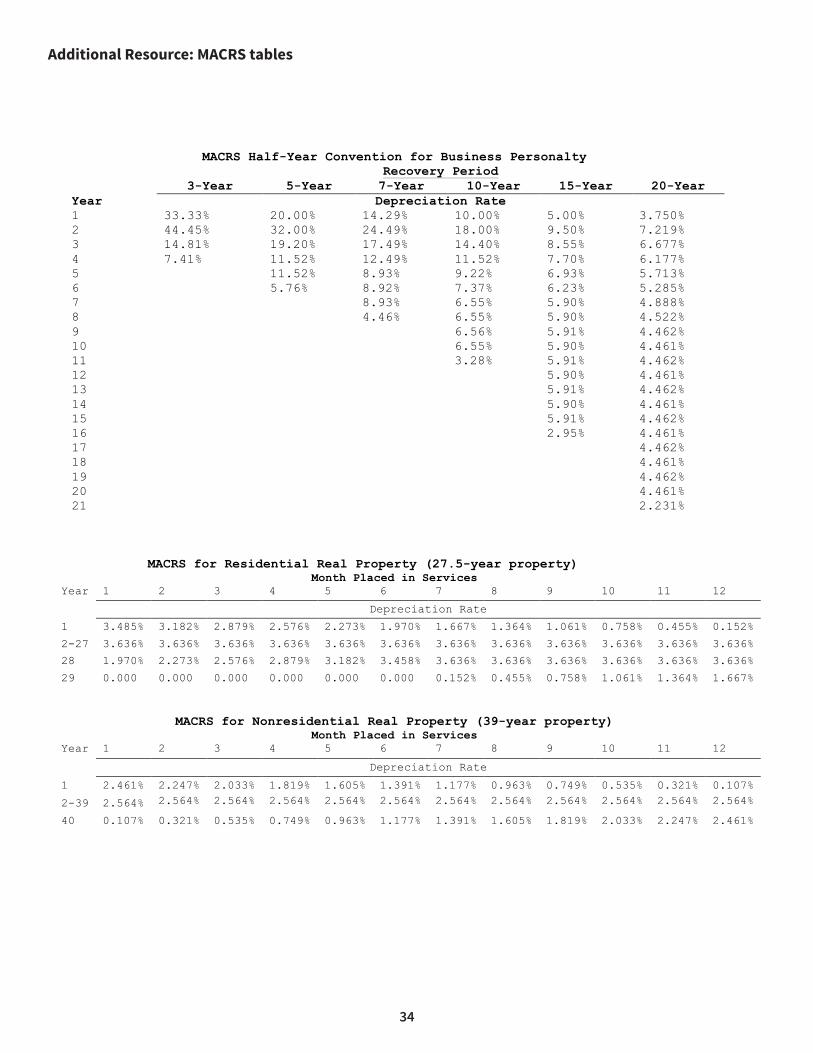

Additional Resources: MACRS tables 33-34

Additional Resource: ADS tables 35

2

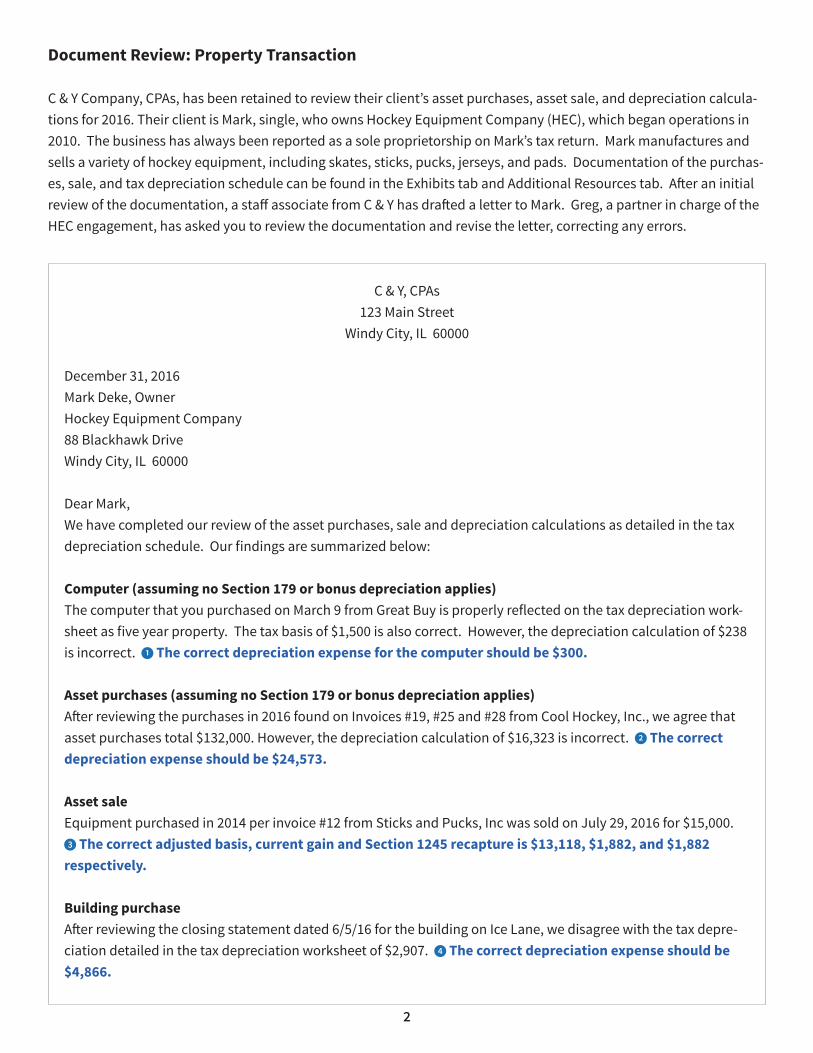

Document Review: Property Transaction

C & Y Company, CPAs, has been retained to review their client’s asset purchases, asset sale, and depreciation calcula-tions for 2016. Their client is Mark, single, who owns Hockey Equipment Company (HEC), which began operations in 2010. The business has always been reported as a sole proprietorship on Mark’s tax return. Mark manufactures and sells a variety of hockey equipment, including skates, sticks, pucks, jerseys, and pads. Documentation of the purchas-es, sale, and tax depreciation schedule can be found in the Exhibits tab and Additional Resources tab. After an initial review of the documentation, a staff associate from C & Y has drafted a letter to Mark. Greg, a partner in charge of the HEC engagement, has asked you to review the documentation and revise the letter, correcting any errors.

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. 1 The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. 2 The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. 3 The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882

respectively.

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depre-ciation detailed in the tax depreciation worksheet of $2,907. 4 The correct depreciation expense should be $4,866.

3

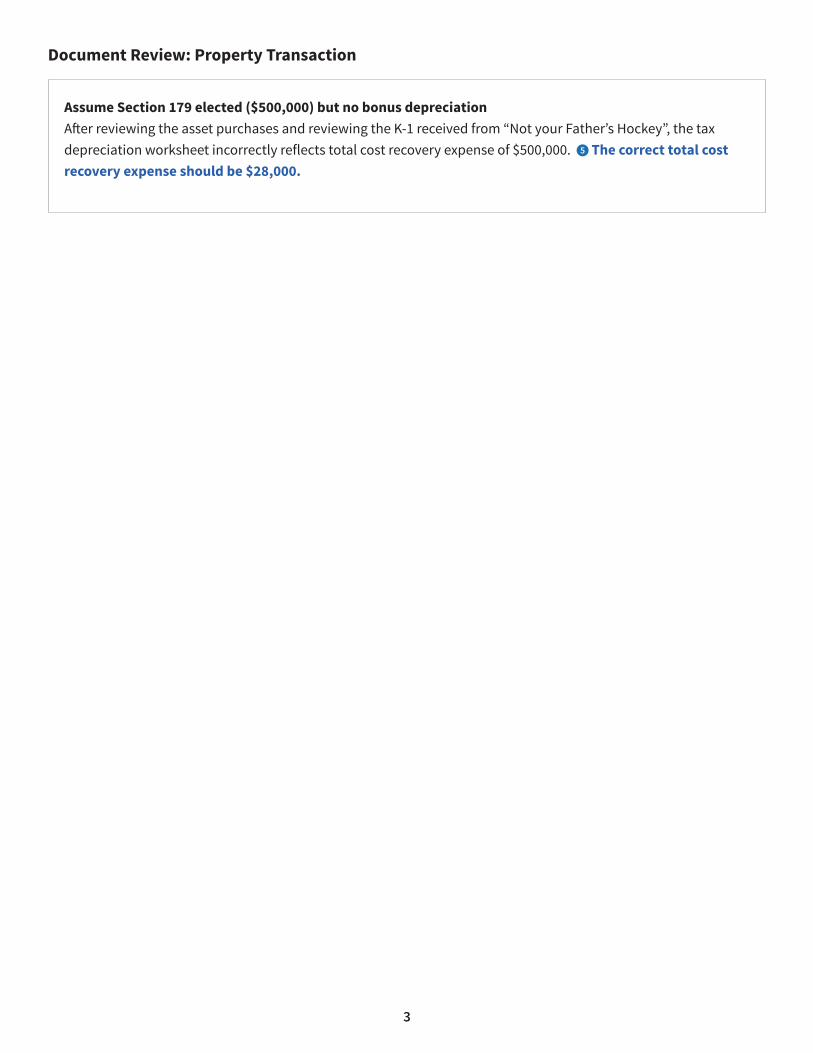

Document Review: Property Transaction

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. 5 The correct total cost recovery expense should be $28,000.

4

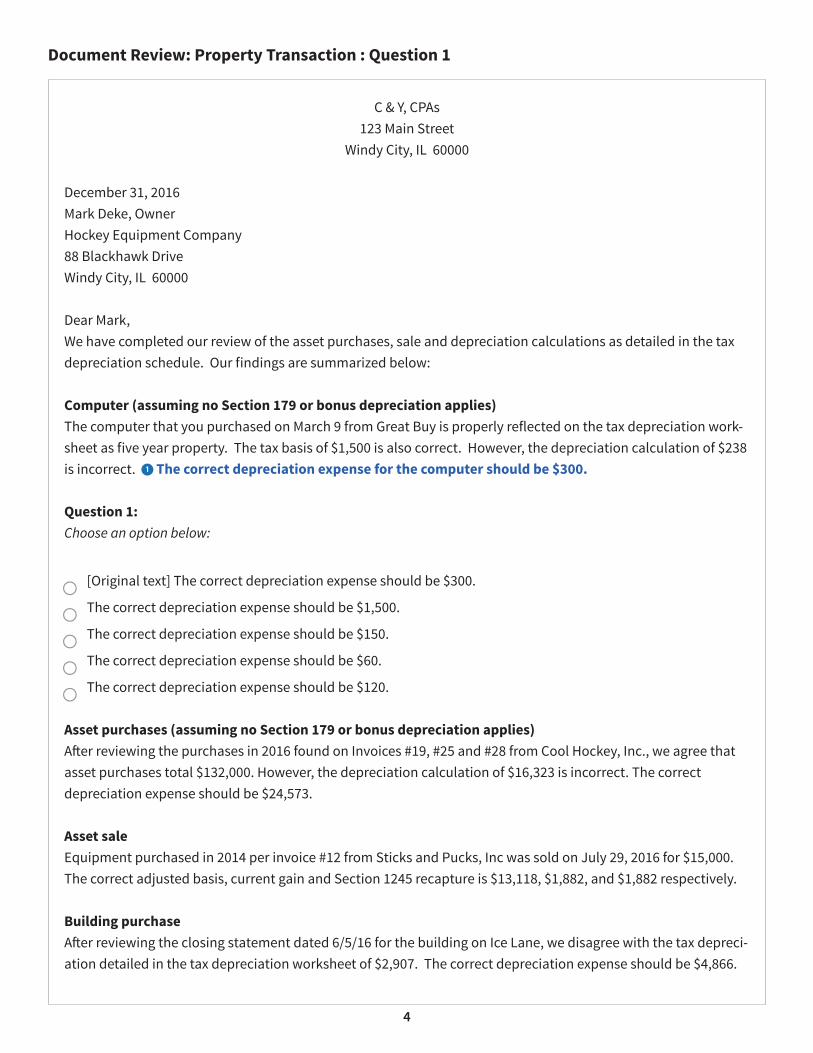

Document Review: Property Transaction : Question 1

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. 1 The correct depreciation expense for the computer should be $300.

Question 1:Choose an option below:

[Original text] The correct depreciation expense should be $300.

The correct depreciation expense should be $1,500.

The correct depreciation expense should be $150.

The correct depreciation expense should be $60.

The correct depreciation expense should be $120.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

5

Document Review: Property Transaction : Question 1

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

6

Document Review: Property Transaction : Question 1 & Rationale

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

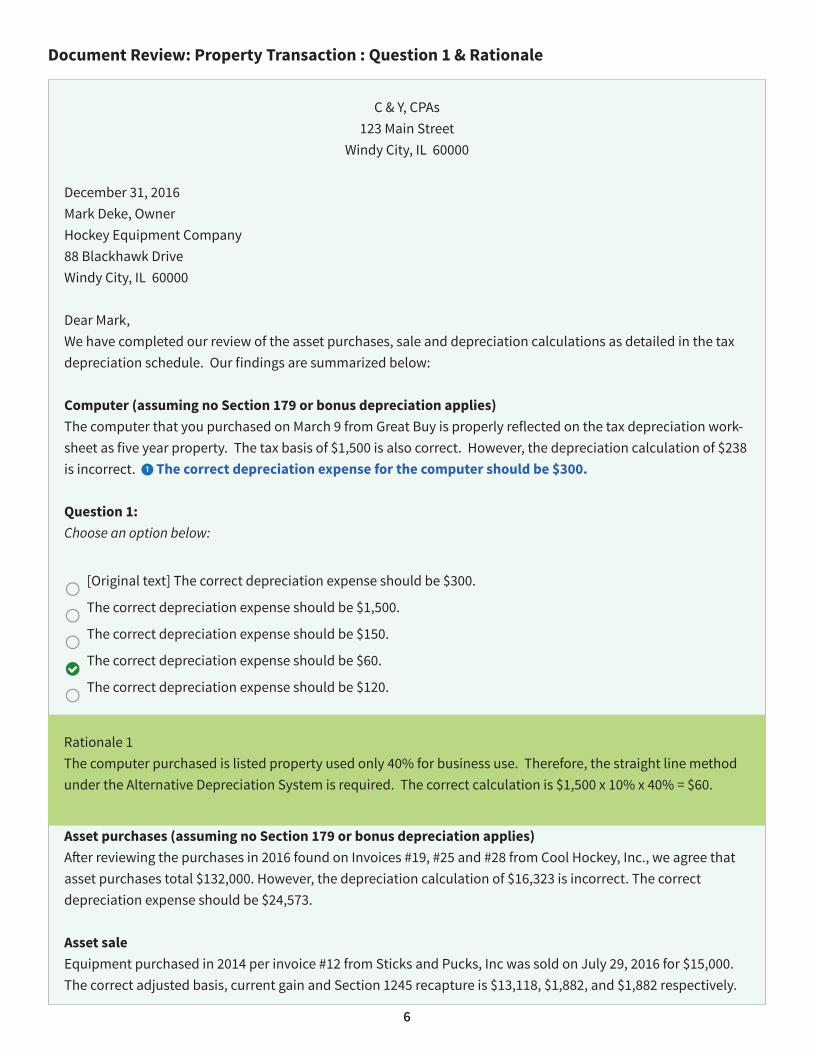

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. 1 The correct depreciation expense for the computer should be $300.

Question 1:Choose an option below:

[Original text] The correct depreciation expense should be $300.

The correct depreciation expense should be $1,500.

The correct depreciation expense should be $150.

The correct depreciation expense should be $60.

The correct depreciation expense should be $120.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

Rationale 1The computer purchased is listed property used only 40% for business use. Therefore, the straight line method under the Alternative Depreciation System is required. The correct calculation is $1,500 x 10% x 40% = $60.

7

Document Review: Property Transaction : Question 1 & Rationale

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

8

Document Review: Property Transaction : Question 2

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

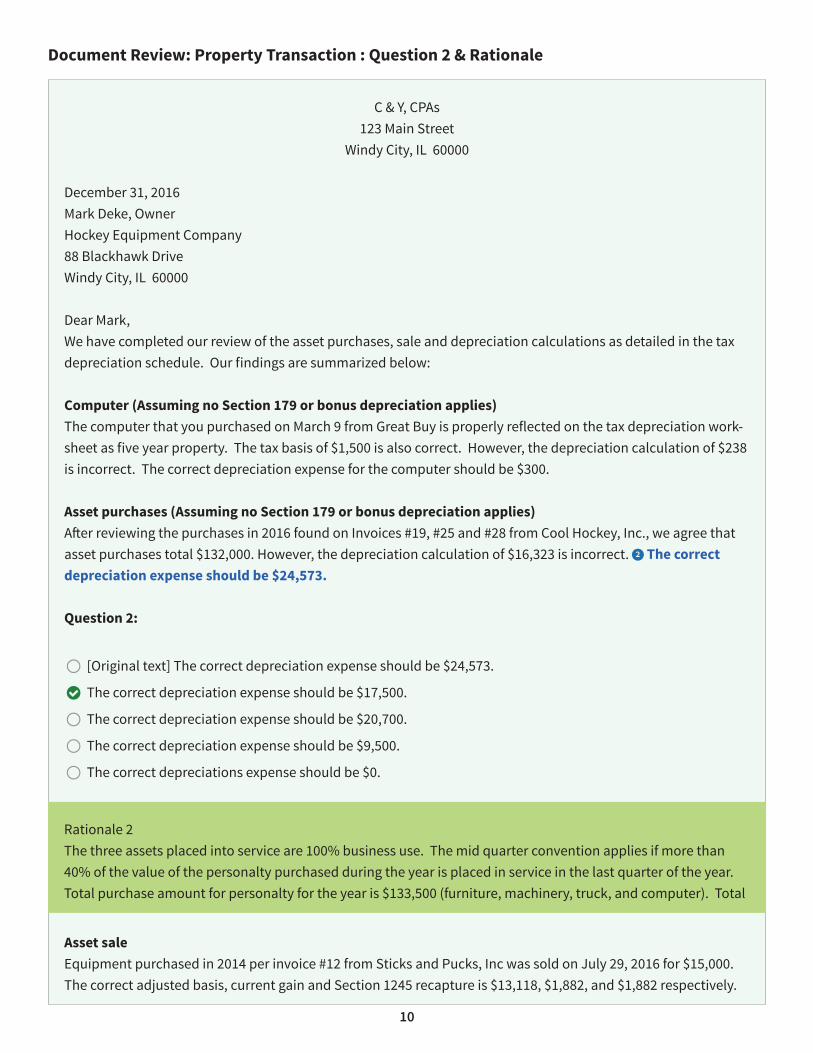

Computer (Assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

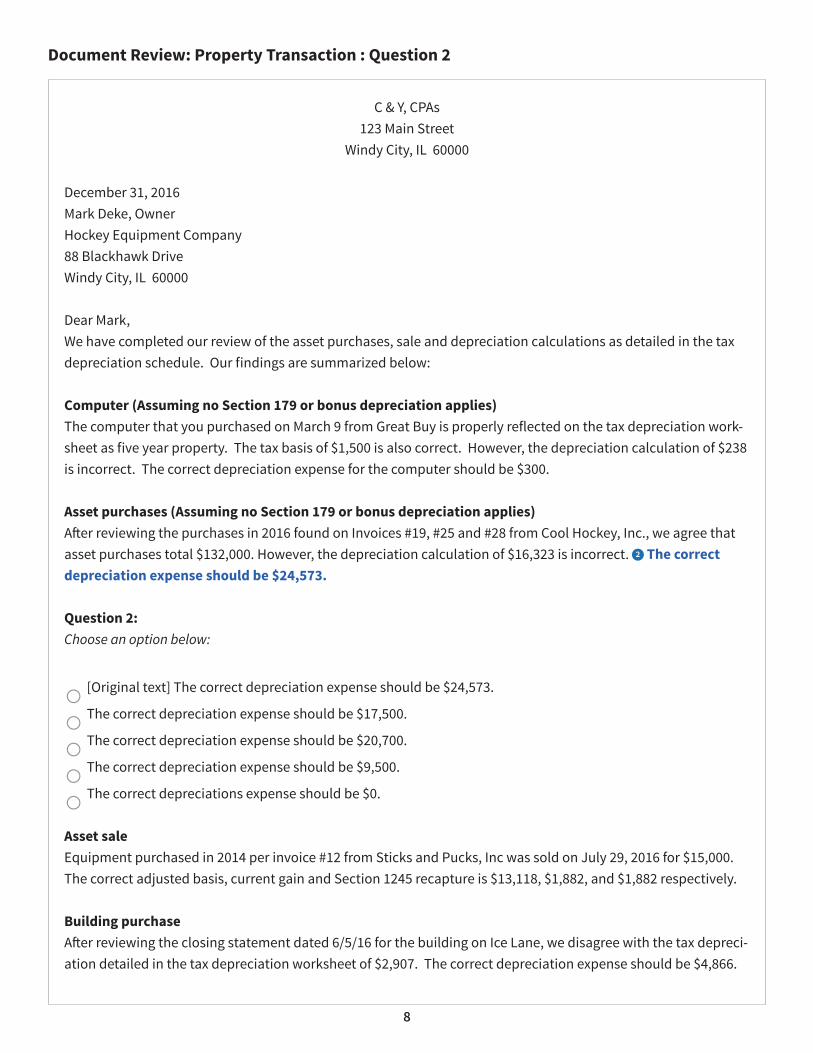

Asset purchases (Assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. 2 The correct depreciation expense should be $24,573.

Question 2:Choose an option below:

[Original text] The correct depreciation expense should be $24,573.

The correct depreciation expense should be $17,500.

The correct depreciation expense should be $20,700.

The correct depreciation expense should be $9,500.

The correct depreciations expense should be $0.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

9

Document Review: Property Transaction : Question 2

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

10

Document Review: Property Transaction : Question 2 & Rationale

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (Assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (Assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. 2 The correct depreciation expense should be $24,573.

Question 2:

[Original text] The correct depreciation expense should be $24,573.

The correct depreciation expense should be $17,500.

The correct depreciation expense should be $20,700.

The correct depreciation expense should be $9,500.

The correct depreciations expense should be $0.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

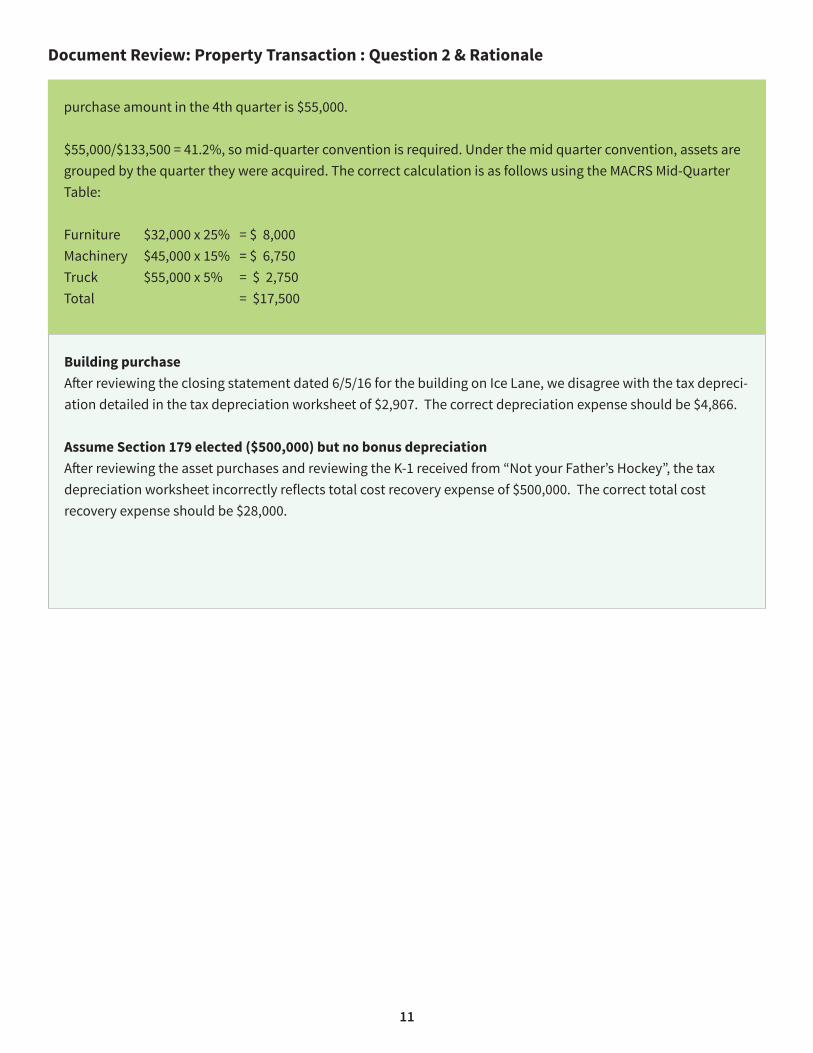

Rationale 2The three assets placed into service are 100% business use. The mid quarter convention applies if more than 40% of the value of the personalty purchased during the year is placed in service in the last quarter of the year. Total purchase amount for personalty for the year is $133,500 (furniture, machinery, truck, and computer). Total

11

Document Review: Property Transaction : Question 2 & Rationale

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

purchase amount in the 4th quarter is $55,000.

$55,000/$133,500 = 41.2%, so mid-quarter convention is required. Under the mid quarter convention, assets are grouped by the quarter they were acquired. The correct calculation is as follows using the MACRS Mid-Quarter Table:

Furniture $32,000 x 25% = $ 8,000Machinery $45,000 x 15% = $ 6,750Truck $55,000 x 5% = $ 2,750Total = $17,500

12

Document Review: Property Transaction : Question 3

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

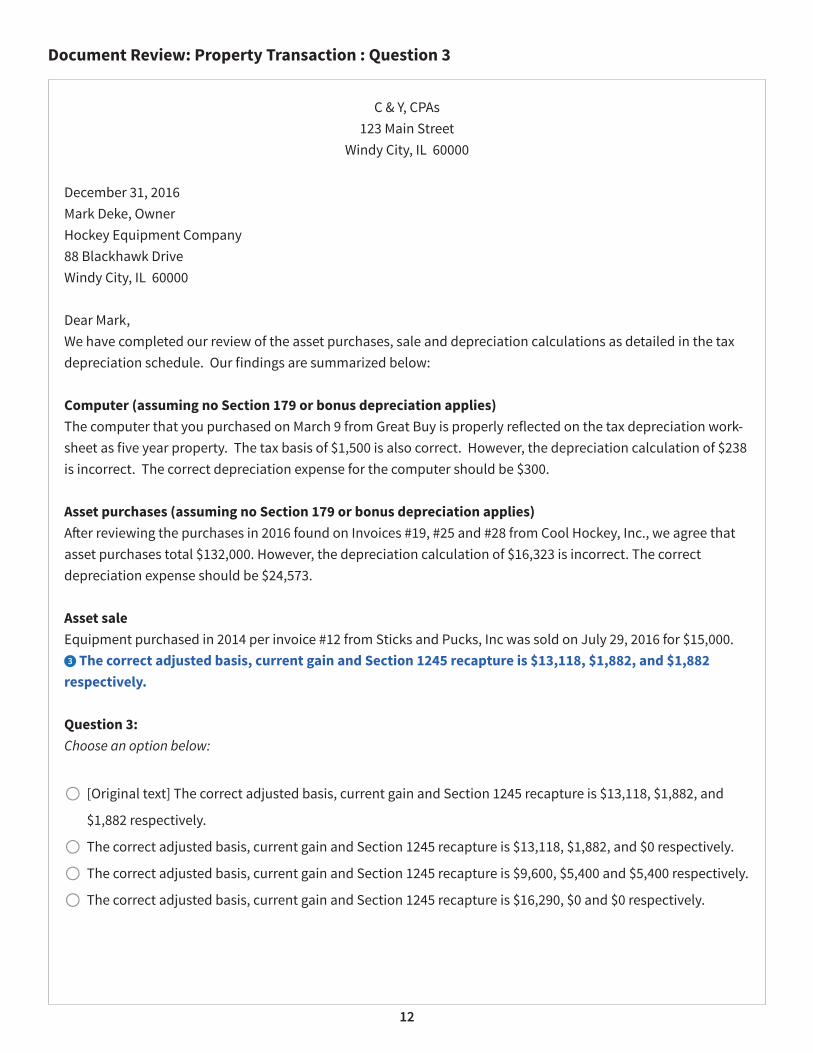

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. 3 The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882

respectively.

Question 3:Choose an option below:

[Original text] The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and

$1,882 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $0 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $9,600, $5,400 and $5,400 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $16,290, $0 and $0 respectively.

13

Document Review: Property Transaction : Question 3

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

14

Document Review: Property Transaction : Question 3 & Rationale

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. 3 The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882

respectively.

Question 3:

[Original text] The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and

$1,882 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $0 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $9,600, $5,400 and $5,400 respectively.

The correct adjusted basis, current gain and Section 1245 recapture is $16,290, $0 and $0 respectively.

15

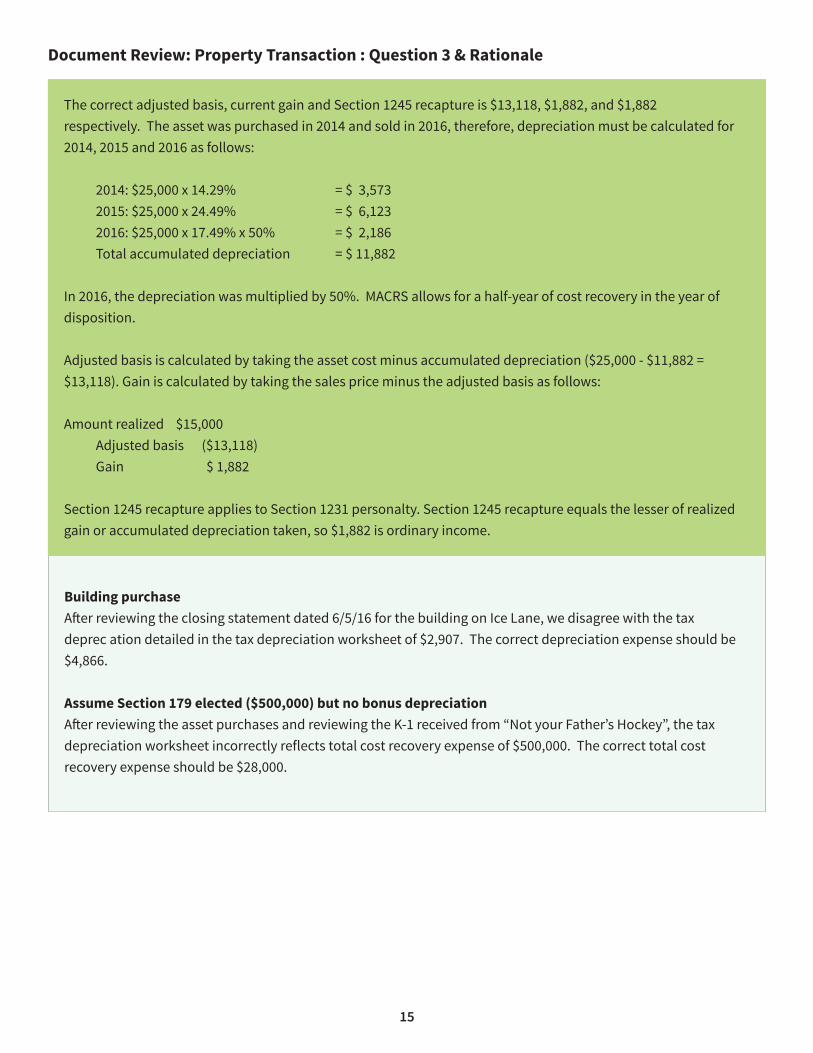

Document Review: Property Transaction : Question 3 & Rationale

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax deprec ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively. The asset was purchased in 2014 and sold in 2016, therefore, depreciation must be calculated for 2014, 2015 and 2016 as follows: 2014: $25,000 x 14.29% = $ 3,573 2015: $25,000 x 24.49% = $ 6,123 2016: $25,000 x 17.49% x 50% = $ 2,186 Total accumulated depreciation = $ 11,882

In 2016, the depreciation was multiplied by 50%. MACRS allows for a half-year of cost recovery in the year of disposition.

Adjusted basis is calculated by taking the asset cost minus accumulated depreciation ($25,000 - $11,882 = $13,118). Gain is calculated by taking the sales price minus the adjusted basis as follows:

Amount realized $15,000 Adjusted basis ($13,118) Gain $ 1,882

Section 1245 recapture applies to Section 1231 personalty. Section 1245 recapture equals the lesser of realized gain or accumulated depreciation taken, so $1,882 is ordinary income.

16

Document Review: Property Transaction : Question 4

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

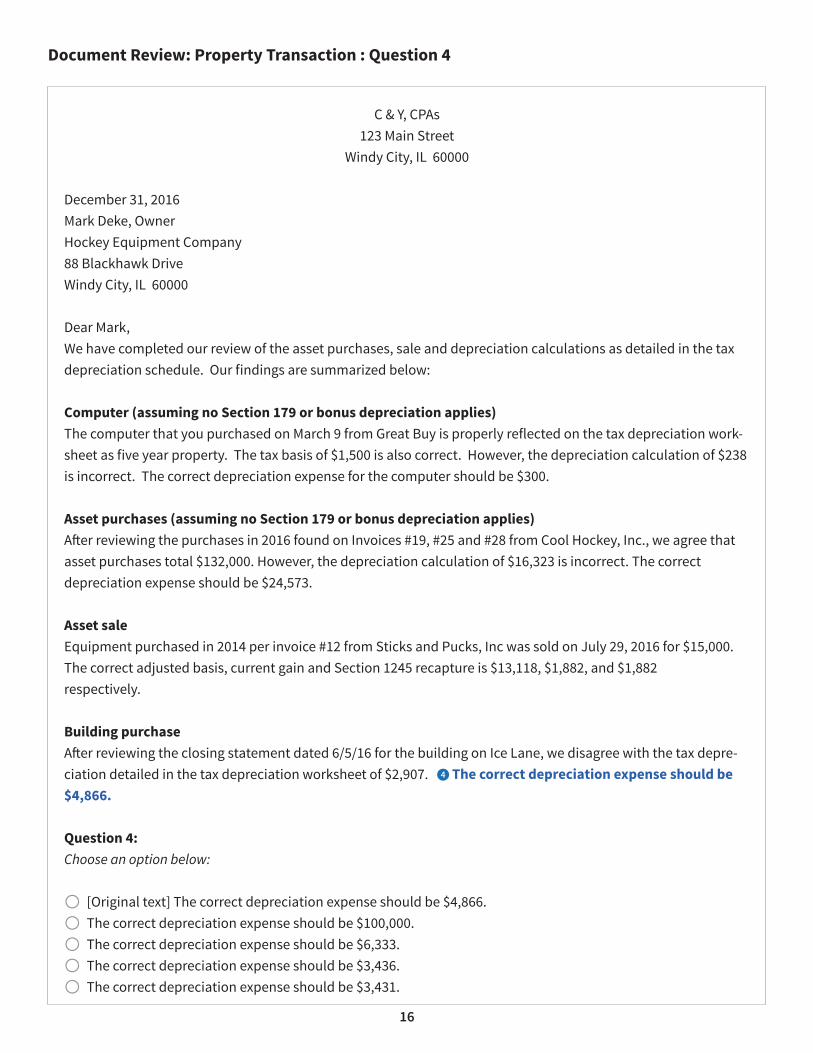

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depre-ciation detailed in the tax depreciation worksheet of $2,907. 4 The correct depreciation expense should be $4,866.

Question 4:Choose an option below:

[Original text] The correct depreciation expense should be $4,866.The correct depreciation expense should be $100,000.The correct depreciation expense should be $6,333.The correct depreciation expense should be $3,436.The correct depreciation expense should be $3,431.

17

Document Review: Property Transaction : Question 4

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

18

Document Review: Property Transaction : Question 4 & Rationale

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

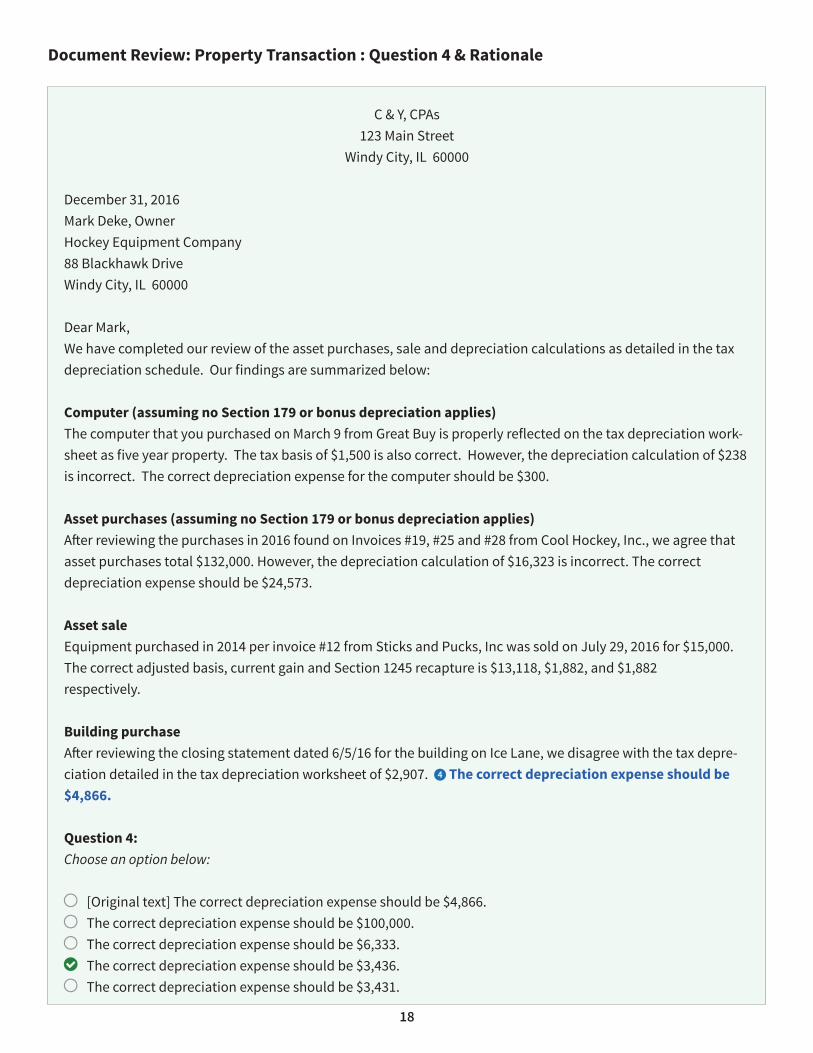

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depre-ciation detailed in the tax depreciation worksheet of $2,907. 4 The correct depreciation expense should be $4,866.

Question 4:Choose an option below:

[Original text] The correct depreciation expense should be $4,866.The correct depreciation expense should be $100,000.The correct depreciation expense should be $6,333.The correct depreciation expense should be $3,436.The correct depreciation expense should be $3,431.

19

Document Review: Property Transaction : Question 4 & Rationale

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. The correct total cost recovery expense should be $28,000.

The building purchased in June was non-residential real estate and is depreciated using the mid-month convention. It is deemed to be placed in service in the middle of the month. The correct calculation is $247,000 x 1.391% = $3,436, per the MACRS Residential Real Estate Table.

20

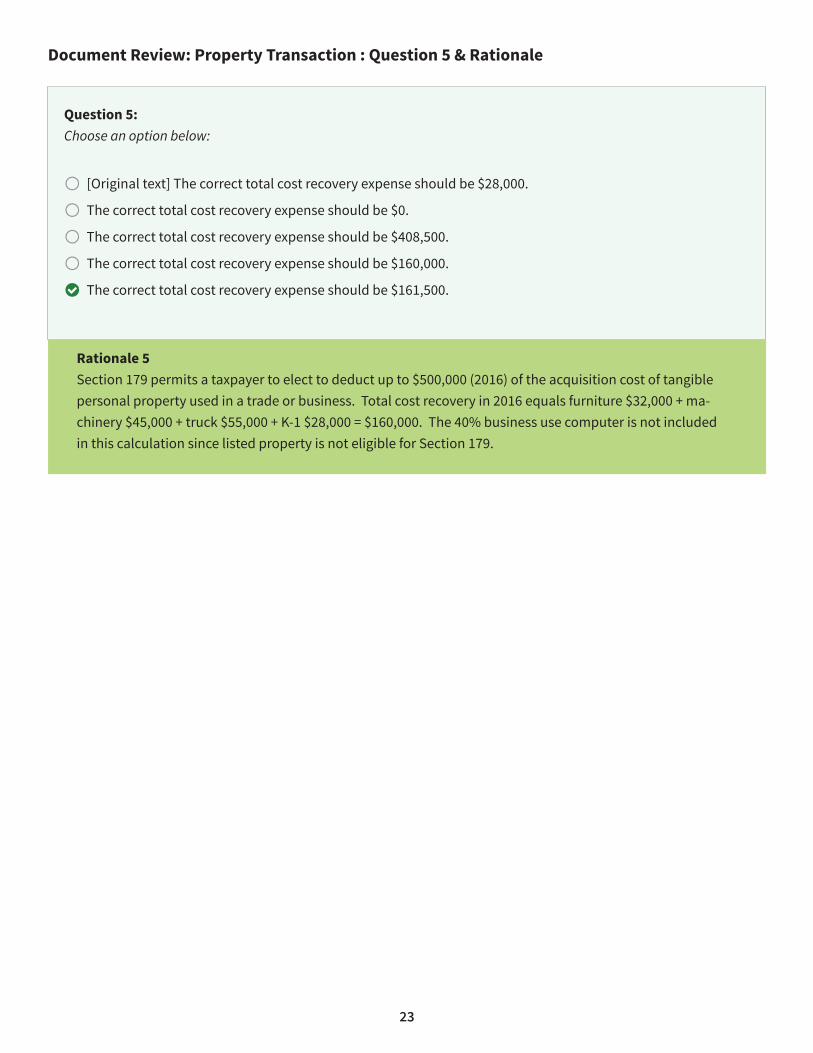

Document Review: Property Transaction : Question 5

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. 5 The correct total cost recovery expense should be $28,000.

21

Document Review: Property Transaction : Question 5

Question 5:Choose an option below:

[Original text] The correct total cost recovery expense should be $28,000.

The correct total cost recovery expense should be $0.

The correct total cost recovery expense should be $408,500.

The correct total cost recovery expense should be $160,000.

The correct total cost recovery expense should be $161,500.

22

Document Review: Property Transaction : Question 5 & Rationale

C & Y, CPAs123 Main Street

Windy City, IL 60000

December 31, 2016Mark Deke, OwnerHockey Equipment Company88 Blackhawk DriveWindy City, IL 60000

Dear Mark,We have completed our review of the asset purchases, sale and depreciation calculations as detailed in the tax depreciation schedule. Our findings are summarized below:

Computer (assuming no Section 179 or bonus depreciation applies)The computer that you purchased on March 9 from Great Buy is properly reflected on the tax depreciation work-sheet as five year property. The tax basis of $1,500 is also correct. However, the depreciation calculation of $238 is incorrect. The correct depreciation expense for the computer should be $300.

Asset purchases (assuming no Section 179 or bonus depreciation applies)After reviewing the purchases in 2016 found on Invoices #19, #25 and #28 from Cool Hockey, Inc., we agree that asset purchases total $132,000. However, the depreciation calculation of $16,323 is incorrect. The correct depreciation expense should be $24,573.

Asset saleEquipment purchased in 2014 per invoice #12 from Sticks and Pucks, Inc was sold on July 29, 2016 for $15,000. The correct adjusted basis, current gain and Section 1245 recapture is $13,118, $1,882, and $1,882 respectively.

Building purchaseAfter reviewing the closing statement dated 6/5/16 for the building on Ice Lane, we disagree with the tax depreci-ation detailed in the tax depreciation worksheet of $2,907. The correct depreciation expense should be $4,866.

Assume Section 179 elected ($500,000) but no bonus depreciationAfter reviewing the asset purchases and reviewing the K-1 received from “Not your Father’s Hockey”, the tax depreciation worksheet incorrectly reflects total cost recovery expense of $500,000. 5 The correct total cost recovery expense should be $28,000.

23

Document Review: Property Transaction : Question 5 & Rationale

Question 5:Choose an option below:

[Original text] The correct total cost recovery expense should be $28,000.

The correct total cost recovery expense should be $0.

The correct total cost recovery expense should be $408,500.

The correct total cost recovery expense should be $160,000.

The correct total cost recovery expense should be $161,500.

Rationale 5Section 179 permits a taxpayer to elect to deduct up to $500,000 (2016) of the acquisition cost of tangible personal property used in a trade or business. Total cost recovery in 2016 equals furniture $32,000 + ma-chinery $45,000 + truck $55,000 + K-1 $28,000 = $160,000. The 40% business use computer is not included in this calculation since listed property is not eligible for Section 179.

24

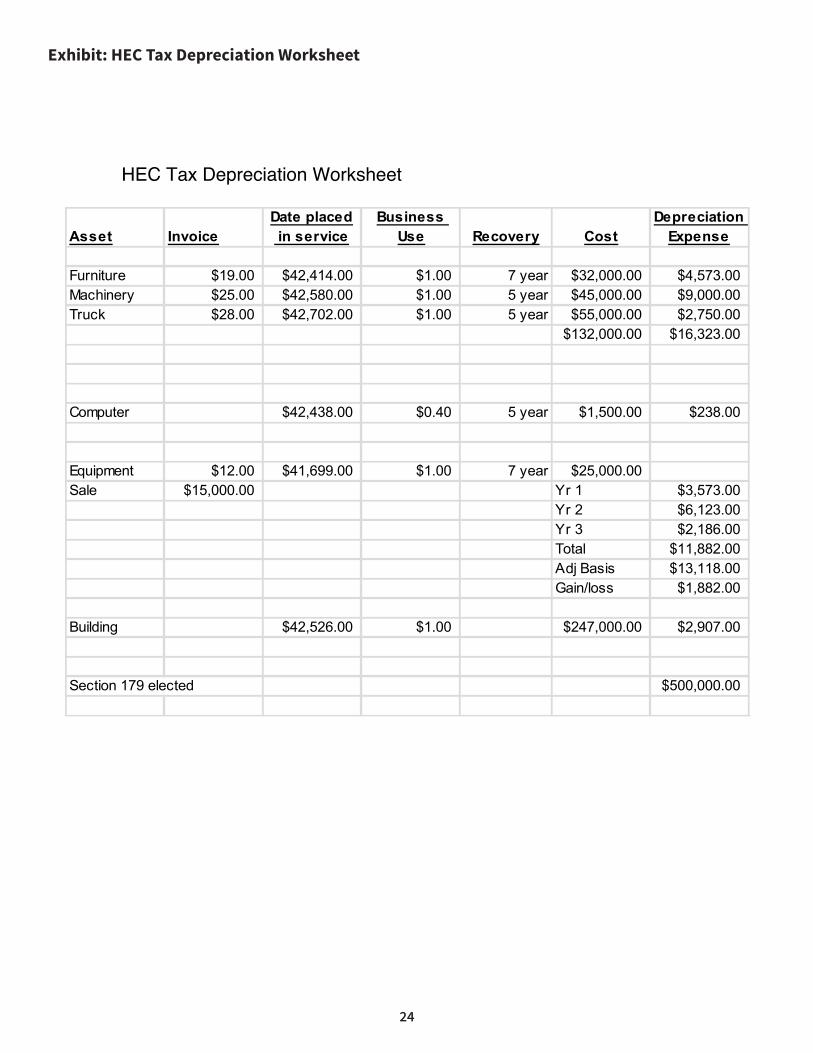

Exhibit: HEC Tax Depreciation Worksheet

HEC Tax Depreciation Worksheet

Asset InvoiceDate placed in service

Business Use Recovery Cost

Depreciation Expense

Furniture $19.00 $42,414.00 $1.00 7 year $32,000.00 $4,573.00Machinery $25.00 $42,580.00 $1.00 5 year $45,000.00 $9,000.00Truck $28.00 $42,702.00 $1.00 5 year $55,000.00 $2,750.00

$132,000.00 $16,323.00

Computer $42,438.00 $0.40 5 year $1,500.00 $238.00

Equipment $12.00 $41,699.00 $1.00 7 year $25,000.00Sale $15,000.00 Yr 1 $3,573.00

Yr 2 $6,123.00Yr 3 $2,186.00Total $11,882.00Adj Basis $13,118.00Gain/loss $1,882.00

Building $42,526.00 $1.00 $247,000.00 $2,907.00

Section 179 elected $500,000.00

25

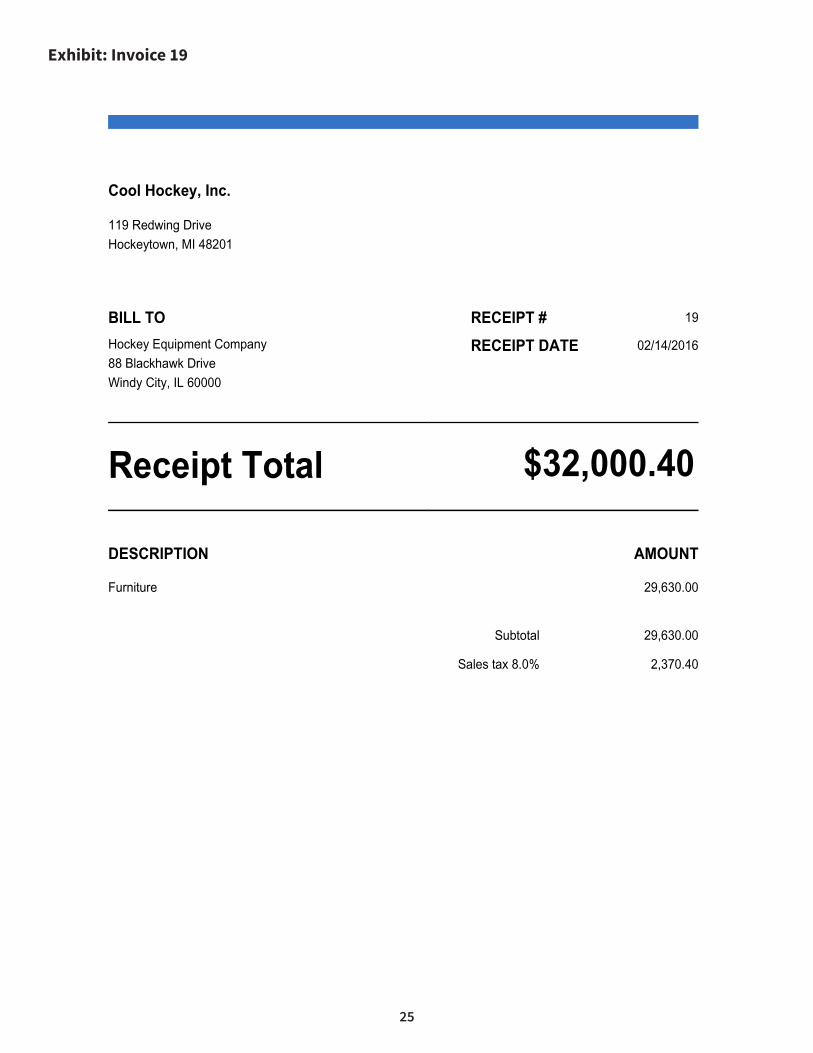

Exhibit: Invoice 19

Cool Hockey, Inc.

119 Redwing Drive

Hockeytown, MI 48201

BILL TO RECEIPT # 19

Hockey Equipment Company

88 Blackhawk Drive

Windy City, IL 60000

RECEIPT DATE 02/14/2016

Receipt Total $32,000.40

DESCRIPTION AMOUNT

Furniture 29,630.00

Subtotal 29,630.00

Sales tax 8.0% 2,370.40

TERMS & CONDITIONS

Payment is due within 15 days

26

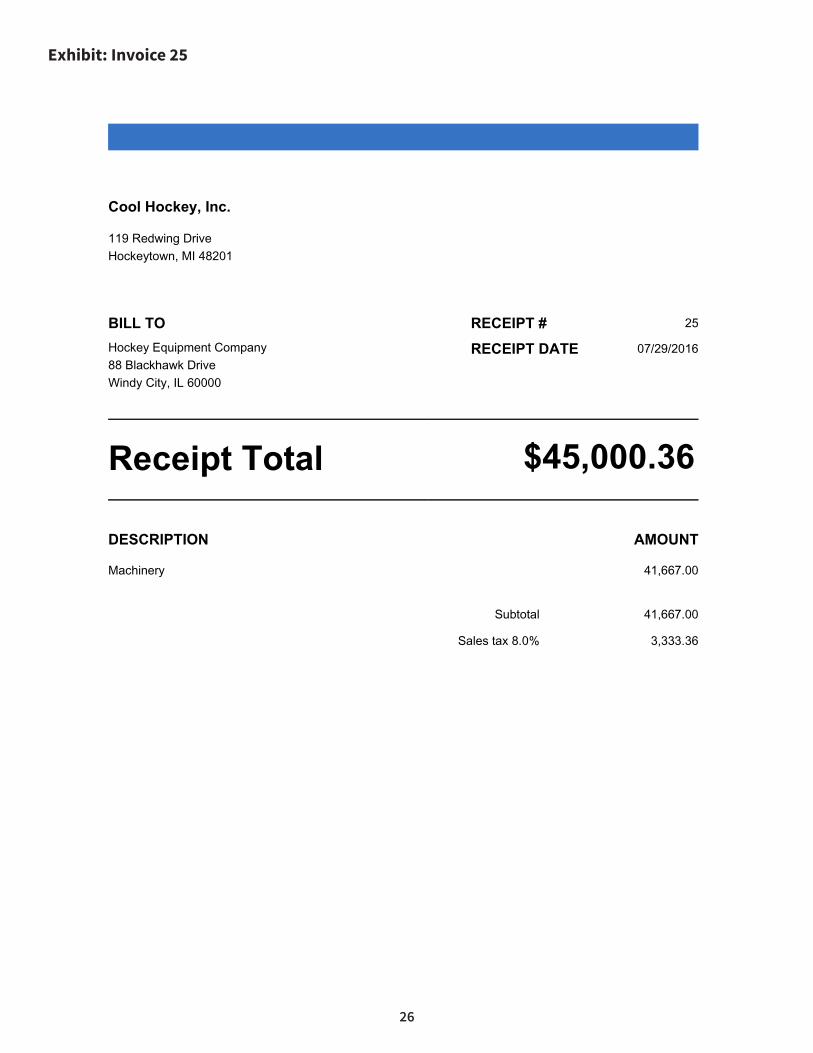

Exhibit: Invoice 25

Cool Hockey, Inc.

119 Redwing Drive

Hockeytown, MI 48201

BILL TO RECEIPT # 25

Hockey Equipment Company

88 Blackhawk Drive

Windy City, IL 60000

RECEIPT DATE 07/29/2016

Receipt Total $45,000.36

DESCRIPTION AMOUNT

Machinery 41,667.00

Subtotal 41,667.00

Sales tax 8.0% 3,333.36

TERMS & CONDITIONS

Payment is due within 15 days

27

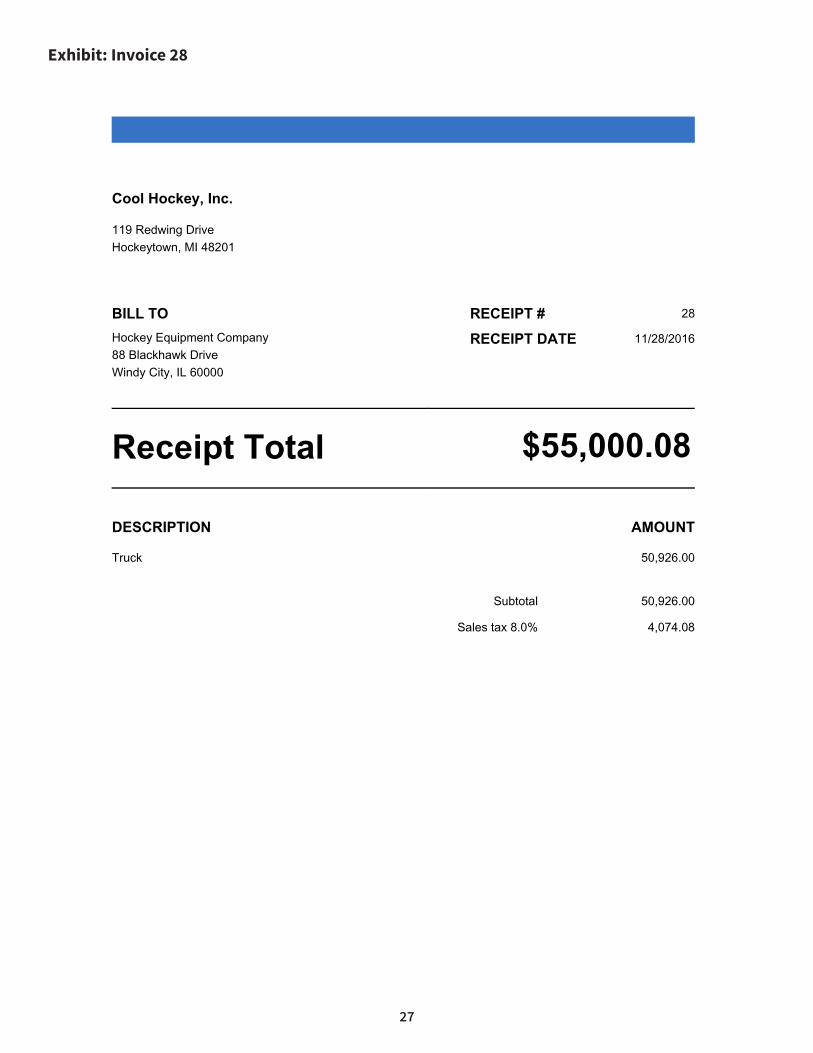

Exhibit: Invoice 28

Cool Hockey, Inc.

119 Redwing Drive

Hockeytown, MI 48201

BILL TO RECEIPT # 28

Hockey Equipment Company

88 Blackhawk Drive

Windy City, IL 60000

RECEIPT DATE 11/28/2016

Receipt Total $55,000.08

DESCRIPTION AMOUNT

Truck 50,926.00

Subtotal 50,926.00

Sales tax 8.0% 4,074.08

TERMS & CONDITIONS

Payment is due within 15 days

28

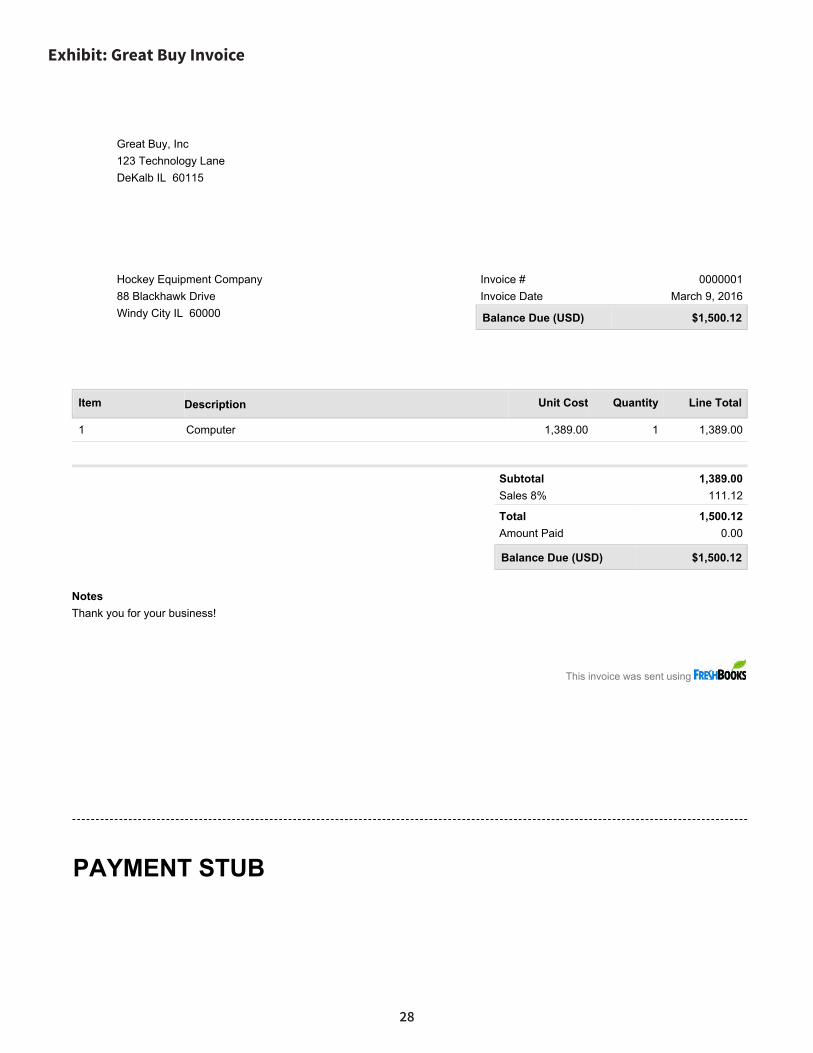

Exhibit: Great Buy Invoice

Hockey Equipment Company88 Blackhawk DriveWindy City IL 60000

Invoice # 0000001Invoice Date March 9, 2016

Balance Due (USD) $1,500.12

Subtotal 1,389.00Sales 8% 111.12

Total 1,500.12Amount Paid 0.00

Balance Due (USD) $1,500.12

This invoice was sent using

Item Description Unit Cost Quantity Line Total

1 Computer 1,389.00 1 1,389.00

NotesThank you for your business!

Great Buy, Inc123 Technology LaneDeKalb IL 60115

PAYMENT STUB

Great Buy, Inc123 Technology LaneDeKalb IL 60115

Client Hockey Equipment CompanyInvoice # 0000001Invoice Date March 9, 2016

Balance Due (USD) $1,500.12

Amount Enclosed

29

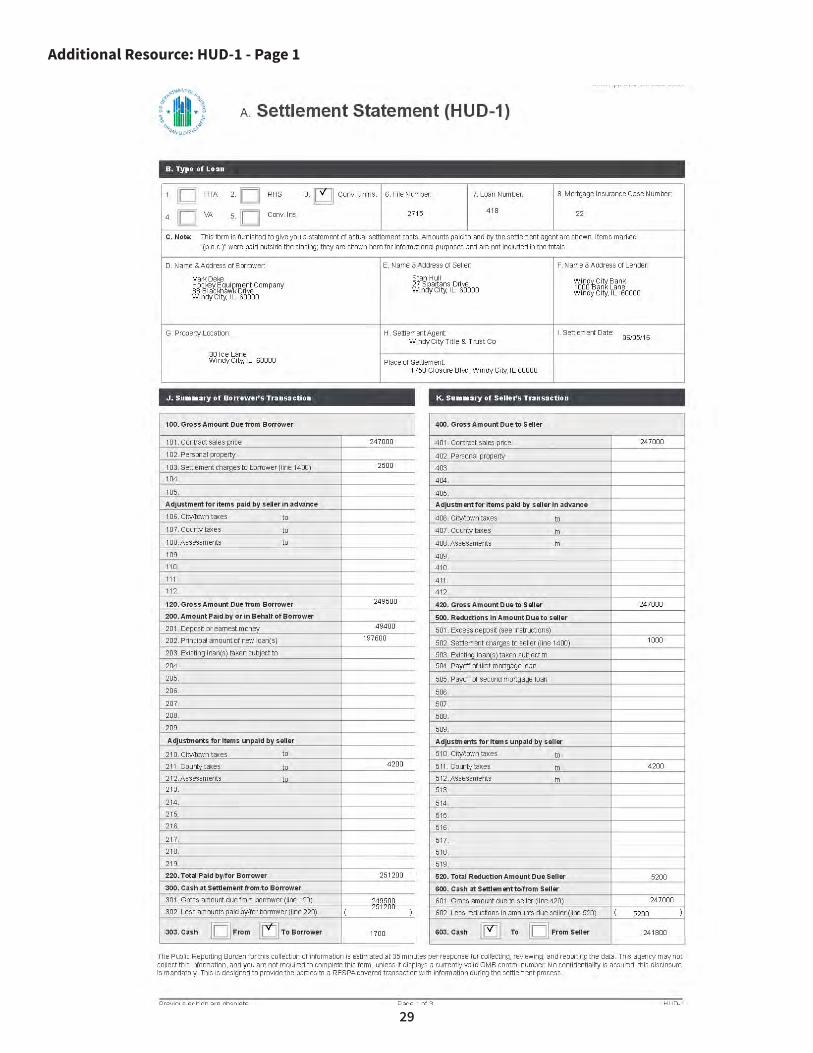

Additional Resource: HUD-1 - Page 1

30

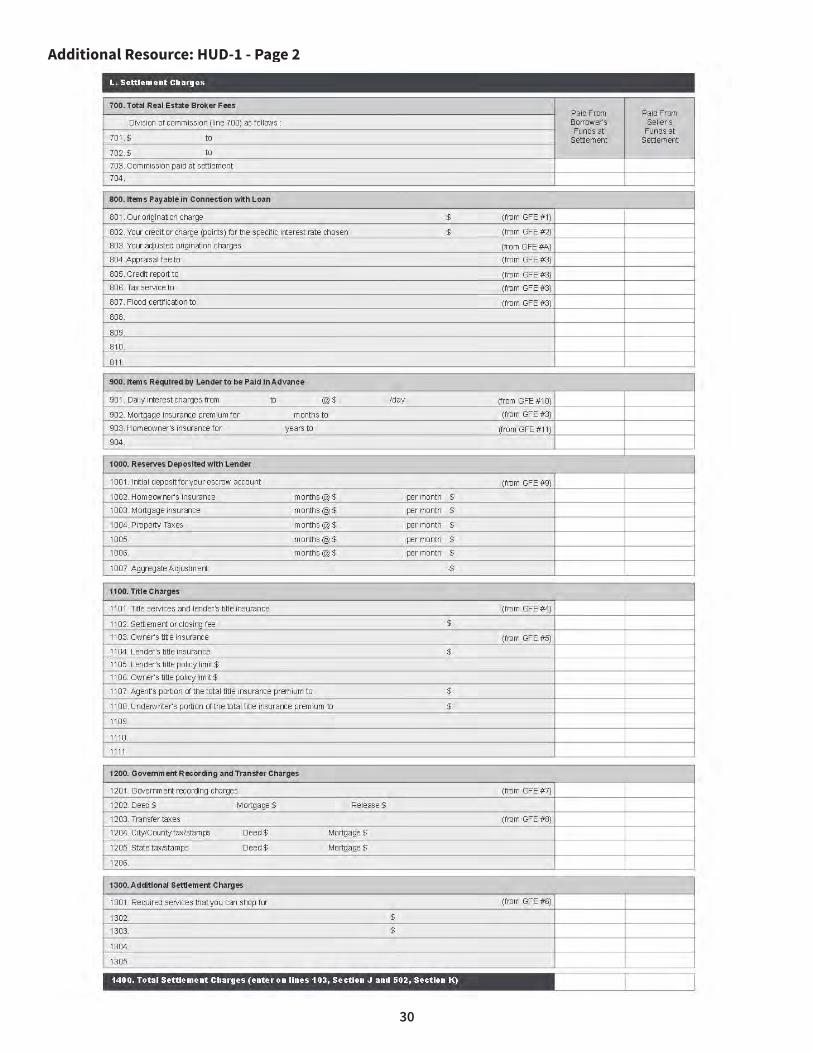

Additional Resource: HUD-1 - Page 2

31

Additional Resource: HUD-1 - Page 3

32

Additional Resource: K-1

33

Additional Resource: MACRS tables

MARS TABLES MACRS: Excerpts from Midquarter Convention Tables – Business Personalty

Mid-Quarter Convention for Business Personalty Placed in Service in First Quarter Depreciation Rate for Recovery Period

Year 3-year 5-year 7-year 10-year 15 year 20-year 1 58.33% 35.00% 25.00% 17.50% 8.75% 6.563% 2 27.78% 26.00% 21.43% 16.50% 9.13% 7.000% 3 12.35% 15.60% 15.31% 13.20% 8.21% 6.482% 4 1.54% 11.01% 10.93% 10.56% 7.39% 5.996% 5 11.01% 8.75% 8.45% 6.65% 5.546% 6 1.38% 8.74% 6.76% 5.99% 5.130% 7 8.75% 6.55% 5.90% 4.746% 8 1.09% 6.55% 5.91% 4.459% Mid-Quarter Convention for Business Personalty Placed in Service in Second Quarter

Depreciation Rate for Recovery Period Year 3-year 5-year 7-year 10-year 15 year 20-year 1 41.67% 25.00% 17.85% 12.50% 6.25% 4.688% 2 38.89% 30.00% 23.47% 17.50% 9.38% 7.148% 3 14.14% 18.00% 16.76% 14.00% 8.44% 6.612% 4 5.30% 11.37% 11.97% 11.20% 7.59% 6.116% 5 11.37% 8.87% 8.96% 6.83% 5.658% 6 4.26% 8.87% 7.17% 6.15% 5.233% 7 8.87% 6.55% 5.91% 4.841% 8 3.33% 6.55% 5.90% 4.478% Mid-Quarter Convention for Business Personalty Placed in Service in Third Quarter

Depreciation Rate for Recovery Period Year 3-year 5-year 7-year 10-year 15 year 20-year 1 25.00% 15.00% 10.71% 7.50% 3.75% 2.813% 2 50.00% 34.00% 25.51% 18.50% 9.63% 7.289% 3 16.67% 20.40% 18.22% 14.80% 8.66% 6.742% 4 8.33% 12.24% 13.02% 11.84% 7.80% 6.237% 5 11.30% 9.30% 9.47% 7.02% 5.769% 6 7.06% 8.85% 7.58% 6.31% 5.336% 7 8.86% 6.55% 5.90% 4.936% 8 5.53% 6.55% 5.91% 4.566% Mid-Quarter Convention for Business Personalty Placed in Service in Fourth Quarter

Depreciation Rate for Recovery Period Year 3-year 5-year 7-year 10-year 15 year 20-year 1 8.33% 5.00% 3.57% 2.50% 1.25% 0.938% 2 61.11% 38.00% 27.55% 19.50% 9.88% 7.430% 3 20.37% 22.80% 19.68% 15.60% 8.89% 6.872% 4 10.19% 13.68% 14.06% 12.48% 8.00% 6.357% 5 10.94% 10.04% 9.98% 7.20% 5.880% 6 9.58% 8.73% 7.99% 6.48% 5.439% 7 8.73% 6.55% 5.90% 5.031% 8 7.64% 6.55% 5.90% 4.654%

34

Additional Resource: MACRS tables

MACRS Half-Year Convention for Business Personalty

Recovery Period 3-Year 5-Year 7-Year 10-Year 15-Year 20-Year Year Depreciation Rate 1 33.33% 20.00% 14.29% 10.00% 5.00% 3.750% 2 44.45% 32.00% 24.49% 18.00% 9.50% 7.219% 3 14.81% 19.20% 17.49% 14.40% 8.55% 6.677% 4 7.41% 11.52% 12.49% 11.52% 7.70% 6.177% 5 11.52% 8.93% 9.22% 6.93% 5.713% 6 5.76% 8.92% 7.37% 6.23% 5.285% 7 8.93% 6.55% 5.90% 4.888% 8 4.46% 6.55% 5.90% 4.522% 9 6.56% 5.91% 4.462% 10 6.55% 5.90% 4.461% 11 3.28% 5.91% 4.462% 12 5.90% 4.461% 13 5.91% 4.462% 14 5.90% 4.461% 15 5.91% 4.462% 16 2.95% 4.461% 17 4.462% 18 4.461% 19 4.462% 20 4.461% 21 2.231%

MACRS for Residential Real Property (27.5-year property) Month Placed in Services

Year 1 2 3 4 5 6 7 8 9 10 11 12

Depreciation Rate

1 3.485% 3.182% 2.879% 2.576% 2.273% 1.970% 1.667% 1.364% 1.061% 0.758% 0.455% 0.152%

2-27 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 28 1.970% 2.273% 2.576% 2.879% 3.182% 3.458% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 29 0.000 0.000 0.000 0.000 0.000 0.000 0.152% 0.455% 0.758% 1.061% 1.364% 1.667%

MACRS for Nonresidential Real Property (39-year property) Month Placed in Services

Year 1 2 3 4 5 6 7 8 9 10 11 12

Depreciation Rate

1 2.461% 2.247% 2.033% 1.819% 1.605% 1.391% 1.177% 0.963% 0.749% 0.535% 0.321% 0.107%

2-39 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564%

40 0.107% 0.321% 0.535% 0.749% 0.963% 1.177% 1.391% 1.605% 1.819% 2.033% 2.247% 2.461%

35

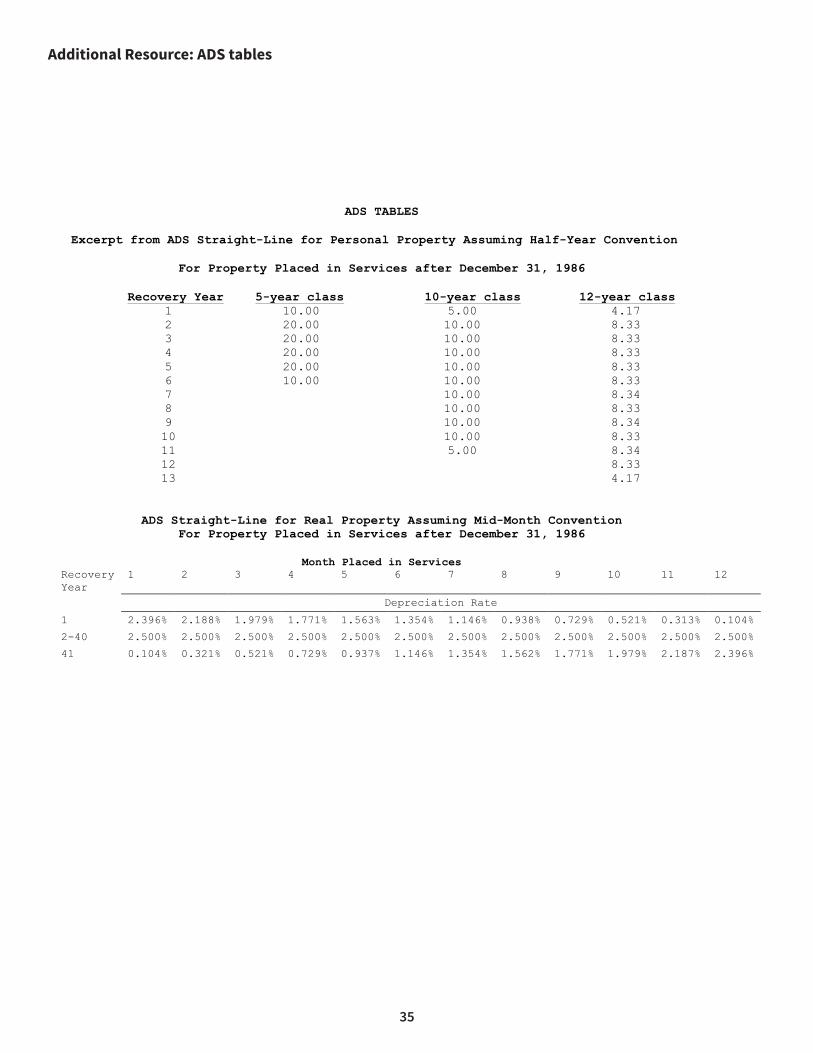

Additional Resource: ADS tables

ADS TABLES

Excerpt from ADS Straight-Line for Personal Property Assuming Half-Year Convention

For Property Placed in Services after December 31, 1986

Recovery Year 5-year class 10-year class 12-year class 1 10.00 5.00 4.17 2 20.00 10.00 8.33 3 20.00 10.00 8.33 4 20.00 10.00 8.33 5 20.00 10.00 8.33 6 10.00 10.00 8.33 7 10.00 8.34 8 10.00 8.33 9 10.00 8.34 10 10.00 8.33 11 5.00 8.34 12 8.33 13 4.17

ADS Straight-Line for Real Property Assuming Mid-Month Convention For Property Placed in Services after December 31, 1986

Month Placed in Services Recovery Year

1 2 3 4 5 6 7 8 9 10 11 12

Depreciation Rate

1 2.396% 2.188% 1.979% 1.771% 1.563% 1.354% 1.146% 0.938% 0.729% 0.521% 0.313% 0.104%

2-40 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 2.500% 41 0.104% 0.321% 0.521% 0.729% 0.937% 1.146% 1.354% 1.562% 1.771% 1.979% 2.187% 2.396%