Embed Size (px)

Citation preview

Effective January 1, 2014 sales taxes must be collected on admission charges to entertainment events and remitted to the N.C. Department of Revenue.

N.C. General Statute 105-164.4(a)(10) imposes a tax on a retailer (including the University) at the current rate of 4.75% general State and applicable local and transit rates (currently 2.25% for Pitt County) of sales and use tax to admission charges to an entertainment activity listed below: ◦ A live performance or other live event of any kind. (most common for

ECU)◦ A motion picture or film.◦ A museum, a cultural site, a garden, an exhibit, a show or a similar

attraction or a guided tour at any of the attractions.

*Admission charge includes charge for a single ticket, a multi-occasion ticket, a seasonal pass, an annual pass and a cover charge

◦ A live performance or other live event of any kind. (most common for ECU)

◦ A motion picture or film.◦ A museum, a cultural site, a garden, an exhibit, a show or a

similar attraction or a guided tour at any of the attractions.

Types of Events◦ Sporting Events◦ Film Screenings◦ Lectures◦ Exhibits◦ Performances

Charges that Generally Do Not Constitute Admission Charges to an entertainment activity subject to tax under N.C. Gen. Stat. § 105-164.4(a)(10):

a.Registration fee to participate in a sporting activity.

b.Tuition or fee for a class or other learning activity that includes instruction.

c.A registration fee for an educational seminar or workshop.

d.Registration to attend summer camp.

e.Fees to bowl, skate, swim, or play miniature golf.

f.Fees paid to fish from a pier and not to observe persons fishing.

g.Golf greens fees or driving range fees.

h.A fee to ride a means of transportation where the purpose is for the transportation.

i.Boat tour, carriage ride, and similar activities where the fee paid does not include admission to an attraction.

j.The retail sale of prepared food as defined in G.S. 105-164.3(28) subject to sales and use tax at the 4.75%general State and applicable local and transit rates of sales and use tax.

k.Admission tickets given away for free that do not constitute bartered transactions.

Departments will need to complete and submit an Evaluation Form-Admission Charged Events

Form can be found on Financial Services website in the Helpful Forms section.

Send questions to [email protected]

Institutional Trust FundsEast Carolina University

Financial Services, MS 203

3800 E. 10th St. 2nd Floor

Sherrilyn Johnson, Financial Director - Institutional Trust Funds/Foundations

Who We AreInstitutional Trust Funds Office

Financial Services

3800 E. 10th St. 2nd Floor

a.k.a. Special Funds

Accountants:

Sharon Cullipher * Cindy Modlin * Virginia Bridgman

http://www.ecu.edu/cs-admin/financial_serv/specialf/index.cfm

What are Institutional Trust Funds?• Are established at the University level by authority

of Chapter 116, Article 1 of the General Statutes• Are set up for specific business purposes as

determined by the approved Fund Authority, and in compliance with UNC-FIT and University guidelines

• Are NOT state appropriated• Are NOT for personal benefit

G.S. 116-36.1

University & Foundation Fund TypesType of Fund Banner Fund Begins With:

State Accounts 111, 112

Institutional Trust Funds12, 14, 15, 23, 24, 25, 27, 310, 311, 312, 316, 317, 2E, 6C, 6R, 6Z

Grants 21ECU Physicians 314, 315Capital Improvement 8, 9ECU Foundation EECU Medical Foundation MECU Educational Foundation PAlumni Association A

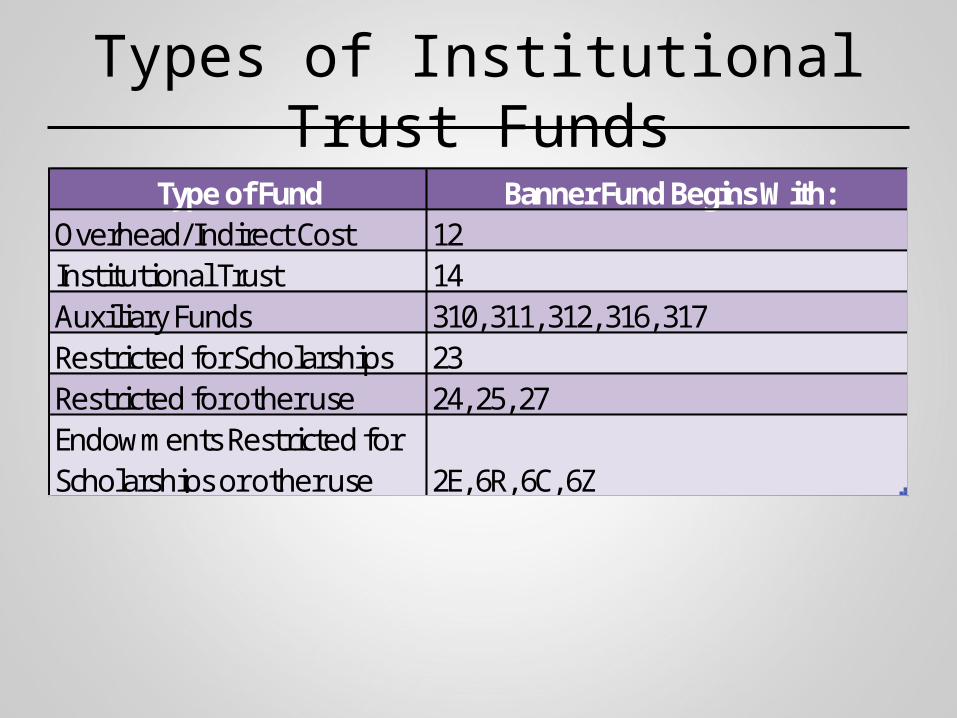

Types of Institutional Trust FundsType of Fund Banner Fund Begins With:

Overhead/Indirect Cost 12Institutional Trust 14Auxiliary Funds 310, 311, 312, 316, 317Restricted for Scholarships 23Restricted for other use 24, 25, 27Endowments Restricted for Scholarships or other use 2E, 6R, 6C, 6Z

Institutional Trust - General• Begin with 141xxx • Must be expended in accordance with approved

fund authority form, University policies, and UNC-FIT guidelines

• Examples– Royalties, patents, copyrights– Student activity programs – Service centers if self-supporting (not captured in

Auxiliary range)– Fees for contract services

Institutional Trust - Residual Funds

• Begin with 143xxx• 143xxx are residual balances transferred from

grants– No other funding should be deposited or transferred

into these funds

• Expenditures must be research related• Established at college or division level

Overhead/Indirect Cost Funds

• Begin with 12xxxx• Indirect cost earned from grants

– No other funding should be deposited or transferred into these funds

• Expenditures must be research related• Established at college or division level

Auxiliary Funds

• Begin with 31xxxx• Includes student auxiliaries, institutional

auxiliaries, and service center operations• Self-supporting entities• Examples

– Parking and Transportation– Student Health Center– Housing and Dining– Student Stores

Restricted Trust Funds• Must be used only for the donor-restricted purpose• Restricted Trust Funds begin with 23, 24, 25, 27• Restricted Endowments begin with 2E, 6C, 6Z, 6R

– 3 parts: Corpus (6C or 6Z), Restricted (6R), Spendable (2E)

– Corpus and Restricted Funds cannot be spent– Principal is invested and interest earned is allocated

annually to the spendable fund in accordance with ECU’s endowment policy.

Virginia Bridgman 737-1138

Scholarships• Due Dates:

– All Summer Scholarships March 15th– Fall/Spring April 15th– Spring Semester Only Sept. 15th

• Must send Scholarship Information Form, Fund Manager Approval, and Scholarship Committee Survey

http://www.ecu.edu/cs-admin/financial_serv/forms/index.cfm

Virginia Bridgman 737-1138

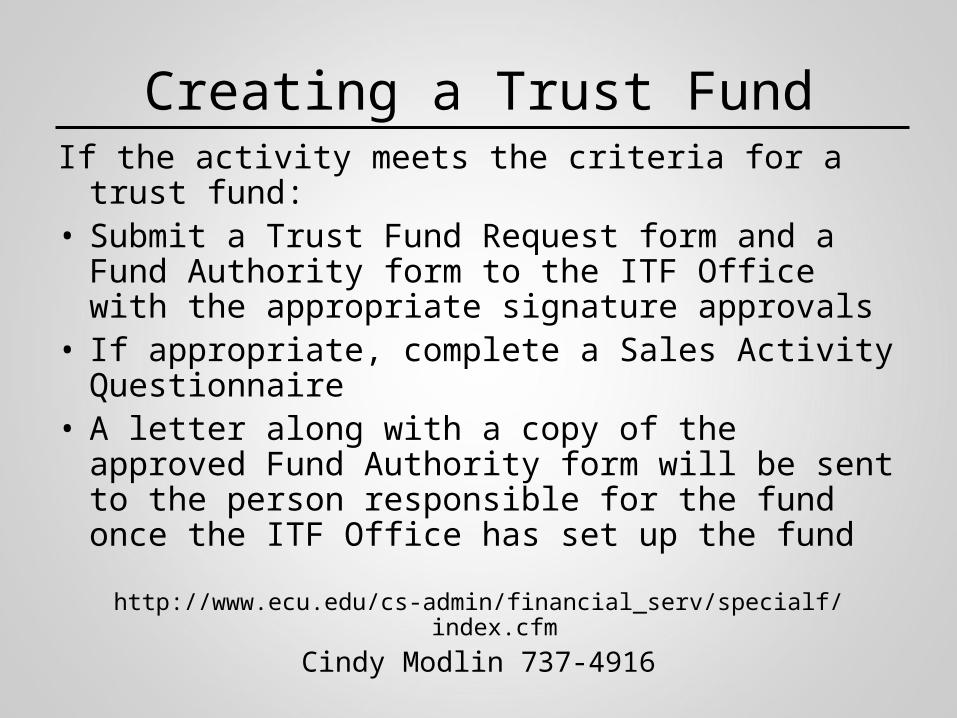

Creating a Trust FundIf the activity meets the criteria for a trust fund:• Submit a Trust Fund Request form and a Fund

Authority form to the ITF Office with the appropriate signature approvals

• If appropriate, complete a Sales Activity Questionnaire

• A letter along with a copy of the approved Fund Authority form will be sent to the person responsible for the fund once the ITF Office has set up the fund

http://www.ecu.edu/cs-admin/financial_serv/specialf/index.cfm

Cindy Modlin 737-4916

Updating a Trust Fund• ORGN changes, responsible party changes,

purpose, source of revenue• Submit a revised Fund Authority form with the

changes and appropriate signature approvals to the ITF Office

• A copy of the approved Fund Authority form will be sent to the person responsible for the fund once the ITF Office has made the changes

• For ORGN changes: move transactions and budget to the new FOAP including payroll redistributions

Operation and Use of Trust Funds• Need to maintain a positive cash balance• Must be used as documented on the approved Fund

Authority• Must follow ECU spending guidelines, and comply

with UNC-FIT and the General Statutes• Requires VC approval to establish• Changes in scope, purpose, source of revenue,

organizational code, etc. must be reported to the ITF Office– Requires an updated Fund Authority– A new fund may be required

Matching Concept

• Revenues must be matched with the associated expenses.

*Revenue-generating Funds should not be set up in the ITF range if the

expenses/resources used to generate that revenue are paid from State or other

Funds.*

Salary and Benefit Budgets• Permanent salary and matching benefits are

budgeted on ITF funds

• Loaded into Banner Finance beginning of fiscal year by ITF Office

• Budgets should include all positions whether filled or vacant

Sharon Cullipher 737-1403

Personnel Actions• PCFs: - all about position budget & funding

- only required for permanent positions• EPAFs: - all about the assigning the employee to the

position

- required for all jobs, special pays and fringe benefits

• PCFs and EPAFs affecting ITF funds must be routed to our office for approval.

• EPAFs are only approved if position budget is available in POSMAN or if a PCF has been submitted.

• Payroll Redistributions that debit an ITF fund should be approved & posted by the ITF Office

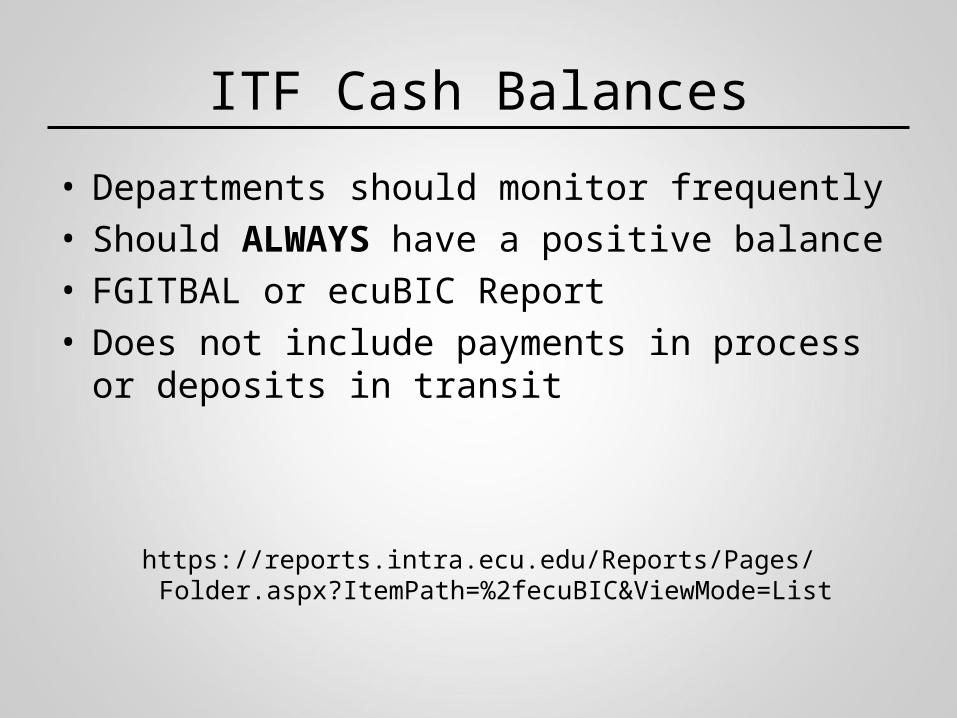

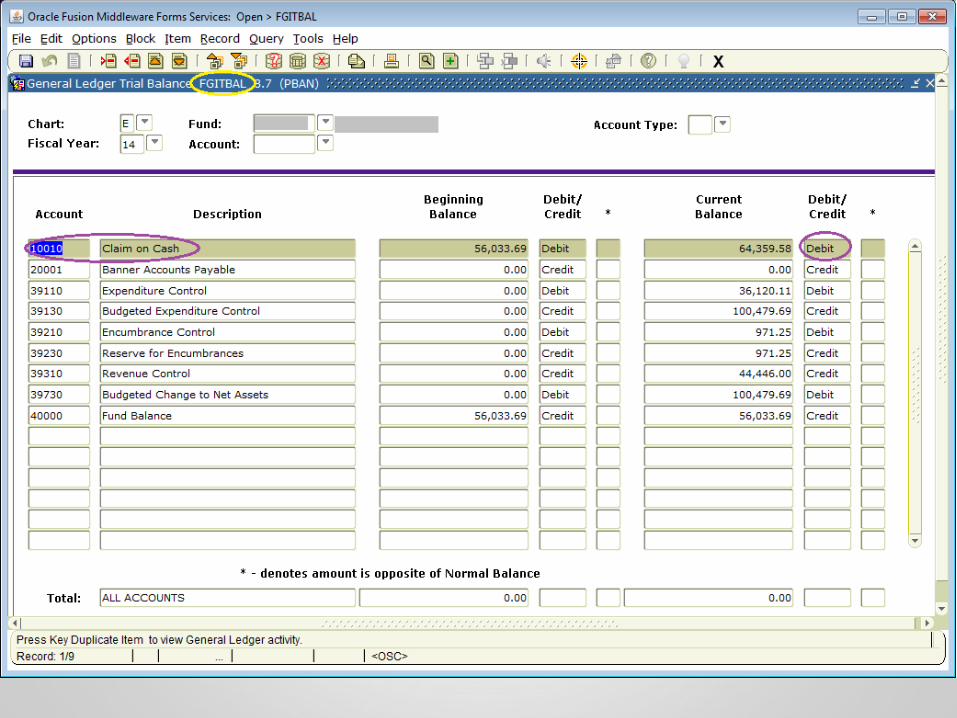

ITF Cash Balances

• Departments should monitor frequently• Should ALWAYS have a positive balance• FGITBAL or ecuBIC Report• Does not include payments in process or deposits

in transit

https://reports.intra.ecu.edu/Reports/Pages/Folder.aspx?ItemPath=%2fecuBIC&ViewMode=List

Cash Balance

Journal Entries/Interdepartmental Transfers

• Must meet UNC-Fit guidelines• Must verify the amount and have a valid business

purpose• Documentation required that supports the

transaction– Examples include Banner screen prints, a copy of an

invoice, a report, or an email

• Accounting staff and/or auditors should be able to clearly understand the purpose of the transaction

JE/IDT Continued• Preparer must sign his/her name or type in name and

initial beside it • Approver must sign his/her full name

– Signed names must be legible!– Approver must be on the Delegation of Authority for the

ORGN being debited.

• Preparer cannot be the approver. Preparer cannot sign as the approver on behalf of someone else

• +/- for budget entries, D/C for journal entries• J51 for Internal Sales and Services, J63 for Journal Entry

Adjustments

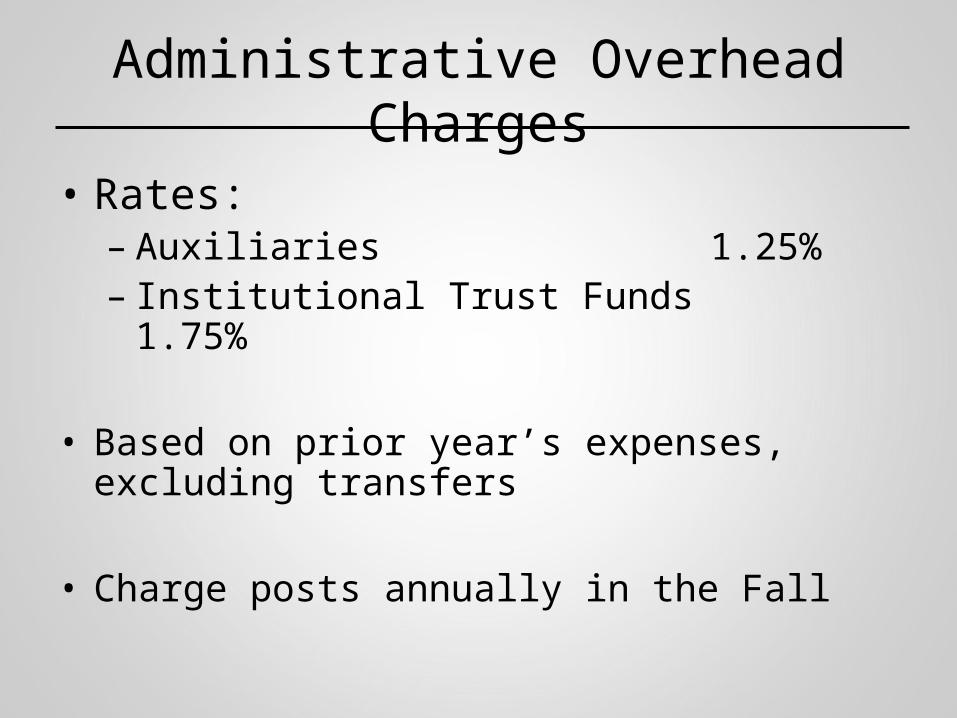

Administrative Overhead Charges

• Often referred to as administrative fees• Are applied to auxiliaries and most trust funds

• Why? Areas receive considerable services from Materials Management, HR, ITCS, and Financial Services beyond which the University receives State appropriation

• Need to have a cash balance available to cover this charge

Administrative Overhead Charges

• Rates:– Auxiliaries 1.25%– Institutional Trust Funds 1.75%

• Based on prior year’s expenses, excluding transfers

• Charge posts annually in the Fall

Calculating Administrative OH Charges

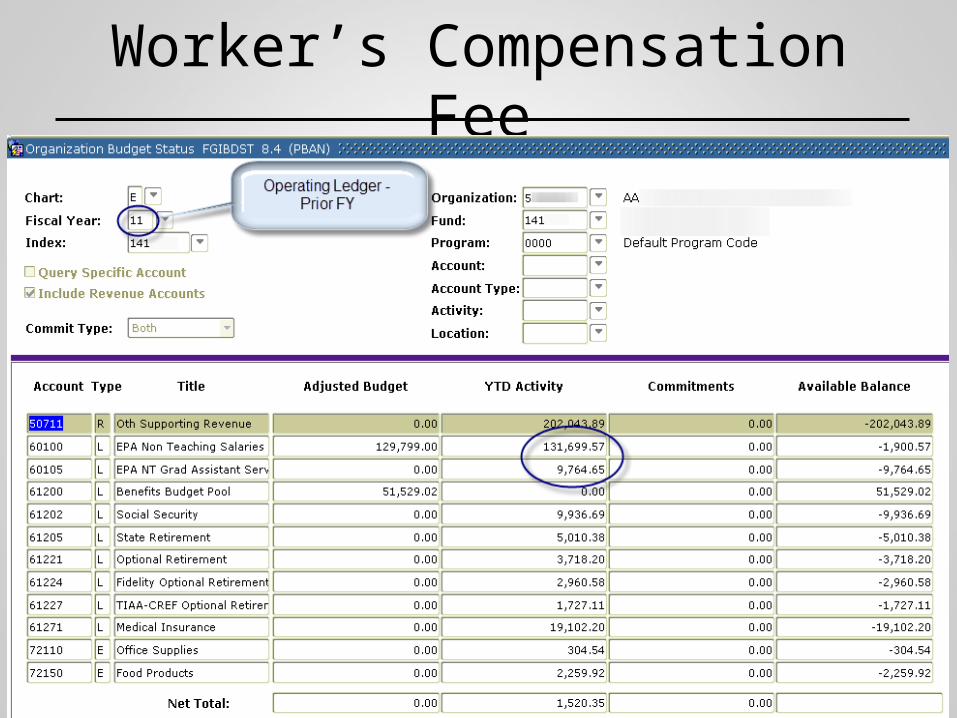

Worker’s Compensation Fee

• University maintains a pool account for supporting non-state worker’s compensation claims

• Charge is based on the amount of prior year’s salary expenditures (not including benefits)

• Charges post in the Fall of every year• Worker’s Comp rate has remained .2% for several

years, but is subject to change based on actual claims

Worker’s Compensation Fee

ORGN Name

Fund Name

Prog Name

Calculating Worker’s Comp Fee

Total Salary $141,464.22

Worker’s Comp Rate X .002

Worker’s Comp Charge $282.93

What to Expect from the ITF Office• Budget office for Institutional Trust Funds• Load salary and benefit budgets annually• Items that require ITF approval

– Journal Entries/IDT’s, Personnel Actions, Direct Pays, ITF Scholarships and Awards

• Create, Update, and Maintain all funds in our range• Process Admin Overhead charges and Worker’s Comp

fees annually• Analysis and Reporting• Enforce General Statutes, Legislation, and University

Guidelines

What Can We Do For You?

Please feel free to call us with any questions or concerns….

We are here to offer guidance and support!

ContactsVirginia Bridgman 737-1138

• Endowments [email protected] • Scholarships• Distinguished Professorships

Cindy Modlin 737-4916• Journal Entries [email protected]• Fund Set-up/Maintenance

Sharon Cullipher 737-1403• Personnel actions

[email protected]• Payroll redistributions• Budget/Financial Information

![BLM9D1822-30B - Ampleon...VDS1 11 [1] drain-source voltage of driver stages n.c. 12 not connected n.c. 13 not connected n.c. 14 not connected n.c. 15 not connected RF_OUT/VDS2 16 RF](https://img.pdfslide.net/doc/110x75/60a72840f38f5e6597029b7f/blm9d1822-30b-ampleon-vds1-11-1-drain-source-voltage-of-driver-stages-nc.jpg)