Embed Size (px)

Citation preview

.

Nationwide YourLife® Indexed UL

Why Nationwide’s Indexed UL? May, 2012

1FLM-0802AO.4 For Insurance professional use

only

Nationwide YourLifeIndexed UL

• Life Insurance issued by Nationwide Life Insurance Company and/or Nationwide Life and Annuity Insurance Company.

• Guarantees are subject to the claims paying ability of Nationwide.

• As your clients' personal situations change (i.e., marriage, birth of a child or job promotion), so will theirlife insurance needs. Care should be taken to ensure this product is suitable for their long-term lifeinsurance needs. They should weigh any associated costs before making a purchase. Life insurance hasfees and charges associated with it that include costs of insurance that vary with such characteristics of theinsured as gender, health and age, and has additional charges for riders that customize a policy to fit theirindividual needs.

• Indexed universal life policies are not stock market investments and do not directly participate in any stock or equity investments. Past index performance of an index is no indication of future crediting rates because you are buying an indexed universal life insurance policy does not involve actually purchasing or owning securities or stock, so it’s not the same as investing directly in the stock market and therefore does not receive dividend or capital gains participation.

• Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution• Not insured by any federal government agency May lose value

• © 2012 Nationwide Financial Services, Inc. All rights reserved

2FLM-0802AO.4 For Insurance professional

use only

Nationwide YourLife® Indexed UL

• S & P 500® is a trademark of Standard & Poor's and has been licensed for use by [Nationwide / Nationwide Life Insurance Company / Nationwide Life and Annuity Insurance Company]. The [Policy / Nationwide YourLife ® Indexed UL / Nationwide MarathonSM Indexed UL] is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's makes no representation regarding the advisability of investing in the Product.

• NASDAQ®, OMX®, NASDAQ OMX®, NASDAQ-100®, and NASDAQ-100 Index® are registered trademarks of The NASDAQ OMX Group, Inc. (which with its affiliates is referred to as the "Corporations") and are licensed for use by [Nationwide / Nationwide Life Insurance Company / Nationwide Life and Annuity Insurance Company]. The Product has not been passed on by the Corporations as to their legality or suitability. The Product is not issued, endorsed, sold, or promoted by the Corporations. The Corporations make no warranties and bear no liability with respect to the product.

• The "Dow Jones Industrial AverageSM" is a product of Dow Jones Indexes, the marketing name and a licensed trademark of CME Group Index Services LLC ("CME"), and has been licensed for use. "Dow Jones®", "Dow Jones Industrial AverageSM" and "Dow Jones Indexes" are service marks of Dow Jones Trademark Holdings, LLC ("Dow Jones") and have been licensed for use for certain purposes by Nationwide / Nationwide Life Insurance Company / Nationwide Life and Annuity Insurance Company. Nationwide's Nationwide YourLife® Indexed UL based on the Dow Jones Industrial AverageSM is not sponsored, endorsed, sold or promoted by CME Indexes, Dow Jones or their respective affiliates, and CME Indexes, Dow Jones and their respective affiliates make no representation regarding the advisability of trading in such product(s)

33FLM-0802AO.4 For Insurance professional

use only

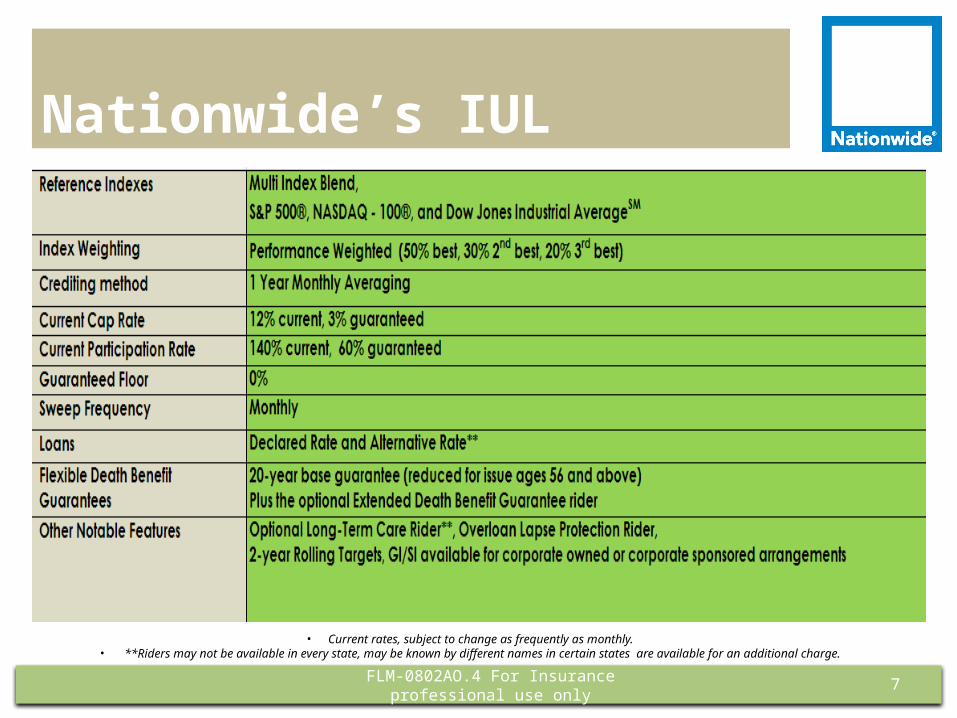

Nationwide’s IUL.

7FLM-0802AO.4 For Insurance professional

use only

• Current rates, subject to change as frequently as monthly. • **Riders may not be available in every state, may be known by different names in certain states are available for an additional charge.

Nationwide Indexed ULRider Highlights

10

Long Term Care rider• Indemnity style – tax-free payments made directly to the policy owner, and no bills or

receipts need to be submitted• Eligibility Requirements – unable to perform two or more of the activities of daily living for

a period of 90 days (elimination period); or have a cognitive impairment• Qualified LTC Services include – Nursing Home Care, Home Health Care and Hospice,

Assisted Living, and Adult Day Care• Monthly Benefit is the lesser of:

- 2% of the long-term care specified amount or- Daily amount allowed by HIPAA ($310/day in 2012) x number of days in the month

Extended Death Benefit Guarantee rider (EDBG)• EDBG Duration – 21 years to Lifetime • EDBG Percentage – 50% to 100% of the Specified Amount• Cumulative premium requirement; Unlimited catch up (no interest)• 100% allocation to Indexed Account only (if EDBG rider elected)• Advanced Payment Premium – discounted premium requirement if paid within

the first ten policy years• Catch Up: Because of our Premium Design - Catch up price is Cumulative

Missed premiums (unlike Shadow Account designs you see on NLG UL's, or for AVIVA and Minn Life's IUL)

Keep in mind that as an acceleration of the death benefit, the LTC rider payout will reduce both the death benefit and cash surrender values. The Long Term Care rider may be known by different names in different states,

may not be available in every state and has an additional charge associated with it.10

FLM-0802AO.4 For Insurance professional use only

Why Nationwide?Monthly Averaging• Potential to minimize market timing risk • Smooth volatility by averaging returns over 12 points in time

vs. 2

Multi-Index Blend• S&P 500®, NASDAQ-100®, Dow Jones Industrial AverageSM

• Performance weighted: 50% (best), 30% (2nd best), 20% (3rd)• Takes the guess work out of allocation

140% current Participation Rate*• Consider current volatile market• Expecting modest market performance – 140% may be ideal

* Current rates are subject to changeNationwide may discontinue any index that becomes unavailable (i.e, is no longer published) or the calculation of which is substantially changed. Nationwide may substitute with a comparable index or may adjust the method of calculating Index Segment Interest.

1111FLM-0802AO.4 For Insurance professional

use only

Coming Soon (June 2012)

New Indexed Strategy • S&P 500® Annual point-to-point *• 100% Participation Rate (current & guaranteed)• 12% Cap Rate (current)

Conditional Return of Premium rider• This rider benefit provides upon surrender the greater of net surrender

value or a percentage of the cumulative premiums, including 1035 premiums, based on policy year:Policy Years 1-3: 100%Policy Year 4: 95%Policy Year 5: 90%

• Eligibility requirements and annual premium requirements must be met

* Current rates are subject to change1212

FLM-0802AO.4 For Insurance professional use only

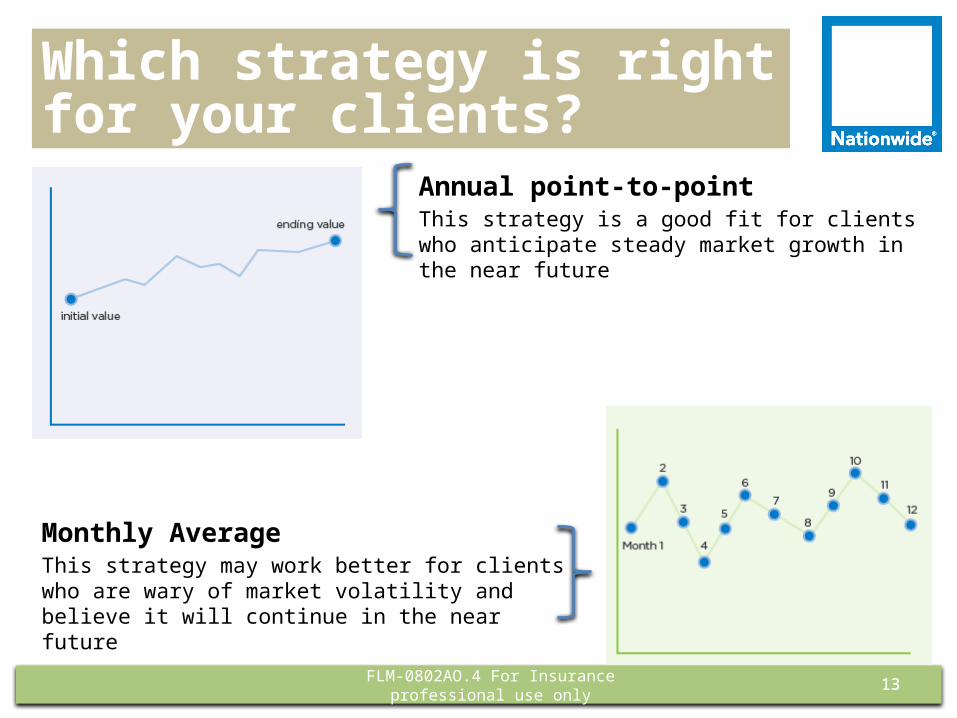

Which strategy is right for your clients?

Annual point-to-pointThis strategy is a good fit for clients who anticipate steady market growth in the near future

1313FLM-0802AO.4 For Insurance professional

use only

Monthly AverageThis strategy may work better for clients who are wary of market volatility and believe it will continue in the near future

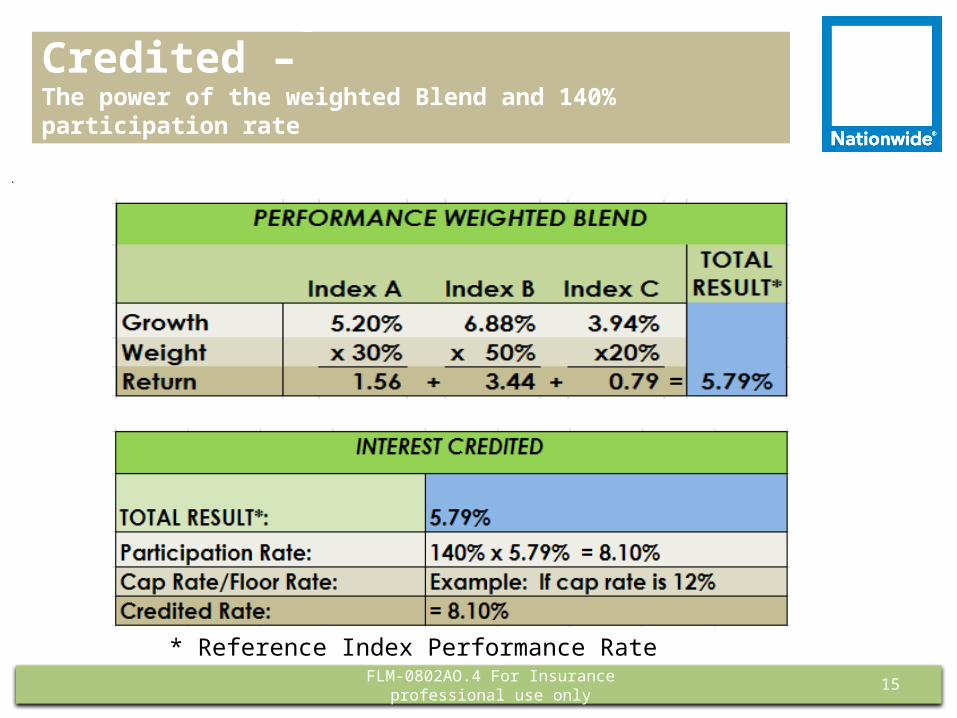

Calculating Interest Credited –The power of the weighted Blend and 140% participation rate

.

15

* Reference Index Performance RateFLM-0802AO.4 For Insurance professional

use only

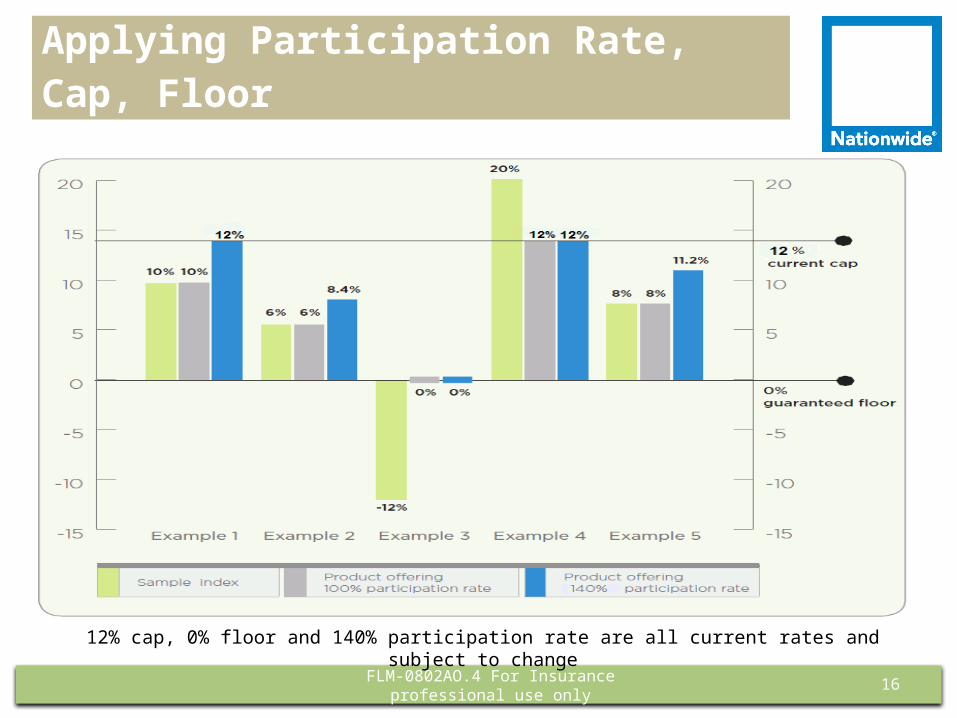

Applying Participation Rate, Cap, Floor

.

16

12% cap, 0% floor and 140% participation rate are all current rates and subject to change

FLM-0802AO.4 For Insurance professional use only

Incorporate IUL into yourExisting Product Solutions

18

Accumulation and Income:

• Alternative to VUL

• Alternative to Accumulation UL’s

IUL can be used for Protection sales:

• Alternative to Current Assumption UL

• Solve to Endow or Solve to Carry ($1)

IUL can be used for Death Benefit Protection sales:

• Alternative to No-Lapse Guaratee UL

• Alternative to VUL (w/ NLG riders)

FLM-0802AO.4 For Insurance professional use only

• IMPORTANT BENCHMARKING INFORMATION: All competitive information is believed to be current as of April 2012. Information was compiled from the latest company software. Aviva v2.9.0.407, ING v2011.07, Lincoln v14.5, Pacific Life v11.04, John Hancock v8.0, Axa v7.1, Penn Mutual 11.1, Nationwide v2.4 and Minnesota Life’s web based software. All information presented is deemed reliable and Nationwide has made every effort to make sure it is accurate; however, it’s possible that there are differences between the products compared which are not reflected and/or of which we are unaware. For this reason, its completeness and accuracy cannot be guaranteed.

20

Disclosure

FLM-0802AO.4 For Insurance professional use only

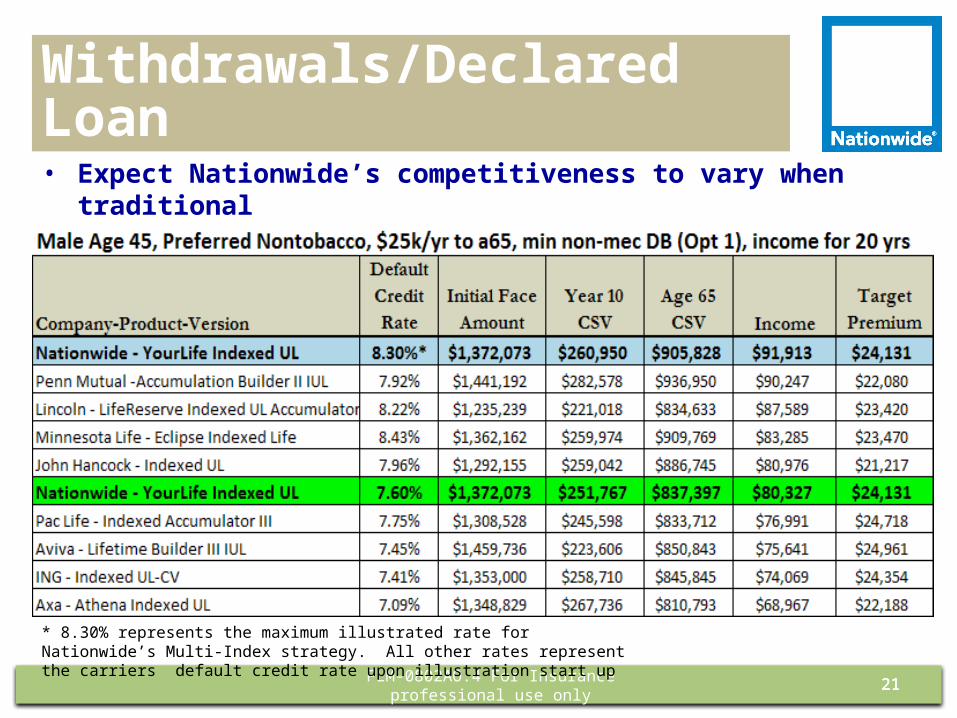

Income solve with Withdrawals/Declared Loan• Expect Nationwide’s competitiveness to vary when

traditional income solves are used

212121FLM-0802AO.4 For Insurance professional

use only

* 8.30% represents the maximum illustrated rate for Nationwide’s Multi-Index strategy. All other rates represent the carriers default credit rate upon illustration start up

Income solve with Withdrawals/Declared Loan• Same scenario as previous except for 7.00% credit rate is

used for all

222222FLM-0802AO.4 For Insurance professional

use only

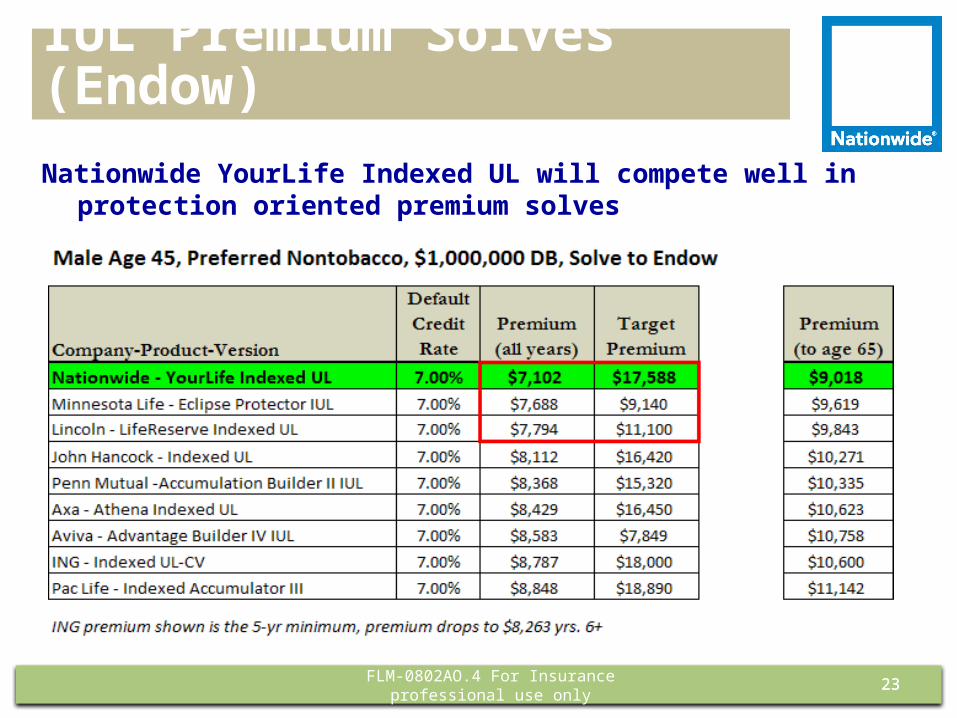

IUL Premium Solves (Endow)

Nationwide YourLife Indexed UL will compete well in protection oriented premium solves

2323FLM-0802AO.4 For Insurance professional

use only

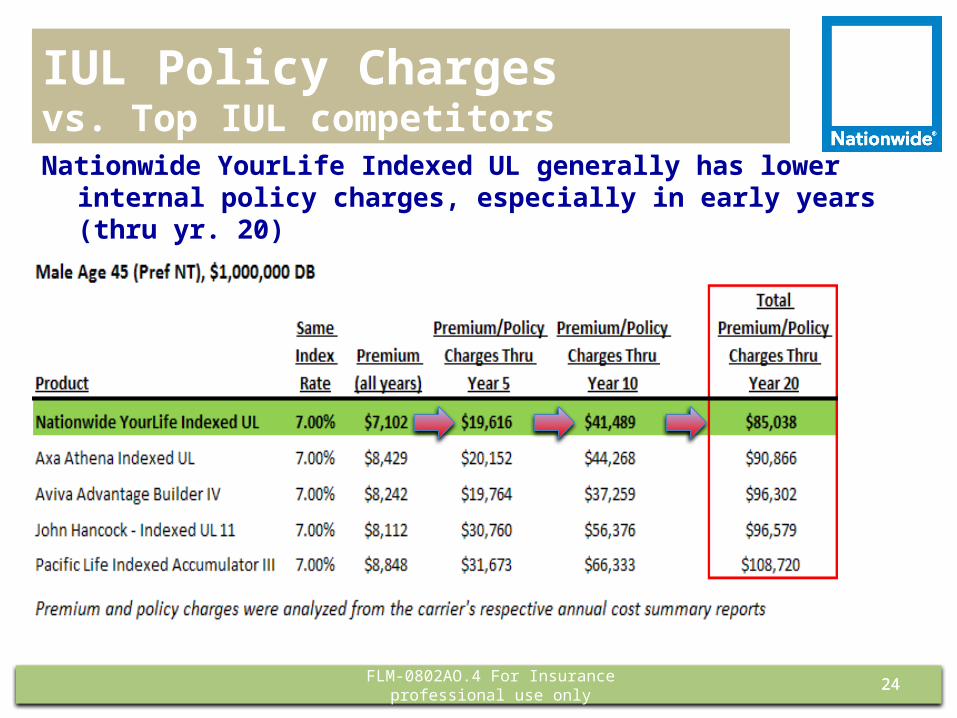

IUL Policy Chargesvs. Top IUL competitorsNationwide YourLife Indexed UL generally has lower

internal policy charges, especially in early years (thru yr. 20)

2424FLM-0802AO.4 For Insurance professional

use only

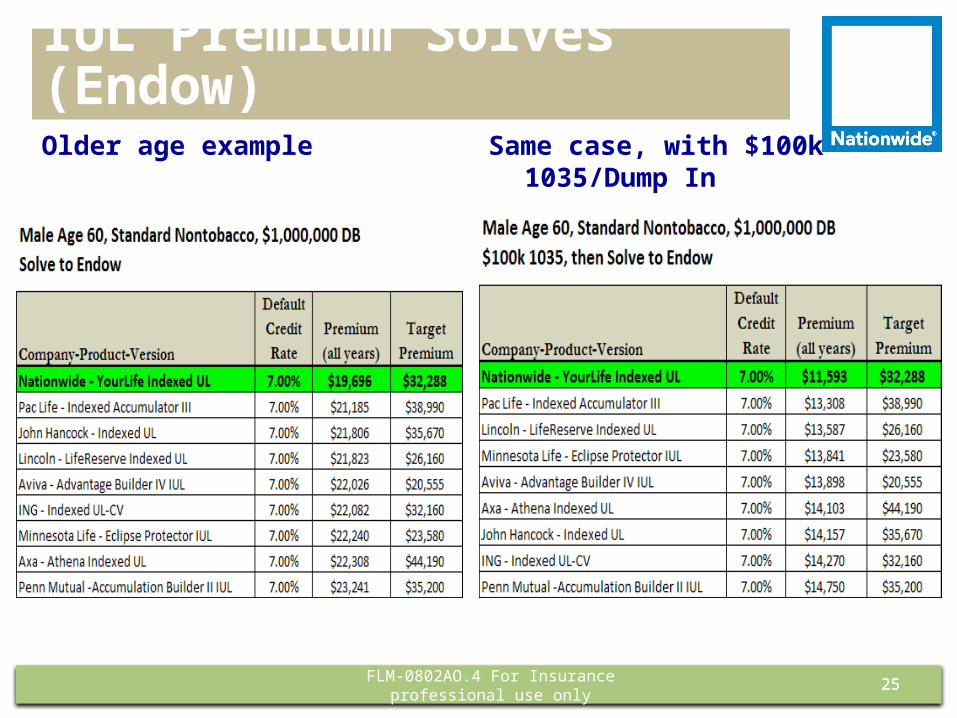

IUL Premium Solves (Endow)Older age

example

2525FLM-0802AO.4 For Insurance professional

use only

Same case, with $100k 1035/Dump In

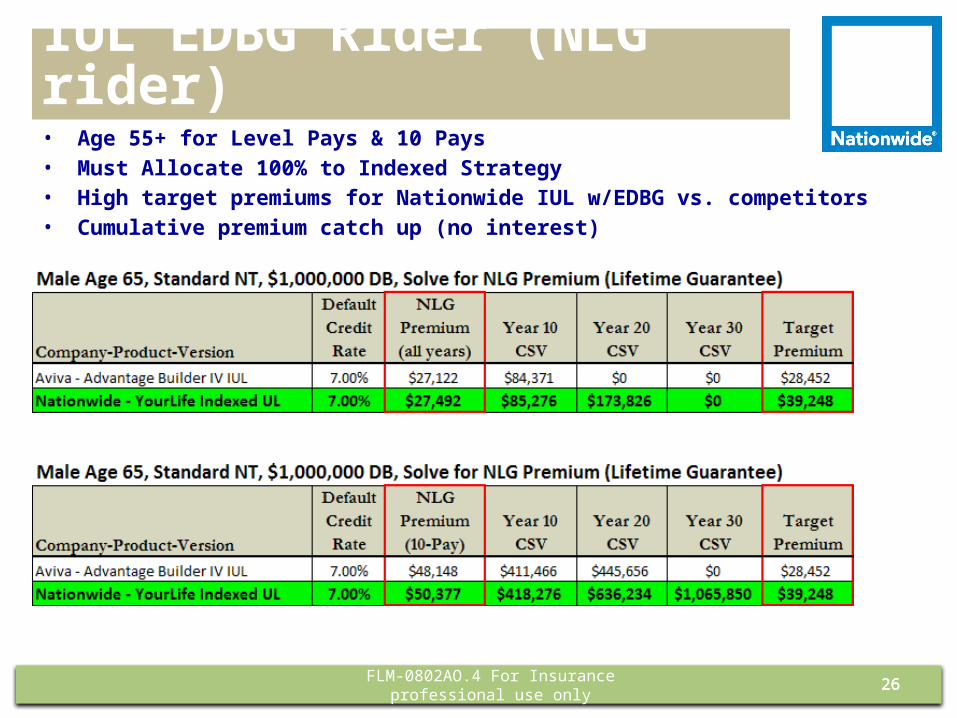

IUL EDBG Rider (NLG rider)• Age 55+ for Level Pays & 10 Pays• Must Allocate 100% to Indexed Strategy• High target premiums for Nationwide IUL w/EDBG vs. competitors• Cumulative premium catch up (no interest)

262626FLM-0802AO.4 For Insurance professional

use only

Quick Summary of Nationwide’s IUL

27

One product to meet many consumer needs:

• Death Benefit Protection (low premium solves)

• Accumulation potential

• Guaranteed Coverage (optional EDBG rider)

• Long Term Care coverage (optional LTC rider)

These riders may be known by different names in different states, may not be in every state and have an additional charge associated with them.

FLM-0802AO.4 For Insurance professional use only

Quick Summary of Nationwide’s IUL Sweet Spots

• Low Premium Solves to Endowo Especially when illustrative rates are same or comparableo Wide range of competitiveness (Age 45 – 65)

• Income Solveso Option 1 DBO (level) more competitive than Option 2o Alternative loans available

• EDBG rider flexibility and targetso Cumulative premium catch up (no interest)o 21 yrs to Lifetime NLG and ability to specify 50% to 100% for NLGo Higher target premiumso All premium must be allocated to Index Strategy with the EDBG rider

• Competitive Target Premiums (2-yr rolling)

FLM-0802AO.4 For Insurance professional use only

28

29

QUESTIONS?

29FLM-0802AO.4 For Insurance professional

use only