Embed Size (px)

Citation preview

Fiscal Sustainability and Debt in Small Open Economies – An Application to the Caribbean

by

DeLisle Worrell (Team Leader), Denisa Applewhaite, Rumile Arana, Elmelynn Croes, Harry Dorinnie, Kari Grenade, Julia Jhinkoo, Jason LaCorbiniere,

Brian Langrin, Edwina Matos-Pereira, Sidonia McKenzie, Ankie Scott-Joseph, Lylia Roberts,

Latoya Smith, Rasheeda Smith and Allan Wright

Caribbean Centre for Money and Finance, 2015

ii | P a g e

Copyright © 2015 by Caribbean Centre for Money and Finance Distributed by the Central Bank of Barbados by permission of the Caribbean Centre for Money and Finance

All rights reserved. Published 2015.

Fiscal sustainability and debt in small open economies: An application to the Caribbean / edited by DeLisle Worrell.

p. cm.

“A collection of research papers produced by a team of regional economists under the auspices of the Caribbean Centre for Money and Finance.”

Printed in Barbados

First Printing, 2015

ISBN: 978-976-602-077-4 paperback ISBN: 978-976-602-078-1 ebook

Central Bank of Barbados Tom Adams Financial Centre Church Village, Bridgetown, St. Michael Barbados BB11126 www.centralbank.org.bb

P a g e | iii

Preface This little volume is remarkable, even before it is read, because it is a model for the future of Caribbean integration. My co-authors are from across the region, from Suriname in the east to Belize in the west, and from The Bahamas in the north to Trinidad and Tobago in the south. Everyone joined the project out of a conviction of the importance of the issue of fiscal sustainability, and for the opportunity to enrich our understanding of this controversial topic. We all worked together enthusiastically, and the experience has been richly rewarding for us all. I would therefore like to say a heartfelt thanks to everyone who participated in the analysis and writing of this book, and to offer congratulations to everyone for helping to produce a study which breaks new ground and makes a persuasive case for a novel and improved way of assessing fiscal sustainability.

Our thanks go also to the Caribbean Centre for Money and Finance, its interim Executive Director, Dr Compton Bourne, and the staff of the Centre, for sponsoring the study, funding the participation of some authors, arranging and hosting conferences for the team, and assuming responsibility for editing and publishing our book. Collaborations of this kind have been among the most enduring outputs of the Centre over the years, and with the effective use of telecommunications they can be undertaken more efficiently than ever before. In this regard we hope our study will set the template for much of the future activity of the CCMF.

iv | P a g e

Our thanks go also to the Governors and presidents of participating central banks, for their endorsement and support of this project, to the staffs of the banks who provided our support, and to our reviewers, Dr Tarron Khemraj, Dr Shelton Nicholls, Dr Winston Moore, and an anonymous referee from the Centro de Estudios Monetarios Latinoamericanos (CEMLA), who all provided comments that helped to improve the book. As always with reviewers, they do not bear any responsibility for the views expressed in this book, and as with all publications of the CCMF, the opinions expressed are not intended to be representative of the views of any participating institution.

DeLisle Worrell November 15, 2014

P a g e | v

List of Contributors

Dr. DeLisle Worrell is Governor of the Central Bank of Barbados, a post he has held since 2009. He was previously Executive Director of the Caribbean Centre for Money and Finance, and spent a decade on the staff of the International Monetary Fund. Dr Worrell is the author of Policies for Stabilization and Growth in Small Very Open Economies (Group of Thirty, Washington, DC, 2012) and Small Island Economies (Praeger, 1987). Dr Worrell’s experience includes fellowships at the Peterson Institute (Washington, D C), the Smithsonian Institute (Washington, D C), Yale University, Princeton University, the Federal Reserve Board and the University of the West Indies. Dr Worrell is a graduate of McGill University (Montreal, Canada), where he obtained his PhD in Economics and the University of the West Indies (BSc Economics). Denisa Applewhaite is a Banking Officer at the Central Bank of Barbados. Rumile Arana is an Economist at the Central Bank of Belize. He holds a BSc and MSc in Economics from the University of the West Indies. He was an awardee of the Thomas de la Rue Scholarship, 2008-2010. Elmelynn Croes is an Economist with the Central Bank of Aruba. She holds an MSc in Finance and BA in Economics from the Florida International University. Harry Dorinnie is an Economist at the Central Bank of Suriname. Dr. Kari Grenade is an Economist at the Caribbean Development Bank. She holds a PhD from Walden University

vi | P a g e

(USA), a Masters in Financial Economics from the University of Toronto, and a BSc from the University of the West Indies. She worked previously at the Eastern Caribbean Central Bank. Her publications on growth, finance and fiscal policy have appeared in international and regional journals. Julia Jhinkoo is Junior Research Fellow with the Caribbean Centre for Money and Finance. She holds an MSc and BSc in Economics from the University of the West Indies. Jason LaCorbiniere is an Economist at the Central Bank of Barbados. He holds an MSc from the University of Nottingham, and a BSc in Economics from the University of the West Indies. His publications are in the area of debt and fiscal policy. Dr. Brian Langrin is Senior Director and Head of the Financial Stability Department of the Bank of Jamaica. He holds a PhD in Economics from Pennsylvania State University (USA), and an MSc and BSc from the University of the West Indies. His publications on finance have appeared in regional and international journals. Edwina Matos-Pereira is Deputy Manager of the Research Department of the Central Bank of Aruba. She holds a Master’s Degree in Economics from the University of Tilburg, the Netherlands. Her work experience includes banking, finance and statistics. She is a PhD candidate of the University of Groningen, the Netherlands. Sidonia McKenzie is an Economist with the Bank of Jamaica. She holds an MSc and BSc in Economics and Statistics from the University of the West Indies.

P a g e | vii

Lylia Roberts is an Economist with the Central Bank of Belize. She holds an MSc in International Trade from the Instituto Politecnico Nacional (Mexico City) and a BSc from San Carlos University, Guatemala City. Dr. Ankie Scott-Joseph is an Economist and Statistician whose work experience includes the Canadian-funded Debt Management Advisory Services to the Eastern Caribbean Central Bank and the St Vincent and the Grenadines Ministry of Finance and Economic Planning. She holds a PhD in Economics from the University of the West Indies, where she earned her BSc. She also holds an MSc from Manchester University. Latoya Smith is a Senior Research Officer with the Central Bank of The Bahamas. She holds an MA in Economics from York University, Toronto, and a BA in Economics from Queens University, Ontario. Rasheeda Smith is an Economist with the International Monetary Fund, Washington, DC. She was previously with the Bank of Jamaica. Dr. Allan Wright is a Senior Economist at the Central Bank of Barbados, on sabbatical with CEMLA, 2012-2014. He holds a PhD, MSc and BSc in Economics from the University of the West Indies. His experience includes Lecturer at the University of the West Indies and pricing, forecasting and research for regional companies in the Caribbean. Dr Wright’s publications on growth, investment and tourism have appeared in regional and international journals.

viii | P a g e

Table of Contents

Preface …………………………………………………. iii

List of Contributors ……………………………………. v

List of Figures …………………………………………. ix

List of Tables ………………………………………….. xii

Introduction ………………….………………………… 1

Chapter 1. Fiscal Sustainability in the Small Open Economy ………………………..………... 11

Chapter 2. A Review of the Literature on Debt and Fiscal Sustainability ………………………. 37

Chapter 3. Fiscal Deficits and Debt in the Caribbean … 63

Chapter 4. A Test of Fiscal Sustainability in the Caribbean ………………………………….. 123

Chapter 5. Fiscal Sustainability in the Caribbean .……. 141

Bibliography …………………………………………… 155

Appendix ………………………………………………. 167

Index …………………………………..……………….. 180

P a g e | ix

List of Figures

Figure 1. Foreign Exchange Market Determined Fiscal Unsustainability …………………………………….. 27

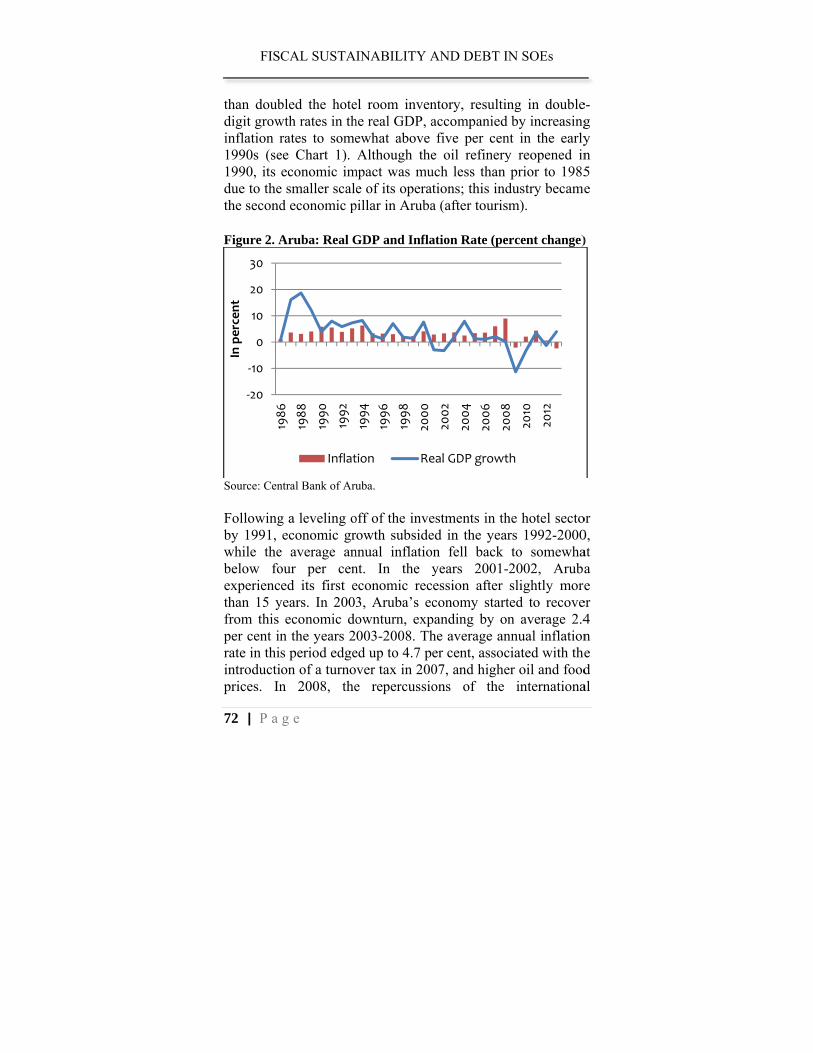

Figure 2. Aruba: Real GDP and Inflation Rate (percentage change) ………………………………… 72

Figure 3. Aruba: Financial Deficit on a Cash Basis ….. 74

Figure 4. Aruba: Government Debt …………………… 75

Figure 5. Overall Balance of the Balance of Payments (BOP) of Aruba ……………………………………. 76

Figure 6. Aruba: Net Foreign Assets (1986-2013)….… 77

Figure 7. The Bahamas: Real GDP Growth (2002-2012) 79

Figure 8. The Bahamas: Debt-to-GDP Ratios (2002-2012) ……………………………………………….. 80

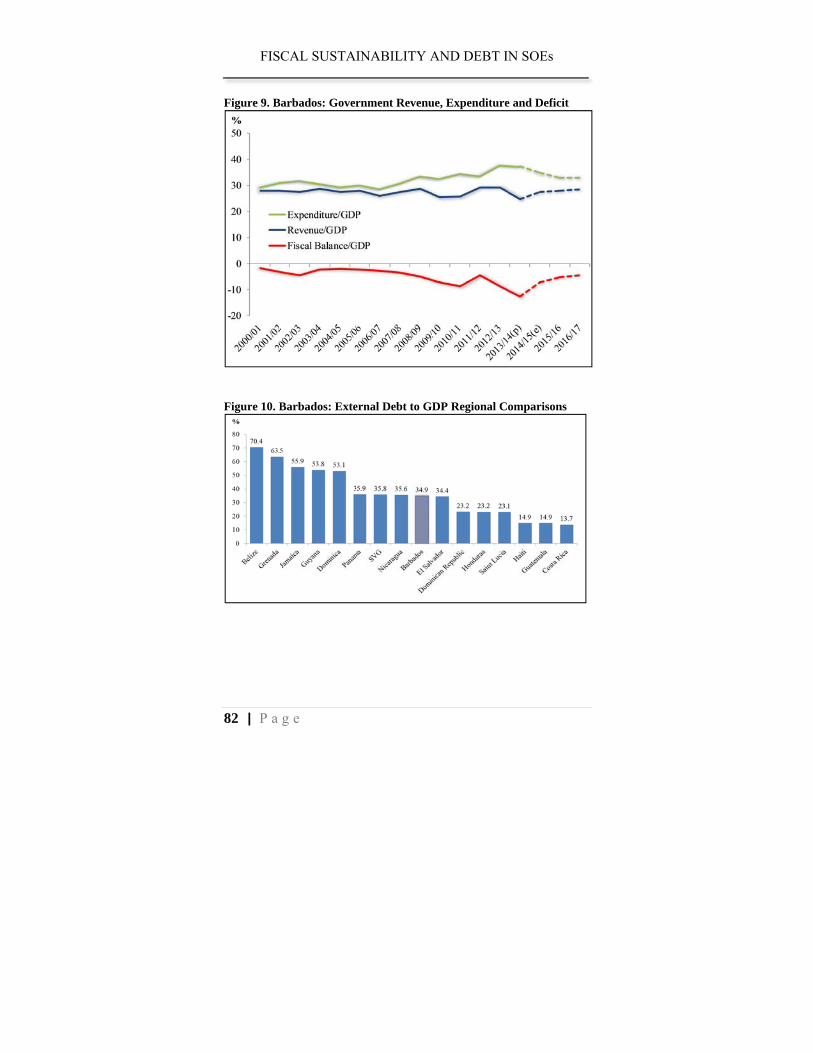

Figure 9. Barbados: Government Revenue, Expenditure and Deficit …………………………………………... 82

Figure 10. Barbados: External Debt to GDP Regional Comparisons ………………………………………… 82

Figure 11. Economic Growth in Suriname …………… 86

x | P a g e

Figure 12. Suriname: Net Official Development Assistance in % of GDP ………….…………….….. 87

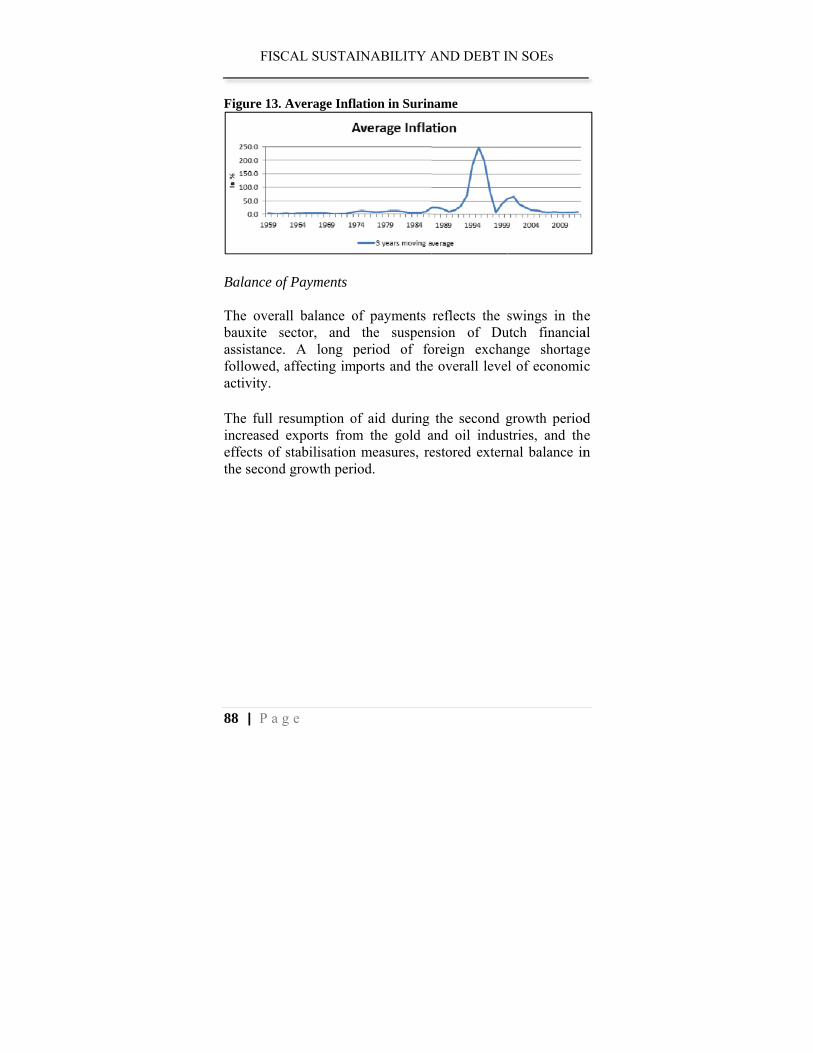

Figure 13. Average Inflation in Suriname ……………. 88

Figure 14. Suriname: Imports, Exports & FDI ………. 89

Figure 15. Suriname: Foreign Exchange Reserves & Import Coverages …………………………………...

90

Figure 16. Suriname: Official Exchange Rate ……….. 90

Figure 17. Suriname: Expenditures & Revenues …….. 92

Figure 18. Suriname: Overall Balance …….…………. 92

Figure 19. Government Debt in Suriname …………… 93

Figure 20. Suriname: CBVS Lending to Government in % of GDP ………………………………….……….. 93

Figure 21. Suriname: Interest & Inflation ……………. 94

Figure 22. Belize: Real GDP Growth versus Fiscal Balance (% of GDP) ……………………………….. 96

Figure 23. Belize: Import Cover (months).………….... 98

Figure 24. Belize: Real GDP Growth versus External Current Account Balance (% of GDP) …………….. 98

Figure 25. Belize: Debt Service Projections ………….. 101

P a g e | xi

Figure 26. Belize: Public Sector Debt-to-GDP Ratio (%) …………………………………………………. 103

Figure 27. Belize: Comparative Debt Service Payment of 2007 vs 2038 Bonds …………………………… 105

Figure 28. Evolution of Jamaica’s Sovereign Credit Ratings …………………………………….………. 113

Figure 29. Foreign Reserves to GDP ………………… 132

Figure 30. Money Creation to GDP ………………….. 133

Figure 31. Impact of Money Creation on Reserves ….. 137

Figure 32. Impact of Monetary Authority Credit on Foreign Reserves …………………………………... 138

xii | P a g e

List of Tables Table 1. The Bahamas: Selected Macroeconomic

Indicators …………………………………………… 79

Table 2. Belize: Evolution of Total External Public Sector Debt (US$Mn)……………..………………..

99

P a g e | xiii

xiv | P a g e

Introduction

The adverse impact of sovereign debt defaults on the international financial system has occasioned intense interest in methodologies for assessing sovereign debt risks. This is manifest in an outpouring of studies, research which has uncovered the fact that the riskiness of sovereign debt is determined in each case by a complex interaction of factors, including Government tax, expenditure and financing policies over time, and the state of domestic and international financial markets. The large number of factors, many of them unique to individual cases, and the fact that social and political considerations enter into the mix, all serve to complicate the task of arriving at generalisations that are robust in application across countries.

The most comprehensive approach to the problem, by the World Bank and the International Monetary Fund (IMF), attempts to address this problem by placing countries in categories, and developing guidelines specific to advanced countries on the one hand, and emerging market and developing countries on the other. They also classify countries by the strength of institutions and other factors that bear on a country's ability to finance high levels of debt. However, the Fund-Bank analysis is flawed in at least two critical dimensions, which may call into question the conclusions drawn from their analysis of sovereign debt: they concern themselves exclusively with the question of sustainability, and they use the same tools for small countries and large.

The fact that a country's fiscal strategy is sustainable, and that debt obligations are serviced fully and on time, is not the only consideration in deciding whether that strategy should be continued. Other considerations relate to the efficiency with

FIS

2 | P a g

which GoGovernmedegree of activity, ato the ovenot easily

There is strategies dissolve ialtered ineven thousense of domestic The princis that fisituation debt, no mthe risk tothe presenrisk, condthe deficit

There remstrategy mservice deis not in thThe procefully infosearch forcircumstaway. Howborrowerssovereigncredit mar

CAL SUSTA

g e

overnment dent involvem

f domestic maamong otherserall developm

y generalised.

therefore athat are not

into crisis if cn the interestsugh they are

the term. Aor abroad, aripal risk to thscal strategyin which govmatter how co be analysed nt study is toditional on tht and the way

mains a risk thmay nonetheleebt in full. Thhe best long ress may be doormed discussr a solution t

ances – or it mwever, lendes from rene

n, among themrkets in the fu

INABILITY A

delivers publiment in commarket distortios. Some of thment of the e

a need to dt sustainable continued – as of economi

perfectly suAgents in fire interested he credit they y will drive vernment wil

committed it min this study.

o provide an he structure oy in which the

hat a sovereigess decide to

hey may do thrun interests oone in a way sion among that is the bemay be done ers have powging, even

m the ability tuture. Soverei

AND DEBT IN

ic services, tmercial servons caused byhese factors meconomy, in

distinguish be– those tha

and those whc and social

ustainable in nancial markin sustainabilprovide to sothe budget tll be unable might be to d. The major cobjective me

f the econome deficit is fina

gn with a sustrenege on its

his for good reof the countrythat is desiraall parties, aest for everyoin an arbitrarwerful weapwhen the bto shut the boign borrowers

N SOEs

the extent oices, and they Governmen

may be relatedways that are

etween fiscaat will fail ohich should be

developmentany practica

kets, whethelity above all

overeign stateto a crisis, ato service it

do so. That icontribution oeasure of thi

my, the size oanced.

tainable fiscas obligation toeason – that iy – or for badable – throughand a genuineone under thery or coercive

pons to deteorrower is a

orrower out os are aware o

of e

nt d e

al or e t, al er l. s a ts s

of is of

al o it d. h e e e

er a

of of

this, and with onlythe Caribb

The focusCaribbeansituation wservice thstatementterm horizexpect, sustainabiparticipanshould takeach counto discusscase of anarrive at ais in the bare issuespursued e

A major cthe discumeasure fiscal straGovernmedebt obligsustainabibecause tby finaninfluencedcalculatiomay judgthe risks

I

have avoidedy a handful ofbean, as we w

s of our studyn sovereigns hwhere, with thheir debt. Ths can be mazon, both in and under

ility in thints need to beke a case-byntry’s circums changes in tn individual ma mutually agbest interests s that are clalsewhere.

contribution oussion of susof sustainabiategy becoment does not hgations. It is ility to a conhe fiscal sustcial marketsd by arbitns, market p

ge sound credin other cre

INTRODUCT

d arbitrary def ill-advised

will show in C

y is fiscal susthave a strategheir best efforhis is a mattade for most

circumstancer worst-cass sense is e concerned ay-case approamstances when

the structure mortgage, the greed maturity

of the countrarified in Ch

of our study istainability. Wility, based o

mes unsustainhave the wherimportant to

ncept that cantainability ins. If the intrary judgmparticipants mdits to be risedits which

TION

efaults in whoexceptions. T

Chapter 3.

tainability, thgy in place tharts, they are uter about wh

countries oves that we mase assumpti

what finanabout. Beyondach, taking funever they arof existing dappropriate p

y and interestry and of the hapter 3, and

s to bring greWe develop on the abilitynable at the rewithal to fu

o limit the non be objectivedicator is clo

ndicator usedments and may be misinky, while unappear soun

P a g e | 3

ole or in partThis is true o

hat is, whetheat will avoid aunable to fullyhich definitivever a mediumay reasonablyions. Fiscancial marked this, lenderull account ore approached

debt. As in theprocedure is tot structure thalender. These

d that will be

eater clarity toan objective

y to pay: thepoint where

ully service itotion of fiscaely measuredosely watchedd is heavilyinappropriate

nformed, andnderestimatingnd. Our study

3

t, of

er a y e

m y al et rs of d e o at e e

o e e e ts al d, d y e d g y

FIS

4 | P a g

therefore sustainabimade, con

Long befomay be dfrom the pThe way inhibit dwealthy bworseningthere maGovernmeintrusive.

It is impofiscal straspecified mentionedmay estimbecause Gsimilar caability to a large eldone in an

Our secoeconomieCaribbeanexport of attain sufcompetitivproducer economy generating

CAL SUSTA

g e

focuses on thility, about wnditional on th

ore this pointdiverting finapoint of view

in which thdevelopment, bondholders frg the distribuay be reasoent is perceiv

ortant to distinategy, which

circumstancd, which cannmate the conGovernment dalculation of adivert financ

lement of judn objective fa

ond innovaties and smaln. A small ecf a limited nufficient produve. Compareand consume

is very larg sufficient

INABILITY A

he objective "which unambhe state of the

t is reached, ancing from

of acceleratinhe fiscal def

by transferrom relativelyution of inco

ons to alter ved to be to

nguish betwemay be obje

es, and the not be determ

nditional probdoes not havea limit on the e from develo

dgment, and tashion.

ion is to dll economiesonomy is obl

umber of comuction size ted to this eer commoditierge. The smt foreign e

AND DEBT IN

"ability to paybiguous stateme world.

the burden oactivities thang economic

ficit is financrring funds y poorer taxpome. Apart f

fiscal strato large, inef

en the sustainectively deteother consid

mined in the sbability of a e the wherewi

size of Goveopment priorthe computati

distinguish bs such as tliged to concmmodities in to become iexport list, tes required bymall economexchange in

N SOEs

y" criterion oments can be

f debt serviceat are prioritydevelopment

ced may alsoto relatively

ayers, therebyfrom all thistegy becausefficient or too

nability of thermined undederations jusame way. Wedefault even

ithal to pay; aernment, or itities, involveion cannot be

etween largethose of theentrate on thewhich it can

internationallythe range oy the growing

my grows bynflows from

of e

e y t. o y y s, e o

e er st e

nt a ts s e

e e e n y

of g y

m

the interincreasinglarge couimport subdomestic assumes alarge coun

Our studobjective of Caribbspecialiseon foreigservice anexcess detime, exhservice thmanner, foreign demethodoloof the poCaribbean

Our studyeconomieimpossiblobligationjudgmentsrates, sociratio of assumptioapplied wor the mac

I

rnationally cg import needuntries have bstitution andconsumption

an importancentries.

dy employs measure of t

bean countried in internatign currency dnd the wealthemand for fohaust the counhe debt. If co

Governmentebt at that poogy which enoint of unsusn countries us

y provides aes, of the rile for Govns. The methos about a foreial stability, pdebt to GD

ons of the cowithout regard

croeconomic

INTRODUCT

competitive ds of the grow

additional d the growth n. The balane for small co

this structurthe sustainabiies, which aonal commerdemand of Gh effects of doreign exchanntry's foreignrrective actiot will be oint. In the cunables us to mstainability, asing this tool.

an objective isk that fiscernment to

odology we decast growth rpolitical will,

DP or any oonventional ad to product omodel prefer

TION

sectors, to wing economy

growth optiof domestic pnce of externountries that i

al reality toility of the fisare all smallrce. If the comGovernment domestic debtnge, Governmn reserves in on is not take

unable to urrent study

make a conditand we do e

measure, focal policy m

fully servidevelop does nrate, interest rinstitutional

of the usual analysis. Theor factor markrred for the an

P a g e | 5

supply they. By contrastions, throughproduction fonal paymentit does not fo

o develop anscal strategiel and highly

mbined impacexternal deb

t results in anment will, inits efforts to

en in a timelyservice the

we develop ational forecasevaluations o

r small openmay render i

ice its debnot depend onrates, discounresilience, the

caveats ande test may beket structuresnalysis.

5

e t, h

or ts or

n s y ct bt n n o y e a st of

n it bt n

nt e d e s,

FIS

6 | P a g

Chapter 1economy"corresponof financunsustainasufficient the debt. Odo not spfocus on t

Our studybe considsustainabibe the opmany nonin decidinof what sustainabiunderstanunsustainacontinue aterm in thChapter 2collapses;slows groidentify adebt are beyond th

Chapter developedunsustainaexchange These cotraded go

CAL SUSTA

g e

1, entitled "F" uses an intnds to the imacial market able when to meet its o

Our concept opeculate on the ability to p

y distinguishedered the opility, and we ptimum fiscan-quantifiableng what is the

is written uility is in fact

nd that word.able at the palong that pathis study. In c2 does not ide; instead, theyowth beyond aa point at whi

optimal, buthat point, and

2 explains d to pinpoable in the plays an ess

ountries expoods and servi

INABILITY A

Fiscal sustaintuitive concep

age in the popagents: the Government

obligations in of sustainabilGovernmentspay.

es between suptimum fiscahave nothing

l strategy, ote factors that me optimum. Wunder the het not about su In normal u

point when yth. That is thecontrast, mucntify a point y argue that a certain threich, in their vt the strategyfor many yea

the logic beoint when

small open sential role inort a limitedices in which

AND DEBT IN

nability in thpt of sustainular mind andfiscal stratedoes not

full and in thlity is an objes' willingness

ustainability aal strategy. Wg to say abouther than to must be taken

We also point eading of fi

ustainability ausage, a stratyou are no loe sense in which of the literat which the the fiscal or

eshold. In othview, the fiscy may be suars.

ehind the tofiscal strateeconomy (Sn the growth

d range of ih they are com

N SOEs

he small opennability whichd in the mindegy becomehave finance

he currency oective one; wes to pay, bu

and what mayWe focus onut what mighpoint out the

n into accounout that muchiscal or deb

as most peopletegy becomeonger able toich we use therature cited infiscal strategydebt strategy

her words theycal deficit andustained wel

ool we haveegy becomeOE). Foreign

h of the SOEinternationallympetitive, and

n h

ds s e

of e

ut

y n

ht e

nt h

bt e s o e n y y y d ll

e s n

E. y d

employ thconsumereconomiescale of pand thersubstitutiodemand fosupply cathe metho

In Chaptethe impaGovernmeGovernme4. The principallyservicing expansionand imposeveral reGovernmefiscal strato achieveservices, of Govern

Chapter sustainabiempirical methodoloare inconsunambiguindicator, offering involve ju

I

he foreign exr and produces do not havproduction forefore there on. It followsfor foreign exannot be sustodology used

er 1 we introdact on the ent debt seent deficit. Thchannels thry affect theof the exte

n and domestorts. In Chapeasons why fent operation

ategy is sustaie greater effiand/or a nati

nment activiti

2 reviews ility, illustrat

approachesogies are all sistent with e

uous concept suite of indicthe most reudgments, so

INTRODUCT

change earnincer goods thve the capacir more than

is virtuallys that a fiscachange that isained. That iin this study.

duce a forecabalance of

ervicing andhe model is frough whiche balance oernal debt, atic financing pter 1 we exfiscal consolins may be winable. Theseiciency of thonal consensies are inappro

the literatuting the divs to the flawed in oneeach other. Aof fiscal sust

ces, or methoeliable guidaometimes abo

TION

ngs to imporhe economy ity to achieva handful of y no scopeal strategy thas in excess ofis the princip

asting model f external d the finanfully articulath the fiscal f paymentsand the impon aggregat

xplain that tidation and twarranted, ev reasons inclu

he delivery ofsus that the siopriate.

ure on debtversity of th

subject. The way or ano

At the end of ttainability emdology can b

ance. The apout things wh

P a g e | 7

rt the range oneeds. Smale an efficiencommodities

e for imporat provokes af the availableple underlying

which showpayments o

ncing of theted in Chapte

deficit wilare via the

pact of fiscae expenditurethere may bethe reform oven when theude the desiref Governmenize and scope

t and fiscaheoretical andhe availablether, and theythe review no

merges, and noe identified approaches alhich are non

7

of ll nt s, rt a e g

ws of e

er ll e

al e e

of e e

nt e

al d e y o o

as ll

n-

FIS

8 | P a g

economicmeet its prequire intergenerparameterobligation

Chapter 3countries on the cothe study on the ineconomicconsolidathis study(CARICOour studiesince 200

Chapter 4methodoloopen econseveral Cunsustainasituation, the curreunsustaina

Our studymarkets aability toGovernmethe overdevelopmGovernme

CAL SUSTA

g e

c in nature, spayment oblig

conceptuallyrational equirs such as rns.

3 reviews the in the last on

ountry. The fihave weaken

ncrease, relatc recession tion is under

y. Four of 15 OM) and the Des) had excha8.

4 is the coreogy for deternomy, and u

Caribbean coability for eand conduct

ent fiscal sability.

y aims to prabout the objeo service theents' willingn

rall fiscal sment of cou

ents that

INABILITY A

such as a gogations. In add troubling ity, and arbirates of disc

fiscal experine and a half tinances of all

ned over time,tive to GDPaggravated

rway in all thcountries in

Dutch Caribbanged or rest

e of the studmining fiscal

use it to evaluountries. We ach country, stress tests t

situation fro

ovide reliablective limits teir debt. Weness to servicetrategy in

untries. Whathave not

AND DEBT IN

overnment's wdition some m

assumptionitrary choicecount of futu

ience of seveto four decadl the countrie, and debt lev

P. The 2008 the situation

he economiesthe Caribbean

bean (the groutructured gov

dy, where wel sustainabilituate the fiscidentify perassess the

to show howom the poi

e informationto Caribbean e have no oe debt, or theterms of tht we do sreached th

N SOEs

willingness tomethodologiens, such a of sensitiveure payment

eral Caribbeandes, dependinges included invels have been

internationan, and fiscas analysed fon Communityup covered byvernment deb

e describe thety in the smalal strategy oriods of pascurrent fisca

w far distant int of fisca

n to financiaGovernments

opinion aboue optimality ohe economicshow is thahe point o

o s

as e ts

n g n n al al or y y

bt

e ll

of st al is al

al s' ut of c

at of

unsustainaobligationGovernme

I

ability do hns. We are aents may lose

INTRODUCT

ave the abilalso able to e the ability to

TION

lity to servicassess the w

o pay.

P a g e | 9

ce their debway in which

9

bt h

FIS

10 | P a

CAL SUSTA

g e

INABILITY A

AND DEBT INN SOEs

FISCAL

Fiscal

The aim ofinancing what impapproach fiscal strasuccessiveexhausts iin this wafiscal strafuture definances tmet in ful

At bottoacceptablygrowth theconomy through fearn foreihigh, and imports reSOEs is lpolicy coincentivestradables.to reduce pushes abeyond tdevaluatioclimate fo

L SUSTAINABI

Sustainabi

of the projecof governme

plications thilends clarity

ategy. The fise deficits drivits ability to ay, the conceategy is unsueficits over to the point wll; the fiscal st

om, economiy low, and hat may be

(SOE), govfiscal expansiign exchange

additional foequired by thled by the trontributes to s and infrast On the distagrowth rates ggregate expthe amount on drives up or investors. T

ILITY IN THE

Chapte

lity in the

t is to measuent deficits ins may have to the discu

scal strategy bve the governfully service ept of sustainustainable if the medium

where debt strategy is sust

ic policy isachieving thsustained overnment canion, because ; in the SOEoreign earnin

he growing ecradable sector

growth to tructure to aaff side, fisca

and generatependiture an

of foreign inflation rat

The key to fis

E SMALL OPE

er 1

Small Ope

ure the practicn small open

for governmssion of the becomes unsunment to the its debt oblig

nability is unthe conditio

m term pushervice obligatainable other

s about kehe highest ratver time. In not drive ecgovernment import prope

ngs are needeconomy. Sustrs of their ecthe extent t

accelerate thel expansion h

e inflation to td the deman

inflows. Thtes and creatscal sustainab

EN ECONOM

P a g e |

en Econom

cal limits to economies, a

ment debt. Tsustainabilityustainable whupper limit tgations. Viewnambiguous: onal forecast hes governmations cannot rwise.

eping inflatte of economthe small op

conomic growservices do

ensities are vd to finance tained growthconomies; fisthat it provide production has the potenthe extent thand for impohe ensuing tes an uncertbility is theref

MY

11

my

the and

This y of hen that wed the of

ment be

tion mic pen wth not

very the

h of scal des

of ntial at it orts

22 tain fore

FI

12 | P a

to ensure and that foreign ex

An essentlarge, relafor SOEsgrowth anthe case ooutput agovernmedomestic proportionexpansiontoo has ingovernmethat is almin fact bemultiplierexpansionpaymentsstimulatedcreate a ddirect imaddition tof moneyimbalanceexchange

Followingdeficit of additionalexceeds threserves demand a

SCAL SUSTA

g e

that fiscal pgovernment

xchange abov

tial differenceatively self-cos the impact nd inflation isof large econnd inflation

ent spendingincome strea

n leaks abron to finance tnflationary effent expansionmost as large e larger thanr effects. Furtn also has its : direct effecd for non-trademand for pact of monto aggregate creation is the of external rate.

g this logic wan SOE beco

l foreign exchhe supply to become depland imports

AINABILITY

policy facilitaactivity does

ve the supply.

e between theontained econof fiscal def

s indirect, vianomies, the im is direct: , whether laam, for the moad via impthe additionafects that are n in the SOE c

as the expann the governmthermore, monlargest poten

cts are limiteddable commoimports. Mor

ney creation spending powherefore modpayments re

we may definomes unsustahange demandsuch an exteleted. The fcomes princ

Y AND DEBT

ates the grows not drive t

e SOEs of thenomies such aficits and deba the balance mpact of fisc

the multiparge or smamost part, anports. If theral governmenmostly domecreates a dem

nsion in most ment expansiney creationtial effects vid to such demodities, but thre important,on imports,

wer. The infldest, until the sults in a dev

ne the point winable, as thed resulting frent that the fofiscal stimulucipally from

IN SOEs

wth of tradablthe demand

e Caribbean aas Brazil, is tbt on economof payments.al expansion lier effects all, add to nd only a smre is monet

nt spending, testic. In contramand for impo

cases, and mion, if there to finance fisia the balancemand as may hey in turn w, though, is because of

lationary imppoint where valuation of

where the fise point when om fiscal poloreign exchanus to aggreg

the impact

les, for

and that mic . In on of

the mall tary that ast, orts may

are scal e of y be will the the

pact the the

scal the

licy nge gate

of

FISCAL

money crecharge to funded enis an impbondholdeand this epaymentsexhaustedoften provand a deep

"Sustainabin this weconomy inevitablebetween tsuch as threached, tpayments do not mthresholdschange at

In order tneed to dbalance oon foreigusing anyOur study2010) uspaymentseconomy estimate paymentsservice. T

L SUSTAINABI

eated to fund service any

ntirely by credpact on the ers have a loeffect will re. At some po

d, the market vokes capital p devaluation

bility" has a way. If fiscal

away from te. It is worthis sustainabhe debt-to-GDthere is a vicrisis ensues

mark any marks are academthe point the

to assess fiscadetermine theof external acn exchange

y appropriate y which introses a simple, but in practis preferabl

the impact ; to this is adThe resulting

ILITY IN THE

the deficit, annew externa

dit from the dforeign balan

ower spendinduce pressurint before forcomes to expflight, the ex

n which amou

clear and spepolicy does

this point, a brth pointing bility indicatoDP ratio: wheniolent markets. In contrastket-driven tramic, because

presumed thr

al sustainabile impact of dcounts, and mreserves. Thimacroecono

oduced this me monetary tice a more fule, if availabof fiscal va

dded the cost g foreign exc

E SMALL OPE

nd there will l debt. If fiscdomestic privnce only to g propensity e on the balareign reservespect a large dexhaustion of funts to overkil

ecific meaninnot succeed

balance of paout the cri

or and convenn the foreign t reaction, ant, the conventansition, and

market agereshold is rea

ity in the opedeficits and fmeasure the ris impact ma

omic model omethodology (

model of tfully articulateble. The moariables on of governme

change surplu

EN ECONOM

P a g e |

be an additiocal expansionvate sector, th

the extent tthan taxpaye

ance of exters are completevaluation. Tforeign reservll.

ng when viewin steering

ayments crisistical differen

ntional measureserves limi

nd a balance tional indicattheir purpor

ents observe ached.

en economy, financing on resulting impay be estimaof the econom(Belgrave et the balance ed model of

odel is used the balance

ent external dus or deficit

MY

13

onal n is here that ers, rnal tely

That ves,

wed the s is nce

ures it is of tors rted

no

we the

pact ated my. al., of

the to of

debt t is

FI

14 | P a

applied toperiod. Iflevel by tunsustainato 12 weelevel withcomfortabmethodoloin the fore

The approis simpleconventiousually athresholdsdefinitionbecomes u

In the SOshould haopinion ntarget a raSuccessfumaintain aand whenmaintainecurrent anFiscal polaggregateit drives exhaust forate targetis the popoint may

SCAL SUSTA

g e

o the level of f, as a result, the end of theable. In Belgeks of imporh which the ble. This is ogy permits ueign exchange

oach to fiscal, intuitive an

onal approachadmitted, soms that are arb

n of sustainaunsustainable

OE, theory anave an exchannowadays is aate or to min

ul exchange raadequate fore

n necessary. Ted, and that nd capital aclicy affects th

e demand. Fisforeign curre

foreign exchat becomes unint where fisy be clearly

AINABILITY

foreign exchathe reserves

e period, the fgrave et al. (2rts is used, b

Barbadian a commonl

us to employe market in ea

sustainabilitynd empiricallh, which is metimes coubitrary. Our aability whiche when failure

nd experiencnge rate objecabout whethenimise the voate targeting reign reserves

That in turn imthe inflows

ccounts are shose outflowscal strategy bency demand

ange reservesobtainable anscal policy bidentified, an

Y AND DEBT

ange reserveslevel falls befiscal deficit2010), a thresbecause that iforeign exchly used thre

y whatever thach country.

y recommendly based, in

more compunter-intuitiveapproach provh is intuitive occurs.

e dictate thatctive. The oner the objectiolatility of therequires that to intervene

mplies that extof foreign ex

sufficient to s, by virtue obecomes unsud to exceed . At this poin

nd there is polbecomes unsund scenarios

IN SOEs

s in the previoelow a threshis deemed to

shold equivalis the minim

hange marketeshold, but

hreshold preva

ded in this stucontrast to

plicated than e, and impovides a clear-ve: the syst

t policy maknly differenceve should bee exchange rathe central baappropriatelyternal balancexchange on cover outflowof its impact ustainable whinflows, andnt the exchanlicy failure. Tustainable. Tand conditio

ous hold o be lent

mum t is the ails

udy the

n is oses -cut tem

kers e of e to ate. ank y as e is the ws. on

hen d to nge

This This onal

FISCAL

forecasts clear of th

Our appmechanismfailure. Tobserve economy Fiscal exeventuallyessential aforeign ecapture parameterMore sopthat incocredibilityexaminatidiscussionthrough th

This apppressure exchange are right inflows anrates whic"A large ait difficuldecreasescontracts linked to (especiallywith negaoutput." T

L SUSTAINABI

can be analyshe point of fai

proach explms by which

The proposedthe economand to obse

pansion geney grows largeammunition fexchange resthe transmi

rs: the fiscal phistication morporate weay, as well as ion of the tran of policy he system.

proach incor(EMP), the reserves; in to do so. Blnd outflows mch can resultappreciation mlt for it to gr. Also, whis denomina

its movementy depreciatioative consequThis paper, c

ILITY IN THE

sed, as to whilure.

licitly incorh the fiscal sd methodolog

mic behaviouerve how it rerates a foree enough to dfor foreign exerves. In thission mechmultiplier an

may be introdalth effects

feedback anansmission me

options, wh

rporates indiexchange ratSOEs people

lanchard et amay cause lat in big disrumay squeeze row back if aen a signif

ated in foreigts), sharp flucns) can causeuences for f

co-authored b

E SMALL OPE

ether they ste

rporates thetrategy drive

gy allows usur which chreaches the peign exchangdeprive the auxchange manahe simplest mhanism thrond the prope

duced with strand indicat

nd second rouechanism len

hose effects

icators of ete and the le care about al. (2010) adarge fluctuatiouptions in ecothe tradable sand when theficant portiongn currency (ctuations in the severe balanfinancial stabby the Econo

EN ECONOM

P a g e |

eer the econo

e transmisses the systems to model aharacterises point of failue deficit whuthorities of agement, thatmodel, we cugh just tnsity to impoructured modtors of polund effects.

nds clarity to may be trac

external marlevel of foreEMP, and th

dmit that capons in exchanonomic activsector and mae exchange rn of domes(or is somehhe exchange rnce sheet effebility, and thomic Counsel

MY

15

omy

ion m to

and the

ure. hich

the t is, can two ort.

dels licy An the ced

rket eign hey

pital nge ity. ake rate stic

how rate ects hus, llor

FI

16 | P a

and head the guidanpolicies, gdecades bsuperior tpeg or a ris highly aware of tthe externlevels gaiwhen they

This apprrespects constraintthe transexchange a foreign above, thdrives thimbalancebalance ois no corrthe conveexpensivetoo fast, default enfailure, beand the prohibitivrelies on rcost of revenue. practical pis not focu

SCAL SUSTA

g e

of the IMF'snce of Fund sgives that insbeen standardtrack record. ate that moveprized in S

the adverse conal account in traction iny involve a co

roach is thethe structur

t. The implicsmission mec

constrained, exchange con

he transmissie economy es, and theref payments cresponding deentional storye it becomes the cost of d

nsues. Howevecause what point at wh

ve cannot berules of thumgovernment These rules policy guidanused on the b

AINABILITY

s Research Dstaff in their astitution's offid practice in s

The exchanges in a predictOEs preciselonsequences and preserv

n these econoontraction in r

appropriate ral nature oations may bchanism in with large ec

nstraint on groon channels to a point is a defined

risis. In a largefined point oy is that the to finance itdebt service ver, there is is “prohibitiv

hich the cosuniquely pa

mb, for exampdebt, as a

of thumb havnce. More seribalance of pay

Y AND DEBT

Department, aanalysis of meicial sanction small open ecge rate target,table way witly because thof failure. Po

ve adequate omies becausreal output.

one for SOof their forbe appreciated

SOEs, whicconomies, whowth. In the Sby which f

of failure ad failure poinge diversifiedof failure andlarger the d

; if the debt becomes prono clearly d

ve” is a mattt of debt searameterised.le with respepercentage

ve proven toiously, becauyments, if app

IN SOEs

and intended ember countrto what has

conomies wit, whether it ith low volatilhey are acutlicies to balanforeign rese

se of that, ev

OEs, becausereign exchand by comparch are forehich do not haSOE, as outlinfiscal expansare via externt, marked byd economy thd crisis. Insteeficit, the mkeeps on ris

ohibitive, anddefined pointter of judgmeervice becom

This approact to the interof governm

oo imprecise use this approaplied to SOE

for ries' for

th a is a ity, tely nce

erve ven

e it nge ring eign ave ned sion rnal y a

here ead,

more sing d a t of ent, mes ach rest

ment for ach

Es it

FISCAL

may suggbalance oBarbados interest/reprecedingthe econo(2010) munsustainabalance oconventio

Converselstrategies balance othe case, relationshThere is nCaribbeanpractical oholds gooon the faeconomicborrowinggrowth-enlevels ofgovernmehigh leveinvestmenproduced therefore the purpothat there IMF has rdebt to Gcountries

L SUSTAINABI

gest that fiscof payments

in 1991, whevenue ratiosg years was clmy to a balan

methodology able in thoseof payments

onal methodol

ly, conventioare unsustai

f payments fain particular

hip between no convincinn or elsewheobservation thod across manact that gov

c infrastructurg to finance nhancing. Hof debt, borrents finance els of debt. nt is in appro

at fair markno surprise t

orted relationsis an optimal

recently uncoGDP and econ

so far tested

ILITY IN THE

cal policy iscrisis is immhen even thos were low, learly unsustance of paymenclearly show

e years, whes crisis cannlogy.

onal analysisinable even tailure even inr, with studigovernment

ng evidence oere, and therehat leads us tony countries. ernment borrre clearly procurrent spend

owever, it dorowing is focurrent spenNor is it thpriate social

ket prices forthat there is ship between l level of deb

overed no relanomic growthd (Pescatori e

E SMALL OPE

sustainable minent. This wough debt-to-

the fiscal ainable, and unts crisis. Thews the fiscaereas the fiscnot be dete

s may suggthough they w

n worst case scies which pudebt and eco

of such a rele is no reasoo expect any The intuitive rowing to b

omotes economding may nooes not follo

for infrastrucnding by borhe case that

and economir products anlittle empiricdebt and gro

t. A test by ecationship betwh, across the t al. 2014). T

EN ECONOM

P a g e |

even thoughwas the case-GDP and tostrategy of ultimately droe Belgrave et

al policy to cal roots of cted using

est SOE fiswill not leadcenarios. Thi

urport to findonomic growationship in on in theory relationship targument rel

uild social amic growth, t necessarily ow that at lcture, and trrowing onlyall governm

ic infrastructund finance. Itcal evidence owth, much lconomists at

ween the ratiowidest range

The exposure

MY

17

h a e in otal the ove t al.

be the the

scal d to s is d a

wth. the or that lies and but be

low that

y at ment ure, t is for

less the

o of e of e of

FI

18 | P a

the flaws cited in economicthe evidepublishedonly six ssince 180definitionfor the Cdiscussed

The convpaper to countries,the net prfor compaforward finterest rBecause pparametergrowth ofachievemthe calculevolution)maturing

The IMFsustainabi2004). It of the deband in thsustainabithresholdsinstitutionstrategy th

SCAL SUSTA

g e

in the Reinhevidence has

cs profession nce is scant

d in 2012, Reitudies globall

00. They all ns, and their rCaribbean app

in Box 1 on p

entional apprIMF staff o

, the suggesteresent valuearison with thfor a decaderates, exchanparameterisatrs are advisedf the economyent of the solation says n), and that thdebt will not

F-World Bankility in low iinvolves "(i)

bt and debt-sehe face of pility guided bs related to ns; and (iii) hat contains t

AINABILITY

hart-Rogoff as been an ac(Herndon, Aand inconsi

inhart, Reinhly that tested

used differeresults are notpears in Greepage 34.

roach is compon debt sustaed methodolog(NPV) of fut

he NPV of thee (IMF, 2008nge rates, gion is largelyd, as well as y. With all th

olvency criternothing abouthe methodolobe rolled ove

k guidance income coun) a standardizervice dynamlausible shoc

by indicative the quality an appropriathe risk of de

Y AND DEBT

analysis that cute embarrash and Pollinstent; in an

hart and Rogothe relationsh

ent methodolt comparableenidge et al.,

plicated. In a ainability forgy involved tture primary e public debt,8). This invogrowth rates y arbitrary, str

a range of shat, the paperria may not bt the level oogy is blind er.

for the assentries is also zed forward-l

mics under a bcks; (ii) assecountry-specof a country

ate borrowingebt distress."

IN SOEs

was previouassment for n, 2013). In faoverview pa

off (2012) fouhip in the perlogies and d. A recent stu, (2013), and

recent guidanr market accthe estimation

fiscal balanc, and forecastolves choice

and deflatoress tests on cenarios for r admits that be feasible, tf debt (only to the risk t

ssment of dcomplex (IM

looking analybaseline scenaessment of dific debt-burdy's policies ag (and lendinSustainability

usly the

fact, aper und riod data udy d is

nce cess n of ces, ting

of ors. the the the

that its

that

debt MF, ysis ario debt den and ng) y is

FISCAL

based onprojected governmerevenue. Tcountries are judged

The convrecently cprofile ofwhereas tpolicy is sustainablto avoid imposes oratios are and Barbinternatioof investmcomparabbe of inve

The convIn the peaccepted mbe a debt-more thadecade, wthe aftermthere wer60 per cefinancial just as arb

L SUSTAINABI

n notional thdebt, the NP

ent revenue, dThe thresholddepending o

d to be poor, m

ventional appcited examplef the UK is there is a geunsustainabl

le by the finathe punitive

on Spain. It isof the same m

bados' policnal comparisoment grade,

ble debt levelsestment grade

entional appreriod before tmaximum lim-to-GDP ratio

an twice the was thought tomath of massre few industrent. A new nmarkets, at le

bitrary as its p

ILITY IN THE

hresholds forPV of debt to debt service tods are differenon whether thmedium or st

proach is some of this is the

currently sieneral percepe, the UK fi

ancial markete debt servics also the casemagnitude as y making on, yet Barbawhereas mo

s and institute.

roach uses ththe recent fin

mit for fiscal o of about 60

maximum, o be the excepsive financialrial countriesnorm of 100 east for develpredecessor.

E SMALL OPE

r the net prexports, the

o exports, andntiated in eveheir institutiotrong.

metimes coune fact that theimilar to thaption that thescal policy is. As a resultce costs whe that Barbadthose of induinstitutions ados' debt is jost industrial tional strength

resholds whicnancial crisesustainability

0 per cent. Japwhich had

ption that prol rescue packs left with rat

per cent haloping countr

EN ECONOM

P a g e |

resent value NPV of debt

d debt serviceery case betweons and polic

nter-intuitive.e fiscal and dt of Spain, e Spanish fiss deemed to t the UK is a

hich the maros' debt-to-Gustrial countriare strong judged not to

countries wh are deemed

ch are arbitras, the genera

y was thoughtpan, with a rapersisted for

oved the rule.kages, howevtios of less th

as taken holdry debt, but i

MY

19

of t to e to een cies

. A debt but

scal be

able rket

GDP ies, by

o be with d to

ary. ally t to atio r a . In ver, han

d in it is

FI

20 | P a

The susta

There is aand whatsustainabiHowever,sustained cause a deGreenidgedebt or fcountries that of coAll other is more, fwell be tocircumstaand certaibenefit offuture.

We have tgrowth rapolicy chpresumedhypotheticoffers no presumedfiscal policarries a term conunderminmarket ac

SCAL SUSTA

g e

inable and th

a considerablt is optimalility these t, it is obviindefinitely,

eviation. Thee et al. (2013)fiscal policy;with a debt-t

ountries with economic cir

for countries wo allow the raances where din contractionf a lower deb

the paradoxicate (by reduc

hange involved benefit fromcal and poorl

useful guidad relationship icy. Using thrisk of impl

nsequences foe domestic fi

ccess.

AINABILITY

e optimal

le difference l. In the reerms have bious that suif there are

e recent study) offers no op their claim to-GDP ratiolower ratios, cumstances awith higher r

atio to remaindebt reductionn of income, wbt-to-GDP rat

cal conclusioncing the debtes a reductionm a reductioly grounded ance for fiscoffers no gui

he ratio as a tlementing po

for growth, inancial mark

Y AND DEBT

between whaecent discussbeen used i

uboptimal pono market fo

y on Caribbeapinion on the

is that the above 56 peall other thin

are not equal, ratios, their ben high, or even would requiwhereas the ptio is hypothe

n that in ordet-to-GDP ratin in growth. on in debt-toin theory and

cal policy. Indance on the trigger for poolicies with dsuch as deb

kets and dama

IN SOEs

at is sustainasions on fisinterchangeabolicies may orces at workan economies sustainabilitygrowth rate

er cent, is belngs being equof course. West policy min to increasere an immediresumed growetical and in

er to enhance io) the requiIn general,

o-GDP ratiosd evidence, an particular, sustainability

olicy adjustmdeleterious lobt haircuts tage internatio

able scal bly.

be k to by

y of in low ual.

What ight , in iate wth the

the ired the

s is and the

y of ment ong that onal

FISCAL

A useful given in th

Is Fisca(Bottom

It is vital the countrtailored tsituation suboptimaunsustainatendenciea point at service thpolicy isalternativeabsence ofrom counthe countrto bear ipresumingstrategies of tax sysfinancial finance, tmarket ddevelopm

L SUSTAINABI

way of reprhe matrix bel

al Policy Optim Answer)

to assess whry’s circumstato the circum

demands a al one. Whaability are cls and under wwhich the au

he national ds hypotheticae fiscal policof a counterfantries and epiry that is the in mind is tg that countriwill have simtems, preferestructures, pr

technology, ledevelopment,

ment, developm

ILITY IN THE

resenting posow:

Is

imal? YES YESYES NO

hich element iance, becausemstances. In

more urgeat is more, wlear, and thatwhat assumptuthorities will debt. In contral: it requircy which profactual, the prsodes which focus of atte

the range ofies are sufficimilar outcomeences for publroduction sysevel of econo

labour marment of the

E SMALL OPE

ssible states

Fiscal Policy (Top answ

S

S

N

YS N

N

in this matrixe the policy ren general, anent responsewe argue that one may deions fiscal polack the whe

rast, the opties a counte

oduces faster ractice is to are presumed

ention. What f assumptioniently alike thes. These inclic provision stems, openneomic developrket flexibiliinstitutions o

EN ECONOM

P a g e |

of the world

y Sustainable?wer) NO

YES NO

NO

x best represeesponse mustn unsustainae than doesat the signs emonstrate wolicy will leaderewithal to fumality of fis

erfactual of growth. In

draw inferend to be similarwe need alwa

ns we make hat similar fislude similaritof public gooess to trade apment, financty, institutioof civil socie

MY

21

d is

?

ents t be able s a

of what d to ully scal

an the

nces r to ays

in scal ties ods, and cial

onal ety,

FI

22 | P a

size of poassumptiowhich is change.

Our studyis unsustaproblem, may be drwaterfall arriving abecause iyour stepsthe literatthe choiceas is the unable to write as th

Sustainab

The appropaper, to where exderived frof expositof insolvethey fall "technicalliabilities technical practical inability ohas harmf

SCAL SUSTA

g e

opulation, lanon that econo

counterintui

y focuses on mainable, for thand the one rawn with canup ahead is

at a fork in tf you chooses. As we shalture ignore the of tributary avoidance ofdistinguish th

hough they ar

bility limits at

oach to fiscaldefine the po

xchange markrom conventiotion, let us cency, i.e. inabdue (Webstel" insolvencexceeds the

government iinterest and

or failure to mful economic

AINABILITY

nd area, etc. omic episodeitive in an

methods of dehe reasons justhat is most rnoeists on an s a signal othe river pos

e the wrong fll see in Chaphe roar of theis a problem f the waterfahe unsustainare the same.

the point of i

l sustainabilitoint of unsustket pressure onal notions oonsider separbility or failur's definitiony, where thvalue of its

insolvency is having no e

meet repaymeconsequence

Y AND DEBT

Most studiess are comparage of rapi

etermining thast cited: it is readily detectunknown riv

of unsustainases a questionfork you willpter 2, not one waterfall, thof the same o

all. Indeed, mable from the

insolvency

ty which is atainability viabecomes expof solvency. Frately a dictio

ure to pay debn), and what he value oassets. We wan academic

economic coent obligations, in contrast.

IN SOEs

s also make rable over timd technologi

at fiscal stratethe most urgted. An analoer. The roar oability, whern of optimal need to retra

nly does mosthey imagine torder of urgen

many writers suboptimal, a

advanced in ta the flash poplosive, may For convenienonary definitbt obligationswe may termf governmen

will show thacuriosum, ofnsequence. T

ns most certai.

the me, ical

egy gent ogy of a reas ity, ace t of that ncy are and

this oint

be nce tion s as m a nt's at a f no The inly

FISCAL

Suppose governmerepay prindomestic of new market intcountry rito GDP, m

Some diffcountry rcapital fliwhere coupast two costs on dthe point that in th(domestictaxes andearners aspayments Naturally,bondholdeaverage) revenue. domestic of incomedistributioa maximudefined in

This logigovernmeproportiontransfer f

L SUSTAINABI

we determent is unable ncipal amouncurrency, repdebt at the terest rate. (Tisk premium.may be refinan

ficulty may emrisk premiumght or for anyuntry risk prdecades. How

domestic debtof unsustainahe aggregatec income earn

benefits froms a group rec

that go tow, within the ers receivingthan the taxThis is the debt are, at be. One cannoon of income um sustainabn this way.

ic applies toent services bn of revenufrom those

ILITY IN THE

mine the poto meet its obnts when thepayment is a

appropriate That is, the rat

) Extremely nced in this w

merge, in them becomes v

y other reasoremiums havew can we deft trigger an ecability? The re, the recipieners) are the m governmenceive the entir

ward interest pgroup of n

g interest arexpayers who

nub of the bottom, a matot observe a becomes too

le debt and d

o concerns aby interest payue. The inte

who would

E SMALL OPE

oint of insobligations to ey fall due. Issured, throuinternationa

te that includelarge stocks

way.

e case of domery large, asn. Jamaica ise been high fine a point aconomic reactreason no sucents of the same collect

nt services. Jare amount copayments onational income fewer (and

contribute tissue: the s

tter affectingdefined poin

o unequal, andebt service

about the cryments whichrest paymen

have benef

EN ECONOM

P a g e |

olvency whpay interest aIf all debt isugh the issuanally competites the prevailof debt, relat

mestic debt, if s a deterrent a case in pofor most of

at which intertion that defin

ch point existsinterest incotive which paamaican incoontributed in n domestic deme earners, d wealthier, to governmenservice costs

the distributnt at which d it follows tlevel cannot

rowding out h absorb a la

nts constitutefitted from

MY

23

here and s in nce tive ling tive

the t to int, the rest nes s is

ome ays

ome tax

ebt. the on

nt's of

tion the

that be

of arge e a the

FI

24 | P a

governmemay not bpoint or ra

In sum, wprivate dointerest oprincipal cannot telpay in fuHowever,willingnes

The circudebt. In obligationexchangeby way oprivate dofinancial wdemand aseriously model, ondeficits anand receipinternatiobalance dpressure difficulty the privat

SCAL SUSTA

g e

ent services be welfare-enange of value

with respect toomestic sourcor principal w

and/or interell whether govfull, at any , sustainabilitss to pay.

umstances arethis case, go

ns because . There is alsof credit proviomestic sourwealth, whichand a demadeplete the

ne may prodnd their imppts, conditionnal economyeteriorates tobecomes exin meeting e

e sector.

AINABILITY

foregone, to nhancing, bu

es at which it b

o domestic debces, there is nowhere governest obligationvernment migpoint, even ty is about th

e quite differovernment mof an inad

o a major proided by the ceces. In this h may be exp

and for foreiforeign rese

uce a forecaact on the bnal on altern. If the foreca the point whxplosive, goexternal debt

Y AND DEBT

bondholdersut there is no becomes unsu

bt raised at mo point or ran

nment is unabns as they beght be unwillwith relativ

he ability to

rent with respmay not be adequate suppblem if domeentral bank, rcase there ispected to stimign exchangerves. Using st of the trajalance of ext

native expectaast indicates there foreign eovernment wt service obli

IN SOEs

s. That transclearly defin

ustainable.

market rates frnge of values ble to pay decome due. Wing to pay, or

vely low ratipay, not ab

pect to exterable to meet ply of foreestic financingrather than frs an additionmulate aggrege, sufficient an appropri

jectory of fisternal paymeations about that the exter

exchange marwill experienigations, as w

sfer ned

rom for

debt We r to ios.

bout

rnal its

eign g is rom n to gate

to iate scal ents the

rnal rket nce will

FISCAL

If we empthe abilityonly unaforecastinpayments which forexternal dno correimbalanceloss of cGovernmethe fiscalexternal mand the emotive tobondholderates. Incpayments they do governmemay chooor externbehaviourlasting effinance fu

The technof liabilittotal of ameasuredof magnidynamicsreal rate ois definedthan the e

L SUSTAINABI

ploy the dictiy to fully seambiguous

ng the impactover the pol

reign exchangdebt service iesponding mes that do notconfidence ient is always policy is crmarket pressuexchange rateo switch ouers are happ

creasing levemay adversenot trigge

ent’s ability toose not to honal, even thour is both unpffects of debtuture investme

nical definitioties over assessets owned , but it will aitude. The f, which com

of interest, is d by the excexcess of natio

ILITY IN THE

ionary definitrvice its extemeasure of t of the fiscalicy horizon, ge market preis likely to bemarket-determt spill over to in economic able to roll o

redible, and ure. If foreige is not exce

ut of domestpy to roll ovels of domesely affect ther any marko service its

nour its debt ough it has thpredictable ant default on ent.

on of governmets – is a theby governme

always exceedflaw in the

mpares the ecothat is assumess of nationonal wealth o

E SMALL OPE

tion of insolvernal debt ob

f fiscal susal strategy on

one may deressure builds tecome problemined limit

the external policy and

over domesticcredibility is

gn reserves ressively volatic assets, a

ver maturing stic debt ande distributionket event tdebt. Of cour

obligations, whe ability to nd irrational, the governm

ment insolveneoretical curient in any cod the nationatextbook aponomic grow

mes, incorrectlnal income oover debt, whi

EN ECONOM

P a g e |

vency, therefobligations is stainability. n the balancerive the pointto an extent tematic. There

to domesbalance throu

d capital fligc debt so longs determined remain adequatile there is and governm

debt at mard rising inter of income, bthat prejudirse, governm

whether domesdo so, but tbecause of

ment’s ability

ncy – the excosum. The s

ountry is seldal debt by ordproach to d

wth rate and ly, that solvenver debt, ratich is the corr

MY

25

ore, the By

e of t at that e is stic ugh ght. g as

by uate

no ment rket rest but

ices ment

stic this the

y to

cess sum dom ders debt the ncy ther rect

FI

26 | P a

measure. rest of thewhich is which it c

Fiscal sus

We build strategy ofrom theexchange authoritietarget is adegree ofFigure 1, the indicainitial levtrajectory not. In thminimumcapital flimarket prpoint at wstudies unforecasts and/or othalternativesustainabi

SCAL SUSTA

g e

A country bee world exceedifficult to

can be valued

stainability an

a methodoloon the basis ofe strategy. T

market pres' exchange

an exchange rf volatility. Twhich uses t

ator of exchvel of reserve

labelled A ihe case of fo

m level Rmin

ight is likelyressure. The which the fiscndertaken foand project thher indices oe scenarios ility.

AINABILITY

ecomes insolveds the total vcalculate bec.

nd the foreign

ogy for testinf the exchangThe fiscal sessure buildsrate target cate anchor orThe procedurthe level of f

hange markets of R0, a fiss sustainable

orecast B, whwith which

y, and an intpoint C may

cal strategy bor the currenheir estimatef external mato stress t

Y AND DEBT

vent only whevalue of the ccause there i

n exchange co

ng the sustainge market pres

trategy is us to the po

cannot be mer achieving anre is shown foreign exchat pressure. Sscal forecast , whereas the

hen foreign rthe market

tensification y therefore beecomes unsu

nt project wed impact on arket pressurthe outer li

IN SOEs

en its debt to ountry’s weais no market

onstraint

nability of fisssure that resuunsustainable oint where et, whether tn acceptably lconceptually

ange reservesStarting with

that follows e trajectory Breserves reachis comfortabof the exter

e considered stainable. In e prepare fisforeign reserve, and we wrimits of fis

the alth, t in

scal ults

if the

that low

y in s as

an the

B is h a ble, rnal the the

scal ves rite scal

FISCAL

Figure 1

Sudden st Small coua "suddeninstitutionmarket prcause thedeterioratgovernmenecessarilof the cumay be re First, if tinvestmenexchange for smal

FXRs

R0

Rmin

L SUSTAINABI

1. Foreign Unsustaina

tops when deb

untries that ben stop", an ns and the privrices, even the balance of e. The fina

ent affected ly within the rrency union

esolved. Let u

the previous nts outside thconstraint ki

ll countries

ILITY IN THE

Exchange Mability

bt is sustainab

elong to a curunwillingnes

vate sector tohough the cou

payments once previous

remains wcountry. The

n will determus consider the

holders of ghe currency ucks in and thethat have

E SMALL OPE

Market Dete

ble

rrency unionss on the pa

o roll over govuntry's fiscal of the union sly made av

within the ue actions of tine how thise possibilities

government punion altogete analysis is ntheir own

F

A

B

C

EN ECONOM

P a g e |

ermined Fis

may experienart of financvernment debstance does as a whole

vailable to union, but the central ba fiscal situats.

paper switchther, the foreno different th

currency. O

Fiscal Deficit

MY

27

scal

nce cial

bt at not to the not ank tion

h to eign han Our

FI

28 | P a

methodolocountry inas a wholunsustainacapital flinvestmenproceeds banking sbank incrrepair govto governreal effect

A shortagwhere thewhich hasof additiofor exampappropriaon centralmay reverby the pconditionastrategy bconfidenc

In circuminvest thewith the central bfinancing the union small, thethe foreigmight be

SCAL SUSTA

g e

ogy will pickn question the. The fiscal able, not beclight. Let usnt stays withfrom maturin

system, the brease by an evernment finanment at markts.

ge of financee central banks accumulatedonal lending tple, the centrate response inl bank lendingrse financial t

private sectoral on the im

by the governce of domestic

mstances wher proceeds in pgovernmentsank would ngap, with imas a whole. I

e fiscal deficign exchange

financial tr

AINABILITY

k up the fact threatens the estance strategcause of “funs consider ohin the uniong governmebanks' treasurequivalent amancing by advket interest ra

e for governk does not redd in banks’ trto governmenal bank does nn this case mig to governmtransfers withr. This centrmplementationment in quesc investors in

re holders of private sectors of other cuneed to crea

mplications fof the impact oit would be c

sustainabilitansfers withi

Y AND DEBT

that the fiscaexternal balangy will in effendamentals”, nly those ca

on. If investoent bonds wiry accounts w

mount. The cevancing this liates. In this c

nment does odirect the addreasury account. In the casnot lend to goight be to relaent; in effect

hin the union tral bank supon of an apstion, designeits sustainabi

maturing govr projects withurrency unionate new mor the balanceon the balanceconsidered suty criterion. in the curren

IN SOEs

al strategy of nce of the unect have beco

but becauseases where ors deposit th the domeswith the cententral bank miquidity increase there are

occur, howevditional liquidunts, in the foe of the ECC

overnments. Tax the restrictthe central bathat are initia

pport would ppropriate fised to restore ility

vernment bonhin the unionn members, ney to fill

e of paymentse of payment

ustainable, usHowever, thncy union as

the nion ome e of

the the stic tral

may ease

no

ver, dity orm CU, The tion ank ated

be scal the

nds , or the the

s of ts is sing here s a

FISCAL

result, witthe countunion.

The reasosharp incfinancing,persistent correctionissued by the extentunion as a

The sustacurrency foreign reis subjectcriterion wmay denystrategy threaching tThe probla strictly countries institutionunion are certain popoint maythe three members be practicthe breach

The Eurobank of th

L SUSTAINABI

th some privtry affected b

on for the locrease in the, or it may be

trend of risn is indicatedthis governmt that investoa whole.

ainability of union like

eserve adequat to the forewill not alert y financing athey lose confthe minimumlem is similar

economic pmay be e

ns, the centranot prepared

oint. Howevey be uniquely

per cent fisof the EU an

cal. In both reh.

pean Centralhe currency u

ILITY IN THE

ate sector funby the sudde

oss of confidee fiscal defie that investorsing fiscal ded. Were the

ment, it might ors lose confi

the aggregatthe ECCU m

acy criterion, beign exchangus to the posst market ratesfidence, even

m foreign reser to that facinerspective theasily financal bank or md to provide fer, no methody determined, scal deficit-tond ECCU havegions this lim

Bank (ECB)union may re

E SMALL OPE

nding being ten stop, to ot

ence by inveicit and the rs have becomeficits. In eitcentral bankbe financing

idence in the

te fiscal stratmay be assebecause the u

ge constraint.sibility that ps to countriesthough there

erve thresholdng the Europehe deficits ofced, but prmember govefinance or tradology existsalthough it i

o-GDP limit ve agreed is tmit is most of

) has shown elieve the fina

EN ECONOM

P a g e |

transferred frthers within

estors may beneed for n

me alarmed bther case, fisk to buy boncapital flight

e stability of

tegy of a smessed using union as a wh However, trivate financi in whose fis

e is no dangerd for the uni

ean Union. Frf small membrivate financernments of ansfers beyons by which ts now clear tto which b

too restrictiveften observed

how the centancial constra

MY

29

rom the

e a new by a scal nds t, to the

mall the

hole this iers scal r of ion. rom

mber cial the

nd a that that

both e to d in

tral aint

FI

30 | P a

on an indcommercifor fiscal small verfinancial impact ofof the unifiscal adjuwould be market pr

Debt mark

The relatinfluencedmeasure differenceinflation. profitablythe funds year. Whrate will the real rawhich thebias towafunding fois severely

Countriesoften finaccounts induced exchange towards tfinance f

SCAL SUSTA

g e

ividual goverial banks, coconsolidation

ry open econaccommodat

f this money cion. The accoustment to blimited so tha

ressure for the

ket structures

tionship betwd by the effiof market e

e between thA high real r

y for the long in ways that yat is more, afind themselvate decrease ae funds are inrds short term

for fixed capity inhibited.

s that experiend themselvehave stabiliseinflation hasrate crisis the

the short endfor fixed inv

AINABILITY

rnment by offonditional on n. In the case nomies like tion would becreation on thommodation we implementeat it does not e union as a w

s and econom

ween fiscal piciency of theefficiency is he nominal inrate of interesterm: the boryield very hig

anyone who bves at a comat any time dunvested. In thm funding emtal formation

ence deep deves in this sied after the ds subsided. e financial m

d of the markvestment drie

Y AND DEBT

fering financethe achievemof central ba

the OECS, ae guided by he foreign exwould be to bed and to takcreate unsust

whole.

mic growth

policy, debt e financial m

the real innterest rate at makes it difrrower wouldgh nominal reborrows at to

mpetitive disaduring the life hese circums

merges, and thn and employm

valuation of ituation, onc

devaluation, aDuring the

markets restrucket: the suppes up, and f

IN SOEs

e, directly or ments of targnk of a union

a limit for suthe prospect

xchange reservbuy time for ke effect, andtainable exter

and growthmarket. A usenterest rate, and the rate fficult to borr

d need to empeturns, year afoday’s high rdvantage shoof the projecttances, a stro

he availabilityment generat

their currencce the exterand devaluatio

period of cture themselvly of long te

funds reposit

via gets n of uch tive ves the d it rnal

h is eful the of

row ploy fter real

ould t in ong y of tion

cies rnal on-the ves erm tion

FISCAL

themselveavailable redress threturns toexchange

It is unlikshort termreal ratesprojects thMoreoverdevaluatioinvests foshort horistuck in ageneratingare no forpath of lo

However,which maincentive attained bcloser to tachieve acontractioHowever,cost of sehigh intetowards tattempts tbring the tight fiscabsorbed that starve

L SUSTAINABI

es to take aat short term

his bias towo the externrate is contai

kely that the m of its own of return ohat are compar, there is theon, an additioor the long teizon offers. Inpath of insuf

g projects. Thrces which drw potential g

, there existsay be stimul

system towby reducing tthe social opta reduction on, supporte, that strategyervicing the erest cost. Bthe short terto reduce therate down p

cal policy. Tmore than haed the country

ILITY IN THE

advantage ofm. However,

wards short-tnal accountsined, and infla

market will accord, becan long term arable to the e ever-presenonal source oferm, thereby n these circumfficient supplyhis is an equrive the econorowth.

s an alternatlated by a reards the lonthe real rate timum. For min the real

ed by convy was repeatgovernment

Because of thrm and unce rate througast a relativeThat in turnalf of all govey of long term

E SMALL OPE

f the high n, there is noterm finances, the depreation rates co

correct this bause it is diff

investment short term re

nt danger of f uncertainty losing the f

mstances the y of finance fuilibrium pathomy away fro

tive path of estructuring ong term. Tha

of interest tomany years, Ja

interest rateventional mtedly frustratdebt, largely he establisheertainty abou

gh monetary ely high thresn meant thaternment reven

m investment

EN ECONOM

P a g e |

nominal retuo mechanism , once balaneciation of me down.

bias towards ficult to achiein fixed cap

eal interest rata new roundfor anyone w

flexibility thacountry may

for employmeh, because thom it, but it i

higher growof the financat path may o a level thatamaica sought

through fismonetary tooted by the h

because of ed market but future ratpolicy failed

shold, even wt interest conues, a situatfinancing.

MY

31

urns m to

nce the

the eve

pital tes.

d of who at a y be ent-here is a

wth, cial be

t is t to scal ols.

high the