Embed Size (px)

Citation preview

1

2

3

4

6

mÉ׸ xÉÇ. / Page No.

IN THIS ISSUE

1. From the Editor’s Desk 1

2. Performance Highlights for the Second Quarter 2 of Financial Year 2016-17

3. Macro Economic Scenario 4

4. S S Mundra, Deputy Governor, RBI, “ABCD of MSME Credit” 9

5. Dr. Raghuram Rajan, Governor, RBI, “Interesting,ProfitableandChallenging:BankinginIndiaToday”16

6. Mutual Funds 23

7. Masala Bonds 27

8. GoldLoanProcedureandPrecautions 32

9. UDAY Scheme 34

10. Cashless Economy 38

11. Guidelines on “Enhancing Credit Supply for 41 Large Borrowers through Market Mechanism”

12. Story 44

13. Synd School 45

14. KeyTakeawaysfromMonetaryPolicyof 46 Major Central Bankers

15. ImportantTerms 48

16. News Scan 50

17. Economic and Financial Indicators 54

{n½‘r BH$Zm°{‘H$ [aì¶y(qg{S>Ho$Q>~¢H$ H$s {V‘mhr Am{W©H$ ~wbo{Q>Z)

Pigmy Economic Review(QuarterlyEconomicBulletinofSyndicateBank)

ZÉÇQû VII eÉÑsÉÉD-ÍxÉiÉqoÉU 2016 xÉÇZrÉÉ 02 VolumeVII July-September2016Number02

1

From the Editor’s DeskIt is indeed a privilege to place Quarterly Economic Bulletin “Pigmy Economic Review”for the Second quarter of FY 2016-17.

The present issue highlights the globaleconomic scenario and performance of Indian economy in the challenging global economicconditions. According to Asian DevelopmentBank (September 27, 2016) the ADB retainsprojections of India’s GDP growth rate at 7.4percentforthecurrentfiscal(2016-17)and7.8percentforthenextfiscal(2017-18).BIJOY KUMAR PANDIT

Further, this issue contains key takeaways from the speeches of RBI Deputy Governor, S S Mundra, on “ABCD of MSME Credit” and RBI former Governor, Dr.RaghuramGRajanon“Interesting,ProfitableandChallenging:BankingInIndiaToday,”togiveinsightontheseimportanttopics.

This issue also emphasizes on Mutual Funds, Masala Bonds, Gold LoanProcedureandPrecautions,UDAYA scheme,Cashless Economy,Guidelineson Enhancing Credit Supply for Large Borrowers through Market Mechanism andmanymoretopicsandeconomicandfinancialindicators.Anattempthasbeenmadetopresentalltheseusefultopicsinasimplemanner,sothatyoufinditeasytounderstand.

I feel our staffmemberswill certainly enrich their knowledge andwill beenthralled by reading this issue. It is our attempt tomake this QuarterlyBulletin reader friendly and useful. I also appeal to all of you to send write-upsrelatedtoeconomy/businessoranyothertopicrelevanttobankingindustry for the next issue.

I also welcome constructive suggestions and views from our readers forimprovingthequalityandcontentofourQuarterlyEconomicBulletin.

BIJOY KUMAR PANDIT

Editor

2

Performance Highlights for the Second Quarter of Financial Year 2016-17

Net Profit:TheBankhasrecordednetprofitof`162 crore for the Half Year ended 30th September2016comparedto`634 crore reported in its corresponding Half Year ended 30thSeptember2015.The net profit for the Q2 (July to Sept 2016) of the current fiscal is at `83 crore as against `332 crore reported during its corresponding period of last year.

Operating Profit:TheoperatingProfitfortheHalf Year ended 30thSeptember2016stoodat`1,791 crore as against `2,234 crore reported during Half Year ended 30th September2015.The operating Profit for Q2 of 2016-17 stood at `1,017 crore as against `1,209 crore reported in Q2 of 2015-16.

Net Interest Income (NII):The Net Interest Income for the Half Year ended 30th September 2016increased to `3,024 crore from `3,007 crore in its corresponding period of previous year.TheNIIforQ2of2016-17marginallydeclinedto`1,545 crore for the Q2 of 2016-17 as against `1,595 crore in Q2 of 2015-16.

Other Income:Theother income increasedby20.61percent to`1,346 crore for the Half Year ended 2016-17 from `1,116 crore during the corresponding Half year.TheotherincomeforQ2of2016-17increasedby28.78percentto 792 crore from `615 crore during the corresponding period of Q2 of 2015-16.

Operating expenses:The operating expenses for theHalf Year ended 30.09.2016 increased to `2,579 crore from `1,889 crore for the corresponding period of 2015. The operating expenses for Q2 of 2016-17 was `1,320 crore as against `1,000 crore for Q2 of 2015-16.

Provisions & Contingencies:Theoverallprovisions for theHalf Year ended 30th September2016stoodat `1,629 crore and increased by 1.81 percent from `1,600 crore during 30.09.2015.TheBankhasmadeprovisionandcontingenciesof`934 crore during Q2 of 2016-17 as against `877croreinitspreviousperiod(2015-16).

3

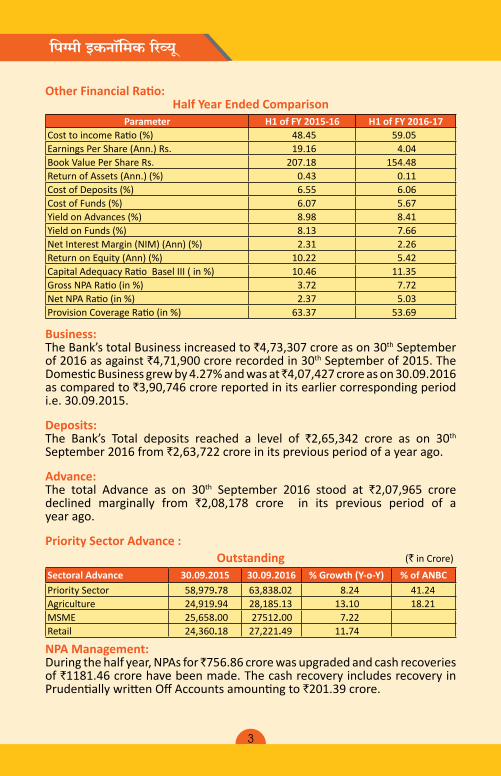

Other Financial Ratio:Half Year Ended Comparison

Parameter H1 of FY 2015-16 H1 of FY 2016-17CosttoincomeRatio(%) 48.45 59.05EarningsPerShare(Ann.)Rs. 19.16 4.04Book Value Per Share Rs. 207.18 154.48ReturnofAssets(Ann.)(%) 0.43 0.11CostofDeposits(%) 6.55 6.06CostofFunds(%) 6.07 5.67YieldonAdvances(%) 8.98 8.41YieldonFunds(%) 8.13 7.66NetInterestMargin(NIM)(Ann)(%) 2.31 2.26ReturnonEquity(Ann)(%) 10.22 5.42CapitalAdequacyRatioBaselIII(in%) 10.46 11.35GrossNPARatio(in%) 3.72 7.72NetNPARatio(in%) 2.37 5.03ProvisionCoverageRatio(in%) 63.37 53.69

Business:TheBank’stotalBusinessincreasedto`4,73,307 crore as on 30thSeptemberof 2016 as against `4,71,900 crore recorded in 30thSeptemberof2015.TheDomesticBusinessgrewby4.27%andwasat 4,07,427 crore as on 30.09.2016 as compared to `3,90,746 crore reported in its earlier corresponding period i.e. 30.09.2015.

Deposits:The Bank’s Total deposits reached a level of `2,65,342 crore as on 30th September2016from`2,63,722 crore in its previous period of a year ago.

Advance:The total Advance as on 30th September 2016 stood at `2,07,965 crore declined marginally from `2,08,178 crore in its previous period of a year ago.

Priority Sector Advance :Outstanding

Sectoral Advance 30.09.2015 30.09.2016 % Growth (Y-o-Y) % of ANBCPriority Sector 58,979.78 63,838.02 8.24 41.24Agriculture 24,919.94 28,185.13 13.10 18.21MSME 25,658.00 27512.00 7.22Retail 24,360.18 27,221.49 11.74

NPA Management:During the half year, NPAs for 756.86 crore was upgraded and cash recoveries of `1181.46crorehavebeenmade.ThecashrecoveryincludesrecoveryinPrudentiallywrittenOffAccountsamountingto`201.39 crore.

(`inCrore)

4

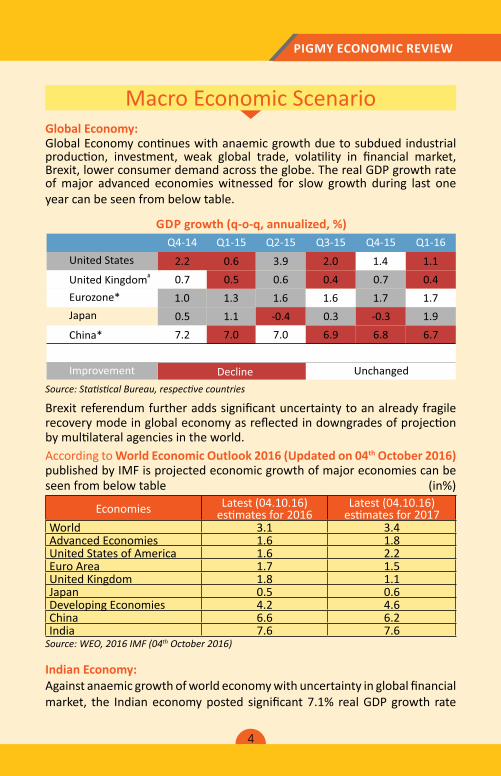

Global Economy:GlobalEconomycontinueswithanaemicgrowthduetosubduedindustrialproduction, investment, weak global trade, volatility in financial market,Brexit,lowerconsumerdemandacrosstheglobe.TherealGDPgrowthrateof major advanced economies witnessed for slow growth during last one yearcanbeseen frombelowtable.

GDP growth (q-o-q, annualized, %)

7.2 7.0 7.0 6.9 6.8 6.7

Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16

2.2 0.6 3.9 2.0 1.4 1.1

0.7 0.5 0.6 0.4 0.7 0.4

1.0 1.3 1.6 1.6 1.7 1.7

0.5 1.1 -0.4 0.3 -0.3 1.9

Improvement Decline Unchanged

United States#United Kingdom

Eurozone*

Japan

China*

Source: Statistical Bureau, respective countries

Brexit referendum furtheraddssignificantuncertaintytoanalreadyfragilerecoverymodeinglobaleconomyasreflectedindowngradesofprojectionbymultilateralagenciesintheworld.According to World Economic Outlook 2016 (Updated on 04th October 2016) publishedbyIMFisprojectedeconomicgrowthofmajoreconomiescanbeseenfrombelowtable (in%)

Economies Latest(04.10.16)estimatesfor2016

Latest(04.10.16)estimatesfor2017

World 3.1 3.4Advanced Economies 1.6 1.8United States of America 1.6 2.2Euro Area 1.7 1.5United Kingdom 1.8 1.1Japan 0.5 0.6Developing Economies 4.2 4.6China 6.6 6.2India 7.6 7.6

Source: WEO, 2016 IMF (04th October 2016)

Indian Economy:Againstanaemicgrowthofworldeconomywithuncertaintyinglobalfinancialmarket, the Indianeconomyposted significant7.1% realGDPgrowth rate

Macro Economic Scenario

5

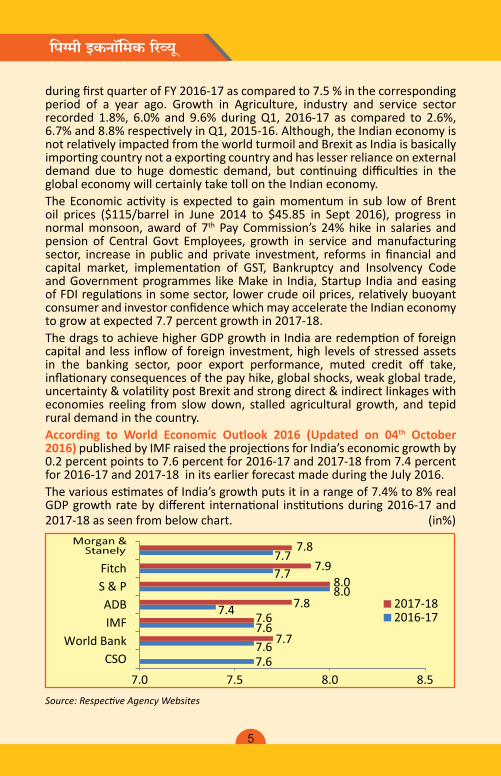

duringfirstquarterofFY2016-17ascomparedto7.5%inthecorrespondingperiod of a year ago. Growth in Agriculture, industry and service sector recorded 1.8%, 6.0% and 9.6% duringQ1, 2016-17 as compared to 2.6%,6.7%and8.8%respectivelyinQ1,2015-16.Although,theIndianeconomyisnotrelativelyimpactedfromtheworldturmoilandBrexitasIndiaisbasicallyimportingcountrynotaexportingcountryandhaslesserrelianceonexternaldemand due to huge domestic demand, but continuing difficulties in theglobaleconomywillcertainlytaketollontheIndianeconomy.TheEconomicactivity is expected togainmomentum in sub lowofBrentoil prices ($115/barrel in June 2014 to $45.85 in Sept 2016), progress innormal monsoon, award of 7th PayCommission’s 24%hike in salaries andpension of Central Govt Employees, growth in service and manufacturing sector, increase in public and private investment, reforms in financial andcapital market, implementation of GST, Bankruptcy and Insolvency Codeand Government programmes like Make in India, Startup India and easing ofFDIregulationsinsomesector,lowercrudeoilprices,relativelybuoyantconsumerandinvestorconfidencewhichmayacceleratetheIndianeconomyto grow at expected 7.7 percent growth in 2017-18. ThedragstoachievehigherGDPgrowthinIndiaareredemptionofforeigncapitaland less inflowofforeign investment,high levelsofstressedassetsin the banking sector, poor export performance, muted credit off take,inflationaryconsequencesofthepayhike,globalshocks,weakglobaltrade,uncertainty&volatilitypostBrexitandstrongdirect&indirectlinkageswitheconomies reeling from slow down, stalled agricultural growth, and tepid rural demand in the country.According to World Economic Outlook 2016 (Updated on 04th October 2016) publishedbyIMFraisedtheprojectionsforIndia’seconomicgrowthby 0.2 percent points to 7.6 percent for 2016-17 and 2017-18 from 7.4 percent for 2016-17 and 2017-18 in its earlier forecast made during the July 2016. ThevariousestimatesofIndia’sgrowthputsitinarangeof7.4%to8%realGDPgrowthratebydifferent international institutionsduring2016-17and2017-18asseenfrombelowchart. (in%)

Source: Respective Agency Websites

6

Banking Sector:The performance of the Scheduled Commercial Banks (SCBs) during Q12016-17postedsatisfactoryresults.Theslowgrowth increditanddepositandcurtailingNPAsthroughrecapitalizationofPSBsandprovidingtoolsforbankstomanagestressedassetsandacceleratingstructuralreformsinthebankingsectorarethemajorreasonstoimprovementinthebalancesheetofthebanksandresultedinnetprofitduringQ12016-17.Asperthelatestavailable data (September 16, 2016), Indian Scheduled Commercial BankdepositsincreasedY-o-Yby9.91%to`97909.66 Billion and credit grew y-o-y by9.33%to`73099.74 Billion up to 16thSeptember2016.

The Indian banks in general and Public Sector Banks (PSBs) in particular,are grappling with the huge stock of stressed assets that has piled up in the system over the years and especially during last three quarters.

Chart: Growth Rate of Deposit and Credit of Scheduled Commercial Banks in India (in % Y-o-Y)

Source: RBI

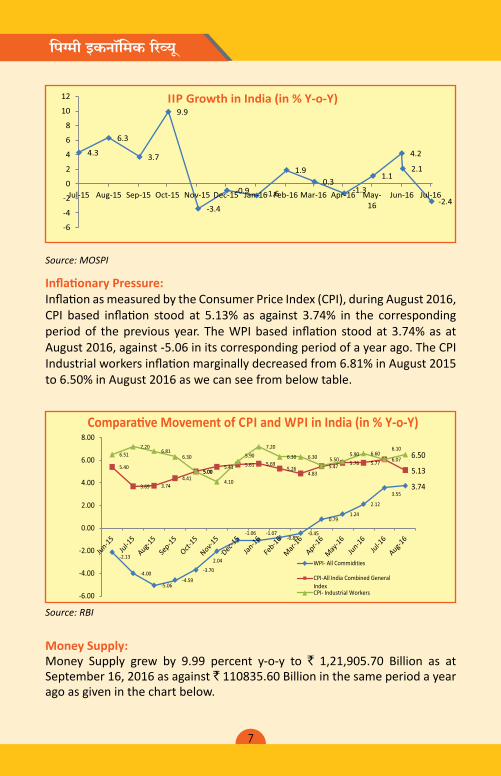

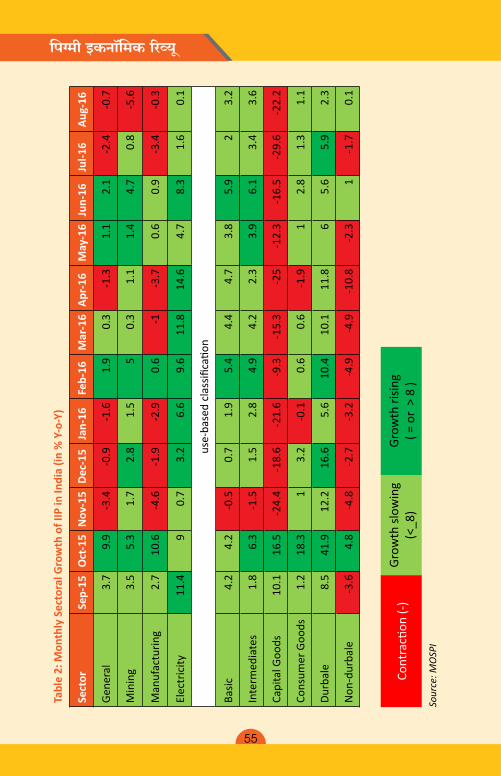

Index of Industrial Productivity (IIP):There is a recovering stage from subdued in Industrial production inthe preceding months. IIP growth recorded at -2.4% during July 2016 asagainst 4.3% in correspondingperiodof theprevious year.Mining (0.8%), Electricity (1.6%), Basic (2%), Intermediates (3.4%) recorded goodperformanceduringJuly2016.Thelacklustreperformanceofmanufacturingsectordipsto-3.4%asattheJuly2016-17ascomparedtoitscorrespondingperiod of previous year.

7

IIP Growth in India (in % Y-o-Y)

Source: MOSPI

Inflationary Pressure:InflationasmeasuredbytheConsumerPriceIndex(CPI),duringAugust2016,CPI based inflation stood at 5.13% as against 3.74% in the correspondingperiodof theprevious year. TheWPIbased inflation stoodat3.74%asatAugust2016,against-5.06initscorrespondingperiodofayearago.TheCPIIndustrialworkersinflationmarginallydecreasedfrom6.81%inAugust2015to6.50%inAugust2016aswecanseefrombelowtable.

Compara e Movement of CPI and WPI in India (in % Y-o-Y)

6.50

5.13

3.74

Source: RBI

Money Supply:Money Supply grew by 9.99 percent y-o-y to ` 1,21,905.70 Billion as at September16,2016asagainst` 110835.60 Billion in the same period a year agoasgiveninthechartbelow.

8

M3 Growth rate in India (in % Y-o-Y)

Source: RBI

Foreign Trade:During August 2016, total exports value stood at `1,44,044.67 crore as compared to `1,40,443.43 crore (higher by 2.56 percent) in the sameperiod of previous year. On the contrary, total imports value recorded at ` 1,95,415.03 crore in August 2016 as against `2,21,126.92crore(lowerby11.63percent) initscorrespondingperiodofpreviousyearasreflectedinbelowchart.

Growth Rate of Export and Import (in % Y-o-Y)

Source: RBI

Overalltradebalancehasimprovedtakingmerchandiseandservicetogether.Tradedeficithasbeenreducedby36.33percentfrom` 80,683.49 crore in August 2015-16 to ` 51,370.36 crore in August 2016-17.

9

ABCD of MSME Credit*

TheAsiaSMEFinanceMonitor2014publishedby theAsianDevelopmentBankhasestimatedthat96%ofallenterprisesintheAsianregionfallundertheMSMEcategory,absorbcloseto2/3rdoftheworkingforceandcontributetoabout42%ofGDP.

1. According to MSME Ministry’s Annual Report for 2015-16, MSME sector in India today is a network of 51 million enterprises providing employment to117.1millionpersonsandcontributing37.5percentofIndia’sGDP.Thedevelopmentofthissectoris,therefore,crucialingeneratingsignificantlevels of employment across the country, more so since we have a large youngandeducatedpopulationwhichisonlookoutforemployment.

MSME – Significance beyond job creation2. While job creation is certainly critical, small businesses play a far

greaterrolethanjustprovidingemployment. TwokeycontributionsofMSME sector.

(i)TheMSMEsectorisanurseryforentrepreneurshipandaschoolforinnovation. Countless medium and large corporates in India haveevolvedoutofbeingmicroandsmallsometimeinnotsodistantpast.Whoownfairlylargebusinessestoday,wouldhavecuttheirteethinbusinessthroughtherouteofmicroandsmallenterprises.

(ii) MSME sector is crucial for the success of the national agendaof Financial Inclusion. Normally, when we talk about financialinclusion,wedoso largely fromtheperspectiveofan individualoratbestahousehold.However,universalfinancialinclusioncannotbeconsideredtohavebeenachievedunlessitisensuredthatthemicroandsmallbusinessesarefinancially included.Creditstothesesmallfamilyrunorindividualrunentitiesfromtheformalfinancialchannelswouldmakethesebusinessessustainableandhelpthemmoveoutofpovertyandpropelthemtoabetterqualityoflife.

The surmise that if this is the sector that is the bulwark for such criticaldevelopmental paradigms, there are compelling enough reasons for all stakeholders - be they the Associations, the Financial Institutions, the

Note* Keynote address delivered by Shri S. S. Mundra, Deputy Governor, Reserve Bank of India at the 2nd CII National Conference on MSME Funding held in New Delhi on August 23, 2016.

10

regulators or the Government, to put all their might together in a convergent fashion so that the right environment is created to propel growth of MSMEs in our country.

For achieving this objective, there is a need to create an ecosystem which can facilitate handholding and nurturing of MSME units particularly at the nascent stages. Also, there is a need to eliminate a host of impediments – of permits, of inspections, of red tape and provide a set of enablers – skill development, infrastructure, markets, technology etc. However, of all the enablers, probably none is more important than Credit. TheIFC/McKinseyhas estimated the credit gap for formal and informal MSMEs worldwideataround$3.9trillionglobally,ofwhich$2.1to2.6trillion is inemergingmarkets.

The ABCD of Credit3. CreditisperhapsthemostcriticalcomponentforMSMEentrepreneurs.

ProvisionforCreditisessentiallydependentonfourpivotalissueswhichI would call ‘ABCD’ of credit.

a) The ‘A’ of Credit –Access/Availability4. The 4thAll India survey ofMSMEs states that close to 90 per cent of

MSMEsaredependentoninformalsources,whichbyanystandardsisaworrisomefigure.As per provisional data for period ended March 2016, total outstanding loan of the banking system to MSME sector stood at around 11.1 trillion rupees in 20.6 million loan accounts. Contrast this to the estimated need of INR 26 trillion and number of MSMEs at 51 million.

5. Animportantpieceoftheproblemisadequacyofbankingoutlets.Smallentrepreneursarespreadacrossremotelocationsinthecountrywherephysicalbankbranchesarenotavailable.Also,thebankingcorrespondentmechanism is yet to mature to a level where they can play a key role in credit disbursal. Second and perhaps amore import dimension is availabilityof credit at a timewhen it is required by the entrepreneur. Ability ofsmall entrepreneurs to withstand life cycle shocks is extremely limited andhenceavailabilityoftimelycreditbecomescriticalfortheirsurvival. The formal financial system, due to a variety of reasons, which mayincludecumbersomeprocedures, lackofunderstandingofthebusinessmodel, inability of the entrepreneur tomeet the requirements of thebanksetc.,isunabletomeetthisimmediateneedoftheentrepreneur.

b)‘B’- Banks and Business6. ‘B’ in the ‘ABCD’ paradigm of credit fundamentally refers to the

informationasymmetrybetween the two Bs – Banks and Business.

11

TheUnitedStatesAgencyforInternationalDevelopment(2009)definesafinanciallyliterateSMEowner/manageras“someonewhoknowswhatare themost suitable financing and financialmanagement options forhis/herbusinessatthevariousgrowthstagesofhis/herbusiness;knowswheretoobtainthemostsuitableproductsandservices;and interactswithconfidencewiththesuppliersoftheseproductsandservices.He/sheis familiar with the legal and regulatory framework and his/her rights and recourseoptions.”

7. Majority of the MSME entrepreneurs in the country today meet the criterion. Financial literacy in the context of a MSME focuses on an individual’s ability to translate financial literacy concepts to businessneeds. Financial literacy is essential for effective money managementandlowlevelsoffinancialliteracyhindertheunderstandingofavailablefinancialproductsandservices. MSE entrepreneurs are also constrained by lack of operational skills, accounting and finance acumen, business planning etc. which underscores a need for facilitation by banks/other agencies.

8. However, it is not a one-way street. Large-scale retirements in banks in recent years have also adversely impacted the collective skill-sets available at the field level in understanding, appraising and monitoring the MSME loan portfolio.Thepoorunderwritingskillsleadstoavoidableunderoroverfinancing,whichcanhaveatellingeffectonthehealthoftheMSMEunits,particularlyinadverselifecyclesituations.

c) ‘C’- Collateral Requirements

9. The formal financial institutions particularly banks consider lending toMSMEs as highly risky since the entrepreneurs often do not possessadequate collateral to support the credit. Very often, the loans arerejected,despitetheprojectprimafacie,beingfeasible.Whilethereareseveral dispensations to tide over the problem, the credit culture hasnotmaturedenoughtoalevelexistingin developed economies where lending is done against the assets of the firm including its movable assets. This also necessitates that we build up strong financial infrastructure, which would support the banks in lending to these sectors without worries and using all types of assets available to secure the loan. It is alsopertinentforbankstorealizethatthoughtheloantotheindividualentitiesinthesectormayberiskieronasolobasis,overallonaportfoliolevel, these are less vulnerablethanloanstocorporate.

12

d) ‘D’- Documentation

10. Many of the MSMEs, particularly the Micro units, do not have adequate documentation to match the rigours of a formal financial system. Absence of documentation drives the small entrepreneurs to informalsourcesthatarewillingtoprovidecreditwithminimumdocumentation.Further,avastmajorityoftheMSMEsareinformal,whichbringsdownthe credit score of the entrepreneur and hinders the ability of theformalfinancialsystemtolendtothem.Banks,ontheirpartwillneedtoleverage on modern technology algorithms and Big data so that they can differentiatebetweenagoodborrowerandanotsogoodoneevenintheabsenceofconventionaldocumentation.

11. Having analyzed various impediments in finance to the sector letmedwellonsomeofthestepstakenbyRBI,GovernmentofIndiaandotherApexinstitutionsinbridgingthesegaps.

(i) Access/ Availability: RBI has initiated several measures to improve the availability of

banking services, especially in the rural and far-flung areas whereaccesstoformalfinanceisarduous.

12. New institutions: twonewuniversalbankshavestartedoperationswhilein-principle approval has been granted to 10 entities to set up SmallFinance Banks that would primarily focus on lending to unserved and undeservedsections includingsmallbusinessunits, smallandmarginalfarmers, micro and small industries and unorganized sector entities. These small finance banks have been mandated to extend 75 per cent of its Adjusted Net Bank Credit (ANBC) to the sectors eligible for classification as priority sector lending (PSL) by the Reserve Bank. At least 50 per cent of its loan portfolio should constitute loans and advances of up to ` 25 lakh. Many of the SFBs have prior experience of workingwithsmallbusinessesasMFIs/NBFCsandwebelievethattheywillbeabletobringintechnologybackedinnovativelastmilepracticestoserve their customers.

13. P2P lending: New players have entered the MSME lending landscape in the form of P2P companies.Theseentitiesuseanonlineplatformtomatchlenderswithborrowerstoprovideunsecuredloansandmostlyforreceivablesfinancing.P2P lendinghasgreatpotentialasanalternativeform of low-cost finance as it can reach to the needy where formalsourcesareunabletoreachorunwillingtolend.RBIhasbeenmindfulof

13

aneedtoregulatetheseentitieswithoutstiflingtheirabilitytoinnovateandiscurrentlyintheprocessofissuingfinalguidelinesonP2Plending.

14. Policy intervention for Life Cycle Issues: Wehaveadvisedthebankstokeepaprovision for additional credit limits (StandbyCredit Facility fortermloansandanadditionalprovisionwithintheoverallworkingcapitallimits) in order to providetimely financial support toMicro and Smallenterprisesfacingfinancialdifficultiesduringtheir lifecycle.Bankshavealsobeenadvisedtocarryoutmid-termreviewofregularworkingcapitallimitsandfixuptimelinesforcreditdecisions

15. Co-origination of loans: WemustbeconsciousthatBankwouldalwaysbe driven by viability assessments/cost considerations. One possiblesolutionforthisproblemcouldbeconvergenceofeffortsbetweenbankson one hand and the NBFCs, MFIs on the other, who have ‘feet on the ground’ in such locations, betterunderstandingof the local conditionsand business viability, better knowledge about the credit worthinessof individuals, their repayment capabilities etc. Could we envisage aframework for co-origination of loans by banks and the NBFCs/MFIs with risk participation? Whileitwouldensureskininthegameforbothparties, it would benefit the entrepreneurs in terms of cost of credit,which on account of blending could be substantially lower. This couldprobablybethemostidealstructuretoservethemicroenterpriseswhoarethemostdeprivedintermsofavailabilityofcredit.

(ii) Banks and Business:

16. Not only are the small entrepreneurs often ignorant about bankingproductsandpractices,severalbankershavelittleunderstandingofthelifecycle credit needs of small businesses. Towards covering this base,RBIhasstartedacapacitybuildinginitiativecalledtheNationalMissionforCapacityBuildingofBankersforfinancingMSMESector(NAMCABS)in a mission mode. The field level functionaries must appreciate theimportanceoftwocriticalpillarsoffinancingMSMEsectorviz.,timelinessand adequacy of credit.

17. Credit Counsellors: For bridging the information asymmetry on theMSMEborrowers side,RBI is initiatingaprocess forputting inplace aframework for accreditation of credit counselorswho are expected toserve as facilitators and enablers for micro and small entrepreneurs.SinceMSMEsaretypicallyenterpriseswithlittlecredithistoriesandwith

14

inadequateexpertiseinpreparingfinancialstatements,creditcounselorswillassisttheborrowersinpreparingtheirprojectreportsandalsohelpbanksmakebetterinformedcreditdecisions.

18. Revival and Rehabilitation of MSMEs: Another key step in the direction of supporting the firms in distress is the issuance of guidelines on the Framework on Revival and Rehabilitation of MSMEs, which provides an institutionalized framework for rehabilitation of enterprises whicharepotentiallyviable,butareundertemporaryduress.TheFrameworkprovidesforastructuredmechanism,whichcouldbetriggeredeitherbythebankerorbytheentrepreneuratthefirstsignsofstress.Theproblemresolutionisscaleduptoacommitteewithatimeboundschedule.Thisisaverypowerfultoolandurgeuponthebankerstogetthisprocessrollingat the earliest.

(iii)The difficult ‘C’s -Credit and Collateral:

19.Theissueoffindingtherightbalanceinsecuringaloanwithoutpushingthe borrower to informal sector has been a bugbear for the bankingsystem.Thisissoughttobeaddressedthroughcreationanddevelopmentofrightinstitutionalstructures.Someoftheseefforts:

20. Movable Asset Registry: Movable assets, as opposed to fixed assetssuchaslandorbuildings,oftenaccountformostofthecapitalstockofprivatefirmsandcompriseanespeciallylargeshareformicro,smallandmedium-size enterprises. Hence,movable assets are themain type ofsecuritiesthatfirmscanpledgetoobtainbankfinancing.CERSAI,inactivecoordinationwithGovernmentofIndiaandReserveBankhasestablishedthemovableassetregistry,whichwhenmaturewouldhaveamultipliereffectinlendingtothesector.

21. TReDS: In order to solve theproblemof delayedpayment toMSMEs,RBI has licensed three entities for operating the Trade ReceivablesDiscountingSystem(TReDS).ThesystemwouldfacilitatethefinancingoftradereceivablesofMSMEenterprisesfromcorporateandotherbuyers,including Government departments and public sector undertakings(PSUs)throughmultiplefinanciers.TheobjectiveistocreateElectronicBill Factoring Exchanges which could electronically accept and settlebills so thatMSMEs could encash their receivableswithout delay. It isexpected that theTReDSwillcommenceoperationswithinthiscurrentfiscal.It would be important that the use of TReDS is made mandatory for, to begin with corporate and PSUs and later for the Government departments. The MSME Ministry to proactively examine this aspect as success of TReDS initiative can be a game changer for the sector.

15

22. Utility of the Credit Guarantee Scheme:Realizing the problems of small borrowersinpostingcollaterals,RBIhasaskedthebanksnottoinsistoncollateral in case of loans up to ` 10 lakh extended to units in the MSE sector.

23. On one hand, the guideline on collateral-free loans has led banks toattimesdevisewaysofdenyingcredit to theMSMEsborrowers,whileon theotherextreme; theprovision for credit guaranteehaspotentialto cause deterioration in quality of credit appraisal and due-diligence,consequently straining the resources of the CGTMSE. Clearly, bothoutcomes are undesirable that borrower is compensated by way of a better pricing in loan for the availability of collateral. Further, the CGTMSE to evolve a framework for making the pricing risk-based rather than having a uniform risk premium related to the past performance and quality of individual portfolios. Eventually, this activity should also move to an open market system.

(iv) The Cumbersome ‘D’- Documentation

24.The absence of credit history and the need for documentation oftenpushes the micro-entrepreneur away from conventional bankingchannelstothemoreinformalsectors.Thishastobeaddressedthroughaconstantprocessofsimplificationofproceduresandmoreimportantlybyleveragingtechnology.

25. Udyami Mitra Portal setupbySIDBIleveragesITarchitectureofStand-UpMitraportalandaimsatinstillingeaseofaccesstoMSMEs’financialandnon-financialserviceneeds.

Conclusion

Our demographics compel us to push forward this agenda and makequantumjumpssothatentrepreneurscanstartanddrivebusinesseswithoutworryingaboutfinance.Weare committed to thisparadigmshiftand theslewofmeasuresthatarebeingtakenbytheRBI,otherapexinstitutionsandstakeholders signify this.

16

Interesting,ProfitableandChallenging:BankinginIndiaToday*

Perhaps the mostimportantissueonthemindsofbankers,giventheresultsseason,istheAssetQualityReviewinitiatedinearly2015-16.IthasimprovedrecognitionofNPAsandprovisioninginbanksenormously,andmanyofyouhavefullyimbibedthespiritofthereview.Somebankshavetakensignificantstepsinrecognizingincipientstressearly.

Now focus should move more to improving the operational efficiencyof stressed assets, and creating the right capital structure so that allstakeholders can benefit. This implies simultaneous action on two fronts.Wherenecessary,newprojectmanagement teamshave tobebrought in,sometimesasowners,andwherethisisnotpossible,asmanagers.A creative search for new management teams, including the possible use of public sector firms or private sector agents, is necessary, as are well-structured performance incentives for non-owner teams such as bonuses for meeting cash flow/profit benchmarks and stock options.

Of course, if the existing promoters are capable and reliable, they shouldbe retained. Equally important, the capital structure should be tailored to what is reasonable, given the project’s situation. If the loan is already anNPA, there is no limit to the kindof restructuring that is possible. If itis standardbut theproject is struggling,wehavea varietyof schemesbywhichamoresensiblecapitalstructurecanbecraftedfortheproject.Theseschemes include the 5/25, the SDR, and the S4A. A caveat is in order, though. SomeofthecurrentdifficultieswithstressedloanscomefromanunrealisticapplicationbybanksofaschemesoastopreventaloanturningNPA,ratherthanbecauseofa carefullyanalyzedbankeffort toeffectmanagementorcapitalstructurechange.RBIwillcontinuemonitoringtoseethatschemesareusedaswarranted,andtargetedatpromoterswhoarecooperativeandableratherthanmisusingthesystem.

To look beyond stressed assets to growthTheseareinteresting,profitable,andchallengingtimesforthefinancialsector.Interestingbecause the levelofcompetition isgoing to increasemanifold,both for customers as well as for talent transforming even the sleepiestareasinfinancialservices.Profitablebecausenewtechnologies,information,and new techniques will open up vastly new business opportunities and

Note: * Address by RBI Governor, Dr. Raghuram Rajan, to the FICCI-IBA Annual Banking Conference, on August 16, 2016, Mumbai.

17

customers. Challenging because competition and novelty constitute aparticularlyvolatilemixintermsofrisk.

Interesting and Profitable

• Overthenextyear,17newnichebankswillbeginbusiness.Inaddition,licensingforuniversalbanksisnowontap,sofitandproperapplicantswithinnovativebusinessplansandgoodtrackrecordswillenter.Financialtechnology will throw up a variety of new ways of accessing the customer and serving her, so new institutions that we have little awarenessof todaywill soonbea sourceof competition. Thesewill finally drawcustomersectors,firms,and individualswithoutaccess today into theformalfinancialsystem.Thosecustomersthatarealreadybeingservedwillbespoiledforchoice.Fortheserviceprovider,eventhoughgreatercompetitionwilltendtoreducespreads,accesstonewcustomersandnew needs will increase volumes.

• Moreover,riskandcostreductionthroughinformationtechnologyandriskmanagementtechniqueswilltendtoincreaseeffectiverisk-adjustedspreads. In sum then, despite increased competition, profitability canincrease.Thecomparativeadvantageofbanksmaylieintheiraccesstolowercostdepositfinancing,thedatatheyhaveoncustomers,thereachoftheirnetwork,theirabilitytomanageandwarehouserisks,andtheirabilitytoaccessliquidityfromthecentralbank.Theseshouldthenbethebasisfortheproductstheyfocuson.

Perhapsacoupleofexamplesmaybeuseful.Indiawillhaveenormousprojectfinancingneedsinthecomingdays.Eventhoughbankersareveryriskaversetoday,andfewprojectsarecomingupforfinancing,thiswillchangesoon.What is in the pipeline is truly enormous – airports, railway lines, power plants,roads,manufacturingplants,etc.Bankerswillremembertheperiodofirrationalexuberancein2007-2008.Herearewaysitcanbedifferentandrisks lowered.

Significantly more in-house expertise can be brought to project evaluation, including understanding demand projections for theproject’soutput,likelycompetition,andtheexpertiseandreliabilityofthe promoter. Bankers will have to develop industry knowledge in key areas since consultants can be biased.

Real risks have to be mitigated where possible, and shared where not. Real risk mitigation requires ensuring that key permissions for landacquisitionandconstructionareinplaceupfront,whilekeyinputsandcustomersaretiedupthroughpurchaseagreements.Wheretheserisks

18

cannotbemitigated,theyshouldbesharedcontractuallybetweenthepromoter and financiers, or a transparent arbitration system agreedupon. So, for instance, if demand falls below projections, perhaps anagreement among promoters and financiers can indicate when newequitywillbebroughtinandbywhom.

Element of project structuring – an appropriately flexible capital structure.Thecapitalstructurehastoberelatedtoresidualrisksoftheproject.Themoretherisks,themoretheequitycomponentshouldbe(genuine promoter equity, not fake borrowed equity, of course), andthe greater the flexibility in the debt structure. Promoters should beincentivized to deliver, with significant rewards for on-time executionand debt repayment.Where possible, corporate debtmarkets, eitherthrough direct issues or securitized project loan portfolios, should beusedtoabsorbsomeoftheinitialprojectrisk.Moresucharm’slengthdebt should typically refinance bank debt when construction is over.Hopefully, some of themeasures taken to strengthen corporate debtmarkets, including the new bankruptcy code, should make all thispossible.

Financiers should put in a robust system of project monitoring and appraisal, including where possible, careful real-time monitoring of costs.Forexample,canprojectinputcostsbemonitoredandcomparedwithcomparableinputselsewhereusingIT,sothatsuspicioustransactionssuggestingover-invoicingareflagged?

The incentive structure for bankers should be worked out so that they evaluate, design, and monitor projects carefully, and get significantrewards if these work out. This means that even while committeesmaytakethefinal loandecision,someseniorbankeroughttoputhernameontheproposal,takingresponsibilityforrecommendingtheloan.ITsystemswithinbanksshouldbeabletopullupoverallperformancerecords of loans recommended by individual bankers easily, and thisshouldbeaninputintotheirpromotion.

Note that none of this is really futuristic, but it requires amuch strongermarriagebetweeninformationtechnologyandfinancialengineering,withanimportantroleforpracticalindustryknowledgeandincentivedesign.Therearealsoinputstomakingprofitableprojectloans–suchastheavailabilityofCASAdeposits–thatwillaccruetothebanksthatbuildouttheirITtoaccessand serve the broader saver cheaply and effectively. Few banks have the in-housetalenttodoallthisnow,butpreparationisimperative.

19

Anareaofmore intensiveuseof ITandanalysis is customer loans,whichis second example. It seems today that, having abandoned project loans, everybankistargetingtheretailcustomer.Clearly,therisksinthisherdingwillmountovertime,asbankscompeteforlessandlesscreditworthycustomers.Butsomeofthisriskcanbemitigatediftheydosufficientduediligence.

Newmeansofcreditevaluationareemerging.Forexample,somelendersareexaminingnot justcredithistoriesfromthecreditbureaubutminingtheirowndataandalsodatafromsocialmediapostsbytheapplicantstoseehowreliable theymight be. Various forms of crowd funding, intermediated bypeer-to-peerlenders,alsoclaimsuperiorcreditevaluation.Ofcourse,muchofthehooplasurroundingthesenewformsoflendinghasyettobetestedbyaseriousdownturn,anditisunclearhowresponsibilitiesforrecoverywilldevolvebetweenintermediaryandinvestoratsuchtimes.

Nevertheless, in this Information age, not only are theremore data withwhich to determine a loan applicant’s creditworthiness, it is also possibletotrackthebehaviourforearlywarningsignsofstress.Furthermore,inthisinterconnectedworld,aborrower’sinabilitytohideadverseinformationsuchasdefaultwhentaggedbyauniqueIDconstitutesabigincentivetorepay.

Importantly,banksnolongerhaveamonopolyoverallcredit-relateddata; Some IT companiesmaydoabetter job inpulling togethereventhebank’sdata,inadditiontotrawlingforotheravailabledata,andanalyzingitalltomakebetterlendingandmonitoringdecisions.Loanapplicationsanddecisionsarenowbeingmadeentirelyonline,withoutaborrowerhavingtostepintoabranch.AlliancesbetweenITcompaniesandbanksarelikelytoincreasesignificantly.

The bottom line is that competition is increasing, and ways ofdeliveringfinancialservicesarechangingtremendously.Bankshaveto discover strategies to use their traditional, although eroding,advantagessuchasconvenience, information,andtrusttoremainonthecompetitivefrontier.Competitionandinnovationconstituteaparticularlyvolatilemixintermsofriskchallengingbanks’traditionalrisk management capabilities. They are also a challenge to theregulator,whowantsthebestforthecustomer(andthereforewantstoencouragecompetitionandexperimentation),whilemaintainingsystemicstability (andthuswantstounderstandrisksbeforetheygettoolargeorwidespread).

20

The Authorities’ DilemmaBefore turning to how the banks should respond to these competitiveand technological forces, letusaskhowthese forcesaffect the regulatorycompact.Ideally,theauthoritiesshouldensuretheiractionsareinstitution,ownership,and technologyneutral soas toensure that themostefficientcustomer-oriented solutions emerge through competition.However, if theauthorities deliberately skew the playing field towards some category ofinstitutionsandawayfromothers,competitionmaynotproducethemostefficientoutcome.

Banks in India have been subject to the grand bargain,whereby they getthebenefitsofraisinglowcostinsureddeposits,liquiditysupportandcloseregulationby the centralbank in return formaintaining reserveswith thecentral bank, holding Government bonds tomeet SLR requirements, andlending to the priority sector.

Inaddition,publicsectorbanksarefurthersubjecttoGovernmentmandatessuch asopeningPMJDYaccounts, ormakingMUDRA loans. They are alsosubject to hiring mandates, in particular the need to hire through open all-India exams rather than from specific campuses or from the localcommunity, and to meet various government diversity mandates. In part compensation, public sector banks do get more Government deposits and business, and are backed by the full faith and credit of the Government. While it is unclear whether the cost of the mandates outweigh the benefits, they do skew the competitive landscape.

Authorities like the central bank and the Government should, over themedium term, reduce the differences in regulatory treatment betweenpublicsectorbanksandprivatesectorbanks,andmoregenerally,betweenbanksandotherfinancialinstitutions.

Challenges Faced by Public Sector Banks Themostpressingtaskforpublicsectorbanks istocleanuptheirbalancesheets, a process which is well under way. A parallel task is to improve their governanceandmanagement. Equally important is tofill out the ranksofmiddle management that have been thinned out by retirements, and torecruittalentwithexpertiseinprojectevaluation,riskmanagement,andIT,includingcybersecurity.

(i) Governance TheBankBoardBureau(BBB),composedofeminentpersonalitieswith

integrity and domain experience, has taken over part of the appointments process in public sector banks. There are two ways the Governmentstill plays a role. First, the final decision on appointments is taken bytheAppointmentsCommitteeoftheCabinet.Second,appointmentsof

21

non-officialdirectorsontobankboardsstill lieoutsidetheBBB.AstheBBB gains experience, it would make sense to allow these decisions also tobetakenbyit.

Managementeffortstotightenpracticesarealsoneeded.Fartoomanyloans are done without adequate due diligence and without adequate followup.Collateralwhenofferedisnotperfected,assetsgivenunderpersonal guarantees not tracked, and post loan monitoring of the accountcanbelax.

(ii) Talent All public sector entities across theworld tend to paymore than the

private sector to lower level employees, and less than the private sector to higher level employees. Thismakes it hard for them to attract toptalent,butmakesiteasiertoattractgoodpeopleatlowerlevels.

(iii) Customers Publicsectorbanksenjoytrustwithcustomers.Anemphasisoncustomer

service and customer-centric advice may allow them to recapture low-costcustomerdepositsthataremigratingelsewhere.PublicsectorbanksshouldtaketheleadinemphasizingtheRBI’s5pointCharterofConsumerRights.Whileitisunderstandablethatwithstressedbalancesheets public sector banks do not want to make too many loans tostressed sectors, it is less clear why their deposit growth is faltering, for thelow-costdepositfranchisewillbethekeytotheirfuturesuccess.

(iv) Structure Some banks may be best off focusing on local activity and in effect,

becoming small finance banks. Others may be best off merging withotherbankssoastoobtainscaleandgeographicdiversification.Asbanksgetcleanedup,andtheirboardsarestrengthened,theirboardsshouldfocus on appropriate structure as part of an overall rethink on strategy.

Back to the Authorities Today, a variety of authorities – Parliament, the Department of FinancialServices, the Bank Board Bureau, the board of the bank, the vigilanceauthorities,andofcoursevarious regulatorsandsupervisors including theRBI –monitor theperformanceof thepublic sector banks.With somanyoverlappingconstituenciestosatisfy,itisawonderthatbankmanagementhas time to devote to themanagement of the bank. It is important that we streamline and reduce the overlaps between the jurisdictions of the authorities, and specify clear triggers or situations where one authority’s oversight is invoked.

22

Inparticular,wehavetomovemuchofthe governance to the bank’s board, withtheGovernmentexercisingitscontrolthroughitsboardrepresentatives(chosenbytheBBB),keepinginmindthebestinterestsofthebankandtheinterests of minority shareholders. Wherever possible, public sector bankboardsshouldbeboundbythesamerulesasprivatesectorbankboards–onereason why the RBI has recently withdrawn the Calendar of Reviews PSBs were asked to follow. Similarly, board membership of public sector banks should pay as well as private sector banks if they are to attract decent talent. As boardstakedecisions,theDepartmentofFinancialServicescouldmoveto

(i) A program role: for example, ensuring Government programs such as PMJDYarewell-designed,appropriatelyremuneratedtobanks,andprogressmonitored

(ii) A co-ordinating role: for example, ensuring financial institutions join acommon KYC registry and

(iii) A developmental role: revitalizing institutions like the Debt RecoveryTribunals through appropriate legislation. RBI would perform a purelyregulatory role, and withdraw its representatives on bank board’s – thiswill require legislative change.Overtime, RBI should also empower boardsmore,for instanceofferingbroadguidelinesoncompensationtoboardsbutnot requiring every top compensation package be approved. Given strongoversight from thebank’sboard, theCVCandCAGwouldget involvedonlyinextraordinarysituationswherethere isevidenceofmalfeasance,andnotwhenlegitimatebusinessjudgmenthasgonewrong.

With changes in technology, cyber security, both at the bank level and atthe system level, has become very important. I think it would be overlycomplacent foranyoneofus to saywearewellprepared tomeetall cyberthreats. A chilling statement by an IT expert is “We have all been hacked,the only question iswhether you know it or you don’t”. RBI isworking onupgrading the capabilities of its inspectors to undertake bank system auditas well as to detect vulnerabilities in them. RBI is also in the process of settingupanITsubsidiary,whichwillbeabletorecruitdirectlyfromindustry,and will give the Reserve Bank better ability to manage and supervisetechnology.

23

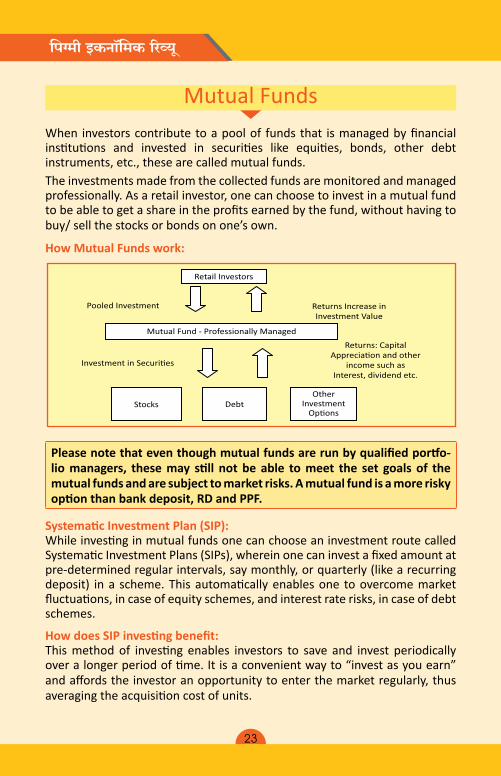

Mutual FundsWhen investorscontributetoapoolof fundsthat ismanagedbyfinancialinstitutions and invested in securities like equities, bonds, other debtinstruments, etc., these are called mutual funds. Theinvestmentsmadefromthecollectedfundsaremonitoredandmanagedprofessionally. As a retail investor, one can choose to invest in a mutual fund tobeabletogetashareintheprofitsearnedbythefund,withouthavingtobuy/sellthestocksorbondsonone’sown.

How Mutual Funds work:

Pooled Investment

Retail Investors

Returns Increase inInvestment Value

Mutual Fund - Professionally Managed

Investment in Securi�es

Returns: CapitalApprecia�on and other

income such asInterest, dividend etc.

Stocks DebtOther

InvestmentOp�ons

Please note that even though mutual funds are run by qualified portfo-lio managers, these may still not be able to meet the set goals of the mutual funds and are subject to market risks. A mutual fund is a more risky option than bank deposit, RD and PPF.

Systematic Investment Plan (SIP):WhileinvestinginmutualfundsonecanchooseaninvestmentroutecalledSystematicInvestmentPlans(SIPs),whereinonecaninvestafixedamountatpre-determined regular intervals, say monthly, or quarterly (like a recurring deposit) ina scheme.Thisautomaticallyenablesone toovercomemarketfluctuations,incaseofequityschemes,andinterestraterisks,incaseofdebtschemes.

How does SIP investing benefit:Thismethodof investing enables investors to save and invest periodicallyoveralongerperiodoftime.Itisaconvenientwayto“investasyouearn”andaffordstheinvestoranopportunity to enter the market regularly, thus averagingtheacquisitioncostofunits.

24

Example:Suppose A invests ` 1000 every month in an equity mutual fund scheme startinginJanuary.Binvests` 12000 in one lump sum in the same scheme inJanuary.Thefollowingtable illustrateshowtheirrespectiveinvestmentswouldhaveperformedfromJanuarytoDecember,2014.

A’s Investment B’s InvestmentMonth NAV Amount Units Amount UnitsJan-14 9.345 1000 107.0091 12000 1284.109Feb-14 9.399 1000 106.3943Mar-14 8.123 1000 123.1072Apr-14 8.012 1000 124.8128May-14 8.75 1000 114.2857Jun-14 8.925 1000 112.0448Jul-14 9.102 1000 109.866Aug-14 8.31 1000 120.3369Sep-14 7.568 1000 132.1353Oct-14 6.462 1000 154.7509Nov-14 6.931 1000 144.2793Dec-14 7.6 1000 131.5789Total1480.601 1284.109

ThusonecanseethatbytakingtheSIProute,Ahaspurchasedtheunitsatvarious intervalsthusallowingAtobenefitfromtimeswhenthepriceperunit was lower. As a result, at the end of the 12 months, A has more units thanB,eventhoughBinvestedthesameamount.That’sbecausetheaveragecost of A’s units is much lower than that of B. B made only one investment and that too when the per-unit price was high.

A’s average unit price = 12000/1480.6012= ` 8.105

B’s average unit price = ` 9.345

“Suppose the NAV amounts had been different. Would A still be better off?” Yes. It has been found that unless NAVs are consistently rising, investingthroughSIPwillusuallydeliverabetteraveragecostperunitthanaone-timeinvestment.Asaresult,anSIPinvestorwillreceiveagreaternumberofunits.

Onceyouidentifytheschemeyouwanttoinvestinandtheamountrequiredto achieve your financial goals, you can decide on themonthly/quarterlyamounttobesetasideandinvestedtoreachthatgoal.Mostinvestorswant

25

tobuystockswhenthepricesarelowandsellthemwhenpricesarehigh. But timing the market is time consuming, risky and a near impossible task to do on a sustained basis. A more successful investment strategy is to adopt the method called Rupee Cost Averaging. Systematic investing i.e. investing through the SIP route can help put the power of compounding and price averaging on your side.

Various Types of Mutual Funds:Eachfundhasapredeterminedinvestmentobjectiveaccordingtowhichthefund’s assets, scope of investment and investment strategies are dictated.

Mutual Funds Classification:

BroadClassifica�on ofMutual Funds

Debt Funds Equity Funds Hybrid Funds Others

Short TermDebt, LongTerm Debt,

Gilt, Income,Liquid,

Floa�ng �ate

EquityDeversified,Index, ELSS,

Sector, Themebased, Large

Cap, Mid Cap,Small Cap, etc

BalancedMonthly

Income Plans

Gold, Commodity,Interna�onal

funds, sociallyresponsible,

exchange traded,real estate, fund

of funds etc.

Types of Mutual Funds:

1. Closed Ended: One’sinvestmentremainslockedinforaspecifiedperiodoftime.

2. Open Ended: Onecaninvestandwithdrawhis/herfundsonanyworkingday.

3. Growth: Theprofitsmadebythefundarereinvestedforoneandthisisreflected

in the value of one’s units.

4. Dividend: Theprofitsofthefundarepaidouttoinvestorsfromtimetotimeinthe

form of dividends.

26

Why Banks sell Mutual Fund to Customers?Banks getmanyadvantagesbycross-sellingmutualfundsamongitscustomers inday-to-daybusiness.Namely,(i)FinancialSuperMarket-Allfinancialproducts–Customersgetunderoneroof(ii)ThrustonNon-interestBasedFeeIncome(iii)ConsistentRevenueatlowcost(iv)CASAbuilding/Stickinesstotheaccount(v)Word-of-MouthPublicity(vi)CustomersEngagement&Delight

PROS:1. Professionally managed investment fund. 2. Reducedriskbecausemostmutualfundshaveadiversifiedportfolio.3. Convenientcomparedtomaintainingone’spersonalportfolioofsecurities.4. Long-term capital gains are tax exempt.5. Low-cost:Mutualfundsareabletotakeadvantageoftheirbuyingandselling

size and thereby reduce transaction costs for investors.When you buy amutual fund, youareable todiversifywithout thenumerous commissioncharges.

6. Mutual funds are typically very liquid investments. Unless they have a pre-specifiedlock-in,yourmoneywillbeavailabletoyouanytimeyouwant.

7. Transparentasmutualfundshavetomakefulldisclosureofinvestmentsonaperiodicbasis.

8. Flexibilityintermsofchoicesastherearenumerousschemetypestosuittheneedsofamultitude.

CONS:1. Higherriskcomparedtoinvestmentoptionslikefixeddeposits.2. Unpredictablecashflows.3. Associated sales charges and other expenses. 4. Short-termcapitalgainsareliabletobetaxed.5. If the manager does not perform as well as you had hoped, you might not

make as much money on your investment as you expected. 6. Variousrisks involved:creditrisk, interestraterisks,marketrisk, inflation,

liquidity and policy risks. Taxation: Different mutual fund schemes are subject to different taxation rules andregulations, depending on the type of mutual fund and term of investment. In some schemes even the dividend is taxed. Accordingly, it is, important to enquireabout theapplicable taxation rulesof theschemeoneselects,beforeone invests in it.

Source: Money Matters –Home Maker to Financial Decision Maker.

27

Masala BondsMasalabondsarerupeedenominateddebt instruments issued inoffshoremarketto investorsby Indiancompaniesandsettlementhappens indollarterms.ARupeedenominatedbond isabond issuedbyan Indianentity inforeignmarkets and the interest payments and principal reimbursementsaredenominated(expressed)inrupeetermsandsettlementmadeindollarterms.Themajorbenefitofthisbondisthatthecurrencyriskisnotbornebytheissuer.AnissuercanissueMasalabondsworthamaximum$750millionayearandthebondsmusthaveaminimummaturityoffiveyears.

For example,IFCissuesMasalabondintheoffshoremarket,thepriceofabondwillbedenominatedinIndiancurrencyandnotintheUS$but,atthetimeofmaturity,itwillbepaidinthetermsofdollarValue.

Particulars ValuePriceofabondinRupeeterms 1050INR/USD rate on the investment date 70AmountInvestedUSD($) 17.5RedemptionAmountinRupeeterms 1200INR/USDrateonRedemptiondate 60RedemptionAmountinUSD($) 20The above table helps one to understand how the bond is issued to anoffshore investor, the investor is required topay in rupee terms i.e.$17.5 (` 1050/Rs.70)atthetimeofpurchasewhereas,onmaturityhereceivesthereturnsinthedollartermsi.e.$20(Rs.60*$20=Rs.1200)forhisinvestments.

History of Masala bonds:International Finance Corporation (IFC) issued a 10-year, 10 billion IndianrupeebondinNovember2014toincreaseforeigninvestmentinIndiaandmobiliseinternationalcapitalmarketstosupportinfrastructuredevelopmentinthecountry.MasalabondwasthefirstIndianbondtogetlistedinLondonStockExchange.IFCnameditMasalabondstogivealocalflavourbycallingtomindIndiancultureandcuisine.Thefollowingcompanieswhoissuedandplanning to issueMasala Bonds in OffshoreMarkets namely, IFC (` 1000 Crore)inNov-2014,IFC(` 170crore)inNov-15,IFC(` 200crore)inNov-16,HDFC($750Million),YesBank($500Million)inDec-16,NTPCLtd($500-$750Million),PowerFinanceCorporation($500-$750Million)andIndianRailwayFinanceCorporation($300-500Million).

28

Benefit to Corporates:

It helps the Indian companies to diversify their bond portfolio. Forexample,earliercompaniesusedtoissueonlycorporatebonds.AMasalabondisanadditiontotheirbondportfolio.

It helps the Indian companies to cut down cost. They can borrow atlow interest rates fromoffshoremarkets. Interests rates in developedcountries are much lower than prevalent in India. If the company issues any bond in India, it carries an interest rate of 7.5%-9.00%whereas;MasalaBondsoutsideIndiaisissuedbelow7.00%interestrate.

It helps the Indian companies to tap a wide investor’s base as thesebondsareissuedintheoffshoremarket.

BeingissuerstheyarenotsubjectedtoFXrisks.Itwillbefullybornebytheinvestors.IndiancorporateshavesufferedconsiderablelossesearlieronECBwhichareusuallyUSDdominatedduetocontinuousstructuraldowntrend of INR against USD since last 2-3 decades.

Benefit to Investors:Masala bond, carrying relativelymuch higher interest rate, is a great

investmentoptionforoffshoreinvestors.They can bet on INR exchange rates. They can benefit when rupee

appreciatesagainstthebond’sredeemable/repayablecurrency.Investors who are reluctant to venture into unknown markets can easily

showinterestinmasalabondsowingtothecredibilityofIFC.AnoffshoreinvestorearnsbetterreturnsbyinvestinginMasalabonds

rather than by investing in his home country. For example, if he hadinvestedinthebondofferedinhishomecountrytheUS,thebondyieldishardly2%whereas ifhe invests inrupeedenominatedmasalaBondtheyieldrangesfrom5.00%to7.00%.

AninvestorwillbenefitfromhisinvestmentinMasalabondsiftherupeeappreciates at the timeofmaturity. For example, if the investor pays$17.5andreceives$30 i.e.the investor isearningaprofitof$12.5onhis investment.

AsitisaRupeedenominatedbond,theriskwillbebornebytheinvestor.The issuerdoesnotcarryanycurrencyriskby issuingthisbond intheforeign market. For example, if the investor pays $17.5 and receives $15.85.Thelossof$1.65onhisinvestmentduetofluctuationinexchangeratehastobebornebytheinvestor.

29

Benefit to India:1. Masalabondswillhelpinbuildingupforeigninvestor’sconfidenceand

knowledge about Indian economyand currencywhichwill strengthenforeign investments in the country.

2. Thiswillcontributetocapitalaccount,thusbalancingBalanceofPayment.

3. Masalabondisagoodwaytotapforeigncapital. IndiahasenvisionedmanyambitiousgoalslikeMakeinIndia,developingsmartcities,DigitalIndia,boostinginfrastructure,climateINDCetc.ForthisIndiawillrequirearound$400billion(INR26lakhcrores)innextfiveyears.Abigchunkofitwillhavetobefinancedbyforeigncapital.Indiahastolookforwaystotapforeignsovereignwealthandattractforeigncapital.

4. InIndiamanylong-termdebtstressedprojectsespeciallyinfrastructureandpowerarestalledduetocapitalshortage,long-termMasalabondsislucrativeforpower,roadandinfracompanies.

5. INRhas been falling in a structural downtrend since last fewdecadesagainstmajorhardcurrencies.GiventhatFXriskisbornebythecreditor,during repayment of bond coupon and maturity amount, if rupeedepreciates,RBIwillrealizemarginalsavingduringrepayment.

Banking Sector:To further encourage the overseas Rupee bond market, Banks are beingpermitted to issueRupeebondsoverseas (MasalaBonds) for their capitalrequirementsandforfinancinginfrastructureandaffordablehousing.

AspertheRBI’sregulationonMasalabonds,themoneycanbeusedonlyforinfrastructurefinancingpurposes inSeptember2015. InAugust2016,theRBIallowedbanks:

(i) To issueRupeedenominatedbonds issuedinoverseas(MasalaBonds)undertheextantframeworkofincentivizingissuanceoflongtermbonds.

(ii) To issue Perpetual Debt Instruments (PDI) qualifying for inclusion asAdditional Tier 1 capital and Debt Capital Instruments qualifying forinclusionasTier2capitalbywayofrupeedenominatedbondsoverseas.

TheoverallguidelinesforrupeedenominatedbondswillbesameasthatforExternal Commercial Borrowings(ECB).

30

Issuance of Rupee denominated bonds overseas

Sr. No.

ECB Parameter Framework

1 Eligibility of borrowers

Any corporate or body corporate is eligible toissue Rupee denominated bonds overseas. RealEstateInvestmentTrusts(REITS)andInfrastructureInvestment Trusts (InvITs) coming under theregulatory jurisdiction of the Securities andExchangeBoardofIndiaarealsoeligible.

2 Type of Instrument

OnlyplainvanillabondsissuedinaFinancialActionTask Force (FATF) compliant financial centres,either placed privately or listed on exchanges as perhostcountryregulations.

3 Recognized Investors

Any investor from a FATF compliant jurisdiction.Banks incorporated in India will not have access to these bonds in any manner whatsoever.Indian Banks, however, can act as arranger and underwriter. In case of underwriting, holding ofIndian banks cannot be more than 5 percent oftheissuesizeafter6monthsofissue.Further,suchholding shall be subject to applicable prudentialnorms.

4 Maturity Minimummaturityperiodof5years.Thecallandputoption,ifanyshallnotbeexercisablepriortocompletionofminimummaturity.

5 All-in-cost The all-in-cost of such borrowings should becommensuratewithprevailingmarketconditions.This will be subject to review based on theexperience gained.

6 End-uses Theproceedscanbeusedforallpurposesexceptfor the following: (i) Real estate activities otherthan for development of integrated township/affordable housing projects. (ii) Investing incapital market and using the proceeds for equity investmentdomestically(iii)Activitiesprohibitedaspertheforeigndirectinvestment(FDI)guidelines. (iv) On-lending to other entities for any of theaboveobjectives.(v)Purchaseofland.

31

7 Amount Under the automatic route the amount will beequivalent of USD 750 million per annum. Cases beyondthislimitwillrequirepriorapprovaloftheReserve Bank.

8 Conversion Rate TheForeigncurrency-Rupeeconversionwillbeatthemarketrateonthedateofsettlementforthepurposeof transactionsundertaken for issueandservicingofthebonds.

9 Hedging The overseas investors will be eligible to hedgetheir exposure in Rupee through permittedderivative products with AD Category-I banks inIndia. The investors canalsoaccess thedomesticmarket through branches/subsidiaries of Indianbanks abroad or branches of foreign bank withIndianpresenceonabacktobackbasis.

10 Leverage The leverage ratio for the borrowing by financialinstitutionswillbeaspertheprudentialnorms,ifany,prescribedbythesectoralregulatorconcerned.

ConclusionOffshorebondshaveitsownsetofadvantagesanddisadvantagesforboththe issuer and the investor aswell as for theeconomy.Competition fromoffshore markets may induce improvements in domestic bonds marketssuchasstrengtheningofdomesticmarketinfrastructure,improvinginvestorprotection and removing tax distortions that hinder domestic marketdevelopment etc. Against these benefits come the risks associated withfinancial openness and sudden shifts in capital flows, and the risk thatoffshoremarketsmaydrawliquidityawayfromthedomesticmarket.

Compilationby: Economic Research Cell, P & D SyndicateBank

32

GoldLoanProcedure&PrecautionsJewelLoans(Goldloans)aresimpleandsecuredloansthatindividualscanavail by offering Gold Jewellery as collateral to lending banks. Gold loansarebestsuitedforthosewhoneedaquicksolutiontoshort-termliquidityissuesanditisrelativelyhassle-freeandquick.OurBankisalsooneofthetoplendersintheGoldloanportfolioamongPSB.LoansextendedagainstGoldmaybecategorizedunderPriorityorNon-Prioritysector advances depending upon the purpose of the credit and nature of its enduse.GoldLoansgrantedtofarmersforagricultureandalliedactivitiesfallunderpriority sectoradvances.Gold loans sanctioned forcropproductionis eligible for interest subvention fromRBI@ 2% for loans granted up to ` 3 lakh.Gold loansgranted forbusinessactivitiesandotherdomesticorpersonal use, fall under Non-Priority sector advances.

General guidelines to be followed for advances against Gold:1. ProperduediligenceandKYCabout theBorrower shall be conducted

beforeextendingGoldLoans.Borrowershouldbeproperly introducedtothebank.

2. Borrowershouldbeanagriculturist foravailing loanunderagricultureand allied activities. In case of other priority sector activities, theborrowershouldbepursuingtherelevantactivity.

3. JewelLoanstoallotherborrowerstobeclassifiedasNon-Prioritysector.4. JewelloansshallbegrantedbyonlythoseBrancheshavingtheservices

of approved Jewel Appraiser.5. Loans to Value Ratio (LTV) on Jewel Loans should be maintained as

perRBI guidelines fromtime totime, atpresent it shouldnot exceed75%of thevalueofgold. Scaleoffinance issued fromRetailBusinessDepartmentfromtimetotimeshallbestrictlyfollowed.

6. Gold Jewellery with purity less than 22 carat should be valuedproportionately.

7. IncaseofGoldLoansgranted foragriculturalpurposes, loansshallbegranted based on the scale of finance applicable for the crop grown.However,forthepurposeofclaiminginterestSubsidytheloanamountshall not exceed ` 3lakhasperRBIdirective.

8. ThemaximumamountstipulatedforextendingGoldLoanisasfollows:a.GoldLoanstoAgriculturists:` 3 lakh per partyb.GoldLoansunderNon-Priority:` 10 lakh per partyc.GoldLoansforBusinessPurposes:` 20 lakh per party

33

Precautions to be taken in lending against Gold:1. It is advisable that advances are to be made to persons properly

introducedtothebank.

2. The Branch should satisfy itself about the ownership of the GoldOrnaments before accepting them for pledge. Branch should obtaindeclaration from the Borrower that the Ornaments are his/her ownproperty and he/she has the fullest right to pledge.

3. TheJewelsshouldbegotappraisedbytheJewelAppraiserattheBranchpremises itself under CCTV surveillance, and under no circumstances,theJewelsshouldbesenttotheJewelAppraiser’splaceforappraisalforthepurposeofgrantingJewelLoan.

4. Thevaluationcertificateof the JewelAppraisershouldclearly indicatethe description of theOrnaments, Grossweight andNetweight. ThevaluationreportshouldbedulysignedbytheAppraiserandCustomerandshouldbekeptalongwiththeLoanDocuments.

5. For extending Gold loans of ` 5lakhandabove,priorclearancefromtheRegionalHeadshallbeobtainedbytheBranches.

6. All Gold Loans with sanctioned limit of ` 1 lakh and above shall be got re-apprised on yearly basis, independent of tenor of the loan. The re-appraisal shall be got done by different Jewel Appraiser, who has not done the first appraisal.

7. IncaseofGoldLoansofabove` 5lakhtheJewelsaretobeappraisedbyotherempanelledJewelAppraiserbeforesanctionanddisbursement.

Restriction in lending:NoLoanshallbearrangedagainstBullions/Bars/Primarygold.

While advancing against the security of specially minted Gold coins, weight of the Gold coins shall not exceed 50 grams per customer.

NoJewelLoanshallnormallybearrangedtobank’sJewelAppraiserortohisrelativesortopersonsintroducedbyhim,unlesstheJewelsproposedtobepledgedareindependentlyappraisedbyotherAppraisers,underinformationtoRegionalOffice.

(Refer Cir No: 297/2013, 248/2014)

Compilationby: Economic Research Cell, P & D SyndicateBank

34

UDAY SchemeThe Ujwal DiscomAssurance Yojana (“UDAY”), a scheme for the financialturnaroundofpowerdistributioncompanies(“Discoms”),wasapprovedbytheCabinetonNovember5,2015,withanobjectivetoimprovetheoperationand financial efficiency of State owned Power Distribution Companies. TheUDAYschemeintendstoachievethisthrough

(a) ImprovingoperationalefficienciesofDiscoms.

(b) ReducingthecostofpowergenerationbyDiscoms.

(c) Financial turnaroundofDiscoms throughState(s) takeoverofDiscomsdebts.

(d) FinancingfuturelossesandworkingcapitalofDiscomsbyState(s)

(e) ReductionininterestcostofDISCOMs.

(f) EnforcingfinancialdisciplineonDISCOMsthroughalignmentwithStatefinances.

Objectives:UDAYisapath-breakingreforminthepowersectorforrealizingaffordableandaccessible24x7PowerforAll.Itisanotherdecisivestepfurtheringthelandmark strides made in the Power sector with the sector witnessing a series ofhistoricimprovementsacrosstheentirevaluechain,fromfuelsupplytogeneration transmission (highest ever increase in transmission lines) andconsumption

Reasons for setting up of UDAY scheme:Theweakestlinkinthevaluechainisdistribution,whereinDISCOMsinthecountry have accumulated losses of approximately ` 3.8 lakh crore and outstanding debt of approximately ` 4.3 lakh crore (as onMarch, 2015).Financially stressed DISCOMs are not able to supply adequate power ataffordablerates,whichhampersqualityoflifeandoveralleconomicgrowthanddevelopment.Efforts towards100%villageelectrification,24x7powersupplyandcleanenergycannotbeachievedwithoutperformingDISCOMs.Poweroutagesalsoadverselyaffectnationalpriorities like“Make in India”and“DigitalIndia”.Inaddition,defaultonbankloansbyfinanciallystressedDISCOMshasthepotential toseriously impactthebankingsectorandtheeconomy at large.

35

Duetolegacyissues,DISCOMsaretrappedinaviciouscyclewithoperationallossesbeing fundedbydebt.OutstandingdebtofDISCOMshas increasedfromabout` 2.4lakhcrorein2011-12toabout` 4.3 lakh crore in 2014-15, withinterestratesupto14-15%.

Salient features of the UDAY scheme:1. To improve operational efficiency, the UDAY scheme has identified

specific areas for improvement (for example, compulsory feeder anddistributiontransformermetering,indexingandmappingoflossesandquarterlytariffrevisions)withinaspecifiedtimeframe,andmeasuredagainstAT&ClossesaspertrajectorytobefinalizedbytheMinistryofPower (“MoP”)andparticipatingState(s).

2. RecognizingcostlypowerasaprimaryreasonforthesystemicfinancialdistressofDiscoms,theUDAYschemehasproposedstepstobetakentoreducecostofpower.Forexample, increasedsupplyofdomesticcoal,coallinkageandcoalpricerationalization,supplyofwashedandcrushedcoalbyCoal India Limited (“CIL”)within specifieddates, allowing coalswapsfrominefficientplantstoefficientplants,etc.

3. ForthefinancialturnaroundofDiscoms,theUDAYschemeseeks:

• ParticipatingStatestotakeover75%ofthedebtsofDiscoms(bywayofgrant),asonSeptember30,2015overaperiodoftwoyears:50%ofsuchdebtswillbetakenover inthefinancialyear2015-16and25%inthefinancialyear2016-17;

• Participating States to issue non-statutory liquidity ratio (“SLR”)bonds, including state development loan (“SDL”) bonds againstDiscoms’ loans,forsubscriptionfirstlybypensionfunds, insurancecompaniesandotherinstitutionalinvestors.Thebalancebonds(nottakenupbypensionfunds,insurancecompanies,etc.)tobeoffereddirectlytolenderbanks/financialinstitutionsinproportiontotheircurrentlendingtoDiscoms.Proceedsofsuchissuesofbondswillbetransferred toDiscoms forpayingoff their loans to lenderbanks/financialinstitutions;

• Lenderbanks/financial institutionsnot to levyprepayment chargeonDiscoms’debts.Lenderstoalsowaiveoffunpaidoverdueinterest(including penal interest) on Discoms’ debt, and to adjust suchoverdue/penalinterestpaidsinceOctober1,2013;and

36

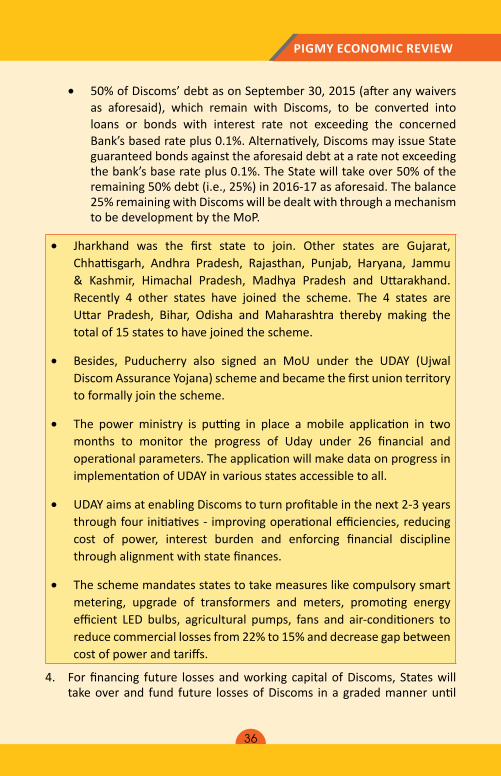

• 50%ofDiscoms’debtasonSeptember30,2015(afteranywaiversas aforesaid), which remain with Discoms, to be converted intoloans or bonds with interest rate not exceeding the concernedBank’sbasedrateplus0.1%.Alternatively,DiscomsmayissueStateguaranteedbondsagainsttheaforesaiddebtataratenotexceedingthebank’sbaserateplus0.1%.TheStatewilltakeover50%oftheremaining50%debt(i.e.,25%)in2016-17asaforesaid.Thebalance25%remainingwithDiscomswillbedealtwiththroughamechanismtobedevelopmentbytheMoP.

• Jharkhand was the first state to join. Other states are Gujarat,Chhattisgarh, Andhra Pradesh, Rajasthan, Punjab, Haryana, Jammu& Kashmir, Himachal Pradesh, Madhya Pradesh and Uttarakhand. Recently 4 other states have joined the scheme. The 4 states are Uttar Pradesh, Bihar, Odisha and Maharashtra thereby making thetotal of 15 states to have joined the scheme.

• Besides, Puducherry also signed an MoU under the UDAY (Ujwal DiscomAssuranceYojana)schemeandbecamethefirstunionterritoryto formally join the scheme.

• The power ministry is putting in place a mobile application in twomonths to monitor the progress of Uday under 26 financial andoperationalparameters.TheapplicationwillmakedataonprogressinimplementationofUDAYinvariousstatesaccessibletoall.

• UDAYaimsatenablingDiscomstoturnprofitableinthenext2-3yearsthroughfour initiatives- improvingoperationalefficiencies,reducingcost of power, interest burden and enforcing financial disciplinethroughalignmentwithstatefinances.

• Theschememandatesstatestotakemeasureslikecompulsorysmartmetering, upgrade of transformers and meters, promoting energyefficient LED bulbs, agricultural pumps, fans and air-conditioners toreducecommerciallossesfrom22%to15%anddecreasegapbetweencostofpowerandtariffs.

4. Forfinancing future lossesandworking capitalofDiscoms, Stateswilltakeoverand fund future lossesofDiscoms inagradedmanneruntil

37

thefinancialyear2020-21.Also, lenderbanks/financial institutionsareno longertoadvanceshort term loanstoDiscomsforfinancing lossesbutmayfinanceDiscoms’workingcapitalrequirementbywayofloans (orbylettersofcreditwhereverpossible),onlyupto25%oftheconcernedDiscom’spreviousyear’sannualrevenue(orasperprudentialnorms).

5. StateswhichachieveoperationalmilestonesoftheUDAYschemewillbeentitledtoadditional/priorityfundingthroughvariousfunds/schemesoftheMoPandMinistryofNewandRenewableEnergy.

Compilationby: Economic Research Cell, P & D SyndicateBank

“NobodyhadreservationsaboutthefundamentalsandtherobustnessofwheretheIndianeconomyispositionedtoday”

ShaktikantaDas,EconomicAffairsSecretary,afterameetingwithForeignPortfolioInvestors

38

Cashless EconomyIndiacontinuestobedrivenbytheuseofcash;lessthan5%ofallpaymentshappen electronically however the Govt and RBI intended to make India a cashlesssociety,withtheaimofcurbingtheflowofblackmoney.EventheRBIhas also recently unveiled a document - “Payments and Settlement Systems in India: Vision 2018”-settingoutaplantoencourageelectronicpaymentsandtoenableIndiatomovetowardsacashlesssocietyoreconomyinthemedium and long term.

Acashlesseconomyisoneinwhichallthetransactionsaredoneusingcardsordigitalmeans.Thecirculationofphysicalcurrencyisminimal.Indiausestoomuchcashfortransactions.Theratioofcashtogrossdomesticproductisoneofthehighestintheworld-12.42%in2014,comparedwith9.47%inChinaor4%inBrazil.Lessthan5%ofallpaymentshappenelectronically.Thenumberofcurrencynotesincirculationisalsofarhigherthaninotherlargeeconomies.Indiahad76.47billioncurrencynotesincirculationin2012-13comparedwith34.5billionintheUS.Somestudiesshowthatcashdominateseveninmalls,whicharevisitedbypeoplewhoarelikelytohavecreditcards,so it is no surprise that cash dominates in other markets as well.

Ways of Payment and Settlements:RTGS, NEFT, Mobile Banking, SMS Banking, Internet Banking, ElectronicClearingSystem,IMPS,SWIFT,andUnifiedPaymentInterface(UPI).

Benefits:Reduced instances of tax avoidance because it is financial institutions

basedeconomywheretransactiontrailsareleft.

Itwillcurbgenerationofblackmoney

ItwillreducerealestatepricesbecauseofcurbsonblackmoneyasmostofblackmoneyisinvestedinRealestatepriceswhichinflatesthepricesof Real estate markets.

In Financial year 2015, RBI spent ` 27 billion on just the activity ofcurrency issuance and management. This could be avoided if we become cashless society.

Itwillpavewayforuniversalavailabilityofbankingservicestoallasnophysical infrastructure is needed other than digital.

Therewillbegreaterefficiencyinwelfareprogrammesasmoneyiswireddirectlyintotheaccountsofrecipients.Thusoncemoneyistransferred

39

directly intoabeneficiary’sbankaccount, theentireprocessbecomestransparent.Paymentscanbeeasilytracedandcollected,andcorruptionwillautomaticallydrop,sopeoplewillnolongerhavetopaytocollectwhatisrightfullytheirs.

Therewillbeefficiencygainsas transactioncostsacross theeconomyshould also come down.

1 in 7 notes is supposed to be fake, which has a huge negative impact on economy, by going cashless, that can be avoided.

In a cashless economy there will be no problem of soiled notes orcounterfeit currency.

ReducedcostsofoperatingATMs.

Speed and satisfaction of operations for customers, no delays andqueues,nointeractionswithbankstaffrequired.

Challenges:

Availabilityofinternetconnectionandfinancialliteracy.

Though bank accounts have been opened through Jan Dhan Yojana,most of them are lying un-operational. Unless people start operatingbankaccountscashlesseconomyisnotpossible.

Thereisalsovestedinterestinnotmovingtowardscashlesseconomy.

Indiaisdominatedbysmallretailers.Theydon’thaveenoughresourcesto invest in electronic payment infrastructure.

Theperceptionofconsumersalsosometimesactsabarrier.Thebenefitof cashless transactions is not evident to even thosewhohave creditcards. Cash, on the other hand, is perceived to be the fastestway oftransacting for82%of credit cardusers. It is universallybelieved thathavingcashhelpsyounegotiatebetter.

Mostcardandcashusersfearthattheywillbechargedmoreiftheyusecards.Further,non-usersofcreditcardsarenotawareofthebenefitsofcredit cards.

Indianbanksaremaking itdifficult fordigitalwallets issuedbyprivatesectorcompaniestobeusedontherespectivebankwebsites.Itcouldberestrictionsonusingbankaccountstorefilldigitalwalletsoralackofaccess to payment gateways. Regulators will have to take a tough stand againstsuchrent-seekingbehaviourbythebanks.

40

Steps taken by RBI and Government to discourage use of cash:LicensingofPaymentbanks

Governmentisalsopromotingmobilewallets.Mobilewalletallowsuserstoinstantlysendmoney,paybills,rechargemobiles,bookmovietickets,sendphysicalande-giftsbothonlineandoffline.Recently,theRBIhadissued certain guidelines that allow the users to increase their limit to `1,00,000basedonacertainKYCverification.

Promotionofe-commercebyliberalizingtheFDInormsforthissector.

GovernmenthasalsolaunchedUPIwhichwillmakeElectronictransactionmuch simpler and faster.

Government has also withdrawn surcharge, service charge on cards and digital payments.

SyndicateBank’s E-Products:Our bank has also introduced E-products/services for our millions ofcustomers to use alternative delivery channel in encouraging cashlesseconomyinthecountry.Asabanker,itisverymuchrequiredtoeducateandencourageourcustomers touse it inday-to-day transactions for seamlessexperienceof customers and reduceouroperational costs. SyndicateBankofferswiderangeofE-productsnamely, InternetBanking,MobileBanking,SMSBanking,MissedCallBanking,TABBanking,NEFT/RTGS,GlobalCreditCard,Debitcard,Onlinetaxpayment,OnlineshoppingandUtilitypayments,POSUtility,E-fillingofincometax,Aadhaarseeding,SWIFT,UnifiedPaymentInterface(UPI),SyndWasiyatEzeeWill,andSyndE-passbook.

Conclusion:Thoughitwilltaketimeformovingtowardsacompletecashlesseconomy,effortsshouldbemadetoconverturbanareasascashlessareas.As70%ofIndia’sGDP comes fromurban areas if Government can convert that intocashless itwill beahugegain. Thereforedifferent trajectoriesneed tobeplanned for migration to cashless for those having bank account and forthose not having.

Compilationby: Economic Research Cell, P & D SyndicateBank

41

Guidelines on “Enhancing Credit Supply for Large Borrowers through Market

Mechanism”Reserve Bank of India (RBI) published guidelines on “Enhancing CreditSupply to largeborrowers throughmarketmechanism through its circularno. RBI/2016-17/50/DBR.BP.BC.No.8/21.01.003/2016-17 dated August 25th, 2016.

Guidelinesaddresstheconcentrationriskofthebankingsystemarisingfromits large exposures towards a single counterparty.

Definitions:

(i) Aggregate Sanctioned Credit Limit (ASCL): Theaggregateofthefundbasedcreditlimitssanctionedoroutstanding;

whichever is higher, to a borrower by the banking system. ASCL alsoincludesunlistedprivatelyplaceddebtwiththebankingsystem.

(ii) Specified Borrower: A. borrowerhavinganASCLofmorethan:

a. ` 25,000croreatanytimeduringFY2017-18.b. ` 15,000croreatanytimeduringFY2018-19c. `10,000croreatanytimeduringApril1,2019onwards

(iii) Reference Date: Thedateonwhichaborrowerbecomesaspecifiedborrower.

(iv) Normally Permitted Lending Limit (NPLL): 50percentof the incremental funds raisedby the specifiedborrower

over and above its ASCL as on the reference date, in the financialyears(FYs)succeedingtheFYinwhichthereferencedatefalls.Forthispurpose,anyfundsraisedbywayofequityshallbedeemedtobepartofincrementalfundsraisedbythespecifiedborrower(fromoutsidethebankingsystem)inthegivenyear.

(v) Banking System: AllbanksinIndiaincludingRRBsandCo-operativebanksandbranchesof

Indianbanksabroad.

42

(vi) Market Instruments: Bonds, debentures, redeemable preference shares and any other

non-creditliability,otherthanequity.

Scope:• These guidelines will be applicable on all single counterparties of

ScheduledCommercialBanks(SCBs),exceptotherSCBs,NBFCsregisteredwithRBI,AFIs(NHB,SIDBI,EXIMBank&NABARD)andHFCsregisteredwith NHB. Banks should apply due diligence while deciding the NPLL for asingleborrowerinorderthatborrowersdonotcircumventthecut-offASCLcriteriabyborrowingthroughdummy/fictitiousgroupcompanies.

• Thiswillcomeintoeffectfromthefinancialyear2017-18onwards.ThebankingsystemshallordinarilykeepitsfutureincrementalexposurestothespecifiedborrowerswithintheNPLL,elsetheywillbesubjecttotheprudentialmeasuresasgivenbelow.

Prudential Measures:From2017-18onwards, incremental exposure of the banking system to aspecifiedborrowerbeyondNPLLshallbedeemedtocarryhigherriskwhichshallberecognizedbywayofadditionalprovisioningandhigherriskweightsas under.(i) Additional provisions of 3 percentage points over and above the

applicableprovisionontheincrementalexposureofthebankingsysteminexcessofNPLLwhichshallbedistributedinproportiontoeachbanksfundedexposuretothespecifiedborrower.

(ii) Additional Risk Weights of 75 percentage points over and above theapplicable riskweight for theexposure to thespecifiedborrower.Theresultant additional riskweighted exposure, in termsof riskweightedassets (RWA) shall bedistributed inproportion toeachbank’s fundedexposuretothespecifiedborrower.