Embed Size (px)

Citation preview

| RETURN TO_ REST RI CTEDI EP<) .. DE5p. Report No. TO-507a

I n wcv I

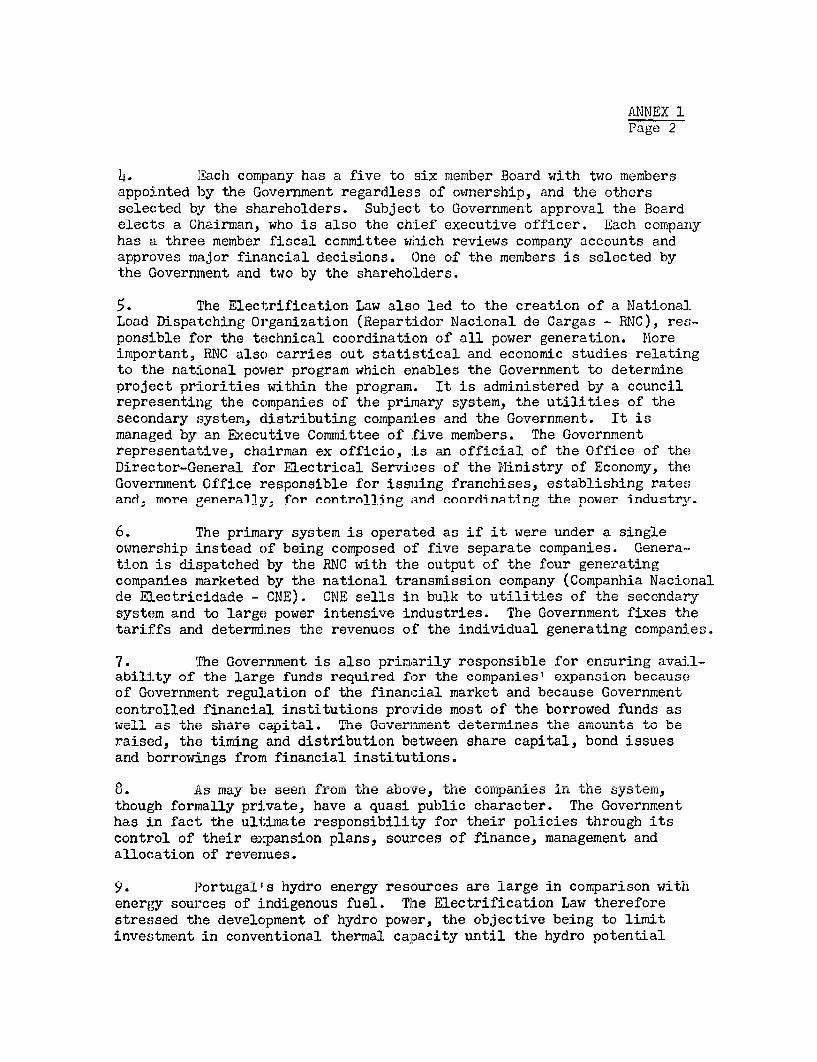

This renorf was arenared for use within 1he Bank and its affilited oraonizations.They do not occept responsibility for its accurcicy or completeness. The report maynot be nihlichein nno may it be quoted as representing their views

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

APPRAISAI, OF THE

GARRAPATELO HYDR.O POWER PROJECT

AND

THE CARREGADO II THEIRMAL POWER PROJECT

POR TJGAL

Ma 8 I 16qA

Pub

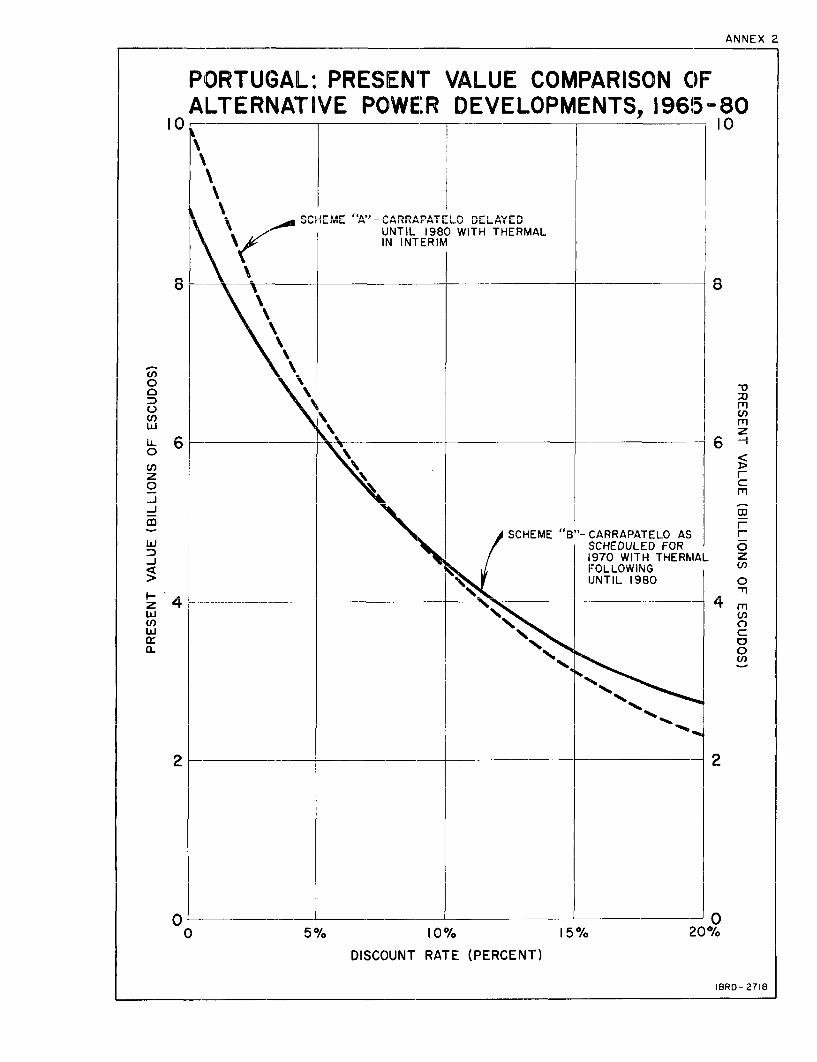

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

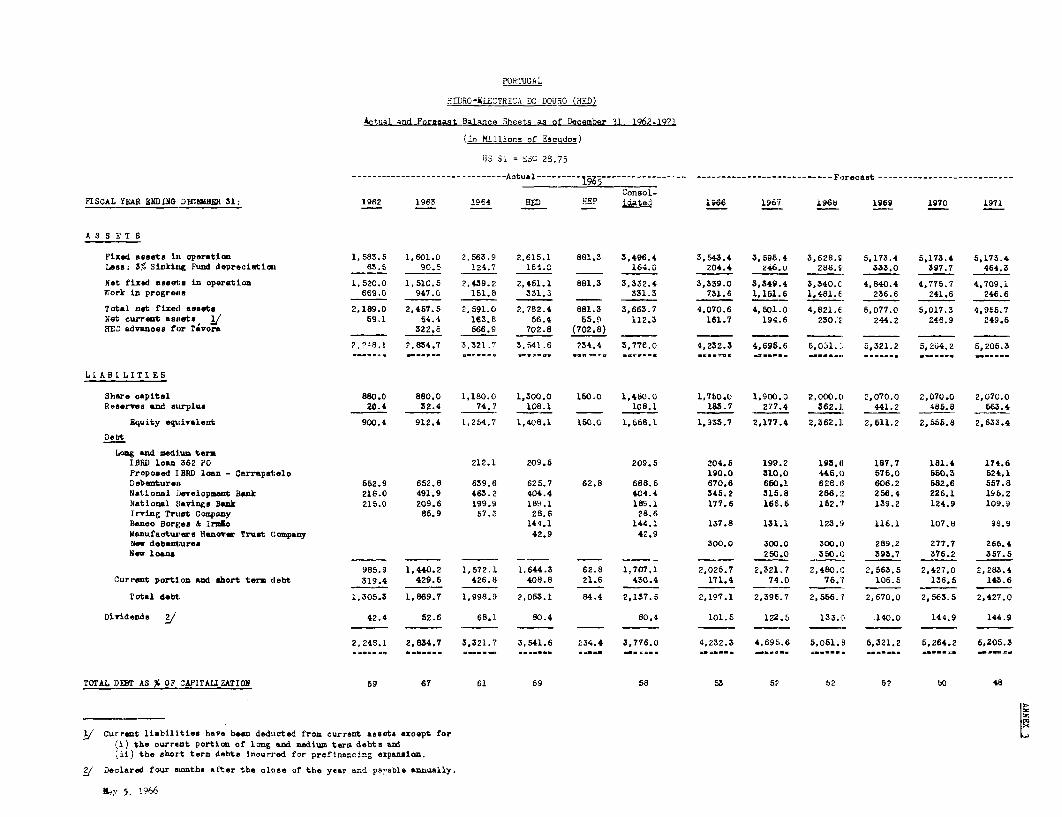

osur

e A

utho

rized

Pub

lic D

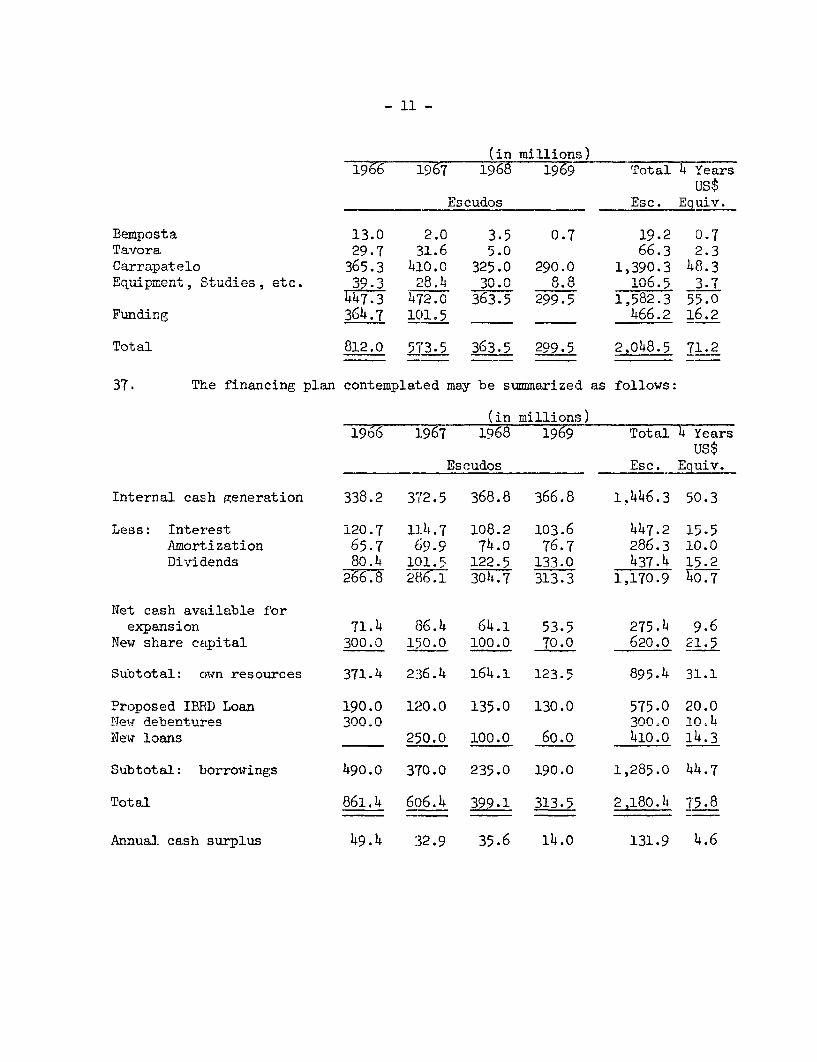

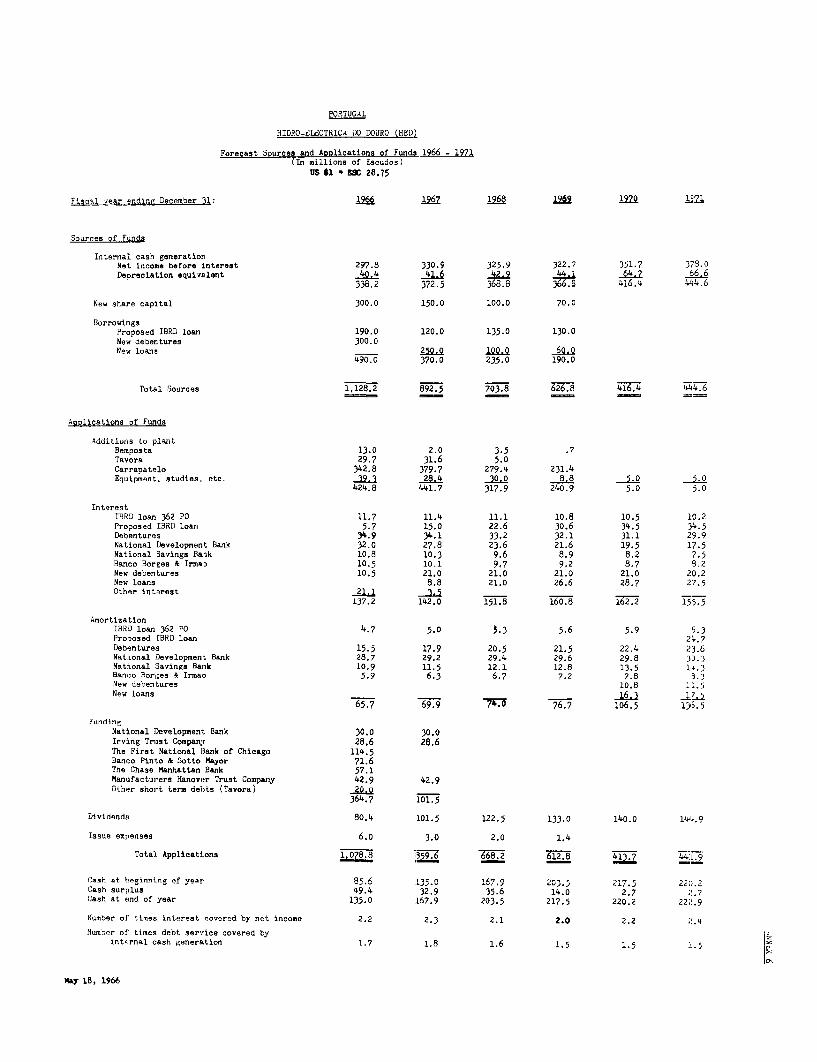

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

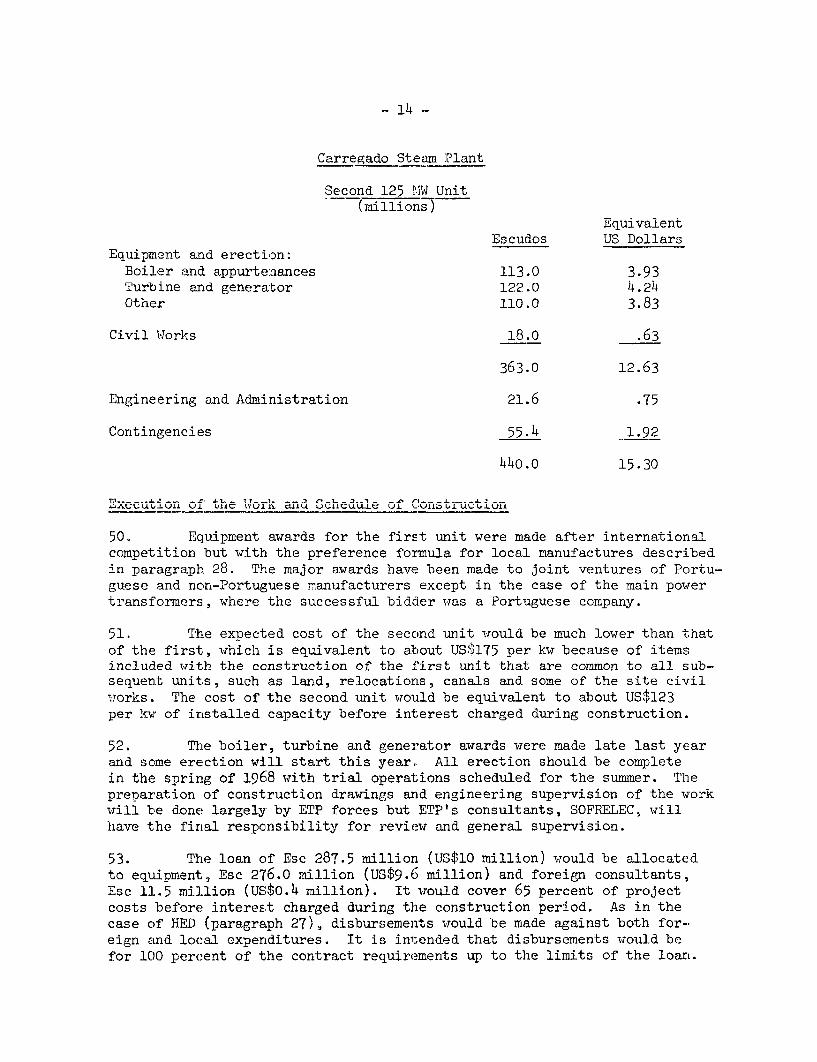

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

U. S. $1 Escudos 28.75Esc 1 = r U.S. C. 035

Esc 1 million = U. S. $34, 783

APPRAISAL OF THECuARRAPATM.&) HYDRO PO'WER PROJECTA AND

THE CARREGADO II THERIUAL POWER PROJECTPOuR;IGAJ

TABLE OF CONTENTS

Page

SUMARY

I. INTRODUCTION 1

II. THE PORTUGtlESE POWER INDUSTRY 1

III. THE POWER MARKET 2

IV. ECONOMIC CONSIDERATIONS 3BackgroundFuture Development of Generating Capacity

V. TALIFFS h

VI. HIDRO-ELECIRICA DO DOURO (HED) 5The ProjectCost EstimateExecution of the Work and Schedule of ConstructionPresent F'inancial PositionP'ast EarningsFinancing PlanThi nannial prospfcts

VTT FMPRE_RSA TERM.OECPThICA PORTT'UT?ESA - ETP 13T'he ProjectCost Est_im-.ate_Execution of the Work and Schedule of ConstructionPi"Apn+. Th1 nn~r.;nl Pr.AQ+. on

Past EarningsFnancint, PlanFinancial Prospects

VIII. PROPOSED FINANCIAL ARRANGEMENTS 18

IX. CONCLUSIONS 19

This report is based upon the findings of an appraisal mission, consistingof E. B. Arnold and Y. Rovani, which visited Portugal in June 1965 and uponup-to-date information submitted recently by HED and ETP.

LIST OF ANNEXES

1 The Portuguese Power Industry

2 Chart - Portugal: Present Value Comparison of Alternative PowerDevelopments, 1965-80

3 Hidro-1aectrica. do Douro (HED), Actual and Forecast Balance Sheets asof December 31, 1962-1971

4 Hidro-Electrica do Douro (HED), Details of Debt as of December 31,1965

5 Hidro-Electrica. do Douro (HED), Actual and Forecast Income Statements1962 - 1971

6 Hidro-Electrica. do Douro (HED), Forecast Sources and Applications of'Funds 1966 - 1971

7 Empresa Termoelectrica Portuguesa (ETP), Actual and Forecast BalanceSheets as of December 31, 1962 - 1970

8 Empresa Termoelectrica Portuguesa (ETP), Actual and Forecast IncomeStatements 1962 - 1970

9 Empresa Termoelectrica Portuguesa (Em'), Forecast Sources andApplications of Funds 1966-1970

Map - Portugal Power Projects

APPRAISAL OF THEl ADDT) A M'Tn TA' vThnD -Ol,1tT7n DDT r%TV4m AIJD

THE CARREGADO II THERJIAL POWER PROJECTDf'rDMTT(-, AT

SUIUXAR'Y

i. Hidro-Electrica do Douro (HED) and Empresa TermoelectricaPortuguesa ( ETTP) have asked for ioans of US$20 million and US$10 miiLionrespectively to help with the financing of HED's 180 MW Carrapatelo hydroproject on the Douro River and with the expansion by 125 N-w of ETP'sCarregado the_rmal project near Lisbon; the Government has expressed itswillingness to guarantee the proposed loans in tne normal manner. hneBank has made three previous loans in Portugal, one to HED and two toETP. The work undertaken as a result of these loans has gone well.The proposed Borrowers are two of the five companies which form thePortuguese primary system of power generation and transmission.

ii. HED and ET-P as well as the other companies of the primarysystem are organized as private stock companies but the Government's con-trol of their policies and supervision of their activities give them aquasi public characte_r. Studies are now being made in Portugal to simplifythe organization of the primary system and to overcome certain disadvan-tages arising from the division of the system into five companies.

iii. The two companies are well organized to undertake the proposedprojects. The projects represent a good balance between hydro and thermaLpower development and are needed to meet growing system requirements.Their total cost exclusive of interest charged during the constructionperiod would be about US$62 million. The proposed loans would providethe equivalent of US$30 million, the balance coming from retained earn-ings, share capital issues and local berrowings.

iv. The level of revenues of HED and ETP, which was increased in 1904

and early 1966, is satisfactory. The financial position of the two companiesis sound and their financial prospects are good.

v. The Carrapatelo project and the Carregado II project are suitablerespectively for:

- a loan of US$20 million to lIED, with a 20 year term, includinga five year Rrace period, andL

- a loan of US$10 million to ET'P, with a 15 year term, includinga three year grace period.

APPRAISAL OF THECARRAPATELO HYDRO POWER PROJECT AND

THE CARREGADO II THERMYAL POWER PROJECTPORTUGAL

I. INTRODUCTION

1. The Bank has made three loans in Portugal. all in the nowersector. The first two, in 1963, were US$7.5 million to Hidro-Electrica doDouro (HED? and US 5 0 mi ll ion tom Innr.Sa Terrn e1(tr.ca Portuguesa (R.TP).

These loans helped to finance HED's Bemposta hydro project and the thirdand final unit. f' ETP's Tanada do Ouiteiro thermal plant. A second loanof US$15 million was made to ETP in 196;5 for the first unit of theGarregado the^ral plant near Lisbon (ultrmate capacity 4 x 125 MU) w New

loans totalling TJS$30 million, of which. US$20 million would be for HED's180 Mv Carrapatelo hydro roJect near Porto nd UST-10 million Tould befor the second 125 MW unit at ETP's Carregado plant, have now been pro-posed. The two proJects would ^otactUS$6 million exclusive _-f

interest charged during the construction -period. The map shows thegnera.l 1 -4-tio4 of Portnguese powrer eln-op-ments.

2. T;i~~1,s re-port- is lase' upon Ile. findigofaaprsl isonCA. L J5CU.1..J -J I. Lit 'J

5.,% IJ..V 'CJ V~LJJnULL16 P u "VOC..DLL 11L;;.V1

consisting of E. B. Arnold and Y. Rovani, which visited Portugal in June1965 d.and u:pon upp-t o-duate inf0or-mt.LiUo sUU1U.LLtAiU recenLtly Uy nEDLlLj U1IU a -Er.

II. THE PORTUGUESE POWER INDUSTRY

3. The organization of the Portuguese power industry has been de-scribed previously (Reports TO 450a anC. 374b), and its main features aresummarized in Annex 1. The proposed RBorrowers are two of the five com-panies of the primary power system, wnich includes three hydro, one tnermaiand one transmission company. All are organized as private stock companies,each with a 75 year concession and similar by-laws. The Government appointstwo of the five to six members of each Board, regardless of ownership, andapproves the Chairman, who is the chief executive officer. The Governmentor government institutions are large shareholders of the companies and.government policies strongly influence the companies' operations and to alarge extent determine their economic eLnd financial performance.

4. Technical operation through coordination between the companies ofthe system is excellent. The division of the system into five companies hashowever certain shortcomings, mainly with regard to system planning and toa rather cumbersome system of tariffs eLnd revenue allocations (see Chapter V).There is also a certain degree of compe.tition between the companies forrights to the development of sites, or the priorities of such developmentonce the rights have been established, which in the past has interfered withthe most desirable development pattern. There is some duplication of staff,both engineering and administrative, which could be avoided were there oneor two companies instead of five, and there are a multiplicity of controlswhich could be simplified.

- 2-

5.~ ~ I. Te 0overnmuent is undertakingaseisostdsthugte

Superior Electricity Council to analyze the structure of the primary systemardl t'o recommend im r-vereUbs S-udle tujd rec-t: erldaV1Utions are also- bein s::L

made on procedures to be followed in the allocation of hydro sites and onthe prinLciples governing concessions.

6. Preliminary information regarding the organization study of theprimary system indicates that a satisfactory solution is in sight, althougha number of complex problems have still to be solved before a new organiza-tion can be clearly defined and implemented. During negotiations agreementwas reached on a program of studies and the Bank;s willingness to considerfurther power lending was made conditional on completion of the studies andagreement on measures of implementing them.

III. THE POWER !MARKET

7. Over 90 percent of the public power supply of Portugal is pro-vided from the primary system. The system is centrally dispatched to maxi-mize economies of generation with the energy so produced marketed by thenational transmission company (CNE) which transmits and sells it in bulkto distribution utilities throughout the country and to certain powerintensive industries. Since their total production is taken by the nationaltransmission company, the individual generating companies of the system haveno direct contact with the market.

8. Historic rlecords of the production and use of electric energy goback many years for -the entire country. These records show that firmenergy requirements have increased at an average annual rate of about 11.3percent since the early 1950's, with extremes of 8.8 percent in 1955 and13.4 percent in 1960. For planning purposes the future growth rate ispresently proJected at 10.7 Dercent annually, indicating the need to doublecapacity about every 7 years. These assumptions are reviewed regularly andchangeed whenever warranted by actual results.

9. The nower and energy requirements on the primary system in 1964were about 800 IMW and 3,700 million kwh, respectively; the correspondingvalues in 19Q70 ar foreeast to rtReah bhont. 1,500 MW Rnd 7000 million kwh.The additional new capacity required during the period would includeCarrapatelo an.d the first, second, third and probably fourth units Pt.Carregado. Final decisions on new plant construction to follow Carregado!I and Carrapatelo are expnected soon. The general princinple tn bh fol-

lowed will be to con-tinue new hydro power construction at about the sameinvestm.ent rat. e + as ir the past Wnd too supply th1e difference in marklet re-

quirements with thermal power. Given the normal exponential rate of marketgrow andwitaU mr or ls ant rte o hydro power constructionit can be seen that -thermal power sources will provide an increasinglyhigher percenLtage of the total power supply system in the future.

- 3 -

!V,. ECONMhIC CONSIDERATIOvNS

Backgron--d

10. FtPcrtugal ',as relatively c- hbydro power resoun ces but practi-

cally no indigenous fuels. Consequently past emphasis was placed on hydropower development.

ll. H1ydtr-ological condi'tons are eharacterized by a pronou,ced lowflow season during six months of the year with July, August and Septemberbeing particularly dry- unf ortunately, t opograpnica l conia uions mae aue-quate river storage impractical. Given these circumstances and writhoutthermal back-up, the hydro installatiorns on the major rivers, which aremostly run-of-river plants, have had to be so sized as to be capable ofmeeting market requirements during even the most adverse water condi-tions. This led to overinstallation in the sense that substantial amountsof surplus energy became available during normal water conditions. Thisis of course economically acceptable as long as the cost of the useablehydro power so produced remains below the cost of equivalent thermalpower.

12. In 1962, when the Bank reviewed the power sector, it was apparentthat even though there were relatively inexpensive hydro sites still avail-able for development, continuation of the past emphasis on hydro would leadto uneconomic system development. Wqhi'Le this view was not accepted offi-.cially it was the subject of considerable debate in planning circlesand the Bankd's observations prevailed in favor of those advocating balanceddevelopment of hydro and thermal resources. As a result, construction of'the Carrapatelo hydro project was delayed in favor of planning for theCarregado thermal plant.

Future Deve-Lonment of Generating Capacity

13. A:Lthough there is estimated to be enough hydro potential remainingto supply Portugal's total power requirements for about the next ten years,it would be extreme'Ly difficult to marshaLl the skills and resources neededto put all sites under construction during the period. In addition, for thereasons given above., it would result in an uneconomic overinstallation ofcapacity. TPhus there is no doubt that thermal power of either the conven-tionaL or nuclear time will be essential in the pattern of future Portuguesepower development. The timing of constructing future hydro additions istherefore all imnortant since a given hydro installation can be economic atcertain stag,es of system development and uneconomic at others.

14. In the circumstances an economic evaluation of Carrapatelohpq best be done by comparing eosts of the total system as it wrm1cl be w-Lth

Carrapatelo on the :Line in 1970 as planned, and w,ith Carrapatelo delayed fora further nu.mber of years. The problem and largest potential source of errorin doing this is in the development of generation schedules to fit assump-tionsLJ±3 .1. .regarding Le t..im&Jing of A. -Li L .add Lf Ai+4ns, sinee theA re isi no.

- 4 -

exact equl valent thermal altr.a+t4ive It.o a r-h 1 IT this

case, the value of Carrapatelo increases year by year as the load base grows*1nti-l- n- 11 the- er.ergy potential-y ava-i.la.l.e ca. b,e -t,lized LA under the IloadLcurve.,

15. Schedules of plant additions, capital costs and incremental pro-il A -4- -- -- - A 41- 4- -- 4-. .n_ _ _ _ _ _4____ UUCCU11 COS"S WeU; IJULCPaIUU 1U W Zuei.liUi UtV±UiJA1IRLiU ;ZDit,tUU3 WIJt lU<VILLg

Carrapatelo on the :Line in 1970 and the other in 1980. Thermal plant capac-ity- was pri,-ied -using LUC expect~ed .xisu:s of Carregado as a guide, that is.,the first unit of a new station at US$174 per kw with subsequent units atUS$122 per liv or an average oI US135 per Kw for a 500 IVW station. Incre-mental thernal production costs were based on fuel at US$20.80 per metricton European port, 9,80u btu per net kwh and maintenance, supplies andlabor at US 0.4 mills per kwh. The cost of transmission for either develop-ment would be about the same. The resulting cost streams were then con-vertedi to present value at 2-1/2, 5, 10, 15 and 20 percent interest ratesand sketched in graphical form as shown by Annex 2. The result indicatesthat system development with Carrapatelo as scheduled is economically advan-tageous at interest rates lower than about 9 percent, where the curves inter-sect. With a higher value of money it would be preferable to delayCarrapatelo, but since 9 percent would be a satisfactory return on anundertaking of this type in Portugal, the early investment in Carrapatelois Justified.

V. TARIFFS

16. Until this year the revenues of the five companies in the primarysystem were derived from two tariffs f'ixed by Government decree, generallyfor three year periods: one, the tariff at which CNE, the transmission andmarketing company, purchased power from the four generating companies inthe primary system, and two, the tarif'fs at which CNE sold this power todistribution companies in the secondary system and to certain industries(see Annex 1). The revenues of CNE resulted from the difference betweenthe gross revenues of the primary system and the cost of power purchasedfrom the generating companies, and the revenues of the individual generatingcompanies resulted from the division, according to percentages fixed bydecree. of the agg2regate revenues frorm their sales to CNE.

17. A decree law of Mlarch 23. 1966 has simDlified this Drocedure andmade it more flexible as there is now only one tariff schedule, namely theone applyvin to sales by COE. This is established from time to time by theSecretary of State for Industry. This tariff schedule is based on closelymreriewpd P;;tiTmnn+.P of' the totnl genpration Fni sales of' the vsytem, anrl of the

operating expenses and fixed charges of the five companies in the system.These estimates will be prepnred annually bar the five companies in the f'uture,with CNE exercising a coordinating ro:Le. The Secretary will then determinet1he percentage a'lloca+4on +o be- used d,uring +he~ followngrn year- fori AiTr4r!irir

the Eggregate revenues among the five companies. There are actually sixpercentages: one fra of the fi ve pri.A system companies, to cover

- 5 -

all of their revernuerequreriuiremnents, except for E'TP's fuel costs and one for

a so-called "Fund for Thermal Support!r which is intended to cover fuel costsand the cost, of -owter purchased in aadverse hydrologicall years from- neighbor=ing countries.

18. Prior to 1964 the regulations provided that the tariffs and revenuea lloca.-tions should btte so calculcat-ed as 4o -rvd eaeh oAh pmr sse

companies with revenues sufficient to cover: (a) all operating expenses, in-cluding taxes; (b) tw-v o pro-v0sions in lieu of depreciation, based on 3 percentnotional sirking funds for (i) renewing equipment over a 25 year period and(ii) redeemidAng the origLnaL Lnvestment over the rellainig ife of thrle cUJ-

cession; (c) interest chargeable to operations at actual rates and (d) divi-dends of at least 6 percent. In accordance with undertakings in ioans 362 P0and 363 P0, which have been renewed in connection with the tuo proposed loans,a decree lawr of 1964 allowed additiona:L revenues to HEu and ETP to (a) coverthe excess, if any, of amortization requirements over the two provisions inlieu of depr^eciatiorn and ('b) provide for the equivalent of not less than10 percent of estimated capital expenditure for expansion. By the decree lawof 1966 already cited, the three other comnanies have now been allowed thesame level of revenues as HED and ETP.

19. Following the recent decree law the tariff charged by CNE wasraised by about 10 percent effective retroactively from January 1, 1966 tocompensate for increased operating expenses of the system and to provide allof the companies in the system with the level of revenues described above,including provision for payment of dividends at 7 percent of par and forself-financing of 10 percent of expansion requirements.

VI. HIDRO-ELECTRICA DO DOURO (HED)

20. HED was established. in 1953 to develop the hydroelectric potentialof the Douro River and some of its tributaries; it is presently the largestof the primary system generating companies. HED's initial efforts wereaimed at the development of the international stretch of the Douro, as aL-located to Portugal by agreement in 1927 with Spain. This was undertakenin three stages: Picote, with three 60 MW units, was completed in 1958;Mliranda. with three 52 MW units in 1960 and Bemposta. with three 70 IW units,the last development of Portugal's section of the international stretchof the river. began operations in l96-. The previous loan to HED helpedwith the financing of Bemposta. In addition, in 1962 HED took over themanagement of the nartiallv comoleted Tavora prolect from Hidro-ElectricaPortuguesa (HEP), a private utility of the secondary system. This projectwas suihtantiaF1v tompleted in IQ64.

21. The Carrapatelo proiect, for which the pr nposed lonn has beenrequested, would be the first of five developments planned on "the NationalDouro," the stretch of the river entirely within Portugal (which wSa re-served for Portuguese exploi-tation by the 1927 agreement with Spain).

- 6 -

22. The Company is well staffed to design and undertake the construc-tion of hydro power projects. Consultants are used for certain specializedwork as, for instance, model testing, but the company generally undertakesall design eLnd engineering supervision of construction with its own forces.

Tre Prolect

23. The site. about 60 kilometers from the mouth of the river, is ac-cessible by road, rail or river transport. The power installation would be18n TWJ in three unit-, with An av r'ate annuAl enprav ranabilitv of about800 million kwh. The dam, with a crest; height of about 55 meters from bed-rock and an over-all crest lenotlf' about 355 meters, is aesizned s a

concrete greLvity structure with the powerhouse on the left hand and naviga-tion locks on the right hand. Thei loc,'k rhnmhbr wrlrlhL be abhit95. Qme tlong by 12 meters wide designed for a riaximum single lift of about 36 meters.Theno cen+atec!;llsr sp.ill1ywoldh bl ont+ lrilo '*lle b six gates dimrenrionedA alnng with

other elements of the structure, for safely handling the design flood of200 ,nori c,r, ,4,! mete-rs per second. MIT - t, -- A pl- uoudehe r.f.rr +although there will be sufficient pondage to meet short peaks of about 130 MWeven Culring "low flow,~s.

_S r, = -- iat_

% veit ~L's L-IL La W L'EW

i~ie ebL±LU~L~ ib UU (JlU W.LJ., PIVJAU:% uArLIie ULI t'..lleP-ZVLU24.~~1 The eti teLMZLte lis based o 1prcseeienced ntepeiu

Douro River projects updated by recent changes in costs of labor and mater-ial. Contirigencies were applied to each item oI the estimate In accurdar,cewith the degree of Lmcertainty associated with estimating the cost of theitem. The indicatecL quantity of excavation wJas increased by 20 percent,and concrete, forms and reinforcing steel by 10 percent. Equipment can bepriced fairly closely, allowing, in th:is case, a contingency of about 5 per-cent. Probably the most difficult item to price is the cost of diversionand management of the river during construction; a contingency of 50 percentwas used.

25. The estimate is summarized below:

- 7 -

Clar-``tcl '-'ro Project

JUUII )CU~X± Lu 11,UbL£j±U.,

S-riarizedu Cost Est l1 iU-t e(millions)

EquivalentEscudos Dollars

Land and relocation of roads and bridges 48.6 1.69

Camps and roads 126.9 4.41

River diversion 41.8 1.46

Civil Siorks:Dam and powerhouse 352.3Nlavigation locks 87.8

440.1 15.31

Equipment:Turbines and generators 180.0';witchyard and transformers 28.6Other 132.5

341.1 11.86Subtotal 998.5 34.73

Administration 161.0 5.6oContingencies 178.5 6.21

Total 1,338.0 46.54

26. The cost estimate has been carefully prepared and should proveadequate. The expected cost would be equivalent to about US$259 per kwof installed capacity exclusive of interest charged during construction.

27. The loan or Esc 575.u million uSPb2U million) would be allocateato equipment, Esc 316.25 million (US$11 million) and to the main civil worksconstruction, Esc 258.75 million (US$9 million). Disbursements would bemade against both foreign and local expenditures. It is intended that dis-bursements for equip!nent contracts would be made for 100 percent of thecontract amounts, up to the equivalent of US$11 million, and that disburse-ments for the main civil works construction would be made for 50 percent ofthe payments due under the main construction contract, or for 100 percentof supply contracts, up to the limit of US$9 million.

Execution of the Work and Schedule of Construction

28. Access roads and preliminary site work have been completed andthe river has been diverted. Bids for the main civil works contract wereinvited on an international basis (without any preference for Portuguesecontractors) last year and an award was made in August to the low bidderwhich -was a Joint venture between French ard Portuguese contractors. Bids

- 8 -

for the main items of equipment are also open to international biddingbut, as in the case of the past Portuguese loans, preference is allowedfor Portuguese manufacturers. The preference formula, which is set forthin the bid invitations, allows the award to be made to any qualified bidder,offering in all or in part locally manufactured goods, whose price did notexceed the price of the lowest qualified bid: (a) by more than 15 percent,if the lowest qualified bid offered only goods manufactured outside Portugal,or (b) by more than 10 percent, if the lowrest qualified bid offered goodsmanufactured both in Portugal and abroa.d.

29. The construction schedule covers substantially a five year period.Preliminary work started in 1964 and first unit operation is scheduled fo:rmid-1969 with the final unit coming into operation in mid-1970. This scheduleis conservative.

Present Financial Position

30. Condensed balance sheets as of December 31, 1962, 1963, 1964 and1965 are shown in Annex 3. At the end of 1965, HED's fixed assets in service,the Picote, Mliranda and Bemposta plants, less reserves in lieu of depreciation(for equipment renewals and investment redemption), totalled about Esc 2,451million (US$85.3 million). construction work in progress was about Esc 331million (US$11.5 million); current assets were about Esc 56 million (US$2million) after deduction of current liabilities (but before deduction ofshort term debts and current portion of long term debt). in addition, HE:Dhad advanced Esc 702.8 million (US$24.4 million) in the construction of theTavora project, the imanagement of which it took over at the end of 1962 fromHIEP. HED has made a nublic offer to buy the Esc 150 million (US$5.2 million)shares of HEP by tendering an equivalent amount of HED shares at par. Thenprchase is emxeted to 'hpe fifni7.pc tbhis vear. The assets taken over byHED wrould consist of Tavora, at a book value of Esc 881.3 million (US$30.7million) and net other assets of Esc 55.9 Qmillion (US$A1l9 million)= Theliabilities taken over consist of (a) L'sc 64.4 million (US$2.2 million)of debentures, the outstanding balanIr of five series with terms rangingbetween 25 and 40 years and interest rates ranging between 4 and 5 percent,&nd- (b) supplier6' Tice,ts ̀otalr) Es200 mnillirn (TS'5.0 7 mnillinn),due in 1966.

31. The capitalization of HIED at the end of 1965 was Esc 3,461 mil-lio (US$120.4 milin) excludine; 4the -apitalzator. of -IP (se Anexfor a proforma balance sheet of HED assuming that HEP had been purchasedfltl tose end of 1965). The main:compone.ts MI this capitali o were asfo]-loiis :

-9-

Long &Reserves -Iedium

Share and Deben- Term ShortSources Capital Surplus tures Loans Term Total

(in millions of Escudos)IBRD Loan 362 P0 214.2 214.2

Social SecurityInstitutions 567.9 372.2 94o.i

National Develop-ment Bank 192.7 30.8 463.2 686.7

National SavingsBank 199.9 199.9

Public 539.4 236.6 776.,D

Commercial Banks 207.2 329.0 536.2

Retained Earnings 108.1 108.1

1,300.0 108.1 639.6 1,o84.5 329.0 3,461.2

Current Portion (13.9) (65.9) 79.8

Total 1300.0 108.1 625.7 1,018.6 408.8 3,461.2

Mlillion US$Equivalent 45.2 3.8 21.8 35.4 14.2 120.4

32. Share capital and reserves totalled Esc 1,408 million or 41 per-cent of the total capitalization. The share capital, last increased byEsc 120 million in 1965, is represented by 1,300,000 shares with a parvalue of Esc 1,000. The shares are nominative (registered) or bearershares. ITwo-thirds must be in the name of Portuguese nationals. About44 percent of the shares were owned by social security institutions, 15percent by the National Development Bank and the balance, or 41 percent,by private investors.

33. About Esc 530 million of unsecured, 5 percent 30 year debentureswere outstanding under eight series issued locally between 1955 and 1960.A ninth series of otherwise similar 25 year debentures, totalling Esc 110million, was sold to social security institutions in 1963 bringing thetotal to Esc 640 million. Sixty-three percent of all debentures are heldby social security institutions and the National Development Bank, thebalance by the public.

- 10 -

34. vE-D's o+hel brrwig totalled Esc 1,1. )0.l io rit in+erest

ranging from 4 percent for the earlier loans (1956-1950) to 7-1/4 percent

million were foreign borrowings, consisting of (a) the Esc 2:L4.2 millionbalance out4Ustanding5 undAer the U IJ I mi.LL.LL1 LL)I.J ±JJULoI JU- 1 0 of. L7963, (Lb)

two 15 year loans, totalling Esc 287.5 million and one 6 year, Esc 60 mil-li,on 'oar, re-'en' to ""TE by the National vl.Irt l rd() i o.a.L±UL. iAd1 LZ±U L. u u U £JI,J uy UILI ±VtU.LUL~± i~v±pIe L D U' LIU kL. Z>J LA UU.J.±dJv

loans with terms of eleven months to four years, totalling Esc 386.2 mil-li on, relent to nED by a private loCal barik. All the local loanls , totall iEngEsc 465.6 million were raised from two government controlled institutions,the National Development Bank and the National Savings Bank, except for one15 year loan, totalling Esc 150 million, from a private local bank.

Past Earnin :s

35. A summary of HED's actual income statements for fiscal years 1962,1963, 1964 and 1965 is shown in Annex 5. Partly as a result of the tariffincrease approved in. 1964, net income rose from Esc 107.2 million in 1963to Esc 197.51 million in 1065 and the coverage of interest charges by netincome imprcoved from. 1.1 times to 1.6 t;imes. Net profit rose from Esc 64.3million in 1963 to E;sc 124.9 million in 1965. Of the latter amount,Esc 34.8 million were set aside as a reserve for expansion which, accordingto a provision in the November, 1964 Decree Law, may not be treated aspart of the shareholders' equity. The net profit available to shareholderswas therefore Esc 9C.1 million, of which Esc 80.4 million were distributedand Esc 9.7 million were set aside as legal reserve or carried over forfuture dividends. Dividends were paid at 5 percent from 1958, the firstyear of operations, through 1960, at 6 percent for fiscal years 1961 and1962 and at 7 percent for fiscal years 1963, 1964 and 1965.

Financing Pan

36. Forecast sources and applications of funds for the six yearsthrough 1971 are given in Annex 6. In the four year period ending 1969,during which the Carrapatelo project would be completed, capital expendi-tures. inclutding capitalized interest, would total about Esc 1,582 million.Funding existing shc,rt and medium term loans as they mature this year and.next year would reauire an additional Esc 466 million (this figure includ.esEsc 446 million of existing HED debts znd Esc 20 million of short term lia-bilities to be taken over from HEP.. as already explained). The year byyear requirements would be as follows for the next four years:

(ir. milliorns'

1966 1967 1968 1969 Total 4 Yearsr7$

Escudos Esc. Equiv.

Bemposta 13.0 2.0 3.5 0.7 19.2 0.7T--,A,_r Onl 7 -:1 -I C K <O J .~~vvxcb ov~2 * * 6} * 66 _ V V.3_ .Carrapatelo 365.3 410.0 325.0 290.0 1,390.3 48.3Equi,;pment, tL,e. 37.3 2. 30.0 8.8 aUU.) 10

447.3 472.0 363.5 299.5 1,582.3 55.0Fwlding 3u4.~~7 1fs1. 46. l'.

r luirig ju~~~.JU. I ±U.L..) ____ ____'U. LU. r

r.i 812. r'% 35 r r 2,048.5 I.c

37. The financing plan contemplated may be summarized as follows:

(in millions)1966 1967 1968 1969 Total 4 Years

Us$Escudos Esc. Equiv.

Internal cash generation 338.2 372.5 368.8 366.8 1,446.3 50.3

Less: Interest 120.7 114.7 108.2 103.6 447.2 15.5Amortization 65.7 69.9 74.0 76.7 286.3 10.0Dividends 80.4 101.5 122.5 133.0 437.4 15.2

2T668 2YET.T 304.7 313.3 1,170.9 t0.77

Net cash avELilable forexpansion 71.4 86 4 64.1 53 5 275 4 9.6

New share capital 300.0 150.0 100.0 70.0 620.0 21.5

Subtotal: own resources 371.4 2:36.4 164.1 123.5 895.4 31.1

Proposed IBRD Loan 190.0 120.0 135.0 130.0 575.0 20.0Neow dbhentures 300.0 300.0 0 n4New loans 250.0 100.0 60.0 410.0 24.3

Subtotal: borrowings 490.0 370.0 235.0 190.0 1,285.0 44.7

Total 861.4 6o6.4 399.1 313.5 2,180.4 75.8

Annual. cash surplus 49.4 :32.9 35.6 14.0 131.9 4.6

- 12 -

Du. HnE would finance aoout Esc 275 miiiion from internaily generatedcash (net of interest chargeable to operations, amortization and dividends)and Esc 620 million from share capital issues. A share capital issue ofEsc 300 rillion will be offered for subscription, at par value, within afew weeks and HEED has agreed that tne full amount of the issue would be sub-scribed, and at least Esc 150 million would be paid in, as conditions tothe effectiveness of the proposed loan. No difficulties are anticipated inraising the estimated Esc 320 million balance of the share capital requiredduring the period.

39. The borrowings contemplated would total Esc 1,285 million, orabout 62.7 percent of the total requirements. The actual increase in debtwouLd, howrever, be smaller than the increase in own resources, since someEsc 466 million of short term debts would be funded and about Esc 286 mil-lion of long term debts would be amortized during the period (see para-graph 44).

40. The proposed Bank loan of US$20 million (Esc 575 million) wasassumed to carry interest at 6 percent and a term of 20 years including afive year grace period. The proposed loan would represent about 36 percentof the cost of the four year expansion (exclusive of funding).

41. 1'ew borrowings amounting to Esc 710 million would have to beobtained in the period, of which Esc 300 million would be needed this year,due to the large amount of funding contemplated. HIED is planning to raisethe latter amount in two issues of 7 nercent, 16 year debentures, the firstof which, for Esc 100 million, would be sold in July, and the second, forthe balancee towardrs the end nf the irepr. It has agreed that effectivenessof the proposed loan should be conditional on the raising of the firstEse ion m-iiin iiuii It T was assme9 that the E' s n 4 niLl ionn of borrow-ings needed in 1967 through 1969, woulcd be in the form of 7 percent, 15y1,ear loans.

42. Fo.recast income statements for the year 19-1971 a shown inAnnex 5. The assumptions regarding the level of future revenues are de-

4 15 z 4 t"e n APL4 .6W

43. Net Jincome in each- of the --- by the -P s would.-1-

be at least twice the annual interest charges. Internal cash generationwo-Uud co-ver debt ServiCeA charges ( uexc .LVui of sot- and medium 'eI debts

to be funded) about 1.5 times each year.

44. Forecast balance sheets as of December 31, 1966 through 1971 areshown in Annex 3. The proportion of debt in the total capitailzation wouldbe reduced from about 58 percent in 1965 to about 48 percent in 1971. Thedebt limitation covenants in the existing and proposed Bank loain agreementswould be met with a correspondingly increasing margin.

- 13 -

1''TT flMRflDCA MA MTn1P 'rTfIrfr TrIA , PTR MTTf'TTT _'A -A -EV L.L. I U1iEIN."IJII. I-VIX± UVUUU:I0

ic rm t. ,,s

f5 ET, hLie mostl recent ComnipUany- in the pray system, was forrmed Lin

1954 with the limited objective of building and operating one small thermalplant near Porto. T-his plant was intended to provide some ins-urance agailspower shortages caused by extreme low water conditions and probably of equalimportance, to provide a market for a low grade coai produced in the DourDbasin. The plant was laid out for three 50 MW units, with one operatingand one under construction at the time of the first Bank loan which Was forthe third unit, now scheduled for completion in mid 1966. Early in 1965the Bank s third power loan in Portugal was made for the first 125 Yi-W unitof the Carregado thermal plant located near Lisbon and the proposed loanwould assist in financing the second 125 MW unit for this plant.

46, Now that the Company has a major role in the future of the powerindustry, the management has been completely reorganized and the staff en-larged. Development is presently concentrated on the Carregado site al-though, for the future, plans are being prepared in conjunction with aSpanish organization for the development of nuclear generating facilitieson the southern border with Spain.

The! Project

47. The Carregado site is about 30 kilometers upstream from Lisbonon the right bank of the Tagus River. This location near the main loadcenter of Lisbon and Setubal will reduce the need for large power transfersfrom the north where most of the hydro capacity is located, with subsequenatsavings in transmission investment and energy losses. Access to the siteis good and fuel can be delivered by pipeline from a refinery located about25 kilometers downstream.

48. The nlant is laid out for four 125 l,Wf units. All necessary landhas been purchased and foundation wrork for the first two units is wellunder way. The units will be of the conventional semi-outdoor type with1,800 p.s.i., 1000°F/10000 F steam conditions. Owing to the relativelyhigh cost of fuel a reheat steam cycle was selected due to its higher

operating efficiency.

Cost Estimate

49. All major equipment awards have been placed for the first unitWit+h non+ti,c for- n c,rond nit+. Prics sn fnr hanr beepn wefll witlhin tlhe

original first unit cost estimates and work is about on schedule. Second.i.t costs can therefore ~~~~~~~~~~~~~~~~~~~~~~~~be es-nmatd wihabttrta nr.ldereo

accuracy. The estimate, which includes adequate provisions for contin-gencies,; _. smmariz.d below.

- 14 -

Carregado Steam Plant

Second i25 riW Unit

EquivalentEscudos US Dollars

Equipment and erection:Boiler and appurtenances 113.0 3.93Turbine and generator 122.0 4.24Other 110.0 3.83

Civil W,7orks 18.0 .63

363.0 12.63

Engineering and Administration 21.6 .75

Contingencies 55.4 1.92

440.0 15.30

ALLxec-LU UI the Vl;.o LA UIU Uedule ofU l u iLt J-uLloi

5.1u±pment awarus for the firc- un.i i were made after ninernati ona!competition but with the preference formula for local manufactures describedin paragraph 28. The major awards have been made to joint ventures of Portu-guese and non-Portuguese manufacturers except in the case of the main powertransformers, where the successful bidder was a Portuguese company.

51.. The expected cost of the second unit would be much lower than thatof the first, which is equivalent to about US$175 per kw because of itemsincluded with the construction of the ifirst unit that are common to all sub-sequent units, such as land, relocations, canals and some of the site civilworks. The cost of the second unit woultd be equivalent to about US$123per kw of installed capacity before interest charged during construction.

52. The boiler, turbine and generator awards were made late last yearand some erection will start this year.. All erection should be completein the spring of 1968 with trial operations scheduled for the summer. Thepreparation of construction drawings and engineering supervision of the workwill be done largely by ETP forces but ETP's consultants, SOFRELEC, willhave the final responsibility for review and general supervision.

53. The loan of Esc 287.5 millioni (US$10 million) would be allocatedto equipment, Esc 276.0 million (US$9.6 million) and foreign consultants,Esc 11.5 million (us$0.4 million). It would cover 65 percent of projectcosts before interest charged during the construction period. As in thecase of HED (paragraph 27), disbursements would be made against both for-.eian Etnd local expenditures. It is intended that disbursements would befor lC)0 percent of the contract requirements up to the limits of the loan.

- 15 -

Present FinpaMcial Position

54. Condensed balance sheets as of December 31, 1-- 2, 1O(- 1964and 1965 are shown in Annex 7. At the end of 1965, ETP's net total assetsviere Esc 9°31- million (TS.i28. .. lin ^4nisin PC^ Esc 49 rlli^n,th

historic cost of plant in service, less reserves in lieu of depreciation,(for eq -4 --Aen reewl dinvest-men` eept-) Esc o36 millon, the

value of work in progress; and Esc 193.6 million, the amount by which cur-rent assets exceeded the tLotal of current l. ± i ,Les , the current portionof long-term. debt and the dividends payable in 1966 for fiscal year 1965.

55. Details of the capitalization are given below:

Escudos(in millions) Percent

Capital, Reserves and Surplus

Share capital, 435,000 shares at Esc 1,000 par 435.0 47.1Reserves and. surplus 70.4 7.6

Total equity 505.4 54.7

Lonig-term Debt

IBRD Loan 363 P0, 5-1/2%, 20 years 67.7 7.3IBRD Loan 412 P0, 5-1/2%, 20 years 51.1 5.5Unsecured debenditures, 5%, 25 years 159.1 17.2National Development Bank loan, 6%, 20 years 23.3 2.5National Savings Bank loan, 6-1/27%, 15 years 127.7 13.8Unemployment Fund loan, no interest, 5 years 2.0 0.3

Debt 430.9 46.6

Less: current portion 13.4 1.3

Total net long-term debt 417.5 45.3

Total Capitalization 922.9 100.0

56. The share capital was increased from Esc 185 million to Esc 435million over the last two years, by two issues of Esc 65 million each in1964 and by one issue of Esc 120 million in December 1965. Forty percentof the last issue was paid in at the time of subscription; the balance willbe naid in this year. The table below shows the present distribution ofownership:

- 16 -

Eseudos(in millions) Percent

C.N.E. 50.7 11.6Other primary system companies 44.9 10.2

95.6 21.8

Nlational Development Bank 101. 23.4Social Security Institutions 69.o 15.9

170.8 39.3

Other power companies 4o.8 9.4Mining companies 7.9 1.8Oil. companies 51.0 11.7Insurance companies 4.5 1.1General public 64.4 14.9

168.6 38.9

Total 435.0 100.0

57. Since Loan 363 PO was made in November 1963, all of ETP's newdebt has been contracted with the Bank while the balance of its requirementswas obtained from issues of new shares and internal cash generation. Loar.363 PO., for IIS$5 million, became effective on February 10, 1964. Loan 412 PO,for US$15 million, WELs declared effective on June 28, 1965.

Past Earnings

58. A summary of ETP's actual income statements for fiscal years 1962,1963, 1964 and 1965 i.s shown in Annex 8. Partly as a result of the tariff'inc:rease approved in 1964, net income rose from Esc 20.7 million in 1963 toEsc 76.6 million in 1.965 and the coverage of interest charges by net incorneimproved from 1.3 times to 3.2 times. NIet profit rose from Esc 15 millionin 1963 to Esc 59.4 million. Of the latter amount, Esc 22 million were setaside as a reserve for expansion which, according to a provision in theNovember 1964 Decree Law, may not be treated as part of the shareholders'equity. The net profit available to shareholders was therefore Esc 37.4million of which Esc 22 million were distributed as dividends and Esc 15.4million were set asid.e as legal reserve or carried over for future dividends.Dividends were naid at 5 nercent in the years 1960 to 1962 and at 7 percentthereafter.

- 17 -

Financiug Plan

59. Forecast sources and application of funds for the five yearsthrough 1970 are given in Annex 9. In the three year period ending 1968,capital expenditures on new plant, including capitalized interest andworking capital requirements, would total Esc 1,688 million, as follows:

(in riillionn)1.966 1967 1968 Total 3 Years

US TEscudos Esc. Equ.iv.

Tapada do OuteiroUnit 3 (the 363 PO -rtct) 144.8 144.8 5.1

CarregadoUnit 1 (the 412 PO proect) 37'0.0 18 8.5 558.5 19.4Unit 2 (the proposed project) 120.0 227.7 118.2 465.9 16.2

Future expansion, etc. 61.0 191.2 225.7 477.9 16.6Increase in working capital .4 23.6 17.2 41.2 1.4

TOTAL 696.2 631.0 361.1 1,688.3 58.7

60. The financing plan contemplated may be summarized as follows:

(n millions)1966 1967 1968 Total 3 Years

US$y

Escudos Esc. Equiv.

Internal cash generation 111.9 162.5 191.1 465.5 16.2

Less: Interest 18.9 34.6 53.0 106.5 3.7^ 1 * n n }. n r r ae r~~~~~~~~~~~% 1 C c-7 Q n nAmortization t3.4. 16.9 C27.5 7.8U 2.0

Dividends 22.0 29.6 42.0 93.6 3.3

Net cash available for expansion ,i7.6 8i.4 68.6 207.6 7.2New share capital 2-37.0 100.0 160.0 497.0 17.3

Sub-total: own resources 294.6 181.4 228.6 4. 24.5

IBRD loan 363 PO 76.1. 76.1 2.7IBRD loan 41.2 PO 225.5 154.6 380.1 13.2Proposed IBED loan 100.0 175.0 12.5 287.5 10.0Future expansion loan 120.0 120.0 240.0 8.3

4o1.6 449.6 132.5 983.7 34.2

TOTAL 696.2 631.0 361.1 1,688.3 58.7

- 18 -

61. rTPi' would - P4 nance about Esc'M) 74. million Irom lts own resourceas,

consisting of Esc 207.6 million from internally generated cash (net of in-LI charga lI t operattionL1s, Wmo0r t izaLti.on nd dividUends, kd:Ui EscU 4'T

million from share capital issues. This includes Esc 72 million to be paidlin thiss yea,r oni ac .ount of the shla,re ciap'taLL s-UbcLriedU 1l 1eLeL'Ue- 1J965,

and a new issue of Esc 165 million planned for the latter part of the year.As in the case of HrEDJ (paragraph 8)), there should be no difficultiles inraising the share capital required during the period.

62. T'he borrowings planned during 1966-68 would total US$34.2 millionconsisting of (a) the US$2.- million balance outstanding at December 31,1965 under Loan 363 PO to finance completion of the Tapada do Outeiro plant;(b) the US$13.2 million balance available under Loan 412 PO for the CarregadoUnit 1 project; (c) the Bank loan of US$10 million nows proposed for financingOf the Carregado Unit 2 project, assumed to carry interest at 6 percent anda term of 15 years, including a 3 year grace period; and (d) initial dis-bursements of US$8.3 million in 1967 and 1968, from future borrowings forCarregado Unit 3.

Financial Prospects

63. Forecast income statements f'or the years 1966-1970 are shown inAnnex 8. Based on existing tariffs, the Company expects to continue Payingdividends Ett the reLte of 7 percent annually.

64. Net income in each of the years covered by the forecasts would. beabout; twice the annual interest charges, with the exception of 1966 when itwould cover interest charges 2.4 times. Internal cash generation couldcover total debt service charges abou-t twice until 1969 when, due to therelatively short amortization period of the proposed loan (12 years), thecoverage would fall] to an annual leveL of about 1.6 times. This coverageis still adiequate.

65. Forecast balance sheets as of December 31, 1966 through 1970 areshown in Annex 7. Debt would increase from 53 percent of the total capitali-zation at -the end of 1965 to a maximum of 58 percent in 1967 when the pro-posed loan would be fully disbursed. This is well within the debt limitationcovenants in the existing and Droposed Bank loan agreements.

VIII. PROPOSED FINAIE[CIAL ABRANGENENTS

66. The continuation of financial undertakings and covenants simi:Larto tlne.- in the 1 T.eng n Ao-retmentq uprp arrePd on during negotiations.

The main provisions are:

- 19 -

(a) The Govermnent has agreed to arrange for the provision offunds required by HED and ETP to carry out respectivelythe Carrapatelo and Carregado II projects should the com-panies be unable to obtain them from other sources;

(b) The Government, HED and ETP would repeat the existingundertakings regarding revenues, as described in para-graph 18;

(c) HED and ET:P would continue to employ accountants satis-factory to the Bank to audit their accounts (both companieshave retained the services of Barton, Mayhew and Co. forthis purpose starting with fiscal year 1963, in the caseof ETP, and 1964, in the case of HED);

(d) The long term indebtedness of HED and ETP would be limitedto twice their respective paid in capital and surplus;

(e) Both companies have agreed to undertake major investmentsonly when they expect to secure the necessary funds onterms reasonably related to future earning capacity andto limit short term borrowings to amounts that could reason-ably be expected to be repaid out of the proceeds of sharecapital issues, long term borrowings or earnings.

IX. CONCLUSIONS

67. The Portuguese power development is being planned along soundlir!es to prov-de an aPdiuate balance hetween hydro and thermnl souree ofproduction. The two projects now proposed are needed to meet load growthan.d are- ecnominicaIlly iiitificd.

68= The projects are techni-ally sou_nd and the cost Pestimat.e arp

realistic.

69. HED and ETP are well organized and managed and there are noqcuest about their a-bilt to construct- nd to operate the proj4 c t s .

70. The revenues o-' the primary system, as increased recently, areexpected to be sufficient to enable the two companies to maintain a sound.L.LnancLa.'L psiL J.L

71. ±e Ca±rrapatelo proJec- is suitab'e for a loan of US$20 millioto HED, for a 20 year term, including a, five year grace period, and theCarregado project is suitable for a loan of US$10 million to ETP for a15 year term, including a three year grace period.

- 20 -

7 T * GoI'uveLLuLIeL, nED and ETP have agCreedu uu proV-bii s±imJllar

to those in the existing agreements (paragraph 66) regarding:

(i) the provision of funds for the two projects;

(ii) the level of revenues to be maintained by the twocomnpanies;

(iii) the continued employment of auditors by the two com-panies;

(iv) the limitation of the two companies' long term indebted-ness; and

(v) the policies to be followed by the two companies withregard to incurrence of short term debts.

73. In addition, HiED has agreed that as conditions to the effective--ness of the Carraoat,elo project loan, it would:

(a) have sold Esc 300 million of new shares and received partialpayment in cash for not less than Esc 150 million; and

(b) have borrowed at least Esc 100 million, repayable over atleast a 15 year period.

May- 1 19IUB, ±ROu

IBRD

ANNEX 1

THE PORTUGUESE lJER TDrTSTP.V

was brought about by the National Electrification.Law of December 1944,whiMr, was later ,o-ified by, a decree-la w, nf Dce-e-roAn Dursuant t+

the more important provisions of the legislation:

(a) power production would be mainly hydroelectric;

(b) companies would be formed w:ith government help toclevelop hydoeecri Aeouce an otas.i~ieviup L~,Y U e.L e LIJ.~Lk IV UULJ._%.U cLLIU UV LI d.Ii,>11ii± U

power throughout the country; the new generating

primary system;

(c) large existing utilities (w:ith generation anddistribution facilities) woulld form the secondarysystem; they would be expected to satisfy theiradditional requirements by purchases from theprimary system;

(d) small existing utilities, engaged in distribution,wqould purchase power from the large utilities orfrom the primary system;

(e) special categories of large consumers (electro-chemicaland electro-metallurgical plants and irrigationundertaltngs) would purchase directly from theprimary system;

(f) the Government would establish tariffs.

2. The primary system created as a result of this legislationconsists at present of the facilities of five companies, establishedbetween 1945 and 1954. There are three hydro companies, each with a75 year concession to develop a specific river basin or area; a thermo-electric company, ETP, and a nation-wide transmission company. At theend of 1964 the installed capacity of the primary system was about 1500 MW.A national network of transmission lines connects the generating plantswith the load centers.

3. The five companies were organized as private stock companiesalong similar lines. The law permits participation for up to 50 percentof the share capital by the Government or its financial institutions.In practice it is hard to determine the precise extent of public andprivate owinership because of the mixed character of the main institutionalshareholders. It is clear, however, that the Government is directly orindirectly the most important shareholder. Government controlled financialinstitutions also hold most of the debt of these companies.

ANNEX 1Page 2

Each company has a five to six member Board with two membersappointed by the Government regardless of ownership, and the othersselected byr the shareholders. Subject to Government approval the Boardelects a Clhairman, who is also the chief executive officer. Each companyhas a three member fiscal committee which reviews company accounts andapproves major financial decisions. One of the members is selected bythe Government and two by the shareholders.

5. The Electrification Law also led to the creation of a NationalLoad Dispatching Organization (Repartidor Nacional de Cargas - RNC), res-ponsible for the technical coordination of all power generation. Moreimportant, RNC also carries out statistical and economic studies relatingto the nat-ional power program which enables the Government to determineproject priorities within the program. It is administered by a councilrepresenting the companies of the primary system, the utilities of thesecondary system, dlistributing companies and the Government. It ismanaged by an Executive Committee of five members. The Governmentrepresentative, chairman ex officio, is an official of the Office of theDirector-General for Electrical Services of the Ministry of Economy, theGovernment Office responsible for issuing franchises, establishing ratesand. more generallvy for controlling and coordinating the nower industry.

6= The primary system is ornrate as- if it. wr iinder a sinrlpownership instead of being composed of five separate companies. Genera-tion is dispatched by the CP>\ with the output of the four cenetfingcompanies marketed by the national transmission company (Companhia Nacionalde Electriciad,ade _ NE). CNTE sellcs in bullk to utillities of the secondAn"r

system and to large power intensive industries. The Government fixes thetariffs ar.dl determines e reverues dual generatir.g cor.parle

7. .I.- 4oer".n is_ -'I-- -ri-m-4i- -epnil -o enurn -avail-I.Le U C.LijJIEiin cL~ .LOV JJJ. ±A %L_Ld.± CjVI U LC .L~.± C1U

ability of the large funds required for the companies' expansion becauseVJ g t V s; iiiiiei U .L CUJ.O UJ.U VJi LsL L|.~ AI|~ Lss'_ V G | J10 a s WwV V' v-S1JsL V

controlled financial institutions provide most of the borrowed funds aswejl dl a IRs t ihe.s e ca.pitl. £Ie GovernmentI detUerILines tLhe Lamounts14 Itob

raised, the timing and distribution between share capital, bond issuesandu Drro-w1Lgs fromn ±±iIda1cUJlaLUIL LU LU±ULU1.

U. iAs may Oe seen rom hne abo-ve, whe co-lmpanes 111 W ysuem,

though formally private, have a quasi public character. The Governmenthas in fact the ultimate responsibiiity Ior their policies through itscontrol of their expansion plans, sources of finance, management andallocation of revenues.

9. PortugalFs hydro energy resources are large in comparison withenergy sources of indigenous fuel. The Electrification Law thereforestressed the development of hydro power, the objective being to limitinvestment in conventional thermal capacity until the hydro potential

ANNEX 1rage 3

has been exploited. Then instead of further investment in conventionalthermal capacity, LI was plannred to snlt to nuclear power. ThIs concepthas been amended du:ring the past three years, as discussed in the body ofthe report, so that now tne development is expected to include sizeabieamounts of oil fired thermal power.

May 18, 1966

ANNEX 2

PORTU(GAL: PRESENT VALUE COMPARISON OFALTERNATIVE POWER DEVELOPMENTS, 19615-80

0F'.( III 1.1

\~~~ ~AP _ SHEM "A=CRAPATELLO DEL AYE

UNTIL 1980 WITH THERMAL'N \y | IN INTERIM

81 ~~ 1 K,I_ 18

OF6 -- F- X 6-

o x'I -o | C

OR -MDCHDLD O

w ~~~~~~~~~~~~~~~m

LL . f OLWN -

-zi m~~~~~~~~~~~~~~

>~~~~~~~~~~~~~~~~~~~17 WI U TIL THEN80 |

z 4 &~~. 1 ° Oo ra

2~~~~~~~~~~~~~~~~~~~NI 198 <

-LJ wn

a. 0~~~N

0L~~~~~~~~~~~~~~NI i9_ 0

0 5% 10% 1 5% 20%DISCOUNT RATE (PERCENT)

IBRD- 2718|

PORTUGAL

HIDRO-GiLECTRICA DO DOURG (HED)

Actua1 Lnd Fo eeast Balance Sheets as of Decexzber -il, 1962-19?

(In Millions of Escudos)

US S1 = h;G Zti.75

--------------------- ---------A 3tual --------- t----------------- --------------- -- ------- F o r. t ----- _____-__________-_

Consol-FISCAL YEAR SINDING D)&BrER 31: 19 62 196!k 1964 PiD datd 966 L967 196ti8 L969 15170 1971

A S S E T S

Fixed assets in operation 1,5 53.5 1,601.0 ,2,563.5 2,615.1 881L.3 3,496.4 3,543.4 3,595.4 3,628.9 5,173.4 5,173.4 5,173.4Loss: 3% Sinkiztg Fund depreciatiox 9.5 90., 124.7 1_4.0 _ 164.0 204.4 246.0 208.5' 333.0 397.7 464.3

Not fixedi assets in operation 1,520.0 1,510.5 2, 439. ! 2,461.1 88].3 3,332.4 3,33i9.0 3,349.4 3,340.C 4,840.4 4,775.7 4,709.1Work in progress 669.0 947.0 151.E1 331.3 331.3 731.6 1,161.6 IL,481. 6 236.6 241.6 246.6

Total ne; fixed assets 2,1S99.0 2,457.5 2,591.0 2,782.4 881.3 3,663.7 4.070.6 4,501.0 41,821.6 5,077.0 5,017.3 4,955.7Net current asBets 5 1S9.1 54.4 163.5 56.4 55.9 112.3 161.7 194.6 230.2 244.2 2.J6.9 249.6RED advanioes for Tavora_ 322.5 5668.51 702.8 (702.8) _____ _

7.?'8.l 7.834.7 5,S21 3, 55416 234.4 3,775.0 4,2Z2.3 4,695.6 15,051.: 5,321.2 5,24A.2 5,205.3

LIABILIT];15S

Share oapital 8190.0 880.0 L,180.0 1,300.0 150.0 1,450.0 1,75,0.0 1,900.0 2,000.0. 2,070.0 2,070.0 2,070.0Recerves and stLrplus 20.4 32.4 74.7 108.1 108.1 183.7 277.4 362.1 441.2 485.8 563.4

Equity equIivLGenit 900.4 912.4 L,254.7 1,408.1 150.0 1,558.1 1,935.7 2,177.4 2,362.1 2,511.2 2,556.8 2,633.4

Debt

Long and medium teriINRD) loan 362 PC 212.1 209.5 209.5 204.5 199.2 193. 6 187.7 131.4 174.6Proposed I BRD loan - Carrapatelo 190.0 310.0 446.0 575.0 b50.3 524.1Debonturs 655Z.9 652.8 639.6 625.7 62.8 688.5 670.6 660.1 628.6 606.2 582.6 557.8National Development Bank 218.0 491.9 463.2 404.4 404.4 345.2 316.8 286.2 256.4 2:26.1 19S6.2NaLtional Savings Bank 215.0 209.6 199.59 189.1 189.1 177.6 165.5 152.7 139.2 124.9 109.9Irving TruLat Company 85.9 57.3 28.6 28.6Banoo Borgem & Iro 144.1 144.1 137.8 131.1 123.9 116.1 107.8 9E.9ManuLfaoturers Hanover Erust C0ompany 42.9 42.9Now debentures 300.0 300.0 300.0 289.2 277.7 265.4,

Ne loa n- 250.0 350.0 393.7 376.2 357 .5

985.9 1,440.2 1,572. L 1.644.3 62.8 1,707.1 2,02 5.7 2,321.7 2,480.0 2, 563.5 2,427.0 2,285.4Current portion and short term debt 319.4 429.5 426. 8 408.8 21.6 430.4 171.4 74.0 76.7 106.5 136.5 143.6

TotaLl debt 1,305.3 1,869.7 1,998.9 2,053.1 84.4 2,137.5 2,197.1 2,395.7 2,566.7 2,670.0 2,563.5 2,427.0

Diridends 42.4 52.6 68.]L 80.4 80.4 101.5 122.5 133.0 .140.0 144.9 144.9

2, 24S.1 2,834.7 5,321. 7 3,541.6 23S4.4 3,776.0 4,232.3 4,695.6 5,051.B 5,321.2 5,264.2 5,208.3

TOTAL DE8r AS % OF CAPITALI ZATION 59 67 61 59 58 53 52 52 62 50 49

Y1 Currant liabilities have beon deducated from current asrsets esoept for(i) thei ourrent portion of long end medium term debts aid(ii) the short term debts incunred for prefinanci-, expany JLO.

2 Declared four months after the lolise of the ye&r and payable annually.

K~y 5. !966

PORTUGAL

HIDRO-ELECTRICA DO DOURO (HED)

Details of Debt as of December 31- 126i

Source Date Origina1 Outstandi.g Interest rerm Anortization Securit(m-illion3 of' Escudos)

Loans

IBRD loan - 362 PO 11/6/63 216.5 .714.2 5.5% 25 years semi .annually 1965-88 Negative pledge

National Development Bank 2/28/56 40.0 27.? 4 & 4.5% 5 to 20 years semi annually 1959-76 Negative pled.ge

National Developmenit Bank 9/4/59 20.0 15.3 4;% 20 years semi mnnually 1962-?8 Negative pledge

National Development Bank 4/20/60 80.0 72.7 6% 5 to 20 years semi annually 1963-80 Negative pledge

National Development Bank 7/27/62 90.0 60.0 ?4 4 to 6 years 3 equl nayments 165/'7

National Development Bank 2/26/64 300.0 2760.0 7.25% 5 to 15 years annually 1964-78 Negative pledge

National Development Bank 9/3/64 27.5 27.5 7.25% 5 to 15 years annually 1966-78 Negative pledge

National Savings Bank 2/1/64 220.0 199.9 5.5% 15 years semi annually 1964-78 Pledge of revenues

Irving Trust Company 4/29/63 114.5 57.2 6.75% 4 years annually 1964-67

Banco Borges & Irmnao 4/15/65 _150, _L50.0 6.75% 5 to 15 years annually 1966-80

Total lcans 1,258.5 1,o84.5

Credits Purpose

Commercial Banks

Banco Pinto & Sotto Mayor 6/19/63 71.6 71.6 6.d11% 1 year Prefinancing of expanslon(due 5/25,/66)

The First NatiLonal Banko£ Chicago (Illinois) 10/28,/63 114.6 57.3 6.5% 1 year Prefinancing of expansion

(due 10/2'8/66)

The First National Bankof Chiicago (London) 10/28,165 57.1 57.1 6.75% 1 year Prefinancing of expansion

(due 10/24/66)

The Chase Manhattan Bank 12/27/65 57.2 57.2 7,11 monthd s Prefinancirig of expansion(due 11/27?/66)

Manufacturers Hanover Trust 12/27,/65 85.3 85.8 6.5j 2 years Prefinancing of expansion(2 equal payments 1966-67)

Total creolits 386.3 :329.0

TOTAL DEBT 1,644= 1i,43.-

May 5, 1966

E'ORTUGAL

H]DRO-ELECTRICA E0 DOURO (HED)

4ctuaL and Forecast Ihcome Statements 1962 I97a

(in Mlillioins of Escudos)

US $1 ESC 28. 75

~~~~~ ~~~~- Actual ------------- ----------------- Forecast --------------------

FISCAL YEAR ENDIiG DECEMBER 31: 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971

Groaa re-emw. 140. 3 i5a.9 265.4 305.4 396.1 441.8 451.iB i4.3 507.8 536.7

Coat ofr operationsOperating expenaes 14.4 15.7 23.2 35.3 36.4 38.5 39.5 41.3 45.6 49.9Tguces 6.3 6.4 25.5 34.2 23.0 32.3 45.0 47.7 47.3 43.7Equipment replacement 10.0 10.0 18.3 20.2 21D08 21.4 22.1 22.7 3 4.1 3 5.1Investmnut redemption 18.3 15.8 14.1 19.0 19.6 20.2 20.8B 21.4 350.6 31.5Subtotal. depreciation equivalent 28.3 25.S 32.4 39.2 4D.4 41.6 42.9 44.1 64.7 66.6

Total 49.0 47.9 81.1 108.7 99.8 112.4 127.4 133.1 157.6 160.2

Neit receipts fromr operations 91.3 106.0 184.3 196.7 296.3 329.4 324.4 321.2 350.2 376.5Other incomo .7 1.2 1.0 1.2 1.5 1.5 1.5 1.5 1.5 1.5

Neit income before interest 92.0 107.2 185.3 197.9 297.8 330.9 325.9 3522.7 351.7 378.0

Interest and otheir financiSl charges 62.8 94.4 125.0D 124.9 143.2 145.0 153.13 162.2 162.2 155.5lA's: Iesue eaxpinses capitalized 3.9 2.0 2.0 3.0 2.0 1.4Intereat capitalised. 22.4 51.5 48.0 49.9 20.5 27.3 43.65 57.2Intereit oharged to operations 40.4 42.9 73.1 73.0 120.7 114.7 1U8.;2 103.6 1652.2 165.5

Net prcofit 51.6 64.3 112.2 124.9 177.1 216.2 217.7 219.1 1139.5 222.5

Disposition of profitShareholders reserve 9.2 11.7 6.5 9.7 5.3 15.4 13.6 16.0 2.3 ir.7Expansion reserves 37.6 34.8 70.3 78.3 71.1 63.1 42.3 69.9Dividends 42.4 52.6 68.1 80.4 101.5 122.5 133.0 L40.0 144.9 144. 9

iay 113, 1966

PORTUGAL

HIDRO-riLrCTRICA DO DOURO (HED)

Forecast Sources and ADolications of Funds 1966 - 19&L(In millions of Escudos)

US $1 ' ESW 28.75

Fiscral vear endino December I: 1967 1968 1

Sources of Funds

Internal cash generationNet income before interest 297.8 330.9 325.9 322.7 351.7 375.0Derreciation equivalent 0.4 421.6 42.9 46 6

338.2 372.5 368.8 366.8 416.A4 .6

New share capital 300.0 150.0 100.0 70.0

BorrowingsProposed IBRD loan 190.0 120.0 135.0 130.0New debentures 300.0New loans 100.60

490.0 370.0 235.0 190.0

Total Sources 1,128.2 892.5 703.8 626.8 416.4 4.44.6

AIoplications of Funds

Additions to plantBemposta 13.0 2.0 3.5 .7Tavora 29.7 31.6 5.0Carranatelo 342.8 379.7 279.4 231.4Equipment, studies, etc. .. 3 28.4 10.0 8.8.0

424.8 441.7 317.9 240.9 5.0 5.0

InterestIBRD loan 362 PO 11.7 11.4 11.1 10.8 10.5 10.2Proposed IBRD loarn 5.7 15.0 22.6 30.6 34.5 34.5Debent-ures 3-'9 34'.i 33.2 32.1 31.1 29.9National Development Bank 32.0 27.8 23.6 21.6 19.5 17.5National Savings BIIk 10.8 10.3 9.6 8.9 8.2 7.5Banco Boreea & Irmao 10.5 10.1 9.7 9.2 8.7 8.2New debentures 10.5 21.0 2i.0 21.0 21.0 20.2New loans 8.8 21.0 26.6 28.7 27.5Other interest 2 1. 1, --

137.2 142.0 151.8 160.8 162.2 155.5

Amortization3R9D loan 362 PO 4.? 5.0 e 5.6 5.9 5.3

Prooosed IBRD loan 24.7Debentures 15.5 17.9 20.5 21.5 22.4 23.6National Development Bank 28.7 29.2 29.4 29.6 29.8 30.3National Savings Bank 10.9 11.5 12.1 12.8 13.5 14.3Banco Borges & Irma) 5.9 6.3 6.7 7.2 7.8 3.3New debentures 10.8 11.5N1ew loans I., 1

65.7 69.9 76.7 106.5 136.5

FundingNational Development Bank 30.0 30.0Irving Trust Compant 28.6 28.6The First National Bank of Chicago 114.5Banco Pinto & Sotto Mayor 71.6The Chase Manhattan Bank 57.1Manufacturers Hanover Trust Companiy 42.9 42.9Other shor-t term debts (Tavora) 20,5

364.7 101.5

Dividends 80,4 101.5 122.5 130 140.0 1' 9

Issue expenses 6.o 3.0 2.0 1.4

Total Applications 1,078, 8 85.2 612.8 413.7 44L.9

C:ash at begLnning of yea! 85.6 135.0 167.9 203.5 217.5 220.2Cash surplus 49.4 32.9 35.6 14.0 2.7 2.7Cash at end of year 135.0 ,167.9 203.5 217.5 220.2 222.9

Number of times interest covered by nel: income 2.2 2.3 2.1 2.0 2.2 2.4Number of times debt service covered by

internal cash generation 17 1.8 1.6 1.5 1.5 :L.5

May L8, 1966

PORTUGA L

EPRESA TERMOELECrRICA PORTUGIUESA (STP)

Actual and Forecast Balance Sheets as of December 311 1962 - 1970

(TIn Mllions of Escados)

US $1 = ESC 28.75

Actual -____________ Forecast

F'ISCAL YEAR E.NDING DECEMER 't]: 1962c 1963 1i64 1265 1 967 1968 196 12970

Fixed assets in operation 311.5 311.5 549.3 549.8 812.0 1482.0 1947.9 2476.3 24715.3Letss: 3% sinking fund depreciation (20.) (24.4)a) (56.1) (70.6) (104.8) (1S7.0) i2.i) (3W.1)Net fixed assets in operation 291.,1 287.1 509.6 493.7 741.4 1377.2 1790.9 2250.7 2172.2Work in crogress 108.4 t 17S. _75.2 235,6 669.2 606.6 4.846 1554 322.7Total net fixetd assets 399.;' 463.0 584.8 729.3 1410.6 1983.8 2275.5 2406.1 2494.9Currpnt assetzi .i 1386 _28.9 279.9 208. 231.9 _249.1 274.3 25S.0

5j36 i, 60o.6 8 1009,2 1618.2 221L 2'524.6 2680.4

LIABILITIES

Share capital 185.0 185.0 315.0 435.0 600.0 700.0 860.0 910.0 910.0Reserves and surplus 45 j.° 31.'t 70.4 1-19 3 171.0 _207.9 2'31 °n 2____

Equity equivalent 189.:3 190.0 348.3 505.4 719.3 871.0 1067.9 1141.0 1161.5

IBRD loan 363 PO 33.7 67.7 143.8 141.1 135.3 129.3 123.0IBRD loaLn 412 PO 51.1 276.6 431.2 423.4 407.2 389.9Proposedi IBRD loan 100.0 275.0 287.5 271.4 254.4Debentures 172.2 168.0 163.7 159.1 154.3 149.2 143.9 138.3 132.5NaLtional Savings Bank 100.0 140.0 134.0 127.7 121.0 113.9 106.3 98.3 89.8NaLtional Development Bank 25.0 2',.0 24.2 23.3 22.4 21.4 20.4 19.3 18.1SuDpliers' credits, etc. 25.2 4.0 3.0 2.0 1.0Future loans: Carregado 3 120.0 240.0 287.5 279.1

Carregado 4 -- z.Debt 322. 4 337.0 158.6 430.5 819. 1 12 51.8 1356.8 1428.3 1473.8Less: current portion (19.IL) (12'.0) jl2.8) (13.4:) (16.2) 2 5.Q_ t3.0) (76,9)

Net long term debt 303-3 325.o ,45.8 417.5; 802.2 1224.3 1303.8 1363.8 1396.9

Cukrrent liabilities 31.6 7,3.6 1o6.6 64.,1 67.8 78.4 103.9 115.4 127.8

Dividends* ]12.0 1 ,o _13.0 22. 29,6 42 0 _ 49.0 - 602 2 1,7

.1> 6]6 .1i"8 .2 "613.7 1009. t 2524.6 27.6

Ne!t long term debt s1S % of' capitalization 62 6,1 50 45 53 '58 55 54 '55

4' Declared f'our months after the close of the year and payable annuually

lay 5, 1966

PORTUGAL

EDlPFXi" TF.JUlp CT=T PrtR-,T!s.icT

Ac Suda arti. ec t Incme Statene 1962 197

, t illions of Escudos)

UJ- -1 = ESC 28.75

_ _ _ __ _ctoa._ _ _ ___ __ __ __ - - - - - - - --------------- ForecaAtFISCAL YTh.R ENDING DECEMBER 11: 2 1963 196 2.P 229 k,.ross revenues 54.4 51.8 13?.1 167.3 144.5 279.6 347.6 41).4''ost of DDerations

Fuel and other variable costs 20.4 179 149.3 6i.6 5j.6 89.5 113.0 i ,,ener&L expenses 4.2 3. 5.06 6.0 .417.4%aintenance and repairs .8 1.] 3.8 3.0 59.0 8.1 17.6 2,.' 30.1Adsinistration a|nd ta;ces 'i.9 13.5 5.2 5.6 12.0 8.1 8.5Euipent reo1la-ement 4. 9 4.9 13.4 13.4 13.4 31.8 48.7' 64.0 73.3Investmeent redemption 4 . 1.1 .,. -u .4 , .2t.,Sub.total: depreciation equivalent 5'.8 5.0 14.5 14.5 14.5 34.2 52.2 68.6 78.5

Total 37.1 31.1 77.8 90.7 47.1 ;513 208.7 260.1 308.4iel: inccrme before interest 17'.3 20.7 59.3 76.6 97.14 228.3 138.9 153.3 160.6lnterest and otier fiLnancial char.ges 144.1 15.6 23.7 23,6 42.7 62.9 74.5 81.5 34.6,ess: issUe eXpMes CsOitWLlized 21.1) (1,1) (2.3) (2.2) (1.4) ( .8) ( .4)interest capitALlised u2) (.LQQ) i5&) .,,3) (1L.) IA,.V) ilgi) ALQAZ) _.7.8).nterest cbarged to operations 6.2 5.6 17.6 17,2 1Ei.9 34.6 53.0 70.0 76.4

bt orofit 1L.1 15.1 41.7 59.4 78.5 93.7 85.9 83.3 84.2isDosition of profit,

Shareholders' reserves ( .9) .3 8.7 15.4 (10.0) (8.9) 2.5 3.2 3.8Ezpansion reserves 20.0 22.0 58l.9 60.6 34.4 19.9 16.7Dividends 12.0 L4.8 13.0 22.0 251.6 42.0 49.0 60.2 63.7

ay 5. 1966

ANNE.Y 0

PORTUGAL

EKPRESA TERMOELECTRICA PORTUGUESA (ETP)

Forecast Sources and ARolications of F-unds 1966 - 1970In millions of Escudos

US $1 = Esc 28.75

Fiscal year ending Deeober 31t 1966 1967 1968 1969 1970

Sources of Funds

Internal cash generationNet income before interest 97.4 128.3 138.9 153.3 160.6Depreciation equivalent _l4 J4.2 _2.2 68.6 78.5

111.9 162.5 191.1 221.9 239.1

New share capital 237.0 100.0 160.0 50.0

Borro.v-.gs

IBRD loan 363 PO 76.1IBRD loan 412 PO 225.5 154.6Prooosed IBRD loan 1(0.0 175.0 12.5Future loarns: Carregado Unit 3 120.0 120.0 47.5

Unit 4 __ 77.0 110.04t0i.6 449.6 132.5 124.5 110.0

Total Sources 7S 712 1 A fQA i ao

Applications of Funds

Additions to plantl'aoada do Outeiro Unit 3 138.9Carregado Unit 1 355.5 176.1

Unit 2 (Proposed Project) 116.6 216.0 107.4Unit 3 50.0 175.0 203.0 76-4Unit 4 99.3 147.1

Studies (Nuclear and other) 11.0 12.0 12.0 12.0 12.0f72-0 579.1 322.4 18?.? 159 1

Net increase or (decrease) in inventories 21.5 15.2 16.0 20.0Interest

IBRD loan 363 'PO 7.3 7.9 7.7 7.4 7.0IBRD loan 412 ?0 13.0 21.8 23.7 23.3 22.3Prooosed IBRD 'Loan 3.0 11.0 16.0 17.0 16.0Debentures 7.5 7.4 7.0 6.7 6.5National Savings Bank 8.2 7.8 7.3 6.8 6.3National Development Bank 1.4 1.3 1.3 1.2 1.1Future loans: Carregado Unit 3 3.5 10.1 16.o 17.2

Carregado Unit 4 _ 40.4 60.7 73.1 80.7 84.2

AmortizationIBRD loan 363 PO 2.7 5.8 6.o 6.3IBRD loan 412 F'0 7.8 16.2 17.3roposed IBRD loar. 16.1 17.0

Debentures 4.8 5.1 5.3 5.6 5.8National Savings Bank 6-.7 7.1 7.6 8.0 8.5National Development Bank .9 1.0 1.0 1.1 1.2Unemployment Fund loan 1. 0 1.0Future loans: Carregado Unit 3 8.4

13.4 16.9 27.5 53.0 64.5

Dividends 22.0 29.6 42.0 49.0 60.2

Issue expenses 2.3 2.2 1.4 .8 .4

Total Applications 771.6 703.7 482.4 391.2 368.4

Cash at beginning of year 94.9 73.8 82.2 83.4 88.6Cash surplus or (deficit) (21.1) 8.4 1.2 5.2 (19.3)Cash at end of year 73.8 82.2 83.4 88.6 69.3

Number of times interest covered bynet income 2.4 2.1 1.9 1.9 1.9

Number of times debt service covered byinternal cash generation 2.1 2.1 1.9 1.7 1.6

May 18, 1966

| Vsf , - -- :<; = ~~~~~~~~:'* - RrasonroO

V0o50 do SLA M ISOESCostelo \ CAN/Ip9

t ! otu° / ~ ~~~~~~~~~~~~~~~~~Es,,sfinq hED plonls i /A~Ai

| ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ - - ~ 871D 7A |Fone fiene on 363PO PO)

VIla Real

|~~~~~~1AARPTL / Ig0/ro S/ uorcr*l~ ~~~~~~~~~~~~~~~~~~~~~~~~~ ''"oa >'a '- -

I C / ./! Coir bro

do Fz i| ~ ~~ ~~~~ . / l CA BRA/L ° 0oc 'C

/ //LeiriO a | % ~ ~_ CosTel_

-_ CAS.ELO DsBODE

| \ ) / Ini// / Portuileore '

ISy / llayorec. * PORTUGAL

ACARR,-EGA DO THERMAL PLAN POWER PROJECTS,.e IjIa/25MW l/limoo CnDnCilV

|Unif t Financed Loon 4/2 PO m Hy ro plnnis, n/i t ornt 2 t pvoec) ner construction

- -or un-l -cestru-tion

g 1 g > * _ =~~~~~~~~~~~. iBRii Project

I ; . Bejo ._1=.,

Setb|I 0 S. 0 60 60BejoI

0 < *0 20 40 60 BO

KILOMETERS

* v I~~~~~~~~~~~~o~

MAY 196: - Ri1AY 1966 ~~~~~~~~~~~~~~~~~~~~~~~IBRD-1138RS

![· 0Jeuow ep Josedsa ep sop ep uqse]dwoo ep odoo sonoqoz uoo sopouêllô] OZIOOW OllYPOl ep sau0410A9J uoo 'DJepow ep sopn6!A ep …](https://img.pdfslide.net/doc/110x75/5b97016309d3f27e758c2ada/-0jeuow-ep-josedsa-ep-sop-ep-uqsedwoo-ep-odoo-sonoqoz-uoo-sopouello-ozioow.jpg)